mental accounting and acceptance of a price discount

TRANSCRIPT

ELSEVIER Acta Psychologica 93 (1996) 149-160

acta psychologica

Mental accounting and acceptance of a price discount

Nicolao Bonini a,*, Rino Rumiati b a lstituto di Psicologia, Universith di Cagliari, Via Basilicata 65, Cagliari, Italy

b . . . . . Dtparttmento dt Pstcologta, Universith degli Studi di Padot,a, Via Venezia 8, 35131 Padot,a, Italy

Abstract

The paper reports five experiments related to a price reduction choice task. In Experiment 1 and in the control condition of Experiment 4, the finding reported by Tversky and Kahneman (1981) with the calculator problem is replicated. People show a difference in the rate of acceptance of a price reduction across the two versions of this problem. This finding has been explained as due to the use of a topical mental account of the offered price reduction. This paper studies the effect on the previous finding of four experimental manipulations of the calculator problem. In these situations, a relationship between the two purchases is provided in order to make their mental segregation difficult and favour the use of a comprehensive mental account of the price discount. Results show that when the two target purchases are embedded in a shopping list, an explicit expense budget is provided, and subjects are reminded that they can also buy the jacket at the other store, the effect reported in the control condition disappears. These results are interpreted by the notion of the focusing mechanism.

P s v c l N F O classif ication: 2340

Keywords: Mental accounting; Choice; Focusing

1. Introduction

W h e n asked to evaluate a price reduction, people may assess it by referring to its absolute value, its relative value or to other expenses. The way people account for the reduct ion will affect its acceptabili ty. An absolute value of $50 may appear more

* Corresponding author. E-mail: [email protected], Tel.: + 39 360 596153, Fax: + 39 49 8276600.

0001-6918/96/$15.00 Copyright © 1996 Elsevier Science B.V. All rights reserved. PII S0001-69 18(96)000 18-2

150 N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160

valuable than the same price reduction related to an expense budget of $1,000 which, in turn, appears less attractive than the same reduction out of an initial price of $100.

As an example of the effect of mental accounting on the acceptance of a price reduction, let us consider the 'calculator problem' (cf. Tversky and Kahneman, 1981, p. 457).

"Imagine that you are about to purchase a jacket for ($125) [$15], and a calculator for ($15) [$125]. The calculator salesman informs you that the calculator you wish to buy is on sale for ($10) [$120] at the other branch of the store, located 20 minutes drive away. Would you make the trip to the other store?"

Results show that when the two versions of this problem are given (one with the figures in parentheses, the other with the figures in brackets), most people (68%) will travel to save the $5 on the cheaper item but not on the more expensive one (29%).

Kahneman and Tversky (1984) interpreted this result as due to the use of a 'topical' mental account of the offered price reduction. In the calculator problem, the relevant topic is whether or not to make a trip to buy a cheaper calculator. By a topical account the calculator initial price would become the reference level to which the advantages and disadvantages of options are assessed. Given that the calculator initial price is different across the two versions of the problem, the advantage associated with driving to the other store will be different across these two versions. This would explain the different rate of acceptance of the offered price reduction across the two versions.

However, one out of two other mental accounts could have been used in the calculator problem: the 'minimal' and the 'comprehensive' accounts. By the former account, the advantage associated with driving to the other store would be the same across the two versions of the problem and would amount to a gain of $5, that is the absolute value of the calculator price reduction. By the latter account, the price of the jacket as well as other expenses would be considered. By the comprehensive account, the advantage associated with driving to the other store would be the same across the two versions of the problem and would amount to the existing wealth plus the jacket and calculator minus $135.

A crucial component of the elaboration of a mental account is the way people segregate~integrate features of choice options. Thaler (1993, p. 2), for example, considers "mental accounting as a collection of aggregation rules - what gets combined with what". Tversky and Kahneman (1981, p. 456) define a psychological account "as an outcome frame which specifies (i) the set of elementary outcomes that are evaluated jointly and the manner in which they are combined and (ii) a reference outcome that is considered neutral or normal" (italics added).

Minimal, topical and comprehensive accounts can be interpreted as a different segregation of available information. Let us consider again the calculator problem. Minimal and topical accounts could be due to a focusing mechanism by which the person considers only one purchase (e.g., the calculator) and the absolute or relative value of its price reduction. However, a comprehensive account could be due to a focusing mechanism by which the person relates the price reduction to other expenses (e.g., the jacket and the calculator). According to this analysis, the crucial difference between the comprehensive account and the minimal and topical ones relates to whether

N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160 151

or not subjects are focused on the planned purchases (cf. Legrenzi et al., 1993, for a discussion of the focusing mechanism).

