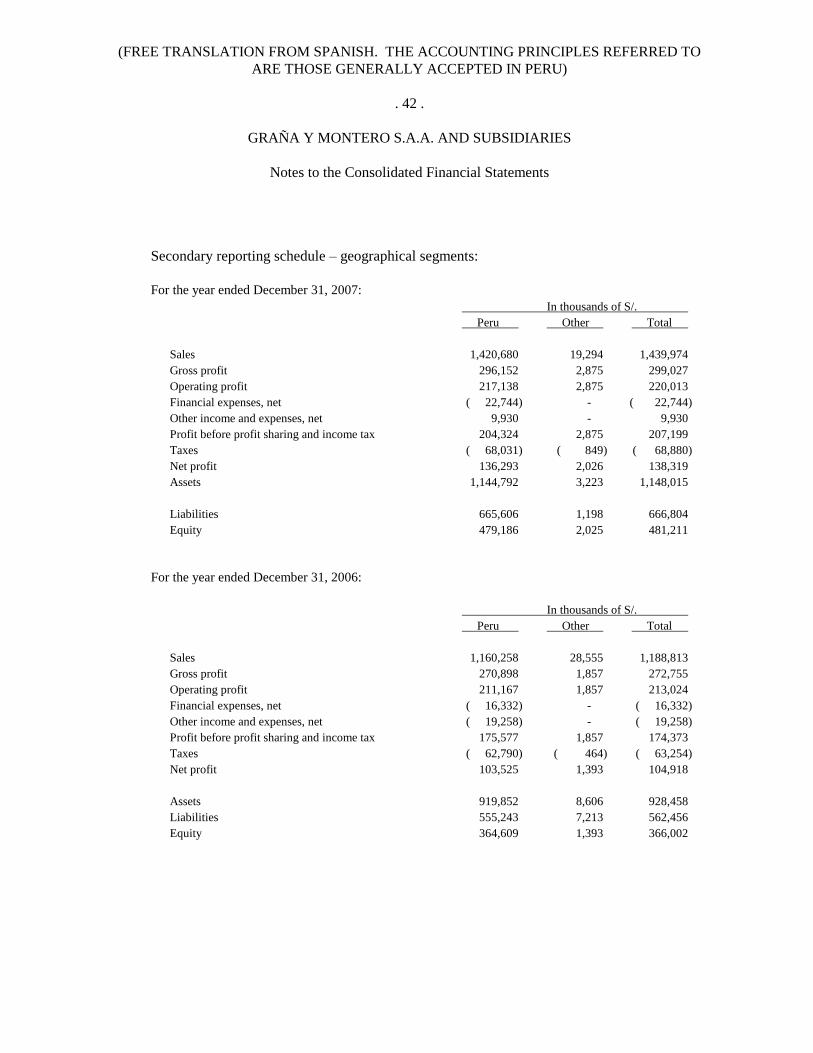

ffss graÑa y montero consolidado...

TRANSCRIPT

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Financial Statements

As of December 31, 2007 and 2006

(With the Independent Auditor’s Report Thereon)

(FREE TRANSLATION FROM SPANISH.THE ACCOUNTING PRINCIPLES REFERRED TOARE THOSE GENERALLY ACCEPTED IN PERU)

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Balance Sheet

As of December 31, 2007 and 2006

(Stated in thousands of nuevos soles)

Assets 2007 2006 Liabilities and Stockholders’ Equity 2007 2006Current assets: Current liabilities:

Cash and banks and restricted funds (note 4) 141,946 150,088 Bank overdrafts and loans (note 15) 21,476 5,151------------ ------------ Trade accounts payable 185,669 136,827

Accounts receivable: Other accounts payable (note 16) 147,030 156,503Trade (note 5) 233,564 188,805 Commercial papers - 5,000Affiliates (note 6) 641 6,261 Current portion of long-term Consortiums (note 7) 1,921 11,828 debt (note 17) 66,052 51,245Other accounts receivable (note 8) 81,256 54,194 ------------ ------------

------------ ------------ Total current liabilities 420,227 354,726317,382 261,088

------------ ------------Inventories, net (note 9) 79,257 37,283 Long-term debt (note 17) 218,469 191,601Prepaid expenses and taxes 44,386 13,615Available-for-sale non-financial assets 2,207 - Deferred income tax (note 21.e) 22,569 12,371

------------ ------------Total current assets 585,178 462,074 Deferred income 5,539 3,758

------------ ------------ ------------ ------------Total liabilities 666,804 562,456

Long-term accounts receivable (note 10) 23,437 12,858 ------------ ------------Stockholders’ equity:

Deferred income tax (note 21.e) 2,314 12,705 Capital stock (note 18) 299,423 235,787Legal reserve (note 19) 13,514 3,373

Investments (note 11) 111,980 89,980 Other reserves (note 19) 4,388 -Retained earnings 130,012 101,386

Property, plant, and equipment (note 12) 328,005 272,836 Minority interest 33,874 25,456------------ ------------

Goodwill (note 13) 34,458 32,497 Total stockholders’ equity 481,211 366,002

Other assets (note 14) 62,643 45,508 Commitments and contingencies (note 22)------------ ------------ ------------ ------------

Total assets 1,148,015 928,458 Total liabilities and stockholders’equity 1,148,015 928,458======= ======= ======= =======

See the accompanying notes to the consolidated financial statements.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Statement of Income

For the years ended December 31, 2007 and 2006

(Stated in thousands of nuevos soles) 2007 2006

Valuation of works (note 23) 1,019,200 834,791Income from services rendered 360,807 277,937Sale of merchandise and property 59,967 76,085

--------------- -------------Total revenue 1,439,974 1,188,813

--------------- -------------

Cost of works (note 23) ( 865,549) ( 668,279)Cost of rendered services ( 222,569) ( 181,085)Cost of sales of merchandise and property ( 52,829) ( 66,694)

--------------- -------------Total cost ( 1,140,947) ( 916,058)

--------------- -------------

Gross profit 299,027 272,755

Operating administrative and general expenses (note 24) ( 79,014) ( 59,731)--------------- -------------

Operating profit 220,013 213,024--------------- -------------

Other (expenses) income:Financial, net (note 25) ( 22,744) ( 25,742)Results attributable to associates 4,029 701Various, net ( 2,525) ( 11,085)Write-off of investments (note 11) - ( 11,935)Exchange difference, net 8,426 9,410

--------------- -------------( 12,814) ( 38,651)--------------- -------------

Profit before workers’ profit sharing and income tax 207,199 174,373

Workers’ profit sharing (note 20) ( 9,721) ( 8,915)Income tax (note 21) ( 59,159) ( 54,339)

--------------- -------------Profit before minority interest 138,319 111,119

Minority interest ( 8,419) ( 6,201)--------------- -------------

Net profit for the year 129,900 104,918======== =======

Earnings per basic share in S/. (note 26) 0.303 0.311======== =======

See the accompanying notes to the consolidated financial statements.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Statements of Changes in Stockholders’ Equity

For the years ended December 31, 2007 and 2006

(Stated in thousands of nuevos soles)

Capital Legal Other stock reserve reserves Retained Minority

(note 18) (note 19) (note 19) earnings interest Total

Balances as of December 31, 2005 206,335 101 - 32,509 23,514 262,459Capitalization 29,452 - - ( 29,452) - -Transfer to legal reserve - 3,272 - ( 3,272) - -Adjustment of subsidiaries - - - ( 3,317) - ( 3,317)Dividends paid - - - - ( 4,259) ( 4,259)Net profit for the year - - - 104,918 6,201 111,119

--------------- ---------------- ---------------- ---------------- --------------- ---------------Balances as of December 31, 2006 235,787 3,373 - 101,386 25,456 366,002Transfer to legal reserve - 10,141 - ( 10,141) - -Dividends - - - ( 20,277) - ( 20,277)Recording of unrestricted reserves - - 7,000 ( 7,000) - -Capitalization 63,970 - - ( 63,970) - -Adjustment - - - 114 - 114Treasury shares (note 18) ( 334) - ( 2,612) - - ( 2,946)Net profit for the year - - - 129,900 8,418 138,318

--------------- ---------------- ---------------- ---------------- --------------- ---------------Balances as of December 31, 2007 299,423 13,514 4,388 130,012 33,874 481,211

========= ========= ========= ========= ========= =========

See the accompanying notes to the consolidated financial statements.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Statement of Cash Flows

For the years ended December 31, 2007 and 2006

(Stated in thousands of nuevos soles)

2007 2006

Operating activities:Net profit for the year 129,900 104,918 Adjustment to net result that do not affect the cash flow of operating activities:

Depreciation 58,528 53,953Deterioration of intangible assets 2,904 2,356Amortization of other assets 5,161 6,270Write-off of investments - 11,935Profit attributable to associates and subsidiaries ( 19,418) ( 562)Adjustments - 177Loss on sale of assets 7,955 3,878

Net variations in assets and liabilities:Trade accounts receivable ( 44,759) ( 2,644)Other accounts receivable ( 23,847) ( 21,741)Inventories ( 41,974) 18,632Prepaid expenses and taxes and other assets ( 30,771) 1,733Trade accounts payable 48,842 3,502Other accounts payable 31,299 59,021

--------------- ----------------Net cash provided by operating activities 123,820 241,428

--------------- ----------------Investing activities:

Sale of property, plant, and equipment 8,630 6,033Acquisition of minority interest ( 4,865) -Purchase of intangible assets ( 12,092) ( 10,050)Purchase of investments ( 3,874) ( 13,735)Purchase of fixed assets ( 149,537) ( 83,880)

--------------- ----------------Net cash used in investing activities ( 161,738) ( 101,632)

--------------- ----------------

(Continued)

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Statement of Cash Flows, (cont.)

