chapter twelve work sheet and adjusting entries. copyright © houghton mifflin company. all rights...

TRANSCRIPT

Chapter Twelve

Work Sheet and Adjusting Entries

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 2

Performance Objectives

1.Prepare an adjustment for supplies

2.Prepare an adjustment for merchandise inventory under the periodic inventory system

3.Prepare an adjustment for unearned revenue

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 3

Performance Objectives

4.Record the following adjustment data in a work sheet:– Merchandise inventory– Unearned revenue– Supplies used– Expired insurance– Depreciation– Accrued wages or salaries

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 4

Performance Objectives

5.Complete the work sheet

6.Journalize the adjusting entries for a merchandising business under the periodic inventory system

7.Journalize the adjusting entry for merchandise inventory under the perpetual inventory system

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 5

Adjustments

• Bring the books “up to date”• Are made every time the financial statements

are produced• Occur simply because time has passed or an

asset has been used up• Each adjustment affects at least one income

statement account– Provides a more accurate net income number

• Each adjustment affects at least one balance sheet account– Makes the fundamental accounting equation (A =

L + OE) more accurate

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 6

Matching Principle and Accrual Accounting

• Matching principle– Revenue for one time period is matched up or

compared with the related expenses for the same time period

– Uses adjusting entries to match unrecorded expenses and revenues in one period to expenses and revenues in that same period that have already been recorded

• Accrual accounting– Record revenue when it is earned, regardless of

when the cash comes in– Record expenses when they are incurred,

regardless of when the cash goes out

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 7

Adjustments

1. Record adjustments in the worksheet1. Label debits and credits for each entry with a

letter reference: (a),( b), (c)

• Record the adjustments in the general journal

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 8

Performance Objective 1

Prepare an adjustment for supplies

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 9

Data for Adjusting Supplies

• Debit Supplies when supplies are purchased throughout the period

• Take inventory to determine the amount of supplies left at the end of the period

• Make an adjusting entry for the amount used (total minus amount left) – Debit Supplies Expense – Credit Supplies

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 10

Performance Objective 2

Prepare an adjustment for merchandise inventory under the periodic inventory system

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 11

Periodic Inventory System

• The system under which the buying of merchandise during the year is recorded as– Debit to Purchases– Credit to Accounts Payable or Cash

• At the end of the year, a physical count of the stock of goods is taken– No changes to Merchandise Inventory account

until physical count is taken

• Adjusting entries are made to record the amount of the physical count

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 12

Physical Inventory

• An actual count of the stock of goods on hand

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 13

Brings Inventory Balance to Counted Total!

DR CR DR CR+ - + -

bal. 77,000 77,000 a) a) 77,000b) 64,900 b) 64,900

64,900

Merchandise Inventory Income Summary

Adjustments forMerchandise Inventory

Step One:Step One:• Remove beginning

inventory– Credit

Merchandise Inventory

– Debit Income Summary

DR CR DR CR+ -

bal. 77,000 77,000 a) a) 77,0000

Merchandise Inventory Income Summary

Step Two:Step Two:• Enter the new

balance from the physical count– Debit

Merchandise Inventory

– Credit Income Summary

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 14

Performance Objective 3

Prepare an adjustment for unearned revenue

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 15

Unearned Revenue

• Revenue received in advance for goods or services to be delivered later

• Classified as a liability until the revenue is earned

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 16

Why We Adjust Unearned Revenue

• When we buy a one-year insurance policy, we record: Prepaid Insurance– Each month, we incur

1/12 of the cost as Insurance Expense

– Adjustments “update our accounts” and make our financial statements more accurate

• When the insurance company receives our check, they record: Unearned Insurance Revenue– Each month, they earn

1/12 of it as Insurance Revenue

– Adjustments “update their accounts” and make their financial statements more accurate

““See both sides of the coin!”See both sides of the coin!”One person’s One person’s expenseexpense is another person’s is another person’s revenuerevenue!!

