padd 2 presentation - platts energy forum november, 2011 padd 2 crude oil market dynamics today’s...

TRANSCRIPT

Katherine Spector

CIBC Commodities Strategy

NY Energy Forum November, 2011

PADD 2 Crude Oil Market DynamicsToday’s Market & Five Year Forward View

New York Energy Forum, November 22, 2011 (K. Spector) 2

• How we got here• Recent new information• Looking five years ahead

PADD 2 Historically, Now, & In the Future

New York Energy Forum, November 22, 2011 (K. Spector) 3

(Where Is PADD 2 Again?)

Alberta, CA

Cushing, OK

New York Energy Forum, November 22, 2011 (K. Spector) 4

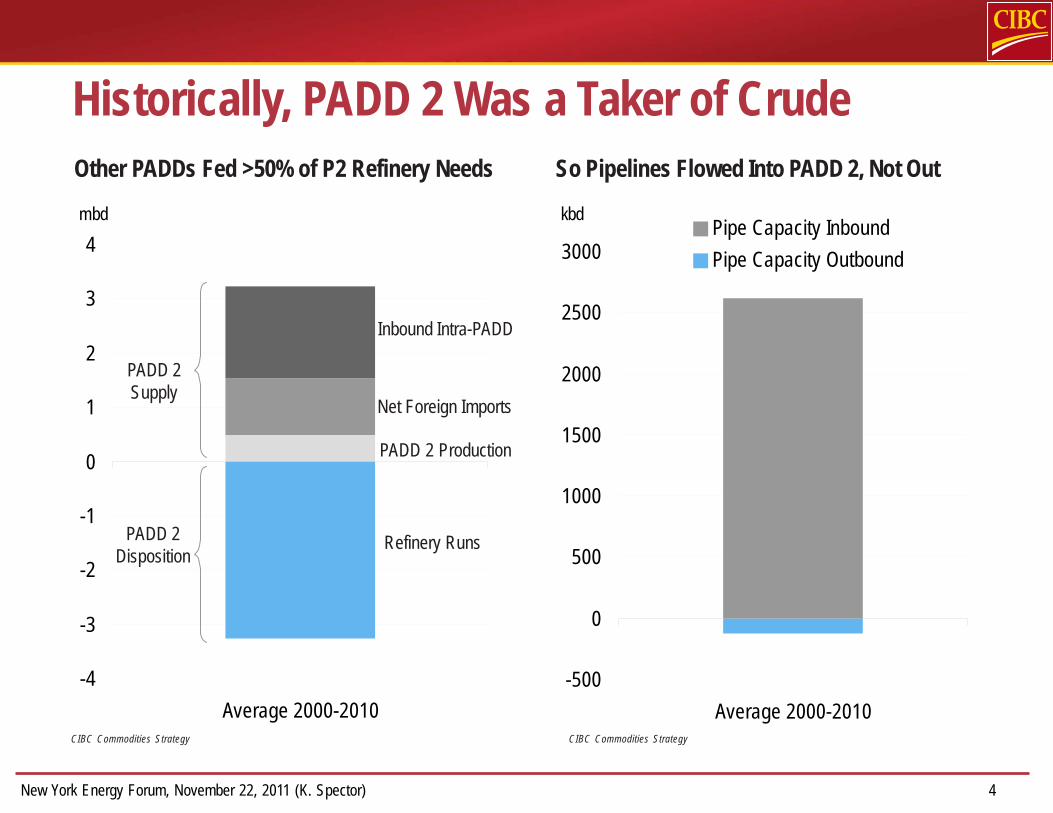

Historically, PADD 2 Was a Taker of Crude

-4

-3

-2

-1

0

1

2

3

4

Average 2000-2010

mbd

Other PADDs Fed >50% of P2 Refinery Needs

CIBC Commodities Strategy

-500

0

500

1000

1500

2000

2500

3000

Average 2000-2010

kbdPipe Capacity Inbound

Pipe Capacity Outbound

So Pipelines Flowed Into PADD 2, Not Out

CIBC Commodities Strategy

PADD 2Supply

PADD 2Disposition

Refinery Runs

PADD 2 Production

Net Foreign Imports

Inbound Intra-PADD

New York Energy Forum, November 22, 2011 (K. Spector) 5

But Quite Suddenly, PADD 2 Supply Took Off

339

491

-100

0

100

200

300

400

500

600

700

800

900

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

kbd

Padd 2 Production (mostly Bakken) Foreign Imports (mostly Canadian)

