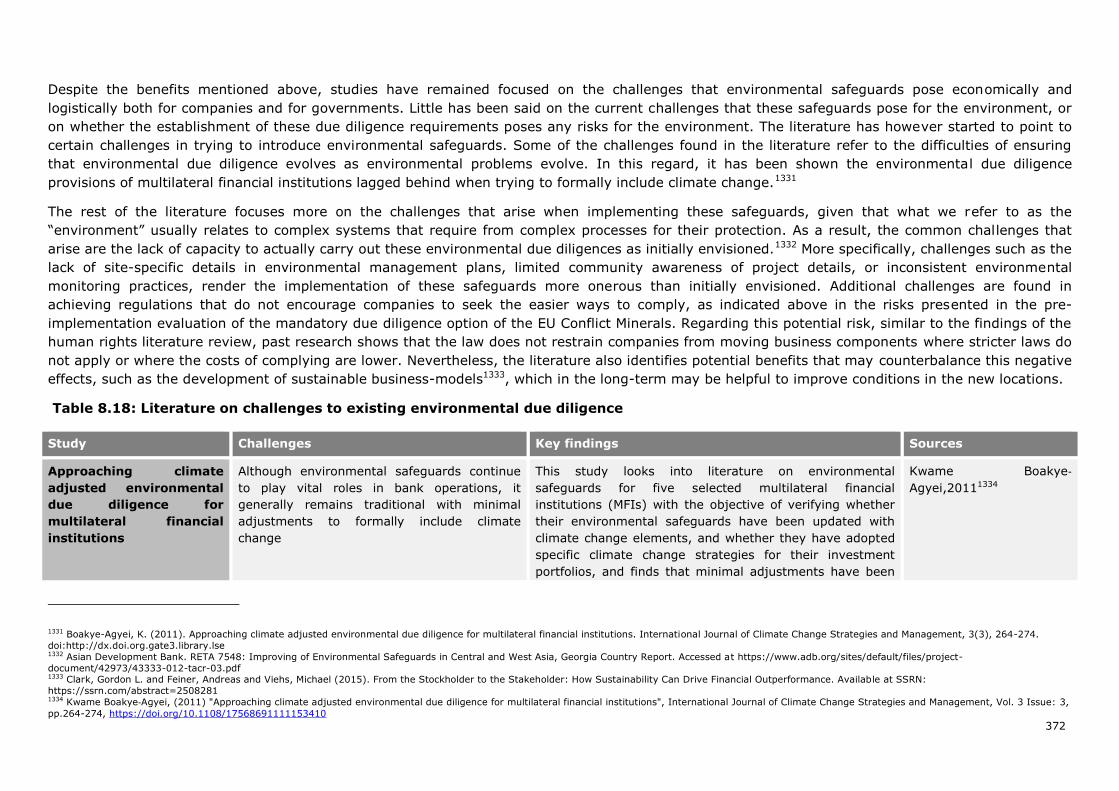

study on due diligence requirements through the supply chain

TRANSCRIPT

Lise Smit, Claire Bright, Robert McCorquodale, Matthias Bauer, Hanna Deringer, Daniela Baeza-

Breinbauer, Francisca Torres-Cortés, Frank Alleweldt, Senda Kara and Camille Salinier and Héctor

Tejero Tobed

January – 2020

Study on due diligence

requirements through the supply chain

FINAL REPORT

2

EUROPEAN COMMISSION

Directorate-General for Justice and Consumers

Directorate— A — Civil and Commercial Justice Unit— A.3 — Company Law

E-mail: [email protected]

European Commission B-1049 Brussels

EUROPEAN COMMISSION

3

Directorate General for Justice and Consumers

Study on due diligence requirements through the

supply chain

Final Report

4

5

LEGAL NOTICE

Printed by the British Institute of International and Comparative Law in United Kingdom Manuscript completed in January 2020 First edition This document has been prepared for the European Commission however it reflects the views only of the authors, and the Commission cannot be held responsible for any use which may be made of the information contained therein.

The European Commission is not liable for any consequence stemming from the reuse of this publication.

Luxembourg: Publications Office of the European Union, 2020

© European Union, 2020 Reuse is authorised provided the source is acknowledged. The reuse policy of European Commission documents is regulated by Decision 2011/833/EU (OJ L 330, 14.12.2011, p. 39).

For any use or reproduction of photos or other material that is not under the copyright of the European Union (*), permission must be sought directly from the copyright holders.

PDF ISBN 978-92-76-15094-7 doi:10.2838/39830 DS-01-20-017-EN-N

6

ACKNOWLEDGEMENTS The authors of this study are Lise Smit, Claire Bright, Robert McCorquodale, Matthias

Bauer, Hanna Deringer, Daniela Baeza-Breinbauer, Francisca Torres-Cortés, Frank

Alleweldt, Senda Kara and Camille Salinier, with case studies by Héctor Tejero Tobed.

Our sincere gratitude to Irene Pietropaoli for her valuable contributions, to Bradley

Dawson for the design and formatting, and to Anthony Wenton for proof-reading.

Country Reports were authored by Geert van Calster and Siel Demeyer (Belgium), Lia

Heasman (Denmark, Finland and Sweden), Elsa Savourey (France), Daniel Augenstein

(Germany), Shane Darcy (Ireland), Giacomo Cremonisi (Italy), Liesbeth Enneking

(Netherlands), Bartosz Kwiatkowski (Poland), Maria Prandi and Daniel Iglesias Márquez

(Spain) and Stuart Neely (United Kingdom).

The information and views set out in this study are those of the author(s) and do not

necessarily reflect the official opinion of the Commission. The Commission does not

guarantee the accuracy of the data included in this study. Neither the Commission nor

any person acting on the Commission’s behalf may be held responsible for the use which

may be made of the information contained therein.

7

ABSTRACT This study for the European Commission focuses on due diligence requirements to

identify, prevent, mitigate and account for abuses of human rights, including the rights

of the child and fundamental freedoms, serious bodily injury or health risks,

environmental damage, including with respect to climate. It was conducted by the British

Institute of International and Comparative Law (lead), Civic Consulting and LSE

Consulting. Through desk research, country analyses, interviews and surveys it identifies

Market Practices (Task 1) and perceptions regarding regulatory options. The Regulatory

Review (Task 2), including twelve Country Reports, shows that UN Guiding Principles on

Business and Human Rights’ standard of due diligence is increasingly being introduced

into legal standards or proposed in Member States. The Problem Analysis, policy

background and intervention logic concludes with the definition of four options for

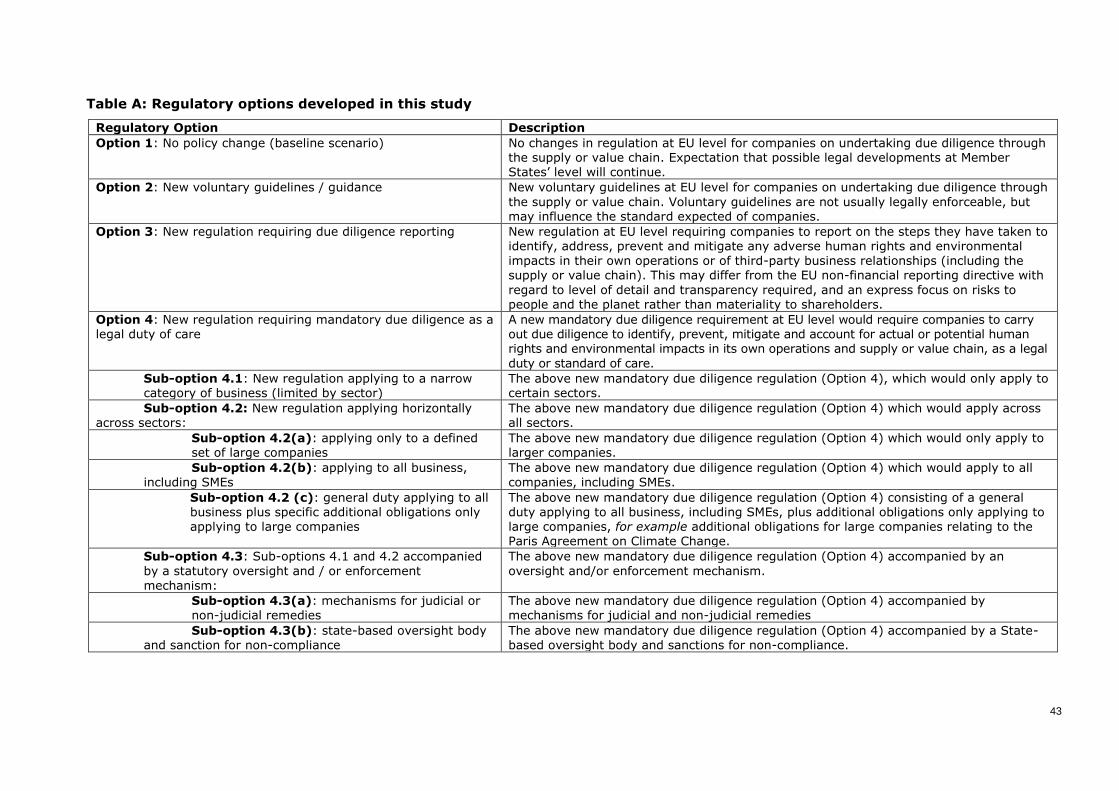

regulatory proposals (Task 3): No change (Option 1), new voluntary guidelines (Option

2), new reporting requirements (Option 3) and mandatory due diligence as a legal

standard of care (Option 4). Option 4 includes sub-options limited to sector and company

size, and enforcement through state-based oversight or judicial / non-judicial remedies.

The assessment of impacts of regulatory options (Task 4) considers economic impacts,

impacts on public authorities, social, human rights and environmental impacts.

8

CONTENTS

LIST OF TABLES........................................................................................................... 12

LIST OF FIGURES ......................................................................................................... 13

EXECUTIVE SUMMARY (ENGLISH) ............................................................................ 15

NOTE DE SYNTHÈSE (FRANÇAIS) ............................................................................. 24

I. INTRODUCTION .................................................................................................... 35

1. Introduction................................................................................................ 35

2. Background ................................................................................................ 35

3. Scope and definitions ................................................................................... 37

3.1 Scope ........................................................................................... 37

3.2 Definitions ..................................................................................... 38

4 Methodology ............................................................................................... 40

5 General Overview ........................................................................................ 40

II. MARKET PRACTICES ............................................................................................ 44

1. Introduction................................................................................................ 44

2. Methodology ............................................................................................... 44

3. General survey data .................................................................................... 45

Business survey respondents ........................................................... 45 3.1

General survey respondents ............................................................ 46 3.2

4. Current due diligence practices ..................................................................... 48

Overview of current practices ........................................................... 48 4.1

Scope of due diligence .................................................................... 50 4.2

CASE STUDY: BASF AND VALUE-TO-SOCIETY .................................................................. 58

Language used to describe due diligence ........................................... 59 4.3

CASE STUDY: VATTENFALL AND LIMITING ENVIRONMENTAL DAMAGE ............................... 61

Due diligence practices in own operations .......................................... 63 4.4

Due diligence practices in supply and value chains .............................. 65 4.5

CASE STUDY: LUNDBECK AND AKORN: RESTRICTING PENTOBARBITAL FOR LETHAL INJECTIONS IN THE US ......................................................................................... 67

Traceability and the scope of the supply chain .................................... 70 4.6

CASE STUDY: MARKS & SPENCER AND MAPPING SUPPLY CHAINS ..................................... 71

CASE STUDY: HENNES & MAURITZ AND TRANSPARENCY IN THE SUPPLY CHAIN ................. 72

Audits ........................................................................................... 73 4.7

Leverage and the ability of individual companies ................................ 74 4.8

CASE STUDY: FAIRPHONE AND TRANSPARENCY IN COMMUNICATIONS .............................. 77

Communication with stakeholders and local experts ............................ 78 4.9

CASE STUDY: NESTLÉ AND NGO PARTNERING................................................................. 79

CASE STUDY: HUAYOU COBALT: ACKNOWLEDGING RISKS IN ARTISANAL AND SMALL-SCALE MINING ..................................................................................................... 81

Buying practices and an integrated approach ..................................... 83 4.10

CASE STUDY: BUYING PRACTICES AND THE FAIRTRADE MINIMUM PRICE FOR COCOA ......... 85

Remedies and grievance mechanisms ............................................... 86 4.11

CASE STUDY: THE BANGLADESH ACCORD AND WORKER SAFETY ...................................... 87

9

Incentives for undertaking due diligence ........................................... 89 4.12

Digital technologies ........................................................................ 91 4.13

Overall views on current due diligence practices ................................. 92 4.14

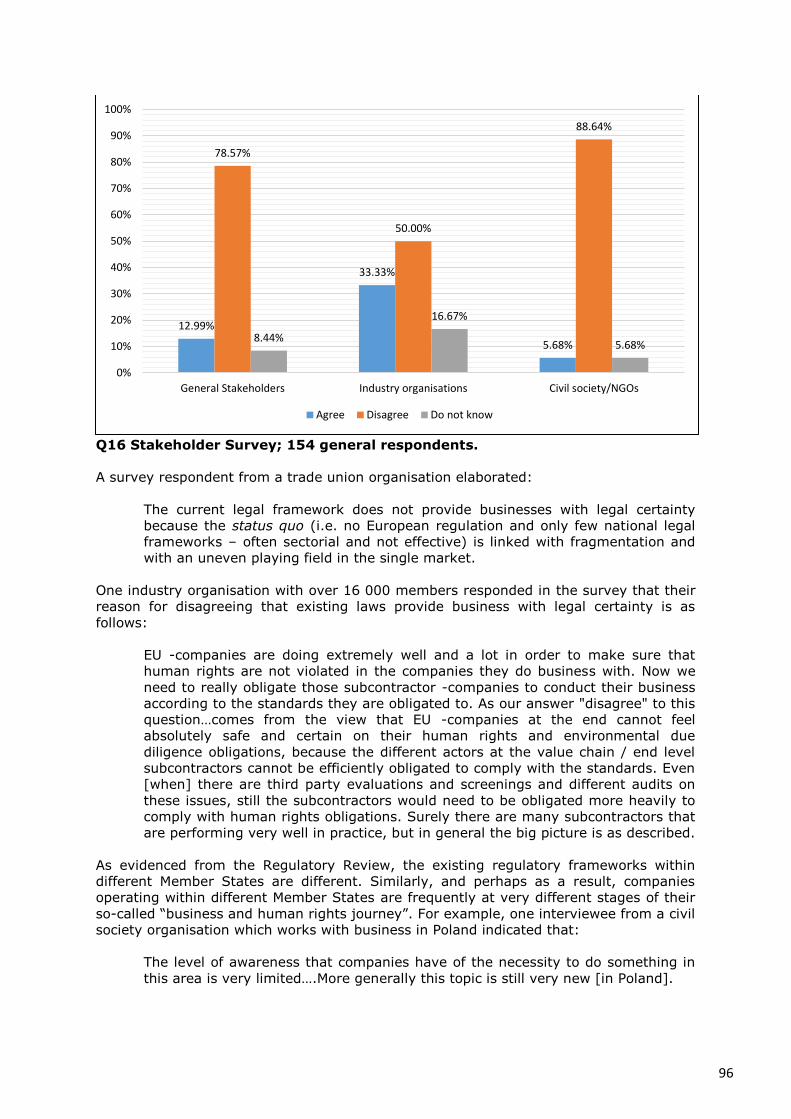

5. Stakeholder views on impacts of regulatory options ......................................... 93

Option 1: No policy change (baseline scenario) .................................. 93 5.1

Option 2: New voluntary guidelines / guidance ................................... 97 5.2

Option 3: New regulation requiring due diligence reporting .................. 99 5.3

Option 4: Regulation requiring mandatory due diligence as a standard 5.4of care ........................................................................................ 105

Sub-options of Option 4 ................................................................ 121 5.5

Overall stakeholder views .............................................................. 141 5.6

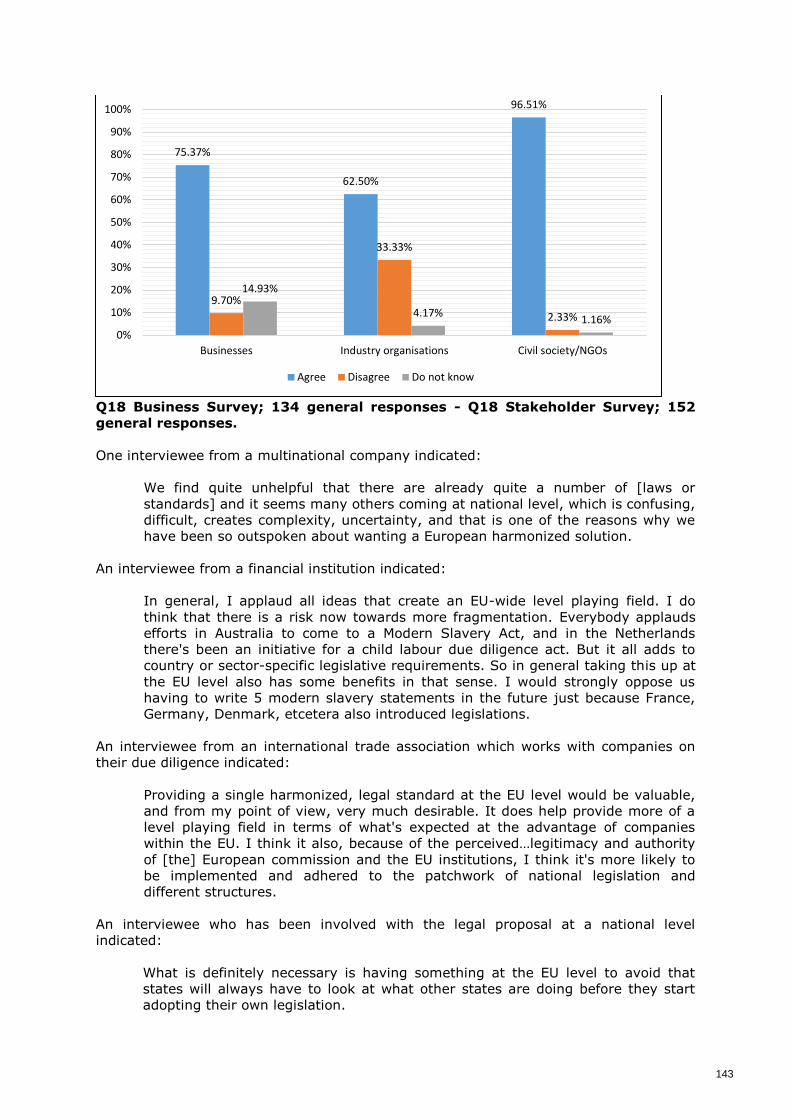

6. Stakeholder views on effects of EU-level regulation ....................................... 142

Harmonisation ............................................................................. 142 6.1

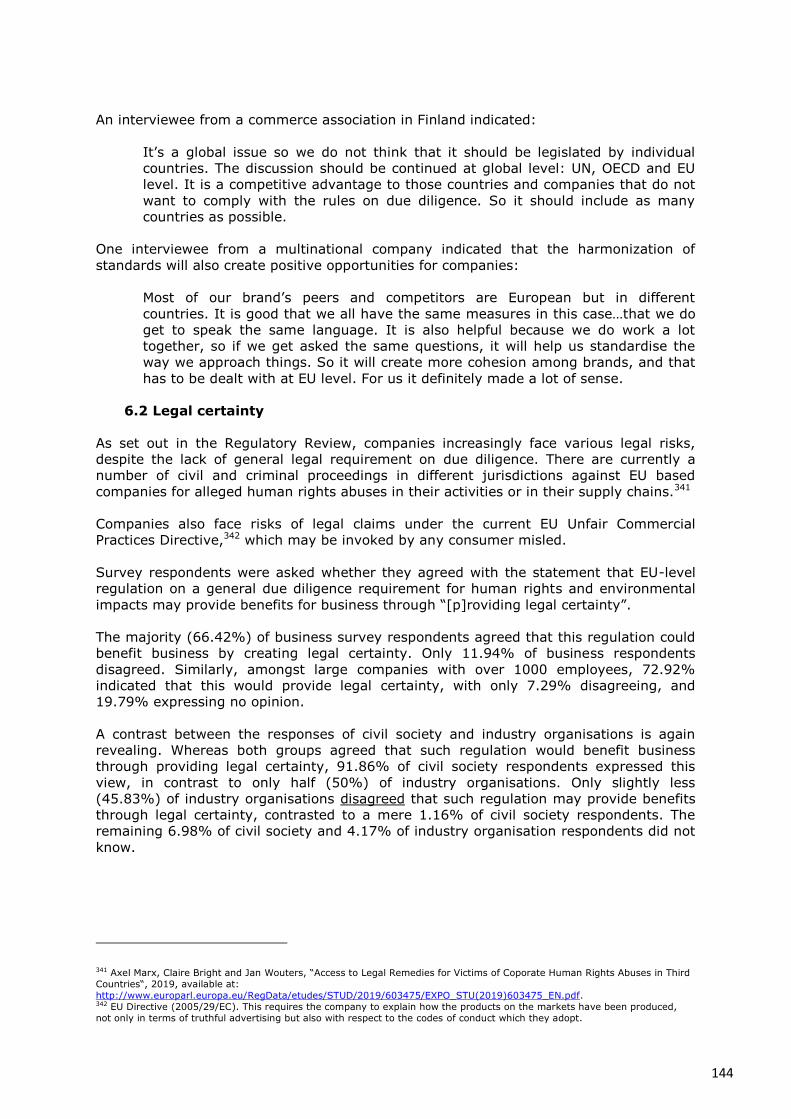

Legal certainty ............................................................................. 144 6.2

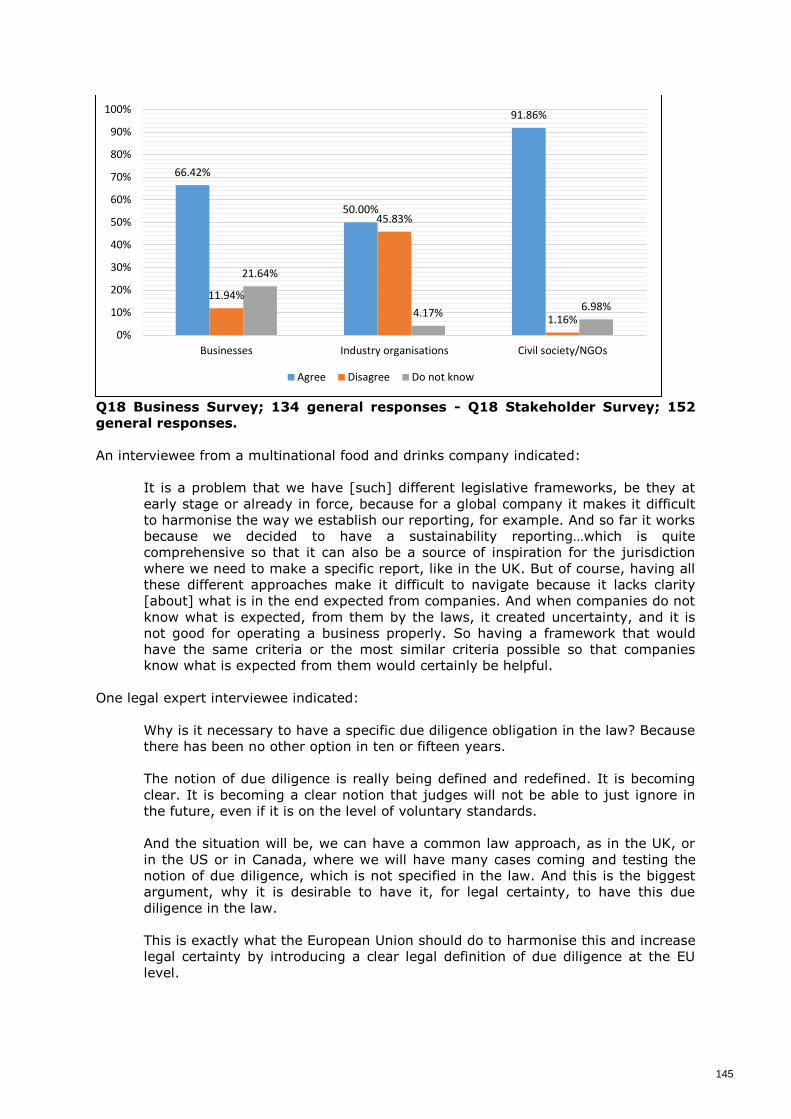

Competitiveness and “levelling the playing field” .............................. 146 6.3

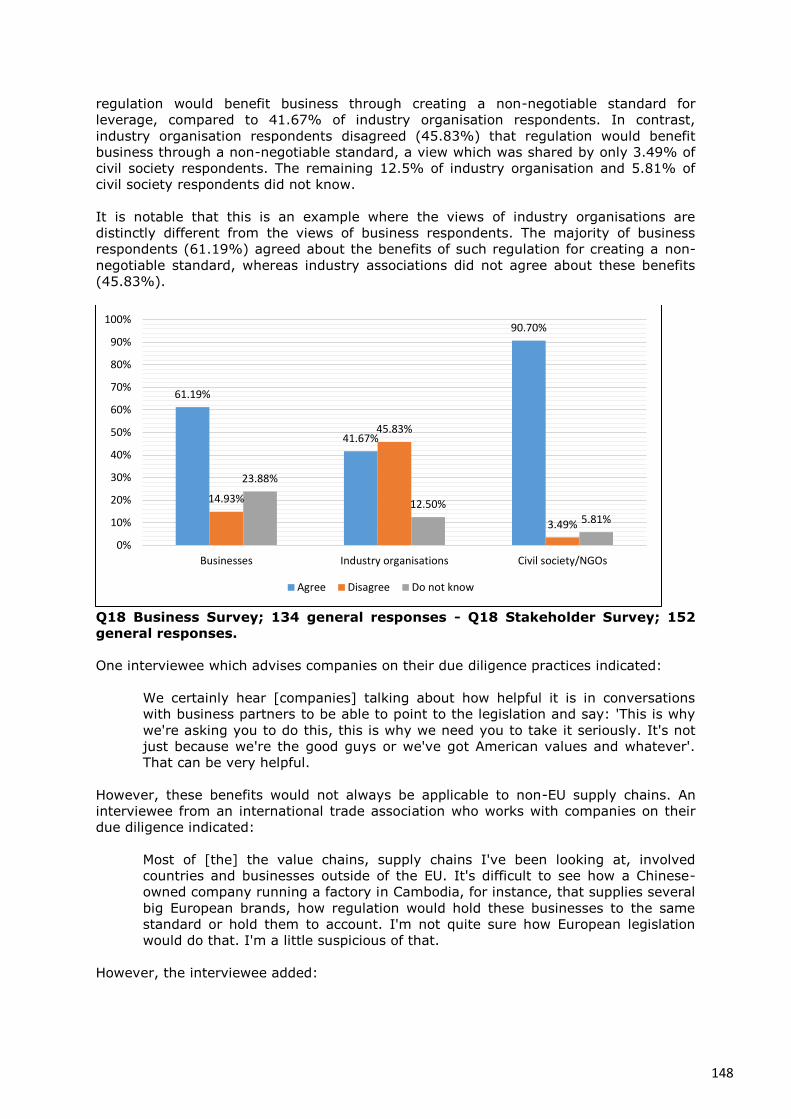

Non-negotiable standard to facilitate leverage .................................. 147 6.4

Access to the European market ...................................................... 149 6.5

The leadership of the EU ............................................................... 150 6.6

III. REGULATORY REVIEW ..................................................................................... 156

1. Introduction.............................................................................................. 156

2. Methodology ............................................................................................. 156

3. The concept of due diligence ....................................................................... 156

3.1 Due diligence as a legal standard of care ......................................... 158

3.2 Developments in due diligence ....................................................... 158

3.2.1 UN Guiding Principles on Business and Human Rights ....................... 158

3.2.2 OECD Guidelines for Multinational Enterprises .................................. 161

3.2.3 The ILO Tripartite Declaration of Principles concerning Multinational Enterprises and Social Policy (ILO MNE declaration) .......................... 164

3.2.4 Other international standards ......................................................... 165

3.2.5 EU-level standards and developments ............................................. 165

3.2.6 Domestic measures regulating due diligence in supply chains ............. 170

3.2.7 Case law ..................................................................................... 175

3.2.8 Due diligence in the Draft Treaty .................................................... 177

3.2.9 The usefulness and establishment of the concept of due diligence 179

3.3 Environmental due diligence and climate change .............................. 180

3.3.1 Environmental due diligence .......................................................... 180

3.3.2 Due diligence and climate change ................................................... 184

3.4 Due Diligence, sustainability and the SDGs ...................................... 189

3.5 Due Diligence and corruption ......................................................... 190

3.6 Due Diligence in the agricultural sector, including coffee, tea and cocoa subsectors .......................................................................... 191

3.7 Due Diligence for child labour......................................................... 191

4. Domestic frameworks ................................................................................ 192

4.1 Country reports: Twelve selected EU Member States ........................ 192

4.2 Other domestic developments ........................................................ 192

4.2.1 Switzerland ................................................................................. 193

4.2.2 Norway ....................................................................................... 195

4.2.3 Canada ....................................................................................... 196

4.2.4 Australia 196

4.2.5 United States of America ............................................................... 197

10

4.2.6 Brazil 197

4.3 Overview and Comparative Analysis of Country Reports .................... 199

4.3.1 Introduction ................................................................................. 199

4.3.2 Areas of law ................................................................................. 200

4.3.3 The Legal Duty ............................................................................. 201

4.3.4 Scope ........................................................................................ 204

4.3.5 Transnational Application............................................................... 206

4.3.6 Corporate Groups ......................................................................... 207

4.3.7 Monitoring, Enforcement and Remedies ........................................... 209

4.3.8 Conclusions ................................................................................. 212

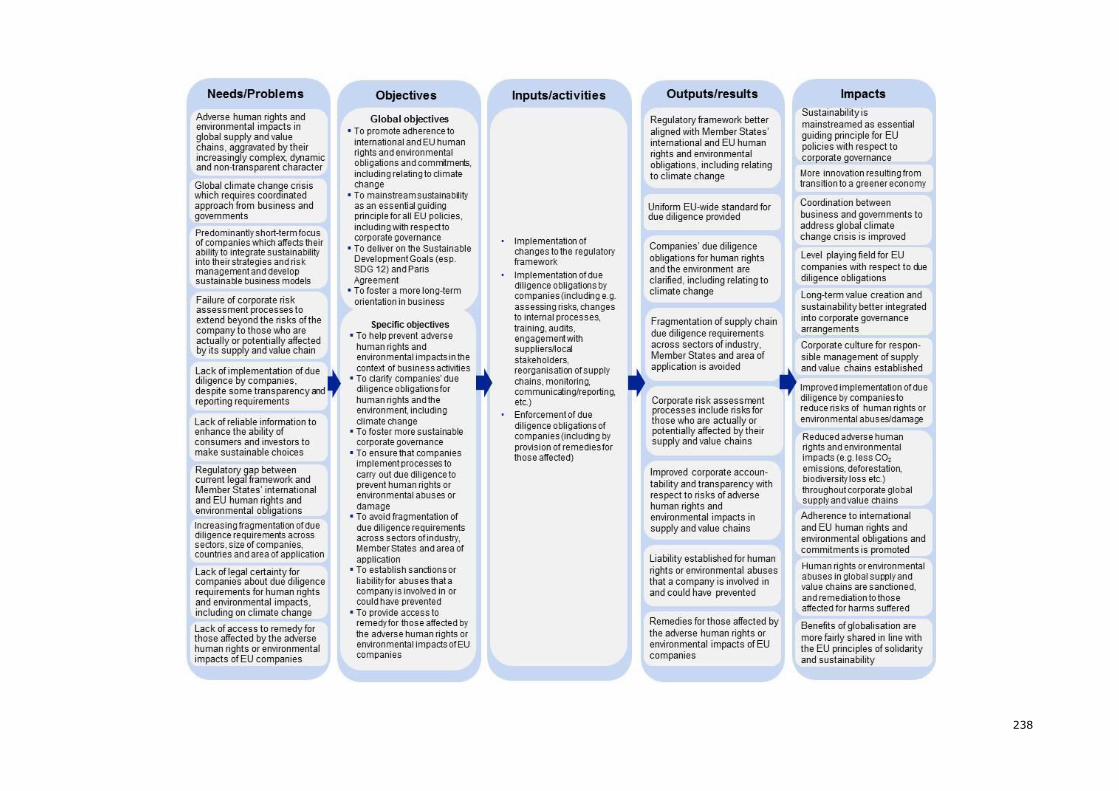

IV. PROBLEM ANALYSIS AND OPTIONS FOR REGULATORY INTERVENTION ........... 214

1. Introduction.............................................................................................. 214

2. Problem analysis ....................................................................................... 214

2.1 Adverse human rights and environmental impacts in global value chains, aggravated by their increasingly complex, dynamic and non-

transparent character ................................................................... 214

2.2 Lack of implementation of due diligence by companies, despite

existing voluntary and legally binding transparency and reporting requirements ............................................................................... 218

2.3 Failure of corporate risk assessment processes to extend beyond the risks of the company to those who are actually or potentially affected by its supply and value chain ......................................................... 221

2.4 Regulatory gap between existing legal framework and Member States’ obligations ................................................................................... 222

2.5 Increasing fragmentation of due diligence requirements across sectors, size of companies, countries, and area of application ............ 225

2.6 Lack of legal certainty about due diligence requirements for human rights and environmental impacts ................................................... 227

2.7 Lack of access to remedy for those affected by the adverse human rights or environmental impacts of EU companies ............................. 228

3. Legal basis for and policy background of a possible future EU intervention ........ 231

3.1 Legal basis for a possible future EU intervention ............................... 231

3.2 Policy background of a possible future EU intervention ...................... 232

3.3 Calls for mandatory due diligence at EU level based on legal and policy background ........................................................................ 234

4. Intervention logic of a possible future EU intervention .................................... 235

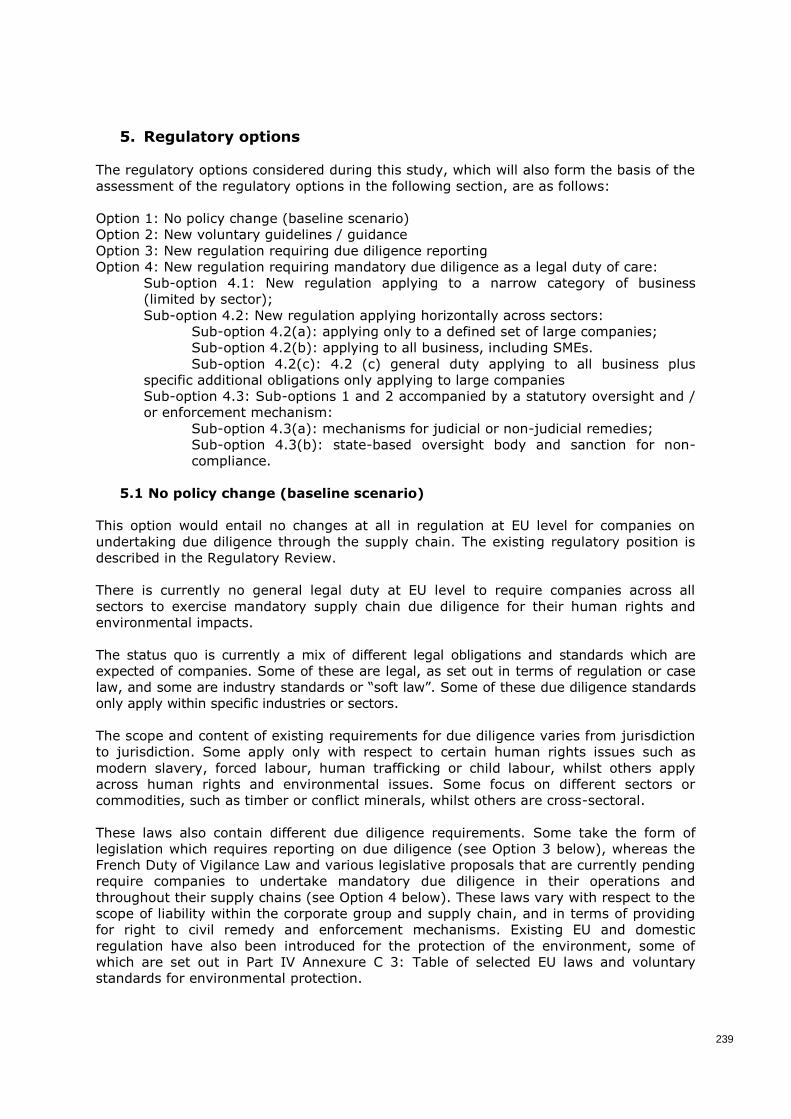

5. Regulatory options .................................................................................... 239

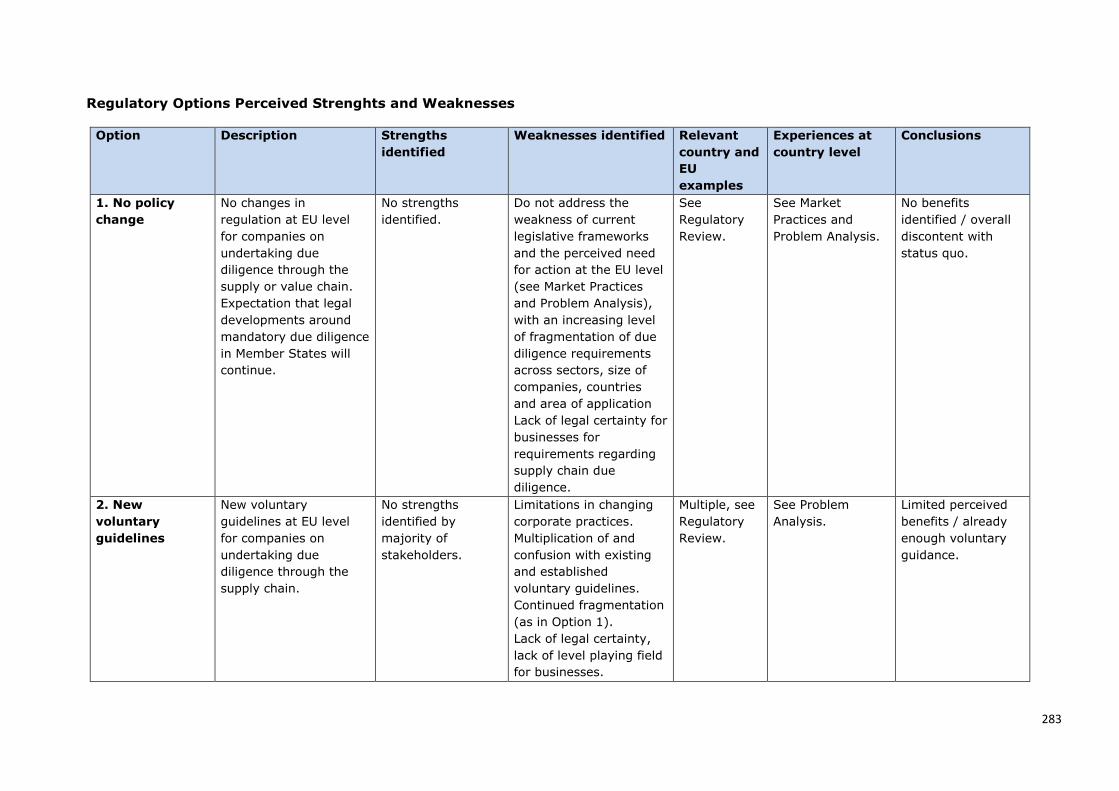

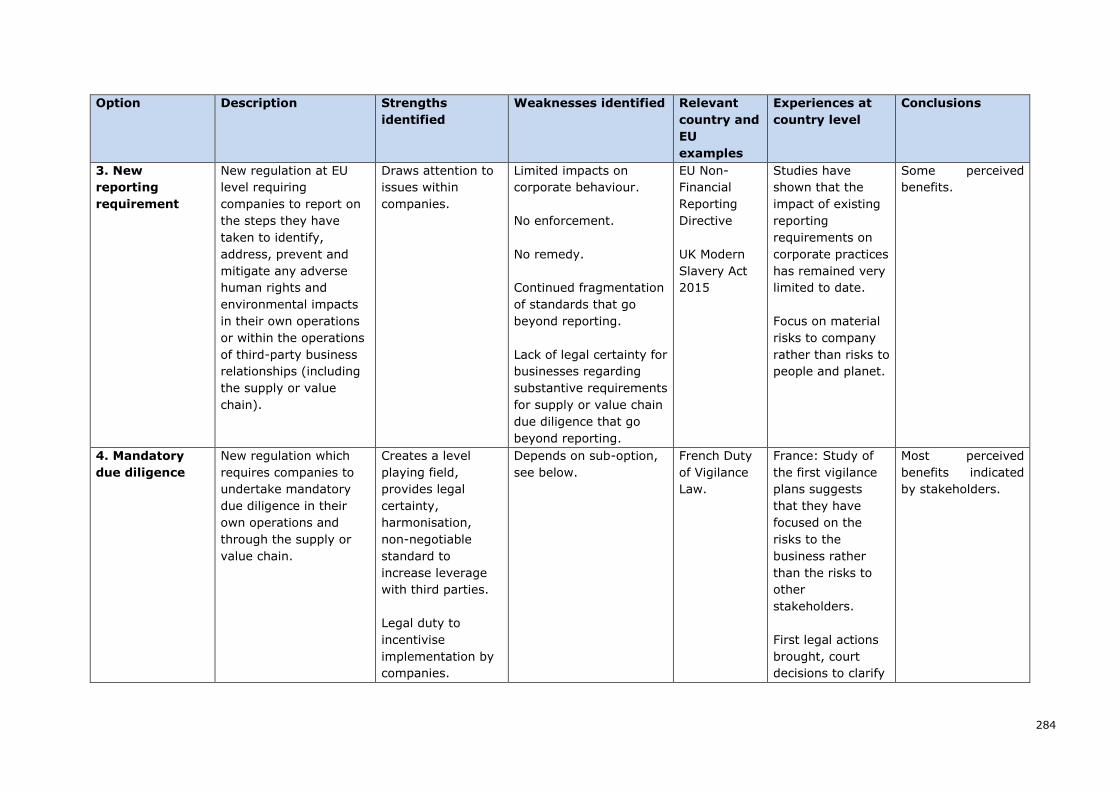

5.1 No policy change (baseline scenario) .............................................. 239

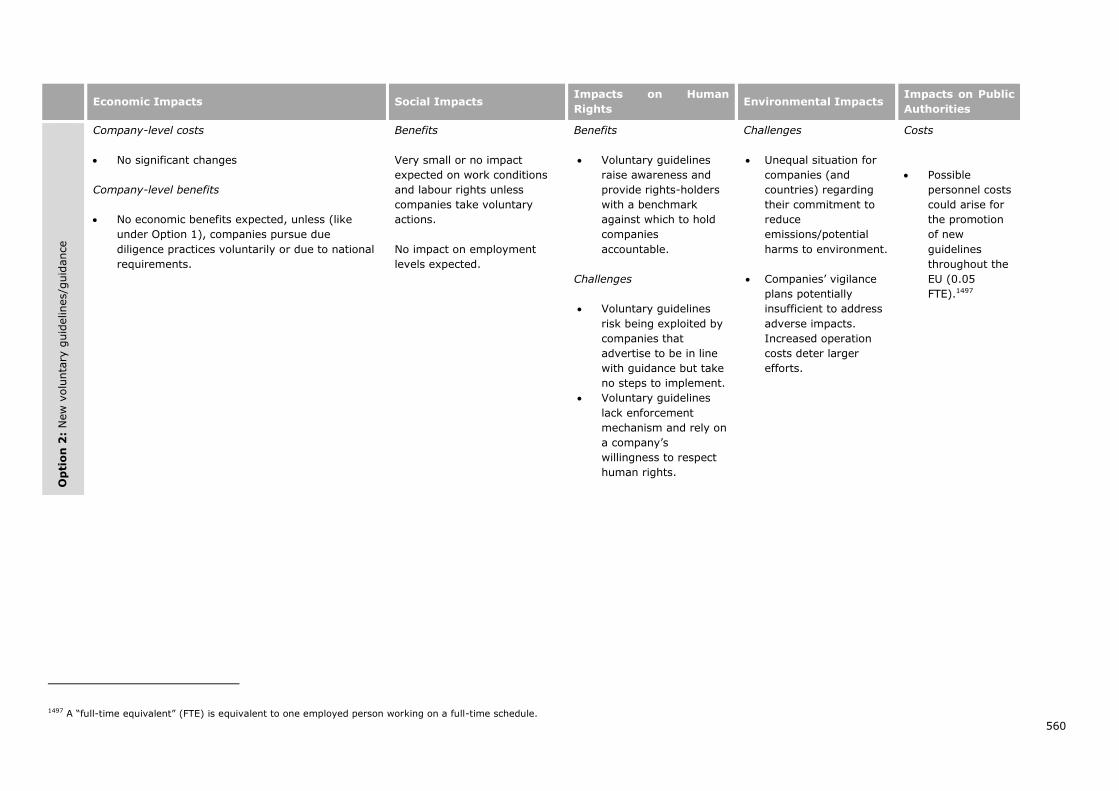

5.2 New voluntary guidelines/guidance (Option 2) ................................. 242

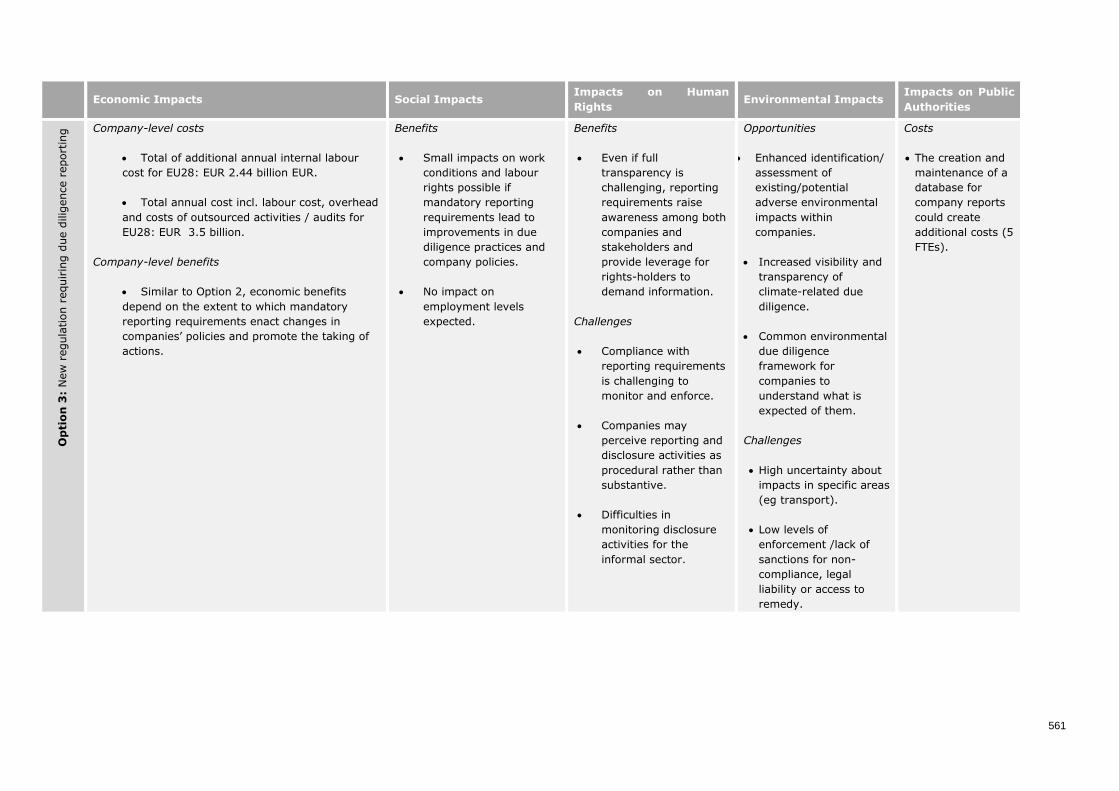

5.3 New regulation requiring due diligence reporting (Option 3) ............... 245

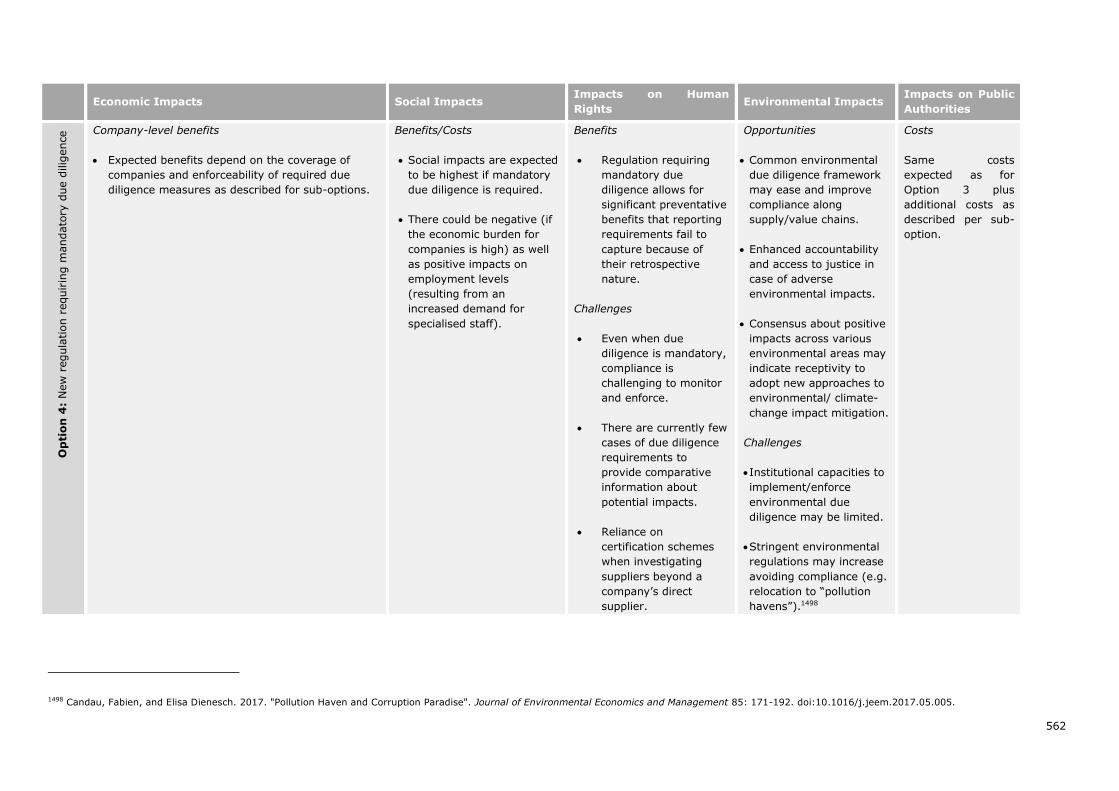

5.4 New regulation requiring mandatory due diligence (Option 4) ............ 250

6. Due diligence as a legal standard of care: Clarification of a few common questions ................................................................................................. 260

