lesotho - poverty reduction support programme … reviewers 1. issa faye ... poverty reduction...

TRANSCRIPT

Language: English Original : English

AFRICAN DEVELOPMENT FUND

PROGRAMME : POVERTY REDUCTION

SUPPORT PROGRAMME (PRSP) COUNTRY : LESOTHO ________________________________________________________________________ APPRAISAL REPORT MARCH 2009

Appraisal Team

Team Leader: Team Members: Sector Manager Sector Director Regional Director:

Mothobi P. S. MATILA, Senior Economist, OSGE.2 (Task Manager) George HONDE, Country Economist, ORSA Marlene KANGA, OSGE.2 Gabriel NEGATU, OSGE Abdirahman BEILEH, ORSA

Peer Reviewers

1. Issa FAYE, Senior Economist, OSGE.2 2. Devinder GOYAL, Public Financial Expert, ORPF.2 3. Suwareh DARBO, Senior Country Economist, ORSA 4. Abdoulaye COULIBALY, Financial Governance

Expert, (OSGE.1)

TABLE OF CONTENTS

FISCAL YEAR OF BUDGET .................................................................................................................i CURRENCY EQUIVALENTS ...............................................................................................................i WEIGHTS AND MEASURES................................................................................................................i ACRONYMS AND ABBREVIATIONS.............................................................................................. ii GRANT AND LOAN INFORMATION .............................................................................................. iii

I. THE PROPOSAL...................................................................................................................1 II. COUNTRY AND PROGRAMME CONTEXT..................................................................1

2.1 GOVERNMENT OVERALL DEVELOPMENT STRATEGY AND MEDIUM TERM REFORMS PRIORITIES.................................................................................................................................1

2.2 RECENT ECONOMIC AND SOCIAL DEVELOPMENT, PERSPECTIVES, CONSTRAINTS AND CHALLENGES.............................................................................................................................2

2.3 BANK GROUP PORTFOLIO STATUS ............................................................................................5 III. RATIONALE, KEY DESIGN ELEMENTS AND SUSTAINABILITY .........................6

3.1 LINK WITH CSP, COUNTRY READINESS ASSESSMENT AND ANALYTICAL WORK UNDERPINNINGS .......................................................................................................................6

3.2 COLLABORATION AND COORDINATION WITH OTHER DONORS.................................................9 3.3 OUTCOMES OF THE PAST AND ONGOING SIMILAR OPERATIONS AND LESSONS .....................11 3.4 RELATIONSHIPS TO ONGOING BANK’S OPERATIONS ..............................................................11 3.5 BANK’S COMPARATIVE ADVANTAGES....................................................................................12 3.6 APPLICATIONS OF GOOD PRACTICES PRINCIPLES AND CONDITIONALITY ..............................12 3.7 APPLICATION OF BANK GROUP NON-CONCESSIONAL BORROWING POLICY ............................13

IV. THE PROPOSED PROGRAMME....................................................................................13 4.1 PROGRAMME’S GOAL AND PURPOSE........................................................................................13 4.2 PROGRAMME PILLARS, SPECIFIC OPERATIONAL POLICY OBJECTIVES AND EXPECTED

RESULTS..................................................................................................................................13 4.3 FINANCING NEEDS AND ARRANGEMENTS ................................................................................16 4.4 PROGRAMME’S BENEFICIARIES................................................................................................16 4.5 IMPACT ON GENDER.................................................................................................................17 4.6 ENVIRONMENTAL ISSUES.........................................................................................................17

V. IMPLEMENTATION, MONITORING AND EVALUATION .....................................17 5.1 IMPLEMENTATION ARRANGEMENTS........................................................................................17 5.2 MONITORING AND EVALUATION ARRANGEMENTS .................................................................18

VI. RISK MANAGEMENT.......................................................................................................18 VII. LEGAL INSTRUMENTS AND AUTHORITY ...............................................................19

7.1 LEGAL DOCUMENTATION ........................................................................................................19 7.2 CONDITIONS ASSOCIATED WITH BANK GROUP INTERVENTIONS.............................................19 7.3 COMPLIANCE WITH ADF POLICIES..........................................................................................20

VIII. RECOMMENDATIONS.....................................................................................................20 ANNEX I LETTER OF DEVELOPMENT POLICY.................................................................................8 ANNEX II PROGRAMME INDICATORS FOR 2009 AND 2010 (EXTRACTED FROM THE PAF).............2 ANNEX III LESOTHO: SELECTED ECONOMIC AND FINANCIAL INDICATORS, 2004–2013.................1 ANNEX IV PREREQUISITES CONDITIONS FOR PRSP.........................................................................1

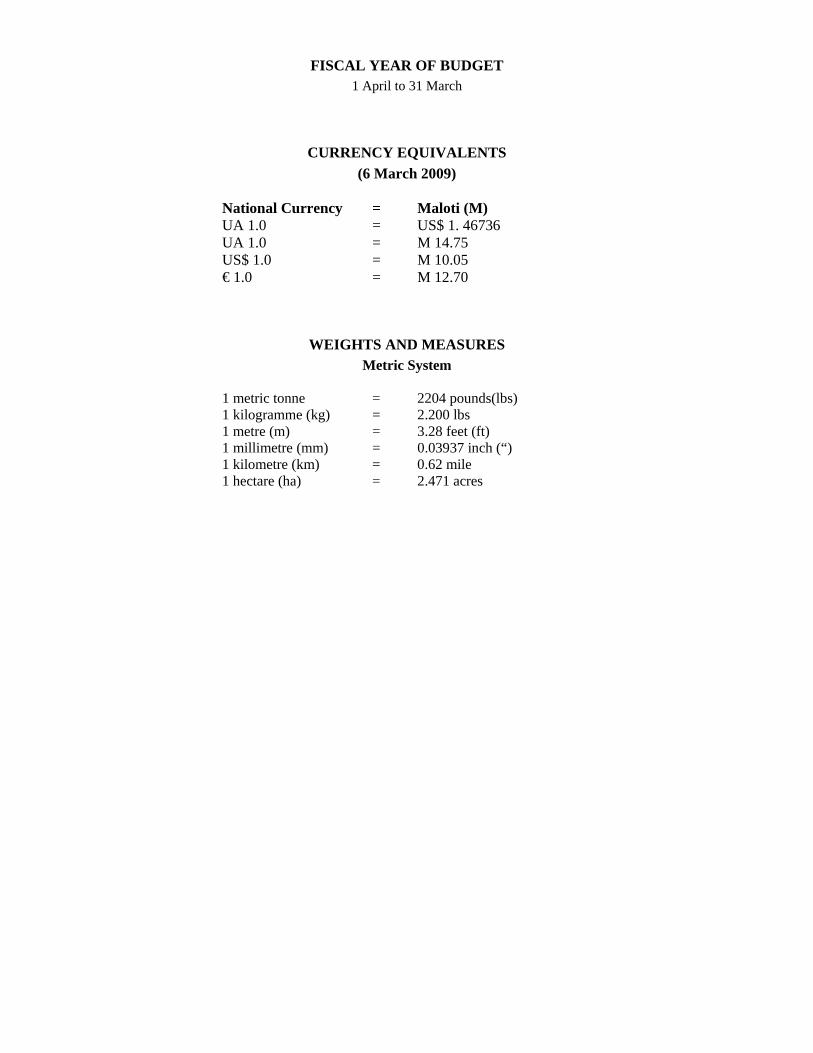

FISCAL YEAR OF BUDGET 1 April to 31 March

CURRENCY EQUIVALENTS (6 March 2009)

National Currency = Maloti (M) UA 1.0 = US$ 1. 46736 UA 1.0 = M 14.75 US$ 1.0 = M 10.05 € 1.0 = M 12.70

WEIGHTS AND MEASURES Metric System

1 metric tonne = 2204 pounds(lbs) 1 kilogramme (kg) = 2.200 lbs 1 metre (m) = 3.28 feet (ft) 1 millimetre (mm) = 0.03937 inch (“) 1 kilometre (km) = 0.62 mile 1 hectare (ha) = 2.471 acres

ii

ACRONYMS AND ABBREVIATIONS ACP : Africa, Caribbean and Pacific ADB : African Development Bank AGOA : African Growth and Opportunities Act CBL : Central Bank of Lesotho CER : Country Economic Review CMA : Common Monetary Area CPAR : Country Procurement Assessment Review CPI : Consumer Price Index CSP : Country Strategy Paper EU : European Union FDI : Foreign Direct Investment FTA : Free Trade Area GBS : General Budget Support GDP : Gross Domestic Product GNI : Gross National Income GoL : Government of the Kingdom of Lesotho GOLFIS : Government of Lesotho Financial Information System HDI : Human Development Index HIV/AIDS : Human Immuno Deficiency Virus/ Acquired Immuno Deficiency

Syndrome IFMIS : Integrated Financial Management Information System LDC : Less Developed Country LNDC : Lesotho National Development Corporation LRA : Lesotho Revenue Authority LHWP : Lesotho Highlands Water Project MCC : Millennium Challenge Corporation MDGs : Millennium Development Goals MFA : Multi-Fibre Agreement MFDP : Ministry of Finance and Development Planning MTEF : Medium Term Expenditure Framework NIR : Net International Reserve PAF : Performance Assessment Framework PEFA : Public Expenditure and Financial Accountability PEMFAR : Public Expenditure Management and Financial Accountability Review PFM : Public Financial Management PPAD : Procurement Policy and Advisory Division PRS : Poverty Reduction Strategy PRSP : Poverty Reduction Support Programme RSA : Republic of South Africa PSIRP : Public Service Improvement and Reform Programme SACU : Southern Africa Customs Union SADC : Southern African Development Community SMMEs : Small, Micro and Medium Enterprises SARB : South African Reserve Bank SSA : Sub-Saharan African T&C : Textile and Clothing U.S. : United States VAT : Value-Added Tax

iii

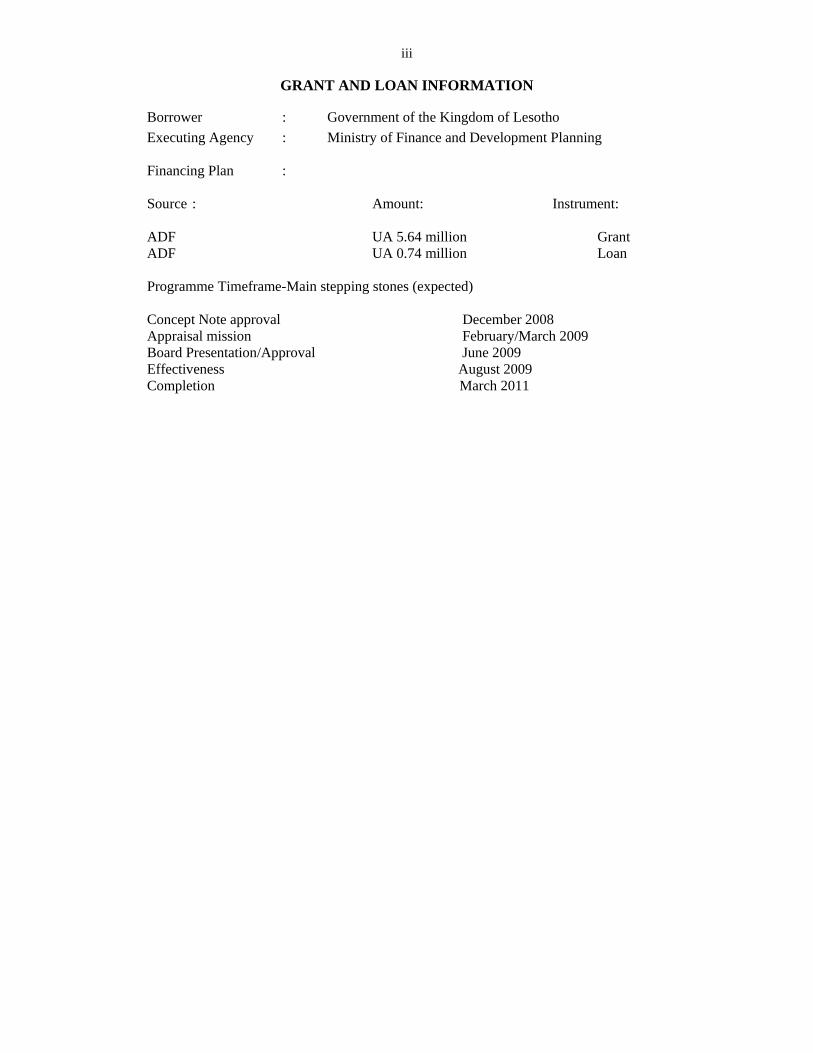

GRANT AND LOAN INFORMATION

Borrower : Government of the Kingdom of Lesotho Executing Agency : Ministry of Finance and Development Planning Financing Plan : Source : Amount: Instrument: ADF UA 5.64 million Grant ADF UA 0.74 million Loan Programme Timeframe-Main stepping stones (expected) Concept Note approval December 2008 Appraisal mission February/March 2009 Board Presentation/Approval June 2009 Effectiveness August 2009 Completion March 2011

