fintech conference presentation

TRANSCRIPT

FinTech

Trends, Opportunities

and Risks in the Age of

Digitization

Alex Rozman

Deloitte Advisory

July 31, 2015

Confidential

2 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Presenter

As used in this document, “Deloitte Advisory” means Deloitte & Touche LLP, which provides audit and enterprise risk services; Deloitte Financial Advisory Services LLP, which provides forensic, dispute, and

other consulting services; and its affiliate, Deloitte Transactions and Business Analytics LLP, which provides a wide range of advisory and analytics services. Deloitte Transactions and Business Analytics LLP

is not a certified public accounting firm. These entities are separate subsidiaries of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its

subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Alex Rozman

Deloitte Advisory

Alex Rozman is a Senior Manager at Deloitte Advisory specializing in FinTech and

anti-money laundering compliance in the emerging payments industry. Prior to

joining Deloitte, Mr. Rozman worked as a Managing Partner for a litigation boutique

law firm, served as a Director for a consulting company, and served as a General

Counsel and Chief Compliance Officer for a forex broker-dealer. He is a frequent

speaker on emerging payments and cryptocurrency issues and has served as an

advisor to the senior management and boards of directors of technology and

financial services institutions. He holds a JD degree from Chicago-Kent College of

Law and a double BA from the University of Illinois at Champaign-Urbana.

3 Copyright © 2015 Deloitte Development LLC. All rights reserved.

In this age of digitization, financial services are in

an era of exponential change.

Pioneering FinTech startups are transforming

traditional banking services.

Banks will need to adapt or reinvent their core

business models to stay competitive.

Fintech payments products are posing new

consumer protection issues such as fraud and

personal data security risks as well as money

laundering and terrorist financing risks prompting a

heightened focus on regulation.

Introduction

Age of Digitization

5

Evolution of the Bookstore: 1994

6

Evolution of the Bookstore: 2003

7

Evolution of the Bookstore: 2007

8 C O N F I D E N T I A L | J U L Y 2 0 1 5

Computing Performance is Improving Exponentially

Source: Graphic: Deloitte University Press

Dropping cost is driving rapid Digitization

9 C O N F I D E N T I A L | J U L Y 2 0 1 5

As Digitization Spreads, Disruption is Happening Faster

0

2

4

6

8

10

12

14

16

18

20

TypicalFortune

500

Google(1998)

Facebook(2004)

Tesla(2003)

Uber(2009)

WhatsApp(2009)

Snapchat(2011)

Oculus Rift(2012)

Source: Ismail, Salim, Exponential Organizations: Why new organizations are ten types better, faster, and cheaper than yours

Characteristics of exponential organizations… 1. ACCESS RESOURCES

THEY DON’T OWN 2. INFORMATION IS THEIR

GREATEST ASSET

Tim

e to

$1

B M

arke

t C

ap (

Year

s)

10 C O N F I D E N T I A L | J U L Y 2 0 1 5

We Don’t Always See Disruption Until It’s Too Late

Time (Years)

Pa

ce

of In

no

va

tio

n

Exponential Technology surges past status quo

Today

Where Exponential

Technology is now

Exponential Business

Innovation

Source: Graphic: Deloitte University Press

11 C O N F I D E N T I A L | J U L Y 2 0 1 5 11

What Happens When Disruption Goes Mainstream?

“What happens when we have an UBER moment in Banking – when tech companies do to banks what UBER has done for taxis: destroying their business before governments get around to regulating them” Mark Carney, Governor of the Bank of England

Spotlight on FinTech

13 Copyright © 2015 Deloitte Development LLC. All rights reserved.

What is FinTech?

New Definition

Recently the term has started to

be used for broader applications of

technology to include:

Front end consumer products

New paradigms such as

Bitcoin and shared ledgers

FinTech is shorthand for

‘innovation in financial services’

new products from new tech

startups

new approaches by existing

players where technology is the

key component

Traditional Definition

A contraction of the words ‘Financial’

and ‘Technology’

Ubiquitous term for any technology

applied to financial services

Technology that was primarily sold to the

financial services sector working for the

back office functions

The definition of the term “Fintech” has evolved over time.

14 C O N F I D E N T I A L | J U L Y 2 0 1 5 14

FinTech is “Hot” and Emerging as 21st Century Finance

Ideas Changing the Financial Services Landscape

Products & Services

Tools and services for financial institutions ranging from alternative trading systems to BPO, financial modeling and analysis software, data analytics and machine learning

Cyber, compliance, and identity and transaction verification platforms and services

Products & Services (e.g., Data Analytics, Cloud

Computing)

Risk & Security

Peer-to-peer lending , captive lending, crowdfunding, underwriter, and landing platforms Lending

Payment processing, billing, and money transfer/ remittance platforms serving B2B and B2C customers

Payments

Potential monetary medium of exchange that requires less processing time and lower fees for online transactions

Digital Currency

Wealth Management Companies that help manage individuals manage their personal bills, accounts and/or credit as well as manage their personal assets and investments

There are immediate and long term implications on the syntax of financial institutions due to FinTech.