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 17

Unearned Revenue—A Liability

• The customer has a claim against the company for the goods or services until the goods are delivered or the services are rendered

• Time Magazine “owes” the customer the magazines

• The insurance company “owes” the customer the insurance coverage

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 18

The Adjustment for Unearned Revenue

• Assume Bell Publishing receives $82,000 in cash for subscriptions covering two years

• At the end of the year $30,750 of the subscriptions have been earned

• Record as– Debit to Unearned Subscriptions– Credit to Subscriptions Income

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 19

The Adjustment for Unearned Revenue

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 20

Performance Objective 4

Record the adjustment data in a work sheet (including merchandise inventory, unearned revenue, supplies used, expired insurance, depreciation, and accrued wages or salaries)

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 21

Adjusted Trial Balance in the Work Sheet

• Eliminate the Adjusted Trial Balance column

• Extend the adjusted amounts to– Income Statement column– Balance Sheet column

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 22

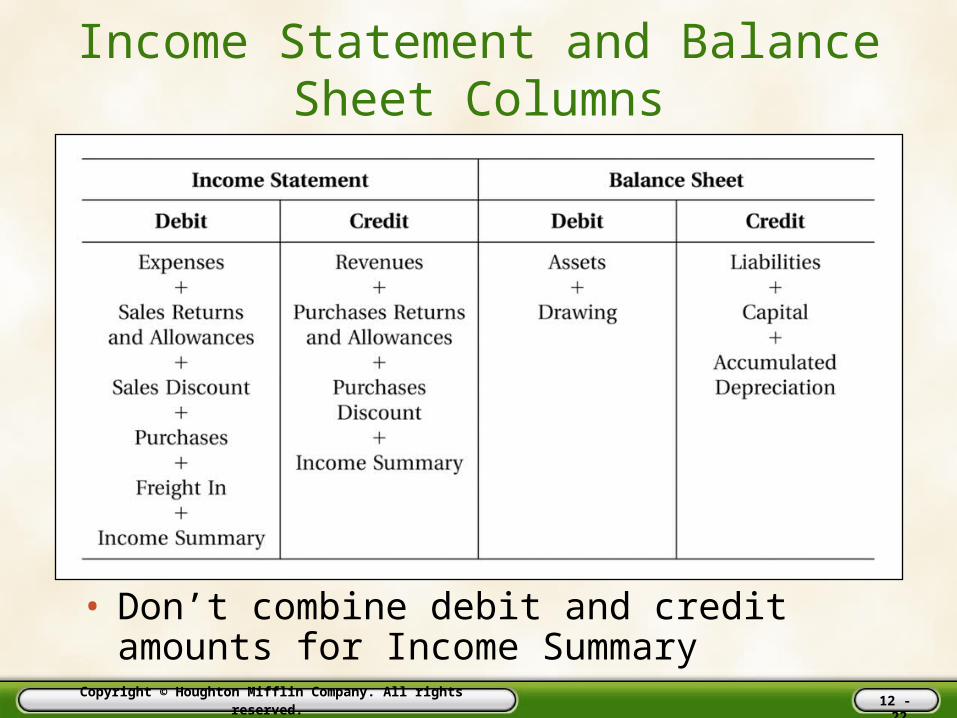

Income Statement and Balance Sheet Columns

• Don’t combine debit and credit amounts for Income Summary

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 23

Complete the Work Sheet

• Take a look in the textbook at the Dodson Plumbing Supply work sheet.– It’s too big to fit into the PowerPoint slides!

