icici prudential indo asia equity fund

TRANSCRIPT

ICICI Prudential Indo Asia Equity Fund

ICICI Prudential Indo Asia Equity Fund (an open ended-diversified equity scheme), the mutual fund Scheme offered under this Offer Document, has been prepared in accordance with the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, as amended from time to time and filed with the Securities and Exchange Board of India (SEBI) and the Units being offered for public subscription have not been approved or disapproved by SEBI nor has SEBI certified the accuracy or adequacy of the Offer Document.

This Offer Document contains information necessary for an investor to make an informed investment decision in the Scheme described herein. Investors should carefully read the Offer Document prior to making an investment decision and retain the Offer Document for future reference. Investors may note that this Offer Document remains effective until a material change occurs. Material changes shall be filed with SEBI and circulated to all Unitholders or may be publicly notified by advertisements in the newspapers subject to the applicable regulations.

New Fund Offer of Units of Rs.10 per unit plus applicable load during New Fund Offer and at NAV based prices subject to load upon re-opening.

Scheme re-opens for continuous sale & repurchase within 30 days from the closing of New Fund Offer.

* The Trustee reserves the right to extend the closing date by suitable notification subject to the condition that the New Fund Offer shall not be kept open for more than 30 days.

An Open Ended Diversified Equity Scheme

New Fund Offer opens on : August 23, 2007

New Fund Offer closes on : September 21, 2007*

Earliest closing on : September 21, 2007

Offer Document

Sponsors: ICICI Bank Limited (erstwhile ICICI Limited), Regd. Office: Landmark, Race Course Circle, Vadodara 390 007, India; and Prudential plc (formerly known as Prudential Corporation Holdings Limited), Laurence Pountney Hill, London EC4ROHH, UK.

Investment Manager: ICICI Prudential Asset Management Company Limited(erstwhile Prudential ICICI Asset Management Company Limited)Corp. Office: 8th Floor, Peninsula Tower, Peninsula Corporate Park, Ganpatrao Kadam Marg, Off Senapati Bapat Marg, Lower Parel, Mumbai 400 013.Regd. Office: 12th Floor, Narain Manzil, 23 Barakhamba Road, New Delhi 110 001.

Trustee: ICICI Prudential Trust Limited(erstwhile Prudential ICICI Trust Limited)Regd. Office: 12th Floor, Narain Manzil, 23 Barakhamba Road, New Delhi 110 001.

SMS INVEST to 8558

CALL 1800 22 2273or apply online at www.icicipruamc.com

2

ICICI Prudential Mutual Fund

IMPORTANT NOTICE

Investing in mutual fund schemes involves certain risks and considerations associated generally with making investments insecurities. The value of the Scheme’s investments may be affected generally by factors affecting financial markets, such asprice and volume, volatility in interest rates, currency exchange rates, changes in regulatory and administrative policies of theGovernment or any other appropriate authority (including tax laws) or other political and economic developments.Consequently, there can be no assurance that the Scheme offered in this Offer Document would achieve the stated objectives.The NAV of the Units of the Scheme may fluctuate and can go up or down. Past performance of the schemes managed by theSponsors or their affiliates or the Asset Management Company is not indicative of the future performance of the Scheme norwill the performance of the Scheme, following the commencement of the operations, be indicative of the Scheme’s futureperformance.

Prospective investors are advised to review this Offer Document carefully and in its entirety and consult their legal, tax andfinancial advisors to determine possible legal, tax and financial or any other consequences of subscribing to, purchasing orholding Units under the Scheme, before making an application to subscribe or purchase the Units.

ICICI Prudential Mutual Fund (the Fund) and the ICICI Prudential Asset Management Company Limited (the AMC), have notauthorized any person to give any information or make any representations, either oral or written, not stated in this OfferDocument in connection with issue of Units under the Scheme. Prospective investors are accordingly advised not to rely uponany information or representations not incorporated in this Offer Document. Any subscription, purchase or sale made by anyperson on the basis of statements or representations which are not contained in this Offer Document or which are inconsistentwith the information contained herein shall be solely at the risk of the investor.

Unitholders / investors are requested to read and understand the Offer Document, Key Information Memorandum and riskfactors furnished with the scheme in which they seek to make investments or in which they have invested. Unitholders /Investors are urged not to rely upon or be misled by any oral promises or statements made by the distributors / intermediariesof the Mutual Fund and it is brought to the special attention of investors that the AMC / Mutual Fund will not be liable formis-statement or communication by agents / distributors which are not previously expressly authorized / approved by theAMC / Mutual Fund.

The AMC, Trust and ICICI Prudential Mutual Fund shall not be responsible for any claims made by the Unitholders / Investorsbased on such oral promises made by the distributors / intermediaries.

The current Regulations impose certain restrictions and conditions on the AMC for entering into transactions with theSponsors and their associates on behalf of the Fund. These restrictions include:

a) Purchase or sale of securities through any broker associated with the Sponsors or through a firm which is an associateof the Sponsor(s) shall not exceed an average of 5% of the aggregate purchases and sale of securities made by the Fundin all its Schemes in a block of any three months.

b) Utilization of the services of the Sponsors or any of their associates, for the purpose of any securities transactions anddistribution and sale of securities shall be made only if a disclosure to this effect is made in the Offer Document and thebrokerage or commission paid is also disclosed in the half yearly annual accounts of the mutual fund.

c) The Mutual Fund Scheme shall not make any investment in:

1. any unlisted security of an associate or group company of the Sponsor; or

2. any security issued by way of private placement by an associate or group company of the Sponsor; or

3. the listed securities of group companies of the Sponsor which is in excess of 25% of its net assets.

In this Offer Document, all references to “$” are to United States of America Dollars, “£” to Pound Sterling of UnitedKingdom and “Rs.” to Indian Rupees. The Reference Exchange Rate between the United States Dollar and the Indian Rupeehas been taken at $1 = Rs.45.76 and UK£ and Indian Rupee at 1£=Rs.81.18.

This Offer Document is dated August 03, 2007.

ICICI Prudential Indo Asia Equity Fund

3

TABLE OF CONTENTS

1. Highlights ---------------------------------------------------------------------------------------------------------------------------------------- 6

2. Risk Factors and Special Considerations ----------------------------------------------------------------------------------------------- 8

3. Due Diligence Certificate ------------------------------------------------------------------------------------------------------------------ 16

4. Definitions -------------------------------------------------------------------------------------------------------------------------------------- 17

5. Summary – ICICI Prudential Indo Asia Equity Fund ------------------------------------------------------------------------------- 19

6. Constitution of the Mutual Fund -------------------------------------------------------------------------------------------------------- 20

a) Sponsors --------------------------------------------------------------------------------------------------------------------- 20

b) The Trustee Company ----------------------------------------------------------------------------------------------------------------- 21

i. Directors --------------------------------------------------------------------------------------------------------------------- 21ii. Rights and Obligations of the Trustee ------------------------------------------------------------------------------------ 22

iii. Trusteeship Fees ---------------------------------------------------------------------------------------------------------------- 24

c) Management of Asset Management Company (AMC) ----------------------------------------------------------------------- 24

i. Board of Directors of the AMC --------------------------------------------------------------------------------------------- 25

ii. Powers, Duties & Responsibilities of the AMC ------------------------------------------------------------------------- 28

iii. Key Employees of AMC & relevant experience -------------------------------------------------------------------------- 29

iv. Fund Manager ------------------------------------------------------------------------------------------------------------------ 35

v. Compliance Officer ------------------------------------------------------------------------------------------------------------ 35

vi. Investor Relations Officer ---------------------------------------------------------------------------------------------------- 35

d) Auditors --------------------------------------------------------------------------------------------------------------------- 35

e) Registrar --------------------------------------------------------------------------------------------------------------------- 35

f) Custodian --------------------------------------------------------------------------------------------------------------------- 35

7. Investment Objectives & Policies ------------------------------------------------------------------------------------------------------- 36

Fundamental Attributes of the Scheme -------------------------------------------------------------------------------------------------- 36

a) Type of the Scheme -------------------------------------------------------------------------------------------------------------------- 36

b) Investment Objective ------------------------------------------------------------------------------------------------------------------ 36

c) Investment Pattern and Investment Plicies --------------------------------------------------------------------------------------- 36

d) Change in Investment Pattern ------------------------------------------------------------------------------------------------------ 39

e) Terms of the Scheme ------------------------------------------------------------------------------------------------------------------ 39

f) Change in Fundamental Attributes ----------------------------------------------------------------------------------------------- 41

g) Securitisation and Portfolio Sale --------------------------------------------------------------------------------------------------- 41

h) Asia and India Market Outlook & Strategy -------------------------------------------------------------------------------------- 43

i) Portfolio Turnover --------------------------------------------------------------------------------------------------------------------- 55

j) Procedure followed for investment decisions ----------------------------------------------------------------------------------- 55

k) Exposure to Derivatives --------------------------------------------------------------------------------------------------------------- 56

l) Investment Restrictions for the Scheme ------------------------------------------------------------------------------------------ 60

m) Underwriting by the Fund ----------------------------------------------------------------------------------------------------------- 62

