tube investments buy - iifl capital

TRANSCRIPT

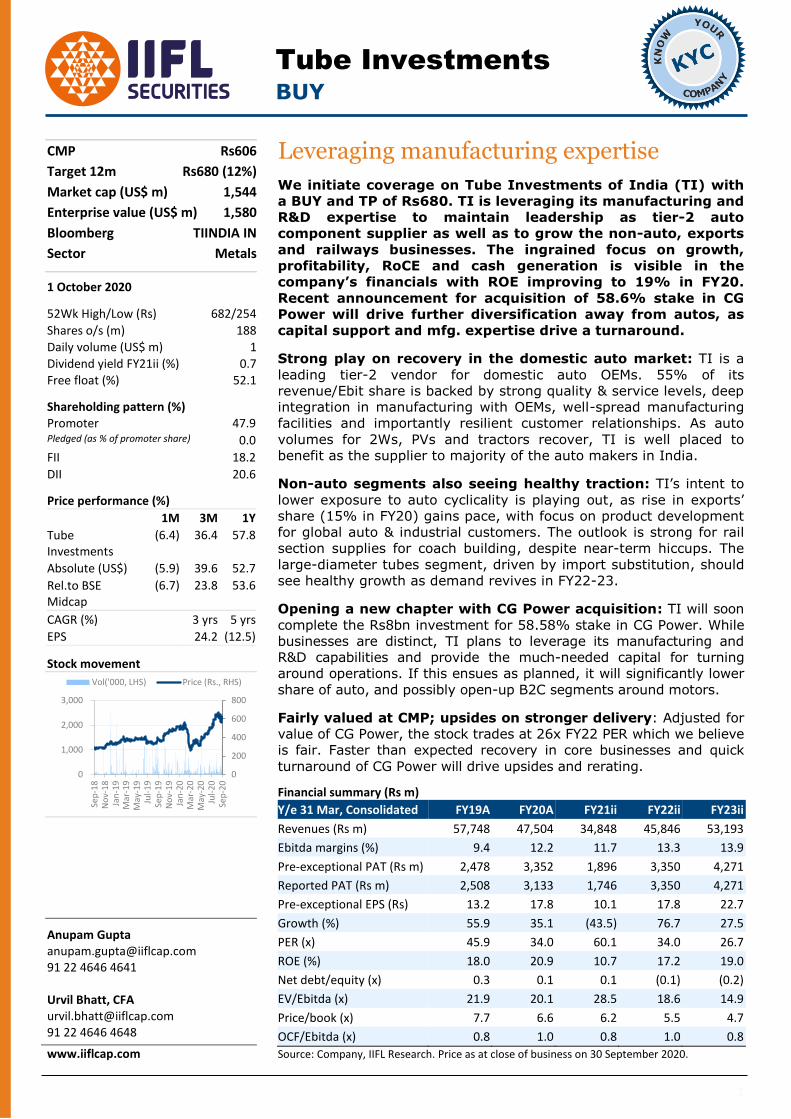

CMP Rs606

Target 12m Rs680 (12%)

Market cap (US$ m) 1,544

Enterprise value (US$ m) 1,580

Bloomberg TIINDIA IN

Sector Metals

1 October 2020

52Wk High/Low (Rs) 682/254

Shares o/s (m) 188

Daily volume (US$ m) 1

Dividend yield FY21ii (%) 0.7

Free float (%) 52.1

Shareholding pattern (%) Promoter 47.9 Pledged (as % of promoter share) 0.0

FII 18.2

DII 20.6

Price performance (%)

1M 3M 1Y

Tube Investments

(6.4) 36.4 57.8

Absolute (US$) (5.9) 39.6 52.7

Rel.to BSE Midcap

(6.7) 23.8 53.6

CAGR (%) 3 yrs 5 yrs

EPS 24.2 (12.5)

Stock movement

Anupam Gupta [email protected] 91 22 4646 4641

Urvil Bhatt, CFA [email protected] 91 22 4646 4648

www.iiflcap.com

www.iiflcap.com

0

200

400

600

800

0

1,000

2,000

3,000

Sep

-18

No

v-1

8Ja

n-1

9M

ar-1

9M

ay-1

9Ju

l-1

9Se

p-1

9N

ov-

19

Jan

-20

Mar

-20

May

-20

Jul-

20

Sep

-20

Vol('000, LHS) Price (Rs., RHS)

Leveraging manufacturing expertise

Tube Investments BUY BUY

1

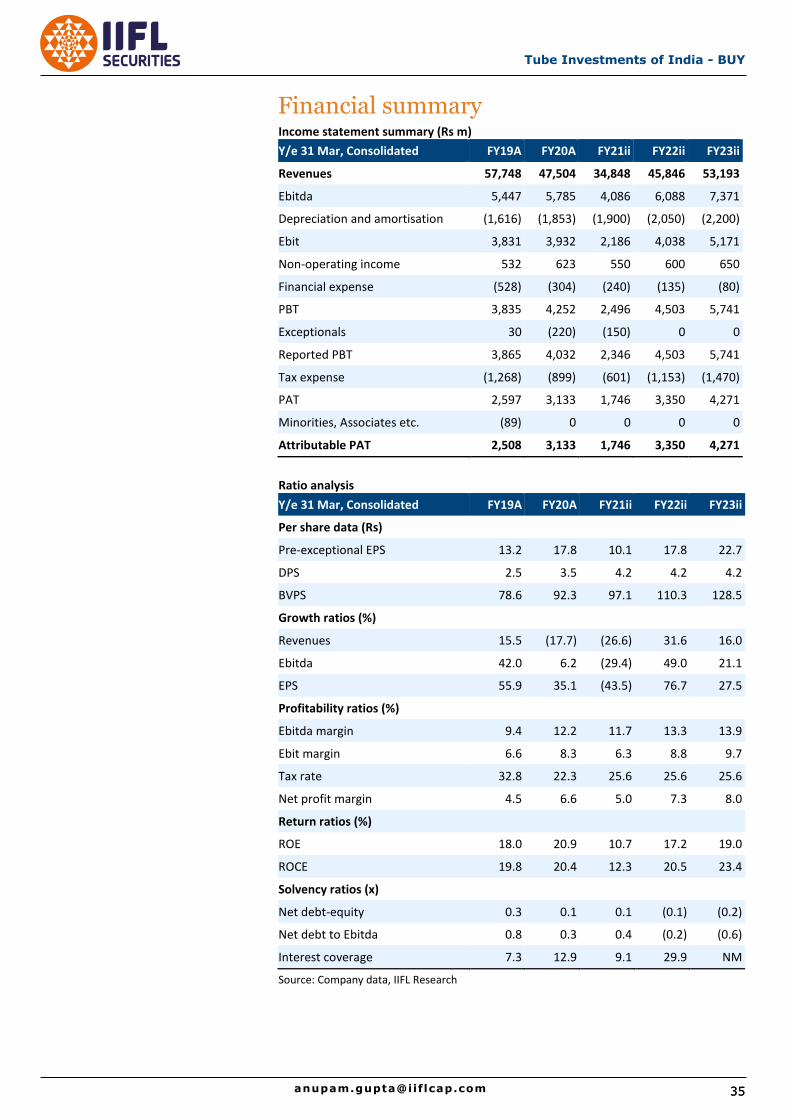

Financial summary (Rs m)

Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Revenues (Rs m) 57,748 47,504 34,848 45,846 53,193

Ebitda margins (%) 9.4 12.2 11.7 13.3 13.9

Pre-exceptional PAT (Rs m) 2,478 3,352 1,896 3,350 4,271

Reported PAT (Rs m) 2,508 3,133 1,746 3,350 4,271

Pre-exceptional EPS (Rs) 13.2 17.8 10.1 17.8 22.7

Growth (%) 55.9 35.1 (43.5) 76.7 27.5

PER (x) 45.9 34.0 60.1 34.0 26.7

ROE (%) 18.0 20.9 10.7 17.2 19.0

Net debt/equity (x) 0.3 0.1 0.1 (0.1) (0.2)

EV/Ebitda (x) 21.9 20.1 28.5 18.6 14.9

Price/book (x) 7.7 6.6 6.2 5.5 4.7

OCF/Ebitda (x) 0.8 1.0 0.8 1.0 0.8

Source: Company, IIFL Research. Price as at close of business on 30 September 2020.

We initiate coverage on Tube Investments of India (TI) with

a BUY and TP of Rs680. TI is leveraging its manufacturing and

R&D expertise to maintain leadership as tier-2 auto

component supplier as well as to grow the non-auto, exports

and railways businesses. The ingrained focus on growth,

profitability, RoCE and cash generation is visible in the

company’s financials with ROE improving to 19% in FY20.

Recent announcement for acquisition of 58.6% stake in CG

Power will drive further diversification away from autos, as

capital support and mfg. expertise drive a turnaround.

Strong play on recovery in the domestic auto market: TI is a

leading tier-2 vendor for domestic auto OEMs. 55% of its

revenue/Ebit share is backed by strong quality & service levels, deep

integration in manufacturing with OEMs, well-spread manufacturing

facilities and importantly resilient customer relationships. As auto

volumes for 2Ws, PVs and tractors recover, TI is well placed to

benefit as the supplier to majority of the auto makers in India.

Non-auto segments also seeing healthy traction: TI’s intent to

lower exposure to auto cyclicality is playing out, as rise in exports’

share (15% in FY20) gains pace, with focus on product development

for global auto & industrial customers. The outlook is strong for rail

section supplies for coach building, despite near-term hiccups. The

large-diameter tubes segment, driven by import substitution, should

see healthy growth as demand revives in FY22-23.

Opening a new chapter with CG Power acquisition: TI will soon

complete the Rs8bn investment for 58.58% stake in CG Power. While

businesses are distinct, TI plans to leverage its manufacturing and

R&D capabilities and provide the much-needed capital for turning

around operations. If this ensues as planned, it will significantly lower

share of auto, and possibly open-up B2C segments around motors.

Fairly valued at CMP; upsides on stronger delivery: Adjusted for

value of CG Power, the stock trades at 26x FY22 PER which we believe

is fair. Faster than expected recovery in core businesses and quick

turnaround of CG Power will drive upsides and rerating.

Tube Investments of India – BUY

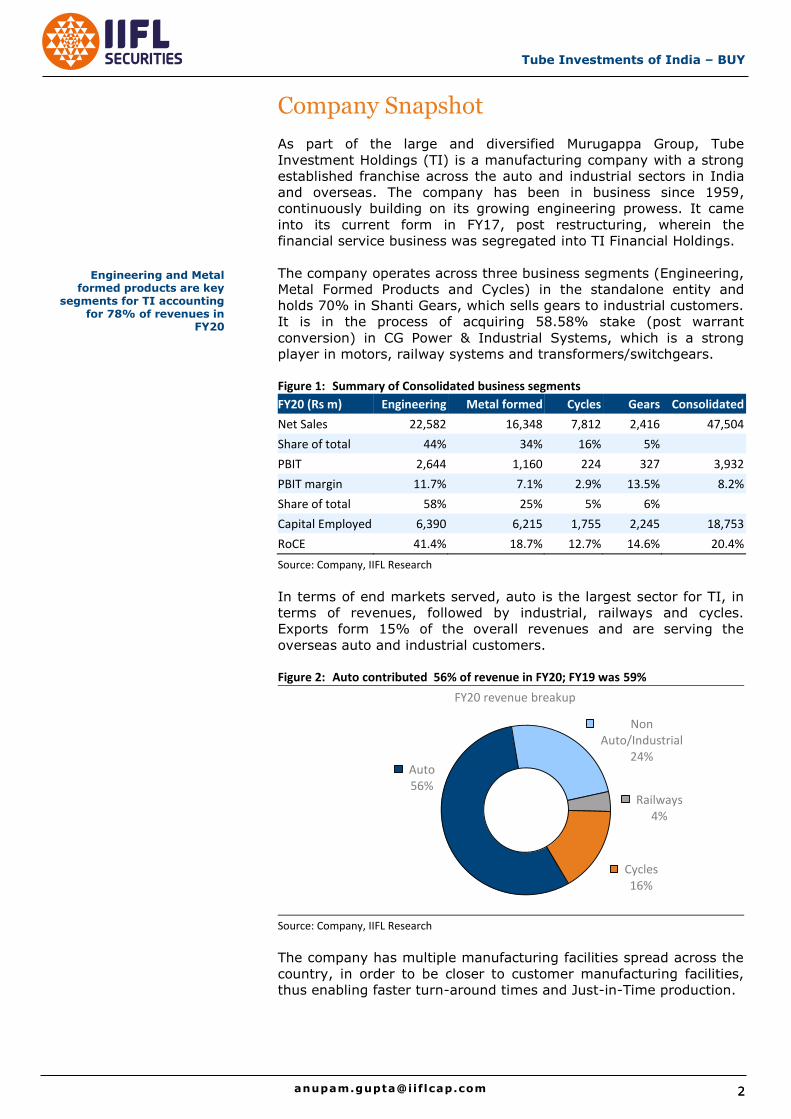

Company Snapshot

As part of the large and diversified Murugappa Group, Tube

Investment Holdings (TI) is a manufacturing company with a strong

established franchise across the auto and industrial sectors in India

and overseas. The company has been in business since 1959,

continuously building on its growing engineering prowess. It came

into its current form in FY17, post restructuring, wherein the

financial service business was segregated into TI Financial Holdings.

The company operates across three business segments (Engineering,

Metal Formed Products and Cycles) in the standalone entity and

holds 70% in Shanti Gears, which sells gears to industrial customers.

It is in the process of acquiring 58.58% stake (post warrant

conversion) in CG Power & Industrial Systems, which is a strong

player in motors, railway systems and transformers/switchgears.

Figure 1: Summary of Consolidated business segments

FY20 (Rs m) Engineering Metal formed Cycles Gears Consolidated

Net Sales 22,582 16,348 7,812 2,416 47,504

Share of total 44% 34% 16% 5%

PBIT 2,644 1,160 224 327 3,932

PBIT margin 11.7% 7.1% 2.9% 13.5% 8.2%

Share of total 58% 25% 5% 6%

Capital Employed 6,390 6,215 1,755 2,245 18,753

RoCE 41.4% 18.7% 12.7% 14.6% 20.4%

Source: Company, IIFL Research

In terms of end markets served, auto is the largest sector for TI, in

terms of revenues, followed by industrial, railways and cycles.

Exports form 15% of the overall revenues and are serving the

overseas auto and industrial customers.

Figure 2: Auto contributed 56% of revenue in FY20; FY19 was 59%

Source: Company, IIFL Research

The company has multiple manufacturing facilities spread across the

country, in order to be closer to customer manufacturing facilities,

thus enabling faster turn-around times and Just-in-Time production.

