russia info kit summary sep2014

TRANSCRIPT

RUSSIA SUMMARY

Table of Contents

Deoffshorization..............................................................1Deoffshorization - summary................................................1

Development of legislative initiative...................................2Key measures in the plan include:.......................................2Allowing Access to “Audit Secrets”......................................3Taxation of profit from the “indirect” sale of immovable property.......4Initiatives of the Federation Council...................................4Implications............................................................6

Controlled Foreign Companies Bill.........................................6Foreign persons affected................................................6CFC profit taxable......................................................7Obligations to report CFCs..............................................8Penalties for violating disclosure requirements.........................8Principle of Tax Residence of Foreign Organizations.....................8Taxation of Income from the Sale of an “Indirect” Interest..............9Impact of the New Rules.................................................9

Sales tax legislation........................................................10Implications.............................................................11

Tax of 13% for debts written off.............................................11Sanctions – implications – Forbes view.......................................11List of offshore zones of Central Bank of Russia.............................12Actual bilateral treaties Russian Federation for the avoidance of double taxation.....................................................................13

Deoffshorization

Deoffshorization - summary"Political order " to combat offshore companies was formulated by President Vladimir Putin in his annual address to the Federal Assembly at the end of last year (2013). He demanded to deprive offshore companies access to any state support: no loans from Vnesheconombank, no state guarantees and state contracts.

The Federation Council decided to extend the limit. The amendments cover the state procurement market for all companies registered in offshore zones (the list, compiled

1

by the Ministry of Finance). Vnesheconombank loans will only be received by Russian business and prohibited to be issued to any foreign companies. In addition, the projectintroduces additional requirements for the registration of legal entities.

Another set of amendments is aimed to strengthen criminal liability for tax evasion using offshore companies and transfer prices. Such a violation will be automatically equated with tax evasion on a large scale, in other words the Violator - the head or the beneficiary of the company - could face up to six years (without these conditions -two years).

During the last 20 years more than $ 800 billion were derived from Russia through offshore zones, (referring to the calculations of experts of the Council of Federation). The same calculations were given earlier in the report of Tax Justice Network: $ 798 billion in 1990-2010.

The government prepares its own laws, including introduction of limited access to statefinances. Since during the crisis, the state refinanced the debt of many holdings, for example, UC Rusal (Jersey) received $ 4.5 billion. Alfa-Bank , owned by ABH Holdings Corp (British Virgin Islands) received a loan of state VneshEconomBank in 2009.

The government insists on mitigation of the Federation Council package: restrict accessto state support, not all foreign companies, but only to those who did not disclose thebeneficiaries.

About 30% of companies that perform large state orders use offshore schemes.

Companies use offshore schemes, not only for the tax savings, but at the request of theforeign partners, says PwC . This is a good moment for deoffshorization. Because of thesanctions, and various restrictions Russian companies have problems with foreign partners. They try to replace European funds with the Russian governmental money. A number of companies have already seriously considered a move to Russian jurisdiction. For example, the retail chain " The Seventh Continent " sold 100% of the shares (previously belonged to the Cyprus Pakva Investments Limited). 100% of the oil and gas contractor "StroiGazM ontazh ", which is now directly owned by Arkady and Boris Rotenberg, until mid-June belonged to Cyprus Milasi Engineering Ltd.

Development of legislative initiative The initiative for the deoffshorization of the Russian economy is threatening to becomethe most momentous event in the field of taxation in recent years. Coupled with the extremely serious plans for a similar toughening of rules in OECD countries and the EU (the OECD’s Base Erosion and Profit Shifting (BEPS) action plan), the initiative is expected to affect a significant portion of Russian business.

According to currently available draft documents, the deoffshorization policy is expected to have the following main consequences: An increase in the tax burden on many Russian holding structures organized with the useof foreign holding companies/ the need for a fundamental review of activities carried on through such holding companies.

An increase in the tax burden on many operating structures, including those associated with foreign sales, financing, etc. Many operating structures will become economically unviable unless significant changes are made to them.

2

Disclosure of beneficial owners in accounting statements. Enforcement of this requirement will be aided by systematic information exchange with EU countries and manyoffshore zones and by allowing Russian tax authorities access to information constituting audit secrets.

In February 2014, the Russian Ministry of Finance developed a 21-point plan (later reduced to 17 points) setting out the key areas of future development in the Government’s fight against the “offshorization” of the Russian economy. The plan has become unofficially known as the “national plan against offshore companies.” The Finance Ministry’s plan sets out general guidelines for the development of tax, accounting and criminal legislation, aimed at “de-offshorization.” According to those guidelines, bills will be drafted in the second quarter of 2014 with a view to making amendments to the Tax Code and other legislation by the end of 2014.

Key measures in the plan include:The introduction in Russian legislation of the concepts of “controlled foreign companies,”(see the summary below) “tax residence of organizations,” “actual recipient (owner) of income” and “offshore company”;

The establishment of measures aimed at combating abuse of double taxation treaties (taxtreaties), including in particular the use of reduced tax rates provided for in such treaties;

The introduction of a requirement for Russian companies to disclose information on their “beneficial owners” in accounting statements, and the introduction of liability of executive bodies for failure to provide data or provision of inaccurate data;

Legislative framing of procedures for the disclosure and exchange between Russian tax authorities and tax authorities of foreign jurisdictions. This involves the conclusion of bilateral international agreements on the exchange of tax information and Russia’s accession to the multilateral Council of Europe Convention Mutual Administrative Assistance in Tax Matters; Allowing Russian tax authorities access to information constituting audit secrets;

Improvement of Russian transfer pricing rules, including raising the effectiveness of control over foreign trade transactions and reducing to zero the aggregate criterion for qualifying transactions where one of the parties of a transaction or its beneficiary is an offshore company;

Introduction of criminal liability of legal entities for actions associated with money laundering and tax evasion. Preparation of a Framework for the Development of the System for Combating the Legitimization (Laundering) of Proceeds of Crime and the Financing of Terrorism in the Russian Federation;

Giving the Investigative Committee of the Russian Federation the right to institute criminal cases without liaising with the tax authorities (abolition of the previously obligatory tax audit report);2

Other amendments to tax legislation, such as: clarifying the provisions of Russian legislation regarding the tax treatment of income of foreign companies from transactions involving the sale of shares in companies which indirectly own Russian immovable property and improving procedures for the charging of assets tax and the

3

recovery of tax and levy arrears from foreign companies which own immovable property inthe Russian Federation;

The possible introduction of regulatory restrictions on the participation of Russian persons in foreign entities classed as trusts or foundations.

Allowing Access to “Audit Secrets”The plan includes measures that would allow Russian tax authorities access to information and documents constituting audit secrets, which were received and/or prepared by an audit organization or an individual audit in the course of providing services.

It is worth pointing out that this initiative is not something new. A bill4 of amendments to the Law Concerning Auditing Activities was drafted back in 2013, presumably in line with OECD recommendations presented in the context of negotiations on Russia’s accession to the OECD.

In addition to the above-mentioned amendment, there is also a plan to prepare guidelines for auditors on checking information on owners of organizations and ultimatebeneficiaries when auditing a company’s accounting (financial) statements. The relevantbill is expected to be submitted to the Government in October 2014.

Beneficial Owner of an Organization and Beneficial Owner of Income: a Confusion of Concepts?

This measure would involve not only introducing a requirement to disclose information on the beneficial owner of a Russian organization, but also creating a centralized register of beneficial owners which would be accessible by the tax authorities, including for the purpose of exchanging information.

The concept of a “beneficial owner” of a company was introduced back in July 2013 in Law No. 134-FZ, which amended various legislative acts, including the law on the countering of illegal financial operations.5 For the purposes of that law a “beneficialowner” is a physical person who whether directly or indirectly owns a company and is able to control it (i.e., a so-called “ultimate beneficial owner”). The law currently affects banks, brokerage companies, insurers, etc. which are required to “take measuresthat are reasonable and practicable in the circumstances for the identification of beneficial owners.” These are the entities that are likely to supply information for the creation of the centralized register. Enforcement of this requirement would be aided by the introduction of criminal liability of managers of banks, insurance companies and other financial organizations for the provision of knowingly false or incomplete information about the real state of affairs.

