trinity capital inc

TRANSCRIPT

PROSPECTUS

Trinity Capital Inc.7,375,274 Shares of Common Stock

We are a specialty lending company that provides debt, including loans and equipment financings, to growth stage companies, including venture-backed companies andcompanies with institutional equity investors. We define “growth stage companies” as companies that have significant ownership and active participation by sponsors, such as institutionalinvestors or private equity firms, and annual revenues of up to $100 million.

We are an internally managed, closed-end, non-diversified management investment company that has elected to be regulated as a business development company (“BDC”)under the Investment Company Act of 1940, as amended (the “1940 Act”). We intend to elect to be treated, and intend to qualify annually thereafter, as a regulated investmentcompany (“RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”), for U.S. federal income tax purposes. As a BDC and a RIC, we are required to comply withcertain regulatory requirements. See “Regulation” and “Certain U.S. Federal Income Tax Considerations.”

Our investment objective is to generate current income and, to a lesser extent, capital appreciation through our investments. We seek to achieve our investment objective bymaking investments consisting primarily of term loans and equipment financings and, to a lesser extent, working capital loans, equity and equity-related investments. In addition, wemay obtain warrants or contingent exit fees at funding from many of our portfolio companies, providing an additional potential source of investment returns.

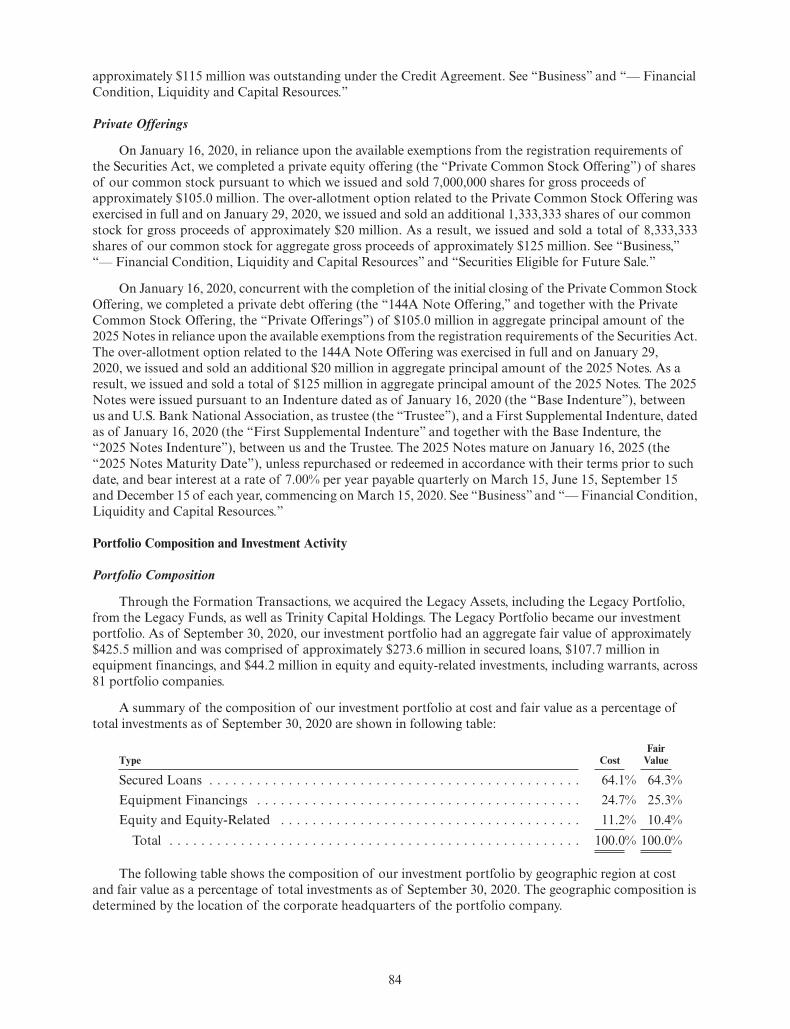

As of September 30, 2020, our investment portfolio had an aggregate fair value of approximately $425.5 million and was comprised of approximately $273.6 million in securedloans, $107.7 million in equipment financings, and $44.2 million in equity and equity-related investments, including warrants, across 81 portfolio companies.

We primarily target investments in growth stage companies that have generally completed product development and are in need of capital to fund revenue growth. Our loansand equipment financings range from $2 million to $30 million. We are not limited to investing in any particular industry or geographic area and seek to invest in under-financedsegments of the private credit markets. The debt in which we invest typically is not rated by any rating agency, but if these instruments were rated, they would likely receive a rating ofbelow investment grade (that is, below BBB- or Baa3), which is often referred to as “high yield” or “junk.” As of September 30, 2020, the debt, including loans and equipment financings,in our portfolio had a weighted average time to maturity of approximately 2.9 years.

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”). As a result, we are subject to reduced publiccompany reporting requirements and intend to take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act.

This is our initial public offering of our shares of common stock, par value $0.001 per share, pursuant to which we are offering 6,900,000 shares of our common stock. Inaddition, this prospectus relates to 475,274 shares of our common stock (the “Secondary Shares”) that may be sold by the selling stockholders identified under “Selling Stockholders”(the “Selling Stockholders”). We will not receive any of the proceeds from the sale of the Secondary Shares by the Selling Stockholders.

Our shares of common stock have no history of public trading. Our common stock has been approved for listing on the Nasdaq Global Select Market under the symbol “TRIN”.

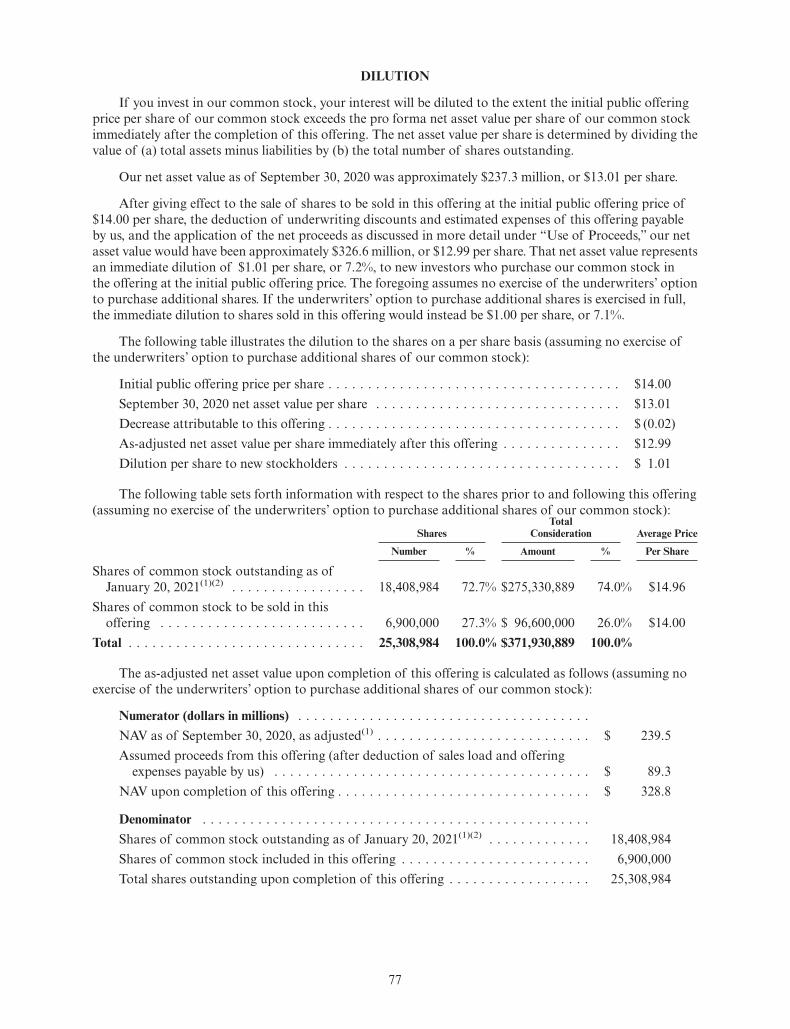

The initial public offering price per share of our common stock is $14.00 per share. At the initial public offering price of $14.00 per share, purchasers in this offering willexperience dilution of approximately $1.01 per share. See “Dilution” for more information. The net asset value per share of our common stock as of September 30, 2020 was $13.01.

Investing in our common stock involves a high degree of risk, including credit risk and the risk of the use of leverage, and is highly speculative. In addition, shares of closed-endinvestment companies, including BDCs, frequently trade at a discount to their net asset values. If shares of our common stock trade at a discount to our net asset value, purchasers in thisoffering will face increased risk of loss. Before buying any shares of our common stock, you should read the discussion of the material risks of investing in our common stock, including therisk of leverage, in “Risk Factors” beginning on page 20 of this prospectus.

