u.s. industrial marketbeat 1q 2018 - texas a&m university · marketbeat u.s. industrial overall...

TRANSCRIPT

cushmanwakefield.com | 1

U.S. IndustrialQ1 2018

MARKETBEAT

U.S. INDUSTRIAL

Overall Vacancy

Net Absorption/Rent NNN 4-QTR TRAILING AVERAGE

Market Indicators

Q1 17 Q1 18 12-Month Forecast

Overall Vacancy 5.3% 5.0%

Net Absorption 56.5M 56.9M

Under Construction 218.4M 251.3M

Weighted Asking Rent (NNN) $5.68 $5.99

Rent Growth (Yr/Yr % Chg.) 4.1% 5.4%

Employment IndicatorsQ1 17 Q1 18 12-Month

Forecast

Total Nonfarm Employment 145.8M 148.1M

Industrial Employment 31.5M 32.3M

Unemployment 4.7% 4.1%

$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

0

10

20

30

40

50

60

70

80

2014 2015 2016 2017 2018Net Absorption, MSF Weighted Asking Rent, $ PSF

Forecast

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2014 2015 2016 2017 2018

Historical Average = 8.4%

Forecast

No Signs of Slowing

Strong Start: U.S. industrial markets absorbed 56.9 million square feet (msf) in the first quarter of 2018 (Q1 2018), making it the fourth strongest start to a year of the past 30 years; only the record-setting 2016 and prior cycle highs of 2007 and 1999 were stronger. Each U.S. region performed well during the quarter, with the South and West leading absorption gains and the Northeast posting the greatest year-over-year improvement. Absorption in the Midwest remained solid, in line with 2016/2017 tallies. Leasing velocity accelerated in half of the U.S. markets, with more than three-quarters of the country registering net occupancy gains. Demand for U.S. industrial space is expected to remain strong throughout 2018, with quarterly net absorption forecast to average 58.1 msf. While that forecast is lower than the quarterly average of 61.6 msf of actual net absorption in 2017, it is higher than the 56.4 msf of quarterly net absorption of the past seven years.

Broad-Based Gains: Occupancy gains were broad-based in Q1 2018, with logistics product absorbing 51.0 msf, manufacturing footprints expanding by 2.4 msf, and flex growing by 2.9 msf. The Midwest led manufacturing and flex activity, while the West and South regions had the strongest warehouse performance. Logistics-related leasing was driven by the Inland Empire, Pennsylvania I-81/I-78 Distribution Corridor, Atlanta, Central New Jersey, Dallas, Miami and Kansas City; these markets combined accounted for more than half the nation’s warehouse absorption. Chicago, Philadelphia, San Jose, Cincinnati, and Hartford registered the best performance in manufacturing product. For flex space, Salt Lake City, Miami, Detroit, Milwaukee, Pittsburgh, Kansas City, and Minneapolis accounted for nearly 90% of the segment’s growth.

Nowhere to Go: The industrial market continued to tighten in Q1 2018 with vacancy rates falling in two-thirds of the country. At 5.0%, the U.S. overall vacancy rate is a full 330 basis points (bps) below the 10-year historical average of 8.4% for all product types. The tightest U.S. markets include Savannah, Los Angeles, San Francisco, Orange County, Fort Myers/Naples, San Jose, Central New Jersey and El Paso, all of which have headline vacancy rates of 3% or lower. Logistics-related vacancy declined by 10 bps in Q1 2018 despite the delivery of 43.3 msf of speculative warehouse product. Space options are particularly tight in the 100,000-to-250,000-square-foot size segment where new supply has lagged, and leasing demand has recently spiked. Deal volume by tenants taking space in the 250,0000-to-500,000-square-foot segments was up 16.9% in the quarter, while activity in the bulk segment of 500,000-square-feet and above continued to decline gradually from its Q3 2017 peak. The amount of available logistics space and its characteristics will remain a key storyline in 2018: 61.2% of available logistics space is more than 20 years old, and over half of it possesses clear heights below 28 feet. That presents limited options for tenants seeking modern space.

Rents Rising Faster: Rent growth accelerated in Q1 2018, with more room to run. U.S. industrial rents increased 5.4% in Q1 2018 from a year ago, rising in 59 of 79 markets tracked by Cushman & Wakefield; 19 markets reported double-digit gains. Among the regions, year-over-year rent growth was strongest in the South (7.1%) and West (6.0%) and more moderate in the Midwest (4.9%) and Northeast (4.1%). The highest rent growth was in Seattle, Sacramento, San Francisco, Jacksonville, Nashville, Raleigh/Durham and Oakland—all markets where rents increased more than 14% year-over-year. Although overall industrial rents currently stand at a record high of $5.99 per square foot (psf), on an inflation-adjusted basis they remain 4.9% below the level at the height of the last cycle. Strong occupier demand for high-quality space and infill sites capable

Source: Cushman & Wakefield Research

Source: BLS

cushmanwakefield.com | 2

U.S. IndustrialQ1 2018

MARKETBEAT

Development Pipeline Is Growing UNDER CONSTRUCTION (MSF)

Supply Will Not Run Away From Demand DELIVERIES BY TYPE AND NET ABSORPTION (MSF)

Tight Market Conditions Continue OVERALL INDUSTRIAL VACANCY RATE

Outlook• Demand drivers point to growth in 2018 with strong absorption

in markets with sufficient supply and robust rent growth in markets facing supply constraints.

• We forecast total retail and food sales to accelerate to 5.2%, and for eCommerce sales to grow by 16.4%, in 2018.

• Net absorption is expected to surpass 230 msf in 2018 for the third year in a row, and eclipse 200 msf in 2019 for a sixth year.

• Developers will exercise caution, with deliveries modestly outpacing demand, allowing vacancy rates to hover in the 5% range through 2018/2019.

• Rent growth will remain strong in 2018, softening slowly late in the year with rent growth gradually decelerating in 2019.

Source: Cushman & Wakefield Research

Source: Cushman & Wakefield Research

Source: Cushman & Wakefield Research

of supporting omnichannel fulfillment amid a historically tight market mean 2018 is expected to be another year of robust rent growth.

Development Picking Up: New construction starts rose by 3.6% nationally in Q1 2018 with 42 markets reporting development levels increasing quarter-over-quarter. The largest uptick in construction activity occurred in the South and West regions, as is often the case during any first quarter when seasonality limits activity in the Northeast and Midwest. Currently, there is 251.3 msf of industrial product under construction, of which 164.1 msf is speculative. Although five markets—Inland Empire, Dallas, Pennsylvania I-81/I-78 Distribution Corridor, Atlanta, and Central Valley California—account for over one-third of the development pipeline, 47 markets have more than 1 msf under construction. Activity is expected to increase, but increasing construction costs, scarcity of entitled land and labor, discerning lenders, and caution among developers diminished the likelihood that supply will outstrip demand.

Full Speed AheadDemand Drivers Look Great: Economic fundamentals remain solid, underpinned by a strong job market. An average of 202,000 new jobs have been created every month in 2018—more than the monthly averages in both 2016 and 2017. Industrial output rose 3.2% in the six months ending February—the largest 6-month growth rate for any period since 2010. Intermodal rail volume—which correlates closely with warehouse demand—rolled to its second highest weekly average ever in February, and March volume following was the strongest March on record. Strength is also evident in U.S. retail sales for March, which recorded an increase in sales at auto dealers, furniture and home stores, and electronic and appliance sellers.

Trade Rhetoric vs. Reality: Trade rhetoric has roiled equity markets and interjected a layer of complexity for logisticians. Trade reality is much different than the rhetoric. Little formal trade policy has taken effect and many countries initially subjected to steel and aluminum tariffs have received exemptions. NAFTA negotiations are showing signs of promise, and recent dialogue between the U.S. and China has taken a more conciliatory tone. Trade policy and geopolitical threats will remain headwinds but a strong job market, rising incomes that allow consumers to purchase more, elevated confidence that emboldens them to spend, and strong corporate earnings that encourage businesses to invest all point to stronger growth in 2018.

0

5

10

15

20

25

30 Build-to-Suit Deliveries Speculative Deliveries

0.0%

1.0%

2.0%

3.0%

4.0%Q1 2018 Vacancy

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 2017 2018F

Build-to-Suit Deliveries Speculative Deliveries Net Absorption

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 3

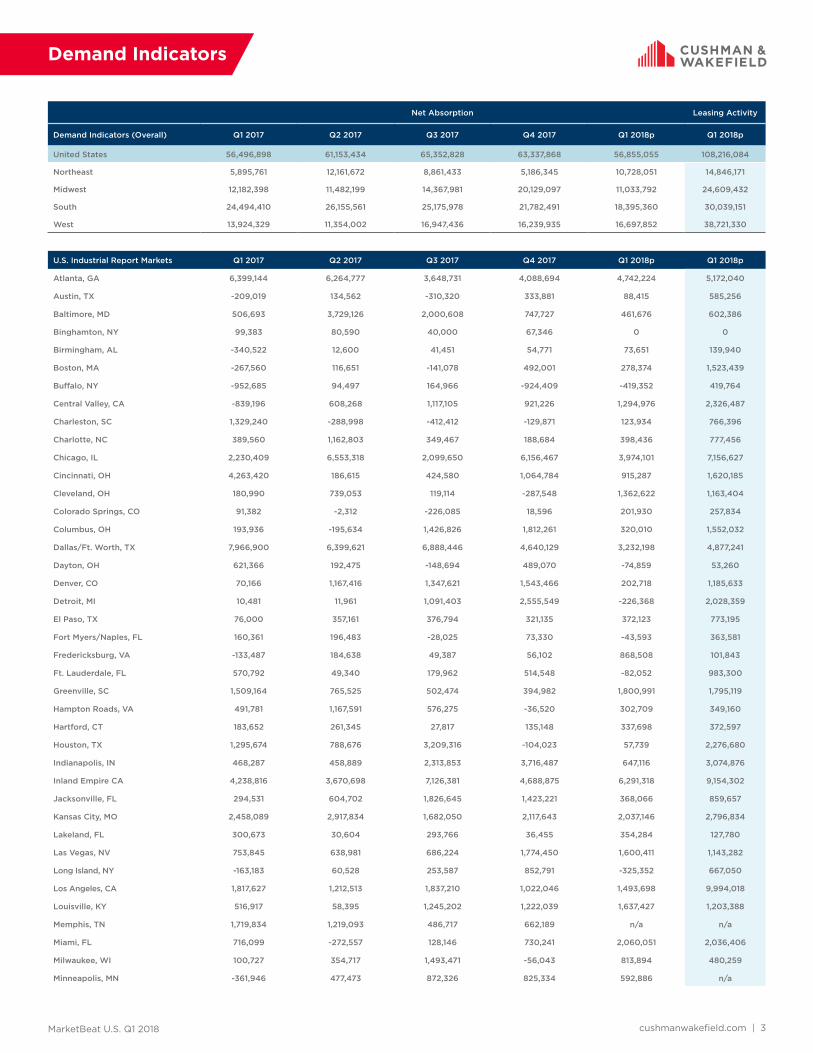

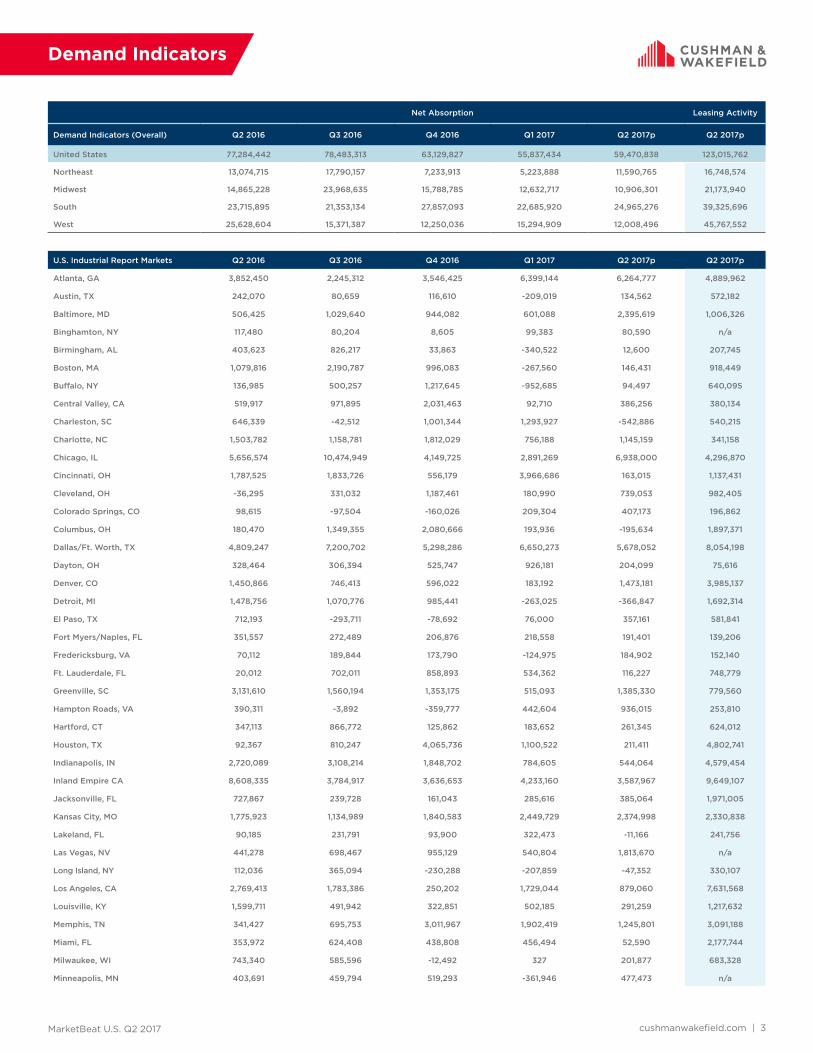

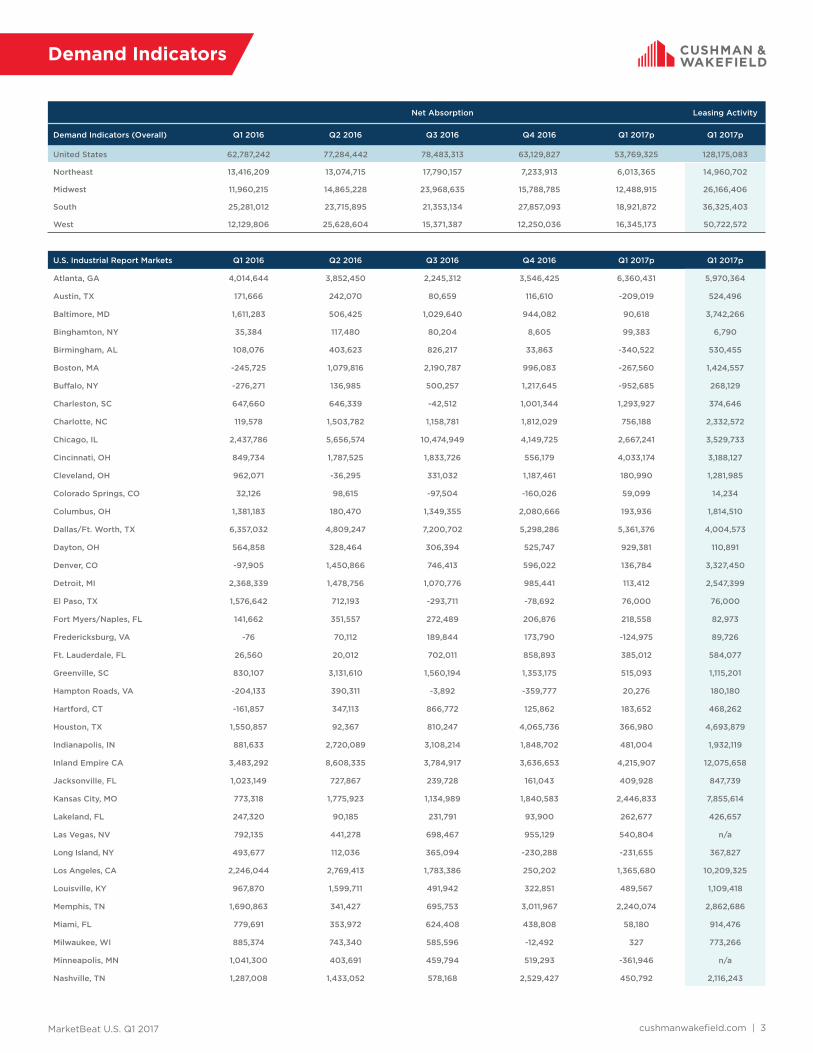

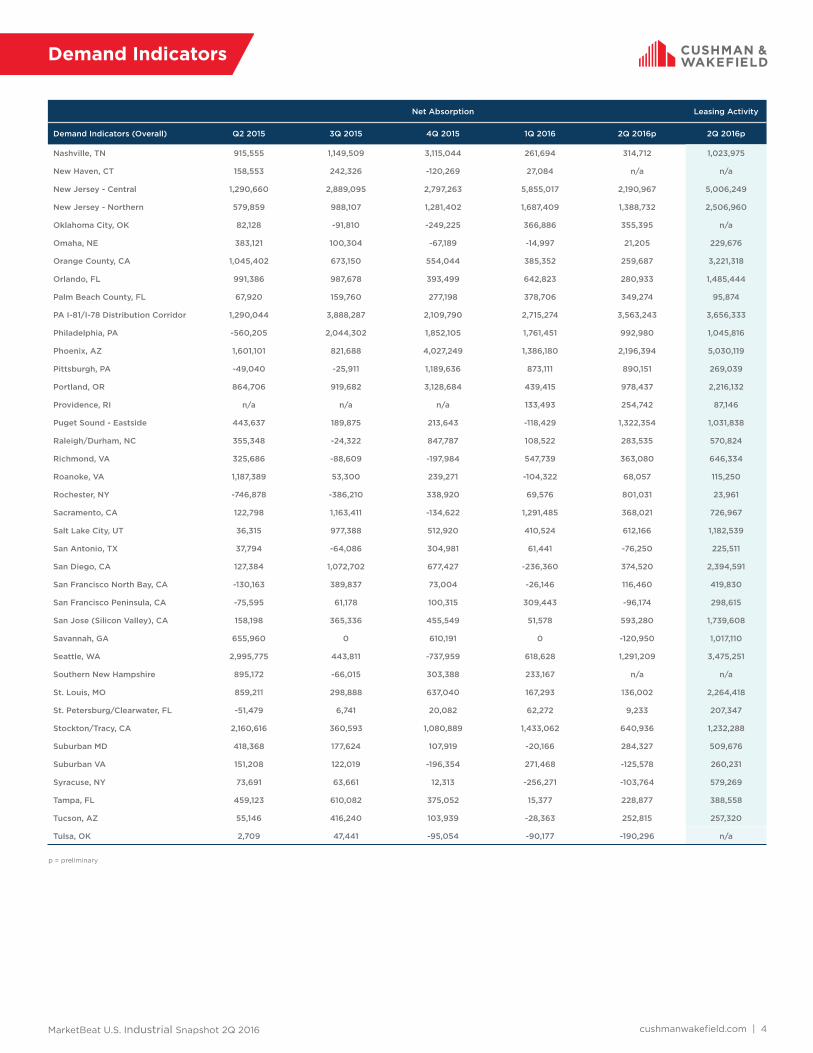

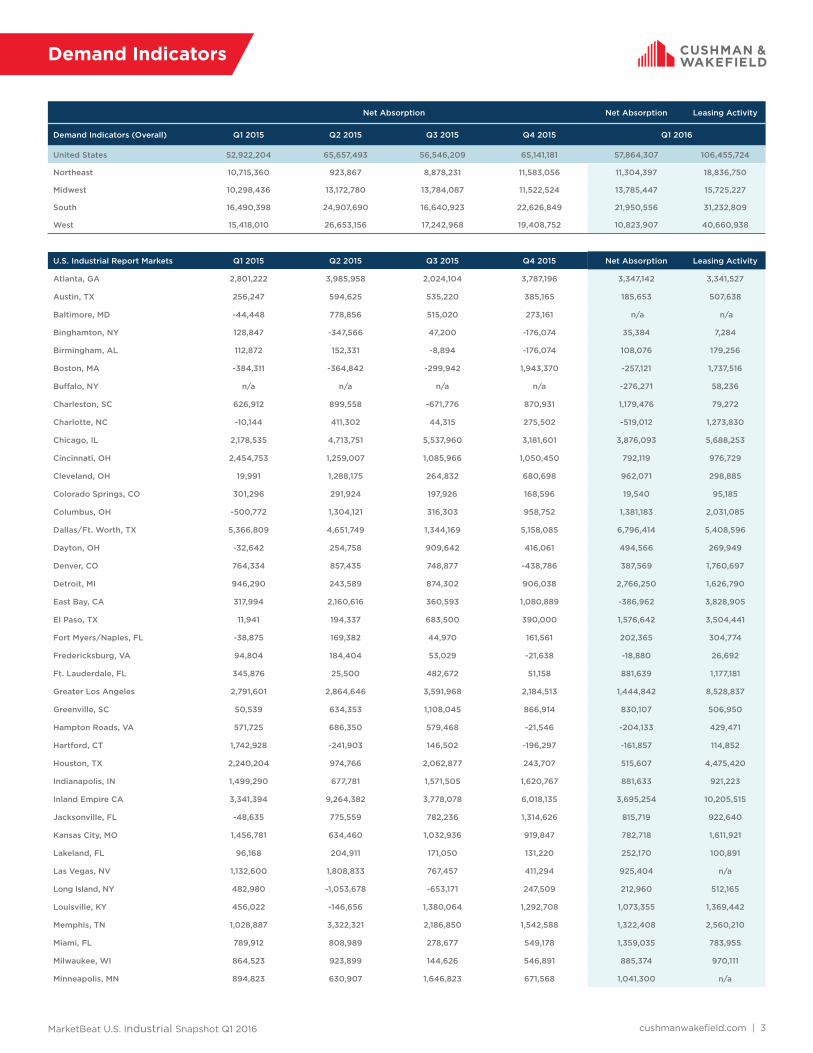

Net Absorption Leasing Activity

Demand Indicators (Overall) Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

United States 56,496,898 61,153,434 65,352,828 63,337,868 56,855,055 108,216,084

Northeast 5,895,761 12,161,672 8,861,433 5,186,345 10,728,051 14,846,171

Midwest 12,182,398 11,482,199 14,367,981 20,129,097 11,033,792 24,609,432

South 24,494,410 26,155,561 25,175,978 21,782,491 18,395,360 30,039,151

West 13,924,329 11,354,002 16,947,436 16,239,935 16,697,852 38,721,330

U.S. Industrial Report Markets Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

