offshoring it to india as an enabler for banking business ... · 2 / 22 offshoring it to india as...

TRANSCRIPT

Offshoring IT to India as an Enabler for Banking Business Transformation

Dr. Wolfgang Messner

2 / 22

Offshoring IT to India as an Enabler for Banking Business Transformation

Dr. Wolfgang Messner

1 INTRODUCTION

Challenges and changes in the world of banking are becoming increasingly more radical. Banking information technology (IT) plays a major role in this process. Against a recent backdrop of capital yields, the main focus of banks is currently to reduce operational costs. Information technology plays an important role in this contest and banks are looking for an IT management framework which will enable them to break themselves down into process components and reassemble themselves along different lines. Outsourcing is a real option to increase effectiveness and efficiency of such business processes, offshoring to India helps to match reduced IT budgets. However, an agenda is required to assess possible chances, consequences and risks prior of taking a decision. Even in an information networked economy, personal communication and understanding of cultural differences is key to success. Following the right path of offshoring, banks can create a momentum to reduce their non-discretionary costs and invest back into strategic capabilities enabling business transformation.

2 BANKING INFORMATION TECHNOLOGY

2.1 Connotation for Banks

Financial service providers are complex institutions; they offer various financial services to their customers based on correlation-rich partnerships with other financial, personnel and information related resources.

In no other industry area has the market framework changed as tremendously as it did for the banking industry in the past five years. Decreasing margins, increasing pressure by competitors, market entry by non- and near-banks, changing customer behaviour are just a few of the trends which are signalling a complete structural change of the banking industry. The progress in information technology (IT) has started this change and also maintained its momentum. At the same time, information technology plays a major role in coping with the challenges of the structural change.1 It offers exceptional opportunities for fast innovators and harbours fundamental risks for laggards.

The importance of banking information technology is based on the fact that banking business is mainly about processing data and information. Thus IT supports and governs the entire value creation process, has an effect on every single activity and corporate function. The banking operations are highly dependent on IT in their day-to-day activities coping with huge amounts of data and for automating the business processes.

3 / 22

An optimal usage of banking IT can only be achieved through implementing adequate strategies which govern the capabilities and the positioning of the bank among the market participants.

2.2 Current Cost Traps

IT budgets in the banking industry are typically around nine percent of earnings. A closer look reveals that roughly 55% is used for non-discretionary IT expenditure, i.e. costs for day-to-day operations and maintenance of existing applications. 10% has to be taken into account for planning, governance and administration. This leaves only 35% for new development.

Non-discretionary IT costs are expected to rise in the future. The complexity of the IT landscape is continuing to increase due to Internet applications, extension of legacy systems to support new services and products and a need to service customer relationship management systems. Since the market downturn began in March 2000, banks have struggled with realigning expenses and revenues. Traditional cost cutting measures, such as headcount and capital expenditure reductions, were the first line of defence.2 But IT budgets are expected to be cut further in the next years. After three consecutive years of cost cutting, banks have little remaining fat and consequently they are expected to fall into an investment trap with less money being available for new development.

Some leading banks still view technology leadership and cost leadership as separate ways of achieving high profits within a given product market. But in the future, a bank’s success may hinge on its ability to provide a leading financial product at lower costs.3

2.3 IT Management Framework

The way out of this dilemma is to develop and strengthen capabilities in the banking IT. The business value of an IT capability comes from its ability to conduct business processes more reliably, faster and at less cost, and to increase revenue, reduce time to market, improve customer service and provide information for better business decisions. These capabilities are to be oriented along a stringent IT management framework.

The IT Management Framework is depicted in Figure 1. It allows comprehensive reshaping of processes to achieve significant improvements in effectiveness and efficiency.

4 / 22

Business Requirements

Building Blocks

Plan Govern Measure

IT Management Framework

IT-Strategy

IT-Governance

• Long-term planning• Allignment of IT with

business requirements

• Definition, building and governing decision making structure

• Business Case• Benefit Management

Application Development

• Disciplined projects• Effective project

management• Quality & timeliness of

delivery• Wide-spread distribution

IT Operation and Maintenance

• Supporting day-to-day operations according to agreed SLAs

• Within budget• User Support

Architecture Landscape

• Flexibility to meet changing business requirements

• Consists of technical, security, data and application architecture components

Management of Resources

• Maximise value of IT investments

• Career development• Knowledge Management• Supplier Management• Quality Assurance

Business Requirements

Building Blocks

Plan Govern MeasurePlan Govern Measure

IT Management Framework

IT-Strategy

IT-Governance

• Long-term planning• Allignment of IT with

business requirements

• Definition, building and governing decision making structure

• Business Case• Benefit Management

Application Development

• Disciplined projects• Effective project

management• Quality & timeliness of

delivery• Wide-spread distribution

IT Operation and Maintenance

• Supporting day-to-day operations according to agreed SLAs

• Within budget• User Support

Architecture Landscape

• Flexibility to meet changing business requirements

• Consists of technical, security, data and application architecture components

Management of Resources

• Maximise value of IT investments

• Career development• Knowledge Management• Supplier Management• Quality Assurance

Figure 1: IT Management Framework

IT Strategy Most modern banks are aware of the importance of IT for creating competitive advantages. But in reality, IT does not always receive clearly defined goals and prioritisation criteria from business. This situation can be improved by a more systematic strategic coordination between business and the IT. Changes have to be made inside and outside the IT organisation. Alternatively, a dynamic optimisation and restructuring of the IT project portfolio would ensure its harmonisation with the business strategies.

IT Governance IT Governance is the key element in developing a successful banking IT as only the combination of all six capability areas brings real success. Medium-sized and small banks are frequently finding it difficult to determine their position and direction because performance measures are not meaningful, not detailed enough or not comprehensive. Reliable instruments are required to ensure that the goals of IT Strategy are actually achieved and maintained in the long run. Projects have to pass a stringent cost/benefit analysis and have to be later monitored by a benefit management ensuring that the promised benefits can actually be realised.