7. Further considerations around scope of application ........................................ 271

7.1 Accompanying non-binding guidance on the mandatory duty ............. 271

7.2 Regulation of transnational corporate activity: foreign-based subsidiaries, suppliers and third parties ........................................... 274

7.3 Implementation at Member State level ............................................ 276

7.4 Material scope of adverse human rights and environmental impacts ... 277

7.5 Conflict of laws considerations ....................................................... 278

7.6 Transitional period ........................................................................ 280

7.7 Mandatory due diligence as part of a package of measures ................ 280

11

8. Discussion of strengths and weaknesses of the options identified .................... 281

V ASSESSMENT OF OPTIONS .................................................................................. 290

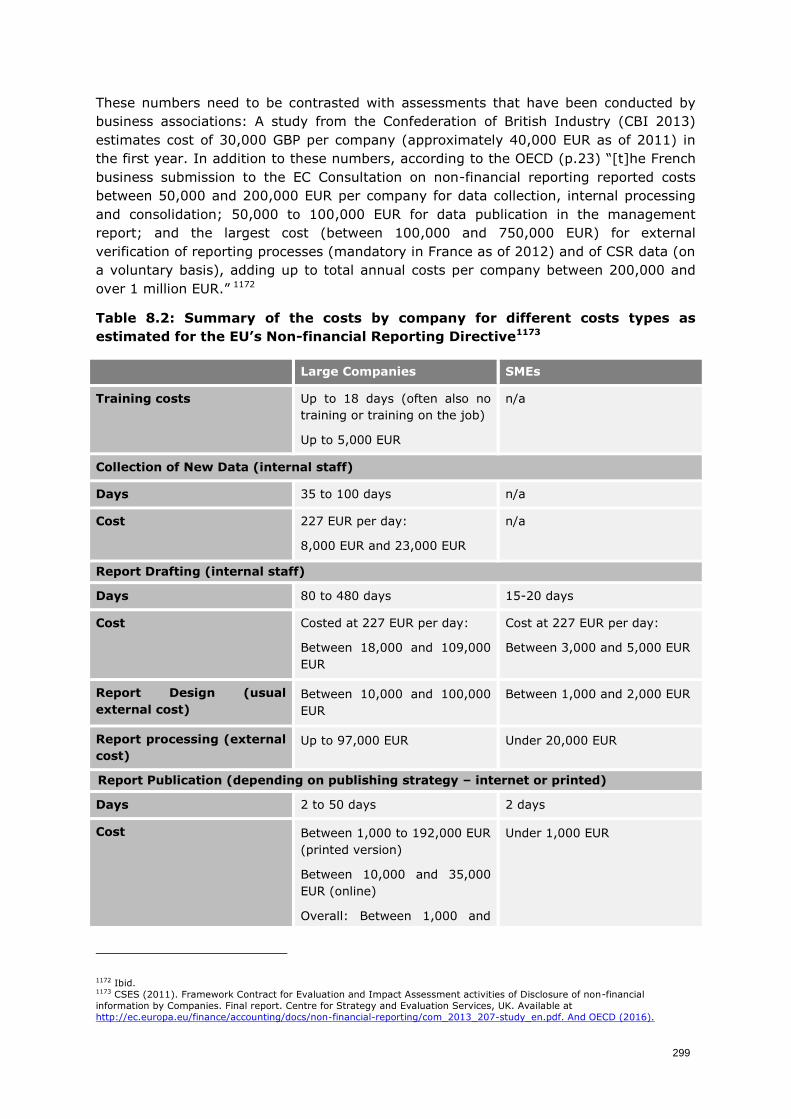

1. Literature Review ...................................................................................... 290

1.1 Economic Impacts ..................................................................................... 290

1.1.1 Company-level Costs .................................................................... 290

1.1.2 Company-level Benefits ................................................................. 301

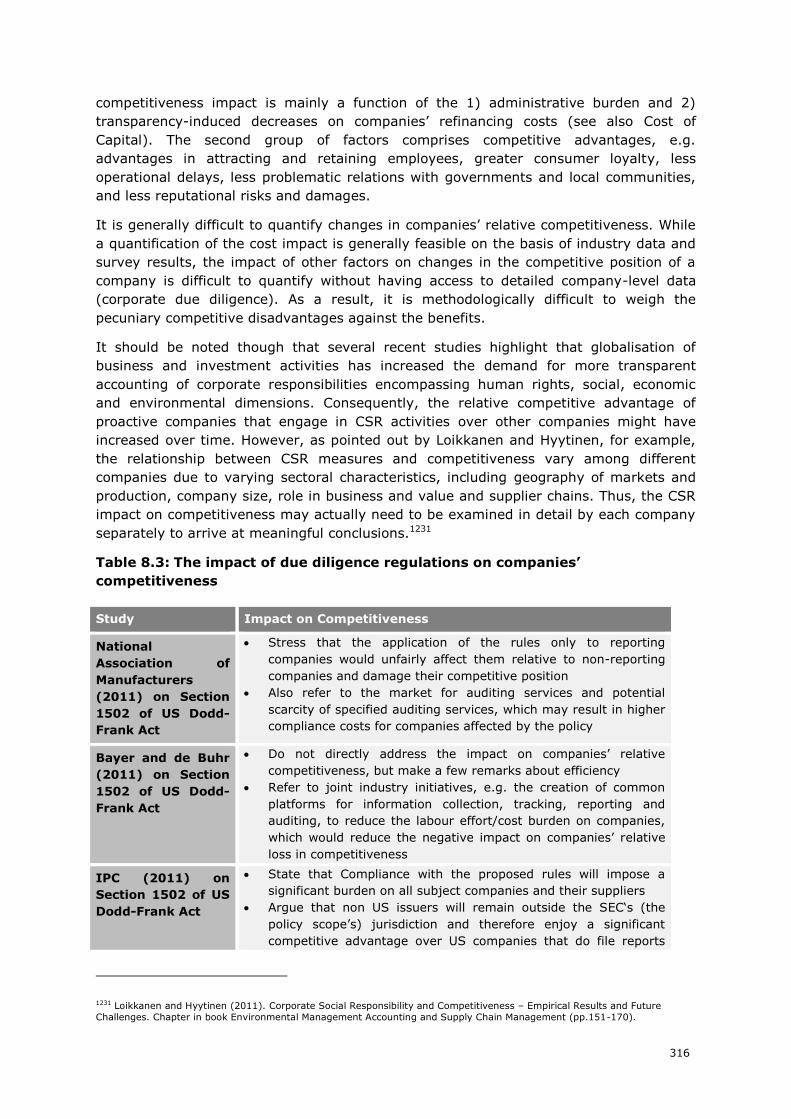

1.1.3 Impact on Company-Level Competitiveness ..................................... 315

1.1.4 Impact on SMEs ........................................................................... 317

1.1.5 Industry and Aggregate Economic Impacts ...................................... 320

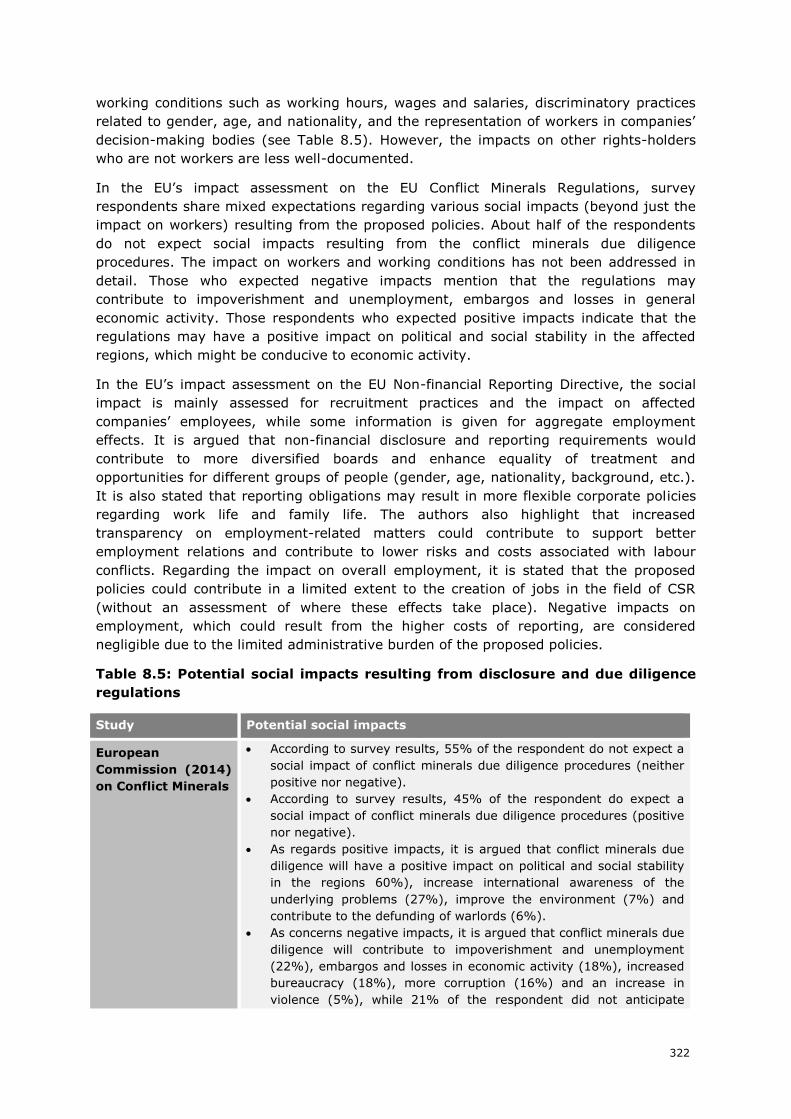

1.2 Social Impacts .......................................................................................... 320

1.3 Impacts on Human Rights .......................................................................... 324

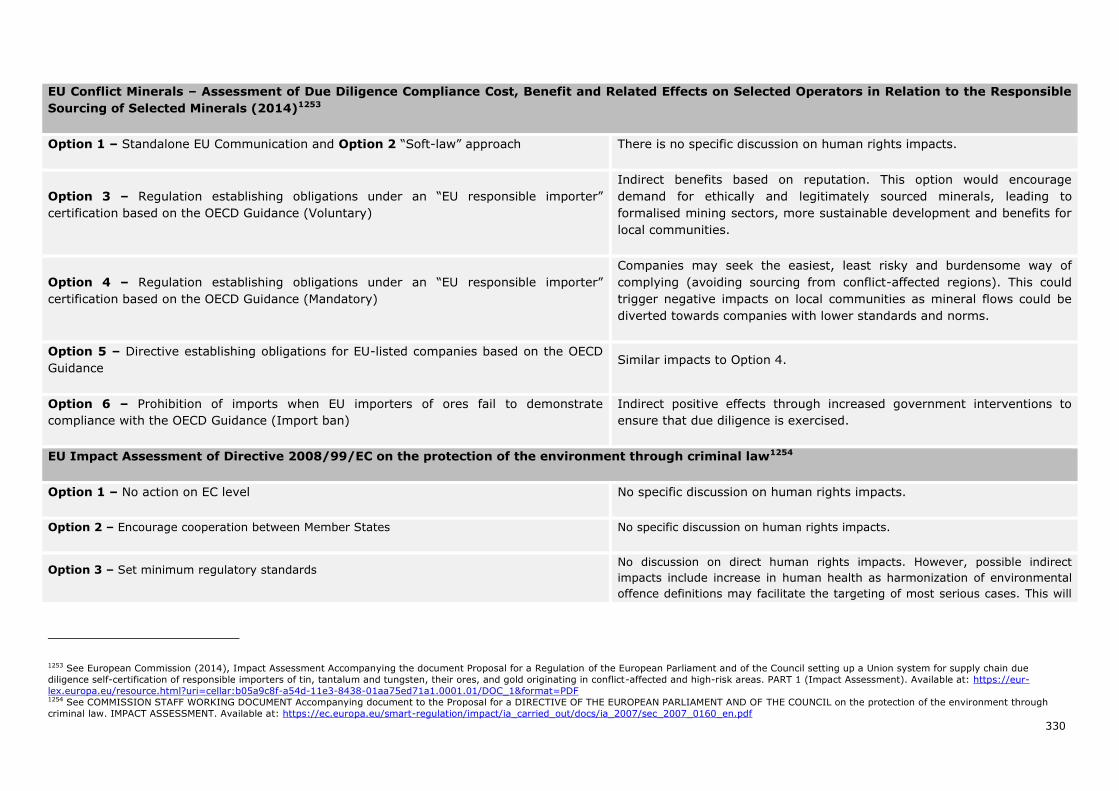

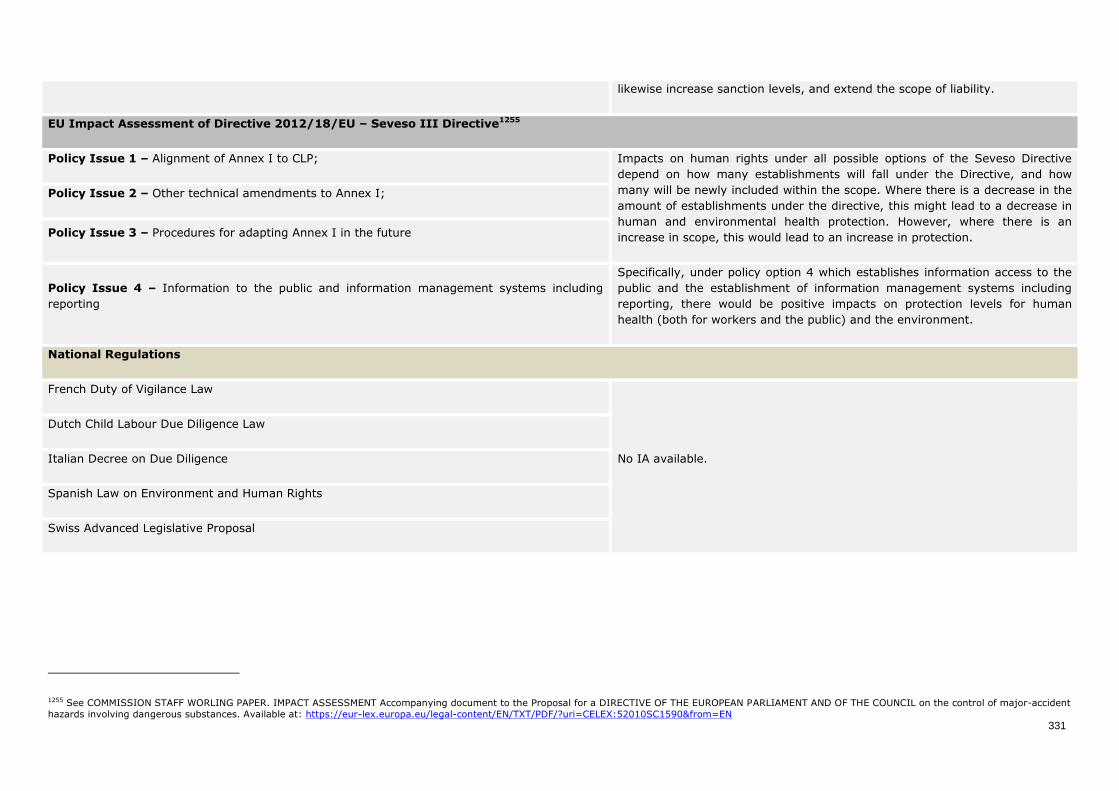

1.3.1 Pre-Implementation Impact Assessment Review ............................... 325

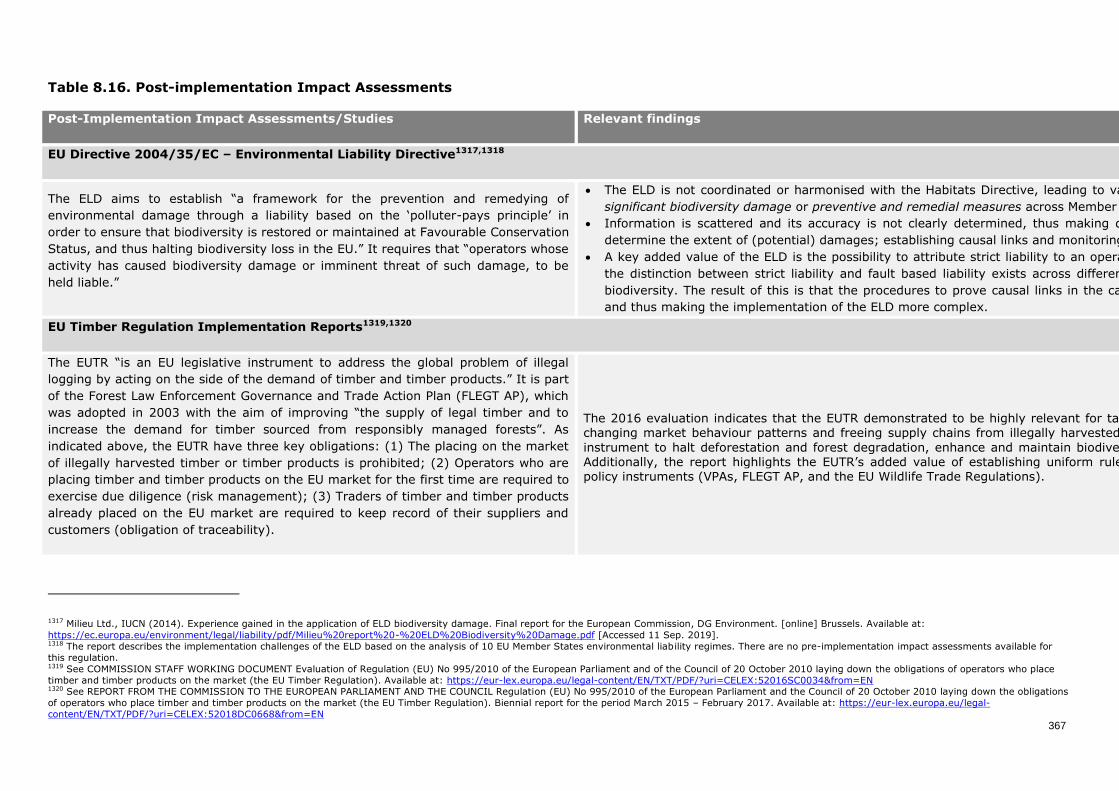

1.3.2 Post-Implementation Impact Assessment Review ............................. 332

1.3.3 Benefits and Challenges of the Different Policy Approaches ................ 333

1.4 Environmental Impacts .............................................................................. 356

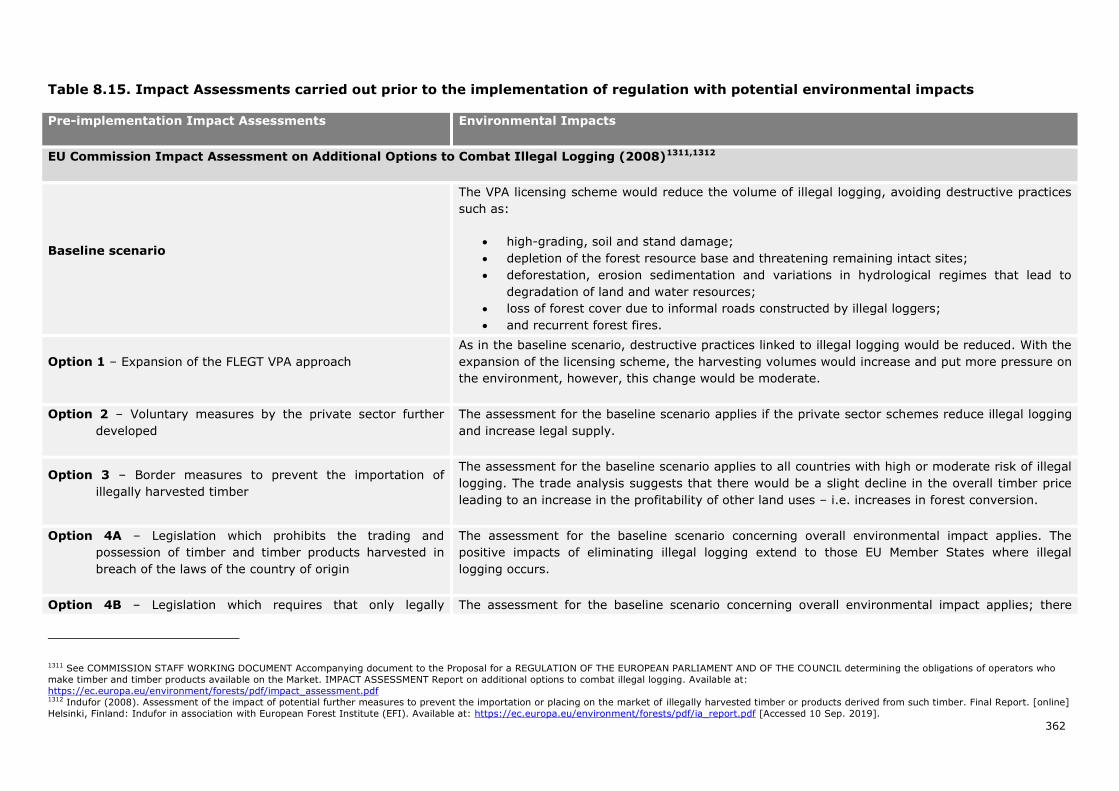

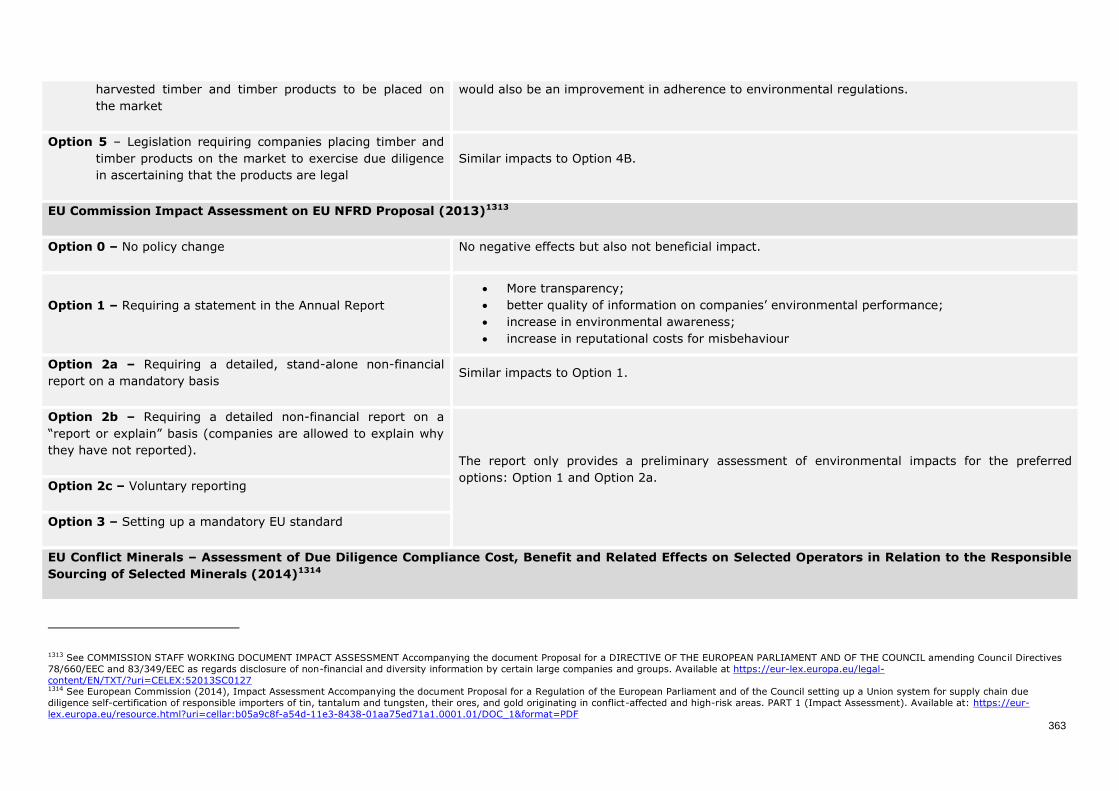

1.4.1 Pre-Implementation Impact Assessment Review ............................... 359

1.4.2 Post-Implementation Impact Assessment Review ............................. 366

1.4.3 Benefits and Challenges of Environmental Due Diligence ................... 368

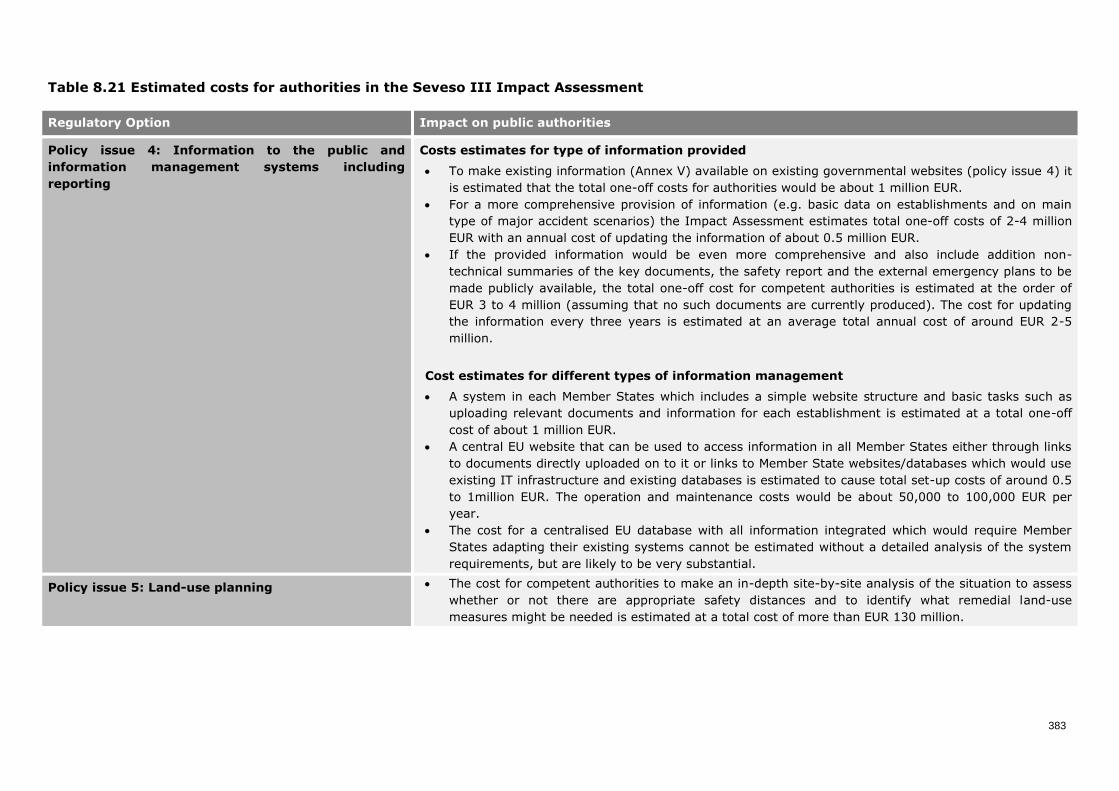

1.5 Impact on Public Authorities ....................................................................... 374

2. METHODOLOGY .................................................................................................. 386

2.1 Economic and Social Impact Assessment ...................................................... 386

2.1.1 Economic Impacts: Company-level, sector- and economy wide impacts ....................................................................................... 386

2.1.2 Social Impacts in the EU and non-EU countries ................................ 388

2.1.3 Impacts on the public authorities in EU Member States ..................... 388

2.2 Human Rights and Environmental Impact Assessment ................................... 388

2.2.1 Impacts on Human Rights ............................................................. 388

2.2.2 Environmental Impacts ................................................................. 389

3. ANALYSIS .......................................................................................................... 390

3.1 Economic Impacts across Regulatory Options ................................................ 398

3.1.1 General remarks .......................................................................... 398

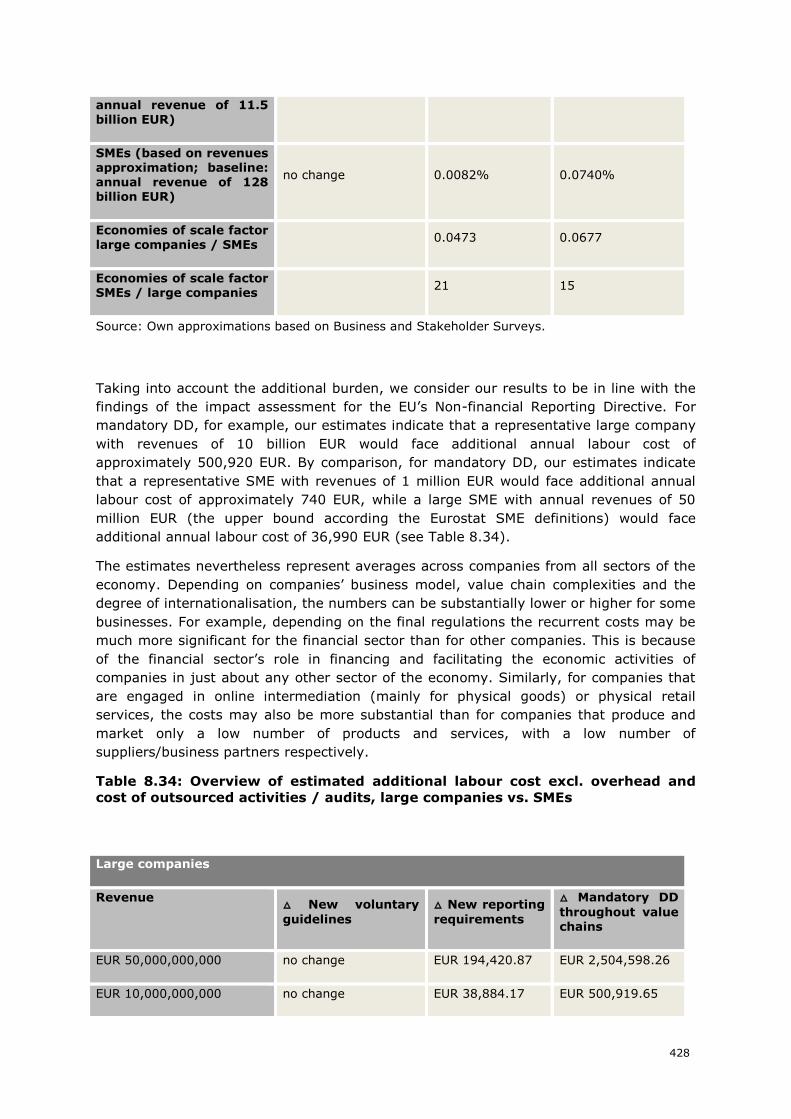

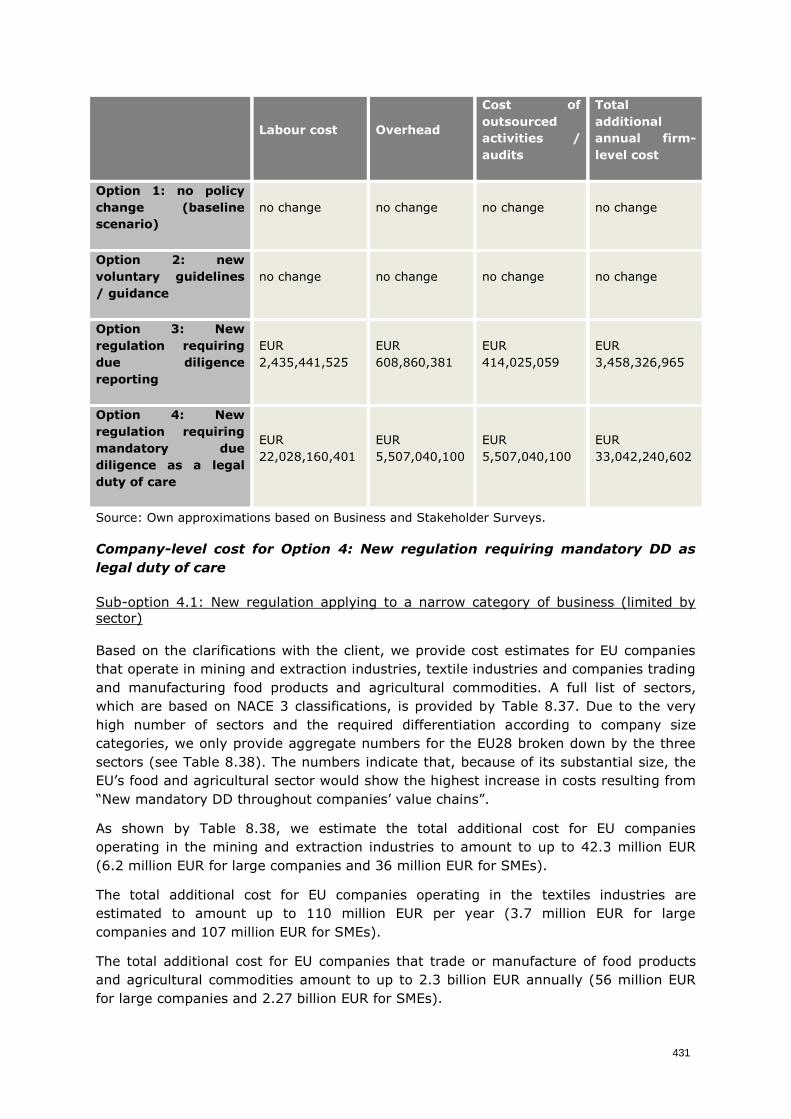

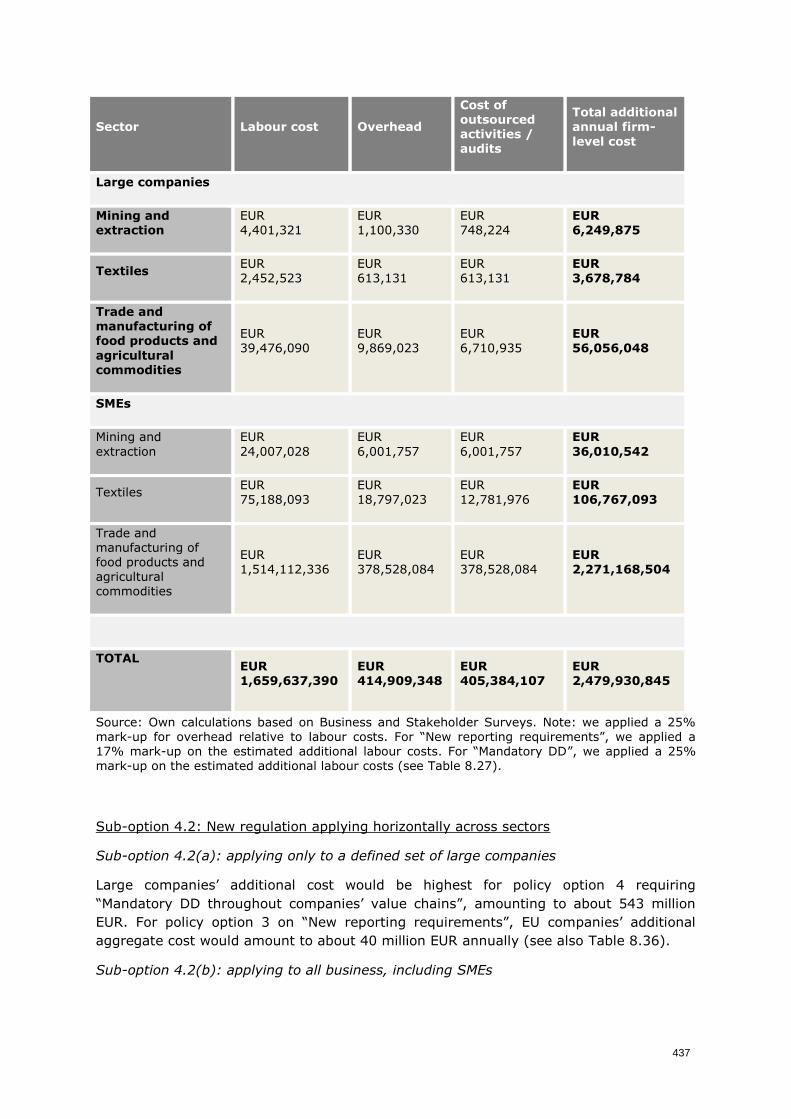

3.1.2 Company-level Costs .................................................................... 401

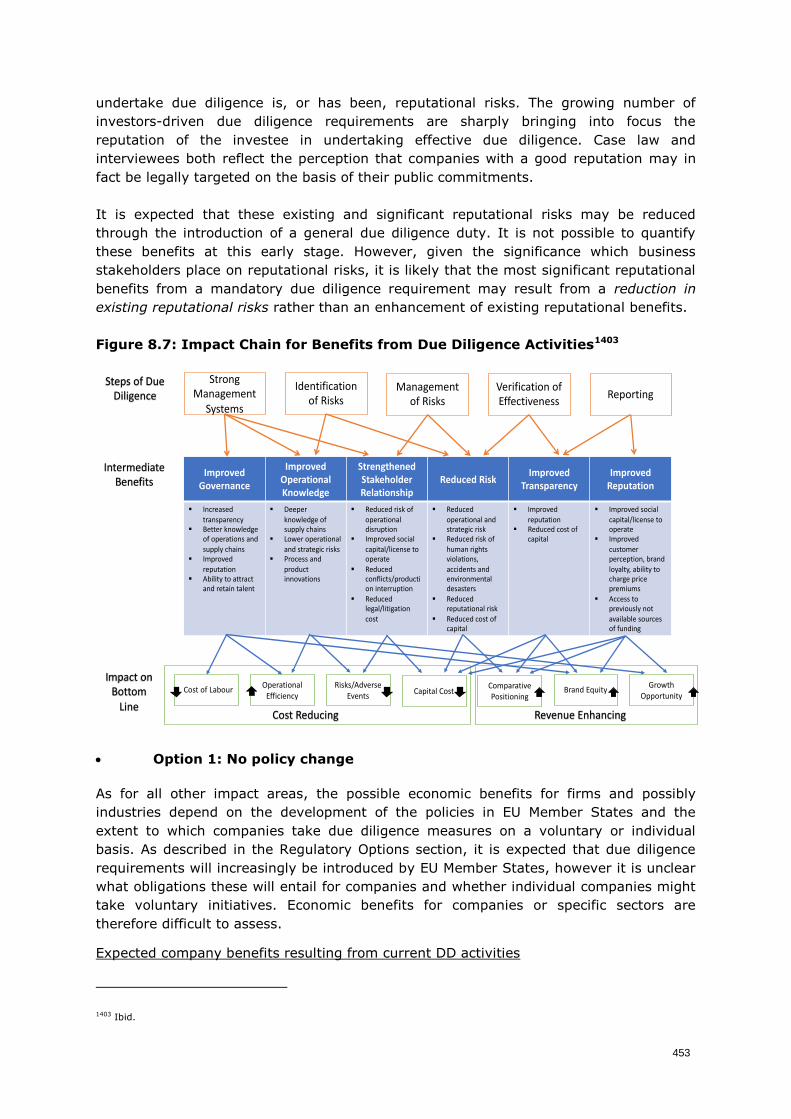

3.1.3 Company-level Benefits ................................................................. 448

3.1.4 Comparison of options and final assessment .................................... 470

3.2 Impacts on non-Economic spheres: Social, Human Rights and Environmental Impacts, and Impacts on Public Administration ............................................. 472