2007 2006

Financing activities:Loans received, net of amortizations 78,140 ( 46,173) Securitization bonds, net of amortization ( 25,140) ( 26,803)Dividends paid ( 20,277) -Repurchase of own shares ( 2,946) -

---------------- ----------------Net cash provided by (used in)

investing activities 29,777 ( 72,976) --------------- ----------------

Net (decrease) increase in cash ( 8,141) 66,820Cash and cash equivalents at the beginning of the year 137,647 48,818 Variation in restricted funds ( 5,780) 22,009

--------------- ----------------Cash at end of year 123,726 137,647

========= =========

See the accompanying notes to the consolidated financial statements.

(Continued)

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

As of December 31, 2007 and 2006

(1) Business ActivityThe Company was incorporated on August 12, 1996 as the holding company of Grupo Graña

y Montero. Its main activity is to invest in subsidiaries and related entities. Additionally, as from September 2005, it renders services of general management, financial management, commercial management, legal advisory and human resources management (prior to that date, it rendered business advisory services) to said companies. Its legal domicile is located at Av. Paseo de la República 4675, Surquillo.

Likewise, as from year 2006, the Company was engaged in the leasing of offices to the Group companies and to third parties.

In conformity with Companies Act, the consolidated financial statements, as of December 31, 2007, have been prepared by the Board of Directors, which will submit them to General Stockholders’ Meeting for their consideration, within the terms established by Law. Consolidated financial statements as of December 31, 2006 were approved by the General Stockholders’ Meeting, held on March 31, 2007.

a) Subsidiaries:The consolidated financial statements of the Company include assets, liabilities,income and expenses of the following subsidiaries:

GyM S.A. is engaged in the business of civil construction, electromechanical assembly, buildings, management and development of real property projects and other related services.

GMP S.A. is engaged in the exploitation, production, treatment, and trading of oil, natural gas and its derivatives, as well as the storage and delivery of fuels.

GMD S.A. is engaged in providing IT solutions in the Peruvian corporate market.

GMI S.A. Ingenieros Constructores is engaged in providing services of advisory and engineering consultancy, execution of surveys and projects, project management and works supervision.

Concar S.A. is engaged in the operation of concession of works and infrastructure.

Fashion Center S.A. is engaged in developing and operating the conditioning and fitting out project for commercial and recreational use of the area of Parque Salazar of the District of Miraflores.

Until June 30, 2007, Larcomar S.A. was engaged in the operation of the project that is currently operated by Fashion Center S.A.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 2 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

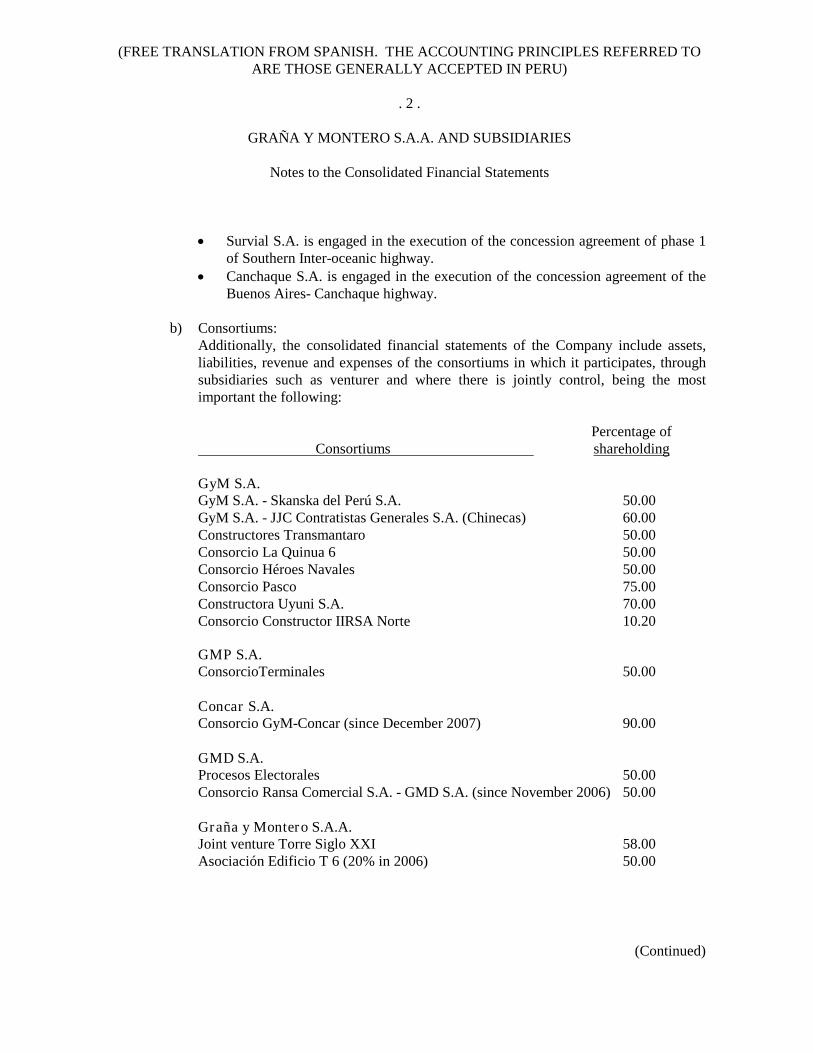

Survial S.A. is engaged in the execution of the concession agreement of phase 1 of Southern Inter-oceanic highway.

Canchaque S.A. is engaged in the execution of the concession agreement of the Buenos Aires- Canchaque highway.

b) Consortiums:Additionally, the consolidated financial statements of the Company include assets, liabilities, revenue and expenses of the consortiums in which it participates, through subsidiaries such as venturer and where there is jointly control, being the most important the following:

Percentage of Consortiums shareholding

GyM S.A.GyM S.A. - Skanska del Perú S.A. 50.00GyM S.A. - JJC Contratistas Generales S.A. (Chinecas) 60.00Constructores Transmantaro 50.00Consorcio La Quinua 6 50.00Consorcio Héroes Navales 50.00Consorcio Pasco 75.00Constructora Uyuni S.A. 70.00Consorcio Constructor IIRSA Norte 10.20

GMP S.A.ConsorcioTerminales 50.00

Concar S.A. Consorcio GyM-Concar (since December 2007) 90.00

GMD S.A. Procesos Electorales 50.00Consorcio Ransa Comercial S.A. - GMD S.A. (since November 2006) 50.00

Graña y Montero S.A.A. Joint venture Torre Siglo XXI 58.00Asociación Edificio T 6 (20% in 2006) 50.00

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 3 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

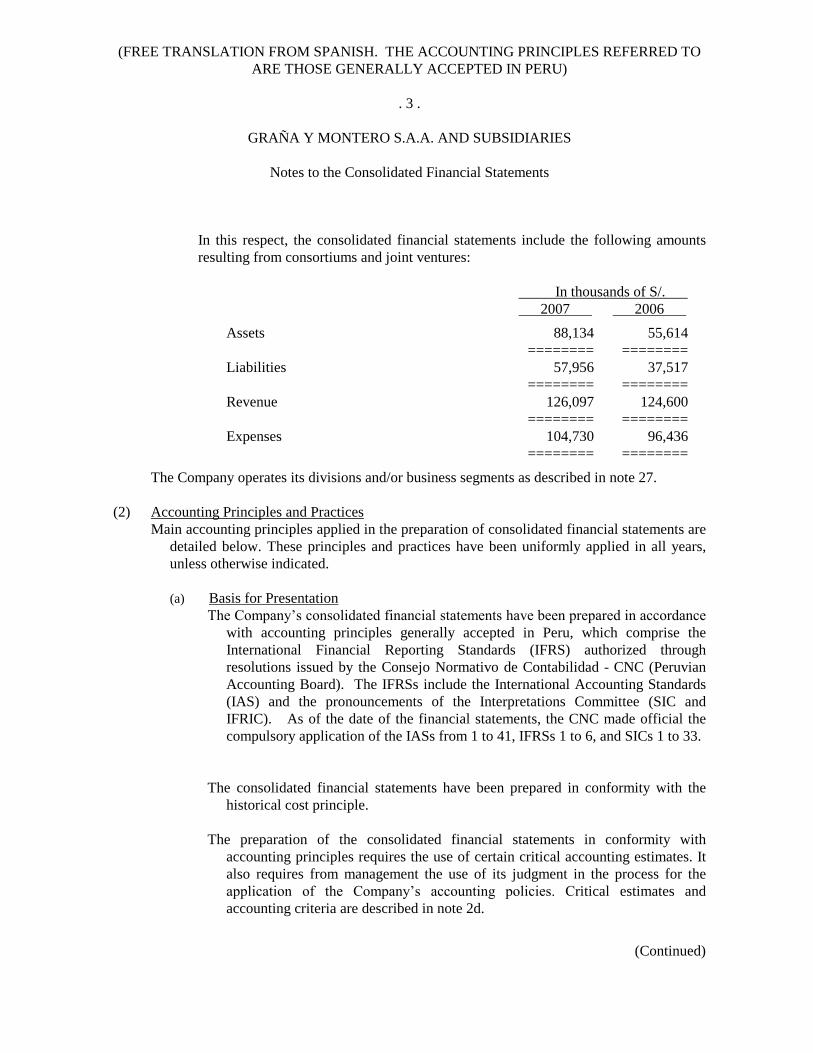

In this respect, the consolidated financial statements include the following amounts resulting from consortiums and joint ventures:

In thousands of S/. 2007 2006

Assets 88,134 55,614======== ========

Liabilities 57,956 37,517======== ========

Revenue 126,097 124,600======== ========

Expenses 104,730 96,436======== ========

The Company operates its divisions and/or business segments as described in note 27.

(2) Accounting Principles and PracticesMain accounting principles applied in the preparation of consolidated financial statements are

detailed below. These principles and practices have been uniformly applied in all years, unless otherwise indicated.