Cumulative Supply Growth Into PADD 2: Thanks To Alberta & The US Bakken

CIBC Commodities Strategy, EIA

New York Energy Forum, November 22, 2011 (K. Spector) 6

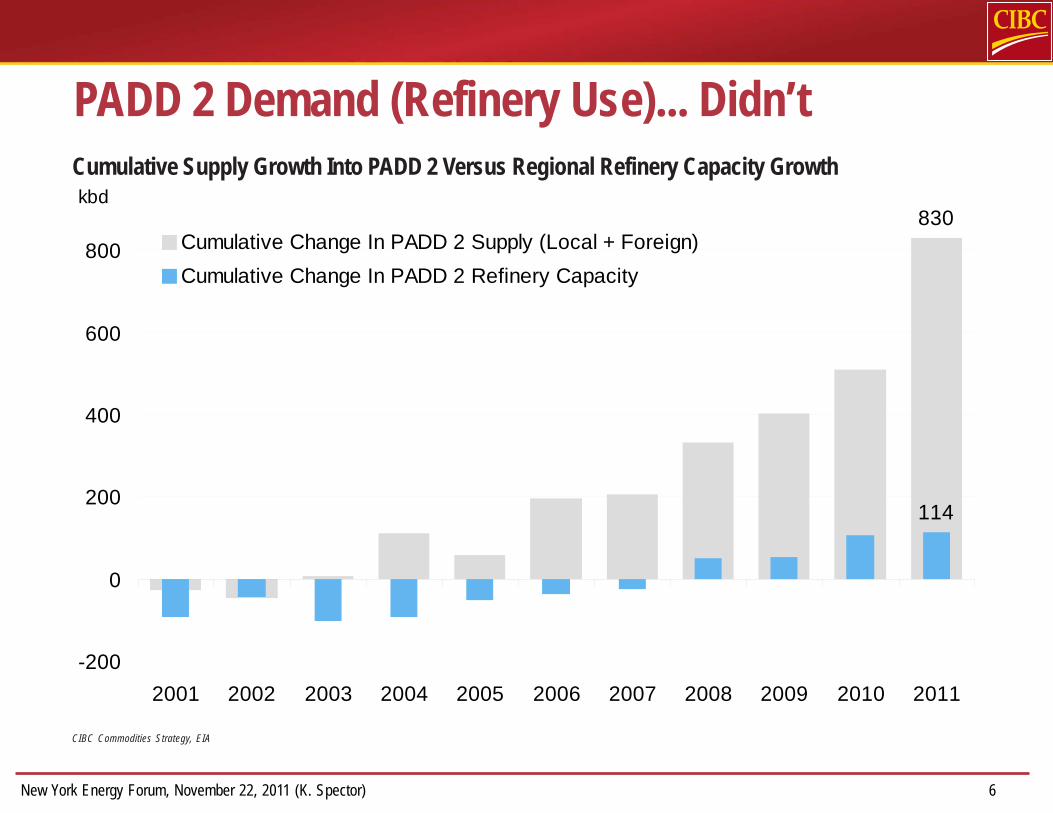

PADD 2 Demand (Refinery Use)... Didn’t

830

114

-200

0

200

400

600

800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

kbd

Cumulative Change In PADD 2 Supply (Local + Foreign)

