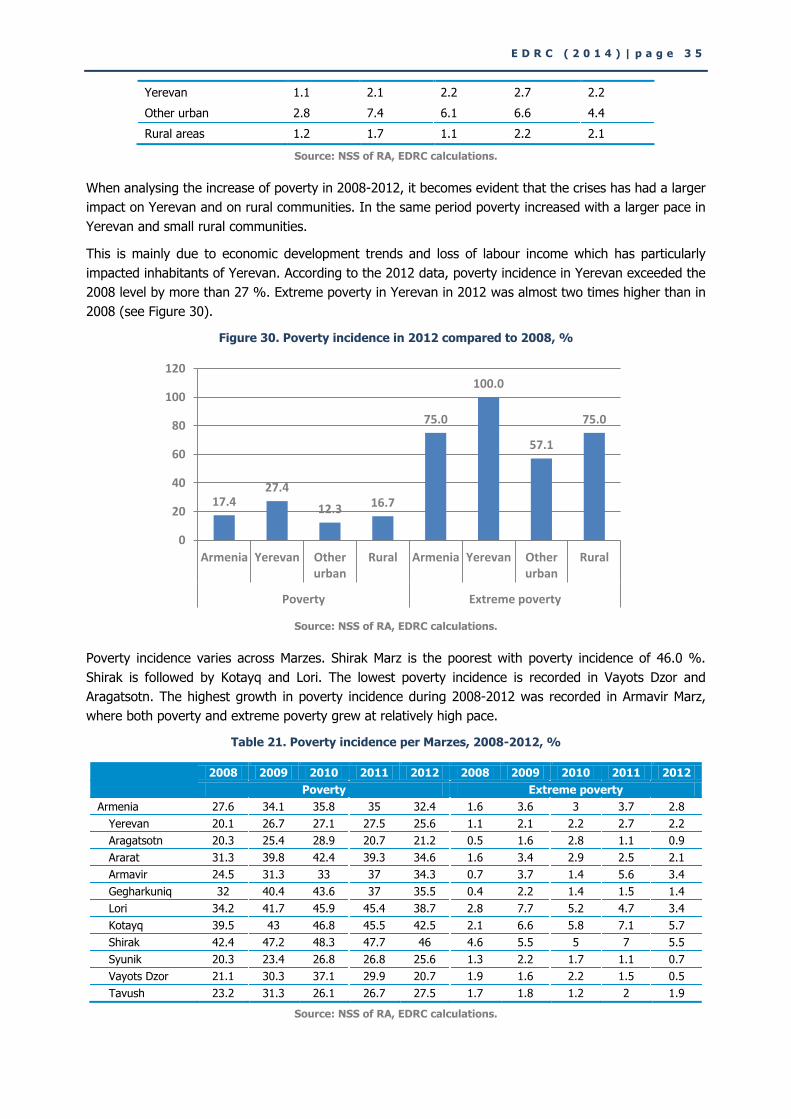

armenia economic report 2014: eurasian integration and trade

TRANSCRIPT

ARMENIA ECONOMIC REPORT 2014

Eurasian Integration and Trade

November 2014

ECONOMIC DEVELOPMENT AND RESEARCH CENTER (EDRC)

RESEARCH TEAM

Mushegh TUMASYAN

Armen GRIGORIAN

Yelena MANUKYAN

Karine HARUTYUNYAN

AER 2014 is drafted and published by the support of Deutsche Gesellschaft fur Internationale

Zusammenarbeit (GIZ).

The authors express their gratitude to the “Republican Union of Employers of Armenia” for their support and

cooperation.

The opinions and conclusions expressed in the Report belong to authors and do not necessarily coincide with official

views or position of any governmental body or GIZ.

Proper reference to the Report when citing is obligatory.

ARMENIA ECONOMIC REPORT 2014

© “ECONOMIC DEVELOPMENT AND RESEARCH CENTER” EDRC, 2014

For questions and suggestion please contact EDRC: +374 (0) 60 540 289, [email protected], www.edrc.am

ABOUT THE ARMENIA ECONOMIC REPORT (AER)

The Armenia Economic Report (hereafter AER or the Report) is an annual analytical periodical which aims

to support accountability and evidence-based decision making culture in Armenia. It particular sets out to

analyse and interpret economic policies and developments, raise awareness, and create a sounder base

for enhanced policy discussions and development.

The Report consists of two main sections. The first section refers to the economic developments of the

previous year. This among others includes global development trends, macroeconomic developments in

Armenia, industrial production, labour market and poverty situation. In addition, economic outlook for

the coming three years are presented in this section.

Section two of the Report is each year dedicated to a certain theme and addresses a specific urgent

issue for Armenia. This part of the Report involves analyses of the chosen topic and discussions on the

direction of economic policy regarding the touched upon thematic.

The general theme of the AER 2014 is Eurasian Integration and Trade. The Report presents (potential)

trade development trends and assessment of the Eurasian Economic Union membership.

Every year, development of the AER involves partnerships and collaboration with various stakeholder

groups, public and private organizations, including governmental bodies and relevant academic and civic

society organizations in Armenia.

AER (2014) is developed by the Economic Development and Research Center (EDRC) which is an

independent analytical center based in Armenia. The Report is prepared with the generous support of the

Deutsche Gesellschaft fur Internationale Zusammenarbeit (GIZ).

The electronic Armenian and English versions of AERs are available at www.edrc.am

Recent Armenia Economic Reports:

AER 2013: Human Capital and Growth Perspectives

AER 2011/2012: Trade Policy and Growth Sustainability

AER 2010: The Necessity in Economy Diversification and Export Expansion

AER 2009: From Crisis to New Development

E D R C ( 2 0 1 4 ) | p a g e 5

TABLE OF CONTENTS

EXECUTIVE SUMMARY .............................................................................................................. 7

ECONOMIC DEVELOPMENT TRENDS ........................................................................................ 9

1.1. Global Economic Trends .............................................................................................. 10

Global Output ........................................................................................................................... 10

Largest Economies .................................................................................................................... 12

Welfare Distribution .................................................................................................................. 13

Commodity Prices ..................................................................................................................... 13

Consumer Prices ....................................................................................................................... 15

1.2. Economic Trends in Armenia ....................................................................................... 16

Economic Growth and GDP ........................................................................................................ 16

GDP Expenditure Structure ........................................................................................................ 17

Foreign Trade and Current Account ............................................................................................ 18

Remittances ............................................................................................................................. 19

Savings and Budget Indicators ................................................................................................... 20

External Debt ........................................................................................................................... 21

Exchange Rates ........................................................................................................................ 22

Consumer Prices ....................................................................................................................... 23

Foreign Investments ................................................................................................................. 23

1.3. Labour Market and Unemployment ............................................................................ 26

Labour Force ............................................................................................................................ 26

Employment Profile ................................................................................................................... 27

Remuneration ........................................................................................................................... 28

Unemployment Trends .............................................................................................................. 29

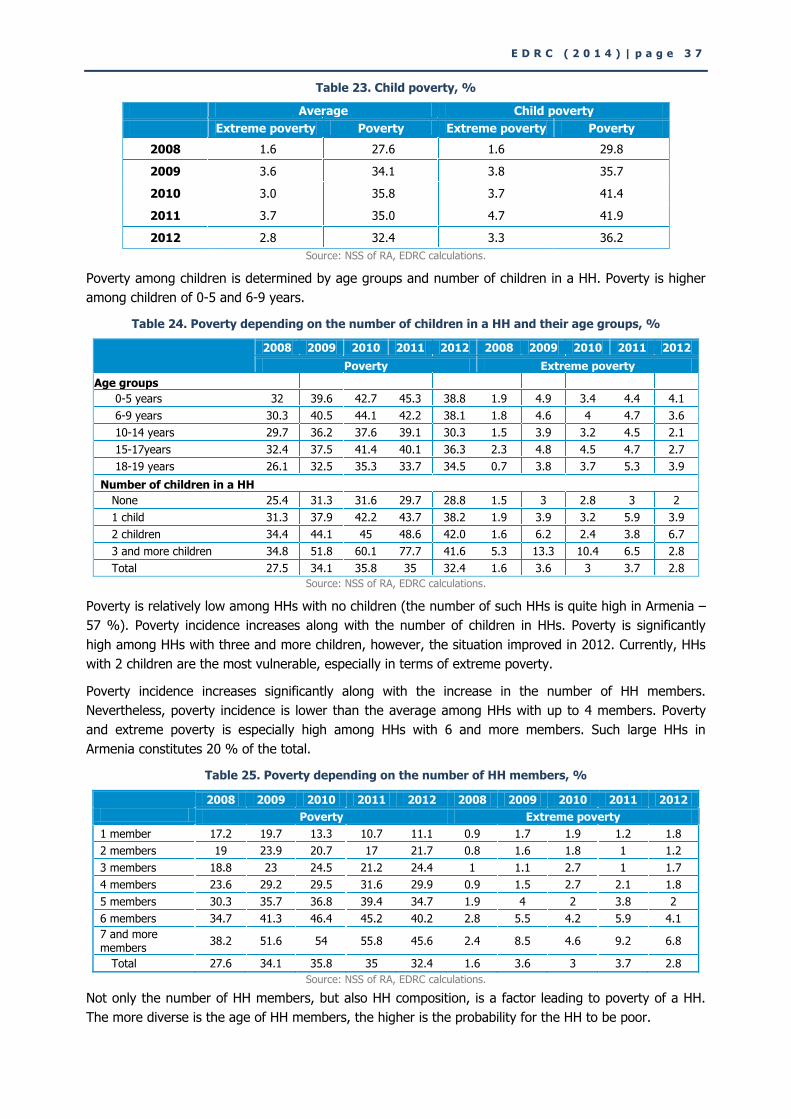

1.4. Poverty and Social Snapshot ....................................................................................... 33

Overall Trends .......................................................................................................................... 33

Regional Picture of Poverty ........................................................................................................ 34

Main Socio-Demographic Characteristics of the Poor .................................................................... 36

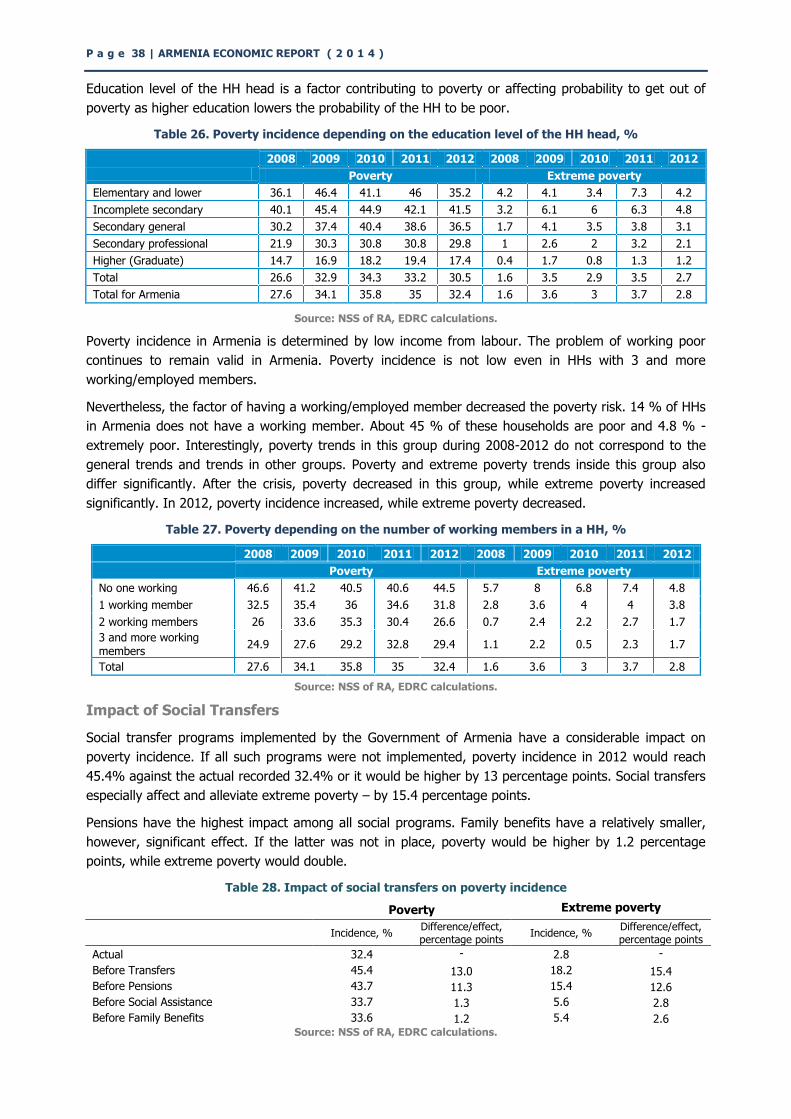

Impact of Social Transfers ......................................................................................................... 38

1.5. Economic Outlook ....................................................................................................... 39

EURASIAN INTEGRATION AND TRADE FLOWS OF ARMENIA ................................................ 43

2.1. Introduction ................................................................................................................ 44

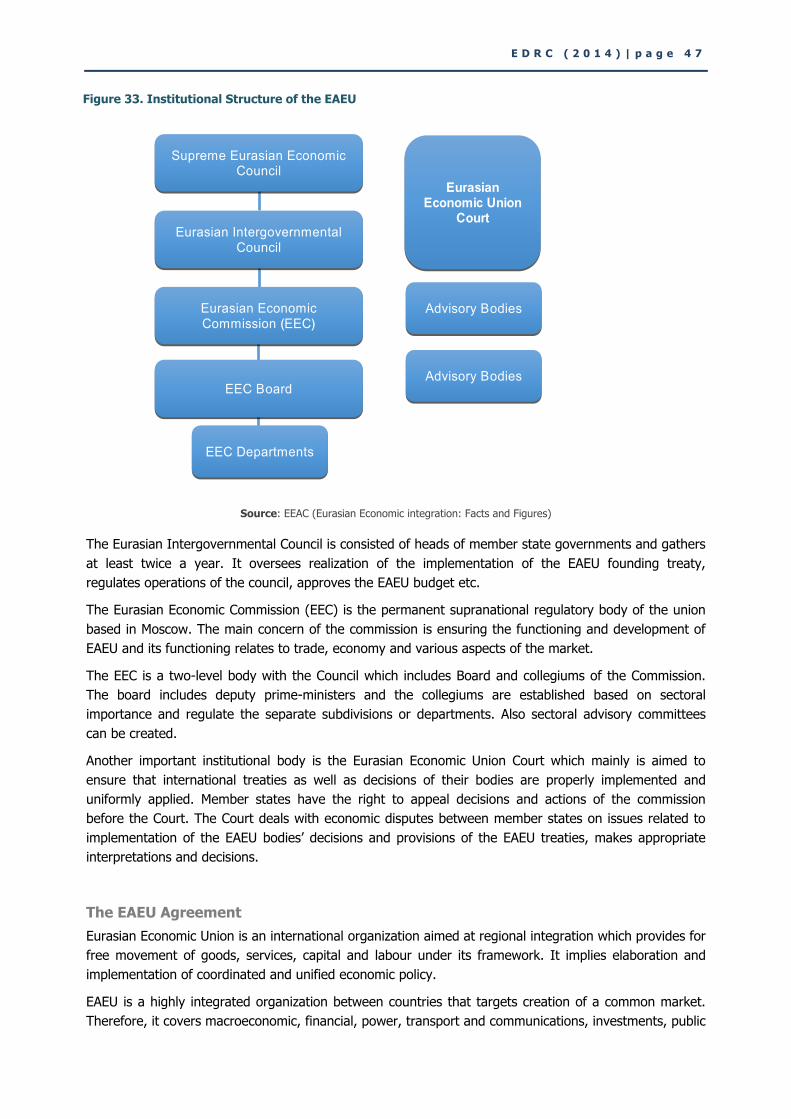

2.2. Eurasian Integration Process ...................................................................................... 46

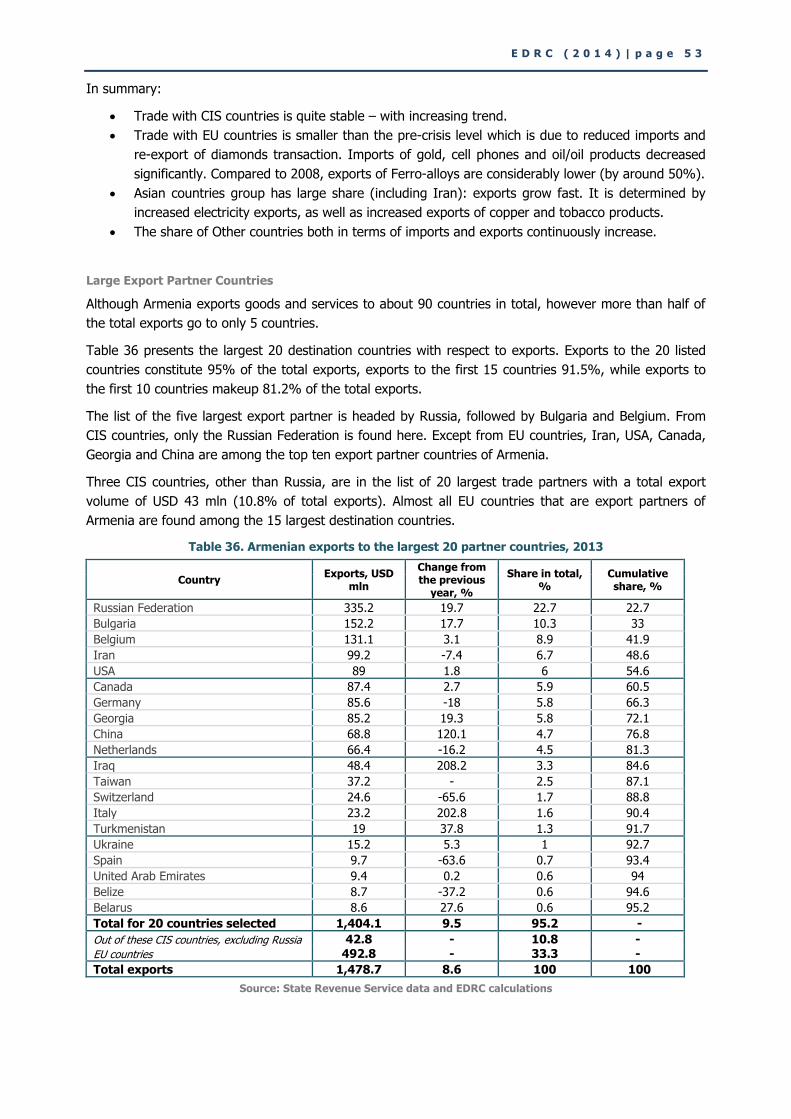

2.3. Foreign Trade of Armenia ........................................................................................... 50

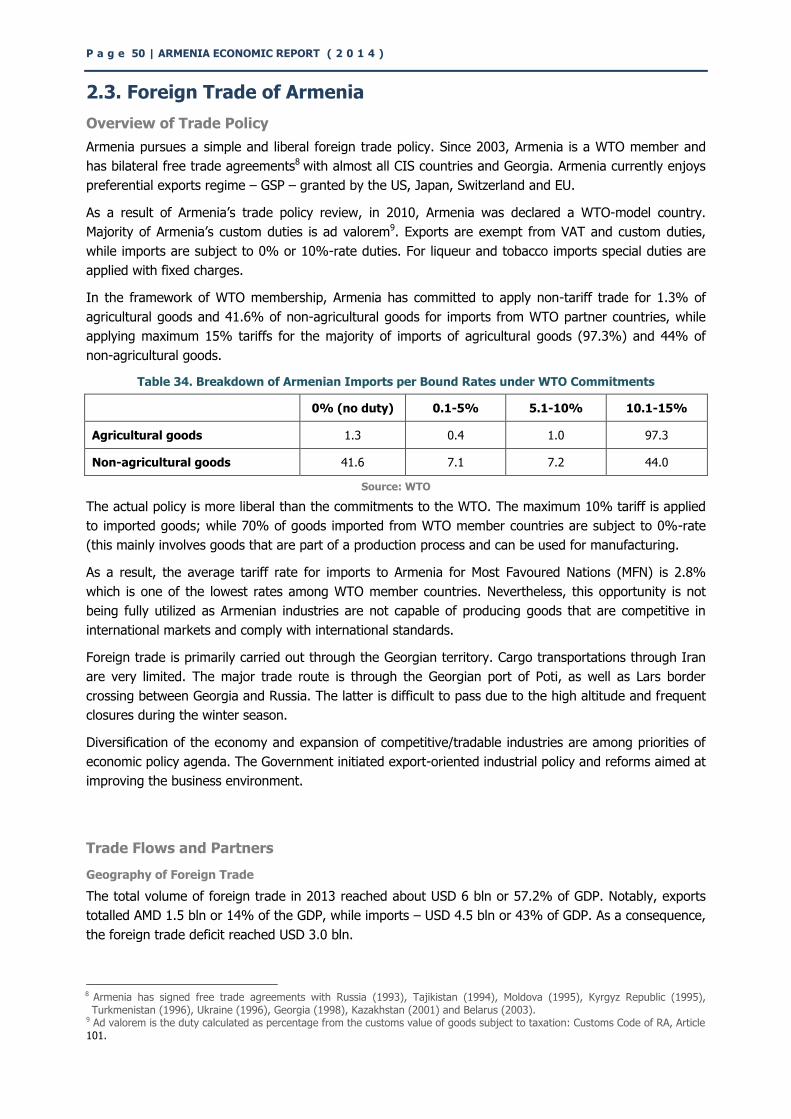

Overview of Trade Policy ........................................................................................................... 50

Trade Flows and Partners .......................................................................................................... 50

General Geography of Foreign Trade .......................................................................................... 50