Atlanta, GA 6,399,144 6,264,777 3,648,731 4,088,694 4,742,224 5,172,040

Austin, TX -209,019 134,562 -310,320 333,881 88,415 585,256

Baltimore, MD 506,693 3,729,126 2,000,608 747,727 461,676 602,386

Binghamton, NY 99,383 80,590 40,000 67,346 0 0

Birmingham, AL -340,522 12,600 41,451 54,771 73,651 139,940

Boston, MA -267,560 116,651 -141,078 492,001 278,374 1,523,439

Buffalo, NY -952,685 94,497 164,966 -924,409 -419,352 419,764

Central Valley, CA -839,196 608,268 1,117,105 921,226 1,294,976 2,326,487

Charleston, SC 1,329,240 -288,998 -412,412 -129,871 123,934 766,396

Charlotte, NC 389,560 1,162,803 349,467 188,684 398,436 777,456

Chicago, IL 2,230,409 6,553,318 2,099,650 6,156,467 3,974,101 7,156,627

Cincinnati, OH 4,263,420 186,615 424,580 1,064,784 915,287 1,620,185

Cleveland, OH 180,990 739,053 119,114 -287,548 1,362,622 1,163,404

Colorado Springs, CO 91,382 -2,312 -226,085 18,596 201,930 257,834

Columbus, OH 193,936 -195,634 1,426,826 1,812,261 320,010 1,552,032

Dallas/Ft. Worth, TX 7,966,900 6,399,621 6,888,446 4,640,129 3,232,198 4,877,241

Dayton, OH 621,366 192,475 -148,694 489,070 -74,859 53,260

Denver, CO 70,166 1,167,416 1,347,621 1,543,466 202,718 1,185,633

Detroit, MI 10,481 11,961 1,091,403 2,555,549 -226,368 2,028,359

El Paso, TX 76,000 357,161 376,794 321,135 372,123 773,195

Fort Myers/Naples, FL 160,361 196,483 -28,025 73,330 -43,593 363,581

Fredericksburg, VA -133,487 184,638 49,387 56,102 868,508 101,843

Ft. Lauderdale, FL 570,792 49,340 179,962 514,548 -82,052 983,300

Greenville, SC 1,509,164 765,525 502,474 394,982 1,800,991 1,795,119

Hampton Roads, VA 491,781 1,167,591 576,275 -36,520 302,709 349,160

Hartford, CT 183,652 261,345 27,817 135,148 337,698 372,597

Houston, TX 1,295,674 788,676 3,209,316 -104,023 57,739 2,276,680

Indianapolis, IN 468,287 458,889 2,313,853 3,716,487 647,116 3,074,876

Inland Empire CA 4,238,816 3,670,698 7,126,381 4,688,875 6,291,318 9,154,302

Jacksonville, FL 294,531 604,702 1,826,645 1,423,221 368,066 859,657

Kansas City, MO 2,458,089 2,917,834 1,682,050 2,117,643 2,037,146 2,796,834

Lakeland, FL 300,673 30,604 293,766 36,455 354,284 127,780

Las Vegas, NV 753,845 638,981 686,224 1,774,450 1,600,411 1,143,282

Long Island, NY -163,183 60,528 253,587 852,791 -325,352 667,050

Los Angeles, CA 1,817,627 1,212,513 1,837,210 1,022,046 1,493,698 9,994,018

Louisville, KY 516,917 58,395 1,245,202 1,222,039 1,637,427 1,203,388

Memphis, TN 1,719,834 1,219,093 486,717 662,189 n/a n/a

Miami, FL 716,099 -272,557 128,146 730,241 2,060,051 2,036,406

Milwaukee, WI 100,727 354,717 1,493,471 -56,043 813,894 480,259

Minneapolis, MN -361,946 477,473 872,326 825,334 592,886 n/a

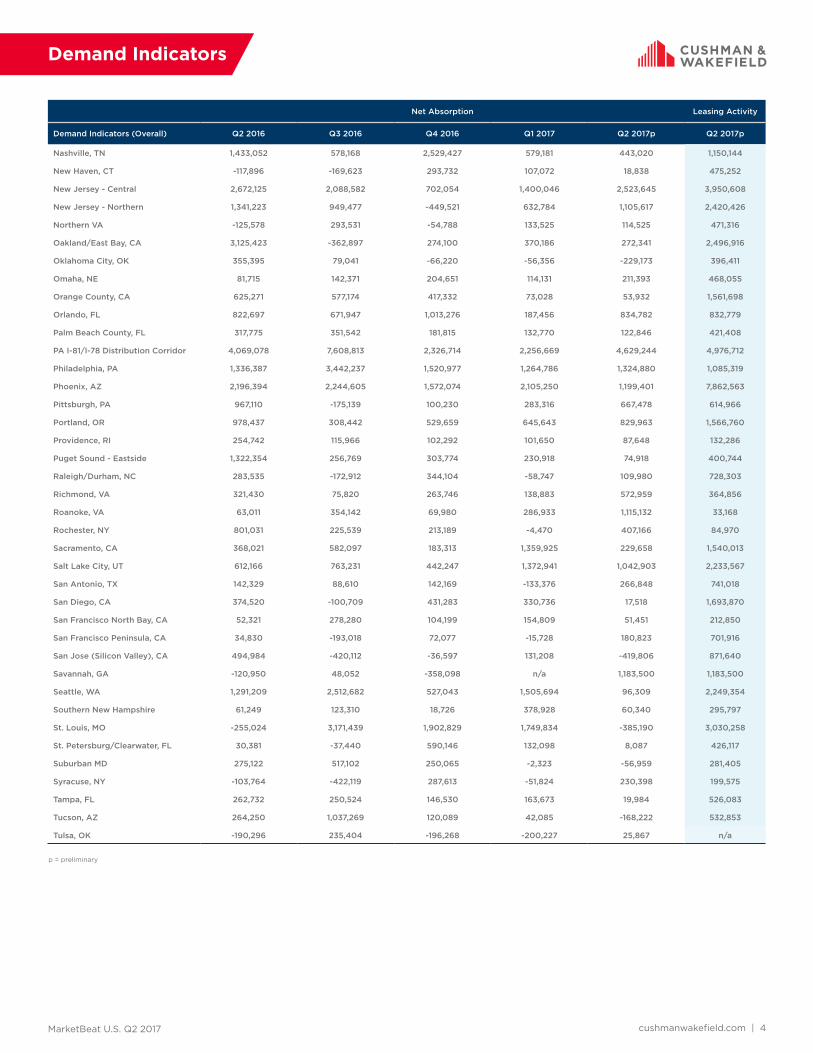

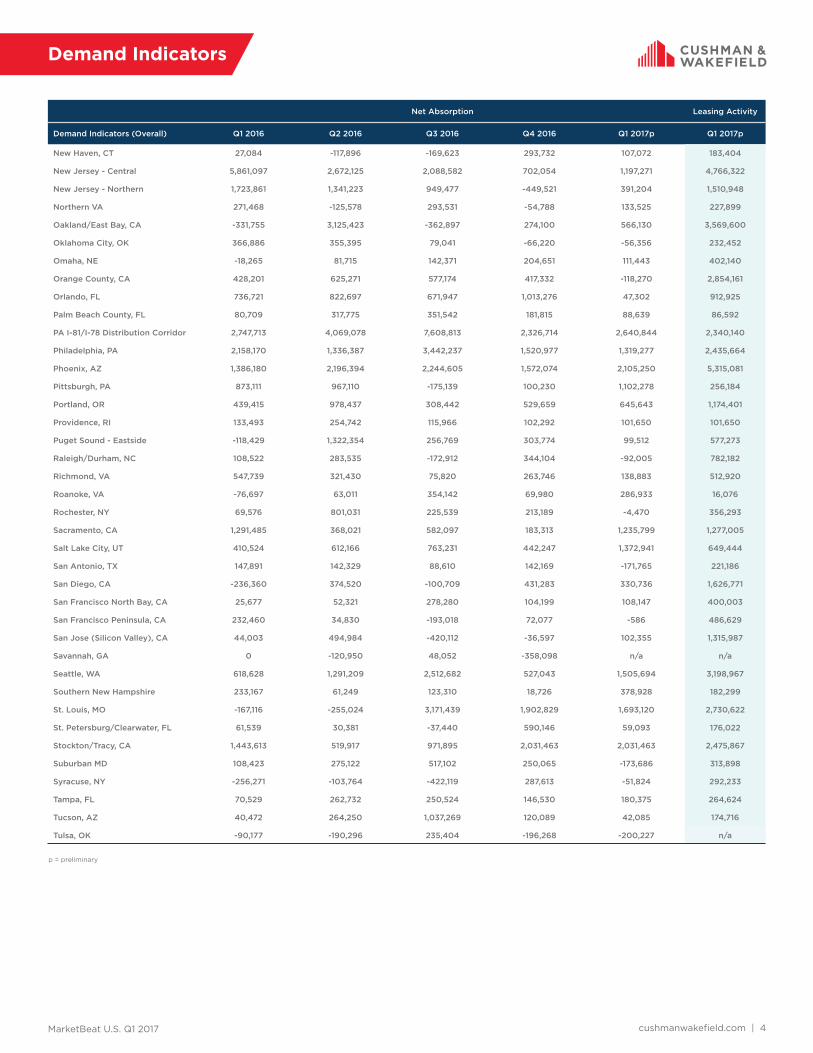

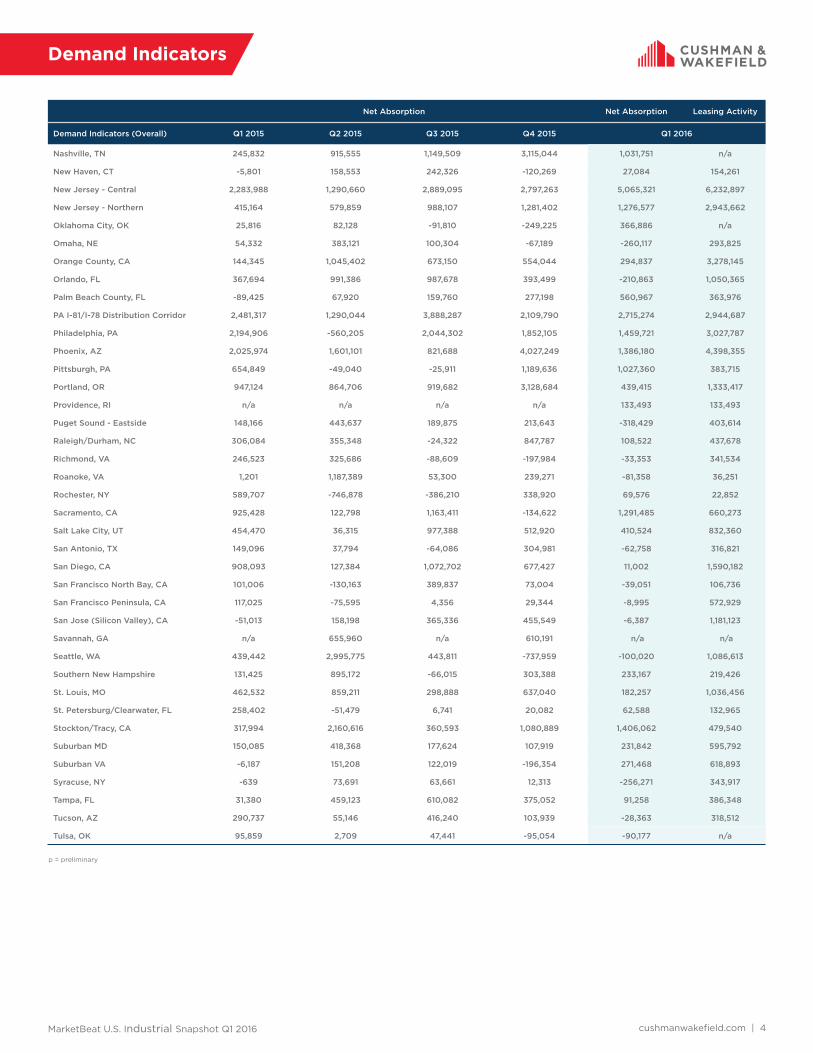

Demand Indicators

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 4

Net Absorption Leasing Activity

Demand Indicators (Overall) Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

Nashville, TN 625,416 -200,280 1,675,012 120,526 363,767 908,645

New Haven, CT 107,072 18,838 5,477 175,696 112,991 197,598

New Jersey - Central 1,765,243 2,548,178 2,809,359 2,184,634 3,890,321 4,173,654

New Jersey - Northern 689,129 1,364,765 497,798 1,664,946 -117,749 2,208,903

Northern VA 133,525 158,067 -20,211 35,291 16,212 558,873

Oakland/East Bay, CA 371,786 210,153 -1,569,379 660,234 -178,872 1,623,432

Oklahoma City, OK -56,356 -229,173 -542,074 N/A -3,545 282,099

Omaha, NE 130,509 146,433 349,921 455,995 -136,317 159,588

Orange County, CA 181,240 166,598 -143,511 -261,531 -130,959 1,740,922

Orlando, FL 169,416 989,386 462,458 789,720 587,900 681,534

Palm Beach County, FL 132,122 174,307 362,784 101,677 73,537 454,298

PA I-81/I-78 Distribution Corridor 2,309,040 4,642,512 3,541,623 844,371 4,777,838 3,109,193

Philadelphia, PA 1,418,070 1,422,735 1,437,888 611,009 1,139,650 1,531,487

Phoenix, AZ 2,105,250 1,199,401 2,571,976 2,600,022 1,394,165 1,836,246

Pittsburgh, PA 283,316 765,481 -650,575 -356,733 912,161 285,801

Portland, OR 645,643 829,963 870,133 -72,333 -633,444 1,452,233

Providence, RI 101,650 87,648 63,199 313,632 71,456 71,456

Puget Sound - Eastside 99,512 74,918 -182,255 220,980 524,863 763,351

Raleigh/Durham, NC -247,778 76,732 317,502 -294,394 143,571 572,717

Richmond, VA 480,166 595,183 705,151 1,022,908 -135,089 555,002

Roanoke, VA -442,290 170,468 95,604 6,011 480,115 241,088

Rochester, NY -4,470 407,166 407,166 -594,469 101,023 34,609

Sacramento, CA 770,177 483,538 1,379,668 1,426,115 1,260,063 1,282,663

Salt Lake City, UT 1,372,941 1,042,903 798,628 723,096 1,039,351 616,141

San Antonio, TX 57,024 439,830 135,180 -203,074 76,360 488,528

San Diego, CA 330,736 17,518 844,640 103,378 -85,162 1,667,853

San Francisco North Bay, CA 105,774 46,381 71,827 39,783 -107,480 106,181

San Francisco Peninsula, CA -15,400 233,572 762 15,292 26,778 162,000

San Jose (Silicon Valley), CA 276,251 -463,286 -177,705 346,282 683,222 1,261,451

