poland – the eu front runner in terms of growth performance bre - bre bank – best – in - class...

TRANSCRIPT

Poland – the EU front runner in terms of growth performance

BRE - BRE Bank – best – in - class financial services’ provider in Poland

Tel Aviv, Dec 12, 2010

Przemysław GdańskiBRE Bank Management Board Member Head of Corporate Banking

2

Poland – the EU front runner in terms of growth performance

3

Poland - the largest from EU new member states in terms of area and population is located at the heart of Europe at the crossroads of major communication corridors, became the EU front runner in terms of growth performance in 2009 as the global crisis wreaked havoc to European economies.

With exports to GDP ratio at about 40% it can be classified as a relatively closed economy, which in times of the crisis turned out to be a blessing rather than a curse. Relatively smaller dependence (as compared to its regional peers) on foreign trade reduced the impact of foreign demand shock.

Key macroeconomic data – features of Polish economy

2009

Area (Sq. Km) 312 679

Population (mn) 38.2

GDP Growth (%) 1.7

Inflation Rate (%) 3.5

Exports volume (% of GDP) 38.9%

Source: StatOffice.

4

Poland – the EU front runner amid the global recession…

Poland’s GDP (% YoY)

Source: StatOffice, European Commission interim forecast (Sep’10), BRE forecast.

European Commission GDP forecasts (%

YoY)

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

2005 2006 2007 2008 2009 2010F 2011F 2012F

BRE forecast 2009 2010F

Germany -4,7 3,4Spain -3,7 -0,3France -2,6 1,6Italy -5,0 1,1Netherlands -3,9 1,9Euro area -4,1 1,7POLAND 1,7 3,4UK -4,9 1,7

EU27 -4,2 1,80,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

2005 2006 2007 2008 2009 2010F 2011F 2012F

BRE forecast

5

-40

-20

0

20

40

09-07 03-08 09-08 03-09 09-09 03-10 09-10

Exports, %YoY Imports, %YoY

-10

-5

0

5

10

15

20

08-08 01-09 06-09 11-09 04-10 09-10

Retail sales, %YoY

-15

-10

-5

0

5

10

15

20

25

08-08 01-09 06-09 11-09 04-10 09-10

Industry, %YoY Construction, %YoY

\

Exports and imports (% YoY)

…currently notes dynamic rebound…

Production in industry and construction (% YoY, wda*)

Retail sales (% YoY)

One-off effects of harsh winter

* wda – working day adjusted.

Source: NBP, StatOffice.

Foreign trade increase stimulates Polish industry

Public investment sustains growth in construction sector

Gradual stabilization on the labour market supports retail sales

6

…based on recovering external demand from Germany

Exports of Poland and Germany (% YoY)

Source: Bloomberg, NBP, Eurostat.

Strong trade relations between Poland and Germany

Germany – the main recipient of Polish exports

Rebound in Germany boosted Polish economy

-40

-30

-20

-10

0

10

20

30

40

01'01 01'02 01'03 01'04 01'05 01'06 01'07 01'08 01'09 01'10

German exports Polish exports

7

2,0

3,0

4,0

5,0

6,0

7,0

8,0

07-09 11-09 03-10 07-10 11-10

220

240

260

280

300

320

340

360

Poland (%), LA Germany (%), LA Spread (bp), RA

Financial markets have confidence in Polish assets

Sou

rce:

NB

P, M

inF

in, B

loom

berg

.

Poland-Germany 10Y T-bond spread (bp)

0

50

100

150

200

250

300

12-06 06-07 12-07 06-08 12-08 06-09 12-09 06-10

40

60

80

100

120

140

03-07 10-07 05-08 12-08 07-09 02-10 09-10

Non-residents’ participation in Polish T-bond market (PLN

bn)

Non-residents’ participation in Polish equity market (PLN

bn)

2,0

4,0

6,0

8,0

10,0

12,0

14,0

05-07 12-07 07-08 02-09 09-09 04-10 11-10Poland Greece Germany Ireland Hungary

10Y T-bond yields (%)

8

25,6

6,8

6,7

6,3

5,7

4,1

3,6

2,6

2,6

2,6

0,3

0 10 20 30

Germany

France

Italy

UK

Czech Rep.

Netherlands

Russia

Hungary

Sweden

Spain

Israel

Poland’s trade with Israel is rather limited …

Main recipients of Polish exports

(EUR bn, 2009)

30,1

9,1

7,1

6,1

5,6

5,0

4,3

3,6

3,4

2,6

0,2

0 10 20 30 40

Germany

Russia

Italy

Netherlands

China

France

Czech Rep.