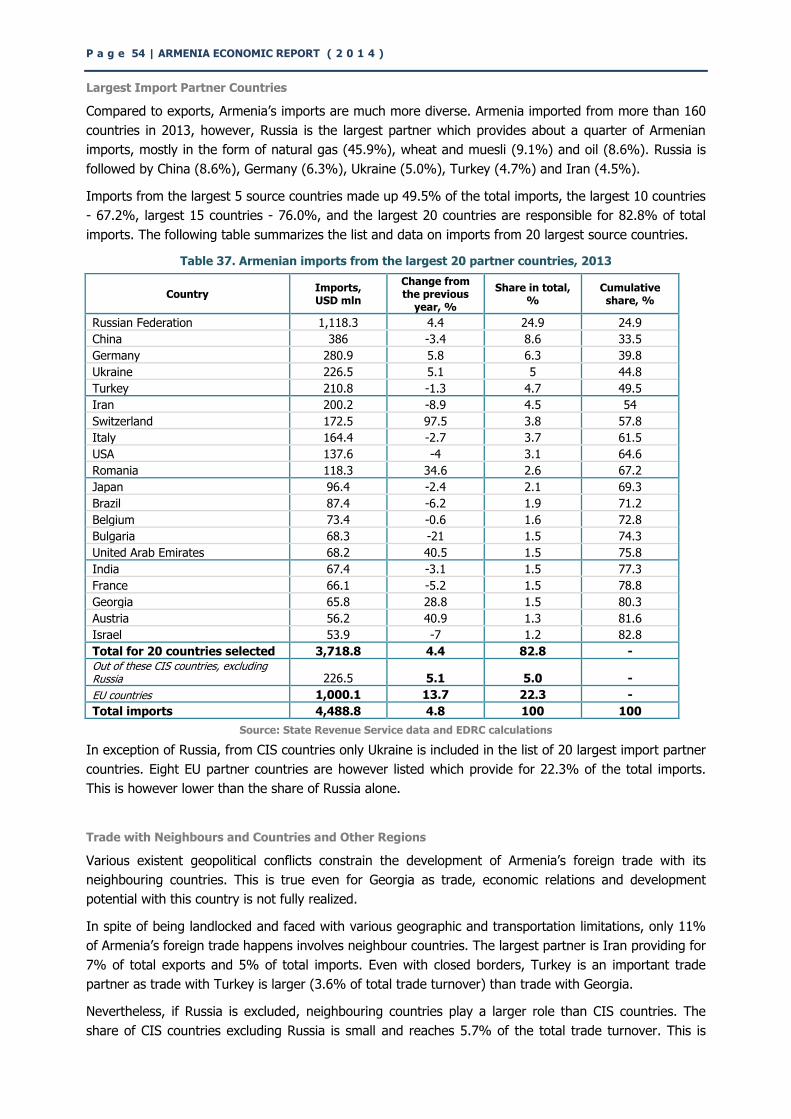

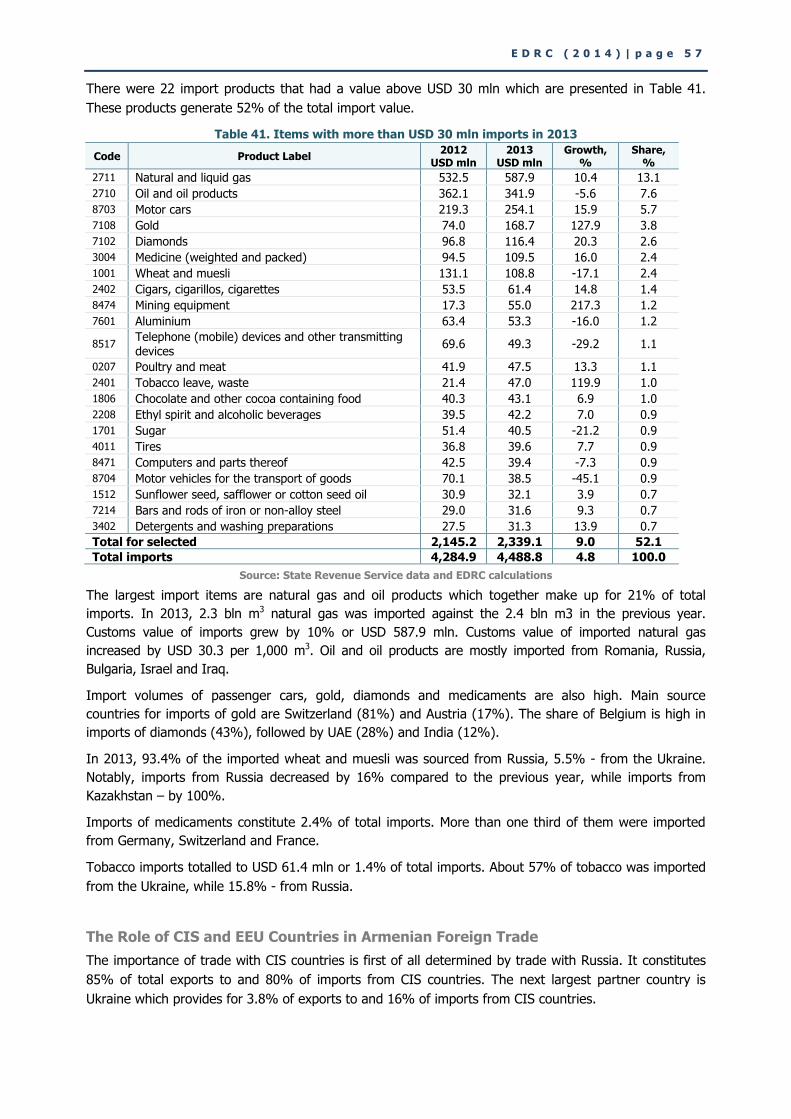

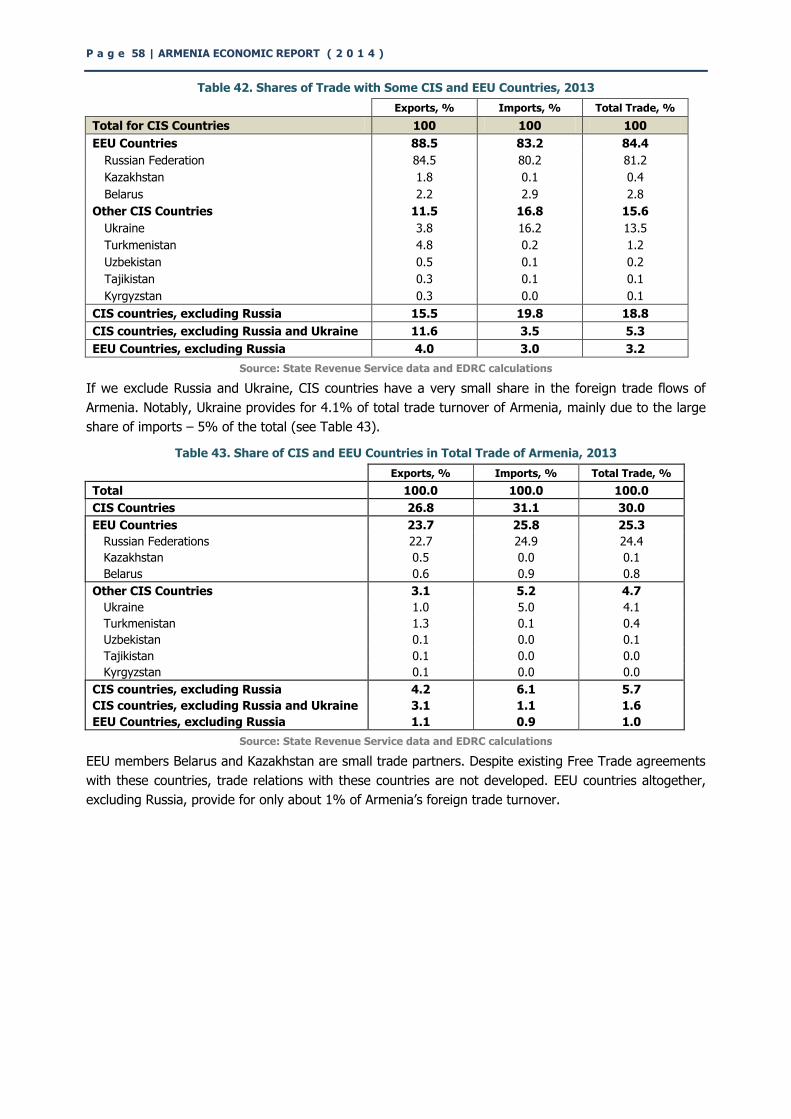

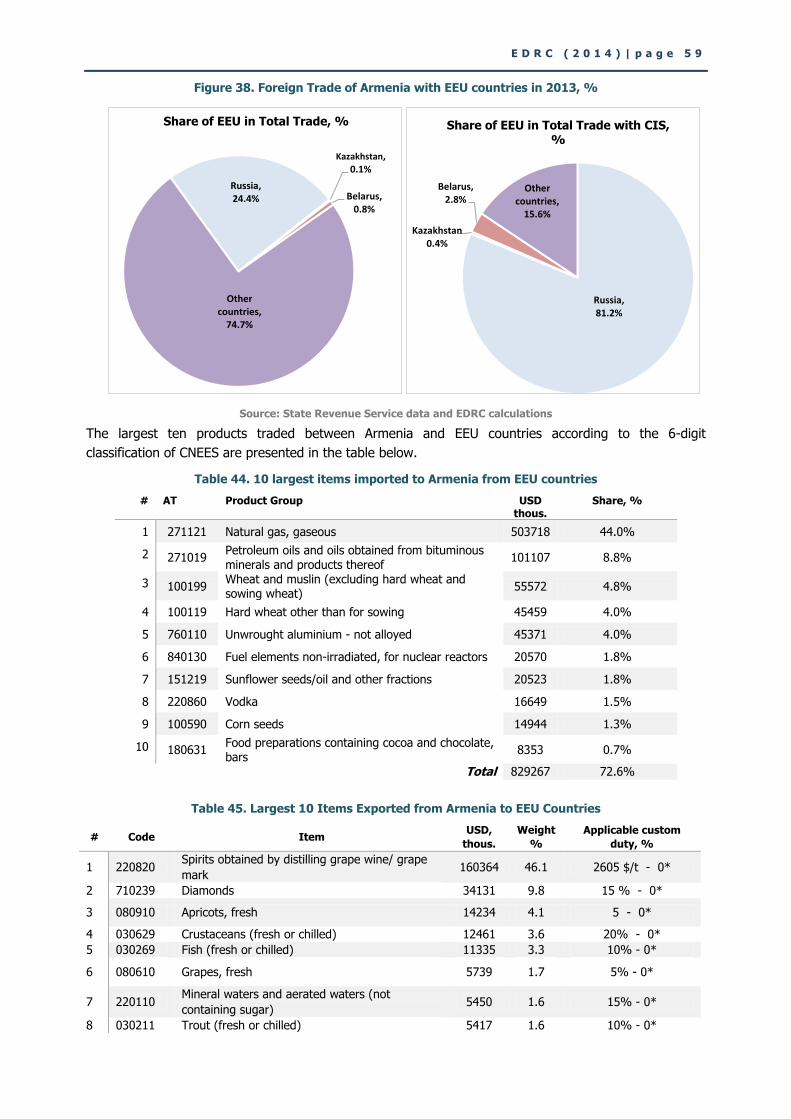

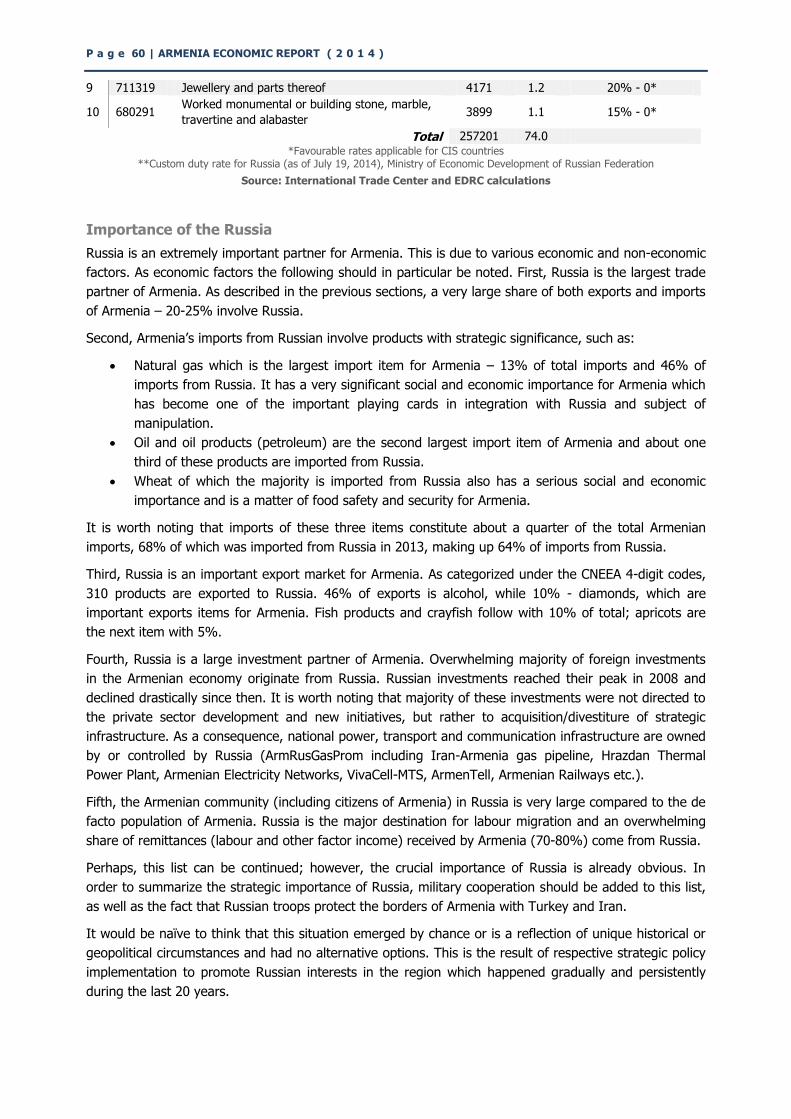

The Role of CIS and EEU Countries in Armenian Foreign Trade ..................................................... 57

Importance of the Russia ........................................................................................................... 60

P a g e 6 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

2.4. Trade Flows Impact Analysis ...................................................................................... 62

Trade Creation and Diversion Effects .......................................................................................... 62

Trade with EAEU Countries ........................................................................................................ 62

Trade with Countries that have Free Trade Agreements with Armenia ........................................... 63

Trade with Third Countries ........................................................................................................ 63

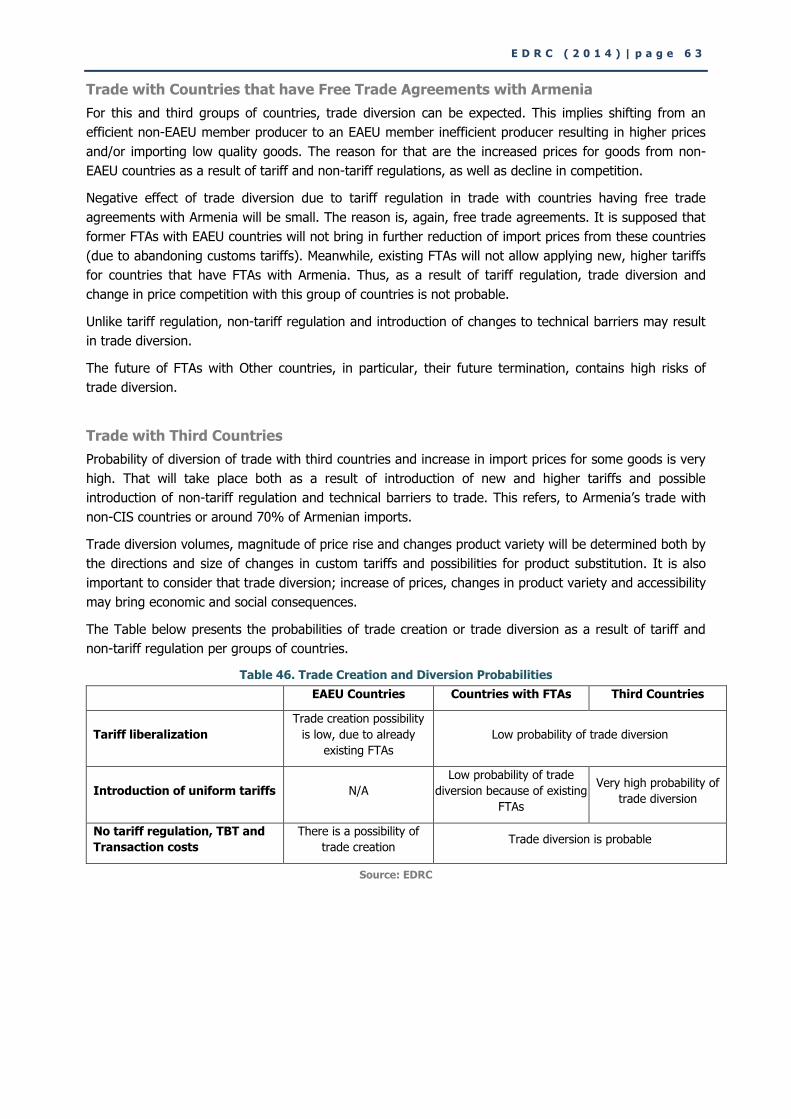

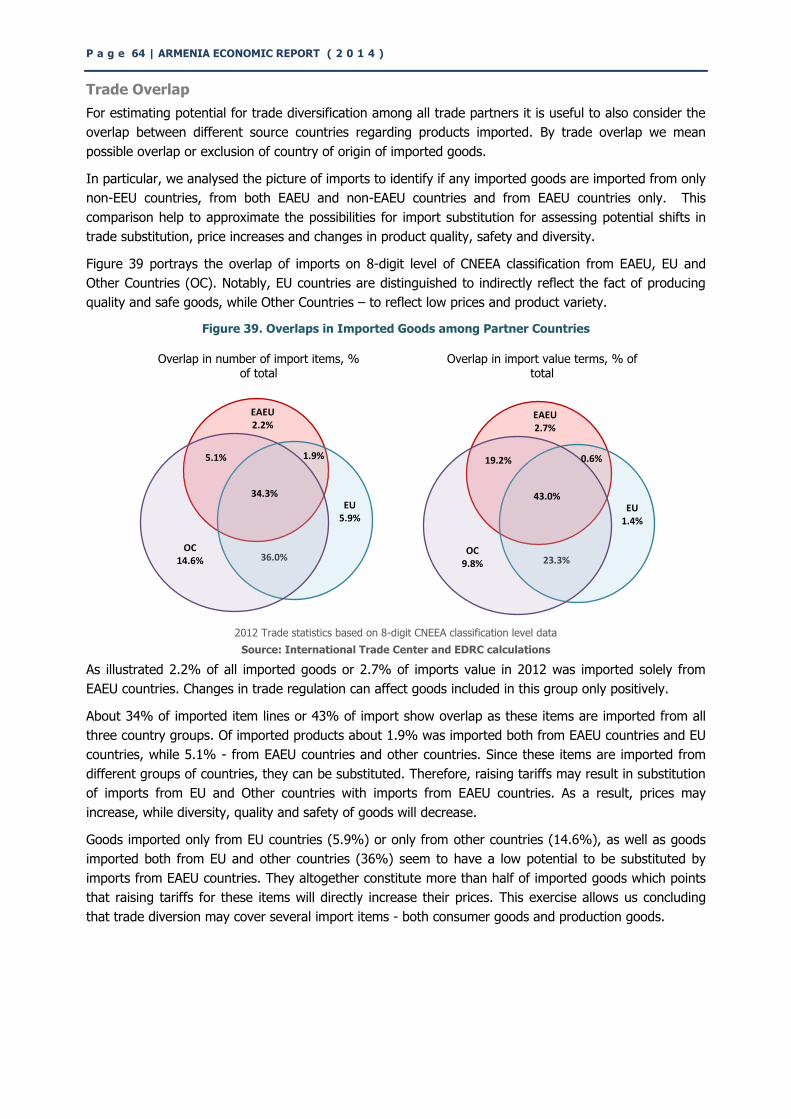

Trade Overlap .......................................................................................................................... 64

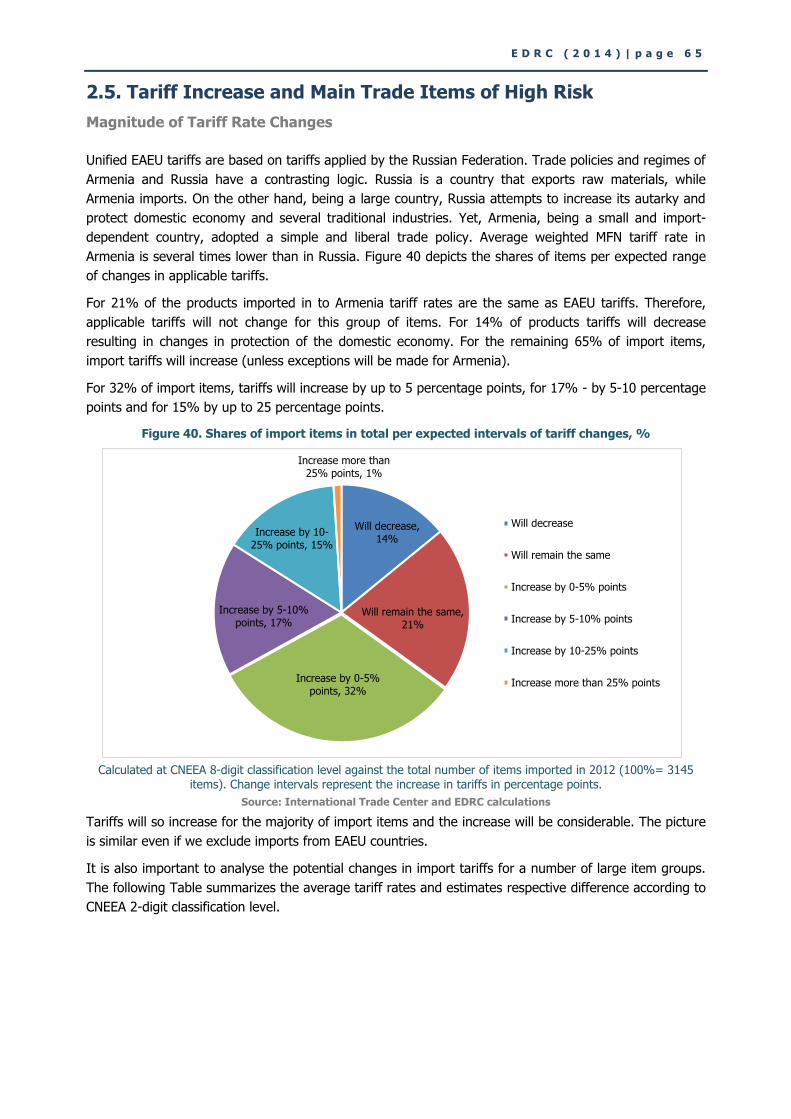

2.5. Tariff Increase and Main Trade Items of High Risk .................................................... 65

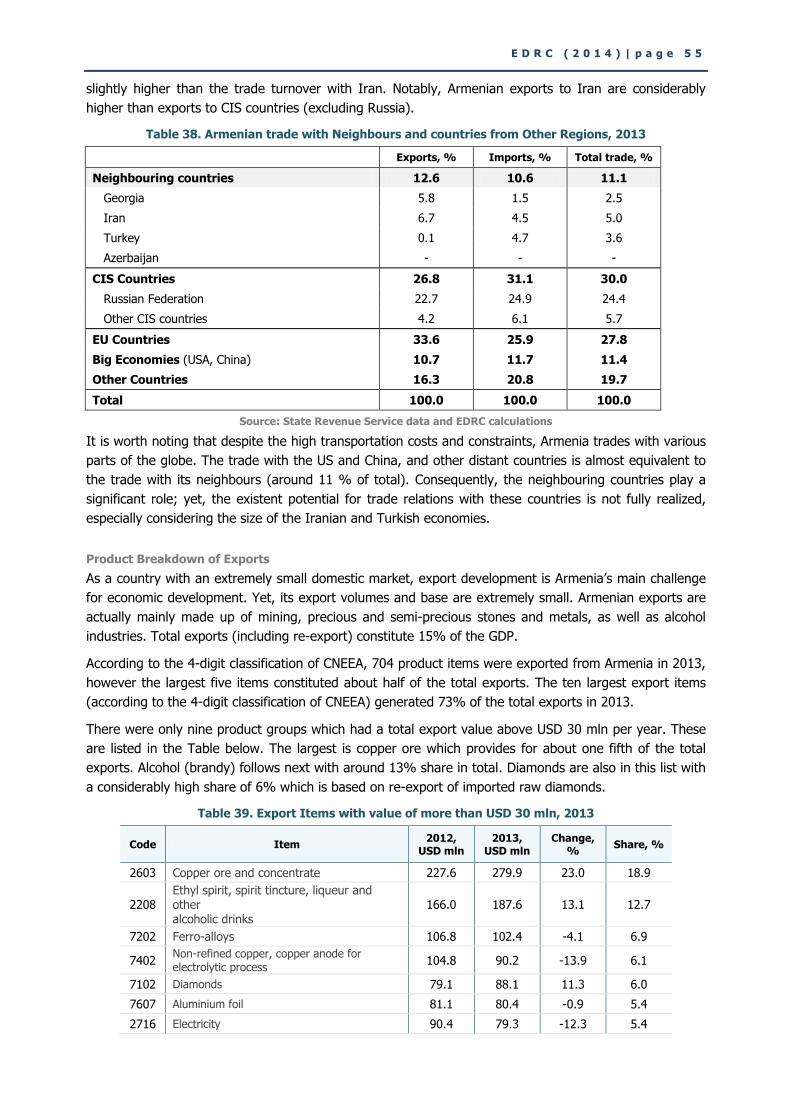

Magnitude of Tariff Rate Changes .............................................................................................. 65

Group of Items with High Consumer Impact Risk ......................................................................... 67

2.6. Summary of the Results and Conclusions ................................................................... 69

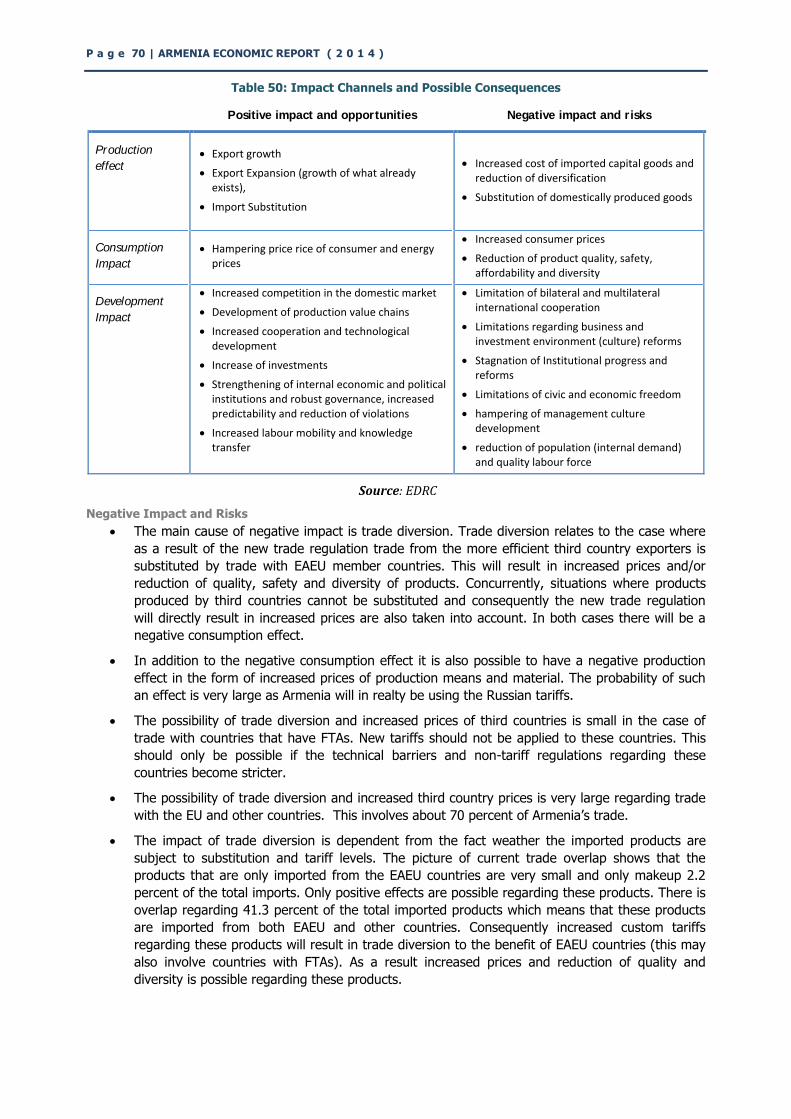

Positive Consequences and Opportunities .................................................................................... 69

Negative Impact and Risks ........................................................................................................ 70

Conclusions .............................................................................................................................. 71

Suggestions for Further Research ............................................................................................... 72

