islami bank bangladesh limited annual report 2015...islami bank bangladesh limited annual report...

TRANSCRIPT

Islami Bank Bangladesh Limited Annual Report 2015175

Islami Bank Bangladesh Limited Annual Report 2015176

Independent Auditors’ Report To the Shareholders of Islami Bank Bangladesh Limited

We have audited the accompanying consolidated financial statements of Islami Bank Bangladesh Limited and its subsidiaries (the “Group”) as well as the separate financial statements of Islami Bank Bangladesh Limited (the “Bank”), which comprise the consolidated and separate balance sheets as at 31 December 2015, and the consolidated and separate profit and loss accounts, consolidated and separate statements of changes in equity and consolidated and separate cash flow statements for the year then ended, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Financial Statements and Internal Controls

Management is responsible for the preparation of consolidated financial statements of the Group and also separate financial statements of the Bank that give a true and fair view in accordance with Bangladesh Financial Reporting Standards (BFRS) as explained in note 2.1 and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements of the Group and also the separate financial statements of the Bank that are free from material misstatement, whether due to fraud or error. The Bank Company Act, 1991 as amended and the Bangladesh Bank regulations require the management to ensure effective internal audit, internal control and risk management functions of the Bank. The management is also required to make a self-assessment on the effectiveness of anti-fraud internal controls and report to Bangladesh Bank on instances of fraud and forgeries.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements of the Group and the separate financial statements of the Bank based on our audit. We conducted our audit in accordance with Bangladesh Standards on Auditing (BSA). Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements of the Group and the separate financial statements of the Bank are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements of the Group and separate financial statements of the Bank. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the consolidated financial statements of the Group and the separate financial statements of the Bank, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of consolidated financial statements of the Group and the separate financial statements of the Bank that give a true and fair view in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion of the effectiveness of the entities internal control systems. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements of the Group and also the separate financial statements of the Bank.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements of the Group and also the separate financial statements of the Bank give a true and fair view of the consolidated financial position of the Group and the separate financial position of the Bank as at 31 December 2015, and of its consolidated and separate financial performance and its consolidated and separate cash flows for the year then ended in accordance with Bangladesh Financial Reporting Standards (BFRS) as explained in note 2.1.

Report on Other Legal and Regulatory Requirements

In accordance with the Companies Act 1994, Securities and Exchange Rules 1987, the Bank Company Act 1991 as amended and the rules and regulations issued by Bangladesh Bank, we also report the following:

Islami Bank Bangladesh Limited Annual Report 2015177

(a) we have obtained all the information and explanation which to the best of our knowledge and belief were necessary for the purpose of our audit and made due verification thereof;

(b) to the extent noted during the course of our audit work performed on the basis stated under the Auditors’ Responsibility section in forming the above opinion on the consolidated financial statements of the Group and the separate financial statements of the Bank and considering the reports of the management to the Bangladesh Bank on anti-fraud internal controls and instances of fraud and forgeries as stated under the Management’s Responsibility for the Financial Statements and Internal Control:

i. internal audit, internal control and risk management arrangements of the Group and the Bank as disclosed in note 3.31 appeared to be adequate;

ii. nothing has come to our attention regarding material instances of forgery or irregularity or administrative error and exception or anything detrimental committed by employees of the Bank and its related entities other than matters disclosed in note 3.31.8;

(c) financial statements of subsidiary companies of the Bank namely Islami Bank Securities Limited have been audited by Kazi Zahir Khan& Co., Chartered Accountants and Islami Bank Capital Management Limited have been audited by Hussain Farhad & Co., Chartered Accountants and have been properly reflected in the consolidated financial statements;

(d) in our opinion, proper books of accounts as required by law have been kept by Islami Bank Bangladesh Limited so far as it appeared from our examination of those books;

(e) the consolidated balance sheet and consolidated profit and loss account of the Group and the separate balance sheet and separate profit and loss account of the Bank dealt with by the report are in agreement with the books of account;

(f) the expenditure incurred was for the purposes of the Bank’s business;

(g) the consolidated financial statements of the Group and the separate financial statements of the Bank have been drawn up in conformity with prevailing rules, regulations and Bangladesh Financial Reporting Standards as explained in note 2.1 as well as with related guidance, circulars issued by Bangladesh Bank and decision taken in tripartite meeting amongst Inspection Team of Bangladesh Bank, External Auditors and the Management of Islami Bank Bangladesh Limited held on 10 April 2016 and subsequent letter no. DBI-4/42(7)/2016-722 dated 19 April 2016 issued by Bangladesh Bank.

(h) adequate provisions as explained in note 17.1 have been made for the investments, other assets and off-Balance Sheet items which are, in our opinion, doubtful of recovery;

(i) the records and statements submitted by the branches have been properly maintained and consolidated in the financial statements;

(j) the information and explanation required by us have been received and found satisfactory and

(k) we have reviewed over 80% of the risk weighted assets of the Bank and we have spent around 9,200 person hours for the audit of the books and accounts of the Bank.

Aziz Halim Khair ChoudhuryChartered Accountants

Syful ShamsulAlam& Co.Chartered Accountants

HowladarYunus& Co.Chartered Accountants

Date:19 April, 2016Place: Dhaka

Islami Bank Bangladesh Limited Annual Report 2015178

Islami Bank Bangladesh Limited and its SubsidiariesConsolidated Balance Sheet

As at 31 December 2015

Particulars Notes 31.12.2015Taka

31.12.2014Taka

Property and Assets

Cash in hand 7(a) 55,256,081,820 46,219,359,839

Cash in hand (including foreign currency) 7(a)(i) 8,625,867,409 7,696,844,962

Balance with Bangladesh Bank & its agent bank(s) (including foreign currency) 7(a)(ii) 46,630,214,411 38,522,514,877

Balance with other banks & financial institutions 8(a) 25,644,591,295 23,615,218,198

In Bangladesh 8(a)(i) 23,974,968,279 21,205,895,651

Outside Bangladesh 8(a)(ii) 1,669,623,016 2,409,322,547

Placement with banks & other financial institutions 9.0 3,000,000,000 2,000,000,000

Investments in shares & securities 10(a) 98,397,090,217 99,677,400,553

Government 10(a)(i) 95,482,757,770 97,435,777,770

Others 10(a)(ii) 2,914,332,447 2,241,622,783

Investments 525,104,502,716 460,385,467,466

General investments etc. 11.1(a) 488,699,301,422 433,004,101,205

Bills purchased & discounted 11.2(a) 36,405,201,294 27,381,366,261

Fixed assets including premises 12(a) 15,838,557,191 15,930,479,589

Other assets 13(a) 2,527,292,915 3,751,558,076

Non - banking assets - -

Total property and assets 725,768,116,154 651,579,483,721

Liabilities and Capital

Liabilities

Placement from banks & other financial institutions 14(a) 17,766,330,139 7,657,500,743

Deposits & other accounts 15(a) 614,877,266,437 559,713,580,029

Mudaraba savings deposits 211,327,625,463 183,125,942,453

Mudaraba term deposits 179,234,913,887 169,288,934,029

Other mudaraba deposits 162,097,188,257 149,300,904,194

Al- wadeeah current and other deposit accounts 57,126,253,285 54,347,905,252

Bills payable 5,091,285,545 3,649,894,101

Mudaraba perpetual bond 16.0 3,000,000,000 3,000,000,000

Other liabilities 17(a) 42,521,807,091 34,220,763,730

Deferred tax liabilities 18(a) 310,066,332 393,276,062

Total liabilities 678,475,469,999 604,985,120,564

Capital/shareholders’ equity 47,292,646,155 46,594,363,157

Paid - up capital 19.0 16,099,906,680 16,099,906,680

Statutory reserve 21.0 16,099,906,680 16,099,906,680

Other reserves 22.0 11,779,818,313 12,007,818,774

Retained earnings 40(a) 3,312,951,535 2,386,670,563

Non-controlling interest 40(b) 62,947 60,460

Total liabilities & shareholders’ equity 725,768,116,154 651,579,483,721

Islami Bank Bangladesh Limited Annual Report 2015179

Islami Bank Bangladesh Limited and its SubsidiariesConsolidated Balance Sheet

As at 31 December 2015

Particulars Notes 31.12.2015Taka

31.12.2014Taka

Off-balance sheet items

Contingent liabilities

Acceptances & endorsements - -

Letters of guarantee 23.0 10,629,688,357 8,839,985,590

Irrevocable letters of credit (including back to back bills) 115,229,781,408 99,102,373,685

Bills for collection 7,496,874,228 4,853,286,313

Other contingent liabilities 23,581,701 23,581,701

Total 133,379,925,694 112,819,227,289

Other commitments

Documentary credits, short term and trade related transactions - -

Forward assets purchased and forward deposits placed - -

Undrawn note issuance, revolving and underwriting facilities - -

Undrawn formal standby facilities, credit lines and other commitments - -

Total - -

Total off-balance sheet items including contingent liabilities 133,379,925,694 112,819,227,289

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015180

Islami Bank Bangladesh Limited and its SubsidiariesConsolidated Profit & Loss Account

For the year ended 31 December 2015

Particulars Notes 2015Taka

2014Taka

Operating incomeInvestment income 24(a) 48,019,361,677 49,109,956,379 Profit paid on mudaraba deposits 25(a) (28,711,803,286) (30,592,937,508)Net investment income 19,307,558,391 18,517,018,871

Income from investments in shares & securities 26(a) 815,154,861 1,847,241,058 Commission, exchange & brokerage income 27(a) 6,212,914,002 5,883,332,280 Other operating income 28(a) 1,729,427,055 1,223,373,942 Total operating income 28,065,054,309 27,470,966,151

Operating expenses Salary & allowances 29(a) 8,884,178,676 8,197,568,114 Rent, taxes, insurances, electricity etc. 30(a) 1,147,142,738 1,000,045,580 Legal expenses 31(a) 44,189,468 16,206,043 Postage, stamps and telecommunication etc. 32(a) 43,895,740 47,306,134 Stationery, printing and advertisement etc. 33(a) 319,978,205 317,612,092 Chief executive’s salary & fees 34.0 8,400,000 8,400,000 Directors’ fees & expenses 35(a) 12,640,292 13,183,767 Shari’ah supervisory committee’s fees & expenses 36.0 3,730,249 2,562,124 Auditors’ fees 37(a) 2,530,000 2,344,118 Charges on investment losses - - Depreciation and repair to bank’s assets 38(a) 961,943,629 866,506,137 Zakat expenses 421,312,940 425,985,241 Other expenses 39(a) 1,649,966,254 1,205,550,108 Total operating expenses 13,499,908,191 12,103,269,458 Profit/ (loss) before provision 14,565,146,118 15,367,696,693 Provision for investments & off- balance sheet exposures 17.1.4 5,393,314,666 4,670,784,729 Provision for diminution in value of investments in shares 17.2(a) 27,069,117 36,184,361 Other provisions 17.4 99,232,276 117,049,502 Total provision 5,519,616,059 4,824,018,592 Total profit/(loss) before taxes 9,045,530,059 10,543,678,101 Provision for taxation for the period 5,895,163,334 6,562,294,743 Current tax 17.7(a) 5,978,373,064 6,367,368,688 Deferred tax 18(b) (83,209,730) 194,926,055 Net profit/ (loss) after tax 3,150,366,725 3,981,383,358 Net profit after tax attributable to: 3,150,366,725 3,981,383,358 Equity holders of IBBL 3,150,364,238 3,981,381,780 Non-controlling interest 40(b) 2,487 1,578

Retained earnings from previous year 2,386,670,563 2,637,858,071 Add: Net profit after tax (attributable to equity holders of IBBL) 3,150,364,238 3,981,381,780 Profit available for appropriation 5,537,034,801 6,619,239,851

