restaurant sector - initiation of coverage - credit suisse

TRANSCRIPT

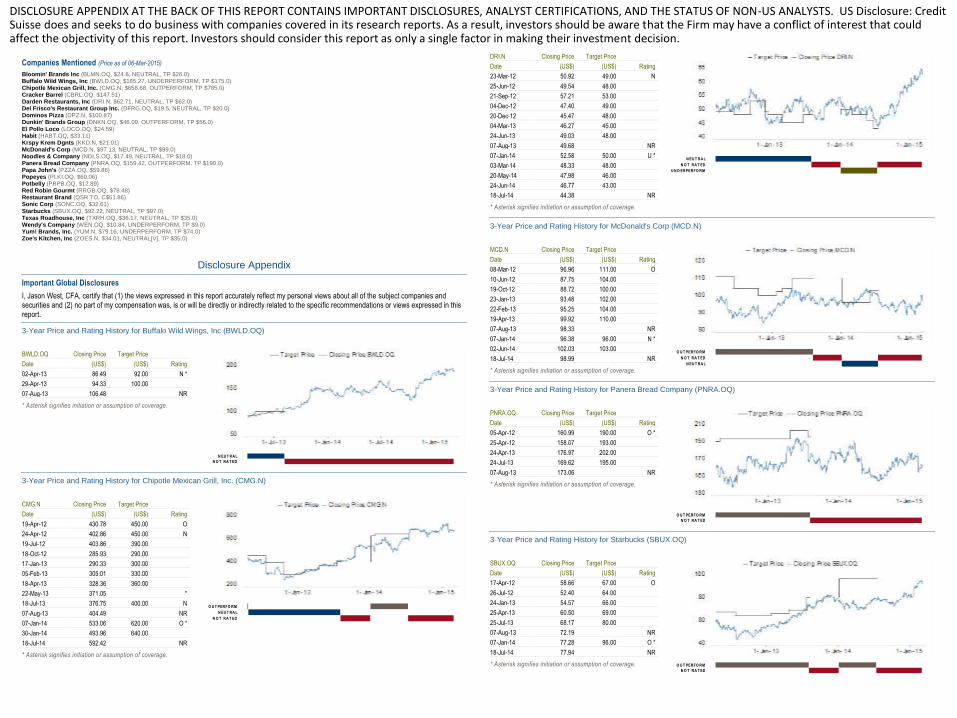

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATU.S.

OF NON-U.S. ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors

should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights and Access

Credit Suisse Equity Research

Americas/United States

Restaurant Sector Initiation of Coverage: Entering Happy Hour, but Without the Discount

March 10, 2015

RESEARCH TEAM

Jason West, CFA

Research Analyst +1 617-556-5745 [email protected]

1

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1999 2001 2003 2005 2008 2010 2012 2014 2016

Knapp CD Industry SSS Listed Restaurants SSS Black Box SSS

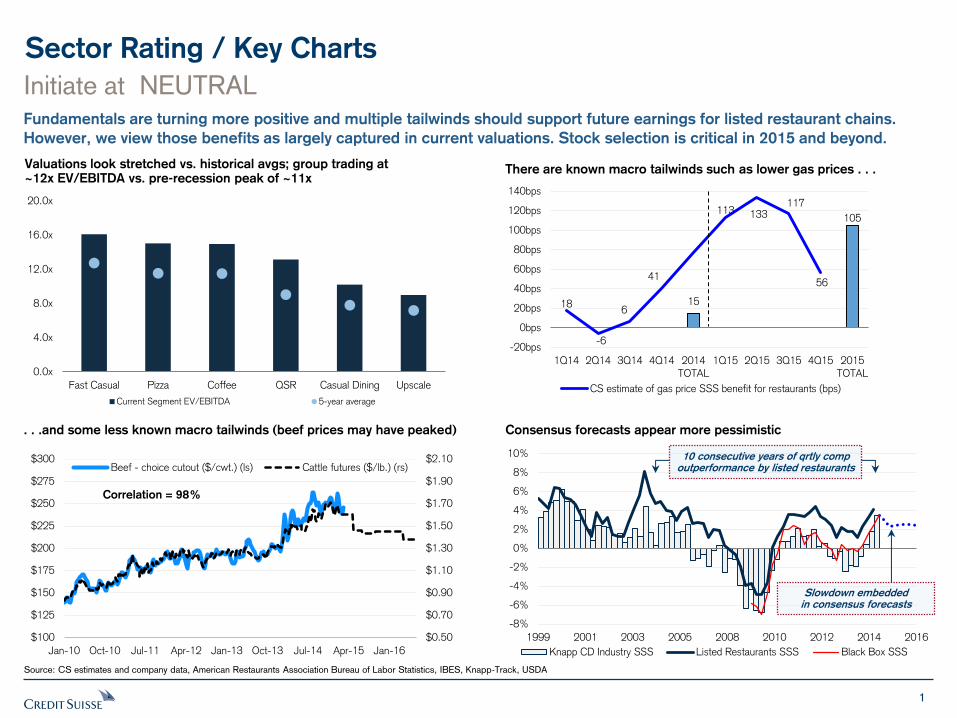

Sector Rating / Key Charts

Initiate at NEUTRAL Fundamentals are turning more positive and multiple tailwinds should support future earnings for listed restaurant chains.

