poland empirical research and contribution to standard...

TRANSCRIPT

1

Poland – Empirical research and contribution to standard setting

prof. Radosław Ignatowski Head of International Accounting Unit

Department of Accounting Management Faculty

University of Lodz, Poland

Presentation prepared for

Accounting and Auditing Education Community of Practice Workshop

Joint Vienna Institute, 16 – 17 January, Vienna

2

Presentation

Accounting Profession, Accounting Regulations, Accounting Theory and Academics’ World

Institutional framework of Polish Accounting System in International Environment – Legal or Environmental (law vs accounting standards, rules based vs principles based regulations)

Standards and IFRSs phenomena in Poland

Impact of Academics and Empirical Research on Standard Setting Process (internal and international level)

Developments in Polish Accounting System and Accounting Research – Obstructions and Challenges

Contents:

3

Accounting and Reality

Accounting Objective

Active and Passive

Depict (present) reality by availably-ideal model – Financial Accounting

Create reality – Managerial (and Financial) Accounting

4

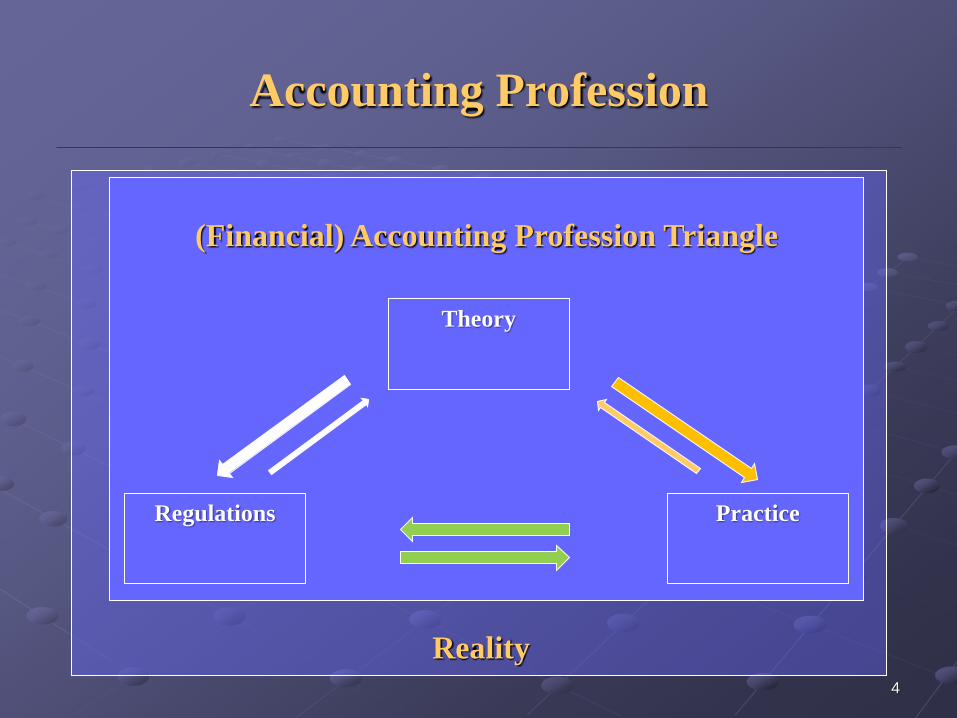

Accounting Profession

(Financial) Accounting Profession Triangle

Theory

Regulations Practice

Reality

5

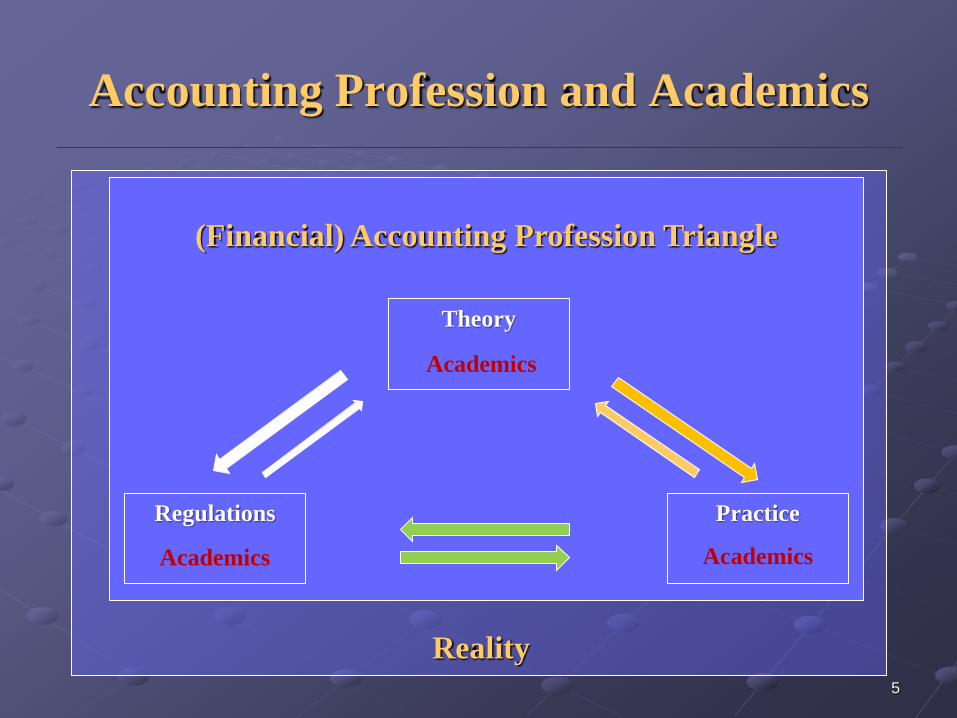

Accounting Profession and Academics

(Financial) Accounting Profession Triangle

Theory

Regulations Practice

Reality

Academics

Academics Academics

6

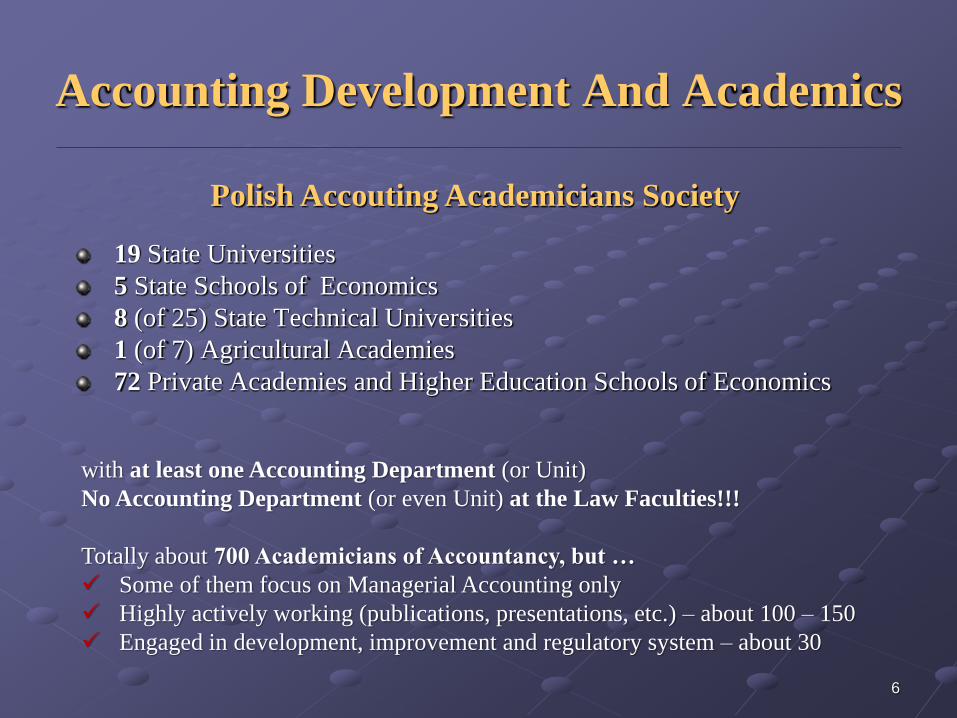

Accounting Development And Academics

19 State Universities

5 State Schools of Economics

8 (of 25) State Technical Universities

1 (of 7) Agricultural Academies

72 Private Academies and Higher Education Schools of Economics

Polish Accouting Academicians Society

with at least one Accounting Department (or Unit)

No Accounting Department (or even Unit) at the Law Faculties!!!

