session 7: insurance basics for transportation professionals

TRANSCRIPT

TRB: Workshop on Transportation Law – July 23, 2013 Kevin Coen CRIS, ARM

Session 7: Insurance Basics for Transportation Professionals

Liberty Mutual Insurance

Agenda • The Nature of Risk • State of the Market • Insurance vs. Surety vs. Letters of Credit • Major Line of Construction Insurance

– Worker’s Compensation – Looking at Liability

• Professional/Environmental • Commercial General Liability • Builder’s Risk

– Umbrella/Excess • The Insurance Tower • Additional Issues

– Named Insured – Construction Defect – TRIA

Liberty Mutual Insurance

The Nature of Risk:

Probability (Occurrence Opportunity)

Frequency (Exposure Opportunity)

Likelihood (Chance of Occurrence)

Severity (Degree of Harm)

RISK

Liberty Mutual Insurance

State of the Market: Combined Ratio / ROE

* 2008 -2012 figures are return on average surplus and exclude mortgage and financial guaranty insurers. 2012 combined ratio including M&FG insurers is 103.2, 2011 combined ratio including M&FG insurers is 108.1, ROAS = 3.5%.

Source: Insurance Information Institute from A.M. Best and ISO data.

100.1 100.8

92.795.7

101.2 101.0

106.5

102.499.5

6.2%4.7%

7.9%

10.9%

9.6%

8.8%

4.3%

7.4%

12.7%

80.0

85.0

90.0

95.0

100.0

105.0

110.0

2003 2005 2006 2007 2008 2009 2010 2011 20120%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s Depressed Investment Environment to Generate Risk Appropriate ROEs

Liberty Mutual Insurance

State of the Market:

• Soft Market from March 2005 until August 2011 • Market begins harding November 2011 • Last Hard Market result of 9/11

Hard vs. Soft Market

Source: MarketScout

Liberty Mutual Insurance

Insurance vs. Surety

Liberty Mutual Insurance

Different Type Project Guarantees

Liberty Mutual Insurance

Photo Use

Major Insurance Lines for Construction

Liberty Mutual Insurance

Workers Compensation Combined Ratio: 1994–2012P

102.

0

97.0 10

0.0

101.

0

112.

6

108.

6

105.

1

102.

7

98.5 10

3.5

104.

5 110.

6 115.

0

115.

0

109.

0

121.

7

107.

0

115.

3

118.

2

8085

9095

100105110

115120

125130

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Workers Comp Results Began to Improve in 2012. Underwriting Results Deteriorated Markedly from 2007-2010/11 and Were the Worst They Had Been in a Decade.

Sources: A.M. Best (1994-2009); NCCI (2010-2012P) and are for private carriers only; Insurance Information Institute.

12/01/09 - 9pm 9

Liberty Mutual Insurance

Workers Compensation Medical Severity Moderate Increase in 2012

10

Annual Change 1991–1993: +1.9% Annual Change 1994–2001: +8.9% Annual Change 2002–2010: +6.0%

Average Medical Cost per Lost-Time Claim

Med

ical

C

laim

Cos

t ($0

00s)

$8.1

$8.2

$8.1

$8.8

$9.2

$9.9

$10.9

$11.8

$13.1

$14.0

$15.9

$17.3

$18.7

$19.7

$21.2

$22.3

$23.7

$25.3

$26.4

$26.7

$27.7

$28.5

+6.8%+1.3%-2.1%+9.0%+5.1%+7.4%

+10.1%+8.3%

+10.6%+7.3%

+13.5%+8.8%

+7.7%+5.4%

+7.8%+5.4%

+6.3%+6.6%

+4.1%+1.4%+3.6%

+3%

5

10

15

20

25

30

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20112012p

2012p: Preliminary based on data valued as of 12/31/2012. 1991-2011: Based on data through 12/31/2011, developed to ultimate

Based on the states where NCCI provides ratemaking services including state funds, excluding WV; Excludes high deductible policies.

