summer internship project report on working capital management

TRANSCRIPT

SUMMER INTERNSHIP PROJECT REPORTON

“WORKING CAPITAL MANAGEMENT IN

MARATHON ELECTRIC INDIA PVT. LTD.”

SUBMITTED IN PARTIAL FULFILLMENT

TOWARDS THE AWARD OF

MASTER OF BUSINESS ADMINISTRATION

(2013 – 15)

SUBMITTED BY:

SUNIL KUMAR

University Roll No. : 138410183

MBA II YEAR (IV TRIMESTER)

1

INSTITUTE OF BUSINESS MANAGEMENT

DECLARATION

I SUNIL KUMAR, student of MBA session 2013-2015,

hereby declare that my work entitled “Analysis

ofworking capital management” at Marathon Electric India

Pvt. Ltd. is the outcome of genuine efforts done

by me under an able guidance of MR. MAHESH

NAGPAL (Finance Controller) and been submitted to

the GLA University, (Mathura) as a dissertation in

partial fulfillment for the award of the

degree of Master of Business Administration (MBA)

comprises only my original work and due

toan acknowledgement has been made in the

text to all other material used.

Date: (SUNIL KUMAR)

2

3

4

ACKNOWLEDGEMENTApplication of theoretical knowledge to a practical

situation is the bonanzas of this survey. Without a

proper combination of inspections and perspirations,

it’s not easy to achieve anything. There is always a

sense of gratitude, which we express to others for

help and the needy service they render during

the different phases of our lives. We would do it

as we really wish to express my gratitude

toward all those who have been helpful to us

directly or indirectly during the

development of this training report.

We would like to thank my supervisor Mr. MAHESH

NAGPAL (Finance Controller) who was always there

to help and guide us when we needed help.

His perceptive criticism kept us working

to make this report more full proof. We are

thankful to him for encouraging and valuable

support. Working under his was an extremely

knowledgeable and enriching experience for me.

We are very thankful to him for all the

value additions and enhancement done to me. I

also thanks to our Assist. Professor (Mr.Ankit Saxena) of

GLA University.

No words can adequately express our overriding

debt of gratitude to my parents, whose support5

helps me in all the way. Above all we shall thank

our colleagues who constantly encouraged

and blessed me so as to enable us to do

this work successfully.

EXECUTIVE SUMMERYThe report basically related to the how to

manage working capital in the company. Cash

is the lifeblood of the company without this

company cannot run successfully. In this we find

out the shortfalls of working capital management

and to find out the company liquidity,

profitability we use some tools to analyze

the financial data of the company for some

future plan. For this study, we collect both types

of data primary data, as well as secondary data also. We

use the descriptive method of the research methodology.

6

To complete this summer training report in a

short time my supervisor and my colleagues also

help to me.

INDEX

SR NO. PARTICULARS PAGE NO.

7

I Front Page i

II Declaration ii

III Company certificate Iii

IV Acknowledgement iv

V Executive Summery v

VI Index vi

1 Chapter – 1About the Company Profile

1 – 10

2 Chapter – 2Introduction to the topic

11 – 19

3 Chapter – 3Objective and Methodology

20 – 25

4 Chapter – 4Data analysis and interpretation

26 – 47

6 Chapter – 5Finding & Conclusions

48 – 50

7 Limitation for further study 51

8 Appendices vii – xi

8

CHAPTER – 1

INTRODUCTION

&

ABOUT

THE COMPANY PROFILE

9

COMPANY PROFILE

Marathon Electric India Pvt. Ltd. Was established in

1913. Since 1913, Marathon Electric has been dedicated to

providing customers with quality products for targeted

applications.

Headquartered:

Wausau, Wisconsin, USA

Regd. Office & Works:

Faridabad (Haryana)

10

Product:

Motors

Nature of business:

Manufacturing & Assembling

Website:

www.marathonelectric.in

INTRODUCTION

In India, Marathon Electric delivers efficient mechanical

power solutions using AC electric motors up to 4.5MW.

Marathon Electric India has manufacturing facilities,

Marathon Electric India Pvt. Ltd. At Faridabad & Marathon

Electric Motors (India) Ltd in Kolkata. Together,

Marathon Electric in India is the Largest Manufacturer &

Exporter of Electric Motors. MEIPL strategic product

lines include Motors and Fans. Our range of Fractional

Horsepower motors serves applications such as Heating,

Ventilating, Air-conditioning & Commercial Refrigeration

(HVAC), General Purpose Applications, Evaporative Coolers

& Cooler Kits, and Washing Machines & Wet Rice Grinders.

MEIPL Integral Horsepower motors range up to 11KV serving

a wide range of applications such as pumps, compressors,11

fans, crushers, conveyors, kilns etc. We also

manufacture Propeller, Axial Flow and Centrifugal Flow

type of industrial fans used for various purposes.

Marathon Electric is part of

Regal Beloit Corporation. The

Regal Beloit Corporation is a

leading manufacturer of

electrical and mechanical motion

control and power generation

products serving markets

throughout the world. Regal

Beloit is headquartered in

Beloit, Wisconsin, and has

manufacturing, sales, and service

facilities throughout North

America and in Mexico, Europe,

and Asia.

Global Technology Center - India (GTCI)

The Global Technology Center (Marathon) - India, also

known as GTCI is located at the ve y heart of the city12

of Hyderabad, the city of pearls. The technology

center is the global hub for Engineering and

Information Technology.

GTCI has world class facilities with Engineering and

IT teams working collaboratively with Regal Beloit

locations globally. This center started its operations

in August 2005. Since then the technological

improvements and world class delivery has made GTCI a

truly competitive advantage for Regal Beloit

Corporation.

Our BrandsMarathon in India is also well known for its brandsGenteq, AUE & Cool Home.

13

Our Products

AC motors, single / Three phase

Cooler motors and Fans

Air Circulator

Wet Rice Grinder

Cage Induction Motors

Roller Table Motors

ECM Motors

14

Fitness Equipment Motors

Marathon Electric – Business units India Headquarter/ MEIPL Faridabad, Haryana

Manufacturing Unit of Fractional Horsepower Motors

MEMIL Kolkata, West Bengal

Manufacturing unit of Integral Horsepower HVAC

Motors

Global Technology Center (Marathon) India –

Hyderabad

The technology center is the global hub of

Engineering and information Technology.

Our Vision

We will clearly differentiate our products and services

as the best value to our customers, as measured by our

customers. We will maintain a sustainable, competitive

advantage through the excellence of our people and our

processes – creating value for all our stakeholders.

Our Mission

We will live our values, demonstrating integrity in all

our actions. We will function with a high level of

15

personal energy, energizing those around us. We will have

the courage to make difficult decisions and execute to

accomplish our vision.

Award and recognitions

Safety Award, 2007

Haryana State Safety and Welfare Awards2007

16

2008 Annual S.A.F.E. Award

Safety Awareness for Employees Award

Award for Export Excellence

ISO 9001:200017

ISO 9001:2008 Certificate from NSF

Award for Excellence in Cost Management

Objectives

To deliver world class performance to customers

through innovation, quality, delivery,

responsiveness and cost.

Develop, attract,& retain the best people by

providing and engaging work environment while

helping them achieves their career goals.

18

Stand top quartile performance in the diversified

industrial sector with respect to revenue growth,

profitability, and cash flow.

Factors of Success

Wide range of motors.

Well advanced manufacturing plant and localization.

Brand value and excellent service after sales.

A developer in FHP motors and hasa major export

marketof India.

80 percent market of market share in India for FHP

motors.

20 percent market share in IHP motors.

19

SWOT Analysis

20

Strength

Innovative products

Largest manufacturing

unit in India

Best technology

Customized product

Indigenous

Weakness

Lack of HRD measure

to retain skilled

professional

Complex organization

structure

Pricing of products

Opportunities

Power sector growth

in India

Global opportunities

Threats

Flood of imports from

china

New competitors

SME built duplicate

products

CHAPTER – 2

INTRODUCTION,

OBJECTIVE AND SCOPE OF STUDY

21

INTRODUCTION

Meaning of Capital

In the ordinary sense of the word capital means an

initial investment invested by a businessman or owner at

the time of commencing the business.

Introduction of Working Capital

It describes about how the company manages its working

capital and the various steps that are required in the

management of working capital.

Cash is the lifeline of a company. If this lifeline

deteriorates, so does the company’s ability to fund

operations, reinvest, and meet capital requirements and

payments. Understanding a company’s cash flow prospects

is to look at its Working Capital Management.

Thus, in very simple words, working capital may be

defined as “capital invested in current assets.” Here

current assets are those assets, which can be converted22

into cash within a short period of time and the cash

received is again invested in these assets. Thus, it is

constantly receiving or circulating. Hence, working

capital is also known as circulating capital or floating

capital.

Meaning of working capital

Working capital means the funds (i.e., capital) available

and used for day to day operation (i.e.; working) of a

company. In Accounting

Working Capital = Current Assets – CurrentLiabilities

Definition of working capital

According to Weston & Brigham

“Working capital refers to a firm’s investment

in short term assets - cash, short term securities,

account receivable, and inventories.”

According to Mead Mallett& Field

“Working capital means currentassets”

The project describes how the management of working

capital takes place at Marathon Electric India Pvt. Ltd.

Classification of working capital

Working capital can be classified are as follows-

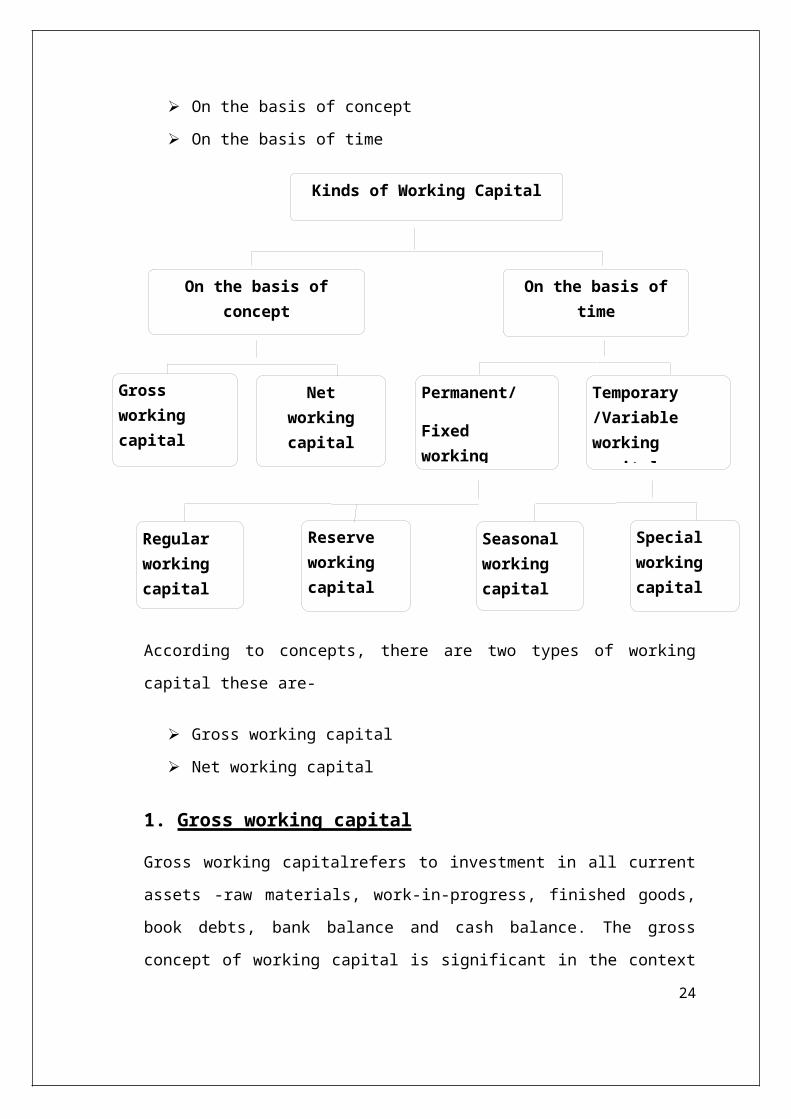

23

On the basis of concept

On the basis of time

According to concepts, there are two types of working

capital these are-

Gross working capital

Net working capital

1. Gross working capital

Gross working capitalrefers to investment in all current

assets -raw materials, work-in-progress, finished goods,

book debts, bank balance and cash balance. The gross

concept of working capital is significant in the context

24

On the basis ofconcept

Gross working capital

On the basis oftime

Networkingcapital

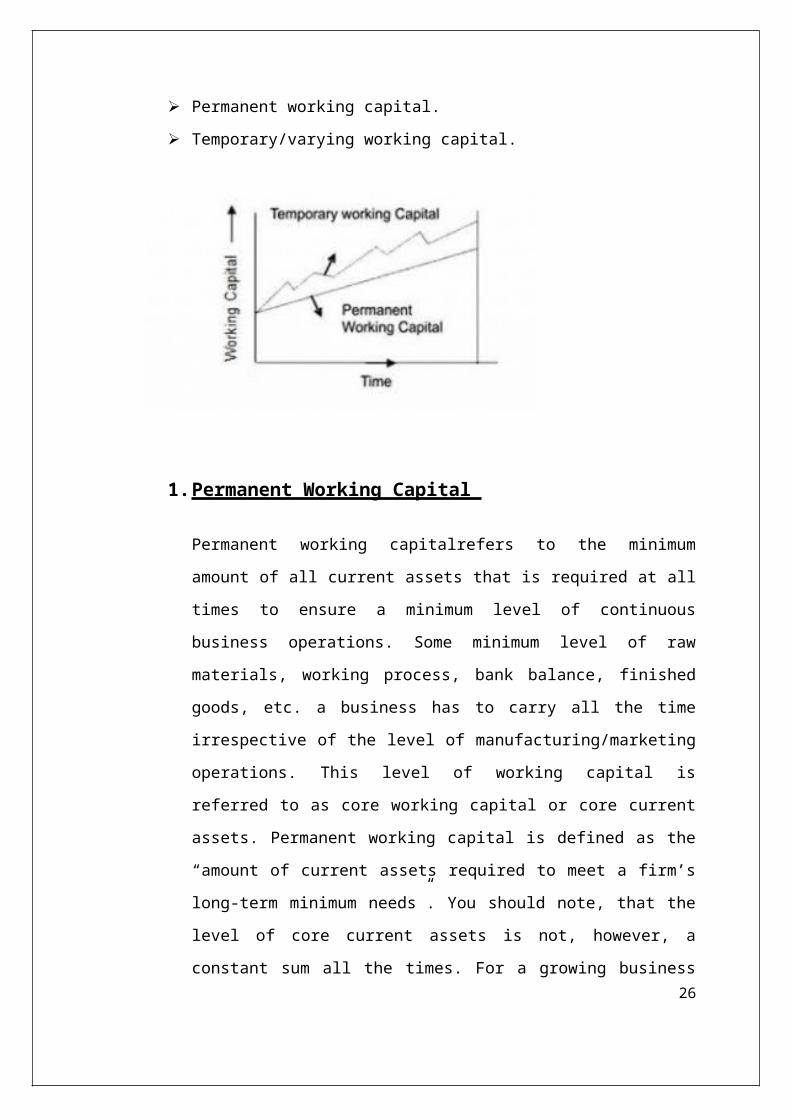

Kinds of Working Capital

Permanent/

Fixed working

Temporary /Variable working capital

Regular working capital

Reserve working capital

Seasonal working capital

Special working capital

of measuring working capital needed, measuring the size

of the business, continued and smooth flow of operations

of the business and the like.

