scek's consulting contents

TRANSCRIPT

SCEK’S CONSULTING

The Formal and Informal Institutional Makings of the Political Economy of the Budget Process in Somaliland

The Political Economy of the Budget in Somaliland

Nairobi 2010

Dr. Scek

2 | P a g e

Contents

Executive summary ........................................................................................................ 4

Background ......................................................................................................................... 8

Methodology ........................................................................................................................ 9

Objectives of the Exercise .............................................................................................. 10

Linkages PEFA and CA .................................................................................................. 10

Framework for the Interaction of Budget Stakeholders .................................................... 11

Key Steps in the Budget Process ....................................................................................... 14

Key Findings from the Analysis of the Budget Process .................................................... 16

Political Factors Affecting Budget Process ........................................................................ 17

Economic Vulnerability ................................................................................................. 18

Power Relation among the Various Actors ................................................................... 19

Budget Analysis: Formulation, Approval, Implementation and Oversight ..................... 21

Stage 1: Budget Formulation Process ............................................................................ 21

How does budget planning and formulation operate in practice ............................................................ 22

Stage II: Budget Approval ............................................................................................. 22

Stage III: Budget Execution .......................................................................................... 23

Stage IV: Budget Monitoring and Control .................................................................... 25

Executive Controls ..................................................................................................................................... 26

House of Representatives Oversight/Control .......................................................................................... 26

Civil Society and Citizen in Budget Oversight/Control ............................................................................ 27

Performance Measurement Framework - PEFA Indicators ............................................. 28

Challenges Facing Somaliland .......................................................................................... 31

Conclusions ....................................................................................................................... 33

Executive Undermining Formal Process ....................................................................... 34

Weak Accountability Institutions .................................................................................. 34

Dr. Scek

3

Weak Demand for Accountability ................................................................................. 34

Development Partners Conflicting Interests ................................................................ 35

Policy Recommendations .................................................................................................. 36

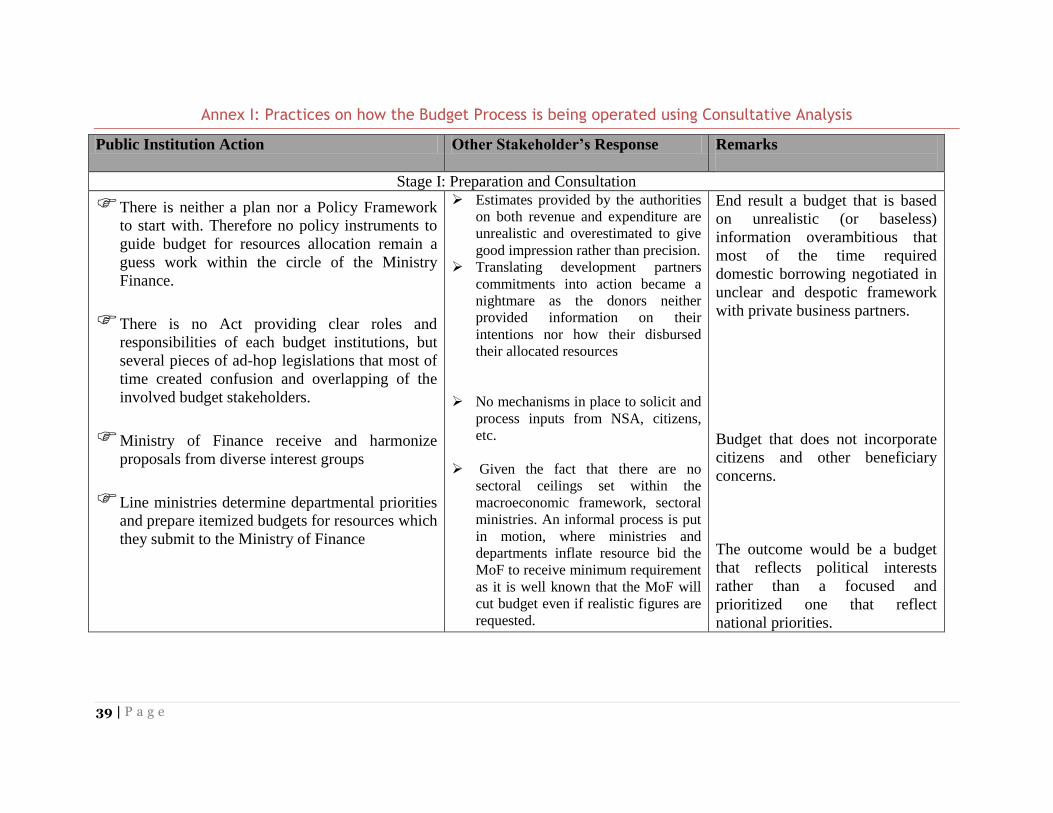

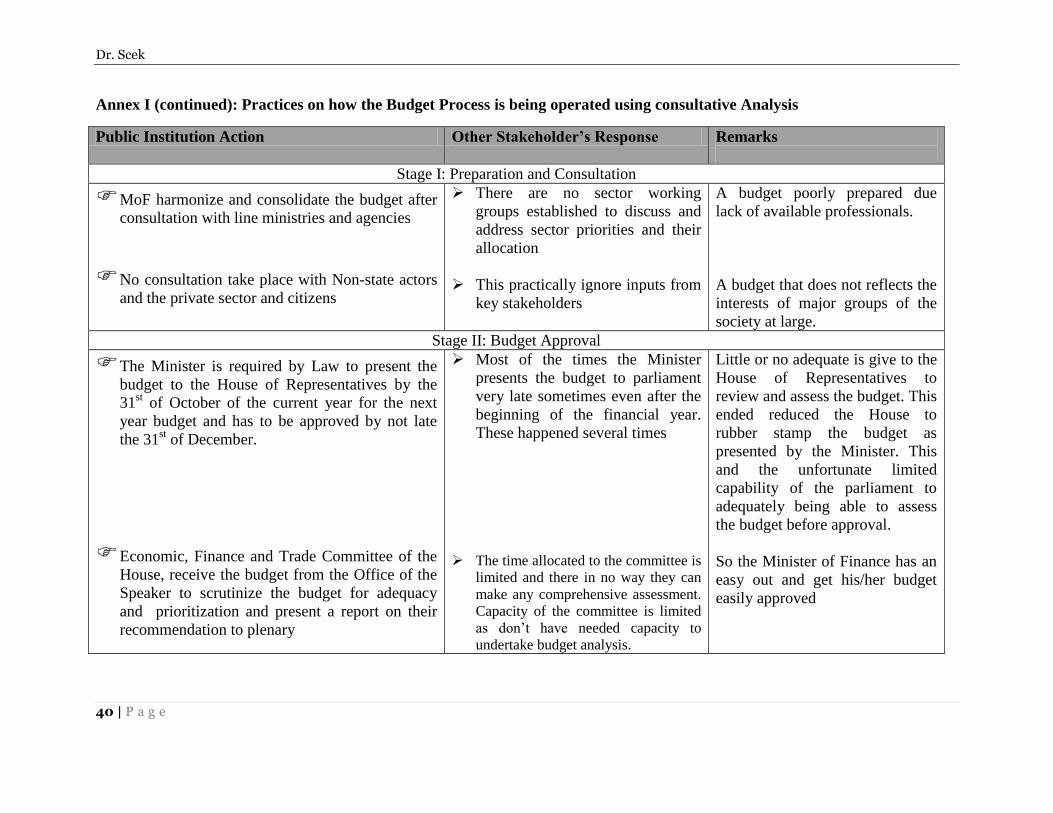

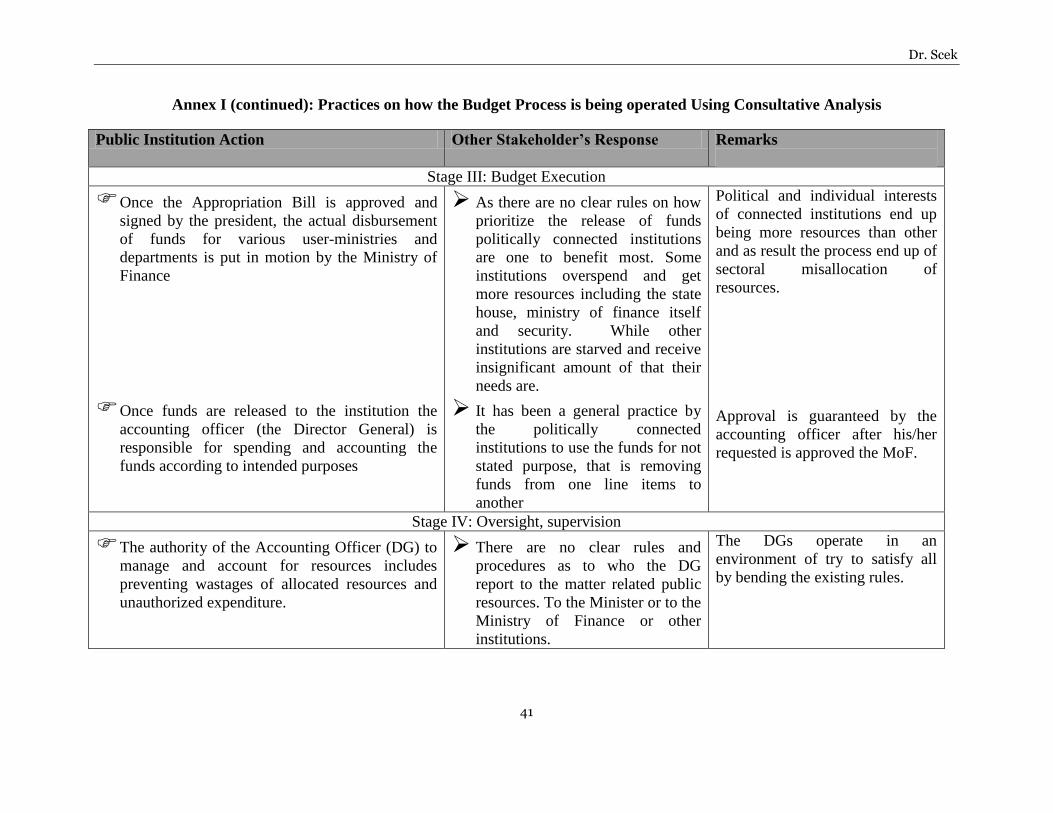

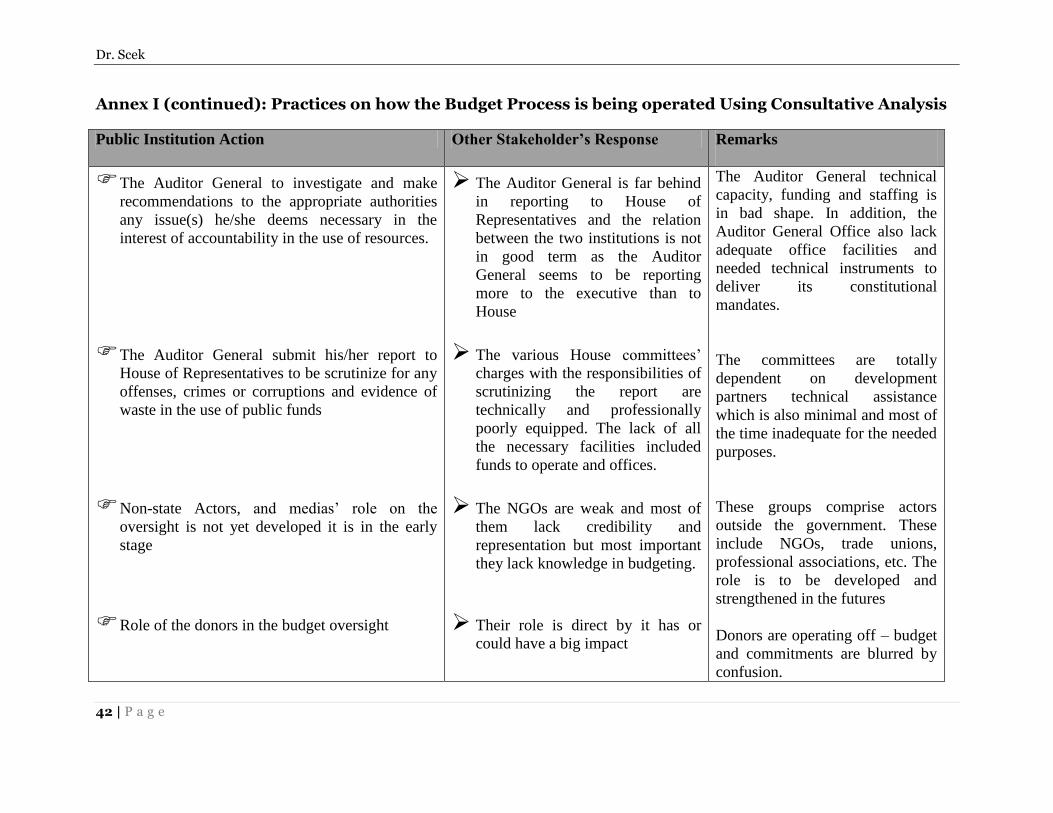

Annexes: Results of the Analysis ...................................................................................... 38

