poland - emis insight - poland ict... · poland's state-run post poczta polska provided nearly...

TRANSCRIPT

- 1 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Produced by:

Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

ICT Sector Poland

July 2015

PL_517_0001_Jul'2015_TO_NY EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 2 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Table of Contents

I. Sector Overview

1. Sector Highlights

2. Economic Importance

3. Sector Forecast

4. Main Sector Indicators

5. EU Comparison

6. Telecom Business Sentiment

7. Postal Services

8. Postal Services (cont’d)

9. Consumer Surveys

10.Bundled Services

11.Investments

12.Government Policy

II. Mobile Telephony

1. Segment Highlights

2. Key Segment Data

3. Market Shares

4. Customer Preferences

5. Roaming

6. Equipment: Brands

7. Equipment: Smartphones

III.Fixed-line Telephony

1. Segment Highlights

2. Basic Data

3. Traffic

4. Customers Preferences

5. VoIP

IV.Internet Access

1. Segment Highlights

2. EMEA Comparison

3. Key Segment Data

4. Internet Services Providers

5. Fixed-line Internet

6. Enterprises & Internet

7. Households & Internet

8. Wholesale Market

9. Internet Content

10.E-commerce

11.E-commerce (cont’d)

12.Segment Forecasts

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 3 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Table of Contents

V. Pay TV

1. Basic Data & Forecasts

2. TV Audience

3. Terrestrial Digital TV

4. Added & Multimedia Services Market

VI. Main Players

1. M&A Activity

2. Top Companies

3. Orange Polska

4. Orange Polska (cont'd)

5. Orange Polska (cont'd)

6. Cyfrowy Polsat

7. T-Mobile Polska

8. P4

9. Netia

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 4 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

I. Sector Overview

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 5 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Sector Highlights

The share of telecom industry in Poland's GDP has remained 2.5%, while the entire ICT account for nearly 8%. According to forecasts, cited by the

Economy Ministry, it should rise to 15% over the next 10 years.

In 2013, Poland’s ICT market ranked 11th and its telecom market - 9th in Europe in terms of value.

ICT Sector

Market Decline

Workforce

Segment Penetration

The telecom market has been declining in value for a second year in a row – by 2.6% in 2014 and by 3.7% in 2013. This trend is expected to be

sustained (e.g. market researcher PMR expects a 1.1% fall in 2015), although others forecast stabilisation (P4 sees a growth of 2%). The declines

are largely due to the results of the mobile telephony segment. Declines in traditional voice services have also been dragging down the fixed-line

segment, even though VoIP and WLL-based services are growing.

As a result of tighter operating conditions, telecoms tend to lay off sizeable parts of their workforce. E.g. group layoffs were implemented in T-

Mobile Polska (340 persons), Netia (350 persons) and Orange Polska has continued its voluntary resignations scheme (1,500 persons).

The highest market penetration is registered in the mobile segment (150.8% in Q1 2015 and growing), while in the fixed-line segment, the decline

that started in 2005 has continued, with market penetration of 14.2%. Meanwhile, the internet access penetration reached 75% in 2014.

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 6 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Comments

Economic Importance

The telecom market continues to play an important role, but its impact on the Polish economy has been decreasing. The country is stronger in consumer

electronics in terms of production facilities and market dynamics. All in all, the market is expected to rebound – possibly already this year.

Key Data

Central Statistical Office (GUS), Electronic Communications Office (UKE)

2009 2010 2011 2012 2013 2014

GDP (real value) PLN bn 1,344.5 1,416.6 1,553.6 1,615.9 1,662.7 1,728.7

GDP (real value) % change 1.6 3.7 4.8 1.8 1.7 3.4

Telecom market, PLN bn 42.0 42.5 43.0 43.5 40.2 39.2

Telecom market, % change -4.0 1.2 1.1 1.5 -3.7 -2.6

Telecom market, % of GDP 3.1 3.0 2.8 2.7 2.4 2.3

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 7 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Sector Forecasts

Forecasts: Nominal Values (mn)

Forecasts: Per 100 People (%)

Forecasts: Revenue* (USD bn)

Pyramid Research, Economist Intelligence Unit (EIU) (left); International Telecommunication Union; OECD; EIU (right)

5.48 5.41 5.05 4.71 4.40

57.47 59.04 60.44 61.74 62.85

2014 2015 2016 2017 2018

Telephone main lines Mobile subscriptions

14.2 14.1 13.2 12.3 11.5

149.3 153.7 157.6 161.4 164.3

2014 2015 2016 2017 2018

Telephone main lines Mobile subscriptions

1.36 1.24

0.99 0.87 0.88 0.89

5.79 5.89

4.95

4.69

5.13

5.64

2013 2014 2015 2016 2017 2018

Fixed-line Mobile

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 8 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

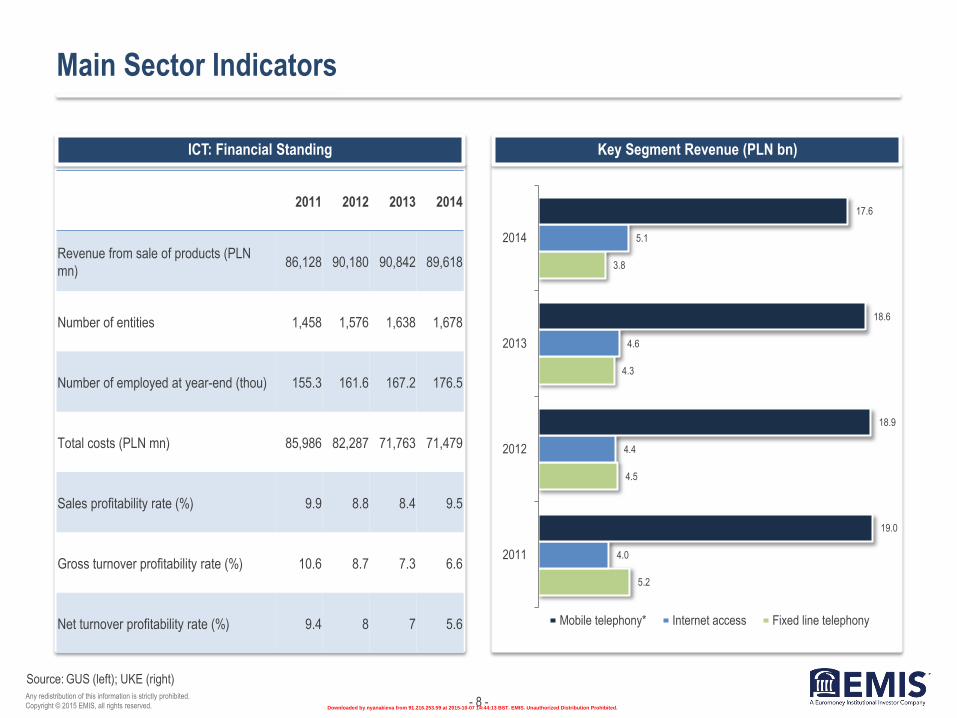

Main Sector Indicators

ICT: Financial Standing Key Segment Revenue (PLN bn)

GUS (left); UKE (right)

2011 2012 2013 2014

Revenue from sale of products (PLN

mn) 86,128 90,180 90,842 89,618

Number of entities 1,458 1,576 1,638 1,678

Number of employed at year-end (thou) 155.3 161.6 167.2 176.5

Total costs (PLN mn) 85,986 82,287 71,763 71,479

Sales profitability rate (%) 9.9 8.8 8.4 9.5

Gross turnover profitability rate (%) 10.6 8.7 7.3 6.6

Net turnover profitability rate (%) 9.4 8 7 5.6

5.2

4.5

4.3

3.8

4.0

4.4

4.6

5.1

19.0

18.9

18.6

17.6

2011

2012

2013

2014

Mobile telephony* Internet access Fixed line telephony

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 9 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

EU Comparison

Syrvey of Households in 2014 (%)

Percentage of Households with Bundled Telecom Services (%)

European Commission

30

68

91

15

44 44

91 92 91 98

92 87

57 65

76 65

55 54

Poland EU avg Germany Czech Rep. Hungary Romania

Households with fixed telephone access Individual mobile telephone access Households with internet access

21

46

61

23

48 47

Poland EU avg Germany Czech Rep. Hungary Romania

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 10 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Comments

Telecom Business Sentiment

Executives from enterprises operating in the area of information and communications have been positive on the business climate since the beginning of

2014.

