liquidity position of citizen bank

TRANSCRIPT

A FIELD REPORT WRITING

ON

LIQUIDITY POSTION

OF

CITIZEN BANK INTERNATIONAL LTD

KATHMANDU, NEPAL

Submitted To:

Office of dean

Faculty of Management

Purbanchal University

Biratnagar

Submitted By:

Smita Shrestha

Asian college of management and technology

P.U Registration No:

Symbol No:

In the partial fulfillment of the requirement for the degree

Of

Bachelor of Business Administration (BBA) fifth semester

April,2014

Acknowledgement

This report has been prepared in partial fulfillment of the requirement for the degree of

Bachelor Administration (BBA) 5th semester. I would like to express my gratitude to

Purbanchal University for providing me with a great opportunity of preparing this project

report in accordance to its syllabus. I was very much anxious, and excited writing a report

of this kind, first time ever in my career. What so ever the situation, this report is finally

prepared with the help and guidance from my teachers and friends. I highly appreciate

and honor the efforts of Purbanchal University to develop required attitude, abilities and

practical skills in students which constitute a foundation for their competent and

responsibilities business managers.

I would like to thanks those who help in this project report .My thanks go to lectures of

field report whose valuable suggestion and advices guided to the completion of this

report.

And lastly I would like to thanks staffs of Citizen Bank International Ltd for

co-operation in providing all the necessary information and data for preparing this report.

Thank you,

Miss Smita Shrestha

Asian College of Management & Technology

TABLE OF CONTENTS

Recommendation

Acknowledgement

Abbreviations

List of Tables and Figures

Page no

Chapter I: INTRODUCTION 1

Title

1.1General background 11.1.1Introduction of banks 11.1.2 Commercial banks in Nepal 21.1.3 Introduction of Citizen Bank International Ltd 2-31.1.4 List of Commercial bank in Nepal 4-51.1.5 Branches of CBIL 5-61.1.6 Nature of study 7

1.1.6.1 Liquidity defined/what is liquidity? 71.1.6.2 The demand and supply of bank ltd 7- 8

1.1.6.2.1demand of bank ltd 71.1.6.2.2 supply of bank ltd 8

1.1.6.3 Why manage liquidity? 9

1.2Area of study 8-9

1.3Issue to be addressed/questions to be answered 9

1.4Objectives of the study 9

1.5Needs of the study 9

1.6 Organization study 9

1.6.1 Chapter plan 9-10

1.6.2 Research Methodology 10

1.6.3 Research Design 10

1.6.4 Nature and sources of Data 11

1.6.4.1 Primary Data 11

1.6.4.2 Secondary Data 11

1.6.5 Data Collection Procedure 11

1.6.5.1 Data presentation 11-12

1.6.5.2 Data analytical tools 12

1.7 Limitation of the study 12

Chapter II: DATA PRESENTATION & ANALYSIS 13

2.1 Data presentation 13

2.1.1Financial Analysis

2.2 Data analysis 14

2.2.1 Ratio Analysis 14

2.2.2 Profitability Ratios 15

2.2.3 Meaning and Concept of profitability 15

2.2.4 Meaning and Concept of profitability ratios 15

2.3 Major finding 27

Chapter III: Summary, Conclusion and Recommendation 28

3.1 Summary 29

3.2 Conclusion 29

3.3 Recommendation 30

Bibliography

Annex

ABBERVATIONS

CBIL Citizen Bank International Limited

& And

% Percentage

No Number

FY Fiscal Year

NRB Nepal Rastriya Bank

BBA Bachelor in Business Administration

NPR Net Profit Ratio

GPR Gross Profit Ratio

OPR Operating Profit Ratio

ROE Return on Assets

ROA Return on Assets

EPS Earning Per Share

ISR Interest Spread Ratio

WWW World Wide Web

NEPSE Nepal Stock Exchange

LIST OF TABLES

Table No Title Page No

Table 2.1 Gross profit ratio 16

Table 2.2 Net profit ratio 18

Table 2.3 Operation profit ratio. 19

Table 2.4 Return on Assets 21

Table 2.5 Return on Equity 22

Table 2.6 Earnings per share 24

Table 2.7 Interest spread Ratios 25

LIST OF FIGURES

Figures No Title Page. No

Figure no 2.1 Gross profit ratio`` 17

Figure no 2.2 Net profit ratio 18

Figure no 2.3 Operation profit ratio. 20

Figure no 2.4 Return on Assets 21

Figure no 2.5 Return on Equity 23

Figure no 2.6 Earnings per share 24

Figure no 2.7 Interest spread Ratios 26

BIBLIOGRAPHY

Annual report of Citizen Bank International Limited

Agrawal, Dr.GR (2000)- “Marketing Management in Nepal”, Kathmandu: M.K Publisher & distributors.

Bajaracharya, B.C (2000)-”Business Statistics and Management”, Kathmandu: M.M Publication, Third Edition.

Panta,Pream Raj,(2012),”Social Science Research and Thesis writing,” Kathmandu: Buddha Publication.

Shrestha M.K & Bhandari D.B (2004),”Financial Market & Institution” Kathmandu: Asmita books & Stationery.

Websites:

www.ctznbank.com

www.google.com

www.financialmarket.com

pg. 8

CHAPTER –I

INTRODUCTION

1.1GENERAL BACKGROUND

1.1.1 INTRODUCTION OF THE BANKSGenerally, bank is an institution which accepts deposits, makes business loans, and offers

related services. Commercial banks also allow for a variety of deposit accounts, such as

checking, saving, and time deposit. There institutions are run to make a profit and owned

by a group of individuals, yet some may be members of the Federal Reserve System.

