socially%responsible%investments:%the% … · · 2015-05-28• accounting & audit quality •...

TRANSCRIPT

Gary Ometer, CPA, CGMA, Chief Financial Officer, Virginia College Savings Plan, North Chesterfield, Virginia Jennifer Cooperman, MBA Treasurer, City of Portland, Oregon

Moderator:

Speakers:

Sunday, May 31, 2015 2:40PM – 3:30PM 1 CPE

Socially Responsible Investments: The Challenges with

Purposeful InvesRng & Divestment

Responsible InvesRng History

5/31/2015 GFOA -‐ SRI 2

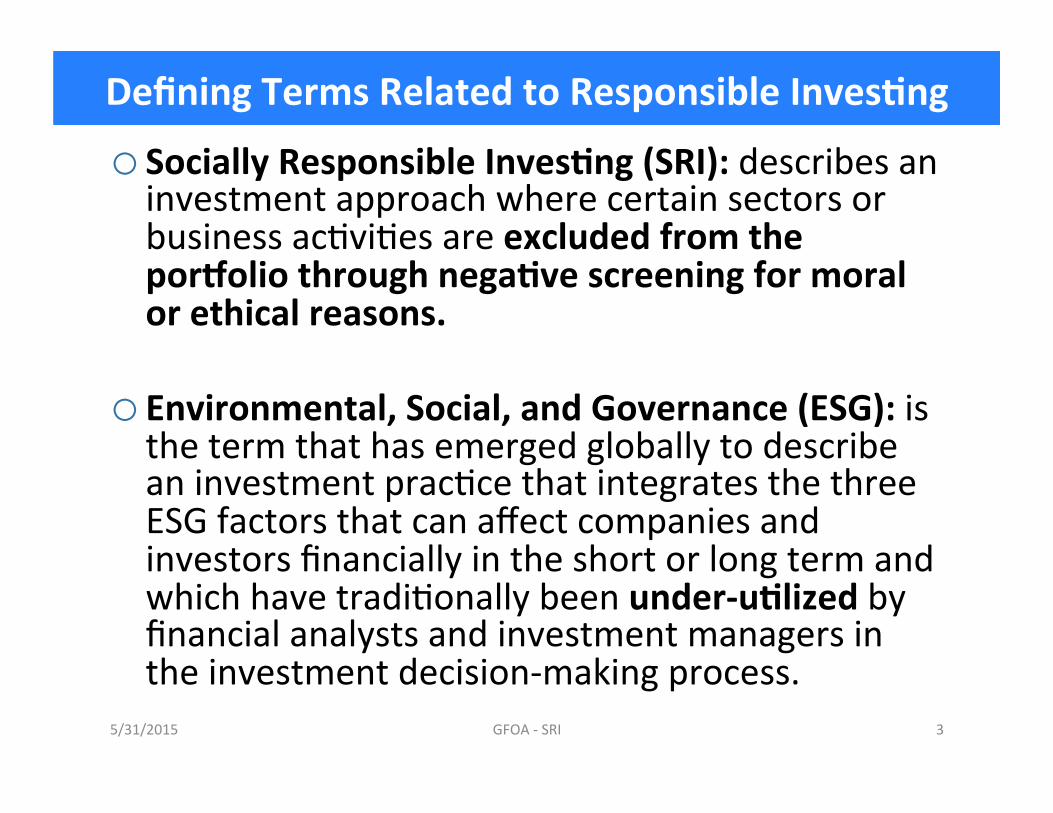

Defining Terms Related to Responsible InvesRng

o Socially Responsible InvesRng (SRI): describes an investment approach where certain sectors or business acAviAes are excluded from the porYolio through negaRve screening for moral or ethical reasons.

o Environmental, Social, and Governance (ESG): is the term that has emerged globally to describe an investment pracAce that integrates the three ESG factors that can affect companies and investors financially in the short or long term and which have tradiAonally been under-‐uRlized by financial analysts and investment managers in the investment decision-‐making process.

5/31/2015 GFOA -‐ SRI 3

Defining Terms Related to Responsible InvesRng (cont.)

o Impact InvesRng: invesAng in projects, companies, funds or organizaAons with the express goal of generaAng and measuring mission-‐related social, environmental or economic change alongside financial return.

o Divestment: a type of exclusionary screening strategy through which investors acAvely exclude companies involved in some acAvity, country or industry from their investment porOolios (e.g., fossil fuel, nuclear, poliAcal).

o Responsible Investment (RI) describes any investment approach and style that integrates ESG factors into the investment decision making process and ownership pracAces (voAng, shareholder acAvism and engagement) with the aim of achieving opRmal risk-‐adjusted returns.

*There is not always a clear delineaRon of these approaches

5/31/2015 GFOA -‐ SRI 4

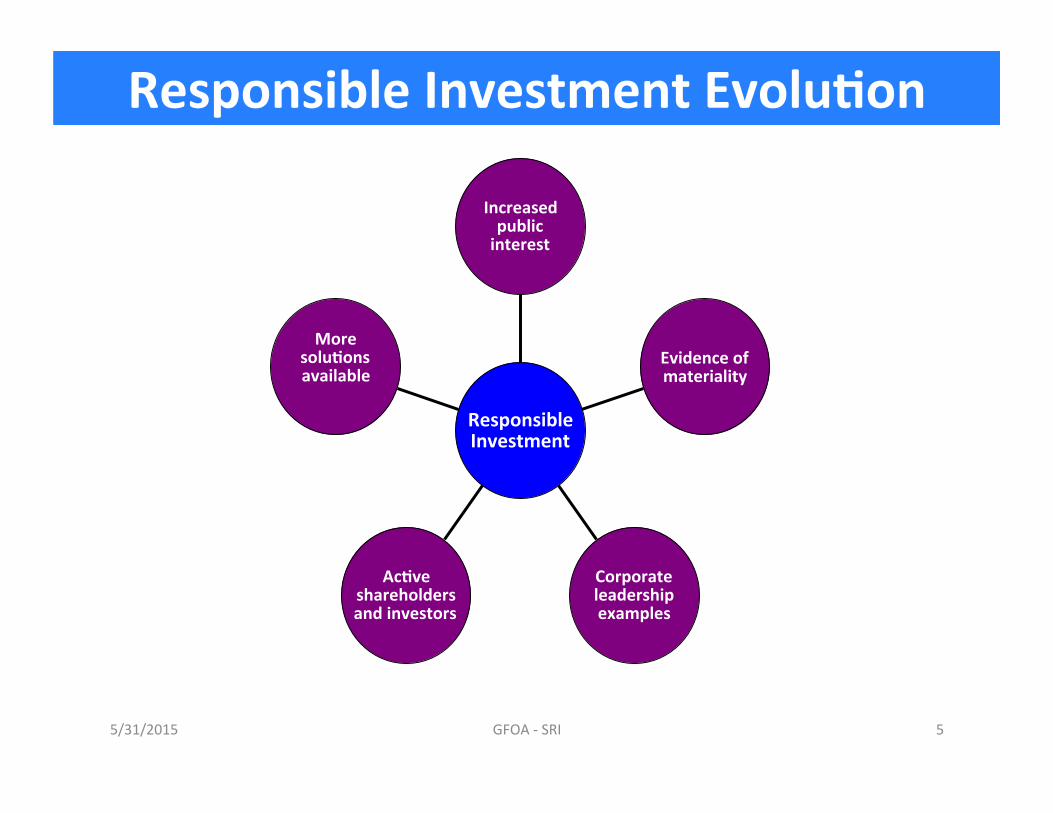

Responsible Investment EvoluRon

More soluRons available

AcRve shareholders and investors

Corporate leadership examples

Evidence of materiality

Increased public interest

Responsible Investment

5/31/2015 GFOA -‐ SRI 5

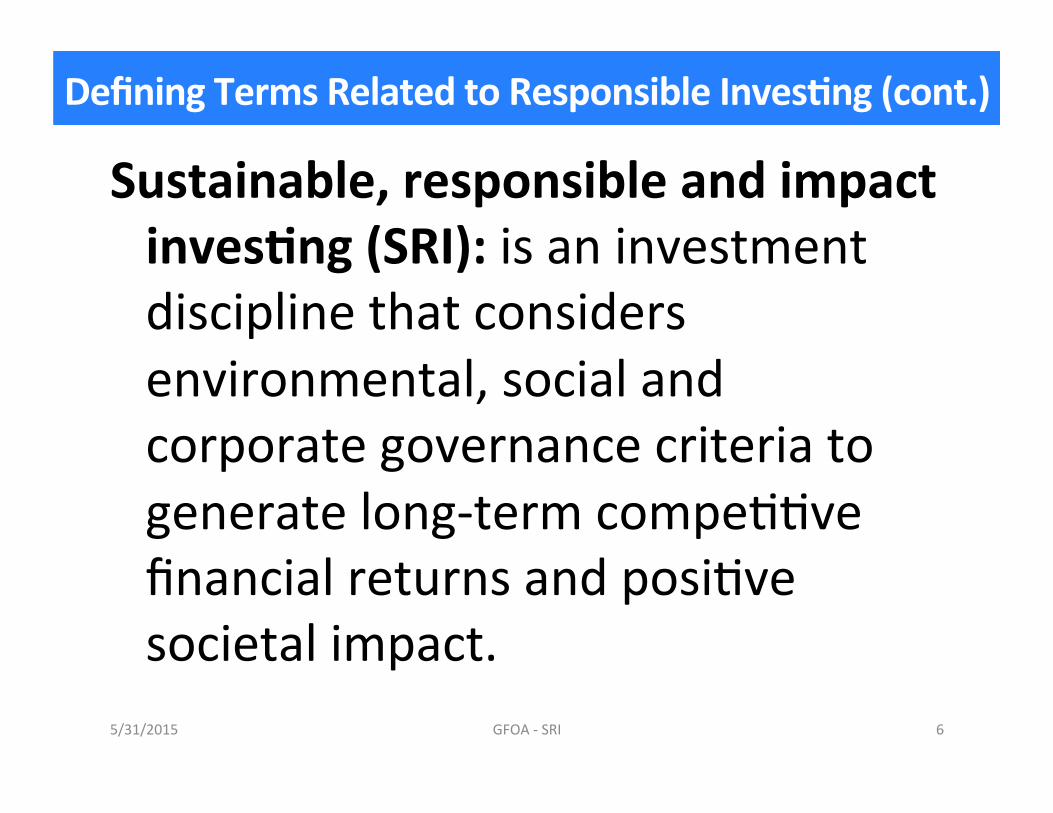

Defining Terms Related to Responsible InvesRng (cont.)

