thesis.pdf - harvard dash

TRANSCRIPT

The Experience of Production: Essays on Customers in Service Operations

CitationBuell, Ryan W. 2012. The Experience of Production: Essays on Customers in Service Operations. Doctoral dissertation, Harvard Business School.

Permanent linkhttps://nrs.harvard.edu/URN-3:HUL.INSTREPOS:37367787

Terms of UseThis article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http://nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of-use#LAA

Share Your StoryThe Harvard community has made this article openly available.Please share how this access benefits you. Submit a story .

Accessibility

T E P : EC S O

A

R W. B

F X. FD CM I. N

A R

D B A

T O M

H UC , M

M

© – R W. BA .

Frances X. Frei Ryan W. Buell

T E P : E CS O

A

Over time, the delivery of services has become increasingly co-productive(customers participate materially in the production of service outcomes) andinseparable from customer view. As a result, a distinctive aspect of service operations isthat they feature production processes in which the experience of productionin uences customer behavior. In particular, operational choices intended to maximizerm pro ts may back re if they diminish customer experiences and, in the process,

alter whether and how customers choose to perform their role in the rm’s operatingsystem. In three studies, my dissertation empirically explores how two speci coperational choices - ) whether and how a rm automates service, and ) the level ofservice quality a rm chooses to provide relative to its competitors - affect theexperiences and behaviors of its customers, and in turn, the rm’s performance.

iii

Contents

T E P. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. eoretical and practical signi cance . . . . . . . . . . . . . . . . . .. Overview of dissertation research . . . . . . . . . . . . . . . . . . .

A S -S C S S ?. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. Literature review and hypothesis development . . . . . . . . . . . . .. Methodological approach . . . . . . . . . . . . . . . . . . . . . . . .. Research se ing and data . . . . . . . . . . . . . . . . . . . . . . . .. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. Managerial implications . . . . . . . . . . . . . . . . . . . . . . . .. Conclusions, limitations, and opportunities for future research . . . .

T L I : H O T IP V. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. Waiting, Effort and Perceived Value . . . . . . . . . . . . . . . . . .. Presentation of Experiments . . . . . . . . . . . . . . . . . . . . . .. General Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . .

H D C R S Q C ?. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. eory and hypothesis development . . . . . . . . . . . . . . . . . .. Research se ing and data . . . . . . . . . . . . . . . . . . . . . . . .. Primary analysis and results . . . . . . . . . . . . . . . . . . . . . .

iv

. Long-run effects of service positioning . . . . . . . . . . . . . . . . .

. Discussion and conclusions . . . . . . . . . . . . . . . . . . . . . . .

R

v

Author List

Chapter was co-authored with Dennis Campbell and Frances X. Frei.Chapter was co-authored with Michael I. Norton.Chapter was co-authored with Dennis Campbell and Frances X. Frei.

vi

Listing of gures

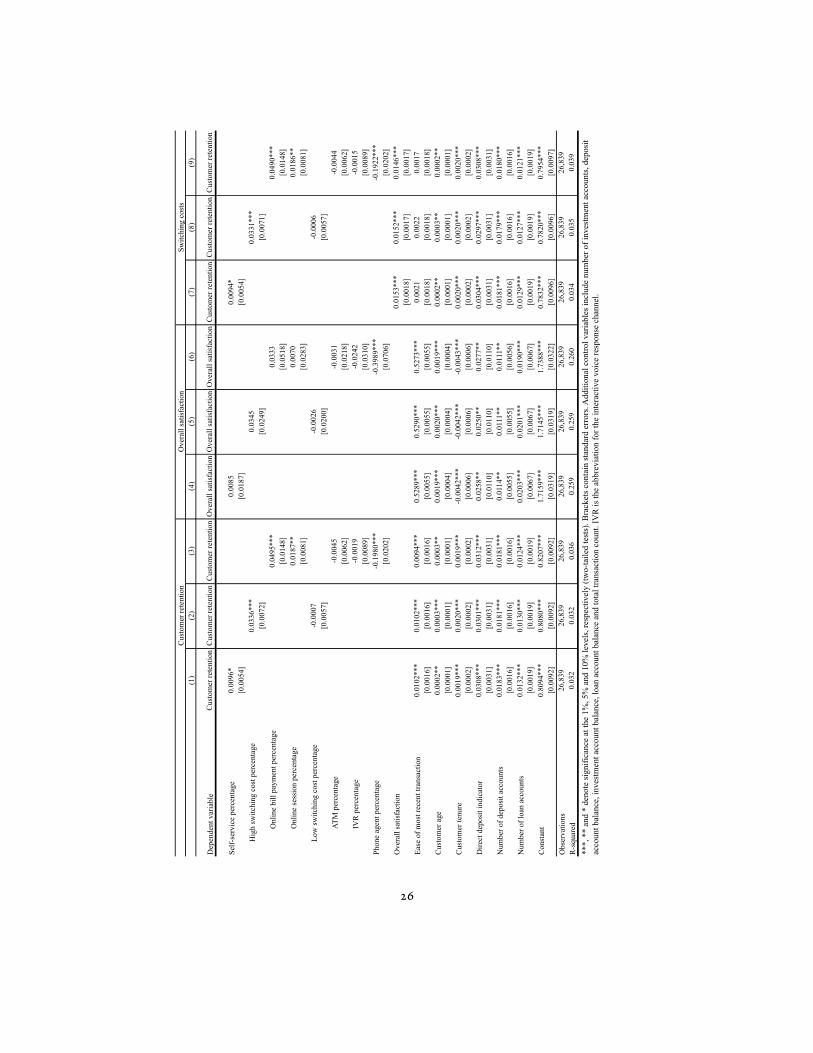

. . Drivers of retention in self-service channels. . . . . . . . . . . . . . .

. . Variable correlations for customer observation period. . . . . . . . . .

. . Summary statistics for customer observation period. . . . . . . . . .

. . e associations among channel usage, customer retention and overallsatisfaction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . e associations among channel usage, customer retention and overallsatisfaction, controlling for ease of most recent transaction. . . . . . .

. . Comparing the effects of aggregated self-service and individual channelusage on the satisfaction of enthusiasts and non-enthusiasts. . . . . .

. . Comparing the effects of aggregated self-service and individual channelusage on the satisfaction of enthusiasts and non-enthusiasts. . . . . .

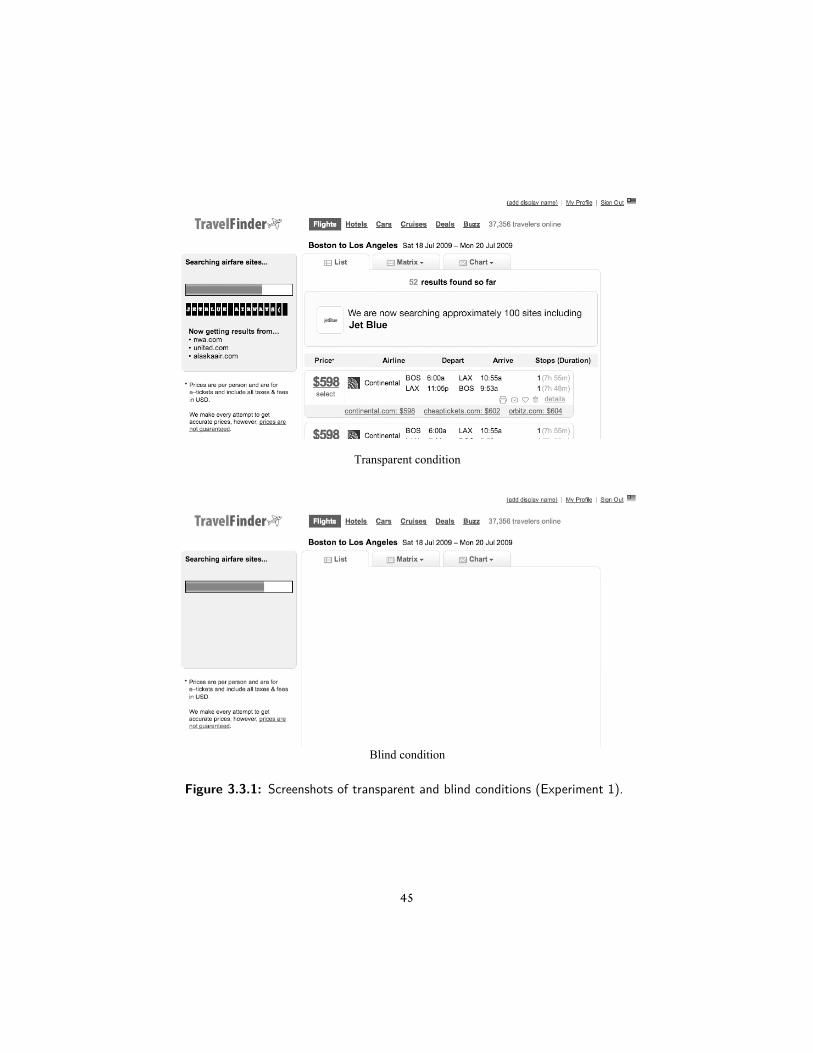

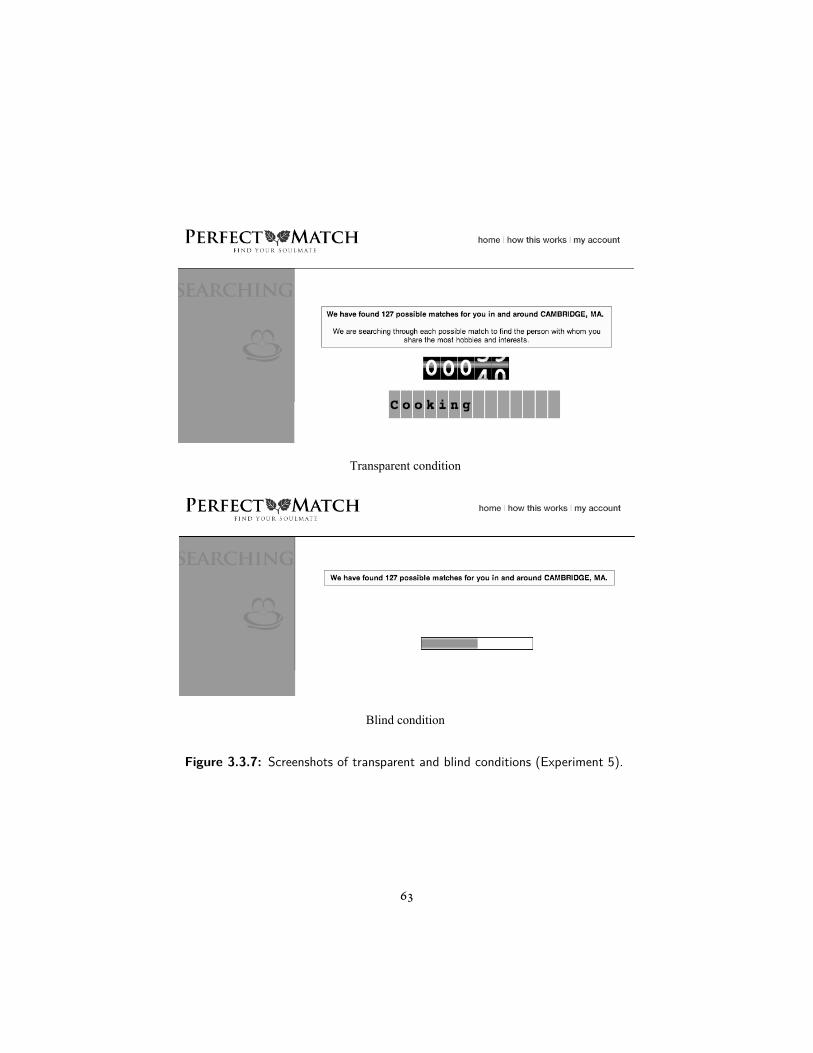

. . Screenshots of transparent and blind conditions (Experiment ). . . .

