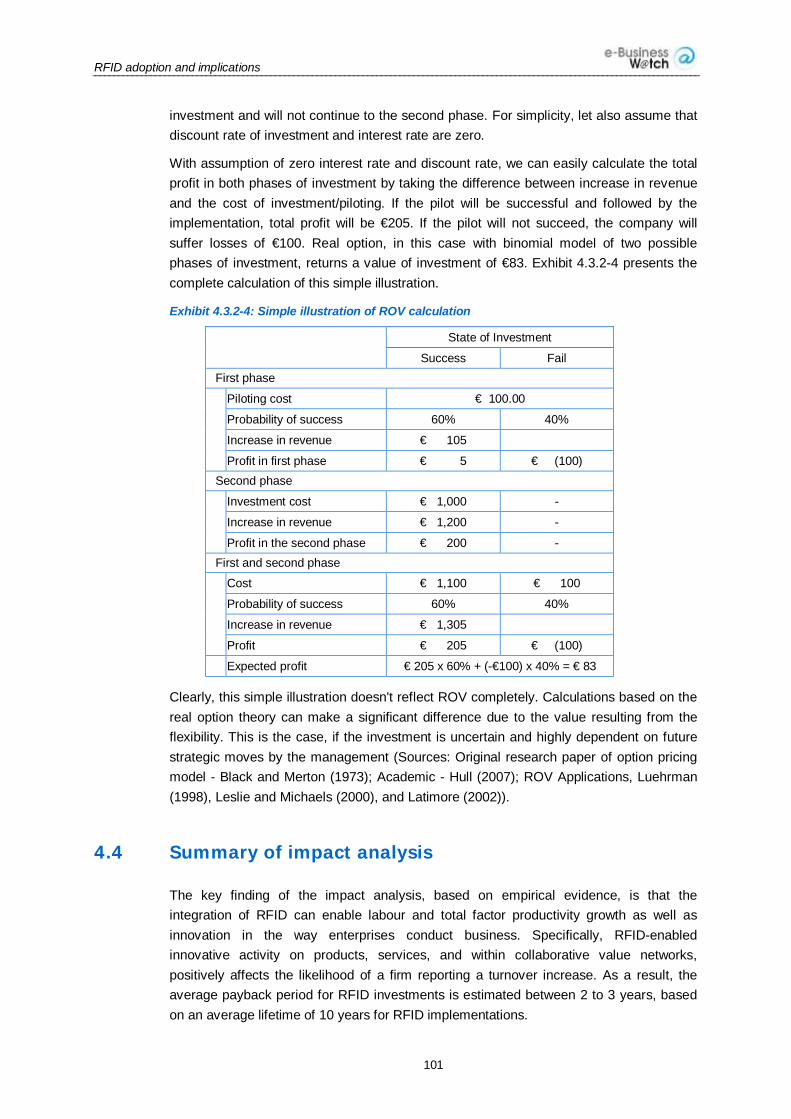

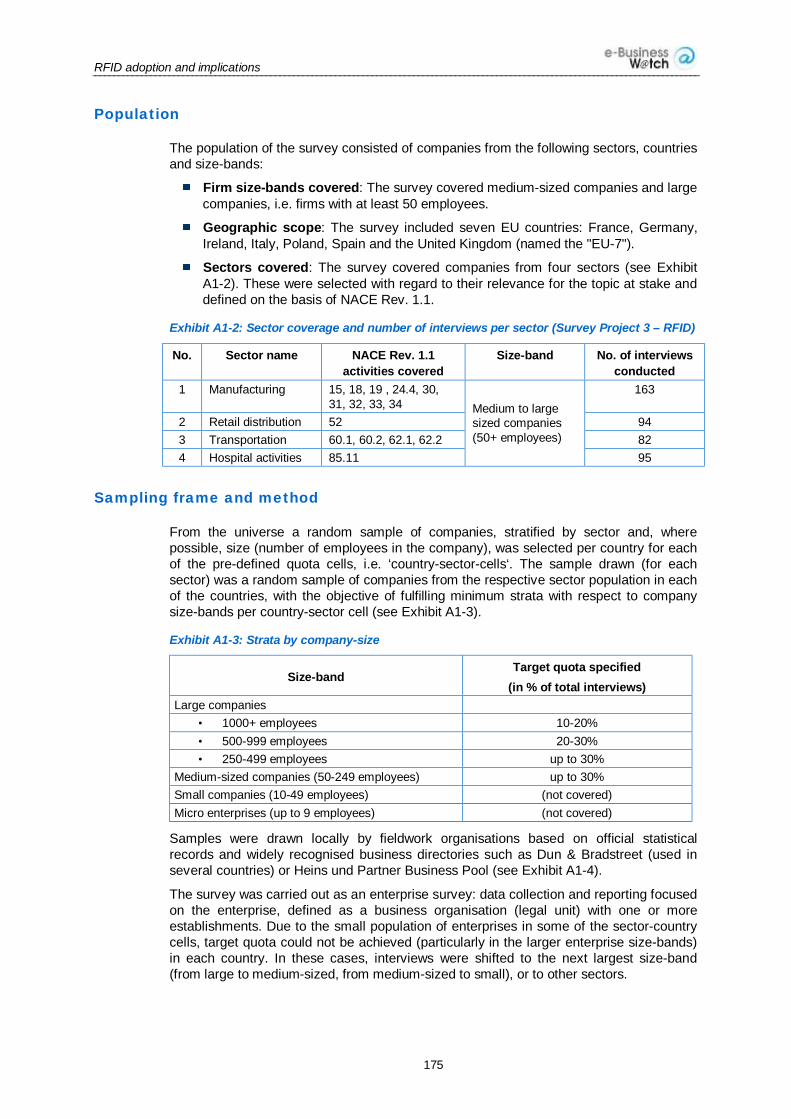

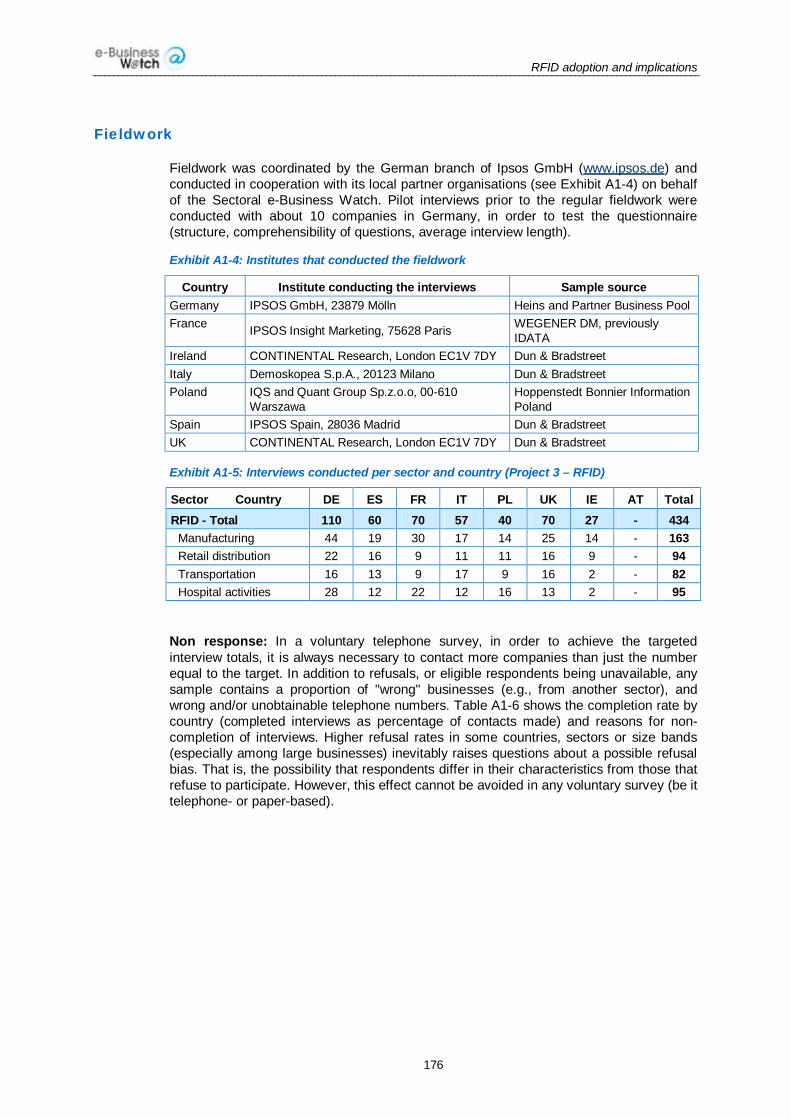

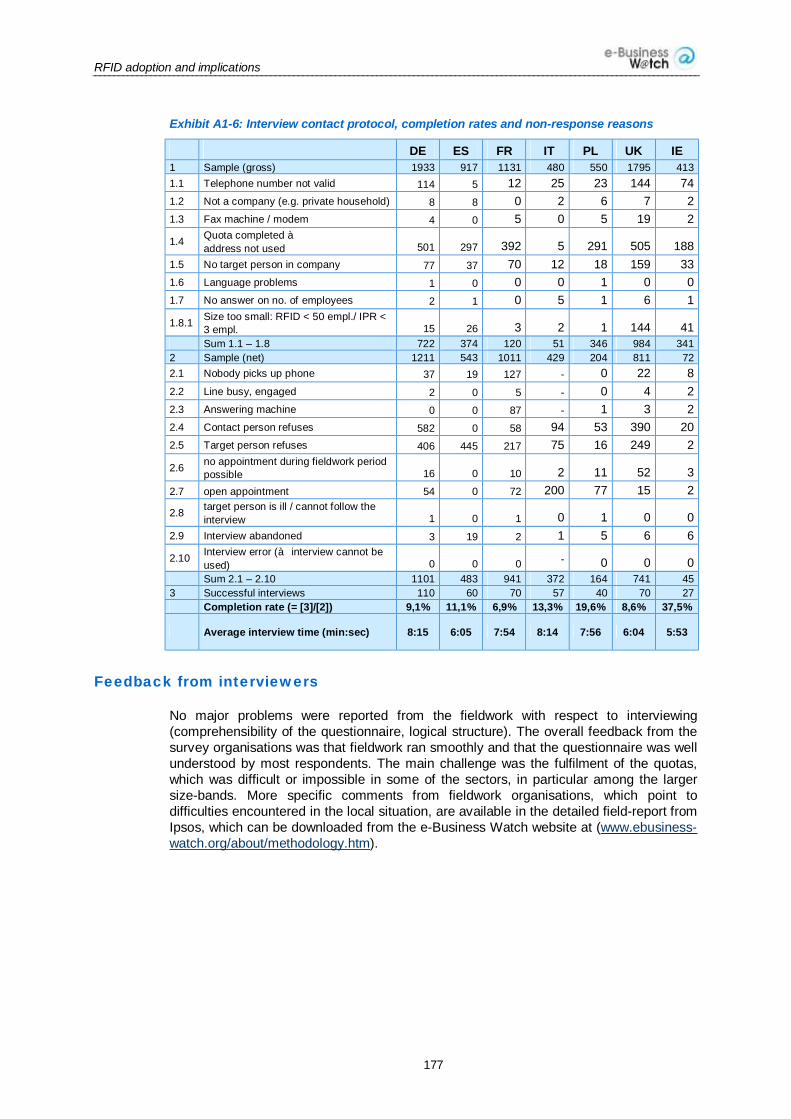

rfid adoption and implications - empirica

TRANSCRIPT

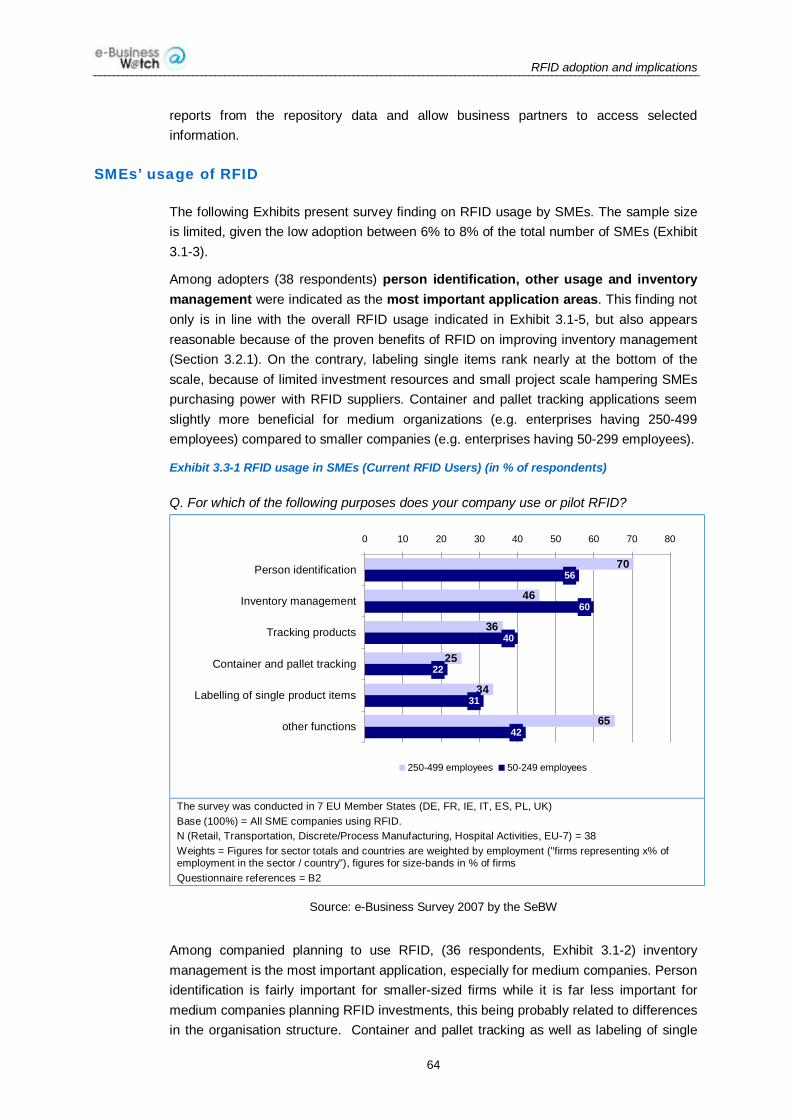

RFID Adoption and Implications

Study reportNo. 07/2008

This report was prepared by IDC EMEA on behalf of the European Commission, Enterprise & Industry Directorate General, in the context of the "Sectoral e-Business Watch" programme. The Sectoral e-Business Watch is implemented by empirica GmbH in cooperation with Altran Group, Databank Consulting, DIW Berlin, IDC EMEA, Ipsos, GOPA-Cartermill and Rambøll Management based on a service contract with the European Commission.