Appropriation: 5,537,034,801 6,619,239,851 Statutory reserve 21.0 - 1,461,293,053 General reserve 22.1 (190,902,736) 136,746,051 Dividend 40.0 2,414,986,002 2,634,530,184 Retained earnings 40(a) 3,312,951,535 2,386,670,563 Consolidated earnings per share 42(a) 1.96 2.47

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015181

Islami Bank Bangladesh Limited and its SubsidiariesConsolidated Cash Flow Statement

For the year ended 31 December 2015

Particulars Note2015Taka

2014Taka

Cash flows from operating activitiesInvestment income 47,915,719,537 49,004,594,914 Profit paid on mudaraba deposits (29,563,685,828) (31,722,869,528)Income/ dividend receipt from investments in shares & securities 2,063,232,961 1,870,699,544 Fees & commission receipt in cash 6,212,914,002 5,883,332,280 Recovery from written off investments 39,909,335 39,350,296 Payments to employees (8,561,139,222) (8,100,074,962)Cash payments to suppliers (326,787,585) (326,348,124)Income tax paid (9,203,786,715) (5,648,297,930)Receipts from other operating activities 2,013,322,283 1,213,407,361 Payments for other operating activities (2,289,395,100) (2,594,835,403)(i) Operating profit before changes in operating assets 8,300,303,668 9,618,958,448 Changes in operating assets and liabilities Increase/(decrease) of statutory deposits - - (Increase)/decrease of net trading securities - - (Increase)/decrease of placement to other banks - - (Increase)/decrease of investments to customers (61,629,035,250) (57,190,662,489)(Increase)/decrease of other assets 1,189,635,579 1,013,868,776 Increase/(decrease) of placement from other banks 10,108,829,396 7,657,500,743 Increase/(decrease) of deposits from other banks 153,938,891 (193,547,298)Increase/(decrease) of deposits received from customers 54,025,872,754 86,764,748,509 Increase/(decrease) of other liabilities account of customers - - Increase/(decrease) of trading liabilities - - Increase/(decrease) of other liabilities 2,075,425,298 2,872,167,220 (ii) Cash flows from operating assets and liabilities 5,924,666,668 40,924,075,461 Net cash flows from operating activities (A)=(i+ii) 14,224,970,336 50,543,033,909

Cash flows from investing activitiesProceeds from sale of securities 1,335,573,339 1,175,692,382 Payment for purchase of securities/BGIIB (117,057,781) (34,768,348,787)Placement to Islamic Refinance Fund Account (1,000,000,000) (2,000,000,000)Payment for purchase of securities/membership - - Purchase/sale of property, plants & equipments (960,327,089) (941,612,274)Purchase/sale of subsidiaries - - Net Cash flows from investing activities (B) (741,811,531) (36,534,268,679)

Cash flows from financing activitiesReceipts from issue of debt instruments - - Payment for redemption of debt instruments - - Receipts from issuing ordinary share/ rights share - - Dividend paid in Cash (2,414,986,002) (1,170,902,304)Net cash flows from financing activities (C) (2,414,986,002) (1,170,902,304)Net increase/(decrease) in cash (A+B+C) 11,068,172,803 12,837,862,926 Add/(less): effects of exchange rate changes on cash & cash equivalent (2,077,725) 5,074,713 Add: cash & cash equivalents at beginning of the year 69,834,578,037 56,991,640,398 Cash & cash equivalents at the end of the year 45(a) 80,900,673,115 69,834,578,037

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015182

Isla

mi B

ank

Bang

lade

sh L

imite

d an

d its

Sub

sidi

arie

sCo

nsol

idat

ed S

tate

men

t of C

hang

es in

Equ

ityFo

r the

year

end

ed 3

1 De

cem

ber 2

015

(Am

ount

in Ta

ka)

Parti

cular

sPa

id-up

capit

alSh

are p

re-

mium

Stat

utor

y re

serve

Gene

ral/

othe

r re

serve

s *

Asse

ts re

valua

-tio

n res

erve

Reva

luatio

n re

serve

of

secu

rities

Reta

ined

earn

ings

Non-c

ontro

lling

inter

est

Tota

l

12

34

56

78

910

(2+3

+4+5

+6+7

+8+9

)Ba

lance

as at

01 J

anua

ry 20

1516

,099,9

06,68

0 1,

989,6

33

16,09

9,906

,680

425,3

57,82

1 11

,498,9

71,32

0 81

,500,0

00

2,38

6,670

,563

60,46

0 46

,594,3

63,15

7 Ch

ange

s in a

ccou

nting

polic

y res

tate

d bala

nce

- -

- -

- -

- -

Surp

lus/ (

defic

it) on

acco

unt o

f rev

aluat

ion of

prop

ertie

s -

- -

- -

- -

- Su

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of in

vestm

ents

(shar

es &

secu

rities

) -

- -

- -

(35,0

20,00

0) -

- (3

5,02

0,00

0)

Curre

ncy t

rans

lation

diffe

renc

es -

- -

(2,07

7,725

) -

- -

(2,0

77,7

25)

Net g

ain an

d los

ses n

ot re

cogn

ized i

n the

inco

me s

tate

men

t -

- -

- -

- -

- -

Net p

rofit

for t

he pe

riod

- -

- -

- -

3,15

0,364

,238

2,48

7 3,

150,

366,

725

Tran

sfer t

o (fro

m) r

eser

ve -

- -

(190

,902,7

36)

- -

190,9

02,73

6 -

- Di

viden

d:

-

- -

- -

- -

B

onus

shar

es -

- -

- -

- -

- -

C

ash d

ivide

nd -

- -

- -

- (2

,414,9

86,00

2) -

(2,4

14,9

86,0

02)

Issue

of sh

are c

apita

l -

- -

- -

- -

- -

Tota

l sha

reho

lder

s’ eq

uity

as on

31 D

ecem

ber 2

015

16,09

9,906

,680

1,98

9,63

3 16

,099

,906

,680

23

2,37

7,36

0 11

,498

,971

,320

46

,480

,000

3,

312,

951,

535

62,9

47

47,2

92,6

46,1

55

Add:

Mud

arab

a per

petu

al bo

nd -

- -

- -

- -

3,00

0,00

0,00

0 Ad

d: Ge

nera

l pro

vision

for u

nclas

sified

inve

stmen

ts an

d off-

ba

lance

shee

t item

s (N

ote-2

.1.3)

- -

- 4,

540,0

47,24

0 -

- -

- 4,

540,

047,

240

Adjus

tmen

t for

curre

ncy t

rans

lation

diffe

renc

es -

- -

(4,31

4,759

) -

- -

(4,3

14,7

59)

Less

: Ass

ets r

evalu

ation

rese

rve (

Note

-2.1.

3) -

- -

- (6

,899,3

82,79

2) -

- -

(6,8

99,3

82,7

92)

Less

: Rev

aluat

ion re

serve

of se

curit

ies (N

ote-2

.1.3)

- -

- -

(13,8

80,00

0) -

- (1

3,88

0,00

0)To

tal e

quity

as on

31 D

ecem

ber 2

015

16,0

99,9

06,6

8 1,

989,

633

16,0

99,9

06,6

80 4,

768,

109,

841

4,59

9,58

8,52

8 32

,600

,000

3,

312,

951,

535

62,9

47

47,9

15,1

15,8

44

*Not

e : G

ener

al / o

ther

rese

rves

Parti

culrs

01.0

1.20

1501

.01.

2014

Gene

ral re

serve

377,1

59,53

2 25

0,219

,286

Divid

end e

quali

zatio

n acc

ount

32,00

0,000

32

,000,0

00

Curre

ncy t

rans

lation

diffe

renc

es 6,

392,4

84

1,31

7,771

To

tal

415,

552,

016

283,

537,

057

Islami Bank Bangladesh Limited Annual Report 2015183

Isla

mi B

ank

Bang

lade

sh L

imite

d an

d its

Sub

sidi

arie

sCo

nsol

idat

ed S

tate

men

t of C

hang

es in

Equ

ityFo

r the

year

end

ed 3

1 De

cem

ber 2

014

(Am

ount

in T

aka)

Parti

cular

sPa

id-u

p cap

ital

Shar

e pr

emiu

mSt

atut

ory

rese

rve

Gene

ral/

othe

r re

serv

es *

Asse

ts

reva

luat

ion

rese

rve

Reva

luat

ion

rese

rve o

f se

curit

ies

Reta

ined

ea

rnin

gs

Non-

cont

rolli

ng

inte

rest

Tota

l

12

34

56

78

910

(2+3

+4+5

+6+7

+8+9

)Ba

lance

as at

01 J

anua

ry 20

14 14

,636

,278

,800

1,

989,

633

14,6

38,6

13,6

27

283,

537,

057

11,4

98,9

71,3

20

62,6

00,0

00

2,63

7,85

8,07

1 61

,332

43

,759

,909

,840

Ch

ange

s in a

ccou

nting

polic

y res

tate

d bala

nce

- -

- -

- -

- -

Surp

lus/ (

defic

it) on

acco

unt o

f rev

aluat

ion of

prop

ertie

s -

- -

- -

- -

- Su

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of in

vestm

ents

(shar

es &

secu

rities

) -

- -

- -

18,90

0,000

-

- 18

,900

,000

Cu

rrenc

y tra

nslat

ion di

ffere

nces

- -

- 5,

074,7

13

- -

- 5,

074,

713

Net g

ain an

d los

ses n

ot re

cogn

ized i

n the

inco

me s

tate

men

t -

- -

- -

- -

- -

Net p

rofit

for t

he pe

riod

- -

- -

- -

3,98

1,381

,780

1,57

8 3,

981,

383,

358

Tran

sfer t

o res

erve

- -

1,46

1,293

,053

136,7

46,05

1 -

- (1

,598,0

39,10

4) -

- Di

viden

d:

-

- -

- -

- -

B

onus

shar

es 1,

463,6

27,88

0 -

- -

- -

(1,46

3,627

,880)

- -

C

ash d

ivide

nd -

- -

- -

- (1

,170,9

02,30

4) (2

,450)

(1,1

70,9

04,7

54)

Issue

of sh

are c

apita

l -

- -

- -

- -

- -

Tota

l sha

reho

lder

s’ eq

uity

as on

31 D

ecem

ber 2

014

16,0

99,9

06,6

80

1,98

9,63

3 16

,099

,906

,680

42

5,35

7,82

1 11

,498

,971

,320

81

,500

,000

2,

386,

670,

563

60,4

60

46,5

94,3

63,1

57

Add:

Mud

arab

a per

petu

al bo

nd -

- -

- -

- -

- 3,

000,

000,

000

Add:

Gene

ral p

rovis

ion fo

r unc

lassif

ied in

vestm

ents

and o

ff- ba

lance

shee

t item

s -

- -

4,75

3,680

,000

- -

- -

4,75

3,68

0,00

0 Ad

justm

ent f

or cu

rrenc

y tra

nslat

ion di

ffere

nces

(6,39

2,484

) -

(6,3

92,4

84)

Less

: 50.0

0% of

asse

ts re

valua

tion r

eser

ve -

- -

- (5

,749,4

85,66

0) -

- -

(5,7

49,4

85,6

60)

Less

: 50.0

0% of

reva

luatio

n res

erve

of se

curit

ies -

- -

- -

(40,7

50,00

0) (4

0,75

0,00

0)To

tal e

quity

as on

31 D

ecem

ber 2

014

16,0

99,9

06,6

80

1,98

9,63

3 16

,099

,906

,680

5,17

2,64

5,33

7 5,

749,

485,

660

40,7

50,0

00

2,38

6,67

0,56

3 60

,460

48

,551

,415

,013

Engr

. Mus

tafa

Anw

ar

Engr

. Md.