At the same time, it is not yet clear how the requirement to disclose the beneficial owner of a company would correlate with the concept of the “actual recipient (owner) ofincome” which is expected to be introduced to tax legislation. In particular, it is notclear how the term is to be interpreted for the purposes of applying tax treaties. It is important to note that, as long ago as 2009, the idea was raised of introducing additions to Article 7 of the Tax Code which would have limited the operation of tax treaties only insofar as “beneficial owners” of income were concerned, but the amendments in question were not considered at that time.

4

It should be noted that the concept of the “beneficial owner” or “actual recipient” of income is actively used in international tax law as an instrument for combating tax treaty abuse. In general terms it essentially means that where a company which receivesincome (such as dividends, interest and royalties) is not the beneficial owner of that income, the company does not have the right to apply tax treaty provisions exempting the income from withholding tax or prescribing reduced rates. The OECD Tax Committee commented on this concept back in 1986 in a special Report devoted to “conduit companies,”6 later in the Commentaries to the OECD Model Tax Convention, and recently in a 2012 Report7 which is specifically devoted to an attempt to define the term “beneficial owner.” The OECD’s position, as set out in those documents, is that a company which receives income cannot be considered as the beneficial owner of that income if it is an agent or a nominee or has limited powers to dispose of the income which effectively renders it a conduit in respect of that income. An important criterion of beneficial ownership is the absence of a legal obligation to transfer income received to a third party.

Quite often in international holding structures the recipient of dividend or interest income from Russia might be a foreign company which is based, for example, in Cyprus, while the ultimate beneficial owner which controls the foreign companies might be located in Russia and control the business through a chain of subholding companies. It is possible that information obtained as a result of the disclosure of the name of the ultimate beneficial owner could be used by the tax authorities to contest the assumption that the foreign companies which directly receive income (such as dividends and income) are the “actual recipients” of that income. Furthermore, the introduction of this requirement would provide a basis for implementing the “controlled foreign companies” rules and the “tax residence” concept.

The adoption of the initiatives described above would probably require Russian groups with a foreign presence to review the level of “actual presence” (substance) of the foreign companies, the structure of their income and expenditure and the management system and operating model of their business. Particular attention would need to be paid to increasing the actual powers that foreign companies within the holding structure have to dispose of the income in question and assessing whether or not they have the attributes of conduit companies.

Taxation of profit from the “indirect” sale of immovable property in Russia

In accordance with current Russian legislation, income of foreign companies from the sale of shares in Russian organizations more than 50% of whose assets consist of immovable property situated in the territory of the Russian Federation is taxable at source in Russia.8 The existing tax rules have resulted in sales being conducted through a foreign company rather than a Russian company as a means of protecting the income received from Russian withholding tax.

Under the amendments proposed by the Ministry of Finance, profit earned from the sale of the above-mentioned shares would be taxed irrespective of the “level of ownership” at which the sale takes place. In other words, “indirect” sales of immovable property (or of companies by which it is owned) would be taxed in Russia under domestic law.

Provisions of this kind are already contained in a number of Treaties (such as those with Luxembourg and Switzerland). Since, however, there are no corresponding provisions

5

in the Russian Tax Code, until amendments are made to Russia’s domestic tax law those treaty provisions cannot be applied in practice, as international treaties cannot establish the principal elements of a tax obligation, but only contain “distributive” provisions defining the tax competence of a state in respect of a particular item of income.

One of the legislative proposals might, therefore, be the introduction of provisions requiring tax obligations to be fulfilled directly by a nonresident seller of such assets, or requiring a nonresident purchaser to withhold tax from resources paid to a seller. In order for the new provisions to be effective, amendments would also have to be made to Article 13 of most Russian tax treaties, similar to those made to the Cyprusand Luxembourg treaties. In addition, mechanisms would need to be provided for collecting tax and obtaining information on transactions, since no such mechanisms are prescribed by law or applied in practice at the present time.

Initiatives of the Federation Council, the Investigative Committee and Individual Deputies of the State Duma

In addition to the proposals being drafted by the Ministry of Finance a number of documents are being prepared by initiative groups of legislative bodies. The FederationCouncil is considering a number of proposals, including the following:

There is a proposal for a provision to be introduced to the Tax Code which would make it inadmissible for a taxpayer to receive an unjustified tax benefit. This would provide a legal framework for the receipt of an unjustified tax benefit to be automatically qualified as a direct violation of law. In this respect, the bill does not propose clear criteria for distinguishing an unjustified tax benefit from legitimate methods of planning activities. There is a risk that the introduction of vague and imprecise concepts which are characteristic of the “unjustified tax benefit” doctrine would lead to even greater uncertainty in tax law enforcement.

There is a proposal for the introduction in Article 21 of the Tax Code, which deals with taxpayers’ rights, the concept of “tax policies” as a document in which a taxpayermay reflect “legal methods of obtaining a tax benefit” which it plans to use in the following year, which would have to be approved by the tax authority before the beginning of the ensuing year. The taxpayer would thus be insured against any claims inregard to the legitimacy of those types of tax benefit which have been disclosed in advance in its tax policies. This would imply that any reduction of the tax burden which has not been disclosed in advance in the tax policies and approved by the tax authority would be at risk of being contested as unjustified.

An addition is proposed to Article 36 of the Budget Code, concerning the principle of budget transparency, which would establish a requirement to disclose information on intermediate holders and beneficial owners of entities which act as suppliers of goods,work and services which are paid for out of State budget resources.

Another proposal is for the inclusion in Article 115.2 of the Budget Code of an additional criterion whereby only persons registered in the Russian Federation would have the right to receive State and municipal guarantees.

There is a proposal to restrict access to participation in the system of State procurements for entities which are registered in or are tax residents of countries which have been “blacklisted” by the Ministry of Finance.9

6

Additions are proposed to Articles 198 and 199 of the Criminal Code of the Russian Federation, which prescribe punishment for tax evasion, whereby they would apply to thereceipt of an unjustified tax benefit as one of the methods of tax evasion.

Initiatives to limit the legal capacity of offshore companies and “offshore-controlled” Russian companies

A number of State Duma deputies have prepared bills for discussion which set out de-offshorization measures through amendments to Federal Law No. 115-FZ of 7 August 2001 “Concerning the Countering of the Legitimization (Laundering) of Proceeds of Crime and the Financing of Terrorism” and a number of other laws:

The bill provides for the introduction of such concepts as “offshore zone,” “offshore-controlled company.” In this respect, a list of offshore zones would be approved by a federal executive body authorized by the Government.

The proposed definitions of an offshore company and an offshore-controlled company are very broad. Specifically, an “offshore company” is a legal entity registered in an offshore zone with a Russian legal entity or physical person as its beneficiary and (or) ultimate (beneficial) owner. An offshore-controlled company is a Russian legal entity which is directly or indirectly controlled by one or more offshore companies. Inthis respect, the control threshold is set at 10% for an open joint stock company and 30% for companies established in other forms. This wording could result in many companies (including some with State participation) being placed in the category of offshore-controlled companies.

The bill proposes the inclusion in the Law of a requirement of mandatory inspection of operations involving monetary resources or other assets where either of the parties involved is an offshore company or an offshore-controlled company and there is information on their involvement in money laundering or tax evasion or their refusal todisclose information on beneficial owners who are public officials. In this respect, the procedure for defining and disseminating such information is to be clarified by theGovernment.

The bill proposes a number of limitations on the legal capacity of the above-mentioned categories of companies, including limitations on the performance of certain export operations, participation in privatization and participation in the capital of companies (the list of which is to be established by the President of the Russian Federation) which produce strategically significant goods, work and services, the receipt of funds from the federal budget and guarantees from the State and certain banks, the supply of goods, work and services for State and municipal requirements and participation in the capital of a specialized depositary, non-State pension funds and (or) management companies thereof. Such transactions and actions may be invalidated by a court.

The bill imposes a prohibition on the participation of a number of companies with Stateparticipation in the charter capital of offshore companies and offshore-controlled companies. Given the broad nature of the proposed wording, many Russian business structures might fall under the scope of this prohibition.