Cumulative Change In PADD 2 Refinery Capacity

Cumulative Supply Growth Into PADD 2 Versus Regional Refinery Capacity Growth

CIBC Commodities Strategy, EIA

New York Energy Forum, November 22, 2011 (K. Spector) 7

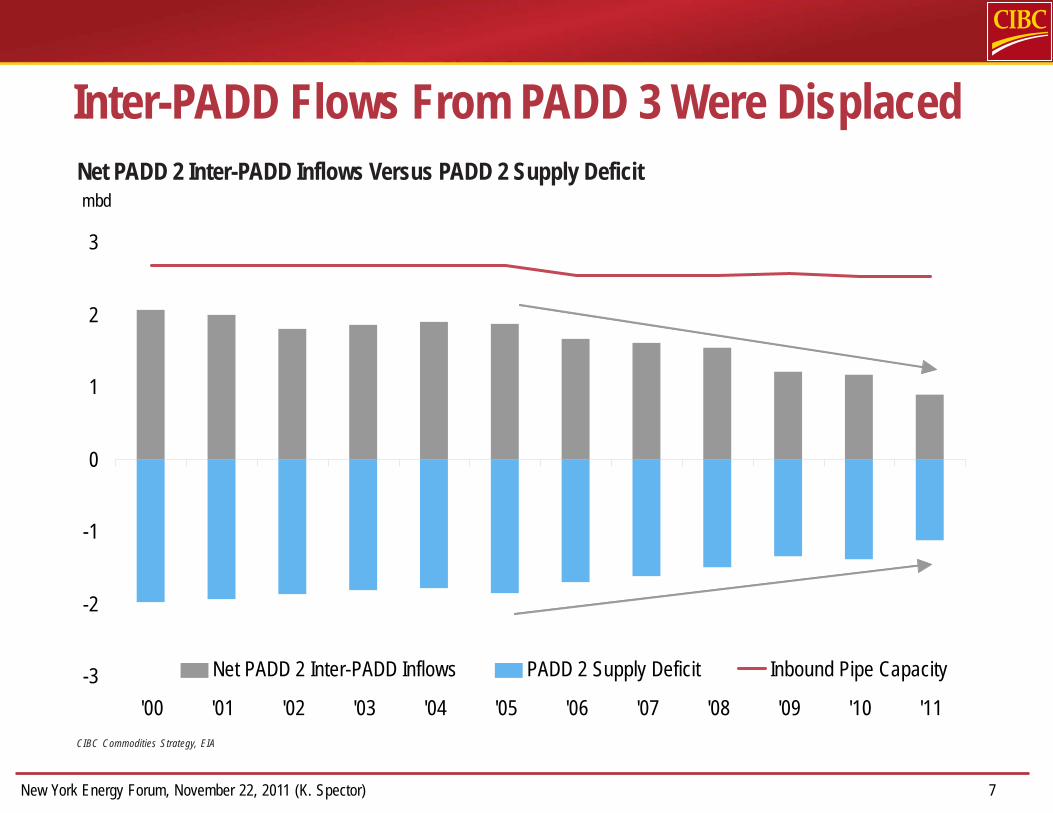

Inter-PADD Flows From PADD 3 Were Displaced

-3

-2

-1

0

1

2

3

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

mbd

Net PADD 2 Inter-PADD Inflows PADD 2 Supply Deficit Inbound Pipe Capacity

Net PADD 2 Inter-PADD Inflows Versus PADD 2 Supply Deficit

CIBC Commodities Strategy, EIA

New York Energy Forum, November 22, 2011 (K. Spector) 8

But Cushing Inventories Still Climbed(Storage Capacity Did, Too)

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011

mb

Average Cushing Crude Stocks Cushing Storage Capacity

Net PADD 2 Inter-PADD Inflows Versus PADD 2 Supply Deficit

CIBC Commodities Strategy, EIA

New York Energy Forum, November 22, 2011 (K. Spector) 9

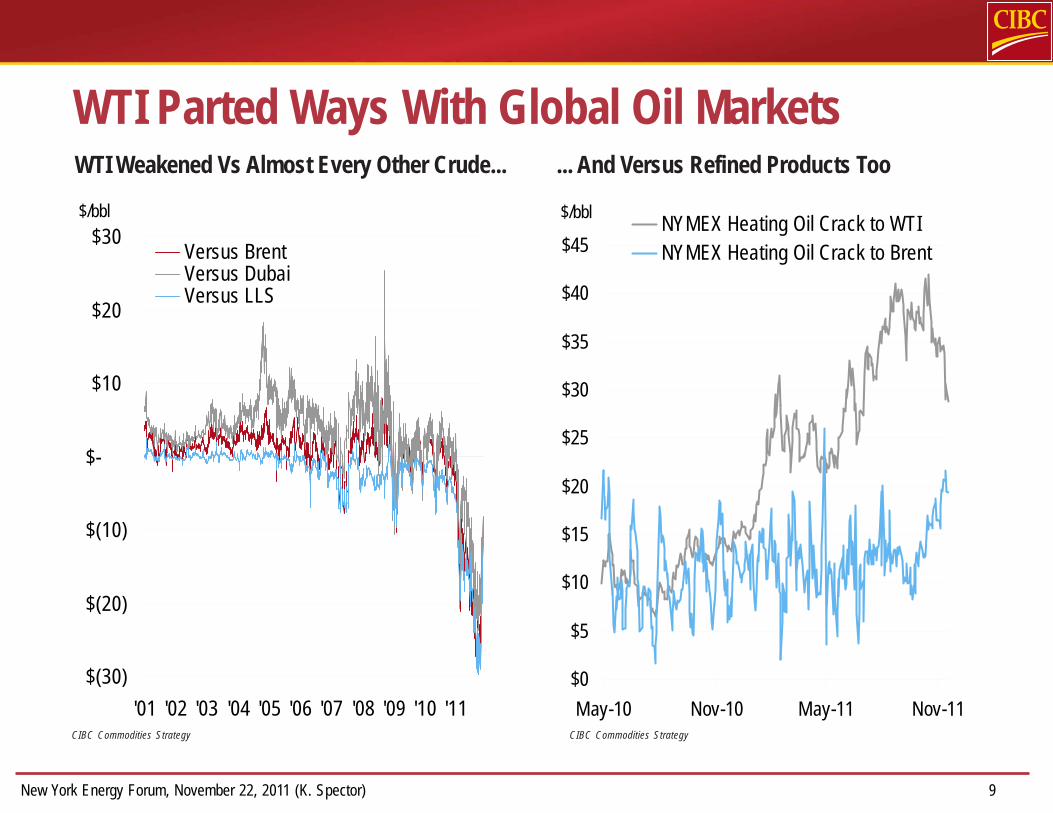

WTI Parted Ways With Global Oil Markets

$(30)

$(20)

$(10)

$-

$10

$20

$30

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

$/bbl

Versus BrentVersus DubaiVersus LLS

WTI Weakened Vs Almost Every Other Crude...