(a) Basis for Presentation The Company’s consolidated financial statements have been prepared in accordance

with accounting principles generally accepted in Peru, which comprise the International Financial Reporting Standards (IFRS) authorized through resolutions issued by the Consejo Normativo de Contabilidad - CNC (Peruvian Accounting Board). The IFRSs include the International Accounting Standards (IAS) and the pronouncements of the Interpretations Committee (SIC and IFRIC). As of the date of the financial statements, the CNC made official the compulsory application of the IASs from 1 to 41, IFRSs 1 to 6, and SICs 1 to 33.

The consolidated financial statements have been prepared in conformity with the historical cost principle.

The preparation of the consolidated financial statements in conformity with accounting principles requires the use of certain critical accounting estimates. It also requires from management the use of its judgment in the process for the application of the Company’s accounting policies. Critical estimates and accounting criteria are described in note 2d.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 4 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(b) Consolidated Financial StatementsThe consolidated financial statements comprise the financial statements of Graña y

Montero S.A.A., the financial statements of the subsidiaries and consortiums detailed in note 1.

SubsidiariesThe subsidiaries are all entities over which the Company has authority to govern

their operating and financial policies generally for being holder of more than one half of voting shares. Subsidiaries are consolidated from the date on which its control is transferred to the Company. They are not consolidated anymore since the date that control ceases.

The Company uses the purchase method to record the acquisition of subsidiaries. The cost of acquisition is measured as the fair value of delivered assets, equity instruments issued, and liabilities incurred or assumed at the date of exchange, plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities assumed in a business combination are initially measured at fair value at the acquisition date. The excess of the cost of acquisition over the fair value of the Company’s interest in identifiable net assets acquired is recorded as goodwill.

Transactions, balances and unrealized gains among the companies that the Company controls are eliminated. Also, unrealized losses are eliminated unless the transaction provides evidence of an impairment of the assets transferred.

ConsortiumsThe Company’s interest in jointly controlled entities is recorded by the

proportionate consolidation method, through which the Company includes in the relevant components of their consolidated financial statements the proportionate shareholding of its interest in revenue and expenses, assets and liabilities and individual cash flows of the joint venture. Significant transactions between the Company and joint ventures have been eliminated.

(c) Functional Currency and Foreign Currency Transactions i) Functional and presentation currency

The items included in the Company’s financial statements are stated in the currency of the primary economic environment in which the entity operates (functional currency). The consolidated financial statements are presented in nuevos soles which is the Company’s functional and presentation currency.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 5 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(ii)Foreign currency transactions and balancesForeign currency transactions are translated into functional currency using exchange rates ruling at the dates of the transactions.

Gains or losses on exchange differences resulting from the collection and/or payment of such transactions and from translating monetary assets and liabilities stated in foreign currency at exchange rates ruling at year-end closing are recognized in the statement of income.

(d) Critical Accounting Estimates and CriteriaThe estimates and criteria used are continuously evaluated and are based on

historical experience and other factors, including the reasonable expectation of occurrence of future events depending on the circumstances.

i) Critical Accounting Estimates and Criteria

The Company makes estimates and assumptions regarding the future. By nature, resulting accounting estimates, very rarely will be the same as the respective actual results. However, it is the opinion of Management that estimates and assumptions applied by the Company do not have significant risk as to produce a material adjustment to the balances of assets and liabilities for next year.

Review of book value and provision for impairmentThe Company applies the guidelines stated in IAS 36 to determine whether a permanent asset requires from a provision for impairment. This determination requires the use of professional judgment by Management to analyze the indicators that might present impairment as well as the determination of value in use. In this last case, it is required to apply judgment in the elaboration of future cash flows that include the projection of future operations level of the Company, projection of economic factors that affect Annual Guaranteed Remuneration, as well as the election of the discount rate to be applied in this flow.

Taxes Interpretations of applicable tax legislation are required in determining obligations and tax expenses. The Company looks for professional counseling in tax matters before taking any decision on it. Although Management considers that its estimates are prudent and appropriate, interpretation differences may arise with tax authorities affecting the charges for future taxes.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 6 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(ii) Critical Judgment in the Application of Accounting PoliciesManagement has exercised its critical judgment when applying accounting policies for the preparation of the accompanying consolidated financial statements, as explained in the corresponding accounting policies.

(e) Cash and Cash Equivalents Cash and cash equivalents comprise cash in hands, overnight, time and sight

deposits held at banks with original maturities between two and three months.

(f) Financial Instruments A financial instrument is as any contract that gives rise to both a financial asset in

one entity and a financial liability, or equity instrument in another. In the case of the Company, financial instruments correspond to primary instruments such as accounts receivable, accounts payable, and shares representing capital share in other companies.

Financial instruments are classified as asset, liability or equity according to the substance of the contract. The interest, dividends, gains, and losses generated by a financial instrument, and classified as liability, are recorded as income or expense in the statement of income. The payment to holders of financial instruments classified as equity is recorded directly against equity. The financial instruments are compensated when the Company has the legal right to compensate them, and management has the intention of paying them on a net basis or negotiating the asset, and paying the liability simultaneously.

Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties, or a liability settled between a debtor and a creditor in an arm’s length transaction.

In management’s opinion, the book value of financial instruments as of December 31, 2007, is substantially similar to their fair values due to their short period of realization and/or maturity. The recognition and valuation criteria of those accounts are disclosed in their respective accounting policies.

(g) Trade Accounts Receivable and Provision for Doubtful Accounts Accounts receivable are initially recorded at their fair value and are subsequently

valued at amortized cost. The provision for deterioration of trade accounts receivable is determined when there is objective evidence that the Company will not collect all the amounts overdue according to terms originally established. Management considers that the balances of trade accounts receivable as of December 31, 2007 do not present uncollectibility risks.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 7 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Trade accounts receivable are presented net of the advances received from clients provided that they are related with the same work agreement and said agreement establishes the possibility of compensation.

(h) Inventories Inventories are valued at construction, acquisition and/or contribution costs, which

do not exceed the net realizable value. The cost of construction materials is determined on a weighted average method, except in the case of inventories in transit, determined by the specific identification method. The net realizable value is the estimated selling price in the ordinary course of business, less cost to sale, and the commercialization costs. For the reductions of inventory book value at net realizable value, inventory impairment is charged to the results of the period when those reductions occur.

(i) Investments The Company classifies its investments in the following categories: i) marketable

financial assets, ii) loans and accounts receivable, iii) Held-to-maturity investments, and iv) available-for-sale financial assets. The classification depends on the purpose for which investments were acquired. Management determines the classification of their investments as of the date of their initial recognition and reassesses this classification as of every closing date.

Marketable financial assetsA financial asset is classified in this category if it was mainly acquired in order to be sold in the short term or if it is so assigned by Management. Derivative financial instruments are also classified as marketable unless they are designated as hedges. Assets in this category are classified as current assets if they are held as marketable or they are expected to be realized within 12 months as from the balance sheet date. During 2007 and 2006, the Company did not hold any investment under this category.

Loans and accounts receivableLoans and accounts receivable are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise when the Company provides with money, goods or services directly to a debtor, with no intention to trading the account receivable. They are included in current assets, except for maturities exceeding 12 months after the date of the balance sheet. These ones are classified as non-current assets. Loans and accounts receivable are included in trade accounts to affiliates and various accounts receivable in the balance sheet (note 2g).

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 8 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Held-to-maturity investmentsHeld-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities acquired with the intention and ability to hold them to maturity. During 2007 and 2006, the Company did not hold any investment under this category.

Available-for-sale financial assets Available-for-sale financial assets are non-derivative financial assets designated in this category or that do not classify in any of the other categories. These assets are shown as non-current assets unless Management has express intention to sell the investment within 12 months after the date of the balance sheet.

Investment purchases and sales are recognized as of the date of negotiation, date on which the Company commits to purchase or sale the asset. Transactions costs related to financial assets recorded at fair value through gains and losses are recognized in the statement of income. Financial assets are not recognized anymore when the rights to receive cash flows from investments have expired or have been transferred, and the Company has substantially transferred all risks and rewards derived from ownership.

Available-for-sale financial assets and marketable financial assets are subsequently recognized at fair value. Loans, accounts receivable, and held-to-maturity investments are recorded at their amortized cost, using the effective interest method.

Realized and unrealized gains and losses arising from changes in the fair value of the “marketable financial assets” category are included in the statement of income, in the period they are originated. Unrealized gains or losses arising from changes in the fair value of non-monetary securities, classified as available-for-sale, are recognized in equity. When securities classified as available-for-sale are sold or impaired, accumulated fair value adjustments are included in the statement of income as gains or losses in investment in securities.

Fair value of quoted investments is based on current bid prices. If market is not active (or securities are not listed), the Company establishes the fair value by using valuation techniques.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 9 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

The Company evaluates at each balance sheet date, if there is objective evidence of the impairment of a financial asset or group of financial assets.

(j) Available-for-Sale Non-Financial Assets Assets are classified as available for sale when their book value is expected to be

recovered through their sale, when there is a plan for such a sale, and it is highly probable that their sale occurs in the short-term. These assets are valued at the lower of their cost or at their realizable value.

If the realizable value is lower than the book value, a provision is recorded and charged to revaluation surplus and deferred income tax and workers’ profit sharing or to results depending if it is a good that has been previously revalued or not, respectively.

(k) Investments in Associates and ConsortiumsThese investments are recorded at acquisition cost, crediting to results the dividends

received in cash.

(l) Property, Plant, and Equipment Property, plant, and equipment are recorded at cost less their depreciation.

Historical cost includes disbursements directly attributable to the acquisition of these entries. Subsequent costs attributable to the goods of the fixed asset increasing the original capacity of goods are capitalized, other costs are recognized in the results.

Lands are not depreciated. Depreciation of plant and equipment and vehicles recognized as “Large Equipment” is calculated based on their use hours, in relation to the estimated useful hours of these assets. The depreciation of other assets that do not qualify as “Large Equipment” is calculated by straight line method to assign its cost less its residual value during the estimated useful life, as follows:

Years __Buildings and premises between 5 and 33Plant and equipment between 5 and 10Vehicles between 5 and 10Furniture and fixtures between 4 and 10Various equipment between 4 and 10

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 10 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Residual values and useful life of assets are reviewed and adjusted, if necessary, at the date of each balance sheet. The assets book value is immediately written off at its recoverable value if the asset book value is higher than the estimated recoverable value. Gains and losses for the sale of goods of the fixed asset correspond to the difference between transaction income and the assets book value. These are included in the statement of income.

