knowledge sharing on indonesia petrochemical...

TRANSCRIPT

Private & Confidential

May 14, 2013

Knowledge Sharing on Indonesia Petrochemical Outlook

By

Mr. Sermsak Sriyaphai EVP – EO-Based Performance Business Unit

2

Private & Confidential

Indonesia petrochemical business outlook

Key opportunities and challenges of petrochemical development

Competitive edge of local producers

Conclusion

Outlines

3

Private & Confidential

Indonesia petrochemical business outlook

Key opportunities and challenges of petrochemical development

Competitive edge of local producers

Conclusion

Outlines

4

Private & Confidential

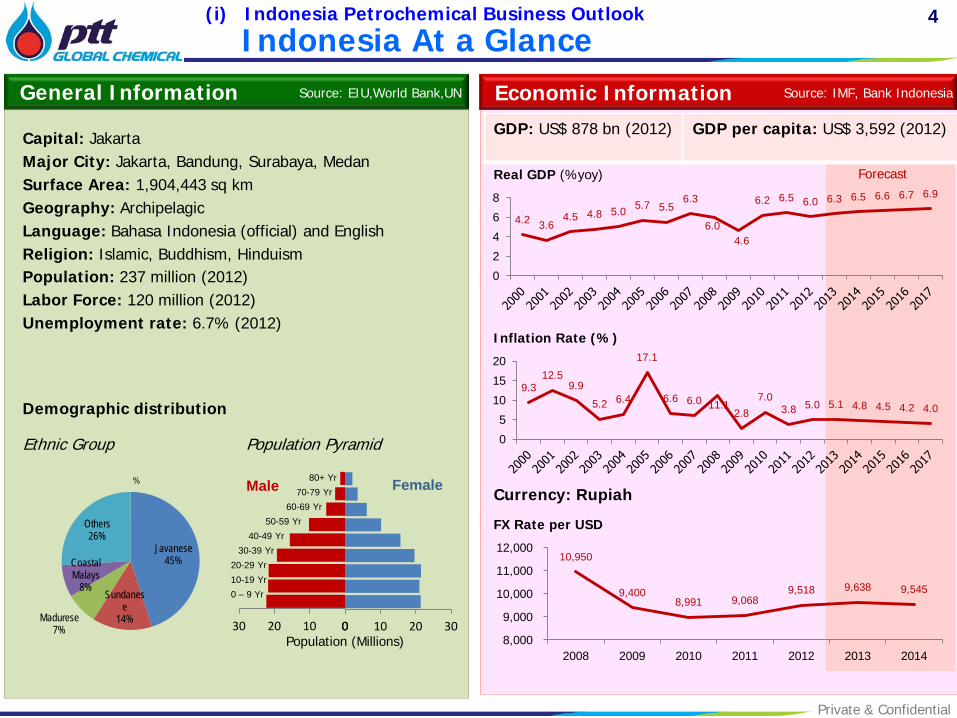

Indonesia At a Glance General Information

Population: 237 million (2012) Labor Force: 120 million (2012) Unemployment rate: 6.7% (2012)

Capital: Jakarta Major City: Jakarta, Bandung, Surabaya, Medan Surface Area: 1,904,443 sq km Geography: Archipelagic Language: Bahasa Indonesia (official) and English Religion: Islamic, Buddhism, Hinduism

Demographic distribution

Ethnic Group Population Pyramid

0 10 20 300102030

Male Female

Population (Millions)

10-19 Yr 20-29 Yr

30-39 Yr 40-49 Yr

50-59 Yr 60-69 Yr

70-79 Yr 80+ Yr

Economic Information

GDP: US$ 878 bn (2012) GDP per capita: US$ 3,592 (2012)

Real GDP (%yoy) Forecast

4.2 3.6 4.5 4.8 5.0 5.7 5.5

6.3

6.0 4.6

6.2 6.5 6.0 6.3 6.5 6.6 6.7 6.9

0

2

4

6

8

Inflation Rate (%)

