construction & infrastructure21jan15

TRANSCRIPT

TRACKCONSTRUCTION & INFRASTRUCTURE

InfraTrack December 16, 2015

Nitin Arora Research [email protected] +91 22 66242491

Kushan ParikhResearch [email protected] +91 22 66121431

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

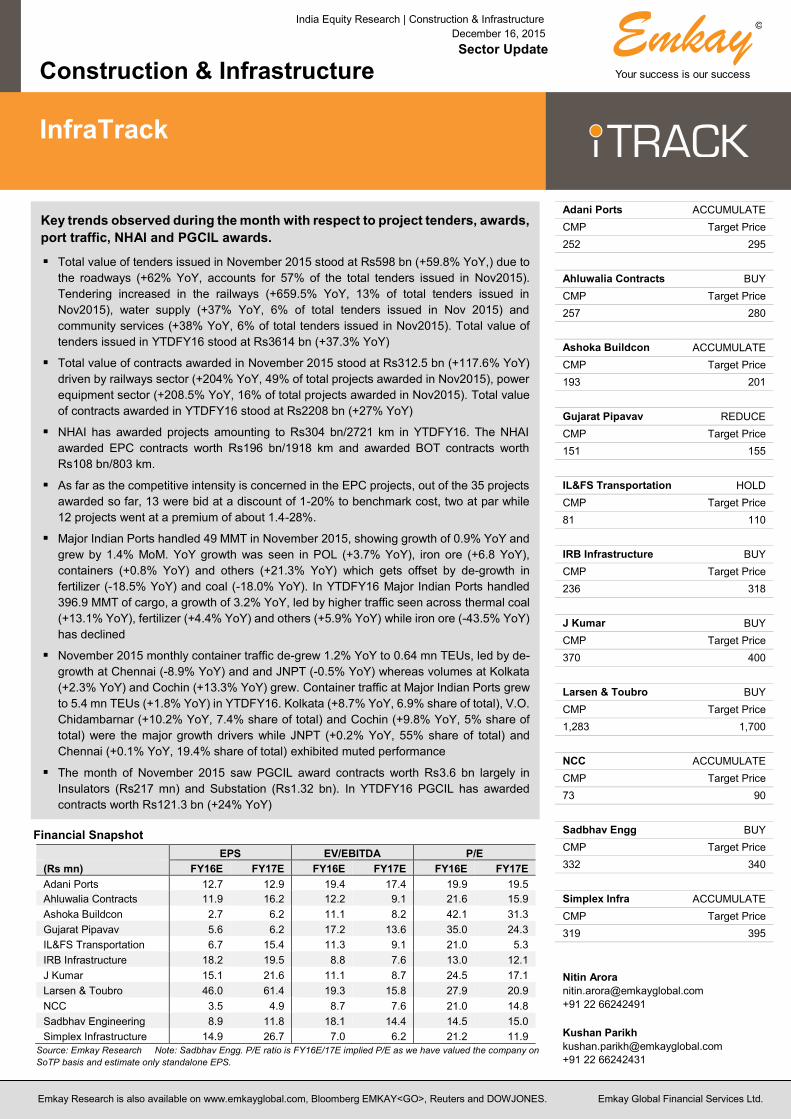

Callout Key trends observed during the month with respect to project tenders, awards,

port traffic, NHAI and PGCIL awards.

Total value of tenders issued in November 2015 stood at Rs598 bn (+59.8% YoY,) due to

the roadways (+62% YoY, accounts for 57% of the total tenders issued in Nov2015).

Tendering increased in the railways (+659.5% YoY, 13% of total tenders issued in

Nov2015), water supply (+37% YoY, 6% of total tenders issued in Nov 2015) and

community services (+38% YoY, 6% of total tenders issued in Nov2015). Total value of

tenders issued in YTDFY16 stood at Rs3614 bn (+37.3% YoY)

Total value of contracts awarded in November 2015 stood at Rs312.5 bn (+117.6% YoY)

driven by railways sector (+204% YoY, 49% of total projects awarded in Nov2015), power

equipment sector (+208.5% YoY, 16% of total projects awarded in Nov2015). Total value

of contracts awarded in YTDFY16 stood at Rs2208 bn (+27% YoY)

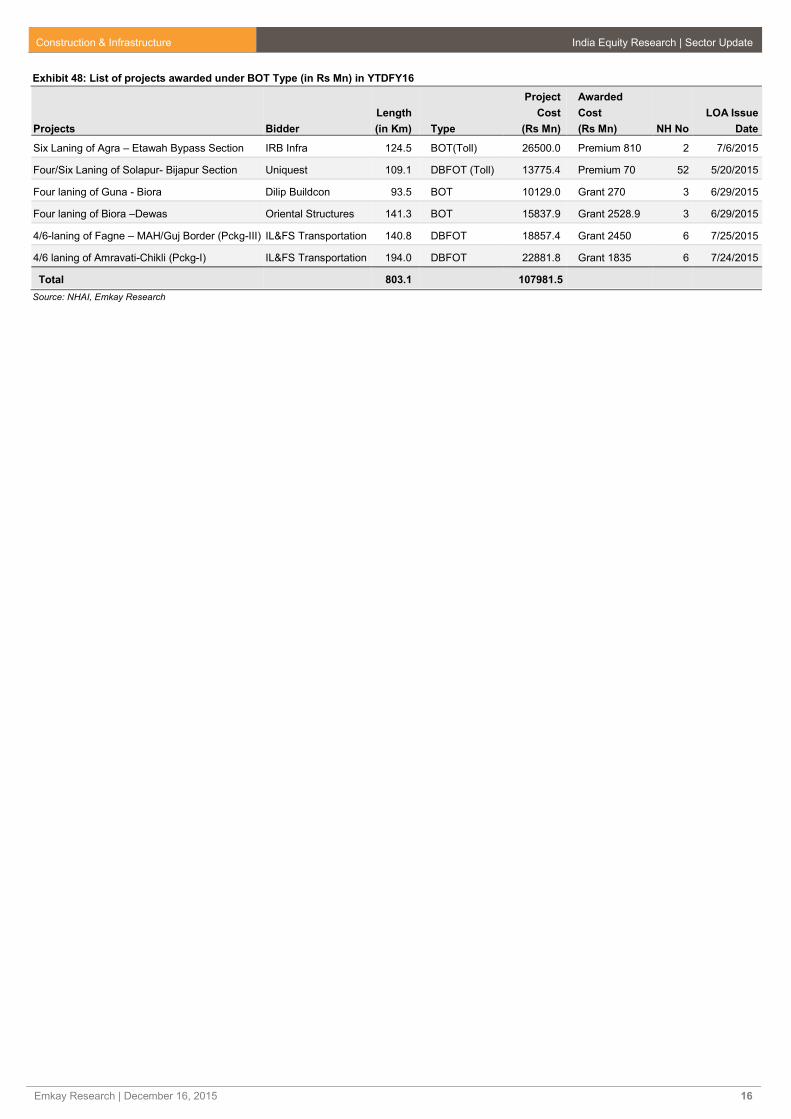

NHAI has awarded projects amounting to Rs304 bn/2721 km in YTDFY16. The NHAI

awarded EPC contracts worth Rs196 bn/1918 km and awarded BOT contracts worth

Rs108 bn/803 km.

As far as the competitive intensity is concerned in the EPC projects, out of the 35 projects

awarded so far, 13 were bid at a discount of 1-20% to benchmark cost, two at par while

12 projects went at a premium of about 1.4-28%.

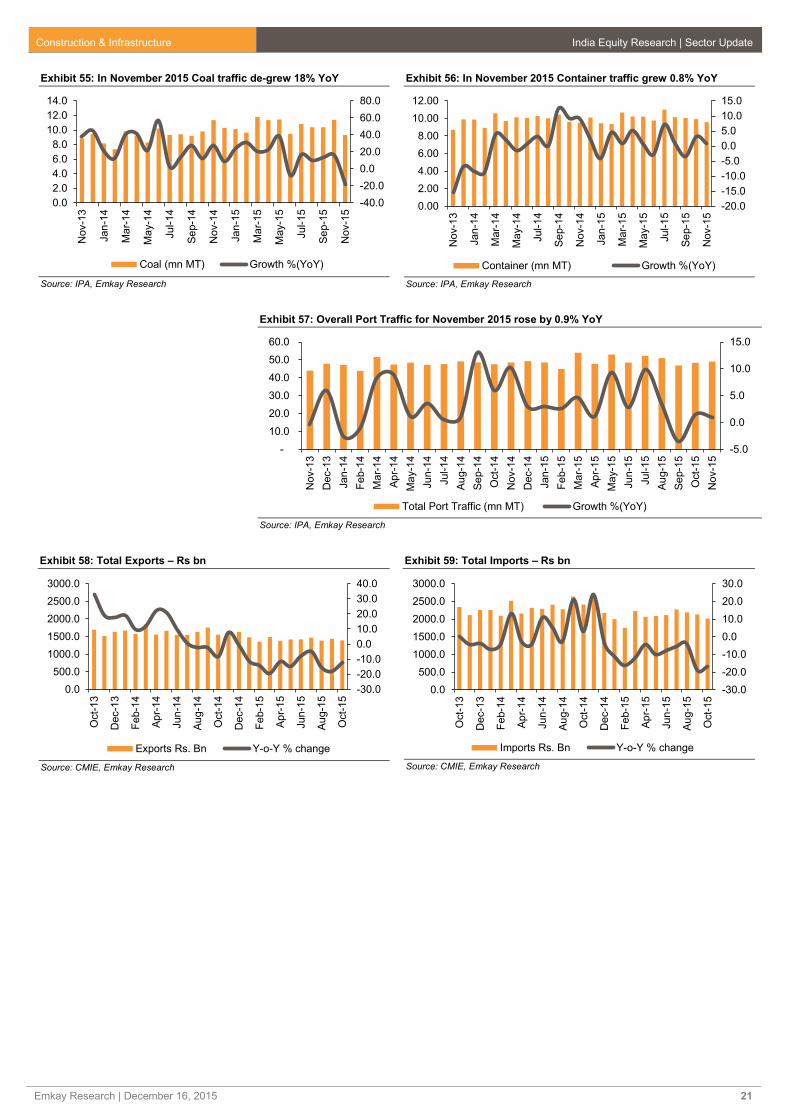

Major Indian Ports handled 49 MMT in November 2015, showing growth of 0.9% YoY and

grew by 1.4% MoM. YoY growth was seen in POL (+3.7% YoY), iron ore (+6.8 YoY),

containers (+0.8% YoY) and others (+21.3% YoY) which gets offset by de-growth in

fertilizer (-18.5% YoY) and coal (-18.0% YoY). In YTDFY16 Major Indian Ports handled

396.9 MMT of cargo, a growth of 3.2% YoY, led by higher traffic seen across thermal coal

(+13.1% YoY), fertilizer (+4.4% YoY) and others (+5.9% YoY) while iron ore (-43.5% YoY)

has declined

November 2015 monthly container traffic de-grew 1.2% YoY to 0.64 mn TEUs, led by de-

growth at Chennai (-8.9% YoY) and and JNPT (-0.5% YoY) whereas volumes at Kolkata

(+2.3% YoY) and Cochin (+13.3% YoY) grew. Container traffic at Major Indian Ports grew

to 5.4 mn TEUs (+1.8% YoY) in YTDFY16. Kolkata (+8.7% YoY, 6.9% share of total), V.O.

Chidambarnar (+10.2% YoY, 7.4% share of total) and Cochin (+9.8% YoY, 5% share of

total) were the major growth drivers while JNPT (+0.2% YoY, 55% share of total) and

Chennai (+0.1% YoY, 19.4% share of total) exhibited muted performance

The month of November 2015 saw PGCIL award contracts worth Rs3.6 bn largely in

Insulators (Rs217 mn) and Substation (Rs1.32 bn). In YTDFY16 PGCIL has awarded

contracts worth Rs121.3 bn (+24% YoY)

India Equity Research | Construction & Infrastructure

December 16, 2015

Sector Update

Construction & Infrastructure

InfraTrack

TRACK

Financial Snapshot

EPS EV/EBITDA P/E

(Rs mn) FY16E FY17E FY16E FY17E FY16E FY17E

Adani Ports 12.7 12.9 19.4 17.4 19.9 19.5

Ahluwalia Contracts 11.9 16.2 12.2 9.1 21.6 15.9

Ashoka Buildcon 2.7 6.2 11.1 8.2 42.1 31.3

Gujarat Pipavav 5.6 6.2 17.2 13.6 35.0 24.3

IL&FS Transportation 6.7 15.4 11.3 9.1 21.0 5.3

IRB Infrastructure 18.2 19.5 8.8 7.6 13.0 12.1

J Kumar 15.1 21.6 11.1 8.7 24.5 17.1

Larsen & Toubro 46.0 61.4 19.3 15.8 27.9 20.9

NCC 3.5 4.9 8.7 7.6 21.0 14.8

Sadbhav Engineering 8.9 11.8 18.1 14.4 14.5 15.0

Simplex Infrastructure 14.9 26.7 7.0 6.2 21.2 11.9

Source: Emkay Research Note: Sadbhav Engg. P/E ratio is FY16E/17E implied P/E as we have valued the company on

SoTP basis and estimate only standalone EPS.

