the new mobile wave - electronic payments international

TRANSCRIPT

•Sibos 2016: Transforming the landscape?

•SWIFT: Europe’s changing payment infrastructure

•Comment: combating professional fraud

•Surveys: New Zealand, South Korea, Ukraine

October 2016 Issue 352 www.electronicpaymentsinternational.com

The new mobile waveAre smartphones about

to make cards redundant?

EPI 352.indd 1 11/11/2016 12:32:10

Multichannel digital solutions for fi nancial services providers

To fi nd out more about us please visit:

www.intelligentenvironments.com

Intelligent Environments is an international provider of innovative mobile and online solutions for fi nancial services providers. Our mission is to enable our clients to always stay close to their own customers.

We do this through Interact®, our single software platform, which enables secure customer acquisition, engagement, transactions and servicing across any mobile and online channel and device. Today these are predominantly focused on smartphones, PCs and tablets. However Interact® will support other devices, if and when they become mainstream.

We provide a more viable option to internally developed technology, enabling our clients with a fast route to market whilst providing the expertise to manage the complexity of multiple channels, devices and operating systems. Interact® is a continuously evolving technology that ensures our clients keep pace with the fast moving digital landscape.

We are immensely proud of our achievements, in relation to our innovation, our thought leadership, our industrywide recognition, our demonstrable product differentiation, the diversity of our client base, and the calibre of our partners.

For many years we have been the digital heart of a diverse range of fi nancial services providers including Atom Bank, Generali Wealth Management, HRG, Ikano Retail Finance, Lloyds Banking Group and Think Money Group.

IE RBI final design.indd 1IE RBI final design.indd 1 05/05/2016 10:36:4105/05/2016 10:36:41

www.electronicpaymentsinternational.com October 2016 y 1

NEW

S

EDITOR’S LETTER

Financial News Publishing, 2012Registered in the UK No 6931627

ISSN 0956-5558Unauthorised photocopying is illegal. The

contents of this publication, either in whole or

part, may not be reproduced, stored in a data

retrieval system or transmitted by any form or

means, electronic, mechanical, photocopying,

recording or otherwise, without the prior

permission of the publishers

Editor: Anna MilneTel: +44 (0)207 406 6701Email: [email protected]

Group Editor: Douglas BlakeyTel: +44 (0)207 406 6523Email: [email protected]

Senior Reporter: Patrick BrusnahanTel: +44 (0)207 406 6526Email: [email protected]

Asia Editorial: Xiou Ann LimTel: +65 6383 4688Email: [email protected]

Group Publisher: Ameet PhadnisTel: +44 (0)207 406 6561Email: [email protected]

Sub-editor: Nick Midgley

Director of Events: Ray GiddingsTel: +44 (0)203 096 2585Email: [email protected]

Head of Subscriptions: Sharon HowleyTel: +44 (0)203 096 2636Email: [email protected]

Sales Executive: Harry HookerTel: +44 (0) 203 096 2622Email: [email protected]

Customer Services:Tel: +44 (0)203 096 2636 or +44 (0)203 096 2622Email: [email protected]

For more information on Timetric, visit our website at www.timetric.com. As a subscriber, you are automatically entitled to online access to Electronic Payments International. For more information, please telephone +44 (0)207 406 6536 or email [email protected]

London Office71-73 Carter Lane London EC4V 5EQ

Asia Office1 Finlayson Green, #09-01Singapore 049246Tel: +65 6383 4688Fax: +65 6383 5433Email: [email protected]

A few landmark events for elec-tronic payments have taken place over the last month. Firstly, and most probably least significantly,

every black cab in London now takes card payment- and they have scrapped the surcharge, instead adding 20p to the base fare. Hardly something that will put people off. Is it too little too late, in light of Uber’s storming success? I wouldn’t like to say.

At more or less the same time there was the world’s highest ever (probably) Apple Pay trans-action in the form of the remote purchase of a vintage car at British auctioneer Coys.

The first ever purchase of a classic car via social media using mobile app Vero for the sale of a 1964 Aston Martin DB5 for £825,000 ($1.01m) was completed by a buyer who made the pay-ment using Apple Pay.

Mobile payments are on the increase and will likely follow an upward trajectory for quite some time longer.

Recent research by Timetric suggests that mobile NFC payments will overtake contactless card transactions both in volume and value, although the latter won’t take much to beat, given the low value maximum limit on contactless card payments. See page 10 for a more comprehensive rundown on the contactless payments landscape, based on this research.

And further west, the US election result has come up trumps for bitcoin. Shortly after mid-

night Eastern Time, during electoral proceed-ings, the cryptocurrency climbed to $732, almost $120 more than the same time a month prior.

Speculation started the night before the elec-tion. If Clinton were to win, this was not expect-ed to have much effect on the value of bitcoin. A Trump win, however, would be a different story.

And true enough, as Trump garnered more and more votes, so the value of bitcoin rose in tandem, rising 3.4% in the two hours after mid-night on 9 November.

A similar spike occurred during Brexit, when bitcoin spiked 7%, resulting in a $100 increase in the price of bitcoin during one trading session. All this amid the pound taking a serious bashing.

In an interview for CoinDesk, a hedge fund manager dealing in bitcoin said a Trump presi-dency, despite being an “epic disaster” in most respects, would be “great for bitcoin”, adding, “in the fear and chaos bitcoin would be a defen-sive asset people could turn to”.

He wasn’t the only one. As a result of Brexit, many analysts had predicted a boost for bitcoin in the event of success for Donald Trump.

Other analysts suggested that even if there was a spike, it would be shortlived. Either way, any positive fluctuation would indicate that bitcoin is a go to measure for many to safeguard against economic uncertainty.<

ANNA MILNE, [email protected]

CONTENTSNEWS

3: NEWS DIGEST

FEATURE

6: SIBOS The theme for this year’s Sibos conference was ‘transforming the landscape’. Anna Milne reports back from Geneva

8: SWIFT With the ECB looking to merge the Target2 real-time gross settlement payment system with the T2S securities settlement mechanism, Anna Milne speaks to SWIFT at Sibos about its plans for 2017

10: CONTACTLESS The global contactless card transaction value will almost quadruple between 2016 and 2020. Why is contactless affecting the payments world with so much vigour? Patrick Brusnahan takes a closer look

SURVEY

13: NEW ZEALAND

14: SOUTH KOREA

15: UKRAINE

COMMENT

2: JOHN MARSDEN, EQUIFAX

16: RALF OHLHAUSEN, PPRO GROUP

EPI 352.indd 1 11/11/2016 12:32:12

www.electronicpaymentsinternational.com 2 y October 2016

COM

MEN

TEQUIFAX Electronic Payments InternationalElectronic Payments International

With some unwanted recent findings regarding fraud, as well as major breaches in cybersecurity, a stronger strategy towards security is needed now more than ever. John Marsden, head of ID and fraud at Equifax, gives an overview of the problem and offers critical advice for individuals and businesses

Recent ONS crime figures show bank-ing and credit fraud is up 13% in the year ending June 2016.

Companies have stepped up their fraud protection with multiple layered fraud defences, but this often moves criminal activ-ity to channels that are less well protected.

Fraud is a surprisingly professional indus-try. The number of cases continues to rise as criminals find new ways to access informa-tion, often fuelled by a deep understanding of their target’s identity. Underlying this is the sharing of knowledge and consumers’ personal information across dark web mar-ketplaces.

Consumers must take steps to protect themselves from falling prey to fraudulent behaviour. People are without doubt con-fused about where to store and share confi-dential information like their bank account number, sort code and even date of birth.

As consumers seek the convenience and speed offered by digital correspondence, they expose themselves to fraudsters who will steal this information to gain access to accounts and financially exploit individuals.

Data shared on the dark web cannot be treated as a one-time event; the data never truly vanishes and can spread glob-ally in a short amount of time, enabling criminals to fraudulently takeover accounts and identities.

To reduce the risks and damage associated with fraudulent activity, more needs to be done to educate the public and give them a stronger chance of protecting themselves.

The advice is very clear: remain vigilant, only share your details when you are sure the channel is secure, and keep the follow-ing guidelines in mind when handling your personal information:1. Do not do your online banking in public

places, and definitely do not use public Wi-Fi – criminals can set up bogus pub-lic Wi-Fi hotspots to access devices and information.

2. Never respond to unprompted banking messages unless you are absolutely certain the request is genuine, for example you have spoken with your bank to confirm.

3. Be very aware of domain names online

and the security signs visible in a brows-er. Make sure you log on to a banking website at a web address you know, not via a link.

