the end of transfer pricing

TRANSCRIPT

canadian tax journal / revue fiscale canadienne (2013) 61:1, 159 - 78

159

Policy Forum: The End of Transfer Pricing?

Robert Couzin*

A B S T R A C T

This article is based on a lecture delivered at the NYU School of Law in September 2012. It puts into question the viability of the prevailing model for the allocation of income within a multinational enterprise (MNE), the system of transfer pricing based on the arm’s-length principle. The author likens transfer pricing to a scientific “paradigm” as discussed by the historian of science Thomas Kuhn, suggesting that its perseverance is due especially to the entrenched interests of its practitioners in both government and the private sector. At the theoretical level, transfer pricing suffers from a conflict with the reality of the MNE; in practical terms, it is challenged in particular on the grounds of complexity and the attendant cost of administration and compliance. The author briefly canvasses possible solutions to the impasse, focusing on profit splits and formulary apportionment.

KEYWORDS: TRANSFER PRICING n POLICY n INTERNATIONAL TAXATION n MULTINATIONALS n

ALLOCATION n APPORTIONMENT

* OfCouzinTaylorLLP,Toronto,alliedwithErnst&YoungLLP(e-mail:[email protected]).Thisarticleformedthebasisofthe17thDavidR.TillinghastLectureonInternationalTaxationpresentedattheNYUSchoolofLawonSeptember13,2012.AnearlierversionwaspresentedattheannualseminaroftheCanadianBranchoftheInternationalFiscalAssociationinOttawaonMay17,2012.Thecommentsare,ofcourse,myownpersonalviews.

C O N T E N T S

An Allegory 160An Analytical Framework 162

Profit Allocation, Profit Shifting, and Base Erosion 162Allocation of Tax Revenues and Transfer Pricing 164The Arm’s-Length Principle 165Methods 166

Challenges to the Paradigm: Practice and Theory 167Practice 167

Cost and Revenue 167Consistency 169Impact on “Real” Transfer Pricing 170

Theory 171A Historical Postscript 173

160 n canadian tax journal / revue fiscale canadienne (2013) 61:1

A N A LLEGO RY

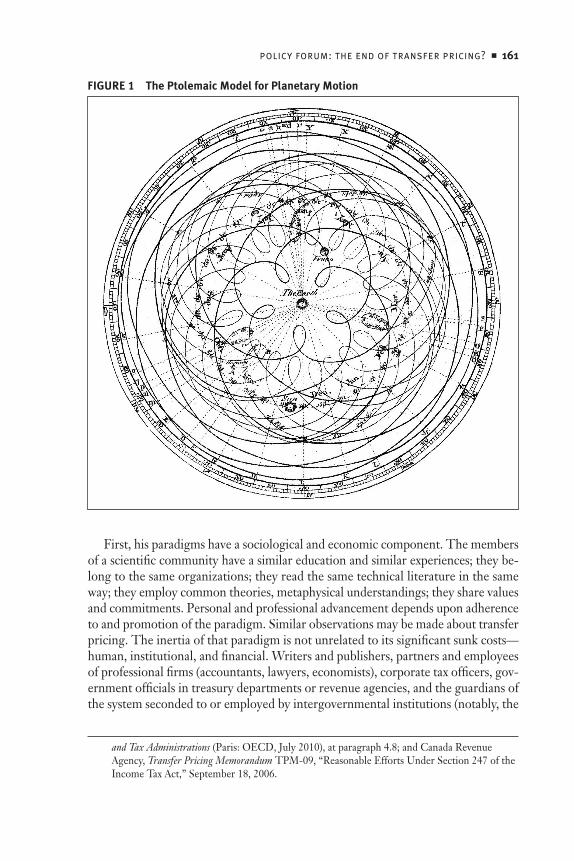

ThePtolemaictheoryservedhumankindwellforoveramillennium,fromantiquitytotheRenaissance,providingaccuratepredictionsofthemotionsofheavenlybod-iesaroundafixed,centredearth.Newobservationswereaccommodatedwithinanincreasinglyelaboratemathematicalmodelunderwhichplanetstracedpathsintheformofcomplicatedloopscalledepicycles(seefigure1).Themodelanditsintel-lectualfoundationssurvivedbytweaking,bending,andadjustingthetheoryanditsgeometricelaboration.

The publication of a treatise on planetary motion by a Polish astronomer in1543usheredintheCopernicanrevolution.Thesignificanceofthateventcanbeproperlyunderstoodonlyinitsfullsocial,philosophical,religious,scientific,andhistoricalcontext,butitissufficientheretonoteafewpurelypracticalaspects.ItsimpactwassubjectedtoacreativereinterpretationbythehistorianofscienceThomasKuhnin1957andgeneralizedinhis1962classic,The Structure of Scientific Revolu-tions.1Kuhnarguedthatscientificprogressreliedontheformulationandeventualabandonmentof“paradigms,”associatingfamousnamesinthehistoryofsciencewithso-calledparadigmshifts.Theircontributionswerenotmerelydiscoveriesbutreorientationsinourunderstandingoftheuniverseanditsoperation—likeLavoisier’sworkontheinteractionofsubstancesorNewton’sopticaltheories.

Attheriskofpassingtooabruptlyfromthesublimetothe,letussay,lesssub-lime,Iinvokethisnotionofscientificrevolutionasametaphororallegoryforthesubjectofthisarticle—namely,the internationaltaxregimeforallocatingprofitswithinanassociatedgroupofcompanies,knownas“transferpricing.”2Itisoftensaidthattransferpricingisnotascience;3Kuhn’sanalysisdoes,nevertheless,offersomeinterestinglessons.

The Solutions on Offer 173Stay the Course 173Change the Tax Base 174Two-Sided and Non-Transactional Approaches 175

Profit Splits and Principled Profit Splits 175Formulary Apportionment 176

1 ThomasS.Kuhn,The Copernican Revolution: Planetary Astronomy in the Development of Western Thought(Cambridge,MA:HarvardUniversityPress,1957);andThe Structure of Scientific Revolutions(Chicago:UniversityofChicagoPress,1962).

2 Thesametermisusedtorefertothemanagerialaccountingtaskofdeterminingintercompanyprices,animportantsubjectthathasseriousramificationsforeconomicefficiency(referredtobrieflybelow).Inthisarticle,however,unlessotherwisestated,“transferpricing”referstotheeponymoustaxregime.

3 Someprefertosaythatitisnotan“exactscience”;see,forexample,OrganisationforEconomicCo-operationandDevelopment,OECD Transfer Pricing Guidelines for Multinational Enterprises

policy forum: the end of transfer pricing? n 161

First,hisparadigmshaveasociologicalandeconomiccomponent.Themembersofascientificcommunityhaveasimilareducationandsimilarexperiences;theybe-longtothesameorganizations;theyreadthesametechnicalliteratureinthesameway;theyemploycommontheories,metaphysicalunderstandings;theysharevaluesandcommitments.Personalandprofessionaladvancementdependsuponadherencetoandpromotionoftheparadigm.Similarobservationsmaybemadeabouttransferpricing.Theinertiaofthatparadigmisnotunrelatedtoitssignificantsunkcosts—human,institutional,andfinancial.Writersandpublishers,partnersandemployeesofprofessionalfirms(accountants,lawyers,economists),corporatetaxofficers,gov-ernmentofficialsintreasurydepartmentsorrevenueagencies,andtheguardiansofthesystemsecondedtooremployedbyintergovernmentalinstitutions(notably,the

FIGURE 1 The Ptolemaic Model for Planetary Motion

and Tax Administrations(Paris:OECD,July2010),atparagraph4.8;andCanadaRevenueAgency,Transfer Pricing MemorandumTPM-09,“ReasonableEffortsUnderSection247oftheIncomeTaxAct,”September18,2006.

162 n canadian tax journal / revue fiscale canadienne (2013) 61:1

OrganisationforEconomicCo-operationandDevelopment[OECD])—allofthesepeopleareengagedinanddependentuponthecontinuedexistenceofaparticularsystem.Wemightcall itan“establishment”or, recallingPresidentEisenhower’sfamousreferenceto“themilitary-industrialcomplex,”4aprivate-publicfiscalcom-plex.Careers,livelihoods,andpersonalself-worthareatstake.