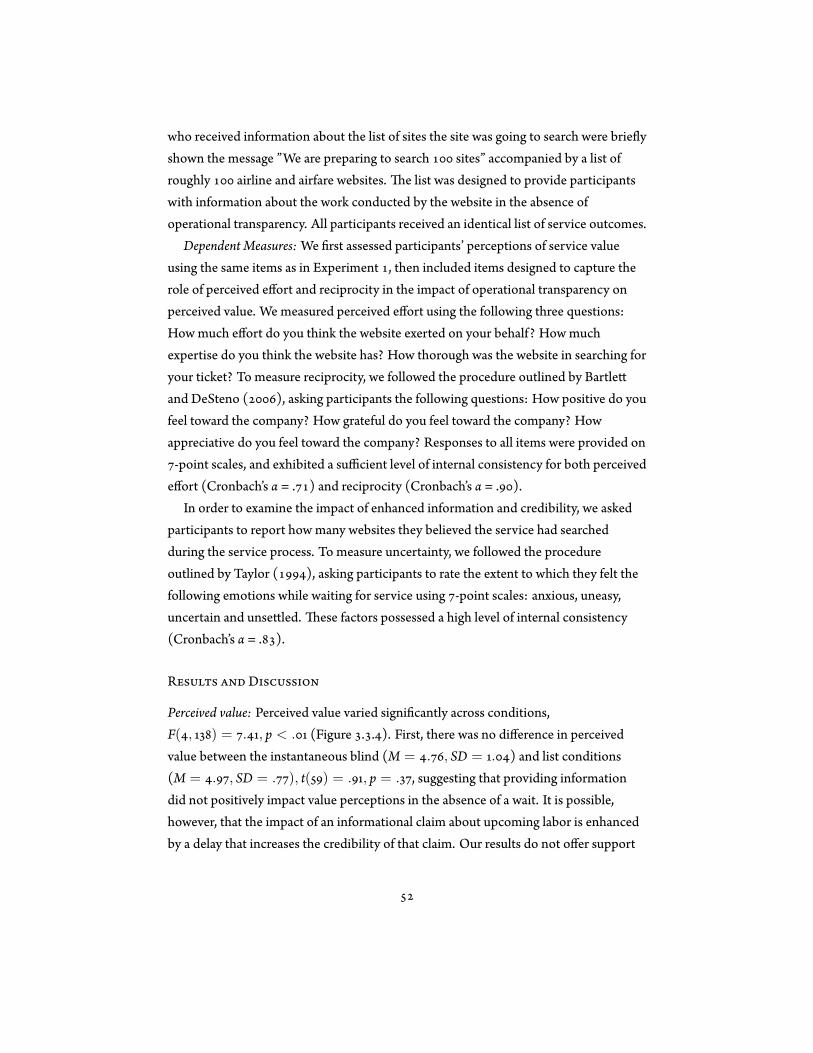

. . e effect of operational transparency andwait time on perceived value(Experiment ). . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

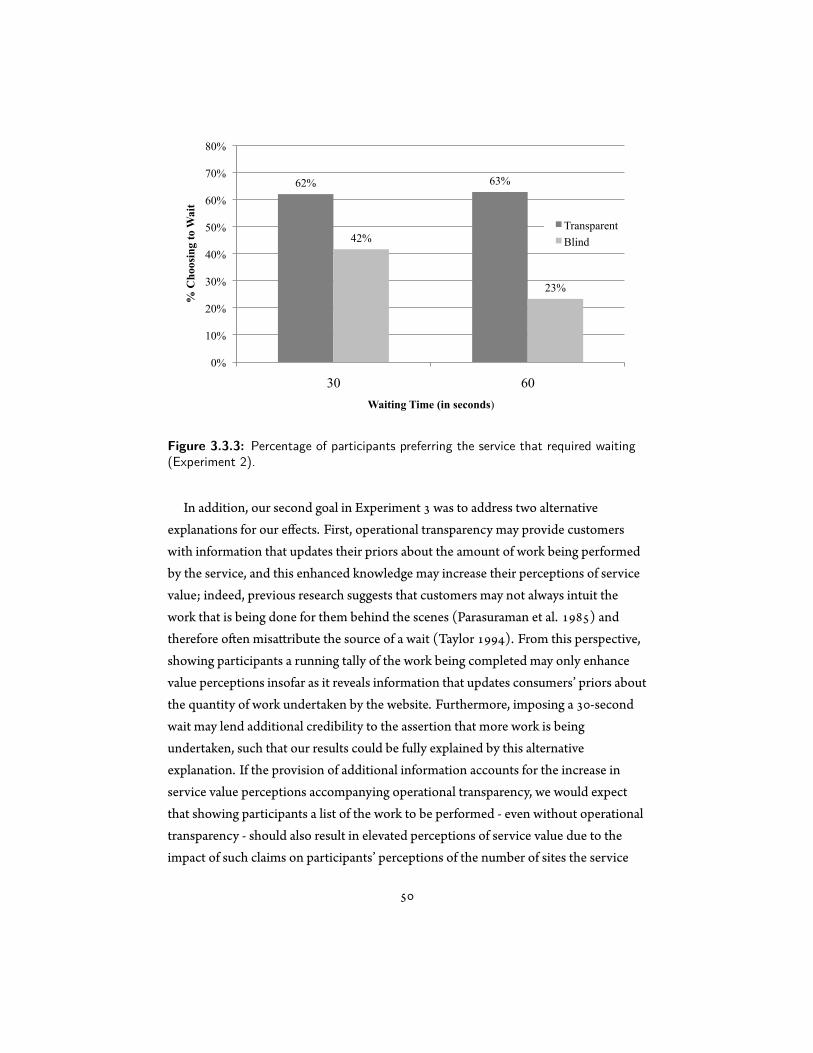

. . Percentage of participants preferring the service that required waiting(Experiment ). . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . e effect of enhanced information and credibility on perceived value(Experiment ). . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

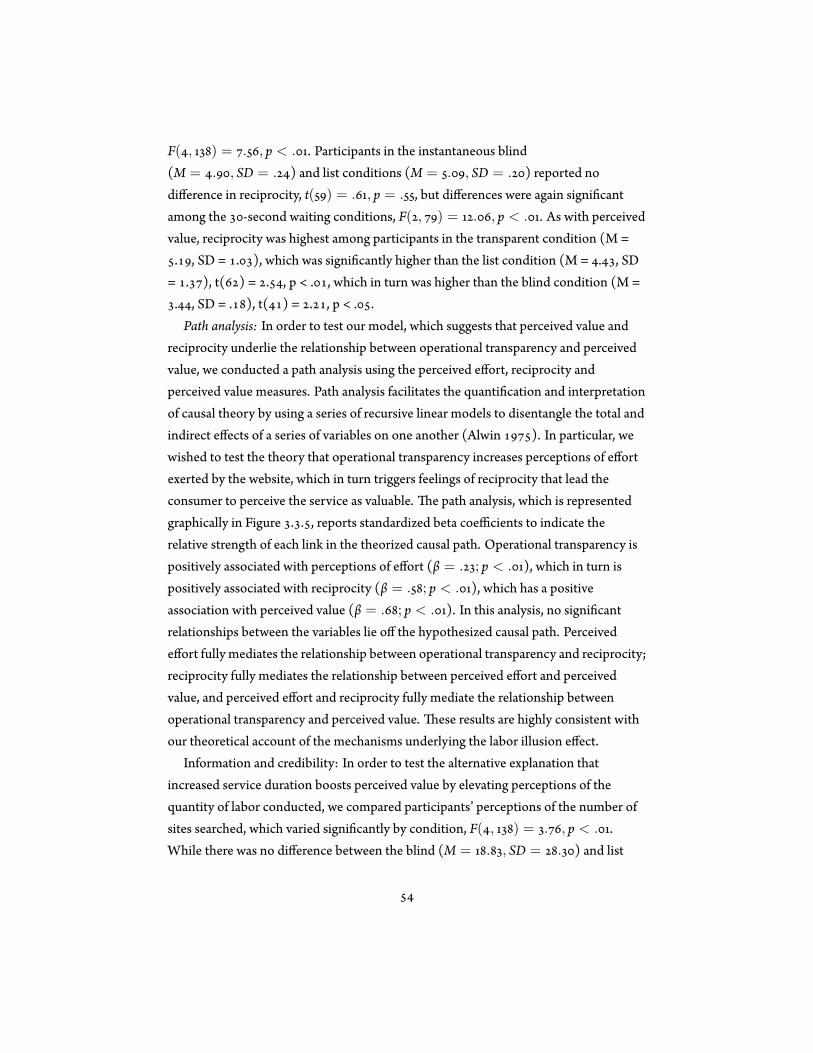

. . Path analysis (Experiments and ). . . . . . . . . . . . . . . . . . .

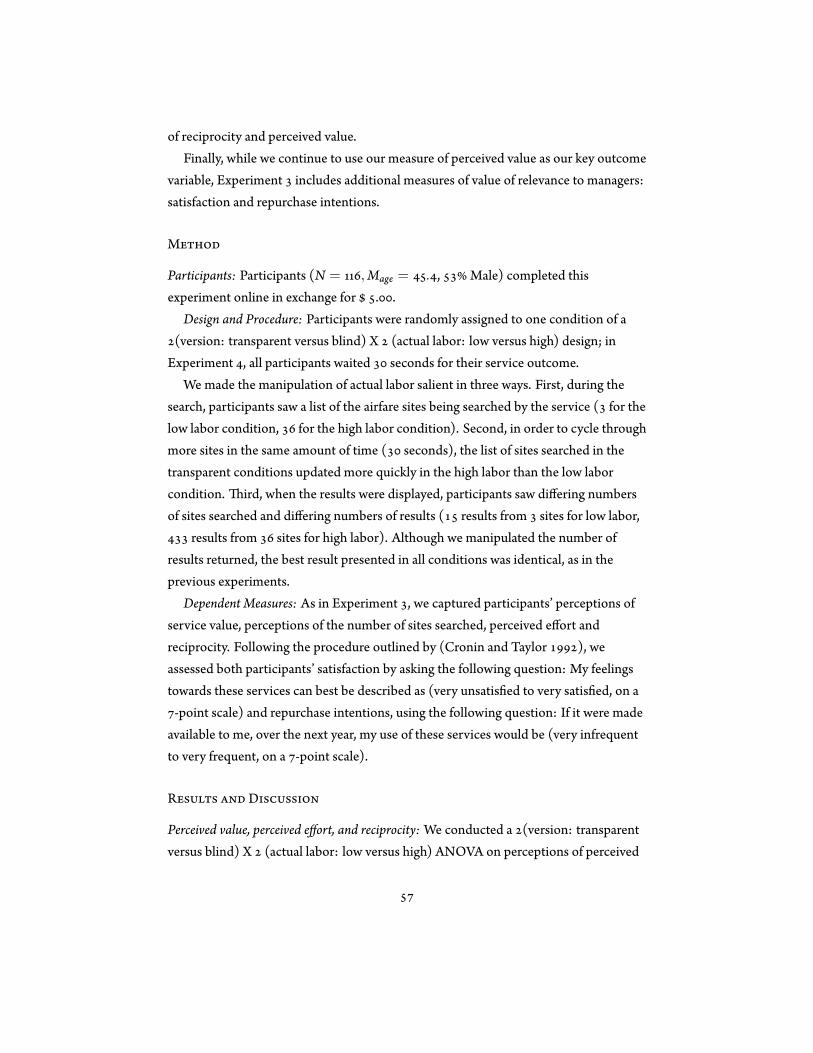

. . e effect of actual labor on perceived value (Experiment ). . . . . .

. . Screenshots of transparent and blind conditions (Experiment ). . . .

. . Perceived value of service by waiting time, outcome andwaiting condi-tion (Experiment ). . . . . . . . . . . . . . . . . . . . . . . . . . .

vii

. . Market summary statistics ( ). . . . . . . . . . . . . . . . . . . .

. . Summary statistics for customer panel ( - ). . . . . . . . . . .

. . Comparison of different types of institutions. . . . . . . . . . . . . .

