indicative 2015 results (unaudited)

TRANSCRIPT

Indicative 2015 Results

(Unaudited)

February 2016

Excellence in Execution

Table of Contents

2

Macro Overview 3 3

Business Overview 3 6

Indicative 2015 Results 3 14

2016 Outlook 3 20

Macro Overview

Section 1

Excellence in Execution

5,14% 5,03%

4,92% 5,01%

4,72% 4,67% 4,73%

5,04%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Macro Overview

4

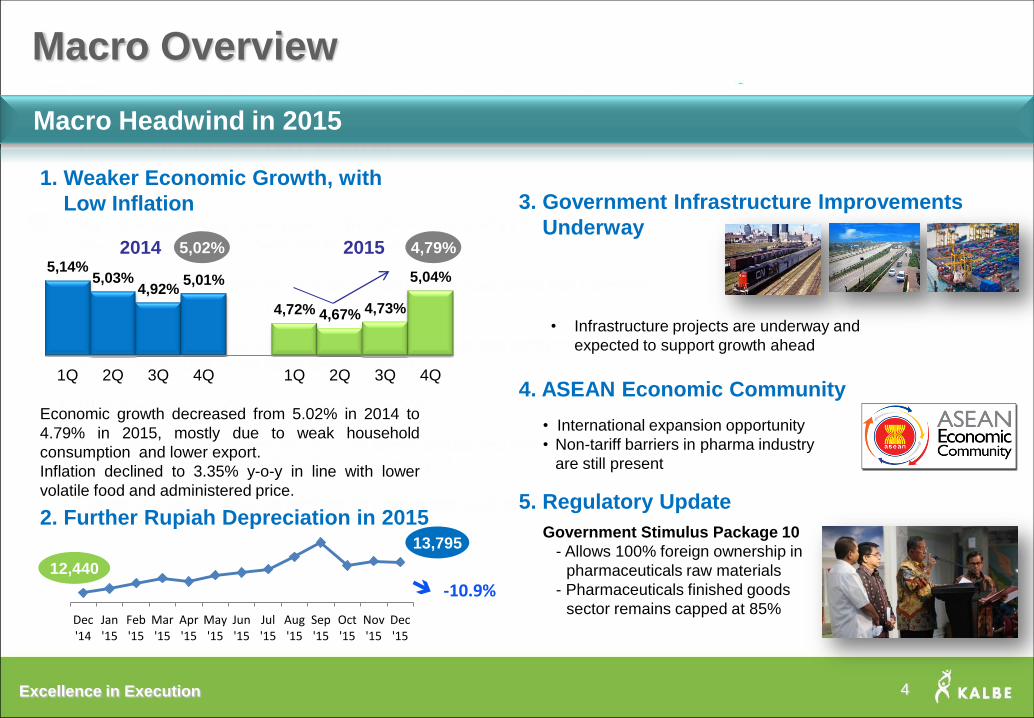

1. Weaker Economic Growth, with

Low Inflation

Economic growth decreased from 5.02% in 2014 to

4.79% in 2015, mostly due to weak household

consumption and lower export.

Inflation declined to 3.35% y-o-y in line with lower

volatile food and administered price.