According to the bill, within six months of the amendments being introduced, offshore companies and offshore-controlled companies must alienate shares in companies which produce strategically significant goods, work and services. Otherwise they will not be

7

able to exercise certain rights, such as voting rights and the right to receive dividends. Given the broad nature of the proposed wording, many Russian business structures might fall under the scope of this prohibition.

If Russia were to conclude an agreement on the exchange of information requiring a foreign state to disclose, inter alia, the beneficiaries of offshore companies, the above-mentioned restrictions on offshore companies and offshore-controlled companies would cease to have effect.

International exchange of tax information

The CFC rules can only be applied effectively in the context of a proper mechanism for the international exchange of tax information which would enable Russian tax authorities to obtain information on ownership of Russian companies in offshore and low-tax states and territories. It is now known that there are plans to conclude a bilateral agreement on the exchange of tax information with the British Virgin Islands.Russia is also expected to ratify this year the Council of Europe and OECD Convention on Mutual Administrative Assistance in Tax Matters (Strasbourg, 1988), which would alsoprovide enhanced scope for international tax co-operation not only in the area of information exchange but also on a broader range of issues.

ImplicationsAt this stage the measures outlined in the “anti-offshore plan” of the Ministry of Finance and in the bills described above reflect the main objectives of Russia’s de-offshorization policy. The initiatives are aimed on one hand at limiting capital outflow from Russia into offshore jurisdictions, and on the other hand represent an attempt to apply Russian taxation to structures which use offshore companies administered from Russia.

Deputy Finance Minister S.D. Shatalov said in an interview on 30 January 201410 that “the Ministry of Finance is by no means demanding that foreign subsidiaries be wound upand all business transferred to Russia. The message on taxes is this: […] make use of convenient jurisdictions if the nature of your business demands it, but do so openly.”

Nevertheless, some of the proposals that have emerged since then indicate the likelihood of a tougher approach which might result in fairly severe restrictions for “offshore-controlled” Russian companies and possibly even restrictions on the creation in the first place of certain offshore foreign legal structures (such as trusts and foundations). It is not yet quite clear what tools might be deployed in Russian legislation for the implementation of such restrictions.

It is recommended that Russian holding structures act immediately to diagnose and evaluate the company’s readiness for the planned changes and to assess the potential risks in order to determine whether it might be worth taking steps to change the business structure. It cannot be ruled out that offshore companies which are on the Finance Ministry’s “blacklist” will need to be eliminated from corporate structures.

As noted above, the proposed provisions might change significantly in the course of thelaw-making process.Endnotes1. http://www.minfin.ru/common/upload/library/2014/03/main/KIK_2014-03-18.docx.2. Draft Federal Law “Concerning the Annulment of Certain Provisions of Legislative Acts of the Russian Federation Based on Articles 198 to 199.2of the Criminal Code,” restoring the common procedure for examining the matter of the institution of criminal proceedings.3. See EY Global Tax Alert of 23 December 2013, Russia’s Anti-Offshore Tax Policies Gain Momentum.

8

4. Draft Federal Law “Concerning the Introduction of Amendments to Article 82 of the Tax Code of the Russian Federation and Article 9 of the Federal Law Concerning Auditing Activities.”5. Federal Law No. 115-FZ of 7 August 2001 “Concerning the Countering of the Legitimization (Laundering) of Proceeds of Crime and the Financing of Terrorism.”6. OECD (2012), “R(6). Double taxation conventions and the use of conduit companies,” in OECD, Model Tax Convention on Income and on Capital 2010: Full Version, OECD, 2010, p. R(6)-8 [DOI:10.1787/9789264175181-99-en].7. OECD Model Tax Convention: Revised Proposals Concerning The Meaning of “Beneficial Owner” in Articles 10, 11 and 12.” 19 October 2012 to 15 December 2012. [http://www.oecd.org/ctp/treaties/Beneficialownership.pdf].8. Article 309, clause 1, subclause 5) of the Tax Code.9. Order No. 108n of the Ministry of Finance of the Russian Federation of 13 November 2007 “Concerning Approval of the List of States and Territories Which Grant Preferential Tax Treatment and (or) Do Not Require the Disclosure and Provision of Information in Relation to Financial Operations (Offshore Zones).”10. http://www.vedomosti.ru/library/news/22065781/my-ischerpali-rezerv-povysheniya-nalogov?full#cut.

Controlled Foreign Companies BillExecutive summary (from 28 march 2014)

On 19 March 2014, in line with the plan for the “de-offshorization” of the Russian economy, the Ministry of Finance published a Bill1 aimed at establishing rules relatingto controlled foreign companies (CFC), tax residence of organizations and the taxation of profit from the “indirect” sale of immovable property. The Bill is one of the key instruments for the implementation of the Government’s policy of de-offshorization of the economy and will be of major significance for the great majority of companies and businessmen with assets or operations outside the Russian Federation.

Application of the CFC rules

The CFC rules will apply to Russian organizations and physical persons which/who are tax residents of the Russian Federation. It is important to note that, at present, the concept of tax residence is used in the Tax Code only in relation to physical persons, while the concept of the tax residence of organizations is a new development along withthe CFC rules.

Foreign persons affected by the CFC rulesAccording to the Bill, CFCs are organizations which are residents of countries traditionally considered as “offshore,” low-tax jurisdictions, and which are controlledby physical persons or organizations who/which are Russian tax residents.

The new rules do not affect all foreign organizations, but only those which are residents of jurisdictions included in a special list approved by the Ministry of Finance. A similar list of offshore jurisdictions was introduced by the Ministry of Finance a few years ago,2 although it is used for other tax regulation purposes, such as transfer pricing and the application of preferential rates of dividend taxation, rather than the application of CFC rules. The Finance Ministry is likely to approve a new, extended list, which may even include certain countries with which international double taxation treaties exist. The Finance Ministry has the power to change the list in the future by adding new jurisdictions. No amendments to the Tax Code would be needed for that purpose. This would create a high degree of uncertainty for taxpayers.

Unlike many examples in global practice, the Bill does not establish any serious exceptions to the CFC category, such as companies which carry on an active business or are involved in industrial projects. The exceptions it does make are for companies whose shares are circulated on stock exchanges (included in a list established by the Central Bank) and companies which are recognized as tax residents of the Russian Federation.

According to the Bill, the CFC rules will apply not only to organizations but also to so-called “structures.” In particular, the CFC category includes “foundations,

9

partnerships, partnership associations and other collective investment vehicles which have the right to carry out entrepreneurial activities in the interests of their beneficiaries,” where they are tax residents of “blacklisted” countries. Although it isnot clear from the proposed wording of this provision whether the definition includes foreign trusts, it appears that it does not rule out the application of the CFC rules to foreign trusts, including certain participants in such arrangements.

Definition of control

The Bill defines control as “the exertion of or the ability to exert influence” on decisions of CFCs in regard to profit distribution, including in particular the direct or indirect possession of more than 10% of the capital of a CFC (including jointly witha spouse, children or other persons). The use of the phrase “in particular” may indicate that a person with a participating interest of less than 10% in a foreign organization may also be deemed to be a controlling person if control is exercised. TheBill does not define the term “other persons.”

Nor does the Bill establish criteria in accordance with which relationships with “otherpersons” may be regarded as grounds for aggregating a participating interest with the participating interests of such persons.

In the case of control over a “structure,” rather than an organization, the term refersto influence over the person who manages the assets of the structure in question with respect to decisions on profit distribution. No level of participating interest is established in this case – it is the existence of influence over the manager’s decisions that matters.

It is important to note that there is a lack of clarity as to the meanings of certain terms, including “control,” “influence” and “structure,” which could result in expansive interpretation by the tax authorities and, consequently, additional risks fortaxpayers.

CFC profit taxable in the Russian FederationA profit share would be included in the tax base of a Russian resident to an extent corresponding to the size of the resident’s direct or indirect participating interest in the CFC and with account taken of the length of time for which the interest has beenheld. The Bill does not establish any mechanism for calculating a profit share for a partial tax period.

Expenses and losses relating to other activities of organizations and tax deductions available to individuals cannot reduce the tax base of those persons for CFC profit.