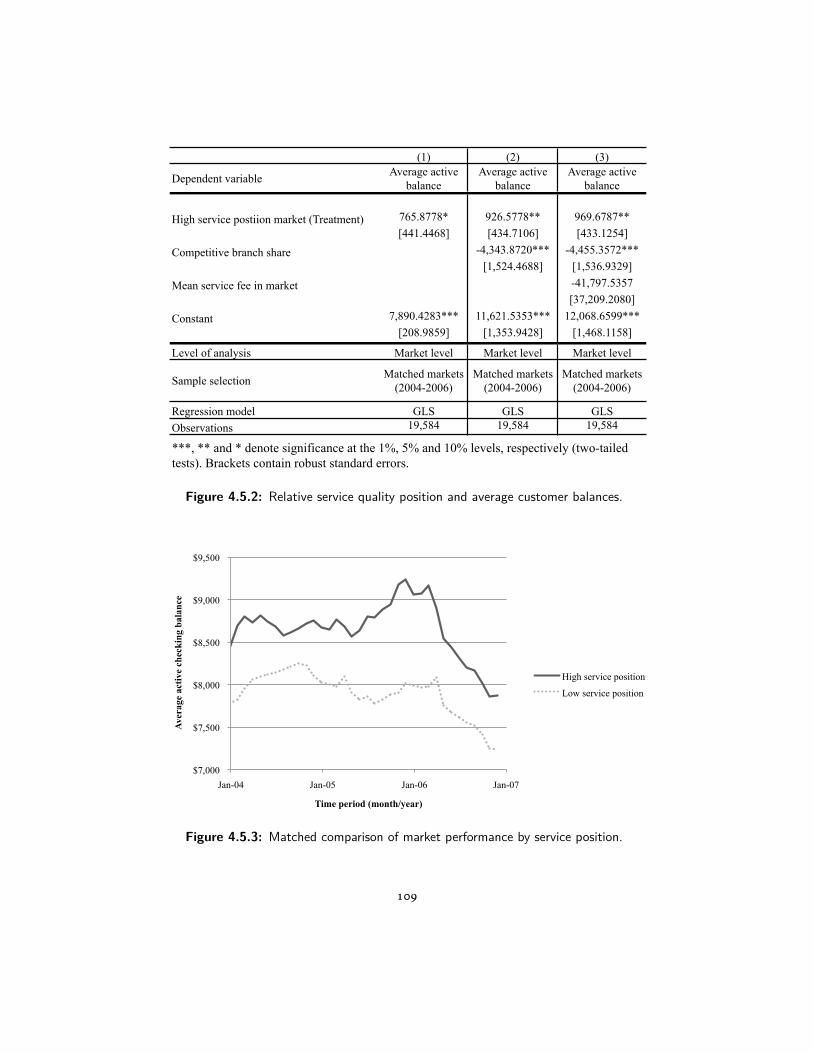

. . Firms trade-off price and service quality. . . . . . . . . . . . . . . . .

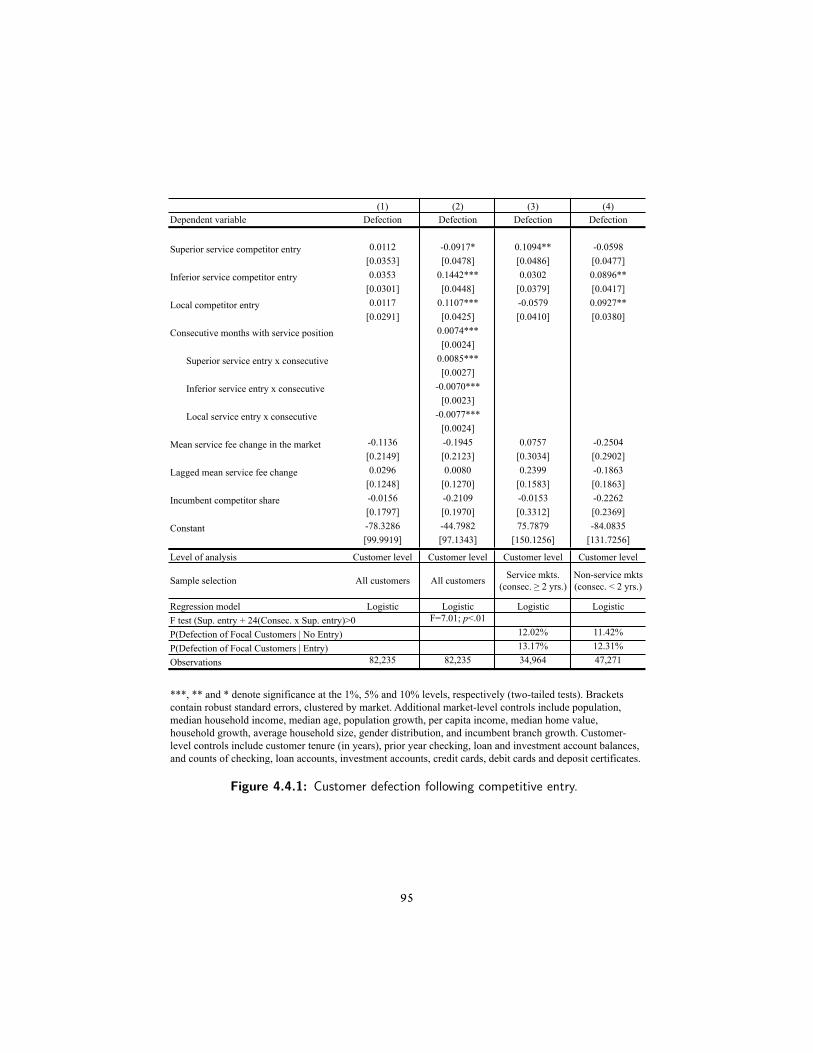

. . Customer defection following competitive entry. . . . . . . . . . . .

. . Customer service sensitivity and objective service quality differencesbased on incumbent service position. . . . . . . . . . . . . . . . . .

. . Which customers defect in response to increased service quality com-petition. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . Predicted defection in service-positioned markets following superiorservice quality entry by customer type. . . . . . . . . . . . . . . . . .

. . Balance statistics. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . Relative service quality position and average customer balances. . . .

. . Matched comparison of market performance by service position. . . .

viii

F T D , , ,,

. T. I , .

ix

Acknowledgments

T , during which I’ve been a student at Harvard Business School,have been my most fun and ful lling so far. It has been my honor to work with anamazing group of colleagues who have deeply enriched my life and challenged me to bea be er scholar. ank you to all of you, from the bo om of my heart. No ma er howlong I spend writing these acknowledgements, I could never adequately express theimmeasurable good you’ve done for me.

I’m grateful to my advisor, Frances Frei, for encouraging me to pursue a doctorateand for taking me on as her student. You’ve taught me countless things, but the twolessons that stand out the most are what a privilege it is to be held to high standards,and what a joy it is to help clear away the pebbles impeding the successes of others.You’ve changed my life in the best and most meaningful of ways, and I’m eager to payforward the investments you have made in me to future generations of graduatestudents. It’s truly a pleasure to be serving with you.

To Dennis Campbell, thank you for your unending generosity. It seems thatvirtually every day of my doctoral student life, I’ve found myself in your office, pouringover the results of a new analysis, white boarding an empirical model, learning about aneconometric technique, or asking your advice on broad range of topics. You are a gi edscholar and talented teacher, a productive collaborator, and a caring advisor. I’velearned so much from you, and I’m eternally grateful.

To Michael Norton, thank you for your passion for ideas, and for welcoming aconsumer-oriented operations student into your remarkable community of socialpsychologists. My world has been a more energizing and exciting place ever since.You’ve taught me how fascinating the humans are, the importance of random thoughts,

x

the art of packaging ideas in a compelling and intuitive way, and, most of all, the sheerjoy that comes from working with enthusiastic, open-minded, brilliant people. Youinspire me to be a be er researcher and person.

To Ananth Raman, thank you for challenging me to think big thoughts and for yourcounsel, clarity, wisdom and mentorship. You have inspired me to be forward thinkingabout the connections in my work and to embrace its intersections with otherdisciplines. You’ve given me the courage to pursue the questions I nd fascinating andhave helped to de ne my yardstick for impact, both within the discipline and inpractice. I have great respect for you, and you’ve had a profound effect on the type ofscholar I aspire to become.

To JoshuaMargolis, YoungmeMoon and omas Steenburgh, thank you for helpingme nd my way to the Harvard Business School Doctoral Program, and for yourongoing guidance and kindness. To Francesca Gino, Jan Hammond, Rakesh Khuranaand Michael Toffel, thank you for always making time for me, and for being soastonishingly supportive and insightful. I am so fortunate to have you in my life, and Icount my blessings every day to have you as colleagues.

To Bill Simpson, thank you for your ongoing guidance, patience and support in myquest to get it right. You taught me how to be a careful researcher, and I rest easier atnight because of you.

To Chris Winter and Hal Beck, thank you for your generosity and trust, and forkeeping me tethered to reality. I look forward to our calls every Friday, and I hope tocontinue looking forward to them long into the future.

I’ve also bene ted tremendously from my amazing colleagues in the HarvardDoctoral Programs over the years, many of whom have gone on to begin successfulcareers at institutions around the world. My deepest thanks to Lalin Anik, SilviaBellezza, Ethan Bernstein, Jillian Berry, Sen Chai, Mika Chance, Zoe Chance, JonathanClark, Nathan Craig, Anil Doshi, Emilie Feldman, Ray Fung, Claudine Gartenberg,Budhaditya Gupta, Andrew Hill, Fern Jira, Sorapop Kiatpongsan, Tami Kim, VenkatKuppuswamy, Clarence Lee, Jeff Lee, Eric Lin, Chris Liu, Maria Loumioti, JolieMartin, Mary Carol Mazza, Anoop Menon, Katherine Milkman, Frank Nagle, ErinReid, Patricia Sa erstrom, Bill Schmidt, George Serafeim, Ovul Sezer, Hee Yeon Shin,Lisa Shu, Sameer Srivastava, Brad Staats, Tina Tang, Chia-Jung Tsay, Kristin Wilsonand Ting Zhang for your friendship and feedback on my work through the years. It’ssuch a privilege to be changing the world with you.

xi

I am grateful to John Korn, Janice McCormick, Deborah Hoss, LuAnn Langan,Dianne Le, Jennifer Mucciarone and Marais Young, who have cultivated andmaintained an exceptional doctoral student community at Harvard Business School. Ialso acknowledge Harvard Business School, the Gipp Ludcke (MBA ) FellowshipFund, Mr. George A. Wiltsee and the MBA Classes of Fund for DevelopingIndustrial Leadership, the MBA Class of Fund for Leadership in Manufacturing,and Mr. Hansjoerg Wyss and the Hansjoerg Wyss Endowment for Doctoral Education,which provided generous fellowships in support of this research through the years.

ank you for supporting my work.I deeply appreciate the suggestions and feedback I have received on this work from

many seminar participants at the University of Michigan, Georgia Tech, the Universityof Minnesota, London Business School, e Wharton School, Dartmouth College,Northwestern University, the Massachuse s Institute of Technology and HarvardBusiness School, as well as participants at the - INFORMS AnnualConferences, the - Manufacturing and Service Operations ManagementAnnual Meetings, the - Production and Operations Management SocietyAnnual Meetings, the Workshop on Empirical Research in OperationsManagement, the QUIS /POMS Service College Meeting, the Societyfor Personality and Social Psychology Annual Meeting, and the Society forJudgement and Decision Making Annual Conference.

I’m grateful to my parents, Richard and Dianne Buell, and my sister, Allison Buellfor their love and enthusiastic support. ank you for going out of your way to keepour connections strong.

Finally, I most want to thank my wife, Trisha Multhaupt-Buell, for her love, sacri ce,and indescribable indulgence as I’ve pursued this passion. I truly could not have donethis without you. I also credit our daughter Darcy, who constantly amazes me andteaches me new things every day. You are the joy I didn’t know I was missing, and mylife is so much be er now that you’re a part of it. I love you both so much.

xii

1e Experience of Production

. I

O , the delivery of services has become increasingly co-productive(customers participate materially in the production of service outcomes) and,

as a consequence, inseparable from customer view. As a result, a distinctive aspect ofservice operations is that they feature production processes in which the experience ofproduction in uences customer behavior.

In such contexts, operational design choices intended to maximize rm pro ts mayback re if they perturb customer experiences and, in the process, alter whether andhow customers choose to perform their role in the rm’s operating system. In my work,which contributes to the growing body of empirical service operations literature, Iexplore how operational choices, made in the service of customers, affect customeractions, and in turn, rm performance.

. T

A considerable body of the extant operations literature explores how customers affectoperating systems. is issue is particularly important in service contexts, where thepotential efficiency of the system is a function of the degree of customer contactentailed in the process (Chase ). Customers subject service systems totremendous variability by showing up when they want, asking for different things,varying in their willingness and ability to help themselves, and valuing different servicedimensions (Frei ). Accordingly, rich streams of research analyze how servicesystems can perform as designed in the face of this variability.

