che trinity inc. unaudited quarterly reporttrinity-health.org/documents/secondquarter2014.pdf ·...

TRANSCRIPT

CHE TRINITY INC.

UNAUDITED QUARTERLY REPORT

For the six months ended December 31, 2013 and 2012

CHE TRINITY INC.

TABLE OF CONTENTS

Page

UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 AND JUNE 30, 2013 AND FOR THE SIX MONTHS ENDED DECEMBER 31, 2013 AND 2012:

Consolidated Balance Sheets (unaudited) 3-4

Consolidated Statements of Operations and Changes in Net Assets (unaudited) 5-7

Summarized Consolidated Statements of Cash Flows (unaudited) 8

Notes to Consolidated Financial Statements (unaudited) 9-21

MANAGEMENT DISCUSSION AND ANALYSIS (unaudited) 22-23

LIQUIDITY REPORT (unaudited) 24

FINANCIAL RATIOS AND STATISTICS (unaudited) 25

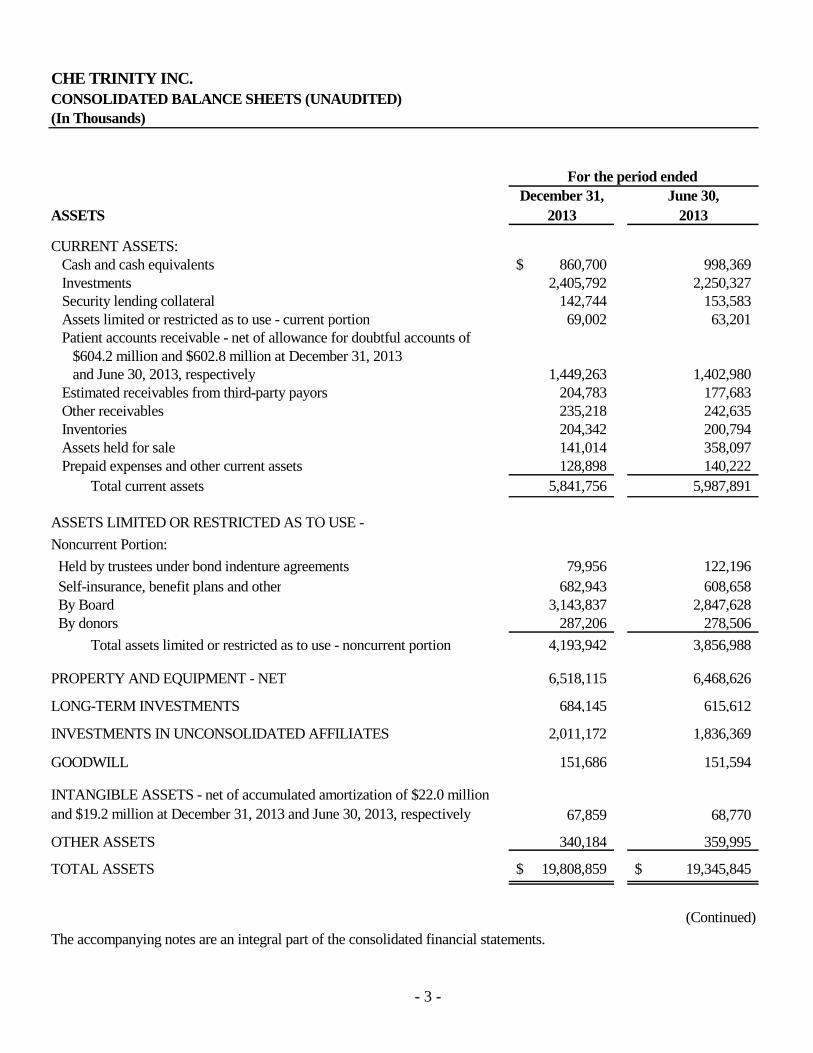

CHE TRINITY INC. CONSOLIDATED BALANCE SHEETS (UNAUDITED) (In Thousands)

For the period ended December 31, June 30,

ASSETS 2013 2013

CURRENT ASSETS: Cash and cash equivalents 860,700 $ 998,369 Investments 2,405,792 2,250,327 Security lending collateral 142,744 153,583 Assets limited or restricted as to use - current portion 69,002 63,201 Patient accounts receivable - net of allowance for doubtful accounts of

$604.2 million and $602.8 million at December 31, 2013 and June 30, 2013, respectively 1,449,263 1,402,980

Estimated receivables from third-party payors 204,783 177,683 Other receivables 235,218 242,635 Inventories 204,342 200,794 Assets held for sale 141,014 358,097 Prepaid expenses and other current assets 128,898 140,222

Total current assets 5,841,756 5,987,891

ASSETS LIMITED OR RESTRICTED AS TO USE -

Noncurrent Portion:

Held by trustees under bond indenture agreements 79,956 122,196 Self-insurance, benefit plans and other 682,943 608,658 By Board 3,143,837 2,847,628 By donors 287,206 278,506

Total assets limited or restricted as to use - noncurrent portion 4,193,942 3,856,988

PROPERTY AND EQUIPMENT - NET 6,518,115 6,468,626

LONG-TERM INVESTMENTS 684,145 615,612

INVESTMENTS IN UNCONSOLIDATED AFFILIATES 2,011,172 1,836,369

GOODWILL 151,686 151,594

INTANGIBLE ASSETS - net of accumulated amortization of $22.0 million and $19.2 million at December 31, 2013 and June 30, 2013, respectively 67,859 68,770

OTHER ASSETS 340,184 359,995

TOTAL ASSETS 19,808,859 $ 19,345,845 $

(Continued)

The accompanying notes are an integral part of the consolidated financial statements.

- 3 -

LIABILITIES AND NET ASSETS For the period ended

December 31, June 30, 2013 2013

CURRENT LIABILITIES: Commercial paper 109,982 $ 368,923 $ Short-term borrowings 1,228,720 896,455 Current portion of long-term debt 124,524 128,273 Accounts payable 554,245 653,137 Accrued expenses 249,558 300,765 Salary, wages, and related liabilities 625,725 624,124 Current portion of self-insurance reserves 117,811 102,292 Payable under security lending agreements 142,744 153,583 Liabilities held for sale 263,359 415,077 Estimated payables to third-party payors 375,617 403,879

Total current liabilities 3,792,285 4,046,508

LONG-TERM DEBT - Net of Current Portion 3,644,912 3,512,404

SELF-INSURANCE RESERVES - Net of Current Portion 872,791 816,538

ACCRUED PENSION AND RETIREE HEALTH COSTS 728,101 921,995

DEFERRED REVENUE FROM ENTRANCE FEES 94,623 91,871

OTHER LONG-TERM LIABILITIES 470,052 511,568

Total liabilities 9,602,764 9,900,884

NET ASSETS: Unrestricted net assets 9,798,742 9,051,595 Noncontrolling ownership interest in subsidiaries 32,962 31,034

Total unrestricted net assets 9,831,704 9,082,629

Temporarily restricted net assets 285,650 269,653

Permanently restricted net assets 88,741 92,679

Total net assets 10,206,095 9,444,961

TOTAL LIABILITIES AND NET ASSETS 19,808,859 $ 19,345,845 $

The accompanying notes are an integral part of the consolidated financial statements. (Concluded)

- 4 -

CHE TRINITY INC.

CONSOLIDATED STATEMENTS OF OPERATIONS AND CHANGES IN NET ASSETS (UNAUDITED) (In Thousands)

Six Months Ended Pro-forma

December 31, December 31, 2013 2012

UNRESTRICTED REVENUE: Patient service revenue - net of contractual and other allowances 6,244,864 $ 6,107,154 $ Provision for bad debts (347,169) (357,425)

Net patient service revenue less provision for bad debts 5,897,695 5,749,729 Capitation and premium revenue 318,404 260,358 Net assets released from restrictions 10,158 8,948 Other revenue 565,122 538,570

Total unrestricted revenue 6,791,379 6,557,605

EXPENSES: Salaries and wages 2,948,960 2,828,321 Employee benefits 594,506 631,287 Contract labor 50,109 60,917

Total labor expenses 3,593,575 3,520,525 Supplies 1,091,792 1,047,081 Purchased services 753,622 712,444 Depreciation and amortization 352,488 335,631 Occupancy 285,612 276,121 Medical claims 127,715 104,221 Interest 85,051 77,239 Other 314,610 281,284

Total expenses 6,604,465 6,354,546

OPERATING INCOME BEFORE OTHER ITEMS 186,914 203,059

CONSOLIDATION COSTS (19,151) (3,231) GAIN ON SALE OF ASSETS - 21,007

OPERATING INCOME 167,763 220,835

NONOPERATING ITEMS: Investment income 379,869 265,278 Equity gains in unconsolidated affiliates 143,544 82,989 Change in market value and cash payments of interest rate swaps 10,501 8,118 Loss on early extinguishment of debt (2,203) -Other, including income taxes (1,281) (645)

Total nonoperating items 530,430 355,740

EXCESS OF REVENUE OVER EXPENSES 698,193 576,575 LESS EXCESS OF REVENUE OVER EXPENSES ATTRIBUTABLE

TO NONCONTROLLING INTEREST 7,491 5,743

EXCESS OF REVENUE OVER EXPENSES - Net of noncontrolling interest 690,702 $ 570,832 $

