corporate update larrain vial second annual investor

TRANSCRIPT

Corporate Update

Larrain Vial Second Annual Investor ConferenceHotel Ritz Carlton, Santiago de ChileMarch 17 – 19, 2008

1

This presentation may include forward-looking comments regarding the Company’s business outlook and

anticipated financial and operating results. These expectations are highly dependent on the

economy, the airline industry, commodity prices, international markets and external events.

Therefore, they are subject to change and we undertake no obligation to publicly update or revise

any forward looking statements to reflect events or circumstances that may arise after the date of

this presentation. More information on the risk factors that could affect our results are contained on

our Form 20-F for the year ended December 31, 2006.

Information, tables and logos contained in this presentation may not be used without consent from LAN

Contents

I. LAN OVERVIEW

II. FINANCIAL RESULTS

III. FUTURE OUTLOOK

2

LAN: A Growth Story

1993 2007 CAGR

AIRCRAFT 13 83 14%

SALES (millions) US$318 US$3,525 19%

PASSENGERS (millions) 1.0 11.1 19%

CARGO TONS (thousands) 48 604 20%

EMPLOYEES 2,227 15,797 15%

3

LAN Overview: A Passenger + Cargo Airline

4

Passenger Business: Capacity Breakdown by Route Type (ASK)

Chile (Dom)14%

International75%

Peru (Dom)7%

Arg. (Dom)4%

Cargo Business: Capacity Breakdown by Route Type

(ATK)Chile (Dom)

3%

Intl97%

Cargo Operations• Sales (2007): US$1.2 billion• Tons transported (2007): 604 thousand• Fleet: 10 dedicated freighters• Companies: Chile, Brazil, Mexico

Passenger Operations• Sales (2007): US$2.2 billion• Passengers transported (2007): 11.1 million• Fleet: 73 aircraft• Companies: Chile, Argentina, Peru & Ecuador

LAN Business Model: Distinct blend enhances returns and reduces risk

Revenue Mix, Selected Companies, 2007Passenger and Cargo Combination

– Lower Break-Even Load Factors– Increased diversification

7%

13%

21%

33%

21%

16%

7%

8%

12%

88%

90%

73%

79%

86%

80%

67%

60%

59%

62%

6%

6%

3%

4%

29%

22%

5%

6%

9%

12%

19%

Delta

American

Iberia

Qantas

BA

Air France

Singapore

Cathay

Korean Air

LAN

Cargo Others PassengerNote: Information for BA, Air France & Singapore for the year ended March 2007.

Note: Information for Qantas for the year ended June 2007.

BELF Differential for passenger + cargo routes (2007)

13%

59%72%

Load

Fac

tor

BELF w/o Cargo

CargoContribution

BELF w/ Cargo

Note: BELF = Break-even load factor

5

LAN’s Diversified Business Model

6

50%

International(Long Haul)

25%

Regional

14%Dom. Chile

7%Dom. Perú

4%Dom. Argentina

62%Passenger

33%

Cargo5%

Others

Diversified Passenger CapacityDiversified Business Model(% Operating Revenues) (% ASKs)

LAN’s business model is diversified among the passenger and cargo businesses, as well as geographically throughout Latin America and the rest of the world.

This allows LAN the flexibility to better withstand unfavorable economic conditions

LAN Operates with High Efficiency Levels

Lan Dom

Thai

Singapore

Qantas

Korean

JAL

EVA

CathayAir Asia

TAM

LAN

COPA

GOLUS Airways

LUVJBU

United AirlinesDelta

COAMRIB

BAAF-KLM

RyanAir

EasyJet

20

30

40

50

60

70

80

90

100

500 1.000 1.500 2.000 2.500 3.000 3.500 4.000 4.500 5.000

Trip Length (Km)

Tota

l Ope

ratin

g C

ost/A

TKCost/ATK industry comparison (2007)

DOM

LAN’s Cost / ATK increased by 2.8% in 2007 and decreased by 0.2% ex-fuel.

