eramo day one keynote ceri 2015 petrochemical conference

DESCRIPTION

Ceri Presentation 2015 Petrochemical confTRANSCRIPT

Global Petrochemical Market Outlook:Impact of Energy at the ExtremesPresented to: CERI 2015 Petrochemical Conference

June 7-9, 2015 • Delta Lodge at Kananaskis • Alberta

Mark EramoVice President - Global Chemical InsightsIHS Chemical, Houston, [email protected]

Agenda

• Chemical Building Blocks• Energy At The Extremes• Investment Trends• Basic Chemical Demand &

Trade• Low Crude Impact On

Profit Cycle• Closing Thoughts

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Automotive /Transportation

• Consumer products

• Packaging

• Building & construction

• Recreation /Sport• Industrial

• Medical• Pharmaceuticals• Personal care

• Textiles• Electrical/

Electronics• Aerospace

• Business equipment

Customers of the Chemical Industry

•Oil•Gas•Coal•Minerals•Renewables

Mining, Drilling, Refining & Gas

Processing

Chemical Intermediates

Commodities

Differentiated Commodities

Technical Specialties

Olefins(ethylene, propylene,

butylene)

Aromatics(benzene, toluene,

xylenes)

Chlor-Alkali(chlorine, caustic

soda)

Others(e.g., ammonia, phosphorous)

Methanol

Basic Chemicals

• Plastics & Engineering Resins− Extruded films, pipe, profiles,

coatings, sheet, foams, sheet− Blow-molded parts− Injection molded parts− Composites

•Synthetic Fibers•Rubber Products•Paints & Coatings•Adhesives & Sealants•Lubricants•Water Treatment products•Cleaning Products• Industrial Chemicals•Flame Retardants•Many others…

Formulated Products / Performance Materials

Chemical Industry Value ChainNatural Resources

End-use Consumer Products

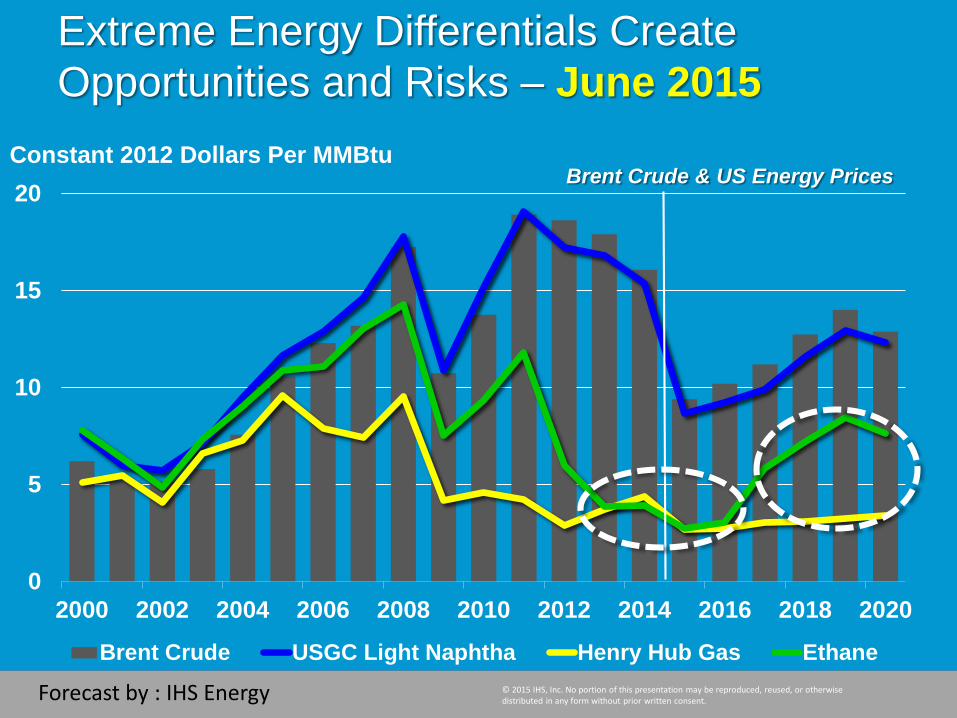

Extreme Energy Differentials Create Opportunities and Risks – June 2015

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

5

10

15

20

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Brent Crude USGC Light Naphtha Henry Hub Gas Ethane

Constant 2012 Dollars Per MMBtuBrent Crude & US Energy Prices

Forecast by : IHS Energy

When Energy Markets Move Chemical Will Markets Respond

• The rapid decline in crude oil pricing causes supply-chains to “pause” as buyers anticipate lower prices “tomorrow”.

