equalization aid emily koczela, brown deer business manager karen kucharz robbe, school financial...

TRANSCRIPT

Equalization AidEmily Koczela,

Brown Deer Business ManagerKaren Kucharz Robbe,

School Financial Services Consultant

Department of Public Instruction

January 23,2014

U.S. Constitution on Education

10th Amendment

“…powers not granted to the federal government by

the Constitution, nor prohibited to the States, are

reserved to the States or the people…”

1791

1848 Wisconsin Constitution

“Each town and city shall be required to raise by tax,

annually, for the support of common schools therein……”

Article X, Section 4.

1848 Wisconsin Constitution

“The legislature shall provide by law for the establishment of

district schools, which shall be as nearly uniform as practicable;

and such schools shall be free and without charge for tuition to all children between the ages of

4 and 20.”Article X, Section 2.

Basic Framework

State ResponsibilityDistrict Schools

As Nearly Uniform as PracticableFree

Local Tax

Supreme Court

Uniformity goes to the “character of education,”

not to the total amount spent.

However, funding “character” cannot result in too great of a

disparity of cash.

Modern-Day Wisconsin

In Wisconsin, the primary funding source for public

schools is the property tax, but we know the property values

across the state are not uniform.

The challenge is defining “uniformity.”

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

10 mil tax(Example: $1,000,000 x

.010)

$10,000

$20,000

$30,000

$40,000

$50,000

What is “uniformity”?

$20,000

$20,000

$20,000

$20,000

$20,000$30,00

0$40,000

$50,000

$60,000

$70,000

(state aid is the same?)

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

What is “uniformity”?

$10,000

$20,000

$30,000

$40,000

$50,000$20,00

0$10,000

$ 0

$-10,000

$-20,000$30,00

0$30,000

$30,000

$30,000

$30,000

(“Robin Hood” principle with local tax?)

NOT LEGAL

Buse vs. Smith(1976)

State cannot “recapture” from local tax base.

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

What is “uniformity”?

$10,000

$20,000

$30,000

$40,000

$50,000$40,00

0$30,000

$20,000

$10,000

$ 0 $50,00

0$50,000

$50,000

$50,000

$50,000

(state aid is related to local value)

Starting to Come Together

More local property wealth means

less aid from the state.

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

Number of Children to Educate

2010 10 10 10$100,000

$400,000 $250,000

$300,000

$200,000

Notice how the tax base per child changes after incorporating the number of children to

educate.

State Formula

Takes into account BOTH property tax base AND number

of children to educate.

2013-14 General Aid*

Equalization $4,295,238,507 98.03%

Special Adjustment

$18,167,259 0.41%

Inter-District $22,239,425 0.51%

Intra-District $45,947,412 1.05%

Total General Aid

$4,381,592,603 100%

Most districts receive only Equalization Aid.

* Prior to Choice/Charter deductions.

16

Property Value per Member

17

Property Value per Member

18

Property Value per Member

Equalization Aid

Property Tax Base

Equalization Aid

What about two-thirds funding?Two-thirds NEVER meant that each district would get 66.7% state aid!

It was a STATE computation that added together several statewide revenue sources, (all local levies, state and categorical aid and levy credit) and multiplied that number by 66.7%. The result of this equation was put into the formula.

Two-thirds is no longer law.