Annex I: Practices on how the Budget Process is being operated using Consultative

Analysis .............................................................................................................................. 39

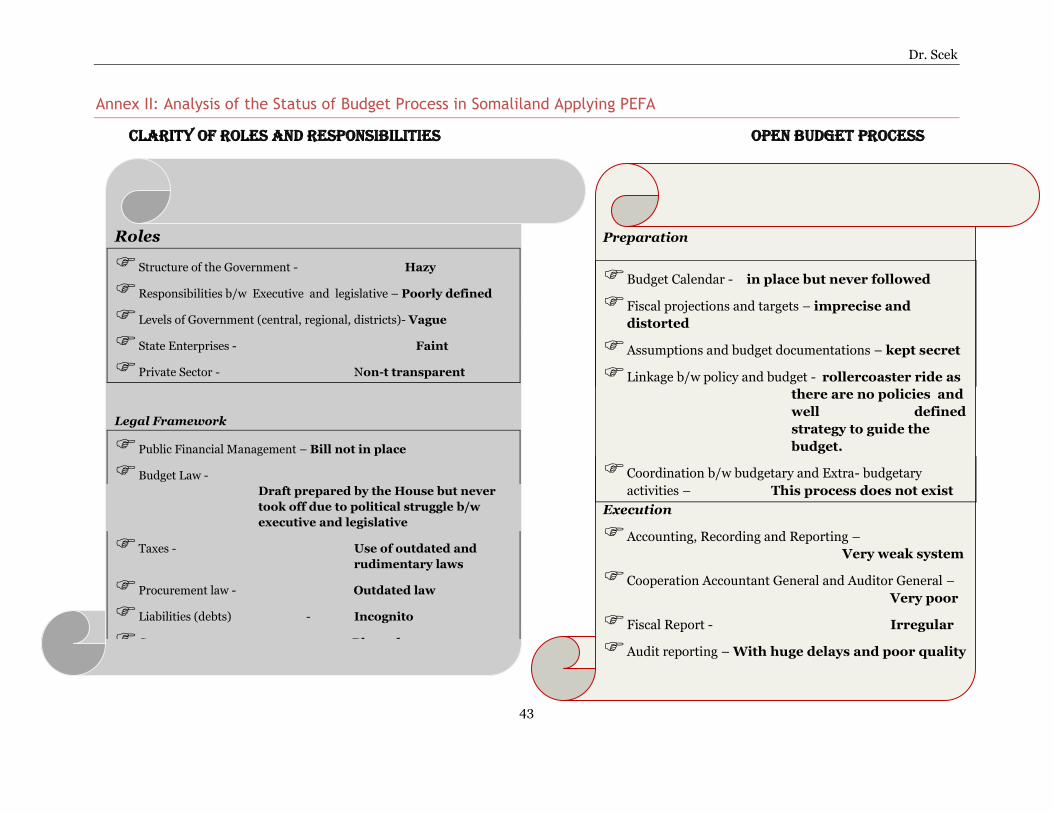

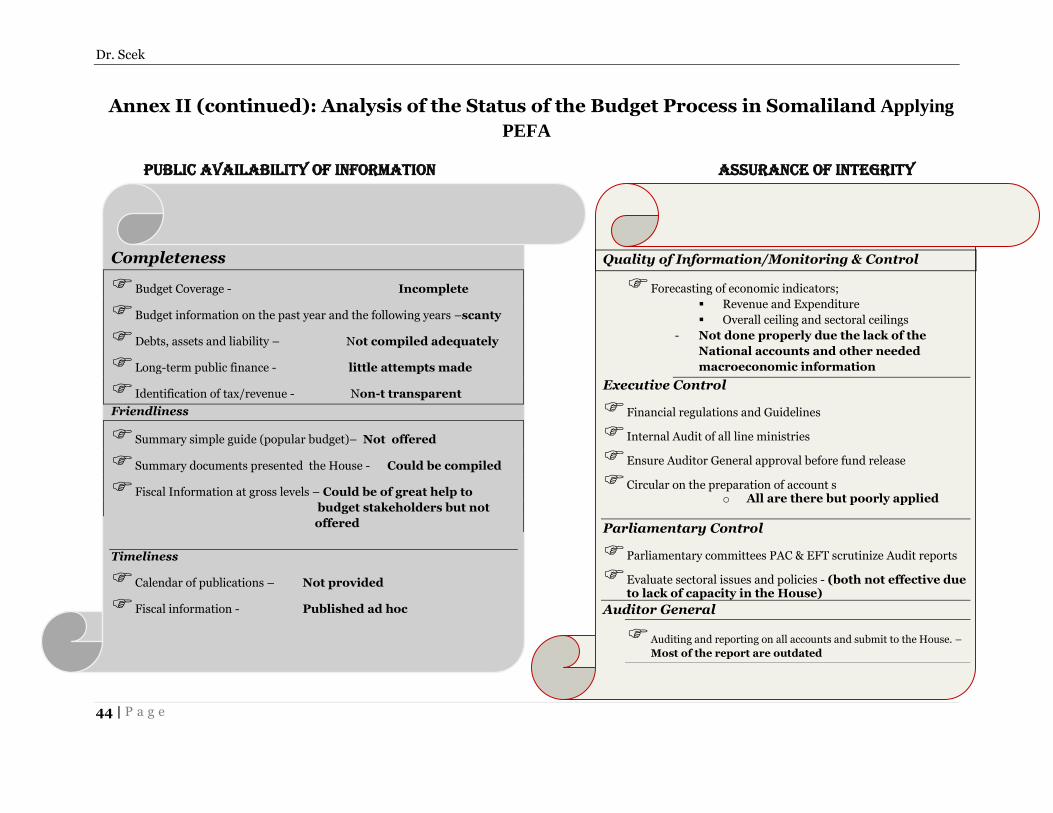

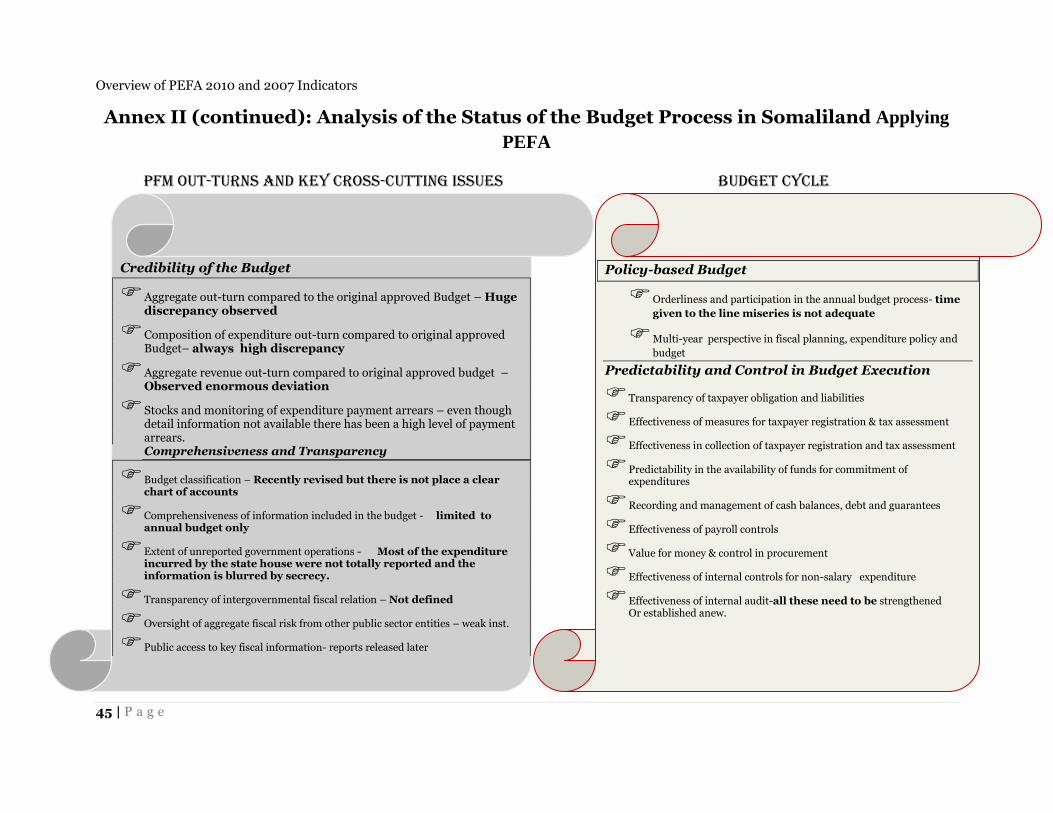

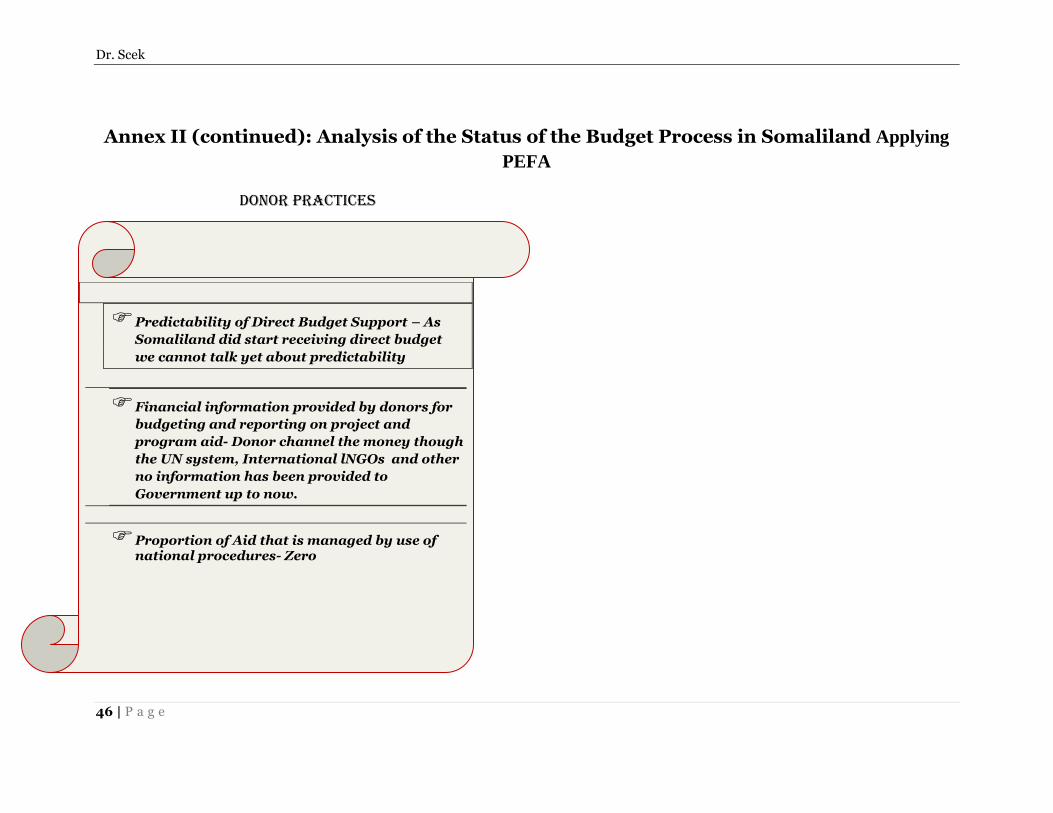

Annex II: Analysis of the Status of Budget Process in Somaliland Applying PEFA ........ 43

Annex III: Statistical Data ................................................................................................. 47

Dr. Scek

4 | P a g e

The Formal and Informal Institutional Makings of

the Political Economy of the Budget Process in

Somaliland

The Political Economy of the Budget in Somaliland

Executive summary

In this exercise, we have been duelling to explain why the apparent weak lack of political will to

formulate, implement and monitor the budget process and in that matter the Public Financial

Management system in accordance with the overall Somaliland strategy since its establishment

in the early 1990s. The study attempts to unpack the concept of political will through an analysis

of the formal and informal institutions and enforcement mechanisms determining how

government, other stakeholders, such as think tanks, the private sector, non-state actors and

development partners in Somaliland may inter-act in the budget process.