• Combination of a pause in demand and the decline in costs for high-cost producers results in price decreases.

• As market prices “chase” falling costs, cash margins for high-cost producers can expand while cash margins for low cost producers will decline.

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

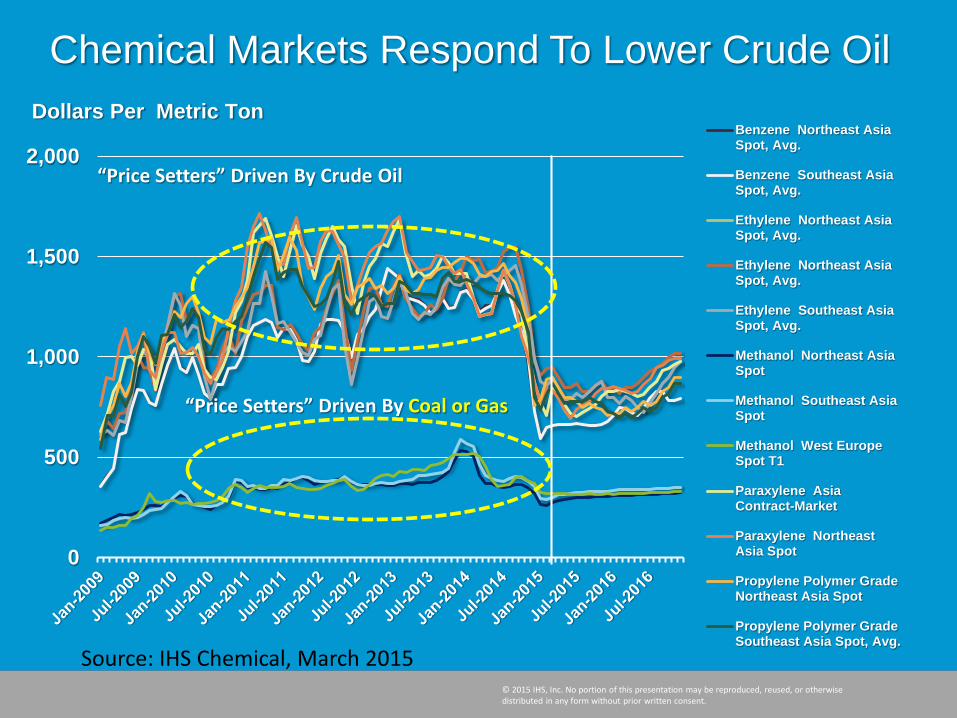

Chemical Markets Respond To Lower Crude Oil

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

500

1,000

1,500

2,000Benzene Northeast AsiaSpot, Avg.

Benzene Southeast AsiaSpot, Avg.

Ethylene Northeast AsiaSpot, Avg.

Ethylene Northeast AsiaSpot, Avg.

Ethylene Southeast AsiaSpot, Avg.

Methanol Northeast AsiaSpot

Methanol Southeast AsiaSpot

Methanol West EuropeSpot T1

Paraxylene AsiaContract-Market

Paraxylene NortheastAsia Spot

Propylene Polymer GradeNortheast Asia Spot

Propylene Polymer GradeSoutheast Asia Spot, Avg.