In this paper, we report four studies that investigate the role played by four experimental manipulations of the calculator problem on the effect reported by Tversky and Kahneman (1981). The experimental strategy underlying these studies can be described as an attempt to manipulate the mental segregability of the planned purchases when a price reduction is assessed. We argue that one way to induce people to use a comprehensive account is to make the segregation of the planned purchases difficult (e.g. by strengthening the relation between them). In such situations, the person should relate the calculator price reduction to the planned purchases rather than to the target one. This, in turn, should wipe out the difference in the rate of acceptance of the price reduction across the two versions of the problem.

There are several ways to strengthen the relation between purchases. One way is to provide a categorical link between them. A person may plan to buy a table and a chair rather than a calculator and a jacket. The categorical link between table and chair (they are both pieces of furniture) may make their mental segregation more difficult. Thinking about one purchase also may induce a person to consider the other purchase because of their categorical link. It should be noted that this sort of 'semantic priming' between concepts characterises the spreading activation model of semantic memory. This model predicts that the activation of a concept spreads to concepts that are more linked to the target one (cf. Collins and Loftus, 1975). Evidence of a semantic priming effect has been found by Meyer and Schvaneveldt (1976). If the categorical link between two purchases avoids their mental segregation, then a price reduction of one purchase should be related to both purchases and the effect reported by Tversky and Kahneman (1981) should disappear.

Another way to strengthen the relation between purchases is to embed them in a shopping list including several products. When the two purchases are inserted in such a list, they and the other listed products may form a sort of 'mental unity'. Let 's consider a perceptual example. When a person sees two stars in the sky, he or she says " I see two stars". However, when a person sees a galaxy he or she does not say " I see millions of stars", but probably he or she will say " I see a galaxy". Just as millions of stars form a phenomenological unit (e.g., the galaxy), so several products may form a psychological unity (e.g., the shopping list). It could also be argued that in the control condition of the calculator problem a shopping list is provided. However, it seems to us that a prototypical shopping list to be used in a big store includes more than two items. If our hypothesis is correct, a person who is planning to buy several products may consider, for example, how much money he or she could spend that day and, conse- quently, be induced to think in terms of a global expense budget. In that case, a price reduction of one purchase should be related to the planned purchases rather than to the target one. In this situation, we expect the effect reported in the calculator problem to disappear.

A third way to strengthen the relation between purchases is to refer them to an explicit expense budget. A person may plan to buy x and y knowing their prices in advance. To that purpose, he or she could get cash equivalent to the sum of the two selling prices. Thinking in terms of a global expense budget may favour the use of a

152 N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160

comprehensive account of a price reduction. In that case, the calculator price reduction should be related to the planned purchases and the effect reported by Tversky and Kahneman should disappear.

Finally, a simpler way to relate the two purchases in the calculator problem is to remind the subjects that they can also buy the jacket at the other store. If we consider the instructions used in the original formulation of the problem, we note that the jacket is mentioned only in the first line. This problem formulation may have induced the subjects to focus their attention only on the calculator purchase. In order to defocus subjects' attention from the calculator, the jacket purchase can be mentioned just before the presentation of the choice dilemma. If the use of a topical account is due to such attentional focusing, then the effect reported by Tversky and Kahneman should disap- pear when a defocusing is provided.

The paper presents five experiments. In Experiment 1, Tversky and Kahneman's (1981) study is replicated. This experiment provides a baseline to which the results of the other experiments are compared. In Experiment 2, a categorical link between the two purchases is provided. In Experiment 3, the two purchases are embedded in a shopping list that includes four products. In Experiment 4, an explicit expense budget is provided. Finally, in Experiment 5 subjects are reminded that they can also buy the jacket at the other store.

2. Experiment 1

2.1. Method

2.1.1. Subjects The subjects taking part in this experiment were 100 students attending a psychology

degree course at the University of Padua (northern Italy)

2.1.2. Experimental design Tversky and Kahneman's (1981) calculator problem was used in this experiment. The

students were equally and randomly assigned to the two versions of the problem. In the first version (low-price calculator), the prices of the jacket and the calculator were respectively 630,000 and 70,000 lire. In the second version (high-price calculator), the prices of the jacket and the calculator were 70,000 and 630,000 lire. In both versions the calculator price reduction was 24,000 lire.