Budget process involves several stages including long-term planning, medium term or Rolling

Plan, Annual Budget preparation by the Ministries of Finance and Planning, submission to the

House of Representatives, approval of the Budget (appropriation bill), implementation, and

oversight. In this study it is implied that the budget, public financial management and

accountability as interlinked processes that manifest in the budget cycle or better said the process

is applied into three main stages, namely:

i) The preparation/formulation of the budget,

ii) Budget Execution, and

iii) Evaluation/budget oversight.

Given the fact of limited availability of quantitative data, the focus will be on the qualitative

aspects of the budget process, by examining what are actually the formal and informal

institutions that affect the budget process in Somaliland.

A qualitative combined with a quantitative approach has been applied to the study and the

findings are drawn from the content of documents, interviews and to some extent, direct

observations of research and of knowledgeable individuals (experts), as well as PEFA indicators

Dr. Scek

5

where data were on hand. A number of key budget stakeholders were interviewed in the budget

process from government (executive), House of Representatives committee members on the

economy, finance and trade, private sector, think tanks and the development partners.

The results suggest that from the process of planning and formulation of the budget, through

approval, to its implementation and oversight, the budget process in Somaliland did not provide

any relativistic or accurate estimates of revenue and expenditure. The budget process has been

more or less a drama that masked the real allocation of resources and spending plans. All the

involved stakeholders, the executive, legislative, think tanks and development partners were

aware that many of their statements and actions have had little bearing on actual distribution of

resources. Yet, all stakeholders „staged‟ as if the budget preparation and formulation would

actually have a bearing on the actual implementation and distribution of resources.

As it was usual at each stage in the budget process, both formal and informal institutions

interacted formally and informally. Though some legislations were introduced to improve the

process and development partners support on capacity-building have partially strengthened some

formal institutions, however decisions continued to be influenced by informal practices rather

than formally established process. Their continued prevalence undermined the formal institutions

of the budget process in Somaliland. Behind the scenes, the stakeholders manoeuvred

strategically to ensure that their interests were protected. As a result, despite good stated

intentions expressed in the government strategies, the observed outcomes of the budget process

in Somaliland is a budget that has secured the interests of the politically connected powerful

actors in the public sector, this included Office of the President, security sector and alike at the

cost of productive and social sectors.

The study suggested that the Government of Somaliland did not comply during the considered

period (1990 to 2010) of study with its contract to its citizens by adhering to a budget process

consistent with the stated objectives. The formulation process resulted in budgets that were

unrealistic, overambitious and did not reflect priorities as identified in the government policies

and strategies. The Government faced incentives allowing the budget formation to reflect

unrealistic fiscal forecasts and ambitions targets. These allowed the Government at the stage of

implementation to undermine the existing rules and regulations by allowing powerful players to

utilize budget resources at their own discretion to serve their own institutional and individual

interests. Again, powerful interests and informal incentives allowed the oversight and integrity

institutions, such as the auditor general and the various parliamentary committees, media and

civil society not to develop their capacity and became unable to fulfill their constitutional

mandates. Examining each stage of the budget process the following issues are identified:

Dr. Scek

6 | P a g e

Budget Formulation At this stage it has been observed that the issues of capacity, commitments and interests played

out very clearly at the budget formulation stage to produce a budget that neither reflected the

country‟s strategy no set priorities if any. Even before the budget formulation was put in motion,

most of the resources expected to be available are committed, allocated or earmarked to specific

institutions and in some cases to domestic debt payment. This led to the fact that funds

earmarked to social sector or pro-poor programs are switched to expenditures that further

political and specific groups‟ interests.

Approval Process At the stage of budget approval, this consists of passing of the vote on account; “debates” and

approval of the Appropriations Bill. Immediately following the approval of the annual estimates

the Appropriation Bill is passed giving statutory sanction for the issue by the Treasury out of

consolidated fund, and the application towards the supply granted for the services for that year of

the total net sum of and its appropriation to the various net recurrent expenditure and

development expenditure votes, including moneys previously authorized by vote on account

procedure. The Bill also statutorily sanctions the application of the various sums contained in the

estimates as Appropriation in Aid of the grants for the services and purposes specified. It has

been observed that due to the weak parliamentary capacity the approval process is mere robber

stamping of the executive proposal without critical review or substantial inputs. Even though the

House in the second half of 2000s has attempted its determination to ensure that all government

finances are allocated according to the rules and as such the House has a say on how the funds

are allocated.

Implementation of the Budget The implementation stage of the budget is most subject to informal influences and interests as

funds are limited. It has been observed at this stage massive budget indiscipline, slippages and

expenditure that bears little resemblance to the priorities set in the budget as it was approved by

the House of Representatives. Furthermore, the cash budget system allows a great deal of

discretion in the allocation of resources to line ministries and public agencies. Powerful

ministries or well connected institutions are the one to receive funds before any others.

Budget oversight

Most Governments tend to operate in secrecy. They share little information concerning their

financial operations and Somaliland has been an exception. Since, it establishment Somaliland in

the early 1990s little is known about the mobilized resources and how these resources are

utilized. Therefore, it is imperative for the organized stakeholders whether they are within the

Government or outside demand not only that their concerns are taken into accounts in the budget

but also the actual performance of the stated commitments in the budget.

In this context it is crucial to examine how the Government managed to implement what it

planned to do so during the considered period. Budget controls ensure that planned and approved

expenditures eventually materialize and that those responsible for budget implementation do not

use resources for unintended purposes.

Dr. Scek

7

The key to exercising the oversight function over the budget process is capacity and commitment

among the main actors. The legal framework as well as the formal rules and regulations in

Somaliland are poorly designed to create sufficient capacity in the budget oversight actors.

However, the Government has not moved much to translate the commitment indicated by

passing new legislation into action.

It has been observed in this study that there were four main reasons for the poor budgeting

process, these included:

a. formal budget processes were undermined at each stage by the executive;

b. Accountability institutions have not been effective, as they were practically

undermined through subversion, under funding and political patronage;

c. Weak or non existence of domestic “demand function” outside government for

improvements of budget which has been a manifestation of deep-rooted. There is at

present insufficient demand for economic accountability from other stakeholders, such

as civil society, think tanks, etc. given the fact of their weaknesses and sometime

credibility, and

d. Weak participation of the development partners in the budget process given the fact

that all donor support goes through off budget.

As entry points for a better budget process it would be worthwhile for the World Bank, in

cooperation with other development partners to undertake a program on economic accountability

which emphasising:

a. Defining clearly the roles and responsibilities of the various budget actors

b. Strengthening of auditor general and other integrity institutions

c. Sstrengthening of the House of Representatives, particularly, the Committees

on the Economy, Finance and Trade and Public Accounts; and

d. Strengthen demand for accountability from all the budget stakeholders

Dr. Scek

8 | P a g e

Background

Since its establishment in the early 1990s the State of Somaliland has placed at the top of its

agenda peace building, security, reconstruction and development with equitable distributions.

Virtually development partners in principle sanctioned to these policies, which culminated in the

development of a joint Government and development partners document “The Reconstruction

Development Program for Somaliland” in 2007. Nevertheless, throughout the considered period

the government has failed to demonstrate its ability to implement the set strategies (except that of

security) as well as to raise, allocate and account properly for public resources. Persistent budget

instability due to lack of development partners support and unpredictable domestic revenue

mobilization combined with domestic borrowing contributed to poor budget performance.

Measures to strengthen Public Financial Management system by the government made little

progress.

Of the few studies undertaken by some donors and the government on Public Financial

Management, it was observed that the government showed little commitment to political will to

implement policies in accordance with the set objectives of proposed policies and strategies. In

this study attempts are made to understand why there has been lack of willingness to formulate,

execute and evaluate a comprehensive budget process that is consistent with the stated objectives

of the government strategies. Identify who are the unwilling stakeholders and why? Attempt will

also be made to unpack how the various institutions interrelate to each other in budget process.

The budget is the most important government tool that has greater impact on the day-to-day life

of every citizen. The impact of the budget on all aspects of the welfare of citizens is felt once the

budget has been approved by the House of Representatives and the measure defined in it starts

being implemented. In fact, taxation measures proposed in the budget might determine the

direction of investment and consumption depending on whether there is a proposed increase or

decrease in taxes. Since this affect the price of commodities and services. This is to say that the

prices of goods and services may rise or decline depending on whether the budget introduced

new taxes or scrapped old ones.

The importance of each sector, program or project is determined by the amount of resources

allocated in the budget. In fact the amount of money allocated to each reflect the order of

government‟s policy commitments and priorities. For instance, a Government policy to improve

security and build peace is best exemplified by the amounts allocated to security forces, to the

reconciliation and related sectors, such as job creation for the youths and unemployed that

contribute towards the improvement of security situation in the country. Similarly failure to

allocate funds for such identified projects may then reflect the gap between Government rhetoric

and its real policy commitment.

Budget process involves several stages among them the most important are: (i) budget

formulation by the executive; (ii) approval by the House of Representatives; (iii) Execution by

line ministries and public agencies; and (iv) Oversight, supervision and control by the legislative

and integrity institutions as well the civil society and the public at large. The focus in this study

Dr. Scek

9

will be both on qualitative and quantitative aspects of the budget process and the involvement of

both formal and informal institutions and how they affect the budget process.

The interactions of the various stakeholders involved in the budget process and how they adhere

to the formal institutional procedures could be explained by the constraints and opportunities

facing each of the stakeholders.

Key stakeholders in the budget process involved in Somaliland include at various stages were:

The Government as public actors;

The private sector, individual business people who had leverage to government by having

provided loans or contribution directly or indirectly to the budget, and

Development partners, even though all donor support was provided either in the form of

projects or through the NGOs and the UN system – off budget.

The interests of each of the group did vary overtime and relation to other actors.

Methodology

Participation and Consultation are two of the key elements for a successful budget process. In

this regard, Somaliland has been evolving slowly in moving from secrecy in budget process

toward an open and consultative process with the attempts of involving key stakeholders and

ordinary people. As a follow-up on this, there is an identified need to involve citizens in the

monitoring of the strategy – one mean of doing this is through a participatory monitoring

exercise.

The study on the Political Economy of the Budget in Somaliland uses a combined consultative

(qualitative analysis) and quantitative approaches that is designed to assess the effectiveness of

budgeting process involving both formal and informal institutions. The Study can best be described

as utilizing a consultative methodology – a complex blend of principles and techniques from various

sources, which combine with quantitative approach used in the PEFA and qualitative or consultative

process. In general, the exercise uses non-standard participatory methods of data collection to elicit

the knowledge, views and opinions of the budget stakeholders. Among the tools used include direct

interviews, discussions, and reviewing existing documents and information available.

As such, the consultative approach (CA) collects qualitative data, which has the benefit of offering

stakeholder‟s perceptions on the budgeting processes, as well as their priorities, constraints and

opportunities for improving the situations. The data is collected by a multi-disciplinary team who,

for the most part, work closely with all budget stakeholders to allow them triangulate and

crosscheck information outside the formal and informal institutions involved in the budgeting

decision-making process.

The type of data generated by CA deepens the understanding of the interaction between the formal

and informal actors, particularly the causality, the multi-dimensionality and the inter-linkages of

influencing factors, as well as defining the priorities of the budget interventions whether linked to

Dr. Scek

10 | P a g e

political patronage or national interests. In general terms, CA is not dissimilar to the other

Consultative/Participatory Assessments, particularly with its move away from trying to solely

provide new insights on the nature of the thinking of key stakeholders, its greater focus on the

impact of policies, and the emphasis on institutional arrangements in its establishment.