Dollars Per Metric Ton

“Price Setters” Driven By Crude Oil

“Price Setters” Driven By Coal or Gas

Source: IHS Chemical, March 2015

0

400

800

1200

1600

SaudiArabiaEthane

U.S. Ethane WesternCanada

China CTO SaudiArabia

Naphtha

NortheastAsia

Naphtha

WestEuropeNaphtha

China MTO

2011 2013 2015US$ / Metric Ton

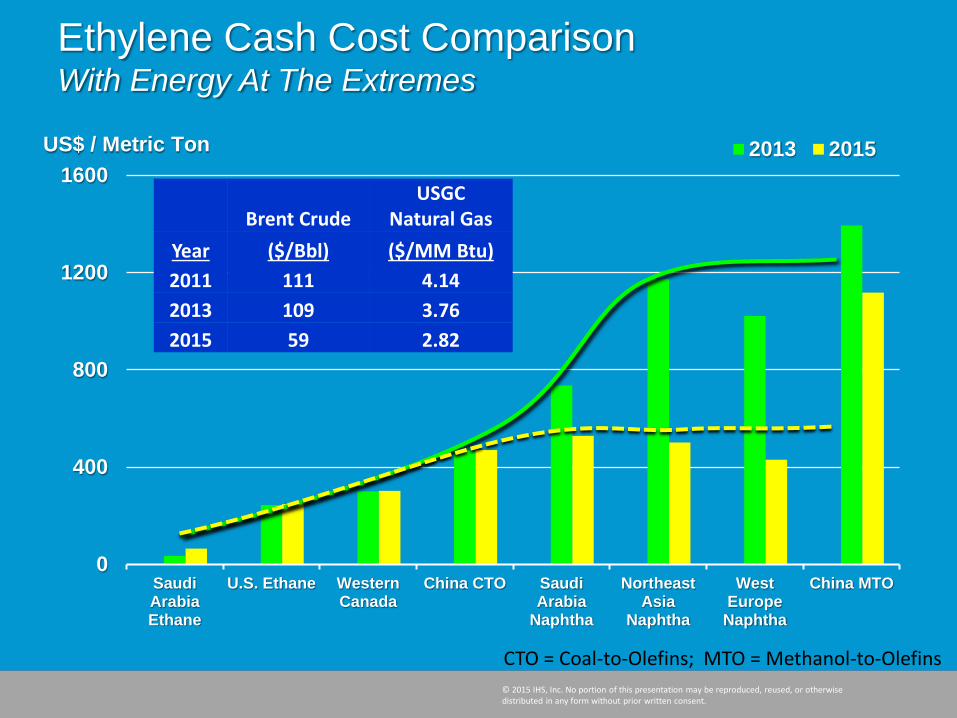

Ethylene Cash Cost Comparison With Energy At The Extremes

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Brent CrudeUSGC

Natural GasYear ($/Bbl) ($/MM Btu)2011 111 4.142013 109 3.762015 59 2.82

CTO = Coal-to-Olefins; MTO = Methanol-to-Olefins

0

400

800

1200

1600

SaudiArabiaEthane

U.S. Ethane WesternCanada

China CTO SaudiArabia

Naphtha

NortheastAsia

Naphtha

WestEuropeNaphtha

China MTO

2011 2013 2015US$ / Metric Ton

Ethylene Cash Cost Comparison With Energy At The Extremes

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Brent CrudeUSGC

Natural GasYear ($/Bbl) ($/MM Btu)2011 111 4.142013 109 3.762015 59 2.82

CTO = Coal-to-Olefins; MTO = Methanol-to-Olefins

Investment Drivers Vary By Region By Value Chain

• North America (USA) Leverage low cost natural gas based chemicals

into investments in ethylene, propylene and methanol based derivatives.

Invest to establish export channels to market that exceed historical norms

• Middle East (Saudi Arabia) Moderated investment pace, diversified feedslate

to support downstream market development and continued industrial expansion well beyond ethylene chemistry

• North East Asia (China) Strong domestic investment focused on reducing

import dependencies. Leverage coal to chemicals technology near term

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Raw Material & Energy

Costs

Demand Growth & Access to Markets

Technology &

Economies of Scale

Chemical Industry Investments Seek A Sustainable Advantage

Top 5 Countries Adding Base Chemical Capacity 231 Million Tons from 2010 to 2020

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

20

40

60

80

100

120

China UnitedStates

SaudiArabia

S. Korea India

Chlorine Paraxylene Benzene

Methanol Propylene Ethylene

Million Metric Tons

Top five will add nearly 75% of base chemical capacity. China will dominate new

capacity, adding 45% of total

Investment capital has shifted to North America, however, the vast majority of new investment continues to accelerate in Asia/Pacific, dominated by China

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Olefin (CTO/MTO Construction)

Olefin (Operating CTO/MTO)

Olefins

PX

MEG (Operating)

MEG (Construction)

Petrochemical Investment In China Moves West

China Unconventional Olefins Capacity Growth

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0%

25%

50%

75%

20

40

60

80

2009 2011 2013 2015 2017 2019

Olefin-Conventional CTO MTO PDH % of Unconventional

Light Olefins Capacity(Million Metric Ton)