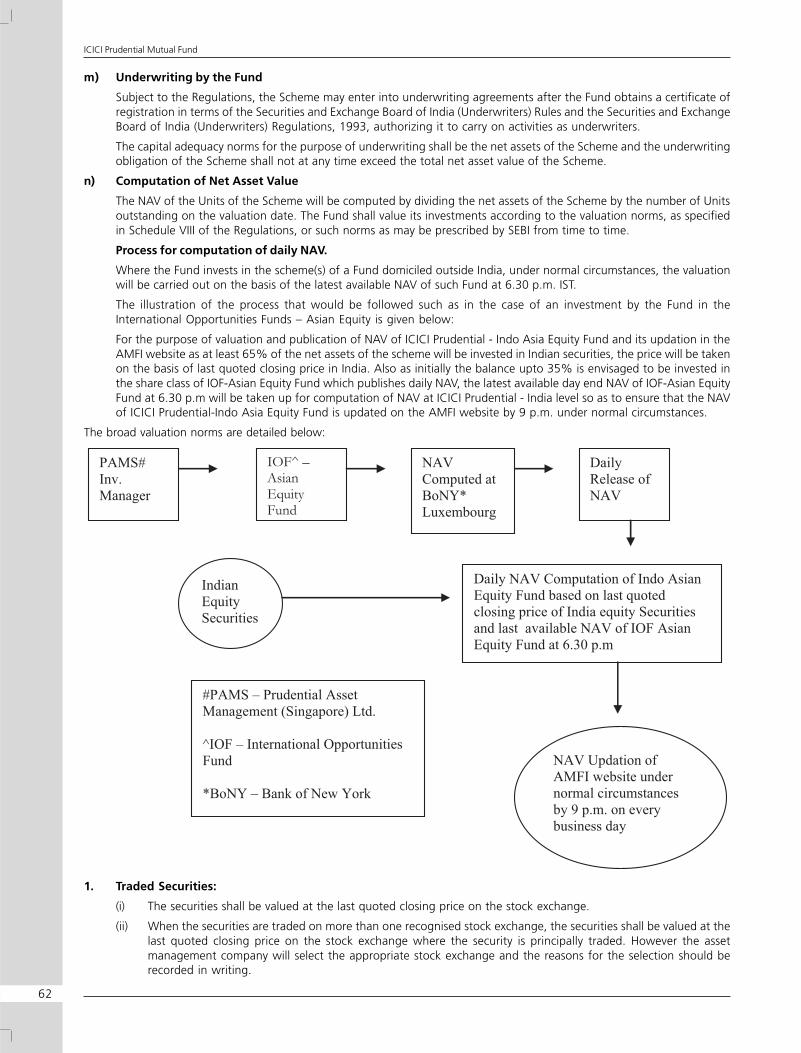

n) Computation of Net Asset Value --------------------------------------------------------------------------------------------------- 62

o) Accounting Policies & Standards --------------------------------------------------------------------------------------------------- 67

8. Units & The New Fund Offer ------------------------------------------------------------------------------------------------------------- 68

General Information -------------------------------------------------------------------------------------------------------------------------- 68

a) Minimum Subscription Amount --------------------------------------------------------------------------------------------------- 68

b) Offer Price ------------------------------------------------------------------------------------------------------------------------------- 68

c) Minimum Amount for Application ------------------------------------------------------------------------------------------------ 68

d) New Fund Offer Expenses ------------------------------------------------------------------------------------------------------------ 68

e) Options offered under the Scheme ----------------------------------------------------------------------------------------------- 68

f) Pledge of Units for Loans ------------------------------------------------------------------------------------------------------------ 68

g) Systematic Investment Plan (SIP) ---------------------------------------------------------------------------------------------------- 68

4

ICICI Prudential Mutual Fund

h) Systematic Withdrawal Plan (SWP) ------------------------------------------------------------------------------------------------- 69

i) Systematic Transfer Plan (STP) ------------------------------------------------------------------------------------------------------- 69

j) How to Switch -------------------------------------------------------------------------------------------------------------------------- 69

k) Who can Invest? ------------------------------------------------------------------------------------------------------------------------ 70

l) How to Apply? -------------------------------------------------------------------------------------------------------------------------- 70

i. New Fund Offer ---------------------------------------------------------------------------------------------------------------- 70

ii. Resident Investors - Mode of Payment ----------------------------------------------------------------------------------- 71

iii. NRIs & FIIs --------------------------------------------------------------------------------------------------------------------- 71

iv. Mode of Payment on Repatriation Basis --------------------------------------------------------------------------------- 72

v. Mode of Payment on Non-Repatriation Basis -------------------------------------------------------------------------- 72

vi. Investment of the minor investor on attaining majority -------------------------------------------------------------- 72

vii. Application under Power of Attorney/Body Corporate/Registered Society/Partnership ---------------------- 72

viii. Joint Applicants ---------------------------------------------------------------------------------------------------------------- 72

ix. Nomination Facility ------------------------------------------------------------------------------------------------------------ 73

m) Issuance of Units/Refund ------------------------------------------------------------------------------------------------------------ 73

n) Account Statements ------------------------------------------------------------------------------------------------------------------- 73

o) Refunds ---------------------------------------------------------------------------------------------------------------------------------- 73

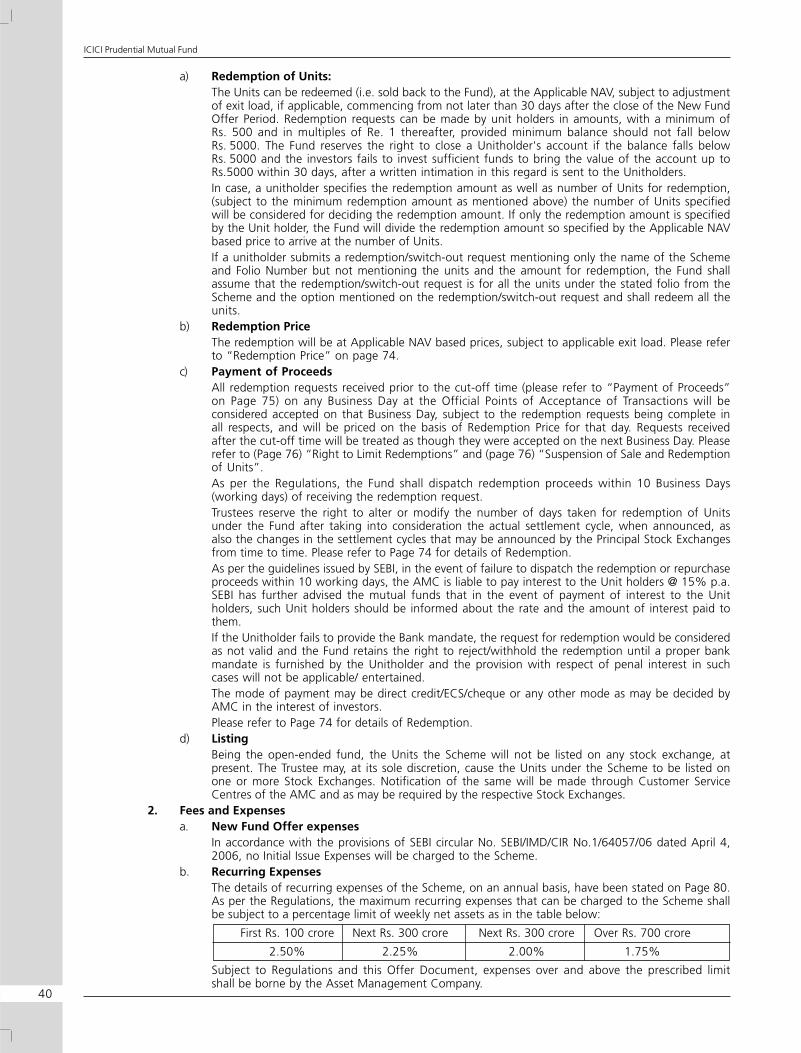

p) Redemption of Units ------------------------------------------------------------------------------------------------------------------ 74

i. Redemption Price -------------------------------------------------------------------------------------------------------------- 74

ii. Applicable NAV ----------------------------------------------------------------------------------------------------------------- 74

iii. Cooling-off period for web based transactions ------------------------------------------------------------------------ 74

iv. How to Redeem? --------------------------------------------------------------------------------------------------------------- 75

v. Payment of Proceeds ---------------------------------------------------------------------------------------------------------- 75

vi. Non receipt of email communication by investors --------------------------------------------------------------------- 76

vii. Redemption by NRIs/FIIs ------------------------------------------------------------------------------------------------------ 76

viii. Effect of Redemptions -------------------------------------------------------------------------------------------------------- 76

ix. Fractional Units ----------------------------------------------------------------------------------------------------------------- 76

x. Signature mismatch cases --------------------------------------------------------------------------------------------------- 76

xi. Right to Limit Redemptions ------------------------------------------------------------------------------------------------- 76

xii. Suspension of Sale and Redemption of Units -------------------------------------------------------------------------- 76

xiii. Permanent Account Number (PAN) ---------------------------------------------------------------------------------------- 77

xiv. Dormant Account Locking --------------------------------------------------------------------------------------------------- 77

xv. Prevention of Money Laundering ------------------------------------------------------------------------------------------ 77

q) Purchase of Units after the New Fund Offer Period --------------------------------------------------------------------------- 78

i. Purchase Price ------------------------------------------------------------------------------------------------------------------- 78

ii. How to Purchase? -------------------------------------------------------------------------------------------------------------- 78

iii. Purchase by NRIs --------------------------------------------------------------------------------------------------------------- 79

iv. Applicable NAV ----------------------------------------------------------------------------------------------------------------- 79

v. Cooling-off period for web based transaction ------------------------------------------------------------------------- 79

9. Load Structure, Fees and Expenses ---------------------------------------------------------------------------------------------------- 80

A) Load Structure of the Scheme ------------------------------------------------------------------------------------------------------ 80

B) Fees and Expenses of the Scheme ------------------------------------------------------------------------------------------------- 80

i. New Fund Offer Expenses ---------------------------------------------------------------------------------------------------- 80

ii. Estimated Recurring Expenses ---------------------------------------------------------------------------------------------- 80

C) New Fund Offer Expenses of the Past Schemes --------------------------------------------------------------------------------- 81

D) Condensed Financial Information ------------------------------------------------------------------------------------------------- 82

ICICI Prudential Indo Asia Equity Fund

5

10. Unitholders Rights & Services ---------------------------------------------------------------------------------------------------------- 105

a) Investor Services ---------------------------------------------------------------------------------------------------------------------- 105

b) Ease of Transactions ----------------------------------------------------------------------------------------------------------------- 105

i. Customer Service Centers in major metros ---------------------------------------------------------------------------- 105

ii. Process transactions in a timely manner ------------------------------------------------------------------------------- 105

c) Problem Resolution ----------------------------------------------------------------------------------------------------------------- 105

d) Information about the Scheme --------------------------------------------------------------------------------------------------- 105

e) NAV Information --------------------------------------------------------------------------------------------------------------------- 105

f) Disclosure of information under the Regulations --------------------------------------------------------------------------- 106

g) Rights of Unitholders of the Scheme ------------------------------------------------------------------------------------------- 106

h) Duration of the Scheme/Winding up ------------------------------------------------------------------------------------------- 106

i) Procedure and manner of Winding up ----------------------------------------------------------------------------------------- 107

j) Tax benefits of investing in the Mutual Fund --------------------------------------------------------------------------------- 107

1) To the Fund -------------------------------------------------------------------------------------------------------------------- 107

2) Securities Transaction Tax -------------------------------------------------------------------------------------------------- 107

