overview of the french public oversight system -...

TRANSCRIPT

Mars 2010

AN OVERVIEW OF THE FRENCH PUBLIC

OVERSIGHT SYSTEM

1

Contents of the presentation

1 - Structure and organization of the H3C

2 – Inspections

2-1 Legal framework of inspections

2-2 General Information related to

inspections

2-3 Process and methodology

2-4 Supervision

2

1 – Structure and organization

3

High Council for Statutory Audit : H3C

Created by the Financial Security Law, written into the Commercial Code (1 August 2003) In line with EU 8th Company Law Directive

Independent public authority with own legal personality- Under the Minister of Justice

Financial independence in budget determination Mandatory contributions from the profession

• Registration

• Audit reports issued

12 members of the Board appointed by Decree for 6-year term

Government Commissioner Appointed by the Minister of Justice

Sits in H3C meetings with consultative powers.

4

Supervision of the statutory

audit profession, with the

assistance of the CNCC

Role of the H3C

Ensure compliance with the

rules of professional ethics,

and independence of the

statutory auditors

Definition as written in

the Commercial Code (Financial Security Law)

5

Responsibilities of the H3C (as defined by law)

Inspections- Define the framework, orientation and modalities for the conduct of inspections, supervise their

implementation to H3C decisions, ensure the proper conduct of these inspections and follow-up by direct supervisory review of inspection files

- Has direct responsibility for the implementation of inspections, and may participate, if necessary, in the inspection operations and issue follow-up recommendations

Auditing standards and professional pratices

- Identify and promote good professional practices and good conduct- Issue an opinion on auditing standards before official approbation by Decree (Minister of Justice)

Professional Code of Ethics

- Issue an opinion on the reviewed Professional Code of Ethics before approval by Conseil d’Etat and published by Decree

International

- Establish and maintain good relations with other foreign oversight authorities that exercise equivalent competences

Jurisdictional

- Appellate authority for decisions by:• Regional registration commissions for registration matters

• Regional chambers on disciplinary matters

6

2 - Inspections

7

8

2-1 Legal framework of inspections

Periodic inspections

All registered statutory auditors and audit firms in Franceare subject to periodic inspections.

9

Inspection Cycles :

3 years for PIE auditors

6 years for other auditors

Specific regulations

Inspections carried out on documents and on-site (R. 821-24)

Inspections carried out at least every six years, with a

three-year delay for statutory auditors who conduct

statutory audits of :

- individuals or public-listed entities or chartitable entities,

- security social organizations as mentioned in Article L. 114-8

of the code de la sécurité sociale,

- credit establishments,

- insurance companies,

- pension funds institutions regulated by Title III of Book IX of

the code de la sécurité sociale,

- private health insurance or mutual unions regulated by Book

II of the code de la mutualité i.e. mutual insurance system (R.

821-26)

10

11

Inspections and Investigations :

INSPECTIONS

Inspections performed byH3C inspectors with theassistance of AMF (forinspections relating to auditors ofpublic-listed entites or collectiveinvestment undertakings)(H3C can delegated a part ofinspections to CNCC)

Inspections performed by CNCCor CRCC

PIE auditors

PIE non auditors

INVESTIGATIONS

Minister of Justice

OR

Autorité des Marchés Financiers

(AMF)