CIBC Commodities Strategy

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

May-10 Nov-10 May-11 Nov-11

$/bblNYMEX Heating Oil Crack to WTINYMEX Heating Oil Crack to Brent

... And Versus Refined Products Too

CIBC Commodities Strategy

New York Energy Forum, November 22, 2011 (K. Spector) 10

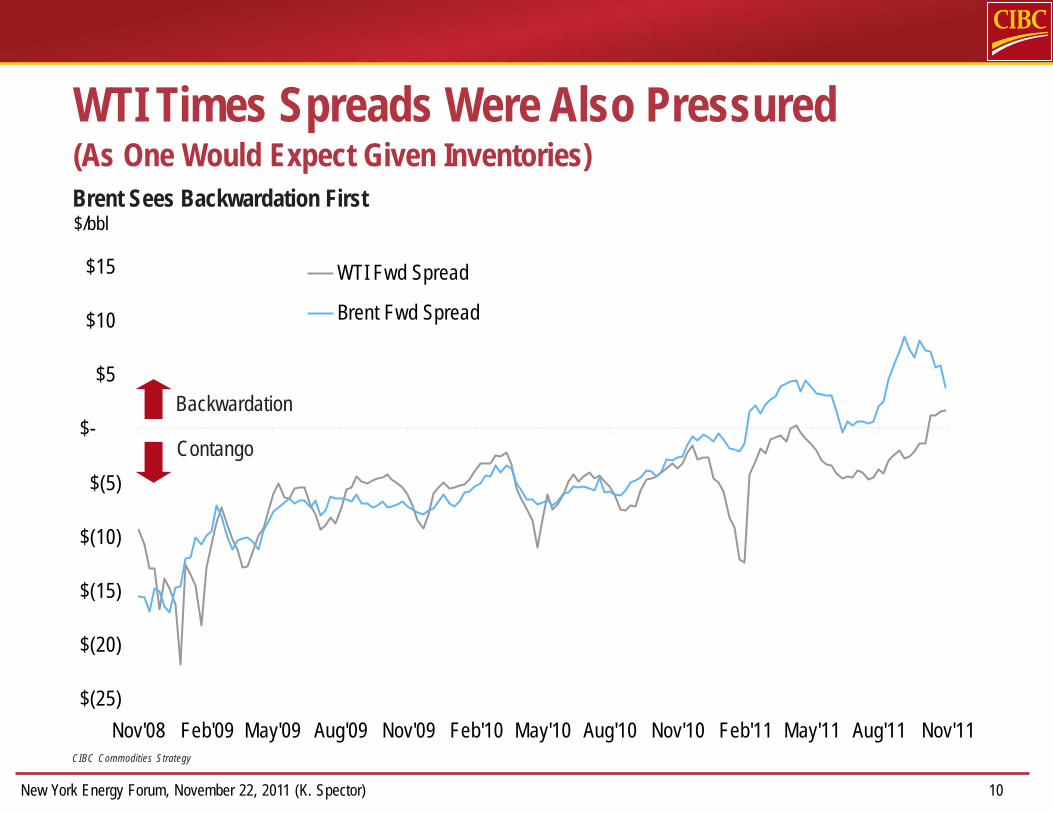

WTI Times Spreads Were Also Pressured(As One Would Expect Given Inventories)Brent Sees Backwardation First

CIBC Commodities Strategy

$(25)

$(20)

$(15)

$(10)

$(5)

$-

$5

$10

$15

Nov'08 Feb'09 May'09 Aug'09 Nov'09 Feb'10 May'10 Aug'10 Nov'10 Feb'11 May'11 Aug'11 Nov'11

$/bbl

WTI Fwd Spread

Brent Fwd Spread

Backwardation

Contango

New York Energy Forum, November 22, 2011 (K. Spector) 11

-1200

-1000

-800

-600

-400

-200

0

200

400

600

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11

kbdCumulative Chg in Bakken + AB Bitumen

Cumulative Change in North Sea

Brent Has Issues Too, But Still Attracted Volumes

-1200

-1000

-800

-600

-400

-200

0

200

400

600

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11

kbdCumulative Chg in Bakken + AB Bitumen

Cumulative Change in North Sea

North Sea Production Only Going One Way

CIBC Commodities Strategy

24%

26%

28%

30%

32%

34%

36%

38%

40%

Oct-07 Oct-08 Oct-09 Oct-10 Oct-11

But Even So Trading Volumes Shifted To Brent

CIBC Commodities Strategy

Brent Volume As % Of Total WTI + Brent Volume

New York Energy Forum, November 22, 2011 (K. Spector) 12

But Wait! The Market Responds to Dislocation

-

10

20

30

40

50

60

70

80

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

kbd

Ex-PADD 2 Barge Volumes Ramp Up

CIBC Commodities Strategy

400

450

500

550

600

650

700

750

800

'08 '09 '10 '11

kbd

$(30)

$(20)

$(10)

$-

$10

$20

$30

$/bbl

Railed Oil (left)WTI-Brent Spread (right)

Railed Volumes Also Rise...