9.3 12.5

9.9

5.2 6.4

17.1

6.6 6.0 11.1 2.8

7.0 3.8 5.0 5.1 4.8 4.5 4.2 4.0

0

5

10

15

20

FX Rate per USD

10,950

9,400 8,991 9,068

9,518 9,638 9,545

8,000

9,000

10,000

11,000

12,000

2008 2009 2010 2011 2012 2013 2014

Currency: Rupiah

Source: EIU,World Bank,UN Source: IMF, Bank Indonesia

Javanese 45%

Sundanese

14% Madurese 7%

Coastal Malays

8%

Others 26%

%

0 – 9 Yr

(i) Indonesia Petrochemical Business Outlook

5

Private & Confidential

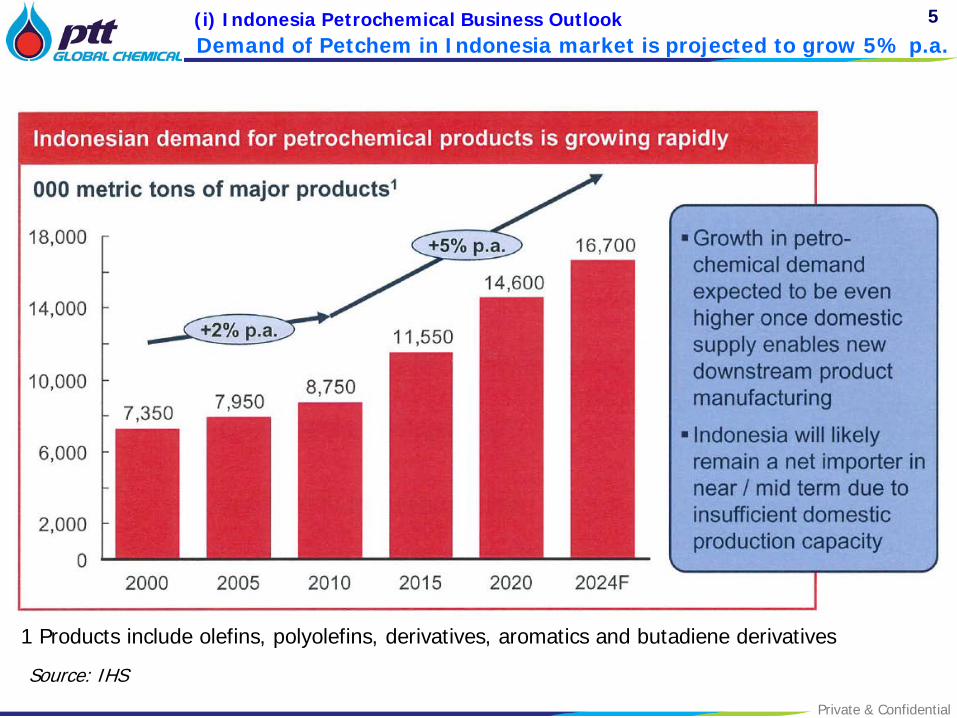

Demand of Petchem in Indonesia market is projected to grow 5% p.a. (i) Indonesia Petrochemical Business Outlook

1 Products include olefins, polyolefins, derivatives, aromatics and butadiene derivatives

Source: IHS

6

Private & Confidential

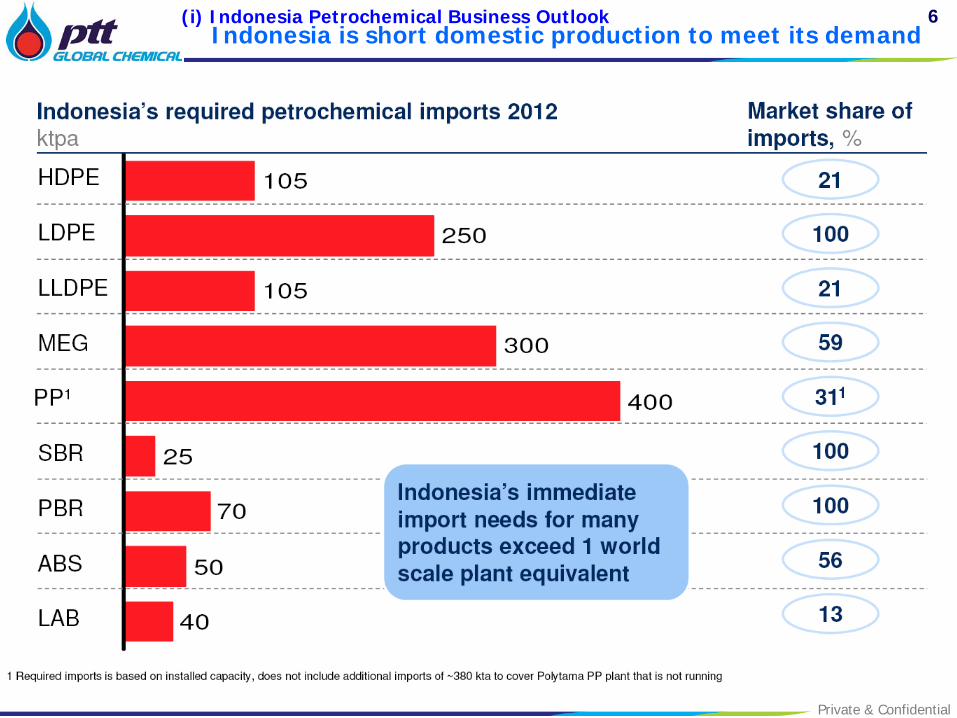

Indonesia is short domestic production to meet its demand (i) Indonesia Petrochemical Business Outlook