While commercial banks offer services to individuals, they are primary concerned with

receiving deposits and lending to businesses. In an economy the bank is regarded as one

of the economic backbone of the country for its development. Bank is a financial

institution that deals in money. The basic function of bank is collecting deposit and

granting the loans. It involves in credit creation that in related to creation of deposit and

loan. In the economy, the banks collects small saving of general people, accumulative it

and lends the productive sectors of the society for the overall economic development.

According to Scholars, “The bank is defined as factory of money for credit where it does

not purchase goods and sells it rather produces credit inform of deposit and sells it

inform of loans.” Thus in conclusion, we can say that bank is an organization which

deals with the monetary transactions for the mobilization of idle money or deposits in

productive sectors, is essentially essential for the development of the whole net.

pg. 9

1.1.2 COMMERCIAL BANK IN NEPALThe history of financial and economic development in Nepal is not very old. It has gone

through different stages, during the PM Ranodip Singh around 1972 A.D. “TEJARATH

ADDA” was introduced, which brought a reform in economic and financial section. The

main purpose of “TEJARATH ADDA” was to provide credit facilities to the general

public at confessional rate. However the installment of “KHUSI KHANA” as a banking

agency during the king Prithivi Narayan Shah could also be regarded as the first step

towards banking in Nepal. After that the first commercial bank of Nepal, Nepal bank

Limited (NBL) was lunched with the cooperation of imperial bank of India in November

1937. Holding 51% government equity. The second commercial bank, Rastriya Banijya

bank come into existence in 1966 A.D. with 100% government ownership. In early 1980,

to meet the need of health completion in the financial system, Nepal allowed to entry of

foreign banks as joint ventures with up to maximum of 50% equity participation.

Nepal Arab bank limited was the first joint venture bank which was established with the

joint venture of Arab bank emirates in 1984. in 1986, Nepal grind lays bank limited (now

chartered bank limited) entered in Nepali financial market as a joint venture with ANZ-

Grind lays.

1.1.3 Introduction of Citizen Bank International LtdCitizen Bank international limited(CBIL) was established on June 21, 2007 and

commenced is commercial operation from 20th April 2007.The head office of the bank is

located at Sharada Sadan, Kamaladi. It is an “A” level financial institution as licensed by

the Nepal Rastra Bank(NRB) as well as a public limited company established under

company act 2056.It is promoted by eminent personalities/business and industrial houses

and reputed individuals having high social standing. It is promoted by prominent

personalities‟ business/industrial house and reputed individuals having high social

standings .It is managed by a team of experienced bankers and professionals. With the

increasing level of liberalization, privatization and globalization in this sector the

commercial bank such as “Citizens bank international ltd.”, are established to aid the

economic growth and development of this nation. Today’s bank plays a vital role for the

pg. 10

economic development of the country Massive changes and developments have taken

place during the past two decades in the financial sector. Amidst all these changes, for

economic growth and development of New Nepal, Liberalization, Privatization and

Globalization in this sector has given birth to the largest commercial bank,.

It is managed by a team of experienced bankers and professionals It provides various

banking services to a wide range of customers including banks, insurance companies,

industrial trading houses, airlines, hotels, and many other sectors

Vision

To be the leading bank known for its service excellence in the region.

Mission

To be a trustworthy partner for the progress of individuals and institutions by designing,

producing and delivering the best financial solutions. The Bank will constantly strive to

inculcate in its services five corporate values as follows:

Customer Focus

we are committed to meet the financial needs of our customers and exceed their

expectations through innovative solutions.

Service Excellence

we promise to deliver customer centered products and services par excellence.

Human Resource

We employ bright, honest, helpful and pleasant people. We nurture and empower them to

achieve their full potential.

Corporate Governance

We believe in being accountable, conducting business ethically and maintaining

transparency.

pg. 11

Social Responsibility

We are committed to take social initiatives for the development of the nation.

1.1.4 LIST OF COMMERCIAL BANK IN NEPAL:

S.No. Name of commercial banks

1 Nepal Bank ltd.

2 Rastriya Banijya Bank Ltd.

3 Agriculture Development Bank Ltd.

4 Nabil Bank Ltd.

5 Nepal Investment Bank Ltd.

6 Standard Chartered Bank Nepal Ltd.

7 Himalayan Bank Ltd.

8 Nepal SBI Bank Ltd.

9 Nepal Bangladesh Bank Ltd.

10 Everest Bank Ltd.

11 Bank of Kathmandu Ltd.

12 Nepal Credit and Commercial Bank ltd.

13 Lumbini Bank Ltd.

14 Nepal Industrial and Commercial Bank Ltd.

15 Machhapuchre Bank Ltd.

16 Kumari Bank Ltd.

17 Laxmi Bank Ltd.

18 Siddhartha Bank Ltd.

19 Global Bank Ltd.

20 Citizens Bank International Ltd.

21 Prime Commercial Bank Ltd.

22 Sunrise Bank Ltd.

23 Bank of Asia Nepal Ltd.

24 DCBL Bank Ltd.

25 NMB Bank Nepal Ltd.

26 Kist Bank Ltd.

27 Janata Bank Nepal Ltd.

pg. 12

28

29

Mega Bank Nepal Ltd.