CIBC Commodities Strategy

New York Energy Forum, November 22, 2011 (K. Spector) 13

Cushing Crude Inventories Fell Accordingly

29

31

33

35

37

39

41

43

Jan'11 Feb'11 Mar'11 Apr'11 May'11 Jun'11 Jul'11 Aug'11 Sep'11 Oct'11

million bblCushing Inventories Fall Nearly 12 mb From Early April Peak

CIBC Commodities Strategy, EIA

41.9 mb

30.1 mb

New York Energy Forum, November 22, 2011 (K. Spector) 14

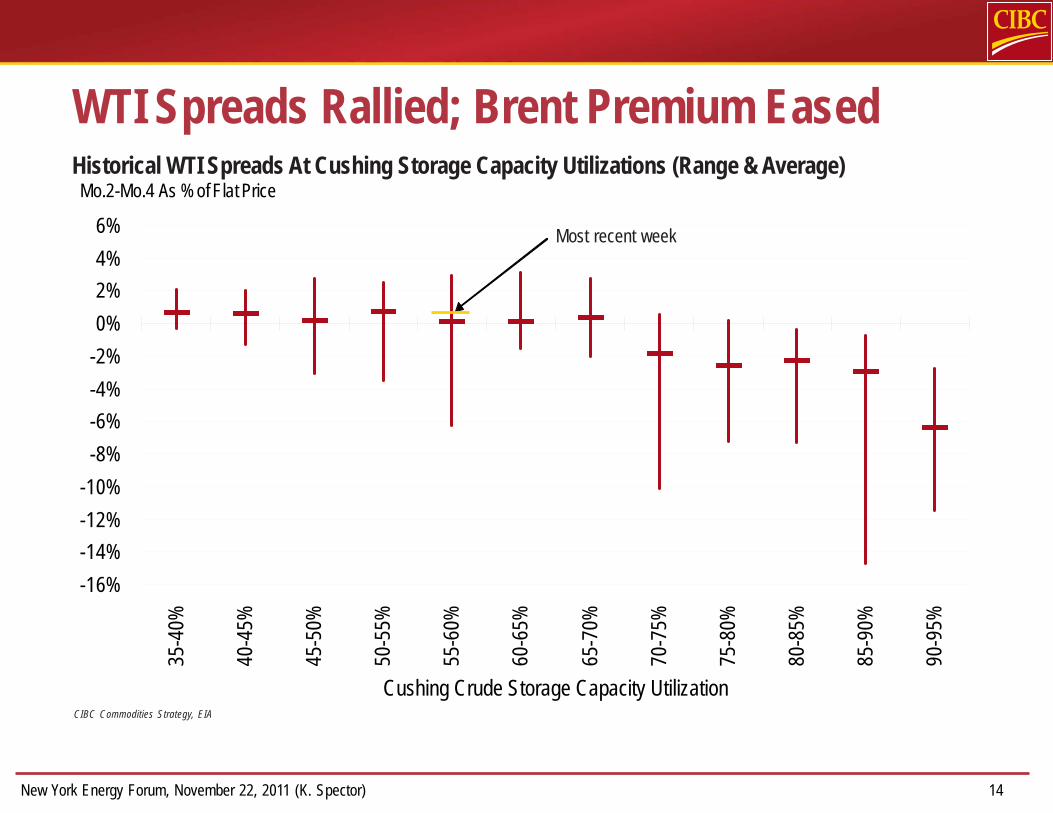

Mo.2-Mo.4 As % of Flat Price

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

35-4

0%

40-4

5%

45-5

0%

50-5

5%

55-6

0%

60-6

5%

65-7

0%

70-7

5%

75-8

0%

80-8

5%

85-9

0%

90-9

5%

Cushing Crude Storage Capacity Utilization

Historical WTI Spreads At Cushing Storage Capacity Utilizations (Range & Average)

