sub-national revenue generation and fiscal management: the case of cape town

TRANSCRIPT

Sub-national Revenue Generation and Fiscal Management: The Case of Cape Town

ICTD Property Taxation Workshop

February 13, 2016

William Attwell

2Overview of Talk

– Local government fiscal powers in South Africa

– Special rating areas

– Property taxes and the budget

– Poverty alleviation mechanisms

– Local government finance challenges

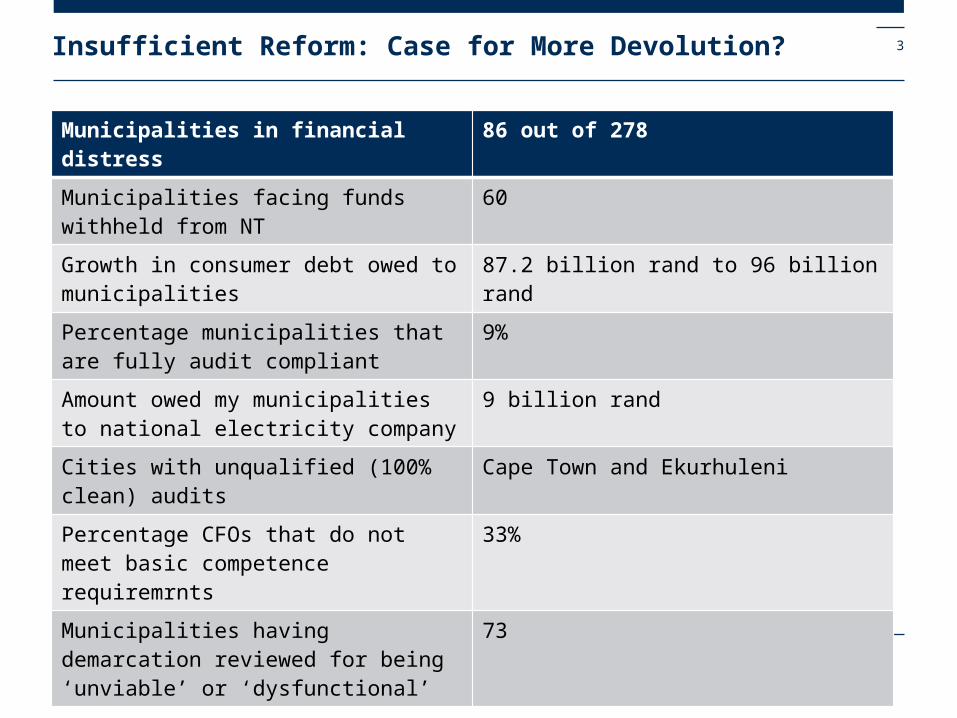

3Insufficient Reform: Case for More Devolution?

Municipalities in financial distress 86 out of 278

Municipalities facing funds withheld from NT 60

Growth in consumer debt owed to municipalities

87.2 billion rand to 96 billion rand

Percentage municipalities that are fully audit compliant

9%

Amount owed my municipalities to national electricity company

9 billion rand

Cities with unqualified (100% clean) audits Cape Town and Ekurhuleni

Percentage CFOs that do not meet basic competence requiremrnts

33%

Municipalities having demarcation reviewed for being ‘unviable’ or ‘dysfunctional’