The accompanying notes are an intergral part of the consolidated financial statements. (Continued)

- 5 -

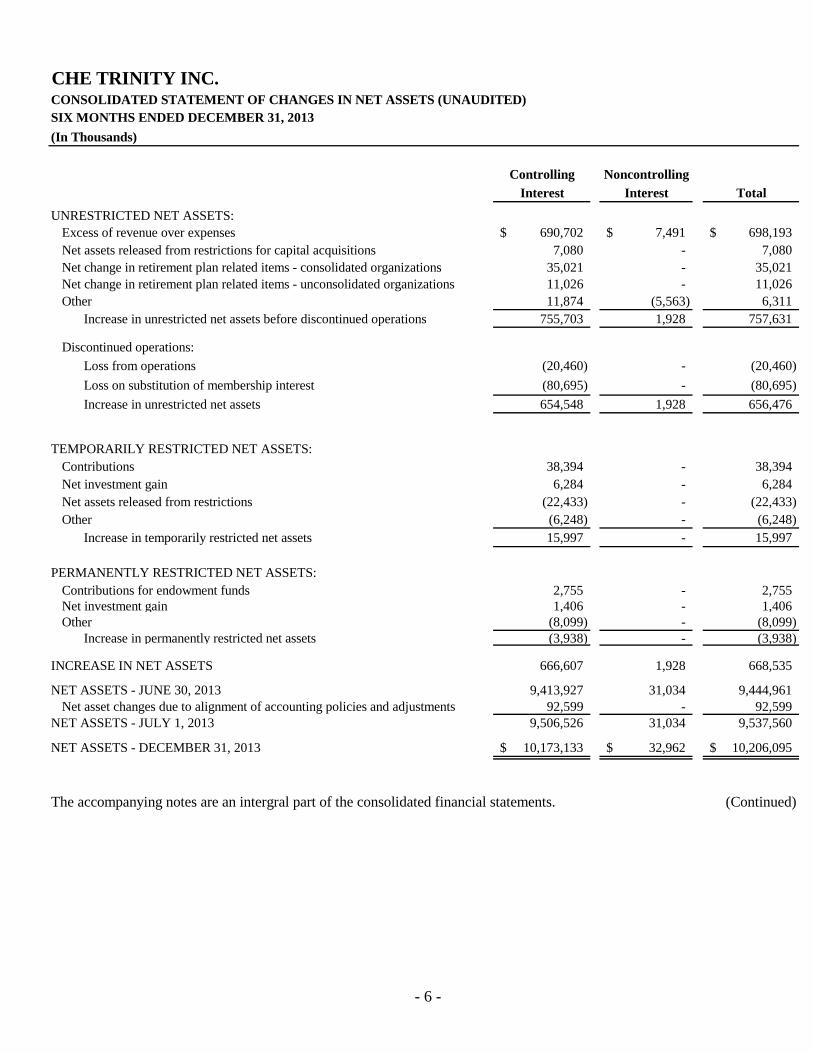

CHE TRINITY INC. CONSOLIDATED STATEMENT OF CHANGES IN NET ASSETS (UNAUDITED) SIX MONTHS ENDED DECEMBER 31, 2013

(In Thousands)

Controlling

Interest

Noncontrolling

Interest Total

UNRESTRICTED NET ASSETS: Excess of revenue over expenses Net assets released from restrictions for capital acquisitions Net change in retirement plan related items - consolidated organizations Net change in retirement plan related items - unconsolidated organizations Other

Increase in unrestricted net assets before discontinued operations

690,702 $ 7,080

35,021 11,026 11,874

755,703

7,491$ ---

(5,563) 1,928

$ 698,193 7,080

35,021 11,026 6,311

757,631

Discontinued operations:

Loss from operations

Loss on substitution of membership interest

Increase in unrestricted net assets

(20,460)

(80,695)

654,548

-

-

1,928

(20,460)

(80,695)

656,476

TEMPORARILY RESTRICTED NET ASSETS: Contributions Net investment gain Net assets released from restrictions Other

Increase in temporarily restricted net assets

38,394 6,284

(22,433) (6,248) 15,997

-----

38,394 6,284

(22,433) (6,248) 15,997

PERMANENTLY RESTRICTED NET ASSETS: Contributions for endowment funds Net investment gain Other

Increase in permanently restricted net assets

2,755 1,406

(8,099) (3,938)

----

2,755 1,406

(8,099) (3,938)

INCREASE IN NET ASSETS 666,607 1,928 668,535

NET ASSETS - JUNE 30, 2013 Net asset changes due to alignment of accounting policies and adjustments

NET ASSETS - JULY 1, 2013

9,413,927 92,599

9,506,526

31,034 -

31,034

9,444,961 92,599

9,537,560

NET ASSETS - DECEMBER 31, 2013 10,173,133 $ 32,962 $ $ 10,206,095

The accompanying notes are an intergral part of the consolidated financial statements. (Continued)

- 6 -

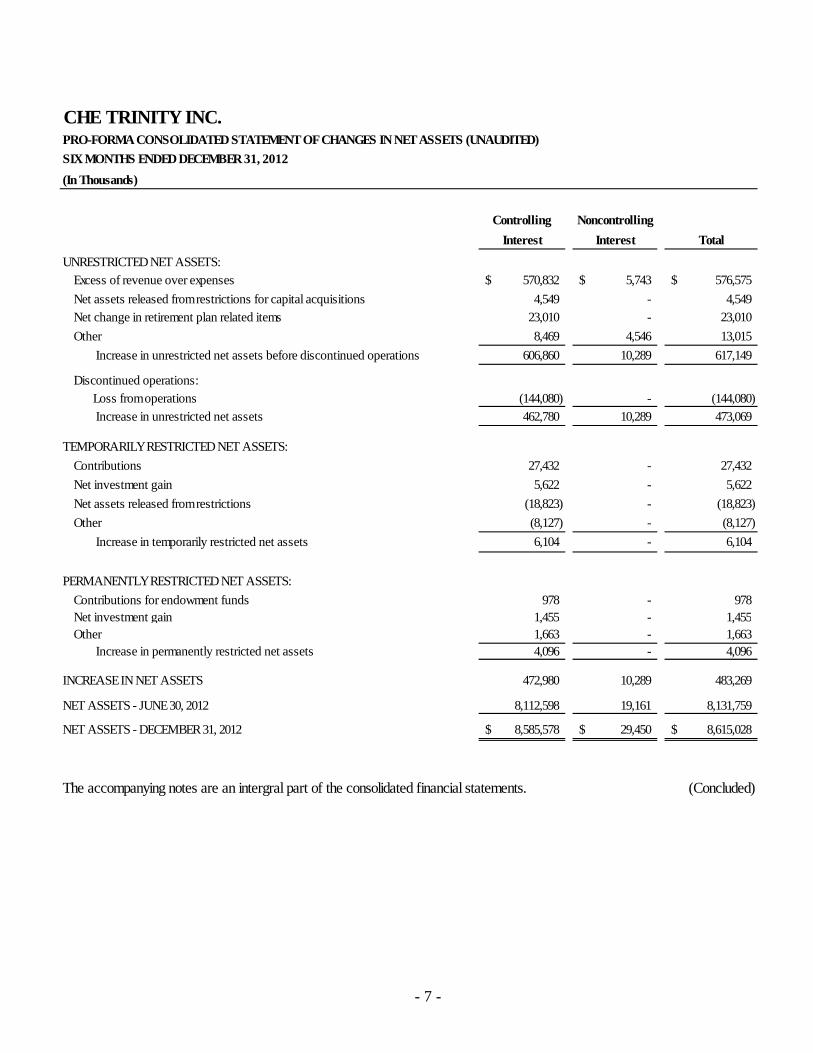

CHE TRINITY INC. PRO-FORMA CONSOLIDATED STATEMENTOF CHANGES INNET ASSETS (UNAUDITED)

SIX MONTHS ENDED DECEMBER 31, 2012

(In Thousands)

Controlling

Interest

Noncontrolling

Interest Total

UNRESTRICTED NET ASSETS: Excess of revenue over expenses

Net assets released fromrestrictions for capital acquisitions Net change in retirement plan related items

Other

Increase in unrestricted net assets before discontinued operations

570,832 $

4,549 23,010

8,469

606,860

5,743 $

--

4,546

10,289

$ 576,575

4,549 23,010

13,015

617,149

Discontinued operations: Loss fromoperations

Increase in unrestricted net assets

(144,080)

462,780

-

10,289

(144,080)

473,069

TEMPORARILYRESTRICTED NET ASSETS:

Contributions

Net investment gain

Net assets released fromrestrictions

Other

Increase in temporarily restricted net assets

27,432

5,622

(18,823)

(8,127)

6,104

-

-

-

-

-

27,432

5,622

(18,823)

(8,127)

6,104

PERMANENTLYRESTRICTED NET ASSETS:

Contributions for endowment funds Net investment gain Other

Increase in permanently restricted net assets

978 1,455 1,663 4,096

----

978 1,455 1,663 4,096

INCREASE IN NET ASSETS 472,980 10,289 483,269

NET ASSETS - JUNE 30, 2012 8,112,598 19,161 8,131,759

NET ASSETS - DECEMBER 31, 2012 8,585,578 $ 29,450 $ $ 8,615,028

The accompanying notes are an intergral part of the consolidated financial statements. (Concluded)

- 7 -

CHE TRINITY INC.

