polsinelli shughart pc in california, polsinelli shughart llp health insurance marketplaces and...

TRANSCRIPT

Polsinelli Shughart PC In California, Polsinelli Shughart LLP

Health Insurance Marketplaces and

Texas UpdateMarch 14, 2013

Emily [email protected]

© 2013 Polsinelli Shughart PC2

Polsinelli Shughart provides this material for informational purposes only. The material provided herein is general and is not intended to be legal advice. Nothing herein should be relied upon or used without consulting a lawyer to consider your specific circumstances, possible changes to applicable laws, rules and regulations and other legal issues. Receipt of this material does not establish an attorney-client relationship.

Polsinelli Shughart is very proud of the results we obtain for our clients, but you should know that past results do not guarantee future results; that every case is different and must be judged on its own merits; and that the choice of a lawyer is an important decision and should not be based solely upon advertisements.

© 2013 Polsinelli Shughart PC. In California, Polsinelli Shughart LLP. Polsinelli Shughart is a registered mark of Polsinelli Shughart PC

© 2013 Polsinelli Shughart PC3

PART I:

MARKETPLACES GENERALLY

© 2013 Polsinelli Shughart PC4

Insurance Market Reforms, v. 1.1

• Temporary High Risk Pool Programs: state-based

• Rate Review Standards

• First-line Coverage Reforms (September 23, 2010)– No Lifetime Limits– Restricted Annual Limits– Restrictions on Rescission– First Dollar Coverage of Preventive Services– Extended Dependent Coverage (age 26)– External Review Organizations: state-regulated– No Pre-Existing Conditions for Children– Disclosure of Justifications for Premium Increases

• Medical Loss Ratios with Rebates

© 2013 Polsinelli Shughart PC5

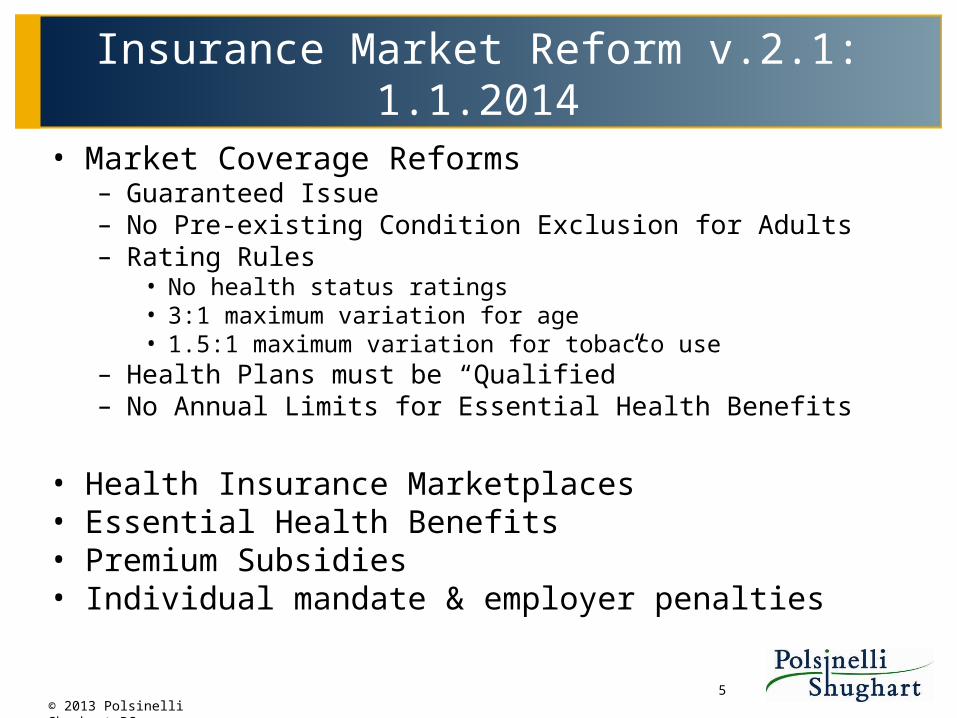

Insurance Market Reform v.2.1: 1.1.2014

• Market Coverage Reforms– Guaranteed Issue– No Pre-existing Condition Exclusion for Adults– Rating Rules