Note: “LAN Dom” refers to the Cost/ATK of LAN’s domestic operation, excluding cargo.

Note: Information for all airlines is for the last full year reported.7

Leading Presence in South American Markets

LAN Market Share in Passenger Markets (December 2007)

Market Size: Passengers Transported 2007(millions)

8Sources: DGAC Chile, DGAC Peru, Undersecretary of Transportation Argentina, DAC Ecuador, LAN Estimates.

2,8

4,93,9

7,5

2,2

4,13,6

5,6

012345678

Ecuador Chile Peru Argentina

International Domestic

Millions ofPassengers

PeruInternational: 27%

Domestic: 68%

ArgentinaInternational: 16%

Domestic: 18%

ChileInternational 50%Domestic: 75%

EcuadorInternational: 21%

Buenos AiresSantiago

Guayaquil

Lima

Guayaquil

Buenos AiresSantiago

Lima

LAN’s Regional Strategy – Passenger Operations

Multi-hub/Multi-airline model– Interlocking hubs protect and

complement each other– Higher asset utilization

1.500 KM

TAM Commercial Agreement– Implemented in December 2007– Main Routes: Santiago, Lima,

Buenos Aires to Sao Paulo– Domestic Markets

• Brazil• Peru• Chile• Argentina

TAM / LAN Agreement

9

Leading South American Passenger Route Network

10

Alliances

TAM

693 destinationsworldwide

Passenger network enhanced with key global strategic alliances

Madrid

Easter Island

Auckland

Papeete

Sydney

Frankfurt

New York

MiamiLos Angeles

Mexico City

Caracas

Sao Paulo

Buenos AiresMontevideo

Cancun

Bariloche

Pta. Arenas

Arica

La Paz

Pto. Montt

Cuzco

Lima

Bogotá

Santiago

Rio de Janeiro

Rosario

Quito

Pta. Cana

Guayaquil

Ushuaia

Salta

Rio Gallegos

Com. Rivadavia

Cordoba

Iguazú

IquiqueAntofagasta

CalamaCopiapo

La Serena

Mendoza

Concepcion

Balmaceda

TemucoValdiviaOsorno

TacnaArequipa

Puerto Maldonado

Iquitos

Piura

TarapatoPucalpa

ChiclayoTrujillo

LAN

Codeshare

DOMESTIC OPERATIONS

New A320 family aircraft

Lower fares

More direct flights

INTERNATIONAL OPERATIONS

New Premium Business Class: first with full flat sleeper seats between Latin America and the United States

