state of play and roadmap concept: mobility sector

TRANSCRIPT

State of Play and

Roadmap Concept:

Mobility Sector RE-SOURCING Deliverable 4.2

Dr. Johannes Betz, Stefanie Degreif, Peter Dolega

Öko-Institut e.V.

07.04.2021

This project has received funding from the European Union‘s Horizon 2020 research and innovation programme under grant agreement Nº 869276

Disclaimer:

This publication is part of a project that has received funding from the European Union’s Horizon 2020

research and innovation programme under grant agreement No 869276.

This publication reflects only the author’s view. Neither the European Commission nor any person

acting on behalf of the Commission is responsible for the use which might be made of the information

contained in this publication.

Reproduction and translation for non-commercial purposes are authorized, provided the source is

acknowledged and the publisher is given prior notice and sent a copy.

Imprint: Date: April 2021 | Johannes Betz, Stefanie Degreif, Peter Dolega (Oeko-Institut)

Work package: WP4 EU State of Play & Roadmaps | Task 4.2 State of Play and Roadmap concepts for mobility sector | Final

| Dissemination level: public

http://re-sourcing.eu

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

1

Contents

List of Abbreviations .................................................................................................................................... 5

Executive Summary ...................................................................................................................................... 9

1 Introduction and Focus ...................................................................................................................... 11

1.1 The RE-SOURCING Project ....................................................................................................................... 11

1.2 The Mobility Sector .................................................................................................................................. 13

2 Key Players in the Selected Global Battery Value Chain Steps ............................................................. 17

2.1 Mining and Processing............................................................................................................................. 19

2.1.1 Lithium ............................................................................................................................................ 20 2.1.2 Cobalt .............................................................................................................................................. 23 2.1.3 Nickel .............................................................................................................................................. 25 2.1.4 Graphite .......................................................................................................................................... 28

2.2 Cell Production ......................................................................................................................................... 30

2.2.1 Companies with producing European battery plants ..................................................................... 32 2.2.2 Companies with planned or under construction European battery plants .................................... 33

2.3 Recycling .................................................................................................................................................. 35

2.3.1 Battery Recycling Plants in the EU .................................................................................................. 35 2.3.2 Battery Recycling Plants outside of the EU ..................................................................................... 36

3 Challenges ......................................................................................................................................... 37

3.1 Mining and Processing............................................................................................................................. 38

3.1.1 Lithium ............................................................................................................................................ 38 3.1.2 Cobalt .............................................................................................................................................. 39 3.1.3 Nickel .............................................................................................................................................. 40 3.1.4 Graphite .......................................................................................................................................... 41

3.2 Cell Production ......................................................................................................................................... 42

3.2.1 Technical Overview ......................................................................................................................... 43 3.2.2 Challenges in Production ................................................................................................................ 45

3.3 Recycling .................................................................................................................................................. 47

3.3.1 Technological Status of Lithium-Ion Battery Recycling ................................................................... 47 3.3.2 Challenges of LIB Recycling ............................................................................................................. 50

4 Standards and Initiatives .................................................................................................................... 53

4.1 General .................................................................................................................................................... 54

4.1.1 Environmental Health and Safety (EHS) Standards in the EU ......................................................... 55 4.1.2 European Bank for Reconstruction and Development ................................................................... 55 4.1.3 Global Reporting Initiative .............................................................................................................. 55 4.1.4 International Finance Corporation, World Bank Group .................................................................. 55 4.1.5 International Labour Organisation (ILO) Conventions and Recommendations .............................. 56 4.1.6 ISO Standards .................................................................................................................................. 56

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

2

4.1.7 OECD Guidelines for Multinational Enterprises & Due Diligence Guidance for Responsible Mineral

Supply Chains ............................................................................................................................................... 57 4.1.8 Sustainable Development Goals (SDG) ........................................................................................... 57 4.1.9 UN Human Rights Principles ........................................................................................................... 57

4.2 Mobility / Battery-Specific Standards and Initiatives .............................................................................. 57

4.2.1 Drive Sustainability ......................................................................................................................... 57 4.2.2 European Battery Alliance .............................................................................................................. 58 4.2.3 European Green Vehicles Initiative (EGVI) ..................................................................................... 58 4.2.4 Global Battery Alliance ................................................................................................................... 58 4.2.5 Proposal for a Regulation of the European Parliament and of the Council Concerning Batteries

and Waste Batteries ..................................................................................................................................... 59

4.3 Mining...................................................................................................................................................... 60

4.3.1 Alliance for Responsible Mining ..................................................................................................... 60 4.3.2 Certified Trading Chains (CTC) Certification Scheme by BGR ......................................................... 61 4.3.3 China Responsible Mineral Supply Chain Due Diligence Management Guide................................ 61 4.3.4 Cobalt Industry Responsible Assessment Framework (CIRAF) ....................................................... 61 4.3.5 EITI Standard ................................................................................................................................... 61 4.3.6 Extractive Waste Directive .............................................................................................................. 61 4.3.7 Fair Cobalt Alliance (FCA) ................................................................................................................ 62 4.3.8 Global Tailings Review .................................................................................................................... 62 4.3.9 ICMM Mining Principles .................................................................................................................. 62 4.3.10 IFC Industry Sector Guidelines .................................................................................................... 63 4.3.11 IRMA – Initiative for Responsible Mining Assurance .................................................................. 63 4.3.12 London Metal Exchange Responsible Sourcing Requirements .................................................. 63 4.3.13 OECD Guidance Documents ....................................................................................................... 64 4.3.14 Responsible Cobalt Initiative ...................................................................................................... 64 4.3.15 Responsible Minerals Initiative .................................................................................................. 64 4.3.16 The European Raw Materials Alliance (ERMA) ........................................................................... 65 4.3.17 The World Bank Climate-Smart Mining Initiative ....................................................................... 65 4.3.18 Towards Sustainable Mining ...................................................................................................... 65

4.4 Recycling .................................................................................................................................................. 66

4.4.1 Basel Convention ............................................................................................................................ 66 4.4.2 ELV Directive ................................................................................................................................... 66 4.4.3 Collection, Logistics, Pre-treatment, Downstream treatment of WEEE (EN 50625-1:2014) .......... 66

5 Narrative Analysis .............................................................................................................................. 67

5.1 Methodology ........................................................................................................................................... 67

5.2 Results ..................................................................................................................................................... 68

6 Vision ................................................................................................................................................ 73

7 Gap Analysis and Focus Areas for the Roadmap Process ..................................................................... 77

7.1 Gap Analysis ............................................................................................................................................ 77

7.2 Focus Areas for the Roadmap Process ..................................................................................................... 78

7.2.1 Level Playing Field ........................................................................................................................... 78 7.2.2 Global Due Diligence ....................................................................................................................... 78 7.2.3 Harmonization of Sustainability Requirements .............................................................................. 79 7.2.4 Responsible Procurement ............................................................................................................... 80

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

3

7.2.5 Resource efficiency ......................................................................................................................... 80 7.2.6 Strengthen Recycling ...................................................................................................................... 81

8 Conclusion & Next Steps .................................................................................................................... 83

9 Acknowledgements ........................................................................................................................... 83

10 References ......................................................................................................................................... 84

Annex: Narrative Analysis on responsible sourcing ..................................................................................... 99

Figures

Figure 1: Greenhouse gas emissions 2018 by sector in the European Union (EU27) (Source: European

Commission 2020a) ............................................................................................................................... 13

Figure 2: Value chain of a Li-ion battery (Source: Oeko-Institut) ......................................................... 16

Figure 3: Global battery market in 2018 (Source: Oeko-Institut 2020) ................................................ 17

Figure 4: Global demand in batteries for electric mobility in 2016, 2030 and 2050 in a two-degree

climate scenario (2DS) (Source: Oeko-Institut 2019) ............................................................................ 18

Figure 5: Overview of the four selected raw materials lithium, cobalt, nickel and graphite .............. 20

Figure 6: Global primary lithium production (Source: Oeko-Institut 2020) ......................................... 21

Figure 7: Global primary cobalt production (Source: Oeko-Institut 2020) ........................................... 24

Figure 8: Nickel mine production by country in 2018 in tonnes (Source: Oeko-Institut) ..................... 26

Figure 9: Natural graphite mine production by country in 2016, 2017 and 2018 in tonnes (Source:

Oeko-Institut) ........................................................................................................................................ 28

Figure 10: Corporate world market shares for natural graphite production in 2018. Data from (Pillot

2019). .................................................................................................................................................... 29

Figure 11: Corporate world market shares for synthetic graphite production in 2018. Data from (Pillot

2019). .................................................................................................................................................... 29

Figure 12: Overview over the companies and their global market share of the LIB pack market (Pillot

2019) ..................................................................................................................................................... 31

Figure 13: Overview of battery cell plants announced in Europe (T&E 2021; Zenn 2021) ................... 32

Figure 14: Schematic illustration of the electrode stack of an LIB; volume distribution true-to-scale

(Redrawn from (Betz et al. 2020)). ....................................................................................................... 43

Figure 15: Cylindric cell with the electrode stack visible. Source: (Winter et al. 2017) ....................... 44

