the panama papers: a discussion of some ethical issues

TRANSCRIPT

1

THE PANAMA PAPERS:

A Discussion of Some Ethical Issues

Robert W. McGee

Fayetteville State University

Working Paper

May 27, 2016

ABSTRACT

The Panama Papers refers to a massive leak of information encompassing more

than 11 million documents involving more than 200,000 offshore entities. The leak

originated in Panama. Some of the documents involve transactions as far back as

the 1970s. Numerous wealthy individuals, including top government officials from

many countries, have been implicated. The release of information and documents

has led to several resignations and numerous lawsuits. The end of litigation is not

in sight, as lawyers and government agencies in several countries continue to read

and digest the information.

Although there is nothing illegal per se about having offshore entities, some

such entities have been used to hide assets, evade income taxes, launder money and

evade sanctions. The whistleblower who leaked the information to Süddeutsche

Zeitung, a German newspaper, called himself John Doe to maintain anonymity. He

leaked the information because of his strong distaste for income inequality and

because of his view that there were many injustices being perpetrated by some of

the entities and individuals who were availing themselves of the entities.

This paper discusses some of the underlying ethical issues that lurk beneath

the surface of most discussions about hiding assets and income offshore. The

discussion will focus on the ethics of parking profits (or hiding assets) offshore, tax

evasion, bribery, and whistle blowers.

This paper also includes links to more than 80 studies on tax evasion and

11 studies on bribery.

Key Words: whistle blowers, tax evasion, tax compliance, bribery, ethics, Panama Papers, offshore

accounts, corruption, scandals, FCPA, money laundering

JEL Codes: D63, E62, G18, G28, G38, H24, H25, H26, H56, J18, K14, K34, K42, L84

2

TABLE OF CONTENTS Introduction 2

Parking Profits Offshore 4

Some Moral Issues 7

Tax Evasion 11

Bribery 19

Whistleblowers 24

Concluding Comments 26

References 27

Author Bio 35

Bibliography – Bribery 36

Bibliography – Tax Evasion 37

INTRODUCTION

Lawrence J. Trautman (2016) has written an excellent manuscript on the Panama Papers.

I will not attempt to critique, duplicate or summarize that paper here. My intent is much more

modest, namely, to address some of the underlying ethical issues that are lurking in the shadows

of any discussions about the Panama Papers and other attempts to hide assets and income from

governments.

Basically, the Panama Papers refers to a massive leak of information encompassing more

than 11 million documents involving more than 200,000 offshore entities. The leak originated in

Panama. Some of the documents involve transactions as far back as the 1970s. Numerous wealthy

individuals, including top government officials from many countries, have been implicated. The

release of information and documents has led to several resignations and numerous lawsuits. The

end of litigation is not in sight, as lawyers and government agencies in several countries continue

to read and digest the information.

Although there is nothing illegal per se about having offshore entities, some such entities

have been used to hide assets, evade income taxes, launder money and evade sanctions. The

whistleblower who leaked the information to Süddeutsche Zeitung, a German newspaper, called

3

himself John Doe to maintain anonymity. He leaked the information because of his strong distaste

for income inequality and because of his view that there were many injustices being perpetrated

by some of the entities and individuals who were availing themselves of the entities.

The International Consortium of Investigative Journalists (ICIJ) assisted in the

dissemination of the documents. Journalists from 107 media outlets in 80 countries combed

through the documents and began publishing articles about them and releasing some of the

documents on April 3, 2016 (Wikipedia, 2016), which triggered a feeding frenzy among the media.

Trautman (2016) has already outlined many of the details in the case, and a search of the

internet makes it easy to get additional information and updates, so there is no need to regurgitate

those details here. Any details I would give here will quickly become outdated anyway, and more

details seem to become available on a daily basis. The purpose of this paper is to discuss policy

and the ethical implications of certain acts and arrangements, not to attempt to keep the reader

informed about recent developments.

The remainder of this paper will discuss some of the underlying ethical issues that lurk

beneath the surface of most discussions about hiding assets and income offshore. The discussion

will focus on the ethics of parking profits (or hiding assets) offshore, tax evasion, bribery, and

whistle blowers. The mainstream media either ignores discussing these topics or, when they are

discussed, they often get it wrong. That is understandable. Journalists need to write copy that

sizzles in order to sell newspapers and magazines. Publishing rational discussions that apply

ethical principles to topics like offshore entities, tax evasion, bribery and whistleblowing would

tend to put readers to sleep, which would not help sales. Furthermore, many journalists, perhaps

most, lack an understanding of ethical principles, and so would not be suited for the job of

analyzing these topics by applying ethical principles.

4

PARKING PROFITS OFFSHORE1

In a recent article, Richard Ruben2 reported that the largest U.S. companies added $206

billion to their stockpiles of offshore profits in 2013, an 11.8 percent increase since 2012. Total

offshore profits for these companies are now $1.95 trillion, which is more than the GDP of all but

the largest nine countries in the world.3 If these multinational corporations formed a separate

nation, they would be slightly larger than India and slightly smaller than Italy in terms of GDP.

Ruben pointed out that large multinational companies will likely continue to keep their profits

offshore until Congress gives them a reason not to.

The scary part of that assessment is that Congress can take several approaches to resolve

this problem, assuming that it is a problem.4 One approach would be to penalize companies for

continuing this practice, which would lead to negative unintended consequences. Another

approach would be to reduce tax rates so that companies would not feel compelled to shelter their

profits from the excessive tax rates the U.S. government and various state governments impose of

them.

Some people would challenge the assertion that U.S. tax rates are excessive. However, a

comparison of U.S. corporate tax rates to those of other developed countries finds that U.S.

1 Some of the material for this part was taken from Robert W. McGee. 2014. Some Thoughts on the Ethics of

Parking Profits Offshore. Journal of Accounting, Ethics & Public Policy 15(1): 165-174.

http://ssrn.com/abstract=2410020

2 Richard Ruben, Corporate Cash Abroad Rises $206 Billion as Multinationals Avoid Taxes. ACCOUNTING TODAY

online, March 13, 2014. www.accountingtoday.com. 3 World Bank http://databank.worldbank.org/data/download/GDP.pdf. The GDP statistics are for 2012. 4 A strong case can be made that parking cash or any other asset offshore is really none of any government’s business,

since having the right to property means that anyone can do whatever they want with their own property. Governments

have no inherent right to claim an ownership interest in the property of others.

5

corporate tax rates are the highest in the world. Table 1 compares corporate tax rates of various

developed countries.

Table 1. Marginal Effective Tax Rate on Capital Investment, OECD Countries5

Marginal Effective Tax Rate

Statutory

Tax Rate*

2013 2012 2011 2010 2009 2008 2007 2006 2005 2013

U.S. 35.3 35.3 35.3 35.3 35.6 35.6 35.6 35.9 35.9 39.1

France 35.2 35.2 35.2 34.0 35.1 35.1 35.1 35.1 35.4 34.4

Korea 30.1 30.1 30.1 30.1 30.1 32.8 32.8 32.8 32.8 24.2

Japan 29.3 31.5 31.5 31.5 31.5 31.5 31.5 31.5 31.5 37.0

Austria 26.2 26.2 26.2 26.2 26.2 26.2 26.2 26.2 26.2 25.0

Spain 26.0 26.0 26.0 26.0 26.0 26.0 28.2 30.3 30.3 30.0

Australia 25.9 25.9 25.9 25.9 25.9 25.9 25.9 25.9 25.9 30.0

UK 25.9 26.9 27.1 29.1 29.0 28.8 30.0 30.0 30.0 23.0

Italy 24.5 24.5 28.0 28.0 28.0 28.1 33.5 33.5 33.5 27.5

Germany 24.4 24.4 24.4 24.4 24.4 24.4 34.0 34.0 34.0 30.2

Norway 24.4 24.4 24.4 24.4 24.4 24.4 24.4 24.4 24.4 28.0

Portugal 22.9 22.9 20.8 20.8 18.8 18.8 18.8 19.6 19.6 31.5

New Zealand 21.6 21.6 21.6 18.2 18.2 18.2 20.5 20.5 20.5 28.0

Denmark 19.1 19.1 19.1 19.1 19.1 19.1 19.1 21.7 21.7 25.0

Canada 18.6 17.4 18.7 19.8 27.3 28.0 30.9 36.2 38.8 26.3

Belgium 18.5 18.5 18.5 18.5 18.5 18.5 18.0 18.0 23.5 34.0

Greece 18.1 11.3 11.3 13.2 13.7 13.7 13.7 15.8 17.5 26.0

Finland 17.5 17.5 18.7 18.7 18.7 18.7 18.7 18.7 18.7 24.5

Switzerland 17.5 17.5 17.5 17.5 17.5 17.5 18.0 18.0 18.0 21.1

Netherlands 17.5 17.5 17.5 17.5 17.5 17.5 17.5 20.7 22.3 25.0

Mexico 17.4 17.4 17.4 17.4 16.0 16.0 16.0 16.7 17.4 30.0

Luxembourg 17.3 17.0 17.0 16.8 16.8 18.5 19.4 19.4 19.9 29.2

Estonia 17.1 17.1 17.1 17.1 17.1 17.1 18.1 19.1 20.2 21.0

Hungary 16.1 16.1 16.1 16.1 16.6 16.6 16.6 15.3 14.7 19.0

Sweden 16.1 19.5 19.5 19.5 19.5 20.9 20.9 20.9 20.9 22.0

Slovak Republic 15.7 12.7 12.7 12.7 12.7 12.7 12.7 12.7 12.7 23.0

Israel 15.0 15.0 14.3 15.0 15.8 16.5 18.0 19.5 19.5 25.0

Poland 14.6 14.6 14.6 14.6 14.6 14.6 14.6 14.6 14.6 19.0

Iceland 14.2 14.2 14.2 12.6 10.4 10.4 12.6 12.6 18.0 20.0

Czech Rep 12.7 12.7 12.7 12.7 13.5 14.2 16.5 16.5 18.0 19.0

Ireland 10.1 10.1 10.1 10.1 10.1 10.1 10.1 10.1 10.1 12.5

Slovenia 9.8 10.5 11.8 11.8 12.4 13.1 13.8 14.5 15.2 17.0

Chile 7.7 7.7 7.7 6.7 6.7 6.9 7.1 7.3 7.3 20.0

Turkey 5.7 5.7 5.7 5.7 5.7 5.7 5.7 5.7 10.9 20.0

OECD Average:

Weighted* 28.5 28.8 29.0 29.1 29.5 29.6 30.8 31.2 31.5 32.9

Unweighted 19.6 19.5 19.7 19.6 19.8 20.1 21.0 21.6 22.4 25.5

5 Adapted from Table 2 of Jack Mintz and Duanjie Chen, Special Report No. 214: The U.S. Effective Corporate Tax

Rate: Myth and the Fact, Washington, DC: Tax Foundation, February 6, 2014. http://taxfoundation.org/article/us-

corporate-effective-tax-rate-myth-and-fact [accessed March 14, 2014].

6

Note: G-7 countries are in bold.

*Weighted by the average GDP for 2005-2011 in 2005 constant U.S. dollars.

--------------------------------------------------------------------------------

It must be pointed out that these U.S. corporate tax rates are for the federal tax only. One

must add the appropriate state and perhaps local tax rates to get the complete picture. Table 2 ranks

the states based on their top marginal corporate income tax rate.

Table 2

Ranking of State Corporate Tax Rates

(as of January 1, 2013)6

RANK STATE RATE

%

1 Iowa 12.0

2 Pennsylvania 9.99

3 D.C. 9.975

4 Minnesota 9.8

5 Illinois 9.5

6 Alaska 9.4

7 Connecticut 9.0

7 New Jersey 9.0

7 Rhode Island 9.0

10 Maine 8.93

11 California 8.84

12 Delaware (see note) 8.7

13 New Hampshire 8.5

13 Vermont 8.5

15 Maryland 8.25

16 Indiana 8.0

16 Louisiana 8.0

16 Massachusetts 8.0

19 Wisconsin 7.9

20 Nebraska 7.81

21 New Mexico 7.6

21 Oregon 7.6

23 Idaho 7.4

24 New York 7.1

25 Kansas 7.0

25 West Virginia 7.0

27 Arizona 6.968

28 North Carolina 6.9

29 Montana 6.75

30 Alabama 6.5

30 Arkansas 6.5

30 Tennessee 6.5

33 Hawaii 6.4

34 Missouri 6.25

35 Georgia 6.0

35 Kentucky 6.0

6 Adapted from Table 15 of Tax Foundation, Facts & Figures: How Does Your State Compare? Washington, DC:

Tax Foundation, 2013. http://taxfoundation.org/sites/taxfoundation.org/files/docs/ff2013.pdf.

7

35 Michigan 6.0

35 Oklahoma 6.0

35 Virginia (see note) 6.0

40 Florida 5.5

41 North Dakota 5.15

42 Mississippi 5.0

42 South Carolina 5.0

42 Utah 5.0

45 Colorado 4.63

46 Nevada 0

46 Ohio (see note) 0

46 South Dakota 0

46 Texas (see note) 0

46 Washington (see note) 0

46 Wyoming 0

Note: Ohio, Texas and Washington do not have a

corporate income tax, but they do have a gross receipts

tax. Delaware and Virginia have both a corporate income

tax and a gross receipts tax. For specifics, see Tax

Foundation, Facts & Figures: How Does Your State

Compare? 2013.

Iowa imposes the highest corporate tax rate, 12 percent, followed by Pennsylvania,

Washington, DC, Minnesota, Illinois, Alaska, Connecticut, New Jersey and Rhode Island, all of

which have a top rate of 9 percent or more. Nevada, Ohio, South Dakota, Texas, Washington and

Wyoming do not have a corporate income tax, although some of these states have other taxes to

compensate for the lack of a corporate income tax.

If one adds the federal, state and (sometimes) local corporate income tax rates, plus some

of the other taxes assessed on corporations in the United States such as property and sales taxes,

the total could come close to, or even exceed, 50 percent of profits in some cases. Thus, up to half

of corporate profits are skimmed off the top by a party (government) that is not even a shareholder.

Some Moral Issues

The underlying assumption of many people who complain about the practice of shifting

profits to low-tax jurisdictions is that there is somehow something wrong or immoral about parking

profits in a foreign country, that there is something unpatriotic about it. Setting aside for a moment

8

the fact that patriotism is the last refuge of a scoundrel,7 if one examines this issue from the

perspective of wertfrei economics, the issue is a little more complex than what may at first appear.

One obvious point to be made is that corporate board members have a fiduciary duty to

their shareholders to safeguard the assets of the corporation. Earning profits in high-tax

jurisdictions tends to dissipate those assets to a greater extent than would be the case if those profits

were instead reported in a lower-tax jurisdiction. Thus, the argument could be made that the top

management of a corporation has a fiduciary duty to export profits if doing so is in the best interests

of the shareholders.

Robert Nozick,8 the eminent Harvard philosopher, took the position that the income tax is

the equivalent of slavery, since it robs the workers of the fruits of their labor. For example, in

substance it does not make much difference whether someone takes 40 percent of your income or

forces you to work for them two days a week. In both cases, you only get to keep 60 percent of the

fruits of your labor and you are someone’s slave two days a week.

It might be argued that the government provides services in exchange for these exactments,

and that there is therefore a moral duty to pay, but the same argument could be made for slave

owners. They provide food, shelter and clothing for their slaves, yet no one argues they have a

duty to work for the slave master. In many cases, government does not even provide services, at

least not for the individuals who have to pay the taxes. What is more likely is that the people who

do not pay taxes receive the benefits.

If there is any moral duty to pay taxes, that duty must be directly related to the extent of

services provided by the government that insists on skimming a portion of the corporation’s profits.

7 Samuel Johnson, April 7, 1775. http://www.samueljohnson.com/refuge.html. 8 ROBERT NOZICK, ANARCHY, STATE & UTOPIA. New York: Basic Books, 1974.

9

One might begin this conversation by asking, “What does the federal government do for the

average multinational corporation?”

It has been argued that the government provides services that corporations benefit from

using. Police and fire are two services that come to mind. However, most police and fire services

are provided by the local governments. In some communities, more than half of the police function

is performed by the private sector through security guards. Many fire departments are volunteer,

and thus are not a burden even on the local government. The argument that the federal government

is morally entitled to receive tax payments because it provides these services falls apart under this

analysis.

The infrastructure argument is another argument that has been used to justify corporate

income taxation at the federal level. However, most infrastructure is provided either by the state

and local governments or by the private sector. State and federal gasoline taxes pay for the roads.

Income taxes do not.

National defense is provided by the federal government. However, the extent to which this

expenditure benefits multinational corporations is questionable. One reason why U.S. citizens and

U.S. corporations feel threatened is because of the U.S. government’s aggressive and

interventionist foreign policy. Such a policy causes some people to hate Americans and American

corporations, making them more likely to be attacked. In the absence of such a foreign policy, the

need to defend the citizenry would be greatly reduced.9 It might also be pointed out that the federal

government does little or nothing to defend multinational corporations, especially the branches

located outside the United States. The federal government sometimes makes them targets, but does

little or nothing to defend them.

9 CHALMERS JOHNSON, BLOWBACK: THE COSTS AND CONSEQUENCES OF AMERICAN EMPIRE, 2nd edition, New York:

Macmillan/Holt, 2010; RON PAUL, A FOREIGN POLICY OF FREEDOM, Rosetta Books, 2010.

10

Table 3 provides a statistical summary of U.S. federal government spending.

Table 3

Federal Government Summary of

Spending (2014)10

Health care 27

Pensions 25

Defense 22

Welfare 11

Interest 6

Education 3

Transportation 3

Protection 1

General government 1

Other 1

Total 100%

It is questionable how much the federal health care system benefits multinational

corporations, especially the branches outside the United States. Even for those locations within the

United States it is questionable how much the federal health care system benefits them. The system

imposes costs, but the benefits are more difficult to assess.

Federal pension payments do not have any visible benefits for multinational corporations.

However, the pension system (Social Security) does impose costs on multinationals as well as on

all other businesses, even those in the nonprofit sector, since they have to pay more than 7 percent

of employee wages into the system, with no visible benefits.

The U.S. tax system taxes American citizens and U.S. corporations on their worldwide

income, which means that American citizens living and working in France and U.S. corporations

doing business in Germany have to pay taxes to support the federal welfare and pension schemes

that benefit people living in the United States, a policy that is inherently unfair. Multinational

corporate units located outside the United States do not benefit from these expenditures, and it is

10 http://www.usgovernmentspending.com/piechart_2014_US_fed. [accessed March 14, 2014]

11

questionable whether their domestic units benefit, either. Since that is the case, where can one find

a moral duty to pay corporate taxes to the U.S. government?