Much of this work has been a natural extension of previous lines of inquiry initiallyconducted in manufacturing contexts. rough the application of insights and toolsfrom traditional operations management, such as queuing theory (Afèche andMendelson , Allon et al. , Anand et al. , de Vèricourt and Zhou ,Dewan and Mendelson , Mandelbaum and Shimkin , Stidham , Zohar etal. ), demand forecasting (Adrangi et al. , Watson , Willemain et al.

), inventory management (Berman et al. , Berman and Kim , Bermanand Sapna ), and capacity planning(Allon and Federgruen , Hall and Porteus

), scholars have been able to make great progress in improving the efficiency ofservice operating systems. In these cases, traditional approaches were extended toaccommodate the important characteristics of services, which include customerparticipation in the service process, intangibility, simultaneity, heterogeneity ofoutputs and perishability (Fitzsimmons and Fitzsimmons ).

However, while service production processes, by de nition, rely on customer inputs(Sampson and Froehle, ), far less work has explored how operational choicesaffect customer behaviors. Broadly speaking, there are two sets of exceptions. e rstset includes analytical papers like (Dana and Petruzzi, ), in which customerschoose where to shop based on a rm’s observable prices and expectations aboutunobserved inventory levels, and (Gans ), which models how customers willallocate spending across providers that vary in service quality. ese studies considerhow anticipated customer responses to operational choices will affect rmperformance. However, while most analytical models assume rational consumerbehavior, actual customers may depart from rationality (Gino and Pisano, ).Where understood, accounting for these departures has been shown to lead to

markedly different results (Huang et al., ). Moreover, there are a plethora offactors at play in a service interaction, and it’s not always clear which operationalchoices will be most salient to customers in the eld. e second set of exceptions,which is much smaller, includes empirical works, like (Olivares et al. ), whichexplores how queues affect the purchase behavior of customers, (Craig et al., ),which studies how supplier reliability affects customer demand, and (Dixon andVerma, ), which investigates how sequence effects in service bundles affectcustomer repurchase decisions. ese studies differ from the earlier examples, in thatthey empirically examine the behaviors of actual customers. My work pursues a similarpath, by employing both the econometric analysis of large-sample datasets, as well asin-lab and online experimental methodologies. rough my research, I endeavor toimprove our discipline’s understanding of how customers respond to operationalchoices, and by extension, improve both the performance of service organizations andthe in-process experiences of their customers.

. O

In three chapters, my dissertation empirically explores how two speci c operationalchoices - ) whether and how a rm automates service, and ) the level of servicequality a rm chooses to provide relative to its competitors - affect the experiences andbehaviors of its customers, and in turn, the rm’s performance.

Chapter , titled, Are Self-Service Customers Satis ed or Stuck?, explores theimplications of service automation for customer outcomes by disentangling thedistinct effects of satisfaction and switching costs on self-service customer retention.

is is a particularly important issue in the nancial services industry whereconsiderable investments have been made in developing, and migrating customers to,self-service distribution channels, which are widely acknowledged to lower the cost ofservice delivery for individual transactions. Numerous studies in the services literaturehave demonstrated that self-service customers are retained with greater frequency thantheir full-service counterparts. ere are two competing explanations for thisphenomenon. Either self-service channel usage promotes customer satisfaction and inturn, loyalty, or it imposes switching costs on customers that make it more difficult forthem to defect. Our empirical analysis of multi-channel banking customers suggeststhe la er - that self-service customers may be retained through switching costs, not

satisfaction effects. In fact, the results of our analysis suggest that self-servicecustomers aren’t just stuck, they’re actually less satis ed.

Dissatis ed customers held captive by switching costs spend less money and arenotoriously difficult and expensive to serve, suggesting that in the near-term, there maybe hidden performance costs associated with self-service strategies. Moreover, theremay be reason to believe that switching cost-imposed ”stickiness” will not beinde nitely sustainable. It has been predicted that over time switching barriers willdrop and companies will have to develop new methods for generating customer loyalty.

e increasing technological capabilities of consumers combined with thestandardization of technology and industry-wide efforts to improve ease-of-use andreduce adoption barriers are all drivers of this change.

Chapter , titled, e Labor Illusion: How Operational Transparency IncreasesPerceived Value, extends the previous paper by exploring how operationally transparentinterfaces can a enuate the negative satisfaction effects of self-service technologies.Self-service technologies are capable of delivering service outcomes more quickly andconveniently than face-to-face alternatives. However, unlike those who transact inface-to-face se ings, self-service customers do not observe physical effort from theservice provider and may not observe other visible cues signaling the value created bythe service. As such, while an automated solution may objectively deliver superiorperformance, customers might not perceive it as valuable if it does not appear to beexerting a sufficient level of effort. Conventional wisdom and operations theorysuggests that the longer customers wait, the less satis ed they become; we demonstratethat due to what we term the labor illusion, when websites engage in operationaltransparency by signaling that they are exerting effort, customers can actually preferwebsites with longer waits to those that return instantaneous results - even when thoseresults are identical. In particular, we show that perceptions of service provider effortinduce feelings of reciprocity, which together mediate the link between operationaltransparency and increased valuation.

ese ndings shed light on the hidden costs of strategies employed by anincreasingly signi cant number of rms to infuse technology into service operations.

ese very strategies, which are designed to enhance the technical efficiency of service,may also counter-intuitively erode consumer perceptions of the value of the servicesthey create. If this is the case, then these strategies may have negative long-termimplications for companies that fail to compensate by investing in initiatives that infuse

additional meaning into each transaction and into their relationships with theircustomers.

Chapter , titled, How Do Customers Respond to Service Quality Competition?, links arm’s choice of service quality relative to local market competitors to the defection

decisions of its customers, and in turn, its nancial performance. Our customer-levelanalysis exploits the varying competitive dynamics in geographically isolated marketsin which a nationwide retail bank conducted business over a ve-year period. We ndthat customers defect at a higher rate from the incumbent following increased servicecompetition only when the incumbent offers high quality service relative to existingcompetitors in a local market. We provide evidence that this result is due to a sortingeffect whereby the incumbent a racts service (price) sensitive customers in marketswhere it has supplied relatively high (low) levels of service quality in the past.Furthermore, we show that it is the high quality incumbent’s most pro tablecustomers, those with the longest tenure, most products, and highest balances, who arethe most a racted by superior service alternatives. Along the way, we also show thatrms trade-off price and service quality and that when the incumbent offers relatively

low service quality in a local market, its customers are more likely to defect in the wakeof entry or expansion by inferior service quality (price) competitors. Our resultsappear to have long run implications whereby sustaining a high level of service relativeto local competitors leads the incumbent to a ract and retain higher value customersover time.

ese results suggest that rms, which make the strategic decision not to competeon service, may not need to be concerned about the entry or expansion of competitorsoffering superior service. ey also highlight the dangers of complacency forservice-positioned rms. e entry of a competitor offering superior service can havesizable short-term implications - increasing defection in our analysis by an average of. in a single year over baseline defection rates - and signi cant long-run

implications as well. Perhaps most crucially, the positive association we demonstratebetween service sensitivity and customer value suggests that models assuming the twoare independent will underestimate the importance of service quality, and prescribesuboptimally low service levels. Initiatives to optimize a rm’s service level must weighthe long-term costs of losing a rm’s most valuable customers against the costs ofperpetuating a level of relative service quality that is sufficient to retain them.

R.W. Buell, Campbell, D., Frei, F.X. . Are Self-Service Cus-tomers Satis ed or Stuck? Production and Operations Manage-ment. ( ) - .

2Are Self-Service Customers Satis ed or Stuck?

. I

T , how satisfaction and switching costs contribute toretention among self-service technology (SST) customers, and more broadly, theoverall impact of self-service usage on customer satisfaction and retention. A numberof studies in the services literature have suggested that self-service customers are moreloyal than their full-service counterparts (Campbell and Frei, ; Hi and Frei,

; Marzocchi and Zammit, ; Mols, ; Wallace, Giese, and Johnson, ;Yen and Gwinner, ). ere are two competing explanations for why this might bethe case. One explanation is that self-service channels offer bene ts over full-serviceofferings that improve customer satisfaction, and by extension, loyalty. e alternativeexplanation is that self-service usage increases switching costs, which improvesretention by making it more difficult for customers to defect to competitors.

It has been well established in the literature that a satis ed customer is more likely toremain loyal to a rm than a dissatis ed one (Anderson, ; Bowen and Chen, ;

Heske , Sasser, and Schlesinger, ; LaBarbera and Mazursky, ; Newman andWerbel, ; Oliver, ). However, a customer who nds it difficult to switch to acompetitor as a result of learning costs, psychological effects, transaction costs, orcontractual obligations, may also remain loyal, despite dissatisfaction (Farrell andKlemperer, ).

Understanding what motivates self-service customers to remain loyal has signi cantimplications for service organizations. Dissatis ed customers held captive by switchingcosts spend less money and are notoriously difficult and expensive to serve (Coylesand Gokey, ; Jones and Sasser, ; Xue and Harker, ). Moreover, they willdefect from a rm over time if switching costs fall (Evans and Wurster, ).Consequently, if switching costs are found to be the driver of increased loyalty amongself-service customers, then managers face a crucial expected value calculation:weighing the near-term cost bene ts of self-service technologies against the potentialreduction in customer lifetime value from those who defect, seeking superior serviceexperiences elsewhere.

As the role of service businesses has grown in prominence, the impact oftechnological innovation in service delivery has received considerable a ention fromthe operations management community (Apte, Maglaras, and Pinedo, ; Roth andMenor, ; Spohrer and Maglio, ). Our paper broadens this existing literaturein two ways. First, the overall impact of self-service usage on satisfaction and retentionremains unresolved. While a signi cant number of prior studies have examined theserelationships, their results have con icted over the direction of the impact. In general,studies that have found that self-service usage increases satisfaction, have also foundthat it increases retention (Marzocchi and Zammit, ; Mols, ; Wallace et al.,

; Yen and Gwinner, ). In contrast, those that have found that it decreasessatisfaction have also found that it decreases retention (Carmel and Sco , ;Meuter, Ostrom, Bitner, and Roundtree, ; Price and Arnould, ). emulti-channel nature of the personal banking industry affords a unique opportunity toanalyze the incremental impact of self-service channel usage on overall customersatisfaction and retention relative to the use of full-service channels. We use actualtransaction data to categorize individual customers by channel. is approach providesgreater clarity into the relationships between self-service usage, satisfaction andretention. Speci cally, it lets us examine the relationship between satisfaction andretention in self-service channels that have varying amounts of switching costs

associated with them.Second, we have disentangled the relative impact of self-service-related satisfaction

and switching costs on actual customer retention, rather than on stated intention tostay with a rm. By combining customer surveys to assess satisfaction withlongitudinal observations of customers to gauge retention, we provide evidence on therelationship between satisfaction and actual retention in a multi-channel se ing.Previous studies examining the impact of self-service channel usage have tended to relyon customer surveys or observational analyses, but not a mix of the two. Studiesexamining the link between self-service usage and satisfaction have addressed retentionby inquiring about customers’ future intentions to remain with the rm (Marzocchiand Zammit, ; Mols, ; Wallace et al., ; Yen and Gwinner, ). It hasbeen demonstrated that self-reported retention measures overstate switching behavior(Garland, ). In contrast, studies focusing speci cally on retention that have beenobservational in nature have not had access to satisfaction data (Chen and Hi , ;Xue and Harker, ).

is study does not employ a direct, customer-reported measure of switching costs.Instead, we infer the relative level of switching costs in various channels by examininggains to retention, controlling for satisfaction and other customer-speci ccharacteristics. is approach is consistent with a number of previous studies(Anderson and Sullivan, ; Fornell, ; Klemperer, ). We employ amediation model to analyze satisfaction survey data and lagged observational data onretention, controlling for proportional channel use. With this approach, we isolatesatisfaction effects from switching costs and provide a more detailed picture of how theimplementation of self-service technology impacts customer behavior.

e remainder of the paper proceeds as follows. A review of the relevant literatureand our hypotheses development are provided in Section . Our methodologicalapproach is described in Section . Section provides a description of our research siteand data collection. Results are discussed in Section . Managerial implications of ourndings are discussed in Section . Section concludes the paper.