This prospectus contains important information you should know before investing in our common stock. Please read this prospectus before investing and keep it for futurereference. We also file periodic and current reports, proxy statements and other information about us with the U.S. Securities and Exchange Commission (the “SEC”). This informationis available free of charge by contacting us at 3075 West Ray Road, Suite 525, Chandler, Arizona 85226, calling us at (480) 374-5350 or visiting our corporate website located atwww.trincapinvestment.com. Information on our website is not incorporated into or a part of this prospectus. The SEC also maintains a website at http://www.sec.gov that contains thisinformation.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation tothe contrary is a criminal offense.

Per Share TotalPublic offering price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14.00 $103,253,836Sales load (underwriting discounts and commissions)(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 0.84 $ 6,195,230Proceeds to us, before expenses(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $13.16 $ 90,804,000Proceeds to the Selling Stockholders, before expenses(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $13.16 $ 6,254,606

(1) See “Underwriting” for a more complete description of underwriting discounts and commissions.(2) We estimate that we will incur offering expenses of approximately $1.5 million, or approximately $0.22 per share, in connection with this offering of shares by us and the Selling

Stockholders.(3) We will pay the fees and expenses incident to the offer and sale of the Secondary Shares by the Selling Stockholders (excluding underwriting discounts and commissions).

We have granted the underwriters an option to purchase up to an additional 1,106,291 shares of our common stock from us, at the public offering price, less the sales load payableby us, within 30 days from the date of this prospectus. If the underwriters exercise their option in full, the total sales load will be approximately $7.1 million and total proceeds to us,before expenses, will be approximately $105.4 million.

The underwriters expect to deliver the shares of our common stock on or about February 2, 2021.

Joint Book-Running Managers

Keefe, Bruyette & WoodsA Stifel Company

Wells Fargo Securities UBS Investment Bank

Co-Managers

Janney Montgomery Scott B. Riley Securities Ladenburg Thalmann Compass Point

The date of this prospectus is January 28, 2021.

TABLE OF CONTENTS

PROSPECTUS SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1THE OFFERING SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10FEES AND EXPENSES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14SELECTED FINANCIAL DATA AND PRO FORMA FINANCIAL INFORMATION . . . . . . . 16RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . 72USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75DISTRIBUTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76DILUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101SENIOR SECURITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117PORTFOLIO COMPANIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126EXECUTIVE COMPENSATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134CERTAIN RELATIONSHIPS AND RELATED-PARTY TRANSACTIONS . . . . . . . . . . . . . . . 140CONTROL PERSONS AND PRINCIPAL STOCKHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . 142DETERMINATION OF NET ASSET VALUE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144DISTRIBUTION REINVESTMENT PLAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS . . . . . . . . . . . . . . . . . . . . . . . 147DESCRIPTION OF OUR CAPITAL STOCK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157REGULATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167SECURITIES ELIGIBLE FOR FUTURE SALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173SELLING STOCKHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179UNDERWRITING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181CUSTODIAN, TRANSFER AND DIVIDEND PAYING AGENT AND REGISTRAR . . . . . . . . 187BROKERAGE ALLOCATION AND OTHER PRACTICES . . . . . . . . . . . . . . . . . . . . . . . . . . . 187LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM . . . . . . . . . . . . . . . . . . . . . . 187AVAILABLE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187INDEX TO FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

You should rely only on the information contained in this prospectus. We have not, and the underwritershave not, authorized anyone to give you any information other than in this prospectus, and we take noresponsibility for any other information that others may give you. We are not, and the underwriters are not,making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You shouldassume that the information appearing in this prospectus is accurate only as of the date on the front cover of thisprospectus. Our business, financial condition, results of operations and prospects may have changed since thatdate. We will update these documents to reflect material changes only as required by law.

In addition, this prospectus contains statistical and market data that has been obtained from industrysources and publications. These industry sources and publications generally indicate that they have obtainedtheir information from sources believed to be reliable, but do not guarantee the accuracy and completeness oftheir information. Although we believe that these sources and publications are reliable, we do not represent thatwe have done a complete search for other industry data and you are cautioned not to give undue weight to

i

such statistical and market data as it involves many assumptions and limitations. Further, neither we nor theunderwriters in this offering have independently verified the accuracy or completeness of the statistical andmarket data obtained from industry sources and publications, and neither we nor the underwriters in this offeringtake any further responsibility for such statistical and market data. Forward-looking information obtainedfrom these sources and publications is subject to the same qualifications and the additional uncertaintiesregarding the other forward-looking statements contained in this prospectus.

ii

PROSPECTUS SUMMARY

This summary highlights some of the information in this prospectus. It is not complete and may notcontain all of the information that you may want to consider before investing in our common stocks. You shouldread our entire prospectus before investing in our common stock.

Throughout this prospectus, except where the context suggests otherwise:

• the terms “we,” “us,” “our,” “Trinity’’ and “Company” refer, collectively, to the Legacy Funds (asdefined below) and their respective subsidiaries, general partners, managers and managing members, asapplicable prior to the consummation of the Formation Transactions (as defined below) and TrinityCapital Inc. after the consummation of the Formation Transactions; and

• “Legacy Funds” refers collectively to Trinity Capital Investment, LLC (“TCI”), Trinity CapitalFund II, L.P. (“Fund II”), Trinity Capital Fund III, L.P. (“Fund III”), Trinity Capital Fund IV, L.P.(“Fund IV”) and Trinity Sidecar Income Fund, L.P. (“Sidecar Fund”) and their respective subsidiaries,general partners, managers and managing members, as applicable.

Trinity Capital Inc.

Overview

Trinity Capital Inc., a Maryland corporation, provides debt, including loans and equipment financings,to growth stage companies, including venture-backed companies and companies with institutional equityinvestors. Our investment objective is to generate current income and, to a lesser extent, capital appreciationthrough our investments. We seek to achieve our investment objective by making investments consistingprimarily of term loans and equipment financings and, to a lesser extent, working capital loans, equity andequity-related investments. Our equipment financings involve loans for general or specific use, includingacquiring equipment, that are secured by the equipment or other assets of the portfolio company. Inaddition, we may obtain warrants or contingent exit fees at funding from many of our portfolio companies,providing an additional potential source of investment returns. The warrants entitle us to purchasepreferred or common ownership shares of a portfolio company, and we typically target the amount of suchwarrants to scale in proportion to the amount of the debt or equipment financing. Contingent exit feesare cash fees payable upon the consummation of certain trigger events, such as a successful change of controlor initial public offering of the portfolio company. See “Business — Investment Philosophy, Strategy andPurpose.”

We target investments in growth stage companies, which are typically private companies, includingventure-backed companies and companies with institutional equity investors. We define “growth stagecompanies” as companies that have significant ownership and active participation by sponsors, such asinstitutional investors or private equity firms, and annual revenues of up to $100 million. Subject to therequirements of the Investment Company Act of 1940, as amended (the “1940 Act”), we are not limited toinvesting in any particular industry or geographic area and seek to invest in under-financed segments of theprivate credit markets. The debt in which we invest typically is not rated by any rating agency, but if theseinstruments were rated, they would likely receive a rating of below investment grade (that is, below BBB- orBaa3), which is often referred to as “high yield” or “junk.”

We primarily seek to invest in loans and equipment financings to growth stage companies that havegenerally completed product development and are in need of capital to fund revenue growth. We believe alack of profitability often limits these companies’ ability to access traditional bank financing, and our in-houseengineering and operations experience allows us to better understand this risk and earn what we believe tobe higher overall returns and better risk-adjusted returns than those associated with traditional bank loans.

Our loans and equipment financings range from $2 million to $30 million. We believe investments ofthis scale are generally sufficient to support near-term growth needs of most growth stage companies. Wegenerally limit each loan and equipment financing to approximately five percent or less of our total assets. Weseek to structure our loans and equipment financings such that amortization of the amount investedquickly reduces our risk exposure. Leveraging the experience of our investment professionals, we seek to

1

target companies at their growth stage of development and to identify financing opportunities ignored bythe traditional direct lending community.

As of September 30, 2020, our investment portfolio had an aggregate fair value of approximately$425.5 million and was comprised of approximately $273.6 million in secured loans, $107.7 million inequipment financings, and $44.2 million in equity and equity-related investments, including warrants, across81 portfolio companies. See “Business” and “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” for additional information.