3) To the Unitholders ----------------------------------------------------------------------------------------------------------- 108

3.1. Income received from mutual fund ------------------------------------------------------------------------------ 108

3.2. Long term capital gains on transfer of units ------------------------------------------------------------------ 108

3.3. Short term capital gains on transfer of units ------------------------------------------------------------------ 108

3.4. Capital Losses --------------------------------------------------------------------------------------------------------- 108

4) Tax deduction at source ---------------------------------------------------------------------------------------------------- 109

4.1. For Income In Respect of Units ----------------------------------------------------------------------------------- 109

4.2. For Capital Gains ---------------------------------------------------------------------------------------------------- 109

5) Rebate Under Section 88E ------------------------------------------------------------------------------------------------- 109

6) Investments by Charitable and Religious Trust ----------------------------------------------------------------------- 109

7) Wealth Tax --------------------------------------------------------------------------------------------------------------------- 109

8) Gift Tax ------------------------------------------------------------------------------------------------------------------------- 109

k) Unclaimed redemption amount -------------------------------------------------------------------------------------------------- 109

11. Other Matters --------------------------------------------------------------------------------------------------------------------------- 110

a) Unitholder Grievances Redressal Mechanism --------------------------------------------------------------------------------- 110

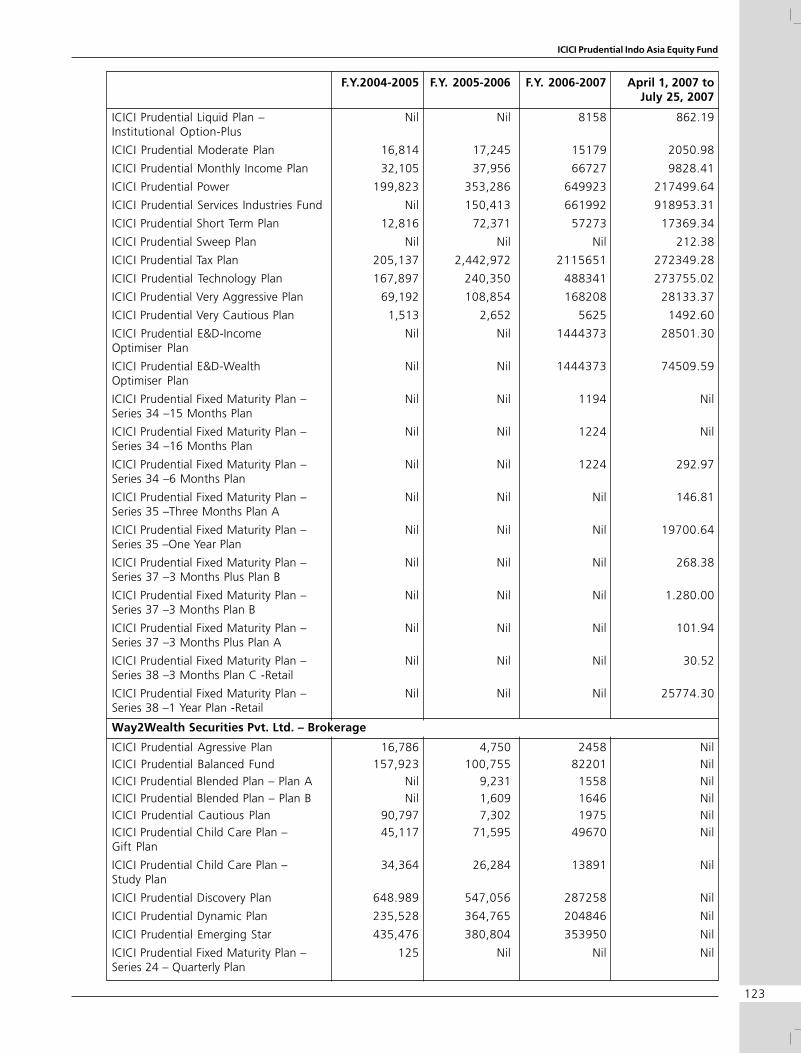

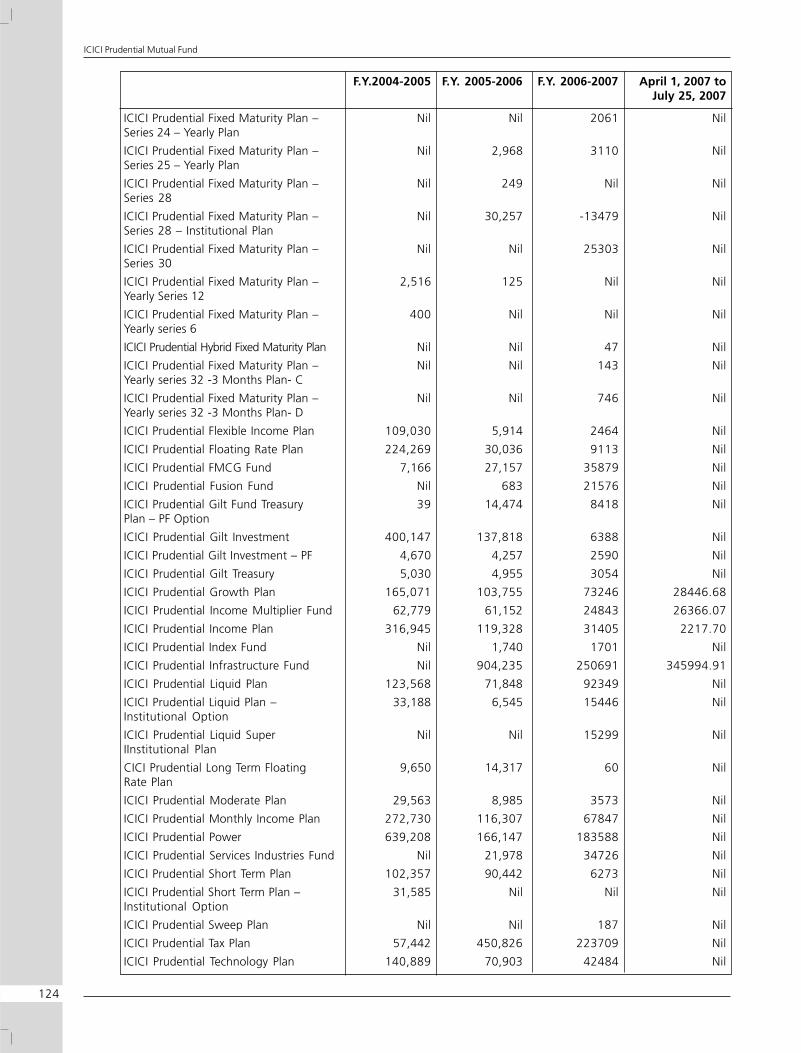

b) Associate Transactions -------------------------------------------------------------------------------------------------------------- 111

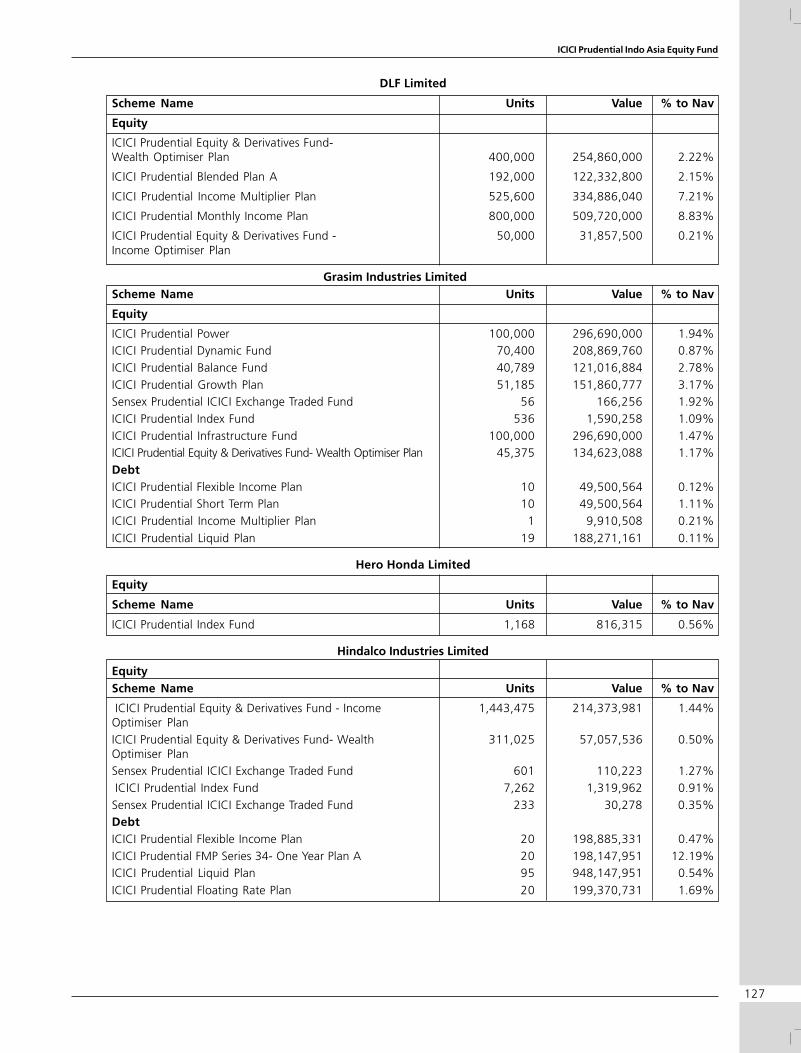

c) Details of Investment in Companies that hold more than 5% ----------------------------------------------------------- 126

of NAV of Schemes managed by the AMC

d) Penalties and Pending Litigations ----------------------------------------------------------------------------------------------- 133

e) Borrowing by the Mutual Fund -------------------------------------------------------------------------------------------------- 152

f) Stock Lending by the Mutual Fund ---------------------------------------------------------------------------------------------- 152

g) Policy on Offshore Investments by the Scheme ------------------------------------------------------------------------------- 152

h) Inter-Scheme Transfers -------------------------------------------------------------------------------------------------------------- 153

i) General Information ---------------------------------------------------------------------------------------------------------------- 153

Power to make Rules -------------------------------------------------------------------------------------------------------- 153

Power to remove Difficulties ---------------------------------------------------------------------------------------------- 153

Scheme to be binding on the Unitholders ---------------------------------------------------------------------------- 153