iv

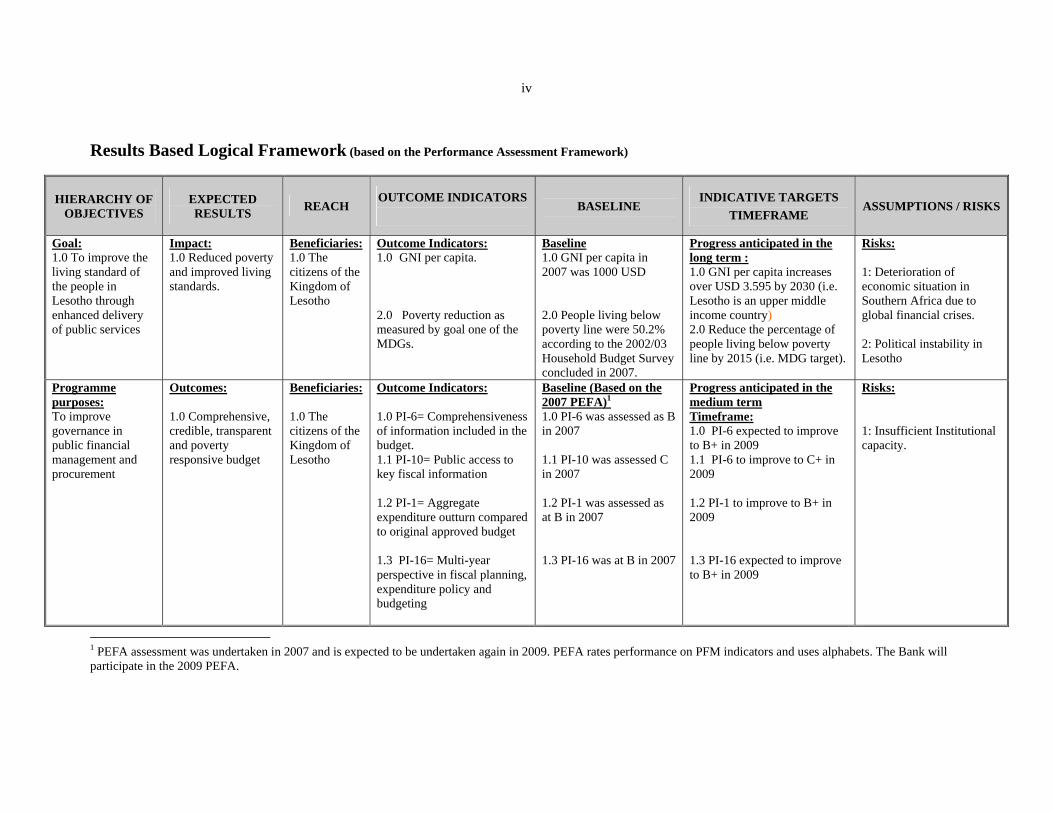

Results Based Logical Framework (based on the Performance Assessment Framework)

HIERARCHY OF OBJECTIVES

EXPECTED RESULTS REACH

OUTCOME INDICATORS

BASELINE

INDICATIVE TARGETS TIMEFRAME

ASSUMPTIONS / RISKS

Goal: 1.0 To improve the living standard of the people in Lesotho through enhanced delivery of public services

Impact: 1.0 Reduced poverty and improved living standards.

Beneficiaries: 1.0 The citizens of the Kingdom of Lesotho

Outcome Indicators: 1.0 GNI per capita. 2.0 Poverty reduction as measured by goal one of the MDGs.

Baseline 1.0 GNI per capita in 2007 was 1000 USD 2.0 People living below poverty line were 50.2% according to the 2002/03 Household Budget Survey concluded in 2007.

Progress anticipated in the long term : 1.0 GNI per capita increases over USD 3.595 by 2030 (i.e. Lesotho is an upper middle income country) 2.0 Reduce the percentage of people living below poverty line by 2015 (i.e. MDG target).

Risks: 1: Deterioration of economic situation in Southern Africa due to global financial crises. 2: Political instability in Lesotho

Programme purposes: To improve governance in public financial management and procurement

Outcomes: 1.0 Comprehensive, credible, transparent and poverty responsive budget

Beneficiaries: 1.0 The citizens of the Kingdom of Lesotho

Outcome Indicators: 1.0 PI-6= Comprehensiveness of information included in the budget. 1.1 PI-10= Public access to key fiscal information 1.2 PI-1= Aggregate expenditure outturn compared to original approved budget 1.3 PI-16= Multi-year perspective in fiscal planning, expenditure policy and budgeting

Baseline (Based on the 2007 PEFA)1 1.0 PI-6 was assessed as B in 2007 1.1 PI-10 was assessed C in 2007 1.2 PI-1 was assessed as at B in 2007 1.3 PI-16 was at B in 2007

Progress anticipated in the medium term Timeframe: 1.0 PI-6 expected to improve to B+ in 2009 1.1 PI-6 to improve to C+ in 2009 1.2 PI-1 to improve to B+ in 2009 1.3 PI-16 expected to improve to B+ in 2009

Risks: 1: Insufficient Institutional capacity.

1 PEFA assessment was undertaken in 2007 and is expected to be undertaken again in 2009. PEFA rates performance on PFM indicators and uses alphabets. The Bank will participate in the 2009 PEFA.

v

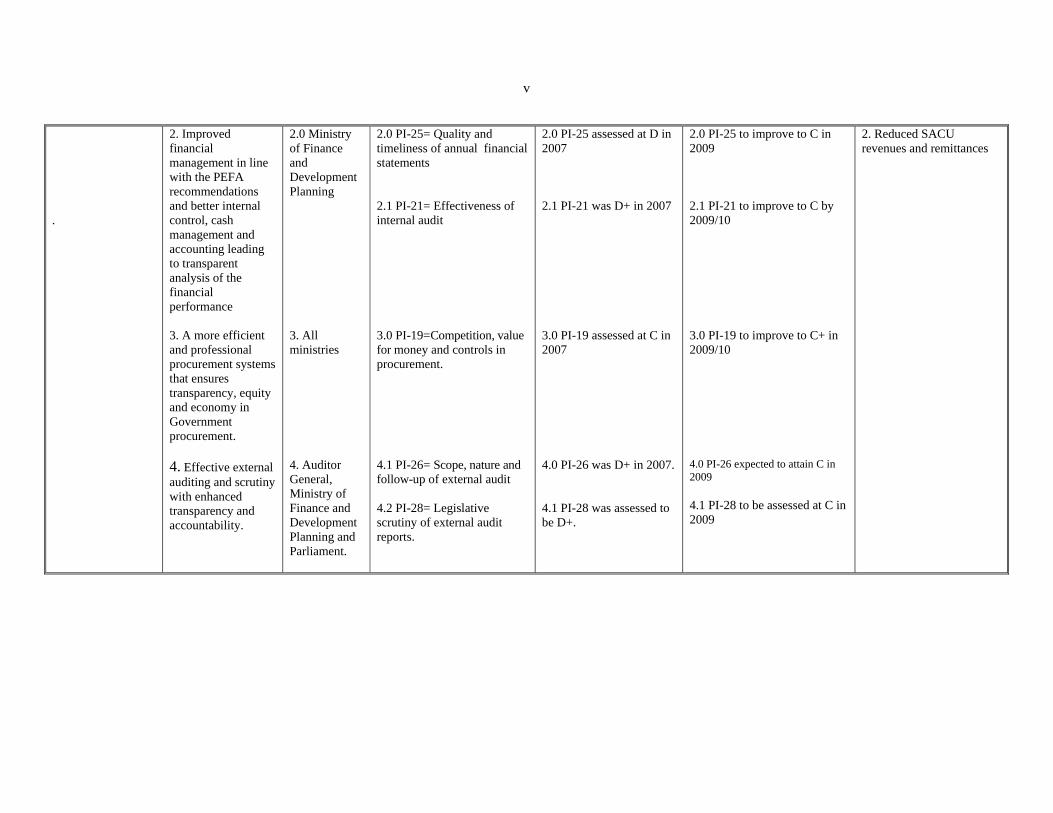

.

2. Improved financial management in line with the PEFA recommendations and better internal control, cash management and accounting leading to transparent analysis of the financial performance 3. A more efficient and professional procurement systems that ensures transparency, equity and economy in Government procurement. 4. Effective external auditing and scrutiny with enhanced transparency and accountability.

2.0 Ministry of Finance and Development Planning 3. All ministries 4. Auditor General, Ministry of Finance and Development Planning and Parliament.

2.0 PI-25= Quality and timeliness of annual financial statements 2.1 PI-21= Effectiveness of internal audit 3.0 PI-19=Competition, value for money and controls in procurement. 4.1 PI-26= Scope, nature and follow-up of external audit 4.2 PI-28= Legislative scrutiny of external audit reports.

2.0 PI-25 assessed at D in 2007 2.1 PI-21 was D+ in 2007 3.0 PI-19 assessed at C in 2007 4.0 PI-26 was D+ in 2007. 4.1 PI-28 was assessed to be D+.

2.0 PI-25 to improve to C in 2009 2.1 PI-21 to improve to C by 2009/10 3.0 PI-19 to improve to C+ in 2009/10 4.0 PI-26 expected to attain C in 2009 4.1 PI-28 to be assessed at C in 2009

2. Reduced SACU revenues and remittances

vi

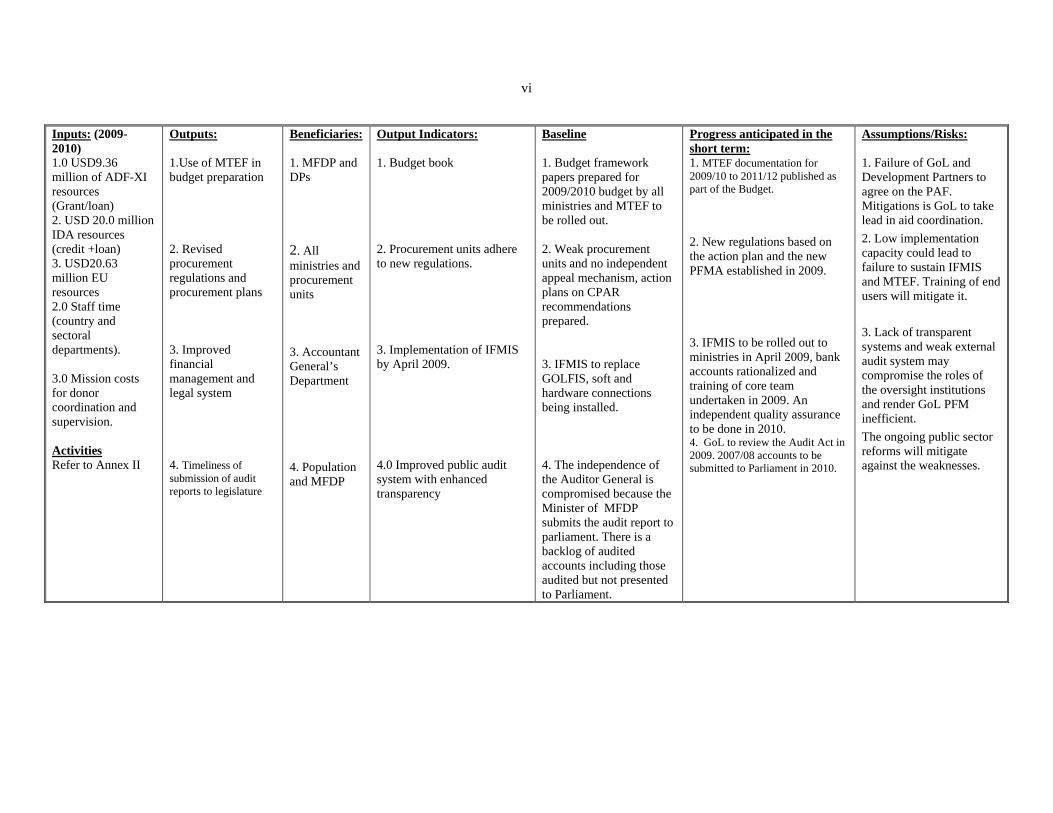

Inputs: (2009-2010) 1.0 USD9.36 million of ADF-XI resources (Grant/loan) 2. USD 20.0 million IDA resources (credit +loan) 3. USD20.63 million EU resources 2.0 Staff time (country and sectoral departments). 3.0 Mission costs for donor coordination and supervision. Activities Refer to Annex II

Outputs: 1.Use of MTEF in budget preparation 2. Revised procurement regulations and procurement plans 3. Improved financial management and legal system 4. Timeliness of submission of audit reports to legislature

Beneficiaries: 1. MFDP and DPs 2. All ministries and procurement units 3. Accountant General’s Department 4. Population and MFDP

Output Indicators: 1. Budget book 2. Procurement units adhere to new regulations. 3. Implementation of IFMIS by April 2009. 4.0 Improved public audit system with enhanced transparency

Baseline 1. Budget framework papers prepared for 2009/2010 budget by all ministries and MTEF to be rolled out. 2. Weak procurement units and no independent appeal mechanism, action plans on CPAR recommendations prepared. 3. IFMIS to replace GOLFIS, soft and hardware connections being installed. 4. The independence of the Auditor General is compromised because the Minister of MFDP submits the audit report to parliament. There is a backlog of audited accounts including those audited but not presented to Parliament.