Adani Ports ACCUMULATE

CMP Target Price

252 295

Ahluwalia Contracts BUY

CMP Target Price

257 280

Ashoka Buildcon ACCUMULATE

CMP Target Price

193 201

Gujarat Pipavav REDUCE

CMP Target Price

151 155

IL&FS Transportation HOLD

CMP Target Price

81 110

IRB Infrastructure BUY

CMP Target Price

236 318

J Kumar BUY

CMP Target Price

370 400

Larsen & Toubro BUY

CMP Target Price

1,283 1,700

NCC ACCUMULATE

CMP Target Price

73 90

Sadbhav Engg BUY

CMP Target Price

332 340

Simplex Infra ACCUMULATE

CMP Target Price

319 395

Nitin Arora

+91 22 66242491

Kushan Parikh

+91 22 66242431

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 3

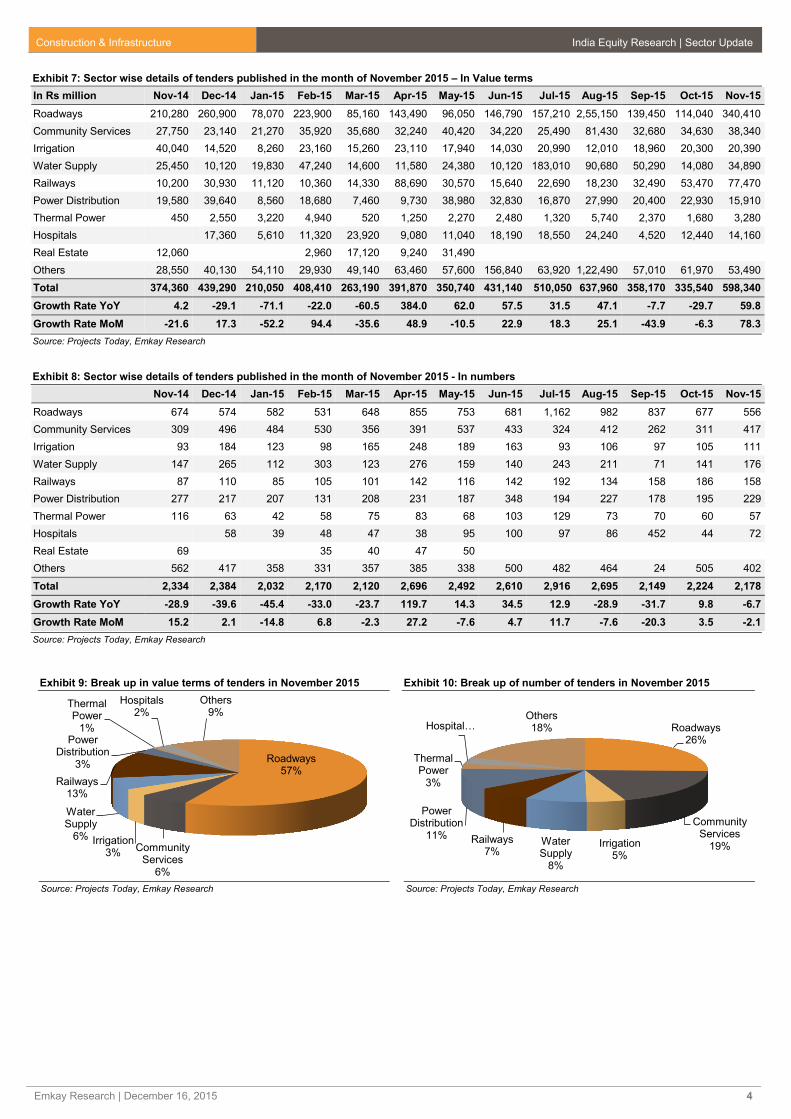

Tenders Issued

Total value of tenders issued in November 2015 stood at Rs598 bn (+59.8% YoY,) due to

the roadways (+62% YoY, accounts for 57% of the total tenders issued in

Nov2015).Tendering increased in the railways (+659.5% YoY, 13% of total tenders issued

in Nov2015), water supply (+37% YoY, 6% of total tenders issued in Nov 2015) and

community services (+38% YoY, 6% of total tenders issued in Nov2015). We witnessed

total number of tenders decreased 6.7% on a YoY basis.

Out of Rs77.5 bn worth tenders, Rs38.1 bn are three orders coming from Ircon

International Ltd. for constructing various tunnel sections, bridges and a station yard of the

Katra-Banihal stretch of the Udhampur-Srinagar-Baramulla new broad gauge railway line

in Jammu & Kashmir.

Water tenders included three tenders worth Rs16.4 bn combined coming from Telangana

state for it Drinking Water Supply project.

Total value of tenders issued in YTDFY16 stood at Rs3614 bn (+37.3% YoY). We

witnessed strong tendering in roadways, railways, community services, hospitals and

water supply projects.

In November 2015, State govt tenders rose to Rs301.6 bn (+51% YoY), while Central govt

tenders were up at Rs296.4 bn (+71% YoY) and private tenders stood at Rs290 mn.

State govt tenders in YTDFY16 increased to Rs2053 bn (+39% YoY), Central govt tenders

increased to Rs1551 bn (+47% YoY) and private domestic tenders increased to Rs9.1 bn.

Exhibit 1: Tenders Published 78.3% MoM in November 2015

Source: Projects Today, Emkay Research

Exhibit 2: Number of tenders decreased by 2.1% MoM to 2178

Source: Projects Today, Emkay Research

Exhibit 3: Tenders Published 59.8% YoY in November 2015

Source: Projects Today, Emkay Research

Exhibit 4: Number of tenders decreased by 6.7% YoY to 2178

Source: Projects Today, Emkay Research

Exhibit 5: YTDFY16, Value of tenders increased by 37.3%

Source: Projects Today, Emkay Research

Exhibit 6: YTDFY16, Number of tenders increased 3.8% to 19960

Source: Projects Today, Emkay Research

-200

-100

0

100

200

0

200000

400000

600000

800000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

MoM

Gro

wth

(%

)

Rs M

illio

n

State Government Central Government

Growth Rate MoM

-100

-50

0

50

100

0

1000

2000

3000

4000

5000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

MoM

Gro

wth

(%

)

No. of T

enders

State Government Central Government

Growth Rate MoM

-200

-100

0

100

200

300

400

500

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

-90

-60

-30

0

30

60

90

120

150

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15YoY

Gro

wth

(%

)

0

500

1000

1500

2000

2500

3000

3500

4000

YT

DF

Y1

1

YT

DF

Y1

2

YT

DF

Y1

3

YT

DF

Y1

4

YT

DF

Y1

5

YT

DF

Y1

6

In R

s b

n

0

5000

10000

15000

20000

25000

30000

YT

DF

Y1

1

YT

DF

Y1

2

YT

DF

Y1

3

YT

DF

Y1

4

YT

DF

Y1

5

YT

DF

Y1

6

No. of T

enders

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 4

Exhibit 7: Sector wise details of tenders published in the month of November 2015 – In Value terms

In Rs million Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

Roadways 210,280 260,900 78,070 223,900 85,160 143,490 96,050 146,790 157,210 2,55,150 139,450 114,040 340,410

Community Services 27,750 23,140 21,270 35,920 35,680 32,240 40,420 34,220 25,490 81,430 32,680 34,630 38,340

Irrigation 40,040 14,520 8,260 23,160 15,260 23,110 17,940 14,030 20,990 12,010 18,960 20,300 20,390

Water Supply 25,450 10,120 19,830 47,240 14,600 11,580 24,380 10,120 183,010 90,680 50,290 14,080 34,890

Railways 10,200 30,930 11,120 10,360 14,330 88,690 30,570 15,640 22,690 18,230 32,490 53,470 77,470

Power Distribution 19,580 39,640 8,560 18,680 7,460 9,730 38,980 32,830 16,870 27,990 20,400 22,930 15,910

Thermal Power 450 2,550 3,220 4,940 520 1,250 2,270 2,480 1,320 5,740 2,370 1,680 3,280

Hospitals 17,360 5,610 11,320 23,920 9,080 11,040 18,190 18,550 24,240 4,520 12,440 14,160

Real Estate 12,060 2,960 17,120 9,240 31,490

Others 28,550 40,130 54,110 29,930 49,140 63,460 57,600 156,840 63,920 1,22,490 57,010 61,970 53,490

Total 374,360 439,290 210,050 408,410 263,190 391,870 350,740 431,140 510,050 637,960 358,170 335,540 598,340

Growth Rate YoY 4.2 -29.1 -71.1 -22.0 -60.5 384.0 62.0 57.5 31.5 47.1 -7.7 -29.7 59.8

Growth Rate MoM -21.6 17.3 -52.2 94.4 -35.6 48.9 -10.5 22.9 18.3 25.1 -43.9 -6.3 78.3

Source: Projects Today, Emkay Research

Exhibit 8: Sector wise details of tenders published in the month of November 2015 - In numbers

Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

Roadways 674 574 582 531 648 855 753 681 1,162 982 837 677 556

Community Services 309 496 484 530 356 391 537 433 324 412 262 311 417

Irrigation 93 184 123 98 165 248 189 163 93 106 97 105 111

Water Supply 147 265 112 303 123 276 159 140 243 211 71 141 176

Railways 87 110 85 105 101 142 116 142 192 134 158 186 158

Power Distribution 277 217 207 131 208 231 187 348 194 227 178 195 229

Thermal Power 116 63 42 58 75 83 68 103 129 73 70 60 57

Hospitals 58 39 48 47 38 95 100 97 86 452 44 72

Real Estate 69 35 40 47 50

Others 562 417 358 331 357 385 338 500 482 464 24 505 402

Total 2,334 2,384 2,032 2,170 2,120 2,696 2,492 2,610 2,916 2,695 2,149 2,224 2,178

Growth Rate YoY -28.9 -39.6 -45.4 -33.0 -23.7 119.7 14.3 34.5 12.9 -28.9 -31.7 9.8 -6.7

Growth Rate MoM 15.2 2.1 -14.8 6.8 -2.3 27.2 -7.6 4.7 11.7 -7.6 -20.3 3.5 -2.1

Source: Projects Today, Emkay Research

Exhibit 9: Break up in value terms of tenders in November 2015

Source: Projects Today, Emkay Research

Exhibit 10: Break up of number of tenders in November 2015

Source: Projects Today, Emkay Research

Roadways57%

Community Services

6%

Irrigation3%

Water Supply

6%

Railways13%

Power Distribution

3%

Thermal Power

1%

Hospitals2%

Others9%

Roadways26%

Community Services

19%Irrigation5%

Water Supply

8%

Railways7%

Power Distribution

11%

Thermal Power

3%

Hospital…Others18%

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 5

Exhibit 11: YTDFY16, improvement seen in most segments (Value terms)

Source: Projects Today, Emkay Research

Exhibit 12: YTDFY16, improvement seen in most segments (No. of Contracts)

Source: Projects Today, Emkay Research

Exhibit 13: Tenders in numbers terms down 17.5% YoY

Source: Projects Today, Emkay Research

Exhibit 14: Road tenders in value terms +61.9% YoY

Source: Projects Today, Emkay Research

Exhibit 15: Tenders in Number terms +19.4% YoY

Source: Projects Today, Emkay Research

Exhibit 16: Irrigation tenders in value terms -49.1% YoY

Source: Projects Today, Emkay Research

Exhibit 17: Tenders in number terms +19.7% YoY

Source: Projects Today, Emkay Research

Exhibit 18: Water supply tenders in value terms up 37.1% YoY

Source: Projects Today, Emkay Research

0 500000 1000000 1500000

Roadways

Community Services

Irrigation

Water Supply

Railways

Power Distribution

Thermal Power

Hospitals

Real Estate

OthersRs Million

YTDFY15 YTDFY16

0 2000 4000 6000 8000

Roadways

Community Services

Irrigation

Water Supply

Railways

Power Distribution

Thermal Power

Hospitals

Real Estate

Others Number of Contacts

YTDFY15 YTDFY16

-100

-50

0

50

100

150

200

0

1000

2000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Roadways YOY - Growth

-200

-100

0

100

200

300

400

500

600

700

0

100000

200000

300000

400000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Roadways YOY - Growth

-150

-100

-50

0

50

100

150

0

50

100

150

200

250

300

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Irrigation YOY - Growth

-150

-100

-50

0

50

100

150

200

0

10000

20000

30000

40000

50000

60000

70000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Irrigation YOY - Growth

-150

-100

-50

0

50

100

0

50

100

150

200

250

300

350

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Water Supply YOY - Growth

-200

0

200

400

600

800

0

50000

100000

150000

200000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Water Supply YOY - Growth

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 6

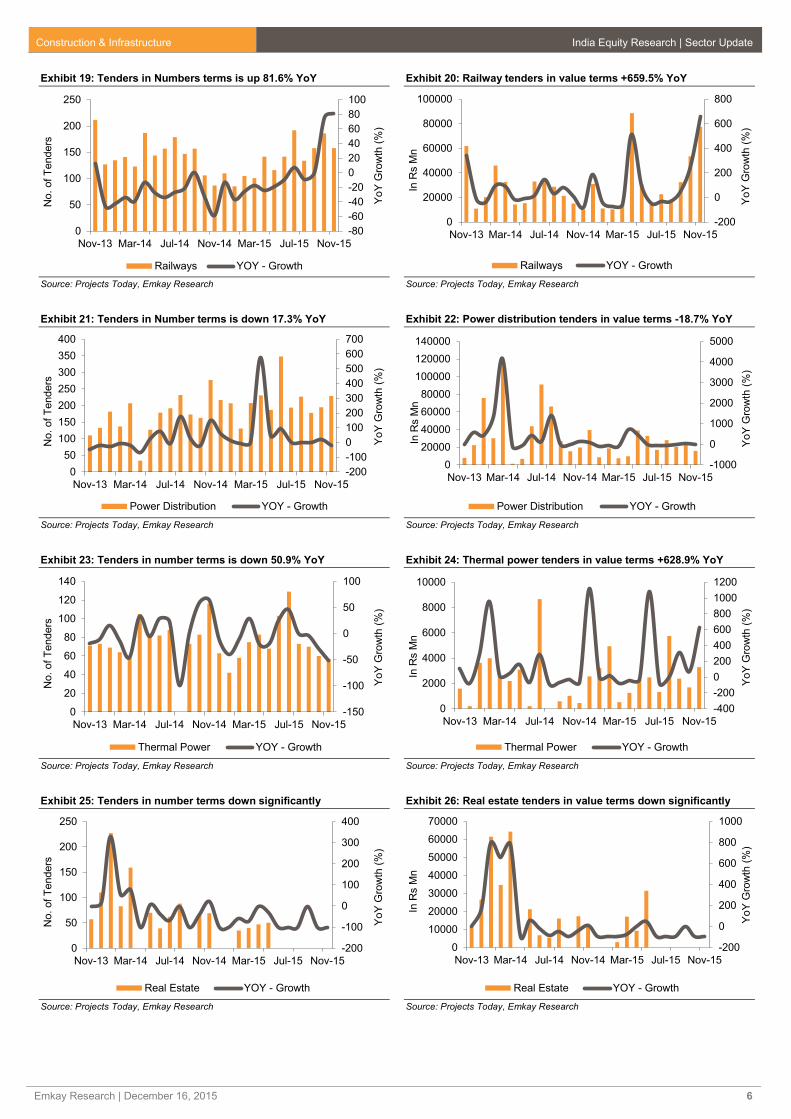

Exhibit 19: Tenders in Numbers terms is up 81.6% YoY

Source: Projects Today, Emkay Research

Exhibit 20: Railway tenders in value terms +659.5% YoY

Source: Projects Today, Emkay Research

Exhibit 21: Tenders in Number terms is down 17.3% YoY

Source: Projects Today, Emkay Research

Exhibit 22: Power distribution tenders in value terms -18.7% YoY

Source: Projects Today, Emkay Research

Exhibit 23: Tenders in number terms is down 50.9% YoY

Source: Projects Today, Emkay Research

Exhibit 24: Thermal power tenders in value terms +628.9% YoY

Source: Projects Today, Emkay Research

Exhibit 25: Tenders in number terms down significantly

Source: Projects Today, Emkay Research

Exhibit 26: Real estate tenders in value terms down significantly

Source: Projects Today, Emkay Research

-80

-60

-40

-20

0

20

40

60

80

100

0

50

100

150

200

250

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Railways YOY - Growth

-200

0

200

400

600

800

0

20000

40000

60000

80000

100000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Railways YOY - Growth

-200

-100

0

100

200

300

400

500

600

700

0

50

100

150

200

250

300

350

400

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Power Distribution YOY - Growth