Esk

ande

r Ali

Khan

M

d. W

ahid

uzza

man

Kha

ndak

er

Moh

amm

ad A

bdul

Man

nan

Ch

airm

an

Dire

ctor

Di

rect

or

Man

agin

g Di

rect

orTh

is is

cons

olid

ated

bal

ance

she

et re

ferre

d to

in o

ur s

epar

ate

repo

rt of

eve

n da

te.

Aziz

Hal

im K

hair

Chou

dhur

y Sy

ful S

ham

sul A

lam

& C

o.

Howl

adar

Yun

us &

Co.

Char

tere

d Ac

coun

tant

s Ch

arte

red

Acco

unta

nts

Char

tere

d Ac

coun

tant

sDh

aka

19 A

pril,

2016

Islami Bank Bangladesh Limited Annual Report 2015184

Islami Bank Bangladesh LimitedBalance Sheet

As at 31 December 2015

Particulars Notes 31.12.2015Taka

31.12.2014Taka

Property and AssetsCash in hand 7.0 55,256,075,599 46,219,359,426

Cash in hand (including foreign currency) 7.1 8,625,861,188 7,696,844,549 Balance with Bangladesh Bank & its agent bank(s) (including foreign currency) 7.2 46,630,214,411 38,522,514,877

Balance with other banks & financial institutions 8.0 19,766,322,649 20,199,350,245

In Bangladesh 8(i) 18,096,699,633 17,790,027,698 Outside Bangladesh 8(ii) 1,669,623,016 2,409,322,547

Placement with banks & other financial institutions 9.0 3,000,000,000 2,000,000,000

Investments in shares & securities 10.0 99,436,769,339 100,856,528,896

Government 10.1 95,482,757,770 97,435,777,770 Others 10.2 3,954,011,569 3,420,751,126

Investments 11.0 530,194,502,716 463,475,467,466

General investments etc. 11.1 493,789,301,422 436,094,101,205 Bills purchased & discounted 11.2 36,405,201,294 27,381,366,261

Fixed assets including premises 12.0 15,836,479,066 15,926,361,916

Other assets 13.0 2,330,975,328 3,744,970,802 Non - banking assets - -

Total property and assets 725,821,124,697 652,422,038,751

Liabilities and Capital

Liabilities

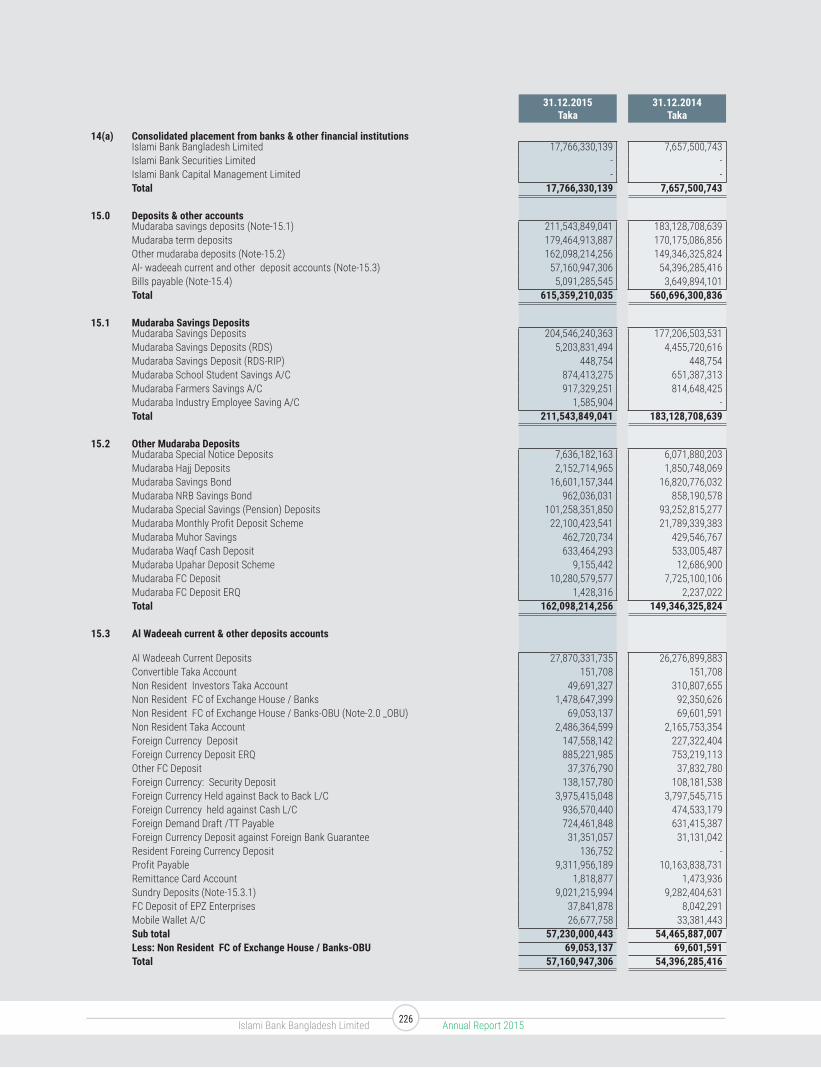

Placement from banks & other financial institutions 14.0 17,766,330,139 7,657,500,743 Deposits & other accounts 15.0 615,359,210,035 560,696,300,836 Mudaraba savings deposits 15.1 211,543,849,041 183,128,708,639 Mudaraba term deposits 179,464,913,887 170,175,086,856 Other mudaraba deposits 15.2 162,098,214,256 149,346,325,824 Al- wadeeah current and other deposit accounts 15.3 57,160,947,306 54,396,285,416 Bills payable 15.4 5,091,285,545 3,649,894,101

Mudaraba perpetual bond 16.0 3,000,000,000 3,000,000,000

Other liabilities 17.0 42,185,241,832 34,052,027,094

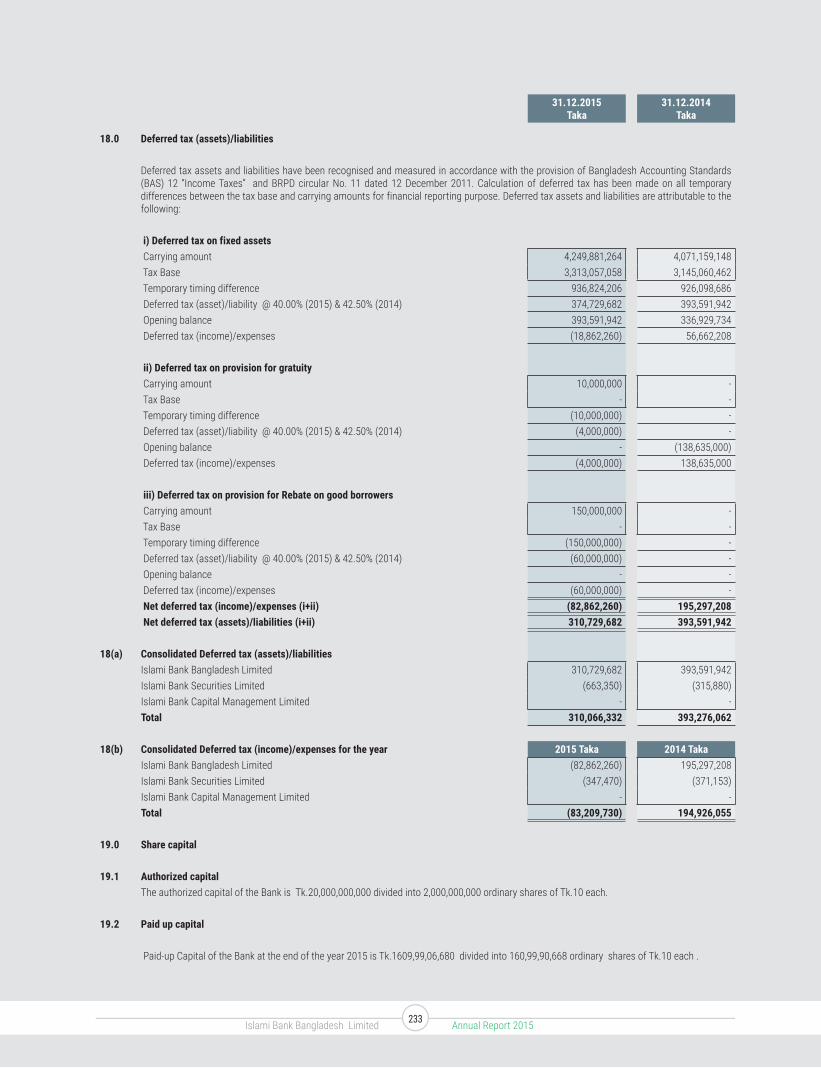

Deferred tax liabilities 18.0 310,729,682 393,591,942

Total liabilities 678,621,511,688 605,799,420,615

Capital/ shareholders’ equity 47,199,613,009 46,622,618,136 Paid - up capital 19.0 16,099,906,680 16,099,906,680 Statutory reserve 21.0 16,099,906,680 16,099,906,680 Other reserves 22.0 11,779,818,313 12,007,818,774 Retained Earnings 40.0 3,219,981,336 2,414,986,002 Total liabilities & shareholders’ equity 725,821,124,697 652,422,038,751

Islami Bank Bangladesh Limited Annual Report 2015185

Islami Bank Bangladesh LimitedBalance Sheet

As at 31 December 2015

Particulars Notes 31.12.2015Taka

31.12.2014Taka

Off-balance sheet itemsContingent liabilitiesAcceptances & endorsements - - Letters of guarantee 23.0 10,629,688,357 8,839,985,590 Irrevocable letters of credit (including back to back bills) 115,229,781,408 99,102,373,685 Bills for collection 7,496,874,228 4,853,286,313 Other contingent liabilities 23,581,701 23,581,701

Total 133,379,925,694 112,819,227,289

Other commitments

Documentary credits, short term and trade related transactions - - Forward assets purchased and forward deposits placed - - Undrawn note issuance, revolving and underwriting facilities - - Undrawn formal standby facilities, credit lines and other commitments - - Total - -

Total off-balance sheet items including contingent liabilities 133,379,925,694 112,819,227,289