Figure 16: Overview cell production (Source: Oeko-Institut) ............................................................... 44

Figure 17: Environmental challenges of current materials and components in state-of-the-art LIB cells

(Dühnen et al. 2020). ............................................................................................................................ 46

Figure 18: Overview of recycling routes of LIBs (Source: Sojka et al. 2020) ......................................... 48

Figure 19: Overview of selected standards and initiatives (Source: Oeko-Institut) ............................. 54

Figure 20: Overview of the European Battery Alliance, Batteries Europe and Battery2030+ (Di Persio

et al. 2020) ............................................................................................................................................ 58

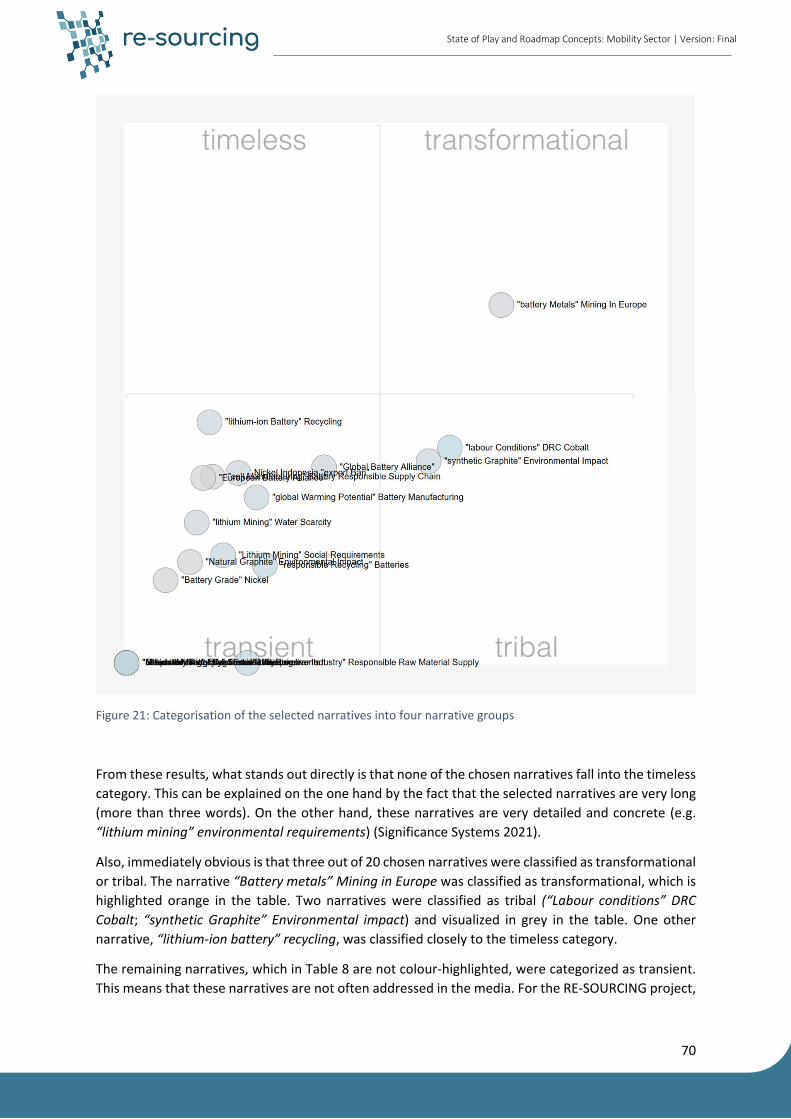

Figure 21: Categorisation of the selected narratives into four narrative groups ................................. 70

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

4

Figure 22: Emotional response to the narrative “battery metals” mining in Europe ........................... 71

Figure 23: Emotional response to the narrative “lithium-ion battery” recycling ................................. 72

Figure 24: Vision for the Mobility Sector by 2050, based on (Kügerl 2021); (WEF Mining & Metals 2014)

(WBCSD 2020) (Franks 2015) ................................................................................................................ 76

Figure 25: Decoupling of resource use and environmental impacts from GDP growth (UNEP 2011) . 81

Figure 26: Generated emotions related to (A) "responsible sourcing", (B) “sustainable raw materials”

(Kügerl 2021) ....................................................................................................................................... 101

Tables

Table 1: Overview of some key players in the automotive supply chain, omitting sourcing and smelting

.............................................................................................................................................................. 14

Table 2: Overview of EU lithium miners in alphabetical order per country (Cornish Lithium 2021; SR

2021; Mining Journal 2019) .................................................................................................................. 22

Table 3: Overview of EU27 cobalt miners ............................................................................................. 25

Table 4: Overview of EU27 nickel miners ............................................................................................. 27

Table 5: Overview of European natural graphite miners ...................................................................... 30

Table 6: Recycling companies for LIBs in the EU27 ............................................................................... 36

Table 7: Selection of 20 narratives for the mobility sector .................................................................. 67

Table 8: Categorisation of the selected narratives into four narrative groups .................................... 69

Table 9: Selection of narratives for responsible sourcing (see Kügerl 2021) ........................................ 99

Table 10: Results of narrative analysis, green – timeless, orange – transformational, yellow – between

transient and timeless, blue - between tribal and transformational, grey – tribal (Kügerl 2021) ...... 102

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

5

List of Abbreviations

2DS two-degree climate scenario

3R reduce, reuse, recycle

3TG tin, tungsten, tantalum, and gold

ACEA European Automobile Manufacturers’ Association

Al aluminium

AMD acid mine drainage

ARM Alliance for Responsible Mining

ASM artisanal and small-scale mining

BEV battery electric vehicle

BGR German Federal Institute for Geosciences and Natural Resources

C carbon

CCCMC China Chamber of Commerce of Metals, Minerals & Chemicals Importers and

Exporters

CI Cobalt Institute

CIRAF Cobalt Industry Responsible Assessment Framework

CMRT Conflict Minerals Reporting Template

Co cobalt

Cr chromium

CRAFT Code of Risk mitigation for ASM engaging in Formal Trade

CRT Cobalt Reporting Template

CSR corporate social responsibility

CSR Europe European Business Network for Corporate Sustainability and Responsibility

CTC certified trading chains

Cu copper

E- electric

EBA European Battery Alliance

EBRD European Bank for Reconstruction and Development

EHS environmental health and safety

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

6

EITI Extractive Industries Transparency Initiative

eLI European Lithium Institute

ELV end-of-life vehicles

EoL end-of-life

ESG environmental, social, governance

EU European Union

EU27 27 Member States of the European Union

EU-OSHA European Union Information Agency for Occupational Safety and Health

EV electric vehicle

FCA Fair Cobalt Alliance

Fe iron

GBA Global Battery Alliance

GHG greenhouse gas

GIZ German Corporation for International Cooperation GmbH

GRI Global Reporting Initiative

H hydrogen

HEV hybrid electric vehicles

HF hydrofluoric acid

ICE internal combustion engine

ICMM International Council on Mining & Metals

IFC International Finance Corporation

ILO International Labour Organisation

IRMA Initiative for Responsible Mining Assurance

ISO International Standards Organisation

ITSCI International Tin Supply Chain Initiative

LFP lithium iron phosphate

Li lithium

LIB lithium-ion batteries

LME London Metal Exchange

LMO lithium ion manganese oxide

LSM large-scale mining

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

7

LTO lithium titanium oxide

Mn manganese

N nitrogen

NABU Nature and Biodiversity Conservation Union

NCA lithium nickel cobalt aluminium oxide

NG natural graphite

NGO non-governmental organisation

Ni nickel

NMC lithium nickel manganese cobalt oxide

NMP N-methyl-2-pyrrolidone

O oxygen

OECD Organisation for Economic Co-operation and Development

OEM original equipment manufacturer

P phosphorus

PCB printed circuit board

PGM platinum group metals

PHEV plugin-hybrid electric vehicles

PVDF polyvinylidene difluoride

R&D research & development

RCI Responsible Cobalt Initiative

RJC Responsible Jewellery Council

RMAP Responsible Minerals Assurance Process

RS responsible sourcing

RSBN Responsible Sourcing Blockchain Network

SDG Sustainable Development Goals

SEI solid-electrolyte interphase

SG synthetic graphite

SoH State of Health

SoP state of play

Ti titanium

TSM Towards Sustainable Mining

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

8

TR thermal runaway

VDA German Association of the Automotive Industry

WBCSD World Business Council for Sustainable Development

WEEE Waste Electrical and Electronic Equipment

WWF World Wide Fund For Nature, or World Wildlife Fund

xEV all types of electric vehicles

Country codes

BE Belgium

CN China

CA Canada

CH Switzerland

D Germany

DRC Democratic Republic of the Congo

HK Hongkong

JP Japan

KOR South Korea

NOR Norway

USA United States of America

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

9

Executive Summary Meeting the Paris Agreement’s goals requires transformation in the mobility sector. Battery electric

vehicle technology today offers a promising technology to achieve the necessary changes and

transform the sector. Yet this transformation goes hand in hand with a significant increase in the raw

material demand for lithium-ion batteries.