Commerce and Trust Bank Nepal Ltd

30 Civil Bank Ltd.

31 Century Commercial Bank Ltd.

Source:” www.nrb.org.np”

1.1.5 Branch of Citizen Bank international Ltd

District Branch location

Banke Nepalgunj Branch Dhambouji Chowk,

Bara Pathalaiya, Pipra Simra – 9

Bhaktapur Khauma-15

Bhaktapur Bayakha Bazar – 7, Thimi

Chitawan Narayanghat Branch Lions Chowk,Bharatpur-4

Dang New Road-11

Dhanusa BhanuChowk-2

Dolakha Bich Bazar

Humla Simikot-2, Mathilo Bazaar

Jhapa Birtamod Branch Kakadvitta Road,Anarmani VDC-3,Birtamod

Kailali Dhangadhi Branch,Main Road,Kailali

Kanchanpur Municipality – 4 (Nearby Buspark)

Kaski Pokhara Branch, Nayasadak,Pokhara-9,Kaski,Nepal

Kathmandu Corporate Office/Kamaladi Branch, Sharada Sadan

Kathmandu Bouddha Branch ,Jorpati -3, Bouddha

Kathmandu New Road Branch,Kathmandu-23, Naya Sadak,Basantapur

pg. 13

Kathmandu Koteshwor Branch,Kathmandu-10,Koteshwor

KathmanduKalanki Branch

Ganesh Man Singh Marg, (Near Kalanki Mandir)

Kathmandu Thahiti Branch,Thahiti Chowk, Thahiti, Kathmandu

Kathmandu Nayabazar Branch,V.S. Complex, Sohrakhutte, Nayabazar,

KathmanduMaitidevi Branch

Setopul, Maitidevi

Kathmandu Saraswatinagar – 6, Kapan Marg

Kathmandu Narayan Gopal Chowk

Kathmandu Naya Bazar – 17

Kathmandu Samakhushi Branch

Lalitpur Kumaripati Branch,Lalitpur-5,Kumaripati

Lalitpur Chayabahal-2

Morang Biratnagar Branch, Dharan Road-8,

Myagdi New Road – 1, Beni Bazar

Parsa Birgunj Branch,Adarsha Nagar Chowk,Main Road

Rupandehi Butwal Branch,Pushpalal Park

Sunsari Itahari-1, Dharan road

Surkhet Sunny Hall Line, Surkhet-6

Udayapur Gaighat Bazar – 4

Source from www.ctznbank.com

pg. 14

1.1.6 Nature of study

1.1.6.1 Liquidity defined/what is liquidity?

Liquidity is the availability of cash amount and at the time of needed at a reasonable cost.

Liquidity can be defined as bank’s capacity to pay cash in exchange of deposits. And

assets is said to be liquid when it is readily converted into cash with little or no capital

loss or price deprecation.

It is the status & part of the assets which can be used to meet the obligation of the banks.

Commercial bank holds liquid assets balances in the form of currency, bank balance,

marketable securities and other assets immediately convertible into cash. Liquidity can be

viewed in terms of liquidity stored in the balance sheet and in terms of liquidity available

through purchase funds.

1.1.6.2 Demand and Supply of Bank Liquidity

1.1.6.2.1 Demand of Bank Liquidity

Commercial banks need liquidity to meet loan demand and deposit withdrawals such as:

Repay deposits:

The various deposits taken by bank are repayable on demand or fixed maturity along with

interest, so demand for liquidity arises.

Meet contingent liability:

Banks carry out off balance sheet activities like letter of credit, acceptance, guarantee,

forward exchange contract etc. For carrying out all those activities, the bank needs

sufficient liquidity.

Disburse loans and advances:

pg. 15

The main profit earing function of banks is by giving loans and advances. Some loans are

disbursed at once while some loans are withdrawn by the customers as per their

requirement.

1.1.6.2.2 Supply of Bank Liquidity

To meet foregoing demands for liquidity, banks can draw upon several potential sources

of supply. The most important sources is receipt of new customer deposits, both from

newly opened accounts and from new deposits placed in exiting accounts. Another

element in the supply of bank liquidity from customers repaying their loans.

These various sources of liquidity demand and supply come together determine each

bank’s net liquidity position at any moment in time.

1.1.6.3 Why manage liquidity?

The purpose of managing liquid assets is to minimize the opportunity cost of holding

cash and maximizes the opportunity cost holding cash and maximize on the portion of the

funds that is not required immediately. Business firms need to maintain a certain degree

of liquidity in the form of cash in hands, bank deposits & marketable securities to meet

daily operating expenses and short term financial obligation.

1.2 Area of study

Liquidity ratios are used to determine a company’s ability to meet its short-term debt

obligations. Investors often take a close look at liquidity ratios when performing

fundamental analysis on a firm. Since a company that is consistently having trouble

meeting its short-term debt is at a higher risk of bankruptcy, liquidity ratios are a good

measure of whether a company will be able to comfortably continue as a going concern

any type of ratio analysis should be looked at within the correct context. For instance,

investors should always look at a company’s ratios against those of its competitors, its

sector and its industry and over a period of several years. In this issue’s Fundamental

pg. 16

Focus, we investigate liquidity ratios using time-series analysis, competitive analysis and

sector and industry analysis.

1.3 Issues to be addressed/question to be answered The question that were from the organization:-

What is the level of current assets related to current liabilities of the bank?

