© tim voorhees, jd, mba 1996-2005 1 best practices session d updated 2/7/2005 conducting discovery...

TRANSCRIPT

© Tim Voorhees, JD, MBA 1996-2005

1

Best Practices Session D Updated 2/7/2005

Conducting Discovery Sessions and Client

Retreats

© Tim Voorhees, JD, MBA 1996-2005

2

1. Engaging clients2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

3

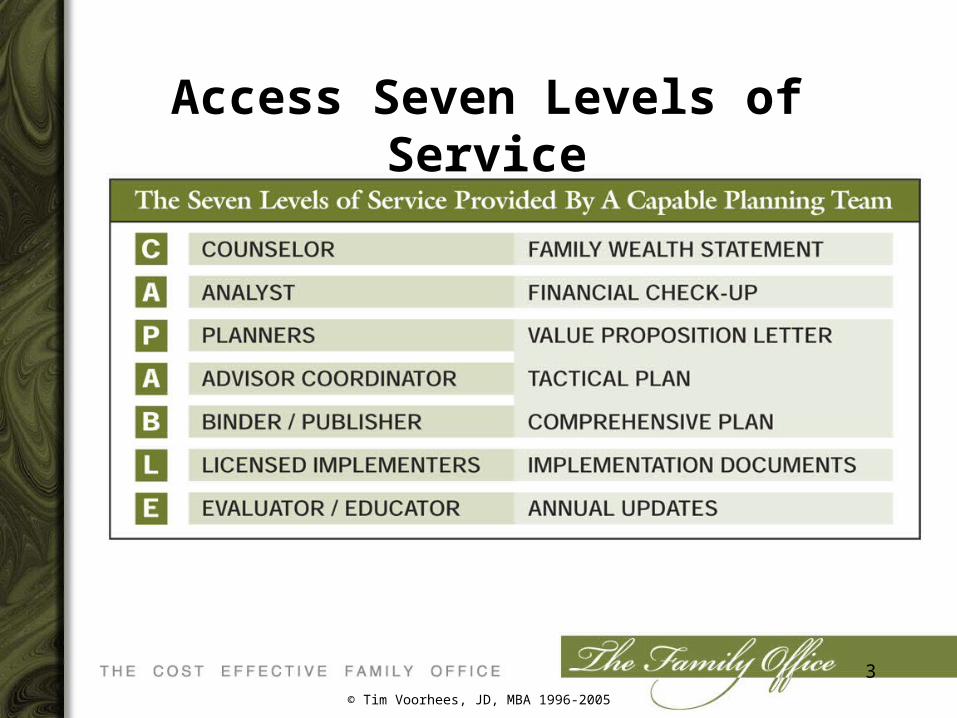

Access Seven Levels of Service

© Tim Voorhees, JD, MBA 1996-2005

4

Provide Clear Value Before

Upgrading the Level of Service

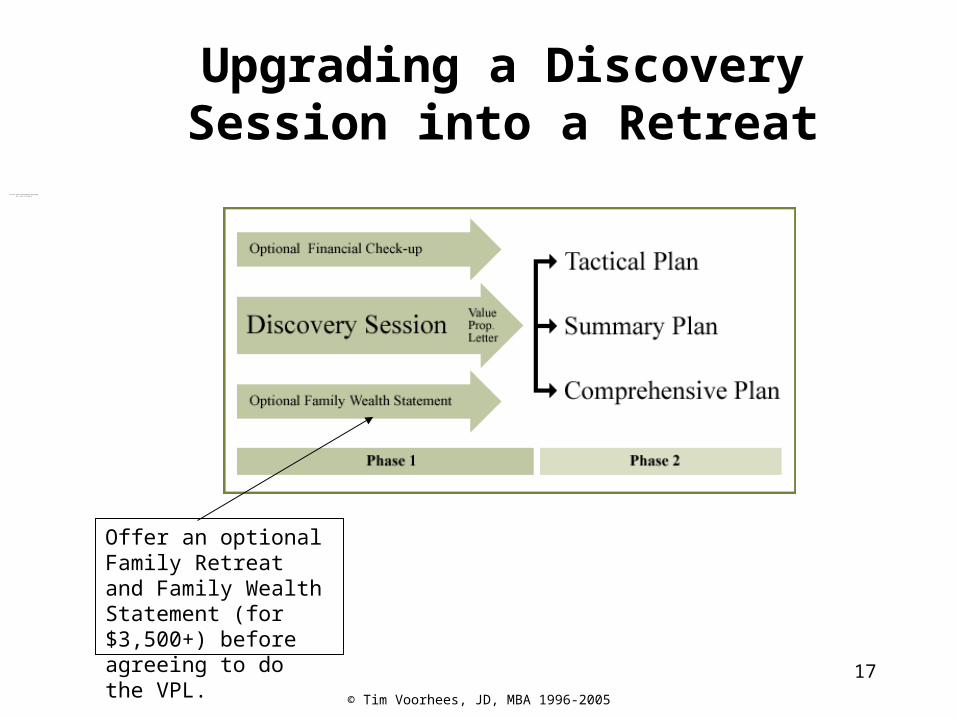

Offer an optional Family Retreat and Family Wealth Statement (for $3,500+) before agreeing to do the VPL.