This document provides an overview on the current status of the mobility sector, focusing on three

selected value-chain steps for lithium-ion batteries – raw material mining, battery cell production and

battery recycling – and four relevant materials: lithium, cobalt, nickel and graphite.

Key players and sustainability challenges along the supply chain steps were identified for this analysis.

Mining faces a wide range of challenges, which are raw-material and site-specific. Overarching

challenges in hard rock or ore mining (for the selected materials lithium, cobalt, nickel and graphite)

include heavy metal pollution, acid mine drainage, energy intensive processing, habitat

fragmentation, disturbance of land areas and dust pollution. For lithium from brines, water scarcity

and connected social tensions as well as dust emissions are major challenges. Social dimensions

related to cobalt mining are an additional issue already in public discourse; the main cobalt-producing

country, the Democratic Republic Congo (DRC), has a relatively high share (10-20% of production from

DRC) of artisanal and small-scale mining (ASM). ASM is the income basis of thousands of families in

the DRC. But the often informal ASM sector is connected to child labour, forced labour, inadequate

health and safety conditions, and funding of armed conflicts.

Battery cell manufacturing also faces challenges. It is a very energy-intensive process and therefore

associated with high greenhouse gas emissions. Furthermore, the toxic substances in the battery cell

require proper handling. As well, high susceptibility to production errors for battery cells lead to high

scrap rates in production.

Recycling of end-of-life Li-ion batteries is indispensable because of the high risk of “thermal runaway”

related to overheating batteries leading to fires. Therefore, adequate collection, storage, transport

and treatment of used Li-ion batteries are essential.

This report also examines existing standards and initiatives addressing these challenges. Various

regulations, standards, initiatives as well as guidelines promoting sustainable practices for the mining

sector were analysed. It was noted that the availability of standards and frameworks for the battery

cell manufacturing and recycling steps are rather limited while other value chain steps are covered in

numerous initiatives.

A gap analysis was conducted to assess whether the standards and initiatives cover the challenges

that exist in the supply chains. In the mining sector, one identified gap is the very large and confusing

number of guidelines. There is no international framework that also provides mutual recognition of

standards. Such a framework would define terms and provide guidance for companies on which

standards to apply. For customers, too, knowing which standards and corporate qualities are relevant

is challenging.

These difficulties in knowing what standards are best also apply to battery cell manufacturing and the

collection and recycling of end-of-life Li-ion batteries. There are no international guidelines addressing

the whole supply chain. The proposal for an EU Regulation on (waste) batteries could offer an

important step to integrate crucial elements of the supply chain in a regulation (supply chain due

diligence, product carbon footprint, material specific recycling targets, recycled content etc.).

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

10

Resource efficiency is a relevant lever to reduce the negative impacts in primary extraction. Especially

when considering the rapidly increasing demand for raw materials in the growing market of electric

vehicles, a decoupling of economic growth from resource consumption is necessary.

As a first step in the Roadmap process, an overarching vision was developed with various goals that

need to be achieved by 2050 to ensure a sustainable and responsible value chain in the mobility sector.

The basis of this vision is built on the concepts of planetary boundaries and strong sustainability.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

11

1 Introduction and Focus This report is the first publication of the in-depth work in the mobility sector. It provides an overview

of the current status of this sector, with a focus on Li-ion batteries, the key players, challenges and

selected standards and initiatives. In the coming months, the mobility Roadmap will be developed

with different stakeholders. In parallel, good practice examples of approaches for responsible sourcing

will be researched. Selected good practice examples – ‘Flagship’ Cases – will be included in the Flagship

Labs at the end of 2021 into early 2022. In these Labs, Flagship Cases will be promoted to other actors

in the value chain for implementation in other companies or institutions. A good-practice guidance

document will summarise these approaches and will be included in the final Roadmap, which will be

published in summer 2022.

1.1 The RE-SOURCING Project Responsible Sourcing (RS) is becoming a reality for more and more businesses and policymakers, and

it is increasingly demanded by both NGOs and civil society. Everyone is striving to keep ahead of rapidly

evolving ecological and social needs, company practices, business models, government regulations,

and initiatives spearheaded by civil society, etc.

In response to the growing challenge of responsible sourcing, the RE-SOURCING Global Stakeholder

Platform has been started in 2020.

RE-SOURCING, funded under the European Union’s (EU) Horizon 2020 programme, is a four-year

project (November 2019 to October 2023) coordinated by the Institute for Managing Sustainability at

the Vienna University of Economics and Business. The project’s consortium consists of 12 international

partners in- and outside the EU, working together to create the RE-SOURCING Platform. The project’s

vision is to advance and establish Responsible Sourcing as a minimum requirement among EU and

international stakeholders. The project fosters the development of a globally accepted definition of

Responsible Sourcing, facilitate the implementation of RS practices through direct knowledge

exchange within its network and beyond, and advocate for Responsible Sourcing in international

political forums.

To guarantee a thorough and comprehensive Responsible Sourcing framework, RE-SOURCING takes a

holistic approach by integrating firms and industries (up- and downstream) across the mineral value

chains of three sectors: Renewable Energy, Mobility and Electronics – all of which play a decisive role

in the EU Green Deal and the clean energy transition. As such, RE-SOURCING equally takes into

account traditional minerals, conflict minerals and green tech minerals in its approach. The main

target groups of the project are the EU and international industry stakeholders, EU policymakers and

civil society.

The RE-SOURCING project’s actions seek to:

▪ facilitate the development of a globally accepted definition of RS;

▪ develop ideas for incentives facilitating responsible business conduct in the EU, supporting RS

initiatives;

▪ enable the exchange of stakeholders for information and promotion of RS;

▪ foster the emergence of RS in international political fora; and

▪ support the European Innovation Partnership on Raw Materials.

RE-SOURCING will deliver:

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

12

▪ For EU and international business stakeholders:

o increased capacity of decisionmakers for implementing responsible business conduct;

o better understanding and awareness of RS in three sectors: renewable energy, mobility and

electric and electronic equipment; and

o facilitated implementation of lasting and stable sectoral framework conditions for RS.

▪ For EU policymakers:

o increased capacity for RS policy design and implementation;

o innovative ideas on policy recommendations for stimulating RS in the private sector; and

o better understanding and awareness on RS in three sectors: renewable energy, mobility and

electric and electronic equipment.

▪ For civil society:

o integration of sustainable development and environmental agendas into the RS discourse;

o an established, global level playing field of RS in international political fora and business

agendas; and

o better understanding and awareness on RS in three sectors: renewable energy, mobility and

electric and electronic equipment.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

13

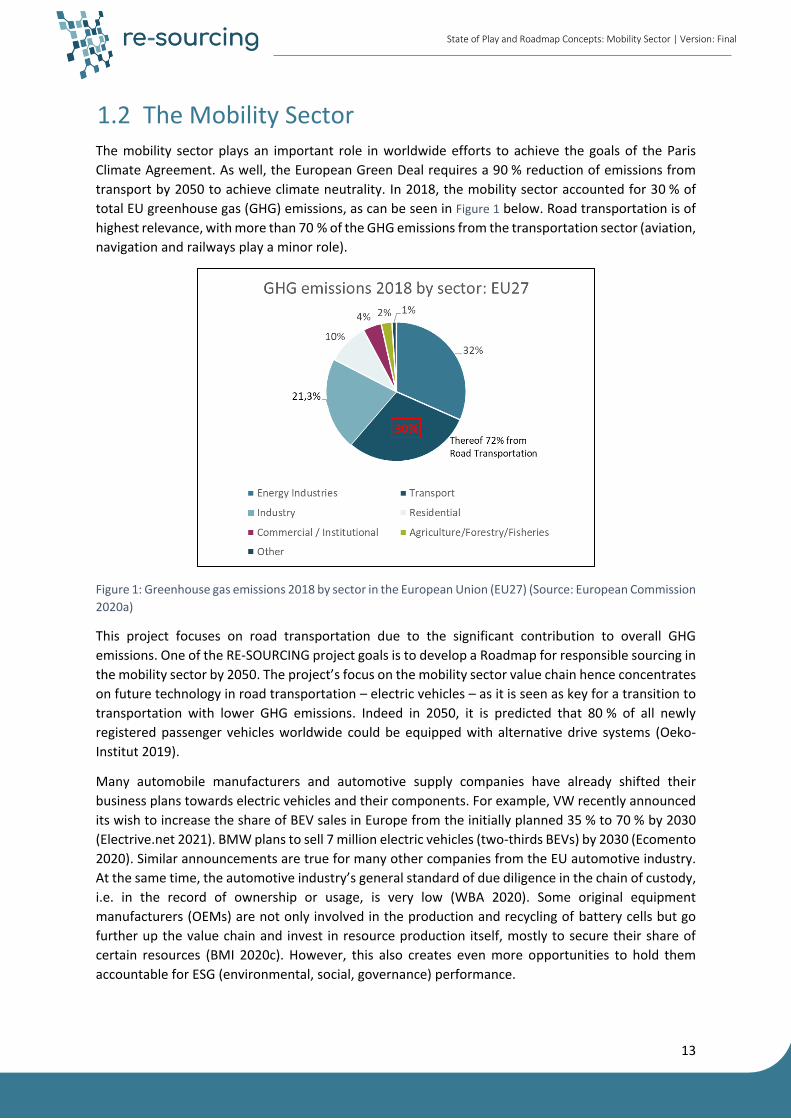

1.2 The Mobility Sector The mobility sector plays an important role in worldwide efforts to achieve the goals of the Paris

Climate Agreement. As well, the European Green Deal requires a 90 % reduction of emissions from

transport by 2050 to achieve climate neutrality. In 2018, the mobility sector accounted for 30 % of

total EU greenhouse gas (GHG) emissions, as can be seen in Figure 1 below. Road transportation is of

highest relevance, with more than 70 % of the GHG emissions from the transportation sector (aviation,

navigation and railways play a minor role).