Savannah, GA 0 1,183,500 0 3,855,811 0 0

Seattle, WA 1,505,694 96,309 561,459 251,674 1,762,853 2,015,848

Southern New Hampshire 378,928 60,340 184,217 -302,661 -118,498 189,254

St. Louis, MO 1,886,130 -360,935 2,643,481 1,279,098 808,274 4,524,008

St. Petersburg/Clearwater, FL 97,885 174,396 123,416 225,964 -179,626 77,306

Suburban MD -2,323 -56,959 37,371 316,522 61,323 423,623

Syracuse, NY -51,824 230,398 219,989 23,043 87,490 61,366

Tampa, FL 187,495 90,095 677,735 587,815 35,773 455,312

Tucson, AZ 42,085 120,470 32,737 218,284 57,423 131,453

Tulsa, OK -200,227 25,867 93,420 N/A 58,275 549,302

Demand Indicators

p = preliminary

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 5

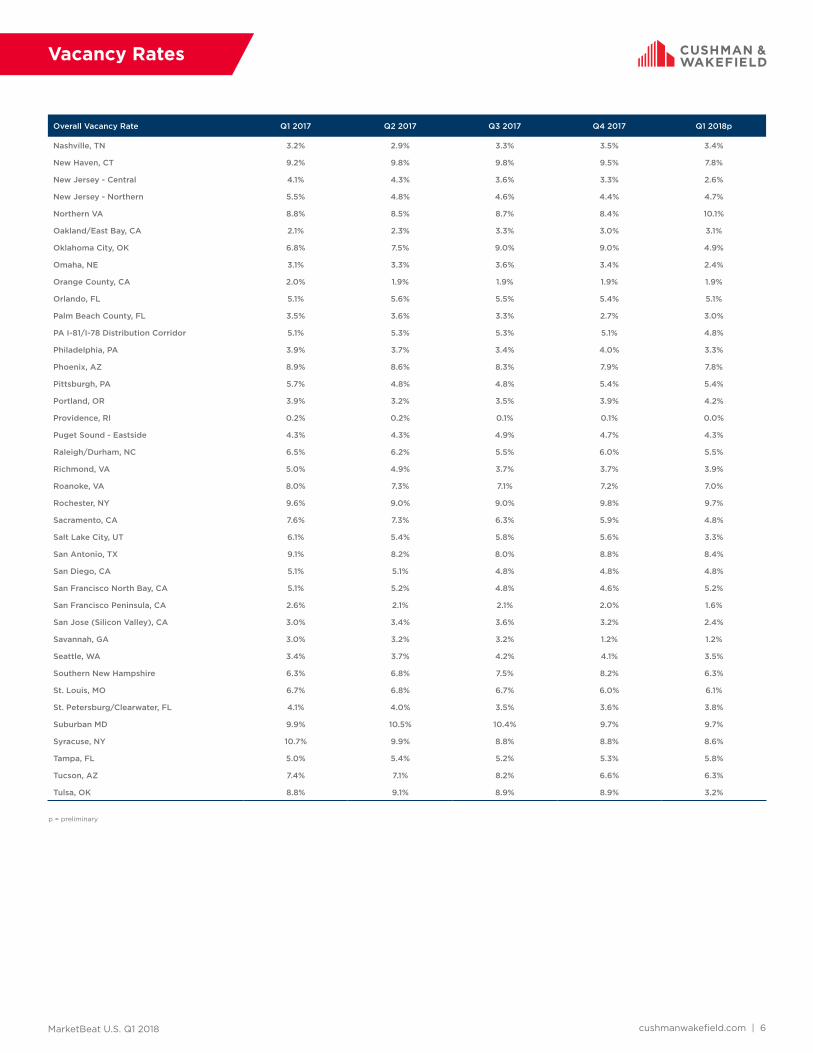

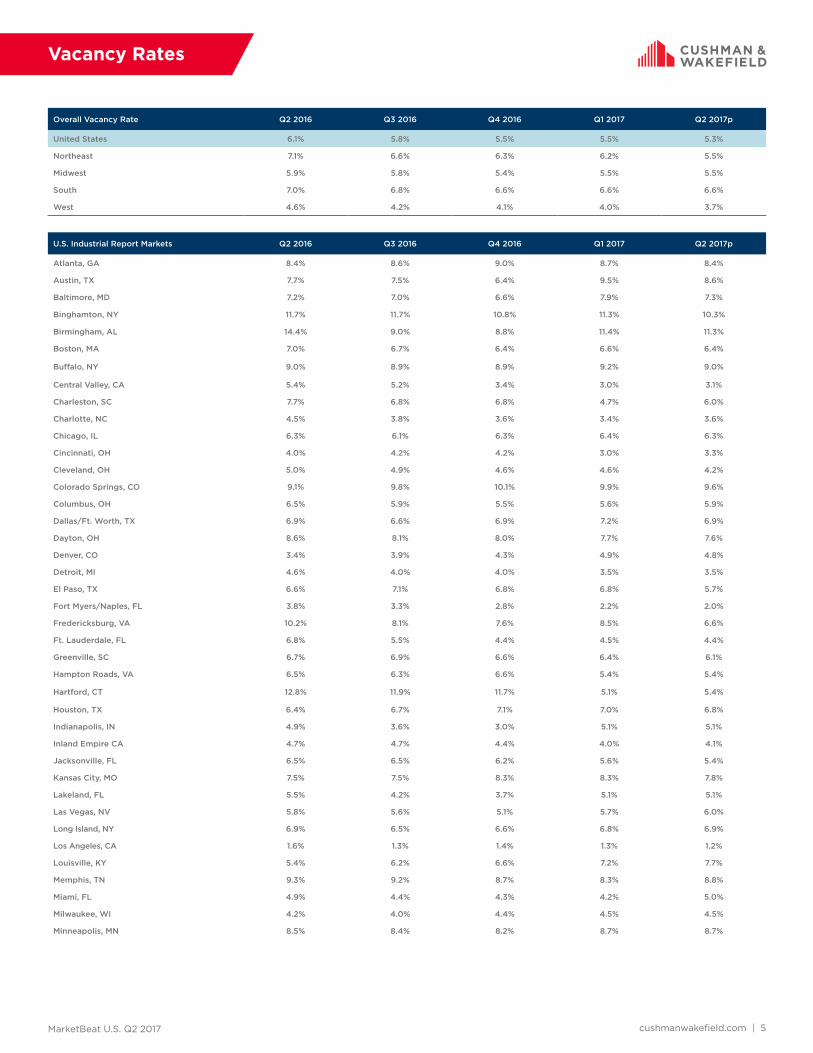

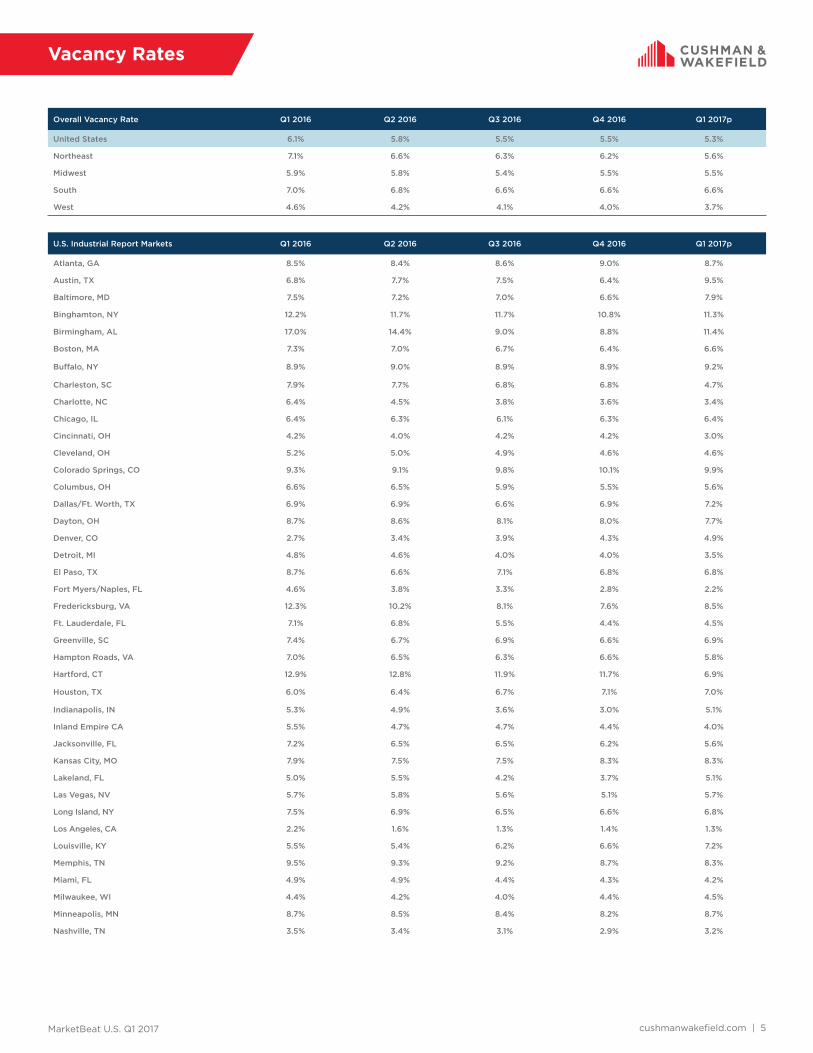

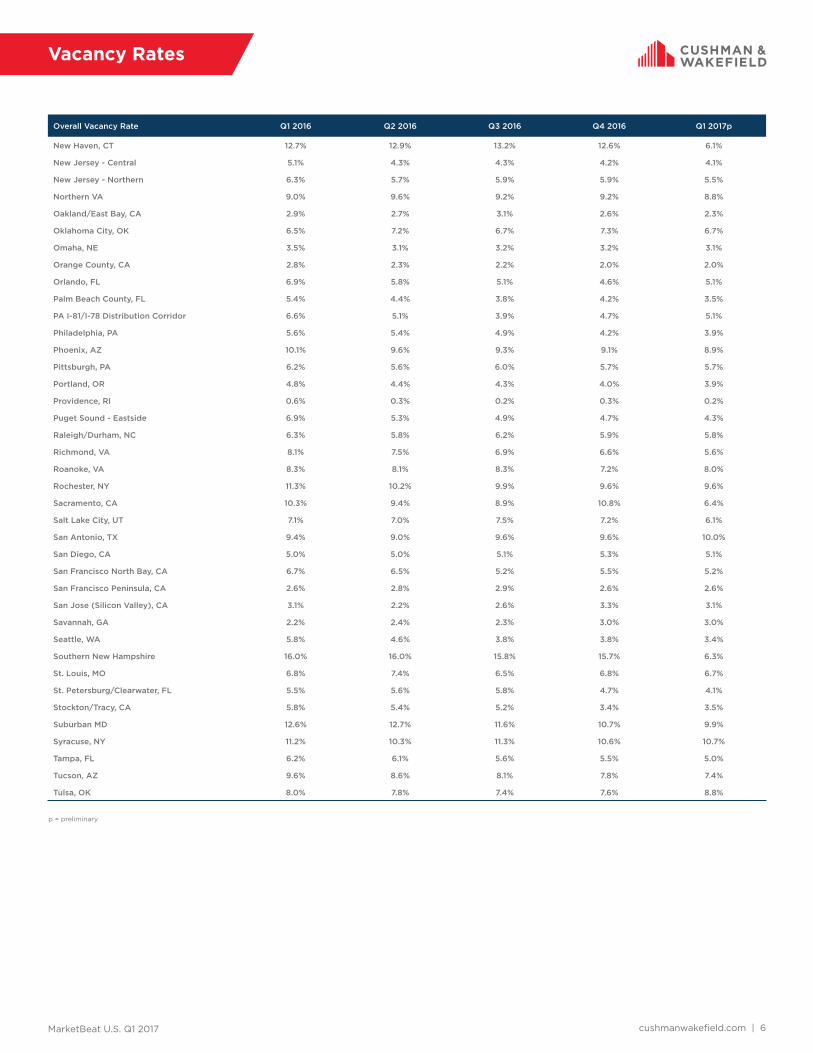

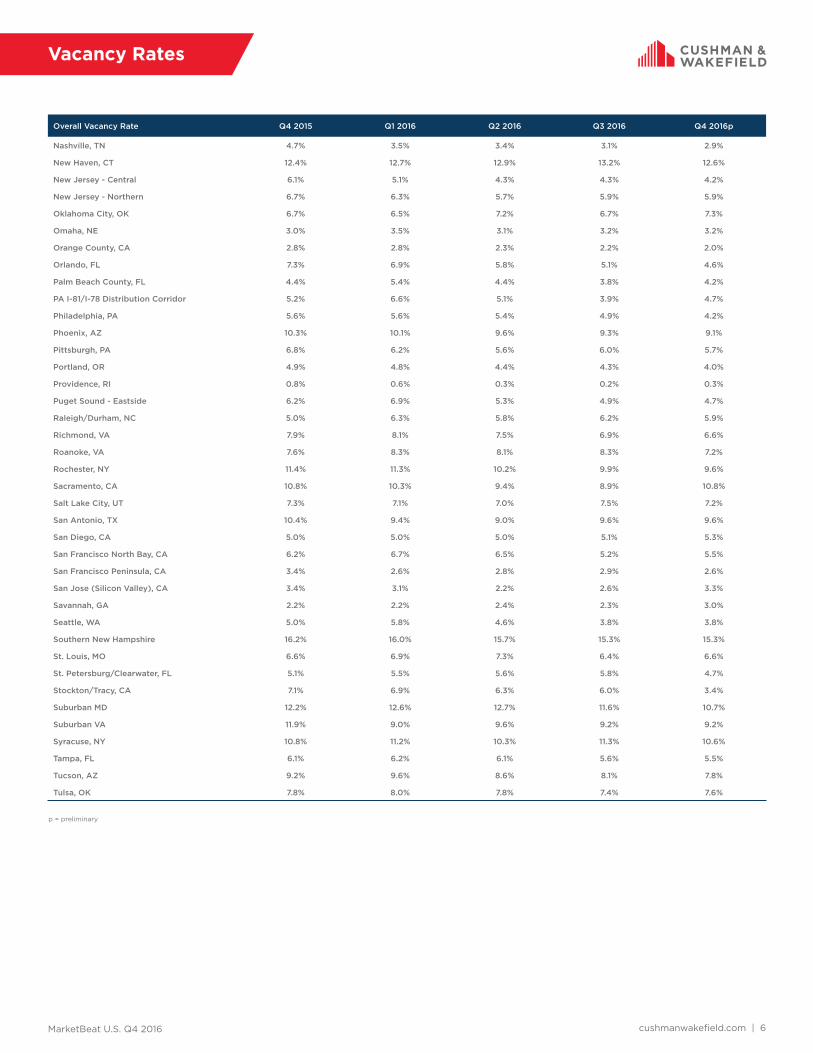

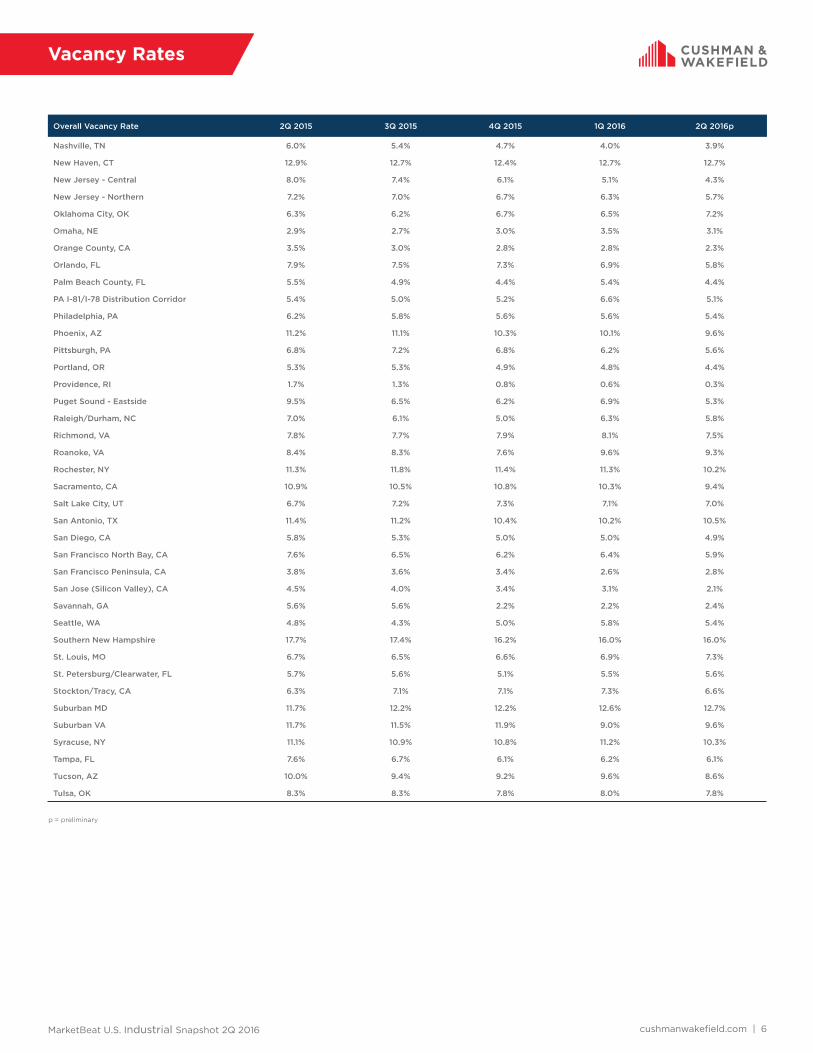

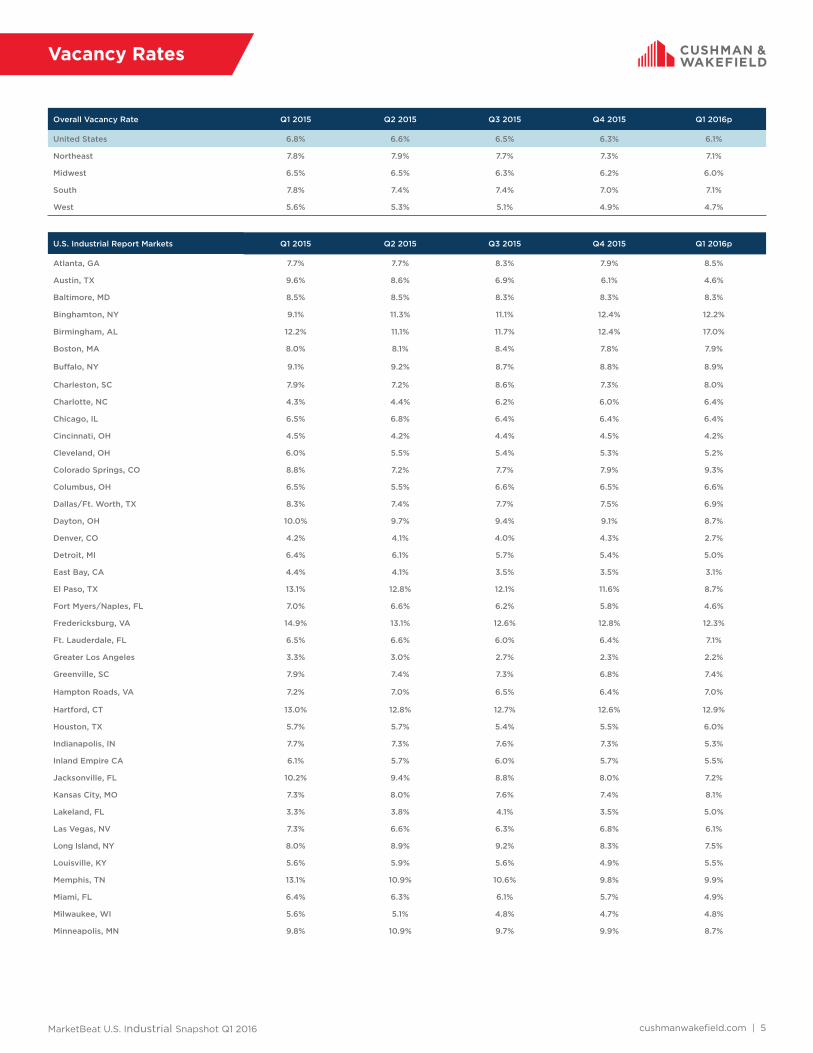

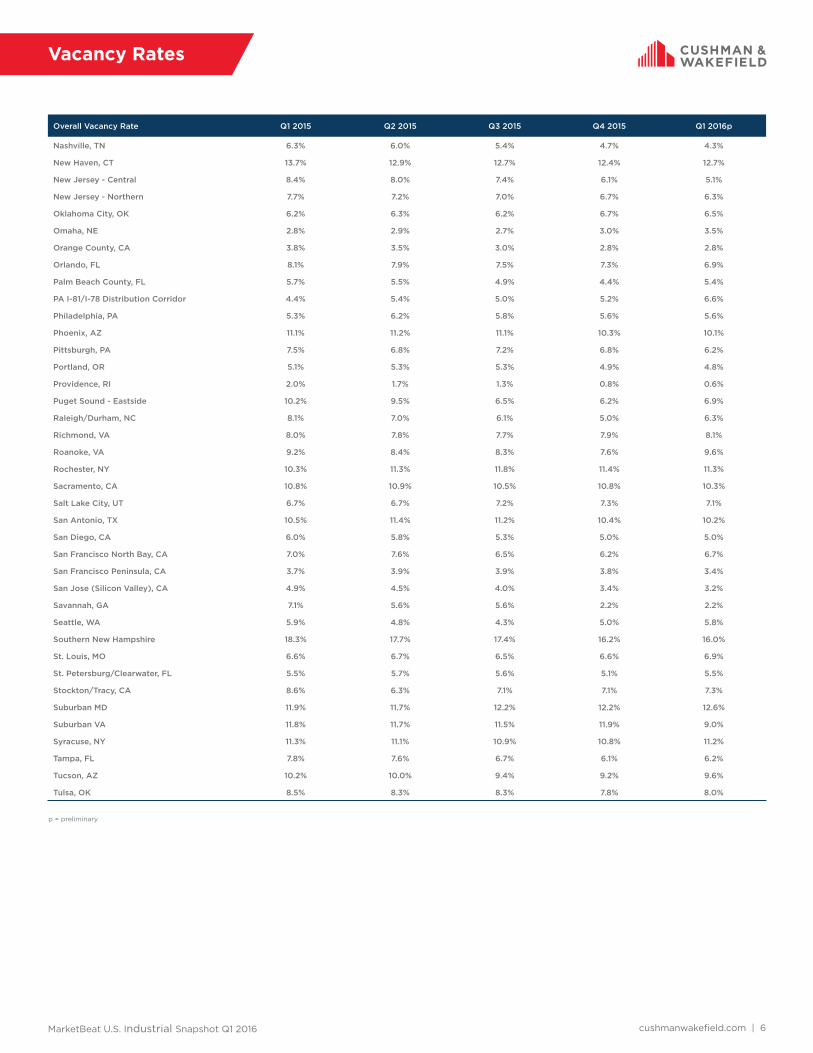

Vacancy Rates

Overall Vacancy Rate Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p

United States 5.3% 5.3% 5.1% 5.1% 5.0%

Northeast 5.7% 5.5% 5.3% 5.3% 4.9%

Midwest 5.5% 5.4% 5.4% 5.3% 5.3%

South 6.5% 6.5% 6.2% 6.1% 6.0%

West 3.7% 3.6% 3.7% 3.7% 3.5%

U.S. Industrial Report Markets Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p