Objectives of the Exercise

The objectives of the exercise is the integration of a “quantitative” approach, known as PEFA

initiative – this exercise examines issues raised in connection the budget processes from the formal

institutional point of view or better said “quantitative” perspective. To this end, the CA or

consultative approach, which deliberately tries to focus its work on qualitative measures to ensure

complementarities are developed with the PEFA initiative by using qualitative approach. Table 1

highlights the objectives.

Table 1: The Objectives and Results of the Exercise

Objective: Consult with the budget stakeholders in the formal and informal institutions to assess the effectiveness of budget, and to make policy recommendations to improve the budget process.

Study Purpose: To test and develop a monitoring tool that clearly establishes the linkages between PEBS (qualitative) and PEFA (quantitative) exercise to provide policy makers with the most comprehensive information possible on the impact and effectiveness of the budget process.

Result 1 Policy initiatives are examined to assess how they operate with resource allocation, based on identified priorities strategy in the budget

Result 2 The information generated is fed back into the policy process in the form of recommendations on improving the decision-making process.

Result 3 Capacity to carry out the exercise is generated amongst government institutions.

Linkages PEFA and CA

The two exercises, the more quantitative PEFA and the qualitative CA offer the potential for

combining “Quantitative” and “Qualitative” approaches to data collection, collation and analysis in

examining the budget process in Somaliland.

CA is foremost about power and interests. It focuses on analyzing social and political processes as

the outcome of the strategy to control over resources and positions. The CA specifically analyzes:

The interests, incentives and power of different groups in the society (political and economic

elites, social classes, ethnic, tribal and religious groups) and how these generate particular policy

outcomes that may encourage or hinder development;

Decision-making and influence on development decision of formal institutions (executive,

legislative and alike) and informal institutions (traditional leaders, interest groups and others)

The influence of social, political and cultural norms, values and ideas and cultural beliefs on

shaping human relations and interactions, political and economic competing claims and

consequent influence on development

This approach suggests that the focus should be to consider not only formal, written rules and

political rhetoric but also informal, unwritten rules, customs and traditional social practices that

determine the rules of the game. In fact, to political and economic resources depends on personal

Dr. Scek

11

ties and the distinction between public and private is mostly observed to be blurred. Therefore, it is

necessary to include informal and less visible arenas as that are where political, economic and social

influence and power is play out.

It became clear that using one approach will be insufficient to gather accurate information on the

interaction between the formal and informal institutions. That‟s the point of bringing qualitative and

quantitative approaches give two different perspectives, each with its own appropriate time and

place and neither with supremacy over the other; however what is really needed is for the two

approaches to be used in such a way that they complement each other and to address different

aspects of the raised issues. In this regard, a combination of the two will yield greater insight than

one on its own, and adds a greater robustness to the findings.

This study make an attempt to a systematic approach at combining the CA and PEFA to analyze the

Somaliland budget processes taking into account both formal and informal institutions. The

approach of combining the two “Qualitative” and “Quantitative” work is suggested to be as follow:

Establishing a Linkage between the quantitative (PEFA) and qualitative methodologies

(CA)

Examining, explaining, confirming, refuting, and/or enriching information from one

approach with that from the other; and

Consolidating the results of the two approaches into one set of policy recommendations

As a means of facilitating this combination, the two exercises

Investigate the same policy areas, which have been selected based on issues raised on

the budget processes.

Utilise the resources of the same institutions, thereby improving the potential for

feedback into the policy system, and creating economies of scale.

It is hoped that the major advantages proposed by this merger between PEFA and CA are that the

results can be used to enriching and explaining the different results, while providing evidence on

different aspects of the same thing.

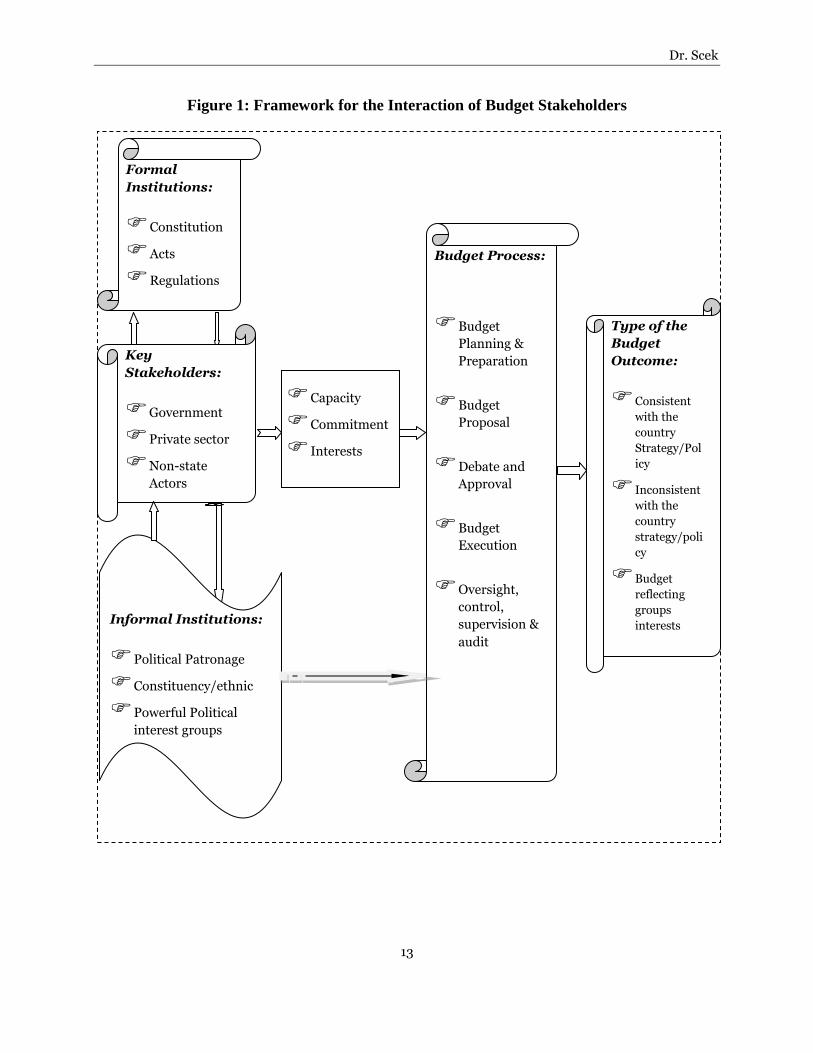

Framework for the Interaction of Budget Stakeholders

It is well known fact that formal state institutions are weak and sometime believed or deemed to

be less legitimate in fragile and conflict-affected contexts; there are often informal institutions

that persist and retain legitimacy. These institutions are diverse and may include community

mechanisms or customary local governance institutions. Often, they fulfil some of the key

functions expected to be implemented by the state and this is also a case in the budgeting process

in Somaliland.

Since its establishment Somaliland focused primarily on rebuilding formal institutions and their

capacities at the central level, sidelining sub-state and informal institutions. This has prevented

Dr. Scek

12 | P a g e

the evolution of an organic process of reform driven by local actors that could allow for greater

resonance and legitimacy with citizens.

There is a growing awareness of a need to pay attention to existing informal institutions. This

may stem from pragmatic acceptance of their existence; a recognition that they represent local

culture and practice; and/or the view that they can provide a bridge between state and society.

Informal institutions may improve public service delivery; help stimulate investment; facilitate

the transition to more inclusive, rules-based governance; and promote social reconciliation in

situations of conflict.

In some cases, informal institutions can work synergistically with formal institutions. In other

cases, however, they may compete with formal institutions in negative ways and undermine

them, particularly in the case of patronage networks. Critics view such informal institutions as

undermining norms of governance and citizenship. Further, local and informal institutions may

not necessarily function better than the state and can in some cases be discriminatory,

particularly towards women and youth and minorities. Working with informal actors does not

necessarily mean endorsement of all their principles and working mechanisms though if one can

engage in dialogue with them with a view to securing inclusive rights could be considered to be

the best approach.

The key to adopting an institutionally diverse approach in budgeting processes is to avoid

competition between informal and formal institutions. It is important to understand the

conditions in which they can be beneficially linked. Figure 1 below propose a framework on the

how to understand and explain the role of the formal and informal institutions in the budget

process and how they interact and influence each other.

Dr. Scek

13

Figure 1: Framework for the Interaction of Budget Stakeholders

Budget Process:

Budget

Planning &

Preparation

Budget

Proposal

Debate and

Approval

Budget

Execution

Oversight,

control,

supervision &

audit

Type of the

Budget

Outcome:

Consistent

with the

country

Strategy/Pol

icy

Inconsistent

with the

country

strategy/poli

cy

Budget

reflecting

groups

interests

Capacity

Commitment

Interests

Informal Institutions:

Political Patronage

Constituency/ethnic

Powerful Political

interest groups

Formal

Institutions:

Constitution

Acts

Regulations

Key

Stakeholders:

Government

Private sector

Non-state

Actors

Donors

Dr. Scek

14 | P a g e

Key Steps in the Budget Process

Somaliland has been preparing its annual budgets since the mid-1990s. The process followed for

budget preparation is not officially documented but it has been largely modeled around processes

that existed before the civil war in the Somali Republic. The process is outlined below and

partially defined in the Financial Accounting Procedures of the State of 1996:

In theory the executive organ of the Somaliland authorities (Council of Ministers) within the

formal institutions discusses issues of the budget and submits recommendations to the

Ministry of Finance. In parallel discussions taking place between the powerful politicians,

political patronage and interest group on how budget resources could allocate/distribute.

Most of the time the initiative is from the Minister of Finance in consultation with some key

allies with the Council of Ministers and the Presidency decide on the budget priorities and

strategies. The Ministry of Finance then issues a Budget Circular to the line ministries and

public agencies to prepare and submit their budget proposals to the Ministry of Finance by a

specified dateline.

Line ministries prepare budget proposals according to their needs and challenges according

to the guidelines specified in the Budget Circular and submit them to MoF. However,

powerful ministers and their ministries already know with some certainty what to expect in

the budget allocation through their patronage or interest groups. The MoF (budget

department) reviews all the proposed proposals from line ministries and consolidates them to

a proposed draft Government budget.

The proposed draft is submitted to the Council of Ministers for review, discussions and

endorsement. After the Cabinet endorsement, the Minister for Finance submits the draft

budget to the House of Representatives through the Speaker‟s Office. The Speaker then

forwards the budget to the Standing Committee for Economic, Finance and Trade issues;

The Economic, Finance and Trade Committee reviews and discusses the proposed draft

budget. The committee can propose rejection of the draft budget, recommend further

amendments to be adjusted by the line ministries or approve the draft budget. The Economic

Finance and Trade Committee, then presents their recommendations to the plenary session of

the House of Representatives for discussion of both the proposed Government budget and

any recommendations made by the committee; and

The plenary session may either reject or approve the draft budget. Once the House of

Representatives approve the budget and the appropriation bill is signed by the President then

budget implementation enters into motion.

Box 1, billow describes the budget cycle and how the interactions among the various key

stakeholders are operated.

Dr. Scek

15

Box 1: Budget Cycle

The budget cycle consists of three broad Stages: (i) Budget formulation and approval

(appropriation); (ii) Budget execution, including budget revisions that might take place during the

execution; and (iii) budget reporting, auditing and evaluation. The budget year in Somaliland

correspond to the calendar year. So in any one calendar year (current year) three overlapping sets of

activities take place. These are the budget for the following year is being prepared and approved; the

budget for the current year is being implemented; and various reporting and auditing activities are

taking place for the current year and the year earlier.

Stage I Budget Formulation and Approval: The formulation and approval of the budget has the

following steps, most of which are set by the Financial and Accounting Procedures of the State of

1996:

30 June – July: Plan Preparation or Macroeconomic Policy Framework to determine guiding

policies and strategies for the budget; determine the overall envelope and set

initial ceilings for budgeting (not specified as yet in any law);

August – September: Issuing of a “Budget Circular” by the Ministry of Finance, this provides

guidelines for the preparation of the budget proposals with budget initial

ceilings (not fully practiced);

30 September Ministry of Finance submits the proposed budget to the Council of Ministers;

31 October Ministry of Finance submits the Draft Budget to the House of Representatives

once the Council of Ministers endorsed;

31 December Deadline for the approval of the Budget and issuing of the Appropriation Act

by the House of Representatives.

Stage II Execution and Revisions: budget execution take place through a quarterly warrant system,

in which funds are released to budget institutions (monthly, quarterly basis depending on cash

availability) and then reported and replenished. In practice, there are delays in releasing of funds,

due to cash constraints and delays in the submission and processing of accounts.