However, we view those benefits as largely captured in current valuations. Stock selection is critical in 2015 and beyond.

Source: CS estimates and company data, American Restaurants Association Bureau of Labor Statistics, IBES, Knapp-Track, USDA

Valuations look stretched vs. historical avgs; group trading at ~12x EV/EBITDA vs. pre-recession peak of ~11x

There are known macro tailwinds such as lower gas prices . . .

. . .and some less known macro tailwinds (beef prices may have peaked) Consensus forecasts appear more pessimistic

Slowdown embedded in consensus forecasts

10 consecutive years of qrtly comp outperformance by listed restaurants

0.0x

4.0x

8.0x

12.0x

16.0x

20.0x

Fast Casual Pizza Coffee QSR Casual Dining Upscale

Current Segment EV/EBITDA 5-year average

$0.50

$0.70

$0.90

$1.10

$1.30

$1.50

$1.70

$1.90

$2.10

$100

$125

$150

$175

$200

$225

$250

$275

$300

Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-14 Apr-15 Jan-16

Beef - choice cutout ($/cwt.) (ls) Cattle futures ($/lb.) (rs)

Correlation = 98%

15

105

18

-6

6

41

113 133 117

56

-20bps

0bps

20bps

40bps

60bps

80bps

100bps

120bps

140bps

1Q14 2Q14 3Q14 4Q14 2014TOTAL

1Q15 2Q15 3Q15 4Q15 2015TOTAL

CS estimate of gas price SSS benefit for restaurants (bps)

2

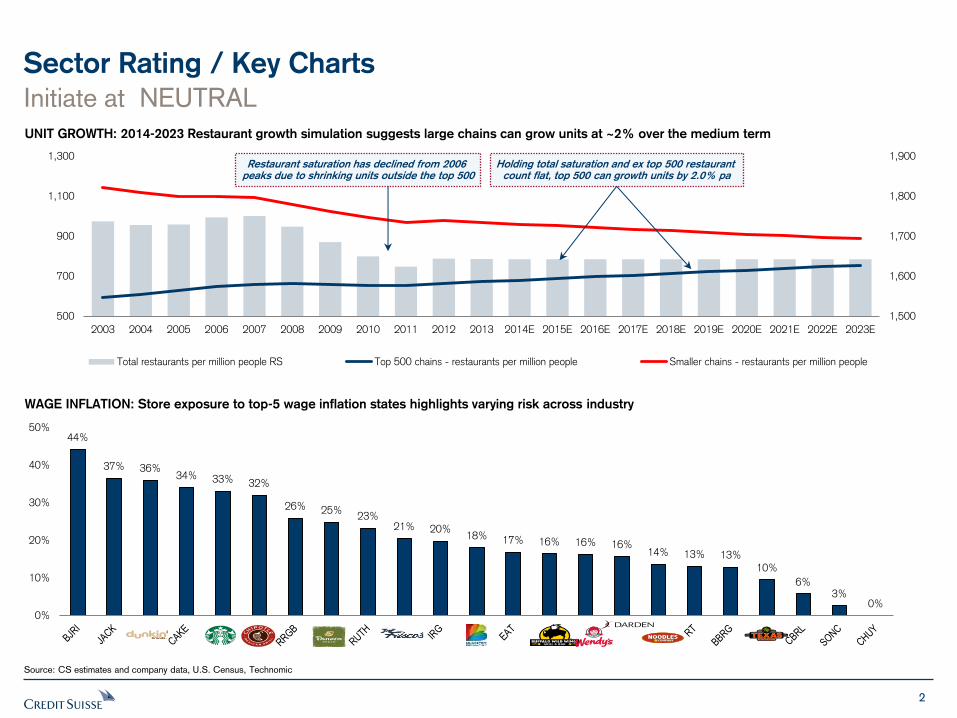

Sector Rating / Key Charts

Initiate at NEUTRAL

Source: CS estimates and company data, U.S. Census, Technomic

UNIT GROWTH: 2014-2023 Restaurant growth simulation suggests large chains can grow units at ~2% over the medium term

