claiming an income protection benefit

TRANSCRIPT

Claiming an Income Protection benefitThis document provides information about making a claim for Income Protection benefit.

Claiming Income Protection benefit

What is Income Protection?

Income protection (IP) insurance pays a monthly income,

while you are unable to work due to illness or injury. Australian

Catholic Superannuation and Retirement Fund’s (Australian

Catholic Superannuation) IP cover is unitised cover, with each

unit covering a ‘Salary’ up to $1,000.

What is the waiting period to claim? The waiting period is the number of consecutive days (either 30,

60 or 90 as applicable) for which you must be totally or partially

disabled before you are eligible to receive benefits.

The Waiting Period commences from the later of the following:

a. the date you were first examined by a Medical Practitioner

as Totally Disabled in relation to an injury or sickness that

gave rise to a claim; and

b. the date you ceased work due to that injury or sickness.

If you had consulted a Medical Practitioner within seven days of

ceasing work due to the injury or sickness, the Waiting Period will

commence from the date you ceased work.

What are the benefit periods?

The benefit period is the maximum amount of time ‘Total

Disability’, and ‘Partial Disability’ benefits may be paid for 2

years, 5 years and up to age 65. For your benefit period please

contact Australian Catholic Superannuation or log onto the

member portal. Login or register at www.catholicsuper.com.au

What is involved when making an IP claim?

The high-level steps of details outlining what is involved in

applying for the IP benefit.

Step 1

You can go online or advise Australian Catholic Superannuation that you wish to claim. You can make a claim through the Member Portal. In the Member Portal you simply click on ‘make a claim’. OR contact the Fund on 1300 658 776.

Step 2Complete lodgement form online OR alternately you can contact Australian Catholic Superannuation to raise a claim on your behalf.

Step 3

Depending on the information in the original forms, you may be required to see an independent doctor or specialist or provide further information. The Insurer may also request additional information from you, your doctors or employers.

Step 4Once all the requested information has been obtained by the insurer. The claim will be assessed. The assessment is undertaken by the Insurer.

Step 5

If the claim is approved, payments are made into your nominated bank account, with the super contribution portion paid into your Australian Catholic Superannuation account.

Step 6

If claim is declined, the information will be sent to the Fund’s Insurance Claims and Complaints Committee (The Trustee) for a decision to be reviewed.

Step 7

If The Trustee agrees with the insurer, a letter will be sent to you to explain why your claim was declined. If the Trustee disagrees with the insurer, they will send it back to the Insurer for further review.

What information do I need to provide to make the claim?

The information that is required to make a IP claim is:

• Declaration and Authority.

• An original certified copy of your ID.

• An Employer’s Statement. This statement will need to be

completed by your employer.

• Medical Attendants Statement.

• An EFT Form so we can be aware of your payment details.

• A Tax File Number Declaration.

The insurer will assess your claim and will request further

information to complete the assessment of the claim.

How to certify a document?

A certified document is a copy of the original proof of

identification document that has been signed and certified as a

true and correct copy of the original. Only authorised people can

certify a document.

A “Certifying your identification documents” flyer will be attached

to the initial claims pack

Will the insurer require further information once the claim is lodged?

More often than not, the insurer will request additional

information be provided. The insurer may request an

independent medical assessment by a medical practitioner of

their choosing, which is at their expense to assist with the review

process.

How long does the assessment take?

We are unable to provide an exact timeframe, as each case

is different however the insurer and Australian Catholic

Superannuation will strive to resolve the claim as quickly as

possible.

However, whilst your claim is being assessed, the insurer or

Australian Catholic Superannuation will contact you to provide

you with updates on your claim.