15 C O N F I D E N T I A L | J U L Y 2 0 1 5 15

Early Disruptors are Just the Start

Financial Services

Banking (Personal) Banking

• Checking accounts Debit cards ATMs

Savings accounts ForEX CDs

• Lending/Credit Loans

Mortgages/Home equity loans

Student loans Payday Other

Credit cards Investing and Wealth Management

Financial planning/advice Investment instruments:

annuities, bonds, IRAs, mutual funds, securities, backed lending, etc.

Other Brick and mortar Online/mobile/tablet banking

Banking (Business) Banking

• Checking accounts • Cash management

Payroll Merchant services ForEX

• Lending/Credit Credit cards Line of credit

Letters of credit Loans

Installments Commercial mortgages

Working capital loans

Capital Markets Investment Banking Sales and Trading Alternate Investments

Insurance Life and Annuity Property and Casualty Specialty

Telematics

Big Data and Machine Learning

Sharing Economy

E-aggregators

Advanced Analytics

Cloud Computing

Equity Crowdfunding

Digital Currency

Online Banking

High Net Worth Wealth Management

Managed portfolios Private equity markets Secondary transactions

Point Of Sale (Credit Cards)

P2P Lending

16 Copyright © 2015 Deloitte Development LLC. All rights reserved.

FinTech Key Themes

Democratization: Leveling the playing field

Disintermediation of Traditional Business Models: New

platforms and technologies changing delivery

Customer Experience: Providing customers with intuitive, mobile-first,

personalized financial offerings

• Simplification

• Transparency

• Analytics

17 Copyright © 2015 Deloitte Development LLC. All rights reserved.

FinTech Future: A Technology Revolution

Internet

Revolution

1990’s

Smartphone

Evolution

2000’s

Blockchain and

Non Traditional

Banking

Products

Emergence

Today

Desktop Computing Mobile Computing Cloud Computing / SaaS

E-Commerce App Economy Blockchain & Shared Ledger

Online Banking P2P Payments Real time payments

Trends

“Eventually mainstream products, companies and industries emerge to commercialize it; its effects become profound;

and later, many people wonder why its powerful promise wasn’t more obvious from the start. What technology am I

talking about? Personal computers in 1975, the Internet in 1993, and – I believe – Bitcoin in 2014.”

Marc Andreessen, Andreessen Horowitz

18 C O N F I D E N T I A L | J U L Y 2 0 1 5 18

Global FinTech Investment Grew 170% in 2014 to

$12B, with 80% in the US “Silicon Valley is coming. There are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking.”

- Jamie Dimon, JPMorgan Chase CEO

“We have a chance to rebuild the system. Financial transactions are just numbers; it’s just information. You shouldn’t need 100,000 people and prime Manhattan real estate ”

- Marc Andreesen, Tech Entrepreneur

“Boardroom conversations at the largest banks and financial institutions are no longer focused only on how they can beat each other; they are increasingly concerned about nontraditional competitors—Paypal, Venmo, Square ” - Stanford Social Innovation Review

Advances in innovative technologies and need for alternative lending for the private sector and individuals are allowing emergence of range of services.

Source: Graphic: Deloitte University Press

19 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Case Study: Goldman Sachs Making Bets on FinTech

FinTech companies have long been financed by venture capital firms, but Wall

Street banks are also starting to place their bets on the future of FinTech

Payments

Investments into Square (including in its

latest $150M round at a $6B valuation),

Payments security firm Bluefin Payments

Payments platform Revolution Money,

acquired by American Express in 2010

Co-led a $25M Series C deal to bill

presentment and payment startup Billtrust in

April.

Bitcoin / Blockchain

Lead investor in bitcoin payments startup

Circle Internet Financial (latest $50M

financing)

Goldman deal is the first investment by

a bulge bracket bank in a blockchain or

digital currency startup

Big Data (deals including)

Deals including social media data analysis

firm Dataminr, valued at $700M

Financial data engineering startup Kensho

Technologies

Predictive data analytics firm Context

Relevant

“big data analytics can be the next wave of

global services and… the market has

tremendous growth potential.”