2. Net working capital

Net working capitalrefers to the excess of current assets

over current liabilities. That is, the value of current

assets minus the value of current liabilities

(currentliabilities includetrade creditors, bills

payable, outstanding expenses such as wages, salaries,

dividend payable and tax payable, bank overdraft, etc.)

The net concept of working capital is significant in the

context of financing of working capital, the short term

liquidity aspects of the business, and the like.

Net working capital may be positive or negative. A

positive net working capital arises when current assets

exceed current liabilities and a negative working capital

occurs when current liabilities are in excess of current

assets. It shows bad liquidity position. This is a

qualitative concept which highlights the character of the

sources from which the funds have been procured to

support that portion of the current assets which is in

excess of current liabilities.

According to time there are two kinds of working

capital. These are-

25

Permanent working capital.

Temporary/varying working capital.

1.Permanent Working Capital

Permanent working capitalrefers to the minimum

amount of all current assets that is required at all

times to ensure a minimum level of continuous

business operations. Some minimum level of raw

materials, working process, bank balance, finished

goods, etc. a business has to carry all the time

irrespective of the level of manufacturing/marketing

operations. This level of working capital is

referred to as core working capital or core current

assets. Permanent working capital is defined as the

“amount of current assets required to meet a firm’s

long-term minimum needs”. You should note, that the

level of core current assets is not, however, a

constant sum all the times. For a growing business26

the permanent working capital will be rising, for a

declining business it will be decreasing and for a

stable business it will be remaining more, or

lessstay-put. So permanent working capital

perennially needs one though not fixed in volume.

This part of the working capital being a permanent

investment needs to be financed through long-term

funds.Depending upon the changes inthe production

and sales, the need for working capital, over and

above the permanent working capital, will fluctuate.

Initial Working Capital :In the initial period ofits operation, a firm must need enough money to pay

certain expenses before the business profits. In the

initial years the banks may not funding loans or

overdrafts, sales may have to be made on credit and

it may be necessary to pay the creditors

immediately. Therefore the owners themselves have to

provide the necessary funds in the initial period,

which may be known as initial working capital.

Regular Working Capital : The firm is always

required to keep certain funds with it to continue

the regular business operations, which is called as

Regular Working Capital. It is required to maintain

regular stock of raw materials and work-in-progress

and also of the finished goods, which must be

maintained permanently at a definite level. Regular

27

working capital is the excess of current assets over

current liabilities. It ensures smooth operation of

business.

2.Temporary or Variable Working Capital

Temporary or variable working capitalvaries with the

volume of operations. If fluctuates with scale of

operations. This is the additional working capital

required during up sessions over the above the fixed

working capital. During seasons more production/sales

takeplace, resulting in larger working capital needs.

The reverse is true during off-seasons. As seasons

alternate, temporary working capital moves up and down

like tides. Temporary working capital is defined as the

“amount of current assets that varies with seasonal

requirements”. Temporary working capital can be

financed through short term funds, i.e. current

liabilities. When the level of temporary working

capital moved up, the business might use short-term

funds and when the level of temporary working capital

recedes, the business might retire its short term

loans.

Seasonal Working Capital :Some business

operations require additional working capital during

a particular season. For example, the groundnut oil

producers may have to purchase groundnut in a

28

particular season and have to employ additional

labor for that purpose. These may require additional

funds for a temporary period, which may be called as

seasonal working capital.

Special Working Capital: In all enterprises,

some unforeseen events do occur like a sudden

increase in demand, downward movement of prices of

raw materials, strike, or natural calamities, when

extra funds are needed to tide over such situation.

Such type of extra funds is called as Special

working capital.

Importance of working capital

Working capital is one of the important measurements of

the financial position. The words of H. G. Guthmann

clearly explain the importance of working capital.

“Working Capital is the lifeblood and the nerve center of

the business.” The object of working capital management

is to manage firm’s current assets and liabilities in

such a way that a satisfactory level of working capital

is maintained. If the firm cannot maintain a satisfactory

level of working capital, it is likely to become

insolvent andmay even be forced into insolvency. Thus,

the need for working capital to run day-to-day business

activities smoothly can’t be overstated.

Requirements of working capital

29

There are no set rules or formula to determine the

working capital requirements of the firms. A large number

of factors influence the working capital need of the

firms. All factors are of different importance and also

an important change for the firm over time. Therefore, an

analysis of the relevant factors should be made in order

to determine the total investment in working capital.

Generally the following factors influence the working

capital requirements of the firm:

• Nature and size of the business

• Seasonal fluctuations

• Production policy

• Taxation

• Depreciation policy

• Reserve policy

• Dividend policy

• Credit policy:

• Growth and expansion

• Price level changes

• Operating efficiency

Sources of working capital

30

The financial manager is always interested in obtaining

the working capital at the right time at a reasonable

cost and at the best possible favorable terms. A part of

the working capital investment is a permanent investment

in fixed assets. These following are the various sources

of working capital:-Source of working capital divided

into two parts

Long - term

Short - term

Sources of long term working capital

Issues of share

Floating of debenture

Public deposit

Loans

Sources of short term working capital

Internal source

Depreciation

Taxation

Accrued expense

Ploughing back of profit

External source

Bank credit

Trade credit

Government assistance

Loan from Director

31

Security of employee

Need of working capital

The need for working capital arises due to the time gap

between production and realization of cash from sales.

Working capital is must for every business for purchasing

raw materials, semi-finished goods, stores & spares etc.

and the following purpose

To purchase raw material, spare parts and othercomponents.

To meet overhead expenses.

To hold finished and spare parts etc.

To pay selling and distributing expenses.

To repair& maintenance both machinery as well asfactory built.

To pay wages, salaries and other charges.

To helpful in maintaining uncertainties involved inbusiness fields.

Working capital management

Working capital management means management or

administrating of all aspects of working capital: current

assets and current liabilities.

In other word of Adam Smith; “working capital management

is concerned with the problems that arise in attempting

32

to manage the current assets, current liabilities and the

interrelationship that exist between them”

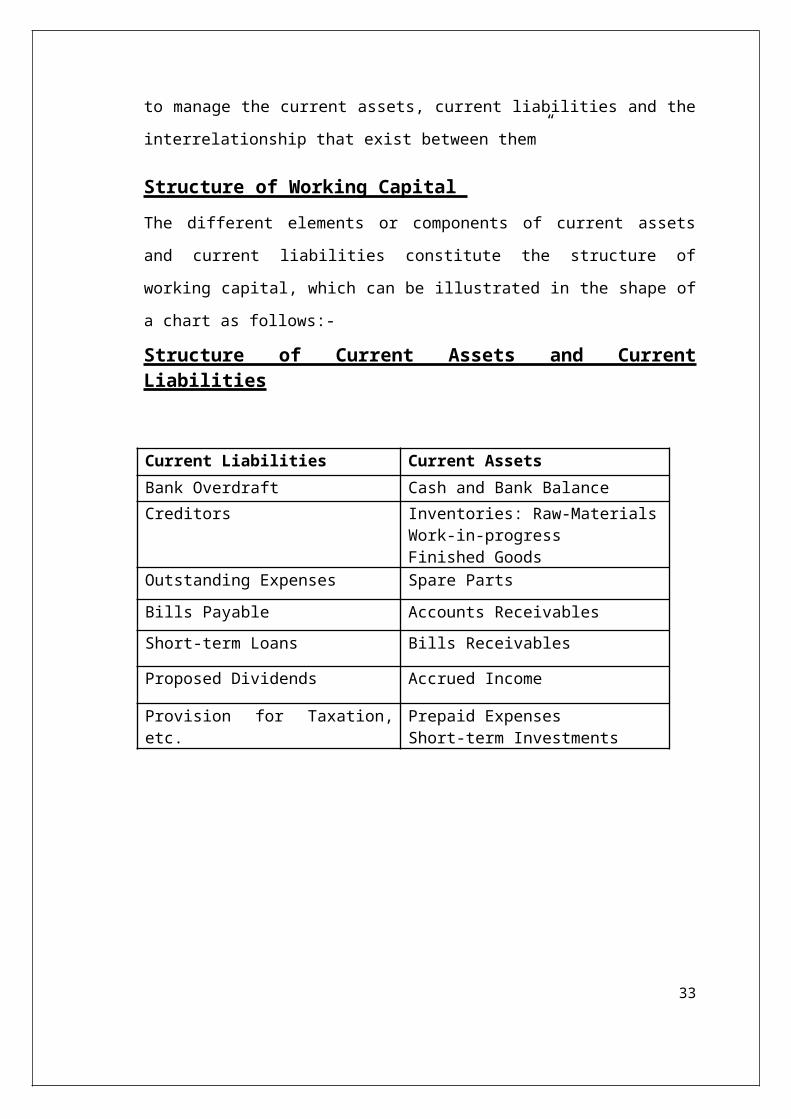

Structure of Working Capital The different elements or components of current assets

and current liabilities constitute the structure of

working capital, which can be illustrated in the shape of

a chart as follows:-

Structure of Current Assets and CurrentLiabilities

Current Liabilities Current AssetsBank Overdraft Cash and Bank BalanceCreditors Inventories: Raw-Materials

Work-in-progressFinished Goods

Outstanding Expenses Spare PartsBills Payable Accounts ReceivablesShort-term Loans Bills Receivables

Proposed Dividends Accrued Income

Provision for Taxation,etc.

Prepaid ExpensesShort-term Investments

33

CHAPTER – 3OBJECTIVE, SCOPE

AND

METHODOLOGY

Need of the Study

34

The need of the study is the important part of the

project. My purpose of doing this study is to find out

the cause of shortage of working capital. Working capital

is the lifeblood and the nerve center of business.

Working capital is very essential to maintain the smooth

running of a business. No business can run successfully

without an adequate amount of working capital. How the

business retain their market share as well as the

goodwill of the company. So that company has to maintain

its cash to run the business and accomplishing their day

to day expenses.

Objective of the study

To study the Working Capital position of Marathon

Electric India Pvt. Ltd.

To study the movement of Working Capital components

( Inventory, Creditor's, Debtor’s )

To evaluate the cash management performance in terms

( Size, Liquidity control ) of Marathon Electric

India Pvt. Ltd.

35

Scope of the study

The scope of study is identified after and during the

study is conducted. The main scope of the study was to

put into practical and theoretical aspect of the study

into real life work experience. The study of working

capital is based on tools like Ratio Analysis, Statement

of change in working capital. Further the study is based

on the last four years, i.e. 2009-2010 to 2012-2013

annual report of Marathon Electric India Pvt. Ltd.

36

INTRODUCTONThe research methodology is a way to systematically solve

the research problem. It may be understood as a science

of studying new research is done systematically. In that

various steps, those are generally adopted by a

researcher in studying his problem along with the logic

behind them.

The procedure by which a researchergoes about their work

of describing, explaining predicting phenomenon is called

methodology.

Research Design

37

A research design is an arrangement of condition for

collection at analysis of data in a manner that combines

relevance to the research purpose with the economy in the

process.

Process of Research

Formulating the objective of the study(What the study

is about and why it is being made)

Designing the method of data collection (What

technique of gathering data will be adopted)

Selecting the sample (How much material will be

needed)

Collecting the data (Where can be required data can

be found and with what time period should the data be

related)

Processing and analysis the data

Reporting and finding

Sampling Design

38

A sample design is a definite plan for obtaining a sample

from a given population. It refers to the technique or

the procedure adopted in selecting items for the sample.

The main constituents of the sampling design below-

Sampling unit

Sample size

Sampling unit

A sampling framework, i.e. developed roe the target

population that will be sampled, i.e. who is to be

surveyed

Sample unit taken by me – Financial statement of the

company

Sample size

It is the substantial portions of the largest population

that are sampled achieve reliable results.

Sample size – the last four years, i.e. 2009-2010 to

2012-2013 financial statements of the company.

A tool used for calculation – MS-Excel.

Data collection

The datahave been collected from two types-39

Primary data

Secondary data

Primary data

Primary data are the data which is collected from first

hand, for the first time which is original in nature.

Secondary data

Secondary data are those data which have already

collected and stored. Secondary data easily get those

secondary data from records annual reports of the

company, etc. It will save the time, money and to collect

the data.

The major source of data of this project was collected

through annual reports, profit and loss account of the

four year period of company, i.e. from 2009-2010 to 2012-

2013 and some more information collected from the

internet and text source.

Tools used for Analysis of data

The data were analyzed using the following tools. They

are-

Ratio Analysis.

40

Statement of changes in working capital.

41

CHAPTER – 4

DATA ANALYSIS

AND

INTERPRETATION

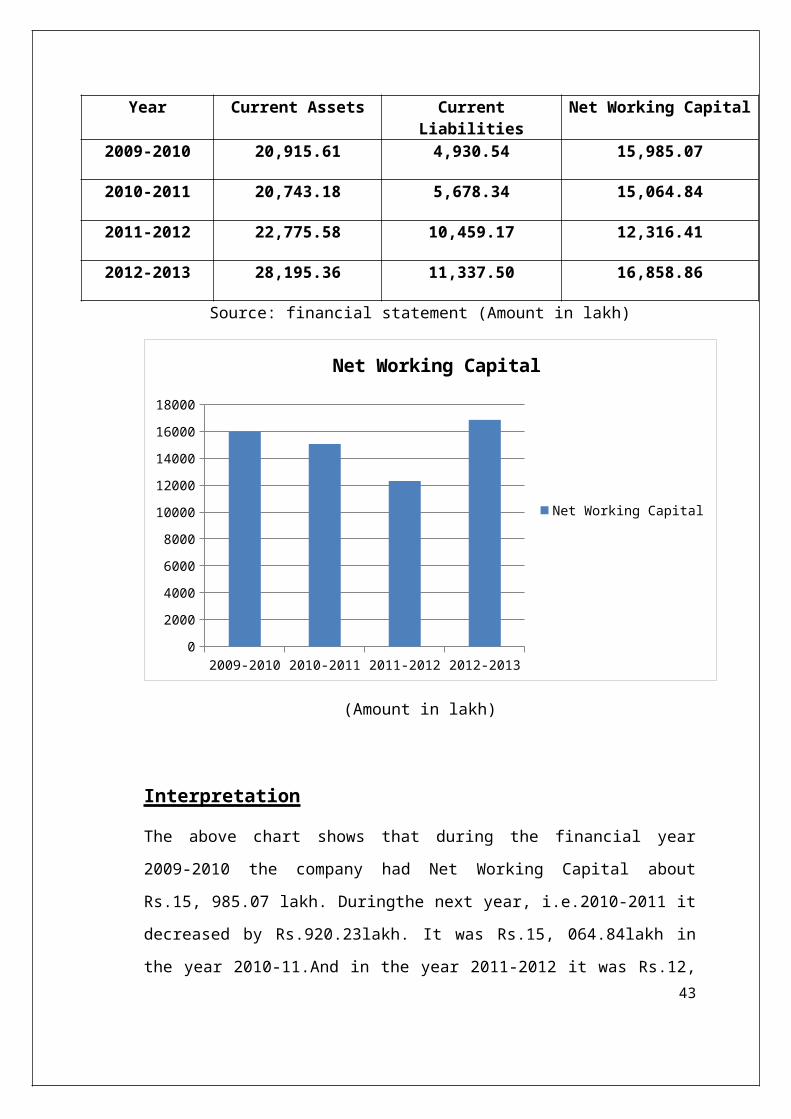

DATA ANALYIS AND INTERPRETATIONAn analysis of working capital will be very helpful for

knowing the operation efficiency of the company. The

following table provides data relating to the net working

capital of MIEPL.