Auto 56%

Non Auto/Industrial

24%

Railways 4%

Cycles 16%

FY20 revenue breakup

Engineering and Metal formed products are key

segments for TI accounting for 78% of revenues in

FY20

3

Tube Investments of India - BUY

Figure 3: Manufacturing presence

Source: Company, IIFL Research. TPI – Tube products of India (Engineering segment), TICI – TI Cycles of India, MFPD – Metal formed product division

Figure 4: Tube Investments of India – Major milestones

Year Major milestones

1949 TI Cycles of India established in collaboration with Tube Investments, UK

1959 Tube Products of India merged with TI Cycles of India to form Tube Investments of India

1960 TI Diamond Chains (TIDC) formed in collaboration with Diamond Chains USA

1965 TI Metal Forming was established as a division of Tube Investments

1969 TI Diamond Chains diversifies into industrial chains

1975 TIDC diversifies into heavy duty chains

1985 Diversification into engineering class chains and mfg. of bike chains

1990 Acquisition of Press Metal Corporation

1995 Setup of the fine blanking division for the auto sector

1996 Indigenously designed tube plant setup near Pune

1998 Sets-up new facility to make car door frames near Gurgaon

2001 Cycle manufacturing plant set up at Nashik, entry into financial services by purchasing 41.8% stake in Cholamandalam Investments and Finance

2004 TI Diamond Chains merged with TI India; metal forming division sets up mfg. facility in Gujarat for making door frames

2006 Hydro forming facility commissioned near Chennai to supply auto components

2010 Commissioned new plant at Sanand, Gujarat and Laksar, Uttarakhand

2017 Demerger of Tube Investment of India with the financial business into TI Financial Holdings

2019 New facility established at Rajpura, Punjab for high strength tubes and telescopic front fork products

2020 Made binding bid for acquisition of 58.58% stake in CG Power & Industrial Systems at Rs8bn

Source: Company, IIFL Research

Punjab (3) – Mohali & Rajpura Uttarakhand (2)

Haryana (1) - Bawal

Gujarat (1) –Sanand

Maharashtra (2) – Shirwal& Pune

Tamil Nadu (8)

Telengana (1) - Medak

TPI

TICI

MFPD

Tube Investments of India – BUY

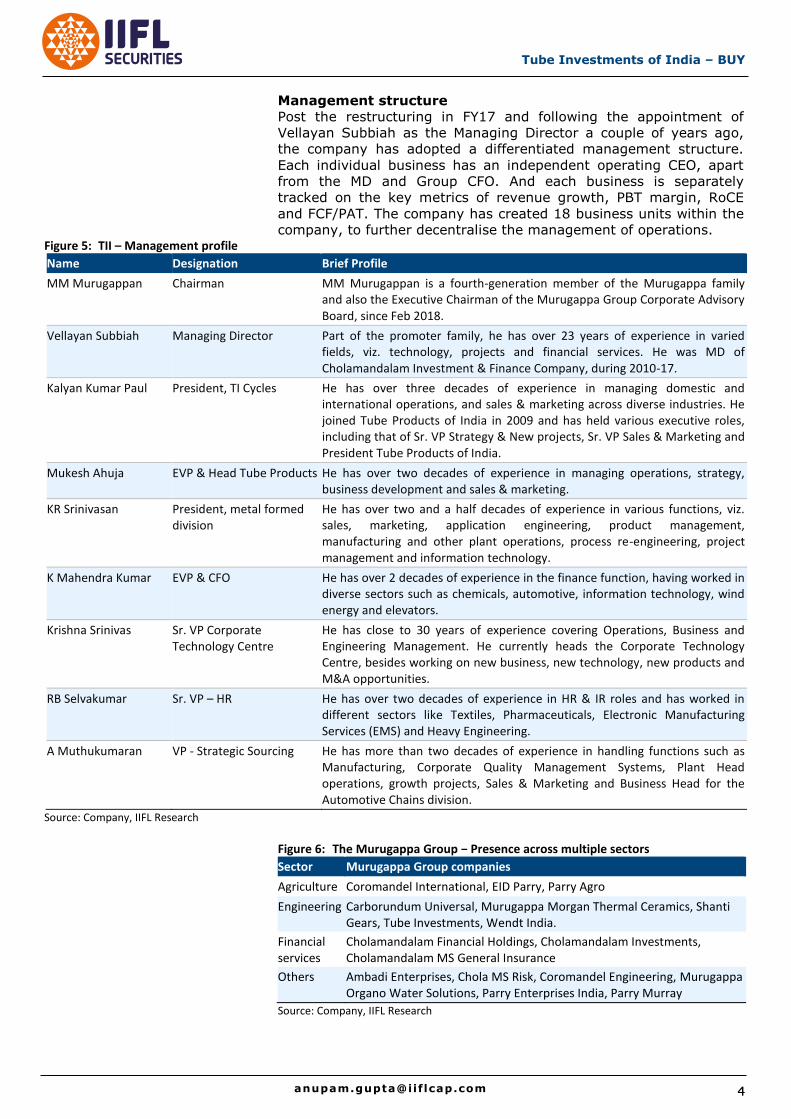

Management structure

Post the restructuring in FY17 and following the appointment of

Vellayan Subbiah as the Managing Director a couple of years ago,

the company has adopted a differentiated management structure.

Each individual business has an independent operating CEO, apart

from the MD and Group CFO. And each business is separately

tracked on the key metrics of revenue growth, PBT margin, RoCE

and FCF/PAT. The company has created 18 business units within the

company, to further decentralise the management of operations. Figure 5: TII – Management profile

Name Designation Brief Profile

MM Murugappan Chairman MM Murugappan is a fourth-generation member of the Murugappa family and also the Executive Chairman of the Murugappa Group Corporate Advisory Board, since Feb 2018.

Vellayan Subbiah Managing Director Part of the promoter family, he has over 23 years of experience in varied fields, viz. technology, projects and financial services. He was MD of Cholamandalam Investment & Finance Company, during 2010-17.

Kalyan Kumar Paul President, TI Cycles He has over three decades of experience in managing domestic and international operations, and sales & marketing across diverse industries. He joined Tube Products of India in 2009 and has held various executive roles, including that of Sr. VP Strategy & New projects, Sr. VP Sales & Marketing and President Tube Products of India.

Mukesh Ahuja EVP & Head Tube Products He has over two decades of experience in managing operations, strategy, business development and sales & marketing.

KR Srinivasan President, metal formed division

He has over two and a half decades of experience in various functions, viz. sales, marketing, application engineering, product management, manufacturing and other plant operations, process re-engineering, project management and information technology.

K Mahendra Kumar EVP & CFO He has over 2 decades of experience in the finance function, having worked in diverse sectors such as chemicals, automotive, information technology, wind energy and elevators.

Krishna Srinivas Sr. VP Corporate Technology Centre

He has close to 30 years of experience covering Operations, Business and Engineering Management. He currently heads the Corporate Technology Centre, besides working on new business, new technology, new products and M&A opportunities.

RB Selvakumar Sr. VP – HR He has over two decades of experience in HR & IR roles and has worked in different sectors like Textiles, Pharmaceuticals, Electronic Manufacturing Services (EMS) and Heavy Engineering.

A Muthukumaran VP - Strategic Sourcing He has more than two decades of experience in handling functions such as Manufacturing, Corporate Quality Management Systems, Plant Head operations, growth projects, Sales & Marketing and Business Head for the Automotive Chains division.

Source: Company, IIFL Research

Figure 6: The Murugappa Group − Presence across multiple sectors

Sector Murugappa Group companies

Agriculture Coromandel International, EID Parry, Parry Agro

Engineering Carborundum Universal, Murugappa Morgan Thermal Ceramics, Shanti Gears, Tube Investments, Wendt India.

Financial services

Cholamandalam Financial Holdings, Cholamandalam Investments, Cholamandalam MS General Insurance

Others Ambadi Enterprises, Chola MS Risk, Coromandel Engineering, Murugappa Organo Water Solutions, Parry Enterprises India, Parry Murray

Source: Company, IIFL Research

5

Tube Investments of India - BUY

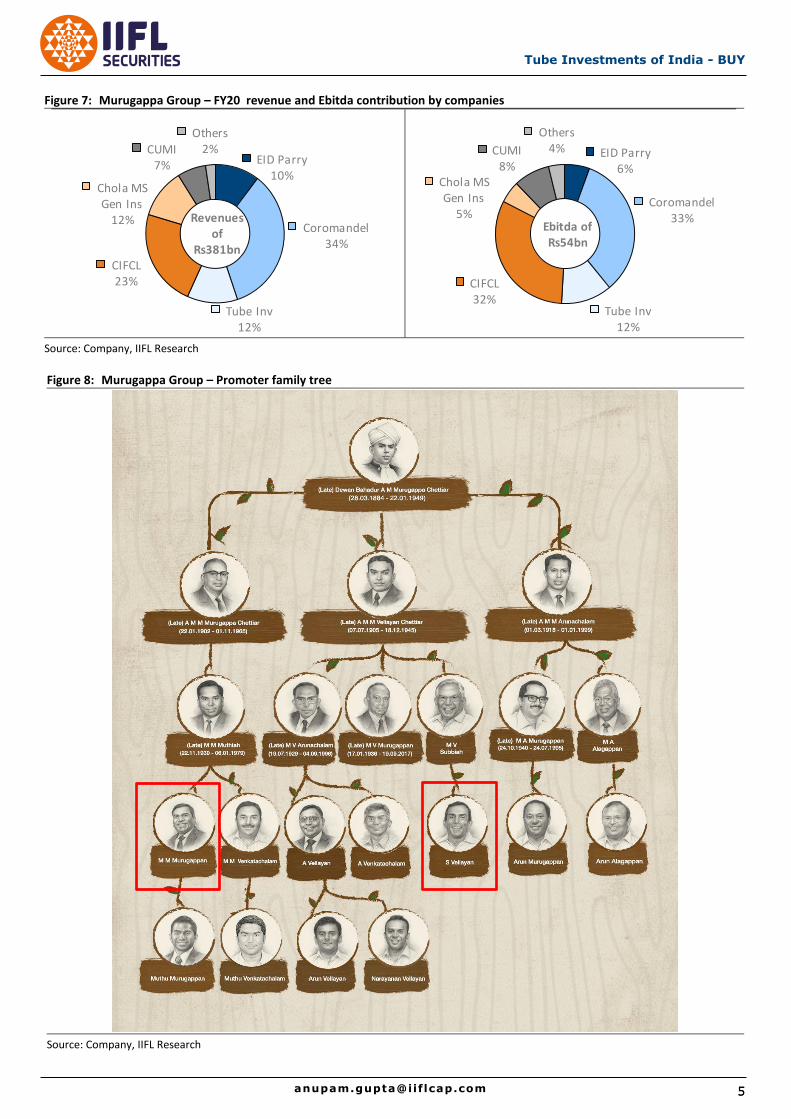

Figure 7: Murugappa Group – FY20 revenue and Ebitda contribution by companies

Source: Company, IIFL Research

Figure 8: Murugappa Group – Promoter family tree

Source: Company, IIFL Research

EID Parry10%

Coromandel34%

Tube Inv12%

CIFCL23%

Chola MS Gen Ins

12%

CUMI7%

Others2%

Revenuesof

Rs381bn

EID Parry6%

Coromandel33%

Tube Inv12%

CIFCL32%

Chola MS Gen Ins

5%

CUMI8%

Others4%

Ebitda ofRs54bn

Tube Investments of India – BUY

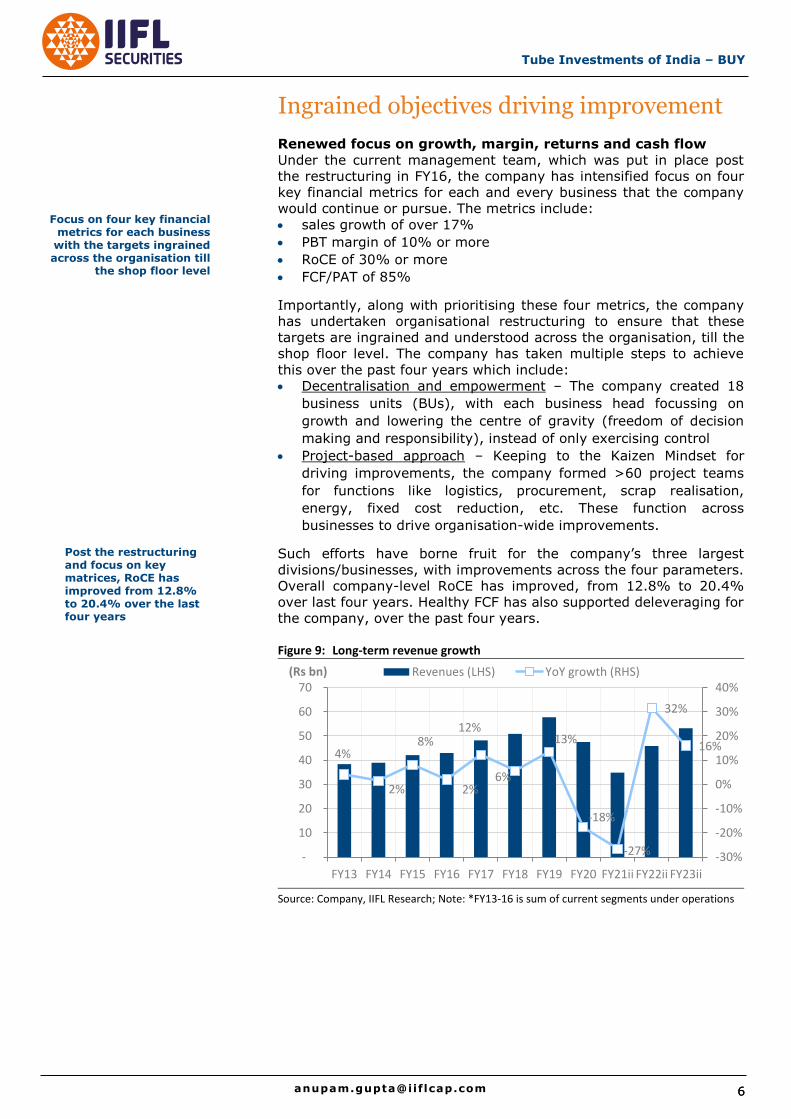

Ingrained objectives driving improvement

Renewed focus on growth, margin, returns and cash flow

Under the current management team, which was put in place post

the restructuring in FY16, the company has intensified focus on four

key financial metrics for each and every business that the company

would continue or pursue. The metrics include:

sales growth of over 17%

PBT margin of 10% or more

RoCE of 30% or more

FCF/PAT of 85%

Importantly, along with prioritising these four metrics, the company

has undertaken organisational restructuring to ensure that these

targets are ingrained and understood across the organisation, till the

shop floor level. The company has taken multiple steps to achieve

this over the past four years which include:

Decentralisation and empowerment – The company created 18

business units (BUs), with each business head focussing on

growth and lowering the centre of gravity (freedom of decision

making and responsibility), instead of only exercising control

Project-based approach – Keeping to the Kaizen Mindset for

driving improvements, the company formed >60 project teams

for functions like logistics, procurement, scrap realisation,

energy, fixed cost reduction, etc. These function across

businesses to drive organisation-wide improvements.

Such efforts have borne fruit for the company’s three largest

divisions/businesses, with improvements across the four parameters.

Overall company-level RoCE has improved, from 12.8% to 20.4%

over last four years. Healthy FCF has also supported deleveraging for

the company, over the past four years.

Figure 9: Long-term revenue growth

Source: Company, IIFL Research; Note: *FY13-16 is sum of current segments under operations

4%

2%

8%

2%

12%

6%

13%

-18%

-27%

32%

16%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-

10

20

30

40

50

60

70

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

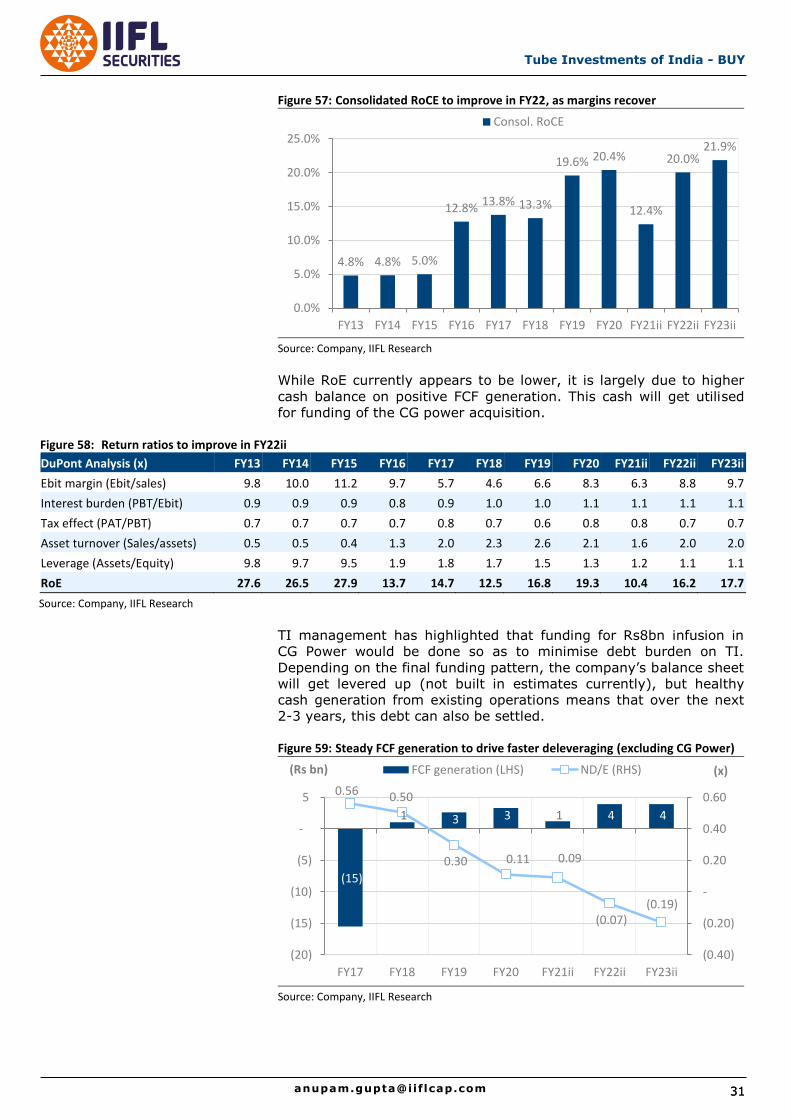

(Rs bn) Revenues (LHS) YoY growth (RHS)

Focus on four key financial metrics for each business

with the targets ingrained across the organisation till

the shop floor level

Post the restructuring and focus on key matrices, RoCE has improved from 12.8% to 20.4% over the last four years

7

Tube Investments of India - BUY

Figure 10: Long term Ebit and margins

Source: Company, IIFL Research; Note: *the FY13-16 margins corresponding to current operational segments

Figure 11: RoCE has steadily improved post restructuring

Source: Company, IIFL Research; Note: *gains from restructuring visible FY17 onwards