European Commission, DG Enterprise & Industry

e-Mail: [email protected], [email protected]

IImmppaacctt SSttuuddyy NNoo.. 0077//22000088

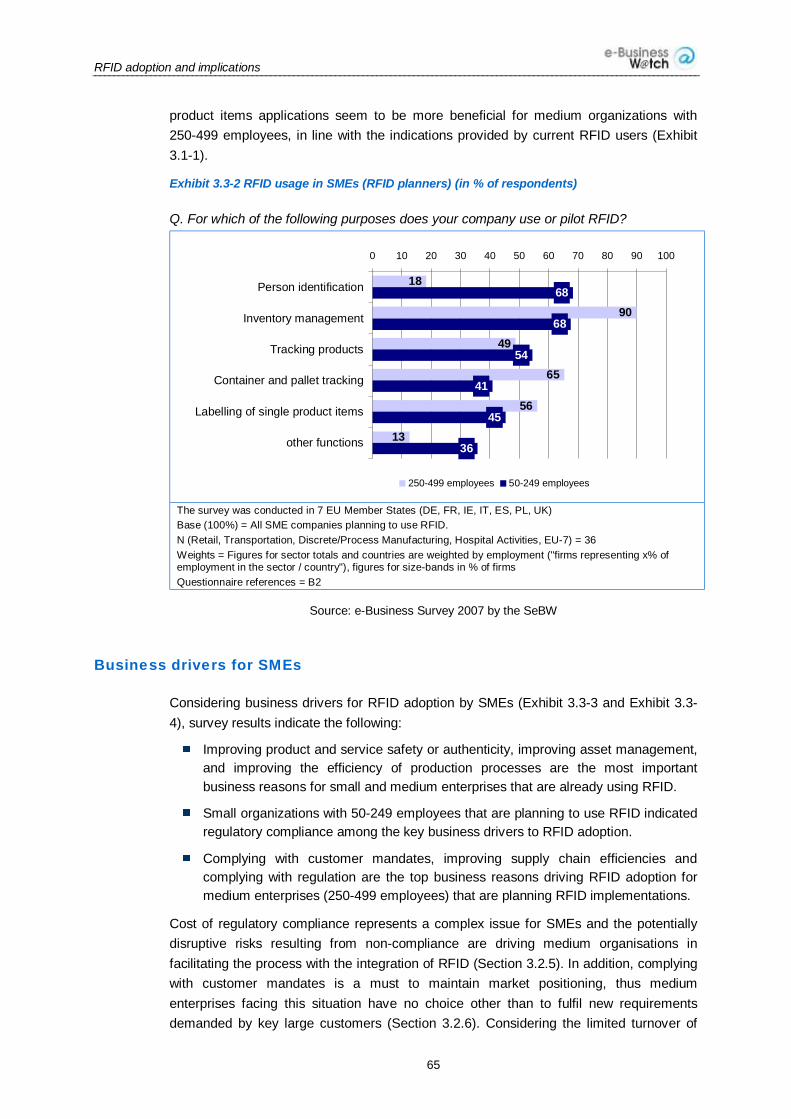

RRFFIIDD AAddooppttiioonn aanndd IImmpplliiccaattiioonnss

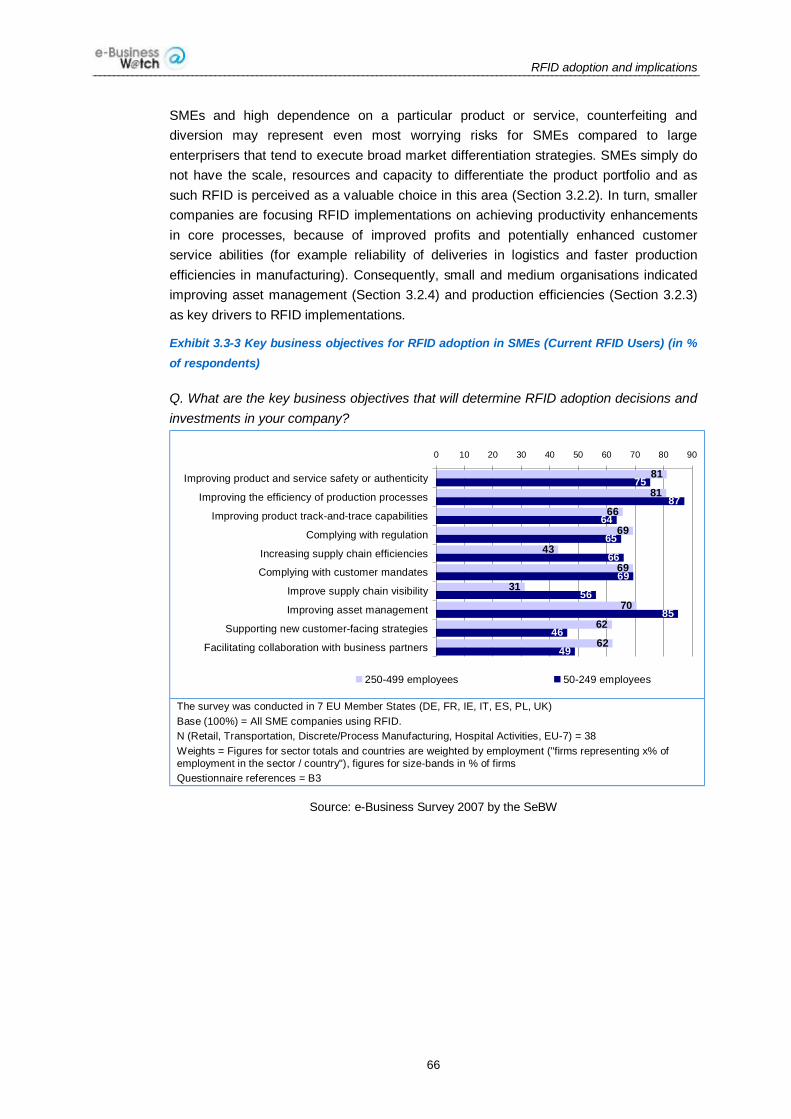

A Sectoral e-Business Watch study by IDC / Global Retail Insights

FFiinnaall RReeppoorrtt Version 4.0

September 2008

RFID adoption and implications

2

About the Sectoral e-Business Watch and this report

The European Commission, Enterprise & Industry Directorate General, launched the Sectoral e-Business Watch (SeBW) to study and assess the impact of ICT on enterprises, industries and the economy in general across different sectors of the economy in the enlarged European Union, EEA and Accession countries. SeBW continues the successful work of the e-Business W@tch which, since January 2002, has analysed e-business developments and impacts in manufacturing, construction, financial and service sectors. All results are available on the internet and can be accessed or ordered via the Europa server or directly at the Sectoral e-Business Watch website (www.europa.eu.int/comm/enterprise/ict/policy/watch/index.htm, or www.ebusiness-watch.org).

This document is a final report of a Topic Impact Study, focusing on the adoption of Radio Frequency Identification (RFID) technologies and their impact on the manufacturing, transportation, retail and healthcare industries. The study describes how companies use ICT for conducting business, and, above all, assesses implications thereof for firms and for the industry as a whole. The elaborations are based on an international survey of enterprises on their use of RFID, econometric analyses, expert interviews and case studies.

Disclaimer

Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of the following information. The views expressed in this report are those of the authors and do not necessarily reflect those of the European Commission. Nothing in this report implies or expresses a warranty of any kind. Results from this report should only be used as guidelines as part of an overall strategy. For detailed advice on corporate planning, business processes and management, technology integration and legal or tax issues, the services of a professional should be obtained.

Acknowledgements

This report was prepared by IDC EMEA on behalf of the European Commission, Enterprise & Industry Directorate General. The main author was Ivano Ortis. The study is a deliverable of the Sectoral e-Business Watch, which is implemented by empirica GmbH in cooperation with Altran Group, Databank Consulting, DIW Berlin, IDC EMEA, Ipsos, GOPA-Cartermill and Rambøll Management, based on a service contract with the European Commission (principal contact and coordination: Dr. Hasan Alkas).

The SeBW would like thank the members of the Advisory Board in 2007/2008 for reviewing the draft report and providing valuable comments and suggestions: Andy Lee (Cisco), Antonio Lasi (Lombardia Informatica) and Jean-Francois Remy (HP).

Contact

For further information about this Sector Study or the Sectoral e-Business Watch, please contact:

Global Retail Insights, IDC Viale Monza, 14 20127 Milan, Italy [email protected]

Sectoral e-Business Watch c/o empirica GmbH Oxfordstr. 2, 53111 Bonn, Germany [email protected]

European Commission Enterprise & Industry Directorate-General, ICT for Competitiveness and Innovation [email protected]

Rights restrictions

Material from this report can be freely used or reprinted but not commercially resold and, if quoted, the exact source must be clearly acknowledged. Milan / Brussels, 2008

RFID adoption and implications

3

Table of contents

Executive Summary ................................................................................................... 5

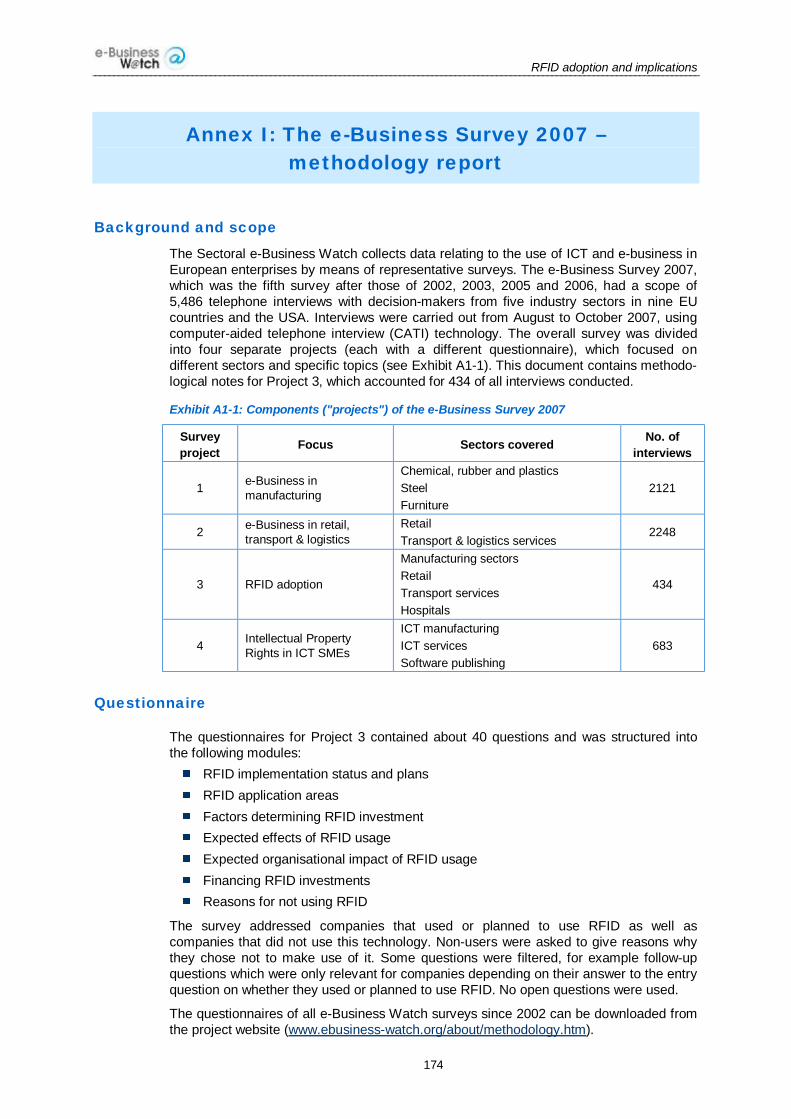

1 Introduction ................................................................................................... 9 1.1 About this report .................................................................................................................. 9 1.2 About the Sectoral e-Business Watch................................................................................ 10 1.3 ICT and e-Business – key terms and concepts .................................................................. 14 1.4 Study objectives and methodology..................................................................................... 19

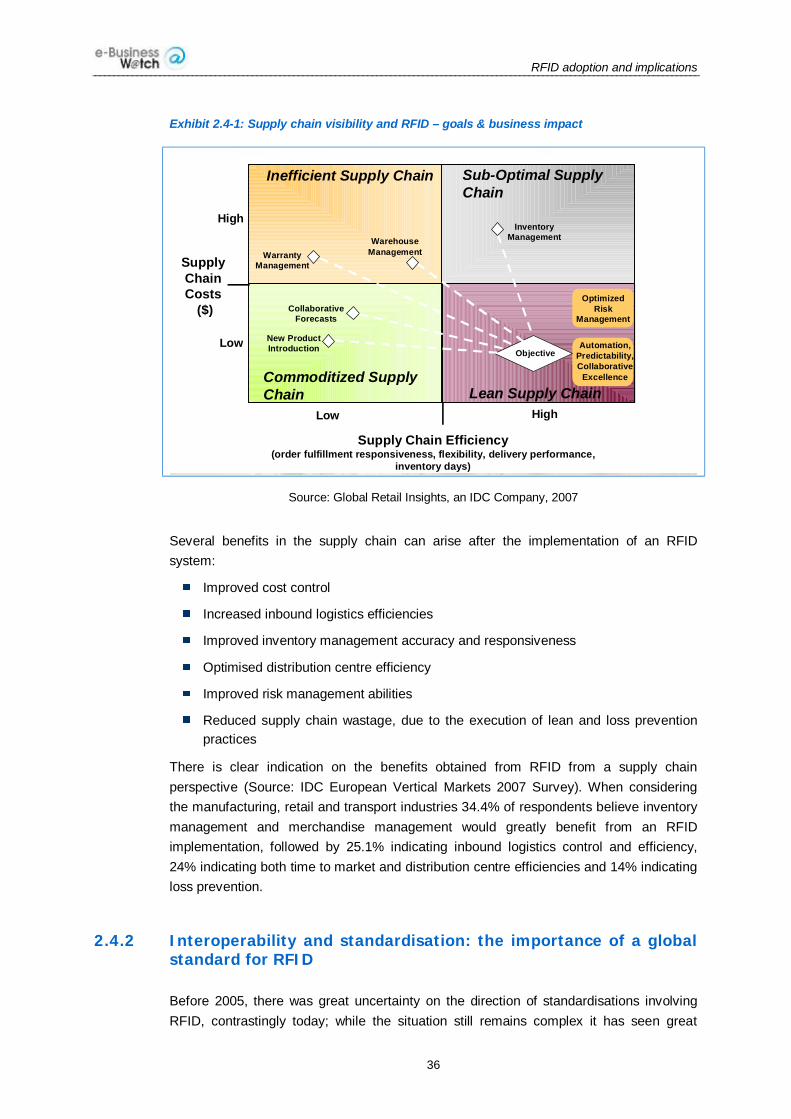

2 Context and background ............................................................................. 21 2.1 Topic definition — main goals and scope of the study ........................................................ 21 2.1.1 Main goals...................................................................................................................................... 21 2.1.2 Scope............................................................................................................................................. 21 2.2 RFID technology................................................................................................................ 22 2.2.1 A basic description of RFID............................................................................................................. 22 2.2.2 Types of RFID tags......................................................................................................................... 25 2.2.3 RFID standards .............................................................................................................................. 27 2.3 RFID benefit and impacts .................................................................................................. 29 2.4 Key trends and challenges for RFID applications ............................................................... 32 2.4.1 Responsive supply chains............................................................................................................... 32 2.4.2 Interoperability and standardisation: the importance of a global standard for RFID ............................ 36 2.4.3 Return on investment (ROI) for RFID – The challenge of creating the business case......................... 37 2.4.4 Value chain collaboration and RFID: opportunities to drive profitable growth strategies ..................... 39 2.4.5 RFID concerns: security, privacy and health risks ............................................................................ 41 2.5 RFID applications in the retail, manufacturing, transportation and healthcare industries ..... 42

3 Deployment of RFID solutions..................................................................... 46 3.1 RFID adoption trends ........................................................................................................ 46 3.1.1 RFID adoption: international comparison ......................................................................................... 46 3.1.2 RFID adoption in the EU ................................................................................................................. 47 3.2 Key business objectives driving RFID adoption.................................................................. 52 3.2.1 Improving supply chain efficiency, visibility, and predictability ........................................................... 57 3.2.2 Improving product or service safety and authenticity ........................................................................ 58 3.2.3 Enabling faster operational turnarounds and improving production processes efficiencies ................. 59 3.2.4 Augmenting asset management capabilities .................................................................................... 60 3.2.5 Regulatory compliance.................................................................................................................... 61 3.2.6 Market-driven mandates.................................................................................................................. 62 3.2.7 Reducing out-of-stock situations...................................................................................................... 62 3.3 Benefits and opportunities for SMEs.................................................................................. 63