(A) Net Working Capital = Current Assets –Current Liabilities

Table showing Net Working Capital

42

Year Current Assets CurrentLiabilities

Net Working Capital

2009-2010 20,915.61 4,930.54 15,985.07

2010-2011 20,743.18 5,678.34 15,064.84

2011-2012 22,775.58 10,459.17 12,316.41

2012-2013 28,195.36 11,337.50 16,858.86

Source: financial statement (Amount in lakh)

2009-2010 2010-2011 2011-2012 2012-20130

200040006000800010000120001400016000

18000

Net Working Capital

Net Working Capital

(Amount in lakh)

Interpretation

The above chart shows that during the financial year

2009-2010 the company had Net Working Capital about

Rs.15, 985.07 lakh. Duringthe next year, i.e.2010-2011 it

decreased by Rs.920.23lakh. It was Rs.15, 064.84lakh in

the year 2010-11.And in the year 2011-2012 it was Rs.12,43

316.41lakh which again decreased by Rs.2, 748.43 lakh as

compared to last year, i.e. 2011-1012. The above chart

interprets that the company iscontinuingdecrease in the

NWC till 2011-2012. But in the year 2012-2013it was

increased by Rs.4, 542.45 lakh. Duringthis year NWC was

about Rs.16, 858.86 lakh. This means that the company is

in a positive position in the year 2012-2013 and it

hassufficient capital to pay off its current liabilities.

(B) Ratio Analysis

Introduction

Ratio analysis is a powerful tool financial analysis.

Ratio analysis is a process of comparison of one figure

against another, which makes a ratio and the appraisal of

the ratios to make a proper analysis about the strengths

and weakness of the firm’s operations. The term ratio

refers to the numerical or quantitative relationship

between two accounting figures. Ratio analysis of

financial statement stands for the process of determining

and presenting the relationship of items and group of

items in the statements.

44

Types of Ratio Analysis

Liquidity Ratio

Turnover/Activity Ratio

1. Liquidity Ratios

Liquidity refers to the ability of a firm to meet its

current obligations as and when these become due. The

short term obligations are met by realizing amounts of

current, floating, or circulating assets.

Following are the ratios which can help to assess the

ability of a firm to meet its current liabilities

1. Current Ratio

2. Acid Test Ratio /Quick Ratio / Liquidity

Ratio

3. Absolute Liquidity Ratio

2. Turnover / Activity Ratios

These are the ratios which indicate the speed with

which assets are converted or turned over into sales.

1. Inventory Turnover Ratio

2. Debtors/Account receivable Turnover Ratio

3. Creditors/Account payable Turnover Ratio

4. Working Capital Turnover Ratio

45

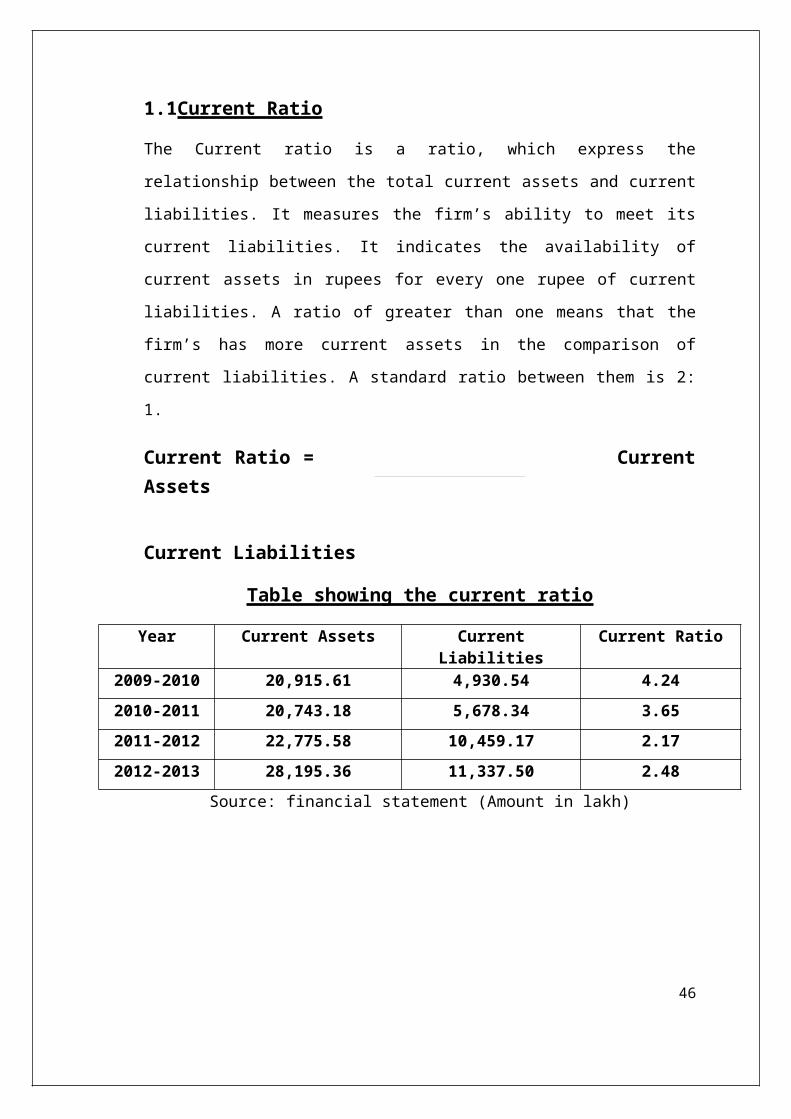

1.1Current Ratio

The Current ratio is a ratio, which express the

relationship between the total current assets and current

liabilities. It measures the firm’s ability to meet its

current liabilities. It indicates the availability of

current assets in rupees for every one rupee of current

liabilities. A ratio of greater than one means that the

firm’s has more current assets in the comparison of

current liabilities. A standard ratio between them is 2:

1.

Current Ratio = CurrentAssets

Current Liabilities

Table showing the current ratio

Year Current Assets CurrentLiabilities

Current Ratio

2009-2010 20,915.61 4,930.54 4.242010-2011 20,743.18 5,678.34 3.652011-2012 22,775.58 10,459.17 2.172012-2013 28,195.36 11,337.50 2.48

Source: financial statement (Amount in lakh)

46

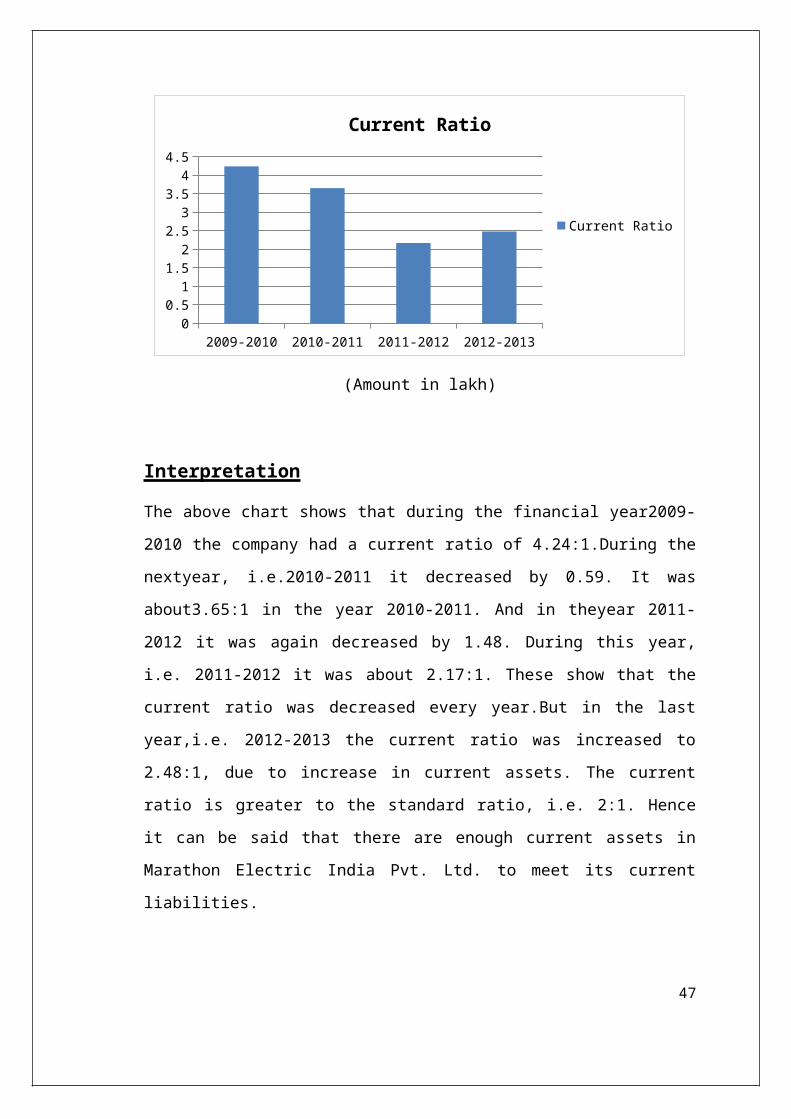

2009-2010 2010-2011 2011-2012 2012-20130

0.51

1.52

2.53

3.54

4.5

Current Ratio

Current Ratio

(Amount in lakh)

Interpretation

The above chart shows that during the financial year2009-

2010 the company had a current ratio of 4.24:1.During the

nextyear, i.e.2010-2011 it decreased by 0.59. It was

about3.65:1 in the year 2010-2011. And in theyear 2011-

2012 it was again decreased by 1.48. During this year,

i.e. 2011-2012 it was about 2.17:1. These show that the

current ratio was decreased every year.But in the last

year,i.e. 2012-2013 the current ratio was increased to

2.48:1, due to increase in current assets. The current

ratio is greater to the standard ratio, i.e. 2:1. Hence

it can be said that there are enough current assets in

Marathon Electric India Pvt. Ltd. to meet its current

liabilities.

47

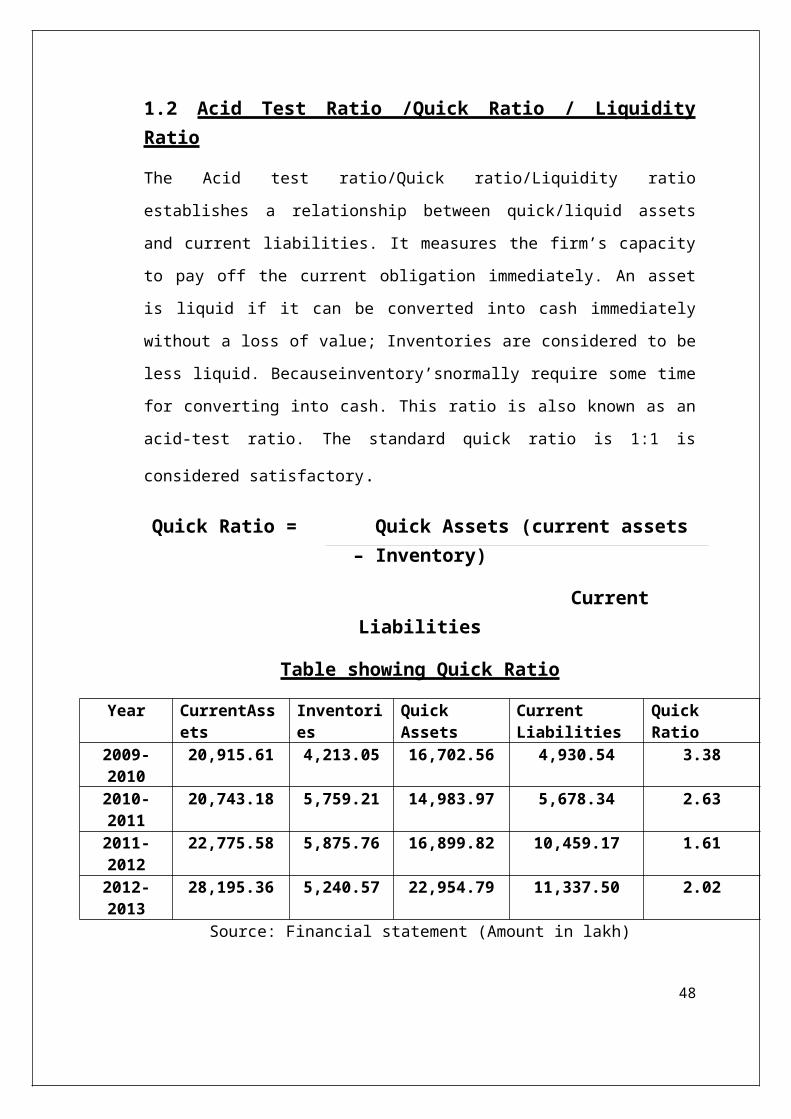

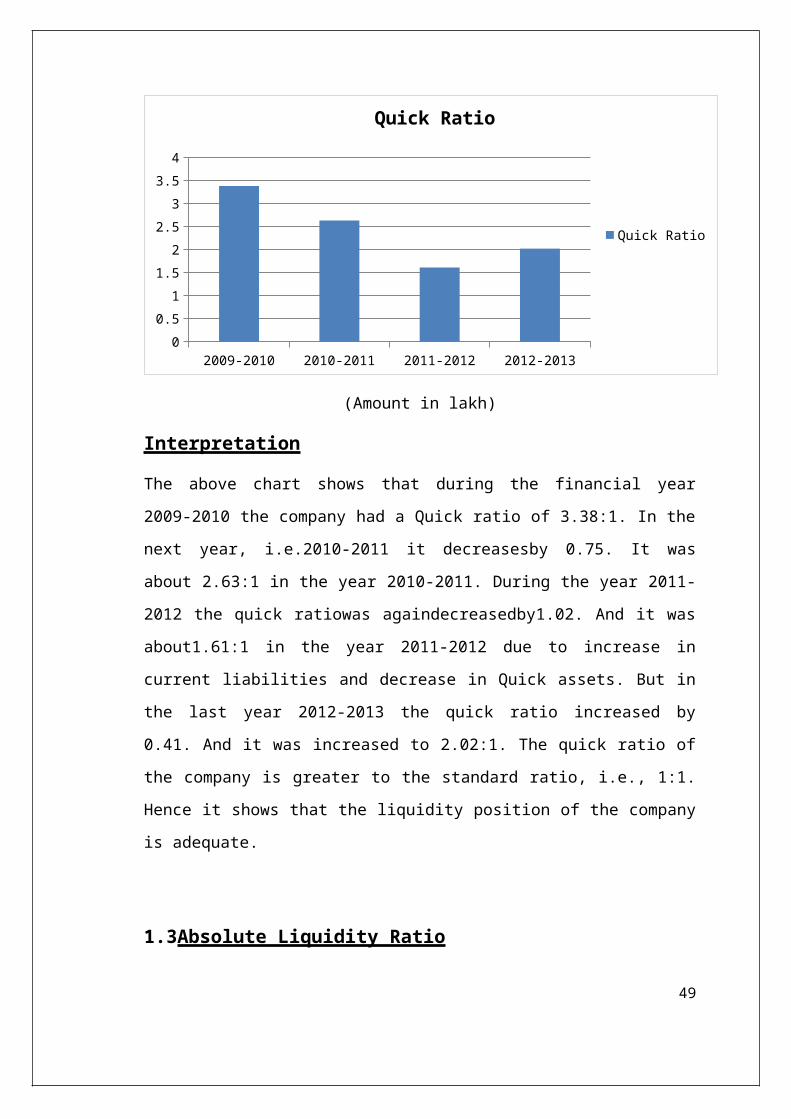

1.2 Acid Test Ratio /Quick Ratio / LiquidityRatio

The Acid test ratio/Quick ratio/Liquidity ratio

establishes a relationship between quick/liquid assets

and current liabilities. It measures the firm’s capacity

to pay off the current obligation immediately. An asset

is liquid if it can be converted into cash immediately

without a loss of value; Inventories are considered to be

less liquid. Becauseinventory’snormally require some time

for converting into cash. This ratio is also known as an

acid-test ratio. The standard quick ratio is 1:1 is

considered satisfactory.