Belgium

UK

Slovakia

Israel

Main suppliers of Polish imports (EUR bn, 2009)

Source: Eurostat.

9

10,5

16,5

47,1

9,0

16,8 Chemicals andrelated products

Manufacturedgoods classifiedchiefly by materialMachinery andtransportequipmentFood and liveanimals

Others

35,1

7,0

22,6

26,5

8,8 Chemicals andrelated products

Manufacturedgoods classifiedchiefly by material

Machinery andtransportequipment

Miscellaneousmanufacturedarticles

Others

Source: Eurostat.

Main export goods:

vehicles

ships, boats

electrical machinery and equipment

Main import goods:

chemical products

arms, ammunition

electrical machinery and equipment

… and characterized with the following structure

Polish exports to Israel - decomposition (%, 2009)

Polish imports from Israel - decomposition (%, 2009)

10

Israeli investors’ engagement in Poland is low

FDI inflow to Poland - decomposition (EUR bn,

2008)*

Source: NBP.

Poland’s liabilities resulting from FDI (EUR bn, 2008)

1,6

1,6

1,3

1,1

0,6

0,5

0,5

0,4

0,4

0,3

0,04

0,0 0,5 1,0 1,5 2,0

Germany

Netherlands

Luxembourg

Sweden

France

Cyprus

Austria

Iceland

USA

UK

Israel

22,0

18,1

12,5

10,0

7,1

5,3

4,4

4,3

4,1

3,8

0,1

0 5 10 15 20 25

Netherlands

Germany

France

Luxembourg

USA

Sweden

UK

Italy

Austria

Belgium

Israel

Possible underestimation due to investment through companies registered in other countries.

11

Summary

Poland – the only EU country without recession in 2009

Poland enjoys strong rebound, so far based mainly on external demand from Germany

Polish assets enjoy strong confidence of financial markets

Small trade volume between Israel and Poland

Limited FDI inflow from Israel to Poland – room for improvement

12

BRE Bank – best – in - class financial services’ provider in Poland

13

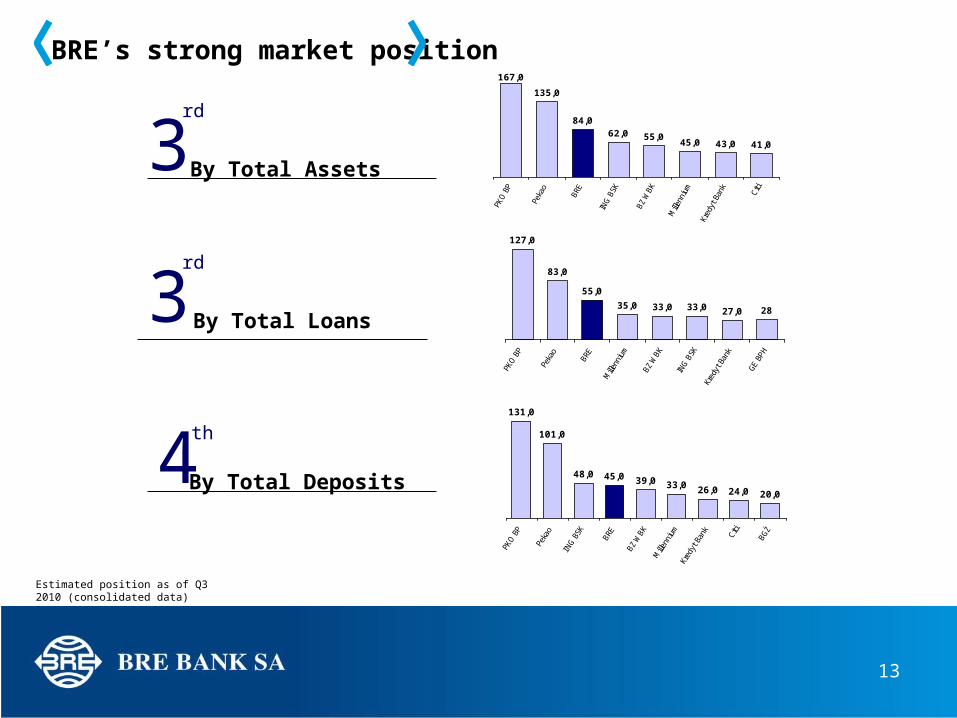

BRE’s strong market position

By Total Assets

By Total Loans

By Total Deposits

3rd

3rd

4th

62,0 55,045,0 43,0 41,0

84,0

135,0

167,0

127,0

83,0

55,0

35,0 33,0 27,0 2833,0

PKO

BP

Peka

o

BRE

Mille

nniu

m

BZ W

BK

ING B

SK

Kred

yt B

ank

GE B

PH

131,0

101,0

48,039,0 33,0 26,0 24,0 20,0

45,0

Estimated position as of Q3 2010 (consolidated data)