RFID adoption and implications

4

3.4 Key barriers to RFID adoption and lessons learned from case studies ............................... 72 3.5 RFID investment plans and adoption roadmap................................................................... 77 3.6 Summary and conclusions of RFID deployment................................................................. 80

4 RFID benefits and business impact............................................................. 83 4.1 Impact on productivity and innovation ................................................................................ 83 4.2 Impact on employment and workforce composition ............................................................ 89 4.3 RFID ROI .......................................................................................................................... 95 4.3.1 RFID costs...................................................................................................................................... 95 4.3.2 Business case assessment ............................................................................................................. 96 4.4 Summary of impact analysis ............................................................................................ 101

5 Case studies .............................................................................................. 103 5.1 METRO Group (Germany)............................................................................................... 105 5.2 Hewlett-Packard (Brazil) .................................................................................................. 112 5.3 Euro Pool System (Belgium)............................................................................................ 118 5.4 Hong Kong International Airport....................................................................................... 123 5.5 Land Rover (UK) ............................................................................................................. 128 5.6 Istituto Nazionale dei Tumori (Italy).................................................................................. 134 5.7 New Look (UK) ................................................................................................................ 144 5.8 Futura Systems (Spain)................................................................................................... 147 5.9 Schuitema (Netherlands) ................................................................................................. 152 5.10 Motol university hospital (Czech Republic)....................................................................... 158 5.11 Summary of case study findings ...................................................................................... 162

6 Conclusions: outlook and policy implications .......................................... 163 6.1 Outlook on further possible RFID developments .............................................................. 164 6.2 Policy implications ........................................................................................................... 165 6.2.1 Supporting RFID skills development to improve European Industry Competitive Performance ......... 166 6.2.2 Long-term regulatory framework for radio frequency standards....................................................... 167 6.2.3 Analyse potential environmental impacts resulting from the diffusion of billions of RFID devices and

provide recycling guidelines for consumer products........................................................................ 168 6.2.4 Promote EU level R&D cooperative research for medium-long term RFID applications and innovations

– a focus on wireless mesh-network communication protocols........................................................ 169

References ............................................................................................................. 170

Annex I: The e-Business Survey 2007 – methodology report ............................... 174

Annex II: RFID standards ....................................................................................... 180

Annex III: RFID standard bodies and regulation.................................................... 182

RFID adoption and implications

5

Executive summary

Key findings

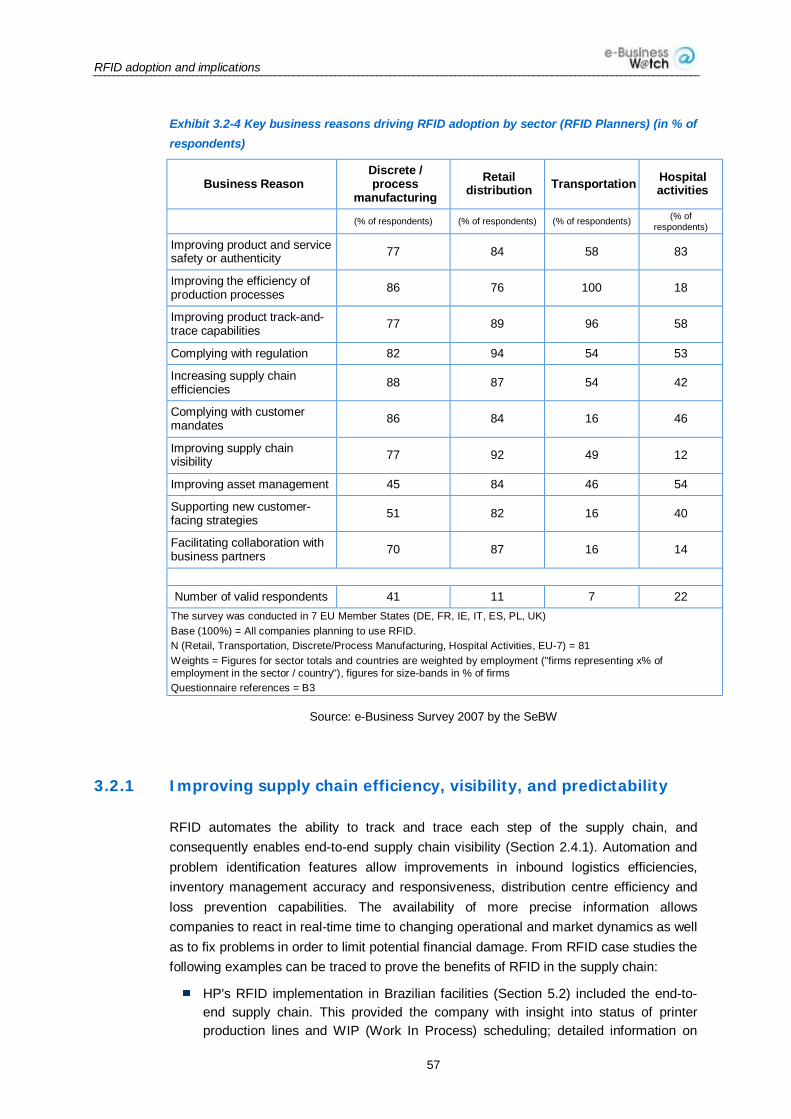

RFID may become mainstream in Europe over the next 5 to 10 years. A significant adoption uptake in the retail, transportation, and logistics sectors over the past years indicates that RFID is expected to grow at a fast pace over the coming 5 to 10 years.

Business stimuli will foster the implementation of RFID. Key business drivers for RFID adoption include mainly operational incentives such as the opportunity to achieve cost reductions and productivity improvements along the supply chain and in production processes. The focus is expected to gradually move from operational execution activities to the optimisation of business planning and intelligence capabilities motivation.

Average payback time for RFID investments is estimated to be between 2 to 3 years. Empirical evidence indicates that the implementation of RFID can enable labour and total factor productivity growth. It also fosters innovative activity leading to increases in turnover. Depending on the implementation scale, companies can expect a 12 to 18 months competitive advantage from the implementation of RFID.

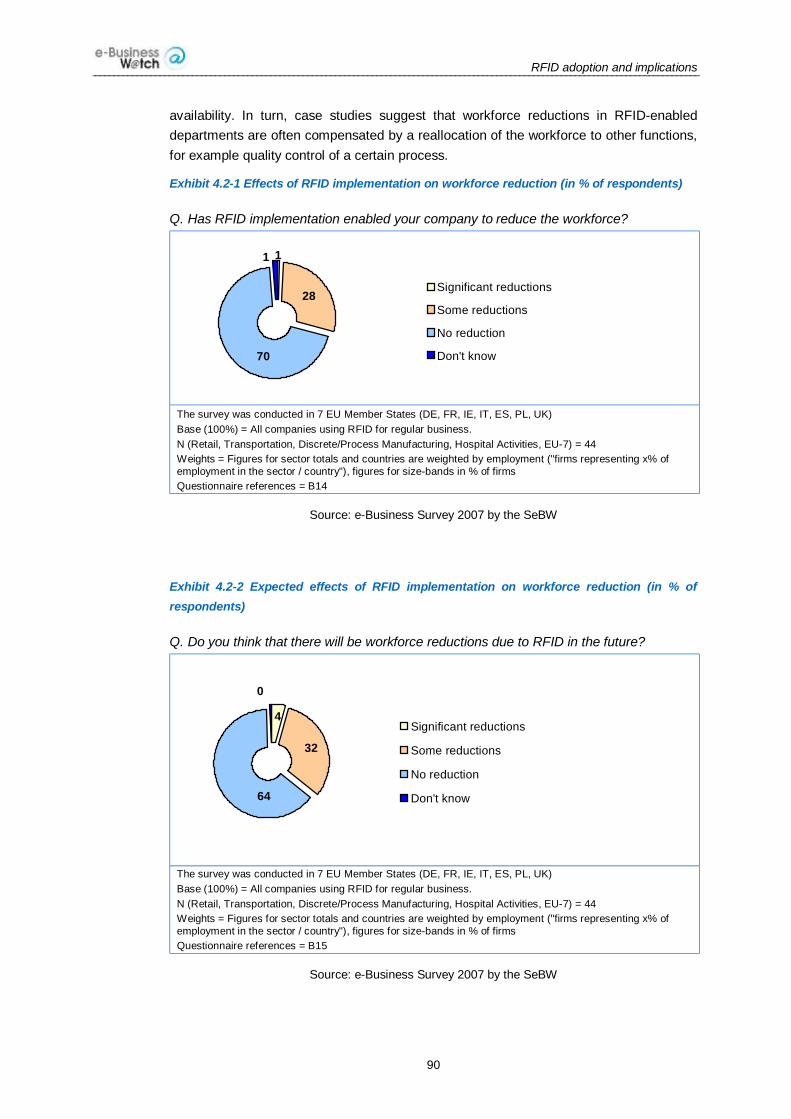

RFID adoption affects workforce composition. About 30% of companies already using RFID report some workforce reductions. These reductions in RFID-enabled departments are often compensated by a reallocation of the workforce to other business functions.

Outlook for further developments. Technological innovations will lead to greater integration of RFID with other technologies, real-time locating systems (RTLS), and business intelligence platforms. Other trends are embedding RFID in products -such as contact-less cards- and incorporating RFID into product packaging, to enable recycling.

Objectives and scope of the study

This document is the Sectoral e-Business Watch study on Radio Frequency Identification (RFID) activities in the manufacturing, transportation, healthcare and retail industries. Its objective is to describe how companies in these industries use RFID for conducting business, to assess impacts of this development for firms and for the industries as a whole, and to indicate possible implications for policy. Findings presented in this report are based on literature, expert interviews, case studies and the results of an international survey of enterprises on their RFID usage conducted by the Sectoral e-Business Watch (SeBW) in August and September 2007 in seven European countries.

The manufacturing, transportation, healthcare and retail industries as defined for the study purpose cover the business activities defined in section 2.1.2.

RFID technology

RFID is mostly used for identifying people, objects, transactions or events through a wireless communication connection. It is an automatic identification and data capture method (AIDC), which not only helps to identify, but also to collect data attributes about a certain object or person, including localisation and environmental measurements when integrated with sensor networks. The development of RFID technology emerges to be one of the most interesting innovations for the improvement of business process efficiency across the manufacturing, transportation & logistics, wholesale distribution and retail trade sectors.

RFID adoption and implications

6

This is due to the fact that RFID systems offer enterprises an advanced way of gathering and processing business data. RFID is becoming a real opportunity to drive business process re-engineering and business models re-thinking through a systematic usage of RFID-collected data in specific-use case scenarios.

RFID may become mainstream in Europe over the next 5 to 10 years

Compared to the estimated RFID adoption rate of 18% of enterprises in 2006 and 25% in 2007 – resulting from a significant adoption uptake in retail, transportation and logistics - adoption of RFID is expected to grow in the EU-7 at a fast pace over the next 5 years (see sections 3.1 and 3.5):

On average, an annual growth of approximately 27% in the number of enterprises adopting RFID is estimated during the period 2007-2009.

By 2011, approximately 44% of enterprises are estimated to have implemented RFID.

Potentially, by 2012 half of EU-7 enterprises may have implemented RFID.

The leading sectors in the usage of RFID are the transport sector (27% of respondents) and the retail sector (26%). The highest percentage of pilots and ongoing implementations was reported in the manufacturing sectors, due to the increased pressure from their retail customers and with the objective of improving production efficiency while safeguarding product safety and authenticity. In the hospital activities sector, only 18% of respondents indicated that they have adopted RFID with 10% that are already using RFID in their regular business.

RFID adoption is positively correlated with company size: diffusion rates vary from 31% for large enterprises (over 1000 employees) to approximately 12-15% for the other enterprise classes.

Projected growth rates in RFID adoption will be driven by key business motivations including the opportunity to achieve cost reductions and productivity improvements along the supply chain, achieving regulatory compliance, increasing quality of service provided to customers and improve enterprise assets management efficiencies (see sections 3.2, 3.3, and 4.1).

The increasing momentum for investment in 2008 is also a consequence of the fact that RFID usage may be driven not only by the opportunity to optimise business process efficiency but also to enable informed decisions across the enterprise effectively. Thus, the focus of RFID implementations is expected to move gradually from operational execution activities to the optimisation of business planning and intelligence capabilities.