Totally about 700 Academicians of Accountancy, but …

Some of them focus on Managerial Accounting only

Highly actively working (publications, presentations, etc.) – about 100 – 150

Engaged in development, improvement and regulatory system – about 30

7

Accounting Development And Academics

Scientific research on applied and potential regulations – verifications of existed and potential models – empirical research, based on classical and pragmatic approaches – logical reasoning vs statistical modelling, case studies, others

Review of existed and potential regulations by individuals and within scientific (academic) organization: Scientific Board of the Accountants Association in Poland (AAP) – 48 Members

Proposals of regulations (legal or professional) by individuals and within scientific organization: Perfection of Regulatory and Accounting Principles Commission of the AAP

Active participation within formal regulatory bodies – e.g. Accounting Standards Committee in Poland (ASC) – 8 of 18 Members are full or part-time academic staff

Contribution of Academics to Polish Accounting Regulatory System Development

8

Accounting Development And Academics

Scientific research on applied and potential regulations – verifications of existed and potential international regulations – empirical research, based on classical and pragmatic approaches – logical reasoning vs statistical modelling, case studies, others

Review of existed and potential regulations by individuals and within scientific and professional organizations: AAP, ASC

Glosses and Opinions on Discussion Papers and Exposure Drafts of IFRSs by individuals and by official bodies: AAP, ASC, National Chamber of Statutory Auditors (NCSA)

Active participation within formal regulatory and professional bodies – IFAC, EFRAG (TEG plus Working Groups), EU Reflection Groups, World Standards Setters Meetings, FEE, UN ISAR, EFAA

Contribution of Academics to International Accounting Regulatory and Profession Systems Development

9

Accounting Development And Academics

Professional National Accounting Standards (NAS) and Statements (SAP) – all of them where prepared by academics: NAS 1 – Separate and Consolidated Cash Flow Statements – University of Łódź

NAS 2 – Income Taxes – Warsaw School of Economics

NAS 3 – Construction Contracts – University of Łódź

NAS 4 – Impairment of Assets – University of Warsaw

NAS 5 – Lease, rental and usage transactions – University of Łódź

NAS 6 – Provisions, Deferred Income and Contingencies – Cracow University of Economics

NAS 7 – Accounting Policy, Estimates and Errors and Events after the balance sheet date – University of Gdańsk

NAS 8 – Real Estate Developments – University of Łódź

NAS 9 – Management Commentary – University of Łódź

(…)

Contribution of Academics to Polish Accounting Regulatory System Development

10

Accounting Development And Academics

Professional National Accounting Standards (NAS) and Statements (SAP) – all of them where prepared by academics:

(…)

SAP-1 – Cost of Production – Warsaw School of Economics

SAP-2 – Emission Rights – University of Łódź

SAP-3 – Green Energy Certificates – University of Łódź

SAP-4 – Electronic Accounting Systems – Wrocław University of Economics

Contribution of Academics to Polish Accounting Regulatory System Development

11

Accounting Development And Academics

Why do academics are (should be) involved in Regulatory Process?

Trust and Authority

Neutrality and Objectivity

Holistic not Individually Oriented Approach

Up-to-date knowledge and international orientation

Ability to explain why, not only how

Academic as an managerial, investor viewer – accounting as a tool for decision making on entity and economy level