Application Development Insufficiencies in IT Strategy and Governance burden the Application Development with cross-departmental clarifications and coordination activities. Thus projects often overshoot in terms of budget, hardly deliver on time and they frequently have redundant content. Reasons are to be found in weak cost estimates, insufficient project reviews and non availability of proven methodologies.

5 / 22

IT Operation and Maintenance Most banks have already put prerequisites in place to position their IT Operation as a reliable service provider. Such prerequisites are commonly agreed service level agreements (SLAs), communication interfaces between business and IT, single point of contact for customer management, business process oriented servicing and needs led volumes.

Architecture Landscape The current status of the architecture landscape in many banks can be described as highly fragmented, heterogeneous and complex. Customer data is stored in different areas making a single integrated view of the customer a dream. System functionality is overlapping and requires the user to do frequent re-keying of the same information into different systems. Different applications run on different databases and use various hardware and software standards. The number of existing systems and interfaces is a good indicator for complexity.

Management of Resources In addition to managing employees and knowledge in the bank, strategic procurement is especially important in this context. It is responsible for decisions on structural adjustments to the depth of the IT value chain, i.e. which parts of the value chain should be covered within the bank and which ones by partners.

Developing a better understanding of the costs and business value of major business applications in partnership with business owners will improve alignment between business and IT. It will also provide a better foundation for considering contributions from investments in the IT landscape and effects of outsourcing.

3 OFFSHORING OPPORTUNITIES

Core competencies are not products or things that banks do extremely well; they are those intellectually-based service activities or systems that the bank offers and delivers better than any competitor. Through them the bank creates uniquely high value for its customers. In an information intensive services industry, like banking, IT generally has a high value. But unless a bank is best-in-world at an IT management capability, it will be someone else’s core competency. Thus the bank would give up competitive edge by not procuring that skill from a best-in-world source.4

Outsourcing therefore is the key for entrepreneurial success. Banks are following an outsourcing strategy mainly in order to

• Achieve cost benefits

• Offer a higher level of service

• Free its resources and focus on its core competencies and goals5

Offshoring takes outsourcing international; tasks are no longer carried out onsite, near-site or near-shore, but they are taken to different parts of the world. Typically, the following tasks are feasible for offshoring:

6 / 22

• Maintenance of existing software packages, including all support levels

• Development of new software modules

• Software testing to reduce bugs prior to roll-out

• Enterprise Application Integration (EAI) to better connect and integrate existing systems with each other

• Data Centre Operations

Different types of banks will consider a different scope and depth of offshoring. Depth is an indicator of the economic penetration of outsourcing. Scope enriches this dimension with aspects of its dynamic and structural character. The scope dimension captures the degree of diversification of offshoring. The rationale for this scope dimension builds upon the notion of psychic distance, which is the degree to which a bank in a country is uncertain of the characteristics of foreign sourcing markets.6

Situational variables of banks have a significant moderating effect on the readiness for and the appropriateness of international outsourcing strategies:

• Product innovation: Under conditions of high product and service innovation activity, banks internalise more new technological knowledge than when the rate of product innovation is lower. Highly innovative banks intensify their global searching activity to obtain and combine best-practices from specialized sources around the world. Therefore, it is expected that during periods of increased product innovation a bank seeks innovative solutions outside the current portfolio of contractors. To obtain this knowledge, a bank is willing to invest in new relationships and to incur economic and emotional costs to overcome the increased psychic distance it faces

• Customer base value: The value of the customer base can be depicted as an aggregated combination of current customer value with the customer’s potential. With high uncertainty about the value of its customer base, the bank might prefer a concentrated low scope outsourcing strategy

• Technology uncertainty: When technology uncertainty is high, banks will have a desire to decrease this uncertainty by cooperating with a world-class supplier

• Internationality and bank size: Larger banks with experiences abroad are more likely to be ready for international outsourcing. A possible partial explanation is that larger banks have more negotiation power

This allows to develop a two-dimensional classification of the degree of offshoring in the context of these situational variables (see Figure 2).

7 / 22

Bounded Player Mature Globalist

Infant Opportunity Taker

Scope

Depth

high

low

low high

• Small sized, local banks• Uncertainty about customer

base value

• Technlogy uncertainty• High product innovation

• Technology certainty• Standard products (low

innovation rate)

• Big multinaltional banks• Awareness of customer base

value

Offsho

ring

Maturity

Figure 2: Offshoring Typology7

It may be expected that ‘Infants’ migrate towards ‘Opportunity Takers’ when technological volatility increases, for example by a need to offer eBusiness services to its customers. Therefore, the typology presented in Figure 2 provides a dynamic perspective on possible expansion paths of offshoring.

4 THE INDIAN OFFSHORING MARKET

4.1 Market Landscape

India started to be taken seriously as a possible outsourcing destination when Indian programmers were showing a quasi omnipresence in major American software companies. Highly qualified, motivated and English speaking, these programmers soon managed to create a niche for themselves in the Silicon Valley. Soon, the American companies started looking at possibilities of developing software in India, where they could add cost reductions to the list of benefits.

In Europe, India as an IT nation was largely unknown till preparations for Y2k bug fix and the European Monetary Union started. Suddenly there was a lack of resources in Europe and companies were hurriedly looking at alternative resource pools.

Another boost was noticed when Western companies started building up development centres in India and Indian companies started exploring the West. After successfully developing their market presence in the U.K. and the U.S., Indian offshore enterprises are now concentrating on enhancing their operations in mainland Europe.8 Driven by the current economic downturn, enterprises are viewing offshore providers as a remedy to optimise the utilisation of their shrinking IT budgets. In order to meet this demand, many large traditional global enterprise service providers – for example Accenture, Bearing Point, Cap Gemini Ernst & Young, Computer Sciences Corp., Deloitte, Electronic Data Systems and IBM Global Services – are also aggressively pursuing global delivery strategies.9 Figure 3 shows the most important Indian players in this market.