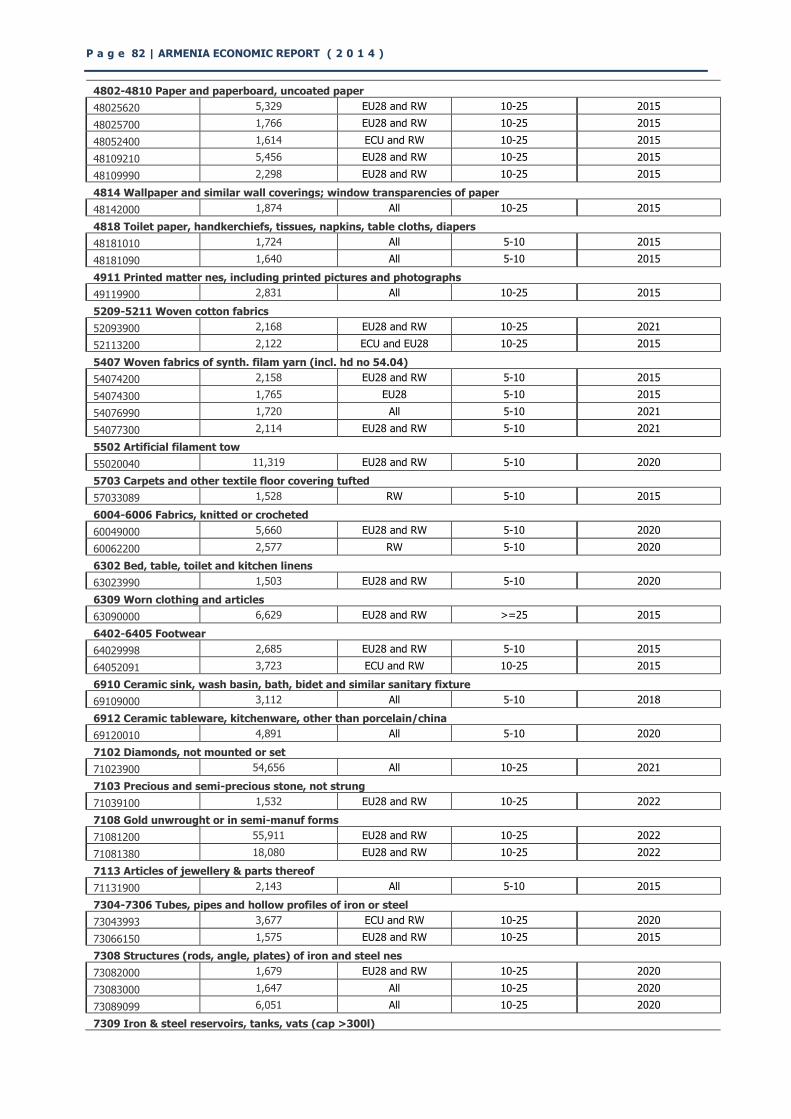

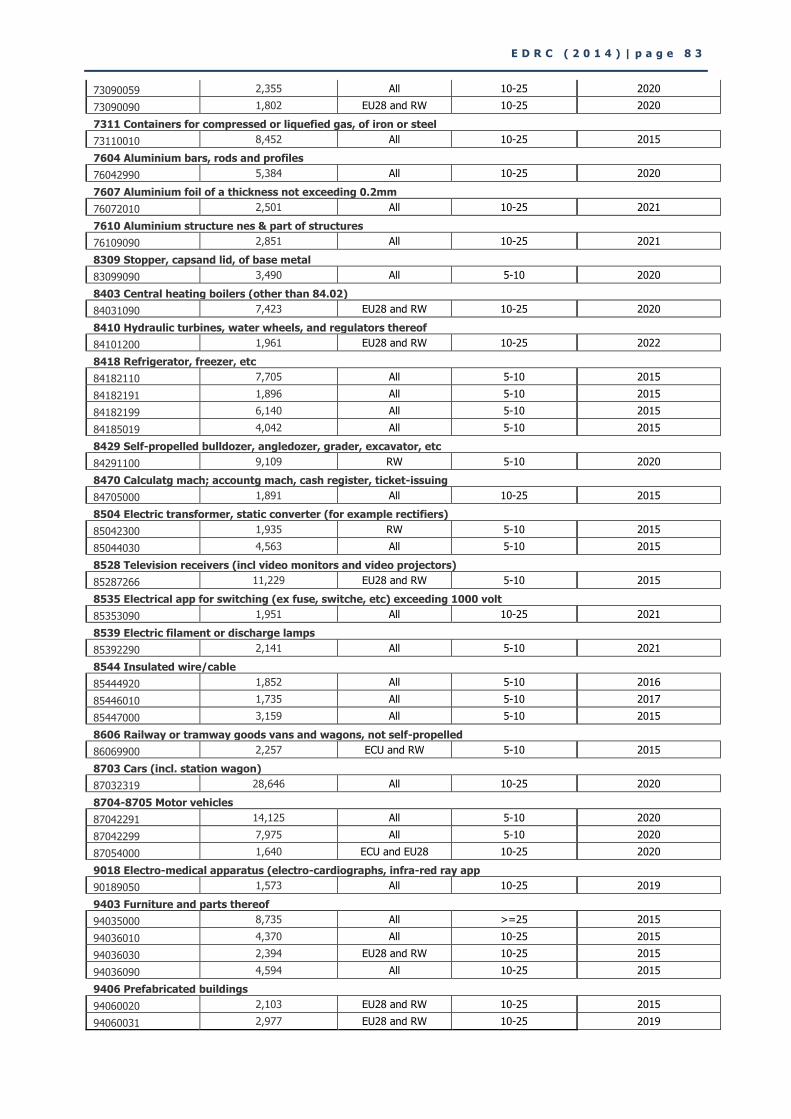

APPENDICES ........................................................................................................................... 73

Appendix 1. The Traditional Theories of Trade Liberalization ........................................... 73

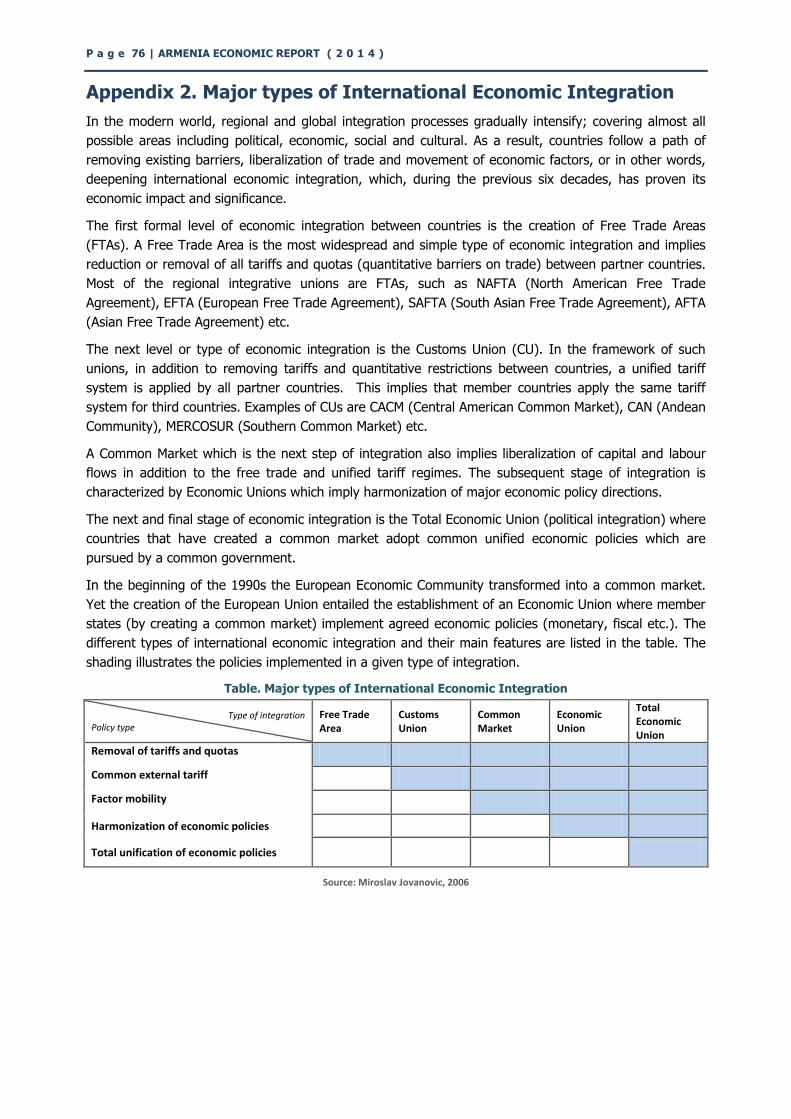

Appendix 2. Major types of International Economic Integration ...................................... 76

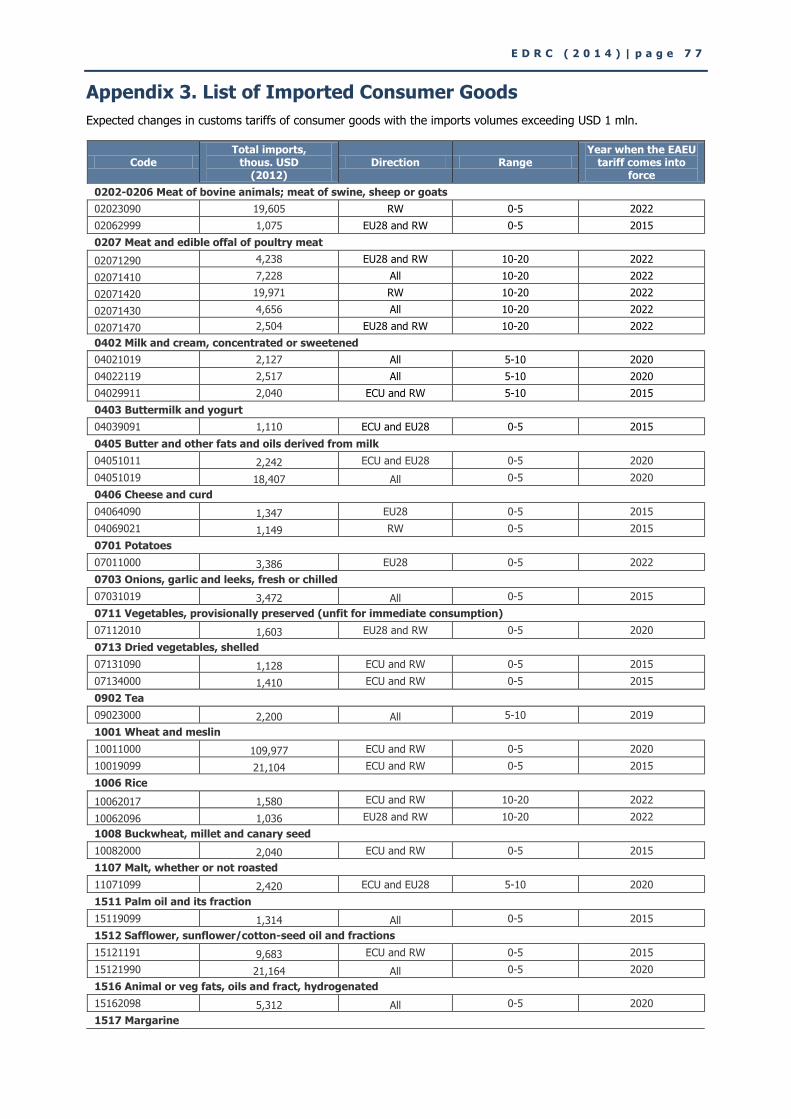

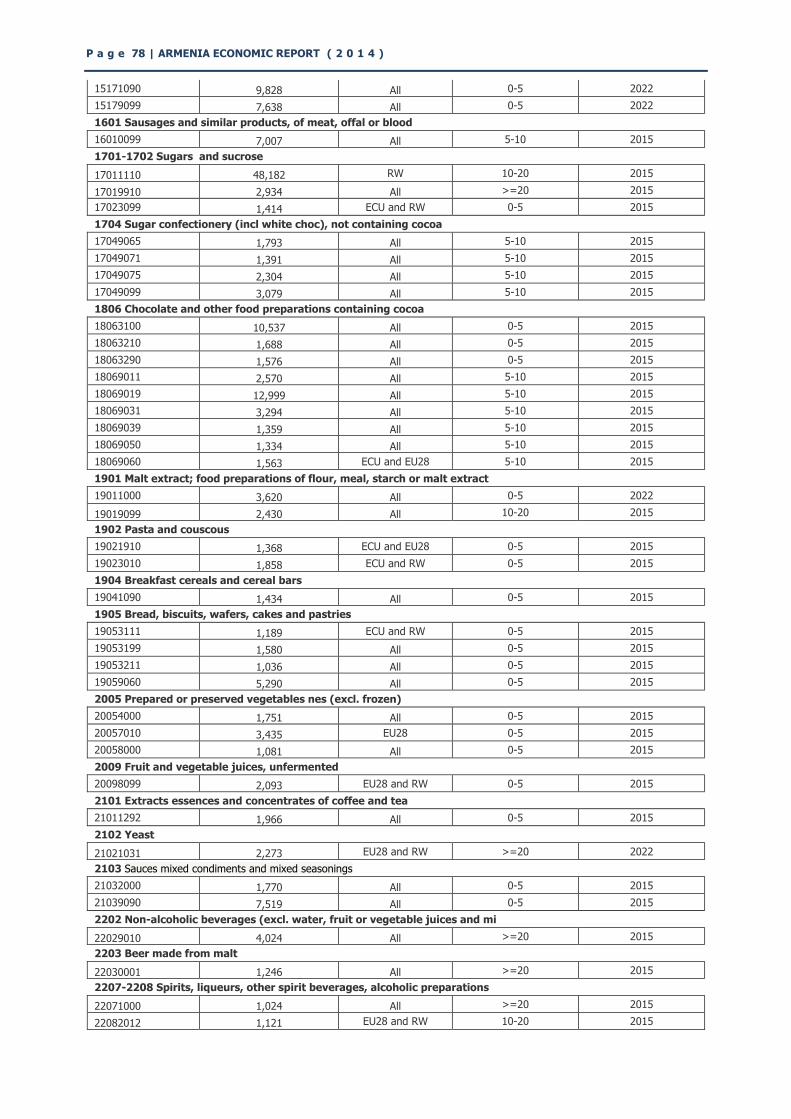

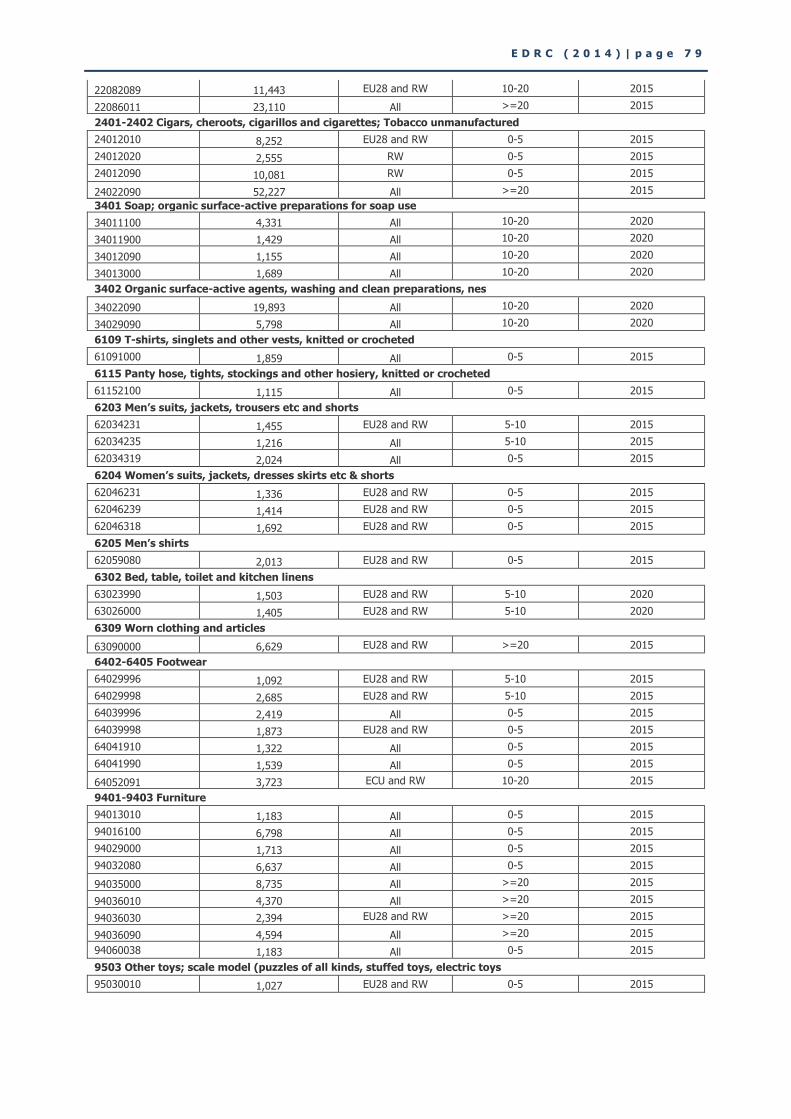

Appendix 3. List of Imported Consumer Goods ................................................................. 77

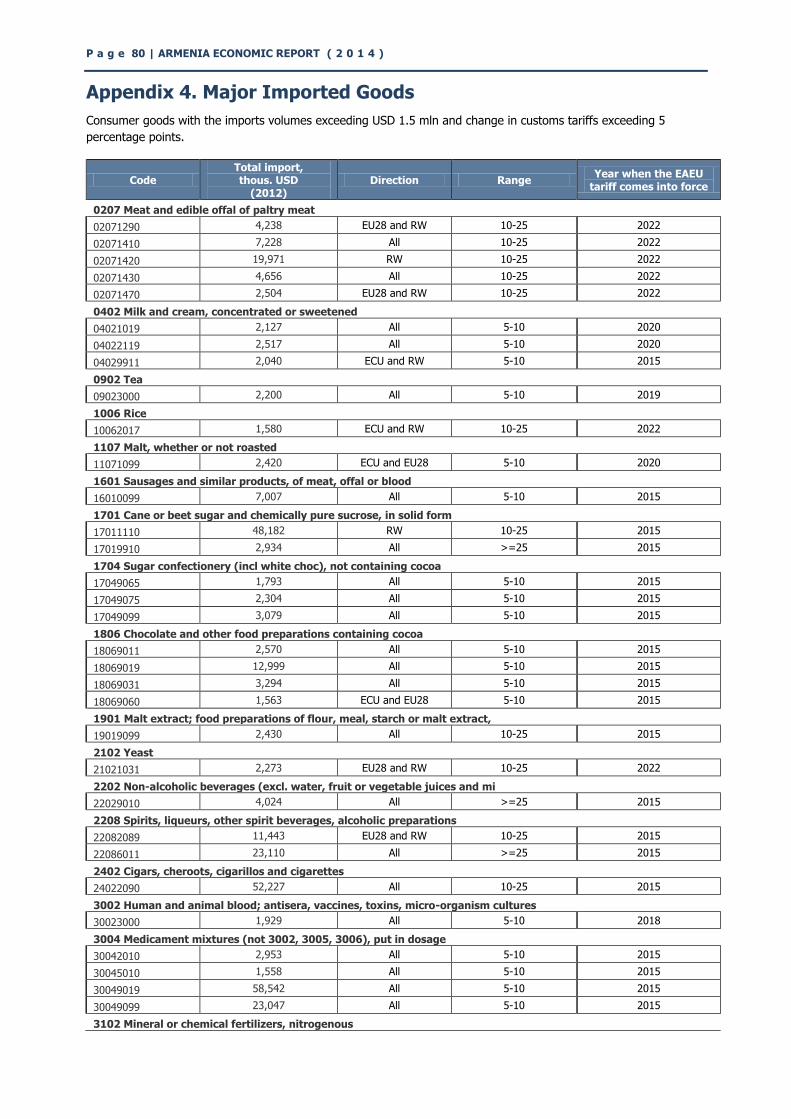

Appendix 4. Major Imported Goods ................................................................................... 80

LIST OF FIGURES .................................................................................................................... 84

LIST OF TABLES ...................................................................................................................... 85

ABBREVIATIONS .................................................................................................................... 86

E D R C ( 2 0 1 4 ) | p a g e 7

EXECUTIVE SUMMARY

Slow global economic growth continued in 2013. Growth in advanced economies is in

a lower gear and developing economies continue to account for a great part of the

growth. In 2013 the global economy exceeded its pre-crisis level by 15.8%.

The Russian and CIS economies are also experiencing a relative weak growth which to a certain

degree was caused by stabilizing or falling commodity prices. Among Armenia’s neighbouring

countries, the highest growth rate was recorded in Azerbaijan where the pre-crisis level was

exceeded by 24%.

Despite the slow average economic growth in advanced economies and extensive expansion

trends in emerging and developing Asia, the global welfare is still distributed unevenly as per

capita GDP of developing countries continues to significantly lag behind developed economies.

Since 2010 the Armenian economy on average grew by 4.4%. Real growth in 2013 reached

3.5% and so the pre-crisis real GDP level is finally recovered and exceeds 2008 levels by 1.9%.

In exception of construction, all major sectors of the economy exceed their pre-crisis levels. Bulk

of the acceleration has come from the service sector which grew by 26%.

Accordingly, structural adjustments of the economic structure in Armenia continue as the

construction sector continues to shrink and some smaller economic sectors such as the hotel and

catering and services sectors experience high growth rates.

Exports in dollar terms grew by 8.6% and reached 15% of the GDP which is quite high for

Armenia. In contrast, imports grew only by 0.2% and equalled 34% of the GDP. As a result the

current account balance improved by 1.6 percentage points of the GDP.

Improvement of the current account balance was also due to increased inflow of private

remittances that totalled USD 1.87 bln. Compared to 2012, remittances grew by 10.8%. About

86% of all remittances came from Russia.

The difference between public savings and investments continues to remain negative. State

budget revenues grew by 13.2%, and the budget deficit decreased significantly.

Nevertheless, the deficit as share of GDP slightly increased, reaching 1.7%. External

public debt increased by 4.3% or USD 160 mln and reached USD 3,899 mln.

Depreciation of the AMD against major currencies continued. Nevertheless, the AMD remains

overvalued. The average annual depreciation rate was 2% against the U.S. Dollar and 5.4%

against the Euro. Dram appreciated against the Russian Rouble by 0.5%.

Consumer prices increased by 5.6% in 2013, and so slightly exceeded the projected levels.

Inflation was specifically high in services (9.7%) and alcohol and tobacco products (6.7%).

Foreign investments decreased compared to 2012 and remained to be small constituting 5.7% of

the GDP (USD 597 mln). Russia continues to be the largest source of investments. Mining and

telecom sectors are the most popular sectors for foreign investments.

Both economic activity and employment level are low in Armenia. During 2008-2013

the labour force shrank by 8%. In 2013, 63% of the labour force (1.4 mln people)

was economically active.The labour market in Armenia is also characterised by long-term

unemployment. Average duration of job search is almost two years.

Majority of the employed are engaged in non-productive and non-tradable sectors. The share of

employment in agriculture remains high, reaching 37%. Trade and education are also large

sectors in terms of employment, with 9.7% and 9% of the total employment respectively.

Education employs more people than the manufacturing industry.

P a g e 8 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Remuneration levels increased as the average monthly salary in 2013 increased by 33.5%.

Salary levels are relatively high in finance and insurance, IT and telecommunication sectors and

lowest in education, healthcare, social service, culture, trade, and agriculture sectors.

Since 2011 there has been steady decline of unemployment. In 2013 unemployment

reached 16.2% which is slightly lower than its pre-crisis level. Unemployment in

Armenia has an urban character as unemployment in towns and cities is very higher

and reached 23.4% in 2013. Unemployment also continues to have a gender and age

dimension as it is higher among women and youth.

The high real growth in 2012 and increased remittances caused a significant decrease of

poverty. Nevertheless, poverty and particularly extreme poverty indicators still exceed pre-crisis

levels and inequality has continuously increased. In 2012, 32.4% of the Armenian households (or

about 1 mln people) were poor, while 2.8% (85 thousand people) were extremely poor.

Poverty incidence is partially determined by low income from labour. The problem of working

poor continues to remain valid in Armenia. Poverty incidence is not low even in households that

have 3 and more working/employed members.

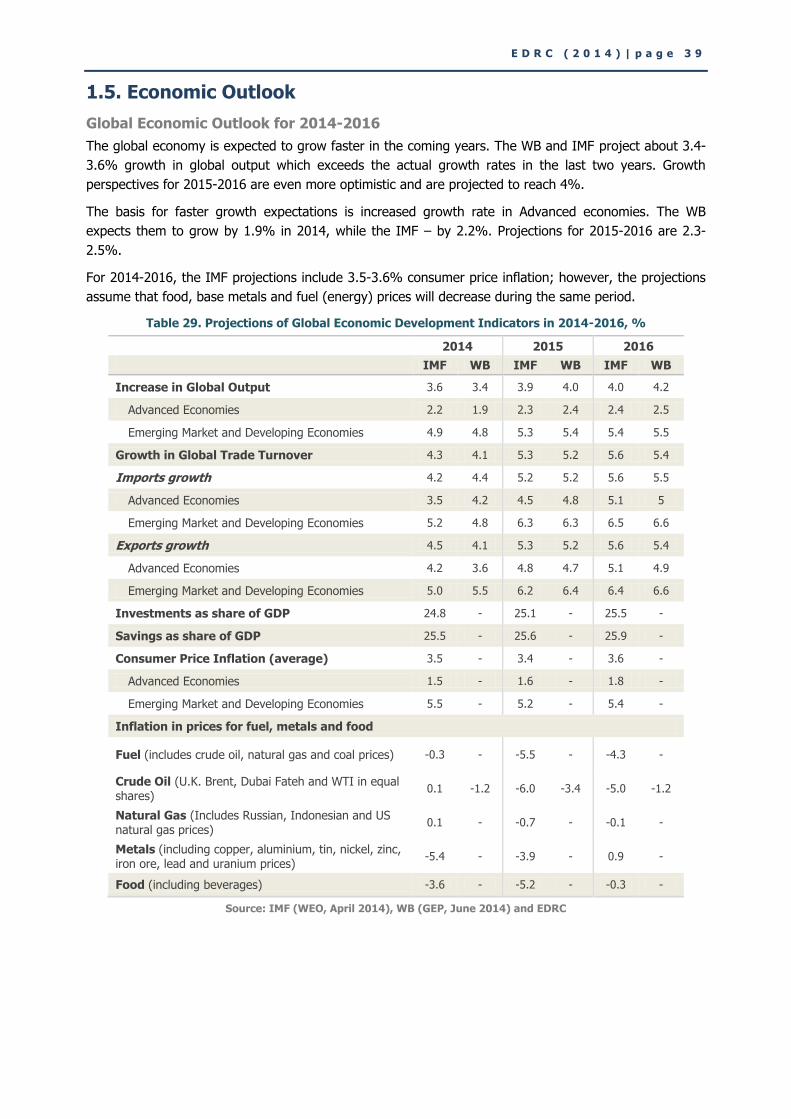

The global economic outlook is more positive as the global economy is expected to

grow faster in the coming years. WB and IMF project about 3.4-3.6% growth in

global output which exceeds actual growth rates of the last two years.