Progress anticipated in the short term: 1. MTEF documentation for 2009/10 to 2011/12 published as part of the Budget. 2. New regulations based on the action plan and the new PFMA established in 2009. 3. IFMIS to be rolled out to ministries in April 2009, bank accounts rationalized and training of core team undertaken in 2009. An independent quality assurance to be done in 2010. 4. GoL to review the Audit Act in 2009. 2007/08 accounts to be submitted to Parliament in 2010.

Assumptions/Risks: 1. Failure of GoL and Development Partners to agree on the PAF. Mitigations is GoL to take lead in aid coordination. 2. Low implementation capacity could lead to failure to sustain IFMIS and MTEF. Training of end users will mitigate it. 3. Lack of transparent systems and weak external audit system may compromise the roles of the oversight institutions and render GoL PFM inefficient. The ongoing public sector reforms will mitigate against the weaknesses.

vii

PROGRAMME EXECUTIVE SUMMARY 1. The Poverty Reduction Support Programme (PRSP I) for Lesotho is a two year programme aimed at assisting the country to implement the Poverty Reduction Strategy (PRS). The programme will be supported by a budget support loan amounting to UA 740 000 and a grant of UA5.64 million to be disbursed in one tranche. The expected outputs are: (i) a Performance Assessment Framework (PAF) agreed and used for managing and monitoring budget support; (ii) Revised procurement regulations and establishment of procurement units in line ministries; (iii) Introduction of Integrated Financial Management Information System (IFMIS) to enhance management of financial accounts: (iv) Medium Term Expenditure Framework (MTEF) aligned to poverty reduction expenditure priorities; (v) Transparent budget formulation and dissemination among stakeholders; (vi) adoption of the Public Financial Management and Accountability Act; and (vii) improved external audit system to enhance fiscal transparency and accountability. 2. The expected outcomes of the programme are: (i) Comprehensive, credible, transparent and poverty responsive budget; (ii) Improved financial management in line with the Public Expenditure Management and Financial Accountability Review (PEMFAR) recommendations and better internal control, cash management and accounting leading to transparent analysis of the financial performance; (iii) A more efficient and professional procurement systems that ensures transparency, equity and economy in government procurement; and (iv) Effective external auditing and scrutiny with enhanced transparency and accountability. This operation will benefit the citizens of Lesotho through improved service delivery, transparency and accountability and management of public resources. The Auditor General, Ministry of Finance and Development Planning and all ministries will benefit from improved financial management and accounting system as a result of introduction of IFMIS. 3. GoL has undertaken reforms in the past which are predicated upon several studies done by different donors. The findings and recommendations of these reports led to the elaboration of the Public Service Improvement and Reform Programme (PSIRP) supported by development partners which aimed at resolving the identified weaknesses. The PFM reform component of the PSIRP focuses on improving the link between the country’s poverty reduction strategy and the annual planning and budgeting processes through introduction of a three year MTEF in six pilot ministries in 2005/06. While the roll out of MTEF to other ministries including training of staff is ongoing, all ministries prepared budget framework papers for 2009/2010-2011/2012 period. Weaknesses have been identified in the legislative, regulatory and institutional framework, as well as in market practices, transparency and integrity of the procurement system. An action plan has been prepared to address these weaknesses. 4. Budget support is suitable for reforms undertaken by a country which has set up a donor coordination mechanism. Lesotho has a framework for budget support management with development partners and a framework for monitoring progress. The Bank will collaborate with other development partners like the World Bank which has already provided budget support last year and is working on its second operation for 2009 and the European Union which is working on its support. The Bank’s allocation to Lesotho is small and could not be split into many sectors and is best used through budget support to augment national resources. The Bank will use its experience of budget support and managing projects in Lesotho as well as in other countries including fragile states to manage this operation. 5. The operation will in particular contribute to institutional development and knowledge building through knowledge sharing during formulation and management of the performance assessment framework.

I. THE PROPOSAL 1.1 We submit the following Report and Recommendation on a proposed loan and grant to Lesotho for UA 6.38 million (Six Million Three Hundred Eighty Thousand Units of Account) to finance the first Poverty Reduction Support Programme (PRSP I) in Lesotho. It is a general budget support programme and will cover twenty two months from June 2009 to March 2011. The programme has been appraised by a Bank mission from 23 February to 6 March, 2009. It results from a request of the Government of the Kingdom of Lesotho (GoL) dated 5 March 2009 and discussions held with previous Bank missions and is in line with the Lesotho PRS and the Bank’s Country Strategy Paper for Lesotho (2008-2012) adopted in December 2008. The PRS has been endorsed by the donors in 2006 when they began discussion for budget support. The design of the programme took into account good practices on conditionality and Bank Group provisions on non-concessional debt accumulation policy for ADF grant and loan, HIPC and MDRI beneficiaries. Lesotho is not a HIPC or MDRI beneficiary. 1.2 The programme goal is to improve the living standard of the people in Lesotho through enhanced delivery of public services. Its policy objective is to reduce poverty and increase economic growth, through improvement in governance and public financial management (PFM). The expected outcomes of the programme are: (i) Comprehensive, credible, transparent and poverty responsive budget; (ii) Improved financial management in line with the PEMFAR recommendations and better internal control, cash management and accounting leading to transparent analysis of financial performance; (iii) A more efficient and professional procurement system that ensures transparency, equity and economy in government procurement; and (iv) Effective external auditing and scrutiny with enhanced transparency and accountability. These outcomes will lead to improved service delivery and, hence, improved living standards of the people.

II COUNTRY AND PROGRAMME CONTEXT

2.1 Government Overall Development Strategy and Medium term Reforms priorities 2.1.1 Lesotho’s Poverty Reduction Strategy (PRS), which originally covered the period 2004/05-2006/07, and has been extended up to April 2011, was prepared through an extensive and elaborate national consultative process. The PRS articulates priorities and strategies for poverty reduction in Lesotho through economic growth and empowerment of the poor. The PRS continues to reflect Lesotho’s priorities and strategies for poverty reduction, within the four key pillars of policy objectives, namely: (i) accelerating shared and sustainable economic growth; (ii) human development; (iii) protecting and enabling disadvantaged groups; and (iv) good governance. The PRS’ priority areas of actions have been identified for each pillar as indicated in Table 1. The PRS links policy, planning and budgeting processes and ensures that there is synergy between key initiatives such

Table 1: PRS in Short PRS Pillars PRS Priority Areas of Action I: Accelerating shared & sustainable economic growth

o Private sector development o Tourism o Mining & quarrying o Agriculture o Economic infrastructure o Protecting & conserving environment

II. Human development

o Education & training o Healthcare o HIV & AIDS epidemic o Social infrastructure

III. Protecting and enabling disadvantaged groups

o Women’s empowerment o Youth & children’s issues o Other disadvantaged groups o Food insecurity

IV. Good governance

o Improving public service delivery o Deepening democratic institutions o Justice, safety & security

2

as the National Vision 2020 published in 2004 which articulates the level of development that Basotho2 aspire to attain by 2020, the Millennium Development Goals (MDGs) to be achieved by 2015 and national goals and PRS priorities. 2.1.2 The PRS will be replaced by a National Development Plan (NDP) because GoL has now decided to move away from a PRS process to a comprehensive planning framework that would not only reflect financial and human capacity issues, but also place emphasis on growth priorities. To complement the PRS during the interim period leading to the development of a National Development Plan, the Government has: (i) introduced budget framework papers in all line ministries for 2009/10-2011/12 period; (ii) finalised a Growth Strategy Paper (GSP) to identify potential drivers of growth; and (iii) completed an Issues Paper for the NDP (2008/09-2009/10) in order to ensure that a strategic document exists to guide the budgeting process during the intervening fiscal years.