-Ankur Sahu, co-head of

private equity at

Goldman Sachs in Asia

Source: https://www.cbinsights.com/blog/goldman-sachs-fin-tech-startups

20 Copy right © 2014 Deloitte Dev elopment LLC. All rights reserv ed.

Wearable Technologies Augmented reality personalizes product information and

offers

Enables instantaneous, “see-and-buy” impulse purchases

Frictionless, hands-free payments, free of plastic,

smartphones or credentials

Secure, bio-authenticated transactions

Internet of Things

Physical objects become active participants in business

processes and conduct transactions

High-speed, automated machine-to- machine (M2M)

payments and settlement

Payments integrated in telematics (congestion pricing,

parking, in-car entertainment), appliances (energy

pricing, automated grocery shopping) and every day

objects

FinTech Innovation Expanding Payments Ecosystem

21 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Current Marketplace Examples

FX Trading Desks Becoming

Automated

• UBS has been ordered by

regulators to automate 95% of its

FX trading as a result of currency

manipulation

• Barclays has automated 90% of its

FX trading

Automating Manual Processes

• Nasdaq is experimenting with

blockchain technology in the

Nasdaq Private Market by

automating informal recordkeeping

previously done by lawyers to verify

transactions by hand

22 C O N F I D E N T I A L | J U L Y 2 0 1 5

Major players are engaging the Fintech ecosystem

via “Labs” and “Accelerators” with mixed results

TECHNOLOGY CAPABILITIES

UBS developed a physical space in their offices that promotes innovative thinking

JP Morgan Chase Financial Services Lab is an internal space dedicated to finding financial management solutions

Deutsche Bank developed a Joint Innovation lab with IBM and Microsoft, focused on internally innovating

Barclays partnership with TechStars to provide funding and mentoring to select FinTech startups

Citi co-sponsoring a “Mobile Challenge” with IBM for FinTech startups to build, test and deploy their solutions

Santander and HSBC created funds for direct investment into startups in the FinTech space

ING built Customer Experience Center dedicated to testing, collaborating, and innovating

BBVA created Innovation centers to drive digital transformation in the industry and foster innovation

Charles Schwab Intelligent Portfolios is a no-fee virtual investment platform invests consumer money without the middle man by obtaining their preferences and managing their money using a proprietary algorithm

Citi Private Bank In View provides clients a comprehensive snapshot of their wealth on all mobile devices, giving bankers and clients extensive amounts of data at their fingertips.

Goldman Sachs and Societe Generale are reportedly planning to purchase P2P loan invoices and repackage them into high yielding assets to create a new offering for their clients

UBS “Idea exchange” allows all employees to submit and vote on internal innovation ideas

JP Morgan Chase QuickPay lets you send, receive or request money using your smartphone, tablet or computer...all you need is the recipient's email address or mobile number.

Results are mixed!

Source: Graphic: Deloitte University Press

Role of Digital

Currencies and the

Blockchain Protocol

24 Copyright © 2015 Deloitte Development LLC. All rights reserved.

A decentralized cryptocurrency is a digital currency in which encryption

techniques are used to regulate the generation of units of currency and

verify the transfer of funds, operating independently of a central bank.

What are Decentralized Cryptocurrencies?

Bitcoin and other cryptocurrencies

are both a network (based on the

Blockchain) and a unit of value

(digital currency). They can be

converted into fiat currencies,

enabling peer-to-peer (P2P)

payment networks reducing the use

of third-parties / intermediaries.

25 C O N F I D E N T I A L | J U L Y 2 0 1 5

Blockchain Could Disintermediate Traditional

Financial Services

Source: Graphic: Deloitte University Press

26

Why is the Blockchain Protocol Interesting?

Technology

Factors Definition

Protocol

An open set of standards that affords global interoperability; A peer to peer network

that uses cryptographic protocol, where messages are digitally signed and time

stamped and broadcast on the network

Interoperability allows anyone to pay anyone globally

Network

A distributed network that is self - regulating; the network timestamps transactions by

including them in blocks of transactions. Any one block cannot be modified without

changing all the blocks since the modification

Self – Regulating prevents double spending

Blockchain/

Shared Ledger

Globally distributed public ledger allows public record keeping of all transactions; all

confirmed transactions are included in the block chain and time stamped

Public Record Keeping does not require trust / dependence in a central authority

Universal Value

Transfer System

Ability to make payments across borders independent of fiat currencies.

Independent of fiat currencies - avoid exchange rate volatilities

27

The combined market capitalization of the top ten most popular

virtual currencies is currently eclipsed by the total value of

physical US currency in circulation2

What is the VC Market Size?

Physical US

Currency

$1.29 Trillion

Top Five Virtual Currencies

$4.45 Billion

Cryptocurrency Market cap (as of 7/21/15)1

Bitcoin $4,004,791,068

Ripple $246,291,261

Litecoin $156,490,278

Dash $20,325,704

Dogecoin $17,000,462

1 http://coinmarketcap.com 2 http://www.federalreserve.gov/paymentsystems/coin_currcircvalue.htm

28

State of Decentralized Cryptocurrency: 2015 Outlook Virtual currencies continue to grow in prominence, with increasing consumer, merchant, and venture capital interest while

traditional financial institutions continue to evaluate the pros and cons.