% of Unconventional Light Olefins Capacity

North America Ethylene Capacity Growth: 2014 – 2020Completed or Firm Projects (Thousand Metric Tons)

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Company Location Total GrowthBASF/Total Port Arthur. TX 128ChevronPhillips Cedar Bayou, TX 1,500Dow Freeport, TX 1,500Dow Plaquemine, LA 220Eastman Longview, TX 17Equistar Various sites 1,112ExxonMobil Baytown, TX 1,500Flint Hills Port Arthur, TX 100Formosa Point Comfort, TX 1,150Oxy/Mexichem Ingleside, TX 550Shin-Etsu Plaquemine, LA 500Sasol Lake Charles, LA 1,550Westlake KY and LA sites 216Williams Geismar, LA 258Braskem Idesa Mexico 1,000Nova Sarnia 168

Total Additions 11,469

North American ethylene capacity will increase to 45+ million metric tons by 2020, driven by low-cost ethane feedstock

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Company Location Total Growth*BASF (MTP) US Gulf Coast 475Dow Freeport, TX 750Enterprise Mont Belvieu, TX 750Ascend Alvin, TX 1,173Formosa Point Comfort, TX 600Williams Redwater, Alberta 500RexTac Odessa 400

Total Additions 4,648

N.America On-Purpose Propylene Capacity Growth: 2014 – 2020Completed or Firm Projects (Thousand Metric Tons)All are PHD Units except for BASF

* MTP = methane to propylene

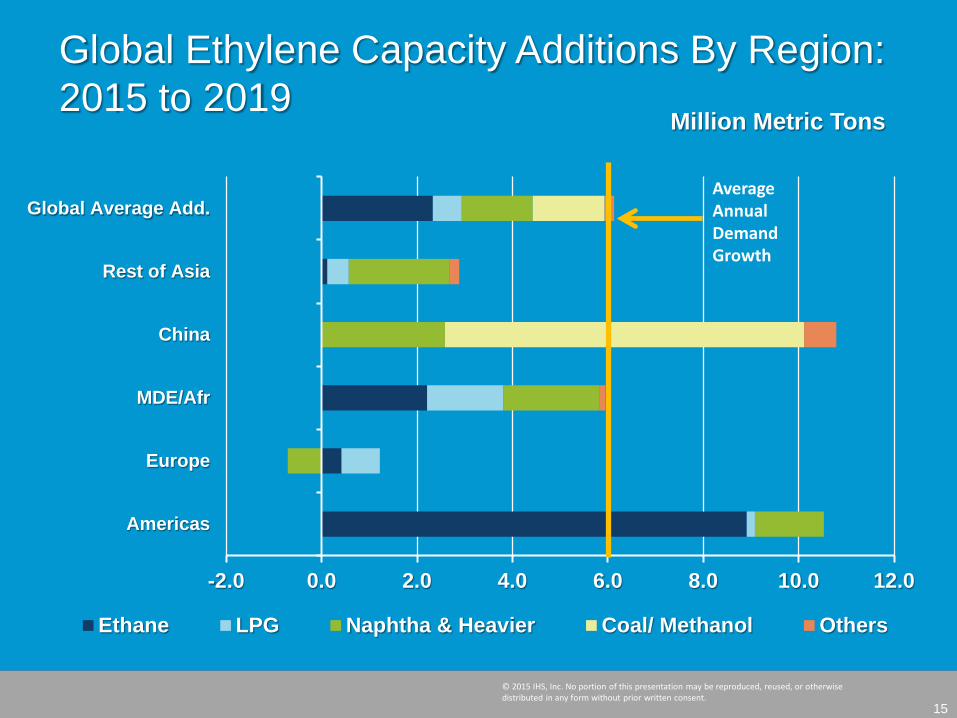

15

Global Ethylene Capacity Additions By Region: 2015 to 2019

Million Metric Tons

-2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0

Americas

Europe

MDE/Afr

China

Rest of Asia

Global Average Add.