Documents available for Inspection ------------------------------------------------------------------------------------- 153

6

ICICI Prudential Mutual Fund

HIGHLIGHTS

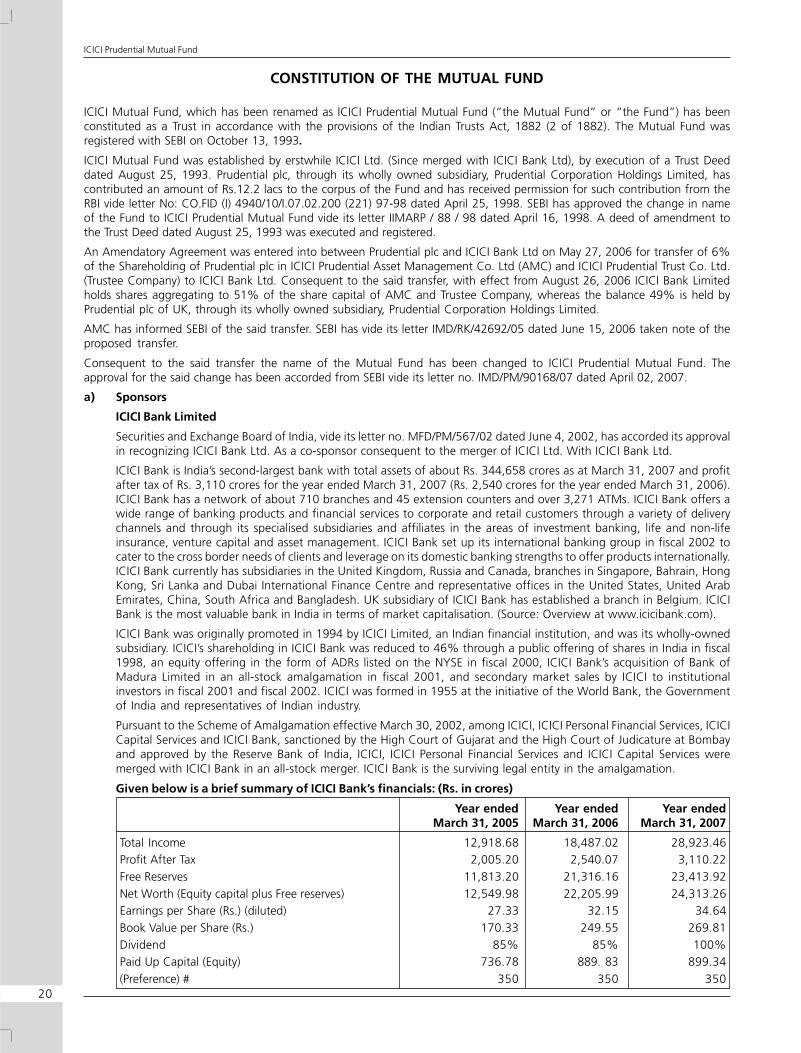

The Sponsors of the Fund are ICICI Bank Limited (erstwhile ICICI Limited) and Prudential plc. of the United Kingdom (UK).

Prudential plc is a leading international financial services group providing retail financial products and services and fundmanagement to many millions of customers worldwide. As a group Prudential plc has, as of December 31, 2006, overGBP251 billion of funds under management, more than 20 million customers and over 23,000 employees worldwide as ofDecember 31, 2006.

Securities and Exchange Board of India, vide its letter no. MFD/PM/567/02 dated June 4, 2002, has accorded its approval inrecognizing ICICI Bank Ltd. as a co-sponsor consequent to the merger of ICICI Ltd. with ICICI Bank Ltd.

ICICI Bank is India’s second-largest bank with total assets of about Rs. 344,658 crores as at March 31, 2007 and profit aftertax of Rs. 3,110 crores for the year ended March 31, 2007 (Rs. 2,540 crores for the year ended March 31, 2006). ICICI Bankhas a network of about 710 branches and 45 extension counters and over 3,271 ATMs. ICICI Bank offers a wide range ofbanking products and financial services to corporate and retail customers through a variety of delivery channels and throughits specialised subsidiaries and affiliates in the areas of investment banking, life and non-life insurance, venture capital andasset management. ICICI Bank set up its international banking group in fiscal 2002 to cater to the cross border needs ofclients and leverage on its domestic banking strengths to offer products internationally. ICICI Bank currently has subsidiariesin the United Kingdom, Russia and Canada, branches in Singapore, Bahrain, Hong Kong, Sri Lanka and Dubai InternationalFinance Centre and representative offices in the United States, United Arab Emirates, China, South Africa and Bangladesh.UK subsidiary of ICICI Bank has established a branch in Belgium. ICICI Bank is the most valuable bank in India in terms ofmarket capitalisation. (Source: Overview at www.icicibank.com).

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial institution, and was its wholly ownedsubsidiary. ICICI’s shareholding in ICICI Bank was reduced to 46% through a public offering of shares in India in fiscal 1998,an equity offering in the form of ADRs listed on the NYSE in fiscal 2000, ICICI Bank’s acquisition of Bank of Madhura Limitedin an all-stock amalgamation in fiscal 2001, and secondary market sales by ICICI to institutional investors in fiscal 2001 andfiscal 2002.

Pursuant to the Scheme of Amalgamation effective March 30, 2002, among ICICI, ICICI Personal Financial Services, ICICICapital Services and ICICI Bank, sanctioned by the High Court of Gujarat and the High Court of Judicature at Bombay andapproved by the Reserve Bank of India, ICICI, ICICI Personal Financial Services and ICICI Capital Services were merged withICICI Bank in an all-stock merger. ICICI Bank is the surviving legal entity in the amalgamation.

Fund Management expertise

Prudential plc is a leading international financial services group providing retail financial products and services andfund management to many millions of customers worldwide. As a group Prudential plc has, as of December 31, 2006,over GBP251 billion of funds under management, more than 20 million customers and over 23,000 employeesworldwide as of December 31, 2006.

ICICI Prudential Asset Management Company Limited, the Investment Manager to the ICICI Prudential Mutual Fund,manages assets over 48,688 crores as on July 31, 2007 through 32 schemes. It is one of the largest asset managementcompanies in the country.

Investment Objectives

ICICI Prudential Indo Asia Equity Fund is an Open-ended equity scheme that seeks to generate long term capitalappreciation by investing in equity, equity related securities and or share classes/units of equity funds of companies,which are incorporated or have their area of primary activity, in the Asia Pacific region. Initially the Scheme will beinvesting in share classes of International Opportunities Fund (I.O.F) Asian Equity Fund and thereafter the Fund Managerof ICICI Prudential Indo Asia Equity Fund may choose to make investment in listed equity shares, securities in the AsiaPacific Region.

However, there can be no assurance that the investment objective of the Scheme will be realized

Transparency –The AMC will calculate and disclose the first NAV not later than 30 days from the closure of the NewFund Offer Period. Subsequently, the NAV will be calculated and disclosed at the close of every Business Day. In addition,the AMC will disclose details of the portfolio at least on a half-yearly basis.

NAV will be determined on every Business Day except in special circumstances described on page 76. NAV of the Schemeshall be made available at all Customer Service Centers of the AMC. The AMC shall also endeavor to have the NAVpublished in a daily newspaper and update on AMC’s website (www.icicipruamc.com).

AMC shall update the NAVs on the website of Association of Mutual Funds in India - AMFI (www.amfiindia.com) by9.00 p.m. every Business Day. In case of any delay, the reasons for such delay would be explained to AMFI and SEBI bythe next day. If the NAVs are not available before commencement of business hours on the following day due to anyreason, the Fund shall issue a press release providing reasons and explaining when the Fund would be able to publishthe NAVs.

ICICI Prudential Indo Asia Equity Fund

7

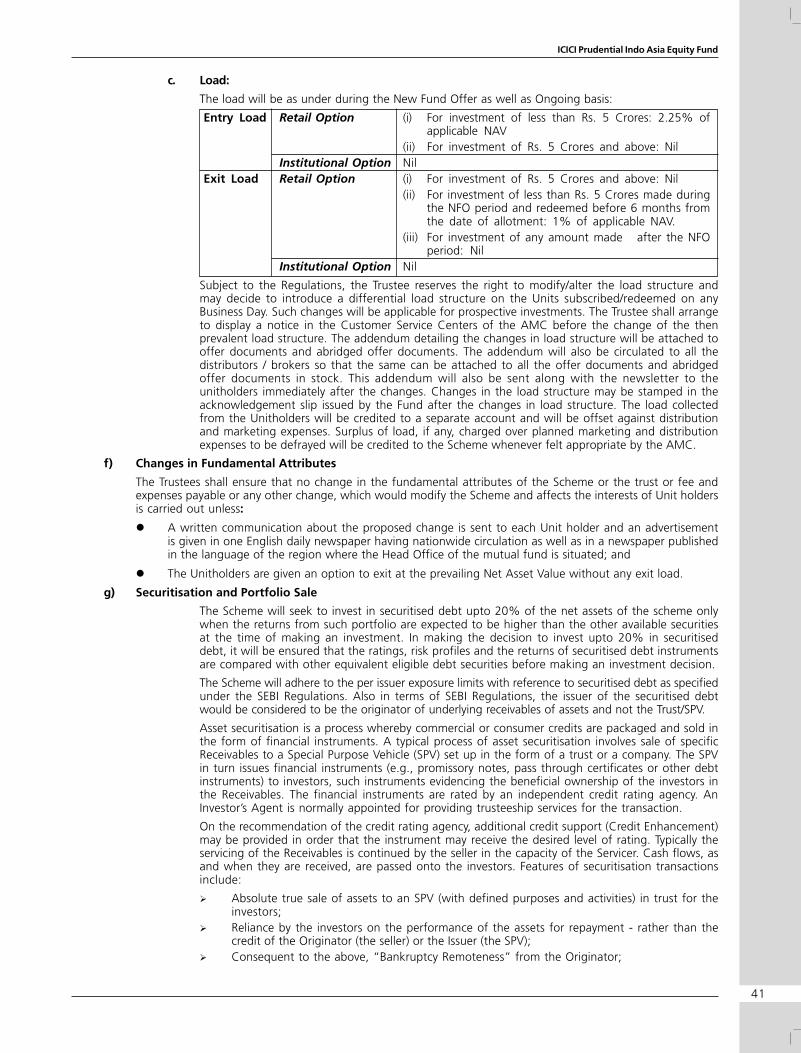

Load (During NFO as well as ongoing basis): –Entry Load Retail Option (i) For investment of less than Rs. 5 Crores: 2.25% of applicable NAV

(ii) For investment of Rs. 5 Crores and above: NilInstitutional Option Nil

Exit Load Retail Option (i) For investment of Rs. 5 Crores and above: Nil(ii) For investment of less than Rs. 5 Crores made during the NFO period

and redeemed before 6 months from the date of allotment: 1% ofapplicable NAV.