3.2.1 General remarks and description of impact areas ............................. 472

3.2.2 Assessment of impacts by policy option ........................................... 476

3.2.3 Comparison of options and final assessment .................................... 548

4. GLOBAL COMPARISON OF REGULATORY OPTIONS .................................................. 556

12

List of Tables

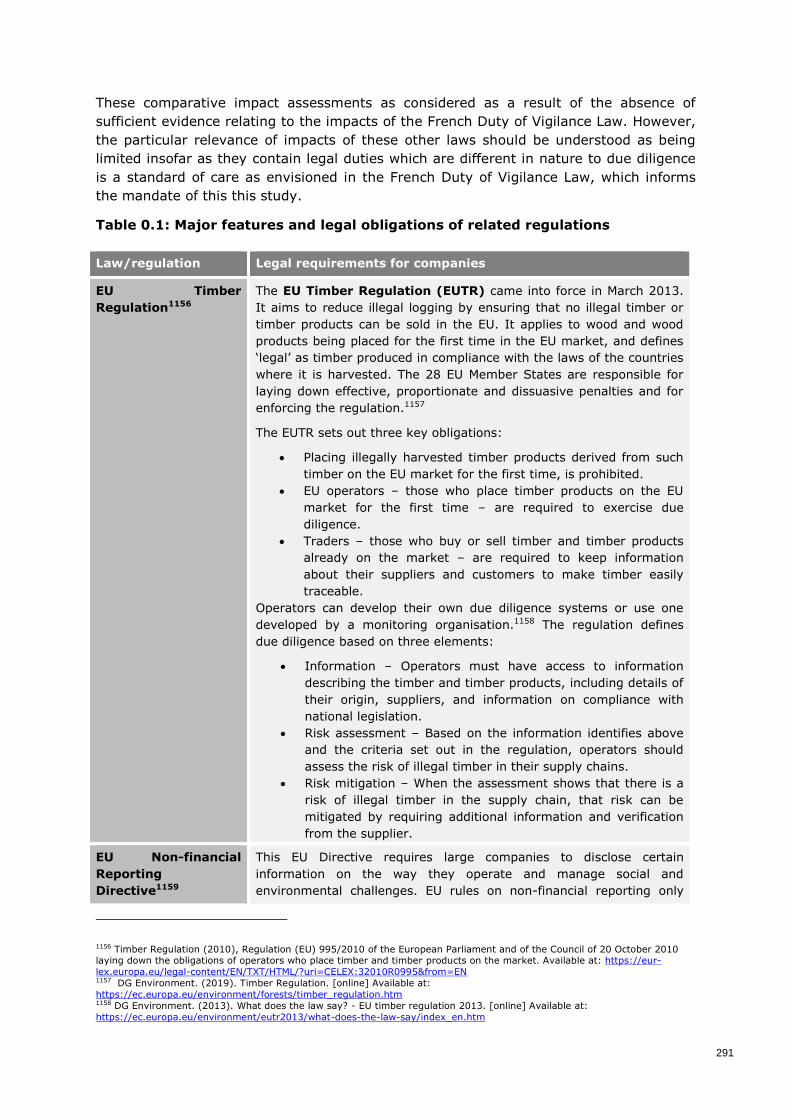

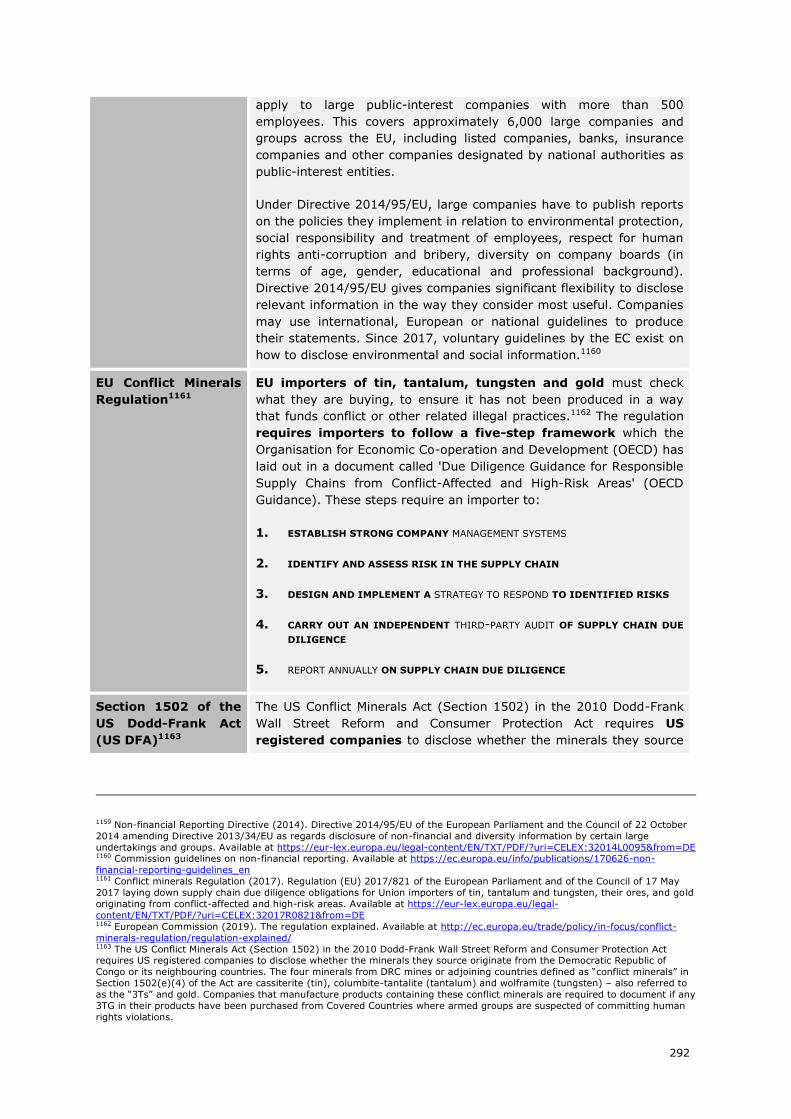

Table 0.1: Major features and legal obligations of related regulations ..................................... 291

Table 0.1: Overview of options analysed in relevant EU impact assessments ........................... 295

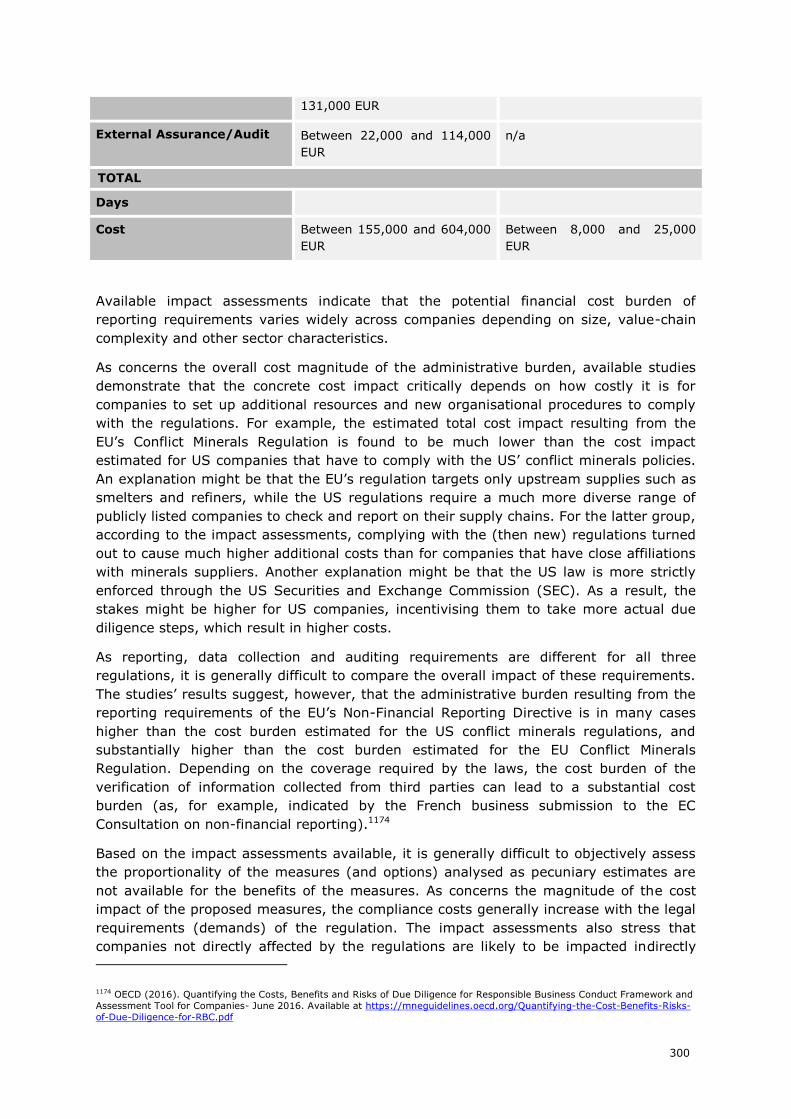

Table 0.2: Summary of the costs by company for different costs types as estimated for the EU’s

Non-financial Reporting Directive ................................................................................ 299

Table 0.3: The impact of due diligence regulations on companies’ competitiveness................... 316

Table 0.4: The impact of due diligence regulations on SMEs .................................................. 319

Table 0.5: Potential social impacts resulting from disclosure and due diligence regulations ........ 322

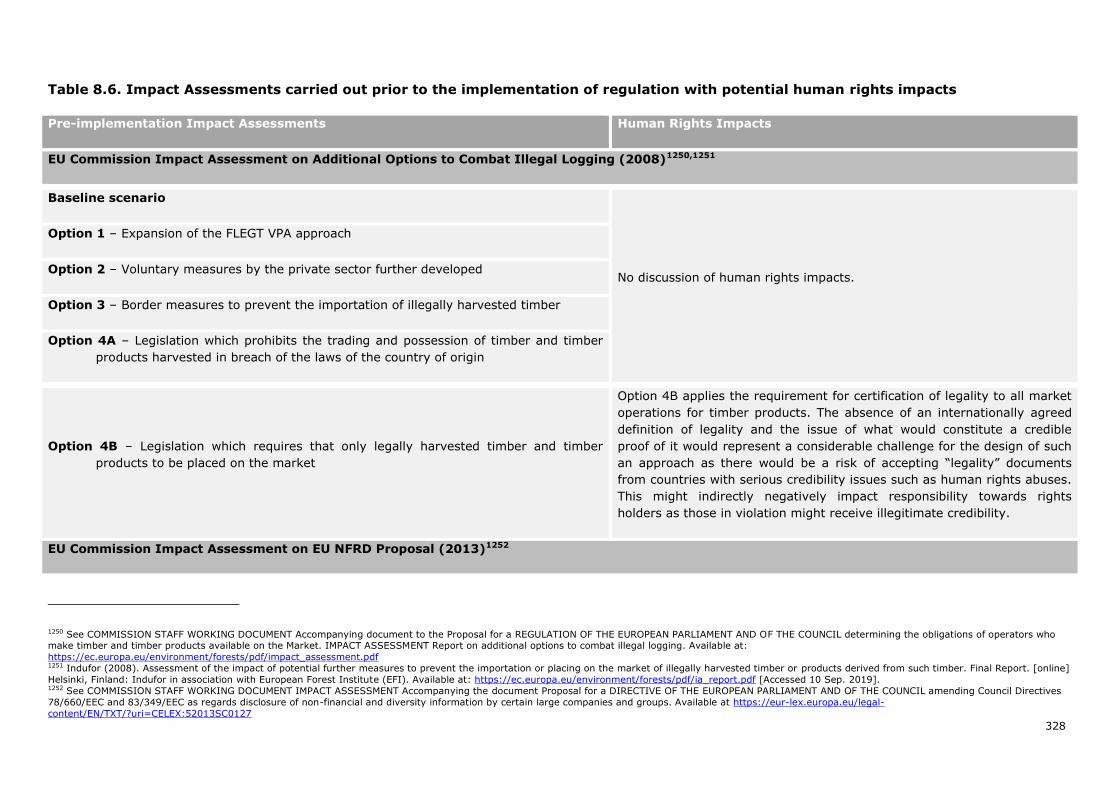

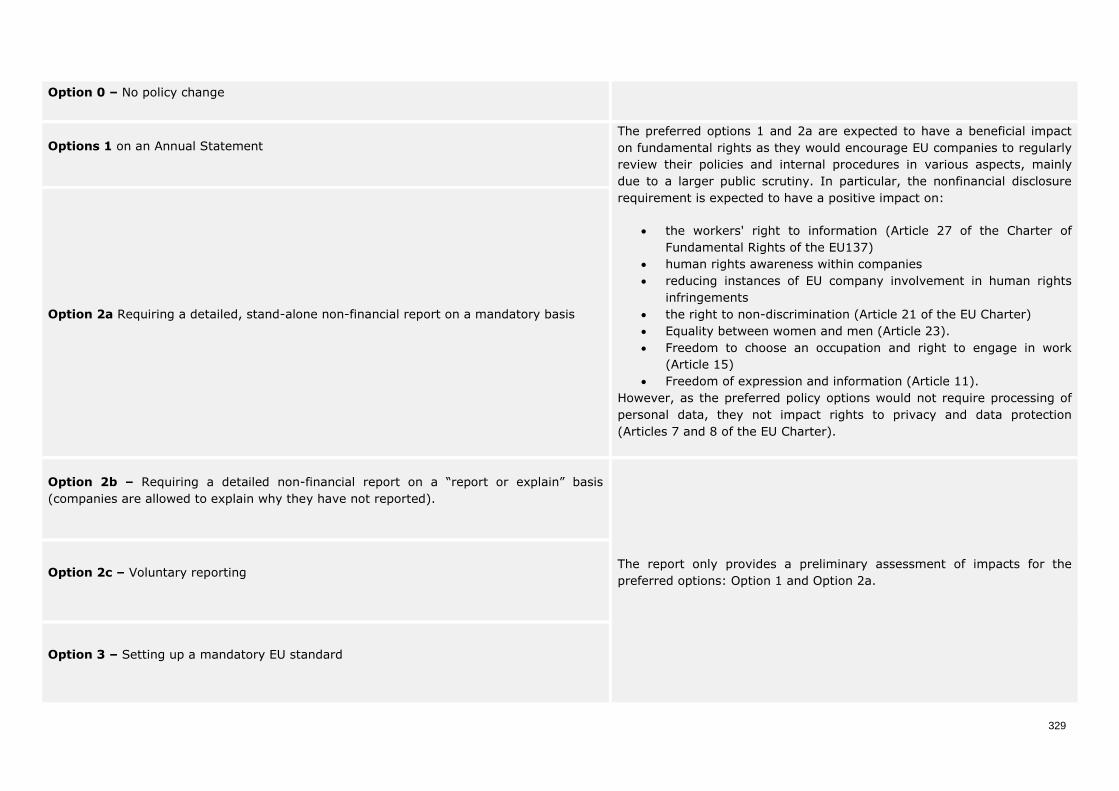

Table 0.6. Impact Assessments carried out prior to the implementation of regulation with potential

human rights impacts ............................................................................................... 328

Table 0.7. Post-implementation Impact Assessments............................................................ 333

Table 0.8: Literature on Positive HR Impacts of Voluntary Due Diligence Approaches ................ 336

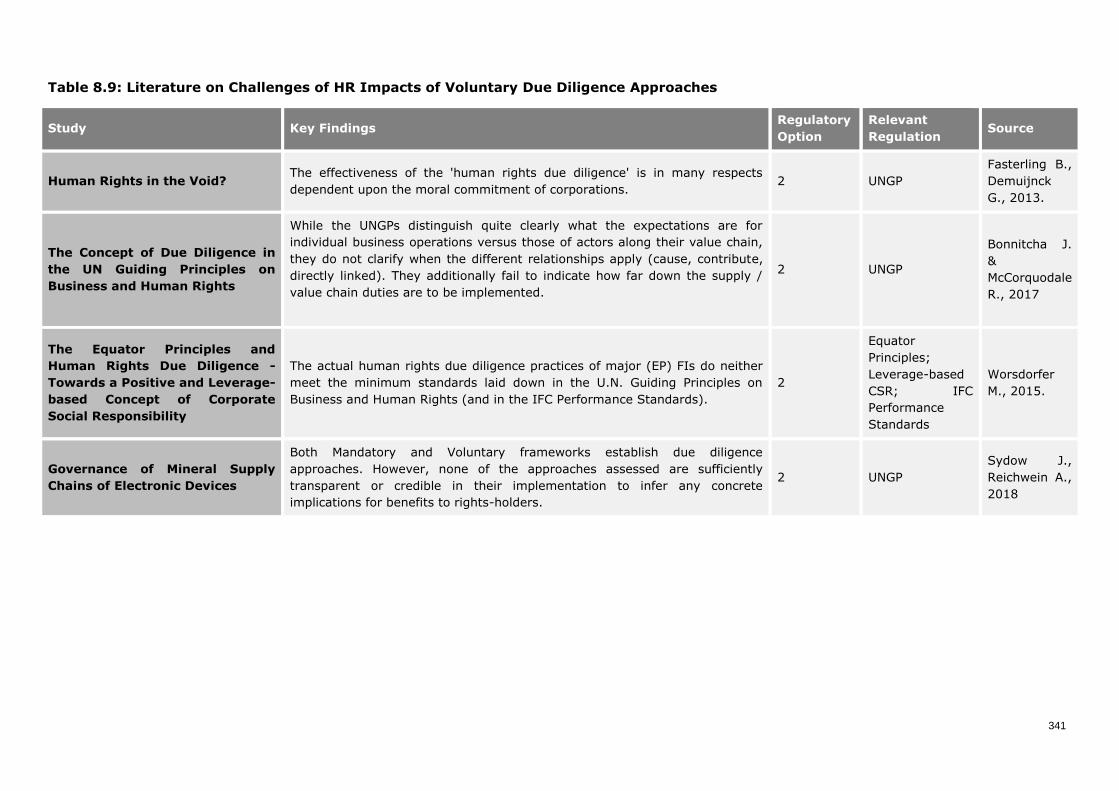

Table 0.9: Literature on Challenges of HR Impacts of Voluntary Due Diligence Approaches ........ 341

Table 0.10: HR Scope and Credibility of Voluntary Approaches .............................................. 343

Table 0.11: Literature on Positive HR Impacts of Mandatory Reporting Requirements as Due

Diligence Approaches ................................................................................................ 345

Table 0.12: Literature on Challenges of HR Impacts of Mandatory Reporting Requirements as Due

Diligence ................................................................................................................. 348

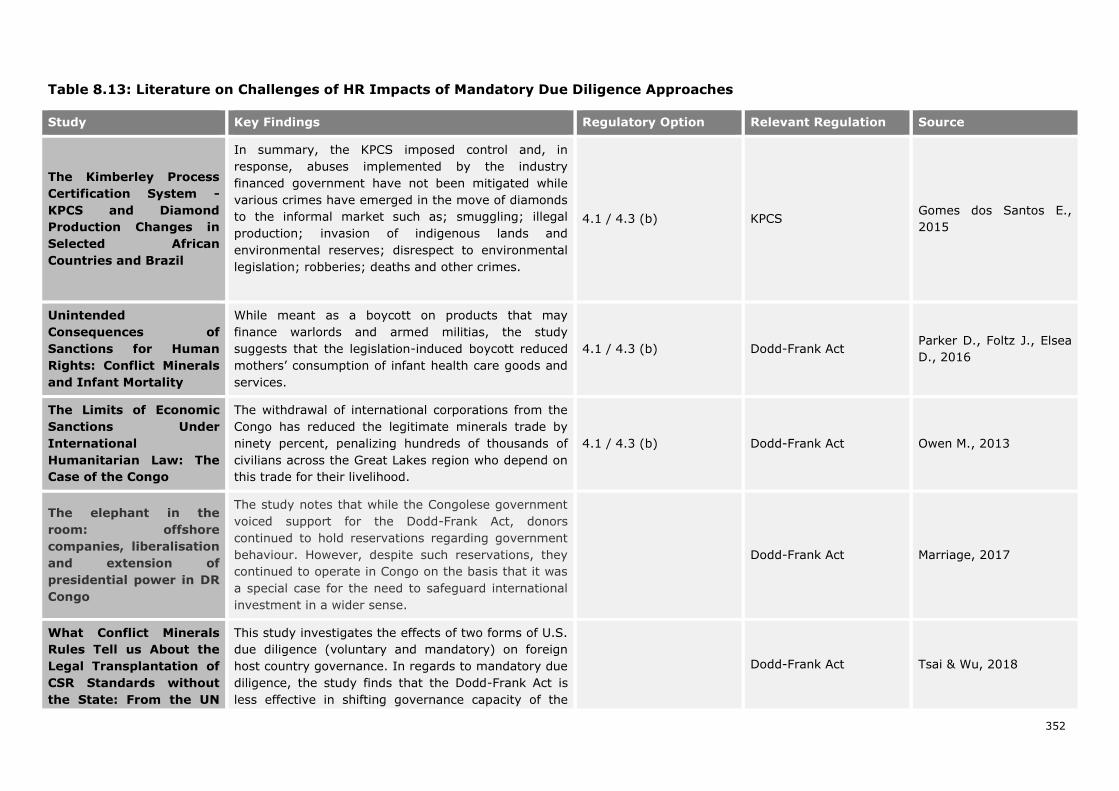

Table 0.13: Literature on Challenges of HR Impacts of Mandatory Due Diligence Approaches .... 352

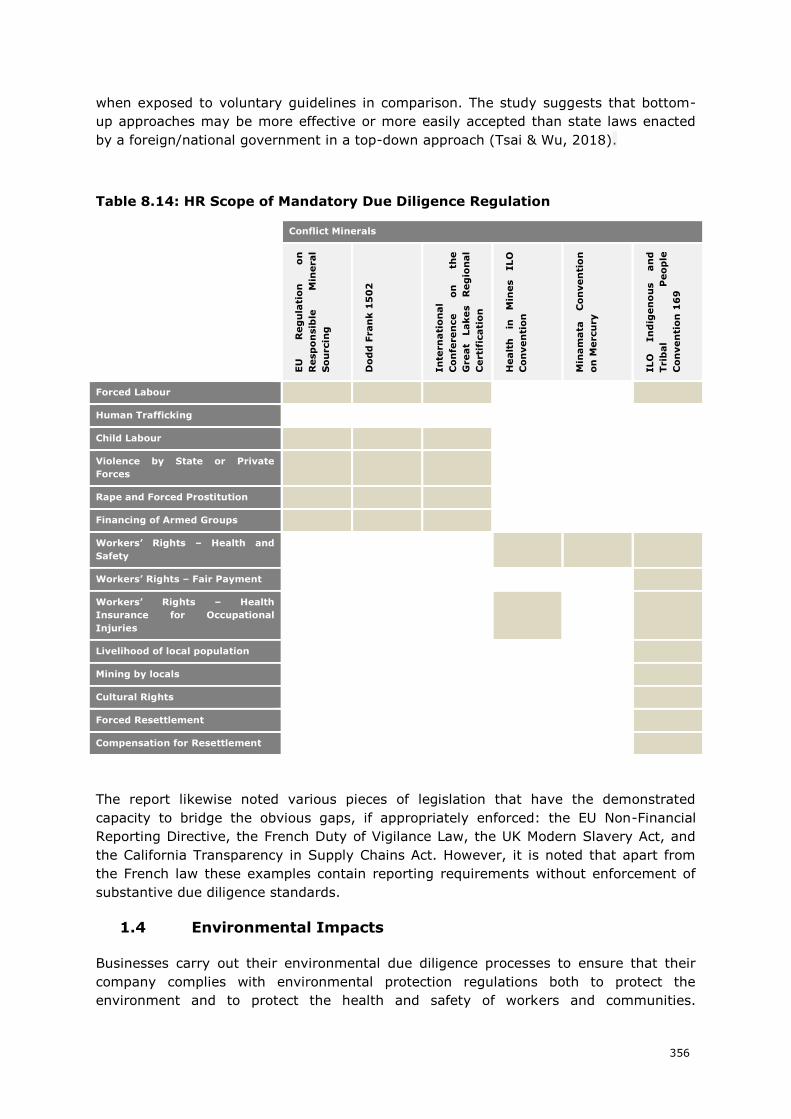

Table 0.14: HR Scope of Mandatory Due Diligence Regulation ............................................... 356

Table 0.15. Impact Assessments carried out prior to the implementation of regulation with

potential environmental impacts ................................................................................. 362

Table 0.16. Post-implementation Impact Assessments .......................................................... 367

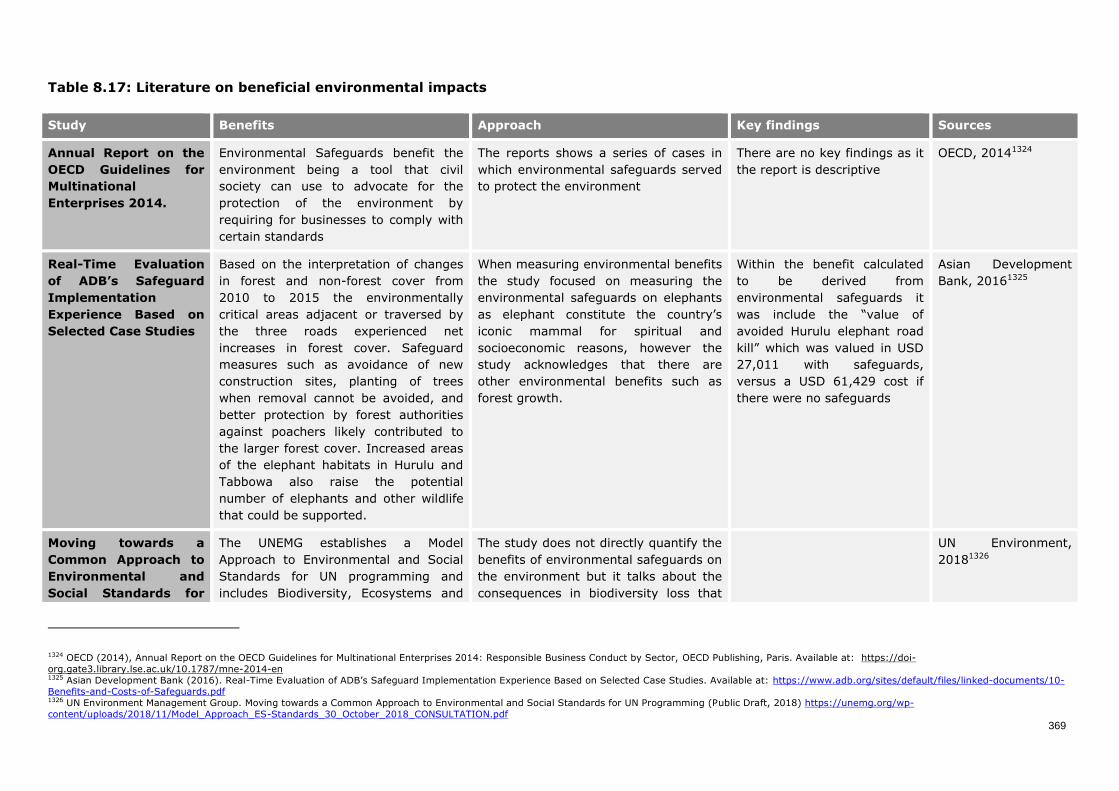

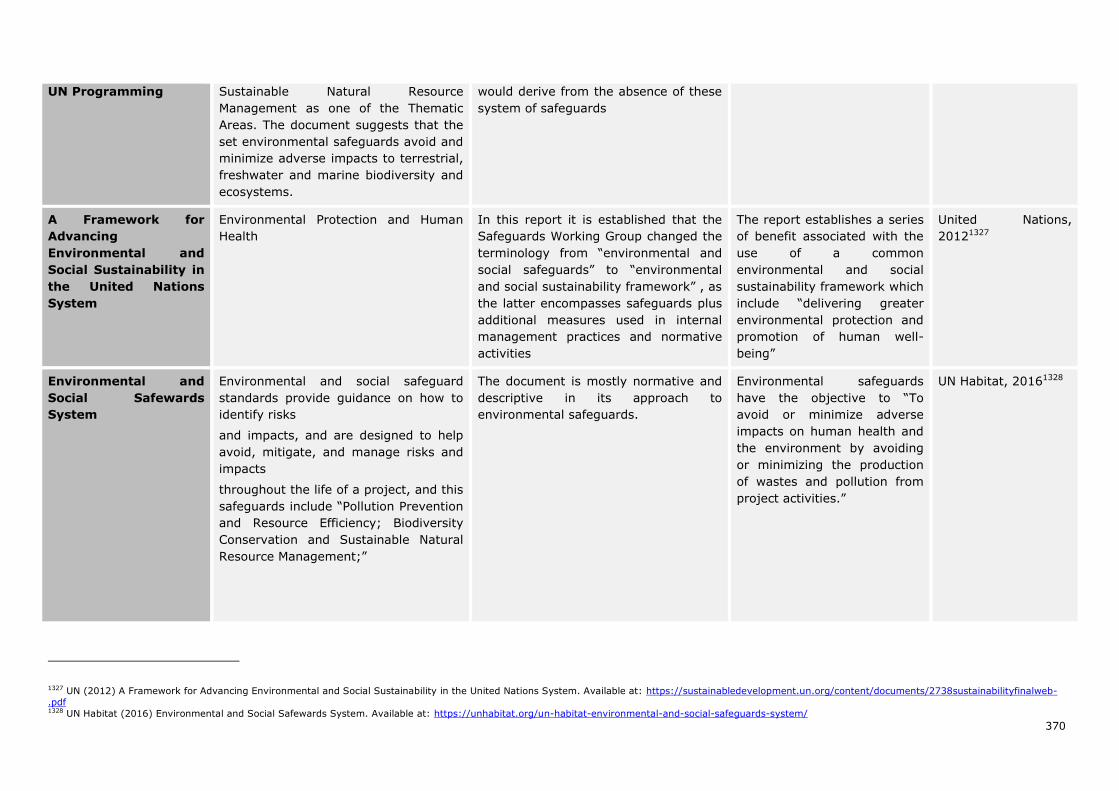

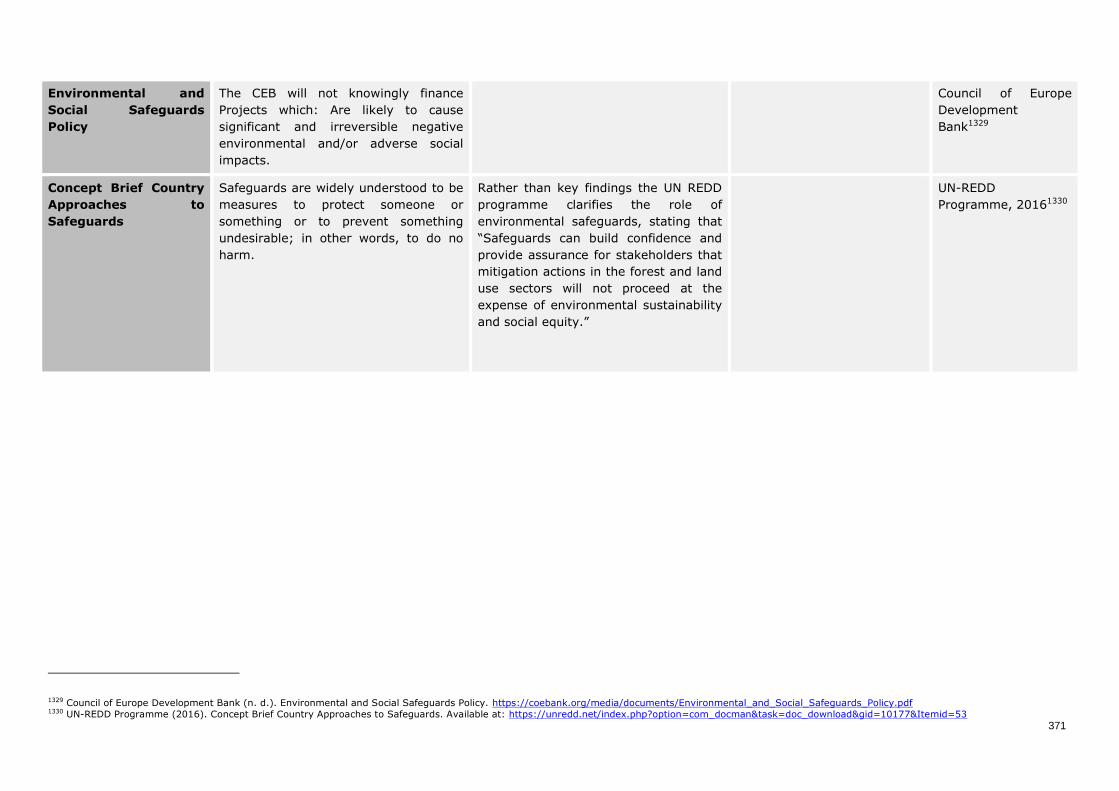

Table 0.17: Literature on beneficial environmental impacts ................................................... 369

Table 0.18: Literature on challenges to existing environmental due diligence ........................... 372

Table 0.19: Estimated economic cost for EU and MS public authorities from the EU Conflict

Minerals Regulation................................................................................................... 375

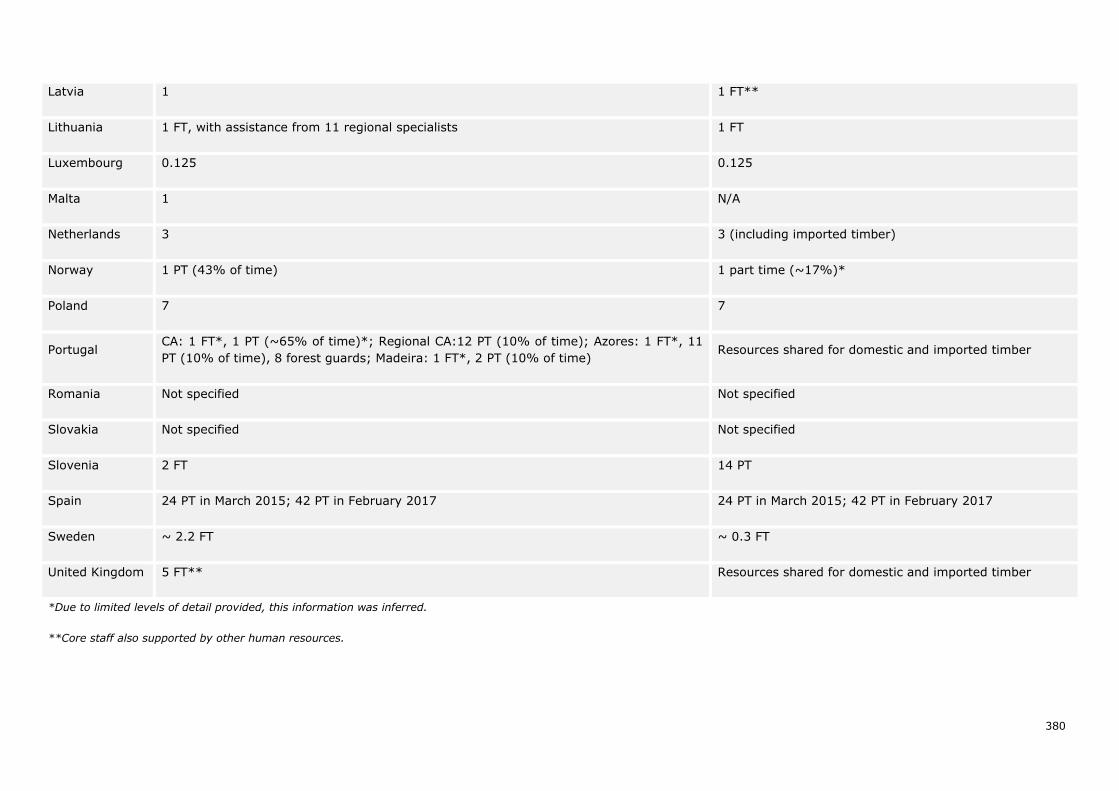

Table 0.20 Human resources available for the implementation and enforcement of the EUTR as

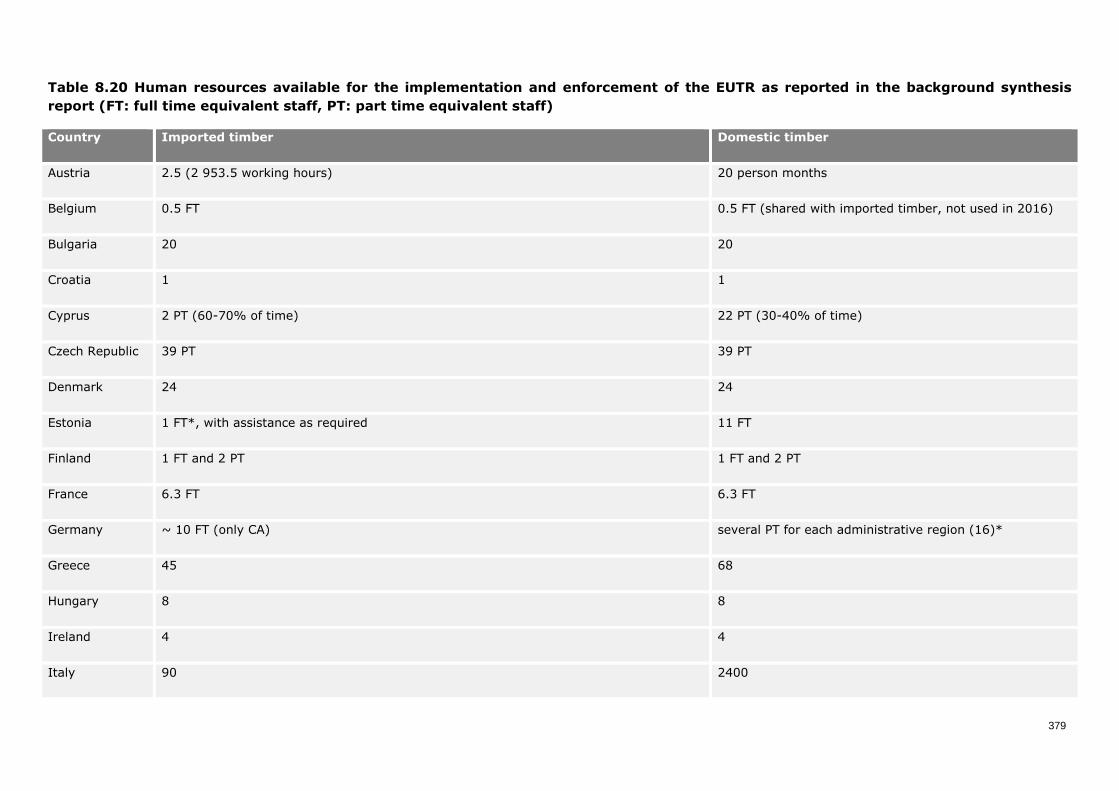

reported in the background synthesis report (FT: full time equivalent staff, PT: part time

equivalent staff) ....................................................................................................... 379

Table 0.21 Estimated costs for authorities in the Seveso III Impact Assessment ...................... 383

Table 0.22 Estimated impacts on public authorities in the Impact Assessment of the EU Directive

on the protection of the environment through criminal law ............................................ 385

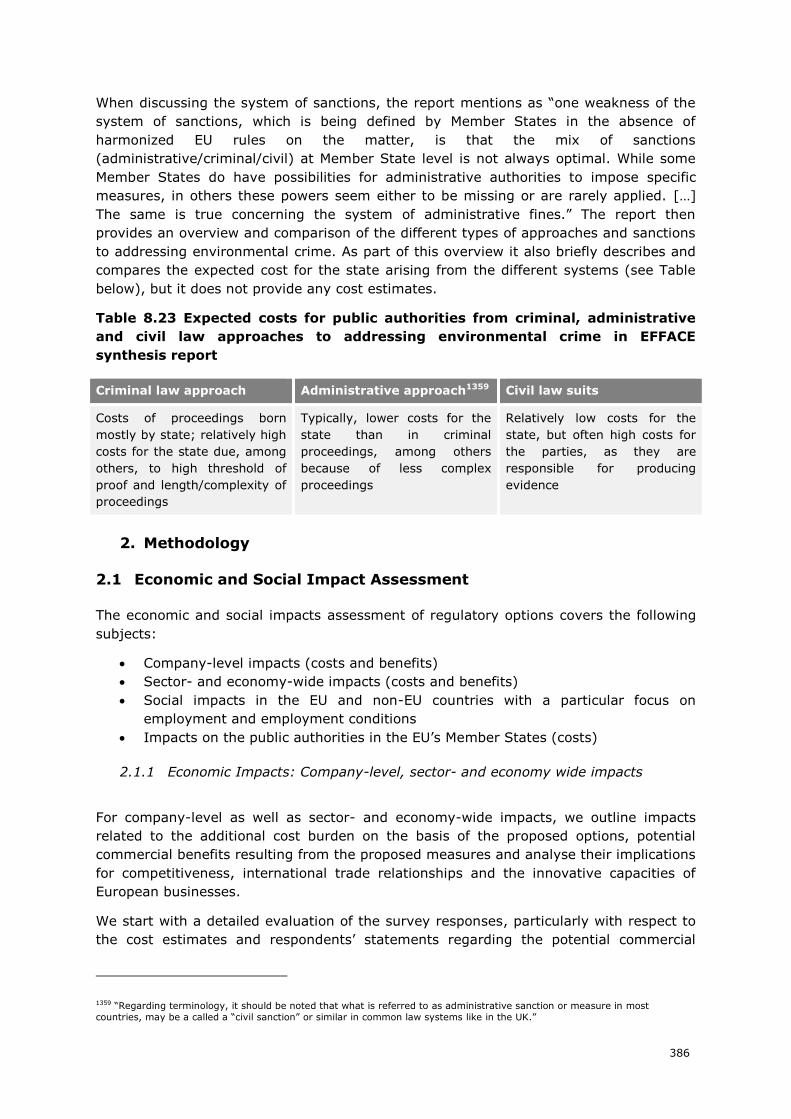

Table 0.23 Expected costs for public authorities from criminal, administrative and civil law

approaches to addressing environmental crime in EFFACE synthesis report ...................... 386

