negotiated transfer pricing and divisional vs. firm-wide performance evaluation

TRANSCRIPT

Negotiated Transfer Pricing and Divisional versus

Firm-Wide Performance Evaluation

Regina M. Anctil

and

Sunil Dutta*

University of California, Berkeley

*Corresponding author. Address: Haas School of Business, University of California, Berkeley,CA 94720; e-mail: [email protected]; phone: 510-643-1229; fax 510-643-1412.

The authors thank Stefan Reichelstein, Jerry Zimmerman, two anonymous referees, andworkshop participants at U. C. Berkeley, University of Chicago, Columbia University, andUniversity of Minnesota for their helpful comments and suggestions.

Negotiated Transfer Pricing and Divisional versus Firm-Wide Performance Evaluation

Abstract

A firm with two divisions, each run by a risk-averse manager, contracts with the twomanagers to operate their divisions and possibly engage in interdivisional trade. Each divisioncan increase the total surplus generated through interdivisional trade by making costlyrelationship-specific investments. The terms of trade are determined through negotiationsbetween the two managers. Managerial compensation contracts are linear functions of divisionalprofit and firm-wide profit. If managers are compensated solely on the basis of their divisionalprofits, they invest less than the first-best amounts. While compensation contracts based on firm-wide profits alone can induce first-best investments, they impose extra risk on risk-aversemanagers. Therefore, we find that optimal linear compensation contracts will contain bothdivisional and firm-wide components. Our analysis also identifies a feature of negotiated transferpricing, namely interdivisional risk-sharing, and characterizes its impact on the design of optimalcontracts.

Key words: Performance evaluation, Transfer pricing, Investment, Hold-up problem.

I. INTRODUCTION

In multidivisional firms, divisional interests often conflict with the goal of firm-wide

profit maximization. Transfer pricing and managerial performance evaluation are two key

instruments that firms use to manage potential conflicts. In this paper we analyze the role of

these two institutions in providing incentives for divisional managers to balance the interests of

their own divisions against the good of the firm. In particular, we examine how managerial

compensation contacts use divisional and firm-wide performance measures in conjunction with

negotiated transfer pricing to influence the way division managers balance divisional and firm-

wide goals.

We characterize the conflict between divisional and firm-wide interests as an investment

“hold-up” problem, identified by Williamson (1985) and others. We model a firm with two

divisions; each division is an autonomous profit-generating entity managed by a risk- and effort-

averse manager. In addition to their independent external operations, the divisions can trade an

intermediate product with each other. Prior to determining the terms of interdivisional trade, the

divisions can make costly, relationship-specific investments to increase the total surplus

generated by their internal trade. For instance, the supplying division may invest in production

technology to reduce the variable cost of production. Similarly, the buying division may enhance

its revenues by investing in market research or advance promotion.

If the firm uses negotiated transfer pricing for the interdivisional transfer, then each

manager invests anticipating that, while his division will have to bear the full cost of its

investment, it will get only a portion of the returns. If the division managers are rewarded on the

basis of their division profits, they will invest less than the first-best amounts. This disincentive

to invest constitutes the investment hold-up problem.

In this paper, we focus on resolution of the investment hold-up problem through

2

managerial performance evaluation. In particular, we consider the role of linear compensation

contracts based on divisional profits and firm-wide profits.1 Our analysis establishes a tradeoff

between inducing efficient investments and imposing risk on risk-averse managers. We

demonstrate that first-best investments can be induced if the managers are rewarded solely on the

basis of firm-wide profit. Such contacts are never optimal, however, since they impose excessive

risks on the managers. It is also not optimal to reward managers only on the basis of their

division profits, as this practice leads to an excessive loss of investment efficiency. Our analysis

shows that the optimal linear contracts will contain both divisional and firm-wide performance

measures.2

We also identify an important characteristic of negotiated transfer pricing that impacts the

design of optimal contracts, but has not been previously recognized in the literature. In our

model, costs and revenues associated with interdivisional trade are subject to random shocks that

are realized after the two managers have negotiated the terms of trade. Consequently, under

negotiated transfer pricing division managers share not only the expected surplus, but also the

residual risk connected with interdivisional trade. If the managers were risk-neutral, this

interdivisional risk-sharing would have no implication for the firm’s welfare. When managers

are risk-averse, however, risk-sharing allows the firm to lower its expected compensation costs.

The impact of interdivisional risk-sharing on the design of optimal contacts can be best

illustrated in a case where only one division, say the buying division, has an investment

opportunity. In this case, there is no need to provide investment incentives to the manager of the

supplying division. We find, however, that the supplying manager’s optimal contract will still

place weight on both divisional and firm-wide profits. The reason is that interdivisional risk-

sharing makes accrued divisional profits positively correlated. This correlation allows the firm to

reduce the amount of risk that needs to be imposed on the manager of the supplying division

3

using relative performance evaluation, that is, by tying a part of the supplying manager’s

compensation to the buying division’s profits.

The buying division manager’s contract optimally places weight on both divisional and

firm-wide performance measures. The optimal weight on firm-wide profit is determined by the

tradeoff between two conflicting goals: to induce investment, and to reduce the risk through

relative performance evaluation. When both managers have the opportunity to invest, a similar

tradeoff determines the optimal weights on firm-wide performance.

As mentioned above, negotiated transfer pricing plays a critical role in determining the

characteristics of optimal contracts. To illustrate the interaction of negotiated transfer pricing and

firm-wide performance evaluation in contracting, we again turn to the case where the buying

division has the investment opportunity. We compare the effect of using negotiated transfer

pricing with that of requiring the buyer simply to reimburse the seller for realized production

costs, which would be more reflective of cost-based transfer pricing.