. L

A growing number of rms are augmenting traditional face-to-face service strategieswith self-service technology. In part, these rms implement SSTs with the intentions of

improving satisfaction and loyalty through increased efficiency, convenience andperceived control for the customer (Hi , Frei, and Harker, ; Meuter, Ostrom,Roundtree, and Bitner, ; Yen, ). Yet, the interrelationships betweenself-service channel usage, retention, switching costs and satisfaction remainunresolved in the literature. is section reviews the literature that shapes ourunderstanding of these interrelationships, and motivates a number of relevanthypotheses. Due to con icting ndings among a portion of the relevant studies we cite,we have adopted the convention of stating non-directional hypotheses in null form anddirectional hypotheses in alternative form.

Our review is divided into three streams. First, we focus on the literatureinvestigating the overall link between self-service channel usage and retention.Numerous studies have explored this relationship in a wide-array of se ings, but theirndings have o en con icted. Second, we highlight two potential sources of this

con ict: switching costs and satisfaction effects. We review a number of theoreticaland empirical analyses that have focused on these effects in various self-service se ings.Finally, we argue that considering either effect on its own provides an incompletepicture of the link between self-service usage and retention.

. . T -

Despite the increasing prevalence of self-service technologies, the link betweenself-service channel usage and retention remains ambiguous in the literature. Severalstudies have found a positive relationship, noting that self-service and online customershave higher repurchase ratios than their full-service and offline counterparts (Hi andFrei, ; Mols, ; Xue and Harker, ). Moreover, to the extent that onlinechannels increase transaction frequency, they have been shown to increase customerretention (Chen and Hi , ). Conversely, going from personal service toself-service has been shown to have a negative effect on bonding and loyalty with lowcomplexity transactions and relationships (Selnes and Hansen, ). Furthermore,customer delight in online self-service channels has been shown not to lead to loyalty(Herington and Weaven, ). Based on these con icting ndings, we hypothesizethat in aggregate, self-service usage has an ambiguous impact on retention. isnon-directional hypothesis is stated in null form:

Hypothesis (H ): Relative to full-service channel usage, there is not a signi cantrelationship between self-service channel usage and retention.

. . T

S

A portion of the ambiguous relationship between self-service usage and retention canbe explained by varying levels of switching costs. Consumers face switching costswhen investments speci c to their current providers must be duplicated for newproviders (Farrell and Klemperer, ). Two types of switching costs seemparticularly relevant in self-service banking environments: start-up costs and learningcosts. Start-up costs exist in channels where customers must setup a product for itsinitial use (Burnham, Freis, and Mahajan, ; Klemperer, ). For example, inretail banking, online bill pay imposes start-up costs by requiring up-front manual dataentry by its users. Learning costs include the time and effort required to acquire thenecessary skills to use a service effectively (Burnham et al., ; Farrell andKlemperer, ; Guiltinan, ; Klemperer, ). Online banking systems imposelearning costs, as customers must familiarize themselves with the bank’s proprietaryweb interface in order to make efficient use of the service. A er start-up and learningcosts have been expended, switching to a competitor requires duplicated effortelsewhere, thereby creating a barrier to defection.

While online bill pay and online banking impose switching costs on customers,other channels like ATM and phone banking, which are basically standardized betweenrms and require no signi cant start-up investment, are not likely to impose such

switching costs. To the extent that high switching cost channels complicate the processof changing banks, ceteris paribus, we would expect customers in low switching costchannels to defect with greater frequency than customers in high switching costchannels. However, switching costs only represent one part of the equation thatconnects self-service channel usage to customer retention. Understanding the netimpact of self-service transactions also requires exploration of the connection betweenself-service usage and retention driven through satisfaction effects. Consequently, wehypothesize that self-service usage, without accounting for satisfaction effects, will beambiguously associated with retention in both high and low switching cost channels.

e following non-directional hypotheses are stated in null form:

Hypothesis (H ): e usage of high switching cost self-service channels is not associatedwith customer retention.

Hypothesis (H ): e usage of low switching cost self-service channels is not associatedwith customer retention.

S

Self-service technology usage has been found to promote customer satisfaction in anumber of se ings, including retail banking (Mols, ), supermarkets (Marzocchiand Zammit, ), online commerce (Szymanski and Hise, ; Zviran, Glezer, andAvni, ) and travel (Yen, ). In one study, of those satis ed withself-service technologies reported that their satisfaction was driven by bene ts that gobeyond full-service offerings (Meuter et al., ). In another, self-service customerswere found to be both more efficient and more satis ed than their full-servicecounterparts (Xue and Harker, ). Ease of use, service performance, perceivedcontrol and convenience have been shown to be signi cant drivers of satisfaction inonline self-service se ings (Yen, ). Moreover, multiple channel interaction,including transactions conducted in self-service channels, has been shown to lead topositive discon rmation, which in turn was found to lead to increased satisfaction andloyalty (Wallace et al., ).

On the other hand, with the wrong model, outsourcing work to customers throughself-service technology can leave them feeling frustrated and annoyed (Moon and Frei,

). Some customers in self-service se ings have been found to report technologyfailures, service design problems, process failures, technology design problems andcustomer driven failures as sources of dissatisfaction (Meuter et al., ). Customerswith technology anxiety are less likely to have a positive self-service technologyexperience, even when things go well (Meuter et al., ). Furthermore, whilenegative feelings towards speci c employees diminish a customer’s global opinion ofthe brand, they also have been shown to increase self-service technology usage, whichsuggests an adverse selection effect may exist among self-service customers (Curran,Meuter, and Surprenant, ).

In order to examine the links between self-service usage and retention driven

Negativeretention effect

Retention effectcontingent on

relative strengthof switching

costs andsatisfaction

effects

Retention effectcontingent on

relative strengthof switching

costs andsatisfaction

effects

Positive retentioneffect

Negative Positive

Low

High

SwitchingCosts

SatisfactionEffects

Figure 2.2.1: Drivers of retention in self-service channels.

through satisfaction effects, we test the following non-directional hypothesis, which isstated in null form:

Hypothesis (H ): Relative to full-service channel usage, there is not a signi cantrelationship between self-service channel usage and satisfaction.

. . D

If switching costs and satisfaction effects jointly in uence the relationship betweenself-service channel usage and customer retention, then both elements must beconsidered in order to understand a channel’s net impact on retention (Figure . . ).Figure . . illustrates the interplay of these factors. In the rst quadrant, negativeretention is predicted, due to the absence of switching barriers and negativesatisfaction effects. In quadrant two, positive satisfaction effects counterbalance theabsence of switching barriers, leading to a net impact on retention that is contingentupon the drivers’ relative effects. In the third quadrant, the outcome is also contingenton the relative strength of each effect, as high switching barriers endeavor to overcomenegative satisfaction effects. Finally, in quadrant four, switching costs and satisfactioneffects reinforce one another, leading to a positive net impact on retention.

Figure . . elucidates both the importance and the challenge of disentangling the

impact of self-service-related satisfaction effects and switching costs on customerretention. As we have described above, to a certain extent, the direction of aself-service channel’s impact on switching costs is knowable from an ex-anteperspective due to inherent characteristics of the channel (e.g. start-up costs arepresent in online bill pay and largely absent in the automated phone channel).However, a speci c channel’s impact on satisfaction may be more difficult to foresee.By examining the impact of self-service channel usage on retention controlling forsatisfaction, we can isolate the portion of retention that is a ributable tonon-satisfaction effects. In congruence with prior studies, we argue that thesenon-satisfaction effects are synonymous with switching costs (Anderson and Sullivan,

; Fornell, ; Klemperer, ). As such, we expect that high switching costchannels will exhibit positive retention net of satisfaction, while low switching costchannels will exhibit insigni cant or negative retention effects net of satisfaction. efollowing directional hypotheses are stated in alternative form:

Hypothesis : (H ): Controlling for satisfaction, self-service customers who transact in highswitching cost channels are more likely to remain loyal to a rm than full-service customers.

Hypothesis : (H ): Controlling for satisfaction, self-service customers who transact in lowswitching cost channels are no more likely to remain loyal to a rm than full-servicecustomers.

By controlling for satisfaction effects, these hypotheses resolve the directionalambiguity in hypotheses and . Moreover, using full-service channels as theirbaseline creates a conservative test of switching costs, as it has been argued in theliterature that face-to-face interactions create relational (psychological) switchingbarriers (Farrell and Klemperer, ; Jones, Mothersbaugh, and Bea y, ).

. M

We conduct our study in the context of the retail banking industry. ere are severalreasons that retail banking is the ideal se ing in which to disentangle the impact ofswitching costs and satisfaction effects on self-service customer retention. First, retailbanks employ multiple channels to serve their customers. ese channels range from

full-service teller interactions to completely automated self-service channels such asonline banking and ATMs. As described above, these channels vary in terms of thelevel and types of switching costs each imposes. Second, retail banking customers are adiverse group, with varying needs, preferences and experiences. is variability createsa rich environment in which to analyze the impact of operational decisions onconsumer behavior. Moreover, the diverse customer base is common to a wide varietyof consumer service rms, broadening the relevance of our analysis. Finally, retailbanks capture and store a considerable amount of data about their customers, for bothstrategic and regulatory purposes. We were able to tap into this resource to conductour empirical analysis.

is study diverges methodologically from past work by analyzing the completepro le of transactions across all channels of service between a bank and a randomlyselected sample of its customers. Our observational dataset includes counts of thenumber of transactions a random sample of customers conducted through eachchannel over a one-year period. Many of the previous analyses have treated self-servicechannel usage as a binary variable, but a precedent exists in the literature forcharacterizing multi-channel customers based on the proportion of overall transactionsconducted through speci c channels (Montoya-Weiss, Voss, and Grewal, ). Wefollow this precedent by characterizing customers based on their proportional channelmix.

We couple this information with customer-level satisfaction data, gathered throughsurveys, and customer-level retention information, provided by the bank one yearfollowing our period of observation, to analyze the incremental impact of channel mixon customer satisfaction and retention. We examine the impact of channel mix onthree levels. First, we compare self-service channel mix to full-service channel mix onan aggregated level. is approach serves as our tests of hypotheses and , enablingus to broadly understand if customer involvement in the production of servicein uences satisfaction and retention. Second, we aggregate transactions conducted inthe high and low switching cost self-service channels we identi ed earlier based onex-ante characteristics. We compare the effects of the use of each type of channel onretention to test hypotheses and , learning if the level of switching costs in aself-service channel differentially drives retention. ird, we analyze the impact of eachchannel separately, to test hypotheses and , and be er understand if all channels arecreated equally with regard to switching costs, satisfaction and retention.

Disentangling the relationships between satisfaction effects, switching costs, andretention in a self-service se ing requires analysis of retention controlling forsatisfaction. No such study has yet been conducted. Prior studies exploring theserelationships have relied on customer surveys or observational analyses, but not both atthe same time. Studies examining the link between self-service usage and satisfactionhave, by necessity, been survey-based, and when these studies have addressed thequestion of retention, they’ve asked customers if they intended to continue patronizingthe rm (Marzocchi and Zammit, ; Mols, ; Wallace et al., ; Yen andGwinner, ). Furthermore, a number of observational studies have been conductedfocusing on retention, but they did not consider satisfaction in their models (Chen andHi , ; Xue and Harker, ). A general model illustrating these approaches isgiven by the following equations.

satisfaction = α + α (self-service) + α (controls) ( . )

retention = β + β (self-service) + β (controls) ( . )

retention = γ + γ (self-service) + γ (satisfaction) + γ (controls) ( . )

While these studies have provided scholars and practitioners with signi cantinsights about the net effects of self-service channel usage as well as other antecedentson each variable, they are limited by an inability to disentangle the impact ofsatisfaction effects and switching costs on customer retention. For this study, weemploy a mediation model that enables us to tease apart these two effects, as well asunderstand the ultimate impact of self-service usage use on satisfaction and retention.We use the following model for our analyses:

In contrast to previous studies, which tend to measure self-service participation as abinary variable, we measure self-service usage disaggregated by channel, based on therelative use of those channels. We estimate all equations through OLS regression. isallows for straightforward interpretation of the coefficients in terms of switching costsand satisfaction effects. In particular, this enables us to assess the direct impact of eachchannel’s use on satisfaction, characterized by α , and retention, characterized by , ourmodel enables us to understand the relative impact of satisfaction effects and switching

costs for each channel. In our model, we de ne switching costs as gains to retentionearned by a channel a er controlling for overall satisfaction. is approach isconsistent with previous theoretical and empirical treatments of switching costs inseveral non-service contexts (Anderson and Sullivan, ; Fornell, ; Klemperer,

). Hence, if γ > for any particular channel, then switching costs exist in thatchannel. α represents the impact a particular channel’s use has on overall satisfactionrelative to face-to-face teller transactions, and γ represents overall satisfaction’s impacton customer retention. erefore, the direct effect of satisfaction on retention(satisfaction effect) for a particular channel is given by α γ . Comparing α and α γenables us to understand the relative impact of switching costs and satisfaction effectson retention for each channel. Moreover, the sum of switching costs and satisfactioneffects for each channel equals the total effect of each self-service channel’s usage oncustomer retention, γ + (α γ ) = β .