Atlanta, GA 8.7% 8.4% 7.8% 7.7% 8.1%

Austin, TX 9.5% 8.6% 9.5% 8.8% 9.2%

Baltimore, MD 7.9% 7.3% 6.9% 6.4% 6.4%

Binghamton, NY 11.3% 10.3% 9.8% 9.9% 8.8%

Birmingham, AL 11.4% 11.3% 10.8% 10.6% 10.2%

Boston, MA 6.6% 6.5% 6.4% 6.2% 5.9%

Buffalo, NY 9.2% 9.0% 8.9% 9.1% 9.2%

Central Valley, CA 3.4% 3.3% 2.8% 3.3% 4.0%

Charleston, SC 4.7% 6.0% 8.0% 8.1% 9.4%

Charlotte, NC 3.4% 3.6% 3.5% 3.4% 5.1%

Chicago, IL 6.4% 6.3% 6.7% 6.8% 6.8%

Cincinnati, OH 3.0% 3.3% 3.4% 3.2% 3.7%

Cleveland, OH 4.6% 4.2% 3.8% 3.9% 3.5%

Colorado Springs, CO 10.1% 10.0% 10.6% 10.7% 9.7%

Columbus, OH 5.6% 5.9% 5.1% 4.7% 4.8%

Dallas/Ft. Worth, TX 7.2% 6.9% 6.8% 7.0% 6.3%

Dayton, OH 7.7% 7.6% 8.2% 8.3% 7.8%

Denver, CO 4.9% 4.8% 4.8% 4.9% 5.0%

Detroit, MI 3.5% 3.5% 3.1% 2.9% 2.9%

El Paso, TX 6.8% 5.7% 5.0% 3.2% 2.7%

Fort Myers/Naples, FL 2.2% 2.0% 1.8% 1.9% 2.1%

Fredericksburg, VA 6.6% 5.3% 4.7% 5.3% 5.5%

Ft. Lauderdale, FL 4.5% 4.4% 4.0% 2.9% 3.8%

Greenville, SC 6.5% 6.2% 5.8% 5.8% 5.5%

Hampton Roads, VA 4.9% 4.7% 4.1% 4.4% 4.2%

Hartford, CT 8.1% 8.3% 8.1% 7.9% 7.1%

Houston, TX 7.0% 6.8% 6.2% 6.3% 6.0%

Indianapolis, IN 5.1% 5.1% 5.5% 5.3% 5.5%

Inland Empire CA 4.0% 4.1% 4.0% 4.1% 3.9%

Jacksonville, FL 5.6% 5.4% 4.8% 4.0% 3.4%

Kansas City, MO 8.3% 7.5% 7.1% 7.2% 7.4%

Lakeland, FL 5.1% 5.1% 3.9% 3.9% 4.9%

Las Vegas, NV 5.2% 5.4% 6.0% 6.2% 6.2%

Long Island, NY 6.8% 6.9% 6.5% 5.6% 5.1%

Los Angeles, CA 1.3% 1.2% 1.2% 1.3% 1.3%

Louisville, KY 7.2% 7.7% 8.1% 7.7% 7.2%

Memphis, TN 8.1% 8.4% 8.2% 7.8% 7.8%

Miami, FL 4.2% 5.0% 4.7% 4.7% 4.3%

Milwaukee, WI 4.5% 4.5% 3.8% 4.1% 4.1%

Minneapolis, MN 8.7% 8.7% 8.0% 8.5% 8.7%

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 6

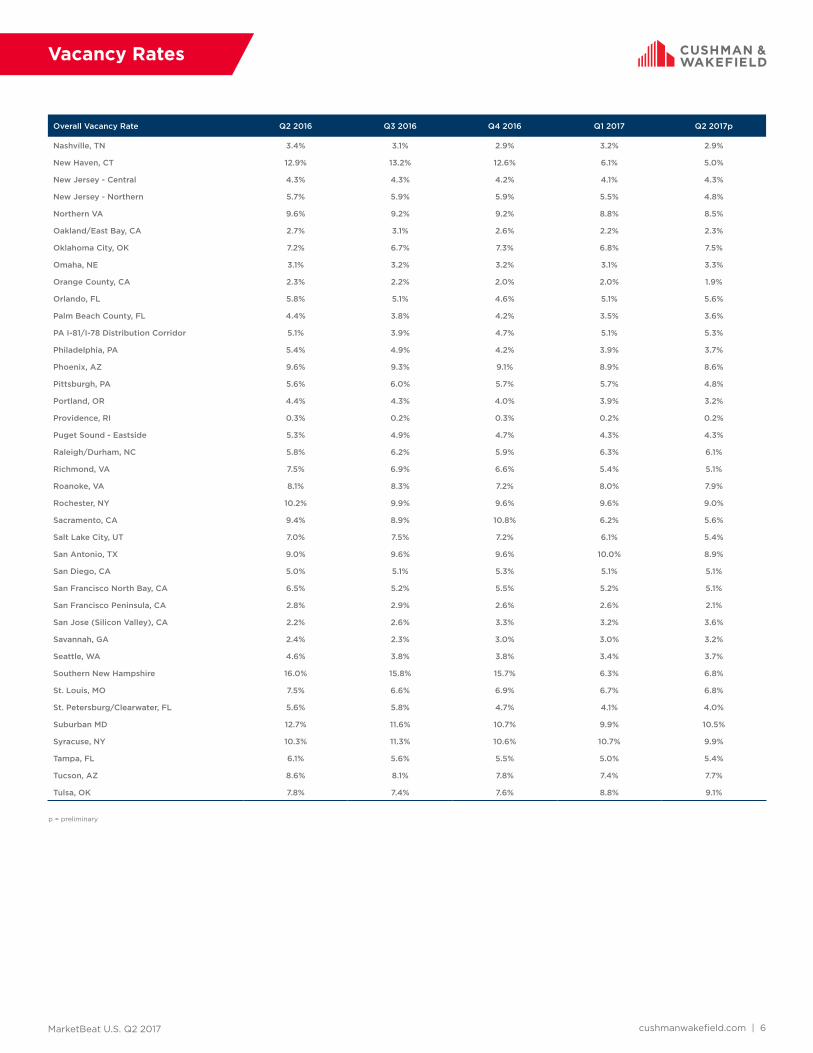

Vacancy Rates

Overall Vacancy Rate Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p

Nashville, TN 3.2% 2.9% 3.3% 3.5% 3.4%

New Haven, CT 9.2% 9.8% 9.8% 9.5% 7.8%

New Jersey - Central 4.1% 4.3% 3.6% 3.3% 2.6%

New Jersey - Northern 5.5% 4.8% 4.6% 4.4% 4.7%

Northern VA 8.8% 8.5% 8.7% 8.4% 10.1%

Oakland/East Bay, CA 2.1% 2.3% 3.3% 3.0% 3.1%

Oklahoma City, OK 6.8% 7.5% 9.0% 9.0% 4.9%

Omaha, NE 3.1% 3.3% 3.6% 3.4% 2.4%

Orange County, CA 2.0% 1.9% 1.9% 1.9% 1.9%

Orlando, FL 5.1% 5.6% 5.5% 5.4% 5.1%

Palm Beach County, FL 3.5% 3.6% 3.3% 2.7% 3.0%

PA I-81/I-78 Distribution Corridor 5.1% 5.3% 5.3% 5.1% 4.8%

Philadelphia, PA 3.9% 3.7% 3.4% 4.0% 3.3%

Phoenix, AZ 8.9% 8.6% 8.3% 7.9% 7.8%

Pittsburgh, PA 5.7% 4.8% 4.8% 5.4% 5.4%

Portland, OR 3.9% 3.2% 3.5% 3.9% 4.2%

Providence, RI 0.2% 0.2% 0.1% 0.1% 0.0%

Puget Sound - Eastside 4.3% 4.3% 4.9% 4.7% 4.3%

Raleigh/Durham, NC 6.5% 6.2% 5.5% 6.0% 5.5%

Richmond, VA 5.0% 4.9% 3.7% 3.7% 3.9%

Roanoke, VA 8.0% 7.3% 7.1% 7.2% 7.0%

Rochester, NY 9.6% 9.0% 9.0% 9.8% 9.7%

Sacramento, CA 7.6% 7.3% 6.3% 5.9% 4.8%

Salt Lake City, UT 6.1% 5.4% 5.8% 5.6% 3.3%

San Antonio, TX 9.1% 8.2% 8.0% 8.8% 8.4%

San Diego, CA 5.1% 5.1% 4.8% 4.8% 4.8%

San Francisco North Bay, CA 5.1% 5.2% 4.8% 4.6% 5.2%

San Francisco Peninsula, CA 2.6% 2.1% 2.1% 2.0% 1.6%

San Jose (Silicon Valley), CA 3.0% 3.4% 3.6% 3.2% 2.4%

Savannah, GA 3.0% 3.2% 3.2% 1.2% 1.2%

Seattle, WA 3.4% 3.7% 4.2% 4.1% 3.5%

Southern New Hampshire 6.3% 6.8% 7.5% 8.2% 6.3%

St. Louis, MO 6.7% 6.8% 6.7% 6.0% 6.1%

St. Petersburg/Clearwater, FL 4.1% 4.0% 3.5% 3.6% 3.8%

Suburban MD 9.9% 10.5% 10.4% 9.7% 9.7%

Syracuse, NY 10.7% 9.9% 8.8% 8.8% 8.6%

Tampa, FL 5.0% 5.4% 5.2% 5.3% 5.8%

Tucson, AZ 7.4% 7.1% 8.2% 6.6% 6.3%

Tulsa, OK 8.8% 9.1% 8.9% 8.9% 3.2%

p = preliminary

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 7

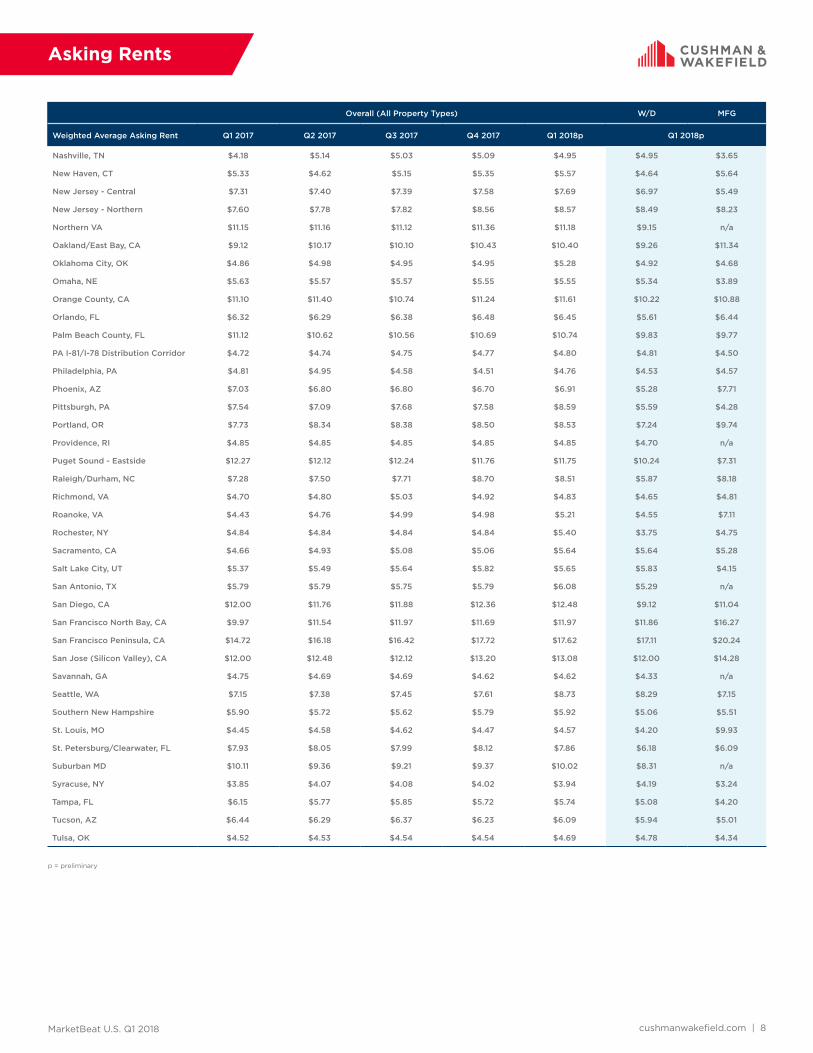

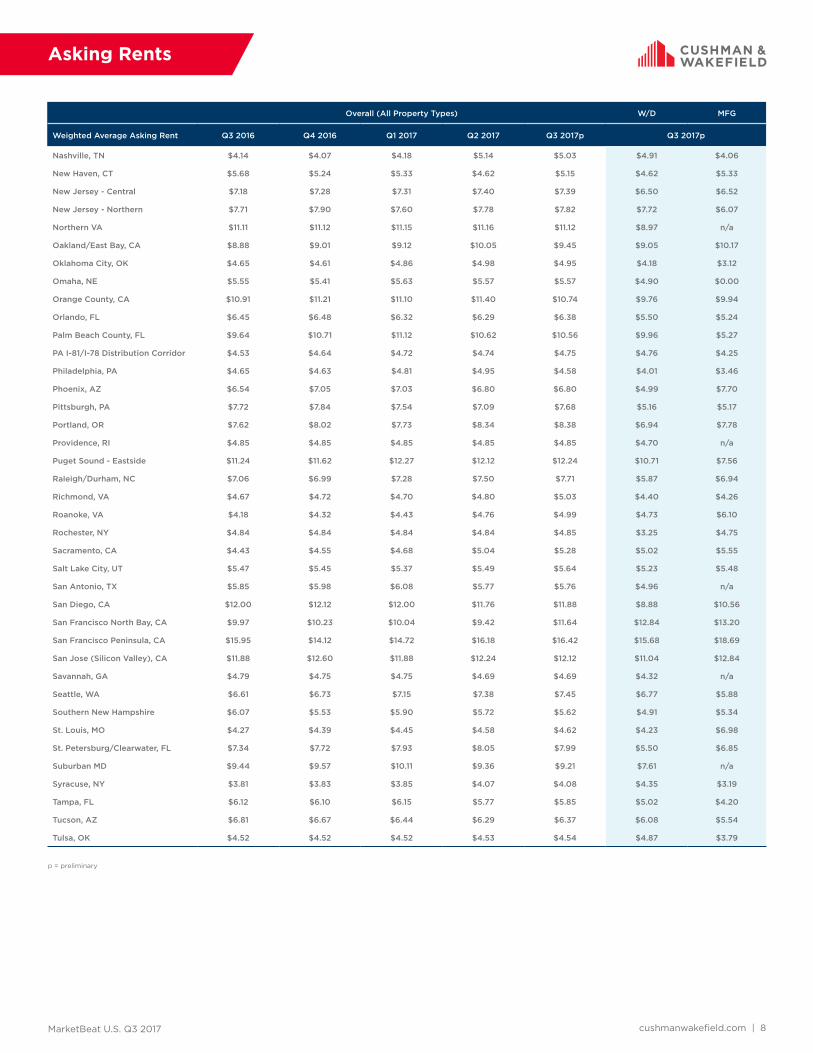

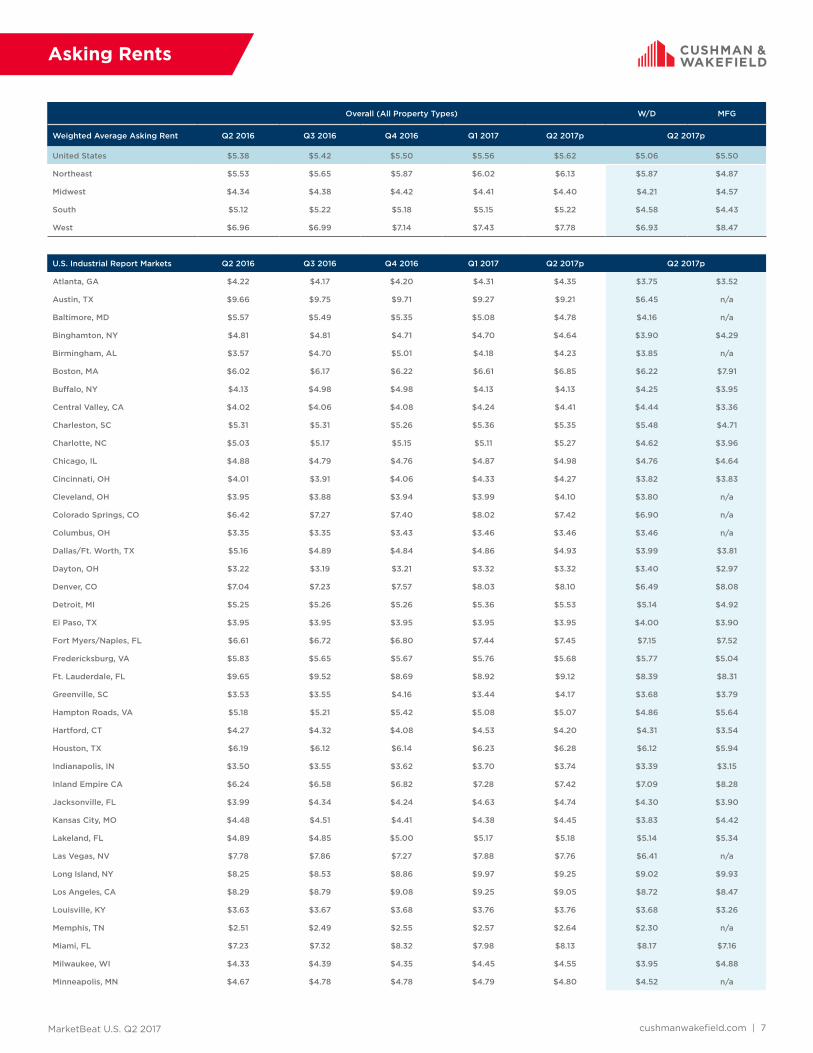

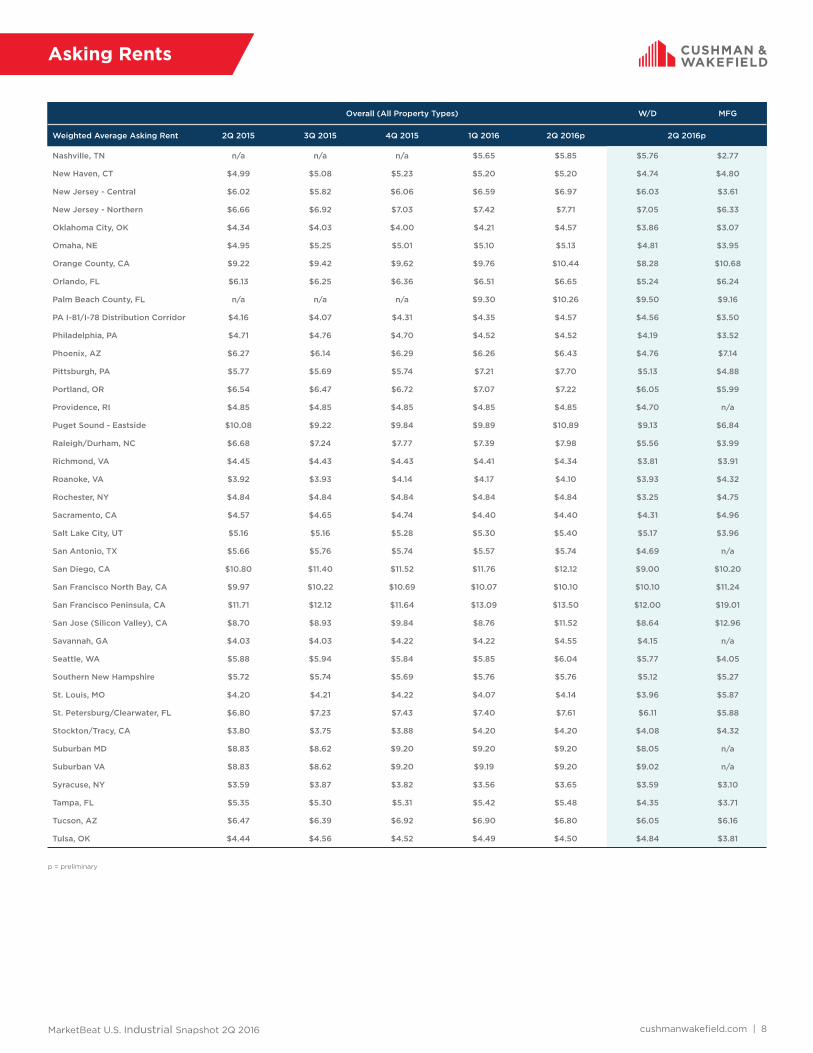

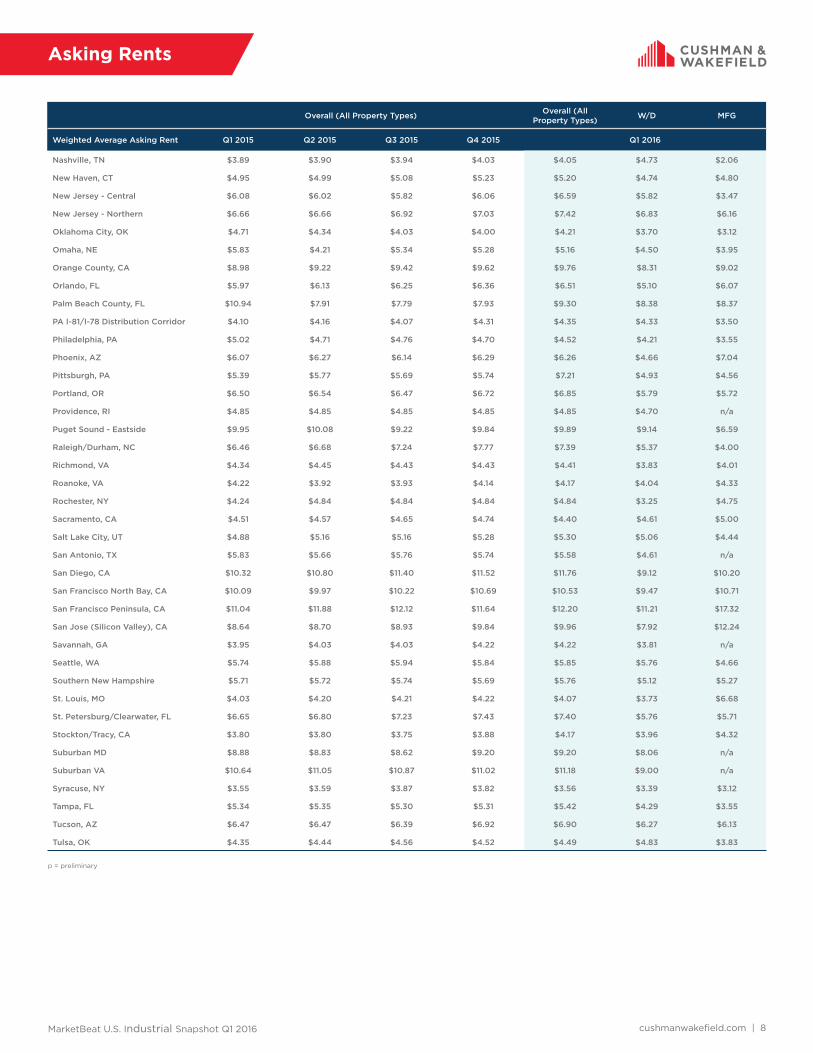

Asking Rents

Overall (All Property Types) W/D MFG

Weighted Average Asking Rent Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

United States $5.68 $5.70 $5.80 $5.84 $5.99 $5.39 $5.77

Northeast $6.17 $6.03 $6.03 $6.17 $6.42 $6.23 $5.15

Midwest $4.48 $4.57 $4.61 $4.61 $4.70 $4.38 $4.65

South $5.23 $5.27 $5.45 $5.41 $5.60 $5.03 $4.69

West $7.83 $7.91 $7.98 $8.12 $8.30 $7.23 $8.68

U.S. Industrial Report Markets Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

Atlanta, GA $4.31 $4.35 $4.54 $4.47 $4.83 $4.08 $3.78

Austin, TX $9.27 $9.21 $9.34 $9.24 $10.08 $8.21 $10.78

Baltimore, MD $5.08 $4.78 $5.10 $5.70 $5.75 $5.21 n/a

Binghamton, NY $4.70 $4.64 $4.58 $4.57 $4.57 $4.09 $4.29

Birmingham, AL $4.18 $4.23 $4.09 $4.02 $3.98 $3.71 n/a

Boston, MA $6.61 $6.85 $6.97 $8.17 $7.45 $6.64 $8.78

Buffalo, NY $4.13 $4.13 $4.13 $4.13 $4.13 $4.25 $3.95

Central Valley, CA $4.32 $4.25 $4.24 $4.75 $4.20 $4.44 $3.36

Charleston, SC $5.36 $5.35 $5.48 $5.52 $5.54 $5.56 $4.70

Charlotte, NC $5.11 $5.27 $5.42 $5.21 $5.27 $4.79 $4.10

Chicago, IL $4.87 $4.98 $5.03 $5.08 $5.19 $4.95 $4.84

Cincinnati, OH $4.33 $4.27 $4.33 $4.25 $4.34 $4.11 $3.50

Cleveland, OH $3.99 $4.10 $4.12 $4.15 $4.30 $3.99 n/a

Colorado Springs, CO $6.78 $7.43 $7.37 $7.85 $8.06 $7.46 $7.19

Columbus, OH $3.46 $3.46 $3.46 $3.50 $3.55 $3.55 n/a

Dallas/Ft. Worth, TX $4.86 $4.93 $5.59 $5.06 $5.40 $4.27 $4.22

Dayton, OH $3.32 $3.32 $3.33 $3.26 $3.29 $3.63 $2.95

Denver, CO $8.03 $8.10 $8.03 $7.96 $7.78 $6.38 $7.24

Detroit, MI $5.36 $5.53 $5.56 $5.57 $5.79 $5.40 $5.10

El Paso, TX $3.95 $3.95 $4.00 $4.10 $4.10 $4.10 $4.00

Fort Myers/Naples, FL $7.44 $7.45 $7.50 $7.61 $7.72 $7.30 $8.65

Fredericksburg, VA $5.71 $5.69 $5.73 $5.73 $5.79 $5.45 $4.62

Ft. Lauderdale, FL $8.92 $9.12 $9.21 $9.27 $9.45 $8.91 $10.18

Greenville, SC $3.58 $3.58 $3.63 $3.60 $3.43 $3.32 $3.21

Hampton Roads, VA $5.08 $5.05 $5.00 $5.28 $5.44 $5.18 $5.97

Hartford, CT $4.53 $4.21 $4.24 $4.28 $4.47 $4.60 $3.89

Houston, TX $6.23 $6.28 $6.40 $6.44 $6.22 $6.12 $5.81

Indianapolis, IN $3.70 $3.74 $3.76 $3.80 $3.88 $3.58 $3.31

Inland Empire CA $7.28 $7.42 $7.52 $7.61 $7.69 $6.92 $8.31

Jacksonville, FL $4.63 $4.74 $4.98 $5.37 $5.52 $4.76 $9.49

Kansas City, MO $4.38 $4.45 $4.43 $4.27 $4.20 $3.57 $4.04

Lakeland, FL $5.17 $5.18 $5.76 $5.54 $5.45 $5.01 $5.95

Las Vegas, NV $7.14 $6.80 $6.81 $6.82 $6.75 $6.60 $6.36

Long Island, NY $9.97 $9.25 $9.21 $9.44 $10.68 $9.98 $10.74

Los Angeles, CA $9.25 $9.05 $9.00 $9.36 $9.85 $9.46 $8.86

Louisville, KY $3.76 $3.76 $3.70 $3.73 $3.81 $3.73 $3.14

Memphis, TN $2.73 $2.81 $2.75 $2.75 $2.75 n/a n/a

Miami, FL $7.98 $8.13 $8.25 $8.45 $8.79 $8.84 $7.32

Milwaukee, WI $4.45 $4.55 $4.59 $4.64 $4.57 $4.00 $4.84

Minneapolis, MN $4.79 $4.80 $4.90 $4.88 $4.90 $4.65 n/a

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 8

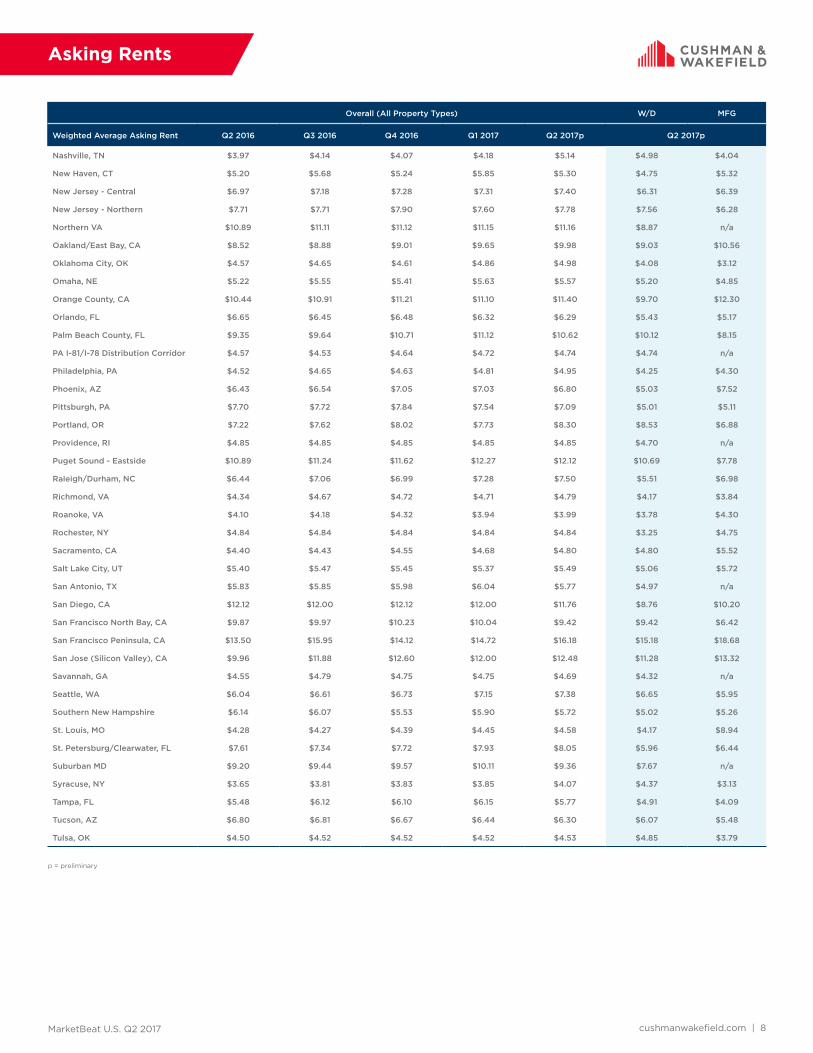

Asking Rents

p = preliminary

Overall (All Property Types) W/D MFG

Weighted Average Asking Rent Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018p Q1 2018p