Increased

Bitcoin

Adoption

Continued

Venture Capital

Investment

Integration with

Traditional

Capital Markets

Regulatory

Landscape

Maturity

Emergence of

the Blockchain

and Shared

Ledgers

Usage of Bitcoin by both consumers

and merchants is increasing at a

steady rate, with an estimated 12mm

Bitcoin wallets by the end of 2015.

Venture capital firms are being joined

by mainstream institutional investors

as investment in the virtual currency

space grows at a rapid pace

Bitcoin and other virtual currencies may

continue to be integrated into traditional

capital markets, with SEC-regulated

exchanges, CFTC-approved derivatives

and OTC financial products

Initial impressions from a majority of

the regulatory authorities in

international financial centers are

expected to be issued by 2016

New use cases for distributed open

ledgers are being explored in a wide

swath of industries

+140k merchants worldwide

projected to accept Bitcoin by 4Q

2015

+$275MM in venture capital

investment raised by virtual currency

businesses in 1Q 2015

NYSE and NASDAQ have

invested in virtual currency

exchanges and new technologies

NYDFS issued finalized

“BitLicense” regulations, setting an

example for other states and foreign

jurisdictions

Possibilities for future uses

of the blockchain include smart

contracts, electronic voting, and anti-

counterfeiting measures

29

Potential Other Use Cases For Blockchain Technology As distributed ledger technology evolves, use cases may impact a wide swath of industries.

Smart Contracts

Electronic contracts with transfer of

ownership provisions coded into the

contract itself. Both tamper-proof and

self-executing, the need for trusted third-

parties to resolve disputes or enforce

settlements is eliminated.

Intellectual Property

Encrypted and time stamped

documents stored on the blockchain

can be used to document ownership

of IP without revealing the

information it contains, and provide

proof that the document was

authored at a particular time.

Medical Records

Patients can hold the

private key used to encrypt

their medical data, using

public keys to share

selected information with

doctors only when desired

Foreign Exchange

The ability to securely clear and settle

transactions bilaterally using the blockchain opens

the FX market to non-bank market makers,

tightening spreads and lowering transaction costs

Transfer of Property

Fractional bitcoins marked with certain properties,

also known as colored coins, are use to represent

digital or physical assets such as a house or a car.

Identity Management

A cryptographic distributed

network could be used to

verify people’s identities,

such as passports, social

security numbers, tax id

numbers and driver’s

licenses

Lower transaction costs

Increased information

sharing

Elimination of requirement

for trusted third-party

intermediaries

IMPACTS

30 C O N F I D E N T I A L | J U L Y 2 0 1 5

Bitcoin Could Take Over Where Monetary Markets

are Less Efficient

Source: Graphic: Deloitte University Press

Risks

32 Copyright © 2015 Deloitte Development LLC. All rights reserved.

“..even if the vast majority of practitioners

may be doing things right, there are –

CFO’s, Controllers, Chief Accounting

Officers, Independent Auditors and

Accountants in other roles – who appear to

be failing in their role as gatekeepers.”

Howard Scheck, former Chief Account

Division of Enforcement U.S. Securities

and Exchange Commission

33 Copyright © 2015 Deloitte Development LLC. All rights reserved.

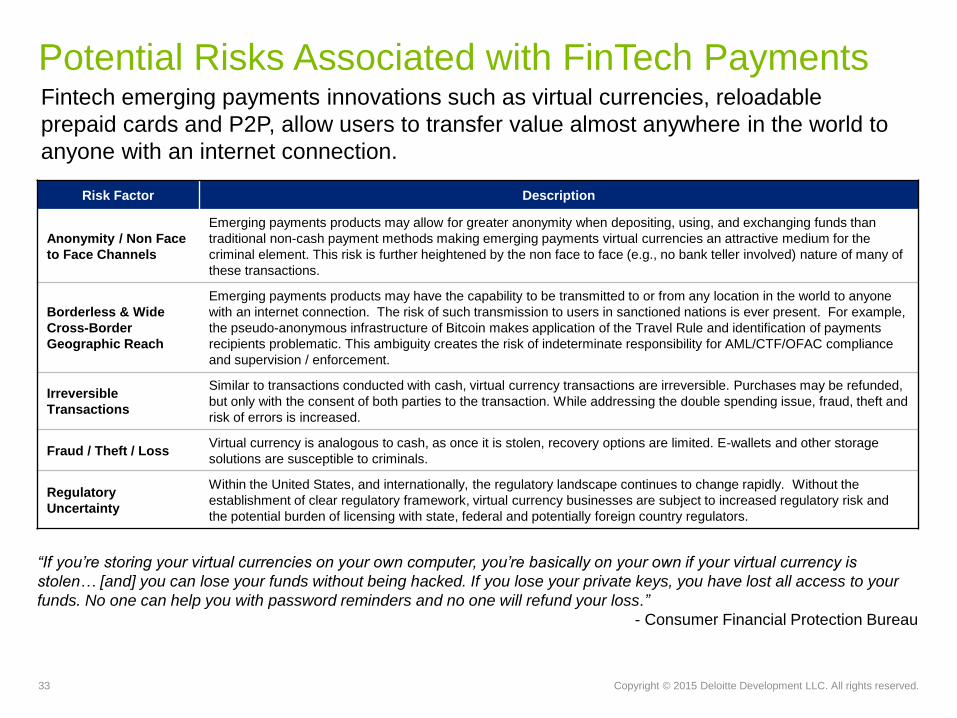

Potential Risks Associated with FinTech Payments

“If you’re storing your virtual currencies on your own computer, you’re basically on your own if your virtual currency is