(iii) For investment of any amount made after the NFO period: NilInstitutional Option Nil

Any redemption/switch arising out of excess holding by an investors beyond 25% of the net assets of the scheme in themanner envisaged under specified SEBI Circular No. SEBI/IMD/CIR No.10/22701/03 dated 12th December 2003, suchredemption / switch will not be subject to exit load.

However, the Trustee shall have a right to prescribe or modify the load structure with prospective effect subject to amaximum prescribed under the Regulations.

High Liquidity - Being an open-ended Scheme, Units may be redeemed on every Business Day at NAV based prices. TheFund will, under normal circumstances, endeavor to dispatch redemption cheques within T+10 Business Days from thedate of acceptance of the redemption request at any of the Customer Service Centers.

New Fund Offer Expenses: In accordance with the provisions of SEBI Circular No. SEBI/IMD/CIR No.1/64057/06 datedApril 4, 2006, no Initial Issue Expenses will be charged to the Scheme.

Options - Investors under the ICICI Prudential Indo Asia Equity Fund shall have two options namely Retail and Institutional.Under Retail Option, investors will have Growth and Dividend sub options with dividend payout and reinvestmentfacility. Under the Institutional Option only Growth Sub–option is available. If any investor fail to specify options underthe scheme then the Retail Option with Dividend reinvestment facility will be default option and if any investor fails tospecify the sub-options under the Retail Option then Dividend Reinvestment shall be default sub–option. Both theOptions under the Scheme will have the same portfolio. The Trustees may at their discretion add one or more additionaloptions/sub-options under the Scheme.

Repatriation – Repatriation benefits would be available to NRIs/ PIOs/ FIIs, subject to applicable Regulations notified byReserve Bank of India from time to time. Repatriation of these benefits will be subject to applicable deductions inrespect of levies and taxes, as may be applicable at present or in future.

For details on tax update, please refer page 107 of this document.

Investors in the Scheme are not being offered any guaranteed returns.

Investors are advised to consult their Legal / Tax and other Professional Advisors in regard to tax/legalimplications relating to their investments in the Scheme and before making decision to invest in the Schemeor redeem the Units in the Scheme.

8

ICICI Prudential Mutual Fund

RISK FACTORS AND SPECIAL CONSIDERATIONS

Mutual Funds and securities investments are subject to market risks and there is no assurance or guarantee that theobjectives of the Scheme will be achieved.

As with any securities investment, the NAV of the Units issued under the Scheme can go up or down depending on thefactors and forces affecting the capital markets.

Past performance of the Sponsors, AMC/Fund does not indicate the future performance of the Scheme of the Fund.

The Sponsors are not responsible or liable for any loss resulting from the operation of the Scheme beyond thecontribution of an amount of Rs. 22.2 lacs collectively made by them towards setting up the Fund and such otheraccretions and additions to the corpus set up by the Sponsors.

ICICI Prudential Indo Asia Equity Fund is the name of the Scheme and does not in any manner indicate either the qualityof the Scheme or its future prospects and returns.

The NAVs of the Scheme may be affected by changes in the general market conditions, factors and forces affectingcapital market, in particular, level of interest rates, various market related factors and trading volumes, settlementperiods and transfer procedures.

In the event of receipt of inordinately large number of redemption requests or of a restructuring of the Scheme’sportfolio, there may be delays in the redemption of Units. Please see page 8 for “Risk Factors and Special Considerations”and page 76 for “Right to Limit Redemptions” in this Offer Document.

The liquidity of the Scheme’s investments is inherently restricted by trading volumes in the securities in which it invests.

The Scheme may use various derivatives and hedging products from time to time, as would be available and permittedby SEBI, in an attempt to protect the value of the portfolio and enhance Unitholders interest. In case the Scheme utilizesany derivatives under the Regulations, the Scheme may, in certain situations, be exposed to risks associated with the useof derivatives.

Investors in the Scheme are not offered any guaranteed returns.

Mutual Funds being vehicles of securities investments are subject to market and other risks and there can be noguarantee against loss resulting from investing in schemes. The various factors which impact the value of schemeinvestments include but are not limited to fluctuations in the equity and bond markets, fluctuations in interest rates,prevailing political and economic environment, changes in government policy, factors specific to the issuer of securities,tax laws, liquidity of the underlying instruments, settlements periods, trading volumes etc. and securities investmentsare subject to market risks and there is no assurance or guarantee that the objectives of the Scheme will be achieved.

As the liquidity of the Scheme’s investments could at times, be restricted by trading volumes and settlement periods, thetime taken by the Fund for redemption of units may be significant in the event of an inordinately large number ofredemption requests or of a restructuring of the Scheme’s portfolio. In view of this the Trustee has the right, at their solediscretion to limit redemptions (including suspending redemption) under certain circumstances, as described under thesection titled “Right to limit Repurchases”.

From time to time and subject to the regulations, the sponsors, the mutual funds and investment Companies managedby them, their affiliates, their associate companies, subsidiaries of the sponsors and the AMC may invest in eitherdirectly or indirectly in the scheme. The funds managed by these affiliates, associates and/ or the AMC may acquire asubstantial portion of the Scheme. Accordingly, redemption of units held by such funds, affiliates/associates andsponsors may have an adverse impact on the units of the Scheme because the timing of such redemption may impactthe ability of other unitholders to redeem their units.

The scheme may invest in other schemes of any other mutual Funds outside India in conformity with the investmentobjectives of the scheme and within prescribed regulatory limits and subject to applicable SEBI Circular no SEBI/IMD/CIRCULAR NO7/73202/06 Dated 2nd August 2006 para 3a &3b permits mutual fund to make investment in unitssecurities issued by overseas mutual fund with sub-ceiling for individual mutual fund which should not exceed 10% ofthe net assets managed by them as on 31st March of the year ,subject to a maximum of US $ 200 million per mutual fund(limit increased by SEBI Circular dated SEBI/IMD/CIR No. 3/93334/07 dated May 14, 2007) and as per the provisions ofpara (h) the limit of 5% of Net Assets and the prohibition of charging of fees shall not be applicable to investments inmutual funds in foreign countries made in accordance with the guidelines as per the above circular . However,management fees and other expenses charged by the mutual fund (s) in foreign countries along with the managementfee and recurring expenses charged to the domestic mutual fund shall not exceed the total limits on expenses asprescribed under Regulation 52 (6).

From time to time and subject to the regulations, the AMC may invest in this Scheme. The decision to invest in theScheme by the AMC will be based on parameters specified by the Board of the AMC.

Further, as per the Regulation, in case the AMC invests in any of the schemes managed by it, it shall not be entitled tocharge any fees on such investments.

ICICI Prudential Indo Asia Equity Fund

9

The provisions of SEBI circular ref SEBI/IMD/CIR No.10/22701/03 dated.12th December 2003 and SEBI/IMD/CIR No.1/42529/05 dated June 14, 2005 The Scheme shall have a minimum of 20 investors and any one of the investor shall nothold more than 25% of Net Assets of the Scheme. In case the scheme on the date of allotment of NFO does not have20 investors and if any one of the investor holds more than 25% of Net Assets of the Scheme, the scheme will endeavorto ensure that within a three months period or the end of the succeeding calendar quarter from the close of NFO of theScheme, whichever is earlier, the Scheme complies with these conditions failing which the provisions of Regulation39(2) of the SEBI (Mutual Funds) Regulations, 1996, would become automatically applicable without any referencefrom SEBI and accordingly the scheme shall be wound up immediately and the units shall be redeemed. The twoconditions mentioned above shall also be complied within each subsequent calendar quarter thereafter, on an averagebasis as specified by SEBI.

Different types of securities in which the scheme would invest as given in the offer document carry different levels andtypes of risk. Accordingly the scheme’s risk may increase or decrease depending upon its investment pattern. E.g.corporate bonds carry a higher amount of risk than Government securities. Further even among corporate bonds,bonds which are AAA rated are comparatively less risky than bonds which are AA rated.

Scheme Specific Risk Factors relating to ICICI Prudential Indo Asia Equity Fund

1. To the extent the assets of the scheme are invested in overseas financial assets, there may be risks associated withcurrency movements, restrictions on repatriation and transaction procedures in overseas market. Further, therepatriation of capital to India may also be hampered by changes in regulations or political circumstances as wellas the application to it of other restrictions on investment. In addition, country risks would include events such asintroduction of extraordinary exchange controls, economic deterioration, bi-lateral conflict leading toimmobilization of the overseas financial assets and the prevalent tax laws of the respective jurisdiction forexecution of trades or otherwise.

2. Investors may note that AMC/Fund Manger’s investment decisions may not be always profitable. The Schemeproposes to invest substantially in equity and equity related securities. The Scheme will, to a lesser extent, alsoinvest in debt and money market instruments. Trading volumes, settlement periods and transfer procedures mayrestrict the liquidity of these investments. Different segments of the Indian financial markets have differentsettlement periods and such periods may be extended significantly by unforeseen circumstances. The inability ofthe Scheme to make intended securities purchases due to settlement problems could cause the Scheme to misscertain investment opportunities. By the same rationale, the inability to sell securities held in the Scheme’sportfolio due to the absence of a well developed and liquid secondary market for debt securities would result, attimes, in potential losses to the Scheme, in case of a subsequent decline in the value of securities held in theScheme’s portfolio.

3. The scheme is also vulnerable to movements in the prices of securities invested by the scheme, which again couldhave a material bearing on the overall returns from the scheme. These stocks, at times, may be relatively less liquidas compared to growth stocks.

4. The liquidity of the Scheme’s investments is inherently restricted by trading volumes in the securities in which itinvests.

5. The value of the Scheme’s investments, may be affected generally by factors affecting securities markets, such asprice and volume volatility in the capital markets, interest rates, currency exchange rates, changes in policies of theGovernment, taxation laws or any other appropriate authority policies and other political and economicdevelopments which may have an adverse bearing on individual securities, a specific sector or all sectors includingequity and debt markets. Consequently, the NAV of the Units of the Scheme may fluctuate and can go up or down.