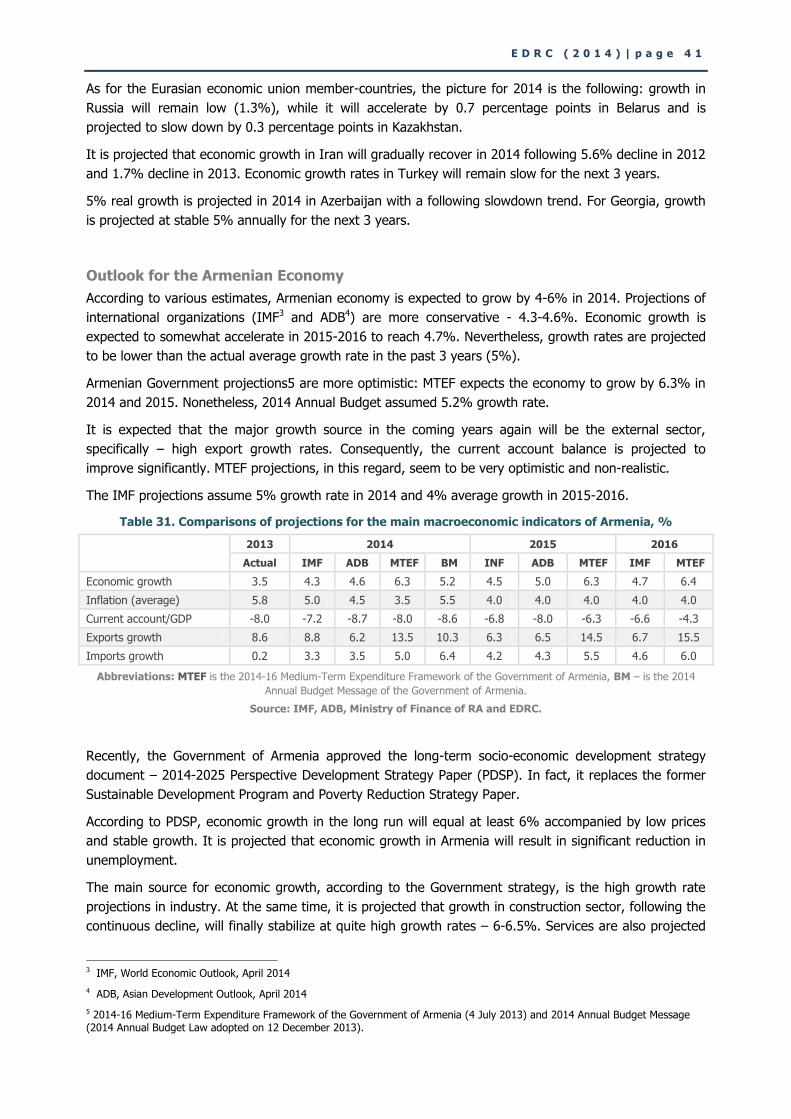

The Armenian economy is expected to grow by 4-6% in 2014. Projections of international

organizations (IMF and ADB) are more conservative and involve 4.3-4.6%. Growth is expected to

somewhat accelerate in 2015-2016 and reach 4.7%, nevertheless projections remain lower than

the actual average growth rate of the past 3 years (5%).

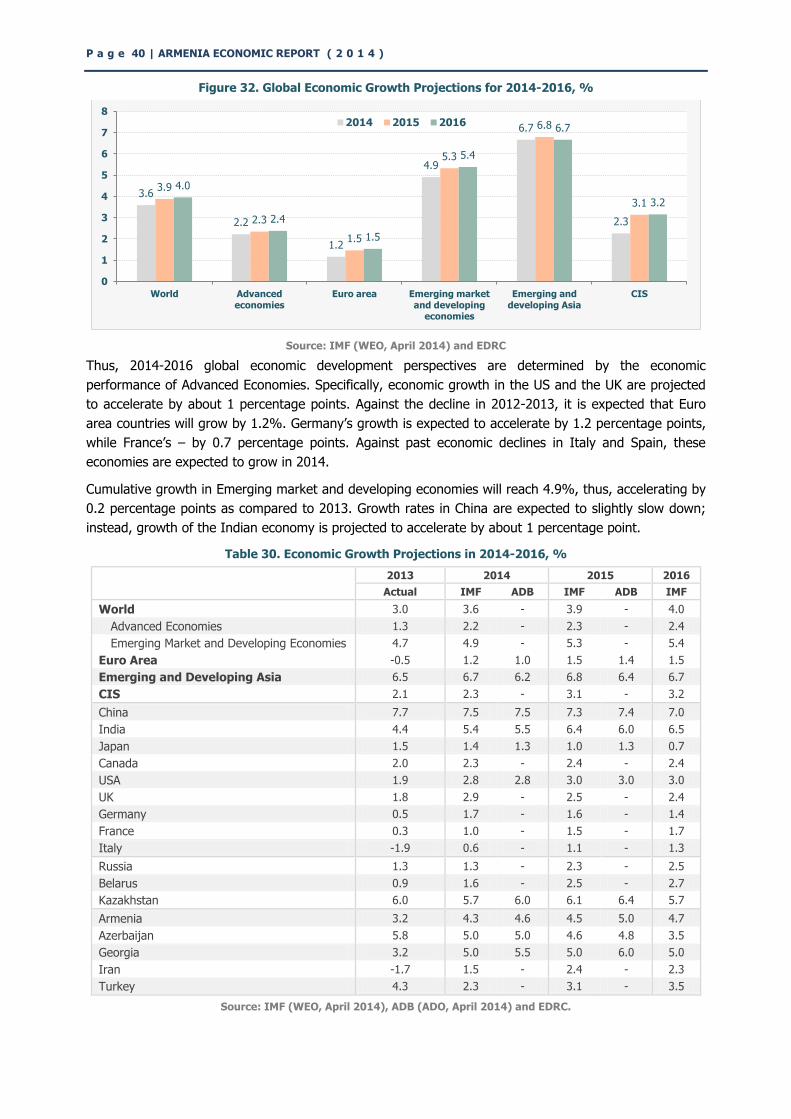

The Eurasian integration is a manifestation of great geopolitical processes which opposes

western processes. Armenia as a small country is anyhow forced to be a part of this process.

With membership in the EAEU, Armenia is forced to significantly change its trade policy with

third countries which is economically not effective for the country. This is made evident by the

large list of exemptions for the 2015-2022 period.

Positive potential economic benefits of membership are limited and this only can be considerable

in case of increased competition, enhanced administration etc. The main source of economic

benefit will be occurrence of long term dynamic effects which also has limitations and particular

analysis on this topic are needed.

Instead the possible price rise of raw material and capital goods will have a negative impact on

Armenia’s economy. The potential for negative impact of trade diversion and increased prices of

products imported from third countries is very high. If exceptions are not made adequately then

socio-economic consequences will be dramatically large.

E D R C ( 2 0 1 4 ) | p a g e 9

Section 1 ECONOMIC DEVELOPMENT TRENDS

1.1. Global Economic Trends

1.2. Economic Trends in Armenia

1.3. Labour Market and Unemployment

1.4. Poverty and Social Snapshot

1.5. Economic Outlook

P a g e 10 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

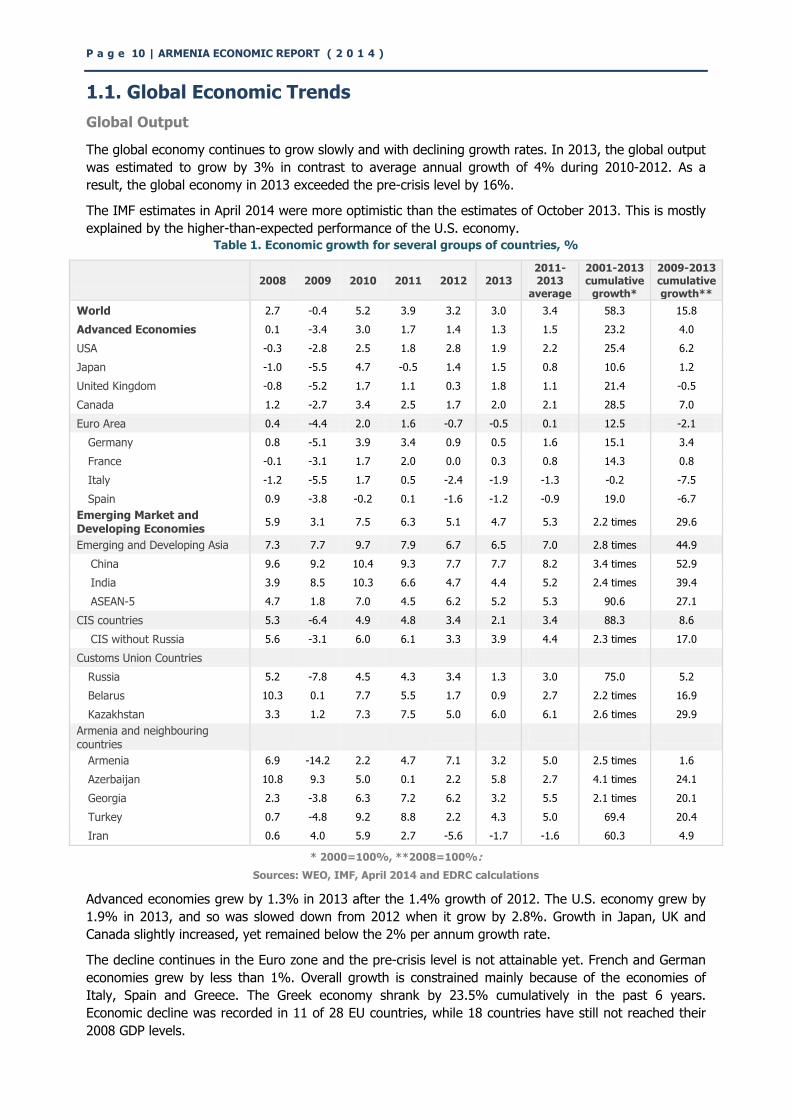

1.1. Global Economic Trends

Global Output

The global economy continues to grow slowly and with declining growth rates. In 2013, the global output

was estimated to grow by 3% in contrast to average annual growth of 4% during 2010-2012. As a

result, the global economy in 2013 exceeded the pre-crisis level by 16%.

The IMF estimates in April 2014 were more optimistic than the estimates of October 2013. This is mostly

explained by the higher-than-expected performance of the U.S. economy.

Table 1. Economic growth for several groups of countries, %

2008 2009 2010 2011 2012 2013

2011-2013

average

2001-2013 cumulative

growth*

2009-2013 cumulative growth**

World 2.7 -0.4 5.2 3.9 3.2 3.0 3.4 58.3 15.8

Advanced Economies 0.1 -3.4 3.0 1.7 1.4 1.3 1.5 23.2 4.0

USA -0.3 -2.8 2.5 1.8 2.8 1.9 2.2 25.4 6.2

Japan -1.0 -5.5 4.7 -0.5 1.4 1.5 0.8 10.6 1.2

United Kingdom -0.8 -5.2 1.7 1.1 0.3 1.8 1.1 21.4 -0.5

Canada 1.2 -2.7 3.4 2.5 1.7 2.0 2.1 28.5 7.0

Euro Area 0.4 -4.4 2.0 1.6 -0.7 -0.5 0.1 12.5 -2.1

Germany 0.8 -5.1 3.9 3.4 0.9 0.5 1.6 15.1 3.4

France -0.1 -3.1 1.7 2.0 0.0 0.3 0.8 14.3 0.8

Italy -1.2 -5.5 1.7 0.5 -2.4 -1.9 -1.3 -0.2 -7.5

Spain 0.9 -3.8 -0.2 0.1 -1.6 -1.2 -0.9 19.0 -6.7

Emerging Market and Developing Economies

5.9 3.1 7.5 6.3 5.1 4.7 5.3 2.2 times 29.6

Emerging and Developing Asia 7.3 7.7 9.7 7.9 6.7 6.5 7.0 2.8 times 44.9

China 9.6 9.2 10.4 9.3 7.7 7.7 8.2 3.4 times 52.9

India 3.9 8.5 10.3 6.6 4.7 4.4 5.2 2.4 times 39.4

ASEAN-5 4.7 1.8 7.0 4.5 6.2 5.2 5.3 90.6 27.1

CIS countries 5.3 -6.4 4.9 4.8 3.4 2.1 3.4 88.3 8.6

CIS without Russia 5.6 -3.1 6.0 6.1 3.3 3.9 4.4 2.3 times 17.0

Customs Union Countries

Russia 5.2 -7.8 4.5 4.3 3.4 1.3 3.0 75.0 5.2

Belarus 10.3 0.1 7.7 5.5 1.7 0.9 2.7 2.2 times 16.9

Kazakhstan 3.3 1.2 7.3 7.5 5.0 6.0 6.1 2.6 times 29.9

Armenia and neighbouring countries

Armenia 6.9 -14.2 2.2 4.7 7.1 3.2 5.0 2.5 times 1.6

Azerbaijan 10.8 9.3 5.0 0.1 2.2 5.8 2.7 4.1 times 24.1

Georgia 2.3 -3.8 6.3 7.2 6.2 3.2 5.5 2.1 times 20.1

Turkey 0.7 -4.8 9.2 8.8 2.2 4.3 5.0 69.4 20.4

Iran 0.6 4.0 5.9 2.7 -5.6 -1.7 -1.6 60.3 4.9

* 2000=100%, **2008=100%:

Sources: WEO, IMF, April 2014 and EDRC calculations

Advanced economies grew by 1.3% in 2013 after the 1.4% growth of 2012. The U.S. economy grew by

1.9% in 2013, and so was slowed down from 2012 when it grow by 2.8%. Growth in Japan, UK and

Canada slightly increased, yet remained below the 2% per annum growth rate.

The decline continues in the Euro zone and the pre-crisis level is not attainable yet. French and German

economies grew by less than 1%. Overall growth is constrained mainly because of the economies of

Italy, Spain and Greece. The Greek economy shrank by 23.5% cumulatively in the past 6 years.

Economic decline was recorded in 11 of 28 EU countries, while 18 countries have still not reached their

2008 GDP levels.

E D R C ( 2 0 1 4 ) | p a g e 1 1

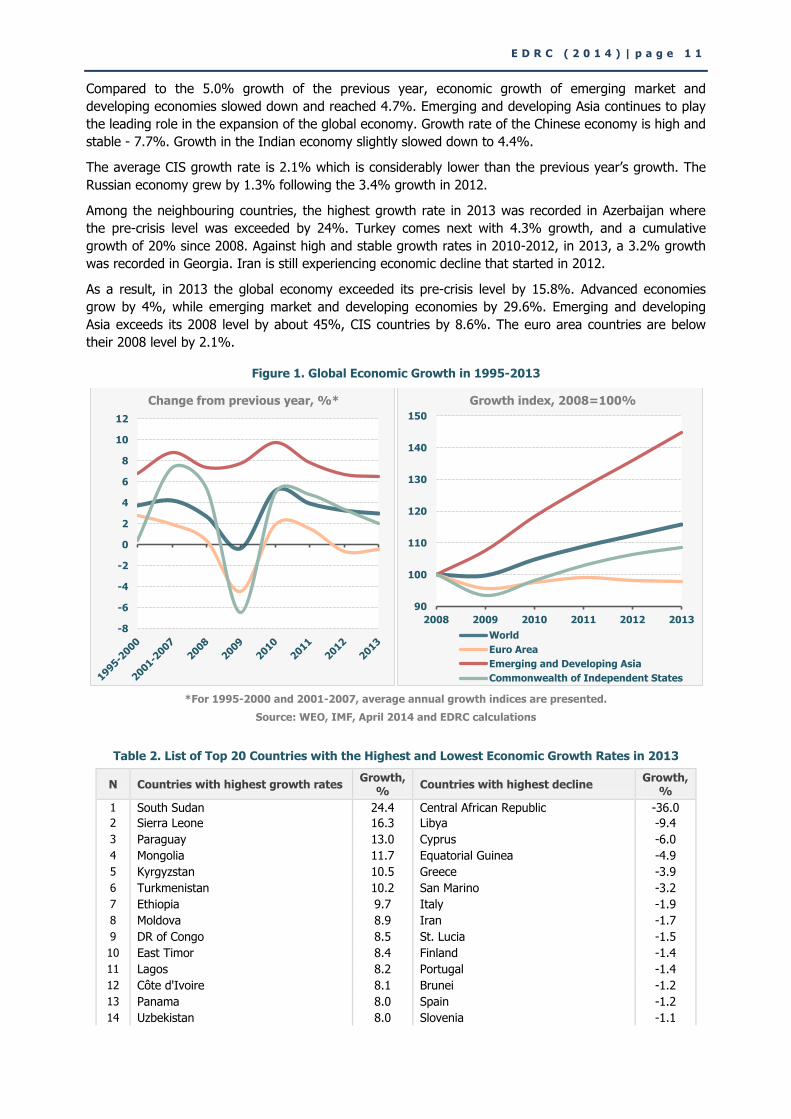

Compared to the 5.0% growth of the previous year, economic growth of emerging market and

developing economies slowed down and reached 4.7%. Emerging and developing Asia continues to play

the leading role in the expansion of the global economy. Growth rate of the Chinese economy is high and

stable - 7.7%. Growth in the Indian economy slightly slowed down to 4.4%.

The average CIS growth rate is 2.1% which is considerably lower than the previous year’s growth. The

Russian economy grew by 1.3% following the 3.4% growth in 2012.

Among the neighbouring countries, the highest growth rate in 2013 was recorded in Azerbaijan where

the pre-crisis level was exceeded by 24%. Turkey comes next with 4.3% growth, and a cumulative

growth of 20% since 2008. Against high and stable growth rates in 2010-2012, in 2013, a 3.2% growth

was recorded in Georgia. Iran is still experiencing economic decline that started in 2012.

As a result, in 2013 the global economy exceeded its pre-crisis level by 15.8%. Advanced economies

grow by 4%, while emerging market and developing economies by 29.6%. Emerging and developing

Asia exceeds its 2008 level by about 45%, CIS countries by 8.6%. The euro area countries are below

their 2008 level by 2.1%.

Figure 1. Global Economic Growth in 1995-2013

*For 1995-2000 and 2001-2007, average annual growth indices are presented.

Source: WEO, IMF, April 2014 and EDRC calculations

Table 2. List of Top 20 Countries with the Highest and Lowest Economic Growth Rates in 2013

N Countries with highest growth rates Growth,

% Countries with highest decline

Growth, %

1 South Sudan 24.4 Central African Republic -36.0

2 Sierra Leone 16.3 Libya -9.4

3 Paraguay 13.0 Cyprus -6.0

4 Mongolia 11.7 Equatorial Guinea -4.9

5 Kyrgyzstan 10.5 Greece -3.9

6 Turkmenistan 10.2 San Marino -3.2

7 Ethiopia 9.7 Italy -1.9

8 Moldova 8.9 Iran -1.7

9 DR of Congo 8.5 St. Lucia -1.5

10 East Timor 8.4 Finland -1.4

11 Lagos 8.2 Portugal -1.4

12 Côte d'Ivoire 8.1 Brunei -1.2

13 Panama 8.0 Spain -1.2

14 Uzbekistan 8.0 Slovenia -1.1

-8

-6

-4

-2

0

2

4

6

8

10

12

Change from previous year, %*

90

100

110

120

130

140

150

2008 2009 2010 2011 2012 2013

World

Euro Area

Emerging and Developing Asia

Commonwealth of Independent States

Growth index, 2008=100%

P a g e 12 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

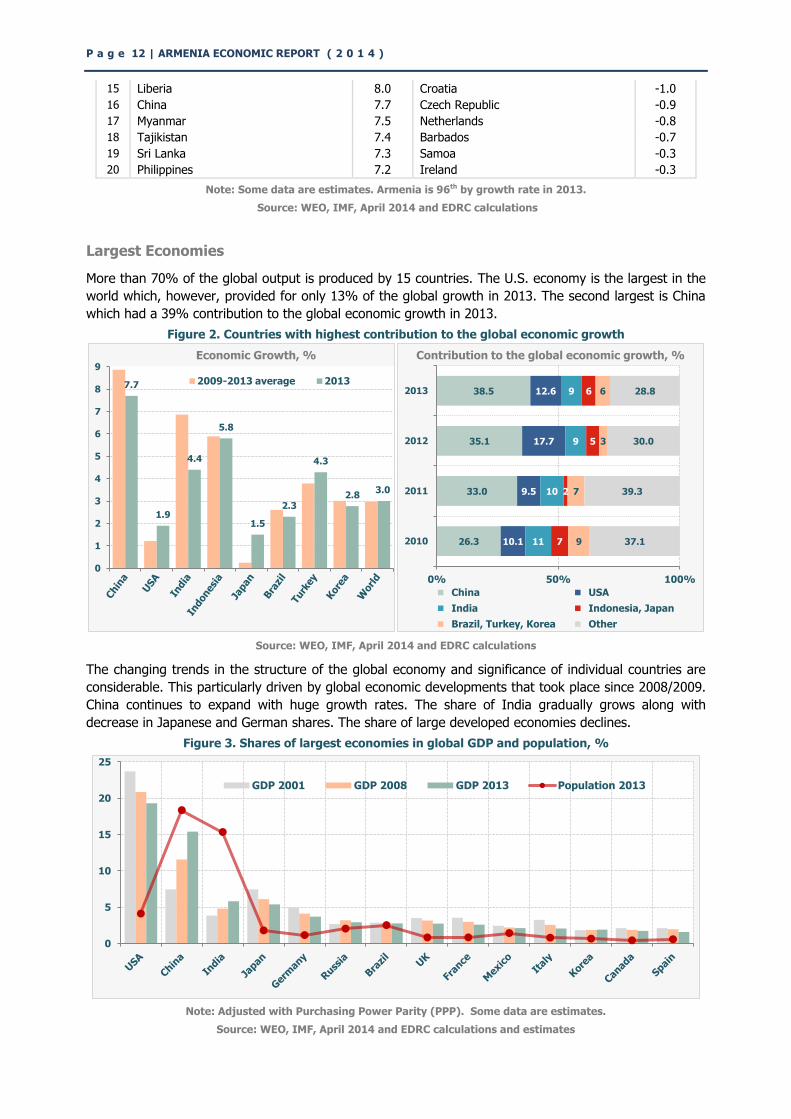

15 Liberia 8.0 Croatia -1.0

16 China 7.7 Czech Republic -0.9

17 Myanmar 7.5 Netherlands -0.8

18 Tajikistan 7.4 Barbados -0.7

19 Sri Lanka 7.3 Samoa -0.3

20 Philippines 7.2 Ireland -0.3

Note: Some data are estimates. Armenia is 96th by growth rate in 2013.

Source: WEO, IMF, April 2014 and EDRC calculations

Largest Economies

More than 70% of the global output is produced by 15 countries. The U.S. economy is the largest in the

world which, however, provided for only 13% of the global growth in 2013. The second largest is China

which had a 39% contribution to the global economic growth in 2013.

Figure 2. Countries with highest contribution to the global economic growth

Source: WEO, IMF, April 2014 and EDRC calculations

The changing trends in the structure of the global economy and significance of individual countries are

considerable. This particularly driven by global economic developments that took place since 2008/2009.

China continues to expand with huge growth rates. The share of India gradually grows along with

decrease in Japanese and German shares. The share of large developed economies declines.

Figure 3. Shares of largest economies in global GDP and population, %

Note: Adjusted with Purchasing Power Parity (PPP). Some data are estimates.

Source: WEO, IMF, April 2014 and EDRC calculations and estimates

7.7

1.9

4.4

5.8

1.5

2.3

4.3

2.8 3.0

0

1

2

3

4

5

6

7

8

9

2009-2013 average 2013

Economic Growth, %

26.3

33.0

35.1

38.5

10.1

9.5

17.7

12.6

11

10

9

9

7

2

5

6

9

7

3

6

37.1

39.3

30.0

28.8

0% 50% 100%

2010

2011

2012

2013

China USA

India Indonesia, Japan

Brazil, Turkey, Korea Other

Contribution to the global economic growth, %

0

5

10

15

20

25

GDP 2001 GDP 2008 GDP 2013 Population 2013

E D R C ( 2 0 1 4 ) | p a g e 1 3

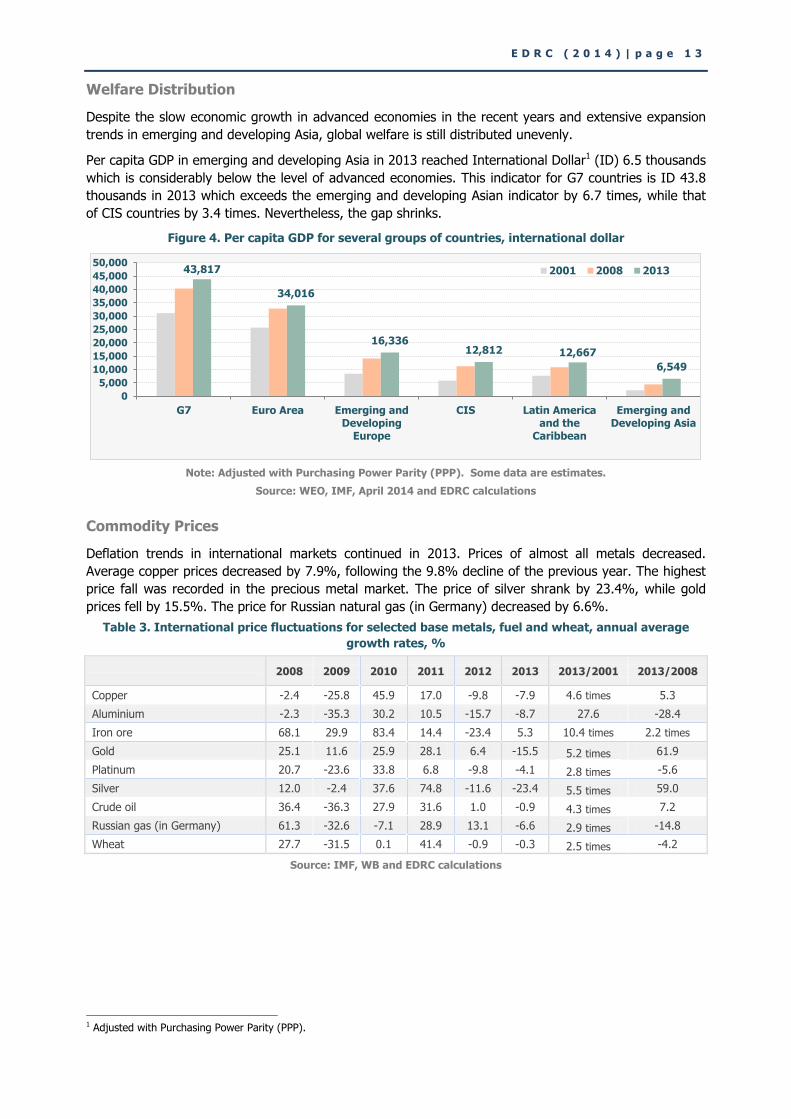

Welfare Distribution

Despite the slow economic growth in advanced economies in the recent years and extensive expansion

trends in emerging and developing Asia, global welfare is still distributed unevenly.

