g hanni act chp 4 study guide

TRANSCRIPT

Chapter 04 - International Financial Reporting Standards: Part I

CHAPTER 4INTERNATIONAL FINANCIAL REPORTING STANDARDS:

PART I CASE 4-1 PROBLEM IS VERY IMPORTANT!!Chapter Outline

I. The International Accounting Standards Board (IASB) had 29 International Accounting Standards (IAS) and 9 International Financial Reporting Standards (IFRS) in force in September 2010.A. In 2002, the IASB and U.S. Financial Accounting Standards Board (FASB) agreed to

work together to reduce differences between IFRS and U.S. GAAP.

II. There are several types of differences between IFRS and U.S. GAAP.A. Definition differences. Differences in definitions can occur even though concepts are

similar. Definition differences can lead to differences in recognition and/or measurement.

B. Recognition differences. Differences in recognition criteria and/or guidance related to (a) whether an item is recognized, (b) how it is recognized, and/or (c) when it is recognized (timing difference).

C. Measurement differences. Differences in approach for determining the amount recognized resulting from either (a) a difference in the method required, or (b) a difference in the detailed guidance for applying a similar method.

D. Alternatives. One set of standards allows a choice between two or more alternative methods; the other set of standards requires one specific method to be used.

E. Lack of requirements or guidance. IFRS do not cover an issue addressed by U.S. GAAP, and vice versa.

F. Presentation differences. Differences in the presentation of items in the financial statements.

G. Disclosure differences. Differences in information presented in the notes to financial statements related to (a) whether a disclosure is required and/or (b) the manner in which a disclosure is required to be made.

III. A variety of differences exist between IFRS and U.S. GAAP with respect to the recognition and measurement of assets.A. Inventory – IFRS require inventory to be reported on the balance sheet at the lower of

cost or net realizable value; U.S. GAAP requires the lower of cost or replacement cost, with net realizable value as a ceiling and net realizable value less a normal profit margin as the floor. U.S. GAAP allows the use of LIFO; IFRS do not.

B. Property, plant and equipment – subsequent to acquisition, IFRS allow fixed assets to be reported on the balance sheet using a cost model (historical cost less accumulated depreciation and impairment losses) or a revaluation model (fair value at the balance sheet date less accumulated depreciation and impairment losses); U.S. GAAP requires the use of the cost model. Component depreciation must be applied under IFRS when items of property, plant and equipment are comprise of significant parts; this is not the case under U.S. GAAP

4-1

Chapter 04 - International Financial Reporting Standards: Part I

C. Impairment of assets – an asset is impaired under IFRS when its carrying amount exceeds its recoverable amount, which is the greater of net selling price and value in use. Value in use is calculated as the present value of future cash flows expected from continued use of the asset and from its disposal. An asset is impaired under U.S. GAAP when its carrying amount exceeds the undiscounted future cash flows expected from the asset’s continued use and disposal.1. Measurement of impairment loss – the impairment loss under IFRS is the

difference between carrying amount and recoverable amount; under U.S. GAAP, the impairment loss is the amount by which carrying amount exceeds fair value. Recoverable amount and fair value are likely to be different.

2. Reversal of impairment loss – if subsequent to recognizing an impairment loss, the recoverable amount of an asset is determined to exceed its new carrying amount, IFRS require the original impairment loss to be reversed; U.S. GAAP does not allow the reversal of a previously recognized impairment loss.

D. Development costs – when certain criteria are met, IFRS require development costs to be capitalized as an asset and then amortized over their useful life; U.S. GAAP requires development costs to be expensed as incurred. An exception exists in U.S. GAAP for software development costs.

E. Borrowing costs – similar to U.S. GAAP, IFRS requires borrowing costs to be capitalized to the extent they are attributable to the acquisition, construction, or production of a qualifying asset. Other borrowing costs are expensed as incurred. However, the amount of borrowing costs to be capitalized differs between IFRS and U.S. GAAP.

F. Leases – both IFRS and U.S. GAAP distinguish between operating and finance (capitalized) leases. U.S. GAAP provides “bright line” tests to determine when a lease must be capitalized; IFRS do not.

IV. A number of IASB standards deal primarily with disclosure and presentation issues, and in some cases requirements differ from U.S. GAAP.A. In the statement of cash flows, IAS 7 allows interest and dividends received to be

classified as operating or investing, whereas these are always classified as operating under U.S. GAAP. IAS 7 allows interest and dividends paid to be classified as operating or financing, whereas interest paid is operating and dividends paid is financing under U.S. GAAP.

B. IAS 10 requires financial statements to be adjusted for so-called adjusting events that occur up to the point that the financial statements have been authorized for issuance. U.S. GAAP uses the date the financial statements are issued or are available to be issued as the cutoff date for adjusting events.

C. IAS 8 establishes a hierarchy of authoritative pronouncements to be considered in selecting an accounting policy. The lowest level in the hierarchy would allow the use of U.S.GAAP. Once selected, accounting policies must be applied consistently unless a change is required by IFRS or would result in more relevant information being reported in the financial statements.

D. IFRS 5 provides a more liberal definition of what qualifies as a discontinued operation than does U.S. GAAP.

E. IAS 34 requires interim periods to be treated as discrete accounting periods, whereas U.S. GAAP treats interim periods as an integral part of the full year.

4-2

Chapter 04 - International Financial Reporting Standards: Part I

Answers to Questions

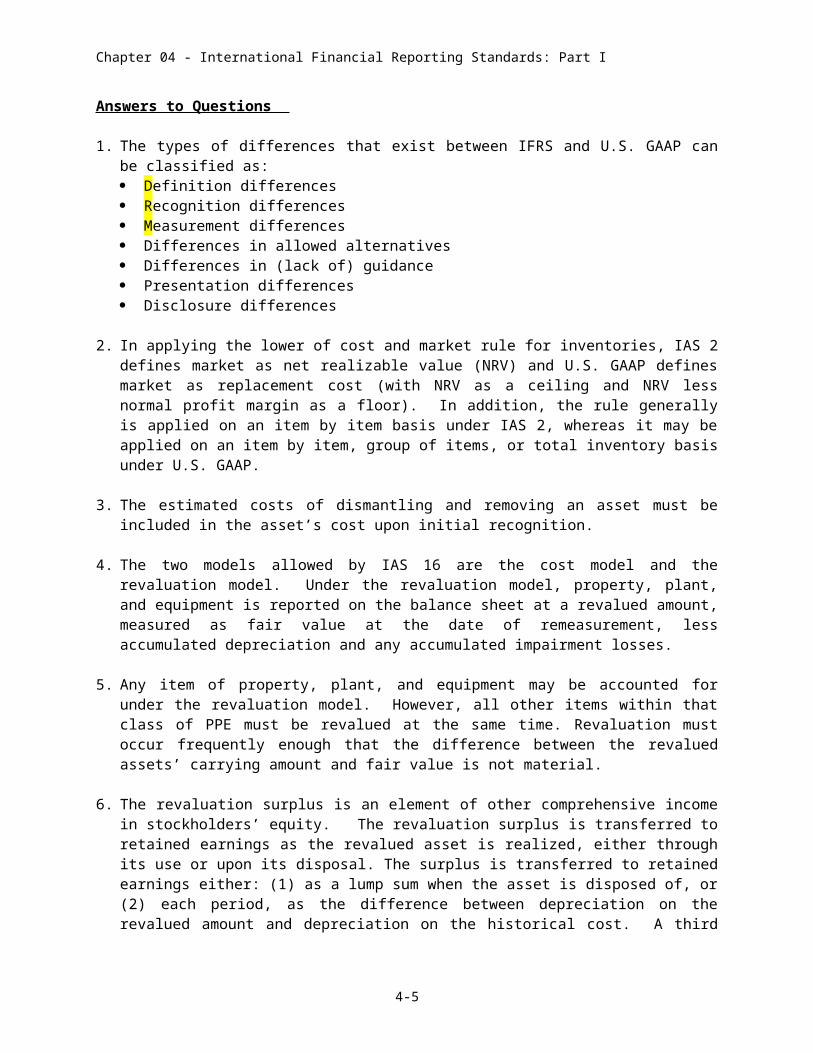

1. The types of differences that exist between IFRS and U.S. GAAP can be classified as: Definition differences Recognition differences Measurement differences Differences in allowed alternatives Differences in (lack of) guidance Presentation differences Disclosure differences

2. In applying the lower of cost and market rule for inventories, IAS 2 defines market as net realizable value (NRV) and U.S. GAAP defines market as replacement cost (with NRV as a ceiling and NRV less normal profit margin as a floor). In addition, the rule generally is applied on an item by item basis under IAS 2, whereas it may be applied on an item by item, group of items, or total inventory basis under U.S. GAAP.

3. The estimated costs of dismantling and removing an asset must be included in the asset’s cost upon initial recognition.

4. The two models allowed by IAS 16 are the cost model and the revaluation model. Under the revaluation model, property, plant, and equipment is reported on the balance sheet at a revalued amount, measured as fair value at the date of remeasurement, less accumulated depreciation and any accumulated impairment losses.

5. Any item of property, plant, and equipment may be accounted for under the revaluation model. However, all other items within that class of PPE must be revalued at the same time. Revaluation must occur frequently enough that the difference between the revalued assets’ carrying amount and fair value is not material.

6. The revaluation surplus is an element of other comprehensive income in stockholders’ equity. The revaluation surplus is transferred to retained earnings as the revalued asset is realized, either through its use or upon its disposal. The surplus is transferred to retained earnings either: (1) as a lump sum when the asset is disposed of, or (2) each period, as the difference between depreciation on the revalued amount and depreciation on the historical cost. A third treatment for revaluation surplus is to allow it to stay in other comprehensive income indefinitely.

7. When an item of property, plant, and equipment is comprised of significant parts that have different useful lives, as is the case for an airplane, the asset must be split into components and each component must be depreciated separately.

8. Under the fair value model for investment property, changes in fair value are recognized in net income, whereas changes in fair value under the revaluation model are taken to other comprehensive income.

4-3

Chapter 04 - International Financial Reporting Standards: Part I

9. Under IAS 36, an impairment loss arises when an asset’s recoverable amount is less than its carrying value, where recoverable amount is the greater of net selling price and value in use. Value in use is determined as the expected future cash flows from use of the asset discounted to present value. The amount of the loss is the difference between carrying value and recoverable amount.

Under U.S. GAAP, an impairment loss arises when the expected future cash flows (undiscounted) from the use of the asset are less than its carrying value. If impairment exists, the amount of the loss is equal to the difference between carrying value and fair value, which can be determined in different ways.

10. A previously impaired asset may be written back up only to what it’s carrying amount would have been if the impairment had never been recognized.

11. The three types of intangible assets are: (1) purchased, (2) acquired in a business combination, and (3) internally generated. (1) and (2) are classified as having a finite or indefinite useful life; (3) can only be classified as finite-lived. Finite-lived intangibles are amortized on a systematic basis over their useful lives. All intangibles are subject to impairment testing. Indefinite-lived intangibles must be tested for impairment at least annually.

12. Under IAS 36, expenditures giving rise to a potential intangible are classified as either research or development expenditures. Research expenditures are expensed as incurred. Development expenditures are recognized as an intangible asset when six criteria are met. Under U.S. GAAP, research and development costs are expensed as incurred. The only exception is for software development costs, which are recognized as an asset when certain criteria have been met.

13. Indefinite-lived intangibles and goodwill are subject to impairment testing at least annually.

14. Goodwill is measured as the excess of (a) consideration transferred plus noncontrolling interest over (b) the fair value of the acquired firm’s net assets. Two alternative methods are available to measure noncontrolling interest; therefore, two different measures of goodwill exist for a given business combination.

15. A gain on bargain purchase exists when (a) consideration transferred plus noncontrolling interest is less than (b) the fair value of the acquired firm’s net assets. The difference between (a) and (b) is sometimes referred to as “negative goodwill.”

16. Goodwill must be tested for impairment annually. Goodwill that can be allocated to a specific cash-generating unit is tested for impairment using a bottom-up test. In this test, the carrying value of the cash-generating unit, including goodwill, is compared with the recoverable amount of the cash-generating unit. If the recoverable amount of a cash-generating unit is less its carrying value, goodwill is deemed to be impaired and is written down.

4-4

Chapter 04 - International Financial Reporting Standards: Part I

17. IAS 23 (revised in 2007) requires borrowing costs to be capitalized to the extent they are attributable to the acquisition, construction, or production of a qualifying asset; other borrowing costs are expensed in the period in which they are incurred.

18. Borrowing costs are defined more broadly in IAS 23 than are interest costs in U.S. GAAP. For example, foreign exchange gains and losses are treated as borrowing costs to the extent they represent adjustments to interest costs. Another difference is that under IFRS interest income earned on short-term investment of borrowed amounts is netted against interest cost to determine the amount of borrowing cost to capitalize. There is no netting of interest income and interest expense under U.S. GAAP.

19. IAS 17 describes five situations that would normally lead to a lease being classified as a finance lease, but does not describe these as being absolute tests. (The standard provides three additional situations that could lead to a lease being classified as a finance lease.) The criteria implied in four of the situations are similar to the specific criteria in U.S. GAAP, but the IAS 17 criteria provide less “bright line” guidance. IAS 17 indicates that a lease would normally be capitalized when the lease term is for the major part of the leased asset’s life – U.S. GAAP specifically defines “major part” as 75%. IAS 17 also indicates that a lease would normally be capitalized when the present value of minimum lease payments is equal to substantially all the fair value of the leased asset – U.S. GAAP specifically defines “substantially all” as 90%. Determining whether a lease should be capitalized is an example of the principles-based approach followed in IFRS versus the rules-based approach of U.S. GAAP.