Contribution of Academics to (Polish) Accounting Regulatory System Development

12

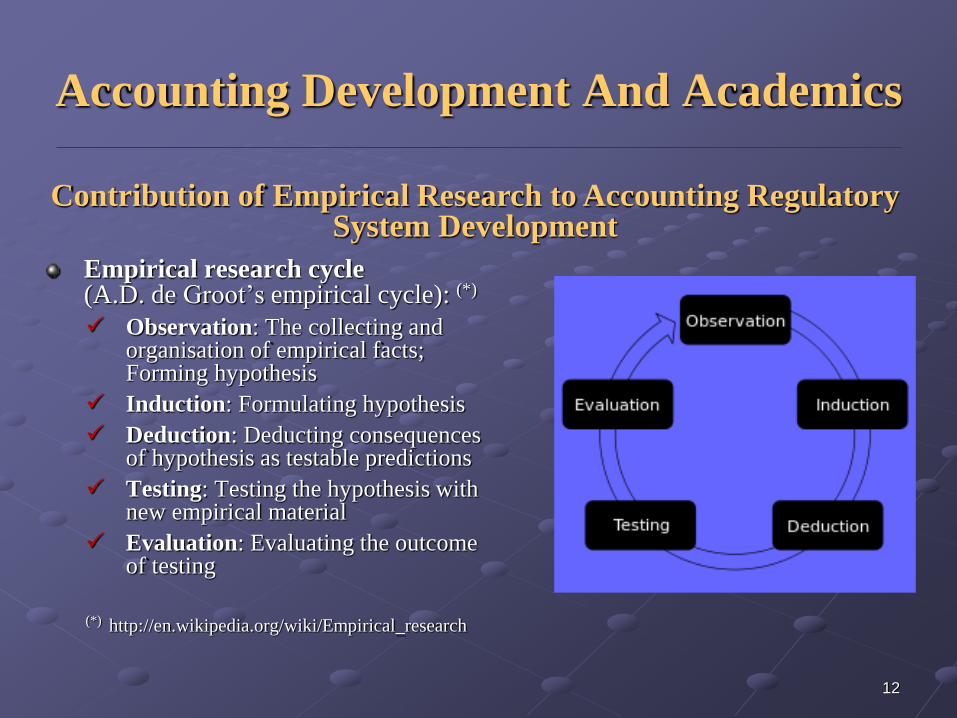

Accounting Development And Academics

Empirical research cycle (A.D. de Groot’s empirical cycle): (*)

Observation: The collecting and organisation of empirical facts; Forming hypothesis

Induction: Formulating hypothesis

Deduction: Deducting consequences of hypothesis as testable predictions

Testing: Testing the hypothesis with new empirical material

Evaluation: Evaluating the outcome of testing

(*) http://en.wikipedia.org/wiki/Empirical_research

Contribution of Empirical Research to Accounting Regulatory System Development

13

Accounting Development And Academics

Empirical research methods to be used:

case study (studies) research

qualitative research

quantitative research

Contribution of Empirical Research to (Polish) Accounting Regulatory System Development

14

Accounting Development And Academics

Pre-setting

Define the constituents needs

Define existing practice

Define available solutions

Setting

Define choosen solution

Verify choosen solution by field tests

Post-setting

Identify existing practice (implemented standard attitude)

Be satisfied or back to the beginning

Contribution of Empirical Research to (Polish) Accounting Regulatory System Development

15

Accounting Development

External Finance – shareholders vs stakeholders, private and public sector

Legal System – normative and legalistic orientation vs non-legalistic approach based on profession regulations

Political and Economic Ties with Other Countries

Size and Complexity of Business Enterprises

Sophistication of Management and the Financial Community,

General Level of Education (on both side: Academics and Students) (Scolatization Factor in Poland: 2013 – 52% (1990) – 13%)

Culture and Individualism and Ambiguity, and Uncertainty Avoidance

Level of Inflation

Main Variables shaping (financial) accounting developments

16

Accounting Development

The Fair Presentation/Full Disclosure Model – Anglo-Saxon Model

The Legal Compliance Model – Continental Model

The Inflation Adjusted Model

Rules (Based) Accounting Model

Principles (Based) Accounting Model

Objective (Based) Accounting Model

Main Accounting Models (Systems)