The latter scheme allocates the entire surplus to the buying division.3 The buyer will

make the first-best investment without any firm-wide component in his or her compensation

contract. The seller has no investment issue and no profit from interdivisional trade. Thus the

selling manager’s contract needs no firm-wide component. This may be an efficient arrangement

if the buying division’s investment has a relatively large impact on the trading surplus. This has

led to the argument that an efficient mechanism allocates the entire trading surplus to the

division with the investment opportunity.4 We show that this argument is not valid when

managers are risk-averse however. Such schemes are inefficient from a risk-sharing perspective

because they allocate all the residual risk of interdivisional trade to the buying division. Central

management may prefer to endure a loss of investment efficiency and use negotiated transfer

pricing rather than distort managerial risk-sharing using the alternative scheme.

4

Other studies have looked at various approaches to dealing with the investment hold-up

problem. Edlin and Reichelstein (1995) show that efficient investments can be achieved when

the managers can commit to contracts prior to making their investment decisions. In this paper,

however, we take the view that prior contracts may be difficult to enforce if all the relevant

characteristics of the transferred good or service cannot be specified in advance. Instead we

focus on the solution of the investment hold-up problem through managerial performance

evaluation.5,6

Holmstrom and Tirole (1991) also examine the investment hold-up problem between two

divisions in a decentralized firm. As in our paper, their analysis focuses on the role of managerial

compensation contracts in inducing investments. In their model, however, managerial

compensation contracts are not allowed to be contingent on firm-wide profits. Their analysis

does not focus on tradeoffs between divisional and firm-wide performance measures.7

In contrast to the approach in this paper, many papers have analyzed the performance

evaluation and transfer-pricing problems using the theory of mechanism design. Under the

mechanism design framework, the main focus is on deriving an optimal mechanism that induces

divisional managers to reveal their private information. This approach has been used by Amershi

and Cheng (1990), Antle and Eppen (1985), Harris et al. (1982), Vaysman (1996), and

Christensen and Demski (1996).

The plan of this paper is as follows. Section II describes the basic setup of the model.

Section III examines the properties of optimal linear contracts under negotiated transfer pricing,

and illustrates how risk sharing, investment incentives, and firm welfare depend on the transfer

pricing scheme. Section IV concludes the paper.

5

II. THE MODEL

Technology

We characterize the performance measurement problem of a two-division firm with a

risk-neutral principal which we call central management and two risk-averse, effort-averse

agents, division managers 1 and 2.

Each division has profit from its own operations. We assume that the net profit of these

operations for division i is a function of manager i’s effort level ai, and a random variable ie~ .

Let iii eaX ~)( + denote this profit for division i. We assume that ),(~ ∞−∞∈ie , has mean 0 and

variance iσ , and that the functions Xi are strictly increasing, concave, and twice differentiable.

In addition to the above operations, an intermediate product can be produced in division 1

and transferred to division 2. We assume that the intermediate product is highly specialized and

has no external market. Throughout the analysis we refer to the transfer of the intermediate good

in terms of its quantity, q. However, the variable q need not be restricted to such a narrow

interpretation. It may also refer to some other characteristic of the transferred good, such as its

quality.

The cost to division 1 of producing q units of the intermediate product is an increasing

function of q, and a decreasing function of a level of investment I1 borne by division 1. This

function takes the form 11~),( uIqC + , where 1

~u has mean 0 and variance 1uσ . Division 2 earns

net revenue R from the transfer, where R is an increasing function of q and a level of investment

I2 borne by division 2. This function takes the form 22~),( uIqR + , where 2

~u has mean 0 and

variance 2uσ . The terms iu~ represent uncertainty in total upstream or downstream costs incurred

on the product. In addition, we assume that if q=0, all revenue and cost is avoided; in particular

6

1~u = 2

~u =0. The function R is assumed to be strictly increasing, concave, and twice differentiable

in q for all I2; and C is strictly increasing, convex, and twice differentiable in q for all I1. Further,

we assume that the expected contribution margin, ),(),( 12 ICIR ⋅−⋅ , is strictly concave in q for

all I1 and I2. We assume that all random variables are independent of one another.

For given investments I1 and I2, let ),( 21* IIq denote the optimal quantity choice for the

firm. That is,

]~),(~),([maxarg),( 11220

21* uIqCuIqREIIq

q

−−+=≥

We assume that q* is an interior point for all 2121 ,,, uuII . And we let ),( 21 IIM denote the

expected contribution margin at the optimal quantity choice. The firm’s investment choice

problem under full information is8

21

2121

,

.),(Maximize

II

IIIIM −−(1)

We further assume the second-order condition,

011 <M and 02122211 >− MMM (A1)

holds for all 21, II . Assumption A1 and the Envelope Theorem imply that the first-best

investments, ),( *2

*1 II , exist and satisfy

1*)*,(

2

2 =∂

∂I

IqR and 1

*)*,(

1

1 =∂

∂−

I

IqC. (2)

In addition, we assume the following:

.0and 02

2

1

2

>∂∂

∂<

∂∂∂

Iq

R

Iq

C(A2)

7

Assumption A2 states that investment increases marginal revenue and decreases marginal cost. It

implies that the optimal quantity function, ),(* ⋅⋅q , is increasing in both its arguments.

Preferences, Information, and Contracts

We assume the division managers are effort and risk averse, with expected utility given

by

)()~

var()~

(),~

( 21

iiiiiiii aVSSEaSEU −−≡ ρ ,

where iρ is the coefficient of risk aversion, Si denotes the manager’s compensation, and )( ii aV is

the manager’s personal cost of supplying effort ai. We assume that )(⋅iV is strictly increasing,

strictly convex, and twice differentiable.9

In our model we assume the firm is decentralized in the sense that central management

cannot observe the agents’ actions or investments. We also assume that, for the purpose of

performance evaluation, central management uses only the aggregate divisional profits,

,~),(~)(~1111111 tIuIqCeaX +−−−+=π (3)

tIuIqReaX −−+++= 2222222~),(~)(~π , (4)

where t denotes the transfer payment from division 2 to division 1 for supplying q units of the

intermediate product.