4. Never provide any banking details to a third party you do not know or are unsure about – in part or as a whole.

5. Avoid unnecessarily sharing details such as your name, address and date of birth.

Fraud losses riseThe latest FFA UK report reveals a 25% year-on-year increase in financial fraud losses for the first half of 2016 to £399.5m.

Cyber and ID fraud dominate the fraud landscape, and online scams and attacks con-tinue to rise. E-commerce is growing, and is a tempting prospect for fraudsters looking to use identity and payment data such as credit and debit card information they have gained via the vast ‘carders’ markets’.

Fraudsters are sophisticated, and can easily gather information which can then be used to open accounts and make purchases online fraudulently. This situation is exacerbated by an increasing frequency of data breaches by hackers who can then sell this data on to other criminals.

In addition, a frightening number of con-sumers are also still being tricked into hand-ing over personal data. This usually occurs when a criminal is able to convince an indi-vidual that they are emailing or calling from a legitimate organisation and they need to verify their personal details. Using this infor-mation, criminal fraud networks can create high-quality ID data to sell via the dark web.

The financial services industry has to work together, educating consumers and sharing information to help collectively tackle this criminal activity.

The focus must be twofold. It is vital that any organisation holding personal data con-tinuously evolves the systems and processes in place to keep that information safe.

Equally, any business handling financial transactions has to take every possible step to ensure the customer they are dealing with is genuine.

It is clear that passwords alone are no longer enough, fraudsters are wise to our

thinking when we create a password, mak-ing them all too easy to crack. This is why businesses need to invest in new technology like biometrics and device recognition creat-ing multiple layers of defence.

The criminals do not stand still, and busi-nesses of all sizes need to work hard to stay ahead.

Stolen passwords and usernamesAround 500m Yahoo passwords and user-names have been stolen since 2014.

Passwords are continuing to topple like dominos, and the rate of major breaches is increasing at an alarming rate. The Yahoo breach is a super-sized domino that is going to have huge effects on people for years to come.

This is a game changer in the online fraud world; aside from Gmail being cracked, there is no other single event that could happen that will cause more fraud and damage over the next five years.

The breach has been a major blow to Yahoo, with personal details of around 0.5bn users now up for sale on the dark web. This information will spread quickly and globally, with no chance of recovery. There will be a long-lasting impact for consumers and busi-nesses as hackers attempt to use the breached data to access other online accounts.

We urge businesses to be on high alert for any customer contacting them from a Yahoo email address, as there is a high chance that their details have been comprised. One par-ticular area to watch are requests to reset passwords; sending a ‘click here to reset pass-word’ link to a Yahoo address is not advis-able given the size of the breach.

Passwords are no longer effective as a standalone measure, and companies must act sooner rather than later to improve their online security.

The normal advice of complex password, numbers and numerals no longer works in a world where there are now billions of cracked passwords; companies should instead introduce a second layer of authenti-cation processing, such as device recognition, to help build the necessary barriers to keep data safe.<

How to combat professional fraud

EPI 352.indd 2 11/11/2016 12:32:13

www.electronicpaymentsinternational.com October 2016 y 3

NEW

S

DIGESTElectronic Payments InternationalElectronic Payments International

STRATEGY

Visa appoints new CEOPayment giant Visa has named Alfred Kelly, Jr, a current Visa board member, as its new CEO.

Kelly will replace Charlie Scharf, who is resigning as CEO with effect from 1 Decem-ber 2016. Kelly is president and CEO of Intersection Co., and the former president of American Express (Amex).

According to the succession plan, Kelly will join the company on 31 October 2016 as CEO designate, while Scharf will act as an advisor to Kelly from 1 December 2016 for several months.

Visa independent chairman Robert Mats-chullat said: “Charlie has been a visionary CEO, highly successful by any set of metrics. He has helped transform Visa, the leading

global payments technology company, into a technology-driven digital commerce com-pany, and has led a strategy that will benefit this company for years to come.“The board of directors is extremely grate-

ful for Charlie’s leadership and wishes to thank him for his outstanding four-year tenure, which saw total shareholder return increase by more than 130%, outperform-ing both the overall stock market and our peer group.”

During his 23-year tenure at Amex Kelly assumed numerous management roles, including president of Amex and head of the global consumer and consumer card ser-vices groups. At present he is on the board of directors at MetLife. <

PAYMENTS

WorldRemit launches remittance service to Cameroon UK-based online money transfer service WorldRemit has partnered with financial company Express Union to launch its instant remittance service to Cameroon.

The deal will enable WorldRemit clients to transfer money instantly, to be picked up as cash at over 700 Express Union locations.

WorldRemit co-founder and executive director Catherine Wines said: “Adding hun-dreds of new cash pickup locations to our Cameroon corridor translates into improved service, better choice and more convenience for our customers and their families.

“WorldRemit remains committed to secure and instant money transfers, tapping into the unrivalled local knowledge and operational excellence of trusted partners like Express Union.”

Express Union general manager Charès Nghoguo added: “For Express Union – the number one money transfer company in Cameroon – the partnership with WorldRe-mit is geared towards providing an addi-tional means of connecting Cameroonian migrants to their relatives back in the coun-try, and local economic actors to foreign ones.

“By opening its 700 points of sale to the beneficiaries of WorldRemit transfers from abroad, Express Union is showing its civic commitment to solidarity, generosity, popu-lation welfare and Cameroonian develop-ment thanks to money transfers”.

According to the World Bank, Cameroon received $244m in remittances in 2015, more than double the amount in 2010.

In May this year WorldRemit partnered with UAE Exchange to expand its reach in Morocco, Uganda, Rwanda, Kenya and Zambia. <

PRODUCTS

Dion introduces instant bank solution Dion Global Solutions has launched a Real Time Payment Engine (RTPE) solution, which will enable banks to comply with new regulatory directives and also meet customer demands.

A modular payment hub, RTPE will sup-port processing of real-time payments and will allow banks to become compliant with new European regulation, European Pay-ment Services Directive, which becomes effective in 2018.

The multi-channel solution, according to the company, will allow banks to connect to customers via corporate, internet, mobile or branch banking.

The solution supports the ISO20022-based Common Global Implementation-Market Praxis standard for customer con-nectivity.

Developed on Dion’s SEPA Gateway solu-tion platform, RTPE’s architecture provides 24-hour availability that supports existing SEPA workflows as well as foreign currency and domestic payments.

Dion Global Solutions chief technology officer Andreas Wagner commented: “The PSD2 directive requires banks to rework the payment processing cycle and implement a far more efficient and quicker method.“Using Dion’s messaging technology,

X-Gen, our RTPE application is a real-time payment hub that will support banks to comply with the upcoming payment initia-tives.“We provide a cost-efficient solution, as

it embeds into the existing application and process landscape.“Due to its modularity customers can select

only what they really need to improve pro-cess efficiency.” <

STRATEGY

Alipay partners with payment platform Zapper in the UK Chinese online payment platform Alipay has collaborated with Zapper, a mobile pay-ments platform, to allow Chinese tourists visiting the UK to pay using the Alipay app at more than 1,000 locations in the country.

The partnership will enable over 450m Alipay users to pay for goods through the Alipay app at affiliated Zapper businesses in the UK, Europe and North America.

Alipay app consumers will be able to use mobile-based QR code technology in the country; nearly 85% of mobile payments in China are made using QR technology.

Alipay’s head of Europe, the Middle East and Africa, Rita Liu, said: “With Zapper as a partner, Alipay can further enhance our user experience as they can conveniently shop

outside of China and pay with Alipay.“Meanwhile merchants, in addition to the

Alipay payment solution, can better connect and understand hundreds of thousands Chi-nese tourists travelling in the UK.”

Zapper CEO of UK and Ireland Gerry Hooper said: “This is an incredibly exciting opportunity for us, pioneering the way by combining our synonymous QR code pay-ment technology.“This is a huge development, enabling Chi-

nese tourists to seamlessly continue using the highly popular Alipay app when travelling to the UK, and our partnered Zapper ven-ues to appeal more favourably to travelling Alipay users and stand out from the competi-tion.”<

EPI 352.indd 3 11/11/2016 12:32:13

www.electronicpaymentsinternational.com 4 y October 2016

NEW

SDIGEST Electronic Payments International

STRATEGY

Payment startup Affirm raises $100m from Morgan Stanley Affirm, the company started by PayPal co-founder Max Levchin, has obtained a $100m lending facility from financial services giant Morgan Stanley.

The financial technology company said it will use the facility to continue its expansion of consumer-friendly POS financing at lead-ing online and offline retailers.

Affirm offers consumers an alternative to traditional credit with a transparent loan product that enables consumers to pay for purchases over time.

Affirm shows customers upfront exactly

what they will owe, with no hidden fees or surprises.

