final final

TRANSCRIPT

1Customer needs and wants from Mobile Banking and the level of

Chapter-1

Introducti

on

Aid-De-Camp

2Customer needs and wants from Mobile Banking and the level of

urrently we are living in the age of competition at

anything in any places. From that tendency recently

Education is also in the age of competition. So the

procedures and standards of teaching are upgraded by

different universities and institutions in our country. In

respect to that, assignment is mandatory for our MBA

program assignned by our course teacher . To do so wehave

completed our assignment on Customer needs and wants from

Mobile Banking and the level of customer satisfaction.

C

Now a day the world is denoted as Global village. The whole

world is considered as a potential market as a every single

product and service. The economical prospective of a

country largely depends on the international trade. With

that view of the volume of international business increase

Aid-De-Camp

1.1 Introduction of the Report

1.2 Objectives of Study

3Customer needs and wants from Mobile Banking and the level of

day by day. The banking sector of the operations is

considered as a key factor of the economy of a country’s

economic development. As a student of MBA another objective

is to get sound knowledge about mobile Banking

To fulfill academic requirement.

To inspect the mobile Banking services by Dutch-Bangla

Bank.

To know the customer needs and wants from mobile banking

To asses the level of customer satisfaction from mobile

banking

To recommend ways and means to solve problems regarding

mobile Banking.

The Report mainly focuses on the following areas:

Mobile Banking and Internet Banking .

What kinds of standard documents are required for account

opening like Mobile account.

1.4.1 To make the Report more meaningful and presentable,

two sources of data and information have been used widely.

Aid-De-Camp

1.3 Scope of the Report

1.4 Methodology

4Customer needs and wants from Mobile Banking and the level of

Both primary and secondary data sources were used to

generate the report.

1.4.2 Primary:

Primary data are root level data and are collected without

correction. These data were collected by

1) Face to face conversation with customer

1.4.3 Secondary:

Annual reports and Mobile Banking of Dutch-Bangla Bank

Limited, Instruction circular of Head Office, Brochures of

different Banks, News Paper & Magazine regarding Mobile

Banking issues, Seminar papers and so on.

Aid-De-Camp

5Customer needs and wants from Mobile Banking and the level of

Investigated the customers' perspectives of mobile banking,

their perceived importance for it, usage patterns and

problems rising on its utilization. The paper discussed the

strategic implications of the research findings. Empirical

data were gathered from bank customers in Kuwait to achieve

the research objectives. All bank customers in Kuwait were

considered as population of research interest. The results

showed the perceived importance of internet banking

services by customers, current and potential use of MB

services in Kuwait and problems perceived by bank customers

in using MB. The researchers' main hypothesis tested that

top five services considered relative important in Kuwait

banks were "Review account balance", "Obtain detailed

transactions histories, "Open accounts", Pay bills" and

Transfer funds between own accounts".

Analyzed the factors affecting the adoption of Mobile

banking by Australian consumers. His sample was from

individual residents and business firms in Australia. The

study focused on the capital cities where use of mobile

internet and population was likely to be high. White and

yellow pages were used as the frame of reference for

Aid-De-Camp

1.5 Literature Review

6Customer needs and wants from Mobile Banking and the level of

personal and business customers, respectively. The findings

suggest that security concerns and lack of awareness about

mobile banking and its benefits stand out as being the

obstacles to the adoption of mobile banking in Australia.

He also suggests some of the ways to address these

impediments. Further, he suggests that delivery of

financial services over the Internet should be a part of

overall customer service and distribution strategy. These

measures could help in rapid migration of customers to

mobile Internet banking, resulting inconsiderable savings

in operating costs for banks. El- Sherbini et al. (2007)

Investigated why corporate customers do not accept mobile

banking, which can assist banks to implement this self-

service technology more efficiently. Many Thai banks are

currently implementing mobile banking. Banks that offer

service via this channel claim that it reduces costs and

makes them more competitive. However, many corporate

customers are not highly enthusiastic about mobile banking.

They used in-depth qualitative interviews methodology for

collecting their data. The interviews with Thai firms

suggested that security of the Internet is a major factor

inhibiting wider adoption. Those already using Internet

banking seem to have more confidence that the system is

reliable, whereas non-users are much more service

conscious, and do not trust financial transactions made via

Internet channels. Non-mobile banking users tend to have

Aid-De-Camp

7Customer needs and wants from Mobile Banking and the level of

more negative management attitudes toward adoption and are

more likely to claim lack of resources. Legal support is

also a major barrier to Internet banking adoption for

corporate customers. Rotchanakitumanuai and Speech (2003)

History of Mobile Banking in Bangladesh

“Dutch-Bangla Bank Limited” (DBBL) has for the first time

introduced its mobile banking service expanding the banking

service from cities to remote areas. Bangladesh Bank

Governor Atiur Rahman yesterday inaugurated the service by

depositing Tk 2,000 and withdrawing Tk 1,500 through

Banglalink and Citycell mobile networks in Motijheel area.

Bangladesh Bank has already allowed 10 banks to initiate

mobile banking. Of them DBBL kicked off first." Mobile

banking is an alternative to the traditional banking

through which banking service can be reached at the

doorsteps of the deprived section of the society,” the

central bank governor said at an inaugural press briefing

at Hotel Purbani. Atiur Rahman said through mobile banking

various banking services including depositing and

withdrawing money, payment of utility bills and reaching

remittance to the recipient would be possible. By going to

the DBBL-approved Citycell and Banglalink agents throughout

the country the subscribers on showing necessary papers and

payment of a fee of Tk 10 can open an account. To avail of

the banking service a subscriber will require owning a cell

phone of any provider and he will be given a four-digit

Aid-De-Camp

8Customer needs and wants from Mobile Banking and the level of

PIN. By using the PIN he can operate all types of banking

services including depositing and withdrawing money

maintaining security and secrecy of his account. The

customer will hand over cash to the agent and the agent

will initiate the transaction from his mobile phone, the

agent will help the account holder to do the banking using

his PIN. A customer can deposit or withdraw money five

times a day and he can deposit or draw Tk 5,000 per day.

One percent of the transaction account or Tk 5, whichever

is higher, will be taken as cash-in-charges. In case of

cash out the charge will be 2 percent of the transaction

amount or Tk 10. However, the registration fee, salary and

remittance disbursement services will be provided free of

cost.

Chief limitation of Internet banking is the requirement of

a PC with an Internet connection.The major limitations of

this study are:

Sufficient records, publications were not available as

per our requirement.

Time constraint

Lack of opportunity to work

Up to date data are not available.

Aid-De-Camp

1.6 Limitations of the Study

9Customer needs and wants from Mobile Banking and the level of

Customers are not free to interview long time.

Chapter-2

Mobile

Banking

”Mobile banking” is not simply another delivery channel butAid-De-Camp

10Customer needs and wants from Mobile Banking and the level of

represents a fundamental shift in the paradigm of consumer

banking.”

Aid-De-Camp

11Customer needs and wants from Mobile Banking and the level of

Internet Banking helps the customer's anytime access to

their banks. Customer's could check out their account

details, get their bank statements, perform transactions

like transferring money to other accounts and pay their

bills sitting in the comfort of their homes and offices.

However the biggest limitation of Internet banking is the

requirement of a PC with an Internet connection, not a big

obstacle if we look at the US and the European countries,

but definitely a big barrier if we consider most of the

developing countries of Asia like Bangladesh. Mobile

banking addresses this fundamental limitation of Internet

Banking, as it reduces the customer requirement to just a

mobile phone. Mobile usage has seen an explosive growth in

most of the Asian economies like Bangladesh. The main

reason that Mobile Banking scores over Internet Banking is

that it enables ‘Anywhere Anytime Banking'. Customers don't

Aid-De-Camp

2.1 Introduction to Mobile Banking

12Customer needs and wants from Mobile Banking and the level of

need access to a computer terminal to access their bank

accounts, now they can do so on-the-go while waiting for

the bus to work, traveling or when they are waiting for

their orders to come through in a restaurant. The scale at

which Mobile banking has the potential to grow can be

gauged by looking at the pace users are getting mobile in

Bangladesh.

The mobile subscriber base in Bangladesh hit 70 million in

2011. The explosion as most analysts say, is yet to come as

Bangladesh has about one of the biggest untapped markets.

We see that in Korea which is now witnessing the roll-out

of some of the most advanced services like using mobile

phones to pay bills in shops and restaurants.

Aid-De-Camp

13Customer needs and wants from Mobile Banking and the level of

Introduction of new technologies

Control costs

To increase online channel customers

Personalize customer interactions

A broad spectrum of Mobile/branchless banking models is

evolving. These models

differ primarily on the question that who will establish

the relationship (account

opening, deposit taking, lending etc.) With the end

customer, the Bank or the Non-

Bank/Telecommunication Company (Telco).

Mobile Banking is a Banking process without bank branch

which provides financial services to un-banked communities

efficiently and at affordable cost. To provide banking and

financial services, such as cash-in, cash out, merchant

Aid-De-Camp

2.2 Reason of Genesis of M-Banking

2.3 Mobile Banking A New Business Models

2.4 Mobile Banking

14Customer needs and wants from Mobile Banking and the level of

payment, utility payment, salary disbursement, foreign

remittance, government allowance disbursement, ATM

money withdrawal through mobile technology devices, i.e.

Mobile Phone, is called Mobile Banking.

Mobile banking (m-banking) involves the use of a mobile

phone or another mobile devices to undertake financial

transactions linked to a client’s account. M-banking is one

of the newest approaches to the provision of financial

services, made possible by the widespread adoption of

mobile phones even in low income people. The roll out of

mobile technology has been rapid, and has extended access

well beyond already connected customers in rural area.

There is mounting evidence of positive social impact on

poorer people and communities as a result.

There are sound reasons for the hope that M-banking could

have similar impact. A mobile network offers a high

technology platform onto which other services can be often

provided at very low cost to deliver an effective result.

Mobile data channels are often under-used and therefore may

be offered at low cost by the network operator. M-banking

services which use channels such as text messaging/ SMS can

be carried at a cost of less. The low cost of using

existing infrastructure makes such channels more amenable

to use by low income customers. M-banking is new in our

country, and there has been limited donor support in this

sector to date. This report considers the case for donors

to support m-banking as a sector. Bangladesh Bank permitted

Aid-De-Camp

15Customer needs and wants from Mobile Banking and the level of

commercial bank to do such kind of mobile banking business

that the rural people who have mobile but haven’t banking

facilities, Service holders can get there salary by the

mobile banking.

Overview of Mobile banking model

Introduction and success of m-banking depends on three key

determinants- policy & regulation, profitable/sustainable

business case for all actors and client uptake. Primarily,

policy and regulation sets the foundation stone of the m-

banking model According to CGAP there are two models of

mobile banking. Both the model use retail agents (e.g.

merchants, supermarkets or post offices) to deliver

financial services outside traditional bank branches but

these models of m- banking systems differ primarily on the

following questions –

⇒ Who will establish the relationship (account opening,

deposit taking, lending etc.) with the end customer? The

answer can be a Bank Nonbank/TelecommunicatioCompany

(Telco).

⇒ What is the nature of agency agreement between bank and

the Non-Bank.

Aid-De-Camp

16Customer needs and wants from Mobile Banking and the level of

i. Bank-based model - Every customer has a direct

contractual relationship with a licensed and supervised

financial institution (whether account-based or involving a

one-off transaction) even though

the customer may deal exclusively with a retail agent who

is equipped to communicate directly with the bank

(typically using either a mobile phone or a point-of-sale

(POS) terminal)

ii. Nonbank-based model- Customers have no direct

contractual relationship with a licensed and

supervised financial institution. Instead, the customer

exchanges cash at a retail agent (or otherwise transfers,

or arranges for the transfer of funds) in return for an

electronic record of value.

Aid-De-Camp

2.5 Objective of Mobile Banking

17Customer needs and wants from Mobile Banking and the level of

Approximately 87% of the total population of Bangladesh is

un-banked. To bring such a huge population into the banking

channel, DBBL is implementing a system to launch mobile

banking soon. The project is in its final stage now. With

this facility any person having a mobile number will be

able to use his number as a bank account. In this mobile

account they will be able to do the following:

● Cash deposit to any Agent of DBBL

● Cash withdrawal from any Agent of DBBL

● Cash withdrawal from DBBL ATMs

● Funds transfer to another mobile account

● Utility bill payment, Tuition fee payment, Air time

top-up.

