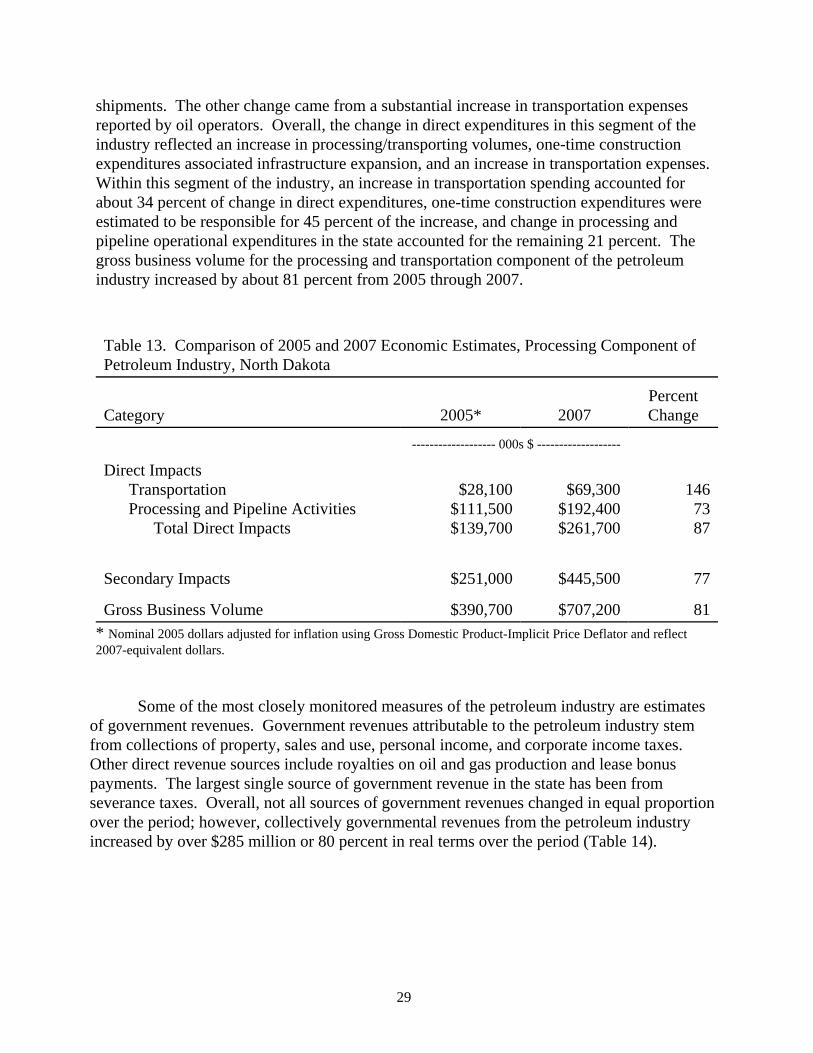

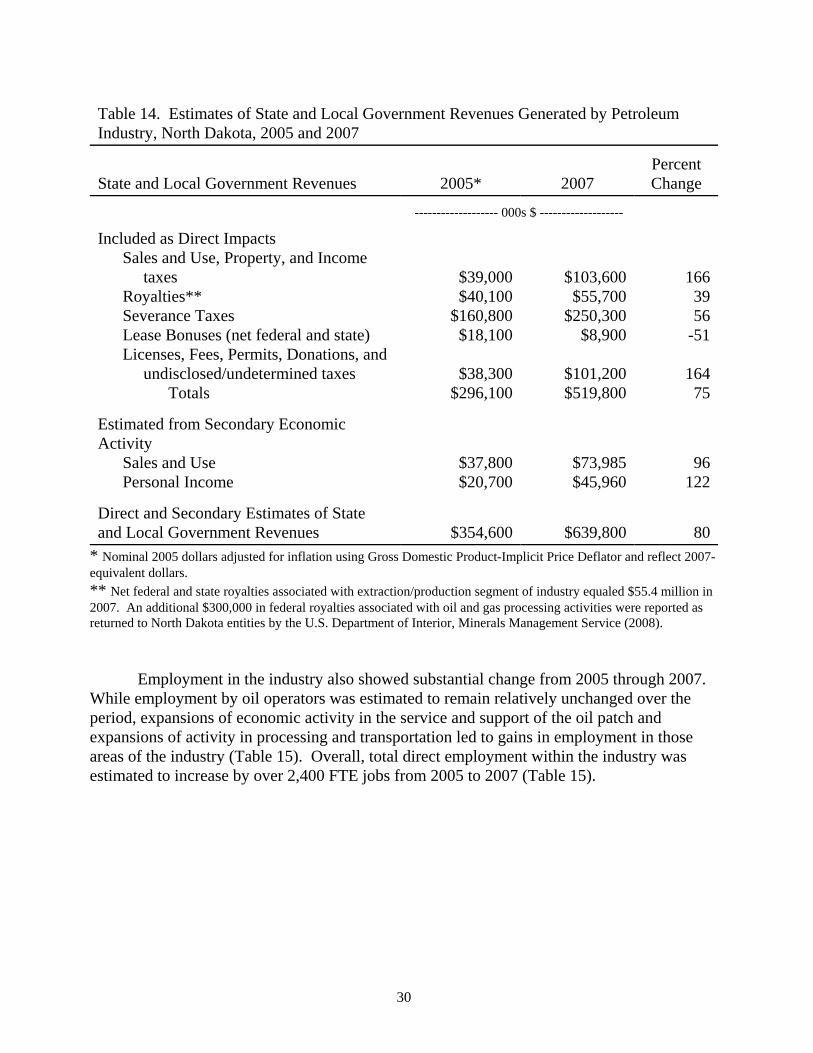

petroleum industry’s economic contribution to north...

TRANSCRIPT

Agribusiness and Applied Economics Report No. 639 January 2009

Petroleum Industry’s EconomicContribution to North Dakota in 2007

Dean A. BangsundF. Larry Leistritz

Department of Agribusiness and Applied EconomicsAgricultural Experiment StationNorth Dakota State University

Fargo, North Dakota 58108

ACKNOWLEDGMENTS

Special thanks are extended to Ron Ness, President, North Dakota Petroleum Council, forhis leadership, guidance, and information throughout the study. The North Dakota PetroleumCouncil also shared responsibility for administering the surveys and soliciting industrycooperation in the study.

Several individuals were helpful at various stages of the study. Our appreciation andthanks are extended to:

Lynn Helms (North Dakota Industrial Commission)Bruce Hicks (North Dakota Industrial Commission)Ryan Kopseng (Missouri River Royalty Corporation)Rick Ross (Whiting Oil and Gas)Wayne Biberdorf (Hess Corporation)Tod Maleckar (Diamond Resources)Steve Pine (Great Northern Energy)Keith Bayley (State Land Department)Kathy Strombeck (Office of State Tax Commissioner)Larry Melvin (U.S. Forest Service)Justin Kringstad (North Dakota Pipeline Authority)Shelly Swandal (Department of Agribusiness and Applied Economics)Norma Ackerson (Department of Agribusiness and Applied Economics)

The study authors and study sponsors would like to thank all the companies andindividuals that took the time to complete and return the survey materials. This study, with itsreliance on industry data, would not have been possible without industry cooperation.

Thanks are given to Norma Ackerson for document preparation, Shelly Swandal for workwith the study surveys, and to our colleagues for reviewing this manuscript.

Financial support was provided by the North Dakota Oil and Gas Research Council andthe North Dakota Petroleum Council. We express our appreciation for their support.

The authors assume responsibility for any errors of omission, logic, or otherwise. Anyopinions, findings, or conclusions expressed in this publication are those of the authors and donot necessarily reflect the views of the North Dakota Petroleum Council or the NDSUDepartment of Agribusiness and Applied Economics.

A single copy of this publication is available free of charge. Please address your inquiryto the Department of Agribusiness and Applied Economics, NDSU Dept 7610, PO Box 6050,Fargo, ND 58108-6050, phone (701-231-7441), fax (701-231-7400), or e-mail:[email protected] . This publication is also available electronically at the following website: http://agecon.lib.umn.edu/

NDSU is equal opportunity institution.

Copyright © 2009 by Bangsund and Leistritz. All rights reserved. Readers may makeverbatim copies of this document for non-commercial purposes by any means, provided thiscopyright notice appears on all such copies.

TABLE OF CONTENTSPage

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Industry Organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Production Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Data Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Oil Operators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Pipelines and Processors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Service and Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Leasing and Brokerage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Estimation Techniques . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Input-Output Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Economic Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Direct Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Exploration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Extraction/Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Total Direct Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Secondary Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Direct Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Secondary Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Government Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Total Economic Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Comparison of 2005 and 2007 Industry Assessments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

AppendicesAppendix A - Questionnaire, Oil Operators, North Dakota, 2007 . . . . . . . . . . . . . . 40Appendix B - Questionnaire, Processors, North Dakota, 2007 . . . . . . . . . . . . . . . . 50Appendix C - Questionnaire, Lease/Brokerage Firms, North Dakota, 2007 . . . . . . 57

i

List of TablesTable Page

1 Basic Production Statistics from Survey of Oil Operators, North Dakota, 2007 . . . . . 9

2 Direct Impacts from General Exploration, Drilling Activities, and LeaseBonuses, North Dakota, 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3 Direct Impacts from Oil and Gas Extraction and Production Activities,North Dakota, 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

4 Direct Impacts from Oil and Gas Processing, North Dakota, 2007 . . . . . . . . . . . . . . 15

5 Total Direct Impacts, Petroleum Industry, North Dakota, 2007 . . . . . . . . . . . . . . . . . 16

6 Total Secondary Impacts, Petroleum Industry, North Dakota, 2007 . . . . . . . . . . . . . 18

7 State and Local Government Revenues Attributable to the Petroleum Industry,North Dakota, 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

8 Total (Direct and Secondary) Economic Impacts, Petroleum Industry, North Dakota, 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

9 Oil and Gas Production Statistics, North Dakota, 2005 and 2007 . . . . . . . . . . . . . . . 25

10 Summary of Oil Operator Surveys, North Dakota, 2005 and 2007 . . . . . . . . . . . . . . 26

11 Comparison of 2005 and 2007 Economic Estimates, ExplorationComponent of Petroleum Industry, North Dakota . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

12 Comparison of 2005 and 2007 Economic Estimates, Oil and GasExtraction/Production Component of Petroleum Industry, North Dakota . . . . . . . . . 28

13 Comparison of 2005 and 2007 Economic Estimates, Processing Componentof Petroleum Industry, North Dakota . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

14 Estimates State and Local Government Revenues Generated by PetroleumIndustry, North Dakota, 2005 and 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

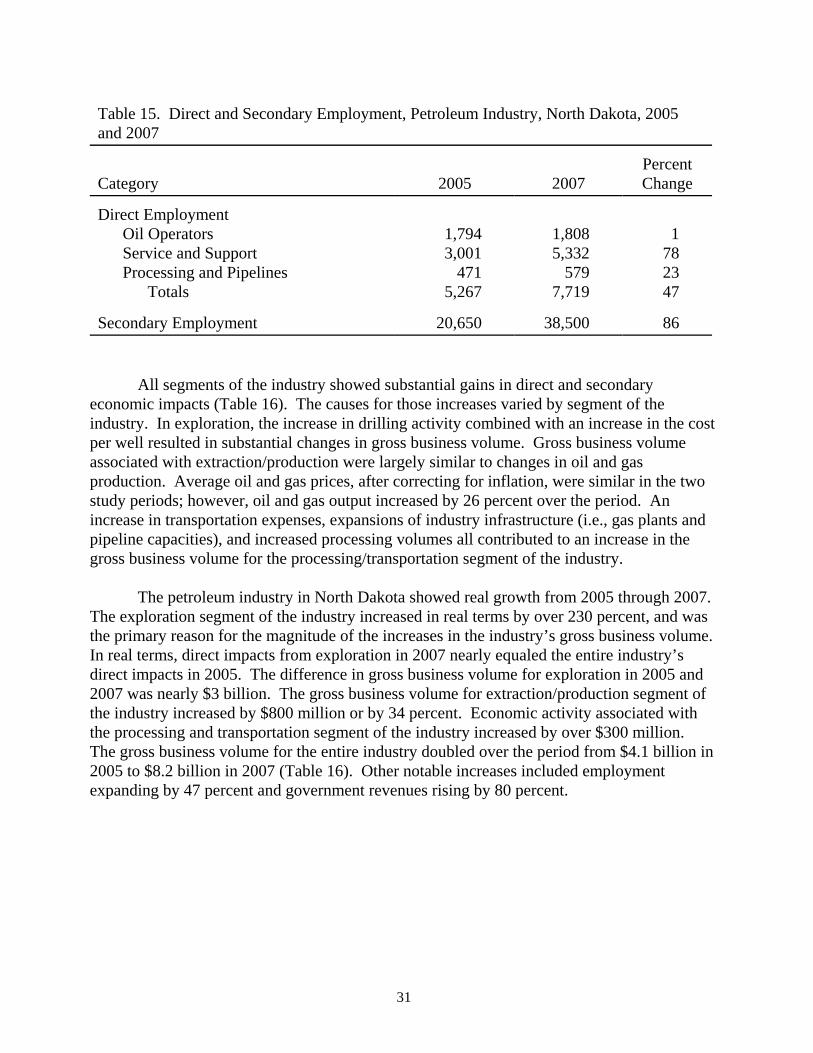

15 Direct and Secondary Employment, Petroleum Industry, North Dakota,2005 and 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

16 Key Economic Values, Petroleum Industry, North Dakota, 2005 and 2007 . . . . . . . 32

ii

List of FiguresFigure Page

1 Oil Producing Counties, North Dakota . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2 Historic Oil Production, Key Counties, North Dakota, 1952 through 2008 . . . . . . . . . 5

3 Top States in Crude Oil Production, United States, 1981 through 2007 . . . . . . . . . . . 5

4 Crude Oil Production, North Dakota, 1951 through 2007 and Projected 2008 . . . . . . 6

5 Production and Market Value of Crude Oil, North Dakota, 1974 through 2007 . . . . . 7

6 Value of Crude Oil Production in Nominal and Real Dollars, North Dakota,1974 through 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

7 Economic Effects of Key Segments of the North Dakota Petroleum Industry, 2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

iii

Executive Summary

The purpose of this study was to estimate the economic contribution of crude oil andnatural gas exploration, extraction, transportation, and processing in North Dakota in 2007. Expenditures made in North Dakota by oil companies represented the direct impacts of theindustry. Secondary economic impacts result from the spending and respending of the directimpacts and were estimated using the North Dakota Input-Output Model.