The point is that the federal government provides little in the way of services to

multinational corporations, although the myriad of federal regulations imposed on them does

increase their cost of doing business. According to one estimate, the cumulative cost of regulations

added between 1949 and 2011 has cost $38 trillion in terms of reduced economic growth.11

The current regulatory and tax system also places U.S. corporations at a competitive

disadvantage worldwide. Their costs of capital and other costs of doing business are higher than

would otherwise be the case, and the regulatory burden makes it more difficult to do business. Can

it be said that there is still a moral obligation to pay the corporate tax when the recipient of that tax

is doing more to you than for you?

TAX EVASION12

Authors have written about the abusive techniques of the Internal Revenue Service

(Burnham, 1989; Hansen, 1984). Others have written about how to protect yourself from the IRS

(Frankel & Fink, 1985; Kaplan, 1999; Wilson, 1980). Studies have been done of how tax dollars

are wasted or how the tax burden is excessive (DioGuardi, 1992; Fitzgerald & Lipson, 1984; Grace,

1984; Payne, 1993; Shlaes, 1999).

11 Kevin Glass, The $38 Trillion Cost of Regulation, June 26, 2013, Townhall.com

http://townhall.com/tipsheet/kevinglass/2013/06/26/the-38-trillion-cost-of-regulation-n1628668; John W. Dawson

and John J. Seater, Federal Regulation and Aggregate Economic Growth, Journal of Economic Growth 18: 137-177

(June, 2013). 12 Some of the material for this part was taken from Adriana M. Ross and Robert W. McGee. 2012. A Demographic

Study of Polish Attitudes toward Tax Evasion, Academy of Accounting and Financial Studies Journal 16(4): 1-40.

http://ssrn.com/abstract=2410020

12

There have been calls for tax reform because of the perception that the tax system is unfair,

but scholars and commentators cannot agree on what reforms should be made. Some authors call

for higher taxes or support the concept of a graduated tax that charges higher rates on the rich

(Johnston, 2003, 2007), while other studies dispute the efficacy of the graduated income tax (Blum

& Kalven, 1953). Some authors have called for the abolition of the income tax and its replacement

with a flat tax or a fair tax (Boortz & Linder, 2005; Champagne, 1994; Hall & Rabushka, 1985).

Others have called for an abolition of all coercive taxes and their replacement with a voluntary

system (Curry, 1982; Sabrin, 1995).

Numerous studies on various aspects of tax collection and tax evasion have been done over

the years. Richard Musgrave is perhaps the most famous theoretical researcher on this topic for

the last half of the twentieth century (Musgrave, 1959, 1986; Musgrave & Musgrave, 1976;

Musgrave & Peacock, 1958). He took a rather statist approach. His basic premise is that the state

is entitled to take more or less whatever it wants to take, at least in a functioning democracy. His

main focus was on how the government should extract taxes. He investigated issues of efficiency

and, although he also addressed fairness at times, his concept of what is fair could be challenged

by those who believe that the graduated income tax is either unfair or inefficient (Blum & Kalven,

1953).

James M. Buchanan, the 1986 Nobel Prize winner in economics, is far less statist in his

approach (Buchanan, 1967; Buchanan & Flowers, 1975). He recognizes, as did James Madison,

one of America’s founding fathers, that the state can get out of control at times, even in a

democracy, and that constitutional limits have to be placed on the legislature. Buchanan and

Musgrave (2001) co-authored a book that presented their two contrasting views on the relationship

between the individual and the state.

13

An examination of the philosophical literature on the ethics of tax evasion found that there

are three basic positions on the issue (McGee, 2006a). Tax evasion is never ethical, sometimes

ethical or always ethical. In terms of frequency, the most popular position in both the philosophical

and empirical literature is that tax evasion is sometimes ethical, although scholars cannot agree on

when tax evasion is ethical and when it is not.

It has been suggested that there may even be a positive duty to evade taxes, at least in some

cases (McGee, 2012). For example, where the state is evil or corrupt or engages in unjust wars

(McGee, 1994; Pennock, 1998), a case can be made that society’s best interests could be served

by evading taxes, because evil regimes would not be fed the tax funds they need to carry on their

evil activities.

Other instances where evasion might be a duty have also been suggested. For example, if

one takes the efficiency strain of utilitarian ethics, which holds that the only ethical act is the one

that is most efficient, a case can be made that keeping money in the more efficient private sector

meets that utilitarian test, because paying taxes shifts the funds to the less efficient government

sector (McGee, 2012).

Another case for advocating a duty to evade taxes is when doing so reduces the property

rights violations that take place in society (McGee, 2012). If one takes the Nozick (1974) position

that taxation is theft, a violation of property rights or a form of slavery, then one may reasonably

conclude that evasion reduces the amount of theft, property rights violations and slavery in society.

Perhaps the strongest argument to justify tax evasion would be the case of Jews living in

Nazi Germany. Surely if tax evasion were ever justified it would be in this case, since arguing that

Jews have a duty to pay taxes to Hitler is unthinkable, or at least so it would seem. Several surveys

have asked participants their opinions on the strength of various arguments that have been given

14

over the centuries to justify tax evasion and the strongest argument in support of the tax evasion

on moral grounds have often been the case of Jews paying taxes to Hitler. However, it was not

always perceived as the strongest argument to justify tax evasion. A survey of students in

Argentina ranked it in first place, tied with the ability to pay argument (McGee & Rossi, 2008).

However, in a survey of Australian students it did not even rank in the top six (McGee & Bose,

2009). The top six reasons to justify tax evasion in the Australian study were in cases where tax

rates were too high, where the tax system is perceived as being unfair, where a large portion of the

money collected is wasted, where the government discriminates against the taxpayer on the basis

of religion, race or ethnic background, where a significant portion of the money collected winds

up in the pockets of corrupt politicians or their families and friends, and where the government

imprisons people for their political opinions.

A survey of Orthodox Jewish students (McGee & Cohn, 2008) ranked the Jewish argument

first place in terms of justifiability out of 18 arguments justifying tax evasion, but even among

Jewish students it was perceived that there was some duty to pay taxes to Hitler, not because Hitler

was worthy of their tax money but because of the perception that there is a duty to God to pay

taxes and a duty to the Jewish community as well. There is a strain of thought within the Jewish

religious and philosophical literature that one must obey the law regardless of what the law might

be – “the law is the law.” The Jewish literature also teaches that one must never do anything to

disparage another Jew. Thus, if one Jew evades taxes it makes all other Jews look bad; therefore,

a Jew must never evade taxes. Another reason for paying taxes is that Jews are obligated to do

good works (mitzvos). Evading taxes might cause one to be imprisoned, where the possibility of

doing good works is greatly reduced. Therefore, a Jew must not evade taxes. (Cohn, 1998; Tamari,

1998; McGee & Cohn, 2008).

15

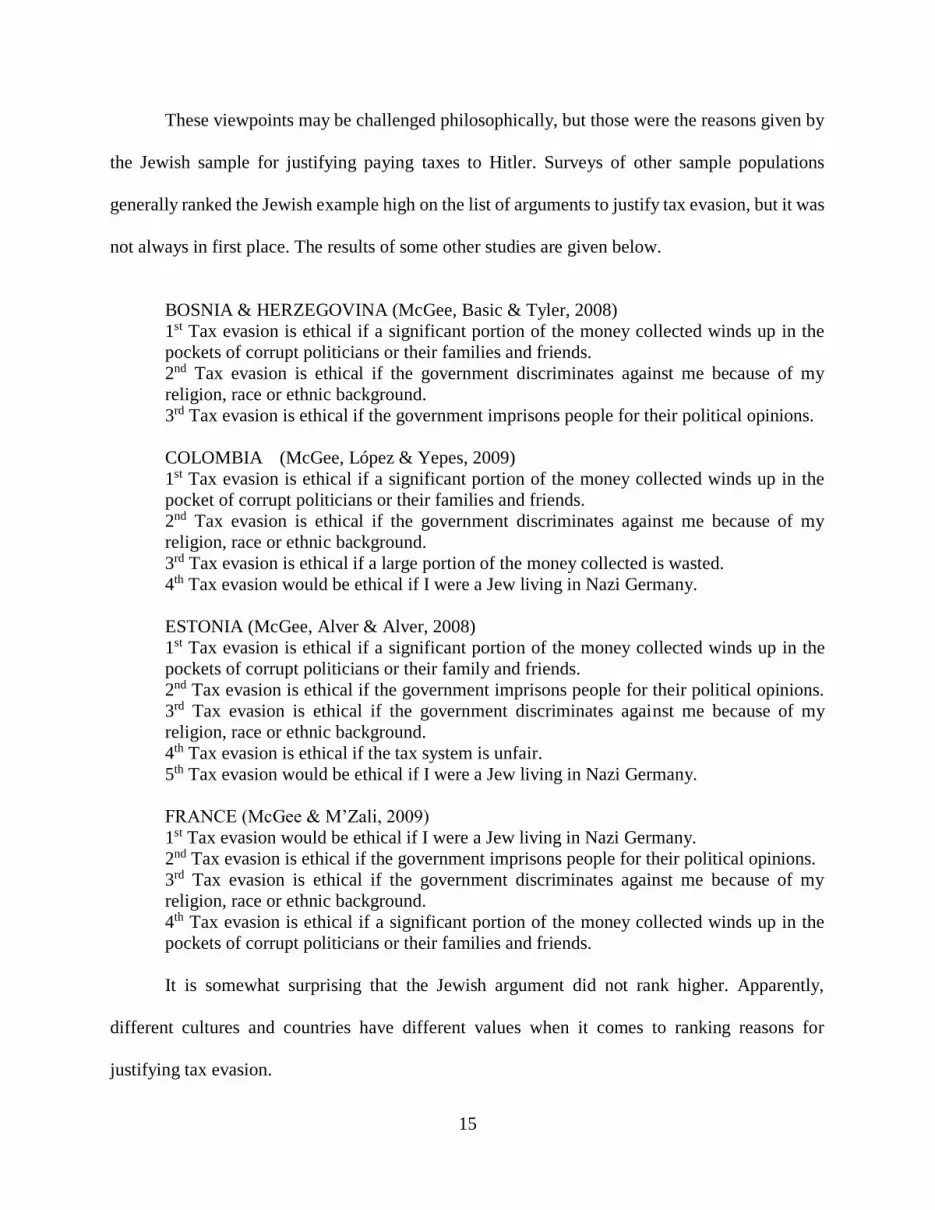

These viewpoints may be challenged philosophically, but those were the reasons given by

the Jewish sample for justifying paying taxes to Hitler. Surveys of other sample populations

generally ranked the Jewish example high on the list of arguments to justify tax evasion, but it was

not always in first place. The results of some other studies are given below.