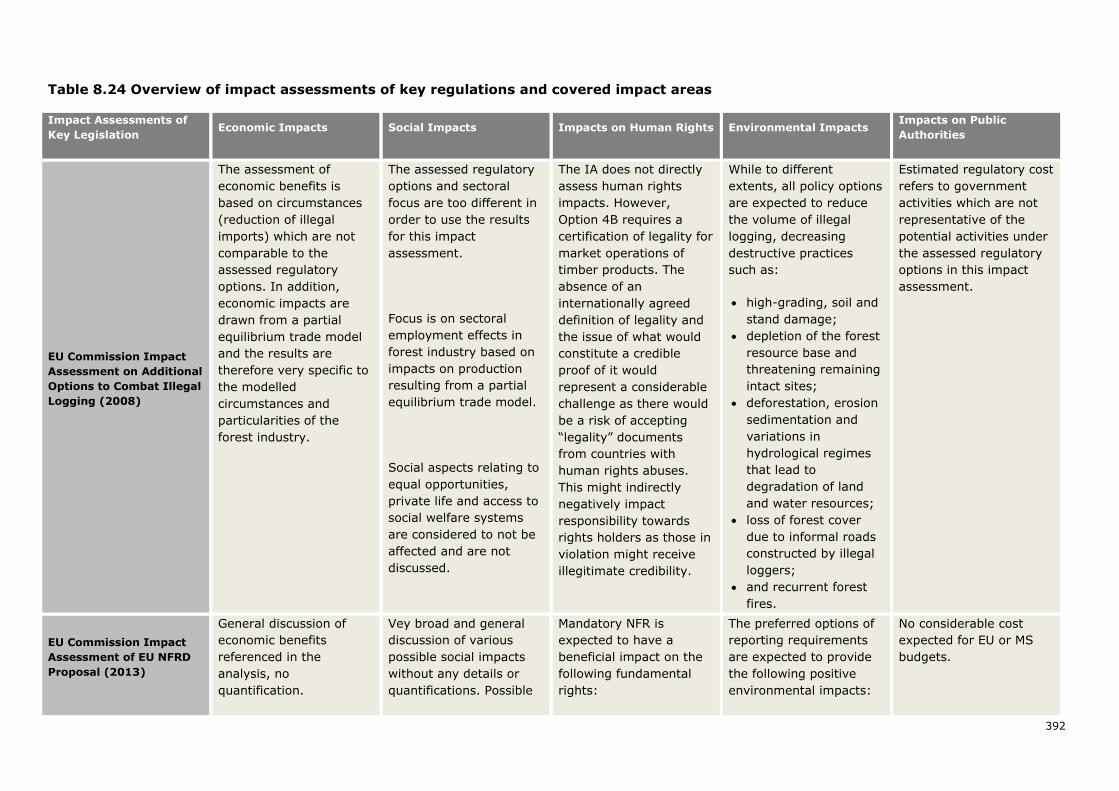

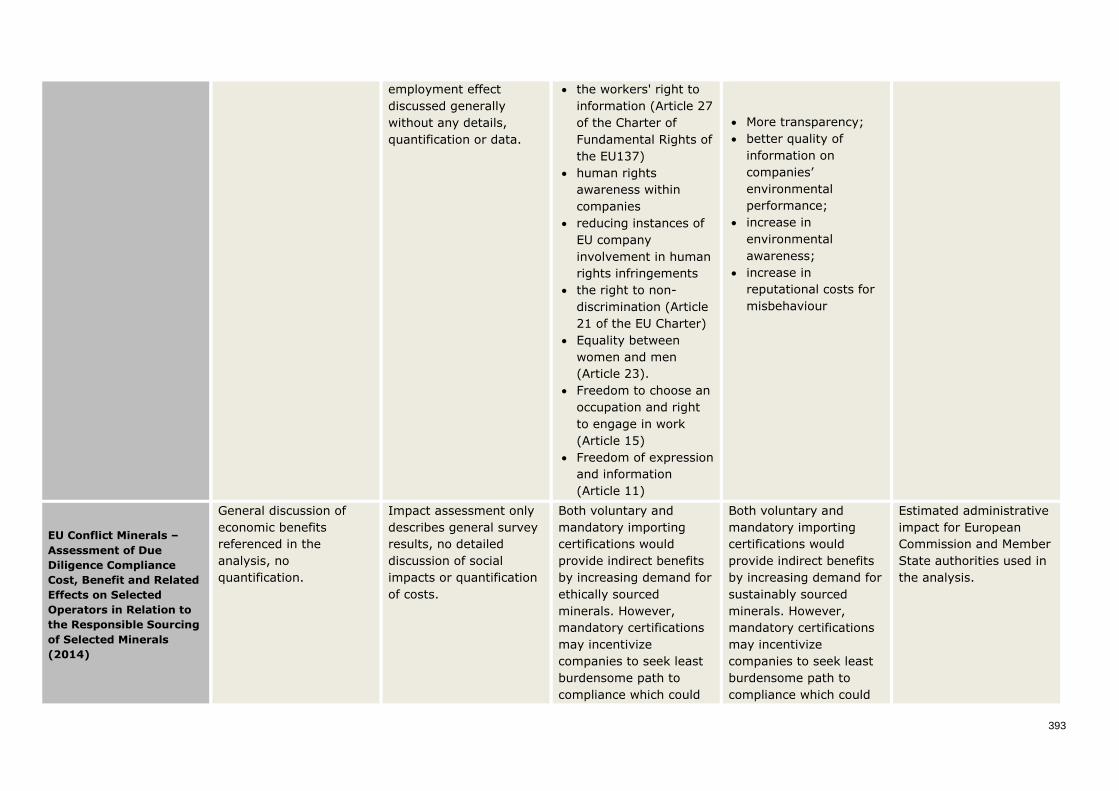

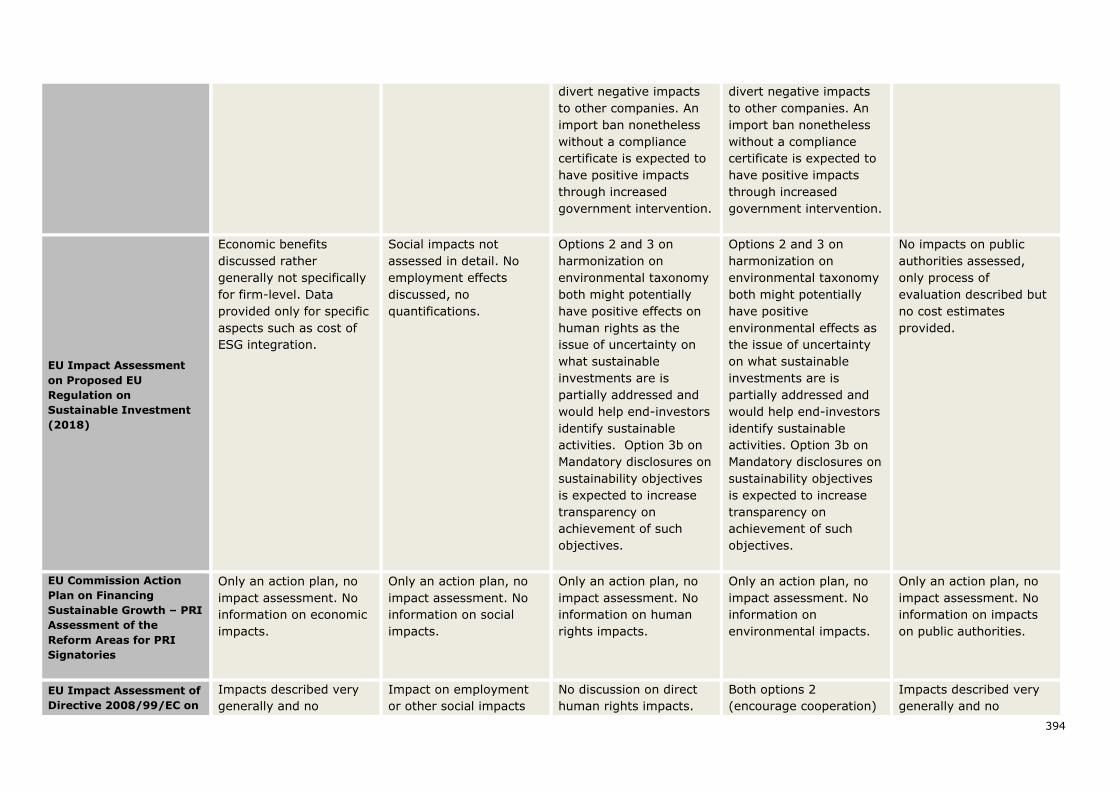

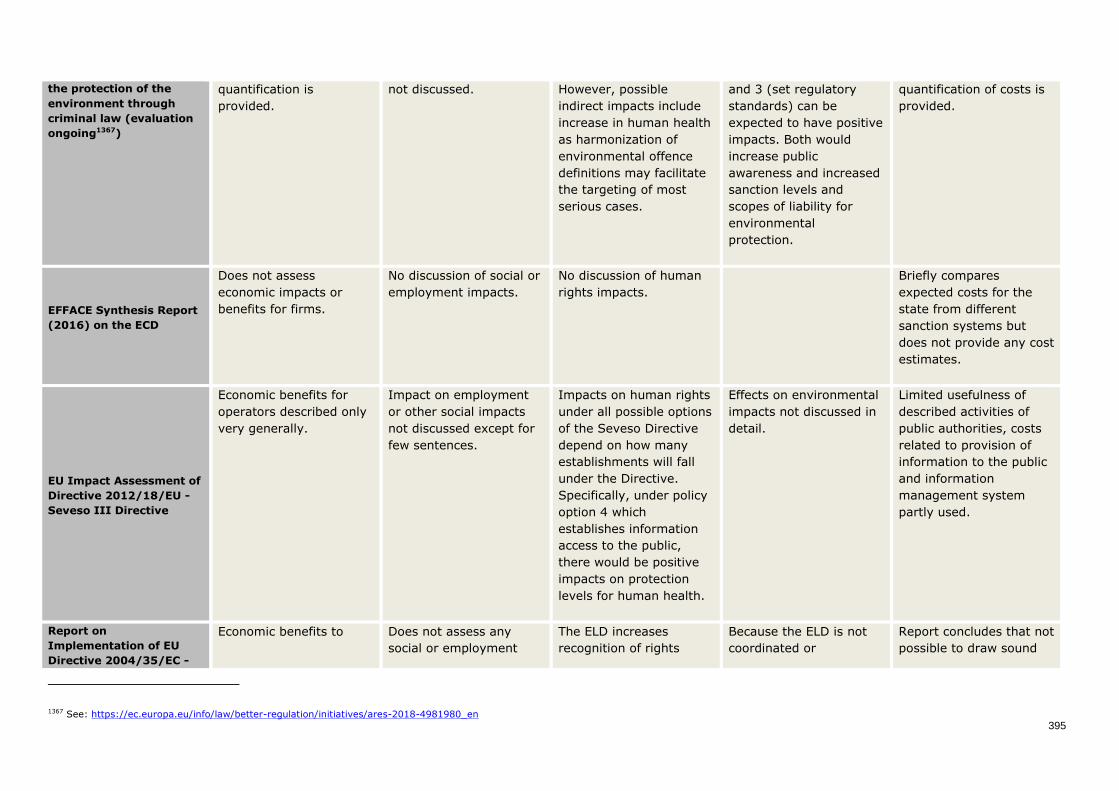

Table 0.24 Overview of impact assessments of key regulations and covered impact areas ......... 392

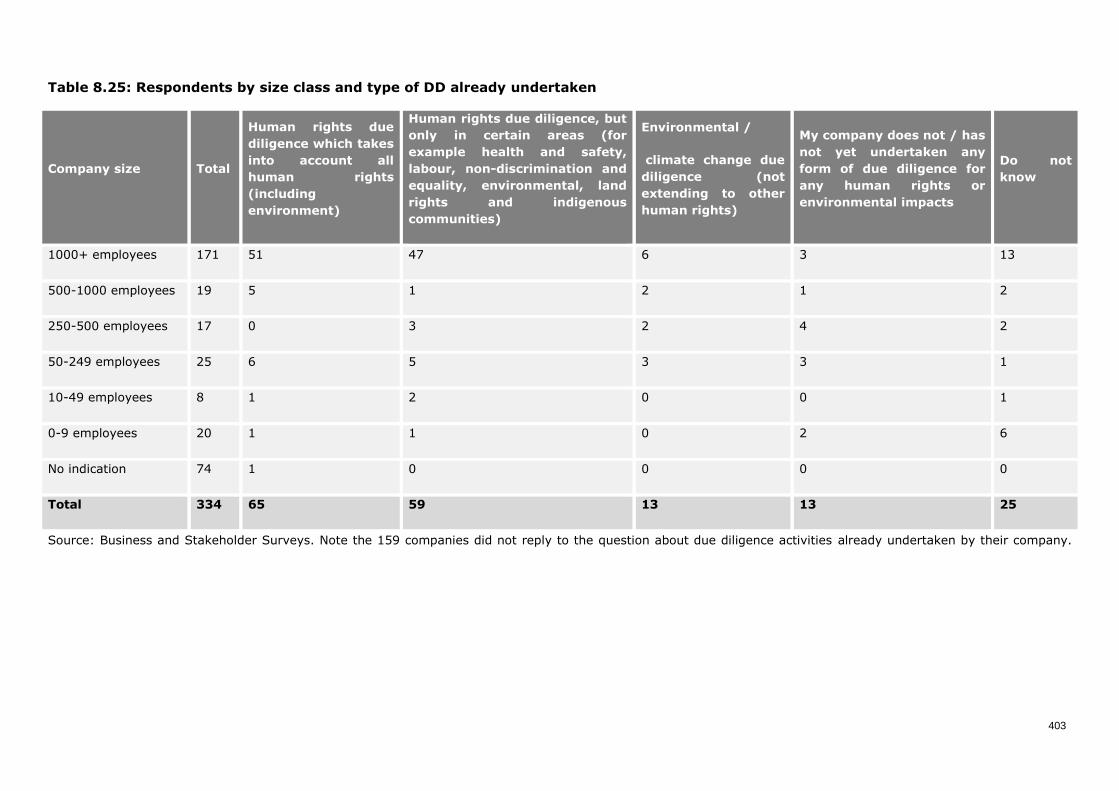

Table 0.25: Respondents by size class and type of DD already undertaken .............................. 403

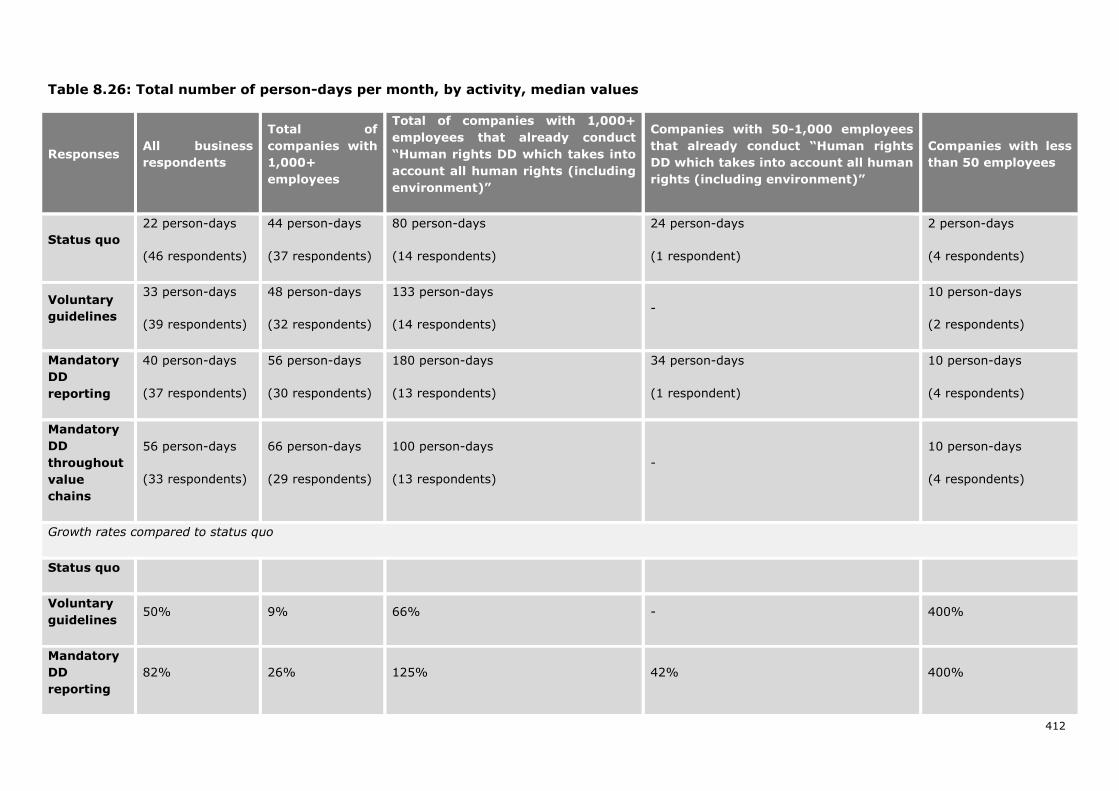

Table 0.26: Total number of person-days per month, by activity, median values ...................... 412

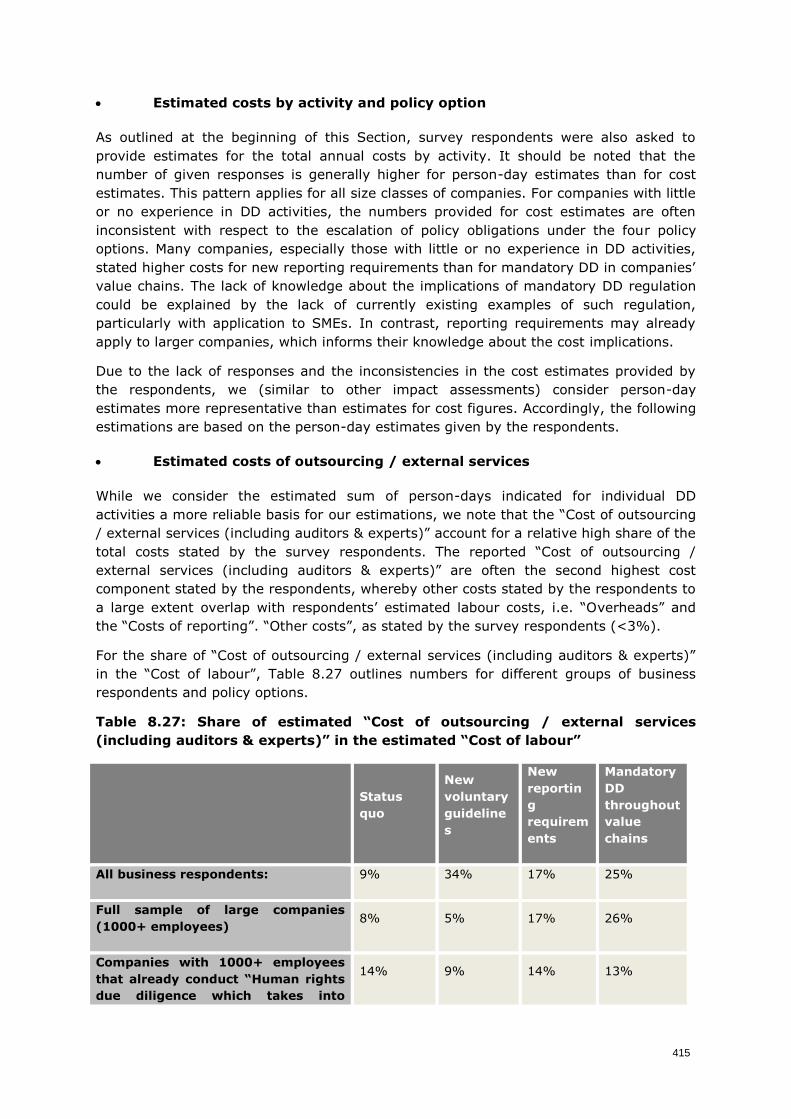

Table 0.27: Share of estimated “Cost of outsourcing / external services (including auditors &

experts)” in the estimated “Cost of labour” .................................................................. 415

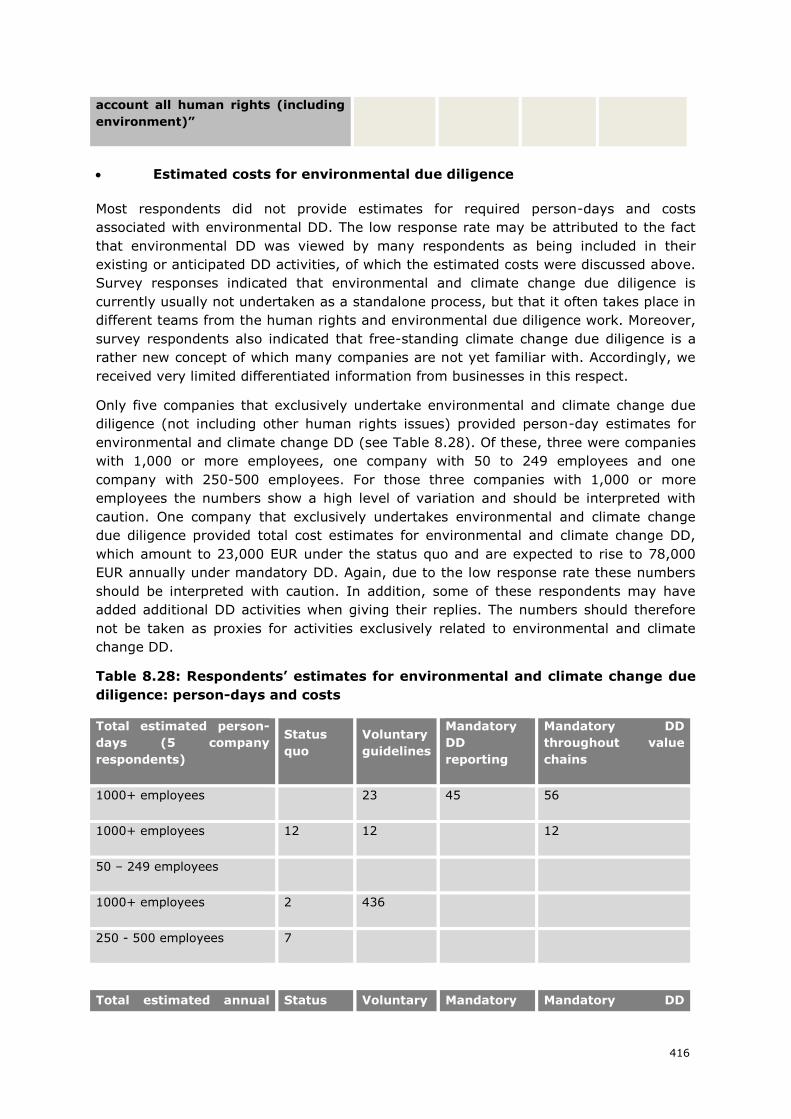

Table 0.28: Respondents’ estimates for environmental and climate change due diligence: person-

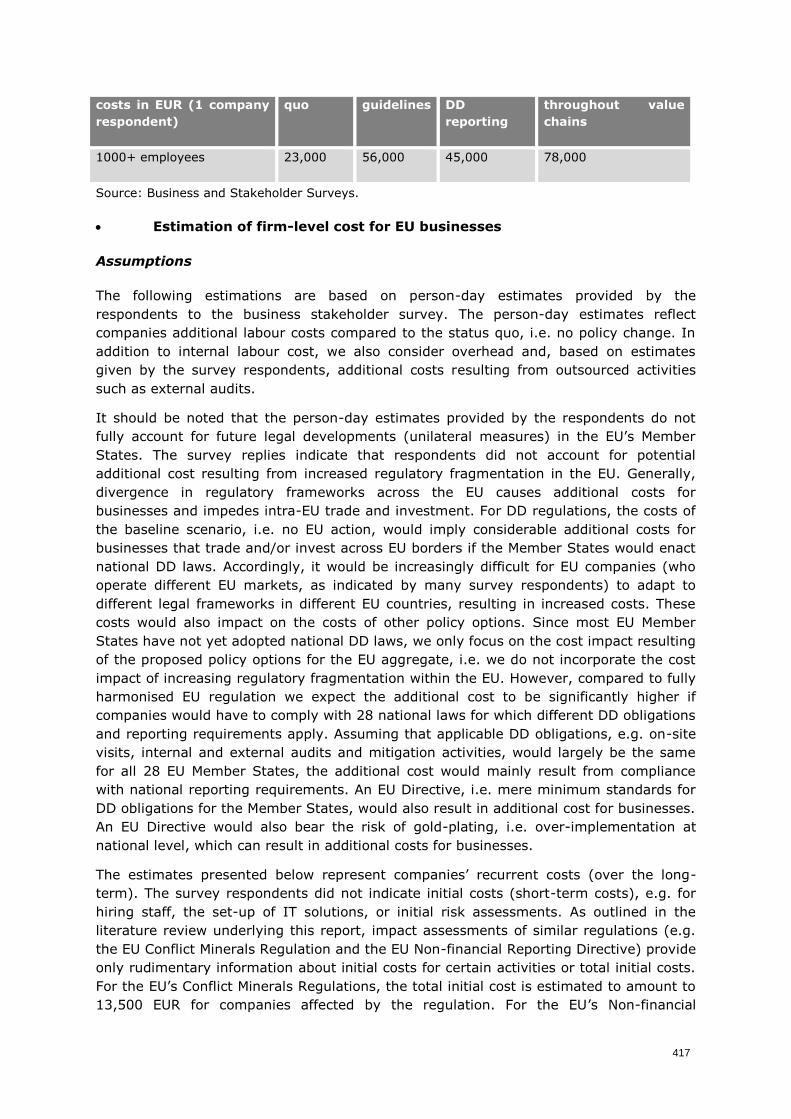

days and costs ......................................................................................................... 416

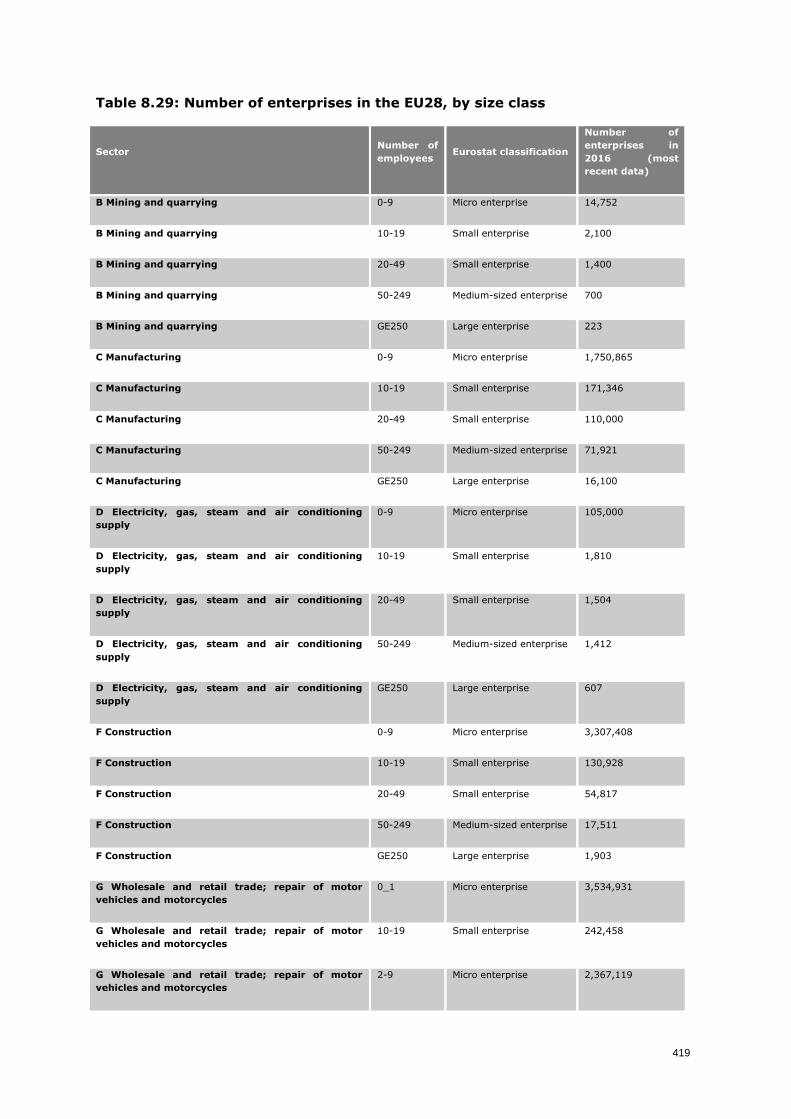

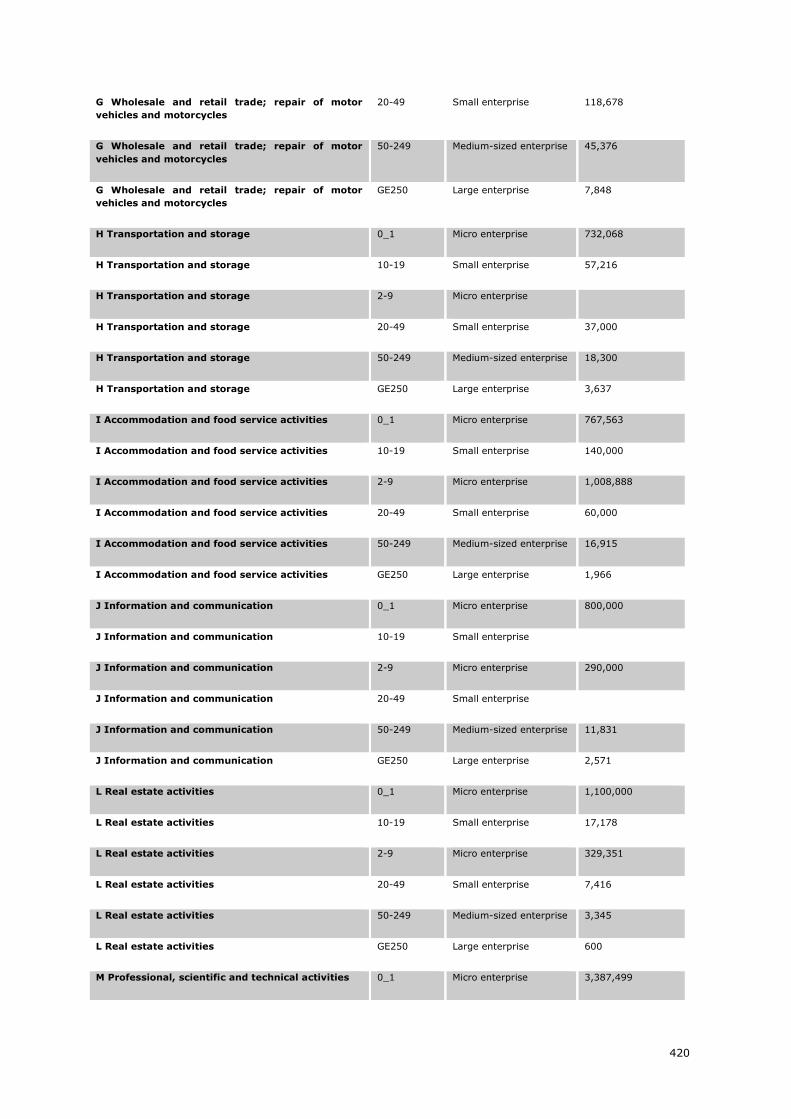

Table 0.29: Number of enterprises in the EU28, by size class ................................................ 419

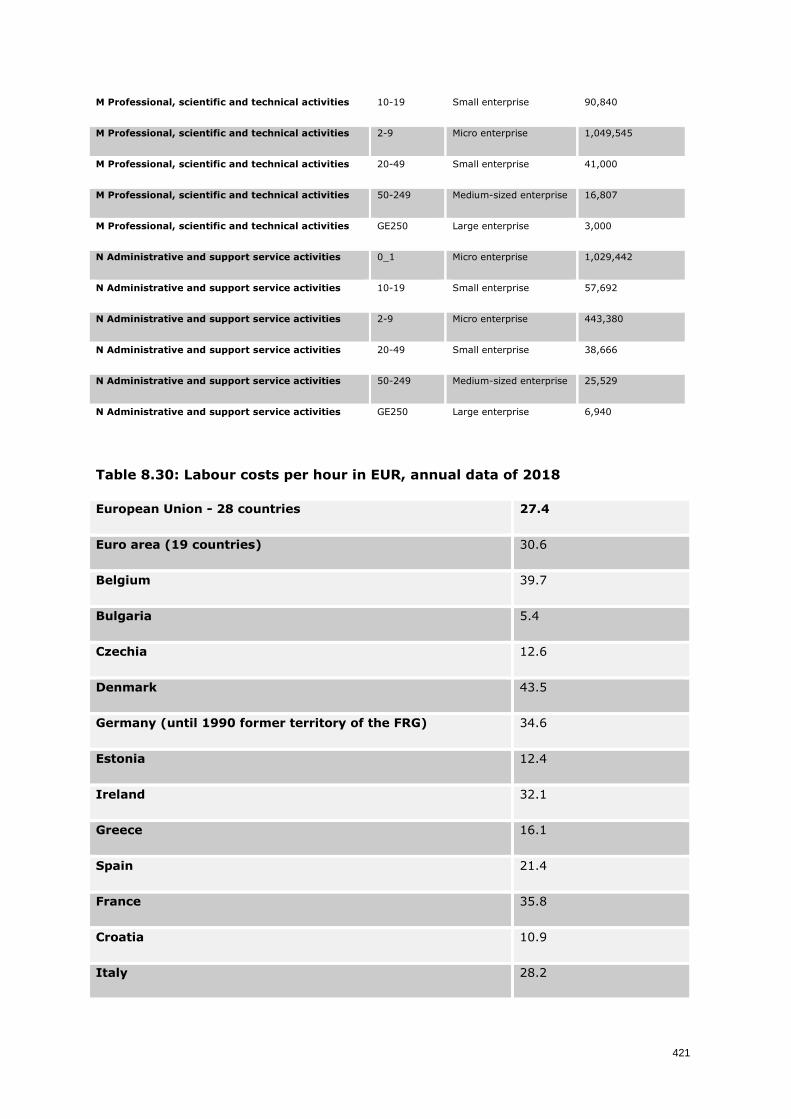

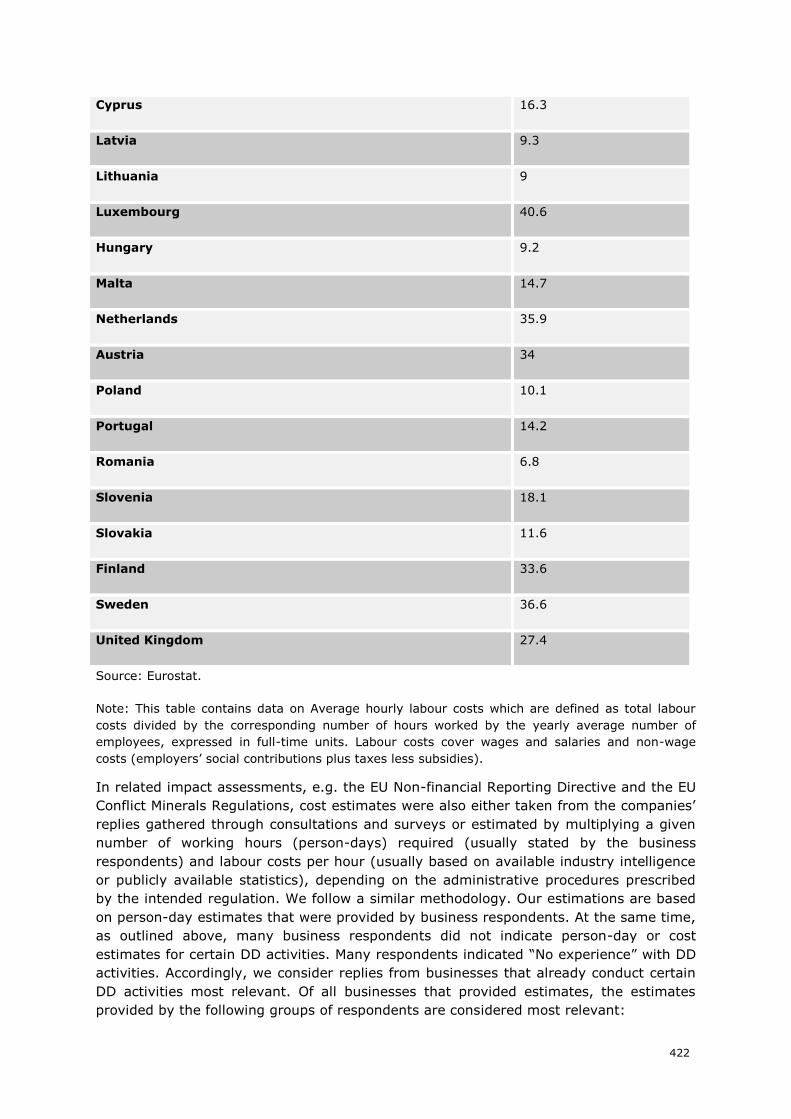

Table 0.30: Labour costs per hour in EUR, annual data of 2018 ............................................. 421

Table 0.31: Firm-level cost based on revenues approximation: large companies with more than

250 employees ......................................................................................................... 424

Table 0.32: Firm-level cost based on revenues approximation: companies with up to 249

employees ............................................................................................................... 425

Table 0.33: Additional firm-level cost as percentages of revenues, large companies vs. SMEs .... 427

Table 0.34: Overview of estimated additional labour cost excl. overhead and cost of outsourced

activities / audits, large companies vs. SMEs ................................................................ 428

Table 0.35: Overview of estimated additional labour cost incl. overhead and cost of outsourced

activities / audits, large companies vs. SMEs ................................................................ 429

13

Table 0.36: Estimated additional firm-level cost, EU aggregate .............................................. 430

Table 0.37: Overview of sectors: mining and extraction industries, food products and agricultural

commodities, textile industries – NACE Level 3 ............................................................. 432

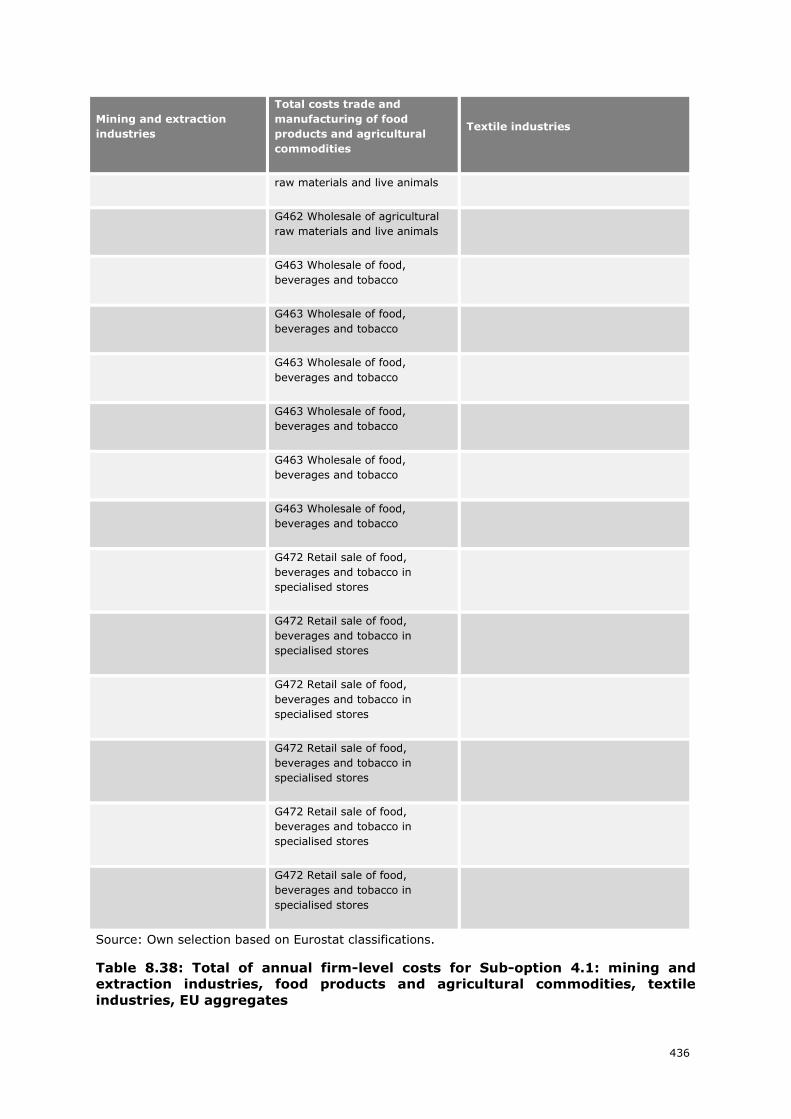

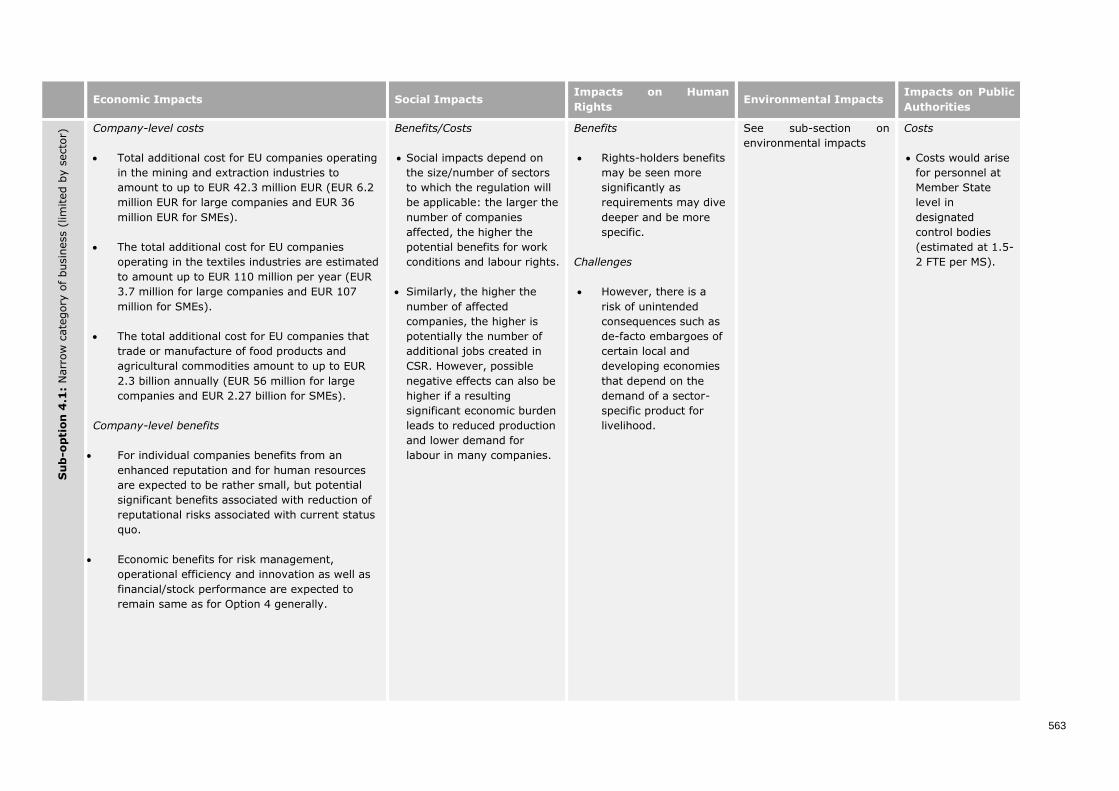

Table 0.38: Total of annual firm-level costs for Sub-option 4.1: mining and extraction industries,

food products and agricultural commodities, textile industries, EU aggregates .................. 436

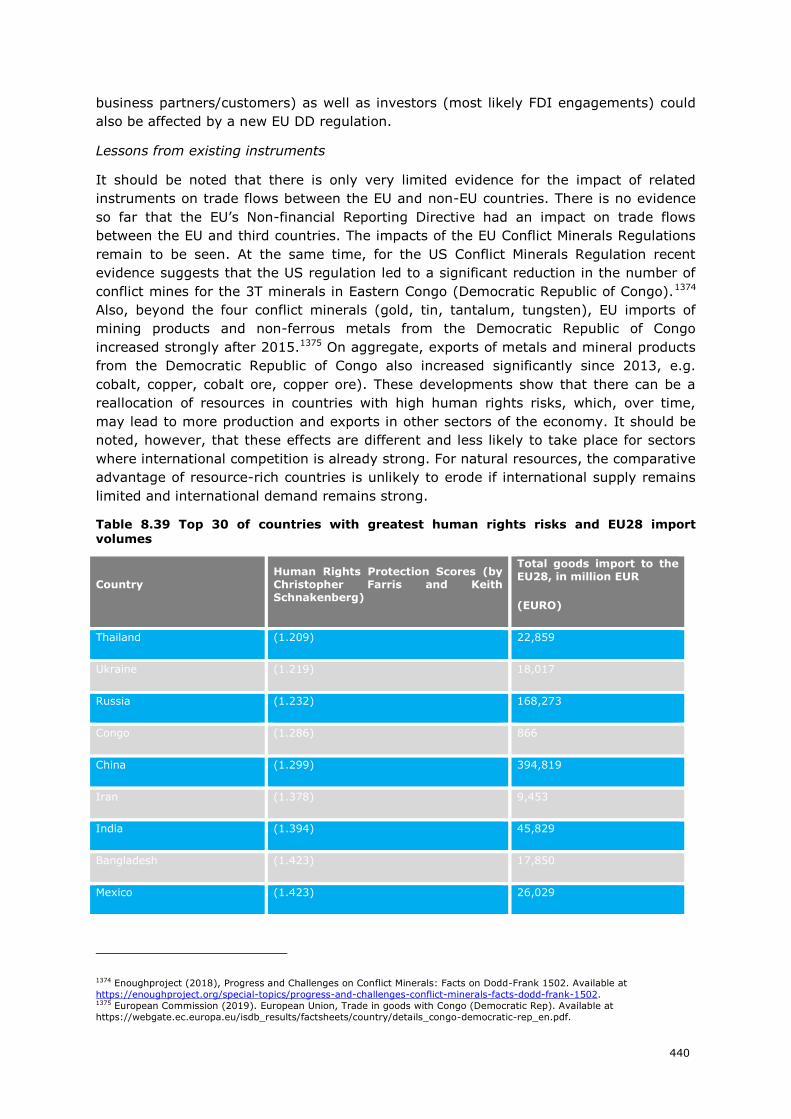

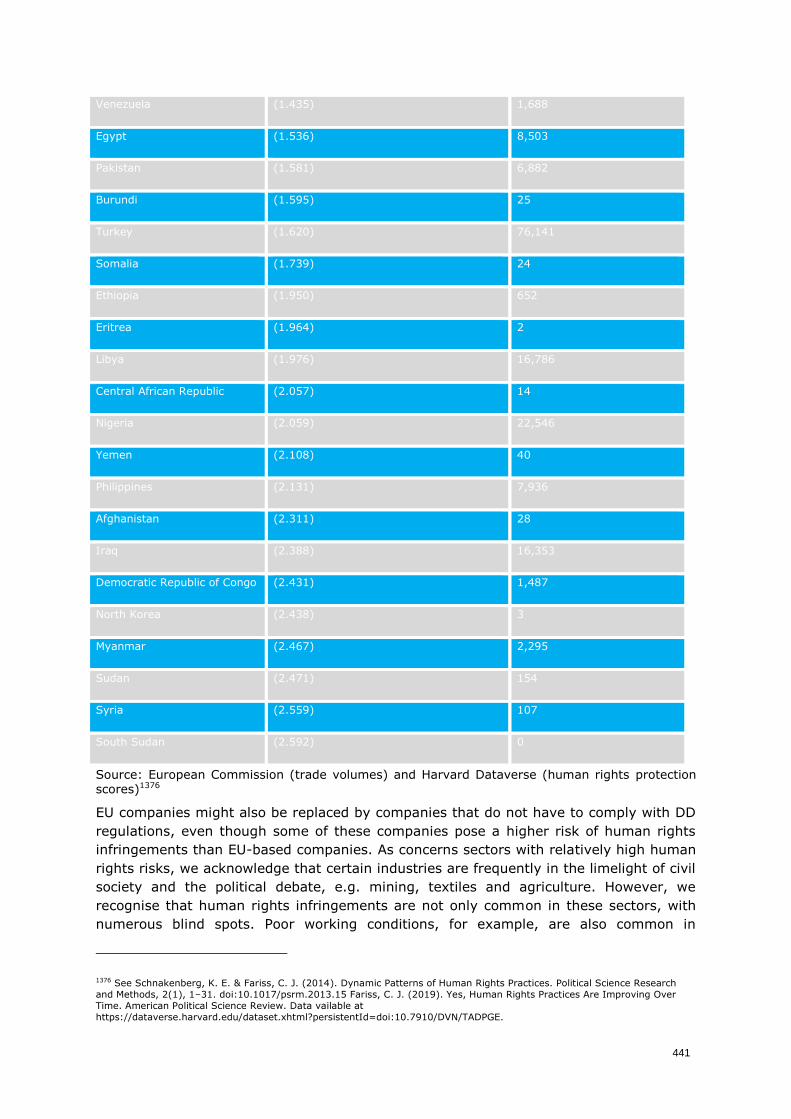

Table 0.39 Top 30 of countries with greatest human rights risks and EU28 import volumes ....... 440