Begin with the Free Discovery Session

Tim Voorhees, JD, MBA, 1996-2005

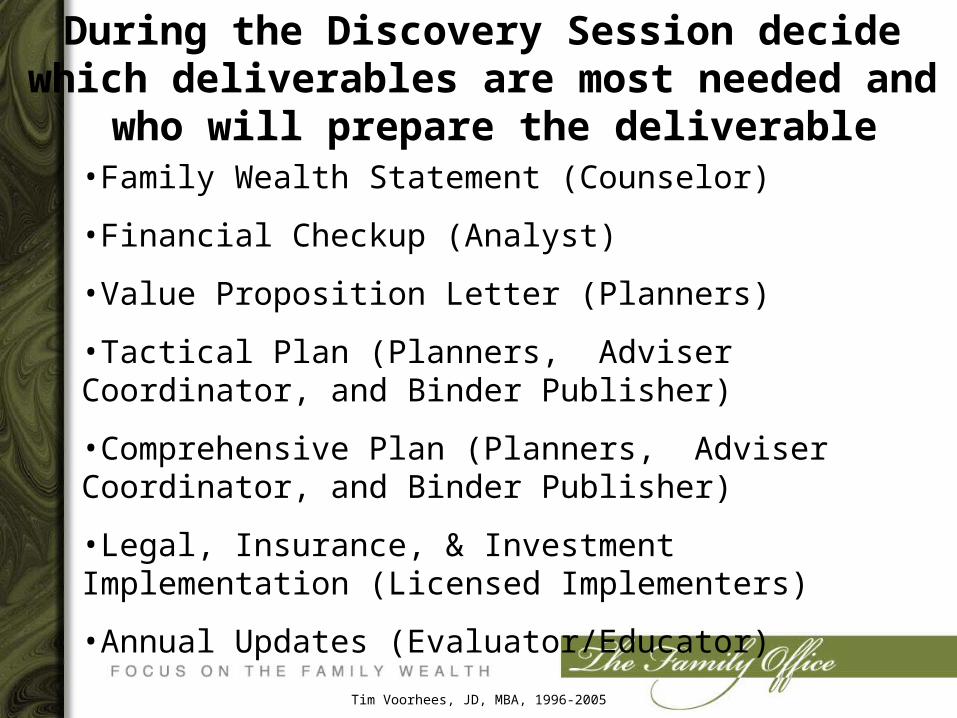

During the Discovery Session decide which deliverables are most needed and

who will prepare the deliverable•Family Wealth Statement (Counselor)

•Financial Checkup (Analyst)

•Value Proposition Letter (Planners)

•Tactical Plan (Planners, Adviser Coordinator, and Binder Publisher)

•Comprehensive Plan (Planners, Adviser Coordinator, and Binder Publisher)

•Legal, Insurance, & Investment Implementation (Licensed Implementers)

•Annual Updates (Evaluator/Educator)

Tim Voorhees, JD, MBA, 1996-2005

Phase 1 Phase 2

Typically offer needed deliverables during four phases

Phase 3 Phase 4

Family Wealth Statement

Financial Checkup

Value Proposition Letter

Tactical Plan

Comprehensive Plan

Legal, Insurance, & Investment Implementation

Annual Updates

© Tim Voorhees, JD, MBA 1996-2005

7

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

Tim Voorhees, JD, MBA, 1996-2005

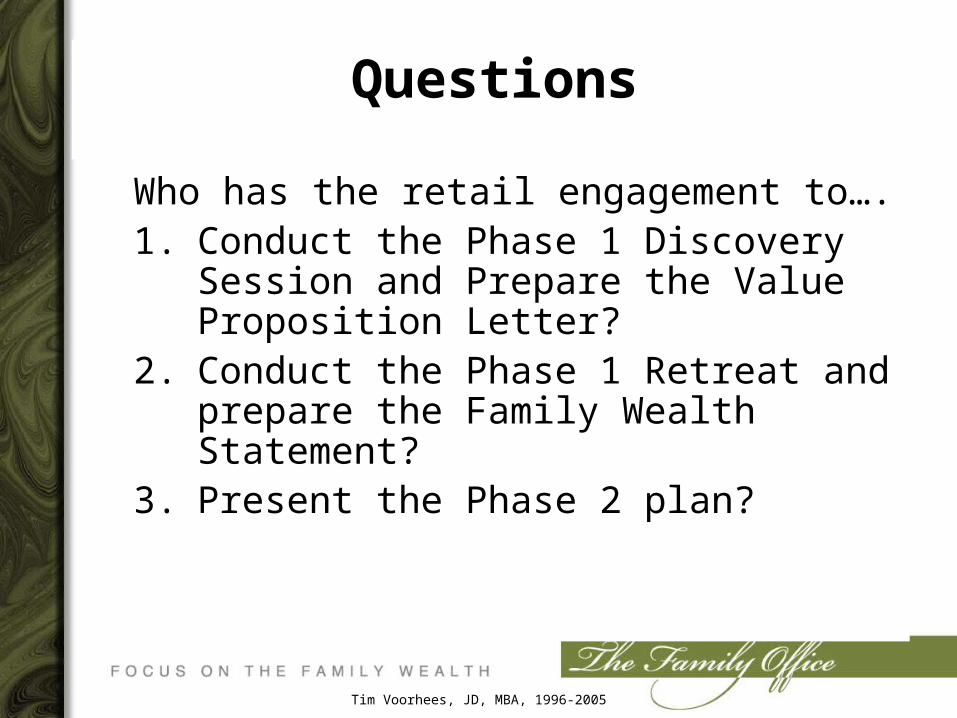

Questions

Who has the retail engagement to….1. Conduct the Phase 1 Discovery

Session and Prepare the Value Proposition Letter?