20. A difference in accounting for a sale-and-leaseback gain exists between IFRS and U.S. GAAP when the lease is classified as an operating lease. Under U.S. GAAP, the gain must be amortized over the life of the lease. Under IAS 17, the portion of the gain equal to the difference between the fair value and the carrying amount of the leased asset is recognized immediately. Any difference between the fair value of the asset and its selling price is amortized over the life of the lease. If the lease is classified as a finance lease, both IFRS and U.S. GAAP require the gain on sale-and-leaseback to be amortized over the life of the lease.

21. U.S. GAAP requires interest paid and received and dividends received to be classified as operating; dividends paid must be classified as financing. IAS 7 allows interest paid and dividends paid to be classified either as operating or financing; interest received and dividends received may be classified as either operating or investing.

22. IAS 10 establishes the date that financial statements are authorized for issuance as the cut-off date for recognition of events after the reporting period. U.S. GAAP uses the date that financial statements are available for issuance as the cut-off date.

4-5

Chapter 04 - International Financial Reporting Standards: Part I

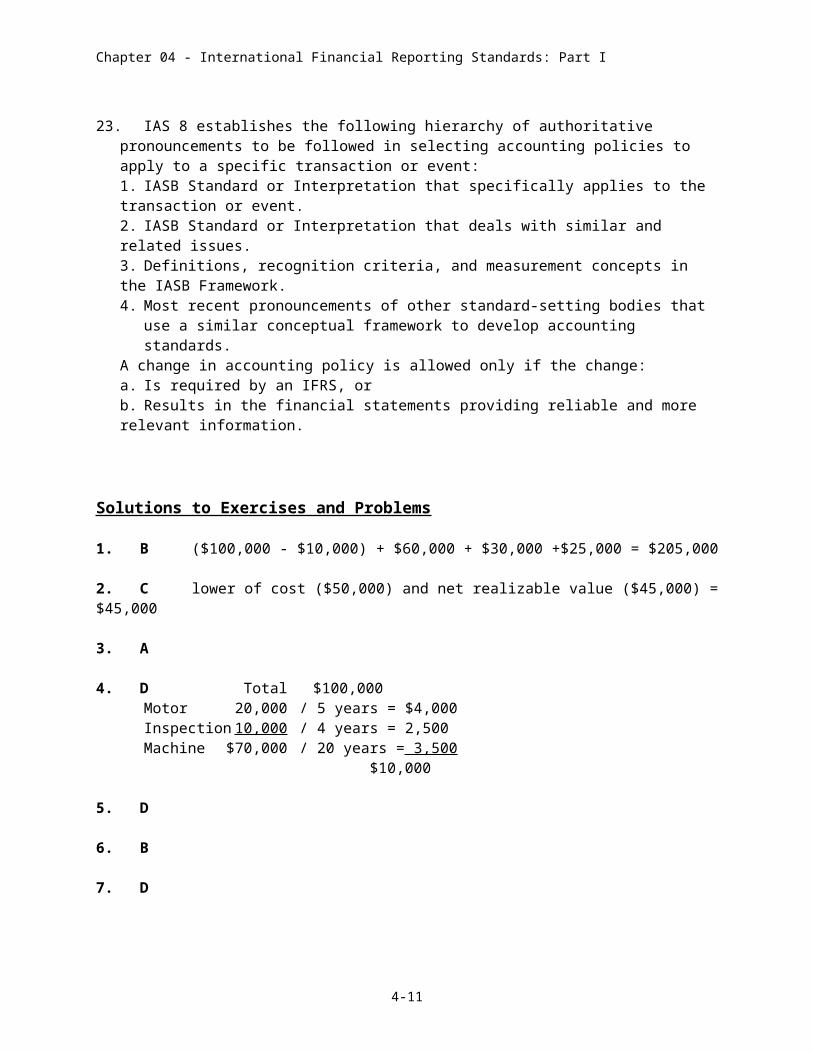

23. IAS 8 establishes the following hierarchy of authoritative pronouncements to be followed in selecting accounting policies to apply to a specific transaction or event:1. IASB Standard or Interpretation that specifically applies to the transaction or event.2. IASB Standard or Interpretation that deals with similar and related issues.3. Definitions, recognition criteria, and measurement concepts in the IASB Framework.4. Most recent pronouncements of other standard-setting bodies that use a similar

conceptual framework to develop accounting standards. A change in accounting policy is allowed only if the change:a. Is required by an IFRS, or b. Results in the financial statements providing reliable and more relevant information.

Solutions to Exercises and Problems

1. B ($100,000 - $10,000) + $60,000 + $30,000 +$25,000 = $205,000

2. C lower of cost ($50,000) and net realizable value ($45,000) = $45,000

3. A

4. D Total $100,000Motor 20,000 / 5 years = $4,000Inspection 10,000 / 4 years = 2,500 Machine $70,000 / 20 years = 3,500

$10,000

5. D

6. B

7. D

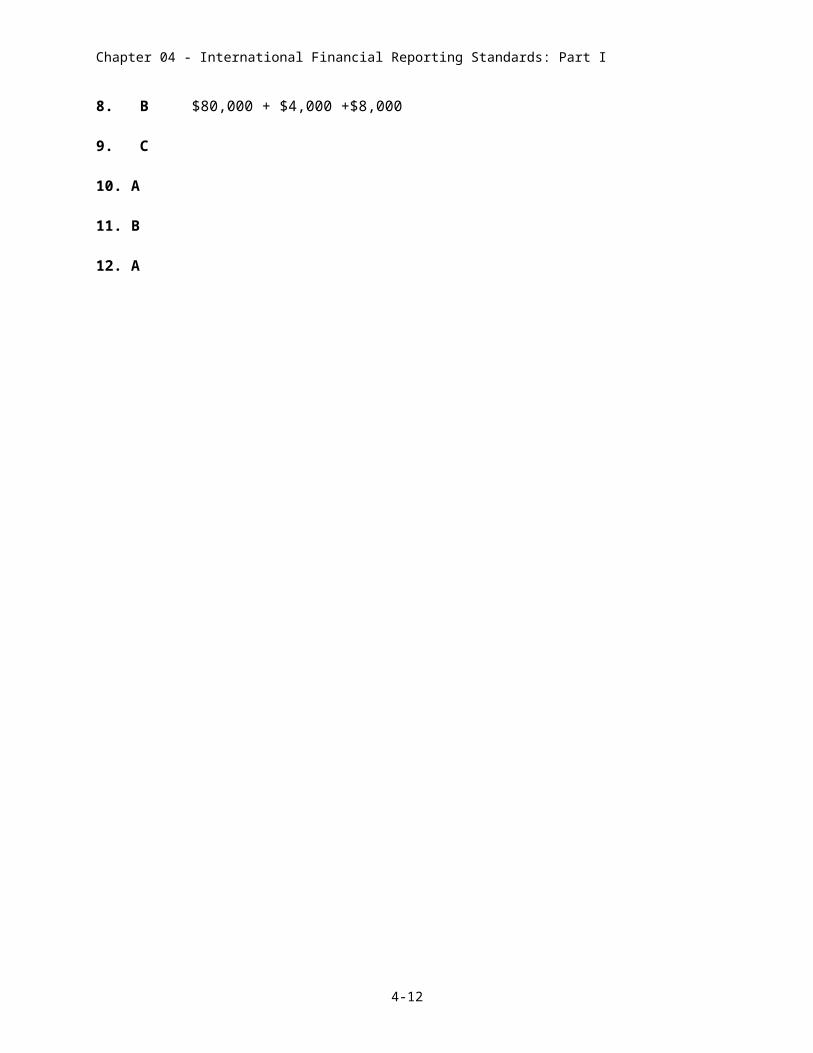

8. B $80,000 + $4,000 +$8,000

9. C

10. A

11. B

12. A

4-6

Chapter 04 - International Financial Reporting Standards: Part I

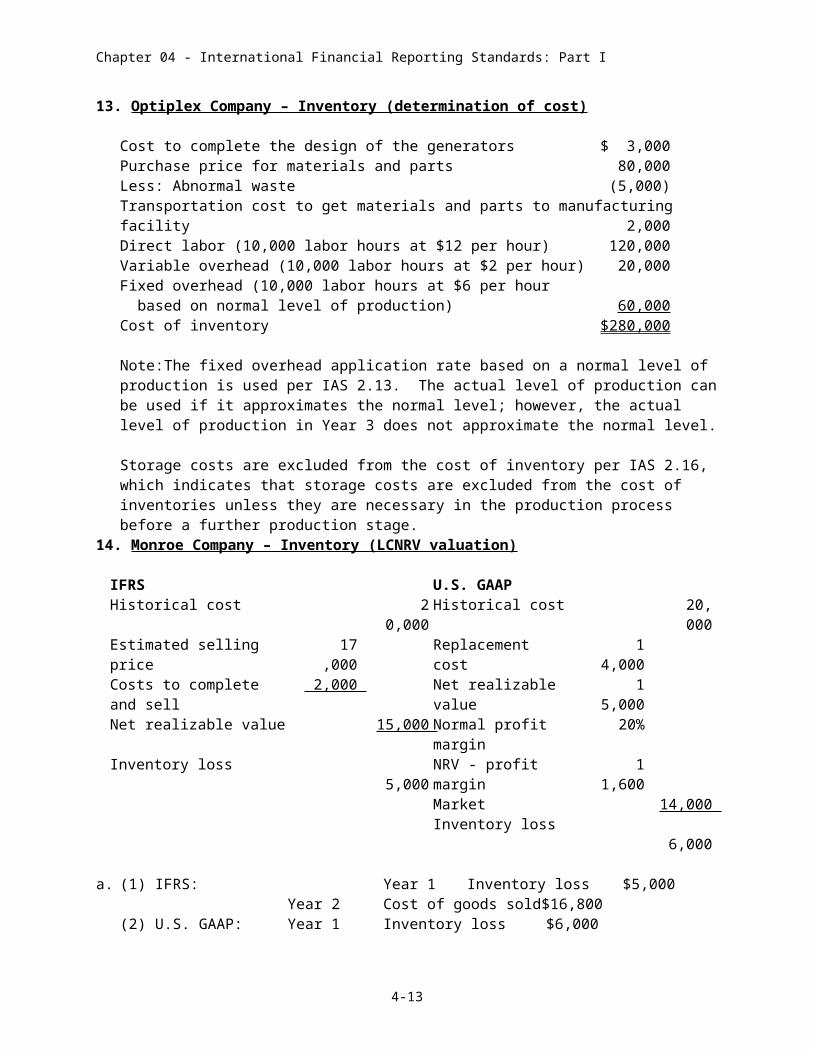

13. Optiplex Company – Inventory (determination of cost)

Cost to complete the design of the generators $ 3,000Purchase price for materials and parts 80,000Less: Abnormal waste (5,000)Transportation cost to get materials and parts to manufacturing facility 2,000Direct labor (10,000 labor hours at $12 per hour) 120,000Variable overhead (10,000 labor hours at $2 per hour) 20,000Fixed overhead (10,000 labor hours at $6 per hour based on normal level of production) 60,000Cost of inventory $280,000

Note:The fixed overhead application rate based on a normal level of production is used per IAS 2.13. The actual level of production can be used if it approximates the normal level; however, the actual level of production in Year 3 does not approximate the normal level.

Storage costs are excluded from the cost of inventory per IAS 2.16, which indicates that storage costs are excluded from the cost of inventories unless they are necessary in the production process before a further production stage.

14. Monroe Company – Inventory (LCNRV valuation)

IFRS U.S. GAAPHistorical cost 20,00

0 Historical cost 20,000

Estimated selling price 17,000 Replacement cost 14,000

Costs to complete and sell 2,000 Net realizable value 15,000

Net realizable value 15,000 Normal profit margin 20%Inventory loss 5,000 NRV - profit margin 11,60

0 Market 14,000 Inventory loss 6,00

0

a. (1) IFRS: Year 1 Inventory loss $5,000Year 2 Cost of goods sold $16,800

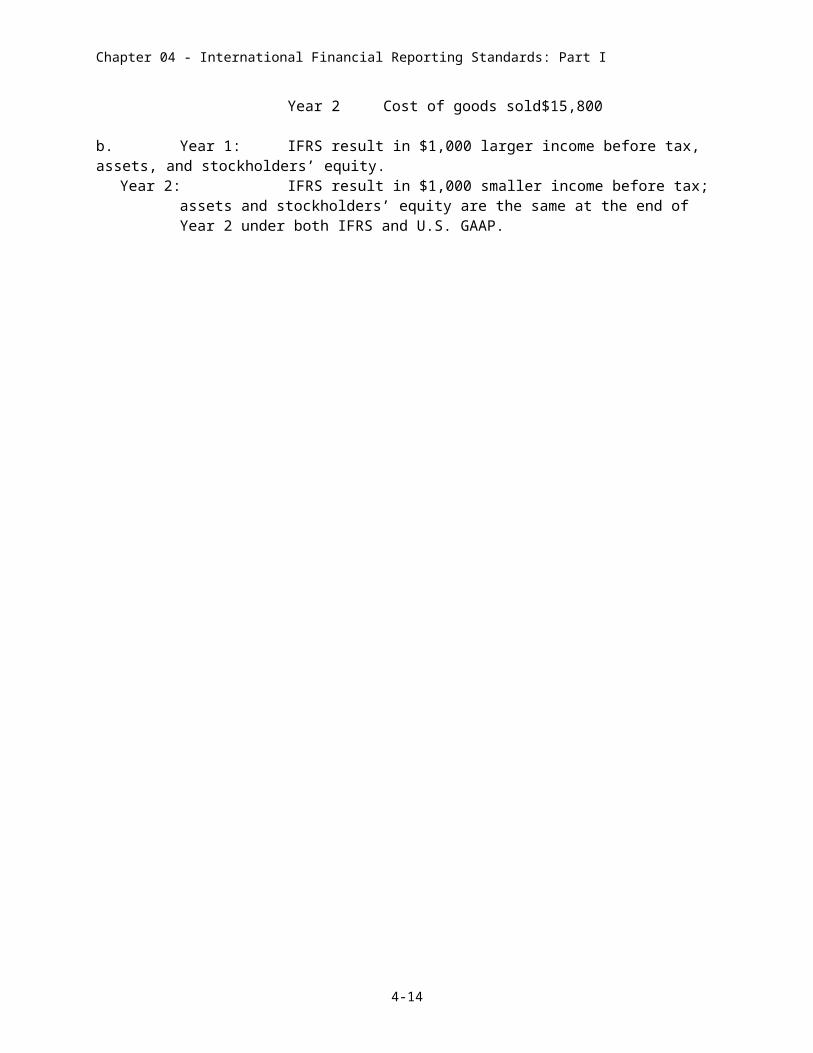

(2) U.S. GAAP: Year 1 Inventory loss $6,000Year 2 Cost of goods sold $15,800

b. Year 1: IFRS result in $1,000 larger income before tax, assets, and stockholders’ equity.Year 2: IFRS result in $1,000 smaller income before tax; assets and stockholders’ equity

are the same at the end of Year 2 under both IFRS and U.S. GAAP.