Why do the banks maintain the liquidity position?

What are benefits of adequate capital of the bank?

1.4 Objectives of the studyThe main objective of the study is to analyze the Citizen Bank International Ltd

liquidity position. Other objectives can be listed below:

To show the level of current assets relative to current liabilities of the bank.

To analyze the financial performance, profitability.

To suggest the amount of the optimum level of liquidity and manage the policy.

1.5 Needs of the study The essence of the liquidity management problem for a bank may be described

into statements:

The demands for bank liquidity are rarely equal to the supply of the liquidity at

any particular moment in time. The bank must continually deal with either a

liquidity deficit or liquidity surplus.

1.6Organization of the study

1.6.1 Chapter plan The study is divided into 3 chapters such as

pg. 17

Introduction

Presentation and analysis of data

Summary, conclusion and recommendation

1.6.2 Research methodology

The method which is use in the research is called research methodology. How the data is

collected and which source the research use for getting the data is under the research

methodology. Research methodology covers the data analysis tools as well. It helps in

carrying out the entire research work in desired way.

1.6.3 Research Design

A research design is the arrangement conditions, for the collection and analysis of data in

a manner that aims to combined relevance to the research purpose with economy in

procedures.

The present study is mainly based on 2 types design ie descriptive and analytical. The

descriptive research presents the general pattern of liquid assets, cash and marketable

securities. The analytical research design makes the analysis of gathered facts and

information and makes critical evaluation of it.This study aims on the financial analysis

of the Nepal investment bank Ltd. This study is mainly based on primary data and

secondary data.

The primary data, which are collected directly from the question answer, direct

interview with customer and office staffs.

The secondary data are collected from respective annual reports especially from

the Citizen bank web sites and various other journals and from security bond Nepal

(SUBO) and Nepal stock exchange (NEPSE).

pg. 18

1.6.4 Nature and Source of Data

There are mainly 2 types of nature of data which are mentioned below:

Primary data:

Primary data are those fresh and original data, which are collected and recorded by the

investigator or researcher. They are collected from face to face dealing with the investors

and members in the organization.

.Secondary data:

Secondary data are those data that have been collected earlier for some purpose.

These data are borrows from others who have collected them for some purpose.

This fieldwork report is total based on the secondary data. The sources of

secondary data are as follows:

CBIL Reports.

Website of CBIL, www.ctznbank.com

1.6.5 Data collection procedure

As stated earlier, this report is purely based on secondary data annual report of the bank

for the study. This report is prepare by using real data obtained from various sources like

financial news newspaper, magazine of commercial work and annual report.

1.6.5.1 Data presentation

Presentation means the presentation of the collected data through table; figure etc.

presentation is the process of understanding the study or the report and calculating the

pg. 19

opinion. An analysis of a data means the process where the statement or the report gets

resolve by breaking them into simple statement. Analysis means to find out something

and give opinion about the presented data.

1.6.5.2 Data analytical tools

Data analysis tools means which tools the research used for present and analyzed the

data. The main tools of analysis are mathematical and statistical tools. In this reports

statistical and financial ratio tools is used for data analysis. Mean and correlation is

calculated for analysis the data as statistical tools

1.7 limitations of the study Different companies operate in different industries each having different

environmental conditions such as regulation, market structure, etc. Such factors

are so significant that a comparison of two companies from different industries

might be misleading.

Financial accounting information is affected by estimates and assumptions.

Accounting standards allow different accounting policies, which impairs

comparability and hence ratio analysis is less useful in such situations

Ratio gives false result, if they are calculated from incorrect accounting data.

Ratios are calculated on the basis of past data. Therefore, they don’t provide

complete information for future forecasting.

pg. 20

Chapter-II

DATA PRESENTATION AND ANALYSIS

2.1Data presentation

2.1.1Financial Analysis:The process of evaluating businesses, projects, budgets and other finance-related entities

to determine their suitability for investment. Typically, financial analysis is used to

analyze whether an entity is stable, solvent, liquid, or profitable enough to be invested in.

When looking at a specific company, the financial analyst will often focus on the income

statement, balance sheet, and cash flow statement. In addition, one key area of financial

analysis involves extrapolating the company's past performance into an estimate of the

company's future performance. Financial analysis can be performance by insiders or by

parties outside the firm visa creditors, investors, government, financial analysis and

others. The primary tools of the financial analysis are financial ratio.

But the reporter isn’t subject to calculation of financial ratio.by the topic. The report is

limited to the calculation of the set of commonly used liquidity ratios and integrated

models analyzing the liquidity position. Generally, the liquidity position is the key of the

creditors to know the firm’s ability to meet there claim over the short period of time.

However the analysis in this report is not interested in analyzing the firm’s ability to meet

their current obligation.

pg. 21

2.2 Data Analysis

2.2.1 Ratio Analysis

A ratio defined as the “relationship between two numbers, amount, or measurement,

which shows how much greater on is than the others.” Ratio helps to summarize the large

quantities of financial data and to make qualitative judgment about the firm’s financial

performance. Quantitative analysis of information contained in a company’s financial

statements. Ratio analysis is based on line items in financial statements like the balance

sheet, income statement and cash flow statement; the ratios of one item – or a

combination of items - to another item or combination are then calculated. Ratio analysis

is used to evaluate various aspects of a company’s operating and financial performance

such as its efficiency, liquidity, profitability and solvency.