Figure 1: Greenhouse gas emissions 2018 by sector in the European Union (EU27) (Source: European Commission

2020a)

This project focuses on road transportation due to the significant contribution to overall GHG

emissions. One of the RE-SOURCING project goals is to develop a Roadmap for responsible sourcing in

the mobility sector by 2050. The project’s focus on the mobility sector value chain hence concentrates

on future technology in road transportation – electric vehicles – as it is seen as key for a transition to

transportation with lower GHG emissions. Indeed in 2050, it is predicted that 80 % of all newly

registered passenger vehicles worldwide could be equipped with alternative drive systems (Oeko-

Institut 2019).

Many automobile manufacturers and automotive supply companies have already shifted their

business plans towards electric vehicles and their components. For example, VW recently announced

its wish to increase the share of BEV sales in Europe from the initially planned 35 % to 70 % by 2030

(Electrive.net 2021). BMW plans to sell 7 million electric vehicles (two-thirds BEVs) by 2030 (Ecomento

2020). Similar announcements are true for many other companies from the EU automotive industry.

At the same time, the automotive industry’s general standard of due diligence in the chain of custody,

i.e. in the record of ownership or usage, is very low (WBA 2020). Some original equipment

manufacturers (OEMs) are not only involved in the production and recycling of battery cells but go

further up the value chain and invest in resource production itself, mostly to secure their share of

certain resources (BMI 2020c). However, this also creates even more opportunities to hold them

accountable for ESG (environmental, social, governance) performance.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

14

In Table 1, there is a list of selected key players (Europe / global) in the automotive supply chain that

focus on electric vehicles.

Table 1: Overview of some key players in the automotive supply chain, omitting sourcing and smelting

Level Europe-based

companies

Companies mainly

based outside Europe

Product

1st tier Volkswagen AG (D),

Renault-Nissan-

Mitsubishi (NL),

Stellantis N. V. (NL)

BMW (D), PSA (F),

Daimler (D)

Toyota (JP), Hyundai

Motor Group (KOR),

GM (USA), BYD (CN),

Suzuki (JP), BAIC Group

(CN), SAIC (CN), Geely

(CN), Tesla (USA)

Original equipment

manufacturer (OEM)

2nd tier BASF (D), Umicore (BE) Johnson Matthey (UK) Catalyst manufacturer

2nd tier ZF (D), Continental (D),

Bosch (D), Magneti

Marelli (I), Valeo (F),

Michelin (F), Mahle

(D), Faurecia (F)

Denso (JP), Magna

(CA), Hyundai Mobis

(KOR), Aisin (JP),

Bridgestone-Firestone

(JP), Lear (USA), Delphi

(USA)

Automotive parts

(motors and others)

2nd tier Siemens (D), VW (D),

Bosch (D), SEW

Eurodrive (D), ZF (D),

Schaeffler (D), Brose

(D), ABB (CH)

Toshiba (USA), Nidec

(JP), Rockwell

Automation (USA),

AMETEK (USA), Regal

Beloit (USA), Johnson

Electric (HK)

E-Motor

2nd tier BMZ (D), Bosch (D),

Akasol (D), Deutsche

Accumotive GmbH (D,

Daimler)

LG Chem (KOR),

Panasonic (JP), Tesla

(USA), Samsung SDI

(KOR), CATL (CN), BYD

(CN), Clarios (USA, PB

Battery)

Battery manufacturer

PSA (F), VW (D),

Northvolt (SWE), Freyr

(NOR), Leclanché (D)

LG Chem (KOR), CATL

(CN), Panasonic (KOR),

Tesla (USA), BYD (CN),

Svolt (CN), Farasis

(USA/CN), Microvast

(CN), SK Innovation

(KOR), Samsung SDI

(KOR)

Cell manufacturer

3rd tier Umicore (BE), BASF (D) Shanshantech (CN),

NEI (USA), Nichia (JP),

Easpring (CN), L&F

(KOR)

Cathode material

producer

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

15

3rd tier SGL Carbon (D) Shenzhen BTR (CN),

Hitachi (JP), Mitsubishi

(JP), Shinzoom (CN),

ShanShan (CN), Sinuo

(CN), Zichen (CN)

Anode material

producer (natural and

synthetic graphite)

Today, the most promising technology for the future of alternative drive systems is the battery electric

vehicle (BEV). In this context, the production of strong, efficient and affordable batteries is essential.

As the traction battery is the most valuable part of an electric car, with 40 % of the value chain (BMWI

2021), the RE-SOURCING project focuses on traction batteries for electric passenger cars. The

immense impact of the electric-vehicle market on the production of lithium-ion batteries (LIBs) is

described in chapter 2. It is not yet clear if other technologies, like hydrogen fuel cell technology, will

gain a higher market share for vehicles in the future or remain a niche product (Hebling et al. 2019).

For vehicle batteries, the research here focused on current lithium-ion technology and

manufacturing processes. This includes graphite anodes and lithium nickel cobalt manganese oxide

(LiNixMnyCozO2, NMC) cathodes. Recent automotive trends use LIBs with a lithium iron phosphate

(LiFePO4, LFP) cathode for small cars, as the battery cells are currently cheaper; LFP batteries are

already very common in China. Whether this trend will continue in Europe or move back towards NMC

cathodes is difficult to project. Future technologies, such as solid-state batteries or non-lithium battery

chemistries, are not part of this document as they do not yet play a role in the battery cell market and

it is difficult to predict whether and to what extent their major technological challenges will be

overcome to allow future use.

The mobility sector as a whole requires a wide range of raw materials. These materials differ according

to application, such as body frame, wheels, cables, motors or batteries. Apart from other materials

like plastics, including rubber for tires, the major metals used in the mobility sector are:

▪ “Traditional” metals, like steel (e.g. for body frame, engine, transmission and wheels), copper

(e.g. for cables, LIBs, electric engine, electronics) and aluminium (e.g. for light weight

construction);

▪ Conflict minerals: 3TGs (tin, tungsten, tantalum, and gold; for e.g. electronics like the battery

management system); and

▪ Green technology materials, like rare earth elements (e.g. for permanent magnets in electric

motors), platinum group metals (e.g. for catalytic converter of fuel cells), cobalt, lithium,

nickel, natural graphite (e.g. for LIBs).

As this project focuses on the traction battery for electric vehicles, the State of Play and Roadmap

will likewise focus on the LIB materials lithium, cobalt, nickel and graphite. Focus on these four

materials results from the fact that the development of the LIB market has a large impact on the

sourcing of these materials, as they are all crucial for the future of LIB. Furthermore, copper is excluded

here since it is part of the renewable energy sector of this project (Kügerl 2021). The value chain of a

LIB is very diverse. As shown in Figure 2, it can be divided into seven simplified steps: mining, precursor

production, electrode material production, cell production, module and pack production, use phase

and finally battery recycling. This State of Play document will focus on three of these steps: mining,

cell production and recycling for traction batteries and the selected LIB materials, as further

illustrated in chapter 2.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

16

Figure 2: Value chain of a Li-ion battery (Source: Oeko-Institut)

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

17

2 Key Players in the Selected Global Battery

Value Chain Steps The mobility sector is critical for the battery market. Demand for lithium-ion batteries (LIBs) is strongly

driven by the increasing demand for electric vehicles of all types, which is in turn promoted as a

mitigation strategy to reduce contributions to climate change. High-performance LIBs (partially)

power all types of electric vehicles, including e-bikes, hybrid electric vehicles (HEV), plugin-hybrid

electric vehicles (PHEV), battery electric vehicles (BEV), electric buses and hybrid or fully electric

lorries.

As depicted in Figure 3, vehicles in general used nearly two thirds of the produced LIBs in 2018, since

a large number of LIBs are needed to move a vehicle compared to powering small devices. As the

battery electric vehicle (BEV) market is expected to grow dramatically, the ratio of LIBs for the mobility

sector is foreseen to significantly increase over the next years.