(m) Finance Lease Agreements Lease and/or sale agreements with a leaseback agreement on plant and equipment,

through which the Company substantially assumes all risks and benefits related to the property of leased assets, are classified as finance lease and are capitalized at the beginning of the agreement at the lesser value resulting from the fair value of leased assets and the present value of the minimum payments of lease fees. Lease fees payments are designated to reduce the liability and the recognition of the financial charge in such a manner as to obtain a constant interest rate on the debts pending of amortization. Obligations for financial and/or sale leases with financial leaseback agreements, net of financial charges, are included in the long-term debt account in the balance sheet. The financial cost is charged to results in the lease period. The cost of assets acquired through financial and/or sale lease with financial leaseback agreement is depreciated in the estimation of its useful life.

(n) GoodwillGoodwill represents the excess of the cost of an acquisition over the fair value of the Company’s shares of the identifiable net assets of a subsidiary as of the date of acquisition. Likewise, the goodwill arising during the acquisition of minority interest in a subsidiary represents the excess of cost of the additional investment over book value of net identifiable assets as of the date of acquisition. Goodwill is reviewed to determine whether a recognition of provisions for impairment is required. It is recorded at cost less accumulated provisions for impairment. Impairment losses are recognized in the statement of income and are not reversed. Gains and losses from the sale of subsidiaries or associates include the book value of goodwill related to the sold entity.

Goodwill is allocated to cash-generating units to conduct impairment tests. Each of those cash generating units represents the Company’s investment in every place where it operates per primary reporting segment (note 13).

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 11 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(o) Other AssetsConcessions included in Other Assets item of the balance sheet are recognized as

such based on the forecast that these will generate future economic benefits for the Company. Concessions are recorded at cost. These fees are amortized at straight-line method based on the remaining maturity of concession agreements. Repairs of highways and works in parking lots are capitalized, and regular maintenance of highways and parking lots are recognized in expenses when they are incurred.

Investments in exploration, development and subscription rights of concession agreements are amortized as from the period when income from its exploitation is obtained until the maturity of the respective agreements. On the other hand, if it were the case, investments in exploration and exploitation, referred to those exploration agreements in which it has been determined that results are not successful, are charged to the results in the period when this situation is determined, after the compensation attributable to the shareholding of third parties in said investments.

Costs related to the development or maintenance of software are recognized in results when incurred. However, costs that are directly related to single and identifiable software, that are controlled by the Company and that will provide future economic benefits higher than their cost in more than one year, are recognized as intangible assets. Direct costs related to the development of software include personnel costs and an aliquot of general expenses. Development costs of capitalized software are amortized by straight-line method in the estimate of its useful life, without exceeding four years.

(p) Impairment of Non-Financial Assets Assets that have an indefinite useful life and are not subject to amortization, are

tested annually for impairment. Assets that are subject to depreciation or amortization are reviewed for impairment whenever events or circumstances indicate that the book value may not be recoverable.

Impairment losses are the amount by which the asset book value exceeds its recoverable amount. The recoverable amount of assets corresponds to the higher net amount that would be obtained from the sale or value in use. In order to assess the impairment, assets are grouped at the lowest levels for which identifiable cash flows are generated (cash-generating units).

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 12 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(q) Loans Loans are initially recognized at their fair value, net of transaction costs incurred.

These loans are subsequently recorded at their amortized cost, and any resulting difference between the funds received (net of transaction costs) and the redemption value is recognized in the statement of income during the period of the loan using the effective interest method.

Loans are classified as current liability unless the Company has the unconditional right to differ settlement of the liability for at least twelve months after the balance sheet date.

(r) ProvisionsProvisions are recognized when the Company has a present legal obligation, either

legal or constructive, as a result of past events, and when it is probable that an outflow of resources will be required to settle the obligation, and it is possible to reliably estimate its amount. Restructuring cost provisions comprise lease termination penalties and employee termination payment.

When there are a number of similar obligations, the probability that an outflow of resources will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognized although the likelihood of outflow of resources for any one item included in the same class of obligations may be small.

Provisions are recognized at present value of expenditures expected to be required to settle the obligation using pre-tax rates that reflect the current market assessment of the time value of money and the risks specific to the obligation. The increase in the provision due to the passage of time is recognized as interest expense in the statement of income.

(s) Share of the ProfitsThe Company recognizes a liability and an expense for workers’ profit sharing in

profits equivalent to 5% and 10% of taxable base determined according to the current tax legislation for each subsidiary.

(t) Income TaxCurrent income tax is determined according to current tax provisions (note 21).

Deferred income tax is recorded using the liability method, recognizing the effect of

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 13 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

of temporary differences that arise between the tax base of assets and liabilities and its balance in the financial statements.

Deferred tax assets are only recognized as it is probable to have taxable benefits in the future against the credits that can be used.

The effect of these temporary differences is also considered in the calculation of workers’ profit sharing.

(u) Capital Common shares are classified as equity.

When the capital stock recognized as equity is repurchased (treasury shares in conformity with the IFRSs), the payment made including any cost directly related (net of taxes) is deducted from the Company’s equity until shares are amortized, reissued or sold (this repurchase has a different connotation under article 105 of Companies Act). When such shares are subsequently reissued or sold, any payment received, net of incremental costs directly attributable to the transaction and effects corresponding to income tax, is included in the equity (note 18).

(v) Dividend Distribution Dividend distribution to stockholders is recognized as liability in the financial statements in the period when dividends are approved by the Company’s stockholders.

(w) Contingent Assets and Liabilities Contingent liabilities are not recognized in financial statements. They are only

disclosed in the notes to financial statements unless the possibility of an outflow of economic resources is remote. Contingent assets are not recognized in financial statements, and they are only disclosed when an inflow of economic benefits is probable.

(x) Revenue RecognitionThe Company recognizes revenues when the amount can be reliably measured, it is

probable that future economic benefits will flow to the Company, and specific criteria are met per type of revenue as described below. Revenues are recognized in the results as follows:

Income for work valuations

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 14 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Income for work valuations and their respective costs are recognized as such when executing them, according to work advances. Additionally, such income and costs are adjusted to recognize the final projected profit margin of works which is monthly reviewed. Income is invoiced prior approval of works owners.

Sale of goodsOrdinary income resulting from sale of goods are recognized and recorded when the products are delivered and the risks and rewards inherent to the ownership of products are transferred to the buyer, and the corresponding collection of accounts receivable is fairly assured.

Income from rendered servicesIncome for services rendered are recognized in the accounting period when they are rendered, regarding the complete specific service, calculated on the service actually provided as a portion of the total of services to be rendered.

Income and costs for rendered services are recognized as such when such services are rendered.

Interest and dividendsInterest income is recognized on a time proportion basis, using the effective interest method.

Revenues from dividends are recognized when the right to receive the payment has been established.

(y) Accounting Pronouncements Pending ApprovalThe International Accounting Standards Board (IASB) has issued certain

International Financial Reporting Standards (IFRS) effective since 2007; however, official approval of these IFRSs in Peru is pending. For information purposes, the IFRS that have been issued but are not yet effective as of December 31, 2007 are detailed below:

- IFRS 7 – Financial Instruments: Disclosures. This IFRS is effective internationally as from January 1, 2007. The objective of IFRS 7 is to include in the financial statements, disclosures that allow users to evaluate the significance of financial instruments for an entity’s financial position and performance, through the understanding of the nature and extent of risk arising from financial instruments as well as the methods used to manage the risks derived from these instruments.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 15 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

- IFRS 8 –Operating Segments (effective for periods beginning on or after January 1, 2008).

- IFRIC 7 –Applying the Restatement Approach under IAS 29 (effective for periods beginning on or after March 1, 2006).

- IFRIC 8 - Scope of IFRS 2 (effective for periods beginning on or after May 2006).

- IFRIC 9 –Reassessment of Embedded Derivatives (effective for periods beginning on or after June 1, 2006).

- IFRIC 10 –Interim Financial Reporting and Impairment (effective for periods beginning on or after January 1, 2007).

- IFRIC 11 –IFRS 2: Group and Treasury Share Transactions (effective for periods beginning on or after March 1, 2007).

- Review of IFRS 3 - Business Combinations and IAS 27 Consolidated and Separate Financial Statements (modifications effective for periods beginning on or after July 1, 2009).

Management estimates that these interpretations will not have a significant effect on the stockholders’ equity or results.

(3) Financial Risk ManagementThe Company’s activities may expose it to a variety of financial risks related to the effects of

fluctuations in the debt and equity market prices, fluctuations in foreign exchange, interest rates, and fair values of financial assets and financial liabilities. The Company’s general program for the administration of risks is mainly focused on financial market unpredictability, and seeks to minimize potential adverse effects on its financial behavior.

Administration and Finance Management is in charge of the administration of risk following the policies approved by the Board of Directors. The Administration and Finance Management identifies, evaluates, and covers the financial risks in close cooperation with operating units. The Board of Directors provides guidelines for the global administration of risks, as well as written policies that cover specific areas, such as risks of fluctuations in foreign exchange rate, in interest rates, credit risks, and the investment of liquidity surplus.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 16 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(i) Currency risk The Company's activities and indebtedness in foreign currency exposes it to exchange rate fluctuation risk, especially concerning the U.S. dollar. In order to reduce the Company’s exposure, it conducts efforts to keep an appropriate balancing between assets and liabilities and between income and expenses in foreign currency.

Complementarily, the Company uses forward foreign exchange contracts, in order to mitigate the risk associated to the exposure arising from the costs in nuevos soles associated to income in foreign currency.