Affirm also offers advanced technology and analytics that look beyond traditional FICO scores. Affirm currently has agree-ments with more than 750 merchants.

The fresh round of funding comes with the news that Affirm has tripled the volume of its loans in the last year.

Levchin co-founded PayPal with Peter Thiel, and was its chief technology officer for four years before it was bought by eBay in 2002. <

MOBILE

Apple Pay arrives to ANZ customers in New Zealand

ANZ Bank New Zealand has announced that customers with a Visa debit or personal ANZ Visa credit card can now use Apple Pay to make transactions in the country.

When a consumer adds a credit card to Apple Pay, the actual card numbers are not stored on the device or on Apple servers. Instead, a unique device account number is assigned, encrypted and securely stored in the secure element on the device.

In stores, Apple Pay works with Apple’s latest iPhones, including the iPhone SE, iPhone 6 and later, the iPad Pro, iPad Air 2, and iPad Mini 3 and later, and Apple Watch.

Customers will be able to use Apple Pay anywhere in New Zealand where contactless payments are available, such as BP, The Warehouse, Warehouse Stationery, Noel Leeming, Torpedo 7, McDonald’s, Domi-no’s Pizza and Burger King. They can also use Apple Pay to purchases online via apps and websites.

ANZ CEO New Zealand David Hisco said: “More than 50% of ANZ Visa trans-

actions are contactless, and this number is steadily increasing as more retailers adopt contactless technology.“Adding Apple Pay to our mobile payment

offering will make it fast and convenient for more customers to securely make everyday purchases wherever there is a contactless terminal.“Following on from our highly success-

ful goMoney mobile banking app, ANZ is pleased to continue leading the industry with innovative solutions for customers.”

ANZ New Zealand head of digital and transformation Liz Maguire said: “Our cus-tomers asked us for Apple Pay and we’re thrilled they can now use it, continuing our commitment to giving our customers innova-tive digital ways to do their banking.“We’re confident they will enjoy this easy,

simple and secure way to pay without having to present cards or cash.”

On 5 October 2016, Russia-based Sber-bank launched Apple Pay for its customers and MasterCard cardholders. <

SECURITY

UK financial fraud losses up 25% in first half Total financial fraud losses in the UK dur-ing the first half of 2016 increased by 25% to £399.5m ($490m) for payment cards, remote banking and cheques, according to new data issued by the Financial Fraud Action UK (FFA UK).

Losses on payment cards, including remote purchase fraud, lost and stolen cards, card-not-received, counterfeit card and card ID theft, grew by 31% to £321.5m, com-pared with £244.6m in the first half of 2015.

The FFA data shows that the prevented loss for cards stood at £475.7m.

Between January and June, remote pur-chase fraud increased by 31% to £224.1m, compared to £171.7m in the first half of 2015, the report said.

Banks’ security systems continued to pre-vent the majority of fraud from taking place, with prevented fraud totalling £678.7m, according to FFA UK. This is equivalent to £6 in every £10 of attempted fraud being stopped.

There was a small increase in remote banking losses, up from £66.2m in the first half of 2015 to £70.6m, with a prevented loss of £103.2m.

FFA UK director Katy Worobec com-mented: “Banks use a range of robust secu-rity systems to protect their customers, but as these systems become more sophisticated, criminals have increasingly been turning to scams and exploiting data breaches to con victims out of their personal and security information, as well as money.“Banks will continue to invest in advanced

verification methods, including biometric validation and dynamic card security codes.“We ask all consumers to be alert to

scammers, which is why we recently launched the Take Five campaign,” Worobec continued.“The industry takes its responsibility to

combat fraud extremely seriously, but banks cannot stop all fraud on their own. It is essential all organisations with a role to play work together to better protect individuals and companies.”

In an attempt to prevent future data breaches, the FFA UK has also requested all organisations that manage personal and financial data to improve their security sys-tems, and urged customers to beware of any unsolicited phone calls, text messages and emails. <

EPI 352.indd 4 11/11/2016 12:32:15

www.electronicpaymentsinternational.com October 2016 y 5

NEW

S

DIGESTElectronic Payments International

PAYMENTS

Seamless launches contactless payment feature in UK Swedish m-commerce software firm Seam-less has introduced a contactless payment feature for its Seqr mobile payment app in partnership with UK-based payment net-work GoCardless.

The contactless feature, called Tap & Pay, will allow Seqr customers to link bank accounts to the app and make payments directly from them.

According to Seamless, the UK is one of Europe’s most advanced markets for contactless payments, with nearly 500,000 terminals currently activated.

Seamless CEO Peter Fredell said: “The launch of these two new features represents a major leap forward for Seqr in terms of customer acquisition and payment accept-ance in the UK. At a global level, Seqr is

rapidly establishing itself as the standard way for customers to pay with their mobile, adding contactless payments and direct bank account linking the UK will cement this posi-tion further.”

Linking bank accounts is facilitated by GoCardless, whose partnership with Seam-less was announced in June. Tap & Pay is available to Android smartphone users.<

STRATEGY

Wells Fargo forms new payment division; shakes up management American banking giant Wells Fargo has cre-ated a new business division that will focus on payments, virtual solutions and innova-tion.

The Payments, Virtual Solutions and Inno-vation group will be headed by Avid Mod-jtabai, who is currently head of the bank’s consumer lending group.

Commenting on the move, Wells Fargo president and COO Tim Sloan said: “Creat-ing this new group will significantly enhance our ability to transform products, services and technologies to deliver simple, reliable and compelling new experiences for today’s and tomorrow’s customers.”

In conjunction with the creation of the new division, the bank also unveiled a raft of management changes.

Franklin Codel, currently head of home lending, will assume an expanded role that

includes dealer services, including indirect auto lending and commercial services, and personal lending, including direct auto, per-sonal lines and loans and student lending.

Perry Pelos, currently head of commercial banking services, has been named head of the banking wholesale banking division.

Codel, Pelos and Mary Mack, head of community banking, have also been added to the group’s Operating Committee.“There is nothing more important to our

leadership team than for our customers and clients to be proud of banking with us,” said Sloan.“I have huge confidence in our leadership

team, and believe these new appointments will enable us to manage our business and engage with customers and clients in compel-ling ways as we serve their varied and evolv-ing needs.”<

M&A

Euronet Worldwide completes YourCash Europe acquisitionElectronic payment provider Euronet World-wide has completed the acquisition of Your-Cash Europe, a UK-based ATM operator.

YourCash Europe operates around 5,000 cash machines in the UK, Netherlands, Bel-gium and Ireland.

The company, which processes millions of transactions every year while dispensing billions of pounds and euros to consumers via its European ATMs, generated revenues of around £29m ($35m) in 2015. The com-bined businesses will operate independent ATM networks in 21 European countries.

Euronet CEO – EFT Europe Nikos Foun-tas said: “YourCash has a management team that shares our vision of bringing financial

convenience to customers, and has a proven track record of delivering strong growth in new and existing markets.

“This is a great opportunity to leverage the benefits that each organisation brings to the partnership in order to expand Euronet’s ATM coverage across Europe, create addi-tional value for all of our customers, accel-erate revenue growth and achieve market synergies across the businesses.”

Jenny Campbell, CEO and principal shareholder of YourCash commented: “We are excited to join the Euronet family. After years of excellent organic growth and expan-sion into new markets, we are excited to be able to leverage Euronet’s global scale.”<

PAYMENTS

Vodafone and PayPal team up to enable UK contactless payments Vodafone has teamed up with payment giant PayPal to allow UK customers to make contactless payments through PayPal accounts with Android smartphones.

The partnership will enable PayPal users to link accounts to Vodafone Pay to make purchases at over 400,000 restaurants and shops that accept contactless payments.

Customers can also make payments on public transport in and around London where contactless and Oyster are accepted.

Customers can also make purchases of up to £30 ($36) at any contactless terminal using a phone integrated with a Vodafone NFC SIM. They can also use Vodafone Pay, a subsidiary of the Vodafone Wallet app, at retailers by using a PIN.

Customers can also add MasterCard bank credit and debit cards to Vodafone Pay.

Vodafone Pay can be used to make a pay-ment even when the phone is switched off or out of battery, because the terminal uses NFC technology embedded in the Vodafone SIM card.

Vodafone UK head of consumer services Kate Wright said: “Our customers told us that being able to use PayPal when making mobile payments was important to them so we’re delighted to now offer this on Vodafone Pay.

“The service also works with any Visa and MasterCard credit or debit card offering cus-tomers greater choice than any other mobile payment service.”