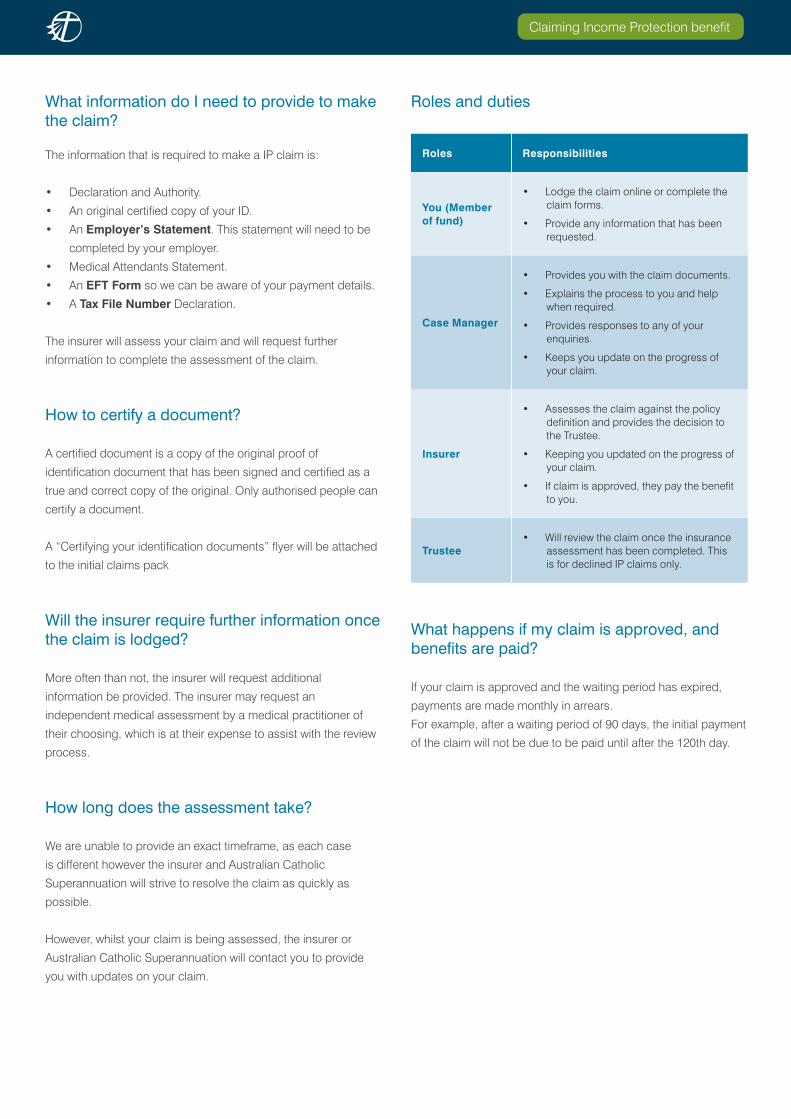

Roles and duties

What happens if my claim is approved, and benefits are paid?

If your claim is approved and the waiting period has expired,

payments are made monthly in arrears.

For example, after a waiting period of 90 days, the initial payment

of the claim will not be due to be paid until after the 120th day.

Roles Responsibilities

You (Member of fund)

• Lodge the claim online or complete the claim forms.

• Provide any information that has been requested.

Case Manager

• Provides you with the claim documents.

• Explains the process to you and help when required.

• Provides responses to any of your enquiries.

• Keeps you update on the progress of your claim.

Insurer

• Assesses the claim against the policy definition and provides the decision to the Trustee.

• Keeping you updated on the progress of your claim.

• If claim is approved, they pay the benefit to you.

Trustee• Will review the claim once the insurance

assessment has been completed. This is for declined IP claims only.

Claiming Income Protection benefit

What are benefit offsets?

Your IP benefit will be offset (reduced), so that the combined

amount of the benefit payable and Benefit Offsets is no more

than the lesser of the monthly equivalent of 85% of:

• the insured Member’s Salary; and

• the Maximum Benefit.

Your benefit will be offset (reduced) by the following:

All benefits or other payments (whether lump sum, periodic or

otherwise) which are paid, or are required to be paid, in relation

to your injury or illness, under any:

• workers’ compensation, motor accident compensation or

similar legislation or scheme;

• Common law settlements for loss of income, loss of earning

capacity or any other economic loss, whether paid as a

lump sum or not;

• Disability income type insurance policy from any other

insurance company;

• sick leave payments.

Any other loss of income, loss of earning capacity or any other

economic loss component of a lump sum payment paid or

required to be paid (except for lump sum received for TPD or a

lump sum superannuation payment).

Any income received from your employer while being paid a

benefit excluding annual leave, redundancy payments and long

service leave entitlements.

For the full information in relation your benefit offsets please refer

to the Insurance Factsheet.

What is the IP benefit?

The IP benefit is the lesser of:

• 85% of your Salary

• 85% of the benefit provided by the number of units you hold.

The benefit is split, so that 75/85ths of the benefit is paid to you

and 10/85ths is paid as a contribution to your Australian Catholic

Superannuation account.