● Receive remittance from home and abroad

● Salary disbursement

● Disbursement of Govt. allowances

● Merchant Payment

● Balance Inquiry

By providing electronic access to money, it is possible to

ultimately alleviate poverty, because of the following

reasons.

Real time on-line banking

Available anytime, anywhere throughout the country

Aid-De-Camp

2.6 Benefits of Mobile Banking

18Customer needs and wants from Mobile Banking and the level of

It’s convenient, affordable and secured

It is much more effective in developing savings

habits

It will make access to banking and advanced payment

transactions at affordable cost

It is much safer, speedy and safeguard against

fraudulent transaction.

While poor people have little money, they are active

managers of what they have. Holding cash comes at high

price to poor people because of the risk of crime in many

poor People, but they often have few alternatives to cash

based services.

Aid-De-Camp

2.7 Some other purpose of Mobile Banking

19Customer needs and wants from Mobile Banking and the level of

In particular, appropriate financial services help poor

people to access usefully large lump sums of money, which

may either enable a pathway out of poverty through

investment in income generating activities (such as micro

enterprises) or asset creation (such as housing); or may

reduce vulnerability to sudden shocks to cash flow, as a

result for example of illness or climate conditions.

In our country, poor people are forced to rely on informal

financial services, which may be unsafe, or fringe formal

financial products which may be expensive as well as

unsafe. In other words, their exclusion from formal

financial services has economic and social impacts which

may exacerbate their poverty.

The cost efficient provision of formal financial services

(payments/ remittances, savings, credit or insurance) is

predicated on customers having access at least to a basic

transactional account, from which electronic transfers can

be made as like purchase product and pay one another by M-

banking and cash withdrawn as necessary.

M-banking holds the prospect of offering a low cost,

accessible transaction banking platform for currently

unbaked and poorer customers. In addition, as mobile

networks expand their coverage, they offer the opportunity

Aid-De-Camp

20Customer needs and wants from Mobile Banking and the level of

of bringing payment and remittance services into that areas

where banking services is unable able.

However, not all m-banking products will be

transformational in the sense of broadening access to

financial services substantially at first or even at all.

However, it is likely that even m-banking services which

start targeted at existing banked customers may over time

extend to un-banked groups.

In low income people, m-banking may enable to use such

kind of Banking where Banking facilities can’t reach

till now the cost and safety of using m-banking is

comparatively low.

M-banking potentially brings new Customer where

banking sector is running as like as dog for there

product marketing; these may be stronger than retail

banks and better placed to reach out to un-banked

customers.

Aid-De-Camp

2.8 Why Mobile Banking is Necessary

21Customer needs and wants from Mobile Banking and the level of

M-banking is still very new, whereas other forms of e-

banking are quite well established; the potential to

influence and adapted to the customer may be higher

compare to former banking because a lot of people use

mobile phone in our country

\

Rapid expansion of Mobile Phone

Nation wide coverage

Enhanced Mobile Phone Services

Failing cost of Technology

Increasing competition in Commercial Banking

Ability to offer low cost banking services

Affordable and secure

High level of Mobile phone literacy among client

Aid-De-Camp

2.9 Why DBBL chose Mobile Banking

22Customer needs and wants from Mobile Banking and the level of

Existing of Mobile payment platform which is save

and secure & recognized by Bangladesh Bank

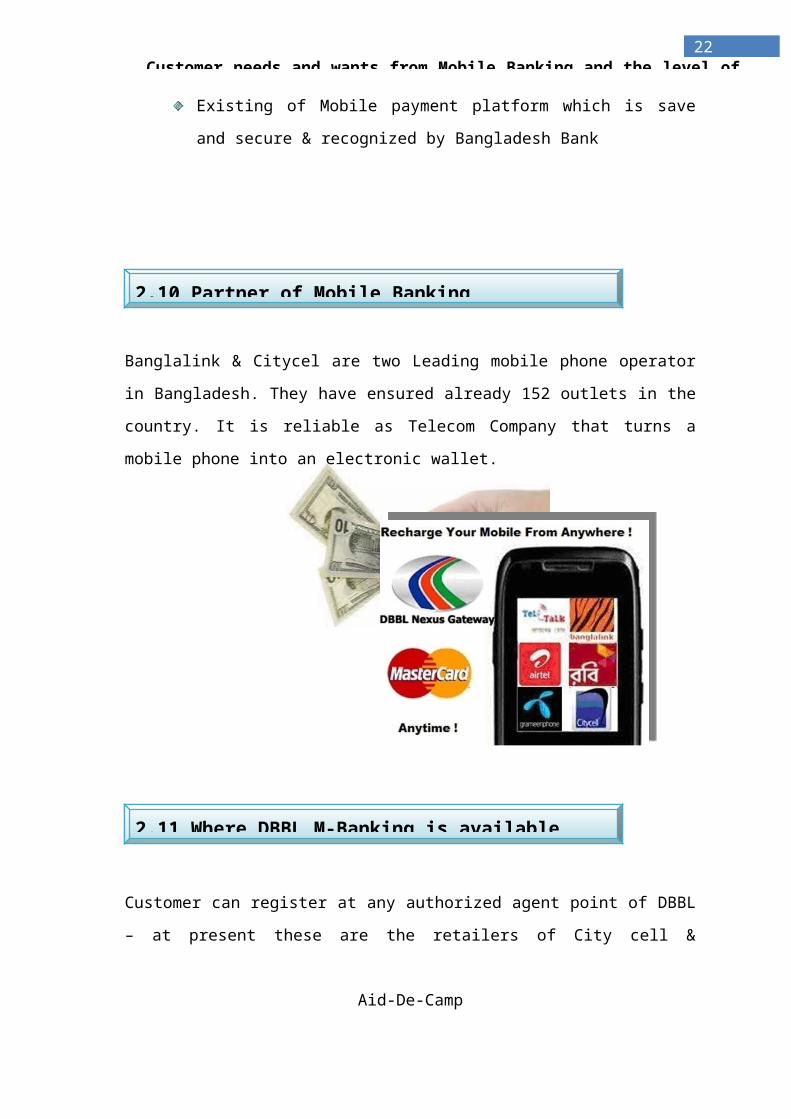

Banglalink & Citycel are two Leading mobile phone operator

in Bangladesh. They have ensured already 152 outlets in the

country. It is reliable as Telecom Company that turns a

mobile phone into an electronic wallet.

Customer can register at any authorized agent point of DBBL

– at present these are the retailers of City cell &

Aid-De-Camp

2.10 Partner of Mobile Banking

2.11 Where DBBL M-Banking is available

23Customer needs and wants from Mobile Banking and the level of

Banglalink throughout the country who can display ‘DBBL

Agent Certificate’ and

‘DBBL Mobile Banking Banner’. Banking is there. Around 152

Banglalink and Citycel agent around the country and all

the DBBL branch is the Mobile Banking place. A Mobile

account holder can deposit money from DBBL permitted

Banglalink and City cell agent and any branch of DBBL,

They also can withdraw money from DBBL Banglalink and City

cell agent and Branch. They also cash out from ATM.

The biggest advantage that mobile banking offers to banks

is that it drastically cuts down the costs of providing

service to the customers.

You can make transactions or pay bills anytime. It

saves a lot of time.

Mobile banking thorough cell phone is user friendly.

The interface is also very simple. You just need to

follow the instructions to make the transaction. It

also saves the record of any transactions made.

Cell phone banking is cost effective. DBBL provide

this facility at a lower cost as compared to banking

by self.

Aid-De-Camp

2.12 Advantages of Mobile Banking

24Customer needs and wants from Mobile Banking and the level of

Banking through mobile reduces the risk of fraud.

You will get an SMS whenever there is an activity in

your account. This includes deposits, cash

withdrawals, funds transfer etc. You will get a notice

as soon as any amount is deducted or deposited in your

account.

Banking through cell phone benefits the banks too. It

cuts down on the cost of tele- banking and is more

economical.

Mobile banking through cell phone is very advantageous

to the banks as it serves as a guide in order to help

the banks improve their customer care services.

Banks can be in touch with their clients with mobile

banking.

Banks can also promote and sell their products and

services like credit cards, loans etc. to a specific

group of customers.

Various banking services like Account Balance

Enquiry , Credit/Debit Alerts, Bill Payment Alerts,

Transaction History, Fund Transfer Facilities, Minimum

Balance Alerts etc. can be accessed from your mobile.

You can transfer money instantly to another account in

the same bank using mobile banking.

Mobile banking has an edge over internet banking. In

case of online banking, you must have an internet

connection and a computer. This is a problem in

developing countries. However, with mobile banking,

Aid-De-Camp

25Customer needs and wants from Mobile Banking and the level of

connectivity is not a problem. You can find mobile

connectivity in the remotest of places also where

having an internet connection is a problem.

Uncertainties over the speed and nature of customer adoption This is

to be expected with any new offering, although the

uncertainty is compounded by the relative lack of knowledge

of the needs of un-banked people in many places, and the

market potential. Consumer education may speed adoption;

but more likely, adoption on scale will happen as it has

happened with mobile phones: by forced to adapt their

offerings as they encounter feedback in the market place.

Therefore, it is necessary to have sufficient providers in

the market who can remain in the market long enough to

ensure that to identify the elements of a successful model.

Hence, support to providers may assist in overcoming this

barrier. Generally available research into the patterns and

needs of the un-banked target market may also help.

Lack of interoperability with existing systems Interoperability of

different payment systems is primarily a question of market

structure and regulation. It arises initially only in

markets where there is an existing payment infrastructure

with which new providers can inter-operate (and later on,

Aid-De-Camp

2.13 Limitations of Mobile Banking

26Customer needs and wants from Mobile Banking and the level of

once new infrastructure becomes the standard). Without

inter-operability, the fixed costs of deploying financial

infrastructure may be much harder to recover, since usage

per item of proprietary infrastructure will fall. Clearly,

one solution may be to give regulators the power to require

interoperability; however, it may be sufficient to

encourage the identification of appropriate standard

upfront. This could take place via support to regulators or

industry bodies, where these exist .

Regulatory barrier Specific regulatory impediments vary by

market; but in general, a lack of openness to new models of

provision and a lack of policy certainty limit the

potential of new models. Increasing openness and certainty

may require support to regulators to outline high level

policy, as well as to amend existing regulations or draft

new ones where and when required.

The case for donor support therefore rests on removing

barriers such as these, thereby making it more likely that

transformational models of M-banking will emerge at all, or

at least, sooner; and that they will develop more rapidly

than otherwise would be the case.

Aid-De-Camp

27Customer needs and wants from Mobile Banking and the level of

Reaching deeper into rural areas without costly

investment in infrastructure

Reducing the costs of servicing

Interoperability

Security risks from robbery & holdup

Scalability & reliability

Personalization

Customer education

Reduce

cost

of

clients

High transecting cost

Lac of cash out late

Cost of cash in and out is high compare to interest

rate on bank deposit

Marketing to convince more people

Merchants and Shops to accept M-cash in payment for

goods and services.

Overcome initial security of customer money.

Aid-De-Camp

2.14 Challenges before Mobile Banking

28Customer needs and wants from Mobile Banking and the level of

Interoperability:

There is a lack of common technology standards for mobile

banking. Many protocols are being used for mobile banking.

It would be a wise idea for the vendor to develop a mobile

banking application that can connect multiple banks. It

would require either the application to support multiple

protocols or use of a common and widely acceptable set of

protocols for data exchange. There are a large number of

different mobile phone devices and it is a big challenge

for banks to offer mobile banking solution on any type of

device.

Security

Security of financial transaction, being executed from some

remote location and transmission of financial information

over the air, are the most complicated challenges that need

to be addressed jointly by mobile application developers,

wireless network service providers and the bank's IT

department. The following aspects need to be addressed to

offer a secure infrastructure for financial transaction

over wireless network:

* Physical security of the handheld device. If the bank

offers smart-card based security, the physical security of

the device is more important.

Aid-De-Camp

29Customer needs and wants from Mobile Banking and the level of

* Security of the thick-client application running on the

device. In case the device is stolen, the hacker should

require ID/Password to access the application.

* Authentication of the device with service provider before

initiating a transaction. This would ensure that

unauthorized devices are not connected to perform financial

transactions.

* User ID / Password authentication of bank's customer.

* Encryption of the data being transmitted over the air.