According to the most recent round of surveys from June 2015, executives assessed current demand, sales and financial situation to be better than in the

previous three months. They did not report any major delays in payments for services. Furthermore, they expect prices to continue to fall in the coming

months (Poland has been experiencing CPI deflation since the middle of 2014). Employment growth in the sector is anticipated to retain its momentum.

Business Climate in ICT Sector

GUS

11 12

16

19 18

21

8 6

5

0

5

10

15

20

25

Jan2014

Feb2014

Mar2014

Apr 2014 May2014

Jun2014

Jul 2014 Aug2014

Sep2014

Oct 2014 Nov2014

Dec2014

Jan2015

Feb2015

Mar2015

Apr 2015 May2015

Jun2015

Indicator Improvement Worsening

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 11 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Postal Services

Postal Services Revenue (Polish Post plus alternative operators (PLN bn)

UKE

Volume of Packages (in domestic and cross-border services, mn items)

Comments

Poland's state-run post Poczta Polska provided nearly 1.8bn postal services (universal services, courier and other services), which translated into revenue

of over PLN 4.6bn (EUR 1.1bn) last year. Alternative operators provided nearly 4.2bn services, generating over PLN 2.9bn in revenue.

5.6 5.8 5.5 5.8 5.8 5.9 5.9

7.5 7.6

5.4 5.6

5.3 5.6

5.6 5.8

5.8

7.4 7.4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Incl. mass mailing

Excl. mass mailing

5,091 5,193 5,411 5,360 5,597 5,750 5,151 4,877 5,973

1,802 1,994 2,003 2,011 2,019 2,019 2,002 2,086

3,991

2006 2007 2008 2009 2010 2011 2012 2013 2014

Incl. mass mailing

Excl. mass mailing

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 12 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Postal Services (cont’d)

Comments

Top Alternative Postal Services Operators both in Volume ad Value Terms

Number of Alternative Operators

Number of Post Offices

UKE

Apart from the Polish Post, who is the designated operator (i.e.

the one responsible for delivering some basic services to the

entire population), there were 294 entities in the post operators

registry, maintained by the Electronic Communications Office

(UKE). However, only 165 alternative operators were actually in

operation last year. 157

164

182

209

244

247

267

275

295

91

100

106

125

152

154

153

163

166

2006

2007

2008

2009

2010

2011

2012

2013

2014

Operating Registered

InPost

InPost Paczkomaty

PGP

Speedmail

ABC Direct Contact

8,553 8,692

8,489 8,378 8,365 8,383

8,459

7,884

7,540

2006 2007 2008 2009 2010 2011 2012 2013 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 13 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Consumer Surveys

Retail: What Telecom Services Do You Use in 2014 (%*) Corporate: What Telecom Services Do You Use in 2014? (%*)

PBS, Indicator, UKE

88

58

72

27

23

mobile phone

internet (in total)

fixed-line internet

mobile internet

fixed-line phone

* - n = 1600 * - n = 423

89

80

52

mobile phone internet (in total) fixed-line phone

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 14 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Bundled Services

Comments

Retail: Telecom Services Bundles in 2014 (%, n = 1600)

Most Popular Bundles in 2014 (%)

Corporate: Telecom Services Bundles (%, n = 418)

UKE (upper); PBS, Indicator, UKE (lower)

More than 4.2 million customers used bundled services in 2014. These

services generated nearly PLN 2bn (EUR 480mn) in revenues.

Customers used 42 types of packages of bundles services.

30.0

18.8

15.2

11.3

10.9

13.7

Fixed-line internet + TV

Fixed-line telephony + fixed-lineinternet + TV

Mobile telephony + mobile internet

Fixed-line internet + TV + VoIPtelephony

Fixed-line telephony + fixed-lineinternet

Others

Mobile phone and internet

47%

Only mobile phone 27%

Fixed-line and mobile

phones, internet 11%

Only fixed-line phone 9%

Fixed-line and mobile phones

4%

Fixed-line phone and internet 0%

No phone and internet 2%

Mobile phone and internet

34%

Only mobile phone 13%

Fixed-line and mobile

phones, internet 35%

Fixed-line and mobile phones

7%

Fixed-line phone and

internet 10%

Only fixed-line phone 1%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 15 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Investments

Investment Breakdown (PLN mn) Market Share of Investments by Technology (%)

BuddeComm based on ITU and regulator data

980

517

845

910

83

99

330

753

10

53

448

2011

2012

2013

2014*

State aid Fibre networks Access networks

* - BuddeCom Communication's estimates for 2014

Sector 2011 2012 2013 2014*

2G/3G 29.4 53.4 55.1 -

LTE - - 14.3 21.6

DSL 62.8 32.9 4.2 4.3

Cable 3.7 7.5 13.0 16.8

FWA - 2.4 - -

Ethernet - 1.6 - 2.2

FttX 1.6 0.7 10.4 41.3

WiMAX 0.2 0.6 - 11.9

Other 0.2 0.9 3.0 1.3

* - BuddeCom Communication's estimates for 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 16 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Government Policy

LTE Auction

The state is currently auctioning off frequencies in the 800MHz and 2600MHz bands suitable for 4G Long Term Evolution (LTE)

technology, but the bidding has dragged on for several months.

The watchdog originally expected the auction to bring at least PLN 1.8bn to the state coffers and market estimates were at up

to PLN 3bn , while on July 20, 2015, the value of the highest bids for all these frequencies totalled PLN 5.19bn.

Even though operators have already broadly covered Poland with LTE services, they expect the new frequencies to provide a

boost for this segment's rapid growth.

MTR Policy

In the past few years, the Polish telecoms regulator UKE implemented new regulations for call termination in mobile networks to introduce symmetric wholesale rates (MTR) based on the operator costs designed to significantly reduce their level.

Over the last six years, MTR cuts (now accomplished) and price wars triggered by no-limit offers have led to a combined revenue decline of the three biggest mobile telephony networks to the tune of 7%. Hence, analysts expect mobile firms' revenue to stabilise already this year, while P4 (operator of the Play network, which was not subject to MTR cuts and thus was able to increase its revenue in the recent years) expects them to post revenue growth of 2%. However, Orange Polska expects the market to post yet another decline.

Universal

Services

The UKE has selected the Poczta Polska to be the provider of universal postal services until 2025. Under the law, the state-owned enterprise was selected as the so-called designated operator (i.e. the one providing universal services) in 2013-2015. During the 2015 tender, no competitor filed a viable offer (although PGP did submit an offer, admitting itself it failed to meet all the requirements of the tender).

The obligation to provide universal postal services involves the offer of posting letters and packages, domestic and foreign, but - as UKE's representatives point out - it also includes the obligation to provide postal services to persons with disabilities or those living in areas where the profitability of postal services is not guaranteed.

Eighth

TV Multiplex

Emitel has recently won the tender for operator of the eighth multiplex (MUX-8) intended for the terrestrial digital broadcasting

or re-broadcasting of TV programmes, for a period of 15 years from the date of delivering the decision on frequency

reservation. MUX-8 will include 3 slots for the public TVP (3 SD channels or 1 HD and 1 SD channel) and four slots for

channels that will be provided by winners of new respective licences. Currently, terrestrial digital TV is available via three

multiplexes: MUX-1 and MUX-2 broadcast thematic channels (8 channels each), while MUX-3 is focused on the public TVP's

channels (also 8 channels, including TVP1 HD, TVP2 HD and 4 thematic channels).

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 17 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

II. Mobile Telephony

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 18 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Segment Highlights

The market declined for a second consecutive year in 2014, but is expected to stabilise in value in 2015, as the MTR cuts that have undermined

revenue in the past few years are over. Mobile operator P4 expects the market to grow by 2% this year, while the Economist Intelligence Unit has

forecast CAGR of around 2.2% in the 2015-2019 period.