We restrict our analysis to compensation contracts in which the wage payments are linear

functions of the performance measures 1~π and 2

~π . Thus, contracts take the form

jiiiiiS πβπαω ++= , where iα is the weight in manager i’s contract on the profit of division i,

8

and iβ is the weight in manager i’s contract on the profit of division j. This means that with two

divisions, the contract places iβ weight on firm-wide income and ii βα − on the profit of

division i. So FiiiiiS πβπγω ++= , where iii βαγ −= and jiF πππ += .

Our assumptions that contracts are linear and based on aggregate division and firm profit

merit further discussion. Following the work of Holmstrom and Milgrom (1987), the literature

on contracting commonly utilizes the linear contract assumption; we adopt it here for tractability

reasons.10 Limiting the set of contracting variables to Fi ππ and is restrictive. For example, it

may be optimal to have contracts based on the transfer payment, or on divisional revenues, or

costs. But such contracts do not appear to be common practice, whereas contracts based on

divisional and firm profit are common (Bushman, et al., 1995). This is perhaps because

increasingly complex contracts are increasingly costly. Similar contract restrictions can be found

in the models of Holmstrom and Tirole (1991), Edlin and Reichelstein (1995), and Baldenius

(1998).11

Contracting in our model is the initial event in the following sequence:

Date 1 Date 2 Date 3 Date 4

Center signsContractswith managers.

( 21 , II ) and ( 21 , aa )chosen.

Managers trade q anddetermine t; 21 and uurealized.

Divisional profit realized;contracts settled.

At date 2 managers choose their investment levels and their division-specific effort

levels. Since no one except the managers observes these, the managers are unable to write

enforceable contracts on them.12 At date 3 the division managers jointly determine the quantity

and transfer payment. At this date, the division managers learn both division’s cost and revenue

through the common observation of the realizations of the iu ’s.

9

The determination of q at date 3 warrants some discussion. We assume that the managers

must wait until date 3 to determine q. The need to postpone the choice of q might arise because q

depends on other events, not modeled here, that take place at date 3. The choice might depend,

for instance, on last minute knowledge of consumer preferences.13

Determining the Transfer Payment

The two division managers are free to choose any quantity and transfer price. While

negotiating the quantity and transfer payment choice at date 3, the divisional managers’

incentives depend on their bonus coefficients βi and αi. These coefficients will determine each

division manager’s concern for his or her own division relative to the good of the firm in

bargaining for the transfer payment. To ensure that there is a well-defined outcome to the

negotiation, we only consider compensation contracts that put non-negative incremental weight

on divisional profits. If βi > αi and βj ≤ αj, in particular, then the manager i would propose a

very large transfer payment from division i to division j which would be accepted by manager j.

We assume that:

ii αβ ≤ for each i. (A3)

Further, we assume that if the contract leaves a manager indifferent, he will bargain in favor of

his own division.

Given this, it follows that the managers will bargain to maximize their own divisional

profits. Note that their ability to carry out their trade agreement does not depend on its

verifiability, but rather on the managers’ common knowledge of their respective environments. It

is in each division’s interest to agree on the ex post surplus-maximizing choice of q at date 3. At

that point the choice of investments has already been made, and the investment outlay of each

10

division is irrelevant in the negotiation of the transfer payment. We represent negotiations by the

Nash bargaining solution in which the two divisions share the surplus generated by the transfer

equally. The transfer payment, which produces this equal sharing, is given by

]~~),(),([21

121*

2* uuIqCIqRt +++= ,

where the buyer reimburses the seller for half the actual cost and pays out half the actual

revenues.

For notational convenience, let 12~~~ uuu −≡ and 21 uuu σσσ +≡ .

Given the above transfer payment, divisional profits are given by

11*

2*

1111 ]~),(),([21~)(~ IuIqCIqReaX −+−++=π (5)

21*

2*

2222 ]~),(),([21~)(~ IuIqCIqReaX −+−++=π (6)

The effect of the investment hold-up problem is apparent in the division-profit measures above.

The marginal benefit accruing to each division of each dollar of investment is only half the

marginal surplus. The selling division yields only half the cost savings per dollar of investment,

while the buying division yields only half the revenue increase per dollar. First-best investment

requires divisional profits to reflect the full cash benefit, cost savings or revenue increase, of

each dollar of investment.

III. DIVISIONAL AND FIRM-WIDE PERFORMANCE EVALUATION

We let )),,(( , iiiii aIaSEU denote manager i’s expected utility for a given contract Si,

effort choice ai, and investment choice Ii. For notational simplicity, we suppress the choices of

manager j in the expected utility of agent i. The Program P1, below, represents central

management’s contracting problem.

11

Program P1

iiiii Ia

EEE

βαωπβαπβαωωππ

,,,,

)()()()()()( maximize 2121212121 +−+−+−+

subject to

111111 )),,(( UaIaSEU ≥ (IR1)

222222 )),,(( UaIaSEU ≥ (IR2)

1

111111 )),,((maxarg

a

aIaSEUa

′′′∈

(IC1)

2

222222 )),,((maxarg

a

aIaSEUa

′′′∈

(IC2)

1

111111 )),,((maxarg

I

aIaSEUI

′′∈

(ICI1)

2

222222 )),,((maxarg

I

aIaSEUI

′′∈

(ICI2)

.iii ∀≤ αβ (CC),

where Uj denotes the manager j’s reservation utility.

Constraints IR1 and IR2 require that managers are guaranteed their reservation utilities.

Constraints IC1 and IC2 ensure that effort choices are incentive compatible. That the two

managers’ investment choices are incentive compatible is assured by constraints ICI1 and ICI2.

The last constraint (CC) reflects assumption A3.