In circumstances where γ > and α γ > for a particular channel, use of thechannel drives retention both by increasing customer switching costs and improvingcustomer satisfaction. On the other hand, when α γ < for a particular channel, useof the channel dissatis es customers, increasing the likelihood of their departure fromthe rm. Similarly, when γ < for any channel, use of the channel facilitatescustomer departure from the rm, irrespective of customer satisfaction.Understanding the direction of satisfaction effects and switching costs for each channelhas signi cant implications for a company’s choice of service strategy. For example,channels characterized by α γ < < γ , where |γ | > |α γ | are net destroyers ofcustomer satisfaction, but have a positive overall impact on retention because β > .Companies serving customers through such channels may nd themselves in a tenuousposition if technology advances and switching costs fall, as dissatis ed customers heldhostage by switching costs would be liberated to seek service elsewhere.

. R

For this study, we observe the behavior of , randomly selected customersperforming a transaction in the branch network of a nationwide U.S. retail bank.(Figures . . and . . ) is bank is one of the largest diversi ed nancial servicesrms in the U.S., and is both highly regarded for its customer service, as well as

respected as an industry leader for its initiatives to provide easy-to-use self-service

options for its customers. It serves millions of account holders through its network ofover , branches and nearly , ATM machines located in more than states.Our dataset includes the number of transactions each customer initiated in each of thebank’s channels for a one-year period during , as well as demographic and accountinformation, customer satisfaction data, and lagged customer retention data for eachcustomer.

. . S -

During our period of observation, the bank conducted all of its transactions withcustomers through six channels, including automated teller machines (ATM), onlinebill payment, online banking, interactive voice response (IVR), phone agentinteractions, and face-to-face teller transactions. We consider ATMs, online billpayment, online banking and IVR to be self-service channels. Phone agent and tellertransactions are considered full-service channels. For each customer, we sum thetransaction counts across self-service channels, and divide by the total number oftransactions to create an aggregated self-service mix variable. We also create channelproportion variables for each channel by dividing the annual transaction count in thechannel by the customer’s total transaction count. When we regress these variables, wecontrol for total transaction count to eliminate frequency-of-use and experience effects.

. . C

Retention was measured on the last day of , one year a er the initial observationperiod. Customers who still held accounts with the bank at that time were counted asretained, and those who had closed all of their accounts for any reason were deemed tohave defected. By this de nition, over the period in question, the bank experienced acustomer defection rate of . , representing the loss of hundreds of thousands ofcustomers across the country. We introduce customer retention into our regressions asa binary, dependent variable.

Varia

ble

corr

elat

ions

for t

he c

usto

mer

obs

erva

tion

perio

d1

23

45

67

89

1011

1213

1415

1617

1O

vera

ll sa

tisfa

ctio

n1.

002

Cus

tom

er re

tent

ion

0.07

1.00

3O

nlin

e bi

ll pa

ymen

t per

cent

age

0.00

0.03

1.00

4O

nlin

e se

ssio

n pe

rcen

tage

-0.0

1-0

.01

0.08

1.00

5AT

M p

erce

ntag

e-0

.01

-0.0

2-0

.07

-0.1

11.

006

IVR

per

cent

age

-0.0

2-0

.04

-0.1

1-0

.22

-0.1

01.

007

Phon

e ag

ent p

erce

ntag

e-0

.06

-0.0

6-0

.06

-0.0

9-0

.08

0.11

1.00

8C

usto

mer

tenu

re-0

.01

0.12

0.00

-0.1

8-0

.08

-0.0

7-0

.01

1.00

9C

usto

mer

age

0.05

0.09

-0.0

2-0

.24

-0.1

4-0

.05

0.02

0.46

1.00

10D

irect

dep

osit

indi

cato

r0.

020.

090.

090.

080.

070.

100.

010.

170.

251.

0011

Num

ber o

f dep

osit

acco

unts

0.02

0.10

0.07

-0.0

3-0

.03

-0.0

80.

020.

200.

150.

071.

0012

Num

ber o

f loa

n ac

coun

ts0.

030.

080.

08-0

.08

-0.0

5-0

.09

0.00

0.19

0.11

0.04

0.17

1.00

13N

umbe

r of i

nves

tmen

t acc

ount

s0.

020.

030.

04-0

.03

-0.0

4-0

.05

0.00

0.12

0.10

0.05

0.13

0.10

1.00

14D

epos

it ac

coun

t bal

ance

0.02

0.05

0.04

-0.0

6-0

.07

-0.0

80.

020.

150.

180.

030.

300.

050.

111.

0015

Loan

acc

ount

bal

ance

0.00

0.03

0.06

-0.0

2-0

.02

-0.0

40.

030.

050.

050.

010.

060.

440.

060.

021.

0016

Inve

stm

ent a

ccou

nt b

alan

ce0.

020.

020.

02-0

.02

-0.0

2-0

.02

0.00

0.08

0.07

0.03

0.05

0.05

0.51

0.14

0.04

1.00

17To

tal t

rans

actio

n co

unt

-0.0

3-0

.03

0.19

0.29

0.12

0.33

0.00

-0.1

2-0

.15

0.12

0.08

-0.0

7-0

.05

-0.0

70.

00-0

.02

1.00

Perc

enta

ge v

aria

bles

repr

esen

t the

pro

porti

on o

f tot

al c

usto

mer

tran

sact

ions

con

duct

ed in

par

ticul

ar c

hann

els t

hrou

ghou

t the

per

iod

of o

bser

vatio

n. IV

R is

the

abbr

evia

tion

for t

he in

tera

ctiv

e vo

ice

resp

onse

ch

anne

l.

Figure 2.4.1: Variable correlations for customer observation period.

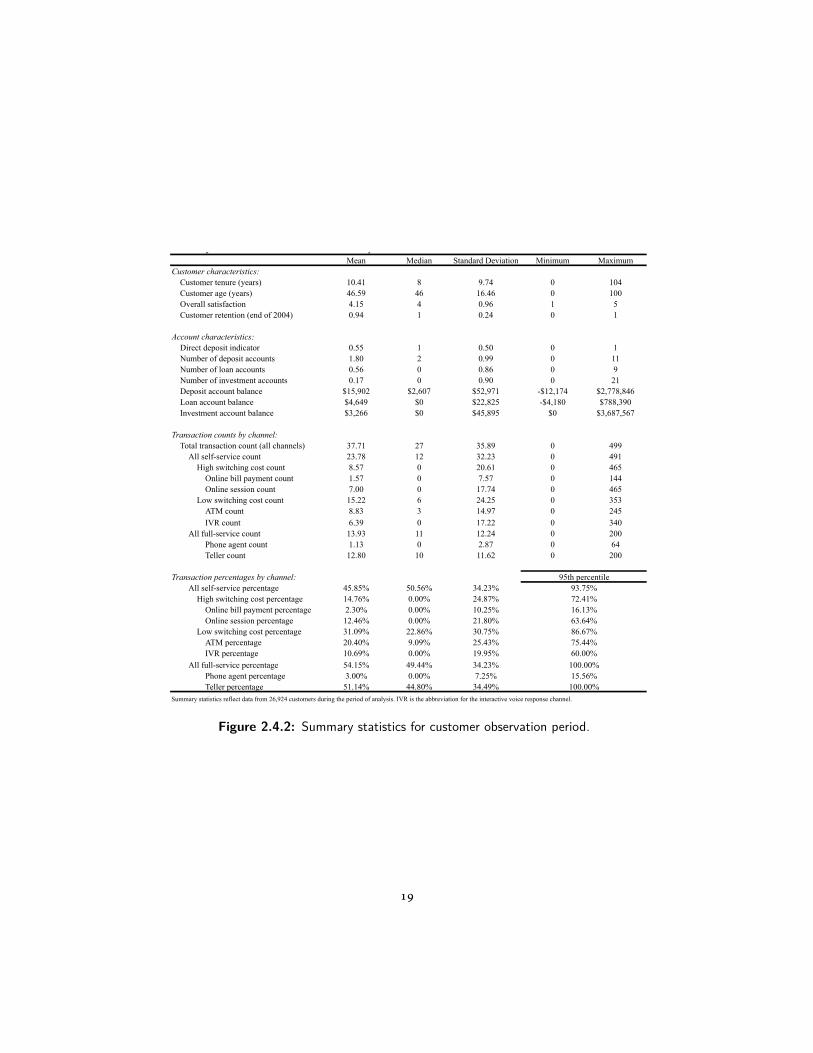

Mean Median Standard Deviation Minimum MaximumCustomer characteristics:

Customer tenure (years) 10.41 8 9.74 0 104Customer age (years) 46.59 46 16.46 0 100Overall satisfaction 4.15 4 0.96 1 5Customer retention (end of 2004) 0.94 1 0.24 0 1

Account characteristics:Direct deposit indicator 0.55 1 0.50 0 1Number of deposit accounts 1.80 2 0.99 0 11Number of loan accounts 0.56 0 0.86 0 9Number of investment accounts 0.17 0 0.90 0 21Deposit account balance $15,902 $2,607 $52,971 -$12,174 $2,778,846Loan account balance $4,649 $0 $22,825 -$4,180 $788,390Investment account balance $3,266 $0 $45,895 $0 $3,687,567

Transaction counts by channel:Total transaction count (all channels) 37.71 27 35.89 0 499

All self-service count 23.78 12 32.23 0 491High switching cost count 8.57 0 20.61 0 465

Online bill payment count 1.57 0 7.57 0 144Online session count 7.00 0 17.74 0 465

Low switching cost count 15.22 6 24.25 0 353ATM count 8.83 3 14.97 0 245IVR count 6.39 0 17.22 0 340

All full-service count 13.93 11 12.24 0 200Phone agent count 1.13 0 2.87 0 64Teller count 12.80 10 11.62 0 200

Transaction percentages by channel:All self-service percentage 45.85% 50.56% 34.23%

High switching cost percentage 14.76% 0.00% 24.87%Online bill payment percentage 2.30% 0.00% 10.25%Online session percentage 12.46% 0.00% 21.80%

Low switching cost percentage 31.09% 22.86% 30.75%ATM percentage 20.40% 9.09% 25.43%IVR percentage 10.69% 0.00% 19.95%

All full-service percentage 54.15% 49.44% 34.23%Phone agent percentage 3.00% 0.00% 7.25%Teller percentage 51.14% 44.80% 34.49%

Summary statistics for the customer observation period

Summary statistics reflect data from 26,924 customers during the period of analysis. IVR is the abbreviation for the interactive voice response channel.

95th percentile93.75%72.41%16.13%63.64%86.67%75.44%60.00%

100.00%15.56%

100.00%

Figure 2.4.2: Summary statistics for customer observation period.

. . C

In January of , randomly selected customers were contacted via phone tocomplete a survey within hours of personally visiting a branch to conduct atransaction. To gauge overall satisfaction, customers were asked, ”Taking into accountall the products and services you receive from [it], how satis ed are you with [thebank] overall?” Customers rated their overall satisfaction on a Likert scale of - , witha score of representing complete satisfaction. e average satisfaction rating reportedwas . . In this study, we have chosen to focus on overall satisfaction rather thanchannel-speci c satisfaction because we believe it more directly relates to a customer’sdecision to remain loyal to the rm.

. . C

e customer demographic and account information factored into our analysisincludes customer age, the length of the customer’s relationship with the bank, thenumbers of different types of accounts the customer had (deposit, loan andinvestment), the aggregate balances for each customer by account type (in thousandsof dollars), and whether or not the customer had signed-up for direct deposit service.

e inclusion of these control variables helps us avoid omi ed variable bias, as severalof them have explanatory power and are correlated with the variables of interest.(Figure . . ) Customer ages in our sample are roughly normally distributed(skewness = . , kurtosis = . ), with a mean of . , and the average customer hada . -year relationship with the bank. Roughly half of all customers sampled usedonline banking and direct deposit. Nearly used online bill payment.