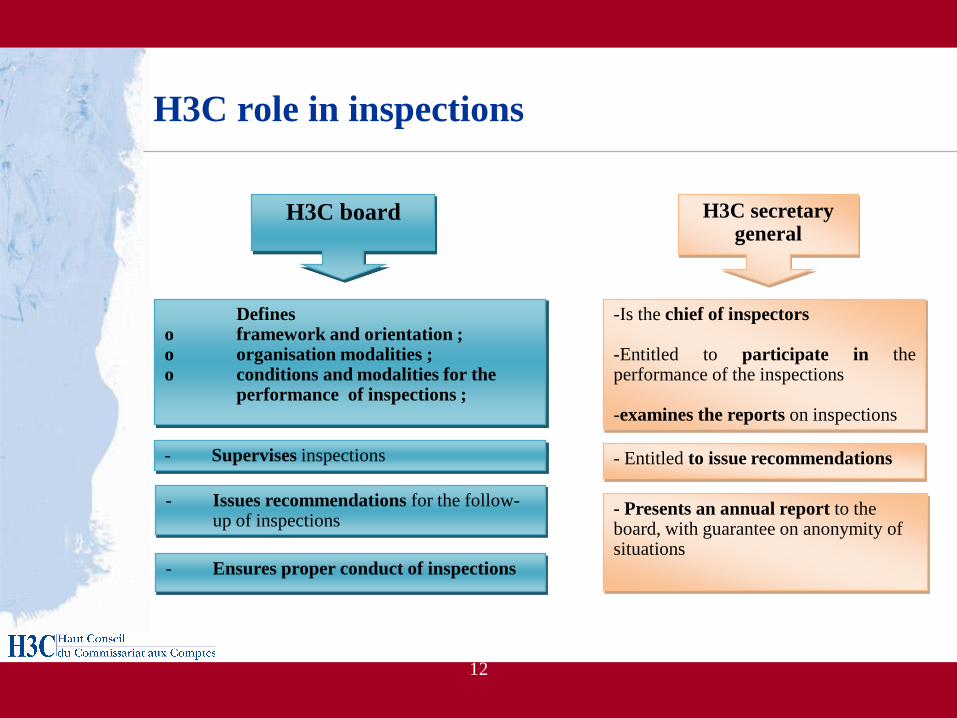

H3C role in inspections

12

Defineso framework and orientation ;o organisation modalities ;o conditions and modalities for the

performance of inspections ;

- Supervises inspections

- Issues recommendations for the follow-up of inspections

- Ensures proper conduct of inspections

H3C secretary general

-Is the chief of inspectors

-Entitled to participate in theperformance of the inspections

-examines the reports on inspections

- Entitled to issue recommendations

- Presents an annual report to the board, with guarantee on anonymity of situations

H3C board

13

2-1 General information related to inspections

2-1-1 Population of auditors and audit

engagements held (2008)

A large number of statutory auditors and audit firms to be

inspected

Significant concentration of public interest entities (PIE)

and public-listed entities (PLE) audit engagements within

the major audit firms

14

Industry overview

15

- High population of registered auditors

- Joint audits for consolidated accounts

• Legal requirement for a minimum of two independent

auditors

TOTAL : 19 100 registered auditorsAudit firms 4 600 ; Statutory auditors 14 500

212 000 audit engagements

Public interest entities

Public listed entities

Auditors : 752

Auditors : 328

Engagements 1241

Engagements 3700

Industry concentration

•Significant concentration of public-listed entities(PLE) audit engagements within major audit firms

Around 600 entities

PLE auditors328

PLE engagements 1241

4 largest audit firms

PLE engagements 559

324 other audit firms

PLE engagements 682

16

2-1-2 Population of auditors under inspection

Inspections performed by H3C directly

- 2 networks with the largest number of PLE audit engagements,

- 285 audit firms with PIEs

A part of these inspections can be delegated to the professional bodies

Inspections performed by professional bodies:

- 1240 audit firms with non PIEs

17

2-2-3 Who are the inspectors ?

Full-time non-practitioner inspectors employed by H3C

The inspectors are qualified professional auditors or

individuals in the financial sector who do not hold any audit

engagements and must comply with independence rules

written by the H3C.

Secretary general ensures the management of the

inspectors

- Assisted by a director recruited by the H3C after mandatory

Board opinion

18

2-2-3 Who are the reviewers ?

QA reviewers are registered statutory auditors in

professional practice :

- about 850 practitioners who consecrate 40 – 100 hours per

year to quality assurance reviews,

- work on average for a period of three to ten years

Work of reviewers are monitored by CNCC and CRCC

and H3C

Time devoted to quality control by the reviewers, CNCC

and CRCC - about 40 000 hours

19

2-2-3 Who are the reviewers ?

Selection of reviewers

- on the basis of criteria determined by the H3C,

- according to their specialisations : technical skills and

practical experience as statutory auditor,

Appointment of reviewers, based on criteria of :