7

Private & Confidential

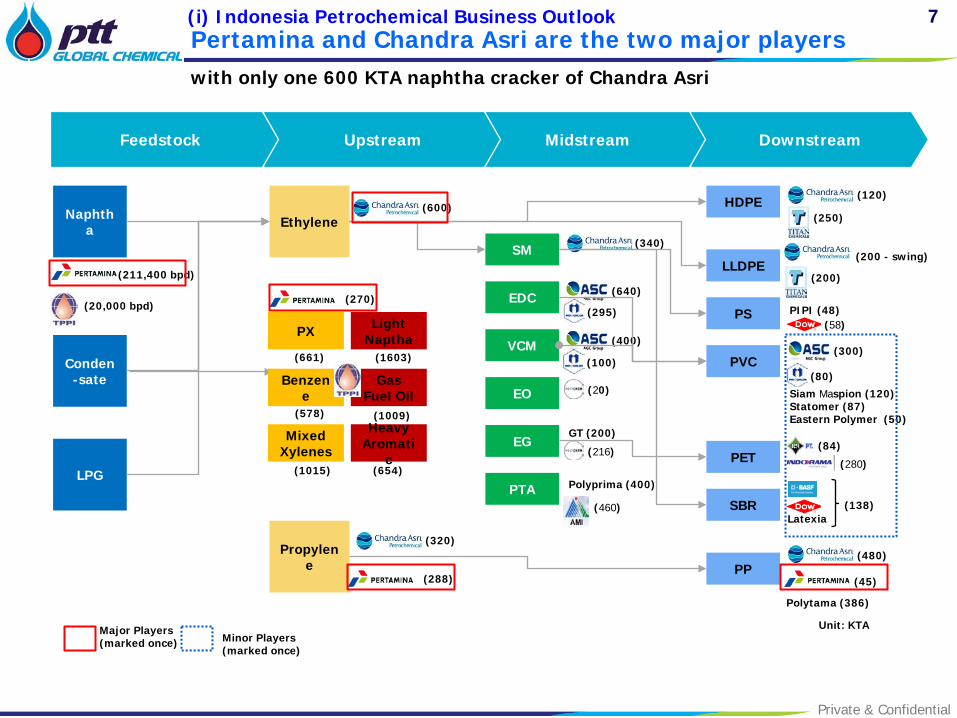

Pertamina and Chandra Asri are the two major players

with only one 600 KTA naphtha cracker of Chandra Asri

Downstream Midstream Upstream Feedstock

Naphtha

Conden-sate

LPG

Ethylene

Propylene

SM

EDC

HDPE

LLDPE

PS

PTA

PVC

PET

SBR

EO

PP

VCM

(600) (120)

(250)

(200 - swing)

(320)

(288)

(340)

Unit: KTA

(480)

(45)

Polytama (386)

Polyprima (400)

EG GT (200)

(200)

PIPI (48)

Siam Maspion (120) Statomer (87) Eastern Polymer (50)

(84)

Latexia

(640)

(400) (300)

(295)

(100) (80)

(20)

(216)

(138)

(20,000 bpd)

(58)

(460)

(280)

(211,400 bpd)

PX

Benzene

Mixed Xylenes

Light Naptha

Gas Fuel Oil

Heavy Aromati

c

(661) (1603)

(1009)

(654) (1015)

(578)

Major Players (marked once) Minor Players

(marked once)

(270)

(i) Indonesia Petrochemical Business Outlook

8

Private & Confidential

0% 50% 100%

Asahimas

CAP

Indorama

Pertamina

Polychem

Polytama

Titan

TPPI

Ethylene HDPE LLDPELDPE MEG PVCPropylene PP BenzenePolystyrene Paraxylene Polyester/PET