We are an internally managed, closed-end, non-diversified management investment company that haselected to be regulated as a business development company (“BDC”) under the 1940 Act. We intend to electto be treated, and intend to qualify annually, as a regulated investment company (“RIC”) under theInternal Revenue Code of 1986, as amended (the “Code”), for U.S. federal income tax purposes. As a BDCand a RIC, we are required to comply with certain regulatory requirements. See “Regulation” and “CertainU.S. Federal Income Tax Considerations.” For example, as a BDC, at least 70% of our assets must be assetsof the type listed in Section 55(a) of the 1940 Act, as described herein.

Our History

On January 16, 2020, through a series of transactions (the “Formation Transactions”), we acquired theLegacy Funds, including their respective investment portfolios (collectively, the “Legacy Portfolio”), andTrinity Capital Holdings, LLC, a holding company whose subsidiaries managed and/or had the right toreceive fees from certain of the Legacy Funds (“Trinity Capital Holdings”). In the Formation Transactions,the Legacy Funds were merged with and into the Company, and we issued 9,183,185 shares of our commonstock at $15.00 per share for an aggregate amount of approximately $137.7 million and paid approximately$108.7 million in cash to the Legacy Investors to acquire the Legacy Funds and all of their respectiveassets, including the Legacy Portfolio.

As part of the Formation Transactions, we also acquired 100% of the equity interests of TrinityCapital Holdings, the sole member of Trinity Management IV, LLC, the investment manager to Fund IVand the sub-adviser to Fund II and Fund III, for an aggregate purchase price of $10.0 million, which wascomprised of 533,332 shares of our common stock at $15.00 per share for an aggregate amount ofapproximately $8.0 million and approximately $2.0 million in cash. As a result of this transaction, TrinityCapital Holdings became a wholly-owned subsidiary of the Company.

For additional information regarding our history and the Formation Transactions, see “Business.”

Borrowings

Through our wholly-owned subsidiary, Trinity Funding 1, LLC, we are a party to a $300 million CreditAgreement (as amended, the “Credit Agreement”) with Credit Suisse AG (“Credit Suisse”). The CreditAgreement matures on January 8, 2022, unless extended, and we have the ability to borrow up to an aggregateof $300 million. Borrowings under the Credit Agreement generally bear interest at a rate of the three-month London Inter-Bank Offered Rate (“LIBOR”) plus 3.25%. As of January 20, 2021, approximately$135 million was outstanding under the Credit Agreement. See “Business” and “Management’s Discussionand Analysis of Financial Condition and Results of Operations.”

In January 2020, we issued $125 million in aggregate principal amount of our unsecured 7.00% Notesdue 2025 (the “2025 Notes”) in reliance upon the available exemptions from the registration requirements ofthe Securities Act (the “144A Note Offering”). The 2025 Notes were issued pursuant to an Indenturedated as of January 16, 2020 (the “Base Indenture”), between us and U.S. Bank National Association, astrustee (the “Trustee”), and a First Supplemental Indenture, dated as of January 16, 2020 (the “FirstSupplemental Indenture” and, together with the Base Indenture, the “2025 Notes Indenture”), between usand the Trustee. The 2025 Notes mature on January 16, 2025 (the “2025 Notes Maturity Date”), unlessrepurchased or redeemed in accordance with their terms prior to such date, and bear interest at a rate of7.00% per year payable quarterly on March 15, June 15, September 15 and December 15 of each year,commencing on March 15, 2020. See “Business,” “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” and “Securities Eligible for Future Sale.”

2

In December 2020, we issued $50 million in aggregate principal amount of our unsecured 6.00%Convertible Notes due 2025 (the “Convertible Notes”) in reliance upon the available exemptions from theregistration requirements of the Securities Act. The Convertible Notes were issued pursuant to the BaseIndenture and a Second Supplemental Indenture, dated as of December 11, 2020 (the “Second SupplementalIndenture” and, together with the Base Indenture, the “Convertible Notes Indenture”), between us and theTrustee. The Convertible Notes mature on December 11, 2025 (the “Convertible Notes Maturity Date”),unless earlier converted or repurchased in accordance with their terms prior to such date. The ConvertibleNotes bear interest at a rate of 6.00% per year, subject to additional interest of 0.75% per annum if we do notmaintain an investment grade rating with respect to the Convertible Notes, payable semiannually on May 1and November 1 of each year, commencing on May 1, 2021. Holders may convert their Convertible Notes, attheir option, at any time on or prior to the close of business on the business day immediately preceding theConvertible Notes Maturity Date. The conversion rate is initially 66.6667 shares of our common stock, per$1,000 principal amount of the Convertible Notes (equivalent to an initial conversion price of approximately$15.00 per share of common stock). The conversion rate is subject to adjustment in some events but will notbe adjusted for any accrued and unpaid interest. Upon conversion of the Convertible Notes, we will pay ordeliver, as the case may be, cash, shares of our common stock, or a combination of cash and shares of ourcommon stock, at our election, per $1,000 principal amount of the Convertible Notes, equal to the thenexisting conversion rate. See “Management’s Discussion and Analysis of Financial Condition and Resultsof Operations” and “Securities Eligible for Future Sale.”

COVID-19 Developments

In March 2020, the outbreak of the novel coronavirus (“COVID-19”) was recognized as a pandemic bythe World Health Organization. Shortly thereafter, the President of the United States declared a NationalEmergency throughout the United States attributable to such pandemic. The pandemic has becomeincreasingly widespread in the United States, including in the Company’s primary markets of operation. Asof the three and nine months ended September 30, 2020, and subsequent to September 30, 2020, theCOVID-19 pandemic has had a significant impact on the U.S. and global economy.

We have and continue to assess the impact of the COVID-19 pandemic on our portfolio companies.We cannot predict the full impact of the COVID-19 pandemic, including its duration in the United Statesand worldwide, the effectiveness of governmental responses designed to mitigate strain to businesses and theeconomy, and the magnitude of the economic impact of the outbreak, including with respect to the travelrestrictions, business closures and other quarantine measures imposed on service providers and otherindividuals by various local, state, and federal governmental authorities, as well as non-U.S. governmentalauthorities. While several countries, as well as certain states, counties and cities in the United States, haverelaxed initial public health restrictions with a view to partially or fully reopening their economies, many citiesworld-wide have since experienced a surge in the reported number of cases, hospitalizations and deathsrelated to the COVID-19 pandemic. These increases have led to the re-introduction of restrictions andbusiness shutdowns in certain states, counties and cities in the United States and globally and could continueto lead to the re-introduction of such restrictions and business shutdowns elsewhere. Additionally, as ofJanuary 2020, travelers from the United States are not allowed to visit Canada, Australia or the majority ofcountries in Europe, Asia, Africa and South America. These continued travel restrictions may prolong theglobal economic downturn. In addition, although the Federal Food and Drug Administration authorizedvaccines produced by Pfizer-BioNTech and Moderna for emergency use starting in December 2020, it remainsunclear how quickly the vaccines will be distributed nationwide and globally or when “herd immunity” willbe achieved and the restrictions that were imposed to slow the spread of the virus will be lifted entirely. Thedelay in distributing the vaccines could lead people to continue to self-isolate and not participate in theeconomy at pre-pandemic levels for a prolonged period of time. Even after the COVID-19 pandemic subsides,the U.S. economy and most other major global economies may continue to experience a recession, and weanticipate our business and operations could be materially adversely affected by a prolonged recession in theUnited States and other major markets. As such, we are unable to predict the duration of any business andsupply-chain disruptions, the extent to which the COVID-19 pandemic will negatively affect our portfoliocompanies’ operating results or the impact that such disruptions may have on our results of operationsand financial condition. Though the magnitude of the impact remains to be seen, we expect our portfoliocompanies and, by extension, our operating results to be adversely impacted by the COVID-19 pandemic and,depending on the duration and extent of the disruption to the operations of our portfolio companies, we

3

expect that certain portfolio companies will experience financial distress and may possibly default on theirfinancial obligations to us and their other capital providers. Some of our portfolio companies have significantlycurtailed business operations, furloughed or laid off employees and terminated service providers, anddeferred capital expenditures, which could impair their business on a permanent basis and additionalportfolio companies may take similar actions. We continue to closely monitor our portfolio companies, whichincludes assessing each portfolio company’s operational and liquidity exposure and outlook; however, anyof these developments would likely result in a decrease in the value of our investment in any such portfoliocompany. In addition, to the extent that the impact to our portfolio companies results in reduced interestpayments or permanent impairments on our investments, we could see a decrease in our net investmentincome, which would increase the percentage of our cash flows dedicated to our debt obligations and couldimpact the amount of any future distributions to our stockholders.