-1000

0

1000

2000

3000

4000

5000

0

20000

40000

60000

80000

100000

120000

140000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Power Distribution YOY - Growth

-150

-100

-50

0

50

100

0

20

40

60

80

100

120

140

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Thermal Power YOY - Growth

-400

-200

0

200

400

600

800

1000

1200

0

2000

4000

6000

8000

10000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Thermal Power YOY - Growth

-200

-100

0

100

200

300

400

0

50

100

150

200

250

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

No. of T

enders

Real Estate YOY - Growth

-200

0

200

400

600

800

1000

0

10000

20000

30000

40000

50000

60000

70000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Real Estate YOY - Growth

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 7

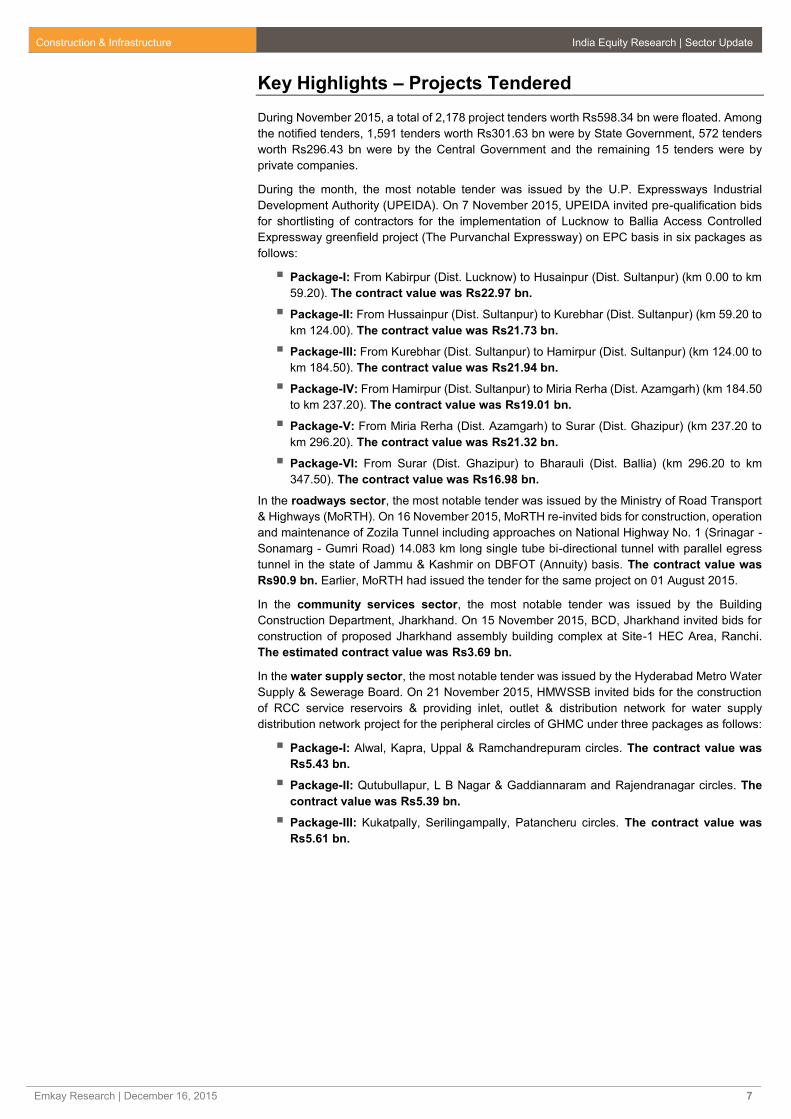

Key Highlights – Projects Tendered

During November 2015, a total of 2,178 project tenders worth Rs598.34 bn were floated. Among

the notified tenders, 1,591 tenders worth Rs301.63 bn were by State Government, 572 tenders

worth Rs296.43 bn were by the Central Government and the remaining 15 tenders were by

private companies.

During the month, the most notable tender was issued by the U.P. Expressways Industrial

Development Authority (UPEIDA). On 7 November 2015, UPEIDA invited pre-qualification bids

for shortlisting of contractors for the implementation of Lucknow to Ballia Access Controlled

Expressway greenfield project (The Purvanchal Expressway) on EPC basis in six packages as

follows:

Package-I: From Kabirpur (Dist. Lucknow) to Husainpur (Dist. Sultanpur) (km 0.00 to km

59.20). The contract value was Rs22.97 bn.

Package-II: From Hussainpur (Dist. Sultanpur) to Kurebhar (Dist. Sultanpur) (km 59.20 to

km 124.00). The contract value was Rs21.73 bn.

Package-III: From Kurebhar (Dist. Sultanpur) to Hamirpur (Dist. Sultanpur) (km 124.00 to

km 184.50). The contract value was Rs21.94 bn.

Package-IV: From Hamirpur (Dist. Sultanpur) to Miria Rerha (Dist. Azamgarh) (km 184.50

to km 237.20). The contract value was Rs19.01 bn.

Package-V: From Miria Rerha (Dist. Azamgarh) to Surar (Dist. Ghazipur) (km 237.20 to

km 296.20). The contract value was Rs21.32 bn.

Package-VI: From Surar (Dist. Ghazipur) to Bharauli (Dist. Ballia) (km 296.20 to km

347.50). The contract value was Rs16.98 bn.

In the roadways sector, the most notable tender was issued by the Ministry of Road Transport

& Highways (MoRTH). On 16 November 2015, MoRTH re-invited bids for construction, operation

and maintenance of Zozila Tunnel including approaches on National Highway No. 1 (Srinagar -

Sonamarg - Gumri Road) 14.083 km long single tube bi-directional tunnel with parallel egress

tunnel in the state of Jammu & Kashmir on DBFOT (Annuity) basis. The contract value was

Rs90.9 bn. Earlier, MoRTH had issued the tender for the same project on 01 August 2015.

In the community services sector, the most notable tender was issued by the Building

Construction Department, Jharkhand. On 15 November 2015, BCD, Jharkhand invited bids for

construction of proposed Jharkhand assembly building complex at Site-1 HEC Area, Ranchi.

The estimated contract value was Rs3.69 bn.

In the water supply sector, the most notable tender was issued by the Hyderabad Metro Water

Supply & Sewerage Board. On 21 November 2015, HMWSSB invited bids for the construction

of RCC service reservoirs & providing inlet, outlet & distribution network for water supply

distribution network project for the peripheral circles of GHMC under three packages as follows:

Package-I: Alwal, Kapra, Uppal & Ramchandrepuram circles. The contract value was

Rs5.43 bn.

Package-II: Qutubullapur, L B Nagar & Gaddiannaram and Rajendranagar circles. The

contract value was Rs5.39 bn.

Package-III: Kukatpally, Serilingampally, Patancheru circles. The contract value was

Rs5.61 bn.

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 8

Projects Awarded

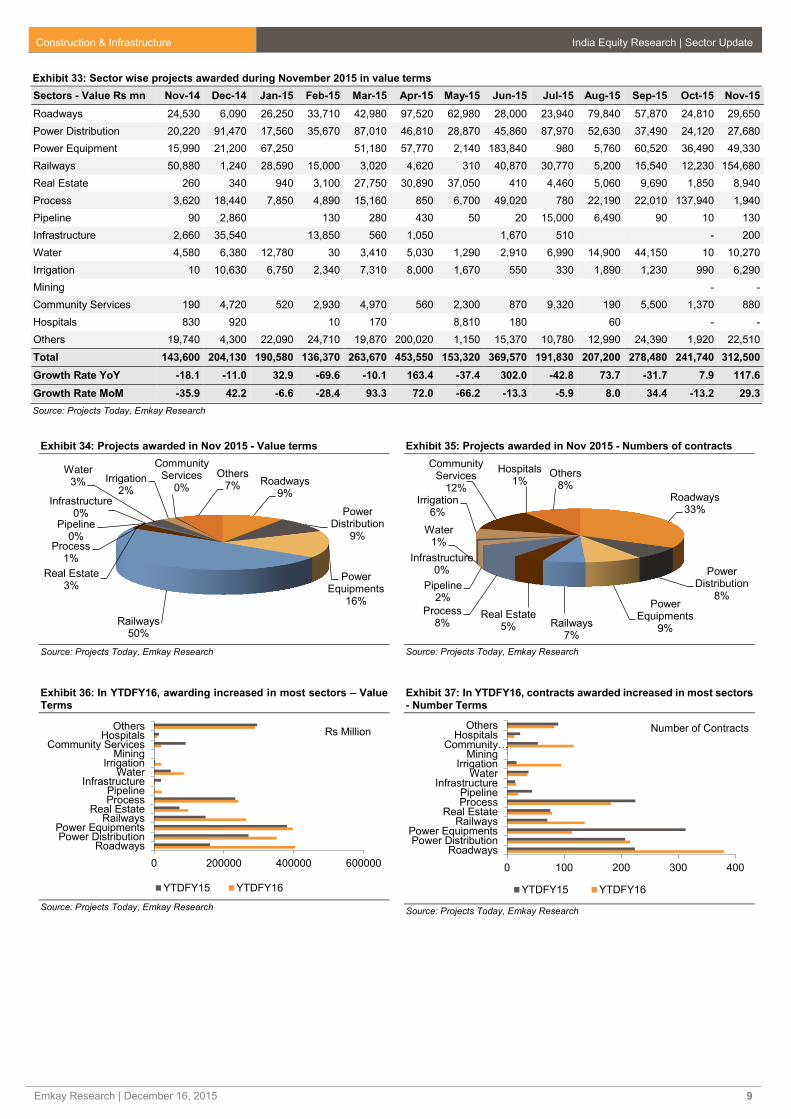

Total value of contracts awarded in November 2015 stood at Rs312.5 bn (+117.6% YoY)

driven by railways sector (+204% YoY, 49% of total projects awarded in Nov2015), power

equipment sector (+208.5% YoY, 16% of total projects awarded in Nov2015). GE Global

Sourcing India Pvt. Ltd was awarded Rs146.6 bn project by Indian Railways for setting up

a diesel locomotive factory in Bihar.

Total value of contracts awarded in YTDFY16 stood at Rs2208 bn (+27% YoY). We

witnessed growth in awarding in roadways (+152.5% YoY), railways (79.2% YoY), water

(+78.8% YoY) and power distribution (30% YoY).

In November 2015, domestic awards increased to Rs284.4 bn (+111.7% YoY,) and

international awards during the month increased to Rs28.1 bn (204.1% YoY).

Domestic awards on YTDFY16 basis stood at Rs1819.5 bn (+45.8% YoY) while

international awards stood at Rs388.7 bn (-20.8% YoY).