It is also interesting to note that where the share of ownership cannot be determined, the full amount of CFC profit will be taxed. If the chain of indirect ownership of a CFC by a taxpayer includes organizations which are Russian tax residents, amounts of CFC profit taken into account by those organizations are deducted from the taxpayer’s base. It is not yet clear what would constitute sufficient evidence that CFC profit hasbeen taken into account by other organizations.

CFC profit is to be calculated in accordance with Chapter 25 of the Tax Code. In practice this means that taxpayers would not only have to obtain financial statements from CFCs, but would also have to adjust those statements in line with Russian taxation

10

rules. It is not quite clear from the text of the Bill how that adjustment is expected to be carried out.

The amount included in a Russian resident’s tax base would be not the entire amount of CFC profit, but profit reduced by the amount of dividends paid out of that profit. Profit in foreign currency must be translated into roubles at the end of a calendar year. In the event that a CFC distributes dividends out of undistributed profit of prior periods, the tax base for the relevant tax in which the dividends received are taken into account would be reduced to an extent corresponding to the taxpayer’s participating interest in the CFC by amounts of profit which were previously taken intoaccount in determining the tax base for the relevant tax.

CFC profit would be taxed at 20% for controlling organizations and 13% for controlling physical persons.

The Bill also contains provisions to exclude double taxation in the case of “cascade” structures where there is more than one CFC in the chain of ownership: CFC profit is reduced by amounts of profit which other controlling persons have taken into account for taxation purposes in proportion to their participating interests. These provisions will probably need to be elaborated upon when the bill is next heard.

Obligations to report CFCsThe Bill requires a resident taxpayer to submit to the tax authority a standard notification of participation in three categories of organizations, and to submit a CFCtax declaration accompanied by appropriate documents.

The first category comprises all CFCs without exception which are located in jurisdictions included in the Finance Ministry’s list, where the direct or indirect participating interest in those organizations amounts to not less than 1%.

The second category comprises types of CFCs whose tax residence cannot be determined and in which, again, there is a participating interest of 1%.

The third category comprises all foreign companies without exception (regardless of whether they are blacklisted) for which the taxpayer is deemed to be a “controlling person,” i.e., where the participating interest is not less than 10%. A notification must also be submitted in relation to “structures” where a Russian resident has a rightto income distributed by them (foundations, partnerships, etc.).

This means that a much broader range of persons will be required to submit notifications than will have obligations to pay tax in respect of CFCs. The need for notifications to be submitted in relation to the last category of organizations is questionable, especially if they are not on the Finance Ministry’s blacklist. It is important to note that no obligation is established to disclose information on “non-offshore” structures (such as foundations, trusts, etc.).

A notification must contain the following data: the period for which information on a CFC is provided, the name of the CFC, registration details of the CFC, information on the participating interest in the CFC’s capital and the dates of the financial statements and of the related auditor’s report (if an audit is compulsory under local law). It should be noted that some offshore jurisdictions do not require local companies to prepare reports, and so it is not quite clear at this point how the Russian authorities will obtain the relevant data. In addition, a notification must indicate the manner of indirect participation of a taxpayer in a CFC; in other words,

11

it must disclose the entire chain of ownership of multiple CFCs. A notification must besubmitted within 20 days from the date on which grounds for submitting it arise (e.g., from the date on which control over a CFC arises), or on 1 March of a calendar year in the case of notifications for which the grounds for submitting them arose or existed without changes in the preceding calendar year.

Taxpayers must also submit a separate tax declaration for a CFC (the form of which is to be established by the Federal Tax Service). The declaration must be accompanied by the CFC’s financial statements and related auditor’s report (if one is required) and legalized translations thereof into Russian.

Penalties for violating disclosure requirementsThe Bill makes amendments to the Tax Code setting out sanctions for the non-disclosure or incomplete disclosure of information on CFCs and the non-payment or underpayment of relevant tax. In particular, in the latter case a fine is established equal to 20% of CFC profit rather than of the amount of unpaid tax.

The Bill does not establish any special provisions concerning administrative or criminal liability.

It should be pointed out that the effective implementation of provisions dealing with the monitoring by tax authorities of compliance with CFC rules is only possible in the context of a proper mechanism for the international exchange of tax information betweenthe Ministry of Finance and the tax authorities of offshore jurisdictions. No such international agreement has yet been concluded by Russia, but the Ministry of Finance has signaled its intention that this should happen soon.

Principle of Tax Residence of Foreign Organizations in the Russian FederationBased on the “Place of Effective Management” Criterion

In addition to the CFC rules, the Bill introduces the concept of the tax residence of organizations. At present, tax is paid by Russian organizations on worldwide profit, and by foreign organizations only on profit from Russian sources, including profit of apermanent establishment of a foreign organization in Russia.

The new provisions create a much stronger connection to the tax jurisdiction of the Russian Federation for profit of foreign persons. This is achieved by the introduction of the concept of the “place of effective management” of a foreign organization in the Russian Federation. This is definitely a new development in Russian tax law. It means that where a foreign organization has a place of effective management in the Russian Federation, it becomes a tax resident of the Russian Federation and is taxable on a parwith Russian organizations, which are tax residents of the Russian Federation by default.

The Bill lists a number of conditions and states that a foreign organization will be considered as having a place of effective management in the Russian Federation if any of those conditions is met (not all of them together):

Meetings of the board of directors are held in the Russian Federation; “Executive management” is exercised in the Russian Federation; Chief (executive) officers are located in the Russian Federation; Accounting records are maintained in the territory of the Russian Federation; and The foreign organization’s archives are kept in the Russian Federation.

12

Remarkably, foreign organizations which are recognized as such under the provisions of double taxation treaties concluded by Russia are also deemed to be Russian tax residents.

Unlike the CFC rules, the tax residence rules apply to all foreign organizations, and not only to jurisdictions on the Finance Ministry’s list. Interestingly, according to the Bill foreign companies are recognized as Russian tax residents only for profits taxpurposes. This means that the status of such companies in relation to other Russian taxes is not established.

Taxation of Income from the Sale of an “Indirect” Interest in Russian Immovable Property

The Bill extends the scope of subsection 5 of clause 1 of Article 309 of the Tax Code, under which tax is charged in the Russian Federation on income from the sale of shares (participating interests) in companies more than 50% of whose assets consists of immovable property located in Russia, to apply not only to shares in Russian companies which are directly owned by the alienating party, but also to cases where such shares (participating interests) are indirectly owned and to sales of shares (participating interests) in foreign companies where 50% of their assets consists of immovable property situated in Russia. In other words, the provision aims to cover capital gains from the sale of shares in any company in a chain of ownership which indirectly (through a chain of foreign or Russian companies) owns immovable property in Russia where that immovable property represents 50% or more its assets.

The provision is clearly intended to eliminate a loophole in the existing rules governing the taxation of profit from the sale of shares in Russian organizations whoseassets consist primarily of immovable property. It is no secret that many transactions on the immovable property market occur at higher levels of the ownership structure outside Russia, and what is bought and sold is not the property itself but shares in a foreign company which in turn has a direct or indirect holding in a Russian company with immovable property.

This change should be viewed in the context of the recent amendments made to the Russia-Switzerland and Russia-Luxembourg tax treaties. Under the amendments to Article 13 of those treaties, rights to tax capital gains from the sale of shares and participating interests in companies which derive their value primarily from immovable property are transferred to the country where the property itself is located (in this case the Russian Federation). It has recently been rumored that similar amendments may be made to the Russia-Netherlands treaty. It is perfectly logical for changes in international treaties to be followed up by the introduction of similar provisions in domestic tax law.

Nevertheless, it is still unclear how the new rules will be implemented. In order for them to be effective it is also necessary to impose obligations to pay or withhold taxes on the foreign seller or purchaser accordingly. Without this, the new rules will have little effect.

Entry into Force

If the Bill were to be adopted and published in 2014, it might enter into force and be applied from 1 January 2015.

13

According to the general rules set out in Article 5 of the Tax Code, tax laws enter into force not earlier than upon the lapse of one month from the date of their officialpublication and not earlier than the first day of the next tax period for the relevant tax. Clause 2 of Article 5 of the Tax Code further states that provisions which establish new obligations or otherwise worsen the position of taxpayers cannot have retroactive force. This means that the Bill is unlikely to be applied retroactively, i.e., to 2014.