2.2. Results and discussion

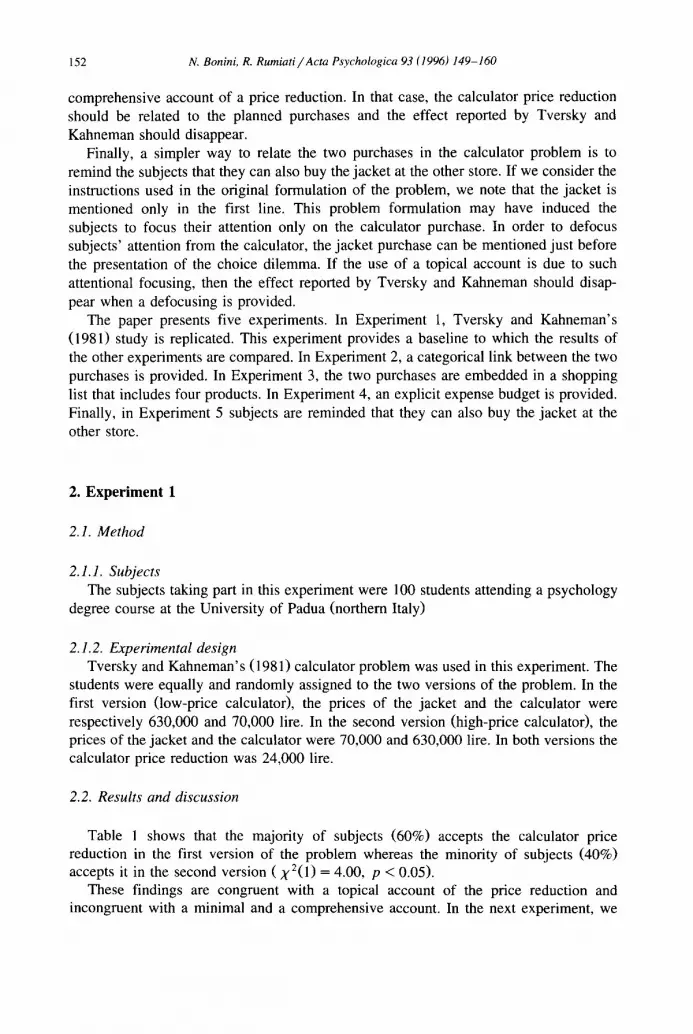

Table 1 shows that the majority of subjects (60%) accepts the calculator price reduction in the first version of the problem whereas the minority of subjects (40%) accepts it in the second version (X2(1) = 4.00, p < 0.05).

These findings are congruent with a topical account of the price reduction and incongruent with a minimal and a comprehensive account. In the next experiment, we

N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160

Table l Numbers (percentages) of acceptance/rejection of a price reduction in the control condition

153

Control

Low-price calculator High-price calculator (70,000 lire) (630,000 lire)

Yes 30 (60%) 20 (40%) No 20 (40%) 30 (60%)

Total 50 50

controlled whether this effect would disappear when a categorical link between the two purchases is provided.

3. Experiment 2

3.1. Method

3.1.1. Subjects The subjects taking part in this experiment were 100 students attending a psychology

degree course at the University of Padua.

3.1.2. Experimental design The students were equally and randomly assigned to the two versions of the problem.

Contrary to the previous experiment, the two purchases (a chair and a little table) belong to the same category (furniture). As in the previous experiment, the prices of the two purchases were 630,000 and 70,000 lire and the price reduction for the target purchase (little table) was 24,000 lire.

The subjects were given the following instructions. Figures in parentheses relate to the first version of the problem (low-price little table) whereas figures in brackets relate to the second version (high-price little table).

"Imagine that you are about to purchase a chair for (630,000 life) [70,000 tire], and a little table for (70,000 lire) [630,000 lire]. The salesman at the furniture department informs you that the little table you wish to buy is on sale for (46,000 lire) [606,000 lire] at the other branch of the store, located 20 minutes drive away. Would you make the trip to the other store?"