Table 0.40 Respondents’ replies regarding distortion of competition due to more equal standards

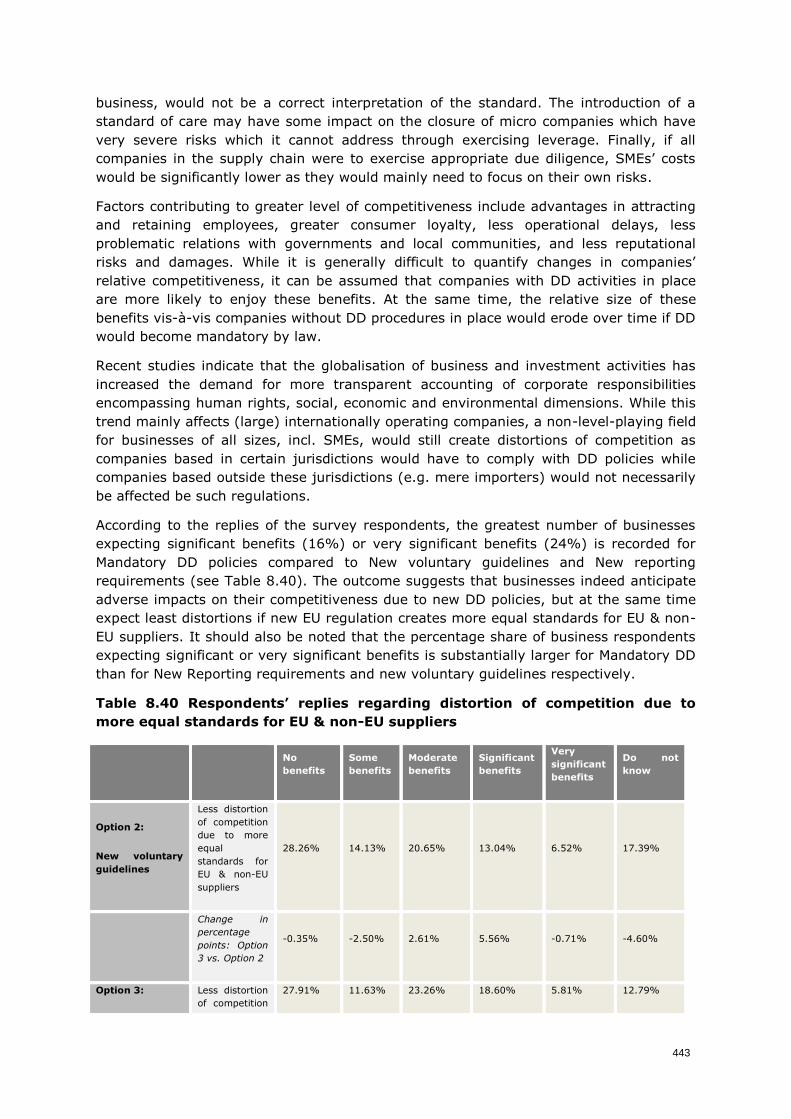

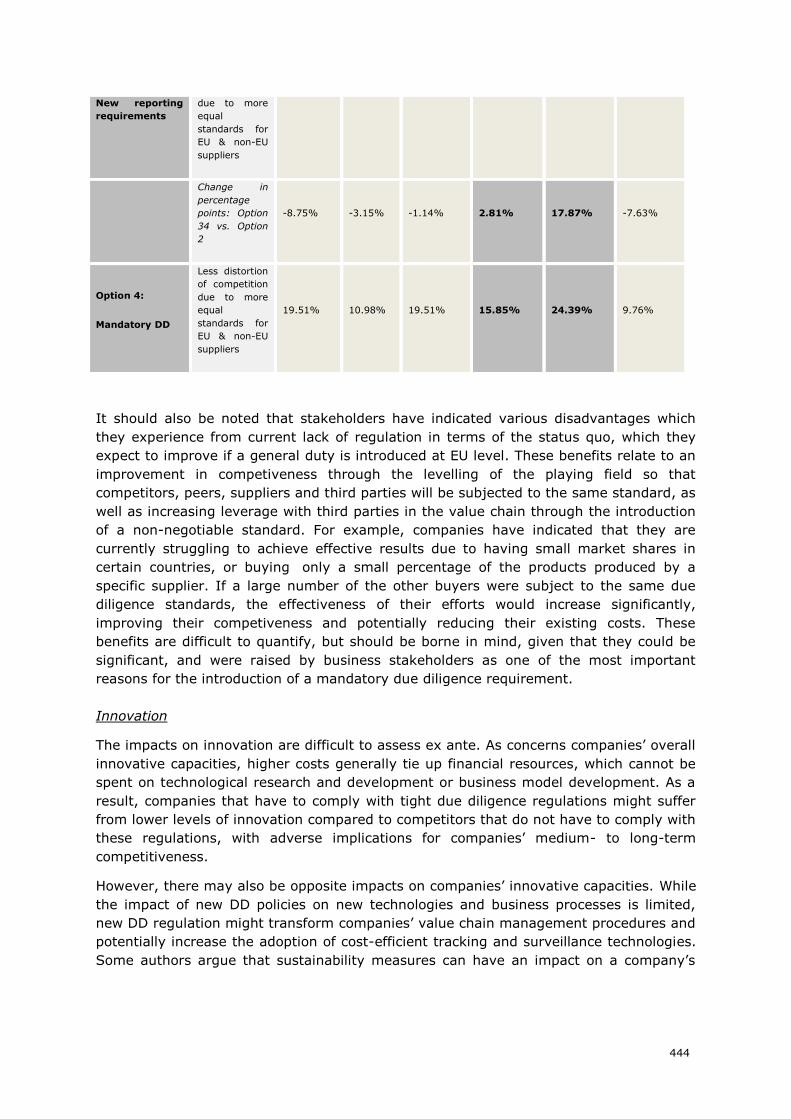

for EU & non-EU suppliers .......................................................................................... 443

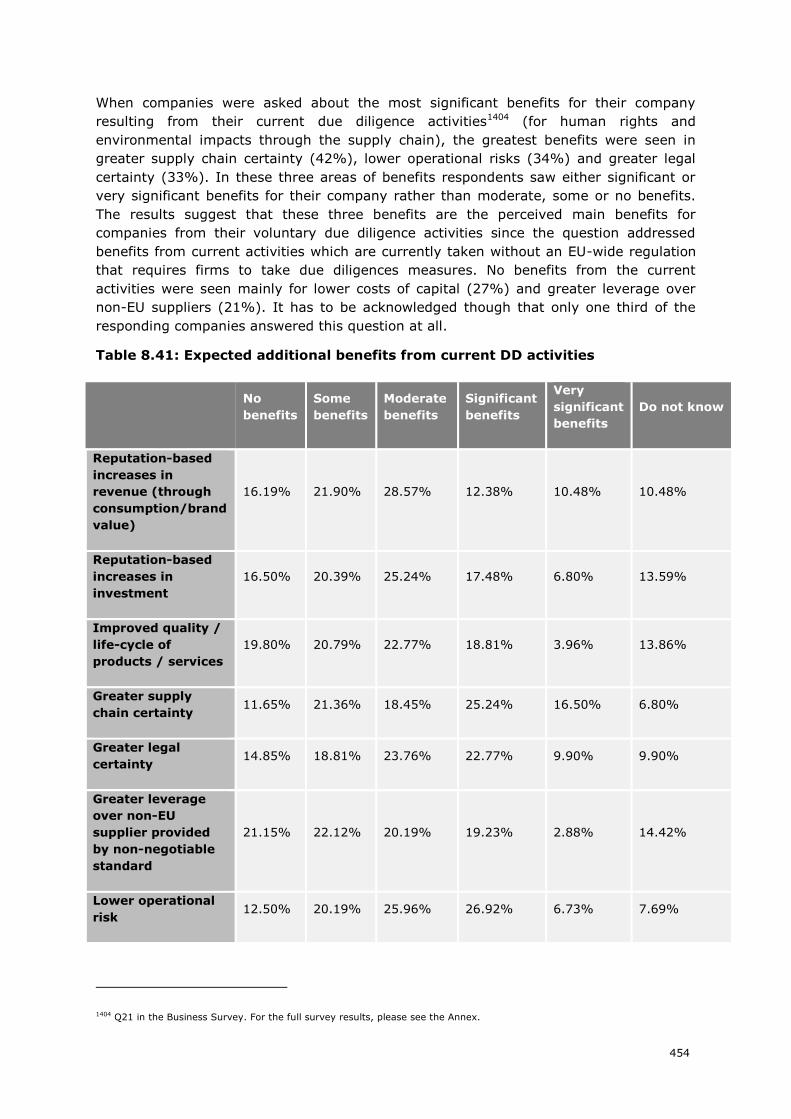

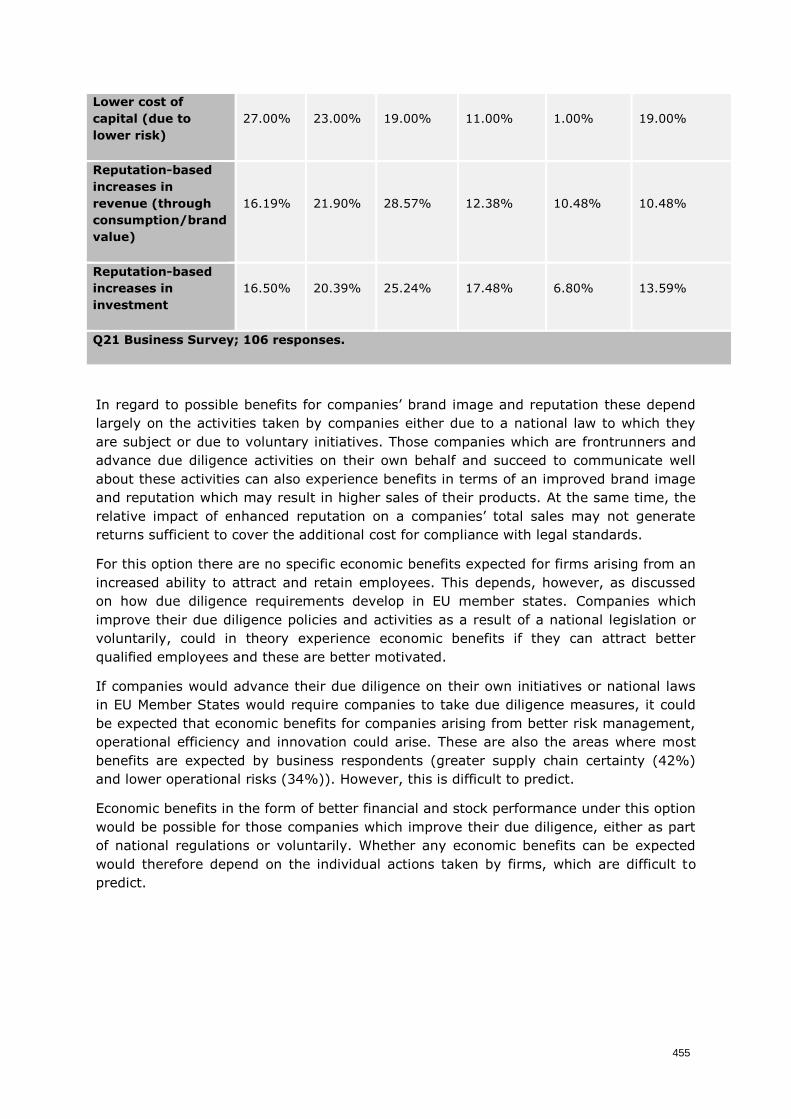

Table 0.41: Expected additional benefits from current DD activities ........................................ 454

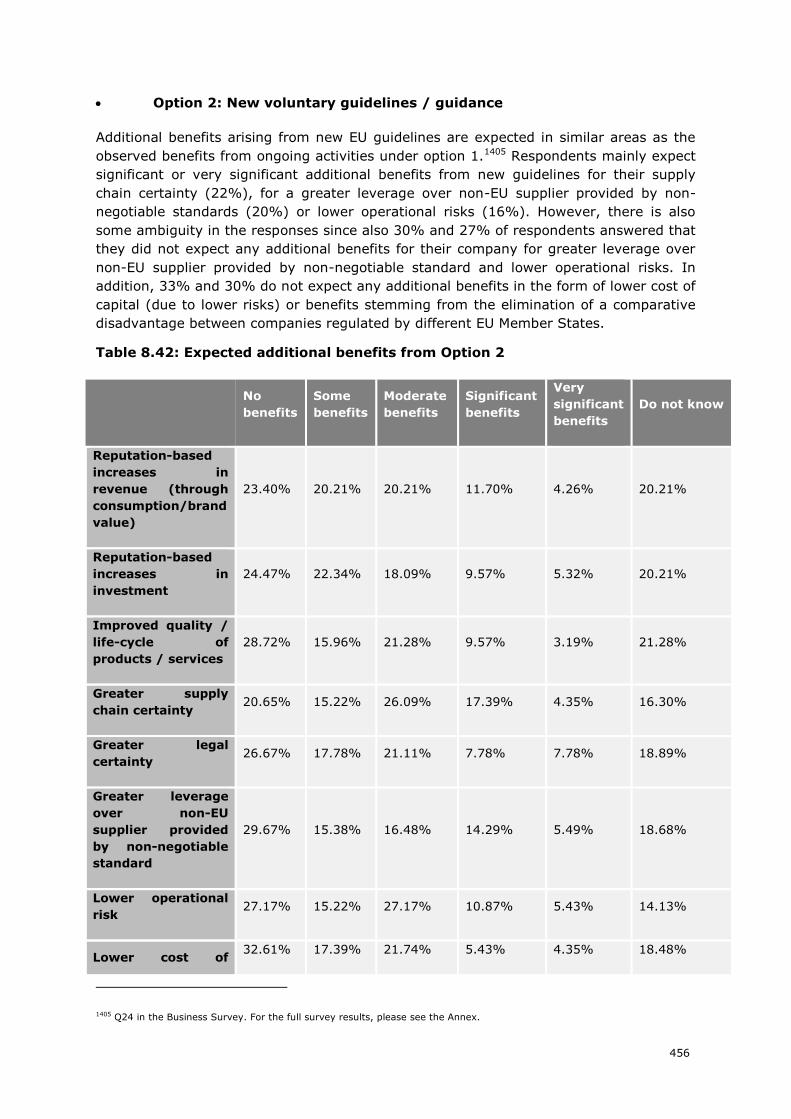

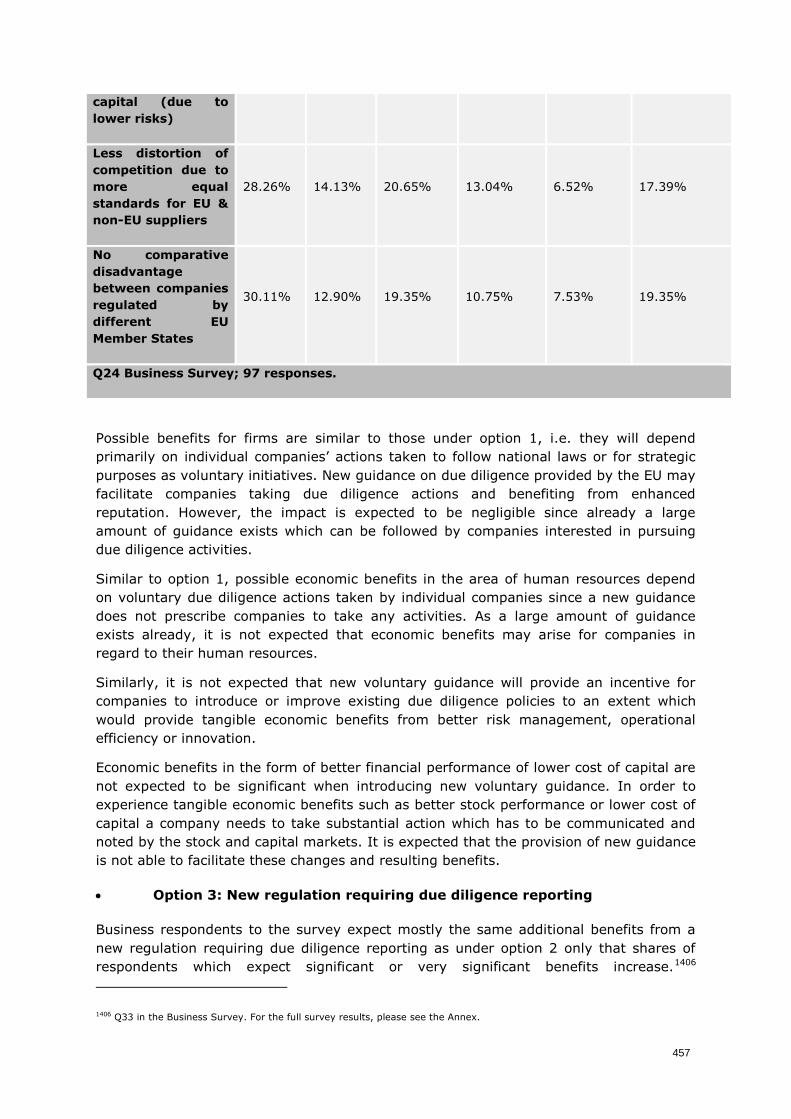

Table 0.42: Expected additional benefits from Option 2 ........................................................ 456

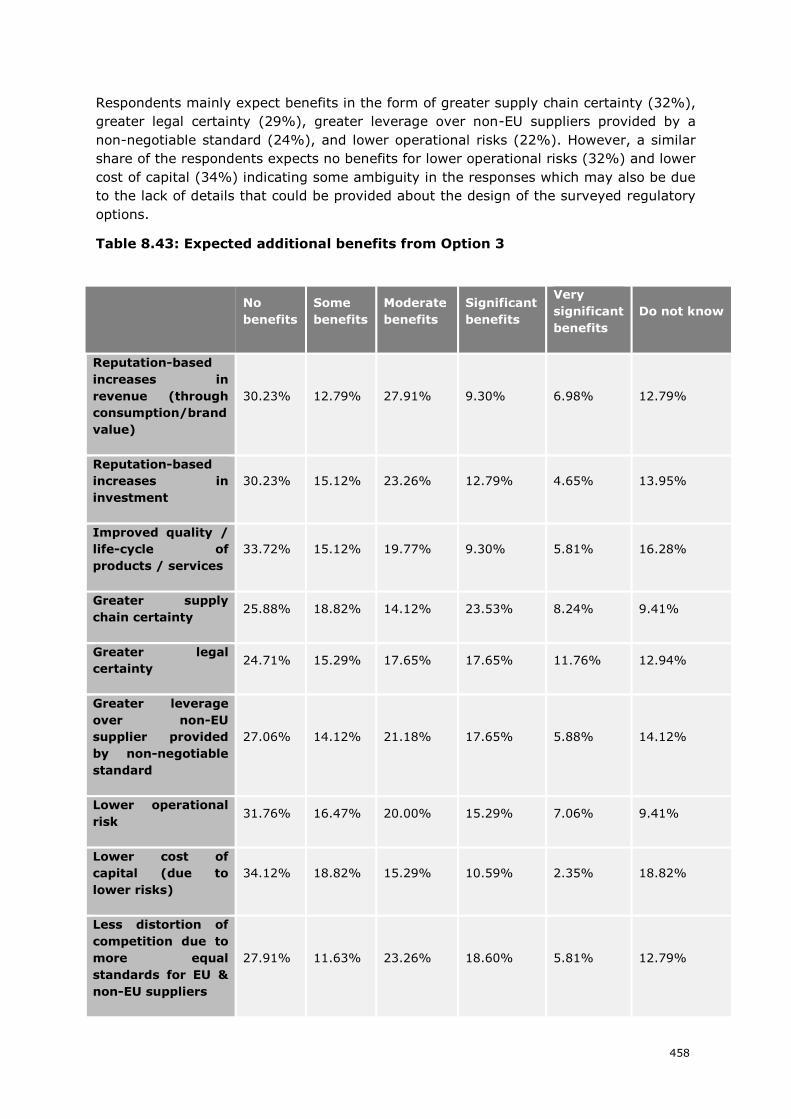

Table 0.43: Expected additional benefits from Option 3 ........................................................ 458

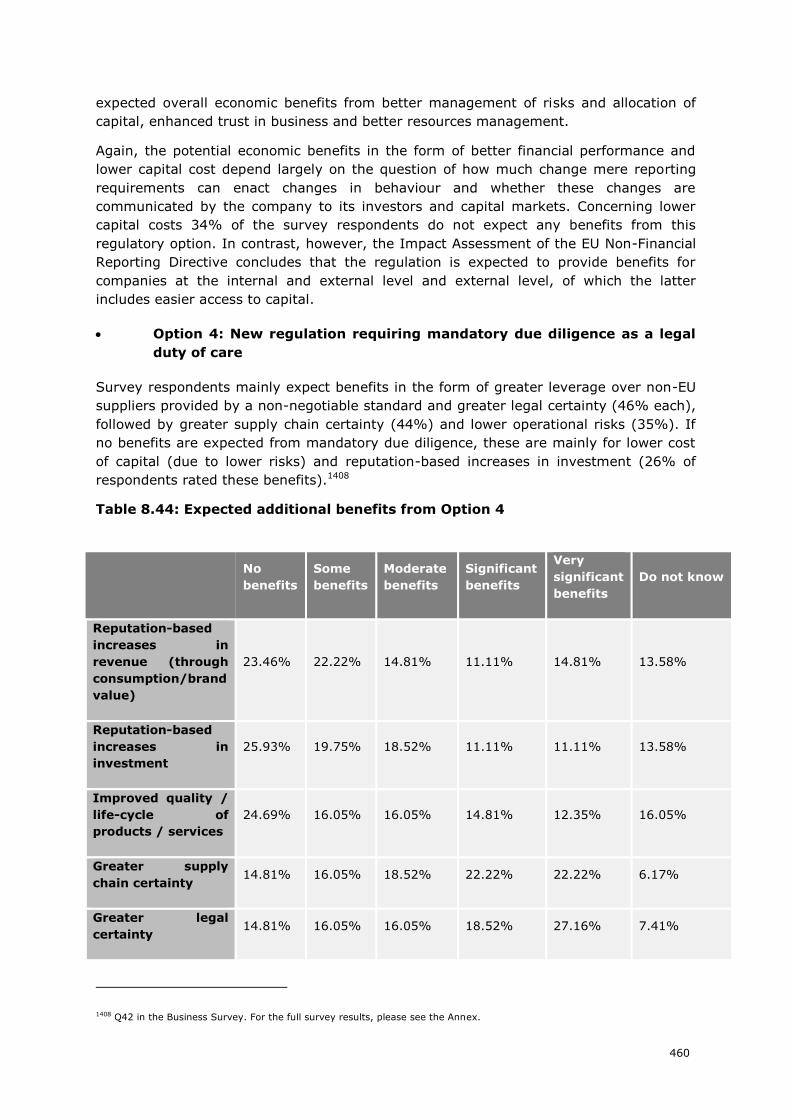

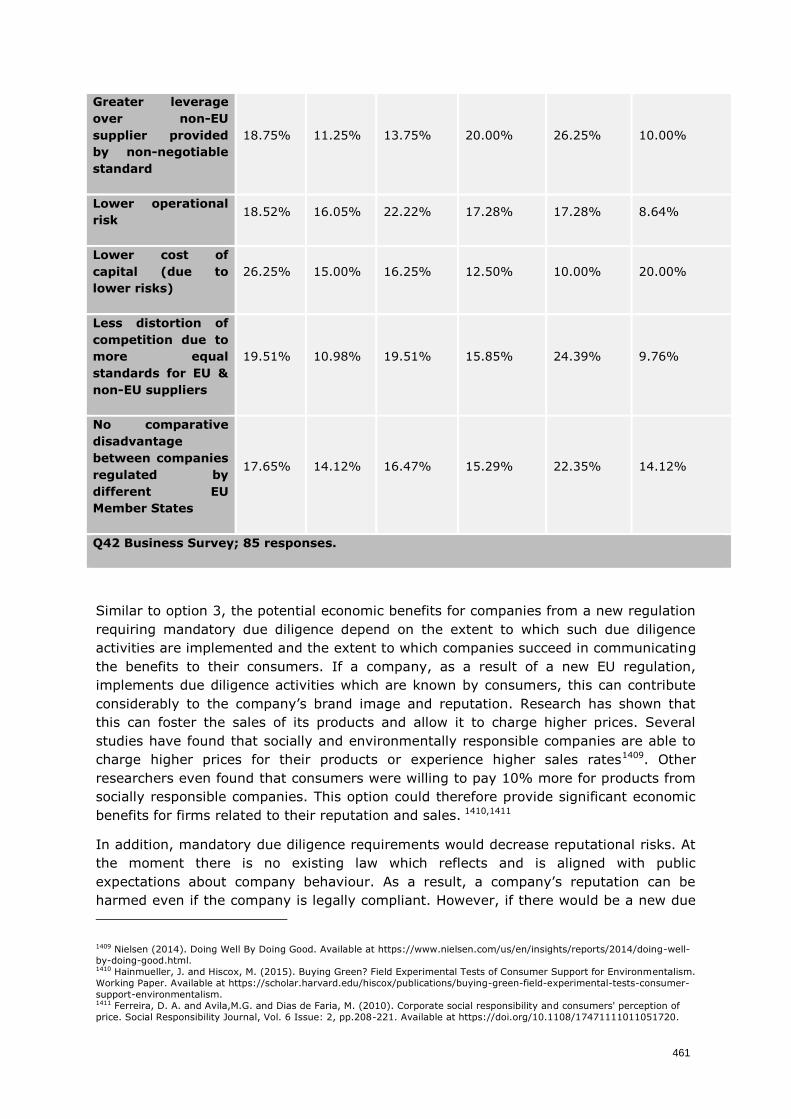

Table 0.44: Expected additional benefits from Option 4 ........................................................ 460

Table 0.45: Potential impact of mandatory DD on small companies’ revenues and profit margins,

by sector, approximated annual cost of mandatory DD based on “alternative total costs”

(median data) .......................................................................................................... 467

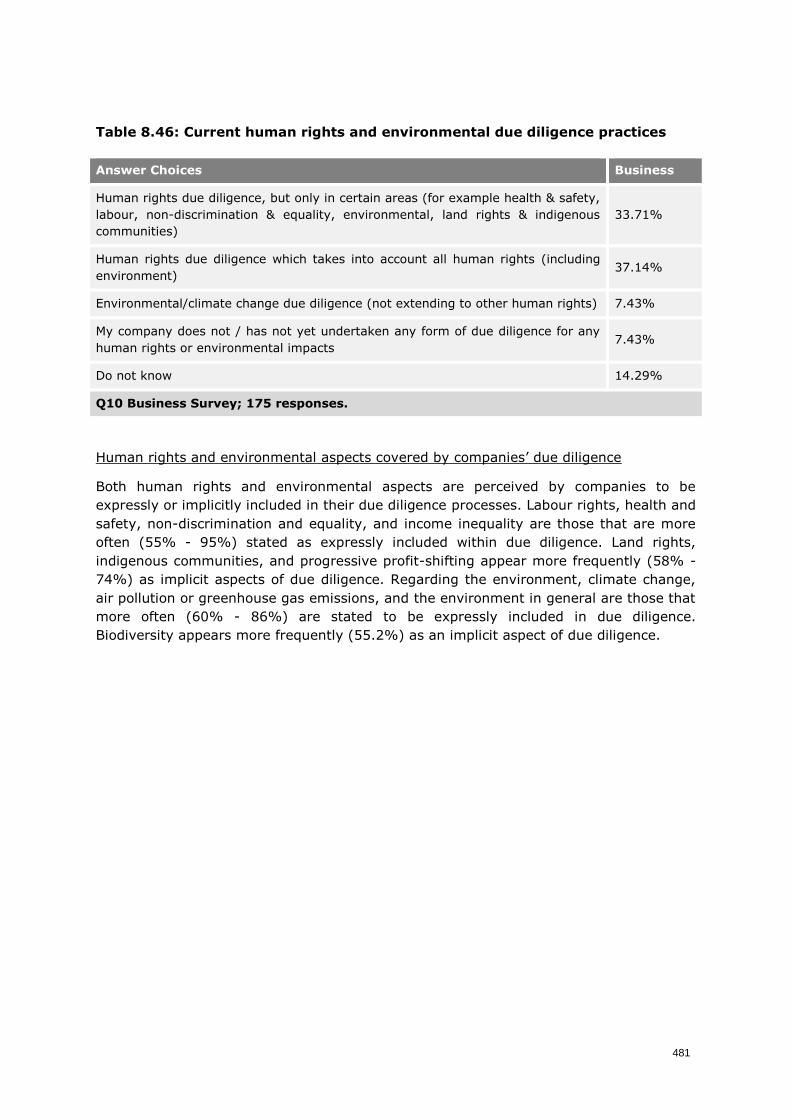

Table 0.46: Current human rights and environmental due diligence practices .......................... 481

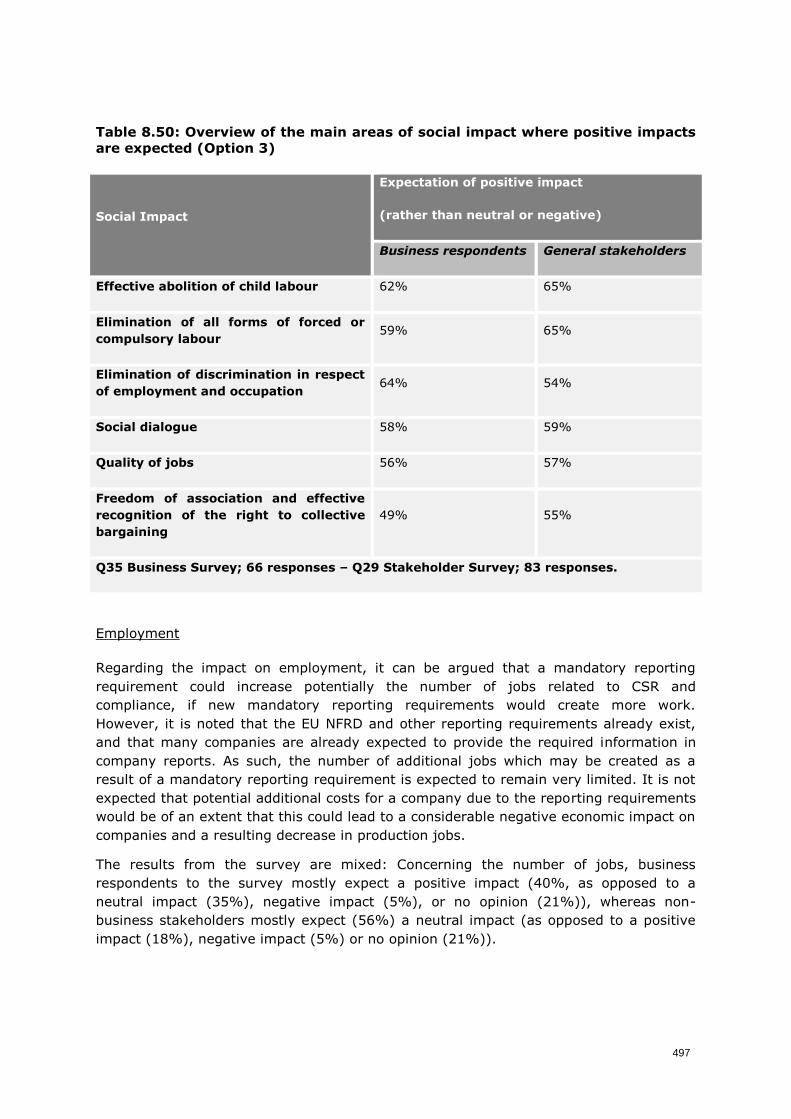

Table 0.47. Overview of the main areas of social impact where positive impacts are expected

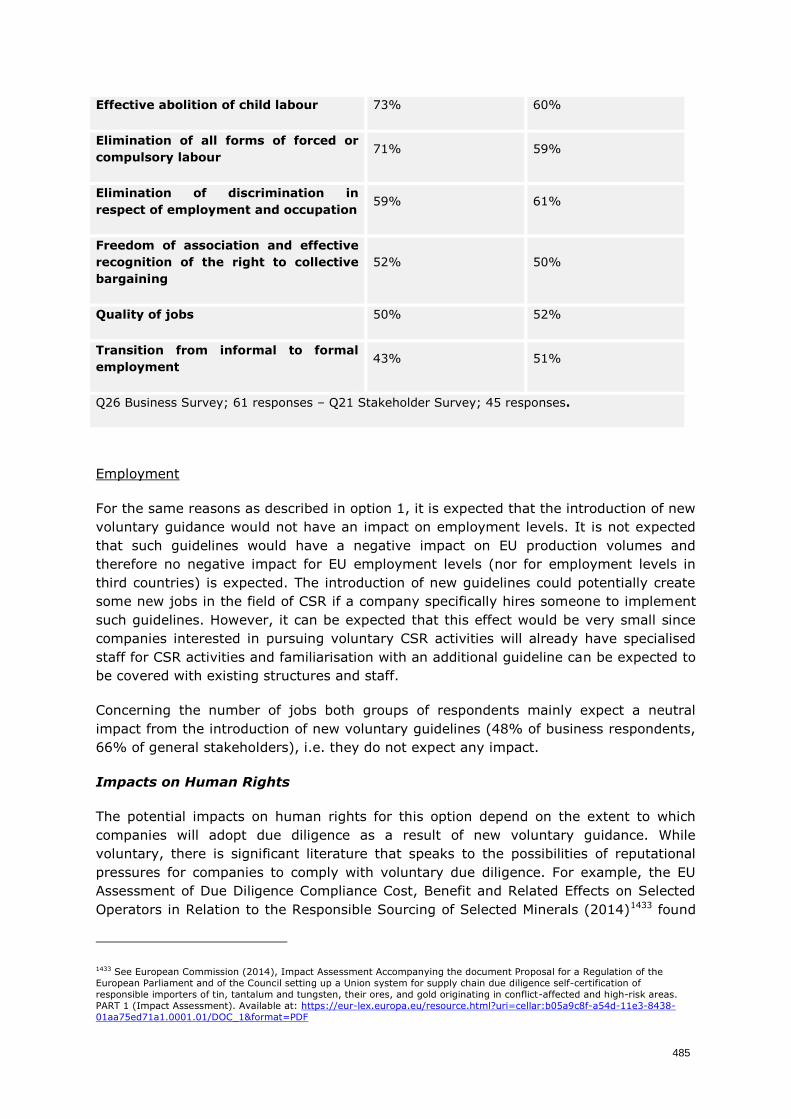

(Option 2) ............................................................................................................... 484

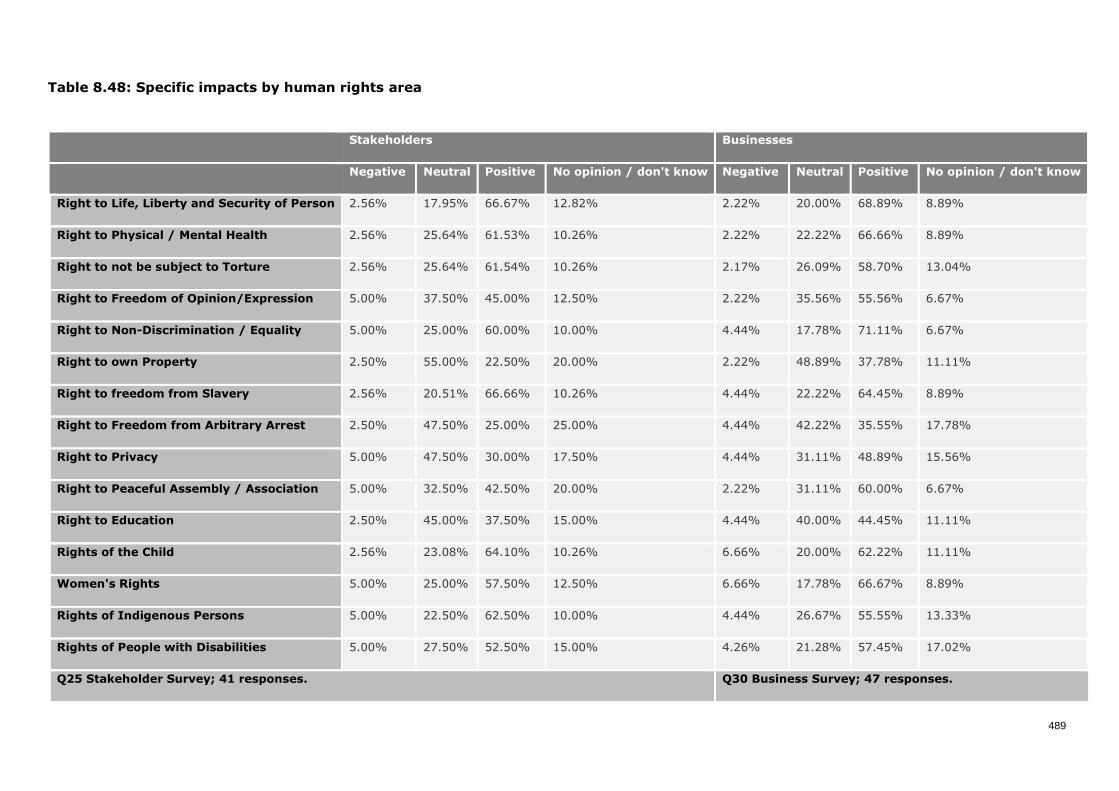

Table 0.48: Specific impacts by human rights area ............................................................... 489

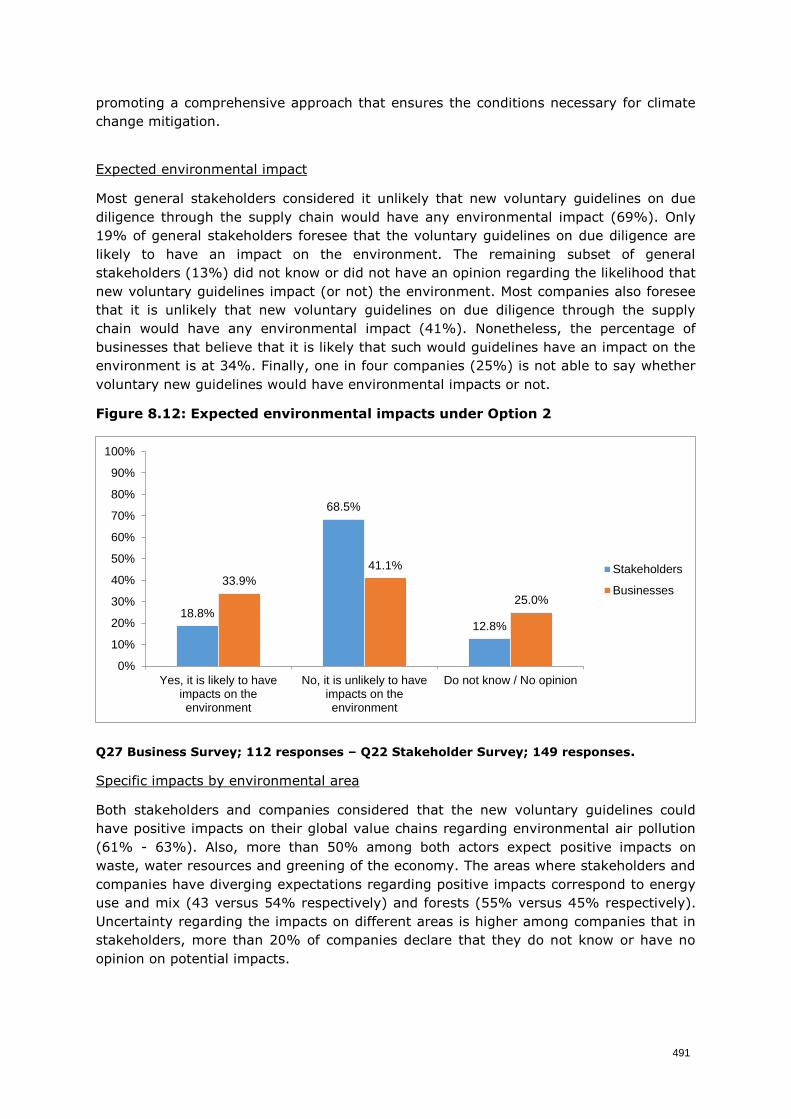

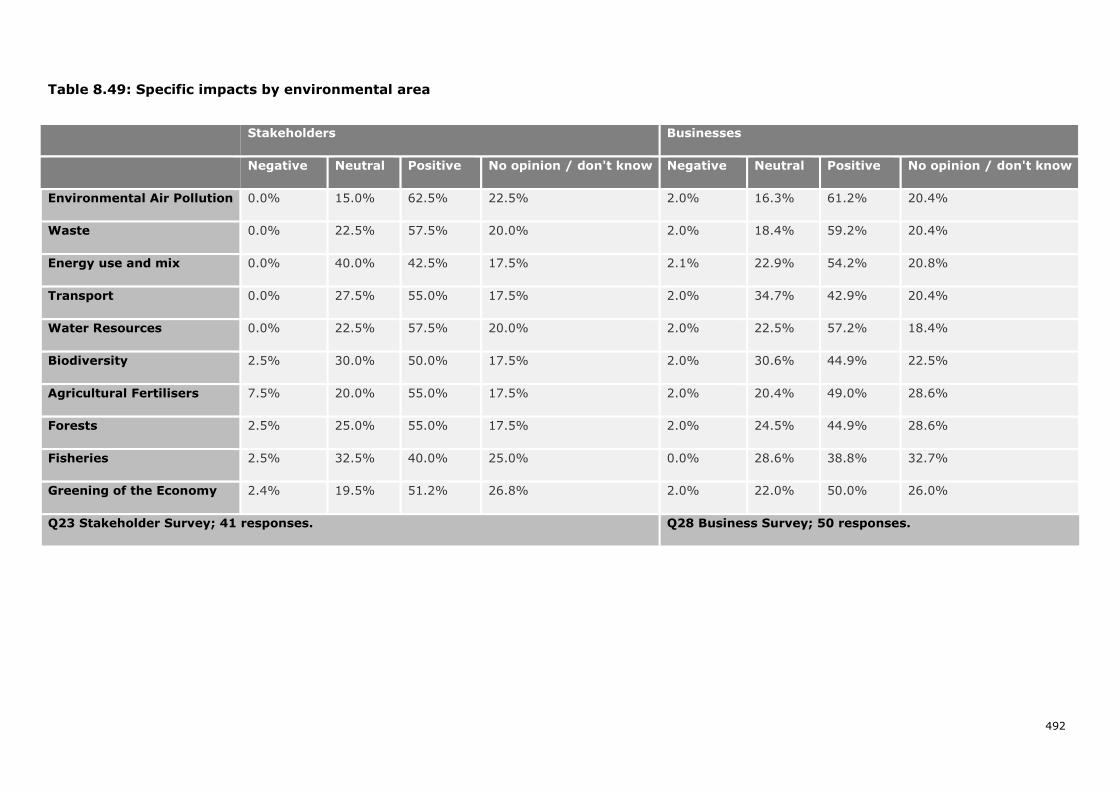

Table 0.49: Specific impacts by environmental area ............................................................. 492