Per capita GDP in emerging and developing Asia in 2013 reached International Dollar1 (ID) 6.5 thousands

which is considerably below the level of advanced economies. This indicator for G7 countries is ID 43.8

thousands in 2013 which exceeds the emerging and developing Asian indicator by 6.7 times, while that

of CIS countries by 3.4 times. Nevertheless, the gap shrinks.

Figure 4. Per capita GDP for several groups of countries, international dollar

Note: Adjusted with Purchasing Power Parity (PPP). Some data are estimates.

Source: WEO, IMF, April 2014 and EDRC calculations

Commodity Prices

Deflation trends in international markets continued in 2013. Prices of almost all metals decreased.

Average copper prices decreased by 7.9%, following the 9.8% decline of the previous year. The highest

price fall was recorded in the precious metal market. The price of silver shrank by 23.4%, while gold

prices fell by 15.5%. The price for Russian natural gas (in Germany) decreased by 6.6%.

Table 3. International price fluctuations for selected base metals, fuel and wheat, annual average

growth rates, %

2008 2009 2010 2011 2012 2013 2013/2001 2013/2008

Copper -2.4 -25.8 45.9 17.0 -9.8 -7.9 4.6 times 5.3

Aluminium -2.3 -35.3 30.2 10.5 -15.7 -8.7 27.6 -28.4

Iron ore 68.1 29.9 83.4 14.4 -23.4 5.3 10.4 times 2.2 times

Gold 25.1 11.6 25.9 28.1 6.4 -15.5 5.2 times 61.9

Platinum 20.7 -23.6 33.8 6.8 -9.8 -4.1 2.8 times -5.6

Silver 12.0 -2.4 37.6 74.8 -11.6 -23.4 5.5 times 59.0

Crude oil 36.4 -36.3 27.9 31.6 1.0 -0.9 4.3 times 7.2

Russian gas (in Germany) 61.3 -32.6 -7.1 28.9 13.1 -6.6 2.9 times -14.8

Wheat 27.7 -31.5 0.1 41.4 -0.9 -0.3 2.5 times -4.2

Source: IMF, WB and EDRC calculations

1 Adjusted with Purchasing Power Parity (PPP).

43,817

34,016

16,336 12,812 12,667

6,549

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

G7 Euro Area Emerging and Developing

Europe

CIS Latin America and the

Caribbean

Emerging and Developing Asia

2001 2008 2013

P a g e 14 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

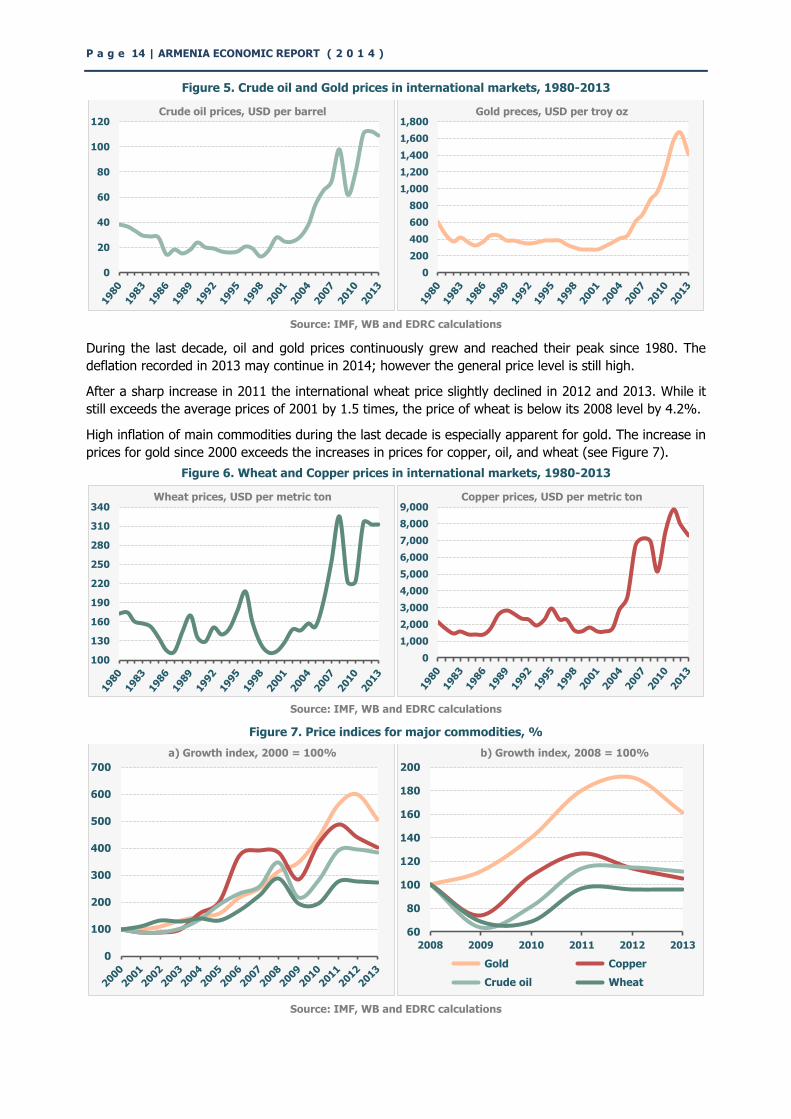

Figure 5. Crude oil and Gold prices in international markets, 1980-2013

Source: IMF, WB and EDRC calculations

During the last decade, oil and gold prices continuously grew and reached their peak since 1980. The

deflation recorded in 2013 may continue in 2014; however the general price level is still high.

After a sharp increase in 2011 the international wheat price slightly declined in 2012 and 2013. While it

still exceeds the average prices of 2001 by 1.5 times, the price of wheat is below its 2008 level by 4.2%.

High inflation of main commodities during the last decade is especially apparent for gold. The increase in

prices for gold since 2000 exceeds the increases in prices for copper, oil, and wheat (see Figure 7).

Figure 6. Wheat and Copper prices in international markets, 1980-2013

Source: IMF, WB and EDRC calculations

Figure 7. Price indices for major commodities, %

Source: IMF, WB and EDRC calculations

0

20

40

60

80

100

120 Crude oil prices, USD per barrel

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800 Gold preces, USD per troy oz

100

130

160

190

220

250

280

310

340 Wheat prices, USD per metric ton

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000 Copper prices, USD per metric ton

0

100

200

300

400

500

600

700

a) Growth index, 2000 = 100%

60

80

100

120

140

160

180

200

2008 2009 2010 2011 2012 2013

b) Growth index, 2008 = 100%

Gold Copper

Crude oil Wheat

E D R C ( 2 0 1 4 ) | p a g e 1 5

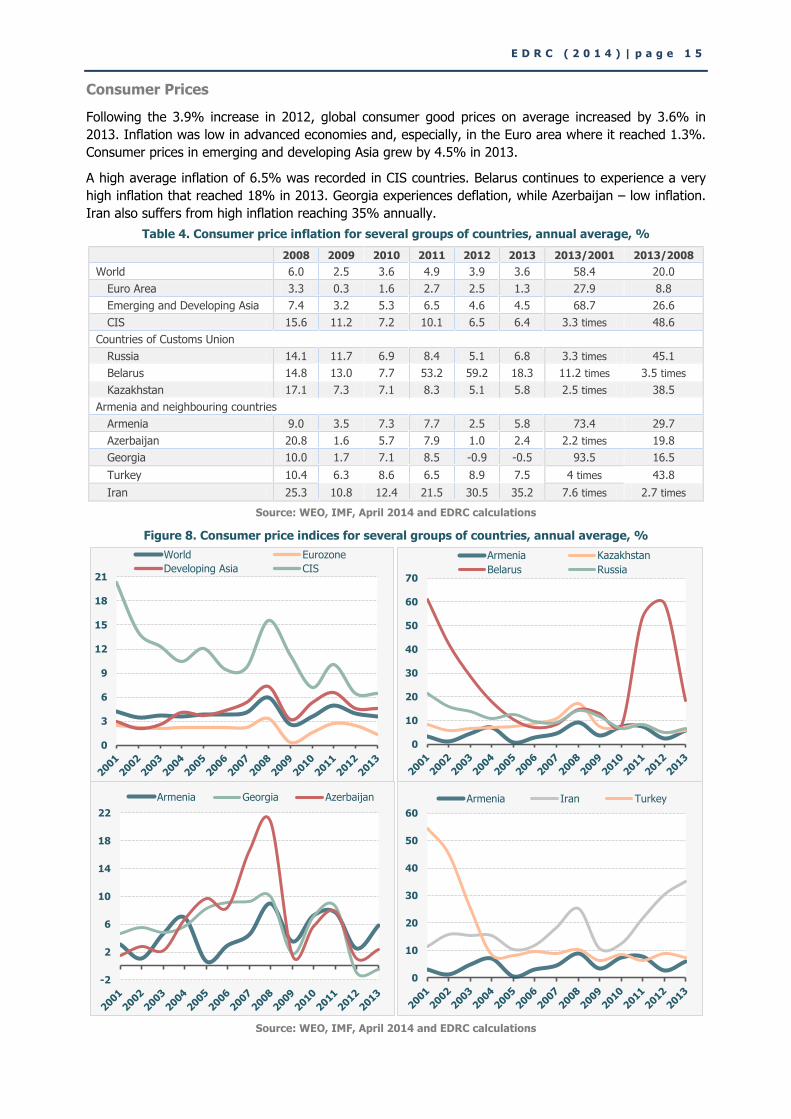

Consumer Prices

Following the 3.9% increase in 2012, global consumer good prices on average increased by 3.6% in

2013. Inflation was low in advanced economies and, especially, in the Euro area where it reached 1.3%.

Consumer prices in emerging and developing Asia grew by 4.5% in 2013.

A high average inflation of 6.5% was recorded in CIS countries. Belarus continues to experience a very

high inflation that reached 18% in 2013. Georgia experiences deflation, while Azerbaijan – low inflation.

Iran also suffers from high inflation reaching 35% annually.

Table 4. Consumer price inflation for several groups of countries, annual average, %

2008 2009 2010 2011 2012 2013 2013/2001 2013/2008

World 6.0 2.5 3.6 4.9 3.9 3.6 58.4 20.0

Euro Area 3.3 0.3 1.6 2.7 2.5 1.3 27.9 8.8

Emerging and Developing Asia 7.4 3.2 5.3 6.5 4.6 4.5 68.7 26.6

CIS 15.6 11.2 7.2 10.1 6.5 6.4 3.3 times 48.6

Countries of Customs Union

Russia 14.1 11.7 6.9 8.4 5.1 6.8 3.3 times 45.1

Belarus 14.8 13.0 7.7 53.2 59.2 18.3 11.2 times 3.5 times

Kazakhstan 17.1 7.3 7.1 8.3 5.1 5.8 2.5 times 38.5

Armenia and neighbouring countries

Armenia 9.0 3.5 7.3 7.7 2.5 5.8 73.4 29.7

Azerbaijan 20.8 1.6 5.7 7.9 1.0 2.4 2.2 times 19.8

Georgia 10.0 1.7 7.1 8.5 -0.9 -0.5 93.5 16.5

Turkey 10.4 6.3 8.6 6.5 8.9 7.5 4 times 43.8

Iran 25.3 10.8 12.4 21.5 30.5 35.2 7.6 times 2.7 times

Source: WEO, IMF, April 2014 and EDRC calculations

Figure 8. Consumer price indices for several groups of countries, annual average, %

Source: WEO, IMF, April 2014 and EDRC calculations

0

3

6

9

12

15

18

21

World Eurozone

Developing Asia CIS

0

10

20

30

40

50

60

70

Armenia Kazakhstan

Belarus Russia

-2

2

6

10

14

18

22

Armenia Georgia Azerbaijan

0

10

20

30

40

50

60

Armenia Iran Turkey

P a g e 16 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

1.2. Economic Trends in Armenia

Economic Growth and GDP

Against quite high growth recorded in 2012, real growth rate in 2013 was lower than projected - 3.5%.

The slowdown in economic growth, again, was a result of sharp decline in construction.

After the recent decline, Armenian economy grew by 18.7% during 2010-2013 or on average by 4.4%

per annum. The largest share in economic recovery and growth belongs to service sector as it grew by

26% and provided for more than half of the economic recovery and growth.

Industrial sectors altogether (including power sector, water supply and mining) expanded by 39% during

the last 4 years, however their contribution to income generation was considerably lower than that of

services. Industrial sectors on average provided for 1.3 percentage points of annual 4.4% average

growth. Agriculture grew cumulatively by 12%, thus, providing for the 0.7 percentage points of annual

average growth.

The construction sector significantly constrained the economic growth. Following the sharp decline in

2009, it continued to decline in 2011 and 2013 by 12.2% and 10.8% respectively. Construction sector is

still 2 times smaller than it was in 2008.

Therefore, the pre-crisis real GDP level is finally recovered and exceeded by 1.9%. Beside construction,

all other major sectors of the economy exceed their 2008 levels.

Table 5. Growth indices in aggregate sectors of the economy, %

2013

Annual growth

2010-2013 2013/2008**

Average Cumulative Contribution*

GDP (real) 3.5 4.4 18.7 4.4 101.9

Agriculture 7.2 3.0 12.4 0.7 119.1

Industry 5.4 8.6 39.0 1.3 129.4

Construction -10.8 -4.0 -15.2 -0.6 49.6

Trade and services 6.2 6.0 26.0 2.5 121.4

Net taxes and FISIM -0.9 4.2 17.7 0.4 88.9

*Contribution to economic growth, percentage points, ** 2013 GDP compared to 2008 GDP in comparable prices.

Source: NSS of RA, EDRC estimates

As it was already noted, construction sector experienced decline. It constrained the total annual growth

by 1.3 percentage points. Low annual growth rate was also determined by low growth recorded in trade

– only 1%. Transport and communications also grew modestly: 3.7% in 2013 after 9.4% in 2012.

Economic growth was quite high in certain sectors. The largest share of economic growth was

contributed to by agriculture – 1.4 percentage points. Manufacturing contributed to 0.7 percentage

points. Finance and insurance, which is two times smaller than manufacturing, provided for 0.6

percentage points of total growth. Growth was also constrained by power and water supply sector which

had almost no contribution to economic growth in 2013.

Table 6. Economic growth in main sectors, 2009-2013, %

2009 2010 2011 2012 2013 2013 2013/2008 2008 2013

Growth rates Contribution* Index** Share in GDP

GDP -14.1 2.2 4.7 7.2 3.5 3.5 101.9 100 100

Agriculture 6.0 -16.0 14.0 9.5 7.2 1.4 119.1 16.3 19.3

Manufacturing -7.1 12.1 12.4 4.1 7.1 0.7 130.4 8.8 10.1

Mining 6.3 22.8 13.9 15.7 5.9 0.2 182.2 1.6 2.4

Power and water supply -13.3 -6.3 16.8 5.9 1.0 0.0 101.4 2.9 4.7

E D R C ( 2 0 1 4 ) | p a g e 1 7

Construction -41.6 3.3 -12.2 4.8 -10.8 -1.3 49.6 25.3 10.5

Trade -4.8 2.9 4.8 4.7 1.0 0.1 108.6 11.6 12.8

Transport and communications -9.9 7.0 2.4 9.4 3.7 0.3 112.1 6.8 6.5

Financial services -1.6 10.6 23.5 19.9 12.9 0.6 182.1 3.4 4.7

Public administration -5.9 -0.7 7.6 -2.1 14.9 0.6 113.1 2.7 4.1

Healthcare, social services -4.0 -1.4 6.6 0.2 5.7 0.2 107.0 2.7 4.2

Education 2.2 4.6 3.4 1.6 -0.0 -0.0 112.2 2.7 3.0

Hotels and catering 23.5 19.6 5.3 23.6 27.8 0.3 245.8 0.4 1.1

Other sectors (including taxes and FISIM)

-15.5 10.0 -0.2 9.0 3.7 0.6 104.8 14.8 16.5

*Contribution to economic growth, percentage points, ** 2013 GDP compared to 2008 GDP in comparable prices.

Source: NSS of RA, EDRC estimates.

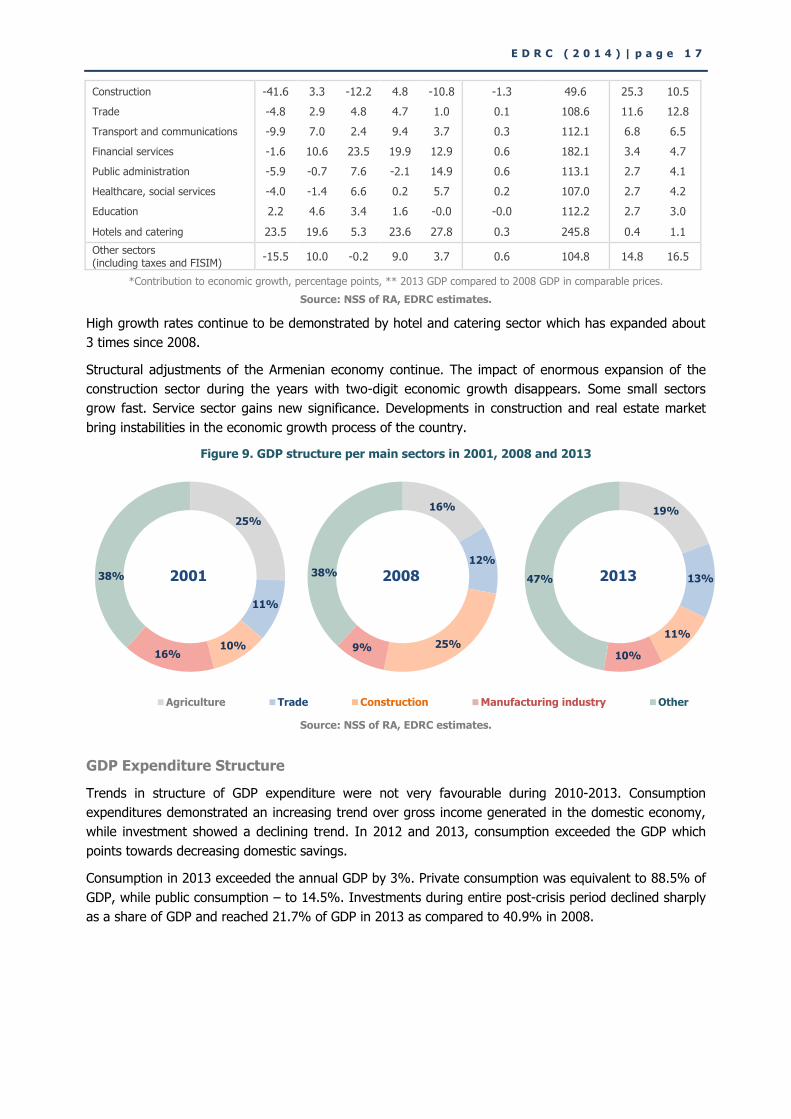

High growth rates continue to be demonstrated by hotel and catering sector which has expanded about

3 times since 2008.

Structural adjustments of the Armenian economy continue. The impact of enormous expansion of the

construction sector during the years with two-digit economic growth disappears. Some small sectors

grow fast. Service sector gains new significance. Developments in construction and real estate market

bring instabilities in the economic growth process of the country.

Figure 9. GDP structure per main sectors in 2001, 2008 and 2013

Source: NSS of RA, EDRC estimates.

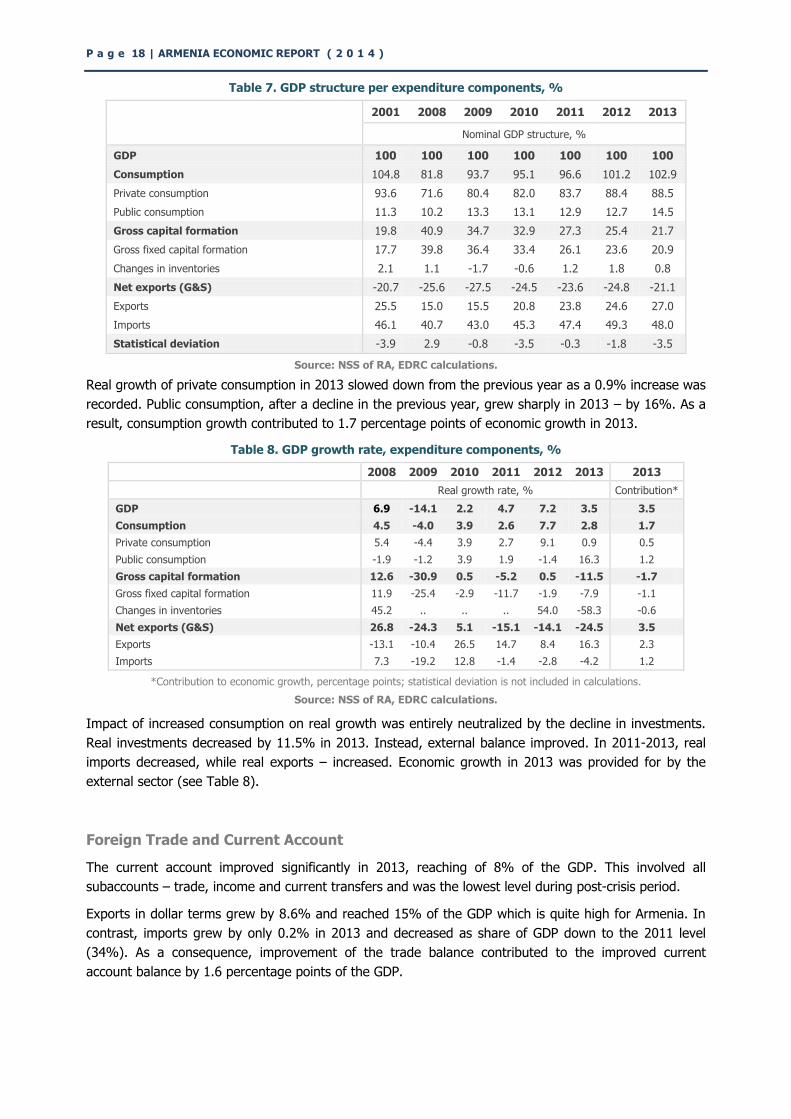

GDP Expenditure Structure

Trends in structure of GDP expenditure were not very favourable during 2010-2013. Consumption

expenditures demonstrated an increasing trend over gross income generated in the domestic economy,

while investment showed a declining trend. In 2012 and 2013, consumption exceeded the GDP which

points towards decreasing domestic savings.

Consumption in 2013 exceeded the annual GDP by 3%. Private consumption was equivalent to 88.5% of

GDP, while public consumption – to 14.5%. Investments during entire post-crisis period declined sharply

as a share of GDP and reached 21.7% of GDP in 2013 as compared to 40.9% in 2008.

Agriculture Trade Construction Manufacturing industry Other

16%

12%

25% 9%

38% 2008

19%

13%

11%

10%

47% 2013

25%

11%

10% 16%

38% 2001

P a g e 18 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Table 7. GDP structure per expenditure components, %

2001 2008 2009 2010 2011 2012 2013

Nominal GDP structure, %

GDP 100 100 100 100 100 100 100

Consumption 104.8 81.8 93.7 95.1 96.6 101.2 102.9

Private consumption 93.6 71.6 80.4 82.0 83.7 88.4 88.5

Public consumption 11.3 10.2 13.3 13.1 12.9 12.7 14.5

Gross capital formation 19.8 40.9 34.7 32.9 27.3 25.4 21.7

Gross fixed capital formation 17.7 39.8 36.4 33.4 26.1 23.6 20.9

Changes in inventories 2.1 1.1 -1.7 -0.6 1.2 1.8 0.8

Net exports (G&S) -20.7 -25.6 -27.5 -24.5 -23.6 -24.8 -21.1

Exports 25.5 15.0 15.5 20.8 23.8 24.6 27.0

Imports 46.1 40.7 43.0 45.3 47.4 49.3 48.0

Statistical deviation -3.9 2.9 -0.8 -3.5 -0.3 -1.8 -3.5

Source: NSS of RA, EDRC calculations.

Real growth of private consumption in 2013 slowed down from the previous year as a 0.9% increase was

recorded. Public consumption, after a decline in the previous year, grew sharply in 2013 – by 16%. As a

result, consumption growth contributed to 1.7 percentage points of economic growth in 2013.