3.2. Results and discussion

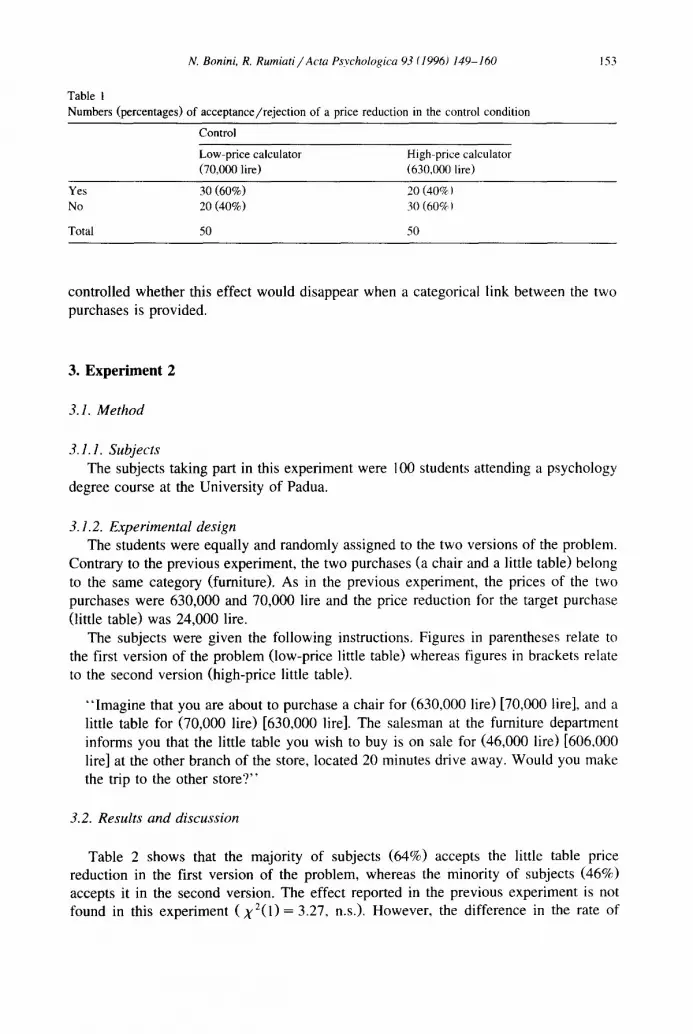

Table 2 shows that the majority of subjects (64%) accepts the little table price reduction in the first version of the problem, whereas the minority of subjects (46%) accepts it in the second version. The effect reported in the previous experiment is not found in this experiment ( X 2 ( I ) = 3.27, n.s.). However, the difference in the rate of

154 N. Bonini, R. Rumiati /Acta Psychologica 93 (1996) 149-160

Table 2 Numbers (percentages) of acceptance/rejection of a price reduction in the 'same category' condition

Same category condition

Low-price little table High-price little table (70,000 lire) (630,000 lire)

Yes 32 (64%) 23 (46%) No 18 (36%) 27 (54%)

Total 50 50

acceptance of the price reduction across the two verstons of the problem (18%) is similar to that reported in the previous experiment (20%).

The presence of a categorical link between the two purchases did not strongly reduce the difference in the rate of acceptance of the price reduction across the two versions of the problem. This finding is surprising. It seemed reasonable that two purchases from the same 'categorical' account would have been integrated. This result could be due to a weak manipulation of the 'categorical link' between the two purchases used in this experiment. Although a chair and a little table may well belong to the same super-ordinate category (i.e., furniture), they do not belong to the same basic category. A better example of categorical link at a basic level would be a 'little table for the kitchen' and a 'little table for the living room'. In that case, the two purchases relate to the same basic category (i.e., tables). Research on semantic memory shows that the strongest link between concepts is at a basic level. Exemplars of a basic category are more closely linked together than exemplars of a super-ordinate category (cf. Rosch et al., 1976). Thus, it is possible that the super-ordinate categorical link used in this experiment is not strong enough to avoid the mental segregation of the two purchases when the price reduction is assessed.

In the next experiment we controlled whether the effect reported in Experiment 1 would disappear when the two purchases are embedded in a shopping list.

4. Experiment 3

4.1. Method

4.1.1. Subjects The subjects taking part in this experiment were 61 students attending a psychology

degree course at the University of Padua.

4.1.2. Experimental design Thirty-three and 28 subjects respectively participated in the first (low-price calcula-

tor) and in the second (high-price calculator) version of the problem. Contrary to Experiment 1, the two purchases (the jacket and the calculator) were inserted in a shopping list covering four products: a jacket, a calculator, a set of coloured pens and a

N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160 155

bottle of shampoo. As in Experiment 1, the prices of the two purchases were 630,000 and 70,000 lire and the calculator price reduction was 24,000 lire.

The subjects were given the following instructions. Figures in parentheses relate to the first version of the problem (low-price calculator) whereas figures in brackets relate to the second version (high-price calculator).

"Imagine that you are about to purchase a jacket for (630,000 lire) [70,000 lire], a calculator for (70,000 lire) [630,000 lire], a set of coloured pens for 20,000 lire and one bottle of shampoo for 7,000 lire. The calculator salesman informs you that the calculator you wish to buy is on sale for (46,000 lire) [606,000 lire] at the other branch of the store, located 20 minutes drive away. Would you make the trip to the other store'?"