2. Conduct the Phase 1 Retreat and prepare the Family Wealth Statement?

3. Present the Phase 2 plan?

© Tim Voorhees, JD, MBA 1996-2005

9

The Biggest Producers Leave Phase 1 and Phase 2 to

Channel Members• It is most profitable when you focus

entirely on Phase 3 implementation of investment and insurance tools.

• If a VFOS Channel Member works with your client to complete Phase 1 and 2 deliverables, we maximize the likelihood that Phase 3 investment and insurance tools will be implemented through you.

© Tim Voorhees, JD, MBA 1996-2005

10

Requirements before you can deliver our deliverables with VFOS only acting as a back

office for you:• You must believe that it is a good

use of your time to go through the training.

• You must complete Best Practices and Best Tools training and sign our Allied Adviser Agreement to access Phase 1 deliverables at wholesale costs.

© Tim Voorhees, JD, MBA 1996-2005

11

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

12

Goals of the Discovery Sessions

• Attract prospects -- create referrals• Convert prospects to clients• Deliver indispensable value• Turn clients into lifelong partners• Establish a foundation for Wealth

Blueprinting• Help clients review 300 tools x 200

services to achieve 100 goals: 6 Million options!

© Tim Voorhees, JD, MBA 1996-2005

13

Min

imiz

e T

axes

Acc

um

ula

te W

ealt

hP

rote

ct A

sset

s fr

om

Cre

dit

ors

Man

age

Ris

k

Mai

nta

in C

on

tro

lM

anag

e C

ash

Flo

wIn

crea

se C

har

itab

le G

ivin

g P

ote

nti

al

Co

ord

inat

e E

stat

e D

istr

ibu

tio

ns

Pro

tect

Ag

ain

st E

stat

e A

dm

in. E

xp./D

elay

s

Man

age

Fam

ily B

usi

nes

s S

ucc

essi

on

Mai

nta

in C

on

tro

l Ove

r P

erso

nal

Aff

airs

Max

imiz

e C

on

tro

l Ove

r S

oci

al C

apit

al

Mo

re S

oci

al C

apit

al L

ever

age

Tax

Opi

nion

Op

inio

n F

irm

PP

M

Con

e of

sile

nce

WORKSHOP TOOLS LISTED BELOW Common Application Target Net worth

Aircraft Acquisition Strategy Business planning 10 million + Y N Y Y Y Y Y N Y N Y Y Y

Charitable LLC Wealth Transfer 10 million + Y Y Y Y Y Y Y Y Y Y Y Y Y

Contingent Swap Income Tax Planning 10 million + Y Y N Y Y Y N N N N N N N

Costless Collar Income Tax Planning 5 million + N N N Y N Y N N N N N N N

Employee Stock Ownership Plan Wealth Transfer 10 million + Y Y Y Y Y Y N Y Y Y Y N N

Exchange Fund Wealth Transfer 5 million + Y Y N Y N N N N N N N N N

Family Split Dollar Wealth Transfer 5 million + N N N N N Y N Y Y Y N N N

Flip CRT Income Tax Planning 3 million + Y Y Y Y Y Y Y N Y N Y Y Y

Hedge Fund Investment Planning 5 million + Y Y N Y N N N N N N N N N

Investor Play Basket Investment Planning 5 million + Y Y Y Y Y Y Y Y Y Y Y N N

Leveraged Retirement Distribution Technique Wealth Transfer 5 million + Y N Y N Y Y N Y Y Y Y N N

Non-Qualified Stock Option Strategies Income Tax Planning 5 million + Y Y Y Y Y N Y N N N Y N N

Offshore Insurance Investment Planning 5 million + Y Y Y Y Y Y N Y Y Y Y N N

Private Equity Investment Planning 5 million + N Y N Y Y Y Y N N N Y Y Y

Receivable Asset Monetization Investment Planning 5 million + Y Y N Y Y Y Y N N N Y N N

Re-Engineered Corporate Balance Sheet Corporate Finance 100 million + Y N N N N N N N N N N N N

SERP SWAP Wealth Transfer 3 million + Y N Y N Y Y N Y Y Y Y N N

Pension Distribution Strategy Wealth Transfer 3 million + Y N Y N Y Y N Y Y Y Y N N

Stretch IRA Wealth Transfer 3 million + Y Y Y N N N N Y N N Y N N

Super CLAT Income Tax Planning 3 million + Y N Y N Y N Y Y Y N Y Y Y

Synthetic Equity Income Tax Planning 10 million + Y Y Y Y Y Y N Y Y Y Y N N

Tax-Free CRT Distributions Charitable Planning 5 million + Y N Y Y N Y Y Y N N N Y Y