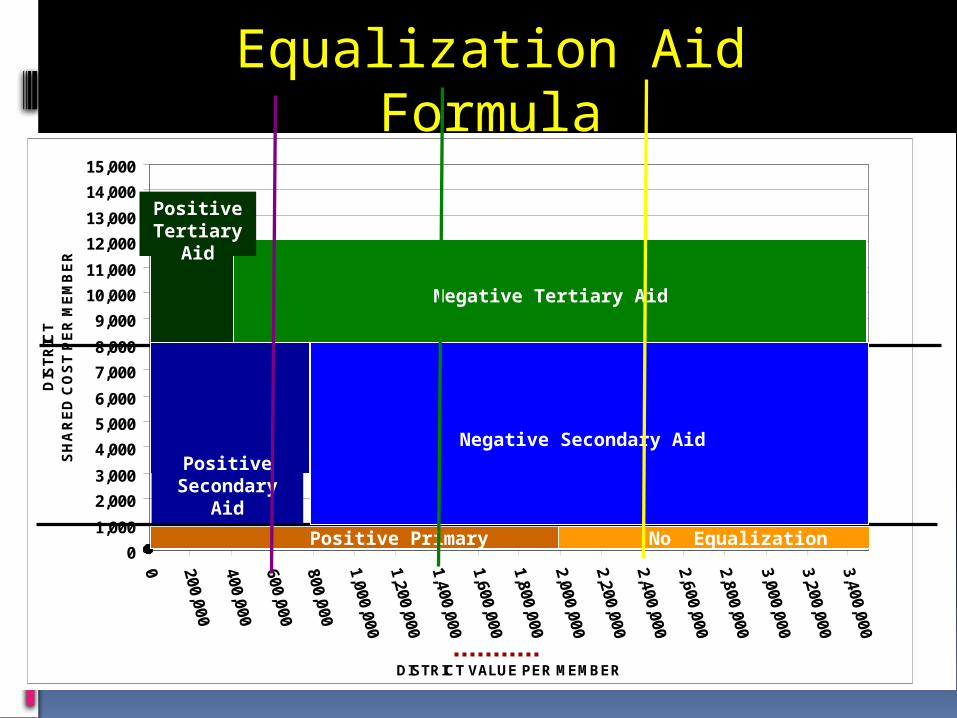

Equalization Aid Formula

A cost-sharing formula that incorporates:

Property Value Number of Students to Educate Spending

General Fund Shared Cost

Local Property

Tax43%

Local Misc. Receipts

1%Other Misc.3%

State General

Aid44%

Categor-ical

State Aid3%

Federal Aid5%

Debt Service Funds Shared Cost

Local Property

Tax98%

Misc Local Revenue

2%

Total General Fund (Fund 10) Expenditures

+ (plus)Total Debt Service Funds (Funds

38 & 39) Expenditures

- (minus)all local misc. revenue, grant

revenue,and categorical aid.

Result is “Shared Cost”

District Factor – Shared Cost

District Factor - Wealth

Property tax base is used to determine district wealth and

ability to support district expenditures.

Uses Equalized Valuation or Fair Market Value.

(NOT Assessed Value)

District Factor – Membership

F.T.E. = full-time equivalent2 halftime kindergarten students = 1 F.T.E.

Average of 3rd Friday F.T.E. - September

2nd Friday F.T.E. - January

+ Summer School F.T.E

Summer School = 48,600 minutes of instruction = 1 F.T.E.

The Computation

…….is actually 3 individual computations……..

The results of all 3 are summed to get the district’s total aid.

3 State Factors

Cost CeilingsGuaranteed Valuations Per Member

Amount of Money to Distribute

3 District Factors

Spending (“Shared Cost”)Wealth/Property Tax BaseStudents (“Membership”)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

District Value per Member

10% 90%

75%25%

50%50%

Equalization Aid Formula

Sample District ResultsPer-Pupil Funding

DISTRICT10% x $1,000

= $100

25% x $7,000

=$1,750

50% x $4,000

=$2,000

$3,850

STATE90% x $1,000

= $900

75% x $7,000

= $5,250

50% x $4,000

= $2,000

$8,150

$3,850 + $8,150 = $12,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

Negative Tertiary Aid

Negative Secondary Aid

No Equalization Aid

Equalization Aid Formula

Where Can I Find This Grid For My District?