2.2 Recent Economic and Social Development, Perspectives, Constraints and Challenges Recent Macroeconomic Performance

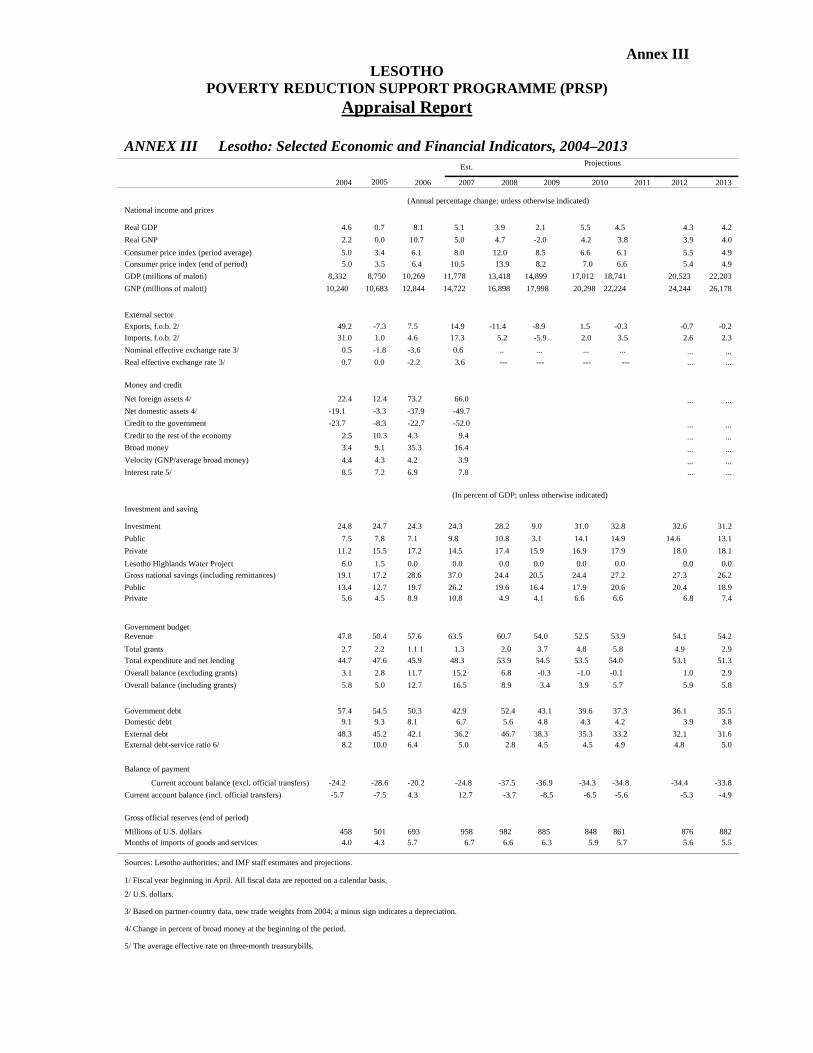

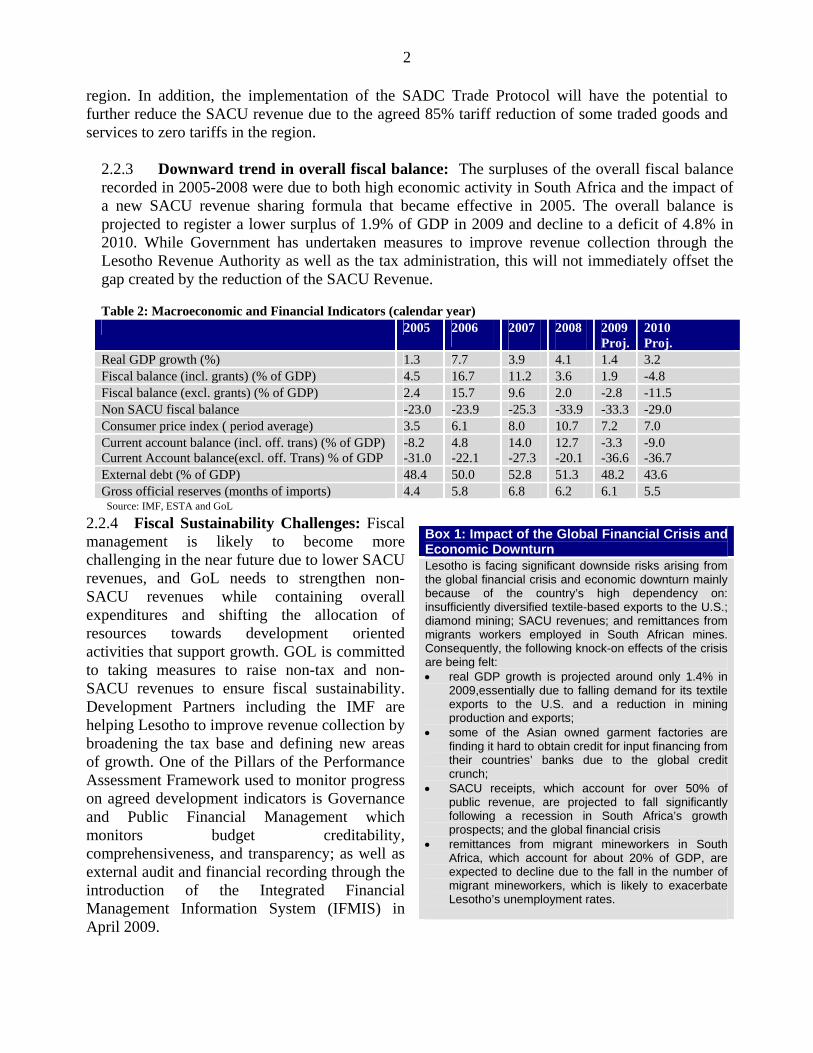

2.2.1 Lesotho has ensured prudent macroeconomic management and economic stability since 2000. Gross Domestic Product real growth was 8.1% in 2006 and declined to 5.1% in 2007 due to drought and agriculture’s negative contribution to GDP growth. However, the economic growth weakened to 3.9% in 2008 in the wake of the global financial crisis and economic downturn. Specifically, manufacturing activity slowed down reflecting a reduction in textile exports to the U.S. by about 11% year-on-year in December 2008, which experienced recession in the latter part of 2008, while mining production and exports also fell due to weak prices for diamonds. By the end of 2008, one mining company had suspended production in response to rapid fall in prices. It is estimated that the economic growth momentum will further slow down to 2.1% in 2009 due to the global financial crisis. Growth will be vulnerable to external shocks, the weak global economy and recession. The reduced diamond mining activities, declining export of the textile sector and the resultant job losses will further weaken economic activities and slow down growth. The current account balance is projected to register deficit from 2008 to 2011 due to declining transfers from the Southern African Customs Union (SACU) resulting from reduced economic activity in South Africa and the SACU region. Implementation of the SADC Trade Protocol will have the potential to reduce the SACU revenue due to the 85% tariff reduction of some traded goods and services to zero tariffs in the region. SACU will be subsumed under the SADC trade protocol and reduce further the revenue pool. (Paragraph 2.2.12) 2.2.2 The fiscal balance (including grants) in 2006/07 was 12.7% and was estimated to be 16.7% of GDP in 2007 due to favourable SACU revenues and under spending of the budget, improved domestic revenue collection, largely reflecting improved tax administration since the establishment of the Lesotho Revenue Authority in 2003, and rapid growth in South African imports leading to increased import and excise duty. Overall fiscal (including grants) balance registered a surplus of about 8.9% of GDP in 2008. The sharp increase in SACU receipts in recent years was due to both high economic activity in South Africa and the impact of a new sharing formula that became effective in 2005. In addition to that, Lesotho received adjustment payments due under the previous sharing arrangements. This was transitory as overall fiscal balance excluding grants is projected to be in deficit from 2009 to 2011 according to the IMF and GoL projections. The 2009/10 GoL budget estimates put the budget deficit at 10.6% partly due to the global downturn and stimulus programmes aimed at retaining employment and is significantly 2 People of Lesotho.

3

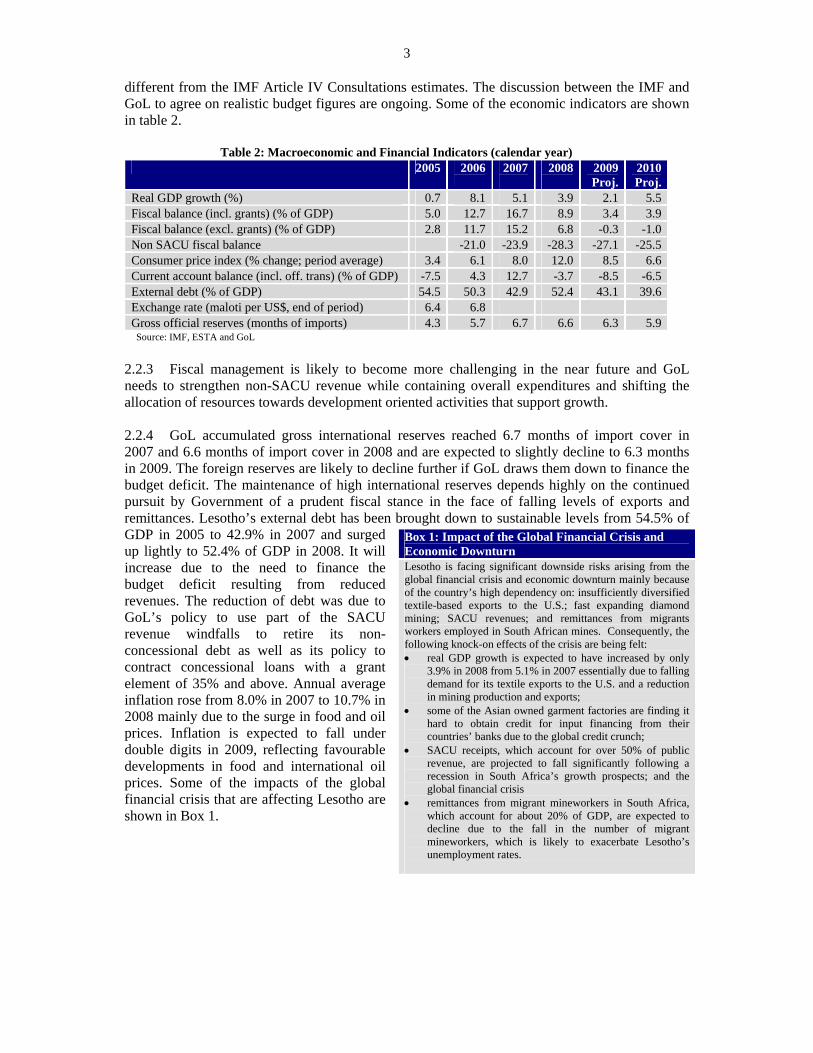

different from the IMF Article IV Consultations estimates. The discussion between the IMF and GoL to agree on realistic budget figures are ongoing. Some of the economic indicators are shown in table 2.

Table 2: Macroeconomic and Financial Indicators (calendar year) 2005 2006

2007 2008

2009 Proj.

2010Proj.

Real GDP growth (%) 0.7 8.1 5.1 3.9 2.1 5.5Fiscal balance (incl. grants) (% of GDP) 5.0 12.7 16.7 8.9 3.4 3.9Fiscal balance (excl. grants) (% of GDP) 2.8 11.7 15.2 6.8 -0.3 -1.0Non SACU fiscal balance -21.0 -23.9 -28.3 -27.1 -25.5Consumer price index (% change; period average) 3.4 6.1 8.0 12.0 8.5 6.6Current account balance (incl. off. trans) (% of GDP) -7.5 4.3 12.7 -3.7 -8.5 -6.5External debt (% of GDP) 54.5 50.3 42.9 52.4 43.1 39.6Exchange rate (maloti per US$, end of period) 6.4 6.8 Gross official reserves (months of imports) 4.3 5.7 6.7 6.6 6.3 5.9 Source: IMF, ESTA and GoL

2.2.3 Fiscal management is likely to become more challenging in the near future and GoL needs to strengthen non-SACU revenue while containing overall expenditures and shifting the allocation of resources towards development oriented activities that support growth. 2.2.4 GoL accumulated gross international reserves reached 6.7 months of import cover in 2007 and 6.6 months of import cover in 2008 and are expected to slightly decline to 6.3 months in 2009. The foreign reserves are likely to decline further if GoL draws them down to finance the budget deficit. The maintenance of high international reserves depends highly on the continued pursuit by Government of a prudent fiscal stance in the face of falling levels of exports and remittances. Lesotho’s external debt has been brought down to sustainable levels from 54.5% of GDP in 2005 to 42.9% in 2007 and surged up lightly to 52.4% of GDP in 2008. It will increase due to the need to finance the budget deficit resulting from reduced revenues. The reduction of debt was due to GoL’s policy to use part of the SACU revenue windfalls to retire its non-concessional debt as well as its policy to contract concessional loans with a grant element of 35% and above. Annual average inflation rose from 8.0% in 2007 to 10.7% in 2008 mainly due to the surge in food and oil prices. Inflation is expected to fall under double digits in 2009, reflecting favourable developments in food and international oil prices. Some of the impacts of the global financial crisis that are affecting Lesotho are shown in Box 1.

Box 1: Impact of the Global Financial Crisis and Economic Downturn Lesotho is facing significant downside risks arising from the global financial crisis and economic downturn mainly because of the country’s high dependency on: insufficiently diversified textile-based exports to the U.S.; fast expanding diamond mining; SACU revenues; and remittances from migrants workers employed in South African mines. Consequently, the following knock-on effects of the crisis are being felt: • real GDP growth is expected to have increased by only

3.9% in 2008 from 5.1% in 2007 essentially due to falling demand for its textile exports to the U.S. and a reduction in mining production and exports;

• some of the Asian owned garment factories are finding it hard to obtain credit for input financing from their countries’ banks due to the global credit crunch;

• SACU receipts, which account for over 50% of public revenue, are projected to fall significantly following a recession in South Africa’s growth prospects; and the global financial crisis

• remittances from migrant mineworkers in South Africa, which account for about 20% of GDP, are expected to decline due to the fall in the number of migrant mineworkers, which is likely to exacerbate Lesotho’s unemployment rates.

4

Recent Developments in Poverty and Social Indicators 2.2.5 The incidence of poverty in Lesotho remains a concern in spite of the strong economic growth in recent years. The 2002/03 Household Budget Survey finalised in 2007, indicated that slightly over half of the population, at 50.2%, still lived below the poverty line in 2002/03, an improvement from 62.1% registered in 1994/95. The leading cause of poverty is rising unemployment, estimated at 23.2% of the total labour force in 2002/03, and underemployment resulting from a series of structural changes which began in early 1990s with the decline of mining employment in RSA that has been worsened by the recent retrenchments in both mining and textiles industries due to the global financial crisis. Income inequality, though still high, has also been showing declining trends, with the Gini coefficient decreasing from 0.57 in 1994/95 to 0.52 in 2002/03. In 2008, Lesotho’s overall human development index (HDI) was 0.496, ranked 155th out of 179 countries, compared to 0.549 and 1138, respectively, in 2007. 2.2.6 On progress in achieving the MDGs, while Lesotho will almost meet the targets for attaining universal primary education and eliminating gender disparity in primary and secondary education, it is unlikely to achieve targets on halving poverty, eradicating hunger, as well as reducing under-five and maternal mortality rates. The slow progress in improving social indicators and attaining MDGs can be attributed to the high HIV/AIDS prevalence rate, chronic drought, reduction in remittances from migrant mineworkers and poor coverage of basic health services. In 2008, about one in four Basotho (15-49 years) were HIV positive, ranking Lesotho the third highest HIV prevalence country in the world. As a result of the impact of AIDS, average life expectancy is estimated to have fallen from 60 years in 1996 to about 43 years by 2008. Business Environment 2.2.7 Although the private sector business climate in Lesotho is complemented by the country’s access to the range of South Africa’s developed infrastructures and wider capital and financial markets, the country has not made any significant strides in improving the investment climate in recent years. Obstacles to private sector development that still exists relate to outdated laws and regulations, which impose unnecessarily long and complex procedures for the registration and licensing of firms, as well as administrative requirements that make it unnecessarily long and cumbersome to obtain work and resident permits. According to the 2009 Ease of Doing Business (EDB) published by the World Bank, it takes 40 days to start a business in Lesotho. Overall, it ranked Lesotho 123 out of 181 countries. Lesotho is ranked below other SACU countries. Recognising these weaknesses, with the support of the World Bank and Millennium Challenge Corporation (MCC), GoL is currently undertaking major policy reforms, including measures to improve the business environment and reduce the costs of doing business by reviewing several obsolete laws and business procedures, increase economic diversification through skills development, improve access to credit and increase the participation of women in the formal sector. A Trade Facilitation and Investment Centre, a one-stop-shop, has also been established to assist investors to rapidly obtain company registration, tax compliance, import and export permits as well as work and residence permits.