14

BRE Bank Group – universal financial services’ provider for financial institutions, corporate customers, HNWI, retail clients

ADVISORY SERVICES AND FINANCING SUUPORTED

BY EU FUNDING

TRANSACTIONALBANKING

RISKMANAGEMENT

STRUCTERED AND MEZZANINEFINANCING

COMPREHENSIVE WEALTHMANAGEMENT

INVESTMENTBANKING

BROKERAGESERVICE

FINANCING OF COMMERCIAL REAL ESTATE

FACTORING

LEASING

TRADITIONALDEPOSITS

FINANCING CURRENTAND INVESTMENT

ACTIVITIES

TRADE FINANCE

BRE Bank Group

15

A leading universal bank in Poland… …with a differentiated value proposition

Multi-brand, multi-channel approach attracting both young and affluent customers

Leading in internet banking

Physical network of retail branches, financial centres and mobile agents

Open-architecture “Investment Fund Supermarket” and insurance supermarket

Continuous product innovation

BRE Bank at a glance

One of the largest universal banking groups in Poland serving over 3.5M retail and 13,000 corporate customers

Strong Corporate and Investment banking business with 3rd/4th largest corporate deposit/loan portfolio in Poland

Dynamically growing Retail Banking business with 3rd/6th largest retail loan/deposit portfolio in Poland

Retail Banking

Corporates &

Markets

Long-standing client relationships across large, medium-sized and small companies

Exclusively dedicated corporate branch and office network

Strengths across corporate and investment banking services

Innovative integrated transactional banking platform

Total assets (PLN B)

Loans(PLN B)

Deposits(PLN B)

PKO BP

Pekao

BRE Bank

ING BSK

BZ WBK

Millenium

Kredyt Bank

BHW

GE BPH

BGZ

Source: BRE Group 3 Q 2010 consolidated financial statements, 3 Q 2010 consolidated financial statements of the banks, Rzeczpospolita

167

135

84

62

55

45

43

41

36

27

127

83

55

33

33

35

27

13

28

19

131

101

45

48

39

33

26

24

14

20

16

Strong Corporate and Investment Banking BusinessExclusively dedicated physical distribution

networkIntegrated and advanced sales approach

Leading, comprehensive ‘one-stop shop’ product offering in Poland

13 thousand customers covered by 200 relationship managers in branches and headquarters

Renowned corporate banking internet platform iBRE

The best integrated bank corporate platform of 2009 in CEE(a)

New customer relationship management (“CRM”) system supports cross selling and upselling activities

Analysis of clients’ potential requirements

Planning and monitoring of sales activities

Transactional banking services available through MultiBank branches (appeal to SMEs)

Transactional banking innovative and tailored products

Short term and long term financing fourth largest corporate loan portfolio

Largest specialized mortgage bank (BRE Bank Hipoteczny)

Leasing No 2 with 9% market share (BRE Leasing)

Factoring market share ~14% (Polfactor)

Securities sales and trading leading market making positions (eg IRS/FRA, FX)

Debt origination market shares in non-government debt >20%

Structured and mezzanine finance services

Trade Finance Products

Brokerage a leader in brokerage and investment advisory (DI BRE)

Corporate Banking

Investment Banking

(a) Highest award in the „World’s Best Internet Bank“ (Global Finance) in the category of “the best integrated bank corporate platform of 2009” in CEE region

Source: Company data

17

Advisory services Advisory services and suportand suport

Transaction Banking - fully fledged product range well fitting to dynamic & expanding companies

Accounts

Liquidity managementZero / target balancing

Pooling

Mass payments identification and

reconciliation

Direct debit

Physical cash processingCash Deposits / transports

LCY and FCY payments (incl.SEPA); individual and

mass payments

Cards incl. prepaid

Cash disbursements

Postal order and other settlements

Sh

ort

term

fin

an

cin

g

(rece

ivab

le

dis

cou

nti

ng

).