4.2. Results and discussion

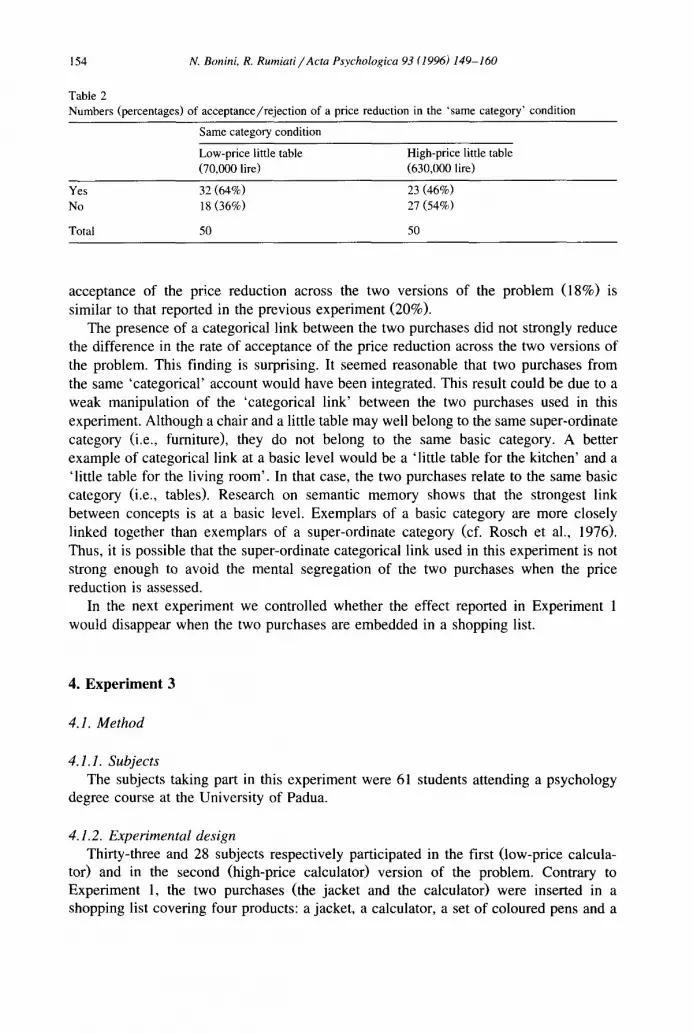

Table 3 shows that nearly half the subjects in both versions of the problem accept the calculator price reduction. The effect reported in Experiment 1 disappears in this experiment (X2(1) = 0.16, n.s.). The difference in the rate of acceptance of the price reduction across the two versions of the problem decreases to 6%.

This finding is incongruent with a topical account. By a topical account, the calculator price reduction radically changes across the two versions of the problem (a 34% and nearly a 4% discount rate respectively). Thus, a difference in the rate of acceptance of the price reduction across the two versions of the problem should be found. However, this finding is congruent with a comprehensive account. By a compre- hensive account, the calculator price reduction does not change across the two versions of the problem (it amounts to 24,000 lire out of 700,000 lire). Thus, a difference in the rate of acceptance of the price reduction across the two versions of the problem should not be found.

A shopping list seems to have made the relationship between the products stronger and induced the subjects to assess the calculator price reduction related to a global expense budget. However, an alternative interpretation of this finding could be ad- vanced. There is a strong match between the savings on the calculator (24,000 lire) and the cost of the pen and shampoo (27,000 lire). This may allow people to interpret the potential savings on the calculator in a very concrete way - the ability to 'get the

Table 3 Numbers (percentages) of acceptance/rejection of a price reduction in the 'shopping list" condition

Shopping list condition

Low-price calculator High-price calculator (70,000 lire) (630,000 lire)

Yes 17 (52%) 13 (46%) No 16 (48%) 15 (54%)

Total 33 28

156 N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160

shampoo and pens for free'. In this interpretation of the result, people would not aggregate across all four purchases, they simply would look at the absolute savings on the target purchase ('minimal account') because there is a very concrete interpretation of the amount that they save. However, if this interpretation is true, in both versions of the problem a high percentage of 'yes answers' should be found. The perspective to get for free two planned purchases should induce people to accept the price reduction. How- ever, as shown in Table 3, nearly 50% of subjects accept it in both versions of the problem.

In the next experiment, we controlled whether the effect reported in Experiment 1 would disappear when an explicit expense budget is provided.