8 / 22

Enterprise Service Provider Total Revenue 2003 Worldwide Headcount

Tata Consultancy Services 1,020 million $ 23,400

Infosys Technologies 754 million $ 15,500

Wipro Technologies 690 million $ 19,800

Satyam Computer Services 459 million $ 9,800

HCL Technologies 333 million $ 9,600

Patni Computer Systems 188 million $ 5,600

NIIT 160 million $ 2,400 Figure 3: Major Indian Enterprise Service Providers10

The market is highly fragmented; the top five firms control 48% of the market, the remainder is split among 2,805 firms.11

There are many theories as to what is behind the success of the Indian IT sector. By and large, the success can be attributed to the following rationales:

• The Educational System: Despite the low literacy levels, India is renowned for its good educational system. To whom it is available, it offers a comprehensive tutoring with an emphasis on mathematics and sciences. This contributes to a large extent to being successful in programming where an analytical mind frame is required. Especially the Indian Institutes of Technology (IIT) and Management (IIM) are regarded as leading universities in the world. Due to a high demand in the IT sector, students are unfortunately encouraged to bend educational goals to suit the market needs

• Language: With Hindi being the official language, India has another 17 officially acknowledged languages and more than 1600 unofficial languages and dialects. Fortunately for the offshoring business, the British colonial legacy has turned India into one of the largest English speaking countries

• The Brain Drain Effect: In the past India has been experiencing an exodus of highly qualified and motivated engineers and programmers to the Western world, mainly the U.S. and U.K. But through this “brain drain” the Indian software industry got exposure to the latest technological advances and business concepts

• Governmental Support: The Indian government is backing efforts of Indian companies to further develop the offshoring business by offering tax holidays, tax exemptions on software exports and duty free hardware imports. The Government has created Software Technology Parks where companies with a hundred percent foreign equities are permitted and bureaucratical obstacles are minimised. Today the IT industry’s centre of attention are the cities of Bangalore, Chennai, Hyderabad and Pune.

9 / 22

4.2 Characteristics of Indian Enterprises

4.2.1 Organisational Considerations Traditionally Indian private companies were owned and managed by a family belonging to one of the traditional business communities, notably the Gujaratis, Parsis, Sindhis and Marwaris. These communities had built up a high level of internal trust with a close network for business opportunities, loans, information and other resources.

As some of these family business grew and endeavoured onto the international business place, their leadership was now reflecting a juxtaposition of heterogeneous elements of two divergent cultures. In many of these companies the top leadership positions – especially that of the CEO – are still in the hands of these family members. However, they have mostly been internationally trained with university education at U.S. or U.K. premier institutes.12

4.2.2 Style of Leadership In spite of these changes, the Indian executive has not yet been fully ‘westernised’, i.e. made compatible with the way ‘Westerners’ are thinking and acting. The adoption of western management style appears to be a surface phenomenon that does not change the core personality. In cases of stress, the Indian manager might turn back to more traditional ways of getting things done.

A recent study reported by Harvard University, INSEAD and INETOP examines the dimensions on which the top leadership of modern Indian business organizations differs from its US counterparts (see Figure 4).

ChallengingAssesses if the leader is able to search for opportunities and to experiment and take risks

InspiringConcerns the leader’s capacity to envision the future and enlist the support of others

EnablingMeasures the leader’s success in planning, empowerment, delegation and building trust

ModelingRates the leader on his success in building teams, setting clear goals, setting an example and ensuring keeping of certain values

EncouragingIndicates the ability to recognize contributions and celebrate accomplishments

Ind

ian

S

amp

le Mean = 24.26

SD = 3.23

US

S

amp

le Mean = 22.38

SD = 4.17

Mean = 23.38

SD = 4.14

Mean = 20.48

SD = 4.90

Mean = 24.91

SD = 3.59

Mean = 23.89

SD = 4.37

Mean = 24.48

SD = 3.58

Mean = 22.18

SD = 4.16

Mean = 20.81

SD = 5.30

Mean = 21.89

SD = 5.22

∆ Ind-US = + 1.88 ∆ Ind-US = + 2.90 ∆ Ind-US = + 1.02 ∆ Ind-US = + 2.30 ∆ Ind-US = - 1.08

Figure 4: Assessment of Leadership Practices in India and US13

10 / 22

The Indian group is characterized by scores that are higher than the American norm for the challenging, inspiring, enabling and modelling dimensions and lower for the dimension of encouraging. It can also be derived from these figures that Indian senior managers will feel more committed to the leadership of their companies than their US counterparts.

A cultural explanation for this phenomenon might be that Indian managers tend to idealize their CEOs. Because of the socialization pattern in the family, Indians are more likely to be more inclined to perceive the leader of a company, the patriarchal elders of the extended family and jat14 as a wise, caring, dependable yet demanding figure. However, today this idealization of the leader is no longer completely blind to his deficiencies or organizational needs that the leader does not fulfil.

4.2.3 The Indian Offshore Team Changes occur not only at the leadership level. At all other levels – right from the junior developer to the senior project manager – employees no longer come from these traditional business communities. However, they are resourced from a vast range of upper and middle class families from urban and small-town India. Most have grown up in nuclear families, but they have been inculcated with the idea and values of an extended family. Through their education at colleges, universities and institutes of engineering or management they have been exposed to Western management techniques. This may sharply differ from the traditional family and cultural values.

In every day project life working together with Indian colleagues some peculiarities will be noticed:15

Delivery Problems Despite the good education and expertise of Indian programmers, there will be discrepancies in delivery.