In response to the COVID-19 pandemic, we instituted a temporary work-from-home policy inMarch 2020, during which our employees primarily worked remotely without disruption to our operations.In May 2020, we began to allow healthy employees to work in the office if they so choose.

Our Business and Structure

Overview

We provide debt, including loans and equipment financings, to growth stage companies, includingventure-backed companies and companies with institutional equity investors. Our investment objective is togenerate current income and, to a lesser extent, capital appreciation through our investments. We makeinvestments consisting primarily of term loans and equipment financings and, to a lesser extent, workingcapital loans, equity and equity-related investments.

We target investments in growth stage companies with institutional investor support, experiencedmanagement teams, promising products and offerings, and large expanding markets. These companiestypically have begun to have success selling their products to the market and need additional capital to expandtheir operations and sales. Despite often achieving growing revenues, these types of companies typicallyhave limited financing options to fund their growth. Equity, being dilutive in nature, is generally the mostexpensive form of capital available, while traditional bank financing is rarely available, given the lifecycle stageof these companies. Financing from us bridges this financing gap, providing companies with growthcapital, which may result in improved profitability, less dilution for all equity investors, and increasedenterprise value. We are not limited to investing in any particular industry or geographic area and seek toinvest in under-financed segments of the private credit markets.

We invest in debt, including loans and equipment financings, that may have initial interest-only periodsof 0 to 24 months and may then fully amortize over a term of 24 to 60 months. These investments are typicallysecured by a blanket first lien, a specific asset lien on mission critical assets or a blanket second lien. Wemay also make a limited number of direct equity and equity-related investments in conjunction with our debtinvestments. We target growth stage companies that have recently issued equity to raise cash to offsetpotential cash flow needs related to projected growth, have achieved positive cash flow to cover debt service,or have institutional investors committed to providing additional funding. A loan or equipment financingmay be structured to tie the amortization of the loan or equipment financing to the portfolio company’sprojected cash balances while cash is still available for operations. As such, the loan or equipment financingmay have a reduced risk of default. We believe that the amortizing nature of our investments will mitigaterisk and significantly reduce the risk of our investments over a relatively short period. We focus on protectingand recovering principal in each investment and structure our investments to provide downside protection.As of September 30, 2020, the debt, including loans and equipment financings, in our portfolio had a weightedaverage time to maturity of approximately 2.9 years.

Certain of the loans in which we invest have financial maintenance covenants, which are used toproactively address materially adverse changes in a portfolio company’s financial performance. However, wehave invested in and may in the future invest in or obtain significant exposure to “covenant-lite” loans,which generally are loans that do not have a complete set of financial maintenance covenants. Generally,covenant-lite loans provide borrower companies more freedom to negatively impact lenders because theircovenants are incurrence-based, which means they are only tested and can only be breached following an

4

affirmative action of the borrower, rather than by a deterioration in the borrower’s financial condition.Accordingly, because we invest in and have exposure to covenant-lite loans, we may have fewer rights againsta borrower and may have a greater risk of loss on such investments as compared to investments in orexposure to loans with financial maintenance covenants.

Management Team

We are an internally managed BDC employing 34 dedicated professionals, including 15 investment,originations and portfolio management professionals, all of whom have experience working on investmentand financing transactions. Our management team has prior management experience, including with earlystage tech startups, and employs a highly systematized approach. Our senior management team, led bySteven L. Brown, comprises the majority of the senior management team that managed the Legacy Fundsand sourced their investment portfolios, and we believe is well positioned to take advantage of the potentialinvestment opportunities available in the marketplace.

• Steven L. Brown, our founder, is our Chairman and Chief Executive Officer and has 25 years ofexperience in venture equity and venture debt investing and working with growth stage companies.

• Gerald Harder, our Chief Credit Officer, has been with Trinity since 2016, and we believe his prior30 years of engineering and operations experience adds significant value in analyzing investmentopportunities.

• Kyle Brown, our President and Chief Investment Officer, has been with Trinity since 2015 and isresponsible for managing Trinity’s investment activities. He has historically managed relationshipswith potential investment partners, including venture capital firms and technology bank lenders,allowing us to nearly triple the number of investment opportunities reviewed by our senior managementafter Mr. Brown joined the senior management of Trinity.

• Ron Kundich, our Senior Vice President — Loan Originations, is responsible for developingrelationships with our referral partners, sourcing potential investments and evaluating investmentopportunities.

• David Lund, our Chief Financial Officer, Executive Vice President of Finance and StrategicPlanning, and Treasurer, has over 35 years of finance and executive leadership experience workingwith both private and publicly traded companies, including serving as Chief Financial Officer at aninternally managed venture lending, publicly traded BDC during its initial stage and subsequent yearsof growth in assets.

All investment decisions are made by our Investment Committee (the “Investment Committee”), whosemembers consist of Steven L. Brown, Gerald Harder, Kyle Brown and Ron Kundich. We consider theseindividuals to be our portfolio managers. The Investment Committee approves proposed investments bymajority consent, which majority must include Steven L. Brown, in accordance with investment guidelinesand procedures established by the Investment Committee. See “Management” and “Executive Compensation”for additional information regarding these individuals.

The members of the Investment Committee have worked together in predecessor investment funds,including the Legacy Funds, and bring decades of combined experience investing in venture debt andventure capital and managing venture-backed start-ups and other public and private entities. As a result, themembers of the Investment Committee have strong backgrounds in venture capital, private equity, investing,finance, operations, management and intellectual property, and have developed a strong working knowledgein these areas and a broad network of contacts. Combined, as of September 30, 2020, the members of theInvestment Committee had over 75 years in aggregate of operating experience in various public and privatecompanies, many of them venture-funded. As a group, they have managed through all aspects of theventure capital lifecycle, including participating in change of control transactions with venture-backedcompanies that they founded and/or served.

Potential Competitive Advantages

We believe that we are one of only a select group of specialty lenders that has our depth of knowledge,experience, and track record in lending to growth stage companies. Further, we are one of an even smallersubset of specialty lenders that offers both loans and equipment financings. Our other potential competitiveadvantages include:

5

• In-house engineering and operations expertise to evaluate growth stage companies’ business productsand plans.

• Direct origination networks that benefit from relationships with venture banks, institutional equityinvestors and entrepreneurs built during the term of operations of the Legacy Funds, which began in2008.

• A dedicated staff of professionals covering credit origination and underwriting, as well as portfoliomanagement functions.

• A proprietary credit rating system and regimented process for evaluating and underwriting prospectiveportfolio companies.

• Scalable software platforms developed during the term of operations of the Legacy Funds, whichsupport our underwriting processes and loan monitoring functions.

For additional information regarding our potential competitive advantages, see “Business.”

Market Opportunity

We believe that an attractive market opportunity exists for providing debt and equipment financing togrowth stage companies for the following reasons:

• Growth stage companies have generally been underserved by traditional lending sources.

• Unfulfilled demand exists for debt, including loans and equipment financings, to growth stagecompanies due to the complexity of evaluating risk in these investments.

• Debt investments with warrants are less dilutive than traditional equity financing and complementequity financing from venture capital and private equity funds.

• Equity funding of growth stage companies, including venture capital backed companies, hasincreased steadily over the last ten years, resulting in new lending and equipment financingopportunities. During the last economic downturn from 2007 – 2009, new venture capital fundingsin the United States decreased less than 15% annually, and totaled almost $60.0 billion. The totalinvestment opportunities we have generated for review increased from approximately $1.14 billion in2015 to $3.28 billion in 2018, and $3.81 billion for the year ended December 31, 2019. During thefirst nine months of 2020, we generated approximately $4.3 billion of investment opportunities forreview. The total investment opportunities we have generated for review from inception of TCI throughSeptember 30, 2020 were approximately $18.3 billion. Notably, our equipment financing businesssaw substantial growth in potential investment opportunities from $50.0 million in 2016 to $1.39billion in 2019, and $1.2 billion for the first nine months of 2020, with more growth projected in 2020and beyond. We believe that our potential investment opportunities year to date signal a continuingrobust market for investment in growth stage companies. During the first nine months of 2020, wefunded investments of approximately $138.0 million, including $71.3 million in secured loans,$64.9 million in equipment financings, and $1.8 million in equity investments.

• We estimate that the annual U.S. venture debt and equipment financing market in 2019 exceeded$20.0 billion and was approximately $17.0 billion as of September 30, 2020. We believe that theequipment financing market is even more fragmented, with the majority of equipment financingproviders unable to fund investments for more than $10 million. We believe there are significant growthopportunities for us to expand our market share in the venture debt market and become a one-stopshop for loans and equipment financing for growth stage companies.