Table 0.50: Overview of the main areas of social impact where positive impacts are expected

(Option 3) ............................................................................................................... 497

Table 0.51. Specific human rights impacts by area (Option 3) ............................................... 502

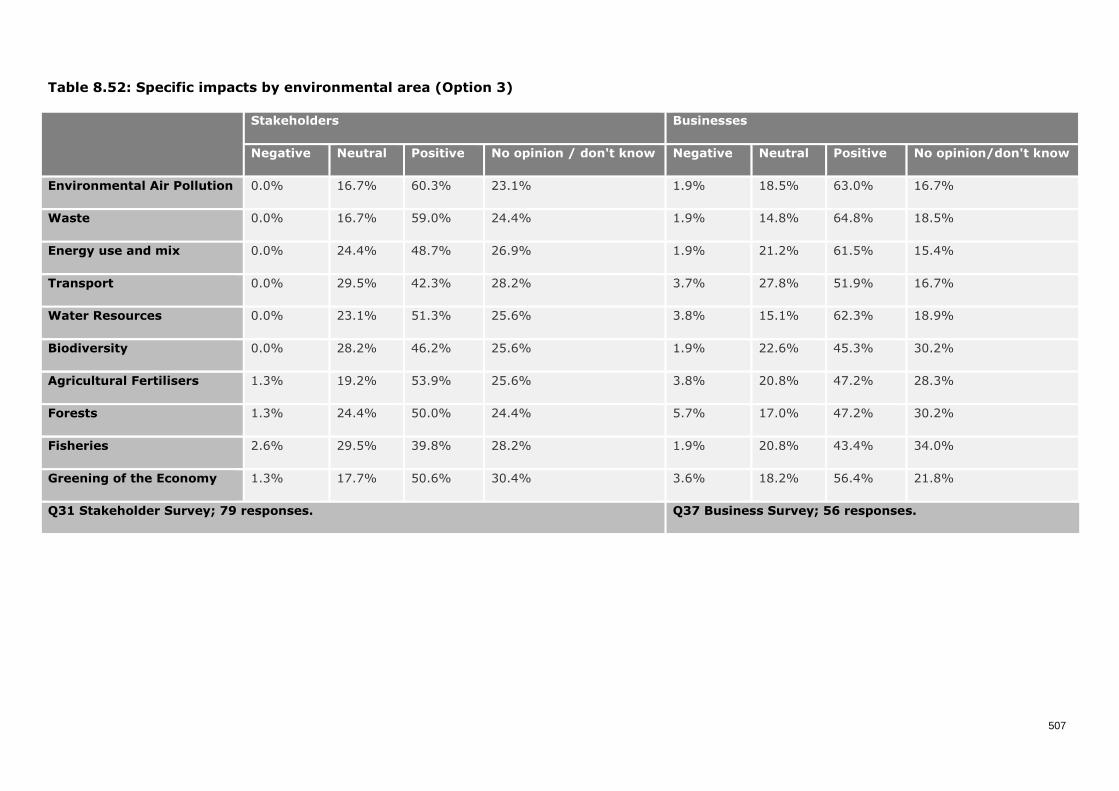

Table 0.52: Specific impacts by environmental area (Option 3) .............................................. 507

Table 0.53: Overview of the main areas of social impact where positive impacts are expected

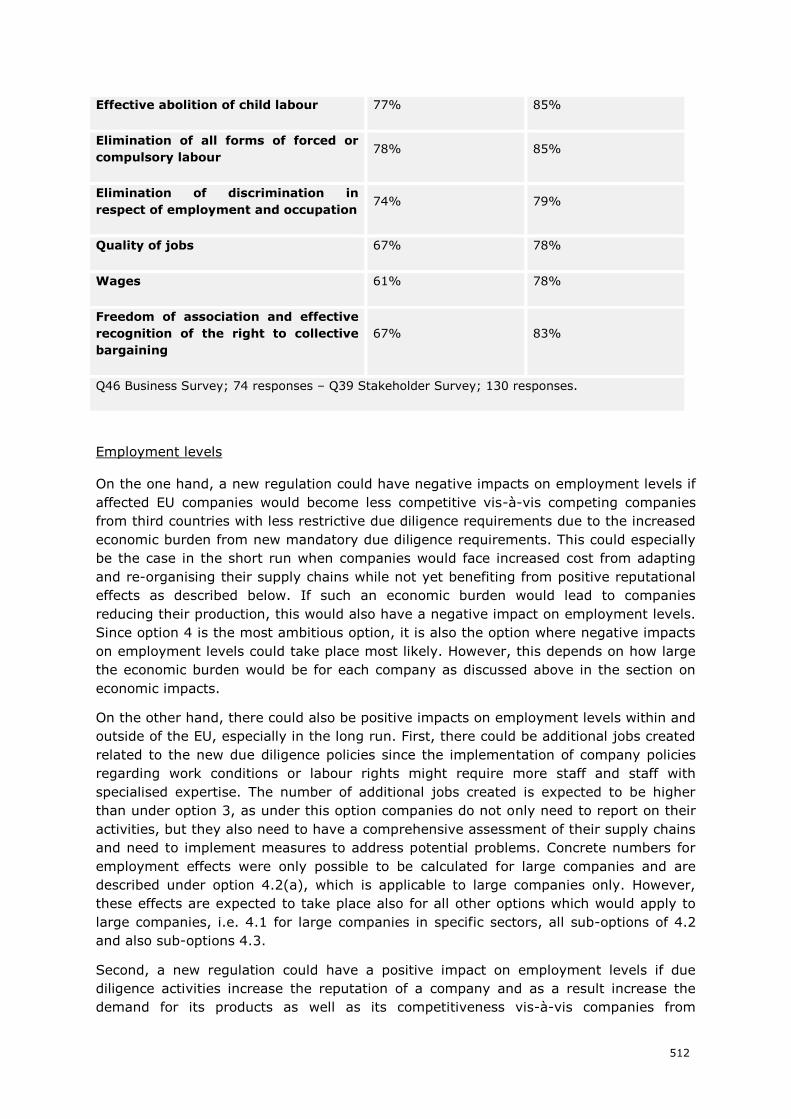

(Option 4) ............................................................................................................... 511

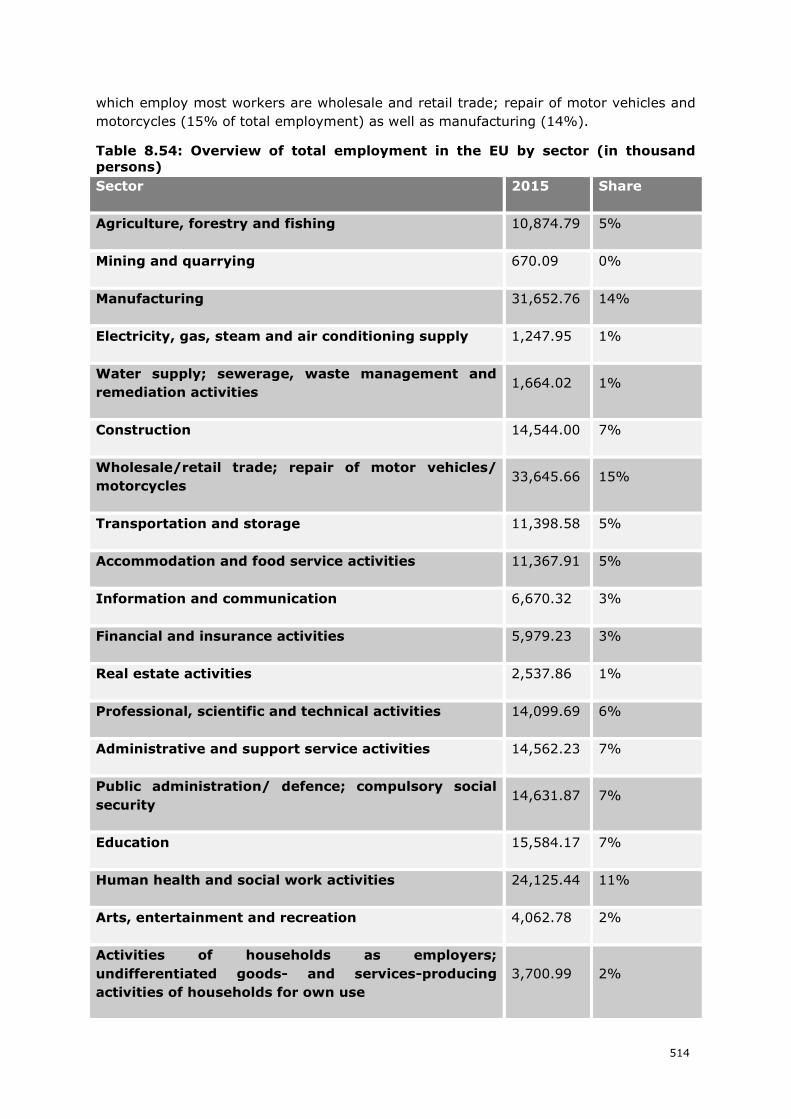

Table 0.54: Overview of total employment in the EU by sector (in thousand persons) ............... 514

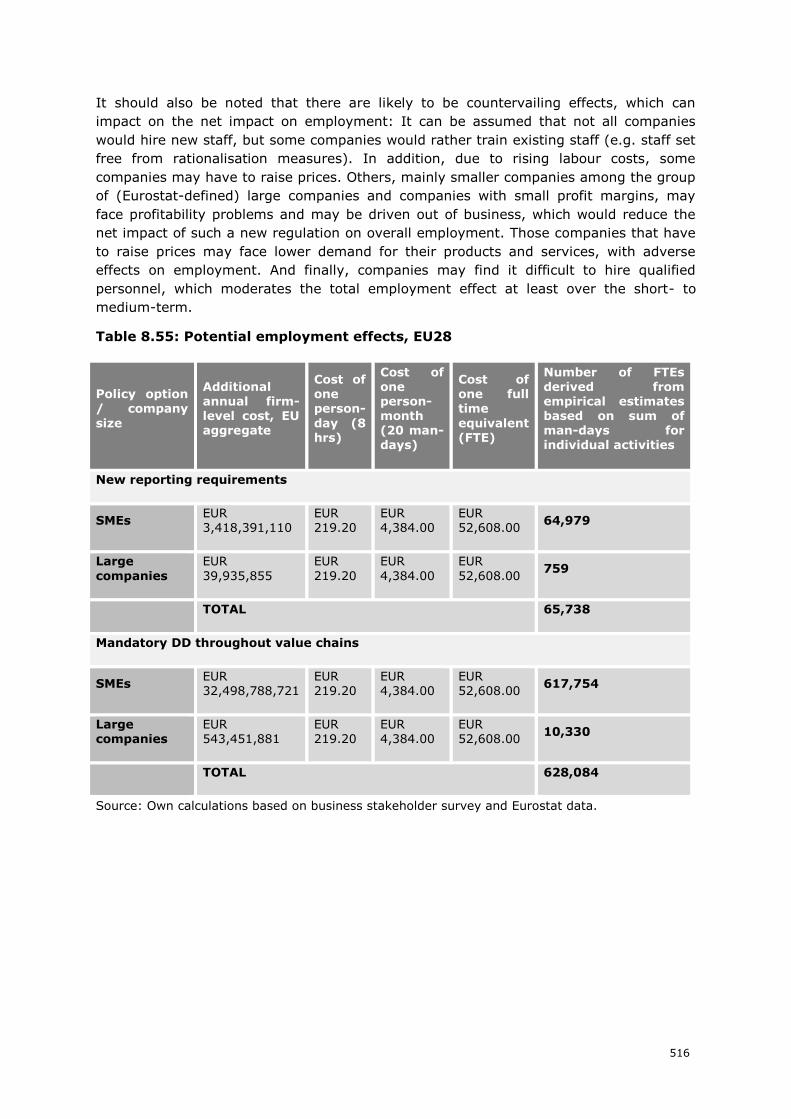

Table 0.55: Potential employment effects, EU28 .................................................................. 516

Table 0.56: Potential employment effects resulting for new mandatory DD throughout companies’

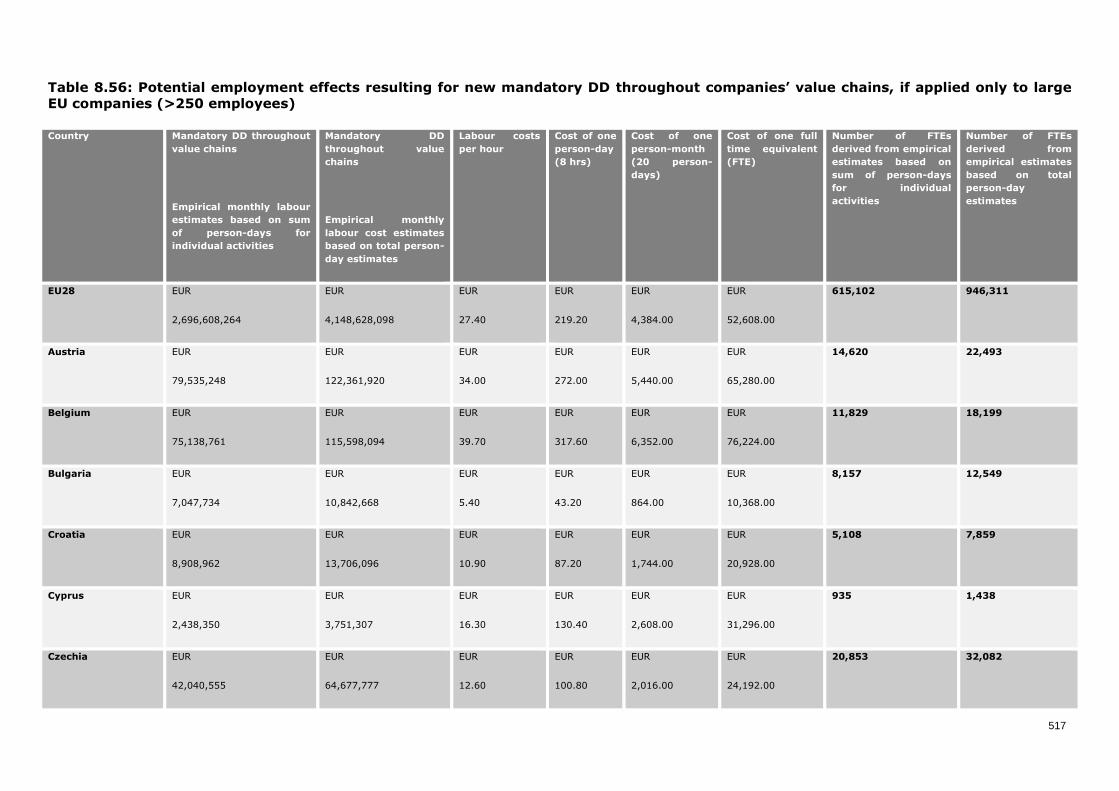

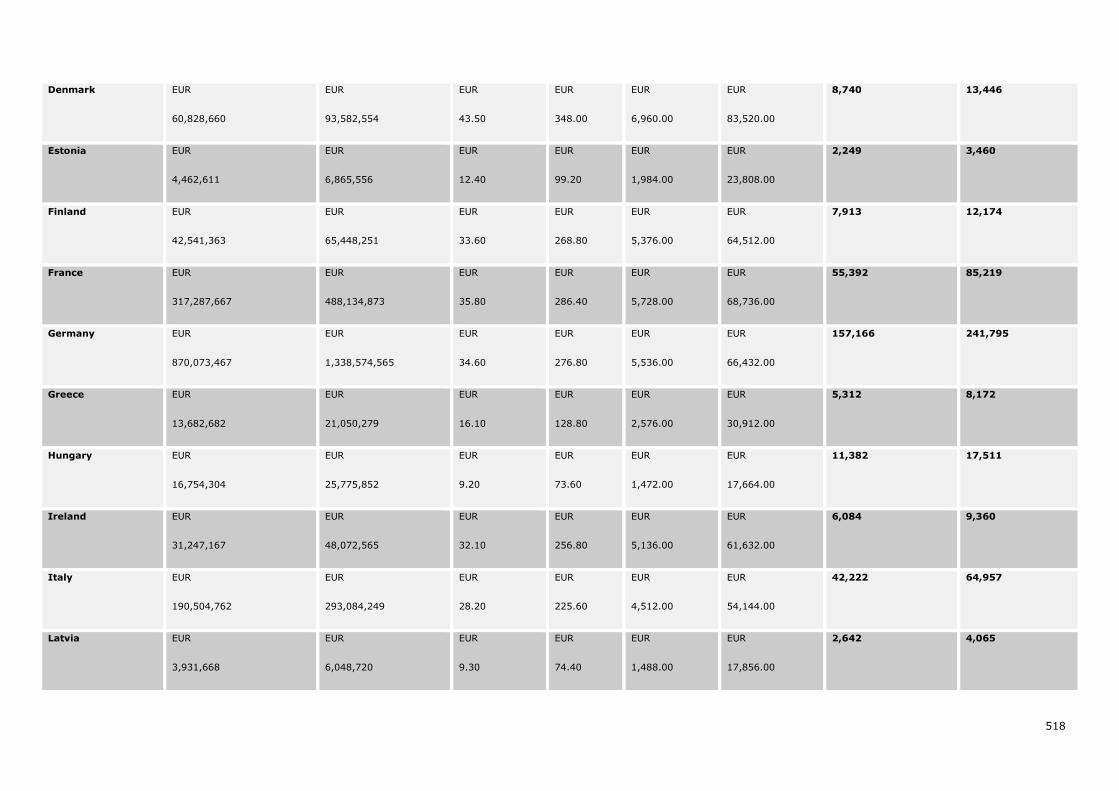

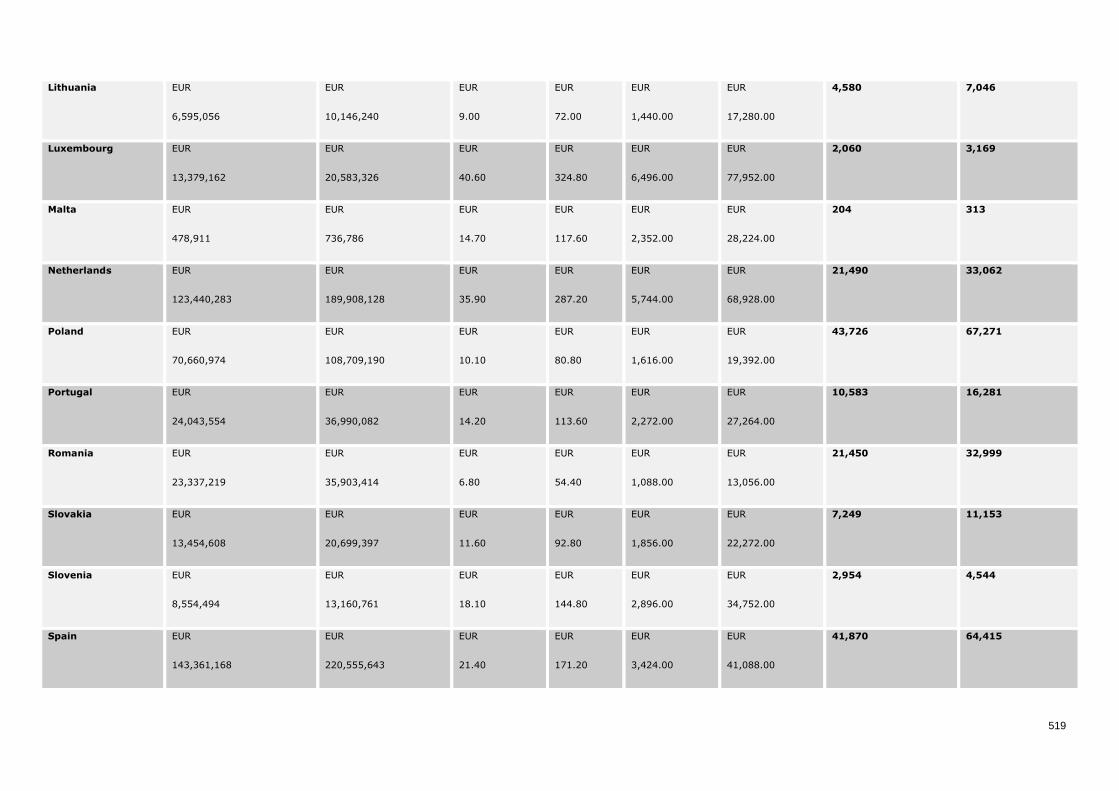

value chains, if applied only to large EU companies (>250 employees) ............................ 517

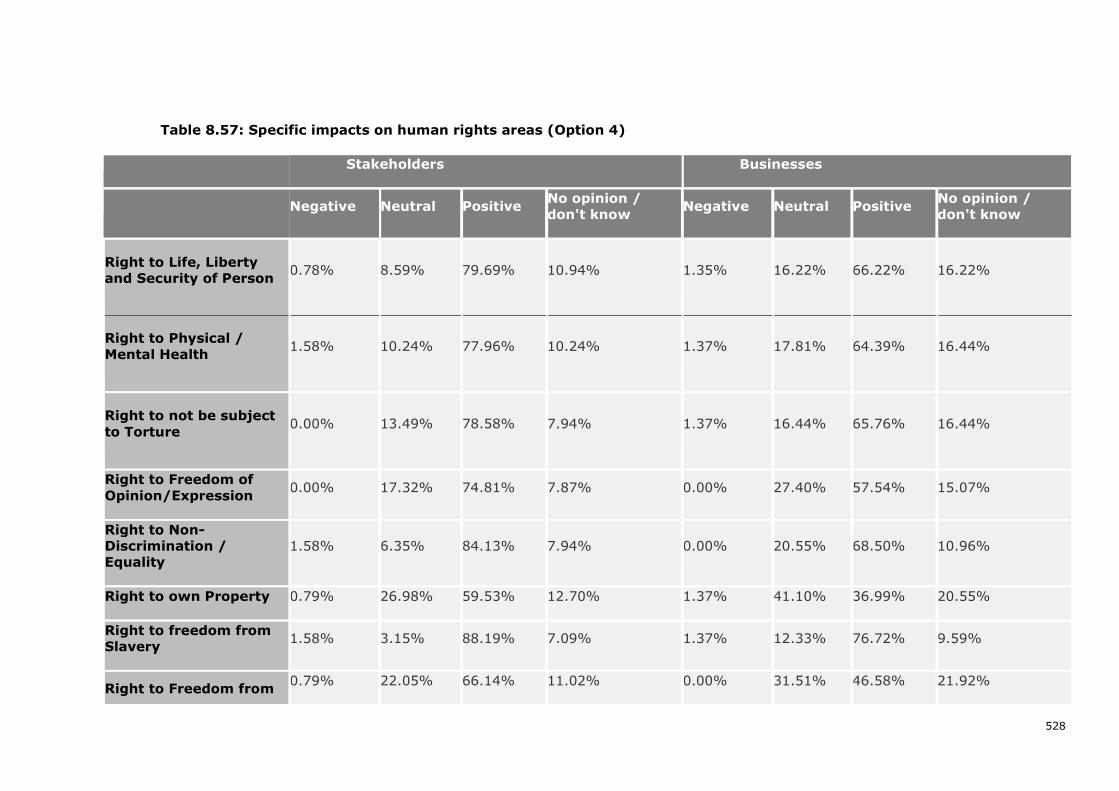

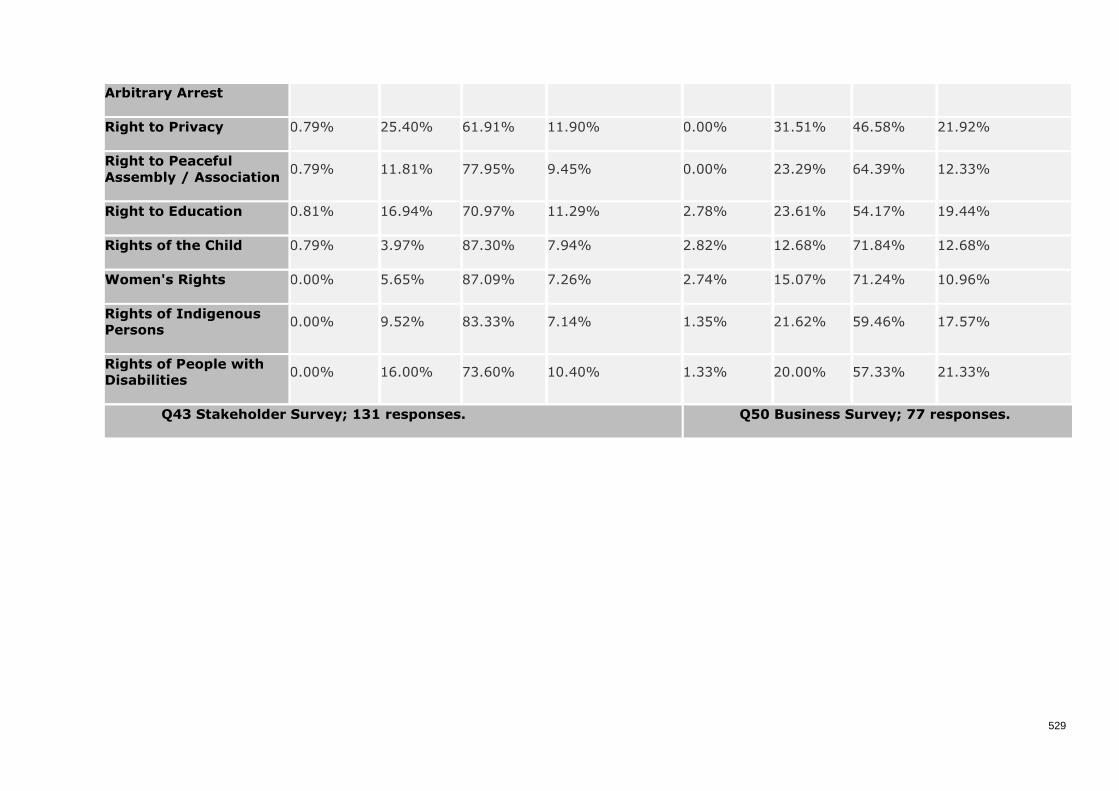

Table 0.57: Specific impacts on human rights areas (Option 4) .............................................. 528

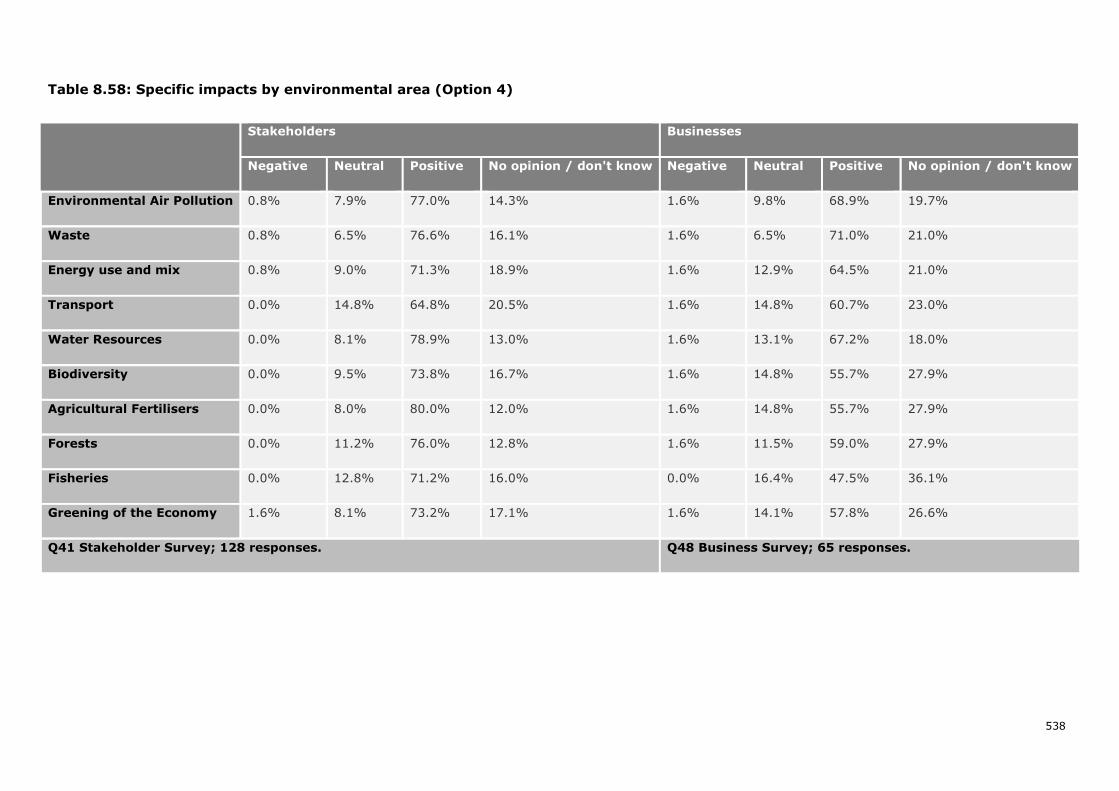

Table 0.58: Specific impacts by environmental area (Option 4) .............................................. 538

Table 0.59: Average labour costs (EUR), in 2018 based on EU-28 .......................................... 542

Table 0.60: Expected costs for public authorities from criminal, administrative and civil law

approaches to addressing environmental crime in EFFACE synthesis report ...................... 546

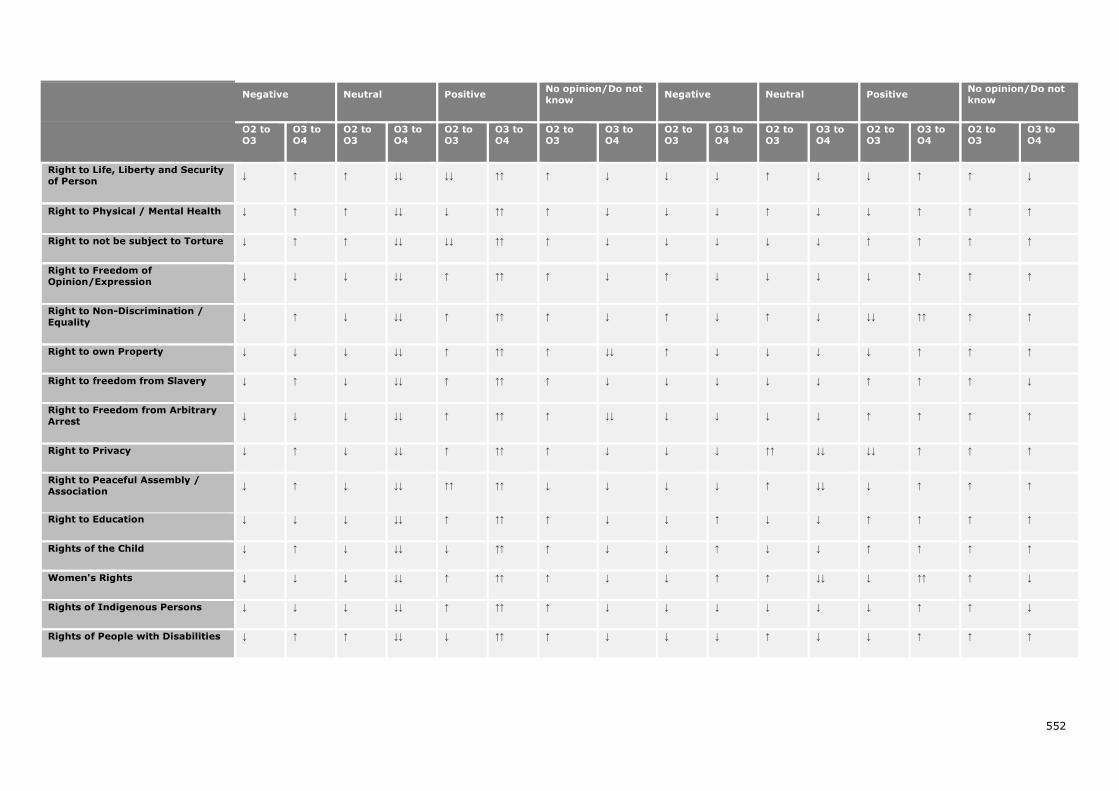

Table 0.61: Summary of respondents’ perceptions about human rights impacts by area ........... 551

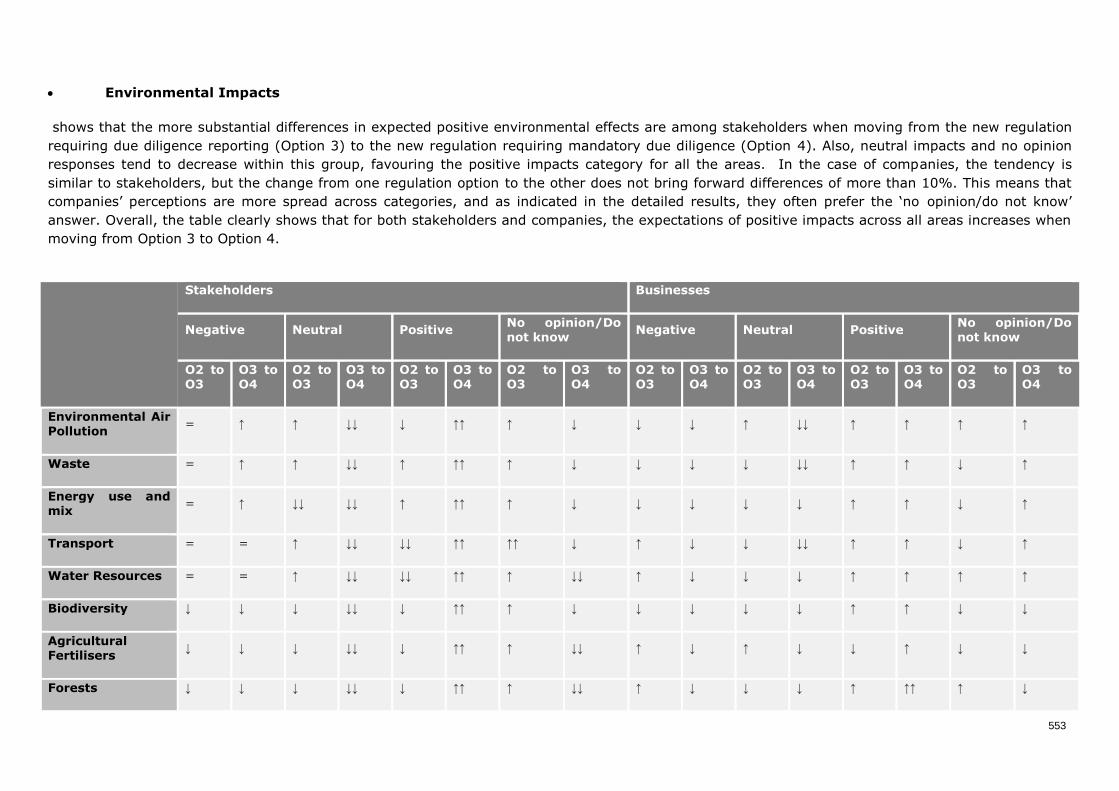

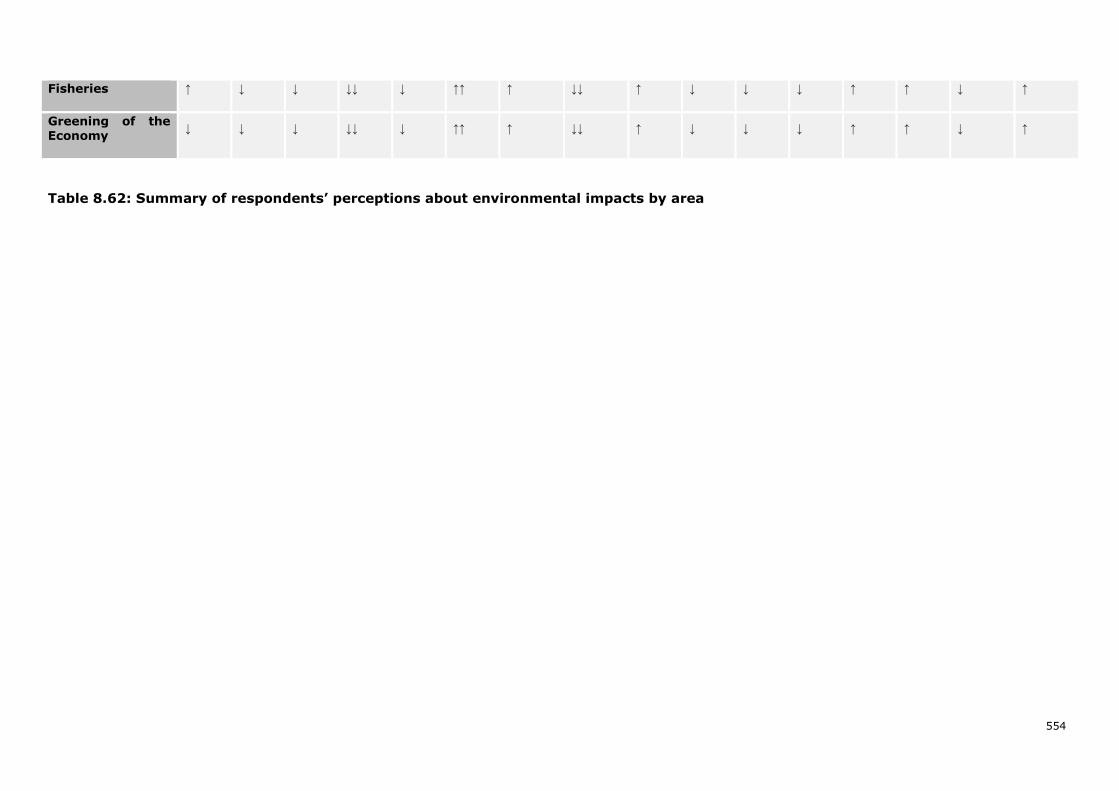

Table 0.62: Summary of respondents’ perceptions about environmental impacts by area .......... 554

Table 0.63: Overview of regulatory options and impacts by area ............................................ 559

List of Figures

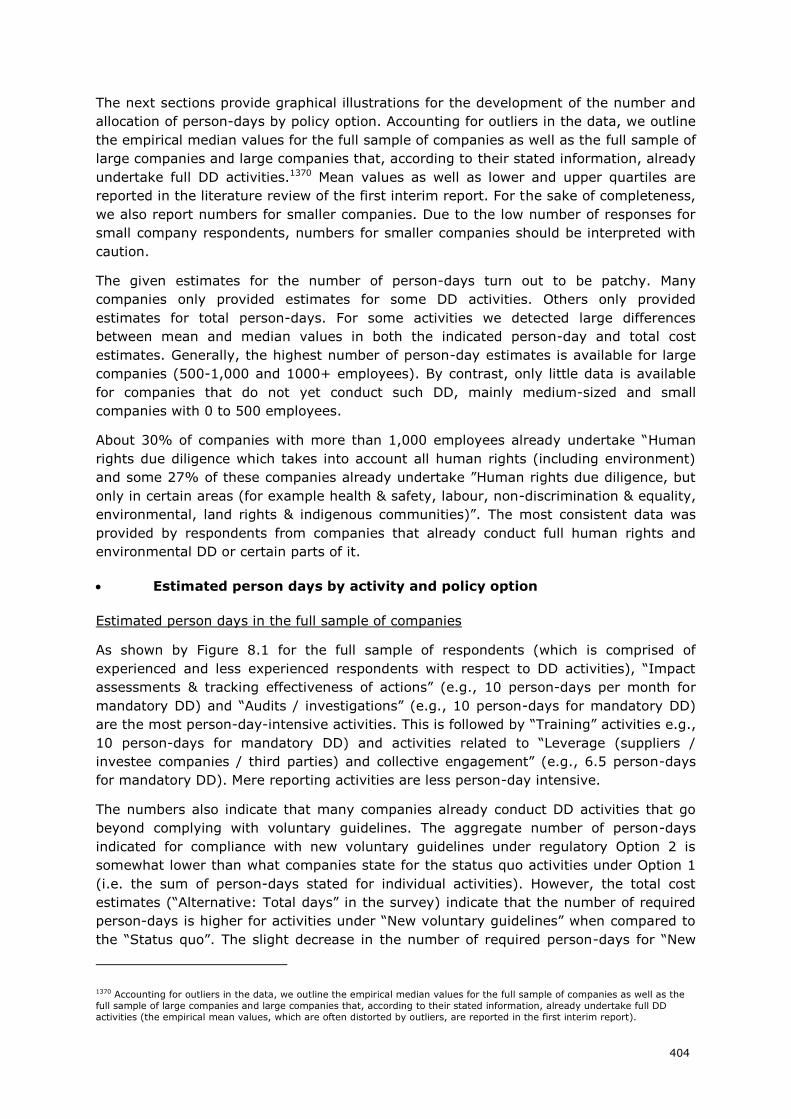

Figure 0.1: Development of number and allocation of person-days by policy option, all business

respondents (in person-days per month) ..................................................................... 405

Figure 0.2: Development of number and allocation of person-days by policy option, total of

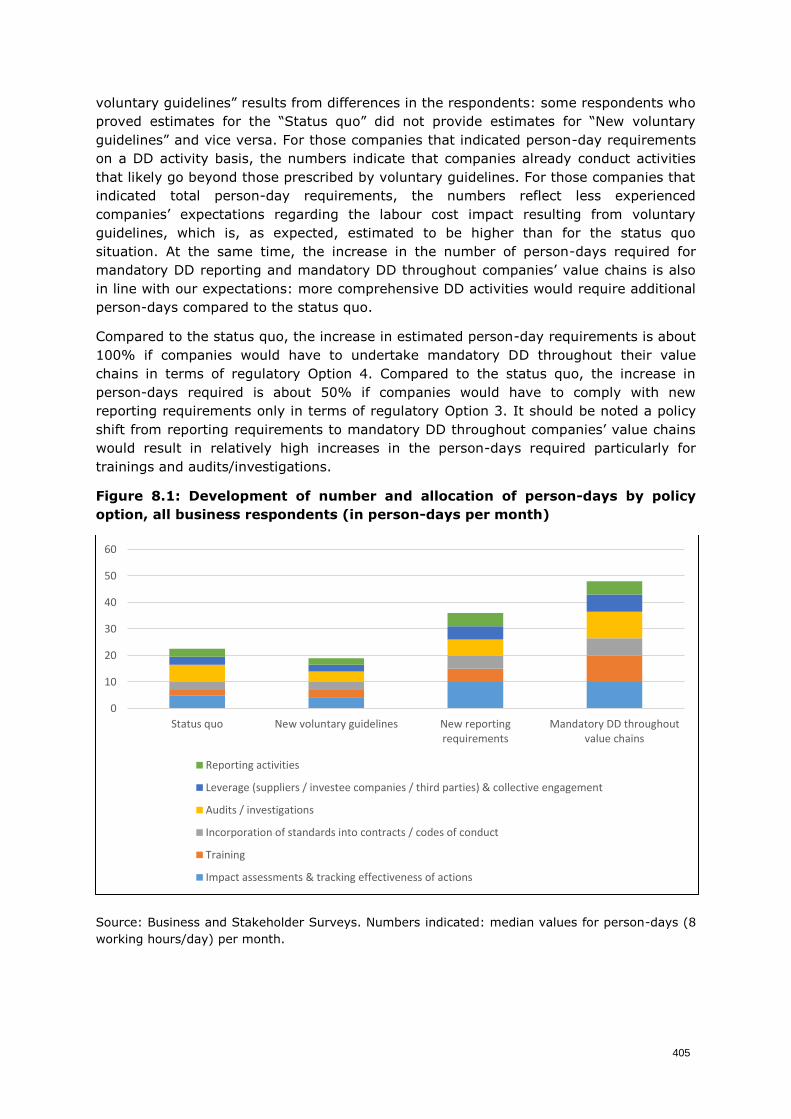

companies with 1000+ employees (in person-days per month) ...................................... 407

