financial entropy, conservation laws and the eurozone crisis

TRANSCRIPT

Financial entropy, conservation laws and the

EuroZone crisis

Who? Paul Cockshott1,

From? 1School of Computer Science: University of Glasgow ,

When? Glasgow 2014

Outline

Quick summaryWhat determines rate of pro�t

TheoryConservation laws

Phase space

Empirical data

Stability pactConclusion on the Stability Pact

I will give a quick account of our analysis and then gointo depth.The crisis is caused by two main mechanisms:

1 the falling rate of pro�t and

2 the polarisation of capital into rentier and productivecapital.

Polarisation

Always a spread of rates of pro�t,

some capitals are obtaining a pro�t below and some abovethe current interest rate.

The higher the interest rate → more capitalists earn lesspro�t than they could earn by simply lending money.

Polarisation of capitalist class into two groups,

net debtorsnet creditors

Polarisation grows → a distinct class of rentiercapitalists arises

There is no net value in �nance

Very important!

Sum of credit is always 0

since the asset of one capitalist is a liability of another.

There is therefore no value held in the �nancial system.

Capital can not 'move into �nance'

Outline

Quick summaryWhat determines rate of pro�t

TheoryConservation lawsPhase space

Empirical data

Stability pactConclusion on the Stability Pact

Laws Governing Growth of value

Growth of value given by product of the rate of pro�tand the share of this pro�t that is accumulated.

Typically in developed capitalist countries the accumulationshare is only abour 20 to 30%.

Fundamentally the rate of accumulation is constrainedby the growth of the working class population.

Marx : �accumulation of capital is growth of theproletariat.�

As the growth of the working class slows down, so must therate of accumulation.

What determines long run rate of pro�t ?

Factors Increasing Pro�t Rate

Rate of growth of working classRate of growth of productivity of labour

Factors Reducing Pro�t Rate

The share of pro�t being accumulated

The more is accumulated the faster the rise in c

v→ the more

pro�t rate falls

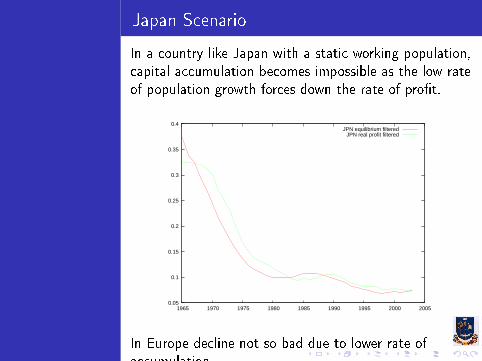

Japan Scenario

In a country like Japan with a static working population,capital accumulation becomes impossible as the low rateof population growth forces down the rate of pro�t.

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

1965 1970 1975 1980 1985 1990 1995 2000 2005

JPN equilibrium filteredJPN real profit filtered

In Europe decline not so bad due to lower rate ofaccumulation.

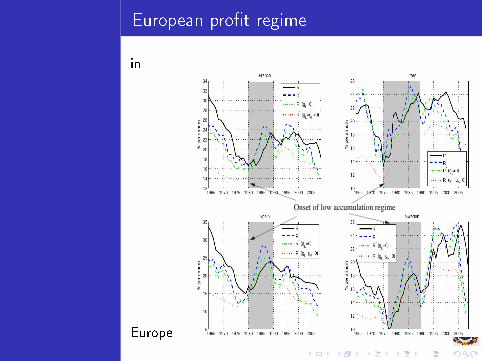

European pro�t regime

in

Europe

Onset of low accumulation regime

Consequence of low pro�ts

If �rms attempt to accumulate under thesecircumstances the law of the falling rate of pro�t cuts in

drives down the rate of pro�t until a large part of capital isearning less than the rate of interest.

These �rms then stop investing and try lending theirpro�ts out via the banking system.

There are not enough pro�table �rms wanting to borrow

the banks seek other unproductive avenues for the deposits:

lending to the state,

lending to consumers,

and speculation in asset markets.