Figure 12: FCF and deleveraging over the past four years, post restructuring

Source: Company, IIFL Research *excludes outflow towards CG Power stake acquisition

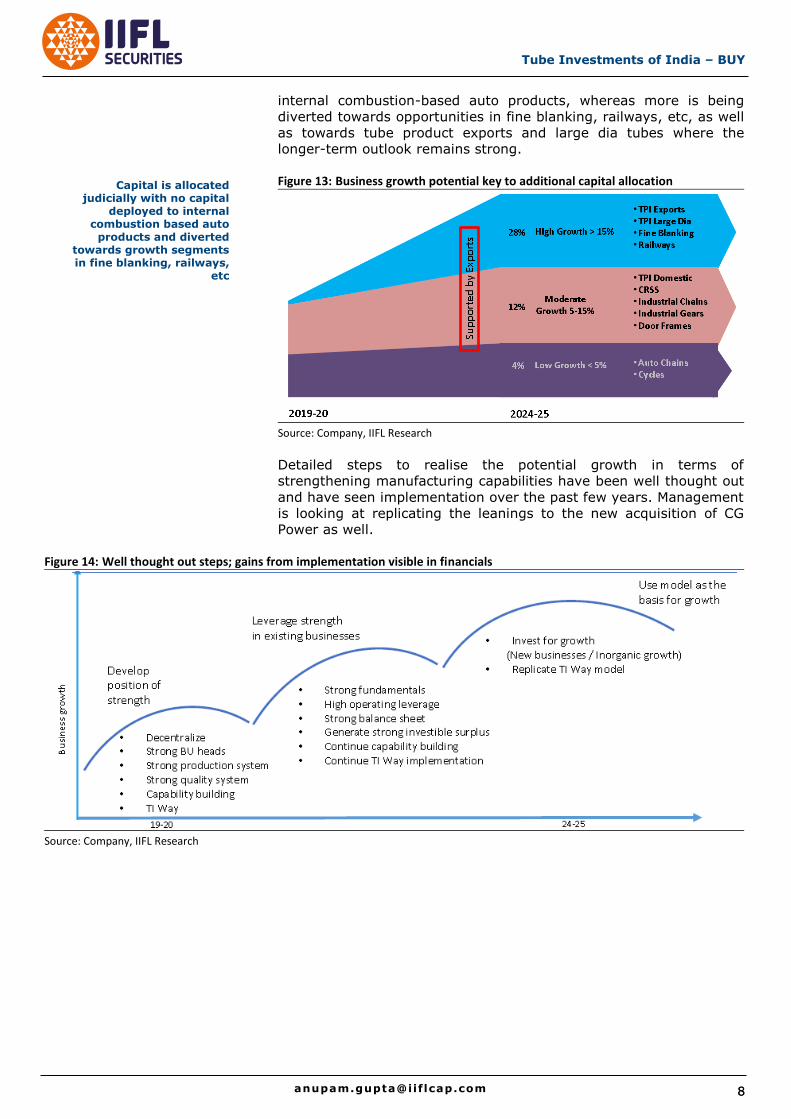

Allocating capital judiciously, across product segments

In order to leverage the strong established manufacturing

capabilities and solution-driven mindset, management has

recognised the market opportunity and possible runway for various

businesses. This is driving capital allocation in a more fruitful way for

the company. For example, no new capital is being deployed towards

3 3 3 3 3 3

4 5

3

5 6

6.5% 6.8%

6.0% 6.6%

6.3% 5.7%

7.6%

9.6%

7.9%

10.1% 10.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-

1

2

3

4

5

6

7

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs bn) Ebit (LHS) Ebit margins (RHS)

4.8% 4.8% 5.0%

12.8% 13.8% 13.3%

19.6% 20.4%

12.4%

20.0% 21.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

Consol. RoCE

(15)

1 3 3 1 4 4

0.56 0.50

0.30 0.11 0.09

(0.07) (0.19)

(0.40)

(0.20)

-

0.20

0.40

0.60

(20)

(15)

(10)

(5)

-

5

FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(x) (Rs bn) FCF generation (LHS) ND/E (RHS)

Tube Investments of India – BUY

internal combustion-based auto products, whereas more is being

diverted towards opportunities in fine blanking, railways, etc, as well

as towards tube product exports and large dia tubes where the

longer-term outlook remains strong.

Figure 13: Business growth potential key to additional capital allocation

Source: Company, IIFL Research

Detailed steps to realise the potential growth in terms of

strengthening manufacturing capabilities have been well thought out

and have seen implementation over the past few years. Management

is looking at replicating the leanings to the new acquisition of CG

Power as well.

Figure 14: Well thought out steps; gains from implementation visible in financials

Source: Company, IIFL Research

Capital is allocated judicially with no capital

deployed to internal combustion based auto

products and diverted towards growth segments in fine blanking, railways,

etc

9

Tube Investments of India - BUY

Strengthening leadership in core operations

Direct play on domestic auto recovery

Strong product portfolio for most auto manufacturers

Over the past several years, TI has built up strong leadership

position in the auto component segment for most of the products it

manufactures and supplies through a combination of excellence in

various aspects, including:

An extensive product portfolio across tubes, tubular components,

CRSS, fine blank products, PV door frames.

Pan India manufacturing presence for closer integration with

customers.

Forming a strong, well-established and transparent relationship

with OEMs, from the product-development phase itself.

Well-developed supply chain and focussed, solution-based

investment in R&D.

Established infrastructure for handling new product development.

Strong financial metrics.

The key products are used in 2-wheelers, 3-wheelers, passenger

vehicles as well as commercial vehicles. With ~56% of consolidated

revenues (75% for engineering products, 67% for metal formed

products) linked to the auto segment, TI is a direct play on the

recovery in auto volumes, domestically.

Figure 15: Both large segments have high dependence on auto market

Source: Company, IIFL Research

Figure 16: Growth for key products links follows volumes growth for 2W, PV and CVs

FY17 FY18 FY19 FY20

Auto sector – Industry volume

2W industry volume growth 7.0% 15.0% 5.0% -18.0%

PV industry volume growth 9.0% 8.0% 3.0% -18.0%

CV industry volume growth 0.0% 13.0% 15.0% -32.0%

Key products for TI

Tubes volume growth 9.0% 18.0% 12.0% -21.0%

CRSS volume growth 6.1% 11.0% 2.0% -16.0%

Automotive chain growth 0.7% 18.0% 6.0% -12.0%

Doorframe volume growth 6.0% 6.0% 12.0% -16.0%

Fine blanking volume growth 12.0% 29.0% 15.0% 2.0%

Source: Company, SIAM, IIFL Research

Auto 75%

Non Auto 25%

Engineering

Auto 67%

Non Auto 22%

Railways

11%

Metal formed product

TI has established strong leadership position in the

auto component segments with key products used in 2

wheeler and passenger vehicles

Tube Investments of India – BUY

10 10 [email protected]

Figure 17: Engineering segment – Key products for 2Ws and passenger vehicles

Source: Company, IIFL Research

Figure 18: Large and high quality client base for engineering products segment

Source: Company, IIFL Research

Figure 19: Metal Formed rolled formed products for the auto business

Source: Company, IIFL Research

11

Tube Investments of India - BUY

Figure 20: Metal formed products –Chains and fine blanked products for auto market

Source: Company, IIFL Research

Figure 21: Key customers for rolled formed products

Figure 22: Key customers for auto chains

Figure 23: Key customers for fine blanking products

Source: Company, IIFL Research

Tube Investments of India – BUY

12 12 [email protected]

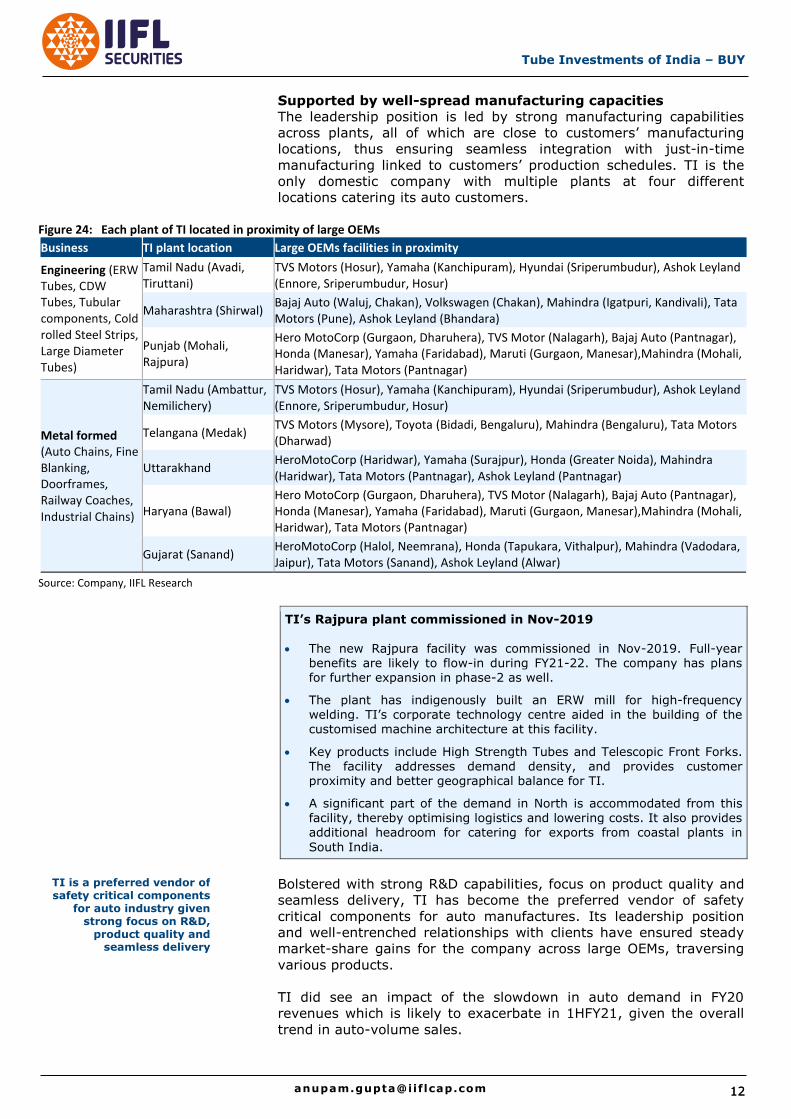

Supported by well-spread manufacturing capacities

The leadership position is led by strong manufacturing capabilities

across plants, all of which are close to customers’ manufacturing

locations, thus ensuring seamless integration with just-in-time

manufacturing linked to customers’ production schedules. TI is the

only domestic company with multiple plants at four different

locations catering its auto customers.

Figure 24: Each plant of TI located in proximity of large OEMs

Business TI plant location Large OEMs facilities in proximity

Engineering (ERW Tubes, CDW Tubes, Tubular components, Cold rolled Steel Strips, Large Diameter Tubes)

Tamil Nadu (Avadi, Tiruttani)

TVS Motors (Hosur), Yamaha (Kanchipuram), Hyundai (Sriperumbudur), Ashok Leyland (Ennore, Sriperumbudur, Hosur)

Maharashtra (Shirwal) Bajaj Auto (Waluj, Chakan), Volkswagen (Chakan), Mahindra (Igatpuri, Kandivali), Tata Motors (Pune), Ashok Leyland (Bhandara)

Punjab (Mohali, Rajpura)

Hero MotoCorp (Gurgaon, Dharuhera), TVS Motor (Nalagarh), Bajaj Auto (Pantnagar), Honda (Manesar), Yamaha (Faridabad), Maruti (Gurgaon, Manesar),Mahindra (Mohali, Haridwar), Tata Motors (Pantnagar)

Metal formed (Auto Chains, Fine Blanking, Doorframes, Railway Coaches, Industrial Chains)

Tamil Nadu (Ambattur, Nemilichery)

TVS Motors (Hosur), Yamaha (Kanchipuram), Hyundai (Sriperumbudur), Ashok Leyland (Ennore, Sriperumbudur, Hosur)

Telangana (Medak) TVS Motors (Mysore), Toyota (Bidadi, Bengaluru), Mahindra (Bengaluru), Tata Motors (Dharwad)

Uttarakhand HeroMotoCorp (Haridwar), Yamaha (Surajpur), Honda (Greater Noida), Mahindra (Haridwar), Tata Motors (Pantnagar), Ashok Leyland (Pantnagar)

Haryana (Bawal) Hero MotoCorp (Gurgaon, Dharuhera), TVS Motor (Nalagarh), Bajaj Auto (Pantnagar), Honda (Manesar), Yamaha (Faridabad), Maruti (Gurgaon, Manesar),Mahindra (Mohali, Haridwar), Tata Motors (Pantnagar)

Gujarat (Sanand) HeroMotoCorp (Halol, Neemrana), Honda (Tapukara, Vithalpur), Mahindra (Vadodara, Jaipur), Tata Motors (Sanand), Ashok Leyland (Alwar)

Source: Company, IIFL Research

TI’s Rajpura plant commissioned in Nov-2019

The new Rajpura facility was commissioned in Nov-2019. Full-year

benefits are likely to flow-in during FY21-22. The company has plans for further expansion in phase-2 as well.

The plant has indigenously built an ERW mill for high-frequency welding. TI’s corporate technology centre aided in the building of the customised machine architecture at this facility.

Key products include High Strength Tubes and Telescopic Front Forks.

The facility addresses demand density, and provides customer proximity and better geographical balance for TI.

A significant part of the demand in North is accommodated from this facility, thereby optimising logistics and lowering costs. It also provides additional headroom for catering for exports from coastal plants in

South India.

Bolstered with strong R&D capabilities, focus on product quality and

seamless delivery, TI has become the preferred vendor of safety

critical components for auto manufactures. Its leadership position

and well-entrenched relationships with clients have ensured steady

market-share gains for the company across large OEMs, traversing

various products.

TI did see an impact of the slowdown in auto demand in FY20

revenues which is likely to exacerbate in 1HFY21, given the overall

trend in auto-volume sales.

TI is a preferred vendor of safety critical components

for auto industry given strong focus on R&D,

product quality and seamless delivery

13

Tube Investments of India - BUY

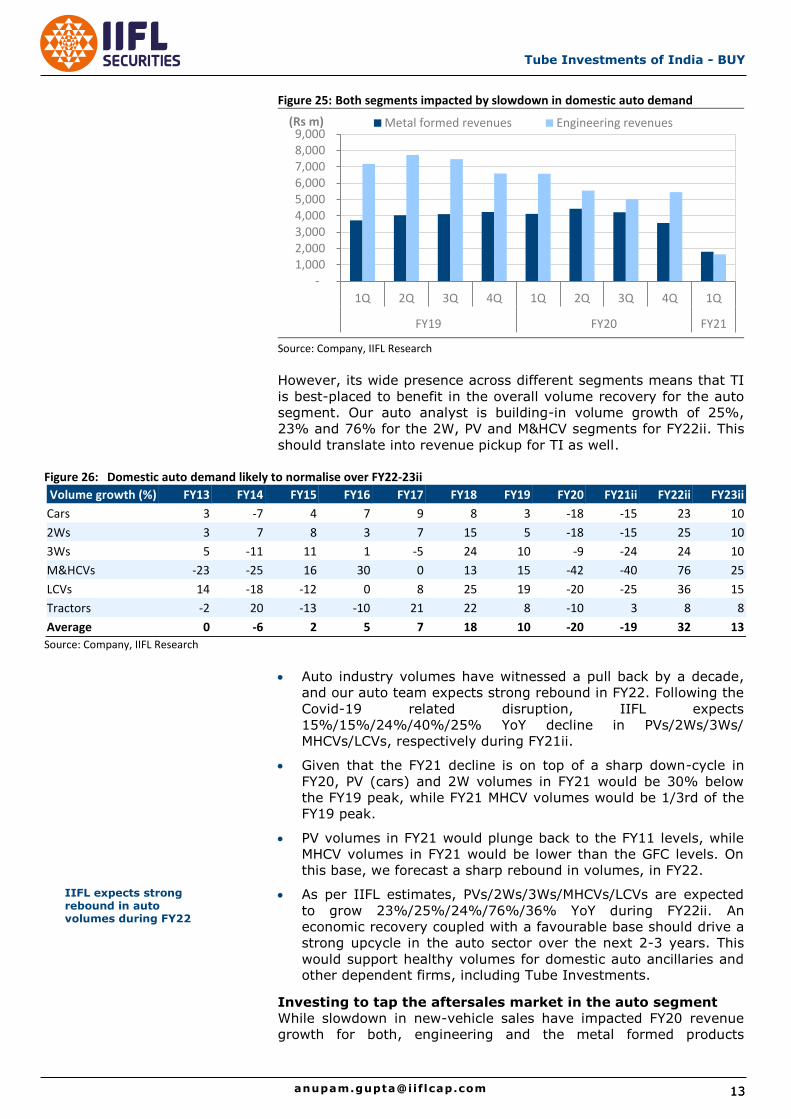

Figure 25: Both segments impacted by slowdown in domestic auto demand

Source: Company, IIFL Research

However, its wide presence across different segments means that TI

is best-placed to benefit in the overall volume recovery for the auto

segment. Our auto analyst is building-in volume growth of 25%,

23% and 76% for the 2W, PV and M&HCV segments for FY22ii. This

should translate into revenue pickup for TI as well.