5. Experiment 4

5.1. Method

5.1.1. Subjects The subjects taking part in this experiment were 135 students from the University of

Aix-en-Provence (France).

5.1.2. Experimental design Sixty-seven and 68 subjects respectively participated in the first (low-price calculator)

and in the second (high-price calculator) version of the problem. Contrary to the control condition, an expense budget that refers to the sum of the prices of the two planned purchases was provided. Subjects were given the following instructions. The figures in parentheses relate to the first version of the problem (low-price calculator) whereas figures in brackets relate to the second version (high-price calculator). As in the control condition, the prices of the two purchases were 320 and 2,680 Frs. and the calculator price reduction was 100 Frs.

"Imagine that you decide to purchase a jacket for (2,680 Frs.) [320 Frs.], and a calculator for (320 Frs.) [2,680 Frs.]. You get out from your house with 3,000 Frs. in your pocket. At the store, the calculator salesman informs you that the calculator you wish to buy is on sale for (220 Frs.) [2,580 Frs.] at the other branch of the store, located 20 minutes drive away. Would you make the trip to the other store?"

5.2. Results and discussion

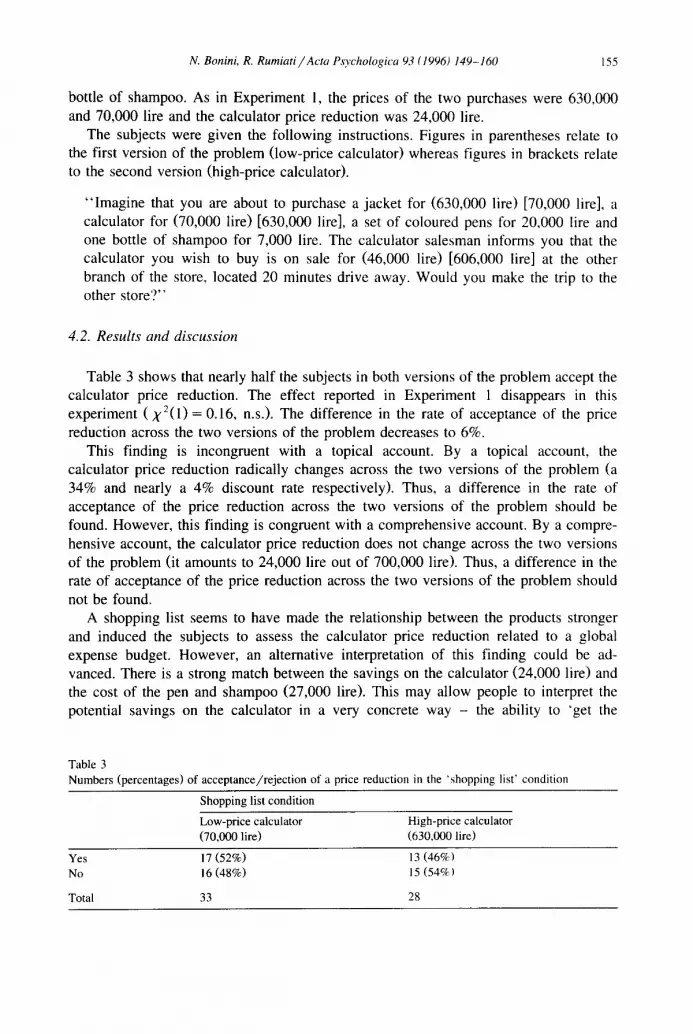

In the control condition, the majority of subjects (76%) accepts the calculator price reduction in the first version of the problem whereas a minority of subjects (40%) accepts it in the second version (X2(1) = 17.67, p < 0.0001). This finding is congruent with a topical account of the offered price reduction and incongruent with both a minimal and a comprehensive account.

Table 4 shows the findings in the expense budget condition. The majority of subjects accepts the calculator price reduction in both versions of the problem (67% and 56%

N. Bonini, R. Rumiati / Acta Psychologica 93 (1996) 149-160

Table 4 Numbers (percentages) of acceptance/rejection of a price reduction in the 'expense budget' condition

157

Expense budget condition

Low-price calculator High-price calculator (320 Frs.) (2,680 Frs.)

Yes 45 (67%) 38 (56cA) No 22 (33%) 30 (44c/,)

Total 67 68

respectively). The effect reported in the control condition disappears in the expense budget condition ( X 2 ( 1 ) = 1.81, n.s.). The difference in the rate of acceptance of the calculator price reduction across the two versions of the problem decreases to 11%.