Sustainable, responsible and impact invesRng (SRI): is an investment discipline that considers environmental, social and corporate governance criteria to generate long-‐term compeAAve financial returns and posiAve societal impact.

5/31/2015 GFOA -‐ SRI 6

The Forum for Sustainable & Responsible Investment

5/31/2015 GFOA -‐ SRI 7

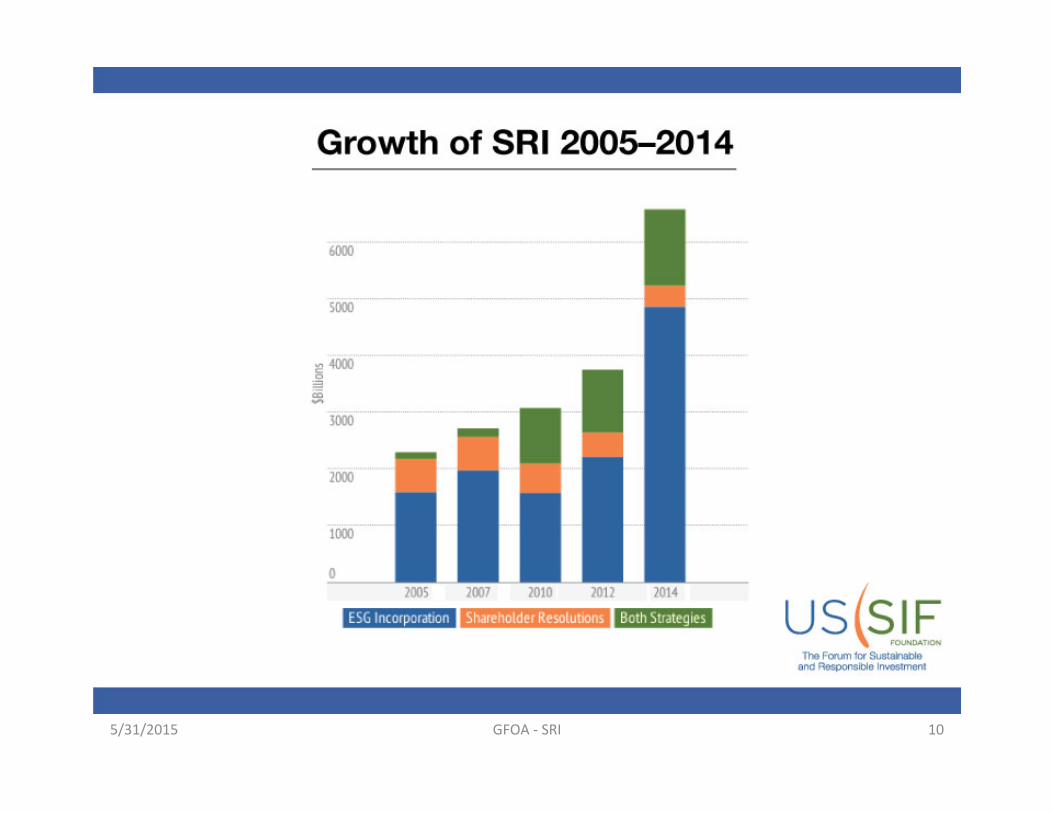

What the US(SIF Trends Report Measures o 2014 Trends Report is snapshot of US-‐domiciled assets engaged in

SRI strategies at year-‐end 2013.

o Two SRI strategies measured: – ESG incorporaAon: consideraAon of environmental, social (including community) and corporate governance (ESG) factors in investment analysis and porOolio selecAon

– Filing of shareholder resoluAons on ESG issues o AddiRonally, quesRons about:

– Why and how investor incorporates ESG – Whether investor engages in dialogue with companies on ESG issues

o US SIF FoundaRon has measured involvement in SRI strategies since 1995

5/31/2015 GFOA -‐ SRI 8

5/31/2015 GFOA -‐ SRI 9

5/31/2015 GFOA -‐ SRI 10

5/31/2015 GFOA -‐ SRI 11

5/31/2015 GFOA -‐ SRI 12

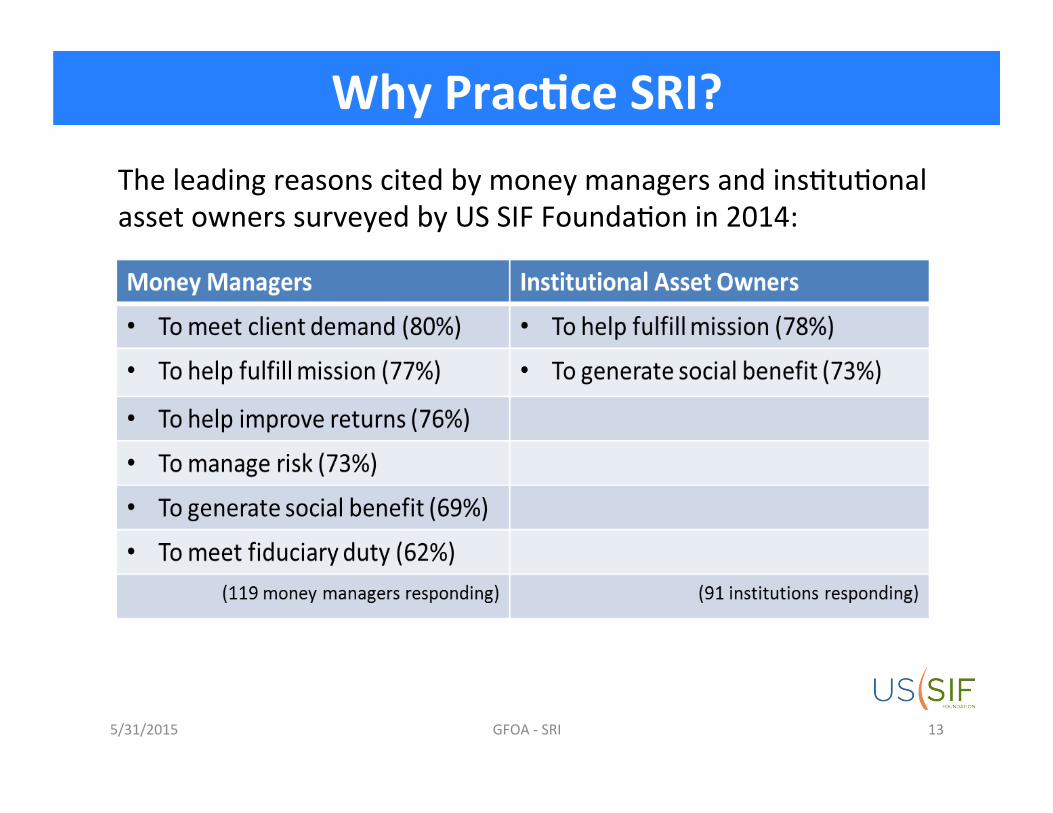

Why PracRce SRI? The leading reasons cited by money managers and insAtuAonal asset owners surveyed by US SIF FoundaAon in 2014:

5/31/2015 GFOA -‐ SRI 13

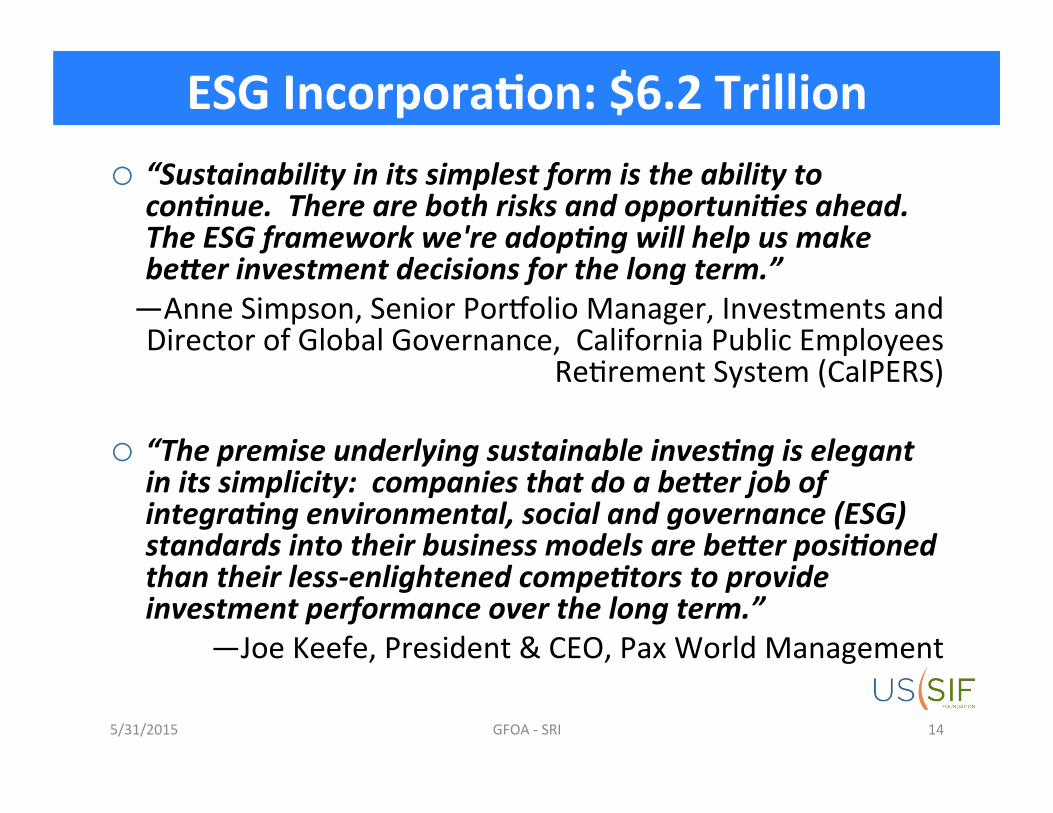

ESG IncorporaRon: $6.2 Trillion o “Sustainability in its simplest form is the ability to

con;nue. There are both risks and opportuni;es ahead. The ESG framework we're adop;ng will help us make beCer investment decisions for the long term.” —Anne Simpson, Senior PorOolio Manager, Investments and Director of Global Governance, California Public Employees

ReArement System (CalPERS)

o “The premise underlying sustainable inves;ng is elegant in its simplicity: companies that do a beCer job of integra;ng environmental, social and governance (ESG) standards into their business models are beCer posi;oned than their less-‐enlightened compe;tors to provide investment performance over the long term.”