Stagnation

Thus the typical pattern in a developed capitalistcountry is

banking system channels funds from productivecompanies and rentier class to

state,working class consumers via consumer credit,and as vast bonuses paid to the bankers themselves.

In the City of London alone there are more than 3000bankers who are paid more than ¿1Million a year.

Since, in Europe and Japan, capitalism is a historicallyobsolete system and can no longer accumulate ( due todemographic reasons ) the �nancial system turns into avast parasitic excressence consuming the surplus productunproductively or channeling it into unproductive uses.

Outline

Quick summaryWhat determines rate of pro�t

TheoryConservation laws

Phase space

Empirical data

Stability pactConclusion on the Stability Pact

Laws of motion

Marx, we suggest, wanted to establish a theory of thecapitalist economy informed by the laws of physics.This comes across in several ways:

his avowed aim to write a book on the `laws of motion'of capitalism; Newtonian

his distinction between the concept of labour and labourpower; Watt

his presentation of value as the crystalisation of humanenergy; von Mayer, Joule

and his analysis of commodity exchange as anequivalence relation.

Engels to Marx 14 July 1858

Another result that would have delighted old Hegel is thecorrelation of forces in physics, or the law wherebymechanical motion, i.e. mechanical force (e.g. throughfriction), is, in given conditions, converted into heat,heat into light, light into chemical a�nity, chemicala�nity (e.g. in the voltaic pile) into electricity, the latterinto magnetism. These transitions may also take placedi�erently, backwards or forwards. An Englishman[Joule] whose name I can't recall has now shown thatthese forces pass from one to the other in quite speci�cquantitative proportions...

Outline

Quick summaryWhat determines rate of pro�t

TheoryConservation lawsPhase space

Empirical data

Stability pactConclusion on the Stability Pact

Phase space

A basic tool of statistical mechanics is the concept ofphase space.Consider a collection of particles in a closed volume.Each particle can be described by 6 numbers:

3 numbers to specify the position and

3 numbers to specify its momentum.

We say that each particle has 6 degrees of freedom.

If you have N particles you have 6N degrees of freedomor dimensions

Why is this relevant to economy?

Again dealing with a system with very large numbers ofagents.

We have analogues of position and momentum.

The total debt/credit position of an agent is analogous toits mass,and the rate of change of its debt/credit position isanalogous to its momentum.

Thus if two billion people in the world are enmeshed indebt/credit relations then the whole system is a phasespace of 2 billion dimensions/degrees of freedom.

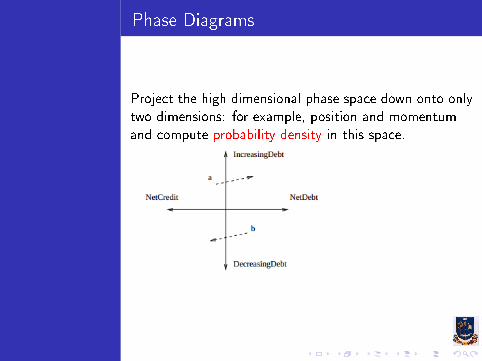

Phase Diagrams

Project the high dimensional phase space down onto onlytwo dimensions: for example, position and momentumand compute probability density in this space.

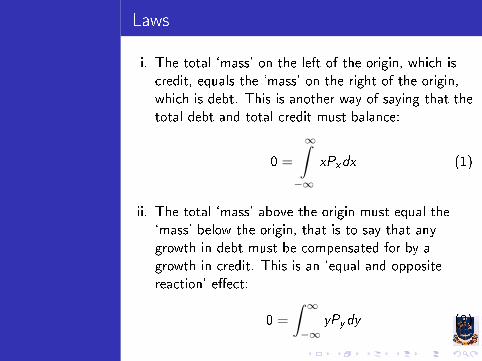

Laws

i. The total `mass' on the left of the origin, which iscredit, equals the `mass' on the right of the origin,which is debt. This is another way of saying that thetotal debt and total credit must balance:

0 =

∞∫−∞

xPxdx (1)

ii. The total `mass' above the origin must equal the`mass' below the origin, that is to say that anygrowth in debt must be compensated for by agrowth in credit. This is an `equal and oppositereaction' e�ect:

0 =

∫ ∞−∞

yPydy (2)

NB

These very basic points establish that there is no netvalue or net wealth embodied in the �nancial system andthat there is no �ow of value into or out of the �nancialsystem. It shows the fallacy of the conception, popularamong some political economists that capital has `movedinto �nance' because of the low rate of pro�t pertainingin industry.