Impact of the New Rules on Russian TaxpayersFrom the point of view of the practical effects on business, the new CFC rules will create requirements for certain groups of Russian taxpayers to present large volumes ofinformation on foreign assets to the tax authorities on a regular basis and to calculate additional taxes. In particular, the CFC rules will affect Russian companies which have foreign asset ownership structures that include companies in blacklisted jurisdictions. This includes large Russian holding companies which own or control foreign companies and “structures” on the Finance Ministry’s “blacklist.”

However, the CFC rules also affect another broad category of persons, namely individuals who are residents of Russia, including both Russian and foreign citizens. It is important to understand that so-called foreign “personal holding mechanisms” which are traditionally used by Russian business owners, including offshore trusts, foundations and other similar structures, are very likely to fall within the scope of the CFC rules. Individuals will encounter restrictions on the use of foreign structuresto defer the payment of personal income tax, but as long as all profit is distributed every year in the form of dividends, the tax burden will not increase. On the other hand, there will be a significantly increased administrative burden associated with thepreparation and filing of returns.

The CFC rules will also affect portfolio investors who invest in foreign collective investment instruments, such as mutual investment funds, partnerships, other investmentfunds and similar structures in which a participating interest of more than 10% is held. It should be said that the 10% participation threshold for the taxation of CFC profits is unreasonably low. In any case all Russian taxpayers will come under a significant administrative burden associated with obtaining or preparing CFC statements. There seems little justification for imposing such a burden on investors starting from a participation threshold as low as 1%.

There is still uncertainty regarding CFC profit which arose before the new rules came into effect. For example, if a Russian taxpayer established its obligation to submit a notification of CFCs starting in 2015, but according to the CFC financial statements its undistributed profit is attributable to earlier years, would that “old profit” be taxable? An overall reading of Chapter 25 of the Tax Code suggests that this is very unlikely, but taxpayers need to be ready for this potential risk.

It is recommended that Russian taxpayers take urgent measures to diagnose and analyze the effect of the CFC rules on their structures of ownership of foreign and Russian assets, and to consider possible ways of modifying those structures. It would also be worthwhile to evaluate the readiness of subdivisions of Russian companies for the task of collecting and preparing documents in the form required by the Bill.

Similarly to the adverse effects of the CFC rules, the introduction of the tax residence rules may likewise lead to an increase in the tax risks associated with the

14

operational management of foreign organizations from Russia. As with the CFC rules, therefore, taxpayers need to act quickly to analyze the structures of management of direct and indirect affiliated companies and evaluate the related tax risks. At the same time, the tax connection criteria of the maintenance of accounting records and thekeeping of archives in the territory of the country are unnecessarily severe and at variance with international practice.

Finally, the introduction of the new rules concerning the taxation of the “indirect” sale of immovable property will make it necessary to analyze and possibly review structures of investment in Russian immovable property. It will also create a need for more scrupulous structuring of transactions involving the indirect sale of such property, including the need for the parties to transactions to agree on terms relatingto allocation of liability and indemnification of tax losses (indemnities).

It is expected that the business community will be actively involved in the discussion of the Bill, and hope that collective efforts will result in changes to some of the Bill’s provisions.Endnotes1. http://www.minfin.ru/common/upload/library/2014/03/main/KIK_2014-03-18.docx2. Order No. 108n of the Ministry of Finance of the Russian Federation of 13 November 2007 “Concerning Approval of the List of States and Territories Which Grant Preferential Tax Treatment and (or) Do Not Require the Disclosure and Provision of Information in Relation to Financial Operations (Offshore Zones).”

Sales tax legislation

During the week of 4 August 2014, the Russian Ministry of Finance prepared draft legislation intended to provide the legal framework within which federal regions may implement a sales tax for discussion within authorities.1

Draft proposals

Implementation of the sales tax is to be allowed with effect from 1 January 2015. The sales tax should be introduced in a particular federal region under a law enacted by the respective region. Taxpayers are organizations and individual entrepreneurs carrying out activities in federal regions where a sales tax has been introduced.

The current draft provides for the implementation of a sales tax at a maximum rate of 3% on goods, services and works supplied to individuals.

The federal regions are to determine:

− The sales tax rate− Procedure and terms of payment− Compliance and reporting formalitiesThe tax base is the price of the goods, services or work, including value-added tax (VAT) and excise duty.

The tax arises on the date of receipt of payment in the seller’s bank account or payment in cash, or the date of provision of the goods, services or work.

Monthly returns are to be filed.

The place of taxation (i.e., the federal region in which sales tax should be reported and paid), is the place of state registration of the organization or private entrepreneur or the place indicated in the charter documents (with respect to a separate subdivision).

15

Certain goods are to be exempt from sales tax. Goods and services subject to a reduced VAT rate or exemption from VAT are generally not subject to sales tax. This includes: certain foodstuffs and dairy products, pharmaceuticals, housing and utilities, certain education services provided by non-profit organizations, textbooks, certain periodicals, services provided by organizations working in the field of culture and arts, healthcare, public transport, financial services and religious services.

ImplicationsIf a sales tax is implemented, companies operating in Russia will have to:

Analyze which products are subject to sales tax (this will likely differ among federal regions)

Adjust their ERP/invoicing systems Implement compliance procedures (compliance obligations will likely differ among

federal regions).

Important questions remain unanswered at this stage, such as:

Should sales tax apply to free of charge supplies of goods (services, works), including the supplies in the frame of loyalty programs?

How the authorities would deal with a situation where a company registered in a low or no sales tax federal region is selling (e.g., via websites and mail order catalogues) to individuals located in the federal regions with higher sales tax rate?

Would it be possible to reverse sales tax in the case of return of goods? How should a seller determine whether the individual is buying goods for himself

or for the company? To what extent the existing VAT case law can be applied to resolve future

disputes regarding sales tax?Endnote1. The Russian Federation has 85 federal regions.

Tax of 13% for debts written off

The Federal Tax Service has sent a letter to their offices, which states that the Russians have to pay tax on debts that they have been forgiven by the bank.

The letter says that "In case of cancellation of debt from the balance sheet of a credit institution a customer receives economic benefits in the form of cost savings since they do not need to repay the amounts of principal and / or interest. Therefore, this income is subject to personal income tax at a rate of 13 %.

The "date of receipt of income by an individual” is defined as the date of writing bad debt from the balance sheet of the credit institution.

Earlier it was reported that over 7 months in 2014 banks have written off a record 113.2 billion rubles of bad debts which is 27% (or 31 billion) higher than in January -July of last year.

It was stated in 2013, that banks must necessarily write off the debts with delay of 360 days.

16

Sanctions – implications – Forbes view

Each new round of development of Ukrainian conflict leads to the introduction of new financial sanctions against Russia, and practically all over the globe from the USA to Australia. How do they work? In early 2014, foreigners are selling weakening ruble, Russian companies are losing access to foreign credit and capital markets, and the projection of GDP in Russia becomes more pessimistic. The Russian stock market suffers losses - investors capitalization falls. For the first six months the RTS index fell by5%. That Europe sanctions push foreign investors to withdraw from Russia and once againconvince the doubters that it is time to exit. The head of the group "Sputnik" Boris Jordan, who works in Russia 20 years old, says that geopolitical conflict affects primarily for long-term investors, they are now looking to the Russian market more negative than in previous years. At the same time, in his opinion, the situation has continued to attract the market speculators.

In July of 2014 the government's forecast of GDP growth for the year was 0.5%, the forecast of the Bank of Russia - 0.4%. HSBC chief economist Alexander Morozov believes that economic growth this year will be zero due to decrease in the second half of the year, but he hopes for a 1% increase in 2015.

What will happen if the United States and the EU will toughen sanctions? Russia may be in the position of South Africa, anti-business and government that the United States imposed strict sanctions in 1985-1986. Sanctions and falling commodity prices have destabilized the South African economy, which subsequently led to a change of the apartheid regime. According to estimates of the then Minister of Finance of South Africa, the sanctions cost the economy a decrease in average annual growth rate from 5.5% to 3.5%, while capital outflows led to a moratorium on debt payments and the introduction of multiple exchange rates.