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 24

Steps for Completing the Work Sheet

1. Record trial balance– Total and rule column– Make sure DR = CR

2. Record adjustments in work sheet; make sure totals are equal

3. Record adjusted balance of each account in Income Statement and Balance Sheet columns– Total and rule columns– DR ≠ CR

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 25

Steps for Completing the Work Sheet

4. In the Income Statement columns, calculate net income or net loss– Subtract the smaller side from the larger side– “Plug” this number to make DR = CR– If there is net income, the credit side of the

columns will be larger and you will place net income on the debit side

– If there is net loss, the debit side of the columns will be larger and you will place net loss on the credit side

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 26

Steps for Completing the Work Sheet

5.In the Balance Sheet columns, calculate net income/loss– Subtract the smaller side from the larger

side– “Plug” this number to make DR = CR

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 27

Performance Objective 6

Journalize the adjusting entries for a merchandising business under the periodic inventory system

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 28

Journalize Adjusting Entry for Supplies

DescriptionPost.Ref. Debit Credit

1 20-- Adjusting Entries2 June 30 Supplies Expense 515 540.003 Supplies 115 540.00

Line #

General Journal Page 4

Date

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 29

Post Adjusting Entry for Supplies

Account: Supplies Account No: 115

Debit Credit1 20--2 June 4 1 800.00 800.00 3 30 Adj. 4 540.00 260.00

Line #

General Ledger

Date CreditBalance

ItemPost.Ref. Debit

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 30

Journalize Adjusting Entry for Merchandise Inventory

DescriptionPost.Ref. Debit Credit

20-- Adjusting EntriesDec. 31 Income Summary 77,000.00

Merchandise Inventory 77,000.00

31 Merchandise Inventory 64,900.00Income Summary 64,900.00

General Journal Page 1

Date

DR CR DR CR+ - + -

bal. 77,000 77,000 a) a) 77,000b) 64,900 b) 64,900

64,900

Merchandise Inventory Income Summary

Update AccountsUpdate Accounts

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 31

Journalize Adjusting Entry for Unearned Revenue

• Insurance company receives cash for a one-year insurance policy

• After a month, the insurance company has earned one month’s revenue

DescriptionPost.Ref. Debit Credit

20-- Adjusting EntriesJan. 31 Unearned Insurance Revenue 100.00

Insurance Revenue 100.00

Date

General Journal Page 16

Page 6

Description Debit Credit20--Jan. 1 Cash 1,200.00

Unearned Insurance Revenue 1,200.00Received Ck. No.3287 from customer for 1-year truck insurance.

General Journal

Date

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 32

Journal Entriesand Posting (T Account Demo)

DescriptionPost. Ref. Debit Credit

20—Jan 1 Cash 1,200.00

Unearned Insurance Revenue 1,200.00Received Ck. No. 3287 from customer for 1-year truck insurance.

Adjusting Entries31 Unearned Insurance Revenue 100.00

Insurance Revenue 100.00

Page 16

Date

General Journal

= +

DR CR DR CR DR CR+ - - + - +

bal. 5,000.001-Jan 1,200.00 31-Jan 100.00 1,200.00 1-Jan 100.00 31-Jan

Cash (1100) Unearned Insurance Revenue (2110) Insurance Revenue (4110)

Owner's EquityLiabilitiesAssets

11002110

2110

4110

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 33

Journal Entries Under the Periodic Inventory System

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 34

Performance Objective 7

Journalize the adjusting entry for merchandise inventory under the perpetual inventory system

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 35

Perpetual Inventory System

• The system under which the buying of merchandise during the year is recorded as:– Debit to Merchandise Inventory– Credit to Accounts Payable or Cash

• When merchandise is sold, the cost of the merchandise is recorded as:– Debit to Cost of Goods Sold– Credit to Merchandise Inventory