Exhibit 27: Nov 2015, projects awarded in value terms +29.3% MoM

Source: Projects Today, Emkay Research

Exhibit 28: Nov 2015, projects awarded in number terms +17.5% MoM

Source: Projects Today, Emkay Research

Exhibit 29: Nov 2015, projects awarded up 117.6% YoY

Source: Projects Today, Emkay Research

Exhibit 30: Nov 2015, projects awarded number terms +53.4% YoY

Source: Projects Today, Emkay Research

Exhibit 31: YTDFY16 projects awarded up 27% YoY

Source: Projects Today, Emkay Research

Exhibit 32: In YTDFY16 projects awarded in number terms +6.4% YoY

Source: Projects Today, Emkay Research

-100

-50

0

50

100

150

200

250

300

0

100000

200000

300000

400000

500000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

In %

Te

rms

Rs M

illio

n

Indian Overseas Growth Rate MoM

-100

-50

0

50

100

150

0

50

100

150

200

250

300

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

In %

Term

s

No. of A

ward

s

Indian Overseas Growth Rate MoM

-100

0

100

200

300

400

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

-100

0

100

200

300

400

500

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

0

500

1000

1500

2000

2500

YT

DF

Y1

1

YT

DF

Y1

2

YT

DF

Y1

3

YT

DF

Y1

4

YT

DF

Y1

5

YT

DF

Y1

6

In R

s b

n

0

200

400

600

800

1000

1200

1400

1600

YT

DF

Y1

1

YT

DF

Y1

2

YT

DF

Y1

3

YT

DF

Y1

4

YT

DF

Y1

5

YT

DF

Y1

6

In N

um

bers

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 9

Exhibit 33: Sector wise projects awarded during November 2015 in value terms

Sectors - Value Rs mn Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

Roadways 24,530 6,090 26,250 33,710 42,980 97,520 62,980 28,000 23,940 79,840 57,870 24,810 29,650

Power Distribution 20,220 91,470 17,560 35,670 87,010 46,810 28,870 45,860 87,970 52,630 37,490 24,120 27,680

Power Equipment 15,990 21,200 67,250 51,180 57,770 2,140 183,840 980 5,760 60,520 36,490 49,330

Railways 50,880 1,240 28,590 15,000 3,020 4,620 310 40,870 30,770 5,200 15,540 12,230 154,680

Real Estate 260 340 940 3,100 27,750 30,890 37,050 410 4,460 5,060 9,690 1,850 8,940

Process 3,620 18,440 7,850 4,890 15,160 850 6,700 49,020 780 22,190 22,010 137,940 1,940

Pipeline 90 2,860 130 280 430 50 20 15,000 6,490 90 10 130

Infrastructure 2,660 35,540 13,850 560 1,050 1,670 510 - 200

Water 4,580 6,380 12,780 30 3,410 5,030 1,290 2,910 6,990 14,900 44,150 10 10,270

Irrigation 10 10,630 6,750 2,340 7,310 8,000 1,670 550 330 1,890 1,230 990 6,290

Mining - -

Community Services 190 4,720 520 2,930 4,970 560 2,300 870 9,320 190 5,500 1,370 880

Hospitals 830 920 10 170 8,810 180 60 - -

Others 19,740 4,300 22,090 24,710 19,870 200,020 1,150 15,370 10,780 12,990 24,390 1,920 22,510

Total 143,600 204,130 190,580 136,370 263,670 453,550 153,320 369,570 191,830 207,200 278,480 241,740 312,500

Growth Rate YoY -18.1 -11.0 32.9 -69.6 -10.1 163.4 -37.4 302.0 -42.8 73.7 -31.7 7.9 117.6

Growth Rate MoM -35.9 42.2 -6.6 -28.4 93.3 72.0 -66.2 -13.3 -5.9 8.0 34.4 -13.2 29.3

Source: Projects Today, Emkay Research

Exhibit 34: Projects awarded in Nov 2015 - Value terms

Source: Projects Today, Emkay Research

Exhibit 35: Projects awarded in Nov 2015 - Numbers of contracts

Source: Projects Today, Emkay Research

Exhibit 36: In YTDFY16, awarding increased in most sectors – Value Terms

Source: Projects Today, Emkay Research

Exhibit 37: In YTDFY16, contracts awarded increased in most sectors - Number Terms

Source: Projects Today, Emkay Research

Roadways9%

Power Distribution

9%

Power Equipments

16%

Railways50%

Real Estate3%

Process1%

Pipeline0%

Infrastructure0%

Water3% Irrigation

2%

Community Services

0%

Others7%

Roadways33%

Power Distribution

8%Power

Equipments9%

Railways7%

Real Estate5%

Process8%

Pipeline2%

Infrastructure0%

Water1%

Irrigation6%

Community Services

12%

Hospitals1%

Others8%

0 200000 400000 600000

RoadwaysPower DistributionPower Equipments

RailwaysReal Estate

ProcessPipeline

InfrastructureWater

IrrigationMining

Community ServicesHospitals

OthersRs Million

YTDFY15 YTDFY16

0 100 200 300 400

RoadwaysPower Distribution

Power EquipmentsRailways

Real EstateProcessPipeline

InfrastructureWater

IrrigationMining

Community…Hospitals

Others Number of Contracts

YTDFY15 YTDFY16

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 10

Exhibit 38: Projects awarded November 2015 up 20.9% YoY

Source: Projects Today, Emkay Research

Exhibit 39: Projects awarded in November 2015 up significantly YoY

Source: Projects Today, Emkay Research

Exhibit 40: Projects awarded November 2015 +124.2% YoY

Source: Projects Today, Emkay Research

Exhibit 41: Projects awarded November 2015 up 2044% YoY

Source: Projects Today, Emkay Research

Exhibit 42: Projects awarded November 2015 up 36.9% YoY

Source: Projects Today, Emkay Research

Exhibit 43: Projects awarded November 2015 up 208.5% YoY

Source: Projects Today, Emkay Research

Exhibit 44: Projects awarded November 2015 up significantly YoY

Source: Projects Today, Emkay Research

Exhibit 45: Projects awarded November 2015 down 13.7% YoY

Source: Projects Today, Emkay Research

-500

0

500

1000

1500

0

20000

40000

60000

80000

100000

120000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Roadways

Roadways YoY - Growth

-20000

0

20000

40000

60000

80000

0

10000

20000

30000

40000

50000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Irrigation

Irrigation YoY - Growth

-5000

0

5000

10000

15000

0

10000

20000

30000

40000

50000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Water

Water YoY - Growth

-500

0

500

1000

1500

2000

2500

0

50000

100000

150000

200000

Nov-13

Mar-14 Jul-14 Nov-14

Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Railways

Railways YoY - Growth

-2000

0

2000

4000

6000

0

20000

40000

60000

80000

100000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Power Distribution

Power Distribution YoY - Growth

-500

0

500

1000

1500

2000

0

50,000

100,000

150,000

200,000

250,000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Power Equipments

Power Equipments YoY - Growth

-1000

0

1000

2000

3000

4000

0

10000

20000

30000

40000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Real Estate

Real Estate YoY - Growth

-2000

0

2000

4000

6000

8000

10000

0

10000

20000

30000

40000

50000

Nov-13 Mar-14 Jul-14 Nov-14 Mar-15 Jul-15 Nov-15

YoY

Gro

wth

(%

)

In R

s M

n

Community Services + Hospitals

Community Services + Hospitals YoY - Growth

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 11

Key Highlights – Projects Awarded

During November 2015, a total of 135 contracts with order value totaling Rs303.01 bn were

awarded. These orders (domestic as well as overseas) were bagged by 102 companies across

various sectors. Further, of the 135 finalized contracts, 5 were bagged by Indian companies to

execute job work overseas.

Indian Railways issued Letter of Award (LoA) for setting up of the Diesel Locomotive Factory at

Marhowra in Saran district of Bihar to USA-based company M/s. GE Global Sourcing India. A

joint venture company between the Ministry of Railways and GE Global Sourcing India will be

created to build and run the factory. The factory to manufacture and supply Modern Diesel

Electric Locomotives of 4500 HP and 6000 HP to Indian Railways. These locos, in combination

can operate as 9000 HP and 12000 HP multiple units (1000 locos to be manufactured in a period

of ten years).

Bharat Heavy Electricals Limited (BHEL) secured the second largest project orders worth

Rs46.14 bn for setting up two Supercritical Thermal Power projects involving one unit each of

800 MW sets, in Andhra Pradesh. The projects are 1x800 MW Dr. Narla Tata Rao Thermal

Power Station (Dr NTTPS) Stage-V of Andhra Pradesh Power Generation Corporation

(APGENCO) and 1x800 MW Sri Damodaram Sanjeevaiah Thermal Power Station (SDSTPS)

Stage-II, popularly known as Krishnapatnam Supercritical Thermal Power Project, of Andhra

Pradesh Power Development Company (APPDCL). The scope of work in the projects includes

supply, erection and commissioning of boilers, turbines, generators and associated auxiliaries.

The third largest contract, valued at Rs10.24 bn, was bagged by Pratibha Industries from

Government of Telangana, Rural Water Supply & Sanitation Department, TWPS., Circle,

Karimnagar (Water Supply Project) for providing drinking water to habitations in LMD-

Karimnagar, Ramadugu Segment & LMD-Manakondur, Husnabad, Huzurabad Segment in

Telangana including operation and maintenance for 10 years. The project was scheduled for

completion in 30 months.

The roadways sector saw the finalization of 40 new contracts worth Rs26.5 bn. The largest

contract in the sector was finalized by National Highways Authority of India (NHAI), for a Rs6.44

bn job to PNC Infratech for improvement / augmentation of Aligarh-Moradabad section of NH-

93 to two lane with paved shoulders from km 85.650 to km 232.020 in Uttar Pradesh under NHDP

Phase-IV on EPC basis. The project is scheduled for completion in 30 months.

During November 2015, fourteen contracts worth Rs27.69 bn were awarded in the power

distribution sector. Power Grid Corporation of India (PGCIL) owned 11 of the 14 contracts

finalized in the month. However, the largest contract in this sector was finalized by the Saudi

Electricity Company. The company awarded a Rs7.18 bn job to Larsen & Toubro (L&T) for

construction of five 132 kV substations at Hail in Saudi Arabia. The scope involves detailed

design, engineering, construction, testing and commissioning of 132 kV gas insulated

switchgear, 132/13.8 kV, 50/67 MVA power transformers, 132/33 kV, 80/100 MVA power

transformers, 13.8 kV switchgears, 33 kV switchgear, control and protection systems, substation

automation systems, HVAC, Novec firefighting system, along with associated auxiliary system

and civil works.

Overseas Contract

In November 2015, Indian companies bagged five overseas contracts worth Rs28.1 bn in

Heavy/Light Commercial Vehicles, Power Distribution, Crude Oil/POL Pipeline & Solar based

Power sectors from countries like the South Africa, Saudi Arabia, USA & Philippines.

The largest overseas contract, valued at Rs13.34 bn was bagged by Ashok Leyland from

Government of Cote D’Ivoire for supply of 3600 vehicles. This contract is being funded by EXIM

Bank of India and the company has to supply the trucks and buses over the next 12 months.

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 12

Other Developments

The last date for submission of bids for the construction of six lane elevated road from

Basaveshwara Circle to Hebbal Flyover via Le-Meridien Hotel and Mekhri Circle in Bengaluru

was extended up to 26 December 2015.

National Highways Authority of India has cancelled its tender issued on 30 October 2014 for four-

laning of Aunta-Simaria (Ganga Bridge with approach road) section of NH 31 from km 197.900

to 206.050 (design chainage) and (existing chainage km 204.741 to km 209.945 of NH-31) [total

design length - 8.150 km] in the state of Bihar on EPC basis due to change in contract model.

The project is now proposed to be taken up on Hybrid Annuity mode instead of EPC mode.

Lack of participation forced tender issuing authorities to extend the last date of submission of

504 project tenders and cancellation of around four tenders during November 2015.

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 13

Highway Pulse

NHAI awards contracts worth Rs304 bn/2721 Km in YTDFY16

NHAI has awarded projects amounting to Rs304 bn/2721 km in YTDFY16. The NHAI

awarded EPC contracts worth Rs196 bn/1918 km and awarded BOT contracts worth

Rs108 bn/803 km.

As far as the competitive intensity is concerned in the EPC projects, out of the 35 projects

awarded so far, 13 were bid at a discount of 1-20% to benchmark cost, two at par while

12 projects went at a premium of about 1.4-28%.

During the month NHAI came out with tenders on additional 10 projects (Rs82.25 bn/409

km) under the Hybrid Annuity model of which 2 projects were earlier tendered in EPC

mode (Rs13.6 bn/60 km) and another 2 projects were earlier tendered as a single BOT

Toll project (Rs18.2 bn/105 km).

Sadbhav Engg won two EPC projects on a continuous stretch, UP/Haryana border-

Yamunanagar-Saha-Barwala-Panchkula Section Packages 1 & 2. In Package 1 (44.3 km),

L1 was Sadbhav Engg at Rs4.68 bn, L2 was PNC Infratech at Rs5.14 bn. In Package 2

(45.2 km) L1 was Sadbhav Engg at Rs4.37 bn, L2 was KSS-Ramky Infra at Rs4.59 bn.

In Solapur-Bijapur BOT project, L1 was Uniquest Infra Ventures at a premium of Rs68 mn,

L2 was Essel Infra at a grant of Rs1700 mn.

In Guna-Biora BOT project, L1 was Dilip Buildcon at a grant of Rs270 mn, L2 was Oriental

Structures at a grant of Rs990 mn, L3 was Sadbhav Engg at a grant Rs1860 mn, L4 was

ITNL at a grant of Rs3545 mn and L5 was IRCON at a grant of Rs3900 mn.

In Biora-Dewas BOT project, L1 was Oriental Structures at a grant of Rs2528.9 mn, L2

was Sadbhav Engg at a grant of Rs4860 mn, L3 was Essel at a grant of Rs4950 mn, and

L4 was ITNL at a grant of Rs5543 mn.

IL&FS Transportation won two BOT projects on a single stretch, National Highway 6. In

Fagne-Maha/Guj border (Package 3), L1 was IL&FS Transportation at a grant of Rs2450

mn, L2 was Essel Infra at a grant of Rs2520 mn, L3 was Sadbhav Engg at a Grant Rs3960

mn and L4 was ACL at a grant Rs6580 mn. In Amravati-Chikli (Package 1), L1 was IL&FS

Transportation at a grant of Rs1835 mn, L2 was Sadbhav Engg at a grant Rs3150 mn, L3

was IRB Infra at a grant Rs5850 mn, L4 was Essel Infra at a grant Rs6030 mn and L5 was

TRIL at a grant of Rs7380 mn.

PNC Infratech declared the L1 Bidders for two roads projects of National Highways

Authority of India for an aggregate project cost of Rs. 15.06 bn (PNC Share Rs9.30 bn).

The projects involve rehabilitation and augmentation of four laning of Koilwar – Bhojpur

won at a project cost of Rs8.25 bn won 1.4% premium to the benchmark cost. Second

lowest bidder (L2) was BSCPL Infrastructure which bid the project at Rs8.7 bn. Third

lowest bidder (L3) was HCC which bid the project at Rs9.2 bn. Bhojpur - Buxar section

won at a project cost of Rs6.81 bn, 6% premium to the benchmark cost. Second lowest

bidder (L2) was Ashoka Buildcon which bid the project at Rs7.09 bn. Third lowest bidder

(L3) was BSCPL which bid the project at Rs7.3 bn

The NHAI has awarded six packages of Eastern peripheral expressway project.

Package 1 -22 km. Sadbhav Engg has quoted project cost of Rs7.92 bn in line with NHAI

benchmark cost of Rs7.71 bn. The L2 in this project was L&T quoted Rs8.39 bn and L3

was GR Infrastructure quoted Rs8.74 bn.