Quick Ratio = Quick Assets (current assets– Inventory)

CurrentLiabilities

Table showing Quick Ratio

Year CurrentAssets

Inventories

Quick Assets

Current Liabilities

Quick Ratio

2009-2010

20,915.61 4,213.05 16,702.56 4,930.54 3.38

2010-2011

20,743.18 5,759.21 14,983.97 5,678.34 2.63

2011-2012

22,775.58 5,875.76 16,899.82 10,459.17 1.61

2012-2013

28,195.36 5,240.57 22,954.79 11,337.50 2.02

Source: Financial statement (Amount in lakh)

48

2009-2010 2010-2011 2011-2012 2012-20130

0.51

1.52

2.53

3.54

Quick Ratio

Quick Ratio

(Amount in lakh)

Interpretation

The above chart shows that during the financial year

2009-2010 the company had a Quick ratio of 3.38:1. In the

next year, i.e.2010-2011 it decreasesby 0.75. It was

about 2.63:1 in the year 2010-2011. During the year 2011-

2012 the quick ratiowas againdecreasedby1.02. And it was

about1.61:1 in the year 2011-2012 due to increase in

current liabilities and decrease in Quick assets. But in

the last year 2012-2013 the quick ratio increased by

0.41. And it was increased to 2.02:1. The quick ratio of

the company is greater to the standard ratio, i.e., 1:1.

Hence it shows that the liquidity position of the company

is adequate.

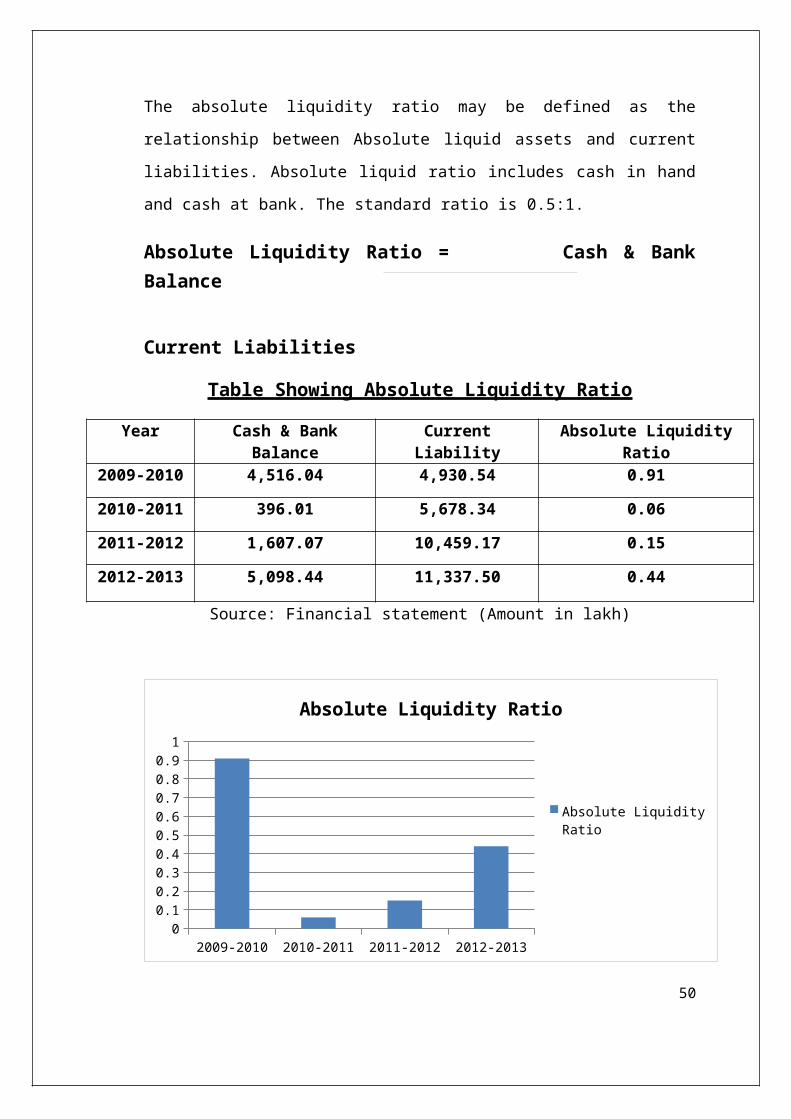

1.3Absolute Liquidity Ratio

49

The absolute liquidity ratio may be defined as the

relationship between Absolute liquid assets and current

liabilities. Absolute liquid ratio includes cash in hand

and cash at bank. The standard ratio is 0.5:1.

Absolute Liquidity Ratio = Cash & BankBalance

Current Liabilities

Table Showing Absolute Liquidity Ratio

Year Cash & BankBalance

CurrentLiability

Absolute LiquidityRatio

2009-2010 4,516.04 4,930.54 0.91

2010-2011 396.01 5,678.34 0.06

2011-2012 1,607.07 10,459.17 0.15

2012-2013 5,098.44 11,337.50 0.44

Source: Financial statement (Amount in lakh)

2009-2010 2010-2011 2011-2012 2012-20130

0.10.20.30.40.50.60.70.80.91

Absolute Liquidity Ratio

Absolute Liquidity Ratio

50

(Amount in lakh)

Interpretation

The above chart shows that during the financial year

2009-2010 the absolute liquidity ratio of the company was

about 0.91:1.In the next year 2010-2011 it decreased by

0.85.It was about 0.06:1, in the year 2010-2011.In the

year2011-2012 absolute liquidity ratio increased by 0.09,

and it was about0.15:1, in the year 2011-2012. In the

last year,i.e. 2012-2013 it increased by 0.29, and it was

about0.44:1. After 2010-2011 the absolute liquidity ratio

of the company is increasingevery year. But besides of

2009-2010 the absolute liquidity ratio of the company is

less thanto the standard rate i.e., 0.5:1. Hence it shows

that the liquidity position of the company is

satisfactory.

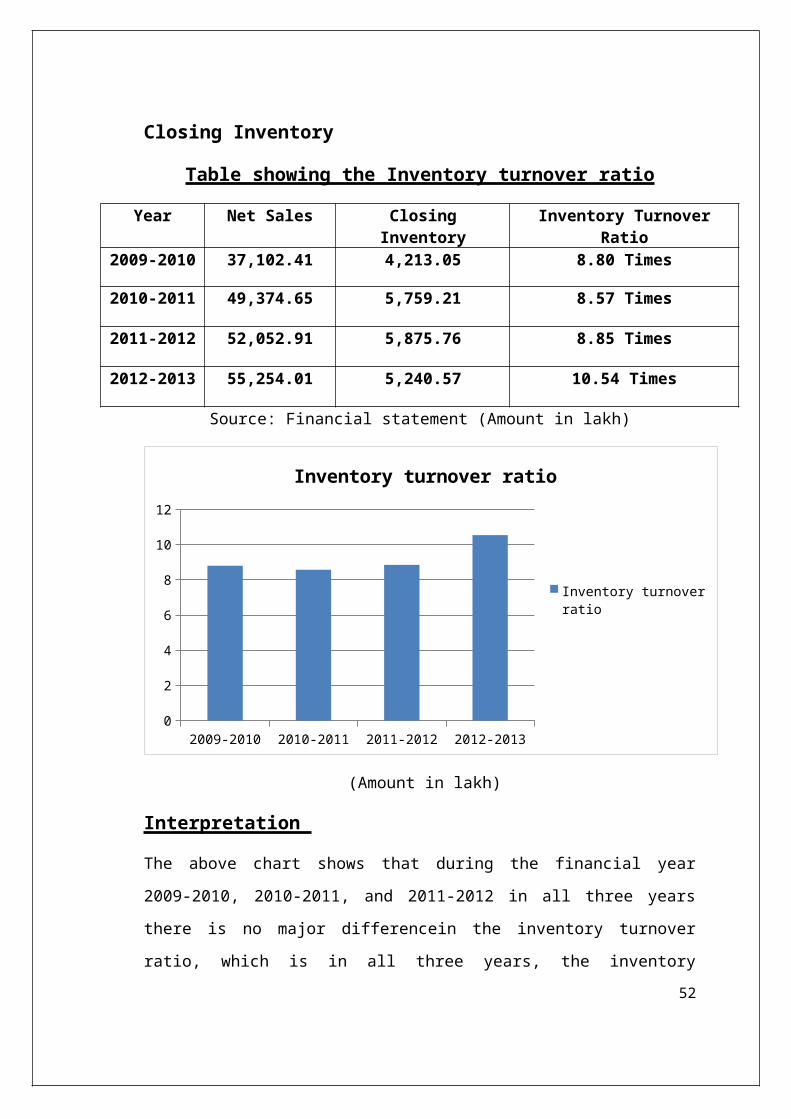

2.1.Inventory Turnover Ratio

The Inventory turnover ratio is the ratio, which

indicates the number of times the stock is turned over

i.e., sales during the year. This measures the efficiency

of the sales and stock levels of the company. A high

ratio means high sales, fast stock turnover, and a low

stock level. A low stock turnover ratio means the

business slows down or with a high stock level.

Inventory Turnover Ratio = Net sales

51

Closing Inventory

Table showing the Inventory turnover ratio

Year Net Sales ClosingInventory

Inventory TurnoverRatio

2009-2010 37,102.41 4,213.05 8.80 Times

2010-2011 49,374.65 5,759.21 8.57 Times

2011-2012 52,052.91 5,875.76 8.85 Times

2012-2013 55,254.01 5,240.57 10.54 Times

Source: Financial statement (Amount in lakh)

2009-2010 2010-2011 2011-2012 2012-20130

2

4

6

8

10

12

Inventory turnover ratio

Inventory turnover ratio

(Amount in lakh)

Interpretation

The above chart shows that during the financial year

2009-2010, 2010-2011, and 2011-2012 in all three years

there is no major differencein the inventory turnover

ratio, which is in all three years, the inventory52

turnover ratio was about 8.80 times,8.57 times, and 8.85

times, respectively.But in the last year, i.e. 2012-2013

it increased by 1.69 times as compared to the previous

year, i.e. 2011-2012. And it was about 10.54 times in the

year 2012-2013. It shows that in all three years the

company had general sales, but in the last year 2012-2013

the company increased in its sales as compared to last

three previous years i.e. 2009-2010, 2010-2011, and 2011-

2012.

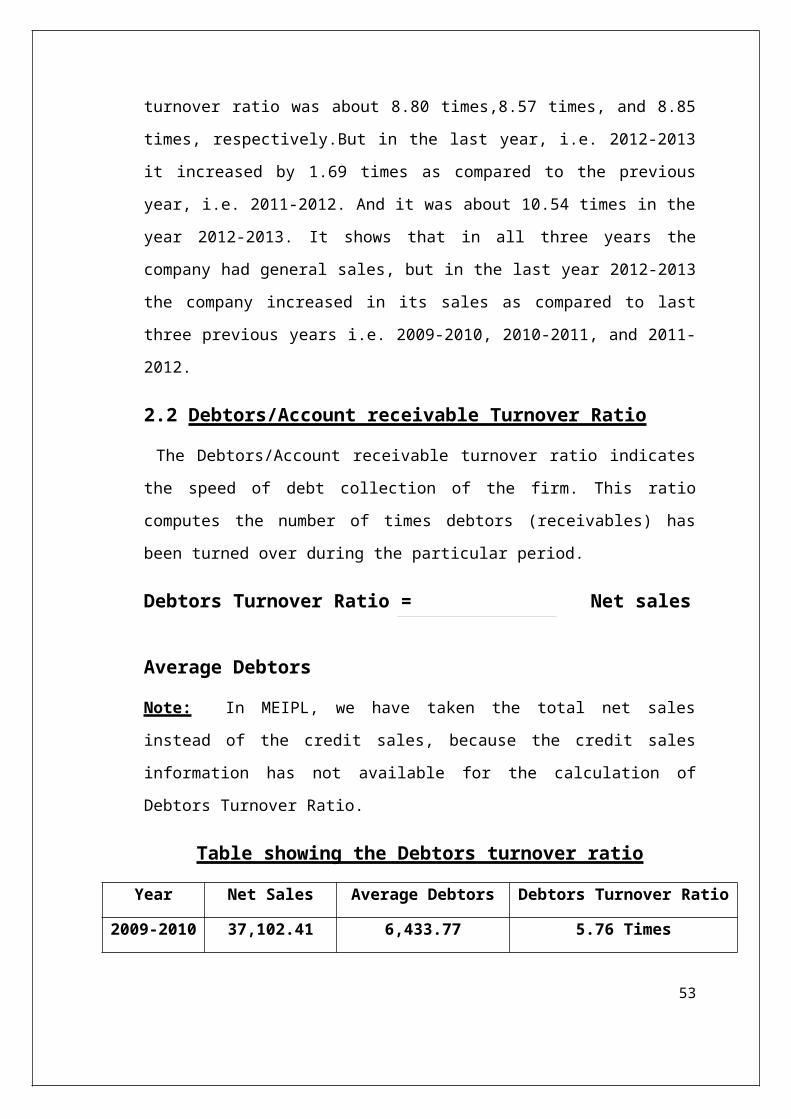

2.2 Debtors/Account receivable Turnover Ratio

The Debtors/Account receivable turnover ratio indicates

the speed of debt collection of the firm. This ratio

computes the number of times debtors (receivables) has

been turned over during the particular period.

Debtors Turnover Ratio = Net sales

Average Debtors

Note: In MEIPL, we have taken the total net sales

instead of the credit sales, because the credit sales

information has not available for the calculation of

Debtors Turnover Ratio.

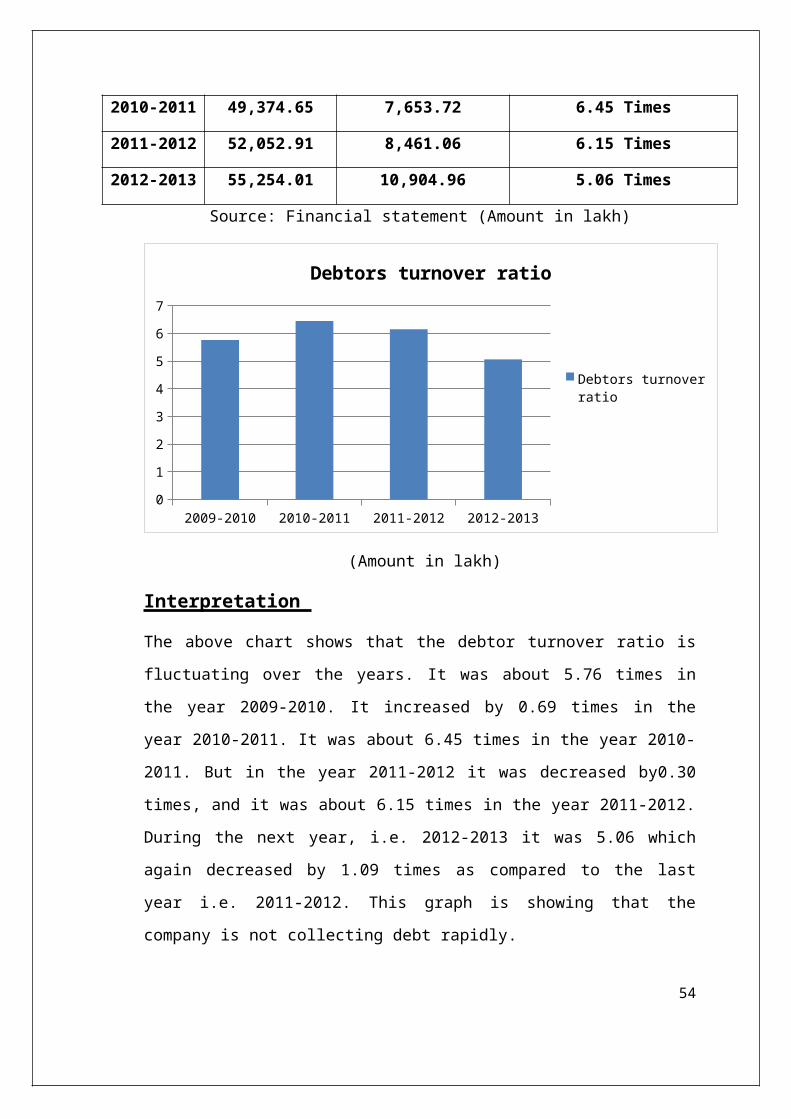

Table showing the Debtors turnover ratio

Year Net Sales Average Debtors Debtors Turnover Ratio

2009-2010 37,102.41 6,433.77 5.76 Times

53

2010-2011 49,374.65 7,653.72 6.45 Times

2011-2012 52,052.91 8,461.06 6.15 Times

2012-2013 55,254.01 10,904.96 5.06 Times

Source: Financial statement (Amount in lakh)

2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

7

Debtors turnover ratio

Debtors turnover ratio

(Amount in lakh)

Interpretation

The above chart shows that the debtor turnover ratio is

fluctuating over the years. It was about 5.76 times in

the year 2009-2010. It increased by 0.69 times in the

year 2010-2011. It was about 6.45 times in the year 2010-

2011. But in the year 2011-2012 it was decreased by0.30

times, and it was about 6.15 times in the year 2011-2012.