—Joe Keefe, President & CEO, Pax World Management

5/31/2015 GFOA -‐ SRI 14

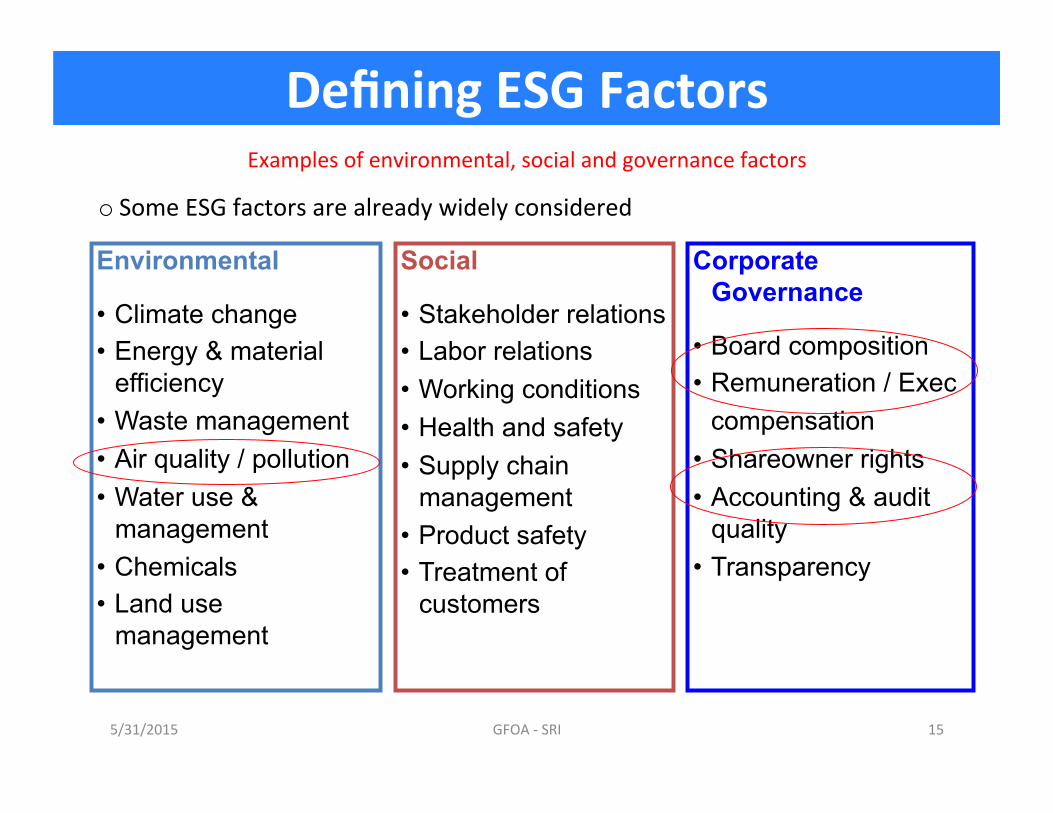

Environmental

• Climate change • Energy & material

efficiency • Waste management • Air quality / pollution • Water use &

management • Chemicals • Land use

management

Social

• Stakeholder relations • Labor relations • Working conditions • Health and safety • Supply chain

management • Product safety • Treatment of

customers

Corporate Governance

• Board composition • Remuneration / Exec compensation

• Shareowner rights • Accounting & audit

quality • Transparency

o Some ESG factors are already widely considered

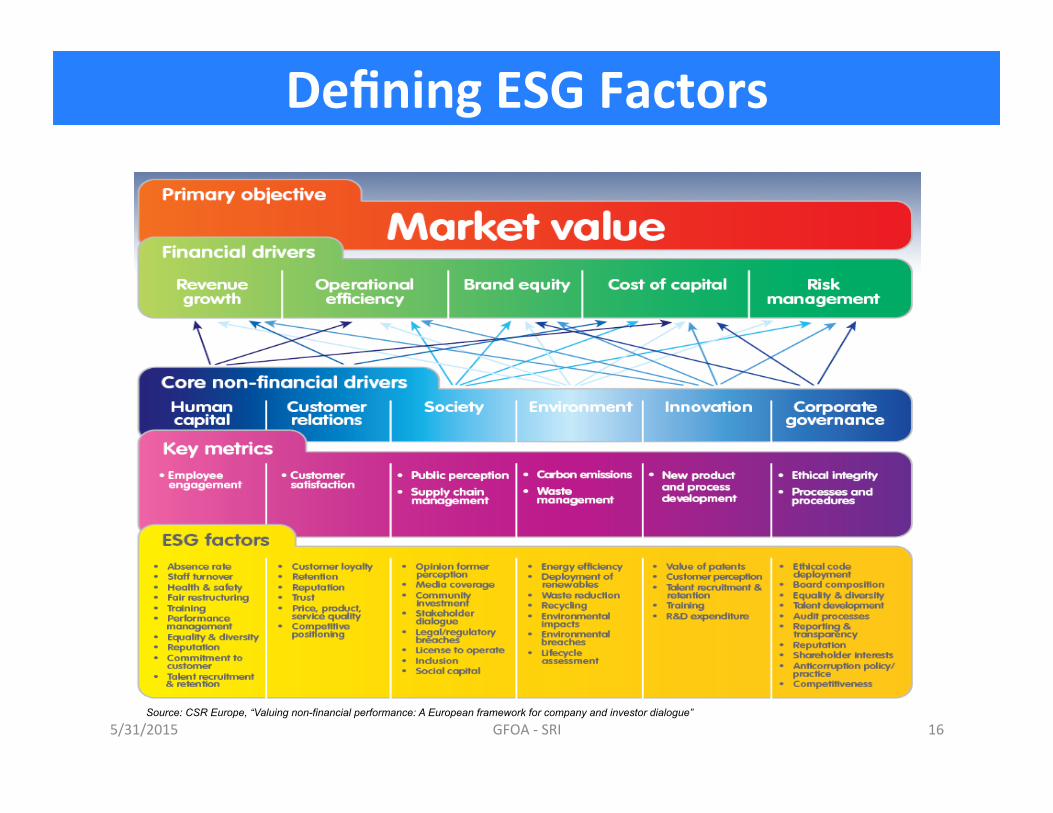

Defining ESG Factors Examples of environmental, social and governance factors

5/31/2015 GFOA -‐ SRI 15

How can ESG factors affect the performance of corporaRons?

Source: CSR Europe, “Valuing non-financial performance: A European framework for company and investor dialogue”

Defining ESG Factors

5/31/2015 GFOA -‐ SRI 16

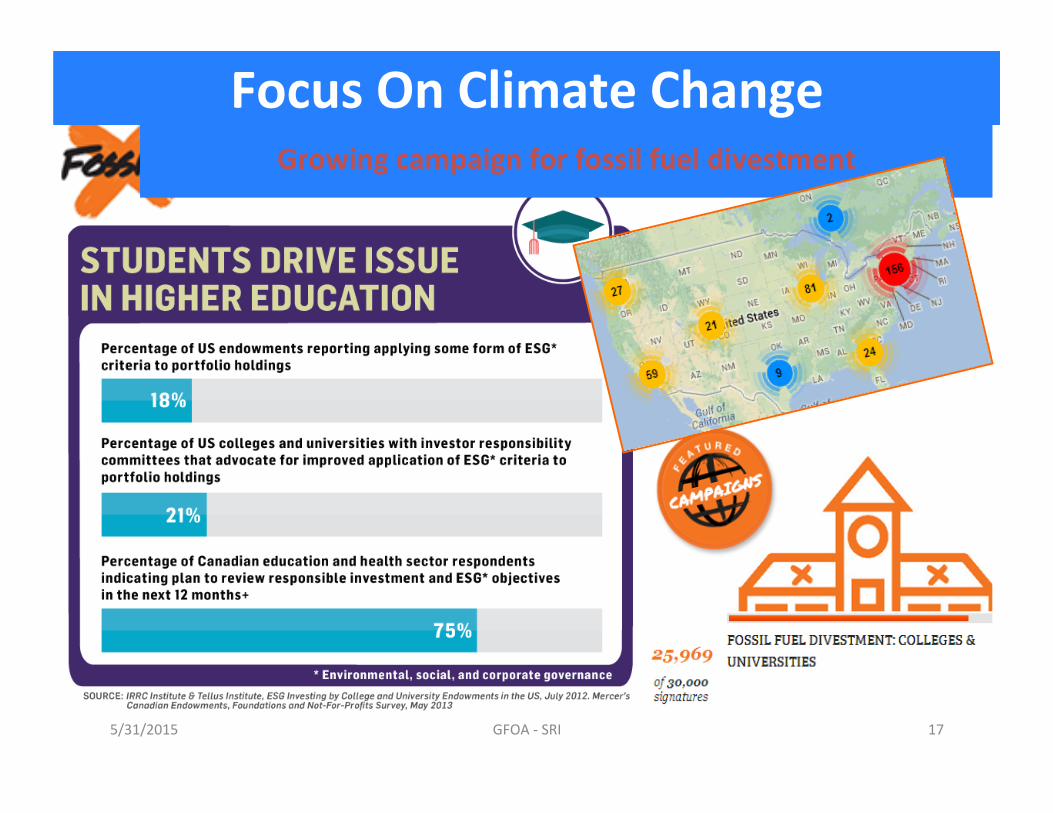

Growing campaign for fossil fuel divestment

Focus On Climate Change

5/31/2015 GFOA -‐ SRI 17

Why now? Financial drivers

o Assess environmental, social and governance (ESG) consideraAons to opAmize risk-‐adjusted returns

o Influence corporate behavior to enhance long-‐term outcomes

o Contribute to the integrity of financial markets

Non-‐financial drivers

o Reflect long-‐term investment horizon

o Reflect concerns and values of stakeholders

o Manage reputaAon, business risk

Why Responsible Investment?