State of the art on board entertainmentsystem

Complete retrofit of B767 fleet in 1H08 –US$80 million investment

Begin retrofit of A340 fleet in 2H08

Differentiated Value Propositions in the Passenger Business

11

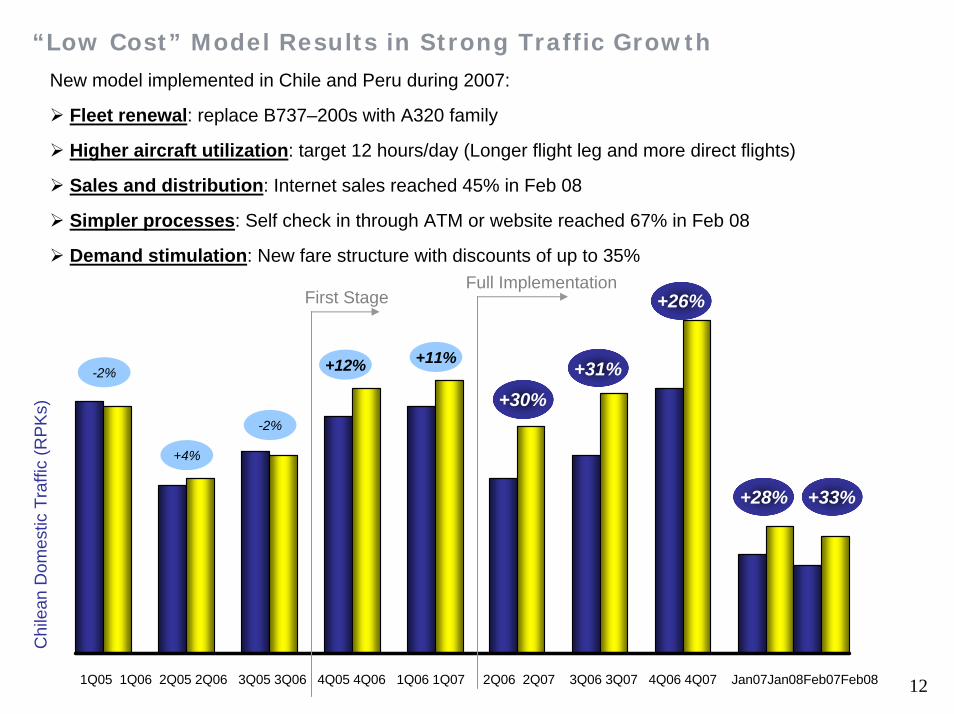

“Low Cost” Model Results in Strong Traffic Growth New model implemented in Chile and Peru during 2007:

Fleet renewal: replace B737–200s with A320 family

Higher aircraft utilization: target 12 hours/day (Longer flight leg and more direct flights)

Sales and distribution: Internet sales reached 45% in Feb 08

Simpler processes: Self check in through ATM or website reached 67% in Feb 08

Demand stimulation: New fare structure with discounts of up to 35%

1Q05 1Q06 2Q05 2Q06 3Q05 3Q06 4Q05 4Q06 1Q06 1Q07 2Q06 2Q07 3Q06 3Q07 4Q06 4Q07 Jan07Jan08Feb07Feb08

+31%+30%

+11%+12%

-2%

+4%

-2%

Chi

lean

Dom

estic

Traf

fic(R

PK

s)

First StageFull Implementation

+26%

+28% +33%

12

Most Complete Cargo Network in Latin America

LAN is the leading cargo operator in Latin America

13

Madrid

Easter Island

Auckland

Papeete

Sydney

FrankfurtLos Angeles

Mexico City

Caracas

Sao Paulo

Buenos AiresMontevideo

Cancun

Bariloche

Pta. Arenas

Arica

La Paz

Pto. Montt

Cuzco

Lima

Bogotá

Santiago

Rosario

Quito

Pta. Cana

Guayaquil

Ushuaia

Salta

Rio Gallegos

Com. Rivadavia

Cordoba

Iguazú

IquiqueAntofagasta

CalamaCopiapo

La Serena

Mendoza

Concepcion

Balmaceda

TemucoValdiviaOsorno

TacnaArequipa

Puerto Maldonado

Iquitos

Piura

TarapatoPucalpa

ChiclayoTrujillo

Houston

San JosePanama

Merida

Rio de Janeiro

Porto Alegre

VitoriaBelo HorizonteSalvador

Manaos

Alliances Passenger networkCargo network

Curitiba

Asunción

Amsterdam

Miami

Dynamics of the Latin America Air Cargo Market

Operational efficiencies must be obtained by managing unbalanced flows and seasonal fluctuations.

Northbound Flows:

dominated by fish, flowers, fruits and vegetables

Southbound Flows:dominated by consumer electronics, machinery,

spare parts and automotive parts

14Source: Boeing World Air Cargo 2006 - 2007

Macro Drivers of the Air Cargo Market:

Product seasonality

GDP growth

Exchange rates

Fuel prices

Eastbound Flows:

dominated by fish and flowers

Westbound Flows:

dominated by consumer electronics, machinery,

spare parts and automotive parts

Contents

I. LAN OVERVIEW

II. FINANCIAL RESULTS

III. FUTURE OUTLOOK

15

Strong Revenue Growth

Operating Revenues 1993 – 2007

3.525

318407

600 694

9721.083

1.237

1.425 1.428 1.4541.639

2.093

2.506

3.034

0

400

800

1.200

1.600

2.000

2.400

2.800

3.200

3.600

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

US$ Million

CAGR24%

CAGR1%

CAGR19%

US$ Millions

16

$11 $15$34 $44

$83$62

$112

$172

$303

$413

$6

$38

$308

$51$46 $50$80

$142

$48

$164

$241

$0

$64

$31$25

$147

$84

$31$11

$48

$0$25$50$75

$100$125$150$175$200$225$250$275$300$325$350$375$400$425

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

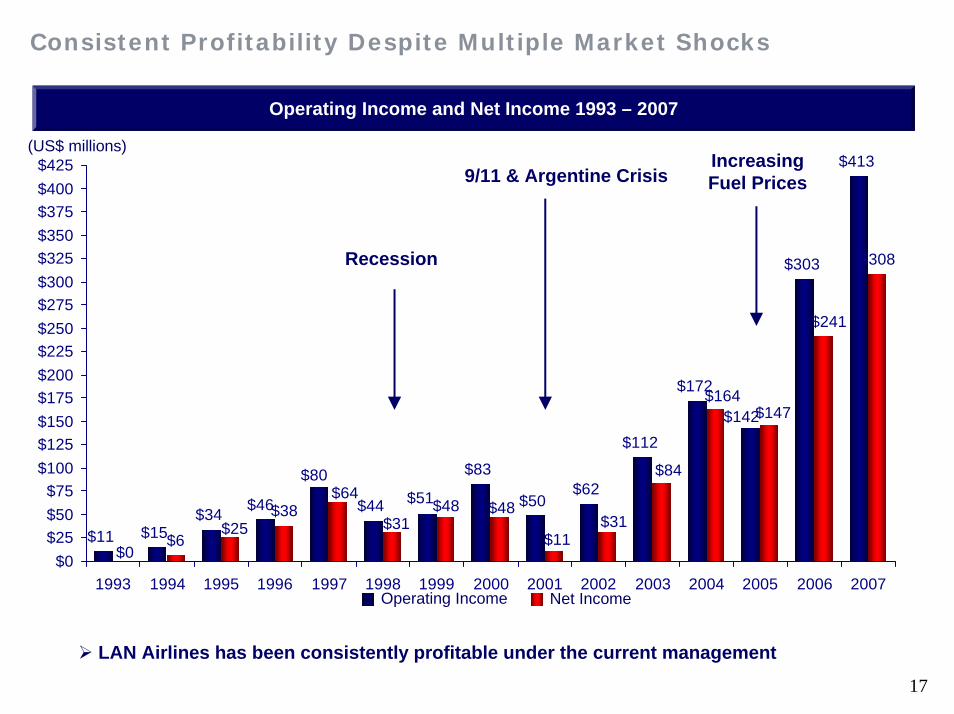

Operating Income and Net Income 1993 – 2007

Operating Income Net Income

(US$ millions)

Recession

9/11 & Argentine CrisisIncreasing Fuel Prices

Consistent Profitability Despite Multiple Market Shocks

LAN Airlines has been consistently profitable under the current management

17

Current Trends in EBITDAR and EBITDAR Margin

$290 $323$382 $370

$583

$726

19,2%20,6%

14,8%

18,3%19,7%19,9%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1.000

2002 2003 2004 2005 20060%

5%

10%

15%

20%

25%

EBIT

DA

R (U

S$m

illio

ns)

EBITDAR

18EBITDAR Margin

EBITD

AR

Margin

(%)

Improvement in EBITDAR margin driven by:“Low cost” model in domestic operationsStrong revenue growth in international passenger businessEfficiencies in cargo business, reduced ACMI, more profitable route mixEfficiency in back office and support areas

Note: EBITDAR = Operating income + depreciation & amortization + aircraft rentals (does not include fuel hedging gains/losses)