Asecondsimilaritybetweentransferpricingandascientificpursuitconcernsthewayinwhicheachcontrolsitsownscope.WhatKuhncalled“normalscience”solvespuzzles,problemsthatariseandaresusceptibleofsolutionwithintheparadigm.Whenacrisisarises,afactorconceptionthatthreatenstounderminetheparadigm,scientistsdonotrenounceit.Todosowouldbetoabandonscienceitselfastheyknowit.Similarly,transfer-pricingpractitionersapproachsuchpracticaldifficultiesasthecrisisofintangiblesbyexpandingoradjustingratherthanreplacingthepara-digm.Liketheetherinphysicsorphlogistoninchemistry,transferpricingisnolongermerelyatechniqueortoolbuthasbecomeawayofunderstandingreality—inthiscase,fiscalreality.

Mythesisisthat21stcenturytransferpricingbearsaneerieresemblancetoasupersededscientificparadigm.AnobservationbyKuhnaboutPtolemaicepicyclesseemsapt.Bythe16thcentury,heobserved,“astronomy’scomplexitywasincreas-ingfarmorerapidlythanitsaccuracy.”5Sotoowithtransferpricing.Paradigmsdochange,generallyafteraperiodofintenseinsecurity.Revolutionsdooccur.

A N A N A LY TIC A L FR A ME WO RK

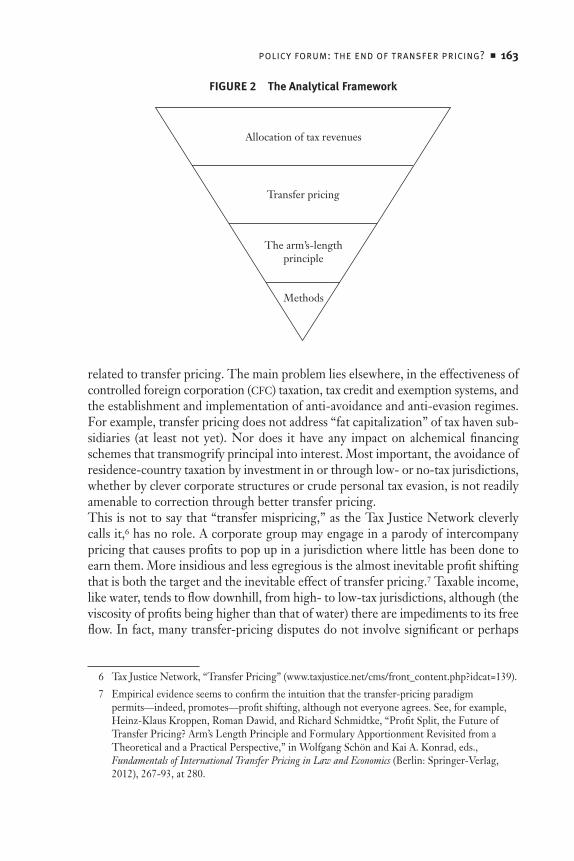

Thetransfer-pricingcomplexhascommandeerednotonlytheleversofinternationalincome allocation but also its vocabulary and conceptual apparatus, by equatingtransferpricingwiththeequitabledistributionoffiscalrevenues.Underthisheading,Iwouldliketorepositiontheconcepts,placingthemwithinahierarchy,illustratedinfigure2.

Asapreliminarymatter, it isusefultodrawadistinctionthatisoftenlost(orburied)bymanycommentators,bothdefendersandcriticsoftheinternationalfiscalorder,betweentransferpricingandtaxavoidance.

Profit Allocation, Profit Shifting, and Base Erosion

Multinationalenterprises (MNEs)earn their incomeglobally,butcountries tax itlocallybyimposingtechniquesofgeographicaldivisionorallocation.Itisunhelpfultoconfusethattaskwiththeequallyimportant,sometimesoverlapping,butnone-thelessdistinctobjectiveofprotectingthedomestictaxbaseagainstundueerosionthroughinternationaltax-avoidancestrategies.Thosestrategiesareonlytangentially

4 DwightD.Eisenhower,“FarewellAddresstotheNation,”January17,1961:“Inthecouncilsofgovernment,wemustguardagainsttheacquisitionofunwarrantedinfluence,whethersoughtorunsought,bythemilitary-industrialcomplex”(http://quod.lib.umich.edu/p/ppotpus/4728424.1960.001?view=toc).

5 Kuhn,supranote1,at68.

policy forum: the end of transfer pricing? n 163

relatedtotransferpricing.Themainproblemlieselsewhere,intheeffectivenessofcontrolledforeigncorporation(CFC)taxation,taxcreditandexemptionsystems,andtheestablishmentandimplementationofanti-avoidanceandanti-evasionregimes.Forexample,transferpricingdoesnotaddress“fatcapitalization”oftaxhavensub-sidiaries (at least not yet). Nor does it have any impact on alchemical financingschemesthattransmogrifyprincipalintointerest.Mostimportant,theavoidanceofresidence-countrytaxationbyinvestmentinorthroughlow-orno-taxjurisdictions,whetherbyclevercorporatestructuresorcrudepersonaltaxevasion,isnotreadilyamenabletocorrectionthroughbettertransferpricing.Thisisnottosaythat“transfermispricing,”astheTaxJusticeNetworkcleverlycallsit,6hasnorole.Acorporategroupmayengageinaparodyofintercompanypricingthatcausesprofitstopopupinajurisdictionwherelittlehasbeendonetoearnthem.Moreinsidiousandlessegregiousisthealmostinevitableprofitshiftingthatisboththetargetandtheinevitableeffectoftransferpricing.7Taxableincome,likewater,tendstoflowdownhill,fromhigh-tolow-taxjurisdictions,although(theviscosityofprofitsbeinghigherthanthatofwater)thereareimpedimentstoitsfreeflow.Infact,manytransfer-pricingdisputesdonotinvolvesignificantorperhaps

FIGURE 2 The Analytical Framework

Allocation of tax revenues

Transfer pricing

Methods

The arm’s-length principle

6 TaxJusticeNetwork,“TransferPricing”(www.taxjustice.net/cms/front_content.php?idcat=139).

7 Empiricalevidenceseemstoconfirmtheintuitionthatthetransfer-pricingparadigmpermits—indeed,promotes—profitshifting,althoughnoteveryoneagrees.See,forexample,Heinz-KlausKroppen,RomanDawid,andRichardSchmidtke,“ProfitSplit,theFutureofTransferPricing?Arm’sLengthPrincipleandFormularyApportionmentRevisitedfromaTheoreticalandaPracticalPerspective,”inWolfgangSchönandKaiA.Konrad,eds.,Fundamentals of International Transfer Pricing in Law and Economics(Berlin:Springer-Verlag,2012),267-93,at280.

164 n canadian tax journal / revue fiscale canadienne (2013) 61:1

anynettaxreduction.Countriescommonlyseekto“repatriate”profitsthattheybelievetoberightfullytheirswithoutregardtowhetherthetaximposedby“theotherside”ishigherorlower.Itisnotunusualforeachoftwojurisdictionstocon-tendthatanMNEhasshiftedprofitstotheother.

Thedistinctionbetweenallocating“real”MNEprofitsandstemmingabusivetaxavoidanceisfundamental.Asystemdesignedtoachievetheformermaynotbebestsuitedtoaddressthelatter,andtheconfusionoftheseobjectivesisinimicaltotheresolutionofeitherone.Aprimeexampleisthetransferofvaluableintangiblestolow-taxsubsidiaries,astrategysowellknownandwidespreadthateventheNew York Timeshasfoundoutaboutit.8Globalmandatoryconsolidationwouldresolvetheissue,asmightcertaintypesofCFCoranti-avoidancelegislation.Addressingitthroughsophisticatedtransfer-pricingmethodologiesdemandstheconstructionofrulesthatareappropriatenotonlytothesetypesoftransactionsbutalsotoeverydayinter-unitlicensing,arecipefordesigningalegislativeresponsethatisinappropri-atetoboth.

Theseremarksaregenerallyrestrictedtothequestionsthatarisebecauseoftheneedtoallocaterealincomeamongjurisdictionsthathaverealfiscalclaimstoit,recognizingthat theirrelativetaxratesorothersystemattributesmaywellhavebeenafactorinMNEpricingstrategies.