Growth Stage Companies are Underserved by Traditional Lenders. We believe many viable growthstage companies have been unable to obtain sufficient growth financing from traditional lenders, includingfinancial services companies such as commercial banks and finance companies, because traditional lendershave continued to consolidate and have adopted a more risk-averse approach to lending. More importantly,we believe traditional lenders are typically unable to underwrite the risk associated with these companieseffectively and generally refrain from lending and/or providing equipment financing to growth stagecompanies, instead preferring the risk-reward profile of traditional fixed asset-based lending.

6

Unfulfilled Demand for Debt and Equipment Financing to Growth Stage Companies. Private capital inthe form of debt and equipment financing from specialty finance companies continues to be an importantsource of funding for growth stage companies. We believe that the level of demand for debt and equipmentfinancing is a function of the level of annual venture equity investment activity, and can be as much as20% to 30% of such investment activity. We believe this market is largely served by a handful of venturebanks, with whom our products generally do not compete, and a relative few term lenders and lessors.

We further believe that demand for debt and equipment financing to growth stage companies is currentlyunderserved, given the high level of activity in venture capital equity market for the growth stage companiesin which we invest, and that this is an opportune time to invest in the debt and equipment financing forgrowth stage companies. Our senior management team has seen a significant increase in the number ofpotential investment opportunities over the last ten years.

Debt Investments with Warrants Complement Equity Financing from Venture Capital and Private EquityFunds. We believe that growth stage companies and their financial sponsors will continue to view debt andequipment financing as an attractive source of capital because it augments the capital provided by venturecapital and private equity funds. We believe that our debt investments, including loans and equipmentfinancings, will provide access to growth capital that otherwise may only be available through incrementalequity investments by new or existing equity investors. As such, we intend to provide portfolio companies andtheir financial sponsors with an opportunity to diversify their capital sources.

For additional information regarding our market opportunity, see “Business.”

Investment Philosophy, Strategy and Process

We lend money in the form of term loans and equipment financings and, to a lesser extent, workingcapital loans to growth stage companies. Investors may receive returns from three sources — the loan’sinterest payments or equipment financing payments and the associated contractual fees; the final principalpayment; and, contingent upon a successful change of control or initial public offering, proceeds from theequity positions or contingent exit fees obtained at loan or equipment financing origination.

We primarily seek to invest in loans and equipment financings to growth stage companies that havegenerally completed product development and are in need of capital to fund revenue growth. We believe alack of profitability often limits these companies’ ability to access traditional bank financing, and our in-houseengineering and operations experience allows us to better understand this risk and earn what we believe tobe higher overall returns and better risk-adjusted returns than those associated with traditional bank loans.

Our loans and equipment financings range from $2 million to $30 million. We believe investments ofthis scale are generally sufficient to support near-term growth needs of most growth stage companies. Wegenerally limit each loan and equipment financing to approximately five percent or less of our total assets. Weseek to structure our loans and equipment financings such that amortization of the amount investedquickly reduces our risk exposure. Leveraging the experience of our investment professionals, we seek totarget companies at their growth stage of development and to identify financing opportunities ignored bythe traditional direct lending community.

We believe good candidates for loans and equipment financings appear in all business sectors. Subjectto the requirements of the 1940 Act, we are not limited to investing in any particular industry or geographicarea and seek to invest in under-financed segments of the private credit markets. We believe in diversificationand do not intend to specialize in any one sector. Our portfolio companies are selected from a wide range ofindustries, technologies and geographic regions. Since we focus on investing in portfolio companiesalongside venture capital firms and technology banks, we anticipate that most of our opportunities willcome from sectors that those sources finance. See “Business” for additional details.

Employees

As of September 30, 2020, we had 34 employees, including 15 investment, originations and portfoliomanagement professionals, all of whom have experience working on investment and financing transactions.

7

Corporate Information

Our principal executive offices are located at 3075 West Ray Road, Suite 525, Chandler, Arizona 85226and our telephone number is (480) 374-5350. Our corporate website is located at www.trincapinvestment.com.Information on our website is not incorporated into or a part of this prospectus.

Preliminary Estimates of Results as of December 31, 2020

From October 1, 2020 through December 31, 2020, we made total investments of approximately$102.1 million. Of these investments, $72.4 million were in secured loans, $29.3 million were in equipmentfinancings, and $0.4 million were in equity securities. Approximately $45.5 million of these investments wereto 7 new portfolio companies and approximately $56.6 million were to 12 existing portfolio companies.The weighted average yield of debt and other income producing securities funded during the period atamortized cost was approximately 13.8%.

From October 1, 2020 through December 31, 2020, we received approximately $43.0 million inprincipal repayments, including approximately $29.0 million of early repayments. During this period werecognized realized losses of approximately $5.0 million primarily related to one investment and reversedpreviously recorded net unrealized depreciation related to such net realized losses of approximately$4.0 million.

The level of our investment activity can vary substantially from period to period depending on manyfactors. Such factors may include the amount of loans, equipment financings and equity capital required bygrowth stage companies, the general economic environment and market conditions, including as a resultof the COVID-19 pandemic, and the competitive environment for the types of investments we make.

For the three-month period ended December 31, 2020, we estimate that our unaudited total investmentincome will be between $15.0 million and $15.7 million and our unaudited net investment income will bebetween $4.8 million and $5.5 million, or between $0.26 and $0.30 per share. For the year ended December 31,2020, we estimate that our unaudited total investment income will be between $54.6 million and$55.3 million and our unaudited net investment income will be between $22.8 million and $23.5 million, orbetween $1.26 and $1.30 per share.The unaudited estimate of the range of the net asset value per share of ourcommon stock as of December 31, 2020 is between $12.93 and $13.03.

The preliminary financial estimates provided herein have been prepared by, and are the responsibilityof, management. Neither Ernst & Young LLP, our independent registered public accounting firm, nor anyother independent accountants, have audited, reviewed, compiled, or performed any procedures with respectto the accompanying preliminary financial data.

These estimates are subject to the completion of our financial closing procedures and are not acomprehensive statement of our financial results or valuations as of December 31, 2020 and have not beenapproved by the Board. We advise you that our actual results may differ materially from these estimates as aresult of the completion of the period and our financial closing procedures, final adjustments, valuationprocess and other developments that may arise between now and the time that our financial results arefinalized.

Risk Factors

An investment in our common stock involves a high degree of risk and may be considered speculative.You should carefully consider the information found in “Risk Factors” in this prospectus and the otherinformation included in this prospectus before deciding to invest in shares of our common stock. Principalrisks involved in an investment in us include:

• we have limited operating history as a BDC;

• we depend upon our senior management team and investment professionals, including the membersof the Investment Committee, and their referral relationships with venture capital sponsors for oursuccess;

8

• economic recessions or downturns, disruptions and instability in capital markets, and political, socialand economic uncertainty including as a result of the COVID-19 pandemic, could impair ourportfolio companies and harm our business and operating results;

• the COVID-19 pandemic has caused severe disruptions in the U.S. economy and has disruptedfinancial activity in the areas in which we or our portfolio companies operate;

• our stockholders may experience dilution if additional shares of our common stock are issued,which could reduce the overall value of an investment in us;

• regulations governing our operation as a BDC and RIC affect our ability to raise capital and the wayin which we raise additional capital or borrow for investment purposes, which may have a negativeeffect on our growth;

• we may borrow money, which may magnify the potential for gain or loss and may increase the risk ofinvesting in us;

• we will be subject to corporate-level U.S. federal income tax if we are unable to qualify or maintainour tax treatment as a RIC under Subchapter M of the Code;

• changes in laws or regulations governing our operations may adversely affect our business or causeus to alter our business strategy;

• any failure in cyber security systems, as well as the occurrence of events unanticipated in our disasterrecovery systems and management continuity planning, could impair our ability to conduct businesseffectively;

• our management team and investment professionals may not be able to achieve the same or similarreturns as those achieved by the Legacy Funds or by such persons while they were employed at priorpositions;

• our investment strategy focuses on growth stage companies, which are subject to many risks,including dependence on the need to raise additional capital, volatility, intense competition, shortenedproduct life cycles, changes in regulatory and governmental programs, periodic downturns, belowinvestment grade ratings, which could cause you to lose all or part of your investment in us;

• we are subject to risks inherent in the equipment financing business that may adversely affect ourability to finance our portfolio on terms which will permit us to generate profitable rates of return forinvestors;

• our investments are geographically concentrated in the Western and Northeastern part of the UnitedStates, including California, which may results in a single occurrence in a particular geographicarea having a disproportionate negative impact on our investment portfolio. For example, portfoliocompanies in California, may be particularly susceptible to certain types of hazards, such asearthquakes, floods, mudslides, wildfires and other national disasters, which could have a negativeimpact on their business and ability to meet their obligations under their debt securities that we hold;

• our investments are very risky and highly speculative and a lack of liquidity in our investments mayadversely affect our business;

• we may be subject to risks associated with our investments in senior loans, junior debt securities andcovenant-lite loans;

• our portfolio may be exposed in part to one or more specific industries, which may subject us to arisk of significant loss in a particular investment or investments if there is a downturn in that particularindustry;

• we are exposed to risks associated with changes in interest rates, including the decommissioning ofLIBOR;

• defaults by our portfolio companies could jeopardize a portfolio company’s ability to meet itsobligations under the debt, equipment financing or equity investment that we hold which couldharm our operating results;

• we may not be able to pay distributions, our distributions may not grow over time and/or a portionof our distributions may be a return of capital;

• investing in our common stock may involve an above-average degree of risk; and• the market price of our common stock may fluctuate significantly.