Nashville, TN $4.18 $5.14 $5.03 $5.09 $4.95 $4.95 $3.65

New Haven, CT $5.33 $4.62 $5.15 $5.35 $5.57 $4.64 $5.64

New Jersey - Central $7.31 $7.40 $7.39 $7.58 $7.69 $6.97 $5.49

New Jersey - Northern $7.60 $7.78 $7.82 $8.56 $8.57 $8.49 $8.23

Northern VA $11.15 $11.16 $11.12 $11.36 $11.18 $9.15 n/a

Oakland/East Bay, CA $9.12 $10.17 $10.10 $10.43 $10.40 $9.26 $11.34

Oklahoma City, OK $4.86 $4.98 $4.95 $4.95 $5.28 $4.92 $4.68

Omaha, NE $5.63 $5.57 $5.57 $5.55 $5.55 $5.34 $3.89

Orange County, CA $11.10 $11.40 $10.74 $11.24 $11.61 $10.22 $10.88

Orlando, FL $6.32 $6.29 $6.38 $6.48 $6.45 $5.61 $6.44

Palm Beach County, FL $11.12 $10.62 $10.56 $10.69 $10.74 $9.83 $9.77

PA I-81/I-78 Distribution Corridor $4.72 $4.74 $4.75 $4.77 $4.80 $4.81 $4.50

Philadelphia, PA $4.81 $4.95 $4.58 $4.51 $4.76 $4.53 $4.57

Phoenix, AZ $7.03 $6.80 $6.80 $6.70 $6.91 $5.28 $7.71

Pittsburgh, PA $7.54 $7.09 $7.68 $7.58 $8.59 $5.59 $4.28

Portland, OR $7.73 $8.34 $8.38 $8.50 $8.53 $7.24 $9.74

Providence, RI $4.85 $4.85 $4.85 $4.85 $4.85 $4.70 n/a

Puget Sound - Eastside $12.27 $12.12 $12.24 $11.76 $11.75 $10.24 $7.31

Raleigh/Durham, NC $7.28 $7.50 $7.71 $8.70 $8.51 $5.87 $8.18

Richmond, VA $4.70 $4.80 $5.03 $4.92 $4.83 $4.65 $4.81

Roanoke, VA $4.43 $4.76 $4.99 $4.98 $5.21 $4.55 $7.11

Rochester, NY $4.84 $4.84 $4.84 $4.84 $5.40 $3.75 $4.75

Sacramento, CA $4.66 $4.93 $5.08 $5.06 $5.64 $5.64 $5.28

Salt Lake City, UT $5.37 $5.49 $5.64 $5.82 $5.65 $5.83 $4.15

San Antonio, TX $5.79 $5.79 $5.75 $5.79 $6.08 $5.29 n/a

San Diego, CA $12.00 $11.76 $11.88 $12.36 $12.48 $9.12 $11.04

San Francisco North Bay, CA $9.97 $11.54 $11.97 $11.69 $11.97 $11.86 $16.27

San Francisco Peninsula, CA $14.72 $16.18 $16.42 $17.72 $17.62 $17.11 $20.24

San Jose (Silicon Valley), CA $12.00 $12.48 $12.12 $13.20 $13.08 $12.00 $14.28

Savannah, GA $4.75 $4.69 $4.69 $4.62 $4.62 $4.33 n/a

Seattle, WA $7.15 $7.38 $7.45 $7.61 $8.73 $8.29 $7.15

Southern New Hampshire $5.90 $5.72 $5.62 $5.79 $5.92 $5.06 $5.51

St. Louis, MO $4.45 $4.58 $4.62 $4.47 $4.57 $4.20 $9.93

St. Petersburg/Clearwater, FL $7.93 $8.05 $7.99 $8.12 $7.86 $6.18 $6.09

Suburban MD $10.11 $9.36 $9.21 $9.37 $10.02 $8.31 n/a

Syracuse, NY $3.85 $4.07 $4.08 $4.02 $3.94 $4.19 $3.24

Tampa, FL $6.15 $5.77 $5.85 $5.72 $5.74 $5.08 $4.20

Tucson, AZ $6.44 $6.29 $6.37 $6.23 $6.09 $5.94 $5.01

Tulsa, OK $4.52 $4.53 $4.54 $4.54 $4.69 $4.78 $4.34

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 9

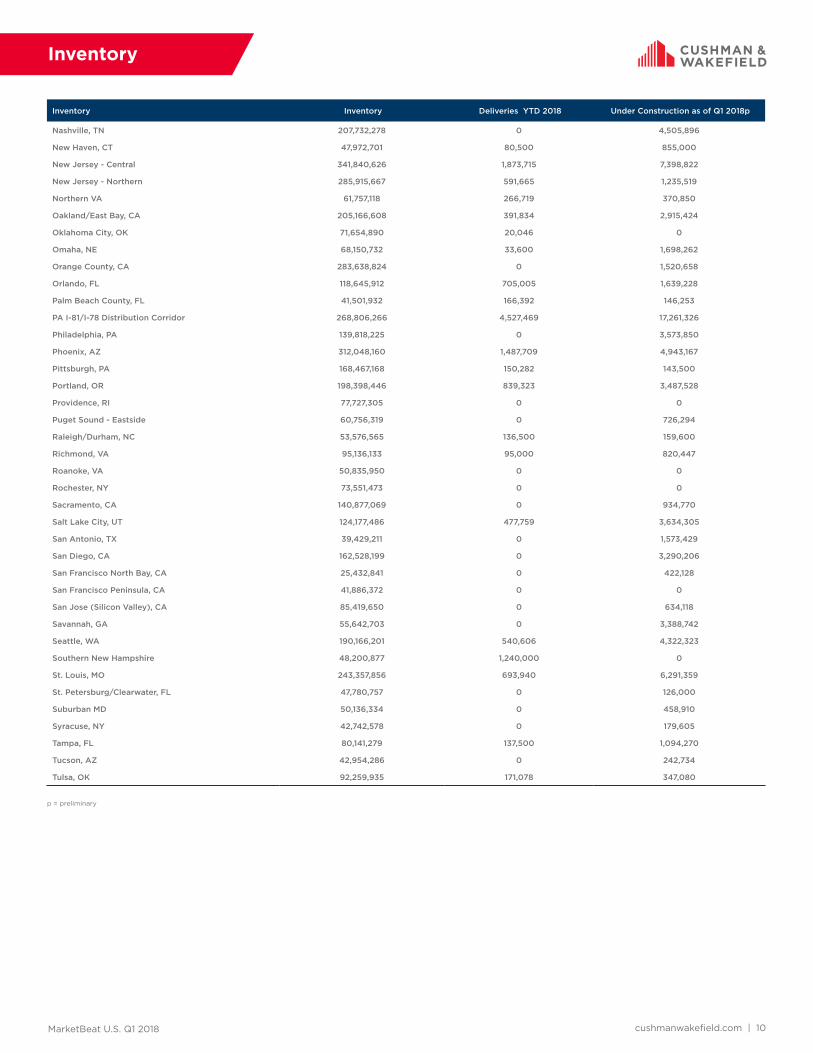

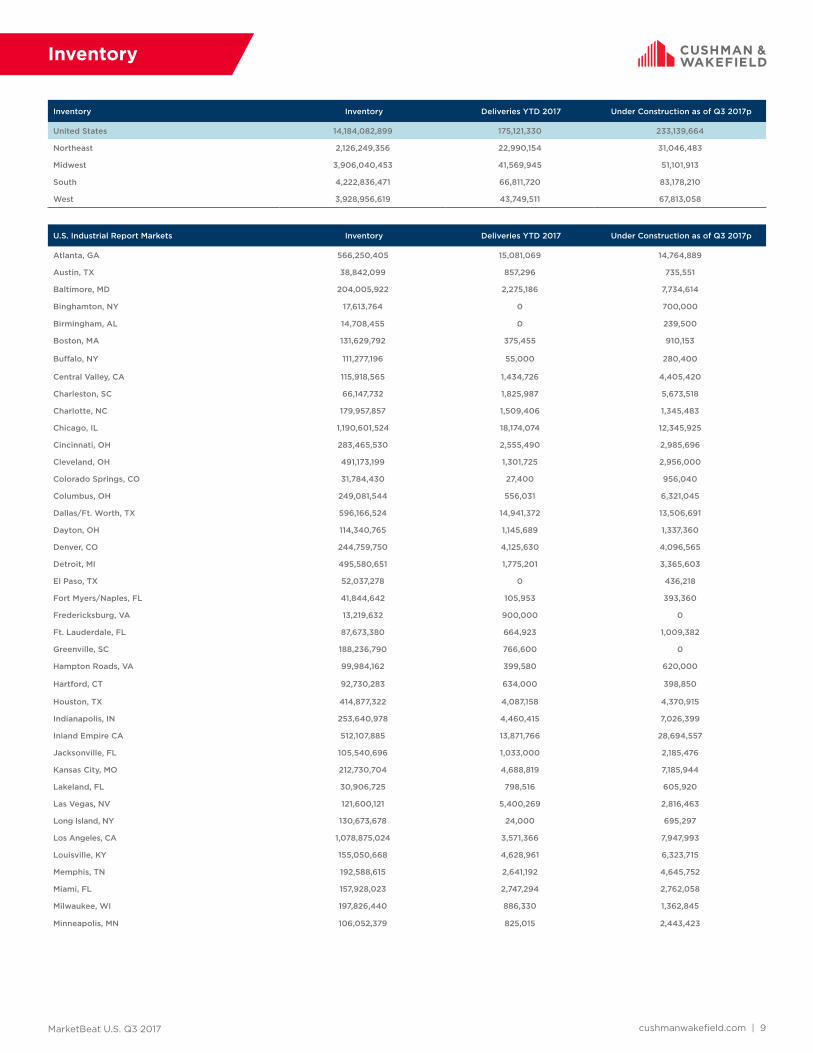

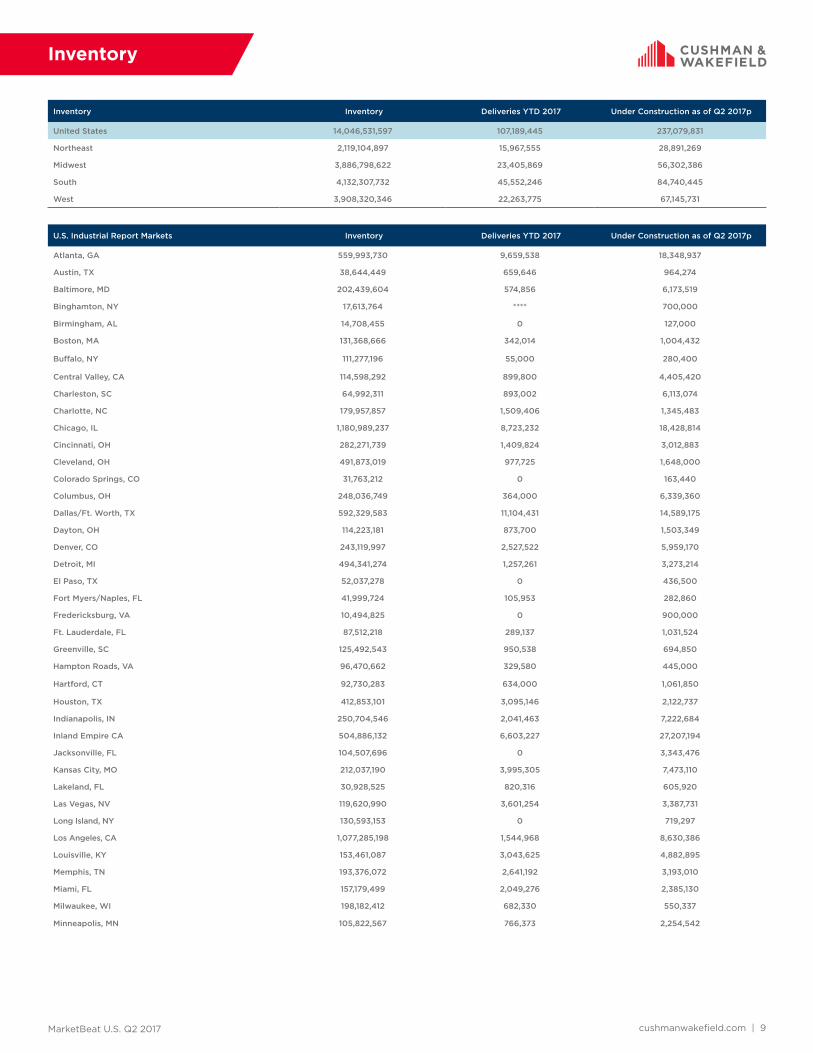

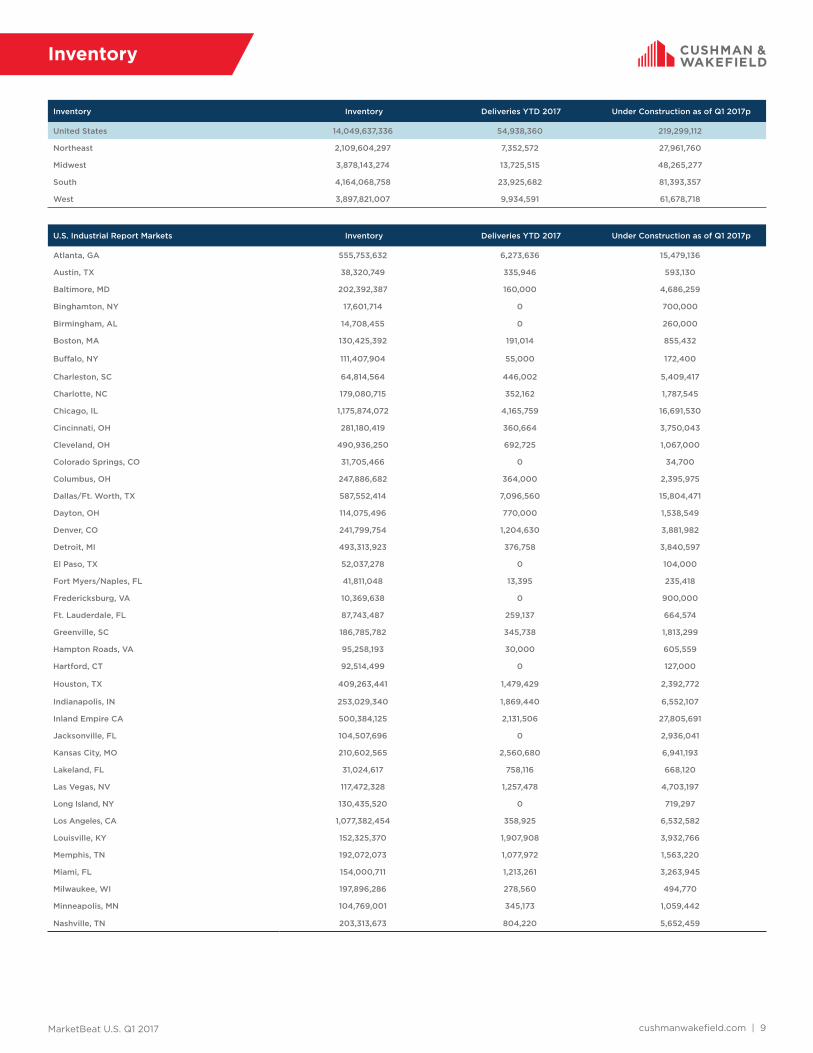

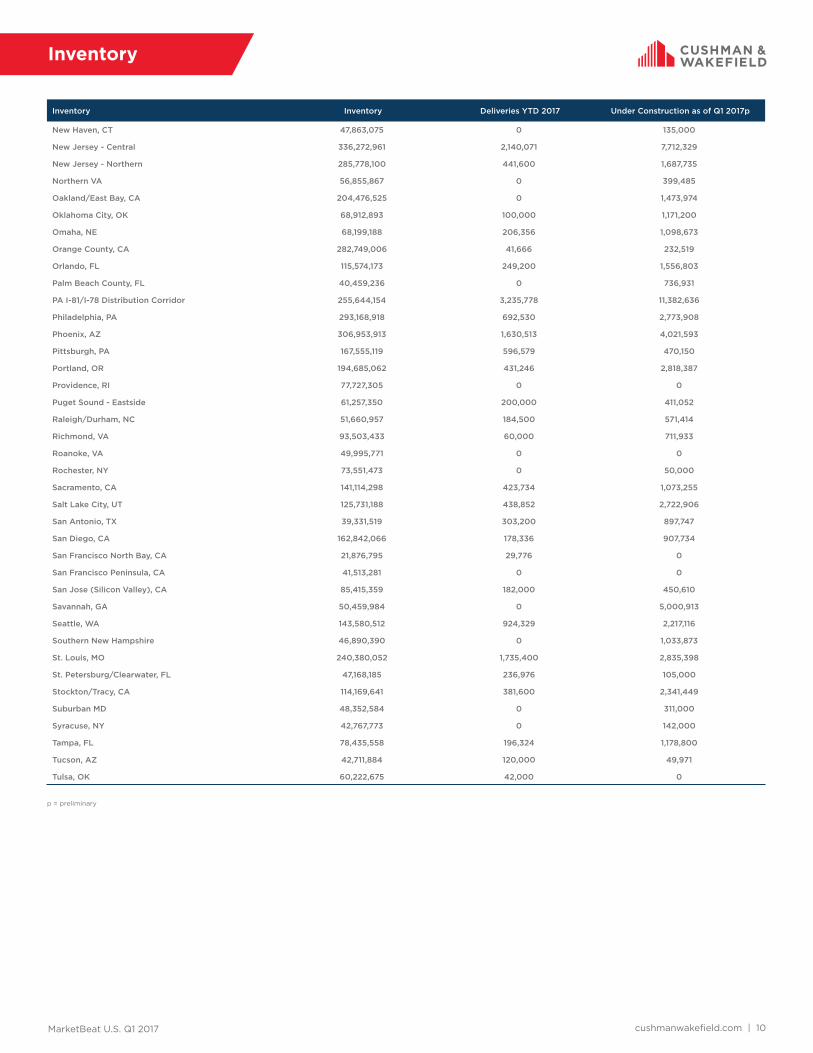

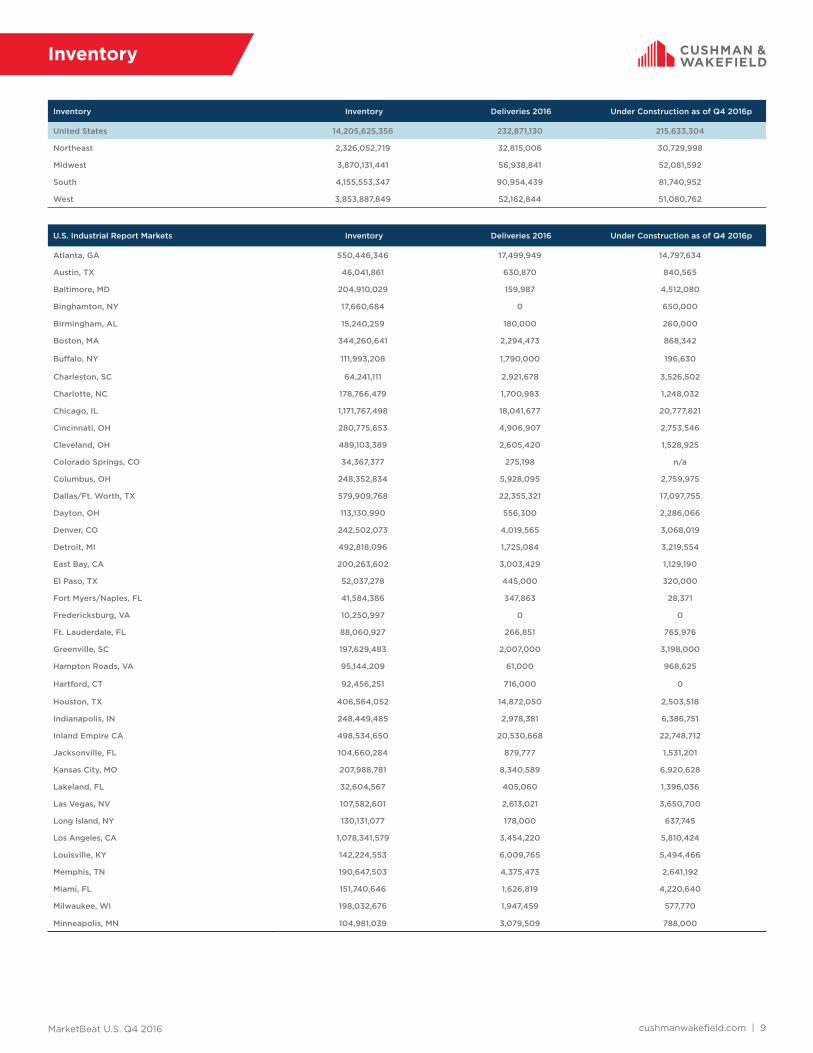

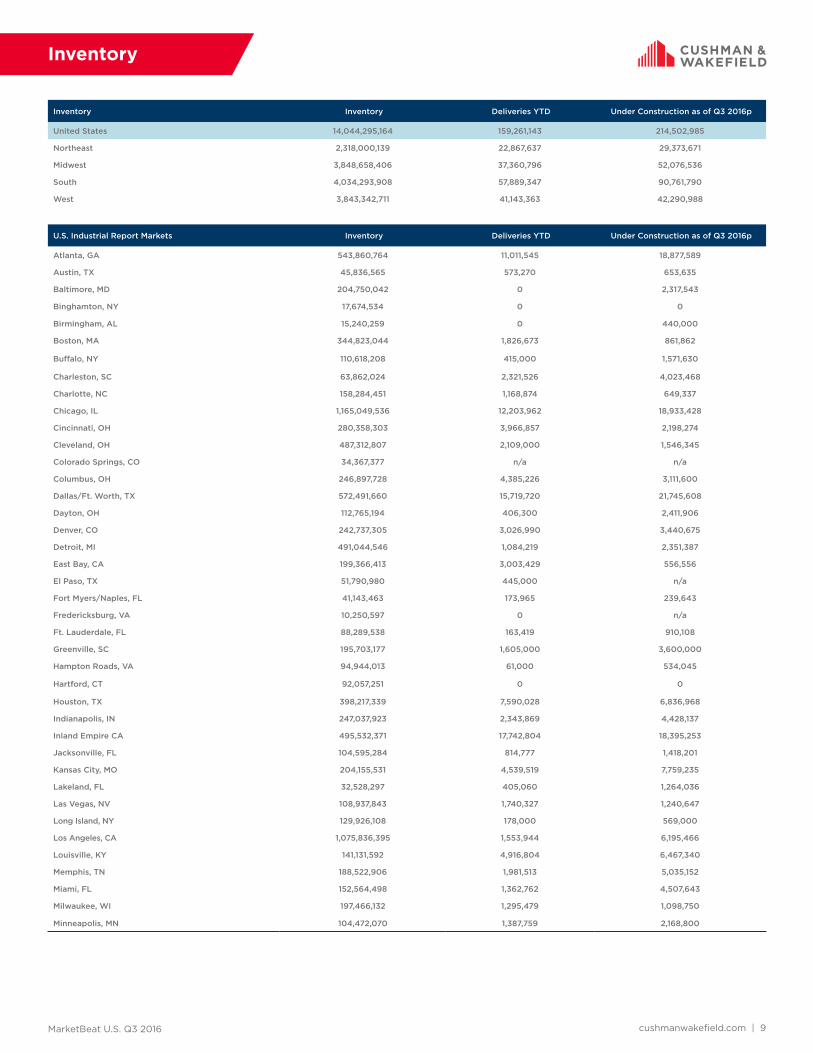

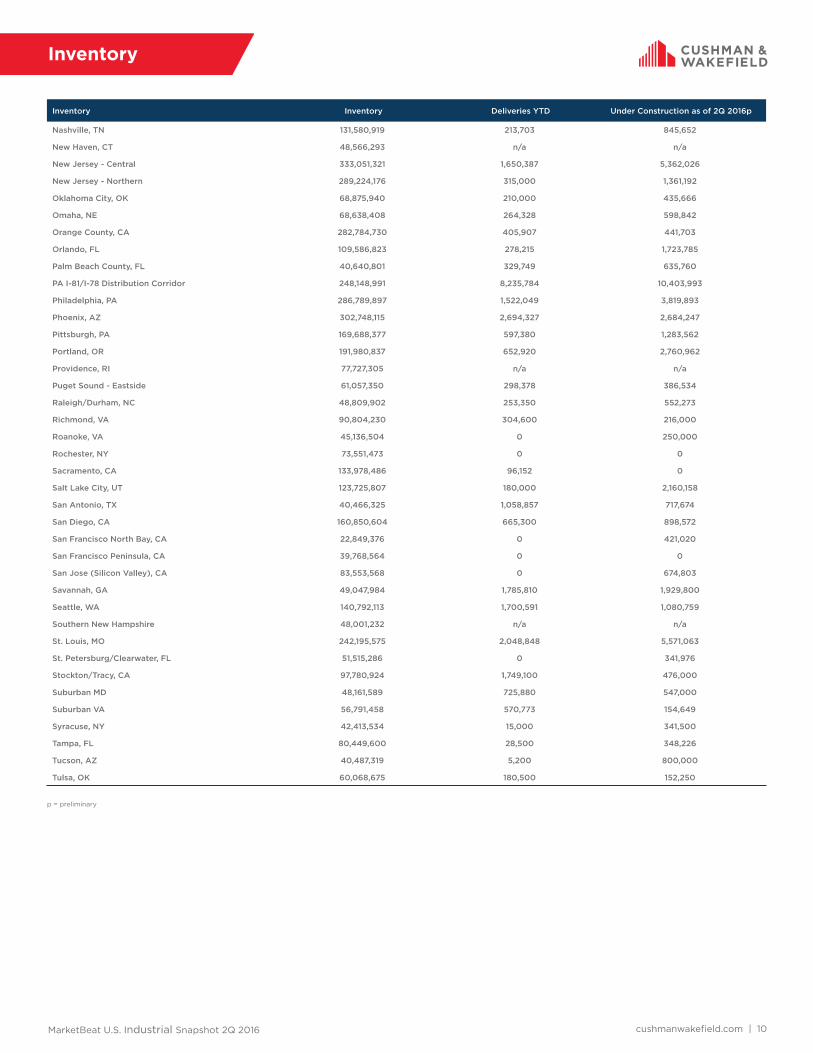

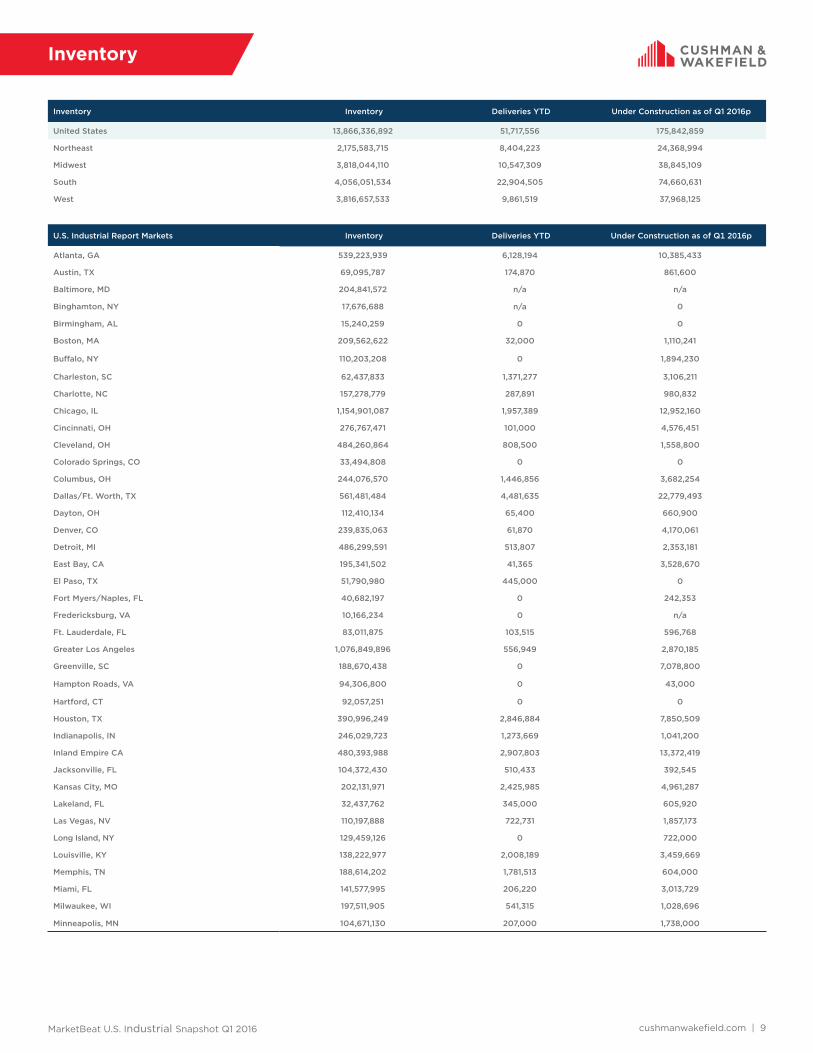

Inventory

Inventory Inventory Deliveries YTD 2018 Under Construction as of Q1 2018p

United States 14,410,824,692 58,799,986 251,252,728

Northeast 1,993,641,042 8,791,831 35,742,136

Midwest 3,980,416,040 13,555,670 46,547,019

South 4,455,891,503 21,504,739 95,617,226

West 3,980,876,107 14,947,746 73,346,347

U.S. Industrial Report Markets Inventory Deliveries YTD 2018 Under Construction as of Q1 2018p

Atlanta, GA 595,218,856 5,295,533 16,455,440

Austin, TX 41,563,750 350,171 1,425,067

Baltimore, MD 206,480,254 839,200 6,206,238

Binghamton, NY 17,266,122 0 0

Birmingham, AL 14,636,022 127,000 872,500

Boston, MA 145,612,419 45,000 3,064,775

Buffalo, NY 110,137,656 108,000 637,157

Central Valley, CA 124,812,694 1,309,285 9,227,339

Charleston, SC 67,701,399 2,004,601 4,586,278

Charlotte, NC 190,510,328 1,679,322 3,042,678

Chicago, IL 1,199,111,877 3,363,887 7,544,990

Cincinnati, OH 286,357,688 2,516,071 3,315,073

Cleveland, OH 493,267,300 755,000 3,668,270

Colorado Springs, CO 27,985,210 0 150,000

Columbus, OH 250,114,480 765,226 6,969,125

Dallas/Ft. Worth, TX 717,443,390 3,077,808 20,172,705

Dayton, OH 118,524,616 83,600 1,013,750

Denver, CO 242,223,330 213,800 4,631,834

Detroit, MI 535,827,638 696,874 4,520,054

El Paso, TX 52,409,401 373,760 697,662

Fort Myers/Naples, FL 41,657,618 42,715 524,521

Fredericksburg, VA 13,547,393 0 0

Ft. Lauderdale, FL 88,377,590 553,693 1,526,763

Greenville, SC 190,880,359 0 2,506,460

Hampton Roads, VA 98,264,807 50,000 195,000

Hartford, CT 93,012,333 133,200 1,255,000

Houston, TX 423,531,502 2,006,427 6,535,264

Indianapolis, IN 257,512,784 669,044 5,760,586

Inland Empire CA 523,896,800 5,909,554 25,649,881

Jacksonville, FL 106,009,294 0 1,175,100

Kansas City, MO 217,905,877 2,618,804 3,695,142

Lakeland, FL 31,571,987 636,120 650,808

Las Vegas, NV 121,262,863 1,275,681 2,460,469

Long Island, NY 132,569,626 42,000 137,582

Los Angeles, CA 1,067,244,749 2,502,195 4,153,169

Louisville, KY 158,118,608 1,411,889 5,590,250

Memphis, TN 192,588,615 N/A 5,261,192

Miami, FL 159,149,333 1,358,260 3,562,595

Milwaukee, WI 200,343,420 627,045 837,874

Minneapolis, MN 109,941,772 732,579 1,232,534

MarketBeat U.S. Q1 2018 cushmanwakefield.com | 10

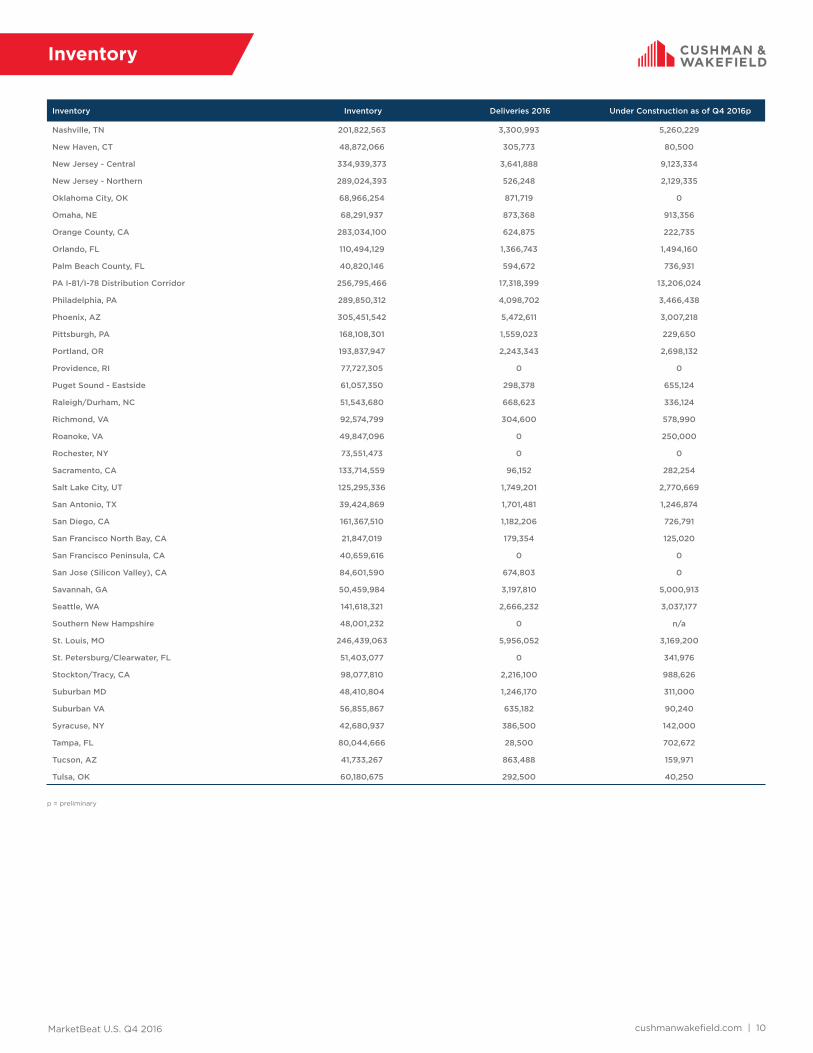

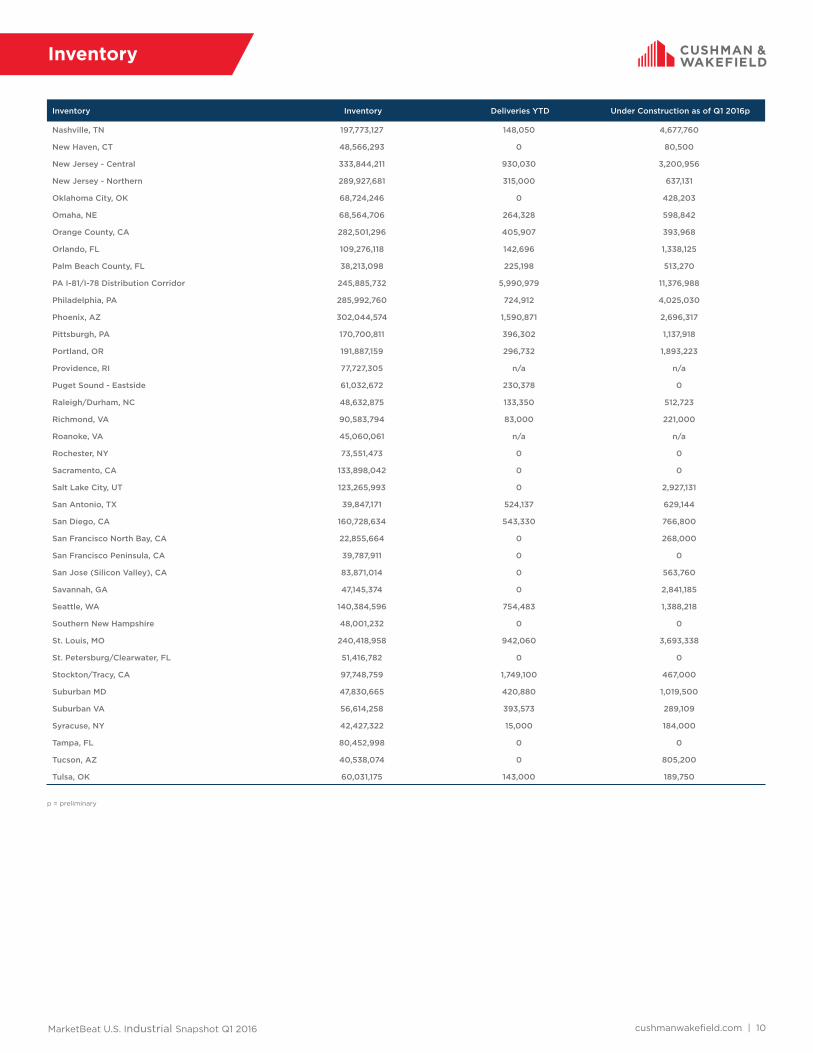

Inventory

Inventory Inventory Deliveries YTD 2018 Under Construction as of Q1 2018p

Nashville, TN 207,732,278 0 4,505,896

New Haven, CT 47,972,701 80,500 855,000

New Jersey - Central 341,840,626 1,873,715 7,398,822

New Jersey - Northern 285,915,667 591,665 1,235,519

Northern VA 61,757,118 266,719 370,850

Oakland/East Bay, CA 205,166,608 391,834 2,915,424

Oklahoma City, OK 71,654,890 20,046 0

Omaha, NE 68,150,732 33,600 1,698,262

Orange County, CA 283,638,824 0 1,520,658

Orlando, FL 118,645,912 705,005 1,639,228

Palm Beach County, FL 41,501,932 166,392 146,253

PA I-81/I-78 Distribution Corridor 268,806,266 4,527,469 17,261,326

Philadelphia, PA 139,818,225 0 3,573,850

Phoenix, AZ 312,048,160 1,487,709 4,943,167

Pittsburgh, PA 168,467,168 150,282 143,500

Portland, OR 198,398,446 839,323 3,487,528

Providence, RI 77,727,305 0 0

Puget Sound - Eastside 60,756,319 0 726,294

Raleigh/Durham, NC 53,576,565 136,500 159,600

Richmond, VA 95,136,133 95,000 820,447

Roanoke, VA 50,835,950 0 0

Rochester, NY 73,551,473 0 0

Sacramento, CA 140,877,069 0 934,770

Salt Lake City, UT 124,177,486 477,759 3,634,305

San Antonio, TX 39,429,211 0 1,573,429

San Diego, CA 162,528,199 0 3,290,206

San Francisco North Bay, CA 25,432,841 0 422,128

San Francisco Peninsula, CA 41,886,372 0 0

San Jose (Silicon Valley), CA 85,419,650 0 634,118

Savannah, GA 55,642,703 0 3,388,742

Seattle, WA 190,166,201 540,606 4,322,323

Southern New Hampshire 48,200,877 1,240,000 0

St. Louis, MO 243,357,856 693,940 6,291,359

St. Petersburg/Clearwater, FL 47,780,757 0 126,000

Suburban MD 50,136,334 0 458,910

Syracuse, NY 42,742,578 0 179,605

Tampa, FL 80,141,279 137,500 1,094,270

Tucson, AZ 42,954,286 0 242,734

Tulsa, OK 92,259,935 171,078 347,080

p = preliminary

Methodology

Cushman & Wakefield’s quarterly estimates are derived from a variety of data sources, including its own proprietary database, and historical data from third party data sources. The market statistics are calculated from a base building inventory made up of industrial properties deemed to be competitive in the local industrial markets. Generally, owner-occupied and federally-owned buildings are not included. Older buildings unfit for occupancy or ones that require substantial renovation before tenancy are generally not included in the competitive inventory. The inventory is subject to revisions due to resampling. Vacant space is defined as space that is available immediately or imminently after the end of the quarter. Sublet space still occupied by the tenant is not counted as available space. The figures provided for the current quarter are preliminary, and all information contained in the report is subject to correction of errors and revisions based on additional data received.