73

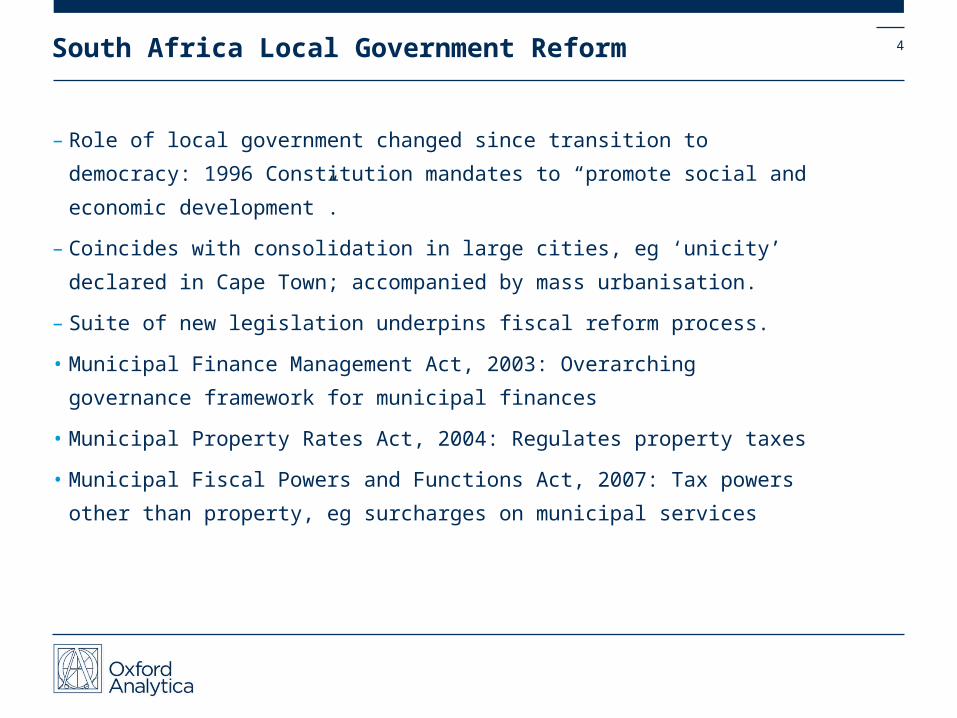

4South Africa Local Government Reform

– Role of local government changed since transition to democracy: 1996 Constitution mandates to “promote social and economic development”.

– Coincides with consolidation in large cities, eg ‘unicity’ declared in Cape Town; accompanied by mass urbanisation.

– Suite of new legislation underpins fiscal reform process.

• Municipal Finance Management Act, 2003: Overarching governance framework for municipal finances

• Municipal Property Rates Act, 2004: Regulates property taxes

• Municipal Fiscal Powers and Functions Act, 2007: Tax powers other than property, eg surcharges on municipal services

5Municipal Property Rates Act, No. 6 of 2004

- Regulates municipalities’ powers to impose property taxes; stipulates standards for “fair” valuation methods and outlines a transparent system for exemptions reductions and rebates), objections and appeals.

- Section 2 (1) “A metropolitan or local municipality may levy a rate on property in its area”

- Section 3 (3) Requires that municipalities formulate their own rates policies

- Equity considerations:

(f) Requires that policies take into account the effect of rates on the poor and include “appropriate” measures to alleviate the rates burden on them;

(g) they must also take into account the effect of rates on organisations undertaking “public benefit” activities;

(h) consider their implications for public services and infrastructure; and

(i) be consistent with the municipality's responsibility to promote local, social and economic development.

- Generally, most effective in wealthier areas where residents have the ability to pay.

6Property taxes: Some considerations

– Benefits:

• Property is immovable: Cannot move away when taxes are increased.

• Inherently local character: Where used to fund basic services, lines of accountability with local authority is clear, helping build legitimacy.

• Value invested by local authority in surrounding land (eg, service infrastructure) is reflected in property value

• Promote productive use of urban land.

• Can help to fund services not easily financed through user charges.

- But:

• Accurate land valuation costly; requires adequate bureaucratic capacity.

• Maintaining real tax rates requires regular updates, possibly spurring resentment.

• Property values inelastic vis a vis GDP performance; can hurt cash-poor but asset-rich residents.

- In OECD countries, property taxes equivalent to 2% of GDP; developing countries between 0.3-0.7%.

- Different valuation approaches: Area-based versus value-based land value assessments.

7Revenues sources (%) CoCT 2015/16 Budget

Property rates, 20.8

Electricity; 35.1

Water; 8.7

Sanitation; 4.6

Refuse; 3.5Other services; 1.8

Rentals; 1.1

Interest (external invest); 0.9

Interest (debtors); 0.7 Fines; 3.1

Permits; 0.1

Agency services; 0.5 Transfers; 11.3

Other revenue; 7.7 PPE disposal; 0.2

8Property Rates Contribution to Revenue (CoCT revenue summary 2015/16)

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/180

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

Property rates Total revenue Elecricity revenue Transfers

9Section 22: Special Rating Areas

- This allows municipalities to:

“…levy an additional rate on property in a specified area for the purpose of raising funds for improving or upgrading that area…”

- Requires that most resident/ businesses/ property owners in that area agree to the SRA.

- First case in SA was Cape Town’s Central City Improvement District:

• Established in 2000 by businesses located in the CBD.

• Founders concerned by degraded state and resulting business ‘flight to the suburbs’.

• For higher than normal rates, the CCID provides extra security (by CCID officers), conducts extra cleaning, engages NGOs on social programmes and markets the CBD as ‘business friendly’.

- New Tygerberg Valley Partnership being considered for secondary CBD.

10Central City Improvement District (CCID)

11City of Cape Town Special Rating Area By-Law, 2012

– Regulates the operations, approvals process and application procedure for establishing an SRA.