WAGE INFLATION: Store exposure to top-5 wage inflation states highlights varying risk across industry

44%

37% 36% 34% 33% 32%

26% 25% 23%

21% 20% 18% 17% 16% 16% 16%

14% 13% 13% 10%

6% 3%

0% 0%

10%

20%

30%

40%

50%

1,500

1,600

1,700

1,800

1,900

500

700

900

1,100

1,300

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

Total restaurants per million people RS Top 500 chains - restaurants per million people Smaller chains - restaurants per million people

Restaurant saturation has declined from 2006 peaks due to shrinking units outside the top 500

Holding total saturation and ex top 500 restaurant count flat, top 500 can growth units by 2.0% pa

3

Table of Contents

Coverage Introduction

Stock Picks / Company Tear Sheets

FOCUS ISSUE: Gasoline Price Impact

Appendix

FOCUS ISSUE: Minimum Wage Analysis

Coverage Introduction

Sector Overview

Valuation & Risks

Tear Sheets

Appendix

Discussion Points

5

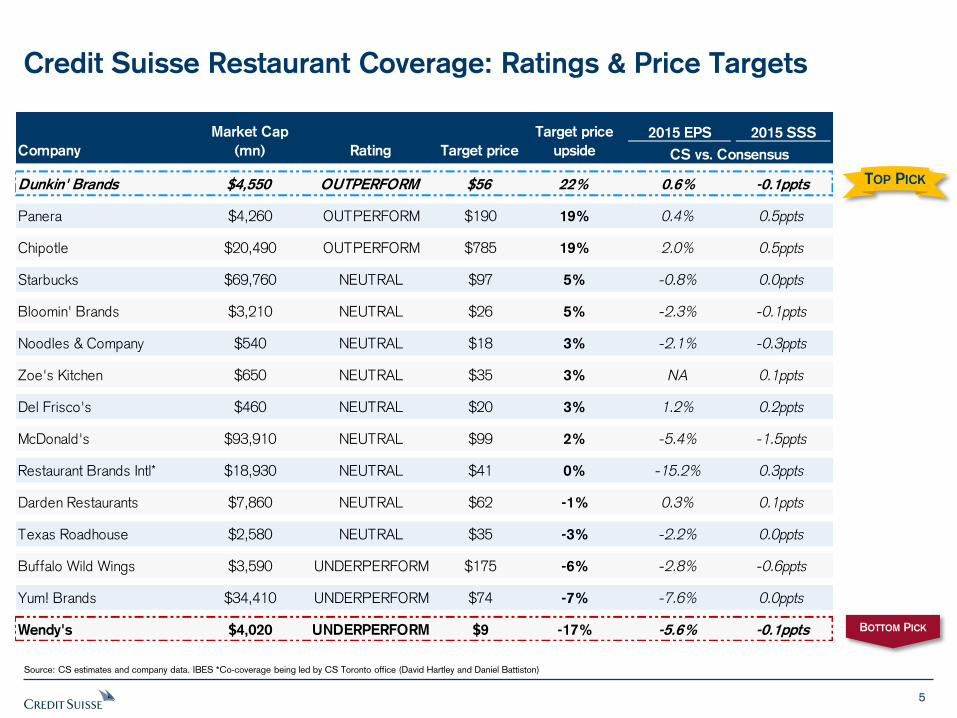

Credit Suisse Restaurant Coverage: Ratings & Price Targets

Source: CS estimates and company data. IBES *Co-coverage being led by CS Toronto office (David Hartley and Daniel Battiston)