Surveys were used to collect production, expenditure, and employment data for thepetroleum industry in North Dakota. Oil operators (i.e., firms that own or operate oil wells)in the state were surveyed to obtain information on in-state expenses for oil and gasexploration, expenses for oil and gas extraction/production, general business expenditures,employment, oil and gas output, and leasing and drilling activity. A similar survey wasconducted for firms engaged in pipeline transportation and processing of crude oil andnatural gas in North Dakota. A third survey of leasing/brokerage firms was used to developestimates of private lease bonuses paid to in-state mineral owners. Key parameters from aprevious study were used with current data to estimate employment and expenditure patternsof firms that provide service and support in the oil fields

The survey of oil operators produced financial data on about 34 percent of NorthDakota’s oil and natural gas production in 2007. Secondary data, obtained from governmentagencies, was combined with survey data to estimate royalties, lease bonuses, and severancetaxes.

Total in-state expenditures in 2007 for oil and gas exploration (e.g., seismic testing,well drilling) were estimated from survey data and statewide drilling statistics. A total of 336wells were drilled in 2007. Average expense per well for oil operators was estimated at $4.3million. The combination of in-state expenses for exploration and lease bonuses resulted in$1.536 billion in direct impacts in 2007. The secondary economic impacts associated withexploration activities were estimated at $2.721 billion. The in-state gross business volume(direct and secondary impacts) of exploration activities was estimated at $4.257 billion in2007.

Estimates of oil and gas extraction/production expenses, general business expenses foroil operators, private and public mineral royalties, and state severance taxes were derivedfrom survey data and secondary information obtained from various government agencies. The state had 3,759 producing wells which combined for over 45 million barrels of oil and70.8 million mcf of natural gas in 2007. Total direct impacts for oil and gas production wereestimated at $1.308 billion in 2007. Total secondary economic impacts associated withextraction activities were estimated at $1.956 billion. The in-state gross business volume ofoil and gas extraction/production was estimated at $3.264 billion in 2007.

In-state expenditures for transportation expenses for crude oil, pipeline operationexpenses, natural gas processing, and crude oil refining were estimated to have a directimpact in North Dakota of $261.7 million in 2007. Total secondary economic impacts

iv

associated with processing and transporting crude oil and natural gas were estimated at $445million. Processing and transporting crude oil and natural gas generated a gross businessvolume of $707 million in 2007.

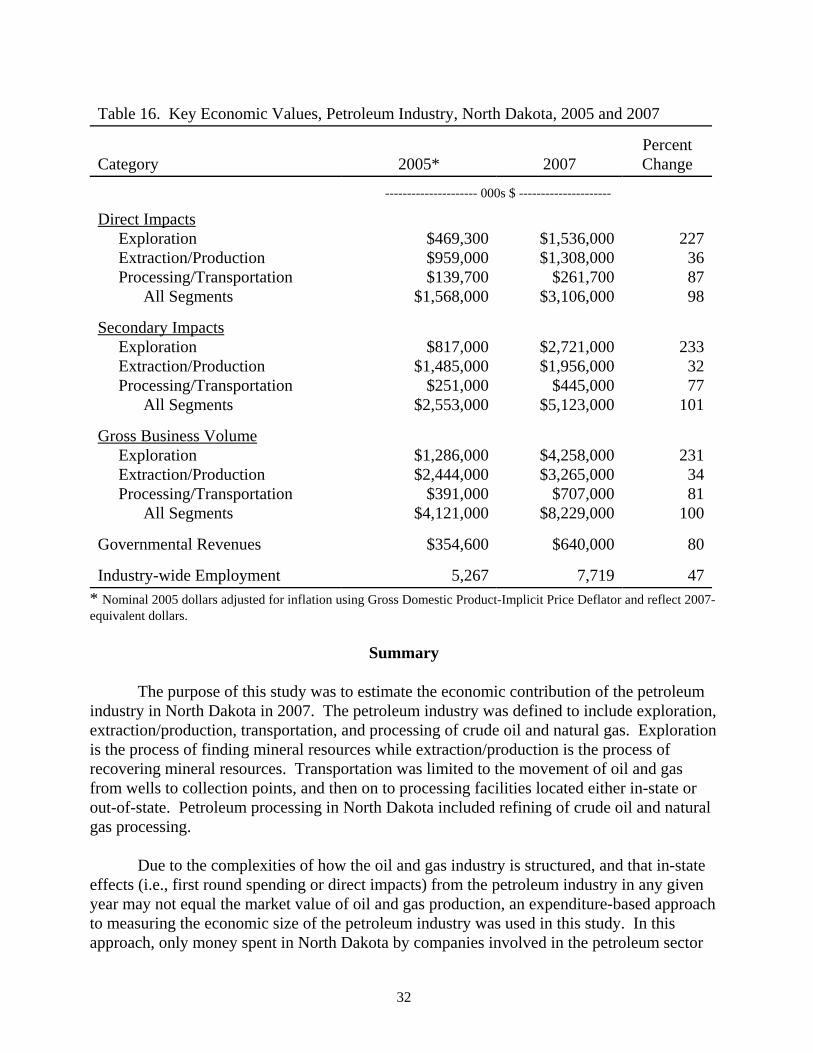

Industry-wide direct and secondary economic impacts from the petroleum industrywere estimated at $3.106 billion and $5.123 billion, respectively. The gross business volumefor the entire industry in North Dakota in 2007 was estimated at $8.229 billion.

Additional measures of the petroleum industry’s economic importance to the stateinclude direct employment for 7,719 full-time jobs, economy-wide personal income of $3.1billion, statewide retail sales of $2 billion, direct contributions to local and state governmenttax revenues of $520 million, indirect contribution of $120 million in state governmentgeneral tax collections, and secondary employment of 38,500 full-time equivalent jobs.

Comparing various production statistics between 2005 and 2007 revealed that thenumber of producing wells, oil and gas production, and drilling activities all increased in thestate. Oil and natural gas prices between the two periods were similar after adjusting 2005figures for inflation. From 2005 to 2007, expenditures for exploration (i.e., well drilling andleasing mineral rights) in the state increased nearly 230 percent in real terms (i.e., correctingfor inflation). By comparison, expenditures for oil and natural gas production over the sameperiod paralleled changes in oil and gas output and were estimated to increase by 36 percentin real terms. Processing and transportation activities also showed substantial growth overthe period due to increased processing and transportation volumes and expansion ofprocessing and pipeline capacity. Economic activity associated with the processing segmentof the industry increased in real terms by 81 percent. Overall, the gross business volume(i.e., direct and secondary economic effects) of the industry was estimated to double in size inreal terms from $4.1 billion in 2005 to $8.2 billion in 2007.

While this study is a snapshot in time, results from this study would suggest thatrecent increases in exploration, processing and pipeline capacity and output, and increases incrude oil and natural gas production, have translated into substantial increases in grossbusiness volume for the state. The economic size of the industry has grown in recent years tobecome one of most single important basic-sector activities in the state. The industryprovides substantial governmental revenues through traditional tax collections, royaltyrevenue, lease bonuses, and severance taxes. In addition to public sector revenues, thepetroleum industry continues to act as a solidifying force in the North Dakota economythrough an expansion of industry-based employment and indirectly through bolsteredsecondary economic activity involving nearly all sectors of the economy.

The sheer size of the industry in 2007 suggests that much of North Dakota’s recenteconomic vitality can be linked to the expansion of petroleum exploration, production, andprocessing in the state. Current activity levels in the petroleum industry clearly make it oneof the key forces in the North Dakota economy.

v

Petroleum Industry’s Economic Contribution to North Dakota in 2007

Dean A. Bangsund and F. Larry Leistritz*

Introduction

North Dakota’s largest basic sector industries, which include agriculture,manufacturing, and energy, provide much of the economic stimuli for the state’s economy. These large industries are generally comprised of distinct sectors or economic groups. Forexample, agriculture in North Dakota is often considered a combination of crop productionand livestock. The energy industry in North Dakota is also comprised of several distinctsectors that are commonly treated as separate activities. North Dakota’s energy industriescan be conveniently separated into the activities that produce and distribute electricity, coal,and petroleum.

While separating the energy industry into similar activities is relatively straightforward, identifying the economic players within those sectors is less clear. In the case ofelectricity generation, a handful of firms and generating facilities exist within the state. Thesame situation exists with coal production–a handful of companies operate at a limitednumber of locations. However, the industrial organization associated with oil and natural gasproduction is very different. Rather than having a handful of firms and a limited number ofsite-specific facilities and locations, the petroleum industry involves hundreds of firms and amultitude of facilities spread out over the western third of North Dakota.

North Dakota’s rank among the nation’s top 10 oil producing states is commonknowledge to those in the petroleum sector, and national oil production statistics are readilyavailable to the general public (U.S. Department of Energy 2008). In 2006, the firstcomprehensive economic assessment of the petroleum industry in the state was conducted(Bangsund and Leistritz 2007). Since that time, much attention has been focused on theindustry; however, much of the attention has less to do with a revelation of the industry’simportance to the state, but rather due to substantial changes in drilling activity, oil output,tax revenues, and dramatic swings in crude oil prices.

Recent upswings in oil activity since 2005, due in part to increased energy prices, theavailability of improved exploration and extraction technology, and substantial potential foroil recovery from various formations in the Williston Basin, have brought new attention tothe petroleum industry in North Dakota. Increase in leasing activity, expansion of welldrilling rigs operating in the state, substantial growth in severance tax collections, and otherfinancial and economic aspects of the industry have all been discussed in the media. Despitea recently completed study of the industry in 2006, another assessment of the industry is

*Research scientist and professor, respectively, Department of Agribusiness and Applied Economics,North Dakota State University, Fargo.

warranted to track the substantial change in physical and economic activity in NorthDakota’s oil patch.

Ongoing and repeated assessments of key industries in North Dakota are notunprecedented. Actually, many key industries periodically re-assess their economicimportance in the state. Examples include several assessments for the wheat and sugarbeetindustries (Bangsund and Leistritz 2005, 2004, 1998, 1995b) and studies of the ligniteindustry in North Dakota (Coon and Leistritz 2008a).

Determining the economic contribution of a given industry quantifies its importanceto state and local economies. Not only can the economic impacts to the state and localeconomies be measured, but the effects on specific economic sectors and related industriesalso can be identified. Also, economic studies can demonstrate the susceptibility of theNorth Dakota economy to fluctuations in factors affecting petroleum exploration andextraction, demonstrate the economic dependence of the state on natural resource-basedindustries, and indicate the economic impacts that could result from potential changes inpolicies which affect the petroleum industry.

Objectives

The purpose of this report is to estimate the economic contribution (direct andsecondary effects) of the petroleum industry to the economy of North Dakota. Specificobjectives include:

1) estimate the economic size of petroleum exploration, extraction, and processingsectors, and

2) provide estimates of industry-wide employment, tax revenues, and other keyeconomic measures.

Background

The industrial organization of the petroleum industry in the United States is oftendivided into upstream and downstream components. The upstream components of thepetroleum industry generally include exploration, development, and production of crude oiland natural gas. The downstream components include transportation, processing,distribution, marketing, and retail delivery of petroleum products.

Industry Organization

The petroleum industry in North Dakota consists of both upstream and downstreamcomponents. For this study, the petroleum industry was defined to only include in-stateexploration, extraction/production, transportation, and processing of crude oil and naturalgas. Exploration can be generally thought of as the process of finding mineral resources. Extraction or production is the process of developing and recovering mineral resources.

2

Transportation components of the industry, in this study, were limited to the movement of oiland gas from wells to collection points, and then on to processing facilities located either in-state or out-of-state. Petroleum processing in North Dakota included refining of crude oiland natural gas processing. The distribution, marketing, and retail sale of processedpetroleum products (e.g., diesel, gasoline, kerosene, motor oil, lubricants, propane, naturalgas) were not included.

The exploration and extraction phases of the petroleum industry are not organized likeother industries in the state. Firms that own producing wells (oil operators) contract much ofthe work of exploration and extraction of oil and gas to other firms that specialize in variousaspects of those processes. As a result, much of the expenditures incurred in the state for oiland gas production start with the oil operator but flow through the various firms engaged inproviding support and service within the oil fields. While oil operators represent a mix ofsmall to large firms, a majority of the prominent oil operators in North Dakota also haveoperations in other states. For many oil operators, their operations in North Dakota do notrepresent the majority of their oil and gas revenues. As a result of having operations and/orheadquarters in other states, net revenues from North Dakota oil and gas production mayleave the state for a variety of reasons. However, North Dakota is still the beneficiary ofexploration and discovery expenses from firms that may have minimal operations in the state.

Oil and gas wells typically have three types of economic interests. These players areoften referred to as royalty interests, owner/operator interests, and working interests. Royaltyinterests receive a share of the value of a well’s output but do not share in the expensesassociated with the well. Owner and working interests share, based on various percentagesor arrangements, the remaining revenues and all of the expenses of a well. The well owner oroperator is generally responsible or in charge of all operations. The owner arranges to havework completed for most of the necessary activities associated with the well, and chargesworking interests for their share of the expenses. As a result of these typical arrangements,the total number of firms receiving revenues and incurring expenses from oil and gas wells inNorth Dakota is unknown. However, the number of oil operators (firms that own or operatewells) is known.

For various reasons, the magnitude of economic effects of oil and gas production arenot necessarily equivalent to the market value (i.e., price times quantity) of oil and gasproduced. Exploration and extraction technologies use specialized inputs and services, manyof which are not available in North Dakota and must be purchased from out-of-state sources. Many oil operators have operations and/or are headquartered in other states, and revenues forsome firms may leave the state to be used for projects elsewhere. The same situation mayexist where firms use resources obtained from out-of-state operations for oil and gasexploration in the state. In addition, oil operators headquartered out-of-state often haveminimal general business expenses in the state. Similarly, firms that only have workinginterests in producing wells may or may not have physical operations in the state. All ofthese factors make it very problematic to base economic importance of the petroleumindustry solely on the value of oil and gas production.