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015186

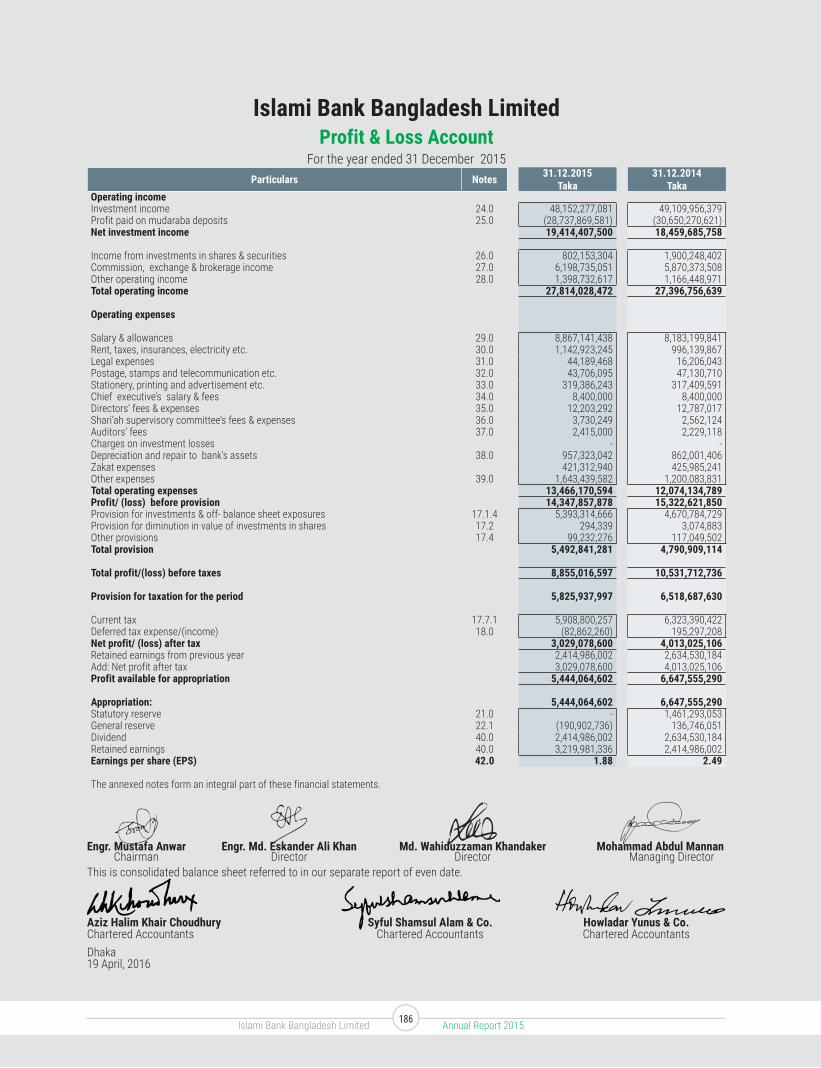

Islami Bank Bangladesh LimitedProfit & Loss Account

For the year ended 31 December 2015Particulars Notes 31.12.2015

Taka31.12.2014

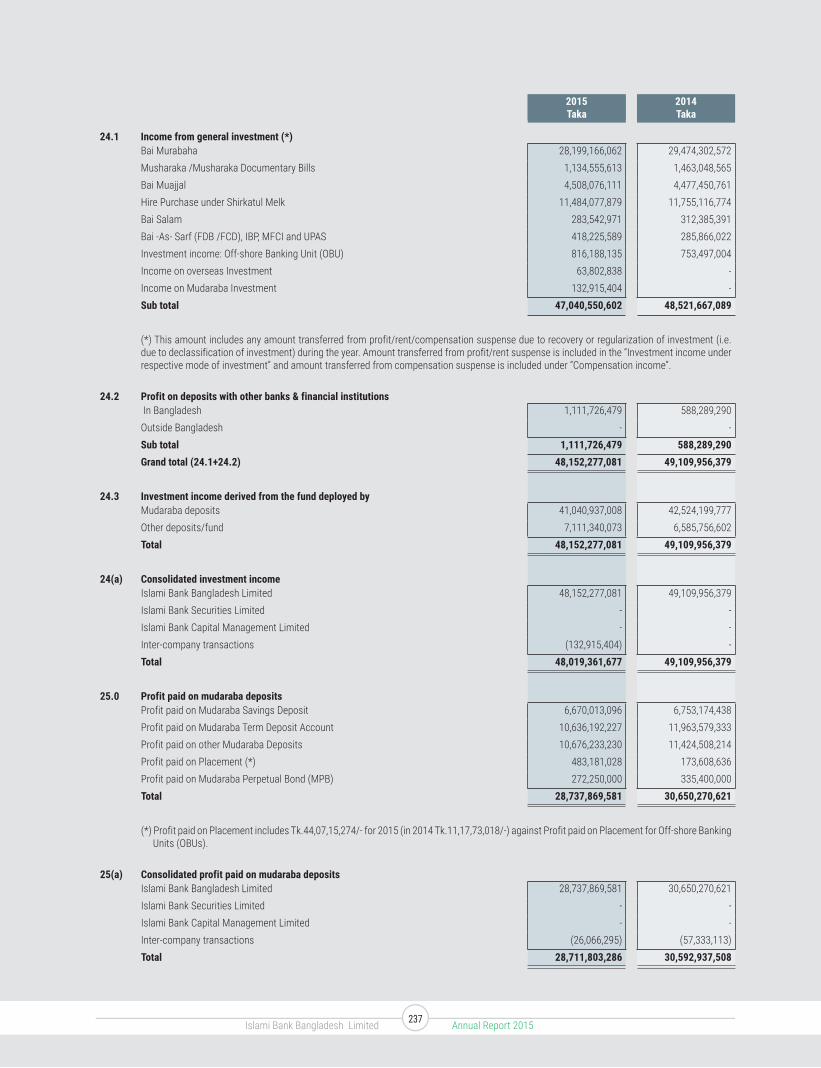

TakaOperating incomeInvestment income 24.0 48,152,277,081 49,109,956,379 Profit paid on mudaraba deposits 25.0 (28,737,869,581) (30,650,270,621)Net investment income 19,414,407,500 18,459,685,758

Income from investments in shares & securities 26.0 802,153,304 1,900,248,402 Commission, exchange & brokerage income 27.0 6,198,735,051 5,870,373,508 Other operating income 28.0 1,398,732,617 1,166,448,971 Total operating income 27,814,028,472 27,396,756,639

Operating expenses

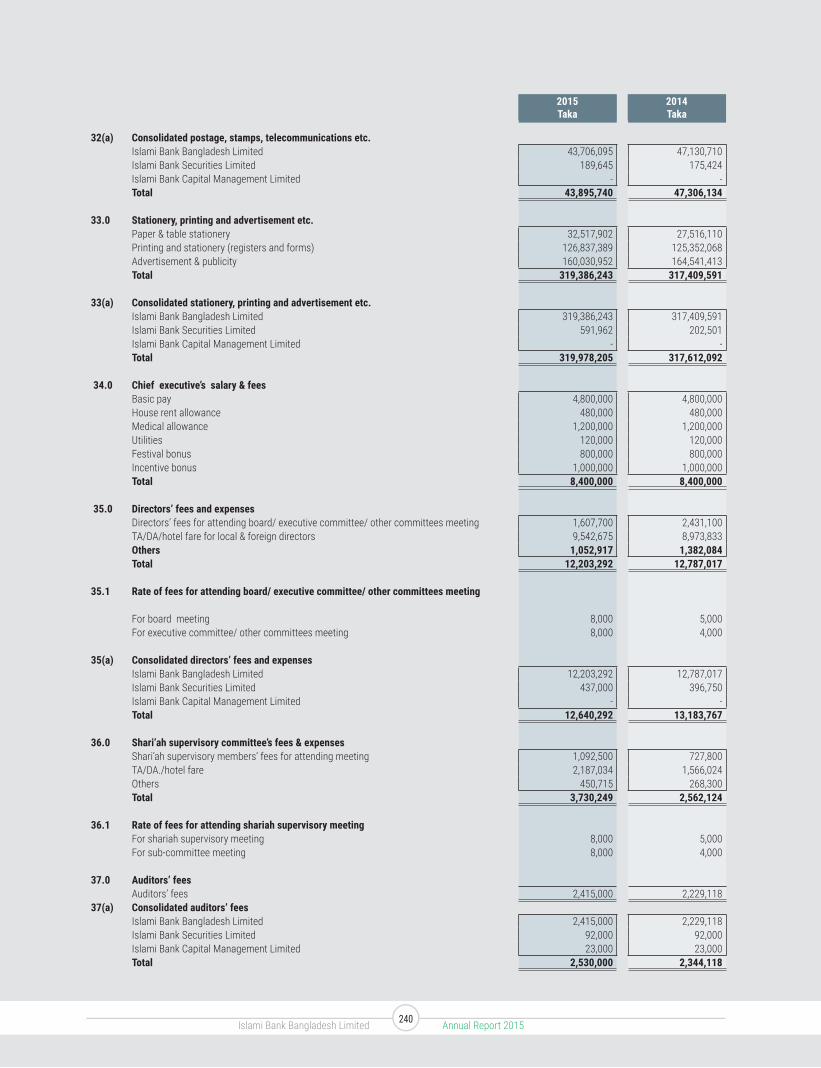

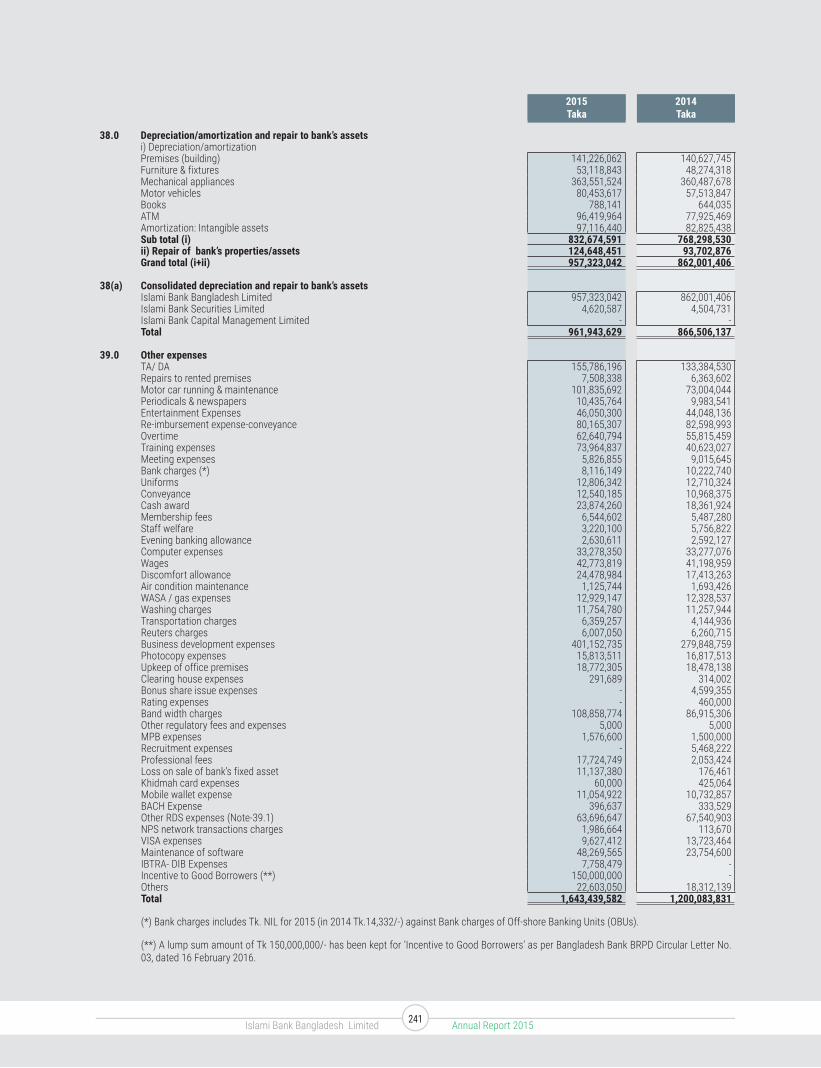

Salary & allowances 29.0 8,867,141,438 8,183,199,841 Rent, taxes, insurances, electricity etc. 30.0 1,142,923,245 996,139,867 Legal expenses 31.0 44,189,468 16,206,043 Postage, stamps and telecommunication etc. 32.0 43,706,095 47,130,710 Stationery, printing and advertisement etc. 33.0 319,386,243 317,409,591 Chief executive’s salary & fees 34.0 8,400,000 8,400,000 Directors’ fees & expenses 35.0 12,203,292 12,787,017 Shari’ah supervisory committee’s fees & expenses 36.0 3,730,249 2,562,124 Auditors’ fees 37.0 2,415,000 2,229,118 Charges on investment losses - - Depreciation and repair to bank’s assets 38.0 957,323,042 862,001,406 Zakat expenses 421,312,940 425,985,241 Other expenses 39.0 1,643,439,582 1,200,083,831 Total operating expenses 13,466,170,594 12,074,134,789 Profit/ (loss) before provision 14,347,857,878 15,322,621,850 Provision for investments & off- balance sheet exposures 17.1.4 5,393,314,666 4,670,784,729 Provision for diminution in value of investments in shares 17.2 294,339 3,074,883 Other provisions 17.4 99,232,276 117,049,502 Total provision 5,492,841,281 4,790,909,114