Market Value

The mobile telephony penetration in Poland is above the average compiled by the Telecom Market Matrix database. In 2014, Poland ranked 8th in

the European Union with a penetration rate of 139.2%, 7.2pps above the EU average. However, according to the Polish statistics office, the

penetration rate exceeded 150%.

Currently, 27 million Poles use mobile telephony services and this number is projected to grow by another 1mn by 2018. The number of mobile

telephony customers increased by 1.4% y/y last year. At the end of 2014, the number of registered SIM cards was 57.8mn.

The number of customers who switched their operators in 2014 stood at 1.81 million, up by 16.8% from the previous year.

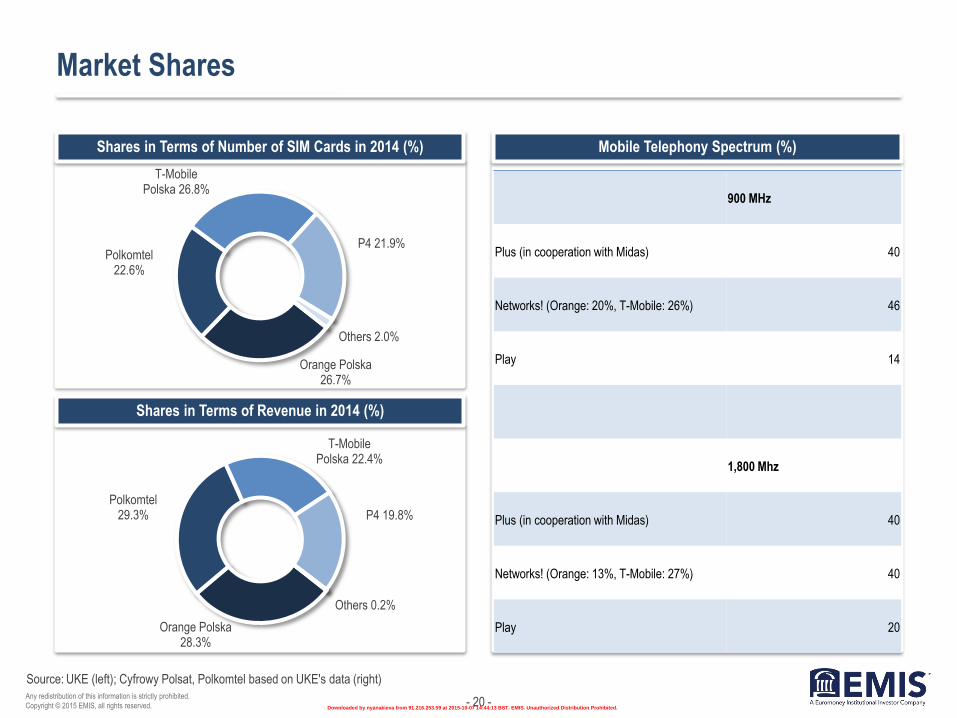

T-Mobile Polska, Deutsche Telekom's Polish business, remained the market leader with a 26.8% share, down by 0.2pps y/y, while the biggest growth was noted by P4 (Play network) - by 1.5 million users, or 14.1%. Operators outside of top 4 (MNO and MVNO) registered a combined fall of revenues by 22.1% y/y.

In terms of revenue, Polkomtel, a unit of media group Cyfrowy Polsat, became the leader, though its share inched down by 0.2pps to 29.3%.

At the end of 2014, as many as 69% of Polish internet users were equipped with smartphones, according to data by IAB Polska, which means that their penetration was equal to that of notebooks. In addition, 27% of them used tablets. The penetration indicators are expected to stabilise in the next two years. According to research firm TNS Polska, the penetration rates in May 2015 were 58% and 21%, respectively. The share of smartphone users surged by a total of 32pps over the last four years.

Penetration

Customer Base

Market Players

Smartphones

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 19 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Key Segment Data

Nominal Number of Users and Mobile Market Penetration in Poland

Share of Pre-paid and Post-paid Customers in Total Number of Subscribers (%)

UKE

41.4 43.9 44.8 47.0 50.1 53.9 57.0 57.8

108.6 115.2 117.4

123.2 131.6

140.0 148.0 150.2

2007 2008 2009 2010 2011 2012 2013 2014

SIM cards (mn)

Penetration (%)

51.2 52.6

54.2 54.2 54.0

48.8 47.3

45.8 45.8 46.0

2010 2011 2012 2013 2014

Pre-paid

Post-paid

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 20 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Market Shares

Shares in Terms of Number of SIM Cards in 2014 (%)

Shares in Terms of Revenue in 2014 (%)

Mobile Telephony Spectrum (%)

UKE (left); Cyfrowy Polsat, Polkomtel based on UKE's data (right)

Orange Polska 26.7%

Polkomtel 22.6%

T-Mobile Polska 26.8%

P4 21.9%

Others 2.0%

Orange Polska 28.3%

Polkomtel 29.3%

T-Mobile Polska 22.4%

P4 19.8%

Others 0.2%

900 MHz

Plus (in cooperation with Midas) 40

Networks! (Orange: 20%, T-Mobile: 26%) 46

Play 14

1,800 Mhz

Plus (in cooperation with Midas) 40

Networks! (Orange: 13%, T-Mobile: 27%) 40

Play 20

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 21 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

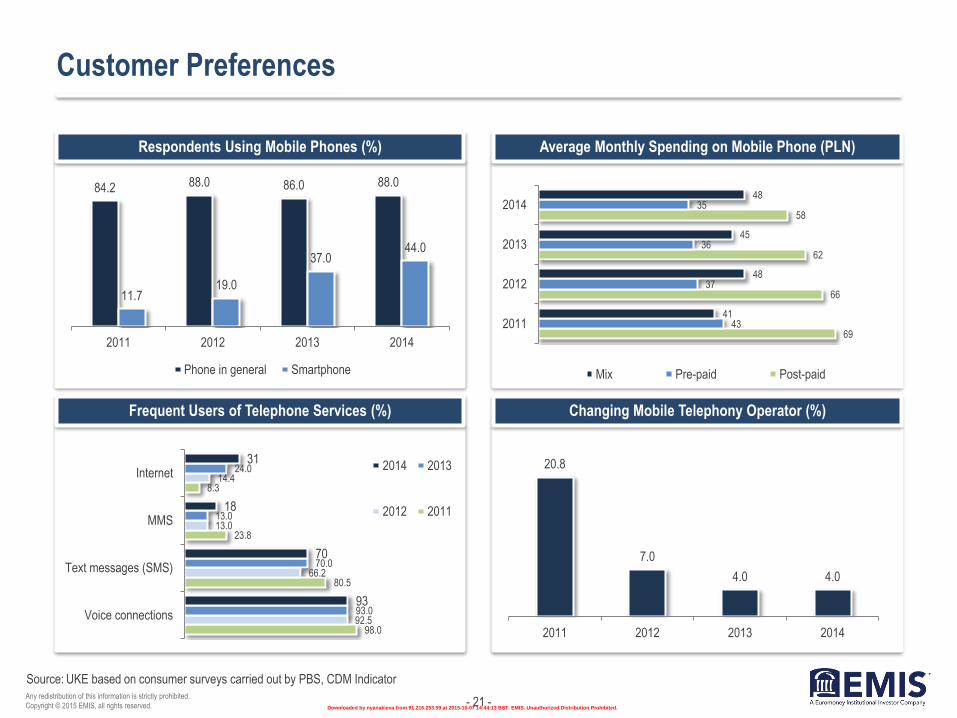

Customer Preferences

Respondents Using Mobile Phones (%)

Frequent Users of Telephone Services (%)

Average Monthly Spending on Mobile Phone (PLN)

Changing Mobile Telephony Operator (%)

UKE based on consumer surveys carried out by PBS, CDM Indicator

84.2 88.0 86.0 88.0

11.7 19.0

37.0 44.0

2011 2012 2013 2014

Phone in general Smartphone

69

66

62

58

43

37

36

35

41

48

45

48

2011

2012

2013

2014

Mix Pre-paid Post-paid

98.0

80.5

23.8

8.3

92.5

66.2

13.0

14.4

93.0

70.0

13.0

24.0

93

70

18

31

Voice connections

Text messages (SMS)

MMS

Internet2014 2013

2012 2011

20.8

7.0

4.0 4.0

2011 2012 2013 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 22 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Roaming