3

BIL

LIN

GS

BOTTINEAU

BOWMAN

BURKE

DUNN

HETTINGER

MCHENRY

MCKENZIEMCLEAN

MOUNTRAIL

SLOPE

STARK

WARD

WILLIAMS

RE

NV

ILL

E

VA

LL

EY

GO

LD

EN

DIVIDE

Production Statistics

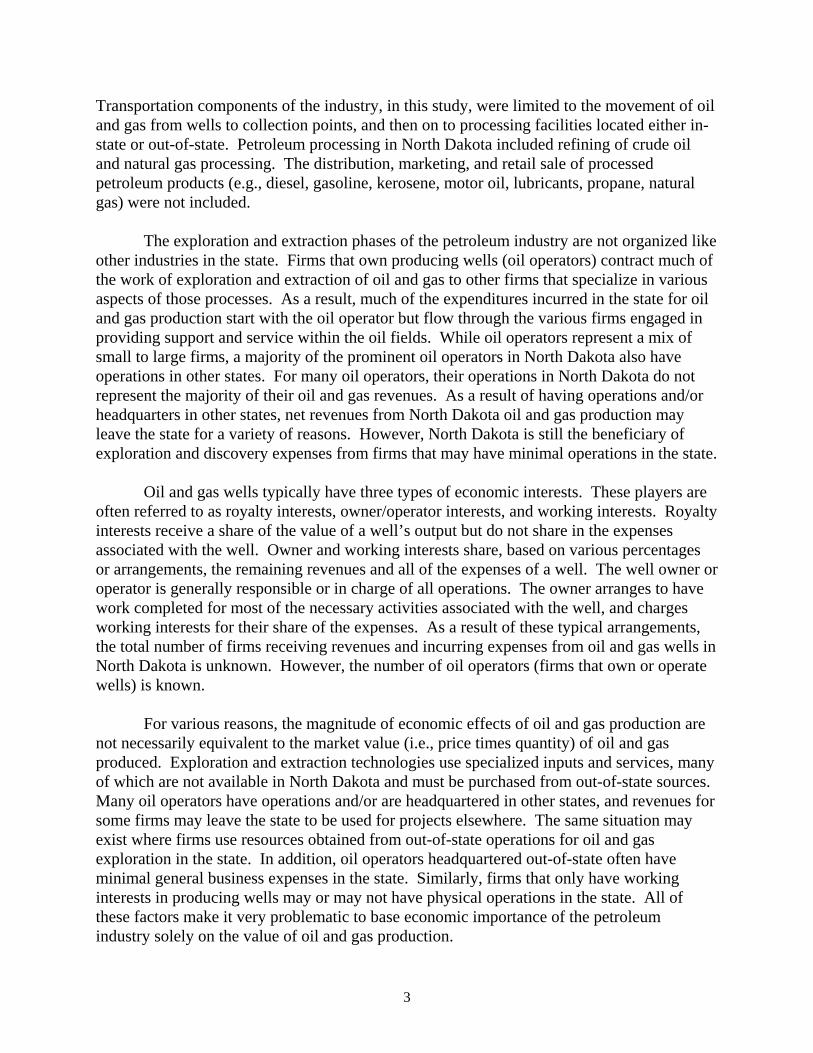

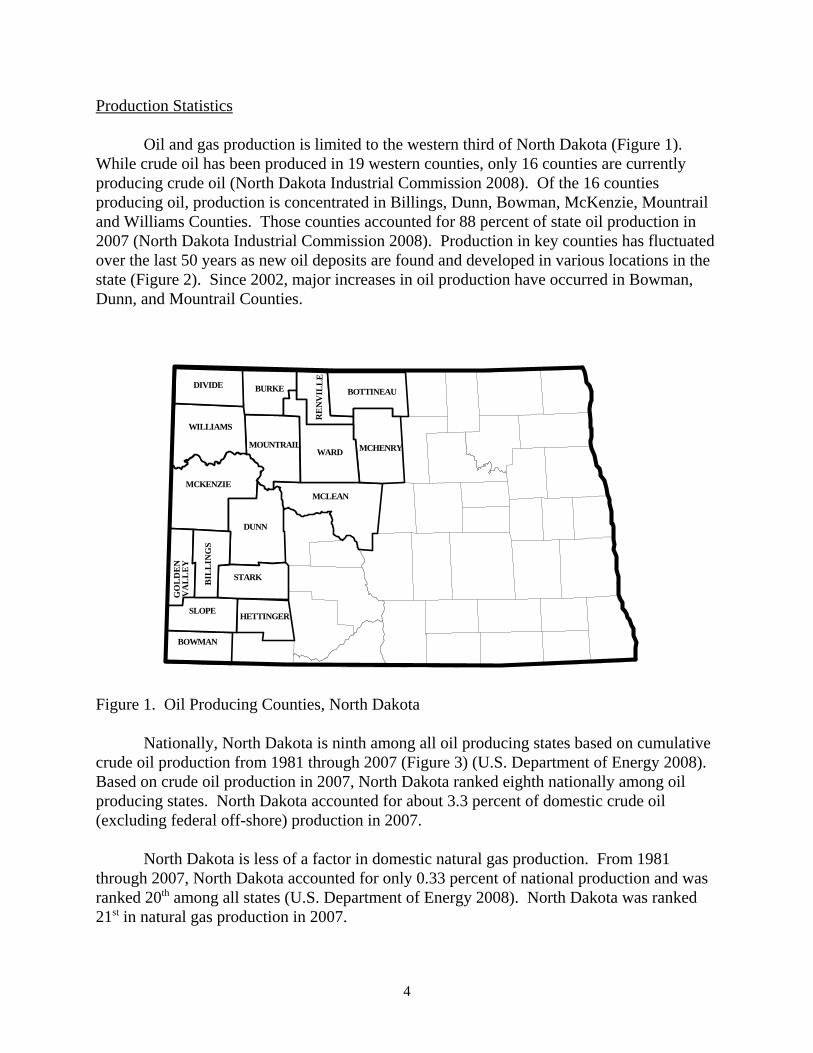

Oil and gas production is limited to the western third of North Dakota (Figure 1). While crude oil has been produced in 19 western counties, only 16 counties are currentlyproducing crude oil (North Dakota Industrial Commission 2008). Of the 16 countiesproducing oil, production is concentrated in Billings, Dunn, Bowman, McKenzie, Mountrailand Williams Counties. Those counties accounted for 88 percent of state oil production in2007 (North Dakota Industrial Commission 2008). Production in key counties has fluctuatedover the last 50 years as new oil deposits are found and developed in various locations in thestate (Figure 2). Since 2002, major increases in oil production have occurred in Bowman,Dunn, and Mountrail Counties.

Figure 1. Oil Producing Counties, North Dakota

Nationally, North Dakota is ninth among all oil producing states based on cumulativecrude oil production from 1981 through 2007 (Figure 3) (U.S. Department of Energy 2008). Based on crude oil production in 2007, North Dakota ranked eighth nationally among oilproducing states. North Dakota accounted for about 3.3 percent of domestic crude oil(excluding federal off-shore) production in 2007.

North Dakota is less of a factor in domestic natural gas production. From 1981through 2007, North Dakota accounted for only 0.33 percent of national production and wasranked 20th among all states (U.S. Department of Energy 2008). North Dakota was ranked21st in natural gas production in 2007.

4

1952 1958 1964 1970 1976 1982 1988 1994 2000 20060

10

20

30

40

50

60

(milli

ons

of b

arre

ls)

McKenzie Billings Williams Bowman Bottineau Stark All Others

ColoradoNorth Dakota

KansasNew Mexico

WyomingOkalahoma

LouisianaCalifornia

AlaskaTexas

0

5,000

10,000

15,000

20,000

(mill

ions

of b

arre

ls)

Figure 2. Historic Oil Production, Key Counties, North Dakota, 1952 through 2007Source: North Dakota Industrial Commission (2008).

Figure 3. Top States in On-Shore Crude Oil Production, United States, 1981 through 2007Source: U.S. Department of Energy (2008).

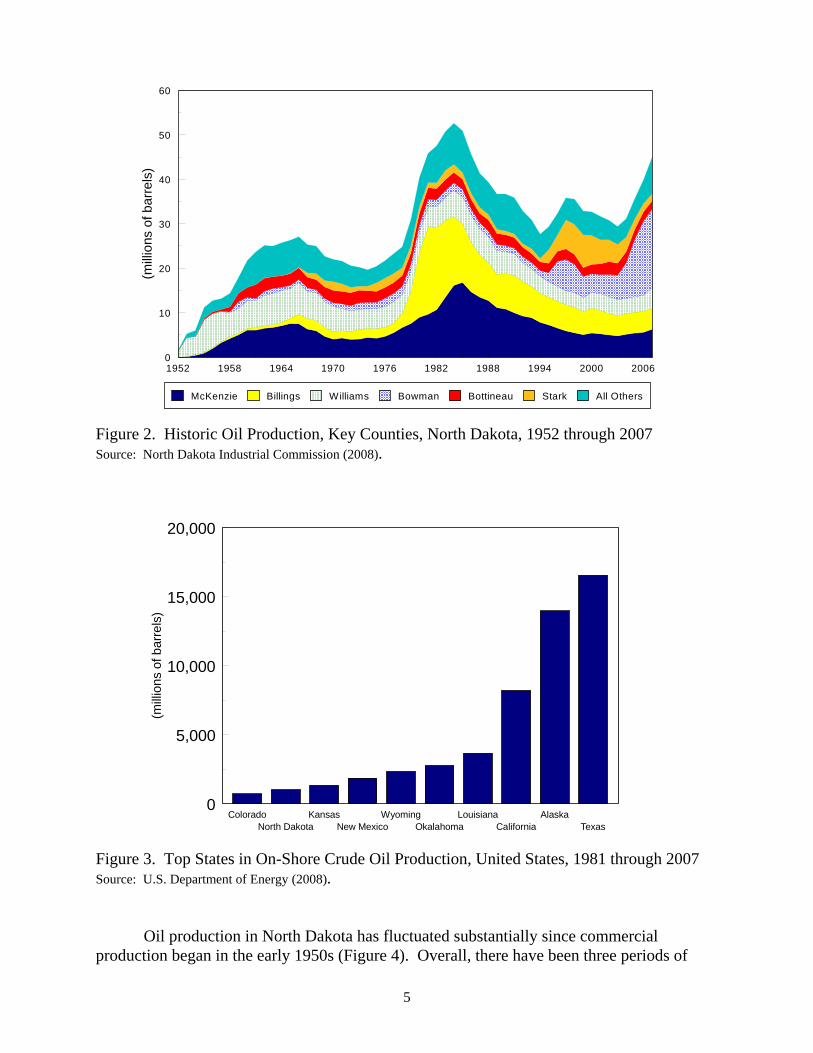

Oil production in North Dakota has fluctuated substantially since commercialproduction began in the early 1950s (Figure 4). Overall, there have been three periods of

5

1954 1960 1966 1972 1978 1984 1990 1996 2002 20080

10

20

30

40

50

60

(mill

ions

of b

arre

ls)

Actual Projected

rapid growth in oil production in North Dakota. The first period was from 1951 through1962, the second period occurred from 1974 to 1984, and the current period which began in2003. After historic highs in 1984, overall oil production in the state declined rapidly for 10years. Since 1994, oil production in the state has seen two periods of expansion and oneperiod of declining production. Crude oil production in the state is currently increasing, andcrude oil production in 2007 was the highest since the early 1980s. Although state totals for2008 were not available when this study was completed, monthly oil output for Januarythrough August of 2008 indicates that oil production in the state will reach an all time high in2008.

Figure 4. Crude Oil Production, North Dakota, 1951 through 2007 and Projected 2008Source: North Dakota Industrial Commission (2008).

The annual value of oil production in North Dakota was estimated using monthlyaverage price and production data from the North Dakota Industrial Commission (2008). Theoverall value of oil production in North Dakota, in nominal terms, has generally paralleled oilproduction despite price fluctuations over time (Figure 5). Nominal oil prices wereconverted to real dollars (2007) using the Gross Domestic Product-Implicit Price Deflator(U.S. Department of Commerce 2008). In real terms, from 1980 to 2000 the value of crudeoil production in North Dakota largely declined (Figure 6). However, in both real terms andnominal terms, the value of crude oil production in the state has increased substantially since2000 (Figure 6).

6

1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 200610

20

30

40

50

60

0

0.5

1

1.5

2

2.5

3

3.5

(mill

ions

of b

arre

lls)

(bill

ions

of n

omin

al d

olla

rs)

Value ofoil output

Oilproduction

1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 20060

1

2

3

4

(bill

ions

of d

olla

rs)

NominalDollars

Real (2007)Dollars

Figure 5. Production and Market Value of Crude Oil, North Dakota, 1974 through 2007Source: North Dakota Industrial Commission (2008).

Figure 6. Value of Crude Oil Production in Nominal and Real Dollars, North Dakota, 1974through 2007

7

Procedures

An economic contribution analysis, as defined in this study, represents an estimate ofall relevant in-state expenditures and returns associated with an industry. The economiccontribution approach to estimating economic activity has been used for several otherindustries in North Dakota (Bangsund and Leistritz 1995a, 1995b, 1998, 1999, 2004, 2005;Coon and Leistritz 2008a).

Data Collection

Due to the complexities of how the oil and gas industry is structured, and that in-stateeffects (i.e., first round spending or direct impacts) from oil and gas production in any givenyear may not equal the market value of oil and gas production, an expenditure-basedapproach to measuring the economic size of the petroleum industry was used in this study. Inthis approach, a sample of firms active in the petroleum industry in North Dakota were askedto provide estimates of the amount of expenditures made to entities (i.e., individuals, firms,and governments) in North Dakota. Two separate survey efforts were conducted for thestudy and provided the basis for most of the economic data needed to complete the study.