• At the end of the year, a physical count of the stock of goods is taken– An adjusting entry is made to record the difference between

the amount of the count and the amount previously recorded

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 36

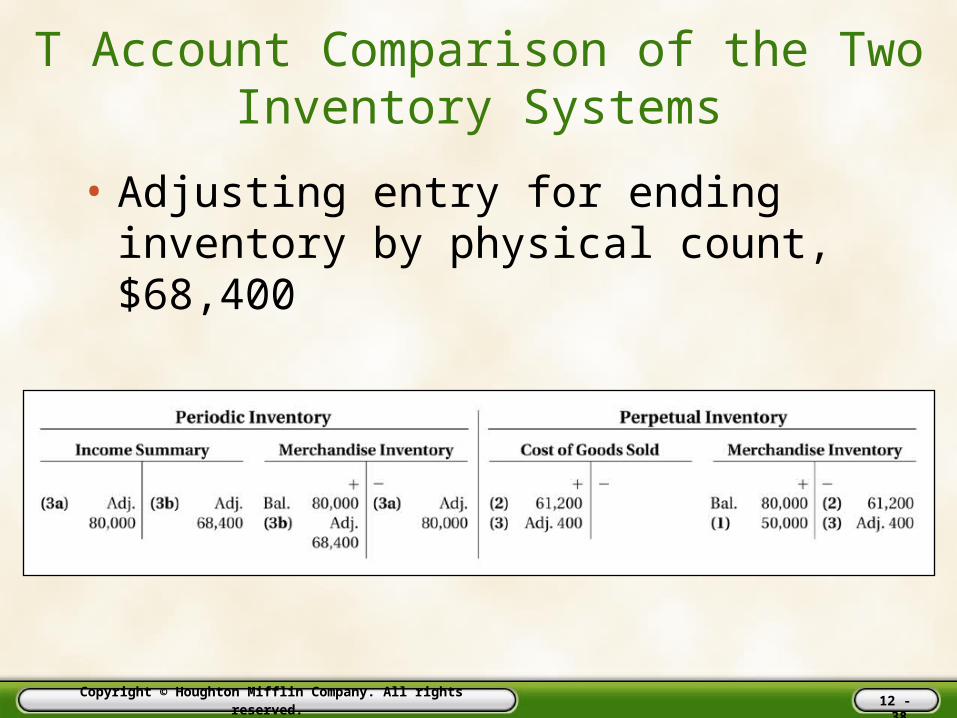

T Account Comparison of the Two Inventory Systems

• Bought merchandise on account, $50,000

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 37

T Account Comparison of the Two Inventory Systems

• Sold merchandise for $82,000 having a cost of $61,200

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 38

T Account Comparison of the Two Inventory Systems

• Adjusting entry for ending inventory by physical count, $68,400

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 39

Journal Entries for Merchandise Inventory Under the Perpetual Inventory System

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 40

Comparison of Income Statements

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 41

Demonstration Problem

We will complete a work sheet and make the adjusting journal entries

a) Merchandise Inventory at Jan. 1, 20-- $120,500.00

b) Merchandise Inventory at Dec. 31, 20-- 104,682.00

c) Store supplies inventory at Dec. 31 900.00

d) Insurance expired during the year 2,040.00

e) Salary accrued at Dec. 31 1,865.00

f) Depreciation of building 2,142.00

g) Depreciation of store equipment 2,731.00

Adjustments for Monty Company

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 42

Work Sheet

DR CR DR CR DR CRCash 12,500.00Accounts Receivable 2,140.00Merchandise Inventory 120,500.00Store Supplies 1,520.00Prepaid Insurance 3,040.00Land 48,000.00Building 108,000.00Accumulated Depreciation, Building 16,600.00Store Equipment 36,400.00Accumulated Depreciation, Store Equipment 11,600.00Accounts Payable 14,650.00Sales Tax Payable 4,192.00Notes Payable 5,000.00B. Monty, Capital 216,135.00B. Monty, Drawing 44,200.00Sales 467,550.00Sales Returns & Allowances 2,634.00Purchases 284,719.00Purchases Returns & Allowances 5,560.00Purchases Discount 3,671.00Freight In 7,868.00Salary Expense 58,673.00Advertising Expense 7,259.00Utilities Expense 5,895.00Miscellaneous Expense 840.00Interest Expense 770.00