Tax-Free S Corporation Sale Strategy Income Tax Planning 5 million + Y Y Y Y N Y N Y Y N Y N N

Unitrust Limited Partnership Income Tax Planning 5 million + Y Y Y N Y Y Y Y N N Y Y Y

Tools/Benefits Grid

A partial list of tools and goals

© Tim Voorhees, JD, MBA 1996-2005

14

Gene

rate

Perso

nal In

come

Tax

Ded

uctio

ns

Gene

rate

Busin

ess I

ncom

e Tax

Ded

uctio

ns

Defer

Tax

able

Incom

eGe

nera

te Fu

ture T

ax-F

avor

ed In

come

Minim

ize C

apita

l Gain

Inco

me

Minim

ize E

state

Taxe

s

Accu

mulat

e Per

sona

l Wea

lth

Prote

ct As

sets

from

Cred

itors

Incre

ase C

urre

nt Sp

enda

ble In

come

Incre

ase C

urre

nt Ch

arita

ble G

iving

Incre

ase F

uture

Cha

ritable

Givi

ng

Coor

dinate

/ Bala

nce E

state

Distr

ibutio

ns

Redu

ce E

state

Expe

nses

and D

elays

Mana

ge F

amily

Bus

iness

Suc

cess

ion

Maint

ain M

axim

um Le

gal C

ontro

l ove

r Ass

ets

Maxim

ize C

ontro

l ove

r Soc

ial C

apita

l

Dive

rsify

Inves

tmen

t Ass

ets

Prov

ide In

centi

ves f

or C

hildr

en

Leve

rage

Qua

lified

Reti

reme

nt Pl

an D

istrib

ution

s

Acqu

ire A

ssets

Mor

e Tax

- Effic

iently

Oper

ate B

usine

ss in

Tax

-Fre

e Env

ironm

ent

Buy L

ife In

sura

nce w

ith P

re-T

ax D

ollar

s

Pursu

e Agg

ress

ive T

ax P

lannin

g

Mana

ge T

iming

of T

axab

le Inc

ome

Redu

ce In

vestm

ent R

isk

1031 Exchange 0 0 3 0 0 0 2 0 2 0 1 1 1 2 2 1 2 0 0 2 01035 Exchange 0 0 3 0 3 0 2 0 2 0 1 1 1 1 2 1 3 1 1 2 3402(e) Rollover 0 0 0 3 0 0 0 0 2 0 0 0 0 0 0 0 0 0 3 2 0412(i) with sale to Family Entity 0 3 3 0 0 3 0 1 0 0 0 2 2 2 1 0 0 1 3 1 0412(i) with rollout to Participant 0 3 3 2 0 0 3 1 0 0 0 1 1 1 1 0 0 0 3 1 0Aircraft Acquisition Strategy 3 0 0 0 2 1 0 1 1 0 2 0 1 0 3 2 1 0 0 3 0Accounts Receivable Financing 0 0 3 3 0 1 3 3 0 0 1 1 2 2 2 0 2 0 0 1 0Asset Allocation 0 0 0 0 1 0 3 0 0 0 0 0 0 0 1 0 3 0 0 1 0Charitable Gift Annuity, Deferred 3 0 2 3 3 3 2 3 3 3 3 1 2 1 1 2 2 1 1 0 0Charitable Gift Annuity, Immediate 3 0 1 3 3 3 0 2 3 2 1 1 2 1 1 2 2 1 1 0 0Charitable Gift Subject to Life Estate 2 0 0 0 0 3 0 1 3 1 3 1 2 1 1 2 2 1 1 2 1Charitable Limited Liability Company 3 0 0 0 3 3 0 3 3 2 2 1 2 2 2 3 2 1 1 1 1Charitable Remainder Unitrust, Standard (SCRUT) 2 0 1 1 3 3 2 1 2 0 3 2 1 0 1 3 2 0 0 1 0Charitable Remainder Unitrust, Standard with Wealth Replacement 2 0 1 1 3 3 1 2 2 1 3 2 1 0 1 3 3 0 0 1 0Charitable Remainder Unitrust, Net Income with Makeup (NIMCRUT) 2 0 1 1 3 3 2 2 2 1 3 2 1 0 1 3 3 0 0 1 0Charitable Remainder Unitrust, with Flip Provision (Flip CRT) 2 0 1 1 3 3 2 2 3 1 3 2 1 0 1 3 3 0 0 1 0Charitable Remainder Unitrust, with private stock redemption 2 0 1 1 3 3 1 2 3 1 3 2 1 3 1 3 3 0 0 1 0Charitable Remainder Annuity Trust (CRAT) 2 0 0 1 3 3 0 2 3 1 3 2 1 0 1 3 3 0 0 1 0Charitable Lead Annuity Trust, Grantor (GCLAT) 3 3 0 0 0 2 0 2 0 3 2 1 1 0 1 3 1 0 0 1 0Charitable Lead Annuity Trust, Nongrantor (CLAT) 0 0 0 0 0 3 0 2 0 3 2 1 1 1 0 3 1 0 0 1 0Charitable Lead Annuity Trust, Super CLAT 3 0 0 0 2 3 0 2 0 3 2 1 1 0 0 3 1 0 0 1 0Charitable Lead Unitrust, Grantor (GCLUT) 3 3 0 0 0 2 0 2 0 3 2 1 1 0 1 3 1 0 0 1 0Charitable Lead Unitrust, Nongrantor (CLUT) 0 0 0 0 0 3 0 2 0 3 2 1 1 1 0 3 1 0 0 1 0Common Trust Fund 3 3 1 0 3 0 2 1 2 1 1 0 1 0 1 0 2 0 0 1 0Costless Collar 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0Defined Benefit Pension Plan 0 3 3 0 0 0 3 3 0 0 1 1 1 1 3 0 2 0 0 1 0Disability Income Trust 0 3 3 0 0 0 3 2 0 0 1 0 0 1 3 0 2 0 0 0 0Dynasty Trust 0 0 0 0 0 3 0 3 0 0 0 2 1 2 0 0 0 0 0 2 0Education Trust 0 0 0 0 0 1 1 2 0 0 0 2 1 0 0 0 0 0 0 0 0Leveraged Employee Stock Ownership Plan with Synthetic Equity 0 3 1 1 3 3 1 2 2 1 1 2 1 3 0 0 3 0 0 2 3

