nestle valuation report - arthur steven · 2019-09-30 · arthur steven asset management limited...

TRANSCRIPT

30th September 2019

Arthur Steven Asset Management Limited

NESTLE VALUATION REPORT

1

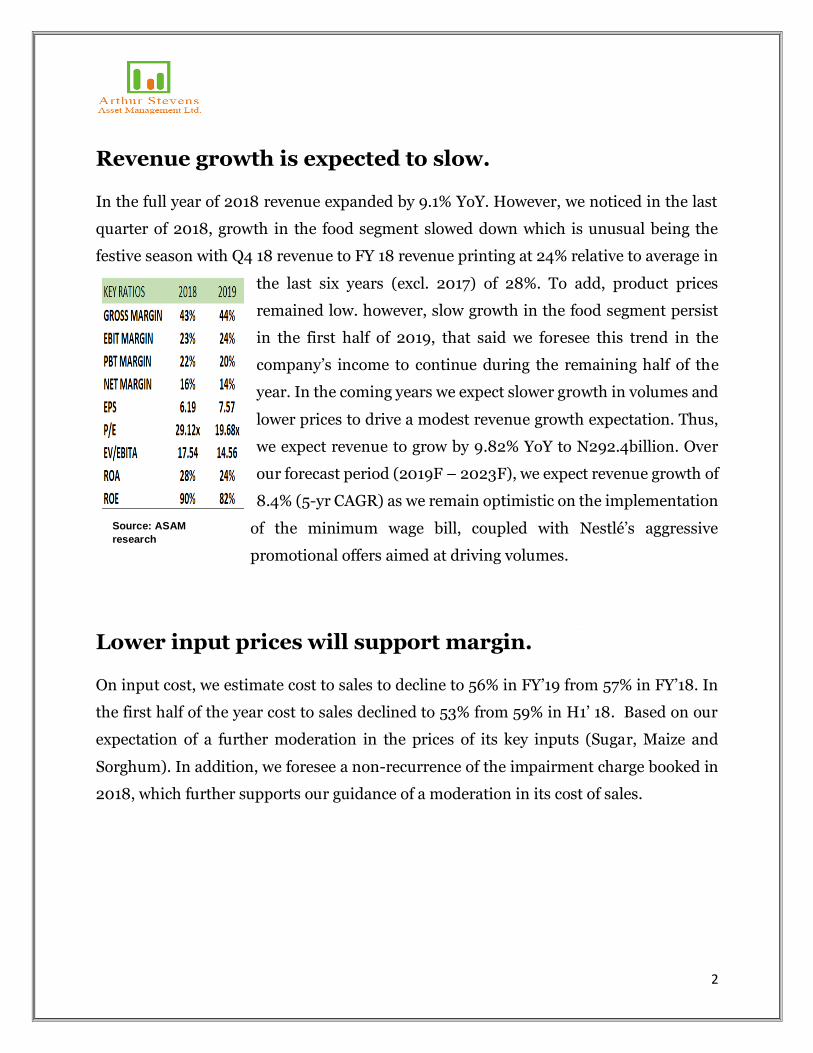

EARNINGS UPDATE│NESTLE|H1:2019

Nestle Nigeria Plc released its Half-year (HY) 2019

financial statement showing an increase of 4.89%

year-on-year (YoY) in revenue ₦141.91 billion while

the Profit Before Tax (PBT) grew marginally by

22.32% YoY to ₦26.25 billion.

Nestlé Nigeria is a food processing group organized

primarily around 2 families of products:- foods

(62.2% of net sales): cereals (Nestlé Nutrend,

Nestlé Cerelac and Nestlé Golden Morn brands),

dairy products (Nido), chocolates and

confectionery (Chocomilo) and seasoning products

(Maggi); - beverages (37.8%): instant coffee

(Nescafé brand), bottled water (Nestlé Pure Life), chocolate beverages (Milo), etc.

Share Price Performance

Year-to-Date, Nestle share price has depreciated by

22.88% with year highest price of N1617.10 and year

lowest price of N1070.00.