Figure 3: Global battery market in 2018 (Source: Oeko-Institut 2020)

This strong growth is also visible in Figure 4, where global demand in batteries for electric mobility in

2016, 2030 and 2050 in a two-degree climate scenario (2DS) is depicted. Starting with ≈85 GWh in

2016, the demand rises to over 1000 GWh in this scenario by 2030 and again more than triples

(6600 GWh) by 2050. This massive demand corresponds with a huge demand for more resources.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

18

Figure 4: Global demand in batteries for electric mobility in 2016, 2030 and 2050 in a two-degree climate

scenario (2DS) (Source: Oeko-Institut 2019)

To more deeply investigate the challenges of the battery value chain, we have divided it into seven

steps. We focused on three of these steps, here marked in bold:

1) Mining: Mining of different materials takes place around the globe; includes the mining and refining of the

key elements for LIBs (e.g. Li, Co, Ni, Cu and graphite). Many socio-economic and environmental challenges

occur during the mining process (see chapter 3.1).

2) Precursor production: Includes e.g. the production of the cathode precursor by co-precipitation of the

transition metals Ni and Co.

3) Electrode material production: Includes the manufacturing of active materials for the anode and cathode,

binders, current collectors, separators and electrolyte including additives.

4) Cell production: Addresses electrode manufacturing and the production and assembly of single battery

cells.

5) Pack & module production: Usually takes place at the automobile manufacturing stage to ensure that

specifications for vehicles are met; includes:

Module production (configuration of cells into larger modules that include some electronic management);

pack assembly (Installation of modules together with systems that manage power, charging and temperature);

and

vehicle integration (integration of the battery pack into the vehicle structure, including the battery-car

interface).

6) Use-phase: Includes use during specified in-vehicle battery lifetime and also the possible battery reuse

(second life in another application like stationary energy storage).

7) Recycling: Includes the entire recycling process of a battery (including collection, transportation, storage,

deconstruction and separation/purification for recycling of materials and components).

To have deeper insights about the most important steps, we concentrated our efforts on mining, cell

production and recycling. Mining has the highest social and environmental impact of all seven steps.

The European market of cell production is growing very fast at the moment, as European countries

have a large focus on strengthening the battery production in Europe and there is also a strong market

pull from the car companies based there, driven by the strong environmental legislation. This and the

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

19

possibility of improving responsible sourcing by regulating cell production makes this a very important

step in the value chain. In order to achieve a circular economy and limit the risk posed by EoL batteries,

they must be recycled, which is therefore a crucial step in the battery value chain. In our research for

the first step ‘mining’, we evaluated the material flows around the globe and the social and

environmental challenges of resource extraction. Our focus on lithium, cobalt, nickel and graphite

results from the fact that the development of the LIB market has a large impact on the sourcing of

these materials, as they are all crucial for the future of LIBs. Research on copper, also used widely in

batteries, is part of the renewable energy sector analysis within this project (Kügerl 2021).

Moving further down the value chain to cell production, we explain the general process for

manufacturing batteries. This includes electrode production, battery cell assembly and quality

management. We then look at the challenges and opportunities for improvement, particularly at the

environmental level.

Finally, we skip to the last step in the cycle, recycling, where we focus on the development of the

recycling industry around the globe as more and more batteries reach their end-of-life (EoL) and the

technological and environmental challenges related to this.

2.1 Mining and Processing Batteries need massive amounts of resources, which are distributed around the globe. As mentioned,

this paper focuses on the four most critical resources related to the battery value chain: lithium,

cobalt, nickel and graphite. To be able to get a better understanding of their origins and the

stakeholders involved in their extraction, this chapter lists the countries and companies mainly

involved in the production of these minerals.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

20

The following figure illustrates global production, EU import and worldwide reserves of the four

selected materials lithium, cobalt, nickel and graphite.

Figure 5: Overview of the four selected raw materials lithium, cobalt, nickel and graphite 1

2.1.1 Lithium

Lithium is essential for LIBs, although it only represents a small percentage of a battery cell’s weight

(≈ 2 % per cell). Nevertheless, LIBs are already responsible for 57 % of lithium demand (ahead of glass

and ceramics, lubricant/grease, metallurgy etc.) (BMI 2020a). In general, the global lithium value chain

has not yet been fully established itself, as demand and also production has been rising strongly over

the last few years and shifted from South America as the strongest producing region to Australia. An

overview of global lithium production is given in Figure 6. While Chile led the primary lithium

production market up through 2016, thereafter Australia has become the largest lithium producer in

the world. For more information about the challenges of lithium production, see chapter 3.1.1.

1 All data refers to 2018 sources: Mine production: Li: (USGS 2020b); Ni, Co, C: (BGS 2021) Import: All data refers to (UN Comtrade 2021):

▪ Nickel: HS 283324 Sulphates; of nickel; HS 2604 Nickel ores and concentrates; ▪ Cobalt: HS 2605 Cobalt ores and concentrates; HS 2822 Cobalt oxides and hydroxides; commercial

cobalt oxides; ▪ Lithium: HS 283691 Carbonates; lithium carbonate; HS 282520 Lithium oxide and hydroxide ▪ Graphite: HS 380110 Graphite; artificial; HS 2504 Graphite; natural

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

21

Figure 6: Global primary lithium production (Source: Oeko-Institut 2020)

Currently, the companies with the highest production figures for lithium extraction are, in alphabetical

order (Schmidt 2017, BMI 2020a, Miningscout 2018):

Albemarle

Albemarle is based in the USA and has three independent operations for primary lithium. The first one

is in Chile. The Salar de Atacama has the largest reserves of lithium in the world; Albemarle is one of

the companies which operates a brine mine there since the 1980s. The second operation is in Silver

Peak, Nevada, USA, which is brine-based plant operated by Albemarle since the 1960s. The last one is

in Australia, where Albemarle attained 49 % share in Talison Lithium in 2014, giving it access to

spodumene resources (Greenbushes). Apart from mining, Albemarle also refines lithium in the USA.

GanfengLithium

Jiangxi GanfengLithium is based in China and the world’s largest lithium producer in 2020, as other

producers did not reach their targeted production capacities (BMI 2020a). It has invested in many

lithium mining projects around the world (Argentina, China, Mexico, Australia) and uses different

methods to extract lithium from various sources (spodumene, brines, recycling). GangfengLithium and

Tianqi are the largest refiners of lithium in the world (USITC 2020).

Livent

Livent, formerly known as FMC Corporation, is based in the USA, but present in many countries, while

mining mainly in Argentina and Canada.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

22

SQM

SQM (Sociedad Química y Minera) is a Chilean company and produces lithium hydroxide and lithium

carbonate from brine. Like Albemarle, SQM mines in the Salar de Atacama in Chile. Apart from Chile,

SQM has also invested in mines in Argentina and Australia (SQM 2018).

Tianqi

Tianqi Lithium is a Chinese company and has the largest lithium production capacities in the world

(BMI 2020a). It is involved in Talison Lithium (Australia, Tianqi (51 %) and Albermarle 49 %) and owns

the largest LiOH plant in the world in Kwinana, Australia (Gov WA 2019). It is the world’s single largest

refiner of lithium materials (USITC 2020).

Mineral Resources Limited

Minerals Resource Limited is an Australian company and has the fifth largest lithium production

capacities in the world. It produces Lithium out of the Mt Marion mine with an initial capacity of

206 000 tonnes of spodumene concentrate per year. The capacity is being extended to 450 000 tonnes

per year (NS Energy 2021).

2.1.1.1 EU Mining Activities:

Today, there is no significant lithium production in the EU27. A mine in Alvarães, Portugal, operated

by Mota Soluções Cerâmicas (MCS), only produces a small amount of lithium for ceramics. However,

as indicted in Table 2, several projects for lithium production in the EU are planned that shall use

different lithium sources.

Table 2: Overview of EU lithium miners in alphabetical order per country (Cornish Lithium 2021; SR 2021;

Mining Journal 2019)

Company Country of planned

operation

Type

European Lithium Austria spodumene

European Metals Czech Republic zinnwaldite

UnLimited Germany thermal brines

Vulcan Energy

Resources

Germany thermal brines

Zinnwald Lithium plc Germany zinnwaldite

Cornish Lithium Great Britain thermal brines

Keliber Oy Finland spodumene

Savannah Resources Portugal spodumene

Rio Tinto Serbia lithium-borate deposit which contains

jadarite, a lithium sodium borosilicate

mineral

Infinity Lithium Spain zinnwaldite

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

23

Leading Edge

Materials

Sweden spodumene

Livista Energy plans to refine lithium and produce initially 30 000 t/a in Europe (Livista 2021); for more

information, see the corporate website2.

2.1.2 Cobalt

Cobalt (Co) is part of NMC (lithium nickel manganese cobalt oxide), which is the main cathode material

for xEVs (all types of electric vehicles). It increases the conductivity of the cathode material and

stabilizes the cathode structure, thereby increasing the cycle life and the power capability of the

battery (Li & Lu 2020). Cobalt is a commodity, which is in most cases a by-product of nickel or copper

mining3, although in different concentrations. Therefore, the production of cobalt is also strongly

related to production of the other metals. However, an increase in cobalt production could also be

achieved by refining the tailings of mines that have not already extracted cobalt due to low market

demand or previous technological barriers.