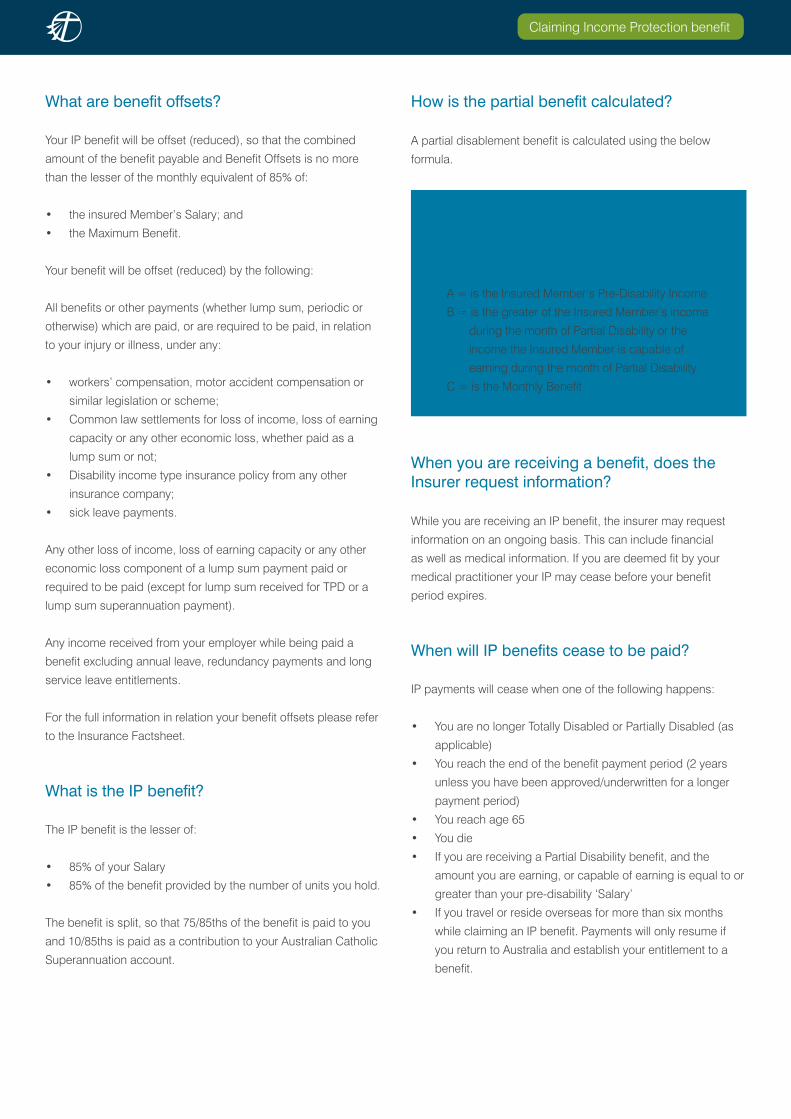

How is the partial benefit calculated?

A partial disablement benefit is calculated using the below

formula.

When you are receiving a benefit, does the Insurer request information?

While you are receiving an IP benefit, the insurer may request

information on an ongoing basis. This can include financial

as well as medical information. If you are deemed fit by your

medical practitioner your IP may cease before your benefit

period expires.

When will IP benefits cease to be paid?

IP payments will cease when one of the following happens:

• You are no longer Totally Disabled or Partially Disabled (as

applicable)

• You reach the end of the benefit payment period (2 years

unless you have been approved/underwritten for a longer

payment period)

• You reach age 65

• You die

• If you are receiving a Partial Disability benefit, and the

amount you are earning, or capable of earning is equal to or

greater than your pre-disability ‘Salary’

• If you travel or reside overseas for more than six months

while claiming an IP benefit. Payments will only resume if

you return to Australia and establish your entitlement to a

benefit.

Claiming Income Protection benefit

A = is the Insured Member’s Pre-Disability Income

B = is the greater of the Insured Member’s income

during the month of Partial Disability or the

income the Insured Member is capable of

earning during the month of Partial Disability

C = is the Monthly Benefit

A – B x CA

What happens if my claim is not approved?

If the Insurer declines your claim, the information will be sent to

the Insurance, Claims and Complaints Committee (The Trustee)

for review to make sure it is fair and reasonable. If they agree

with the insurer’s decision, a letter will be sent to you explaining

why the claim was declined. If the Trustee disagrees with the

insurer’s decision, they will send the claim back to the insurer for

assessment.

What do I do if you disagree with the decision?

You may appeal the decision and provide further information to

support your appeal through our internal complaint’s procedure.

Once the new information is received your claim will be re-

assessed. The assessment will be undertaken by the Insurer.

Once a decision has been made, the information will once again

be sent to The Trustee. If you are unhappy with the outcome,

a complaint can be forwarded to the Australian Financial

Complaints Authority (AFCA).

AFCA is an independent external disputes resolution scheme to

assist members to resolve certain superannuation complaints.

Definitions

Employer member(s) means you are enrolled into Australian

Catholic Superannuation by an employer sponsor (i.e., an

employer who has completed an Employer application form),

who makes super contributions to the Fund on your behalf.