The trend of these ratios over time is studied to check whether they are improving or

deteriorating. Ratios are also compared across different companies in the same sector to

see how they stack up, and to get an idea of comparative valuations. Ratio analysis is a

cornerstone of fundamental analysis.

2.2.2 Types of Ratios

The ratios are calculates to serve the objectives of the users or the analyisis.to

suit the need of the analysis ratios have been grouped as below:

1. Liquidity ratios

2. Leverage ratios

3. Activity ratios

4. Profitability ratios

5. Market value ratios

Liquidity ratios measure the firm’s ability to meet current obligations.

Leverage ratios show the proportions of the debt & equity in financing the firm’s asset

this ratio is known as debt management ratio.

Activity ratio also known as asset management ratios, measure how effectively the firm

managing its assets.

pg. 22

Profitability ratios measure the overall performance & the effective ness of the firm. It

shows the combined effects of the liquidity, assets management and debt management on

operating results.

2.3. Meaning and Concept of profitabilityProfitability is the primary goal of all business ventures. Without profitability the

business will not survive in the long run. So measuring current and past profitability and

projecting future profitability is very important. Every firm is most concerned with its

profitability. One of the most frequently used tools of financial ratio analysis is

profitability ratios which are used to determine the company's bottom line and its return

to its investors. Profitability measures are important to company managers and owners

alike. If a small business has outside investors who have put their own money into the

company, the primary owner certainly has to show profitability to those equity investors.

2.3.1Meaning and Concept of profitability ratiosProfitability is an indicator of success in business. Measurement of profitability is the

main concern for all interested parties, i.e. creditors, investors, owners and management.

Net sales are taken as a denominator in calculating all the ratios for return. Gross profit

margin, operating profit margin and net profit margin represent the company’s ability to

translate sales into profit at different stages of measurement. Some major profitability

ratios are performed below :

1) Gross Profit Ratio (GPR)

2) Net Profit Ratio (NPR)

3) Operation Profit Ratio (OPR)

4) Return on Assets (ROA)

5) Return on Equity (ROE)

6) Earnings per Share (EPS)

7) Interest Spread Ratio (ISR)

pg. 23

2.2.3.1 Gross Profit Ratio (GPR):

The gross profit margin looks at cost of goods sold as a percentage of sales. This ratio

looks at how well a company controls the cost of its inventory and the manufacturing of

its products and subsequently passes on the costs to its customers. The larger the gross

profit margin, the better for the company

The formula for calculating gross profit margin is

Table:2.1

Gross Profit Ratio (In millions)

Fiscal Year Gross Profit Total Interest

Revenue

GPR

2065/66 150.64 758.256 19.87%

2066/67 305.14 1398.83 21.97%

2067/68 312.37 1795.23 17.41%

2068/69 355.39 1980.32 17.94%

2069/70 627.02 2211.98 28.34%

Source: Annual report of CBIL( FY 2065/66- 2069/70)

Table shows the change in gross profit ratio of Citizen Bank International Limited from

the period 2065/66 to 2069/70. The highest GPR was 28.34% in the fiscal year 28.34%

and the lowest was 17.41% in the fiscal year 2067/68.

pg. 24

GPM=Gross Profit

x 100Sales

Figure 2.1

Gross profit ratio

2065/66 2066/67 2067/68 2068/69 2069/700

500

1000

1500

2000

2500

Gross profit ratio

The above bar diagram shows the GPR of CBIL which is decreasing at first year 2065/66

and slowly increasing at last 4 years.

2.2.2.2Net Profit Ratio (NPR):

When doing a simple profitability ratio analysis, net profit margin is the most often

margin ratio used. It is ratio between net income and sales. The net profit margin shows

how much of each sales dollar shows up as net income after all expenses are paid.

The formula for net profit margin is:

NPR =Net Profit

x 100Sales

pg. 25

Table 2.2

Net Profit Ratio (NPR): (In millions)

Fiscal Year Net Profit Total Interest

Revenue

NPR

2065/66 95.809 758.256 12.68%

2066/67 193.56 1398.83 13.87%

2067/68 198.56 1795.23 11.06%

2068/69 224.79 1980.32 11.35%

2069/70 413.24 2211.98 18.68%

Source: Annual report of CBIL( FY 2065/66- 2069/70)

Table and chart shows the change in net profit ratio of Citizen Bank International Ltd.

from the period 2065/66 to 2069/70. The highest NPR was 18.68 % in the fiscal year

2069/70 and the lowest was 11.06 % in the fiscal year 2067/68.

Figure 2.2

Net profit ratio

2065/66 2066/67 2067/68 2068/69 2069/700%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Net profit ratio

Series4NPRTotal Intrest Revenue

pg. 26

The above bar diagram shows the PR of CBIL which is decreasing at first year 2065/66

and slowly increasing at last 4 years.