Figure 26: Domestic auto demand likely to normalise over FY22-23ii

Volume growth (%) FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

Cars 3 -7 4 7 9 8 3 -18 -15 23 10

2Ws 3 7 8 3 7 15 5 -18 -15 25 10

3Ws 5 -11 11 1 -5 24 10 -9 -24 24 10

M&HCVs -23 -25 16 30 0 13 15 -42 -40 76 25

LCVs 14 -18 -12 0 8 25 19 -20 -25 36 15

Tractors -2 20 -13 -10 21 22 8 -10 3 8 8

Average 0 -6 2 5 7 18 10 -20 -19 32 13

Source: Company, IIFL Research

Auto industry volumes have witnessed a pull back by a decade,

and our auto team expects strong rebound in FY22. Following the

Covid-19 related disruption, IIFL expects

15%/15%/24%/40%/25% YoY decline in PVs/2Ws/3Ws/

MHCVs/LCVs, respectively during FY21ii.

Given that the FY21 decline is on top of a sharp down-cycle in

FY20, PV (cars) and 2W volumes in FY21 would be 30% below

the FY19 peak, while FY21 MHCV volumes would be 1/3rd of the

FY19 peak.

PV volumes in FY21 would plunge back to the FY11 levels, while

MHCV volumes in FY21 would be lower than the GFC levels. On

this base, we forecast a sharp rebound in volumes, in FY22.

As per IIFL estimates, PVs/2Ws/3Ws/MHCVs/LCVs are expected

to grow 23%/25%/24%/76%/36% YoY during FY22ii. An

economic recovery coupled with a favourable base should drive a

strong upcycle in the auto sector over the next 2-3 years. This

would support healthy volumes for domestic auto ancillaries and other dependent firms, including Tube Investments.

Investing to tap the aftersales market in the auto segment

While slowdown in new-vehicle sales have impacted FY20 revenue

growth for both, engineering and the metal formed products

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

FY19 FY20 FY21

(Rs m) Metal formed revenues Engineering revenues

IIFL expects strong rebound in auto volumes during FY22

Tube Investments of India – BUY

14 14 [email protected]

business, the company has tried to counter this hit through higher

focus on after-sales market demand for spares. In the metal formed

products business, auto chains, under the brand Diamond Chains,

have seen healthy traction. Focus has been on innovative products

such as chains for higher CC bikes as well as various types of

innovative chains for standard segment bikes. The company also

leveraged the multi-layered distribution infrastructure, to deepen its

market presence.

Figure 27: TI is investing in its aftermarket chains brand and its distribution

Source: Company, IIFL Research

Tapping into the global auto supply chain

Given the leadership position in the core engineering business (ERW

tubes, CRSS and door frames) as well as in the overall auto volume

prospects, both on a domestic scale, management expects growth

for these products to range between 5% and 15% over the medium-

to-long term at the national level. This would clearly be below the

target growth levels for any business.

To leverage its manufacturing prowess and diversify away from the

domestic auto segment, the company has increased focus on exports

of auto products. The past few years have seen the share of exports

grow steadily.

Figure 28: Export revenue growth and share of consolidated revenue

Source: Company, IIFL Research

0.0%

5.0%

10.0%

15.0%

20.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY14 FY15 FY16 FY17 FY18 FY19 FY20

(Rs m) Export revenues (LHS) Export revenue share (RHS)

TI has increased its focus on tapping into the global

auto supply chain to reduce dependence on domestic

auto segment

15

Tube Investments of India - BUY

This is likely to accelerate, supported by fresh approvals from global

OEMs. Majority of the exports, currently, are in the engineering

segment, to customers in Europe, South East Asia and China. Metal

formed products export growth is led by building new distributors

and channel partners in Central America and SAARC.

Commissioning of the Rajpura plant in Punjab, in Nov-2019, provides

the company significant headroom to increase focus on exports, as

this frees up capacity at the plants in Tamil Nadu, which have an

added advantage of proximity to ports. The Rajpura plant has now

been configured to meet the tighter specifications needed for the

export markets.

Management highlights that the approval process for more products

has already commenced, even as the company invests to garner the

opportunities emerging from the Euro-6 changeover as well as from

electric vehicles. Importantly, tighter specifications and lower

competition will translate into higher margins vs the domestic auto

business for TI’s engineering products. Additionally, management

expects gains from the China Plus One strategy for global auto

OEMs, post the supply-chain disruptions due to Covid-19.

Commissioning of the Rajpura plant allows

headroom to increase exports from its plants in

Tamil Nadu

Tube Investments of India – BUY

16 16 [email protected]

Healthy traction in non-auto business

Efforts on, to grow non-auto revenues for engineering and

metal formed product

Over the last four years, the company has seen steady growth in the

non-auto business, including railway coaches and large dia tubes for

off-road vehicle applications. This has been a conscious choice by the

management for diversifying revenue streams to reduce dependence

and, hence, the cyclicality from exposure to the auto sector.

In the engineering products segment, large dia tubes for

construction equipment as well as tractors are the key offering.

Opportunity in the large dia non-auto segment is due to import

substitution, given only few competitive manufacturers domestically.

Investment in R&D to develop products that meet specifications has

been a key trend for the company in this segment.

Figure 29: Engineering products – Large diameter tubes for off-road applications

Source: Company, IIFL Research

Figure 30: Large dia tube volumes have seen steady increase since FY16

Source: Company, IIFL Research

15,303

21,733

35,425

44,989

33,292

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

FY16 FY17 FY18 FY19 FY20

(tonnes) Large Dia tube volumes

Non auto businesses such as railways, large dia tubes

have seen increased traction over the past few

years

17

Tube Investments of India - BUY

In the metal formed segment, the industrial chains business

contributes meaningful revenues. Growth is led by demand from

industries, including construction equipment, material handling,

agricultural equipment, cement, power, conveyor manufacturers,

food processing and multi-level car parking. Overall, growth here

would be subdued but steady, and the company will likely benefit

from the entrenched position with key large clients.

Figure 31: Metal Formed – Industrial chains’ product portfolio

Power transmission/conveying chains

Agricultural chains

Engineering class chains

Source: Company, IIFL Research

Figure 32: Industrial chains – Key customers

Source: Company, IIFL Research

Figure 33: Industrial Chains have seen steady growth in the past two years

Source: Company, IIFL Research

Strong traction in railway coach building

In the railways segment, while the company has been a supplier for

decades, there has been steady uptick in the flow of orders for

sections for railway coaches from the three Railway Coach factories

over the past 3-4 years. Demonstration − of the latest technologies

(robotic welding) in manufacturing − to railways has set new

benchmarks for tendering, providing TI the lead in a not-so-crowded

9.0% 8.0%

19.0%

10.0%

0.0%

5.0%

10.0%

15.0%

20.0%

FY17 FY18 FY19 FY20

Industrial chains growth

Tube Investments of India – BUY

18 18 [email protected]

market. Also, dedicated manufacturing plants in close proximity to

the Rail Coach factories have provided an advantage to the

company.

Figure 34: Railway factory locations and TI plants for railways

Railway factories TI plants catering for the Railways

Integral Coach Factory, Chennai (Tamil Nadu) TI Metal Forming, Kakkalur

Rail Coach Factory, Kapurthala (Punjab) TI Metal Forming - Uttarakhand

Modern Coach Factory, Raebareli (UP) TI Metal Forming Uttarakhand

Source: Company, IIFL Research

Figure 35: Metal formed products used in rail coaches

Source: Company, IIFL Research

FY20 witnessed 49% YoY revenue growth for the railways business,

supported by healthy coach build-out by the Indian Railways and TI’s

leadership position in the segment. While the near term is uncertain

due to stressed financials of railways, coach build-out plans remain

strong, as per various releases by the government.

Figure 36: Coach build-out plan announced by the Indian Railways (IR)

No. of coaches FY19* FY20* FY20R FY21* FY21R FY22*

LHB 4,238 4,034 5,784 4,079 6,631 4,099

Self-propelled 1,729 1,856 2,192 2,405 1,765 2,546

Others 91 50 50 50 279 50

Total 6,058 5,940 8,026 6,534 8,675 6,695

Source: IR; Note: *original plan announced in Jan-19; R - revised production plan for respective years, announced later

Additionally, increase in domestic sourcing of train-sets, as

announced for 44 Vande Bharat trains, will aid ordering for the TI

railway business.

TI’s railway business grew 49% YoY in FY20 on

healthy coach building by the Indian Railways

19

Tube Investments of India - BUY

Tender for 44 Vande Bharat trains

The Indian Railways has floated the revised Tender of semi high-

speed 44 Vande Bharat trains-sets. The Tender is for 3-phase

Propulsion, Control and other Equipment, along with bogies for the

trains-sets. The main features of the Tender are as under:

Train-sets shall be manufactured at ICF/Chennai,

RCF/Kapurthala and MCF/Raebareli

It shall be a local (indigenous) tender

A two-stage, reverse auction shall take place

The revised Tender is in line with Government of India’s preference

for the Make in India policy; the minimum local content percentage

has been revised to 75%. It is the first big tender under the revised

DPIIT norms of AtmaNirbhar Bharat and has at least 75% domestic

components. This tender is now a Domestic Tender, with only the

companies registered in India eligible to apply, and would have to

quote in Indian Rupees.

The company has also started supplying parts for metro train

manufacturing in both, India and overseas. This has been a

remunerative business with healthy return ratios, despite being a

B2G (business-to-government) business.

Cycles – Turnaround on track

TI manufactures and markets a wide range of bicycles and

accessories − from standard to premium − including performance

bicycles for the fitness and adventure space.

Figure 37: Cycles − Key brands for TI

Source: Company, IIFL Research

It was a pioneer in the retail format of experiential stores – Track &

Trail Urban, Track & trail Sport and BSA Hercules Rural outlets. It

currently has ~225 Track & Trail stores across India. Its overall

distribution network is spread across 8,500 dealers. It has an omni-

channel presence, with unified in-store and online experience.

Tube Investments of India – BUY

20 20 [email protected]

Figure 38: Retail experience at Track & Trail

Source: Company, IIFL Research

The company enjoys a stronger position in the specials category,

which has higher value addition, realisation and profitability

compared with standard cycles. Differentiation through innovation

has aided this, e.g. handles with integrated headlights, anti-slip

chains, etc.

Figure 39: TI enjoys a larger share in the specials segment

Source: Company, IIFL Research; Note: Market share, as of Nov-2019

Figure 40: TI has 28% market share in the domestic cycles market

Source: ACMA, IIFL Research *FY20 market share as of Nov-2019

54.0% 60.0% 61.0% 63.0% 66.0%

72.0% 72.0% 72.0%

FY17 FY18 FY19 FY20

Share of specials for industry Share of specials for TI

31% 28% 31% 35%

27% 29% 23% 28%

17% 16% 17% 7%

10% 10% 11% 12%

15% 17% 18% 18%

FY17 FY18 FY19 FY20

Hero TI Atlas Avon Others

Exit from the institutional business in FY17 and high focus on specials category has improved profitability

for the cycles business

21

Tube Investments of India - BUY

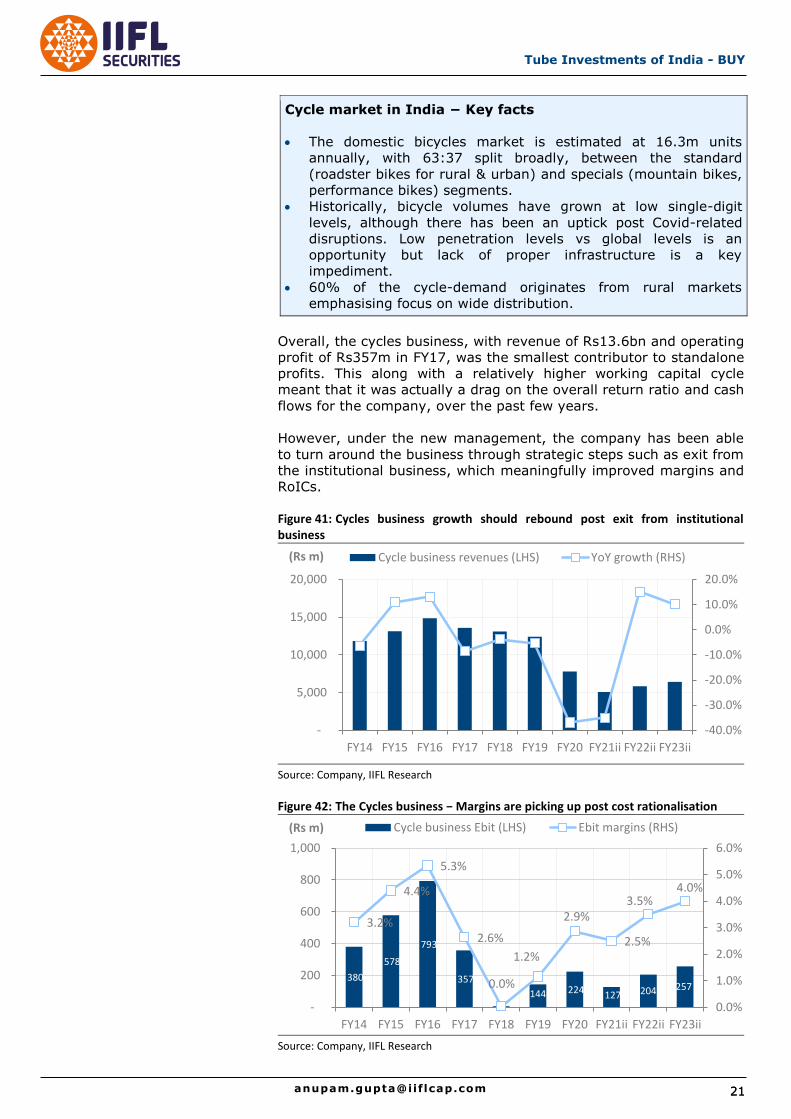

Cycle market in India − Key facts

The domestic bicycles market is estimated at 16.3m units

annually, with 63:37 split broadly, between the standard

(roadster bikes for rural & urban) and specials (mountain bikes,

performance bikes) segments.

Historically, bicycle volumes have grown at low single-digit

levels, although there has been an uptick post Covid-related

disruptions. Low penetration levels vs global levels is an

opportunity but lack of proper infrastructure is a key

impediment.

60% of the cycle-demand originates from rural markets

emphasising focus on wide distribution.

Overall, the cycles business, with revenue of Rs13.6bn and operating

profit of Rs357m in FY17, was the smallest contributor to standalone

profits. This along with a relatively higher working capital cycle

meant that it was actually a drag on the overall return ratio and cash

flows for the company, over the past few years.

However, under the new management, the company has been able

to turn around the business through strategic steps such as exit from

the institutional business, which meaningfully improved margins and

RoICs.

Figure 41: Cycles business growth should rebound post exit from institutional business

Source: Company, IIFL Research

Figure 42: The Cycles business − Margins are picking up post cost rationalisation

Source: Company, IIFL Research

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

-

5,000

10,000

15,000

20,000

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs m) Cycle business revenues (LHS) YoY growth (RHS)

380

578

793

357

6 144 224 127 204 257

3.2%

4.4%

5.3%

2.6%

0.0%

1.2%

2.9%

2.5%

3.5% 4.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

-

200

400

600

800

1,000

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs m) Cycle business Ebit (LHS) Ebit margins (RHS)

Tube Investments of India – BUY

22 22 [email protected]

Other significant steps and initiatives include:

Rationalising of the product portfolio towards

affordability/specialities. New product development through

innovation has benefited overall revenue growth over FY19-20.

Rationalisation of the cost structure to reduce breakeven

volumes, from ~0.18m cycles annually to ~0.145m cycles.

Streamlining and rationalising the distribution network through

optimised warehousing.

Consolidation of manufacturing footprint post commissioning of

the 250,000-unit capacity Rajpura plant, as the company was

able to close down the Nashik facility for bicycles.

Investments in marketing and distribution, with steady increase

in Track & trail stores. Leveraging rapid increase in internet

penetration through its omni-channel strategy.

However, given the state of the market, management admits that

these steps can only help the company cover some distance, in

terms of growth potential, segment margins and RoICs. Further

measures to meet overall company-level targets would involve

playing on the manufacturing strength to tap newer markets. This

will primarily be targeted towards generating volumes so as to sweat

the assets, including the new Rajpura plant.