12

Given the structure of compensation contracts and utility,

+++−−++= 222

, )(4

1

2

1)()()()),(( iiujiiiiiijiiiiiiiii aVEEaIaSEU βασσβσαρπβπαω

(7)

Without loss of generality, we normalize Uj to 0 for each i. We know that the individual

rationality constraints will hold with equality, so that the fixed payment to agent i will be,

+++++−−= 222 )(

4

1

2

1)()()( iiujiiiiiijiiii aVEE βασσβσαρπβπαω .

Thus, we can simplify program P1 by substituting the fixed portions of the agents’ wages

directly into the principal’s objective function. Further, IC1, IC2, ICI1, and ICI2 can be replaced

with their first order conditions. These simplifications lead to the following maximization

problem:

Program P2

iiii

iiiiujiiiiiiii

aI

IqCIqRIaVaXMax

βα

βασσβσαρ

,,,

),(),()(4

1

2

1)()( 1

*2

*2

1

222 −+

−

+++−−∑

=

subject to:

iaVaX iiiii ∀=′−′ 0)()(α (ICi)

0)(2

11

111 =−

∂∂

+− αβαI

C(ICI1)

0)(2

12

222 =−

∂∂

+ αβαI

R(ICI2)

iii ∀≥ βα (CC)

13

To ensure that the principal always finds it optimal to induce positive efforts from both

managers, we make the following technical assumption:

0

)(

→∀∞→′

i

ii

a

iaXLim (A4)

It can be easily verified that (A4), in combination with the principal’s first-order conditions for

the effort choices, implies that 0* >iα for each i.

Before we discuss the results of this analysis, it is worthwhile to return briefly to our

discussion of contracting based solely on divisional and firm-wide profit. As we state above,

central management does not contract upon individual components of divisional profits in this

model, but clearly if it could, it would benefit from doing so. In particular, one useful contracting

variable in this model would be the transfer payment, ]~~),(),([2

12112 uuIqCIqRt +++= , itself.

Consider what would happen if contracts took the form tS ijiiiii τπβπαω +++= . The variable

t is a less noisy contracting variable than is firm-wide profit. In this case, it can be shown that the

optimal linear contract will place zero weight on firm-wide profit (i.e., 0* =iβ ). In our simple

two-division firm it is clear that it would be worthwhile for contracts to utilize the transfer price

rather than using firm-wide profit. But if a firm contained many divisions with different

interdivisional transactions, contracting on each transfer payment would quickly become

cumbersome. Firm-wide profit, on the other hand, remains a single contracting variable.

A pure firm-wide profit-sharing contract for a given agent in our model is one where

equal weight is placed on the measured profit of each division. In other words, there is no

incremental weight on division i’s profit in agent i’s contract, beyond that which comes through

14

the firm-wide measure. Proposition 1 establishes the benchmark that such contracts yield first-

best investment.

Proposition1

Divisional investments are first best if and only if 2,1, == iii βα .

Proof

(All proofs are in the appendix)

The proof shows that a pure profit-sharing contract induces each manager to internalize

fully the surplus generated by the interdivisional transaction. Proposition 1 provides the

benchmark contracts with which to compare the optimal contracts and investments. It also shows

why central management will never choose contracts where ii αβ > for both division managers.

The firm would always be able to improve both risk sharing and investment by decreasing the

firm-wide profit coefficient.

In our model, the underlying moral hazard problem is two dimensional. In addition to the

familiar effort-choice problem, the managers choose the levels of monetary investments in their

divisions. Proposition 1 distinguishes the problem of inducing a monetary investment from that

of inducing a manager to undertake personally costly effort. This contrasts with Feltham and Xie

(1994) which examines a setting in which the agent faces a multidimensional choice of

personally costly efforts. Superficially our two problems are similar. However, the manager

considering an effort investment internalizes its cost fully because of effort aversion, whereas the

same manager internalizes the monetary cost of investment only through its endogenous effect, if

any, on his compensation. For this reason, by designating measured performance to be firm-wide

profit, central management can insure first-best investment by paying the manager any fraction

15

thereof. On the other hand, if the investment is personal effort rather than the firm’s capital, the

only way to achieve first-best investment is if the firm is sold to the manager.

The design of agents’ contracts in this model balances the benefits from inducing more

efficient investment choices against the cost of imposing firm-wide risk on risk-averse managers.

In our initial examination of this tradeoff, we turn to a special case where only division 2, the

buying division, invests.14 We will assume that )(),( 1 qCIqC ≡ . This simpler setting retains

most of the ingredients of the problem, but holds constant the reaction of each agent’s investment

choice to that of the other agent. Note that, absent any contract weight on firm-wide

performance, negotiated transfer pricing still motivates some revenue-enhancing investment by

giving division 2 a share in the surplus. The following proposition describes the managers’

optimal contracts when there is no risk associated with the interdivisional trade, in other words,

when 0=uσ .

Proposition 2

If only division 2 invests, and 0=uσ , then

.0*.

**0.

1

22

=<<

βαβ

ii

i

Proposition 2 shows that manager 2’s optimal contract will contain both divisional and firm-wide

performance measures. Thus, it is not optimal to compensate manager 2 solely on the basis of

firm-wide profit and induce the first-best investment. It is also not optimal to reward him only on

the basis of his division profit as it leads to an excessive loss of investment efficiency. This result

illustrates a basic tradeoff between inducing efficient investment and imposing risk on risk-

averse managers. Since manager 1 has no investment opportunity, his optimal contract will

16

include no firm-wide profit component.

The next proposition, however, shows that placing no weight on firm-wide profit is, in

general, suboptimal in the contract of both managers, even if only one manager has the

opportunity to invest.

Proposition 3

If only division 2 invests, and 0>uσ , then

0*.

**.

1

22

<<<−

βαβ

ii

bi

where b is some positive number.

When there is residual uncertainty associated with interdivisional trade, there is an

additional consideration that impacts the optimal weight on the firm-wide profit. A consequence

of negotiated transfer pricing is that the division managers share not only the expected surplus,

but also the residual risk associated with the interdivisional trade. This offers the firm an

opportunity to reduce its expected compensation costs through relative performance evaluation.