2007

Solid Financial Position

LAN is one of the few Investment Grade airlines in the world (BBB rating)

LAN successfully completed a US$320 million equity offering in June 2007

LAN has no short term debt; long-term debt only related to aircraft financing

Low interest rates, over 90% of interest bearing debt is fixed

Diversified revenue stream: different businesses and different countries

60%

65%

70%

75%

80%

1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07

Leve

rag

e

0%2%4%6%8%10%12%14%16%18%20%

Leverage Liquidity

19

Fuel pass-through in cargo businesses

Change in passenger fuel pass-through table in December 2007

Fuel Strategy: Fuel Cost Pass-Through Mechanism

Regional (US$) Long Haul (US$) Regional (US$) Long Haul (US$)< 40 0 0 <40 0 0

40 - 45 10 20 40-50 10 20 45 - 50 13 30 50-60 15 40 50 - 55 15 40 60-70 20 60 55 - 60 18 50 70-80 25 80 60 - 65 20 60 80-90 30 100 65 - 70 23 70 90< * * 70 - 75 25 80 75 - 80 28 90 80 - 85 30 100 85 - 90 33 110 90 - 95 35 120 95 - 100 38 130 100 - 105 40 140 105 - 110 43 150

Referencia WTI US$

Fuel Surcharge Internacional (OW) Referencia WTI US$

Fuel Surcharge Internacional (OW)International Fuel Surcharge

Note: Fuel surcharges are per segment (ie.one way).

< 40 040 – 50 050 – 60 2,50060 – 70 5,00070 – 80 7,50080 – 90 10,00090 – 100 12,500100 – 110 15,000110 – 120 7,500

Domestic Chile WTI US$ Fuel Surcharge (Ch$)

International US$ 1.00 / Kg.

From Europe Euro 0.80 / Kg.

20

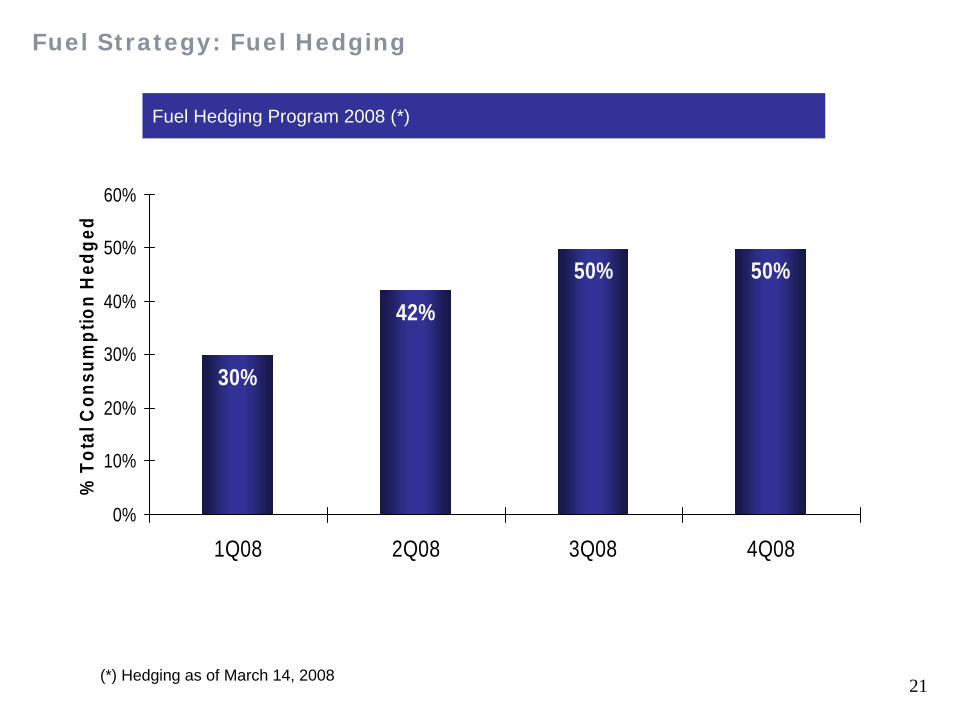

Fuel Hedging Program 2008 (*)