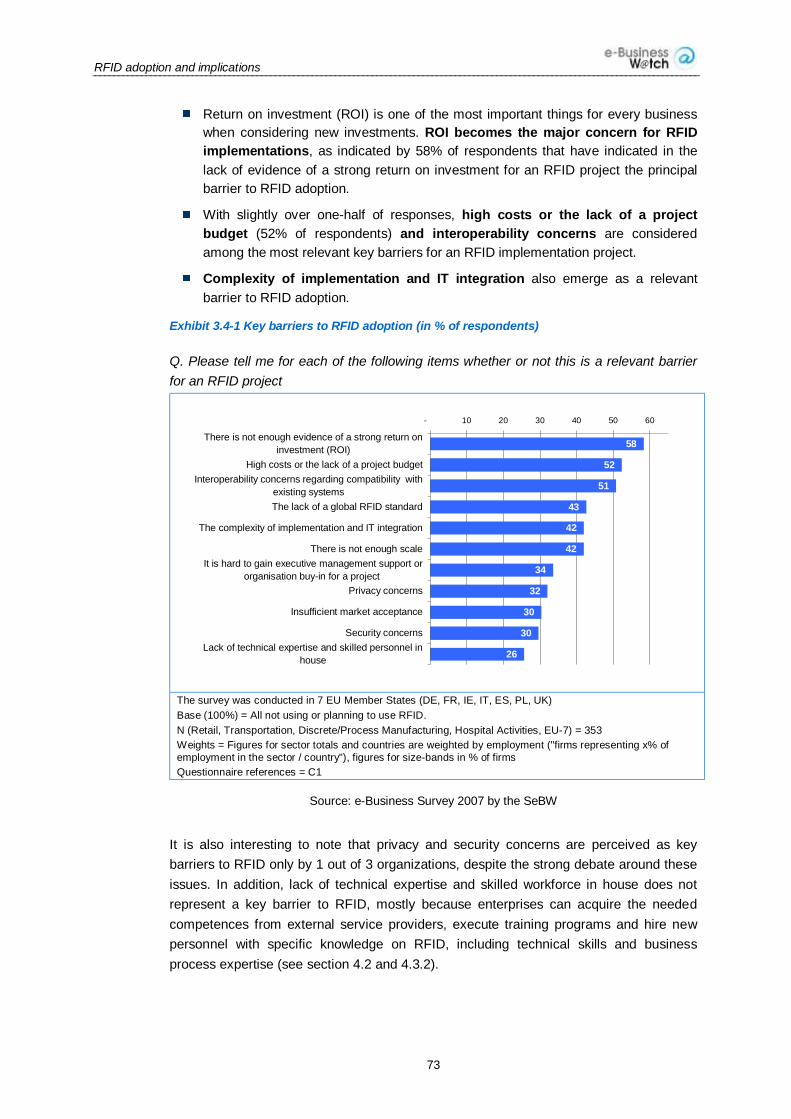

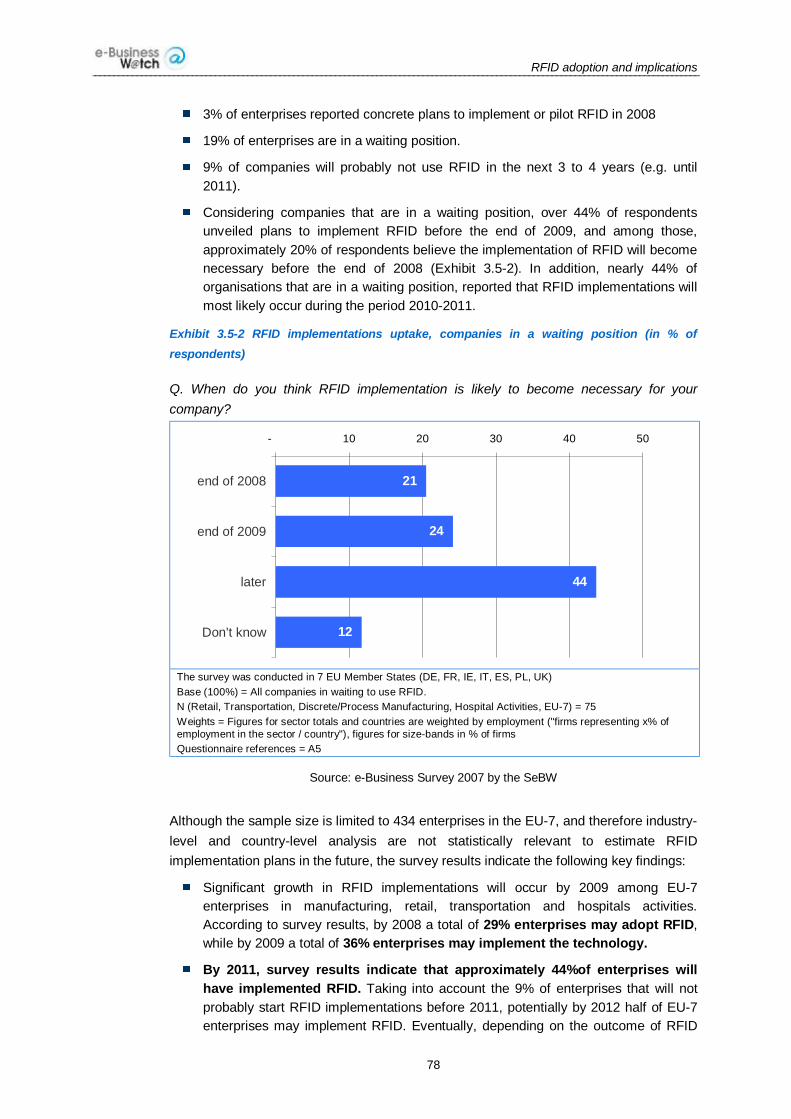

Among the key lesson learned from RFID case studies and best practices is that the required process re-engineering effort always turns out to be more than companies would initially expect. However, this shall not cause enterprises to stop innovation, as RFID is a tangible opportunity to drive new value creation and improve enterprise competitiveness.

Short-term business drivers to RFID adoption

As illustrated in more detail in sections 3.2 and 3.3, key drivers to RFID adoptions in the short-term include:

Improving product and service safety or authenticity.

Improving the efficiency of production processes.

Improving product track-and-trace capabilities and increasing supply chain efficiencies and visibility. Warehouse and logistics productivity improvements emerge as the major supply chain goal in the short-term. Global traceability represents a major medium to long-term objective for the industry, with RFID

RFID adoption and implications

7

holding the potential to increase consumers' safety.

Achieve regulatory compliance in a more efficient way.

Improving asset management efficiencies.

Market-driven mandates issued by large retail companies (for example WalMart and the METRO Group) are expected to further stimulate RFID adoption among consumer product goods manufacturers.

Impact of RFID

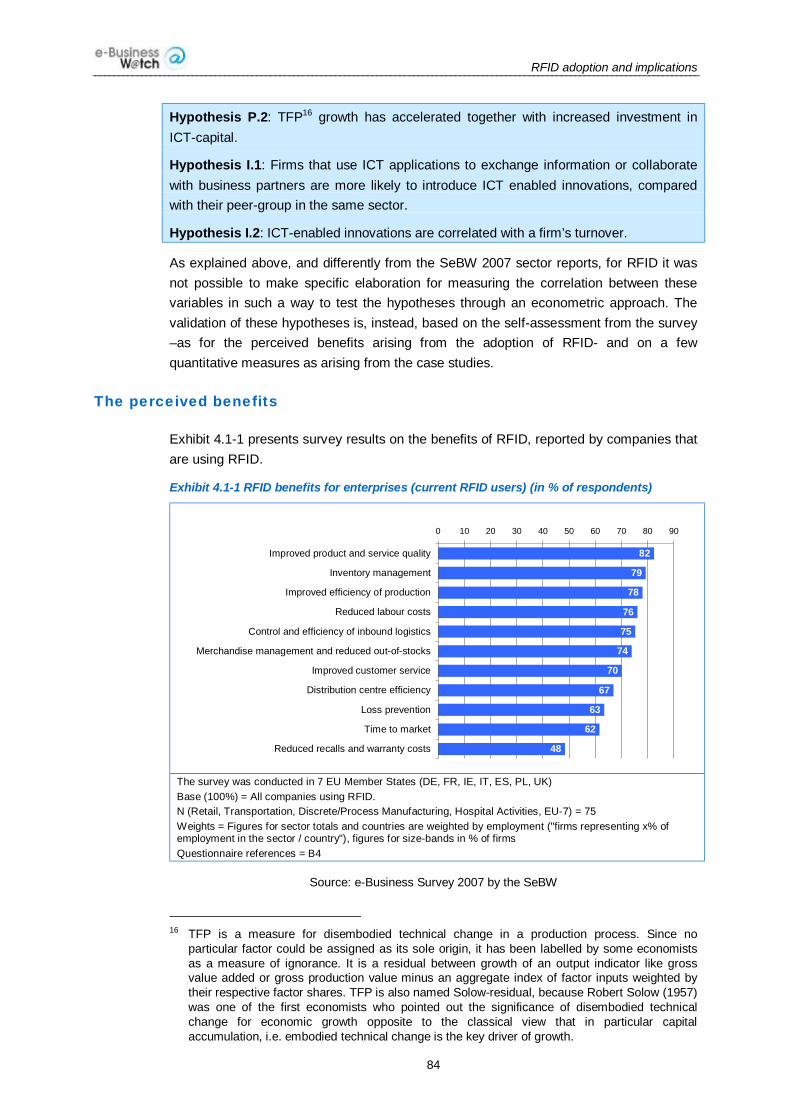

RFID-enabled companies can achieve on average a 12 to 18 months competitive advantage depending on the implementation scale, as demonstrated, for example, with the RFID projects conducted by the METRO Group, Royal Ahold and NYK Logistics.

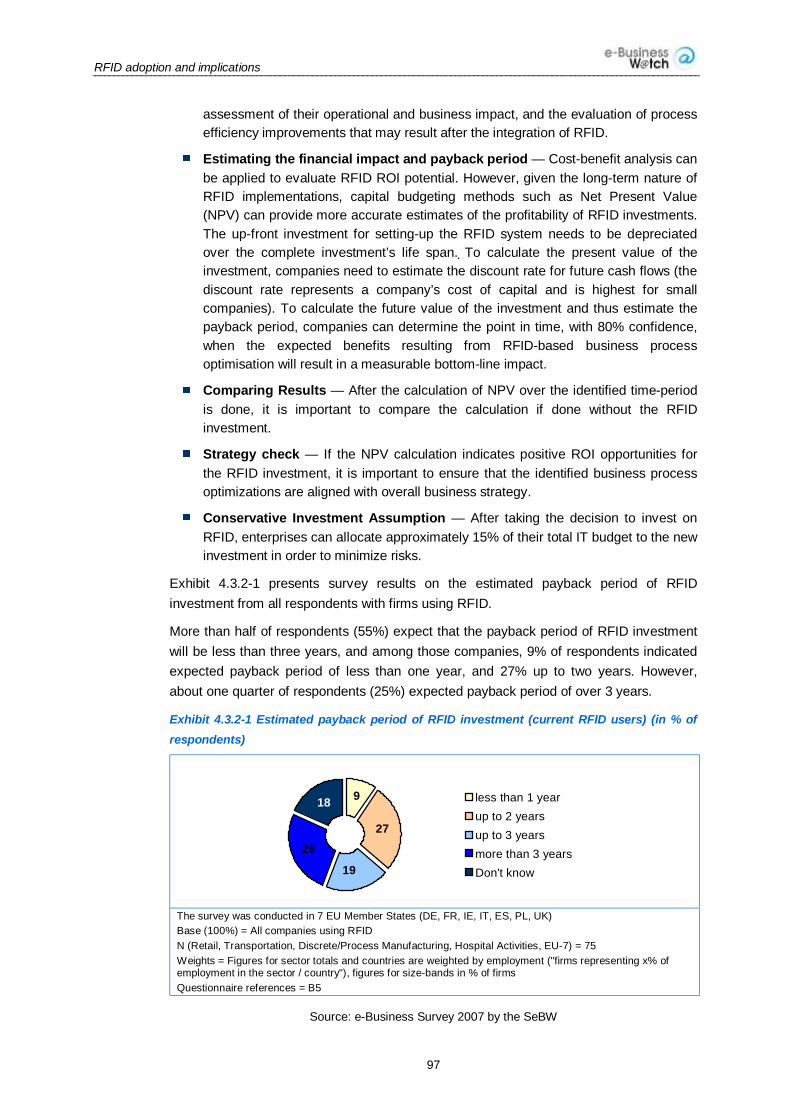

Empirical evidence indicates the implementation of RFID can enable labour and total factor productivity growth as well as innovation in the way enterprises conduct business. RFID-enabled innovative activity on products, services and within collaborative value networks, positively affects the likelihood of a firm reporting a turnover increase. As a result, the average payback period for RFID investments is estimated between 2 to 3 years, based on an average lifetime of 10 years for RFID implementations.

About 30% of companies already using RFID have experienced some workforce reductions. Companies piloting or planning to use RFID expect even slightly higher reductions. In turn, workforce reductions in RFID-enabled departments are often compensated for by a reallocation of the workforce to other business functions. A minority of enterprises created new technical (22%) or business process oriented (18%) jobs.