• No health status ratings• 3:1 maximum variation for age• 1.5:1 maximum variation for tobacco use

– Health Plans must be “Qualified”– No Annual Limits for Essential Health Benefits

• Health Insurance Marketplaces• Essential Health Benefits• Premium Subsidies• Individual mandate & employer penalties

© 2013 Polsinelli Shughart PC6

Health Insurance (Exchange) Marketplaces

Marketplace for health insurance – like Expedia

Provide coverage options for individuals & small businesses – increased transparency

Site to manage new federal tax credits for certain individuals who do not have coverage through their employer

Enrollment “facilitators” for public programs

© 2013 Polsinelli Shughart PC7

Marketplace Basics

• Every state must have a Marketplace) for individuals and small businesses (up to 50 employees), effective January 1, 2014; number will be raised to 100 employees in 2016

• “Qualified” health plans must offer a minimum level of coverage

• Each state must define (and be approved by the government) the “Essential Health Benefits” to be offered by marketplace plans

© 2013 Polsinelli Shughart PC8

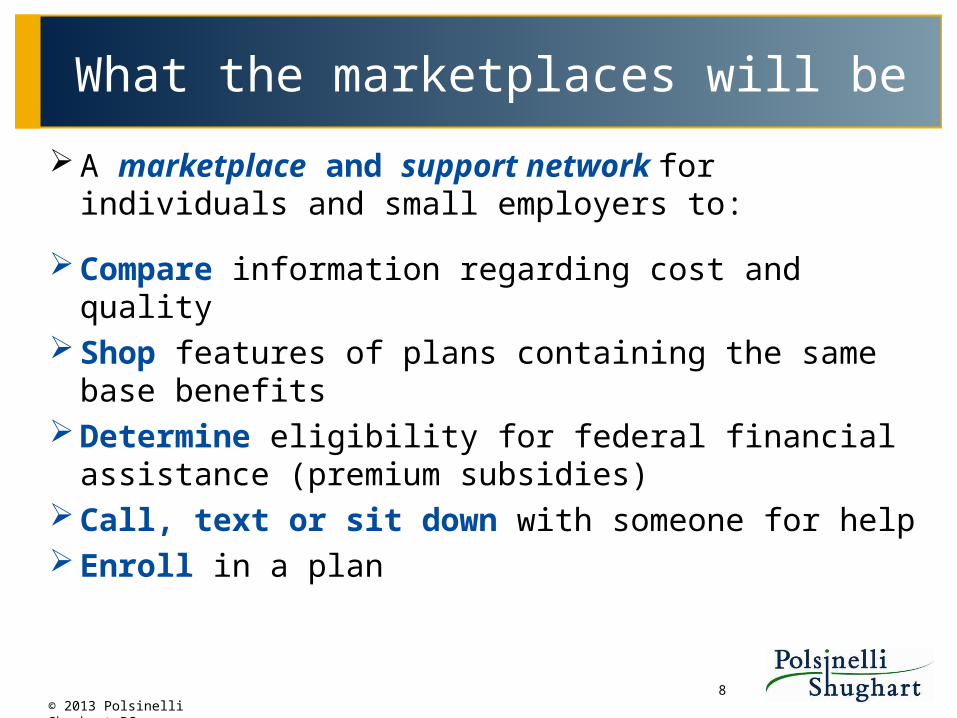

What the marketplaces will be

A marketplace and support network for individuals and small employers to:

Compare information regarding cost and quality Shop features of plans containing the same base

benefits Determine eligibility for federal financial

assistance (premium subsidies) Call, text or sit down with someone for help Enroll in a plan