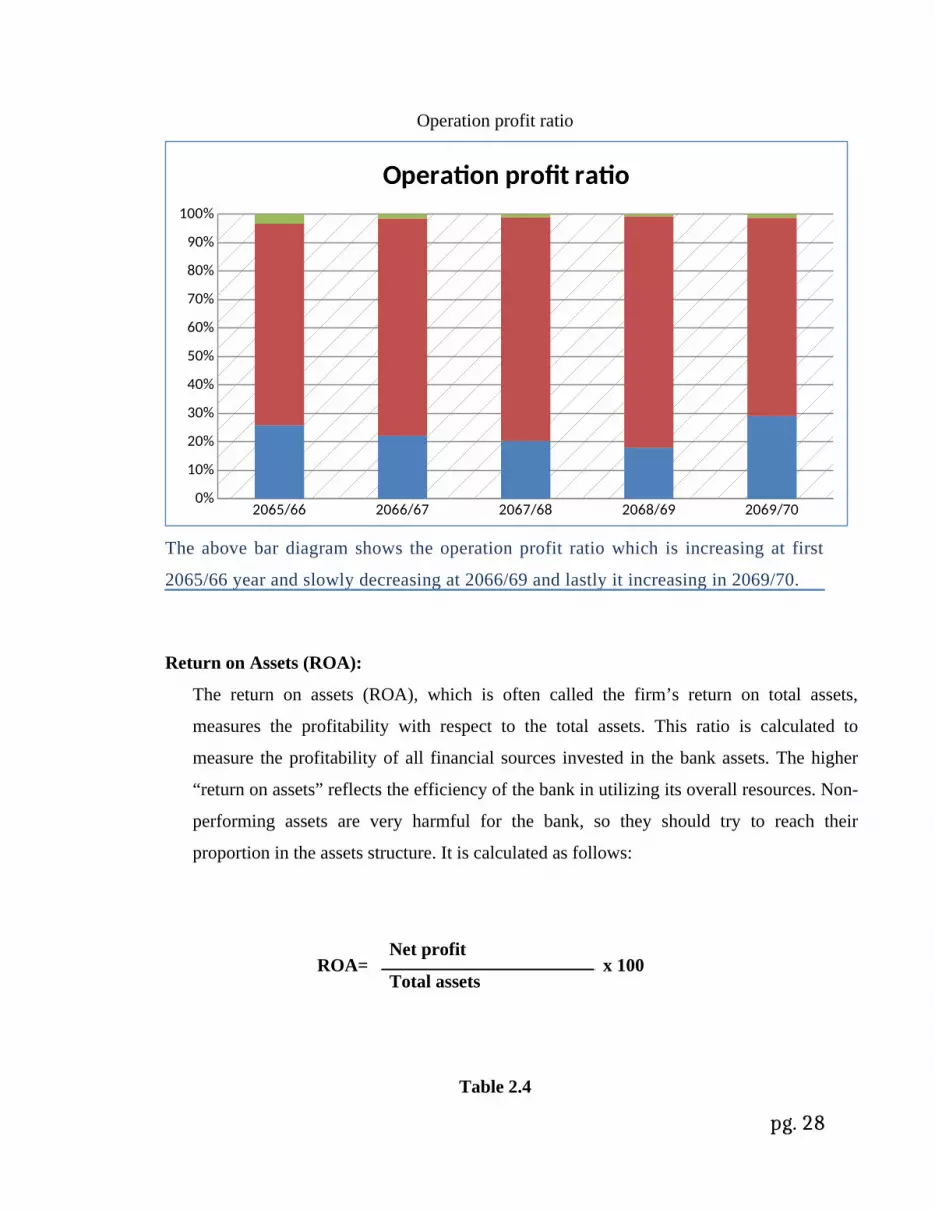

Operation Profit Ratio:

It shows the relationship between operating profit and sales and indicates operating profit

of a firm. Higher operating profit ratio is preferred because it is good sign of operating

efficiency of a firm.

The formula for operating profit margin is:

OPR =Operating Profit

x 100Sales

Table 2.3

Operation Profit Ratio: (in millions)

Fiscal Year Operation Profit Total Interest

Revenue

Operation Profit

Ratio

2065/66

275.74

758.256 36.36%

2066/67 405.51 1398.83 28.98%

2067/68 461.90 1795.23 25.79%

2068/69 435.22 1980.32 21.97%

2069/70 919.10 2211.98 41.55%

Source: Annual report of CBIL( FY 2065/66- 2069/70)

Table shows the change in operating profit ratio of CBIL from the period 2065/66to

2069/70. The highest OPR was 41.55% in the fiscal year 2069/70 and the lowest was

21.97% in the fiscal year 2068/69.

Figure 2.3

pg. 27

Operation profit ratio

2065/66 2066/67 2067/68 2068/69 2069/700%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Operation profit ratio

The above bar diagram shows the operation profit ratio which is increasing at first

2065/66 year and slowly decreasing at 2066/69 and lastly it increasing in 2069/70.

Return on Assets (ROA):

The return on assets (ROA), which is often called the firm’s return on total assets,

measures the profitability with respect to the total assets. This ratio is calculated to

measure the profitability of all financial sources invested in the bank assets. The higher

“return on assets” reflects the efficiency of the bank in utilizing its overall resources. Non-

performing assets are very harmful for the bank, so they should try to reach their

proportion in the assets structure. It is calculated as follows:

Table 2.4

pg. 28

ROA=Net profit

x 100Total assets

Return on Assets

( in millions)

Fiscal Year Net Profit Total Assets ROA

2065/66 95.809 12966.04 0.00735

2066/67 193.56 16516.88 0.0117

2067/68 198.56 16816.49 0.0118

2068/69 224.79 20068.50 0.0112

2069/70 413.24 25979.51 0.0159

Source: Annual report of CBIL( FY 2065/66- 2069/70)

From above table we can see that total assets is increasing all over the year and the net profit

is increasing process which makes ROA process. The highest ROA obtained is 0.0159 which

is in the year 2069/70 and the lowest is 0.00735 which is in the year 2065/70.