TOP PICK

BOTTOM PICK

2015 EPS 2015 SSS

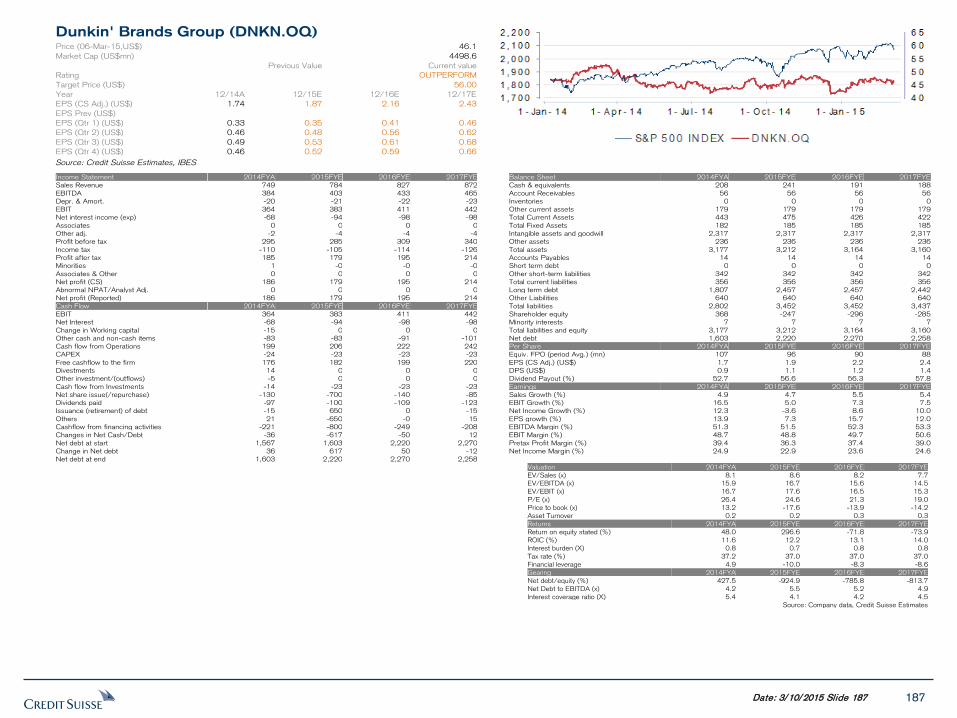

Dunkin' Brands $4,550 OUTPERFORM $56 22% 0.6% -0.1ppts

Panera $4,260 OUTPERFORM $190 19% 0.4% 0.5ppts

Chipotle $20,490 OUTPERFORM $785 19% 2.0% 0.5ppts

Starbucks $69,760 NEUTRAL $97 5% -0.8% 0.0ppts