Since inducing efficient investment is not a concern for the selling division, this role of

firm-wide performance evaluation is most apparent in the contract of manager 1. Interdivisional

risk-sharing makes division profits positively correlated, providing central management an

opportunity to reduce the firm’s expected compensation costs. The negative weight *1β reflects

the firm’s use of this opportunity. In other words, the signal 2π is used in manager 1’s contract to

remove the effect of common uncontrollable events that affect the interdivisional trade and,

therefore, the accrued profit of division 1. We must stress that, in the absence of interdivisional

risk-sharing, there is no scope for relative performance evaluation in this model since we assume

17

that division cash flows are not correlated.

In manager 2’s contract the optimal weight on firm-wide profit is determined by the

relative magnitudes of the two opposing effects. A positive weight induces the manager to make

more efficient investment; but it also distorts risk sharing. A negative weight sacrifices better

investment for improved risk sharing. The sign of the coefficient depends on the relative

importance of investment and risk premium reduction to the firm.

As with Proposition 2, Proposition 3 rules out pure profit-sharing contracts. This again

implies that *11 II < . One might suppose from Proposition 3 that if both managers had investment

opportunities, then ** αβ < would be true for both managers, and both would underinvest. We

find, however, that if both managers can invest, then the principal might write a contract where

** ii αβ = , and induce manager i to undertake first-best investment. The reason is that if

investment is bilateral, then the investments of the two divisions become complements.

Investment on the part of division i increases the productivity of the investment of division j,

providing more investment incentive to that manager. Proposition 4 provides the only restriction

on the optimal contract weights in the case of bilateral investment.

Proposition 4

If both agents have investment opportunities, then ** ii αβ < for at least one i.

Proposition 4 establishes that optimal contracts will always induce at least one manager

to underinvest, relative to the first-best investment level that would result if ** ii αβ = for both i.

But it allows for first-best investment on the part of one manager. This result is unique to the

setting where agents are risk averse. When managers are risk averse it may be cheaper to induce

18

manager i to invest, by increasing the weight on the firm-wide profit in j’s contract, than by

imposing greater firm-wide performance risk on manager i. This the case particularly if iρ or

jσ is large. If managers were risk neutral both direct and indirect investment incentives would

be equally costly.

In their analysis of the investment incentives of risk-averse division managers,

Holmstrom and Tirole (1991) do not consider contracts with a firm-wide performance evaluation

component, iβ , conjecturing that it would merely make contracts more costly. But our analysis

has shown that firm-wide performance evaluation contributes to contracting in two significant

ways. First, profit sharing induces managers to sacrifice divisional welfare and coordinate with

other divisions for the firm. Second, it provides an incremental risk-sharing opportunity between

central management and each manager. Moreover, the existence of complementarity between

divisions allows central management indirect means of motivating costly investment, which is

incrementally valuable when managers are risk averse.

We have assumed, up to this point, that the firm uses negotiated transfer pricing, allowing

the managers to bargain over the terms of trade. We have observed how contracts are able to take

advantage of interdivisional risk sharing that is one result of this bargaining.

To illustrate this role of negotiated transfer pricing on the design of optimal contracts and

firm welfare, we return to the case where only the buying division has an investment

opportunity. It would seem to make sense, in this case, to use some form of cost-based transfer

price that reimburses division 1 for the incremental production cost of any level of the

intermediate good. At the same time the profit of division 2 fully reflects the trade surplus.

Formally, if 1~)( uqCt += , then 1111

~)(~ eaX +=π and uqCIqReaX ~)(),(~)(~22222 +−++=π . It

follows that optimal contracts will set 021 == ββ . For convenience, we refer to this type of

19

transfer payment as cost-based and the underlying system as cost-based transfer pricing.15

Cost-based transfer pricing eliminates the usefulness of firm-wide performance

evaluation both for investment and for risk sharing. Manager 2 internalizes the trade surplus and

will choose the first-best levels of q and I2 as long as 02 >α . If managers were risk neutral, the

firm would clearly be better off using cost-based transfer pricing. We also make the formal

observation that, if there were no risk associated with interdivisional trade, cost-based transfer

pricing would dominate negotiated transfer pricing.

Observation

If 0=uσ and only the buying division invests, then central management prefers cost-

based transfer pricing to negotiated transfer pricing.

The observation highlights the value of negotiated transfer pricing, relative to cost-based transfer

pricing; its value lies in the potential for risk-averse managers to share the residual risk

connected with interdivisional trade. If 0=uσ , then there is no such potential. If, however,

0>uσ , then the relative rank of these two transfer pricing regimes will depend on the relative

magnitude of two opposing forces: risk sharing and investment incentives. Negotiated transfer

pricing is efficient with respect to risk sharing, but it leads to distorted investment incentives. On

the other hand, cost-based transfer pricing leads to first-best investment without firm-wide

performance evaluation. But this arrangement is inefficient from a risk-sharing perspective,

because one party bears all the risk related to the interdivisional transfer. If this risk is more

costly than the loss of division 2’s investment efficiency, the firm is actually better off using

negotiated transfer pricing.