Allocation of Tax Revenues and Transfer Pricing

Statesneedtodefraythecostsofpublicgoodslikedefence,healthcare,education,pensions,enforcingcontracts,maintainingpublicorder,andregulation,forwhichtheyrelymainlyoncaptive,relativelyimmobiletaxbases—propertyandpayrolls,consumption,andtheincomeofresidents.Someluckystatescollecteconomicrentsinrespectofnaturalresources.Inaddition,mostofthemtaxprofitsofMNEsthattheyregardasallocabletotheirjurisdictions.

Transferpricing—alongwiththesystemwithinwhichitisembedded,includingthepermanentestablishment(PE)threshold,PEprofitallocationmethodology,andsourcerules—isameans,notanend.Thepremiseunderlyingtheparadigmisthatifthepriceisright,theinterstateallocationoftaxrevenuewillalsoberight,thatthesimultaneousandharmoniousapplicationoftransfer-pricingrequirementsbymul-tiplejurisdictionswillresultinthefairandaccuratedistributionofMNEtaxrevenuesamongstates.InthewordsofarecentOECDrelease,transferpricingissupposed“toensurethateachcountryreceivesitsfairshareoftax.”9

Agreatdealofefforthasbeendirectedtothefirstofthesetwo“rights”(therightprice)andratherlesstothesecond(therightresult).Inthesimplestofworlds—one

8 See,forexample,CharlesDuhiggandDavidKocieniewski,“HowAppleSidestepsBillionsinTaxes,”New York Times,April28,2012,atA1.

9 OrganisationforEconomicCo-operationandDevelopment,“Tax:OECDToSimplifyTransferPricingRules,”March28,2012(www.oecd.org/document/31/0,3746,en_21571361_44315115_49995807_1_1_1_1,00.html).

policy forum: the end of transfer pricing? n 165

farsimplerthanours,evenbackwhenthesenotionswerefirstelaborated—itmayseemintuitivethattotalgroupprofitwillbefairlyallocatedifintercompanypricesarecorrectlydetermined.Thisisnotalwaystrueeveninthesimplestcase,anditishighly suspect inmorecomplexand realistic situations.For reasons thatwillbediscussedbelow,correcttransferpricing,whateverismeantbythatexpression,isnotlogicallyidenticaltothecorrectallocationoffiscalrevenues,whateverismeantbythatexpression.

Discussionsof the fairallocationof taxingrightswithrespect toMNEprofitspresumethatallocativefairnessistobejudgedbyhowwellthesystemrespondstothequestion“Are theprofitsbeingtaxedwhere theyareearned?”Thetransfer-pricingparadigmrespondswithatautologybyassertinganaffirmativeanswersolongasitsrulesarefollowed.Moresubtly,considerationsofthisallocationques-tioncommonlyequate“earned”with“produced,”assumingthatprofitsshouldbesituatedwhere“productiveactivities”occur.Butincometax,asLordMacnaghtenfamouslysaid,isataxonincome.10Itisnotataxonproduction.Someargumentsaboutthelocalizationofincome,especiallyfromservices,arereallyaboutwhatwemeanby“earned.”

The Arm’s-Length Principle

Thearm’s-lengthprinciple11isthechosenmeansforapplyingtransferpricing.Itispremisedonthedeterminationofthehypotheticalprofitsofahypotheticalseparateentity under the conditions that would hypothetically prevail if there were no“association.”12

Otherprinciplescouldbeandinsomecircumstancesareapplied.Forexample,theintroductionofthecomparableprofitsmethod(CPM)intheUnitedStateswasvigorouslyresistedbysomegovernmentsinthemid-1990sbecausetheyfeltthatitdidnotconformtothearm’s-lengthprinciple(or,indeed,wasnotatransfer-pricingmethodatall).13Ivividlyrecallheateddiscussionsbetweenbusinessrepresentatives

10 Attorney General v. London County Council(1900),4TC265,at293.

11 Sometimescalledthearm’s-lengthmethodorthearm’s-lengthstandard.“Standard”impliesacomparisonwithsomethingthatismeasurable,while“method”isusedinthisarticletorefertocertainoperationaltools.Mypreferencefortheterm“principle”servestoemphasizethatwearedealingwithsomethingmoreconceptualthanastandardormethod.

12 OrganisationforEconomicCo-operationandDevelopment,Model Tax Convention on Income and on Capital: Condensed Version(Paris:OECD,July2010),article9.

13 TheCanadiangovernmentexpresseditsconcerninajointpressreleasebytheministersoffinanceandnationalrevenue:“TheMinistersnotedthatdifficultiesmayarisewhereaforeignjurisdictionadoptsanotherapproach—suchasthe‘comparableprofitsmethod’(CPM)setoutinthenewU.S.regulations—whichmaygeneratetransferpricesthatdonotconformtothearm’slengthprincipleand,hence,wouldnotbeacceptableforCanadiantaxpurposes.”(Canada,DepartmentofFinance,“TransferPricingRulesandGuidelinesClarified,”News Release94-003,January7,1994.)Atthe1993annualconferenceoftheCanadianTaxFoundation,theCanadaRevenueAgency(CRA)wasevenmorenegative:“TheCPMredeterminesataxpayer’sprofit,

166 n canadian tax journal / revue fiscale canadienne (2013) 61:1

andtheOECDthatledtoacreativecompromiseinthenewtransfer-pricingguide-lines,includingboththe“lastresort”languageandtheso-calledtransactionalnetmarginmethod,whichisonlyCPMindrag.Itisdifficulttoargue(althoughtheUSgovernmentandothersdo)thatCPMisanapplicationofthearm’s-lengthprinciple.14

Ofspecialinterestistheriseofprofitsplits,particularly(althoughnotexclusively)in the context of one-off negotiations within the mutual agreement procedure(MAP)andadvancepricingagreements(APAs).15Thetransfer-pricingestablishmentconsidersthatthesesolutionsfallwithinthearm’s-lengthprinciple,whichisnowbeingappliedtodealings involving“uniquecontributions.”This is typical intra-paradigmjargon.Ifthecontributionis“unique,”thenarm’s-lengthpartieswouldnothavemadeit,soanyarm’s-lengthpriceisfanciful.Moregenerally,commercialactorsdonotseektosharetheaggregateprofitattributabletotheirdealingsinanequitablefashion.Profitsplitsareattemptstodividethebaby,generallymadeingoodfaithalthoughoflessthanSolomonicsimplicity.

Thus,thearm’s-lengthprincipleshouldberegardednotasadefinitionoftransferpricingbutinsteadasaparticularandnotinevitabledecisionabouthowitmaybecontrolled.

Methods

Withinthearm’s-lengthprinciple,various“methods”havebeenconstructeduponwhich practitioners, enterprises, and tax administrations principally focus theirintensive—andexpensive—attention.Thesemethodsareintendedtoprovideamech-anicalandobjectivemeansofimplementingthearm’s-lengthprinciple.Theyallrelyonanexternalcomparison—witheitherapriceoramargin—inordertodeterminewhatonepartofanMNEwouldhavechargedanotherintheabsenceofassociation.

Thedifficultiesinapplyingthesemethodsandthemultipleandcompoundinghypothesesuponwhichtheyrestarereflectedintheirincreasingcomplexity.Just

ratherthanitstransferprice....BecauseoftheweaknessesoftheCPMasabasisofcomputingtransferprices,thedepartmentstronglyrecommendsthatcorporationsusethetraditionalpricingmethodsdiscussedinInformation Circular87-2,whichcontinuestoreflectitsviewsonthedeterminationoftransferprices.”(“RevenueCanadaRoundTable,”inReport of Proceedings of the Forty-Fifth Tax Conference,1993ConferenceReport(Toronto:CanadianTaxFoundation,1994),58:1-76,question33,at58:18-19.)Bowingtothepressuresofcross-borderrealpolitik,theCRAtookamoregenerouspositioninthesubsequentrevisionoftheinformationcircular,acceptingCPMwherecomparabilityrequirementsaremet(Information Circular87-2R,“InternationalTransferPricing,”September27,1999,atparagraphs114-15).