stolen… [and] you can lose your funds without being hacked. If you lose your private keys, you have lost all access to your

funds. No one can help you with password reminders and no one will refund your loss.”

- Consumer Financial Protection Bureau

Risk Factor Description

Anonymity / Non Face

to Face Channels

Emerging payments products may allow for greater anonymity when depositing, using, and exchanging funds than

traditional non-cash payment methods making emerging payments virtual currencies an attractive medium for the

criminal element. This risk is further heightened by the non face to face (e.g., no bank teller involved) nature of many of

these transactions.

Borderless & Wide

Cross-Border

Geographic Reach

Emerging payments products may have the capability to be transmitted to or from any location in the world to anyone

with an internet connection. The risk of such transmission to users in sanctioned nations is ever present. For example,

the pseudo-anonymous infrastructure of Bitcoin makes application of the Travel Rule and identification of payments

recipients problematic. This ambiguity creates the risk of indeterminate responsibility for AML/CTF/OFAC compliance

and supervision / enforcement.

Irreversible

Transactions

Similar to transactions conducted with cash, virtual currency transactions are irreversible. Purchases may be refunded,

but only with the consent of both parties to the transaction. While addressing the double spending issue, fraud, theft and

risk of errors is increased.

Fraud / Theft / Loss Virtual currency is analogous to cash, as once it is stolen, recovery options are limited. E-wallets and other storage

solutions are susceptible to criminals.

Regulatory

Uncertainty

Within the United States, and internationally, the regulatory landscape continues to change rapidly. Without the

establishment of clear regulatory framework, virtual currency businesses are subject to increased regulatory risk and

the potential burden of licensing with state, federal and potentially foreign country regulators.

Fintech emerging payments innovations such as virtual currencies, reloadable

prepaid cards and P2P, allow users to transfer value almost anywhere in the world to

anyone with an internet connection.

34 Copyright © 2015 Deloitte Development LLC. All rights reserved.

FinTech / Emerging Payments Product Risk Factors (1 of 2)

Red Flag Recommended Risk Mitigation Factors

A customer with an excessive number of accounts (based on program

parameters)

• Enhanced Due Diligence to confirm the customer’s

identity and anticipated activity

A customer who is unwilling to provide information required by the CIP • Enhanced Due Diligence to confirm the customer’s

identity

• Consideration for account closure or termination

A customer who presents unusual or suspicious identification

documents that cannot readily be verified

• Enhanced Due Diligence to confirm the customer’s

identity and anticipated activity

• Consideration for account closure or termination

A customer who requests a shipment/transfer of payment products

outside of the United States

• Collect and confirm the identity and location of all third

parties involved in the prepaid card program, including

any subagents

A customer uses different tax identification numbers with variations of

his or her name

• Enhanced Due Diligence to confirm the customer’s

identity

• Consideration for account closure or termination

A customer who is reluctant to provide the information needed for a

mandatory report, to have the report filed, or to proceed with a

transaction after being informed that the report must be filed

• Enhanced Due Diligence to confirm the customer’s

identity

• Consideration for account closure or termination

A customer that coerces or attempts to coerce a bank employee to not

file any required recordkeeping or reporting forms

• Enhanced reporting processes and staff training

High dollar deposits followed by numerous small withdrawals • Enhanced Transaction Monitoring

• Potential SAR filing

A Cardholder who makes multiple value loads on the same day at

different load locations

• Enhanced Transaction Monitoring

• Potential SAR filing

Large number of failed authorizations • Enhanced Transaction Monitoring

• Potential SAR filing

35 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Red Flag Recommended Risk Mitigation Effort