Balances in foreign currency as of December 31 are summarized as follows:

In thousands of US$ 2007 2006

Assets:Cash and banks and restricted funds 32,065) 44,400)Trade accounts receivable 38,680) 29,921)Other accounts receivable 45,232) 24,073)

--------------- --------------115,977) 98,394)

--------------- --------------

Liabilities:Bank loans ( 14,805) ( 1,611)Trade accounts payable ( 35,908) ( 20,219)Other accounts payable ( 29,073) ( 10,427)Long-term debts (including current portion) ( 67,559) ( 66,779)

--------------- --------------( 147,345) ( 99,036)

--------------- --------------Net liability position ( (31,368)) ( 642)

======== ========

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 17 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Those balances have been stated in S/. at the following free market exchange rate, ruling as of December 31:

In S/. 2007 2006

1 US$ - Exchange rate established by the Superintendency of Banking, Insurance and Private Pension Fund Administrators (AFP) - purchase (assets) 2.995 3.194

1 US$ - Exchange rate established by the Superintendency of Banking, Insurance and AFP - sale (liabilities) 2.997 3.197

As of December 31, 2007 and 2006, the Company and its subsidiaries recorded gains on exchange for S/. 65,704,000 and S/. 97,148,000 and losses on exchange for S/. 57,278,000 and S/. 87,738,000, respectively.

(ii) Interest rate riskThe Company’s income and operating cash flows are independent from the changes in the market interest rates because the Company’s debt is substantially subject to fixed rate. Only the short-term debt corresponding to bank loans that finance working capital are subject to fluctuation of interest rates.

(iii) Credit risk The Company does not have significant credit concentration risk. Concerning the loans to its related parties, the Company has established measures aimed at assuring recoverability of such loans.

The Company’s certificates of time deposits are limited to four sound financial entities in order to avoid risk concentration.

(iv) Liquidity riskPrudent management of liquidity risk implies keeping enough cash and marketable

securities, financing available through a proper number of credit sources, and the capacity of closing positions in the market.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 18 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

The Company maintains an average debt maturity greater than the DEBT/ EBITDA ratio; additionally, the Company holds overnight deposits and certificates of time deposits for an approximate amount of US$ 18 million destined to face cash demands that new projects or investments may require.

Finally, the program of commercial papers obtained during 2006 has enabled lines amounting to US$ 20 million that contribute to reduce the dependence on lines granted by the financial system, diversifying financing sources.

(4) Cash and Banks and Restricted FundsThey comprise the following:

In thousands of S/. 2007 2006

Cash and checking accounts 51,861 36,027Overnight and time deposits 71,865 101,620

--------------- --------------123,726 137,647

Collateral account 4,743 3,292Restricted funds 13,477 9,149

--------------- --------------Total 141,946 150,088

======== ========

As of December 31, 2007, the Company holds checking accounts and time deposits at local banks in local and foreign currency for approximately S/. 58.4 million and US$ 21.6 million, respectively (S/. 7.1 million and US$ 9 million, respectively, as of December 31, 2006).

As of December 31, 2007, the collateral account amounting to S/. 4.7 million (equivalent to US$ 1.6 million) corresponds to a fund held at Banco de Crédito del Perú as a collateral for the compliance bond of the Concession Agreement of the “Eje Multimodal Sur, Tramo 3 (IIRSA Sur Tramo 3)”. The Company expects to recover this collateral during 2008.

As of December 31, 2007, GMP S.A. holds at Banco de Crédito del Perú a restricted fund for US$ 4.5 million that guarantees obligations of a related company. As of December 31, 2006, restricted funds corresponded to a collateral for US$ 2.9 million granted in favor of Merrill-Lynch for the financing of the Southern Interoceanic highway.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 19 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(5) Trade Accounts Receivable Trade accounts receivable correspond mainly to revenue from work valuations. Trade

accounts receivable have current maturity, and do not accrue interest, and do not have specific guarantees.

The detail of the aging of accounts receivable is as follows:

In thousands of S/. 2007 2006

Current 231,951 187,019Overdue until 30 days 433 1,124Overdue over 30 days 1,180 662

--------------- --------------233,564 188,805

======== ========(6) Related Parties

The movement of accounts receivable and payable with related entities for the period ended December 31, 2007, is as follows:

In thousands of S/.Name of affiliates and Initial Final

related parties balances Additions Deductions balances

Receivable:GME S.A. 1,436 - ( 1,332) 104Norvial S.A. 3,977 362 ( 3,977) 362Other minor 848 174 ( 847) 175

----------- ----------- ----------- -----------6,261 536 ( 6,156) 641

====== ====== ====== ======Payable:

GME S.A. 5,647 - ( -) 5,647Norvial S.A. - 7 ( - 7Other minor - 12 ( - 12

----------- ----------- ----------- -----------5,647 19( -) 5,666

====== ====== ====== ======

Accounts receivable and payable have current maturity and do not have specific guarantees.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 20 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

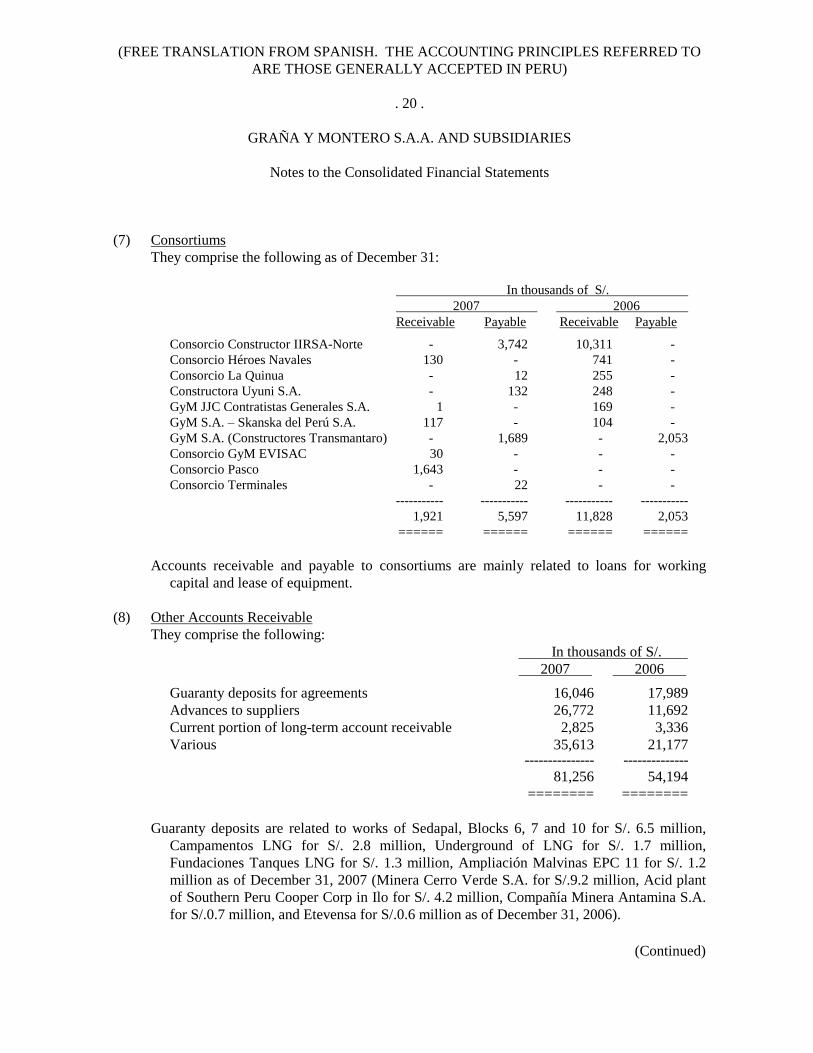

(7) ConsortiumsThey comprise the following as of December 31:

In thousands of S/. 2007 2006Receivable Payable Receivable Payable

Consorcio Constructor IIRSA-Norte - 3,742 10,311 -Consorcio Héroes Navales 130 - 741 -Consorcio La Quinua - 12 255 -Constructora Uyuni S.A. - 132 248 -GyM JJC Contratistas Generales S.A. 1 - 169 -GyM S.A. – Skanska del Perú S.A. 117 - 104 -GyM S.A. (Constructores Transmantaro) - 1,689 - 2,053Consorcio GyM EVISAC 30 - - -Consorcio Pasco 1,643 - - -Consorcio Terminales - 22 - -

----------- ----------- ----------- -----------1,921 5,597 11,828 2,053

====== ====== ====== ======

Accounts receivable and payable to consortiums are mainly related to loans for working capital and lease of equipment.

(8) Other Accounts ReceivableThey comprise the following:

In thousands of S/. 2007 2006

Guaranty deposits for agreements 16,046) 17,989)Advances to suppliers 26,772) 11,692)Current portion of long-term account receivable 2,825) 3,336)Various 35,613) 21,177)

--------------- --------------81,256) 54,194)

======== ========

Guaranty deposits are related to works of Sedapal, Blocks 6, 7 and 10 for S/. 6.5 million, Campamentos LNG for S/. 2.8 million, Underground of LNG for S/. 1.7 million, Fundaciones Tanques LNG for S/. 1.3 million, Ampliación Malvinas EPC 11 for S/. 1.2 million as of December 31, 2007 (Minera Cerro Verde S.A. for S/.9.2 million, Acid plant of Southern Peru Cooper Corp in Ilo for S/. 4.2 million, Compañía Minera Antamina S.A. for S/.0.7 million, and Etevensa for S/.0.6 million as of December 31, 2006).

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 21 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Advances given to suppliers correspond to Golf Millenium works for S/. 6.2 million, Línea de Transmisión de San Gaban for S/. 0.8 million, Edificio Santo Toribio for S/.1.1 million,Hotel Novotel for S/.0.9 million, Clinica Ricardo Palma for S/.0.55 million, Ministry of Transportation and Communications for S/. 5.1 million, and advances for imports and their pertinent proceedings for S/. 7.2 million, as of December 31, 2007 (Sedapal Block 7 for S/. 1 million, Edificio Real Diez for S/.0.9 million, Cerro Verde S.A. for S/. 0.8 million, EPC 11 Malvinas for S/. 0.5 million, extension of Larcomar S.A. for S/. 0.3 million, and advances for imports for S/. 1.3 million as of December 31, 2006).