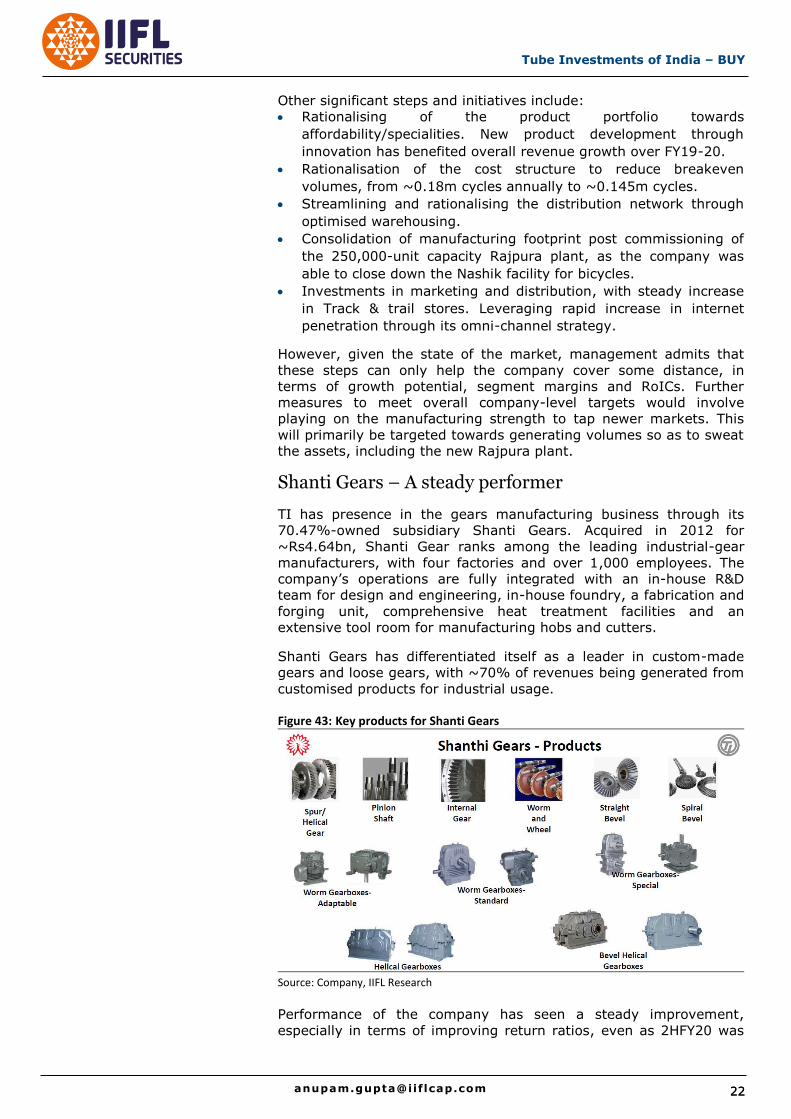

Shanti Gears – A steady performer

TI has presence in the gears manufacturing business through its

70.47%-owned subsidiary Shanti Gears. Acquired in 2012 for

~Rs4.64bn, Shanti Gear ranks among the leading industrial-gear

manufacturers, with four factories and over 1,000 employees. The

company’s operations are fully integrated with an in-house R&D

team for design and engineering, in-house foundry, a fabrication and

forging unit, comprehensive heat treatment facilities and an

extensive tool room for manufacturing hobs and cutters.

Shanti Gears has differentiated itself as a leader in custom-made

gears and loose gears, with ~70% of revenues being generated from

customised products for industrial usage.

Figure 43: Key products for Shanti Gears

Source: Company, IIFL Research

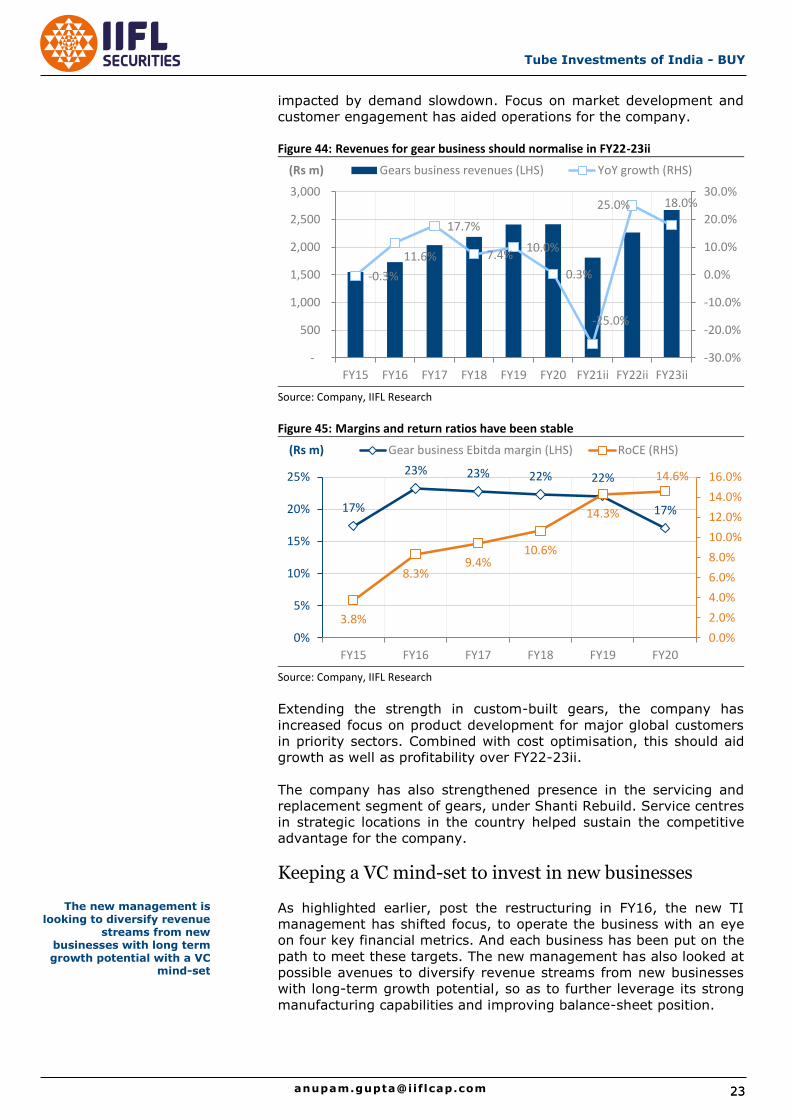

Performance of the company has seen a steady improvement,

especially in terms of improving return ratios, even as 2HFY20 was

23

Tube Investments of India - BUY

impacted by demand slowdown. Focus on market development and

customer engagement has aided operations for the company.

Figure 44: Revenues for gear business should normalise in FY22-23ii

Source: Company, IIFL Research

Figure 45: Margins and return ratios have been stable

Source: Company, IIFL Research

Extending the strength in custom-built gears, the company has

increased focus on product development for major global customers

in priority sectors. Combined with cost optimisation, this should aid

growth as well as profitability over FY22-23ii.

The company has also strengthened presence in the servicing and

replacement segment of gears, under Shanti Rebuild. Service centres

in strategic locations in the country helped sustain the competitive

advantage for the company.

Keeping a VC mind-set to invest in new businesses

As highlighted earlier, post the restructuring in FY16, the new TI

management has shifted focus, to operate the business with an eye

on four key financial metrics. And each business has been put on the

path to meet these targets. The new management has also looked at

possible avenues to diversify revenue streams from new businesses

with long-term growth potential, so as to further leverage its strong

manufacturing capabilities and improving balance-sheet position.

-0.3%

11.6%

17.7%

7.4% 10.0%

0.3%

-25.0%

25.0% 18.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

-

500

1,000

1,500

2,000

2,500

3,000

FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs m) Gears business revenues (LHS) YoY growth (RHS)

17%

23% 23% 22% 22%

17%

3.8%

8.3% 9.4%

10.6%

14.3%

14.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0%

5%

10%

15%

20%

25%

FY15 FY16 FY17 FY18 FY19 FY20

(Rs m) Gear business Ebitda margin (LHS) RoCE (RHS)

The new management is looking to diversify revenue

streams from new businesses with long term growth potential with a VC

mind-set

Tube Investments of India – BUY

24 24 [email protected]

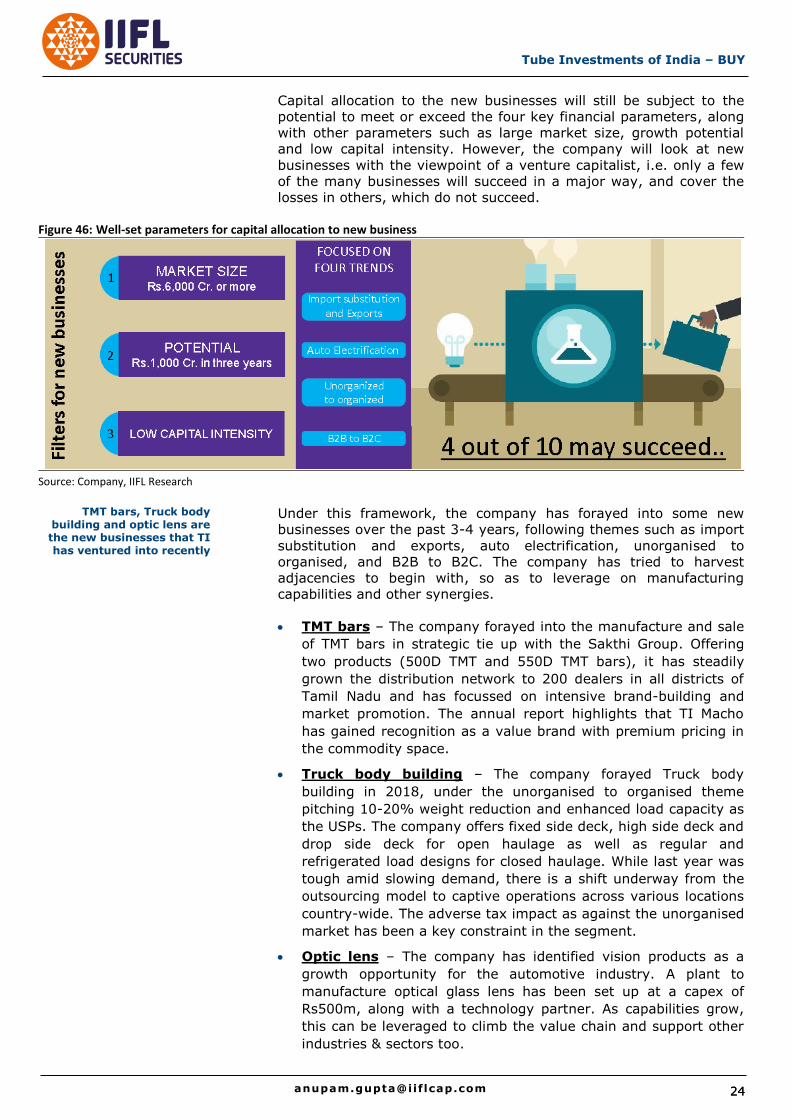

Capital allocation to the new businesses will still be subject to the

potential to meet or exceed the four key financial parameters, along

with other parameters such as large market size, growth potential

and low capital intensity. However, the company will look at new

businesses with the viewpoint of a venture capitalist, i.e. only a few

of the many businesses will succeed in a major way, and cover the

losses in others, which do not succeed.

Figure 46: Well-set parameters for capital allocation to new business

Source: Company, IIFL Research

Under this framework, the company has forayed into some new

businesses over the past 3-4 years, following themes such as import

substitution and exports, auto electrification, unorganised to

organised, and B2B to B2C. The company has tried to harvest

adjacencies to begin with, so as to leverage on manufacturing

capabilities and other synergies.

TMT bars – The company forayed into the manufacture and sale

of TMT bars in strategic tie up with the Sakthi Group. Offering

two products (500D TMT and 550D TMT bars), it has steadily

grown the distribution network to 200 dealers in all districts of

Tamil Nadu and has focussed on intensive brand-building and

market promotion. The annual report highlights that TI Macho

has gained recognition as a value brand with premium pricing in

the commodity space.

Truck body building – The company forayed Truck body

building in 2018, under the unorganised to organised theme

pitching 10-20% weight reduction and enhanced load capacity as

the USPs. The company offers fixed side deck, high side deck and

drop side deck for open haulage as well as regular and

refrigerated load designs for closed haulage. While last year was

tough amid slowing demand, there is a shift underway from the

outsourcing model to captive operations across various locations

country-wide. The adverse tax impact as against the unorganised

market has been a key constraint in the segment.

Optic lens – The company has identified vision products as a

growth opportunity for the automotive industry. A plant to

manufacture optical glass lens has been set up at a capex of

Rs500m, along with a technology partner. As capabilities grow,

this can be leveraged to climb the value chain and support other

industries & sectors too.

TMT bars, Truck body building and optic lens are the new businesses that TI has ventured into recently

25

Tube Investments of India - BUY

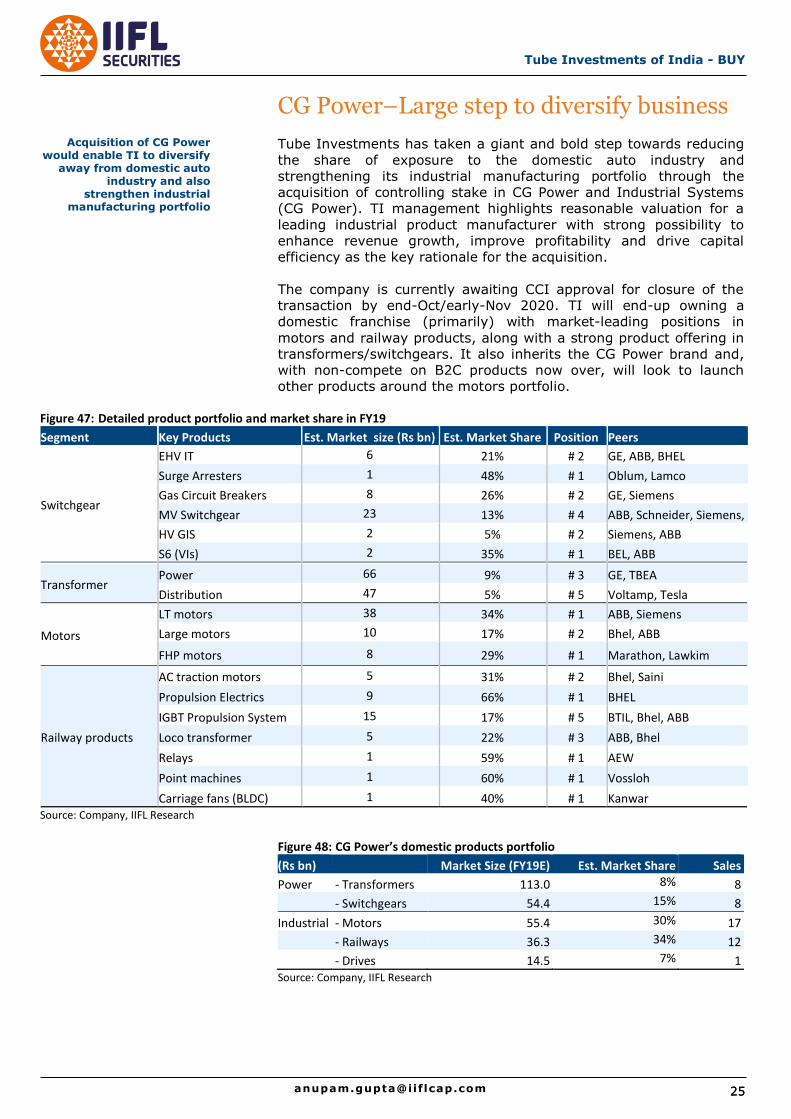

CG Power–Large step to diversify business

Tube Investments has taken a giant and bold step towards reducing

the share of exposure to the domestic auto industry and

strengthening its industrial manufacturing portfolio through the

acquisition of controlling stake in CG Power and Industrial Systems

(CG Power). TI management highlights reasonable valuation for a

leading industrial product manufacturer with strong possibility to

enhance revenue growth, improve profitability and drive capital

efficiency as the key rationale for the acquisition.

The company is currently awaiting CCI approval for closure of the

transaction by end-Oct/early-Nov 2020. TI will end-up owning a

domestic franchise (primarily) with market-leading positions in

motors and railway products, along with a strong product offering in

transformers/switchgears. It also inherits the CG Power brand and,

with non-compete on B2C products now over, will look to launch

other products around the motors portfolio.