Package 2 -24 km. Sadbhav Engg has quoted project cost of Rs7.56 bn in line with NHAI

benchmark cost of Rs7.85 bn. The L2 in this project was L&T quoted Rs8.20 bn and L3

was GR Infrastructure quoted Rs8.34 bn.

Package 3 – 24.5 km L1 Lowest bidder JP associates Quoted project cost at 7.47 bn

5% below the NHAI benchmark cost , L2 was Corson corivam at Rs7.76 bn

Package 4 - 22 km L1 Ashoka Buildcon quoted project cost at Rs7.89 bn in line NHAI

benchmark cost , L2 Oriental structures quoted at 7.98 bn

Package 5 - 21 km L1 Oriental structures bid 1% below the NHAI benchmark cost ,

and L2 was Ashoka Buildcon at Rs6.84 bn

Package 6 – 22 Km L1 Gayatri projects bid the project 12% below the benchmark cost,

L2 was GR Infrastructure at Rs6.98 bn.

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 14

Gayatri Projects won another 4 EPC projects in the state of West Bengal, 2 projects on

the contiguous stretch of NH-233, 4 laning Ghaghra Bridge to Varanasi section, package

1, 60 kms at a premium of 11.1% and package 2, 59 kms at a premium of 14.3%.

L&T won its second NHAI project for the year, in EPC mode, 4 laning of Baharagora to

Singhara section of NH-6 at adiscount of 18.2%.

In September 2015, NHAI awarded the 4 packages of JNPT roads (57 kms) in EPC mode,

of which one package was won by Ashoka Buildcon (10.6 kms, awarded cost Rs4.14 bn)

at a premium of 4.7% while the other three packages were won by a JV of J. Kumar

Infraprojects and J.M. Mhatre Infra (46.3 kms, awarded cost Rs16.34 bn) where J. Kumar

Infra’s share is Rs10.65 bn.

PNC Infratech was declared L1 in the Aligarh Moradabad Road Project (146.4 kms),

awarded at Rs6.45 bn (+28% premium to benchmark), L2 was NCC at Rs7 bn.

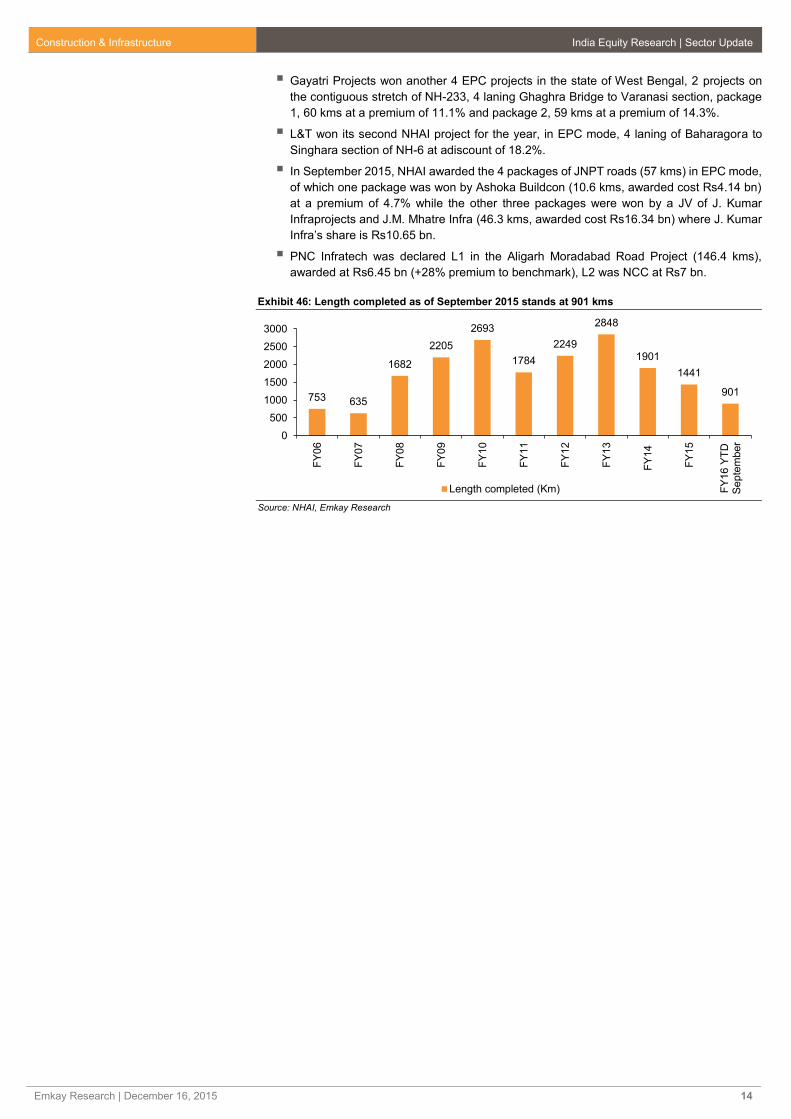

Exhibit 46: Length completed as of September 2015 stands at 901 kms

Source: NHAI, Emkay Research

753 635

1682

2205

2693

1784

2249

2848

1901

1441

901

0

500

1000

1500

2000

2500

3000

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16 Y

TD

Se

pte

mber

Length completed (Km)

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 15

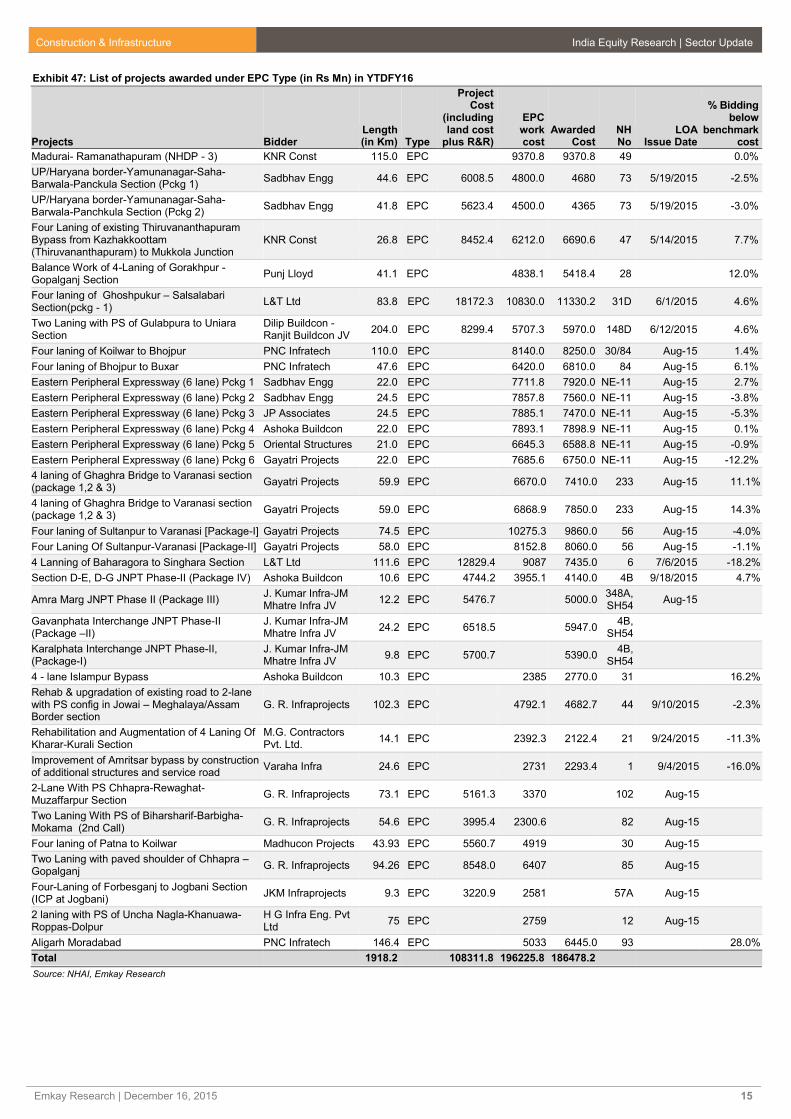

Exhibit 47: List of projects awarded under EPC Type (in Rs Mn) in YTDFY16

Projects Bidder Length (in Km) Type

Project Cost

(including land cost

plus R&R)

EPC work cost

Awarded Cost

NH No

LOA Issue Date

% Bidding below

benchmark cost

Madurai- Ramanathapuram (NHDP - 3) KNR Const 115.0 EPC 9370.8 9370.8 49 0.0%

UP/Haryana border-Yamunanagar-Saha-Barwala-Panckula Section (Pckg 1)

Sadbhav Engg 44.6 EPC 6008.5 4800.0 4680 73 5/19/2015 -2.5%

UP/Haryana border-Yamunanagar-Saha-Barwala-Panchkula Section (Pckg 2)

Sadbhav Engg 41.8 EPC 5623.4 4500.0 4365 73 5/19/2015 -3.0%

Four Laning of existing Thiruvananthapuram Bypass from Kazhakkoottam (Thiruvananthapuram) to Mukkola Junction

KNR Const 26.8 EPC 8452.4 6212.0 6690.6 47 5/14/2015 7.7%

Balance Work of 4-Laning of Gorakhpur - Gopalganj Section

Punj Lloyd 41.1 EPC 4838.1 5418.4 28 12.0%

Four laning of Ghoshpukur – Salsalabari Section(pckg - 1)

L&T Ltd 83.8 EPC 18172.3 10830.0 11330.2 31D 6/1/2015 4.6%

Two Laning with PS of Gulabpura to Uniara Section

Dilip Buildcon - Ranjit Buildcon JV

204.0 EPC 8299.4 5707.3 5970.0 148D 6/12/2015 4.6%

Four laning of Koilwar to Bhojpur PNC Infratech 110.0 EPC 8140.0 8250.0 30/84 Aug-15 1.4%

Four laning of Bhojpur to Buxar PNC Infratech 47.6 EPC 6420.0 6810.0 84 Aug-15 6.1%

Eastern Peripheral Expressway (6 lane) Pckg 1 Sadbhav Engg 22.0 EPC 7711.8 7920.0 NE-11 Aug-15 2.7%

Eastern Peripheral Expressway (6 lane) Pckg 2 Sadbhav Engg 24.5 EPC 7857.8 7560.0 NE-11 Aug-15 -3.8%

Eastern Peripheral Expressway (6 lane) Pckg 3 JP Associates 24.5 EPC 7885.1 7470.0 NE-11 Aug-15 -5.3%

Eastern Peripheral Expressway (6 lane) Pckg 4 Ashoka Buildcon 22.0 EPC 7893.1 7898.9 NE-11 Aug-15 0.1%

Eastern Peripheral Expressway (6 lane) Pckg 5 Oriental Structures 21.0 EPC 6645.3 6588.8 NE-11 Aug-15 -0.9%

Eastern Peripheral Expressway (6 lane) Pckg 6 Gayatri Projects 22.0 EPC 7685.6 6750.0 NE-11 Aug-15 -12.2%

4 laning of Ghaghra Bridge to Varanasi section (package 1,2 & 3)

Gayatri Projects 59.9 EPC 6670.0 7410.0 233 Aug-15 11.1%

4 laning of Ghaghra Bridge to Varanasi section (package 1,2 & 3)

Gayatri Projects 59.0 EPC 6868.9 7850.0 233 Aug-15 14.3%

Four laning of Sultanpur to Varanasi [Package-I] Gayatri Projects 74.5 EPC 10275.3 9860.0 56 Aug-15 -4.0%

Four Laning Of Sultanpur-Varanasi [Package-II] Gayatri Projects 58.0 EPC 8152.8 8060.0 56 Aug-15 -1.1%

4 Lanning of Baharagora to Singhara Section L&T Ltd 111.6 EPC 12829.4 9087 7435.0 6 7/6/2015 -18.2%

Section D-E, D-G JNPT Phase-II (Package IV) Ashoka Buildcon 10.6 EPC 4744.2 3955.1 4140.0 4B 9/18/2015 4.7%

Amra Marg JNPT Phase II (Package III) J. Kumar Infra-JM Mhatre Infra JV

12.2 EPC 5476.7 5000.0 348A, SH54

Aug-15

Gavanphata Interchange JNPT Phase-II (Package –II)

J. Kumar Infra-JM Mhatre Infra JV

24.2 EPC 6518.5 5947.0 4B,

SH54

Karalphata Interchange JNPT Phase-II, (Package-I)

J. Kumar Infra-JM Mhatre Infra JV

9.8 EPC 5700.7 5390.0 4B,

SH54

4 - lane Islampur Bypass Ashoka Buildcon 10.3 EPC 2385 2770.0 31 16.2%

Rehab & upgradation of existing road to 2-lane with PS config in Jowai – Meghalaya/Assam Border section

G. R. Infraprojects 102.3 EPC 4792.1 4682.7 44 9/10/2015 -2.3%

Rehabilitation and Augmentation of 4 Laning Of Kharar-Kurali Section

M.G. Contractors Pvt. Ltd.