The vast majority of cobalt production occurs in the Democratic Republic of the Congo (DRC),

providing over 70 % of worldwide production (see Figure 7). Although artisanal and small-scale mining

(ASM) is strongly represented in the media, it is estimated that cobalt production in the year 2020 in

the DRC from large-scale mining (LSM) operations rose to a share of over 90 %. ASM extraction of

cobalt in the DRC during 2020 provided less than 5 % of the world cobalt supply (BMI 2020b). However,

this is unusual and correlated to the low cobalt price and the Corona pandemic. The ratio of ASM

compared to LSM in the DRC has been much higher in the past (closer to 25 %) (Mancini et al. 2020).

ASM cobalt production has historically been strongly linked to market demand. Previous trends

indicate that, as prices rise in a tighter market, the ASM sector for cobalt increases production to

provide the ‘swing supply’ to the market. Although currently cobalt prices are drastically lower than

their peak in April 2018, and likewise ASM shares in the market have significantly contracted, this

could change with the market demands.

Counteracting this trend, stronger regulations of mining practices are expected to slow ASM reactivity

to these market forces. This would in turn limit the ability of ASM to provide a swing supply and

perhaps then impact prices (BMI 2020b). Nevertheless, ASM is still very important, as it provides

income for a large number of people and at the same time can have a highly negative social and

environmental impact.4

2 https://livista.energy/ (15.03.2021) 3 There is only one mine in Morocco, which produces cobalt as main product. (Shedd et al. 2017). 4 Cobalt is not itself classified as a conflict mineral. Yet, since artisanal mining accounts for a significant share of all cobalt production in the DRC, it nonetheless carries a number of environmental and social risks (Al Barazi 2017). In light of this and the broader context of cobalt mining in the DRC, cobalt might be classified under the minerals where due diligence along the supply chain is required.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

24

Figure 7: Global primary cobalt production (Source: Oeko-Institut 2020)

There are many companies involved in cobalt production. Currently, the largest are (in alphabetical

order):

China Molybdenum

China Molybdenum (China Moly) is based in China and the second largest producer of cobalt (Argus

Media 2020). It operates the Tenke Fungurume mine (owns 80 % since 2019), producing copper and

cobalt, and it took over the Kisanfu project (95 %, remaining 5 % belong to the DRC government; in

development to produce copper and cobalt), both mining projects in the DRC (Reuters 2020a).

Chemaf

Chemaf (Chemical of Africa) is a subsidiary of Shalina Resources, a company operating mainly in the

DRC, while their headquarters are in the United Arabic Emirates. It operates several mines producing

cobalt in the DRC.

Gécamines

Gécamines (Générale des Carrières et Mines) is an enterprise owned by the DRC government, which

is heavily invested in several copper-cobalt mines (Boss, Kolwezi, Lubumbashi Slag Hill, Ruashi) in the

DRC (Gecamines 2017). In most cases, however, it is not the main mine operator.

Glencore

Glencore is the largest miner of cobalt in the world. In 2019, it produced about 42 200 t of Co

hydroxide in Katanga (DRC), 3 400 t Co metal in Murrin Murrin (Australia) and 700 t Co metal in

Nikkelverk (Norway). Mutanda, a large copper-cobalt mine in the DRC, is currently (as of 2020) placed

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

25

on care and maintenance. All in all, Glencore is responsible for about 25 – 30 % of global cobalt

production.

Huayou Cobalt

Huayou Cobalt, based in China, reports that they are the largest cobalt refiner in the world. It has

Congo Dongfang International Mining (CDM) as a subsidiary, which has the right of first refusal for the

entire ASM cobalt (copper) ore production from Kasulo in the DRC.

Vale

Vale S. A. is a Brazilian mining company operating several large iron and nickel mines around the world,

with some of the nickel mines also producing cobalt as a by-product (e.g. in New Caledonia and

Canada).

2.1.2.1 EU Mining Activities

Most cobalt from the EU27 is produced in Finland (Statista 2018). Although they do not play a major

role in the global cobalt market, the following companies are looking for cobalt in the EU (not

necessarily an exhaustive list):

Table 3: Overview of EU27 cobalt miners

Name Mining in Status Metals

Terrafame Oy Finland Producing Nickel, zinc, cobalt,

copper

Eurobattery Minerals Sweden,

Finland,

Spain

In development Nickel, cobalt,

copper, rare earth

elements

European Cobalt Ltd Slovakia,

Finland

In development Copper, nickel,

cobalt, gold, silver

Talga Resources Sweden In development Copper, cobalt

Umicore refines cobalt in Kokkola, Finland. It is the largest cobalt refinery outside of China (15 000 t/a)

(Chemical Engineer 2019).

2.1.3 Nickel

The global production of nickel (Ni) is much more distributed around the world than other battery

materials, as can be seen in Figure 8. Since most nickel is used in steel production, LIBs only use a

fraction of global nickel production. Other nickel applications relate to defence systems, prompting

countries around the world to consider securing their own supply. In general, nickel demand for

batteries can be easily covered by the available supply. However, LIBs need nickel with a very high

degree of purification, which is only performed in certain countries.

Nickel is used as the most common cathode material for traction batteries, as part of lithium nickel

cobalt manganese oxide (NMC). This cathode material comes with different ratios of transition metals

(nickel, cobalt and manganese), although many producers tend to prefer high nickel ratios, as they

increase the battery’s energy density. This also goes along with lower cobalt and manganese ratios.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

26

Figure 8: Nickel mine production by country in 2018 in tonnes (Source: Oeko-Institut)

There are many companies involved in nickel production. The largest are (in alphabetical order)

(McCrae 2018):

Anglo American

Anglo American, with its headquarters in England, mines nickel in two Brazilian mines: Barro Alto and

Codemin.

BHP

BHP (Broken Hill Proprietary Company), formerly known as BHP Billiton, and its subsidiary Nickel West

are both based in and operate several nickel mines and refineries in Western Australia (BHP 2021). It

is an Australian-British commodities group and, together with Vale and Rio Tinto, one of the world's

three largest mining companies. BHP was the world's fifth largest nickel producer in 2019 (Statista

2020).

Glencore

Based in Switzerland, Glencore has invested in nickel mines in Canada, New Caledonia and Australia.

It refines nickel and cobalt in their refinery Nikkelverk in Norway, which they state is the largest nickel

refinery in the western world (Glencore 2021).

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

27

Jinchuan

The Jinchuan Group Ltd. is a Chinese resourcing company producing different minerals like nickel,

copper, cobalt and others. Jinchuan produced about 150 000 tonnes of Nickel in 2019 and is,

therefore, the third biggest nickel producer in the world (Statista 2020).

Nornickel

Nornickel (former Norilsk Nickel) operates some of the largest nickel mines in the world. It is based in

Russia but also has operations in Finland and South Africa. In Harjavalta, Finland, it refines about

66 000 t of metals a year (not only nickel, but also copper and platinum group metals) (Nornickel

2021). In 2019, Nornickel was the second largest nickel producer with around 166 thousand tonnes

(Statista 2020).

Vale

Vale S. A. is a Brazilian mining company operating several large iron and nickel mines around the world.

Its biggest nickel mines are in Canada, but it also operates nickel mines in Indonesia, New Caledonia

and Brazil (McCrae 2018). In 2019, Vale was the largest nickel producing company with around 208

000 tonnes (Statista 2020).

2.1.3.1 EU Mining Activities

Production of nickel ore from mining in the EU27, occurring in Finland and Greece, contributed to

2.1 % of the global mine supply in 2019 and totalled 71.8 kt of primary refined nickel (including Class 1

metal5 and primary nickel sulphate). The entire EU27 intermediate nickel production in 2020 is

expected to have increased, to 62 kt, providing 5.7 % of global intermediate nickel supply. Finland

produced about 95 % of the EU27’s intermediate nickel in 2020, coming from Boliden operations in

Harjavalta, Terrafame operations in Talvivaara and the smaller Mondo Minerals operation for crude

nickel sulphate in Vuonos (JRC 2021).

The majority of the EU’s refined primary nickel production also occurs in Finland, accounting for about

76 % of the 2020 refined output. France, Austria, Belgium and Germany also refine nickel.

Although they do not play a major role on the global nickel market, the companies listed in Table 4

are exploring for and/or producing nickel in the EU. The supply of nickel is also relevant for the defence

sector, as mentioned earlier, and, thus, also of major interest for the EU.

Table 4: Overview of EU27 nickel miners

Name Mining in Status Metals

Boliden Finland Producing nickel, copper, gold,

platinum,

palladium

Mondo Minerals Finland Producing Nickel as part of talc

mines

5 Class 1 nickel products correspond mainly to electrolytic nickel, powders and briquettes with a nickel purity of at least 99.8 %. About 55 % of the total nickel mine production is Class 1. Class 2 resembles mostly nickel products for e.g. steel production with high contents of other metals like iron.

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

28

Terrafame Oy Finland Producing Nickel, zinc, cobalt,

copper

Eurobattery Minerals Sweden,

Finland,

Spain

In development Nickel, cobalt,

copper, rare earth

elements

European Cobalt Ltd Slovakia,

Finland

In development Copper, nickel,

cobalt, gold, silver

2.1.4 Graphite

LIBs typically use graphite as their anode material. Natural graphite (NG) can either be mined in open

pits or underground. Its counterpart, synthetic graphite (SG), can be produced by heating coke or

other carbon-based precursors. Both graphite forms must then be processed further before they can

be used as anode materials. The different origins of NG and SG contribute to differences in their post-

processing purity and their electrochemical properties.