– SRA’s require a realistic business plan, proof of consent of the majority of affected owners/ affected residents, and payment of a fee.

– A management body is then established to oversee the running of the SRA; it can receive payments from the CoCT subject to MFMA requirements; CoCT may also impose administrative charges.

–Management body’s immediate reporting line is to the Subcouncil.

– This ensures a direct accountability link with local elected representatives.

– The SRA business plan is usually time-bound; it must reapply to the CoCT to renew.

– A majority of owners affected by the SRA may apply have SRA dissolved.

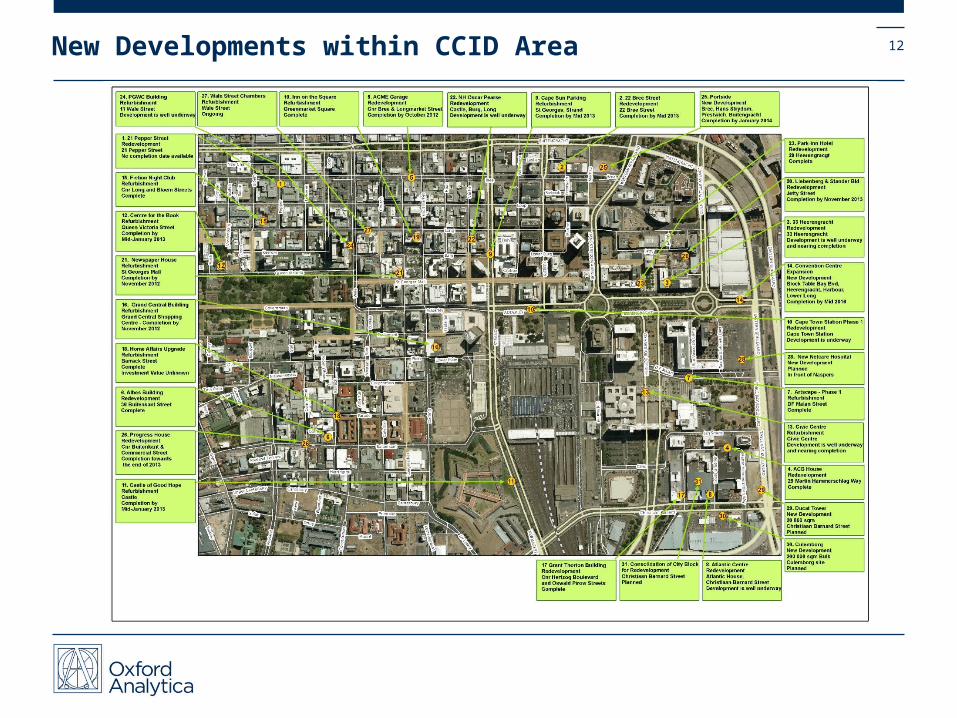

12New Developments within CCID Area

13CoCT 2015/16 Budget: Stylized facts

– Total budget: 38.2 billion rand (82% operating; 18% capital budget)

– Operating revenue increased form 28.4 billion to 31.7 billion during 2014/15 to 2015/16.

– Largest contributions came from electricity (11.1 billion), property taxes (6.6 billion) and transfers from national government (3.6 billion). The latter includes the “equitable share” (calculated on population) and transfers for various national policy priorities, eg EPWP, health initiatives and skills development linked to the national infrastructure programme.

– Staff costs represent the largest expenditure item (30.6%), followed by materials and bulk purchases (25.9%) and contracted services (15.1%).

– Capital budget provides for various forms of pro-poor spending:

• Broadband infrastructure: 191 million rand

• Basic services for ‘backyarders’: 80 million rand

• Development of District 6: 76 million rand

14Poverty Relief and Taxes

– Residents can receive free basic services if (i) their property is worth below a given amount (ii) they earn below certain thresholds and apply to the CoCT for an ‘indigent grant’.

– The property-linked benefits operate as a sliding scale, ranging from 100,000 rand (100% free) up to 400,000 rand.

– It provides ‘lifeline’ electricity (60 kWh per month), water and sanitation supplies for very low income households; and

– The latter in funded by national government transfers; topped up with rates account.

– Section 67 grants for niche social projects.