“2013-14 Equalization Aid Formula Position”

http://sfs.dpi.wi.gov/sfs_buddev_eq

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

District Value per Member

Negative Tertiary Aid

Negative Secondary Aid

No Equalization Aid

Equalization Aid Formula

Watch Value Per Member Over Time

Where Can I Find Value Per Member Over Time

For My District?

http://sfs.dpi.wi.gov/sfs_buddev_valuation

“School Aid Property Valuation” (Used in the Equalization Aid

Formula)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

District Value per Member

Negative Tertiary Aid

Negative Secondary Aid

No Equalization Aid

Equalization Aid Formula

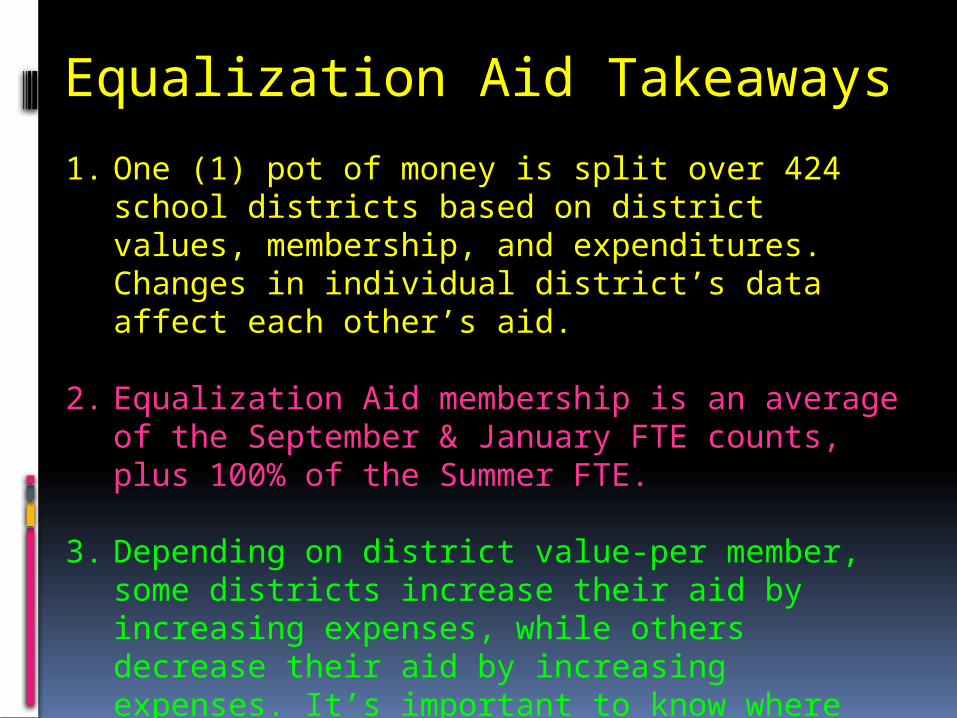

Equalization Aid Takeaways

1. One (1) pot of money is split over 424 school districts based on district values, membership, and expenditures. Changes in individual district’s data affect each other’s aid.

2. Equalization Aid membership is an average of the September & January FTE counts, plus 100% of the Summer FTE.

3. Depending on district value-per member, some districts increase their aid by increasing expenses, while others decrease their aid by increasing expenses. It’s important to know where your district is in the formula.

4. Be aware of what is happening to your district over time.

Equalization Aid

Knowing where your district is in the formula will help you better explain

how changes in local finances might affect your state aid.

What if we

underspend

our budget?

How does

that affect

our aid?

If we go to referendum, how will our aid

change?

Thanks to WASB, WASDA and WASBO for the opportunity to speak to you

today!

* * *DPI School Financial Services

Homepage

WASBO Homepage

…..whew! you made it!....

http://dpi.wi.gov/sfs/index.html

http://www.wasbo.com/

Please feel free to stop by the DPI booth if you’d like to chat more about your

specific district data!

We’ll have the 2013-14 Equalization Aid and 2013-14 Revenue Limit data available so you can continue the

conversation with us……..

See you later!

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

District Value per Member

10% 90%

75%25%

50%50%Negative Tertiary Aid

Negative Secondary Aid

No Equalization Aid

Equalization Aid Formula

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive Tertiary

Aid

District Value per Member

10% 90%

75%25%

50%50%Negative Tertiary Aid

Negative Secondary Aid

No Equalization Aid

Equalization Aid Formula