20

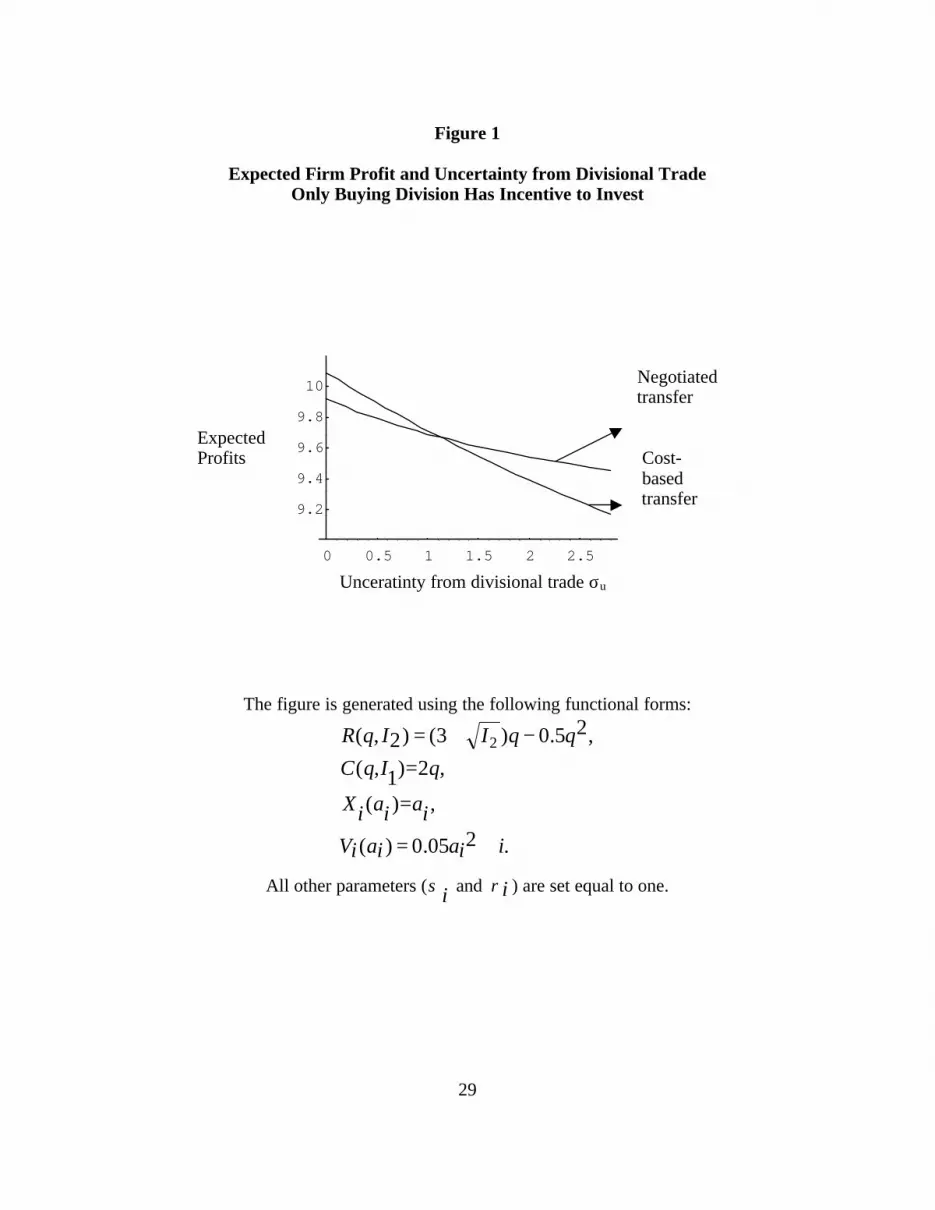

To illustrate this tradeoff, figure 1 depicts the firm’s welfare under each regime as a

function of uσ in the case of unilateral investment. It shows that if uσ is relatively large, the

desirable risk-sharing properties of negotiated transfer pricing can more than offset its adverse

effect on investment incentives.

[Insert Figure 1 about here]

The above tradeoffs also exist in the case of bilateral investment, but the welfare

comparison is also a function of the importance of the second investment.

IV. CONCLUSION

This analysis has examined how a decentralized firm can use divisional and firm-wide

incentives to guide division managers to engage in interdivisional transactions and make costly

divisional investments for the benefit of the firm. Underlying these incentive contracts is a

fundamental tradeoff between efficient risk sharing, which calls for division-based performance

evaluation, and profit enhancing coordination, which calls for firm-wide performance evaluation.

We have demonstrated that optimal compensation contacts will contain both divisional and firm-

wide performance measures. Our analysis has also identified a characteristic of negotiated

transfer pricing, namely interdivisional risk-sharing, that impacts the design of optimal

compensation contacts, and reduces the firm’s expected compensation costs.

We have shown that the need for firm-wide performance evaluation can be eliminated

only if one manager somehow captures the entire surplus from the interdivisional trade. The

desirability of implementing such a scheme, however, depends on the relative importance of

interdivisional risk sharing and relationship-specific investments.

21

APPENDIX

Proof of Proposition 1

First best investments satisfy:

01),(

2

*2

*

=−∂

∂I

IqR(a1)

01),(

1

*1

*

=−∂

∂−

I

IqC. (a2)

If investments are first best, then ICI1 and ICI2 in program P2 imply that

iii αβα =+ )(2

1 for each i. This proves the “only if” part.

Substituting ii βα = in ICI1 and ICI2 in program P2 yields (a1) and (a2), and thus

proving the “if” part.

Proof of Proposition 2

In this case, Program P2 simplifies to

( )iii

jiiiiiiiii

aI

IqCIqRaVaXMax

βα

σβσαρ

,,,

)(),(2

1)()(

2

2*

2*22

2

1

−−++−−∑=

subject to:

iaVaX iiiii ∀=′−′ 0)()(α (IC)

0)(2

12

222 =−

∂∂

+ αβαI

R(ICI2)

iii ∀≥ βα (CC)

Let 2, µλi denote the Lagrange multipliers on ICi and ICI2, respectively. The first-order

22

conditions with respect to 212 and,, ββI yield

02

1 2222

22

=+

+

−

∂∂

MI

R βαµ (a3)

0211 ≥− σβρ (a4)

0][2

1

22122 ≥

∂∂

+−I

Rµσβρ (a5)

Note that (a4) and (a5) hold with equality if the constraints CC are not binding. First note from

(a4) that 01 >β cannot be a solution; therefore 11 αβ < and (a4) holds with equality, giving ii. To

show i, suppose that 22 αβ = . Then ICI2 implies that 01),(

2

*2

*

=−∂

∂I

IqR. Substituting this into

(a3) implies 02 =µ . Substituting 02 =µ into (a5) implies 02 ≤β , a contradiction. Therefore

22 αβ < and (a5) holds with equality. This implies

12

22

2 2 σρ

µβ

I

R

∂∂

= , which is positive since it can be shown that 02 >µ , proving i.