This finding is incongruent with a topical account of the offered price reduction whereas it is congruent with a comprehensive account. To ask somebody to consider the cash needed to buy the planned purchases may induce him or her to assess the calculator price reduction related to a global expense budget. In this case, the offered price reduction is the same across the two versions of the problem and its rate of acceptance should not differ across these versions. However, an alternative interpretation of this result could be advanced. If subjects think there is anything else they want to do that day besides buy a jacket and a calculator, they may want to make sure that they do not spend the entire 3,000 frs. on the jacket and calculator. Thus, the expense budget factor may not really be an expense budget, but a liquidity constraint factor. If this hypothesis is true, in both versions of the problem an high percentage of 'yes answers' should be found. A need of liquidity for extra expenses should induce the subjects to accept the offered price reduction. However, as can be seen from Table 4, only 67% and 56% of subjects accept it.

In the next experiment, we controlled whether the effect reported in Experiment 1 would disappear when subjects are reminded that they can also buy the jacket at the other store.

6. Experiment 5

6.1. Method

6.1.1. Subjects The subjects taking part in this experiment were 100 students from the Universities of

Padua and Trento (Northern Italy).

6.1.2. Experimental design The students were equally and randomly assigned to the two versions of the

calculator problem. As in Experiment 1, the prices of the two purchases were 630,000 and 70,000 lire and the calculator price reduction was 24,000 lire. Contrary to

158 N. Bonini, R. Rumiati /Acta Psychologica 93 (1996) 149-160

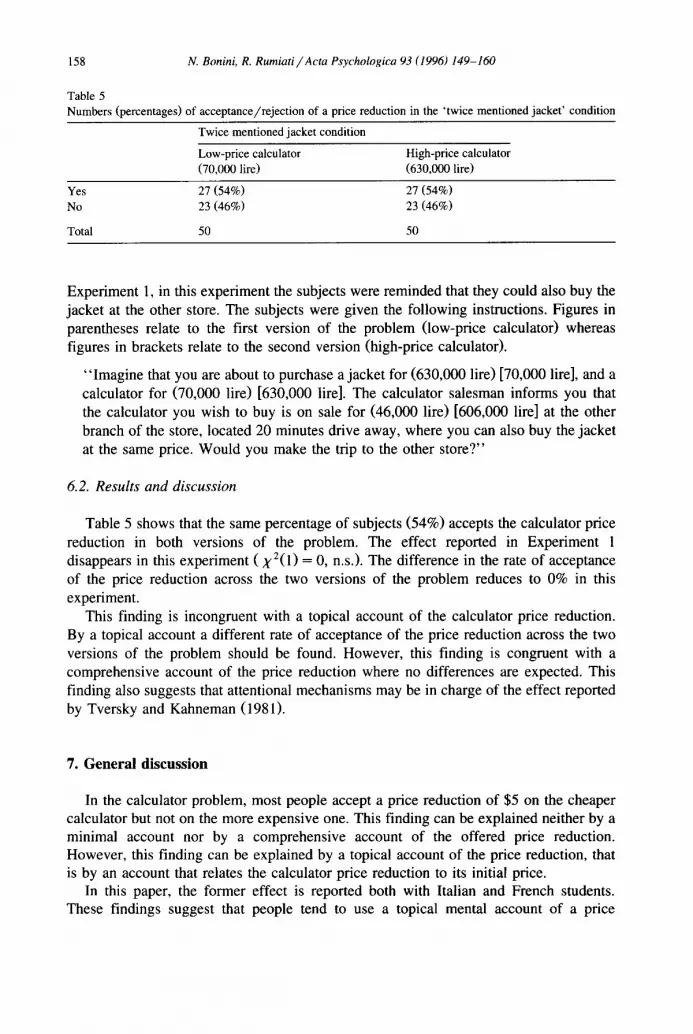

Table 5 Numbers (percentages) of acceptance/rejection of a price reduction in the 'twice mentioned jacket' condition

Twice mentioned jacket condition

Low-price calculator High-price calculator (70,000 lire) (630,000 lire)

Yes 27 (54%) 27 (54%) No 23 (46%) 23 (46%)

Total 50 50

Experiment 1, in this experiment the subjects were reminded that they could also buy the jacket at the other store. The subjects were given the following instructions. Figures in parentheses relate to the first version of the problem (low-price calculator) whereas figures in brackets relate to the second version (high-price calculator).

"Imagine that you are about to purchase a jacket for (630,000 life) [70,000 lire], and a calculator for (70,000 lire) [630,000 lire]. The calculator salesman informs you that the calculator you wish to buy is on sale for (46,000 lire) [606,000 lire] at the other branch of the store, located 20 minutes drive away, where you can also buy the jacket at the same price. Would you make the trip to the other store?"