During this stage numerous adjustments are made to the original (approved) budget either through

small adjustment approved by the minister of Finance or large scale that requires approval of the

House of Representatives but in most case done with legislative approval.

Stage III Budget Reporting, Auditing and Evaluation: Budget institutions report on their budget

execution during the course of the year, which they have to do in order to replenish their accounts

under the warrant system. The Financial and Accounting Procedures of the State requires the budget

institutions to report on a quarterly basis to House of Representatives.

Evaluation of the Budget Performance is a not a routine but rather ad hoc and sporadic issue.

Attempt to regularize and institutionalize these processes are being thought and legal framework for

that purpose being developed.

Dr. Scek

16 | P a g e

Key Findings from the Analysis of the Budget Process

From the description above of the budget process and the interactions among and within the key

budget stakeholders, it can be inferred that the budget process has been a purely political process

that engaged on one side a group of stakeholders within the formal institutions (ministries) and

the informal institutions (powerful political interest groups, political patronage) on the others and

as such the various actors responded to incentives in the formal and informal institutions.

However, considering from the perspective of the process of planning and formulating the

budget through implementation and oversight, it can be concluded that the budget process in

Somaliland mostly provided unrealistic estimates of both revenue and expenditure throughout

the considered period. These meant that the budget process has been like a drama that masked

the real allocation (distribution) and spending of resources. To no one surprise of the

stakeholders in the process all the actors, government, private sector, political parties and to

some extend the development partners seemed that they were aware that all their statements and

actions have had no bearing on the distribution and disbursement of the budget resources. Yet all

of them (stakeholders) behaved purposefully as if the budget planning and formulation had had a

bearing on the actual implementation of the budget.

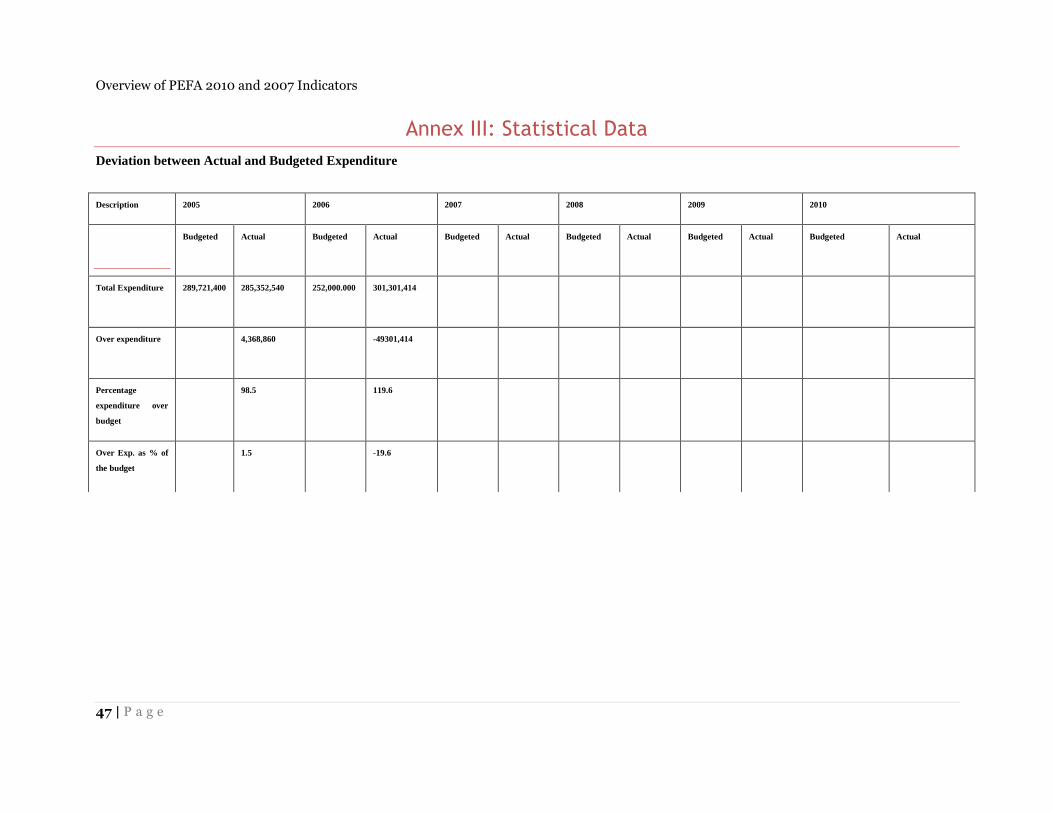

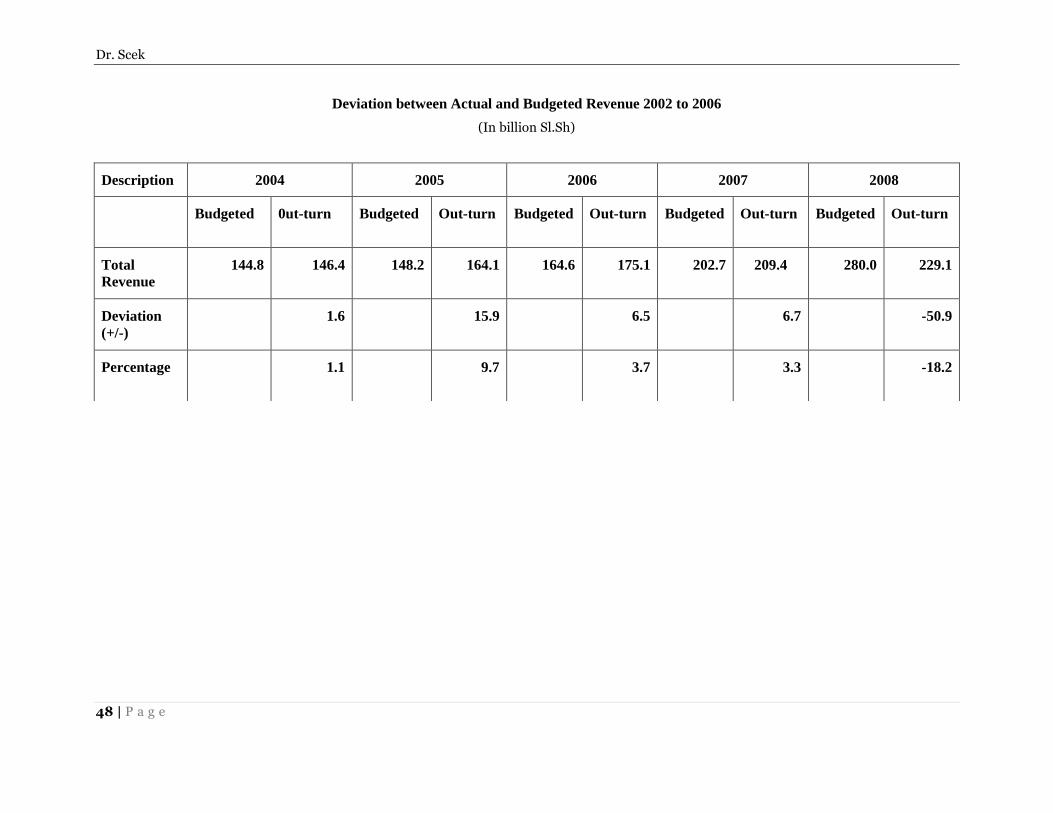

From the quantitative side (PEFA) at the end of the financial year few are surprised to observe

that the actual disbursements or outturns totally differed from the planned/approved budget

expenditures. From the limited information available since the early 2000; it is evident that the

actual expenditure outturns have been significantly differing from originally approved budgets,

both in level and composition. In fact, considering the 2004 budget, which had an approved

estimate of $21 million, had an extra - budgetary expenditure in the amount of $24 million that is

three million more than the budgeted expenditures. Likewise, extra-budgetary revenues were

almost double the budgeted figures, suggesting ultraconservative budget planning or poor ability

to forecast fiscal aggregates. Consequently, this budget cannot be considered as a realistic and

credible policy instrument to guide future government policy implementation. This has been so,

because of weaknesses in the budget preparation, execution and control processes, as well as, the

impact of regional shocks, border problems with Puntland. Most import also the practice of

prepared and executing the budget outside the formal institutions. Non-existence of

macroeconomic forecasting, in particular estimates of Gross Domestic Product (GDP) has also

contributed to unreliable estimates. Rough estimates made by UNDP/World Bank (2003)

indicate that per capita GDP for the Somaliland areas was in the range of the $250 to 300 of

which over 60% is derived from remittances. These patterns of the economic structure has not

changed and the economy is still dominated by remittances and related activities.

From this brief analysis it became clear that estimates of domestic revenues, have been

drastically underestimated either intentionally or poor ability to forecast. Significant budgetary

pressures have been created by under-budgeting of non-discretionary expenditures, especially of

private domestic debt, causing a shortfall of resources for social sector expenditures. Non-

compliance in budget execution has encouraged repeated within-year adjustments in resource

allocation leading to un-authorized and overspending by certain key Ministries, whereas other

Ministries had to cope with significant reduction in budget allocations.

Dr. Scek

17

During the considered period of this study, there have been continuous interactions at each

budget stage between formal and informal institutions. Legislative changes, capacity building

and the development partner‟s attitude have changed formal institutions with the introduction of

new acts and procedures on the budgeting process, but still decision continue to be influenced by

the practices of the informal institutions. Their continued prevalence undermined the reform in

the public financial institutions of the budget process. Behind the scene, interest groups

maneuvered strategically to represent their interests to be kept on board. Despite some good

intentions expressed by the Government in its development strategies the politically powerful

managed to secure their interests in the budget.

Political Factors Affecting Budget Process

Somaliland‟s decade-long experience with democracy displays a number of the democratic

shortcoming, similarly observed across sub-Saharan Africa‟s new democracies and more

specifically in post-conflict countries. Somaliland‟s young democracy also displays several

unique features, which consists of a hybrid system of governance combining tribal traditional

balanced local democracy with western style democracy. At its establishment in the early 1990s

it moved from the style of tribal democracy to a multi-party system modeled to the western style

democracy. In a series of inter-clan peace negotiations which led to the culmination in the

Borame conference in 1993 to the establishment of a clan/traditional system of government.

This was late followed by the National Congress, which adopted the Charter for a transitional

period and established a bi-cameral system of legislation composed with upper and lower houses.

The Upper House or Guurti was entrusted to safeguard peace among the clans and lower House

or House of Representatives was entrusted with the legislative issues. The congress elected the

first President of Somaliland.

In the late 1990s (1996/1997) a third National Congress took place in Hargeisa, which developed

and adopted a Constitution that legalized the structure proposed in the earlier at National

Congress. The Constitution established a bi-cameral system, composed of 82 Council of Elders

(House of Guurti) and 82 elected members of the House of Representatives. The Congress

elected the President and the Vice President for a five years term. The transition from the

traditional democracy to a multi-party system of democracy was completed with district council

elections that were contested by several national and local parties. In the early 2000s there were

three major parties, namely UDUB party, which won the 2003 presidential election for a five

years term, followed by Kulmiye, which won the recent presidential election and Ucid party and

some small ones that are operating at regional and local levels.

Overall, several local and national elections took place; three Presidents were elected in a fair

and transparent elections and powers changed hands in a peacefully manner and without

violence. Virtually all political actors and parties respect in principles, the basic tenants of

democracy, human rights and the country‟s constitution. Nonetheless, the political culture at both

the top and grassroots levels raises a number of serious questions with regard to the depth of

democratization. The limited institutionalization of the democratic process is witnessed by the

lack of full respect for opposing views; weakness of political parties indicated by rapidly

changing alliance and leaderships and the most important weak institutionalization of the

Dr. Scek

18 | P a g e

oversight institutions. At this point in time it is difficult distinguishing the role of the government

and that of the governing parties.

In other words, it can be said that Somaliland has made remarkable progress on many fronts, not

least through a unique reconciliation process, creation and operationalization of functioning

governance, such as judiciary systems, and a democratization process that has led to free and fair

elections and a multiparty Presidential system. This has been made possible primarily through

active involvement of a vibrant private sector, non-governmental organizations (NGOs), civil

society and large inflows of remittances, as well as the active involvement of traditional and

religious leaders that has enabled the democratization process to be entrenched in the

constitution.