Another example from the recent past. In 2012, the United States and other developed countries have imposed tough sanctions against Iran, which has refused to halt its nuclear program. As a result, this has led to the fact that its oil exports fell by 40%of GDP - by 5.6%, the inflation rate reached the index is above 40%, in comparison to the year 2011 imports increased by 13%, exports declined by more than a quarter an unemployment rate of 12%. And in 2013, the citizens voted against the government of President Mahmoud Ahmadinejad, replacing it with a cabinet, ready to negotiate with theUnited States. This year, Iran pledged to reduce their stockpiles of enriched uranium by 20%.

Are the reasons for optimism?

Managing Director of Arbat Capital Julia Bushueva believes that the Russian market is so much negative that the slightest positive news could lead to a serious increase. Although in the case of long-term sanctions and the lack of reform, it does not excludethe transformation of the Russian stock market in underdeveloped, as in Argentina. Former partner of George Soros, head of Rogers Holdings, Jim Rogers says that he is interested in precisely such markets, so he buys Russian indices and stocks. He believes that Russia has a lot of neighbours who are interested in its resources and assets, and they will continue business in the country.

The smallest positive change in American policy towards Russia can dramatically increase the amount of investment, as the growth potential due to inherent risks will be enormous. As an example, stock index Iran TEPIX, which in 2013 increased by 130%

17

after it was announced that sanctions can be eased. Now on the market of Iran is almostno foreigners.

How to get investors into the financial market? This is what we asked the owners of bigbusiness, which are being traded on stock exchanges. The main piece of advice: before you invest, is to understand in what business you are investing, and make maximum use of the skills learned from the management of real assets.

An interesting trend - billionaires came to independent trading due to the fact that the crisis with their means unsuccessfully worked professional management.

At the same time, the Russian authorities undertook deoffshorization business. On the one hand, the stock market will suffer, because most of the calculations are carried out with offshore accounts. For example, the head of Spectrum Partners Dmitry Yevenko already liquidated its management company hedge funds because they do not see any prospects in the work in the "gray zone." However there's a downside of deoffshorization: Russian officials and businessmen have begun to return money to Russia. And not only in the decision of the Russian authorities, owners of large statesfear for their money, because the possible new sanctions and arrests of their assets abroad.

List of offshore zones of Central Bank of Russia

Direction CBR August 7, 2003 N 1317-U "On the procedure for establishing the authorizedbanks of correspondent relations with non-resident banks, registered in the states and territories, offering preferential tax treatment and (or) not requiring the disclosure and provision of information on financial operations (offshore) "(As amended July 15, 2011)

LIST of States and territories, offering preferential tax regime and (or) not requiringthe disclosure and providing information when financial transactions (offshoring) 1 The first group:1.1. Separate administrative units of the United Kingdom of Great Britain and Northern Ireland:- Channel Islands (Guernsey, Jersey, Sark)- On the Isle of Man1.2. Ireland (Dublin, Shannon)1.3. Malta1.5. China (Hong Kong (Hong Kong))1.7. The Swiss Confederation1.8. Singapore1.9. Montenegro 2 The second group:2.1. Antigua and Barbuda2.2. Commonwealth of the Bahamas2.3. Barbados2.4. State of Bahrain2.5. Belize2.6. Brunei - Darussalam

2.7. Dependence on the United Kingdom ofGreat Britain and Northern Ireland area:- Anguilla- Bermuda- British Virgin Islands- Montserrat- Gibraltar- Turks and Caicos

18

- Cayman Islands2.8. Grenada2.9. Djibouti2.10. Commonwealth of Dominica2.11. China (Macau (Macao))2.12. Costa - Rica2.13. Lebanese Republic2.14. Mauritius2.15. Malaysia (about. Labuan)2.16. The Republic of Maldives2.17. The Principality of Monaco2.18. Netherlands Antilles2.19. New Zealand:- Cook Islands- Niue2.20. United Arab Emirates (Dubai)2.21. Portuguese Republic (about. Madeira)2.22. Independent State of Western Samoa2.23. Seychelles2.24. Saint - Kitts and Nevis2.25. Saint - Lucia

2.26. Saint - Vincent and the Grenadines2.27. USA:- Virgin Islands USA- Commonwealth of Puerto - Rico- Wyoming- Delaware2.28. Kingdom of Tonga2.29. Democratic Socialist Republic of Sri - Lanka2.30. Palau 3 The third group:3.1. The Principality of Andorra3.2. Federal Islamic Republic of the Comoros:- Anzhuanskie Islands3.3. Aruba3.4. The Republic of Vanuatu3.5. The Republic of Liberia3.6. The Principality of Liechtenstein3.7. The Marshall Islands3.8. Nauru

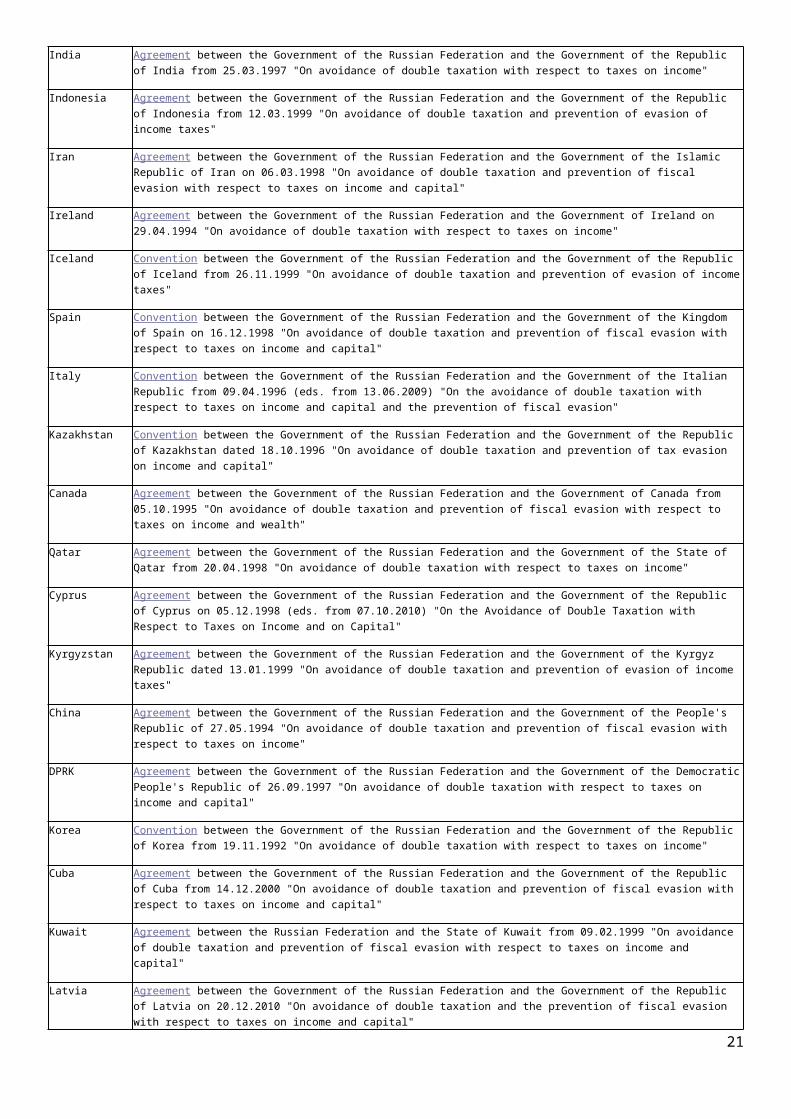

Actual bilateral treaties Russian Federation for the avoidance of doubletaxation

Lists of international treaties of the Russian Federation on other issues, see. In the Help information .