Ethane LPG Naphtha & Heavier Coal/ Methanol Others

Average AnnualDemand Growth

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Global Ethylene Supply Will Need More From Naphtha Cracking

-36%

-24%

-12%

0%

12%

24%

36%

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023

Ethylene Supply Growth from Naphtha

Percentages on lines are period averages

Million Metric Tons

23% 30%

11%

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

North America Middle East China

West Europe Others Annual Demand Increase

Global Propylene Capacity Growth To Exceed Demand Growth Near Term

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Million Metric TonsGlobal Propylene Capacity Growth By Region

Agenda

• Chemical Building Blocks• Energy At The Extremes• Investment Trends• Basic Chemical Demand

& Trade• Low Crude Impact On The

Profit Cycle• Closing Thoughts

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Ethylene Methanol Propylene Chlorine Paraxylene Benzene

Million Metric Tons

Global Base Chemicals Cumulative Demand Growth2010 - 2020 = 224 Million Metric Tons

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Total Growth

MM TonsAAGR: 2010/20

MM Tons/YrAAGR:

2010/20, %Ethylene 61.6 5.6 3.5Methanol 52.4 4.8 6.9Propylene 47.8 4.3 4.2Chlorine 28.1 2.6 3.6Paraxylene 19.4 1.8 4.5Benzene 14.7 1.3 2.3

Regional Trade Is Critical To Success

• Trade is an essential element of basic chemical supply chains

• Low cost regions such as North America and the Middle East will export increasing volumes

• On-purpose technology will change propylene trade patterns

• Significant investment in ships, ports, and infrastructure is needed to support increasing trade volumes

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

5 Countries Adding 75% of Base Chemical Capacity: 2010 to 2020 (231 MM Metric Tons)

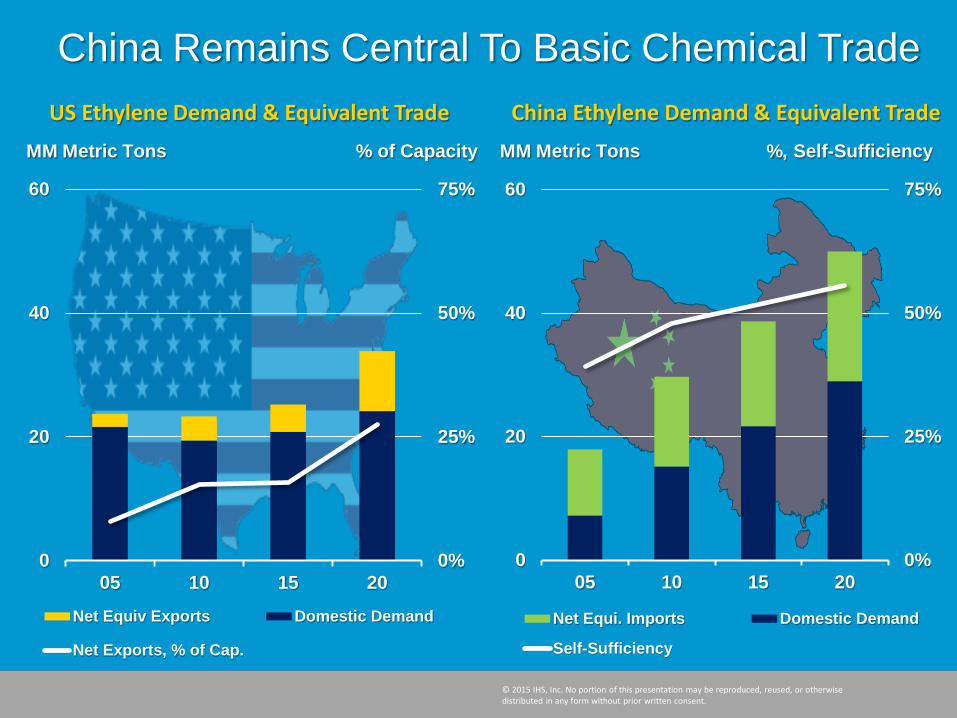

China Remains Central To Basic Chemical Trade

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0%

25%

50%

75%

0

20

40

60

05 10 15 20

Net Equi. Imports Domestic Demand

Self-Sufficiency

MM Metric Tons %, Self-Sufficiency

0%

25%

50%

75%

0

20

40

60

05 10 15 20

Net Equiv Exports Domestic Demand

Net Exports, % of Cap.