5/31/2015 GFOA -‐ SRI 18

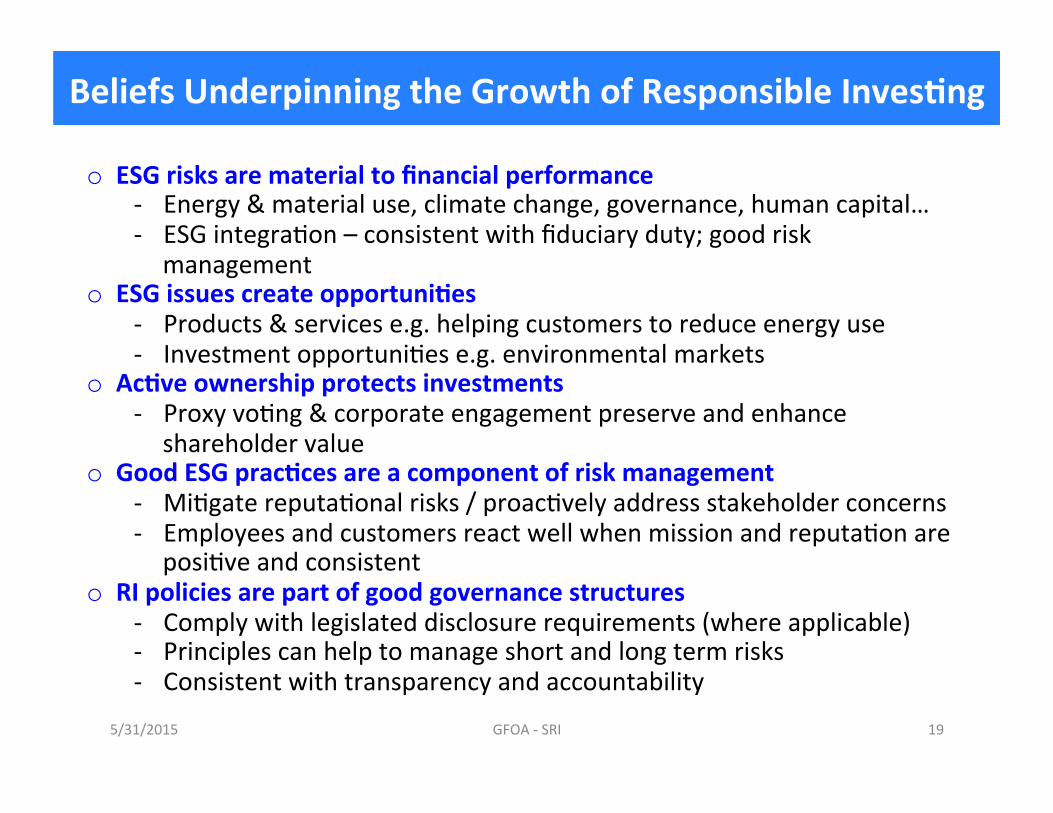

Beliefs Underpinning the Growth of Responsible InvesRng

o ESG risks are material to financial performance -‐ Energy & material use, climate change, governance, human capital… -‐ ESG integraAon – consistent with fiduciary duty; good risk

management o ESG issues create opportuniRes

-‐ Products & services e.g. helping customers to reduce energy use -‐ Investment opportuniAes e.g. environmental markets

o AcRve ownership protects investments -‐ Proxy voAng & corporate engagement preserve and enhance

shareholder value o Good ESG pracRces are a component of risk management

-‐ MiAgate reputaAonal risks / proacAvely address stakeholder concerns -‐ Employees and customers react well when mission and reputaAon are

posiAve and consistent o RI policies are part of good governance structures

-‐ Comply with legislated disclosure requirements (where applicable) -‐ Principles can help to manage short and long term risks -‐ Consistent with transparency and accountability

5/31/2015 GFOA -‐ SRI 19

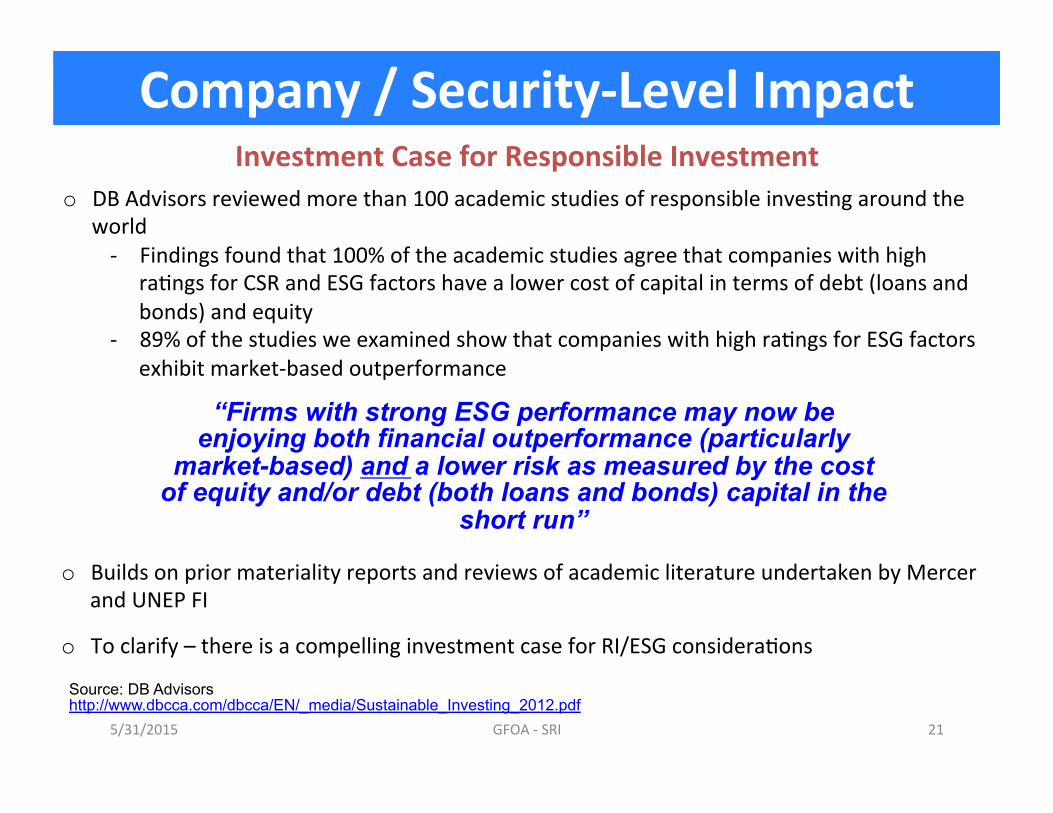

Company / Security-‐Level Impact Investment Case for Responsible Investment

5/31/2015 GFOA -‐ SRI 20

Company / Security-‐Level Impact Investment Case for Responsible Investment

o DB Advisors reviewed more than 100 academic studies of responsible invesAng around the world -‐ Findings found that 100% of the academic studies agree that companies with high

raAngs for CSR and ESG factors have a lower cost of capital in terms of debt (loans and bonds) and equity

-‐ 89% of the studies we examined show that companies with high raAngs for ESG factors exhibit market-‐based outperformance

“Firms with strong ESG performance may now be enjoying both financial outperformance (particularly

market-based) and a lower risk as measured by the cost of equity and/or debt (both loans and bonds) capital in the

short run”

o Builds on prior materiality reports and reviews of academic literature undertaken by Mercer and UNEP FI

o To clarify – there is a compelling investment case for RI/ESG consideraAons

Source: DB Advisors http://www.dbcca.com/dbcca/EN/_media/Sustainable_Investing_2012.pdf

5/31/2015 GFOA -‐ SRI 21

UN PRI

The United NaAons-‐supported Principles for Responsible Investment (PRI) IniAaAve is an internaAonal network of investors working together to put the six Principles for Responsible Investment into pracAce. Its goal is to understand the implicaAons of sustainability for investors and support signatories to incorporate these issues into their investment decision making and ownership pracAces.

5/31/2015 GFOA -‐ SRI 22

5/31/2015 GFOA -‐ SRI 23

UN PRI – The Six Principles Principle 1: We will incorporate ESG issues into investment analysis and decision-‐making processes.

Principle 2: We will be acAve owners and incorporate ESG issues into our ownership policies and pracAces.

Principle 3: We will seek appropriate disclosure on ESG issues by the enAAes in which we invest.

Principle 4: We will promote acceptance and implementaAon of the Principles within the investment industry.

Principle 5: We will work together to enhance our effecAveness in implemenAng the Principles.

Principle 6: We will each report on our acAviAes and progress towards implemenAng the Principles.