Mining operations for NG are mostly found in China, where over 60 % of the world’s NG was produced

in 2019 (see Figure 9; USGS 2020). Other countries have been increasing their NG mining; in 2018,

Mozambique mined the second largest amount of natural graphite in the world, contributing about

9 % of the worldwide market share, although their production is refined in China as well (Pillot 2019).

Figure 9: Natural graphite mine production by country in 2016, 2017 and 2018 in tonnes (Source: Oeko-Institut)

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

29

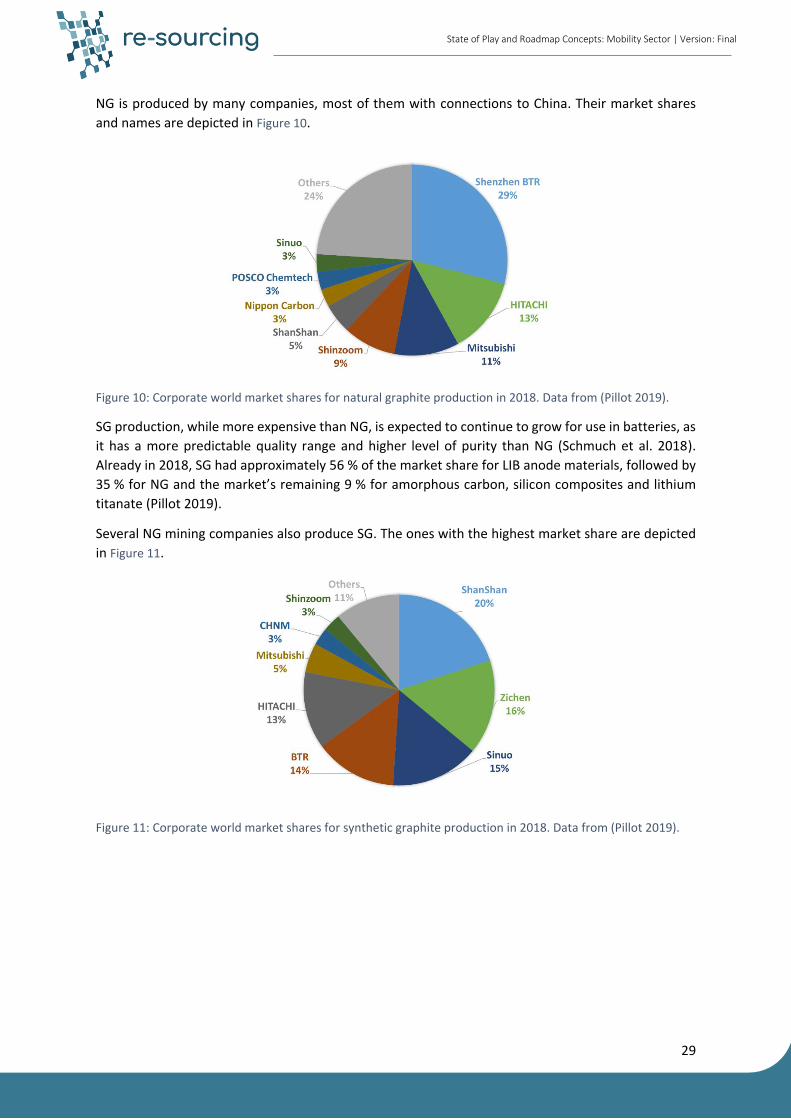

NG is produced by many companies, most of them with connections to China. Their market shares

and names are depicted in Figure 10.

Figure 10: Corporate world market shares for natural graphite production in 2018. Data from (Pillot 2019).

SG production, while more expensive than NG, is expected to continue to grow for use in batteries, as

it has a more predictable quality range and higher level of purity than NG (Schmuch et al. 2018).

Already in 2018, SG had approximately 56 % of the market share for LIB anode materials, followed by

35 % for NG and the market’s remaining 9 % for amorphous carbon, silicon composites and lithium

titanate (Pillot 2019).

Several NG mining companies also produce SG. The ones with the highest market share are depicted

in Figure 11.

Figure 11: Corporate world market shares for synthetic graphite production in 2018. Data from (Pillot 2019).

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

30

2.1.4.1 European Mining Activities

Natural graphite is mined in several European countries, as can be seen in Table 5. However, as

illustrated before, there are no major European companies refining natural graphite for anode

materials.

Table 5: Overview of European natural graphite miners

Name Mining in Status

Graphit Kropfmühl (Dutch Advanced Metallurgical

Group N.V. (AMG))

Germany Producing

Grafitbergbau Kaisersberg Austria Producing

Leading Edge Materials Sweden Producing

Mineral Commodities Ltd (MRC) Norway Producing

Skaland Graphite AS Norway Producing

Talga Resources Sweden Producing

Zavalyevskiy Graphite6 Ukraine Producing

The only synthetic graphite production in Europe to our knowledge, is SGL Carbon, a German company

with sites around the world. SGL Carbon produces not only synthetic graphite, but also other advanced

carbon products (SGL 2021).

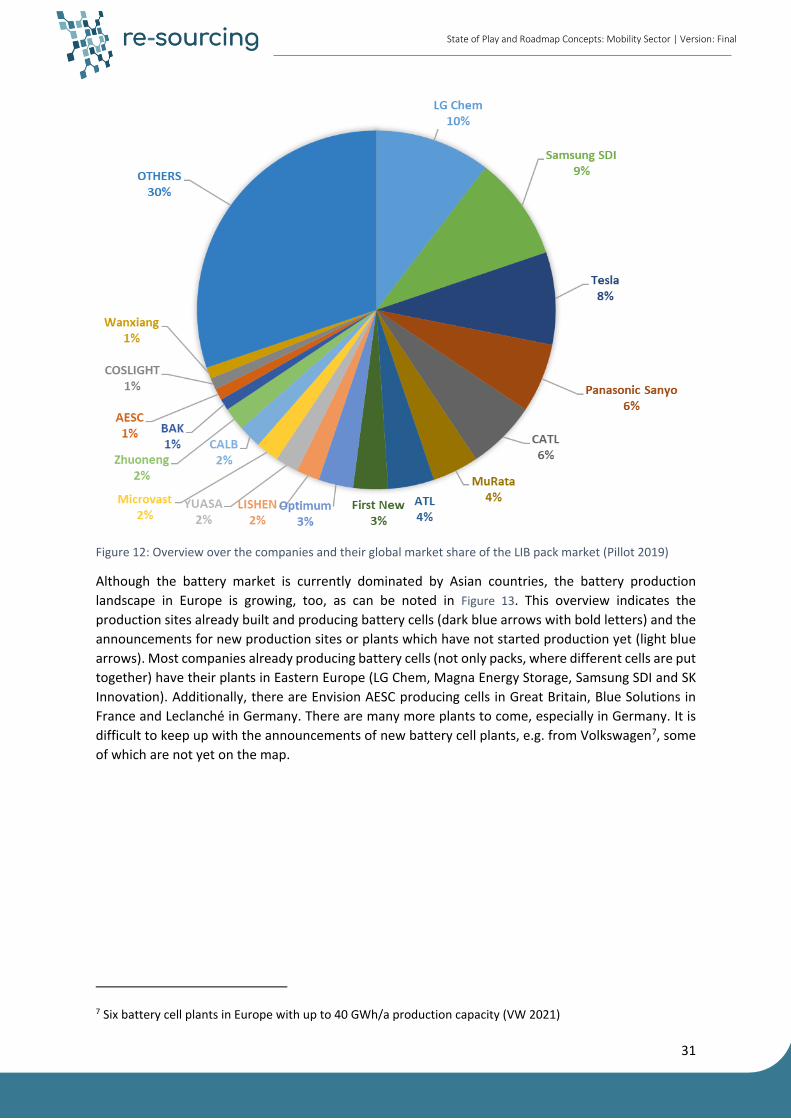

2.2 Cell Production Current battery cell production is dominated by Asian countries. An overview of the companies with

the highest share (in US dollars) of the global battery pack market is shown in Figure 12. There the

diversity of the market with the high number of companies becomes visible. The largest is LG, a South

Korean chemical company, followed by Samsung SDI, also from South Korea. Tesla in third place is

mainly a car manufacturer based in the US, but also produces LIBs, mainly in collaboration with

Panasonic, the company with the fourth highest market share. CATL is also one of the largest battery

cell manufacturers, based in China and expanding massively. However, the battery market is very

dynamic and constantly changing, with new battery cell factories being planned, built and starting

production all the time. Therefore, and for the reason that these figures refer to 2018, the order

should be taken with caution.