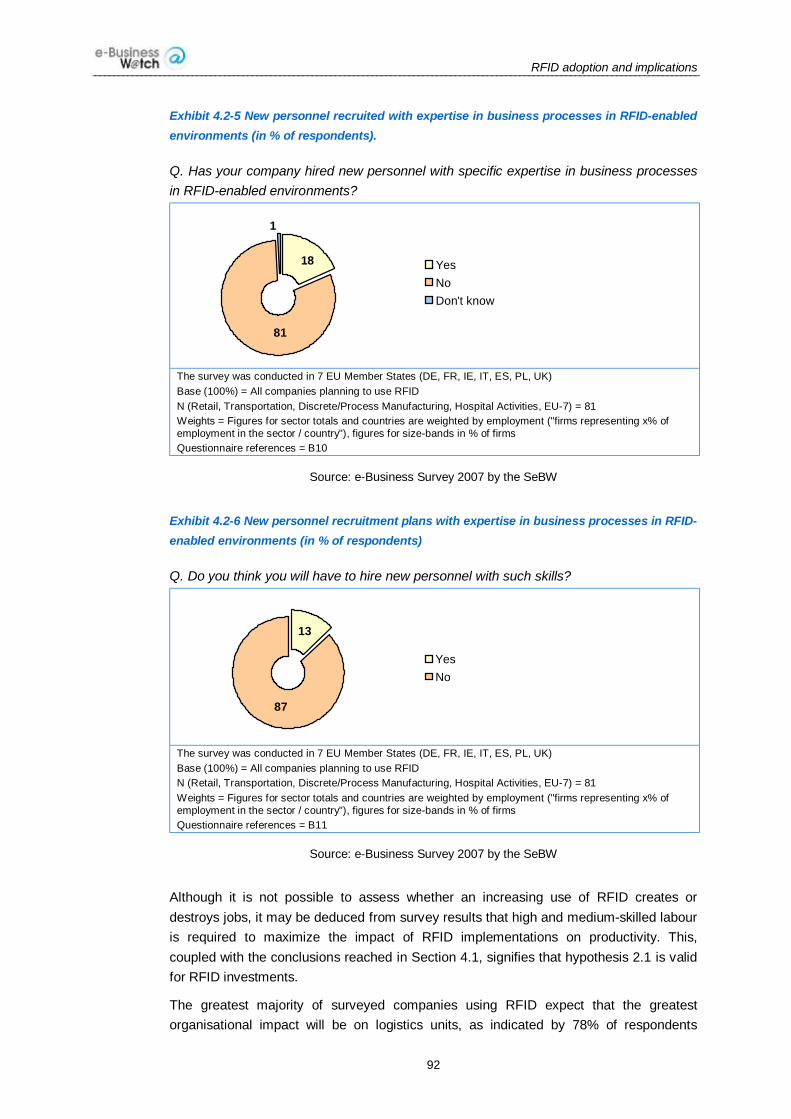

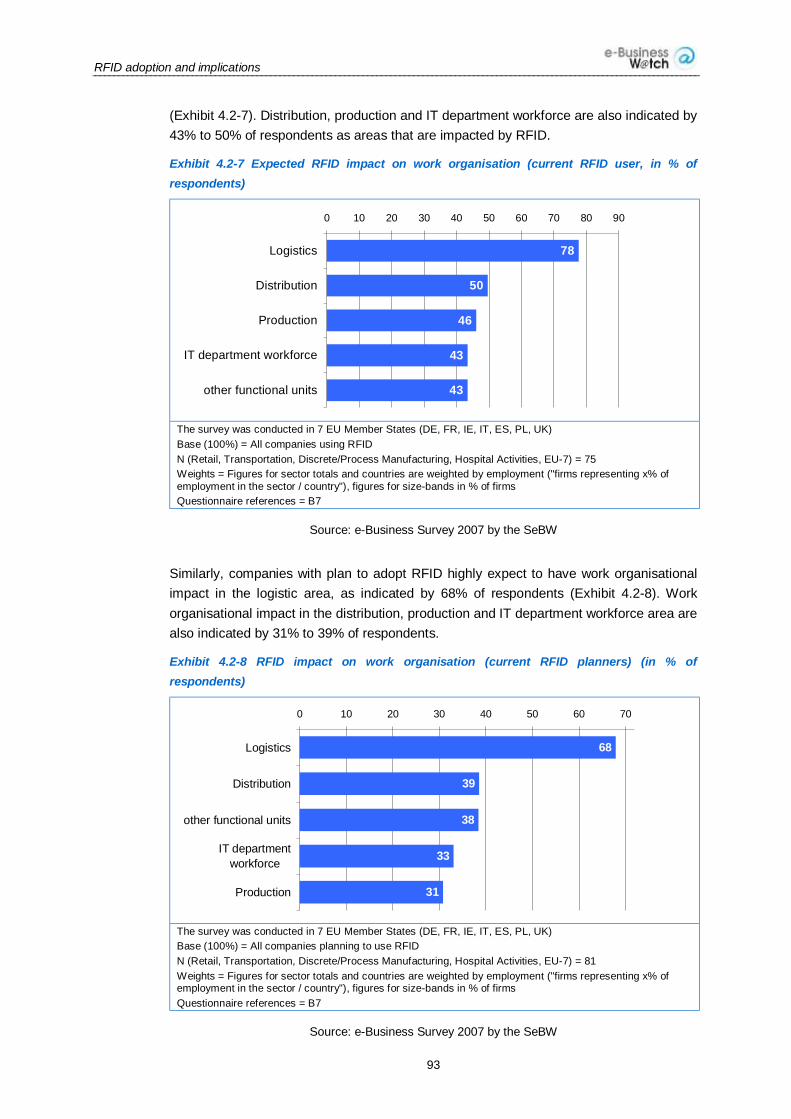

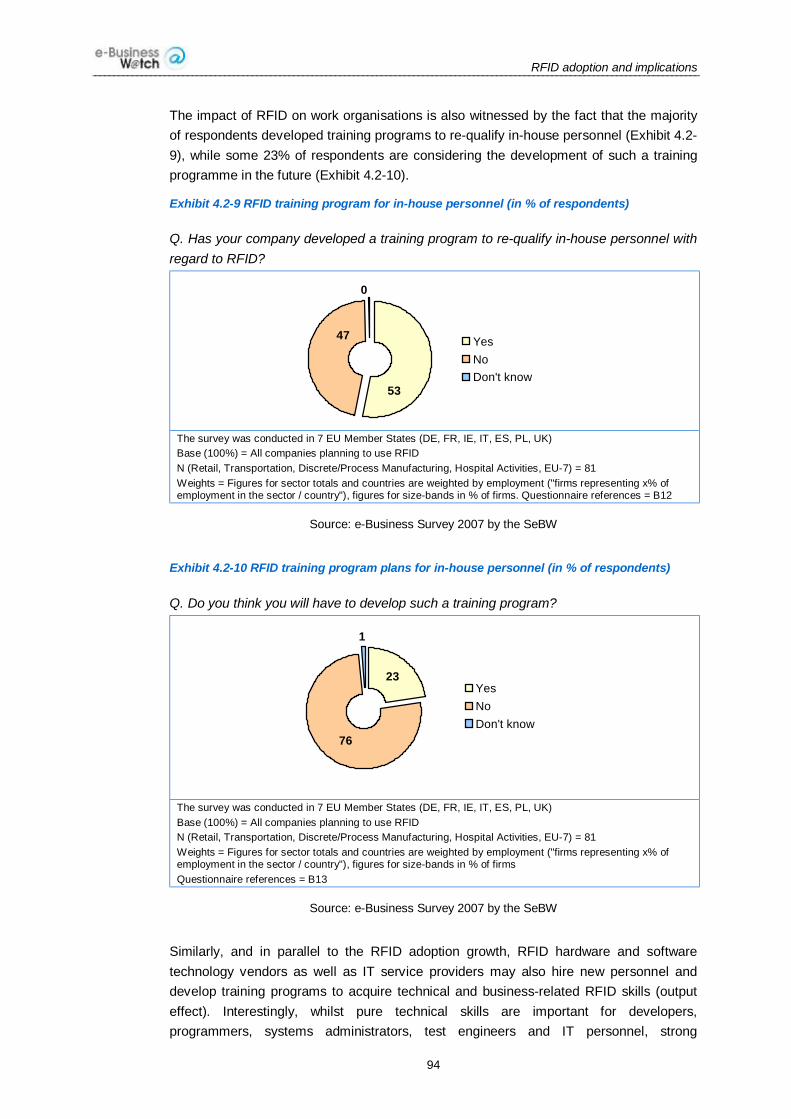

Although it is difficult to assess whether an increasing use of RFID creates or destroys jobs, it may be deduced from empirical

evidence that high and medium-skilled labour is required to maximise the impact of RFID implementations on productivity, both on the demand-side (e.g. within end-user organisations) and the output-side (e.g. within technology vendor organisations).

Strategic recommendations to approach RFID investments

Understanding whether a company can achieve concrete competitive advantage from RFID and whether RFID is the right solution to implement requires detailed assessments. The implementation of RFID is a business journey, and as such, enterprises should not position RFID as a new and complex technology project to run, because business performance improvements may result.

What drives companies' performance after the implementation of RFID data collection is the automated use of accurate information that is available in real-time, not the availability of the data in itself.

The following emerge as key trends:

Actual productivity improvements that are obtainable by enterprises depend upon a number of variables that are specific to the actual use case scenario. A phased implementation approach seems the most viable solution to enable quick ROI opportunities (e.g. between 12 to 36 months) while ensuring the attainment of long-term strategic goals.

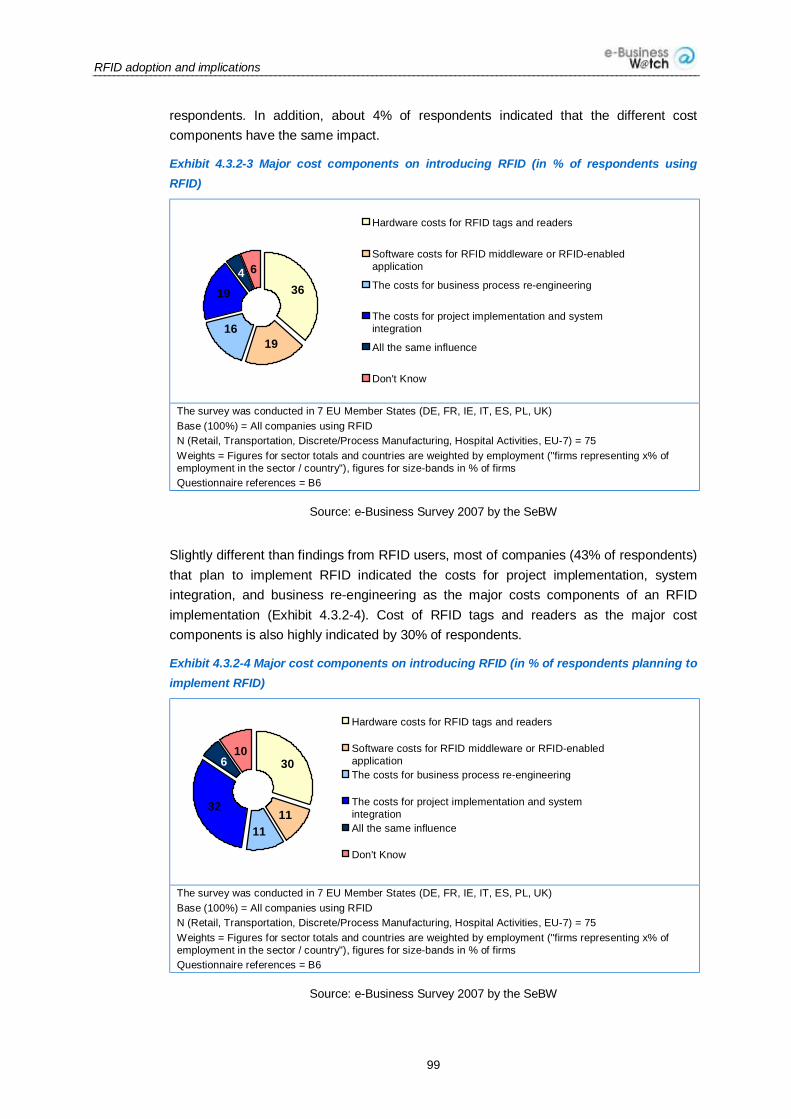

The major cost component of the total value of an RFID project seems to be the cost of project implementation, system integration and business process re-engineering. Cost for RFID tags and readers is the second major component of the total investment while software costs come third.

RFID-enabled innovations are correlated with company size. As opposed to large-scale enterprise implementation scenarios, RFID applications by SMEs

RFID adoption and implications

8

tend to focus on enabling productivity improvements that have a positive business impact in the short-term.

RFID will run parallel to barcodes for many years.

RFID is not the sole technology choice available to enterprises. Therefore, enterprises are recommended to assess RFID ROI following the guideline provided in the study (see section 4.3), whilst assessing the impact of selected technology options on the specific use case and their eventual synergies. The development of multigenerational RFID programs to accommodate new technologies when they become available is highly advisable.

Extending supply chain visibility and performance objectives to the edges, in other words beyond the "4-walls" of an enterprise, will be instrumental to maximise RFID ROI. Therefore, the recommendation is to move gradually from a closed-loop implementation scenario to include the extended boundaries.

Outlook for further developments

Technological innovation will lead to greater integration of RFID with other technologies such as sensor network technologies, real-time locating systems (RTLS), and business intelligence platforms. This may enable innovations such as the self-service totally automated store. Trends towards embedding RFID in products -such as contact-less cards- and incorporation of RFID into product

packaging, to enable recycling can also be envisaged.

Policy implications

In the light of the current policy context for RFID, considering the key barriers to RFID, as well as the expected impact on employment and workforce composition, the following political activities are suggested to the European Commission, national and regional governments as well as European and national industry associations:

Supporting RFID skills development to improve European Industry Competitive Performance (section 6.2.1)

Developing a regulatory framework promoting radio standards for the medium to long term (present standards are too fragmented and valid only up to 10 years horizon) (section 6.2.2).

Analyse potential environmental impacts resulting from the diffusion of billions of RFID devices and provide recycling guidelines for consumer products (section 6.2.3).

Invest in EU level R&D cooperative research for medium-long term RFID applications and innovations (section 6.2.4). In sight of the emerging wireless and universal communication scenario, a possible need may arise for interoperability guidelines and a new wireless communication protocol standard based on mesh-networks.

RFID adoption and implications

9

1 Introduction

1.1 About this report

Purpose, sources and addressees

This is the final report of the “Sectoral e-Business Watch” (SeBW) study on Radio Frequency Identification (RFID) in the healthcare, manufacturing, transportation and retail industries. The study analyses how companies from these industries use RFID for managing their business processes, both internally and in exchange with suppliers and customers. It identifies related opportunities, possible barriers for RFID adoption and digital integration and assesses the impact of RFID integration for firms and for the industry as a whole. Possible implications for policy actions are indicated.

Findings presented in this report are based on literature, expert interviews, case studies and the results of an international survey of enterprises on their RFID usage conducted by the SeBW in August and September 2007 in seven European countries. The study addresses, in particular, policy makers in the fields of innovation and RFID-related policies and in sectoral economic policy. It also addresses representatives of the retail, manufacturing, transportation and healthcare industries, notably decision makers in industry associations as well as firm managers in marketing, procurement, ICT and e-solutions, and human resources.

Study structure

This report is structured into six main sections. Chapter 1 explains the background and context why this study is being conducted: it introduces the Sectoral e-Business Watch (SeBW) programme of the European Commission, a conceptual framework for the analysis of e-business, and the specific methodology used for this study. Chapter 2 provides some general information and key figures about RFID in Europe and beyond. Chapter 3 analyses the current state-of-play of RFID adoption and plans for adoption in this industry, focusing on specific ICT-related issues that were found to be particularly relevant. Chapter 4 assesses the impact of RFID developments on productivity and innovation, work processes and employment, and on Return on Investment (ROI). Chapter 5 presents case studies which provide further evidence for the issues discussed in chapters 3 and 4. The final Chapter 6 provides an outlook to future developments and draws conclusions on policy implications.

Combining exploratory, descriptive and explanatory approaches

The study approach is exploratory, descriptive and explanatory, thus applying a broad and sound methodological basis: A qualitative case study approach (chapter 5) is combined with a descriptive presentation of quantitative survey data (chapter 3) and an economic analysis of ICT adoption and its impacts (chapter 4). This threefold approach is meant to produce an in-depth understanding of current e-business issues in the

RFID adoption and implications

10

industry (the "practitioner's view") as well as the state of the art of e-business practice (the “empiricist’s view”), while also assessing the economic effects of this practice, for instance on firm productivity and innovation (the "economist's perspective"). While the results from these different approaches are presented like self-sustained pieces of research in separate chapters, they are intertwined and cross-referenced.

1.2 About the Sectoral e-Business Watch

Mission and objectives

The "Sectoral e-Business Watch" (SeBW) explores the adoption, implication and impact of electronic business practices in different sectors across the European economy. It represents the continued effort of the European Commission, DG Enterprise and Industry to support policy in the fields of ICT and e-business, which started with "e-Business W@tch" in late 2001.

In ICT-related fields, DG Enterprise and Industry has a twofold mission: "to enhance the competitiveness of the ICT sector, and to facilitate the efficient uptake of ICT for European enterprises in general." The services of the SeBW are expected to contribute to these goals. This mission can be broken down into the following main objectives pertaining to this study:

to assess the impact of RFID on enterprises, industries and the economy in general;

to highlight barriers for RFID uptake, i.e. issues that are hindering a faster and/or more effective use of ICT by enterprises in Europe;

to assess the role of RFID;

to identify and discuss policy challenges stemming from the observed develop-ments, notably at the European level;

to engage in dialogue with stakeholders from industry and policy institutions, providing a forum for debating relevant issues.

By delivering evidence on RFID uptake and impact, the SeBW is supporting informed policy decision-making, in particular in the fields of innovation, competition and structural policy.

Policy context

The initial e-Business W@tch programme was rooted in the eEurope Action Plans of 2002 and 2005. The eEurope 2005 Action Plan had defined the goal "to promote take-up of e-business with the aim of increasing the competitiveness of European enterprises and raising productivity and growth through investment in information and communication technologies, human resources (notably e-skills) and new business models".1

1 "eEurope 2005: An information society for all". Communication from the Commission,

COM(2002) 263 final, 28 May 2002, chapter 3.1.2.

RFID adoption and implications

11

The i2010 policy2, a follow-up to eEurope, also stresses the critical role of ICT for productivity and innovation, stating that "… the adoption and skilful application of ICT is one of the largest contributors to productivity and growth throughout the economy, leading to business innovations in key sectors" (p. 6). The Communication anticipates "a new era of e-business solutions", based on integrated ICT systems and tools, which will lead to an increased business use of ICT. However, it also warns that businesses "still face a lack of interoperability, reliability and security", which could hamper the realisation of productivity gains (p. 7).

In February 2005, the European Commission proposed a new start for the Lisbon Strategy. While it recommended changes in the governance structures, i.e. the way objectives are to be addressed, the overall focus on growth and jobs remained unchanged. Some of the policy areas of the renewed Lisbon objectives address ICT-related issues. Central Policy Area No. 6 deals with facilitating ICT uptake across the European economy. Policy-makers in this area will require thorough analysis of ICT uptake based on accurate and detailed information on the most recent developments. Such evidence-based analysis is also needed when targeting individual sectors to fully exploit the technological advantages, in alignment with Central Policy Area No. 7 “Contributing to a strong European industrial base”. Furthermore, Guideline No. 9, addressed to Member States, encouraging the widespread use of ICT,3 can be effectively addressed only if actions are based on understanding of the potential for and probable effectiveness of interventions.

"ICT are an important tool …"

"More efforts are needed to improve business processes in European enterprises if the Lisbon targets of competitiveness are to be realised. European companies, under the pressure of their main international competitors, need to find new opportunities to reduce costs and improve performance, internally and in relation to trading partners. ICT are an important tool to increase companies’ competitiveness, but their adoption is not enough; they have to be fully integrated into business processes."

Source: European Commission (2005): Information Society Benchmarking Report

Also in 2005, in consideration of globalisation and intense international competition, the European Commission launched a new industrial policy4 to create better framework conditions for manufacturing industries in the coming years. Some of the policy strands

2 "i2010 – A European Information Society for growth and employment." Communication from the

Commission, COM(2005) 229 final. 3 "Working Together for Growth and Jobs: a New Start for the Lisbon Strategy", Communication,

COM (2005) 24, Brussels, 02.02.2005. Available at http://europa.eu.int/growthandjobs/pdf/COM2005_024_en.pdf.

4 "Implementing the Community Lisbon Programme: A Policy Framework to Strengthen EU Manufacturing - towards a more integrated approach for Industrial Policy." Communication from the Commission, COM(2005) 474 final, 5.10.2005.

RFID adoption and implications

12

described have direct links to ICT usage, recognising the importance of ICT for innovation, competitiveness and growth.