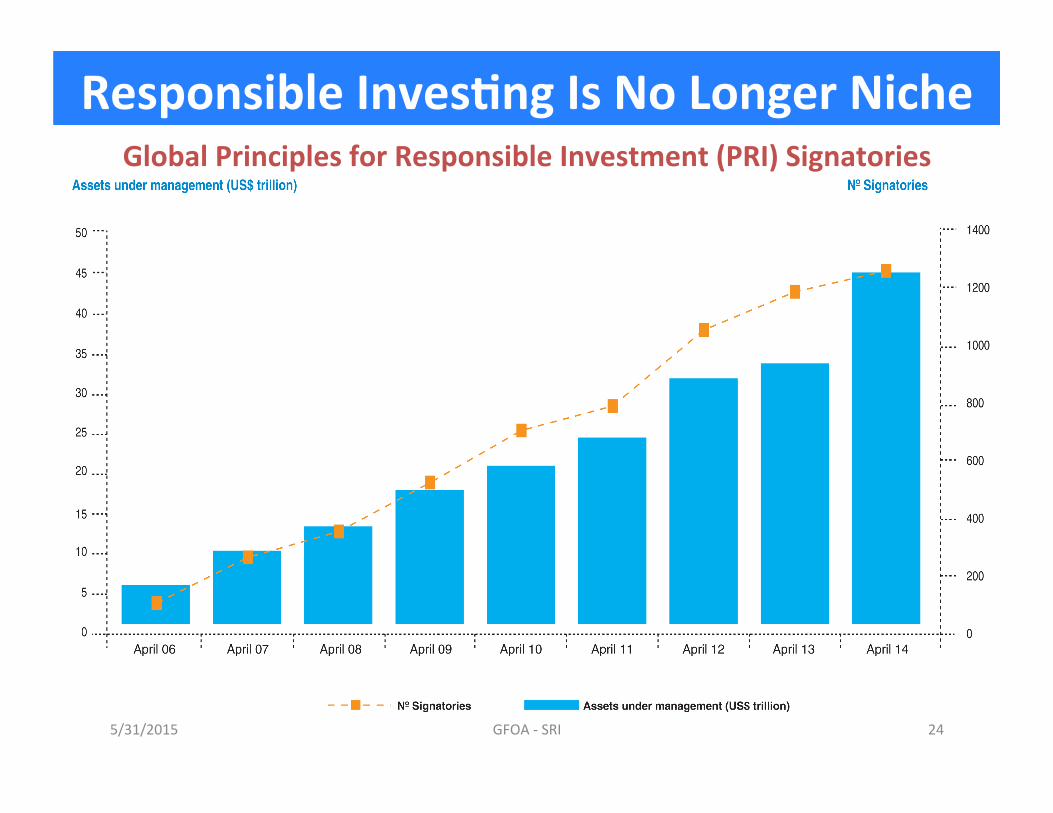

Responsible InvesRng Is No Longer Niche Global Principles for Responsible Investment (PRI) Signatories