Bloomin' Brands $3,210 NEUTRAL $26 5% -2.3% -0.1ppts

Noodles & Company $540 NEUTRAL $18 3% -2.1% -0.3ppts

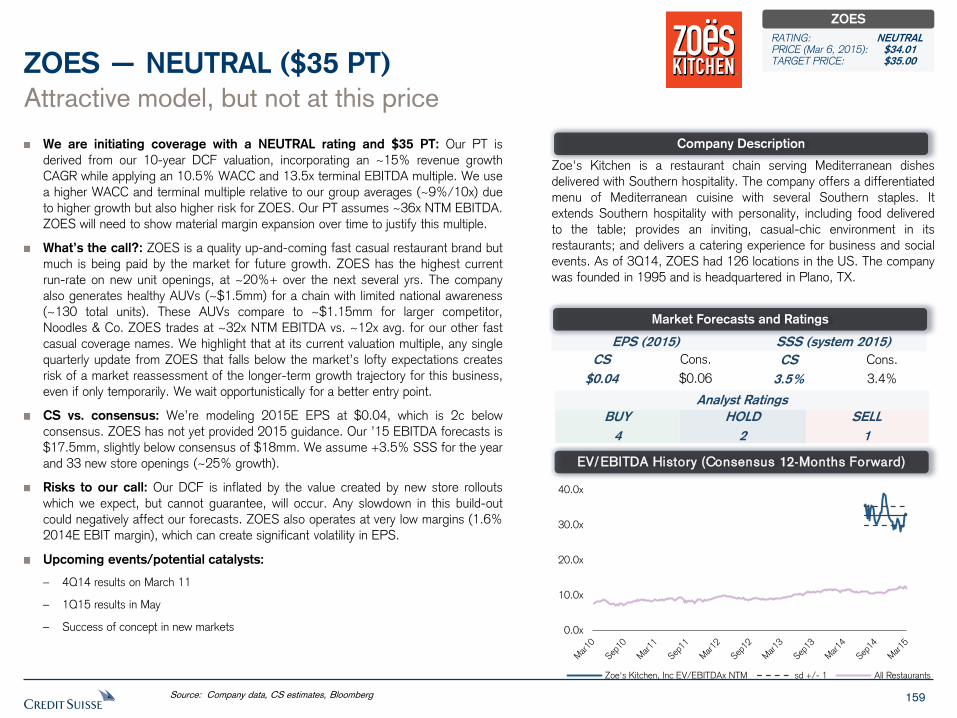

Zoe's Kitchen $650 NEUTRAL $35 3% NA 0.1ppts

Del Frisco's $460 NEUTRAL $20 3% 1.2% 0.2ppts