4-7

Chapter 04 - International Financial Reporting Standards: Part I

15. Beech Corporation – Inventory (LCNRV valuation)

IAS 2.29 indicates that inventories are usually written down to NRV item by item. Grouping is acceptable when several criteria are met, including relating to the same product line. Because these three products relate to three different product lines, grouping would not be allowed.

Product Cost

Selling price

12/31/Y1

Selling costs (5%)

NRV12/31/Y1

LCNRV (item by item)

12/31/Y1101 $130 $160 $8 $152 $130202 160 $140 $7 $133 133303 100 $100 $5 $95 95Item-by-item total

$390 $358

Cost $390LCNRV 358Write-down $ 32

Inventory write-down expense $32 Inventory valuation allowance $32

Note: The use of the contra-account “Inventory valuation allowance” facilitates a possible reversal of the write-down as is allowed under IAS 2.

16. Beech Corporation – Inventory (reversal of write-down)

IAS 2 indicates that an inventory write-down is reversed when, for example, inventory is still on hand and its selling price has increased. The reversal is limited to the amount of the original write-down. The new carrying amount should be the lower of original cost and current NRV.

Product

Carrying Amount 12/31/Y1 Cost

Selling price

12/31/Y2

Selling costs (5%)

NRV12/31/Y2

LCNRV12/31/Y2

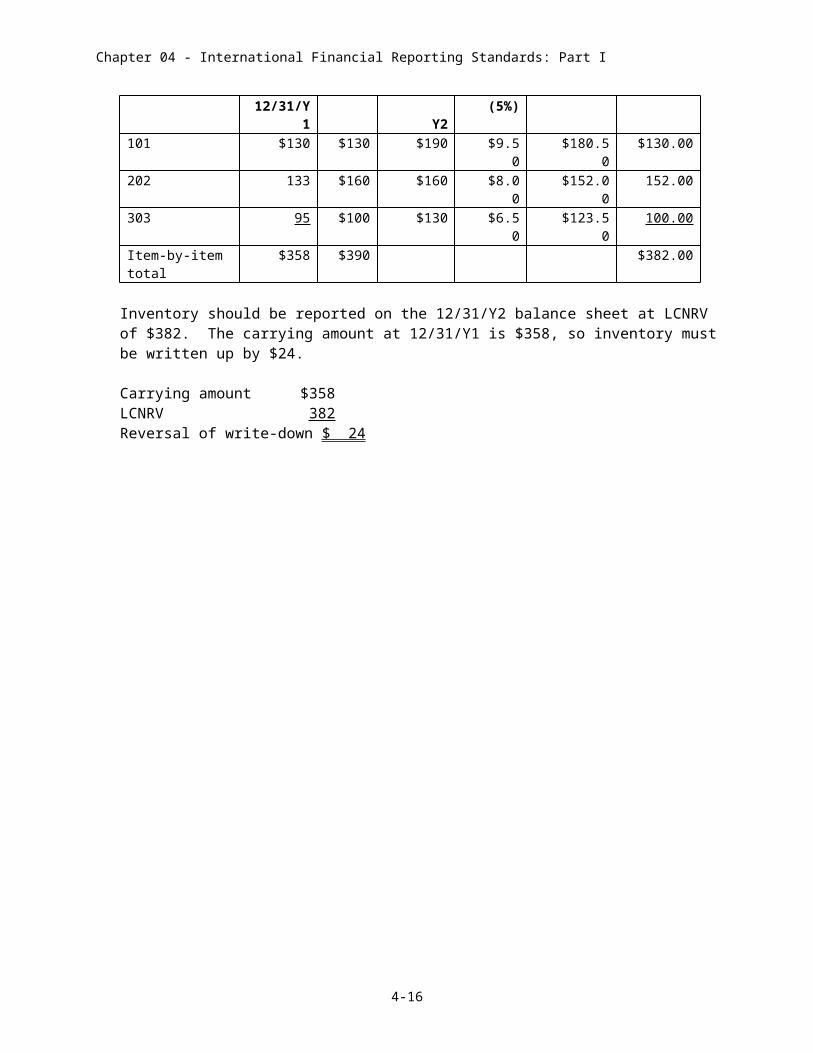

101 $130 $130 $190 $9.50 $180.50 $130.00202 133 $160 $160 $8.00 $152.00 152.00303 95 $100 $130 $6.50 $123.50 100.00Item-by-item total $358 $390 $382.00

Inventory should be reported on the 12/31/Y2 balance sheet at LCNRV of $382. The carrying amount at 12/31/Y1 is $358, so inventory must be written up by $24.

Carrying amount $358LCNRV 382Reversal of write-down $ 24

4-8

Chapter 04 - International Financial Reporting Standards: Part I

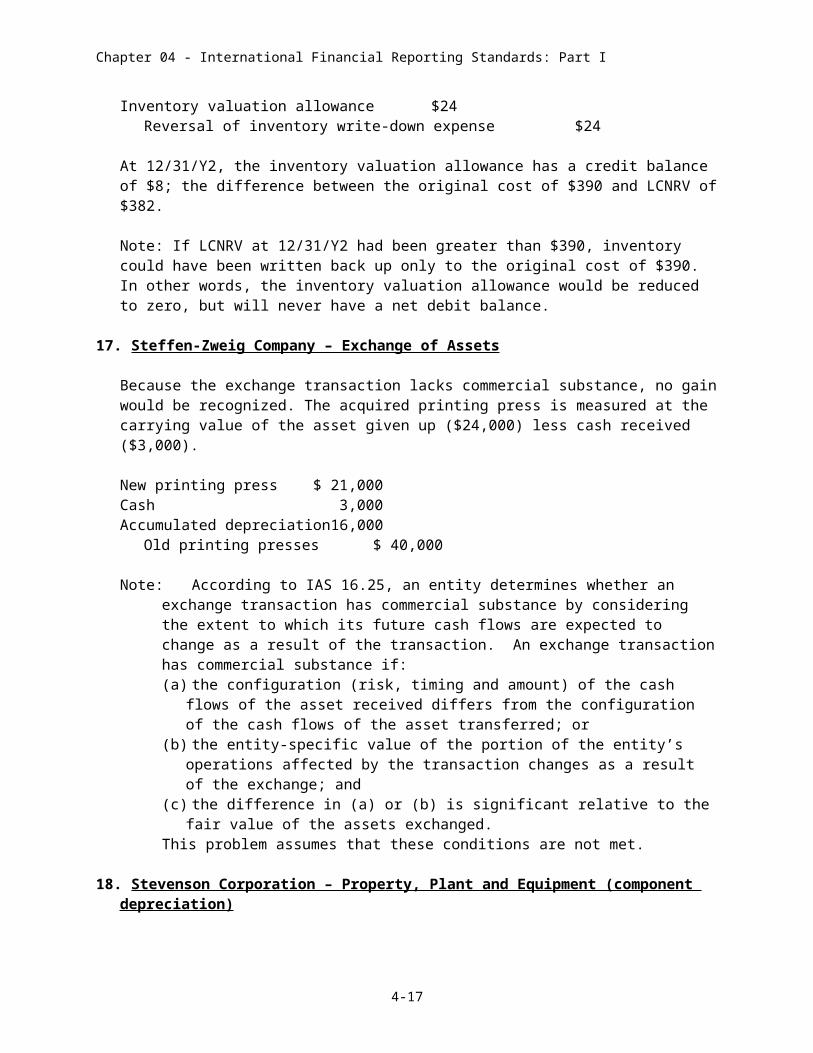

Inventory valuation allowance $24Reversal of inventory write-down expense $24

At 12/31/Y2, the inventory valuation allowance has a credit balance of $8; the difference between the original cost of $390 and LCNRV of $382.

Note: If LCNRV at 12/31/Y2 had been greater than $390, inventory could have been written back up only to the original cost of $390. In other words, the inventory valuation allowance would be reduced to zero, but will never have a net debit balance.

17. Steffen-Zweig Company – Exchange of Assets

Because the exchange transaction lacks commercial substance, no gain would be recognized. The acquired printing press is measured at the carrying value of the asset given up ($24,000) less cash received ($3,000).

New printing press $ 21,000Cash 3,000Accumulated depreciation 16,000

Old printing presses $ 40,000

Note: According to IAS 16.25, an entity determines whether an exchange transaction has commercial substance by considering the extent to which its future cash flows are expected to change as a result of the transaction. An exchange transaction has commercial substance if: (a) the configuration (risk, timing and amount) of the cash flows of the asset received

differs from the configuration of the cash flows of the asset transferred; or(b) the entity-specific value of the portion of the entity’s operations affected by the

transaction changes as a result of the exchange; and(c) the difference in (a) or (b) is significant relative to the fair value of the assets

exchanged.This problem assumes that these conditions are not met.

18. Stevenson Corporation – Property, Plant and Equipment (component depreciation)

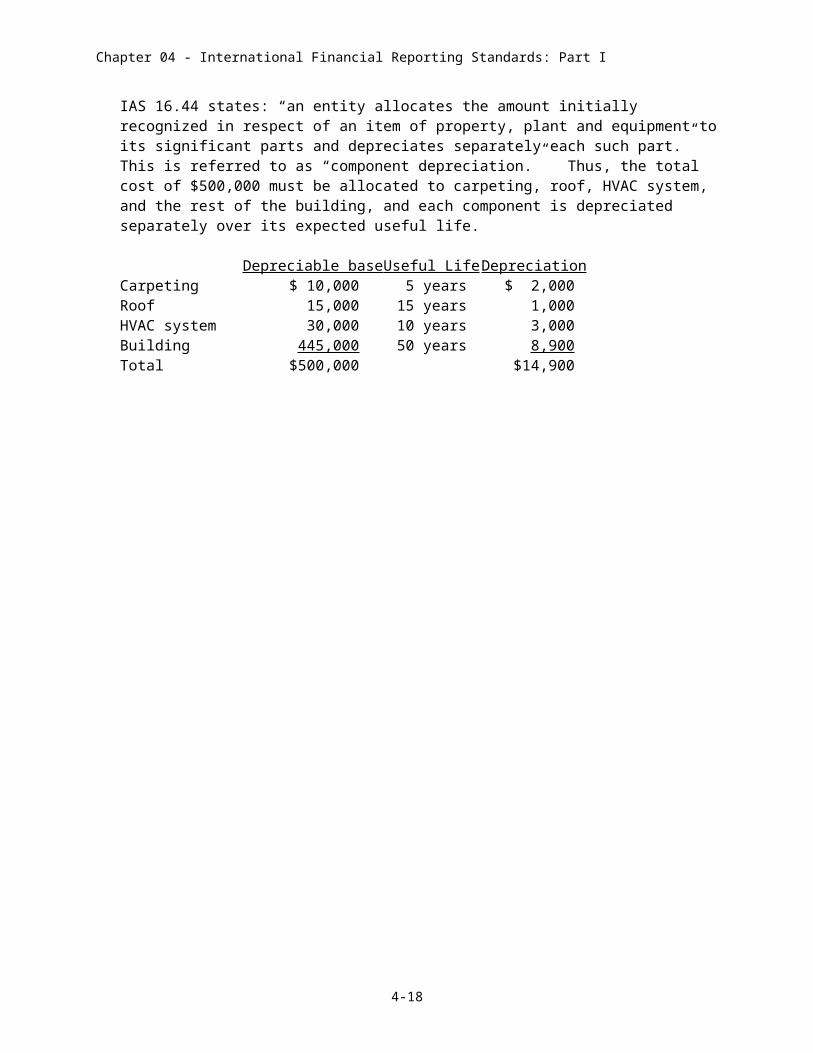

IAS 16.44 states: “an entity allocates the amount initially recognized in respect of an item of property, plant and equipment to its significant parts and depreciates separately each such part.” This is referred to as “component depreciation.” Thus, the total cost of $500,000 must be allocated to carpeting, roof, HVAC system, and the rest of the building, and each component is depreciated separately over its expected useful life.