5/31/2015 GFOA -‐ SRI 24

ESG IncorporaRon by Money Managers & CLLs

5/31/2015 GFOA -‐ SRI 25

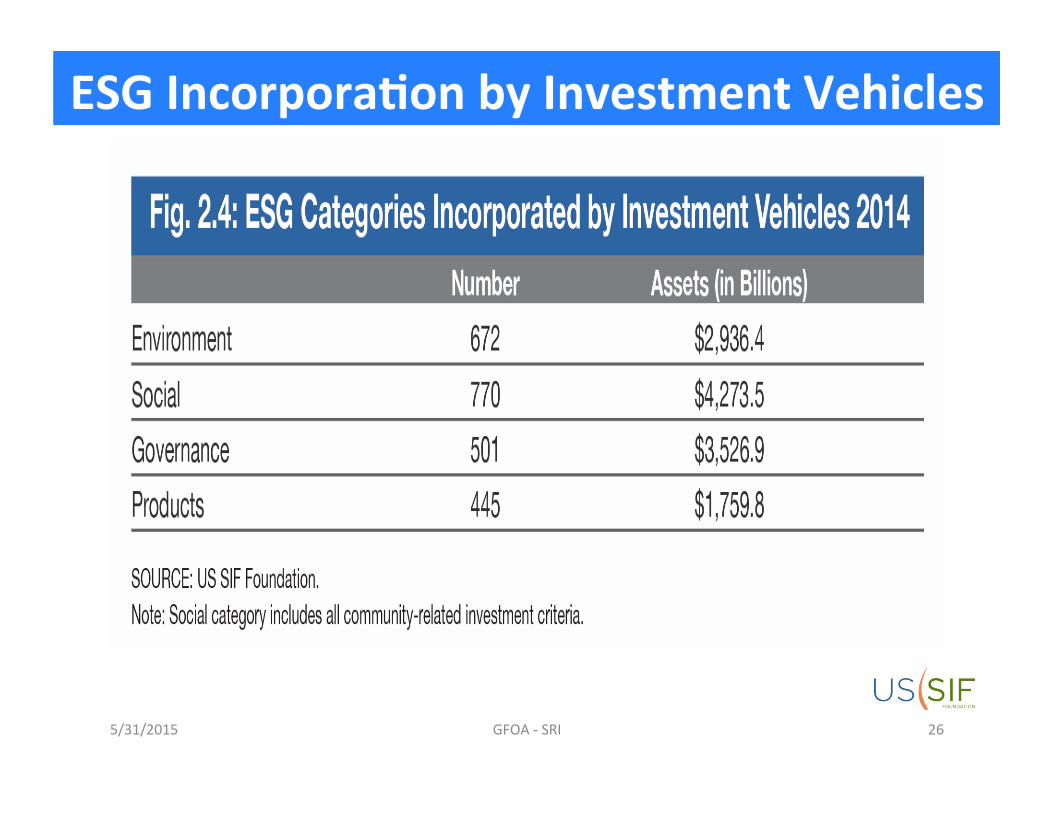

ESG IncorporaRon by Investment Vehicles

5/31/2015 GFOA -‐ SRI 26

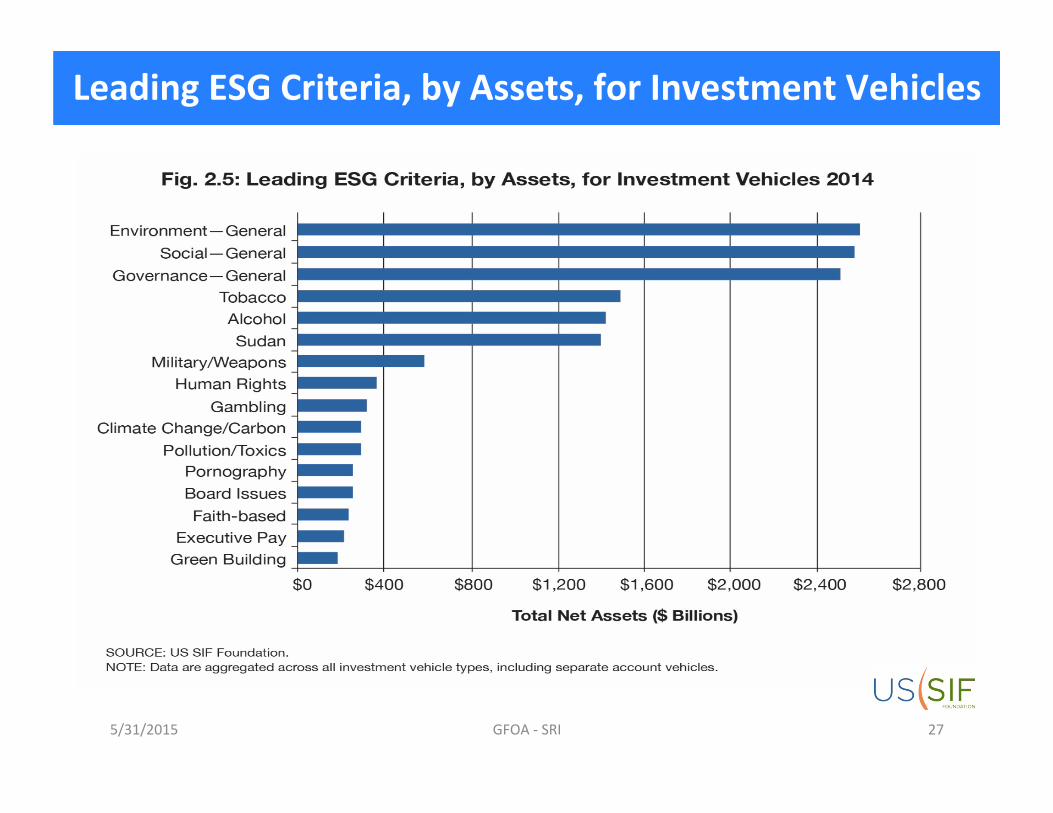

Leading ESG Criteria, by Assets, for Investment Vehicles

5/31/2015 GFOA -‐ SRI 27

Number of Shareholder Proponents 2012-‐14, by Investor Type

5/31/2015 GFOA -‐ SRI 28

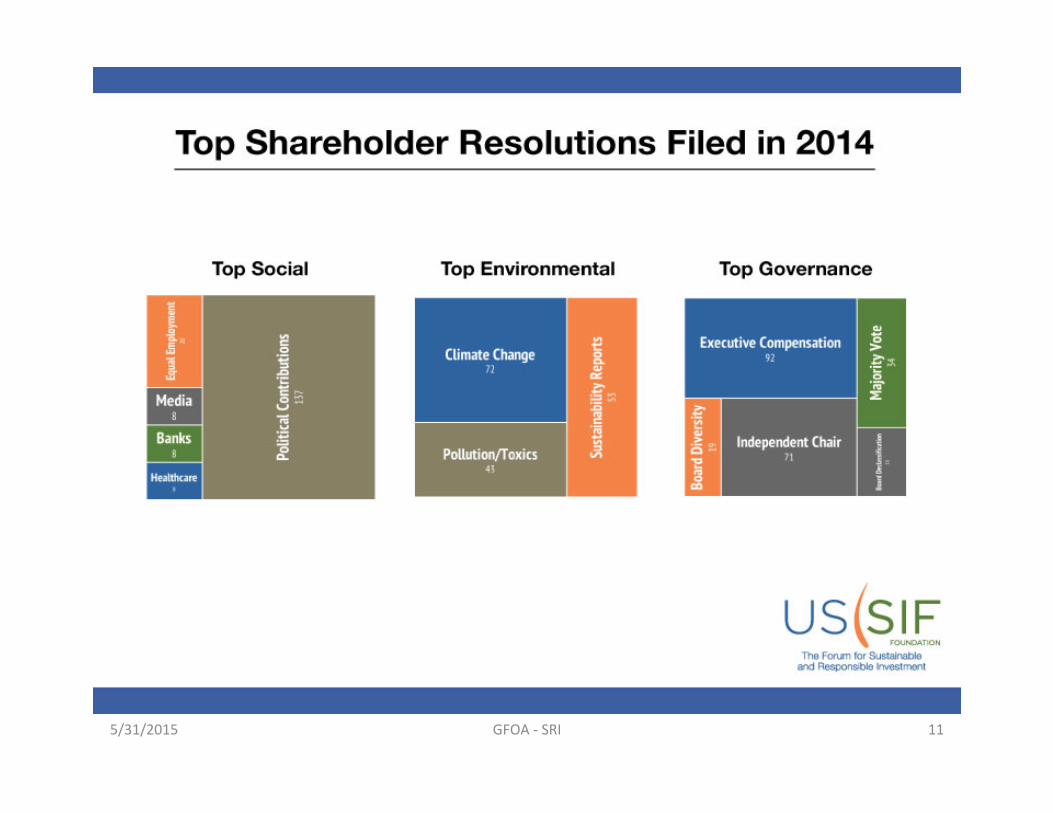

Leading Categories of Environmental & Social Shareholder Proposals, 2012-‐14

5/31/2015 GFOA -‐ SRI 29

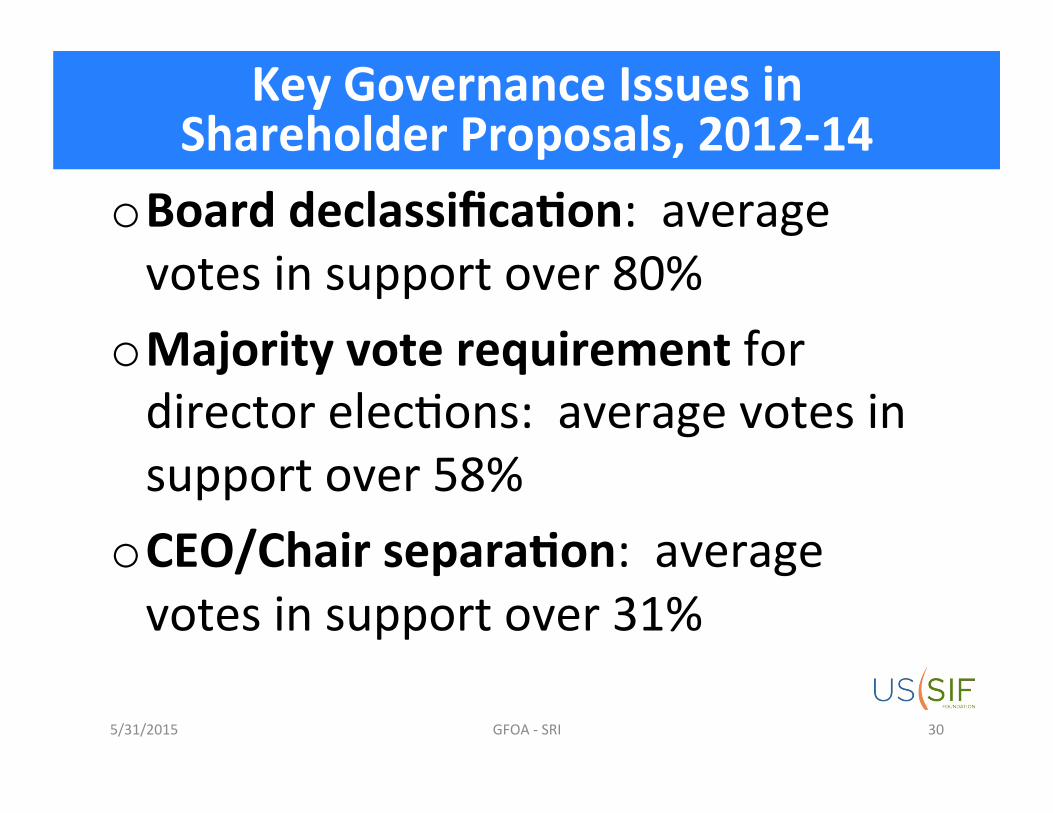

Key Governance Issues in Shareholder Proposals, 2012-‐14

o Board declassificaRon: average votes in support over 80%

o Majority vote requirement for director elecAons: average votes in support over 58%

o CEO/Chair separaRon: average votes in support over 31%

5/31/2015 GFOA -‐ SRI 30

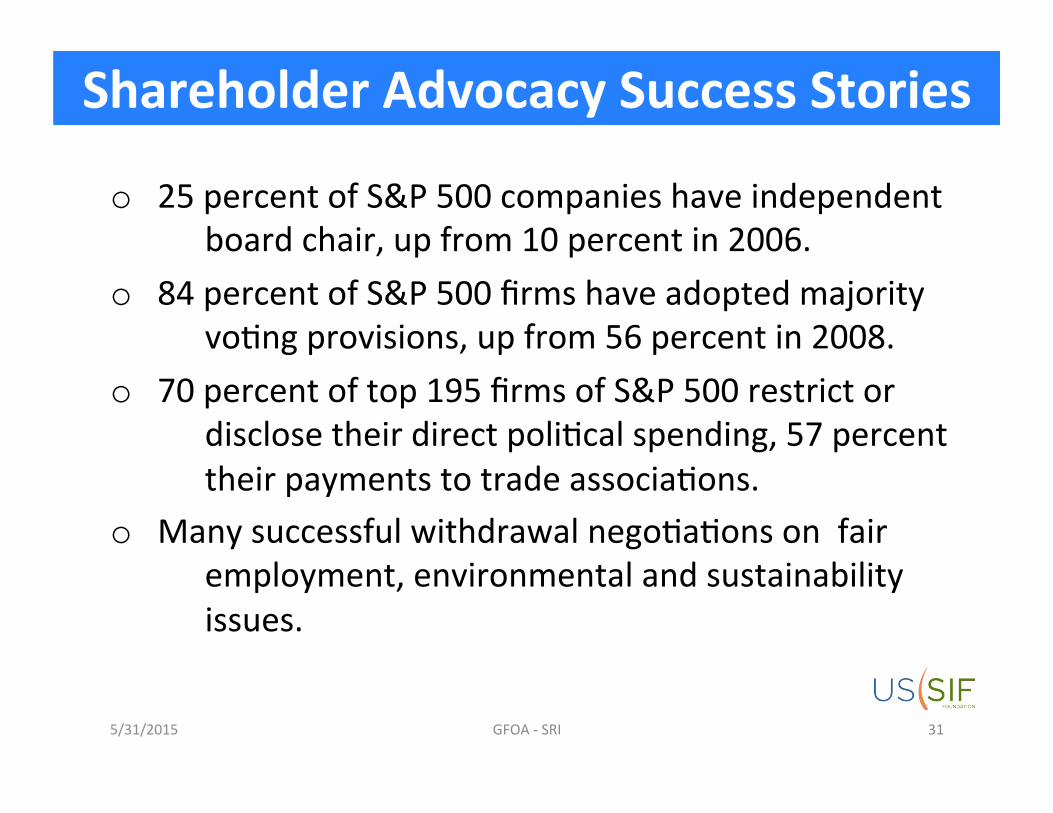

Shareholder Advocacy Success Stories

o 25 percent of S&P 500 companies have independent board chair, up from 10 percent in 2006.

o 84 percent of S&P 500 firms have adopted majority voAng provisions, up from 56 percent in 2008.

o 70 percent of top 195 firms of S&P 500 restrict or disclose their direct poliAcal spending, 57 percent their payments to trade associaAons.

o Many successful withdrawal negoAaAons on fair employment, environmental and sustainability issues.

5/31/2015 GFOA -‐ SRI 31

Thank You

5/31/2015 GFOA -‐ SRI 32

ImplemenRng Socially Responsible InvesRng in the

City of Portland, OR

Jennifer Cooperman, MBA City Treasurer

Agenda

o Portland, OR investment program o City’s Investment Advisory Comminee (IAC) o SRI process/framework o IAC observaRons/concerns o Other consideraRons o Appendix: City’s Investment Policy – Corporate Debt

5/31/2015 34

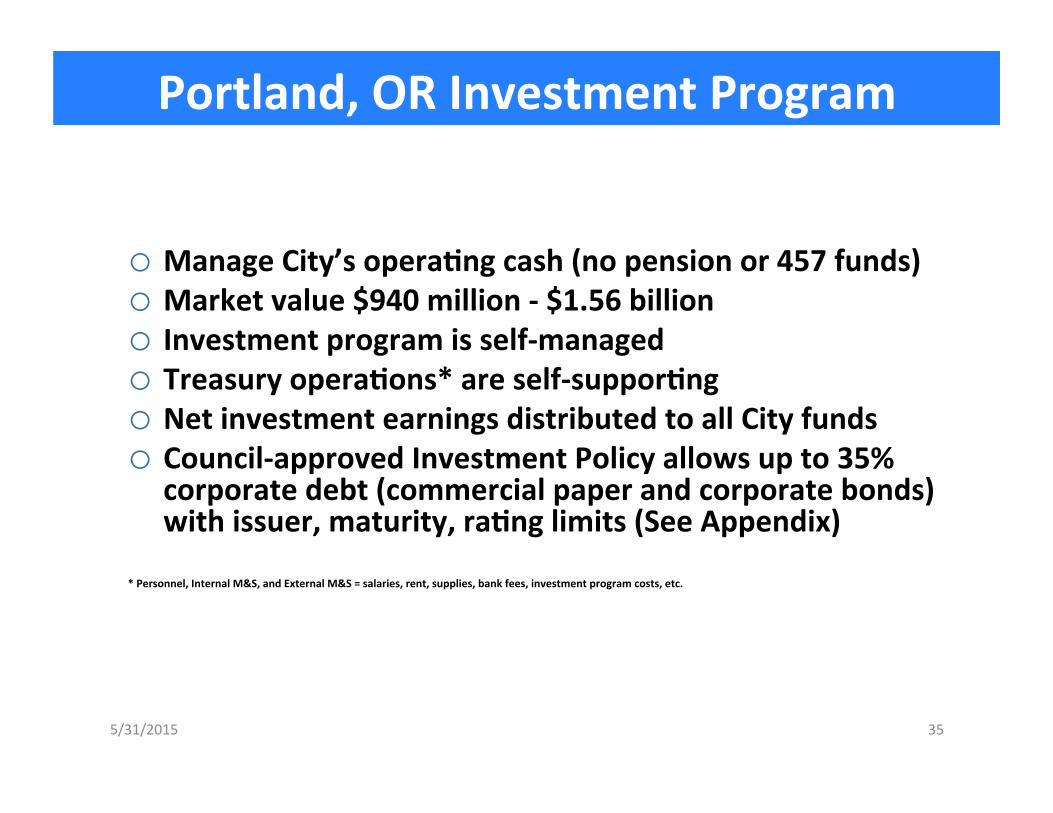

Portland, OR Investment Program

o Manage City’s operaRng cash (no pension or 457 funds) o Market value $940 million -‐ $1.56 billion o Investment program is self-‐managed o Treasury operaRons* are self-‐supporRng o Net investment earnings distributed to all City funds o Council-‐approved Investment Policy allows up to 35%

corporate debt (commercial paper and corporate bonds) with issuer, maturity, raRng limits (See Appendix)

* Personnel, Internal M&S, and External M&S = salaries, rent, supplies, bank fees, investment program costs, etc.