© 2013 Polsinelli Shughart PC9

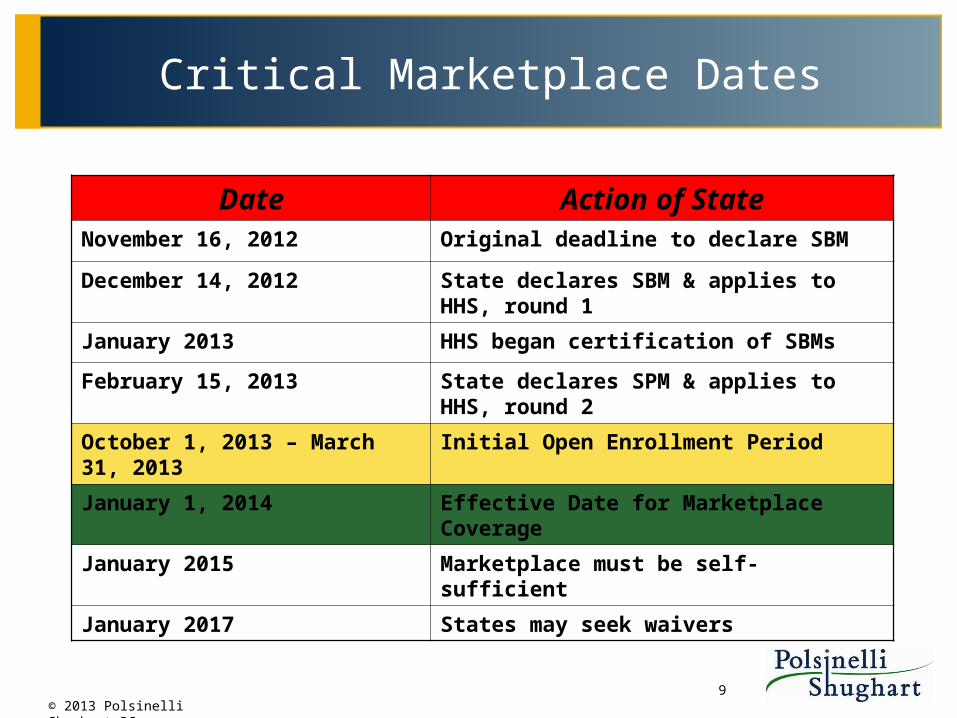

Critical Marketplace Dates

Date Action of StateNovember 16, 2012 Original deadline to declare SBM

December 14, 2012 State declares SBM & applies to HHS, round 1

January 2013 HHS began certification of SBMs

February 15, 2013 State declares SPM & applies to HHS, round 2

October 1, 2013 – March 31, 2013 Initial Open Enrollment Period

January 1, 2014 Effective Date for Marketplace Coverage

January 2015 Marketplace must be self-sufficient

January 2017 States may seek waivers

© 2013 Polsinelli Shughart PC10

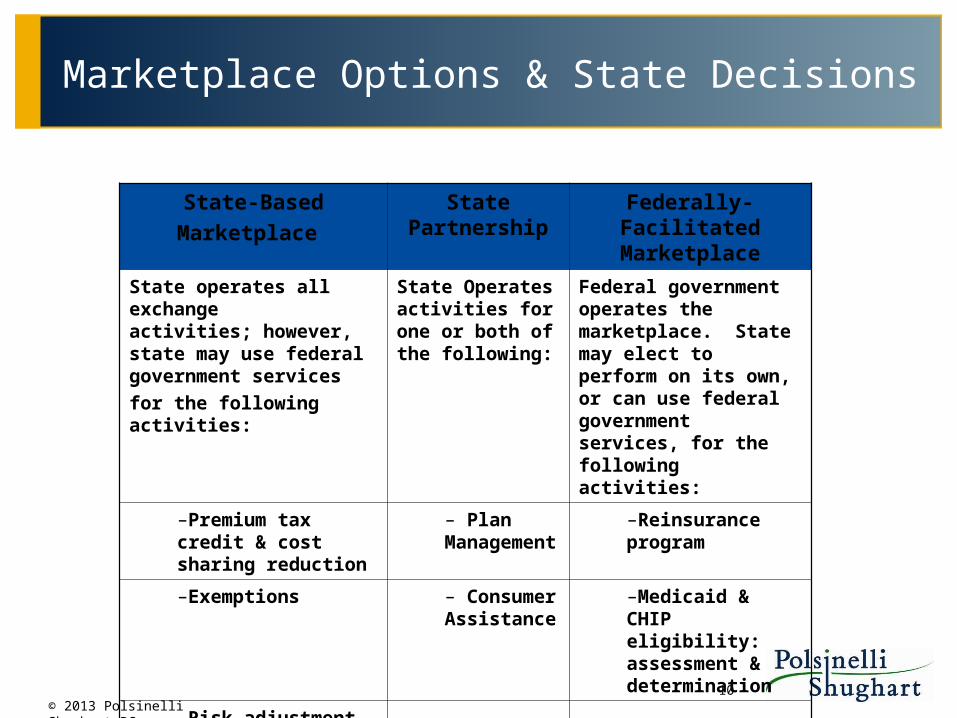

Marketplace Options & State Decisions

State-Based

Marketplace

State Partnership

Federally-Facilitated Marketplace

State operates all exchangeactivities; however, state may use federal government services

for the following activities:

State Operates activities for one or both of the following:

Federal government operates the marketplace. State may elect to perform on its own, or can use federal government services, for the following activities:

–Premium tax credit & cost sharing reduction

– Plan Management

–Reinsurance program

–Exemptions – Consumer Assistance

–Medicaid & CHIP eligibility: assessment & determination

–Risk adjustment program

–Reinsurance

© 2013 Polsinelli Shughart PC11

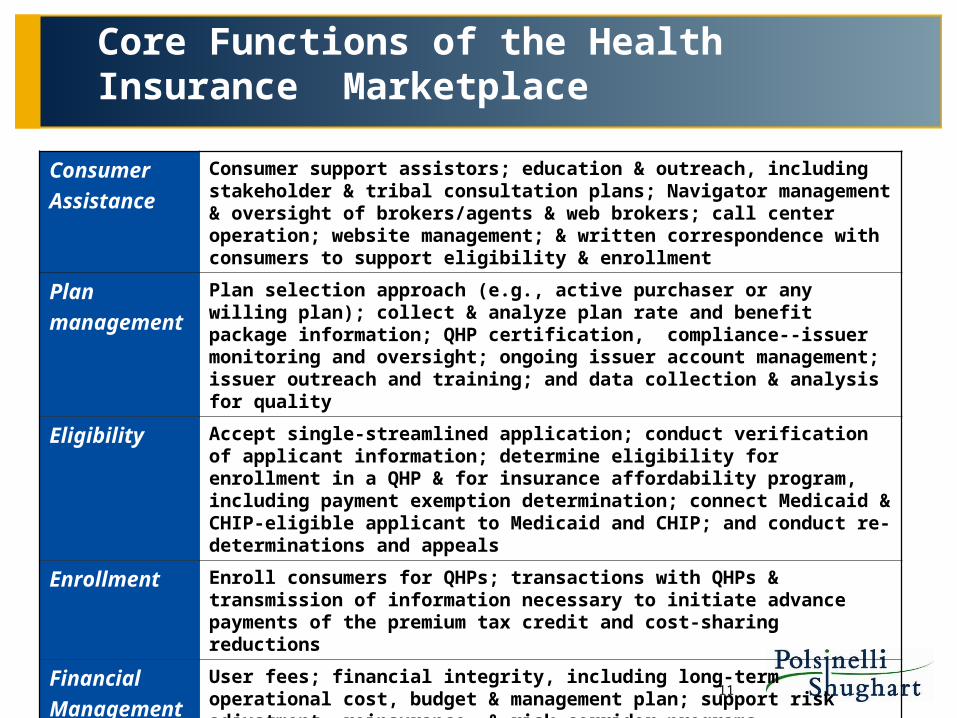

Core Functions of the Health Insurance Marketplace

Consumer

Assistance

Consumer support assistors; education & outreach, including stakeholder & tribal consultation plans; Navigator management & oversight of brokers/agents & web brokers; call center operation; website management; & written correspondence with consumers to support eligibility & enrollment

Plan

management

Plan selection approach (e.g., active purchaser or any willing plan); collect & analyze plan rate and benefit package information; QHP certification, compliance--issuer monitoring and oversight; ongoing issuer account management; issuer outreach and training; and data collection & analysis for quality

Eligibility Accept single-streamlined application; conduct verification of applicant information; determine eligibility for enrollment in a QHP & for insurance affordability program, including payment exemption determination; connect Medicaid & CHIP-eligible applicant to Medicaid and CHIP; and conduct re-determinations and appeals

Enrollment Enroll consumers for QHPs; transactions with QHPs & transmission of information necessary to initiate advance payments of the premium tax credit and cost-sharing reductions

Financial

Management

User fees; financial integrity, including long-term operational cost, budget & management plan; support risk adjustment, reinsurance, & risk corridor programs.