Economic Vulnerability

Poverty levels are high compared to East African standards, but lower than in many other post-

conflict countries in Africa. This indicates that Somaliland has moved further along the

development continuum. Per capita income was estimated at US$ 250 in 2004, with 73 percent

of the population living below the poverty line (i.e. less than $2 per day), and 43 percent living in

extreme poverty (i.e. less than $1 per day). The above figures reveal large geographic disparities,

with per capita income ranging from about US$ 201-250 in Sahil; and US$ 251-300 in Sool and

Sanaag; to US$ 301-350 in Awdal, Hargeisa and Togdher regions. In addition, the figures show

clear urban-rural disparities, with urban populations far better off than their rural counterparts.

Unemployment is high and associated with poverty, poor social indicators and prevalent use of

khat (mild drug). Unemployment is both a cause for and result from heavy abuse of Khat, and

the two problems are closely linked. Young males in particular spend their days chewing, and are

left incapacitated and unable to perform their duties. This also has severe gender aspects, as

women are left as sole providers for large families. Although traditional mechanisms still

continue to provide coverage for unemployed, these are far from sufficient, and being

undermined by the increased urbanization and changing society (breaking out of the traditional

networking system).

The traditional livestock and agriculture sectors dominate the economy of Somaliland and hence

the employment of its people, since much of it is labor intensive. Livestock sector represent the

dominant productive activity, followed by fishery and crops. The main features of the livestock

sub-sector in Somaliland are the significance of disease and the dependence on an almost tree-

less rangeland that is extremely sensitive to drought and has been depleted and destroyed over

time. Livestock earnings, which contribute substantially to the budget through export taxation,

were seriously damaged by the 2000 drought, which lasted until 2004, and the livestock export

ban in Saudi Arabia, but has since returned to its previous levels. In addition, Somaliland has a

promising fishing sector with most of the potential in fairly good condition except for the lobster

resource which is considered to be in a state of depletion.

Crop production is sizable, but plagued by many of the same problems as the livestock sector.

About 39,000 farm families are involved in rain-fed and irrigated crop production in Somaliland,

cultivating about one-third of the area suitable for agricultural production. Rain-fed crops

Dr. Scek

19

include sorghum, maize, cowpeas, groundnut and sesame. Irrigated crops are citrus, papaya,

guava, water melons and vegetables such tomato, onion, cabbage, carrot, and peppers. The sector

has been vulnerable to droughts and increasingly constrained by the huge damage done to the

environment and the lack of available land for cultivation, and is plagued by low efficiency and

productivity. Given the deteriorated state of the cultivatable farm land the sector‟s economic

potential is limited, but it will continue to impact the domestic market due to high labor intensity

and importance for local market activity.

Somaliland has a strong and vibrant private sector operating in Hargeisa and other urban centers

as a result of the prolonged peace and achievement of relative security, the sector is involved in a

large range of economic activities and import-export businesses. Investments by the private

sector in all these cities resulted in the delivery of goods and services such as electricity,

telecommunications, domestic water supplies, and urban waste disposal. At the same time the

livestock and fisheries industries also flourished.

However, it has been observed that the cost of doing business in Somaliland is extremely high

due in part to the lack of international recognition. Business people do not have access to regular

bank financing, and cannot borrow at international market rates. Import and export activity also

face large constraints, as traders cannot obtain international insurance or guarantees. Remittance

companies are however prevalent and some have even started the transition towards regular

banking operations, including offering savings accounts and limited forms of guarantees.

Power Relation among the Various Actors

Somaliland has a relatively developed democratic and electoral system. The legitimacy of

elected authorities as well as democratic institutions has been reinforced and people in

Somaliland are more aware of their rights. However, deepening of democratic values and

institutions will require strengthening and institutionalizing political systems, strengthening of

civil society and media institutions that can ensure greater accountability and engage in the

decision making process.

Political participation in local communities that can contribute to the fulfillment of the

democratic process should be an urgent priority that will require further work. This would

include research on promotion of the inclusion of women, young adults and other under-

represented groups, research on civic and human rights and perceptions on institutions and non-

state actors. An important aspect of this will be the design of civic education programs and

public information campaigns.

Somaliland Non-state actors are currently suffering from a range of constraints and the question

of legitimacy of the sector emerges as a key constraint to the effective operation and impact of

civil society. Legitimacy is inextricably linked to lack of accountability and inadequate

transparency, and problems include the proliferation of „briefcase NGOs‟ that undermine the

credibility of the NGO sector as a whole. Their power to interact with the authorities and other

budget stakeholders is limited at this moment in time. To improve bottom-up accountability,

priority actions would include developing legal regulation and system of official registration of

civil society organizations and NGOs that could guide and clarify their involvement in public

Dr. Scek

20 | P a g e

affairs, and programs of training for human rights institutions and CSO‟s in civic education,

with special attention to gender issues and disadvantaged groups.

Media institutions are still constrained by weak information delivery capacity, lacking

professional skills of investigative journalists, and close links to political factions. Their power

of leverage to shaping the budget is still at initial stage for them to demand for information from

the budget authorities.

House of Representatives Oversight: oversight of the budget by the House has improved

drastically in recent time, despite being poorly funded by the executive. A limited number of

development partners have supported the various House committees and sub-committees and

made them able to operationalize their activities to provide their mandated constitutional

functions. This has produced significant changes in the way the members of the House perceive

they job as parliamentarians. The committees still lack technical staff and their capability is still

limited.

Chamber of Commerce: as representatives of part of the private sector, their power to shape the

budget is immense. Big companies have been providing loan or contribution to the government

to finance it operations. As private citizens business or company are also involved in politics

and have a stake or interests in how public resources are allocated or distributed.

Dr. Scek

21

Budget Analysis: Formulation, Approval, Implementation and

Oversight

Theoretically, the basis for formulating the budget in Somaliland is a Policy Framework Paper,

which articulates the country‟s development policies. There has not been such a Policy

Framework in the past, but in the mid 2000s the government has adopted a Reconstruction and

Development Program (RDP) as such a policy. Since 2007 it was assumed that the RDP would

be the government policy document to determine the policy issues that the budget should address

and also the levels of funding that can be mobilized both domestically and from the development

partners.

The RDP and under it several sectoral documents that were developed by the line ministries was

supposed to be the guiding policy document for development planning and funding. In practice

conflicting interest groups have acted against it. In the first place the development partners who

contributed to the development of the RDP and promised financing the large component never

delivered their commitments. The situation continued as usual, development partners provided

they support either through the UN system or through NGOs with little or no government

involvement.

The government on its side continued with it is effort to mobilize domestic resources and the

strategy for allocation or distribution didn‟t changes much. Most of the funds went for security

and administration and an insignificant part to development projects focusing on reconstruction

and poverty reduction.

Stage 1: Budget Formulation Process

Generally, budget formulation should be preceded by a plan preparation. In Somaliland the plan

is formulated by the Ministry of Planning alongside other players as of today this process is still

partial (the formulation of the plan has not been complete yet) as there is no a development plan

or strategy for Somaliland. The plan (should) provides broad policy directions for what the

government intends to implement in the next three or five years. The actual budget preparation

phase starts with the

preparation of

macroeconomic framework,

where estimates of revenue

and expenditure are made

and initial budget ceilings

set. This is followed by the

issuance of a “Budget

Circular” by the Ministry of

Finance to all ministries and

government agencies. The

circular define broad

parameters of the budget and

sets sectoral expenditure

ceilings (not fully applied today) to be adhered to by the ministries and line agencies. This

Box 2: What role do various stakeholders play in budget planning and preparation?

Are stakeholders (public institutions, agencies, private sector,

NSAs, etc.) inputs solicited and incorporated in setting up budget

priorities?

Are there mechanisms in place for soliciting and integrating

stakeholders‟ proposals?

Are the ministerial budgets processes open to the stakeholders or

interested parties?

Is the budget preparation accorded any form of publicity?

Dr. Scek

22 | P a g e

generally happen in the third quarter of the fiscal year. The circular requests budget institutions

to forward their expenditure proposals outlining their proposed activities during the considered

financial year. The line ministries and public agencies prepare and submit their budget proposals

to the Ministry of Finance. The Budget Department of the Ministry of Finance reviews and

harmonizes all the ministerial proposals in accordance with the national priorities and availability

of the resources.

Theoretically, after the review of the proposals and consolidation of the budget by Budget

Department of the Ministry of Finance, negotiations between the Ministry of Finance and line

ministries take place and decisions are made on the resource allocations. During these

“negotiation meetings”, ministries present

their justifications on their need of

resources on the basis of national

priorities. Allocations are made on the

basis of national priorities as set in the

national plan or sectoral strategies. After

the completion of the negotiations the

Ministry of Finance revises the budget

accordingly and submits it to the cabinet

for endorsement. Once endorsed by the

Cabinet the budget is tabled to the House

of Representatives for discussions and

approval.

How does budget planning and formulation operate in practice

As suggested in the previous sections, there are no clear processes followed in the formulation of

the budget. In fact, there is no plan or Policy Framework Paper that articulates government

policies that are required to guide the budget preparation. Budget envelope is also defined

informally as there is no macroeconomic framework in place that could provide estimates of key

forecasts of economic indicators, such as revenue, expenditure forecasts and overall economic

growth. A tabular presentation is given in Box 1 on how the budget formulation process is

operated and who are the major stakeholders involved in both the formal and informal

institutions.

Stage II: Budget Approval

At this stage the Minister of Finance is required by law to present the Budget on the 31st of

October in accordance with the Budget Calendar to House of Representatives. The Minister

generally presents a summary document in the form of “Budget Speech”, which emphasizes

broad government policy objectives, intended in the ensuring fiscal policy and the measures

necessary to achieve them. The document or the budget speech in theory should be accompanied

by the Appropriation Bill, which contains proposed expenditure allocations; Finance Bill,

which contains taxation proposals, and the Statistical Annexes to the budget which contains,

among other things, a statement of the government‟s indebtedness to various lending entities. In

practice not all these documents are prepared and submitted to the House. What is submitted is

the budget document with scratchy and ad hoc related and poorly prepared documents.

Box 3: Power of House of Representatives

Does the House have sufficient time to study the budget

prior to presentation by the Minister?

Does the House have access to an effective research and

information and resources to enable the members to

contribute meaningfully to the budget debates?

Does the House have adequate powers to alter budget

proposals in any way it may deem necessary?

Dr. Scek

23

This is followed by a debate in the House of Representatives on the broad policy proposals

contained in the Minister Budget Speech. This is generally done by Economic, Finance and

Trade committee of the House, which reviews and presents it recommendations to the plenary of

the House through the office of the speaker. The review and the debate at the House committees

and at in the plenary session focus on the issues related to the government‟s economic policy and

strategies as they are outlined in the financial statements and the Budget. As it has been the case

the budget has never been submitted to the House according to the Budget Calendar, but with

several months of delays going even beyond start of fiscal year. Due to this and other factors, the

Minister each year seek approval from the House to spend up to 50% (according the rules) of the

allocated expenditure pending the substantive ministerial vote-by-vote debate. The purpose of

approving this advance expenditure is to guarantee continuity of government operations.

The House continues discussing on the proposed taxation proposals contained in the budget

(Finance Bill) along with other laws affecting the proposed revenue collection. This culminates

in the passing of the Finance Act, which authorize the Government to raise revenue from a wide

range of taxation measures.

The House debates and approves the Appropriation Bill on Ministry-by-ministry basis. During

the process members of the House of Representatives have the opportunity to propose reduction

or increase on specific items on the basis of the budget objectives and national priorities. The

Budget procedures require that the debate on the budget conclude by but not late than the 31st of

December of the current budget year.

This is the formal institutional budgeting procedures as prescribed partly in the constitution and

in the Financial and Accounting Procedures of the State. The informal structure used in the

process of budget approval is the one that links the Minister of Finance and some interest groups

that are composed of some members of the House from the same party, business people in the

private sector and senior government officials and in some case members of the ethnic group.

This group tries to maneuver the approval process by convincing or manipulating the House

committees‟ members and members of the House to guide or misguide them to approve the

budget. The outcome might then be a budget that reflect a group interest rather than a budget

that reflect the interest of the nation and to all the citizens.