. R

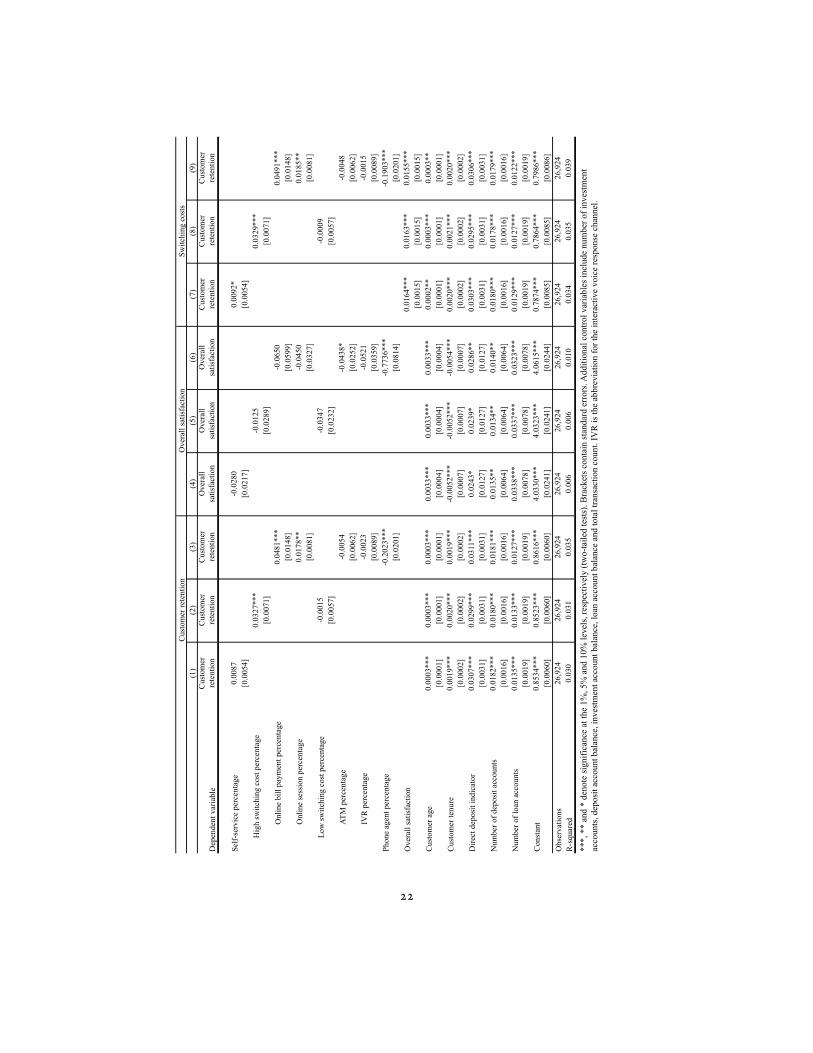

. . T -

We begin by testing the overall impact of self-service usage on customer retention.(Figure . . ) In column , our analysis reveals that the aggregate proportion of acustomer’s total transactions conducted through self-service channels has a marginallyinsigni cant impact on customer retention (. , p=. ; two-tailed). is nding

is consistent with hypothesis .In column , we examine how the proportional usage of high and low switching cost

self-service channels impacts customer retention. We nd that customers who increasethe proportion of their transactions in high switching cost self-service channels areretained with statistical signi cance (. , p<. ; two-tailed), while those whoincrease the proportion of their transactions in low switching cost self-service channelsare no more or less likely to be retained (- . , p=. ; two-tailed). Consistently,a test on the joint null hypotheses that the coefficients on online bill payment andonline session usage in column are both zero yielded a signi cant F-statistic: F( ,

)= . ; p<. , while the same test conducted on ATM and IVR usage yielded aninsigni cant F statistic: F( , )=. ; p=. . ese ndings do not supporthypothesis , but are consistent with hypothesis .

To summarize, these results suggest that relative to using full-service channels, theusage of self-service channels in aggregate has a statistically insigni cant impact oncustomer retention. However, customers who use high switching cost self-servicechannels relative to other channels are more likely to be retained, while those who uselow switching cost self-service channels relative to other channels are no more likely tobe retained.

. . T -

Our next set of tests addresses the impact of self-service usage on customersatisfaction. In column , we do not nd that aggregated self-service usage impactssatisfaction (-. , p=. ; two-sided). ese ndings support hypothesis .Moreover, in column , we see that there are not systematic differences in the impact ofhigh and low switching cost self-service channels on satisfaction (high switching costchannels: -. , p=. ; two-sided, and low switching cost channels: -. ,p=. two-sided). Column reveals the association between individual channels andcustomer satisfaction. Customers who utilized the phone agent channel, were lesssatis ed relative to customers engaging in face-to-face transactions (-. , p<. ;

Figure 2.5.1 (following page): The associations among aggregated self-servicechannel usage, high and low switching cost self-service channel usage, individualchannel usage, customer retention, overall satisfaction, and switching costs.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

Dep

ende

nt v

aria

ble

Cus

tom

er

rete

ntio

nC

usto

mer

re

tent

ion

Cus

tom

er

rete

ntio

nO

vera

ll sa

tisfa

ctio

nO

vera

ll sa

tisfa

ctio

nO

vera

ll sa

tisfa

ctio

nC

usto

mer

re

tent

ion

Cus

tom

er

rete

ntio

nC

usto

mer

re

tent

ion

Self-

serv

ice

perc

enta

ge0.

0087

-0.0

280

0.00

92*

[0.0

054]

[0.0

217]

[0.0

054]

Hig

h sw

itchi

ng c

ost p

erce

ntag

e0.

0327

***

-0.0

125

0.03

29**

*[0

.007

1][0

.028

9][0

.007

1]O

nlin

e bi

ll pa

ymen

t per

cent

age

0.04

81**

*-0

.065

00.

0491

***

[0.0

148]

[0.0

599]

[0.0

148]

Onl

ine

sess

ion

perc

enta

ge0.

0178

**-0

.045

00.

0185

**[0

.008

1][0

.032

7][0

.008

1]Lo

w sw

itchi

ng c

ost p

erce

ntag

e-0

.001

5-0

.034

7-0

.000

9[0

.005

7][0

.023

2][0

.005

7]AT

M p

erce

ntag

e-0

.005

4-0

.043

8*-0

.004

8[0

.006

2][0

.025

2][0

.006

2]IV

R p

erce

ntag

e-0

.002

3-0

.052

1-0

.001

5[0

.008

9][0

.035

9][0

.008

9]Ph

one

agen

t per

cent

age

-0.2

023*

**-0

.773

6***

-0.1

903*

**[0

.020

1][0

.081

4][0

.020

1]O

vera

ll sa

tisfa

ctio

n0.

0164

***

0.01

63**

*0.

0155

***

[0.0

015]

[0.0

015]

[0.0

015]

Cus

tom

er a

ge0.

0003

***

0.00

03**

*0.

0003

***

0.00

33**

*0.

0033

***

0.00

33**

*0.

0002

**0.

0003

***

0.00

03**

[0.0

001]

[0.0

001]

[0.0

001]

[0.0

004]

[0.0

004]

[0.0

004]

[0.0

001]

[0.0

001]

[0.0

001]

Cus

tom

er te

nure

0.00

19**

*0.

0020

***

0.00

19**

*-0

.005

2***

-0.0

052*

**-0

.005

4***

0.00

20**

*0.

0021

***

0.00

20**

*[0

.000

2][0

.000

2][0

.000

2][0

.000

7][0

.000

7][0

.000

7][0

.000

2][0

.000

2][0

.000

2]D

irect

dep

osit

indi

cato

r0.

0307

***

0.02

99**

*0.

0311

***

0.02

43*

0.02

39*

0.02

86**

0.03

03**

*0.

0295

***

0.03

06**

*[0

.003

1][0

.003

1][0

.003

1][0

.012

7][0

.012

7][0

.012

7][0

.003

1][0

.003

1][0

.003

1]N

umbe

r of d

epos

it ac

coun

ts0.

0182

***

0.01

80**

*0.

0181

***

0.01

35**

0.01

34**

0.01

40**

0.01

80**

*0.

0178

***

0.01

79**

*[0

.001

6][0

.001

6][0

.001

6][0

.006

4][0

.006

4][0

.006

4][0

.001

6][0

.001

6][0

.001

6]N

umbe

r of l

oan

acco

unts

0.01

35**

*0.

0133

***

0.01

27**

*0.

0338

***

0.03

37**

*0.

0323

***

0.01

29**

*0.

0127

***

0.01

22**

*[0

.001

9][0

.001

9][0

.001

9][0

.007

8][0

.007

8][0

.007

8][0

.001

9][0

.001

9][0

.001

9]C

onst

ant

0.85

34**

*0.

8523

***

0.86

16**

*4.

0330

***

4.03

23**

*4.

0615

***

0.78

74**

*0.

7864

***

0.79

86**

*[0

.006

0][0

.006

0][0

.006

0][0

.024

1][0

.024

1][0

.024

4][0

.008

5][0

.008

5][0

.008

6]O

bser

vatio

ns26

,924

26,9

2426

,924

26,9

2426

,924

26,9

2426

,924

26,9

2426

,924

R-s

quar

ed0.

030

0.03

10.

035

0.00

60.

006

0.01

00.

034

0.03

50.

039

The

asso

ciat

ions

am

ong

aggr

egat

ed se

lf-se

rvic

e ch

anne

l usa

ge, h

igh

and

low

switc

hing

cos

t sel

f-se

rvic

e ch

anne

l usa

ge, i

ndiv

idua

l cha

nnel

usa

ge, c

usto

mer

re

tent

ion,

ove

rall

satis

fact

ion,

and

switc

hing

cos

ts

***,

**

and

* de

note

sign

ifica

nce

at th

e 1%

, 5%

and

10%

leve

ls, r

espe

ctiv

ely

(two-

taile

d te

sts)

. Bra

cket

s con

tain

stan

dard

err

ors.

Add

ition

al c

ontro

l var

iabl

es in

clud

e nu

mbe

r of i

nves

tmen

t ac

coun

ts, d

epos

it ac

coun

t bal

ance

, inv

estm

ent a

ccou

nt b

alan

ce, l

oan

acco

unt b

alan

ce a

nd to

tal t

rans

actio

n co

unt.

IVR

is th

e ab

brev

iatio

n fo

r the

inte

ract

ive

voic

e re

spon

se c

hann

el.

Cus

tom

er re

tent

ion

Ove

rall

satis

fact

ion

Switc

hing

cos

ts

two-sided). Phone interviews with executives at the bank suggested that customersmay systematically choose to interact with the bank through the phone agent channelto communicate when there is a problem. is factor likely explains the statisticallysigni cant relationship between phone agent transactions and dissatisfaction.Customers who used the other channels we analyzed were neither more nor lesssatis ed than customers who transacted with full-service tellers. ese ndings suggestthat self-service channel transactions do not promote satisfaction relative toface-to-face channel usage.

. . T - -

To disentangle the impact of satisfaction effects and switching costs on customerretention, we analyze the impact of channel usage on customer retention, controllingfor satisfaction. In this series of regressions, the coefficients on channel mix variablesindicate the level of customer retention that is unexplained by differences in customersatisfaction. Channels with positive retention net of satisfaction exhibit characteristicsconsistent with switching costs. In column , we nd that on an aggregate basis,self-service channel usage has a marginally insigni cant impact on retention net ofsatisfaction (. , p=. ; two-tailed). Column illustrates that customers in highswitching cost channels are retained with an intensity greater than that explained bytheir satisfaction (. , p<. ; one-sided), while those transacting in low switchingcost channels do not exhibit the same pa ern (-. , p=. ; one-sided). esendings offer support for hypotheses and . Column shows retention net of

satisfaction on a channel-by-channel basis. Usage of online bill payment (. ,p<. ; one-sided) and online banking (. , p<. ; one-sided) corresponds withstatistically signi cant retention net of satisfaction, while usage of other self-servicechannels has no such effect.