744,958.00 744,958.00Income SummaryStore Supplies ExpenseInsurance ExpenseDepreciation Expense, BuildingDepreciation Expense, Store EquipmentSalaries Payable

0.00 0.00 0.00 0.00 0.00 0.00Net Income 0.00 0.00

0.00 0.00 0.00 0.00

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name CRDR

Adjustments

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 43

Empty Inventory Account

DR CR DR CR DR CRCash 12,500.00Accounts Receivable 2,140.00Merchandise Inventory 120,500.00 a) 120,500.00Store Supplies 1,520.00Prepaid Insurance 3,040.00Land 48,000.00Building 108,000.00Accumulated Depreciation, Building 16,600.00Store Equipment 36,400.00Accumulated Depreciation, Store Equipment 11,600.00Accounts Payable 14,650.00Sales Tax Payable 4,192.00Notes Payable 5,000.00B. Monty, Capital 216,135.00B. Monty, Drawing 44,200.00Sales 467,550.00Sales Returns & Allowances 2,634.00Purchases 284,719.00Purchases Returns & Allowances 5,560.00Purchases Discount 3,671.00Freight In 7,868.00Salary Expense 58,673.00Advertising Expense 7,259.00Utilities Expense 5,895.00Miscellaneous Expense 840.00Interest Expense 770.00

744,958.00 744,958.00Income Summary a) 120,500.00Store Supplies ExpenseInsurance ExpenseDepreciation Expense, BuildingDepreciation Expense, Store EquipmentSalaries Payable

120,500.00 120,500.00 0.00 0.00 0.00 0.00Net Income 0.00 0.00

0.00 0.00 0.00 0.00

CRDRAdjustments

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 44

Place Counted Inventory into Merch. Inv. Account

DR CR DR CR DR CRCash 12,500.00Accounts Receivable 2,140.00Merchandise Inventory 120,500.00 b) 104,682.00 a) 120,500.00Store Supplies 1,520.00Prepaid Insurance 3,040.00Land 48,000.00Building 108,000.00Accumulated Depreciation, Building 16,600.00Store Equipment 36,400.00Accumulated Depreciation, Store Equipment 11,600.00Accounts Payable 14,650.00Sales Tax Payable 4,192.00Notes Payable 5,000.00B. Monty, Capital 216,135.00B. Monty, Drawing 44,200.00Sales 467,550.00Sales Returns & Allowances 2,634.00Purchases 284,719.00Purchases Returns & Allowances 5,560.00Purchases Discount 3,671.00Freight In 7,868.00Salary Expense 58,673.00Advertising Expense 7,259.00Utilities Expense 5,895.00Miscellaneous Expense 840.00Interest Expense 770.00

744,958.00 744,958.00Income Summary a) 120,500.00 b) 104,682.00Store Supplies ExpenseInsurance ExpenseDepreciation Expense, BuildingDepreciation Expense, Store EquipmentSalaries Payable

225,182.00 225,182.00 0.00 0.00 0.00 0.00Net Income 0.00 0.00

0.00 0.00 0.00 0.00

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name CRDR

Adjustments

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 45

Record All Adjustments

DR CR DR CR DR CRCash 12,500.00Accounts Receivable 2,140.00Merchandise Inventory 120,500.00 b) 104,682.00 a) 120,500.00Store Supplies 1,520.00 c) 900.00Prepaid Insurance 3,040.00 d) 2,040.00Land 48,000.00Building 108,000.00Accumulated Depreciation, Building 16,600.00 f) 2,142.00Store Equipment 36,400.00Accumulated Depreciation, Store Equipment 11,600.00 g) 2,731.00Accounts Payable 14,650.00Sales Tax Payable 4,192.00Notes Payable 5,000.00B. Monty, Capital 216,135.00B. Monty, Drawing 44,200.00Sales 467,550.00Sales Returns & Allowances 2,634.00Purchases 284,719.00Purchases Returns & Allowances 5,560.00Purchases Discount 3,671.00Freight In 7,868.00Salary Expense 58,673.00 e) 1,865.00Advertising Expense 7,259.00Utilities Expense 5,895.00Miscellaneous Expense 840.00Interest Expense 770.00