9

THE OFFERING SUMMARY

Common Stock Offered by Us . . . . . . 6,900,000 shares (or 8,006,291 shares if the underwritersexercise their option to purchase additional shares of ourcommon stock).

Common Stock Offered by the SellingStockholders . . . . . . . . . . . . . . . . 475,274 shares (the “Secondary Shares”). The Secondary

Shares offered pursuant to this prospectus were issued by us inthe Private Common Stock Offering (as defined in thisprospectus), the Formation Transactions and pursuant to ourdistribution reinvestment plan, and are being registered forresale pursuant to the Common Stock Registration RightsAgreement (as defined in this prospectus). See “SellingStockholders” and “Securities Eligible for Future Sale.”

Common Stock to be Outstandingafter this Offering . . . . . . . . . . . . . 25,308,984 shares, (or 26,415,275 shares if the underwriters

exercise their option to purchase additional shares of ourcommon stock).

Use of Proceeds . . . . . . . . . . . . . . . . Our net proceeds from this offering will be approximately$89.3 million (or approximately $103.9 million if theunderwriters exercise their option to purchase additionalshares of our common stock), based on an offering price of$14.00 per share, after deducting the underwriting discountsand commissions and estimated offering costs of approximately$1.5 million.

We intend to use the net proceeds of this offering to pay downa portion of our existing indebtedness outstanding under theCredit Agreement, to make investments in accordance with ourinvestment objective, and for general corporate purposes.

We will not receive any of the proceeds from the sale of theSecondary Shares.

Pursuant to the Common Stock Registration RightsAgreement, we will pay the fees and expenses incurred inoffering and disposing of the Secondary Shares, including allregistration and filing fees, any other regulatory fees, printingand delivery expenses, listing fees and expenses, fees andexpenses of counsel, independent certified public accountants,and any special experts retained by us, and reasonable anddocumented fees and expenses of counsel to the SellingStockholders in an amount not to exceed $75,000. The SellingStockholders will be responsible for (i) all brokers’ andunderwriters’ discounts and commissions, transfer taxes, andtransfer fees relating to the sale or disposition of the SecondaryShares, and (ii) the fees and expenses of any counsel to theSelling Stockholders exceeding $75,000. See “Use of Proceeds.”

Symbol on the Nasdaq Global SelectMarket . . . . . . . . . . . . . . . . . . . . Our common stock has been approved for listing on the

Nasdaq Global Select Market under the symbol “TRIN”.

Distributions . . . . . . . . . . . . . . . . . . We generally intend to make quarterly distributions and todistribute, out of assets legally available for distribution,substantially all of our available earnings, as determined byour board of directors (the “Board”) in its sole discretion and

10

in accordance with RIC requirements. The distributions thatwe pay may represent a return of capital. A return of capitalwill (i) lower a stockholder’s tax basis in our shares andthereby increase the amount of capital gain (or decrease theamount of capital loss) realized upon a subsequent sale orredemption of such shares, and (ii) reduce the amount of fundswe have for investment in portfolio companies. A distributionor return of capital does not necessarily reflect our investmentperformance, and should not be confused with yield orincome. See “Distributions” and “Certain Material U.S.Federal Income Tax Considerations.”

On November 9, 2020, the Board declared a quarterlydistribution of $0.27 per share, which was paid on December 4,2020 to stockholders of record as of November 20, 2020. OnDecember 22, 2020, the Board declared a dividend of $0.27 pershare, which was paid on January 15, 2021 to stockholders ofrecord as of December 30, 2020. See “Management'sDiscussion and Analysis of Financial Condition and Resultsof Operations — Recent Developments.”

We can offer no assurance that we will achieve investmentreturns that will permit us to make distributions or that theBoard will declare any distributions in the future.

To maintain our tax treatment as a RIC, we must makecertain distributions. See “Certain U.S. Federal Income TaxConsiderations — Taxation as a Regulated InvestmentCompany.”

Taxation . . . . . . . . . . . . . . . . . . . . . We intend to elect to be treated as a RIC for U.S. federalincome tax purposes, and we intend to operate in a manner soas to qualify annually for the tax treatment applicable toRICs. Our tax treatment as a RIC will enable us to deductqualifying distributions to our stockholders, so that we will besubject to corporate-level U.S. federal income taxation onlyin respect of earnings that we retain and do not distribute.

To maintain our status as a RIC and to avoid being subject tocorporate-level U.S. federal income taxation on our earnings,we must, among other things:

• maintain our election under the 1940 Act to be treated asa BDC;

• derive in each taxable year at least 90% of our grossincome from dividends, interest, gains from the sale orother disposition of stock or securities and other specifiedcategories of investment income; and

• maintain diversified holdings.

In addition, to receive tax treatment as a RIC, we must timelydistribute (or be treated as distributing) in each taxable yeardividends for tax purposes equal to at least 90% of ourinvestment company taxable income and net tax-exemptincome for that taxable year.

As a RIC, we generally will not be subject to corporate-levelU.S. federal income tax on our investment company taxable

11

income and net capital gains that we distribute to stockholders.If we fail to distribute our investment company taxableincome or net capital gains on a timely basis, we will be subjectto a nondeductible 4% U.S. federal excise tax. We maychoose to carry forward investment company taxable incomein excess of current year distributions into the next tax year andpay the 4% U.S. federal excise tax on such income. Anycarryover of investment company taxable income or net capitalgains must be timely declared and distributed as a dividendin the taxable year following the taxable year in which theincome or gains were earned. See “Distributions” and “CertainU.S. Federal Income Tax Considerations.”

Leverage . . . . . . . . . . . . . . . . . . . . . As a BDC, we are permitted under the 1940 Act to borrowfunds or issue “senior securities” to finance a portion of ourinvestments. As a result, we are exposed to the risks of leverage,which may be considered a speculative investment technique.

Leverage increases the potential for gain and loss on amountsinvested and, as a result, increases the risks associated withinvesting in our securities. With certain limited exceptions, wemay issue “senior securities,” including borrowing moneyfrom banks or other financial institutions only in amounts suchthat the ratio of our total assets (less total liabilities otherthan indebtedness represented by senior securities) to our totalindebtedness represented by senior securities plus preferredstock, if any, is at least 150% after such incurrence or issuance.This means that generally, we can borrow up to $2 for every$1 of investor equity. The costs associated with our borrowingsare borne by our stockholders. In connection with ourorganization, the Board and our initial sole stockholderauthorized us to adopt the 150% asset coverage ratio. See“Regulation.” As of September 30, 2020, our asset coverageratio was approximately 198.6%. We target a leverage range ofbetween 1.15x to 1.35x.

As of January 20, 2021, approximately $135 million wasoutstanding under the Credit Agreement. We have the abilityto borrow up to $300 million under the Credit Agreement andborrowings thereunder generally bear interest at a rate of thethree-month LIBOR plus 3.25%.

As of January 20, 2021, $125 million in aggregate principalamount of the 2025 Notes was outstanding. The 2025 Notesbear interest at a rate of 7.00% per year payable quarterly onMarch 15, June 15, September 15 and December 15 of eachyear, commencing on March 15, 2020.

As of January 20, 2021, $50 million in aggregate principalamount of the Convertible Notes was outstanding. TheConvertible Notes bear interest at a rate of 6.00% per year,subject to additional interest of 0.75% per annum if we do notmaintain an investment grade rating with respect to theConvertible Notes, payable semiannually on May 1 andNovember 1 of each year, commencing on May 1, 2021.