Oil Operators

Firms that own or operate oil wells in the state were surveyed to obtain information onexpenses for oil and gas exploration and extraction/production, general business expenses inthe state, employment, physical measures of oil and gas production, and leasing and drillingactivity (Appendix A). The North Dakota Petroleum Council provided names and addressesfor 140 oil operators in the state. The survey process started with sending cover letters and aquestionnaire to each firm on the mailing list. A second mailing was conducted for all firmsthat had not responded1 to the first mailing. After two mailings, dissemination of surveymaterials and solicitation of industry cooperation was deferred to the study sponsor.

The combination of two mailings and personal contacts of oil operators conducted bythe study sponsor resulted in useable information from 14 firms. The firms’ production fromowned/operated wells represented about 34 percent of the state’s 2007 production of crudeoil and natural gas (Table 1).

1Firms with non-deliverable addresses, those who responded with completed questionnaires, and those whoindicated they would not or could not participate were excluded in the second mailing.

8

Table 1. Basic Production Statistics from Survey of Oil Operators, North Dakota, 2007

Number of firms responding with useful information 14

Number of wells owned or operated in North Dakota (14 firms) 1,897

Crude oil production in 2007 in North Dakota (14 firms) 13,503,595 barrelsa

Natural gas production in 2007 in North Dakota (14 firms) 34,360,934 mcfa

Number of oil wells drilled in 2007 (9 firms) 126a Output from wells operated or owned. Does not include production from working interests.

Pipelines and Processors

Another survey was conducted for firms engaged in pipeline transportation of crudeoil and unprocessed natural gas produced in North Dakota and for firms involved withprocessing of crude oil and natural gas in North Dakota. The survey was used to obtainestimates of the amount and type of expenditures made in North Dakota and in-stateemployment by those firms (Appendix B). A mailing list of 10 firms operating pipelines, gasprocessing plants, and oil refineries were provided by the North Dakota Petroleum Council. The firms on the mailing list received two mailings, with some firms being contactednumerous times by industry representatives. A total of four firms provided useableinformation. While representative data for industry activities in this segment of the industrywas obtained through the survey, a breakout of survey data for crude oil pipelines, natural gasprocessing plants and pipelines, and crude oil refineries is not possible due to confidentialityreasons. Firms operating pipelines for the transport of refined or processed petroleumproducts were not included in the study.

Service and Support

Information from firms that provide service and support to oil operators in the statewas obtained from Bangsund and Leistritz (2007). Key parameters from the surveyconducted in 2006 were used in this study. When applicable, financial coefficients from2005 data were adjusted to correct for effects of inflation using the Gross Domestic Product-Implicit Price Deflator (U.S. Department of Commerce 2008).

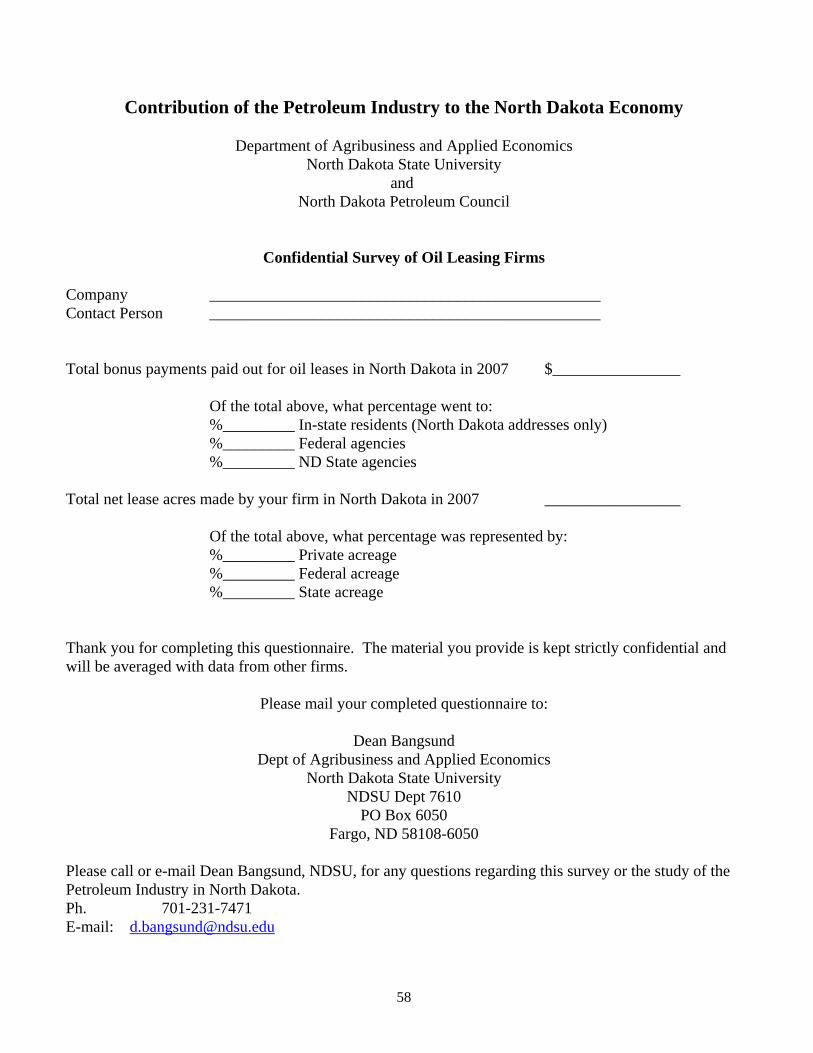

Leasing and Brokerage

A survey of companies providing leasing services to petroleum sector firms wasconducted to obtain information on oil leasing activities in North Dakota. A questionnairewas developed to obtain information necessary to estimate the amount of lease bonuses onprivate land paid to North Dakota entities (Appendix C). The study sponsor distributed thequestionnaire to five firms. The survey resulted in obtaining useable financial information

9

from three firms. Lease bonuses for government mineral ownership were obtained bycontacting the respective federal and state agencies in the state.

Estimation Techniques

The survey of oil operators and processors/pipeline operators and information fromBangsund and Leistritz (2007) provided data for two critical aspects of the study. First, datafrom the oil operator and processor surveys was used to set the level of spending in NorthDakota. In other words, the data was used to determine the magnitude of spending within thestate. Second, data from both current surveys and previous surveys (Bangsund and Leistritz2007) was used to determine the type and distribution of spending among various sectors ofthe North Dakota economy.

The survey of oil operators provided financial data on about one-third of all oil andgas production in the state. In addition, survey respondents provided information onexploration expenses, wells drilled, and leasing data. Benchmark expenses forextraction/production, transportation, and operational expenses (e.g., general administrativecosts) were estimated per barrel of oil equivalent (BOE). Total state production in 2007,expressed in BOE, was then used with survey estimates of in-state expenditures per BOE togenerate state-level estimates for extraction, transportation, and administrative spending. In-state employment by oil operators was estimated in the same manner. Benchmark expensesfor exploration were estimated on a per-well drilled basis and were used with data on thenumber of wells drilled in North Dakota in 2007. Data from the survey of oil lease/brokeragefirms was used with data from the North Dakota State Land Department to estimate in-statebonus payments for private leases. Other economic components of the petroleum industry’sdirect impacts, such as severance taxes, public lease bonuses, and royalty revenuesrepresented a combination of survey data, state-level statistics, and information obtainedfrom various state and federal governmental agencies.

The survey of service and support firms for oil and gas production in North Dakotaprovided estimates of in-state spending by various types of expenses (e.g., salaries/wages,utilities, office supplies, business services) (Bangsund and Leistritz 2007). The percentage ofspending in various categories, obtained from Bangsund and Leistritz (2007), was used toallocate state-level expenditures for exploration and extraction to various economic sectors ofthe North Dakota Input-Output Model. The amount of spending was determined using datafrom the survey of oil operators, while data from Bangsund and Leistritz (2007) providedinsights on how those dollars impacted various sectors of the North Dakota economy.

Input-Output Analysis

Economic activity from a project, program, policy, or activity can be categorized intodirect and secondary impacts. Direct impacts are those changes in output, employment, orincome that represent the initial or first-round effects of the project, program, policy, oractivity. Secondary impacts (sometimes further categorized into indirect and induced effects)result from subsequent rounds of spending and respending within the economy. This process

10

of spending and respending is sometimes termed the multiplier process, and the resultantsecondary effects are sometimes referred to as multiplier effects (Leistritz and Murdock1981).

Input-output (I-O) analysis is an economic tool that traces linkages among sectors ofan economy and calculates the total business activity resulting from a direct impact in a basicsector (Coon et al. 1985). The North Dakota I-O Model has 17 economic sectors, is closedwith respect to households (households are included in the model), and was developed fromprimary (survey) data from firms and households in North Dakota. Empirical testing hasshown the North Dakota Input-Output Model is sufficiently accurate in estimating grossbusiness volume, personal income, retail activity, and gross receipts in major economicsectors in North Dakota (Coon and Leistritz 2008b).

Economic Impacts

The economic contribution of the petroleum industry was primarily based onestimates of in-state expenditures from exploration, extraction, transportation, and processingof crude oil and natural gas. Estimates of in-state expenditures were combined withestimates of oil and gas royalties, state severance taxes, and lease bonuses to determine totaldirect impacts. Subsequently, the direct impacts were applied to the North Dakota Input-Output Model to estimate the secondary impacts. Secondary impacts result from therespending of direct impacts within the economy. The following section is divided into fivemajor parts: (1) direct impacts, (2) secondary impacts, (3) employment, (4) tax revenue, and(5) total economic impacts.

Direct Impacts

From an economic perspective, direct impacts are those changes in economic output,employment, or income that represent the initial or first-round effects of a project, program,or activity. The direct impacts from the petroleum industry in North Dakota includedexpenditures for (1) oil and gas exploration, (2) oil and gas extraction/production, (3)transportation of crude oil and unprocessed gas, and (4) processing crude oil and natural gas. Direct impacts also included various revenue streams originating from either oil and gasexploration, such as lease bonuses, or oil and gas production, such as severance taxes androyalty payments. The following sections describe these direct economic impacts.

Exploration

The economic effects of exploration come from expenditures within North Dakota fora variety of activities that involve searching and discovering viable oil and gas resources. Exploration was defined to include, but not limited to, seismic testing, geological research,lease expenses, other environmental research, land survey work, excavation, road building,construction of drill site, construction and delivery of electricity, pipeline development, andall other activities associated with drilling oil and/or gas wells (Appendix A).

11

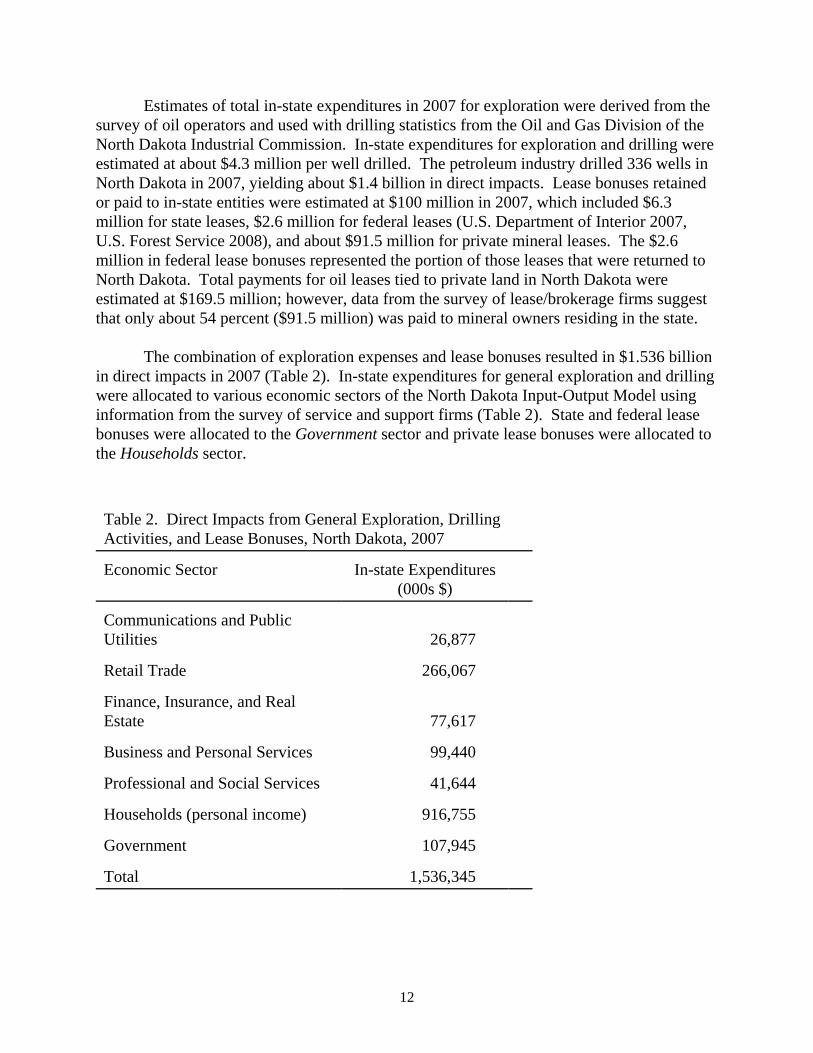

Estimates of total in-state expenditures in 2007 for exploration were derived from thesurvey of oil operators and used with drilling statistics from the Oil and Gas Division of theNorth Dakota Industrial Commission. In-state expenditures for exploration and drilling wereestimated at about $4.3 million per well drilled. The petroleum industry drilled 336 wells inNorth Dakota in 2007, yielding about $1.4 billion in direct impacts. Lease bonuses retainedor paid to in-state entities were estimated at $100 million in 2007, which included $6.3million for state leases, $2.6 million for federal leases (U.S. Department of Interior 2007,U.S. Forest Service 2008), and about $91.5 million for private mineral leases. The $2.6million in federal lease bonuses represented the portion of those leases that were returned toNorth Dakota. Total payments for oil leases tied to private land in North Dakota wereestimated at $169.5 million; however, data from the survey of lease/brokerage firms suggestthat only about 54 percent ($91.5 million) was paid to mineral owners residing in the state.