Source: ASAM research

Source: ASAM research

2

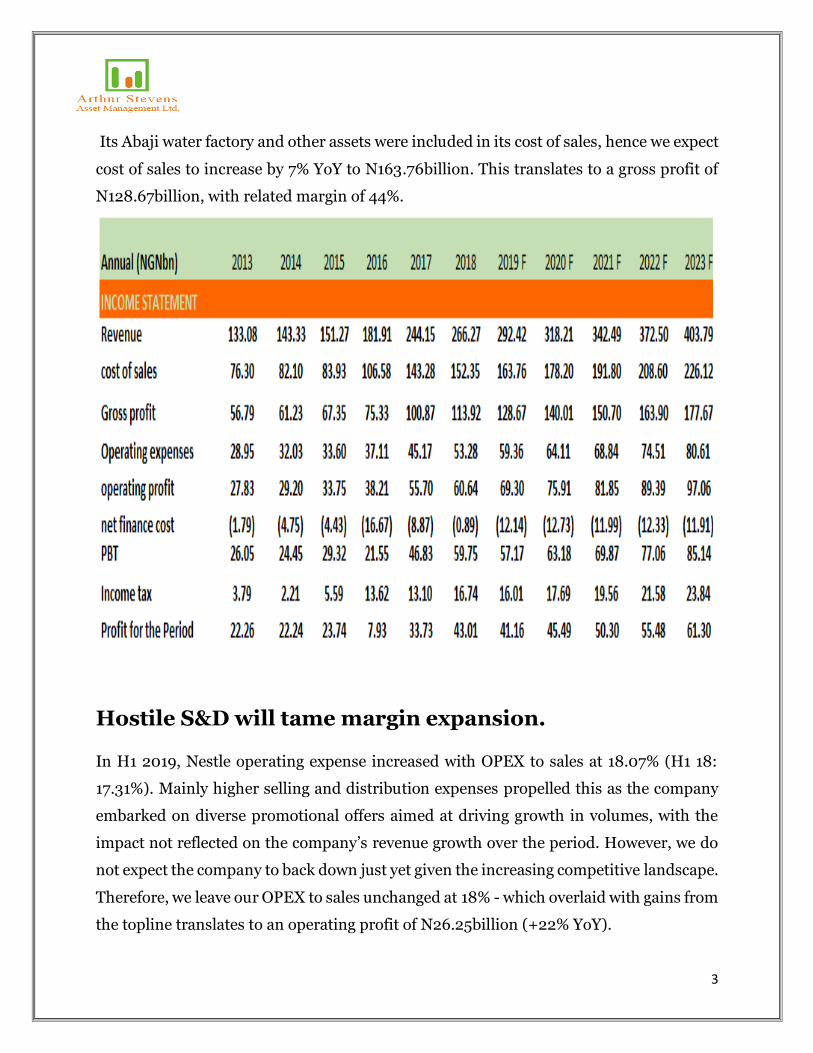

Revenue growth is expected to slow.

In the full year of 2018 revenue expanded by 9.1% YoY. However, we noticed in the last

quarter of 2018, growth in the food segment slowed down which is unusual being the

festive season with Q4 18 revenue to FY 18 revenue printing at 24% relative to average in

the last six years (excl. 2017) of 28%. To add, product prices

remained low. however, slow growth in the food segment persist

in the first half of 2019, that said we foresee this trend in the

company’s income to continue during the remaining half of the

year. In the coming years we expect slower growth in volumes and

lower prices to drive a modest revenue growth expectation. Thus,

we expect revenue to grow by 9.82% YoY to N292.4billion. Over

our forecast period (2019F – 2023F), we expect revenue growth of

8.4% (5-yr CAGR) as we remain optimistic on the implementation

of the minimum wage bill, coupled with Nestlé’s aggressive

promotional offers aimed at driving volumes.

Lower input prices will support margin.

On input cost, we estimate cost to sales to decline to 56% in FY’19 from 57% in FY’18. In

the first half of the year cost to sales declined to 53% from 59% in H1’ 18. Based on our

expectation of a further moderation in the prices of its key inputs (Sugar, Maize and

Sorghum). In addition, we foresee a non-recurrence of the impairment charge booked in

2018, which further supports our guidance of a moderation in its cost of sales.

Source: ASAM

research

3

Its Abaji water factory and other assets were included in its cost of sales, hence we expect

cost of sales to increase by 7% YoY to N163.76billion. This translates to a gross profit of

N128.67billion, with related margin of 44%.

Hostile S&D will tame margin expansion.

In H1 2019, Nestle operating expense increased with OPEX to sales at 18.07% (H1 18:

17.31%). Mainly higher selling and distribution expenses propelled this as the company

embarked on diverse promotional offers aimed at driving growth in volumes, with the

impact not reflected on the company’s revenue growth over the period. However, we do

not expect the company to back down just yet given the increasing competitive landscape.

Therefore, we leave our OPEX to sales unchanged at 18% - which overlaid with gains from

the topline translates to an operating profit of N26.25billion (+22% YoY).

4

5

Conclusion

For the remaining half year of 2019, we

remain optimistic on the company’s

earnings, driven by moderation in the

prices of its key inputs with expectations of

stable/declining product prices. This

should translate into expansion in gross

margin by 122bps YoY to 44.5%. However,

with our forecast OPEX to sales maintained increased to 18% YOY from 17% H1’ 18 and

this is propelled significantly by higher selling and distribution expenses as the company

embarked on diverse promotional offers aimed at driving growth in volumes. With the

impact not reflected on the company’s revenue growth over the period, we do not expect

the company to back down just yet given the increasing competitive landscape

promotional offers. Further down, the company was able to extinguish its FCY loans in

the first half of the year and thereby making gains on FY of 38.6 billion reducing net

finance cost nearly to zero percent. Overall, we lower our EPS estimate to N52.45 in 2019.