PayPal UK director of mobile commerce Rob Harper said: “Mobile payments have long been at the heart of what we do; this year marks 10 years since we first launched a mobile payment service in the UK.“As mobile technology continues to evolve,

we will continue to look at new ways to make it easier and faster for our customers to pay.” <

EPI 352.indd 5 11/11/2016 12:32:15

www.electronicpaymentsinternational.com 6 y October 2016

FEAT

URE

SIBOS Electronic Payments International

The theme for this year’s conference programme at Sibos in Geneva in late September was ‘transforming the landscape’. Anna Milne reports back with an essential overview of the main points made by key industry participants during the Payment Strategies for the Future panel discussion

Banks have two questions to ask themselves as they move into an open banking environment: where are they sourcing their products and

services, and how are they distributing them?Previously a bank would only produce and

develop its own products and services, and distribute them to its own customers.

Now they can bring in other providers’ offerings, and there are also platforms as well, providing interplay between products and services.

During the Payment Strategies for the Future panel at Sibos, the EBA Group out-lined some very real prospects for banks with regard to evolving in the emerging ‘open banking’ and PSD2 landscape.

“At EBA we have a four-point focus,” explained Vincent Brennan, head of group operations at Bank of Ireland and deputy chairman of the EBA Group.

The four points are:

• To produce more collateral to help members navigate the field

• To monitor development in the market• To use regulation and technology to

inform business model• To produce papers informing whether

the environment now is actually new, or whether it is a matter of pulling the strands of themes together from the last few years

Daniel Szmukler, MD at the EBA Group, said the EBA workgroups do not value block-chain in itself, but aim to evaluate use cases of how beneficial it would be to financial services, particularly in transaction banking.

They analysed possible use cases on inter-bank and intrabank transactions, but could not find much of a use case for interbank; it was, however, much more relevant to intra-bank, for example in cases where a parent company distributes among subsidiaries.

There is a whole raft of opportunities in

trade finance, because this area has a lot of paper-based processes, and stakeholders in different areas need information to proceed with the next stage.

The instant exchange of information there-fore makes a massive difference, and speeds things up tenfold; goods can be sent sooner once transactions are transparent.

A pertinent use case: a permissioned ledger There is a huge mountain to climb to trans-form this. How do you make it interoperable?

The view was that blockchain/DLT will not replace the entire legacy environment with something new unless a whole new environment is put in. It would just be tanta-mount to spending a whole lot of money just to do something in a different way.

Stakeholders need to build new value ser-vices to exploit the technology.

The role of a bank has always been to fill a gap, provide a service; this needs to evolve.

The two big questions for banks

www.privatebankerinternational.com

Don’t have online account details?

You and your associates may be entitled to online login credentials. The benefits of full online access are as follows:

• Timely daily news updates

• Access the latest analysis

• Monthly editions sent directly to your inbox

• News alerts direct to your inbox

• Comments from key industry influencers and leaders

• Search for specific, relevant content

• Access the archive

To create or activate your account please contact:

[email protected] touch briefings ad copy - CI 18042016.indd 1 18/04/2016 11:17:37

Sibos soundbitesBlockchain hype has died down somewhat, or rather the camps have become distinctly more polarised.

There are those who are happy to dismiss it outright, and those who proclaim its profundity in shaping the future.

It must be said, however, that there is a little more understanding around the different types of blockchain: permission/permissionless, mutable/immutable (thanks to Accenture’s curveball release last week), and so on.

IBM’s CEO Ginni Rometty said: “This will have profound impact on how the world works. Efficiency will be improved [to the tune of] over $100bn. Blockchain will do for transactions what the internet did for information.”

She was referring to IBM’s work on and with the Linux Foundation and Hyperledger, for which IBM has contributed significant amounts of code, open source, so anyone can work with it.

To summarise it differently: “IBM puts 38% of its revenue ($31bn) into helping clients become digital,” Rometty added.

Standards, standards, standardsIf one word echoed around the conference hall, it was standards.

Everybody is in agreement about the need to agree on a common standard in payments, so it is just a matter of time.

Segmentation of banksBanks need to figure out what they are best at and, based on this, decide who to partner with.

CBW Bank is coming to Europe, and had a “great week” drumming up business at Sibos. Watch this space.

IBM’s Rometty: “Very few will be able to keep up with our cloud development – the amount we invest.

“Banks need to make strategic decisions about partnership, for those segments they decide they will not and should not specialise in, and then focus on what they are good at.”

SWIFT’s gpi vs Ripple’s global payments steering group Despite fierce gossip to the contrary, Ripple has not been throwing down the gauntlet quite

as aggressively as it might have seemed.

It was only too keen to point out there will be a point in time, if it is not already here, where Ripple would be only too delighted to join forces with SWIFT, and possibly vice versa. They have market share and scalability respectively to be play for.

The futureIBM calls it Cognitive Business: digital today, cognitive tomorrow.

“It is more than machine learning,” said Rometty. Augmented intelligence, or, as futurologist Gerd Leonhard, speaking at the Innotribe arena, referred to it (in a human evolutionary way), exponential humanism.

Leonhard explained: “There will be a shift of value from selling commodities to creating experience. Airbnb doesn’t own property; Uber doesn’t own cars.

“The future of the financial industry is creating experiences – value trust and relationships, and having tech support it.”<

EPI 352.indd 6 11/11/2016 12:32:17

FEAT

URE

SIBOSElectronic Payments International

It might not be just based on transactions or account holding fees; the business model is intimately linked to the opportunity that technology can bring.

Thomas Egner, board member, CEO and CFO at EBA Group, said: “The point is to rethink the process and then seek to digit-ise, rather than give in to the temptation to digitise the process and then rethink the pro-cesses.

“There is not a common view on what open banking really means.”

Brennan added: “The topics now all require collaboration, even within the bank. Cards practitioners, channel, IT, products, they all need to coalesce, and it is intertwined with cybercrime and data. Banks have had to become very good at dealing with regulation – fintechs are not as good at this.

“KPMG research stated that 80% banks expected to be disintermediated by a third -party player.”

Szmukler said: “Who would have thought we would be sitting here today talking about cryptocurrencies six years ago? Such lingo would not have even been acceptable in a bank six years ago.

“We need to think outside the box, which is difficult in the day job when bound by the culture of the organisation in the day job. Culture comes into play – everything is pulled into play.

“Also, you cannot build everything your-self, otherwise you become a jack of all trades, master of none. The culture inherent in banks, however, is to own the process, end to end.”

Brennan added: “Firms once considered competitors are now potential partners and colleagues.”

This led to the question of whether it was possible to provide a clearer picture of how banking might evolve, in terms of rethink-ing the processes before digitising rather than vice versa.

“It is about everything: the pricing model, the strategy, the revenue strategy,” Brannan explained.

“For example, who is going to pay for instant payments? Are we going to introduce a flat fee? We cannot charge the customer for an instant payment, therefore something else has to give.

“Also you need to break it down in terms

of short, medium and longer term. In the short to medium term, banks are tied to complying with upcoming deadlines, tech standards and PSD2; that has to take prior-ity. Real change will not happen between now and 2018.

“There are multiple layers to this answer,” Brennan continued. “For our bank we have made life far too complicated for ourselves, and that is not disclosing sensitive informa-tion; we are not the only ones.

“Banks need to think out the journey in stages, need to take a view at product level, at channel level, etcetera.”

Egner continued: “At EBA Day there was a question put to bankers on PSD2 and whether it was a strategic or compliance proposition.

“The majority view was that it was com-pliance. Now you ask the same question and the answer is ‘strategic’; this between May and September.

“Something has changed and banks are realising they need to act and react, introduce an element of proactivity in response to regu-lation, from a strategic point of view, and not just trot out the requirements.” <

www.privatebankerinternational.com

Don’t have online account details?

You and your associates may be entitled to online login credentials. The benefits of full online access are as follows:

• Timely daily news updates

• Access the latest analysis

• Monthly editions sent directly to your inbox

• News alerts direct to your inbox

• Comments from key industry influencers and leaders

• Search for specific, relevant content

• Access the archive

To create or activate your account please contact:

[email protected] touch briefings ad copy - CI 18042016.indd 1 18/04/2016 11:17:37EPI 352.indd 7 11/11/2016 12:32:19

www.electronicpaymentsinternational.com 8 y October 2016

SIBOS Electronic Payments International

With the ECB telling Sibos that it is looking at merging the Target2 real-time gross settlement payment system with the T2S securities settlement mechanism, providing a single platform for cash and securities processing in the eurozone, Anna Milne speaks to SWIFT’s Carlo Palmers to get the gen on its plans for 2017

If the ECB’s proposed merger of Tar-get2 and T2S goes ahead, SWIFT stands to lose its status as sole pro-vider of the Target2 network, which

it has had since 2004 when the central bank selected SWIFT.