The combination of exploration expenses and lease bonuses resulted in $1.536 billionin direct impacts in 2007 (Table 2). In-state expenditures for general exploration and drillingwere allocated to various economic sectors of the North Dakota Input-Output Model usinginformation from the survey of service and support firms (Table 2). State and federal leasebonuses were allocated to the Government sector and private lease bonuses were allocated tothe Households sector.

Table 2. Direct Impacts from General Exploration, DrillingActivities, and Lease Bonuses, North Dakota, 2007

Economic Sector In-state Expenditures(000s $)

Communications and PublicUtilities 26,877

Retail Trade 266,067

Finance, Insurance, and RealEstate 77,617

Business and Personal Services 99,440

Professional and Social Services 41,644

Households (personal income) 916,755

Government 107,945

Total 1,536,345

12

Extraction/Production

The economic effects of extraction come from expenditures within North Dakota for avariety of activities that involve bringing crude oil and natural gas from undergroundformations to the earth’s surface. Extraction/production was defined to include, but notlimited to, all activities associated with the removal of crude oil and natural gas from theground, and maintenance and periodic inspections of equipment used to extract oil and gas,and other production related activities, such as well work overs, well idling, shutdown, andabandonment activities (Appendix A). Also included in this segment of the industry are thegeneral business expenditures incurred by oil operators in North Dakota. Examples of theseexpenditures include, but are not limited to, office rent, office supplies, wages and salaries,communications, public utilities, business and professional services, insurance, and interestexpenses (Appendix A). Royalty revenues, both private and public, were included as directimpacts in the extraction/production segment of the petroleum industry. Collections fromstate severance taxes, which include the gross production tax and extraction tax, also wereincluded in the direct impacts.

Estimates of total in-state expenditures in 2007 for extraction/production and generalbusiness expenses were derived from the survey of oil operators and estimated on a BOEbasis. North Dakota produced 45,057,874 barrels of oil and 70,799,663 mcf of natural gas in2007. Those volumes of oil and gas production resulted in an estimated $441.5 million forin-state expenditures for extraction/production and $362.5 million for general businessexpenses. State oil and gas royalties were about $36.1 million (North Dakota State LandDepartment 2007). Total federal royalties returned to North Dakota were about $19.3 million(U.S. Department of the Interior 2008, U.S. Forest Service 2008).

Private royalties were based on data obtained from the survey of lease/brokerage firmsand on production data obtained from the survey of oil operators. Total royalties reported byoil operators were estimated at 14.9 percent and 14.2 percent of well output for oil and gas,respectively. Private royalties were estimated by subtracting state and gross federal royaltiesfrom estimated total royalties. Private royalties (i.e., both in-state and out-of-state mineralowners) from oil and gas production in North Dakota in 2007 were estimated at $369.2million. In-state payments of private royalties were estimated by applying the percentage ofin-state versus out-of-state mineral owners (53.8 percent) to the estimated total privateroyalties ($369.2 million). In-state private royalties in 2007 were estimated at $198.7million.

Total collections from the gross production tax and extraction tax in calendar year2007 were $141.9 million and $108.4 million, respectively (Office of State TaxCommissioner 2008). Those tax collections were included in the extraction/productionsegment of the petroleum industry.

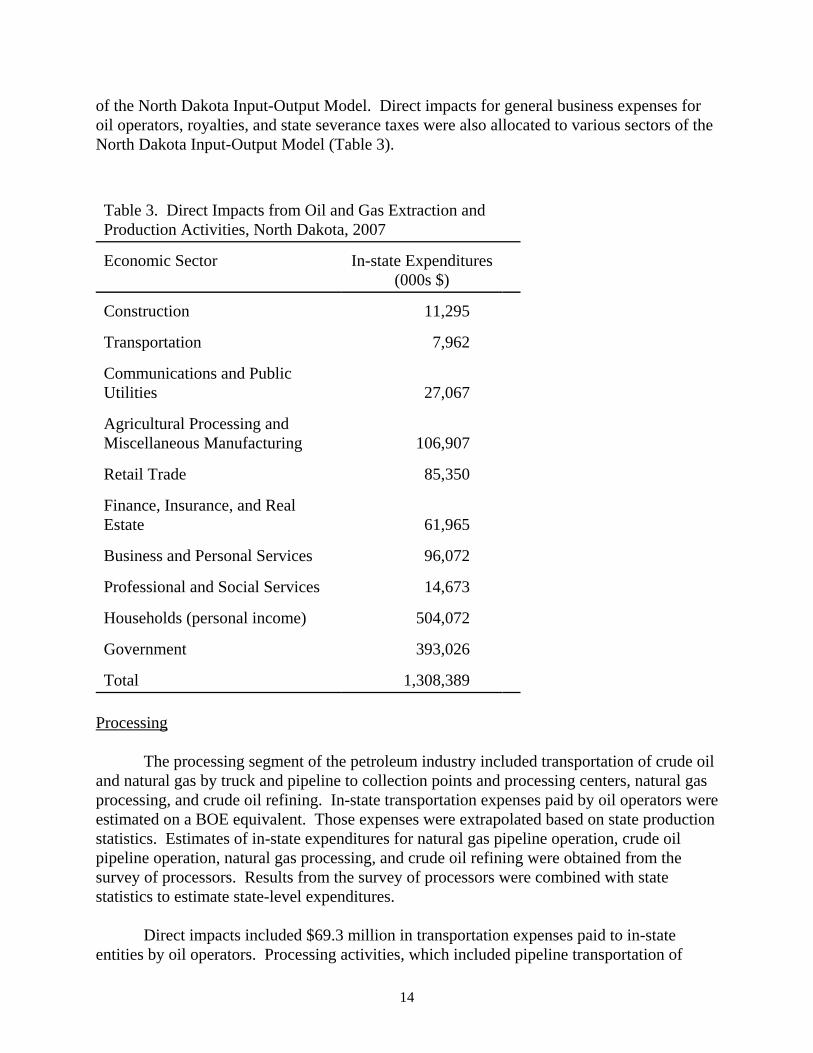

Total direct impacts in the extraction/production segment of the petroleum industry inNorth Dakota in 2007 were estimated at $1.3 billion (Table 3). Data from Bangsund andLeistritz (2007) was used to allocate the in-state expenditures for extraction to various sectors

13

of the North Dakota Input-Output Model. Direct impacts for general business expenses foroil operators, royalties, and state severance taxes were also allocated to various sectors of theNorth Dakota Input-Output Model (Table 3).

Table 3. Direct Impacts from Oil and Gas Extraction andProduction Activities, North Dakota, 2007

Economic Sector In-state Expenditures(000s $)

Construction 11,295

Transportation 7,962

Communications and PublicUtilities 27,067

Agricultural Processing andMiscellaneous Manufacturing 106,907

Retail Trade 85,350

Finance, Insurance, and RealEstate 61,965

Business and Personal Services 96,072

Professional and Social Services 14,673

Households (personal income) 504,072

Government 393,026

Total 1,308,389

Processing

The processing segment of the petroleum industry included transportation of crude oiland natural gas by truck and pipeline to collection points and processing centers, natural gasprocessing, and crude oil refining. In-state transportation expenses paid by oil operators wereestimated on a BOE equivalent. Those expenses were extrapolated based on state productionstatistics. Estimates of in-state expenditures for natural gas pipeline operation, crude oilpipeline operation, natural gas processing, and crude oil refining were obtained from thesurvey of processors. Results from the survey of processors were combined with statestatistics to estimate state-level expenditures.

Direct impacts included $69.3 million in transportation expenses paid to in-stateentities by oil operators. Processing activities, which included pipeline transportation of

14

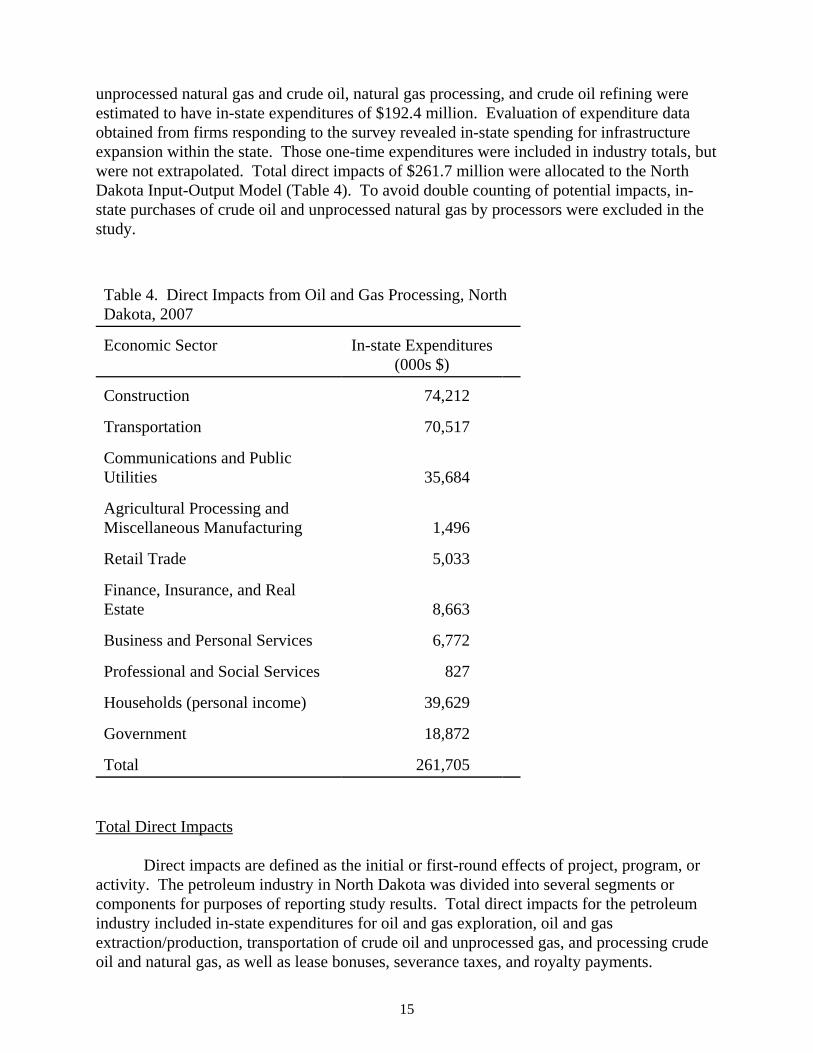

unprocessed natural gas and crude oil, natural gas processing, and crude oil refining wereestimated to have in-state expenditures of $192.4 million. Evaluation of expenditure dataobtained from firms responding to the survey revealed in-state spending for infrastructureexpansion within the state. Those one-time expenditures were included in industry totals, butwere not extrapolated. Total direct impacts of $261.7 million were allocated to the NorthDakota Input-Output Model (Table 4). To avoid double counting of potential impacts, in-state purchases of crude oil and unprocessed natural gas by processors were excluded in thestudy.

Table 4. Direct Impacts from Oil and Gas Processing, NorthDakota, 2007

Economic Sector In-state Expenditures(000s $)

Construction 74,212

Transportation 70,517

Communications and PublicUtilities 35,684

Agricultural Processing andMiscellaneous Manufacturing 1,496

Retail Trade 5,033

Finance, Insurance, and RealEstate 8,663

Business and Personal Services 6,772

Professional and Social Services 827

Households (personal income) 39,629

Government 18,872

Total 261,705

Total Direct Impacts

Direct impacts are defined as the initial or first-round effects of project, program, oractivity. The petroleum industry in North Dakota was divided into several segments orcomponents for purposes of reporting study results. Total direct impacts for the petroleumindustry included in-state expenditures for oil and gas exploration, oil and gasextraction/production, transportation of crude oil and unprocessed gas, and processing crudeoil and natural gas, as well as lease bonuses, severance taxes, and royalty payments.

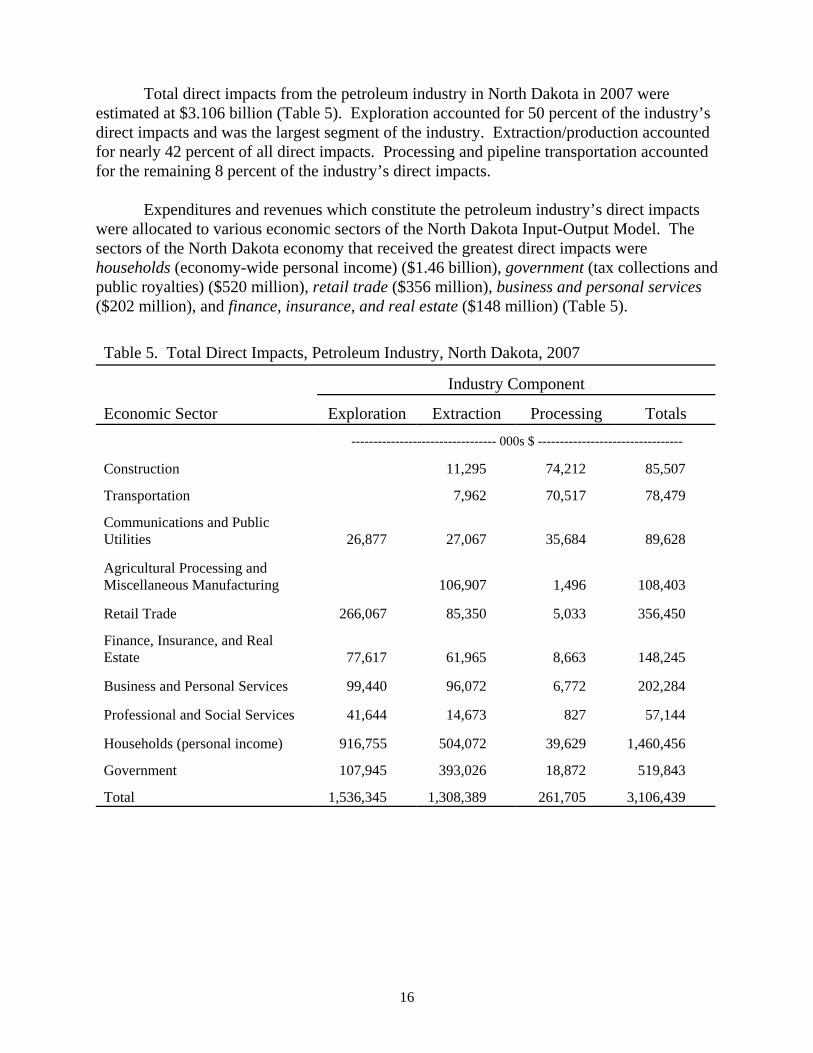

15

Total direct impacts from the petroleum industry in North Dakota in 2007 wereestimated at $3.106 billion (Table 5). Exploration accounted for 50 percent of the industry’sdirect impacts and was the largest segment of the industry. Extraction/production accountedfor nearly 42 percent of all direct impacts. Processing and pipeline transportation accountedfor the remaining 8 percent of the industry’s direct impacts.