First, agreed final delivery dates are almost never adhered to. This may be an outcome of cultural differences, probably best expressed by the two different meanings of the Hindi word kal which means either yesterday or tomorrow. It would best to allow the offshoring team to set their own mini-milestones and to trace every such deadline progressively.

Second, the delivered application might not exactly follow the requirements. This hints for a lack of communication in the initial stages of the project and will be discussed later in section 4.3.7. It could also be a lack of skilled resources or missing technology updates. Sometimes Western companies are getting overwhelmed by the outlook of cost saving when offshoring to India. In India rampant competition is causing the different vendors to undercut each other – there will always be another vendor who will offer the same service at half the price. However, these embarrassingly low rates will somehow have to be balanced out again, i.e. the vendor will miss-out on technology updates, backup solutions etc. He might hire less skilled staff; as mentioned above there are some very good premium Indian educational institutes and also a huge number of ‘village universities’ and non-accredited ‘training institutes’. Eventually the company will have to spend more time and money to make the offshoring contract workable – and it will frequently be questioned.

11 / 22

Attrition Problems Companies also have to get used to the idea that the attrition rate of Indian software staff will be higher than commonly known in the Western world. Generally career development is faster and is also expected to be faster in India. Frequently Indians take up a job in a renowned Indian company only to get abroad experience and finally move abroad. If this kind of IT tourism is not provided – because offshoring is still more cost efficient than remote people sourcing – the employee will very soon reconsider his career choice. Secondly, in the boom time of Indian software industry, every developer could at any point of time secure himself another job which would probably come with a pay hike of 20% and more. No doubt, this is tempting. It will need to be monitored closely how the salary situation in India is developing in the next years.

Attrition is happening faster as well. If an employee quits, he has quit for good and might be leaving the day after for a better opportunity abroad. With his plane ticket already booked, he does not care about his appraisal any more and there is no way of making him keep to the contractually agreed notification period.

Communication Issues Issues will almost never be communicated openly. There is a big fear of losing face in the Indian culture, problems are communicated only when it is far too late to take corrective action.

Communication is less direct; e.g., a ‘yes’ might only denote ‘yes, I understand you’, a ‘done’ could stand for ‘I will start doing it tomorrow’.

Working Hours Western employees are regularly shocked by the number of hours their Indian colleagues spent in office. It has to be understood, that this is just another aspect where the Indian work culture is different from the Western one. A lot of social life is happening at the work place, colleagues become friends, lunch breaks are prolonged to catch up on social life and surfing the Internet is a frequent means of entertainment during office hours. Likewise Indian employees are surprised by the Western concept of a home-office.

4.3 Best Practice Approach for Launching IT Offshoring Initiatives

4.3.1 Taking the Offshoring Decision For European organizations, a greater proportion of outsourcing decisions are made at board level, whilst for US companies, more decisions are made by senior line and, or, by senior functional managers.16 The following activities are proposed:

• Analyse and define the bank’s strategic framework: strategic goals, product and service portfolio, necessary core competencies, evaluation of existing competencies

• Analyse and evaluate options for outsourcing, offshoring and cooperation

• Internal offshoring analysis: define information technology areas and processes which can be offshored, evaluate necessary resources and define a target price, benchmark with competitors

12 / 22

• External market analysis: identify and evaluate offshoring countries, identify vendors (request for information)

An alternative to offshore outsourcing would be offshore insourcing where banks are setting up their own offshore development centres.17 Captive structures were first developed in India during the initial 1990s offshore boom. Back then, this was the only way to go, primarily because local suppliers had little experience and global third-party providers had not yet fully developed their offshore capabilities.18 Examples are Citibank, American Express, HSBC’s development centre in Pune and Deutsche Bank’s former subsidiary Deutsche Software (India) Ltd. in Bangalore, which has now been taken over by HCL and renamed to DSL. However, “it is difficult to keep captive business models operating efficiently and competitively within a maturing third-party supplier market.” (Bierce, 2004, p 6).

4.3.2 Vendor Evaluation Offshoring involves contracting with an external provider for the provision of a service which has previously been provided using the bank’s in-house staff. Typically, the outsourcing process involves some form of bidding, as in competitive tendering and contracting (CTC) or direct negotiation between the transacting parties.19 CTC seeks out the most efficient service provider from the market and is particularly suited when cost reduction is a key objective. Direct negotiation offers the opportunity to emphasize quality and contract performance by closely matching the bank’s requirements with the capabilities of the offshore service provider.

For both cases criteria to evaluate the prospective providers need to be put up:

• Infrastructure: Broadband communication facilities with a guaranteed uptime need to link the bank to the locations of the offshore service provider. Will the development work be done on the bank’s computer systems or on the vendor’s? Are the vendor’s machines equipped and configured properly? Are the vendor’s premises secure?

• Onsite / Offshore Activities: For activities like business requirement gathering, staff from the service provider will need to be onsite at the bank’s site. Likewise, for acceptance testing staff from the bank might need to go to the offshore location. As described later in chapter 4.3.7 such travel should be encouraged. Questions arise around visa requirements and ease of reach by non-stop international flights

• 24x7 Support: Will the offshore vendor be able to bridge time differences and provide 24x7 support?

• Customs and Legal Issues: Can the vendor navigate the customs office easily for software deliveries? What rights will the bank have to software that is developed in India? Where will litigation take place?

• Service contingency: Are there any backup centres – within and outside India – in case of natural disasters or political turmoil? Will it be possible to ‘back-source’ all activities to the bank again?

13 / 22

• Methodologies: Indian companies pride themselves in using industry standard methodologies for application development. Due to the added complexity of offshoring these methodologies might need to be augmented. What steps has the vendor taken in this respect? Is he willing to incorporate pieces of the bank’s methodologies?