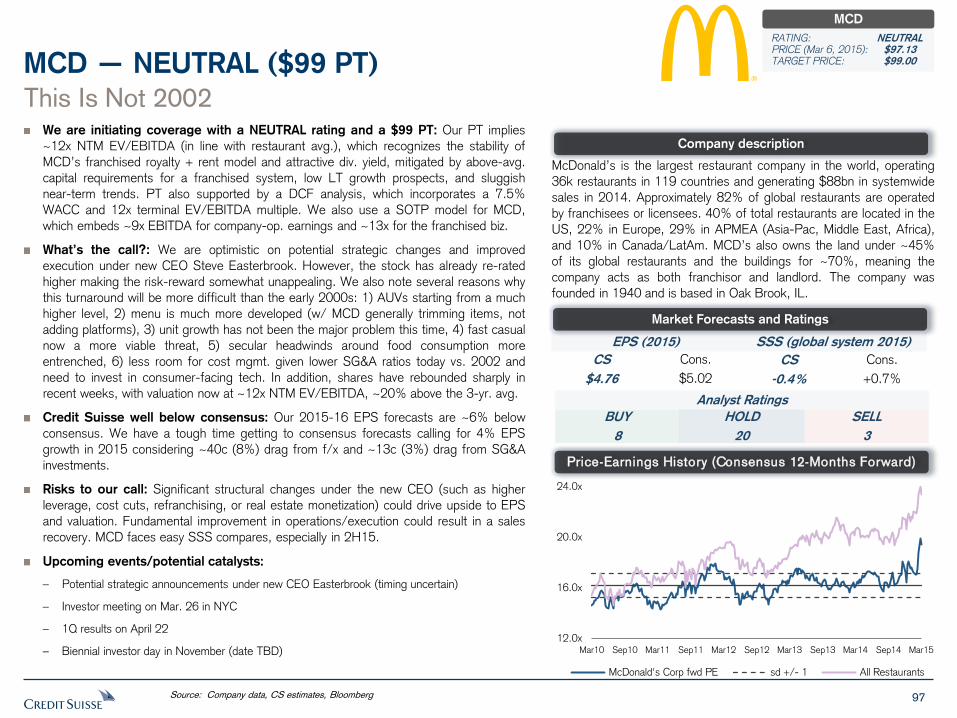

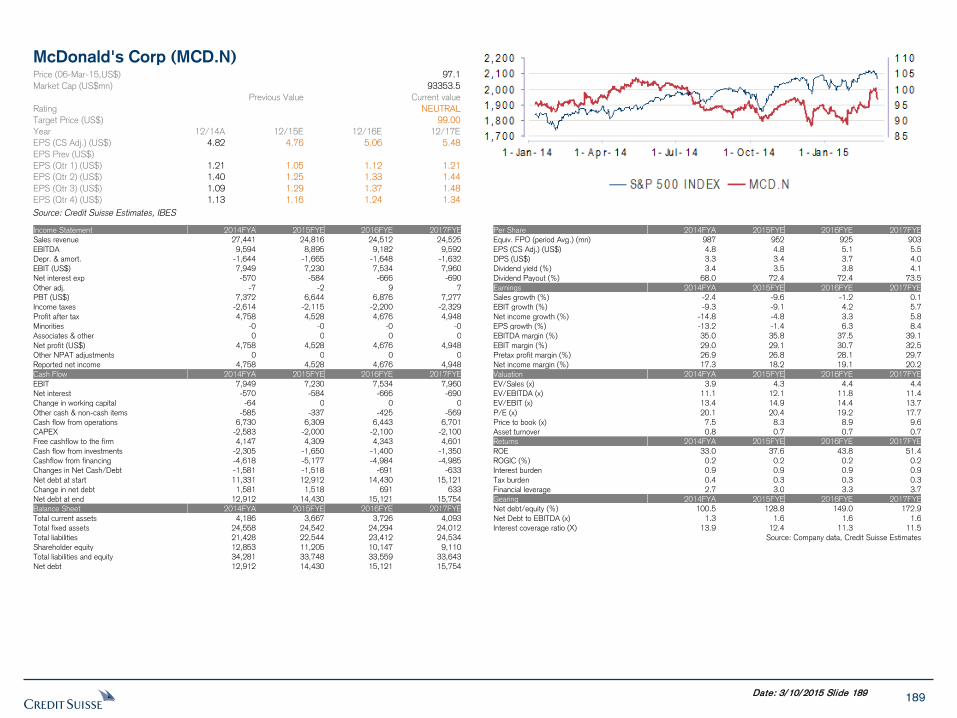

McDonald's $93,910 NEUTRAL $99 2% -5.4% -1.5ppts

Restaurant Brands Intl* $18,930 NEUTRAL $41 0% -15.2% 0.3ppts

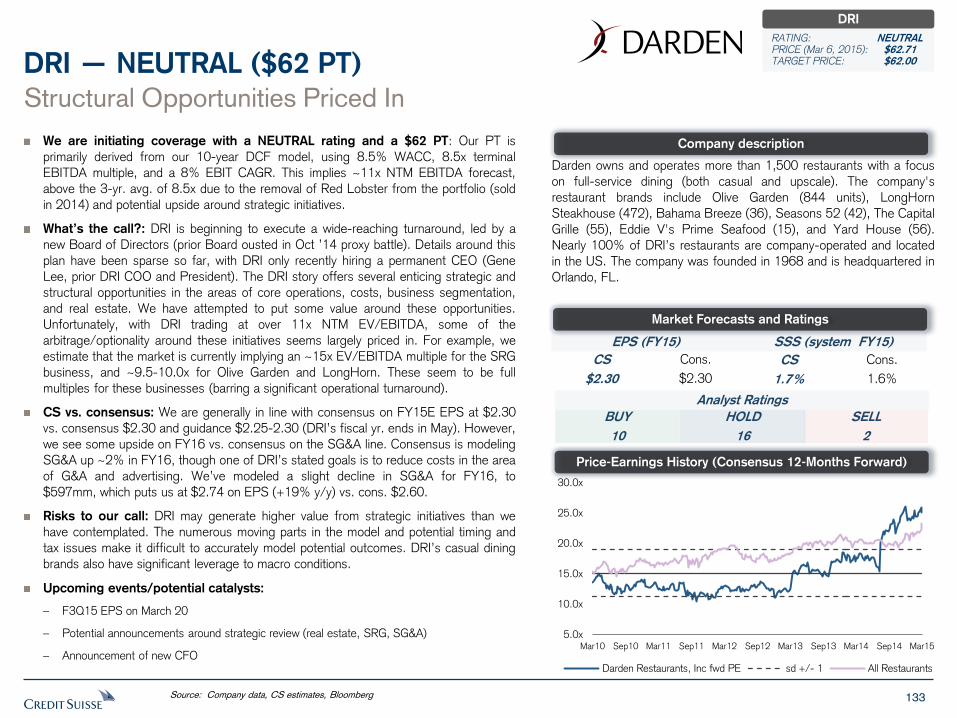

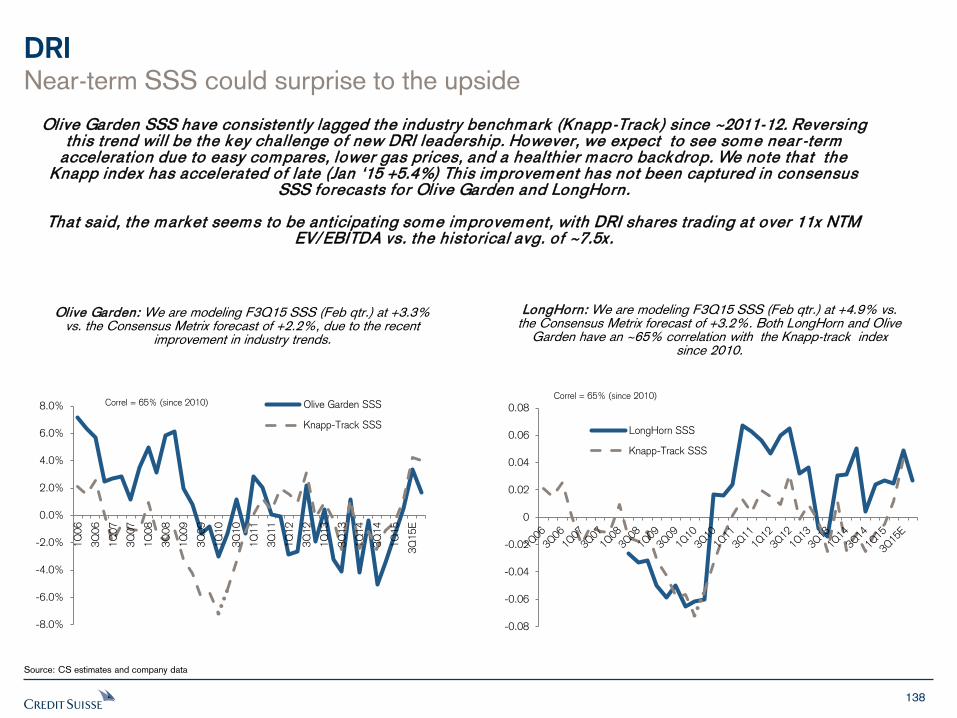