SUMMARIZED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED (In Thousands)

Six Months Ended Pro-forma

December 31, December 31,

2013 2012

OPERATING ACTIVITIES: Increase in net assets $ 668,535 $ 483,269 Adjustments to reconcile change in net assets to net cash provided

by operating activities: Depreciation and amortization 352,488 335,631

Provision for bad debts 347,169 357,425 Asset impairment charge discontinued operations - 110,427 Loss on substitution of membership interest 80,695 -

Change in net unrealized and realized gains and losses on investments (344,383) (222,402) Change in market values of interest rate swaps (20,689) (17,463) Undistributed equity earnings from unconsolidated affiliates (175,236) (147,563)

Restricted contributions and investment income received (4,847) (19,848) Deferred retirement items (11,026) 24,094 Gain on sale of assets - (26,006)

Return on investment in health plan equity interests - 23,987 Other adjustments (2,456) (1,755)

Changes in: Patient accounts receivable (392,141) (339,149) Other assets 6,645 (57,739)

Accounts payable and accrued expenses (60,094) (25,885) Estimated receivables from third-party payors (53,461) (7,536)

Accrued pension and retiree health costs (70,441) (176,257)

Self-insurance and other liabilities 29,159 55,646

Net cash (used in) provided by operating activities of discontinued operations (1,147) 42,542

Total adjustments (319,765) (91,851)

Net cash provided by operating activities 348,770 391,418

INVESTING ACTIVITIES:

Net purchases of investments (200,644) (45,175)

Net purchases of property and equipment (482,226) (472,956)

Physician practice acquisitions, net of cash - (22,341)

Proceeds from disposal of property and equipment 7,304 24,078 Dividends received from unconsolidated affiliates and other changes 15,830 15,168 Increase in assets limited as to use (5,631) (465) Net cash used in investing activities of discontinued operations (3,249) (9,317)

Net cash used in investing activities (668,616) (511,008) FINANCING ACTIVITIES:

Proceeds from issuance of long-term debt 652,517 79,761 Repayments of debt (208,100) (124,442) Net change in commercial paper (258,941) 99,965 Increase in financing costs (3,711) -Proceeds from restricted contributions and restricted investment income 4,847 19,848 Net cash used in financing activities of discontinued operations (4,435) (6,249)

Net cash provided by financing activities 182,177 68,883

NET DECREASE IN CASH AND CASH EQUIVALENTS (137,669) (50,707)

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 998,369 993,735

CASH AND CASH EQUIVALENTS, END OF PERIOD $ 860,700 $ 943,028

The accompanying notes are an integral part of the consolidated financial statements.

- 8 -

CHE TRINITY INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) SIX MONTHS ENDED DECEMBER 31, 2013 AND 2012

1. ORGANIZATION AND MISSION

Effective May 1, 2013, CHE Trinity Inc. ("the Corporation") became the sole member of Catholic Health East, a Pennsylvania nonprofit corporation ("CHE"), and Trinity Health Corporation, an Indiana nonprofit corporation ("Trinity Health") creating a unified Catholic national health system that enhances the mission of service to people and communities across the United States. This transaction was accounted for as a merger and thus the Corporation's balance sheet is recorded at its historical basis under the carryover method. For comparative purposes, consolidated unaudited pro-forma financial results of the Corporation are presented for the six month period ended December 31, 2012. Transition and integration are on-going with the Corporation incurring approximately $19.2 million and $3.2 million of expenses for the six months ended December 31, 2013 and 2012, respectively, as a result of the transaction, which are included in consolidation costs in the statement of operations and changes in net assets. In addition, in July 2013, the Corporation recorded adjustments to net assets totaling $92.6 million to align accounting policies and assumptions related to the valuation of pension and insurance liabilities.

The Corporation has adopted a fiscal year end of June 30. Effective July 1, 2013, CHE changed its fiscal year end from December 31 to June 30 in order to align CHE's year end with the Corporation. These statements reflect the adoption of a June 30 fiscal year end.

The Corporation is sponsored by Catholic Health Ministries, a Public Juridic Person of the Holy Roman Catholic Church. The Corporation operates a comprehensive integrated network of health services including inpatient and outpatient services, physician services, managed care coverage, home health care, long-term care, assisted living care and rehabilitation services located in twenty states. The operations are organized into Regional Health Ministries ("RHMs"). The mission statement for the Corporation is as follows:

We, CHE Trinity Health, serve together in the spirit of the Gospel as a compassionate and transforming healing presence within our communities.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United Statements of America ("GAAP") for interim financial reporting information. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments considered necessary for a fair presentation have been included and are of a normal and recurring nature. Operating results for the six months ended December 31, 2013 are not necessarily indicative of the results to be expected for the year ending June 30, 2014.

Principles of Consolidation - The consolidated financial statements include the accounts of the Corporation, and all wholly-owned, majority-owned and controlled organizations. Investments where the Corporation holds less than 20% of the ownership interest are accounted for using the cost method. All other investments that are not controlled by the Corporation are accounted for using the equity method of accounting. The Corporation has included its equity share of income or losses from investments in unconsolidated affiliates in other revenue and nonoperating items in the consolidated statements of operations and changes in net assets. All material intercompany transactions and account balances have been eliminated in consolidation.

Use of Estimates - The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management of the Corporation to make assumptions,

- 9 -

estimates and judgments that affect the amounts reported in the consolidated financial statements, including the notes thereto, and related disclosures of commitments and contingencies, if any. The Corporation considers critical accounting policies to be those that require more significant judgments and estimates in the preparation of its consolidated financial statements, including the following: recognition of net patient service revenue, which includes contractual allowances and provisions for bad debts and charity care; recorded values of investments, goodwill and intangible assets; reserves for losses and expenses related to health care professional and general liability; and risks and assumptions for measurement of pension and retiree medical liabilities. Management relies on historical experience and other assumptions believed to be reasonable in making its judgment and estimates. Actual results could differ materially from those estimates.

Cash and Cash Equivalents – For purposes of the consolidated statements of cash flows, cash and cash equivalents include certain investments in highly liquid debt instruments with original maturities of three months or less.

Investments - Investments, inclusive of assets limited or restricted as to use, include marketable debt and equity securities. Investments in equity securities with readily determinable fair values and all investments in debt securities are measured at fair value and are classified as trading securities. Investments also include investments in commingled funds, hedge funds and other investments structured as limited liability corporations or partnerships. Commingled funds and hedge funds that hold securities directly are stated at the fair value of the underlying securities, as determined by the administrator, based on readily determinable market values or based on net asset value, which is calculated using the most recent fund financial statements. Limited liability corporations and partnerships are accounted for under the equity method.

Investment Earnings – Investment earnings include interest, dividends, realized gains and losses on investments, holding gains and losses, and equity earnings. Investment earnings on assets held by trustees under bond indenture agreements, assets designated by the Board for debt redemption, assets held for borrowings under the intercompany loan program, and assets deposited in trust funds by a captive insurance company for self-insurance purposes, and certain assets held by grant making foundations in accordance with industry practices are included in other revenue in the consolidated statements of operations and changes in net assets. Investment earnings from all other investments and board designated funds are included in nonoperating investment income, unless the income or loss is restricted by donor or law.

Derivative Financial Instruments – The Corporation periodically utilizes various financial instruments (e.g. options and swaps) to hedge interest rate, equity downside risk and other exposures. The Corporation’s policies prohibit trading in derivative financial instruments on a speculative basis. The Corporation recognizes all derivative instruments in the balance sheets at fair value.

Securities Lending – The Corporation participates in securities lending transactions whereby a portion of its investments are loaned, through its agent, to various parties in return for cash and securities from the parties as collateral for the securities loaned. Each business day the Corporation, through its agent, and the borrower determine the market value of the collateral and the borrowed securities. If on any business day the market value of the collateral is less than the required value, additional collateral is obtained as appropriate. The amount of cash collateral received under securities lending is reported as an asset and a corresponding payable in the consolidated balance sheets and is up to 105% of the market value of securities loaned. At December 31, 2013 and June 30, 2013, the Corporation had securities loaned of $268.4 million and $223.7 million, respectively, and received collateral (cash and noncash) totaling $275.0 million and $230.3 million, respectively, relating to the securities loaned. The fees received for these transactions are recorded in investment income on the consolidated statements of operations and changes in net assets.

Assets Limited as to Use – Assets set aside by the Board for future capital improvements, future funding of retirement programs and insurance claims, retirement of debt, held for borrowings under the intercompany loan program, and other purposes over which the Board retains control and may at its discretion subsequently use for other purposes and self-insurance trust and benefit plan arrangements are included in assets limited as to use.

- 10 -

Donor-Restricted Gifts – Unconditional promises to give cash and other assets to the Corporation’s various RHMs are reported at fair value at the date the promise is received. Conditional promises to give and indications of intentions to give are reported at fair value at the date the gift is received. The gifts are reported as either temporarily or permanently restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the consolidated statements of operations and changes in net assets as net assets released from restrictions. Donor-restricted contributions whose restrictions are met within the same year as received are reported as unrestricted contributions in the consolidated statements of operations and changes in net assets.