At the time it made sense for SWIFT to be the network provider as it already had a sys-tem in place, but it meant SWIFT employed its own proprietary solutions, differentiating it from the network-agnostic T2S, the single pan-European platform for securities settle-ment in central bank money.

The ECB now wants to consolidate the two systems in an open, agnostic solution, and is even looking at blockchain as a means by which to achieve this.

For now, SWIFT’s stance is clear: “We’re eagerly watching how the ECB study will evolve; how far will the ECB step into the European market, we really don’t know,” says Carlo Palmers, market infrastructures solution manager at SWIFT.

“For us it will be one of the potential cus-tomers we would be able to provide a solu-tion for, but we really don’t know and I’m not sure they know either, which is why they are studying it.”

SWIFT is currently working intensively on its Australia rollout, for which testing has

started. The system will be going live next year, after stress tests.

The SWIFT board said in June that any solution should be applicable across differ-ent communities.

Palmers explains that there are slight dif-ferences everywhere, so the board said to analyse differences and come up with a com-mon solution harmonising different sets of requirements for all parties.

If sufficient community support is gar-nered by June 2017, SWIFT will rebuild the Australian solution and build the standard-ised system. But what does Palmers expect thereafter?

“That depends on what community sup-port we achieve but, for example, we are closely following Europe, where there are lots of systems – Nets, Equens, EBA.

“In Hong Kong we are closely following the UK as it looks to revive Faster Payments and also anything not on CHAPS.

We will look at Canada later, after it has built its new payments platform.

“In the UK you have Bacs and ACH, so [it involves] looking at whether it makes sense to harmonise into one single solution for all retail payments. Who will build and operate, potentially bringing people together? The PSR is looking at this.”

SWIFT is also eagerly watching how the announcement Yves Mersch made pans out regarding the consolidation of the T2 and T2S platforms. How would this affect SWIFT?

T2 runs on SWIFT. The new system is likely to go multi-network so SWIFT would no longer have exclusivity, and the harmo-nised solution SWIFT would build for retail payments would also have to support ECB real-time payments.

“We need to see the development first to make sure we build the right thing,” adds Palmers.

Asked whether there is more uncertainty now than ever before, Palmers replies: “Last year we had uncertainty as to whether there would be real-time payments in Europe.

“Now we know for certain real-time pay-ments are going to happen, but the question is how it will happen,” he explains.

To what extent do the banks need to work together? As far as SWIFT is concerned, this is essential. Palmers worked in standards at SWIFT for many years, and drew compari-son with this.

“We need to bring the banks round the table to build a messaging standard. We need to get the operators round the table in the same way.”

The future of Europe’s payment infrastructure – an update

FEAT

URE

EPI 352.indd 8 11/11/2016 12:32:20

www.electronicpaymentsinternational.com October 2016 y 9

FEAT

URE

SIBOSElectronic Payments International

But how do you get everyone together? Do they not just sit and watch, and wait for the first movers?

“We have talked to a number of opera-tors this week and they are prepared to work together. It makes it easier for them; they have to do it.

“There is a necessity, definitely in the eurozone, for operators to be interoperable. Banks being connected to different operators need to be able to exchange the payment in seconds – it’s not up to the consumer.

We believe only a common solution can support that.”

So what, briefly, are the different systems and how do they differ?

“That’s the million-dollar question. That is the task at hand, to establish the differences. It is very detailed.

“Specifically in the eurozone, interoper-ability across currencies is a different story. A common settlement scheme has been agreed with the ECB. A scheme on service levels, SEPA credit transfer and now ECT SEPA Credit Transfer Inst. have also been agreed,” Palmers explains.

“All the details – including how quickly the payment will happen, how to reject it if need be, how to abort, how to decide if the payment is too slow, how to stop execution – all this has all been agreed, but technically

how this will be achieved between two oper-ators needs to be figured out.

“The UK, Denmark, Sweden and Australia do not need this, but across Europe we do.”

US market plansThe US is already working on instant pay-ments, and TCH has chosen VocaLink as the operator – using its own network, not relying on the SWIFT network.

SWIFT’s approach is to see if there is demand for a connecting platform for larger institutions.

“Our interface – AMH, for larger institu-tions – needs to be upgraded for real time, but we are seeing if there is demand for a connector to hook up to TCH,” explains Palmers.

“The other thing about AMH is that it is one thing to build a connector, but AMH is a multi-network interface not bound to the SWIFT network.

“Larger institutions in the US have said if they used AMH they would also use it in other communities with real-time systems, which is yet another reason for us to harmo-nise the communities to come up with the same real-time payments offer so all banks have the same connector, and therefore a similar experience when connecting to dif-ferent systems.

“Otherwise it’s very difficult for the bank each time they want to connect to a new or different real-time network because they have launched a full-scale project.”

On blockchainWe know, and Palmers reiterates, that SWIFT is looking into blockchain, however he remains sceptical as to its current potential capacity for real-time retail payments.

“It doesn’t seem to be ready yet today to step into the real-time retail market for high-volume, low-latency, high-capacity traffic; it does not seem ready to handle this yet.

“Maybe in the future, but other areas, such as trade finance and correspondent banking, are areas where blockchain is more appropri-ate right now than real-time payments.

“It’s good in those areas because you dis-tribute the proof of the data, but in real time, because of the speed it requires, it doesn’t seem to be the right solution at the moment.”

If someone said the SWIFT network was old-fashioned, how would Palmers respond?

“Speak to Wim Raymaekers! I didn’t think anyone holding real-time payment systems in the retail space was looking at Ripple; only once they go cross-border, cross-currency do they look at Ripple.”

Common standardOne of SWIFT’s goals is standardisation in the financial services industry.

“It has always been, and we’ll do every-thing we can to achieve that.

“Members don’t want to kick off big pro-jects from scratch for every community they want to connect to each time they want to connect to a new real-time system,” Palmers explains.

“The challenge now is there is no time to do conversions; before there was time when systems were off, for example at night.

“Everyone now seems to agree on ISO 20022 as a common payments standard, but next come different protocols such as for security and tech, and if these are not har-monised the end consumer standing in the shop wanting to pay on their mobile won’t be able to do so in real time.”

So who is doing what and where? Palmers explains that Belgium has issued a request for proposals and is choosing a system that will serve the Belgian market.

In the Netherlands each bank is choosing its own operator, already assuming that these operators will be able to work together.

“Otherwise you will never be able to do a five-second payment in the Netherlands.

“The ECB is saying you should not look at this domestically; you need to look at it eurozone-wide. They don’t like the fact they are all choosing their own solution.” <

Anatomy of an instant payment

The key points of the Single Euro Payments Area (SEPA) Instant Credit Transfer (SCT Inst.) scheme are as follows:

• SEPA Inst. will cover the largest area in the world for an interoperable instant payments scheme.

• The EBC has set a maximum time of 20 seconds for a real-time payment. An additional five seconds can be applied for a reply to come back.

• A maximum still needs to be set, but SLAs will expect much faster figures – this is up to individual banks and operators.

• 99.999% of payments will be expected to be completed within two to four seconds.

• In Australia it was agreed that 99% of payments have to be made within one second, and 90% in five seconds; beyond 10 seconds the payment is aborted.<

EPI 352.indd 9 11/11/2016 12:32:23

www.electronicpaymentsinternational.com 10 y October 2016

CONTACTLESS Electronic Payments InternationalFEAT

URE

In the mid-term, contactless cards are set to dominate the global contactless payment environment, according to a recent report from Timetric.

However, smartphone penetration is destined to increase, causing mobile NFC capability becoming more widespread, pos-sibly leading to mobile NFC overtaking contactless card payments.

A number of European countries, as well as Australia and Canada, are outpacing the rest of the world in terms of adoption of contactless; these countries currently account for most of the world’s contactless payment activity.

Europe is also ahead of the US in terms of contactless adoption. According to MasterCard, contactless transactions in Europe grew by 150% in 2015 from the pre-vious year.

Global demand for NFC acceptance is accelerating, and in May 2016 Visa Europe reported 3bn contactless transactions on both cards and mobile devices. In addition, one in five in-store Visa-processed card pay-ments were contactless during the 12 months to April 2016.

Visa reported 165m contactless cards in circulation and 3.2m NFC-enabled POS terminals in Europe, and has mandated that all Visa-accepting POS terminals should be NFC-enabled by 2020.

Contactless payments have become commonplace in the UK. The number of

contactless card transactions in the UK rose by 212.2% year on year in January 2016.

The number of bank-owned contactless POS terminals in the UK reached 309,706 in December 2015, representing roughly 17.8% of the overall number of POS terminals.