According to the Financial and Accounting Procedures of the State, the budget should be tabled

to the House by the Minister of Finance by the 31st of October each year, but unfortunately this

has not been followed by the executive, just to give some recent examples, the 2007 Budget was

submitted and resubmitted to the House on March 19th

, 2007 but never approved as the executive

and the legislative couldn‟t reconcile their interests. The 2008 budget was presented to the House

on May 6, 2008. The House due to its priority of holding elections passed the budget without

delays.

Stage III: Budget Execution

This stage of the budget process entails the actual disbursement of the funds (money, money) for

the various user-departments and ministries. Upon approval of the budget and passing of all

related bills, the government (Ministry of Finance) is authorized to raise revenue through taxes

Dr. Scek

24 | P a g e

and related measures and spend the funds according to the approved budget estimates. In

exceptional cases, however, ministries or agencies may exceed the approved allocations during

unpredictable events and in the case of Somaliland for certain institutions this has been the rule

rather than exception. It is said that in such situations the Ministry of Finance authorizes the

withdrawals and then presents the Supplementary Estimates to the House of Representatives for

approval before the end of the prevailing financial year.

Somaliland has been preparing, executing budgets for over a decade and half. The basic

financial and accounting environment in which the Somaliland government operates with is

governed by a set of legislations, namely:

1. The Financial and Accounting Procedures of the State; and

2. Regulations for the Accounts of the State.

The former is the formal Act assented by the President on the 15th

May, 1996 while the later is

the accompanying Regulations. The Financial and Accounting Procedures constitute the basic

underlying legal framework governing budget preparation; revenues of the state; budget

execution; expenditure; annual accounts; administrative and accounting control; the duties of the

auditor general and accounting responsibility.

Once the budget is approved and the authority to expand is given, warrants are issued as follow:

Warrants: The authority to start spending an approved budget is by way of:

1. Expenditure Warrants for MDAs in Hargeisa

2. Departmental Warrants for Regional ministerial departments.

Expenditure Warrants: Each MDA is responsible for the execution of their budget as approved

by the House of Representatives. Budget amounts are disbursed to MDAs by way of expenditure

warrants. Expenditure warrants are notification to the MDA allowing them to expend for the

ensuing Quarter, such amounts as indicated on the warrant. The amount on the warrant is arrived

at taking the yearly budgeted amount and dividing it by three to arrive at the amount for the

quarter.

The MDA initiates the process by drawing the Warrant which details the expenditure for the

quarter including salaries. The Warrants contain sub-heads of expenditure for the quarter. The

Warrant is then sent to the Ministry of Finance in the Budget Department for scrutiny and to

generally assess whether or not the expenditures conform to the budget. Upon approval the

Warrant is sent to the Auditor General, again for scrutiny and approval.

Once the Auditor General has approved the Warrant is then sent to the Accountant General who

proceeds to enter the warrant value in the MDA‟s Vote Book maintained in the Accountant

General‟s Office ready for effecting payments as appropriate, A copy of the warrant is sent to the

originating MDA for it to be enter the approved amount in its counterpart Vote Book.

In the Accountant General‟s Office there is a Vote Book control office manned by officers who

have been assigned to cater for various MDAs payments. Thus each officer is allocated a certain

Dr. Scek

25

number of MDAs for which they are responsible for processing their payments as well as

ensuring that the two vote books are reconciled whenever there is a discrepancy.

Departmental Warrants: These are warrants that are issued by MDAs to their upcountry

stations. These are a subset of the expenditure warrants earlier approved by the Budget

Department and the Auditor General‟s office. These too cover the expenditure of the regional

office for the quarter including salaries and are entered in the respective Vote Books. As for

salaries the names of payees are typed on the back of the warrants and no separate payroll is

provided.

A copy of the warrant is sent to the Regional Accountant (staff of Accountant General) for

recording in the respective regional office‟s Vote Book for control purposes.

The formal institutions in the implementation process includes those institutions that are

involved in collecting revenue, allocating and disbursing this to line ministries, government

agencies and departments using a system of cash budget. Controlling expenditure within the line

ministries and agencies and maintaining accounting records about expenditure, and conducting

audits that enable accounting offers (directors general) to oversee are leading to the effective

execution of the budget.

The formal institutions at this stage of budget process are all ministries and agencies, the

accounting offers (directors general), revenue department, accountant general, auditor general.

While the informal institutions are like invisible hands, which are always there but you don‟t see

them. They originate from the interactions among the formal institutions and individuals or

institutions representing specific interests. This is usually the most complex stage and also a

source for fraud through disregards of existing procedures in the release of funds to certain

powerful institutions and undermining others, which have little political and manipulative

leverage to the Ministry of Finance. The quarterly/or monthly warrants are the major cause of

informality linked to the various interests for the various institutions. It has been observed that

there is ample political pressure on the accounting officers to allocate released funds more to

political objectives rather than priority activities as approved by the House. This always led to

continuously revising the budget throughout the year to accommodate the wishes of the powerful

interest groups. The recording of the disbursement became a nightmare as one has to reconcile

the information as approved in the appropriation bill and one provided or collected through

warrants of the funds released to the line ministries and their disbursement. The end result is that

the accounting and auditing become practically futile as the accounting and auditing personnel

respond to political pressure of the powerful and the records are either incomplete or made

disappear.

Stage IV: Budget Monitoring and Control

Budgeting and public financial management functions are guided by the Constitutions (to limited

extend) and two legislations introduced or up-dated during the second half of 1990s, namely: (i)

The Financial and Accounting Procedures of the State; and (ii) Regulations for the Accounts of

the State. Most of these rules and regulations are outdated and not relevant or adaptable to the

prevailing situation in Somaliland.

Dr. Scek

26 | P a g e

In the current system there are a number of organizations that have the legal and institutional

responsibility for holding the government to account for its performance. These include the

House of Representatives and its number of the House committees, such as the Public Account

Committee, Economic and Finance and Trade Committee, the Auditor General and many more.

The media, Civil Societies and the public at large also have a critical role in overseeing and

scrutinizing the activities of the government, whilst professional accounting bodies have also an

important role to play in ensuring the integrity of the public service, even though they are not yet

well established in Somaliland.

Budgetary controls can be exercised at three levels, these are:

1. Executive controls mainly by the Ministry of Finance

2. House of Representatives controls through the various House committees, Auditor

General, and

3. Citizens controls through advocacy and whistle blowing by individual citizens and

media.

Executive Controls

The Ministry of Finance has on papers a range of control measures on the budget execution.

These are in the form of operational instructions, circulars, directives and regulations that are

issued to the accounting officers in line ministries and public agencies on regular basis.

Some of the control measures in place are those described in the Financial Accounting

Procedures of the State, Government procurement guidelines even outdated but still there;

internal audit, which is most concerned with monitoring compliance with the government

regulations; and the Auditor General who exercise his/her control mandate by scrutinizing and

approving withdrawals from the consolidating fund.

House of Representatives Oversight/Control

The House, working through its committees exercises the ultimate oversight role on the budget.

The House as the legitimate representative arm of government is required by the Constitution

and other laws and procedures to approve all sources of revenue and the proposed expenditure

measures. The Executive is obliged by law to report on how it has utilized all the moneys raised

from taxes and other sources during the year to House. In this context the Minister of Finance

must present all the accounts and statements of all government ministries and agencies to the

Auditor General for audit before presenting them to the House of Representatives

The Auditor General approves all expenditure warrants before they are forwarded to the

Ministries and receives monthly as well as annual financial reports from the Accountant General.

He/She is required to conduct independent audits of the Government Ministries and public

agencies‟ accounts, and issue an audit report within six months of the close of the year. The

minister also issues a circular to all public and statutory bodies requesting them to present their

accounts to the auditor general.

Dr. Scek

27

These are practically the formal guiding instruments of budget controls and oversight. The key

statutes among other include the Constitution, the Financial and Accounting Procedures of the

State. These provide a framework (it does not matter how weak the laws are) on public officers

(accounting offices, and other) should operate in managing public funds.

Unfortunately, there is plenty of evidence that the laws, procedures in place are not being

enforced. In fact, overspending have been the norm in most institutions (particularly) powerful

ones, failing to respect financial reporting datelines, including audit report presented to the

House with huge delays or when they become outdated for more details see Annex I: Stage IV.

The key to exercise the oversight function over the budget process is definitely capacity and

commitment among the main actors. From our observations these two factors were not there, in

fact the capacity is severally weak and it has undermined the effectiveness of the oversight

institutions. The Auditor General Office is understaffed, underfunded and also lack technical

capacity to undertake and implement audit plans.

The House of Representatives has no mechanisms for continuous monitoring of the budget, but it

continues to heavily relay on the reports on the Economic, Financial and Trade Committee and

the Public Account committees, which are of post – mortem value. In addition, the House in its

current format lacks in both research and information gathering capacity, as a result the House

cannot effectively challenge the executive on its budget proposals.

During the past two decades, the government has not moved much to translate its commitments

into needed legislations and reforms to address the weaknesses on the ground. This could be

interpreted to the lack of ownership from the government to the reform agenda to reestablish and

establish needed oversight institutions. This could be explained that some development partners

were active in defining reform agendas, to the extent that they supported design initiatives on

behalf of the government, as results these never took off. The fact was that the development

partners were also not committed to that extends of supporting their own initiatives as evidenced

by the fact that all the support they provided went through off budget.

Civil Society and Citizen in Budget Oversight/Control

Monitoring the implementation of the budget does not merely end with the implementation of the

projects. The extent to which implemented projects attain the desired objectives of the allocation

is an important consideration for all budget beneficiaries. Since civil society groups are closely

integrated with the grassroots among stakeholders and are generally closest to the

implementation units, they retain a strategic role in assessing whether the projects were useful,

Dr. Scek

28 | P a g e

acceptable and sustainable to beneficiaries. There is need for greater and deliberate integration of

local communities and other grassroots stakeholders in the implementation and decision making

in the entire budget process.