Though earnings growth story looking attractive, it looks expensive from a valuation

standpoint. Accordingly, we recommend our SELL recommendation with FVE of

N1,022.54.

Valuation Summary and Recommendation

We used the Free Cash Flow to Equity (FCFE), which gave us ₦1127.89, and the Dividend

Discount Model (DDM), which gave us ₦917.20 for our valuation. On our revised

numbers, we now have a blended fair value of ₦1022.54 per share using a blend of FCFE

and DDM with respective weights at 50% each.

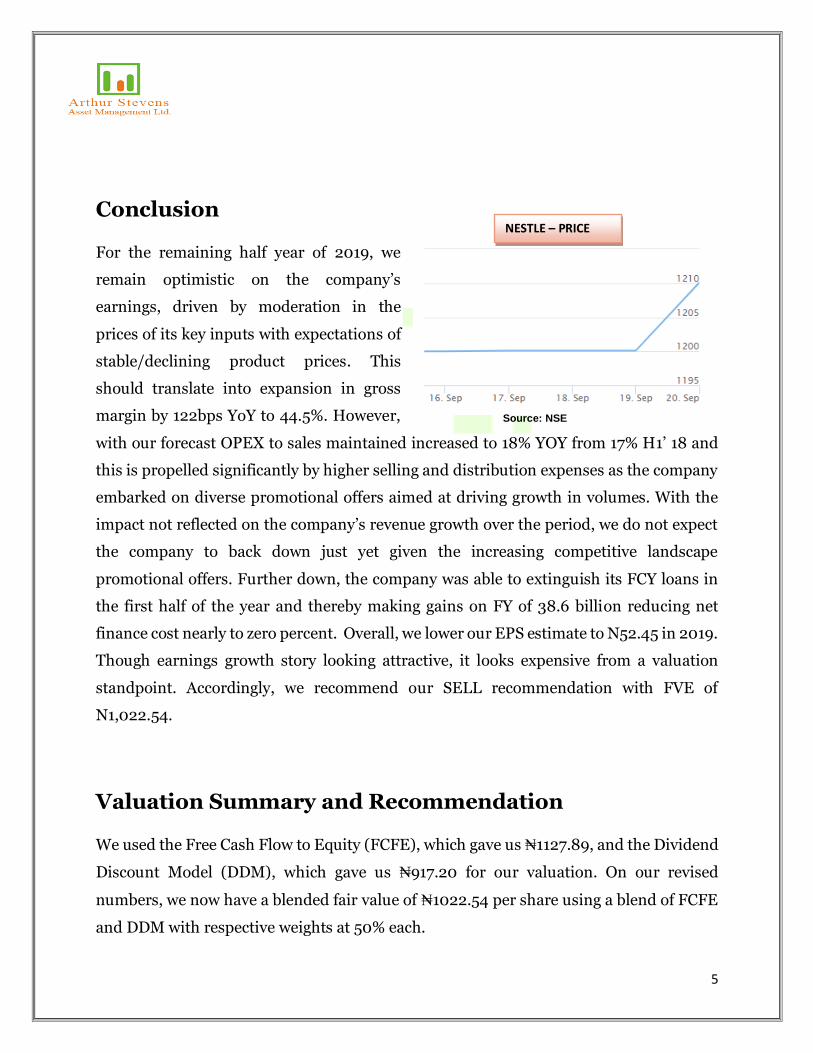

NESTLE – PRICE

MOVEMENT

Source: NSE

6

Relative to last closing price, this translates to -14.80% DOWNSIDE POTENTIAL and a

SELL rating on the shares. The company currently trades at a forward P/E of 36.24x,

which is at a discount to peer average of 22.16x.

7

Ratings Specification

BUY: Target Price of the stock is above the current market price by at least 10 percent

HOLD: Target Price of the stock ranges between -10 percent and 10 percent from the

current market price.

SELL: Target Price of the stock is more than 10 percent below the current market price.

The information, opinions and recommendations

contained herein are and must be construed solely as

statements of opinion and not statements of fact. No warranty, express or implied,

as to the accuracy, timeliness, completeness, merchantability or fitness for any

particular purpose of any such recommendation or information is given or made by

Arthur Stevens Asset Management Ltd in any form or manner whatsoever. Each

recommendation or opinion must be weighed solely as one factor in any investment

or other decision made by or on behalf of any user of the information contained

herein. S uch user must accordingly make its own study and evaluation of each

strategy / security that it may consider purchasing, holding or selling and should

appoint its own investment or financial or other advisors to assist the user in reaching

any decision. Arthur Stevens Asset Management Ltd will accept no responsibility

of any nature in respect of any statement, opinion, recommendation or information

contained in this document.

Disclaimer

8

Arthur Stevens Asset Management Ltd.

(MEMBER OF THE NIGERIAN STOCK EXCHANGE)

… Succeeding Together

Address:

86 Raymond Njoku Street,

SW Ikoyi, Lagos, Nigeria.

Telephone:

+234 9036881136

+234 9035996606

+234 8091054142

9

https://sec.gov.ng/non-mandated/