Depreciable base Useful Life DepreciationCarpeting $ 10,000 5 years $ 2,000Roof 15,000 15 years 1,000HVAC system 30,000 10 years 3,000Building 445,000 50 years 8,900Total $500,000 $14,900

4-9

Chapter 04 - International Financial Reporting Standards: Part I

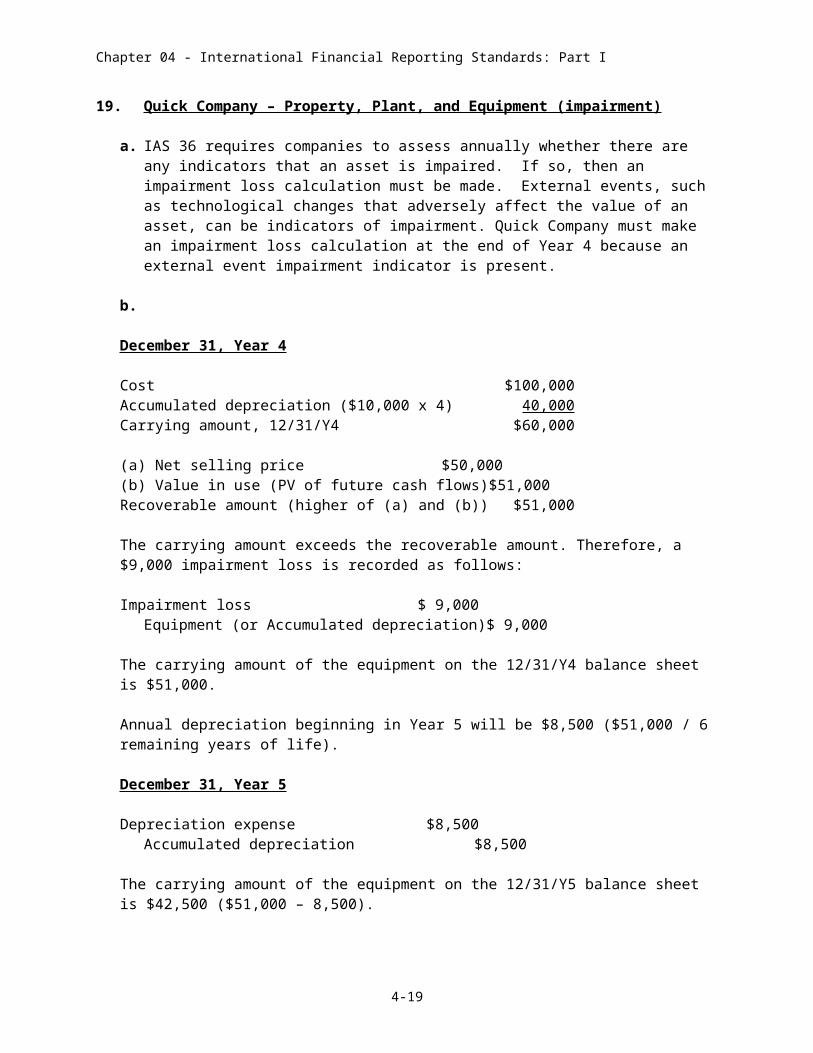

19. Quick Company – Property, Plant, and Equipment (impairment)

a. IAS 36 requires companies to assess annually whether there are any indicators that an asset is impaired. If so, then an impairment loss calculation must be made. External events, such as technological changes that adversely affect the value of an asset, can be indicators of impairment. Quick Company must make an impairment loss calculation at the end of Year 4 because an external event impairment indicator is present.

b.

December 31, Year 4

Cost $100,000Accumulated depreciation ($10,000 x 4) 40,000Carrying amount, 12/31/Y4 $60,000

(a) Net selling price $50,000(b) Value in use (PV of future cash flows) $51,000Recoverable amount (higher of (a) and (b)) $51,000

The carrying amount exceeds the recoverable amount. Therefore, a $9,000 impairment loss is recorded as follows:

Impairment loss $ 9,000Equipment (or Accumulated depreciation) $ 9,000

The carrying amount of the equipment on the 12/31/Y4 balance sheet is $51,000.

Annual depreciation beginning in Year 5 will be $8,500 ($51,000 / 6 remaining years of life).

December 31, Year 5

Depreciation expense $8,500Accumulated depreciation $8,500

The carrying amount of the equipment on the 12/31/Y5 balance sheet is $42,500 ($51,000 – 8,500).

4-10

Chapter 04 - International Financial Reporting Standards: Part I

December 31, Year 6

Depreciation expense $8,500Accumulated depreciation $8,500

The carrying amount of the equipment on the 12/31/Y6 balance sheet is $34,000 ($42,500 – 8,500), prior to any evaluation of whether the impairment has reversed.

Because the technological innovations related to the equipment are not as effective as expected, there is an indicator that the equipment might no longer be impaired. The company must compare the carrying amount of the equipment at 12/31/Y6 with its recoverable amount.

Carrying amount, 12/31/Y6 $34,000

Recoverable amount, 12/31/Y6:(a) Net selling price $42,000(b) Value in use (PV of future cash flows) $44,000Recoverable amount (higher of (a) and (b)) $44,000

The recoverable amount exceeds the carrying amount, thus the equipment is no longer impaired. The equipment is written-up and the impairment loss reversed, but only up to the point where the resulting carrying amount is equal to what it would have been if no impairment had been recorded. This is calculated as:

Cost $100,000Accumulated depreciation ($10,000 x 6 years) 60,000Carrying amount, 12/31/Y6 without impairment $40,000

In this case, the asset is written up from $34,000 to $40,000. The following journal entry is recorded at December 31, Year 6:

Equipment (or Accumulated depreciation) $6,000Reversal of impairment loss (gain) $6,000

4-11

Chapter 04 - International Financial Reporting Standards: Part I

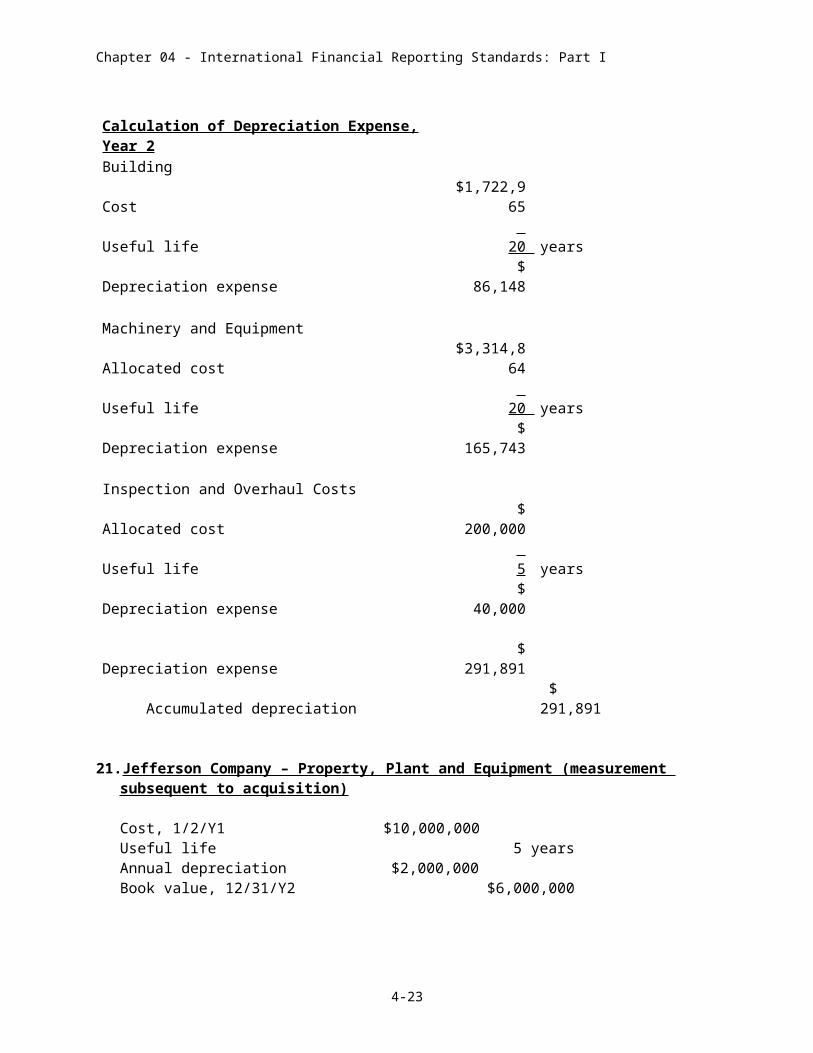

20. Godfrey Company – Property, Plant and Equip (dismantling and inspection costs)

Calculation of Initial Cost, January 1, Year 2: AmountPV Factor

(10%)Building Construction cost $ 1,500,000 Present value of dismantling and removal costs 222,965 1,500,000 0.14864Total cost of the building $ 1,722,965

Machinery and EquipmentConstruction cost $ 3,500,000 Present value of dismantling and removal costs 14,864 100,000 0.14864Total cost of the machinery and equipment $ 3,514,864 Less: Cost of inspection and overhaul 200,000 Cost allocated to machinery and equipment $ 3,314,864

Journal entry at January 1, Year 2:Building $ 1,722,965 Machinery and equipment 3,314,864 Inspection and overhaul costs 200,000 Cash $ 5,000,000

Provision for dismantling and removal 237,83

0

4-12

Chapter 04 - International Financial Reporting Standards: Part I

Calculation of Depreciation Expense, Year 2BuildingCost $1,722,965 Useful life 20 yearsDepreciation expense $ 86,148

Machinery and EquipmentAllocated cost $3,314,864 Useful life 20 yearsDepreciation expense $ 165,743

Inspection and Overhaul CostsAllocated cost $ 200,000 Useful life 5 yearsDepreciation expense $ 40,000

Depreciation expense $ 291,891 Accumulated depreciation $ 291,891

21. Jefferson Company – Property, Plant and Equipment (measurement subsequent to acquisition)

Cost, 1/2/Y1 $10,000,000Useful life 5 yearsAnnual depreciation $2,000,000Book value, 12/31/Y2 $6,000,000

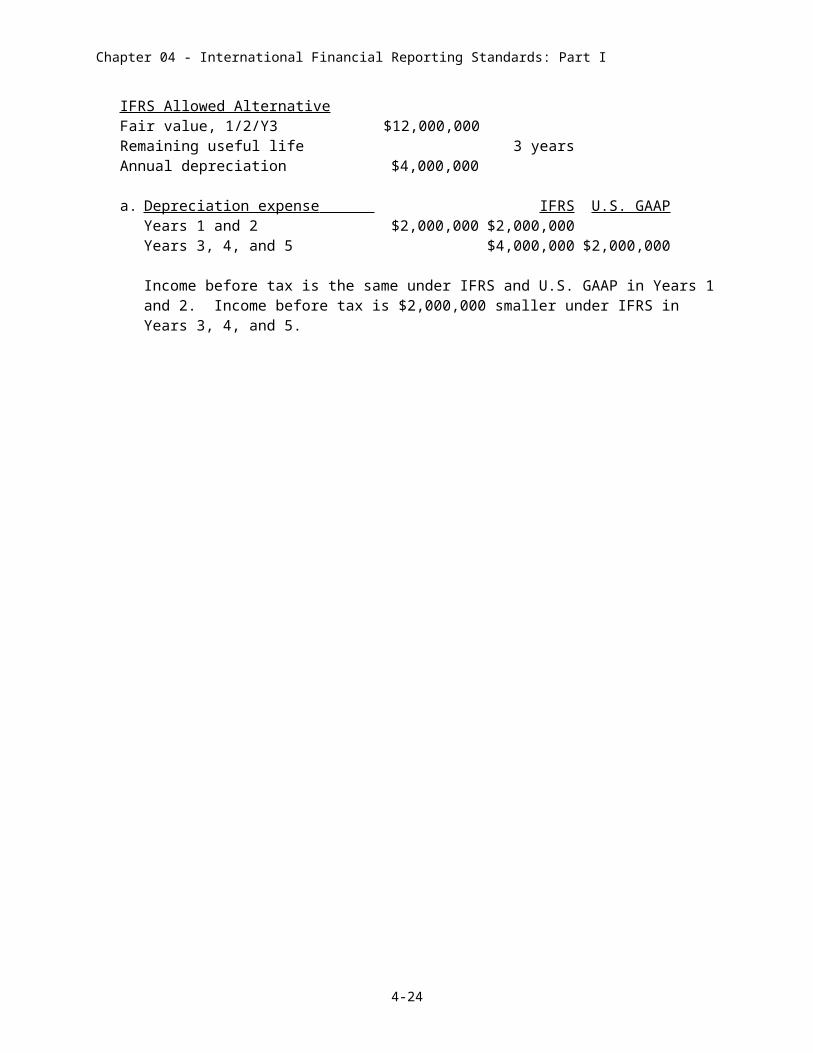

IFRS Allowed AlternativeFair value, 1/2/Y3 $12,000,000Remaining useful life 3 yearsAnnual depreciation $4,000,000

a. Depreciation expense IFRS U.S. GAAPYears 1 and 2 $2,000,000 $2,000,000Years 3, 4, and 5 $4,000,000 $2,000,000

Income before tax is the same under IFRS and U.S. GAAP in Years 1 and 2. Income before tax is $2,000,000 smaller under IFRS in Years 3, 4, and 5.