The SeBW is one of several policy instruments used by DG Enterprise and Industry in this context. Other instruments include

the e-Business Support Network (eBSN), a European network of e-business policy makers and business support organisations,

the eSkills Forum, a task force established in 2003 to assess the demand and supply of ICT and e-business skills and to develop policy recommendations,

the ICT Task Force, a group whose work is to draw together and integrate various activities aiming to strengthen Europe's ICT sector, and

activities in the areas of ICT standardisation, as part of the general standardisation activities of the Commission.5

In parallel to the work of the SeBW, the "Sectoral Innovation Watch" (see www.europe-innova.org) analyses sectoral innovation performance and challenges across the EU from an economic perspective. Studies cover, inter alia, the following sectors: chemical, automotive, aerospace, food, ICT, textiles, machinery and equipment.

Within the policy context for ICT and the Information Society, the EU Commission supports widespread deployment of RFID through a set of policies and legal frameworks, after a public consultation opened in 2006, involving five thematic expert workshops and an online consultation to which 2190 participants contributed. Among the most relevant actions are:

'Radio Frequency Identification (RFID) in Europe: steps towards a policy framework', EU Communication, March 2007 – identify actions concerning security, radio spectrum policy, standardization and research & innovation policy as instrumental factors to drive RFID adoption by European enterprises. Of particular relevance are 'ethical implications, the need to protect privacy and security; governance of the RFID identity databases; availability of radio spectrum; the establishment of harmonised international standards; and concerns over the health and environmental implications'. The 2007-08 work programme of the ICT theme of the 7th Framework Programme (2007-2013) 'has identified four challenges which mention RFID in a number of situations (healthcare, intelligent vehicle and mobility systems, micro and nanosystems, organic electronics, and future networks) as well as the eMobility22 Platform. In the future, the Commission will stimulate research on security of RFID systems, including light-weight security protocols and advanced key distribution mechanisms, with a view to preventing direct attacks on the tag, the reader and the tag-reader communication.'

Draft Recommendation on the implementation of privacy, data protection and information security principles in applications supported by Radio Frequency Identification (RFID) – following a public consultation open until April 25, 2008, the Commission expects to adopt a final recommendation by the summer of 2008.

5 The 2006 ICT Standardisation Work Programme complements the Commission's "Action Plan

for European Standardisation" of 2005 by dealing more in detail with ICT matters.

RFID adoption and implications

13

Commission Decision 2006/804/EC of 23 November 2006 on harmonisation of the radio spectrum for radio frequency identification (RFID) devices operating in the ultra high frequency (UHF) band.

Decision No 676/2002/EC of the European Parliament and of the Council of 7 March 2002 on a regulatory framework for radio spectrum policy in the European Community (Radio Spectrum Decision).

2008 ICT Policy Support Programme (PSP) in CIP – 'A European concerted effort on RFID' is part of the 2008 work programme. The platform aims at federating existing initiatives in a European initiative on RFID, maintaining a roadmap of the relevant technologies, their applications and potential privacy and security threats; creating the environment for progress in related European standardisation and critical infrastructure governance issues; monitoring and, where appropriate, linking to RFID policy initiatives in other regions of the world; identifying best practices to achieve progress towards a single market for RFID applications by raising awareness and removing barriers to its effective, secure and privacy-friendly deployment; supporting the EU/US transatlantic "Lighthouse priority project" on RFID. The first instrument is the promotion of a thematic network to 'explore new ways to implement RFID solutions and identify potential areas for future RFID pilot projects'

Scope of the programme

Since 2001, the SeBW and its predecessor "e-Business W@tch" have published e-business studies on about 25 sectors6 of the European economy, annual comprehensive synthesis reports about the state-of-play in e-business in the European Union, statistical pocketbooks and studies on specific ICT issues. All publications can be downloaded from the programme's website at www.ebusiness-watch.org. In 2007/08, the main studies of the SeBW focus on the following 10 sectors and specific topics:

No. Sector / topic in focus NACE Rev. 1.1 Reference to earlier

studies by SeBW 1 Chemical, rubber and plastics 24, 25 2004, 2003 2 Steel 27.1-3, 27.51+52 -- 3 Furniture 36.12-14 -- 4 Retail 52 2004, 2003 5 Transport and logistics services 60, 63 (parts thereof) -- 6 Banking 65.1 2003 7 RFID adoption and implications (several sectors) -- 8 Intellectual property rights for

ICT-producing SMEs 30.01+02, 32.1-3, 33.2+3; 64.2; 72 (parts thereof)

--

9 Impact of ICT and e-business on energy use

--

10 Economic impact and drivers of ICT adoption

--

6 see overview at www.ebusiness-watch.org/studies/on_sectors.htm.

RFID adoption and implications

14

The SeBW presents a 'wide-angle' perspective on the adoption and use of ICT in the sectors studied. They assess how ICT is having an influence on business processes, notably by enabling electronic data exchanges between a company and its customers, suppliers, service providers and business partners. (The underlying conceptual framework is explained in more detail in the following section.) In addition, the studies also provide some background information on the respective sectors, including a briefing on current trends. Readers, however, should not mistakenly consider this part as the main topic of the analysis. The introduction to the sector is neither intended, nor could it be a substitute for more detailed industrial analysis.

1.3 ICT and e-Business – key terms and concepts

A definition of ICT

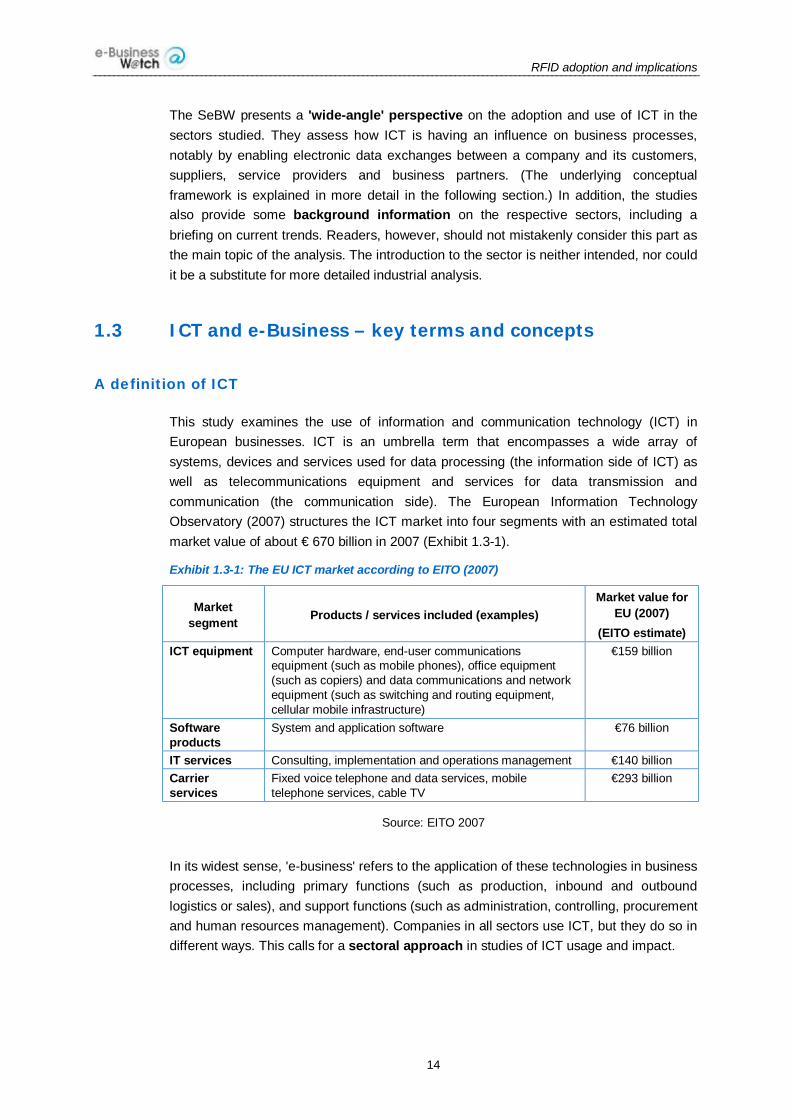

This study examines the use of information and communication technology (ICT) in European businesses. ICT is an umbrella term that encompasses a wide array of systems, devices and services used for data processing (the information side of ICT) as well as telecommunications equipment and services for data transmission and communication (the communication side). The European Information Technology Observatory (2007) structures the ICT market into four segments with an estimated total market value of about € 670 billion in 2007 (Exhibit 1.3-1).

Exhibit 1.3-1: The EU ICT market according to EITO (2007)

Market segment Products / services included (examples)

Market value for EU (2007)

(EITO estimate) ICT equipment Computer hardware, end-user communications

equipment (such as mobile phones), office equipment (such as copiers) and data communications and network equipment (such as switching and routing equipment, cellular mobile infrastructure)

€159 billion

Software products

System and application software €76 billion

IT services Consulting, implementation and operations management €140 billion Carrier services

Fixed voice telephone and data services, mobile telephone services, cable TV

€293 billion

Source: EITO 2007

In its widest sense, 'e-business' refers to the application of these technologies in business processes, including primary functions (such as production, inbound and outbound logistics or sales), and support functions (such as administration, controlling, procurement and human resources management). Companies in all sectors use ICT, but they do so in different ways. This calls for a sectoral approach in studies of ICT usage and impact.

RFID adoption and implications

15

Gaining momentum after a phase of disappointment

When the bust phase of the previous economic cycle – commonly referred to as the 'new economy' – started in 2001, the former internet hype was suddenly replaced by a widespread disappointment with e-business strategies. Companies adopted a more reserved and sceptical attitude towards investing in ICT. Nevertheless, ICT has proved to be the key technology of the past decade (OECD 2004, p. 8), and the evolutionary development of e-business has certainly not come to an end. The maturity of ICT-based data exchanges between businesses and their suppliers and customers, fostered by progress in the definition and acceptance of standards, has substantially increased across sectors and regions over the past five years. In parallel, recent trends such as "Web 2.0" and social networking are widely discussed in terms of their business implications and it is widely recognised that 'e'-elements have become an essential component of modern business exchanges. In short, e-business has regained momentum as a topic for enterprise strategy both for large multinationals and SMEs.

"Measurement of e-business is of particular interest to policy makers because of the potential productivity impacts of ICT use on business functions. However, the ongoing challenges in this measurement field are significant and include problems associated with measuring a subject which is both complex and changing rapidly."

OECD (2005): ICT use by businesses. Revised OECD model survey, p. 17

Companies use ICT in their business processes mainly for three purposes: to reduce costs, to better serve the customer, and to support growth (e.g. by increasing their market reach). In essence, all e-business projects in companies explicitly or implicitly address one or several of these objectives. In almost every case, introducing e-business can be regarded as an ICT-enabled process innovation. Understanding one's business pro-cesses and having a clear vision of how they could be improved (be it to save costs or to improve service quality) are therefore critical requirements for firms to effectively use ICT.

The increasing competitive pressure on companies, many of which operate in a global economy, has been a strong driver for ICT adoption. Firms are constantly searching for opportunities to cut costs and ICT holds great promise in this respect as it increases the efficiency of a firm’s business processes, both internally and between trading partners in the value chain. While cutting costs continues to motivate e-business activity, innovative firms have discovered and begun to exploit the potential of ICT for delivering against key business objectives. They have integrated ICT into their production processes and quality management and, most recently, in marketing and customer services. These last sectors are widely considered key to improve competitiveness in the current phase of development of European economies. Competing in mature markets requires not only optimised cost structures, maximal efficiency, and products or services of excellent quality but also the ability to communicate effectively and cooperate with business partners and potential customers.

RFID adoption and implications

16

A definition of e-business

As part of this maturing process, electronic business has progressed from a specific to a very broad topic. A central element is certainly the use of ICT to accomplish business transactions, i.e. exchanges between a company and its suppliers or customers. These can be other companies ('B2B' – business-to-business), consumers ('B2C' – business-to-consumers), or governments ('B2G' – business-to-government). In the broad sense, transactions include commercial as well as other exchanges such as sending tax return forms to the tax authorities.

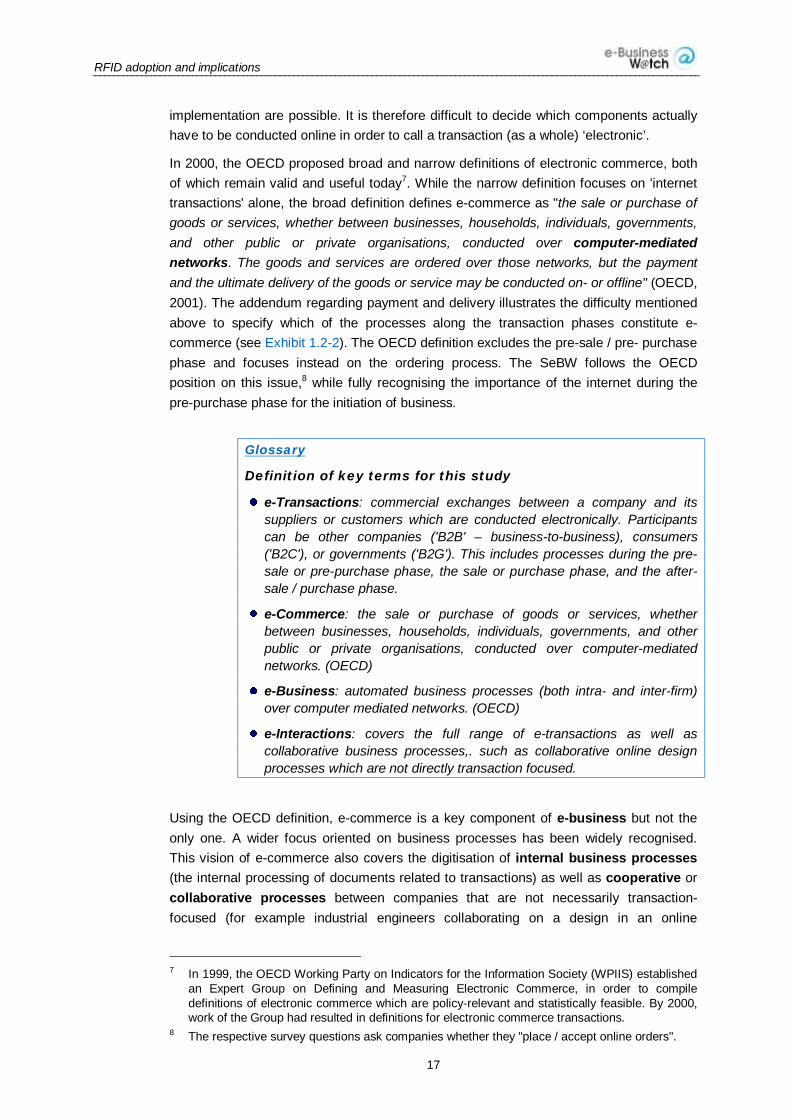

If transactions are conducted electronically ('e-transactions'), they constitute e-commerce. Transactions can be broken down into different phases and related business processes, each of which can be relevant for e-commerce (see Exhibit A.V-2). The pre-sale (or pre-purchase) phase includes the presentation of (or request for) information on the offer, and negotiations over the price. The sale / purchase phase covers the ordering, invoicing, payment and delivery processes. Finally, the after sale / purchase phase covers all processes after the product or service has been delivered to the buyer, such as after sales customer services (e.g. repair, updates).