* Encryption of the data that will be stored in device for

later / off-line analysis by the customer.

Scalability & Reliability

Another challenge for the banks is to scale-up the mobile

infrastructure to handle exponential growth of the customer

base. With mobile banking, the customer may banking be

sitting in banking more and more useful, their expectations

from the solution will increase. Banks unable to meet the

performance and reliability expectations may lose customer

confidence any part of the world (a true anytime, anywhere

banking). As customers will find mobile.Aid-De-Camp

30Customer needs and wants from Mobile Banking and the level of

Application Distribution

Due to the nature of the connectivity between bank and its

customers, it would be impractical to expect customers to

regularly visit banks or connect to a web site for regular

upgrade of their mobile banking application. It will be

expected that the mobile application itself check the

upgrades and updates and download necessary patches.

However, there could be many issues to implement this

approach such as upgrade / synchronization of other

dependent components.

Increasing faster transmission via GPRS 3G technology to be

lunched soon in Bangladesh is expected to bring in a mobile

revaluation.

Users are slowly getting used to the concept of mobile in

hand held device as digital cash or wallet to carry out

purchase.

Presently low value M-commerce transecting is happening.

Aid-De-Camp

2.15 Prospective

31Customer needs and wants from Mobile Banking and the level of

Chapter-3

Findings And

Analysis

Aid-De-Camp

32Customer needs and wants from Mobile Banking and the level of

3.0 Findings:

Dutch-Bangla Bank Limited (DBBL) has for the first time

introduced its mobile banking service, expanding the

banking service from cities to remote areas. [Bangladesh

Bank Governor Atiur Rahman inaugurated the service in July,

2011 by depositing Tk 2,000 and withdrawing Tk 1,500

through Banglalink and Citycell mobile networks in

Motijheel area. Bangladesh Bank has already allowed 10

banks to initiate mobile banking. Of them DBBL kicked off

first. "Mobile banking is an alternative to the traditional

banking through which banking service can be reached at the

doorsteps of the deprived section of the society,” the

central bank governor said at an inaugural press briefing

at Hotel Purbani. Atiur Rahman said through mobile banking

various banking services including depositing and

withdrawing money, payment of utility bills and reaching

remittance to the recipient would be possible. By going to

the DBBL-approved Citycell and Banglalink agents throughout

the country, the subscribers can open an account provided

they show the necessary papers and pay a fee of Tk 10. To

use the banking service, subscribers must own a cell phone

from any provider. The bank gives subscribers a four-digit

PIN. By using the PIN, subscribers can use a number of

banking services, including depositing and withdrawingAid-De-Camp

3. Findings and Analysis:

33Customer needs and wants from Mobile Banking and the level of

money, while maintaining account security. Customers may

hand over cash to agents in the bank's network, and agents

can coordinate the transaction from their mobile phones,

helping account holders securely complete banking tasks

using their PINs. Customers can deposit or withdraw money

up to five times per day, up to Tk 5,000 per day. One

percent of the transaction account or Tk 5, whichever is

greater, will be deducted as a cash-in charge. The charge

for cash-out is 2 percent of the transaction amount or Tk

10, whichever is greater. There are no fees for

registration, salary or remittance disbursement services.

In this assignment we can see some findings:

Mobile Banking drastically cuts down the costs of

providing service to the customers.

Service providers are increasingly using the

complexity of their supported mobile banking services

to attract new customers and retain old ones.

A very effective way of improving customer service

could be to inform customers better. Credit card fraud

is one such area.

The banks add to this personalized communication

through the process of automation. Mobile banking is

not available on every device.

Some banks do not provide Mobile Banking at all. The

cost of mobile banking might not appear significant if

we already have a compatible.

Aid-De-Camp

34Customer needs and wants from Mobile Banking and the level of

Reaching deeper into rural areas without costly

investment in infrastructure

Reducing the costs of servicing

Interoperability

Security risks from robbery & holdup

Scalability & reliability

Personalization

Customer education

Reduce cost of clients

High transecting cost

Lack of cash out late

Aid-De-Camp

35Customer needs and wants from Mobile Banking and the level of

Demographic information analysis of the

respondents

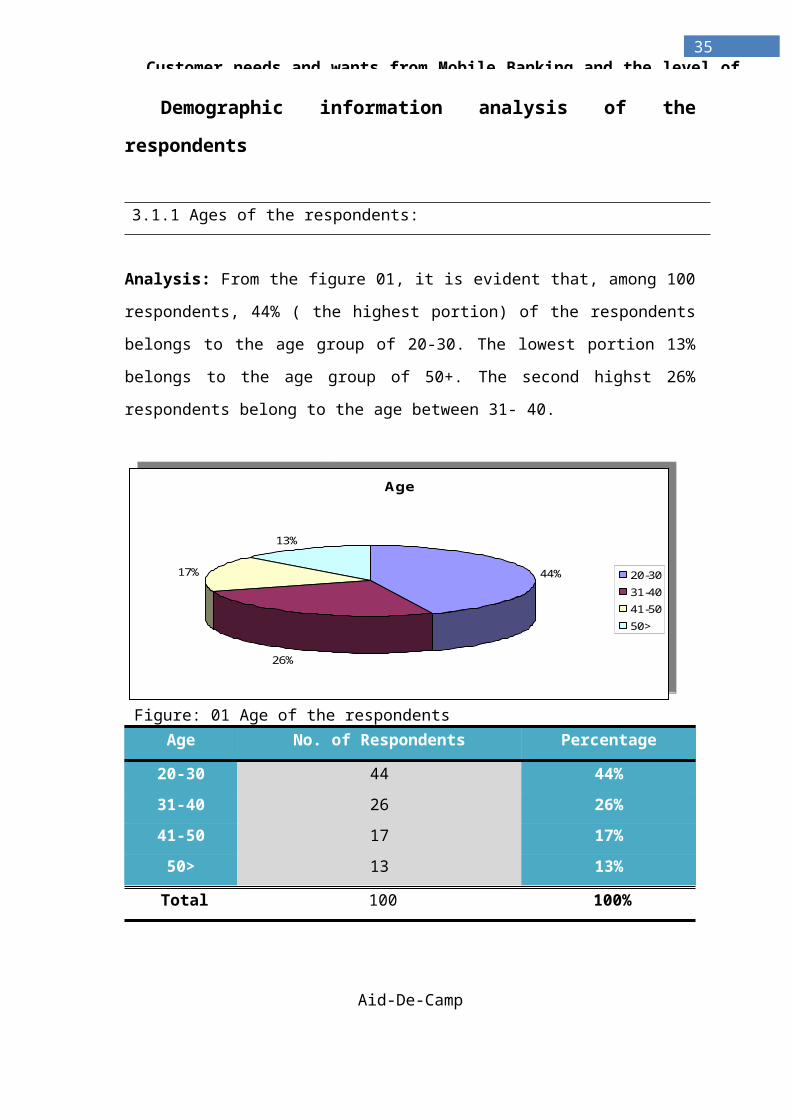

3.1.1 Ages of the respondents:

Analysis: From the figure 01, it is evident that, among 100

respondents, 44% ( the highest portion) of the respondents

belongs to the age group of 20-30. The lowest portion 13%

belongs to the age group of 50+. The second highst 26%

respondents belong to the age between 31- 40.

Figure: 01 Age of the respondents

Age No. of Respondents Percentage

20-30 44 44%31-40 26 26%41-50 17 17%50> 13 13%

Total 100 100%

Aid-De-Camp

Age

44%

26%

17%

13%

20-3031-4041-5050>

36Customer needs and wants from Mobile Banking and the level of

Table: 01 Age of the respondent

Aid-De-Camp

37Customer needs and wants from Mobile Banking and the level of

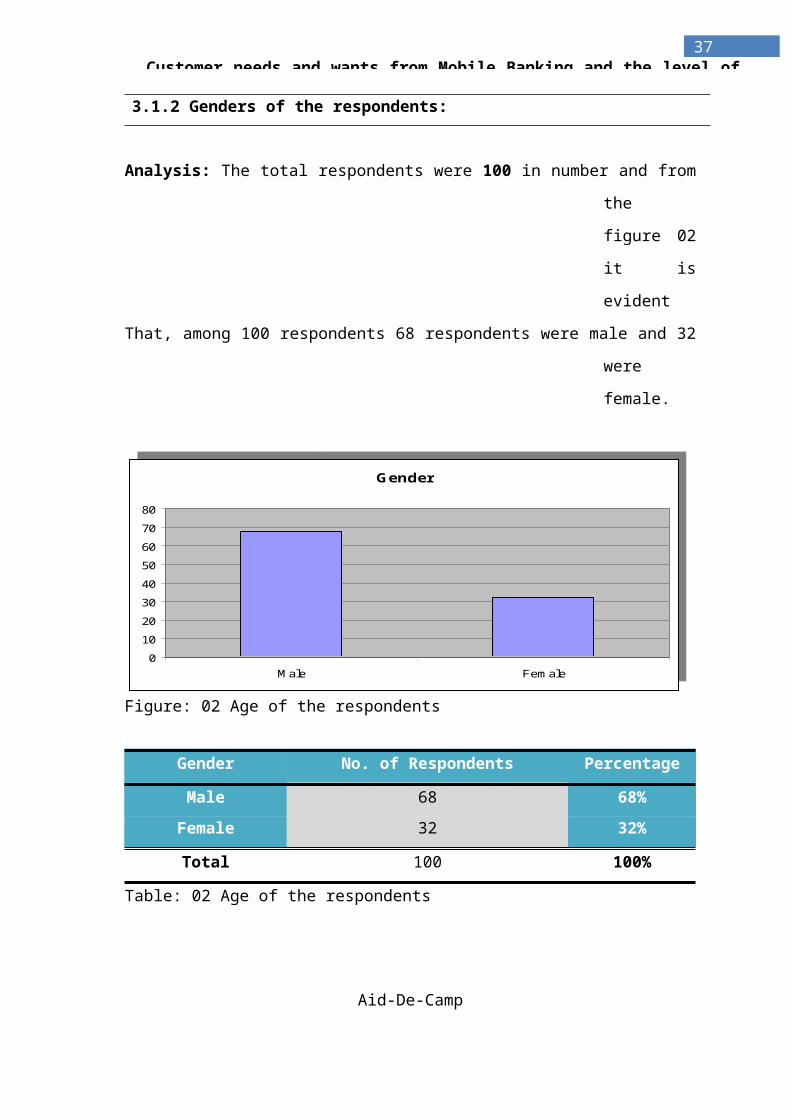

3.1.2 Genders of the respondents:

Analysis: The total respondents were 100 in number and from

the

figure 02

it is

evident

That, among 100 respondents 68 respondents were male and 32

were

female.