BOSNIA & HERZEGOVINA (McGee, Basic & Tyler, 2008)

1st Tax evasion is ethical if a significant portion of the money collected winds up in the

pockets of corrupt politicians or their families and friends.

2nd Tax evasion is ethical if the government discriminates against me because of my

religion, race or ethnic background.

3rd Tax evasion is ethical if the government imprisons people for their political opinions.

COLOMBIA (McGee, López & Yepes, 2009)

1st Tax evasion is ethical if a significant portion of the money collected winds up in the

pocket of corrupt politicians or their families and friends.

2nd Tax evasion is ethical if the government discriminates against me because of my

religion, race or ethnic background.

3rd Tax evasion is ethical if a large portion of the money collected is wasted.

4th Tax evasion would be ethical if I were a Jew living in Nazi Germany.

ESTONIA (McGee, Alver & Alver, 2008)

1st Tax evasion is ethical if a significant portion of the money collected winds up in the

pockets of corrupt politicians or their family and friends.

2nd Tax evasion is ethical if the government imprisons people for their political opinions.

3rd Tax evasion is ethical if the government discriminates against me because of my

religion, race or ethnic background.

4th Tax evasion is ethical if the tax system is unfair.

5th Tax evasion would be ethical if I were a Jew living in Nazi Germany.

FRANCE (McGee & M’Zali, 2009)

1st Tax evasion would be ethical if I were a Jew living in Nazi Germany.

2nd Tax evasion is ethical if the government imprisons people for their political opinions.

3rd Tax evasion is ethical if the government discriminates against me because of my

religion, race or ethnic background.

4th Tax evasion is ethical if a significant portion of the money collected winds up in the

pockets of corrupt politicians or their families and friends.

It is somewhat surprising that the Jewish argument did not rank higher. Apparently,

different cultures and countries have different values when it comes to ranking reasons for

justifying tax evasion.

16

Several religious literatures address the issue of tax evasion. The religion that comes out

strongest against tax evasion is the Church of Jesus Christ of Latter-Day Saints (Mormons). There

is absolutely no excuse for tax evasion in their literature (Smith & Kimball, 1998). The religion

ranked in second place in terms of lack of support for tax evasion is the Baha’i faith. Its religious

literature would justify tax evasion only in cases where the government persecutes members of the

Baha’i faith (DeMoville, 1998).

Other religions are more mixed on the issue. The Jewish religious literature frowns on tax

evasion in general but does provide justification in some cases. Where a king usurps power or

where the laws are discriminatory or capricious the king may be disobeyed, including in the area

of tax laws (Tamari, 1998). There is no moral duty to pay taxes where a king forces himself onto

a country if the people do not accept him. There is no duty to pay taxes where the leadership or

government is not legitimate (Cohn 1998). In cases where evasion is not justifiable, tax evasion is

regarded as theft (Tamari, 1998).

Not much has been written on Muslim religious views regarding tax evasion. Murtuza and

Ghazanfar (1998) have discussed Zakat, the moral duty to provide for the poor, but they did not

address the ethics of tax evasion directly. Ahmad (1995) and Yusuf (1971) addressed the ethics of

tax evasion in their books on Islamic business ethics and economic justice. Their views basically

coincided. In fact, Ahmad cited Yusuf several times. According to these Muslim scholars, there is

no duty to pay customs duties, restrictive tariffs, court fees, revenue stamps, or any tax on income.

Their reason for opposing income taxation is because it curbs initiative and it assumes the

illegitimacy of the income of the rich. They suggest that the state should levy a proportional tax

along the lines of Zakat on accumulated wealth.

17

They were also against indirect taxation, since they believed all taxes should be direct.

There is no justification for the death tax. Any tax that causes prices to rise artificially is

illegitimate. Presumably, that would include sales and use taxes as well as tariffs and attempts to

fix prices. McGee (1997; 1998a&b) discussed the work of these two scholars from a non-Muslim

perspective.

Jalili (2012) wrote a response to these studies and presented a different view. According to

Jalili, in cases where the state is an Islamic state that follows Shariah law there is an absolute duty

to pay whatever taxes the legitimate rulers demand without question. Thus, income taxes, sales

taxes, death taxes, etc., are all legitimate and must be paid, provided one is paying to a legitimate

Islamic state. Where the state is not a pure Islamic state or where the state is not Islamic at all, the

ethics of paying taxes is less clear. Where the funds are spent on good deeds or the prevention of

bad deeds it seems like there is a duty to pay. Where the state violates Islamic law or engages in

bad deeds, it appears that there is no duty to pay. It may even be argued that there is a duty not to

pay, although Jalili does not go into this possibility.

The Christian literature (other than the Mormon literature, which has already been

discussed) is the most eclectic on the ethics of tax evasion. The most comprehensive treatise on

the duty to pay taxes from a Catholic perspective was a doctoral dissertation written by Martin

Crowe (1944). He reviewed 500 years of Catholic literature, some of it in Latin. There is no way

to summarize this body of literature briefly. Basically, one might attempt a summary by stating

that there is somewhat of a duty to pay just taxes and somewhat less of a duty to pay unjust taxes.

Payment may be forgiven where there is no ability to pay. It might be acceptable to evade taxes

imposed on the necessities of life in certain situations.

18

There is some Catholic literature to the effect that a person should pay taxes based on

benefits received. If the state confers no benefits on a particular taxpayer, there is no moral duty

to pay taxes (Crowe, 1944, pp. 24-25). There is some duty to government but that duty is not

absolute. Where tax funds are used to provide for the common good there is some duty to pay but

where they are not used for the common good there is no duty to pay, according to some Catholic

scholars.

Schansberg (1998) discusses the duty of paying unto Caesar what is Caesar’s but he does

not identify quite what Caesar is entitled to receive. Pennock (1998) discusses the issue of whether

there is a duty to pay taxes to a state that is engaging in an unjust war. Gronbacher (1998) discusses

Catholic social thought from the perspective of classical liberalism.

Several secular studies have been done on the ethics of tax evasion. Martinez (1994) wrote

a wide-ranging treatise, which cited an earlier article by McGee (1994). An edited book on the

ethics of tax evasion (McGee, 1998c) included several secular studies. Block (1989, 1993)

conducted studies of the public finance literature but could not find an adequate justification for

taxation, presumably because the authors of public finance texts begin with the assumption that

taxation is justified. Leiker (1998) discussed Rousseau’s view on taxation. Morales (1998)

discussed tax evasion from the viewpoint of Mexican workers and concluded that at times feeding

the family takes precedence over paying taxes.

Some empirical studies have been done on attitudes toward tax evasion. Alm, Martinez-

Vazquez and Torgler (2005) investigated Russian tax morale. Alm and Torgler (2006) discussed

cultural differences and tax morale in the United States and Europe. Torgler and Valev (2010)

examined public attitudes toward corruption and tax evasion from the perspective of gender.

19

A number of survey research studies have been done to discover student views on the ethics

of tax evasion. Surveys were completed for students in Armenia (McGee & Maranjyan, 2006),

China (McGee & Guo, 2007; McGee & An, 2008), Poland (McGee & Bernal, 2006), Puerto Rico

(McGee & López, 2007) and Romania (McGee, 2006b). In each of those studies, various

arguments that had been used in the past to justify tax evasion were ranked. In some cases,

comparisons were also made based on gender, age, academic major, student status to determine

whether those demographic variables made any difference. In some cases they did make a

difference and in other cases they did not make a difference.

BRIBERY13

Both the literature and business practice view bribery in negative terms, and with good

reason. Much of the bribery that occurs involves a one-way transfer, where the recipient of the

bribe does not give any value or render any service in exchange for the payment. Government

officials merely use their office to abuse their power and enrich themselves at the expense of those

who pay, as well as the general public.

The Organisation for Economic Cooperation and Development (2011) and others (Bonucci

& Moulette, 2007; Cuervo-Cazurra, 2006, 2008; Darrough, 2010; Moran, 1999; Pacini, Swingen

& Rogers, 2002; Scharf, 2008) have taken this position, which seems reasonable, in general.

Popular opinion suggests that bribery is always unethical. However, such a conclusion is

premature. Before one can arrive at the ethics of giving or accepting a bribe, one must apply ethical

13 Some of the material for this part was taken from Teresa Hernandez and Robert W. McGee. 2012. A Longitudinal

Study of French Attitudes on Accepting Bribes. Published in the Proceedings of the Allied Academies Summer

International Conference, July, 2012.