Proof of Proposition 3

In this case, program P2 simplifies to:

( )iii

iiujiiiiiiiii

aI

IqCIqRaVaXMax

βα

βασσβσαρ

,,,

)(),()(41

2

1)()(

2

2*

2*222

2

1

−−++++−−∑=

23

subject to:

iaVaX iiiii ∀=′−′ 0)()(α (IC)

0)(2

12

222 =−

∂∂

+ αβαI

R(ICI2)

iii ∀≥ βα (CC)

Let 2, µλi be defined as in Proposition 2. Then first order conditions with respect to I1, β1, and β2

yield

02

1 2222

22

=+

+

−

∂∂

MI

R βαµ (a6)

0)(4

111211 ≥

++− uσβασβρ (a7)

0][2

1)(

4

1

2222122 ≥

∂∂

+

++−

I

Ru µσβασβρ (a8)

Note that (a7) and (a8) will hold with equality if constraints (CC) are not binding.

Since α1 >0, it follows from (a7) that β1 < 0. This proves part (ii).

To prove part (i), suppose, to the contrary, β2 = α2. Then ICI2 implies that

01),(

2

*2

*

=−∂

∂I

IqR. Substituting this in (a6) yields µ2 = 0. Substituting this in (a8) gives

β2 < 0 which is a contradiction.

Hence, (a8) can be rearranged to yield

]4

[

][24

12

2

222

1u

u

I

R

σσρ

µσαρ

β+

∂∂

+−= .

24

It can be easily verified that µ2 > 0 and, therefore, β2 > -b where ]

4[

4

12

22

u

u

bσ

σρ

σαρ

+≡ .

Proof of Proposition 4

Let ii µλ , denote the Lagrange multipliers on constraints IC and ICI in program P2. Then

first order conditions with respect to I1, I2, β1, β2, µ1, and µ2 yield

022

1 1222

21111

11

=+

++

+

−

∂∂

− MMI

C βαµ

βαµ (a9)

022

1 2222

21211

12

=+

++

+

−

∂∂

MMI

R βαµ

βαµ (a10)

0][2

1)(

4

1

1111211 ≥

∂∂

−+

++−

I

Cu µσβασβρ (a11)

0][2

1)(

4

1

2222122 ≥

∂∂

+

++−

I

Ru µσβασβρ (a12)

0)(2

11

111 =−

∂∂

+− αβαI

C(a13)

0)(2

12

222 =−

∂∂

+ αβαI

R(a14),

where 22

2

22I

MM

∂∂

≡ < 0 and 21

2

12II

MM

∂∂∂

≡ > 0.

Suppose, to the contrary, β1 =α1 and β2 = α2. Then, it follows from (a13) and (a14) that

investments are first best. Substituting (a1) and (a2) into (a9) and (a10), we get

022 12

22211

111 =

++

+MM

βαµ

βαµ (a15)

25

022 22

22212

111 =

++

+MM

βαµ

βαµ . (a16)

Since 02122211 >− MMM by assumption, (a15) and (a16) imply that µ1 = µ2 = 0. However, if µ1

= µ2 = 0, then (a11) and (a12) imply that β1 < 0 and β2 < 0. Therefore, we have a contradiction.

Hence it must be the case that βi < αi for at least one i.

Proof of observation

Note that the ex post quantity choice is optimal under both cost-based and negotiated

transfer pricing. Negotiated transfer pricing leads to an equal sharing of the maximized

contribution margin, uIqCIqR +− ),(),( 1*

2* . Under cost-based transfer pricing, the buyer

extracts the entire surplus.

If ]1,0[∈γ denotes the fraction of maximized contribution margin that is credited to

division 1, then negotiated transfer pricing corresponds to the case of γ =1/2 whereas cost-based

transfer pricing corresponds to the case of γ = 0. To prove the result, therefore, it suffices to

show that the principal’s expected profits are strictly decreasing in γ.

For a given γ, the principal’s contacting problem is:

( ) ( ) ( )iii

iiiii

aI

IqCIqRaVaXMax

βα

σβσαρσβσαρ

,,,

2

1

2

1)(),()()(

2

12

222

2222

112

112*

2*

2

1

+−+−−−+−∑

=

Subject to:

iaVaX iiiii ∀=′−′ 0)()(α (IC)

0))1(( 22

22 =−∂∂

+− αγβγαI

R(ICI2)

26

iii ∀≥ βα (CC)

Let L denote the Lagrangian of the above maximization problem with multipliers iλ on

constraints (IC) and 2µ on constraint (ICI2). For a given γ, let Π (γ) denote the value of the

principal’s objective function evaluated at the optimal choices of investment, efforts, and bonus

coefficients. Then, the Envelope Theorem implies that

.)(2

222 I

R

L

d

d

∂∂

−−=

∂∂

=Π

βαµ

γγ

It can be easily verified that 22 βα > , 2µ > 0 if γ > 0 and β2 = 2µ = 0 if γ = 0.

Hence principal’s expected profits are decreasing in γ.

27

REFERENCES

Amershi, A., and P. Cheng. 1990. Intrafirm resource allocation: The economies of transferpricing and cost allocation in accounting. Contemporary Accounting Research 7(Fall): 61-99.

Antle, R., and G. Eppen. 1985. Capital rationing and organizational slack in capitalbudgeting. Management Science 31 (February): 163-174.

Baiman, S., and M. Rajan. 1995. Centralization, delegation, and shared responsibility in theassignment of capital investment decision rights. Journal of Accounting Research 33(Supplement): 135-164.