© 2013 Polsinelli Shughart PC12

CURRENT STATE DECISIONS

• 17 & DC State Based Marketplaces:– CA, CO, CT, DC, HI, ID, KY, MA, MD, MN, NM, NV, NY, OR, RI,

UT**, VT, WA

• 7 State Partnership Marketplaces (February 15, 2013):– AR, DE, IA, IL, MI, NH, WV

• 26 Federally Facilitated Marketplaces– AK, AL, AZ, FL, GA, IN, KS, LA, ME, MO, MS**, MT, ND,NE, NH,

NJ, OH, OK, PA, SC, SD, TN, TX, VA, WI, WY

• * UT wants to operate a small employer group marketplace only• **Secretary rejected MS application from DOI because Governor refused to

implement SBM letter

© 2013 Polsinelli Shughart PC13

Essential Health Benefits

• Health plans participating in the marketplaces (called “Qualified Health Plans”) must offer a certain package of benefits, called “Essential Health Benefits”

• Each state has chosen an existing insurer’s plan as a benchmark plan

• Information on benchmark plans for each state available at http://cciio.cms.gov/resources/data/ehb.html

• Member costs may vary for benefits (e.g., “bronze” vs. “platinum” coverage)

© 2013 Polsinelli Shughart PC14

QHP PLAN LEVELS

• Qualified Health Plan Actuarial Values – “Metal” Levels

• Bronze = 60% actuarial value• Silver = 70% actuarial value• Gold = 80% actuarial value• Platinum = 90% actuarial value

– Catastrophic Plan

© 2013 Polsinelli Shughart PC15

Access to premium subsidies

• Who qualifies?– Individual earning ~ $14,858 to $44,680/ year – Couple earning ~ $20,123 to $60,520/ year– Family of 4 earning ~ $30,657 to $92,200/ year– Small businesses with 25 or fewer employees earning

on average less than $50,000, sliding scale up to 50% of premium

• Managed by the IRS• Applied up-front for individuals as a premium

reduction

© 2013 Polsinelli Shughart PC16

10 Essential Health Benefits Categories

• Ambulatory patient services• Emergency services• Hospitalization• Maternity and newborn care• Mental health and substance use disorder services,

including behavioral health treatment• Prescription drugs• Rehabilitative and habilitative services and devices• Laboratory services• Preventive and wellness services and chronic

disease management• Pediatric services, including oral and vision care

© 2013 Polsinelli Shughart PC17

Potential Marketplace Effects

• Subsidies available to help with affordability – Low uptake could lessen the benefit of the subsidies

• Less cost shifting – result of broader base of insured population

• Premium increases may result, both in and outside of the exchanges– Underlying medical costs increase because more are covered– Essential benefits mandates may increase costs to insurers

• Insurer demands on marketplace participants: effects on providers– Payment rates may go down - transparency– Benefit designs (coverage OR payment levels) could disadvantage

providers

© 2013 Polsinelli Shughart PC18

Practical concerns for payers

• Are we going to play? Answer seems to be “yes”, at least for the Big 5 (Blues, CIGNA, UHC, Aetna, Humana)

• Increased dealings with the federal government – federal fraud and abuse laws

• Network Adequacy– Amending current contracts to specify addition of exchange

products– Contracting with more providers in the market– Careful network structuring and payment

• Benefit plan structure – EHBs! If only thinking about this now, very late to the game.

• Transparency – are payers ready to share pricing?

© 2013 Polsinelli Shughart PC19

Practical concerns for providers

• Network Participation– Amending current contracts to specify addition of

exchange products– Contracting with new QHPs in the market– Be proactive in approaching payers – avoid network de-

selection• Relationships with new payers – be open to new

QHPs• Benefit plan education – knowing new product

characteristics• Transparency – are providers ready to share

pricing?