Table 8. GDP growth rate, expenditure components, %

2008 2009 2010 2011 2012 2013 2013

Real growth rate, % Contribution*

GDP 6.9 -14.1 2.2 4.7 7.2 3.5 3.5

Consumption 4.5 -4.0 3.9 2.6 7.7 2.8 1.7

Private consumption 5.4 -4.4 3.9 2.7 9.1 0.9 0.5

Public consumption -1.9 -1.2 3.9 1.9 -1.4 16.3 1.2

Gross capital formation 12.6 -30.9 0.5 -5.2 0.5 -11.5 -1.7

Gross fixed capital formation 11.9 -25.4 -2.9 -11.7 -1.9 -7.9 -1.1

Changes in inventories 45.2 .. .. .. 54.0 -58.3 -0.6

Net exports (G&S) 26.8 -24.3 5.1 -15.1 -14.1 -24.5 3.5

Exports -13.1 -10.4 26.5 14.7 8.4 16.3 2.3

Imports 7.3 -19.2 12.8 -1.4 -2.8 -4.2 1.2

*Contribution to economic growth, percentage points; statistical deviation is not included in calculations.

Source: NSS of RA, EDRC calculations.

Impact of increased consumption on real growth was entirely neutralized by the decline in investments.

Real investments decreased by 11.5% in 2013. Instead, external balance improved. In 2011-2013, real

imports decreased, while real exports – increased. Economic growth in 2013 was provided for by the

external sector (see Table 8).

Foreign Trade and Current Account

The current account improved significantly in 2013, reaching of 8% of the GDP. This involved all

subaccounts – trade, income and current transfers and was the lowest level during post-crisis period.

Exports in dollar terms grew by 8.6% and reached 15% of the GDP which is quite high for Armenia. In

contrast, imports grew by only 0.2% in 2013 and decreased as share of GDP down to the 2011 level

(34%). As a consequence, improvement of the trade balance contributed to the improved current

account balance by 1.6 percentage points of the GDP.

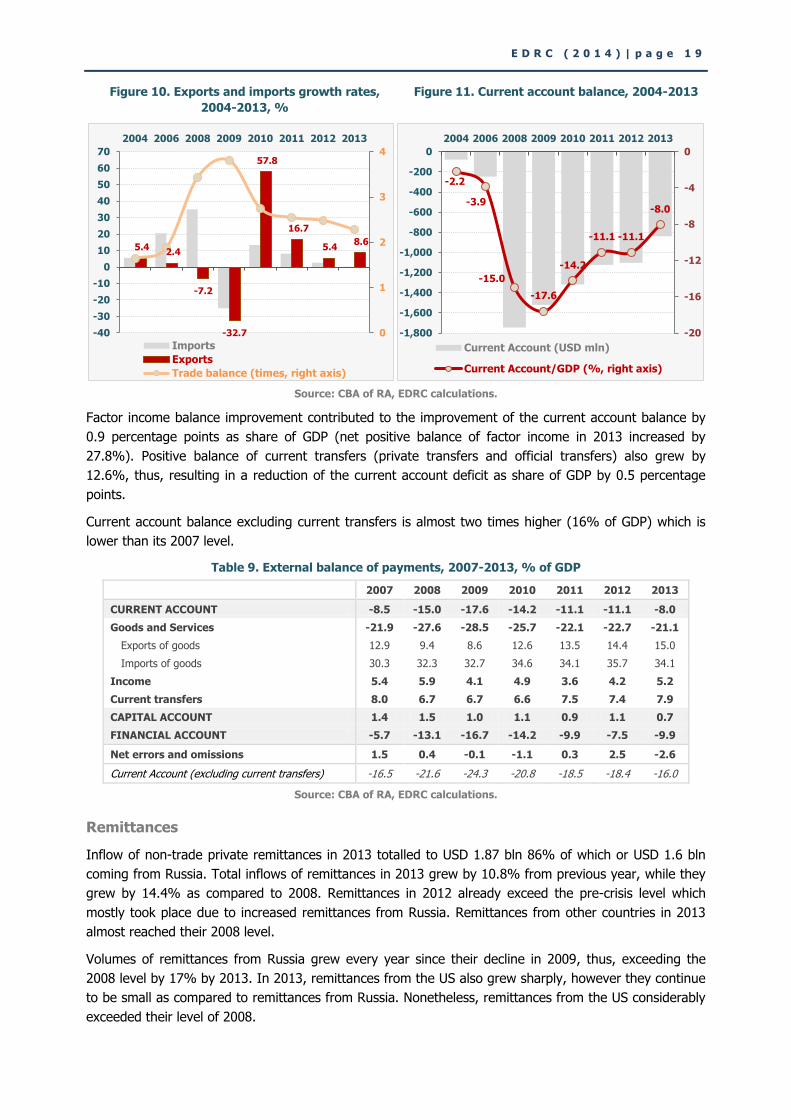

E D R C ( 2 0 1 4 ) | p a g e 1 9

Figure 10. Exports and imports growth rates,

2004-2013, %

Figure 11. Current account balance, 2004-2013

Source: CBA of RA, EDRC calculations.

Factor income balance improvement contributed to the improvement of the current account balance by

0.9 percentage points as share of GDP (net positive balance of factor income in 2013 increased by

27.8%). Positive balance of current transfers (private transfers and official transfers) also grew by

12.6%, thus, resulting in a reduction of the current account deficit as share of GDP by 0.5 percentage

points.

Current account balance excluding current transfers is almost two times higher (16% of GDP) which is

lower than its 2007 level.

Table 9. External balance of payments, 2007-2013, % of GDP

2007 2008 2009 2010 2011 2012 2013

CURRENT ACCOUNT -8.5 -15.0 -17.6 -14.2 -11.1 -11.1 -8.0

Goods and Services -21.9 -27.6 -28.5 -25.7 -22.1 -22.7 -21.1

Exports of goods 12.9 9.4 8.6 12.6 13.5 14.4 15.0

Imports of goods 30.3 32.3 32.7 34.6 34.1 35.7 34.1

Income 5.4 5.9 4.1 4.9 3.6 4.2 5.2

Current transfers 8.0 6.7 6.7 6.6 7.5 7.4 7.9

CAPITAL ACCOUNT 1.4 1.5 1.0 1.1 0.9 1.1 0.7

FINANCIAL ACCOUNT -5.7 -13.1 -16.7 -14.2 -9.9 -7.5 -9.9

Net errors and omissions 1.5 0.4 -0.1 -1.1 0.3 2.5 -2.6

Current Account (excluding current transfers) -16.5 -21.6 -24.3 -20.8 -18.5 -18.4 -16.0

Source: CBA of RA, EDRC calculations.

Remittances

Inflow of non-trade private remittances in 2013 totalled to USD 1.87 bln 86% of which or USD 1.6 bln

coming from Russia. Total inflows of remittances in 2013 grew by 10.8% from previous year, while they

grew by 14.4% as compared to 2008. Remittances in 2012 already exceed the pre-crisis level which

mostly took place due to increased remittances from Russia. Remittances from other countries in 2013

almost reached their 2008 level.

Volumes of remittances from Russia grew every year since their decline in 2009, thus, exceeding the

2008 level by 17% by 2013. In 2013, remittances from the US also grew sharply, however they continue

to be small as compared to remittances from Russia. Nonetheless, remittances from the US considerably

exceeded their level of 2008.

5.4 2.4

-7.2

-32.7

57.8

16.7

5.4 8.6

0

1

2

3

4

-40

-30

-20

-10

0

10

20

30

40

50

60

70

2004 2006 2008 2009 2010 2011 2012 2013

Imports

Exports

Trade balance (times, right axis)

-2.2

-3.9

-15.0

-17.6

-14.2

-11.1 -11.1

-8.0

-20

-16

-12

-8

-4

0

-1,800

-1,600

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

2004 2006 2008 2009 2010 2011 2012 2013

Current Account (USD mln)

Current Account/GDP (%, right axis)

P a g e 20 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Figure 12. Inflows of non-trade remittances, 2008-2013

Source: CBA of RA, EDRC calculations.

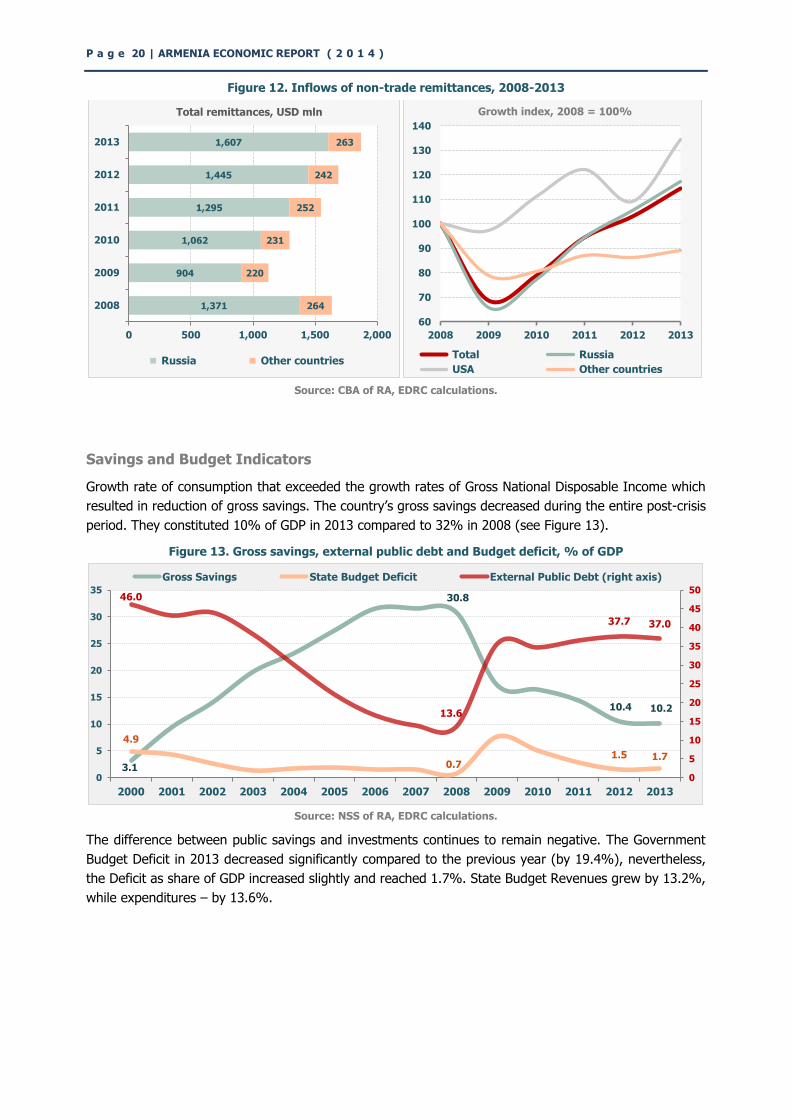

Savings and Budget Indicators

Growth rate of consumption that exceeded the growth rates of Gross National Disposable Income which

resulted in reduction of gross savings. The country’s gross savings decreased during the entire post-crisis

period. They constituted 10% of GDP in 2013 compared to 32% in 2008 (see Figure 13).

Figure 13. Gross savings, external public debt and Budget deficit, % of GDP

Source: NSS of RA, EDRC calculations.

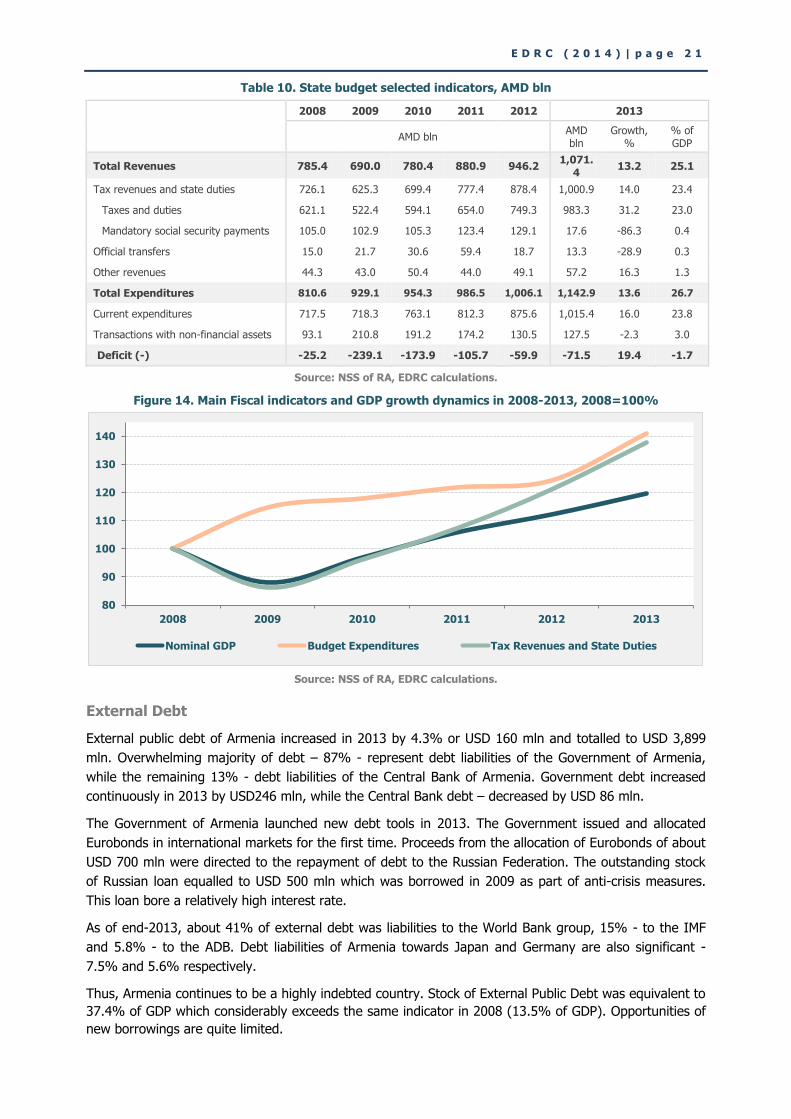

The difference between public savings and investments continues to remain negative. The Government

Budget Deficit in 2013 decreased significantly compared to the previous year (by 19.4%), nevertheless,

the Deficit as share of GDP increased slightly and reached 1.7%. State Budget Revenues grew by 13.2%,

while expenditures – by 13.6%.

1,371

904

1,062

1,295

1,445

1,607

264

220

231

252

242

263

0 500 1,000 1,500 2,000

2008

2009

2010

2011

2012

2013

Russia Other countries

Total remittances, USD mln

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013

Total Russia

USA Other countries

Growth index, 2008 = 100%

3.1

30.8

10.4 10.2

4.9

0.7 1.5 1.7

46.0

13.6

37.7 37.0

0

5

10

15

20

25

30

35

40

45

50

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gross Savings State Budget Deficit External Public Debt (right axis)

E D R C ( 2 0 1 4 ) | p a g e 2 1

Table 10. State budget selected indicators, AMD bln

2008 2009 2010 2011 2012 2013

AMD bln

AMD bln

Growth, %

% of GDP

Total Revenues 785.4 690.0 780.4 880.9 946.2 1,071.

4 13.2 25.1

Tax revenues and state duties 726.1 625.3 699.4 777.4 878.4 1,000.9 14.0 23.4

Taxes and duties 621.1 522.4 594.1 654.0 749.3 983.3 31.2 23.0

Mandatory social security payments 105.0 102.9 105.3 123.4 129.1 17.6 -86.3 0.4

Official transfers 15.0 21.7 30.6 59.4 18.7 13.3 -28.9 0.3

Other revenues 44.3 43.0 50.4 44.0 49.1 57.2 16.3 1.3

Total Expenditures 810.6 929.1 954.3 986.5 1,006.1 1,142.9 13.6 26.7

Current expenditures 717.5 718.3 763.1 812.3 875.6 1,015.4 16.0 23.8

Transactions with non-financial assets 93.1 210.8 191.2 174.2 130.5 127.5 -2.3 3.0

Deficit (-) -25.2 -239.1 -173.9 -105.7 -59.9 -71.5 19.4 -1.7

Source: NSS of RA, EDRC calculations.

Figure 14. Main Fiscal indicators and GDP growth dynamics in 2008-2013, 2008=100%

Source: NSS of RA, EDRC calculations.

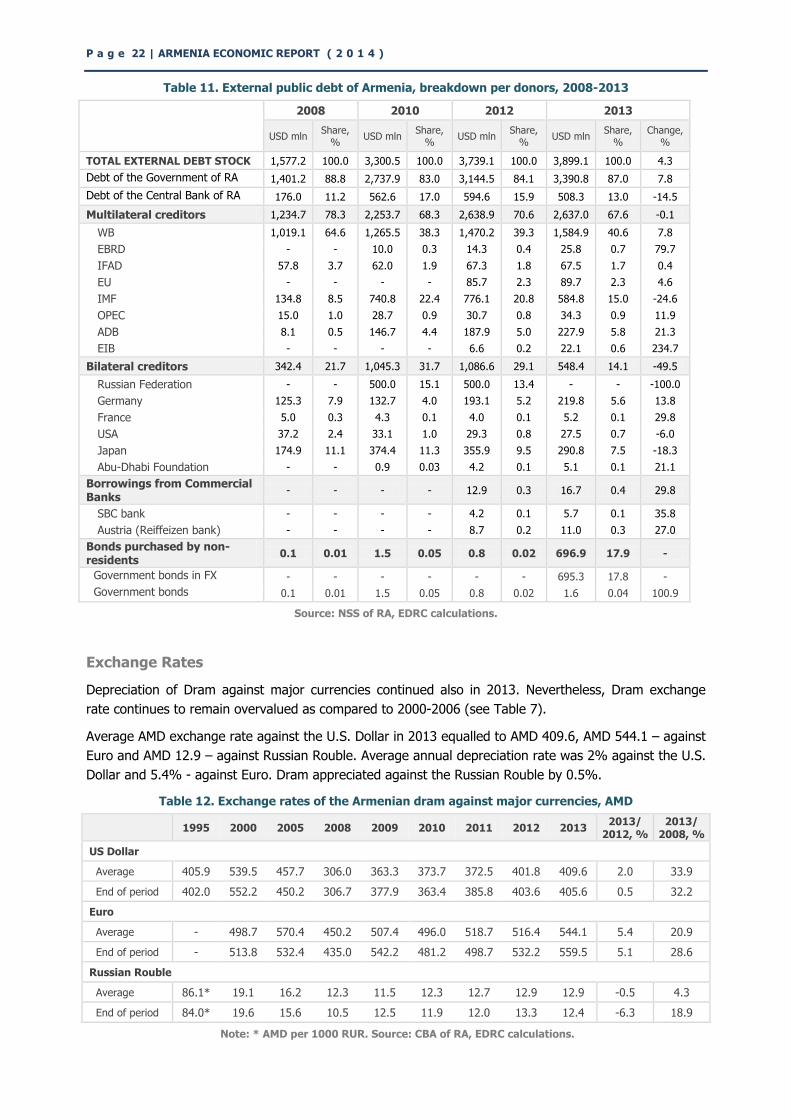

External Debt

External public debt of Armenia increased in 2013 by 4.3% or USD 160 mln and totalled to USD 3,899

mln. Overwhelming majority of debt – 87% - represent debt liabilities of the Government of Armenia,

while the remaining 13% - debt liabilities of the Central Bank of Armenia. Government debt increased

continuously in 2013 by USD246 mln, while the Central Bank debt – decreased by USD 86 mln.

The Government of Armenia launched new debt tools in 2013. The Government issued and allocated

Eurobonds in international markets for the first time. Proceeds from the allocation of Eurobonds of about

USD 700 mln were directed to the repayment of debt to the Russian Federation. The outstanding stock

of Russian loan equalled to USD 500 mln which was borrowed in 2009 as part of anti-crisis measures.

This loan bore a relatively high interest rate.

As of end-2013, about 41% of external debt was liabilities to the World Bank group, 15% - to the IMF

and 5.8% - to the ADB. Debt liabilities of Armenia towards Japan and Germany are also significant -

7.5% and 5.6% respectively.

Thus, Armenia continues to be a highly indebted country. Stock of External Public Debt was equivalent to

37.4% of GDP which considerably exceeds the same indicator in 2008 (13.5% of GDP). Opportunities of

new borrowings are quite limited.

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013

Nominal GDP Budget Expenditures Tax Revenues and State Duties

P a g e 22 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Table 11. External public debt of Armenia, breakdown per donors, 2008-2013

2008 2010 2012 2013

USD mln

Share, %

USD mln Share,

% USD mln

Share, %

USD mln Share,

% Change,

%

TOTAL EXTERNAL DEBT STOCK 1,577.2 100.0 3,300.5 100.0 3,739.1 100.0 3,899.1 100.0 4.3

Debt of the Government of RA 1,401.2 88.8 2,737.9 83.0 3,144.5 84.1 3,390.8 87.0 7.8

Debt of the Central Bank of RA 176.0 11.2 562.6 17.0 594.6 15.9 508.3 13.0 -14.5

Multilateral creditors 1,234.7 78.3 2,253.7 68.3 2,638.9 70.6 2,637.0 67.6 -0.1

WB 1,019.1 64.6 1,265.5 38.3 1,470.2 39.3 1,584.9 40.6 7.8

EBRD - - 10.0 0.3 14.3 0.4 25.8 0.7 79.7

IFAD 57.8 3.7 62.0 1.9 67.3 1.8 67.5 1.7 0.4

EU - - - - 85.7 2.3 89.7 2.3 4.6

IMF 134.8 8.5 740.8 22.4 776.1 20.8 584.8 15.0 -24.6

OPEC 15.0 1.0 28.7 0.9 30.7 0.8 34.3 0.9 11.9

ADB 8.1 0.5 146.7 4.4 187.9 5.0 227.9 5.8 21.3

EIB - - - - 6.6 0.2 22.1 0.6 234.7

Bilateral creditors 342.4 21.7 1,045.3 31.7 1,086.6 29.1 548.4 14.1 -49.5

Russian Federation - - 500.0 15.1 500.0 13.4 - - -100.0

Germany 125.3 7.9 132.7 4.0 193.1 5.2 219.8 5.6 13.8

France 5.0 0.3 4.3 0.1 4.0 0.1 5.2 0.1 29.8

USA 37.2 2.4 33.1 1.0 29.3 0.8 27.5 0.7 -6.0

Japan 174.9 11.1 374.4 11.3 355.9 9.5 290.8 7.5 -18.3

Abu-Dhabi Foundation - - 0.9 0.03 4.2 0.1 5.1 0.1 21.1

Borrowings from Commercial Banks

- - - - 12.9 0.3 16.7 0.4 29.8

SBC bank - - - - 4.2 0.1 5.7 0.1 35.8

Austria (Reiffeizen bank) - - - - 8.7 0.2 11.0 0.3 27.0

Bonds purchased by non-residents

0.1 0.01 1.5 0.05 0.8 0.02 696.9 17.9 -

Government bonds in FX - - - - - - 695.3 17.8 -

Government bonds 0.1 0.01 1.5 0.05 0.8 0.02 1.6 0.04 100.9

Source: NSS of RA, EDRC calculations.

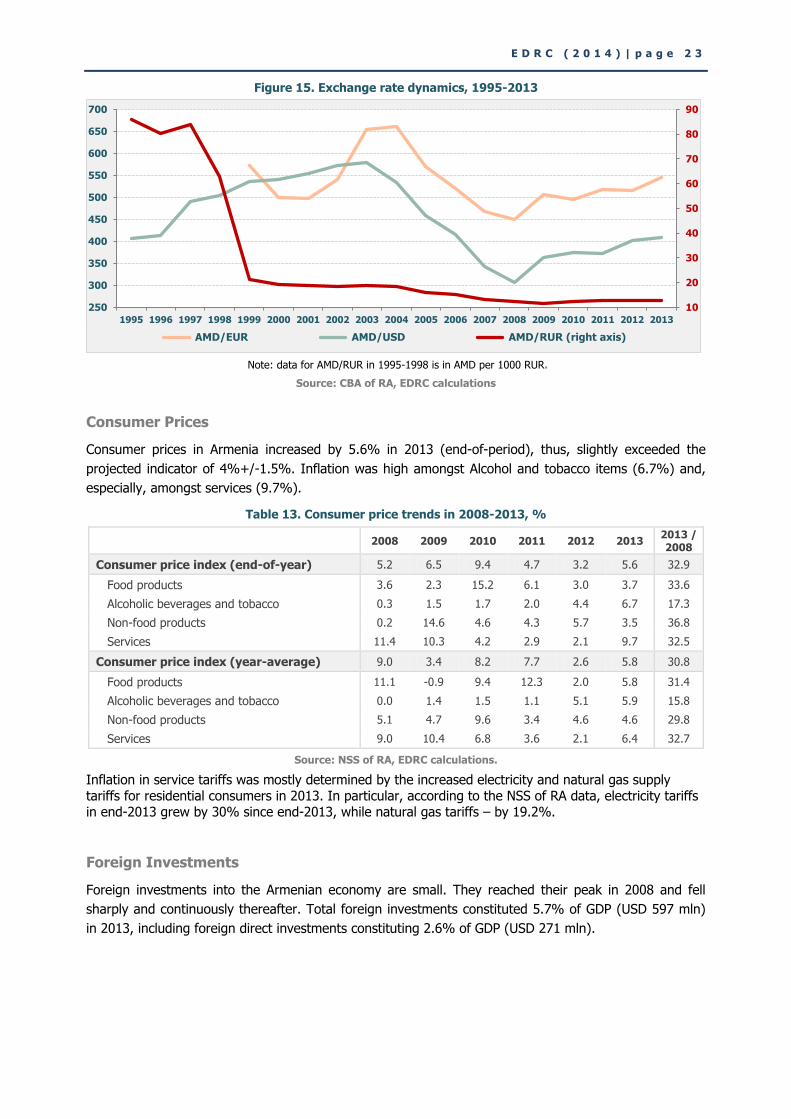

Exchange Rates

Depreciation of Dram against major currencies continued also in 2013. Nevertheless, Dram exchange

rate continues to remain overvalued as compared to 2000-2006 (see Table 7).

Average AMD exchange rate against the U.S. Dollar in 2013 equalled to AMD 409.6, AMD 544.1 – against

Euro and AMD 12.9 – against Russian Rouble. Average annual depreciation rate was 2% against the U.S.

Dollar and 5.4% - against Euro. Dram appreciated against the Russian Rouble by 0.5%.