17

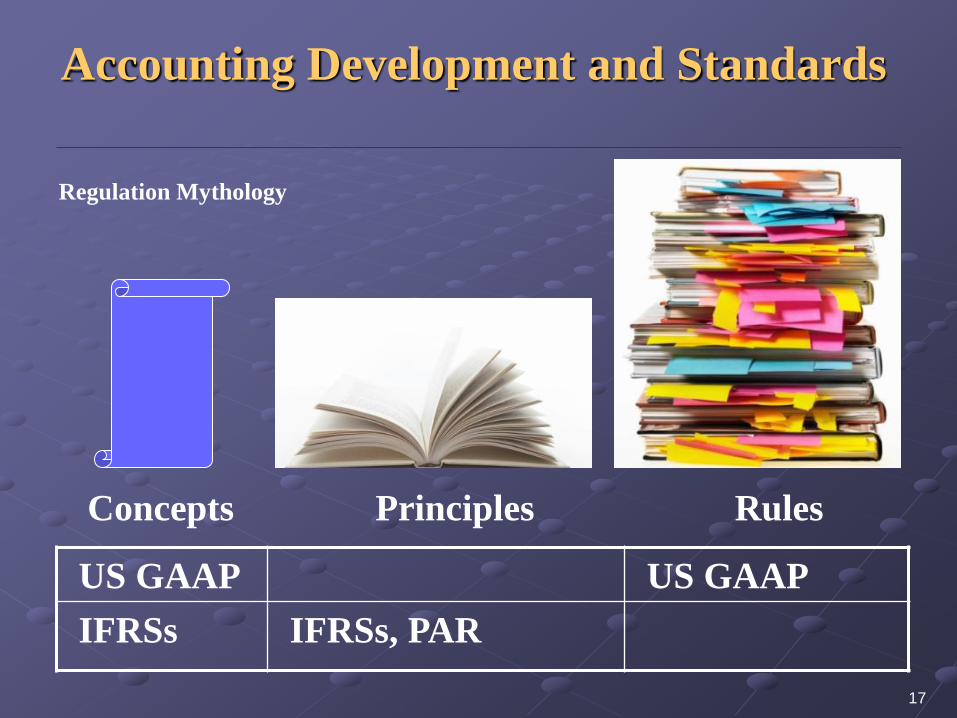

Concepts Principles Rules

US GAAP US GAAP

IFRSs IFRSs, PAR

Regulation Mythology

Accounting Development and Standards

18

Accounting Development and Academics

Purpose – development and rigorous application of globally accepted, high quality reporting standards, being the base of reliable and transparent information provided by entities’ general purpose financial statements for decision making by external users

Realization – Do it by yourself or Use experience and authority of scholars, who did it by theirselves earlier

Harmonization of Accounting and Globalisation

19

Accounting Development

Languages

Different purposes of accounts (financial statements): pro investments and decision making versus pro fiscal (tax) purposes

Different legal systems – some countries require certain policies and outlaw others

Different (orientation on) users of financial information provided – capital market investors versus government (state)

Nationalism

Weak education systems

Lack of strong accountancy bodies – lack of independence

Barriers to International Harmonization

20 20

General Remarks on Financial Reporting

Obligation to prepare and present general purposes financial statements comes from:

Act on Accounting 1994 and

Regulations on Publicly Traded Entities 2006

mostly approved and applied consistently in conformity with EU Directives and other EU regulations

The way the entity fulfil its obligation on financial statutory reporting depends on whether:

entity is covered by UE Regulation 1606/2002 on application of international accounting standards,

entity is not covered by above EU Regulation, and

parent company or its investors have some special needs on statutory financial reporting.

21

Polish Regulatory Framework and IFRS

Entities which are covered by UE Regulation 1606/2002 on application of international accounting standards have to follow entire set of IFRSs (full IFRSs application) approved by EC

Other entities, to whom Act on Accounting is entirely in force, but there are some areas of accounting not covered by AoA or National Accounting Standards (KSR), where some selected IFRSs are permitted (selected IFRSs application).

Two different scope of IFRSs application:

22

Polish Regulatory Framework and IFRS

Obligatory Full Usage of IFRSs adopted by the EU Currently publicly traded companies within the scope of EU markets Banks for preparation and presentation of theirs Consolidated Financial Statements

Facultative Full Usage of IFRSs Currently publicly traded companies within the scope of EU markets

Banks

for preparation and presentation of theirs Separate or Individual Financial Statements

Future publicly traded companies within the scope of EU markets

Members of Groups preparing and presenting Consolidated Financial Statements in conformity with the IFRSs

for preparation and presentation of theirs Individual, Separate and Consolidated Financial Statements

Entities’ scope of IFRSs Application

23

Polish Regulatory Framework and IFRSs

Facultative Selected Usage of IFRSs Any entity

Entities’ scope of IFRSs Application

for preparation and presentation of its Individual, Separate and Consolidated Financial Statements

In matters and issues not covered by Polish Accounting Regulations

24

Regulatory Framework, IFRSs and Academics

Act on Accounting 1994, fully amended in 2000 complied with IASs existed at that time in all material aspects and matters

Lots of amendments to IASs and new IFRSs distinct Polish Accounting Regulations and today’s IFRSs

Not all of IFRSs provisions are suitable and able to be implemented in PAR

Ministry of Finance has established a Working Group on PAR Amendments

There is no way out from IFRSs worldwide implementation

Main objective is to implement as much as possible IASs and IFRSs provisions on a reasonable and law level

Internationalization of accounting profession requires existance of academics and theirs researches on regulatory level and development of accounting profession

Differences, Similarities, Harmonisation and Academics

25

Regulatory Framework, IFRS and Academics

Thank you for your attention and welcome

Q&A