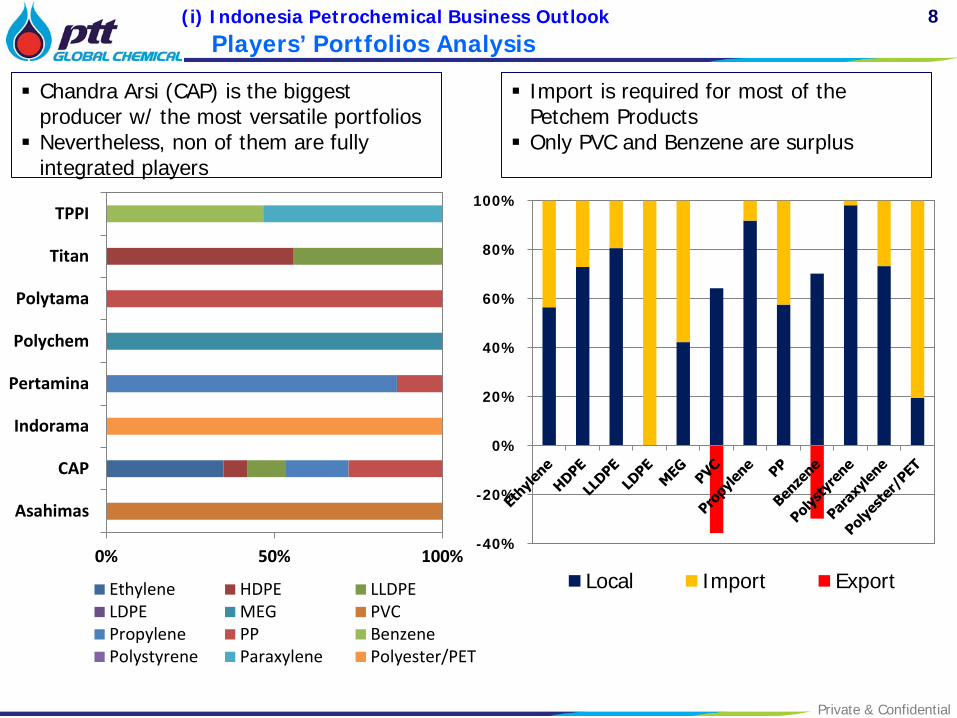

Chandra Arsi (CAP) is the biggest producer w/ the most versatile portfolios Nevertheless, non of them are fully

integrated players

Import is required for most of the Petchem Products Only PVC and Benzene are surplus

Players’ Portfolios Analysis (i) Indonesia Petrochemical Business Outlook

-40%

-20%

0%

20%

40%

60%

80%

100%

Local Import Export

9

Private & Confidential

SOUTH CHINA SEA PACIFIC OCEAN

SUMATRA

JAVA

JAVA OCEAN

KALIMANTAN

SULAWESI

PAPUA

SINGAPORE

Arun P. Brandan

Medan

Palembang

Dumai

Plaju

Balikpapan

Bontang

Jakarta

Balongan Cepu

Cilacap Bali

Banten

Tuban

Most of Petrochemical Players are also located in Java Island where end use industries are located

(i) Indonesia Petrochemical Business Outlook

SUMATRA

Players in Java

10

Private & Confidential

Indonesia petrochemical business outlook

Key opportunities and challenges of petrochemical development

Competitive edge of local producers

Conclusion

Outlines

11

Private & Confidential

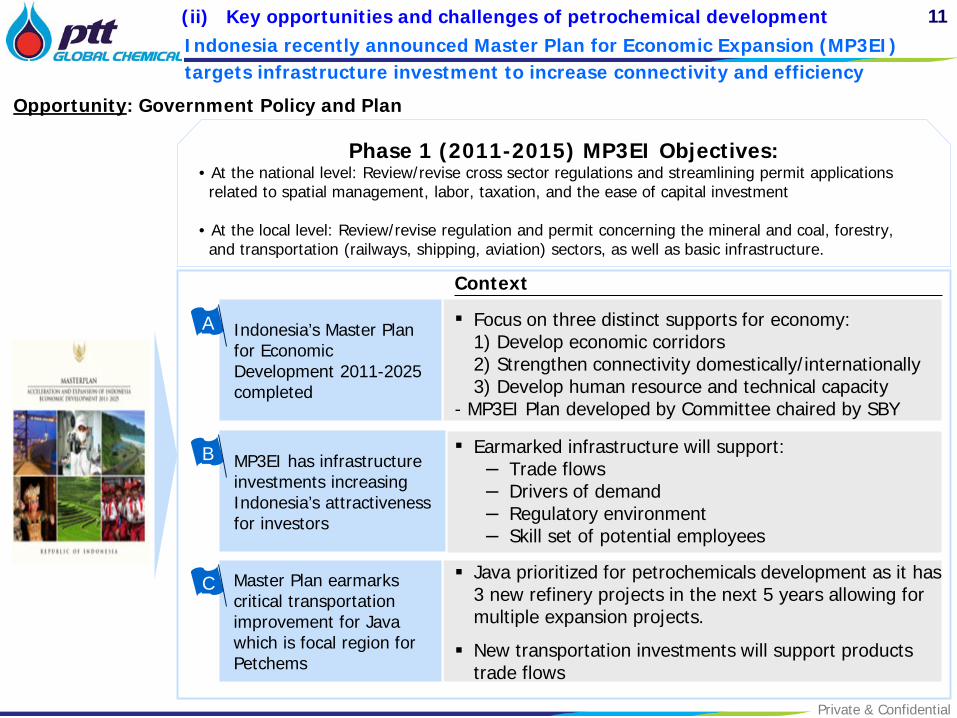

Indonesia recently announced Master Plan for Economic Expansion (MP3EI) targets infrastructure investment to increase connectivity and efficiency