6. Trading volumes, settlement periods and transfer procedures may restrict the liquidity of the investments made bythe Scheme. Different segments of the Indian financial markets have different settlement periods and suchperiods may be extended significantly by unforeseen circumstances leading to delays in receipt of proceeds fromsale of securities. The NAV of the Scheme can go up and down because of various factors that affect the capitalmarkets in general.

7. The NAV of the Scheme to the extent invested in Debt and Money market securities, are likely to be affected bychanges in the prevailing rates of interest.

8. Securities, which are not quoted on the stock exchanges, are inherently illiquid in nature and carry a largeramount of liquidity risk, in comparison to securities that are listed on the exchanges or offer other exit options tothe investor, including a put option. Within the Regulatory limits, the AMC may choose to invest in unlistedsecurities that offer attractive yields. This may however increase the risk of the portfolio.

9. While securities that are listed on the stock exchange carry lower liquidity risk, the ability to sell these investmentsis limited by the overall trading volume on the stock exchanges. Money market securities, while fairly liquid, lacka well-developed secondary market, which may restrict the selling ability of the Scheme(s) and may lead to theScheme(s) incurring losses till the security is finally sold.

10

ICICI Prudential Mutual Fund

10. Investment decisions made by the AMC may not always be profitable, as actual market movements may be atvariance with anticipated trends.

11. The Scheme may use various derivative products as permitted by the Regulations. Use of derivatives requires anunderstanding of not only the underlying instrument but also of the derivative itself. Other risks include, the riskof mis-pricing or improper valuation and the inability of derivatives to correlate perfectly with underlying assets,rates and indices.

12. Different segments of the Indian financial markets have different settlement periods and such periods may beextended significantly by unforeseen circumstances. The inability of the Scheme to make intended securitiespurchases due to settlement problems could cause the Scheme to miss certain investment opportunities. By thesame rationale, the inability to sell securities held in the Scheme’s portfolio due to the absence of a well developedand liquid secondary market for debt securities would result, at times, in potential losses to the Scheme, in caseof a subsequent decline in the value of securities held in the Scheme’s portfolio.

13. The Scheme may also invest in ADRs / GDRs / Foreign Debt Securities as permitted by Reserve Bank of India andSecurities and Exchange Board of India. To the extent that some part of the assets of the Schemes may be investedin securities denominated in foreign currencies, the Indian Rupee equivalent of the net assets, distributions andincome may be adversely affected by the changes in the value of certain foreign currencies relative to the IndianRupee. The repatriation of capital also may be hampered by changes in regulations concerning exchange controlsor political circumstances as well as the application to it of other restrictions on investment.

14. The Fund may use derivatives instruments like Stock Index Futures, Interest Rate Swaps, Forward Rate Agreementsor other derivative instruments for the purpose of hedging and portfolio balancing, as permitted under theRegulations and guidelines. Usage of derivatives will expose the Scheme to certain risks inherent to such derivatives.Please refer page 11 & 58 for details.

15. The performance of the scheme will be affected in case of unforeseen circumstances like political crisis, naturalcalamities, and changes in currency exchange rates or interest rates.

16. Fund manager tries to generate returns based on certain past statistical trend. The performance of the schememay get affected if there is a change in the said trend. There can be no assurance that such historical trends willcontinue.

17. As the Fund will invest in securities which are denominated in foreign currencies (e.g. US Dollars), fluctuations inthe exchange rates of these foreign currencies may have an impact on the income and value of the fund. Theinvestment Manager in India may hedge the currency risk based on his view on the forex markets.

18. As the portfolio will invest in stocks of different countries, the portfolio shall be exposed to the political,economic and social risks with respect to each country. However, the portfolio manager shall ensure that hisexposure to each country is limited so that the portfolio is not exposed to one country. Investments in variouseconomies will also diversify and reduce this risk.

19. In case of abnormal circumstances it will be difficult to complete the square off transaction due to liquidity beingpoor in stock futures/spot market. However fund will aim at taking exposure only into liquid stocks where therewill be minimal risk to square off the transaction.

20. The fund will be exposed to settlement risk, as different countries have different settlement periods.

Fixed Income Securities:

Interest Rate Risk: As with all debt securities, changes in interest rates may affect the Scheme’s Net Asset Value as theprices of securities generally increase as interest rates decline and generally decrease as interest rates rise. Prices of long-term securities generally fluctuate more in response to interest rate changes than do short-term securities. Indian debtmarkets can be volatile leading to the possibility of price movements up or down in fixed income securities and therebyto possible movements in the NAV.

Liquidity or Marketability Risk: This refers to the ease with which a security can be sold at or near to its valuation yield-to-maturity (YTM). The primary measure of liquidity risk is the spread between the bid price and the offer price quotedby a dealer. Liquidity risk is today characteristic of the Indian fixed income market.

Credit Risk: Credit risk or default risk refers to the risk that an issuer of a fixed income security may default (i.e. will beunable to make timely principal and interest payments on the security). Because of this risk corporate debentures aresold at a yield above those offered on Government Securities, which are sovereign obligations and free of credit risk.Normally, the value of a fixed income security will fluctuate depending upon the changes in the perceived level of creditrisk as well as any actual event of default. The greater the credit risk, the greater the yield required for someone to becompensated for the increased risk.

Reinvestment Risk: This risk refers to the interest rate levels at which cash flows received from the securities in theScheme are reinvested. The additional income from reinvestment is the “interest on interest” component. The risk isthat the rate at which interim cash flows can be reinvested may be lower than that originally assumed.

ICICI Prudential Indo Asia Equity Fund

11

Money Market Securities are subject to the risk of an issuer’s inability to meet interest and principal payments on itsobligations and market perception of the creditworthiness of the issuer

Risks attached with the use of derivatives: As and when the Scheme trade in the derivatives market there are riskfactors and issues concerning the use of derivatives that Investors should understand. Derivative products are specializedinstruments that require investment techniques and risk analyses different from those associated with stocks andbonds. The use of a derivative requires an understanding not only of the underlying instrument but also of thederivative itself. Derivatives require the maintenance of adequate controls to monitor the transactions entered into, theability to assess the risk that a derivative adds to the portfolio and the ability to forecast price or interest rate movementscorrectly. There is the possibility that a loss may be sustained by the portfolio as a result of the failure of another party(usually referred to as the “counter party”) to comply with the terms of the derivatives contract. Other risks in usingderivatives include the risk of mis pricing or improper valuation of derivatives and the inability of derivatives to correlateperfectly with underlying assets, rates and indices.

Thus, derivatives are highly leveraged instruments. Even a small price movement in the underlying security could have alarge impact on their value. Also, the market for derivative instruments is nascent in India.

Derivatives products are leveraged instruments and provide disproportionate gains as well as disproportionate losses tothe investor. Execution of such strategies depends upon the ability of the fund manager to identify such opportunities.Identification and execution of the strategies to be pursued by the fund manager involve uncertainty and decision of thefund manager may not always be profitable. No assurance can be given that the fund manager will be able to identifyto execute such strategies.

The risks associated with the use of derivatives are different from or possibly greater than, the risks associated withinvesting directly in securities and other traditional investments.

The specific risk factors arising out of a derivative strategy used by the Fund Manager may be as below:

����� Lack of opportunity available in the market.

����� The risk of mispricing or improper valuation and the inability of derivatives to correlate perfectly with underlyingassets, rates and indices.

����� Execution Risk: The prices which are seen on the screen need not be the same at which execution will take place

Also please refer to Page 56 for example on Derivatives.

Risk Analysis on underlying asset classes in Securitisation:

Generally available Asset Classes for securitisation in India

Commercial Vehicles

Auto and Two wheeler poolsMortgage pools (residential housing loans)Personal Loan, credit card and other retail loans

Corporate loans/receivables

In terms of specific risks attached to securitisation, each asset class would have different underlying risks, however, residentialmortgages are supposed to be having lower default rates as an asset class. On the other hand, repossession and subsequentrecovery of commercial vehicles and other auto assets is fairly easier and better compared to mortgages. Some of the assetclasses such as personal loans, credit card receivables etc., being unsecured credits in nature, may witness higher defaultrates. As regards corporate loans/receivables, depending upon the nature of the underlying security for the loan or thenature of the receivable the risks would correspondingly fluctuate. However, the credit enhancement stipulated by ratingagencies for such asset class pools is typically much higher and hence their overall risks are comparable to other AAA ratedasset classes.

The rating agencies have an elaborate system of stipulating margins, over collateralisation and guarantees to bring risk limitsin line with the other AAA rated securities.

It is relevant to note here that predominantly the scheme intends to invest in only AAA rated securitised debt. This comparesfavourably with a portfolio which is constructed on the basis of AA rated securitised debt.

Some of the factors, which are typically analyzed for any pool are as follows:

Size of the loan: generally indicates the kind of assets financed with loans. Also indicates whether there is excessive relianceon very small ticket size, which may result in difficult and costly recoveries. To illustrate, the ticket size of housing loans isgenerally higher than that of personal loans. Hence in the construction of a housing loan asset pool for say Rs.1,00,00,000/-it may be easier to construct a pool with just 10 housing loans of Rs.10,00,000 each rather than to construct a pool ofpersonal loans as the ticket size of personal loans may rarely exceed Rs.5,00,000/- per individual. Also to amplify thisillustration further, if one were to construct a pool of Rs.1,00,00,000/- consisting of personal loans of Rs.1,00,000/- each,the larger number of contracts(100 as against one of 10 housing loans of Rs.10 lakh each) automatically diversifies the riskprofile of the pool as compared to a housing loan based asset pool.

12

ICICI Prudential Mutual Fund

Average original maturity of the pool: indicates the original repayment period and whether the loan tenors are in line withindustry averages and borrower’s repayment capacity. To illustrate, in a car pool consisting of 60 month contracts, theoriginal maturity and the residual maturity of the pool viz. number of remaining installments to be paid gives a better idea ofthe risk of default of the pool itself. If in a pool of 100 car loans having original maturity of 60 months, if more than 70% ofthe contracts have paid more than 50% of the installments and if no default has been observed in such contracts, this is a farsuperior portfolio than a similar car loan pool where 80% of the contracts have not even crossed 5 installments.