14.1 EPC 2392.3 2122.4 21 9/24/2015 -11.3%

Improvement of Amritsar bypass by construction of additional structures and service road

Varaha Infra 24.6 EPC 2731 2293.4 1 9/4/2015 -16.0%

2-Lane With PS Chhapra-Rewaghat-Muzaffarpur Section

G. R. Infraprojects 73.1 EPC 5161.3 3370 102 Aug-15

Two Laning With PS of Biharsharif-Barbigha-Mokama (2nd Call)

G. R. Infraprojects 54.6 EPC 3995.4 2300.6 82 Aug-15

Four laning of Patna to Koilwar Madhucon Projects 43.93 EPC 5560.7 4919 30 Aug-15

Two Laning with paved shoulder of Chhapra – Gopalganj

G. R. Infraprojects 94.26 EPC 8548.0 6407 85 Aug-15

Four-Laning of Forbesganj to Jogbani Section (ICP at Jogbani)

JKM Infraprojects 9.3 EPC 3220.9 2581 57A Aug-15

2 laning with PS of Uncha Nagla-Khanuawa-Roppas-Dolpur

H G Infra Eng. Pvt Ltd

75 EPC 2759 12 Aug-15

Aligarh Moradabad PNC Infratech 146.4 EPC 5033 6445.0 93 28.0%

Total 1918.2 108311.8 196225.8 186478.2

Source: NHAI, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 16

Exhibit 48: List of projects awarded under BOT Type (in Rs Mn) in YTDFY16

Projects Bidder

Length

(in Km) Type

Project

Cost

(Rs Mn)

Awarded

Cost

(Rs Mn) NH No

LOA Issue

Date

Six Laning of Agra – Etawah Bypass Section IRB Infra 124.5 BOT(Toll) 26500.0 Premium 810 2 7/6/2015

Four/Six Laning of Solapur- Bijapur Section Uniquest 109.1 DBFOT (Toll) 13775.4 Premium 70 52 5/20/2015

Four laning of Guna - Biora Dilip Buildcon 93.5 BOT 10129.0 Grant 270 3 6/29/2015

Four laning of Biora –Dewas Oriental Structures 141.3 BOT 15837.9 Grant 2528.9 3 6/29/2015

4/6-laning of Fagne – MAH/Guj Border (Pckg-III) IL&FS Transportation 140.8 DBFOT 18857.4 Grant 2450 6 7/25/2015

4/6 laning of Amravati-Chikli (Pckg-I) IL&FS Transportation 194.0 DBFOT 22881.8 Grant 1835 6 7/24/2015

Total 803.1 107981.5

Source: NHAI, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 17

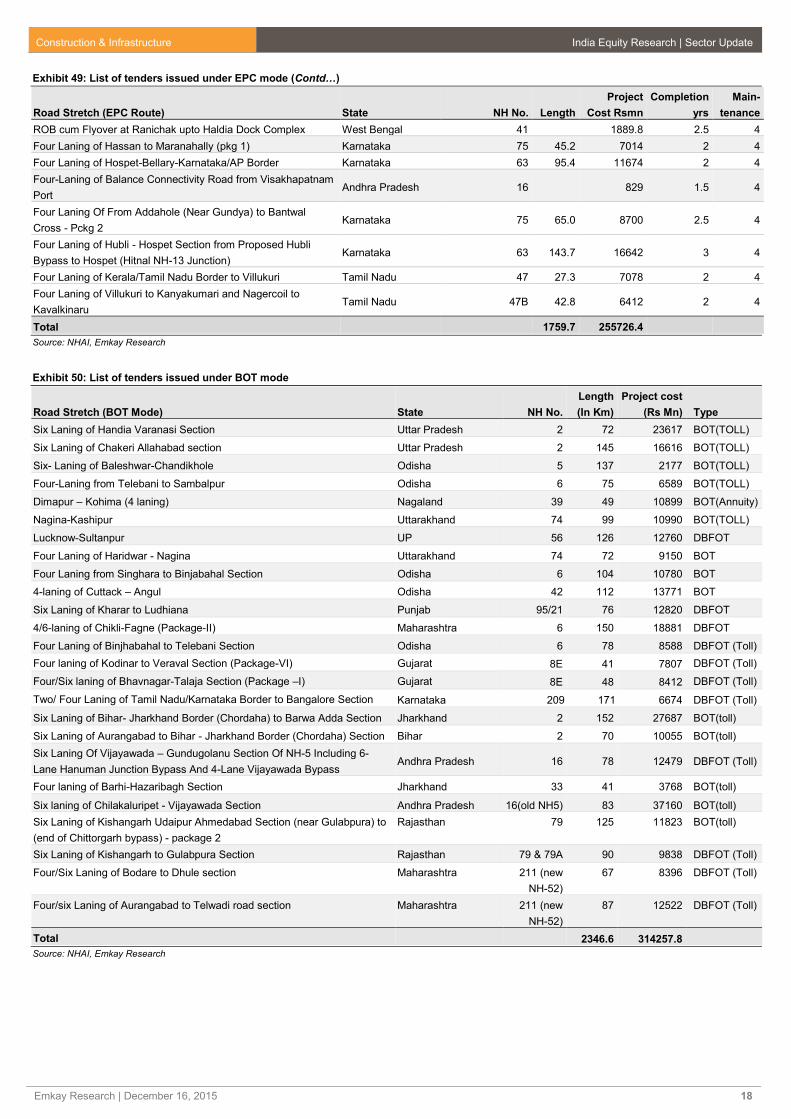

Exhibit 49: List of tenders issued under EPC mode

Road Stretch (EPC Route) State NH No. Length

Project

Cost Rsmn

Completion

yrs

Main-

tenance

4-laning of Varanasi Gorakhpur section [Package-III Birnon

Village To Amilla Village] Uttar Pradesh 29 60.0 8523.2 2.5 4

4-laning of Varanasi Gorakhpur section [Package-IV Amilla

Village to Gorakhpur] Uttar Pradesh 29 60.3 10381.5 2.5 4

Four laning of Ghoshpukur – Salsalabari Section (pckg - 2) West Bengal 31D 71.1 9720.0

Two Laning with paved shoulder of Chhapra – Gopalganj Bihar 85 94.3 6406.8

Four laning of Yadgiri- Warangal Section Telangana 163 99.1 11410.0

Four laning of Bakhtiyarpur – Mokama section Bihar 31 44.6 9861.4

Four laning of Simaria- Khagaria Bihar 31 60.2 6072.5

Four laning of Aunta – Simaria (Ganga bridge with approach rd) Bihar 31 8.2 4898.9 2.5 4

Four Laning of Nerchowk-Kullu stretch [Aut-Takoli Section

(Tunnel), Package-V] Himachal Pradesh 21 6.7 5561.1 2.5 4

Four laning of Nerchowk - Kullu stretch [Rehukaldhar - Aut

Section (Tunnel), Package-IV] Himachal Pradesh 21 4.6 5751.4 2.5 4

Nerchowk-Kullu stretch [Bata-Rehukaldhar Section (Tunnel),

Package-III] Himachal Pradesh 21 2.6 3774.3 2.5 4

Four laning of Nerchowk-Kullu stretch [Pandoh-Bata Section

(Tunnel), Package-II] Himachal Pradesh 21 13.0 6907.8 2.5 4

Dalkhola Bypass section from Design Chainage West Bengal 34 5.4 809.3 2 4

4-laning of Varanasi Gorakhpur [package-II from Sandah to

Birnon] Uttar Pradesh 29 76.0 8566.4 2.5 4

Service Road and RCC Drain incld. Storage Lane at Chat

Junction on Ambala-Chandigarh Punjab

22

(new NH-152) 2.8 240.6

Upgradation of Kullu-Manali section from Km 272.00 to Km

309.345 (Designed Chainage) Himachal Pradesh

NH-21

(now NH-3) 37.3 2184.7 2 4

Rehabilitation and upgradation of Birmitrapur – Barkote section

by Two/Four laning of NH – 23 Odisha 23 126.0 8600.5 2.5 4

Four Laning With PS From Chichra To Kharagpur West Bengal 6 50.8 7696.3 2.5 4

Six laning of Kamrej - Chalthan Section Gujarat 8 16.3 2994.4 2 3

Flyover at (km 544/650), including ROB incld Services Roads,

Footpath for RCC drains on Urban link to Nagpur-Raipur road Maharashtra 6 4086 3 4

Four laning of Chandigarh-Kharar section from Sector-39

(Round about) at Chandigarh to Kharar Punjab 21 & 95 10.2 4473 2.5 4

Rehab & Upgradation of Four Laning with PS of Talibani to

Sambalpur Section Odisha 6 50.7 5228 2.5 4

4 Laning of Sargaon- Bilaspuraa (Package III) Chhattisgarh 200

(new NH130) 35.5 4132 2 4

4 Laning of Simga - Sargaon (Package II) Chhattisgarh

200 (new

NH130) 42.4 4784 2 4

4/6 laning of Raipur- Simga (Package I) Chhattisgarh

200 (new

NH130) 48.6 5867 2 4

4- Laning of Vijayawada – Machilipatnam Andhra Pradesh 9 64.6 8711 2 4

Rehab & upgrade of Jharpokharia Baripada Baleshwar section Odisha 5 80.6 8571 2.5 4

Four laning of Haridwar Nagina section Uttarakhand/UP 74 73.0 9895 2.5 4

Four Laning of Nagina-Kashipur section Uttarakhand/UP 74 102.0 12908 2.5 4

Six laning of Kamrej - Chalthan Section Gujarat 8 16.3 2994 2 3

New 4 lane Bridge across Varsova Creek & its approaches with

Interchange on NH-8 (New NH-48) between Surat –Dahisar

section

Maharashtra 8 (New NH-

48) 1651 2 4

Four Laning of Mahulia-Baharagora- JH/WB Border Section of

NH-33 & NH-6 Jharkhand 33 & 6 71.6 8233 2.5 4

ROB cum Flyover at Ranichak upto Haldia Dock Complex West Bengal 41 1889.8 2.5 4

New 4 lane Bridge across Varsova Creek & its approaches with

Interchange on NH-8 (New NH-48) between Surat –Dahisar Maharashtra

8 (New NH-

48) 1651 2 4

Four Laning of Mahulia-Baharagora- JH/WB Border Section of

NH-33 & NH-6 Jharkhand 33 & 6 71.6 8233 2.5 4

Source: NHAI, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 18

Exhibit 49: List of tenders issued under EPC mode (Contd…)

Road Stretch (EPC Route) State NH No. Length

Project

Cost Rsmn

Completion

yrs

Main-

tenance

ROB cum Flyover at Ranichak upto Haldia Dock Complex West Bengal 41 1889.8 2.5 4

Four Laning of Hassan to Maranahally (pkg 1) Karnataka 75 45.2 7014 2 4

Four Laning of Hospet-Bellary-Karnataka/AP Border Karnataka 63 95.4 11674 2 4

Four-Laning of Balance Connectivity Road from Visakhapatnam

Port Andhra Pradesh 16 829 1.5 4

Four Laning Of From Addahole (Near Gundya) to Bantwal

Cross - Pckg 2 Karnataka 75 65.0 8700 2.5 4

Four Laning of Hubli - Hospet Section from Proposed Hubli

Bypass to Hospet (Hitnal NH-13 Junction) Karnataka 63 143.7 16642 3 4

Four Laning of Kerala/Tamil Nadu Border to Villukuri Tamil Nadu 47 27.3 7078 2 4

Four Laning of Villukuri to Kanyakumari and Nagercoil to

Kavalkinaru Tamil Nadu 47B 42.8 6412 2 4

Total 1759.7 255726.4

Source: NHAI, Emkay Research

Exhibit 50: List of tenders issued under BOT mode

Road Stretch (BOT Mode) State NH No.

Length

(In Km)

Project cost

(Rs Mn) Type

Six Laning of Handia Varanasi Section Uttar Pradesh 2 72 23617 BOT(TOLL)

Six Laning of Chakeri Allahabad section Uttar Pradesh 2 145 16616 BOT(TOLL)

Six- Laning of Baleshwar-Chandikhole Odisha 5 137 2177 BOT(TOLL)

Four-Laning from Telebani to Sambalpur Odisha 6 75 6589 BOT(TOLL)

Dimapur – Kohima (4 laning) Nagaland 39 49 10899 BOT(Annuity)

Nagina-Kashipur Uttarakhand 74 99 10990 BOT(TOLL)

Lucknow-Sultanpur UP 56 126 12760 DBFOT

Four Laning of Haridwar - Nagina Uttarakhand 74 72 9150 BOT

Four Laning from Singhara to Binjabahal Section Odisha 6 104 10780 BOT

4-laning of Cuttack – Angul Odisha 42 112 13771 BOT

Six Laning of Kharar to Ludhiana Punjab 95/21 76 12820 DBFOT

4/6-laning of Chikli-Fagne (Package-II) Maharashtra 6 150 18881 DBFOT

Four Laning of Binjhabahal to Telebani Section Odisha 6 78 8588 DBFOT (Toll)

Four laning of Kodinar to Veraval Section (Package-VI) Gujarat 8E 41 7807 DBFOT (Toll)

Four/Six laning of Bhavnagar-Talaja Section (Package –I) Gujarat 8E 48 8412 DBFOT (Toll)

Two/ Four Laning of Tamil Nadu/Karnataka Border to Bangalore Section Karnataka 209 171 6674 DBFOT (Toll)

Six Laning of Bihar- Jharkhand Border (Chordaha) to Barwa Adda Section Jharkhand 2 152 27687 BOT(toll)

Six Laning of Aurangabad to Bihar - Jharkhand Border (Chordaha) Section Bihar 2 70 10055 BOT(toll)

Six Laning Of Vijayawada – Gundugolanu Section Of NH-5 Including 6-

Lane Hanuman Junction Bypass And 4-Lane Vijayawada Bypass Andhra Pradesh 16 78 12479 DBFOT (Toll)

Four laning of Barhi-Hazaribagh Section Jharkhand 33 41 3768 BOT(toll)

Six laning of Chilakaluripet - Vijayawada Section Andhra Pradesh 16(old NH5) 83 37160 BOT(toll)

Six Laning of Kishangarh Udaipur Ahmedabad Section (near Gulabpura) to

(end of Chittorgarh bypass) - package 2

Rajasthan 79 125 11823 BOT(toll)

Six Laning of Kishangarh to Gulabpura Section Rajasthan 79 & 79A 90 9838 DBFOT (Toll)

Four/Six Laning of Bodare to Dhule section Maharashtra 211 (new

NH-52)

67 8396 DBFOT (Toll)

Four/six Laning of Aurangabad to Telwadi road section Maharashtra 211 (new

NH-52)

87 12522 DBFOT (Toll)