Inventories – Inventories are stated at the lower of cost or market. The cost of inventories is determined principally by the weighted average cost method.

Assets and Liabilities Held of Sale – The Corporation has classified certain long-lived assets as assets held for sale in the consolidated balance sheets when the assets have met applicable criteria for this classification. The Corporation has also classified as held for sale those liabilities related to assets held for sale.

Property and Equipment – Property and equipment, including internal-use software, are recorded at cost, if purchased, or at fair value at the date of donation, if donated. Depreciation is provided over the estimated useful life of each class of depreciable asset and is computed using either the straight-line or an accelerated method and includes capital lease and internal-use software amortization. The useful lives of these assets range from 2 to 50 years. Interest costs incurred during the period of construction of capital assets are capitalized as a component of the cost of acquiring those assets.

Gifts of long-lived assets such as land, buildings, or equipment are reported as unrestricted support and are excluded from the excess of revenue over expenses, unless explicit donor stipulations specify how the donated assets must be used. Gifts of long-lived assets with explicit restrictions that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long-lived assets are reported as restricted support.

Goodwill – Goodwill represents the future economic benefits arising from assets acquired in a business combination that are not individually identified and separately recognized.

Intangible Assets – Intangible assets include both definite and indefinite-lived intangible assets. The majority of the net balance of definite-lived intangibles include non-compete agreements and physician guarantees with finite lives amortized using the straight-line method over their estimated useful lives, which range from 2 to 23 years and 2 to 12 years, respectively. Indefinite-lived intangible assets include trade names and renewable licenses.

Asset Impairment:

Property and Equipment - Impairment testing is performed following a triggering event or whenever events or changes in circumstances indicate an asset’s carrying value may not be recoverable.

Goodwill – Goodwill is tested for impairment on an annual basis or when an event or a change in circumstance indicates the value of a reporting unit may have changed. Testing is conducted at the reporting unit level. There is a two-step process for determining goodwill impairment. Step one compares the carrying value of each reporting unit with its fair value. If this test indicates the fair value is less than the carrying value, then step two is required. Step two compares the implied fair value of the reporting unit’s goodwill with the carrying value of reporting unit’s goodwill. The Corporation estimates the fair value of its reporting units using a discounted cash flow analysis.

Intangible Assets:

Definite-Lived - Impairment testing is performed if events or changes in circumstances indicate that the asset might be impaired. The impairment test consists of a comparison of the fair value of an intangible

- 11 -

asset with its carrying amount. The Corporation estimates the fair value of its intangible assets using an undiscounted cash flow analysis.

Indefinite-Lived - Impairment testing is performed on an annual basis or more frequently if events or changes in circumstance indicate the asset may be impaired. The impairment test consists of a comparison of the fair value of an intangible asset with its carrying amount. The Corporation estimates the fair value of its intangible assets using a discounted cash flow analysis including the use of net revenue associated with the trade names.

Deferred Revenue from Entrance Fees - Certain RHMs operate residential facilities for the elderly. Fees paid by residents upon entering into continuing care contracts, net of the portion that is refundable to the resident, are recorded as deferred revenue and amortized to income using the straight-line method over the estimated remaining life expectancy of the resident.

Temporarily and Permanently Restricted Net Assets – Temporarily restricted net assets are those whose use by the Corporation has been limited by donors to a specific time period or purpose. Permanently restricted net assets have been restricted by donors to be maintained by the Corporation in perpetuity.

Patient Accounts Receivable, Estimated Receivables from and Payables to Third-Party Payors and Net Patient Service Revenue – The Corporation has agreements with third-party payors that provide for payments to the Corporation’s RHMs at amounts different from established rates. Patient accounts receivable and net patient service revenue are reported at the estimated net realizable amounts from patients, third-party payors, and others for services rendered. Estimated retroactive adjustments under reimbursement agreements with third-party payors are included in net patient service revenue and estimated receivables from and payables to third-party payors. Retroactive adjustments are accrued on an estimated basis in the period the related services are rendered and adjusted in future periods, as final settlements are determined. Estimated receivables from third-party payors include amounts receivable from Medicare and state Medicaid meaningful use programs.

Allowance for Doubtful Accounts – The Corporation recognizes a significant amount of patient service revenue at the time the services are rendered even though the Corporation does not assess the patient's ability to pay at that time. As a result, the provision for bad debts is presented as a deduction from patient service revenue (net of contractual provisions and discounts). For uninsured patients that do not qualify for charity care, the Corporation establishes an allowance to reduce the carrying value of such receivables to their estimated net realizable value. This allowance is established based on the aging of accounts receivable and the historical collection experience by RHM and for each type of payor. A significant portion of the Corporation's provision for doubtful accounts relates to self-pay patients, as well as co-payments and deductibles owed to the Corporation by patients with insurance.

Charity Care – The Corporation provides services to all patients regardless of ability to pay. In accordance with the Corporation's policy, a patient is classified as a charity patient based on income eligibility criteria as established by the Federal Poverty Guidelines. Charges for services to patients who meet the Corporation's guidelines for charity care are not reflected in the accompanying consolidated financial statements.

Short-term borrowings – Short-term borrowings include puttable variable rate demand bonds supported by self-liquidity or liquidity facilities considered short-term in nature.

Other Long-Term Liabilities – Other long-term liabilities include accrued payments for the acquisition of Loyola University Health System ("LUHS") as stipulated in the Definitive Agreement related to Trinity Health's acquisition of LUHS, deferred compensation, asset retirement obligations and interest rate swaps.

Premium and Capitation Revenue – The Corporation has certain RHMs that arrange for the delivery of health care services to enrollees through various contracts with providers and common provider entities. Enrollee contracts are negotiated on a yearly basis. Premiums are due monthly and are recognized as revenue during the period in which the Corporation is obligated to provide services to enrollees. Premiums received prior to the

- 12 -

period of coverage are recorded as deferred revenue and included in accrued expenses in the consolidated balance sheet.

Certain of the Corporation’s RHMs have entered into capitation arrangements whereby they accept the risk for the provision of certain health care services to health plan members. Under these agreements, the Corporation’s RHMs are financially responsible for services provided to the health plan members by other institutional health care providers. Capitation revenue is recognized during the period for which the RHM is obligated to provide services to health plan enrollees under capitation contracts. Capitation receivables are included in other receivables in the consolidated balance sheets.

Reserves for incurred but not reported claims have been established to cover the unpaid costs of health care services covered under the premium and capitation arrangements. The premium and capitation arrangement reserves are classified with accrued expenses in the consolidated balance sheets. The liability is estimated based on actuarial studies, historical reporting, and payment trends. Subsequent actual claim experience will differ from the estimated liability due to variances in estimated and actual utilization of health care services, the amount of charges, and other factors. As settlements are made and estimates are revised, the differences are reflected in current operations.

Income Taxes – The Corporation and substantially all of its subsidiaries have been recognized as tax-exempt pursuant to Section 501(a) of the Internal Revenue Code. The Corporation also has taxable subsidiaries, which are included in the consolidated financial statements. Certain of the taxable subsidiaries have entered into tax sharing agreements and file consolidated federal income tax returns with other corporate taxable subsidiaries. The Corporation includes penalties and interest, if any, with its provision for income taxes in other nonoperating items in the consolidated statements of operations and changes in net assets.

Excess of Revenue Over Expenses – The consolidated statement of operations and changes in net assets includes excess of revenue over expenses. Changes in unrestricted net assets which are excluded from excess of revenue over expenses, consistent with industry practice, include the effective portion of the change in market value of derivatives that meet hedge accounting requirements, permanent transfers of assets to and from affiliates for other than goods and services, contributions of long-lived assets received or gifted (including assets acquired using contributions, which by donor restriction were to be used for the purposes of acquiring such assets), net change in retirement plan related items, discontinued operations, extraordinary items and cumulative effects of changes in accounting principles.

Adopted Accounting Pronouncements –

On July 1, 2013, the Corporation adopted Accounting Standard Update ("ASU") 2011-11, “Disclosures About Offsetting Assets and Liabilities." This guidance contains new disclosure requirements regarding the nature of an entity’s rights of setoff and related arrangements associated with its financial instruments and derivative instruments. The adoption of this guidance had no impact on the Corporation's consolidated financial statements.

On July 1, 2013, the Corporation adopted ASU 2012-02, “Intangibles Goodwill and Other (Topic 350): Testing Indefinite-lived Intangible Assets for Impairment.” This guidance provides entities the option of first assessing qualitative factors about the likelihood that an indefinite-lived intangible asset is impaired to determine whether further impairment assessment is necessary. It also enhances the consistency of the impairment testing guidance among long-lived asset categories by permitting entities to assess qualitative factors to determine whether it is necessary to calculate the asset’s fair value when testing an indefinite-lived intangible asset for impairment. The adoption of this guidance had no impact on the Corporation's consolidated financial statements.