As of May 2016, there were a total of 460,000 contactless POS terminals in the country, equivalent to a 50% annual increase.

Contactless card shipments more than trebled between 2012 and 2015, indicating a rapid increase in the global adoption of contactless card payments.

History and progressContactless has certainly come a long way from its origins. The first incarnation of contactless was launched in the US in 1997 through Speedpass. Introduced by Exxon and Mobil, it was a key chain powered by Radio Frequency Identification (RFID).

Technological advances, the shift from cash to electronic payments, media attention and an evolving retail environment have all contributed to the rise of contactless from its humble beginnings.

However, in terms of use case, mass public transport has proven to be a crucial catalyst

Contactless mobile makes waves

The global contactless card transaction value will almost quadruple between 2016 and 2020, while the global mobile NFC transaction value will grow more than fivefold, Timetric’s latest research reveals. What are the factors contributing to this change? Patrick Brusnahan takes a closer look

n EMV CARDS AS A PROPORTION OF TOTAL CARDS IN THE US, 2012-2016

0

10

20

30

40

50

20122013

20152016E

2014

%

Source: Timetric

n EMV/NFC CAPABLE-POS TERMINALS IN THE US (MILLION), 2012-2016

0

1

2

3

4

5

6

7

8

20122013

20152016E

2014

m

Source: Timetric

EPI 352.indd 10 11/11/2016 12:32:28

www.electronicpaymentsinternational.com October 2016 y 11

FEAT

URE

CONTACTLESSElectronic Payments International

for adoption wherever it has been imple-mented.

EMV migration is another key driver. Mer-chants, PSPs and schemes can take advan-tage of a mandated upgrade to terminals by matching it with an upgrade to NFC-capable terminals. In many cases, the shift from EMV to contactless is a simple software upgrade.

As a default, many major POS terminal manufacturers such as VeriFone and Ingen-ico are integrating contactless technology in all newly distributed EMV POS terminals.

The smartphone factor Smartphones are another crucial factor. According to the Ericsson Mobility Report 2016, there are more than 3.2bn smartphone subscriptions worldwide, equivalent to around half of the world’s total population; the figure is expected to reach 6.3bn in 2021.

Following the adoption of smartphones was the launch of the ‘Pays’, Apple Pay, Sam-sung Pay, and Android Pay.

The entry of payment solutions from some of the world’s most valuable brands, includ-ing the ‘Pays’, instantly raised consumer awareness of new payment technology.

The decision by Apple – seen by Forbes as the world’s most valuable brand – to adopt

contactless was a huge boost. The attention gathered by anything launched by Apple is huge, and Apple Pay directed a huge spot-light onto contactless.

The USContactless cards may have missed their golden opportunity in the US. Due to a lack of migration of cards to EMV in the US, mobile payments have picked up the slack.

Main players in the US payments indus-try are focusing on mobile NFC payments. This could lead to the region going straight to mobile NFC payments, leapfrogging contactless cards.

Acquirers and card schemes have taken various initiatives to expedite the migra-tion process and support merchants. For example, to promote EMV adoption among merchants, schemes announced that if more than 75% of merchants’ Visa or MasterCard transactions originated from EMV-compliant POS terminals which support both contact and contactless, they may apply for relief of PCI audit requirements.

Many want an accelerated rate of NFC acceptance expansion. Bundled deals are being offered by POS vendors and acquirers so merchants can simultaneously upgrade terminals to EMV and NFC.

As a result of the US EMV liability shift in October 2015, EMV adoption rates grew from 7.7% in 2014 to 42.3% in 2015.

What is stopping contactless cards?Companies such as Ingenico and VeriFone have already distributed thousands of EMV-enabled POS terminals in the US, the major-ity of which are equipped with contactless technology.

Merchants can also benefit by making a single investment that would result in the delivery of combined EMV and NFC pay-ments. Also, as consumers increasingly make payments using mobile wallets, merchants could actually lose customers if mobile-based contactless options are not available.

As a result, banks and issuers are not push-ing contactless cards to customers; instead, they are promoting NFC-enabled mobile payments.

The price of NFC chips is offputting for banks. In addition, the huge level of mar-keting from mobile players highlighting NFC solutions has eclipsed campaigns for contactless cards; there is little incentive for banks to roll out contactless EMV cards.

More work also needs to be done with pub-lic transit systems to push contactless cards, but with so many different state systems and a general cultural preference for driving over public transport in most US states, there has not been a push for contactless cards.

However, mobile NFC has taken the initia-tive once again. In a recent announcement, the Metropolitan Transport Authority of New York launched a mobile ticketing app, eTix, enabling commuters to use smart-phones to buy tickets and board transit on certain routes on the system. Apple Pay and MasterCard were recently added to the app.

This is likely to accelerate growth in mobile NBC, particularly if similar initiatives are taken up in the rest of the US.

In addition, from a merchant perspective, contactless was not a priority when upgrad-ing terminals ahead of the October 2015 lia-bility shift. This was attributed in part to the higher costs of hybrid EMV and contactless terminals.

Canada leads in North America

Contactless has quietly become a mainstream payment method in Canada.During 2015 contactless transactions in Canada grew by one percentage point a month on average to reach around 10% of total domestic card transactions at the end of the year.The Canadian government has been fully supporting this, which has helped contactless to gain traction.According to Visa, the average proportion of in-store contactless purchases rose from 12.1% in June 2014 to an estimated 25% in June 2015.MasterCard has also captured a significant market share, with 27% of its in-store purchases in September 2015 being contactless.The launch of Apple Pay achieved a higher profile in Canada than in the US, and this only helped the contactless market to grow.<

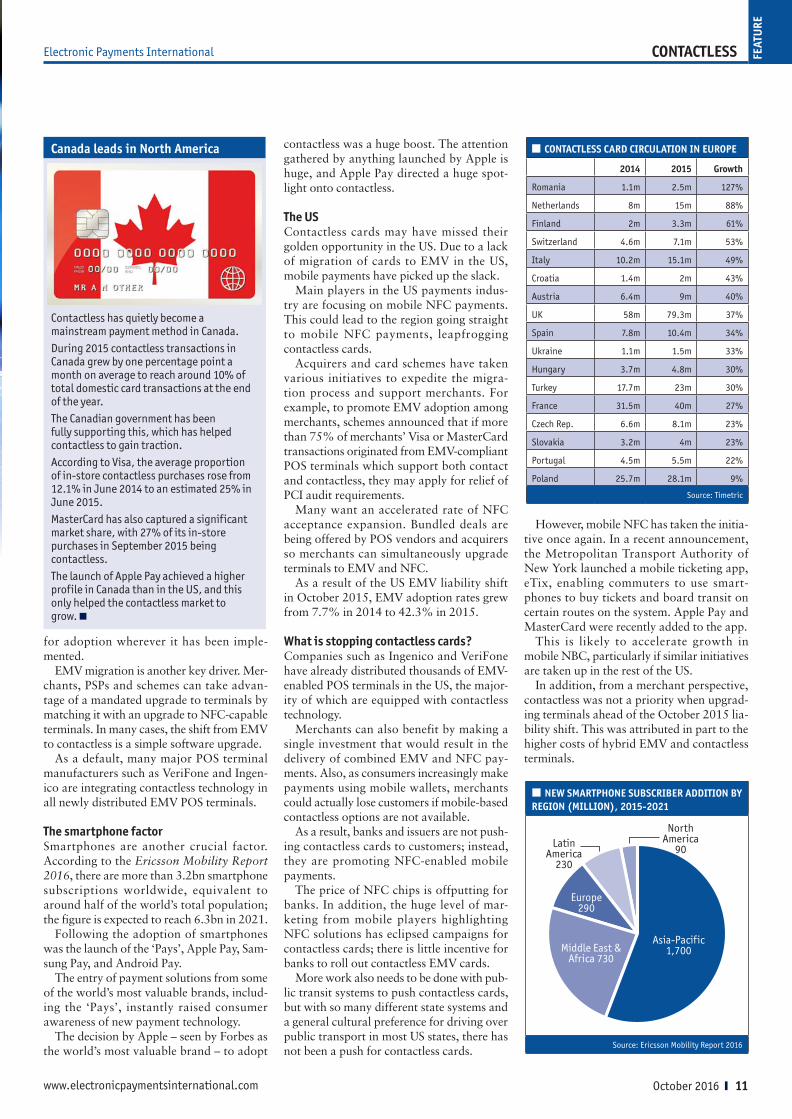

n CONTACTLESS CARD CIRCULATION IN EUROPE

2014 2015 Growth

Romania 1.1m 2.5m 127%

Netherlands 8m 15m 88%

Finland 2m 3.3m 61%

Switzerland 4.6m 7.1m 53%

Italy 10.2m 15.1m 49%

Croatia 1.4m 2m 43%

Austria 6.4m 9m 40%

UK 58m 79.3m 37%

Spain 7.8m 10.4m 34%

Ukraine 1.1m 1.5m 33%

Hungary 3.7m 4.8m 30%

Turkey 17.7m 23m 30%

France 31.5m 40m 27%

Czech Rep. 6.6m 8.1m 23%

Slovakia 3.2m 4m 23%

Portugal 4.5m 5.5m 22%

Poland 25.7m 28.1m 9%

Source: Timetric

n NEW SMARTPHONE SUBSCRIBER ADDITION BY REGION (MILLION), 2015-2021

Asia-Pacific1,700Middle East &

Africa 730

Europe290

LatinAmerica

230

NorthAmerica

90

Source: Ericsson Mobility Report 2016

EPI 352.indd 11 11/11/2016 12:32:31

www.electronicpaymentsinternational.com 12 y October 2016

FEAT

URE

The marketing and promotion of NFC via the ‘Pays’ has driven more merchants to focus on EMV and NFC device capabilities.