Total 2346.6 314257.8

Source: NHAI, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 19

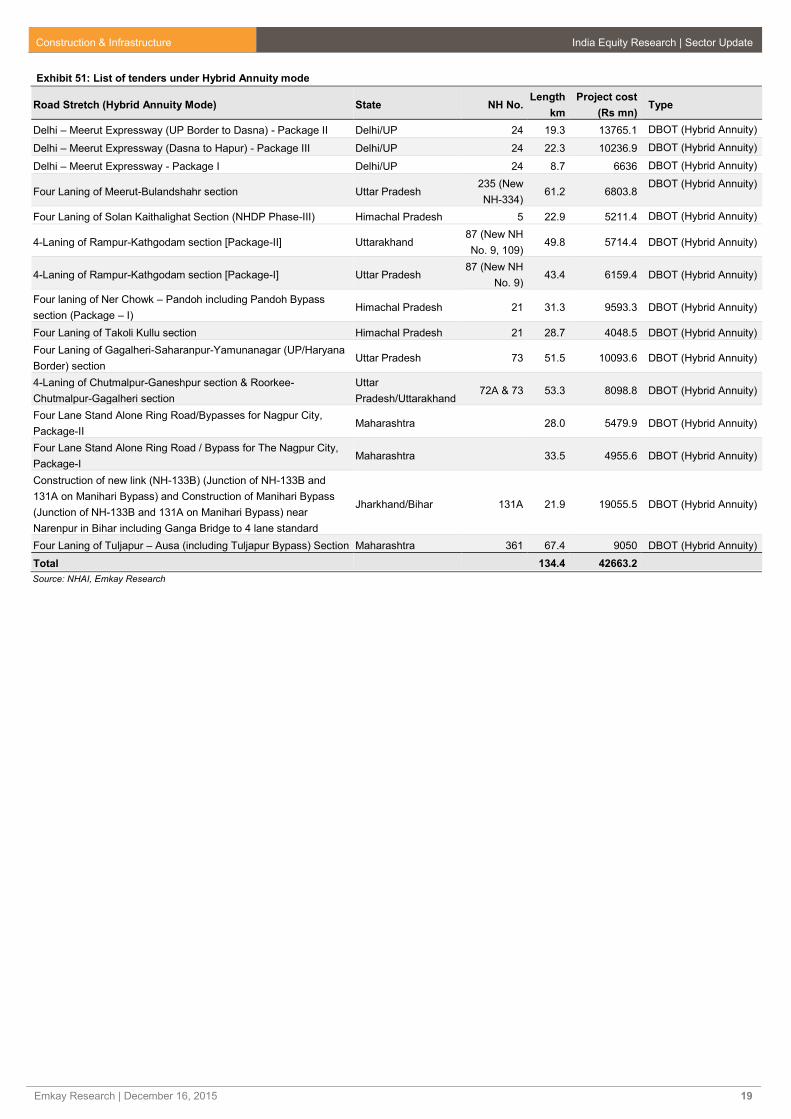

Exhibit 51: List of tenders under Hybrid Annuity mode

Road Stretch (Hybrid Annuity Mode) State NH No. Length

km

Project cost

(Rs mn) Type

Delhi – Meerut Expressway (UP Border to Dasna) - Package II Delhi/UP 24 19.3 13765.1 DBOT (Hybrid Annuity)

Delhi – Meerut Expressway (Dasna to Hapur) - Package III Delhi/UP 24 22.3 10236.9 DBOT (Hybrid Annuity)

Delhi – Meerut Expressway - Package I Delhi/UP 24 8.7 6636 DBOT (Hybrid Annuity)

Four Laning of Meerut-Bulandshahr section Uttar Pradesh 235 (New

NH-334) 61.2 6803.8

DBOT (Hybrid Annuity)

Four Laning of Solan Kaithalighat Section (NHDP Phase-III) Himachal Pradesh 5 22.9 5211.4 DBOT (Hybrid Annuity)

4-Laning of Rampur-Kathgodam section [Package-II] Uttarakhand 87 (New NH

No. 9, 109) 49.8 5714.4 DBOT (Hybrid Annuity)

4-Laning of Rampur-Kathgodam section [Package-I] Uttar Pradesh 87 (New NH

No. 9) 43.4 6159.4 DBOT (Hybrid Annuity)

Four laning of Ner Chowk – Pandoh including Pandoh Bypass

section (Package – I) Himachal Pradesh 21 31.3 9593.3 DBOT (Hybrid Annuity)

Four Laning of Takoli Kullu section Himachal Pradesh 21 28.7 4048.5 DBOT (Hybrid Annuity)

Four Laning of Gagalheri-Saharanpur-Yamunanagar (UP/Haryana

Border) section Uttar Pradesh 73 51.5 10093.6 DBOT (Hybrid Annuity)

4-Laning of Chutmalpur-Ganeshpur section & Roorkee-

Chutmalpur-Gagalheri section

Uttar

Pradesh/Uttarakhand 72A & 73 53.3 8098.8 DBOT (Hybrid Annuity)

Four Lane Stand Alone Ring Road/Bypasses for Nagpur City,

Package-II Maharashtra 28.0 5479.9 DBOT (Hybrid Annuity)

Four Lane Stand Alone Ring Road / Bypass for The Nagpur City,

Package-I Maharashtra 33.5 4955.6 DBOT (Hybrid Annuity)

Construction of new link (NH-133B) (Junction of NH-133B and

131A on Manihari Bypass) and Construction of Manihari Bypass

(Junction of NH-133B and 131A on Manihari Bypass) near

Narenpur in Bihar including Ganga Bridge to 4 lane standard

Jharkhand/Bihar 131A 21.9 19055.5 DBOT (Hybrid Annuity)

Four Laning of Tuljapur – Ausa (including Tuljapur Bypass) Section Maharashtra 361 67.4 9050 DBOT (Hybrid Annuity)

Total 134.4 42663.2

Source: NHAI, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 20

Port Pulse

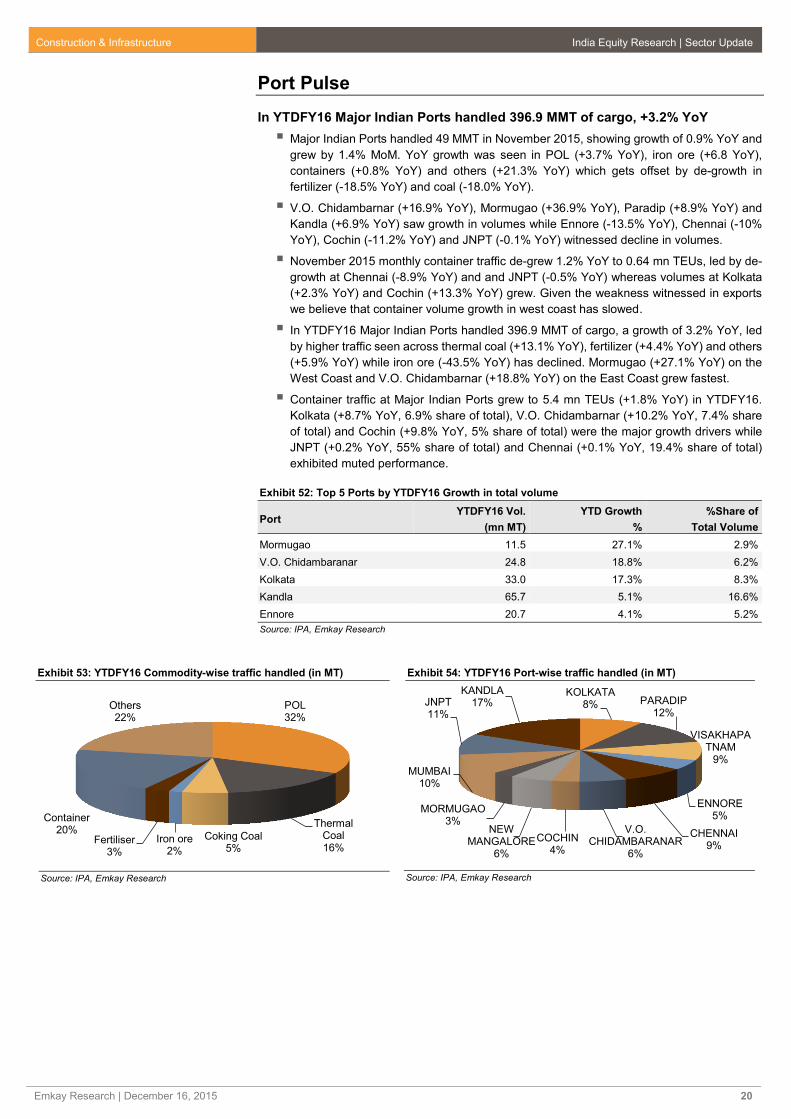

In YTDFY16 Major Indian Ports handled 396.9 MMT of cargo, +3.2% YoY

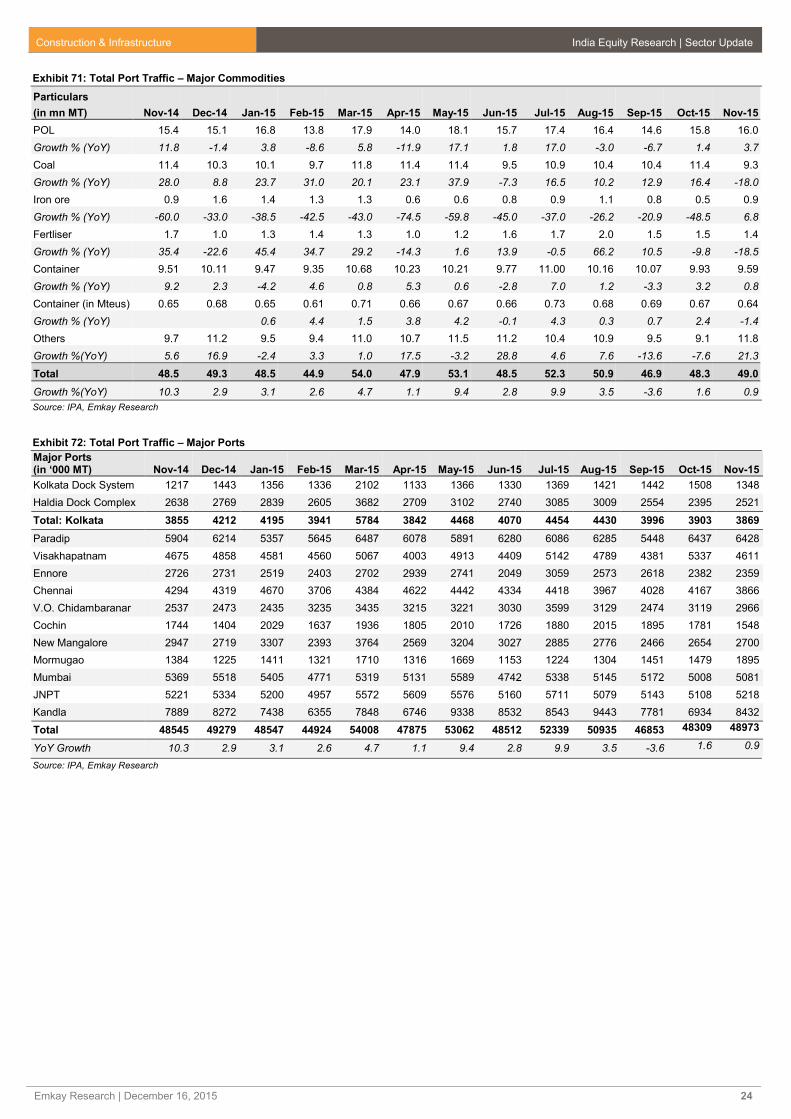

Major Indian Ports handled 49 MMT in November 2015, showing growth of 0.9% YoY and

grew by 1.4% MoM. YoY growth was seen in POL (+3.7% YoY), iron ore (+6.8 YoY),

containers (+0.8% YoY) and others (+21.3% YoY) which gets offset by de-growth in

fertilizer (-18.5% YoY) and coal (-18.0% YoY).

V.O. Chidambarnar (+16.9% YoY), Mormugao (+36.9% YoY), Paradip (+8.9% YoY) and

Kandla (+6.9% YoY) saw growth in volumes while Ennore (-13.5% YoY), Chennai (-10%

YoY), Cochin (-11.2% YoY) and JNPT (-0.1% YoY) witnessed decline in volumes.

November 2015 monthly container traffic de-grew 1.2% YoY to 0.64 mn TEUs, led by de-

growth at Chennai (-8.9% YoY) and and JNPT (-0.5% YoY) whereas volumes at Kolkata

(+2.3% YoY) and Cochin (+13.3% YoY) grew. Given the weakness witnessed in exports

we believe that container volume growth in west coast has slowed.

In YTDFY16 Major Indian Ports handled 396.9 MMT of cargo, a growth of 3.2% YoY, led

by higher traffic seen across thermal coal (+13.1% YoY), fertilizer (+4.4% YoY) and others

(+5.9% YoY) while iron ore (-43.5% YoY) has declined. Mormugao (+27.1% YoY) on the

West Coast and V.O. Chidambarnar (+18.8% YoY) on the East Coast grew fastest.

Container traffic at Major Indian Ports grew to 5.4 mn TEUs (+1.8% YoY) in YTDFY16.

Kolkata (+8.7% YoY, 6.9% share of total), V.O. Chidambarnar (+10.2% YoY, 7.4% share

of total) and Cochin (+9.8% YoY, 5% share of total) were the major growth drivers while

JNPT (+0.2% YoY, 55% share of total) and Chennai (+0.1% YoY, 19.4% share of total)

exhibited muted performance.

Exhibit 52: Top 5 Ports by YTDFY16 Growth in total volume

Port YTDFY16 Vol.