Partial Disability means solely as a result of Injury or illness you

are:

a. incapable or performing one or more duties of your usual

occupation necessary to produce income but has returned

to work in your usual occupation or is working in another

occupation and has a monthly salary less than your Pre-

Disability Salary; and

b. following the advice of a Medical Practitioner in relation to

your illness or Injury for which they are claiming.

Personal Members means you have joined Australian Catholic

Superannuation and you were not enrolled by an employer who

completed an application form to participate in the fund.

Total Disability means solely as a result of Injury or illness, you

are:

a. medically certified as being incapable of performing one or

more duties of your usual occupation necessary to produce

income:

a. not engaged in any occupation: and

b. under the care of a Medical Practitioner.

Salary

a. if you are in permanent employment: The annual

cash salary remuneration you were receiving from your

employer(s) for your personal exertion immediately prior to

becoming disabled. It includes non-cash benefits or fringe

benefits provided as a direct substitute for salary as well as

performance related commission and bonuses.

b. If you are a ‘casual’ or not employed: The annual

cash remuneration which you received from your

employer(s) for your personal exertion over the 12-month

period immediately prior to your disability (or since you

commenced employment if the period is less than 12

months). It includes non-cash benefits or fringe benefits

provided as a direct substitute for remuneration as well

performance related commission and bonuses received

by you during the 12-month period immediately prior to

your disability (or since you commenced employment if the

period is less than 12 months).

c. If you are self-employed: The total amount earned by your

business over the financial year (or proportion of a financial

year) as a direct result of your personal exertion or activities

through your usual occupation, less your share of business

expenses, but before income tax, (or the relevant proportion

for part of a financial year). Salary includes income from all

employment sources.

Waiting Period

Means the number of consecutive days (either 30, 60 or 90 as

applicable) for which you must be Totally Disabled or Partially

Disabled, as the case may be, before a disability benefit is

payable.

The Waiting Period commences from the later of the following:

a. the date you are first examined by a Medical Practitioner

as Totally Disabled in relation to your injury or sickness that

gave rise to the claim; and

b. the date you ceased work due to that injury or sickness.

If you consult a Medical Practitioner within seven days of ceasing

work due to the injury or sickness, the Waiting Period will

commence from the date you ceased work.

Insured Member

Means you have been accepted for insurance cover, or remains

covered, under this Policy and whose cover has neither been

terminated nor ceased.

For full definitions please refer to our insurance factsheet which

is available on our website www.catholicsuper.com.au.

Claiming Income Protection benefit

We’re here to help

If you require any assistance or information regarding the claims process, don’t hesitate to contact us on 1300 658 776 or email

Once you have lodged a claim you can contact AIA claims team on 03 9009 4850 if you require further assistance.

For the full terms and conditions, please refer to the Insurance Factsheet available on the Australian Catholic Superannuation website.

At the date of this publication Insurance is provided under group insurance policies taken out by the Trustee and issued by AIA Australia Ltd ABN 79 004 837 861 AFSL No. 230043 (Insurer). The document details the terms and conditions effective on and from 1 January 2021.

All cover is subject to the terms and conditions of the insurance policies. If there is any conflict between the information contained in this document and the insurance policies, the terms and conditions of the insurance policies will prevail.

You can request a free copy of the policy documents if you require details of the terms and conditions by contacting the Fund.

The information contained in this document does not take into account your specific needs or circumstances. Whilst all due care has been taken in the preparation of this document, the Trustee reserves the right to correct any errors or omissions.

Brisbane, Canberra, Perth, Port Macquarie, Sydney, Townsville

t 1300 658 776 PO Box 656 Burwood, NSW 1805

e [email protected] w www.catholicsuper.com.au

SCS Super Pty Limited, ABN 74 064 712 607, AFSL 230544, RSE

L0002264 Trustee of Australian Catholic Superannuation &

Retirement Fund, ABN 24 680 629 023, RSE R1055436

Any advice contained in this document is of a general nature only, and does not take into account your personal objectives, financial situation or needs. Prior to acting on any information in this document, you need to take into account your own financial circumstances, consider the Product Disclosure Statement and Target Market Determination for any product you are considering, and seek independent financial advice if you are unsure of what action to take.

This document was issued in March 2022.

This document has been prepared by SCS Super Pty Ltd, ABN 74 064 712 607, AFSL 230544, RSE L0002264 Trustee of Australian Catholic Superannuation & Retirement Fund, ABN 24 680 629 023, RSE R1055436. 33 Burwood Rd Burwood, NSW, 2134, Australia.

Claiming Income Protection benefit