4-13

Chapter 04 - International Financial Reporting Standards: Part I

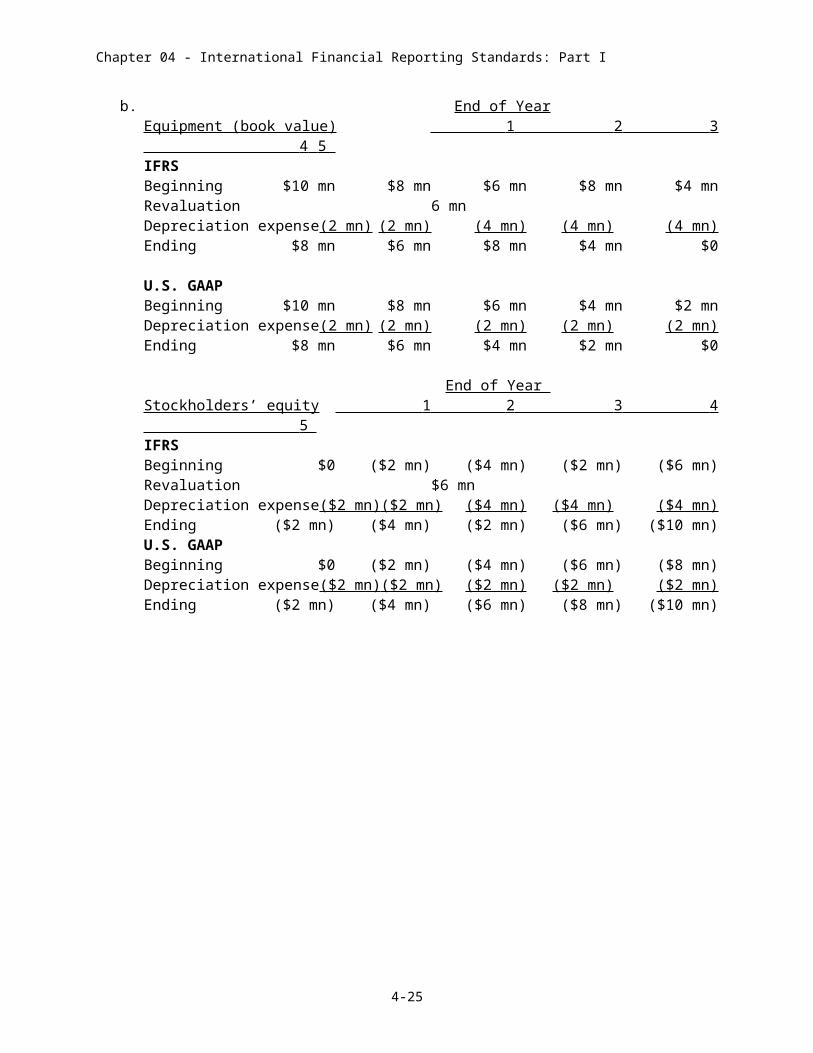

b. End of YearEquipment (book value) 1 2 3 4 5 IFRS

Beginning $10 mn $8 mn $6 mn $8 mn $4 mnRevaluation 6 mn Depreciation expense (2 mn) (2 mn) (4 mn) (4 mn) (4 mn)Ending $8 mn $6 mn $8 mn $4 mn $0

U.S. GAAP Beginning $10 mn $8 mn $6 mn $4 mn $2 mn

Depreciation expense (2 mn) (2 mn) (2 mn) (2 mn) (2 mn)Ending $8 mn $6 mn $4 mn $2 mn $0

End of Year Stockholders’ equity 1 2 3 4 5 IFRS

Beginning $0 ($2 mn) ($4 mn) ($2 mn) ($6 mn)Revaluation $6 mn Depreciation expense($2 mn) ($2 mn) ($4 mn) ($4 mn) ($4 mn)Ending ($2 mn) ($4 mn) ($2 mn) ($6 mn) ($10 mn)U.S. GAAP

Beginning $0 ($2 mn) ($4 mn) ($6 mn) ($8 mn)Depreciation expense($2 mn) ($2 mn) ($2 mn) ($2 mn) ($2 mn)Ending ($2 mn) ($4 mn) ($6 mn) ($8 mn) ($10 mn)

4-14

Chapter 04 - International Financial Reporting Standards: Part I

22. Madison Company – Property, Plant and Equipment (impairment)

IFRS U.S. GAAPCarrying amount 10,000,000 Carrying amount 10,000,000Net selling price 7,500,000 Future cash flows 10,000,000Discounted future cash flows 8,000,000 No impairment 0Value in use (larger amount) 8,000,000Impairment loss 2,000,000

a. (1) IFRS: Year 1 Depreciation expense 2,000,000

Impairment loss 2,000,000

Years 2 - 6 Depreciation expense 1,600,000 (8,000,000/5 years)

(2) U.S. GAAP: Years 1-6 Depreciation expense 2,000,000

b. Income before taxIFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Depreciation expense (2,000,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000)

Impairment loss (2,000,000) 0 0 0 0 0

Impact on income (4,000,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000)

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Depreciation expense (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000)

Impact on income (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000)

Diff. (IFRS-U.S. GAAP) (2,000,000) 400,000 400,000 400,000 400,000 400,000

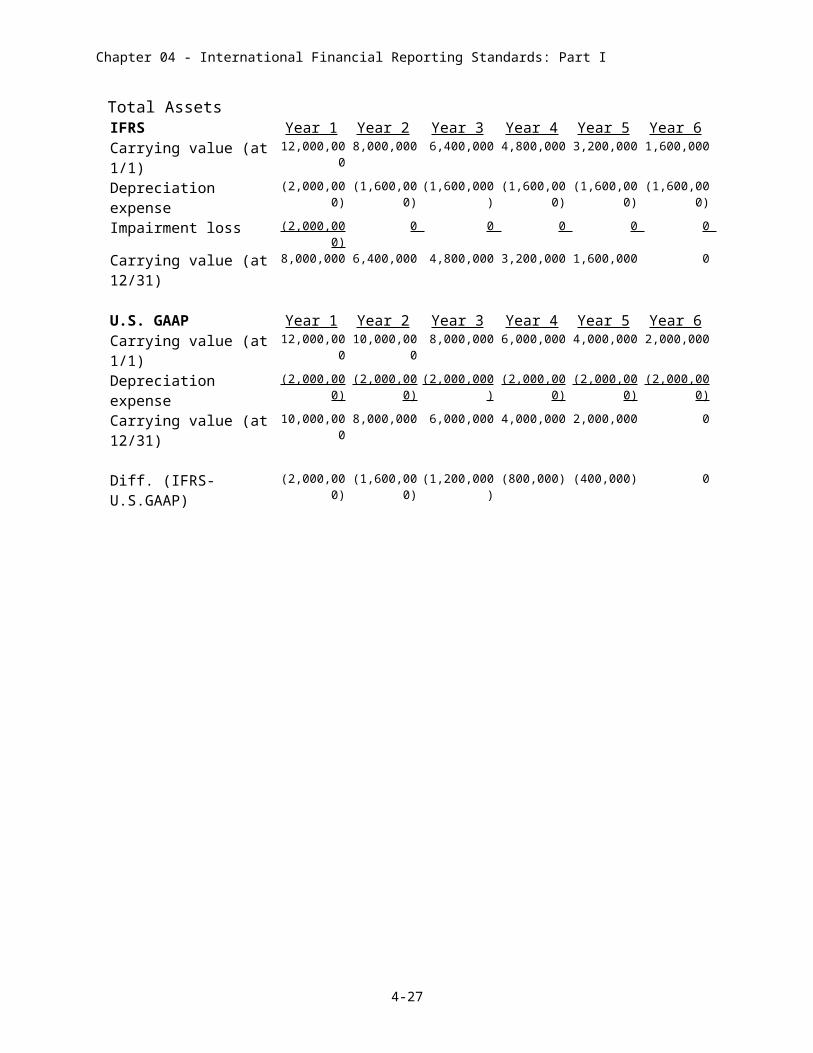

Total AssetsIFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Carrying value (at 1/1) 12,000,000 8,000,000 6,400,000 4,800,000 3,200,000 1,600,000

Depreciation expense (2,000,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000)

Impairment loss (2,000,000) 0 0 0 0 0

Carrying value (at 12/31) 8,000,000 6,400,000 4,800,000 3,200,000 1,600,000 0

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Carrying value (at 1/1) 12,000,000 10,000,000 8,000,000 6,000,000 4,000,000 2,000,000

Depreciation expense (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000)

Carrying value (at 12/31) 10,000,000 8,000,000 6,000,000 4,000,000 2,000,000 0

Diff. (IFRS-U.S.GAAP) (2,000,000) (1,600,000) (1,200,000) (800,000) (400,000) 0

4-15

Chapter 04 - International Financial Reporting Standards: Part I

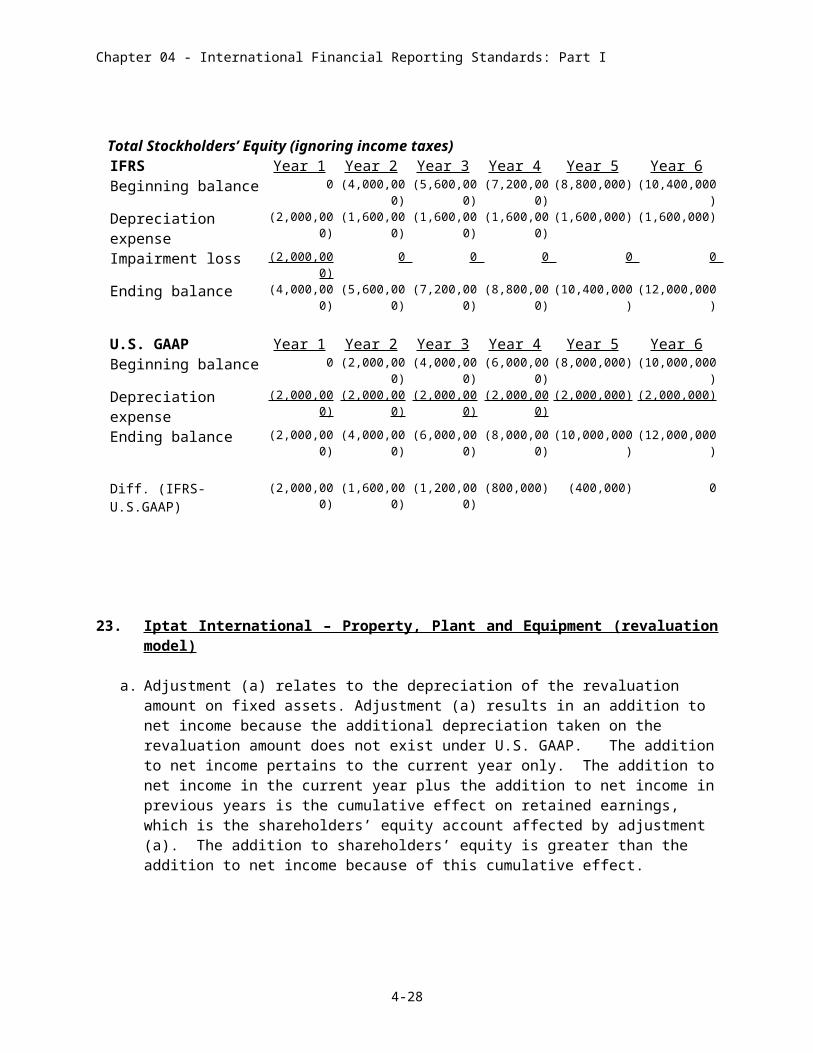

Total Stockholders’ Equity (ignoring income taxes)IFRS Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Beginning balance 0 (4,000,000) (5,600,000) (7,200,000) (8,800,000) (10,400,000)

Depreciation expense (2,000,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000) (1,600,000)

Impairment loss (2,000,000) 0 0 0 0 0

Ending balance (4,000,000) (5,600,000) (7,200,000) (8,800,000) (10,400,000) (12,000,000)

U.S. GAAP Year 1 Year 2 Year 3 Year 4 Year 5 Year 6Beginning balance 0 (2,000,000) (4,000,000) (6,000,000) (8,000,000) (10,000,000)

Depreciation expense (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000) (2,000,000)

Ending balance (2,000,000) (4,000,000) (6,000,000) (8,000,000) (10,000,000) (12,000,000)

Diff. (IFRS-U.S.GAAP) (2,000,000) (1,600,000) (1,200,000) (800,000) (400,000) 0

23. Iptat International – Property, Plant and Equipment (revaluation model)

a. Adjustment (a) relates to the depreciation of the revaluation amount on fixed assets. Adjustment (a) results in an addition to net income because the additional depreciation taken on the revaluation amount does not exist under U.S. GAAP. The addition to net income pertains to the current year only. The addition to net income in the current year plus the addition to net income in previous years is the cumulative effect on retained earnings, which is the shareholders’ equity account affected by adjustment (a). The addition to shareholders’ equity is greater than the addition to net income because of this cumulative effect.

b. Adjustment (b) relates to the revaluation surplus (increase in shareholders’ equity) that is recorded when fixed assets are revalued. This increase does not exist under U.S. GAAP and shareholders’ equity must be reduced accordingly. In this case, the shareholders’ equity account affected is Revaluation Surplus.

24. Lincoln Company – Research and Development Costs

a. IFRS Year 1 Year 2Research expense $6 millionDeferred development costs (asset) $4 millionAmortization expense – deferred development costs $800,000

U.S. GAAPResearch and development expense $10 million --

4-16

Chapter 04 - International Financial Reporting Standards: Part I

b. IFRS result in $4 million larger income before tax in Year 1 and $800,000 smaller income before tax in Years 2-6 compared to U.S. GAAP.