Figure 2.4

Return on Assets

2065/66 2066/67 2067/68 2068/69 2069/700

5000

10000

15000

20000

25000

30000

Return on assets

The above bar diagram shows the Return on ratio which is decreasing at first 2065/66year

and increasing at last 4 years.

pg. 29

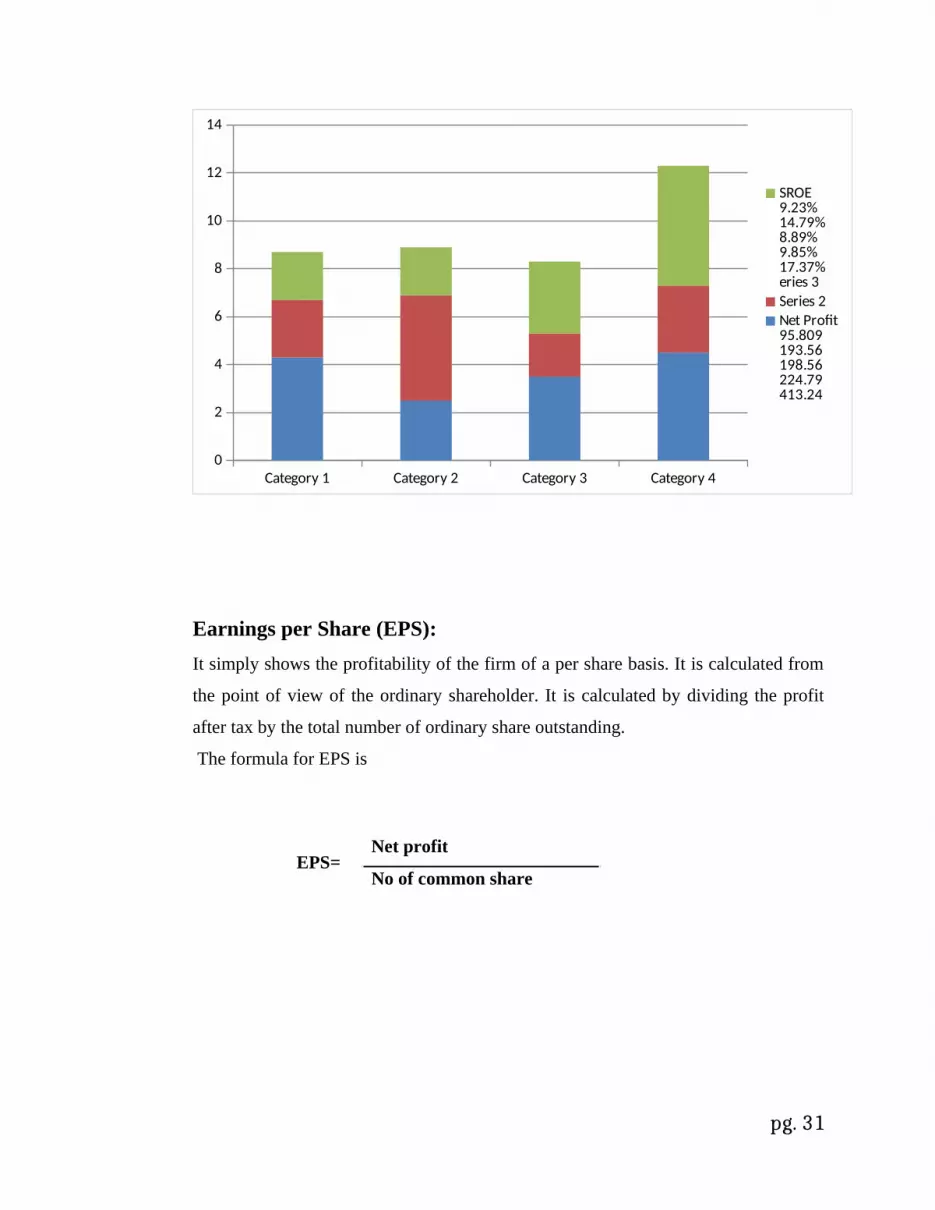

Return on Equity (ROE)

The return on equity (ROE) measures the return on the owner’s investment in the firm.

Higher ratio of return on equity is better for owner.

ROE is calculated as follows:

ROE =

Table 2.5

Return on Equity

(in millions)

Fiscal Year Net Profit Equity ROE

2065/66 95.809 9.23%

2066/67 193.56 14.79%

2067/68 198.56 8.89%

2068/69 224.79 9.85%

2069/70 413.24 17.37%

Source: Annual report of CBIL( FY 2065/66- 2069/70)

pg. 30

Net profitx 100

Total equity

Category 1 Category 2 Category 3 Category 40

2

4

6

8

10

12

14

SROE9.23%14.79%8.89%9.85%17.37%eries 3Series 2Net Profit95.809193.56198.56224.79413.24

Earnings per Share (EPS):It simply shows the profitability of the firm of a per share basis. It is calculated from

the point of view of the ordinary shareholder. It is calculated by dividing the profit

after tax by the total number of ordinary share outstanding.