CIBC Commodities Strategy, EIA

Most recent week

WTI Spreads Rallied; Brent Premium Eased

New York Energy Forum, November 22, 2011 (K. Spector) 15

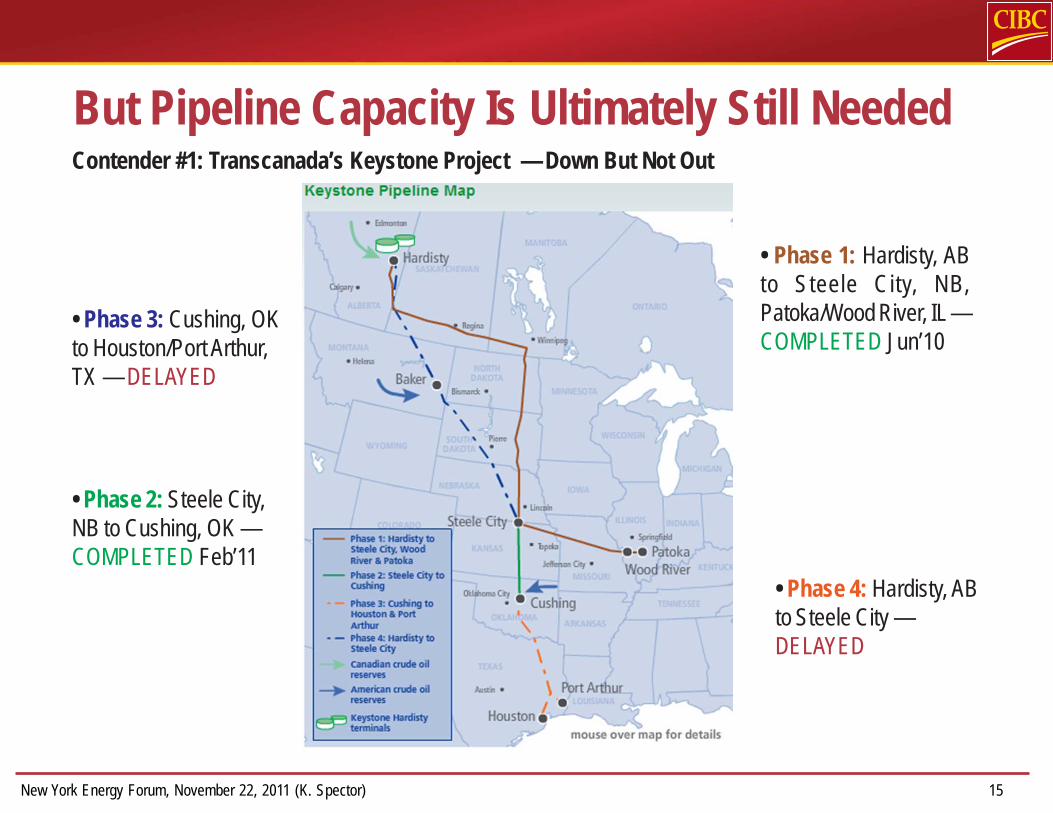

But Pipeline Capacity Is Ultimately Still NeededContender #1: Transcanada’s Keystone Project — Down But Not Out

• Phase 1: Hardisty, ABto Steele City, NB,Patoka/Wood River, IL —COMPLETED Jun’10

• Phase 2: Steele City,NB to Cushing, OK —COMPLETED Feb’11

• Phase 3: Cushing, OKto Houston/Port Arthur,TX — DELAYED

• Phase 4: Hardisty, ABto Steele City —DELAYED

New York Energy Forum, November 22, 2011 (K. Spector) 16

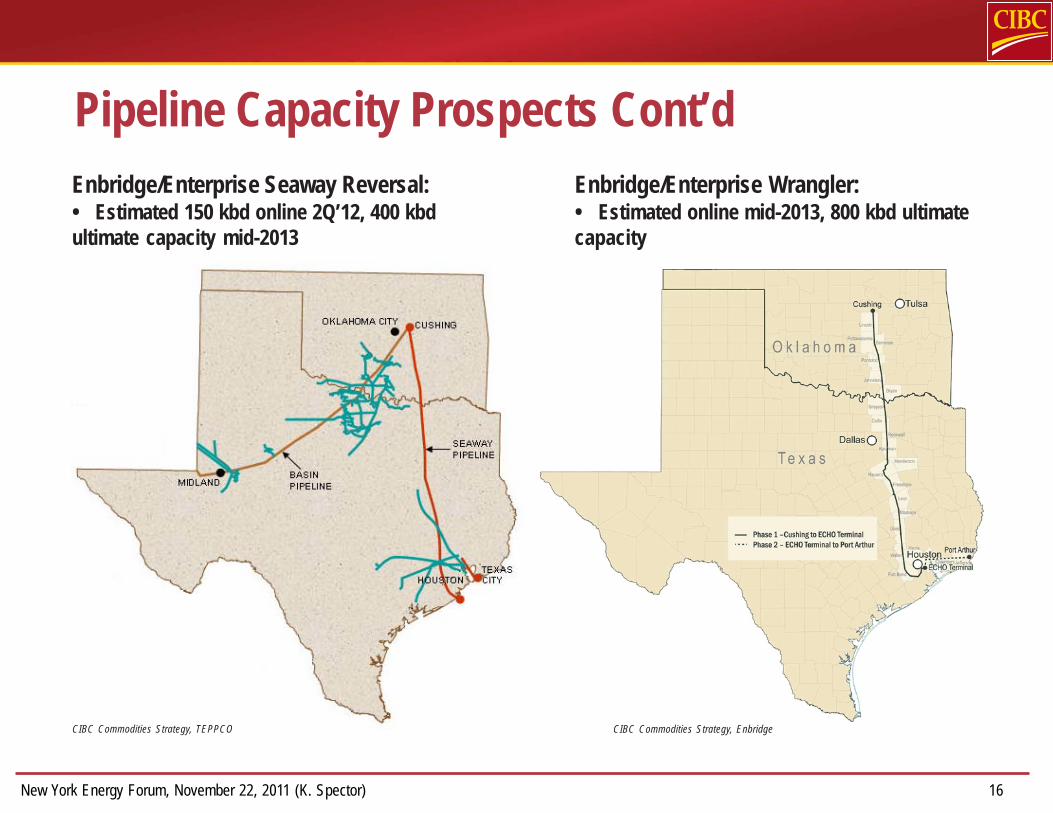

Pipeline Capacity Prospects Cont’dEnbridge/Enterprise Wrangler:• Estimated online mid-2013, 800 kbd ultimatecapacity

Enbridge/Enterprise Seaway Reversal:• Estimated 150 kbd online 2Q’12, 400 kbdultimate capacity mid-2013

CIBC Commodities Strategy, TEPPCO CIBC Commodities Strategy, Enbridge

New York Energy Forum, November 22, 2011 (K. Spector) 17

So Where Does This Leave Us?

-4.0-3.5-3.0-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.03.54.0

Average 2000-2010 2011 2016 est.

mbd

Intra-PADD Inbound

Foreign Imports

PADD 2 Production

Refinery Runs

PADD 2 Production & Canadian Imports Will Displace More USG Crude

CIBC Commodities Strategy, EIA

New York Energy Forum, November 22, 2011 (K. Spector) 18

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

PADD 2 Production Foreign Imports PADD 2 Refinery Capacity

Regional PADD 2 Crude Supply Versus Refinery Capacity

CIBC Commodities Strategy, EIA, CAPP

PADD 2 May Not Need Any PADD 3 Crude At All...