Total profit/(loss) before taxes 8,855,016,597 10,531,712,736

Provision for taxation for the period 5,825,937,997 6,518,687,630

Current tax 17.7.1 5,908,800,257 6,323,390,422 Deferred tax expense/(income) 18.0 (82,862,260) 195,297,208 Net profit/ (loss) after tax 3,029,078,600 4,013,025,106 Retained earnings from previous year 2,414,986,002 2,634,530,184 Add: Net profit after tax 3,029,078,600 4,013,025,106 Profit available for appropriation 5,444,064,602 6,647,555,290

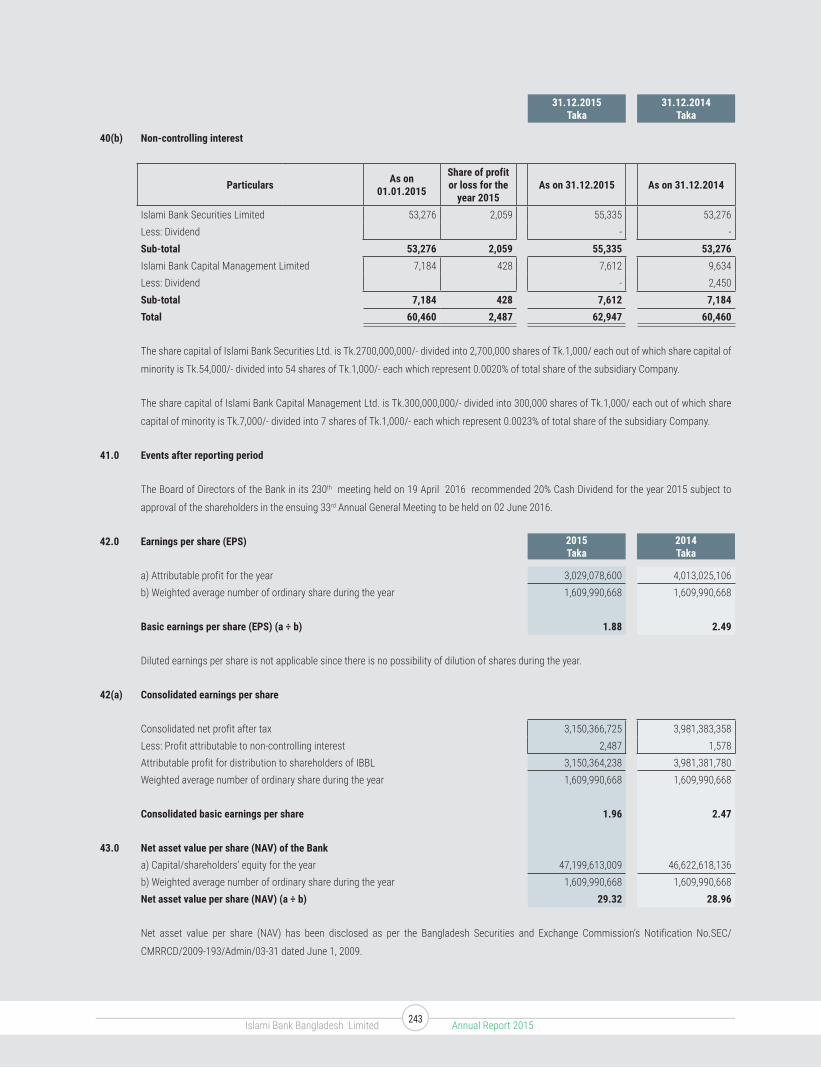

Appropriation: 5,444,064,602 6,647,555,290 Statutory reserve 21.0 - 1,461,293,053 General reserve 22.1 (190,902,736) 136,746,051 Dividend 40.0 2,414,986,002 2,634,530,184 Retained earnings 40.0 3,219,981,336 2,414,986,002 Earnings per share (EPS) 42.0 1.88 2.49

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015187

Islami Bank Bangladesh LimitedCash Flow Statement

For the year ended 31 December 2015

Particulars Note 2015Taka

2014Taka

Cash flows from operating activitiesInvestment income 48,048,634,941 49,004,594,914 Profit paid on mudaraba deposits (29,589,752,123) (31,780,202,641)Income/ dividend receipt from investments in shares & securities 1,945,233,854 1,713,711,788 Fees & commission receipt in cash 6,198,735,051 5,870,373,508 Recovery from written off investments 39,909,335 39,350,296 Payments to employees (8,544,101,984) (8,085,706,689)Cash payments to suppliers (326,195,623) (326,145,623)Income tax paid (9,126,557,598) (5,597,112,182)Receipts from other operating activities 1,682,627,845 1,166,448,971 Payments for other operating activities (2,276,437,791) (2,583,191,009)(i) Operating profit before changes in operating assets 8,052,095,907 9,422,121,333

Changes in operating assets and liabilities

Increase/(decrease) of statutory deposits - - (Increase)/decrease of net trading securities - - (Increase)/decrease of placement to other banks - - (Increase)/decrease of investments to customers (66,719,035,250) (60,280,662,489)(Increase)/decrease of other assets 1,244,475,022 1,025,213,295 Increase/(decrease) of placement from other banks 10,108,829,396 7,657,500,743 Increase/(decrease) of deposits from other banks 153,938,891 (193,547,298)Increase/(decrease) of deposits received from customers 54,508,970,308 87,748,893,103 Increase/(decrease) of other liabilities account of customers - - Increase/(decrease) of trading liabilities - - Increase/(decrease) of other liabilities 4,246,550,417 2,153,192,172 (ii) Cash flows from operating assets and liabilities 3,543,728,784 38,110,589,526 Net cash flows from operating activities (A)=(i+ii) 11,595,824,691 47,532,710,859

Cash flows from investing activities

Proceeds from sale of securities - - Payment for purchase of securities/BGIIB 1,384,739,557 (33,626,229,928)Placement to Islamic Refinance Fund Account (1,000,000,000) (2,000,000,000)Payment for purchase of securities/membership - - Purchase/sale of property, plants & equipments (959,811,944) (940,778,952)Purchase/sale of subsidiaries - - Net cash flows from investing activities (B) (575,072,387) (36,567,008,880)

Cash flows from financing activities

Receipts from issue of debt instruments - - Payment for redemption of debt instruments - - Receipts from issuing ordinary share/ rights share - - Dividend paid in Cash (2,414,986,002) (1,170,902,304)Net cash flows from financing activities (C) (2,414,986,002) (1,170,902,304)

Net increase/(decrease) in cash (A+B+C) 8,605,766,302 9,794,799,675

Add/(Less): effects of exchange rate changes on cash & cash equivalent (2,077,725) 5,074,713 Add: cash & cash equivalents at beginning of the year 66,418,709,671 56,618,835,283

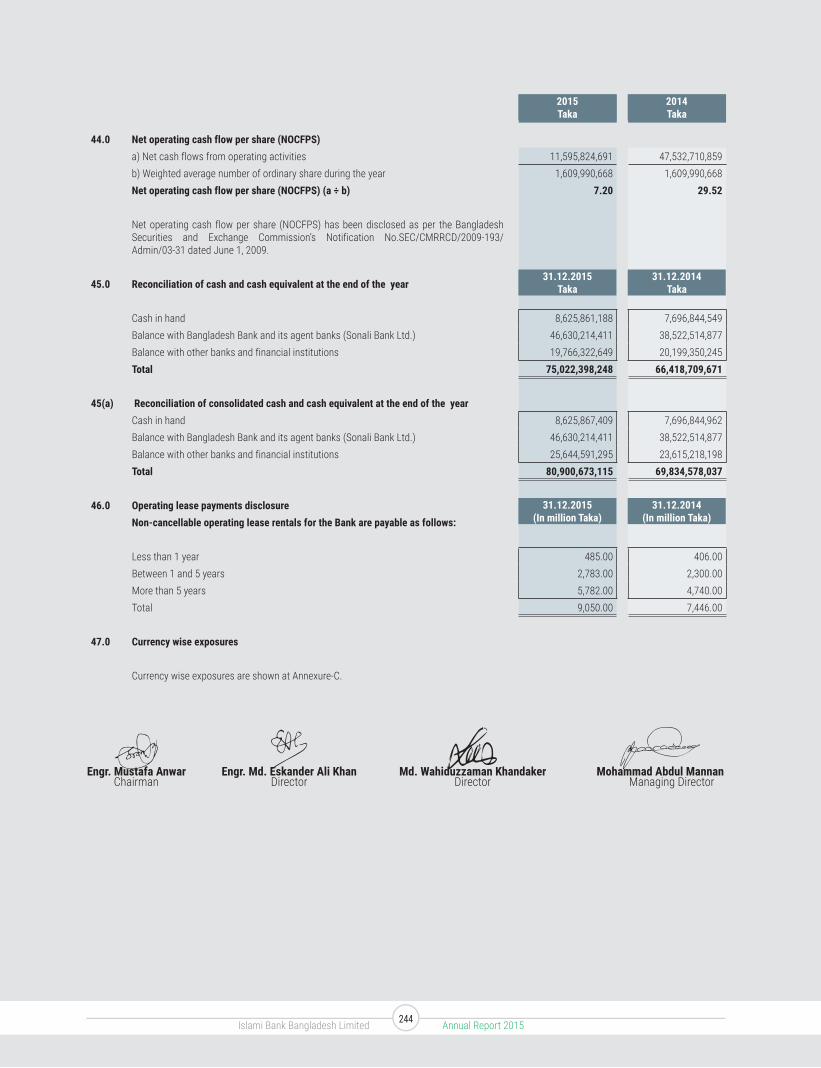

Cash & cash equivalents at the end of the year 45.0 75,022,398,248 66,418,709,671

The annexed notes form an integral part of these financial statements.

Engr. Mustafa Anwar Engr. Md. Eskander Ali Khan Md. Wahiduzzaman Khandaker Mohammad Abdul Mannan Chairman Director Director Managing DirectorThis is consolidated balance sheet referred to in our separate report of even date.