Perspective, Constraints and Challenges 2.2.8 Lesotho faces a number of challenges, which emanate partly from its geographical location and landlocked position. It is completely surrounded by South Africa and has no access to the sea and any other country without passing through South Africa. Its small population of about 2.0 million makes it unattractive to large investors. Hence, it largely depends on South Africa on trade, business, infrastructure, etc. Unemployment remains high, which is exacerbated by the retrenchment of migrant mineworkers from South Africa due to reduced mining activities

5

resulting from the global economic downturn, as well as lack of education, skills and opportunities. 2.2.9 Lesotho’s growth prospects remain extremely vulnerable to external risks, including slowdowns in its markets and exchange rate fluctuations. This is aggravated by the country’s high dependency on an insufficiently diversified textile-based industry. In spite of the expansion in diamond mining, the country needs to further diversify its export base in order to ensure sustainable economic growth. The weak competitiveness of the Lesotho economy, low levels of infrastructural facilities, including inadequate road transport network and lack of reasonably priced and efficient utilities (electricity, water and telecommunication services), continue to constrain private sector development and economic growth in Lesotho. Institutional capacity is also a constraint to service delivery. GoL through its growth strategy intends to address these constraints. 2.2.10 Regional Integration: Lesotho’s challenges and opportunities are greatly influenced by its inherent geographic integration in the economy of South Africa. Lesotho is a member of the Southern African Customs Union (SACU) which governs trade between member countries namely; Botswana, Lesotho, Namibia, South Africa and Swaziland. Lesotho’s revenue from the SACU Revenue Pool represented 35% of GDP in 2006/07 and its high dependence on the foreign taxes for fiscal revenue and its geographical location means that it cannot implement a trade policy and undertake trade liberalization without consultation with members of SACU as per the 2002 Agreement. Lesotho is also a member of the Common Monetary Area (CMA) comprising South Africa and smaller countries, namely Lesotho, Namibia and Swaziland (LNS states) which integrates them into the South African money and capital markets. The LNS states membership of CMA limits their discretion in monetary and exchange rate policies due to the free circulation of the South African rand in their territories. The pegging of their currencies at par to the rand makes it difficult for them to adjust quickly to external shocks other than through coordinated decisions with RSA. However, on the positive side, LNS states benefit from the policy creditability of the South African Reserve Bank and the CMA allows an unrestricted transfer of funds without any transaction costs and foreign exchange risks, whether for current or capital transactions, between CMA member states, which has facilitated cross-border trade among them. 2.2.11 Lesotho is also a member of the Southern African Development Community (SADC) and has joined the SADC Free Trade Area (FTA), which was launched in August 2008. Although this will open up markets for Lesotho’s products, the FTA will reduce the SACU revenue as other SADC members become eligible for free trade and not pay the SACU external tariff. The FTA precedes a customs union planned for 2010, a common market by 2015, monetary union by 2016 and a single currency by 2018. Lesotho has already met all the macroeconomic convergence criteria under SADC. In addition to the FTA, together with Botswana, Namibia, Mozambique and Swaziland, Lesotho also signed an interim (goods only) Economic Partnership Agreement with the EU in November 2007. This allows for duty-free and quota-free access to the EU market as of 1 January 2008.

2.3 Bank Group Portfolio Status 2.3.1 Since 1974, the Bank Group has funded 52 operations in Lesotho with a total net commitment amounting to UA 253.53 million. In terms of sectoral distribution, transport (36%), social sectors (27.2%) and public utilities (18%) are the largest recipients of Bank financing. As at 31 March 2009, six operations were at varying stages of implementation consisting of one project in transport (34.5%), two in social sector (31.71%), one in power (21.8%), one in agriculture and rural development (10.4%) and one in multi-sector (1.6%). The financial commitment relating to ongoing operations amounted to UA 50.36 million, of which UA 21.79 million was disbursed.

6

2.3.2 The 2007 Country Portfolio Performance Review Report (CPPR) rated the quality of the Bank Group portfolio in Lesotho as satisfactory. The common problems that were highlighted by the CPPR as contributing to project implementation delays included: start-up delays essentially relating to the fulfillment of conditions; communication difficulties between the Bank and Government; capacity constraints and weak project management; frequent changes to project management teams; and difficulties in adhering to Bank Group’s rules of procedures for procurement and disbursement. GoL has been making progress to address these generic problems by, among other things: putting in place mechanisms that would ensure that procurement and disbursement documents sent to the Bank Group are in conformity with Bank procedures; and encouraging regular meetings involving the Ministry of Finance and Development Planning (MFDP), line ministries and executing agencies to appraise each other on portfolio implementation issues and iron out any problems, as well as share experiences. The transition of the Bank’s Regional Office from Mozambique to South Africa will benefit Lesotho given its close links with that country.

III RATIONALE, KEY DESIGN ELEMENTS AND SUSTAINABILITY

3.1 Link with CSP, Country Readiness Assessment and Analytical Work Underpinnings Links with CSP

3.1.1 The 2008-2012 Country Strategy Paper (CSP) for Lesotho focuses on two Pillars, namely: (i) improving transparency and accountability in management and use of public resources; and, (ii) promoting economic growth and diversification. The proposed operation (PRSP I) is linked to the first pillar of the CSP whose objective is to support the implementation of the PRS by establishing a sound fiscal policy management that includes transparency and accountability in the management of public resources. It also supports one of the PRS’ priorities, namely Improving Public Service Delivery. 3.1.2 The expected outcomes identified in the CSP are: improved monitoring and evaluation of GoL service delivery; improved budget preparation and execution; improved financial management and reporting; and strengthened external audit and public oversight. The CSP indicated that the Bank operation under the pillar of “Improving transparency and accountability in management and use of public resources” will be in the form of general budget support, which this operation is addressing.

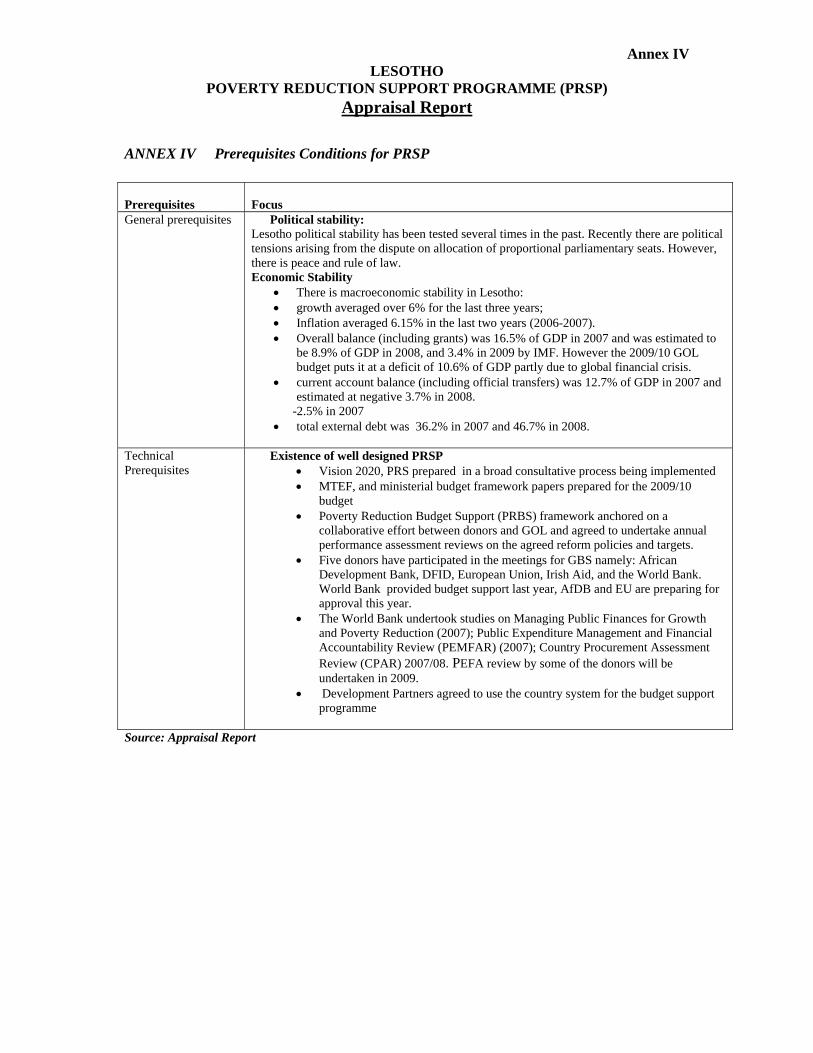

Analytical Works Underpinnings 3.1.3 GoL has undertaken reforms in the past which were based on several analytical studies. The PFM reforms, which are anchored on the PSIRP supported by development partners, focus on improving the link between the country’s poverty reduction strategy and the annual planning and budgeting processes through introduction of the three year Medium Term Expenditure Framework (MTEF) in six pilot ministries in 2005/06. While work is currently underway, including training of staff, to roll out the MTEF to other ministries for the 2010/11-2011/12 period, all ministries have already prepared budget framework papers for 2009/2010-2011/2012 period. 3.1.4 The effectiveness of the public expenditure and financial management has been assessed by many donors. The fiduciary assessments led to the adoption of the Public Sector Improvement and Reform Programme which includes integration of planning and budgeting, accounting and reporting as well as oversight bodies like the Auditor General and the Public Accounts Committee of Parliament, procurement reforms and internal audit. In 2005, Irish Aid provided

7

support for reforms of the PFM including procurement. The European Commission in 2007 provided support for PFM reforms especially on the introduction and implementation of the Integrated Financial Management Information System (IFMIS) which is to replace the outdated Government of Lesotho Financial Information System (GOLFIS) in April 2009. The World Bank undertook studies on Managing Public Finances for Growth and Poverty Reduction, Public Expenditure Management and Financial Accountability Review (PEMFAR 2007); and Country Procurement Assessment Review (CPAR) 2007/08, with the involvement of the African Development Bank (ADB), the United Kingdom’s Department for International Development (DFID) and Irish Aid. The Government, with support from DFID, in 2005/06 prepared the Public Financial Management (PFM) Inception Report and subsequent period reviews of the PFM implementation programme. These reports identified strengths and weaknesses of Lesotho’s fiduciary system and have guided the development of Government’s PFM reform programme over the past two years. 3.1.5 Some of the shortcomings/weaknesses identified included: existence of incremental budgeting based on inputs rather than outcomes; weak alignment of the budget and the PRS priorities and activities. The PEMFAR proposed introduction of the MTEF to improve linkages between budget and expenditure. The CPAR findings noted some improvements in regulatory and institutional frameworks following the adoption of the Public Procurement Regulations in 2007 and establishment of the Procurement Policy and Advisory Division (PPAD). Further weaknesses were identified in legislative and regulatory framework, institutional framework and management as well as in market practices, transparency and integrity of the procurement system. An action plan has been drawn based on the recommendations of the CPAR, including the review of the legislation which will set the basis for a new procurement law and the establishment of a more autonomous procurement structure. 3.1.6 In addition to the aforementioned reforms, in the context of the PSIRP, Lesotho is also gradually implementing a decentralised system of devolving functions, resources and authority from the central government to local authorities. The decentralisation and community empowerment reform is a result of the Local Governance, Decentralisation and Demand Driven Service Delivery Report of 2007. Following the first elections of local government structures in April 2005, progress has been made, particularly on the establishment of the Local Government Service Commission and capacity building activities for District and Community Councils. The major challenges GoL continue to face include delays in the development of the fiscal decentralization strategy. However, the ongoing public sector reforms are expected to improve capacity and service delivery.

Country Readiness Assessment 3.1.7 The prerequisites for budget support including political stability, economic stability and government commitment, and existence of a PRSP have been analysed and found adequate for budget support. (Annex IV). 3.1.8 The fiduciary system of Lesotho has been found adequate overall to receive Policy Based Lending in the form of budget support. Lesotho has adopted a comprehensive PFM reform programme whose implementation is supported by DfID, EU, Ireland and World Bank. The reform covers budget execution, financial accounting and recording, accountability and transparency, auditing and procurement. The PEFA Framework Assessment was concluded in 2007 and scored Lesotho well in seven (7) areas (above C) which included creditability and comprehensiveness of the budget, orderliness and participation in the budget process, introduction of the MTEF and predictability of the flow of funds. The main areas of weakness were in management of expenditure arrears, oversight of fiscal risk, effectiveness of internal control and internal audit, accounting, recording and reporting, external audit and donor practices.