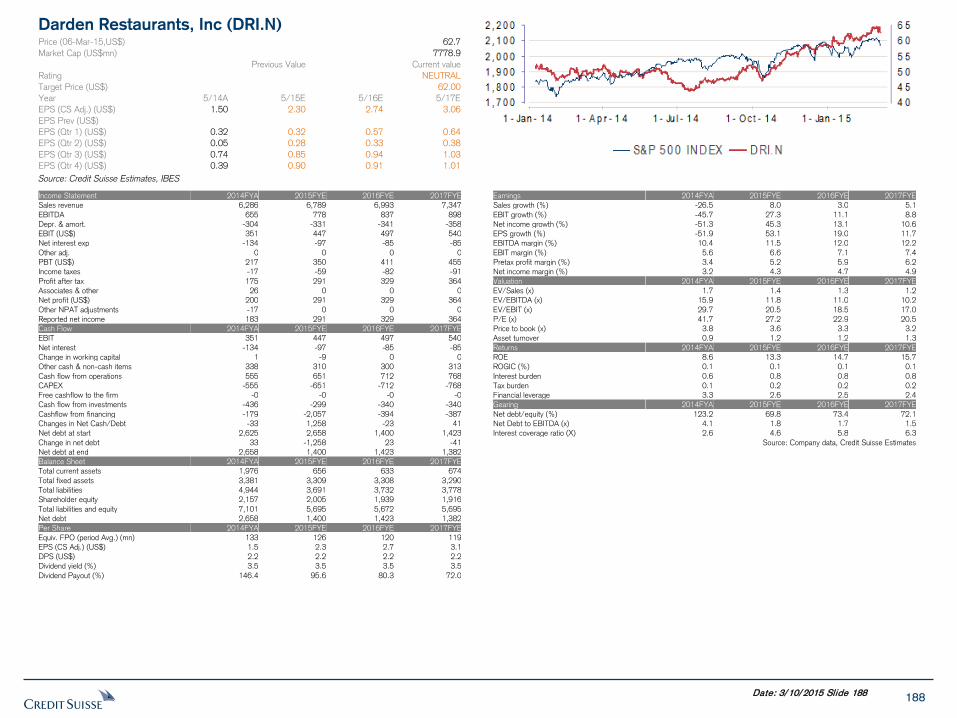

Darden Restaurants $7,860 NEUTRAL $62 -1% 0.3% 0.1ppts

Texas Roadhouse $2,580 NEUTRAL $35 -3% -2.2% 0.0ppts

Buffalo Wild Wings $3,590 UNDERPERFORM $175 -6% -2.8% -0.6ppts

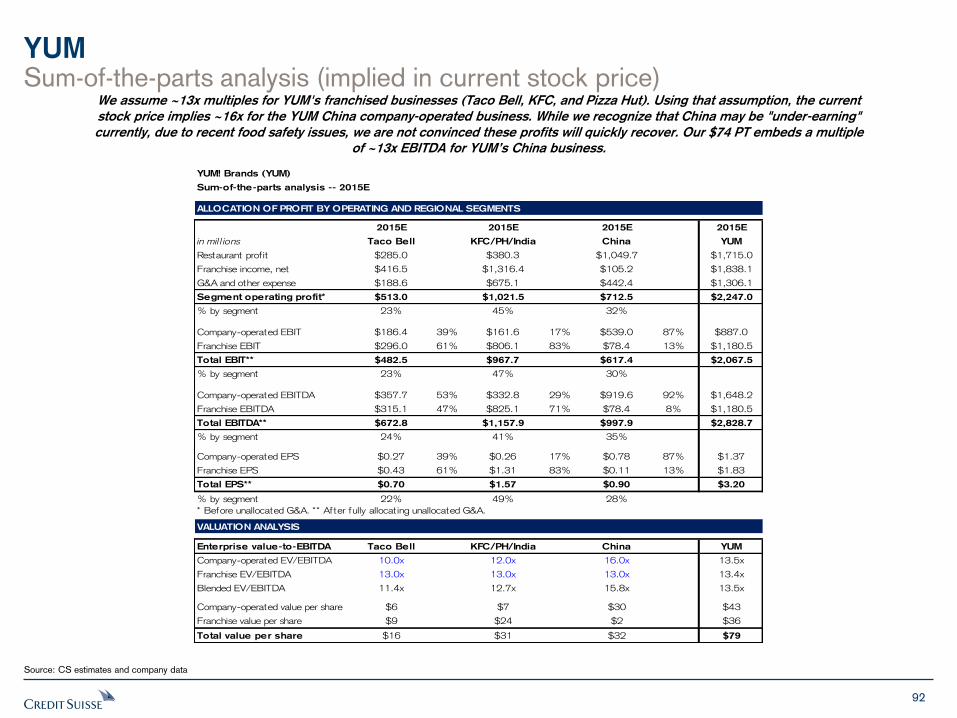