Aziz Halim Khair Choudhury Syful Shamsul Alam & Co. Howladar Yunus & Co. Chartered Accountants Chartered Accountants Chartered AccountantsDhaka19 April, 2016

Islami Bank Bangladesh Limited Annual Report 2015188

Isla

mi B

ank

Bang

lade

sh L

imite

dSt

atem

ent o

f Cha

nges

in E

quity

For t

he ye

ar e

nded

31

Dece

mbe

r 201

5(A

mou

nt in

Tak

a)

Parti

cular

sPa

id-up

capit

alSh

are p

re-

mium

Stat

utor

y res

erve

Gene

ral/

othe

r re

serve

s *

Asse

ts re

valua

-tio

n res

erve

Reva

luatio

n re

serve

of

secu

rities

Reta

ined

earn

ings

Tota

l

12

34

56

78

9 (2+

3+ 4+

5+6+

7+ 8)

Balan

ce as

at 0

1 Jan

uary

2015

16,0

99,9

06,6

80

1,98

9,63

3 16

,099

,906

,680

42

5,35

7,82

1 11

,498

,971

,320

81

,500

,000

2,

414,

986,

002

46,6

22,6

18,1

36

Chan

ges i

n acc

ount

ing po

licy r

esta

ted b

alanc

eSu

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of pr

oper

ties

- -

- -

- -

- Su

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of in

vestm

ents

(shar

es &

secu

rities

) -

- -

- -

(35,0

20,00

0) -

(35,

020,

000)

Curre

ncy t

rans

lation

diffe

renc

es -

- -

(2,07

7,725

) -

- -

(2,0

77,7

25)

Net g

ain an

d los

ses n

ot re

cogn

ized i

n the

inco

me s

tate

men

t -

- -

- -

- -

- Ne

t pro

fit fo

r the

perio

d -

- -

- -

3,02

9,078

,600

3,02

9,07

8,60

0 Tr

ansfe

r to (

from

) res

erve

- -

- (1

90,90

2,736

) -

- 19

0,902

,736

- Di

viden

d: -

B

onus

shar

es -

- -

- -

- -

-

Cas

h divi

dend

- -

- -

- -

(2,41

4,986

,002)

(2,4

14,9

86,0

02)

Issue

of sh

are c

apita

l -

- -

- -

- -

- To

tal s

hare

hold

ers’

equi

ty as

on 31

Dec

embe

r 201

5 16

,099

,906

,680

1,

989,

633

16,0

99,9

06,6

80

232,

377,

360

11,4

98,9

71,3

20

46,4

80,0

00

3,21

9,98

1,33

6 47

,199

,613

,009

Ad

d: M

udar

aba p

erpe

tual

bond

- -

- -

- -

- 3,

000,

000,

000

Add:

Gene

ral p

rovis

ion fo

r unc

lassif

ied in

vestm

ents

and o

ff- ba

lance

shee

t ite

ms

(Not

e-2.1.

3) -

- -

4,56

3,295

,624

- -

- 4,

563,

295,

624

Adjus

tmen

t for

curre

ncy t

rans

lation

diffe

renc

es -

- -

(4,31

4,759

) -

- -

(4,3

14,7

59)

Less

: Ass

ets r

evalu

ation

rese

rve (

Note

-2.1.

3) -

- -

- (6

,899,3

82,79

2) -

- (6

,899

,382

,792

)Le

ss: R

evalu

ation

rese

rve of

secu

rities

(Not

e-2.1.

3) -

- -

- -

(13,8

80,00

0) -

(13,

880,

000)

Tota

l equ

ity as

on 31

Dec

embe

r 201

5 16

,099

,906

,680

1,

989,

633

16,0

99,9

06,6

80

4,79

1,35

8,22

5 4,

599,

588,

528

32,6

00,0

00

3,21

9,98

1,33

6 47

,845

,331

,082

*Not

e : G

ener

al / o

ther

rese

rves

Parti

culrs

01.0

1.20

1501

.01.

2014

Gene

ral re

serve

377,1

59,53

2 25

0,219

,286

Divid

end e

quali

zatio

n acc

ount

32,00

0,000

32

,000,0

00

Curre

ncy t

rans

lation

diffe

renc

es 6,

392,4

84

1,31

7,771

To

tal

415,

552,

016

283,

537,

057

Islami Bank Bangladesh Limited Annual Report 2015189

Isla

mi B

ank

Bang

lade

sh L

imite

dSt

atem

ent o

f Cha

nges

in E

quity

For t

he ye

ar e

nded

31

Dece

mbe

r 201

4(A

mou

nt in

Taka

)

Parti

cular

sPa

id-up

capit

alSh

are

prem

iumSt

atut

ory r

eser

veGe

nera

l/ ot

her

rese

rves

*As

sets

reva

lua-

tion r

eser

ve

Reva

luatio

n re

serve

of

secu

rities

Reta

ined e

arnin

gsTo

tal

12

34

56

78

9 (2+

3+ 4+

5+6+

7+ 8)

Bala

nce a

s at

01 Ja

nuar

y 201

4 14

,636

,278

,800

1,

989,

633

14,6

38,6

13,6

27

283,

537,

057

11,4

98,9

71,3

20

62,6

00,0

00

2,63

4,53

0,18

4 43

,756

,520

,621

Ch

ange

s in a

ccou

nting

polic

y res

tate

d bala

nce

- Su

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of pr

oper

ties

- -

- -

- -

- Su

rplus

/ (de

ficit)

on ac

coun

t of r

evalu

ation

of in

vestm

ents

(shar

es &

secu

rities

) -

- -

- -

18,90

0,000

-

18,9

00,0

00

Curre

ncy t

rans

lation

diffe

renc

es -

- -

5,07

4,713

-

- -

5,07

4,71

3 Ne

t gain

and l

osse

s not

reco

gnize

d in t

he in

com

e sta

tem

ent

- -

- -

- -

- -

Net p

rofit

for t

he pe

riod

- -

- -

- 4,

013,0

25,10

6 4,

013,

025,

106

Tran

sfer t

o res

erve

- -

1,46

1,293

,053

136,7

46,05

1 -

- (1

,598,0

39,10

4) -

Divid

end:

-

Bon

us sh

ares

1,46

3,627

,880

- -

- -

- (1

,463,6

27,88

0) -

C

ash d

ivide

nd -

- -

- -

- (1

,170,9

02,30

4) (1

,170

,902

,304

)Iss

ue of

shar

e cap

ital

- -

- -

- -

- -

Tota

l sha

reho

lder

s’ eq

uity

as on

31 D

ecem

ber 2

014

16,0

99,9

06,6

80

1,98

9,63

3 16

,099

,906

,680

42

5,35

7,82

1 11

,498

,971

,320

81

,500

,000

2,

414,

986,

002

46,6

22,6

18,1

36

Add:

Mud

arab

a per

petu

al bo

nd -

- -

- -

- -

3,00

0,00

0,00

0 Ad

d: Ge

nera

l pro

vision

for u

nclas

sified

inve

stmen

ts an

d off-

balan

ce sh

eet it

ems

- -

- 4,

753,6

80,00

0 -

- -

4,75

3,68

0,00

0 Ad

justm

ent f

or cu

rrenc

y tra

nslat

ion di

ffere

nces

(6,39

2,484

) (6

,392

,484

)Le

ss: 5

0.00%

of as

sets

reva

luatio

n res

erve

- -

- -

(5,74

9,485

,660)

- -

(5,7

49,4

85,6

60)

Less

: 50.0

0% of

reva

luatio

n res

erve

of se

curit

ies -

- -

- -

(40,7

50,00

0) -

(40,

750,

000)

Tota

l equ

ity as

on 31

Dec

embe

r 201

4 16

,099

,906

,680

1,

989,

633

16,0

99,9

06,6

80

5,17

2,64

5,33

7 5,

749,

485,

660

40,7

50,0

00

2,41

4,98

6,00

2 48

,579

,669

,992

Engr

. Mus

tafa

Anw

ar

Engr

. Md.

Esk

ande

r Ali

Khan

M

d. W

ahid

uzza

man

Kha

ndak

er

Moh

amm

ad A

bdul

Man

nan

Ch

airm

an

Dire

ctor

Di

rect

or

Man

agin

g Di

rect

orTh

is is

cons

olid

ated

bal

ance

she

et re

ferre

d to

in o

ur s

epar

ate

repo

rt of

eve

n da

te.

Aziz

Hal

im K

hair

Chou

dhur

y Sy

ful S

ham

sul A

lam

& C

o.

Howl

adar

Yun

us &

Co.

Char

tere

d Ac

coun

tant

s Ch

arte

red

Acco

unta

nts

Char

tere

d Ac

coun

tant

sDh

aka

19 A

pril,

2016

Islami Bank Bangladesh Limited Annual Report 2015190

Isla

mi B

ank

Bang

lade

sh L

imite

dLi

quid

ity S

tate

men

tAs

sets

& lia

bilit

ies

anal

ysis

As a

t 31

Dece

mbe

r 201

5

Parti

cula

rsUp

to 1

Mon

th1

- 3 M

onth

s3

- 12

Mon

ths

1 - 5

yea

rsM

ore

than

5 y

ears

Tota

l 31.

12.2

015

Tota

l 31.

12.2

014

12

34

56

7=(2

+ 3

+ 4

+ 5

+ 6

)8

ASSE

TSCa

sh in

han

d 1

1,69

0,71

4,73

6 -

- -

43,

565,

360,

863

55,

256,

075,

599

46,

219,

359,

426

Bala

nce

with

oth

er b

anks

& fi

nanc

ial in

stitu

tions

(N

ote-

8.2)

13,

471,

322,

649

6,1

25,0

00,0

00

170

,000

,000

-

- 1

9,76

6,32

2,64

9 2

0,19

9,35

0,24

5

Plac

emen

t with

Ban

ks &

oth

er F

inan

cial

Inst

itutio

ns -

3,0

00,0

00,0

00

- -

- 3

,000

,000

,000

2

,000

,000

,000

In

vest

men

ts (i

n sh

ares

& s

ecur

ities

) (No

te-1

0.4)

39,

338,

915,

569

47,

860,

000,

000

8,4

50,0

00,0

00

700

,000

,000

3

,087

,853

,770

9

9,43

6,76

9,33

9 1

00,8

56,5

28,8

96

Gene

ral in

vest

men

ts e

tc.

(Not

e-11

.1.1

) 7

1,76

2,60

7,48

7 8

2,93

9,45

7,43

1 1

37,2

51,3

22,6

03

106

,267

,162

,619

9

5,56

8,75

1,28

2 4

93,7

89,3

01,4

22

436

,094

,101

,205

Bi

lls p

urch

ased

& d

iscou

nted

(No

te-1

1.2.

1) 9

,450

,946

,060

1

2,69

0,49

1,61

0 1

4,26

3,76

3,62

4 -

- 3

6,40

5,20

1,29

4 2

7,38

1,36

6,26

1 Fi

xed

asse

ts in

clud

ing

prem

ises

(land

& b

uild

ing)

, fu

rnitu

re a

nd fi

xtur

es

(Not

e-12

.3)

- -

740

,411

,968

2

,617

,898

,904

1

2,47

8,16

8,19

4 1

5,83

6,47

9,06

6 1

5,92

6,36

1,91

6

Othe

r ass

ets

(Not

e-13

.1)

192

,736

,905

1

,044

,334

,650

5

72,4

51,8

12

348

,686

,845

1

72,7

65,1

16

2,3

30,9

75,3

28

3,7

44,9

70,8

02

Non

- ban

king

asse

ts -

- -

- -

- -

Tota

l ass

ets

145

,907

,243

,406

1

53,6

59,2

83,6

91

161

,447

,950

,008

1

09,9

33,7

48,3

68

154

,872

,899

,225

7

25,8

21,1

24,6

97

652

,422

,038

,751

LI

ABIL

ITIE

SPl

acem

ent f

rom

ban

ks &

oth

er f

inan

cial

inst

itutio

ns 1

4,36

3,36

2,99

6 8

69,5

06,9

35

2,5

33,4

60,2

08

- -

17,

766,

330,

139

7,6

57,5

00,7

43

Depo

sits

(Not

e-15

.5)

109

,919

,107

,672

1

25,6

66,1

83,2

43

144

,689

,435

,299

1

05,3

99,7

14,2

84

129

,684

,769

,537

6

15,3

59,2

10,0

35

560

,696

,300

,836

Ot

her a

ccou

nts

- -

- -

- -

- Pr

ovisi

on &

oth

er lia

bilit

ies

(No

te-1

7.9)

2,9

00,0

67,2

96

12,

594,

135,

013

3,8

30,5

26,5

91

1,7

79,1

30,7

04

21,

081,

382,

228

42,

185,

241,

832

34,

052,

027,

094

Defe

rred

tax l

iabi

lity/

(ass

ets)

- -

- -

310

,729

,682

3

10,7

29,6

82

393

,591

,942

M

udar

aba

perp

etua

l bon

d -

- -

- 3

,000

,000

,000

3

,000

,000

,000

3

,000

,000

,000

To

tal l

iabi

litie

s 1

27,1

82,5

37,9

64

139

,129

,825

,191

1

51,0

53,4

22,0

98

107

,178

,844

,988

1

54,0

76,8

81,4

47

678

,621

,511

,688

6

05,7

99,4

20,6

15

Net l

iqui

dity

gap

18,

724,

705,

442

14,

529,

458,

501

10,

394,

527,

910

2,7

54,9

03,3

80

796

,017

,778

4

7,19

9,61

3,00

9 4

6,62

2,61

8,13

6

Engr

. Mus

tafa

Anw

ar

Engr

. Md.