20

analysis. Doing so may not be easy, since several ethical systems have evolved over the centuries,

and the tools of ethical analysis they use are not identical.

Baron, Pettit and Slote (1997) discuss three ethical systems. Graham (2004) discusses

eight. The main ethical systems in use today include utilitarianism (Baron, Pettit & Slote, 1997;

Brandt, 1992; Frey, 1984; Goodin, 1995; Graham, 2004; McGee, 2012a), rights theory (Baron,

Pettit & Slote, 1997; Brandt, 1992; Frey, 1984; Graham, 2004; McGee, 2012a & c), virtue ethics

(Aristotle, 2002; Baron, Pettit & Slote, 1997; Graham 2004) and duty ethics (Baron, Pettit & Slote,

1997; Brandt, 1992; Graham, 2004; Kant, 1952, 1983). There is a lot of overlap between and

among these main ethical systems, and this paper will not explore their similarities and differences

in depth. However, we will discuss ethical principles from time to time, since any discussion of

bribery is incomplete without a mention of ethics.

The vast majority of economists are utilitarians, either all of the time or most of the time.

Many policy makers and legal scholars also embrace utilitarian ethics to a greater or lesser extent.

Thus, any discussion of ethics from an economic or legal perspective would be incomplete without

a discussion of utilitarian ethics.

There are several approaches to utilitarian ethics. Economists would conclude that an act

or policy is good if the result is a positive-sum game, which means there are more winners than

losers. Such an approach might be a good starting point for analysis. However, there are some

structural difficulties that must be overcome. For example, it is not always easy, or even possible,

to identify all the winners and losers.

Another problem is measurement. What if a few benefit a great deal, while the vast majority

lose just a little? How can one tell if the result is a positive-sum game? Another deficiency of

21

utilitarian ethics is that it totally ignores rights violations, or if it considers them, it lists them as a

negative in the utilitarian calculus.

One strand of utilitarian thought holds that an act or policy is ethical if the result is an

increase in efficiency. Richard Posner, the eminent legal scholar, is one proponent of this view

(Posner, 1983, 1998). The efficiency approach has its critics (McGee, 2012a), but we will not go

into the merits and demerits of the efficiency argument here.

The rights approach is another way to look at ethics. This approach basically holds that an

act or policy might be ethical if no one’s rights are violated, while violating one’s rights always

constitutes unethical conduct, even if the result is a positive-sum game, or even if the majority

benefits (McGee, 2012a, b & c).

Virtue ethics holds that a policy or act is ethical if the result is human flourishing (Aristotle,

2002; Baron, Pettit & Slote, 1997; Graham, 2004). Sometimes such a result is easier to see than at

other times.

Another approach is to look at duty (Kant, 1952, 1983). If one has a duty to perform or not

perform and one does not do one’s duty, one is acting unethically. This approach is used to

determine whether the agent is acting in the principal’s best interest, for example.

One may justify bribing a prison guard to release a political prisoner (Roy & Singer, 2006),

if the prisoner is being kept by a corrupt or evil regime. The fact that the guard (agent) is working

against the interest of the employer (government) can be disregarded in such cases. Bribing guards

to pass along food or medicine to a prisoner might also be considered an ethical act. Thus, one

cannot say categorically that bribery always constitutes unethical conduct.

22

However, Logue (2005) takes the position that bribery is always unethical because it

violates absolute moral principles that cannot be compromised. He discussed the unfairness of

bribery, the inefficient allocation of resources it produces, and the violation of a divine paradigm.

Carson (1987) concluded that accepting a bribe is almost always unacceptable because it

violates an implicit or explicit duty associated with the role one is in. If breaking promises is prima

facie wrong, then bribery is wrong because it involves the breaking of a promise. However, he

makes exceptions in cases of conscripted soldiers, some prostitutes and those who are held as

virtual slaves.

Colombatto (2003) take the approach that corruption is a rational approach to institutional

failures. Houston (2007) examined whether corruption might expand a country’s economic activity

in some cases. For example, bribery might be used to circumvent a bad law or to lubricate

commerce when few other options are available. Bribery and other forms of corruption are

beneficial when they result in trade and productive investments that would not otherwise be

possible. He sees corruption as having a positive effect when it is a substitute for bad governance.

What about the case of bribing tax officials to reduce the tax liability? This act presents

some interesting ethical issues, especially in cases where there is no moral duty to pay the tax

anyway. Is it unethical to bribe a tax official in a case where there is no moral duty to pay the tax

in the first place?

In some cases, there may be a moral duty not to pay the tax. A popular example in the tax

evasion literature is the case where the tax funds collected will be used to prosecute an unjust war

(McGee, 2012). If there is a moral duty not to pay such a tax, could it be said that bribing a tax

official to reduce the tax burden constitutes an unethical act? An even more outrageous example

(one of my favorites, which I have used many times in my articles on tax evasion) is the case of a

23

Jew living in Nazi Germany evading taxes. If it is not unethical for a Jew living in Nazi Germany

to evade taxes, would it be unethical for that same Jew to bribe a tax official to reduce the tax that

is legally but not morally owed?

The acceptability of bribery sometimes has cultural dimensions (Armstrong, 1996; Getz &

Volkema, 2001). A study of a Korean company found that bribery was not unethical because it

served a higher utilitarian purpose (Aupperle & Camarata, 2007). Husted (1999) found that

corruption is correlated to per capita GNP, power distance, masculinity, and uncertainty avoidance.

Napal (2005) found that giving gifts to government officials in Mauritius was a normal way of

doing business. Sanyal and Samanta (2004) examined bribe indices for 19 countries and found that

factors such as per capita income, degree of economic freedom in the country, and cultural factors,

such as power distance and masculinity, and legal factors, such as accounting and tax treatment,

played a role in determining the acceptability of bribery. A few other studies have also used the

Hofstede approach to examine the bribery issue (Chen, Yasar & Rejesus, 2008; Sanchez, Gomez

& Wated, 2008).

Whether corruption and bribery enhance or reduce foreign direct investment (FDI) is

subject to debate. Several studies have concluded that bribery decreased FDI (Cuervo-Cazurra,

2006, 2008; Mauro, 1995), while Egger and Winner (2005) found that it enhances FDI. Egger and

Winner’s study of 73 developed and less developed countries found that corruption stimulates FDI,

which supports the view that corruption can be beneficial in circumventing regulatory and

administrative restrictions. Sanyal and Samanta (2010) found that bribery has a negative effect on

economic growth.

Weitzel and Berns (2006) examined 4979 cross-border and domestic takeovers and found

that host country corruption was negatively associated with target company premiums. They

24

concluded that local corruption does not constitute a significant market barrier to foreign investors,

but rather represents a discount on local takeover synergies.

Johnsen (2009, 2010) viewed bribery from a utilitarian perspective and concluded that

bribery sometimes has positive effects on the economy or on individuals or groups. One way of

looking at bribery from a utilitarian perspective is whether it involves a helping hand or a grabbing

hand. If the person on the receiving end of the bribe does nothing to help the payer, it is a grabbing

hand by someone who merely abuses his or her power. The result is a negative-sum game because

it does not involve a mutually beneficial exchange. However, when the bribe receiver performs

valuable services in exchange for the payment, it is a helping hand scenario, which can justify the

payment of the bribe on ethical grounds (Egger & Winner, 2005; Wong & Beckman, 1992).

A few prior studies have been made using the World Values data. A comparative study of

the USA, Brazil, Germany and China (Hernandez & McGee, 2012a) found that, although

opposition to bribery was strong in all four countries, the Brazilians were significantly less opposed

to bribery than were participants in the other three countries.

A comparative study of Argentina, Brazil and Colombia found that accepting a bribe was

least acceptable in Argentina and most acceptable in Brazil (Hernandez & McGee, 2012b). A third

study was conducted of Egyptian attitudes (Hernandez & McGee, 2012c).

WHISTLE BLOWERS

The morality of whistleblowing – A lot of people think that whistleblowers perform a

valuable function because they expose corruption. For example, Edward Snowden is viewed by

some as an American patriot because he blew the whistle on government officials who were

25

violating the U.S. Constitution on a regular and systematic basis. However, others think he was a

traitor because he weakened national security and revealed classified documents and state secrets.

How should we view the people who revealed the existence of offshore accounts, etc.? If

we begin with the premise that governments do not have a moral claim on 100% of a person’s

income, then it follows that some people who resort to offshore accounts to protect their property

from greedy, evil and/or corrupt governments are acting morally, and that those who place other

people’s property in jeopardy by revealing the existence and location of their assets and offshore

accounts are assisting in the violation of their property rights. In other words, just because someone

is hiding assets from some government does not automatically means they are acting unethically.

In some cases they are merely protecting their property from greedy or evil governments.

The bottom line is that we cannot say categorically that a whistleblower is always acting

morally or always acting immorally. It depends on the facts and circumstances. Whistleblowers

who violate someone’s rights are acting unethically. Those who do not violate anyone’s rights may

be acting ethically.

If we apply utilitarian ethics to the question of tax evasion, one might conclude that evading

taxes can be an ethical act if the result is to keep assets in the more productive private sector rather

than shifting those assets into the less productive public (government) sector. There is a strain of

thought within utilitarian ethics that the ethical outcome is the most efficient outcome (Posner,

1983, 1998). Since it is more efficient to keep assets in the private sector because the private sector

is more productive than the government sector, tax evasion is ethical (McGee, 2012). If one accepts

this premise, then whistleblowers who inhibit this evasion are acting unethically because they

facilitate the government’s efforts to confiscate private wealth, with the result that assets will be

26

transferred from the more efficient and productive private sector into the less productive and less

efficient government sector.