Accident Year

Liberty Mutual Insurance

Workers Comp/Employer’s Liability

• WC Statutory Limits – Occupational Injury/Disease – USL&H – Monopolistic States: ND, OH, WA, WY

• Employer’s Liability – Common Law suits against employer arising out of injury – NY Labor Law, usually CGL exposure

• Effective Plan for Large Project Exposure (+$100m) – Loss Sensitive/Retro – Controlled Insurance Programs (CIP)

• Owner’s or Contractor controlled • Key feature: uniform & enforceable safety program

Liberty Mutual Insurance

Looking at the Liability Picture:

• Commercial General Liability: General Contractor (GC) – Trigger: Bodily Injury(BI)/Property Damage (PD) arising from an

occurrence – 3rd party

• Professional: Designer/Engineering – Trigger: Negligence/Standard of Care, doesn’t need occurrence – 1st and/or 3rd party

• Builder’s Risk: Owner or GC on behalf of – Trigger: Named Perils during course of construction arising from an

occurrence – 3rd but can work as 1st Party

• Owner & Contractor • May exclude Designers and Manufacturers

Liberty Mutual Insurance

General Liability Combined Ratio: 2005–2015F

112.

9

95.1 99

.0

94.2

101.

4

104.

4

105.

8

108.

3

107.

1 110.

8

99.8

80

85

90

95

100

105

110

115

05 06 07 08 09 10 11 12 13F 14F 15F

Commercial General Liability Underwriting Performance Has Been Volatile in Recent Years

Source: Conning Research and Consulting.

12/01/09 - 9pm 13

Liberty Mutual Insurance 14

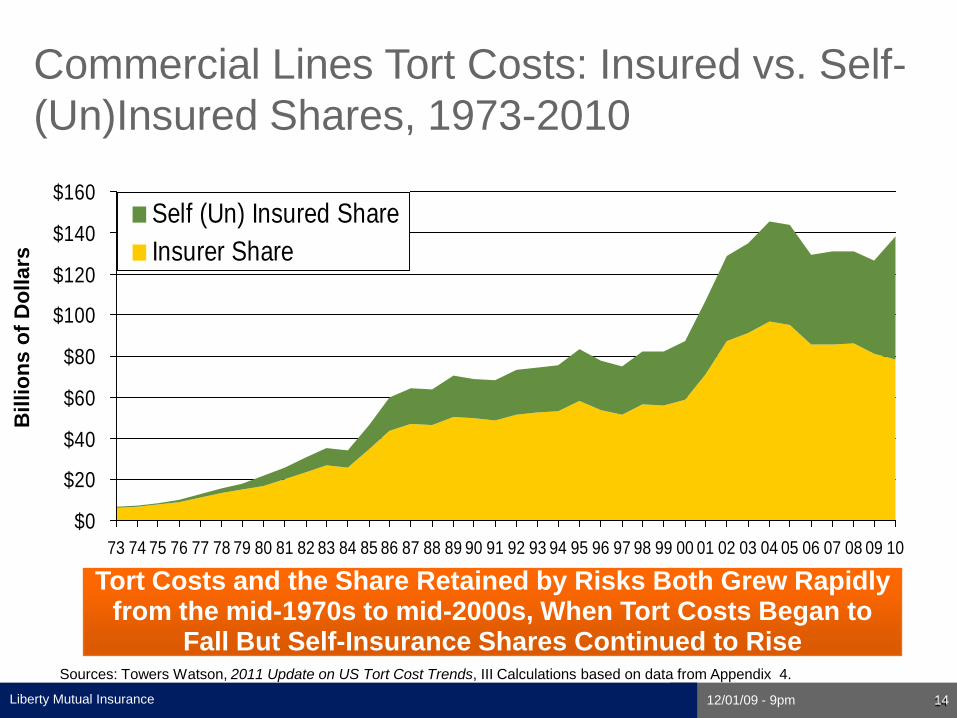

Commercial Lines Tort Costs: Insured vs. Self-(Un)Insured Shares, 1973-2010

Bill

ions

of D

olla

rs

$0

$20

$40

$60

$80

$100

$120

$140

$160

73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Self (Un) Insured ShareInsurer Share

Tort Costs and the Share Retained by Risks Both Grew Rapidly from the mid-1970s to mid-2000s, When Tort Costs Began to

Fall But Self-Insurance Shares Continued to Rise Sources: Towers Watson, 2011 Update on US Tort Cost Trends, III Calculations based on data from Appendix 4.