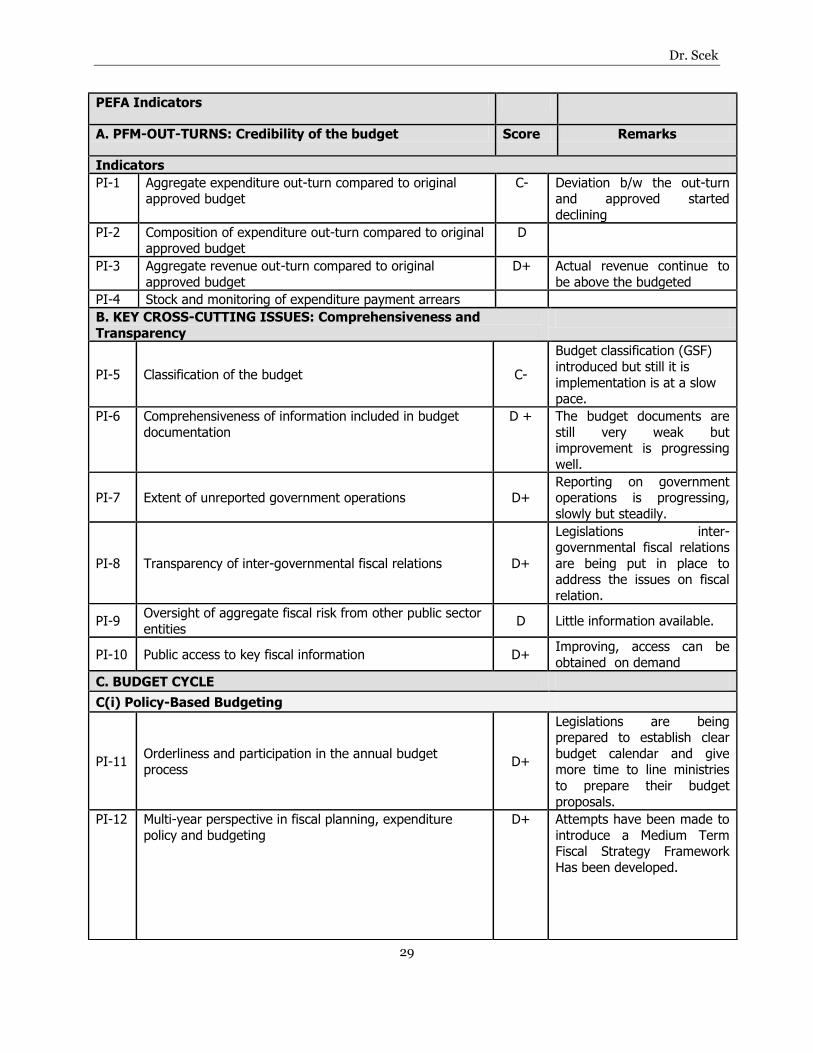

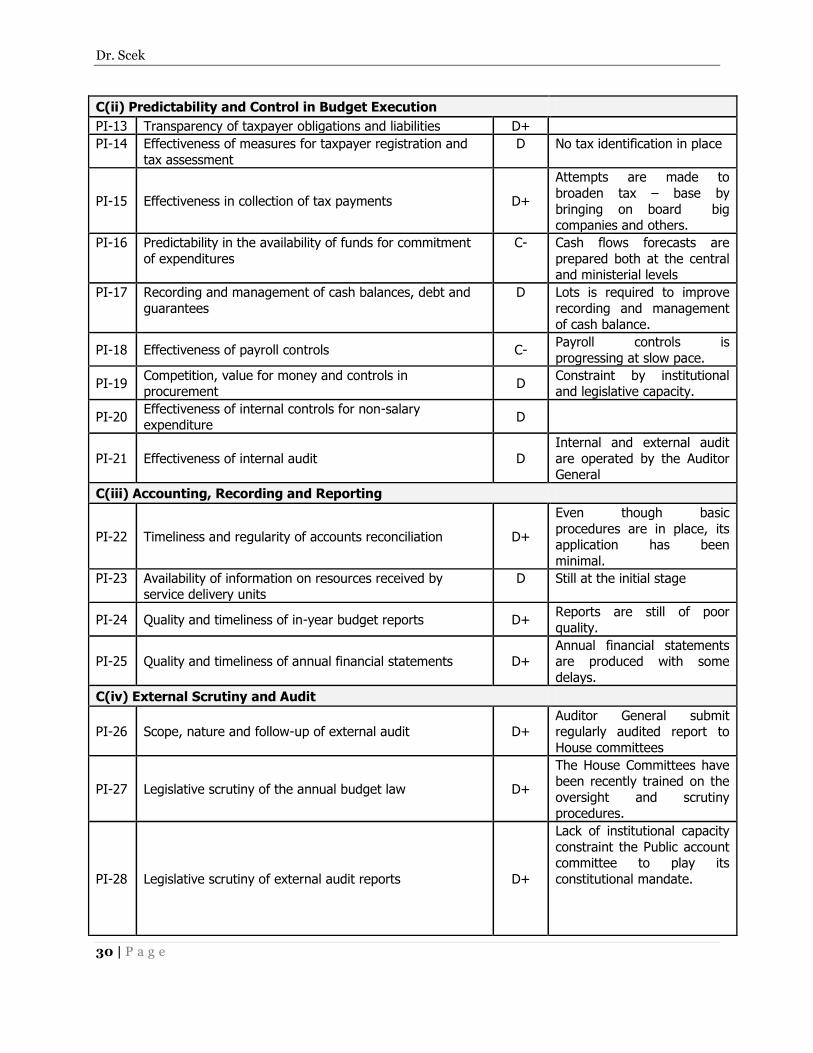

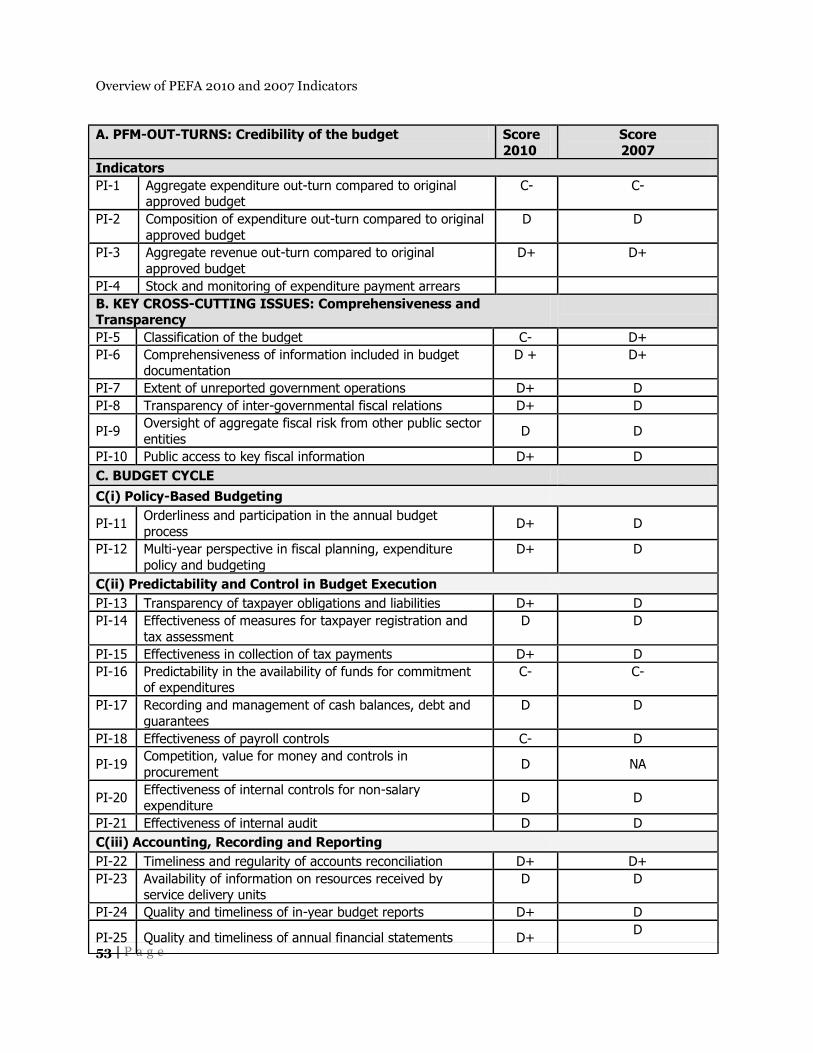

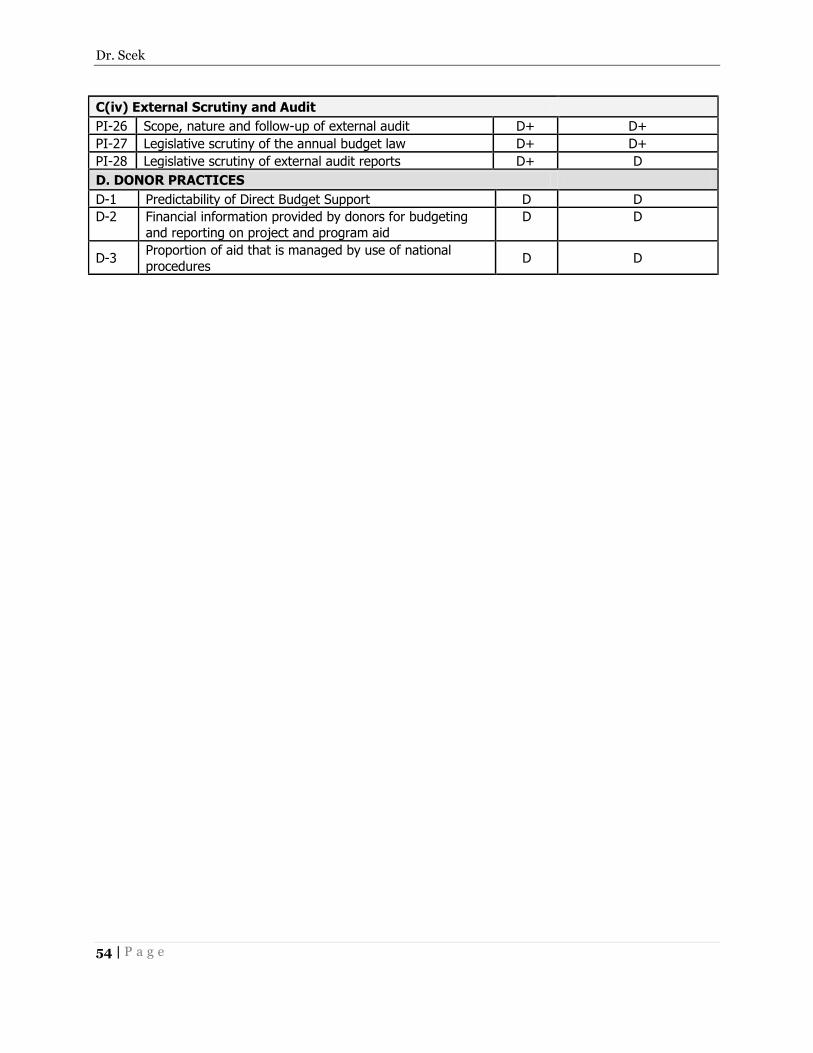

Performance Measurement Framework1 - PEFA Indicators

PEFA Performance Measurement Framework developed by PEFA partners in collaborative

efforts with the OECD Joint Venture on PFM as a tool that can provide reliable information on

the performance of PFM systems, processes and institutions at a point of time. The information

provided by the framework contribute to the formulation of government‟s reforms process by

determining the extent to which reforms are yielding improved performance and by increasing

ability to identify and learn from reform success.

Using the PEFA measurement framework the following indicators are estimated here bellow:

1 Public Expenditure and Financial Accountability (PEFA): Public Financial Management Performance Measurement

Framework, PEFA Secretariat, June 2005. The methodology is available at the PEFA website: www.pefa.org.

Dr. Scek

29

PEFA Indicators

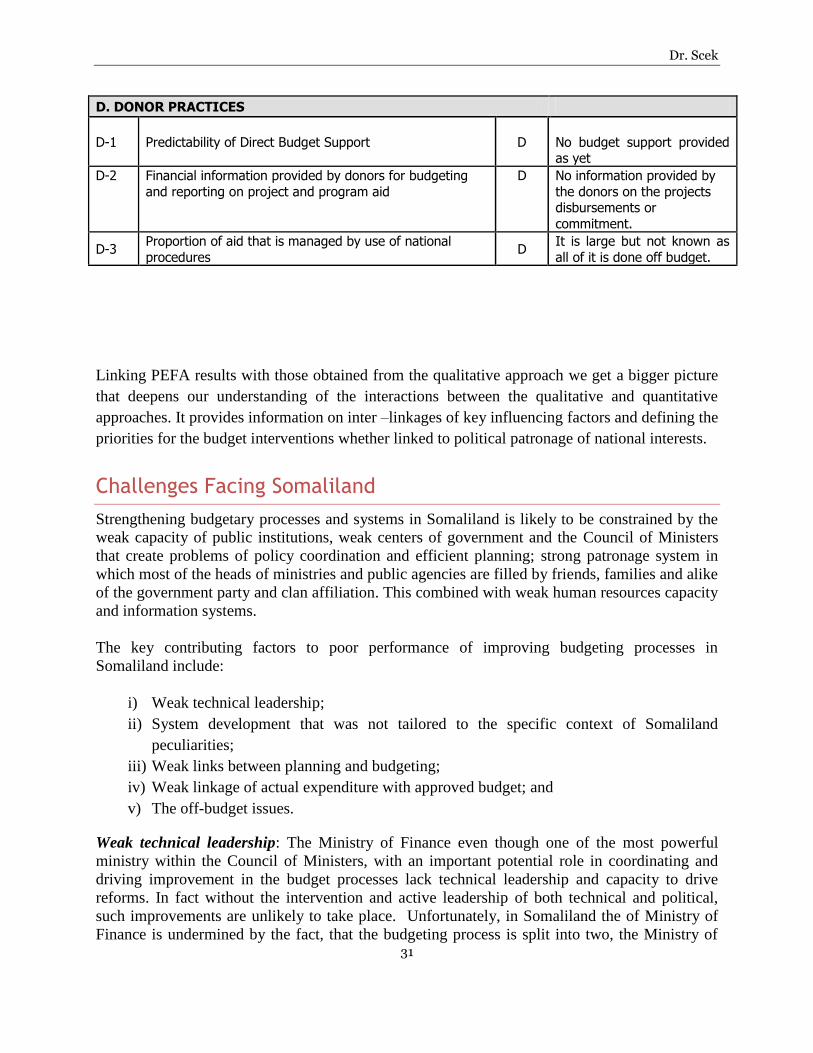

A. PFM-OUT-TURNS: Credibility of the budget Score Remarks

Indicators PI-1 Aggregate expenditure out-turn compared to original