Roaming Volumes Maximum Rates - Retail Level (PLN, incl. VAT)

UKE

1.70

1.48

1.48

1.22

1.22

0.97

0.54

0.41

0.41

0.36

0.36

0.25

0.54

0.46

0.46

0.41

0.41

0.31

3.57

2.3

2.3

1.02

H1/2012

H2/2012

H1/2013

H2/2013

H1/2014

H2/2014

Data transmission (MB) SMS sent

Incoming calls (min) Outgoing calls (min)

357

543 544

791

601

406

457

502

539 570

6 9 16 39

139

2010 2011 2012 2013 2014

Voice connections (mn minutes) Text messages (SMS) (mn)

Data transmission (MB)

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 23 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

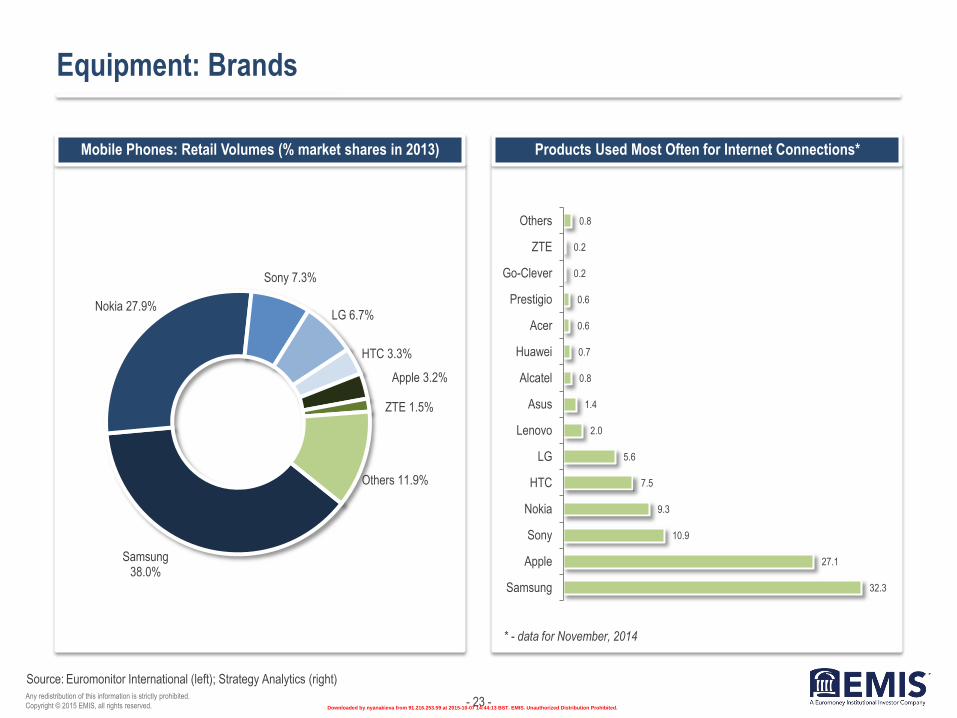

Equipment: Brands

Mobile Phones: Retail Volumes (% market shares in 2013) Products Used Most Often for Internet Connections*

Euromonitor International (left); Strategy Analytics (right)

Samsung 38.0%

Nokia 27.9%

Sony 7.3%

LG 6.7%

HTC 3.3%

Apple 3.2%

ZTE 1.5%

Others 11.9%

32.3

27.1

10.9

9.3

7.5

5.6

2.0

1.4

0.8

0.7

0.6

0.6

0.2

0.2

0.8

Samsung

Apple

Sony

Nokia

HTC

LG

Lenovo

Asus

Alcatel

Huawei

Acer

Prestigio

Go-Clever

ZTE

Others

* - data for November, 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 24 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Equipment: Smartphones

Growth Dynamics of Mobile Devices* (%)

Smartphones Penetration in Poland (%)

Smartphone Operating Systems in 2014 (%)

Main Players

IAB Polska Mobile (upper left); TNS Polska (upper left and right)

Around 10% of the internet traffic in Poland is estimated to be generated

by mobile devices. A total of 60% of the local smartphone and tablet

users take to devices produced by Samsung and Apple.

53

15 22 5

167

125

66

15

2013 2014 2015 2016

Smartphones Tablets

* - Q1 of each year, among internet users aged 15 and above

25

31

44

55

61 64

9

19

40

51

57 60

Jan 2012 Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jun 2016

Declarations Parameters

Android 65%

Windows Phone 16%

iOS 4%

Others 3%

Don't know 12%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 25 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

III. Fixed-line Telephony

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 26 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Segment Highlights

The segment's value continued to decline in 2014 when it fell by 12.7% to PLN 3.8bn (EUR 0.92bn). The number of fixed-line telephony users was

6.2mn (down by 8.4% y/y) and has remained on a downward trend since 2005.

Market Value

According to surveys, the main reason for owning a fixed-line telephone is being accustomed to having one. At the same time, fixed-to-mobile

substitution is increasingly accompanied by fixed-to-VoIP substitution.

The average monthly revenue per user in the segment declined by nearly 5% y/y to PLN 50.3 (EUR 12.19) in 2014 and was down by around PLN 7

since 2010.

The length of voice connections in the fixed-line segment amounted to 10.4bn minutes, down by over 1bn compared to 2013. The length of calls

per user was 145 minutes per year.

The market leader was Orange Polska (a unit of France's Orange), with 56.1% of the segment's users and 54.1% of its revenue, followed by Netia,

with 8.0% and 20.5%, respectively, and UPC with 8.7%. Other major players are UPC and Telefonia Dialog.

Substitution

ARPU

Traffic

Key Players

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 27 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Basic Data

Market Shares in Terms of Number of Subscribers (%)

Key Market Data

Market Shares in Terms of Revenue (%)

UKE

7.2 6.0

5.2 4.5 4.3 3.8

9.2 8.7 7.9 7.4 6.8 6.2

17.6

16.1 14.7

13.0 11.5

10.4

2009 2010 2011 2012 2013 2014

Revenue (PLN bn) Users (mn) Minutes (bn)

62.6

10.7

3.8

5.5

3.4

55.7

11.2

6.3

5.3

3.6

56.9

10.8

7.7

4.7

3.5

56.1

8

8.7

2.2

3.4

Orange

Netia

UPC

Telefonia Dialog

T-Mobile2014

2013

2012

2011

60.6

15.7

5.5

2.5

1.7

57.4

14.6

5.8

4.4

2.4

52.1

22.3

4.8

4.8

2.3

54.1

20.5

4.1

4.7

1.9

Orange

Netia

Telefonia Dialog

UPC

Telekomunikacja Novum 2014

2013

2012

2011

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 28 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Traffic

ARPU, Traffic

Average Monthly Use (minutes)

Revenue Structure by Service Elements (%)

UKE

65.2 57.4 55.4 51.1 52.7 50.3

160 154 154 147 141 145

2009 2010 2011 2012 2013 2014ARPU (PLN) Min per user/ month

108

8

28

Domestic calls International calls Fixed-to-mobile calls

50.1

51.2

62.6

62.9

62.3

37.8

34.7

33.3

26.4

25.5

12.1

14.0

4.1

10.7

12.1

2010

2011

2012

2013

2014

Others Calls Subscription fees

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 29 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Customers Preferences

Comments

Uninterested in Fixed-to-Mobile Substitution (%)

Owners & Spenders

Interested in Fixed-to-VoIP Substitution (%)

UKE

The owners of fixed-line telephones were mostly aged 60 and above

(51% from all age groups) as well as old-age and disability pensioners

(52% of all professional groups). Merely 7% of the people aged 15-24

used fixed-line telephony services and 8% in the 25-34 years bracket. 39

31

31

23

62

49

51

51

2011

2012

2013

2014

Average monthly spending (PLN)

Share of respondents owning fixed-line phone (%)

68.6

25.0

39.0 45.0

2011 2012 2013 2014

7.1

6.0

8.0

9.0

2011 2012 2013 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 30 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

VoIP

Traffic Volumes (bn min)

Number of Subscribers (mn)

Market Shares - Operators Offering VoIP in Own Network (%)

UKE

0.47 0.48

0.70

0.84

0.93

0.59

0.37 0.42

0.34

0.42

2010 2011 2012 2013 2014

In own operator's network

In other operator's network

0.75 0.92

1.05

1.47

1.89

0.26 0.40

0.52 0.59 0.63

2010 2011 2012 2013 2014

In own operator's network In other operator's network

Orange Polska 57.1%

Multimedia Polska 16.4%

Netia 12.9%

Telefonia Dialog 1.7%

Others 11.9%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 31 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

IV. Internet Access

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 32 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Segment Highlights

Broadband internet access continues to be more popular than mobile access services, but market penetration in both types of access exceeds

70%. In the case of the mobile segment, last year saw a rise of unlimited offers.