14 ClausingandAvi-YonahsupporttheUSargumentthatCPMisconsistentwiththearm’s-lengthstandard“eventhoughnocomparablescanbefound.”(KimberleyA.ClausingandReuvenS.Avi-Yonah,Reforming Corporate Taxation in a Global Economy: A Proposal To Adopt Formulary Apportionment,HamiltonProjectDiscussionPaper2007-08(Washington,DC:BrookingsInstitution,June2007),at23-24.)Howevertheissueisnot,ornotonly,thelackofcomparablesbutratherwhethertheconditionsmadebetweenthetwoassociatedenterprisesdifferfromthosethatwouldbemadebetweenindependententerprises.

15 Kroppenetal.,supranote7,at269-71.

policy forum: the end of transfer pricing? n 167

lookattheapparentlysimplenotionof“comparability.”16Thesemattershavebeenthesubjectofconsiderablecommentary,andIwillnotrepeattheincisiveandsome-timescausticobservationsofothers.

Farfromheraldingthestrengthofthearm’s-lengthprinciple,theprevalenceofprofitsplitsinMAPsandAPAssignalsthefailureofthetraditionalmethodsand,forthe reasons already remarked, theprinciple itself.The expression “profits-basedmethods”isaparadigmaticallyOrwelliannonsequitur:negotiatedallocationsarenota“method.”Profitsplitsareusedincomplex,integratedsituationswheremean-ingfulcomparabledataarenotavailable—thatistosay,wherethereisnowaytodeterminewhatarm’s-lengthpartieswouldhavedone.

CH A LLENGE S TO THE PA R A DIGM: PR AC TICE A ND THEO RY

Thereisanoldjokeabouttheeconomistwhomuses,“Iknowitworksinpractice,butdoesitworkintheory?”Transferpricingischallengedinbothrespects.

Practice

Ilimitmycommentstothreeaspects:money,consistency,andpotentialforeco-nomicinefficiency.

Cost and RevenueTransferpricingisanexpensivehobby.Ihavefoundnodataspecifictoitsadminis-trationandcompliance,butweknowthatcorporateincometax(CIT)ingeneralisless efficiently imposed than personal income tax (PIT), and consumption tax ischeapestofall.17Researchconfirms,asonewouldexpect,thattherelativecostsof

16 Theincorporationofthe2012comparabilityrecommendationsintotheOECDtransfer-pricingguidelineswastheculminationofaseven-yearprojectbeginningwithpublicconsultationsbasedona78-pagediscussiondraft(www.oecd.org/ctp/transferpricing/36651642.pdf ).Thedraftersaretobecomplimentedonreducingthefinalproducttoonly27paragraphsintheguidelines,comparedwith20inthe1995version.The1979guidelineshadnoseparatepresentationoftheissue,althoughafewparagraphsweredevotedtoitintheconsiderationofthecomparableuncontrolledpricemethod.(OrganisationforEconomicCo-operationandDevelopment,Transfer Pricing and Multinational Enterprises(Paris:OECD,1979)andTransfer Pricing Guidelines for Multinational Enterprises and Tax Administrations(Paris:OECD,1995.)

17 SeeFrançoisVaillancourtandJasonClemens,“ComplianceandAdministrativeCostsofTaxationinCanada,”inJasonClemens,ed.,The Impact and Cost of Taxation in Canada: The Case for a Flat Tax Reform(Vancouver:FraserInstitute,2008),55-102.RegardingtheUnitedStates,seeUnitedStatesGovernmentAccountabilityOffice,Tax Policy: Summary of Estimates of the Costs of the Federal Income Tax System,GAO-05-878(Washington,DC:GAO,August2005)(www.gao.gov/assets/250/247539.pdf ).PITcompliancemeetsreasonableefficiencystandards(perhaps2percentto3percentofrevenueinCanadaaccordingtoVaillancourtandClemens,supra).ComplianceestimatesforCITvarywidely,fromaslittleas2.5timesPITcostsupto25percentofrevenuescollected,orevenhigher.

168 n canadian tax journal / revue fiscale canadienne (2013) 61:1

CITcompliancearehigherforsmallandmedium-sizedbusinesses,butevenwithrespecttothelarge,concentratedpoolsofincomewheretransferpricingisconcen-trated,efficiency isnot impressive.SomeUSstudies indicate that foreign-sourceincomeaccounts foradisproportionately largeshareofcompliancecosts.18Thismustreflectthecomplexforeigntaxcreditrules,buttransferpricingisalsopartoftheequation.

Theburdenoftransfer-pricingcomplianceisconfirmedbyanecdotalevidence.In surveys, corporate tax officers regard it as significant, excessive, and rising.19They cite the cost of multi-country documentation requirements, unpredictableandunquantifiableauditrisks,penalties,andcontroversymanagement.20Thisisnotparanoia.Documentationrequirements,forexample,beganwithonecountryin1994andspreadtoaround20overthenext10years.Today,theyhaveinfectedasmanyas60(dependinguponwhatoneregardsasadocumentationrequirement).21Theserulesareoftenonerousandinevitablyuncoordinated.Asforauditandcontroversy,theultimateriskofdoubletaxationmaybeoflessconcernthanthecostofprevent-ingit.Finally,itshouldbenotedthatunlikedomesticandevenmostinternationaltaxrules,transferpricingdemandsdoubleandsometimesmultiplecomplianceandadministrationwithrespecttothesamerevenue.

TheOECDconcedesthat“thetimehascometosimplifytherulesandalleviatethecomplianceburdenforbothtaxauthoritiesandtaxpayers”because“complicatedrulescanbeabarriertocross-bordertradeandinvestmentandplaceaheavyburdenon tax administrations and businesses.”22 The predictable, paradigm-protectingresponseisto“simplifyandstrengthen”theexistingruleswitha“how-tomanual”of“goodpractices.”23

Theflipsideofcostisrevenue.Iftransfer-pricingadministrationandcompliancecostsarehighrelativetotherevenueproducedforgovernments,whatabouttheabsolutedollars?Peopleliketothinkthatwhattheydoisimportant,andbillion-dollartaxcaseshaveundoubtedlyswelledtheheadsofmanypractitioners.Buthowfiscallyimportantistransferpricingreally?

18 SeethereferencesinKroppenetal.,supranote7,at282.

19 Thesesurveyresultsrelatetocompliance,andwhilethereisnothingcomparableonthegovernmentside,thecostsofadministrationpresumablyfollowsuit.

20 See,forexample,Ernst&Young,2010 Global Transfer Pricing Survey: Addressing the Challenges of Globalization(Ernst&Young,2011)(www.ey.com/Publication/vwLUAssets/Global_transfer_pricing_survey_-_2010/$FILE/2010-Globaltransferpricingsurvey_17Jan.pdf ).

21 AccordingtoGlobalTransferPricingConsulting,58countrieshave“atleastsomeformofrequirementstojustifytheapplicationofthearm’slengthprinciple,”butsincethisfirmhasapecuniaryinterestinsellingdocumentationservices,theestimatemaybegenerous.(GlobalTransferPricingConsulting,“TransferPricingDocumentation”(www.globaltpconsulting.com/index.php/en/transfer-pricing-documentation).)

22 Supranote9.

23 Ibid.

policy forum: the end of transfer pricing? n 169

Yetagain,directevidenceisdifficulttoproduce,butwecanbeginwithCITasawhole.OECD-wide,CITproducedarelativelystable8percentto10percentcontri-butiontototaltaxrevenuesbetween1965and2009,24althoughthismaskssomeglaringnationaldifferences(in2010,4.2percentinGermanyand23.5percentinNorway).ForCanada,thesharecontributedbyCIThasfallenfrom15percentintheearlyyearstoaround10percentinthelastdecade.25MostofthisCITisundoubtedlyattributabletogarden-varietydomesticactivityunaffectedbycross-bordertrans-actionsordealings.Thisisespeciallytrueineconomies,suchastheUnitedStates,thatarelessdependentoninternationaltrade.

Non-governmentalorganizationscontendthatCITrevenueswouldbefarhigherwereitnotfor“transfermispricing.”Largenumbersarethrownabout,buttheyoftenfailtodisaggregateindividualtaxevasion,taxhavenabuse,andtransferpricing.26Amorecarefully targeted studyestimated that totalCITrevenues in theUnitedStatesarereducedby35percentasaresultoftransfer-pricingprofitshifting.27Thissoundssignificant,butitisactuallyrathermodest,fortworeasons.First,mostofthe“shiftedprofits”aretaxedsomewhereelse,andnotalwaysatamuchlowerrate.Forthisreason,MAPnegotiationsareoftenazero-sumgame(orevenanegative-sumgame, taking intoaccount thecosts incurredonall sides).Thus, theglobalincrementaltaxrevenuesmaybesignificantlylowerthan35percent.Second,evenatthatpercentage,thegainwouldbeabout3percentoftaxrevenuesacrosstheOECD—hardly irrelevant, especially in these lean times, but as dramatic as onemightexpect.