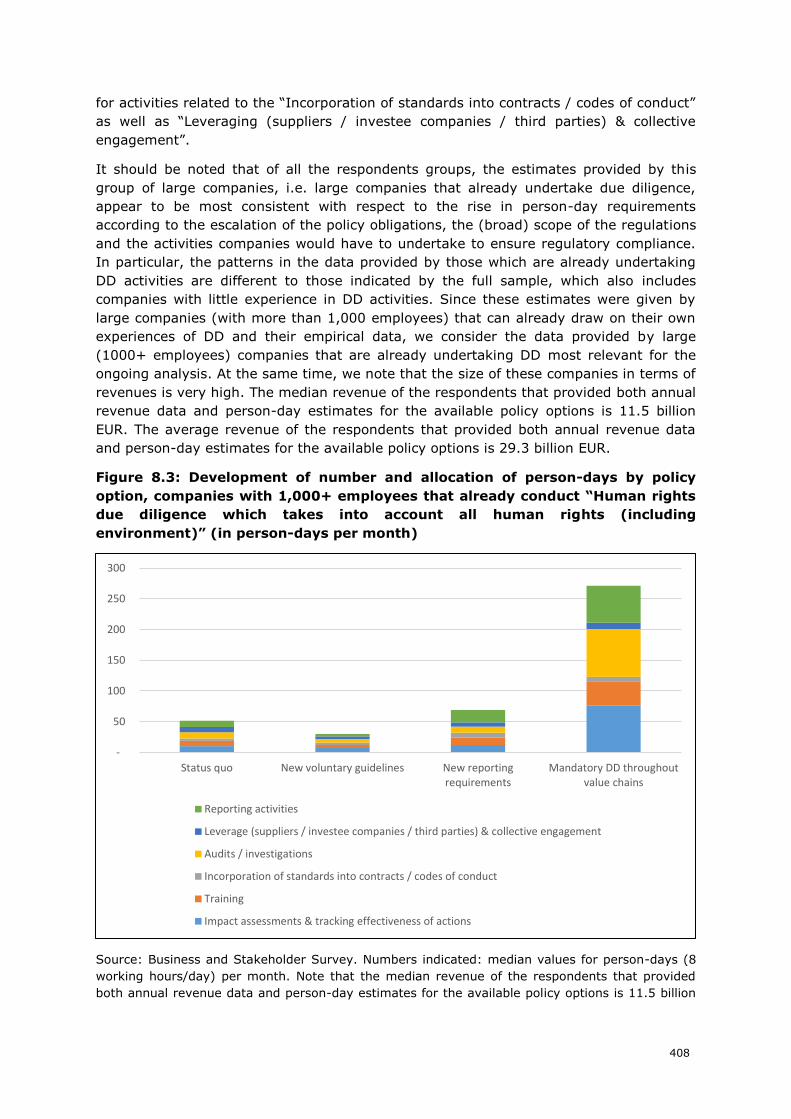

Figure 0.3: Development of number and allocation of person-days by policy option, companies

with 1,000+ employees that already conduct “Human rights due diligence which takes into

account all human rights (including environment)” (in person-days per month) ................ 408

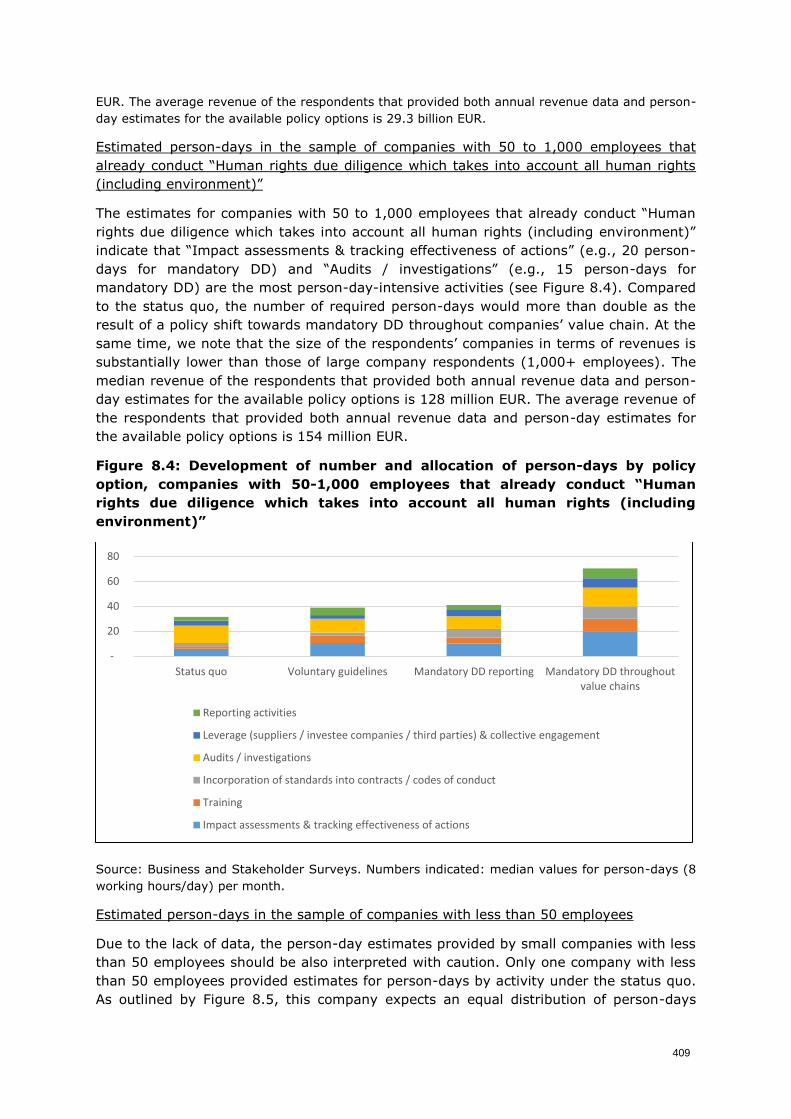

Figure 0.4: Development of number and allocation of person-days by policy option, companies

with 50-1,000 employees that already conduct “Human rights due diligence which takes into

account all human rights (including environment)” ....................................................... 409

Figure 0.5: Development of number and allocation of person-days by policy option, companies

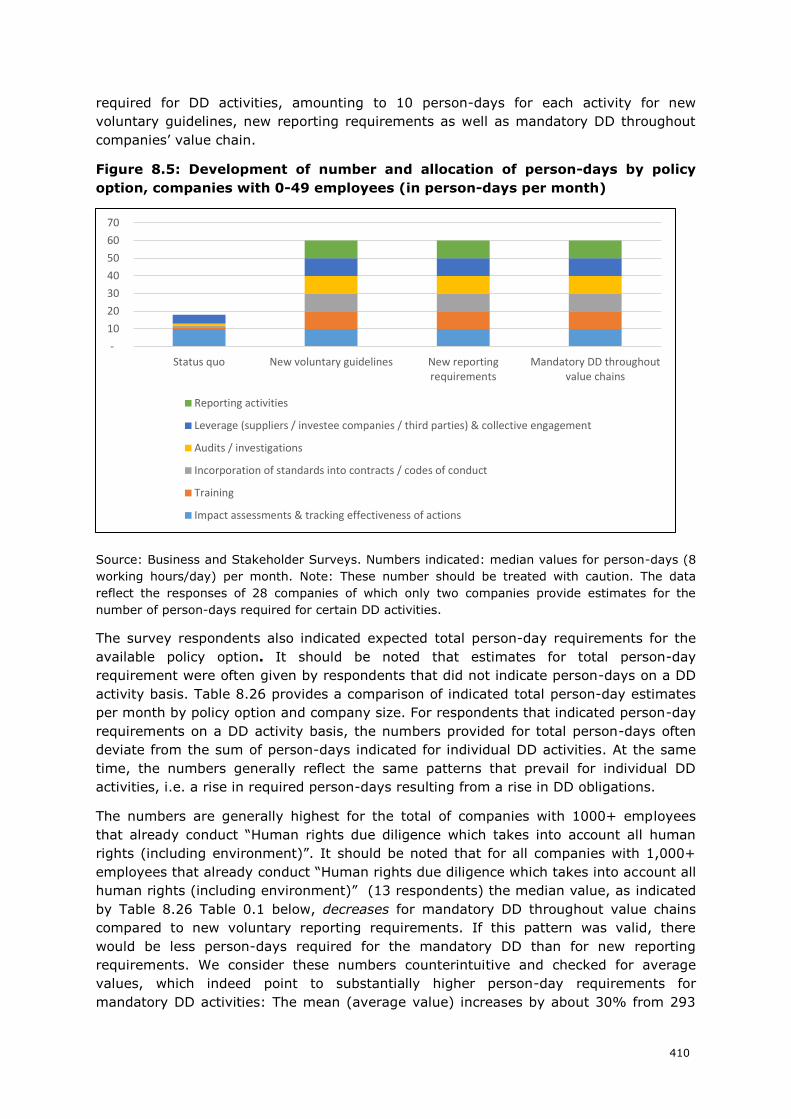

with 0-49 employees (in person-days per month) ......................................................... 410

14

Figure 0.6: Total estimated person-days, large companies (1000+ employees) that already

conduct “Human rights due diligence which takes into account all human rights (including

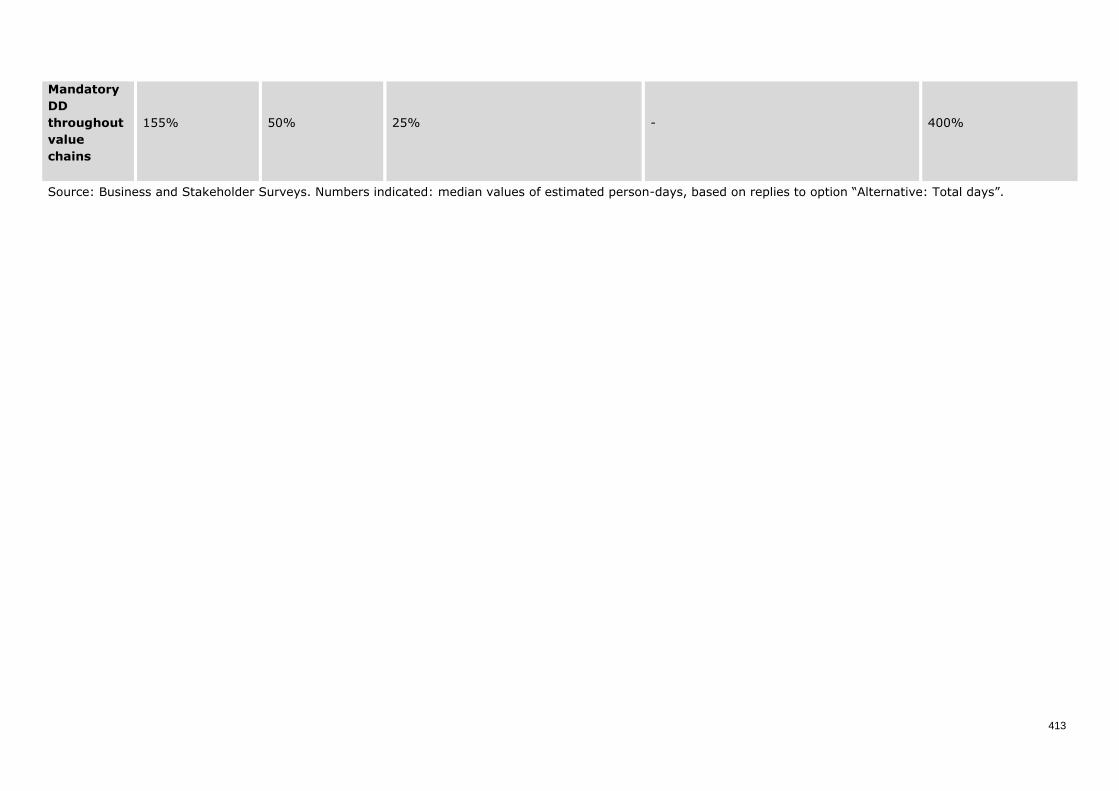

environment)” .......................................................................................................... 414

Figure 0.7: Impact Chain for Benefits from Due Diligence Activities ........................................ 453

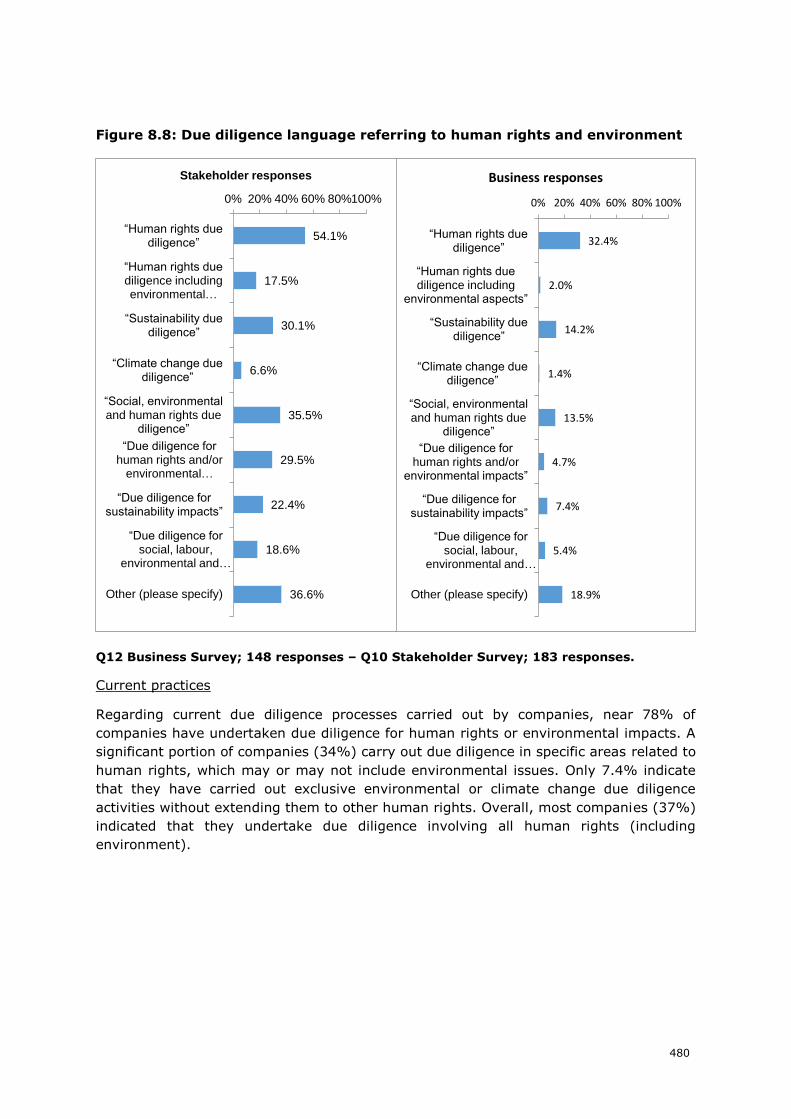

Figure 0.8: Due diligence language referring to human rights and environment ....................... 480

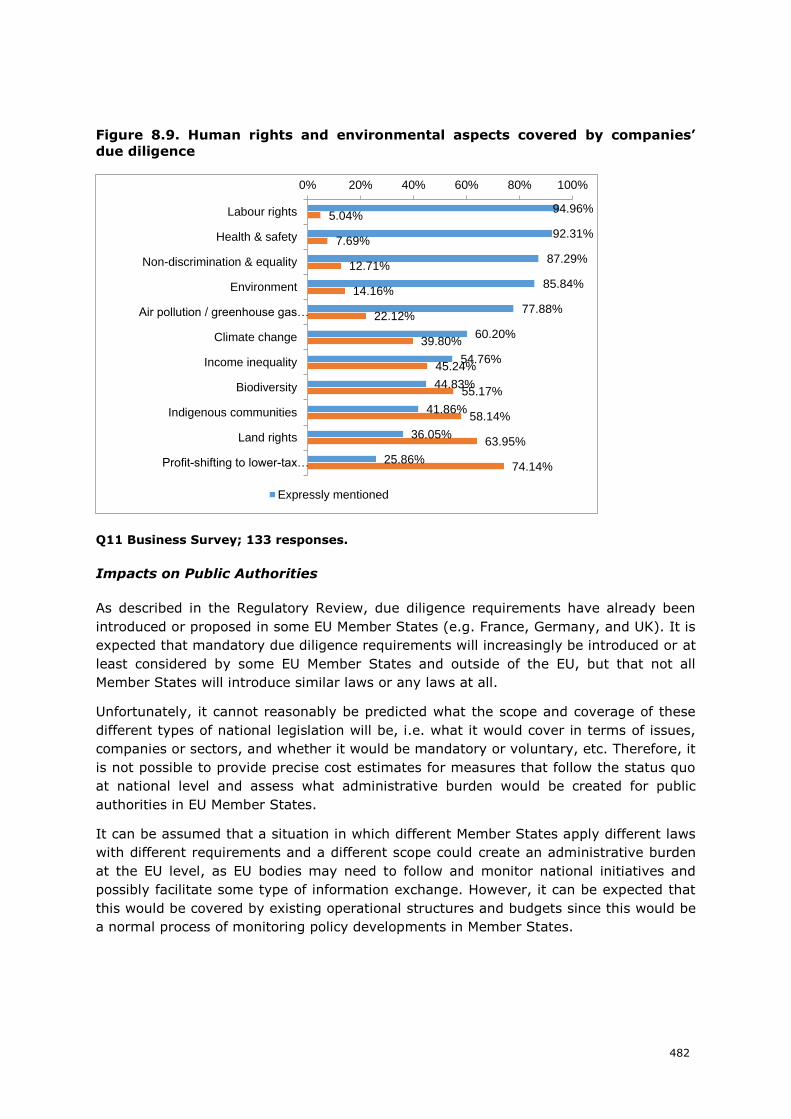

Figure 0.9. Human rights and environmental aspects covered by companies’ due diligence ....... 482

Figure 0.10: Expected social impacts for Option 2 ................................................................ 483

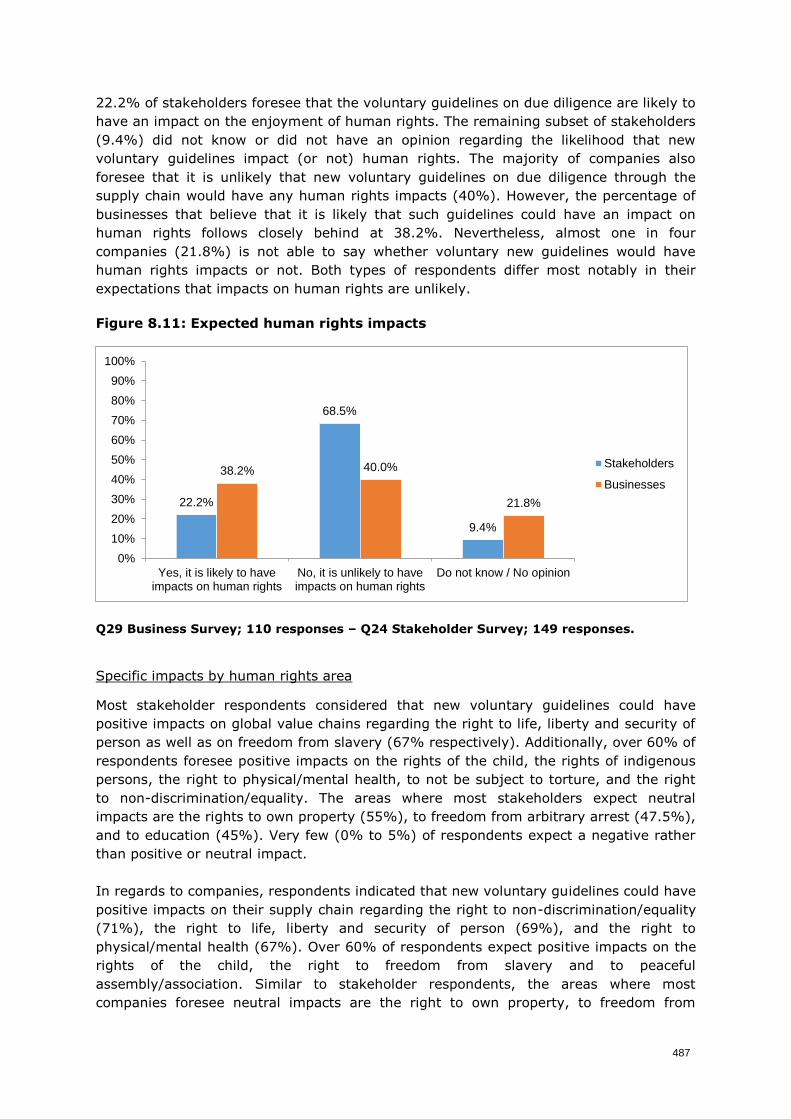

Figure 0.11: Expected human rights impacts ....................................................................... 487

Figure 0.12: Expected environmental impacts under Option 2 ............................................... 491

Figure 0.13: Expected social impacts for Option 3 ................................................................ 494

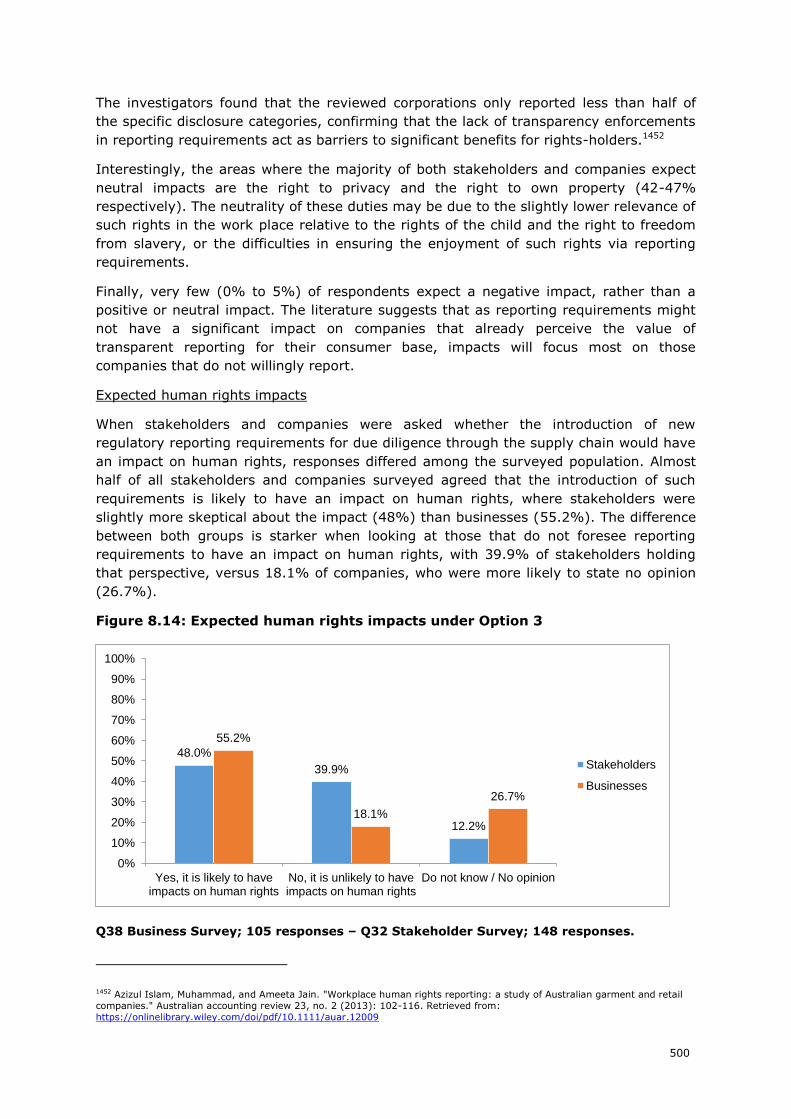

Figure 0.14: Expected human rights impacts under Option 3 ................................................. 500

Figure 0.15: Expected environmental impacts under Option 3 ............................................... 506

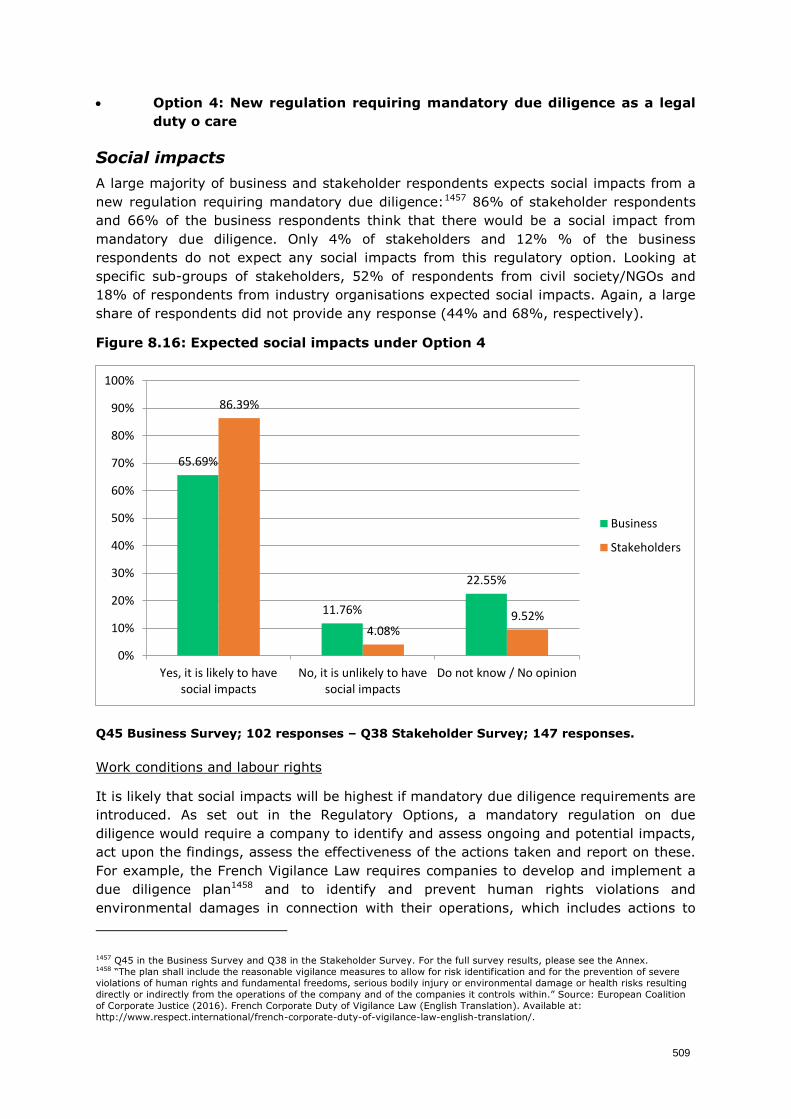

Figure 0.16: Expected social impacts under Option 4 ............................................................ 509

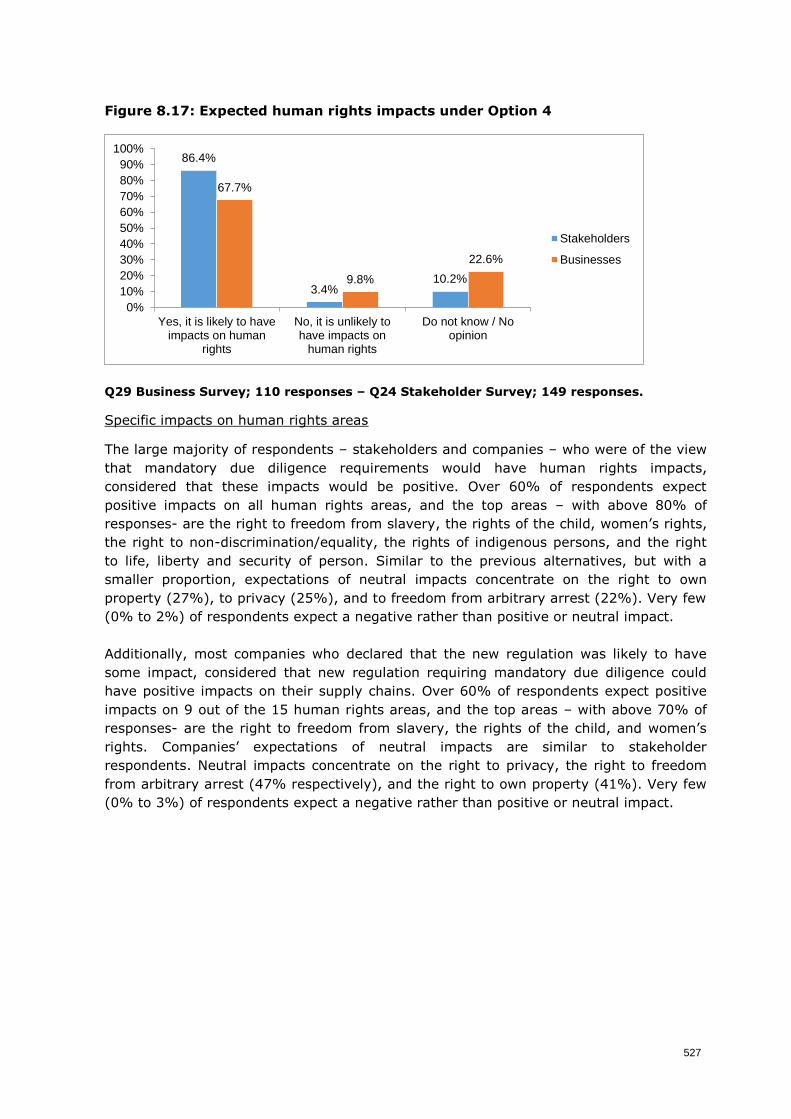

Figure 0.17: Expected human rights impacts under Option 4 ................................................. 527

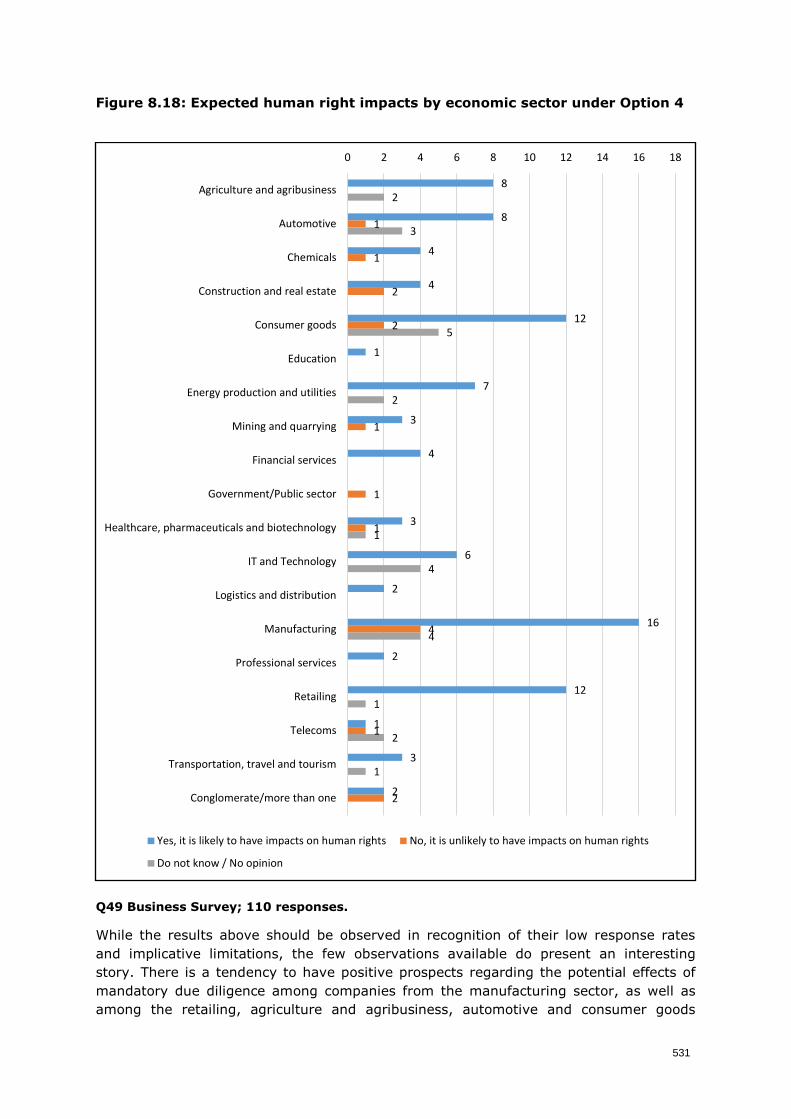

Figure 0.18: Expected human right impacts by economic sector under Option 4 ...................... 531

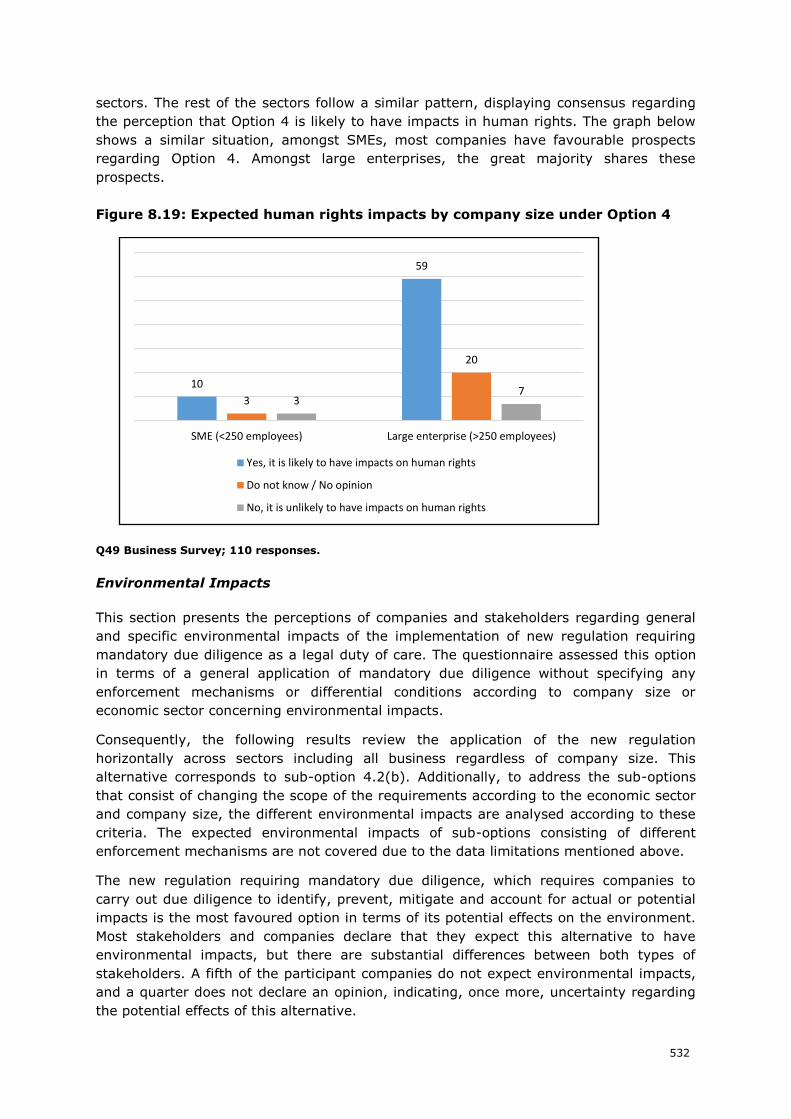

Figure 0.19: Expected human rights impacts by company size under Option 4 ......................... 532

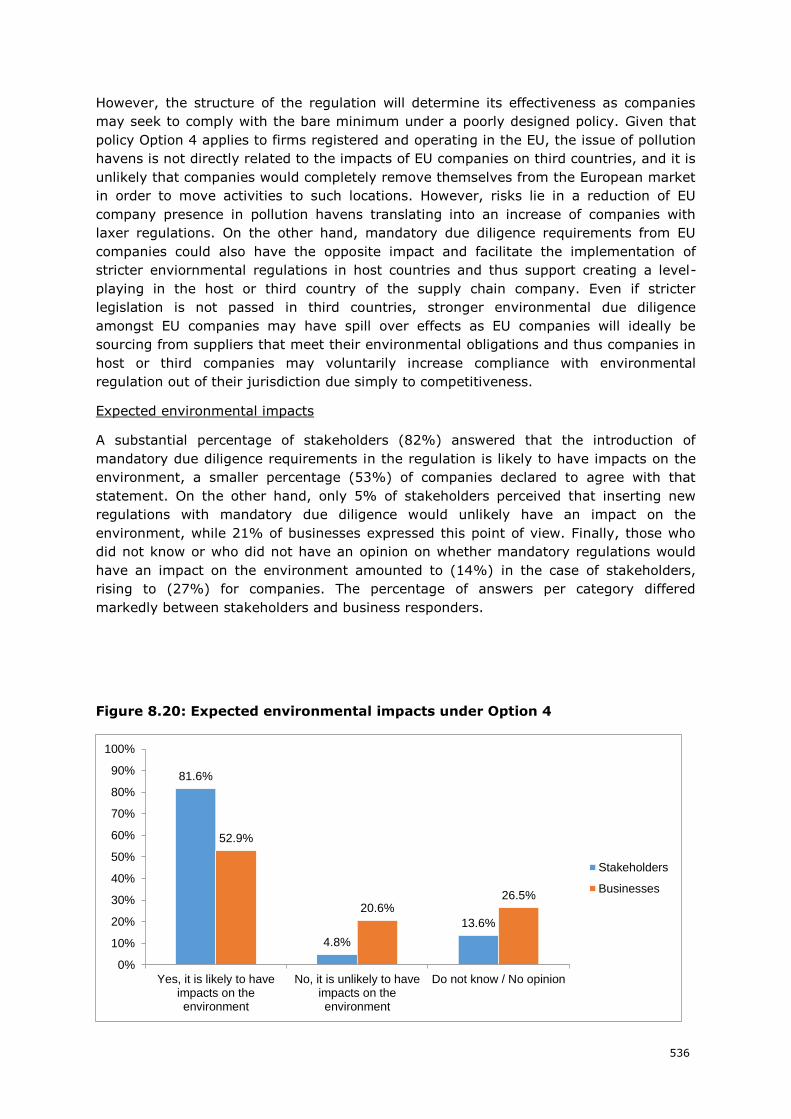

Figure 0.20: Expected environmental impacts under Option 4 ............................................... 536

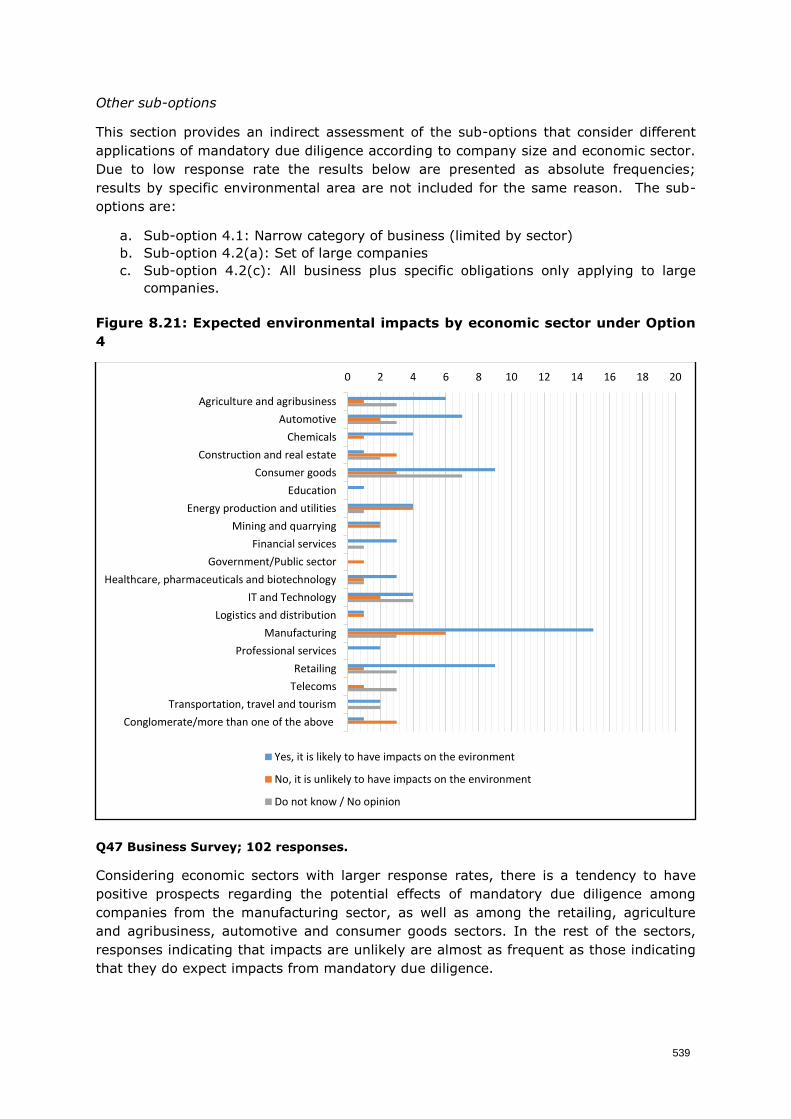

Figure 0.21: Expected environmental impacts by economic sector under Option 4.................... 539

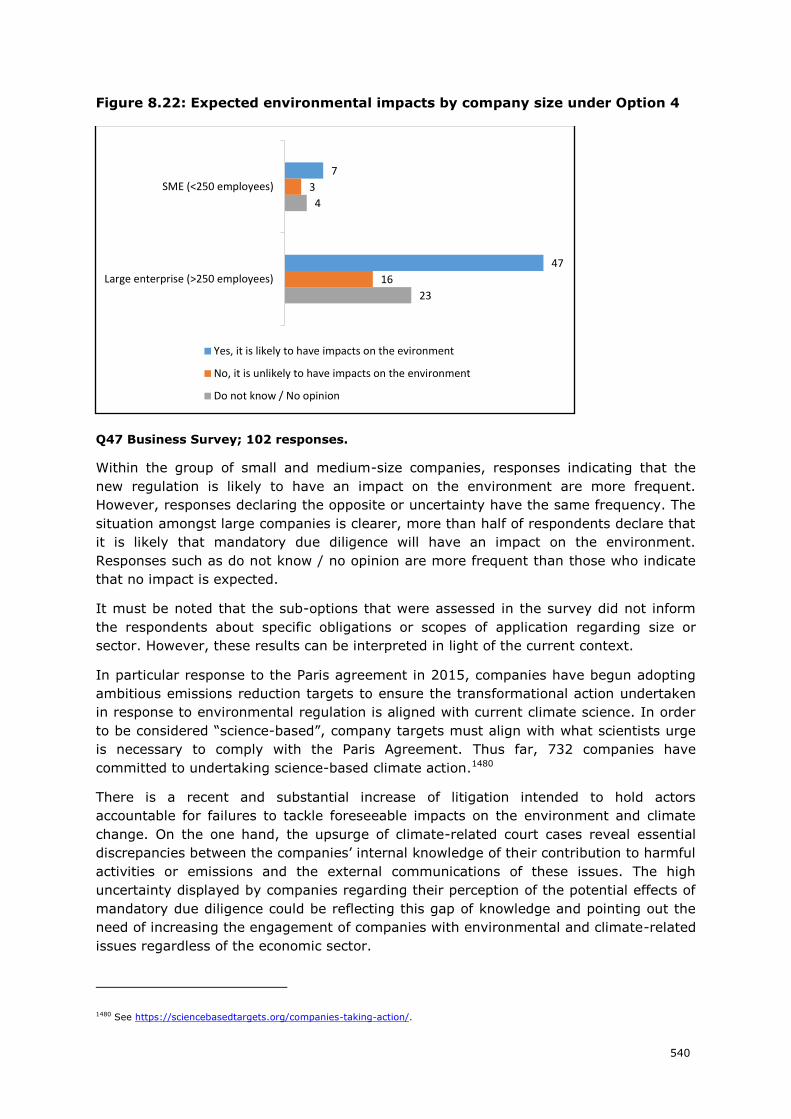

Figure 0.22: Expected environmental impacts by company size under Option 4 ....................... 540

15

EXECUTIVE SUMMARY (English)1

1. Background

This is a study for the European Commission DG Justice and Consumers on due diligence

through the supply chain, undertaken by the British Institute of International and

Comparative Law (BIICL) in partnership with Civic Consulting and LSE Consulting.

The mandate for this study derives from Action 10 of the European Commission Action

Plan on Financing Sustainable Growth of 8 March 2018,2 to:

[C]arry out analytical and consultative work with relevant stakeholders to assess:

(i) the possible need to require corporate boards to develop and disclose a

sustainability strategy, including appropriate due diligence throughout the supply

chain, and measurable sustainability targets; and (ii) the possible need to clarify

the rules according to which directors are expected to act in the company's long-

term interest. [Italics added]

The mandate further derives from the May 2018 European Parliament Report on

Sustainable Finance, which calls for a “legislative proposal” for “an overarching,

mandatory due diligence framework including a duty of care to be fully phased-in within

a transitional period and taking into account the proportionality principle”. 3

The concept of due diligence relevant to this study, to “identify, prevent, mitigate and

account for” adverse corporate impacts on human rights and the environment, was

introduced by the UN Guiding Principles on Business and Human Rights (“UNGPs”),4 and

incorporated into the OECD Guidelines for Multinational Enterprises (“OECD Guidelines”)5

to extend to other areas of responsible business conduct such as the environment and

climate change, conflict, labour rights, bribery and corruption, disclosure and consumer

interests,6 as well as in the ILO Tripartite declaration of principles concerning

multinational enterprises and social policy (“MNE Declaration”).7 It is also the foundation

for the French Duty of Vigilance Law, which requires “reasonable vigilance measures” as

a standard of care for human rights and environmental harms, and which the European

Parliament report states should be the basis for the “pan-European framework”.