Figure 47: Detailed product portfolio and market share in FY19

Segment Key Products Est. Market size (Rs bn) Est. Market Share Position Peers

Switchgear

EHV IT 6 21% # 2 GE, ABB, BHEL

Surge Arresters 1 48% # 1 Oblum, Lamco

Gas Circuit Breakers 8 26% # 2 GE, Siemens

MV Switchgear 23 13% # 4 ABB, Schneider, Siemens,

HV GIS 2 5% # 2 Siemens, ABB

S6 (VIs) 2 35% # 1 BEL, ABB

Transformer

Power 66 9% # 3 GE, TBEA

Distribution 47 5% # 5 Voltamp, Tesla

Motors

LT motors 38 34% # 1 ABB, Siemens

Large motors 10 17% # 2 Bhel, ABB

FHP motors 8 29% # 1 Marathon, Lawkim

Railway products

AC traction motors 5 31% # 2 Bhel, Saini

Propulsion Electrics 9 66% # 1 BHEL

IGBT Propulsion System 15 17% # 5 BTIL, Bhel, ABB

Loco transformer 5 22% # 3 ABB, Bhel

Relays 1 59% # 1 AEW

Point machines 1 60% # 1 Vossloh

Carriage fans (BLDC) 1 40% # 1 Kanwar Source: Company, IIFL Research

Figure 48: CG Power’s domestic products portfolio

(Rs bn)

Market Size (FY19E) Est. Market Share Sales

Power - Transformers 113.0 8% 8 - Switchgears 54.4 15% 8

Industrial - Motors 55.4 30% 17 - Railways 36.3 34% 12 - Drives 14.5 7% 1 Source: Company, IIFL Research

Acquisition of CG Power would enable TI to diversify

away from domestic auto industry and also

strengthen industrial manufacturing portfolio

Tube Investments of India – BUY

26 26 [email protected]

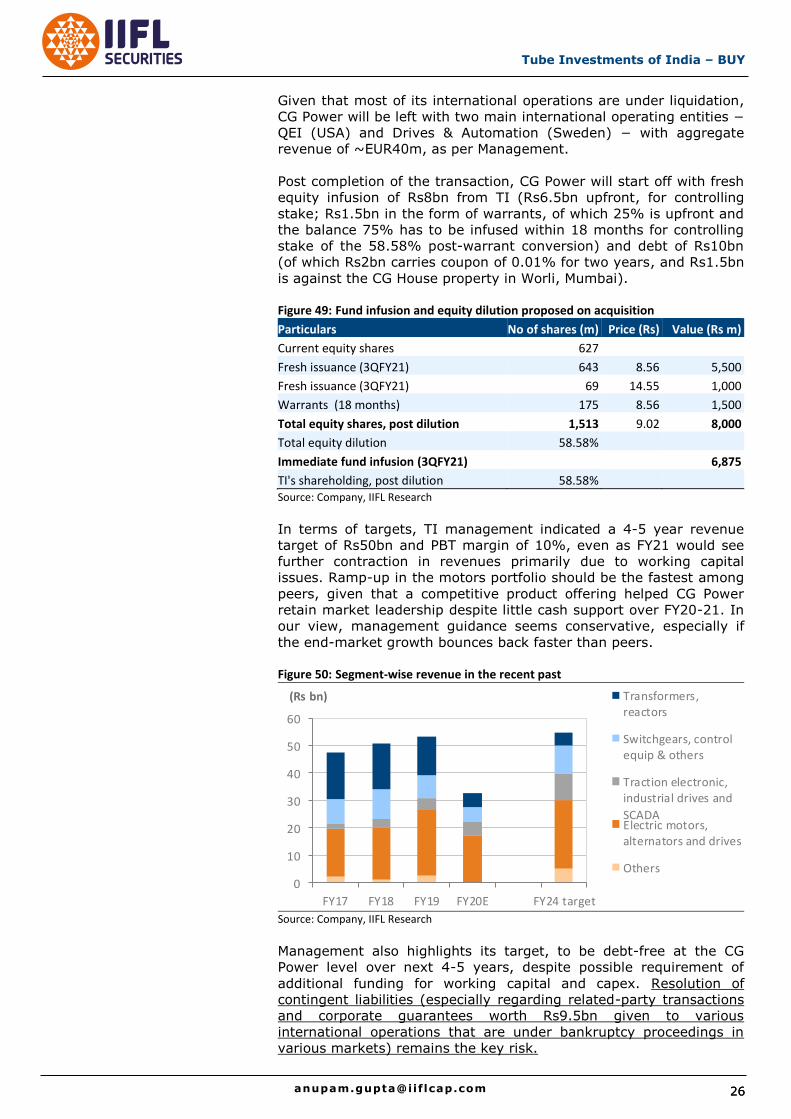

Given that most of its international operations are under liquidation,

CG Power will be left with two main international operating entities −

QEI (USA) and Drives & Automation (Sweden) − with aggregate

revenue of ~EUR40m, as per Management.

Post completion of the transaction, CG Power will start off with fresh

equity infusion of Rs8bn from TI (Rs6.5bn upfront, for controlling

stake; Rs1.5bn in the form of warrants, of which 25% is upfront and

the balance 75% has to be infused within 18 months for controlling

stake of the 58.58% post-warrant conversion) and debt of Rs10bn

(of which Rs2bn carries coupon of 0.01% for two years, and Rs1.5bn

is against the CG House property in Worli, Mumbai).

Figure 49: Fund infusion and equity dilution proposed on acquisition

Particulars No of shares (m) Price (Rs) Value (Rs m)

Current equity shares 627

Fresh issuance (3QFY21) 643 8.56 5,500

Fresh issuance (3QFY21) 69 14.55 1,000

Warrants (18 months) 175 8.56 1,500

Total equity shares, post dilution 1,513 9.02 8,000

Total equity dilution 58.58%

Immediate fund infusion (3QFY21)

6,875

TI's shareholding, post dilution 58.58%

Source: Company, IIFL Research

In terms of targets, TI management indicated a 4-5 year revenue

target of Rs50bn and PBT margin of 10%, even as FY21 would see

further contraction in revenues primarily due to working capital

issues. Ramp-up in the motors portfolio should be the fastest among

peers, given that a competitive product offering helped CG Power

retain market leadership despite little cash support over FY20-21. In

our view, management guidance seems conservative, especially if

the end-market growth bounces back faster than peers.

Figure 50: Segment-wise revenue in the recent past

Source: Company, IIFL Research

Management also highlights its target, to be debt-free at the CG

Power level over next 4-5 years, despite possible requirement of

additional funding for working capital and capex. Resolution of

contingent liabilities (especially regarding related-party transactions

and corporate guarantees worth Rs9.5bn given to various

international operations that are under bankruptcy proceedings in

various markets) remains the key risk.

0

10

20

30

40

50

60

FY17 FY18 FY19 FY20E FY24 target

(Rs bn) Transformers,reactors

Switchgears, controlequip & others

Traction electronic,industrial drives and

SCADAElectric motors,alternators and drives

Others

27

Tube Investments of India - BUY

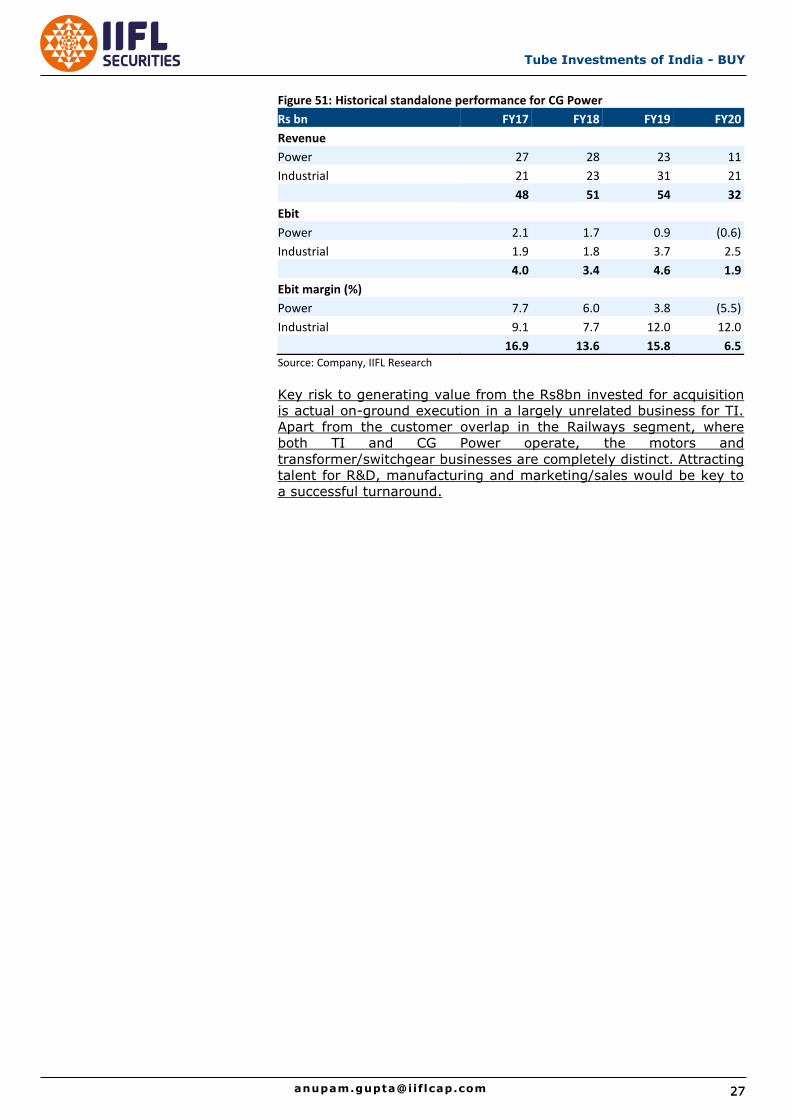

Figure 51: Historical standalone performance for CG Power

Rs bn FY17 FY18 FY19 FY20

Revenue

Power 27 28 23 11

Industrial 21 23 31 21

48 51 54 32

Ebit

Power 2.1 1.7 0.9 (0.6)

Industrial 1.9 1.8 3.7 2.5

4.0 3.4 4.6 1.9

Ebit margin (%)

Power 7.7 6.0 3.8 (5.5)

Industrial 9.1 7.7 12.0 12.0

16.9 13.6 15.8 6.5

Source: Company, IIFL Research

Key risk to generating value from the Rs8bn invested for acquisition

is actual on-ground execution in a largely unrelated business for TI.

Apart from the customer overlap in the Railways segment, where

both TI and CG Power operate, the motors and

transformer/switchgear businesses are completely distinct. Attracting

talent for R&D, manufacturing and marketing/sales would be key to

a successful turnaround.

Tube Investments of India – BUY

28 28 [email protected]

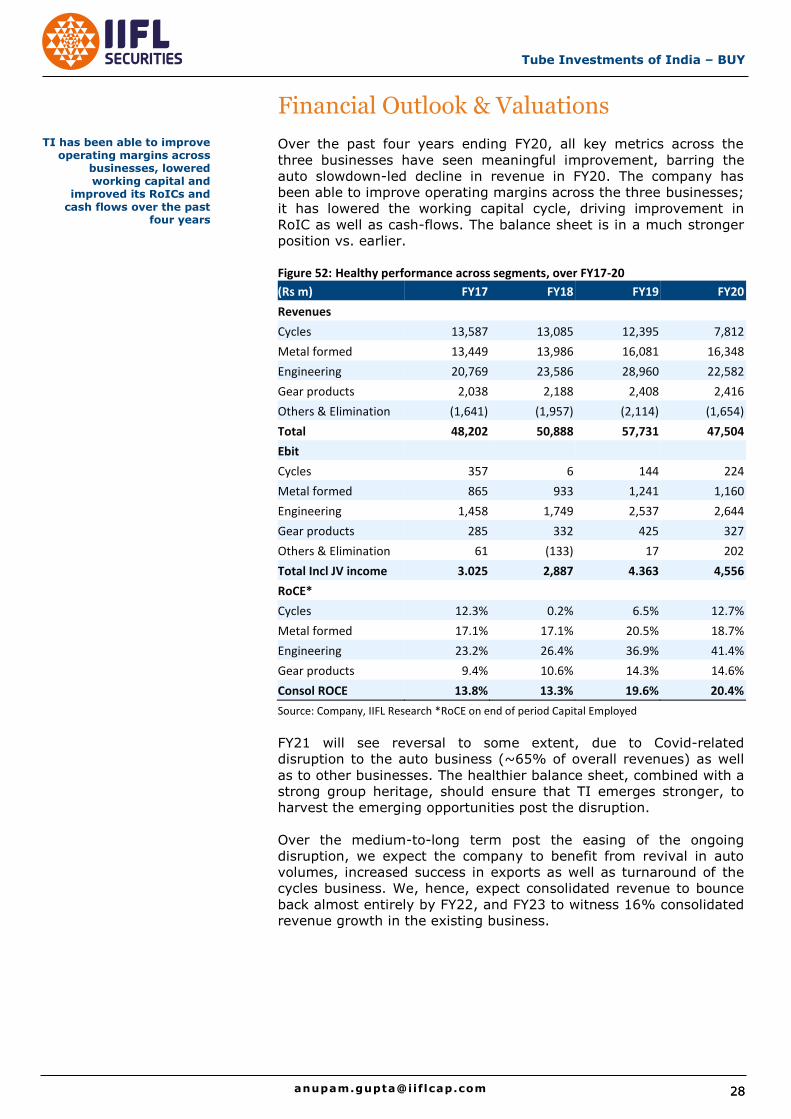

Financial Outlook & Valuations

Over the past four years ending FY20, all key metrics across the

three businesses have seen meaningful improvement, barring the

auto slowdown-led decline in revenue in FY20. The company has

been able to improve operating margins across the three businesses;

it has lowered the working capital cycle, driving improvement in

RoIC as well as cash-flows. The balance sheet is in a much stronger

position vs. earlier.

Figure 52: Healthy performance across segments, over FY17-20

(Rs m) FY17 FY18 FY19 FY20

Revenues

Cycles 13,587 13,085 12,395 7,812

Metal formed 13,449 13,986 16,081 16,348

Engineering 20,769 23,586 28,960 22,582

Gear products 2,038 2,188 2,408 2,416

Others & Elimination (1,641) (1,957) (2,114) (1,654)

Total 48,202 50,888 57,731 47,504

Ebit

Cycles 357 6 144 224

Metal formed 865 933 1,241 1,160

Engineering 1,458 1,749 2,537 2,644

Gear products 285 332 425 327

Others & Elimination 61 (133) 17 202

Total Incl JV income 3.025 2,887 4.363 4,556

RoCE*

Cycles 12.3% 0.2% 6.5% 12.7%

Metal formed 17.1% 17.1% 20.5% 18.7%

Engineering 23.2% 26.4% 36.9% 41.4%

Gear products 9.4% 10.6% 14.3% 14.6%

Consol ROCE 13.8% 13.3% 19.6% 20.4%

Source: Company, IIFL Research *RoCE on end of period Capital Employed

FY21 will see reversal to some extent, due to Covid-related

disruption to the auto business (~65% of overall revenues) as well

as to other businesses. The healthier balance sheet, combined with a

strong group heritage, should ensure that TI emerges stronger, to

harvest the emerging opportunities post the disruption.

Over the medium-to-long term post the easing of the ongoing

disruption, we expect the company to benefit from revival in auto

volumes, increased success in exports as well as turnaround of the

cycles business. We, hence, expect consolidated revenue to bounce

back almost entirely by FY22, and FY23 to witness 16% consolidated

revenue growth in the existing business.

TI has been able to improve operating margins across

businesses, lowered working capital and

improved its RoICs and cash flows over the past

four years

29

Tube Investments of India - BUY

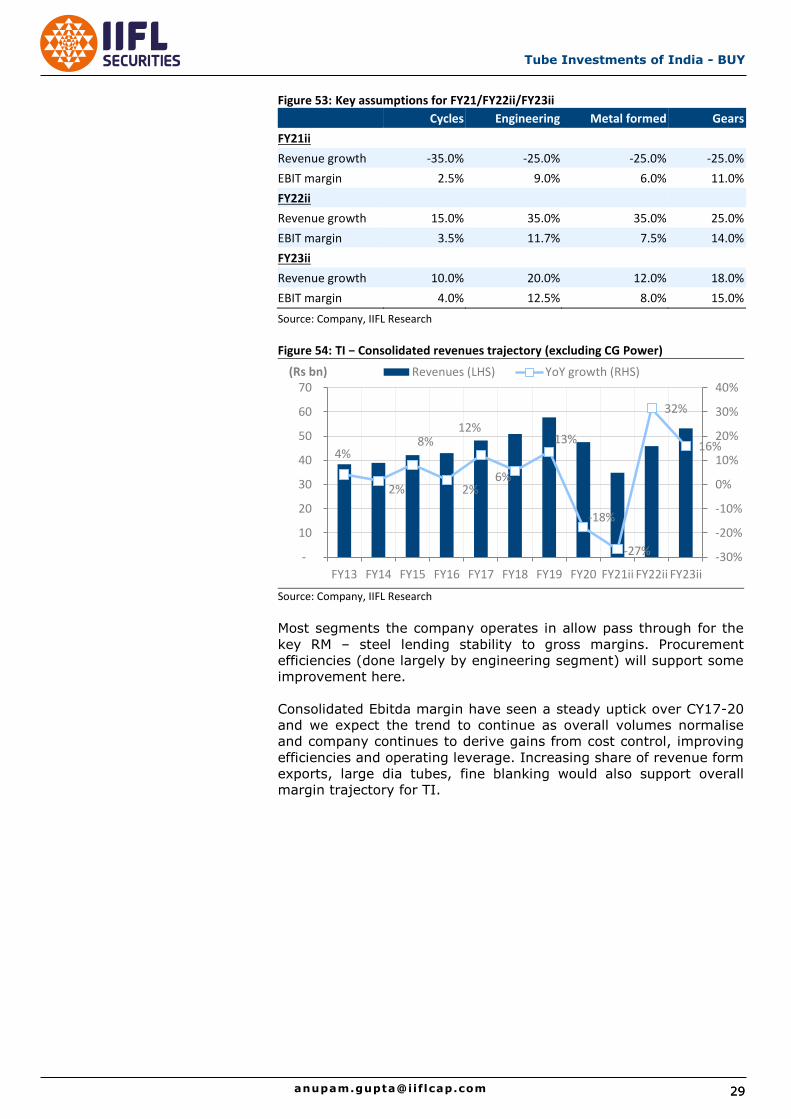

Figure 53: Key assumptions for FY21/FY22ii/FY23ii

Cycles Engineering Metal formed Gears

FY21ii

Revenue growth -35.0% -25.0% -25.0% -25.0%

EBIT margin 2.5% 9.0% 6.0% 11.0%

FY22ii

Revenue growth 15.0% 35.0% 35.0% 25.0%

EBIT margin 3.5% 11.7% 7.5% 14.0%

FY23ii

Revenue growth 10.0% 20.0% 12.0% 18.0%

EBIT margin 4.0% 12.5% 8.0% 15.0%

Source: Company, IIFL Research

Figure 54: TI − Consolidated revenues trajectory (excluding CG Power)

Source: Company, IIFL Research

Most segments the company operates in allow pass through for the

key RM – steel lending stability to gross margins. Procurement

efficiencies (done largely by engineering segment) will support some

improvement here.