On July 1, 2013, the Corporation adopted ASU 2012-05, “Statement of Cash Flows (Topic 230): Not-for-Profit Entities: Classification of the Sale Proceeds of Donated Financial Assets in the Statement of Cash Flows.” This guidance provides clarification on how entities classify cash receipts arising from the sale of certain donated financial assets in the statement of cash flows. The adoption of this guidance had no impact on the Corporation's consolidated statement of cash flows.

- 13 -

On July 1, 2013, the FASB issued ASU 2013-01, “Clarifying the Scope of Disclosures About Offsetting Assets and Liabilities.” This guidance provides clarification on the scope of the offsetting disclosure requirements in ASU 2011-11. The adoption of this guidance did not have a material impact on the Corporation's consolidated financial statements.

Forthcoming Accounting Pronouncements –

In February 2013, the FASB issued ASU 2013-04, “Obligations Resulting From Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the Reporting Date.” This guidance requires entities to measure obligations resulting from the joint and several liability arrangements for which the total amount of the obligation within the scope of this guidance is fixed at the reporting date. This guidance is effective for the Corporation beginning July 1, 2014 with early adoption permitted. The Corporation has not yet evaluated the impact this guidance may have on its consolidated financial statements.

In July 2013, the FASB issued ASU 2013-11. "Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists." This guidance requires entities to present an unrecognized tax benefit, or a portion of an unrecognized tax benefit, in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit, with some exceptions. This guidance is effective for the Corporation beginning July 1, 2014 with early adoption permitted. The Corporation does not expect this guidance to have an impact on its consolidated financial statements.

3. INVESTMENTS IN UNCONSOLIDATED AFFILIATES, BUSINESS DIVESTITURES AND DISCONTINUED OPERATIONS

Investments in Unconsolidated Affiliates – The Corporation and certain of its RHMs have investments in entities that are recorded under the cost and equity methods of accounting. The Corporation’s share of equity earnings from entities accounted for under the equity method was $175.2 million and $101.9 million for the six months ended December 31, 2013 and 2012, respectively, of which $31.7 million and $18.9 million, respectively, is included in other revenue and $143.5 million and $83.0 million, respectively, is included in nonoperating items in the consolidated statements of operations and changes in net assets. The most significant of these investments include the following.

BayCare Health System – The Corporation has a 50.4% interest in BayCare Health System Inc. and Affiliates ("BayCare"), a Florida not-for-profit corporation exempt from state and federal income taxes. BayCare was formed in 1997 pursuant to a Joint Operating Agreement ("JOA") among the not-for-profit, tax-exempt members of the Catholic East BayCare Participants, Morton Plant Mease Health Care, Inc, and South Florida Baptist Hospital, Inc. (collectively, the Members). BayCare consists of three community health alliances located in the Tampa Bay area of Florida including St. Joseph's-Baptist Healthcare Hospital, St. Anthony's Health Care, and Morton Plant Mease Health Care. The Corporation has the right to appoint nine of the twenty-one voting members of the Board of Directors of BayCare. At December 31, 2013, the Corporation's investment in BayCare totaled $1,575.9 million, excluding wholly owned subsidiaries and other beneficial interests.

Catholic Health System, Inc. – The Corporation has a one-third interest in Catholic Health System, Inc. and Subsidiaries ("CHS"). CHS, formed in 1998, is a not-for-profit integrated delivery healthcare system in Western New York jointly sponsored by the Sisters of Mercy, Ascension Health System, the Franciscan Sisters of St. Joseph, and the Diocese of Buffalo. CHE, Ascension Health System, and the Diocese of Buffalo are the corporate members of CHS. CHS operates several organizations, the largest of which are four acute care hospitals located in Buffalo, New York, Mercy Hospital of Buffalo, Kenmore Mercy Hospital, Sisters of Charity Hospital, and St. Joseph Hospital. At December 31, 2013, the Corporation's recorded investment in CHS totaled $22.6 million.

- 14 -

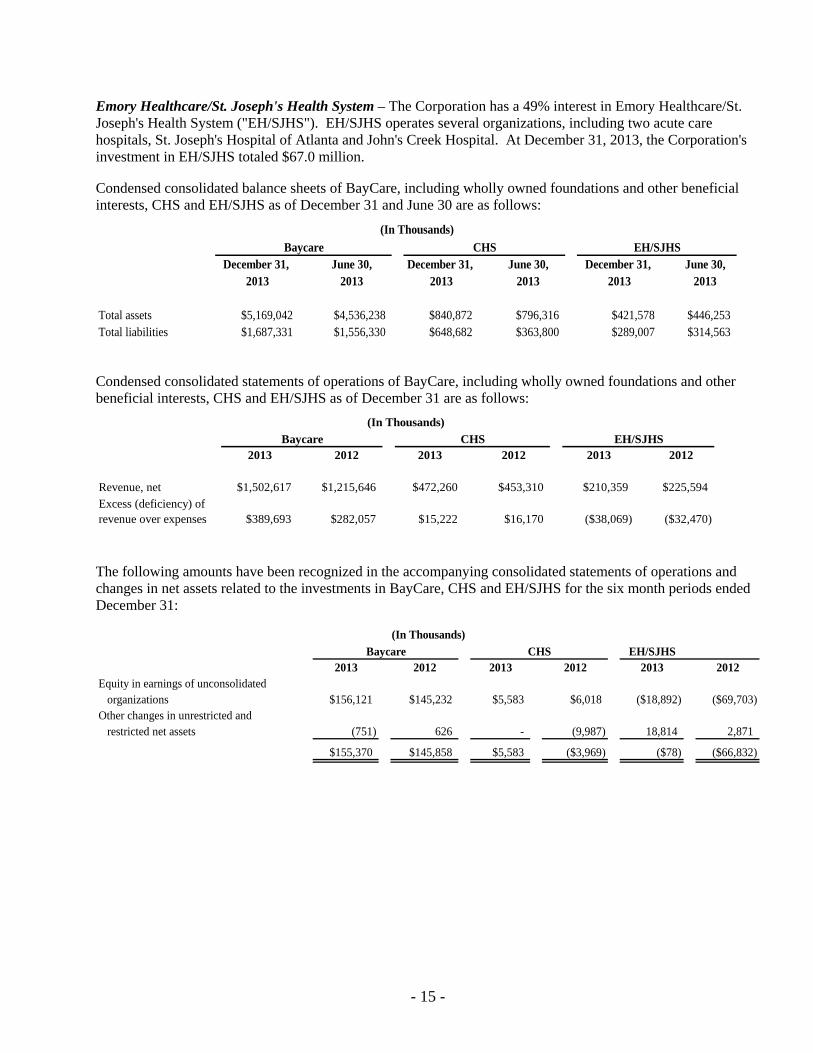

Emory Healthcare/St. Joseph's Health System – The Corporation has a 49% interest in Emory Healthcare/St. Joseph's Health System ("EH/SJHS"). EH/SJHS operates several organizations, including two acute care hospitals, St. Joseph's Hospital of Atlanta and John's Creek Hospital. At December 31, 2013, the Corporation's investment in EH/SJHS totaled $67.0 million.

Condensed consolidated balance sheets of BayCare, including wholly owned foundations and other beneficial interests, CHS and EH/SJHS as of December 31 and June 30 are as follows:

(In Thousands)

Baycare CHS EH/SJHS December 31, June 30, December 31, June 30, December 31, June 30,

2013 2013 2013 2013 2013 2013

Total assets $5,169,042 $4,536,238 $840,872 $796,316 $421,578 $446,253 Total liabilities $1,687,331 $1,556,330 $648,682 $363,800 $289,007 $314,563

Condensed consolidated statements of operations of BayCare, including wholly owned foundations and other beneficial interests, CHS and EH/SJHS as of December 31 are as follows:

(In Thousands)

Baycare CHS EH/SJHS 2013 2012 2013 2012 2013 2012

Revenue, net $1,502,617 $1,215,646 $472,260 $453,310 $210,359 $225,594 Excess (deficiency) of revenue over expenses $389,693 $282,057 $15,222 $16,170 ($38,069) ($32,470)

The following amounts have been recognized in the accompanying consolidated statements of operations and changes in net assets related to the investments in BayCare, CHS and EH/SJHS for the six month periods ended December 31:

(In Thousands)

2013 Baycare

2012 2013 CHS

2012 EH/SJHS

2013 Equity in earnings of unconsolidated

organizations Other changes in unrestricted and

restricted net assets

$156,121

(751)

$145,232

626

$5,583

-

$6,018

(9,987)

($18,892)

18,814

($69,703)

2,871

$155,370 $145,858 $5,583 ($3,969) ($78) ($66,832)

- 15 -

2012

Business Divestitures:

Mercy Health System of Maine ("Mercy Maine") – Effective October 1, 2013, Mercy Maine was assumed by Eastern Maine Health System ("EMHS") via a membership substitution. Substantially all assets and liabilities transferred to EMHS on that date. As a result of the transfer, a loss on disposal of $77.3 million was recorded in unrestricted net assets. The consolidated financial statements for all periods present the operations of Mercy Maine as a discontinued operation. For the six month periods ended December 31, 2013 and 2012, the Corporation reported revenue of $55.6 million and $104.2 million, respectively, and income/(losses) on operations of $0.4 million and ($5.6) million, respectively, in discontinued operations in the statement of changes in net assets. As of June 30, 2013, assets held for sale were $219.1 million and liabilities held for sale were $128.7 million. The majority of assets and liabilities held for sale consisted of:

(In Thousands)

Cash and investments $ 3,381 Current liabilities 17,623

Patient accounts receivable 34,015 Accounts payable and accrued expenses 29,276

Other current assets 10,647 Current portion of long-term debt 13,476

Estimated receivables from third parties 28,083 Long-term debt, net of current portion 63,767

Property and equipment

Assets limited or restricted as to use

Other assets

Total assets $ 213,269

Discontinued Operations:

Saint Michael's Medical Center – On February 8, 2013, Saint Michael's Medical Center entered into an asset purchase agreement under which the hospital would be acquired by Prime Healthcare Services. Certain assets and liabilities of Saint Michael's Medical Center have been classified as held for sale on the consolidated balance sheet. The transaction is expected to be completed in fiscal year 2014. The consolidated financial statements for all periods present the operations of Saint Michael's Medical Center as a discontinued operation. For the six month periods ended December 31, 2013 and 2012, the Corporation reported revenue of $193.0 million and $201.7 million, respectively, and losses on operations of $7.9 million and $139.6 million which includes an asset impairment charge of $110.4M, respectively, in discontinued operations in the statement of changes in net assets. As of December 31, 2013 and June 30, 2013, assets held for sale were $112.0 million and $107.1 million, respectively, and liabilities held for sale were $263.4 million and $267.1 million, respectively. The majority of assets and liabilities held for sale consisted of:

(In Thousands) December 31, June 30, December 31, June 30,

98,601 Other liabilities 18,060

35,827 Total liabilities 142,202$

2,715

2013 2013 2013 2013 Cash and investments Patient accounts receivable Other current assets Property and equipment

Other assets

Assets limited or restricted as to use

$ 15,939 21,029 10,042 80,761

19,223 23,126

18,982 $ 16,709 15,360 80,853

18,990 27,664

Due to CHE Current portion of long-term debt Accounts payable & accrued expenses Other current liabilities Long-term debt, net of current portion Other liabilit ies

Total liabilit ies $

116,160 5,276

17,435 13,890

238,301 7,855

398,917 $

113,499 5,464

18,495 11,929

243,061 7,839

400,287

T otal assets $ 170,120 $ 178,558

Saint James Mercy Hospital ("SJMH") – During December 2013, the Board of Directors of SJMH approved a plan to undergo a visioning plan and to transfer substantially all of the operations of SJMH. Certain assets and liabilities of SJMH have been classified as held for sale on the consolidated balance sheet. The consolidated financial statements for all periods present the operations of SJMH as a discontinued operation. For the six

- 16 -

month periods ended December 31, 2013 and 2012, the Corporation reported revenue of $20.0 million and $24.1 million, respectively, and losses on operations of $3.7 million and $2.7 million, respectively, in discontinued operations in the statement of changes in net assets. As of December 31, 2013 and June 30, 2013, assets held for sale were $6.0 million and $6.1 million, respectively. The majority of assets held for sale consisted of property and equipment.

4. PROPERTY AND EQUIPMENT

A summary of property and equipment at December 31, 2013 and June 30, 2013 is as follows:

December 31, June 30, 2013 2013

(In Thousands)

Land $ 320,848 $ 320,392 Buildings and improvements 7,563,742 7,517,102 Equipment 5,134,519 5,039,511 Capital leased assets 154,556 87,022

Total 13,173,665 12,964,027 Accumulated depreciation and amortization (7,417,108) (7,109,784) Construction in progress 761,558 614,383

Property and equipment, net $ 6,518,115 $ 6,468,626

As part of the acquisition of LUHS that occurred in fiscal year 2012, the Corporation has committed to spend at least $300 million on capital projects for LUHS through fiscal year ending June 30, 2018. This amount may be increased to $400 million if certain operating thresholds are met. Through December 31, 2013, approximately $130 million of capital expenditures have been incurred on capital projects for LUHS. In addition, as part of the acquisition of Mercy Health System of Chicago (MHSC) that occurred in fiscal year 2012, the Corporation has committed to spend at least $140 million for capital, information systems and equipment needs to support the operations of MHSC through the fiscal year ending June 30, 2017. This amount may be increased to $150 million if certain operating thresholds are met. Through December 31, 2013 approximately $53 million of capital expenditures have been incurred on such MHSC projects.

5. LONG-TERM DEBT AND OTHER FINANCING ARRANGEMENTS

Obligated Group and Other Requirements – The Corporation has debt outstanding under a Master Trust Indenture dated October 3, 2013, as amended and supplemented, the Amended and Restated Master Indenture (“ARMI”). The ARMI permits the Corporation to issue obligations to finance certain activities. Obligations issued under the ARMI are general, joint and several obligations of the Corporation, CHE and Trinity Health (the "Obligated Group"). Proceeds from tax-exempt bonds and refunding bonds are to be used to finance the construction, acquisition and equipping of capital improvements. Certain RHMs of the Corporation constitute designated affiliates and the Corporation covenants to cause each designated affiliate to pay, loan or otherwise transfer to the Obligated Group such amounts necessary to pay the amounts due on all obligations issued under the ARMI. The Obligated Group and the designated affiliates are referred to as the Credit Group.

The Obligated Group shall cause Designated Affiliates representing, when combined with the then-current Members of the Obligated Group, not less than 85% of the consolidated net revenues of the Credit Group to grant to the Master Trustee security interests in their Pledged Property, in order to secure all Obligations issued under the Master Indenture.

- 17 -

The Credit Group does not include certain Affiliates that borrow on their own or are members of a separate New York obligated group, but which are included in the Corporation's consolidated financial statements. St. Peter's Hospital of the City of Albany ("St. Peter's") currently is the sole member of an obligated group created under that certain Master Trust Indenture dated as of January 1, 2008, between St. Peter's and Manufacturers and Traders Trust Company, as Master Trustee. St. Peter's has received contingent approval from the New York State Department of Health to permit the entry into that obligated group of additional entities within St. Peter's Health Care Services, Northeast Health, Inc. and Seton Health System, Inc.

There are several conditions and covenants required by the ARMI with which the Corporation must comply, including covenants that require the Corporation to maintain a minimum debt service coverage and limitations on liens or security interests in property, except for certain permitted encumbrances, affecting the property of the Corporation or any material designated affiliate (a designated affiliate whose total revenues for the most recent fiscal year exceed 5% of the combined total revenues of the Corporation for the most recent fiscal year). Long-term debt outstanding as of December 31, 2013 and June 30, 2013, excluding amounts issued under the ARMI, is generally collateralized by certain property and equipment.

Mercy Health System of Chicago ("MHSC") has a commitment from the U.S. Department of Housing and Urban Development (“HUD”) to insure an approximate $66 million mortgage loan, under the Federal Housing Administration’s Section 242 Hospital Mortgage Insurance Program. At December 31, 2013 and June 30, 2013, the outstanding obligation was $62 million and $63 million, respectively. MHSC’s main hospital campus and two satellite facilities are collateral for the mortgage. The mortgage loan agreement with HUD contain various covenants including those relating to limitations on incurring additional debt, disposing of designated property, financial performance, insurance coverage, and timely submission of specified financial reports.

The CHE Trinity Health credit group issued $627 million in tax-exempt variable rate hospital revenue bonds (the “Series 2013 Bonds”) and remarketed $89 million in legacy CHE tax-exempt, variable rate hospital revenue bonds under the ARMI. Proceeds were used to retire $44 million of CHE’s then outstanding fixed rate hospital revenue bonds, $120 million of CHE’s then outstanding variable rate hospital revenue bonds and $269 million of Trinity Health's then outstanding taxable commercial paper obligations. The remaining proceeds of the Series 2013 Bonds will be used to finance, refinance and reimburse a portion of the costs of acquisition, construction, renovation and equipping of health facilities, and to pay related costs of issuance. These transactions resulted in a loss from extinguishment of debt of $1.4 million.

Commercial Paper – The Corporation has a commercial paper program authorized for borrowings up to $600 million. Proceeds from this program are used for general purposes of the Corporation. Notes issued under the commercial paper program are payable from the proceeds of subsequently issued commercial paper notes and from other funds available to the Corporation, including funds derived from the liquidation of securities held by the Corporation in the investment portfolios.

Liquidity Facilities – In July 2013, the Corporation renewed the Trinity Health credit agreements (collectively, the "Credit Agreements") previously entered into between Trinity Health and U.S. Bank National Association, which acts as an administrative agent for a group of lenders thereunder. The Credit Agreements establish a revolving credit facility for the Corporation, under which that group of lenders agree to lend to the Corporation amounts that may fluctuate from time to time. In October 2013, the Corporation exercised its option to increase by $200 million the 2013 Credit Agreements from $731 million to $931 million. Amounts drawn under the 2013 Credit Agreements can only be used to support the Corporation’s obligation to pay the purchase price of bonds which are subject to tender and that have not been successfully remarketed, and the maturing principal of and interest on commercial paper notes. Of the $931 million available balance, $150 million expires in July 2014, $175 million expires in July 2015, $321 million expires in July 2016 and $285 million expires in July 2017. The Credit Agreements are secured by Obligations under the Master Indenture. There were no draws on these credit agreements during the periods ended December 31, 2013 and June 30, 2013.