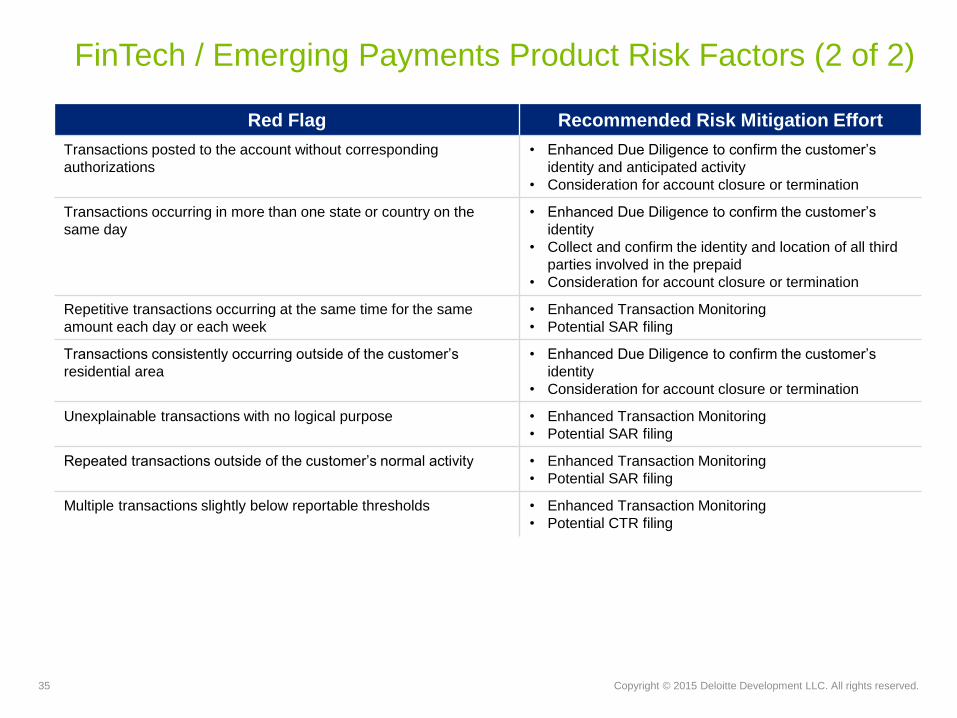

Transactions posted to the account without corresponding

authorizations

• Enhanced Due Diligence to confirm the customer’s

identity and anticipated activity

• Consideration for account closure or termination

Transactions occurring in more than one state or country on the

same day

• Enhanced Due Diligence to confirm the customer’s

identity

• Collect and confirm the identity and location of all third

parties involved in the prepaid

• Consideration for account closure or termination

Repetitive transactions occurring at the same time for the same

amount each day or each week

• Enhanced Transaction Monitoring

• Potential SAR filing

Transactions consistently occurring outside of the customer’s

residential area

• Enhanced Due Diligence to confirm the customer’s

identity

• Consideration for account closure or termination

Unexplainable transactions with no logical purpose • Enhanced Transaction Monitoring

• Potential SAR filing

Repeated transactions outside of the customer’s normal activity

• Enhanced Transaction Monitoring

• Potential SAR filing

Multiple transactions slightly below reportable thresholds • Enhanced Transaction Monitoring

• Potential CTR filing

FinTech / Emerging Payments Product Risk Factors (2 of 2)

Two Case Studies Based on Real Examples ML/TF risks for UR Bank – Pass the antacid

Shut down in August 2015, Gold Reserve was a Costa Rican-based centralized digital currency service noted to have laundered more than $6 billion in criminal proceeds during its history. The site is known for allowing its users to transfer funds from wire transfers to other users with only a name, e-mail address, and birth date. The lack of required KYC information made Gold Reserve an attractive payments processor for criminals. Payments for the sale of child pornography where linked to the service. The money was traced to the criminal’s account with UR Bank. UR Bank is embroiled in negative publicity…

Cotton Road is an online black market, best known as a platform for buying and selling drugs, weapons, stolen identification information, etc. The site worked as an online market place in the Deep Web, operating as a Tor hidden service and accepting Bitcoins as a form of payment. In early August 2015, the site was shutdown and the owner arrested. Law Enforcement has traced the transactions to Bitcoin exchanges where money was sent via ACH & wires from UR Bank. Regulators are knocking on UR Bank’s door…

Cotton Road Gold Reserve

Gold Reserve Scheme The Gold Reserve case demonstrates how a typical series of transactions

in a centralized virtual currency market occur

Bad Guy A

Bad Gal B

Bad Guy A

Exchanger

Exchanger

Personal UR Bank Account

Cash / Check

Bank Wire

Gold Reserve Funds

Gold Reserve Funds

Liberty Reserve Funds

Bank Wire or Debit

Card

Bad Gal B

Cotton Road Website on the Deep Web Cotton Road, a global black-market cyber bazaar, brokered anonymous

criminal transactions with Bitcoins as the main form of currency

Cotton

Cotton Road Scheme The Cotton Road case demonstrates how a typical series of transactions

in a decentralized virtual currency market occur

Illicit Drugs Buyer

Illicit Drugs Seller

Bitcoin Exchanger

Cash / Check/Credit

Card/Bank Wire

Cotton Road

Bitcoin Buyer Wallet

Cotton Road Escrow Account

Cotton Road

Bitcoin Seller Wallet

UR Bank

Every Cotton Road user was required to establish a bitcoin account with Cotton Road to conduct transactions due to anonymity of Bitcoin.