Table 12. Exchange rates of the Armenian dram against major currencies, AMD

1995 2000 2005 2008 2009 2010 2011 2012 2013

2013/ 2012, %

2013/ 2008, %

US Dollar

Average 405.9 539.5 457.7 306.0 363.3 373.7 372.5 401.8 409.6 2.0 33.9

End of period 402.0 552.2 450.2 306.7 377.9 363.4 385.8 403.6 405.6 0.5 32.2

Euro

Average - 498.7 570.4 450.2 507.4 496.0 518.7 516.4 544.1 5.4 20.9

End of period - 513.8 532.4 435.0 542.2 481.2 498.7 532.2 559.5 5.1 28.6

Russian Rouble

Average 86.1* 19.1 16.2 12.3 11.5 12.3 12.7 12.9 12.9 -0.5 4.3

End of period 84.0* 19.6 15.6 10.5 12.5 11.9 12.0 13.3 12.4 -6.3 18.9

Note: * AMD per 1000 RUR. Source: CBA of RA, EDRC calculations.

E D R C ( 2 0 1 4 ) | p a g e 2 3

Figure 15. Exchange rate dynamics, 1995-2013

Note: data for AMD/RUR in 1995-1998 is in AMD per 1000 RUR.

Source: CBA of RA, EDRC calculations

Consumer Prices

Consumer prices in Armenia increased by 5.6% in 2013 (end-of-period), thus, slightly exceeded the

projected indicator of 4%+/-1.5%. Inflation was high amongst Alcohol and tobacco items (6.7%) and,

especially, amongst services (9.7%).

Table 13. Consumer price trends in 2008-2013, %

2008 2009 2010 2011 2012 2013

2013 / 2008

Consumer price index (end-of-year) 5.2 6.5 9.4 4.7 3.2 5.6 32.9

Food products 3.6 2.3 15.2 6.1 3.0 3.7 33.6

Alcoholic beverages and tobacco 0.3 1.5 1.7 2.0 4.4 6.7 17.3

Non-food products 0.2 14.6 4.6 4.3 5.7 3.5 36.8

Services 11.4 10.3 4.2 2.9 2.1 9.7 32.5

Consumer price index (year-average) 9.0 3.4 8.2 7.7 2.6 5.8 30.8

Food products 11.1 -0.9 9.4 12.3 2.0 5.8 31.4

Alcoholic beverages and tobacco 0.0 1.4 1.5 1.1 5.1 5.9 15.8

Non-food products 5.1 4.7 9.6 3.4 4.6 4.6 29.8

Services 9.0 10.4 6.8 3.6 2.1 6.4 32.7

Source: NSS of RA, EDRC calculations.

Inflation in service tariffs was mostly determined by the increased electricity and natural gas supply tariffs for residential consumers in 2013. In particular, according to the NSS of RA data, electricity tariffs in end-2013 grew by 30% since end-2013, while natural gas tariffs – by 19.2%.

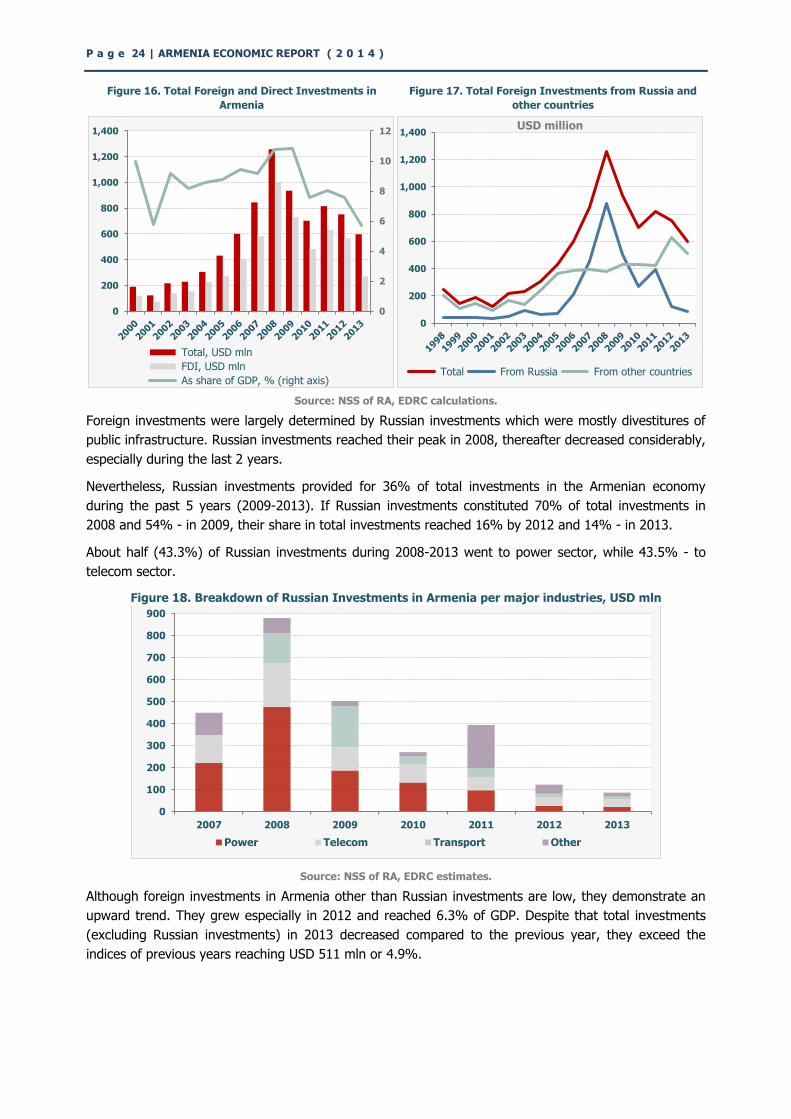

Foreign Investments

Foreign investments into the Armenian economy are small. They reached their peak in 2008 and fell

sharply and continuously thereafter. Total foreign investments constituted 5.7% of GDP (USD 597 mln)

in 2013, including foreign direct investments constituting 2.6% of GDP (USD 271 mln).

10

20

30

40

50

60

70

80

90

250

300

350

400

450

500

550

600

650

700

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

AMD/EUR AMD/USD AMD/RUR (right axis)

P a g e 24 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Figure 16. Total Foreign and Direct Investments in

Armenia

Figure 17. Total Foreign Investments from Russia and

other countries

Source: NSS of RA, EDRC calculations.

Foreign investments were largely determined by Russian investments which were mostly divestitures of

public infrastructure. Russian investments reached their peak in 2008, thereafter decreased considerably,

especially during the last 2 years.

Nevertheless, Russian investments provided for 36% of total investments in the Armenian economy

during the past 5 years (2009-2013). If Russian investments constituted 70% of total investments in

2008 and 54% - in 2009, their share in total investments reached 16% by 2012 and 14% - in 2013.

About half (43.3%) of Russian investments during 2008-2013 went to power sector, while 43.5% - to

telecom sector.

Figure 18. Breakdown of Russian Investments in Armenia per major industries, USD mln

Source: NSS of RA, EDRC estimates.

Although foreign investments in Armenia other than Russian investments are low, they demonstrate an

upward trend. They grew especially in 2012 and reached 6.3% of GDP. Despite that total investments

(excluding Russian investments) in 2013 decreased compared to the previous year, they exceed the

indices of previous years reaching USD 511 mln or 4.9%.

0

2

4

6

8

10

12

0

200

400

600

800

1,000

1,200

1,400

Total, USD mln

FDI, USD mln

As share of GDP, % (right axis)

0

200

400

600

800

1,000

1,200

1,400 USD million

Total From Russia From other countries

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013

Power Telecom Transport Other

E D R C ( 2 0 1 4 ) | p a g e 2 5

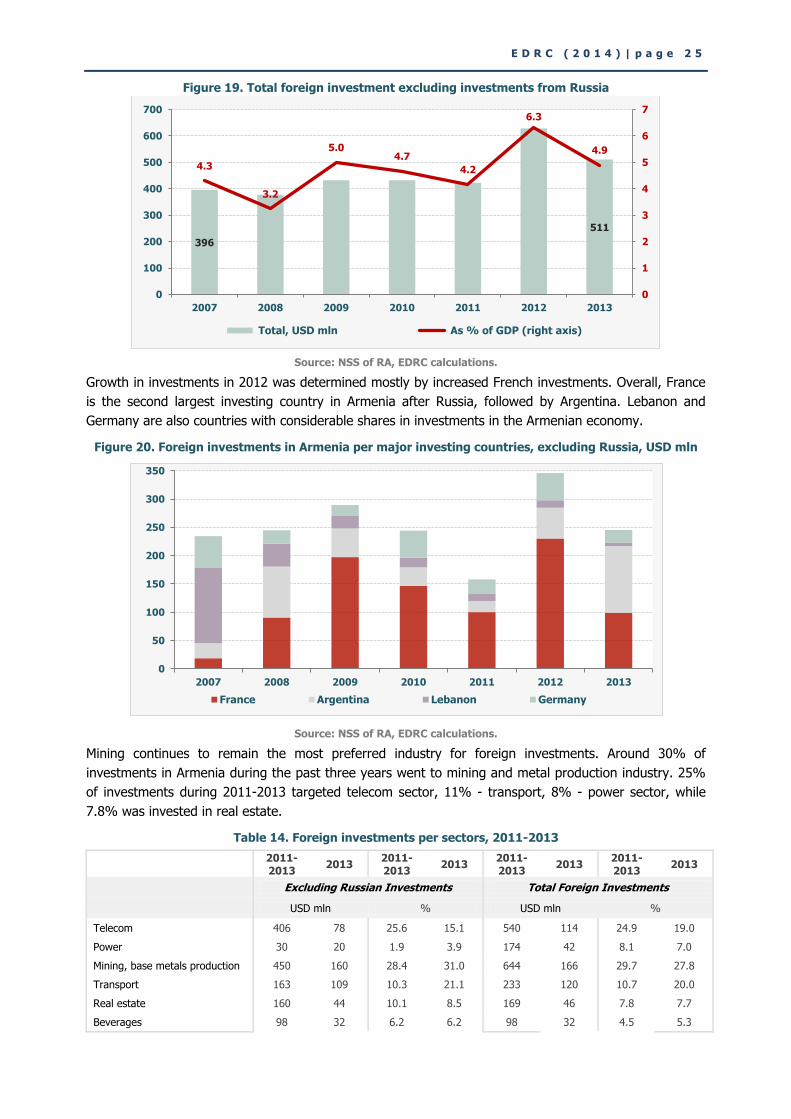

Figure 19. Total foreign investment excluding investments from Russia

Source: NSS of RA, EDRC calculations.

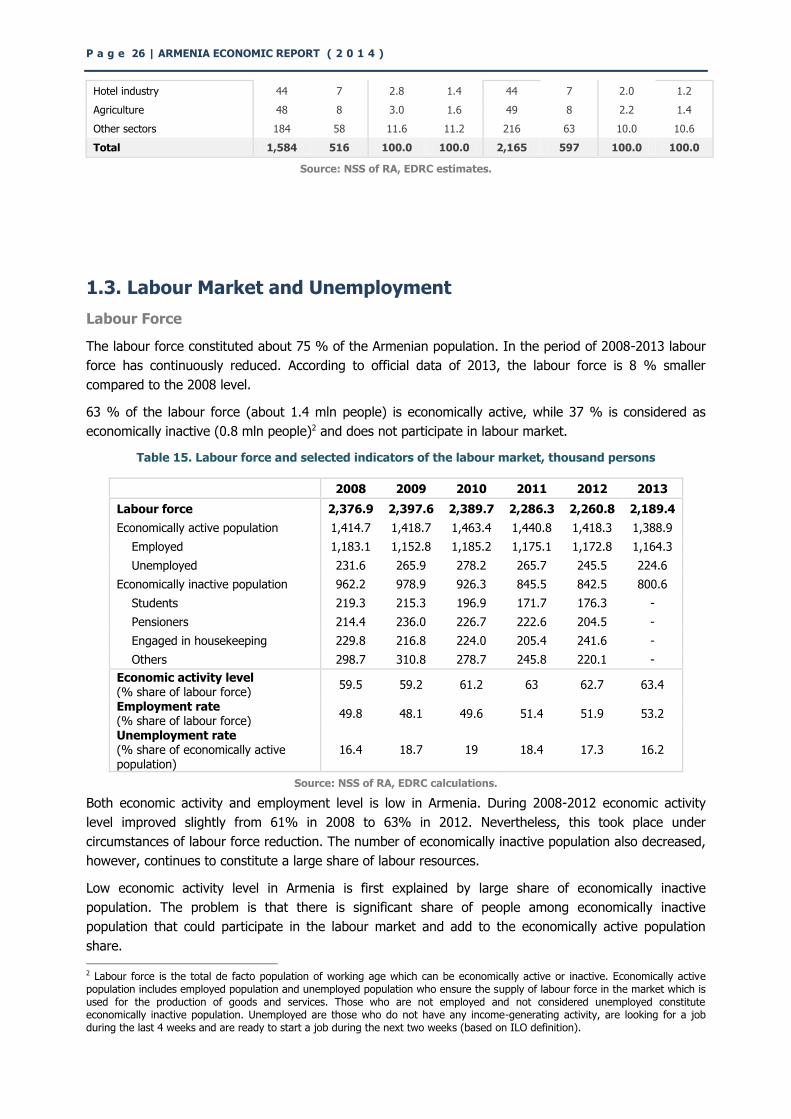

Growth in investments in 2012 was determined mostly by increased French investments. Overall, France

is the second largest investing country in Armenia after Russia, followed by Argentina. Lebanon and

Germany are also countries with considerable shares in investments in the Armenian economy.

Figure 20. Foreign investments in Armenia per major investing countries, excluding Russia, USD mln

Source: NSS of RA, EDRC calculations.

Mining continues to remain the most preferred industry for foreign investments. Around 30% of

investments in Armenia during the past three years went to mining and metal production industry. 25%

of investments during 2011-2013 targeted telecom sector, 11% - transport, 8% - power sector, while

7.8% was invested in real estate.

Table 14. Foreign investments per sectors, 2011-2013

2011-2013

2013 2011-2013

2013 2011-2013

2013 2011-2013

2013

Excluding Russian Investments Total Foreign Investments

USD mln % USD mln %

Telecom 406 78 25.6 15.1 540 114 24.9 19.0

Power 30 20 1.9 3.9 174 42 8.1 7.0

Mining, base metals production 450 160 28.4 31.0 644 166 29.7 27.8

Transport 163 109 10.3 21.1 233 120 10.7 20.0

Real estate 160 44 10.1 8.5 169 46 7.8 7.7

Beverages 98 32 6.2 6.2 98 32 4.5 5.3

396

511

4.3

3.2

5.0 4.7

4.2

6.3

4.9

0

1

2

3

4

5

6

7

0

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013

Total, USD mln As % of GDP (right axis)

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013

France Argentina Lebanon Germany

P a g e 26 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Hotel industry 44 7 2.8 1.4 44 7 2.0 1.2

Agriculture 48 8 3.0 1.6 49 8 2.2 1.4

Other sectors 184 58 11.6 11.2 216 63 10.0 10.6

Total 1,584 516 100.0 100.0 2,165 597 100.0 100.0

Source: NSS of RA, EDRC estimates.

1.3. Labour Market and Unemployment

Labour Force

The labour force constituted about 75 % of the Armenian population. In the period of 2008-2013 labour

force has continuously reduced. According to official data of 2013, the labour force is 8 % smaller

compared to the 2008 level.

63 % of the labour force (about 1.4 mln people) is economically active, while 37 % is considered as

economically inactive (0.8 mln people)2 and does not participate in labour market.

Table 15. Labour force and selected indicators of the labour market, thousand persons

2008 2009 2010 2011 2012 2013

Labour force 2,376.9 2,397.6 2,389.7 2,286.3 2,260.8 2,189.4

Economically active population 1,414.7 1,418.7 1,463.4 1,440.8 1,418.3 1,388.9

Employed 1,183.1 1,152.8 1,185.2 1,175.1 1,172.8 1,164.3

Unemployed 231.6 265.9 278.2 265.7 245.5 224.6

Economically inactive population 962.2 978.9 926.3 845.5 842.5 800.6

Students 219.3 215.3 196.9 171.7 176.3 -

Pensioners 214.4 236.0 226.7 222.6 204.5 -

Engaged in housekeeping 229.8 216.8 224.0 205.4 241.6 -

Others 298.7 310.8 278.7 245.8 220.1 -

Economic activity level (% share of labour force)

59.5 59.2 61.2 63 62.7 63.4

Employment rate (% share of labour force)

49.8 48.1 49.6 51.4 51.9 53.2

Unemployment rate (% share of economically active population)

16.4 18.7 19 18.4 17.3 16.2

Source: NSS of RA, EDRC calculations.

Both economic activity and employment level is low in Armenia. During 2008-2012 economic activity

level improved slightly from 61% in 2008 to 63% in 2012. Nevertheless, this took place under

circumstances of labour force reduction. The number of economically inactive population also decreased,

however, continues to constitute a large share of labour resources.

Low economic activity level in Armenia is first explained by large share of economically inactive

population. The problem is that there is significant share of people among economically inactive

population that could participate in the labour market and add to the economically active population

share.

2 Labour force is the total de facto population of working age which can be economically active or inactive. Economically active population includes employed population and unemployed population who ensure the supply of labour force in the market which is used for the production of goods and services. Those who are not employed and not considered unemployed constitute economically inactive population. Unemployed are those who do not have any income-generating activity, are looking for a job during the last 4 weeks and are ready to start a job during the next two weeks (based on ILO definition).

E D R C ( 2 0 1 4 ) | p a g e 2 7

About a quarter of the economically inactive population were students, while one fifth – retired

pensioners. The remaining part of economically inactive population are those who are engaged in

housekeeping (mostly women) – 29 %, and others who are not employed and are not considered

unemployed (26 %).

Weak prospects of finding a decent job are seen as the main reason for not working and not looking for

a job. There are numerous cases when people do not know how to look for a job or there are various

social and family reasons, as well as health issues.

Labour market in Armenia is characterised by long-term unemployment. Average duration of job search

is almost two years. Interestingly, education level of economically inactive population is quite high as 36

% of them have graduate or professional education, while 44.8 % have secondary education.

Out of the economically active population 83.8 % (or 53 % of the labour force) is employed and the

remaining 16.2 % is unemployed.

Employment Profile

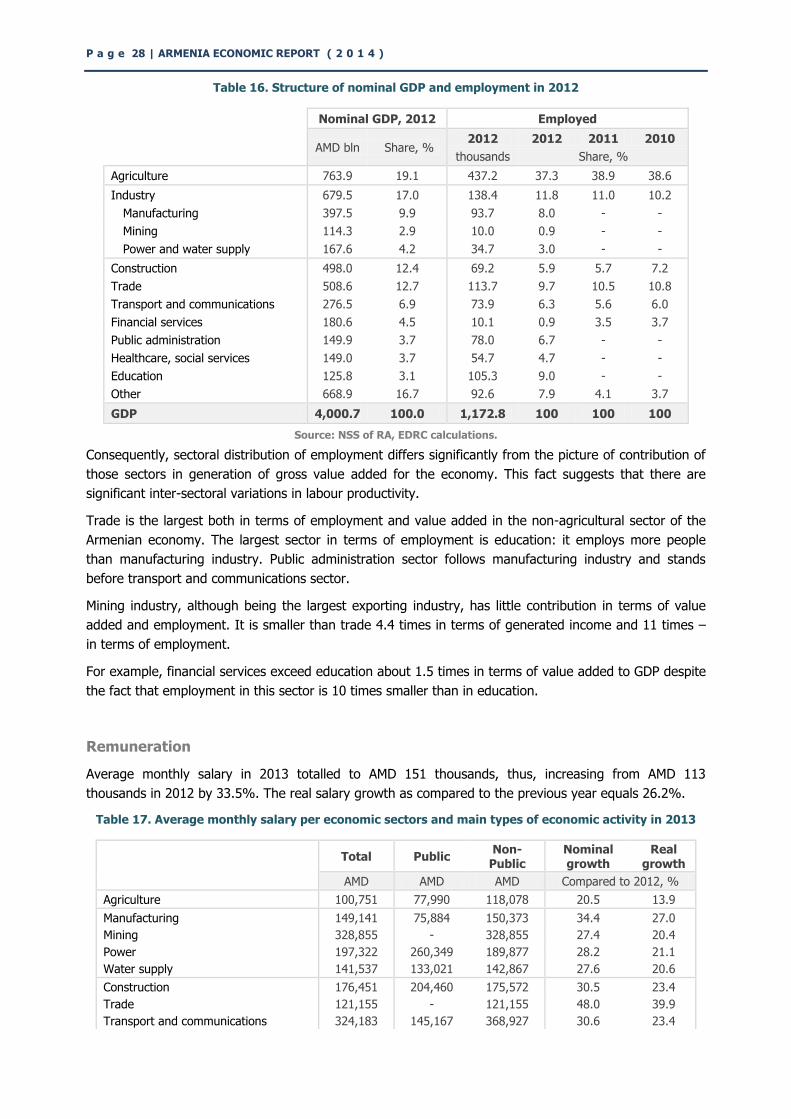

In 2013 employment rate in Armenia equalled 53 %. In other words, only half of the labour force is

employed. This is quite low, although it slightly improved during the recent years. With labour force

decreasing at a faster pace than the number of employed population, the net result was increase in the

employment rate. Thus, labour force declined by 8%, while the number of employed – by 1.6% in 2008-

2013.

Figure 21. Employment trends in Armenia in 2008-2013

Source: NSS of RA, EDRC calculations.

Majority of employed are engaged in non-productive and non-tradable sectors of the economy. The

share of those employed in agriculture is very high, despite a certain decline in recent years.

Agriculture provides around 37 % of employment, while its contribution to GDP is only 19.1 %. About 12

per cent of the employed is engaged in 3 main subsectors of industry which altogether produce 17 % of

the GDP.

Trade and education are large sectors in terms of employment, respectively with 9.7 % and 9 %

employment. Construction, with 12.4 % of GDP, accounts for only 5.9 % of employment.

49.8

48.1

49.6

51.4 51.9

53.2

45

46

47

48

49

50

51

52

53

54

1,130

1,140

1,150

1,160

1,170

1,180

1,190

2008 2009 2010 2011 2012 2013

Employed population, thousands Employment rate, % (right axis)

P a g e 28 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Table 16. Structure of nominal GDP and employment in 2012

Nominal GDP, 2012 Employed

AMD bln Share, % 2012 2012 2011 2010

thousands Share, %

Agriculture 763.9 19.1 437.2 37.3 38.9 38.6

Industry 679.5 17.0 138.4 11.8 11.0 10.2

Manufacturing 397.5 9.9 93.7 8.0 - -

Mining 114.3 2.9 10.0 0.9 - -

Power and water supply 167.6 4.2 34.7 3.0 - -

Construction 498.0 12.4 69.2 5.9 5.7 7.2

Trade 508.6 12.7 113.7 9.7 10.5 10.8

Transport and communications 276.5 6.9 73.9 6.3 5.6 6.0

Financial services 180.6 4.5 10.1 0.9 3.5 3.7

Public administration 149.9 3.7 78.0 6.7 - -

Healthcare, social services 149.0 3.7 54.7 4.7 - -

Education 125.8 3.1 105.3 9.0 - -

Other 668.9 16.7 92.6 7.9 4.1 3.7

GDP 4,000.7 100.0 1,172.8 100 100 100

Source: NSS of RA, EDRC calculations.

Consequently, sectoral distribution of employment differs significantly from the picture of contribution of

those sectors in generation of gross value added for the economy. This fact suggests that there are

significant inter-sectoral variations in labour productivity.

Trade is the largest both in terms of employment and value added in the non-agricultural sector of the

Armenian economy. The largest sector in terms of employment is education: it employs more people

than manufacturing industry. Public administration sector follows manufacturing industry and stands

before transport and communications sector.

Mining industry, although being the largest exporting industry, has little contribution in terms of value

added and employment. It is smaller than trade 4.4 times in terms of generated income and 11 times –

in terms of employment.

For example, financial services exceed education about 1.5 times in terms of value added to GDP despite

the fact that employment in this sector is 10 times smaller than in education.

Remuneration

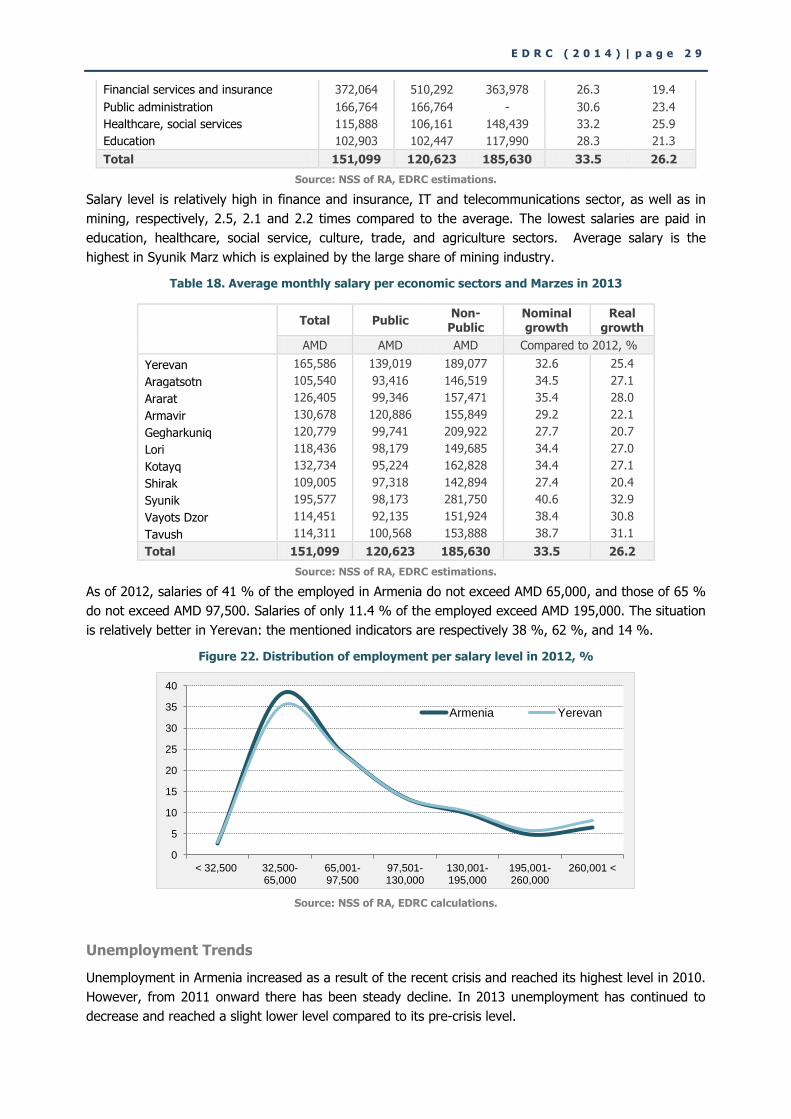

Average monthly salary in 2013 totalled to AMD 151 thousands, thus, increasing from AMD 113

thousands in 2012 by 33.5%. The real salary growth as compared to the previous year equals 26.2%.