Esk

ande

r Ali

Khan

M

d. W

ahid

uzza

man

Kha

ndak

er

Moh

amm

ad A

bdul

Man

nan

Ch

airm

an

Dire

ctor

Di

rect

or

Man

agin

g Di

rect

orTh

is is

cons

olid

ated

bal

ance

she

et re

ferre

d to

in o

ur s

epar

ate

repo

rt of

eve

n da

te.

Aziz

Hal

im K

hair

Chou

dhur

y Sy

ful S

ham

sul A

lam

& C

o.

Howl

adar

Yun

us &

Co.

Char

tere

d Ac

coun

tant

s Ch

arte

red

Acco

unta

nts

Char

tere

d Ac

coun

tant

sDh

aka

19 A

pril,

2016

Islami Bank Bangladesh Limited Annual Report 2015191

Islami Bank Bangladesh Limited and its SubsidiariesNotes to the consolidated financial statements

For the year ended 31 December 20151.0 The Bank and its activities

1.1 Islami Bank Bangladesh Limited (hereinafter referred to as “the Bank” or “IBBL”) was established as a Public Limited Banking Company in Bangladesh in 1983 as the first Shari’ah based Scheduled Commercial Bank in the South East Asia. Naturally, its modus operandi is substantially different from those of other conventional Commercial Banks. The Bank conducts its business on the Shari’ah principles of Mudaraba, Musharaka, Bai-Murabaha, Bai-Muajjal, Hire Purchase under Shirkatul Melk, Bai-Salam and Bai-as-Sarf etc. There is a Shari’ah Supervisory Committee in the Bank which ensures that the activities of the Bank are being conducted on the precepts of Islam.

The shares of the Bank are listed with both Dhaka Stock Exchange (DSE) Limited and Chittagong Stock Exchange (CSE) Limited. The Bank carries out its business activities through its Head Office in Dhaka, 14 Zonal Offices, 304 branches including 57 Authorised Dealer (AD) branches and 3 Off-shore Banking Units (OBUs) in Bangladesh. The Principal place of business is the Registered Office of the Bank situated at Islami Bank Tower, 40, Dilkusha Commercial Area, Dhaka-1000, Bangladesh.

These financial statements as at and for the year ended 31 December 2015 include the consolidated and separate financial statements of the Bank. The consolidated financial statements comprise the financial statements of the Bank and its subsidiaries (mentioned in Note - 1.4, together referred to as “the Companies”).

1.2 Nature of business/principal activities of the Bank1.2.1 Commercial banking services

All kinds of commercial banking services are provided by the Bank to the customers following the principles of Islamic Shari’ah, the provisions of the Bank Company Act, 1991 as amended, Bangladesh Bank’s directives and directives of other regulatory authorities.

1.2.2 Islamic micro-finance

Islamic micro-finance represents micro-finance and the Islamic finance industry. Under Islamic micro-finance, major focus is given on improvement of living standard of poor people. The projects are closely monitored so that the members are really benefited. IBBL provides this services under the umbrella of Rural Development Scheme (RDS) and Urban Poor Development Scheme (UPDS).

1.2.3 Mobile financial services -”mCash”

IBBL has launched mobile financial services on 27 December 2012 under the name “Islami Bank mCash” as per Bangladesh Bank approval (reference no. DCMPS/PSD/37/(W)/2012-321 dated 14 June 2012). Islami Bank mCash offers different services through Mobile phone that include deposit and withdrawal of cash money, fund transfer from one account to another, receiving remittance from abroad, knowing account balance and mini-statement, giving and receiving salary, mobile recharge and payment of utility bill, merchant bill payment etc.

1.3 Off-shore banking unit (OBU)

Bangladesh Bank has approved the operation of Off-Shore Banking Unit (OBU) of Islami Bank Bangladesh Limited located at Head Office Complex Branch- Dhaka, Uttara Branch- Dhaka and Agrabad Branch- Chittagong through letter no. BRPD (P-3)744(111)/2010-1032 dated 28 March, 2010. The Bank commenced the operation of its Off-shore Banking Unit from 08.02.2011 at Head Office Complex Branch, Dhaka, and from 27.09.2011 at Agrabad Branch, Chittagong. Operations of OBU located at Uttara Branch, Dhaka has not yet been started. Due to having different functional currency (Note 2.3), the operation of OBU has been considered as “foreign operation” for reporting purposes and relevant financial reporting standards have been applied accordingly (Note 3.2.2). The financial statements of the OBU are included in the separate financial statements of the Bank and eventually in the consolidated financial statements. The sole financial statements of OBU are shown both in the currency in which it operates (i.e. USD) and in the presentation currency of the Bank (i.e. BDT) in Annexure - E.

Islami Bank Bangladesh Limited Annual Report 2015192

1.4 Subsidiaries of the Bank1.4.1 Islami Bank Securities Limited (IBSL)

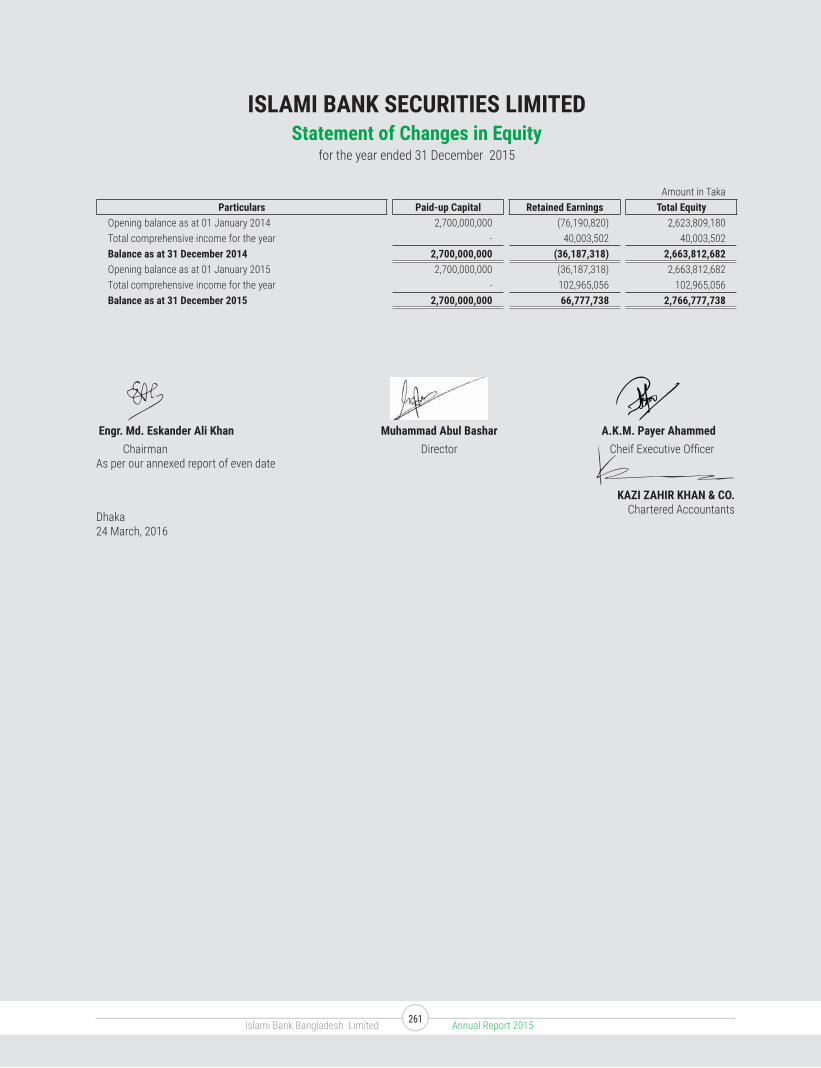

As per Bangladesh Securities and Exchange Commission’s (BSEC) Letter No. SEC/Reg/CSE/MB/ 2009/444 dated 20.12.2009 and approval of Bangladesh Bank through Letter No. BRPD (R-1)717/2010-47 dated 07.02.2010; IBBL established a subsidiary Company named “Islami Bank Securities Limited” to operate stock broker and stock dealer activities.

The share capital of Islami Bank Securities Ltd. is Tk. 2,700,000,000/- divided into 2,700,000 shares of Tk.1,000/ each out of which share capital of IBBL is Tk.2,699,946,000/- divided into 2,699,946 shares of Tk.1,000/- each which represent 99.998% of total share of the subsidiary Company.

IBSL was incorporated on 22.03.2010 and date of commencement of business was 23.05.2010. Required capital was transferred to IBSL on 25.05.2010 which is operating business under the license issued by the Bangladesh Securities & Exchange Commission (BSEC). As a stock broker, IBSL acts as an agent in the purchase and sale of Shari’ah approved listed securities and realizes commission on transactions in accordance with approved commission schedule.

1.4.2 Islami Bank Capital Management Limited (IBCML)

As per Bangladesh Bank BRPD Circular No. 12 dated 14.10.2009 and approval of Bangladesh Bank through Letter No. BRPD (R-1)717/2010-47 dated 07.02.2010, IBBL established another subsidiary Company named “Islami Bank Capital Management Limited” to operate portfolio management, underwriting, issue management etc. IBCML was incorporated on 01.04.2010 and required capital was transferred on 06.07.2010.

The share capital of Islami Bank Capital Management Ltd. is Tk.300,000,000/- divided into 300,000 shares of Tk.1,000/- each out of which share capital of IBBL is Tk.299,993,000/- divided into 299,993 shares of Tk.1,000/- each which represent 99.998% of total share of the subsidiary Company. Permission of Bangladesh Securities and Exchange Commission (BSEC) is yet to be received for the core operation of IBCML.

1.4.3 IBBL Exchange Singapore Pte. Ltd.

‘IBBL Exchange Singapore Pte. Ltd.’ has been incorporated in Singapore, as a subsidiary of Islami Bank Bangladesh Limited for remittance services and things incidental thereto under the Companies Act, CAP. 50 of the Republic of Singapore. Till 31 December 2015, no share capital of the subsidiary has been paid by its parent company i.e. Islami Bank Bangladesh Limited. Therefore, the financial statements of IBBL Exchange Singapore Pte. Ltd. has not been consolidated with that of the parent i.e. IBBL.

2.0 Basis of preparation2.1 Statement of compliance

The Bank and its subsidiaries are being operated in strict compliance with the rules of Islamic Shari’ah. The consolidated and separate financial statements of the Bank have been prepared basically as per provisions of the “Guidelines for Islamic Banking” issued by Bangladesh Bank through BRPD Circular No. 15 dated 09.11.2009 with reference to the provisions of the Bank Company Act, 1991 as amended and by Bangladesh Bank BRPD Circular No.14 dated 25.06.2003 & Bangladesh Bank’s other circulars/instructions and in accordance with International Financial Reporting Standards (IFRSs) adopted as Bangladesh Financial Reporting Standards (BFRSs) by the Institute of Chartered Accountants of Bangladesh (ICAB); the Companies Act, 1994; the Securities and Exchange Rules, 1987; Dhaka and Chittagong Stock Exchanges (Listing) Regulations, 2015, Financial Reporting Act 2015 and other laws and rules applicable in Bangladesh and Standards issued by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), as a member of that organization.