Iconcludethatputtingasidetheproblemofaggressivetaxavoidance,taxevasion,andtaxhavens,thecarvingupofMNEprofitsnowproducesandcanonlyproducearelativelymodestproportionoftherevenuesthatcountriesneedtoprovidepublicgoods.

ConsistencyItwouldbedisingenuousandungracioustodenythetremendousstrides inthecoordinationoftransfer-pricingpracticeachievedinthelastquarter-century.Yetconsistencyremainselusive.Inthedocumentalreadycited,theOECDexpressesa

24 OrganisationforEconomicCo-operationandDevelopment,Revenue Statistics: 1965-2010(Paris:OECD,2011),at22,tableC.

25 Ibid.,at23and92,table12.CITinCanadawas15percentoftotaltaxrevenuein1965,fellto8percentby1982,roseto12percentin2000,andhashoveredbetween10percentand11percenteversince.Thefigureinanysingleyearisnotnecessarilymeaningfulsinceitispositivelyornegativelyaffectedbytheyieldofothertaxbases,thestateoftheeconomy,etc.

26 TaxJusticeNetwork,“Magnitudes:DirtyMoney,LostTaxesandOffshore”(www.taxjustice.net/cms/front_content.php?idcat=103).

27 Clausingreachedthisfigurebyaregressionanalysisbasedonrelativetaxrates,aquestionablemethodologybutperhapsthebestavailable.(KimberlyA.Clausing,Multinational Firm Tax Avoidance and U.S. Government Revenue,workingpaper(Portland,OR:ReedCollege,2007),citedbyClausingandAvi-Yonah,supranote14,at10,note7.)

170 n canadian tax journal / revue fiscale canadienne (2013) 61:1

goalforthefuture:reachinganinternationalconsensus“toensurethattheruleswillbeappliedinagloballyconsistentmanner.”28Iinferthatthetransfer-pricingsystemisnotcurrentlybeingsoapplied.

Internationalfiscalharmonizationisnotalwaysnecessaryorevendesirable,buttransferpricingisdifferent.Ifitsrulesandpracticeareoutofjoint,whatdotheyaccomplish?Theparadigmaticreaction,ofcourse,istoencouragecontinuousgeo-graphicalexpansionandprogressivenationalconformity—aquestforuniversal,orasPtolemymighthavesaid,celestial,harmony.Onewondershowmuchfurtherharmonizationcango,ormoretothepoint(oratleastmoretomypoint),whypar-ticular countries in particular circumstances would want to adopt a system thatproduceswhattheyregardasinequitableresults.29

Impact on “Real” Transfer PricingIftherewerenotaxes,MNEswouldstillhavetopricetheinternaltransferofgoodsandserviceswithaviewtomaximizingeconomicefficiency.Enterprisesoftenarguethattheyshouldbeallowedtousetheirnon-taxtransferpricingtodeterminelocaltaxliabilities,avoidingaduplicationofeffortandcost.Insomerespects,thisisarepriseoftheoldargumentaboutconformitybetweenfinancialormanagerialandtaxaccounting.30Theadvantageofusingasinglesystemissimplicity;thedisadvan-tagesariseoutofthedifferentialgoalsandpracticesoffiscalandcommercialprofitmeasurement.Ofparticular importance is thepotential for incometaxrulesandrequirementstoskewmeasuredandreportedfinancialresults.

Thesameconceptualissuesapplywithrespecttotransferpricing,buttherearealsoadditionalconcerns.First,becausetransferpricesareinherentlyinternational,morethanonejurisdictionisinvolved.Absentperfectconsistency,itisimpossibletoconformtaxandmanagerialprices.Second,thedeterminationofinternalpricesismeanttooptimizetheallocationofresourcesonanafter-taxbasis,andasophis-ticatedconsiderationoffiscaltransferpricingdoestaketaxratesintoaccount.31One

28 Supranote9.

29 HintsofthispushbackcanbefoundinUnitedNations,UN Practical Manual on Transfer Pricing for Developing Countries(NewYork:UnitedNations,October2012),inboththesubstantivediscussionsandthecountryappendixes.

30 Theissuesarediscussedbymanycommentatorsonmanyjurisdictions,andwerecanvassedwellintwoCanadianpaperspublishedmorethan30yearsago:RobertC.Reed,“TheDilemmaofConformity:TaxandFinancialReporting—APerspectivefromRevenueCanada,”inCurrent Developments in Measuring Business Income for Tax Purposes,1981CorporateManagementTaxConference(Toronto:CanadianTaxFoundation,1982),1-21;andGlenE.Cronkwright,“TheDilemmaofConformity:TaxandFinancialReporting—APerspectivefromthePrivateSector,”ibid.,22-40.

31 Aninterestingillustrationisexample19inOrganisationforEconomicCo-operationandDevelopment,Discussion Draft: Revision of the Special Considerations for Intangibles in Chapter VI of the OECD Transfer Pricing Guidelines and Related Provisions(Paris:OECD,June6,2012),atparagraphs250-58(www.oecd.org/tax/transferpricing/50526258.pdf ).

policy forum: the end of transfer pricing? n 171

wonders,however,whethertaxadministrationsinreallifearequicktoaccepttheimplications.Forexample,supposethatauniqueserviceisprovidedbycompanyB,residentincountryB,tocompanyA,residentincountryA,andbothcompaniesaremembersofanassociatedgroup.Assumingthattheserviceisbeingproperlyremuner-ated,thepricepaidbycompanyAshouldriseif,allotherthingsremainingthesame,thetaxrateincountryBincreases.WouldthetaxadministrationincountryAagree?

Moregenerally, the correct price signalswithin the MNE—that is, those thatpromotethehighestlevelofeconomicefficiency—maynotcoincidewithanyinter-nationallyaccepteddeterminationoffiscaltransferpricingforanumberofreasonsthatareunrelatedtoanyarm’s-lengthprinciple.ItseemsthatcostandsimplicityarestrongmotivatorsleadingmostMNEstoconformtheirmanagementandtaxprices,but in doing so, they both run the risk of challenge by tax administrations andsimultaneouslycreateperverseinternalincentives.

Theory

OtherswiththeeconomicexpertiseIlackhavealreadybroachedmanyofthetheor-eticalchallengestothetransfer-pricingparadigm.32Thecentralissue,towhichthecommentsbelowarelimited,concernstheinabilityofthearm’s-lengthprinciple,ortransferpricingingeneral,tocontendwiththeinherentvalueofthefirm.

In1937,Coaseprovocativelyasked,whydofirmsexist?33Theanswer,hesaid,isthatthereisacosttotheuseofthepricemechanism.Firmsaredifferentfromandsometimessuperiortomarketexchange.Coase’s“transactioncost”theoryhasbeenfurtherexamined, itsmechanismshavebeenreconsidered,andthemodelhasbeenrefinedtoincludegroupsornetworks,butthefundamentalpointisgener-allyaccepted.Thearm’s-lengthprinciplenonethelesstriestohypothesizeitswayaround the economic integration of the firm while taking its legal and financialstructureatfacevalue.34

32 Theliteratureisextensive.Forarecentexampleaccessibletothelayreader,seeErikRöder,“ProposalforanEnhancedCCCTBasAlternativetoaCCCTBwithFormularyApportionment”(2012)4:2World Tax Journal125-50.TheUN Practical Manual on Transfer Pricing for Developing Countries,supranote29,atchapter2,includesausefuldiscussionofthetheoryofthefirmandthelegalstructureofMNEswithout,however,raisingtheimplicitissuesfortheapplicationofthetransfer-pricingparadigm.

33 R.H.Coase,“TheNatureoftheFirm”(1937)4:16(newseries)Economica386-405.Coase’sarticleandlaterpapersarereproducedinOliverE.WilliamsonandSidneyG.Winter,eds.,The Nature of the Firm: Origins, Evolution, and Development(NewYork:OxfordUniversityPress,1991).Coase’sworkwaseventuallyrecognizedbytheawardoftheNobelPrizeforEconomicsin1991.