During the next year, i.e. 2012-2013 it was 5.06 which

again decreased by 1.09 times as compared to the last

year i.e. 2011-2012. This graph is showing that the

company is not collecting debt rapidly.

54

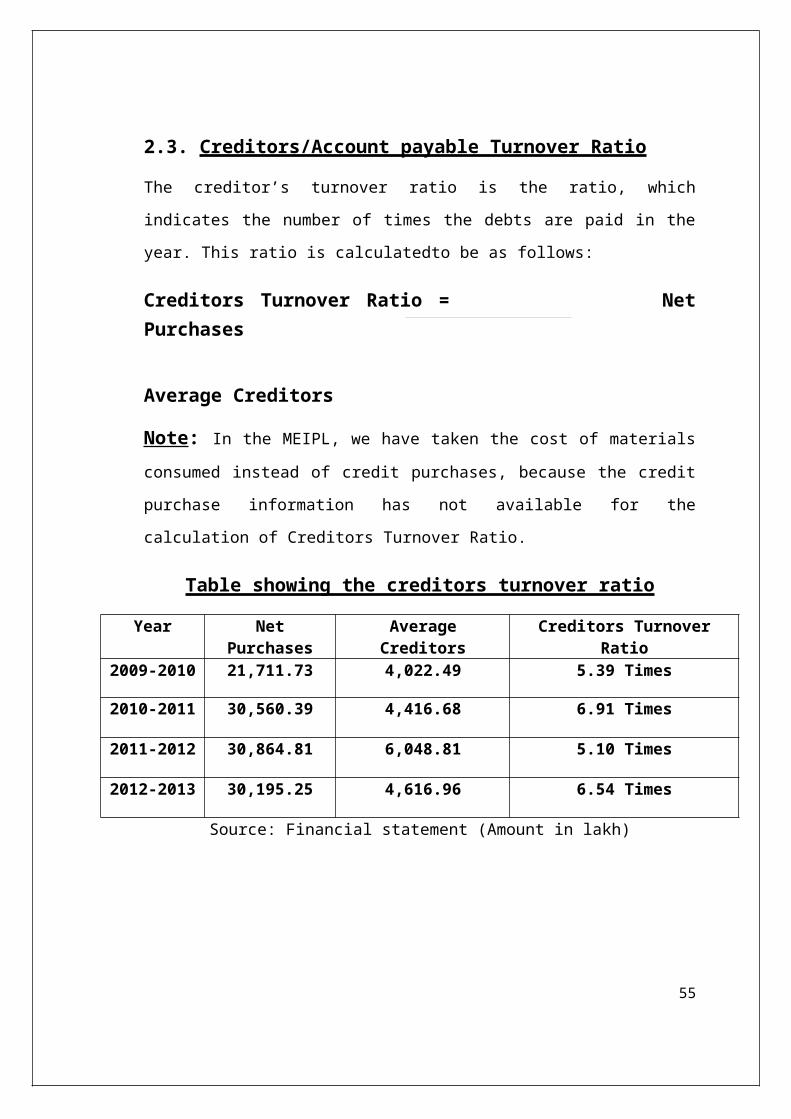

2.3. Creditors/Account payable Turnover Ratio

The creditor’s turnover ratio is the ratio, which

indicates the number of times the debts are paid in the

year. This ratio is calculatedto be as follows:

Creditors Turnover Ratio = NetPurchases

Average Creditors

Note: In the MEIPL, we have taken the cost of materialsconsumed instead of credit purchases, because the credit

purchase information has not available for the

calculation of Creditors Turnover Ratio.

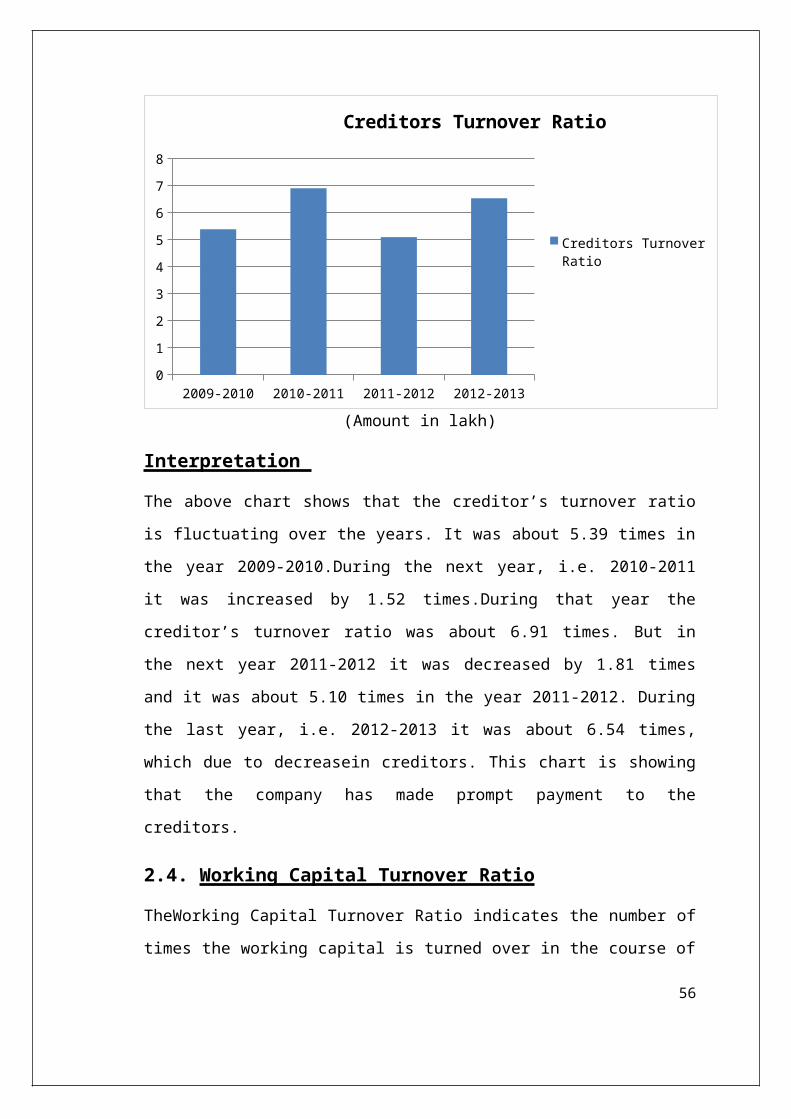

Table showing the creditors turnover ratio

Year NetPurchases

AverageCreditors

Creditors TurnoverRatio

2009-2010 21,711.73 4,022.49 5.39 Times

2010-2011 30,560.39 4,416.68 6.91 Times

2011-2012 30,864.81 6,048.81 5.10 Times

2012-2013 30,195.25 4,616.96 6.54 Times

Source: Financial statement (Amount in lakh)

55

2009-2010 2010-2011 2011-2012 2012-20130

1

2

3

4

5

6

7

8

Creditors Turnover Ratio

Creditors Turnover Ratio

(Amount in lakh)

Interpretation

The above chart shows that the creditor’s turnover ratio

is fluctuating over the years. It was about 5.39 times in

the year 2009-2010.During the next year, i.e. 2010-2011

it was increased by 1.52 times.During that year the

creditor’s turnover ratio was about 6.91 times. But in

the next year 2011-2012 it was decreased by 1.81 times

and it was about 5.10 times in the year 2011-2012. During

the last year, i.e. 2012-2013 it was about 6.54 times,

which due to decreasein creditors. This chart is showing

that the company has made prompt payment to the

creditors.

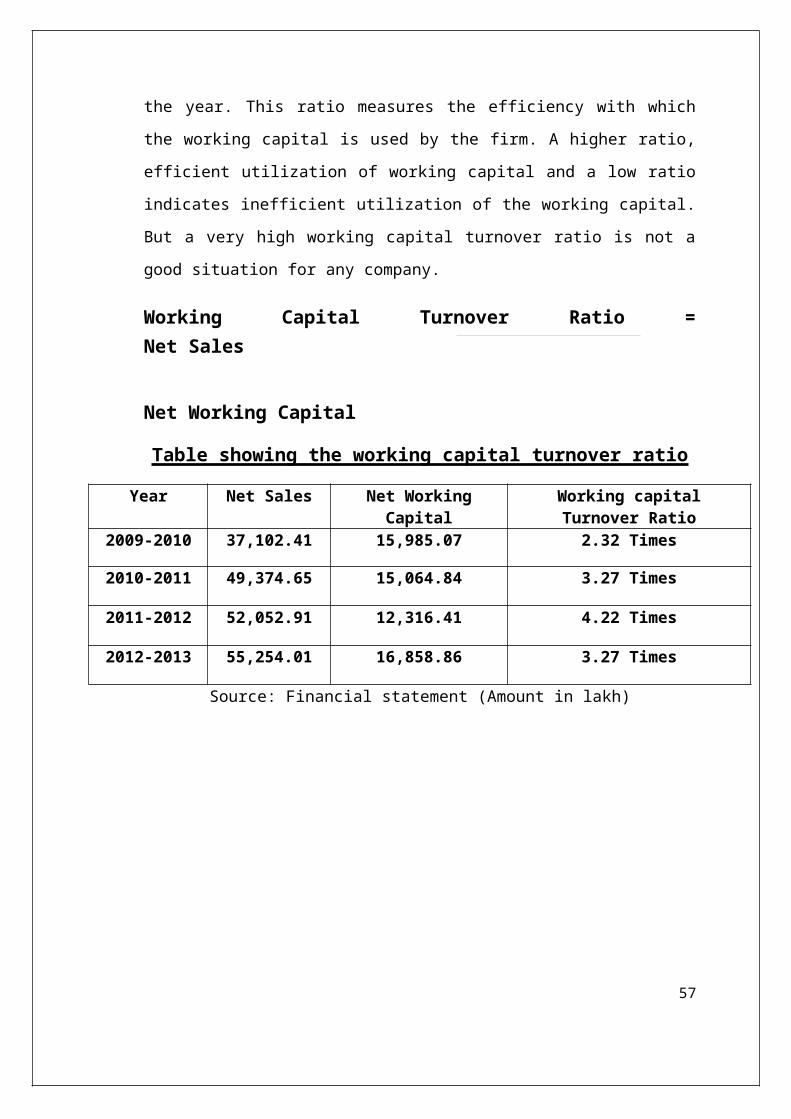

2.4. Working Capital Turnover Ratio

TheWorking Capital Turnover Ratio indicates the number of

times the working capital is turned over in the course of

56

the year. This ratio measures the efficiency with which

the working capital is used by the firm. A higher ratio,

efficient utilization of working capital and a low ratio

indicates inefficient utilization of the working capital.

But a very high working capital turnover ratio is not a

good situation for any company.

Working Capital Turnover Ratio =Net Sales

Net Working Capital

Table showing the working capital turnover ratio

Year Net Sales Net WorkingCapital

Working capitalTurnover Ratio

2009-2010 37,102.41 15,985.07 2.32 Times

2010-2011 49,374.65 15,064.84 3.27 Times

2011-2012 52,052.91 12,316.41 4.22 Times

2012-2013 55,254.01 16,858.86 3.27 Times

Source: Financial statement (Amount in lakh)

57

2009-2010 2010-2011 2011-2012 2012-20130

0.51

1.52

2.53

3.54

4.5

Working Capital Turnover Ratio

Working Capital Turnover Ratio

(Amount in lakh)

Interpretation

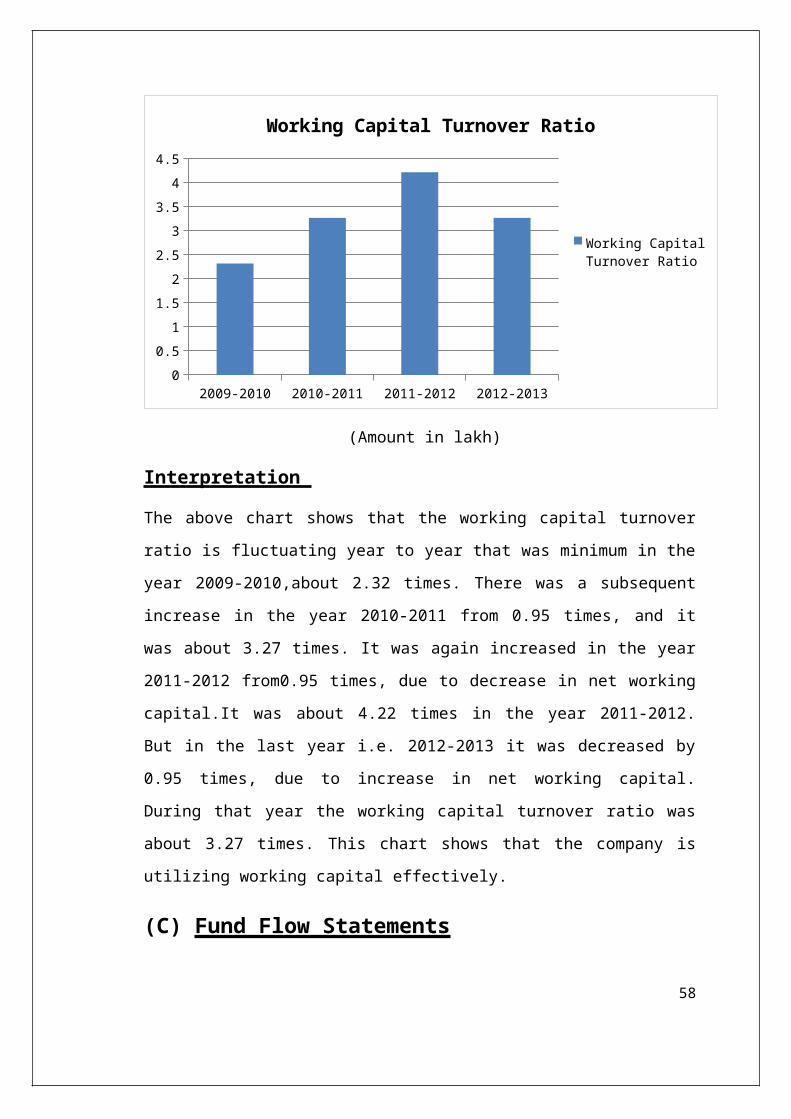

The above chart shows that the working capital turnover

ratio is fluctuating year to year that was minimum in the

year 2009-2010,about 2.32 times. There was a subsequent

increase in the year 2010-2011 from 0.95 times, and it

was about 3.27 times. It was again increased in the year

2011-2012 from0.95 times, due to decrease in net working

capital.It was about 4.22 times in the year 2011-2012.