Broadband vs. Mobile

Among internet service providers, Orange Polska remained the leader with a market share of 29.1% (down by 3pps y/y), followed by Polkomtel

(Plus network) with an 8.8% share and T-Mobile Polska with an 8.3% share.

In December 2014, a total of 21.5mn people used the internet in Poland, up by 17.5% from December 2010, according to data from a Megapanel

PBI/Gemius survey. Data from pollster CBOS shows that 96% of local people aged 18-24 and 94% of those aged 25-34 used the internet, while in

the 55-64 years bracket the share was 42%; it was 20% in the case of users aged 65 and above.

According to Eurostat, 75% of the Polish households had internet access in 2014, which is a rise of 16pps from 2009. The statistics office reports

that nearly 75% of households in 2014 had at least one computer and 74.8% of them - internet access (up by 2pps y/y).

In 2014, a total of 94.4% of local enterprises used computers including almost all large enterprises. In 2014, 65% of the Polish enterprises had a

website, 75% of them placed orders via computer networks and 10% of them received orders via the internet.

Key Players

Internet Users

Households

Enterprises

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 33 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

EMEA Comparison

Internet Access Penetration at EU Households (%) EMEA Average Peak Connection Speeds in Q1 2015 (Mbps)

Eurostat (left); akamai (right)

54

61

67

65

73

78

59 63 67

70 72

75

55 60

65

69 71

75

66

70 73

76

79 81

2009 2010 2011 2012 2013 2014

Cech Rep. Poland Hungary EU average

17.4

13.6

12.8

10.2

9.8

9.4

9.4

9.4

3.4

Ireland

Czech Rep.

Romania

Germany

Poland

Russia

Slovakia

Hungary

South Africa

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 34 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Key Segment Data

Actual Number of Internet Users (mn)

Internet Speed

Average Monthly Cost of Internet Access (PLN)

Frequency of Using Internet (%)

UKE (polls data based on consumer surveys carried out by PBS, CDM Indicator)

2.8 3.3 3.6

4.3

5.8 6.2 6.5

7.1 7.6 7.2

2010 2011 2012 2013 2014

Mobile Fixed-line

57

54

55

53

56

55

52

53

2011 2012 2013 2014

Fixed-line Mobile

2011 2012 2013 2014

up to 1.99 Mb/s 26.0 7.0 5.0 1.0

2-9.99 Mb/s 44.8 29.0 17.0 12.5

10-29.99 Mb/s 9.9 17.0 24.0 27.4

30 Mb/s and above 4.2 8.0 18.0 19.3

40.6

41.0

44.0

43.0

15.2

14.0

11.0

12.0

3.8

6.0

3.0

3.0

0.5

0

1

0

2011

2012

2013

2014

Several times a year Several times a monthSeveral times a week Everyday

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 35 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Internet Services Providers

Internet Services Providers in Total - Market Shares (%)

UKE

31.8

8.3

9.5

8.5

8.4

3.9

4.0

4.1

3.8

2.2

1.2

1.0

1.0

0.9

11.5

29.1

8.8

8.3

7.6

7.0

4.9

4.4

3.9

3.4

3.0

1.0

0.9

0.8

0.8

16.1

Orange Polska

Polkomtel

T-Mobile Polska

UPC

P4

Aero2

Netia

Vectra

Multimedia Polska

Cyfrowy Polsat

Inea

Telefonia Dialog

Internetia

Toya

Others

2014 2013

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 36 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Fixed-line Internet

Retail Market Penetration (%) Fixed-line Providers' Revenue Breakdown (%)

UKE

21.3 23.0 24.5 25.6 24.3 24.9 27.3

29.4 30.2 31.6

61.0

65.9 70.0

73.3 69.3 70.9

77.7

83.6 86.1

90.0

Per 100 inhabitants Of all households

38.0

18.2

23.1

9.3

6.4

5.0

32.3

23.3

22.9

9.7

6.9

4.9

30.1

26.8

22.4

8.8

6.4

5.4

27.1

31.8

20.7

7.5

7.5

5.5

xDSL

2G/3G modem

CATV modem

LAN-Ethernet

WiFi

other2014 2013 2012 2011

other - incl. fixed wireless access, leased

lines, satellite links, CDMA and WiMax

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 37 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Enterprises & Internet

Share of Firms Where Employees Use Computers* (%)

Share of Firms with Computers with Internet Access* (%)

Share of Firms with Internet by Types of Activity (%)

GUS

* - at least once a week in 2010-2013; without specifying frequency in 2014

33.3

35.2 36.1 37.2 36.3 33.6

34.3 35.7 36.4

34.6 30.8

34.4 34.1

36.0 36.1

34.8

36.2 37.6 38.6 37.7

2010 2011 2012 2013 2014

Total Small Medium Large

DSL Computer with 3G

modem 3G handset

Manufacturing 85.6 53.9 41.5

Electricity, gas, steam and air

conditioning supply 95.7 67.9 62.4

Water supply; sewerage, waste

management and remediation

activities

92 54.4 39.8

Construction 79.8 56.4 39.5

Trade; repair of motor vehicles 84 55.4 41.7

Transportation and storage 83.7 54.8 37

Accommodation and catering 78.3 50.1 32.6

Information and communication 95.6 79.2 74.5

Financial and insurance activities 97.7 60.4 50.8

Real estate activities 91.3 44.1 30.8

Professional, scientific and technical

activities 91.4 64.5 50.8

Administrative and support service

activities 84.8 62.4 43.6

Repair of computer and

communication equipment 98.7 75.3 70.1

37.1 38.3 39.0 39.4 37.6 34.6

39.1 39.3 40.4 39.8

45.9 46.8

47.9 48.7 46.7

40.1

42.3 42.8

43.8

42.1

2010 2011 2012 2013 2014

Small Medium Large Total

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 38 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Households & Internet

Type of Internet Connections in Households in 2014 (%) Households with Broadband Access to Internet at Home (%)

GUS

Mobile narrowband connection

4.4%

Connection over normal

telephone line or digital

connection 2.8%

Mobile wideband connection

24.6%

Fixed connection

with wideband access 59.7%

56.8

61.1

67.0

68.8

71.1

75.2

81.7

87.8

89.9

89.7

47.6

51.0

56.6

58.1

61.8

2010

2011

2012

2013

2014

Households without children Households with children Total

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 39 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Wholesale Market

Alternative Operators – Market Share by BSA Lines, 2014 (%)

Alternative Operators – Market Shares by LLU Lines in 2014

Structure of Market - Type of Infrastructure Used (%)

UKE

67.3

62.9 63.9

71.2

10.5 14.7 14.4

10.3

17.8 16.5

15.8 12.4

4.4 5.9 5.9 6.0

2010 2011 2012 2013

Orange Polska AO's own infrastructure BSA LLU

Netia 84.7%

T-Mobile 11.0%

Telestrada 1.9%

Telefonia Dialog 1.4%

Others 0.9%

98.9

1.1

Netia

Others

%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 40 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Comments

Source:

Internet Content

The value of the Polish online advertisement market was estimated at USD 2.7bn in 2014 and according to global consultancy firm PwC should exceed

USD 4.0bn in 2018.

According to PwC, the share of online ads in the entire market should increase to around 36% in 2018, becoming its biggest segment.

Research firm IAB Polska forecasts 2014-2015 CAGR of the online ads segment at 5.3-7.8% (and 7.7-10.0% in its dynamic scenario) to PLN 2.56bn in

2014 an PLN 2.76bn in 2015.