(ii) Key opportunities and challenges of petrochemical development

Indonesia’s Master Plan for Economic Development 2011-2025 completed

MP3EI has infrastructure investments increasing Indonesia’s attractiveness for investors

Context

A

B

Master Plan earmarks critical transportation improvement for Java which is focal region for Petchems

Java prioritized for petrochemicals development as it has 3 new refinery projects in the next 5 years allowing for multiple expansion projects.

New transportation investments will support products trade flows

▪ Earmarked infrastructure will support: – Trade flows – Drivers of demand – Regulatory environment – Skill set of potential employees

▪ Focus on three distinct supports for economy: 1) Develop economic corridors 2) Strengthen connectivity domestically/internationally 3) Develop human resource and technical capacity - MP3EI Plan developed by Committee chaired by SBY

C

Phase 1 (2011-2015) MP3EI Objectives: • At the national level: Review/revise cross sector regulations and streamlining permit applications related to spatial management, labor, taxation, and the ease of capital investment • At the local level: Review/revise regulation and permit concerning the mineral and coal, forestry, and transportation (railways, shipping, aviation) sectors, as well as basic infrastructure.

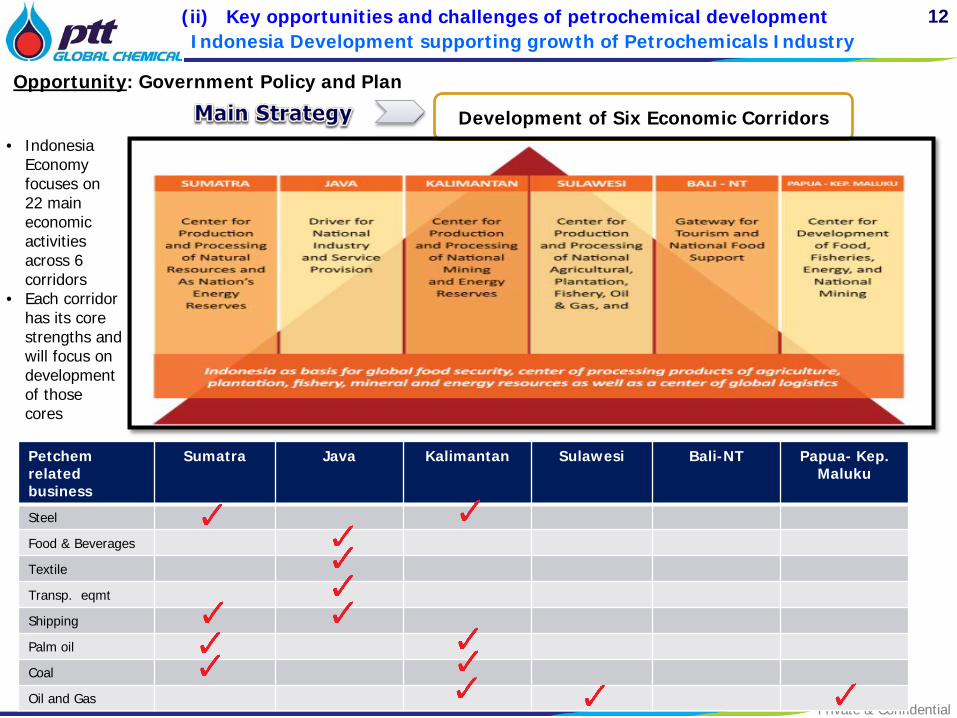

Opportunity: Government Policy and Plan

12

Private & Confidential

Indonesia Development supporting growth of Petrochemicals Industry (ii) Key opportunities and challenges of petrochemical development

Development of Six Economic Corridors • Indonesia

Economy focuses on 22 main economic activities across 6 corridors

• Each corridor has its core strengths and will focus on development of those cores