(mn MT)

YTD Growth

%

%Share of

Total Volume

Mormugao 11.5 27.1% 2.9%

V.O. Chidambaranar 24.8 18.8% 6.2%

Kolkata 33.0 17.3% 8.3%

Kandla 65.7 5.1% 16.6%

Ennore 20.7 4.1% 5.2%

Source: IPA, Emkay Research

Exhibit 53: YTDFY16 Commodity-wise traffic handled (in MT)

Source: IPA, Emkay Research

Exhibit 54: YTDFY16 Port-wise traffic handled (in MT)

Source: IPA, Emkay Research

POL32%

Thermal Coal16%

Coking Coal5%

Iron ore2%

Fertiliser3%

Container20%

Others22%

KOLKATA8% PARADIP

12%

VISAKHAPATNAM

9%

ENNORE5%

CHENNAI9%

V.O. CHIDAMBARANAR

6%

COCHIN4%

NEW MANGALORE

6%

MORMUGAO3%

MUMBAI10%

JNPT11%

KANDLA17%

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 21

Exhibit 55: In November 2015 Coal traffic de-grew 18% YoY

Source: IPA, Emkay Research

Exhibit 56: In November 2015 Container traffic grew 0.8% YoY

Source: IPA, Emkay Research

Exhibit 57: Overall Port Traffic for November 2015 rose by 0.9% YoY

Source: IPA, Emkay Research

Exhibit 58: Total Exports – Rs bn

Source: CMIE, Emkay Research

Exhibit 59: Total Imports – Rs bn

Source: CMIE, Emkay Research

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Nov-1

3

Jan

-14

Ma

r-14

Ma

y-1

4

Jul-1

4

Se

p-1

4

Nov-1

4

Jan

-15

Ma

r-15

May-1

5

Jul-1

5

Se

p-1

5

Nov-1

5

Coal (mn MT) Growth %(YoY)

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Nov-1

3

Jan

-14

Mar-

14

Ma

y-1

4

Jul-1

4

Se

p-1

4

Nov-1

4

Jan

-15

Ma

r-15

Ma

y-1

5

Jul-1

5

Se

p-1

5

Nov-1

5

Container (mn MT) Growth %(YoY)

-5.0

0.0

5.0

10.0

15.0

-

10.0

20.0

30.0

40.0

50.0

60.0

Nov-1

3

Dec-1

3

Jan

-14

Fe

b-1

4

Mar-

14

Ap

r-14

Ma

y-1

4

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-15

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Total Port Traffic (mn MT) Growth %(YoY)

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Exports Rs. Bn Y-o-Y % change

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

Oct-

13

Dec-1

3

Feb-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Imports Rs. Bn Y-o-Y % change

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 22

Exports of Major Commodities

Exhibit 60: Agriculture & Allied Products – Rs bn

Source: CMIE, Emkay Research

Exhibit 61: Chemical and Related products – Rs bn

Source: CMIE, Emkay Research

Exhibit 62: Total Manufactured Goods – Rs bn

Source: CMIE, Emkay Research

Exhibit 63: Engineering Goods – Rs bn

Source: CMIE, Emkay Research

Exhibit 64: Textiles – Rs bn

Source: CMIE, Emkay Research

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Agricultural and allied products Rs Bn YoY % change

-10.0

0.0

10.0

20.0

30.0

40.0

0.0

50.0

100.0

150.0

200.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Chemicals & related products Rs Bn YoY % change

-20.0-10.00.010.020.030.040.050.060.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Total Manufactured goods Rs Bn YoY % change

-40.0

-20.0

0.0

20.0

40.0

60.0

0.0

100.0

200.0

300.0

400.0

500.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Engineering goods Rs Bn YoY % change

-10.00.010.020.030.040.050.060.070.0

0.0

50.0

100.0

150.0

200.0

250.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Textiles Rs Bn YoY % change

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 23

Imports of Major Commodities

Exhibit 65: Agriculture & Allied Products – Rs bn

Source: CMIE, Emkay Research

Exhibit 66: Chemicals & Related Products – Rs bn

Source: CMIE, Emkay Research

Exhibit 67: Total Manufactured Goods – Rs bn

Source: CMIE, Emkay Research

Exhibit 68: Engineering Goods – Rs bn

Source: CMIE, Emkay Research

Exhibit 69: Electronic Goods – Rs bn

Source: CMIE, Emkay Research

Exhibit 70: Coking & Non-Coking Coal – mn MT

Source: CMIE, Emkay Research

-20.0

0.0

20.0

40.0

60.0

80.0

0.020.040.060.080.0

100.0120.0140.0160.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Agricultural and allied products Rs Bn YoY % change

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Chemicals & related products Rs Bn YoY % change

-30.0-20.0-10.00.010.020.030.040.050.060.0

0.0

500.0

1,000.0

1,500.0

2,000.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Total Manufactured goods Rs Bn YoY % change

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

0.0

100.0

200.0

300.0

400.0

500.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Engineering goods Rs Bn YoY % change

0.0

10.0

20.0

30.0

40.0

50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Electronic goods Rs Bn YoY % change

-

5.0

10.0

15.0

20.0

25.0

Ap

r-14

Ma

y-1

4

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Fe

b-1

5

Ma

r-15

Ap

r-15

Ma

y-1

5

Jun

-15

Jul-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Coking & Non-Coking Coal - mn MT

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 24

Exhibit 71: Total Port Traffic – Major Commodities

Particulars

(in mn MT) Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

POL 15.4 15.1 16.8 13.8 17.9 14.0 18.1 15.7 17.4 16.4 14.6 15.8 16.0

Growth % (YoY) 11.8 -1.4 3.8 -8.6 5.8 -11.9 17.1 1.8 17.0 -3.0 -6.7 1.4 3.7

Coal 11.4 10.3 10.1 9.7 11.8 11.4 11.4 9.5 10.9 10.4 10.4 11.4 9.3

Growth % (YoY) 28.0 8.8 23.7 31.0 20.1 23.1 37.9 -7.3 16.5 10.2 12.9 16.4 -18.0

Iron ore 0.9 1.6 1.4 1.3 1.3 0.6 0.6 0.8 0.9 1.1 0.8 0.5 0.9

Growth % (YoY) -60.0 -33.0 -38.5 -42.5 -43.0 -74.5 -59.8 -45.0 -37.0 -26.2 -20.9 -48.5 6.8

Fertliser 1.7 1.0 1.3 1.4 1.3 1.0 1.2 1.6 1.7 2.0 1.5 1.5 1.4

Growth % (YoY) 35.4 -22.6 45.4 34.7 29.2 -14.3 1.6 13.9 -0.5 66.2 10.5 -9.8 -18.5

Container 9.51 10.11 9.47 9.35 10.68 10.23 10.21 9.77 11.00 10.16 10.07 9.93 9.59

Growth % (YoY) 9.2 2.3 -4.2 4.6 0.8 5.3 0.6 -2.8 7.0 1.2 -3.3 3.2 0.8

Container (in Mteus) 0.65 0.68 0.65 0.61 0.71 0.66 0.67 0.66 0.73 0.68 0.69 0.67 0.64

Growth % (YoY) 0.6 4.4 1.5 3.8 4.2 -0.1 4.3 0.3 0.7 2.4 -1.4

Others 9.7 11.2 9.5 9.4 11.0 10.7 11.5 11.2 10.4 10.9 9.5 9.1 11.8

Growth %(YoY) 5.6 16.9 -2.4 3.3 1.0 17.5 -3.2 28.8 4.6 7.6 -13.6 -7.6 21.3

Total 48.5 49.3 48.5 44.9 54.0 47.9 53.1 48.5 52.3 50.9 46.9 48.3 49.0

Growth %(YoY) 10.3 2.9 3.1 2.6 4.7 1.1 9.4 2.8 9.9 3.5 -3.6 1.6 0.9

Source: IPA, Emkay Research

Exhibit 72: Total Port Traffic – Major Ports

Major Ports (in ‘000 MT) Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15

Kolkata Dock System 1217 1443 1356 1336 2102 1133 1366 1330 1369 1421 1442 1508 1348

Haldia Dock Complex 2638 2769 2839 2605 3682 2709 3102 2740 3085 3009 2554 2395 2521

Total: Kolkata 3855 4212 4195 3941 5784 3842 4468 4070 4454 4430 3996 3903 3869

Paradip 5904 6214 5357 5645 6487 6078 5891 6280 6086 6285 5448 6437 6428

Visakhapatnam 4675 4858 4581 4560 5067 4003 4913 4409 5142 4789 4381 5337 4611

Ennore 2726 2731 2519 2403 2702 2939 2741 2049 3059 2573 2618 2382 2359

Chennai 4294 4319 4670 3706 4384 4622 4442 4334 4418 3967 4028 4167 3866

V.O. Chidambaranar 2537 2473 2435 3235 3435 3215 3221 3030 3599 3129 2474 3119 2966

Cochin 1744 1404 2029 1637 1936 1805 2010 1726 1880 2015 1895 1781 1548

New Mangalore 2947 2719 3307 2393 3764 2569 3204 3027 2885 2776 2466 2654 2700

Mormugao 1384 1225 1411 1321 1710 1316 1669 1153 1224 1304 1451 1479 1895

Mumbai 5369 5518 5405 4771 5319 5131 5589 4742 5338 5145 5172 5008 5081

JNPT 5221 5334 5200 4957 5572 5609 5576 5160 5711 5079 5143 5108 5218

Kandla 7889 8272 7438 6355 7848 6746 9338 8532 8543 9443 7781 6934 8432

Total 48545 49279 48547 44924 54008 47875 53062 48512 52339 50935 46853 48309 48973

YoY Growth 10.3 2.9 3.1 2.6 4.7 1.1 9.4 2.8 9.9 3.5 -3.6 1.6 0.9

Source: IPA, Emkay Research

Construction & Infrastructure India Equity Research | Sector Update

Emkay Research | December 16, 2015 25

Power T&D Pulse

For YTDFY16 PGCIL awarding up 24% YoY at Rs121.3 bn

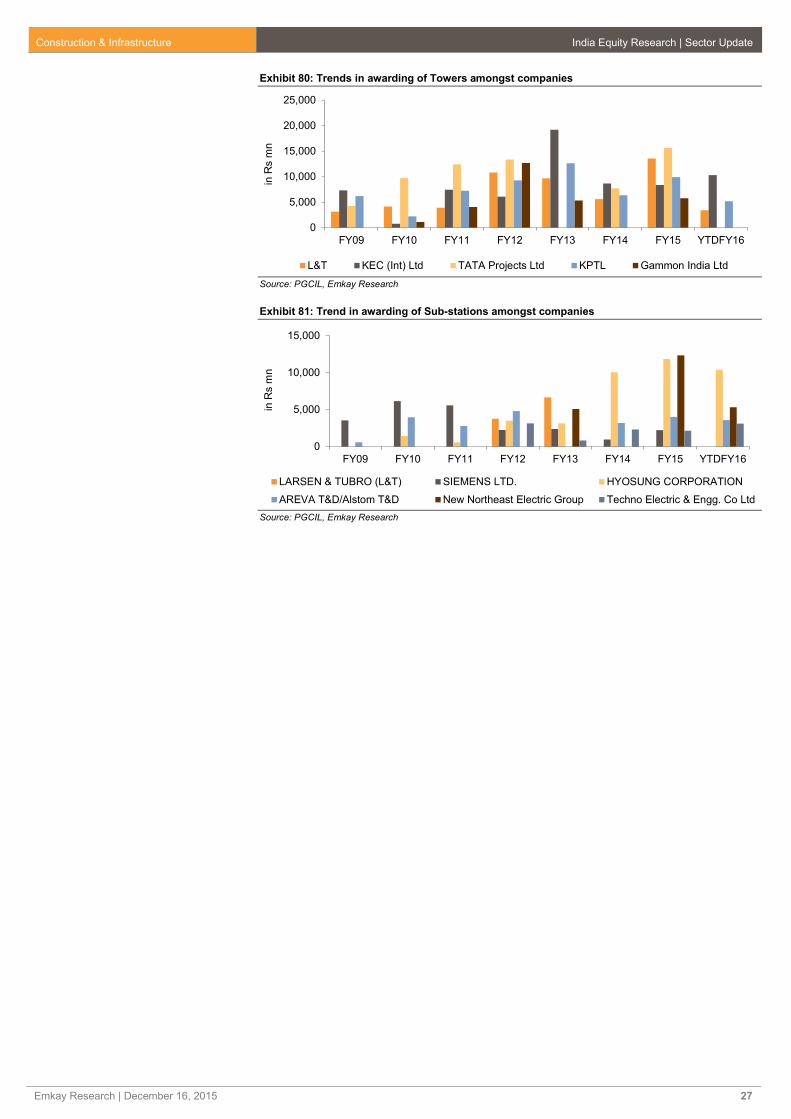

The month of November 2015 saw PGCIL award contracts worth Rs3.6 bn largely in

Insulators (Rs217 mn) and Substation (Rs1.32 bn).

In YTDFY16 PGCIL has awarded contracts worth Rs121.3 bn (+24% YoY).

Substations category saw orders worth Rs34.7 bn (+125% YoY) in YTDFY16 with Chinese

players dominating the market at 65% market share (Hyosung Corp. – 30%, New

Northeast Electric Group High Voltage Switchgear Co. Ltd. – 15%, Rongxin Power

Electronic Co. Ltd. – 14%, Xian XD Switchgear Electric Co. Ltd. – 6%).

Towers category saw orders worth Rs31.6 bn (-2.8% YoY) in YTDFY16 with KEC Intl.

leading the pack at 33% mkt share followed by EMC (17% mkt share), Kalpataru Power

Transmission (16% mkt share), L&T (11% mkt share) and Skipper Ltd. (9% mkt share).

Exhibit 73: YTDFY16, PGCIL orders are up 24% YoY

Source: PGCIL, Emkay Research

Exhibit 74: PGCIL monthly awarding trend

Source: PGCIL, Emkay Research

Exhibit 75: Product-wise ordering activity

Source: PGCIL, Emkay Research

-50%

0%

50%

100%

150%

200%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000Y

TD

FY

09

YT

DF

Y1

0

YT

DF

Y1

1

YT

DF

Y1

2

YT

DF

Y1

3

YT

DF

Y1

4

YT

DF

Y1

5

YT

DF

Y1

6

in R

s m

n

PGCIL Orders Growth YoY

0

10,000

20,000

30,000

40,000

50,000

60,000

Ap

ril

Ma

y

Jun

e

July

Au

gust

Se

pte

mb

er

Octo

ber

Novem

ber

Decem

ber

Jan

uary

Fe

bru

ary

Ma

rch

in R

s m

n

FY14 FY15 YTDFY16

0

20,000

40,000

60,000

80,000

100,000

To

wer

Tra

nsfo

rme

rs

Su

bsta

tio

n

Conducto

rs

Insula

tors

Reacto

rs

Cable

s

Pile

Fo

undatio