744,958.00 744,958.00Income Summary a) 120,500.00 b) 104,682.00Store Supplies Expense c) 900.00Insurance Expense d) 2,040.00Depreciation Expense, Building f) 2,142.00Depreciation Expense, Store Equipment g) 2,731.00Salaries Payable e) 1,865.00

234,860.00 234,860.00 0.00 0.00 0.00 0.00Net Income 0.00 0.00

0.00 0.00 0.00 0.00

CRDRAdjustments

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 46

Carry Over to Income Statement Column

DR CR DR CR DR CRCash 12,500.00Accounts Receivable 2,140.00Merchandise Inventory 120,500.00 b) 104,682.00 a) 120,500.00Store Supplies 1,520.00 c) 900.00Prepaid Insurance 3,040.00 d) 2,040.00Land 48,000.00Building 108,000.00Accumulated Depreciation, Building 16,600.00 f) 2,142.00Store Equipment 36,400.00Accumulated Depreciation, Store Equipment 11,600.00 g) 2,731.00Accounts Payable 14,650.00Sales Tax Payable 4,192.00Notes Payable 5,000.00B. Monty, Capital 216,135.00B. Monty, Drawing 44,200.00Sales 467,550.00 467,550.00Sales Returns & Allowances 2,634.00 2,634.00Purchases 284,719.00 284,719.00Purchases Returns & Allowances 5,560.00 5,560.00Purchases Discount 3,671.00 3,671.00Freight In 7,868.00 7,868.00Salary Expense 58,673.00 e) 1,865.00 60,538.00Advertising Expense 7,259.00 7,259.00Utilities Expense 5,895.00 5,895.00Miscellaneous Expense 840.00 840.00Interest Expense 770.00 770.00

744,958.00 744,958.00Income Summary a) 120,500.00 b) 104,682.00 120,500.00 104,682.00Store Supplies Expense c) 900.00 900.00Insurance Expense d) 2,040.00 2,040.00Depreciation Expense, Building f) 2,142.00 2,142.00Depreciation Expense, Store Equipment g) 2,731.00 2,731.00Salaries Payable e) 1,865.00

234,860.00 234,860.00 498,836.00 581,463.00 0.00 0.00Net Income 82,627.00 0.00

581,463.00 581,463.00 0.00 0.00

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name CRDR

Adjustments

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 47

Carry Over to Balance Sheet Column

DR CR DR CR DR CRCash 12,500.00 12,500.00Accounts Receivable 2,140.00 2,140.00Merchandise Inventory 120,500.00 b) 104,682.00 a) 120,500.00 104,682.00Store Supplies 1,520.00 c) 900.00 620.00Prepaid Insurance 3,040.00 d) 2,040.00 1,000.00Land 48,000.00 48,000.00Building 108,000.00 108,000.00Accumulated Depreciation, Building 16,600.00 f) 2,142.00 18,742.00Store Equipment 36,400.00 36,400.00Accumulated Depreciation, Store Equipment 11,600.00 g) 2,731.00 14,331.00Accounts Payable 14,650.00 14,650.00Sales Tax Payable 4,192.00 4,192.00Notes Payable 5,000.00 5,000.00B. Monty, Capital 216,135.00 216,135.00B. Monty, Drawing 44,200.00 44,200.00Sales 467,550.00 467,550.00Sales Returns & Allowances 2,634.00 2,634.00Purchases 284,719.00 284,719.00Purchases Returns & Allowances 5,560.00 5,560.00Purchases Discount 3,671.00 3,671.00Freight In 7,868.00 7,868.00Salary Expense 58,673.00 e) 1,865.00 60,538.00Advertising Expense 7,259.00 7,259.00Utilities Expense 5,895.00 5,895.00Miscellaneous Expense 840.00 840.00Interest Expense 770.00 770.00