The formula for EPS is

pg. 31

EPS=Net profit

No of common share

Table 2.6

Earnings per share

Source:

Annual

report

of

CBIL( FY 2065/66- 2069/70)

Table shows the change in EPS of Citizen Bank from the period 2065/66 to 2069/70. The

highest EPS was 35.63 in the fiscal year 2064/65 and the lowest was 12.68 in the fiscal year

2068/68. Therefore from above analysis we can say that the earning power of NCCB is in

good condition

Figure 2.6

Earnings per share

2065/66 2066/67 2067/68 2068/69 2069/700%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Earnings per share

Axis Title

pg. 32

Fiscal Year Net profit No. of common

share

EPS

2065/66 95.809 100.00 0.95%

2066/67 193.56 120.69 1.60%

2067/68 198.56 210.00 0.94%

2068/69 224.79 210.18 1.06%

2069/70 413.24 210.18 1.96%

Interest Spread Ratio (ISR):

Interest spread ratio (ISR) shows the relationship between interests to total assets of

the firm. Spread is the difference between interest income and interest expenses. So

higher this value, higher will be this ratio. Higher value of this ratio indicates better

financial position of the organization. It is calculated as follows:

Table 2.7

Interest spread Ratios

Year Interest Income Interest expenses Total AssetsInterest Spread

Ratio (in %)

2065/66 758.25 508.80 12966.04 758.21%

2066/67 1398.83 950.90 16516.88 1398.77%

2067/68 1795.23 1236.32 16816.49 1795.15%

2068/69 1980.32 1405.86 20068.50 1980.25%

2069/70 2211.98 1176.91 25979.51 2211.93%

Source: Annual report of CBIL( FY 2065/66- 2069/70)

pg. 33

ISR = (INTEREST INCOME – INTEREST EXPENSE)

TOTAL ASSETS

2065/66 2066/67 2067/68 2068/69 2069/700

5000

10000

15000

20000

25000

30000

Interest IncomeInterest expenenseTotal Assets

Interest Spread

pg. 34

2.3 Major Finding

The major finding from primary data can be outlined as under:

From the primary sources, the liquidity position of CIBL is in good position. It

maintains its financial position in every situation. The customers of this bank are

satisfied with this bank.

The legal documents demanded by bank in regard loans and deposit is bound to

make any genuine costumer fill irritated, so the banks should appropriate

stapes toward it.

The bank should give immediate response to the new starting business by

lowering the loans provided.

The

pg. 35

CHAPTER-III

SUMMARY, CONCLUSION AND RECOMMENDATION

3.1 Summary It is growing and doing well with sound participate management and efficiency of

employees. It has made its unique position in the competition of commercial bank.

Liquidity is defined as bank’s capacity to pay cash in exchange of deposit. Liquidity

position of the banks is the key factor of sound operating position. The banks having

maintain sufficient amount of liquidity because there will be large proportion of deposits

payable on demand, inability of banks to pay deposits on demand damages the credit

worthiness of the bank .This in turns, may lead to run in bank and collapse of the bank.

This study is confined to Citizen Bank International Limited is done with the main purpose of

analyzing the profitability performance of this bank from the FY 2065/66 to FY 2069/70. The

data presented in the tabular and graphical forms. A ratio analysis has been used to evaluate

the profitability performance of this company. Thus, this report gives the general idea about

the profitability position of CIBL.

3.2 Conclusion

pg. 36

The main objective of this study is to analyze the liquidity position of CBIL and to

provide recommendation based on the study. From the analysis of primary and

secondary, we have rough idea about the liquidity position trend of CBIL for the period

2065/66 to 2069/70 .the ratio of cash and bank balance to current assets of CBIL is

getting stronger and better. . The detailed conclusion of every ratio is as follows

The highest GPR is 28.34% in the FY 2069/70 and the lowest is 17.41% in the FY

2067/68. It declines due to high margin between gross profit and total interest

revenue (sales).

The highest NPR is 18.68% in the FY 2069/ 70 and it lowest NPR is 11.06% in

FY 2067/68. NPR is regularly declining due to large margin between the net profit

and the total interest revenue.

The highest OPR is 41.55% in the FY 2069/70 and the lowest is 21.97% in the

year 2068/69. It declines due to high margin between earning and sales (interest

revenue).

The ROA of the starting FY 2065/66 is 0.00735 and it increasing throughout the

year and at the end FY 2069/70 it becomes 0.0159. Here, ROA increasing due to

heavy investment on assets and getting returns.

The ROE of NCCB is in declining position. The ROE of the starting FY 2064/65 is

0.7280 which is good enough but in the ending FY 2068/69 it declines to 0.0924

which shows the companies ineffectiveness towards returns of net profit.

The Earning Per Share (EPS) of CBIL at starting FY 2065/66 is 9.95% 1.60%

and 0.94% but it increase to 1.06% and 1.96% at last 2 years.

The interest spread ratio of CIBL at first year 758.21 % and it regularly increasing.

The lowest ISR is 758.21% at the beginning year FY 2065/66. ISR increase due to

having the large margin between interest in deposit and interest while providing

loan

pg. 37

3.3 Recommendation

From the above study, it can be considered that the current position of liquidity of CIBL

is fairly well enough. However, the following recommendation can be made based on the

study.

CIBL should maintain the current ratio of cash and bank balance to current assets

ratio.

Formulate the clear vision, mission of the organization to attract customers and

make aware to employees and customers.

Show the interest rate on deposits and create awareness of the service of the

organization for landing to customers by displaying in notice board.

Standardize the operations of the various departments in all branches of the banks.

Improve service quality of official so as to maintain customer faith and image of

the bank.

pg. 38