Expenditures and revenues which constitute the petroleum industry’s direct impactswere allocated to various economic sectors of the North Dakota Input-Output Model. Thesectors of the North Dakota economy that received the greatest direct impacts werehouseholds (economy-wide personal income) ($1.46 billion), government (tax collections andpublic royalties) ($520 million), retail trade ($356 million), business and personal services($202 million), and finance, insurance, and real estate ($148 million) (Table 5).

Table 5. Total Direct Impacts, Petroleum Industry, North Dakota, 2007

Industry Component

Economic Sector Exploration Extraction Processing Totals--------------------------------- 000s $ ---------------------------------

Construction 11,295 74,212 85,507

Transportation 7,962 70,517 78,479

Communications and PublicUtilities 26,877 27,067 35,684 89,628

Agricultural Processing andMiscellaneous Manufacturing 106,907 1,496 108,403

Retail Trade 266,067 85,350 5,033 356,450

Finance, Insurance, and RealEstate 77,617 61,965 8,663 148,245

Business and Personal Services 99,440 96,072 6,772 202,284

Professional and Social Services 41,644 14,673 827 57,144

Households (personal income) 916,755 504,072 39,629 1,460,456

Government 107,945 393,026 18,872 519,843

Total 1,536,345 1,308,389 261,705 3,106,439

16

Secondary Impacts

Secondary economic impacts result from subsequent rounds of spending andrespending within an economy. Input-output (I-O) analysis traces linkages (i.e., the amountof spending and respending) among sectors of an economy and calculates the total businessactivity resulting from a direct impact in a basic sector (Coon et al. 1985). An economic sector is a group of similar economic units (e.g., communications and public utilities, retailtrade, construction).

This process of spending and respending can be explained by using an example. Asingle dollar from an in-state wheat producer (Households sector) may be spent for a loaf ofbread at the local store (Retail Trade sector); the store uses part of that dollar to pay for thenext shipment of bread (Transportation and Agricultural Processing sectors) and part to paythe store employee (Households sector) who shelved or sold the bread; the bread supplieruses part of that dollar to pay for the grain used to make the bread (Agriculture-Crops sector)... and so on (Hamm et al. 1993).

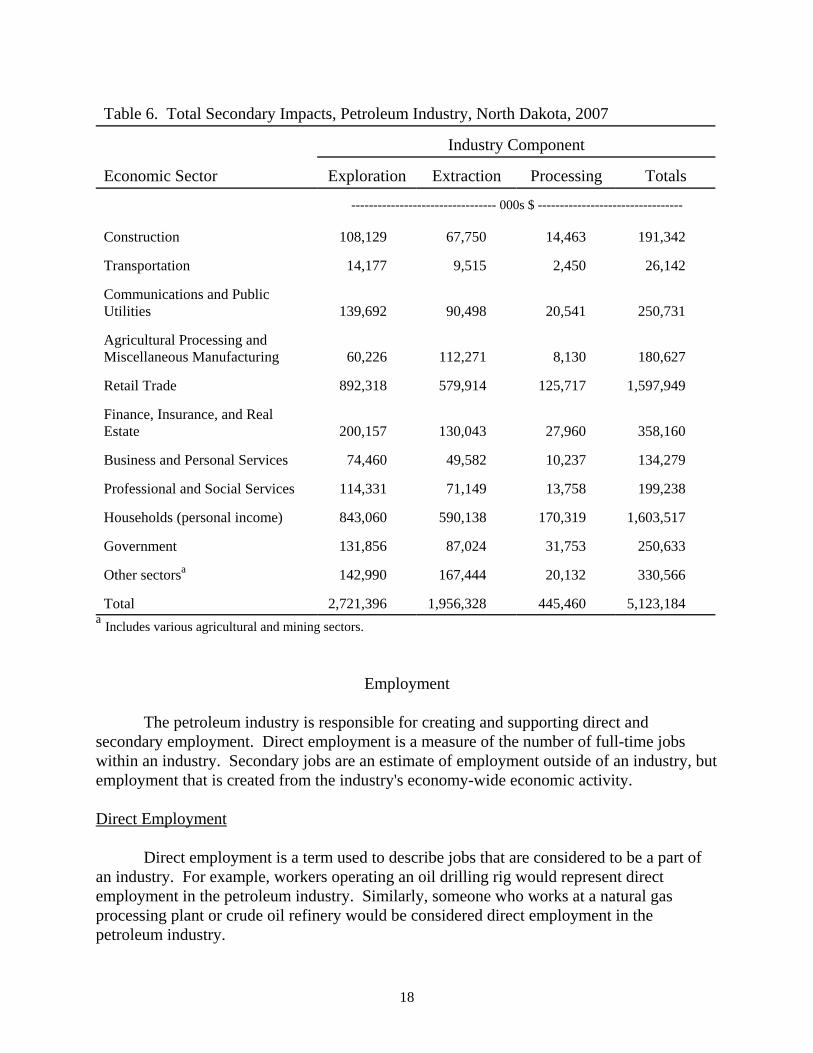

Secondary economic impacts were estimated separately for exploration, extraction,and processing components of the petroleum industry. Results from the North Dakota Input-Output Model revealed that secondary economic impacts from exploration in North Dakotain 2007 would be about $2.7 billion (Table 6). The $1.3 billion in direct impacts for oil andgas extraction (production) activities produced an estimated $1.96 billion in secondaryeconomic impacts. Finally, the transportation and processing segment of the petroleumindustry was responsible for $445 million in secondary economic impacts. Total secondaryeconomic impacts from all components of the petroleum industry were estimated at $5.1billion. Across all three major components of the petroleum industry, considerable secondaryimpacts were generated in the households (economy-wide personal income) ($1.6 billion),retail trade ($1.6 billion), finance, insurance, and real estate ($358 million), communicationsand public utilities ($251 million), and government ($251 million) (Table 6).

17

Table 6. Total Secondary Impacts, Petroleum Industry, North Dakota, 2007

Industry Component

Economic Sector Exploration Extraction Processing Totals

--------------------------------- 000s $ ---------------------------------

Construction 108,129 67,750 14,463 191,342

Transportation 14,177 9,515 2,450 26,142

Communications and PublicUtilities 139,692 90,498 20,541 250,731

Agricultural Processing andMiscellaneous Manufacturing 60,226 112,271 8,130 180,627

Retail Trade 892,318 579,914 125,717 1,597,949

Finance, Insurance, and RealEstate 200,157 130,043 27,960 358,160

Business and Personal Services 74,460 49,582 10,237 134,279

Professional and Social Services 114,331 71,149 13,758 199,238

Households (personal income) 843,060 590,138 170,319 1,603,517

Government 131,856 87,024 31,753 250,633

Other sectorsa 142,990 167,444 20,132 330,566

Total 2,721,396 1,956,328 445,460 5,123,184a Includes various agricultural and mining sectors.

Employment

The petroleum industry is responsible for creating and supporting direct andsecondary employment. Direct employment is a measure of the number of full-time jobswithin an industry. Secondary jobs are an estimate of employment outside of an industry, butemployment that is created from the industry's economy-wide economic activity.

Direct Employment

Direct employment is a term used to describe jobs that are considered to be a part ofan industry. For example, workers operating an oil drilling rig would represent directemployment in the petroleum industry. Similarly, someone who works at a natural gasprocessing plant or crude oil refinery would be considered direct employment in thepetroleum industry.

18

While employment figures are frequently reported by various governmental agenciesand are broken into a hierarchy of categories (e.g., North American Industry ClassificationSystem), deriving specific estimates of employment for large basic-sector industries can beproblematic. Much of the problem arises in defining the type of job, and attributing to whichindustry(s) created that employment. For example, the process of drilling an oil welltypically requires developing a road and a drilling site; work that requires heavy constructionwith earth moving or excavating equipment. Most oil companies will contract that work tolocal firms that specialize in heavy construction or excavating. The individuals performingthe road building and preparation of the drill site are likely to be employed with some type ofconstruction firm, and as a result, those jobs are typically classified and reported bygovernment agencies as construction. Government agencies (e.g., Bureau of the Census,Bureau of Labor Statistics) that track employment often base the classification of those jobson the type of activities that generate the most revenue for a firm (primary activities). In thisexample, the primary activity for this firm is likely to be construction, even if the specificactivities are road building and drill site preparation. However, in the case of assigningwhich basic-sector industry created that employment, it may be more accurate to suggestthose jobs exist as a result of the petroleum industry rather than the construction industry. Yet, in other cases, the level of oil well drilling activity may be insufficient to sustainemployment in heavy construction for an entire year. Those situations result in seasonal orpart-time job creation. The challenge is to measure or estimate the total number of full-timejobs created and sustained by the petroleum industry, even if those jobs appear to be part ofanother industry or are only created for part of a year.

Estimates of direct employment were generated from the survey of oil operators andprocessors, and from key parameters obtained from the survey of service and support firms(Bangsund and Leistritz 2007). The survey of oil operators and processors specifically askedfor the number of full-time jobs in North Dakota (Appendices A and B). Employmentfigures from the survey of oil operators were extrapolated to state totals based on a BOEbasis, while employment data from the survey of processors was extrapolated based on state-level statistics for those operations (e.g., processing volumes). Thus, estimating full-timeemployment by oil operators, pipeline firms, and processors in North Dakota was relativelystraightforward.

Oil operators (firms owning or operating wells) contract much of the work ofexploration and extraction of oil and gas to firms that specialize in various aspects of thethose processes. While some of the work in the oil fields is performed by firms located inother states, much of the work is performed by firms located in close proximity toproduction. One of the difficulties of estimating employment in the service and supportcapacities is determining those jobs that are fully supported versus those jobs that are onlypartially supported by the petroleum industry. An additional complexity is to only attributefull-time employment to the petroleum activities located in North Dakota. For many firmslocated in the oil producing region of North Dakota, the obvious possibility is that someemployment by those firms could be partially or wholly supported by petroleum activities inMontana, Canada, or possibly in other states.

19

The questionnaire used in the service and support survey was designed to address thedegree of job support from the petroleum industry and the level of job support attributable toonly petroleum activities in North Dakota (Bangsund and Leistritz 2007). Data on the grossrevenue needed to support one-full time position within the oil field in North Dakota wasadjusted for inflation using the Gross Domestic Product-Implicit Price Deflator (U.S.Department of Commerce 2008). Total state employment for work in the oil fields was thenestimated based on an adjusted level of spending per FTE job and combined with data fromthe oil operator survey for contract work in the areas of exploration, extraction/production,and transportation in North Dakota.

Employment in North Dakota by oil operators in 2007 was estimated at 1,808 full-time equivalent (FTE) positions. Employment in the processing segment of the industry,which included some pipeline employment, was estimated at 579 FTE jobs. Totalemployment in the oil field for contract work, which includes exploration and extractionsegments of the industry, was estimated at 5,332 FTE jobs. The petroleum industry2, asdefined and evaluated in this study, was estimated to create and support 7,719 FTE positionsin North Dakota in 2007.

Secondary Employment

Secondary employment is a term used to describe jobs that are created and supportedby the volume of business activity generated by an industry, but does not include jobs that arepart of the industry. Direct employment and secondary employment are two distinctlydifferent measures. Productivity ratios3 were used with estimates of business activity invarious sectors of the North Dakota economy to obtain estimates of secondary employment. The petroleum industry in North Dakota was estimated to generate an additional $5.1 billionin secondary business activity, which was sufficient to support 38,500 FTE jobs.

2 The petroleum industry in this study did not include employment associated with transportation ofprocessed petroleum products, marketing, or retail sales. In many cases, those downstream componentsof the industry generate substantial employment. Unfortunately, breakout of jobs by segment of theindustry previously reported are no longer available. In 2006, the petroleum industry in North Dakotawas responsible for over 9,200 jobs, excluding jobs in petroleum refining activities due to non-disclosurerules (American Petroleum Institute 2007). However, industry-wide direct employment in 2006 included507 jobs in transportation (jobs in retail distribution also were not disclosed) and 1,671 jobs in wholesaleoperations; two components of the petroleum industry that were only partially included in this study. TheAmerican Petroleum Institute also estimated that retail gasoline stations in the state were responsible for4,058 jobs in 2006; employment that was considered in addition to the 5,179 jobs attributable to othersegments of the petroleum industry (American Petroleum Institute 2007). While similar data for 2007 isnot available, employment changes reported by the American Petroleum Institute from 2005 to 2006 areconsistent with changes observed in this study from 2005 to 2007.

3A measure of the amount of business activity needed in an economic sector to support one full-timejob.

20

Government Revenues

Governmental revenues, usually based on tax collections, are another importantmeasure of the economic impact of an industry on an economy. The petroleum industry inNorth Dakota, specifically oil and gas production, is responsible for substantial amounts ofstate and local government revenues. One distinction is that unlike many other industries inNorth Dakota, severance taxes (taxes placed on the value of oil and gas removed from theground) collect money based on gross revenues produced by the industry. In contrast,taxation for most other industries is more traditional and usually limited to real property andnet income. Another distinction that makes the petroleum industry different from otherindustries in the state is that governments can hold oil and gas leases and receive royaltiesfrom the value of oil and gas production. Of course, the petroleum industry also generatesrevenues from traditional sources, such as personal income, corporate income, sales and use,and property tax collections.