State The International Treaty

Australia Agreement between the Government of the Russian Federation and the Government of Australia on 07.09.2000 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Austria Convention between the Government of the Russian Federation and the Government of the Republic of Austria from 13.04.2000 "On avoidance of double taxation with respect to taxes on income andcapital"

Azerbaijan Agreement between the Government of the Russian Federation and the Government of the Republic of Azerbaijan dated 03.07.1997 "On avoidance of double taxation with respect to taxes on incomeand property"

Albania Convention between the Government of the Russian Federation and the Government of the Republic of Albania from 11.04.1995 "On avoidance of double taxation with respect to taxes on income andproperty"

Algeria Convention between the Government of the Russian Federation and the Government of the Algerian People's Democratic Republic of 10.03.2006 "On avoidance of double taxation with respect to taxes on income and property"

Argentina Convention between the Government of the Russian Federation and the Government of the ArgentineRepublic from 10.10.2001 "On avoidance of double taxation with respect to taxes on income and capital"

Armenia Agreement between the Government of the Russian Federation and the Government of the Republic

19

of Armenia on 28.12.1996 (eds. from 24.10.2011) "On the elimination of double taxation on income and property"

Belarus Agreement between the Government of the Russian Federation and the Government of the Republic of Belarus of 21.04.1995 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income and property." An integral part of the Agreement is the protocol of 24.01.2006

Belgium Convention between the Government of the Russian Federation and the Government of the Kingdom of Belgium on 16.06.1995 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income and wealth"

Bulgaria Agreement between the Government of the Russian Federation and the Government of the Republic of Bulgaria from 08.06.1993 "On avoidance of double taxation with respect to taxes on income and property"

Botswana Convention between the Government of the Russian Federation and the Government of the Republic of Botswana from 08.04.2003 "On avoidance of double taxation with respect to taxes on income"

Attention! Entry into force of the Convention between the Government of the Russian Federation and the Government of the Federative Republic of Brazil on 22.11.2004, see. letterRussian Finance Ministry of 12.02.2014, the N 03-08-06 / 5641

Brazil Convention between the Government of the Russian Federation and the Government of the Federative Republic of Brazil on 22.11.2004 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

United Kingdom

Convention between the Government of the Russian Federation and the Government of the United Kingdom of Great Britain and Northern Ireland of 15.02.1994 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital gains" (together with the Exchange of Notes dated 15.02.1994 "Between the plenipotentiary Ambassador of the United Kingdom of Great Britain and Northern Ireland to the Russian Federation and the Deputy Minister of Foreign Affairs of the Russian Federation ")

Hungary Convention between the Government of the Russian Federation and the Government of the Republic of Hungary from 01.04.1994 "On avoidance of double taxation with respect to taxes on income andproperty"

Venezuela Convention between the Government of the Russian Federation and the Government of the Bolivarian Republic of Venezuela from 22.12.2003 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Vietnam Agreement between the Government of the Russian Federation and the Government of the Socialist Republic of Vietnam from 27.05.1993 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Germany Agreement between the Russian Federation and the Federal Republic of Germany on 29.05.1996 (eds. dated 15.10.2007) "On the avoidance of double taxation with respect to taxes on income and property"

Greece Convention between the Government of the Russian Federation and the Government of the Hellenic Republic from 26.06.2000 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income and capital"

Denmark Convention between the Government of the Russian Federation and the Government of the Kingdom of Denmark on 08.02.1996 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income and wealth"

Egypt Agreement between the Government of the Russian Federation and the Government of the Arab Republic of Egypt from 23.09.1997 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Israel Convention between the Government of the Russian Federation and the Government of the State of Israel from 25.04.1994 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

20

India Agreement between the Government of the Russian Federation and the Government of the Republic of India from 25.03.1997 "On avoidance of double taxation with respect to taxes on income"

Indonesia Agreement between the Government of the Russian Federation and the Government of the Republic of Indonesia from 12.03.1999 "On avoidance of double taxation and prevention of evasion of income taxes"

Iran Agreement between the Government of the Russian Federation and the Government of the Islamic Republic of Iran on 06.03.1998 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Ireland Agreement between the Government of the Russian Federation and the Government of Ireland on 29.04.1994 "On avoidance of double taxation with respect to taxes on income"

Iceland Convention between the Government of the Russian Federation and the Government of the Republic of Iceland from 26.11.1999 "On avoidance of double taxation and prevention of evasion of incometaxes"

Spain Convention between the Government of the Russian Federation and the Government of the Kingdom of Spain on 16.12.1998 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Italy Convention between the Government of the Russian Federation and the Government of the Italian Republic from 09.04.1996 (eds. from 13.06.2009) "On the avoidance of double taxation with respect to taxes on income and capital and the prevention of fiscal evasion"

Kazakhstan Convention between the Government of the Russian Federation and the Government of the Republic of Kazakhstan dated 18.10.1996 "On avoidance of double taxation and prevention of tax evasion on income and capital"

Canada Agreement between the Government of the Russian Federation and the Government of Canada from 05.10.1995 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and wealth"

Qatar Agreement between the Government of the Russian Federation and the Government of the State of Qatar from 20.04.1998 "On avoidance of double taxation with respect to taxes on income"

Cyprus Agreement between the Government of the Russian Federation and the Government of the Republic of Cyprus on 05.12.1998 (eds. from 07.10.2010) "On the Avoidance of Double Taxation with Respect to Taxes on Income and on Capital"

Kyrgyzstan Agreement between the Government of the Russian Federation and the Government of the Kyrgyz Republic dated 13.01.1999 "On avoidance of double taxation and prevention of evasion of income taxes"

China Agreement between the Government of the Russian Federation and the Government of the People's Republic of 27.05.1994 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

DPRK Agreement between the Government of the Russian Federation and the Government of the DemocraticPeople's Republic of 26.09.1997 "On avoidance of double taxation with respect to taxes on income and capital"

Korea Convention between the Government of the Russian Federation and the Government of the Republic of Korea from 19.11.1992 "On avoidance of double taxation with respect to taxes on income"

Cuba Agreement between the Government of the Russian Federation and the Government of the Republic of Cuba from 14.12.2000 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Kuwait Agreement between the Russian Federation and the State of Kuwait from 09.02.1999 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Latvia Agreement between the Government of the Russian Federation and the Government of the Republic of Latvia on 20.12.2010 "On avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and capital"

21

Lebanon Convention between the Government of the Russian Federation and the Government of the Lebanese Republic from 08.04.1997 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income"

Lithuania Agreement between the Government of the Russian Federation and the Government of the Republic of Lithuania 29.06.1999 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Luxembourg Agreement between the Russian Federation and the Grand Duchy of Luxembourg on 28.06.1993 (eds. from 02.11.2011) "On the avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and property"

Macedonia Agreement between the Government of the Russian Federation and the Government of the Republic of Macedonia on 21.10.1997 "On avoidance of double taxation with respect to taxes on income andproperty"

Malaysia Agreement between the Government of the USSR and the Government of Malaysia on 31.07.1987 "On avoidance of double taxation with respect to taxes on income"

Mali Convention between the Government of the Russian Federation and the Government of the Republic of Mali from 25.06.1996 "On avoidance of double taxation and the establishment of rules for mutual assistance with respect to taxes on income and property"

Malta Convention between the Government of the Russian Federation and the Government of Malta for theavoidance of double taxation and prevention of fiscal evasion with respect to taxes on income

Morocco Agreement between the Government of the Russian Federation and the Government of the Kingdom ofMorocco on 04.09.1997 "On avoidance of double taxation with respect to taxes on income and property"

United Mexican States

Agreement between the Government of the Russian Federation and the Government of the United States Meksikanskansih dated 07.06.2004 "On avoidance of double taxation with respect to taxes on income"

Moldova Agreement between the Government of the Russian Federation and the Government of the Republic of Moldova of 12.04.1996 "On avoidance of double taxation of income and property and preventionof tax evasion"

Mongolia Agreement between the Government of the Russian Federation and the Government of Mongolia on 05.04.1995 "On avoidance of double taxation with respect to taxes on income and property"

Namibia Convention between the Government of the Russian Federation and the Government of the Republic of Namibia on 31.03.1998 "On avoidance of double taxation and prevention of fiscal evasion withrespect to taxes on income"

The Netherlands

Agreement between the Government of the Russian Federation and the Government of the Kingdom ofthe Netherlands on 16.12.1996 "On avoidance of double taxation and prevention of fiscal evasionwith respect to taxes on income and wealth"