A fair amount of coverage has been given to the risks of contactless cards. Particularly given the ability for card skimmers to extract personalised card data from the contactless chip by walking near someone’s wallet with an RFID card reader.

This has caused much concern among

consumers and has likely driven banks and issuers away from contactless technology on plastic products. The heightened security of mobile NFC is still heavily advertised, and is expected to push consumers and issuers alike towards the solution.

Contactless payment cards have actually been available in the US since 2009. Unfor-tunately a lack of contactless-enabled POS terminals meant adoption was not high.

According to estimates, only around 2% of POS terminals were contactless-enabled in the US in 2013. However, with the launch of the ‘Pays’ from 2014, the proportion of ena-bled terminals has since increased to around 20%.

Brazil now ready for contactlessBrazil is no stranger to adopting payment systems into its infrastructure. Various multi-plank strategies to further increase contactless penetration and capture the unbanked population have been undertaken.

Banco Santander has issued more than 3m Santander University Smart cards with Gemalto, using MasterCard’s PayPass fea-tures. The cards include digital IDs to access university facilities, enable users to make low-value purchases for everyday needs, and offer discounts and other student services.

Due to high rates of robbery and theft in the country – Brazil ranks ninth in the world in terms of fear of crime – Brazilians prefer to not carry cash; secure transactions are there-fore a strong consumer preference.

In addition, Brazil is undergoing an eco-nomic recession and political upheaval, which may challenge payment companies already struggling with an unstable internet and contactless payment infrastructure in many areas.

Contactless was introduced in 2013 when banks started EMV migration with dual upgrades, making terminals simultaneously contactless-enabled.

As a result, NFC payments on mobile phones have entered the market. Banks and schemes, in conjunction with the Banco Central do Brasil have steadily introduced various payment products to gain market share.<

CONTACTLESS Electronic Payments International

Mexico and Banamex

Banamex, the Mexican arm of Citibank, first introduced contactless payments in 2012.

As part of the launch it upgraded 30,000 merchant terminals with VeriFone devices. The number of contactless terminals has since increased, reaching 70,000 in 2016.

In February 2016, Banamex and MasterCard, launched a new digital wallet in Mexico and developed a mobile contactless payment app for Android smartphones. Banamex was the first bank in Mexico to implement this technology.

Mexico was also the first country in which Citibank and MasterCard launched a digital wallet using HCE technology as part of their global digital payments initiative agreement. <

Brazilian potential

A number of factors mean the potential for contactless payments in Brazil is huge:

• Brazil has an unbanked population of more than 65m over the age of 15.

• Around 80% of the adult population use some type of card for 30% of all household expenditure, according to the Brazilian Association of Credit Card Companies.

• In 2015, Brazil had more than 2m contactless-enabled POS terminals.

• Around 15.3m smartphones were NFC-enabled in Brazil in 2015, representing 15% of total smartphones.

• Around 37% of Brazil’s 278m active mobile phones were smartphones in 2015. <

EPI 352.indd 12 11/11/2016 12:32:38

www.electronicpaymentsinternational.com October 2016 y 13

NEW ZEALANDElectronic Payments International

New Zealand’s cards and payments industry is well developed, and consumers are prolific users of payment cards.

The country had the highest frequency of use among its Asia-Pacific peers, with 116.2 transactions per card per year in 2015. It was followed by Australia (109.6), South Korea (63.3), Singapore (40.9), Hong Kong (28.0), Japan (13.4) and Taiwan (12.6).

New Zealand has the lowest cash use among OECD countries. According to a sur-vey by MasterCard in February 2016, 49% of participants expect cash payments to cease in the next 10 years. The country leads other OECD countries in terms of cashless payments, with four of every five payments made electronically.

Banks and payment companies are taking regular initiatives to improve financial litera-cy in New Zealand, leading to high banking penetration and driving demand for current accounts and debit cards. The share of New Zealanders aged 15 or above with a bank account reached 99.5% in 2014, according to the World Bank’s Global Findex survey.

Banks and non-bank companies drive growthConsumers in New Zealand have traditional-ly been debt-conscious, and are more inclined to use debit cards than pay later cards.

In terms of transaction value, debit cards accounted for 61.9% of the overall payment

card market in 2015. Debit card penetration in New Zealand is 238.3 cards per 100 indi-viduals, higher than Singapore (206.3), Aus-tralia (178.7) and Hong Kong (77.4).

In contrast, pay later card penetration remains low, at 57.1 cards per 100 individu-als, the lowest in the region.

To increase consumer uptake of pay later cards, banks offer various benefits such as balance-transfer services and low interest rates.

Bank of New Zealand offers the Low Rate MasterCard, providing an interest-free bal-ance transfer service for 12 months, and a standard rate thereafter. ANZ Bank’s Low Rate MasterCard charges annual interest of 13.90% on purchases, 22.95% on cash advances and 1.99% on balance transfers.

Non-banking companies are pushing for share in New Zealand’s pay later card mar-ket. Financial service provider Gem offers credit cards, personal loans, insurance and

interest-free and promotional retail finance, with pricing benefits such as low interest rates and reward programmes.

Gem Visa cardholders are offered 0% interest for the first six months on transac-tions above $250 (NZD357.4).

Focus on innovation to stay afloatWith the growing importance of self-service channels, banks in New Zealand are intro-ducing digital solutions to attract customers and remain competitive.

Westpac launched the Westpac One digi-tal banking platform in February 2015, which can be used on smartphones, tablets and desktops to apply for everyday banking products such as accounts, term deposits, home and personal loans, and credit cards.

The launch led to a 7% annual rise in the number of digital consumers, which reached 705,000 in September 2015. The bank also reported that more than half of its customers used digital channels, and 67% used mobile phones to connect with it in 2015.

ANZ Bank updated its FastPay mobile banking app in October 2015. FastPay was launched in October 2013, and allows busi-ness customers to process payments made through Visa, MasterCard and Eftpos using smartphones or tablets.

With ANZ FastPay, users can have more than one card reader, smartphone or tablet linked to a single business account. <

It has the lowest use of cash in the OECD and an almost fully banked population, and according to a survey in February nearly half of consumers expect cash transactions to die out within a decade. Timetric researchers recently took a closer look at the cards and payments industry in New Zealand

n NEW ZEALAND CARD TRANSACTION VALUE BY CHANNEL ($BN), 2011–2020

ATM POS

2011 13.4 48.7

2012 13.5 52.4

2013 13.3 56.0

2014 13.3 59.4

2015 10.9 52.6

2016 10.0 51.8

2017 9.8 54.3

2018 9.6 57.0

2019 9.4 59.7

2020 9.3 62.9

Source: Timetric

n NEW ZEALAND PAYMENT CARDS BY CARD TYPE (MILLION), 2011–2020

Debit Cards Pay Later Cards

2011 6.6 2.7

2015 11.0 2.6

2016 11.7 2.7

2020 13.5 2.9

Source: Payments New Zealand and Timetric

n NEW ZEALAND CARD TRANSACTION VOLUME BY CHANNEL (MILLION), 2011–2020

ATM POS

2011 112.2 1,197.2

2012 109.1 1,259.6

2013 103.4 1,330.1

2014 98.7 1,405.7

2015 94.6 1,489.9

2016 91.0 1,578.2

2017 87.9 1,667.7

2018 85.3 1,758.7

2019 83.1 1,851.4

2020 81.3 1,949.1

Source: Timetric

n NUMBER OF ATMS AND POS TERMINALS IN NEW ZEALAND (THOUSAND), 2011–2020

ATM POS

2011 2.7 136.1

2012 2.6 141.1

2013 2.6 144.0

2014 2.6 151.8

2015 2.5 158.5

2016 2.5 164.9

2017 2.5 171.0

2018 2.5 176.8

2019 2.4 182.0

2020 2.4 186.7

Source: Timetric

New Zealand on track for cashlessness

COU

NTR

YSU

RVEY

EPI 352.indd 13 11/11/2016 12:32:40

www.electronicpaymentsinternational.com 14 y October 2016

SOUTH KOREA Electronic Payments International

South Korea’s mobile payments boom

South Korea has long been a well-developed payment card market. Its consumers are among the most prolific users of payment cards in

the region, with a frequency of use of 63.3 per card per year – higher than Sin-gapore with 40.9, Hong Kong with 28.0, Japan with 13.4 and Taiwan with 12.6.