5/31/2015 35

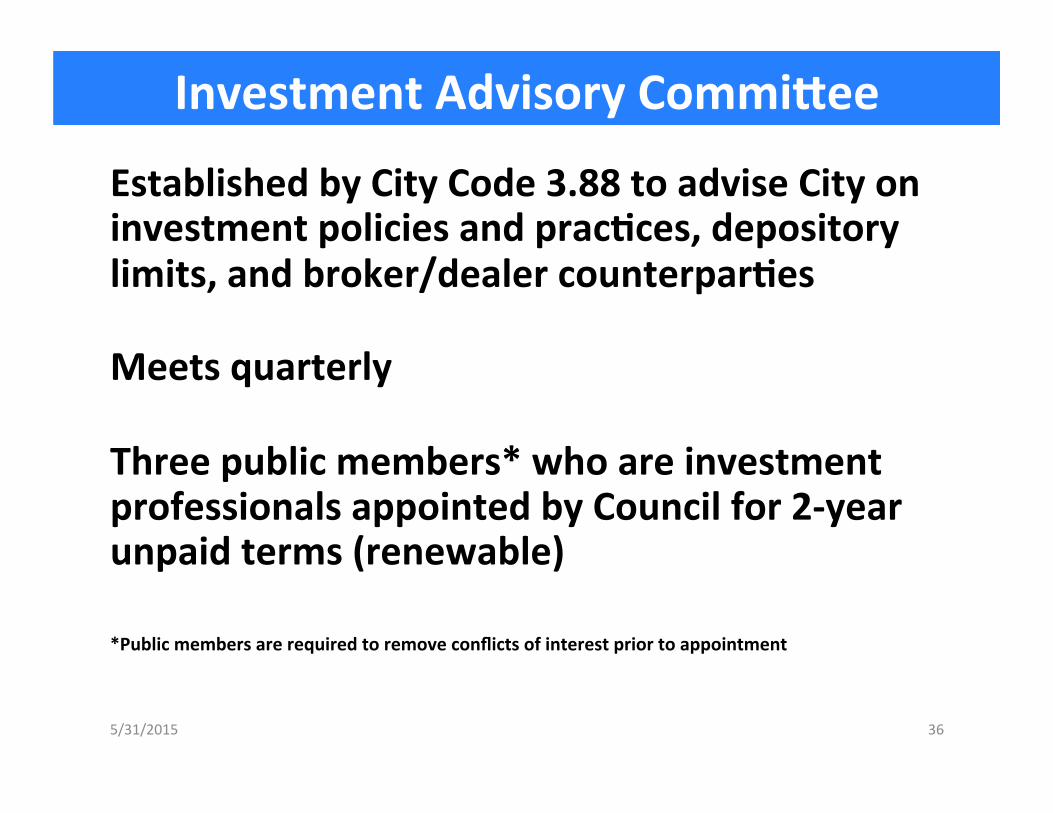

Investment Advisory Comminee

Established by City Code 3.88 to advise City on investment policies and pracRces, depository limits, and broker/dealer counterparRes

Meets quarterly

Three public members* who are investment professionals appointed by Council for 2-‐year unpaid terms (renewable) *Public members are required to remove conflicts of interest prior to appointment

36 5/31/2015

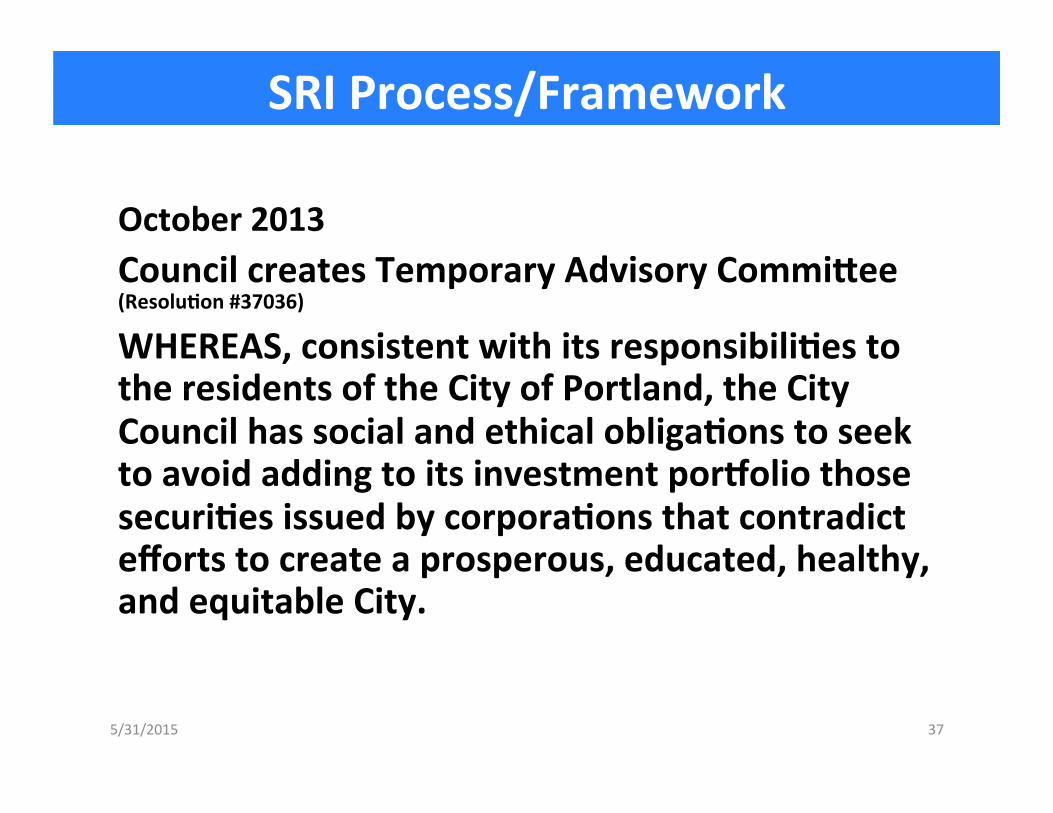

SRI Process/Framework

October 2013 Council creates Temporary Advisory Comminee (ResoluRon #37036)

WHEREAS, consistent with its responsibiliRes to the residents of the City of Portland, the City Council has social and ethical obligaRons to seek to avoid adding to its investment porYolio those securiRes issued by corporaRons that contradict efforts to create a prosperous, educated, healthy, and equitable City.

5/31/2015 37

SRI Framework/Process (cont’d)

October 2013 Council creates Temporary Advisory Comminee (ResoluRon #37036)

Council’s social and ethical concerns: – Environmental concerns – Health concerns including weapons producAon – Concerns about abusive labor pracAces – Concerns about corrupt corporate ethics and governance – Concerns about extreme tax avoidance – Concerns about exercise of such a level of market dominance as to disrupt normal compeAAve market forces.

5/31/2015 38

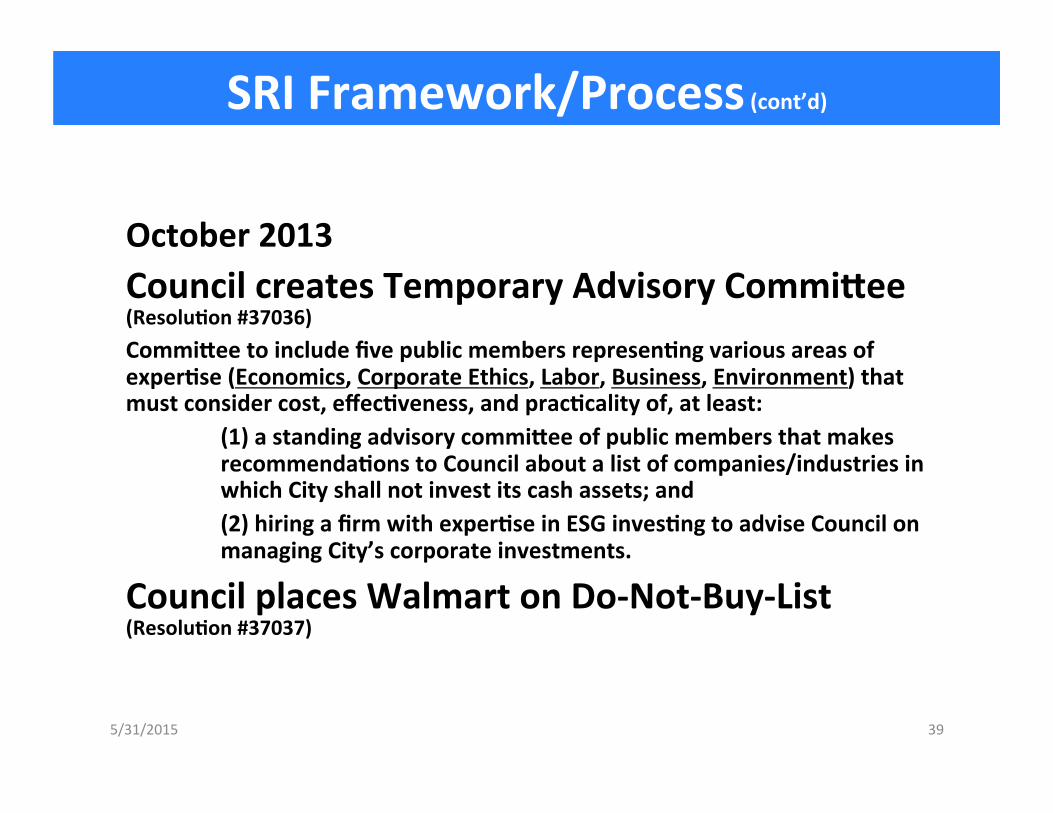

SRI Framework/Process (cont’d)

October 2013 Council creates Temporary Advisory Comminee (ResoluRon #37036) Comminee to include five public members represenRng various areas of experRse (Economics, Corporate Ethics, Labor, Business, Environment) that must consider cost, effecRveness, and pracRcality of, at least:

(1) a standing advisory comminee of public members that makes recommendaRons to Council about a list of companies/industries in which City shall not invest its cash assets; and (2) hiring a firm with experRse in ESG invesRng to advise Council on managing City’s corporate investments.