Loan to Value Ratio: Indicates how much % value of the asset is financed by borrower’s own equity. The lower LTV, the betterit is. This Ratio stems from the principle that where the borrowers own contribution of the asset cost is high, the chances ofdefault are lower. To illustrate for a Truck costing Rs.20 lakhs, if the borrower has himself contributed Rs.10 lakh and hastaken only Rs.10 lakh as a loan, he is going to have lesser propensity to default as he would lose an asset worth Rs.20 lakhsif he defaults in repaying an installment. This is as against a borrower who may meet only Rs.2 lakh out of his own equity fora truck costing Rs.20 lakh. Between the two scenarios given above, the latter would have higher risk of default than theformer.

Average seasoning of the pool: indicates whether borrowers have already displayed repayment discipline. To illustrate, in thecase of a personal loan, if a pool of assets consist of those who have already repaid 80% of the installments without default,this certainly is a superior asset pool than one where only 10% of installments have been paid. In the former case, theportfolio has already demonstrated that the repayment discipline is far higher.

Default rate distribution: Indicates how much % of the pool and overall portfolio of the originator is current, how much is in0-30 DPD (days past due), 30-60 DPD, 60-90 DPD and so on. The rationale here is very obvious, as against 0-30 DPD, the 60-90 DPD is certainly a higher risk category.

Unlike in plain vanilla instruments, in securitisation transactions it is possible to work towards a target credit rating, whichcould be much higher than the originator’s own credit rating. This is possible through a mechanism called ‘Creditenhancement’. The purpose of credit enhancement is to ensure timely payment to the investors, if the actual collection fromthe pool of receivables for a given period are short of the contractual payouts on securitisation. Securitisation are normallynon-recourse instruments and therefore, the repayment on securitisation would have to come from the underlying assetsand the credit enhancement. Therefore, the rating criteria centrally focus on the quality of the underlying assets.

World over, the quality of credit ratings is measured by default rates and stability. An analysis of rating transition and defaultrates, witnessed in both international and domestic arena, clearly reveals that structured finance ratings have been characterizedby far lower default and transition rates than that of plain vanilla debt ratings. Further, internationally, in case of structuredfinance ratings, not only are the default rates low but post default recovery is also high.

In the Indian scenario, also, more than 95% of issuances have been AAA rated issuances indicating the strength of theunderlying assets as well as adequacy of credit enhancement.

Investment exposure of the Scheme with reference to Securitised Debt:

The Scheme will predominantly invest only in those securitisation issuances which have AAA rating indicating the highestlevel of safety from credit risk point of view at the time of making an investment. The Scheme will not invest in foreignsecuritised debt.

The Scheme may invest in various type of securitisation issuances, including but not limited to Asset Backed Securitisation,Mortgage Backed Securitisation, Personal Loan Backed Securitisation, Collateralized Loan Obligation / Collateralized BondObligation and so on.

The Scheme does not propose to limit its exposure to only one asset class or to have asset class based sub-limits as it willprimarily look towards the AAA rating of the offering.

The Scheme will conduct an independent due diligence on the cash margins, collateralisation, guarantees and other creditenhancements and the portfolio characteristic of the securitisation to ensure that the issuance fits in to the overall objectiveof the investment in high investment grade offerings irrespective of underlying asset class.

Risk Factors specific to investments in Securitised Papers:

Types of Securitised Debt vary and carry different levels and types of risks. Credit Risk on Securitised Bonds depends upon theOriginator and varies depending on whether they are issued with Recourse to Originator or otherwise.

Even within securitised debt, AAA rated securitised debt offers lesser risk of default than AA rated securitised debt. Astructure with Recourse will have a lower Credit Risk than a structure without Recourse.

Underlying assets in Securitised Debt may assume different forms and the general types of receivables include Auto Finance,Credit Cards, Home Loans or any such receipts, Credit risks relating to these types of receivables depend upon various factorsincluding macro economic factors of these industries and economies. Specific factors like nature and adequacy of propertymortgaged against these borrowings, nature of loan agreement/ mortgage deed in case of Home Loan, adequacy ofdocumentation in case of Auto Finance and Home Loans, capacity of borrower to meet its obligation on borrowings in caseof Credit Cards and intentions of the borrower influence the risks relating to the asset borrowings underlying the securitiseddebt.

ICICI Prudential Indo Asia Equity Fund

13

Holders of the securitised assets may have low credit risk with diversified retail base on underlying assets especially whensecuritised assets are created by high credit rated tranches, risk profiles of Planned Amortisation Class tranches (PAC),Principal Only Class Tranches (PO) and Interest Only class tranches (IO) will differ depending upon the interest rate movementand speed of prepayment.

Unlike in plain vanilla instruments, in securitisation transactions, it is possible to work towards a target credit rating, whichcould be much higher than the originator’s own credit rating. This is possible through a mechanism called ‘Creditenhancement’. The process of ‘Credit enhancement’ is fulfilled by filtering the underlying asset classes and applying selectioncriteria, which further diminishes the risks inherent for a particular asset class. The purpose of credit enhancement is toensure timely payment to the investors, if the actual collection from the pool of receivables for a given period is short of thecontractual payout on securitisation. Securitisation is normally non-recourse instruments and therefore, the repayment onsecuritisation would have to come from the underlying assets and the credit enhancement. Therefore the rating criteriacentrally focus on the quality of the underlying assets.

The change in market interest rates – prepayments may not change the absolute amount of receivables for the investors, butmay have an impact on the re-investment of the periodic cash flows that the investor receives in the securitised paper.

Limited Liquidity & Price risk

Presently, secondary market for securitised papers is not very liquid. There is no assurance that a deep secondary market willdevelop for such securities. This could limit the ability of the investor to resell them. Even if a secondary market develops andsales were to take place, these secondary transactions may be at a discount to the New Fund Offer price due to changes inthe interest rate structure.

Limited Recourse, Delinquency and Credit Risk

Securitised transactions are normally backed by pool of receivables and credit enhancement as stipulated by the ratingagency, which differ from issue to issue. The Credit Enhancement stipulated represents a limited loss cover to the Investors.These Certificates represent an undivided beneficial interest in the underlying receivables and there is no obligation of eitherthe Issuer or the Seller or the originator, or the parent or any affiliate of the Seller, Issuer and Originator. No financial recourseis available to the Certificate Holders against the Investors’ Representative. Delinquencies and credit losses may causedepletion of the amount available under the Credit Enhancement and thereby the Investor Payouts may get affected if theamount available in the Credit Enhancement facility is not enough to cover the shortfall. On persistent default of a Obligorto repay his obligation, the Servicer may repossess and sell the underlying Asset. However many factors may affect, delay orprevent the repossession of such Asset or the length of time required to realize the sale proceeds on such sales. In addition,the price at which such Asset may be sold may be lower than the amount due from that Obligor.

Risks due to possible prepayments: Weighted Tenor / Yield

Asset securitisation is a process whereby commercial or consumer credits are packaged and sold in the form of financialinstruments Full prepayment of underlying loan contract may arise under any of the following circumstances;

����� Obligor pays the Receivable due from him at any time prior to the scheduled maturity date of that Receivable; or

����� Receivable is required to be repurchased by the Seller consequent to its inability to rectify a material misrepresentationwith respect to that Receivable; or

����� The Servicer recognizing a contract as a defaulted contract and hence repossessing the underlying Asset and selling thesame

In the event of prepayments, investors may be exposed to changes in tenor and yield.

Bankruptcy of the Originator or Seller

If originator becomes subject to bankruptcy proceedings and the court in the bankruptcy proceedings concludes that thesale from originator to Trust was not a sale then an Investor could experience losses or delays in the payments due. Allpossible care is generally taken in structuring the transaction so as to minimize the risk of the sale to Trust not beingconstrued as a “True Sale”. Legal opinion is normally obtained to the effect that the assignment of Receivables to Trust intrust for and for the benefit of the Investors, as envisaged herein, would constitute a true sale.

Bankruptcy of the Investor’s Agent

If Investor’s agent, becomes subject to bankruptcy proceedings and the court in the bankruptcy proceedings concludes thatthe recourse of Investor’s Agent to the assets/receivables is not in its capacity as agent/Trustee but in its personal capacity,then an Investor could experience losses or delays in the payments due under the swap agreement. All possible care isnormally taken in structuring the transaction and drafting the underlying documents so as to provide that the assets/receivables if and when held by Investor’s Agent is held as agent and in Trust for the Investors and shall not form part of thepersonal assets of Investor’s Agent. Legal opinion is normally obtained to the effect that the Investors Agent’s recourse toassets/receivables is restricted in its capacity as agent and trustee and not in its personal capacity.

14

ICICI Prudential Mutual Fund

Credit Rating of the Transaction / Certificate

The credit rating is not a recommendation to purchase, hold or sell the Certificate in as much as the ratings do not commenton the market price of the Certificate or its suitability to a particular investor. There is no assurance by the rating agencyeither that the rating will remain at the same level for any given period of time or that the rating will not be lowered orwithdrawn entirely by the rating agency.

Risk of Co-mingling

The Servicers normally deposit all payments received from the Obligors into the Collection Account. However, there could bea time gap between collection by a Servicer and depositing the same into the Collection account especially considering thatsome of the collections may be in the form of cash. In this interim period, collections from the Loan Agreements may not besegregated from other funds of the Servicer. If the Servicer fails to remit such funds due to Investors, the Investors may beexposed to a potential loss.

Due care is normally taken to ensure that the Servicer enjoys highest credit rating on stand alone basis to minimizeCo-mingling risk.

Investors are urged to study the terms of the Offer Document carefully before investing in this Scheme, and to retain thisOffer Document for future reference.

Investors in the Scheme are not being offered any guaranteed returns.

Investors are advised to consult their Legal /Tax and other Professional Advisors in regard to tax/legalimplications relating to their investments in the Scheme and before making decision to invest in the Schemeor redeem the Units in the Scheme.