6 operating the Zavalye graphite field, the largest mine (flake graphite) in Europe (DERA & ICMNR 2020)

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

31

Figure 12: Overview over the companies and their global market share of the LIB pack market (Pillot 2019)

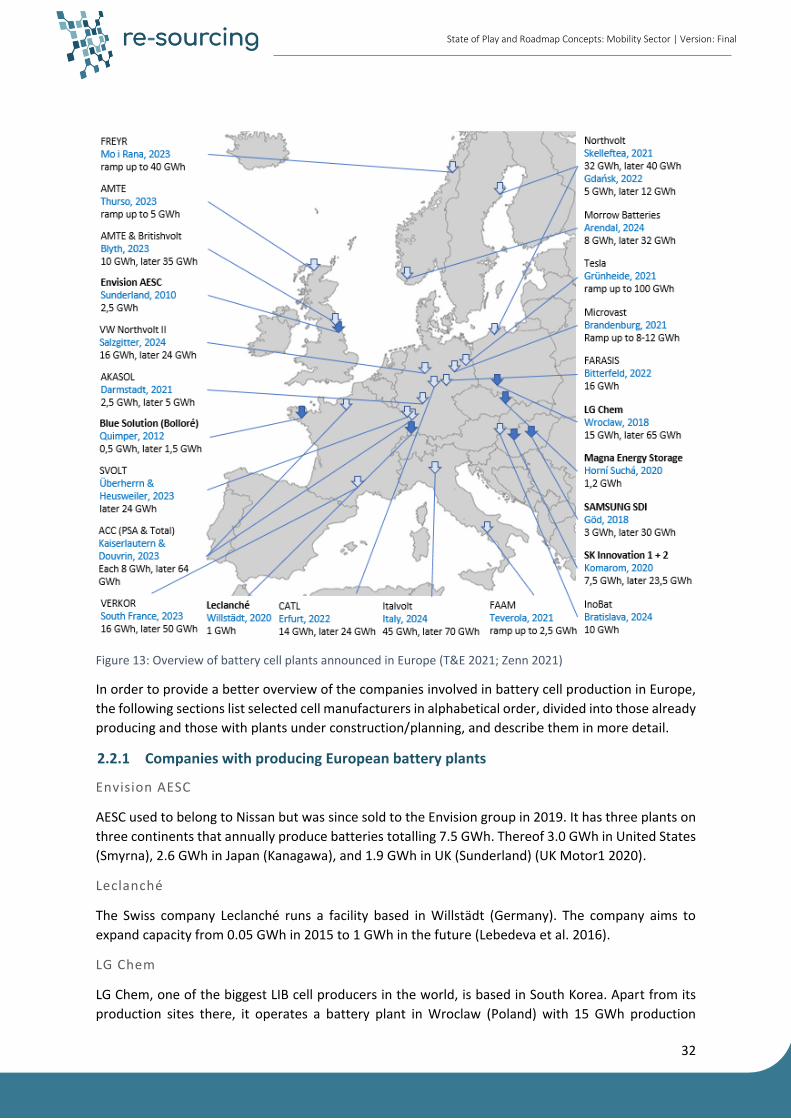

Although the battery market is currently dominated by Asian countries, the battery production

landscape in Europe is growing, too, as can be noted in Figure 13. This overview indicates the

production sites already built and producing battery cells (dark blue arrows with bold letters) and the

announcements for new production sites or plants which have not started production yet (light blue

arrows). Most companies already producing battery cells (not only packs, where different cells are put

together) have their plants in Eastern Europe (LG Chem, Magna Energy Storage, Samsung SDI and SK

Innovation). Additionally, there are Envision AESC producing cells in Great Britain, Blue Solutions in

France and Leclanché in Germany. There are many more plants to come, especially in Germany. It is

difficult to keep up with the announcements of new battery cell plants, e.g. from Volkswagen7, some

of which are not yet on the map.

7 Six battery cell plants in Europe with up to 40 GWh/a production capacity (VW 2021)

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

32

Figure 13: Overview of battery cell plants announced in Europe (T&E 2021; Zenn 2021)

In order to provide a better overview of the companies involved in battery cell production in Europe,

the following sections list selected cell manufacturers in alphabetical order, divided into those already

producing and those with plants under construction/planning, and describe them in more detail.

2.2.1 Companies with producing European battery plants

Envision AESC

AESC used to belong to Nissan but was since sold to the Envision group in 2019. It has three plants on

three continents that annually produce batteries totalling 7.5 GWh. Thereof 3.0 GWh in United States

(Smyrna), 2.6 GWh in Japan (Kanagawa), and 1.9 GWh in UK (Sunderland) (UK Motor1 2020).

Leclanché

The Swiss company Leclanché runs a facility based in Willstädt (Germany). The company aims to

expand capacity from 0.05 GWh in 2015 to 1 GWh in the future (Lebedeva et al. 2016).

LG Chem

LG Chem, one of the biggest LIB cell producers in the world, is based in South Korea. Apart from its

production sites there, it operates a battery plant in Wroclaw (Poland) with 15 GWh production

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

33

capacity and the plan to scale up to 65 GWh. According to its website: LG Chem currently supplies 13

of the 20 major car brands, including Volkswagen, Renault, General Motors and Hyundai. The Group

has presently five battery plants in South Korea, China, the United States and Poland with a total

capacity of 70 GWh. In total, the South Koreans plan to invest around 3 trillion won (about 2.25 billion

euros) in battery plants this year, increasing capacity to 100 GWh before the end of the year

(Electrive.com 2020c).

Magna Energy Storage (MES)

Magna Energy Storage (MES) operates a battery plant in Horní Suchá (Czech Republic), which has the

production capacity of 1.2 GWh per year (CzechTrade 2020).

Samsung SDI

Samsung SDI is based in South Korea and is one of the largest battery cell manufacturers in the world.

Additionally, it has cell production in Göd (Hungary) with production capacity of 4 million battery cells

per month. At the end of 2018, Samsung line 1 entered into operation; lines 2-4 began operating

between March and September 2019. The construction of a second plant in Göd is underway, with

operations scheduled to begin in 2021 and an expected annual capacity of 12 million cells in four

production lines (THELEC 2020a, THELEC 2020b).

SK Innovation

SK Innovation is based in South Korea. Apart from LIB production, its main focus is the exploration and

production of crude oil and natural gas. SK Innovation built a battery factory in Komarom (Hungary),

which started production in 2020 with an annual capacity of 7.5 GWh; a second battery factory with

a capacity of 9,8 GWh (Yonhap 2020) is being built by 2022 and a third factory is planned (Battery-

News 2020). Later, the second plant will likely be extended to a capacity of 16 GWh (Reuters 2020b).

2.2.2 Companies with planned or under construction European battery plants

AMTE

The common project of the two start-ups Britishvolt and AMTE Power is a production facility in St.

Athan, Wales (UK) for batteries for electric cars. The site’s first development stage should be

completed by 2023 with a capacity of 1-5 GWh per year and will be further extended until it reaches

the intended final capacity of 30-35 GWh (Electrive.com 2020a).

Automotive Cells Company (ACC)

The Automotive Cells Company (ACC) is a joint venture of PSA/Opel and Total/Saft. It has planned two

giga factories in Kaiserslautern (Germany) and Douvrin (France), with production starting in 2023. The

total planned production capacity of both plants combined is 48 GWh by 2030. The goals are a low

carbon footprint, 95 % recyclability, ethical supply chain and green factories using renewable energy

sources (ACC 2021).

CATL

Contemporary Amperex Technology Co. Limited (CATL) is one of the largest producers of LIBs for

electric vehicles (EVs) in the world and based in China. Guangdong Brunp, a LIB recycler, is a subsidiary.

CATL was the first producer to announce a LIB factory in Germany, which is now being built (initially

with 14 GWh and up to 24 GWh in a later expansion stage) near Erfurt (Electrive.com 2019, CATL

2020).

State of Play and Roadmap Concepts: Mobility Sector | Version: Final

34

Farasis

Frarasis is planning a plant in Bitterfeld-Wolfen, Sachsen-Anhalt (Germany). In 2022, the plant shall

begin with producing 6 GWh and an extension to 10 GWh has already be announced (Electrive.net

2019). Daimler bought shares of Farasis to secure battery cells for their BEV production (Farasis 2020).

Freyr

According to its website, FREYR is a Norwegian LIB company that develops, finances, constructs and

operates LIB facilities. It plans to produce ‘green battery cells’ that are made using power from its own

wind park and other energy sources. It is developing a pilot plant that will be ‘scalable and

modularized’ with a ‘2-25 GWh fast-track facility and a 32 GWh giga-factory’ (Freyr 2021).

InoBat

InoBat is building a pilot-scale battery cell production plant (100 MWh/a) in Košice (Slovakia) with the

plan to scale production with another plant up to 10 GWh in 2024 (Electrive.com 2020b).

Microvast

Microvast, founded in Texas (USA) has its European headquarters in Ludwigsfelde (Germany) and has

announced a battery plant to be built in Brandenburg (Germany) (Electrive.com 2020d).

Morrow Batteries

The Norwegian company Morrow Batteries is developing a battery cell factory in Arendal in the

southern Norwegian region of Agder. In 2024, the first stage of 8 GWh will be completed and further

developed in three further stages of 8 GWh each, to a final capacity of 32 GWh capacity (Electrive.com

2020e).

Northvolt

Northvolt is a start-up battery producer based in Sweden, which is building a battery factory in

Skellefteå (Northvolt Ett, northern Sweden). According to its website, “large-scale manufacturing will