• Banking Domain Expertise: India’s banking sector has long been under currency exchange restrictions and banking products offered were not comparable with the international market. Thus domain expertise could only be built up recently through onsite assignments. How well versed is the offshore staff with international banking business and with the bank’s specific business practices?

• Employee Retention Rates: As pointed out in chapter 4.2.3, attrition and knowledge retention has become a major issue in Indian companies.20 What are the expected turnover rates? What measures and reward schemes have been put in place to combat this?

• Volume Variation: How will the provider deal with substantial volume variation?

• Capital Investment: How much capital investment and consequently business risk is the vendor willing to bear?

4.3.3 Considering Hidden Costs Most banks offshoring their information technology for the first time are not aware of the costs involved. Only those who had a bad experience take preventive measures the next time; they want to know where the money will be going before taking the formal decision.

• Thinking about Offshoring: This initial step alone already incurs project costs of around $ 500,000 on average21

• Vendor Search and Contracting: Most of the search and contracting costs are fixed costs independent of the contract size. Cost-cutting should not take place at this stage because time and effort spent can significantly reduce the other hidden costs later on. A good idea would be to exchange vendor information with other banks as not every bank will have the opportunity and luxury to go through several low-risk offshoring projects with a set of vendors

• Transitioning: Transition costs incur as long as the offshore vendor has not fully taken over from the bank’s internal IT departments. It can take months and years until the vendor finally knows as much about the IT landscape and the business as the bank itself. Most banks do not realize how much they spend on transitioning. Not only the time internal employees spend on assisting the vendor, but also costs due to disruption, inflexibility and slower reaction are transition costs. Banks can estimate for a transitioning period of 10 to 18 months based on the complexity of the outsourced development area. It is becoming increasingly common that the offshore provider will offer to bear some parts of the transition costs in order to acquire customer share22

14 / 22

• Managing the Vendor: These costs are not readily apparent, but they average around $ 300,000 per year.23 They incur in three areas: monitoring the vendor, bargaining & sanctioning and negotiating contract amendments

Overlooking these hidden costs will be detrimental to the success of the offshoring effort. It is key to manage these four cost areas proactively and holistically right from the beginning.

4.3.4 Designing the Contract Rules and regulations currently do not prescribe how banks must outsource or offshore functions and tasks. However, this should not be mistaken for a laissez-faire regulatory approach. The European Commission is catching up on this and established the Committee of European Banking Supervisors (CEBS) on 1st January 2004. CEBS is promoting convergence across the financial services sectors and aiming for an international regulatory definition of outsourcing and commonly accepted principles.24 National regulations prescribe further procedures.25 In practice, offshore service providers should always be viewed jointly responsible for complying with the law.26 Also, banks sometimes sign pre-written contracts the Indian vendors lay out for them. Especially for banks and lawyers in non-English speaking environments it is extremely difficult to decipher the actual contents of the contract. Indians sometimes pride themselves in using written English that has a high level of sophistication and is sometimes difficult to understand. Many offshoring deals have ended in clashes on the interpretation of service levels,27 hidden costs and penalties. It can be recommended to jointly write the offshoring contract ensuring a minimum level of ambiguity. To be effective, the contract must reflect the type of relationship required – focussed on operational efficiency, cost reduction, effectiveness or building competitive advantage. An exit possibility in case of poor service or non-updating of technology standards simultaneously with market standards should also be defined.

4.3.5 Transitioning A prerequisite for a successful transition from the bank’s internal IT department to the offshore service provider is a ruthless internal process reengineering and reorganisation. Homogenous tasks have to be clustered and well-defined interfaces have to be established in the organisational structure. On all levels, the output to the offshore provider and the expected return needs to be clearly specified. This requires standardisation and a proper implementation of the IT capability framework. If a management framework as described in chapter 2.3 does not exist yet, it is mandatory to establish it before starting any outsourcing or even offshoring discussion. As a side effect this will lead to permanent synergies in the bank. If an implementation of the IT management framework is not done before offshoring, this would mean, that an internally not manageable area is transferred to a third party where it will be even less manageable.28

15 / 22

4.3.6 Change Management The introduction of offshoring will cause the bank’s IT department to react. Some groups become paralysed, other employees jockey for surviving positions or become indecisive under “change fatigue” and others attempt to prove their value to the bank. The employee question can be effectively tackled by setting up a change management office which attempts to involve the employees based on their experience and needs. This is surely the bank’s responsibility as staff will need to be retained for critical functions and the bank can not expect the offshore provider to safeguard its business interests.