Consolidated Ebitda margin have seen a steady uptick over CY17-20

and we expect the trend to continue as overall volumes normalise

and company continues to derive gains from cost control, improving

efficiencies and operating leverage. Increasing share of revenue form

exports, large dia tubes, fine blanking would also support overall

margin trajectory for TI.

4%

2%

8%

2%

12%

6%

13%

-18%

-27%

32%

16%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-

10

20

30

40

50

60

70

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs bn) Revenues (LHS) YoY growth (RHS)

Tube Investments of India – BUY

30 30 [email protected]

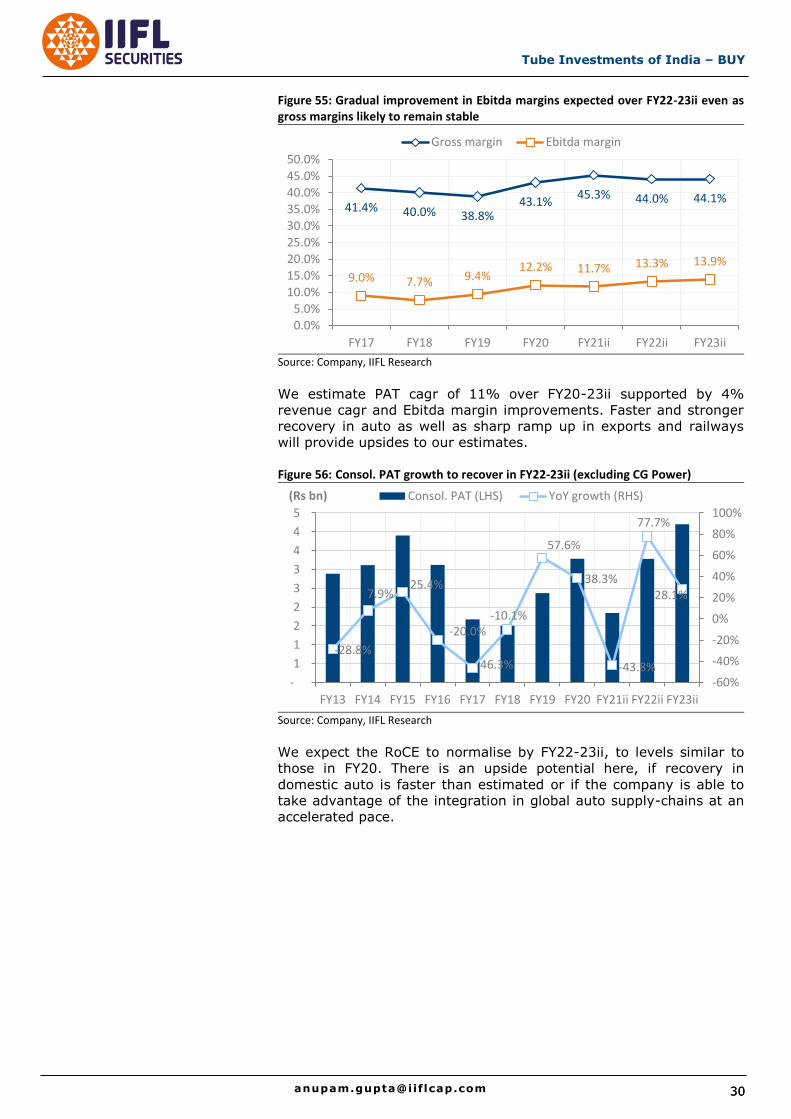

Figure 55: Gradual improvement in Ebitda margins expected over FY22-23ii even as gross margins likely to remain stable

Source: Company, IIFL Research

We estimate PAT cagr of 11% over FY20-23ii supported by 4%

revenue cagr and Ebitda margin improvements. Faster and stronger

recovery in auto as well as sharp ramp up in exports and railways

will provide upsides to our estimates.

Figure 56: Consol. PAT growth to recover in FY22-23ii (excluding CG Power)

Source: Company, IIFL Research

We expect the RoCE to normalise by FY22-23ii, to levels similar to

those in FY20. There is an upside potential here, if recovery in

domestic auto is faster than estimated or if the company is able to

take advantage of the integration in global auto supply-chains at an

accelerated pace.

41.4% 40.0% 38.8% 43.1%

45.3% 44.0% 44.1%

9.0% 7.7% 9.4% 12.2% 11.7% 13.3% 13.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

Gross margin Ebitda margin

-28.8%

7.9% 25.4%

-20.0%

-46.3%

-10.1%

57.6%

38.3%

-43.8%

77.7%

28.1%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-

1

1

2

2

3

3

4

4

5

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(Rs bn) Consol. PAT (LHS) YoY growth (RHS)

31

Tube Investments of India - BUY

Figure 57: Consolidated RoCE to improve in FY22, as margins recover

Source: Company, IIFL Research

While RoE currently appears to be lower, it is largely due to higher

cash balance on positive FCF generation. This cash will get utilised

for funding of the CG power acquisition.

Figure 58: Return ratios to improve in FY22ii

DuPont Analysis (x) FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

Ebit margin (Ebit/sales) 9.8 10.0 11.2 9.7 5.7 4.6 6.6 8.3 6.3 8.8 9.7

Interest burden (PBT/Ebit) 0.9 0.9 0.9 0.8 0.9 1.0 1.0 1.1 1.1 1.1 1.1

Tax effect (PAT/PBT) 0.7 0.7 0.7 0.7 0.8 0.7 0.6 0.8 0.8 0.7 0.7

Asset turnover (Sales/assets) 0.5 0.5 0.4 1.3 2.0 2.3 2.6 2.1 1.6 2.0 2.0

Leverage (Assets/Equity) 9.8 9.7 9.5 1.9 1.8 1.7 1.5 1.3 1.2 1.1 1.1

RoE 27.6 26.5 27.9 13.7 14.7 12.5 16.8 19.3 10.4 16.2 17.7

Source: Company, IIFL Research

TI management has highlighted that funding for Rs8bn infusion in

CG Power would be done so as to minimise debt burden on TI.

Depending on the final funding pattern, the company’s balance sheet

will get levered up (not built in estimates currently), but healthy

cash generation from existing operations means that over the next

2-3 years, this debt can also be settled.

Figure 59: Steady FCF generation to drive faster deleveraging (excluding CG Power)

Source: Company, IIFL Research

4.8% 4.8% 5.0%

12.8% 13.8% 13.3%

19.6% 20.4%

12.4%

20.0% 21.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

Consol. RoCE

(15)

1 3 3 1 4 4

0.56 0.50

0.30 0.11 0.09

(0.07) (0.19)

(0.40)

(0.20)

-

0.20

0.40

0.60

(20)

(15)

(10)

(5)

-

5

FY17 FY18 FY19 FY20 FY21ii FY22ii FY23ii

(x) (Rs bn) FCF generation (LHS) ND/E (RHS)

Tube Investments of India – BUY

32 32 [email protected]

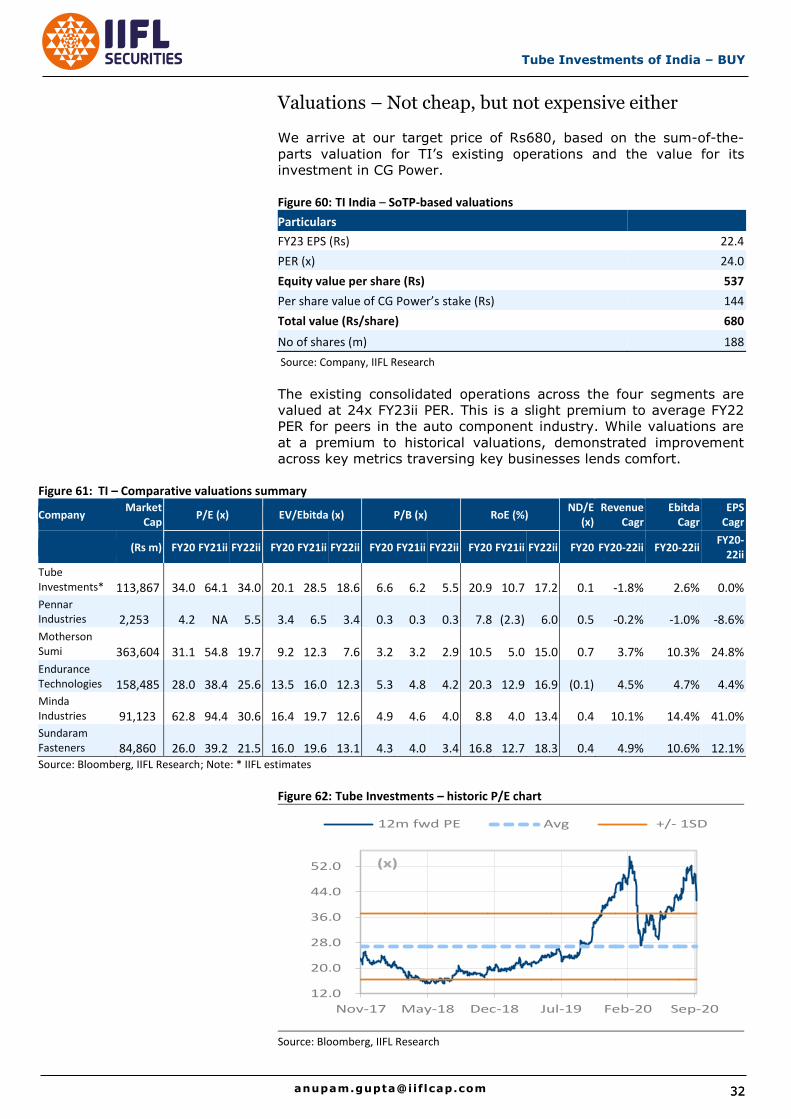

Valuations – Not cheap, but not expensive either

We arrive at our target price of Rs680, based on the sum-of-the-

parts valuation for TI’s existing operations and the value for its

investment in CG Power.

Figure 60: TI India – SoTP-based valuations

Particulars

FY23 EPS (Rs) 22.4

PER (x) 24.0

Equity value per share (Rs) 537

Per share value of CG Power’s stake (Rs) 144

Total value (Rs/share) 680

No of shares (m) 188

Source: Company, IIFL Research

The existing consolidated operations across the four segments are

valued at 24x FY23ii PER. This is a slight premium to average FY22

PER for peers in the auto component industry. While valuations are

at a premium to historical valuations, demonstrated improvement

across key metrics traversing key businesses lends comfort.

Figure 61: TI – Comparative valuations summary

Company Market

Cap P/E (x) EV/Ebitda (x) P/B (x) RoE (%)

ND/E (x)

Revenue Cagr

Ebitda Cagr

EPS Cagr

(Rs m) FY20 FY21ii FY22ii FY20 FY21ii FY22ii FY20 FY21ii FY22ii FY20 FY21ii FY22ii FY20 FY20-22ii FY20-22ii FY20-

22ii

Tube Investments*

113,867 34.0 64.1 34.0 20.1 28.5 18.6 6.6 6.2 5.5 20.9 10.7 17.2 0.1 -1.8% 2.6% 0.0%

Pennar Industries 2,253 4.2 NA 5.5 3.4 6.5 3.4 0.3 0.3 0.3 7.8 (2.3) 6.0 0.5 -0.2% -1.0% -8.6% Motherson Sumi

363,604 31.1 54.8 19.7 9.2 12.3 7.6 3.2 3.2 2.9 10.5 5.0 15.0 0.7 3.7% 10.3% 24.8%

Endurance Technologies

158,485 28.0 38.4 25.6 13.5 16.0 12.3 5.3 4.8 4.2 20.3 12.9 16.9 (0.1) 4.5% 4.7% 4.4%

Minda Industries 91,123 62.8 94.4 30.6 16.4 19.7 12.6 4.9 4.6 4.0 8.8 4.0 13.4 0.4 10.1% 14.4% 41.0% Sundaram Fasteners 84,860 26.0 39.2 21.5 16.0 19.6 13.1 4.3 4.0 3.4 16.8 12.7 18.3 0.4 4.9% 10.6% 12.1% Source: Bloomberg, IIFL Research; Note: * IIFL estimates

Figure 62: Tube Investments – historic P/E chart

Source: Bloomberg, IIFL Research

12.0

20.0

28.0

36.0

44.0

52.0

Nov-17 May-18 Dec-18 Jul-19 Feb-20 Sep-20

12m fwd PE Avg +/- 1SD

(x)

33

Tube Investments of India - BUY

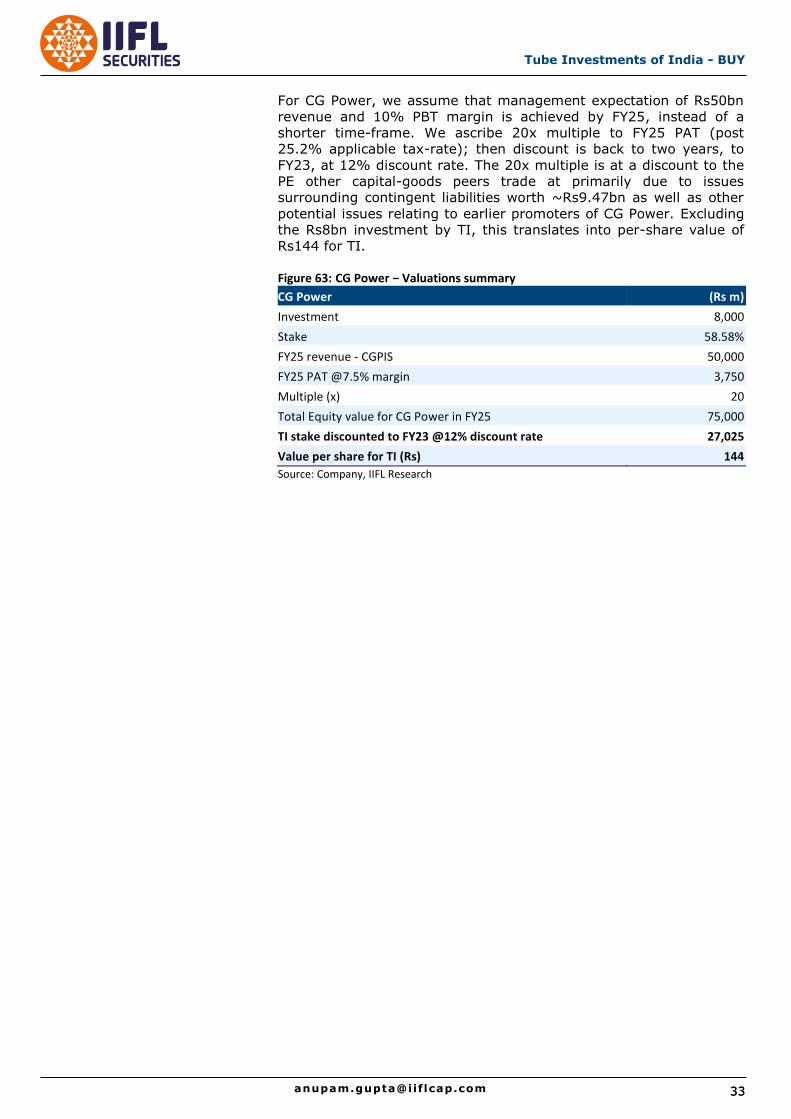

For CG Power, we assume that management expectation of Rs50bn

revenue and 10% PBT margin is achieved by FY25, instead of a

shorter time-frame. We ascribe 20x multiple to FY25 PAT (post

25.2% applicable tax-rate); then discount is back to two years, to

FY23, at 12% discount rate. The 20x multiple is at a discount to the

PE other capital-goods peers trade at primarily due to issues

surrounding contingent liabilities worth ~Rs9.47bn as well as other

potential issues relating to earlier promoters of CG Power. Excluding

the Rs8bn investment by TI, this translates into per-share value of

Rs144 for TI.