Glossary

Definitions by standardisation groups (ISO, ebXML)

The term 'business transaction' is a key concept underlying the development of e-standards for B2B exchanges. Therefore, definitions have been developed by standards communities to underpin their practical work. Examples include:

Business: "a series of processes, each having a clearly understood purpose, involving more than one party, realised through the exchange of information and directed towards some mutually agreed upon goal, extending over a period of time" [ISO/IEC 14662:2004]

Business transaction: "a predefined set of activities and/or processes of parties which is initiated by a party to accomplish an explicitly shared business goal and terminated upon recognition of one of the agreed conclusions by all the involved parties even though some of the recognition may be implicit" [ISO/IEC 14662:2004]

e-Business transaction: "a logical unit of business conducted by two or more parties that generates a computable success or failure state" [ebXML Glossary]

Exhibit 1.3-2: Process components of transactions

Pre-sale / pre-purchase phase

Sale / purchase phase After sale / after-purchase phase

Request for offer/proposal Offer delivery Information about offer Negotiations

Placing an order Invoicing Payment Delivery

Customer service Guarantee management Credit administration Handling returns

Practically each step in a transaction can either be pursued electronically (online) or non-electronically (offline), and all combinations of electronic and non-electronic

RFID adoption and implications

17

implementation are possible. It is therefore difficult to decide which components actually have to be conducted online in order to call a transaction (as a whole) ‘electronic’.

In 2000, the OECD proposed broad and narrow definitions of electronic commerce, both of which remain valid and useful today7. While the narrow definition focuses on 'internet transactions' alone, the broad definition defines e-commerce as "the sale or purchase of goods or services, whether between businesses, households, individuals, governments, and other public or private organisations, conducted over computer-mediated networks. The goods and services are ordered over those networks, but the payment and the ultimate delivery of the goods or service may be conducted on- or offline" (OECD, 2001). The addendum regarding payment and delivery illustrates the difficulty mentioned above to specify which of the processes along the transaction phases constitute e-commerce (see Exhibit 1.2-2). The OECD definition excludes the pre-sale / pre- purchase phase and focuses instead on the ordering process. The SeBW follows the OECD position on this issue,8 while fully recognising the importance of the internet during the pre-purchase phase for the initiation of business.

Glossary

Definition of key terms for this study

e-Transactions: commercial exchanges between a company and its suppliers or customers which are conducted electronically. Participants can be other companies ('B2B' – business-to-business), consumers ('B2C'), or governments ('B2G'). This includes processes during the pre-sale or pre-purchase phase, the sale or purchase phase, and the after-sale / purchase phase.

e-Commerce: the sale or purchase of goods or services, whether between businesses, households, individuals, governments, and other public or private organisations, conducted over computer-mediated networks. (OECD)

e-Business: automated business processes (both intra- and inter-firm) over computer mediated networks. (OECD)

e-Interactions: covers the full range of e-transactions as well as collaborative business processes,. such as collaborative online design processes which are not directly transaction focused.

Using the OECD definition, e-commerce is a key component of e-business but not the only one. A wider focus oriented on business processes has been widely recognised. This vision of e-commerce also covers the digitisation of internal business processes (the internal processing of documents related to transactions) as well as cooperative or collaborative processes between companies that are not necessarily transaction-focused (for example industrial engineers collaborating on a design in an online

7 In 1999, the OECD Working Party on Indicators for the Information Society (WPIIS) established

an Expert Group on Defining and Measuring Electronic Commerce, in order to compile definitions of electronic commerce which are policy-relevant and statistically feasible. By 2000, work of the Group had resulted in definitions for electronic commerce transactions.

8 The respective survey questions ask companies whether they "place / accept online orders".

RFID adoption and implications

18

environment). The OECD WPIIS9 proposes a definition of e-business as "automated business processes (both intra-and inter-firm) over computer mediated networks" (OECD, 2004, p. 6). In addition, the OECD proposed that e-business processes should integrate tasks and extend beyond a stand-alone or individual application. 'Automation' refers here to the substitution of formerly manual processes. This can be achieved by replacing the paper-based processing of documents by electronic exchanges (machine-to-machine) but it requires the agreement between the participants on electronic standards and processes for data exchange.

e-Business and a company's value chain

In some contexts, the term c-commerce (collaborative commerce) is used. Although this concept was mostly abandoned when the 'new economy' bubble burst in 2001, it had the merit of pointing towards the role of ICT in cooperations between enterprises and the increasing digital integration of supply chains. These developments go beyond simple point-to-point exchanges between two companies.

Despite dating back 20 years to the pre-e-business era, Michael Porter's framework of the company value chain and value system between companies10 remains useful to understand the relevance of e-business in this context. A value chain logically presents the main functional areas ('value activities') of a company and differentiates between primary and support activities. However, these are "not a collection of independent activities but a system of interdependent activities", which are "related by linkages within the value chain".11 These linkages can lead to competitive advantage through optimisation and coordination. This is where ICT can have a major impact, in the key role of optimising linkages and increasing the efficiency of processes.

The value system expands this concept by extending its scale beyond the single company. The firm's value chain is linked to the value chains of (upstream) suppliers and (downstream) buyers; the resulting larger set of processes is referred to as the value system. All e-commerce and therefore electronic transactions occur within this value system. Key dimensions of Porter’s framework (notably inbound and outbound logistics, operations, and the value system) are reflected in the Supply Chain Management (SCM) concept. Here, the focus is on optimising the procurement-production-delivery processes, not only between a company and its direct suppliers and customers, but also aiming at a full vertical integration of the entire supply chain (Tier 1, Tier 2, Tier n suppliers). In this concept, each basic supply chain is a chain of sourcing, production, and delivery processes with the respective process interfaces within and between companies.12 Analysing the digital integration of supply chains in various industries has been an important theme in most sector studies by the SeBW.

ICT, e-business and RFID

9 Working Party on Indicators for the Information Society. 10 Porter, Michael E. (1985). Competitive Advantage. New York: Free Press. Page references in

quotations refer to the Free Press Export Edition 2004. 11 ibid., p. 48. 12 cf. SCOR Supply-Chain Council: Supply-Chain Operations Reference-model. SCOR Version

7.0. Available at www.supply-chain.org (accessed in March 2006).

RFID adoption and implications

19

Companies use ICT and RFID mainly for three purposes: to reduce cost, to better serve customers, and to support business growth through for example increasing market share and reach. In essence, the majority of RFID projects in organisations explicitly or implicitly address one or several of these objectives. In almost every case, RFID introduction can be regarded as an ICT-enabled process innovation. Understanding one's business processes, and having a clear vision how they could be improved (be it to save costs or to improve service quality), are therefore critical requirements for firms to effectively use RFID.

The increasing competitive pressure on companies, many of them operating in a global economy, has been a strong driver for ICT adoption in general and RFID in particular. Firms are in constant search for opportunities to cut costs, and this has exactly been a major promise of ICT: enabling firms to cut costs by increasing the efficiency of their business processes, internally and between trading partners in the value chain.

While cutting costs is still a valid motive for e-business activity, innovative firms have discovered and begun to exploit the potential of ICT for delivering key business objectives. These firms have, for example, integrated ICT and RFID into their production processes and quality management, and in more recent times in marketing with the aim to improving customer service. The latter objectives are widely considered key to improving competitiveness in the current phase of development of European economies. Competing in mature markets requires not only optimised cost structures, maximal efficiency, and products or services of excellent quality, but also the ability to communicate effectively and indeed cooperate with business partners and potential customers. Chapter 2 provides background information about RFID and the relevance of this technology to enterprises.

1.4 Study objectives and methodology

Progress towards analysing impacts of ICT and e-business

The methodological framework of the SeBW builds upon the methodology established for the previous implementation of the e-Business W@tch. However, the methodology has been adapted to the new focus of activity, supporting the progress to the evidence-based analysis of RFID adoption trends and impact of this technology for enterprises, in terms of productivity, innovation, competitiveness and workforce.

Data analysis and information sources

The Sectoral e-Business Watch approach is based on a well-tuned composition of data collection instruments, including the use of existing sources (e.g. the Eurostat Community Survey on ICT usage in enterprises) as well as primary research (notably the SeBW Survey and case studies). The main sources of information used for this study are:

SeBW CATI Survey (2007): The SeBW conducted in 2007 a decision-maker survey about RFID activity in the sectors covered in this study. 434 interviews were conducted in seven countries. This survey was the main source for analysing the state of play in RFID adoption, process integration, and impact on the workforce

RFID adoption and implications

20

and return on investment expectations. The survey approach is described in detail in the methodology annex.

Case studies: Ten case studies on RFID adoption in companies from the sectors covered have been conducted specifically for this study. The selection was made with a view to achieve a balanced mix of cases in terms of countries, business activities (sub-sectors), and company size-bands. Cases include best practices, innovative RFID approaches, as well as typical examples of RFID activity (state-of-the-art) in the sectors.

In-depth interviews: In addition to the interviews conducted with firm representatives as part of the case study work, in-depth interviews with company representatives, industry and e-business experts have been conducted.

Literature analysis: SeBW evaluates literature from various sources, including scientific books, journal articles and conference presentations, websites, and newspaper articles.

For data analysis, descriptive and analytical statistical methods have been used.

Validation of results by an advisory board

The study was conducted in consultation with an Advisory Board that was specifically implemented to critically accompany the study from the start. Members of the Advisory Board for this study were (by order of membership approval):

Antonio Lasi, General Manager, Lombardia Informatica.

Andy Lee, RFID program manager, Cisco Systems.

Jean Francois Remy, Business Development Director, manufacturing and retail distribution, HP.

For each Advisory Board, in addition to informal exchanges with the respective study teams during the research phase (e.g. via telephone, e-mail and in bilateral meetings), three meetings were foreseen. The first meeting took place on 29/30 May 2007 in Brussels, during the inception phase. At this meeting, the study exposé and research plan was discussed. A second meeting was held on 5 February in Milano with the objective to discuss and validate the key findings of the interim report. A third meeting, on 20 May 2008 in Brussels was held to discuss the final findings of this report.

The authors of the study wish to thank the advisory board members and the Commission for the constructive feedback and the valuable support given to the study. Any mistake remains of course full responsibility of the authors.

RFID adoption and implications

21

2 Context and background

2.1 Topic definition — main goals and scope of the study

2.1.1 Main goals

This study analyses the use of RFID (Radio Frequency Identification) by companies active in the Retail Distribution, Transportation, Discrete and Process Manufacturing sectors, as well as by organisations active in the human health services (see Exhibit 2.1-1). The study provides a top-down view of RFID adoption roadmap and challenges, starting from the overall picture at European level. It also illustrates adoption patterns and drivers across the various sectors addressed, with a focus on benefits and opportunities for SMEs. In addition, overviews of specific industry segments are provided, leveraging from case studies across covered sectors.

The topic is utterly relevant, as RFID technology is a major driver for the improvement of efficiency and effectiveness of business processes; being essentially a new data acquisition platform for enterprises -possibly integrating diverse platforms of value chain partners- RFID technology is a key enabler of supply chain productivity enhancements and end-to-end visibility, thus also allowing for product tracking and tracing applications. Beyond supply chain efficiencies, innovative applications are also emerging in the areas of mobile payments and ticketing, location based and context-sensitive mobile services, by providing access to digital content in the physical world.

The report is structured as follows. This chapter describes the context and background of the study. The third chapter analyses the diffusion and usage of RFID, based mainly on field research results. Chapter 4 looks at the main benefits and business impacts of RFID in the analysed sectors. Chapter 5 presents in detail the 10 case studies carried out for the study. Chapter 6 presents the final conclusions and policy implications.

2.1.2 Scope

The sectors covered by this study are defined as follows, according to the General Industrial Classification of Economic Activities within the European Union Divisions, i.e., NACE Rev. 1:

Retail Distribution — Retail trade, except of motor vehicles and motorcycles; repair of personal and household goods (NACE 52)

Transportation, including: Railways (NACE 60.1), other land transport (e.g., urban transport and land transport including freight transport by road – NACE 60.2), and Air transport (NACE 62.1 and 62.2).

Discrete and Process Manufacturing — DG 24.5 - Manufacture of soap and detergents cleaning and polishing preparations, perfumes and toilet preparations; 15.1-15.8 - Manufacture of Food products; 15.9 - Manufacture of beverages; 18 Manufacture of wearing apparel; 19 Manufacture of leather and leather products (e.g. footwear); 24.4 Manufacture of pharmaceuticals; 34 Manufacture of computer, electronic and optical products.

RFID adoption and implications

22

Human health services – Hospital activities, medical practice activities, dental practice activities, and other human health activities (NACE Rev 1.1, 85.1).

These sectors cover quite diverse business activities. The respective NACE Rev. 2 groups and their correspondence in NACE Rev. 1 are shown in Exhibit 1.1-1. The names of business activities refer to NACE Rev. 1.

Exhibit 2.1-1: Business activities covered by the RFID topic study

NACE Rev. 2

NACE Rev. 1 Business activity:

10 15 Manufacture of food and beverages 14 15

18 19

Manufacture of wearing apparel Manufacture of leather and leather products (e.g. footwear)

21.1-21.2 24.4 Manufacture of pharmaceuticals 26-27 30/31/32/33

Manufacture of computer, electronic and optical products 29 (excluding 29.31)

34 Manufacture of motor vehicles, trailers and semi-trailers

47 (excluding 47.3)

52 Retail trade, except of motor vehicles and motorcycles

49.10-49.20 60.1 Passenger and Freight Rail transport 49.3-49.4 60.2 Other land transport 51.10-51.21 62.1-62.2 Air transport 86.1-86.2 85.1 Human health services

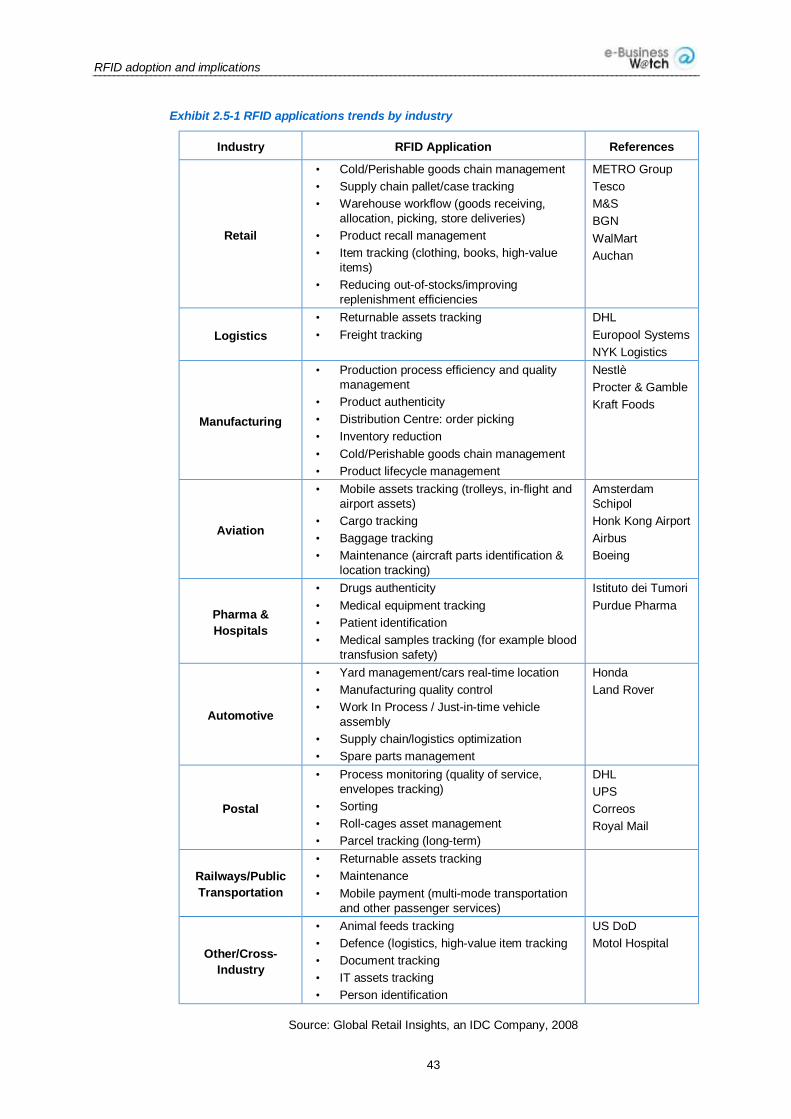

Within this chapter in section 2.1, a definition of RFID along with background information has been included. Section 2.2 illustrates the main technological features and trends of RFID and briefly discusses industry challenges and RFID application patterns. Section 2.3 illustrates benefits and impacts associated to RFID. Section 2.4 analyses key trends and challenges for the implementation of RFID to enable responsive supply chains, successful Return on Investment (ROI) and advanced value chain collaboration frameworks. Finally, Section 2.5 presents RFID applications in the retail, manufacturing, transportation and healthcare industries.