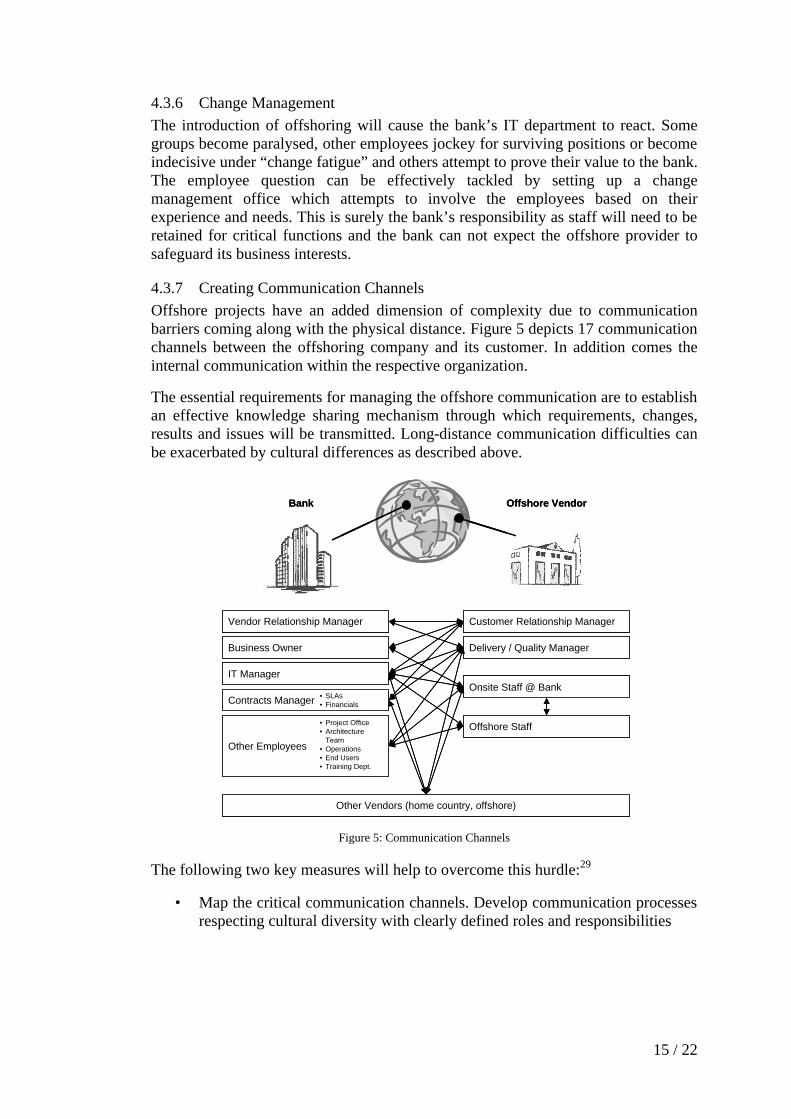

4.3.7 Creating Communication Channels Offshore projects have an added dimension of complexity due to communication barriers coming along with the physical distance. Figure 5 depicts 17 communication channels between the offshoring company and its customer. In addition comes the internal communication within the respective organization.

The essential requirements for managing the offshore communication are to establish an effective knowledge sharing mechanism through which requirements, changes, results and issues will be transmitted. Long-distance communication difficulties can be exacerbated by cultural differences as described above.

Vendor Relationship Manager

Business Owner

IT Manager

Contracts Manager • SLAs• Financials

Other Employees

• Project Office• Architecture

Team• Operations• End Users• Training Dept.

Bank Offshore Vendor

Customer Relationship Manager

Delivery / Quality Manager

Onsite Staff @ Bank

Offshore Staff

Other Vendors (home country, offshore)

Vendor Relationship Manager

Business Owner

IT Manager

Contracts Manager • SLAs• Financials

Other Employees

• Project Office• Architecture

Team• Operations• End Users• Training Dept.

Bank Offshore Vendor

Customer Relationship Manager

Delivery / Quality Manager

Onsite Staff @ Bank

Offshore Staff

Other Vendors (home country, offshore) Figure 5: Communication Channels

The following two key measures will help to overcome this hurdle:29

• Map the critical communication channels. Develop communication processes respecting cultural diversity with clearly defined roles and responsibilities

16 / 22

• Ensure additional resources and costs are built into the project management structure to provide for effective management of the required communication channels. Plan for face-to-face meetings to build a common understanding and respect. In an information network, regular and friendly face-to-face contact is the backbone of an efficient operation

And last but not least, an adequate communication infrastructure with leased high-quality telephone lines etc. will encourage communication between the two different cultures.

4.3.8 Migration Finally, the migration phase will transfer responsibilities and activities from the bank to the offshore vendor. In this phase it is essential to have tested (!) fall-back scenarios.

4.3.9 Controlling In order to ensure the market adequacy of the offshoring agreement in the future, a rigorous controlling process covering the strategic and operational level has to be put into place:

• Strategic level

- Monitoring the offshoring strategy

- Permanent evaluation of the offshoring market

- Continuous benchmarking against the bank’s main competitors and new market entrants

• Operational level

- Controlling of interfaces, costs and quality

- Monitoring of provider as a company

17 / 22

5 OFFSHORING TO INDIA – IS IT WORTH IT?

Compared with prior economic trends of moving work from countries with high labour rates to regions with lower labour rates, contracting out IT development work to India has become a mainstream reality that will not disappear – even once the Western economies fully recover from their current paralysis.

The adoption of offshore services creates both chances and challenges for the bank and the home economy.

5.1 Chances for the Bank’s Business Transformation

Traditionally capabilities are reduced short-term during periods of recession. After an economic recovery they have to be re-acquired at high cost in the long term. Offshoring frees funds by optimising non-discretionary expenditure. This approach focuses on the future because valuable capabilities can be retained (see Figure 6).

Cost-CuttingPeriod

Today TransitioningPeriod

TodayTime Time

IT B

udge

t

IT B

udge

t

non-discretionaryexpenditure

totalexpenditure

non-discretionaryexpenditure

totalexpenditure

Cost-CuttingPeriod

TodayTime

IT C

apab

ilitie

s

existingcapabilities

necessarycapabilities

Cost-CuttingPeriod

TodayTime

IT C

apab

ilitie

s

existingcapabilities

necessarycapabilities

discretionaryexpenditure

capabilitygap

Traditional Cost Cutting Approach Funding IT Transformationthrough Offshoring

Cost-CuttingPeriod

Today TransitioningPeriod

TodayTime Time

IT B

udge

t

IT B

udge

t

non-discretionaryexpenditure

totalexpenditure

non-discretionaryexpenditure

totalexpenditure

Cost-CuttingPeriod

TodayTime

IT C

apab

ilitie

s

existingcapabilities

necessarycapabilities

Cost-CuttingPeriod

TodayTime

IT C

apab

ilitie

s

existingcapabilities

necessarycapabilities

discretionaryexpenditure

capabilitygap

Traditional Cost Cutting Approach Funding IT Transformationthrough Offshoring

Figure 6: Costs of IT Capabilities

Once all costs are taken into account, there is a 30 percent saving potential in the cost base (Figure 7). Process reengineering along the IT management framework can further increase this saving potential to 40 percent. Given a required offshore vendor margin of 15 percent and an estimated 10 percent towards depreciation of initial investment costs and the costs of the transition phase, offshore vendors need to run their business at 35 percent of the bank’s IT department.