The Corporation also maintains a CHE general purpose facility of $300 million, of which $37 million is related to letters of credit. At the Corporation's option, this general purpose facility may be increased to $350 million.

- 18 -

As of December 31, 2013 and June 30, 2013, draws on this general purpose credit facility totaled $61 million and $54 million, respectively.

In addition, in July 2013, the Corporation renewed a Trinity Health three year general purpose credit facility of $200 million. As of December 31, 2013 and June 30, 2013, there were no amounts outstanding under this credit facility.

6. PROFESSIONAL AND GENERAL LIABILITY PROGRAMS

The Corporation operates wholly owned insurance companies that qualify as captive insurance companies (Stella Maris Insurance Company, Ltd. (“Stella Maris”) and Venzke Insurance Company, Ltd. (“Venzke”)). Both insurance companies provide certain insurance coverage to the Corporation's RHMs. The Corporation is self-insured for certain levels of general and professional liability, workers’ compensation and certain other claims. The Corporation has limited its liability by purchasing reinsurance and commercial coverage from unrelated third-party insurers.

As of October 1, 2013, all insurance policies, except workers compensation and auto liability, are being provided to the RHMs under a consolidated program. Workers compensation and auto liability will be consolidated in the third quarter of fiscal year 2014. All assets and liabilities of Stella Maris will be merged into Venzke effective January 1, 2014. Policies issued and reinsurance purchased by Stella Maris prior to January 1, 2014 and all losses previous to January 1, 2014 will be assumed by Venzke.

The Corporation’s current self-insurance program includes $20 million per occurrence for the first layers of professional liability, as well as $10 million per occurrence for hospital government liability, $5 million per occurrence for errors and omission liability, and $1 million per occurrence for directors’ and officers’ liability. Additional layers of professional liability insurance are available with coverage provided through other insurance carriers and various reinsurance arrangements. The total amount available for these subsequent layers is $100 million in aggregate. The Corporation also self-insures up to $500,000 in property damage liability with commercial insurance providing coverage up to $1 billion.

The liability for self-insurance reserves represents estimates of the ultimate net cost of all losses and loss adjustment expenses which are incurred but unpaid at the consolidated balance sheet date. The reserves are based on the loss and loss adjustment expense factors inherent in the Corporation’s premium structure. Independent consulting actuaries determined these factors from estimates of the Corporation’s expenses and available industry-wide data. The Corporation discounts the reserves to their present value using a discount rate of 3.0%. The reserves include estimates of future trends in claim severity and frequency. Although considerable variability is inherent in such estimates, management believes that the liability for unpaid claims and related adjustment expenses is adequate based on the loss experience of the Corporation. The estimates are continually reviewed and adjusted as necessary.

Claims in excess of certain insurance coverage and the recorded self-insurance liability have been asserted against the Corporation by various claimants. The claims are in various stages of processing, and some may ultimately be brought to trial. There are known incidents occurring through December 31, 2013, that may result in the assertion of additional claims, and other claims may be asserted arising from services provided in the past. While it is possible that settlement of asserted claims and claims which may be asserted in the future could result in liabilities in excess of amounts for which the Corporation has provided, management, based upon the advice of Counsel, believes that the excess liability, if any, should not materially affect the consolidated financial position, operations or cash flows of the Corporation.

- 19 -

7. PENSION AND OTHER POSTRETIREMENT BENEFIT PLANS

Defined Contribution Benefits – The Corporation sponsors defined contribution pension plans covering substantially all of its employees. These programs vary by location and are funded by employee voluntary contributions, subject to legal limitations. Employer contributions to these plans include varying levels of matching and non-elective contributions. The employees direct their voluntary contributions and employer contributions among a variety of investment options. Trinity Health suspended the majority of employer matching contributions for the calendar years 2013 and 2014. Contribution expense under the plans totaled $27.6 million and $58.4 million for the six month periods ended December 31, 2013 and 2012, respectively.

Defined Benefit Pension Plans – The Corporation sponsors non-contributory defined benefit pension plans. Certain of the plans have been amended to freeze benefit accruals. The remaining active defined benefit pension plan is structured as a cash balance plan. The Corporation recognizes in its consolidated balance sheets the funded status of its defined benefit pension and other post retirement plans, measured as the difference between the fair value of plan assets and the benefit obligation as of June 30. Further, actuarial gains and losses that are not recognized in net periodic pension cost when they arise are recognized as a component of unrestricted net assets and are amortized as a component of net periodic pension cost over the average future working lifetime of active participants, or the average future life expectancy of all participants for plan with frozen benefits.

Other Post Retirement Benefit Plans – The Corporation also sponsors both funded and unfunded contributory retiree health plans for certain hourly and salaried employees who are retired from or will retire from certain regional health ministries. Benefits provided under these plans and required retiree contributions differ by regional health ministry. The funded plans provide benefits to certain retirees at fixed dollar amounts in Health Reimbursement Account arrangements for Medicare eligible participants. As of January 1, 2002, all such plans were closed to additional participants.

Components of net periodic benefit cost for the six month periods ended December 31 consisted of the following:

Pension Plans Postretirement Plans

2013 2012 2013 2012 (In Thousands) (In Thousands)

Service cost $ 74,569 $ 77,558 $ 314 $ 442 Interest cost 162,647 154,501 2,648 2,686 Expected return on assets (195,337) (191,846) (3,057) (2,855) Amortization of prior service cost (13,441) (14,306) (2,881) (3,659) Recognized net actuarial loss 51,755 69,414 (84) 621

Net periodic benefit cost (income) $ 80,193 $ 95,321 $ (3,060) $ (2,765)

8. CONTINGENCIES

On September 21, 2007, in Boise, Idaho a jury awarded $58.9 million in damages to MRI Associates, LLP, an Idaho limited partnership (“MRIA”) against Saint Alphonsus Regional Medical Center and its subsidiary Saint Alphonsus Diversified Care, Inc. (together, “Saint Alphonsus”). The lawsuit involved Saint Alphonsus’ withdrawal from the MRIA partnership. The jury award was reduced by the trial judge to $36.3 million, which was offset by the award of $4.6 million to Saint Alphonsus, the value of its partnership interest in MRIA. Saint Alphonsus appealed and, in October 2009, the Idaho Supreme Court overturned the trial court decision and remanded the case for a new trial. The second trial was held during October 2011 with a jury awarding approximately $52 million in damages to MRIA. After Saint Alphonsus filed an objection, the trial court entered amended judgments indicating that the plaintiffs could execute alternative judgments which vary in amount from approximately $20 million to $52 million. Saint Alphonsus continues to have an offset of $4.6 million plus 10%

- 20 -

interest running from September 21, 2007. Saint Alphonsus filed a Notice of Appeal to the Idaho Supreme Court in May 2012, because the Corporation believes that the proof of damages is insufficient to sustain the jury’s award under Idaho law. The oral arguments were presented to the Court on February 19, 2014. The Corporation recorded management’s estimation for damages of $20 million in the 2007 consolidated statement of operations and changes in net assets for the year ended June 30, 2007. As of December 31, 2013 and June 30, 2012, the liability is included in other long-term liabilities in the consolidated balance sheets in the event of an unfavorable resolution of this matter.

CHE and Merrill Lynch, Pierce, Fenner & Smith, one of the Corporation’s underwriters, are named as defendants in an action filed by Emmet & Co, Inc. and First Manhattan Co. (together “Plaintiffs”) with respect to three series of bonds issued for the benefit of CHE. Plaintiffs allege that CHE breached the Indentures relating to those bonds and violated the covenant of good faith and fair dealing in the exercise of its optional redemption rights for those bonds in connection with its tender offer for those bonds. CHE filed a motion to dismiss this complaint. On September 25, 2013 the Court granted CHE’s Motion to Dismiss the Complaint. Plaintiffs’ appeal to the New York Supreme Court Appellate Division was denied by Order entered on February 27, 2014. It is uncertain if the Plaintiffs will attempt a further appeal. On March 12, 2014, the Corporation received a copy of a letter sent by counsel to the Plaintiffs to Bank of New York Mellon Trust Company, N.A. as trustee on one of the series of bonds. The letter reasserts the Plaintiffs' argument that the CHE acted improperly in the tender offer and redemption of those bonds. The Corporation believes that the tender and redemption process was properly conducted and will respond to any request for information from the trustee. The Corporation’s management does not believe that this matter, if decided adversely, would have a material adverse effect on the financial condition of the Corporation. In June 2013, CHE received a notice from the IRS that these transactions were under audit, asking for information. CHE does not believe it has any direct exposure as these bonds are held by Merrill Lynch and is fully cooperating in the investigation.

On March 29, 2013, the CHE was notified that it is a defendant in a lawsuit which challenges the church plan status of the CHE Employee Pension Plan. In response thereto, CHE has filed a motion to dismiss the complaint which is now pending before the United States District Court for the Eastern District of Pennsylvania. At this point, it is not possible to assess the exposure, if any, related to these claims and no amount has been reserved at this time.

The Corporation is involved in other litigation and regulatory investigations arising in the course of doing business. After consultation with legal Counsel, management estimates that these matters will be resolved without material adverse effect on the Corporation’s future consolidated financial position or results of operations.