Incomes below 3500 rand

100% rebate

Incomes 3501-4000 rand 75% rebate

Incomes 4001-4500 rand 50% rebate

Incomes 4501-5000 rand 25% rebate

Pensioners/disabled below 3500 rand

100% rebate

Maximum pensioner/disabled threshold 12000 rand

10%

15Participation and Oversight

– Budget is approved by full Council (executive and legislative)

– Follows an extensive public participation process

– ‘Town halls’

– Hard copies available in public libraries

– Communicated through social media: Facebook, Twitter, Podcasts

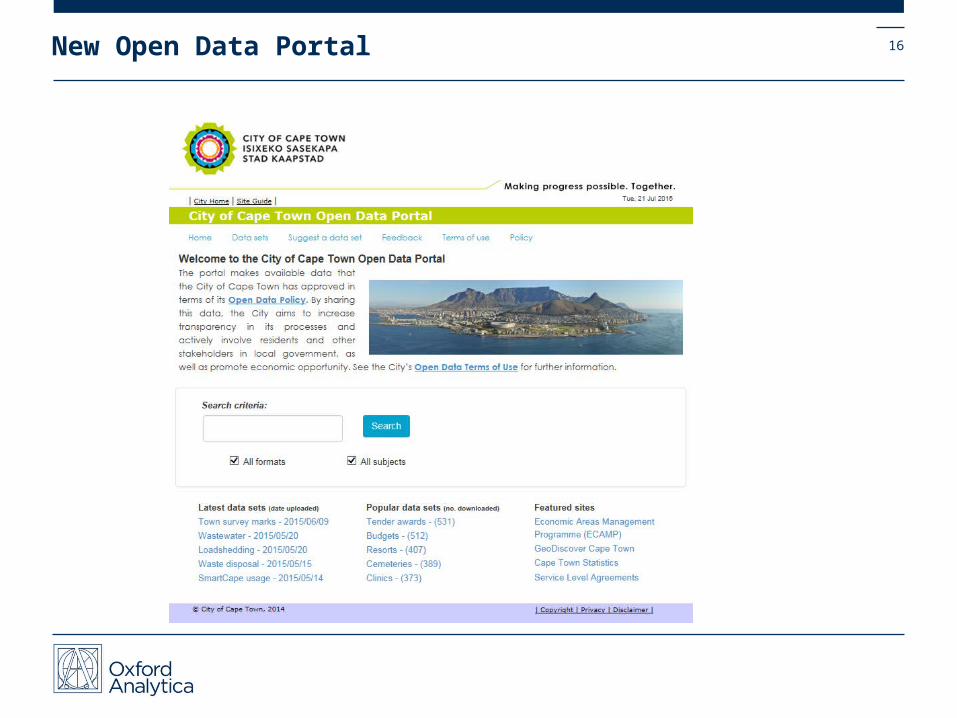

– Extensive budget data available through new Open Data Portal.

16New Open Data Portal

17Some Wider Lessons

– Devolution of more fiscal powers works, but only where accompanied by necessary financial and accounting skills.

– Local governments need strong debt collection and monitoring systems.

– Not all local governments can be financially viable; consolidation an option.

Mayor’s Delivery UnitHow to direct resources to serve policy priorities

18

19Role of ‘Delivery Units’

What is a delivery unit?

- Management tool to ensure that change/ reforms prioritised by political/ executive leadership actually occur.

- Provides the link between the political sphere and the professional civil service.

- Functions can include strategy development, priority identification, systems analysis, problem solving, intra-government coordination, target-setting, M&E.

- Does not replace existing performance management; works within and around, sometimes informally.

- Works by applying pressure to strategic ‘inflection points’ within public sector systems to remove obstacles to delivery.

- Keeps track of departmental performance and ratchets up targets, incentives and sanctions as necessary.

- Located in ‘apex’ office, eg president, prime minister, governor or mayor.

Prominent examples: Tony Blair’s PMDU, Malaysia’s PEMANDU, World Bank’s PDU

20City of Cape Town

MOCT Strategic Policy Unit (SPU)

- Combines policy planning functions with implementation of strategic priorities and M&E.

- SPU members ‘proxies’ for mayor; extends mayor’s influence throughout the organization.

- Aims to overcome institutional inertia, silos.

- Develops overarching strategies (e.g. EGS) and intervenes to align department policies/ protocols; adjusts targets and incentives to change behavior.

- Coordination point for political heads and senior management for major projects; manages, advises on and tracks major cross-department projects.

- Adjusts internal processes and reporting requirements to influence outcomes.

- Works within existing systems; also pursues innovative projects, e.g. Open Data.

- ‘Things you have to do’, e.g. routine services, continue without SPU intervention.

But:

- Some resistance from departments, silo mentality persists, inter-govt coordination.

21Projected populations in largest cities (in ‘000s) Source: UN

22

Oxford Analytica5 Alfred StreetOxford OX1 4EHUnited Kingdom

T +44 (0)1865 261600F +44 (0)1865 242018www.oxan.com

Contact