Figure: 02 Age of the respondents

Gender No. of Respondents Percentage

Male 68 68%Female 32 32%

Total 100 100%

Table: 02 Age of the respondents

Aid-De-Camp

Gender

01020304050607080

M ale Fem ale

38Customer needs and wants from Mobile Banking and the level of

Profession

0510152025303540

Student

Professionals

Business Man

Services Holder

Housewife

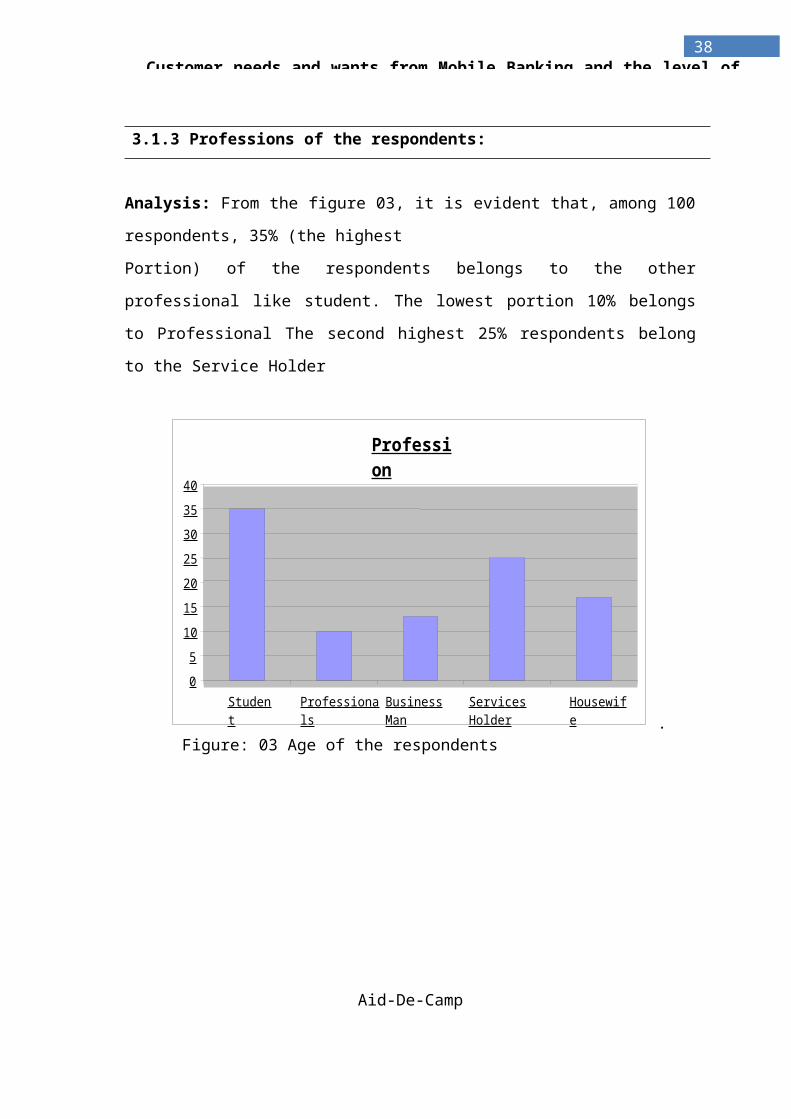

3.1.3 Professions of the respondents:

Analysis: From the figure 03, it is evident that, among 100

respondents, 35% (the highest

Portion) of the respondents belongs to the other

professional like student. The lowest portion 10% belongs

to Professional The second highest 25% respondents belong

to the Service Holder

. Figure: 03 Age of the respondents

Aid-De-Camp

39Customer needs and wants from Mobile Banking and the level of

Table: 03 Qualification of the res

Aid-De-Camp

Reason of join in

mobile banking

No. of Respondents Percentage

Required 53 53%Attractiveness 14 14%

Facilities 21 21%Availability 12 12%

Total 100 100%

40Customer needs and wants from Mobile Banking and the level of

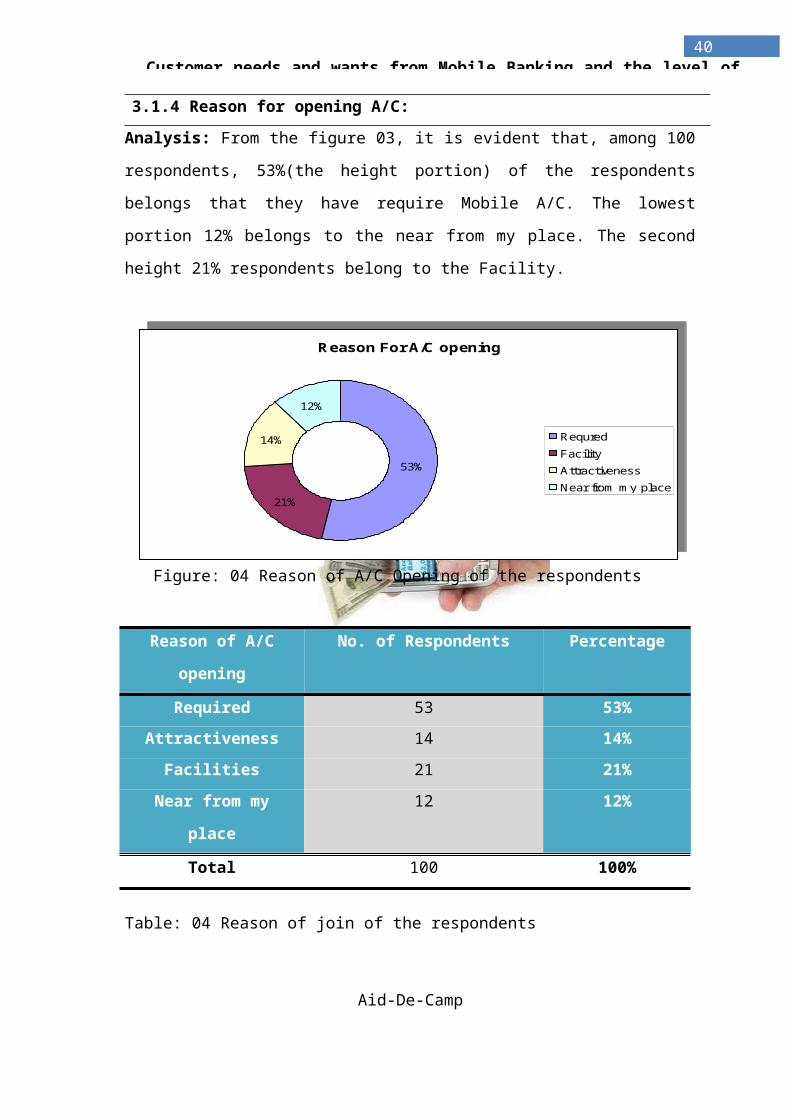

3.1.4 Reason for opening A/C:Analysis: From the figure 03, it is evident that, among 100

respondents, 53%(the height portion) of the respondents

belongs that they have require Mobile A/C. The lowest

portion 12% belongs to the near from my place. The second

height 21% respondents belong to the Facility.

Figure: 04 Reason of A/C Opening of the respondents

Table: 04 Reason of join of the respondents

Aid-De-Camp

Reason For A/C opening

53%

21%

14%

12%

RequredFacilityAttractivenessNear from m y place

Reason of A/C

opening

No. of Respondents Percentage

Required 53 53%Attractiveness 14 14%

Facilities 21 21%Near from my

place

12 12%

Total 100 100%

41Customer needs and wants from Mobile Banking and the level of

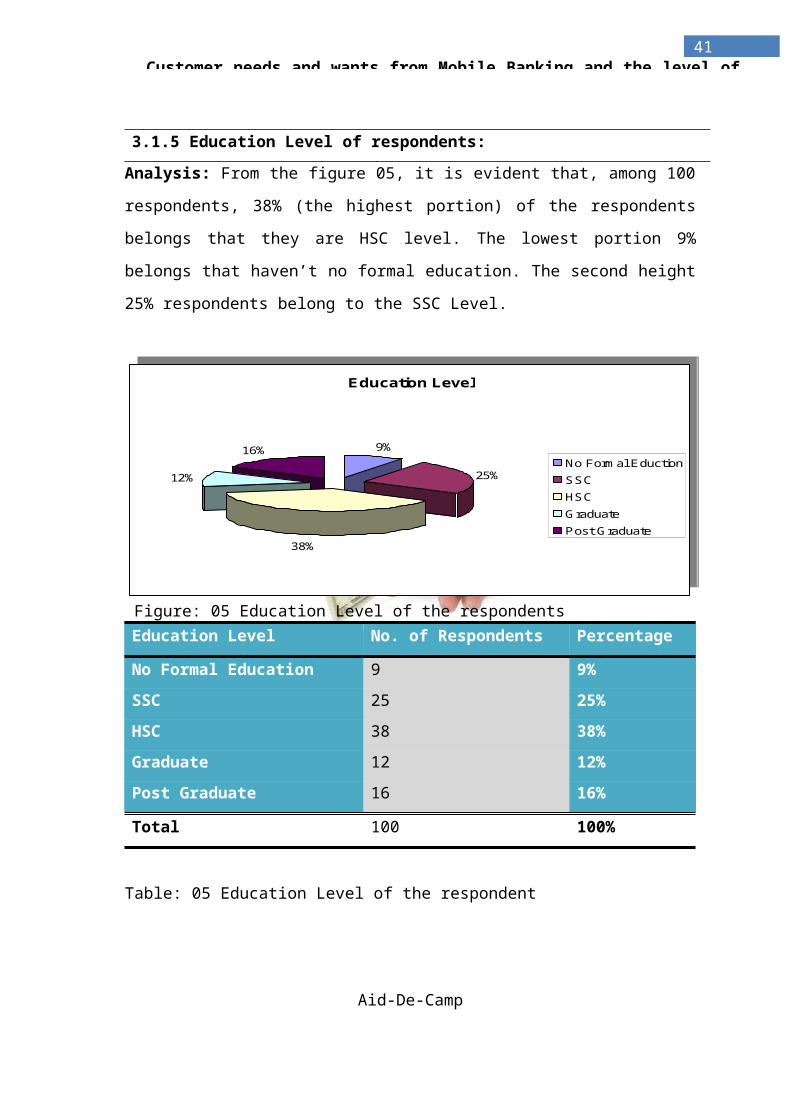

3.1.5 Education Level of respondents:Analysis: From the figure 05, it is evident that, among 100

respondents, 38% (the highest portion) of the respondents

belongs that they are HSC level. The lowest portion 9%

belongs that haven’t no formal education. The second height

25% respondents belong to the SSC Level.

Figure: 05 Education Level of the respondentsEducation Level No. of Respondents Percentage

No Formal Education 9 9%SSC 25 25%HSC 38 38%Graduate 12 12%Post Graduate 16 16%

Total 100 100%

Table: 05 Education Level of the respondent

Aid-De-Camp

Education Level

9%

25%

38%

12%

16%No Form al EductionSSCHSCG raduatePost G raduate

42Customer needs and wants from Mobile Banking and the level of

3.1.6 Responses analysis from the survey questionnaire:

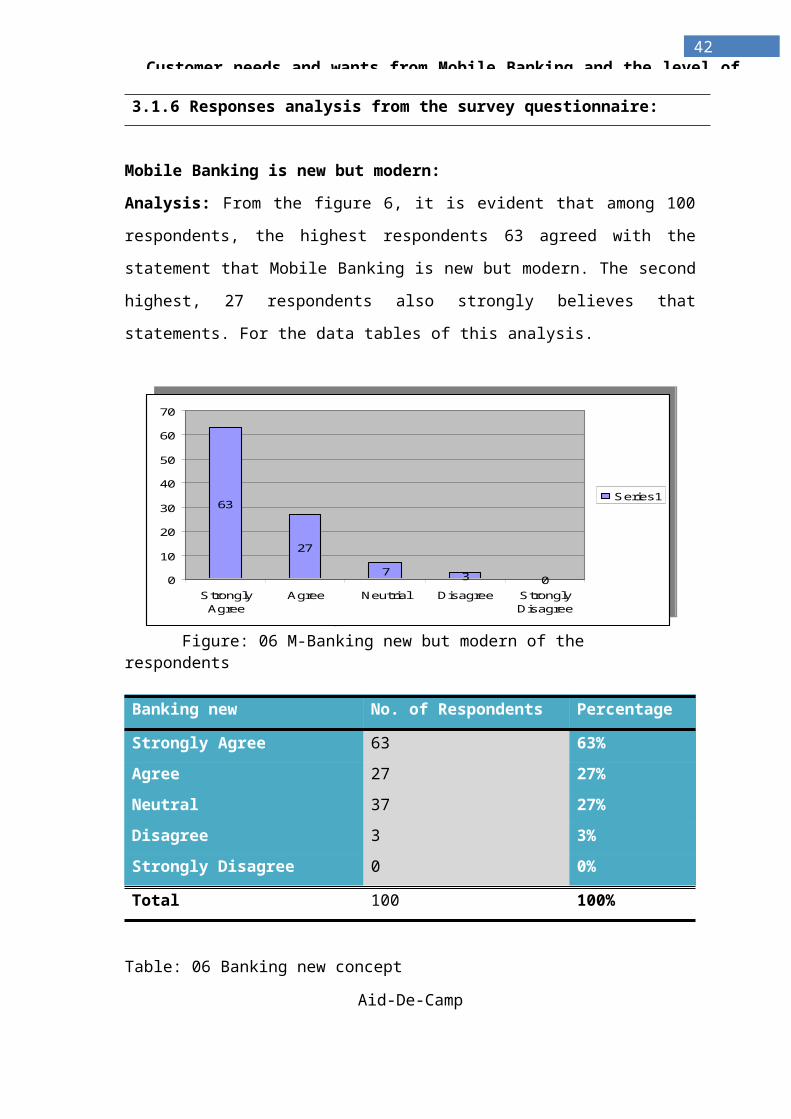

Mobile Banking is new but modern:

Analysis: From the figure 6, it is evident that among 100

respondents, the highest respondents 63 agreed with the

statement that Mobile Banking is new but modern. The second

highest, 27 respondents also strongly believes that

statements. For the data tables of this analysis.