New York Energy Forum, November 22, 2011 (K. Spector) 19

-3000

-2000

-1000

0

1000

2000

3000

Average 2000-2010 2011 2016 est.

kbdPipe Capacity Inbound Pipe Capacity Outbound

PADD 2 Pipeline Capacity: Inbound Versus Outbound

CIBC Commodities Strategy, EIA, CAPP

How Would Those Pipeline Additions Stack Up?

Keystone XL

Wrangler

Seaway

New York Energy Forum, November 22, 2011 (K. Spector) 20

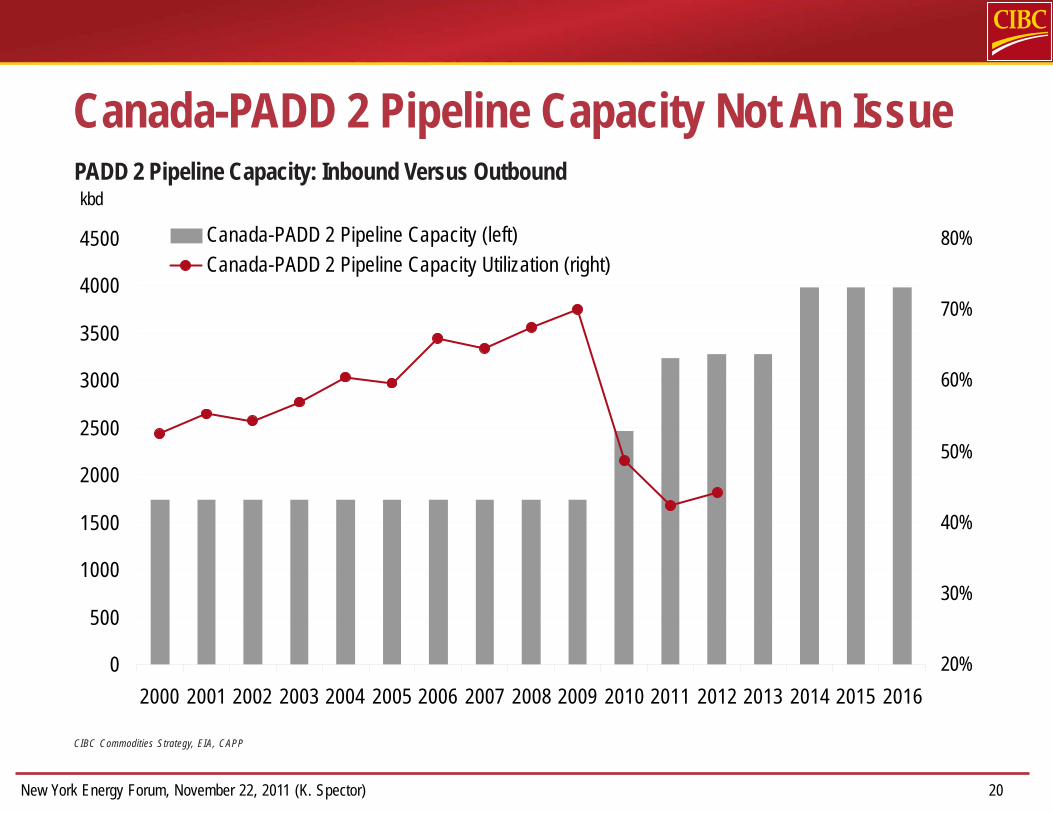

Canada-PADD 2 Pipeline Capacity Not An Issue

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

kbd

20%

30%

40%

50%

60%

70%

80%Canada-PADD 2 Pipeline Capacity (left)Canada-PADD 2 Pipeline Capacity Utilization (right)

PADD 2 Pipeline Capacity: Inbound Versus Outbound

CIBC Commodities Strategy, EIA, CAPP

New York Energy Forum, November 22, 2011 (K. Spector) 21

Origin of PADD 3 Imports, Average 2000-2010

CIBC Commodities Strategy, EIA

What PADD 3 Imports Could Be Displaced?

North America

Sub-Sah. Africa

Latam/S. America

MENA

W. Europe

E. Europe

OPEC(58%)

Non-OPEC(42%)

New York Energy Forum, November 22, 2011 (K. Spector) 22

Other Odds & Ends...• A greenfield refinery in PADD 2?Dakota Oil Processing is planning a (small) 20 kbd refinery in North Dakota geared towards supplyingdiesel to support Bakken production (rigs, trucks).

• Could Canada focus attention west?Proposed pipeline capacity from Edmonton to the West Coast includes Enbridge Gateway project,KinderMorgan’s Northern Leg of the Trans Mountain system, and other TMX expansions. Canadacurrently exports just ~50 kbd to Asia.