744,958.00 744,958.00Income Summary a) 120,500.00 b) 104,682.00 120,500.00 104,682.00Store Supplies Expense c) 900.00 900.00Insurance Expense d) 2,040.00 2,040.00Depreciation Expense, Building f) 2,142.00 2,142.00Depreciation Expense, Store Equipment g) 2,731.00 2,731.00Salaries Payable e) 1,865.00 1,865.00

234,860.00 234,860.00 498,836.00 581,463.00 357,542.00 274,915.00Net Income 82,627.00 82,627.00

581,463.00 581,463.00 357,542.00 357,542.00

CRDRAdjustments

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 48

Work Sheet

DR CR DR CR DR CRCash 12,500.00 12,500.00Accounts Receivable 2,140.00 2,140.00Merchandise Inventory 120,500.00 b) 104,682.00 a) 120,500.00 104,682.00Store Supplies 1,520.00 c) 900.00 620.00Prepaid Insurance 3,040.00 d) 2,040.00 1,000.00Land 48,000.00 48,000.00Building 108,000.00 108,000.00Accumulated Depreciation, Building 16,600.00 f) 2,142.00 18,742.00Store Equipment 36,400.00 36,400.00Accumulated Depreciation, Store Equipment 11,600.00 g) 2,731.00 14,331.00Accounts Payable 14,650.00 14,650.00Sales Tax Payable 4,192.00 4,192.00Notes Payable 5,000.00 5,000.00B. Monty, Capital 216,135.00 216,135.00B. Monty, Drawing 44,200.00 44,200.00Sales 467,550.00 467,550.00Sales Returns & Allowances 2,634.00 2,634.00Purchases 284,719.00 284,719.00Purchases Returns & Allowances 5,560.00 5,560.00Purchases Discount 3,671.00 3,671.00Freight In 7,868.00 7,868.00Salary Expense 58,673.00 e) 1,865.00 60,538.00Advertising Expense 7,259.00 7,259.00Utilities Expense 5,895.00 5,895.00Miscellaneous Expense 840.00 840.00Interest Expense 770.00 770.00

744,958.00 744,958.00Income Summary a) 120,500.00 b) 104,682.00 120,500.00 104,682.00Store Supplies Expense c) 900.00 900.00Insurance Expense d) 2,040.00 2,040.00Depreciation Expense, Building f) 2,142.00 2,142.00Depreciation Expense, Store Equipment g) 2,731.00 2,731.00Salaries Payable e) 1,865.00 1,865.00

234,860.00 234,860.00 498,836.00 581,463.00 357,542.00 274,915.00Net Income 82,627.00 82,627.00

581,463.00 581,463.00 357,542.00 357,542.00

CRDRAdjustments

Monty CompanyWork Sheet

For Year Ended June 30, 20—

Balance SheetTrial Balance Income StatementAccount Name

For Year Ended December 31, 20--

Copyright © Houghton Mifflin Company. All rights reserved. 12 - 49

Journal Entries Before Posting

DescriptionPost.Ref. Debit Credit

1 Adjusting Entries2 20--3 Dec. 31 Income Summary 120,500.004 Merchandise Inventory 120,500.0056 31 Merchandise Inventory 104,682.007 Income Summary 104,682.0089 31 Store Supplies Expense 900.00

10 Store Supplies 900.001112 31 Insurance Expense 2,040.0013 Prepaid Insurance 2,040.001415 31 Depreciation Expense, Building 2,142.0016 Accumulated Depreciation, Building 2,731.001718 31 Depreciation Expense, Store Equipment 2,731.0019 Accumulated Depreciation, Store Equipment 2,731.002021 31 Salary Expense 1,865.0022 Salaries Payable 1,865.00

General Journal

Date

Page 43Line #

2,142.00