MM Metric Tons % of Capacity

US Ethylene Demand & Equivalent Trade China Ethylene Demand & Equivalent Trade

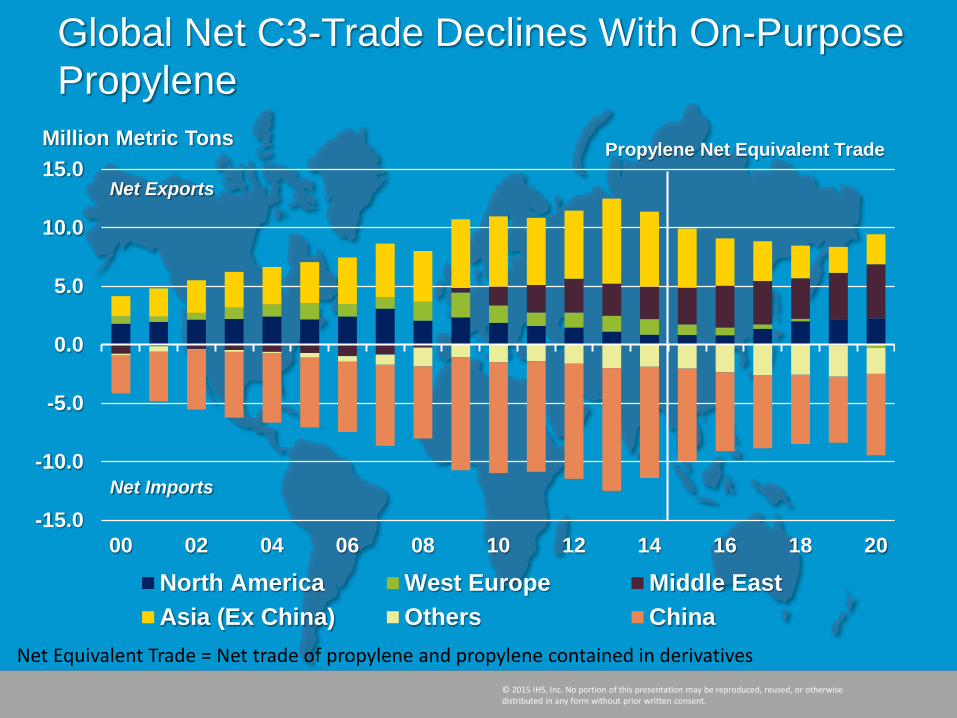

Global Net C3-Trade Declines With On-Purpose Propylene

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

00 02 04 06 08 10 12 14 16 18 20

North America West Europe Middle EastAsia (Ex China) Others China

Propylene Net Equivalent Trade

Net Exports

Net Imports

Million Metric Tons

Net Equivalent Trade = Net trade of propylene and propylene contained in derivatives

Agenda

• Chemical Building Blocks• Energy At The Extremes• Investment Trends• Basic Chemical Demand &

Trade• Low Crude Impact On The

Profit Cycle• Closing Thoughts

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-220

0

220

441

661

882

1,102

1,323

-10

0

10

20

30

40

50

60

00 02 04 06 08 10 12 14 16 18 20

US Ethane to PE Chain Margin Asia Naphtha to PE Chain Margin

Margin, Cents Per Pound Margin, Dollars Per Metric Ton

Polyethylene Integrated Cash MarginsUS Ethane Vs. Asia Naphtha

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Ethane-based margins decline; maintain strong advantage

• Basic chemicals and derivatives markets adjust to “new energy”

• Price setters have lower cost…prices decline seeking new steady state; impact on trade

• Integrated margins for low-cost producers decline, some high-cost producer margins improve

• Approved “advantaged” projects advance; new projects may pause

• Demand declines followed by demand surge; trade patterns shift; potential upcycle in ethylene; propylene oversupply

The Impact of Energy At The Extremes…

Conclusions

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Availability of low-cost ethane and propane in North America to support continued investments; both domestic and international

• Developments in on-purpose technology for olefins versus traditional routes, including the use of methanol as a route to olefins.

• Impact of coal-to-chemicals and on-purpose propylene in China: private/provincial investment versus state-owned; self-sufficiency and surplus capacity impacting trade with China.

• Need for ethylene supplied from naphtha cracking: both higher operating rates for existing assets and investments in new naphtha cracking

The Impact of Energy At The Extremes…

Beyond 2020…

© 2015 IHS, Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Global Petrochemical Market Outlook:Impact of Energy at the ExtremesPresented to: CERI 2015 Petrochemical Conference

June 7-9, 2015 • Delta Lodge at Kananaskis • Alberta

Mark EramoVice President - Global Chemical InsightsIHS Chemical, Houston, [email protected]

THANK YOU!