Online Ad Spending (PLN bn) Internet Companies in Poland: Number of Users (end-2014)

0.743

1.216 1.373

1.582

2.003

2.206

2.432 2.609

2007 2008 2009 2010 2011 2012 2013 2014

20.2

16.8 16.4 15.6 15.3 15.3 12.6

11.1

mn users

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 41 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Comments

Source:

E-commerce

The value of the e-commerce market grew to EUR 7.4bn in 2014 from EUR 5.2bn in 2012, according to data by the Boston Consulting Group. BCG

expects this growth to continue and forecasts the market's value at EUR 22.6bn in 2020.

Poles spending online is smaller than the EU average: at EUR 535 and EUR 1,376, respectively, in 2013.

Persons Buying Online in Last 12 months (% of population) Devices Used for E-Shopping in 2014 (%)

GUS (left); mShopper Mobile Institute (right)

28.9

29.7

30.3

31.6

34.2

31.7

32.6

32.4

34.0

35.9

26.4

27.1

28.5

29.5

32.7

2010

2011

2012

2013

2014

Women Men Total

Computer 65%

Smartphone 17%

Tablet 12%

Other equipment 6%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 42 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

E-commerce (cont’d)

What Was Purchased Online (% of individuals ordering) Number of E-Commerce Services Users by Type in 2014 (mn)

GUS (left); Megapanel PBI/ Gemius (right)

2010 2011 2012 2013 2014

Clothes, sports goods 48.7 52.3 53.2 57.4 60.6

Other equipment* 43.5 40.9 45.3 44.3 41.6

Books, magazines 31 29.4 27.3 27.6 22.9

Electronic equipment excl. computers 19.9 16.2 19.1 17.5 19

Food and cosmetics 19.4 18.9 21.5 24.3 23.8

Films, music 19.8 15.9 16.7 16.5 11.6

Computer hardware 11.8 10.1 11.1 10.9 13.8

Tickets for sports or cultural events 16.7 14.4 14.9 16.5 16.3

Software (incl. games) 18.1 15.6 15.9 15.6 13.6

Holidays, tours, accommodation and

tickets 13 17.1 12 19.4 19.3

* Furniture, vehicles, household appliances, garden goods, hobby goods, tools,

toys, jewellery, works of art and collectibles

13.1

12.9

8.0

2.9

2.7

2.5

1.4

Shops

Auctions

Price comparison

Shopping hubs

Group buying

Discount sales

Opinions on shops and products

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 43 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

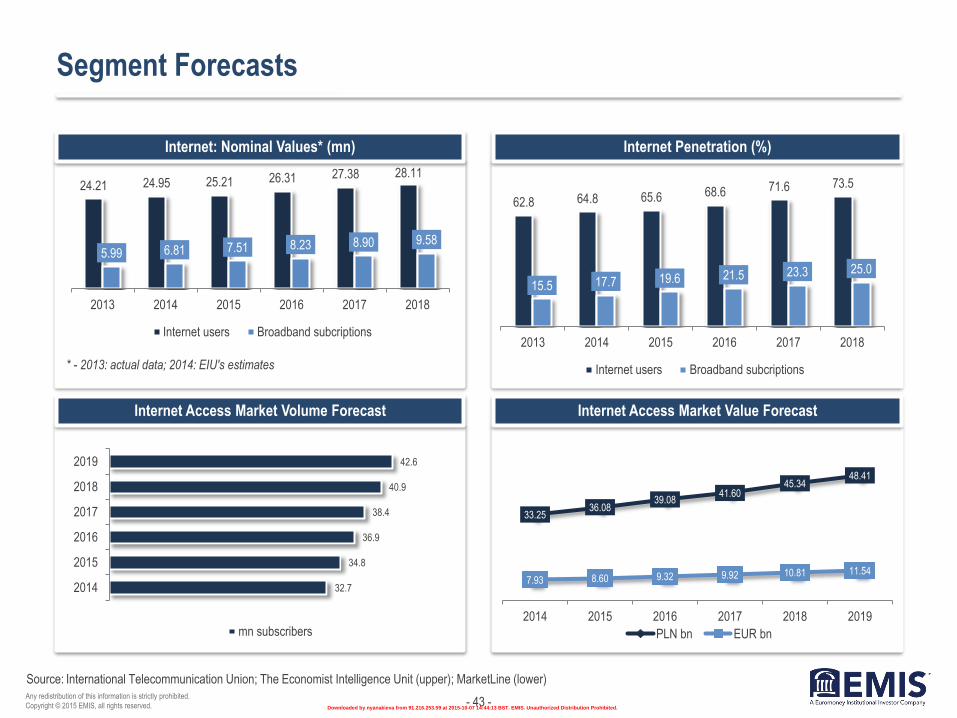

Segment Forecasts

Internet: Nominal Values* (mn)

Internet Access Market Volume Forecast

Internet Penetration (%)

Internet Access Market Value Forecast

International Telecommunication Union; The Economist Intelligence Unit (upper); MarketLine (lower)

24.21 24.95 25.21 26.31 27.38 28.11

5.99 6.81 7.51 8.23 8.90 9.58

2013 2014 2015 2016 2017 2018

Internet users Broadband subcriptions

* - 2013: actual data; 2014: EIU's estimates

62.8 64.8 65.6 68.6 71.6 73.5

15.5 17.7 19.6 21.5 23.3 25.0

2013 2014 2015 2016 2017 2018

Internet users Broadband subcriptions

32.7

34.8

36.9

38.4

40.9

42.6

2014

2015

2016

2017

2018

2019

mn subscribers

33.25 36.08

39.08 41.60

45.34 48.41

7.93 8.60 9.32 9.92 10.81 11.54

2014 2015 2016 2017 2018 2019

PLN bn EUR bn

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 44 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

V. Pay TV

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 45 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Basic Data & Forecasts

Number of Households with Pay TV (mn) Top Cable TV Operators (in Q4/2014, % market share)

PwC (left);

4.7 4.6 4.6 4.5 4.5 4.5

5.8 5.8 5.8 5.8 5.7 5.7

0.2 0.3 0.4 0.4 0.5 0.6

2012 2013 2014 2015 2016 2017

Cable Sat IPTV

UPC Polska 31.25%

Vectra 19.98%

Multimedia Polska 17.83%

Inea 4.54%

Toya 3.70%

Others 22.70%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 46 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Comments

Source:

TV Audience

The average Polish citizen watched TV for 4 hours and 48 minutes per day in Q1 2015, which is 3 minutes more than a year earlier. The growth trend is

attributed to the wider number of offered channels.

Viewers interest in the so-called big four channels, i.e. TVP1, TVP2, TVN, and Polsat, continues to fall: their combined share was 44.9% of the market in

Q1 2015, down by 3.1pps on the year.

TV Channels' Shares (according to audience) in Q1 2015 (%) Ad Market Shares (%, Q4 of each year)

National Broadcasting Council (KRRiT) (left); Starlink for the market, own data for TVN, airtime and sponsoring (right)

12.9

11.6

10.9

9.4

3.4

3.2

3.1

3.0

2.9

TVP1

Polsat

TVN

TVP2

TVN7

TV Puls

TVP Info

TV 4

TVN24

23.7

23.0 23.1

24.5

22.9 22.6

2013 2014

TVP Polsat TVN

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 47 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

Terrestrial Digital TV

Viewing Figures: Shares in Q1 2015 (%)

Viewing Figures: Shares in Q1 2015 (%) (cont’d)

At the end of Q1 2015, nearly 15.9mn Poles had access to

terrestrial digital TV services compared to 14.5mn a year

before. The number of people who used exclusively such

services (i.e. they had no access to cable or sat TV) was

close on 11.5mn vs. slightly above 10mn a year earlier.

In Q1 2015, the public TV channels (TVP1, TVP2, TV

Polonia, TVP Info, TVP Regionalna, TVP Rozrywka, TVP

Kultura, TVP Seriale, TVP Sport, TVP HD, TVP Historia,

and TVP ABC) held a 32% market share vs. 33% a year

earlier.

The average viewing audience of top 4 channels in Q1

2015 was 1.25mn.