8

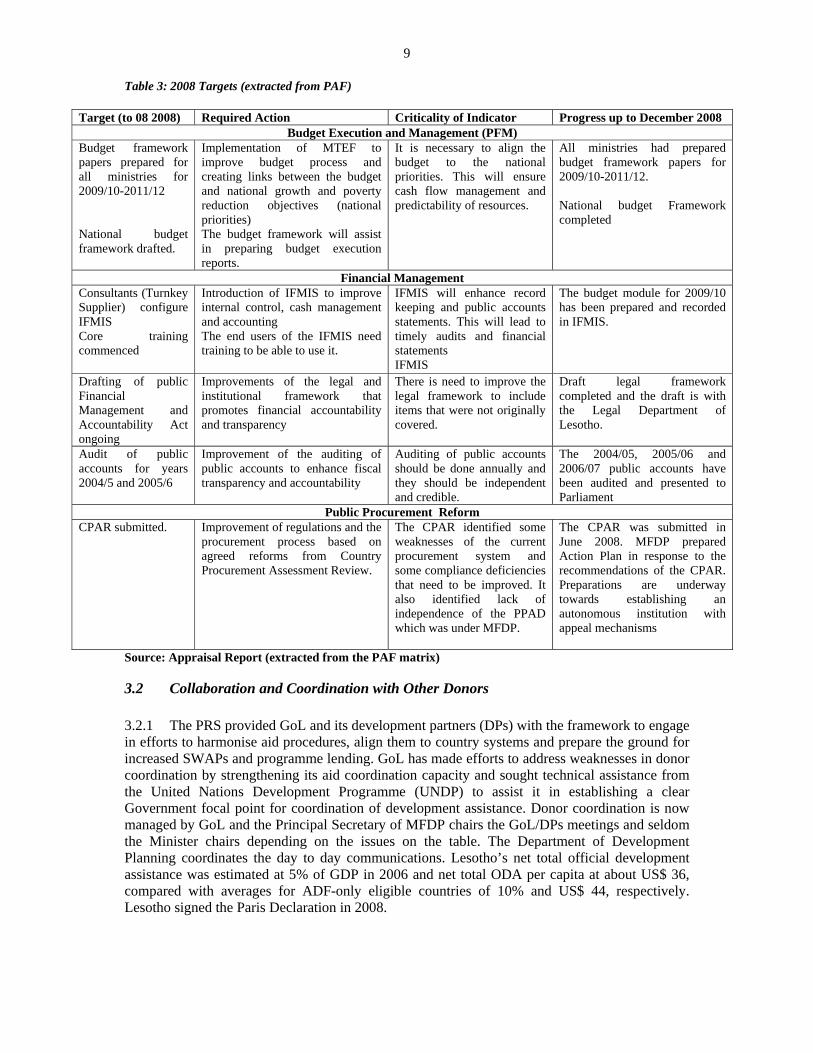

Several steps to improve PFM management have already been taken including deepening of MTEF, drafting of the Public Financial Management and Accountability Bill, launching of a project for the design and implementation of IFMIS, preparation of outstanding accounts up to 2006/07, auditing of public accounts (2004/05) and adoption of the procurement regulations. Introduction of IFMIS will replace the inadequate and weak GOLFIS in April 2009. The 2009/10 budget has been presented in the IFMIS system and the roll out scheme to ministries is planned for April 2009. All logistics, both hardware and software are in place. IFMIS is expected to improve management and record keeping as well as speed up preparation of financial accounts. The draft Financial Management and Accountability Act has been finalised and is expected to be presented to Parliament this year to legalise the operation and utilization of IFMIS. The Bank and other development partners namely, DFID, European Commission and Irish Aid are preparing to undertake a PEFA assessment during the second and third quarter of 2009 to inform the September 2009 annual assessment review. 3.1.9 In 2007 Lesotho adopted a new procurement system and prepared the Public Procurement Regulations of 2007. The regulations provided for a Procurement Policy and Advice Division (PPAD) in the Ministry of Finance and Development Planning whose objectives were to provide policy guidance and information, training and professional development and performance measurement. All line Ministries were required to have Tender Panels, Procurement Units and Evaluation Teams. The CPAR identified weaknesses in the system, notably lack of an independent authority and no oversight and appeal mechanisms because the Advisory Division was under the MFDP. An Action Plan has been drawn based on the recommendations of the CPAR. GoL has accepted the recommendations and wants to professionalise the procurement system. A proposal to transform the PPAD into an autonomous entity has been submitted to Cabinet, while the provisions and coverage of the 2007 Public Procurement Regulations are being reviewed. 3.1.10 The Bank participated in the Joint Budget Support (JBS) group meetings held between the Government and Development Partners interested in providing budget support. The Bank was part of the process that established the Performance Assessment Framework in 2008 including targets that Government was to meet in 2008, 2009 and 2010. The 2008 targets were meant partly to be used as pre-requisites for GoL’s willingness and capability to implement the PAF policies and targets. A joint assessment of these targets took place in November 2008 and a report was prepared in December 2008 providing progress as indicated in Table 4 below. The Bank did not participate in the assessment but found progress to be satisfactory, although requiring improvements. The 2008 targets indicated in Table 4 below reflects areas of focus and have been used as baseline data for this operation.

9

Table 3: 2008 Targets (extracted from PAF)

Target (to 08 2008) Required Action Criticality of Indicator Progress up to December 2008 Budget Execution and Management (PFM)

Budget framework papers prepared for all ministries for 2009/10-2011/12 National budget framework drafted.

Implementation of MTEF to improve budget process and creating links between the budget and national growth and poverty reduction objectives (national priorities) The budget framework will assist in preparing budget execution reports.

It is necessary to align the budget to the national priorities. This will ensure cash flow management and predictability of resources.

All ministries had prepared budget framework papers for 2009/10-2011/12. National budget Framework completed

Financial Management Consultants (Turnkey Supplier) configure IFMIS Core training commenced

Introduction of IFMIS to improve internal control, cash management and accounting The end users of the IFMIS need training to be able to use it.

IFMIS will enhance record keeping and public accounts statements. This will lead to timely audits and financial statements IFMIS

The budget module for 2009/10 has been prepared and recorded in IFMIS.

Drafting of public Financial Management and Accountability Act ongoing

Improvements of the legal and institutional framework that promotes financial accountability and transparency

There is need to improve the legal framework to include items that were not originally covered.

Draft legal framework completed and the draft is with the Legal Department of Lesotho.

Audit of public accounts for years 2004/5 and 2005/6

Improvement of the auditing of public accounts to enhance fiscal transparency and accountability

Auditing of public accounts should be done annually and they should be independent and credible.

The 2004/05, 2005/06 and 2006/07 public accounts have been audited and presented to Parliament

Public Procurement Reform CPAR submitted. Improvement of regulations and the

procurement process based on agreed reforms from Country Procurement Assessment Review.

The CPAR identified some weaknesses of the current procurement system and some compliance deficiencies that need to be improved. It also identified lack of independence of the PPAD which was under MFDP.

The CPAR was submitted in June 2008. MFDP prepared Action Plan in response to the recommendations of the CPAR. Preparations are underway towards establishing an autonomous institution with appeal mechanisms

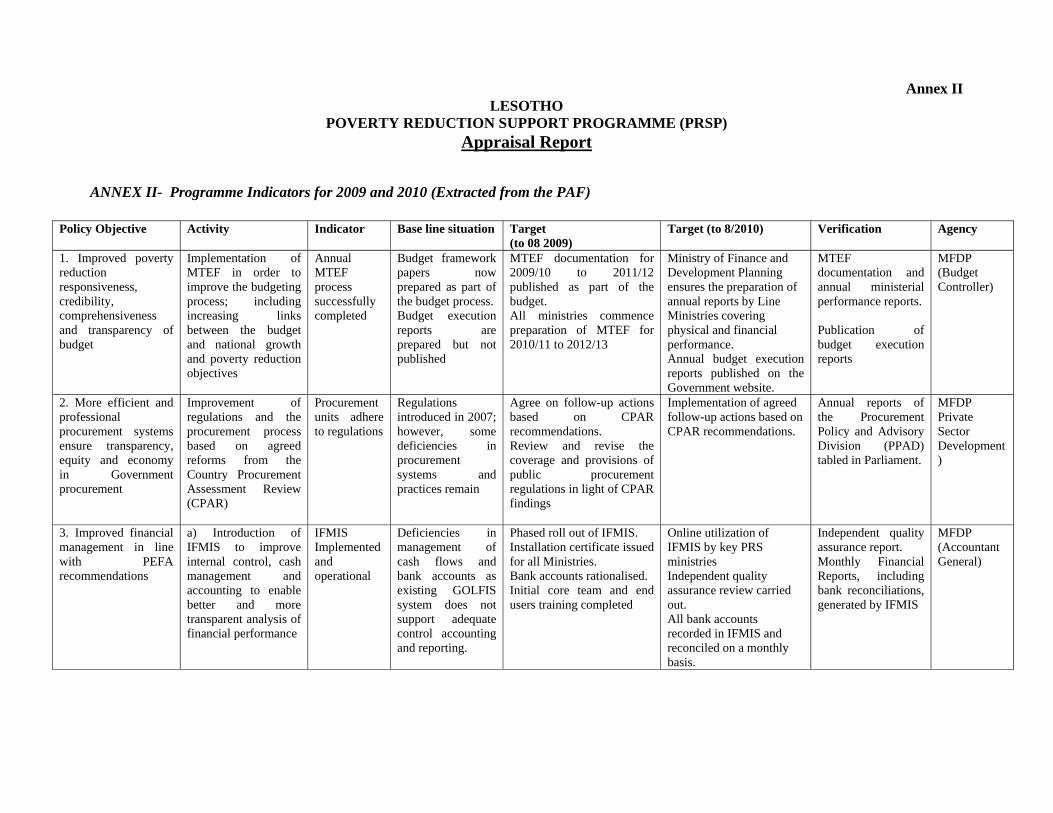

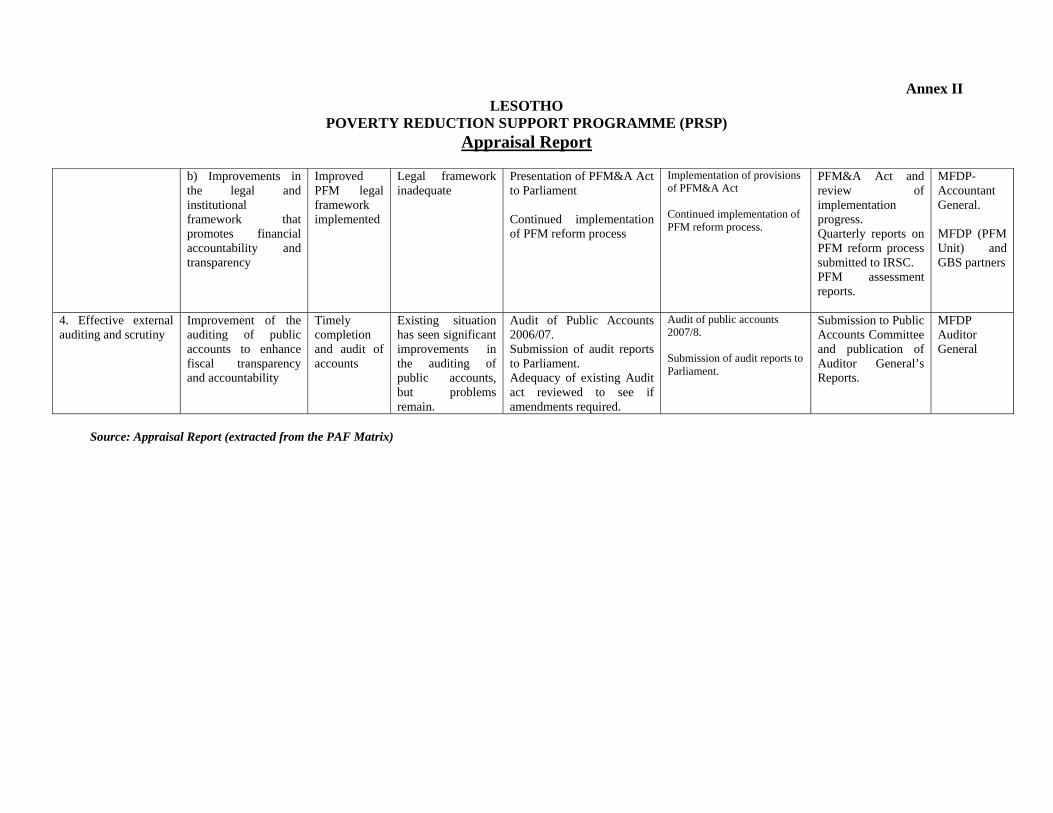

Source: Appraisal Report (extracted from the PAF matrix)

3.2 Collaboration and Coordination with Other Donors 3.2.1 The PRS provided GoL and its development partners (DPs) with the framework to engage in efforts to harmonise aid procedures, align them to country systems and prepare the ground for increased SWAPs and programme lending. GoL has made efforts to address weaknesses in donor coordination by strengthening its aid coordination capacity and sought technical assistance from the United Nations Development Programme (UNDP) to assist it in establishing a clear Government focal point for coordination of development assistance. Donor coordination is now managed by GoL and the Principal Secretary of MFDP chairs the GoL/DPs meetings and seldom the Minister chairs depending on the issues on the table. The Department of Development Planning coordinates the day to day communications. Lesotho’s net total official development assistance was estimated at 5% of GDP in 2006 and net total ODA per capita at about US$ 36, compared with averages for ADF-only eligible countries of 10% and US$ 44, respectively. Lesotho signed the Paris Declaration in 2008.