New Zealand Agreement between the Government of the Russian Federation and the Government of New Zealand on05.09.2000 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Norway Convention between the Government of the Russian Federation and the Government of the Kingdom of Norway on 26.03.1996 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Poland Agreement between the Government of the Russian Federation and the Government of the Republic of Poland of 22.05.1992 "On avoidance of double taxation of income and property"

Portugal Convention between the Government of the Russian Federation and the Government of the Portuguese Republic from 29.05.2000 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Romania Convention between the Government of the Russian Federation and the Government of Romania on 27.09.1993 "On avoidance of double taxation with respect to taxes on income and property"

22

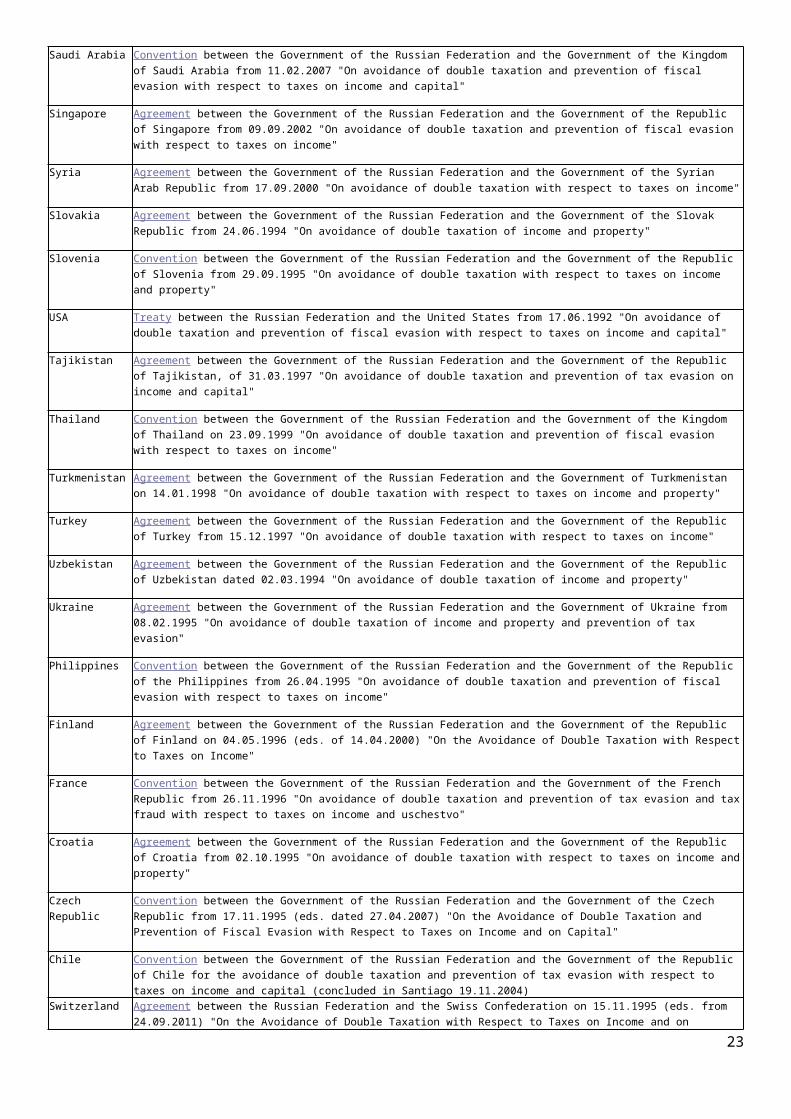

Saudi Arabia Convention between the Government of the Russian Federation and the Government of the Kingdom of Saudi Arabia from 11.02.2007 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Singapore Agreement between the Government of the Russian Federation and the Government of the Republic of Singapore from 09.09.2002 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Syria Agreement between the Government of the Russian Federation and the Government of the Syrian Arab Republic from 17.09.2000 "On avoidance of double taxation with respect to taxes on income"

Slovakia Agreement between the Government of the Russian Federation and the Government of the Slovak Republic from 24.06.1994 "On avoidance of double taxation of income and property"

Slovenia Convention between the Government of the Russian Federation and the Government of the Republic of Slovenia from 29.09.1995 "On avoidance of double taxation with respect to taxes on income and property"

USA Treaty between the Russian Federation and the United States from 17.06.1992 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income and capital"

Tajikistan Agreement between the Government of the Russian Federation and the Government of the Republic of Tajikistan, of 31.03.1997 "On avoidance of double taxation and prevention of tax evasion on income and capital"

Thailand Convention between the Government of the Russian Federation and the Government of the Kingdom of Thailand on 23.09.1999 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Turkmenistan Agreement between the Government of the Russian Federation and the Government of Turkmenistan on 14.01.1998 "On avoidance of double taxation with respect to taxes on income and property"

Turkey Agreement between the Government of the Russian Federation and the Government of the Republic of Turkey from 15.12.1997 "On avoidance of double taxation with respect to taxes on income"

Uzbekistan Agreement between the Government of the Russian Federation and the Government of the Republic of Uzbekistan dated 02.03.1994 "On avoidance of double taxation of income and property"

Ukraine Agreement between the Government of the Russian Federation and the Government of Ukraine from 08.02.1995 "On avoidance of double taxation of income and property and prevention of tax evasion"

Philippines Convention between the Government of the Russian Federation and the Government of the Republic of the Philippines from 26.04.1995 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Finland Agreement between the Government of the Russian Federation and the Government of the Republic of Finland on 04.05.1996 (eds. of 14.04.2000) "On the Avoidance of Double Taxation with Respectto Taxes on Income"

France Convention between the Government of the Russian Federation and the Government of the French Republic from 26.11.1996 "On avoidance of double taxation and prevention of tax evasion and taxfraud with respect to taxes on income and uschestvo"

Croatia Agreement between the Government of the Russian Federation and the Government of the Republic of Croatia from 02.10.1995 "On avoidance of double taxation with respect to taxes on income andproperty"

Czech Republic

Convention between the Government of the Russian Federation and the Government of the Czech Republic from 17.11.1995 (eds. dated 27.04.2007) "On the Avoidance of Double Taxation and Prevention of Fiscal Evasion with Respect to Taxes on Income and on Capital"

Chile Convention between the Government of the Russian Federation and the Government of the Republic of Chile for the avoidance of double taxation and prevention of tax evasion with respect to taxes on income and capital (concluded in Santiago 19.11.2004)

Switzerland Agreement between the Russian Federation and the Swiss Confederation on 15.11.1995 (eds. from 24.09.2011) "On the Avoidance of Double Taxation with Respect to Taxes on Income and on

23

Capital"

Sweden Convention between the Government of the Russian Federation and the Government of the Kingdom of Sweden from 15.06.1993 "On avoidance of double taxation with respect to taxes on income"

Sri Lanka Agreement between the Government of the Russian Federation and the Government of the DemocraticSocialist Republic of Sri Lanka on 02.03.1999 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

South Africa Agreement between the Government of the Russian Federation and the Government of the Republic of South Africa from 27.11.1995 "On avoidance of double taxation and prevention of fiscal evasion with respect to taxes on income"

Yugoslavia (Serbia and Montenegro)

Convention between the Government of the Russian Federation and the Union Government of the Federal Republic of Yugoslavia from 12.10.1995 "On avoidance of double taxation with respect totaxes on income and property"

Japan Convention between the Government of the USSR and the Government of Japan on 18.01.1986 "On avoidance of double taxation with respect to taxes on income"

http://www.consultant.ru/document/cons_doc_LAW_63276/

Sources:

http://www.vedomosti.ru/finance/news/33178991/gosdengi-tolko-dlya-rossii?full#cut

http://www.ey.com/GL/en/Services/Tax/International-Tax/Alert--An-update-on-legislative-initiatives-for--de-offshorization--of-the-Russian-economy

http://www.ey.com/GL/en/Services/Tax/International-Tax/Alert--Russia-publishes-Controlled-Foreign-Companies-Bill

http://www.ey.com/GL/en/Services/Tax/International-Tax/Alert--Russia-plans-to-introduce-sales-tax-legislation

24