34 ThecomplexrelationshipbetweentheintegrationoftheMNEandtransferpricingisexploredinanunpublishedpaperbyAndrewClarksonandThomasTsiopoulos,“TheVerticalBoundariesoftheFirm:ImplicationsfortheArm’sLengthPrinciple,”March17,2006.IthankTomTsiopoulosforbringingthisessaytomyattentionandprovidingmewithacopy.SeealsoJ.ScottWilkie,“Reflectingonthe‘Arm’sLengthPrinciple’:WhatIsthe‘Principle’?WhereNext?”inFundamentals of International Transfer Pricing in Law and Economics,supranote7,137-56,at143.

172 n canadian tax journal / revue fiscale canadienne (2013) 61:1

Thisproblemhasnosolutionwithintheparadigm.Theessenceofthefirm—itsquiddity,asaphilosophermighthavecalledit—isnotanintangiblesusceptibleofbeingpriced;normayitbegeographicallylocalized.Theparadigmrestsuneasilyonitscounterfactualassumptionthatassociatedenterprisesarenotassociated;inreality,integrationisfundamentaltotheveryexistenceofthefirmandcannotreadilybeignored.Thetensioncausedbythiscontradictionisapparentinthetransfer-pricing system and its application. Notwithstanding the supposed rigour of thearm’s-length,separateentityassumption,sometimestheappurtenanceofacorpor-ationtoamultinationalgroupcreepsbackintotheanalysis.35

Treatingthefirm’sconstituentandinextricablepartsasifthecompositeentityweremerely the sumofdiscrete transactions anddealingsbetween independentactors isnot amerepeccadillo. Ignoring the “firmness”of thefirmhas seriousconsequences.Itnotonlyfailstoaddressdirectlythevalueofintegration;equallyimportant, it ignores the inescapable fact thatmanyactivities, relationships, andtransactionsoccurwithinanMNEbutneveroutsideone.

Asymptomofthislatterproblemappearsintherecognitionoftheoccasionalneedto“recharacterize”atransaction,asispermittedundertheOECDguidelineswherethetransactiondiffersfromwhatindependententerpriseswoulddoanditcannotbepricedaccordingtothearm’s-lengthprinciple.36Insuchacase,thetaxadministrationmaydisregard theactual transactionandrecast it as theone thatarm’s-lengthpartieswouldreasonablybeexpectedtohavedone.37Inasimplecom-parisoncase(saleorlease,forexample),thissoundsalmostplausible,butinmostcasesitissophistry.38

ThepeculiarityofMNEbehaviour isnowheremoreevidentthanin“businessrestructuring.”Thetransfer-pricingcomplexhasexpendedconsiderableeffortandbeenhighlycreativeingrapplingwiththeissuesgroupedunderthisrubric,butthefundamentaldifficultyremainsbecausethesysteminsistsonseeingfirmsdifferentlyfromhowtheyseethemselves.Iftaxadministrationstookthebusinessrestructuringargument to its logical conclusion, they would demand a toll charge on everychangeofrisk,everyreallocationoffunction—forthatmatter,everyrelocationof

35 ComparetheacceptancebyCanada’sFederalCourtofAppealof“implicitsupport”forsubsidiaryindebtednesswithinagroupofcompaniesinCanada v. General Electric Capital Canada Inc.,2010FCA344.

36 OECD Transfer Pricing Guidelines,supranote3,atparagraph1:65.

37 Paragraph247(2)(b)oftheCanadianIncomeTaxAct,RSC1985,c.1(5thSupp.),asamended,enactsaslightlydifferentrule,substitutinga“dominanttaxbenefit”testfortheOECD’s“unpriceability,”althoughwhetherthesearereallydifferentisagoodquestion.TheOECDguidelinesdonotrefertotaxavoidanceinthiscontext,butthetextseemstosuggestit.WhataboutbonafidecommercialtransactionsthathavenoequivalentoutsidetheMNE?Iftaxauthoritiescanneitherrecharacterizetransactionsnorapplythearm’s-lengthprinciple,whataretheycalledupontodo?

38 H.DavidRosenbloom,InternationalFiscalAssociationTransferPricingSeminarattheUniversityofMelbourneFacultyofLaw(August2005).

policy forum: the end of transfer pricing? n 173

anemployeeoradjustmenttocapitalstructure.Perhapseverycross-borderconversa-tionshouldbepriced.Suchathoroughgoingsystemwouldbeimpossibletoenforce,entailenormousefficiencylossestoMNEs,andimposeseriouscostsontheecon-omy.The conundrum illustratesonce again the theoreticalweaknessof transferpricing.Theallocationoftaxingrightsinrespectoftheprofitsofafirmshouldnotdependonhoworwhythatfirmreorganizesitsinternalcommercialstructuresandrelationships.

A Historical Postscript

Beforeturningfromproblemstosolutions,Ipausebrieflytoreflectonhowthisparadigm-challengingsituationarose,probably in the1980sandaccelerating inthe1990s,afteralongperiodofrelativetranquility.Afullhistoricalconsiderationmustbelefttoanotherday,butIoffertwobriefobservations.First,MNEsandtheiradvisersdiscoveredthattransferpricingofferedopportunitiesforsignificantglobaltaxratereductiontoolucrativetoignore.Thisepiphanywaspartlyserendipitous,aby-productofthescrambletotightenthemanagementofsupplychainsandtrans-formbusinessenterprisesfromcollectionsoflocalnetworkpointsintotrulyglobalinstitutions.TaxadviserspresentedmanagementwithtemptationsthatwouldhavechallengedaSaintAnthony.Second,governmentsandgovernmentalorganizations—partly inresponsetotaxpayerbehaviourandpartlyasthenaturalresultofmoresophisticated thinkingabout transferpricing—began tocogitate aboutproblemstheyhadpreviouslyignored.Thesewerepuzzlesthat,unbeknownsttothem,hadnosolutionswithintheparadigm.Theprimeexampleis“intangibles,”aproteanandmalignantgrowthonthetransfer-pricingregime.Thelabel“intangible”hasbeenappliedtowhateveritisabouttheMNEthatdemandsareallocationoftaxrev-enues,oreventheestablishmentoftaxingjurisdiction.39

THE SO LUTIO NS O N O FFER

Inevaluatingsolutions,onemustkeepinmindwhattheyaremeanttosolve.Thegoalisneithertopreservetransferpricingnortoburyit.Ifthesystemcanpromoteafairallocationoftaxrevenuesortaxingrights,thenbyallmeansfixit.Butifitcannotaccomplishthisobjectiveatareasonablecost,itshouldbereplaced.Keepinmindthatfairallocationis itselfamatterthatrequiresconsiderableexaminationandcandidinternationaldiscussion.

Stay the Course

Likeanyentrenchedparadigm, transferpricinghas responded tochallenges theseriousnessofwhichitreadilyadmitsbymodificationsandimprovements.These

39 WhentheearlierversionofthisarticlewaspresentedattheInternationalFiscalAssociation(Canadianbranch)seminarinOttawainMay2012,onelistenersuggestedthatIcouldsimplycitetheOECDintangiblesprojectandsitdown,andthatwasbeforethereleaseoftheweightydiscussiondraftonJune6,2012,supranote31.

174 n canadian tax journal / revue fiscale canadienne (2013) 61:1

havebeensuccessful inthesensethattransferpricinghas, indeed,becomemoreeffectiveataccomplishingitsintra-paradigmtask,althoughatever-increasingcost,not only financially but also in terms of complexity and strains at the margins.Guidelinesandregulationsalwaysgetlonger,nevershorter.

Theseeffortshavefocusedmainlyonimprovingthetraditionalmethods,em-bracingthepreviouslyleprousprofitsplit,andbringingintangiblesintothetent.Solongastransferpricingandthearm’s-lengthprinciplereign,suchprojectswillcon-tinue.Forthereasonsalreadyexpressed,itseemsunlikelythattheseendeavourswillresolvethefundamentalpracticalandconceptualchallenges.

Evenstayingthecourse,however,couldaccommodateimprovementsapartfromthemethods,notablyindisputeresolution,apieceofthepuzzledeartotheheartsoflawyers.Toomuchtimeandmoneyisspentontransfer-pricingcontroversies.Arbitrationismakingheadwayasanalternativetojudicialremedies.Itisstillslowandexpensive,andnopanacea.Asoftenremarked,arbitrationisperhapsmostuse-fulinterroremagainstgovernmentalintransigence.