KRRiT

Channel Share (%)

TVP1 16

Polsat 14.83

TVP2 11.49

TVN 10.63

TVP Info 5.65

TV Puls 5.13

TV4 4.23

TVN7 4.11

Puls 2 3.86

TV6 2.54

TTV 2.43

TVP Regionalna 1.92

Channel Share (%)

TVP Rozrywka 1.85

TVP ABC 1.71

Stopklatka 1.62

Fokus TV 1.57

ATM Rozrywka 1.56

Polo TV 1.32

TVP Historia 1.23

Eska TV 0.92

TVP Polonia 0.9

TVP Kultura 0.81

Polsat Sport News 0.56

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 48 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Comments

Added & Multimedia Services Market

The added and multimedia services market includes pay TV, mobile internet, fixed-line and mobile added services. Its growth is expected to accelerate this

year, which market researcher PMR attributes to the mobile internet segment.

Research firm PMR expects the Polish telecom market to drop in value by 1.1% in 2015, while the entire telecom and multimedia market (i.e. including also

pay TV) is expected to fall by 0.5%. Analysts expect the pay TV market to grow this year, though the outflow of customers to the terrestrial digital TV (that

offers over 20 channels already) may mean that this segment would have to fight declines.

Market Value & Dynamics

PMR

9.0 10.0

10.8 11.5

12.3 13.3

13.8

11.4

8.3

6.7 6.5

8.1

2010 2011 2012 2013 2014 2015

PLN bn % y/y change

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 49 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

VI. Main Players

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 50 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

M&A Activity

M&A Deals of 2015

EMIS DealWatch

Date Target Company Deal Type Buyer Seller EUR mn Stake %

03/06/2015 NextWeb Media Acquisition Wirtualna Polska Holding SA NextWeb Holdings Sarl 4.72 100.00

27/05/2015 OpenFM; PolskaStacja Acquisition Wirtualna Polska Holding SA GG Network; Polska Stacja sc 0.97 100.00

08/05/2015 Data center in Warsaw of MNI Acquisition Expedite Advisors Ltd MNI SA 4.37 100.00

08/05/2015 TK Telekom Privatization Netia SA Polskie Koleje Panstwowe SA 55.37 100.00

07/05/2015 Wirtualna Polska Holding SA IPO Institutional and private investors, EBRD Innova Capital Sp z oo 72.53 32.54

05/05/2015 3S SA Acquisition Enterprise Investors PCC SE; Polish private investors 22.00 76.00

13/04/2015 Ertel Acquisition Leon EDF SA 100.00

24/03/2015 Grupa Nokaut SA Acquisition HubStyle 2.54 53.33

16/03/2015 TVN SA Acquisition Scripps Networks Interactive Inc Grupa ITI SA; Canal Plus Group SA 584.00 52.70

25/02/2015 CallFreedom Acquisition Aspenta

04/02/2015 Wykop Acquisition Garvest BV Naspers Ltd 100.00

29/01/2015 Unizeto Technologies SA Acquisition Asseco Poland SA 4.57 81.30

14/01/2015 Gruper.pl Acquisition Zumzi.com Polskapresse

13/01/2015 Grupa Bankier.pl Acquisition Bonnier AB Naspers Ltd 4.70 100.00

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 51 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Source:

Top Companies

Top 10 Companies (according to 2014 sales revenue)

WSE-listed Companies from Telecom Sector

Incurred and Planned Investments (PLN mn)

Company data, Rzeczpospolita

12,212

7,410

6,245

4,392

1,674

1,594

1,483

1,000

706

617

Orange Polska

Cyfrowy Polsat

T-Mobile Polska

P4

Netia

TVN

UPC Polska

FH Kar-Tel

Multimedia Polska

Vectra

Company 12m price change Market value (PLN mn)

Cyfrowy Polsat -3.78 14,837

Hawe -55.48 143

Hyperion 31.48 117

Midas 12.73 917

MNI -2.99 129

Mediatel 100 222

Netia -0.89 1,963

Orange Polska -14.16 10,499

Tele-Polska Holding -58.6 28

2,335

432

1,511

367

279

1,916

711

1,091

358

280

1,775

491

1,230

511

232

2000

910

1000

520

200

Orange Polska

Polkomtel*

T-Mobile Polska

P4

Netia

2015 2014 2013 2012

* - in 2015, combined data for Polkomtel and Cyfrowy Polsat (the latter is now

the former's owner)

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 52 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

Orange Polska

Financial performance (PLN mn)

Employment Evolution

TPSA is a successor of state-owned enterprise Polska

Poczta, Telegraf i Telefon (Polish Post, Telegraph and

Telephone) that was established in 1947. TPSA started its

operations (after parting with the Polish Post) in 1992 and

debuted on the Warsaw Stock Exchange (WSE) in 1998. In

2000, the consortium of France Telecom and Kulczyk

Holding purchased 35% in the telecom in the first phase of

its privatisation and increased the share to 47.5% in 2001.

In 2004, Kulczyk sold his stake to France Telecom.

Currently, FT holds 49.79% in TPSA.

Telekomunikacja Polska and PTK Centertel merged at the

end of 2013: since then they have been operating as a

single company, Orange Polska. The merger was designed

to improve operational efficiency and enhance customer

care.

In March, 2014, Orange Polska and Commerzbank's

mBank announced the setting up of a mobile retail bank

earmarked for smartphone and tablet users. The services

will be delivered under the Orange brand; their debut has

been planned for H2/2014.

In February, 2014, Orange Polska finalised the sale of

Wirtualna Polska, one of the country's most popular general

interest internet portals, for PLN 383mn to private equity

fund Innova Capital.

Company data

16,560 15,715 14,922 14,147 12,923 12,212

6,280 4,711

5,928 4,845 4,084 3,921

1,281 107

1,918 855 294 535

2009 2010 2011 2012 2013 2014

Revenue EBITDA Net income

68,437

27,075 24,913 23,286 21,920 19,923 18,047

2001 2009 2010 2011 2012 2013 2014

workforce

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 53 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

Orange Polska (cont'd)

Group Revenue Evolution (% y/y; excl. regulatory impact)

Financial indicators

The group's revenue decline last year was limited to 2.5%

y/y excluding regulatory impact (i.e. impact of regulation of

rates, such as Mobile Termination Rate, Fixed Termination

Rate, Fixed-to-Mobile rate, customer and visitor roaming

rates, Bitstream Access rates). Overall, its revenue dropped

by 4.5% y/y to PLN 12.79bn.

Its pre-regulatory 2014 mobile revenues went up by 1.4%

y/y, driven by customer base increase, growing usage and

higher sales of equipment.

Restated EBITDA for 2014 amounted to PLN 3,921mn and

stood at 32.1% of revenues, i.e. they decreased by PLN

125mn on the year, however, the margin improved by 0.5

pp. The pre-regulatory decline resulted mainly from lower

revenues (an impact of PLN 319mn) and from higher

interconnect costs (PLN 171mn).

Company data

-6.4 -7.2

-9.9 -7.9

-9.3 -7.9 -5.4

-3.6

-0.8

-6.0

-9.6 -10.4

-10.9 -10.9

-5.4 -3.9

0.3 1.7

-18.5 -16.9 -17.0 -15.9 -15.6 -15.1 -13.1 -12.2

-14.2

6.0

9.4 6.6 6.0

3.7

-0.2 -1.2 -1.7

-2.6 Q4/2012 Q1/2013 Q2/2013 Q3/2013 Q4/3013 Q1/2014 Q2/2014 Q3/2014 Q4/2014

Group Mobile

Fixed voice Fixed broadband, TV and VoIP

0.7 0.4 1.0 1.1 1.1 3.8

1.7

5.0 4.5 4.1

21

11

28 26 25

2010 2011 2012 2013 2014

net debt/EBITDA net debt (PLN bn) net gearing (%)

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 54 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Comments

Source:

Orange Polska (cont'd)

Organic cash flow amounted to PLN 1,149mn in 2014, up by PLN 44mn versus 2013, and was in line with the group's full-year guidance (i.e. keeping this

figure at least stable at the 2013 level of PLN 1.1bn). The target for 2015 is around PLN 900mn (including cash capex for fibre access network project).