Information is not value

This idea of capital moving into �nance a fundamentalmisconception, capital is value, and it can not �ow intothe �nancial system, since the sum of value here isalways zero. A moment's thought about the materialityof value con�rms this. Real-economic value � what theclassical economists understood to be the labour contentof physical goods and services � can not be convertedinto �nancial instruments which are just informationstructures.

Growth of entropy

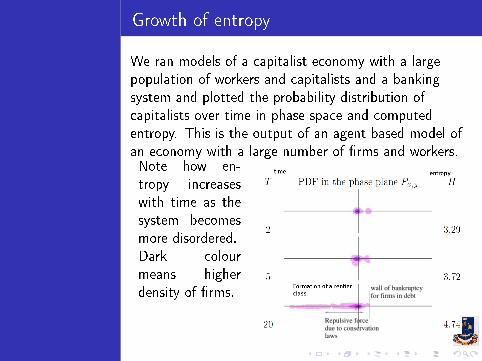

We ran models of a capitalist economy with a largepopulation of workers and capitalists and a bankingsystem and plotted the probability distribution ofcapitalists over time in phase space and computedentropy. This is the output of an agent based model ofan economy with a large number of �rms and workers.Note how en-tropy increaseswith time as thesystem becomesmore disordered.Dark colourmeans higherdensity of �rms.

Repulsive forcedue to conservationlaws

wall of bankruptcyfor firms in debt

Explanation

Since the rentier �rms try to accumulate credits with thebanks somebody has to borrow these.

If insu�cient �rms voluntarilly borrow from the banks,conservation laws force �rms to go into debtinvoluntarily due to making losses.

Unless some other source absorbs the funds available forlending the sytem tends to collapse at this point.

There are 3 possible absorbers of the rentier funds:

1 Working class consumption on credit2 State borrowing3 Borrowing by other countries.

The breakdown occured when loans to working classfailed in the sub-prime mortgage crisis.

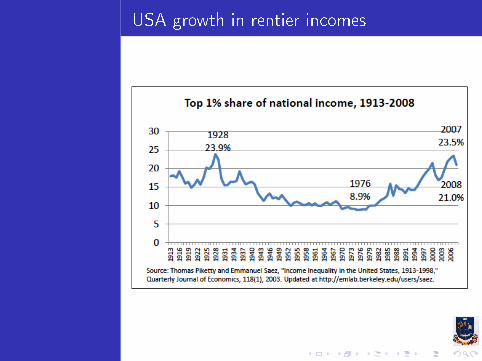

USA growth in rentier incomes

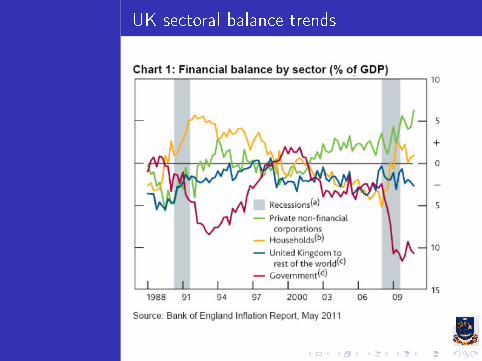

UK sectoral balance trends

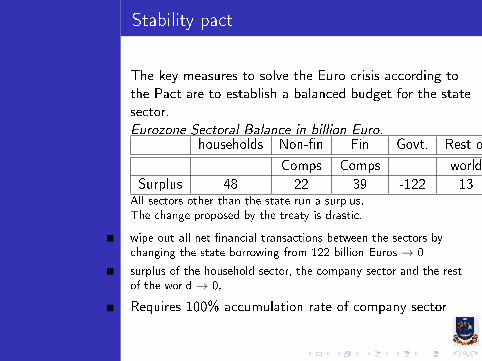

Stability pact

The key measures to solve the Euro crisis according tothe Pact are to establish a balanced budget for the statesector.Eurozone Sectoral Balance in billion Euro.