Regional Map

WestMidwestSouthNortheast

Jason Tolliver Head of Logistics & Industrial Research Americas Tel: +1 317.639.0549 cushmanwakefield.com

Explanation of Terms

Total Inventory: The total amount of industrial space (in buildings of a

predetermined size by market) that can be rented by a third party.

Overall Vacancy Rate: The amount of unoccupied space (new, relet, and

sublet) expressed as a percentage of total inventory.

Absorption: The net change in occupied space between two points in time.

(Total occupied space in the present quarter minus total occupied space from

the previous quarter, quoted on a net, not gross, basis.)

Leasing Activity: The sum of all leases over a period of time. This includes

pre-leasing activity as well as expansions. It does not include renewals.

Overall Weighted Asking Rents: NNN average asking rents weighted by the

amount of available direct and sublease space in industrial properties.

W/D: Warehouse and or distribution properties.

MFG: Manufacturing properties.

About Cushman & Wakefield

Cushman & Wakefield is a leading global real estate services firm with 45,000 employees in more than 70 countries helping occupiers and investors optimize the value of their real estate. Cushman & Wakefield is among the largest commercial real estate services firms with revenue of $6 billion across core services of agency leasing, asset services, capital markets, facility services (C&W Services), global occupier services, investment & asset management (DTZ Investors), project & development services, tenant representation, and valuation & advisory. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

Cushman & Wakefield Copyright 2018. No warranty or representation, express or implied, is made to the accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any special listing conditions imposed by the property owner(s). As applicable, we make no representation as to the condition of the property (or properties) in question.

Carolyn Salzer Analyst, Logistics & Industrial Research Americas Tel: +1 847.518.3212 cushmanwakefield.com

cushmanwakefield.com | 1

U.S. IndustrialQ4 2017

MARKETBEAT

U.S. INDUSTRIAL

Overall Vacancy

Net Absorption/Rent NNN 4-QTR TRAILING AVERAGE

Market Indicators

Q4 16 Q4 17 12-Month Forecast

Overall Vacancy 5.5% 5.1%

Net Absorption 63.1M 63.3M

Under Construction 215.6M 242.5M

Weighted Asking Rent (NNN) $5.63 $5.84

Rent Growth (Yr/Yr % Chg.) 4.1% 3.7%

Employment IndicatorsQ4 16 Q4 17 12-Month

Forecast

Total Nonfarm Employment 145.2M 147.2M

Industrial Employment 25.4M 25.9M

Unemployment 4.7% 4.1%

$4.00

$4.50

$5.00

$5.50

$6.00

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016 2017 2018Net Absorption, MSF Weighted Asking Rent, $ PSF

Forecast

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2013 2014 2015 2016 2017 2018

Historical Average = 8.4%

Forecast

Industrial Market Shows No Signs of Slowing

Another Banner Year: U.S. industrial markets absorbed 63.3 million square feet (msf) in the fourth quarter of 2017, boosting net occupancy gains for the year to over 246.3 msf. The U.S. industrial market has now recorded over 240 msf of absorption for four consecutive years—the strongest run on record. The national industrial vacancy rate held at 5.1% for all product types—the lowest rate on record—with market conditions tightening slightly in the Midwest and South. The greatest growth markets in 2017 were Dallas/Ft Worth, Atlanta, the Inland Empire, Chicago and the Pennsylvania I-81/I-78 Distribution Corridor, and together they accounted for 38% of overall U.S. net absorption.

Firing on All Cylinders: Every industrial segment remained in growth mode. Through Q4 2017, warehouse product posted 224.9 msf of net absorption, manufacturing registered 10.2 msf of growth, flex occupancy grew by 7.2 msf and high technology occupancy increased by 2.4 msf. The current industrial expansion is one for the record book. As of January 2018, the industrial sector has registered 31 consecutive quarters of net occupancy gains—the longest expansion ever. It is also among the strongest with net absorption since 2010 surpassing 1.4 trillion square feet.

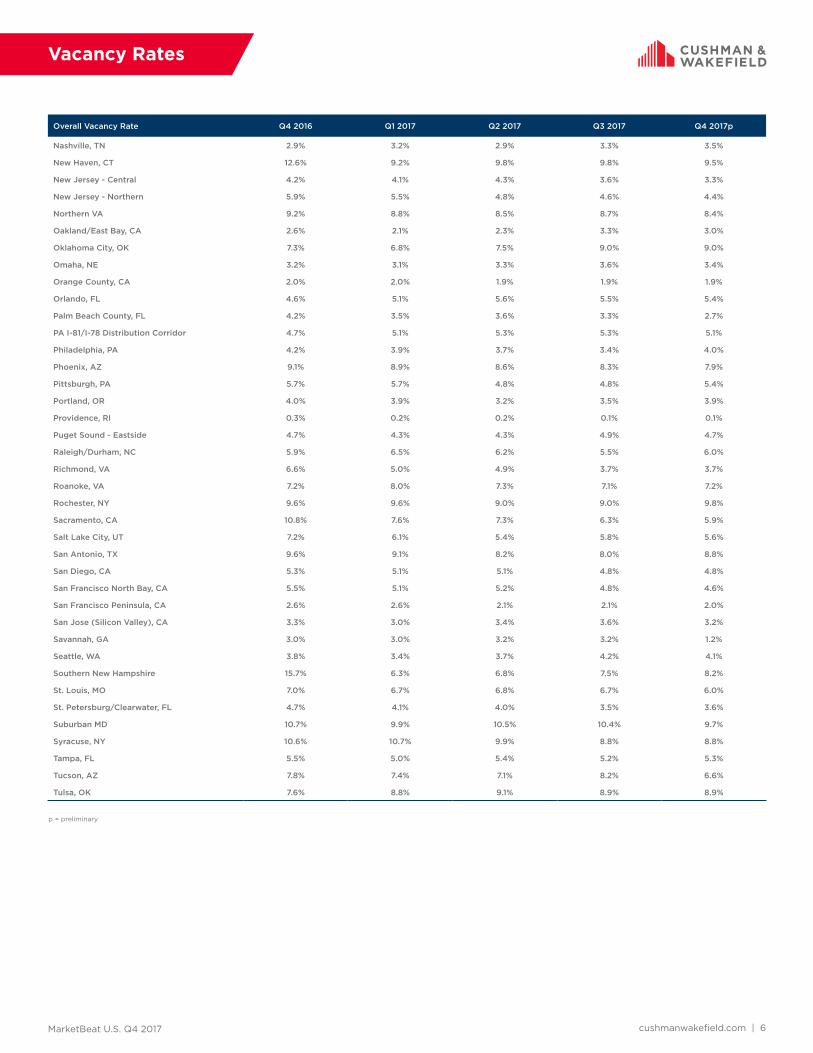

Tight Conditions: At 5.1%, the U.S. industrial vacancy rate is a full 330 basis points (bps) below the 10-year historical average of 8.4% for all product types. The warehouse market remains tight with vacancy tracking at 5.2% in Q4 2017. Over the past year, logistics-related vacancy has declined 50 bps (from 5.7% to 5.2%) despite the delivery of 168.6 msf of new speculative warehouse product. Strikingly, warehouse vacancy rates remain below prior cycle lows in many industrial markets, with conditions tightening further in Q4 2017 as rates track below 5% in nearly half of all U.S. markets. At year-end 2017, the tightest U.S. markets included Savannah, Los Angeles, Orange County, the San Francisco Peninsula, and Oakland/East Bay, all of which have vacancy rates at 3% or below.

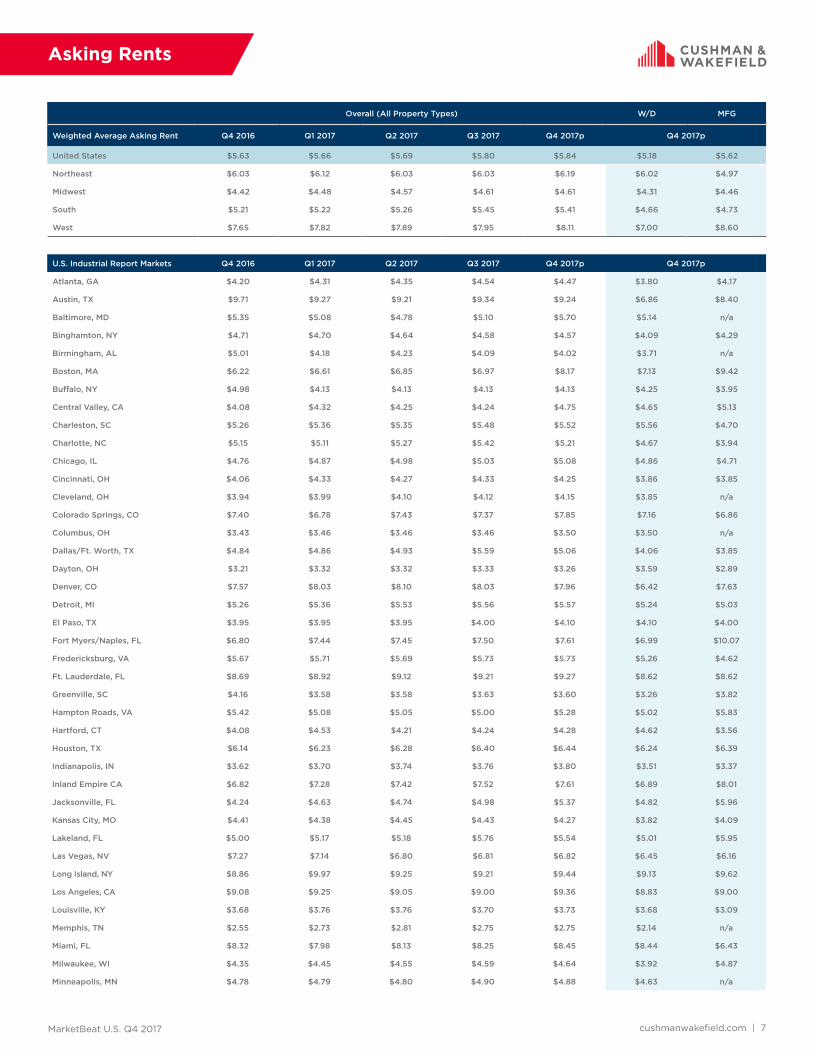

Rents Continue to Run: Healthy demand from logistics and distribution users is fueling rent growth. U.S. industrial rents increased 3.7% in Q4 2017 from a year ago to a record high of $5.84 per square foot (psf). Industrial rents rose in 62 of 79 markets tracked by Cushman & Wakefield during the same period, with many port-proximate industrial markets reporting double-digit gains. Among the regions, year-over-year rent growth in Q4 2017 was strongest in the West (6.1%), followed by the Midwest (4.4%), South (4.1%) and Northeast (2.6%). Rent growth was strongest in Jacksonville, San Francisco, Nashville, Raleigh/Durham, Oakland/East Bay and Seattle—all markets where rents grew more than 12% in 2017.

Conservative Development: New construction starts rose slightly—by 3.5%—in Q4 2017. Currently, there is 242.5 msf of industrial product under construction, of which 161.6 msf is speculative. Although development remains concentrated in major industrial markets, 42 of the 79 markets tracked have over 1 msf under construction. Given the tight market conditions and strong underlying fundamentals, developers are expected be conservative in breaking ground on additional speculative projects, which will slowly bring supply and demand fundamentals closer into balance. Nevertheless, concern over the length of the current economic cycle, the increased institutional nature of developers and financial partners, and lack of land and rising construction costs are likely to prevent dramatic increases in speculative development in most markets.

Source: Cushman & Wakefield Research

Source: BLS

cushmanwakefield.com | 2

U.S. IndustrialQ4 2017

MARKETBEAT

Demand in Line with Supply in Many Markets 2017 NET ABSORPTION & NEW DELIVERIES (ALL TYPES, % OF INVENTORY)

Rebalancing of Vacancy Will Occur Slowly CURRENT CONSTRUCTION COMPARED TO 5-YR ABSORPTION AVERAGE

Few Signs of Overbuilding 2017 DELIVERIES BY TYPE & YEAR-OVER-YEAR CHANGE IN VACANCY

Outlook• Logistics-related leasing will continue to benefit from solid

economic fundamentals that spur increased consumer spending.

• Net absorption will once again surpass 200 msf for a fifth year in a row.

• Increased speculative supply will place upward pressure on vacancy as supply/demand begin to slowly rebalance. We forecast average annual vacancy to rise 20 bps in 2018 to 5.3% for all industrial product types.

• Rental rate appreciation will continue, although rent growth will slowly begin to decelerate in 2018. We anticipate average annual rent gains of 2.9% in 2018 for all industrial product types.

Source: Cushman & Wakefield Research

Source: Cushman & Wakefield Research

Source: Cushman & Wakefield Research

Don’t Bet Against the U.S. Economy, More Upside than Downside

Solid Footing: The U.S. economy and industrial market are positioned to perform well in 2018. For the fourth quarter, job gains averaged 204,000 a month, the most since the third quarter of 2016. For all of 2017, U.S. firms created nearly 2.1 million net new jobs, down from 2.2 million in 2016 but almost equal to the 2012-2016 average. Renewed confidence in the economy and higher levels of real discretionary income are anticipated to boost retail sales while a stronger U.S. housing market will buttress leasing demand among firms associated with home building and furnishings. Stronger global growth is also expected to support economic growth and leasing fundamentals. In short, the U.S. economy and industrial market enter 2018 on the strongest footing of any year in the current expansion with few signs of slowing.

Paying-Up: Since 2016, the Employment Cost Index—a quarterly economic series detailing the changes in the costs of labor for businesses in the economy—has risen at a faster pace for warehouse workers than for all civilian workers. This trend is mirrored in forecasts for income: the largest growth in real per capita income is projected to be in industrial markets, particularly those in Florida and distribution-centric markets in Pennsylvania and the Midwest. Since labor typically accounts for at least half of traditional warehouse operating costs, the relationship between labor costs and warehouse operations will remain a key theme in 2018, with occupiers increasingly required to pay-up to ramp-up or keep-up warehousing and fulfillment operations.

Churning it Out: The U.S. manufacturing sector ended 2017 on a strong note with the ISM manufacturing index rising to 59.7 in December—the second fastest pace of expansion in six years. Buoyed by both domestic and international demand, new orders are surging at their fastest pace in more than 13 years. The ISM index expanded at a torrid pace in the third and fourth quarters of 2017. Since August 2017, the index has consistently tracked above 58.2, a rare occurrence. The only other period in the past 40 years that the ISM registered 58 or higher for that many consecutive months was a streak that lasted from November 2003 to August 2004. The rapid pace of expansion and rising backlog of orders indicates continued production and demand for manufacturing and logistics-related real estate in 2018

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%5.0%

Net Absorption New Deliveries

0

4

8

12

16

20

24

28

32

Speculative Deliveries (MSF) Build-to-Suit Deliveries (MSF)

+10 – YoY change in vacancy, basis points

+50

-30-130

+40

+230 -90 -110 +60 -10 -120-20-110-20-100+110 -180 +110 -80 +60

0

4

8

12

16

20

24

28Q4 2017 Under Construction (MSF) 5-Year Absorption Average (MSF)

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 3

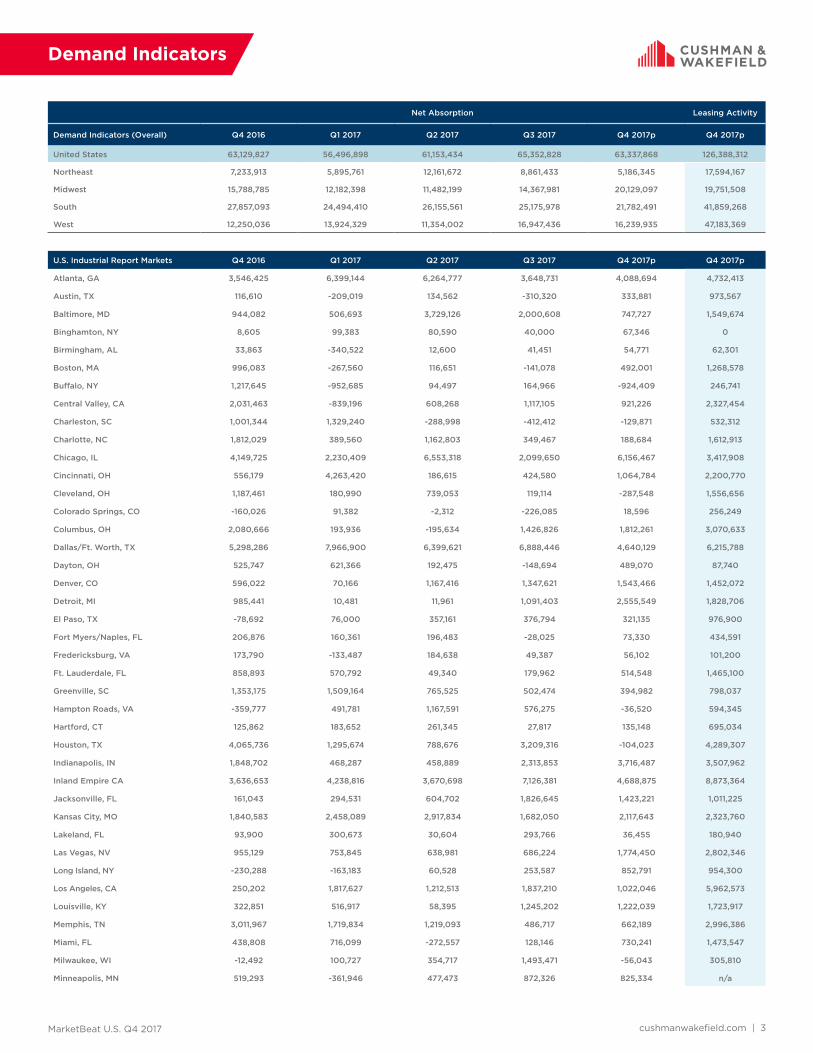

Net Absorption Leasing Activity

Demand Indicators (Overall) Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

United States 63,129,827 56,496,898 61,153,434 65,352,828 63,337,868 126,388,312

Northeast 7,233,913 5,895,761 12,161,672 8,861,433 5,186,345 17,594,167

Midwest 15,788,785 12,182,398 11,482,199 14,367,981 20,129,097 19,751,508

South 27,857,093 24,494,410 26,155,561 25,175,978 21,782,491 41,859,268

West 12,250,036 13,924,329 11,354,002 16,947,436 16,239,935 47,183,369

U.S. Industrial Report Markets Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

Atlanta, GA 3,546,425 6,399,144 6,264,777 3,648,731 4,088,694 4,732,413

Austin, TX 116,610 -209,019 134,562 -310,320 333,881 973,567

Baltimore, MD 944,082 506,693 3,729,126 2,000,608 747,727 1,549,674

Binghamton, NY 8,605 99,383 80,590 40,000 67,346 0

Birmingham, AL 33,863 -340,522 12,600 41,451 54,771 62,301

Boston, MA 996,083 -267,560 116,651 -141,078 492,001 1,268,578

Buffalo, NY 1,217,645 -952,685 94,497 164,966 -924,409 246,741

Central Valley, CA 2,031,463 -839,196 608,268 1,117,105 921,226 2,327,454

Charleston, SC 1,001,344 1,329,240 -288,998 -412,412 -129,871 532,312

Charlotte, NC 1,812,029 389,560 1,162,803 349,467 188,684 1,612,913

Chicago, IL 4,149,725 2,230,409 6,553,318 2,099,650 6,156,467 3,417,908

Cincinnati, OH 556,179 4,263,420 186,615 424,580 1,064,784 2,200,770

Cleveland, OH 1,187,461 180,990 739,053 119,114 -287,548 1,556,656

Colorado Springs, CO -160,026 91,382 -2,312 -226,085 18,596 256,249

Columbus, OH 2,080,666 193,936 -195,634 1,426,826 1,812,261 3,070,633

Dallas/Ft. Worth, TX 5,298,286 7,966,900 6,399,621 6,888,446 4,640,129 6,215,788

Dayton, OH 525,747 621,366 192,475 -148,694 489,070 87,740

Denver, CO 596,022 70,166 1,167,416 1,347,621 1,543,466 1,452,072

Detroit, MI 985,441 10,481 11,961 1,091,403 2,555,549 1,828,706

El Paso, TX -78,692 76,000 357,161 376,794 321,135 976,900

Fort Myers/Naples, FL 206,876 160,361 196,483 -28,025 73,330 434,591

Fredericksburg, VA 173,790 -133,487 184,638 49,387 56,102 101,200

Ft. Lauderdale, FL 858,893 570,792 49,340 179,962 514,548 1,465,100

Greenville, SC 1,353,175 1,509,164 765,525 502,474 394,982 798,037

Hampton Roads, VA -359,777 491,781 1,167,591 576,275 -36,520 594,345

Hartford, CT 125,862 183,652 261,345 27,817 135,148 695,034

Houston, TX 4,065,736 1,295,674 788,676 3,209,316 -104,023 4,289,307

Indianapolis, IN 1,848,702 468,287 458,889 2,313,853 3,716,487 3,507,962

Inland Empire CA 3,636,653 4,238,816 3,670,698 7,126,381 4,688,875 8,873,364

Jacksonville, FL 161,043 294,531 604,702 1,826,645 1,423,221 1,011,225

Kansas City, MO 1,840,583 2,458,089 2,917,834 1,682,050 2,117,643 2,323,760

Lakeland, FL 93,900 300,673 30,604 293,766 36,455 180,940

Las Vegas, NV 955,129 753,845 638,981 686,224 1,774,450 2,802,346

Long Island, NY -230,288 -163,183 60,528 253,587 852,791 954,300

Los Angeles, CA 250,202 1,817,627 1,212,513 1,837,210 1,022,046 5,962,573

Louisville, KY 322,851 516,917 58,395 1,245,202 1,222,039 1,723,917

Memphis, TN 3,011,967 1,719,834 1,219,093 486,717 662,189 2,996,386

Miami, FL 438,808 716,099 -272,557 128,146 730,241 1,473,547

Milwaukee, WI -12,492 100,727 354,717 1,493,471 -56,043 305,810

Minneapolis, MN 519,293 -361,946 477,473 872,326 825,334 n/a

Demand Indicators

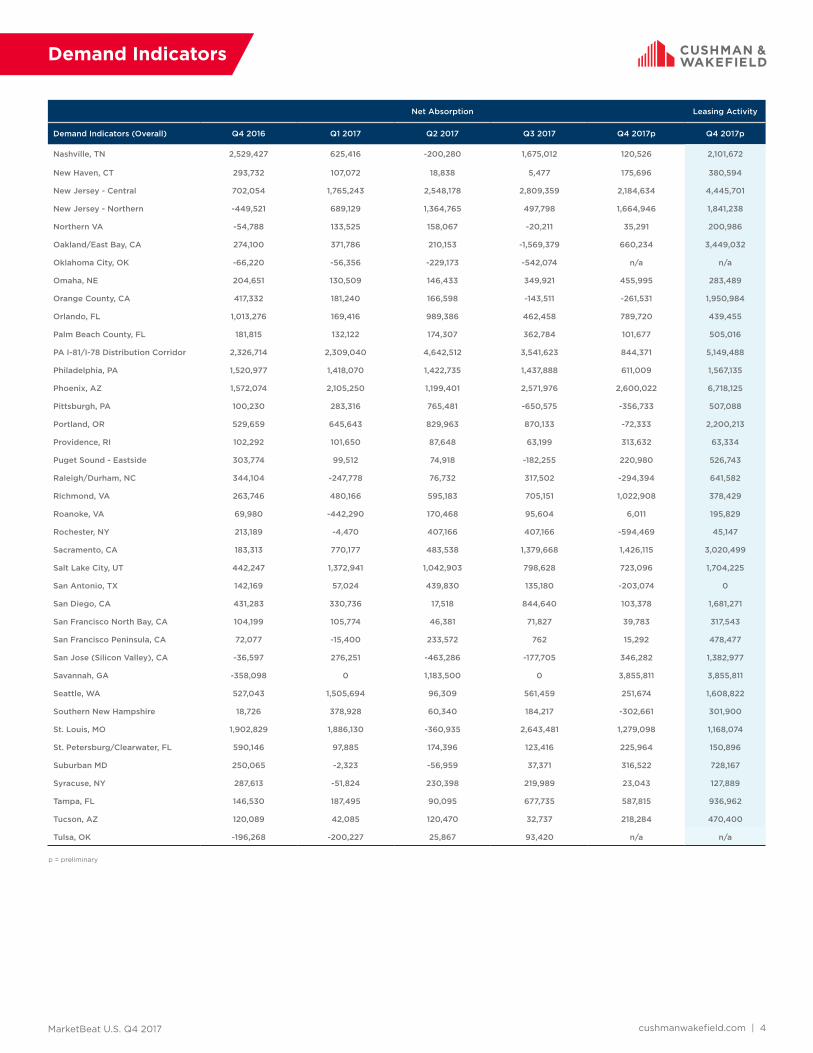

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 4

Net Absorption Leasing Activity

Demand Indicators (Overall) Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

Nashville, TN 2,529,427 625,416 -200,280 1,675,012 120,526 2,101,672

New Haven, CT 293,732 107,072 18,838 5,477 175,696 380,594

New Jersey - Central 702,054 1,765,243 2,548,178 2,809,359 2,184,634 4,445,701

New Jersey - Northern -449,521 689,129 1,364,765 497,798 1,664,946 1,841,238

Northern VA -54,788 133,525 158,067 -20,211 35,291 200,986

Oakland/East Bay, CA 274,100 371,786 210,153 -1,569,379 660,234 3,449,032

Oklahoma City, OK -66,220 -56,356 -229,173 -542,074 n/a n/a

Omaha, NE 204,651 130,509 146,433 349,921 455,995 283,489

Orange County, CA 417,332 181,240 166,598 -143,511 -261,531 1,950,984

Orlando, FL 1,013,276 169,416 989,386 462,458 789,720 439,455

Palm Beach County, FL 181,815 132,122 174,307 362,784 101,677 505,016

PA I-81/I-78 Distribution Corridor 2,326,714 2,309,040 4,642,512 3,541,623 844,371 5,149,488