18 / 22

100%

Orig

inal

cos

t bas

ebe

fore

offs

horin

g

- 60%

Fac

tor

cost

sav

ings

+ 20%

Add

ition

al c

omm

unic

atio

n an

d m

aang

emen

t cos

ts

Add

ition

al V

AT

+ fe

es

+ 10%

70%

Long

-ter

m c

ost b

ase

afte

r of

fsho

ring

40%Savings

60%

Fur

ther

red

uctio

n th

roug

h pr

oces

s im

prov

emen

t and

ta

sk a

ggre

gatio

n

Estimate

100%

Orig

inal

cos

t bas

ebe

fore

offs

horin

g

- 60%

Fac

tor

cost

sav

ings

+ 20%

Add

ition

al c

omm

unic

atio

n an

d m

aang

emen

t cos

ts

Add

ition

al V

AT

+ fe

es

+ 10%

70%

Long

-ter

m c

ost b

ase

afte

r of

fsho

ring

40%Savings

60%

Fur

ther

red

uctio

n th

roug

h pr

oces

s im

prov

emen

t and

ta

sk a

ggre

gatio

n

EstimateEstimate Figure 7: Savings through Offshoring

5.2 Risks

Offshoring is a potentially risky endeavour and all banks will face some core risk factors. It is important to identify and implement mitigating factors to help off-set these risks.

Business Disruption and Disaster The spectre of business disruption is raised by geopolitical risk, natural catastrophes, concerns about infrastructure quality and pandemic diseases. Only recently the outbreak of severe acute respiratory syndrome (SARS) has made this all to clear. Entire commercial facilities in Asia had to be shut down as a precautionary measure to help prevent the spread of the disease. Attacks by terrorists provide further evidence of this risk.

This risk can only be mitigated by maintaining a blend of onshore and offshore facilities, capabilities, resources and knowledge

Loss of Domain Expertise Offshore employees may lack banking expertise as this is a highly regulated industry with strict adherence to policies and procedures. This may lead to a project execution risk and increase the cost of implementation.

This risk can only be overcome by a careful implementation of the knowledge transfer process. Expatriates with multicultural fluency might help to bridge the cultural gap and leverage the knowledge process. The bank and offshore vendor need to find the right mix of expatriates and internal controls. If the bank and vendor employs experienced expatriates with substantial India experience, usually one or two expatriates should be sufficient to ensure effective outcomes.

Employee Morale The process of moving jobs to India can severely impact the morale of the bank’s own employees. Fearing unemployment in tough economic times often causes the bank’s employees to torpedo the offshoring plan.

19 / 22

Banks should come up with a clearly defined policy for keeping domain expertise in the bank and focussing its key employees on strategic initiatives. They should also communicate openly and set realistic expectations.

5.3 Effects on the Economy of the Home Country

Offshoring is expected to grow at the rate of 30 to 40 percent a year over the next 5 years. Consequently a huge number of jobs from the IT industry is expected to go offshore. Such projections have led to discussions about job safety and continuing prosperity of the Western world.

It is to be hoped that the Western world will be dynamic enough to generate new jobs. In the past not only offshoring has resulted in job displacement: also technological change, economic recession, changes in customer behaviour, consolidation of banks have had and will continue to have an effect on the job market.

Earlier it has been stated that offshoring is a kind of innovation that will help banks to free parts of their non-discretionary IT spending and use it to build up competitive capabilities. Through these capabilities, the bank will become more competitive and will eventually be forced by competition to pass these benefits on to its customers. If the employees capture new jobs in the banking industry, a momentum will be created to generate additional services that did not exist before.

Offshore providers will also have to procure equipment (such as hardware, software, telecommunication) and services (legal, financial and marketing) from the Western economy. Thereby they are creating exports and extra revenue. Some offshore providers are incorporated in the Western world. These providers repatriate their earnings.

Going forward, the Western population is ageing. Either an increase in the number of workers through increased immigration or productivity gains – for example through offshoring – will be required to balance the decreasing ratio of workers to the total population and thus to maintain the Western standard of living. Most likely, offshoring will be easier to embrace. On the other hand, the population explosion has not yet been contained in India. The percentage of young Indians between 15 and 24 years is steadily increasing by 1.6% p.a. Industry has to provide another 10 million new jobs for them, requiring an annual economic growth of 10%.30

Thus, today’s major challenge is to firmly believe in the resilience of the Western economy, stay optimistic and not pander to protectionism.

20 / 22

REFERENCES

J. Barthélemy, ‘The Hidden Costs of IT Outsourcing’, MIT Sloan Management Review, (Spring 2001) 60-9.

A. Bierce, S. Spohr, R. Shah, ‘Captive No More’, Executive Agenda, A.T. Kearney (2nd Quarter 2004) 5-13.

CEBS, ‘Committee of European Banking Supervisors Consultation Paper on High Level Principles on Outsourcing’, www.c-ebs.org/25802/29602.html, last accessed 09/06/2004, (30th April 2004).

S. Domberger, P. Fernandez, D. Fiebig, ‘Modelling the Price, Performance and Contract Characteristics of IT Outsourcing’, Journal of Information Technology, Vol. 15 (2000) 107-18.

K. Friemel, ‘Aufstieg der Mittelklasse’, Financial Times Deutschland, (30th Jan 2004) 33.

M. Hignett, M. Rude, I. Grossman, L. Berk-Lidsky: ‘Funding Transformational Change through Offshoring’, Journal of Financial Transformation, Vol 8 (2003) 119-28.