© 2013 Polsinelli Shughart PC20

PART II:

TEXAS MARKETPLACE

© 2013 Polsinelli Shughart PC21

Texas Health Insurance Facts

• Texas has the largest proportion of citizens in the nation without health care at approximately 25%, or 6.2 million people– Roughly equal to the population of Massachusetts

• Insurance rates are largely unregulated– Texas does not require insurers in the individual market to sell to

anyone who applies for a policy, nor does it limit “rating” of customers, where insurance carriers charge more to older subscribers and women, who tend to have higher health care costs

• Texas legal immigrants tend to have a higher rate of uninsurance than non-immigrants – Of the 1.2 million foreign-born, naturalized U.S. citizens in Texas,

31% are uninsured, compared to 22% of U.S.-born Texans

© 2013 Polsinelli Shughart PC22

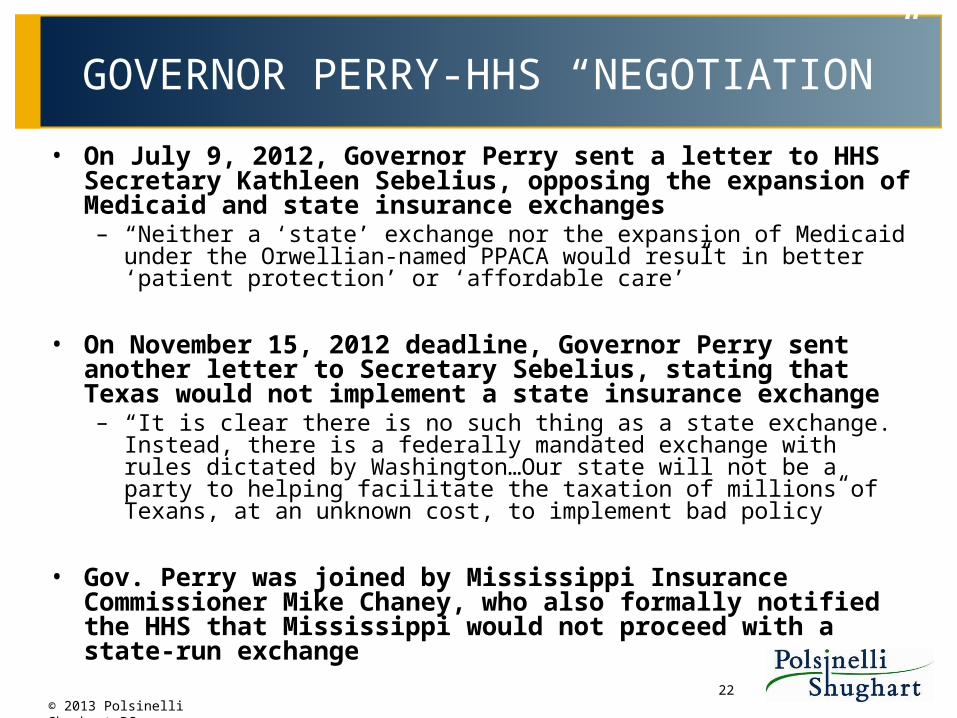

GOVERNOR PERRY-HHS “NEGOTIATION”

• On July 9, 2012, Governor Perry sent a letter to HHS Secretary Kathleen Sebelius, opposing the expansion of Medicaid and state insurance exchanges– “Neither a ‘state’ exchange nor the expansion of Medicaid under the

Orwellian-named PPACA would result in better ‘patient protection’ or ‘affordable care’”

• On November 15, 2012 deadline, Governor Perry sent another letter to Secretary Sebelius, stating that Texas would not implement a state insurance exchange– “It is clear there is no such thing as a state exchange. Instead, there is a

federally mandated exchange with rules dictated by Washington…Our state will not be a party to helping facilitate the taxation of millions of Texans, at an unknown cost, to implement bad policy”

• Gov. Perry was joined by Mississippi Insurance Commissioner Mike Chaney, who also formally notified the HHS that Mississippi would not proceed with a state-run exchange