Between 2011 and 2015, South Korea’s payment card market changed rapidly, with the centre of innovation shifting from prod-ucts to channels and services.

Although issuers continue to develop new products, this tends to be little more than the fine-tuning and modification of exist-ing products. Strategies such as personalised card designs and segment-specific promo-tions and benefits were increasingly used in the past five years.

Telecoms and mobile push contactlessGrowth in contactless mobile payments (m-payment) is expected to accelerate in South Korea, as telecoms and mobile opera-tors promote the technology as part of efforts to improve the user experience and retain customers.

The companies are increasingly positioning themselves as competitors rather than part-ners to payment companies. Major handset manufacturers such as Samsung and LG, and telecom operators such as SK Telecom have all launched contactless payment solutions.

Samsung launched m-payment service Samsung Pay in South Korea in August 2015, and transactions worth $1bn (KRW1.2trn) have since been made. LG introduced the LG Pay contactless m-payment solution in November 2015, allowing users to make pay-ments using LG smartphones. SK Telecom launched contactless m-payment service T-Pay in March 2016, and has already reg-istered over 100,000 subscribers.

Regulations curb credit card issueThe South Korean credit card market was heavily affected by security concerns follow-ing leaks of customer data between 2011 and 2015. In January 2014, the FSS announced that the information of 20m credit card users had been stolen by a temporary employee at the Korea Credit Bureau.

In a separate incident in April 2014, the FSS announced that hackers had stolen the personal data of 200,000 credit card users,

using some to make fake cards to transact around $113,859. The regulator ordered all credit card companies to upgrade fraud detection to prevent similar data thefts.

The government also enforced stringent regulations to curb rising credit card debt and illicit marketing. Korean financial authorities and card issuers developed the Best Practices on Issuance of New Credit Cards and the Setting of Credit Lines in October 2012, limiting eligibility for new credit cards to adults with minimum credit ratings, and making it mandatory to consider the disposable income of a cardholder when establishing credit. Issuers are also required to periodically monitor cardholders’ statuses in this regard, to ensure compliance.

Growing e-commerce marketThe combined e-commerce transaction value in South Korea was $29.7bn in 2015, reg-istering a compound annual growth rate of 15.44% between 2011 and 2015.

E-commerce growth in the country pro-vides significant potential for payment cards, as it continues to be the preferred payment method among online shoppers. As a result, issuers are offering new card features with enhanced security measures.

KB Kookmin Card launched a virtual cred-it card scheme, SecurePay, in association with MasterCard in September 2014, protecting users against personal information theft. <

Frequency of card use has historically been high, but mobile payments are arguably the area where activity in South Korea is most intense, to the extent that many mobile manufacturers and telecoms companies now consider themselves to be direct competitors to payment companies

n SOUTH KOREAN CARD TRANSACTION VALUE BY CHANNEL ($BN), 2011–2020

ATM POS

2011 322.5 476.3

2012 326.0 506.7

2013 343.1 545.4

2014 374.4 598.9

2015 362.6 605.3

2016 350.0 611.9

2017 359.3 660.8

2018 365.5 708.6

2019 370.5 757.3

2020 374.5 805.5

Source: Timetric

n SOUTH KOREAN CARD TRANSACTION VOLUME BY CHANNEL (MILLION), 2011–2020

ATM POS

2011 692.8 8,365.0

2012 738.0 9,893.6

2013 761.9 11,477.7

2014 787.6 13,150.2

2015 801.7 15,107.2

2016 815.6 17,292.2

2017 829.5 19,660.2

2018 843.1 22,122.9

2019 856.3 24,578.6

2020 868.9 27,036.7

Source: Timetric

n NUMBER OF ATMS AND POS TERMINALS IN SOUTH KOREA (THOUSAND), 2011–2020

ATM POS

2011 118.5 2,195.0

2012 122.9 2,214.2

2013 124.2 2,225.8

2014 122.2 2,235.2

2015 121.7 2,243.5

2016 122.0 2,253.6

2017 122.7 2,265.6

2018 123.7 2,278.4

2019 124.9 2,291.2

2020 126.3 2,302.9

Source: Timetric

n SOUTH KOREAN PAYMENT CARDS BY CARD TYPE (MILLION), 2011–2020

Debit Cards Pay Later Cards

2011 141.5 122.1

2015 158.2 93.1

2016 162.2 94.6

2020 175.6 102.9

Source: Timetric

COU

NTR

YSU

RVEY

EPI 352.indd 14 11/11/2016 12:32:45

www.electronicpaymentsinternational.com October 2016 y 15

UKRAINEElectronic Payments International

Payroll and public transport drive cards

Ukraine’s economy was severely affected by the global economic cri-ses, and the country was extended a financial bailout package by the

IMF and the EU to restore growth and revive its beleaguered banking sector.

However, prospects to 2020 are uncertain as a result of the conflict in Crimea.

The Ukrainian government is taking sever-al initiatives to foster banking sector growth in the form of financial inclusion, payment infrastructure modernisation and the adop-tion of technologically advanced payment cards.

The government has also supported mod-ernisation, with regulations in September 2010 requiring all retailers of goods and services to accept card-based payments. This contributed to growth in the overall payment card transaction volume between 2011 and 2015.

Payroll programmes lead debit card issue In Ukraine, payroll programmes have lead to widespread issuance of debit cards, account-ing for 80.4% of all payment cards in circu-lation in 2015.

All major banks in the country – such as PrivatBank, Oschadbank, Raiffeisen Bank Aval and UkrSibbank – offer payroll cards. For instance PrivatBank, through its Salary Project, offers salary packages with benefits such as free cash withdrawals at any of its

ATMs. Accountholders are offered Visa or MasterCard-branded debit cards.

Oschadbank offers the MasterCard Electronic, MasterCard Cirrus Maestro, MasterCard Electronic ZP and Visa Electron for salary accountholders.

Pay later steadily gaining groundPay later card transactions at ATMs were very high until 2013, as Ukrainian consumers used cards to help meet short-term financing needs and avoid liquidity constraints.

To encourage pay later transactions at POS terminals, banks launched a number of marketing programmes and introduced con-venient payment options such as instalment facilities. As a result, pay later card transac-tion volumes and frequency of use at POS terminals increased significantly from 2014.

However, pay later average transaction values at POS terminals fell, signifying pru-dent consumer spending.

Gradual uptake of contactlessContactless technology is expected to gain prominence among Ukrainian consumers. The Ukrainian government is also actively involved in promoting contactless technol-ogy, especially on public transport.

In September 2015, the Kiev Municipal State Administration introduced contactless payments on the city’s subway, enabling passengers to pay fares with MasterCard contactless cards while passing through turnstiles. As of July 2016, 17 of a total 52 subway stations in Kiev offered contactless payments; the remainder will be equipped with contactless terminals in phases.

Banks are also keen to promote contactless technology, and are launching new services to increase uptake. These include a contactless m-payment solution by PrivatBank in Febru-ary 2014. Alfa Bank launched a contactless m-payment pilot project in partnership with Kyivstar in January 2014.

Ukraine’s e-commerce transaction value stood at $1.3bn in 2015. According to the Ukrainian Processing Centre, there was growth in the number of online shops and purchases with payment cards on the internet between 2014 and 2015. The number of sites that accept Visa and MasterCard payments grew by 27% during the same period.

MasterCard’s launch of MasterPass in July 2016 is expected to drive online card-based transactions. <

Severely affected by the global economic crises and currently locked in an ongoing dispute with its superpower neighbour, Ukraine has seen more prosperous times. However, payroll programmes mean debit card use is widespread, and contactless is gaining traction on the Kiev metro

n UKRAINIAN CARD TRANSACTION VALUE BY CHANNEL ($BN), 2011–2020