3. Government Infrastructure Improvements

Underway

4. ASEAN Economic Community

• International expansion opportunity

• Non-tariff barriers in pharma industry

are still present

Government Stimulus Package 10

- Allows 100% foreign ownership in

pharmaceuticals raw materials

- Pharmaceuticals finished goods

sector remains capped at 85%

4,79%

2. Further Rupiah Depreciation in 2015

Dec '14

Jan '15

Feb '15

Mar '15

Apr '15

May '15

Jun '15

Jul '15

Aug '15

Sep '15

Oct '15

Nov '15

Dec '15

Macro Headwind in 2015

5,02%

13,795

12,440

5. Regulatory Update

• Infrastructure projects are underway and

expected to support growth ahead

-10.9%

2014 2015

4

Excellence in Execution

Healthcare Industry

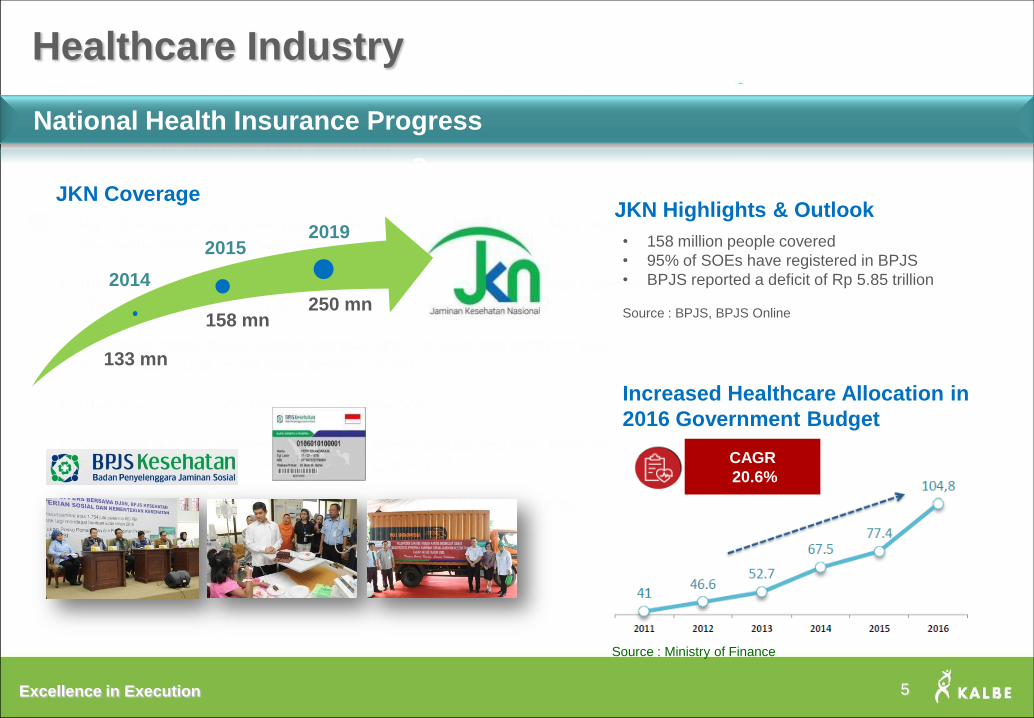

National Health Insurance Progress

133 mn

158 mn 250 mn

JKN Coverage JKN Highlights & Outlook

• 158 million people covered

• 95% of SOEs have registered in BPJS

• BPJS reported a deficit of Rp 5.85 trillion

Source : BPJS, BPJS Online

Increased Healthcare Allocation in

2016 Government Budget

2019 2015

2014

Source : Ministry of Finance

5

CAGR

20.6%

Business

Overview

Section 2

Excellence in Execution 7

What Business

Are We In

To be the best Indonesian Global Health Care company driven by innovation, strong brands and excellent management

To improve health for a better life

We are an Innovative Health Care Business providing Health Care Products & Its Related Services

1. Sustainable Growth

2. Innovation, Quality, and Productivity

3. World Class Competence & Organization

Mission

Vision

Strategy

Values We believe in : Trust, Mindfulness, Innovation, Strive to be the best,

Interconnectedness

Our Business

Strengthening Our Footprints as a Health Care Company

Excellence in Execution

Leadership Development

Business Structure &

Portfolio

Collaborative Innovation

8

Our Strategic Focus

2016 Corporate Initiatives

*ERM : Enterprise Risk Management SCM : Supply Chain Management

Excellence in Execution 9

2016 Corporate Initiatives

Key Achievements & Activities

Kalbe Middle

Management Program Finance Officer

Development Program

Leadership Development

Business Structure & Portfolio

Training Programs Kalbe

Learning Center

Visit of the Minister of

Research & Technology and

Higher Education to SCI

Excellence in Execution 10

Kalbe e-Store

Kalbe Home Delivery

Kalbe Family Rewards Card KALCare

Experiential Store

Kalbe Customer Care

Integrated Service to Consumers

KalbeMed

Mobile Application

Mommychi

Mom & Child

Mobile Application

Mobile Applications Utilization

Diabetes Solution

Center Mobile

Application

Customer Engagement

Events 2015

Dunia Generasi Platinum

Morinaga Mall to Mall Fitbar Fun Activation

(FIFA)

AntioksiDANCE

Entrasol

Prenagen Pregnancy

Education Journey

2016 Corporate Initiatives

Business Structure & Portfolio

Key Achievements & Activities

Excellence in Execution 11

Pharma Actvities in Oncology Department Kalbe Morinaga

Pharmacy Branding Mixagrip in Pharmacy

Gathering Milna Massive Sampling Selling

in Medical Channel

Fitbar Massive

Sampling Activities

Diabetasol in Nutritionist and Dietitians

Associations of the Philippines

Hydro Coco Product Display in UAE

Philippines

Nigeria Myanmar Vietnam

Malaysia

Woods Horizontal Banner in KL Sentral

Key Achievements & Activities

2016 Corporate Initiatives

Business Structure & Portfolio

International Expansion

UAE

Excellence in Execution 12

2016 Corporate Initiatives

Key Achievements & Activities

Visit of the Minister of Industry to Biosimilar Factory Construction

JV Kalbe Genexine

Collaborative Innovation

JV Kalbe Blackmores

Excellence in Execution 13

Quality Assurance & Financial Compliance

2016 Corporate Initiatives

Enterprise Risk Management (ERM)