© 2013 Polsinelli Shughart PC23

Behind the scenes practicality – Texas prepares

• Despite Gov. Perry’s opposition to a state marketplace, officials at Texas’ Department of Insurance (DOI) have been planning for an exchange

– “We’ve been going full speed ahead on implementation, doing the due diligence so that we can be on time with what the law says” - John Greeley, Public Information Officer at the Texas Department of Insurance

• The Texas Department of Insurance received a federal “Exchange Planning Grant” of $1 million in 2010

– However, Texas has since returned $900,000 of the grant to the federal government because of its decision not to run its own marketplace

• In February 2011, the Texas DOI and the Health and Human Services Commission held an “Exchange Planning Symposium”, seeking guidance from stakeholders regarding the exchange

– Should Texas establish an exchange or defer to the federal government?

© 2013 Polsinelli Shughart PC24

Federal Marketplace Deadlines – Texas

• States were required to notify the HHS whether they planned to establish a state-based exchange by February 15, 2013

• If HHS did not receive notification by that date the state was deemed to have deferred to a federally-facilitated exchange

• Governor Perry’s final decision was not to implement a state-based health insurance marketplace in Texas, instead deferring to the federal government to set up and run the marketplace– HHS will assume full responsibility for running a health insurance

exchange in Texas, beginning in 2014 (but many preparations taking place now)

– Note: HHS’ largest contractor (to which it has delegated FFE responsibility) is a UnitedHeathcare subsidiary, QSSI – data hub

© 2013 Polsinelli Shughart PC25

Federally-Facilitated Exchange (“FFE”)

• Since Texas declined to set up a state-based exchange or partnership, PPACA will require HHS to establish a “federally-facilitated exchange” (“FFE”)

• Can be implemented by HHS alone, or a state can enter into a “partnership” combining state and federal operations and functions (IF state applied)

• Partnerships are considered a subset of an FFE; HHS retains authority over partnerships– Texas did not submit a Declaration Letter or Exchange Blueprint

application before the February 2013 deadline, and thus does not have federal approval to operate its own marketplace OR partner with HHS

© 2013 Polsinelli Shughart PC26

Federally-Facilitated Exchanges, cont.

• The final rule establishing marketplaces does not include provisions specific to the operation of FFEs – more details to come?

• FFEs: are required to carry out many of the same functions as

state-based marketplaces must adhere to many of the standards outlined in the

Affordable Care Act and the final rule are required to offer the same tools to help consumers

access an exchange and assess their plan options through an exchange

© 2013 Polsinelli Shughart PC27

Policy Objectives of the Federally-Facilitated Exchanges

• HHS has published key core functions of an FFE, including:– Offering a positive consumer experience– Creating an attractive and viable market for issuers– Working quickly and effectively with States– Reducing administrative and operational burdens on all

marketplace participants– Developing safeguards and processes to protect and

oversee public dollars spent for advance payments of the premium tax credit and cost-sharing reductions

© 2013 Polsinelli Shughart PC28

Administration of the Federally-Facilitated Exchanges

• HHS is developing a comprehensive administrative infrastructure capable of addressing a wide range of state needs (“plan management”)

• Plan management will include: – QHP certification, recertification, and decertification– Eligibility determinations– Accreditation and quality reporting– Benefit and payment parameters– Technical and other assistance through “Account Managers”– General monitoring and oversight of the FFE

• Again, unprecedented degree of control to actual player in the market

© 2013 Polsinelli Shughart PC29

Big FFE Consequence: QHP Certification Process

• HHS will evaluate each potential QHP against all applicable certification standards, either by confirming the outcome of a state’s review (as in the case of licensure) or by performing the review itself.

• HHS intends to certify as a QHP any health plan that meets all certification standards (sort of an “Any Willing QHP” standard)– ***In future years, HHS will analyze the QHP certification process

and may identify improvements or changes to the process.