Figure: 06 M-Banking new but modern of the respondents Banking new No. of Respondents Percentage

Strongly Agree 63 63%Agree 27 27%Neutral 37 27%Disagree 3 3%Strongly Disagree 0 0%

Total 100 100%

Table: 06 Banking new concept

Aid-De-Camp

63

27

7 3 00

10

20

30

40

50

60

70

StronglyAgree

Agree Neutrial Disagree StronglyDisagree

Series1

43Customer needs and wants from Mobile Banking and the level of

Aid-De-Camp

44Customer needs and wants from Mobile Banking and the level of

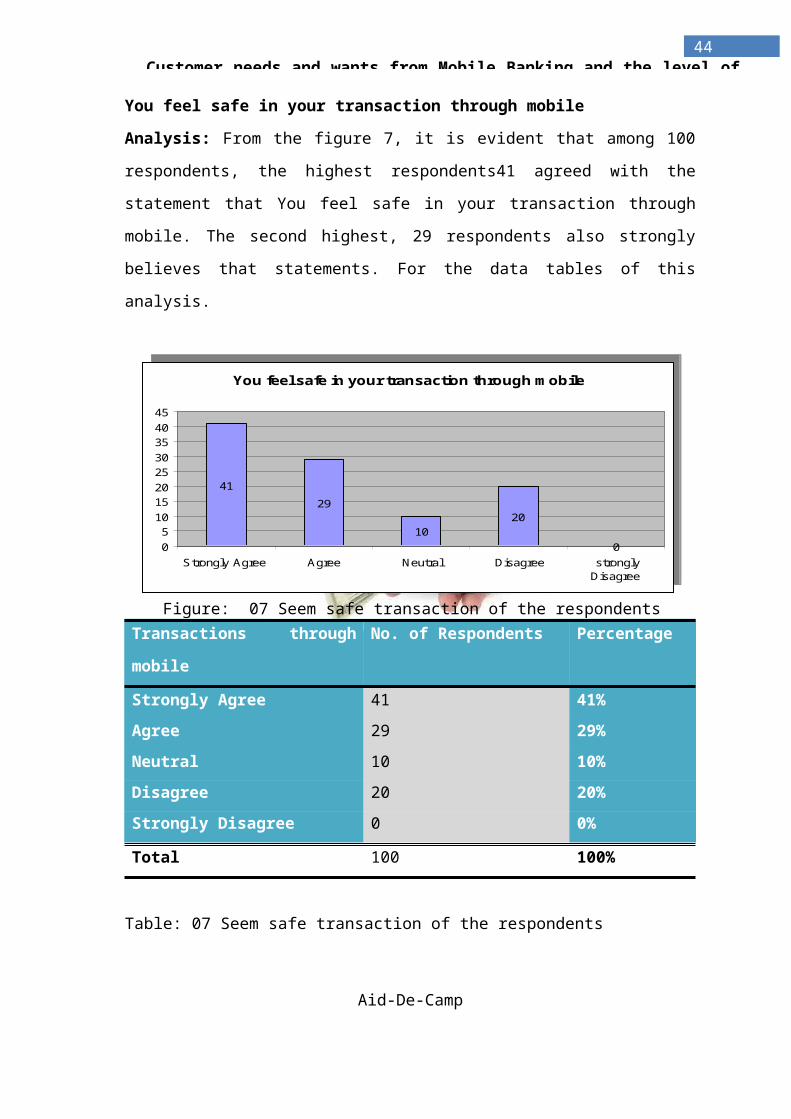

You feel safe in your transaction through mobile

Analysis: From the figure 7, it is evident that among 100

respondents, the highest respondents41 agreed with the

statement that You feel safe in your transaction through

mobile. The second highest, 29 respondents also strongly

believes that statements. For the data tables of this

analysis.

Figure: 07 Seem safe transaction of the respondents Transactions through

mobile

No. of Respondents Percentage

Strongly Agree 41 41%Agree 29 29%Neutral 10 10%Disagree 20 20%Strongly Disagree 0 0%

Total 100 100%

Table: 07 Seem safe transaction of the respondents

Aid-De-Camp

You feel safe in your transaction through m obile

4129

1020

0051015202530354045

Strongly Agree Agree Neutral Disagree stronglyDisagree

45Customer needs and wants from Mobile Banking and the level of

Aid-De-Camp

46Customer needs and wants from Mobile Banking and the level of

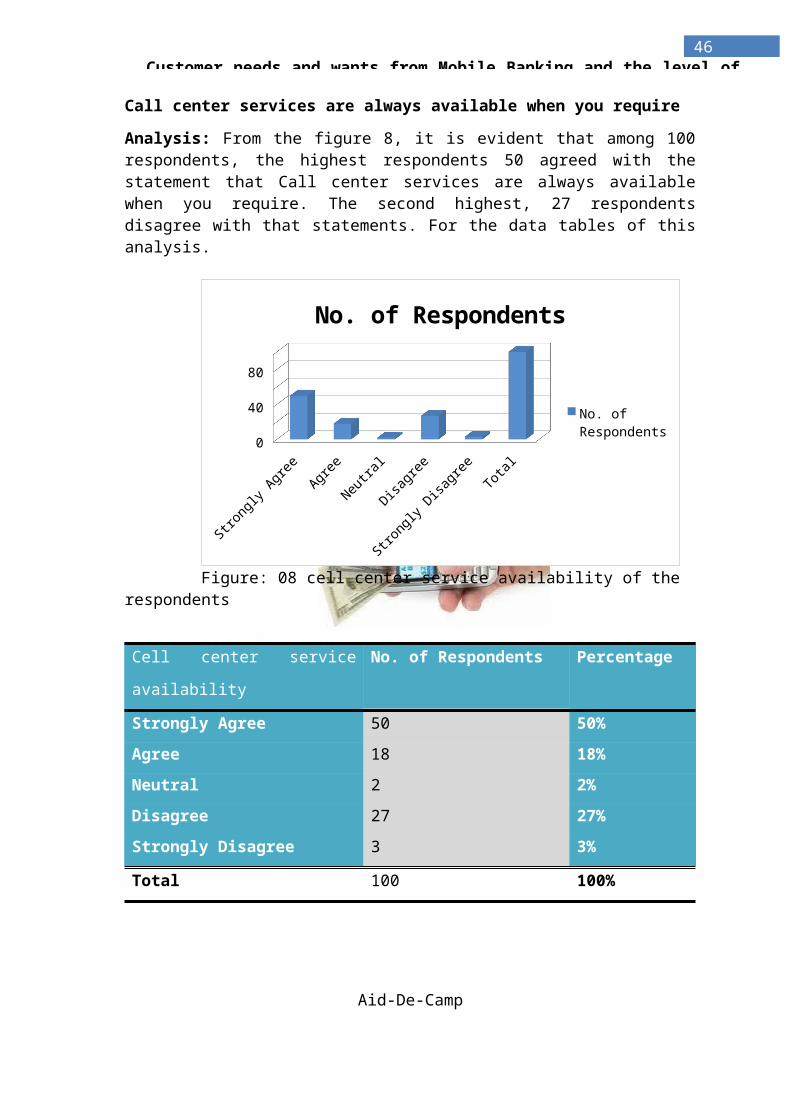

Call center services are always available when you require

Analysis: From the figure 8, it is evident that among 100respondents, the highest respondents 50 agreed with thestatement that Call center services are always availablewhen you require. The second highest, 27 respondentsdisagree with that statements. For the data tables of thisanalysis.

Strongly Agree

Agree

Neutral

Disagree

Strongly Disagree

Total

0

40

80

No. of Respondents

No. of Respondents

Figure: 08 cell center service availability of the respondents

Cell center service

availability

No. of Respondents Percentage

Strongly Agree 50 50%Agree 18 18%Neutral 2 2%Disagree 27 27%Strongly Disagree 3 3%

Total 100 100%

Aid-De-Camp

47Customer needs and wants from Mobile Banking and the level of

Table: 8 cell center service availability of the

respondents

Aid-De-Camp

48Customer needs and wants from Mobile Banking and the level of

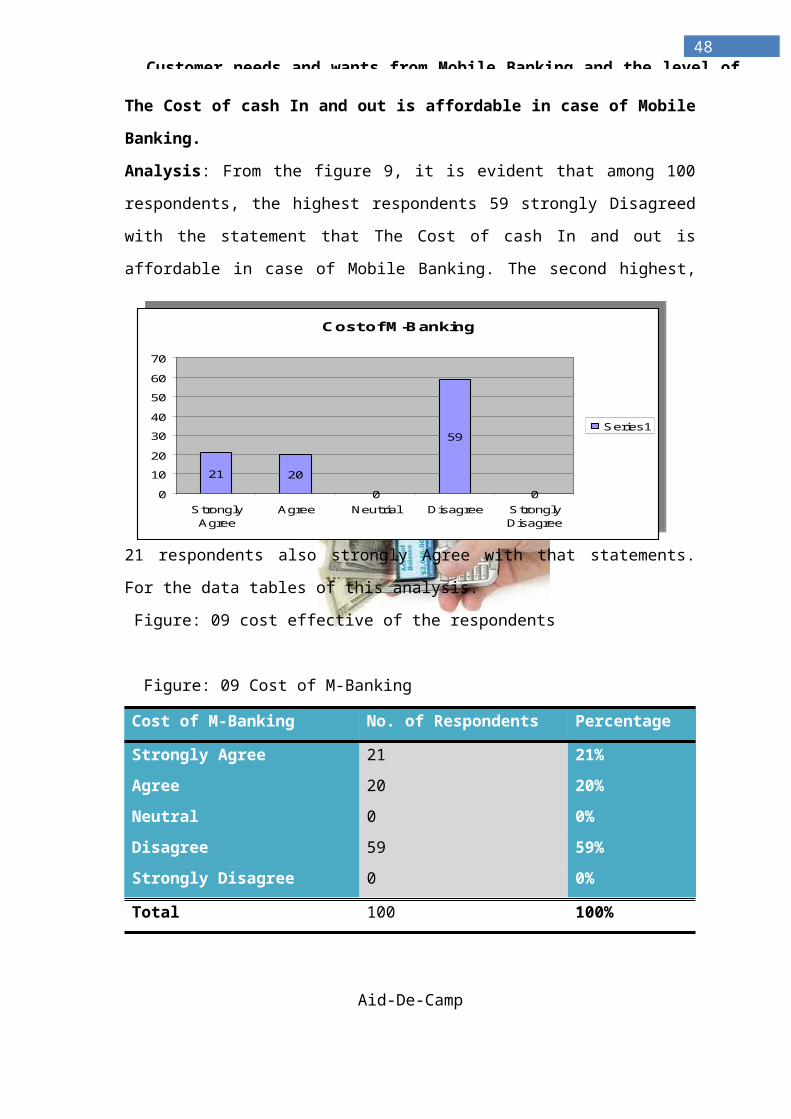

The Cost of cash In and out is affordable in case of Mobile

Banking.

Analysis: From the figure 9, it is evident that among 100

respondents, the highest respondents 59 strongly Disagreed

with the statement that The Cost of cash In and out is

affordable in case of Mobile Banking. The second highest,

21 respondents also strongly Agree with that statements.

For the data tables of this analysis.