2.2 RFID technology

2.2.1 A basic description of RFID

RFID stands for Radio Frequency Identification and it is mostly used for identifying people, objects, transactions or events through a wireless communication connection. RFID is an automatic identification and data capture method (AIDC), which not only helps to identify, but also to collect data attributes about a certain object or person, including localisation and environmental measurements when integrated with sensor networks. All automatically captured data can then be entered directly into a computer system, avoiding less efficient and more error prone human intervention required to execute operational tasks and business intelligence analysis. The temporarily stored information is then processed to feed other internal IT systems (for example store or factory systems)

RFID adoption and implications

23

and external systems alike (for example suppliers portals, business partners and clients information services). Essentially, an RFID system comprises 3 components (Exhibit 2.2-1):

Multiple RFID tags, also called transponders, a term that comes from the short form of transmitter-responder

A number of readers or interrogators, also called transceivers,

The supporting ICT infrastructure (including data communication networks, other hardware such as servers and storage, as well as software components including RFID middleware and information server, front-end RFID-capable applications and back-end systems)

A tag embodies a microchip containing limited processing power, memory storage, a built-in antenna and an encapsulating material that allows the tag to:

Carry on a unique identifier to associate the tag with the "tagged" object, thus allowing for unique object identification

Receive, amplify and retransmit signals on a set of pre-determined frequencies

Transmit a predetermined message in response to a predefined received signal

Generate a reply signal upon proper electronic interrogation

Exhibit 2.2-1: RFID system, automated data collection, information flow

Source: Global Retail Insights, an IDC Company, 2007

RFID tags can be read-only or read-write. A read-only tag includes a programmed identification code, recorded at the time of manufacture or when the tag is allocated to an object. Once programmed, the data on the tag cannot be modified or appended but it

RFID adoption and implications

24

may be read multiple times. Read-Write tags can have their memory changed, or written to, many times. Because their identification codes can be changed, they offer greater functionality albeit at higher price.

Electronic Product Code

In consumer products and retail distribution applications, the Electronic Product Code (EPC), is the coding scheme used to identify an individual object along the supply chain. EPC includes a general identifier (GID), serialized global trade identification number (SGTIN), the serialized shipper container code (SSCC), global location number (GLN), global returnable asset identifier (GRAI) and global individual asset identifier (GIAI). SGTIN is the standard identifier for cases of products and allows each case to be uniquely identified with a serial number. In contrast, the typical Universal Product Code (UPC) or European Article Number (EAN) used in barcodes only provides information about the product but does not uniquely identify each case. The EPC was created by the MIT Auto-ID Center, a consortium of over 120 global corporations and university labs. The EPC system is currently managed by EPCglobal, a subsidiary of GS1, creators of the UPC barcode.

RFID middleware

An important component of RFID infrastructures is the RFID-specific software – named RFID middleware - that translates the raw data from the tag into useful enterprise information. This information can then be fed into other databases and applications (for example inventory management) for further processing. In the case of read-write tags, software is also required to control whether data can be written to the tag, which tag should contain the data and to initiate the process of adding data to, or changing data in the tag.

The RFID middleware in EPC-compliant application conforms to the EPCIS (Electronic Product Code Information Services) standard, designed to enable EPC-related data sharing within and across enterprises. In addition, the Object Naming Service (ONS) standard specifies how the Domain Name System (DNS) is used to locate authoritative metadata and services associated with the SGTIN portion of a given electronic product code. EPCIS provides authorised users access to unique product information, such as type of merchandise, shipping date, manufacturer, price, weight, best-before date, and retail unit (pallet, carton, package, article). These product attributes are then entered into a merchandise management system (MMS), which no longer require manual intervention, as operations are automated. Provided that at the foundation is a solid master data management infrastructure, greater accuracy into products' life-time management will result.

One of the attributes that makes RFID such an innovative feature is that tags can be fit or embedded into almost anything, products, animals or even people, widening possibilities for RFID applications. Companies currently have several options when implementing RFID. They can use static RFID portals, which create a set read field at discrete choke points such as a dock door or sales floor door. Companies may also use mobile devices

RFID adoption and implications

25

such as forklift readers or handheld readers. The type of data one wants to capture dictates the choice of technology.

2.2.2 Types of RFID tags

Tags can be categorised according to key attributes including power, communication frequency, and attachment.

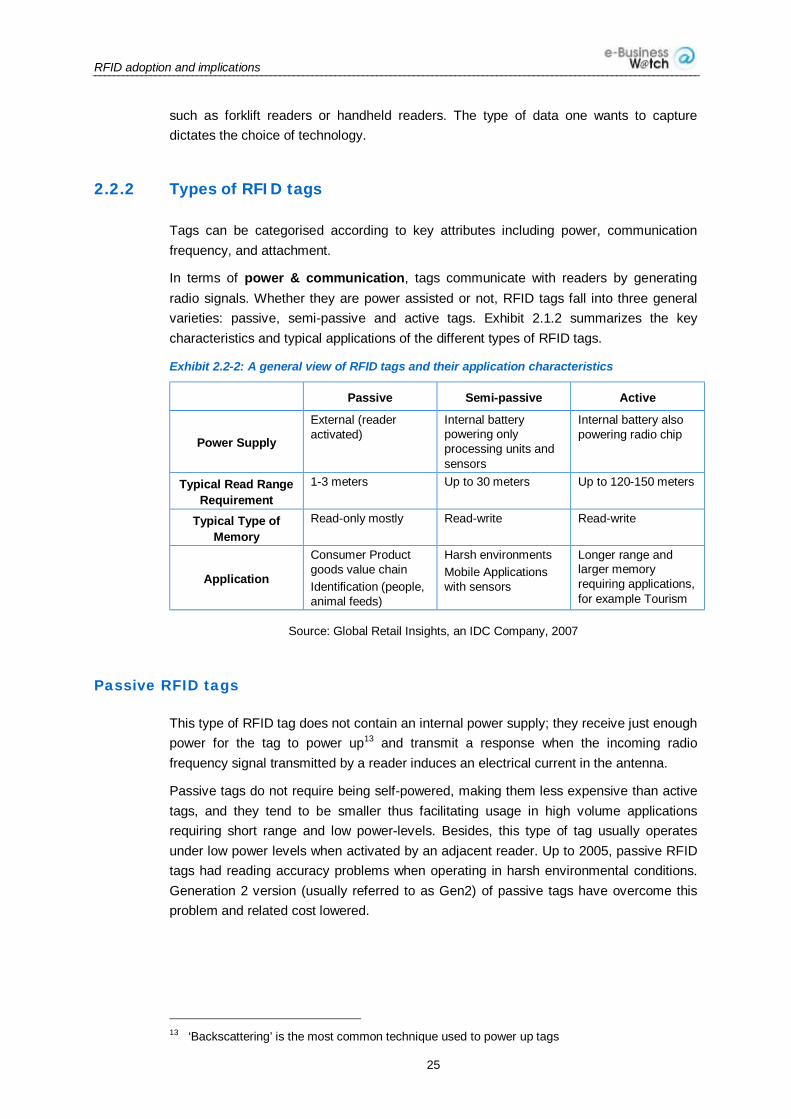

In terms of power & communication, tags communicate with readers by generating radio signals. Whether they are power assisted or not, RFID tags fall into three general varieties: passive, semi-passive and active tags. Exhibit 2.1.2 summarizes the key characteristics and typical applications of the different types of RFID tags.

Exhibit 2.2-2: A general view of RFID tags and their application characteristics

Passive Semi-passive Active

Power Supply

External (reader activated)

Internal battery powering only processing units and sensors

Internal battery also powering radio chip

Typical Read Range Requirement

1-3 meters Up to 30 meters Up to 120-150 meters

Typical Type of Memory

Read-only mostly Read-write Read-write

Application

Consumer Product goods value chain Identification (people, animal feeds)

Harsh environments Mobile Applications with sensors

Longer range and larger memory requiring applications, for example Tourism

Source: Global Retail Insights, an IDC Company, 2007

Passive RFID tags

This type of RFID tag does not contain an internal power supply; they receive just enough power for the tag to power up13 and transmit a response when the incoming radio frequency signal transmitted by a reader induces an electrical current in the antenna.

Passive tags do not require being self-powered, making them less expensive than active tags, and they tend to be smaller thus facilitating usage in high volume applications requiring short range and low power-levels. Besides, this type of tag usually operates under low power levels when activated by an adjacent reader. Up to 2005, passive RFID tags had reading accuracy problems when operating in harsh environmental conditions. Generation 2 version (usually referred to as Gen2) of passive tags have overcome this problem and related cost lowered.

13 ‘Backscattering’ is the most common technique used to power up tags

RFID adoption and implications

26

Semi-passive RFID tags

Semi-passive tags have their own power source, although the battery included only powers the embedded microchip and attached sensors. For a semi-passive tag to transmit information, the radio frequency (RF) energy is reflected back to the reader as is the case with a passive tag. These tags also employ manipulating techniques permitting the device to store energy from the reader so that it is possible to emit a response in the future.

Among the positive features, semi-passive tags have greater sensitivity compared to passive ones. Next to active tags, semi-passive tags can operate whether the reader is present or not, proving a longer battery life-span particularly when used in mobile applications.

Active RFID tags

These RFID tags have their own internal power source to power up the integrated circuits and transmit the signal to the reader. Active tags tend to be more reliable than passive tags due to their ability to transmit at higher power levels with a reader, particularly relevant under challenging environmental conditions like water, metal or under long distances. However, real-life examples demonstrate that reading accuracy targets can be achieved also in harsh situations with passive tags. Compared to passive tags, active tags in general generate stronger responses from weak requests and have a much longer range as well as a larger memory. Nevertheless, active tags have a shorter life span and are more expensive to manufacture.

Attachment characteristics

In terms of attachment characteristics, RFID tags are attachable, implantable or insert-able according to the object and purpose. Tags can also be reusable or disposable according to the nature of use.

Attachable tags: These tags have a broad and diverse application range due to their flexibility and attachment properties. Smart label, a pressure sensitive label, is one of the most common types of attachable tags, which can be also permanent, semi-permanent or temporary.

Implantable tags: Also called embedded, are usually considered for permanent or long-term implantations. They are most common in animal traceability and machine-readable travel documents (MRTD) types of applications.

Inserted tags: This type of tag has little, if no contact at all with the identified object. Without a specific attachment process or tampering the identified object, these tags run the identification process while leaving objects at their original state. Physically, inserted tags are non-adhesive labels, normally used in printed materials.

RFID adoption and implications

27

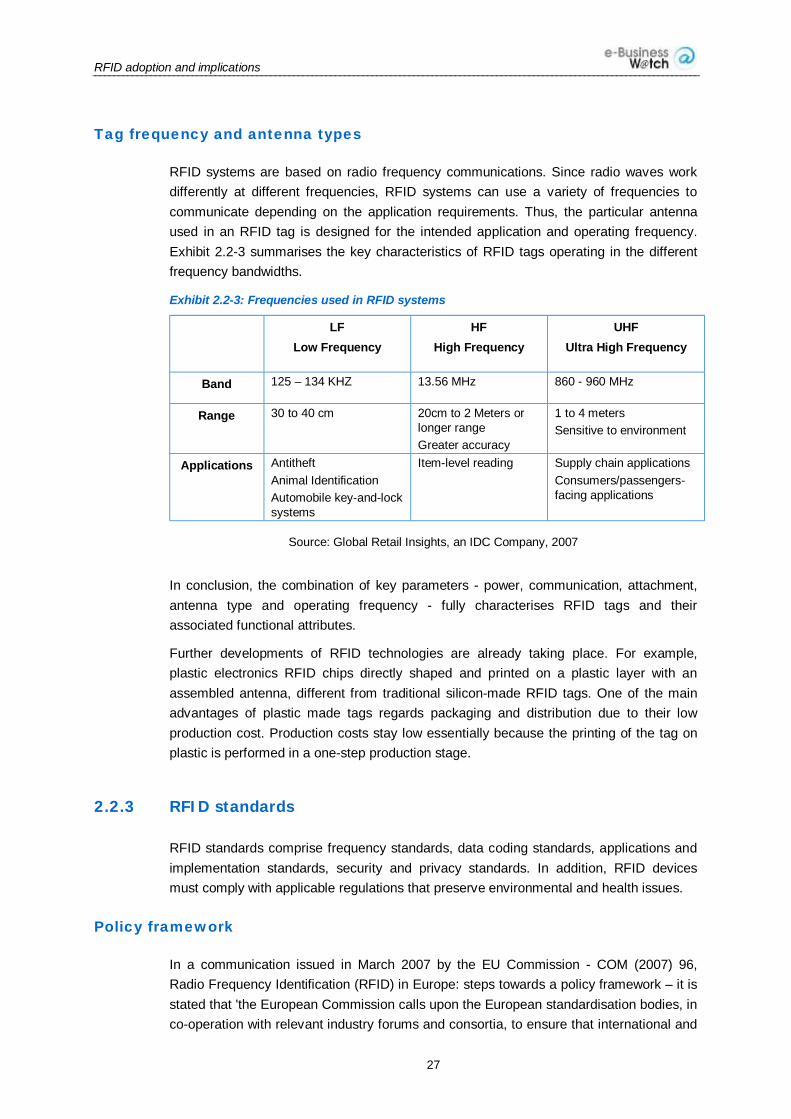

Tag frequency and antenna types

RFID systems are based on radio frequency communications. Since radio waves work differently at different frequencies, RFID systems can use a variety of frequencies to communicate depending on the application requirements. Thus, the particular antenna used in an RFID tag is designed for the intended application and operating frequency. Exhibit 2.2-3 summarises the key characteristics of RFID tags operating in the different frequency bandwidths.

Exhibit 2.2-3: Frequencies used in RFID systems

LF Low Frequency

HF High Frequency

UHF Ultra High Frequency

Band 125 – 134 KHZ 13.56 MHz 860 - 960 MHz

Range 30 to 40 cm 20cm to 2 Meters or longer range Greater accuracy

1 to 4 meters Sensitive to environment

Applications Antitheft Animal Identification Automobile key-and-lock systems

Item-level reading Supply chain applications Consumers/passengers-facing applications

Source: Global Retail Insights, an IDC Company, 2007

In conclusion, the combination of key parameters - power, communication, attachment, antenna type and operating frequency - fully characterises RFID tags and their associated functional attributes.

Further developments of RFID technologies are already taking place. For example, plastic electronics RFID chips directly shaped and printed on a plastic layer with an assembled antenna, different from traditional silicon-made RFID tags. One of the main advantages of plastic made tags regards packaging and distribution due to their low production cost. Production costs stay low essentially because the printing of the tag on plastic is performed in a one-step production stage.

2.2.3 RFID standards

RFID standards comprise frequency standards, data coding standards, applications and implementation standards, security and privacy standards. In addition, RFID devices must comply with applicable regulations that preserve environmental and health issues.

Policy framework

In a communication issued in March 2007 by the EU Commission - COM (2007) 96, Radio Frequency Identification (RFID) in Europe: steps towards a policy framework – it is stated that 'the European Commission calls upon the European standardisation bodies, in co-operation with relevant industry forums and consortia, to ensure that international and

RFID adoption and implications

28