Key3 indicates a primary benefit. A major reason that someone would implement this strategy.2 indicates a secondary benefit--not the only reason but a plus in the decision-making process1 indicates an ancillary benefit--not a significant positive or negative factor.0 indicates the benefit is irrelevant to the strategy or the strategy may actually be a detriment.

Tools/Benefits Grid (partial)

© Tim Voorhees, JD, MBA 1996-2005

15

Summarize the Value Proposition sample diagram

CurrentCurrent ProposedProposed

Estate Taxes $14,300,000 $100,000

Benefit to Heirs

$15,200,000 $18,900,000

Income Tax Savings

$0 $200,000

Benefit to Charity

$0 $21,300,000

Example:

© Tim Voorhees, JD, MBA 1996-2005

16

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

17

Provide Clear Value Before Upgrading the Level of Service

Offer an optional Family Retreat and Family Wealth Statement (for $3,500+) before agreeing to do the VPL.

Upgrading a Discovery Session into a Retreat

© Tim Voorhees, JD, MBA 1996-2005

18

Integrating Retreats into Your Practice

• Offer a service not available elsewhere in your community.

• Cover Discovery Session materials in much greater details.

• Deliver indispensable value• Turn clients into lifelong partners• Establish a foundation for Wealth

Blueprinting• Address issues that can only be

addressed in a 4-6 hour session.

© Tim Voorhees, JD, MBA 1996-2005

19

Learning from the Models

• Scott Fithian – The Family Financial Philosophy

• Jay Link – Family Wealth Letter of Intent

• Scott Farnsworth – Family Wealth Declaration

• Esperti Peterson – Discovery Document• Tim Voorhees – Family Wealth

Statement

© Tim Voorhees, JD, MBA 1996-2005

20

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

21

Developing Wealth Counseling Skills?

• Understanding both the emotional and technical issues

• Drawing out the client’s purpose• Briefly explaining relevant planning tools• Mediating conflicts efficiently• Facilitating interaction of retreat

attendees

© Tim Voorhees, JD, MBA 1996-2005

22

Identifying the Right Clients

• Choosing the right clients • Considering influence of existing

advisers• Understanding dysfunctional

environments • Involving children in the retreat

process• Screening for emotional issues or

potential litigation

© Tim Voorhees, JD, MBA 1996-2005

23

Explaining the Process

• Deciding which advisers will provide wise counsel

• Sharing case histories of successful families

• Giving references if necessary• Discussing roles of existing advisers • Obtaining a commitment of time and

money• Scheduling a retreat

© Tim Voorhees, JD, MBA 1996-2005

24

Motivating Clients to Schedule a Retreat

• Executive Officer and Emotional Officer need agreement

• One day in a lifetime• The Power of Purpose: Genesis 11:6• The need to overcome problems

– Affluenza– Lawsuit risks– Etc.

© Tim Voorhees, JD, MBA 1996-2005

25

Establishing the Price

• Explain how the cost is much less than the benefits

• Discuss business topics to qualify for deduction

• Choose the appropriate engagement letter

© Tim Voorhees, JD, MBA 1996-2005

26

Preparing the Client

• Husband and wife complete the questionnaires separately

• Husband and wife should not compare notes

• Urge the client to schedule at least a half day without interruptions.

― Schedule 4 to 6 hours for the retreat ― Schedule ample time after the

retreat

© Tim Voorhees, JD, MBA 1996-2005

27

Preceding the First Retreat

• Prepare the client(s)• Choose a location • Decide which family members to

include• Schedule one or two days• Bring an assistant• Prepare an agenda• Prepare a list of questions

© Tim Voorhees, JD, MBA 1996-2005

28

During the Retreat • Discuss the power of purpose and mission• Review questions• Use Soft Data Questionnaire• Prepare custom list of questions

− Examine common problems for families with wealth

− Clarify who owns what. Address emotional ownership versus legal ownership

− Look for common communication and trust breakdowns

− Spot indications that family members lack a common mission

− Spot differing, but undisclosed, standards− Look for unprepared heirs

© Tim Voorhees, JD, MBA 1996-2005

29

Story-telling

• Harness emotional energy• Encourage a free-flowing discussion • Cover all the questions without

sticking to a rigid agenda.• Reflect on who inspired husband

and wife they were 10 years old. • Clarify a story that has a beginning

in youth, positive influence today, and great hope for the future.