Therearealsoanumberofcreativeideasfloatingaround.Almost10yearsago,KristerAnderssonof theConfederationofSwedishEnterpriseproposedanovelapproach.40Insteadofdukingitoutwithnationaltaxingauthoritiesandthenhov-eringatthefringesoftheintergovernmentalMAP,theMNEwoulddepositwithafinancialintermediaryanamountequaltothemaximumtaxthatwouldbedueifthetransfer-pricingadjustmentwereupheldanddoubletaxationfullyeliminated.Thegovernmentswouldthenworkouttheirdifferences—ornot—buttheMNE’sexpos-urewouldbelimitedtoitsdeposit.Thiscouldreducethecostofdisputeresolutionandresolvethenaggingproblemofdoubletaxation.

Itisjustanidea.Thereisobviouslymorethinkingtobedone.

Change the Tax Base

TherelativelymodestcontributionofcorporateandspecificallyMNEprofitstaxa-tiontogovernmentcoffersandthedisproportionatelyhighcostofenforcement/compliancecouldsuggestadrasticsolution:eliminatetheCIT.Transferpricingisnot,ofcourse,eitheranecessaryorasufficientreasontoconsidersuchacourse.Anotherreasonwouldbetoavoidembeddedandpotentiallydangerouspolicydeci-sions:CITmaynotproducemuchrevenue,butitiseasytogetwrong,causingrealdamagetotheeconomy.

Themainchallengestoeliminatingcorporateorbusinesstaxationwouldbe

1. fiscal—replacingtheforgonerevenues;and 2. sociopolitical—avoidingevengreaterinequities,bothvertical(exacerbating

income inequality) and horizontal (between the taxation of income fromlabourandincomefromcapital).

40 KristerAndersson,“ANewMethodforResolvingTransferPricingCasesintheEU,”Svensk Skattetidning,2003.

policy forum: the end of transfer pricing? n 175

Thesimplestconceptualsolutionwouldbeanewcorporate-leveltaxproducingthesamerevenuebutwithoutattemptingtomeasureincome—forexample,ataxbasedonapresumptivereturnoncapitalemployedinajurisdiction.Therearemanypos-sibilities.Alternatively,onecoulddecidenottobothertaxingcorporationsandfindsomeotherwaytocapturetheresultingbenefitthatwouldflowtotheownersofcapital(totheextentthatthisiswherethecorporateincometaxlands).41

Whiletheintra-nationincomeinequalitythatwouldresultfromrepealingCITmaybeaddressedbynewapproachestotaxingcapitalincome,theownersofcapitaloftendonotliveinthecountriesthatbearthecostofeducating,andotherwisepro-vidingpublicgoodsfor,theconsumerswhosustainMNEprofits.Eliminatingbusinesstaxationcouldthereforeshiftglobaltaxrevenuesfrompoortorichnations.ThiswouldlikelyleadtoanincreaseinothermeanstoaccessMNEprofits,likethecrudegrosswithholdingtaxessodecriedbymanypolicyexperts.Ifsuchtaxesproducerev-enue,perhapsthissuggeststhatthedomesticmarketisasourceofeconomicrent.

Thefutureofcorporatetaxationisobviouslyalargeandopenquestion.Transferpricingisanillustrationofitsfragility.

Two-Sided and Non-Transactional Approaches

AssumingthatMNEprofitscontinuetobetaxed,theymustsomehowbedividedamongjurisdictions.Thetwocompetitorsmostoftendiscussedaspotentialreplace-mentsfortraditionaltransferpricingareprofitsplitsandformularyapportionment.Humansareattractedbybinarychoices,butreallifeismoreanaloguethandigital;thesetwoapproachesarebetterseenasfuzzycategories,eachcomprisingarangeofpossibilitiesandeventouchingatcertainpoints.

Profit Splits and Principled Profit SplitsProfitsplitsarehardlynew.Asalreadyremarked,this“method”isoftenpromotedasasolutioncommonlyadoptedinMAPandAPAnegotiations.Anumberofcom-mentatorshavebecomeinterestedin(nottosayenamouredoforobsessedwith)atransfer-pricingsystembasedonanenhancedand“principled”profit-splitmethod-ology.Thiscouldbepartofahybridsystem,withthearm’s-lengthprinciplebeingusedinsomecasesandaformularytransaction-basedprofitsplitbeingreservedforthedifficultcases.42Oraprofit-splitapproachcouldofferamoregeneralreplace-menttotransferpricingascurrentlyunderstood.

41 Therehavelongbeendebatesaboutwhethercapitalincomeshouldbetaxedatall.Ifonebelievesitshouldnot,thatsimplifiesthediscussion,butIamnotpreparedtomakethatleap.Somerecenteconomicresearchsuggestingthecontraryviewisdiscussedin“EconomistsAreRethinkingtheViewThatCapitalShouldNotBeTaxed,”The Economist,May5,2012,74(www.economist.com/capitaltax12).

42 ThehybridsystemwasproposedanddefendedbyReuvenAvi-YonahandIlanBenshalom,“FormularyApportionment—MythsandProspects,”apaperdeliveredattheconferenceontransferpricing:alternativemethodsoftaxationofmultinationals,Helsinki,June13-14,2012(www.taxjustice.net/cms/upload/pdf/Ilan_Benshalom__Reuvan_Avi_Yonah_ppt_1206_Helsinki.pdf ).

176 n canadian tax journal / revue fiscale canadienne (2013) 61:1

Asignificantdifficultyrelatesbacktothepurposeoftheexercise,whichisget-tingtherightallocationofprofits.Judgingtheadequacyofaprofitsplit,principledorotherwise,requiressomestandardfordeterminingwhethertheresultisreason-able.Thereis,however,noindependentorobjectivecriterion,otherthantheprofitsplititself.Inthebestcase,themeritoftheprofitsplitisjudgedbywhatthenego-tiators think is the fair remuneration of relative contributions. That judgmentcontainsmanyimportantembeddedassumptions.

Considerinnovation.Inacapitalisteconomy,thecreativepersonownsandbene-fitsfinanciallyfromtheresultsofhisorherefforts,butitdoesnotinexorablyfollowthatthejurisdictioninwhichthatpersonlivesandworksshouldhavefirstclaimtothetaxrevenueattributabletoprofitsfromtheglobalexploitationofsuccessfulre-searchanddevelopment(R&D).This,however,isapremiseofthetransfer-pricingparadigm,includingprofitsplits.Itamountstoaforce-of-attractiontheoryforrichcountries.ThejurisdictionwhereR&Doccursmayprovidesomefinancialsupport,butthenumberofpeopleinvolvedintheactivityisgenerallymodest.Thus,thehost country probably spends much less from the public purse than the marketcountries,whichhavetoprovidehealthyandeducatedconsumers.Sowhatshouldbethestandardforsplittingprofits?Andwhatistheobjectiveofdoingso?

Another issuewith the formulaicprofit splitgoesbeyondthe fourcornersoffiscalpolicy.TheMAPsystem,inwhichtheprofitsplithasmadegreatstrides, isoftenderidedasopaqueandunfair.MNEsworrythatintergovernmentalbargainingmaydisplaceobjectivedeterminations.Lessdevelopedtaxadministrations—often,butnotalways,locatedinlessdevelopedeconomies—worryaboutbeingoutgunnedbythosewithgreaterexperience,resources,orchutzpah.UnliketheMAP,APAsaretransparentforthetaxpayersaswellasthegovernmentsinvolved,butnotforothertaxpayers,includingcompetitors.Underaprincipledbutflexibleprofitsplit,eachdealcouldbedifferent.However,ifthecurrentsystemistoemergefromthewin-dowless rooms of competent authority negotiations to become the standard fornormaltaxpayercomplianceandadministration,itmustberule-based,reasonablypredictable,notreliantondiscretionarydecisionmakingorone-offdeals,andsus-ceptibletoeffectivejudicialappeal.Otherwiseitrisksoffendingtheruleoflaw.43Secretarrangementsspawninconsistency,suspicion,andcorruption.