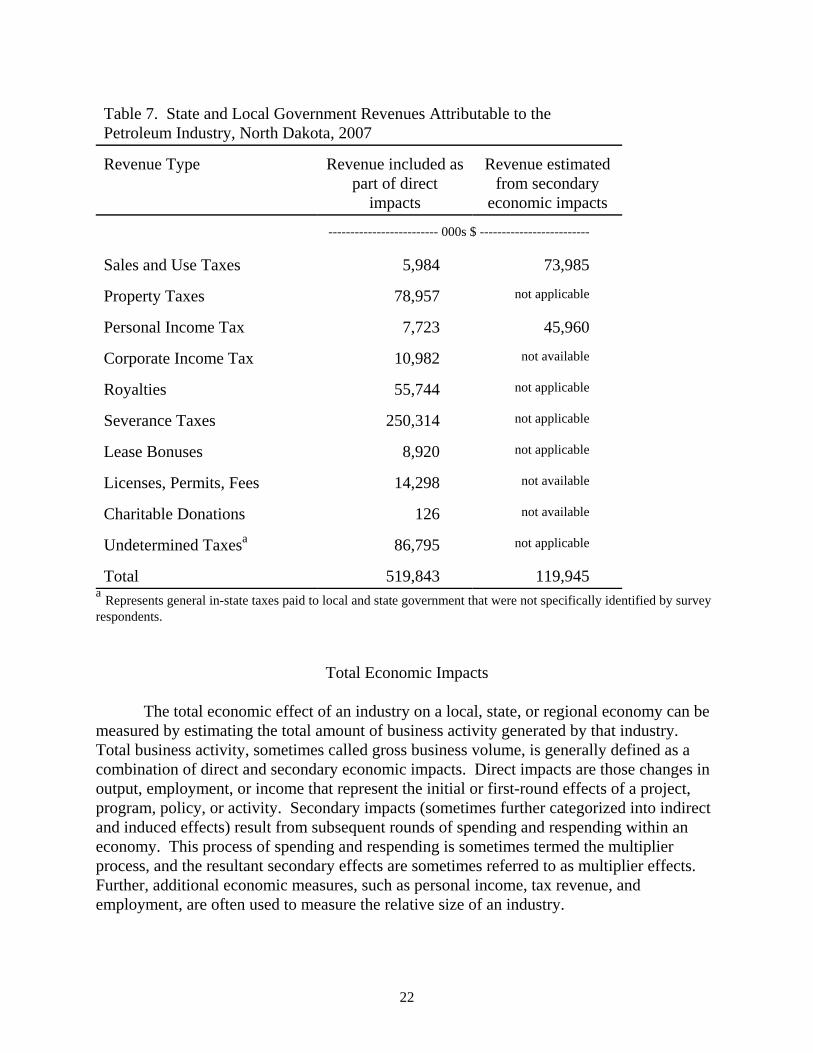

Severance taxes, sales and use taxes, personal income taxes, corporate income taxes,property taxes, royalties, lease bonuses, charitable donations, and licenses, fees, and permitscombined for $519.8 million in government revenues that were directly attributable to thepetroleum industry in North Dakota in 2007 (Table 7). Exploration, extraction/production,and processing segments of the industry were responsible for about 21, 76, and 3 percent,respectively, of the total government revenues from the petroleum industry in North Dakota.

Severance taxes accounted for nearly half (48 percent) of all government revenuesfrom the petroleum industry in North Dakota in 2007. The second largest source was themost common general taxes (i.e., property, personal income, sales and use, and corporateincome) at 36 percent, followed by royalties at 11 percent. The remainder of governmentrevenues represented lease bonuses, permits/fees/licenses, miscellaneous revenues.

In addition to the government revenues that were included as direct impacts,collections from personal income and sales and use taxes were estimated based on thesecondary economic activity generated by the petroleum industry. Secondary economicimpacts in the Retail Trade sector were used to estimate revenue from sales and use taxes. Economic activity in the Households sector (which represents economy-wide personalincome) was used to estimate personal income tax collections. Total collections of personalincome and sales and use taxes arising from secondary economic activity were estimated at$119.9 million (Table 7).

21

Table 7. State and Local Government Revenues Attributable to the Petroleum Industry, North Dakota, 2007

Revenue Type Revenue included aspart of direct

impacts

Revenue estimatedfrom secondary

economic impacts

------------------------- 000s $ -------------------------

Sales and Use Taxes 5,984 73,985

Property Taxes 78,957 not applicable

Personal Income Tax 7,723 45,960

Corporate Income Tax 10,982 not available

Royalties 55,744 not applicable

Severance Taxes 250,314 not applicable

Lease Bonuses 8,920 not applicable

Licenses, Permits, Fees 14,298 not available

Charitable Donations 126 not available

Undetermined Taxesa 86,795 not applicable

Total 519,843 119,945a Represents general in-state taxes paid to local and state government that were not specifically identified by surveyrespondents.

Total Economic Impacts

The total economic effect of an industry on a local, state, or regional economy can bemeasured by estimating the total amount of business activity generated by that industry. Total business activity, sometimes called gross business volume, is generally defined as acombination of direct and secondary economic impacts. Direct impacts are those changes inoutput, employment, or income that represent the initial or first-round effects of a project,program, policy, or activity. Secondary impacts (sometimes further categorized into indirectand induced effects) result from subsequent rounds of spending and respending within aneconomy. This process of spending and respending is sometimes termed the multiplierprocess, and the resultant secondary effects are sometimes referred to as multiplier effects. Further, additional economic measures, such as personal income, tax revenue, andemployment, are often used to measure the relative size of an industry.

22

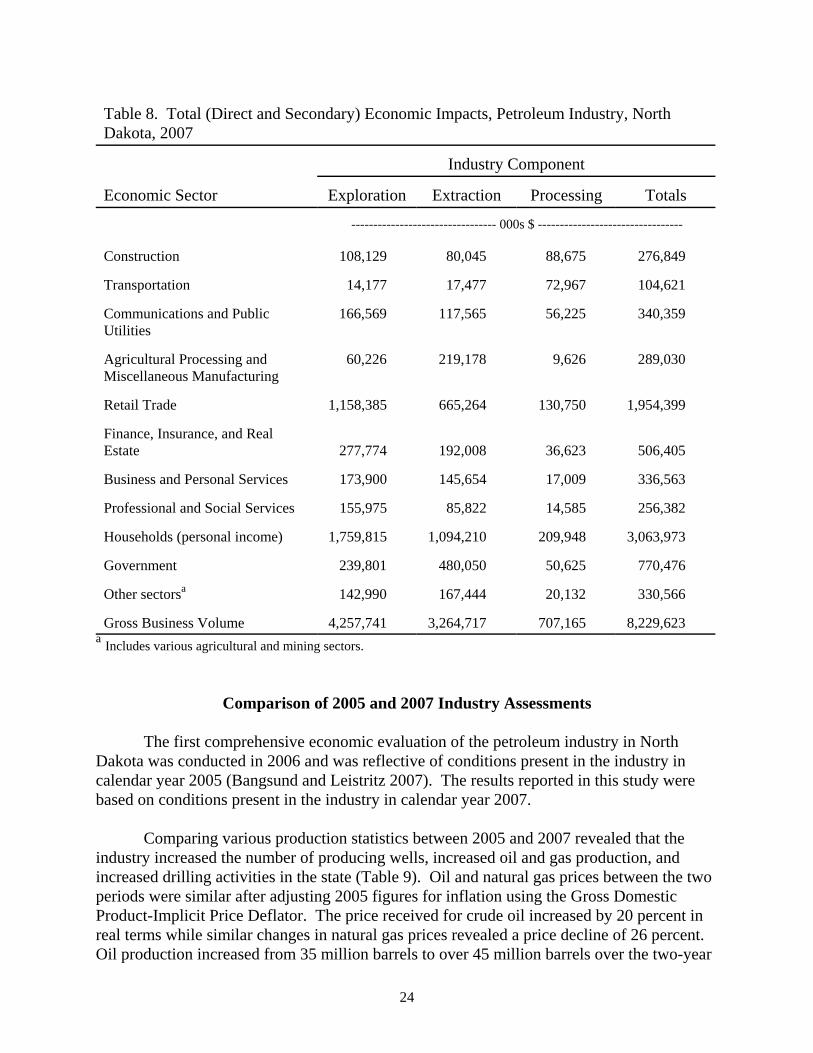

The petroleum industry in North Dakota was defined to include exploration,extraction/production, transportation, and processing of crude oil and natural gas. Directimpacts were based on in-state expenditures, private and public royalties, taxes, and leasebonuses. Direct impacts were allocated to various sectors of the North Dakota Input-OutputModel to generate estimates of the secondary economic impacts.

The direct impact of exploration in 2007 was estimated at $1.5 billion. Totalsecondary economic impacts associated with exploration activities were estimated at $2.7billion. The in-state gross business volume of exploration activities was estimated at $4.26billion in 2007 (Table 8).

The direct impact of extraction/production in 2007 was estimated at $1.3 billion. Total secondary economic impacts associated with extraction and production activities wereestimated at $1.96 billion. The in-state gross business volume of oil and gas extraction wasestimated at $3.26 billion in 2007 (Table 8).

The processing component of the petroleum industry was estimated to have a directimpact in North Dakota of $262 million. Total secondary economic impacts associated withprocessing and transporting crude oil and natural gas were estimated at $445 million. The in-state gross business volume of processing and transporting crude oil and natural gas wasestimated at $707 million in 2007 (Table 8).

Industry-wide direct impacts from the petroleum industry were estimated at $3.106billion in 2007. Total secondary economic impacts associated with the industry wereestimated at $5.123 billion. The gross business volume for the petroleum industry in NorthDakota in 2007 was estimated at $8.23 billion (Table 8).

Additional measures of the petroleum industry’s economic importance to the stateinclude direct employment for 7,719 full-time jobs, economy-wide personal income of $3.06billion, statewide retail sales of nearly $2 billion, direct contributions to local and stategovernment revenues of $520 million, indirect contribution of $120 million in stategovernment tax collections, and secondary employment of 38,500 full-time equivalent jobs. For every dollar spent in the state by the petroleum industry, another $1.65 in additionalbusiness activity was generated.

Some very generic or average impact figures can be produced for basic oil and gasproduction statistics. Based on a gross business volume of $8.23 billion for the petroleumindustry, total economic effects in North Dakota would be about $145 per BOE, or if impactswere only evaluated for crude oil production, total effects would be nearly $183 per barrel. Based on active wells in the state, the overall economic effect (direct and secondary impactsfrom all segments of the industry) per well (averaged for all producing wells) would be about$2.19 million annually.

23

Table 8. Total (Direct and Secondary) Economic Impacts, Petroleum Industry, NorthDakota, 2007

Industry Component

Economic Sector Exploration Extraction Processing Totals

--------------------------------- 000s $ ---------------------------------

Construction 108,129 80,045 88,675 276,849

Transportation 14,177 17,477 72,967 104,621

Communications and PublicUtilities

166,569 117,565 56,225 340,359

Agricultural Processing andMiscellaneous Manufacturing

60,226 219,178 9,626 289,030

Retail Trade 1,158,385 665,264 130,750 1,954,399

Finance, Insurance, and RealEstate 277,774 192,008 36,623 506,405

Business and Personal Services 173,900 145,654 17,009 336,563

Professional and Social Services 155,975 85,822 14,585 256,382

Households (personal income) 1,759,815 1,094,210 209,948 3,063,973

Government 239,801 480,050 50,625 770,476

Other sectorsa 142,990 167,444 20,132 330,566

Gross Business Volume 4,257,741 3,264,717 707,165 8,229,623a Includes various agricultural and mining sectors.

Comparison of 2005 and 2007 Industry Assessments

The first comprehensive economic evaluation of the petroleum industry in NorthDakota was conducted in 2006 and was reflective of conditions present in the industry incalendar year 2005 (Bangsund and Leistritz 2007). The results reported in this study werebased on conditions present in the industry in calendar year 2007.