households Non-�n Fin Govt. Rest of

Comps Comps worldSurplus 48 22 39 -122 13

All sectors other than the state run a surplus,

The change proposed by the treaty is drastic.

wipe out all net �nancial transactions between the sectors by

changing the state borrowing from 122 billion Euros → 0

surplus of the household sector, the company sector and the rest

of the world → 0,

Requires 100% accumulation rate of company sector

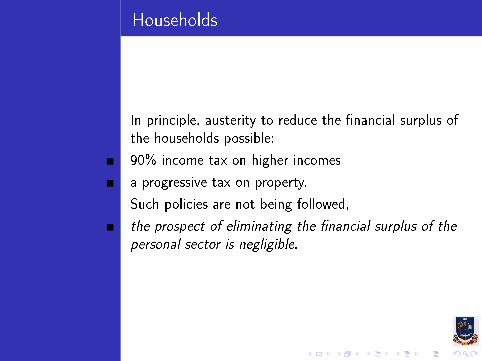

Households

In principle, austerity to reduce the �nancial surplus ofthe households possible:

90% income tax on higher incomes

a progressive tax on property.

Such policies are not being followed,

the prospect of eliminating the �nancial surplus of thepersonal sector is negligible.

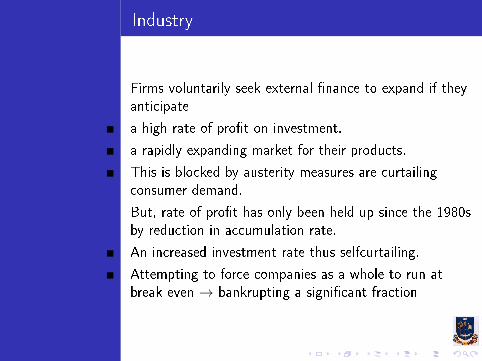

Industry

Firms voluntarily seek external �nance to expand if theyanticipate

a high rate of pro�t on investment,

a rapidly expanding market for their products.

This is blocked by austerity measures are curtailingconsumer demand.

But, rate of pro�t has only been held up since the 1980sby reduction in accumulation rate.

An increased investment rate thus selfcurtailing.

Attempting to force companies as a whole to run atbreak even → bankrupting a signi�cant fraction

Banks

Banks in the Euro-zone are running a surplus of some160 billion Euros

a thus responsible for 13 of the total de�cit of the state

sector.

There is almost nothing that the individual Euro zonegovernments can do to eliminate this.

Whole thrust of economic policy has been to protect theinterests ofbanks.

States could levy heavy taxes on �nancial �rms,

But

Countries in the Euro-zone in the worst �nancial positionhave least pro�table banks.

Rest of world

One e�ective tool that national governments havetraditionally been able to exercise to overcome tradede�cits is now out of reach for the Eurozone.

They can no longer devalue to bring their trade backinto balance.

The ECB again could force a devaluation if itsystematically buys up large quantities of dollarsecurities.

But the national governments can not instruct it to doso.

Outline

Quick summaryWhat determines rate of pro�t

TheoryConservation lawsPhase space

Empirical data

Stability pactConclusion on the Stability Pact

Conclusion

The structure set up under monetary union e�ectivelymakes it impossible for national governments to meetthe obligations that they have undertaken in the pact.Any serious attempt to impose balanced budgets byausterity measures will be ine�ective in its professed aim,and would as a side e�ect engender a downward spiral ofbankruptcies, rising unemployment and deepeningeconomic ruin.Only radical change in production and property relationscan restore European prosperity.