Ignoring income taxes, total assets and total stockholders’ equity are larger under IFRS by the following amounts:

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 $4,000,000 $3,200,000 $2,400,000 $1,600,000 $800,000 $0

25. Xanxi Petrochemical Company – Deferred development costs; Gain on sale and leaseback

Under IFRS, Xanxi apparently has capitalized some development costs as an asset (IAS 38), which would not be acceptable under U.S. GAAP. Adjustment (a) adds back the current year’s amortization expense on the deferred development costs that was deducted in determining IFRS net income. This adjustment results in a larger amount of U.S. GAAP net income. The addition to income flows through to retained earnings increasing shareholders’ equity. The addition to net income pertains to the current year only. The addition to net income in the current year plus the addition to net income in previous years is the cumulative effect on retained earnings. The addition to shareholders’ equity is greater than the addition to net income because of this cumulative effect.

If the lease in a sale-leaseback transaction is classified as an operating lease, IAS 17 requires the gain on such a transaction to be reported in income immediately, whereas U.S. GAAP requires the gain to be amortized over the life of the lease. Adjustment (b) subtracts the gain on sale/leaseback in the current year that was recognized in full under IFRS. The amount of adjustment (b) is the difference between the entire gain recognized under IFRS and the portion of the gain that would be recognized under U.S. GAAP (including amortization of gains that might have been generated in earlier years). The same amount should be subtracted from retained earnings reducing shareholders’ equity. From the fact that adjustment (b) reduced shareholders’ equity by a larger amount than it reduces net income, we can infer that Xanxi had one or more sale/leaseback gains in previous years.

4-17

Chapter 04 - International Financial Reporting Standards: Part I

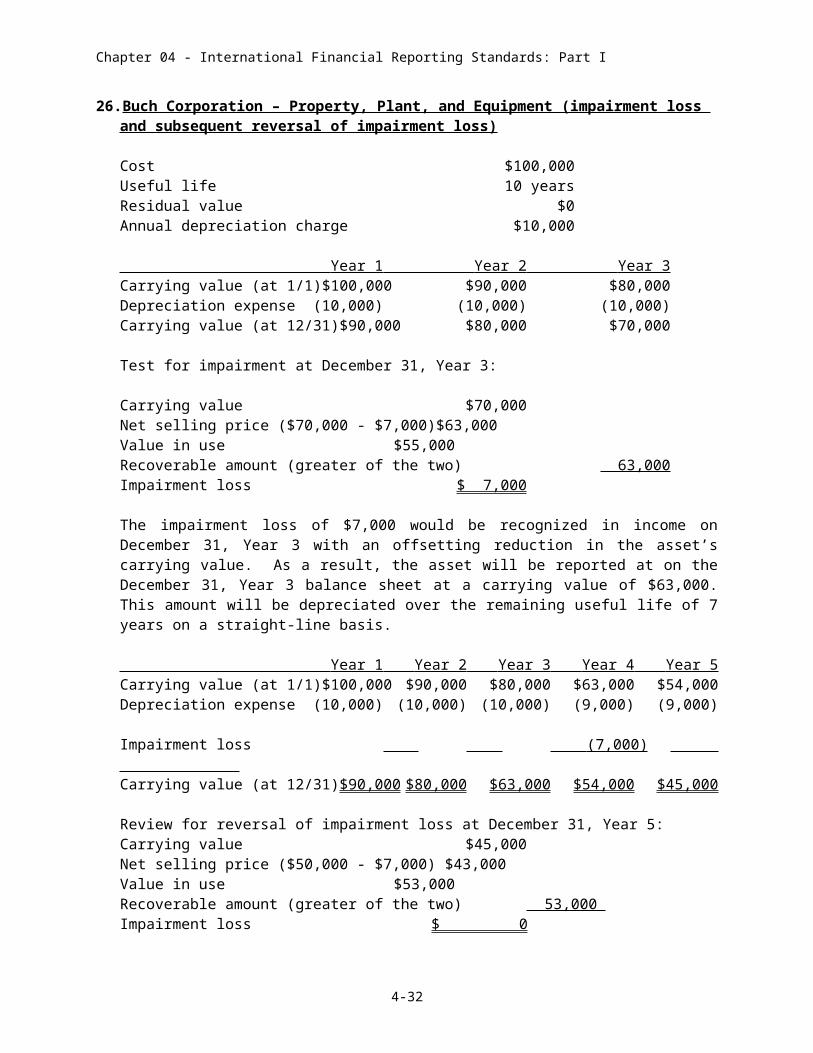

26. Buch Corporation – Property, Plant, and Equipment (impairment loss and subsequent reversal of impairment loss)

Cost $100,000Useful life 10 yearsResidual value $0Annual depreciation charge $10,000

Year 1 Year 2 Year 3 Carrying value (at 1/1) $100,000 $90,000 $80,000Depreciation expense (10,000) (10,000) (10,000)Carrying value (at 12/31) $90,000 $80,000 $70,000

Test for impairment at December 31, Year 3:

Carrying value $70,000Net selling price ($70,000 - $7,000) $63,000Value in use $55,000Recoverable amount (greater of the two) 63,000Impairment loss $ 7,000

The impairment loss of $7,000 would be recognized in income on December 31, Year 3 with an offsetting reduction in the asset’s carrying value. As a result, the asset will be reported at on the December 31, Year 3 balance sheet at a carrying value of $63,000. This amount will be depreciated over the remaining useful life of 7 years on a straight-line basis.

Year 1 Year 2 Year 3 Year 4 Year 5 Carrying value (at 1/1) $100,000 $90,000 $80,000 $63,000 $54,000Depreciation expense (10,000) (10,000) (10,000) (9,000) (9,000)

Impairment loss (7,000) Carrying value (at 12/31) $90,000 $80,000 $63,000 $54,000 $45,000

Review for reversal of impairment loss at December 31, Year 5:Carrying value $45,000Net selling price ($50,000 - $7,000) $43,000Value in use $53,000Recoverable amount (greater of the two) 53,000 Impairment loss $ 0

4-18

Chapter 04 - International Financial Reporting Standards: Part I

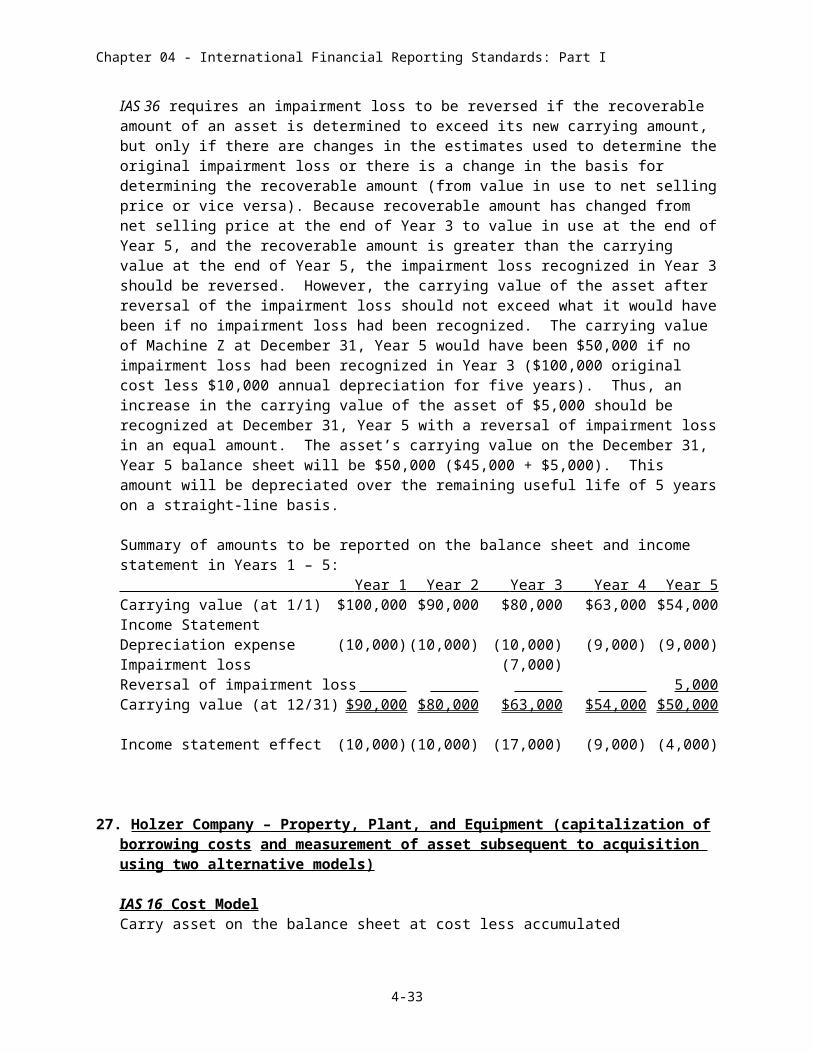

IAS 36 requires an impairment loss to be reversed if the recoverable amount of an asset is determined to exceed its new carrying amount, but only if there are changes in the estimates used to determine the original impairment loss or there is a change in the basis for determining the recoverable amount (from value in use to net selling price or vice versa). Because recoverable amount has changed from net selling price at the end of Year 3 to value in use at the end of Year 5, and the recoverable amount is greater than the carrying value at the end of Year 5, the impairment loss recognized in Year 3 should be reversed. However, the carrying value of the asset after reversal of the impairment loss should not exceed what it would have been if no impairment loss had been recognized. The carrying value of Machine Z at December 31, Year 5 would have been $50,000 if no impairment loss had been recognized in Year 3 ($100,000 original cost less $10,000 annual depreciation for five years). Thus, an increase in the carrying value of the asset of $5,000 should be recognized at December 31, Year 5 with a reversal of impairment loss in an equal amount. The asset’s carrying value on the December 31, Year 5 balance sheet will be $50,000 ($45,000 + $5,000). This amount will be depreciated over the remaining useful life of 5 years on a straight-line basis.

Summary of amounts to be reported on the balance sheet and income statement in Years 1 – 5: Year 1 Year 2 Year 3 Year 4 Year 5 Carrying value (at 1/1) $100,000 $90,000 $80,000 $63,000 $54,000Income StatementDepreciation expense (10,000) (10,000) (10,000) (9,000) (9,000)Impairment loss (7,000)Reversal of impairment loss 5,000 Carrying value (at 12/31) $90,000 $80,000 $63,000 $54,000 $50,000

Income statement effect (10,000) (10,000) (17,000) (9,000) (4,000)

27. Holzer Company – Property, Plant, and Equipment (capitalization of borrowing costs and measurement of asset subsequent to acquisition using two alternative models)

IAS 16 Cost Model Carry asset on the balance sheet at cost less accumulated depreciation and any accumulated impairment losses.

Capitalize borrowing costs borrowing costs attributable to the construction of qualifying assets.

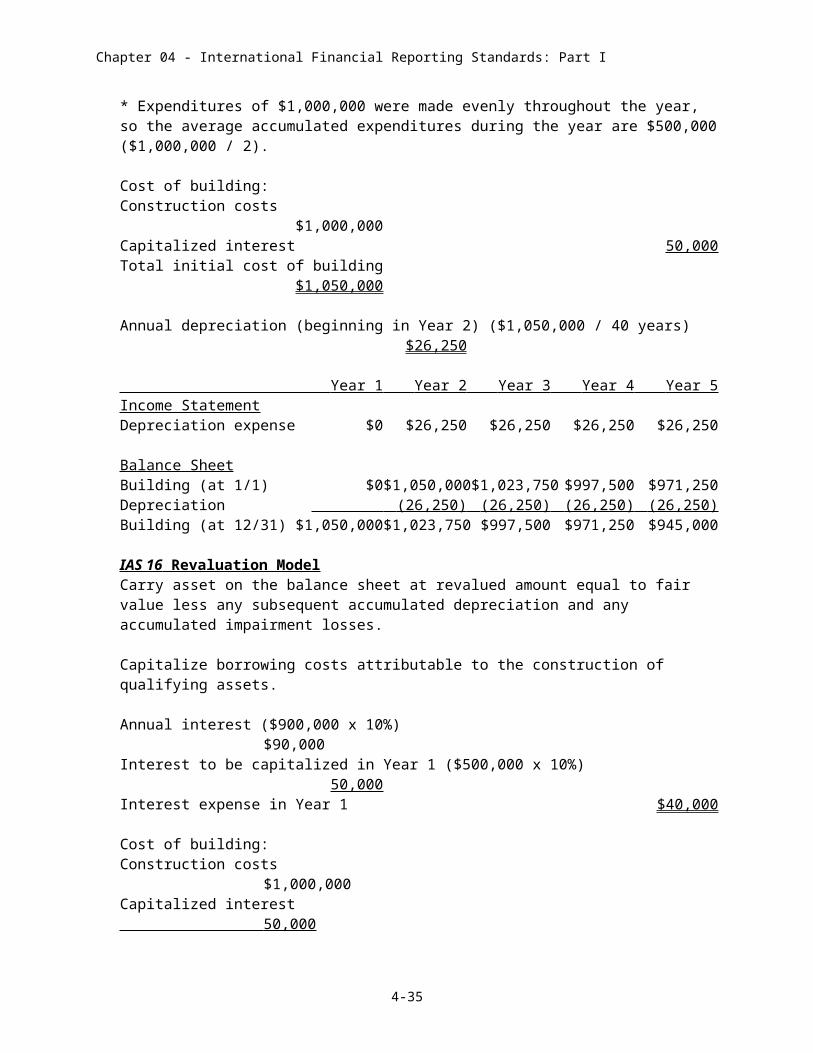

Annual interest ($900,000 x 10%) $90,000Interest to be capitalized in Year 1 ($500,000* x 10%) 50,000Interest expense in Year 1 $40,000

4-19

Chapter 04 - International Financial Reporting Standards: Part I

* Expenditures of $1,000,000 were made evenly throughout the year, so the average accumulated expenditures during the year are $500,000 ($1,000,000 / 2).