Petchem related business

Sumatra Java Kalimantan Sulawesi Bali-NT Papua- Kep. Maluku

Steel

Food & Beverages

Textile

Transp. eqmt

Shipping

Palm oil

Coal

Oil and Gas

Opportunity: Government Policy and Plan

13

Private & Confidential

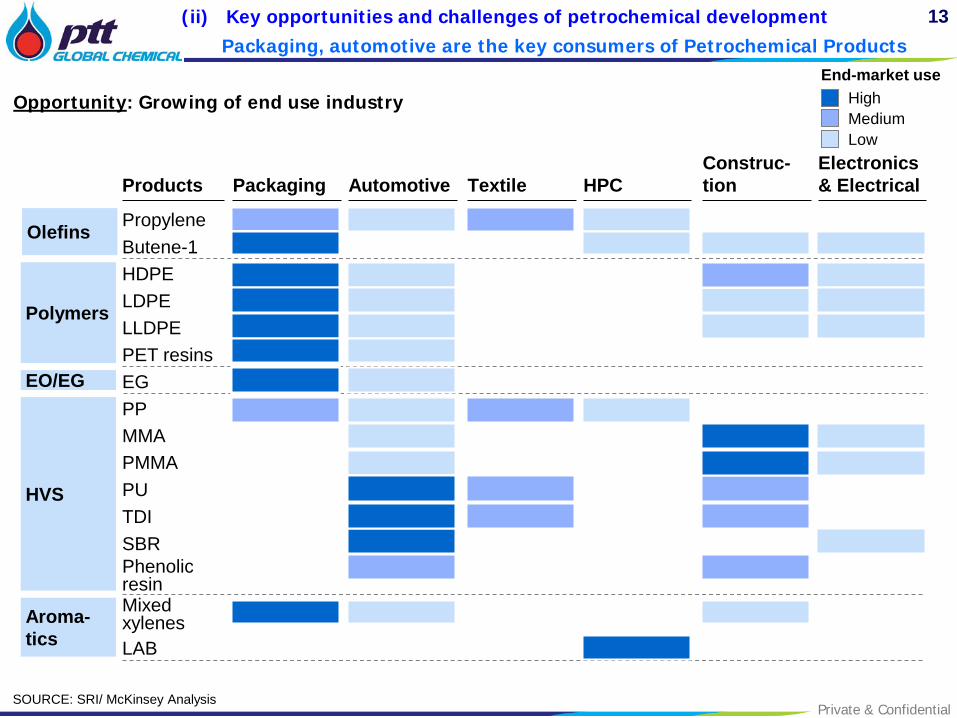

Packaging, automotive are the key consumers of Petrochemical Products (ii) Key opportunities and challenges of petrochemical development