Council places Walmart on Do-‐Not-‐Buy-‐List (ResoluRon #37037)

5/31/2015 39

SRI Framework/Process (cont’d)

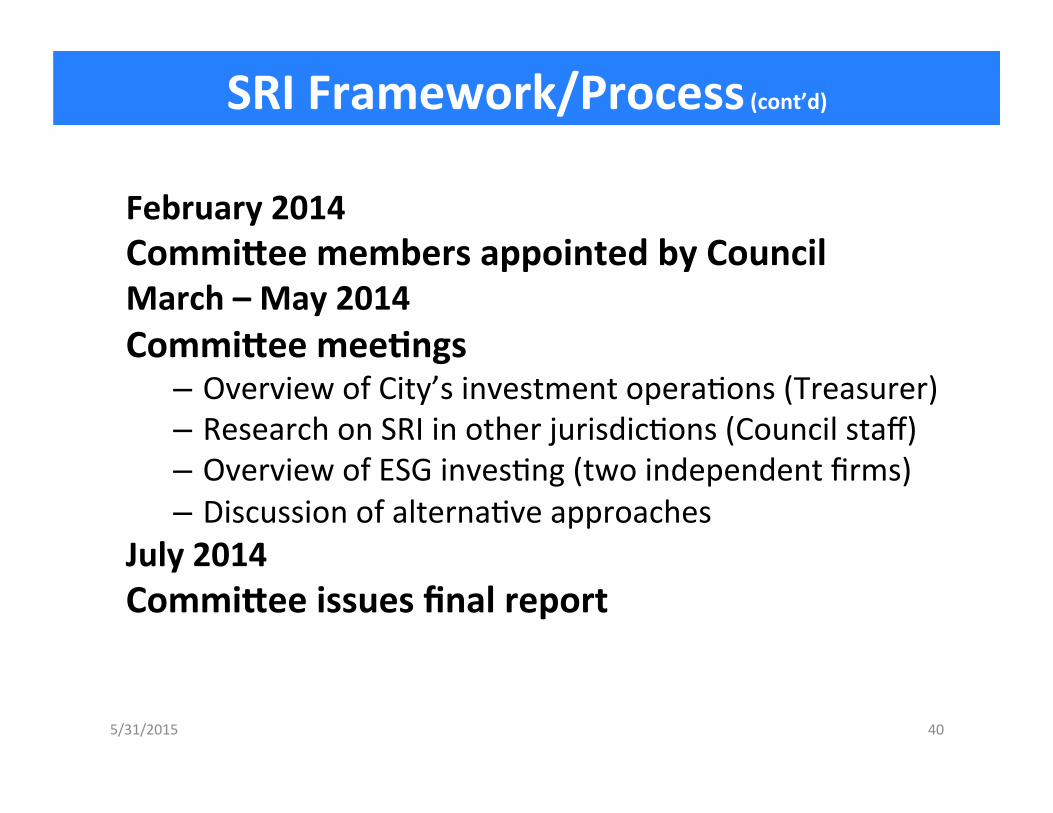

February 2014 Comminee members appointed by Council March – May 2014 Comminee meeRngs

– Overview of City’s investment operaAons (Treasurer) – Research on SRI in other jurisdicAons (Council staff) – Overview of ESG invesAng (two independent firms) – Discussion of alternaAve approaches

July 2014 Comminee issues final report

5/31/2015 40

Temporary Comminee’s RecommendaRons

o Create a permanent comminee of 7-‐10 public members represenRng environment and conservaRon, labor pracRces, corporate ethics and governance, corporate taxaRon, economics, public health and safety, business/commerce

o Contract with third-‐party vendor for SRI research o Permanent comminee to define measurable criteria based on Council-‐approved principles, and determine minimum scoring thresholds to recommend companies for inclusion on do-‐not-‐buy list

o Permanent comminee to consider public input in its recommendaRons to Council

5/31/2015 41

SRI Framework/Process (cont’d)

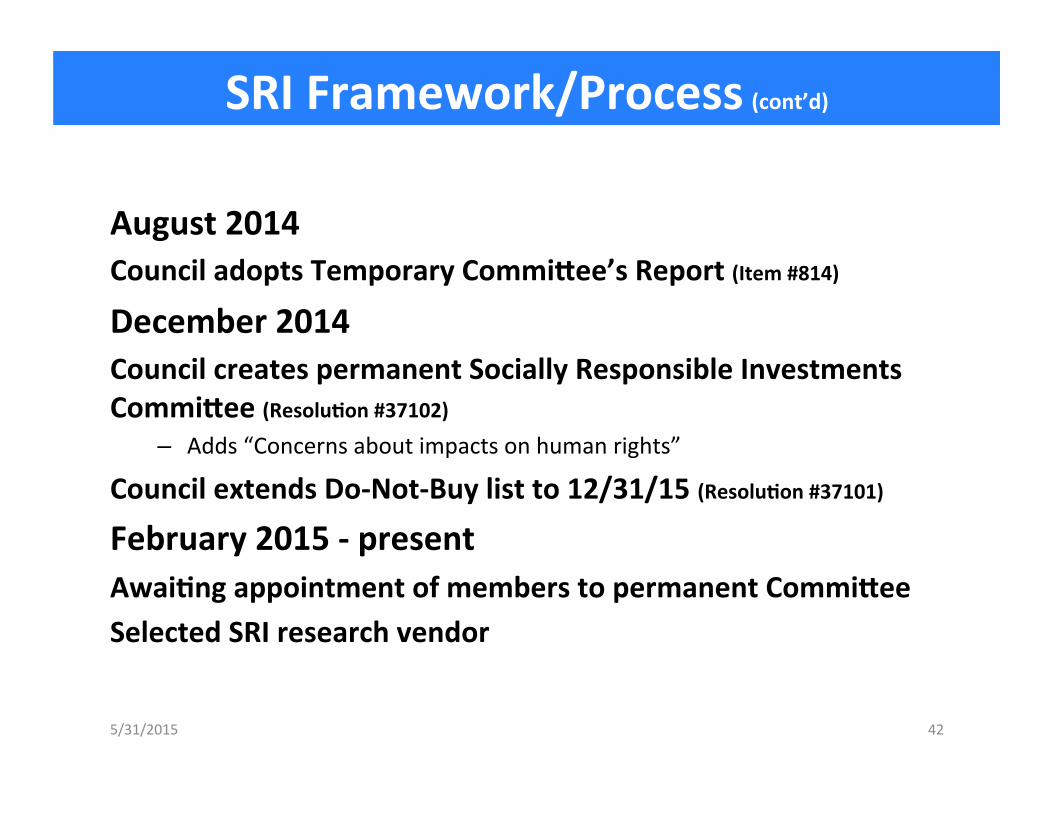

August 2014 Council adopts Temporary Comminee’s Report (Item #814)

December 2014 Council creates permanent Socially Responsible Investments Comminee (ResoluRon #37102)

– Adds “Concerns about impacts on human rights”

Council extends Do-‐Not-‐Buy list to 12/31/15 (ResoluRon #37101)

February 2015 -‐ present AwaiRng appointment of members to permanent Comminee Selected SRI research vendor 5/31/2015 42

IAC ObservaRons/Concerns

o NegaRve impact on porYolio returns due to reduced investment universe.

o Treasurer to provide analysis of financial impact. o Cost of SRI research. o Scoring of companies vis-‐à-‐vis principles may be difficult. o Council retains fiduciary responsibiliRes. Comminee is

making recommendaRons only. o IAC doesn’t want its process to become poliRcized. o How to give companies credit for good work? o Is effort only symbolic? Are there metrics to measure

impact on corporate behavior? o PoliRcal and business recruitment consideraRons as

companies are added to Do-‐Not-‐Buy list.

5/31/2015 43

Other ConsideraRons

o Framework addresses only direct investments (not LGIP) o Do-‐not-‐buy limits are prospecRve and sunset at end of

following calendar year unless Council re-‐adopts o Need for educaRon about ORS allowable investments and

limited universe of eligible corporate investments o Challenge of using “principles” regarding corporate

behavior rather than idenRfying industries or specific firms o Reminders that Treasury is self-‐funded and that

investment limits will reduce interest earnings paid out to City bureaus

o Council-‐owned process o Comminee needs staff support (Treasury is SME)

5/31/2015 44

Appendix: City’s Investment Policy Corporate Debt

(commercial paper and corporate bonds)

Maximum percent of porYolio (total) Maximum percent of porYolio (per

issuer) Commercial Paper Maximum maturity Minimum raRngs (at least one)

Corporate Bonds Maximum maturity Minimum raRngs (at least two)* *Oregon issuers may be A-‐, A3

35% 5% 9 months A-‐1,P-‐1,F-‐1

3 years AA-‐, Aa3

45 5/31/2015

QUESTIONS

Please provide feedback on the session

o Quick Text Feedback 1. Step 1 -‐ Text “GFOA” to 22333 2. Step 2 -‐ Did the session meet your expectaAons

for being high quality and relevant to your job? • Exceeded ExpectaAons– Text “S9EXC” • Met ExpectaAons – Text “S9MET” • Did Not Meet – “S9NOT”

o To provide more detailed evaluaRon on the session or full conference go to www.gfoa.org/evals