Figure: 09 cost effective of the respondents

Figure: 09 Cost of M-Banking

Cost of M-Banking No. of Respondents Percentage

Strongly Agree 21 21%Agree 20 20%Neutral 0 0%Disagree 59 59%Strongly Disagree 0 0%

Total 100 100%

Aid-De-Camp

Cost of M -Banking

21 200

59

0010203040506070

StronglyAgree

Agree Neutrial Disagree StronglyDisagree

Series1

49Customer needs and wants from Mobile Banking and the level of

Table: 09 Cost of M-Banking

Aid-De-Camp

50Customer needs and wants from Mobile Banking and the level of

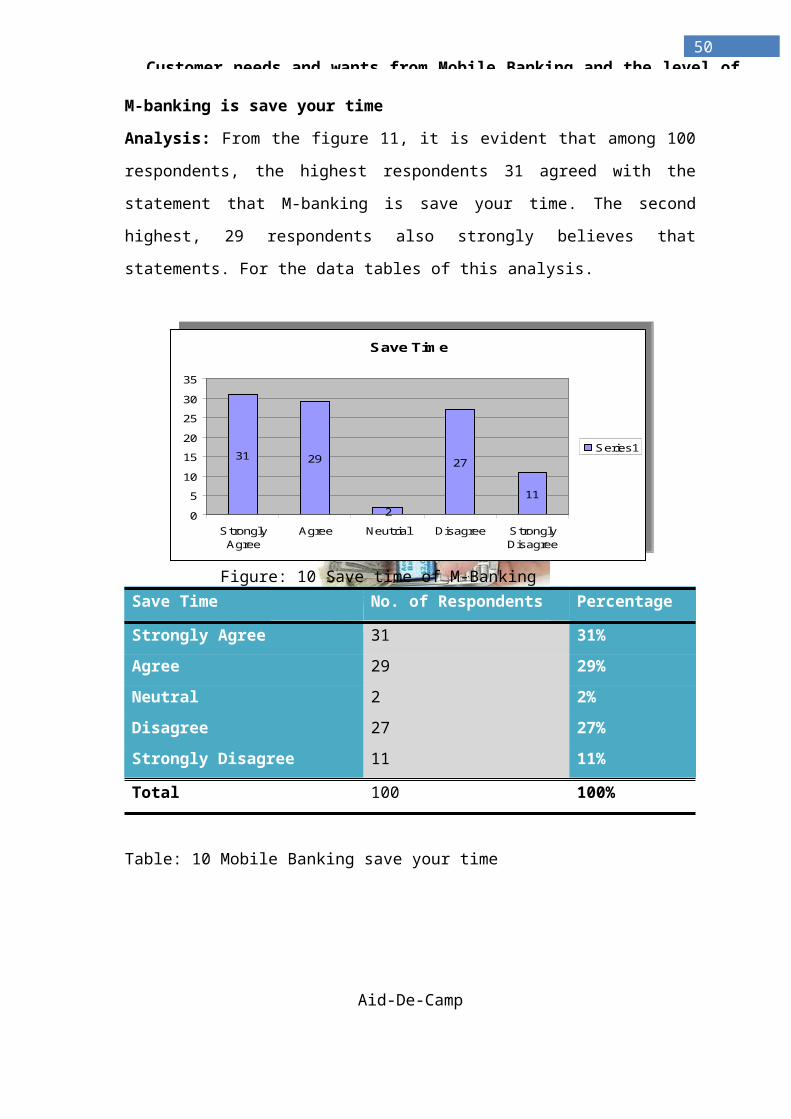

M-banking is save your time

Analysis: From the figure 11, it is evident that among 100

respondents, the highest respondents 31 agreed with the

statement that M-banking is save your time. The second

highest, 29 respondents also strongly believes that

statements. For the data tables of this analysis.

Figure: 10 Save time of M-BankingSave Time No. of Respondents Percentage

Strongly Agree 31 31%Agree 29 29%Neutral 2 2%Disagree 27 27%Strongly Disagree 11 11%

Total 100 100%

Table: 10 Mobile Banking save your time

Aid-De-Camp

Save Tim e

31 29

2

27

11

05101520253035

StronglyAgree

Agree Neutrial Disagree StronglyDisagree

Series1

51Customer needs and wants from Mobile Banking and the level of

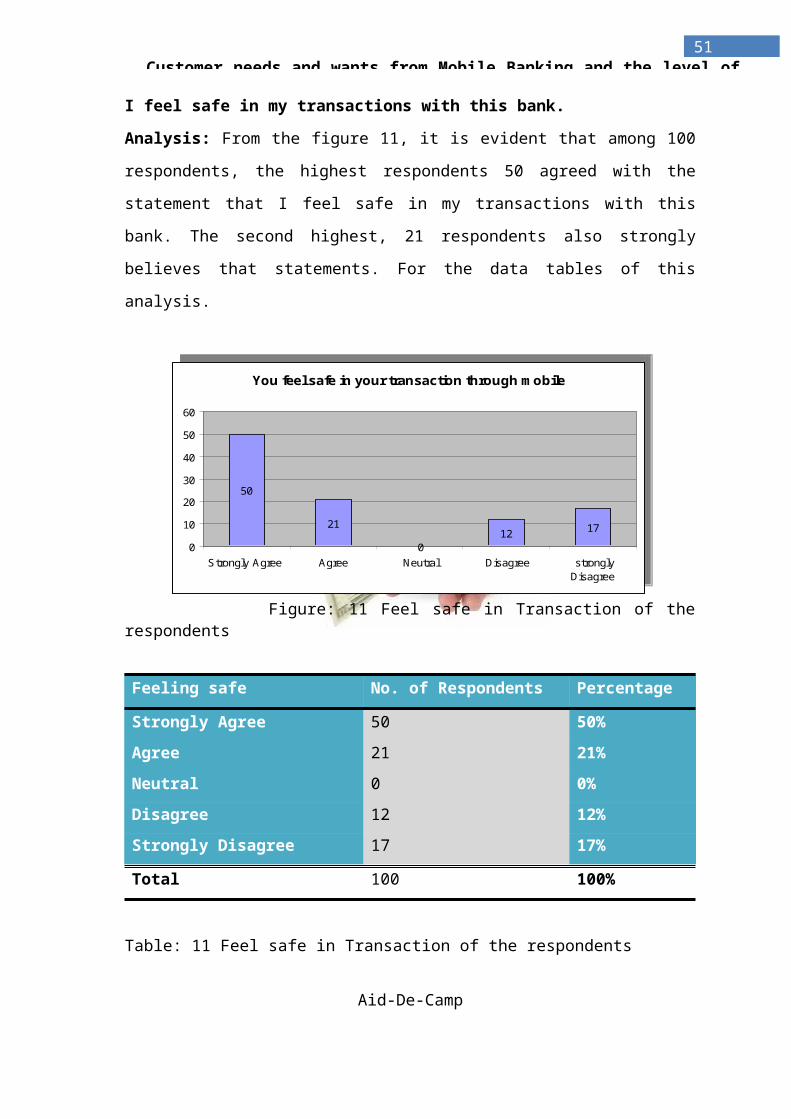

I feel safe in my transactions with this bank.

Analysis: From the figure 11, it is evident that among 100

respondents, the highest respondents 50 agreed with the

statement that I feel safe in my transactions with this

bank. The second highest, 21 respondents also strongly

believes that statements. For the data tables of this

analysis.

Figure: 11 Feel safe in Transaction of therespondents

Feeling safe No. of Respondents Percentage

Strongly Agree 50 50%Agree 21 21%Neutral 0 0%Disagree 12 12%Strongly Disagree 17 17%

Total 100 100%

Table: 11 Feel safe in Transaction of the respondents

Aid-De-Camp

You feel safe in your transaction through m obile

50

21

012 17

0

10

20

30

40

50

60

Strongly Agree Agree Neutral Disagree stronglyDisagree

52Customer needs and wants from Mobile Banking and the level of

Aid-De-Camp

53Customer needs and wants from Mobile Banking and the level of

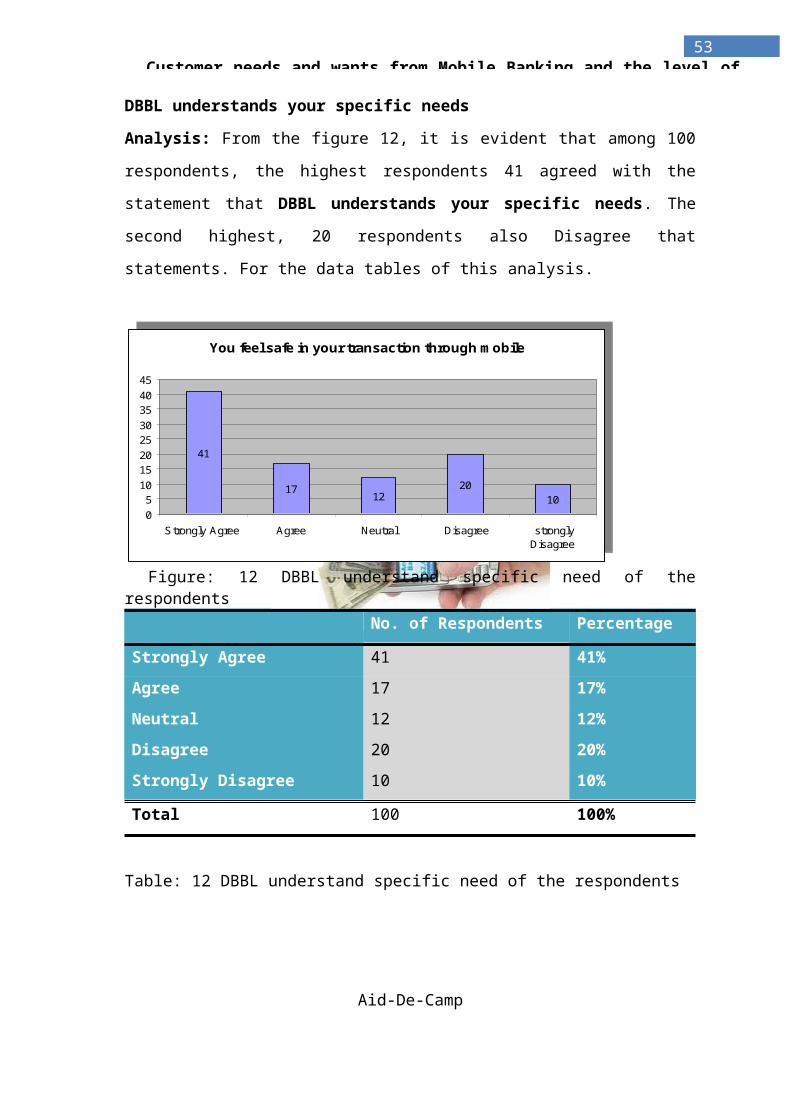

DBBL understands your specific needs

Analysis: From the figure 12, it is evident that among 100

respondents, the highest respondents 41 agreed with the

statement that DBBL understands your specific needs. The

second highest, 20 respondents also Disagree that

statements. For the data tables of this analysis.

Figure: 12 DBBL understand specific need of therespondents

No. of Respondents Percentage

Strongly Agree 41 41%Agree 17 17%Neutral 12 12%Disagree 20 20%Strongly Disagree 10 10%

Total 100 100%

Table: 12 DBBL understand specific need of the respondents

Aid-De-Camp

You feel safe in your transaction through m obile

41

17 1220

10051015202530354045

Strongly Agree Agree Neutral Disagree stronglyDisagree

54Customer needs and wants from Mobile Banking and the level of

Aid-De-Camp

55Customer needs and wants from Mobile Banking and the level of

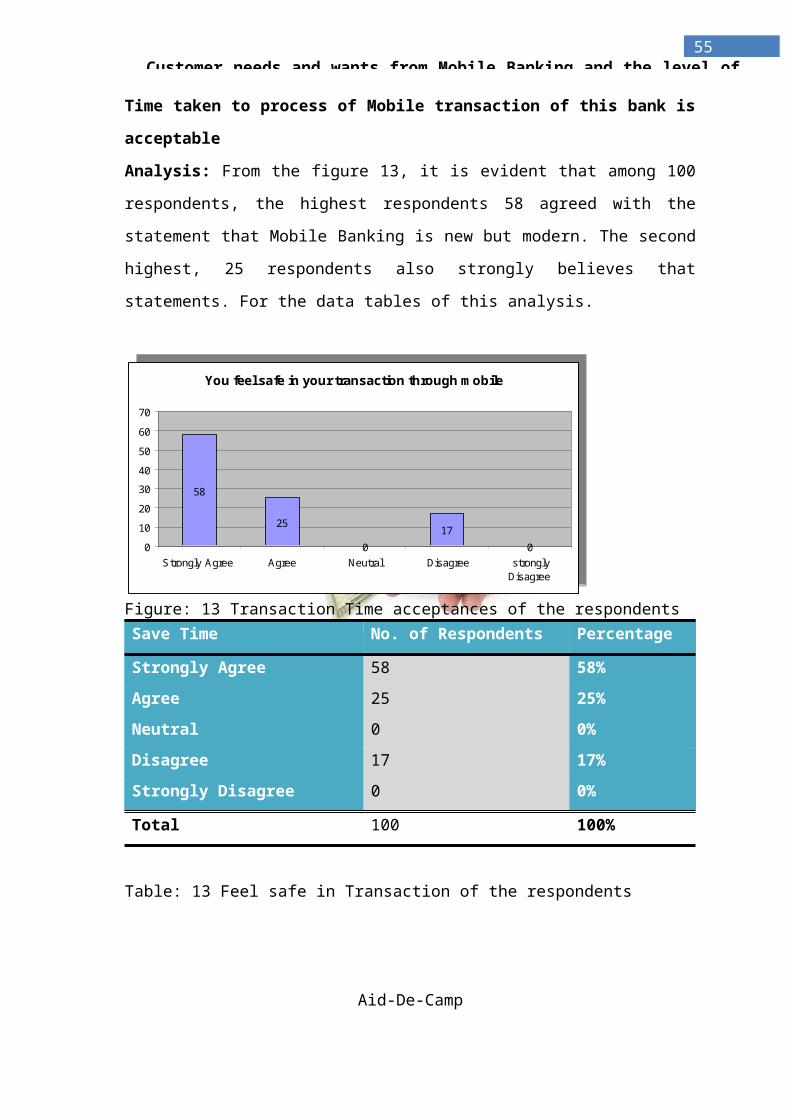

Time taken to process of Mobile transaction of this bank is

acceptable

Analysis: From the figure 13, it is evident that among 100

respondents, the highest respondents 58 agreed with the

statement that Mobile Banking is new but modern. The second

highest, 25 respondents also strongly believes that

statements. For the data tables of this analysis.