EO/EG EG

Olefins Butene-1 Propylene

Polymers LDPE LLDPE

HDPE

PET resins

Aroma-tics LAB

Mixed xylenes

HVS PU TDI SBR

MMA PMMA

PP

Phenolic resin

Packaging HPC Automotive Electronics & Electrical Textile Products

Construc-tion

High Medium Low

End-market use

SOURCE: SRI/ McKinsey Analysis

Opportunity: Growing of end use industry

14

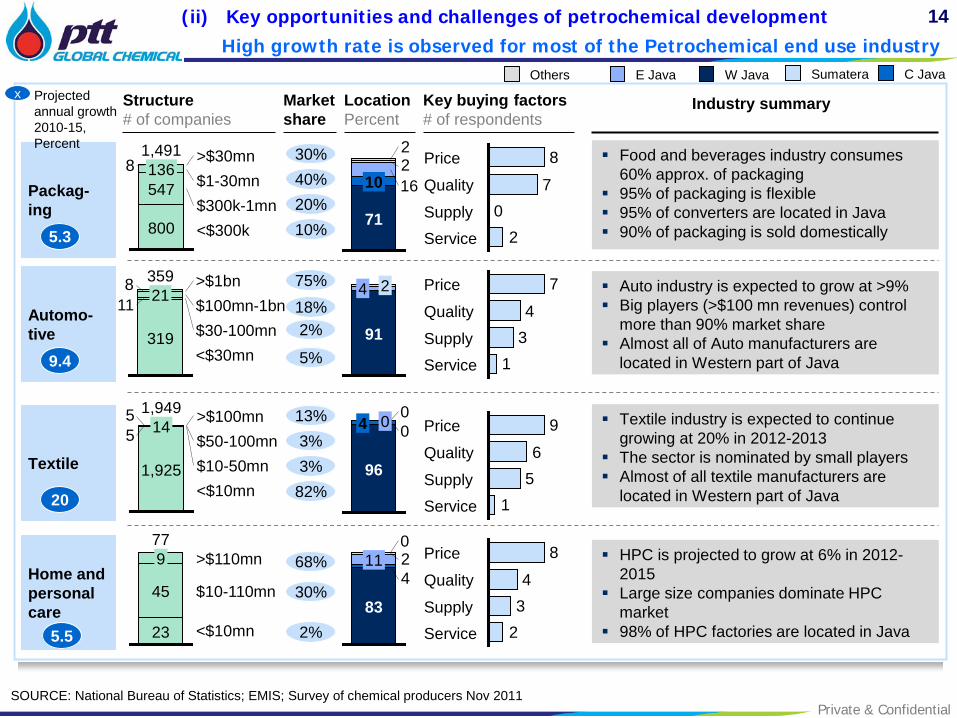

Private & Confidential SOURCE: National Bureau of Statistics; EMIS; Survey of chemical producers Nov 2011

Packag-ing

Automo-tive

Structure # of companies

5.3

Location Percent

Key buying factors # of respondents

8

800

547 136

<$300k $300k-1mn $1-30mn >$30mn 1,491

9.4

22

71

10 16

x Projected annual growth 2010-15, Percent

8

<$30mn $30-100mn $100mn-1bn >$1bn 359

319

11 21

91

4 2

W Java C Java E Java Sumatera Others

Textile

20

55

<$10mn $10-50mn $50-100mn >$100mn 1,949

1,925

14

96

4 0 0 0

Home and personal care

5.5 <$10mn

$10-110mn

>$110mn 77

23

45

9 42

83

11 0

20

7

8

Service Supply

Quality

Price

156

9

Service Supply

Quality

Price

134

7

Service Supply

Quality

Price

234

8

Service Supply

Quality

Price

Market share

30%

10%

40% 20%

13%

82%

3% 3%

75%

5%

18% 2%

68%

2%

30%

Industry summary

Food and beverages industry consumes 60% approx. of packaging

95% of packaging is flexible 95% of converters are located in Java 90% of packaging is sold domestically

Auto industry is expected to grow at >9% Big players (>$100 mn revenues) control

more than 90% market share Almost all of Auto manufacturers are

located in Western part of Java

Textile industry is expected to continue growing at 20% in 2012-2013

The sector is nominated by small players Almost of all textile manufacturers are

located in Western part of Java

HPC is projected to grow at 6% in 2012-2015

Large size companies dominate HPC market

98% of HPC factories are located in Java

High growth rate is observed for most of the Petrochemical end use industry

(ii) Key opportunities and challenges of petrochemical development

15

Private & Confidential

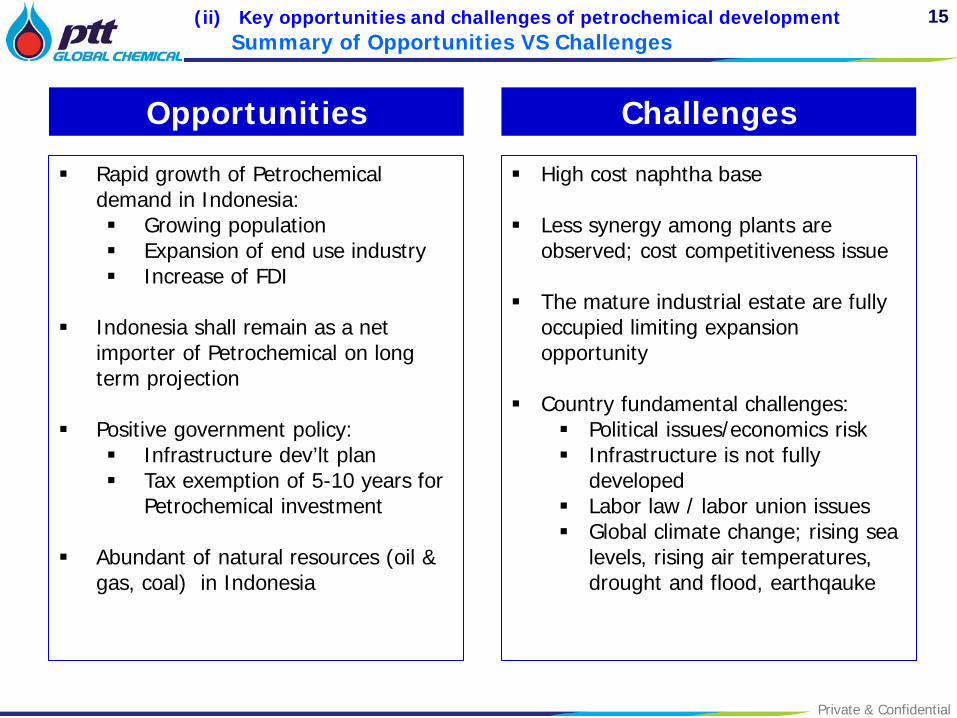

Summary of Opportunities VS Challenges (ii) Key opportunities and challenges of petrochemical development