This study is an initial study for the possible development of regulatory options at the EU

level.

2. Market Practices (Task 1) The methodology for the collection of evidence on market practices consisted of surveys,

interviews, case studies, and desktop and legal research of relevant materials.

1 For brevity, this Executive Summary summarises the content of the study with only limited footnoted references. For

references, please see the Main Report or Synthesis Report. 2 Action 10 of the Communication from the Commission to the European Parliament, the European Council, the Council, the

European Central Bank, the European Economic and Social Committee and the Committee of the Regions Action Plan:

Financing Sustainable Growth, COM/2018/097 final, 8 March 2018. 3 European Parliament Report on Sustainable Finance, 2018/2007(INI) at para 6. 4 UN Office of the High Commissioner for Human Rights “Guiding Principles on Business and Human Rights: Implementing the

‘Protect, Respect and Remedy’ Framework” (“UNGPs”), HR/PUB/11/04, 2011. 5 OECD Guidelines on Multinational Enterprises, 2011 6 OECD Guidelines ibid Commentary on General Policies at para 14. 7 ILO, Tripartite Declaration of Principles concerning Multinational Enterprises and Social Policy, Adopted by the Governing Body

of the International Labour Office at its 204th Session (Geneva, November 1977) and amended at is 279th (November 2000),

295th (March 2006) and 329th (March 2017) Sessions (“MNE Declaration”).

16

The 334 business survey respondents ranged from all sectors, and represented

enterprises of all sizes. Business respondents operated across the EU and the world, with

only 15.32% of respondents indicating that they only operate within the EU, and at least

40 respondents operating in each Member State.

The 297 general survey respondents (including business associations and industry

organisations, civil society, worker representations or trade unions, legal practitioners

and government bodies) similarly provided a representative and balanced sample.

General survey respondents indicated that their work covers all sectors and company

sizes. The largest group indicated that their work is not sector-specific or that it spans

across sectors. All EU Member States were selected by general survey respondents as

being relevant to their work.

Just over one-third of business respondents indicated that their companies undertake

due diligence which takes into account all human rights and environmental impacts, and

a further one-third undertake due diligence limited to certain areas. However, the

majority of business respondents which are undertaking due diligence include first tier

suppliers only. Due diligence practices beyond the first tier and for the downstream value

chain were significantly lower. The vast majority of business stakeholders cover

environmental impacts, including climate change, in their due diligence, although the

term “climate change due diligence” for a self-standing process is currently rarely used,

and human rights and climate change processes often take place in “silos”.

The most frequently used due diligence actions include contractual clauses, codes of

conduct and audits. Divestment was the least selected due diligence action by both

business and general respondents.

When asked about the primary incentives for undertaking due diligence, business

respondents and industry organisations selected the same top three incentives as being:

reputational risks; investors requiring a high standard; and consumers requiring a high

standard. Presumably because of the existing lack of regulatory or legal requirements to

undertake due diligence, business and industry organisation respondents indicated that

regulation or legal requirements are currently, or have been in the past, the least

selected incentives for companies to undertaking due diligence. In contrast, general

stakeholders and civil society respondents viewed regulatory incentives as the top

incentives for due diligence.

Survey respondents indicated that the current legal landscape (Option 1) does not

provide companies with legal certainty about their human rights and environmental due

diligence obligations, and is not perceived as efficient, coherent and effective.

Interviewees across business and other stakeholders agreed that there is already enough

voluntary guidance (Option 2) in existence, and survey respondents overall seemed

unconvinced that new voluntary guidance would have notable social, environmental and

human rights impacts. In contrast, survey respondents from industry organisations

expressed a preference for voluntary guidelines, drawing attention to the influential

nature of existing soft law mechanisms. Stakeholders however suggested that voluntary

guidance could be helpful to supplement and clarify any legal obligations, particularly

relating to the specificities of certain sectors or issues.

Survey respondents were more positive about the likely sustainability impacts of new

regulatory reporting requirements (Option 3). Perceived shortcomings stated by survey

respondents were that reporting requirements do not usually provide for effective

sanctions for non-compliance, and do not substantively require appropriate due diligence

for compliance with the regulatory obligation. It was nevertheless highlighted that

reporting requirements in this area have had a positive impact in raising awareness, and

that some are relatively new.

17

The majority of stakeholders indicated that mandatory due diligence as a legal standard

of care (Option 4) may provide potential benefits to business relating to harmonization,

legal certainty, a level playing field, and increasing leverage in their business

relationships throughout the supply chain through a non-negotiable standard. The level

playing field and legal certainty were amongst the most important considerations for

business interviewees, whereas general interviewees highlighted its potential to address

the lack of access to remedies for affected parties and improve implementation of due

diligence. Almost all interviewees were in principle in favour of a policy change to

introduce a general standard at the EU level, although they differed on aspects of liability

and methods of enforcement. However, industry organisation survey respondents were

overall not in favour of the introduction of new policy changes, including mandatory due

diligence.

Within this option, the overall preference appears for a general cross-sectoral regulation,

but which takes into account the specificities of the sector, and the size of the company

in its application to specific cases. Survey respondents expressed an overall preference

for a standard which applies regardless of size, but views varied in this respect: many

noted a concern about the potential burden for SMEs, whilst other argued that many of

the risks in their supply chain relate to the activities of SMEs.

Stakeholders further indicated that the legal mechanism should be based on a standard

of care rather than a procedural (frequently described as “tick box”) requirement, and

they indicated that a company should be able to avoid legal liability by showing that it

has undertaken the due diligence required in the circumstances (the due diligence

defence). Interviewees also highlighted that mandatory due diligence laws should form

part of a “smart mix” of measures. Some stakeholders remarked that a transitional

period would be helpful. A few interviewees indicated that an EU-level regulation linked

to legal requirements for operating in or access to the European market would be a

powerful incentive. Many stakeholders emphasized the global importance of the EU

leadership in this area.

It is also noted that, increasingly, individual multinational companies support the

introduction of mandatory due diligence regulation, although there is no agreement on

the form of liability and enforcement mechanisms. In contrast, the majority of industry

organisation survey respondents appear to be in favour of the least enforceable

regulatory options. In this respect, industry organisation’s views on regulatory options

are contradictory to those of individual multinational companies on some of these key

questions.

Stakeholders across the spectrum seemed to be in consensus, with many expressing

strong views, that the UNGPs concept of due diligence should not be abandoned for

something that is more "vague". Instead, stakeholders suggested that any regulatory

mechanism should build upon the influence and strength of the due diligence concept of

the UNGPs.

3. Regulatory Review (Task 2)

The study reviewed the regulatory framework applicable to due diligence for human

rights and environmental impacts internationally, in the EU as well as in some non-EU

jurisdictions, and in 12 selected Member States through Country Reports by legal

experts.

18

The UNGPs state that in order to meet their responsibility to respect human rights,

business enterprises should carry out human rights due diligence8 to “identify, prevent,

mitigate and account for”9 actual or potential adverse human rights impacts a company

may be involved in through its own activities or business relationships. This responsibility

applies regardless of size, sector or where the company operates.10 The UNGPs refer to

the value chain (not the supply chain),11 and extends the responsibility to those impacts

that “the business enterprise may cause or contribute to through its own activities, or

which may be directly linked to its operations, products or services by its business

relationships”.12 The concept of leverage is used to determine whether the company has

taken “appropriate action” in circumstances where it may contribute or be directly linked

to an impact.13 Leverage is “considered to exist where the enterprise has the ability to

effect change in the wrongful practices of an entity that causes a harm”.14 The UNGPs

state that human rights due diligence should be ongoing (not once-off), context-specific

(not a one-size fits all “tick-box”), and cover all human rights,15 although certain risks

may be prioritised based on severity.16 Risks should be defined as risks to rights-holders

(i.e. people and the planet), thereby extending beyond risks to the company.17

The influence of the UNGPs is evident in the widespread adoption of the concept and

terminology of due diligence in other subsequent standards. For example, the OECD

Guidelines for Multinational Enterprises,18 were revised in 2011 to align with the

UNGPs,19 and its guidance on Responsible Business Conduct incorporates a similar

standard of due diligence as the UNGPs, including application "in all stages of the supply

chain or value chain".20 The OECD Guidelines extend the concept of due diligence

expressly to other areas of responsible business conduct, including environment and

climate change, as well as risks related to conflict, labour rights, bribery and corruption,

disclosure and consumer interests.21 OECD member states are required to set up

National Contact Points (“NCPs”), to which complaints may be made that a company is in

breach of the OECD Guidelines.

The EU has instituted a number of initiatives imposing certain due diligence-related

obligations for human rights and environmental impacts, including climate impacts.

Sector-specific examples include the EU Timber Regulation (“EUTR”)22 (which predates

the UNGPs), as well as the EU Conflict Minerals Regulation,23 which will come into force

on 1 January 2021. The EU has also adopted the EU Non-Financial Reporting Directive,24

which requires reporting on due diligence, and is accompanied by Non-Binding

8 UNGPs 15-21. 9 UNGP 15. 10 UNGPs 14 and 23. 11 UNGP 13 and its Commentary. 12 UNGP 17. 13 UNGP 19 and its Commentary. 14 Commentary to UNGP 19. 15 UNGP 17 and its Commentary. 16 Ibid. 17 UN Human Rights Council, “Report of the Special Representative of the Secretary-General on the issue of human rights and

transnational corporations and other business enterprises: ‘Protect, Respect and Remedy: a Framework for Business and Human Rights’”, A/HRC/8/5, 7 April 2008, at para 6. 18 OECD Guidelines above n 5. 19 John Ruggie and Tamaryn Nelson, “Human Rights and the OECD Guidelines for Multinational Enterprises: Normative

Innovations and Implementation Challenges“, Corporate Social Responsibility Initiative Working Paper No. 66 (May 2015) at

13. 20 OECD “OECD Guidelines for Multinational Enterprises: Responsible Business Conduct Matters” (“OECD RBC Guidance”),

available at: http://mneguidelines.oecd.org/MNEguidelines_RBCmatters.pdf at 61. 21 OECD Guidelines above n 5Commentary on General Policies at para 14. 22 Regulation (EU) No 995/2010 of the European Parliament and of the Council of 20 October 2010 laying down the obligations of operators who place timber and timber products on the market (“EU Timber Regulation”). 23 Regulation (EU) 2017:821 of the European Parliament and of the Council of 17 May 2017 laying down supply chain due

diligence obligations for Union importers of tin, tantalum and tungsten, their ores, and gold originating from conflict-affected

and high-risk areas (“EU Conflict Minerals Regulation”). 24 Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 (“EU Non-Financial Reporting

Directive”).

19

Guidelines on non-financial reporting,25 and the recent Supplement on corporate climate-

related information reporting.26

Various domestic legislative measures address supply chain due diligence, but they are

often sector- or issue-specific. The 2017 French Duty of Vigilance Law27 is the only

legislative example to date which imposes a general mandatory due diligence

requirement for human rights and environmental impacts. As this law is new, there are

not yet any court judgments to clarify how this law will be interpreted and applied, but

the first legal actions have just been instituted.28 The 2019 Dutch Child Labour Due

Diligence Law requires due diligence for child labour,29 and the 2015 UK Modern Slavery

Act30 requires reporting on due diligence for modern slavery and human trafficking.

There are also currently pending proposals or campaigns for mandatory human rights

and environmental due diligence laws in 13 European countries, including 11 EU Member

States. Other existing domestic laws with due diligence requirement include those

relating to anti-corruption laws, product safety, public procurement, anti-money

laundering, and directors’ duties. Due diligence requirements are also contained in the

Revised Draft of the UN Business and Human Rights Treaty.31

As there is currently no general duty on companies to undertake due diligence for their

human rights and environmental harms in most EU jurisdictions, case law has developed

various possible avenues to bring claims for adverse human rights and environmental

harms in indirect ways, including in tort, criminal law, and consumer protection laws. A

few claims to date have been instituted against companies for climate change

contributions.

Recent developments are clarifying the content of due diligence requirements for

companies’ climate change impacts, many of which took place as this study was being

undertaken. In particular, in April 2019 the Netherlands OECD National Contact Point for

the first time clarified concrete ways in which companies’ individual due diligence actions

can include targets to address climate change.32 Reference was made to the relevant

company’s steps in terms of the Paris Agreement on climate change.33

4. Problem Analysis and Regulatory Options (Task 3)

This task consisted of an analysis of the problems, an intervention logic and the

identification of the possible regulatory intervention options at EU level.34

Option 1: No policy change (baseline scenario)

25 European Commission, Guidelines on non-financial reporting (methodology for reporting non-financial information) (2017/C

215/01). 26 European Commission, Guidelines on non-financial reporting: Supplement on reporting climate-related information (2019/C

209/01). 27 Loi no. 2017-399 du 27 Mars 2017 relative au devoir de vigilance des sociétés mères et des entreprises donneuses d’ordre 28 See Regulatory Review, section 3.2.6. 29 Kamerstukken I, 2016/17, 34 506, A. See Regulatory Review and Netherlands Country Report. 30 Section 54 of the UK Modern Slavery Act 2015. See Regulatory Review and UK Country Report. 31 UN Human Rights Council open-ended intergovernmental working group on transnational corporations and other business

enterprises with respect to human rights (“OEIGWG”), “Legally Binding Instrument to Regulate, in International Human Rights

Law, the Activities of Transnational Corporations and Other Business Enterprises”, 16 July 2019, (“Revised Draft”), available

at: https://www.ohchr.org/Documents/HRBodies/HRCouncil/WGTransCorp/OEIGWG_RevisedDraft_LBI.pdf 32 The Netherlands National Contact Point for the OECD Guidelines for Multinational Enterprises, Oxfam Novib, Greenpeace

Netherlands, BankTrack and Friends of the Earth Netherlands (Milieudefensie) versus ING, Final Statement, 19 April 2019,

available at: https://www.oecdguidelines.nl/documents/publication/2019/04/19/ncp-final-statement-4-ngos-vs-ing. 33 See Paris Agreement on Climate Change, available at: https://unfccc.int/process-and-meetings/the-paris-

agreement/d2hhdC1pcy. 34 Further considerations identified as relevant to the introduction of a new regulatory intervention are discussed in the full

report and include the possibility of accompanying non-binding guidance, the regulation of transnational corporate activity, the

application to corporate groups and the supply chain, implementation at Member State level, material scope relating to the

definition of human rights and environmental impacts, potential conflict of laws, and a transitional period.

20

This option would entail no changes in regulation at EU level for companies on

undertaking due diligence through the supply chain. It is expected that current national

level developments will continue to result in mandatory due diligence legislation in at

least some Member States.

Option 2: New voluntary guidelines / guidance

This option would entail new voluntary guidelines at EU level for companies on

undertaking due diligence through the supply chain. Voluntary guidelines are by their

nature not usually legally enforceable but may influence the standard expected of

companies.

Option 3: New regulation requiring due diligence reporting

This option would entail new regulation at EU level requiring companies to report on the

steps they have taken to identify, address, prevent and mitigate any adverse human

rights and environmental impacts in their own operations or of third-party business

relationships (including the supply chain or value chain).35 This option may differ from

the EU Non-Financial Reporting Directive with regard to level of detail and transparency

required, and an express focus on risks to people and the planet rather than materiality

to shareholders.

Option 4: New regulation requiring mandatory due diligence as a legal duty of

care

This option would entail a new mandatory due diligence requirement at EU level which

would require companies to carry out due diligence to identify, prevent, mitigate and

account for actual or potential human rights and environmental impacts in their own

operations and supply or value chain36, as a legal duty or standard of care. It would allow

for a company to demonstrate, in its defence, that it has met this standard by undertaking

the level of due diligence required in the particular circumstances, i.e. this would be a

context-specific risk-based approach. The due diligence standard would allow for

prioritisation of those risks which are the most “severe”,37 the “most significant”,38 or the

most “salient”.39

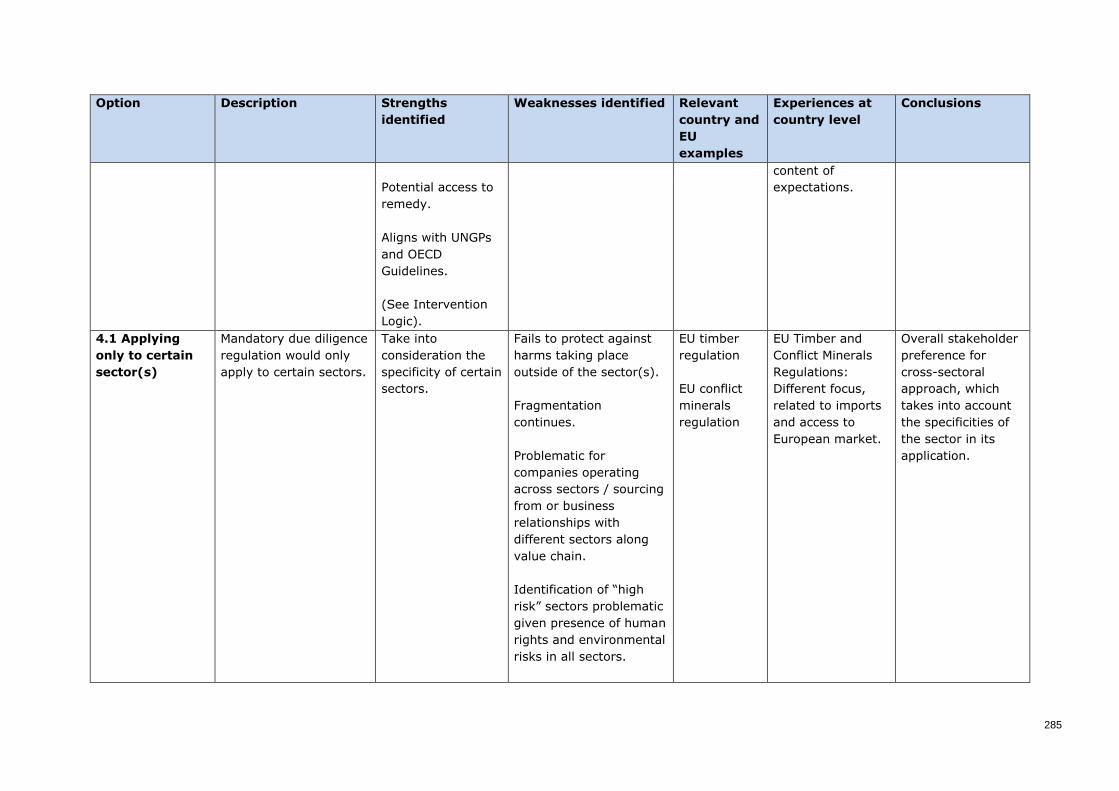

Sub-option 4.1: New regulation applying to a narrow category of business

(limited by sector)

This sub-option would entail a substantive legal duty to meet a standard of due diligence,

applicable only to a certain sector or commodity.

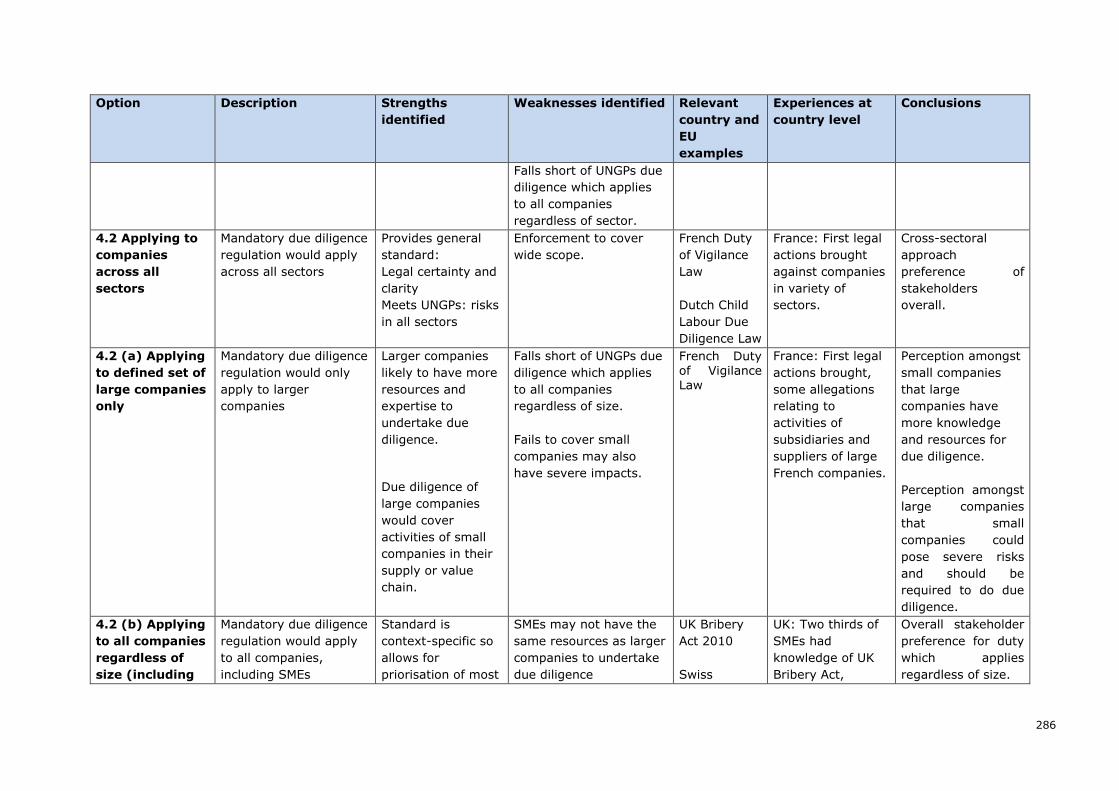

Sub-option 4.2: New regulation applying horizontally across sectors

In terms of this sub-option, the above new mandatory due diligence regulation (Option

4) would apply across all sectors, either (a) to a defined set of large companies; (b) to

all companies regardless of size and so including SMEs, or (c) a general duty for all

companies plus an additional duty for large companies only.

Sub-option 4.2(a): applying only to a defined set of large companies

35 This will depend on the scope of the regulatory intervention. The title of the study in terms of the TOR refers to supply chain

but the scope of the mandate described therein envisions an application to the entire value chain. Survey respondents were

provided with definitions when asked about details relating to their “upstream supply chain” and “downstream value chain” respectively. 36 Ibid. 37 UNGP 17(b). 38 OECD Guidelines above n 5Chapter II, Commentary at para 16. 39 Shift and Mazars, “UN Guiding Principles Reporting Framework with implementation guidance”, available at:

https://www.ungpreporting.org/wp-content/uploads/UNGPReportingFramework_withguidance2017.pdf at 22.

21

This would entail a general legal duty to undertake due diligence (Option 4), applicable only

to a certain defined set of large companies.

Sub-option 4.2(b): applying to all business, including SMEs.

This sub-option would entail a general legal duty to undertake due diligence (Option 4),

applicable to all companies, including SMEs.

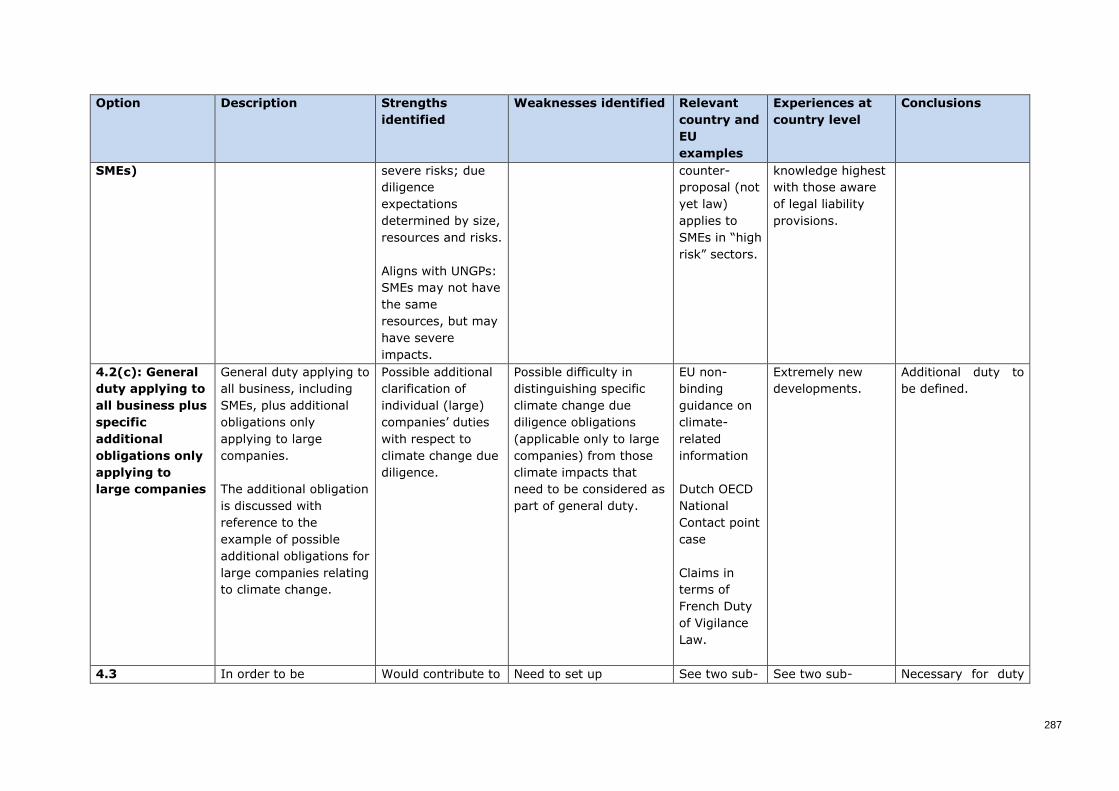

Sub-option 4.2 (c): general duty applying to all business plus specific additional

obligations only applying to large companies

This sub-option is would entail a general due diligence duty applying to all business

(including SMEs) plus an additional specific obligation applicable only to large companies.

By way of one example, this could take the form of a general due diligence duty applying to

all business, (including SMEs), plus an additional obligation linked to climate change targets

for large companies.

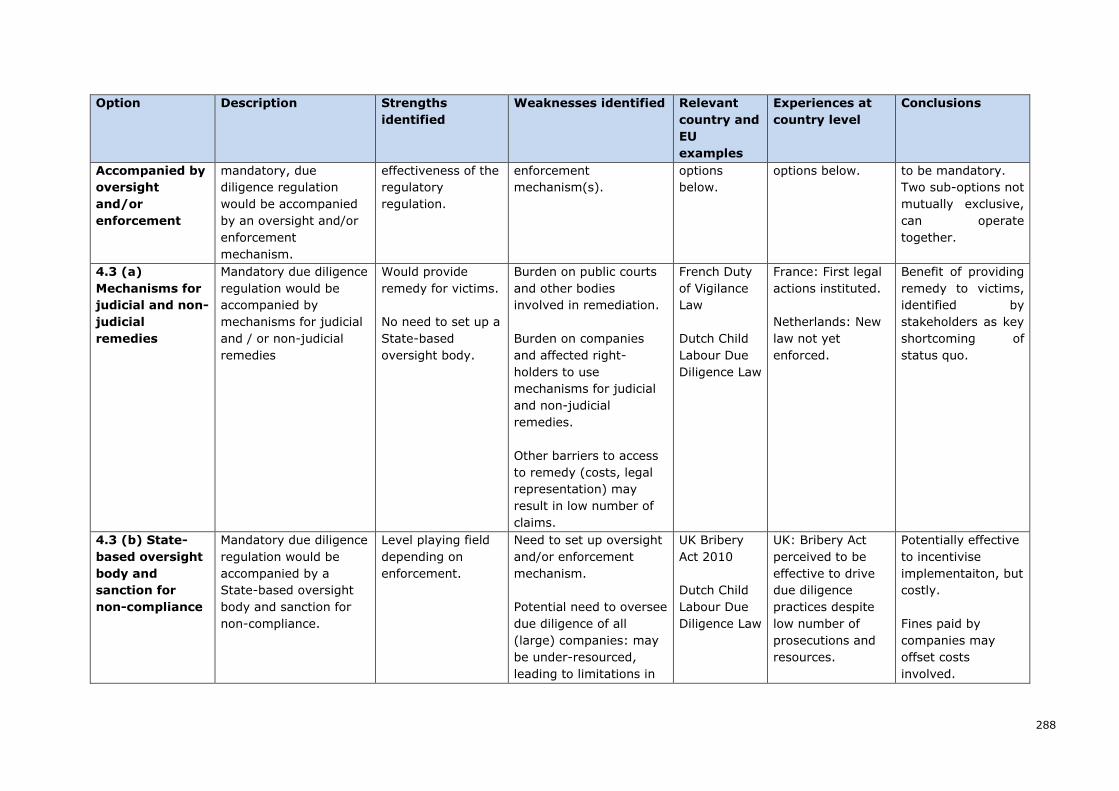

Sub-option 4.3: Sub-options 4.1 and 4.2 accompanied by a statutory oversight

and/or enforcement mechanism

In order to be mandatory, the above new mandatory due diligence regulation (Option 4)

would need to be accompanied by an oversight and/or enforcement mechanism. This

sub-option considers two sub-sub-options for the enforcement and oversight of such a

mechanism, namely (a) through judicial or non-judicial remedies, or (b) through a State-

based oversight body and sanctions for non-compliance. These two sub-sub-options are

not mutually exclusive and could both apply to the same instrument.

Sub-sub-option 4.3(a): mechanisms for judicial or non-judicial remedies

This sub-sub-option would consist of the above new mandatory due diligence regulation

(Option 4) accompanied by mechanisms for judicial and non-judicial remedies for those

affected by the company’s failure to exercise due diligence.

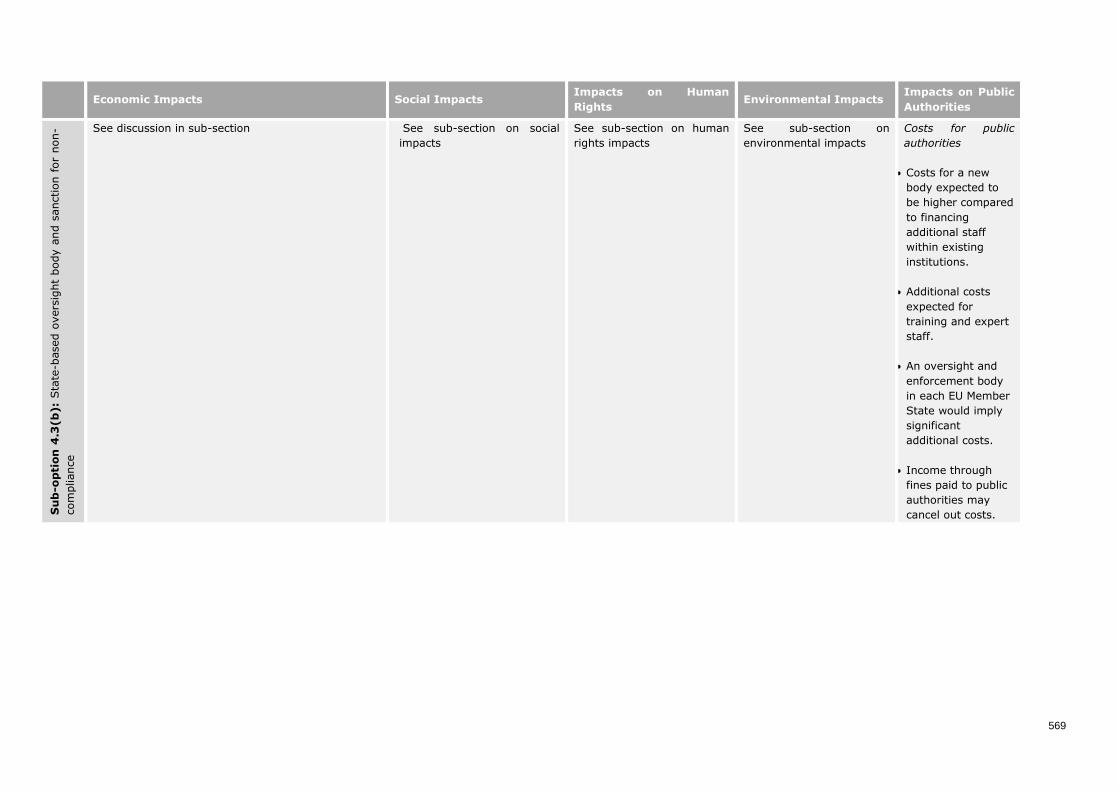

Sub-sub-option 4.3(b): State-based oversight body and sanction for non-

compliance

This sub-option would consist of the above new mandatory due diligence regulation

(Option 4) accompanied by a State-based oversight body and sanctions for non-

compliance. Oversight and enforcement bodies (often called administrative bodies) can be

created at EU and/or Member State level, within existing state departments, or by newly

established bodies. Enforcement mechanisms could include fines, the appointment of

monitors, withdrawal of licences or trade concessions, or even the dissolution of the

company. However, none of these enforcement mechanisms include remedy to the victim,

although this could be expressly provided for in addition to the State-based oversight.

5. Assessment of Options

The assessment of the regulatory options was undertaken by LSE Consulting, based on a

literature review and an assessment of the survey results. It combines quantitative and

qualitative approaches, and aims to discuss and assess, at this preliminary stage,40

possible costs and benefits of the different regulatory options in the following areas:

economic impacts; social impacts; environmental impacts; impacts on human rights;

40 This is only a preliminary study of regulatory options and not a full-scale impact assessment accompanying a regulatory

proposal. As such, the following impact assessment should be taken as a general discussion of potential impacts which could

arise if and when a new regulation is designed.

22

and impacts on public authorities in the EU.41 It is important to point out that the various

stakeholders had different experiences of laws, some of which relate to due diligence

reporting and administrative requirements (and not a standard of care). The lack of

existing comparative legislative examples resulted in varying expectations among survey

respondents.

The quantifications of economic impacts are based on person-day estimates that were

given by the surveyed business respondents for each of the four main regulatory

options. Generally, businesses’ estimates indicate that the number of required person-

days, and related costs respectively, would increase moderately with a shift from the

status-quo to new reporting requirements, and increase more substantially with a shift

from the status-quo to mandatory due diligence. We estimate that the total EU 28

additional annual company-level cost impact (labour cost, overhead and cost of

outsourced activities) would be proportionally highest for policy Option 4, with variations

depending on company size and sector depending on scope of application.

The impact on competition and innovation is difficult to assess ex-ante. Generally, no

significant distortions in intra-EU competition are expected if all companies that operate

in the EU are governed by the same set of regulations. While EU companies might be at

a relative disadvantage in cost competitiveness compared to non-EU companies,

additional firm-level costs as percentages of companies’ revenues are relatively low

compared to, for example, the applied average tariff for goods imported to the EU.

Therefore, no significant negative distortions for EU exporters that result from increased

recurrent administrative cost are expected. Business survey respondents expect

significant benefits or very significant benefits through decreased distortions, if the new

EU regulation creates more equal standards for EU and non-EU suppliers.

Moreover, stakeholders indicated various disadvantages which they experience from the

current lack of regulation in terms of the status quo, which they expect to improve if a

general duty is introduced at EU level. These benefits include an improvement in

competiveness through the levelling of the playing field, so that competitors, peers,

suppliers and third parties will be subjected to the same standard, as well as increasing

leverage with third parties in the value chain through the introduction of a non-

negotiable standard. These benefits are difficult to quantify at this stage, but should be

borne in mind, given that they could be significant, and were raised by business

stakeholders as one of the most important reasons for the introduction of a mandatory

due diligence requirement.

Similarly, business respondents indicated that reputational risk is their top incentive to

undertake due diligence under the current status quo. It is expected that these existing

reputational risks may be reduced through the introduction of a general due diligence

duty. Accordingly, it is likely that the most significant reputational benefits from a

mandatory due diligence requirement may result from a reduction in existing

reputational risks.

Digitalisation and new technology tools hold the potential to provide unprecedented

solutions to identify, address and eliminate human rights infringements and

environmental challenges. However, these technological advancements have not been

taken into consideration by the vast majority of the respondents.

Cost impacts on public authorities in terms of Options 2 and 3 are expected to remain

limited. The additional costs for the monitoring of the implementation of the regulation

under Option 4 are expected to be significant, especially if enforcement is to take place

41 Due to the relative newness of comparable laws which require due diligence as a legal standard of care, it has proven

challenging to find impact assessments which have been carried out for similar legislation, and where these were found they

did not necessarily include information and/or data which could be used for this analysis.

23

at Member State or EU level (sub-option 4.3(b)). By comparison, judicial remedies as

foreseen in sub-option 4.3(a) are likely to have significantly less additional costs for

Member States, insofar as these costs would fall within existing budgets for courts and

the judicial system.

Options 2 and 3 are expected to have only a minor positive social impacts. Since these

options only provide new guidance or require reporting but do not substantively require

companies to take any due diligence measures, it is not expected that substantial

additional measures would be taken by companies to address social matters. Both

options are also expected not to have any major negative or positive impacts on

employment levels. Social impacts from Option 4 are expected to be most significant

because the regulatory options require due diligence practices. However, the magnitude

and the type of social impacts depends on the design and application of the new

regulation, on the social issues which are addressed by the regulation, as well as on the

effectiveness of the enforcement mechanisms.

Similarly, the human rights and environmental impacts from Option 4 are expected to be

most significant, with positive impacts dependent on proper monitoring and

enforcement. However, when comparing Options 2 and 3, respondents foresee voluntary

guidelines to be more effective than reporting requirements in delivering positive

impacts. The expected positive results are consistent with previous EU assessments.

24

NOTE DE SYNTHÈSE (Français)42

1. Contexte

Cette étude sur le devoir de diligence dans les chaînes d'approvisionnement a été

réalisée par le British Institute of International and Comparative Law (BIICL), en

partenariat avec Civic Consulting et LSE Consulting, sur requête de la Commission

européenne et plus particulièrement de la Direction générale de la justice et des

consommateurs.

Le mandat relatif à cette étude émane de l’Action 10 du Plan d’action de la Commission

européenne sur le financement de la croissance durable du 8 mars 2018,43 qui prévoit

que:

La Commission procèdera à des analyses et à des consultations auprès des

parties intéressées, pour évaluer: i) l'éventuelle nécessité d'imposer aux conseils

d'administration l'obligation d'élaborer une stratégie de croissance durable,

prévoyant notamment l'exercice d'une diligence appropriée tout au long de la

chaîne d'approvisionnement, et des objectifs mesurables en matière de durabilité,

et l'obligation de la publier; et ii) l'éventuelle nécessité de clarifier les règles en

vertu desquelles les administrateurs sont censés agir dans l'intérêt à long terme

de l'entreprise. [Italique ajouté].

Le mandat émane également du Rapport du Parlement européen de mai 2018 sur la

finance durable qui invite la Commission à élaborer une « proposition de loi » visant à

mettre en place « un cadre général et obligatoire de diligence raisonnable comprenant un

devoir de vigilance à mettre en place progressivement dans les limites d’une période de

transition et en tenant compte du principe de proportionnalité. » 44

Le concept de diligence raisonnable dont il est fait référence dans le cadre de la présente

étude vise un ensemble de procédures permettant aux entreprises d'« identifier, de

prévenir, d'atténuer et de rendre compte » des incidences négatives qu'elles peuvent

avoir sur les droits de l'homme et sur l'environnement, tel qu'il a été introduit par les

Principes directeurs de l’Organisation des Nations Unies relatifs aux entreprises et aux droits de l’homme (« Principes directeurs des Nations Unies »)45 et intégré dans les

Principes directeurs de l'Organisation de coopération et de développement économique

(OCDE) à l'intention des entreprises multinationales (« Principes directeurs de

l’OCDE »),46 où il a été étendu à d'autres domaines tels que l'environnement et le

changement climatique, l'emploi et les relations professionnelles, la lutte contre la

corruption, les pots-de vin et autres formes d'extorsion, et les intérêts

des consommateurs, ainsi que dans la Déclaration de principes tripartite sur les

entreprises multinationales et la politique sociale de l'Organisation Internationale du

Travail (OIT) (« Déclaration de l'OIT sur les entreprises multinationales »).47 Il constitue

également le fondement de la loi française sur le devoir de vigilance qui exige des entreprises la mise en place des « mesures de vigilance raisonnables » en tant que

42 À des fins de concision, cette note de synthèse présente un abrégé de la teneur de l’étude et les notes de bas de pages sont

limitées. Pour obtenir les références complètes, veuillez vous reporter au Rapport principal ou au Rapport de synthèse. 43 L’Action 10 de la Communication de la Commission au Parlement européen, au Conseil Européen, au Conseil, à la Banque

centrale européenne, au Comité économique et social européen, et au Comité des régions. Plan d'action: financer la croissance

durable, COM(2018)97 final, 8 mars 2018. 44 Rapport du Parlement européen sur la finance durable (2018/2007(INI) au paragraphe 6. 45 Haut-Commissariat aux droits de l’homme de l’ONU « Principes directeurs relatifs aux entreprises et aux droits de l’homme »

mettant en œuvre le cadre « Protéger, respecter et réparer » HR/PUB/11/04 2011 46 OCDE, Principes directeurs de l'OCDE à l'intention des entreprises multinationales, 2011. 47 OIT, Déclaration de principes tripartite sur les entreprises multinationales et la politique sociale, Adoptée par le Conseil

d'administration du Bureau International du Travail à sa 204e session (Genève, novembre 1977) et amendée à ses 279e

(novembre 2000) 295e (mars 2006) et 329e (mars 2017) sessions.

25

norme de conduite, et qui, selon le rapport du Parlement européen, pourrait former le

fondement du « cadre paneuropéen ».

La présente étude constitue une étude initiale en vue du développement éventuel

d’options réglementaires en la matière au niveau européen.

2. Pratiques du marché (Tâche 1) La méthodologie employée pour cette partie de l'étude a reposé sur des enquêtes, des

entretiens et des études de cas, ainsi que sur une recherche documentaire des

ressources pertinentes ayant permis d'identifier les pratiques des entreprises en matière

de diligence raisonnable.

S'agissant des 334 répondants à l’enquête destinée aux entreprises, ils sont constitués

de professionnels provenant d'entreprises de toutes tailles et de tous secteurs d'activité.

Ces entreprises exercent des activités à la fois dans l’UE et dans le monde. Seuls

15,32 % des répondants à cette enquête ont indiqué que leurs entreprises ne déploient

d'activité qu'au sein de l’UE, et au moins 40 répondants ont indiqué que leurs entreprises

déploient une activité dans chacun des États membres de l'UE.

S'agissant des 297 répondants à l’enquête générale, ils sont constitués de membres

d'associations d’entreprises et d'organisations industrielles, de membres de la société

civile, de représentants des employés ou syndicats, d'avocats et d'organismes

gouvernementaux et forment également un échantillon représentatif et équilibré. Ces

répondants ont indiqué que leur travail couvre tous les secteurs d'activité et concerne

des entreprises de toutes tailles. La majorité des répondants ont précisé que leur travail

n’est pas spécifique à un secteur en particulier, mais qu’il englobe plusieurs secteurs. Les

répondants à l’enquête générale ont sélectionné tous les États membres de l’UE comme

étant pertinents pour leur travail.

A peine plus du tiers des répondants à l’enquête destinée aux entreprises ont indiqué

que leurs entreprises mettent en place des procédures de diligence raisonnable couvrant

les incidences négatives relatives à l'ensemble des droits de l’homme et l’environnement,

tandis qu'un autre tiers a précisé que leurs entreprises limitent leur exercice de la

diligence raisonnable à certains domaines particuliers. Une majorité de répondants à

l’enquête destinée aux entreprises n'incluent dans leur exercice de diligence raisonnable

que leurs fournisseurs de premier rang. Les pratiques en matière de diligence

raisonnable allant au-delà du premier rang et incluant les entités situées en aval de la

chaîne de valeur sont nettement plus rares. La très grande majorité des parties

prenantes issues des entreprises incluent les impacts environnementaux, et notamment

ceux liés au changement climatique, dans leurs procédures de diligence raisonnable bien

que la « diligence raisonnable en matière de changement climatique » en tant que

processus autonome soit rarement utilisée en l'état actuel et que les mesures de

diligence raisonnable relatives aux droits de l’homme et celles relatives au changement

climatique soient souvent réalisés de manière parallèle.

Les clauses relatives aux droits de l'homme insérées dans les contrats

d'approvisionnement, les codes de conduite et les audits figurent parmi les mesures les

plus communément mises en oeuvre par les entreprises dans le cadre de l'exercice de

leur diligence raisonnable. Le recours au désinvestissement a été la mesure la moins

sélectionnée aussi bien par les répondants à l’enquête destinée aux entreprises que par

les répondants à l’enquête générale.

Quant aux incitations principales à la mise en oeuvre de mesures de diligence

raisonnable, les trois mêmes réponses ont été sélectionnées par les répondants à

l’enquête destinée aux entreprises et les organisations industrielles, à savoir, les risques

réputationnels, les exigences des investisseurs et les exigences des consommateurs en

26

faveur d'un standard plus élevée. Les répondants à l’enquête destinée aux entreprises et

les organisations industrielles ont indiqué accorder une importance moindre aux