Various accounts receivable include leasing of equipment and reimbursable expenses receivable from CONIRSA for S/. 10.1 million, accounts receivable from Transportadora de Gas del Perú for S/. 1.7 million, Colegio Fe y Alegría for S/. 1.2 million, Proyectos Inmobiliarios Consultores for S/.1.3 million, Red Vial 5 for S/.2.7 million, MTC –Canchaque for S/.2.8 million, Petróleos del Perú for S/.0.7 million, Transportadora de Gas del Perú for S/. 1.7 million, and ICCGSA for S/.0.9 million (CONIRSA for S/.4.7 million, Minera San Cristóbal for S/.1.1 million, Transportadora de Gas del Perú S.A.for S/.1.7 million, Real Once S.A. for S/.1.9 million, Intertítulos Sociedad Titulizadora S.A. for S/.2.6 million, and Consorcio Terminales for S/.2.2 million as of December 31, 2006).

(9) InventoriesThis item as of December 31, comprises:

In thousands of S/. 2007 2006

Property and land 16,074) 8,851)Construction materials 51,939)) 17,426)Supplies 6,388) 5,246)Merchandise 4,128) 5,644)Inventories in transit 873) 278)

--------------- --------------79,402) 37,445)

Provision for inventory impairment ( 145) ( 162)--------------- --------------

79,257 37,283======== ========

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 22 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Property and Land This item comprises lands T2, T8 and T9 of Centro Empresarial Camino Real amounting to

S/. 5.5 million, property Balta, Golf los Incas and Malecón Cisneros for S/. 8.3 million, the lands of Playa Las Lomas for S/.2.2 million (lands T2, T8 and T9 of Centro Empresarial Camino Real for S/.5.5 million and lands from Playa Las Lomas for S/. 3.3 million as of December 31, 2006).

Construction MaterialsAs of December 31, 2007, these materials correspond mainly to the following works: Andoas

for S/.5.7 million, Parques de El Agustino for S/. 16.2 million, Ampliación Malvinas EPC 11 for S/. 3.1 million, Línea de Transmisión San Gaban for S/. 1.3 million, Javier Prado for S/. 4.9 million, Red Vial for S/. 2.7 million, Sedapal for S/. 2.0 million, Telecommunications for S/. 1.4 million, Brocal for S/. 1.2 million, Cashiriari for S/. 0.9 million, and Cerro Corona for S/. 0.8 million (Andoas Plus for S/.3.8 million, Brocal IV for S/.1.3 million, Sedapal Block 7 for S/. 1.4 million, Edificio Real 10 for S/. 4.5 million as of December 31, 2006.

Supplies and MerchandiseThey mainly comprise spare parts, drilling equipment and supplies in general for the

exploitation of lots and gas plant, as well as accessories and supplies for computing and communications equipment.

(10) Long-term Accounts ReceivableThey comprise the following:

In thousands of US$ Authorized In thousands of S/.

Type of and used Total Current Non-currentName of Debtor operation Maturity amount 2007 2006 2007 2006 2007 2006

Consorcio Terminales (1) Loan August 2011 3,800 8,118 10,481 2,112 2,207 6,006 8,274

Petróleos del Perú S.A. (2) Agreement Various 794 8,274 3,464 713 686 7,561 2,778

Proyectos Inmobiliarios

Consultores S.A. Loans 2008 - 1,276 1,141 - - 1,276 1,141Philip Morris S.A. Agreement October 672 - 1,108 - 443 - 665TGP S.A. Various 1,655 1,655 - - - 1,655 -Inversiones Larcomar

S.A. (3) - - 3,024 - - - 3,024 -Sunat (4) Claim - - 1,655 - - - 1,655 -Proyecto Especial

Kovire Agreement - - 1,646 - - - 1,646 -Other - - 614 - - - 614 -

----------- ----------- ----------- ----------- ----------- -----------26,262 16,194 2,825 3,336 23,437 12,858

====== ====== ====== ====== ====== ======

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 23 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(1) In August 2003, the Company granted to Consorcio Terminales S.A. a loan for US$ 9.2 million with funds obtained in the issuance process of securitization bonds. This balance is shown at consolidation percentage of the Consortium (50%) for S/. 8,118,000 as of December 31, 2007 (S/. 10,481,000 in 2006). This account receivable accrues interest at an annual rate of 9.65%.

(2) Long-term accounts receivable from Petróleos del Perú for S/. 8,274,000 (S/. 3,464,000 as of December 31, 2006) represent additional investments finished by Consorcio Terminales and destined to the modernization and enlargement of the terminals under the agreement. These investments will be transferred and invoiced at cost and discounted from the monthly payment for right of use of terminals.

During 2007, said Consortium has incurred in additional investments for S/. 4,810,000 (S/. 3,314,000 in 2006).

(3) In June 2007, Inversiones Larcomar S.A. acquired from Larcomar S.A. several brands which have non-current maturity.

(4) Claim filed by Larcomar S.A. against the payment of the Temporary Tax on Net Assets of years 2005, 2006 and 2007. Tax Court has not issued a definite resolution; however, Management considers that the recognition of the balance compensation is possible.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 24 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

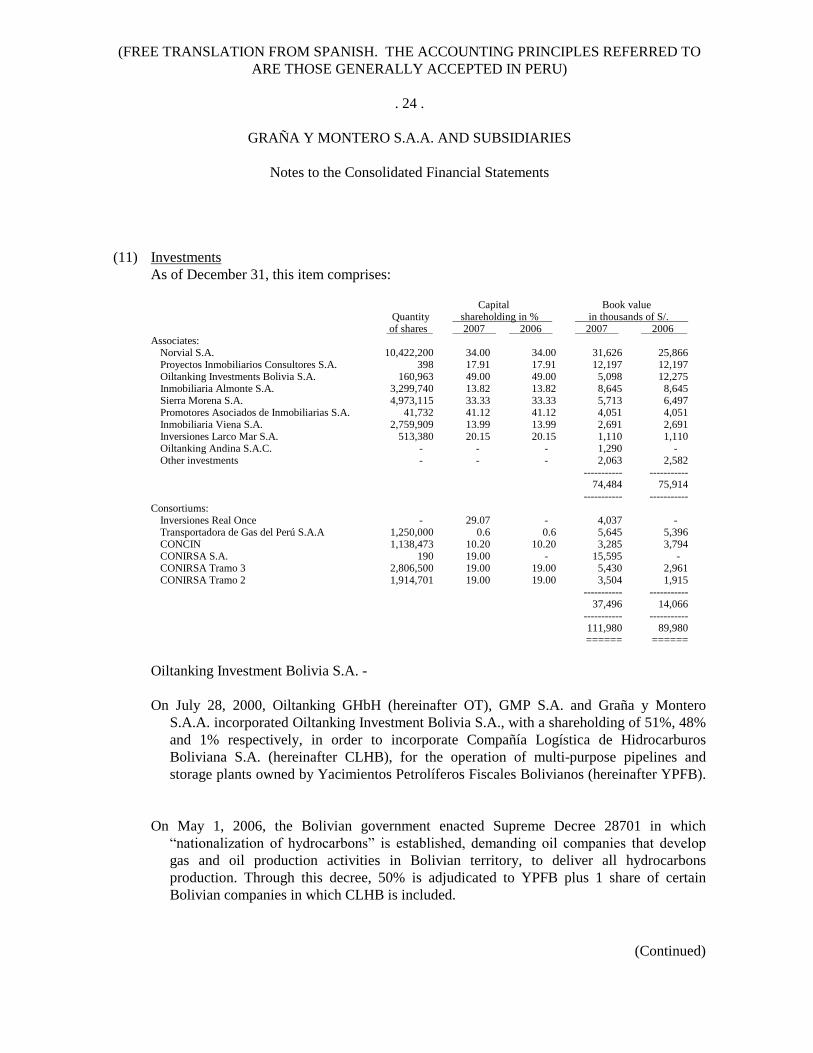

(11) InvestmentsAs of December 31, this item comprises:

Capital Book value Quantity shareholding in % in thousands of S/.of shares 2007 2006 2007 2006

Associates:Norvial S.A. 10,422,200 34.00 34.00 31,626 25,866Proyectos Inmobiliarios Consultores S.A. 398 17.91 17.91 12,197 12,197Oiltanking Investments Bolivia S.A. 160,963 49.00 49.00 5,098 12,275Inmobiliaria Almonte S.A. 3,299,740 13.82 13.82 8,645 8,645Sierra Morena S.A. 4,973,115 33.33 33.33 5,713 6,497Promotores Asociados de Inmobiliarias S.A. 41,732 41.12 41.12 4,051 4,051Inmobiliaria Viena S.A. 2,759,909 13.99 13.99 2,691 2,691Inversiones Larco Mar S.A. 513,380 20.15 20.15 1,110 1,110Oiltanking Andina S.A.C. - - - 1,290 -Other investments - - - 2,063 2,582

----------- -----------74,484 75,914

----------- -----------Consortiums:

Inversiones Real Once - 29.07 - 4,037 -Transportadora de Gas del Perú S.A.A 1,250,000 0.6 0.6 5,645 5,396CONCIN 1,138,473 10.20 10.20 3,285 3,794CONIRSA S.A. 190 19.00 - 15,595 -CONIRSA Tramo 3 2,806,500 19.00 19.00 5,430 2,961CONIRSA Tramo 2 1,914,701 19.00 19.00 3,504 1,915

----------- -----------37,496 14,066

----------- -----------111,980 89,980====== ======

Oiltanking Investment Bolivia S.A. -

On July 28, 2000, Oiltanking GHbH (hereinafter OT), GMP S.A. and Graña y Montero S.A.A. incorporated Oiltanking Investment Bolivia S.A., with a shareholding of 51%, 48% and 1% respectively, in order to incorporate Compañía Logística de Hidrocarburos Boliviana S.A. (hereinafter CLHB), for the operation of multi-purpose pipelines and storage plants owned by Yacimientos Petrolíferos Fiscales Bolivianos (hereinafter YPFB).