- competence,

- independence and absence of conflict of interest in relation to

the reviewed audit firm

Allocation of hours budgeted per inspection

Supervision of reviewers’ work

Training of reviewers

20

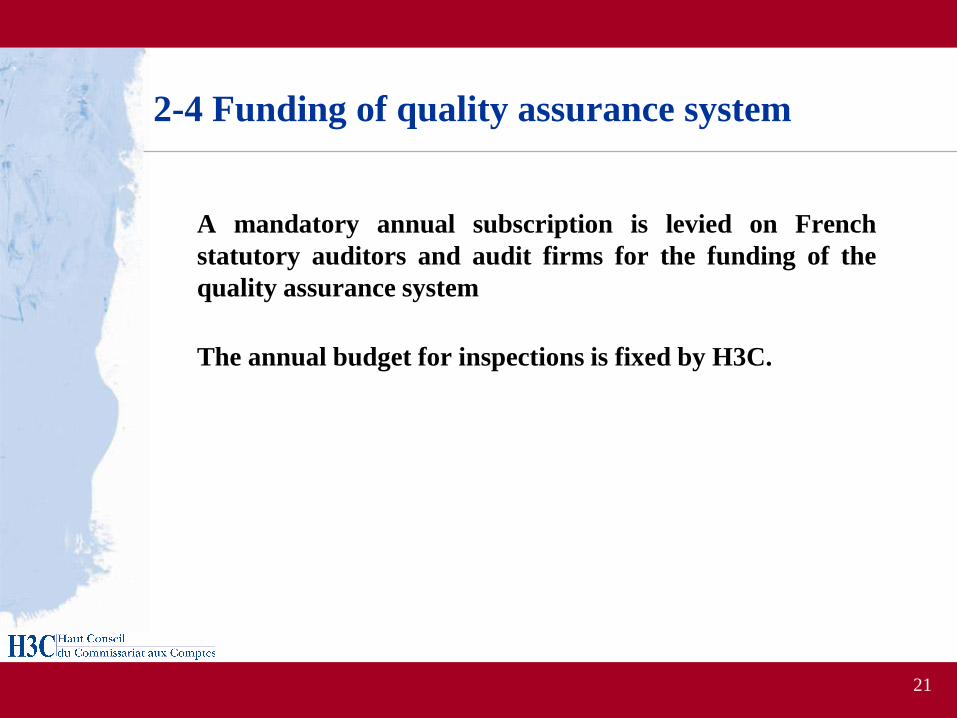

2-4 Funding of quality assurance system

A mandatory annual subscription is levied on French

statutory auditors and audit firms for the funding of the

quality assurance system

The annual budget for inspections is fixed by H3C.

21

22

2-3 Process and methodology

23

3-1 Inspection Program

Decisions of the H3C :

- Single framework of inspections leading to an “overall” inspection of

an auditor (i.e statutory auditor or audit firm)

- Number and type of auditors subject to inspections – according to the

size of their professional activities ;

- Focus on audits of entities that correspond to certain sectors, specific

situations and themes

Secretary general of H3C establish an inspection program

according to H3C decisions :

- Selection of auditors to be inspected

- Selection of audit engagements to be inspected within the selected

auditors

24

Review of firm policy and procedures

Focus on :

- Respect of legislative and regulatory demands, notably to

independence, incompatibilities (Commercial Code, decrees,

Professional Code of Ethics)

- Acceptation of statutory audits and examination of maintenance

of the statutory audit missions

- Professional training

- Existence and use of appropriate methodology tools for the

conduct of statutory audit (compliance with auditing standards)

- Existence and recourse to recent technical

documentation/information

May involve, where firm policy and procedures provide for such, for

an independent review of issued opinions and internal quality control

systems

25

Review of selected audit engagements

Focus on :

- Respect of professional practice standards, legislative texts and

regulations in application

- Compatibility of non-audit services provided with the applicable

ethics rules (Commercial Code and Professional Code of Ethics)

- Appropriate documentation of work carried out, includes the

examination of accounting principles applied by audited entity

and verification of issued financial information

- Consistency of issued opinion with findings presented in

compiled audit files

- Verification of application of firm policy and procedures

26

3-3 Process of inspections

Review of inspections

Exchange of views

Report on results of each inspection

analyse risk on audit firms and engagements

Firm policy and proceduresSelected audit engagements

By H3C (EIP) or CNCC or CRCC (Non EIP)

Between auditor and inspectors or reviewer

• Meeting of Commission members, in the presence ofrepresentatives of the reviewed auditor (optional), inspectorsor reviewers, supervisor, and an AMF representative(when necessary)

Evaluation of results by H3C or CNCC or CRCC commissions

Written by inspectors or reviewers,addressed to auditor

Conduct of inspections

Preparation of inspections

27

2-4 Supervision

Supervision

28

H3C supervise inspections and ensures proper performance (L. 821-1)

Option 1. Direct inspections by

H3C team

Option 2. inspections delegated to

reviewers under supervision H3C

Option 3. inspections by CNCC et

CRCC

Independent team ofnon practionners

employed and managed by H3C secretary general

Secretary general examines the documents retracing the inspection opérations which are carried out by the CNCC

and the CRCC have undertaken

H3C Secretary general : - presents an annual report to the board, with guarantee on anonymity on specific situations- issues recommendations on inspections

Public listed entities and credit

establishments

Non PIE Other PIE

more information : www.h3c.org

29