Bitcoins used for transactions were stored on “wallets” maintained by Cotton Road servers (deposited on account with Cotton Road)

To achieve an extra layer of anonymity Cotton Road sent Bitcoin payments through a “complex, semi-random series of dummy transactions” known as a tumblers which made it difficult to trace individual transactions to Bitcoins leaving the site

40 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Commonly Found AML Program Weaknesses Regulatory enforcement actions give us a glimpse into what regulators

are interested in and where common weaknesses may lie

Insufficient resources dedicated to compliance and internal audit that understand

complex FinTech products

Risk Assessments lack quantitative analysis and support

Inadequate KYC procedures, including limited view of entire customer relationship

especially for global banks (inadequate “feedback loop”)

Employees, Board and management have not received relevant and targeted AML

compliance training, specifically for FinTech products and inherent risks

Inexperienced internal audit and compliance staff

Inadequate program status reporting to the Board and management

Failure to identify and periodically monitor high risk accounts or activity

Suspicious activity investigations not properly documented

AML systems and supporting technology not stress tested

Failure to file timely and accurate required regulatory reports

41 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Commonly Found Overall Program Weaknesses A culture of compliance and sufficient training for all employees are critical

steps to elevating AML compliance programs

Fundamentals and Mechanics of Sound Management

In March 2013, at a testimony before the Committee on Banking, Housing, and Urban Affairs of the

U.S. Senate. Thomas Curry, Comptroller of the Currency identified the following as a part of the

causes of a breakdowns in the fundamentals and mechanics of sound management of operational

risk for AML compliance programs:

Lack of strong corporate governance principles necessary to create a “culture of compliance”

within the organization

Lack of sufficient staffing, high turnover rates, and cutbacks in the compliance area as

common factors that have impeded the effectiveness of banks’ AML programs

Key Takeaways From Recent Enforcement Actions

On Aug. 11, 2014, FinCEN’s Advisory highlighted the importance of maintaining a strong culture of

BSA / AML compliance for senior management, leadership and owners of all financial institutions –

regardless of size or industry sector. Recent AML enforcement actions appear to suggest:

Leadership should actively support and understand compliance efforts

Efforts to manage and mitigate AML deficiencies and risks should not be compromised by

revenue interests

Compliance programs may be more effective by, among other things, ensuring that it is tested by

an independent and competent party

Regulation

43 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Regulators Addressing FinTech Payments Innovations

FinCEN

“Working closely with our delegated BSA examiners at the Internal

Revenue Service (IRS), FinCEN recently launched a series of

supervisory examinations of businesses in the virtual currency

industry. […] Where we identify problems, we will use our supervisory

and enforcement authorities to appropriately penalize non-compliance

and drive compliance improvements.”

CFPB & Federal Reserve

On July 9, 2015, the Consumer Financial Protection Bureau ("CFPB")

continued its focus on payment processing and joined the Federal

Reserve's efforts to develop faster and more secure payment systems

by releasing its "Vision of Consumer Protection in New Faster

Payment Systems" ("Principles").

OCC

Acknowledging that the current legal framework for addressing money

laundering and counter-terrorist financing should be updated to remain

effective, the OCC stated: “The current regulatory regime, which is

rooted in 20th century concepts and approaches, will need to

change and adopt in order to remain relevant into the 21st

century."

SEC

OCC

44 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Examples of State Virtual Currencies Regulatory Landscape

44

Without finalized regulatory guidance from populous technology and financial services hubs such as California and New York,

the majority of US States have hesitated to establish independent viewpoints on how to define and regulate virtual currency

creating industry uncertainty.

Regulatory Guidance Issued

No Guidance or Regulation

Regulation Pending

Washington Department

of Financial Institutions

Guidance issued December

8, 2014 states that virtual

currency is included in the

definition of “money

transmission” under state

law

California State Assembly

Passed AB129 on June 28,

2014 repealing a section of

state code that may have

been interpreted to prohibit

virtual currency

Proposed AB1326 on

February 27, 2015 that

provides a legal definition of

“virtual currency” and

mandates licensing of most

virtual currency businesses

by the California

Department. of Business

Oversight

Texas Department of

Banking

Guidance issued April 3,

2014 states that third-

party exchange of virtual

currency for sovereign

currency is considered

“money transmission”

under state law

New York Department of

Financial Services

Final ruling of “BitLicense”

issued on June 5, 2015 that

provides a regulatory

definition of “virtual

currency” and requires that

all persons engaged in

“virtual currency business

activity” obtain a license

from the NYDFS.