Philadelphia, PA 1,520,977 1,418,070 1,422,735 1,437,888 611,009 1,567,135

Phoenix, AZ 1,572,074 2,105,250 1,199,401 2,571,976 2,600,022 6,718,125

Pittsburgh, PA 100,230 283,316 765,481 -650,575 -356,733 507,088

Portland, OR 529,659 645,643 829,963 870,133 -72,333 2,200,213

Providence, RI 102,292 101,650 87,648 63,199 313,632 63,334

Puget Sound - Eastside 303,774 99,512 74,918 -182,255 220,980 526,743

Raleigh/Durham, NC 344,104 -247,778 76,732 317,502 -294,394 641,582

Richmond, VA 263,746 480,166 595,183 705,151 1,022,908 378,429

Roanoke, VA 69,980 -442,290 170,468 95,604 6,011 195,829

Rochester, NY 213,189 -4,470 407,166 407,166 -594,469 45,147

Sacramento, CA 183,313 770,177 483,538 1,379,668 1,426,115 3,020,499

Salt Lake City, UT 442,247 1,372,941 1,042,903 798,628 723,096 1,704,225

San Antonio, TX 142,169 57,024 439,830 135,180 -203,074 0

San Diego, CA 431,283 330,736 17,518 844,640 103,378 1,681,271

San Francisco North Bay, CA 104,199 105,774 46,381 71,827 39,783 317,543

San Francisco Peninsula, CA 72,077 -15,400 233,572 762 15,292 478,477

San Jose (Silicon Valley), CA -36,597 276,251 -463,286 -177,705 346,282 1,382,977

Savannah, GA -358,098 0 1,183,500 0 3,855,811 3,855,811

Seattle, WA 527,043 1,505,694 96,309 561,459 251,674 1,608,822

Southern New Hampshire 18,726 378,928 60,340 184,217 -302,661 301,900

St. Louis, MO 1,902,829 1,886,130 -360,935 2,643,481 1,279,098 1,168,074

St. Petersburg/Clearwater, FL 590,146 97,885 174,396 123,416 225,964 150,896

Suburban MD 250,065 -2,323 -56,959 37,371 316,522 728,167

Syracuse, NY 287,613 -51,824 230,398 219,989 23,043 127,889

Tampa, FL 146,530 187,495 90,095 677,735 587,815 936,962

Tucson, AZ 120,089 42,085 120,470 32,737 218,284 470,400

Tulsa, OK -196,268 -200,227 25,867 93,420 n/a n/a

Demand Indicators

p = preliminary

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 5

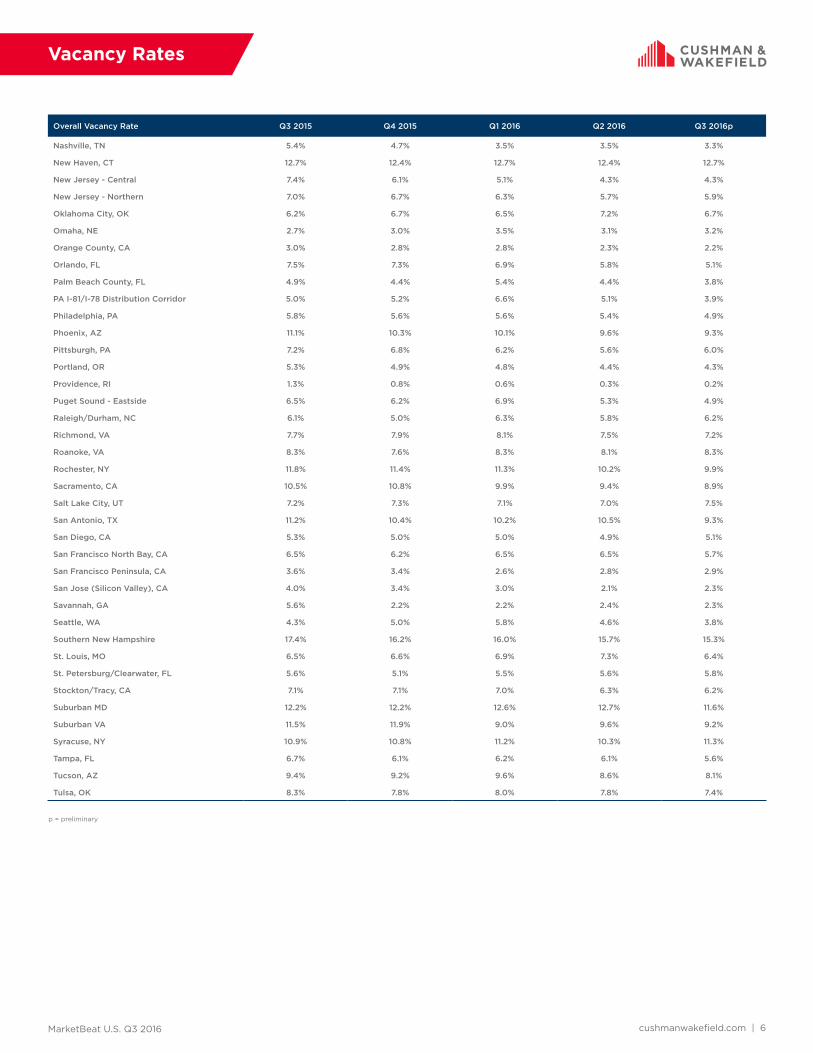

Vacancy Rates

Overall Vacancy Rate Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p

United States 5.5% 5.3% 5.3% 5.1% 5.1%

Northeast 6.2% 5.7% 5.5% 5.3% 5.3%

Midwest 5.5% 5.5% 5.4% 5.4% 5.3%

South 6.6% 6.5% 6.5% 6.2% 6.1%

West 4.0% 3.7% 3.7% 3.7% 3.7%

U.S. Industrial Report Markets Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p

Atlanta, GA 9.0% 8.7% 8.4% 7.8% 7.7%

Austin, TX 6.4% 9.5% 8.6% 9.5% 8.8%

Baltimore, MD 6.6% 7.9% 7.3% 6.9% 6.4%

Binghamton, NY 10.8% 11.3% 10.3% 9.8% 9.9%

Birmingham, AL 8.8% 11.4% 11.3% 10.8% 10.6%

Boston, MA 6.4% 6.6% 6.5% 6.4% 6.2%

Buffalo, NY 8.9% 9.2% 9.0% 8.9% 9.1%

Central Valley, CA 3.4% 3.4% 3.3% 2.8% 3.3%

Charleston, SC 6.8% 4.7% 6.0% 8.0% 8.1%

Charlotte, NC 3.6% 3.4% 3.6% 3.5% 3.4%

Chicago, IL 6.3% 6.4% 6.3% 6.7% 6.8%

Cincinnati, OH 4.2% 3.0% 3.3% 3.4% 3.2%

Cleveland, OH 4.6% 4.6% 4.2% 3.8% 3.9%

Colorado Springs, CO 10.1% 10.1% 10.0% 10.6% 10.7%

Columbus, OH 5.5% 5.6% 5.9% 5.1% 4.7%

Dallas/Ft. Worth, TX 6.9% 7.2% 6.9% 6.8% 7.0%

Dayton, OH 8.0% 7.7% 7.6% 8.2% 8.3%

Denver, CO 4.3% 4.9% 4.8% 4.8% 4.9%

Detroit, MI 4.0% 3.5% 3.5% 3.1% 2.9%

El Paso, TX 6.8% 6.8% 5.7% 5.0% 3.2%

Fort Myers/Naples, FL 2.8% 2.2% 2.0% 1.8% 1.9%

Fredericksburg, VA 7.6% 6.6% 5.3% 4.7% 5.3%

Ft. Lauderdale, FL 4.4% 4.5% 4.4% 4.0% 2.9%

Greenville, SC 6.6% 6.5% 6.2% 5.8% 5.8%

Hampton Roads, VA 6.6% 4.9% 4.7% 4.1% 4.4%

Hartford, CT 11.7% 8.1% 8.3% 8.1% 7.9%

Houston, TX 7.1% 7.0% 6.8% 6.2% 6.3%

Indianapolis, IN 3.0% 5.1% 5.1% 5.5% 5.3%

Inland Empire CA 4.4% 4.0% 4.1% 4.0% 4.1%

Jacksonville, FL 6.2% 5.6% 5.4% 4.8% 4.0%

Kansas City, MO 8.3% 8.3% 7.5% 7.1% 7.2%

Lakeland, FL 3.7% 5.1% 5.1% 3.9% 3.9%

Las Vegas, NV 5.1% 5.2% 5.4% 6.0% 6.2%

Long Island, NY 6.6% 6.8% 6.9% 6.5% 5.6%

Los Angeles, CA 1.4% 1.3% 1.2% 1.2% 1.3%

Louisville, KY 6.6% 7.2% 7.7% 8.1% 7.7%

Memphis, TN 8.7% 8.1% 8.4% 8.2% 7.8%

Miami, FL 4.3% 4.2% 5.0% 4.7% 4.7%

Milwaukee, WI 4.4% 4.5% 4.5% 3.8% 4.1%

Minneapolis, MN 8.2% 8.7% 8.7% 8.0% 8.5%

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 6

Vacancy Rates

Overall Vacancy Rate Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p

Nashville, TN 2.9% 3.2% 2.9% 3.3% 3.5%

New Haven, CT 12.6% 9.2% 9.8% 9.8% 9.5%

New Jersey - Central 4.2% 4.1% 4.3% 3.6% 3.3%

New Jersey - Northern 5.9% 5.5% 4.8% 4.6% 4.4%

Northern VA 9.2% 8.8% 8.5% 8.7% 8.4%

Oakland/East Bay, CA 2.6% 2.1% 2.3% 3.3% 3.0%

Oklahoma City, OK 7.3% 6.8% 7.5% 9.0% 9.0%

Omaha, NE 3.2% 3.1% 3.3% 3.6% 3.4%

Orange County, CA 2.0% 2.0% 1.9% 1.9% 1.9%

Orlando, FL 4.6% 5.1% 5.6% 5.5% 5.4%

Palm Beach County, FL 4.2% 3.5% 3.6% 3.3% 2.7%

PA I-81/I-78 Distribution Corridor 4.7% 5.1% 5.3% 5.3% 5.1%

Philadelphia, PA 4.2% 3.9% 3.7% 3.4% 4.0%

Phoenix, AZ 9.1% 8.9% 8.6% 8.3% 7.9%

Pittsburgh, PA 5.7% 5.7% 4.8% 4.8% 5.4%

Portland, OR 4.0% 3.9% 3.2% 3.5% 3.9%

Providence, RI 0.3% 0.2% 0.2% 0.1% 0.1%

Puget Sound - Eastside 4.7% 4.3% 4.3% 4.9% 4.7%

Raleigh/Durham, NC 5.9% 6.5% 6.2% 5.5% 6.0%

Richmond, VA 6.6% 5.0% 4.9% 3.7% 3.7%

Roanoke, VA 7.2% 8.0% 7.3% 7.1% 7.2%

Rochester, NY 9.6% 9.6% 9.0% 9.0% 9.8%

Sacramento, CA 10.8% 7.6% 7.3% 6.3% 5.9%

Salt Lake City, UT 7.2% 6.1% 5.4% 5.8% 5.6%

San Antonio, TX 9.6% 9.1% 8.2% 8.0% 8.8%

San Diego, CA 5.3% 5.1% 5.1% 4.8% 4.8%

San Francisco North Bay, CA 5.5% 5.1% 5.2% 4.8% 4.6%

San Francisco Peninsula, CA 2.6% 2.6% 2.1% 2.1% 2.0%

San Jose (Silicon Valley), CA 3.3% 3.0% 3.4% 3.6% 3.2%

Savannah, GA 3.0% 3.0% 3.2% 3.2% 1.2%

Seattle, WA 3.8% 3.4% 3.7% 4.2% 4.1%

Southern New Hampshire 15.7% 6.3% 6.8% 7.5% 8.2%

St. Louis, MO 7.0% 6.7% 6.8% 6.7% 6.0%

St. Petersburg/Clearwater, FL 4.7% 4.1% 4.0% 3.5% 3.6%

Suburban MD 10.7% 9.9% 10.5% 10.4% 9.7%

Syracuse, NY 10.6% 10.7% 9.9% 8.8% 8.8%

Tampa, FL 5.5% 5.0% 5.4% 5.2% 5.3%

Tucson, AZ 7.8% 7.4% 7.1% 8.2% 6.6%

Tulsa, OK 7.6% 8.8% 9.1% 8.9% 8.9%

p = preliminary

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 7

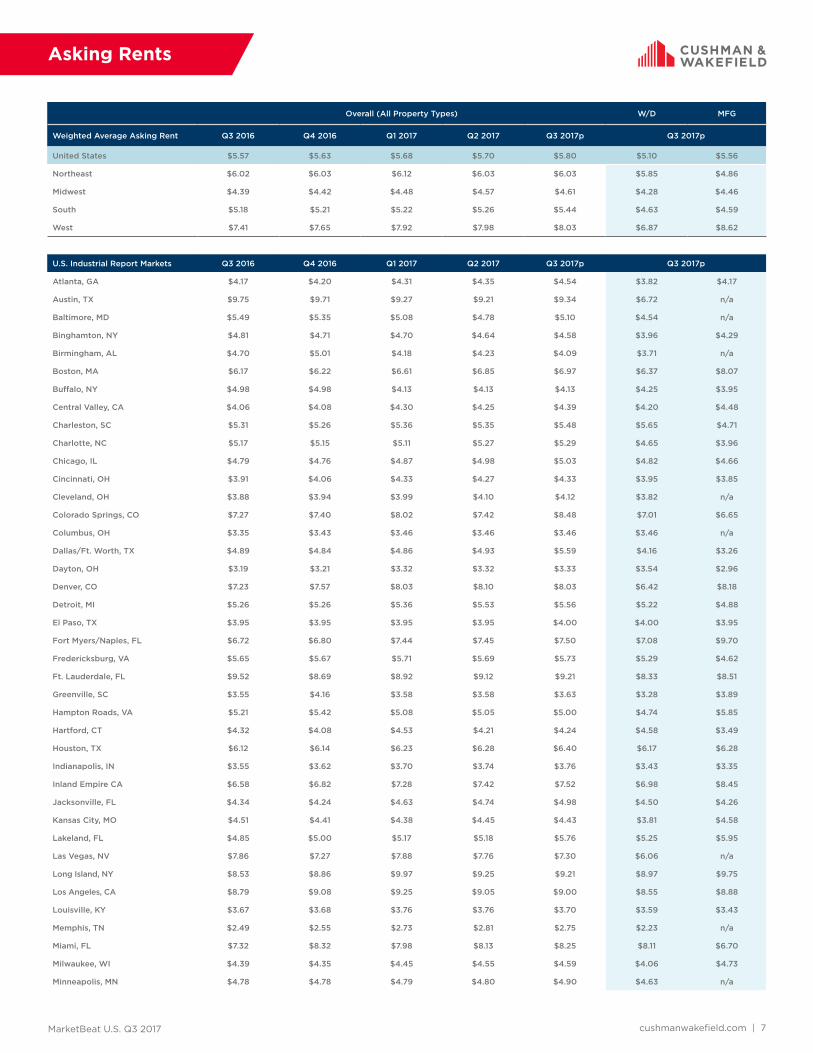

Asking Rents

Overall (All Property Types) W/D MFG

Weighted Average Asking Rent Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

United States $5.63 $5.66 $5.69 $5.80 $5.84 $5.18 $5.62

Northeast $6.03 $6.12 $6.03 $6.03 $6.19 $6.02 $4.97

Midwest $4.42 $4.48 $4.57 $4.61 $4.61 $4.31 $4.46

South $5.21 $5.22 $5.26 $5.45 $5.41 $4.66 $4.73

West $7.65 $7.82 $7.89 $7.95 $8.11 $7.00 $8.60

U.S. Industrial Report Markets Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

Atlanta, GA $4.20 $4.31 $4.35 $4.54 $4.47 $3.80 $4.17

Austin, TX $9.71 $9.27 $9.21 $9.34 $9.24 $6.86 $8.40

Baltimore, MD $5.35 $5.08 $4.78 $5.10 $5.70 $5.14 n/a

Binghamton, NY $4.71 $4.70 $4.64 $4.58 $4.57 $4.09 $4.29

Birmingham, AL $5.01 $4.18 $4.23 $4.09 $4.02 $3.71 n/a

Boston, MA $6.22 $6.61 $6.85 $6.97 $8.17 $7.13 $9.42

Buffalo, NY $4.98 $4.13 $4.13 $4.13 $4.13 $4.25 $3.95

Central Valley, CA $4.08 $4.32 $4.25 $4.24 $4.75 $4.65 $5.13

Charleston, SC $5.26 $5.36 $5.35 $5.48 $5.52 $5.56 $4.70

Charlotte, NC $5.15 $5.11 $5.27 $5.42 $5.21 $4.67 $3.94

Chicago, IL $4.76 $4.87 $4.98 $5.03 $5.08 $4.86 $4.71

Cincinnati, OH $4.06 $4.33 $4.27 $4.33 $4.25 $3.86 $3.85

Cleveland, OH $3.94 $3.99 $4.10 $4.12 $4.15 $3.85 n/a

Colorado Springs, CO $7.40 $6.78 $7.43 $7.37 $7.85 $7.16 $6.86

Columbus, OH $3.43 $3.46 $3.46 $3.46 $3.50 $3.50 n/a

Dallas/Ft. Worth, TX $4.84 $4.86 $4.93 $5.59 $5.06 $4.06 $3.85

Dayton, OH $3.21 $3.32 $3.32 $3.33 $3.26 $3.59 $2.89

Denver, CO $7.57 $8.03 $8.10 $8.03 $7.96 $6.42 $7.63

Detroit, MI $5.26 $5.36 $5.53 $5.56 $5.57 $5.24 $5.03

El Paso, TX $3.95 $3.95 $3.95 $4.00 $4.10 $4.10 $4.00

Fort Myers/Naples, FL $6.80 $7.44 $7.45 $7.50 $7.61 $6.99 $10.07

Fredericksburg, VA $5.67 $5.71 $5.69 $5.73 $5.73 $5.26 $4.62

Ft. Lauderdale, FL $8.69 $8.92 $9.12 $9.21 $9.27 $8.62 $8.62

Greenville, SC $4.16 $3.58 $3.58 $3.63 $3.60 $3.26 $3.82

Hampton Roads, VA $5.42 $5.08 $5.05 $5.00 $5.28 $5.02 $5.83

Hartford, CT $4.08 $4.53 $4.21 $4.24 $4.28 $4.62 $3.56

Houston, TX $6.14 $6.23 $6.28 $6.40 $6.44 $6.24 $6.39

Indianapolis, IN $3.62 $3.70 $3.74 $3.76 $3.80 $3.51 $3.37

Inland Empire CA $6.82 $7.28 $7.42 $7.52 $7.61 $6.89 $8.01

Jacksonville, FL $4.24 $4.63 $4.74 $4.98 $5.37 $4.82 $5.96

Kansas City, MO $4.41 $4.38 $4.45 $4.43 $4.27 $3.82 $4.09

Lakeland, FL $5.00 $5.17 $5.18 $5.76 $5.54 $5.01 $5.95

Las Vegas, NV $7.27 $7.14 $6.80 $6.81 $6.82 $6.45 $6.16

Long Island, NY $8.86 $9.97 $9.25 $9.21 $9.44 $9.13 $9.62

Los Angeles, CA $9.08 $9.25 $9.05 $9.00 $9.36 $8.83 $9.00

Louisville, KY $3.68 $3.76 $3.76 $3.70 $3.73 $3.68 $3.09

Memphis, TN $2.55 $2.73 $2.81 $2.75 $2.75 $2.14 n/a

Miami, FL $8.32 $7.98 $8.13 $8.25 $8.45 $8.44 $6.43

Milwaukee, WI $4.35 $4.45 $4.55 $4.59 $4.64 $3.92 $4.87

Minneapolis, MN $4.78 $4.79 $4.80 $4.90 $4.88 $4.63 n/a

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 8

Asking Rents

p = preliminary

Overall (All Property Types) W/D MFG

Weighted Average Asking Rent Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017p Q4 2017p

Nashville, TN $4.07 $4.18 $5.14 $5.03 $5.09 $5.01 $4.09

New Haven, CT $5.24 $5.33 $4.62 $5.15 $5.35 $4.80 $5.33

New Jersey - Central $7.28 $7.31 $7.40 $7.39 $7.58 $6.84 $5.70

New Jersey - Northern $7.90 $7.60 $7.78 $7.82 $8.56 $8.41 $8.21

Northern VA $11.12 $11.15 $11.16 $11.12 $11.36 $9.16 n/a

Oakland/East Bay, CA $9.01 $9.12 $10.17 $10.10 $10.43 $9.74 $11.21

Oklahoma City, OK $4.61 $4.86 $4.98 $4.95 $4.95 n/a n/a

Omaha, NE $5.41 $5.63 $5.57 $5.57 $5.55 $4.91 n/a

Orange County, CA $11.21 $11.10 $11.40 $10.74 $11.24 $10.06 $10.35

Orlando, FL $6.48 $6.32 $6.29 $6.38 $6.48 $5.64 $5.59

Palm Beach County, FL $10.71 $11.12 $10.62 $10.56 $10.69 $9.65 $9.64

PA I-81/I-78 Distribution Corridor $4.64 $4.72 $4.74 $4.75 $4.77 $4.78 $4.25

Philadelphia, PA $4.63 $4.81 $4.95 $4.58 $4.51 $4.10 $3.43

Phoenix, AZ $7.05 $7.03 $6.80 $6.80 $6.70 $5.02 $7.57

Pittsburgh, PA $7.84 $7.54 $7.09 $7.68 $7.58 $5.55 $4.69

Portland, OR $8.02 $7.73 $8.34 $8.38 $8.50 $7.15 $7.74

Providence, RI $4.85 $4.85 $4.85 $4.85 $4.85 $4.70 N/A

Puget Sound - Eastside $11.62 $12.27 $12.12 $12.24 $11.76 $10.29 $8.27

Raleigh/Durham, NC $6.99 $7.28 $7.50 $7.71 $8.70 $5.78 $8.64

Richmond, VA $4.72 $4.70 $4.80 $5.03 $4.92 $4.33 $4.16

Roanoke, VA $4.32 $4.43 $4.76 $4.99 $4.98 $4.50 $6.83

Rochester, NY $4.84 $4.84 $4.84 $4.84 $4.84 $3.25 $4.75

Sacramento, CA $4.55 $4.66 $4.93 $5.08 $5.06 $4.97 $5.63

Salt Lake City, UT $5.45 $5.37 $5.49 $5.64 $5.82 $5.34 $5.79

San Antonio, TX $5.98 $5.79 $5.79 $5.75 $5.79 $4.98 n/a

San Diego, CA $12.12 $12.00 $11.76 $11.88 $12.36 $9.00 $11.16

San Francisco North Bay, CA $10.23 $9.97 $11.54 $11.97 $11.69 $11.70 $14.26

San Francisco Peninsula, CA $14.12 $14.72 $16.18 $16.42 $17.72 $16.85 $21.28

San Jose (Silicon Valley), CA $12.60 $12.00 $12.48 $12.12 $13.20 $12.24 $13.80

Savannah, GA $4.75 $4.75 $4.69 $4.69 $4.62 $4.33 n/a

Seattle, WA $6.73 $7.15 $7.38 $7.45 $7.61 $7.07 $5.90

Southern New Hampshire $5.53 $5.90 $5.72 $5.62 $5.79 $5.00 $5.36

St. Louis, MO $4.39 $4.45 $4.58 $4.62 $4.47 $4.19 $7.17

St. Petersburg/Clearwater, FL $7.72 $7.93 $8.05 $7.99 $8.12 $5.84 $6.69

Suburban MD $9.57 $10.11 $9.36 $9.21 $9.37 $7.69 n/a

Syracuse, NY $3.83 $3.85 $4.07 $4.08 $4.02 $4.28 $3.25

Tampa, FL $6.10 $6.15 $5.77 $5.85 $5.72 $5.00 $4.20

Tucson, AZ $6.67 $6.44 $6.29 $6.37 $6.23 $6.17 $5.08

Tulsa, OK $4.52 $4.52 $4.53 $4.54 $4.54 n/a n/a

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 9

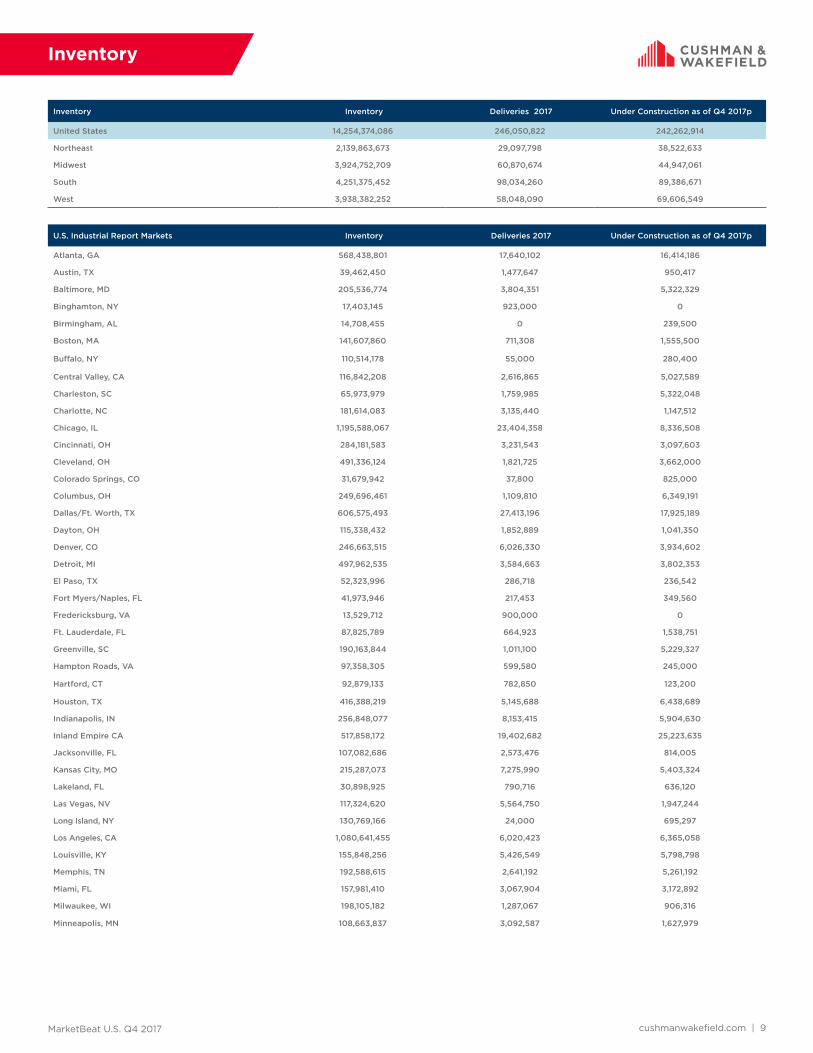

Inventory

Inventory Inventory Deliveries 2017 Under Construction as of Q4 2017p

United States 14,254,374,086 246,050,822 242,262,914

Northeast 2,139,863,673 29,097,798 38,522,633

Midwest 3,924,752,709 60,870,674 44,947,061

South 4,251,375,452 98,034,260 89,386,671

West 3,938,382,252 58,048,090 69,606,549

U.S. Industrial Report Markets Inventory Deliveries 2017 Under Construction as of Q4 2017p