© Tim Voorhees, JD, MBA 1996-2005

30

Bonding with the Client

• Listening to the client's personal history• Connecting to the client’s current

opportunities and threats• Inspiring the client to build on strengths

and overcome weaknesses• Uniting family members around a

common vision • Clarifying “WOTS MOST IMPORTANT?”

© Tim Voorhees, JD, MBA 1996-2005

31

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

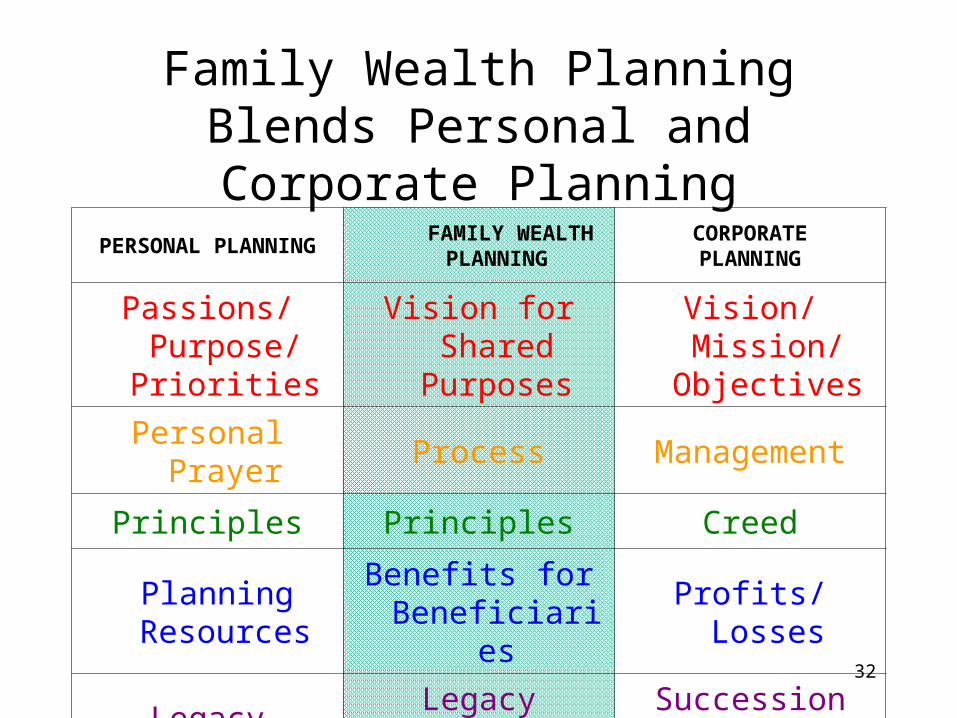

32

Family Wealth Planning Blends Personal and Corporate

PlanningPERSONAL

PLANNING FAMILY WEALTH

PLANNINGCORPORATEPLANNING

Passions/ Purpose/ Priorities

Vision for Shared

Purposes

Vision/ Mission/

Objectives

Personal Prayer

Process Management

Principles Principles Creed

Planning Resources

Benefits for Beneficiaries

Profits/Losses

LegacyLegacy Directives

Succession Plan

© Tim Voorhees, JD, MBA 1996-2005

33

Personal Planning Paradigm:

Passions, Purpose, Priorities, Planning Resources, and Planning Tools

Your Planning Resources

© Tim Voorhees, JD, MBA 1996-2005

34

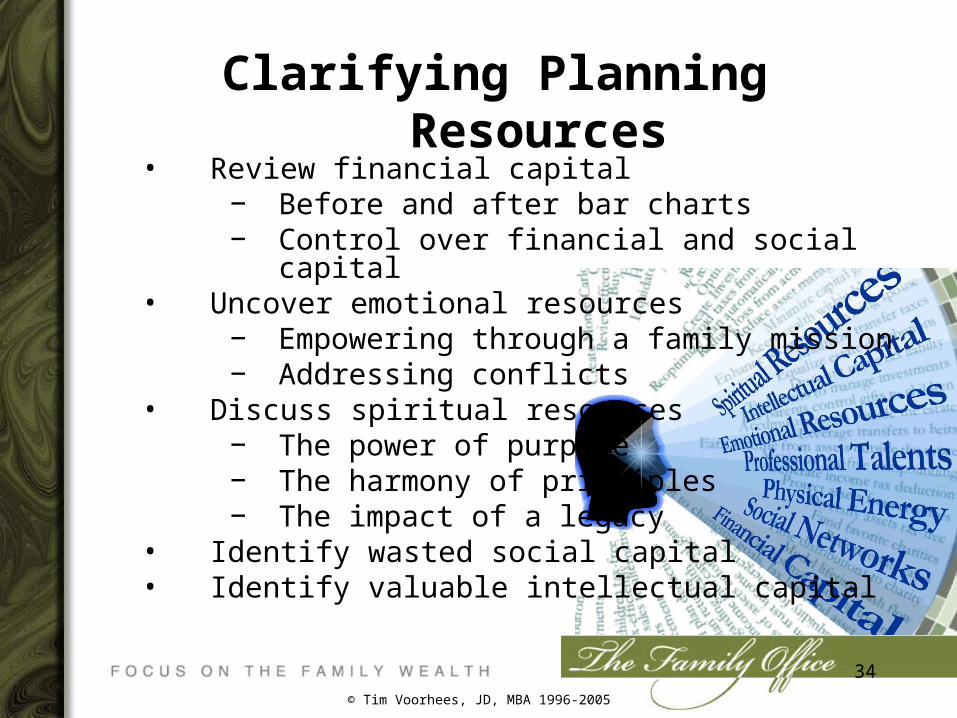

Clarifying Planning Resources

• Review financial capital− Before and after bar charts− Control over financial and social capital

• Uncover emotional resources− Empowering through a family mission− Addressing conflicts

• Discuss spiritual resources− The power of purpose− The harmony of principles− The impact of a legacy

• Identify wasted social capital• Identify valuable intellectual capital

© Tim Voorhees, JD, MBA 1996-2005

35

Explaining Benefits of the Planning Tools

• Clarifying root issues and suggesting financial, legal, or tax tools

• Integrating tools to create a zero-tax plan

• Drafting documents in light of spiritual, intellectual, emotional, and other issues

© Tim Voorhees, JD, MBA 1996-2005

36

Matching Planning Tools with Benefits

• See the tools/benefits grid• See the sample plans• Discuss scenarios

• Income tax deductions this year?• Exercising stock options?• Making lifetime wealth transfers?• Etcetera

© Tim Voorhees, JD, MBA 1996-2005

37

Personal

• Passions

• Purpose

• Priorities

• Principles (Cardinal Virtues)

Corporate

• Vision

• Mission

• Objectives

• Creed (Core Values)

© Tim Voorhees, JD, MBA 1996-2005

38

Corporate Planning Paradigm:

WOTS MOST IMPORTANT?• Review the Weaknesses, Opportunities, Threats, and

Strengths (“WOTS”)

• Clarify the Mission, Objectives, Strategies, and Tactics (“MOST”).

MISSIONOBJECTIVESSTRATEGIESTACTICS

™

© Tim Voorhees, JD, MBA 1996-2005

39

Family Wealth Planning Paradigm: Vision, Mission, and Shared Purposes

• Vision is bigger than mission• Mission is coalesced from individual purpose

statements• Mission is a summary of shared purposes• Mission Statement has 3 critical elements

− Who we are− What we do− Whom we serve

• Purpose Statements are individual and often hard to define but purpose statements should be defined before preceding with Family Wealth Planning.

Proverbs 20:5 - The purposes of a man's heart are deep waters, but a man of understanding draws them out.

© Tim Voorhees, JD, MBA 1996-2005

40

Family Wealth Planning Blends Personal and Corporate

PlanningPERSONAL

PLANNING FAMILY WEALTH

PLANNINGCORPORATEPLANNING

Passions/ Purpose/ Priorities

Vision for Shared Purposes

(Summarized in a Family Mission)

Vision/ Mission/ Objectives

Personal Prayer Process Management

Principles Principles Creed

Planning Resources

Benefits for Beneficiaries

Profits/Losses

Legacy Legacy Directives Succession Plan

© Tim Voorhees, JD, MBA 1996-2005

41

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations

8. Drafting a Family Wealth Statement

9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

42

Picking Scabs?• Does somebody refuse to develop a

mission and vision?• Is somebody avoiding accountability?• Is somebody undermining the family?

(See, e.g., Proverbs 6:16-19)

BEHAVIOR EXAMPLEHaughty eyes Unwilling to listen to counselA lying tongue Misrepresenting factsHands that shed innocent blood Slandering associates or leadersA heart that devises wicked schemes Cheating on taxesFeet that are quick to rush into evil Compromising corporate vision and objectives for personal gainA false witness who pours out lies Bad-mouthingA man who stirs up dissension Engaging in peace-breaking and peace- faking rather than peacemaking

© Tim Voorhees, JD, MBA 1996-2005

43

Addressing Challenging Situations

• The disinherited child• The child from a past relationship• Sons fighting for control of the

family business• Unmotivated kids• Intra-family lawsuits

© Tim Voorhees, JD, MBA 1996-2005

44

Involving Professional Help

• Wealth Counselor Network• Peacemaker Ministries – Certified

Christian Conciliators™• Others

− Roy Williams− Rick Harig− Etc.

© Tim Voorhees, JD, MBA 1996-2005

45

Collecting Relevant Documents

• Ideally have balance sheet before retreat begins

• Get commitments during the retreat to collect documents

• Get permission to work with CPA to gather documents

© Tim Voorhees, JD, MBA 1996-2005

46

Preparing the Client for After the Retreat

• Discuss phases of the CAPABLE model • Offer ideas about forming a team with

unique abilities relevant to the client• Discuss roles of insurance agent,

attorney, CPA, and other existing advisers.