Baldenius, T. 1998. Intrafirm trade, bargaining power, and specific investments. Workingpaper, University of Vienna, Austria.

Bushman, R., R. Indjejikian, and A. Smith. 1995. Aggregate performance measures in businessunit manager compensation: The role of intrafirm interdependencies. Journal ofAccounting Research 33 (Supplement): 101-128.

Christensen, J., and J. Demski. 1996. Transfer pricing in a limited communication setting.Working paper, University of Florida, Gainsville, FL.

Darrough M., and N. Melumad. 1995. Divisional versus company-wide focus: The trade-Offbetween allocation of managerial attention and screening of talent. Journal ofAccounting Research 33 (Supplement): 65-94.

Edlin, A., and S. Reichelstein. 1995. Specific investment under negotiated transfer pricing:An efficiency result. The Accounting Review 70 (April): 275-291.

Feltham, G., and J. Xie. 1994. Performance measure congruity and diversity in multi-taskprincipal/agent relations. The Accounting Review 69 (July): 429-453.

Grossman, S., and O. Hart. 1986. The Costs and benefits of ownership: A theory of verticaland lateral integration. Journal of Political Economy 94 (August): 691-719.

Harris, M., C. Kriebel, and A. Raviv. 1982. Asymmetric information, incentives, and intrafirmresource allocation. Management Science 28 (June): 604-620.

Hart, O. 1995. Firms, Contracts, and Financial Structure. Oxford, U.K.: Claredon Press.

Holmstrom, B., and P. Milgrom. 1987. Aggregation and linearity in the provision ofintertemporal incentives. Econometrica 55 (March): 303-328.

Holmstrom, B., and J. Tirole. 1991. Transfer pricing and organizational form. Journal of Law,Economics, & Organization 7: 201-228.

28

Sahay, S. 1997. Studies in the theory of transfer pricing. Ph.D. dissertation, University ofCalifornia at Berkeley.

Vaysman, I. 1996. A model of cost-based transfer pricing. Review of Accounting Studies 1(March): 73-108.

Williamson, O. 1985. The Economic Institutions of Capitalism. New York, N.Y.: Free Press.

29

Figure 1

Expected Firm Profit and Uncertainty from Divisional TradeOnly Buying Division Has Incentive to Invest

Negotiated transfer

Expected Profits Cost-

based transfer

Unceratinty from divisional trade σu

The figure is generated using the following functional forms:

.205.0)(

,)(

,2)1,(

,25.0)3()2,( 2

iiaiaiV

iaiaiX

qIqC

qqIIqR

∀=

=

=

−+=

All other parameters ( iσ and iρ ) are set equal to one.

0 0.5 1 1.5 2 2.5

9.2

9.4

9.6

9.8

10

30

1 We are primarily interested in factors that influence the trade-off between firm-wide and

divisional performance measures. Thus, we do not consider more disaggregated performance

measures. We simply assume that firms write linear contracts on division profit, firm-wide profit

or a combination of the two.

2 In our analysis, we assume that divisional cash flows are not correlated. Consequently, in the

absence of an investment hold-up problem, there is no need for firm-wide performance

evaluation. In a setting without investment, the optimal linear contract for each manager will be

based only on his or her division profits.

3This scheme can also be implemented in our setting by an asymmetric assignment of decision

rights. For instance, if the buying division is assigned complete authority over the terms of trade,

then it will extract the entire surplus by paying the supplying division its variable costs.

4 See, for instance, Grossman and Hart (1986).

5 Edlin and Reichelstein (1995) do not consider the issue of risk-sharing as the managers are

assumed to be risk neutral. Under the assumption of risk neutrality, compensating divisional

managers on the basis of firm-wide profits alone can also solve the investment hold-up problem.

6 Sahay (1997) shows that a selling division’s investment incentives can be improved by

allowing for markups on variable cost transfers.

7 Other studies examining the tradeoffs between divisional and firm-wide performance evaluation

with risk-averse managers are Bushman et al. (1995), and Darrough and Melumad (1995).

8 While our model deals with investments, it is a one-period model. This means that divisional

and firm profits are reduced by the full cost of investments.

9 In the case where the random variables ie~ and iu~ are normally distributed and contracts are

31

linear, we may derive this function as a certainty equivalent by assuming a utility function given

by )]([ iiii aVSe −−− ρ .

10 See also Feltham and Xie (1994).

11 A formal model that incorporates contracting costs is beyond the scope of this paper. For a

paper that models these costs, see Melumad et al. (1997).

12 Edlin and Reichelstein (1995), Baiman and Rajan (1995), Grossman and Hart (1986), and

Holmstrom and Tirole (1991) make similar assumptions. See Hart (1995) for an overview of the

incomplete contracting literature.

13 This uncertainty can be formally introduced in our model. For example, we may let

111~~

)(ˆ)~

,,( uqICIqC +≡ θθ and 222

22~~

21~

)(ˆ)~

,,( uqqIRIqR +−≡ θθθ , where 0~

>θ is some

common shock that realizes at date 3. Then the optimal quantity is given by

θ~

/))(ˆ)(ˆ(* 12 ICIRq −= , and the contribution margin at the optimal quantity will be

122

12 )](ˆ)(ˆ[21 uuICIR −+− . In this case, the optimal quantity choice is a function of the

stochastic parameter θ~

. Any contract made at date 2, prior to the realization of θ~

, might be

improved through renegotiations at date 3.

14 The results where only the seller invests are analogous to those we derive here. In that case, the

problem resembles the textbook issue of how to motivate a production department to cut costs

when some of those costs are being passed on to another department.

15 When we refer to cost-based transfer pricing, we are interested in any scheme with the

property that the seller is reimbursed for actual production costs. The practice of cost-based

transfer pricing involves the unitization of costs and can encompass many refinements that we do

not characterize here.