New York Energy Forum, November 22, 2011 (K. Spector) 23

This communication, including any attachment(s), is confidential and has been prepared by the Macro Strategy Desk within the Fixed Income, Currencies and Commodities Group at CIBC World Markets Inc., wholly-owned subsidiary and wholesale banking arm of Canadian Imperial Bank of Commerce. The contents of this communication are based on macro and issuer-specific analysis, issuer news, market events and generalinstitutional desk discussion. The author(s) of this communication is not a Research Analyst and this communication is not the product of any CIBC World Markets Inc. Research Department nor should it be construedas a Research Report. The author(s) of this communication is not a person or company with actual, implied or apparent authority to act on behalf of any issuer mentioned in the communication. The commentary andany attachments (other than any attached CIBC World Markets Inc. branded Research Reports) and opinions expressed herein are solely those of the individual author(s), except where the author expressly states themto be the opinions of CIBC World Markets Inc. The author(s) may provide short-term trading views or ideas on issuers, securities, commodities, currencies or other financial instruments but investors should not expectcontinuing analysis, views or discussion relating to the securities, securities, commodities, currencies or other financial instruments discussed herein. Any information provided herein is not intended to represent anadequate basis for investors to make an informed investment decision and is subject to change without notice. CIBC World Markets Inc. or its affiliates may engage in trading strategies or hold positions in the issuers,securities, commodities, currencies or other financial instruments discussed in this communication and may abandon such trading strategies or unwind such positions at any time without notice.This communication,including any attachment(s), is confidential and has been prepared by the Macro Strategy Desk within the Fixed Income, Currencies and Commodities Group at CIBC World Markets Inc., wholly-owned subsidiary andwholesale banking arm of Canadian Imperial Bank of Commerce. The contents of this communication are based on macro and issuer-specific analysis, issuer news, market events and general institutional deskdiscussion. The author(s) of this communication is not a Research Analyst and this communication is not the product of any CIBC World Markets Inc. Research Department nor should it be construed as a ResearchReport. The author(s) of this communication is not a person or company with actual, implied or apparent authority to act on behalf of any issuer mentioned in the communication. The commentary and any attachments(other than any attached CIBC World Markets Inc. branded Research Reports) and opinions expressed herein are solely those of the individual author(s), except where the author expressly states them to be the opinionsof CIBC World Markets Inc. The author(s) may provide short-term trading views or ideas on issuers, securities, commodities, currencies or other financial instruments but investors should not expect continuing analysis,views or discussion relating to the securities, securities, commodities, currencies or other financial instruments discussed herein. Any information provided herein is not intended to represent an adequate basis forinvestors to make an informed investment decision and is subject to change without notice. CIBC World Markets Inc. or its affiliates may engage in trading strategies or hold positions in the issuers, securities,commodities, currencies or other financial instruments discussed in this communication and may abandon such trading strategies or unwind such positions at any time without notice.The contents of this message are tailored for particular client needs and accordingly, this message is intended for the specific recipient only. Any dissemination, re-distribution or other use of this message or the marketcommentary contained herein by any recipient is unauthorized. If you are not the intended recipient, please reply to this e-mail and delete this communication and any copies without forwarding them.The contents of thismessage are tailored for particular client needs and accordingly, this message is intended for the specific recipient only. Any dissemination, re-distribution or other use of this message or the market commentarycontained herein by any recipient is unauthorized. If you are not the intended recipient, please reply to this e-mail and delete this communication and any copies without forwarding them.Distribution in Hong Kong: This communication has been approved and is issued in Hong Kong by Canadian Imperial Bank of Commerce, Hong Kong Branch, a registered institution under the Securities and FuturesOrdinance (the “SFO”) to “professional investors” as defined in clauses (a) to (h) of the definition thereof set out in Schedule 1 of the SFO. Any recipient in Hong Kong who has any questions or requires further informationon any matter arising from or relating to this communication should contact Canadian Imperial Bank of Commerce, Hong Kong Branch at Suite 3602, Cheung Kong Centre, 2 Queen’s Road Central, Hong Kong (telephonenumber: +852 2841 6111).Distribution in Hong Kong: This communication has been approved and is issued in Hong Kong by Canadian Imperial Bank of Commerce, Hong Kong Branch, a registered institution under theSecurities and Futures Ordinance (the SFO) to professionalinvestors as defined in clauses (a) to (h) of the definition thereof set out in Schedule 1 of the SFO. Any recipient in Hong Kong who has any questions orrequires further information on any matter arising from or relating to this communication should contact Canadian Imperial Bank of Commerce, Hong Kong Branch at Suite 3602, Cheung Kong Centre, 2 Queen’s RoadCentral, Hong Kong (telephone number: +852 2841 6111).Distribution in Singapore: This communication is intended solely for distribution to accredited investors, expert investors and institutional investors (each, an “eligible recipients”). Eligible recipients should contact DannyTan at Canadian Imperial Bank of Commerce, Singapore Branch at 16 Collyer Quay #04-02 Singapore 049318 (telephone number + 65-6423 3806) in respect of any matter arising from or in connection with thisreport.Distribution in Singapore: This communication is intended solely for distribution to accredited investors, expert investors and institutional investors (each, an eligiblerecipients). Eligible recipients should contactDanny Tan at Canadian Imperial Bank of Commerce, Singapore Branch at 16 Collyer Quay #04-02 Singapore 049318 (telephone number + 65-6423 3806) in respect of any matter arising from or in connection with thisreport.