In case the requirements of guidelines and circulars issued by Bangladesh Bank differ with those of other regulatory authorities and financial reporting standards, the guidelines and circulars issued by Bangladesh Bank prevails. As such the Bank has departed from those requirements of BFRSs in order to comply with the rules and regulations of Bangladesh Bank which are disclosed below:

i) Provision on investments and off-balance sheet exposures

BFRS: As per BAS 39 “Financial Instruments: Recognition and Measurement” an entity should start the impairment assessment by considering whether objective evidence of impairment exists for financial assets that are individually significant. For financial assets that are not individually significant, the assessment can be performed on an individual or collective (portfolio) basis.

Islami Bank Bangladesh Limited Annual Report 2015193

Bangladesh Bank: As per BRPD circular No.14 dated 23 September 2012, BRPD circular No. 19 dated 27 December 2012, BRPD circular No. 05 dated 29 May 2013 and BRPD circular No. 16 dated 18 November 2014 a general provision at 0.25% to 5% under different categories of unclassified investments (good/standard investments) has to be maintained regardless of objective evidence of impairment. Also provision for sub-standard, doubtful and bad & loss investments have to be provided at 20%, 50% and 100% respectively (except short-term agricultural and micro-credits where 5% for sub-standard and doubtful investments and 100% for bad & loss investments) depending on the duration of overdue. Again as per BRPD Circular No.14 dated 23 September 2012 and BRPD Circular No.19 dated 27 December 2012, a general provision at 1% is required to be provided for all off-balance sheet exposures. Such provision policies are not specifically in line with those prescribed by “BAS 39” Financial Instruments: Recognition and Measurement.

ii) Recognition of investment income in suspense

BFRS: Investment to customers are generally classified as ‘loans and receivables’ as per BAS 39 “Financial Instruments: Recognition and Measurement” and investment income is recognised through effective interest rate method over the term of the investment. Once an investment is impaired, investment income is recognised in profit and loss account on the same basis based on revised carrying amount.

Bangladesh Bank: As per BRPD circular no. 14 dated 23 September 2012, once an investment is classified, investment income on such investment are not allowed to be recognised as income, rather the corresponding amount needs to be credited to an investment income in suspense account, which is presented as liability in the balance sheet.

iii) Investment in shares and securities

BFRS: As per requirements of BAS 39 “Financial Instruments: Recognition and Measurement” investment in shares and securities generally falls either under “at fair value through profit and loss account” or under “available for sale” where any change in the fair value (as measured in accordance with BFRS 13) at the year-end is taken to profit and loss account or revaluation reserve respectively.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June 2003 investments in quoted shares and unquoted shares are revalued at the year end at market price and as per book value of last audited balance sheet respectively. Provision should be made for any loss arising from diminution in value of investment; otherwise investments are recognised at cost.

iv) Revaluation gains/losses on Government securities

BFRS: As per requirement of BAS 39 “Financial Instruments: Recognition and Measurement” where securities will fall under the category of Held for Trading (HFT), any change in the fair value of held for trading assets is recognised through profit and loss account. Securities designated as Held to Maturity (HTM) are measured at amortised cost method and interest income is recognised through the profit and loss account.

Bangladesh Bank: HFT securities are revalued on the basis of mark to market and at year end any gains on revaluation of securities which have not matured as at the balance sheet date are recognised in other reserves as a part of equity and any losses on revaluation of securities which have not matured as at the balance sheet date are charged in the profit and loss account. Profit on HFT securities including amortisation of discount are recognised in the profit and loss account. HTM securities which have not matured as at the balance sheet date are amortised at the year end and gains or losses on amortisation are recognised in other reserve as a part of equity.

v) Other comprehensive income

BFRS: As per BAS 1 “Presentation of Financial Statements” Other Comprehensive Income (OCI) is a component of financial statements or the elements of OCI are to be included in a single Other Comprehensive Income statement.

Bangladesh Bank: Bangladesh Bank has issued templates for financial statements which will strictly be followed by all banks. The templates of financial statements issued by Bangladesh Bank do not include Other Comprehensive Income nor are the elements of Other Comprehensive Income allowed to be included in a single Other Comprehensive Income (OCI) Statement. As such the Bank does not prepare the other comprehensive income statement. However, elements of OCI, if any, are shown in the statements of changes in equity.

Islami Bank Bangladesh Limited Annual Report 2015194

vi) Financial instruments - presentation and disclosure

In several cases Bangladesh Bank guidelines categorise, recognise, measure and present financial instruments differently from those prescribed in BAS 39 “Financial Instruments: Recognition and Measurement”. As such full disclosure and presentation requirements of BFRS 7 “Financial Instruments: Disclosures” and BAS 32 “Financial Instruments: Presentation” cannot be made in the financial statements.

vii) Financial guarantees

BFRS: As per BAS 39 “Financial Instruments: Recognition and Measurement”, financial guarantees are contracts that require an entity to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the terms of a debt instrument. Financial guarantee liabilities are recognised initially at their fair value, and the initial fair value is amortised over the life of the financial guarantee. The financial guarantee liability is subsequently carried at the higher of this amortised amount and the present value of any expected payment when a payment under the guarantee has become probable. Financial guarantees are included within other liabilities.

Bangladesh Bank: As per BRPD 14 dated 25 June 2003, financial guarantees such as letter of credit, letter of guarantee will be treated as off-balance sheet items. No liability is recognised for the guarantee except the cash margin.

viii) Balance with Bangladesh Bank: (Cash Reserve Requirement)

BFRS: Balance with Bangladesh Bank that are required to be kept as part of cash reserve requirement, should be treated as other asset as it is not available for use in day to day operations as per BAS 7 “Statement of Cash Flows”.

Bangladesh Bank: Balance with Bangladesh Bank is treated as cash and cash equivalents.

ix) Cash flow statement

BFRS: The Cash flow statement can be prepared using either the direct method or the indirect method. The presentation is selected to present these cash flows in a manner that is most appropriate for the business or industry. The method selected is applied consistently.

Bangladesh Bank: As per BRPD 14 dated 25 June 2003 and BRPD 15 dated 09 November 2009, cash flow statement is to be prepared following a mixture of direct and indirect methods.

x) Non-banking asset

BFRS: No indication of Non-banking asset is found in any BFRS.

Bangladesh Bank: As per BRPD 14 dated 25 June 2003 and BRPD 15 dated 09 November 2009, there must exist a face item named Non-banking asset.

xi) Presentation of intangible asset

BFRS: An intangible asset must be identified and recognised, and the disclosure must be given as per BAS 38 “Intangible Assets”.

Bangladesh Bank: There is no regulation for intangible assets in BRPD 14 dated 25 June 2003 and BRPD 15 dated 09 November 2009.

xii) Off-balance sheet items

BFRS: There is no concept of off-balance sheet items in any BFRS; hence there is no requirement for disclosure of off-balance sheet items on the face of the balance sheet.

Bangladesh Bank: As per BRPD 14 dated 25 June 2003 and BRPD 15 dated 09 November 2009, off balance sheet items (e.g. Letter of credit, Letter of guarantee etc.) must be disclosed separately on the face of the balance sheet.

Islami Bank Bangladesh Limited Annual Report 2015195

xiii) Investments net of provision

BFRS: Investments should be presented net of provision.

Bangladesh Bank: As per BRPD 14 dated 25 June 2003 and BRPD 15 dated 09 November 2009, provision on investments are presented separately as liability and can not be netted off against investments.

xiv) Revenue

As per BAS 18 “Revenue”, revenue should be recognized on accrual basis but due to the unique nature of Islamic Banks, income from investment under Mudaraba, Musharaka, Bai-Salam, Bai-as-Sarf and Ujarah modes is accounted for on realization basis as per AAOIFI and Bangladesh Bank guidelines.

[Note 4 includes Compliance with Financial Reporting Standards as applicable in Bangladesh]

2.1.1 Authorization of the financial statements for issue

The consolidated financial statements and the separate financial statements of the Bank have been authorized for issue by the Board of Directors on 19 April 2016.

2.1.2 Changes in accounting standards

No new International Financial Reporting Standards (IFRSs) have been adopted by The Institute of Chartered Accountants of Bangladesh (ICAB) as Bangladesh Financial Reporting Standards (BFRSs) during the year that are effective for the first time for the financial year 2015 that have a significant impact on the Companies and accordingly no new accounting standards have been applied in preparing these financial statements.

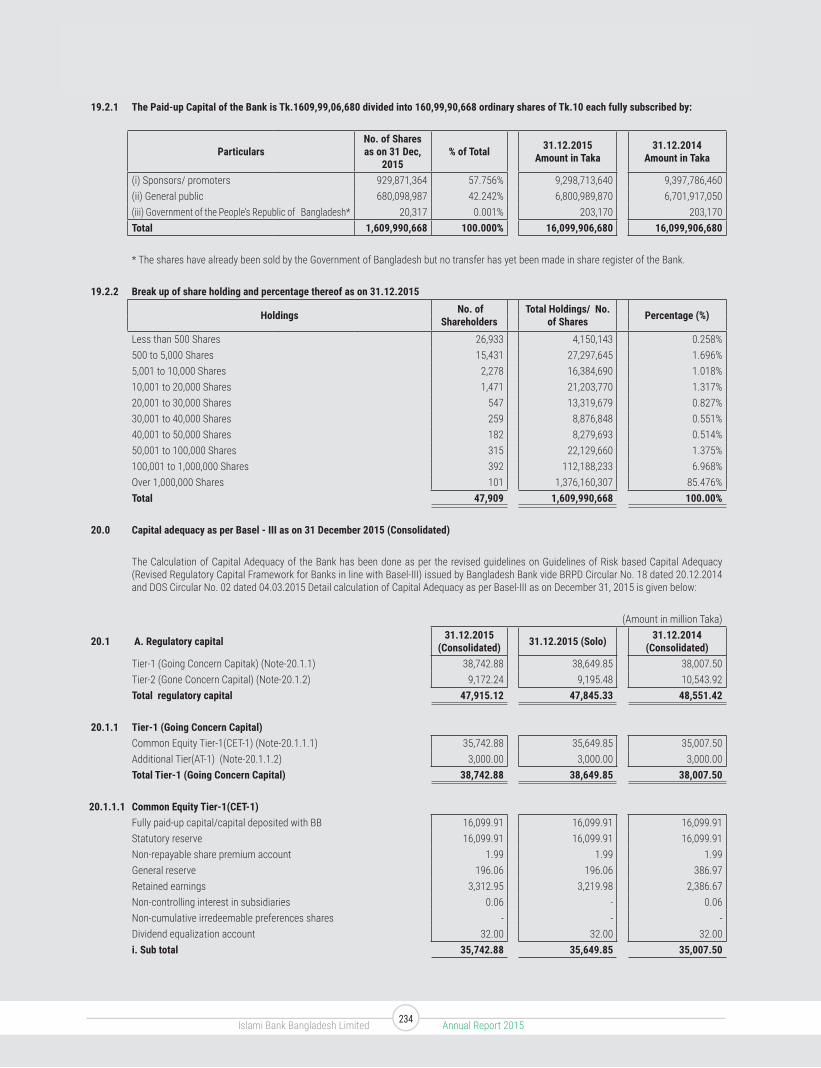

2.1.3 Regulatory capital in line with Basel-III