9. SUBSEQUENT EVENTS

Management has evaluated subsequent events through March 14, 2014, the date the quarterly report was issued. The following subsequent events were noted:

Letter of Intent with Siouxland Surgery Center ("SSC") – On January 17, 2014, the Corporation entered into a nonbinding letter of intent through its operating division Mercy Medical Center, Sioux City to increase its ownership interest in SSC from 30.9% to 51%. The letter of intent will remain in effect until March 31, 2014 unless the term is extended by written agreement of the parties.

- 21 -

CHE Trinity Inc. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management of the Corporation to make assumptions, estimates and judgments that affect the amounts reported in the financial statements, including the notes thereto, and related disclosures of commitments and contingencies, if any. The Corporation considers critical accounting policies to be those that require the more significant judgments and estimates in the preparation of its financial statements, including the following: recognition of net patient service revenue, which includes contractual allowances, provisions for bad debt and charity care; recorded values of investments, goodwill and intangible assets; reserves for losses and expenses related to health care professional and general liability; and risks and assumptions for measurement of pension and retiree medical liabilities. Management relies on historical experience and on other assumptions believed to be reasonable under the circumstances in making its judgment and estimates. Actual results could differ materially from those estimates.

The Patient Protection and Affordable Care Act (“ACA”) was enacted in March 2010. This legislation addresses almost all aspects of hospital and provider operations and health care delivery, and is changing how health care services are covered, delivered, and reimbursed. These changes will result in new payment models with the risk of lower hospital reimbursement from Medicare, utilization changes, increased government enforcement and the necessity for health care providers to assess, and potentially alter, their business strategy and practices, among other consequences. While many providers may receive reduced payments for care, millions of previously uninsured Americans may have coverage.

Management of the Corporation has analyzed the ACA and will continue to do so in order to assess the effects of the legislation and evolving regulations on current and projected operations, financial performance and financial condition. However, management of the Corporation cannot predict with any reasonable degree of certainty or reliability any interim or ultimate effects of the legislation.

Effective May 1, 2013, CHE Trinity Inc. (the "Corporation") became the sole member of Catholic Health East, a Pennsylvania nonprofit corporation ("CHE"), and Trinity Health Corporation, an Indiana nonprofit corporation ("Trinity Health") creating a unified Catholic national health system that enhances the mission of service to people and communities across the United States. This transaction was accounted for as a merger and thus the Corporation's balance sheet is recorded at its historical basis under the carryover method. For comparative purposes, consolidated unaudited pro-forma financial results of the Corporation are presented for the six month period ended December 31, 2012. Transition and integration are on-going with the Corporation incurring approximately $19.2 million and $3.2 million of expenses for the six months ended December 31, 2013 and 2012, respectively, as a result of the transaction, which are included in consolidation costs in the statement of operations and changes in net assets. In addition, in July 2013, the Corporation recorded adjustments to net assets totaling $92.6 million to align accounting policies and assumptions, primarily those related to the valuation of pension and insurance liabilities.

Historical Performance: Six Months Ended December 31, 2013 and 2012

Operating Income. Operating income for the first six months of fiscal year 2014 of $187 million, prior to $19 million of costs incurred as a result of the consolidation, decreased $16 million compared to the same period in fiscal year 2013. Operating cash flow margin and operating margin, prior to consolidation expenses, were 9.2% and 2.8%, respectively, for the six months ended December 31, 2013, compared to 9.4% and 3.1% for the same period in fiscal year 2013. Excess of revenue over expenses was $698 million for the six months ended December 31, 2013, compared to $577 million for the same period in fiscal year 2013, an improvement of $121 million, primarily due to a $115 million increase in investment income.

Revenue. Operating revenue has continued to grow in fiscal year 2014. Total unrestricted revenue of $6.8 billion increased $234 million, or 3.6%, for the six months of fiscal year 2014, compared to the same period in fiscal year 2013. Contributors to the increase were due primarily to the following: (i) $183 million in volume

- 22 -

growth, (ii) payment rate increases of $21 million in net patient service revenue, and (iii) premium revenue of $26 million. These increases were partially offset by a decrease of $36 million in charity care at charges. Volumes were mixed compared to prior year among the RHMs with increases in case-mix adjusted equivalent discharges and surgeries offset by decreases in discharges.

Expenses. Total operating expenses of $6.6 billion, excluding consolidation costs, increased $250 million, or 3.9%, for the first six months of fiscal year 2014, compared to the same period in fiscal year 2013. Contributors to the increase were due primarily to the following: (i) labor expense of $73 million (salaries and wages $121 million primarily due to a 3.4% increase in rate and a 0.5% increase FTEs, partially offset by a $37 million decrease in pension costs), (ii) supplies of $45 million, (iii) purchased services of $41 million, and (iv) medical claims of $23 million. Depreciation and amortization, occupancy, and interest expense did not materially change during the six months ended December 31, 2013 compared to the same period in fiscal year 2013.

Nonoperating Items. The Corporation reported gains in nonoperating items of $530 million for the first six months of fiscal year 2014, compared to gains of $356 million for the same period of fiscal year 2013. The increase of $174 million was primarily due to an increase in investment income of $115 million and equity gains in unconsolidated affiliates of $61 million primarily due to nonoperating investment income at BayCare.

Balance Sheet Trends. The Corporation’s total assets of $19.8 billion increased $463 million, or 2.4%, as of December 31, 2013, compared to June 30, 2013. The most significant increases include: (i) assets limited or restricted as to use, non-current portion, of $337 million, (ii) investments in unconsolidated affiliates of $175 million, (iii) current portion of investments of $155 million, (iv) long-term investments of $69 million, (v) property and equipment - net of $49 million and (vi) patient accounts receivable, net of allowance for doubtful accounts of $46 million. These increases were partially offset by decreases in assets held for sale of $217 million and cash and cash equivalents of $138 million.

Total liabilities of $9.6 billion decreased $298 million, or 3.0%. The most significant decreases included: (i) commercial paper of $259 million, (ii) accrued pension and retiree health costs of $194 million, (iii) liabilities held for sale of $152 million, (iv) accounts payable of $99 million, (v) accrued expenses of $51 million, and (vi) other long-term liabilities of $42 million. These decreases were partially offset by increases in short-term borrowings of $332 million, long-term debt - net of current portion, of $133 million and self-insurance reserves - net of current portion, of $56 million.

Statement of Cash Flows. Cash and cash equivalents decreased $138 million during the six months ended December 31, 2013. During that period, operating activities provided $349 million of cash. Investing activities used $669 million of cash including $482 million for purchases of property and equipment and $201 million for net purchases of investments. Financing activities generated $182 million, primarily as a result of the issuance of long-term debt of $653 million, offset by the repayment of commercial paper of $259 million and the repayment of debt $208 million.

- 23 -

CHE Trinity Inc. Liquidity Reporting Summary as of December 31, 2013

ASSETS

($ in millions) (unaudited)

Daily Liquidity

Money Market Funds (Moody's rated Aaa) Repurchase Agreements U.S. Treasuries & Aaa-rated Agencies Dedicated Bank Lines

Subtotal Daily Liquidity (Cash & Securities)

$

$

1,007 2

26 931

1,965

Undrawn Portion of $600M Taxable Commercial Paper Program 490

Subtotal Daily Liquidity Including Taxable Commercial Paper Program $ 2,455

Weekly Liquidity Exchange Traded Equity Publicly Traded Fixed Income Securities Rated at least Aa3 and Bond Funds Equity Funds Other

Subtotal Weekly Liquidity

$ 1,009 1,196

819 179

3,203

TOTAL DAILY AND WEEKLY LIQUIDITY $ 5,659

Longer Term Liquidity

Funds, vehicles, investments that allow withdrawals with less than one month notice Funds, vehicles, investments that allow withdrawals with one month notice or longer

Total Longer Term Liquidity

245 2,110

$ 2,355

LIABILITIES (Self-liquidity Variable Rate Demand Bonds & Commercial Paper)

Weekly Put Bonds

VRDO Bonds (7-day) $ 385

Long-Mode Put Bonds

VRDO Bonds (Commerical Paper Mode)

Taxable Commercial Paper Outstanding

442

110

TOTAL SELF-LIQUIDITY DEBT AND COMMERCIAL PAPER $ 937

- 24 -

CHE Trinity Inc. Financial Ratios and Statistics (Unaudited)

Pro-forma December 31, December 31,

2013 2012

Financial Indicators

Liquidity Ratios (at December 31) Days Cash on Hand 209 197 Days in Accounts Receivable 43 42

Leverage Ratios (at December 31) Debt to Capitalization 34.2% 36.3% Cash to Debt 139.7% 137.3%

Profitability Ratios (For the Six Months Ended December 31) Prior to Consolidation Costs Operating Margin 2.8% 3.1% Operating Cash Flow Margin 9.2% 9.4%

Statistical Indicators (For the Six Months Ended December 31) (in thousands)

Discharges 260 270 Patient Days 1,194 1,249 Outpatient Visits 6,935 6,598 Emergency Room Visits 1,039 1,053

Continuing Care Home Health Visits 827 746 Patient Days 644 635

- 25 -