Cost of building:Construction costs $1,000,000Capitalized interest 50,000Total initial cost of building $1,050,000

Annual depreciation (beginning in Year 2) ($1,050,000 / 40 years) $26,250

Year 1 Year 2 Year 3 Year 4 Year 5 Income StatementDepreciation expense $0 $26,250 $26,250 $26,250 $26,250

Balance SheetBuilding (at 1/1) $0 $1,050,000 $1,023,750 $997,500 $971,250Depreciation (26,250) (26,250) (26,250) (26,250) Building (at 12/31) $1,050,000 $1,023,750 $997,500 $971,250 $945,000

IAS 16 Revaluation Model Carry asset on the balance sheet at revalued amount equal to fair value less any subsequent accumulated depreciation and any accumulated impairment losses.

Capitalize borrowing costs attributable to the construction of qualifying assets.

Annual interest ($900,000 x 10%) $90,000Interest to be capitalized in Year 1 ($500,000 x 10%) 50,000Interest expense in Year 1 $40,000

Cost of building:Construction costs $1,000,000Capitalized interest 50,000 Total initial cost of building $1,050,000

Annual depreciation (beginning in Year 2) ($1,050,000 / 40 years) $26,250

Year 1 Year 2 Year 3 Year 4 Year 5 Income StatementDepreciation expense $0 $26,250 $26,250 $25,526 2 $25,526 Subtotal $0 $26,250 $26,250 $25,526 $25,526Loss on revaluation 27,500Reversal of revaluation loss (27,500) Total expense (income) $0 $26,250 $43,750 $25,526 $(1,974)

4-20

Chapter 04 - International Financial Reporting Standards: Part I

Balance SheetBuilding (at 1/1) $0 $1,050,000 $1,023,750 $970,000 $944,474Depreciation (26,250) (26,250) (25,526) (25,526) Building (at 12/31) $1,050,000 $1,023,750 $997,500 $944,474 $918,948Loss on revaluation (27,500)1

Reversal of revaluation loss 27,5003

Revaluation surplus 3,552 3 Building (at 12/31) $1,050,000 $1,023,750 $970,000 $944,474 $950,000

1 At December 31,Year 3, the fair value of the building is determined to be $970,000. The carrying value of the building is decreased by $27,500, with a loss on revaluation recognized in Year 3 net income.

2 Depreciation in Year 4 is $25,526 ($970,000 / 38 remaining years).3 At December 31,Year 5, the fair value of the building is determined to be $950,000. The

carrying value of the building is increased by $31,052. A reversal of revaluation loss of $27,500 is recognized in income and $3,552 ($31,052 – 27,500) is recorded as revaluation surplus in shareholders’ equity.

28. Quantacc Company – Reconciliation to U.S. GAAP

Year 5Net income under IFRS $100,000Adjustments:

Reversal of depreciation on revaluation of fixed assets 3,500Reversal of amortization of deferred development costs 16,000Reversal of gain on sale and leaseback (150,000)Amortization of gain on sale and leaseback 7,500

Net income (loss) under U.S. GAAP $ (23,000 )

December 31, Year 5Stockholders’ equity under IFRS $500,000Adjustments:

Reversal of revaluation of fixed assets (35,000)Reversal of accumulated depreciation on revaluation of fixed assets 10,500Reversal of deferred development costs (80,000)Reversal of accumulated amortization on deferred development costs 16,000Reversal of gain on sale and leaseback (150,000)Accumulated amortization of gain on sale and leaseback 7,500

Stockholders’ equity under U.S. GAAP $ 269,000

4-21

Chapter 04 - International Financial Reporting Standards: Part I

29. Stratosphere Company – Property, Plant, and Equipment (revaluation model)

Amounts in parentheses represent credits.

Date CostAccumulated depreciation

Carrying Amount

Revaluation Surplus Income

Retained Earnings

January 1, Year 1 4,000,000 4,000,000 December 31, Year 1 4,000,000 (200,000) 3,800,000 200,000 200,000December 31, Year 2 4,000,000 (200,000) 3,600,000 200,000 200,000December 31, Year 2 (220,000) 400,000 180,000 (180,000) Balance 3,780,000 0 3,780,000 (180,000) 400,000December 31, Year 3 3,780,000 (210,000)* 3,570,000 10,000 210,000 200,000 Balance 3,780,000 (210,000) 3,570,000 (170,000) 600,000Sale, Jan 2, Year 4 (3,780,000) 210,000 (3,570,000) 170,000 70,000 (100,000) Balance $ – $ – $ – $ – 70,000 500,000

* Calculated as $3,780,000 divided by remaining life of 18 years.

Note: The net impact on retained earnings over the life of the equipment is negative $500,000 (debit), which is the difference between the purchase price of $4,000,000 and the selling price of $3,500,000.

Journal entries to account for the building under the revaluation model

January 1, Year 1Building 4,000,000

Cash 4,000,000

December 31, Year 1Depreciation expense 200,000

Accumulated depreciation 200,000

December 31, Year 2Depreciation expense 200,000

Accumulated depreciation 200,000

Accumulated depreciation 400,000Building 220,000Revaluation surplus 180,000

December 31, Year 3Depreciation expense 210,000

Accumulated depreciation 210,000

Revaluation surplus 10,000Retained earnings 10,000

4-22

Chapter 04 - International Financial Reporting Standards: Part I

January 2, Year 4Cash 3,500,000Accumulated depreciation 210,000Loss on sale 70,000

Building 3,780,000

Revaluation surplus (OCI) 170,000Retained earnings 170,000

Note: if the asset hadn’t been revalued, the carrying amount of the building would have been $3,400,000 (cost of $4,000,000 less $200,000 depreciation x3 years) at the date of sale. If the building was sold for $3,500,000, there would have been a gain of $100,000.

Since the building was revalued, the depreciation expense over the three years was $610,000 ($200,000 in Year 1 and Year 2 and $210,000 in Year 3). Revaluation surplus was reduced by $10,000 during this period with the credit applied directly to retained earnings. Therefore, after reversing the remaining revaluation surplus of $170,000 to retained earnings, the resulting loss is $70,000.

30. Reforce Company – Intangible Assets (determination of cost)

IntangibleCost Asset

Market research costs, Year 1 $ 25,000 No

Research costs, Year 1 100,000 NoResearch costs, 1st Quarter, Year 2 70,000 NoLegal fees to register patent, April, Year 2 25,000 YesDevelopment costs for initial prototype, 2nd Quarter, Year 2 500,000 NoTesting of initial prototype, June, Year 2 50,000 NoManagement time to develop business plan, 2nd Quarter, Year 2 15,000 NoCost of revisions and second prototype, 3rd Quarter, Year 2 175,000 YesLegal fees to defend patent, October, Year 2 50,000 YesProduction costs, 4th Quarter, Year 2 400,000 NoMarketing campaign, 4th Quarter, Year 2 80,000 No

The legal fees to register and defend the patent are capitalized as an intangible asset (Patent, $75,000).

Development costs incurred after both (a) technical feasibility has been established and (b) a business plan has been developed are capitalized (Deferred Development Costs, $175,000).

Production costs will be capitalized as Inventory; not as an intangible asset.

Note: Under U.S. GAAP, only the costs associated with obtaining and defending the patent would be recognized as an asset.

4-23

Chapter 04 - International Financial Reporting Standards: Part I

31. Philosopher Stone – Intangible Assets (web site development costs)

Because Philosopher Stone’s intranet will only be used to share information about company personnel, demonstrating future economic benefits might be difficult. SIC 32 talks about a company using a web site to generate revenue, which is not the purpose of the intranet in this case. Even if future economic benefits can be demonstrated, only the costs incurred beyond the “planning stage” are eligible for capitalization. In addition, SIC 32 indicates that the estimated useful life of a web site should be short, meaning that whatever amount of costs are capitalized they will be amortized over a short period of time.

32. Bartholomew Corporation – Goodwill (impairment)

Calculation of Recognized Noncontrolling InterestFair value of net assets (excluding goodwill) $5,000,000Noncontrolling interest % 20%Noncontrolling interest $1,000,000

Calculation of Unrecognized Noncontrolling InterestImplied fair value of 100% of Samson Company $5,000,000 / 80% = $6,875,000Noncontrolling interest % 20%Fair value of noncontrolling interest $1,375,000Recognized noncontrolling interest 1,000,000Unrecognized noncontrolling interest $ 375,000

Calculation of GoodwillConsideration transferred $5,500,000Plus: Noncontrolling interest (recognized) 1,000,000Subtotal $6,500,000Less: Fair value of net assets (excluding goodwill) ,5,000,000Goodwill $1,500,000

The summary journal entry to recognize the acquisition of Samson’s shares would be:Samson’s net assets $5,000,000Goodwill 1,500,000

Cash $5,500,000Noncontrolling interest 1,000,000

Impairment Test, End of Year 1 Net assets Goodwill TotalCarrying amount $5,000,000 $1,500,000 $6,500,000

Unrecognized noncontrolling interest 0 375,000 375,000Adjusted carrying amount $5,000,000 $1,875,000 $6,875,000

Determination of recoverable amount:Fair value less costs to sell (a) $5,000,000 - $200,000 = $4,800,000Present value of future cash flows (b) 4,750,000Recoverable amount (higher of (a) and (b)) 4,800,000Impairment loss (adjusted carrying amount less recoverable amount) $2,075,000

4-24

Chapter 04 - International Financial Reporting Standards: Part I

Allocation of impairment lossGoodwill $1,875,000Samson’s net assets 200,000Total $2,075,000

The allocation of impairment loss to goodwill is shared between the controlling and noncontrolling interest. Thus, $1,500,000 (80%) is allocated to the parent’s investment in Samson Company; the remaining $375,000 (20%) is attributed to the noncontrolling interest but is not recognized. Bartholomew will reflect Goodwill of zero on its December 31, Year 1 balance sheet, and Samson’s net assets will be included in the consolidated amounts at a total of $4,800,000 ($5,000,000 – $200,000).

33. Rocker Division – Goodwill (impairment)

Part A.

Calculation of impairment loss, 12/31/Y5:Carrying amount $2,775Recoverable amount 1,560Impairment loss $1,215

The impairment loss is allocated first to goodwill, until it is reduced to zero. The remaining $215 of loss is allocated to the other assets on the basis of relative carrying amounts:

Property, plant, and equipment $1,375 / $1,775 x $215 = $167Other intangibles $400 / $1,775 x $215 = $ 48

GoodwillProperty, Plant, and Equipment

Other Intangibles Total

Carrying amount, 12/31/Y4 $1,000 $1,500 $500 $3,000Amortization expense, Year 5 0 (125) (100) (225)Subtotal $1,000 $1,375 $400 $ 2,775Impairment loss (1,000) (167) (48) (1,215)Carrying amount, 12/31/Y5 $ 0 $1,208 $352 $1,560

Part B.

Amortization expense is calculated for Year 6 using the revised carrying amounts and estimated remaining useful lives of 11 years and 4 years, respectively:

Property, plant, and equipment $1,208 / 11 years = $110Other intangibles $352 / 4 years = $48 The improvement in export laws results in a potential impairment recovery of $470 = $1,930 – $1,560. However, carrying amounts may only be written-up to the original cost less accumulated amortization (that would have occurred without the impairment loss).

4-25

Chapter 04 - International Financial Reporting Standards: Part I

Carrying amount of PPE is limited to historical cost $1,500 less depreciation of $250 (2 years at $125) = $1,250; carrying amount of Other Intangibles is limited to historical cost of $500 less amortization of $200 (2 years at $100) = $300; the carrying amount for total assets at 12/31/Y6 is limited to $1,550 ($1,250 + $300). Therefore, recovery of impairment loss is $148 ($1,550 - $1,402), which will be prorated to PPE and Other Intangibles based on relative carrying amounts. No recovery of impairment on goodwill is allowed.

Property, plant, and equipment $1,098 / $1,402 x $148 = $116Other intangibles $304 / $1,402 x $148 = $ 32

GoodwillProperty, Plant, and Equipment

Other Intangibles Total

Carrying amount, 12/31/Year 5 $ 0 $1,208 $352 $1,560Amortization expense, Year 6 (110) (48) (158)Subtotal $ 0 $1,098 $304 $1,402Impairment loss/recovery 116 32 148Carrying amount, 12/31/Year 6 $ 0 $1,214 $336 $1,550

34. Complete Company – Goodwill (measurement and impairment)

Part A.

Alternative 1 – Noncontrolling Interest Measured at Proportionate Share of Fair Value of Acquired Firm’s Net Assets

Calculation of Noncontrolling InterestFair value of net assets (excluding goodwill) ($2,000,000 - $500,000) $1,500,000Noncontrolling interest % 40%Noncontrolling interest $600,000

Calculation of GoodwillConsideration transferred $1,200,000Plus: Noncontrolling interest 600,000Subtotal $1,800,000Less: Fair value of net assets (excluding goodwill) 1,500,000Goodwill $ 300,000

4-26

Chapter 04 - International Financial Reporting Standards: Part I

Alternative 2 – Noncontrolling Interest Measured at Fair Value

Calculation of Noncontrolling InterestImplied fair value of 100% of Partial Company $1,200,000 / 60% = $2,000,000Noncontrolling interest % 40%Noncontrolling interest $800,000

Calculation of GoodwillConsideration transferred $1,200,000Plus: Noncontrolling interest 800,000Subtotal $2,000,000Less: Fair value of net assets (excluding goodwill) 1,500,000Goodwill $ 500,000

Goodwill of $500,000 is comprised of $300,000 purchased by Complete plus $200,000 attributed to the Noncontrolling interest ($500,000 - $300,000).