To the extent that the funds sitting offshore are the result of ill-gotten gains, the

whistleblowers have performed an ethical act – if ill-gotten gains are the result of bribery, etc. Tax

evasion is a different issue, because not all tax evasion is unethical, as has been pointed out

elsewhere.

CONCLUDING COMMENTS

It remains to be seen whether the John Doe who blew the whistle on activities that were

illegal was acting ethically or unethically. There is nothing ethically improper about exposing

government corruption, so exposing bribery would be considered ethical, and even praiseworthy

in cases where the bribery was of the greedy hand variety. However, where the bribery was of the

helping hand variety, the conclusion is less clear. In helping hand situations, both parties to the

transaction benefit. It is a mutually beneficial exchange. The fact that the transaction might be

illegal is irrelevant from an ethical perspective. As Martin Luther King used to say, everything

Hitler did was legal, and everything Gandhi did was illegal. Just because something is illegal does

not mean it is unethical, and vice versa.

If the John Doe happened to be an employee of the company from which the documents

were retrieved, he is probably guilty of a breach of fiduciary duty. He was expected to remain

silent, and he did not remain silent. However, the moral duty not to disclose information where

there is a fiduciary duty involved is less than absolute.

27

REFERENCES Adams, C. (1982). Fight, Flight and Fraud: The Story of Taxation. Curacao: Euro-Dutch

Publishers.

Adams, C. (1993). For Good or Evil: The Impact of Taxes on the Course of Civilization. London,

New York & Lanham: Madison Books.

Ahmad, M. (1995). Business Ethics in Islam. Islamabad, Pakistan: The International Institute of

Islamic Thought & The International Institute of Islamic Economics.

Akaah, I. P. (1989). Differences in Research Ethics Judgments between Male and Female

Marketing Professionals. Journal of Business Ethics, 8(5), 375-381.

Alm, J., J. Martinez-Vazquez & B. Torgler. (2005). Russian Tax Morale in the 1990s. Proceedings

of the 98th Annual Conference on Taxation of the National Tax Association, 287-292.

Aristotle (2002). Nichomachean Ethics. Oxford: Oxford University Press.

Armstrong, R. W. (1996). The relationship between culture and perception of ethical problems in

international marketing. Journal of Business Ethics 15(11): 1199-1208.

Aupperle, K. E. & Camarata, M. (2007). Searching for Cross-cultural, Moral and Ethical Reality:

A Case of Bribery in an International and Entrepreneurial Context. International Journal

of Organization Theory and Behavior 10(3): 333-349.

Babakus, E., T. B. Cornwell, V. Mitchell & B. Schlegelmilch (2004). Reactions to Unethical

Consumer Behavior across Six Countries. The Journal of Consumer Marketing 21(4/5):

254-263.

Barnett, J. H. & M. J. Karson. (1987). Personal Values and Business Decisions: An Exploratory

Investigation. Journal of Business Ethics, 6(5), 371-382.

Barnett, J. H. & M. J. Karson. (1989). Managers, Values, and Executive Decisions: An Exploration

of the Role of Gender, Career Stage, Organizational Level, Function, and the Importance

of Ethics, Relationships and Results in Managerial Decision-Making. Journal of Business

Ethics, 8(10), 747-771.

Baron, M.W., P. Pettit & M. Slote (1997). Three Methods of Ethics. Malden, MA & Oxford, UK:

Blackwell Publishing.

Beito, D.T. (1989). Taxpayers in Revolt: Tax Resistance during the Great Depression. Chapel Hill,

NC: University of North Carolina Press.

Betz, M., L. O’Connell & J. M. Shepard. (1989). Gender Differences in Proclivity for Unethical

Behavior. Journal of Business Ethics, 8(5), 321-324.

Block, W. (1989). The Justification of Taxation in the Public Finance Literature: A Critique.

Journal of Public Finance and Public Choice, 3, 141-158.

Block, W. (1993). Public Finance Texts Cannot Justify Government Taxation: A Critique.

Canadian Public Administration/Administration Publique du Canada, 36(2), 225-262,

reprinted in revised form under the title “The Justification for Taxation in the Economics

Literature” in Robert W. McGee (Ed.), The Ethics of Tax Evasion (pp. 36-88) The Dumont

Institute for Public Policy Research, Dumont, NJ, 1998.

Blum, W. J. & H. Kalven, Jr. (1953). The Uneasy Case for Progressive Taxation. Chicago &

London: University of Chicago Press.

Bonucci, N., & Moulette, P. (2007). The OECD Anti-Bribery Convention 10 years on. The

OECD Observer No. 264-265.

Boortz, N. & J. Linder (2005). The Fair Tax Book: Saying Goodbye to the Income Tax and the

I.R.S. New York: HarperCollins.

28

Brandt, R.B. (1992). Morality, Utilitarianism, and Rights. Cambridge, UK & New York:

Cambridge University Press.

Brown, B.S. & P. Choong (2005). An Investigation of Academic Dishonesty among Business

Students at Public and Private United States Universities. International Journal of

Management 22(2): 201-214.

Browning, J. & N. B. Zabriskie. (1983). How Ethical Are Industrial Buyers? Industrial Marketing

Management, 12(4), 219-224.

Buchanan, J.M. (1967). Public Finance in Democratic Process. Chapel Hill, NC: University of

North Carolina Press.

Buchanan, J.M. & M.R. Flowers. (1975). The Public Finances, 4th edition. Homewood, IL:

Richard D. Irwin, Inc.

Buchanan, J.M. & R.A. Musgrave. (2001). Public Finance and Public Choice: Two Contrasting

Visions of the State. Cambridge, MA & London. MIT Press.

Burnham, David (1989). A Law unto Itself: Power, Politics and the IRS. New York: Random

House.

Callan, Victor J. (1992). Predicting Ethical Values and Training Needs in Ethics. Journal of

Business Ethics, 11(10), 761-769.

Carson, T. L. (1987). Bribery and Implicit Agreements: A Reply to Philips. Journal of Business

Ethics 4, 249–251.

Champagne, Frank (1994). Cancel April 15th! The Plan for Painless Taxation. Mount Vernon,

WA: Veda Vangarde.

Chen, Y., Yasar, M., & Rejesus R. M. (2008). Factors Influencing the Incidence of Bribery

Payouts by Firms: A Cross-Country Analysis. Journal of Business Ethics 77: 231-244.

Cohn, G. (1998). The Jewish View on Paying Taxes. Journal of Accounting, Ethics & Public

Policy, 1(2), 109-120, reprinted in Robert W. McGee (Ed.), The Ethics of Tax Evasion (pp.

180-189). Dumont, NJ: The Dumont Institute for Public Policy Research, 1998.

Colombatto, E. (2003). Why is Corruption Tolerated? The Review of Austrian Economics 16(4):

363-379.

Cuervo-Cazurra, A. (2006). Who cares about corruption? Journal of International Business

Studies 37: 807-822.

Cuervo-Cazurra, A. (2008). The effectiveness of laws against bribery abroad. Journal of

International Business Studies 39: 634-651.

Crowe, M. T. (1944). The Moral Obligation of Paying Just Taxes, The Catholic University of

America Studies in Sacred Theology No. 84.

Curry, B. (1982). Principles of Taxation of a Libertarian Society. Glendale, CA: BC Publishing

Company.

Darrough, M. N. (2010). The FCPA and the OECD Convention: Some Lessons from the U.S.

Experience. Journal of Business Ethics 93: 255–276.

Dawson, L. M. (1997). Ethical Differences between Men and Women in the Sales Profession.

Journal of Business Ethics, 16(11), 1143-1152.

DeMoville, W. (1998). The Ethics of Tax Evasion: A Baha’i Perspective. Journal of Accounting,

Ethics & Public Policy, 1(3), 356-368, reprinted in Robert W. McGee (Ed.), The Ethics of

Tax Evasion (pp. 230-240). Dumont, NJ: The Dumont Institute for Public Policy Research,

1998.

DioGuardi, J. J. (1992). Unaccountable Congress. Washington, DC: Regnery Gateway.

29

Egger, P., & Winner, H. (2005). Evidence on corruption as an incentive for foreign direct

investment. European Journal of Political Economy 21: 932-952.

Fitzgerald, R. & G. Lipson (1984). Pork Barrel: The Unexpurgated Grace Commission Story of

Congressional Profligacy. Washington, DC: Cato Institute.

Frankel, S. & R. S. Fink (1985). How to Defend Yourself against the IRS. New York: Simon &

Schuster.

Frey, R.G. (Ed.) (1984). Utility and Rights. Minneapolis: University of Minnesota Press.

Friedman, W. J., A. B. Robinson & B. L. Friedman. (1987). Sex Differences in Moral Judgments?

A Test of Gilligan’s Theory. Psychology of Women Quarterly, 11, 37-46.

Fritzsche, D. J. (1988). An Examination of Marketing Ethics: Role of the Decision Maker,

Consequences of the Decision, Management Position, and Sex of the Respondent. Journal

of Macromarketing, 8(2), 29-39.

Getz, K. A., & Volkema, R. J. (2001). Culture, Perceived Corruption, and Economics. Business

& Society 40(1): 7-30.

Glover, S. H., M. A. Bumpus, G. F. Sharp & G. A. Munchus. (2002). Gender Differences in Ethical

Decision Making. Women in Management Review, 17(5), 217-227.