Table 17. Average monthly salary per economic sectors and main types of economic activity in 2013

Total Public

Non-Public

Nominal growth

Real growth

AMD AMD AMD Compared to 2012, %

Agriculture 100,751 77,990 118,078 20.5 13.9

Manufacturing 149,141 75,884 150,373 34.4 27.0

Mining 328,855 - 328,855 27.4 20.4

Power 197,322 260,349 189,877 28.2 21.1

Water supply 141,537 133,021 142,867 27.6 20.6

Construction 176,451 204,460 175,572 30.5 23.4

Trade 121,155 - 121,155 48.0 39.9

Transport and communications 324,183 145,167 368,927 30.6 23.4

E D R C ( 2 0 1 4 ) | p a g e 2 9

Financial services and insurance 372,064 510,292 363,978 26.3 19.4

Public administration 166,764 166,764 - 30.6 23.4

Healthcare, social services 115,888 106,161 148,439 33.2 25.9

Education 102,903 102,447 117,990 28.3 21.3

Total 151,099 120,623 185,630 33.5 26.2

Source: NSS of RA, EDRC estimations.

Salary level is relatively high in finance and insurance, IT and telecommunications sector, as well as in

mining, respectively, 2.5, 2.1 and 2.2 times compared to the average. The lowest salaries are paid in

education, healthcare, social service, culture, trade, and agriculture sectors. Average salary is the

highest in Syunik Marz which is explained by the large share of mining industry.

Table 18. Average monthly salary per economic sectors and Marzes in 2013

Total Public

Non-Public

Nominal growth

Real growth

AMD AMD AMD Compared to 2012, %

Yerevan 165,586 139,019 189,077 32.6 25.4

Aragatsotn 105,540 93,416 146,519 34.5 27.1

Ararat 126,405 99,346 157,471 35.4 28.0

Armavir 130,678 120,886 155,849 29.2 22.1

Gegharkuniq 120,779 99,741 209,922 27.7 20.7

Lori 118,436 98,179 149,685 34.4 27.0

Kotayq 132,734 95,224 162,828 34.4 27.1

Shirak 109,005 97,318 142,894 27.4 20.4

Syunik 195,577 98,173 281,750 40.6 32.9

Vayots Dzor 114,451 92,135 151,924 38.4 30.8

Tavush 114,311 100,568 153,888 38.7 31.1

Total 151,099 120,623 185,630 33.5 26.2

Source: NSS of RA, EDRC estimations.

As of 2012, salaries of 41 % of the employed in Armenia do not exceed AMD 65,000, and those of 65 %

do not exceed AMD 97,500. Salaries of only 11.4 % of the employed exceed AMD 195,000. The situation

is relatively better in Yerevan: the mentioned indicators are respectively 38 %, 62 %, and 14 %.

Figure 22. Distribution of employment per salary level in 2012, %

Source: NSS of RA, EDRC calculations.

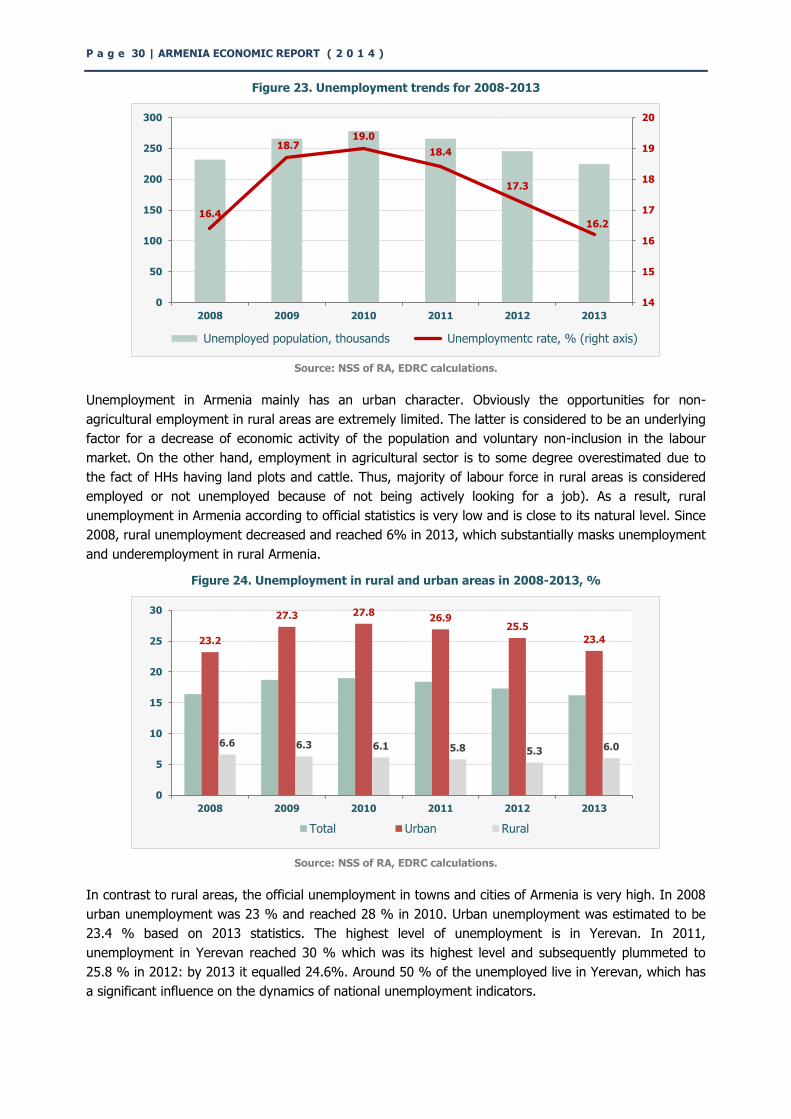

Unemployment Trends

Unemployment in Armenia increased as a result of the recent crisis and reached its highest level in 2010.

However, from 2011 onward there has been steady decline. In 2013 unemployment has continued to

decrease and reached a slight lower level compared to its pre-crisis level.

0

5

10

15

20

25

30

35

40

< 32,500 32,500- 65,000

65,001- 97,500

97,501- 130,000

130,001- 195,000

195,001- 260,000

260,001 <

Armenia Yerevan

P a g e 30 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Figure 23. Unemployment trends for 2008-2013

Source: NSS of RA, EDRC calculations.

Unemployment in Armenia mainly has an urban character. Obviously the opportunities for non-

agricultural employment in rural areas are extremely limited. The latter is considered to be an underlying

factor for a decrease of economic activity of the population and voluntary non-inclusion in the labour

market. On the other hand, employment in agricultural sector is to some degree overestimated due to

the fact of HHs having land plots and cattle. Thus, majority of labour force in rural areas is considered

employed or not unemployed because of not being actively looking for a job). As a result, rural

unemployment in Armenia according to official statistics is very low and is close to its natural level. Since

2008, rural unemployment decreased and reached 6% in 2013, which substantially masks unemployment

and underemployment in rural Armenia.

Figure 24. Unemployment in rural and urban areas in 2008-2013, %

Source: NSS of RA, EDRC calculations.

In contrast to rural areas, the official unemployment in towns and cities of Armenia is very high. In 2008

urban unemployment was 23 % and reached 28 % in 2010. Urban unemployment was estimated to be

23.4 % based on 2013 statistics. The highest level of unemployment is in Yerevan. In 2011,

unemployment in Yerevan reached 30 % which was its highest level and subsequently plummeted to

25.8 % in 2012: by 2013 it equalled 24.6%. Around 50 % of the unemployed live in Yerevan, which has

a significant influence on the dynamics of national unemployment indicators.

16.4

18.7 19.0

18.4

17.3

16.2

14

15

16

17

18

19

20

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013

Unemployed population, thousands Unemploymentc rate, % (right axis)

23.2

27.3 27.8 26.9

25.5

23.4

6.6 6.3 6.1 5.8 5.3 6.0

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013

Total Urban Rural

E D R C ( 2 0 1 4 ) | p a g e 3 1

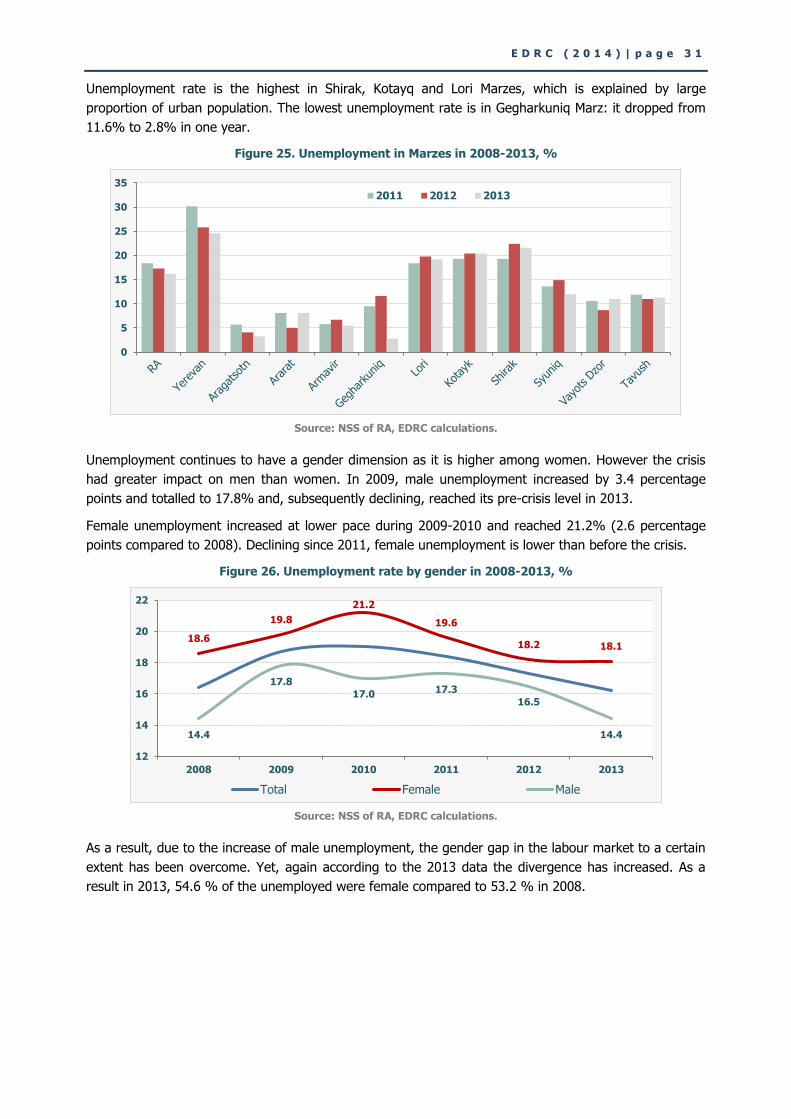

Unemployment rate is the highest in Shirak, Kotayq and Lori Marzes, which is explained by large

proportion of urban population. The lowest unemployment rate is in Gegharkuniq Marz: it dropped from

11.6% to 2.8% in one year.

Figure 25. Unemployment in Marzes in 2008-2013, %

Source: NSS of RA, EDRC calculations.

Unemployment continues to have a gender dimension as it is higher among women. However the crisis

had greater impact on men than women. In 2009, male unemployment increased by 3.4 percentage

points and totalled to 17.8% and, subsequently declining, reached its pre-crisis level in 2013.

Female unemployment increased at lower pace during 2009-2010 and reached 21.2% (2.6 percentage

points compared to 2008). Declining since 2011, female unemployment is lower than before the crisis.

Figure 26. Unemployment rate by gender in 2008-2013, %

Source: NSS of RA, EDRC calculations.

As a result, due to the increase of male unemployment, the gender gap in the labour market to a certain

extent has been overcome. Yet, again according to the 2013 data the divergence has increased. As a

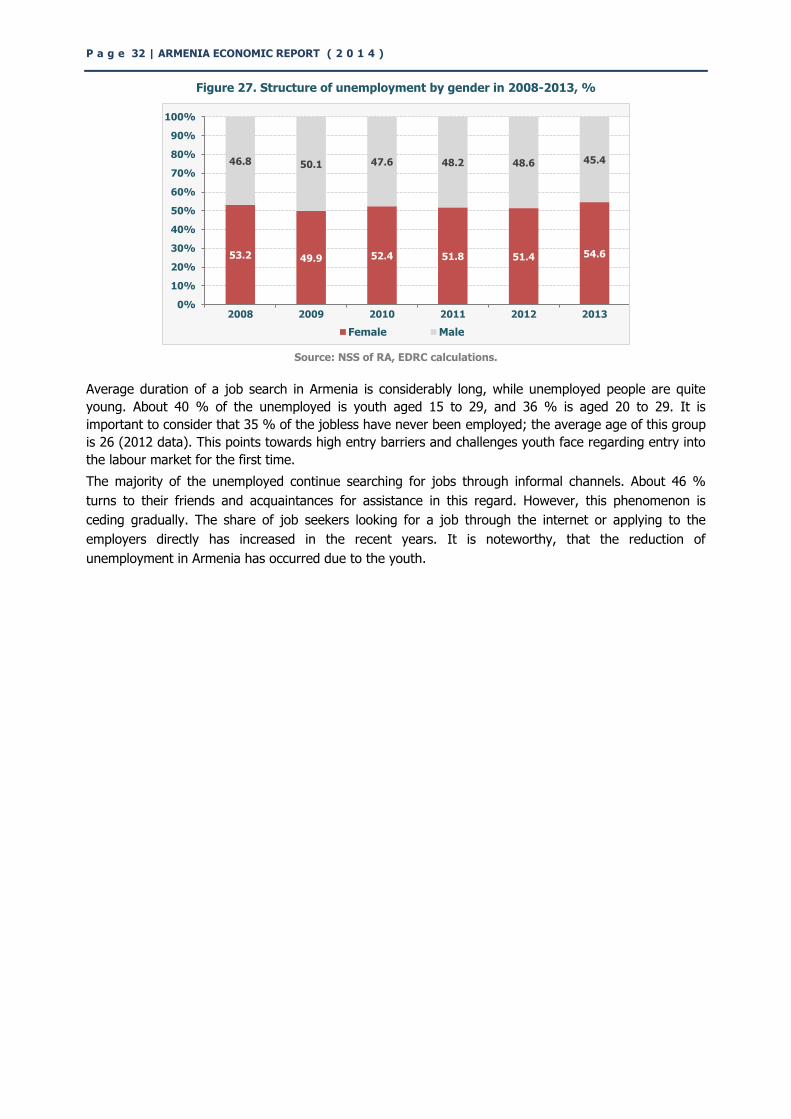

result in 2013, 54.6 % of the unemployed were female compared to 53.2 % in 2008.

0

5

10

15

20

25

30

35

2011 2012 2013

18.6

19.8

21.2

19.6

18.2 18.1

14.4

17.8

17.0 17.3

16.5

14.4

12

14

16

18

20

22

2008 2009 2010 2011 2012 2013

Total Female Male

P a g e 32 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

Figure 27. Structure of unemployment by gender in 2008-2013, %

Source: NSS of RA, EDRC calculations.

Average duration of a job search in Armenia is considerably long, while unemployed people are quite

young. About 40 % of the unemployed is youth aged 15 to 29, and 36 % is aged 20 to 29. It is

important to consider that 35 % of the jobless have never been employed; the average age of this group

is 26 (2012 data). This points towards high entry barriers and challenges youth face regarding entry into

the labour market for the first time.

The majority of the unemployed continue searching for jobs through informal channels. About 46 %

turns to their friends and acquaintances for assistance in this regard. However, this phenomenon is

ceding gradually. The share of job seekers looking for a job through the internet or applying to the

employers directly has increased in the recent years. It is noteworthy, that the reduction of

unemployment in Armenia has occurred due to the youth.

53.2 49.9 52.4 51.8 51.4 54.6

46.8 50.1 47.6 48.2 48.6 45.4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013

Female Male

E D R C ( 2 0 1 4 ) | p a g e 3 3

1.4. Poverty and Social Snapshot

Overall Trends

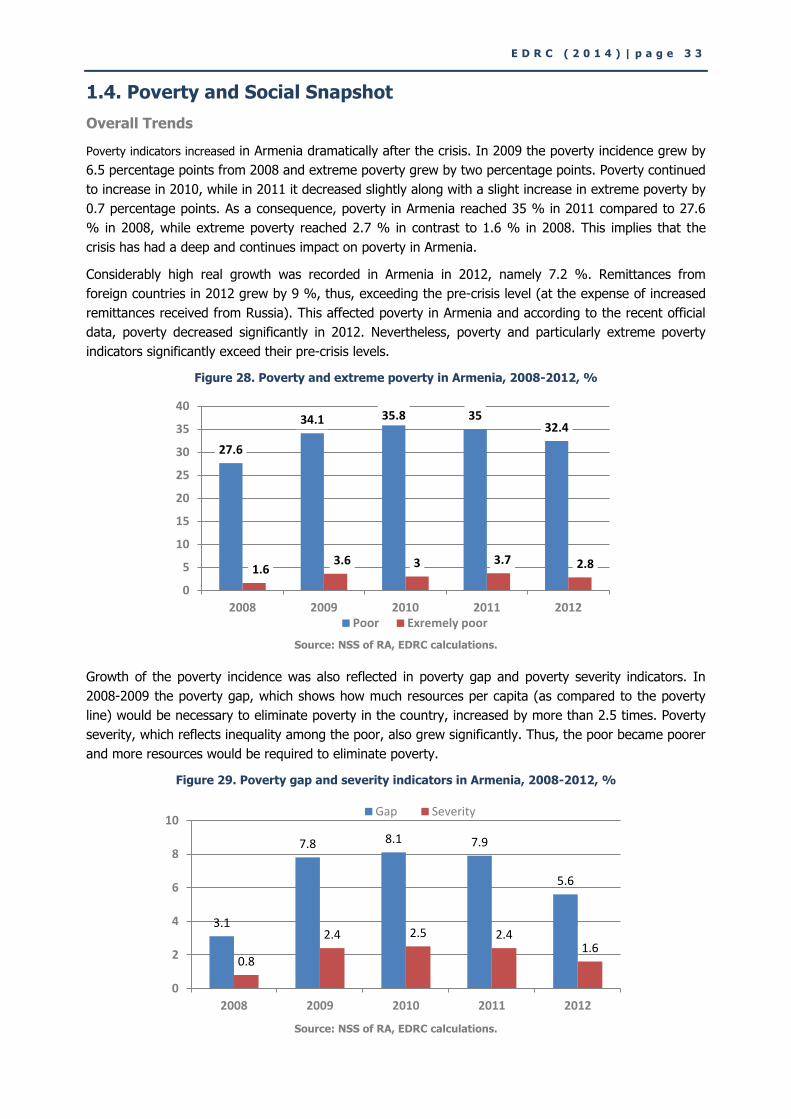

Poverty indicators increased in Armenia dramatically after the crisis. In 2009 the poverty incidence grew by

6.5 percentage points from 2008 and extreme poverty grew by two percentage points. Poverty continued

to increase in 2010, while in 2011 it decreased slightly along with a slight increase in extreme poverty by

0.7 percentage points. As a consequence, poverty in Armenia reached 35 % in 2011 compared to 27.6

% in 2008, while extreme poverty reached 2.7 % in contrast to 1.6 % in 2008. This implies that the

crisis has had a deep and continues impact on poverty in Armenia.

Considerably high real growth was recorded in Armenia in 2012, namely 7.2 %. Remittances from

foreign countries in 2012 grew by 9 %, thus, exceeding the pre-crisis level (at the expense of increased

remittances received from Russia). This affected poverty in Armenia and according to the recent official

data, poverty decreased significantly in 2012. Nevertheless, poverty and particularly extreme poverty

indicators significantly exceed their pre-crisis levels.

Figure 28. Poverty and extreme poverty in Armenia, 2008-2012, %

Source: NSS of RA, EDRC calculations.

Growth of the poverty incidence was also reflected in poverty gap and poverty severity indicators. In

2008-2009 the poverty gap, which shows how much resources per capita (as compared to the poverty

line) would be necessary to eliminate poverty in the country, increased by more than 2.5 times. Poverty

severity, which reflects inequality among the poor, also grew significantly. Thus, the poor became poorer

and more resources would be required to eliminate poverty.

Figure 29. Poverty gap and severity indicators in Armenia, 2008-2012, %

Source: NSS of RA, EDRC calculations.

27.6

34.1 35.8 35 32.4

1.6 3.6 3 3.7 2.8

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012 Poor Exremely poor

3.1

7.8 8.1 7.9

5.6

0.8

2.4 2.5 2.4 1.6

0

2

4

6

8

10

2008 2009 2010 2011 2012

Gap Severity

P a g e 34 | ARMENIA ECONOMIC REPORT ( 2 0 1 4 )

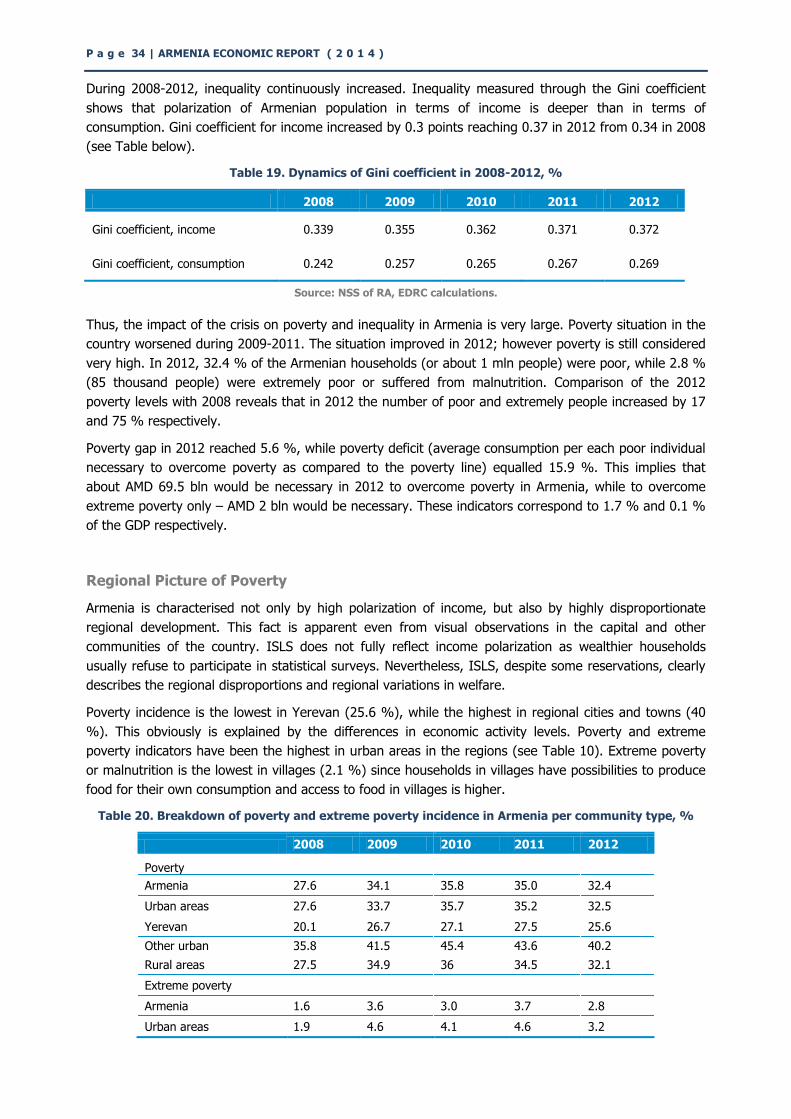

During 2008-2012, inequality continuously increased. Inequality measured through the Gini coefficient

shows that polarization of Armenian population in terms of income is deeper than in terms of

consumption. Gini coefficient for income increased by 0.3 points reaching 0.37 in 2012 from 0.34 in 2008

(see Table below).

Table 19. Dynamics of Gini coefficient in 2008-2012, %

2008 2009 2010 2011 2012

Gini coefficient, income 0.339 0.355 0.362 0.371 0.372

Gini coefficient, consumption 0.242 0.257 0.265 0.267 0.269

Source: NSS of RA, EDRC calculations.

Thus, the impact of the crisis on poverty and inequality in Armenia is very large. Poverty situation in the

country worsened during 2009-2011. The situation improved in 2012; however poverty is still considered

very high. In 2012, 32.4 % of the Armenian households (or about 1 mln people) were poor, while 2.8 %

(85 thousand people) were extremely poor or suffered from malnutrition. Comparison of the 2012

poverty levels with 2008 reveals that in 2012 the number of poor and extremely people increased by 17

and 75 % respectively.

Poverty gap in 2012 reached 5.6 %, while poverty deficit (average consumption per each poor individual

necessary to overcome poverty as compared to the poverty line) equalled 15.9 %. This implies that

about AMD 69.5 bln would be necessary in 2012 to overcome poverty in Armenia, while to overcome

extreme poverty only – AMD 2 bln would be necessary. These indicators correspond to 1.7 % and 0.1 %