Distribution Reinvestment Plan . . . . . We have adopted an “opt out” distribution reinvestment planfor our stockholders. As a result, if we declare a cash dividend

12

or other distribution, each stockholder that has not “optedout” of our distribution reinvestment plan will have theirdividends or distributions automatically reinvested in additionalshares of our common stock rather than receiving cashdistributions. There are no brokerage charges or other chargesto stockholders who participate in the distributionreinvestment plan.

Stockholders who receive dividends and other distributions inthe form of shares of common stock generally are subject tothe same U.S. federal tax consequences as stockholders whoelect to receive their distributions in cash; however, sincetheir cash dividends will be reinvested, those stockholders willnot receive cash with which to pay any applicable taxes onreinvested dividends. See “Distribution Reinvestment Plan.”

Trading at a Discount . . . . . . . . . . . . Shares of closed-end investment companies, including BDCs,frequently trade at a discount to their net asset value. We arenot generally able to issue and sell our common stock at aprice below our net asset value per share unless we havestockholder approval. The risk that our shares may trade at adiscount to our net asset value is separate and distinct from therisk that our net asset value per share may decline. Wecannot predict whether our shares will trade above, at orbelow net asset value. See “Risk Factors.”

Custodian, Transfer and DividendPaying Agent and Registrar . . . . . . Wells Fargo Bank, National Association, serves as our

custodian. American Stock Transfer & Trust Company, LLCserves as our transfer agent, plan administrator, dividend payingagent and registrar. See “Custodian, Transfer and DividendPaying Agent and Registrar.”

Independent Registered PublicAccounting Firm . . . . . . . . . . . . . Ernst & Young LLP acts as our independent registered public

accounting firm.

Available Information . . . . . . . . . . . . We have filed with the SEC a registration statement onForm N-2, of which this prospectus is a part, under theSecurities Act. This registration statement contains additionalinformation about us and the shares of our common stockbeing offered by this prospectus. We are also required to fileperiodic reports, current reports, proxy statements and otherinformation with the SEC. This information is available on theSEC’s website at http://www.sec.gov.

We maintain a website at www.trincapinvestment.com andmake all of our periodic and current reports, proxy statementsand other information available, free of charge, on or throughour website. Information on our website is not incorporatedinto or part of this prospectus. You may also obtain suchinformation free of charge by contacting us in writing at 3075West Ray Road, Suite 525, Chandler, Arizona 85226,Attention: Investor Relations, or through the “Contact”section of our website athttps://trincapinvestment.com/contact/.

13

FEES AND EXPENSES

The following table is intended to assist you in understanding the costs and expenses that you will beardirectly or indirectly. We caution you that some of the percentages indicated in the table below are estimatesand may vary. The expenses shown in the table under “Annual expenses” are based on estimated amountsfor our current fiscal year and assume that we issue 6,900,000 shares of common stock in the offering, basedon an offering price of $14.00 per share. The following table should not be considered a representation ofour future expenses. Actual expenses may be greater or less than shown. Except where the context suggestsotherwise, whenever this prospectus contains a reference to fees or expenses paid by “us” or “the Company”or that “we” will pay fees or expenses, you will indirectly bear these fees or expenses as an investor in theCompany.

Stockholder transaction expenses:Sales load (as a percentage of offering price) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.00%(1)

Offering expenses (as a percentage of offering price) . . . . . . . . . . . . . . . . . . . . . . . . . . 1.55%(2)

Distribution reinvestment plan expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $15.00(3)

Total stockholder transaction expenses (as a percentage of offering price) . . . . . . . . . . . . 7.55%

Annual expenses (as a percentage of net assets attributable to common stock):Operating expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.63%(4)

Interest payments on borrowed funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.34%(5)

Total annual expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9.97%(6)

(1) The sales load (underwriting discount and commission) with respect to the shares of our commonstock sold in this offering, including by us and the Selling Stockholders, which is a one-time fee paid tothe underwriters, is the only sales load paid in connection with this offering.

(2) Amount reflects estimated offering expenses of approximately $1.5 million for the offer and sale ofshares by us and the Selling Stockholders. We will pay the fees and expenses incident to the offer andsale of the Secondary Shares by the Selling Stockholders (excluding underwriting discounts andcommissions). See “Use of Proceeds.”

(3) The expenses of our distribution reinvestment plan are included in “Operating expenses.” The planadministrator’s fees will be paid by us. There will be no brokerage charges or other charges to stockholderswho participate in our distribution reinvestment plan except that, if a participant elects by writtennotice to the plan administrator prior to termination of the participant’s account to have the planadministrator sell part or all of the shares held by the plan administrator in the participant’s accountand remit the proceeds to the participant, the plan administrator is authorized to deduct a $15.00transaction fee plus a $0.12 per share brokerage commission from the proceeds. For additionalinformation, see “Distribution Reinvestment Plan.”

(4) Operating expenses represent the estimated annual operating expenses of the Company and itsconsolidated subsidiaries based on annualized operating expenses estimated for the current fiscal year,which considers the actual expenses for the first nine months ended September 30, 2020, annualized, andadjusted for any additional and non-recurring expenses in the quarter ended December 31, 2020. Wedo not have an investment adviser and are internally managed by our executive officers under thesupervision of the Board. As a result, we do not pay investment advisory fees, but instead we pay theoperating costs associated with employing investment management professionals including, withoutlimitation, compensation expenses related to salaries, discretionary bonuses and grants of options andrestricted stock, if any.

Operating expenses include the fees and expenses incident to the offer and sale of (i) any other sharesof our common stock registered for resale pursuant to the Common Stock Registration RightsAgreement, (ii) the 2025 Notes registered for resale pursuant to the 2025 Notes Registration RightsAgreement (as defined in this prospectus), and (iii) any Convertible Notes and/or shares of our commonstock issued upon conversion of such notes registered for resale pursuant to the Convertible Notes

14

Registration Rights Agreement (as defined in this prospectus). For such offerings, we estimate that wewill incur an aggregate of approximately $450,000 of such fees and expenses.

(5) Interest payments on borrowed funds represents an estimate of our annualized interest expense basedon borrowings under the Credit Agreement with Credit Suisse, the 2025 Notes and the ConvertibleNotes. The assumed weighted average interest rate on our total debt outstanding was 7.11%. Assumeswe had $70 million outstanding under the Credit Agreement, $125 million in aggregate principal amountof the 2025 Notes outstanding and $50 million in aggregate principal amount of the ConvertibleNotes outstanding. We may borrow additional funds from time to time to make investments to theextent we determine that the economic situation is conducive to doing so. We may also issue additionaldebt securities or preferred stock, subject to our compliance with applicable requirements under the1940 Act.

(6) The holders of shares of our common stock indirectly bear the cost associated with our annualexpenses.

Example

The following example demonstrates the projected dollar amount of total cumulative expenses overvarious periods with respect to a hypothetical investment in our common stock. In calculating the followingexpense amounts, we have assumed we would have no additional leverage and that our annual operatingexpenses would remain at the levels set forth in the table above. The stockholder transaction expensesdescribed above are included in the following example.

1 year 3 years 5 years 10 years

You would pay the following expenses on a $1,000 investment, assuming a5% annual return from realized capital gains . . . . . . . . . . . . . . . . . . . $165 $332 $482 $798

The foregoing table is to assist you in understanding the various costs and expenses that an investor inour common stock will bear directly or indirectly. While the example assumes, as required by the SEC, a 5%annual return, our performance will vary and may result in a return greater or less than 5%. In addition,while the example assumes reinvestment of all dividends and distributions at net asset value, if our Boardauthorizes and we declare a cash dividend, participants in our distribution reinvestment plan who have nototherwise elected to receive cash will receive a number of shares of our common stock, determined by dividingthe total dollar amount of the dividend payable to a participant by the market price per share of ourcommon stock at the close of trading on the valuation date for the dividend. See “Distribution ReinvestmentPlan” for additional information regarding our distribution reinvestment plan.

This example and the expenses in the table above should not be considered a representation of ourfuture expenses, and actual expenses (including the cost of debt, if any, and other expenses) may be greateror less than those shown.

15

SELECTED FINANCIAL DATA AND PRO FORMA FINANCIAL INFORMATION

The following tables set forth our selected historical financial information and other data at and for thenine months ended September 30, 2020 and the fiscal year ended December 31, 2019, including on a proforma basis for the fiscal year ended December 31, 2019. On January 16, 2020, through the FormationTransactions, we acquired the Legacy Funds and all of their respective assets (the “Legacy Assets”), includingthe Legacy Portfolio, pursuant to which the Legacy Funds were merged with and into the Company.