Figure: 13 Transaction Time acceptances of the respondentsSave Time No. of Respondents Percentage

Strongly Agree 58 58%Agree 25 25%Neutral 0 0%Disagree 17 17%Strongly Disagree 0 0%

Total 100 100%

Table: 13 Feel safe in Transaction of the respondents

Aid-De-Camp

You feel safe in your transaction through m obile

58

25

017

0010203040506070

Strongly Agree Agree Neutral Disagree stronglyDisagree

56Customer needs and wants from Mobile Banking and the level of

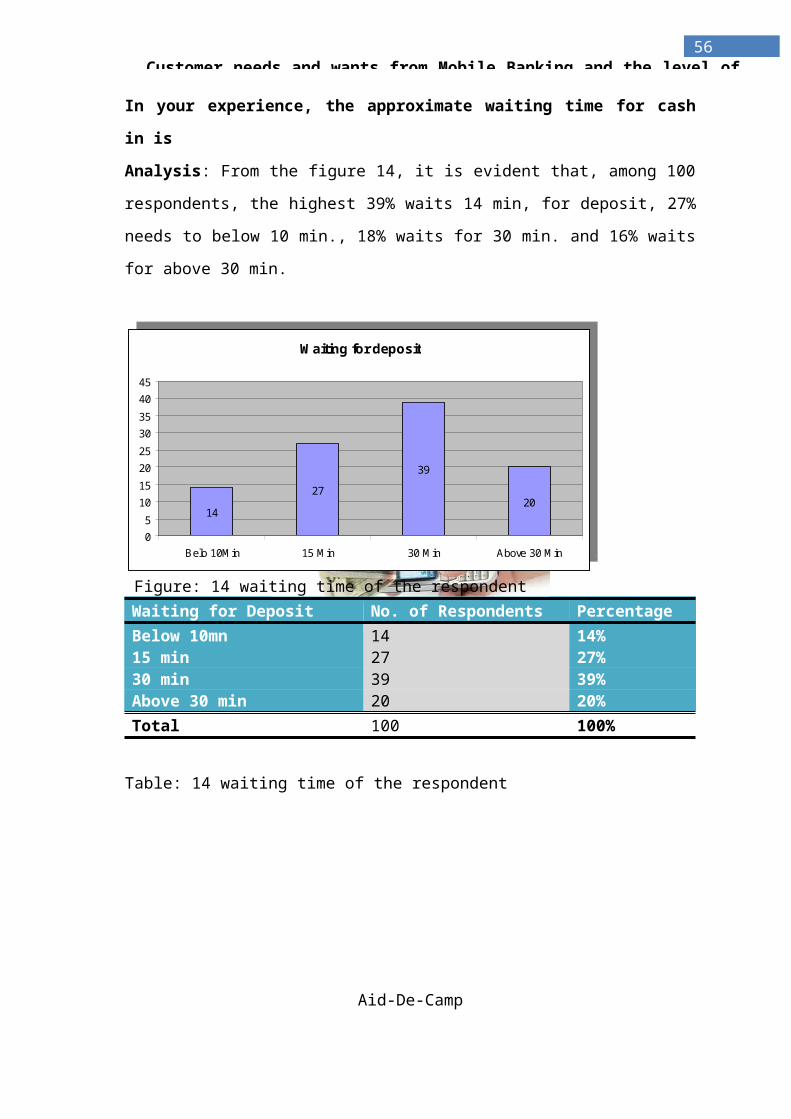

In your experience, the approximate waiting time for cash

in is

Analysis: From the figure 14, it is evident that, among 100

respondents, the highest 39% waits 14 min, for deposit, 27%

needs to below 10 min., 18% waits for 30 min. and 16% waits

for above 30 min.

Figure: 14 waiting time of the respondentWaiting for Deposit No. of Respondents PercentageBelow 10mn 14 14%15 min 27 27%30 min 39 39%Above 30 min 20 20%Total 100 100%

Table: 14 waiting time of the respondent

Aid-De-Camp

W aiting for deposit

1427

39

20

051015202530354045

Belo 10M in 15 M in 30 M in Above 30 M in

57Customer needs and wants from Mobile Banking and the level of

Waiting for Cash Out

50

18 1220

0

10

20

30

40

50

60

Belo 10Min

15 Min

30 Min

Above 30 Min

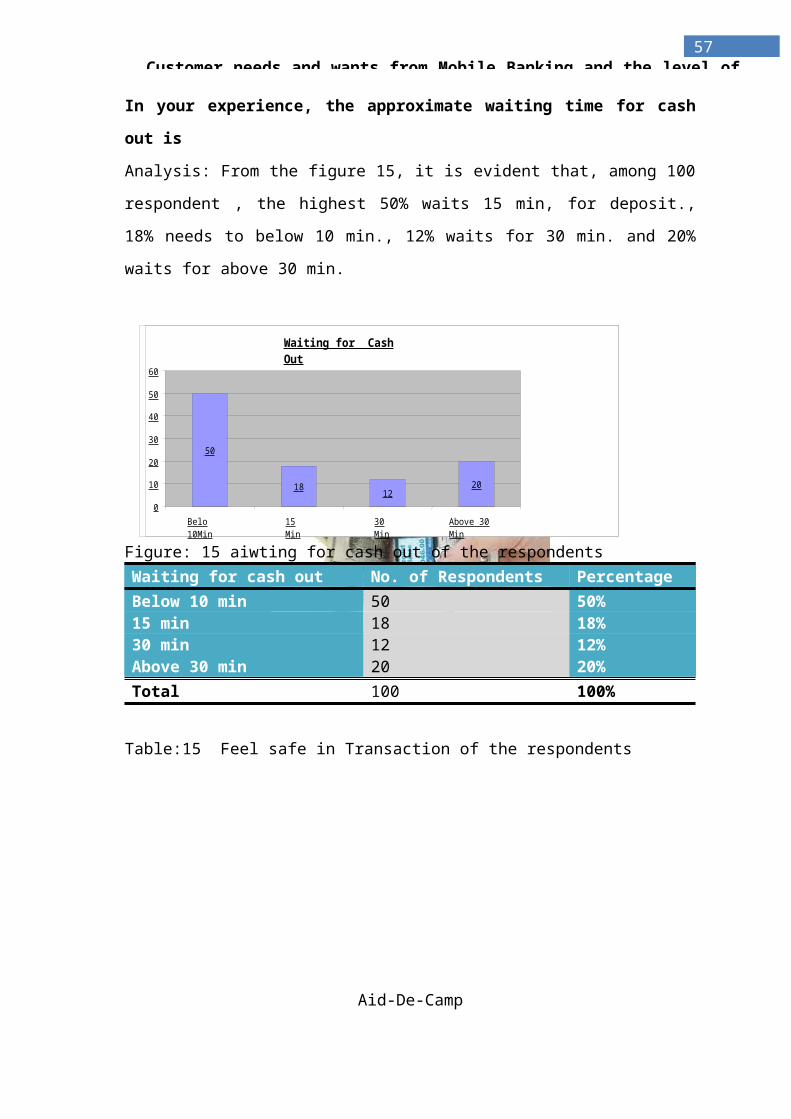

In your experience, the approximate waiting time for cash

out is

Analysis: From the figure 15, it is evident that, among 100

respondent , the highest 50% waits 15 min, for deposit.,

18% needs to below 10 min., 12% waits for 30 min. and 20%

waits for above 30 min.

Figure: 15 aiwting for cash out of the respondentsWaiting for cash out No. of Respondents PercentageBelow 10 min 50 50%15 min 18 18%30 min 12 12%Above 30 min 20 20%Total 100 100%

Table:15 Feel safe in Transaction of the respondents

Aid-De-Camp

58Customer needs and wants from Mobile Banking and the level of

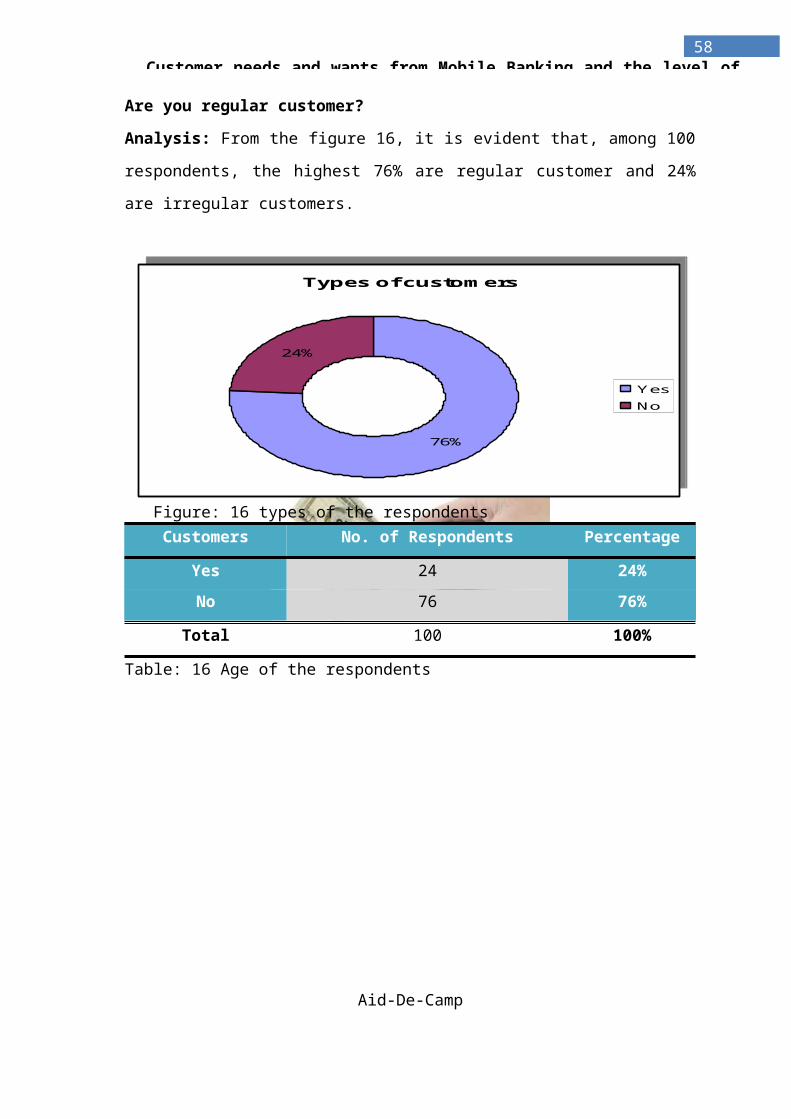

Are you regular customer?

Analysis: From the figure 16, it is evident that, among 100

respondents, the highest 76% are regular customer and 24%

are irregular customers.