Kansas Office of the State

Banking Commissioner

Guidance issued June 6,

2014 states that third-party

exchange of virtual currency

for sovereign currency is

considered “money

transmission” under state

law

Connecticut State

Assembly

Passed House Bill 6800 on

June 19, 2015 provides a

legal definition of “virtual

currency” and requires bond

for applicants and licensees

transmitting virtual currency,

45 Copyright © 2015 Deloitte Development LLC. All rights reserved.

NYDFS “Bitlicense” May Serve as a Model

Cost of applying for licensure: $5,000

Who is covered under the BitLicense

program?

Businesses covered include those

“controlling, administering or issuing a

virtual currency” with the following

exemptions:

Blockchain technology for non-currency

purposes

Software developers that aren’t engaged

directly in money transmission or

exchange

Miners

Individual investors

Merchants who accept bitcoin

Licensed banks

TITLE 23. DEPARTMENT OF FINANCIAL SERVICES

CHAPTER I. REGULATIONS OF THE SUPERINTENDENT OF FINANCIAL SERVICES

PART 200. VIRTUAL CURRENCIES

On June 3, 2015 the New York State Department of Financial Services (NYDFS) released the

final version of the BitLicense regulations

AML program requirements (highlights)

Licensee is required to comply with all applicable

federal and state laws, rules, and regulations.

Licensee must have an overall compliance

officer(s)

Licensee must maintain and enforce written

compliance policies, including policies with

respect to anti-fraud, anti-money laundering, cyber

security, privacy and information security

Reviewed and approved the Board of

Directors

Preserve all of its books and records in their

original form or native file format for a period of at

least 7 years from the date of their creation

Report within 24 hours to NYDFS ≥ $10,000 one-

day transactions by one person

Report suspicious activity

Maintain Customer Identification Program

Verify the customer’s identity and check against

the OFAC SDN list

46 Footer Copyright © 2015 Deloitte Development LLC. All rights reserved.

Illustrative FinTech Enforcement Actions Summary The majority of enforcement actions related to FinTech products such as Bitcoin to this point have been related to criminal

activities, rather than regulatory requirement issues, but that trend may be changing as money transmitters are being held to

an increasingly higher compliance standard.

Company Reason For Enforcement Action Penalty Enforcement

Agency

Silk Road

INTENTIONAL SALE OF CONTRABAND: Silk Road was an

online black market, best known as a platform for buying and

selling drugs, weapons, stolen identification information, etc.

The site worked as an online market place in the Deep Web,

operating as a Tor hidden service and accepting Bitcoins as a

form of payment.

Fine / CND /

Arrest

Joint Law

Enforcement

Erik T.

Voorhees

FAILURE TO REGISTER: Voorhees published prospectuses

on the Internet and actively solicited investors to buy shares in

his two ventures, SatoshiDICE and FeedZeBirds. However,

Voorhees failed to register the offerings with the SEC as

required under the federal securities laws.

Fine / CND SEC

Trendon

Shavers

PONZI SCHEME: Trendon T. Shavers and his company

Bitcoin Savings and Trust (BTCST) charged with offering and

selling investments in violation of the anti-fraud and

registration provisions of the securities laws.

Fine / CND SEC

Ripple Labs FAILURE TO REGISTER / LACK OF AML PROGRAM: Ripple

Labs sold its virtual currency “XRP” without timely registration

as an MSB, or maintaining an adequate AML program. Ripple

Labs and its subsidiary XRP II, LLP were fined $700,000 by

FinCEN, and entered into a settlement agreement with the

U.S. Attorney’s Office.

Fine US DOJ

FinCEN

47 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Aggressive race to acquire FinTech startups between Wall Street and Silicon

Valley VC

Cybersecurity professionals will be in even greater demand

FX and rates automation will eliminate human trading jobs

Aggressive use of risk and compliance technology: Banks becoming more

opportunistic (tied with driving the business) rather than defensive (responding to

regulatory demands).

Rise of the Chief Digital Officer in banks: Engage with new FinTech ecosystems

as technology has deconstructed the walls that once surrounded capital markets

and access to information, price and liquidity

Painful banking transition to cloud computing: Despite the oft cited security

concerns, the biggest obstacle of moving bank’s large infrastructure to cloud

computing model is internal politics

2015-2016 Trends to Watch

48 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Questions

49 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Disclaimer

This presentation contains general information only and Deloitte Advisory is not, by

means of this presentation, rendering accounting, business, financial, investment,

legal, tax, or other professional advice or services. This presentation is not a

substitute for such professional advice or services, nor should it be used as a basis

for any decision or action that may affect your business. Before making any decision

or taking any action that may affect your business, you should consult a qualified

professional advisor.

Deloitte Advisory shall not be responsible for any loss sustained by any person who

relies on this presentation.

Contact Information

Deloitte Advisory 30 Rockefeller Plaza, 40th FL New York, NY USA Tel +1 646 640 6557 [email protected]

Alex Rozman Senior Manager Global Anti-Money Laundering and Sanctions Practice