Part B.

Alternative 1 – Noncontrolling Interest Measured at Proportionate Share of Fair Value of Acquired Firm’s Net Assets Excluding Goodwill

Calculation of Noncontrolling InterestFair value of net assets (excluding goodwill) ($2,000,000 - $500,000) $1,500,000Noncontrolling interest % 20%Noncontrolling interest $300,000

Calculation of GoodwillConsideration transferred $1,100,000Plus: Noncontrolling interest 300,000Subtotal $1,400,000Less: Fair value of net assets (excluding goodwill) 1,500,000Gain on bargain purchase $(100,000)

In this case, Complete would recognize a gain from a bargain purchase in net income in the year in which the acquisition takes place.

Alternative 2 – Noncontrolling Interest Measured at Fair Value

Calculation of Noncontrolling InterestImplied fair value of 100% of Partial Company $1,100,000 / 80% = $1,375,000Noncontrolling interest % 20%Noncontrolling interest $275,000

4-27

Chapter 04 - International Financial Reporting Standards: Part I

Calculation of GoodwillConsideration transferred $1,100,000Plus: Noncontrolling interest 275,000Subtotal $1,375,000Less: Fair value of net assets (excluding goodwill) 1,500,000Gain on bargain purchase $(125,000)

Note: IFRS 3.34 indicates that the gain on bargain purchase is attributable to acquirer. Therefore, it does not appear that any of the gain would be allocated to the noncontrolling interest.

Part C. Assume that Complete Company adopted Alternative 1 in Part A to account for noncontrolling interest

Impairment loss is determined as follows:

Partial Co. Partial Co.Net assets Goodwill Total

Carrying amount $1,500,000 $300,000 $1,800,000

Unrecognized noncontrolling interest 0 200,000 200,000Adjusted carrying amount $1,500,000 $500,000 $2,000,000

Determination of recoverable amount:Fair value less costs to sell (a) $1,900,000 - $20,000 = $1,880,000Present value of future cash flows (b) 1,860,000Recoverable amount (higher of (a) and (b)) 1,880,000Impairment loss (adjusted carrying amount less recoverable amount) $ 120,000

Allocation of impairment loss:

All of the impairment loss is allocated to goodwill. Because Partial Company is a CGU, the impairment loss is shared between the controlling and noncontrolling interest. Thus, $72,000 (60%) is allocated to the parent’s investment in Partial Company; the remaining $48,000 (40%) is attributed to the noncontrolling interest but is not recognized.

Partial Co. Partial Co.Net assets Goodwill Total

Carrying amount $1,500,000 $300,000 $1,800,000

Impairment loss 0 72,000 72,000Carrying amount after impairment loss $1,500,000 $228,000 $1,728,000

Impairment loss $72,000 Goodwill $72,000

4-28

Chapter 04 - International Financial Reporting Standards: Part I

Year 1 Income StatementImpairment loss $72,000

End of Year 1 Consolidated Balance Sheet (amounts related to Partial Company)Net assets $1,500,000Goodwill 228,000Noncontrolling interest (600,000)

35. Thurstone Company – Borrowing Costs (capitalization)

Interest cost (£300,000 x 4% = £12,000 x $2.10 exchange rate on 3/31/Y1) $25,200Less: Income earned on temporary investment (£5,000 x $2.10) (10,500)Net interest cost $14,700Plus: Exchange rate loss (£300,000 x ($2.10 - $2.00)) 30,000Total borrowing cost to be capitalized at 3/31/Y1 $44,700

36. Atlanta Tours Company – Leases (classification)

Finance Lease Criteria Criterion met?Ownership is transferred to the lessee by the end of the lease term.

No.There is no indication that title transfers to the lessee.

The lease contains a bargain purchase option.

No.$4,000 purchase option > $3,500 estimated residual value

The lease term is a major part of the estimated economic life of the leased property.

Perhaps.5 years / 8 years = 62.5%; might be judged as “major part”

The PV of MLP is substantially all of the fair value of the leased property.

Perhaps.$8,930* / $10,000 = 89.3%; might be judged as “substantially all”

The leased assets are of such a specialized nature such that only the lessee can use them without major modifications being made.

Perhaps.Duck Boats Inc. probably would need to remove the wood carving to be able to sell or lease the vehicle to another customer. It is unclear whether this would be considered a major modification.

The lessee bears the lessor’s losses if the lessee cancels the lease.

No.The lease is non-cancelable

The lessee absorbs the gains or losses from fluctuations in the fair value of the residual value of the asset.

No.

The lessee may extend the lease for a secondary period at a rent substantially below the market rent.

No.The lease may not be extended.

4-29

Chapter 04 - International Financial Reporting Standards: Part I

* Calculation of PV of MLPPresent value factor for annuity due, 5 payments, 6% = 4.4651: $2,000 x 4.4651 = $8,930

It is unclear whether Atlanta Tours Company should classify this lease as a finance lease or as an operating lease; ultimately, it will be up to management’s judgment. Collectively, the three criteria that perhaps have been met might lead to a decision that finance lease classification is appropriate. This exercise demonstrates the judgment needed to apply IAS 17.Note: Under U.S. GAAP this lease definitely would not be capitalized, because it does not meet any of the capital lease criteria.

37. Fields Company – Sale-and-Leaseback (recognition of gain)

Part A.Because the leaseback is an operating lease and the sales price approximates fair value, Fields would record a sale and recognize a gain of $100,000 ($500,000 selling price - $400,000 carrying amount).

Part B.Because the leaseback is an operating lease and the sales price of $500,000 is greater than the fair value of $470,000, $30,000 would be deferred and amortized at the rate of $10,000 per year ($30,000 / 3 years) over the three-year term of the lease. The remaining gain of $70,000 ($470,000 fair value - $400,000 carrying amount) would be recognized immediately in net income.

Part C.Because this is a finance lease and there is no indication of impairment, Fields would defer the gain of $100,000 ($500,000 selling price - $400,000 carrying amount) and amortize it over the term of the lease at the rate of $5,000 per year ($100,000 / 20 years).

38. Bridget’s Bakery – Operating Lease

Total consideration for rent over the lease term is $292,500 ($2,500 for 117 months). This consideration must be recognized on a straight-line basis (unless another systematic basis is more representative of the time pattern of the lessee’s benefit from using the leased asset) over the entire lease period of 10 years (120 months), resulting in a monthly lease expense of $2,437.50 ($292,500 / 120 months).

Monthly journal entry for each of the first three months of the lease:

Lease expense $2,437.50Deferred rent payable $2,437.50

Deferred rent payable has a balance of $7,312.50 at the end of three months. This balance is amortized over the remaining 117 months at the rate of $62.50 per month ($7,312.50 / 117 months).

4-30

Chapter 04 - International Financial Reporting Standards: Part I

Journal entry in months 4 through 120:

Lease expense $2,437.50Deferred rent payable 62.50

Cash $2,500.00

Note: SIC-15 Operating Leases-Incentives directly relates to this situation.

39. Acceptable Treatments

Acceptable underIFRS U.S. GAAP Both Neither

A company takes out a loan to finance the construction of a building that will be used by the company. The interest on the loan is capitalized as part of the cost of the building.

X

Inventory is reported on the balance sheet using the last-in, first-out (LIFO) cost flow assumption. X

The gain on a sale and leaseback transaction classified as an operating lease is deferred and amortized over the lease term.

X

A company writes a fixed asset down to its recoverable amount and recognizes an impairment loss in Year 1. In a subsequent year, the recoverable amount is determined to exceed the asset’s carrying amount, and the previously recognized impairment loss is reversed.

X

A company pays less than the fair value of net assets in the acquisition of another company. The acquirer recognizes the difference as a gain on purchase of another company.

X

A company enters into an eight-year lease on equipment that is expected to have a useful life of ten years. The lease is accounted for as an operating lease.

X1

An intangible asset with an active market that was purchased two years ago is carried on the balance sheet at fair value.

X

In preparing interim financial statements, interim periods are treated as discrete reporting periods rather than as an integral part of the full year.

X

Research and development costs are capitalized when certain criteria are met. X2

Interest paid on borrowings is classified as an operating activity in the statement of cash flows. X

4-31

Chapter 04 - International Financial Reporting Standards: Part I

1 This would be acceptable under IAS 17 if 80% of the life of the lease is not viewed as the “major part” of the lease.

2 Neither IFRS nor U.S. GAAP allows capitalization of research costs.

CASE 4-1 Bessrawl Corporation- THIS IS ON THE FINAL TEST! STUDY THIS BECAUSE HE WILL NOT GO OVER IT AND MOST PEOPLE FAILED BECAUSE OF THIS QUESTION!!

Reconciliation from U.S. GAAP to IFRS 2011

Income under U.S. GAAP $1,000,0

00 Adjustments:

Reversal of writedown of inventory to replacement cost 10,000

Additional depreciation on revaluation of equipment (25,000)

Impairment loss on intangible asset (brand) (5,000)

Recognition of deferred development costs 80,000

Reversal of amortization of deferred gain on sale and leaseback (30,000)

Income under IFRS $1,030,000

2011

Stockholders’ equity under U.S. GAAP $8,000,0

00 Adjustments:

Reversal of writedown of inventory to replacement cost 10,000

Original revaluation surplus on equipment 600,000

Accumulated depreciation on revaluation of equipment (25,000)

Impairment loss on intangible assets (brand) (5,000)

Recognition of deferred development costs 80,000

Recognition of gain on sale and leaseback in 2009 150,000

Accumulated amortization of deferred gain on sale and leaseback (2009-2011) (90,000)

Stockholders’ equity under IFRS $8,720,000

Explanation of Adjustments

Inventory. Under U.S. GAAP, the company reports inventory on the balance sheet at the lower of cost or market, where market is defined as replacement cost ($180,000), with net realizable value ($190,000) as a ceiling and net realizable value less a normal profit ($152,00) as a floor.

4-32

Chapter 04 - International Financial Reporting Standards: Part I

In this case, inventory was written down to replacement cost and reported on the December 31, 2011 balance sheet at $180,000. A $70,000 loss was included in 2011 income.

4-33

Chapter 04 - International Financial Reporting Standards: Part I

In accordance with IAS 2, the company would report inventory on the balance sheet at the lower of cost ($250,000) and net realizable value ($190,000). Inventory would have been reported on the December 31, 2011 balance sheet at net realizable value of $190,000 and a loss on writedown of inventory of $60,000 would have been reflected in net income.

IFRS income would be $10,000 larger than U.S. GAAP net income. IFRS retained earnings would be larger by the same amount.

Equipment. Under U.S. GAAP, the company reports depreciation expense of $100,000 [($2,750,000 – $250,000) / 25 years] in 2010 and in 2011.

Under IAS 16’s revaluation model, depreciation expense on equipment in 2010 was $100,000, resulting in a book value at the end of 2010 of $2,650,000. The equipment then would be revalued upward at the beginning of 2011 to its fair value of $3,250,000.

The appropriate journal entry to recognize the revaluation would be:Equipment $600,000

Revaluation Surplus (a stockholders’ equity account) $600,000

In 2011, depreciation expense would be $125,000 [($3,250,000 - $250,000)/24 years].

The additional depreciation under IFRS causes IFRS-based income in 2011 to be $25,000 smaller than U.S. GAAP income. IFRS-based stockholders’ equity is $575,000 larger than U.S. GAAP stockholders’ equity. This is equal to the amount of the revaluation surplus ($600,000) less the additional depreciation in 2011 under IFRS ($25,000), which reduced retained earnings.

Intangible Assets. Under U.S. GAAP, an asset is impaired when its carrying amount exceeds the undiscounted future cash flows expected to arise from continued use of the asset. The brand acquired in 2008 has a carrying amount of $40,000 and future expected cash flows are $42,000, so it is not impaired under U.S. GAAP.

Under IAS 36, an asset is impaired when its carrying amount exceeds its recoverable amount, which is the greater of net selling price and value in use. The brand’s recoverable amount is $35,000; the greater of net selling price of $35,000 and value in use (present value of future cash flows) of $34,000. As a result, an impairment loss of $5,000 would be recognized under IFRS.

IFRS income and retained earnings would be $5,000 less than U.S. GAAP income and retained earnings.

Research and Development Costs. Under U.S. GAAP, research and development expense in the amount of $200,000 would be recognized in determining 2011 income.Under IAS 38, $120,000 (60% x $200,000) of research and development costs would be expensed in 2011, and $80,000 (40% x $200,000) of development costs would be capitalized as an intangible asset (deferred development costs).

4-34

Chapter 04 - International Financial Reporting Standards: Part I

IFRS-based income in 2011 would be $80,000 larger than U.S. GAAP income. Because the new product has not yet been brought to market, there is no amortization of the deferred development costs under IFRS in 2011.

Sale and Leaseback. Under U.S. GAAP, the gain on the sale and leaseback (operating lease) is recognized in income over the life of the lease. With a lease term of five years, $30,000 of the gain would be recognized in 2011. $30,000 also would have been recognized in 2009 and 2010, resulting in a cumulative amount of retained earnings at year-end 2011 of $90,000.

Under IAS 17, the entire gain on the sale and leaseback of $150,000 would have been recognized in income in 2009. This resulted in an increase in retained earnings of $150,000 in that year. No gain would be recognized in 2011. IFRS income in 2011 would be $30,000 smaller than U.S. GAAP income, but stockholders’ equity at December 31, 2011 under IFRS would be $60,000 larger than under U.S. GAAP.

4-35