On May 1, 2006, the Bolivian government enacted Supreme Decree 28701 in which “nationalization of hydrocarbons” is established, demanding oil companies that develop gas and oil production activities in Bolivian territory, to deliver all hydrocarbons production. Through this decree, 50% is adjudicated to YPFB plus 1 share of certain Bolivian companies in which CLHB is included.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 25 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Therefore, in May 2006, Management took the decision to change the investment accounting method in Bolivia, from Valuation at Equity Sharing to Cost Method. As of December 31, 2006, 50% of investment value related to CLHB was considered as accounts receivable and fully recorded for S/. 11.9 million, which was presented as investment write-off in the statement of income of year 2006. As of December 31, 2007, the balance of the investment exposure in CLHB amounts to S/. 5.1 million. As of December 31, 2007, CLHB is still operated and managed by the Company and its partner OT, while transfer of shares is made achieved.

As of December 31, 2007 and 2006, financial Statements do not include assets, liabilities, revenue and expenses of OTIB due to the jointly control loss as a consequence of the decrease of its shares, resulting from nationalization.

(12) Property, Plant, and EquipmentThe movement of the Property, Plant, and Equipment account and the corresponding

accumulated depreciation for the year ended December 31, 2007 and 2006 is the following:

Year 2007:

In thousands of S/. Initial Deductions Final

balances Additions and/or adjustments balancesCost:

Land 1,665) - ( 5) 1,660Buildings and other constructions 157,117) 73,906 ( 90,397) 140,626Plant and equipment 294,239) 50,850 ( 108,751) 236,338Furniture and fixtures 17,283) 3,331 ( 4,895) 15,719Vehicles, various equipment and other 110,715) 35,276 ( 18,941) 127,050Units in transit 3,596) 2,507 (- ) 6,103Works-in-progress 9,522) 58,459 ( 20,737) 47,244

------------ ------------ ------------ ------------594,137 224,329 ( 243,726) 574,740

------------ ======= ======= ------------Accumulated depreciation:

Buildings and other constructions 24,549) 3,464 ( 12,389) 15,624Plant and equipment 218,175) 37,226 ( 107,305) 148,096Furniture and fixtures 9,297) 2,886 ( 4,113) 8,070Vehicles, various equipment and other 69,280) 14,952 ( 9,287) 74,945

------------ ------------ ------------ ------------ 321,301) 58,528 ( 133,094) 246,735

------------ ======= ======= ------------Net cost 272,836) 328,005

======= =======

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 26 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Year 2006: In thousands of S/.

DeductionsInitial and/or Uncon- Final

balances Additions adjustments solidated balancesCost:

Land 6,634) 1,014 ( 1,841) ( 4,142) 1,665Buildings and other constructions 134,951) 28,189 - ( 6,023) 157,117Plant and equipment 289,319) 32,061 ( 8,880) ( 18,261) 294,239Furniture and fixtures 16,909) 1,595 ( 935) ( 286) 17,283Vehicles, various equipment and other 102,993) 20,586 ( 6,471) ( 6,393) 110,715Units in transit 1,242) 2,354 - - 3,596Works-in-progress 8,796) 11,198 ( 6,571) ( 3,901) 9,522

------------ ------------ ------------ ------------ ------------560,844) 96,997 ( 24,698) ( 39,006) 594,137

------------ ------------ ------------ ------------ ------------Accumulated depreciation:

Buildings and other constructions 21,459) 3,603 - ( 513) 24,549Plant and equipment 196,114) 34,667 ( 8,466) ( 4,140) 218,175Furniture and fixtures 8,636) 1,560 ( 816) ( 83) 9,297Vehicles, various equipment and other 60,376) 14,123 ( 2,780) ( 2,439) 69,280

------------ ------------ ------------ ------------ ------------286,585) 53,953 ( 12,062) ( 7,175) 321,301

------------ ======= ======= ======= ------------Net cost 274,259) 272,836

======= =======

As of December 31, 2007, property, plant, and equipment accounts include assets acquired under the modality of finance lease and sale with finance leaseback agreement for approximately S/. 63.95 million (S/.32.6 million in 2006).

As of December 31, 2006, the Company transferred costs related to conditioning of wells from the works-in-progress account to the intangibles item for approximately S/. 7 million (S/. 5 million as of December 31, 2005).

(13) GoodwillIt comprises the highest value paid by the Company to obtain the total capital stock of GMA

S.A. regarding the value of its corresponding interest in stockholders’ equity. The balance as of December 31, 2007 of S/. 29.6 million (S/. 32.5 million in 2006) is shown net of loss for impairment of S/. 2.9 million.

Likewise, in February 2007, the Company acquired 1,103,509 shares at market value that represented an additional shareholding of 5.47% in the subsidiary GMD S.A., paying an amount of S/.4.9 million and thus, increasing its shareholding from 83.21% to 88.68%.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 27 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

The highest value paid on net assets acquired through this share block was S/. 4.8 million and was recognized as goodwill in the balance sheet.

The evaluation of impairment of goodwill was made using the value in use of the corresponding cash-generating unit. The key criteria for the calculation of the value in use have been: a) projection period: 10 years, b) Growth rate: 6% and perpetual growth up to 3%, and c) discount rate: 11%. The results of this evaluation did not determine impairment in book value.

(14) Other AssetsThe annual movement of the other assets item comprises the following:

Year 2007: In thousands of S/.

Initial Deductions and/or Finalbalances Additions adjustments balances

Cost:Arequipa - Matarani highway concession (a) 41,681 - - 41,681Block I 32,296 - 17,489 49,785Block V (c) 8,752 - 1,588 10,340Oracle (d) 14,352 2,022 4,691 21,065CT Concession and rights 9,545 - - 9,545Parque Ovalo Gutiérrez Concession (b) 9,512 - ( 9,512) -Licenses and software projects 3,592 1,748 ( 297) 5,043Surface rights (e) 12,383 11,537 ( 8,180) 15,740Other minor 4,795 1,819 ( 4,795) 1,819

------------ ------------ ------------ ------------136,908 17,126 984 155,018

------------ ======= ======= ------------

Accumulated amortization:Arequipa - Matarani highway concession 41,681 - - 41,681Block I 16,981 2,206 - 19,187Block V 6,878 376 ( 30) 7,224Oracle 12,647 936 1,994 15,577CT Concessions and Rights 5,454 682 ( 2) 6,134Parque Ovalo Gutiérrez Concession 2,948 254 ( 3,202) -Licenses and software projects 497 257 1,349 2,103Surface rights 839 389 ( 819) 409Other minor 3,475 60 ( 3,475) 60

------------ ------------ ------------ ------------91,400 5,160 ( 4,185) 92,375

------------ ======= ======= ------------Net cost 45,508 62,643

======= =======

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 28 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Year 2006: In thousands of S/.

DeductionsInitial and/or Uncon- Final

balances Additions adjustments solidated balancesCost:

Arequipa - Matarani highway concession 41,681 - - - 41,681Block I 25,468 88 6,740 - 32,296Block V 8,442 162 148 - 8,752Software 13,852 500 - - 14,352CT Concessions and Rights 9,545 - - - 9,545Parque Ovalo Gutiérrez Concession 9,512 - - - 9,512CLHB Concessions 6,673 - - ( 6,673) -Licenses and software projects 1,644 1,948 - - 3,592Surface rights 5,742 6,641 - - 12,383Other minor 4,453 711 ( 369) - 4,795

------------ ------------ ------------ ------------ ------------127,012 10,050 6,519 ( 6,673) 136,908

------------ ======= ======= ======= ------------Accumulated amortization:

Arequipa - Matarani highway concession 40,095 1,586 - - 41,681Block I 15,502 1,479 - - 16,981Block V 6,395 483 - - 6,878Software 11,659 988 - - 12,647CT Concessions and Rights 4,771 683 - - 5,454Parque Ovalo Gutiérrez Concession 2,631 317 - - 2,948CLHB Concessions 1,556 - - ( 1,556) -Licenses and software projects 142 355 - - 497Surface rights 685 154 - - 839Other minor 3,941 225 ( 691) - 3,475

------------ ------------ ------------ ------------ ------------87,377 6,270 ( 691) ( 1,556) 91,400

------------ ======= ======= ======= ------------Net cost 39,635 45,508

======= =======

Costs capitalized in the balance of this account are mainly referred to:

(a) The cost incurred in the fitting out of the Arequipa-Matarani highway whose concession of maintenance, fitting out and exploitation matured in May 2006; however, due to modifications in the agreement, the term of this concession was extended until May 2007. As of December 31, 2006, the Company had amortized the total of these assets.

(b) The cost incurred in the execution of the remodeling project of Parque Ovalo Gutiérrez that grants the right of concession on parking lots and other services for a period of 30 years beginning as from September 1997.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 29 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

General Stockholders’ Meeting, held on October 19, 2007, approved the spin-off of the equity block composed of assets and liabilities related to said concession for the exploitation of an underground parking lot denominated “Playa Óvalo Gutierrez”, which entered in force on the same date and had as consequence the reduction of capital of Concar S.A.

(c) Investment expenses in exploration, development and subscription rights obtained through oil exploitation agreements of blocks I and V and the right obtained for the concession in the administration of oil distribution terminals owned by PETROPERU S.A.

(d) Costs related to the acquisition of certain software licenses and Oracle implementation.

(e) Surface rights – Fashion Center S.A., correspond to the value of concession of the right of use of surfaces granted by Municipality of Miraflores in December 1995, for a term of 60 years. Until May 2007, the surface right was granted in favor of Larcomar S.A.