Fuel Strategy: Fuel Hedging

30%

42%

50% 50%

0%

10%

20%

30%

40%

50%

60%

1Q08 2Q08 3Q08 4Q08

% T

otal

Con

sum

ptio

n H

edge

d

(*) Hedging as of March 14, 2008 21

Passenger Capacity and Traffic Evolution

Recent Traffic Trends

78%

81%80%

77%78%

71%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

1Q07 2Q07 3Q07 4Q07 Jan 08 Feb-08

Gro

wth

(%)

64%

66%

68%

70%

72%

74%

76%

78%

80%

82%

Load

Fac

tor (

%)

ASK GrowthRPK GrowthLoad Factor

Cargo Capacity and Traffic Evolution

73%

71%

76%

74%74%74%

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

14,00%

16,00%

1Q07 2Q07 3Q07 4Q07 Jan 08 Feb-08

Gro

wth

(%)

68%

69%

70%

71%

72%

73%

74%

75%

76%

77%

Load

Fac

tor

(%)

ATK GrowthRTK GrowthLoad Factor

22

Contents

I. LAN OVERVIEW

II. FINANCIAL RESULTS

III. FUTURE OUTLOOK

23

Fleet Plan

24

0

2226 28 28 28 28

3750

5766 66

55

5

5

99

9

92

3

4

9

51

32

59

9

0

30

60

90

120

150

2007 2008 2009 2010 2011 2012-16Boeing 737-200 Boeing 767-300ER Airbus A320/A319/A318Boeing 787 Airbus 340-300 Boeing 767-300F CargoBoeing 777-200F Cargo Boeing 737-200F Cargo

1

1

FREIGHTERS

PASSENGERAIRCRAFT

83

139

+ 67%

FLEET CAPEX(USD MM) 471 865 365 243 660 3500

US$6.1 Billion

2 4

Estimated Capacity Expansion

Passenger ASK Growth Cargo ATK Growth

25

0%

5%

10%

15%

2006 2007 2008E

7.0%6.9%

8-10%

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008E

19.5%

20-22%

11.5%

Planes Hours Seats

Importantes iniciativas....crecimiento fuera de Chile....Passenger Business 2008

• Additional frequencies on long-haul routes to Europe and the South Pacific.

• Consolidation of position on regional routes.

• Sustained growth on routes between Latin America and NorthAmerica.

Growing Routes Action Plans

+34%

+20%

+13%

+8%

26

27

0

10

20

30

40

50

60

70

2007 Q12008 Q4

2010 Q32012 Q2

2014 Q12015 Q4

2017 Q32019 Q2

2021 Q12022 Q4

2024 Q32026 Q2

2028 Q12029 Q4

N° Aircraft LH

MIN MAX PLAN

-34 %

-22 %

-52 %

-36 %

Fleet Plan: LAN Maintains the Flexibility to Adjust its Fleet SizeN

umbe

rofL

ong

Hau

lPas

seng

erA

ircra

ft

LAN is Well Positioned for Future Growth

28

Strong footprint in Latin America

Proven business model resilient to adverse economic conditions

Undergoing significant fleet expansion and renewal

Proven ability to operate in a high fuel price environment with “jet fuel pass-through” mechanism

Adjusting value propositions to better serve short haul and long haul passengers

Implementation of new “low cost model” in domestic and regional operations

LAN Investor Relations Contact Information

29

Gisela Escobar, Head of Investor RelationsTel. (562) 565 8785 / (562) 565 [email protected]

Gaelle Duret, Head of ResearchTel. (562) 565 [email protected]

Juan Jose Irarrázaval, Investor Relations AnalystTel. (562) 565 [email protected]