10

3.2.2 The Bank collaborated closely with other DPs in the formulation of this proposed programme, through joint meetings of DPs and with GoL. The Government first requested for general budget support (GBS) during the Ninth Donor Roundtable Conference held in November 2006 in order to ensure that the implementation of its poverty reduction strategy is underpinned by predictable flow of resources. In recognition of recent reform efforts by the GoL to improve fiduciary systems and in support of the implementation of Lesotho’s poverty reduction strategy, three DPs have confirmed their participation in budget support, namely the ADB, EU and World Bank. On the other hand, DFID and Irish Aid are not at the moment providing budget support partly due to lack of resources but may join at a later stage and will remain members of the group. DP’s intending to provide budget support have been meeting since 2006 to discuss issues related to budget support and have jointly developed a Performance Assessment Framework (PAF) with GoL. The four policy areas of the PAF are as indicated in the Table 4 below and indicators are in Annex V. While all other donors support the whole PAF, the Bank has selected a subset of PAF policies and indicators. Table 4: PAF Policy objectives and Action

Policy Action Growth and Macroeconomic Performance Enhancement of the investment climate; improved road maintenance; and

enhanced industrial infrastructure Governance and Public Finance Management

Improved poverty reduction responsiveness, creditability, comprehensiveness and transparency of the budget; more efficient and professional procurement systems; and improved financial management; improvements in the legal and institutional framework that promotes financial accountability and transparency; improvement in preparation and processing of the annual financial statements; improved effectiveness of internal audit; improving the auditing of public accounts; reduction of corruption in the public sector; civil service reform and decentralization.

Human Development and HIV and AIDS Improved primary education; improved coverage of secondary education; improvements in child nutrition; sustained disease prevention; improvements in disease treatments; improved coverage and reliability of rural water supply; improved support to orphaned and vulnerable children; and extension of ARV treatment.

Capacity Development strengthening monitoring and evaluation; and development of national statistical capacity.

Source: PRSP I Appraisal Report 3.2.3 The World Bank has approved a budget support operation for an amount of US$ 8.7 million credit and US$ 7.2 million grant totaling US$15.9 million in May 2008 and is preparing the second operation for an amount of USD10.0 million for 2009. The EU is also preparing its support for an amount of Euro 15.5 million for 2009 and 2010. The annual review of the PAF will be done in September and donors will be expected to indicate their commitments for the following year which will be included in the budget. Examples of good practices in Lesotho are indicated in Box 2. Box 2: Lesotho’s Good practices of Aid Coordination

Source: PRSP I Appraisal Report

In 2006, Government of Lesotho started meeting with donors to established a mechanism to coordinate donors activities and harmonise their programmes. GoL and donors prepared a Memorandum of understanding which is yet to be finalized. A Performance Assessment Framework was completed in November 2008 which sets out the areas of focus for the budget support programme and agreed targets for the three years (2008, 2009, 2010.) Five donors have indicated willingness to support budget support with World Bank already providing budget support based on the agreed areas and others yet to provide support namely African Development Bank and European Union. In education and health DPs have pooled funds to support the Ministries of Health and Education through sector budget support The DPs and GoL agreed to support the public sector reforms through the budget support which is based on the PRS.

11

3.3 Outcomes of the Past and Ongoing Similar Operations and Lessons 3.3.1 The Agricultural Sector Adjustment Programme (ASAP), which was approved in March 1999 for a total amount of UA 4.83 million, is the only Policy Based Lending operation that the Bank Group has ever provided to Lesotho. The operation was closed in July 2003 after achieving a disbursement rate of 49 percent. The lessons that were learnt from the implementation of the ASAP include: (i) Government ownership of development interventions and aligning them to the socio-economic environment in the country; (ii) participation of relevant stakeholders in project identification and other phases of project implementation; (iii) setting of attainable realistic targets and quantifiable indicators for future assessment of project progress and impact; (iv) provision of timely and appropriate support to the project implementation team; (v) complicated conditions imposed on Government prior to disbursement of loans and grants can have a negative implication on the timeliness of project start-up; and (vii) effective donor coordination 3.3.2 The proposed programme is based on the fiduciary assessment made by the team during appraisal and other development partners interested or already providing budget support. It takes into account the lessons derived from ASAP and the following issues:

• It should be selective and have limited conditionalities/milestones and indicators that are to be monitored during the life of the programme.

• The program should focus on reform areas that will have a significant impact when completed.

• The program should be realistic as to what can be achieved, mindful of capacity constraints.

• It should be aligned with the Government’s budget timetable. • It should be monitorable.

3.3.3 The proposed Bank operation also draws from the lessons of the past projects, some of which are contained in the 2005-2007 CSP Completion Report. During the previous CSP period two projects were approved by the Bank on infrastructure development (road project) and enhancing human capital (education) and are ongoing. Three projects approved during the previous CSP on health reforms, capacity building and natural resources income enhancement are also ongoing. All the three operations experienced start-up delays which will be avoided in this programme. Lesotho has institutional capacity weaknesses and it is expected that the reforms under implementation will improve service delivery. Lessons learnt on budget support from other countries that have been considered point to the need for few and explicit conditions as well as to make budget support a fast disbursing operation.

3.4 Relationships to Ongoing Bank’s Operations Out of the 52 projects supported since 1974 only six projects are currently ongoing: one in agriculture and rural development on Highlands Natural Resources & Rural Income Enhancement aimed at reducing poverty; one multi-sector, Institutional Support to the Ministries of Finance and Development Planning and Works and Transport on capacity building; two in the social sector, Support to Health Reforms Programme and the Education Quality Enhancement (Education III); and two in infrastructure, Likalaneng-Thaba Tseka Road Project and Lesotho Electricity Supply Project. The projects are at different stages of implementation. The target for budget execution and financial management will improve overall project management. The proposed operation will also complement the ongoing projects in achieving the country’s PRS and MDGs objectives and service delivery through the ongoing public finance management and governance reforms including the recently approved electricity supply project. GOL has also increased use of the Bank’s Regional Office in Mozambique, which facilitates implementation of Bank projects in Lesotho.

12

3.5 Bank’s Comparative Advantages The Bank has been operating in Lesotho since 1974 and has a good understanding of the country systems. The Bank also participated in the CPAR for Lesotho done by the World Bank as well as in the formulation of an MOU and PAF by donors interested in providing budget support assistance to Lesotho. This made the Bank aware of constraints as well as ongoing reforms in financial management. The Bank will use experience on designing and managing poverty reduction support programmes gained elsewhere to design and manage this programme. The transition of regional office functions from the Mozambique office to the new office in Pretoria, South Africa, will have positive spillovers on Lesotho in terms of the quality of its Bank Group portfolio given the country’s closer proximity and strong links to South Africa.

3.6 Applications of Good Practices Principles and Conditionality The Bank is a member of the budget support donors group in Lesotho and will use the areas defined by the group, as well as select targets/conditions from the PAF. The group use good practices of conditionality, which have been agreed in the PAF in advance. The Bank will also participate in the annual review of the PAF scheduled for September of each year. The operation is fully aligned to these principles of good practice of conditionality as indicated in Box 3. Box 3: Applications of Good Practices Principles and Conditionality Principle 1: Reinforce Ownership The proposed operation supports implementation o f Lesotho’s PRS adopted by the government in 2004 after extensive consultations with broad spectrum of stakeholders. Government is preparing the NDP to replace the PRS based on the lessons learnt from its implementation experience and the development of a home grown growth strategy. It requested joint donor budget support for implementation of its PRS, using the PAF which provides a basis for monitoring the program of overall budget support. The PAF has four broad areas consisting of a number of relevant, monitorable, time-bound, and realistic targets related to priority policy objectives. Principle 2: Agree up front with the Government and other financial partners on a coordinated accountability framework An MOU between the Government and the Joint Budget Support Donor Group has been drafted. All missions have been held jointly and joint aide memoires have been prepared and agreed with the Government. The broad principles o f budget support were agreed in November 2008 and are contained in the December 2008 PAF progress report by GoL. Reviews will be carried out jointly in September each year, to fit in with the Government’s budget preparation timeline. Disbursements of budgetary support will be based on the outcome of the joint annual reviews. Principle 3: Customise the accountability framework and modalities of Bank support to country circumstances The joint budget support review will be aligned to the country’s budget cycle and will be held in September each year. Disbursements are expected to be made in the next financial year based on progress in the agreed realistic targets for the PAF. Disbursement for the proposed PRSP will be based on only targets and actions relating to its selected areas, although the decision on progress will be made collectively by all members. Principle 4: Choose only actions critical for achieving results as conditions for disbursement One of the principles of the joint budget support is that the PAF should consist o f a few monitorable and realistic targets. The targets for the proposed operation covering only four issues have been selected from the twenty PAF targets. Principle 5: Conduct transparent progress reviews conducive to predictable and performance-based financial support In order to improve predictability of budgetary support from donors, the Joint Budget Support (JBS) framework requires donors to indicate levels of budgetary support that they are planning to disburse well in advance before the start of the fiscal year, such that the amounts can be included in the Government Budget submitted to Parliament. Once the main annual PAF review in September has been concluded, all the JBS donors in Lesotho will indicate to the Government how much they’re planning to disburse in the following. Source: Appraisal Report and other documents including World Bank PSRC.

13

3.7 Application of Bank Group non-concessional borrowing policy Lesotho’s external and public debts are projected to be sustainable, it currently stands at 52.3% of GDP and there is a moderate risk of debt distress. The IMF-World Bank joint debt sustainability analysis (DSA) report of January 2009 shows a decline of public sector debt to 43.1% of GDP at end of 2007. The decline is attributed to the authorities’ early repayment of non concessional loans. Lesotho as a blend (loan/grant) country contracts concessional loans with a grant element of 35% as a policy. The NPV of external debt stood at 21.9% at end of 2007 and remained below the policy based indicative thresholds including the HIPC initiative threshold of 150% for PV of debt to export ratio. However, with a projected 10% budget deficit and reduced SACU revenue this trend could change and therefore the country should be prudent in contracting and managing new loans even if they are concessional. The programme design took into account the Bank’s non concessional borrowing policy. However, the Bank has not adopted the hardening of terms to Lesotho because it has not yet benefited from the HIPC and MDRI and it is not in debt stress. Most of Lesotho’s debts (92%) are with multi-lateral creditors on concessional terms.

IV. THE PROPOSED PROGRAMME

4.1 Programme’s goal and purpose The programme’s goal is to improve the living standard of the people in Lesotho through enhanced delivery of public services. The programmes purpose is to improve governance in public financial management and procurement. The expected outcomes of the operation are: (i) improved poverty reduction responsiveness, credibility, comprehensiveness and transparency of the budget; (ii) improved financial management in line with the PEMFAR recommendations; (iii) a more efficient and professional procurement system that will ensure transparency, equity and economy in government procurement; and (iv) an effective external auditing function and scrutiny.

4.2 Programme Pillars, Specific Operational Policy Objectives and Expected Results 4.2.1 The PEMFAR highlighted deficiencies in budget execution, internal control, accounting delays, inadequate cash flow and bank accounts management, audit backlogs and poor fiscal reporting as well as inadequate legal framework. In order to address the above weaknesses, the Government has embarked on a comprehensive PFM reform program. The identified areas of weakness included areas of planning and budgeting, accounting and reporting as well as audit and oversight. The Government established three Task Forces, covering these areas. The task forces have each developed a program of deliverables and report to an overarching PFM Improvement and Reform Steering Committee, chaired by the Principal Secretary of MFDP and comprising senior officials of MFDP and some donors. The planning and budgeting task force focuses on integrating planning and budgeting processes through a medium-term expenditure framework (MTEF). The accounting and reporting task force aims to develop effective budget execution and reporting systems while the work of the audit and oversight task force focuses on: (i) providing technical support to the Auditor-General’s office to increase its technical capacity; and (ii) providing technical support to upgrade the capacity of the Public Accounts Committee. 4.2.2 The pillar for this operation is public reforms in public finance management including procurement. The operation focuses on the following policy areas under Public Financial Management: (i) Budget process-improved poverty reduction responsiveness, comprehensiveness and transparency of the budget; (ii) Procurement-efficient and professional procurement system that ensures transparency, equity and economy in government procurement; (iii) Audits-effective