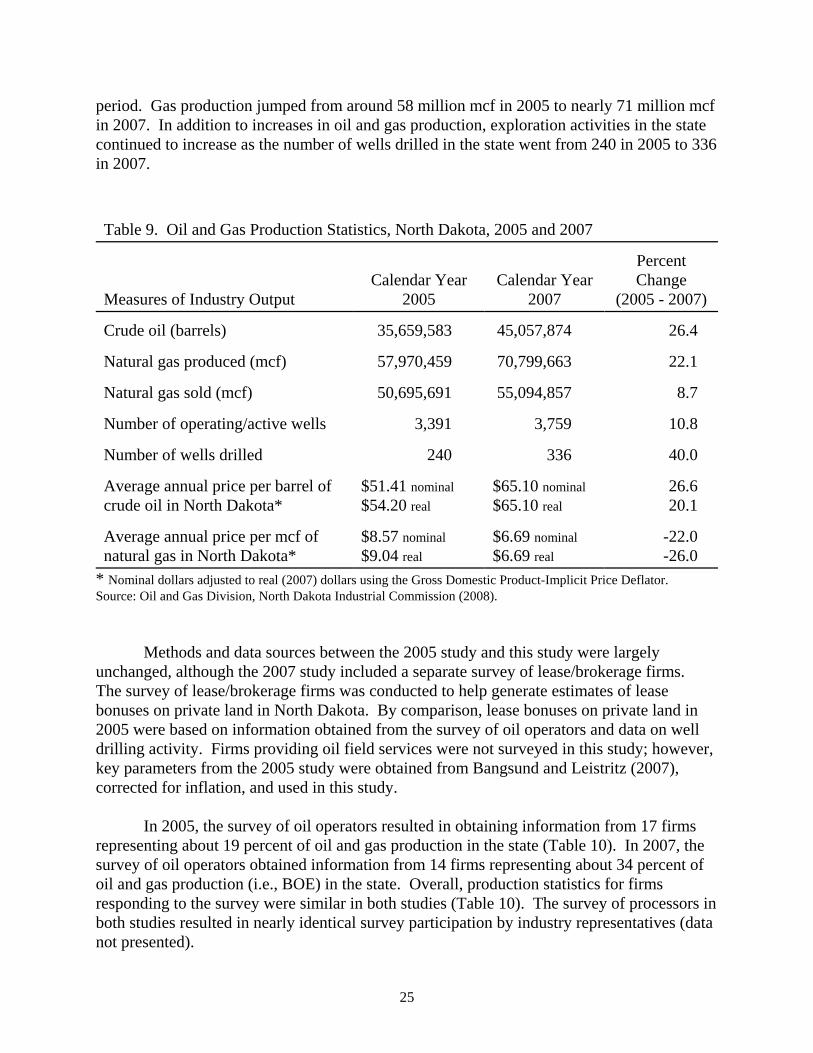

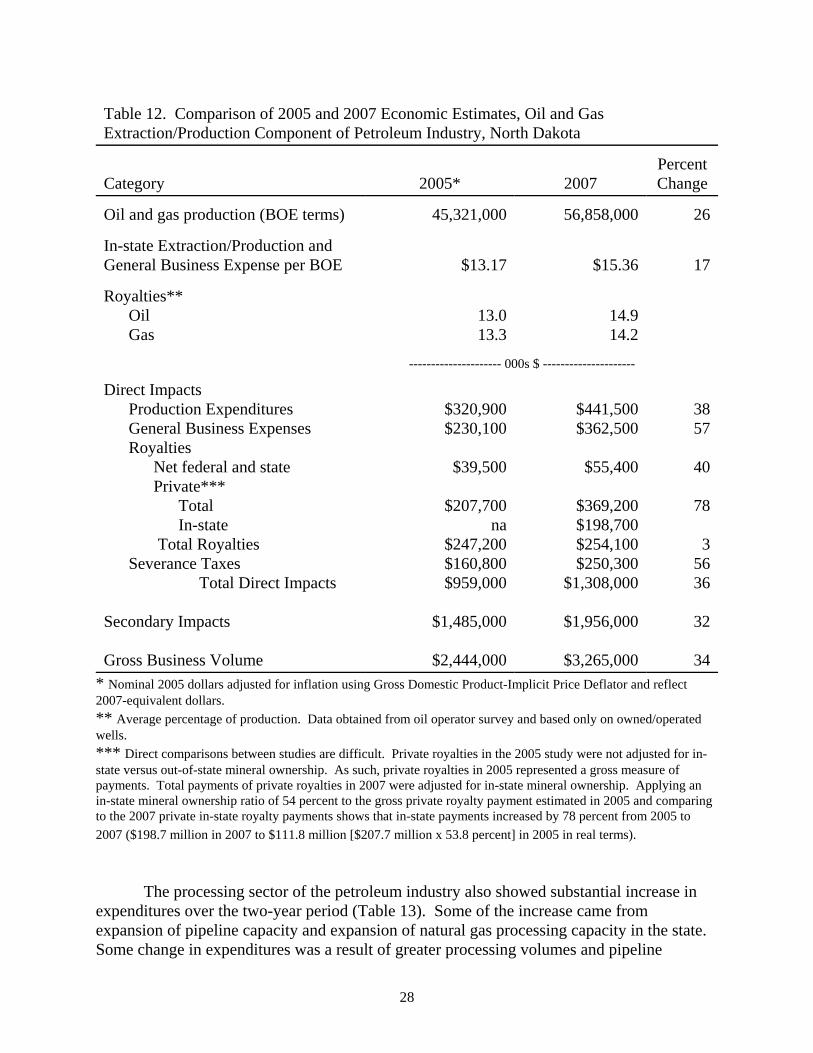

Comparing various production statistics between 2005 and 2007 revealed that theindustry increased the number of producing wells, increased oil and gas production, andincreased drilling activities in the state (Table 9). Oil and natural gas prices between the twoperiods were similar after adjusting 2005 figures for inflation using the Gross DomesticProduct-Implicit Price Deflator. The price received for crude oil increased by 20 percent inreal terms while similar changes in natural gas prices revealed a price decline of 26 percent. Oil production increased from 35 million barrels to over 45 million barrels over the two-year

24

period. Gas production jumped from around 58 million mcf in 2005 to nearly 71 million mcfin 2007. In addition to increases in oil and gas production, exploration activities in the statecontinued to increase as the number of wells drilled in the state went from 240 in 2005 to 336in 2007.

Table 9. Oil and Gas Production Statistics, North Dakota, 2005 and 2007

Measures of Industry OutputCalendar Year

2005Calendar Year

2007

PercentChange

(2005 - 2007)

Crude oil (barrels) 35,659,583 45,057,874 26.4

Natural gas produced (mcf) 57,970,459 70,799,663 22.1

Natural gas sold (mcf) 50,695,691 55,094,857 8.7

Number of operating/active wells 3,391 3,759 10.8

Number of wells drilled 240 336 40.0

Average annual price per barrel ofcrude oil in North Dakota*

$51.41 nominal$54.20 real

$65.10 nominal$65.10 real

26.620.1

Average annual price per mcf ofnatural gas in North Dakota*

$8.57 nominal$9.04 real

$6.69 nominal$6.69 real

-22.0-26.0

* Nominal dollars adjusted to real (2007) dollars using the Gross Domestic Product-Implicit Price Deflator.Source: Oil and Gas Division, North Dakota Industrial Commission (2008).

Methods and data sources between the 2005 study and this study were largelyunchanged, although the 2007 study included a separate survey of lease/brokerage firms. The survey of lease/brokerage firms was conducted to help generate estimates of leasebonuses on private land in North Dakota. By comparison, lease bonuses on private land in2005 were based on information obtained from the survey of oil operators and data on welldrilling activity. Firms providing oil field services were not surveyed in this study; however,key parameters from the 2005 study were obtained from Bangsund and Leistritz (2007),corrected for inflation, and used in this study.

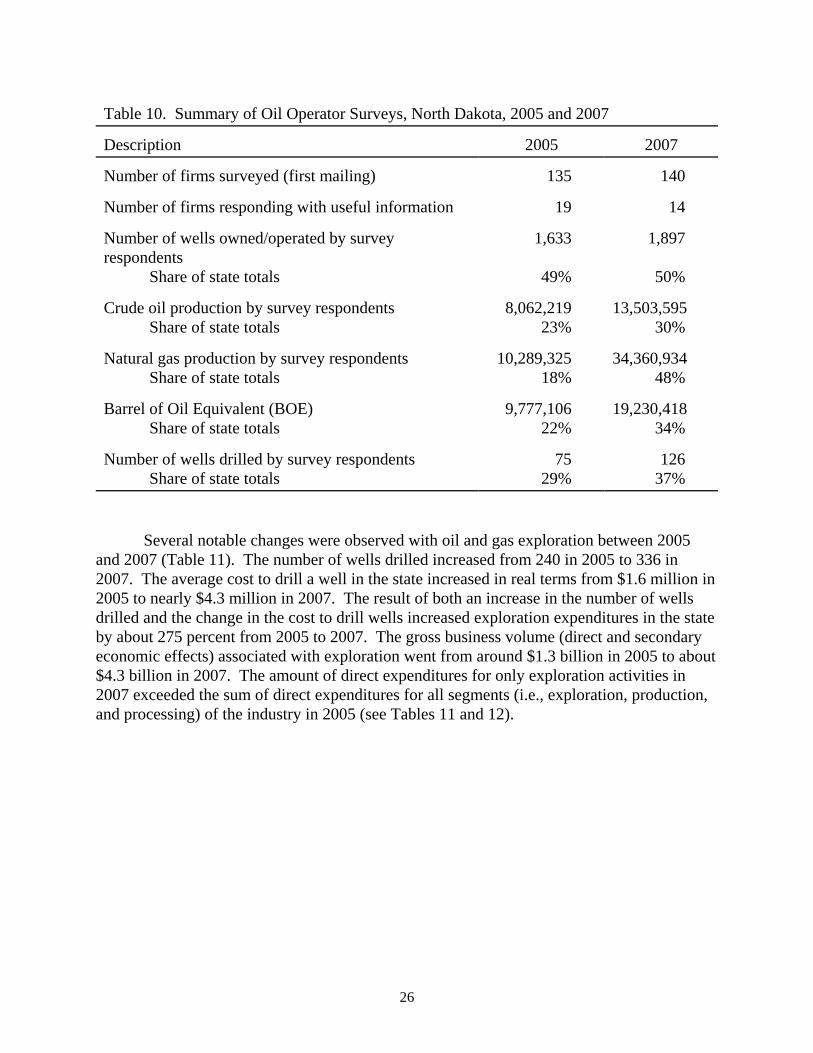

In 2005, the survey of oil operators resulted in obtaining information from 17 firmsrepresenting about 19 percent of oil and gas production in the state (Table 10). In 2007, thesurvey of oil operators obtained information from 14 firms representing about 34 percent ofoil and gas production (i.e., BOE) in the state. Overall, production statistics for firmsresponding to the survey were similar in both studies (Table 10). The survey of processors inboth studies resulted in nearly identical survey participation by industry representatives (datanot presented).

25

Table 10. Summary of Oil Operator Surveys, North Dakota, 2005 and 2007

Description 2005 2007

Number of firms surveyed (first mailing) 135 140

Number of firms responding with useful information 19 14

Number of wells owned/operated by surveyrespondents Share of state totals

1,633

49%

1,897

50%

Crude oil production by survey respondents Share of state totals

8,062,21923%

13,503,59530%

Natural gas production by survey respondents Share of state totals

10,289,32518%

34,360,93448%

Barrel of Oil Equivalent (BOE) Share of state totals

9,777,10622%

19,230,41834%

Number of wells drilled by survey respondents Share of state totals

7529%

12637%

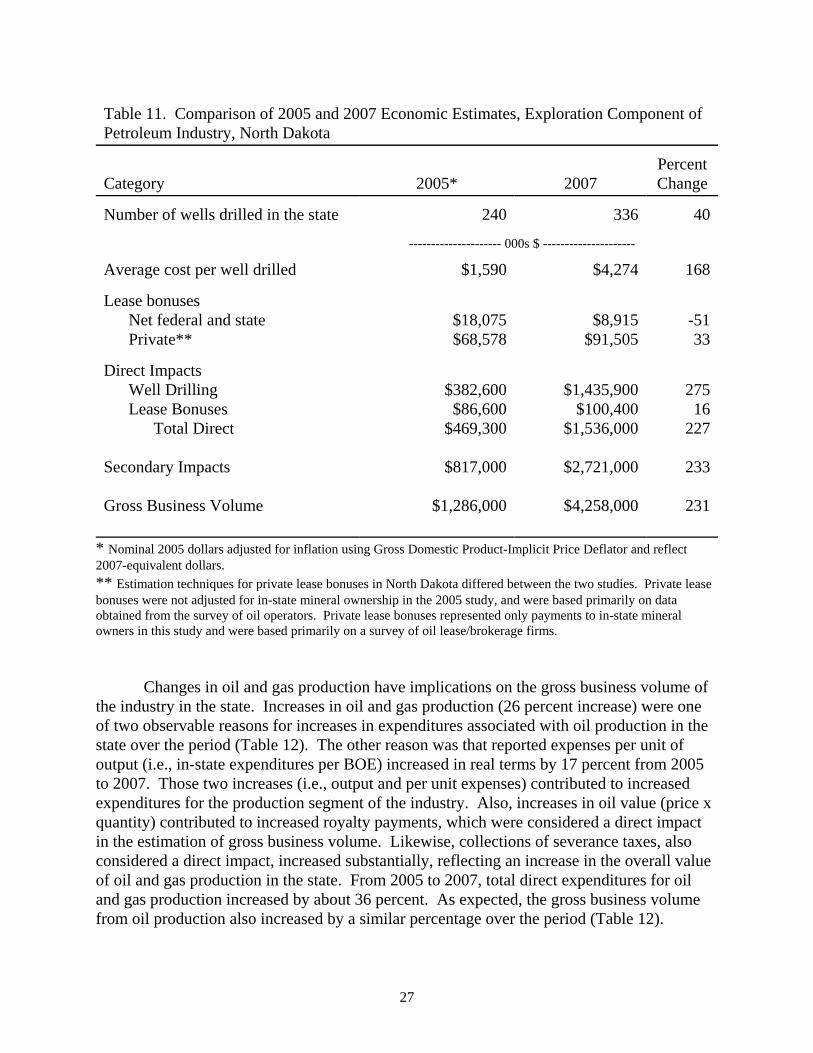

Several notable changes were observed with oil and gas exploration between 2005and 2007 (Table 11). The number of wells drilled increased from 240 in 2005 to 336 in2007. The average cost to drill a well in the state increased in real terms from $1.6 million in2005 to nearly $4.3 million in 2007. The result of both an increase in the number of wellsdrilled and the change in the cost to drill wells increased exploration expenditures in the stateby about 275 percent from 2005 to 2007. The gross business volume (direct and secondaryeconomic effects) associated with exploration went from around $1.3 billion in 2005 to about$4.3 billion in 2007. The amount of direct expenditures for only exploration activities in2007 exceeded the sum of direct expenditures for all segments (i.e., exploration, production,and processing) of the industry in 2005 (see Tables 11 and 12).

26

Table 11. Comparison of 2005 and 2007 Economic Estimates, Exploration Component ofPetroleum Industry, North Dakota

Category 2005* 2007PercentChange

Number of wells drilled in the state 240 336 40

--------------------- 000s $ ---------------------

Average cost per well drilled $1,590 $4,274 168

Lease bonuses Net federal and state Private**

$18,075$68,578

$8,915$91,505

-5133

Direct Impacts Well Drilling Lease Bonuses Total Direct

Secondary Impacts

Gross Business Volume

$382,600$86,600

$469,300

$817,000

$1,286,000

$1,435,900$100,400

$1,536,000

$2,721,000

$4,258,000

27516

227

233

231

* Nominal 2005 dollars adjusted for inflation using Gross Domestic Product-Implicit Price Deflator and reflect2007-equivalent dollars.** Estimation techniques for private lease bonuses in North Dakota differed between the two studies. Private leasebonuses were not adjusted for in-state mineral ownership in the 2005 study, and were based primarily on dataobtained from the survey of oil operators. Private lease bonuses represented only payments to in-state mineralowners in this study and were based primarily on a survey of oil lease/brokerage firms.