Supply Chain Management (SCM)

Powdered milk

capacity expansion New liquid milk factory Distribution Infrastructure

Key Achievements & Activities

Indicative 2015

Results

Section 3

Excellence in Execution

4.329 2.924

4.581 5.535

17.369

4.293 3.066

5.114 5.415

17.888

Prescription Pharmaceuticals

Consumer Health Nutritionals Distribution & Logistics

Consolidation

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

15

Net Sales - Unaudited (in Rp Bn)

-0.8% 4.9%

11.6% -2.2%

3.0%

Consolidated Operational Performance

Overall Weaker Results in Challenging Time

Excellence in Execution

8.476 8.574

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

15,9%

14,8%

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

26,9% 26,9%

5,2% 5,3%

0,8% 0,9%

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

Selling & Marketing

General & Administrative

Research & Development

• Marketing efforts to drive brand awareness

• Research & development activities to support product

development

Operating Expenses to Net Sales Ratios -

Unaudited

Operating Profit - Unaudited

(in Rp bn)

1.2%

-4.3%

32.9%

2,761

33.2%

2,641

48.8% 47.9%

2,641

Gross Profit - Unaudited

(in Rp bn)

Consolidated Operational Performance

Pressure on Operating Margin

16

Excellence in Execution

2.065 1.975

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

2.764 2.709

31 Dec 2014 (Audited)

31 Dec 2015 (Unaudited)

Income Before Tax - Unaudited

(in Rp bn)

Net Income - Unaudited

(in Rp bn)

• Income before tax margin decreased from 15.9% in FY

2014 to 15.1% in FY 2015, mostly due lower gross profit.

-2.0%

• Net income margin decreased from 11.9% in FY 2014

to 11.0% in FY 2015, in line with lower income before

tax margin.

-4.3%

15.9% 15.1% 11.0% 11.9%

Consolidated Operational Performance

Negative Impact on Bottom Line

17

Excellence in Execution

43 45 44 50 48 48 49 48

142 122

110 115 107

132 125 116

27 38 35

57 41

50 46 44

158

129 120 108 114

131 128 120

2008 (Audited)

2009 (Audited)

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

2015 (Unaudited)

Days of Account Receivables

Days of Inventories

Days of Account Payables

Net Operating Cycle

18

End-to-end supply chain

management will be implemented

to overcome fluctuation in

inventory

No. of days

Working Capital Management

Improving Inventory Days

Net Operating Cycle has been

reduced by 38 days from 158

days to 120 days

Excellence in Execution

470 469

783 994

852 945

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

2015 (Unaudited)

14,0 19,0 19,0 17,0 19,0

51% 60% 51% 42% 43%

0% 20% 40% 60% 80%

0,0 5,0

10,0 15,0 20,0

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

Cash Dividend* (Rp/share) Dividend Payout Ratio (%)

19

Total Debt and Gearing Ratio Cash & Net Cash Balance

Dividend Payment Capital Expenditure

* in Rp Billion

*For Fiscal Year *Cash dividend are adjusted for stock split impact

340 25

141 205

584

296 394

7,9%

0,5% 2,3% 2,9%

7,2%

3,2% 3,8%

0,0%

5,0%

10,0%

15,0%

0 100 200 300 400 500 600

2009 (Audited)

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

2015 (Unaudited)

Total Debt in Rp Billion Gearing Ratio

1.562 1.902

2.291 1.860 1.895 1.895

2.704

1.222

1.877 2.151

1.655 1.311

1.598

2.309

2009 (Audited)

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

2015 (Unaudited)

Cash and Cash Equivalent in Rp Billion Net Cash in Rp Billion

Working Capital Management

Strong Balance Sheets

2016 Outlook

Section 4

Excellence in Execution

Capex of Rp 1 – 1.5 Tn for production capacity and distribution network expansion.

21

1. Year-on-year Sales Growth 8% - 10%

2. Operating Profit Margin 14% - 15%

3. Earnings per Share Growth 8% - 10%

4. Dividend Payout Ratio 40% - 50%

Outlook 2016

2016 Earnings Guidance

Excellence in Execution

THANK YOU For further information:

PT Kalbe Farma Tbk.

Jalan Let.Jend. Suprapto Kav. 4

Jakarta 10510, Indonesia

Tel. : 62-21-42873888

Fax. : 62-21-42873678

Email : [email protected]

Website : www.kalbe.co.id

22