Furthermore, by comparing the coefficients on channel mix variables in columns -with those in columns - , we can disentangle the relative magnitude of satisfactioneffects and switching costs in each context. e negative magnitude of the change ofthese coefficients represents the strength of satisfaction effects promoted by thecorresponding channel. In all cases, the magnitudes of the channel mix coefficientsincrease a er controlling for satisfaction. Hence, we nd that while switching costs do

serve as a driver of self-service retention, satisfaction effects do not.

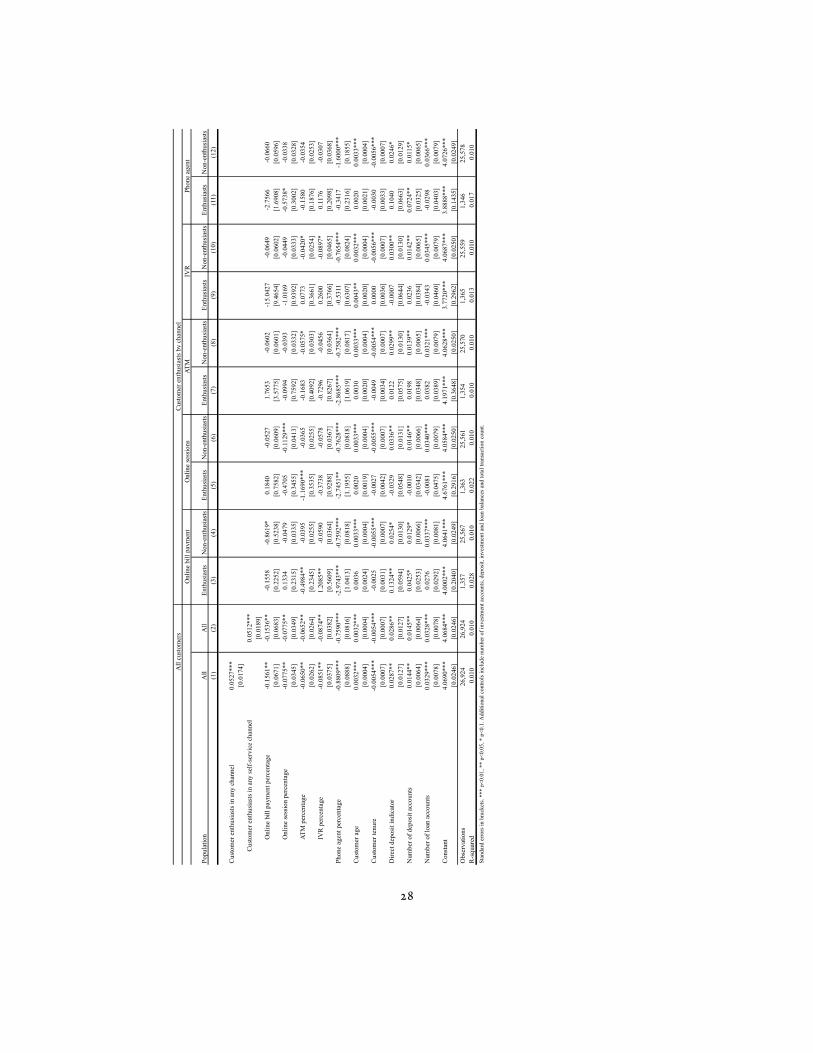

. . A

e signi cant coefficients on a number of the control variables in our regressions areconsistent with previous studies examining customer behavior in the nancial servicessector (Hi and Frei, ). We nd that age, direct deposit participation and thenumber of deposit and loan accounts a customer has are all positively associated withsatisfaction and retention. We also observe that customer tenure is negativelyassociated with overall satisfaction, but positively associated with retention. Consistentwith prior studies, these results suggest that tenure imposes switching barriers onexperienced customers that can override marginal declines in satisfaction.

. . E -

It is worth noting that although we observed statistically signi cant relationshipsbetween the proportional use of speci c channels and customer satisfaction andretention, a considerable portion of the variation in a customer’s satisfaction andretention remains unexplained by factors accounted for in our model. is is evidencedby the low R-squared values reported in Figure . . . As with prior research inbusiness-to-consumer service contexts, customer satisfaction and retention remainshighly heterogeneous a er controlling for characteristics that can be reliably observedand consistently quanti ed across a large sample of customers. In this context, theexplanatory power of our models, while relatively low, is generally consistent with priorstudies investigating such metrics (Hi and Frei, ; I ner and Larcker, ;Verhoef, ).

Previously published papers using customer-level performance metrics withextremely high explanatory power (e.g. - ) include lagged values of theperformance measures of interest in their empirical models. Not surprisingly, laggeddependent variables account for the majority of the explained variation in thesemodels. Including lagged dependent variables in our retention analysis is not possiblesince, by de nition, all customers remaining in the sample each period would have alagged retention value equal to , and those who are not retained would drop from thesample and not be analyzed in future periods. In our retention regressions, the

R-squared values range from - . It should be noted that the papers cited abovewhich examine retention typically do so using probit or logit based regression ratherthan OLS. As a result, these papers report various ”pseudo R-squared” measures ratherthan the traditional R-squared measures from OLS that we report. To make our resultsmore comparable with those of previous studies, we re-estimated our retention modelsusing logit regression and the pseudo R-squared measures range from - , whichis well in line with these previous studies.

e R-squared values we report for our satisfaction regressions are smaller, whichoffers a measure of support for our results by highlighting how li le of the variation insatisfaction is driven by differences in a customer’s proportional use of variouschannels. To our knowledge, the literature provides no benchmark for appropriateR-squared measures in regressions that model satisfaction primarily as a function ofactual customer characteristics and transaction histories. Most of the regressionsmodeling satisfaction in prior literature that we are aware of rely in part onsurvey-based measures of customer perceptions of recent experiences with the serviceprovider. Understandably, a customer’s perceptions of recent experiences with acompany drive a considerable portion of the variation in their overall satisfaction. Wewere able to obtain a measure of the customer’s perception of the ease of their mostrecent transaction with the bank we studied in our paper. When we include thismeasure in the satisfaction regressions as a robustness check, the R-squared valuesclimb to approximately (Figure . . ). All of the results we report are robust tothe inclusion of this variable.

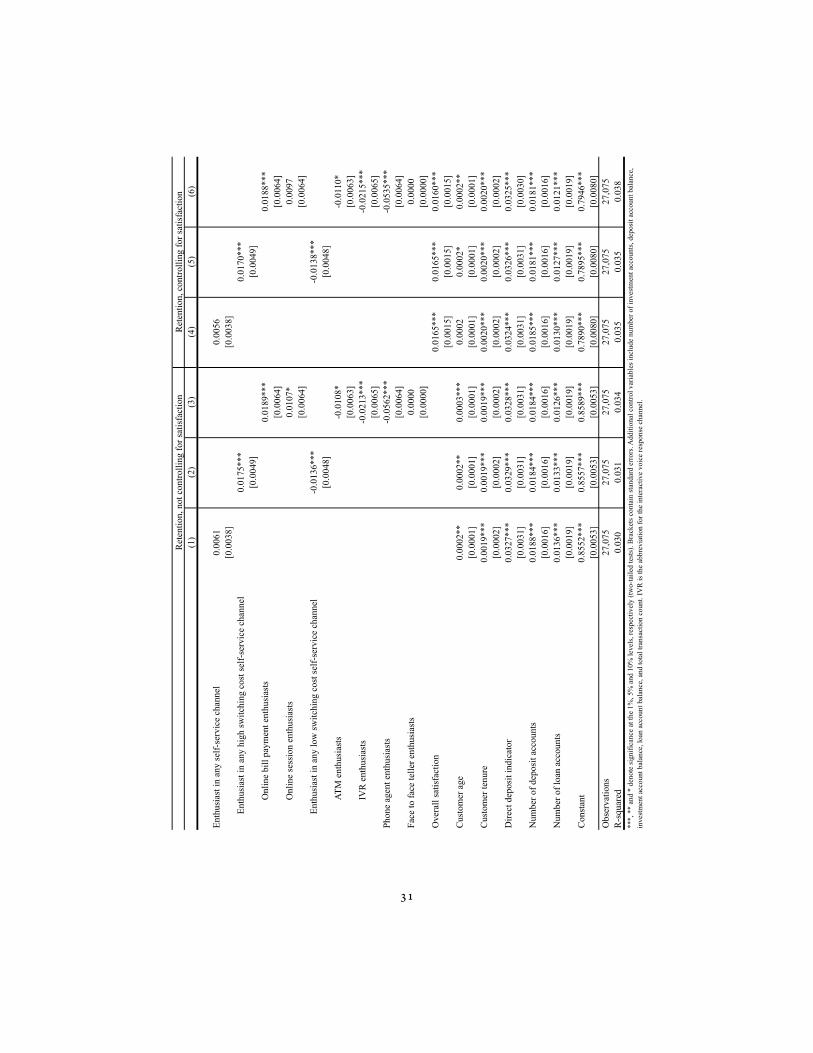

. . C :

Our primary results suggest that self-service channel usage does not necessarilypromote satisfaction or retention relative to transactions conducted in full-servicechannels. We nd that self-service usage contributes positively to loyalty only in

Figure 2.5.2 (following page): The associations among aggregated self-servicechannel usage, high and low switching cost self-service channel usage, individualchannel usage, customer retention, overall satisfaction, and switching costs control-ling for ease of most recent transaction.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

Dep

ende

nt v

aria

ble

Cus

tom

er re

tent

ion

Cus

tom

er re

tent

ion

Cus

tom

er re

tent

ion

Ove

rall

satis

fact

ion

Ove

rall

satis

fact

ion

Ove

rall

satis

fact

ion

Cus

tom

er re

tent

ion

Cus

tom

er re

tent

ion

Cus

tom

er re

tent

ion

Self-

serv

ice

perc

enta

ge0.

0096

*0.

0085

0.00

94*

[0.0

054]

[0.0

187]

[0.0

054]

Hig

h sw

itchi

ng c

ost p

erce

ntag

e0.

0336

***

0.03

450.

0331

***

[0.0

072]

[0.0

249]

[0.0

071]

Onl

ine

bill

paym

ent p

erce

ntag

e0.

0495

***

0.03

330.

0490

***

[0.0

148]

[0.0

518]

[0.0

148]

Onl

ine

sess

ion

perc

enta

ge0.

0187

**0.

0070

0.01

86**

[0.0

081]

[0.0

283]

[0.0

081]

Low

switc

hing

cos

t per

cent

age

-0.0

007

-0.0

026

-0.0

006

[0.0

057]

[0.0

200]

[0.0

057]

ATM

per

cent

age

-0.0

045

-0.0

031

-0.0

044

[0.0

062]

[0.0

218]

[0.0

062]

IVR

per

cent

age

-0.0

019

-0.0

242

-0.0

015

[0.0

089]

[0.0

310]

[0.0

089]

Phon

e ag

ent p

erce

ntag

e-0

.198

0***

-0.3

989*

**-0

.192

2***

[0.0

202]

[0.0

706]

[0.0

202]

Ove

rall

satis

fact

ion

0.01

53**

*0.

0152

***

0.01

46**

*[0

.001

8][0

.001

7][0

.001

7]Ea

se o

f mos

t rec

ent t

rans

actio

n0.

0102

***

0.01

02**

*0.

0094

***

0.52

89**

*0.

5290

***

0.52

73**

*0.

0021

0.00

220.

0017

[0.0

016]

[0.0

016]

[0.0

016]

[0.0

055]

[0.0

055]

[0.0

055]

[0.0

018]

[0.0

018]

[0.0

018]

Cus

tom

er a

ge0.

0002

**0.

0003

***

0.00

03**

0.00

19**

*0.

0020

***

0.00

19**

*0.

0002

**0.

0003

**0.

0002

**[0

.000

1][0

.000

1][0

.000

1][0

.000

4][0

.000

4][0

.000

4][0

.000

1][0

.000

1][0

.000

1]C

usto

mer

tenu

re0.

0019

***

0.00

20**

*0.

0019

***

-0.0

042*

**-0

.004

2***

-0.0

043*

**0.

0020

***

0.00

20**

*0.

0020

***

[0.0

002]

[0.0

002]

[0.0

002]

[0.0

006]

[0.0

006]

[0.0

006]

[0.0

002]

[0.0

002]

[0.0

002]

Dire

ct d

epos

it in

dica

tor

0.03

08**

*0.

0301

***

0.03

12**

*0.

0258

**0.

0250

**0.

0277

**0.

0304