Atlanta, GA 568,438,801 17,640,102 16,414,186

Austin, TX 39,462,450 1,477,647 950,417

Baltimore, MD 205,536,774 3,804,351 5,322,329

Binghamton, NY 17,403,145 923,000 0

Birmingham, AL 14,708,455 0 239,500

Boston, MA 141,607,860 711,308 1,555,500

Buffalo, NY 110,514,178 55,000 280,400

Central Valley, CA 116,842,208 2,616,865 5,027,589

Charleston, SC 65,973,979 1,759,985 5,322,048

Charlotte, NC 181,614,083 3,135,440 1,147,512

Chicago, IL 1,195,588,067 23,404,358 8,336,508

Cincinnati, OH 284,181,583 3,231,543 3,097,603

Cleveland, OH 491,336,124 1,821,725 3,662,000

Colorado Springs, CO 31,679,942 37,800 825,000

Columbus, OH 249,696,461 1,109,810 6,349,191

Dallas/Ft. Worth, TX 606,575,493 27,413,196 17,925,189

Dayton, OH 115,338,432 1,852,889 1,041,350

Denver, CO 246,663,515 6,026,330 3,934,602

Detroit, MI 497,962,535 3,584,663 3,802,353

El Paso, TX 52,323,996 286,718 236,542

Fort Myers/Naples, FL 41,973,946 217,453 349,560

Fredericksburg, VA 13,529,712 900,000 0

Ft. Lauderdale, FL 87,825,789 664,923 1,538,751

Greenville, SC 190,163,844 1,011,100 5,229,327

Hampton Roads, VA 97,358,305 599,580 245,000

Hartford, CT 92,879,133 782,850 123,200

Houston, TX 416,388,219 5,145,688 6,438,689

Indianapolis, IN 256,848,077 8,153,415 5,904,630

Inland Empire CA 517,858,172 19,402,682 25,223,635

Jacksonville, FL 107,082,686 2,573,476 814,005

Kansas City, MO 215,287,073 7,275,990 5,403,324

Lakeland, FL 30,898,925 790,716 636,120

Las Vegas, NV 117,324,620 5,564,750 1,947,244

Long Island, NY 130,769,166 24,000 695,297

Los Angeles, CA 1,080,641,455 6,020,423 6,365,058

Louisville, KY 155,848,256 5,426,549 5,798,798

Memphis, TN 192,588,615 2,641,192 5,261,192

Miami, FL 157,981,410 3,067,904 3,172,892

Milwaukee, WI 198,105,182 1,287,067 906,316

Minneapolis, MN 108,663,837 3,092,587 1,627,979

MarketBeat U.S. Q4 2017 cushmanwakefield.com | 10

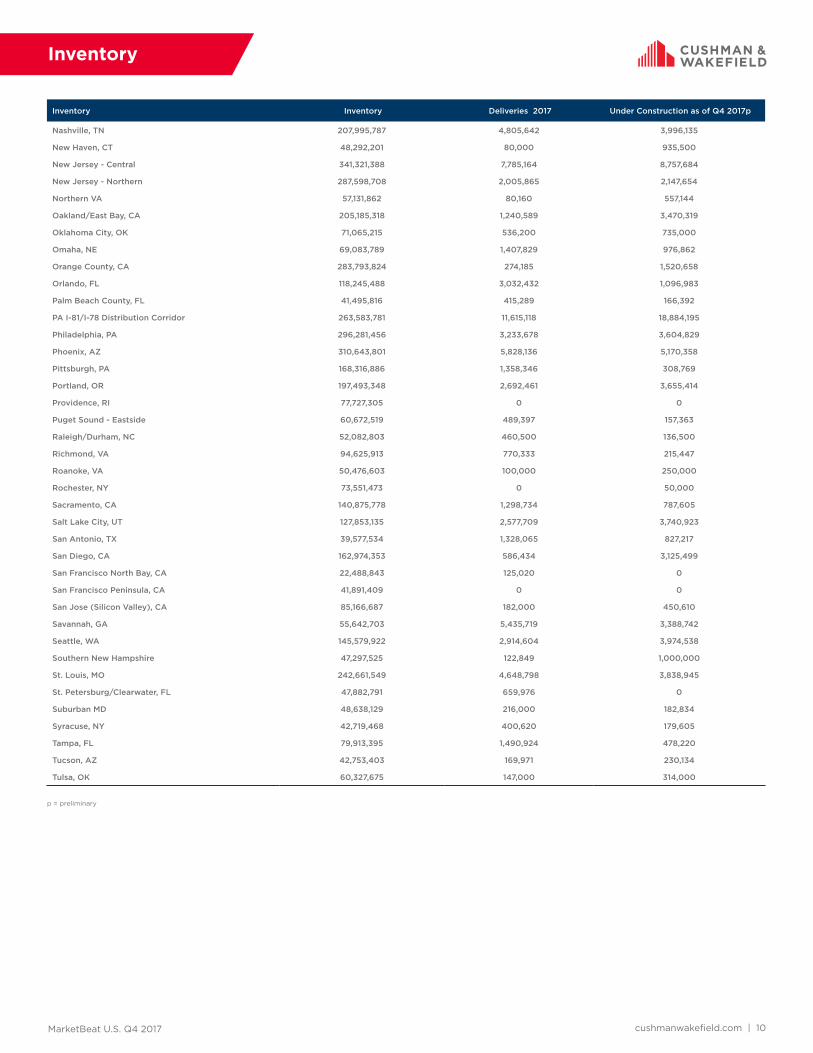

Inventory

Inventory Inventory Deliveries 2017 Under Construction as of Q4 2017p

Nashville, TN 207,995,787 4,805,642 3,996,135

New Haven, CT 48,292,201 80,000 935,500

New Jersey - Central 341,321,388 7,785,164 8,757,684

New Jersey - Northern 287,598,708 2,005,865 2,147,654

Northern VA 57,131,862 80,160 557,144

Oakland/East Bay, CA 205,185,318 1,240,589 3,470,319

Oklahoma City, OK 71,065,215 536,200 735,000

Omaha, NE 69,083,789 1,407,829 976,862

Orange County, CA 283,793,824 274,185 1,520,658

Orlando, FL 118,245,488 3,032,432 1,096,983

Palm Beach County, FL 41,495,816 415,289 166,392

PA I-81/I-78 Distribution Corridor 263,583,781 11,615,118 18,884,195

Philadelphia, PA 296,281,456 3,233,678 3,604,829

Phoenix, AZ 310,643,801 5,828,136 5,170,358

Pittsburgh, PA 168,316,886 1,358,346 308,769

Portland, OR 197,493,348 2,692,461 3,655,414

Providence, RI 77,727,305 0 0

Puget Sound - Eastside 60,672,519 489,397 157,363

Raleigh/Durham, NC 52,082,803 460,500 136,500

Richmond, VA 94,625,913 770,333 215,447

Roanoke, VA 50,476,603 100,000 250,000

Rochester, NY 73,551,473 0 50,000

Sacramento, CA 140,875,778 1,298,734 787,605

Salt Lake City, UT 127,853,135 2,577,709 3,740,923

San Antonio, TX 39,577,534 1,328,065 827,217

San Diego, CA 162,974,353 586,434 3,125,499

San Francisco North Bay, CA 22,488,843 125,020 0

San Francisco Peninsula, CA 41,891,409 0 0

San Jose (Silicon Valley), CA 85,166,687 182,000 450,610

Savannah, GA 55,642,703 5,435,719 3,388,742

Seattle, WA 145,579,922 2,914,604 3,974,538

Southern New Hampshire 47,297,525 122,849 1,000,000

St. Louis, MO 242,661,549 4,648,798 3,838,945

St. Petersburg/Clearwater, FL 47,882,791 659,976 0

Suburban MD 48,638,129 216,000 182,834

Syracuse, NY 42,719,468 400,620 179,605

Tampa, FL 79,913,395 1,490,924 478,220

Tucson, AZ 42,753,403 169,971 230,134

Tulsa, OK 60,327,675 147,000 314,000

p = preliminary

Methodology

Cushman & Wakefield’s quarterly estimates are derived from a variety of data sources, including its own proprietary database, and historical data from third party data sources. The market statistics are calculated from a base building inventory made up of industrial properties deemed to be competitive in the local industrial markets. Generally, owner-occupied and federally-owned buildings are not included. Older buildings unfit for occupancy or ones that require substantial renovation before tenancy are generally not included in the competitive inventory. The inventory is subject to revisions due to resampling. Vacant space is defined as space that is available immediately or imminently after the end of the quarter. Sublet space still occupied by the tenant is not counted as available space. The figures provided for the current quarter are preliminary, and all information contained in the report is subject to correction of errors and revisions based on additional data received.

Regional Map

WestMidwestSouthNortheast

Jason Tolliver Head of Logistics &Industrial Research Americas Tel: +1 317.639.0549 cushmanwakefield.com

Explanation of Terms

Total Inventory: The total amount of industrial space (in buildings of a

predetermined size by market) that can be rented by a third party.

Overall Vacancy Rate: The amount of unoccupied space (new, relet, and

sublet) expressed as a percentage of total inventory.

Absorption: The net change in occupied space between two points in time.

(Total occupied space in the present quarter minus total occupied space from

the previous quarter, quoted on a net, not gross, basis.)

Leasing Activity: The sum of all leases over a period of time. This includes

pre-leasing activity as well as expansions. It does not include renewals.

Overall Weighted Asking Rents: NNN average asking rents weighted by the

amount of available direct and sublease space in industrial properties.

W/D: Warehouse and or distribution properties.

MFG: Manufacturing properties.

About Cushman & Wakefield

Cushman & Wakefield is a leading global real estate services firm with 45,000 employees in more than 70 countries helping occupiers and investors optimize the value of their real estate. Cushman & Wakefield is among the largest commercial real estate services firms with revenue of $6 billion across core services of agency leasing, asset services, capital markets, facility services (C&W Services), global occupier services, investment & asset management (DTZ Investors), project & development services, tenant representation, and valuation & advisory. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

Cushman & Wakefield Copyright 2018. No warranty or representation, express or implied, is made to the accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any special listing conditions imposed by the property owner(s). As applicable, we make no representation as to the condition of the property (or properties) in question.

Carolyn Salzer Analyst, Logistics & Industrial Research Americas Tel: +1 847.518.3212 cushmanwakefield.com

cushmanwakefield.com | 1

U.S. IndustrialQ3 2017

MARKETBEAT

U.S. INDUSTRIAL

Overall Vacancy

Net Absorption/Rent NNN 4-QTR TRAILING AVERAGE

Market Indicators

Q3 16 Q3 17 12-Month Forecast

Overall Vacancy 5.5% 5.1%

Net Absorption 78.5M 66.5M

Under Construction 214.6M 233.1M

Weighted Asking Rent (NNN) $5.57 $5.80

Rent Growth (Yr/Yr % Chg.) 5.1% 4.1%

Employment IndicatorsQ3 16 Q3 17 12-Month

Forecast

Total Nonfarm Employment 144.7M 146.6M

Industrial Employment 25.2M 25.6M

Unemployment 4.9% 4.3%

$4.00

$4.50

$5.00

$5.50

$6.00

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016 2017 2018Net Absorption, MSF Weighted Asking Rent, $ PSF

Forecast

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2013 2014 2015 2016 2017 2018

Historical Average = 8.2%

Forecast

Strong Occupier Demand Surmounts Wave of Historic Supply

Another Solid Year for Industrial: 175.1 million square feet (msf) of new deliveries have hit the market through the first three quarters of 2017, the largest wave of new space delivered in the first nine months of any year. Even so, industrial tenants have absorbed 187.4 msf of space, pushing the vacancy rate downward by 40 basis points (bps) year-over-year to a historic low of 5.1%. Average industrial asking rents for all product types have risen by 4.1% year-over-year to a new high of $5.80 per square foot (psf). Every industrial segment remains in growth mode with warehousing posting 167.2 msf of net absorption, manufacturing registering 11.3 msf of growth, and flex product experiencing 4.8 msf of net occupancy gains from January through September of this year.

Bigger the Market, Bigger the Leasing and Development: The U.S. industrial market remains on track to eclipse 230 msf of absorption for a fourth consecutive year. Considering that the annual average since 2010 has been 196.8 msf, 2017 will undoubtedly be another solid year. Over one-third of year-to-date absorption is attributable to five core markets: Dallas/Ft. Worth, Atlanta, Inland Empire, Chicago, and the Pennsylvania I-81/I-78 Distribution Corridor—an indication that, despite widespread occupancy gains, the bulk of activity remains concentrated in primary industrial cities. This is also the case with industrial development, as these same five markets account for over one-third of both year-to-date deliveries and product currently under construction.

Strong Fundamentals in Secondary Markets: Strengthening fundamentals in secondary markets have given rise to solid occupancy growth in Kansas City, Greenville, Baltimore, Phoenix, and Cincinnati, among other markets. Over 30 secondary markets have registered more than 1 msf of net absorption through Q3 2017. Notably, average annual rent growth for warehouse space is forecast to be stronger in secondary markets (5.5%) than in primary ones (4.8%) in 2017, although rent growth will be historically strong in both.

Supply Not Overpowering Demand: The construction pipeline is at its highest level this cycle. Despite the increase, supply and demand remain in relative equilibrium in most markets. Speculative projects account for 121.6 msf (or 69.5%) of year-to-date deliveries, and given the tight market, developers continue to break ground. Currently, there is 233.1 msf under construction, of which 150.9 msf is speculative. The greatest concentration of speculative projects is in the South and West regions (52.4 msf and 50.8 msf, respectively). Nationally, 34 markets have over 1 msf of speculative product in the pipeline, but in over half of them, vacancy rates continue to tighten, indicating a need for new supply.

Rents Continue to Run: Strong leasing activity by both traditional industrial users and eCommerce-related occupiers continues to fuel rent growth. U.S. average annual industrial warehouse asking rents have increased 23.7% since 2010, and in Q3 2017 rose 4.5% year-over-year to $5.10 psf. Among the regions, year-over-year rent growth in Q3 2017 was strongest in the West (8.4%), followed by the Midwest (5.0%) and the South (4.9%). Rents in the Northeast were virtually unchanged (0.2%). Asking rents increased quarter-over-quarter in 48 of the 79 markets tracked by Cushman & Wakefield, with the most notable increases occurring in coastal markets where a lack of available space and fierce competition are pushing rents higher.

Source: Cushman & Wakefield Research

Source: BLS

cushmanwakefield.com | 2

U.S. IndustrialQ3 2017

MARKETBEAT

Solid Demand in Primary and Secondary Markets YEAR-TO-DATE NET ABSORPTION (MSF)

Few Signs of Overbuilding YEAR-TO-DATE DELIVERIES BY TYPE: (MSF), VACANCY (YOY CHG, BPS)

New Demand Reflects eCommerce Dominance/Rise Q1 2008 = 100

Outlook• Logistics-related leasing will continue to benefit from solid

economic fundamentals that spur increased consumer spending.

• Net absorption will eclipse 230 msf for a fourth year in a row, and will reach 218 msf in 2018.

• Increased speculative supply will place upward pressure on vacancy as supply/demand begin to slowly rebalance in Q4 2017. We forecast average annual vacancy to rise 30 bps in 2018 to 5.3% for all industrial product types.

• Look for continued rental rate appreciation in Q4 2017, with rent growth slowly beginning to decelerate in 2018. We anticipate average annual rent gains of 3.7% in 2017, and 2.9% in 2018, for all industrial product types.

Source: U.S. Census Bureau, Cushman & Wakefield Research

Source: Cushman & Wakefield Research

Source: Cushman & Wakefield Research

U.S. Economy Powers Through Headwinds

Continued Growth on Horizon: The expansion is sailing forward despite economic uncertainty spurred by multiple hurricanes this season. Although weather snapped the 83-month streak of consecutive job gains, with firms shedding 33,000 nonfarm payrolls in September, it is important not to read too much into a single monthly report. We expect hiring to bounce back. On another positive note, the Institute for Supply Management’s (ISM) Purchasing Managers’ Index—a measure of the manufacturing sector’s health—rose to 60.8 in September, its highest reading since 2004. Seventeen of the 18 manufacturing industries the ISM tracks reported growth while the new orders component rose to a multi-year high (64.6). Those results suggest that the manufacturing sector will continue to churn out goods and drive related logistics demand in the months ahead.

Bustling Ports and Busy Railroads: Other important indicators that correlate well with the industrial sector, such as containerized retail imports, intermodal rail volume, and consumer spending, also continue to trend in a positive direction. Ports are bustling. In August 2017 (the most recent month for which data is available), U.S. retail container ports collectively handled 1.80 million TEUs—the highest monthly containerized import volume on record—surpassing the previous high of 1.78 million TEUs set one month earlier in July. This places Q3 2017 among the strongest quarters ever for containerized retail import activity. Railroads are also setting records. Average weekly intermodal rail volume in September was the second highest ever (behind 2015), with the last two weeks of that month the strongest in the history of U.S. railroads.

Confident Consumers Bode Well for Logistics: Consumer sentiment and spending also bode well for logistics and industrial demand. We anticipate consumer spending to grow by 2.7% in 2017, the same rate as last year, a pace that has translated into strong eCommerce-driven leasing fundamentals. Since the second quarter of 2016, eCommerce sales are up by more than 16%, the highest rate in five years. Retail sales are expected to pick up as we head into a holiday season that could be the best one in years. We anticipate overall retail sales will grow by 3.8% in 2017, compared to 3.0% in 2016, before accelerating to 4.1% in 2018.

02468

1012141618

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000 eCommerce Sales Index (RHS)Cumulative Retail Space Demand IndexCumulative Industrial Space Demand Index

0

4

8

12

16

20

Speculative Build-to-Suit

+60 – YoY change in vacancy, basis points

-80 +20-70

+140

-70 +50 -30 +190 +190 -100 +90 0 -50 +20 -10 +40 +30 -150 -100

MarketBeat U.S. Q3 2017 cushmanwakefield.com | 3

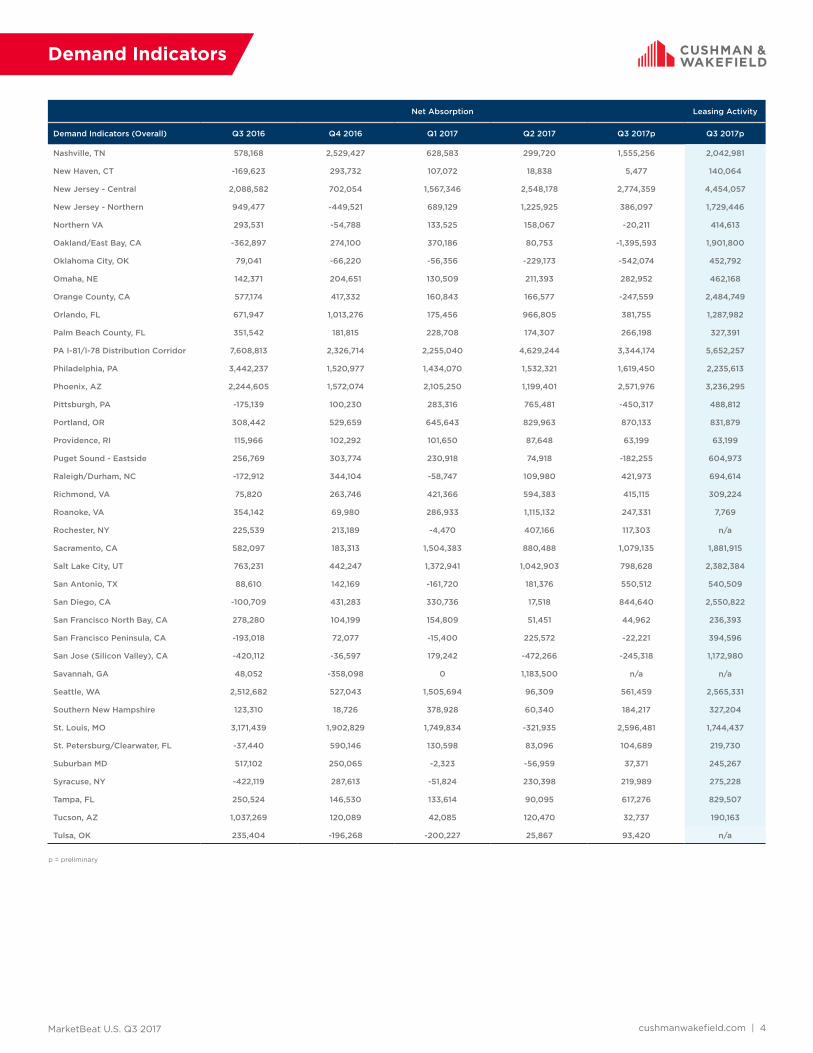

Net Absorption Leasing Activity

Demand Indicators (Overall) Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017p Q3 2017p

United States 78,483,313 63,129,827 58,229,698 62,638,053 66,513,919 118,981,266

Northeast 17,790,157 7,233,913 5,748,978 12,011,270 8,472,310 17,159,732

Midwest 23,968,635 15,788,785 13,095,694 12,254,016 15,432,229 18,697,924

South 21,353,134 27,857,093 24,562,079 26,155,357 24,810,369 39,194,870

West 15,371,387 12,250,036 14,822,947 12,217,410 17,799,011 43,928,740

U.S. Industrial Report Markets Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017p Q3 2017p

Atlanta, GA 2,245,312 3,546,425 6,399,144 6,264,777 3,648,731 6,414,640

Austin, TX 80,659 116,610 -209,019 134,562 -310,320 516,135

Baltimore, MD 1,029,640 944,082 506,693 2,913,206 2,573,184 1,778,967

Binghamton, NY 80,204 8,605 99,383 80,590 40,000 40,000

Birmingham, AL 826,217 33,863 -340,522 12,600 70,051 174,362

Boston, MA 2,190,787 996,083 -267,560 116,651 -141,078 351,738

Buffalo, NY 500,257 1,217,645 -952,685 94,497 164,966 288,683

Central Valley, CA 971,895 2,031,463 -421,586 90,068 647,686 994,709

Charleston, SC -42,512 1,001,344 1,211,292 -273,598 -182,081 418,901

Charlotte, NC 1,158,781 1,812,029 756,188 1,145,159 332,705 n/a

Chicago, IL 10,474,949 4,149,725 3,051,662 7,466,514 3,612,071 3,330,265

Cincinnati, OH 1,833,726 556,179 4,407,420 199,615 426,950 1,217,160

Cleveland, OH 331,032 1,187,461 180,990 739,053 119,114 749,456

Colorado Springs, CO -97,504 -160,026 -54,690 29,210 651,506 234,241

Columbus, OH 1,349,355 2,080,666 193,936 -195,634 1,426,826 2,672,048

Dallas/Ft. Worth, TX 7,200,702 5,298,286 6,771,134 5,587,211 4,758,387 5,541,158

Dayton, OH 306,394 525,747 971,866 204,599 -499,194 135,682

Denver, CO 746,413 596,022 161,477 1,272,015 1,537,380 1,690,291

Detroit, MI 1,070,776 985,441 -59,666 89,640 1,311,972 1,477,521

El Paso, TX -293,711 -78,692 76,000 357,161 376,794 1,178,035

Fort Myers/Naples, FL 272,489 206,876 218,558 191,401 -31,237 92,915

Fredericksburg, VA 189,844 173,790 -130,887 176,438 73,387 53,081

Ft. Lauderdale, FL 702,011 858,893 570,792 49,340 179,962 870,828

Greenville, SC 1,560,194 1,353,175 1,784,144 1,856,762 2,373,548 637,388

Hampton Roads, VA -3,892 -359,777 473,881 1,001,321 724,245 291,335

Hartford, CT 866,772 125,862 183,652 261,345 27,817 412,282

Houston, TX 810,247 4,065,736 1,288,474 603,380 2,771,280 6,031,173

Indianapolis, IN 3,108,214 1,848,702 381,033 424,423 2,130,644 3,509,689

Inland Empire CA 3,784,917 3,636,653 4,238,816 3,666,936 7,042,746 11,816,138

Jacksonville, FL 239,728 161,043 288,006 442,976 1,484,796 255,831

Kansas City, MO 1,134,989 1,840,583 2,449,729 2,756,998 1,667,542 2,897,265

Lakeland, FL 231,791 93,900 300,673 -6,466 336,566 832,390

Las Vegas, NV 698,467 955,129 540,804 1,813,670 1,481,844 n/a

Long Island, NY 365,094 -230,288 -74,069 -47,352 233,960 701,149

Los Angeles, CA 1,783,386 250,202 1,770,796 1,031,454 1,727,125 8,759,081

Louisville, KY 491,942 322,851 502,185 56,395 1,219,602 2,138,200

Memphis, TN 695,753 3,011,967 1,719,834 1,219,093 486,717 3,463,589

Miami, FL 624,408 438,808 716,099 -272,557 128,146 1,133,563