F. Karamouzis, ‘A Look at India for Offshore Sourcing Options’, Gartner Group Article Top View, AV-18-8057 (2003).

A. Kakabadse, N. Kakabadse, ‘Trends in Outsourcing – Contrasting USA and Europe’, European Management Journal, Vol 20 No 2 (April 2002) 189-98.

S. Kakar, M. Kets de Vries, S. Kakar, P. Vrignaud, ‘Leadership in Indian Organizations from a Comparative Perspective’, IJCCM International Journal of Cross Cultural Management, Vol 2(2) (2002) 239-50.

A.T. Kearney, ‘Making Offshore Decisions’, A.T. Kearney’s 2004 Offshore Location Attractiveness Index, www.atkearney.com, last accessed 15/06/04, (2004)

M. Lacity, L. Willcocks, D. Feeny, ‘IT Outsourcing – Maximize Flexibility and Control’, Harvard Business Review, May-June (1995).

C. Locher, J. Mehlau, ‘Der ibi Kubus – Ein multikausales Entscheidungsmodell für das Outsourcing unter Berücksichtigung spezifischer Rahmenbedingungen in der Finanzdienstleistungsbranche’, in: Bartmann, D. (ed.), Bankinformatik 2004, Gabler-Verlag (2003) 285-92.

M. Mol, P. Matthyssens, P. Pauwels, L. Quintens, ‘A technological Contingency Perspective on the Depth and Scope of International Outsourcing’, Proceedings of the 4th IGMS CIBER Research Forum, Temple University Philadelphia (USA), (March 2003).

H.-G. Penzel, ‘Reengineering und Outsourcing – Die zwei Seiten einer Medaille’, BIT Banking and Information Technology, Vol 4 No. 3 (September 2003) 55-65.

A. Pohl, B. Onken, ‘Outsourcing und Offshoring mit indischen IT-Unternehmen’, Study by Deloitte & Touche Corporate Finance, (Munich, September 2003).

J. Quinn, ‘Strategic Outsourcing – Leveraging Knowledge Capabilities’, MIT Sloan Management Review, (Summer 1999) 9-21.

J. Roberts, ‘Communicating with Offshore Application Developers’, Gartner Group Research Note, TU-19-2428 (2003).

21 / 22

R. Scholl, S. Chohan, ‘Offshore Insourcing vs. Offshore Outsourcing’, Gartner Group Research Note, COM-20-4614 (2003).

G. Schmidt, E. Porteus, ‘Sustaining Technology Leadership Can Require both Cost Competence and Innovative Competence’, Stanford University, Research Paper No. 1431R (October 1998).

J. Sviokla, ‘Harnessing Service Price Deflation’, Presentation at The Exchange – The Boulders, Diamondcluster, (7th April 2003).

E. Stahl, A. Wimmer, ‘Informationsverarbeitung in Banken – Innovative Technologien und Konzepte’, in: Bartmann, D. (ed.), Bankinformatik 2004, Gabler-Verlag (2003) 173-82.

G. Tramacere, I. Marriott, ‘Indian Offshore Focus on Europe – Threat or Opportunity?’, Gartner Group Research, Note M-15-4227 (2002).

THE AUTHOR

Wolfgang Messner, Dr. rer. pol. (University of Kassel, Germany), Dipl.-Inform. (Techn. Univ. Munich, Germany and Univ. of Newcastle-upon-Tyne, U.K.), M.B.A. (Univ. of Wales, U.K.) is a Senior Management Consultant with Softlab GmbH in Frankfurt (Germany) concentrating on financial institutions. He has had similar positions with other leading consulting companies. Starting from December 2005, he is also a visiting faculty at the IIM-B (Indian Institute of Management, Bangalore). Earlier he was a project manager with Deutsche Software (India) Ltd. in Bangalore (India) and a business analyst with Deutsche Bank AG in Frankfurt (Germany). He has published several articles with magazines and books and is a frequent speaker on international conferences.

1 See (Stahl/Wimmer, 2003, p. 173)

2 See (Hignett et al., 2003) 3 See (Schmidt/Porteus, 1998) 4 See (Kakabadse/Kakabadse 2002; Quinn, 1999)

5 See (Pohl/Onken, 2003) 6 (Mol et al., 2003) have conducted and tested a technological contingency perspective on the two dimensions of international outsourcing (depth and scope) with 189 Dutch firms. 7 Based on (Mol et al., 2003)

8 See (Tramacere/Marriott, 2002) 9 See (Karamouzis, 2003) 10 See (Karamouzis, 2003; Pohl/Onken, 2003) 11 See (Sviokla, 2003)

12 See (Kakar et al., 2002)

22 / 22

13 In 1999 a study was carried out by (Kakar et al., 2002) involving 23 hybrid companies in India based on the Leadership Practices Inventory (LPI), a widely used 360-degree instrument for leadership evaluation in the organizational world. The figures in this diagram are taken from this study. 14 jat (Hindi) = caste 15 From personal experience of the author as an offshore project manager in India as well as a customer of offshoring services 16 See (Kakabadse/Kakabadse, 2002) 17 For further discussion see (Scholl/Chohan, 2003)

18 See (Bierce et al., 2004, p 6) 19 See (Domberger et al., 2000) 20 See the low employee retention rating of India in (A.T. Kearney, 2004, p 6)

21 See (Barthélemy, 2001) 22 See (Hignett et al., 2003) 23 See (Barthélemy, 2001)

24 See (CEBS, 2004) 25 For example, in Germany the Bundesanstalt für Finanzdienstleistungsaufsicht (BAFin) and the Deutsche Bundesbank have to be informed (!) about outsourcing of core or essential areas, see (Locher/Mehlau, 2003, p 286). 26 See (Hignett et al., 2003)

27 See (Lacity et al., 1995) 28 See (Penzel, 2003) 29 See (Roberts 2003)

30 See (Friemel, 2004)