Goodin, R.E. (1995). Utilitarianism as a Public Philosophy. Cambridge, UK: Cambridge

University Press.

Grace, J. P. (1984). Burning Money: The Waste of Your Tax Dollars. New York: Macmillan

Publishing Company.

Graham, G. (2004). Eight Methods of Ethics. London & New York: Routledge.

Gronbacher, G.M.A. 1998. Taxation: Catholic Social Thought and Classical Liberalism. Journal

of Accounting, Ethics & Public Policy, 1(1), 91-100, reprinted in Robert W. McGee (Ed.),

The Ethics of Tax Evasion (pp. 158-167). Dumont, NJ: The Dumont Institute for Public

Policy Research, Dumont, NJ, 1998.

Gupta, Ranjana & Robert W. McGee (2010). A Comparative Study of New Zealanders’ Opinion

on the Ethics of Tax Evasion: Students v. Accountants. New Zealand Journal of Taxation

Law and Policy 16(1): 47-84.

Hall, R.E. & A. Rabushka. (1985). The Flat Tax. Stanford: Hoover Institution Press.

Hansen, G. (1984). To Harass Our People: The IRS and Government Abuse of Power. Washington,

DC: Positive Publications.

Harris, J.R. (1989). Ethical Values and Decision Processes of Male and Female Business Students.

Journal of Education for Business, 8, 234-238, as cited in Galbraith & Stephenson (1993).

Harris, J. R. (1990). Ethical Values of Individuals at Different Levels in the Organizational

Hierarchy of a Single Firm. Journal of Business Ethics, 9(9), 741-750.

Hernandez, Teresa and Robert W. McGee (2012a). The Ethics of Accepting a Bribe: An

Empirical Study of Opinion in the USA, Brazil, Germany and China. Proceedings of the

International Academy of Business and Public Administration Disciplines 9(2): 817-836

(2012). Dallas, April 19-22, 2012.

Hernandez, Teresa and Robert W. McGee (2012b). Ethical Attitudes toward Taking a Bribe: A

Study of Three Latin American Countries. Proceedings of the International Academy of

Business and Public Administration Disciplines 9(2): 837-862 (2012). Dallas, April 19-22,

2012.

Hernandez, Teresa and Robert W. McGee (2012c). Egyptian Attitudes on Accepting Bribes.

Proceedings of the International Academy of Business and Public Administration

Disciplines 9(2): 863-884 (2012). Dallas, April 19-22, 2012.

30

Houston, D. A. (2007). Can Corruption Ever Improve an Economy? Cato Journal 27(3): 325-

342.

Husted, B. (1999). Wealth, Culture, and Corruption. Journal of International Business Studies

30(2): 339-359.

International Consortium of Investigative Journalists.

https://en.wikipedia.org/wiki/International_Consortium_of_Investigative_Journalists

Izraeli, D. (1988). Ethical Beliefs and Behavior among Managers: A Cross-Cultural Perspective.

Journal of Business Ethics, 7(4), 263-271.

Jalili, A. R. (2012). The Ethics of Tax Evasion: An Islamic Perspective. In Robert W. McGee

(Ed.), The Ethics of Tax Evasion in Theory and Practice (forthcoming). New York:

Springer.

Johnsen, D. B. (2009). The Ethics of “Commercial Bribery”: Integrative Social Contract Theory

Meets Transaction Cost Economics. Journal of Business Ethics. doi: 10.1007/s10551-

009-0323-6.

Johnsen, D. B. (2010). Mutual Funds. In Finance Ethics: Critical Issues in Theory and Practice.

John R. Boatright (ed.). Hoboken, New Jersey: John Wiley & Sons.

Johnston, D.C. (2003). Perfectly Legal: The Covert Campaign to Rig Our Tax System to Benefit

the Super Rich – and Cheat Everybody Else. New York: Penguin.

Johnston, D.C. (2007). Free Lunch: How the Wealthiest Americans Enrich Themselves at

Government Expense (and Stick You with the Bill). New York: Penguin.

Kant, I. (1952). Fundamental Principles of the Metaphysics of Morals. Great Books of the

Western World, Vol. 42 (pp. 251-287), Chicago: Encyclopedia Britannica.

Kant, I. (1983). Ethical Philosophy. J.W. Ellington, translator. Indianapolis & Cambridge:

Hackett Publishing Company.

Kaplan, M. (1999). What the IRS Doesn’t Want You to Know. New York: Villard.

Kidwell, J. M., R. E. Stevens & A. L. Bethke. (1987). Differences in Ethical Perceptions between

Male and Female Managers: Myth or Reality? Journal of Business Ethics, 6(6), 489-493.

Leiker, B. H. (1998). Rousseau and the Legitimacy of Tax Evasion. Journal of Accounting, Ethics

& Public Policy, 1(1), 45-57, reprinted in Robert W. McGee (Ed.), The Ethics of Tax

Evasion (pp. 89-101). Dumont, NJ: The Dumont Institute for Public Policy Research, 1998.

Logue, N. C. (2005). Cultural Relativism or Ethical Imperialism? Dealing with Bribery Across

Cultures. CBFA Conference.

Martinez, L. P. (1994). Taxes, Morals, and Legitimacy. Brigham Young University Law Review,

1994, 521-569.

Mauro, P. (1995). Corruption and Growth. The Quarterly Journal of Economics 110(3): 681-

712.

McDonald, G.M. & P.C. Kan (1997). Ethical Perceptions of Expatriate and Local Managers in

Hong Kong. Journal of Business Ethics 16(15): 1605-1623.

McGee, Robert W. (1994). Is Tax Evasion Unethical? University of Kansas Law Review, 42(2),

411-35. Reprinted at http://ssrn.com/abstract=74420 McGee, Robert W. (1997). The Ethics of Tax Evasion and Trade Protectionism from an Islamic

Perspective, Commentaries on Law & Public Policy, 1, 250-262. Reprinted at

http://ssrn.com/abstract=461397

McGee, Robert W. (1998a). The Ethics of Tax Evasion in Islam, in Robert W. McGee (Ed.), The

Ethics of Tax Evasion (pp. 214-219). Dumont, NJ: The Dumont Institute.

31

McGee, Robert W. (1998b). The Ethics of Tax Evasion in Islam: A Comment. Journal of

Accounting, Ethics & Public Policy, 1(2), 162-168, reprinted in Robert W. McGee (Ed.),

The Ethics of Tax Evasion (pp. 214-219). Dumont, NJ: The Dumont Institute for Public

Policy Research, 1998.

McGee, Robert W. (Ed.). (1998c). The Ethics of Tax Evasion. Dumont, NJ: The Dumont Institute

for Public Policy Research.

McGee, Robert W. (2006a). Three Views on the Ethics of Tax Evasion. Journal of Business Ethics,

67(1), 15-35. Reprinted at http://ssrn.com/abstract=841526

McGee, Robert W. (2006b). The Ethics of Tax Evasion: A Survey of Romanian Business Students

and Faculty. The ICFAI Journal of Public Finance, 4(2), 38-68. Reprinted in Robert W.

McGee & Galina G. Preobragenskaya, Accounting and Financial System Reform in

Eastern Europe and Asia (pp. 299-334). New York: Springer, 2006. Reprinted at

http://ssrn.com/abstract=813345 A Comparative Study of Romania and Bosnia may be

found at http://ssrn.com/abstract=1019252

McGee, Robert W. (2006c). A Survey of International Business Academics on the Ethics of Tax

Evasion. Journal of Accounting, Ethics & Public Policy, 6(3), 301-352. Reprinted at

http://ssrn.com/abstract=803964

McGee, Robert W. & A. Bernal (2006). The Ethics of Tax Evasion: A Survey of Business Students

in Poland. In Mina Baliamoune-Lutz, Alojzy Z. Nowak & Jeff Steagall (Eds.), Global

Economy -- How It Works (pp. 155-174). Warsaw: University of Warsaw & Jacksonville:

University of North Florida. Reprinted at http://ssrn.com/abstract=875434.

McGee, Robert W. & Tatyana Maranjyan (2006). Tax Evasion in Armenia: An Empirical Study.

Working Paper No. 06/10, Armenian International Policy Research Group, Washington,

DC. Reprinted at http://ssrn.com/abstract=869309

McGee, Robert W. & Zhiwen Guo (2007). A Survey of Law, Business and Philosophy Students

in China on the Ethics of Tax Evasion. Society and Business Review, 2(3), 299-315.

Reprinted at http://ssrn.com/abstract=869304

McGee, Robert W., Carlos Noronha & Michael Tyler (2007). The Ethics of Tax Evasion: a Survey

of Macau Opinion. Euro Asia Journal of Management, 17(2), 123-150. Reprinted in Robert

W. McGee (Ed.), Readings in Accounting Ethics (pp. 283-313), Hyderabad, India: ICFAI

University Press, 2009. Other studies of tax evasion in Macau may be found at

http://ssrn.com/abstract=1015882 and http://ssrn.com/abstract=890355

McGee, Robert W. & S. López Paláu (2007). The Ethics of Tax Evasion: Two Empirical Studies

of Puerto Rican Opinion. Journal of Applied Business and Economics, 7(3), 27-47. Reprinted in Robert W. McGee (Ed.), Readings in Accounting Ethics (pp. 314-342).