Figure: 16 types of the respondentsCustomers No. of Respondents Percentage

Yes 24 24%No 76 76%

Total 100 100%

Table: 16 Age of the respondents

Aid-De-Camp

Types of custom ers

76%

24%

YesNo

59Customer needs and wants from Mobile Banking and the level of

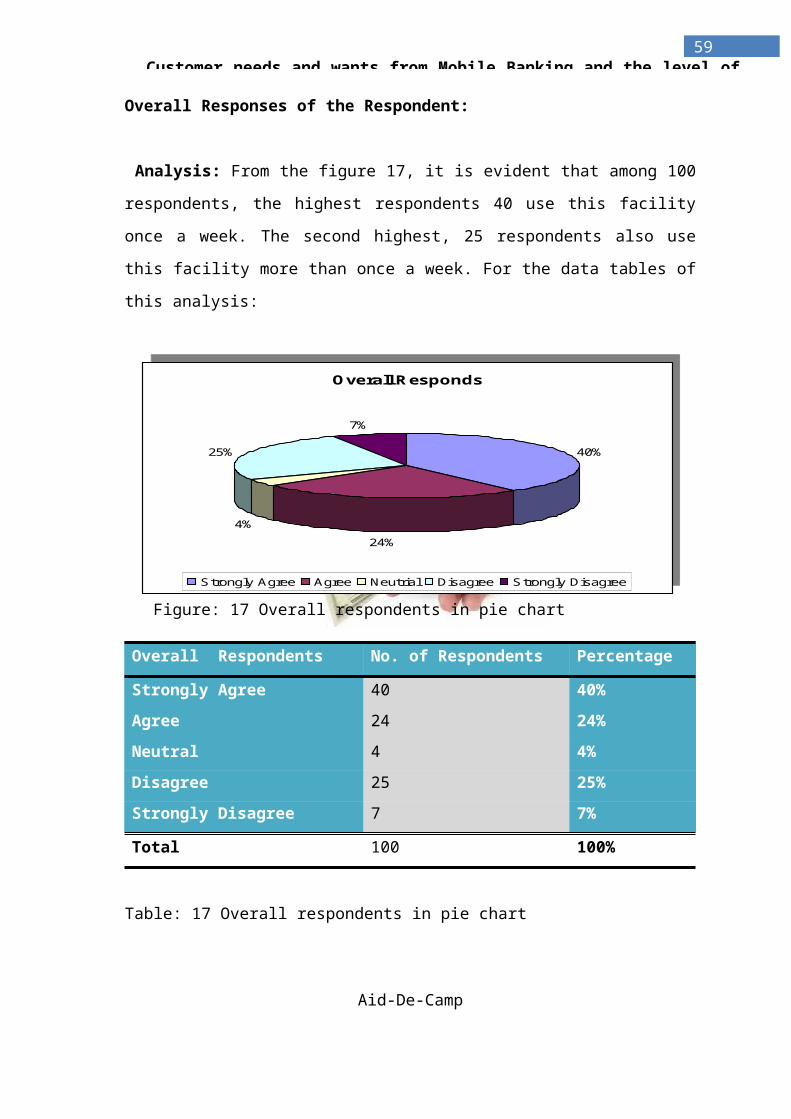

Overall Responses of the Respondent:

Analysis: From the figure 17, it is evident that among 100

respondents, the highest respondents 40 use this facility

once a week. The second highest, 25 respondents also use

this facility more than once a week. For the data tables of

this analysis:

Figure: 17 Overall respondents in pie chart Overall Respondents No. of Respondents Percentage

Strongly Agree 40 40%Agree 24 24%Neutral 4 4%Disagree 25 25%Strongly Disagree 7 7%

Total 100 100%

Table: 17 Overall respondents in pie chart

Aid-De-Camp

Overall Responds

40%

24%4%

25%

7%

Strongly Agree Agree Neutrial Disagree Strongly Disagree

60Customer needs and wants from Mobile Banking and the level of

Chpter-4

Conclusion

&

Recommendation

Aid-De-Camp

61Customer needs and wants from Mobile Banking and the level of

Aid-De-Camp

62Customer needs and wants from Mobile Banking and the level of

For service providers, Mobile banking offers the next

surest way to achieve growth. Countries like Bangladesh

where mobile penetration is nearing saturation, mobile

banking is helping service providers increase revenues from

the now static subscriber base. Also service providers are

increasingly using the complexity of their supported mobile

banking services to attract new customers and retain old

ones. For the fact is that one day, in most of the world

emerging markets, more people will use mobile telephones

than use fixed telephone lines. Businesses that are based

on mobile financial serviced will thus be a natural fit for

these economies.

What is more, there is no need to wait for the next

generation mobile networks; these businesses can be built

using today's technology. But to capture this significant

opportunity, financial firms and telecommunications

companies will have to partnerships with one another and,

possibly, with merchants and retail chains as well. Dutch-

Bangla Bank is pioneer of Mobile Banking in Bangladesh and

it has a lot of possibility to reach customers door as well

as banking in the hand of customers.

Like in many other countries, people in Bangladesh started

believing in mobile banking, which was introduced on May 15

by Dutch Bangla Bank Ltd (DBBL).Aid-De-Camp

4.1 Conclusion

63Customer needs and wants from Mobile Banking and the level of

BRAC Bank introduced the service on July 21. Mercantile

Bank and Trust Bank are also going to introduce m-banking

throughout the country with the help of the

government union information centers.

A total of 12 banks are in the race to introduce the

service, while two are in the final lap of implementation.

It was possible for approval from Bangladesh Bank and the

telecom operators have also come forward to help the banks.

Basic mobile handsets are being used as bank accounts and

will serve as a wallet for the transaction of money,

especially for the un-banked people.

As 99 percent of the people of Bangladesh are under

the mobile phone network, almost all will have access to

the formal financial channel.

On the other hand, more than 7.5 crore people are

using mobile phones. If the banks can reach out to the un-

banked people, the dream of more people having bank

accounts can be fulfilled.

Aid-De-Camp

4.2 Recommendation

64Customer needs and wants from Mobile Banking and the level of

Continue Mobile Banking in the rural areas to increase the

use of E-Money especially in commercial applications.

Continuous pilot testing of the other M-Banking services to

model cost effective ways of reaching more and more people

in areas farther away from bank. Develop a mobile banking

website as information portal particularly for M-Banking.

Continuous support and training workshop on Mobile Banking.

Procedures develops on going .Developed M-banking system to

automated transecting.

A major problem in a business arises when it’s new.

The officer should observe that whether there is loss

of the top executive, demand, or any other most

important new one has entered and often the change may

be worse.

Bank and concern partner should advertise more for

attracting all level of customers.

Bank should encourage students for Mobile account

opening because students are a potential source for a

bank.

Bank should increase facility to fulfillment

customers need.

Bank should also be aware of significant changes in

the training of M-Banking officer and concern Partners

employee.

Changes in industry trends may directly affect

business so that it can no longer completely

profitable. Therefore, the Bank should keep

Aid-De-Camp

65Customer needs and wants from Mobile Banking and the level of

information about the environment of each industry in

which its customers operate

Against big willful defaulters legal action should be

taken promptly for customer M-Money Security.

Should arrange more and more campaign in public place

to increase M-Banking customer.

References and

Appendix

Aid-De-Camp

66Customer needs and wants from Mobile Banking and the level of

Books:

• Bingham, Eugene F, ‘Essential of Managerial Finance’ TwelfthEdition.• Syed Ashrf Ali & R.A Howlader “Banking Low & Practice” FirstEdition November 2009• Annual Report 2010 DBBL• Ross, Westerfield, Jaffe Corporate Finance Sixth Edition• Gitman, J Lawrence (2003), ‘Principal of Finance’ Tenth Edition

Web Site:

• Official website www.dbbl.bd.com• www.theprofriton.com • www.linkedin.com• www.blog.com

Others:

• Dutch-Bangla Bank Ltd.2010 Annual Report• Prospectus of DBBL• Mobile Banking PDF

Vaidya (2011): “Emerging Trends on Functional Utilization ofMobile Banking in Developed Markets in Next 3-4 Years”

Tiwari, Rajnish and Buse, Stephan(2007): The Mobile Commerce Prospects:A Strategic Analysis of Opportunities in the Banking Sector, Hamburg UniversityPress (E-Book as PDF to be downloaded)

Tiwari, Rajnish; Buse, Stephan and Herstatt, Cornelius (2007):Mobile Services in Banking Sector: The Role of Innovative Business Solutions inGenerating Competitive Advantage, in: Proceedings of the InternationalResearch Conference on Quality, Innovation and KnowledgeManagement, New Delhi, pp. 886–894.

Tiwari, Rajnish; Buse, Stephan and Herstatt, Cornelius (2006):Customer on the Move: Strategic Implications of Mobile Banking for Banks and FinancialEnterprises, in: CEC/EEE 2006, Proceedings of The 8th IEEE

Aid-De-Camp

References

67Customer needs and wants from Mobile Banking and the level of

International Conference on E-Commerce Technology and The 3rdIEEE International Conference on Enterprise Computing, E-Commerce, and E-Services (CEC/EEE'06), San Francisco, pp. 522–529.

Tiwari, Rajnish; Buse, Stephan and Herstatt, Cornelius (2006):Mobile Banking as Business Strategy: Impact of Mobile Technologies on CustomerBehavior and its Implications for Banks, in: Technology Management for theGlobal Future - Proceedings of PICMET '06.

Owens, John and Anna Ban tug-Herrera (2006): Catching theTechnology Wave: Mobile Phone Banking and Text-A-Payment in thePhilippines ̂ "DBBL branches to reach 79, ATMs 850 by yr-end".Financial Express.http://www.thefinancialexpress-bd.com/2009/09/29/80133.html.Retrieved 2009-09-02.

Dutch-Bangla Bank Limited

Customer Satisfaction Survey questionnaire:

It’s really appreciable if you would take just a few

minutes to respond to the questioner below. As a valuable

customer of DBBL Mobile Banking, how you rate our service,

is very important information for us. It is to be noted

that all answers here will be treated confidentially & no

individual data will be disclose. Please read the

statements, which some people agree with, and do not.

Whether you Strongly Agree (SA), Agree (A), Neutral (N),

Disagree (D), strongly Disagree (SD) with each statement.

Name:

Demographic Information:Aid-De-Camp

Appendix

68Customer needs and wants from Mobile Banking and the level of

1 Age

a) 20-30 years c) 31-40 years

d) 41-50 years e) above 50 years

2 Gender.

a) Male b) Female

3 Occupation.

a) Professionals b)

Service Holder

c) Business man d) Housewife

e) others

4. Reason for opening A/C.

a) Required b) Facility

c) Attractiveness d) Near from my place

5. Education level.

a) No formal education b) SSC

c) HSC d) Graduation e) Post

Graduation

8. Would you like to use mobile banking services?

a) Yes b) No

Please circle/mark the number you choice- Partic

ulars

SA A N D SD

Aid-De-Camp

69Customer needs and wants from Mobile Banking and the level of

1. Mobile Banking is new but modern 5 4 3 2 1

2. You feel safe in your transaction

through mobile

5 4 3 2 1

3. Call center services are always

available when you require.

5 4 3 2 1

4. The Cost of cash In and out is

affordable in case of Mobile Banking.

5 4 3 2 1

5. Available agent and branch for m-

banking.

5 4 3 2 1

6. M-banking is save your time. 5 4 3 2 1

7. I feel safe in my transactions with this

bank.

5 4 3 2 1

8. DBBL understands your specific needs 5 4 3 2 1

9. Time taken to process of Mobile

transaction of this bank is acceptable

5 4 3 2 1

9. DBBL provides prompt services to its

customers.

5 4 3 2 1

10. DBBL Mobile Banking is very effective

for you

5 4 3 2 1

Please check one best alternative-

Aid-De-Camp

70Customer needs and wants from Mobile Banking and the level of

In your experience, the approximate waiting time for cash

in is

Δ Below 10 min

Δ 15 min

Δ 30 min

Δ Above 30 min

In your experience, the approximate waiting time for cash

out is

Δ Below 10 min

Δ 15 min

Δ 30 min

Δ Above 30 min

Are you regular customer?

Δ Yes

Δ No

How often do you use this facility?

Δ once a week

Δ More than once a week

Δ once a month

Δ Infrequently

Your valuable comment regarding the service:

Aid-De-Camp

71Customer needs and wants from Mobile Banking and the level of

……………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………

Your precious suggestions to improve the services:

……………………………………………………………………………………………………………………………………………………………

………………………………………………………………………………………………………………………………....

Thank you very much for sharing valuable time

Interview Guideline:

Who: Customer of Mobile Banking

What: Satisfaction level of Mobile Banking

Aid-De-Camp