ICICI Prudential Indo Asia Equity Fund

15

Sponsors

ICICI Bank LimitedLandmark, Race Course Circle,Vadodara 390 007, India

Prudential plcLaurence Pountney Hill,London EC4R 0HH, United Kingdom

Asset Management Company

ICICI Prudential Asset Management Company Limited

Registered Office:12th Floor, Narain Manzil, 23,Barakhamba Road, New Delhi – 110 001Telephone: 011 - 23752515-18; Fax: 011-23358582

Corporate Office:8th Floor, Peninsula Tower, Peninsula Corporate Park,Ganpatrao Kadam Marg, Off Senapati Bapat Marg,Lower Parel, Mumbai 400 013.Telephone: 022 - 24997000; Fax : 022 - 24997029

Trustee

ICICI Prudential Trust Limited12th Floor, Narain Manzil,23, Barakhamba Road,New Delhi-110 001

RegistrarComputer Age Management Services Private LimitedUnit : ICICI Prudential Mutual FundFloor IV, Tower 1, Rayala Towers, 158,Anna Salai, Chennai - 600 002

Auditors to the SchemeN. M. Raiji & CompanyUniversal Insurance BuildingSir Phiroze Shah Mehta Road,Mumbai 400 001

CustodianThe Hongkong and Shanghai Banking Corporation Limited/ Its counterpart in other countries18, S. K . Ahire MargWorli, Mumbai 400 030

Legal AdvisorsA.R.A. LAWAdvocates & Solicitors3/F, Mahatma Gandhi Memorial Building,7, Netaji Subhash Road,Churni Road (West), Mumbai – 400 004

16

ICICI Prudential Mutual Fund

DUE DILIGENCE CERTIFICATE

It is confirmed that:

i) The draft Offer Document forwarded to SEBI is in accordance with the SEBI (Mutual Funds) Regulations, 1996 and theguidelines and directives issued by SEBI from time to time.

ii) All legal requirements connected with the launching of the Scheme and also the guidelines, instructions, etc. issued bythe Government of India and any other competent authority in this behalf, have been duly complied with.

iii) The disclosures made in the Offer Document are true, fair and adequate to enable the investors to make a well-informeddecision regarding investment in the proposed Scheme.

iv) The intermediaries named in the Offer Document, according to the information given to the AMC, are registered withSEBI and till date such registration is valid.

Place : Mumbai Ranganath AthreyaDate : October 13, 2006 Sr. Vice President – Compliance,

Legal & Company Secretary

Note: The Due Diligence Certificate as stated above was submitted to SEBI on October 13, 2006

ICICI Prudential Indo Asia Equity Fund

17

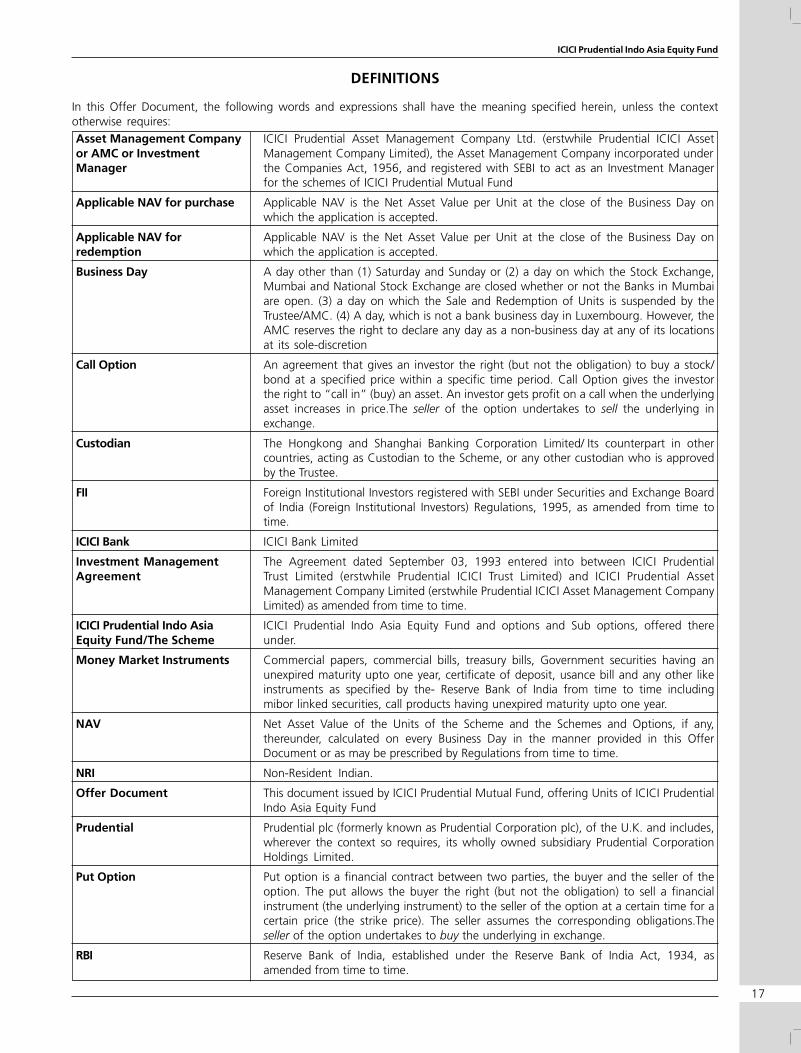

DEFINITIONS

In this Offer Document, the following words and expressions shall have the meaning specified herein, unless the contextotherwise requires:Asset Management Company ICICI Prudential Asset Management Company Ltd. (erstwhile Prudential ICICI Assetor AMC or Investment Management Company Limited), the Asset Management Company incorporated underManager the Companies Act, 1956, and registered with SEBI to act as an Investment Manager

for the schemes of ICICI Prudential Mutual Fund

Applicable NAV for purchase Applicable NAV is the Net Asset Value per Unit at the close of the Business Day onwhich the application is accepted.

Applicable NAV for Applicable NAV is the Net Asset Value per Unit at the close of the Business Day onredemption which the application is accepted.

Business Day A day other than (1) Saturday and Sunday or (2) a day on which the Stock Exchange,Mumbai and National Stock Exchange are closed whether or not the Banks in Mumbaiare open. (3) a day on which the Sale and Redemption of Units is suspended by theTrustee/AMC. (4) A day, which is not a bank business day in Luxembourg. However, theAMC reserves the right to declare any day as a non-business day at any of its locationsat its sole-discretion

Call Option An agreement that gives an investor the right (but not the obligation) to buy a stock/bond at a specified price within a specific time period. Call Option gives the investorthe right to “call in” (buy) an asset. An investor gets profit on a call when the underlyingasset increases in price.The seller of the option undertakes to sell the underlying inexchange.

Custodian The Hongkong and Shanghai Banking Corporation Limited/ Its counterpart in othercountries, acting as Custodian to the Scheme, or any other custodian who is approvedby the Trustee.

FII Foreign Institutional Investors registered with SEBI under Securities and Exchange Boardof India (Foreign Institutional Investors) Regulations, 1995, as amended from time totime.

ICICI Bank ICICI Bank Limited

Investment Management The Agreement dated September 03, 1993 entered into between ICICI PrudentialAgreement Trust Limited (erstwhile Prudential ICICI Trust Limited) and ICICI Prudential Asset

Management Company Limited (erstwhile Prudential ICICI Asset Management CompanyLimited) as amended from time to time.

ICICI Prudential Indo Asia ICICI Prudential Indo Asia Equity Fund and options and Sub options, offered thereEquity Fund/The Scheme under.

Money Market Instruments Commercial papers, commercial bills, treasury bills, Government securities having anunexpired maturity upto one year, certificate of deposit, usance bill and any other likeinstruments as specified by the- Reserve Bank of India from time to time includingmibor linked securities, call products having unexpired maturity upto one year.

NAV Net Asset Value of the Units of the Scheme and the Schemes and Options, if any,thereunder, calculated on every Business Day in the manner provided in this OfferDocument or as may be prescribed by Regulations from time to time.

NRI Non-Resident Indian.

Offer Document This document issued by ICICI Prudential Mutual Fund, offering Units of ICICI PrudentialIndo Asia Equity Fund

Prudential Prudential plc (formerly known as Prudential Corporation plc), of the U.K. and includes,wherever the context so requires, its wholly owned subsidiary Prudential CorporationHoldings Limited.

Put Option Put option is a financial contract between two parties, the buyer and the seller of theoption. The put allows the buyer the right (but not the obligation) to sell a financialinstrument (the underlying instrument) to the seller of the option at a certain time for acertain price (the strike price). The seller assumes the corresponding obligations.Theseller of the option undertakes to buy the underlying in exchange.

RBI Reserve Bank of India, established under the Reserve Bank of India Act, 1934, asamended from time to time.

18

ICICI Prudential Mutual Fund

SEBI Securities and Exchange Board of India established under Securities and ExchangeBoard of India Act, 1992, as amended from time to time.

Source scheme Source scheme means the scheme from which the investor is seeking to switch-out hisinvestments to enable switch-in under the Scheme (ICICI Prudential Indo Asia EquityFund) during the New Fund Offer

The Fund or The Mutual Fund ICICI Prudential Mutual Fund (erstwhile Prudential ICICI Mutual Fund), a trust set upunder the provisions of the Indian Trusts Act, 1882. The Fund is registered with SEBIvide Registration No.MF00393/6 dated October 13, 1993 as ICICI Mutual Fund andhas obtained approval from SEBI for change in name to ICICI Prudential Mutual Fundvide SEBI’s letter dated April 2,2007.

The Trustee ICICI Prudential Trust Limited (erstwhile Prudential ICICI Trust Limited), a company setup under the Companies Act, 1956, and approved by SEBI to act as the Trustee for theschemes of ICICI Prudential Mutual Fund

The Regulations Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, as amendedfrom time to time.

Trust Deed The Trust Deed dated August 25, 1993 establishing ICICI Mutual Fund (subsequentlyrenamed ICICI Prudential Mutual Fund), as amended from time to time.

Trust Fund Amounts settled/contributed by the Sponsors towards the corpus of the ICICI PrudentialMutual Fund and additions/accretions thereto.

Unit The interest of an investor, which consists of one undivided share in the Net Assets ofthe Scheme.

Unit holder A holder of Unit(s) in the scheme of ICICI Prudential Indo Asia Equity Fund as containedin this Offer Document.

ICICI Prudential Indo Asia Equity Fund

19

Summary – ICICI Prudential Indo Asia Equity Fund

Name of the Scheme ICICI Prudential Indo Asia Equity Fund

Structure Open Ended Diversified Equity Scheme

Features ICICI Prudential Indo Asia Equity Fund is an open ended equity fund that seeks togenerate long term capital appreciation by investing in equity, equity related securitiesShare classes / units of Equity Fund of companies which are incorporated or have theirarea of primary activity, in Asia –Pacific region.