14

external auditing; and (iv) Accounts- improved financial management in line with the PEMFAR recommendations. Public Finance Management 4.2.3 Budget Process: The Public Expenditure Management and Financial Accountability Review (PEMFAR) conducted in 2007 by the World Bank indicated that there were some improvements in the budgetary process. It further noted that Lesotho has a participatory budget process, which involves both the spending agencies and the political leadership and follows a pre-determined budget calendar. Following budget discussion and consolidation by respective ministries the budget is submitted to a Cabinet Budget Committee, chaired by the Deputy Prime Minister and comprising the Minister of Finance and eight other ministers. Lesotho has a low absorption capacity although revenue outcomes are not significantly different from budget estimates. Under-spending in many line ministries, especially on the capital budget, reflects lack of implementation capacity within Government. 4.2.4 Efforts have been made to align the budget to public expenditure priorities of the PRS. There has been noticeable increased participation and engagement of the public in the budget process and budget information has been made available to the extent possible. Budget comprehensiveness and delivery has also improved. The introduction of IFMIS will improve the timely availability of budget implementation and accounting information to line Ministries. While Budget framework papers have been prepared as part of the budget process for the 2009/10 budget, work is underway to introduce MTEF in all ministries beyond the six pilot ministries. Budget preparation and execution reports are prepared but not published. 4.2.5 The proposed operation will support budget preparation and execution under the PFM reform programme. The Budget execution will encompass budget preparation, execution and outturn reporting. The operation will ensure a responsive budget to needy areas and alignment to Government priorities and responsive to the needs of vulnerable groups including gender mainstreaming in the budget preparation. The operation will also ensure that the budget is comprehensive, transparent and credible by encouraging Government to continue involving other stakeholders in budget discussions to enable them to demand accountability from Government with regard to programme implementation and budget execution and overall Government expenditures. 4.2.6 The expected outcome of the above activities is a link of the budget to poverty reduction, a transparent and comprehensive budget and publication of the budget execution reports. The target/indicator to be monitored by the Bank as part of the common assessment framework by members of the budget support group will be: preparation of a budget framework paper for all ministries for 2008, 2009, 2010 and 2011; publication of MTEF documentation for 2009; preparation of MTEF for 2010/11 by all ministries in 2009; and publication of the annual budget execution reports in 2010. (Annex II). 4.2.7 Accounts: Lesotho has a backlog of financial accounts due to inadequate record keeping, weak legal framework in financial management as well as the inadequacy of the GOLFIS, an old no longer efficient GoL accounting system. The proposed programme will address these inadequacies by supporting the reform programmes aimed at improving financial management, control and record keeping. There is need for improvement of the financial management in line with the PEMFAR recommendations to achieve better internal control, cash management and accounting leading to transparent analysis of the financial performance. Introduction of IFMIS will improve the public accounts management, record keeping and preparation of quarterly and annual accounts.

15

4.2.8 The current system (GOLFIS) does not provide adequate control, accounting and reporting hence deficiencies in management of cash flows and bank accounts. The existing legal framework is also inadequate and needs to be reviewed before introduction of IFMIS so that the new regulations can be backed by an Act of Parliament. Preparation of annual accounts takes time and is normally submitted after the stipulated period of six months after end of the fiscal year. 4.2.9 The poverty reduction support programme will support improvements in the financial management in line with the PEMFAR recommendations. The expected outcome is improved internal control, cash management and accounting leading to transparent analysis of the financial performance and easy preparation of public accounts. The outcome indicator for this activity is implementation of the IFMIS by April 2009 while targets to be monitored during the programme life period include: installation of IFMIS in all ministries and initial core team and end users training completed; presentation of the Public Financial Management and Accountability Act to Parliament for implementation in 2010; presentation of the draft Public Accounts for 2007/2008 to Auditor General; and presentation of 2008/09 accounts to Auditor General in 2010 (Annex II). 4.2.10 Audit: The main weaknesses of the public sector audit in Lesotho is the delay in preparation of accounts and capacity. The Public Accounts Committee of Parliament is also weak and needs strengthening so that it can efficiently review reports prepared by the Auditor General. The existing situation has seen significant improvements in the auditing of public accounts, but there are problems resulting from preparation of accounts and presentation of the accounts to Parliament which takes time, as well as the capacity of the Public Accounts Committee to effectively deliver on its oversight role. 4.2.11 The operation will support strengthening the external auditing and scrutiny to improve management and accountability of public resources. The expected outcome is improved auditing of public accounts for enhancement of fiscal transparency and accountability. The indicators to be monitored in 2009 are: an audit of public accounts for 2006/7; and a review of the existing Audit Act to determine whether amendments are required. In 2010, they are: audit of accounts for 2007/08; and submission of audit accounts to Parliament. (Details in Annex I). 4.2.12 Procurement: Lesotho adopted the Public Procurement Regulations (PPR) in 2007, which aimed at reforming and modernizing public procurement. The PPR is based on a decentralized system which ensures transparency and accountability and aimed at ensuring consistency with international practices and procedures. Procurement Units have been established in ministries and districts to manage procurement issues in the respective institutions. All procurement entities were required to establish Tender Panels and Tender Evaluation Teams. The then Central Tender Board was disbanded and replaced by the Procurement Policy and Advisory Division (PPAD), whose aim was to support, monitor and enforce compliance at ministerial and districts levels. It was also to provide and develop relevant legislation, means of controlling and enforcing compliance through audits as well as managing training and providing an appeal mechanism. It provided guidance and advice to procurement units. Regulations were introduced in 2007 and implementation commenced and some deficiencies in procurement systems and practices were noticed. 4.2.13 The CPAR identified areas where further reforms were needed and these included legislative and regulatory framework, institutional framework and improved management capacity. The provisions of the constitution of the Appeals Panels were insufficient to establish an independent institution. The procurement management, budgeting and financial management were not integrated or linked because of lack of procurement plans which would make cash flow management predictable.

16

4.2.14 The PRSP I will support activities towards establishment of an efficient and professional procurement system that ensures transparency, equity and economy in government procurement. The expected outcome of this reform is to establish a procurement process based on the action plan drawn from the agreed reforms from the CPAR. The indicator to be monitored during the implementation of the programme in 2009 is: a follow up on agreed actions based on the CPAR and review of the Public Procurement Regulations and for 2010 is the implementation of agreed follow up actions based on the CPAR recommendations. (PRSP I targets in Annex II).

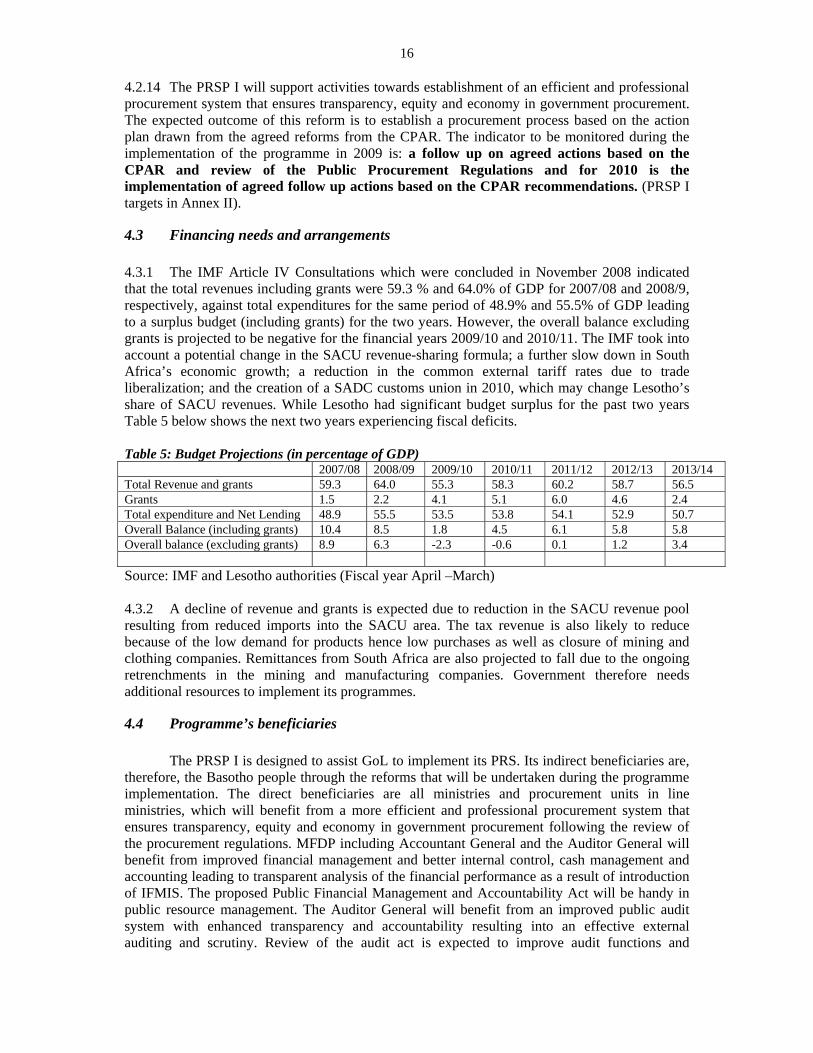

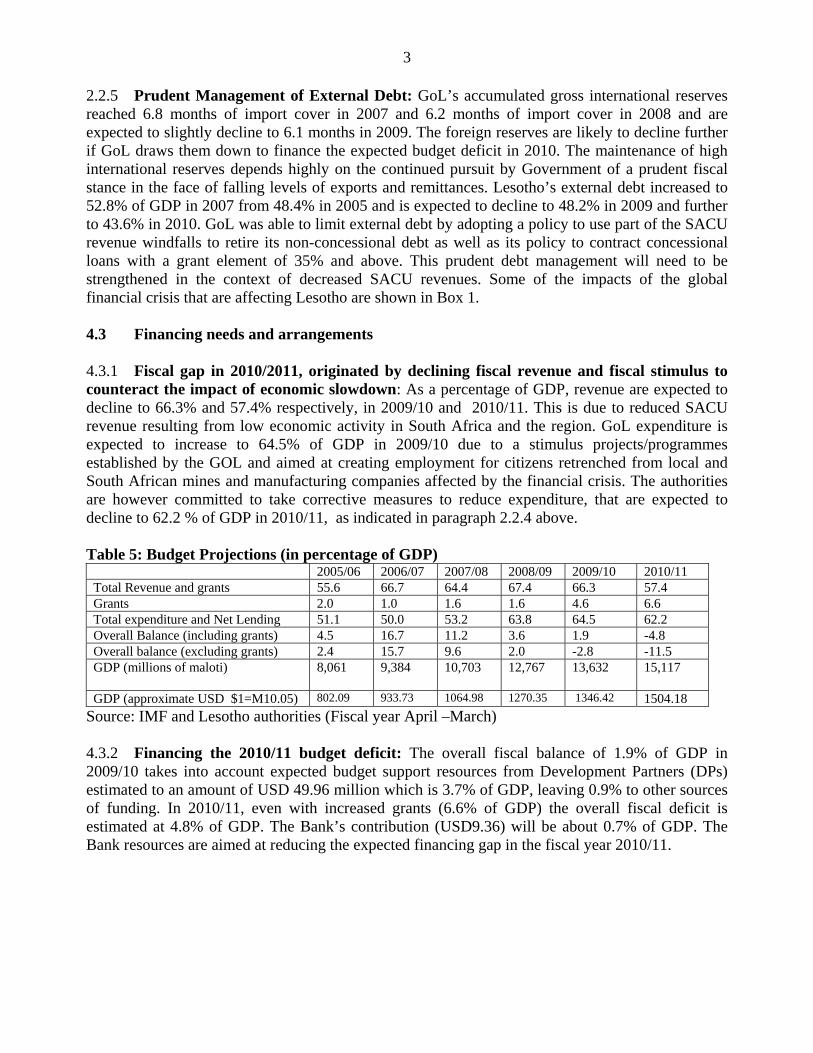

4.3 Financing needs and arrangements 4.3.1 The IMF Article IV Consultations which were concluded in November 2008 indicated that the total revenues including grants were 59.3 % and 64.0% of GDP for 2007/08 and 2008/9, respectively, against total expenditures for the same period of 48.9% and 55.5% of GDP leading to a surplus budget (including grants) for the two years. However, the overall balance excluding grants is projected to be negative for the financial years 2009/10 and 2010/11. The IMF took into account a potential change in the SACU revenue-sharing formula; a further slow down in South Africa’s economic growth; a reduction in the common external tariff rates due to trade liberalization; and the creation of a SADC customs union in 2010, which may change Lesotho’s share of SACU revenues. While Lesotho had significant budget surplus for the past two years Table 5 below shows the next two years experiencing fiscal deficits. Table 5: Budget Projections (in percentage of GDP) 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 Total Revenue and grants 59.3 64.0 55.3 58.3 60.2 58.7 56.5 Grants 1.5 2.2 4.1 5.1 6.0 4.6 2.4 Total expenditure and Net Lending 48.9 55.5 53.5 53.8 54.1 52.9 50.7 Overall Balance (including grants) 10.4 8.5 1.8 4.5 6.1 5.8 5.8 Overall balance (excluding grants) 8.9 6.3 -2.3 -0.6 0.1 1.2 3.4 Source: IMF and Lesotho authorities (Fiscal year April –March) 4.3.2 A decline of revenue and grants is expected due to reduction in the SACU revenue pool resulting from reduced imports into the SACU area. The tax revenue is also likely to reduce because of the low demand for products hence low purchases as well as closure of mining and clothing companies. Remittances from South Africa are also projected to fall due to the ongoing retrenchments in the mining and manufacturing companies. Government therefore needs additional resources to implement its programmes.