• Establish checks and balances for team members

© Tim Voorhees, JD, MBA 1996-2005

47

Following the First Retreat

• Develop Family Wealth Statement and goal statement

• Prepare report card to show if current plan achieves goals

• Prepare Value Proposition Letter• Prepare the family for periodic

Family Meetings

© Tim Voorhees, JD, MBA 1996-2005

48

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

49

Drafting the Family Wealth Statement

• Develop a meaningful structure• Use Covenant model?

− Purpose− Process− Principles− Beneficiaries− Vision and Directives

© Tim Voorhees, JD, MBA 1996-2005

50

Clarifying the Purpose• Start by reflecting back statements

that impassion the client• Crystallize statements about passion

into a purpose• Meld purpose statements into a Family

Mission• Be sure that family members have

ownership in the mission

© Tim Voorhees, JD, MBA 1996-2005

51

The Purpose Statement is Important Because It…

• Inspires unity• Articulates unique characteristics• Clarifies functions• Establishes direction• Guides decision-making• Shapes strategy• Enhances effectiveness• Facilitates evaluation• Focuses the future• Summarizes complex concepts

concisely• Promotes long-term thinking

© Tim Voorhees, JD, MBA 1996-2005

52

Affirming Principles in the FWS

• Financial Security• Wealth Accumulation• Cash Flow and Income• Budgeting• Liquidity • Investment Time

Horizons• Taxes• Charitable gifts of

money• Charitable gifts of time• Diversification• Education funding

• Control• Complexity• Risk Management

and insurance• Asset Protection• Trustee and

fiduciary selection• Loans to family

members and close friends

• Providing for medical needs

• Retirement planning

• Grant-making• Stewardship

training

© Tim Voorhees, JD, MBA 1996-2005

53

Writing the FWS Efficiently• Use boilerplate templates • Use color-coding• Code the husband’s answers in blue, code

wife’s answers in pink, and code similar answers in yellow

• Develop pink-blue-yellow “PBY” document• Combine His and Her answers • Add in retreat notes using a colored font• Use the client’s actual words• Reference trustee, executor, guardian, and

beneficiary language in legal documents

© Tim Voorhees, JD, MBA 1996-2005

54

Preparing the Family for Meetings Following the

First Retreat • Conducting investment seminars• Training board members• Providing stewardship education• Clarifying authority, power, and

influence• Using observable and measurable

standards• Tracking success in realizing goals• Updating the Financial Checkup and VPL

© Tim Voorhees, JD, MBA 1996-2005

55

Access Seven Levels of Service

© Tim Voorhees, JD, MBA 1996-2005

56

1. Engaging clients for retreats2. Asking practice management

questions3. Discussing goals and tools 4. Upgrading a Discovery Session

into a Retreat5. Conducting a Retreat6. Differentiating Personal,

Corporate, and Family Wealth Planning

7. Addressing challenging situations8. Drafting a Family Wealth

Statement9. Accessing the best resources

© Tim Voorhees, JD, MBA 1996-2005

57

Best Practices CD - Session D Resources

4 Case Study: CRT5 Case Study: Super CLAT6 Case Study: ESOP7 Case Study: GDOT8 Case Study- Comprehensive Family Wealth Blueprint9 Engagement Kit Soft Data Questionnaire10 Engagement Kit Hard Data Questionnaire - Long34 Short Soft Data Fact finder35 Short Hard Data Fact finder36 Qualified Plan Fact finder40 200 Tools List

© Tim Voorhees, JD, MBA 1996-2005

58

Best Practices CD - Session D Resources

41 100 Goals List42 70 Best Tools Descriptions44 Tools Benefit Grid - Simple45 Tools Benefit Grid - Comprehensive71 How to charge fees (article)89 Prospecting Letter - Discovery Session 114 Best Practices Session D119 Consent to Share Info - Permission Grid124 Steps to develop Family Wealth Statement240 Follow-up Letter -- offer retreat309 Conducting a Family Retreat812 FAQs regarding free Discovery Sessions

© Tim Voorhees, JD, MBA 1996-2005

59

Best Practices Training

Session AAdapting to Planning Trends and Presenting Valuable Deliverables to Clients

Session B Charging Fees and Using Appropriate Engagement Letters

Session CDelegating Technical Work to a Virtual Back Office and Advanced Sales Department

Session DDeveloping the Value Proposition Letter after a Discovery Session, and Preparing the Family Wealth Statement During/After a Client Retreat

Session EDeveloping Relationships With CPAs, Bankers, Lawyers, Charitable Development Officers, and Other Referral Sources

Session FPresenting Your Materials During Client Seminars, Training Workshops, and One-On-One Presentations

Session GComplying with IRS, SEC, NASD, AICPA, ABA, FPA, and Other Relevant Guidelines

Session HFocusing on Your Unique Talents by Delegating “Administrivia” to a Relationship Manager

Session IConducting a Strategy Session to Integrate Tools Needed to Achieve All of Your Clients' Wealth Optimization Goals

Session JTracking cases and portfolios with web-based project management and CRM systems

© Tim Voorhees, JD, MBA 1996-2005

60

Phone: 800-447-7090 (949-453-2900 in CA)

Fax: 866-447-7090Voicemail: 877-447-7090Email: [email protected]

Contacting Family Office Services