But in the last year i.e. 2012-2013 it was decreased by

0.95 times, due to increase in net working capital.

During that year the working capital turnover ratio was

about 3.27 times. This chart shows that the company is

utilizing working capital effectively.

(C) Fund Flow Statements

58

Principles of working capital for calculating purposes

Current Assets

If the current assets increase as a result of this,

working capital also increases. If the current assets

decrease as a result of this, working capital also

decreases.

Current liabilities

If the current liabilities increase as a result of this,

working capital also decreases. If the current

liabilities decrease as a result of this, working capital

also increases.

Statement of Change in Working Capital:

The purpose of preparing this statement is for finding

out the increase or decrease in working capital and to

make a comparison between two financial years.

59

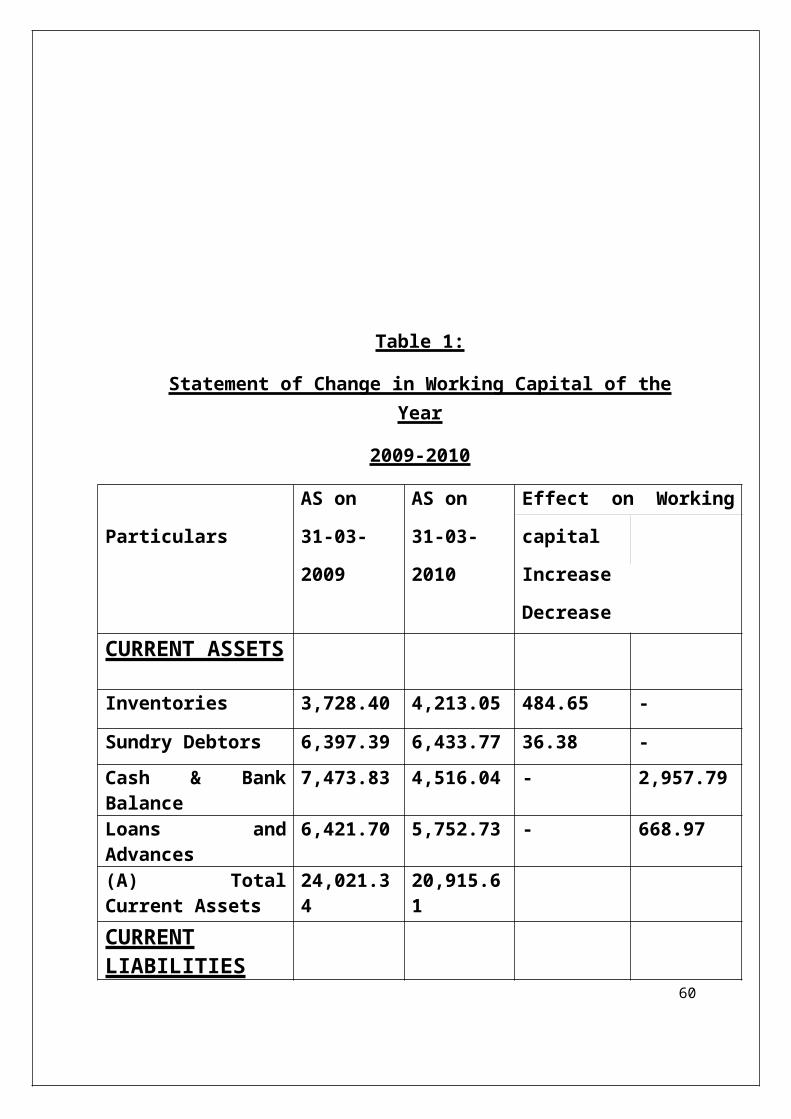

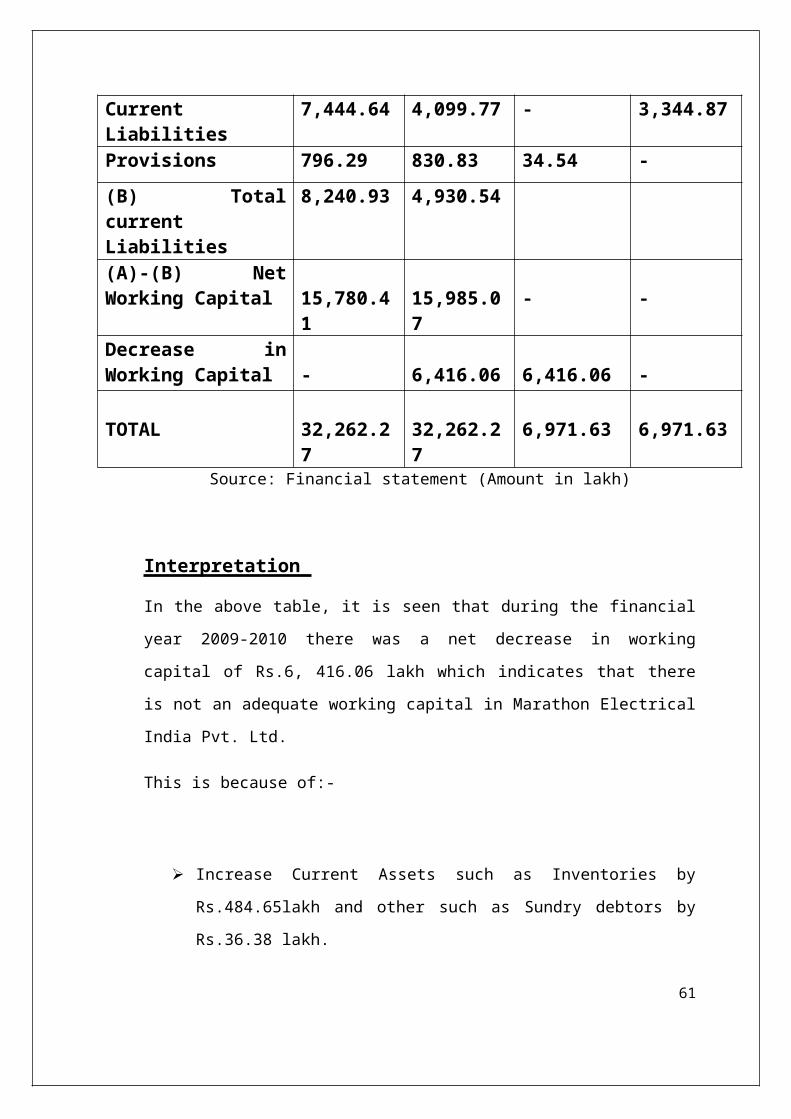

Table 1:

Statement of Change in Working Capital of theYear

2009-2010

Particulars

AS on

31-03-

2009

AS on

31-03-

2010

Effect on Working

capital

Increase

DecreaseCURRENT ASSETS

Inventories 3,728.40 4,213.05 484.65 -

Sundry Debtors 6,397.39 6,433.77 36.38 -Cash & BankBalance

7,473.83 4,516.04 - 2,957.79

Loans andAdvances

6,421.70 5,752.73 - 668.97

(A) TotalCurrent Assets

24,021.34

20,915.61

CURRENTLIABILITIES

60

CurrentLiabilities

7,444.64 4,099.77 - 3,344.87

Provisions 796.29 830.83 34.54 -(B) TotalcurrentLiabilities

8,240.93 4,930.54

(A)-(B) NetWorking Capital 15,780.4

115,985.07

- -

Decrease inWorking Capital - 6,416.06 6,416.06 -

TOTAL 32,262.27

32,262.27

6,971.63 6,971.63

Source: Financial statement (Amount in lakh)

Interpretation

In the above table, it is seen that during the financial

year 2009-2010 there was a net decrease in working

capital of Rs.6, 416.06 lakh which indicates that there

is not an adequate working capital in Marathon Electrical

India Pvt. Ltd.

This is because of:-

Increase Current Assets such as Inventories by

Rs.484.65lakh and other such as Sundry debtors by

Rs.36.38 lakh.

61

Decrease in Cash & Bank Balance by Rs.2, 957.79

lakh. And other current assets such as Loans and

Advances by Rs.668.97 lakh.

Decrease in Current Liabilities by Rs.3, 344.87lakh.

Increase in provisions by Rs.34.54 lakh.

Table 2:

Statement of Change in Working Capital of theYear

2010-2011

62

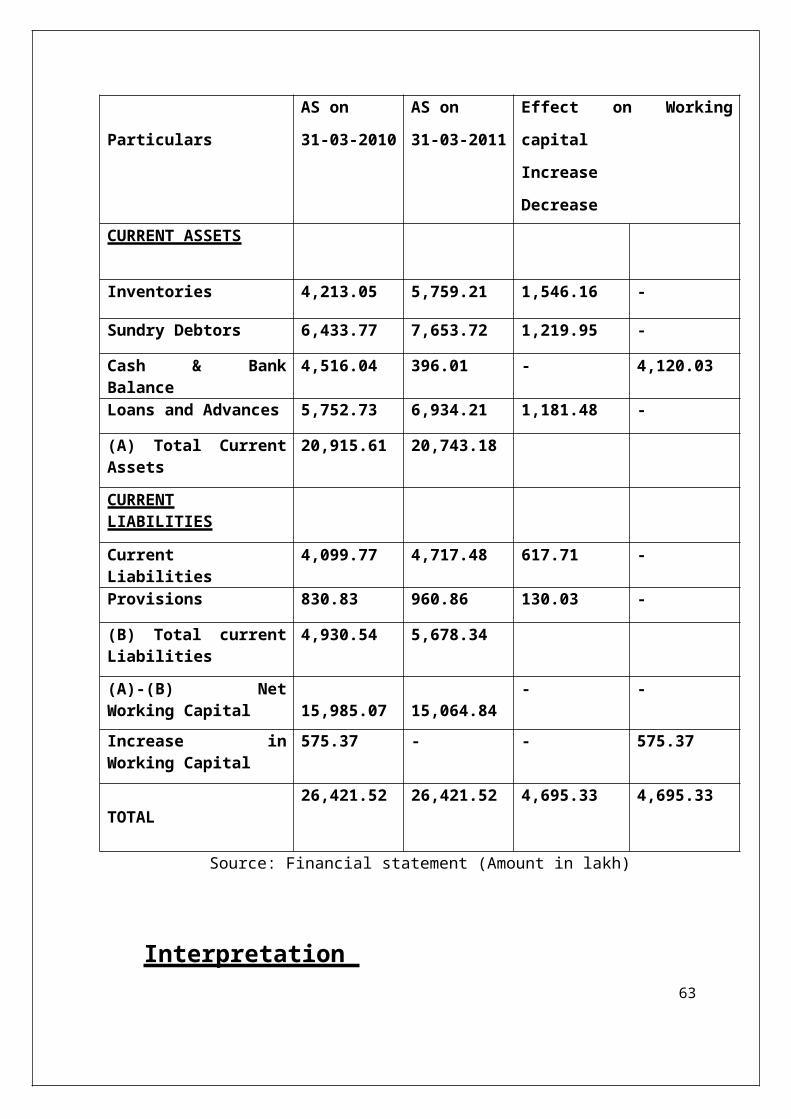

Particulars

AS on

31-03-2010

AS on

31-03-2011

Effect on Working

capital

Increase

DecreaseCURRENT ASSETS

Inventories 4,213.05 5,759.21 1,546.16 -

Sundry Debtors 6,433.77 7,653.72 1,219.95 -

Cash & BankBalance

4,516.04 396.01 - 4,120.03

Loans and Advances 5,752.73 6,934.21 1,181.48 -

(A) Total CurrentAssets

20,915.61 20,743.18

CURRENTLIABILITIES

CurrentLiabilities

4,099.77 4,717.48 617.71 -

Provisions 830.83 960.86 130.03 -

(B) Total currentLiabilities

4,930.54 5,678.34

(A)-(B) NetWorking Capital 15,985.07 15,064.84

- -

Increase inWorking Capital

575.37 - - 575.37

TOTAL26,421.52 26,421.52 4,695.33 4,695.33

Source: Financial statement (Amount in lakh)

Interpretation 63

In the above table, it is seen that during the financial

year 2010-2011 there was a net increase in working

capital of Rs.575.37 lakh. It indicates that an adequate

working capital in Marathon Electrical India Pvt. Ltd.

This is because of:-

Increase in Current Assets such as Inventories by

Rs.1, 546.16 lakh, Sundry debtors by Rs.1, 219.95

lakh, and Loans and advances by Rs.1, 181.48 lakh.

Decrease in Cash and bank balance of Rs.4, 120.03.

Increase in Current Liabilities by Rs 617.71lakh,

and Provisions by Rs.130.03 lakh.

64

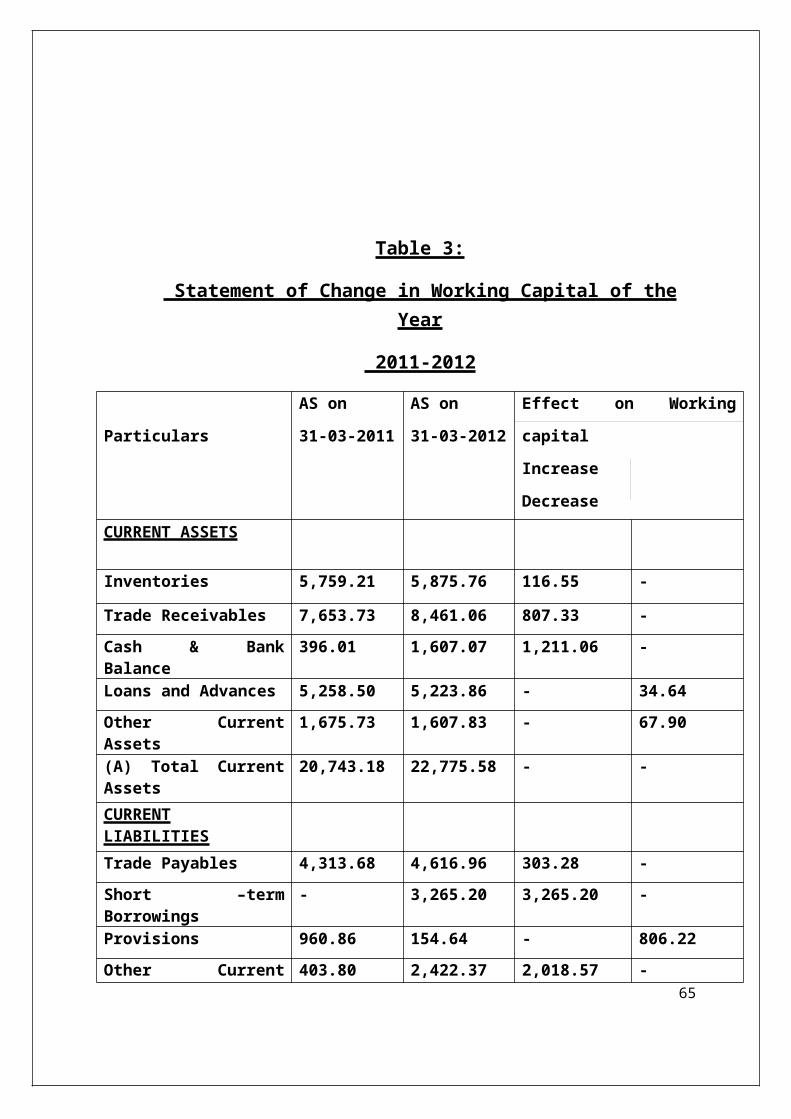

Table 3:

Statement of Change in Working Capital of theYear

2011-2012

Particulars

AS on

31-03-2011

AS on

31-03-2012

Effect on Working

capital

Increase

DecreaseCURRENT ASSETS

Inventories 5,759.21 5,875.76 116.55 -

Trade Receivables 7,653.73 8,461.06 807.33 -Cash & BankBalance

396.01 1,607.07 1,211.06 -

Loans and Advances 5,258.50 5,223.86 - 34.64Other CurrentAssets

1,675.73 1,607.83 - 67.90

(A) Total CurrentAssets

20,743.18 22,775.58 - -

CURRENTLIABILITIESTrade Payables 4,313.68 4,616.96 303.28 -Short –termBorrowings

- 3,265.20 3,265.20 -

Provisions 960.86 154.64 - 806.22Other Current 403.80 2,422.37 2,018.57 -

65

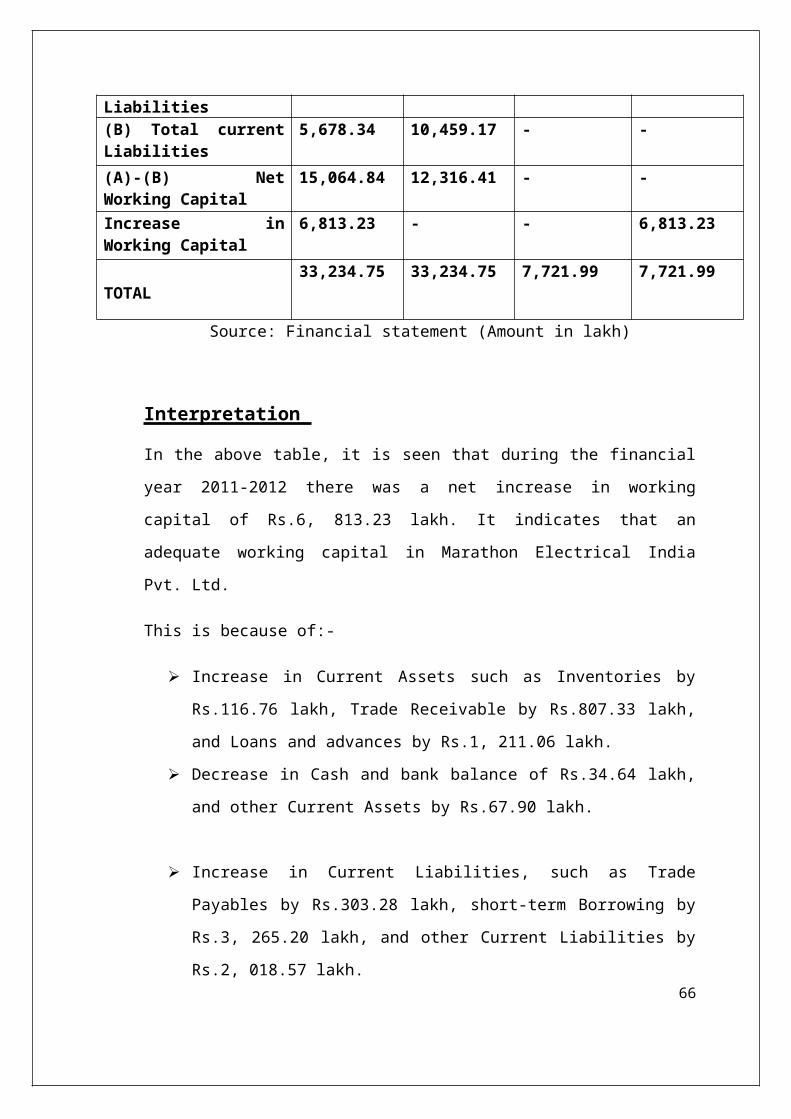

Liabilities(B) Total currentLiabilities

5,678.34 10,459.17 - -

(A)-(B) NetWorking Capital

15,064.84 12,316.41 - -

Increase inWorking Capital

6,813.23 - - 6,813.23

TOTAL33,234.75 33,234.75 7,721.99 7,721.99

Source: Financial statement (Amount in lakh)

Interpretation

In the above table, it is seen that during the financial

year 2011-2012 there was a net increase in working

capital of Rs.6, 813.23 lakh. It indicates that an

adequate working capital in Marathon Electrical India

Pvt. Ltd.

This is because of:-

Increase in Current Assets such as Inventories by

Rs.116.76 lakh, Trade Receivable by Rs.807.33 lakh,

and Loans and advances by Rs.1, 211.06 lakh.

Decrease in Cash and bank balance of Rs.34.64 lakh,

and other Current Assets by Rs.67.90 lakh.

Increase in Current Liabilities, such as Trade

Payables by Rs.303.28 lakh, short-term Borrowing by

Rs.3, 265.20 lakh, and other Current Liabilities by

Rs.2, 018.57 lakh.66

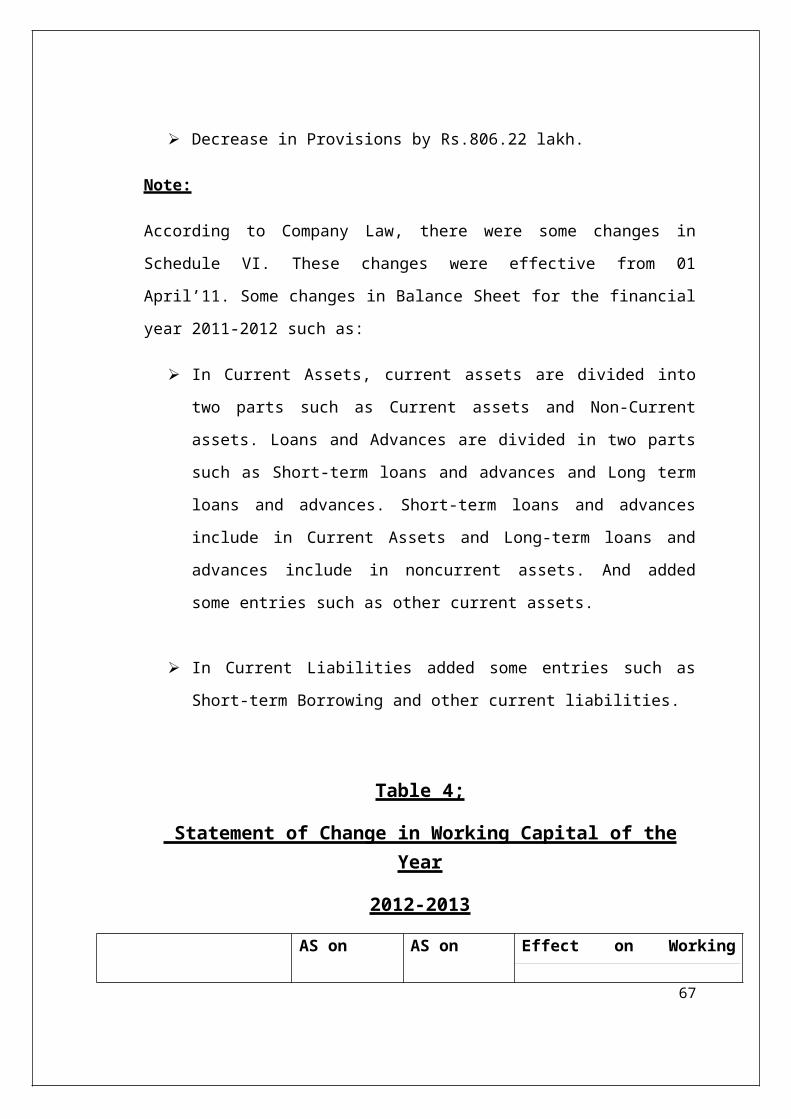

Decrease in Provisions by Rs.806.22 lakh.

Note:

According to Company Law, there were some changes in

Schedule VI. These changes were effective from 01

April’11. Some changes in Balance Sheet for the financial

year 2011-2012 such as:

In Current Assets, current assets are divided into

two parts such as Current assets and Non-Current

assets. Loans and Advances are divided in two parts

such as Short-term loans and advances and Long term

loans and advances. Short-term loans and advances

include in Current Assets and Long-term loans and

advances include in noncurrent assets. And added

some entries such as other current assets.

In Current Liabilities added some entries such as

Short-term Borrowing and other current liabilities.

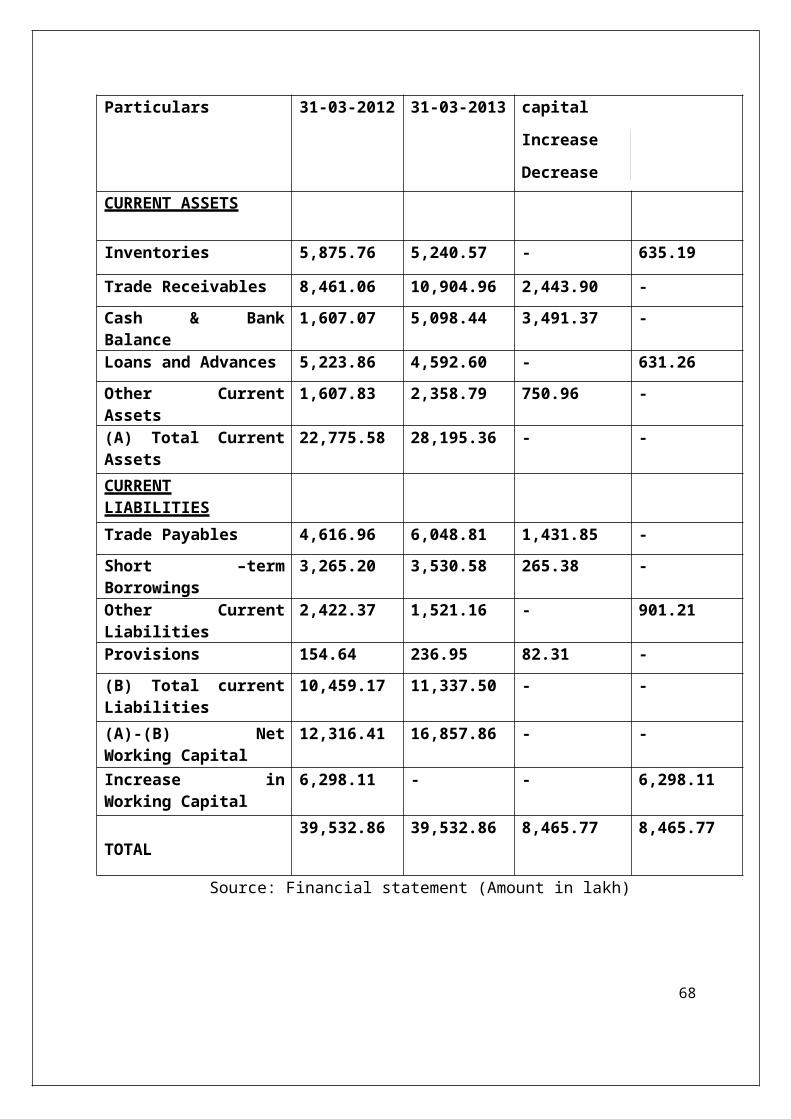

Table 4;

Statement of Change in Working Capital of theYear

2012-2013

AS on AS on Effect on Working

67

Particulars 31-03-2012 31-03-2013 capital

Increase

DecreaseCURRENT ASSETS

Inventories 5,875.76 5,240.57 - 635.19

Trade Receivables 8,461.06 10,904.96 2,443.90 -Cash & BankBalance

1,607.07 5,098.44 3,491.37 -

Loans and Advances 5,223.86 4,592.60 - 631.26Other CurrentAssets

1,607.83 2,358.79 750.96 -

(A) Total CurrentAssets

22,775.58 28,195.36 - -

CURRENTLIABILITIESTrade Payables 4,616.96 6,048.81 1,431.85 -Short –termBorrowings

3,265.20 3,530.58 265.38 -

Other CurrentLiabilities

2,422.37 1,521.16 - 901.21

Provisions 154.64 236.95 82.31 -(B) Total currentLiabilities

10,459.17 11,337.50 - -

(A)-(B) NetWorking Capital

12,316.41 16,857.86 - -

Increase inWorking Capital

6,298.11 - - 6,298.11

TOTAL39,532.86 39,532.86 8,465.77 8,465.77

Source: Financial statement (Amount in lakh)

68

Interpretation

In the above table, it is seen that during the financial

year 2012-2013 there was net increasing in working

capital of Rs.6, 298.11 lakh. It indicates that an

adequate working capital in Marathon Electrical India

Pvt. Ltd.

This is because of:-

Increase in Current Assets such as Trade Receivable

by Rs.2, 443.90 lakh, Cash, and bank balance of

Rs.3, 491.37 lakh. And other Current Assets by

Rs.750.96 lakh.

Decrease in Current Assets such as Inventories by

Rs.635.19 lakh, and Loans and advances by Rs.631.26

lakh.

Increase in Current Liabilities, such as Trade

Payables by Rs.1, 431.85 lakh, Short-term Borrowing

by Rs.265.38 lakh, and Provisions by Rs.82.31lakh.

Decrease in other Current Liabilities by Rs.901.21

lakh.

69

CHAPTER – 5FINDINGS

AND 70

CONCLUSIONS

FINDINGS Working capital of Marathon Electric India Pvt. Ltd

was decreasing every year showing the negative

working capital, besides of 2012-2013. After that

the company is higher than standard rate, i.e. 2:1,

and the position of the company is satisfactory.

The Marathon Electric India Pvt. Ltd. hada higher

Current ratio being 4.24:1 and Quick ratio was

3.38:1.

The MEIPL hadan Absolute liquidity ratiovery low in

the year 2010-2011. During the next year, it was

71

increased by 0.09 times as compared to 2010-2011.

And in the last year, i.e. 2012-2013 it was again

increased.

The MEIPL had an inventory turnover ratio very low

in the year 2010-2011. During the next year, it was

increased by 0.28 times as compared to 2010-2011.And

in the last year, i.e. 2012-2013 it was again

increased.

The MEIPL had Debtor’s turnover ratio very high in

the year 2010-2011. During the next year, it was

decreased by 0.30 times as compared to 2010-2011.And

in the last year, i.e.2012-2013 it was again

decreased.

The Creditor’s turnover ratio of MEIPL was

fluctuating year to year. It was very high in the

year 2010-2011. During the next year, i.e. 2011-2012

it was decreased by 1.81 times as compared to 2010-

2011. And in the last year 2012-2013 it was again

increased.

The MEIPL hada working capital turnover ratio very

low in the year 2009-2010. During the next two

years, i.e. 2010-2011 & 2011-2012, it was increased

by 0.95 & 0.95 times respectively, as compared to

72

the previous year, i.e.2009-2010. And in the last

year, i.e. 2012-2013 it was decreased by 0.95 times

as compared to the previous year, i.e. 2011-2012.

CONCLUSIONS

The study on working capital management conducted in

Marathon Electric India Pvt. Ltd. to analyze the

financial position of the company. The company’s

financial position is analyzed by using the tool of

financial statements from 2009-2010 to 2012-2013.

The financial status of Marathon Electric India Pvt.

Ltd is good. In the last year i.e., 2012-2013 the

inventory turnover ratio has increased, this is a

good sign for the company.

The company’s liquidity position is not good with

regard to the investment in current assets as there

are adequate funds invested in it.

The company is managing its financial position in a

better way. There is a balance between Current

assets and current liabilities and also current

ratio is always above the standard rate.