© 2013 Polsinelli Shughart PC30

QHP Certification Process – Issuer-Level Review

• HHS will look to the QHP Issuer Application to assess at least the following certification standards:– Licensure and good standing: confirm state licensure and

compliance with state solvency and other related requirements

– Network adequacy: in states meeting minimum federal standards, verify state review. Otherwise, review network adequacy data submitted in QHP Issuer Application

– Essential Community Providers (ECPs): collect information on inclusion of ECPs in provider networks and review for sufficiency

– Accreditation: confirm accreditation status, depending on certification year

– Program attestations: ensure submission of required attestations (e.g., attestation of compliance with marketing standards)

© 2013 Polsinelli Shughart PC31

QHP Certification Process – Plan-Level Review

• HHS will look to the rate and benefit data submissions to assess at least the following certification standards:

– Essential health benefits: confirm coverage of essential health benefits

– Actuarial value standards: confirm actuarial value levels of potential QHPs, including compliance with standards related to cost-sharing reductions, cost-sharing limits, and variations to cost-sharing structures

– Discriminatory benefit design: conduct plan-level analysis to determine where discrimination would most likely occur

– Meaningful difference: conduct review for meaningful difference across QHPs offered by the same issuer to ensure that a manageable number of distinct plan options are offered

– Service area: confirm that service area is at least one county or that smaller service area is necessary, non-discriminatory, and in the interest of consumers

– Rates (new and increases): review new rates and rate increase justifications for reasonableness, including confirmation of compliance with market rating reforms

© 2013 Polsinelli Shughart PC32

FFE: Potential Texas Complications

• Establishment and operation of FFEs may come with a number of complicated issues ahead of the October 2013 open enrollment deadline, including:– Consequences of Texas choosing not to expand

Medicaid– Overlap of state and federal regulations regarding

health plans– Adverse Selection– Availability of subsidies– Consumer assistance– Funding (marketplaces are to be self-sufficient by 2015)

© 2013 Polsinelli Shughart PC33

Small Business Health Options Program

• The Affordable Care Act also calls for states to establish a Small Business Health Options Program (“SHOP”)

• Intended to provide an array of affordable, high-quality health insurance plans for small businesses and their employees

• States can also choose to combine the individual and small business or SHOP exchanges

• SHOP exchanges will be competing with insurance offered in the outside market, so they’ll need to offer health plans that are high quality and cost-effective

© 2013 Polsinelli Shughart PC34

Small Business Health Options Programs

• A SHOP has responsibilities similar to an individual exchange:– Collect and verify information from employers and

employees (both considered applicants)• A qualified employee is an employee who receives an offer of

coverage from a qualified employer• A qualified employer is a small group employer that elects to

make all full-time employees eligible for one or more QHPs or offers coverage to each eligible employee through the SHOP serving the employee’s worksite

– Process applications– Determine eligibility– Facilitate enrollment

© 2013 Polsinelli Shughart PC35

Federally-Facilitated SHOP

• Similar to state SHOP exchanges; will provide a number of tools and resources to assist employers and

employees to evaluate coverage options and select a health plan allow employers to model various plan scenarios (i.e., changing

the employer contribution percentage) before making a final selection

collect an aggregated payment from each employer and distribute that payment to QHPs based on participating employees’ plan selections

• Other functions:– Health plan data collection– Offer coverage to multi-state employers– Administrative support– Consumer services– Facilitate agent and broker interface with the exchange

© 2013 Polsinelli Shughart PC36

Practical concerns for payers

• Are we going to play? Resounding “yes” from BCBSTX– “Be Covered Texas” – BCBS will “spend what it takes” to get 6

million lives onto the marketplace– Acting almost as the exchange operator in Texas

• Increased dealings with the federal government – federal fraud and abuse laws

• Network Adequacy– Amending current contracts to specify addition of exchange

products– Contracting with more providers in the market– Careful network structuring and payment

• Benefit plan structure – EHBs! If only thinking about this now, very late to the game.

• Transparency – are payers ready to share pricing?

© 2013 Polsinelli Shughart PC37

Practical concerns for providers

• Network Participation Amending current contracts to specify addition of exchange

products Contracting with new QHPs in the market Be proactive in approaching payers – avoid network de-selection Stay on good terms with BCBSTX

• Relationships with new payers – be open to new QHPs• Benefit plan education – knowing new product

characteristics• Transparency – are providers ready to share pricing?