Figure 63: CG Power − Valuations summary

CG Power (Rs m)

Investment 8,000

Stake 58.58%

FY25 revenue - CGPIS 50,000

FY25 PAT @7.5% margin 3,750

Multiple (x) 20

Total Equity value for CG Power in FY25 75,000

TI stake discounted to FY23 @12% discount rate 27,025

Value per share for TI (Rs) 144

Source: Company, IIFL Research

Tube Investments of India – BUY

34 34 [email protected]

Company snapshot

P/E

EV/Ebitda

0100200300400500600700800

No

v-1

7

Jan

-18

Mar

-18

May

-18

Jul-

18

Sep

-18

No

v-1

8

Jan

-19

Mar

-19

May

-19

Jul-

19

Sep

-19

No

v-1

9

Jan

-20

Mar

-20

May

-20

Jul-

20

Sep

-20

Price TP/Reco changed date(Rs)

#N/A

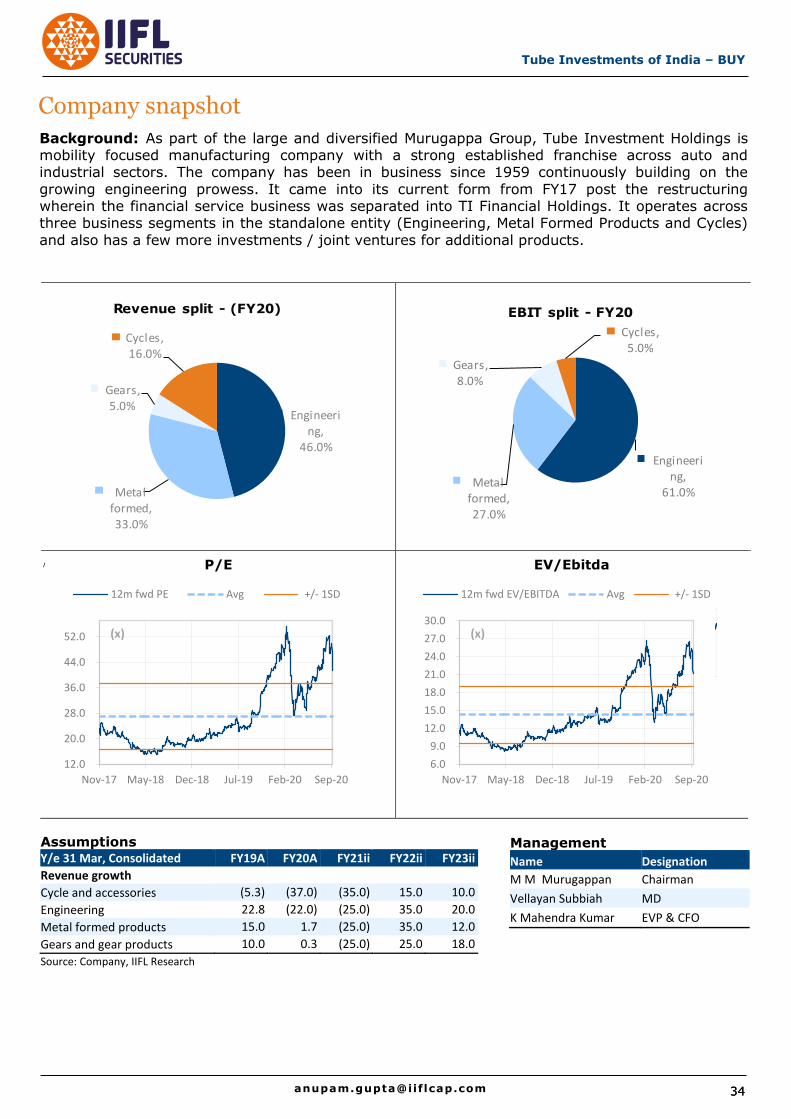

Background: As part of the large and diversified Murugappa Group, Tube Investment Holdings is mobility focused manufacturing company with a strong established franchise across auto and industrial sectors. The company has been in business since 1959 continuously building on the

growing engineering prowess. It came into its current form from FY17 post the restructuring wherein the financial service business was separated into TI Financial Holdings. It operates across three business segments in the standalone entity (Engineering, Metal Formed Products and Cycles)

and also has a few more investments / joint ventures for additional products.

Assumptions Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Revenue growth

Cycle and accessories (5.3) (37.0) (35.0) 15.0 10.0

Engineering 22.8 (22.0) (25.0) 35.0 20.0

Metal formed products 15.0 1.7 (25.0) 35.0 12.0

Gears and gear products 10.0 0.3 (25.0) 25.0 18.0

Source: Company, IIFL Research

Engineering,

61.0%Metal

formed, 27.0%

Gears, 8.0%

Cycles, 5.0%

EBIT split - FY20

6.0

9.0

12.0

15.0

18.0

21.0

24.0

27.0

30.0

Nov-17 May-18 Dec-18 Jul-19 Feb-20 Sep-20

12m fwd EV/EBITDA Avg +/- 1SD

(x)

Engineering,

46.0%

Metal formed, 33.0%

Gears, 5.0%

Cycles, 16.0%

Revenue split - (FY20)

/

12.0

20.0

28.0

36.0

44.0

52.0

Nov-17 May-18 Dec-18 Jul-19 Feb-20 Sep-20

12m fwd PE Avg +/- 1SD

(x)

Management

Name Designation

M M Murugappan Chairman

Vellayan Subbiah MD

K Mahendra Kumar EVP & CFO

35

Tube Investments of India - BUY

Income statement summary (Rs m)

Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Revenues 57,748 47,504 34,848 45,846 53,193

Ebitda 5,447 5,785 4,086 6,088 7,371

Depreciation and amortisation (1,616) (1,853) (1,900) (2,050) (2,200)

Ebit 3,831 3,932 2,186 4,038 5,171

Non-operating income 532 623 550 600 650

Financial expense (528) (304) (240) (135) (80)

PBT 3,835 4,252 2,496 4,503 5,741

Exceptionals 30 (220) (150) 0 0

Reported PBT 3,865 4,032 2,346 4,503 5,741

Tax expense (1,268) (899) (601) (1,153) (1,470)

PAT 2,597 3,133 1,746 3,350 4,271

Minorities, Associates etc. (89) 0 0 0 0

Attributable PAT 2,508 3,133 1,746 3,350 4,271

Ratio analysis

Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Per share data (Rs)

Pre-exceptional EPS 13.2 17.8 10.1 17.8 22.7

DPS 2.5 3.5 4.2 4.2 4.2

BVPS 78.6 92.3 97.1 110.3 128.5

Growth ratios (%)

Revenues 15.5 (17.7) (26.6) 31.6 16.0

Ebitda 42.0 6.2 (29.4) 49.0 21.1

EPS 55.9 35.1 (43.5) 76.7 27.5

Profitability ratios (%)

Ebitda margin 9.4 12.2 11.7 13.3 13.9

Ebit margin 6.6 8.3 6.3 8.8 9.7

Tax rate 32.8 22.3 25.6 25.6 25.6

Net profit margin 4.5 6.6 5.0 7.3 8.0

Return ratios (%)

ROE 18.0 20.9 10.7 17.2 19.0

ROCE 19.8 20.4 12.3 20.5 23.4

Solvency ratios (x)

Net debt-equity 0.3 0.1 0.1 (0.1) (0.2)

Net debt to Ebitda 0.8 0.3 0.4 (0.2) (0.6)

Interest coverage 7.3 12.9 9.1 29.9 NM

Source: Company data, IIFL Research

Financial summary

Tube Investments of India – BUY

36 36 [email protected]

Balance sheet summary (Rs m)

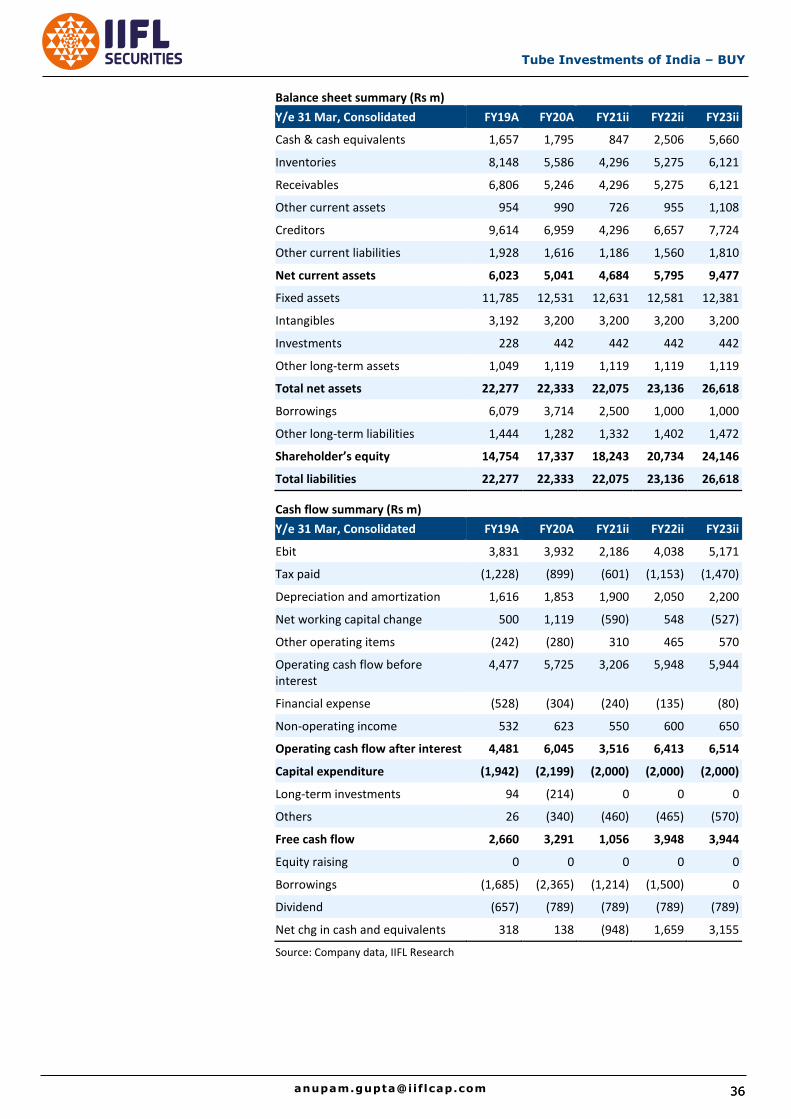

Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Cash & cash equivalents 1,657 1,795 847 2,506 5,660

Inventories 8,148 5,586 4,296 5,275 6,121

Receivables 6,806 5,246 4,296 5,275 6,121

Other current assets 954 990 726 955 1,108

Creditors 9,614 6,959 4,296 6,657 7,724

Other current liabilities 1,928 1,616 1,186 1,560 1,810

Net current assets 6,023 5,041 4,684 5,795 9,477

Fixed assets 11,785 12,531 12,631 12,581 12,381

Intangibles 3,192 3,200 3,200 3,200 3,200

Investments 228 442 442 442 442

Other long-term assets 1,049 1,119 1,119 1,119 1,119

Total net assets 22,277 22,333 22,075 23,136 26,618

Borrowings 6,079 3,714 2,500 1,000 1,000

Other long-term liabilities 1,444 1,282 1,332 1,402 1,472

Shareholder’s equity 14,754 17,337 18,243 20,734 24,146

Total liabilities 22,277 22,333 22,075 23,136 26,618

Cash flow summary (Rs m)

Y/e 31 Mar, Consolidated FY19A FY20A FY21ii FY22ii FY23ii

Ebit 3,831 3,932 2,186 4,038 5,171

Tax paid (1,228) (899) (601) (1,153) (1,470)

Depreciation and amortization 1,616 1,853 1,900 2,050 2,200

Net working capital change 500 1,119 (590) 548 (527)

Other operating items (242) (280) 310 465 570

Operating cash flow before interest

4,477 5,725 3,206 5,948 5,944

Financial expense (528) (304) (240) (135) (80)

Non-operating income 532 623 550 600 650

Operating cash flow after interest 4,481 6,045 3,516 6,413 6,514

Capital expenditure (1,942) (2,199) (2,000) (2,000) (2,000)

Long-term investments 94 (214) 0 0 0

Others 26 (340) (460) (465) (570)

Free cash flow 2,660 3,291 1,056 3,948 3,944

Equity raising 0 0 0 0 0

Borrowings (1,685) (2,365) (1,214) (1,500) 0

Dividend (657) (789) (789) (789) (789)

Net chg in cash and equivalents 318 138 (948) 1,659 3,155

Source: Company data, IIFL Research

37

Tube Investments of India - BUY

Disclosure: Published in 2020, © IIFL Securities Limited (Formerly ‘India Infoline Limited’) 2020

India Infoline Group (hereinafter referred as IIFL) is engaged in diversified financial services business including equity broking, DP services, merchant

banking, portfolio management services, distribution of Mutual Fund, insurance products and other investment products and also loans and finance business. India Infoline Ltd (“hereinafter referred as IIL”) is a part of the IIFL and is a member of the National Stock Exchange of India Limited

(“NSE”) and the BSE Limited (“BSE”). IIL is also a Depository Participant registered with NSDL & CDSL, a SEBI registered merchant banker and a

SEBI registered portfolio manager. IIL is a large broking house catering to retail, HNI and institutional clients. It operates through its branches and

authorised persons and sub-brokers spread across the country and the clients are provided online trading through internet and offline trading through

branches and Customer Care.

a) This research report (“Report”) is for the personal information of the authorized recipient(s) and is not for public distribution and should not be reproduced or redistributed to any other person or in any form without IIL’s prior permission. The information provided in the Report is from

publicly available data, which we believe, are reliable. While reasonable endeavors have been made to present reliable data in the Report so far

as it relates to current and historical information, but IIL does not guarantee the accuracy or completeness of the data in the Report.

Accordingly, IIL or any of its connected persons including its directors or subsidiaries or associates or employees shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained, views and opinions

expressed in this publication.

b) Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or

implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment of its original

date of publication by IIFL and are subject to change without notice. The price, value of and income from any of the securities or financial

instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments.

c) The Report also includes analysis and views of our research team. The Report is purely for information purposes and does not construe to be

investment recommendation/advice or an offer or solicitation of an offer to buy/sell any securities. The opinions expressed in the Report are our current opinions as of the date of the Report and may be subject to change from time to time without notice. IIL or any persons connected with

it do not accept any liability arising from the use of this document.

d) Investors should not solely rely on the information contained in this Report and must make investment decisions based on their own investment objectives, judgment, risk profile and financial position. The recipients of this Report may take professional advice before acting on this

information.

e) IIL has other business segments / divisions with independent research teams separated by 'Chinese walls' catering to different sets of customers having varying objectives, risk profiles, investment horizon, etc and therefore, may at times have, different and contrary views on

stocks, sectors and markets.

f) This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to local law, regulation or which

would subject IIL and its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or

may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this Report may come are

required to inform themselves of and to observe such restrictions.

g) As IIL along with its associates, are engaged in various financial services business and so might have financial, business or other interests in other entities including the subject company(ies) mentioned in this Report. However, IIL encourages independence in preparation of research

report and strives to minimize conflict in preparation of research report. IIL and its associates did not receive any compensation or other

benefits from the subject company(ies) mentioned in the Report or from a third party in connection with preparation of the Report. Accordingly,

IIL and its associates do not have any material conflict of interest at the time of publication of this Report.

h) As IIL and its associates are engaged in various financial services business, it might have:-

(a) received any compensation (except in connection with the preparation of this Report) from the subject company in the past twelve months; (b) managed or co-managed public offering of securities for the subject company in the past twelve months; (c) received any compensation for

investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (d) received any

compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in

the past twelve months; (e) engaged in market making activity for the subject company.

i) IIL and its associates collectively do not own (in their proprietary position) 1% or more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report.

j) The Research Analyst engaged in preparation of this Report or his/her relative:-

(a) does not have any financial interests in the subject company (ies) mentioned in this report; (b) does not own 1% or more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report; (c)

does not have any other material conflict of interest at the time of publication of the research report.

k) The Research Analyst engaged in preparation of this Report:-