Further, Company’s creditor’s turnover ratio is not

so good because of this company may face the

73

shortage of the funds to pay off its debts. To avoid

such situation, companies should use their funds in

a productive way and there should be timely payment

of creditors.

Company net working capital is decreasing, but in

the last year i.e., 2012-2013 it was increased,

still the company is in a better management

position, and the company present status of

maintaining current liabilities and current assets

is satisfactory.

They are able to manage their cash, funds, and

debts. By adopting better management practices, the

company may attain a sound financial position in the

future and will be able to manage its working

capital very effectively and efficiently.

LIMITATIONS OF THE STUDY The study is conducted in very short duration

(summer training).

The analysis is limited to just 4 years of data

study (from 2009 to 2013) for financial analysis.

Limited interaction with the concerned head due to

their busy schedule.

74

The findings of the study are based on the

information retrieved from the selected unit.

Very less information and time spent with the

company staff.

This study is done on the basis of the historical

data not in the actual workplace.

The financial data sensitive in nature the same

could not acquire easily.

Every personhas its own preparation to analyze the

financial data so maybe it varies from person to

person.

The companyhas not provided their financial data

properly because of it is confidential in nature.

75

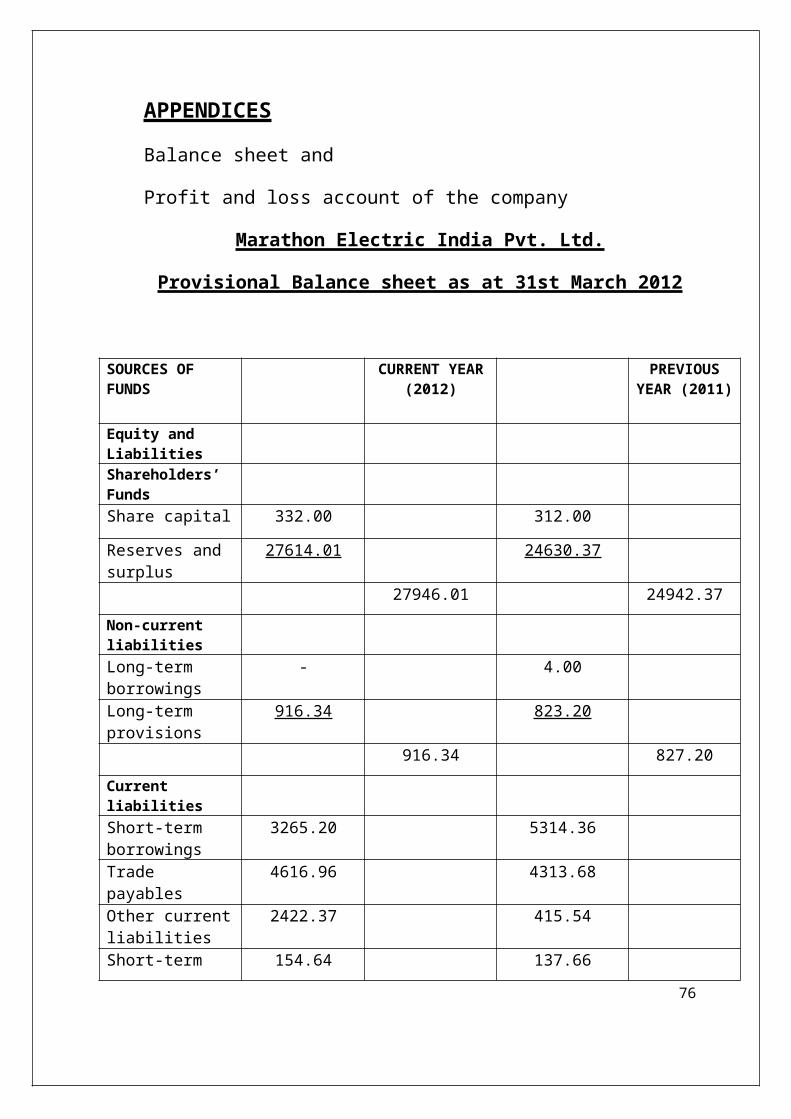

APPENDICES

Balance sheet and

Profit and loss account of the company

Marathon Electric India Pvt. Ltd.

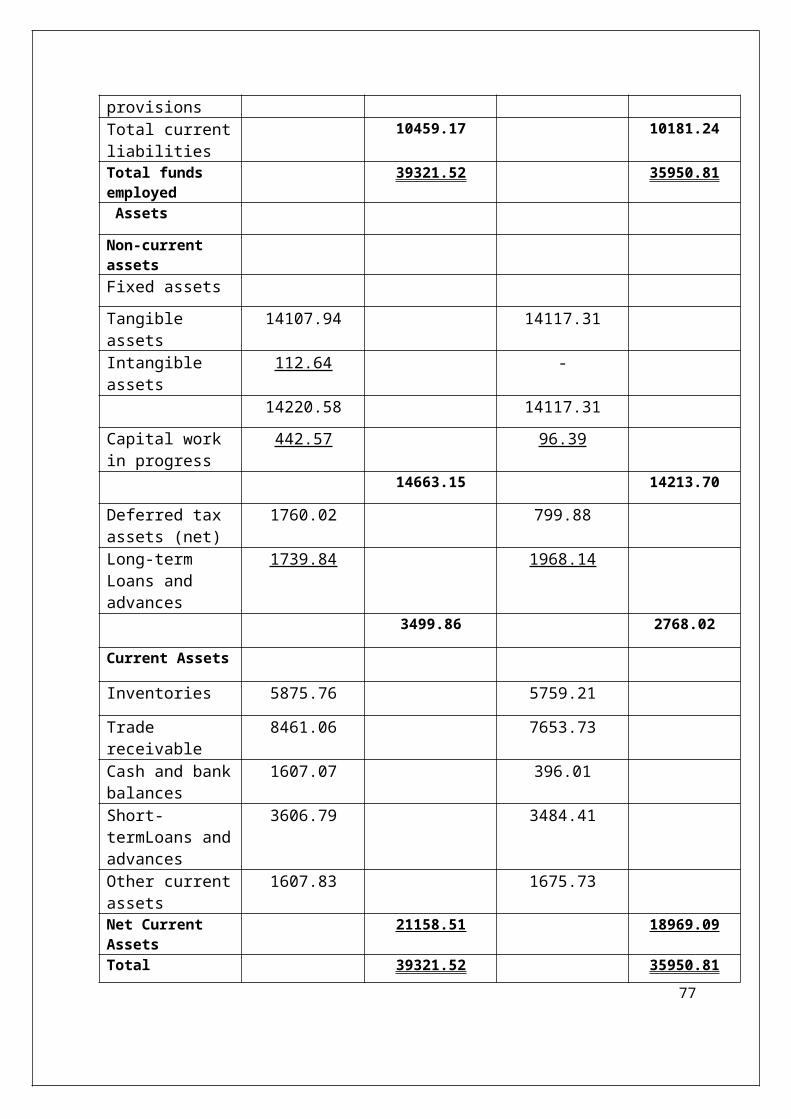

Provisional Balance sheet as at 31st March 2012

SOURCES OF FUNDS

CURRENT YEAR(2012)

PREVIOUSYEAR (2011)

Equity and LiabilitiesShareholders’ FundsShare capital 332.00 312.00

Reserves and surplus

27614.01 24630.37

27946.01 24942.37Non-current liabilitiesLong-term borrowings

- 4.00

Long-term provisions

916.34 823.20

916.34 827.20Current liabilitiesShort-term borrowings

3265.20 5314.36

Trade payables

4616.96 4313.68

Other currentliabilities

2422.37 415.54

Short-term 154.64 137.66

76

provisionsTotal currentliabilities

10459.17 10181.24

Total funds employed

39321.52 35950.81

Assets

Non-current assetsFixed assetsTangible assets

14107.94 14117.31

Intangible assets

112.64 -

14220.58 14117.31Capital work in progress

442.57 96.39

14663.15 14213.70

Deferred tax assets (net)

1760.02 799.88

Long-term Loans and advances

1739.84 1968.14

3499.86 2768.02

Current Assets

Inventories 5875.76 5759.21

Trade receivable

8461.06 7653.73

Cash and bankbalances

1607.07 396.01

Short-termLoans andadvances

3606.79 3484.41

Other currentassets

1607.83 1675.73

Net Current Assets

21158.51 18969.09

Total 39321.52 35950.8177

application ofFunds

Source: Financial statement (Amount in lakh)

Marathon Electric India Pvt. Ltd.

Provisional Balance sheet as at 31st March 2013

SOURCES OF FUNDS

CURRENTYEAR(2013)

PREVIOUSYEAR (2012)

Equity and LiabilitiesShareholders’ FundsShare capital 332.00 332.00

Reserves and surplus

31360.10 27614.01

31692.10 27946.01

Non-current liabilitiesLong-term provisions

994.90 916.34

994.90 916.34

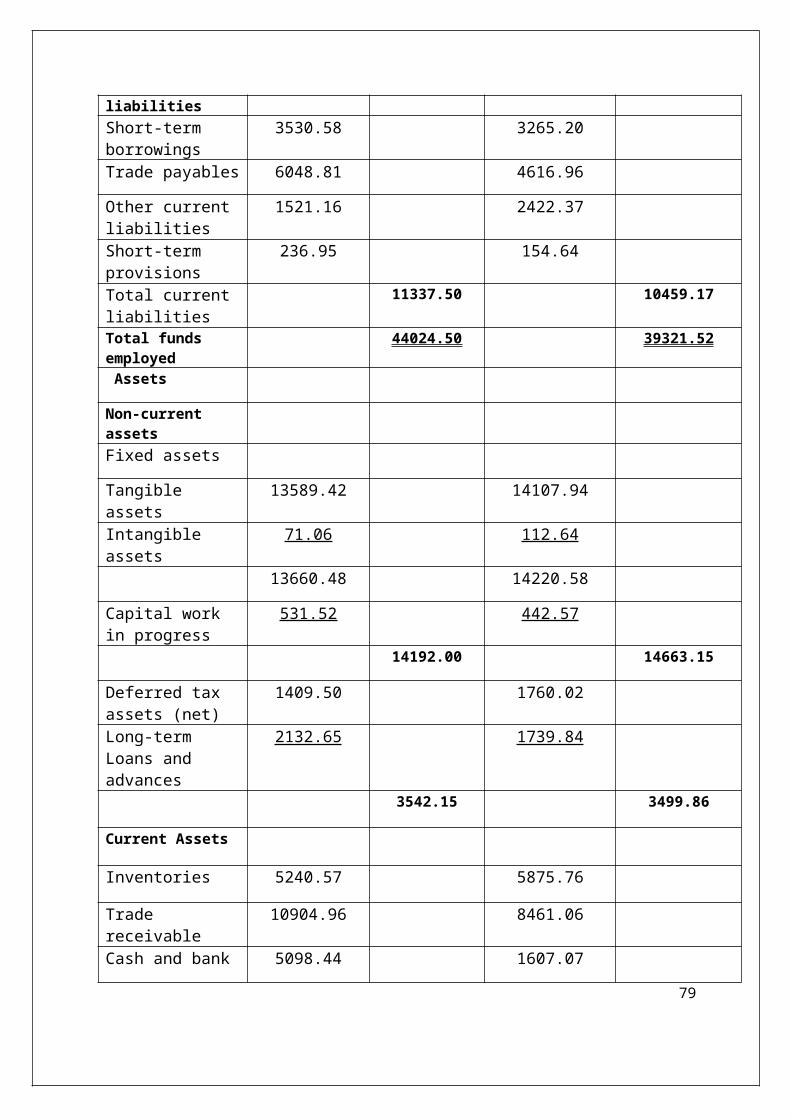

Current 78

liabilitiesShort-term borrowings

3530.58 3265.20

Trade payables 6048.81 4616.96

Other current liabilities

1521.16 2422.37

Short-term provisions

236.95 154.64

Total current liabilities

11337.50 10459.17

Total funds employed

44024.50 39321.52

Assets

Non-current assetsFixed assets

Tangible assets

13589.42 14107.94

Intangible assets

71.06 112.64

13660.48 14220.58

Capital work in progress

531.52 442.57

14192.00 14663.15

Deferred tax assets (net)

1409.50 1760.02

Long-term Loans and advances

2132.65 1739.84

3542.15 3499.86

Current Assets

Inventories 5240.57 5875.76

Trade receivable

10904.96 8461.06

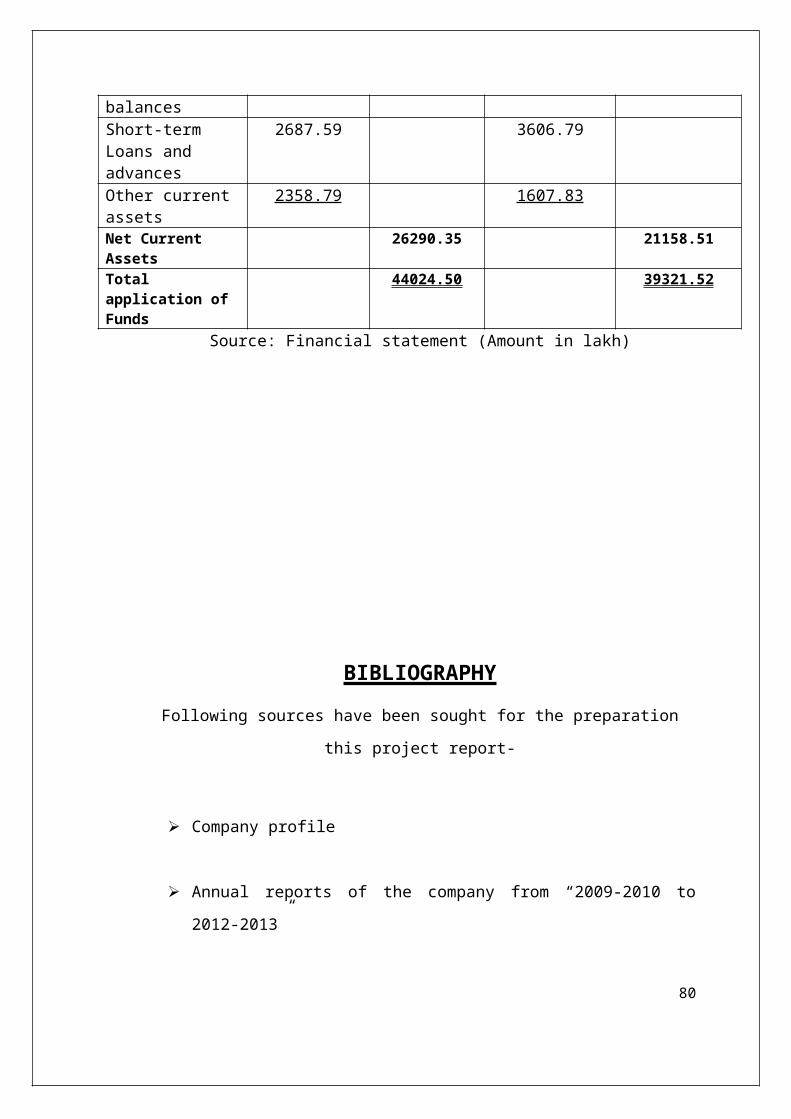

Cash and bank 5098.44 1607.07

79

balancesShort-term Loans and advances

2687.59 3606.79

Other current assets

2358.79 1607.83

Net Current Assets

26290.35 21158.51

Total application of Funds

44024.50 39321.52

Source: Financial statement (Amount in lakh)

BIBLIOGRAPHYFollowing sources have been sought for the preparation

this project report-

Company profile

Annual reports of the company from “2009-2010 to

2012-2013”

80

Direct interaction with the employees of the

company.

Internet-

www.marathonelectric.in

www.google.com

www.wikipidea.org

81