Our selected historical financial information and other data at and for the nine months endedSeptember 30, 2020 has been derived from our unaudited financial statements for the nine months endedSeptember 30, 2020, and the selected historical financial information and other data for the fiscal year endedDecember 31, 2019 has been derived from the audited financial statements of the Legacy Funds for thefiscal year ended December 31, 2019, which are included elsewhere in this prospectus and our SEC filings.In the opinion of management, all adjustments, consisting solely of normal recurring accruals, considerednecessary for the fair presentation of the financial statements for our interim period, have been included. Ourresults for the interim period may not be indicative of our results for any future interim period or the fullfiscal year.

The selected historical financial information and other data presented below should be read inconjunction with the financial statements and notes thereto and “Management’s Discussion and Analysis ofFinancial Condition and Results of Operations,” which are included elsewhere in this prospectus.

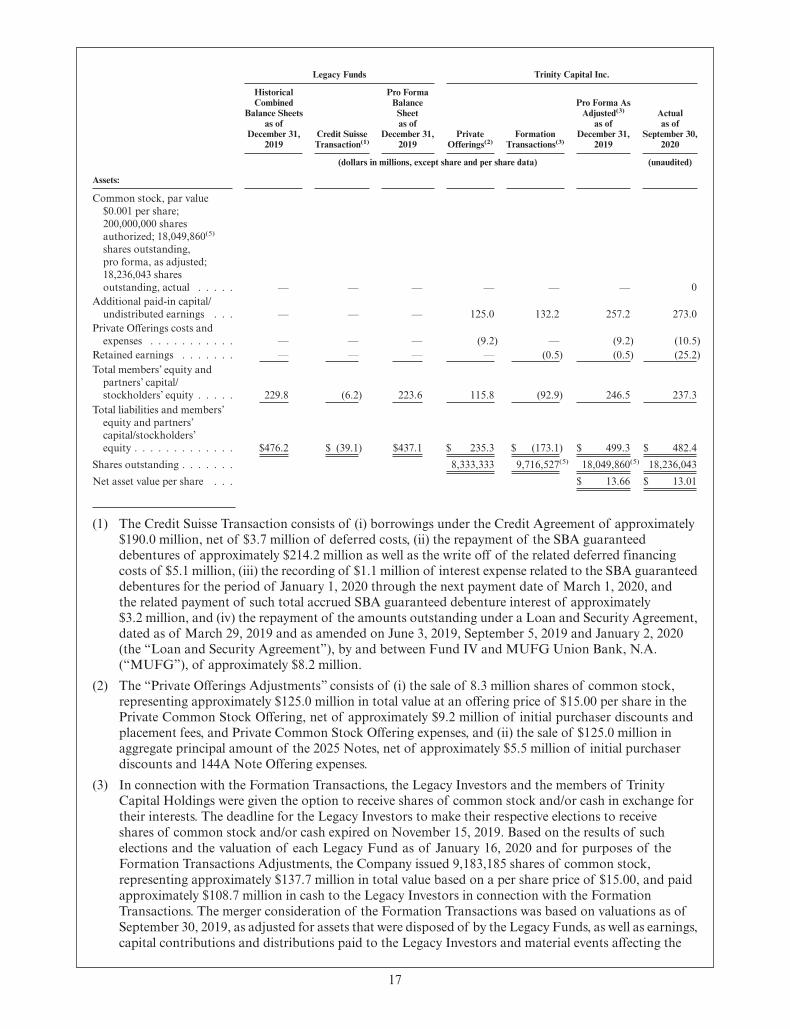

Actual and Pro Forma As Adjusted Balance Sheet

The following unaudited actual and pro forma as adjusted balance sheet is based on our balance sheetas of September 30, 2020 and the historical audited balance sheet of the Legacy Funds as of December 31,2019 included with this prospectus, and pro forma as adjusted to give effect to the borrowings under theCredit Agreement with Credit Suisse and repayment of the SBA guarantee debentures and the Loan andSecurity Agreement with MUFG, the completion of the Private Common Stock Offering and the 144A NoteOffering, and completion of the Formation Transactions discussed in this prospectus.

Legacy Funds Trinity Capital Inc.

HistoricalCombined

Balance Sheetsas of

December 31,2019

Credit SuisseTransaction(1)

Pro FormaBalance

Sheetas of

December 31,2019

PrivateOfferings(2)

FormationTransactions(3)

Pro Forma AsAdjusted(3)

as ofDecember 31,

2019

Actualas of

September 30,2020

(dollars in millions, except share and per share data) (unaudited)

Assets:

Investments, at fair value . . . $419.3 $ — $419.3 $ — $ — $ 419.3 $ 425.5Cash and cash equivalents . . . 52.9 (39.1) 13.8 235.3 (173.3)(4) 75.8 36.3Restricted cash(6) . . . . . . . . — — — — — — 16.3Interest receivable . . . . . . . 3.3 — 3.3 — — 3.3 3.2Other assets . . . . . . . . . . . 0.7 — 0.7 — 0.2 0.9 1.1Total Assets . . . . . . . . . . . $476.2 $ (39.1) $437.1 $ 235.3 $ (173.1) $ 499.3 $ 482.4Liabilities and Members’

Equity and Partnerships’Capital:

Accounts payable and accruedexpenses . . . . . . . . . . . $ 3.1 $ (1.9) $ 1.2 $ — $ 1.6 $ 2.8 $ 5.0

SBA debentures, net . . . . . . 209.1 (209.1) — — — — —Promissory Notes payable,

net . . . . . . . . . . . . . . 21.8 — 21.8 — (21.8) — —2025 Notes, net . . . . . . . . . — — — 119.5 — 119.5 120.2Credit facilities, net . . . . . . 8.2 178.1 186.3 — (60.0) 126.3 112.4Other liabilities . . . . . . . . . 4.2 — 4.2 — — 4.2 7.5Total Liabilities . . . . . . . . . 246.4 (32.9) 213.5 119.5 (80.2) 252.8 245.1Members’ equity and partners’

capital contributions . . . . 229.8 (6.2) 223.6 — (224.6) (1.0) —

16

Legacy Funds Trinity Capital Inc.

HistoricalCombined

Balance Sheetsas of

December 31,2019

Credit SuisseTransaction(1)

Pro FormaBalance

Sheetas of

December 31,2019

PrivateOfferings(2)

FormationTransactions(3)

Pro Forma AsAdjusted(3)

as ofDecember 31,

2019

Actualas of

September 30,2020

(dollars in millions, except share and per share data) (unaudited)

Assets:

Common stock, par value$0.001 per share;200,000,000 sharesauthorized; 18,049,860(5)

shares outstanding,pro forma, as adjusted;18,236,043 sharesoutstanding, actual . . . . . — — — — — — 0

Additional paid-in capital/undistributed earnings . . . — — — 125.0 132.2 257.2 273.0

Private Offerings costs andexpenses . . . . . . . . . . . — — — (9.2) — (9.2) (10.5)

Retained earnings . . . . . . . — — — — (0.5) (0.5) (25.2)Total members’ equity and

partners’ capital/stockholders’ equity . . . . . 229.8 (6.2) 223.6 115.8 (92.9) 246.5 237.3

Total liabilities and members’equity and partners’capital/stockholders’equity . . . . . . . . . . . . . $476.2 $ (39.1) $437.1 $ 235.3 $ (173.1) $ 499.3 $ 482.4

Shares outstanding . . . . . . . 8,333,333 9,716,527(5) 18,049,860(5) 18,236,043Net asset value per share . . . $ 13.66 $ 13.01

(1) The Credit Suisse Transaction consists of (i) borrowings under the Credit Agreement of approximately$190.0 million, net of $3.7 million of deferred costs, (ii) the repayment of the SBA guaranteeddebentures of approximately $214.2 million as well as the write off of the related deferred financingcosts of $5.1 million, (iii) the recording of $1.1 million of interest expense related to the SBA guaranteeddebentures for the period of January 1, 2020 through the next payment date of March 1, 2020, andthe related payment of such total accrued SBA guaranteed debenture interest of approximately$3.2 million, and (iv) the repayment of the amounts outstanding under a Loan and Security Agreement,dated as of March 29, 2019 and as amended on June 3, 2019, September 5, 2019 and January 2, 2020(the “Loan and Security Agreement”), by and between Fund IV and MUFG Union Bank, N.A.(“MUFG”), of approximately $8.2 million.