Hyderabad, India: ICFAI University Press, 2009. Reprinted at

http://ssrn.com/abstract=964048

McGee, Robert W., Jaan Alver & Lehte Alver (2008). The Ethics of Tax Evasion: A Survey of

Estonian Opinion, in Robert W. McGee (Ed.), Taxation and Public Finance in Transition

and Developing Economies (pp. 461-480). New York: Springer. Another study of tax

evasion opinion in Estonia may be found at http://ssrn.com/abstract=988506

McGee, Robert W. & Yuhua An (2008). A Survey of Chinese Business and Economics Students

on the Ethics of Tax Evasion, in Robert W. McGee (Ed.), Taxation and Public Finance in

Transition and Developing Economies (pp. 409-421). New York: Springer. Reprinted at

http://ssrn.com/abstract=869280

32

McGee, Robert W., Meliha Basic & Michael Tyler (2008). The Ethics of Tax Evasion: A

Comparative Study of Bosnian and Romanian Opinion, in Robert W. McGee (Ed.),

Taxation and Public Finance in Transition and Developing Economies (pp. 167-183). New

York: Springer. Reprinted at http://ssrn.com/abstract=1019252. Another study of Bosnian

opinion may be found at http://ssrn.com/abstract=899609

McGee, Robert W. & Y.Y. Butt (2008). An Empirical Study of Tax Evasion Ethics in Hong Kong.

Proceedings of the International Academy of Business and Public Administration

Disciplines (IABPAD), Dallas, April 24-27, 72-83. Reprinted at

http://ssrn.com/abstract=1131314

McGee, Robert W. & Gordon M. Cohn (2008). Jewish Perspectives on the Ethics of Tax Evasion.

Journal of Legal, Ethical and Regulatory Issues, 11(2), 1-32. Reprinted at

http://ssrn.com/abstract=929027 . Other studies on the Jewish perspective may be found at

http://ssrn.com/abstract=251469 and http://ssrn.com/abstract=461399

McGee, Robert W. & Cris Lingle (2008). The Ethics of Tax Evasion: A Survey of Guatemalan

Opinion, in Robert W. McGee (Ed.), Taxation and Public Finance in Transition and

Developing Economies (pp. 481-495). New York: Springer. Reprinted at

http://ssrn.com/abstract=813288. For a comparative study of Guatemala and the USA, see

http://ssrn.com/abstract=892323

McGee, Robert W. & Carlos Noronha (2008). The Ethics of Tax Evasion: A Comparative Study

of Guangzhou (Southern China) and Macau Opinions. Euro Asia Journal of Management,

18(2), 133-152. Reprinted at http://ssrn.com/abstract=1015882. For another study

involving Macau, see http://ssrn.com/abstract=890355

McGee, Robert W. & Galina G. Preobragenskaya (2008). A Study of Tax Evasion Ethics in

Kazakhstan, in Robert W. McGee, editor, Taxation and Public Finance in Transition and

Developing Economies (pp. 497-510). New York: Springer. Reprinted at

http://ssrn.com/abstract=1018513

McGee, Robert W. & M. J. Rossi (2008). A Survey of Argentina on the Ethics of Tax Evasion, in

Robert W. McGee (Ed.), Taxation and Public Finance in Transition and Developing

Economies (pp. 239-261). New York: Springer. Reprinted at

http://ssrn.com/abstract=875892

McGee, Robert W. & R. Tusan (2008). The Ethics of Tax Evasion: A Survey of Slovak Opinion,

in Robert W. McGee, editor, Taxation and Public Finance in Transition and Developing

Economies (pp. 575-601). New York: Springer. Reprinted at

http://ssrn.com/abstract=932990

McGee, Robert W. & Sanjoy Bose (2009). The Ethics of Tax Evasion: A Survey of Australian

Opinion, in Robert W. McGee, Readings in Business Ethics (pp. 143-166). Hyderabad,

India: ICFAI University Press. Reprinted at http://ssrn.com/abstract=979410. For a study

involving Australia, New Zealand and the USA, see http://ssrn.com/abstract=979408.

McGee, Robert W., S. López Paláu & G. A. Yepes Lopez (2009). The Ethics of Tax Evasion: An

Empirical Study of Colombian Opinion, in Robert W. McGee, Readings in Business Ethics

(pp. 167-184). Hyderabad, India: ICFAI University Press. Reprinted at

http://ssrn.com/abstract=973762

McGee, Robert W. & Bouchra M’Zali (2009). The Ethics of Tax Evasion: An Empirical Study of

French EMBA Students, in R.W. McGee, Readings in Business Ethics (pp. 185-199).

Hyderabad, India: ICFAI University Press. Reprinted at http://ssrn.com/abstract=956956

33

McGee, Robert W. & Serkan Benk (2011). The Ethics of Tax Evasion: A Study of Turkish Opinion.

Journal of Balkan & Near Eastern Studies 13(2): 249-262.

McGee, Robert W. Serkan Benk, H. Yildirim & M. Kayikçi (2011). The Ethics of Tax Evasion:

A Study of Turkish Tax Practitioner Opinion. European Journal of Social Sciences 18(3):

468-480.

McGee, Robert W. (Ed.) (2012). The Ethics of Tax Evasion in Theory and Practice. New York:

Springer.

McGee, Robert W. & Tatyana B. Maranjyan (2012). Attitudes toward Tax Evasion: An

Empirical Study of Florida Accounting Practitioners. In R.W. McGee (Ed.), The Ethics of

Tax Evasion: Perspectives in Theory and Practice (pp. 247-265). New York: Springer.

McGee, Robert W. (2012a). Property Rights v. Utilitarian Ethics. In C. Lütge (ed.), Handbook of

the Philosophical Foundations of Business Ethics. Dordrecht: Springer (2012), 1263-1274.

McGee, Robert W. (2012b). The Body as Property Doctrine. In C. Lütge (ed.), Handbook of the

Philosophical Foundations of Business Ethics. Dordrecht: Springer (2012), 1275-1304.

McGee, Robert W. (2012c). Property Rights v. Governments. In C. Lütge (ed.), Handbook of the

Philosophical Foundations of Business Ethics. Dordrecht: Springer (2012), 1305-1323.

McGee, Robert W. (Ed) (2012d). The Ethics of Tax Evasion: Perspectives in Theory and

Practice. New York: Springer.

McGee, Robert W. (2014). Some Thoughts on the Ethics of Parking Profits Offshore. Journal of

Accounting, Ethics & Public Policy 15(1): 165-174. http://ssrn.com/abstract=2410020

McGee, Robert W. (2016). The Panama Papers: A Discussion of Some Ethical Issues. Working

Paper (May 27). http://ssrn.com/abstract=2785954

Mocan, N. (2004). What Determines Corruption? International Evidence from Micro Data.

NBER Working Paper Series, No. 10460, Cambridge, MA.

Morales, A. (1998). Income Tax Compliance and Alternative Views of Ethics and Human Nature.

Journal of Accounting, Ethics & Public Policy, 1(3), 380-399, reprinted in Robert W.

McGee (Ed.), The Ethics of Tax Evasion (pp. 242-258). The Dumont Institute for Public

Policy Research: Dumont, NJ, 1998.

Moran, J. (1999). Bribery and Corruption: the OECD Convention on Combating the Bribery of

Foreign Public Officials in International Business Transactions. Business Ethics: A

European Review 8(3): 141-150.

Murtuza, A. & S.M. Ghazanfar (1998). Taxation as a Form of Worship: Exploring the Nature of

Zakat. Journal of Accounting, Ethics & Public Policy, 1(2), 134-161, reprinted in Robert

W. McGee (Ed.), The Ethics of Tax Evasion (pp. 190-212). The Dumont Institute for Public

Policy Research: Dumont, NJ, 1998.

Musgrave, R.A. (1959). The Theory of Public Finance: A Study in Public Economy. New York:

McGraw-Hill.

Musgrave, R.A. (1986). Public Finance in a Democratic Society. Volume II: Fiscal Doctrine,

Growth and Institutions. New York: New York University Press.

Musgrave, R.A. & P.B. Musgrave (1976). Public Finance in Theory and Practice, 2nd edition.

New York: McGraw-Hill.

Musgrave, R.A. & A.T. Peacock (Eds.) (1958). Classics in the Theory of Public Finance. London

& New York: Macmillan.

Napal, G. (2005). Is bribery a culturally acceptable practice in Mauritius? Business Ethics: A

European Review 14(3): 231-249.

34

Nasadyuk, Irina & Robert W. McGee (2007). The Ethics of Tax Evasion: Lessons for

Transitional Economies. In G.N. Gregoriou & C. Reed (Eds), International Taxation (pp.

291-310). Elsevier.

Nozick, R. (1974). Anarchy, State & Utopia. New York: Basic Books.

Organization for Economic Co-operation and Development. (2011). Convention on Combating

Bribery of Foreign Public Officials in International Business Transactions and Related

Documents (Paris: OECD).

Pacini, C., Swingen, J. A., & Rogers, H. (2002). The Role of the OECD and EU Conventions in

Combating Bribery of Foreign Public Officials. Journal of Business Ethics 37: 385–405.

Payne, J. L. (1993). Costly Returns: The Burdens of the U.S. Tax System. San Francisco: ICS Press.

Pennock, R. T. (1998). Death and Taxes: On the Justice of Conscientious War Tax Resistance.

Journal of Accounting, Ethics & Public Policy, 1(1), 58-76, reprinted in Robert W. McGee

(Ed.), The Ethics of Tax Evasion (pp. 124-142). Dumont, NJ: The Dumont Institute for

Public Policy Research (1998).

Posner, R.A. (1983). The Economics of Justice. Cambridge, MA: Harvard University Press.

Posner, R.A. (1998). Economic Analysis of Law, 5th ed. New York: Aspen Law & Business.