Receivable managementDisbursements management

Dep

osi

ts

(in

cl

au

tom

ate

d

O/N

)

Electronic/internet baking (iBRE)

Reporting/intergration services

18

Transaction Banking - comprehensive catalogue of products & services satisfying the most complex businesses

Account Management Products Integrated Bank Account Agreement Current Accounts – LCY / FCY accounts Pay-roll accounts Escrow accounts Fiduciary accounts iBRE Account Management module

Concentration / Consolidation Products BRE Balancing – zero-balancing services BRE Pooling - notional BRE Pooling – physical International (X-border) Pooling with Commerzbank iBRE Liquidity Management and planning module iBRE Depo Plus – micro deposits management

Disbursements Management Products LCY Payments FCY Payments SEPA Payments BRE Mass Payments BRE Payroll Payments MT101 – Request for Transfer BRE Cards - Business Payment Cards Pre-paid Cards Physical Cash disbursements Cheques iBRE Banking, iBRE Cash, iBRE Cards - modules

Receivables Management Products BRE Collect – identification of incoming payments BRE Mass Collect – identification of bill payments / mass pymts BRE Collect Plus – identification, matching and reconciliation of incoming payments BRE Direct Debit – B2B and B2C direct debit BRE Direct Debit Consent Management EBPP with Retail Banking BRE Cash– 5 different models of cash collection services iBRE Collections and Direct Debit modules Cash Management reporting system – tailor made transaction reporting following individual needs

(Short Term) Financing Products Invoice Discounting (factoring) iFactoring – iBRE Invoice.net iBRE Trade Finance

(Short term) Investments Products BRE Auto-overnight LCY / FCY deposits Longer term deposits iBRE Deposit module

19

Transactional Banking Services

Account management LCY and FCY payment management Cash Management orders management

Other Banking Services

Letters of credit, bank guarantees, collections Treasury Custody services Information management Customized reporting & analyses Electronic invoices and debt discount

iBRE – Internet financial platform aggregating all financial services, within one access channel

iBRE – universal, integrated solution facilitating management of entire company’s financials

20

Treasury*

FX Spot FX forward FX Swap IR SWAP Real-time quoting

eDeposits Tenor declared by the client Current and customized rates

iBRE – universal, integrated solution facilitating management of entire company’s financials

21

BRE’s products & services in practice – x’border client case

Foreign conglomerate

Subsidary 1 Subsidary 2 Subsidary 3

Polish client Leading comapny

of the group

Subsidary 1 Subsidary 2 Subsidary 3

Subsidary 2

Subsidary Subsidary

Bo

rde

rB

ord

er

One of the leading logistic companies operating in over 100 countries with its headquarter in Western Europe’s country and subsidaries in Poland.

Group Revenue : ca. EUR 30 bn

Revenue in Poland: PLN 3 bn

One of the leading logistic companies operating in over 100 countries with its headquarter in Western Europe’s country and subsidaries in Poland.

Group Revenue : ca. EUR 30 bn

Revenue in Poland: PLN 3 bn

22

BRE’s products & services in practice – x’border client case (continued)

Client’s expectations: cash collections and withdrawals invoices’s and pay-roll and

payments (LCY and FCY) consolidation of financial means of

the group enabling effective management of group liquidity

automated financial data exchange between the company and the bank

guarantees credit and pre-paid cards

BRE Bank solutions offered to the client: cash operations – cash collections and withdrawals iBRE-internet based transactional system domestic, international payments and additional, complex cash management solutions international cash pooling comprehensive, fully automated financial data exchange – client’s financial system itegrated with iBRE platform comprehensive Trade Finance solutions wide range of payment and credit cards incl. pre-paid cards

23

Selection of awards and distinctions 2010

iBRE platform - the winner in five categories of prestigious international contest „World Best Internet Banks 2010” run by Global Finance magazine:

Best Corporate/Institutional Internet

Bank Central & Eastern Europe

Best Corporate/Institutional Internet

Bank Poland

Best Integrated Corporate Bank Site

Central & Eastern Europe

Best Consumer Internet Bank - mBank

Czech Republic

Best Integrated Consumer Bank Site –

mBank and Multibank Central &

Eastern Europe

24

Award of Euromoney Magazine 2010:

The Management Board won the second place

in

the category „Bank with most accessible

Senior

Management”

Selection of awards and distinctions 2010