12/01/09 - 9pm 14

Liberty Mutual Insurance

Commercial General Liability (CGL)

• CGL Trigger: Bodily Injury(BI)/Property Damage (PD) arising from an occurrence – Defense obligation is broader than indemnity coverage with defense

costs outside of limits – Course of construction and completed operations – Not regulated like WC – coverages may vary (manuscripted policies) – CG 2243 – full professional liability exclusion – CG 2279 – excludes professional services (except means and methods) – CG 2280 – offers limited design related errors (contractor is the builder) – “Other Insurance” clause – Who is insured: Insured vs. Additional Insured

• Yes: Gain Rights • But you also must support hold harmless and indemnity obligations • And policy forms may not be standard but manuscripted

Liberty Mutual Insurance

Builders Risk

• Builder’s Risk: Named Perils during course of construction arising from an occurrence – transfer accidental physical damage and resulting loss to work in the

course of construction – “All-risk” except those specifically excluded (manuscripted policies) – Usually Owners pays deductibles – Policy may require “direct physical” loss – “property which will or has become a permanent part” of the project – “temporary structures, scaffolds, construction forms, falsework…” – Property locations to be covered: on/off site – Delay in Start Up – time element coverage (soft costs + business

income) – “Other Insurance” clause – Additional Insured: should be parties with insurable interest – Additional Insured: ATIMA “as their interest may appear”

Liberty Mutual Insurance

BR covers Named Perils:

Forecast Parameter Median (1981-2010)

2013F

Named Storms 12.0 18 Named Storm Days 60.1 95 Hurricanes 6.5 9 Hurricane Days 21.3 40 Major Hurricanes 2.0 4 Major Hurricane Days 3.9 9 Accumulated Cyclone Energy 92.0 165 Net Tropical Cyclone Activity 103% 175%

Source: Philip Klotzbach and Dr. William Gray, Colorado State University, April 10, 2013, accessed at http://tropical.atmos.colostate.edu/forecasts/2013/apr2013/apr2013.pdf ; Insurance Information Institute..

Outlook for 2013 Hurricane Season:75% Worse Than Average

Liberty Mutual Insurance

Professional Coverage;

• Professional: complex coverages with many insuring agreements – Trigger: Negligence/Standard of Care, doesn’t need occurrence – Covers economic damage as well as BI/PD

• Delay/cost overruns/loss of use/underperformance – Combined with environmental coverage – Combined PL & CPL (Turnkey Env. Services Firm) – Is it Design/Build or Builder with Design Assist? – CM@Risk: project scheduling, material selection, health & safety – GC’s: CGL does not cover value engineering, constructability reviews,

supervision of professional services – 3rd Party PL: contractor liable whether self-performed or subcontracted – 1st Party Indemnity: Contractor provides excess over E&O or DIC – Rectification & mitigation

Liberty Mutual Insurance

Excess/Umbrella

• Excess Provides Three Main Protections: 1. Additional insurance when liability exceeds per occurrence limit of

underlying policy. 2. Pay liability claims that exhaust underlying policy aggregate limits. 3. Cover claims outside of scope of underlying policy.

• Umbrella Excess Liability Policy – Covers 1&2 but not 3 – Requires insured to maintain underlying coverages to agreed limits

Liberty Mutual Insurance

The Insurance Tower; • OCIP • CCIP • Project Specific

Contractor Coverages

Liberty Mutual Insurance

Additional Issues:

• Additional Insured/Additional Named Insured – “arising out of” replaced with “caused in whole or in part” – AI can change “other insurance” (vertical vs. horizontal exhaustion) – AI vs. contractual indemnification (state anti-indemnity statutes)

• Construction Defect – An “Occurrence”? State by State – Faulty work exception limited to work performed by subcontractor – Don’t rely on insurance – project management is critical!!!

• TRIA – Expires 12-31-2014, US will no longer “certify” acts of terrorism – Insurable Risk?

Liberty Mutual Insurance

IRMI: International Risk Management Institute

http://www.irmi.com/conferences/crc/agenda/default.aspx