Formulary ApportionmentFormularyapportionmentisanoldideathathasbeenadoptedonarestrictedbasis,particularlywithin federal states.Frommyperspective, the experiencehasbeenbothsobering(theUnitedStates)andpotentiallyencouraging(Canada).Theexten-sionoradaptationofsuchasystemtointernationaltaxationofMNEsposesadirectchallengetothetransfer-pricingcomplex,whichhas, inconsequence,neglected,

43 AusefulandperceptiveanalysisoftheconceptwaspresentedbyLordBinghamofCornhill,“TheRuleofLaw,”SixthSirDavidWilliamsLecture,November16,2006(www.cpl.law.cam.ac.uk/past_activities/the_rt_hon_lord_bingham_the_rule_of_law.php).

policy forum: the end of transfer pricing? n 177

disdained,orderidedit.Onepolemicaltacticistoappendtheadjective“global,”arguingthatworldwideagreementisimpossible,asitundoubtedlyis.44However,universalparticipationisunnecessary.ACanada-USwater’sedgesystem,forexample,wouldresolvethelion’sshareoftheCanadiancross-borderallocationquestion.AddEurope,ortherestoftheOECD,andtheexclusionsbecomefiscallymarginal.Anapportionmentsystemalsoreliesonsomeagreementregardingthetaxbase.Thisisnotasutopianasitissometimesmadeouttobe.Businessincometaxbasesareconverginganyway.

Aformularyagreementamongthesesortsofcountriesleavesoutthosestatesthatarepoorerinbothincomeandadministrativeresources,manyofwhichwouldhavesomethingtogain.45Ifearthattheywouldbereluctanttosignon.ToadaptawiseobservationofGrouchoMarx,poorercountriesmaynotwanttojoinanywealthyclubsthatwouldbewillingtohavethemasmembers.Thatwouldbeunfortunate.Formularyapportionmentamongrichcountries—liketheproposedcommoncon-solidatedcorporatetaxbaseintheEuropeanUnion—maymakethemevenricher

44 TheuseoflanguageintheOECD Transfer Pricing Guidelines,supranote3,isillustrativeofthepolemic.Notonlyis“global”addedto“formularyapportionment,”butthetextnotesthatthemethod“hasbeenattemptedbysomelocaltaxingjurisdictions”(ibid.,atparagraph1.16,emphasisadded)andcommentsthatitwouldbebasedon“apredeterminedandmechanisticformula”(ibid.,atparagraph1.17).Agreementonapportionment“wouldbetime-consumingandextremelydifficult”(ibid.,atparagraph1.22).Asiftransferpricingisnottime-consuminganddifficult.Theultimatedefenceofaparadigmisalwaysinertia:thetransitiontoapportionmentwould“presentenormouspoliticalandadministrativecomplexity”(ibid.,atparagraph1.24).Indeferencetotheconcernsofadifferentconstituency,theUN Practical Manual on Transfer Pricing for Developing Countries,supranote29,ismorenuancedinitscomments.Itaccepts(orsuccumbsto)thearm’s-lengthstandardastheapproachrequiredunderarticle9oftheUNmodelconvention(ibid.,atparagraph1.4.3)butisagnosticaboutlargerissues:“Inrecognisingthepracticalrealityofthewidespreadsupportfor,andrelianceon,thearm’slengthstandardamongbothdevelopinganddevelopedcountries,thedraftersoftheManualhavenotfounditnecessary,orhelpful,forittotakeapositiononwiderdebatesaboutotherpossiblestandards”(ibid.,foreword).Seealsoibid.,atparagraph1.4.13,whereitisrecognizedthatformularyapportionment(withthequalifier“global”again)“mightbe”analternative,pointingtoitsuseinsomefederalstatesandtheproposedsystemintheEuropeanUnion,withoutdrawinganyconclusions.

45 ClausingandAvi-Yonah,supranote14,at25-26,discussthedistributiveissuesofmovingfromtransferpricingtoformularyapportionmentusingasinglesalesfactor(seealsotheirtable1).ComparingtheshareofsalesandtheshareofincomeofUSMNEsamonganumberofdevelopedanddevelopingcountries,theyestimatethatsuchachangewouldberoughlyneutralformostAfricancountries,whileAsianandLatinAmericancountrieswouldgainandEuropeancountrieswouldlose.Thissummaryisexpressedbyregion,andindividualcountrieswithinthemfaredifferently.Idonotknowiftheresultsfornon-US-basedMNEswouldbedifferent.Guttentaghasarguedinfavourofbettertransfer-pricingenforcementforthesecountries,includingenactmentofgeneralanti-avoidancerules.( JosephH.Guttentag,“TaxAdministrationinSub-SaharanCountries:TransferPricingIssues,”apaperdeliveredattheHelsinkiconferenceontransferpricing,supranote42(www.taxjustice.net/cms/upload/pdf/Joe_Guttentag_1206_Helsinki.pdf ).)Ifindhisassessmentofthepotentialbenefitsveryoptimisticandparadigm-defensive.

178 n canadian tax journal / revue fiscale canadienne (2013) 61:1

throughgreaterfiscalefficiency(althoughtherearedoubtersinthecaseofEurope),butitwouldnotalleviateinequitiesintheworldwideapportionmentoftaxrevenues.

Inadditiontothesedifficultiesofimplementation,criticsalsoraisetheoreticalobjections.Formulaicfactors, it issaid,arecrudeandopentounanticipatedandimplausibleresults.YetifthegoalistoallocatereceiptsinawaythatiscommensuratewithlocalpublicexpendituresandreasonablyrelatedtoMNEincomeoractivity,factorslikewagesandsalesarenotsowacky.OnecouldarguethattheycomeclosertotheseobjectivesthanthepretensethattheMNEdoesnotexist,thebasisofthearm’s-lengthprincipleandtransferpricing.Formulasmayalsobecriticizedassus-ceptibletomanipulation,butforthetransfer-pricingcomplextoraisethatargumentis,asthesayinggoes,likethepotcallingthekettleblack.

Tobepractical,onemustconsiderthefiscal implicationsofformularyappor-tionmentfortheimportantdevelopedcountriesthatwouldhavetoadoptit.Underaformulaicsystem,theshareofthepiereceivedbymanyoftheserichcountrieswouldbelessthantheythinktheydeserve(recall,forexample,thediscussionofin-novation).However,thepiewouldbefarlarger.EntitiesinintermediatefacilitatingjurisdictionsthatadministerintangiblesorprovidegroupfinancingwouldattractaminusculeportionofMNErevenue,leavingmoreforeveryoneelse.Asinanysuchdramatic shift, a revenue-neutral solution will result in winners and losers. Onemightarguethattheextraefficiencycouldcompensate,butthatisunlikelytoas-suageconservativegovernmentofficials,whonaturallypreferthestatusquo.Fearofunknownandpotentially adverse consequences reinforces their inclination todefendtheparadigm.

If,however,thatparadigmbecomesimpossibletomaintain,whetherthroughitsinherentweaknessesorbecauseofexternalchallengesfromcountriesthatwillnotbuyin,itwouldbehelpfultohaveathoughtfulalternative.Formularyapportion-mentneedssomecreativere-examinationinplaceoftheusualadversarialdebatesamongacademicsanddefensiveposturingbythetransfer-pricingestablishment.Forexample,apportionmentcouldlearnsomethingimportantfromtheprincipledprofitsplit: one size need not fit all. The Canadian income tax regulations governinginterprovincialallocationrecognizethespecialcircumstancesofalimitednumberofcommercialandindustrialsectors(reflectingtheeconomyasitwasmanydecadesago)—financial institutions, transportation, grain elevators, and pipelines. A farmoresophisticatedsystemispossiblewithoutnegatingthebasicprincipleofalloca-tionwithouttransferpricing.

Paradigmshiftsarenotalwaysabrupt.Sometimestheycanberecognizedonlywiththebenefitofhindsight.Gradualism, reformrather than revolution, isprobablynecessary inthepoliticallychargedfieldof taxation.Transparentandmandatoryformulascouldbedevisedwiththeresultingsystemdescribedasaprofitsplit.IfIampermittedtoswitchmetaphorsattheendoftheseremarksfromthehistoryofsciencetothehistoryofpoliticalinstitutions,IimaginethatthisfiscalrevolutionwouldbemoreintheEnglishthantheFrenchstyle.Whichisnottosayitwouldbebloodless.