Capex Reduction Key Investment Areas in 2014 (%)

Company data

2.2

2.7

2.6

2.3

1.9

1.8

13.3

17.3

17.5

16.5

14.8

14.5

2009

2010

2011

2012

2013

2014

Capex/sales PLN bnFixed access network (incl.

fibre) 24%

Mobile network 20%

Core network 9%

IT systems and infrastructure

32%

Other 5%

CPE 10%

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 55 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

Cyfrowy Polsat

Revenue (PLN mn)

Customer Base (mn)

Cyfrowy Polsat is one of the largest Polish companies and a

leading media and telecommunications group in the region. It

provides 16.5mn services to 6.1mn customers.

The Group consists of the following companies and brands:

* Cyfrowy Polsat - Poland's largest and Europe's fourth-

biggest satellite TV platform (with a 32% market share in Poland in

2014)

* Polkomtel - the operator of the Plus mobile telephony

network (with a 28.1% market share in terms of contract SIM

cards in 2014, i.e. the leader of this segment)

* Polsat TV - the leading commercial broadcaster in Poland in

terms of both audience and ad market shares (its flagship channel

achieved 13.3% all-day audience share in 2014 vs. 13.0% of its

major competitor's main channel TVN).

* ipla - the leader of the online video market in Poland (with

over 1,600 feature films and over 100 TV series).

Recently, Cyfrowy Polsat has successfully issued corporate

unsecured series A bearer bonds having with the nominal

value of PLN 1bn. On Jul 10, the bonds were allocated to 52

investors who included numerous investment and pension

funds as well as the European Bank for Reconstruction and

Development (EBRD). In June, 2015, the company and a

group of financial institutions commenced negotiations that are

intended to provide Cyfrowy Polsat with financial resources

which will enable refinancing of the outstanding indebtedness

of the company and its subsidiaries.

Company data

7,773

7,673

7,312

7,133

6,682

6,570

1,266

1,482

2,366

2,778

2,521

7,410

2009

2010

2011

2012

2013

2014

Cyfrowy Polsat Polkomtel

Note: Cyfrowy Polsat has not consolidated Polkomtel fully yet.

14.04

3.20

14.06

3.44

13.99

3.55

13.84

3.57

14.13

3.54

n.a.

4.40

Polkomtel Cyfrowy Polsat

2009 2010 2011 2012 2013 2014

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 56 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

T-Mobile Polska

Financial Results (PLN mn)

Customer Groups

T-Mobile Polska (until May, 2013 - Polska Telefonia

Cyfrowa, PTC) was founded in 1995 as a limited liability

company and was transformed into a joint-stock company

in 2011. Its current sole owner, Deutsche Telekom Group,

was one of its co-founders. In 2011, it replaced the Era

brand with the T-Mobile brand.

T-Mobile and PTK Centertel, operator of the Orange

network, signed an agreement in 2011 to share their radio

access networks. The agreement covers management,

planning, support, development and maintenance of the

joint networks. They established NetWorkS!, a company in

which both operators hold an equal 50% of shares. They

stress that each party remains the owner of their networks

and frequencies. Both operators will continue to compete in

the wholesale and retail market of telecommunications

services under their existing brands.

In the spring of 2014, T-Mobile Polska and Alior Bank

launched what they called the most advanced bank-

telecom cooperation in Europe: "T-Mobile Usługi Bankowe,

dostarczane przez Alior Bank" (T-Mobile Banking Services,

delivered by Alior Bank), which replaced Alior Sync - the

bank's internet-only offer.

Company data

7,602 7,345 7,157 7,023 6,648

6,245

2,661 2,758 2,595 2,454 2,516 2,420

2009 2010 2011 2012 2013 2014

Revenue EBITDA

7.00 7.01 7.04 7.06 7.05 6.99 6.93 6.89 6.82 6.78 9.04 8.91 8.93 8.61 8.51 8.76 8.75 8.84 8.88 9.01

16.04 15.92 15.97 15.67 15.56 15.75 15.68 15.73 15.70 15.79

2006 2007 2008 2009 2010

Post-paid Pre-paid Total

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 57 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

P4

Financial results (PLN bn)

Customer Groups (mn)

In 2005, Netia Mobile – backed by Icelandic tycoon Thor

Bjorgolfsson - won the tender for the fourth infrastructure-

based mobile telephony operator in Poland, (beating e.g.

Hutchison Whampoa). Later that year, Bjorgolsson's

Novator Telecom Poland SARL merged with Netia Mobile.

Still in 2005, the company was renamed P4 (limited liability

company). P4's current shareholders are Novator (49.7%)

and Tollerton (50.3%). According to media reports, the

owners have invested PLN 2.61bn in the company, of

which PLN 2.3bn (EUR 0.6bn) was in cash and the

remaining part - by a contribution in kind (telecom

equipment shop chain Germanos).

In March, 2007, P4 launched its Play network for retail

customers (an in October - for business customers). In

January, 2008, it reached the first 1mn customers. In early

2013, P4 announced it had 8.7mn customers. In October,

2013, P4 announced it reached 10mn customers and

became the 20th biggest operator in the EU.

At the end of Q1 2015, its customer base grew to 12.7mn

(i.e. by 15.9% y/y), while the share of post-paid custoemrs

rose to 48.3% from 45.0% a year before. Thus, Play's

market share increased by 2.6pps to 21.9%. At the same

time, it had 75% of Poland's territory within its LTE services

network.

Company data

2.00

2.67

3.58 3.72

4.39

0.46 0.87

0.56 0.71 1.07

2010 2011 2012 2013 2014Revenue Adjusted EBITDA

2.93 3.96

4.81 5.96

6.48

2.24

3.12 3.88

4.77 5.81

5.16

7.08

8.69

10.73

12.29

2006 2007 2008 2009 2010

Pre-paid Post-paid Total

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 58 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Highlights

Source:

Netia

Financial Results (PLN mn)

Operating Results (thou)

R.P. Telekom (Netia's predecessor) was set up in 1990. In 1991, the company received its first license for delivering telecom services - in the city of Pila. In 1999, it received licenses for offering data transmission and internet access services; also that year, Netia debuted on NASDAQ. In 2000, it debuted on the Warsaw Stock Exchange (WSE).

In 2008, Netia sold a minority stake in P4 - the operator of the Play mobile network - and took over Tele2 Polska. In 2011, it carried out acquisitions of Crowley Data Poland and Telefonia Dialog.

Netia has around 14 thousand km of fibre-optic infrastructure and around 70% of Polish offices within the reach of its network.

In late July, 2015, Netia signed a final agreement to acquire 100% shares of TK Telekom from the Polish state railways PKP. for "just below" PLN 222mn. The transaction has been funded from available credit lines and Netia’s own resources (earlier, Netia secured a PLN 400mn loan from mBank and DNB, earmarked for, among others, paying for TK Telekom). Thanks to this deal, the reach of the Netia group's own fiber backbone network will grow by around 7,5 thousand kilometers. The transaction will scale up the Netia Group's operations in the B2B segment even by over 28% (pro-forma data for 2014).

Netia also stressed that after paying out dividends of PLN 0.60 per share and canvassing TK Telekom the financial leverage of the company remains on a comfortable level.

Company data

1,506 1,569 1,619

2,121 1,876

1,674

304 359 408 591 551 493

2009 2010 2011 2012 2013 2014

Revenue Adjusted EBITDA

559

690

912

875

849

790

1,158

1,218

1,745

1,644

1,489

1,331

n.a.

n.a.

2,789

2,688

2,526

2,305

2009

2010

2011

2012

2013

2014

Services (RGUs) Fixed voice subscribers Broadband subscribers

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.

- 59 - Any redistribution of this information is strictly prohibited.

Copyright © 2015 EMIS, all rights reserved.

Contact:

Corporate Headquarters

6-8 Bouverie Street

London EC4Y 8DD

UK

Voice: +44 20 7779 8100

Fax: +44 20 7779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

US

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No.

III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2015 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organisations, and others.

EMISPDF nyanakieva from 91.216.253.59 on 2015-10-07 14:44:13 BST. DownloadPDF.

Downloaded by nyanakieva from 91.216.253.59 at 2015-10-07 14:44:13 BST. EMIS. Unauthorized Distribution Prohibited.