(15) Bank Overdrafts and LoansThey comprise the following:

In thousands of S/. 2007 2006

Banco de Crédito del Perú 21,476 2,946Interbank - 2,081Banco Interamericano de Finanzas S.A. - 124

--------------- --------------21,476 5,151

======== ========

As of December 31, 2007, the Company held loans for working capital for the financing of works for S/. 21 million.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 30 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

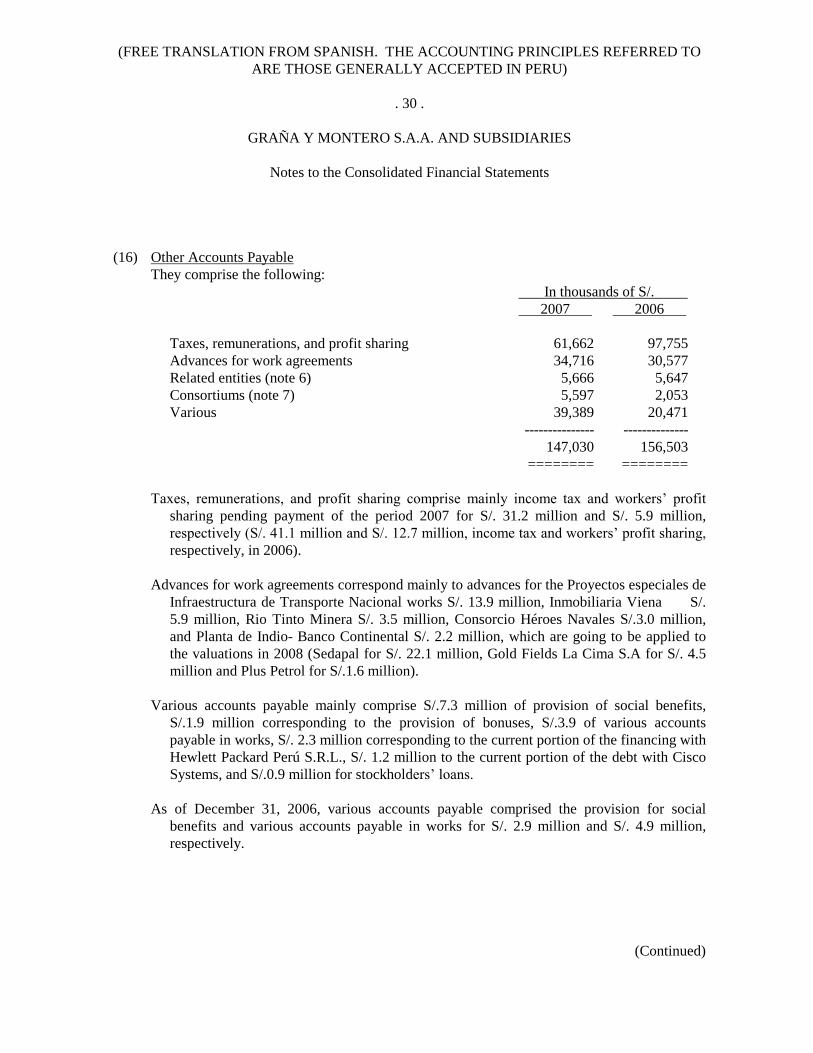

(16) Other Accounts PayableThey comprise the following:

In thousands of S/. 2007 2006

Taxes, remunerations, and profit sharing 61,662 97,755Advances for work agreements 34,716 30,577Related entities (note 6) 5,666 5,647Consortiums (note 7) 5,597 2,053Various 39,389 20,471

--------------- --------------147,030 156,503

======== ========

Taxes, remunerations, and profit sharing comprise mainly income tax and workers’ profit sharing pending payment of the period 2007 for S/. 31.2 million and S/. 5.9 million, respectively (S/. 41.1 million and S/. 12.7 million, income tax and workers’ profit sharing, respectively, in 2006).

Advances for work agreements correspond mainly to advances for the Proyectos especiales de Infraestructura de Transporte Nacional works S/. 13.9 million, Inmobiliaria Viena S/. 5.9 million, Rio Tinto Minera S/. 3.5 million, Consorcio Héroes Navales S/.3.0 million, and Planta de Indio- Banco Continental S/. 2.2 million, which are going to be applied to the valuations in 2008 (Sedapal for S/. 22.1 million, Gold Fields La Cima S.A for S/. 4.5 million and Plus Petrol for S/.1.6 million).

Various accounts payable mainly comprise S/.7.3 million of provision of social benefits, S/.1.9 million corresponding to the provision of bonuses, S/.3.9 of various accounts payable in works, S/. 2.3 million corresponding to the current portion of the financing with Hewlett Packard Perú S.R.L., S/. 1.2 million to the current portion of the debt with Cisco Systems, and S/.0.9 million for stockholders’ loans.

As of December 31, 2006, various accounts payable comprised the provision for social benefits and various accounts payable in works for S/. 2.9 million and S/. 4.9 million, respectively.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 31 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(17) Long-term DebtAs of December 31, this item comprises:

In thousands of S/.Total Current Non-current

2007 2006 2007 2006 2007 2006

Bank debt (a) 159,893 90,534 38,424 18,501 121,469 72,033Securitization bonds 91,731 116,871 27,628 27,148 64,103 89,723

----------- ----------- ----------- ----------- ----------- -----------Financial debt 251,624 207,405 66,052 45,649 185,572 161,756Debt with third parties 26,197 28,741 - 5,596 26,197 23,145Various provisions 6,700 6,700 - - 6,700 6,700

----------- ----------- ----------- ----------- ----------- -----------284,521 242,846 66,052 51,245 218,469 191,601====== ====== ====== ====== ====== ======

(a) Bank debt In thousands of S/.

Type of Total Current Non-current Name of the creditor obligation Maturity 2007 2006 2007 2006 2007 2006

Banco de Crédito de Bolivia Loan 2010 14,483 1,153 4,906 1,153 9,577 -Banco Continental Leasing 2010 8,719 8,148 1,572 2,373 7,147 5,775Citileasing Leasing 2014 27,402 - 2,860 - 24,542 -Interbank Leasing 2014 46,506 12,489 2,021 1,376 44,485 11,113Banco de Crédito del Perú Guarantee 2009 6,403 - - - 6,403 -Banco de Crédito del Perú Leasing 2010 22,322 3,999 13,751 1,002 8,571 2,997Banco de Crédito del Perú Promissory note 2009 - 9,591 - 3,197 - 6,394Interleasing Leasing 2010 19,182 7,041 5,758 3,739 13,424 3,302América Leasing Leasing 2010 5,752 4,527 2,523 1,100 3,229 3,427Banco Interamericano de Finanzas Leasing 2009 2,500 3,359 1,152 1,049 1,348 2,310Scotiabank Leasing 2010 3,380 - 1,093 - 2,287 -Scotiabank Syndicated loans 2013 - 22,305 - 1,804 - 20,501Interbank Syndicated loans 2013 - 17,223 - 1,393 - 15,830Interbank Loan 2008 2,245 - 2,245 - - -Banco de Crédito del Perú Leasing - 999 - 543 - 456 -Other minor - 699 - 315 - 384

---------- ---------- ---------- ---------- ---------- ----------159,893 90,534 38,424 18,501 121,469 72,033====== ====== ====== ====== ====== ======

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 32 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

(b) Securitization BondsIn October 2003, by means of public bid, the totality of “Securitization Bonds from

Graña y Montero and Subsidiaries”- First Issuance were placed for US$50 million, with maturity in 2011 and with a return of 7.5% of annual nominal interest rate.

The amortized cost of debt for the “Securitization Bonds from Graña y Montero and Subsidiaries” item has been determined as follows:

In thousands of 2007 2006

US$ S/. US$ S/.

Original capital 50,000) 149,847) 50,000) 159,850)Amortized capital ( 19,940) ( 59,757) ( 13,709) ( 43,828)

------------- ------------- ------------- -------------Total debt 30,060) (90,090) 36,291(( 116,022

------------- ------------- ------------- -------------Plus:Accrued interest 13,518) 40,513) 11,009) 35,196)Transaction costs (6,681) (20,023) 5,363) 17,146

------------- ------------- ------------- -------------) (20,199) 60,536) 16,372) 52,342)

------------- ------------- ------------- -------------Less:Prepaid costs ( 2,572) ( 7,708) ( 2,582) ( 8,255)Amortization of transaction costs ( 4,193) ( 12,566) ( 3,264) ( 10,435)Amortized interest ( 12,874) ( 38,621) ( 10,261) ( 32,803)

------------- ------------- ------------- -------------( 19,639) ( 58,895) ( 16,107) ( 51,493)

------------- ------------- ------------- -------------Total amortized cost 30,620) 91,731) 36,556) 116,871)Less current portion ( 9,222) ( 27,628) ( 8,450) ( 27,148)

------------- ------------- ------------- -------------Non-current amortized cost 21,398) 64,103) 28,106) 89,723

======= ======= ======= =======

Bondholders’ Meeting, dated October 2007, agreed on the spin off of the equity block composed of the concession of Ovalo Gutierrez from originator Concar S.A. This spin off did not affect future flows of originator Concar S.A. since the aforementioned concession did not take part of the trust fund.

(FREE TRANSLATION FROM SPANISH. THE ACCOUNTING PRINCIPLES REFERRED TO ARE THOSE GENERALLY ACCEPTED IN PERU)

. 33 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(Continued)

Bondholders’ Meeting, dated November 10, 2006, approved some modifications to the initial conditions of the bond issuance process, basically, to generate a reduction in the financial cost and maintain bonds under an AAA rating. Such changes were also ratified by Inter-American Development Bank (IDB) and Nederlanse Financiering-Maatschappij Voor Ontwikkelingslanden N.V. (FMO), guarantors of the securitization process. The main changes are detailed as follows:

Reduction of the partial guarantee of IDB and FMO to 37.5% of the pending balance of bonds.

Release of the reserve account; said funds then have free withdrawal option for the Group (note 4).