6.2. Results and discussion

Table 5 shows that the same percentage of subjects (54%) accepts the calculator price reduction in both versions of the problem. The effect reported in Experiment 1 disappears in this experiment (X2(1) = 0, n.s.). The difference in the rate of acceptance of the price reduction across the two versions of the problem reduces to 0% in this experiment.

This finding is incongruent with a topical account of the calculator price reduction. By a topical account a different rate of acceptance of the price reduction across the two versions of the problem should be found. However, this finding is congruent with a comprehensive account of the price reduction where no differences are expected. This finding also suggests that attentional mechanisms may be in charge of the effect reported by Tversky and Kahneman (1981).

7. General discussion

In the calculator problem, most people accept a price reduction of $5 on the cheaper calculator but not on the more expensive one. This finding can be explained neither by a minimal account nor by a comprehensive account of the offered price reduction. However, this finding can be explained by a topical account of the price reduction, that is by an account that relates the calculator price reduction to its initial price.

In this paper, the former effect is reported both with Italian and French students. These findings suggest that people tend to use a topical mental account of a price

N. Bonini, R. Rurniati / Acta Psychologica 93 (1996) 149-160 159

reduction. However, there are situations where other types of mental account are more psychologically appropriate than the topical one. Results of Experiments 3, 4, and 5 show that the previous effect disappears when the two planned purchases are embedded in a shopping list, when an explicit expense budget is provided, or when subjects are reminded that they can also buy the not-target product at the other store. These findings cannot be explained by a topical mental account of the price reduction. They also show how manipulations of the features of the choice problem induce people to change the level of account of an offered price reduction.

Despite a plausible alternative interpretation of findings reported in the 'shopping list' condition (Experiment 3), we argue that results reported in the 'expense budget' (Experiment 4) and 'twice mentioned jacket' (Experiment 5) conditions can be inter- preted by a comprehensive mental account of the calculator price reduction. By that account, the price reduction is related to other expenses such as those concerning the planned purchases. These global expenses are constant across the two versions of the problem and this would explain why the rate of acceptance of the calculator price reduction is similar across the two versions of the problem. The use of a comprehensive account would be determined by a perceived relationship between the planned purchases that would make their mental segregation difficult. For example, the presentation of an expense budget related to the two purchases may induce people to think in terms of global expenses and savings. Also, the presence of a shopping list may strengthen the relation between the purchases favouring such global considerations.

Evidence that shows how the level of account adopted is itself contingent on characteristics of the choice problem and that subjects tend to frame problems with a higher jacket price at a more comprehensive level has been reported by Ranyard and Abdel-Nabi (1993).

We suggest that the issue related to the conditions favouring a certain kind of mental accounting should be approached in terms of focusing mechanisms (cf. Legrenzi et al., 1993). A way to control such mechanisms is to explicate the relationships (categorical, temporal, spatial, etc.) between purchases. Future research should specify the rules that control the elaboration of a mental account and by this theoretical framework list the conditions that would favour the use of one kind of mental account rather than another.

Acknowledgements

This research was supported by a CNR grant, Comitato 8 and 11. The authors are grateful to two anonymous referees for their comments on a previous version of the paper.

References

Collins, A.M. and E.F. Loftus, 1975. A spreading activation theory of semantic processing. Psychological Review 82, 407-428.

160 N. Bonini, R. Rumiati /Acta Psychologica 93 (1996) 149-160

Kahneman, D. and A. Tversky, 1984. Choices, values and frames. American Psychologist 39, 341-350. Legrenzi P., V. Girotto and P.N. Johnson-Laird, 1993. Focussing in reasoning and decision making. Cognition

49, 37-66. Meyer, D.E. and R.W. Schvaneveldt, 1976. Meaning, memory structure and mental processes. Science 192,

27-33. Ranyard, R. and D. Abdel-Nabi, 1993. Mental accounting and the process of multiattribute choice. Acta

Psychologica 84, 161-177. Rosch, E., C.B. Mervis, W.D. Gray, D.M. Johnsen and P. Boyes-Braem, 1976. Basic objects in natural

categories. Cognitive Psychology 8, 382-440. Thaler, R., 1993. Mental accounting matters. Paper presented at the conference on Subjective Probability

Utility and Decision Making, Aix-en-Provence, August, 1993. Tversky, A. and D. Kahneman, 1981 The framing of decisions and the psychology of choice. Science 211,

453-458.