Rapid growth of Petrochemical demand in Indonesia: Growing population Expansion of end use industry Increase of FDI

Indonesia shall remain as a net importer of Petrochemical on long term projection

Positive government policy:

Infrastructure dev’lt plan Tax exemption of 5-10 years for

Petrochemical investment

Abundant of natural resources (oil & gas, coal) in Indonesia

High cost naphtha base Less synergy among plants are

observed; cost competitiveness issue

The mature industrial estate are fully occupied limiting expansion opportunity

Country fundamental challenges:

Political issues/economics risk Infrastructure is not fully

developed Labor law / labor union issues Global climate change; rising sea

levels, rising air temperatures, drought and flood, earthqauke

Opportunities Challenges

16

Private & Confidential

Indonesia petrochemical business outlook

Key opportunities and challenges of petrochemical development

Competitive edge of local producers

Conclusion

Outlines

17

Private & Confidential

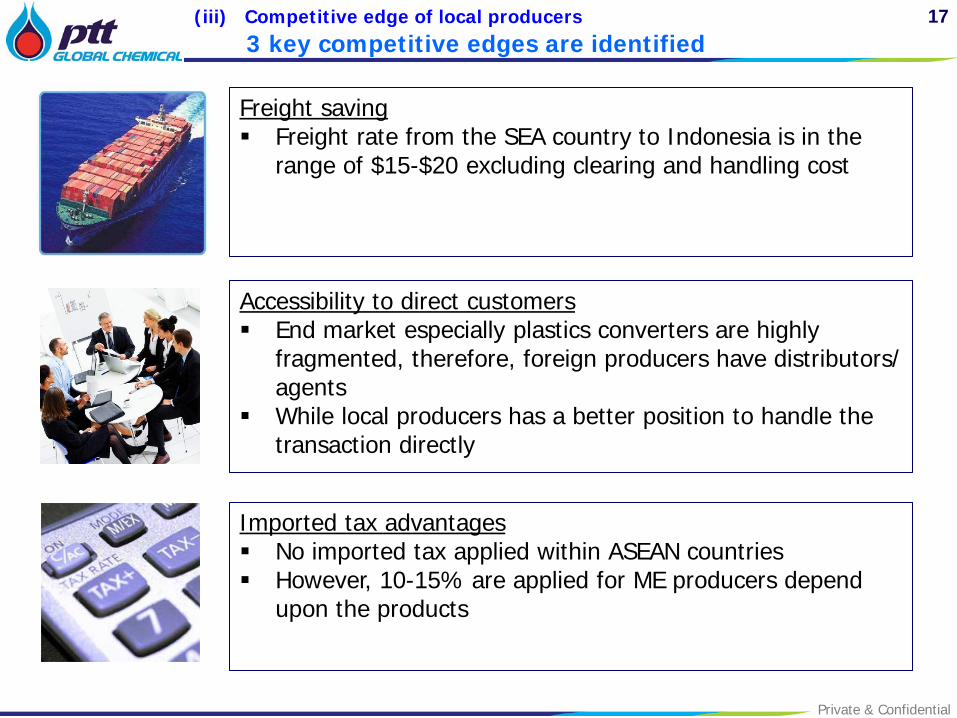

3 key competitive edges are identified (iii) Competitive edge of local producers

Freight saving Freight rate from the SEA country to Indonesia is in the

range of $15-$20 excluding clearing and handling cost

Accessibility to direct customers End market especially plastics converters are highly

fragmented, therefore, foreign producers have distributors/ agents

While local producers has a better position to handle the transaction directly

Imported tax advantages No imported tax applied within ASEAN countries However, 10-15% are applied for ME producers depend

upon the products

18

Private & Confidential

Indonesia petrochemical business outlook

Key opportunities and challenges of petrochemical development

Competitive edge of local producers

Conclusion

Outlines

19

Private & Confidential

Conclusion

Promising petrochemical demand is observed in Indonesia due to several factors i.e. growing of population, expansion of end use industries.

As far as 2025 projection, Indonesia is still be a net importer of Petrochemical products.

Domestic players has a competitive position to access to direct customers due to very fragmented market structure, import tax barrier and freight cost saving.

In addition to high market growth, key opportunities of Petrochemical business in Indonesia are abundant of natural oil and gas feedstock, and support from the government i.e. infrastructure/ logistics system development and investment incentives.

While the challenges could be overcome by creating synergy through fully integrated upstream and downstream complex as well as implementation of operational excellence.