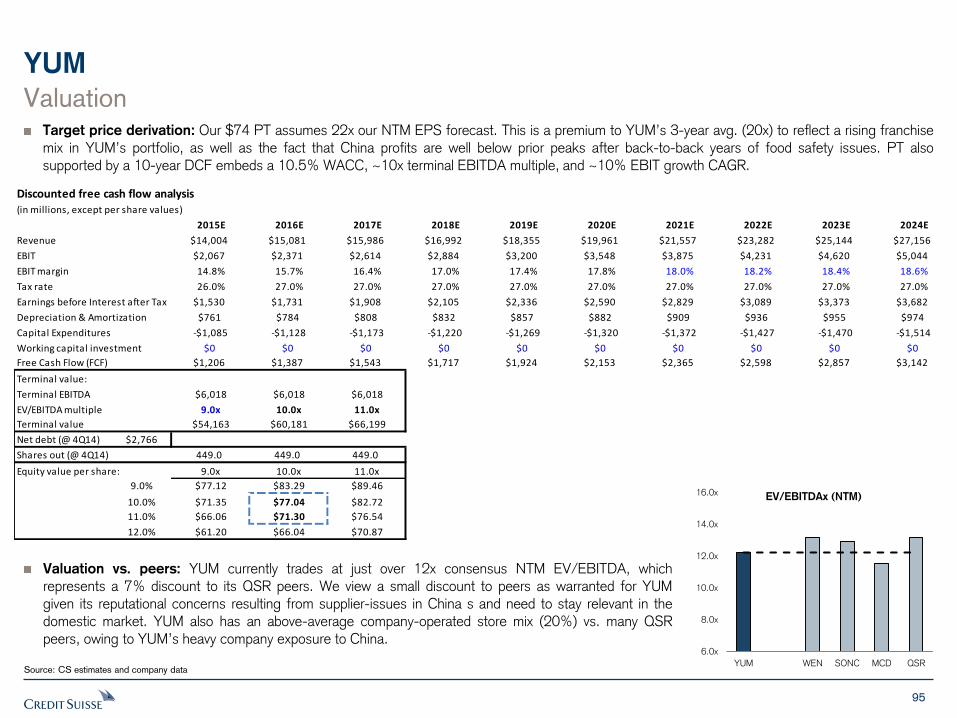

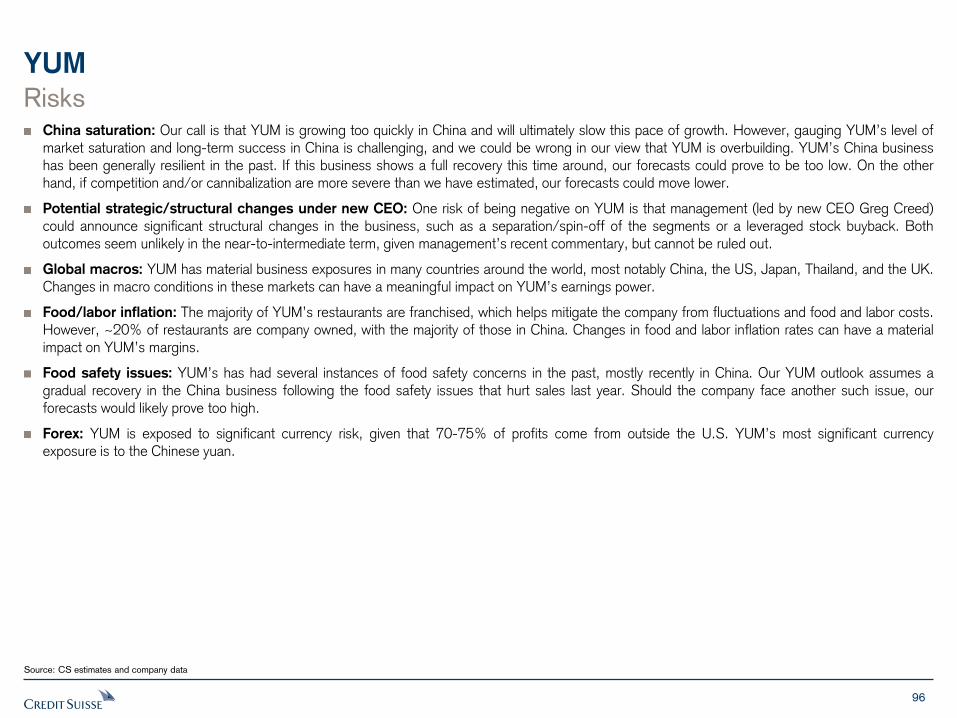

Yum! Brands $34,410 UNDERPERFORM $74 -7% -7.6% 0.0ppts

Wendy's $4,020 UNDERPERFORM $9 -17% -5.6% -0.1ppts

CS vs. ConsensusCompany

Market Cap

(mn) Rating Target price

Target price

upside

6

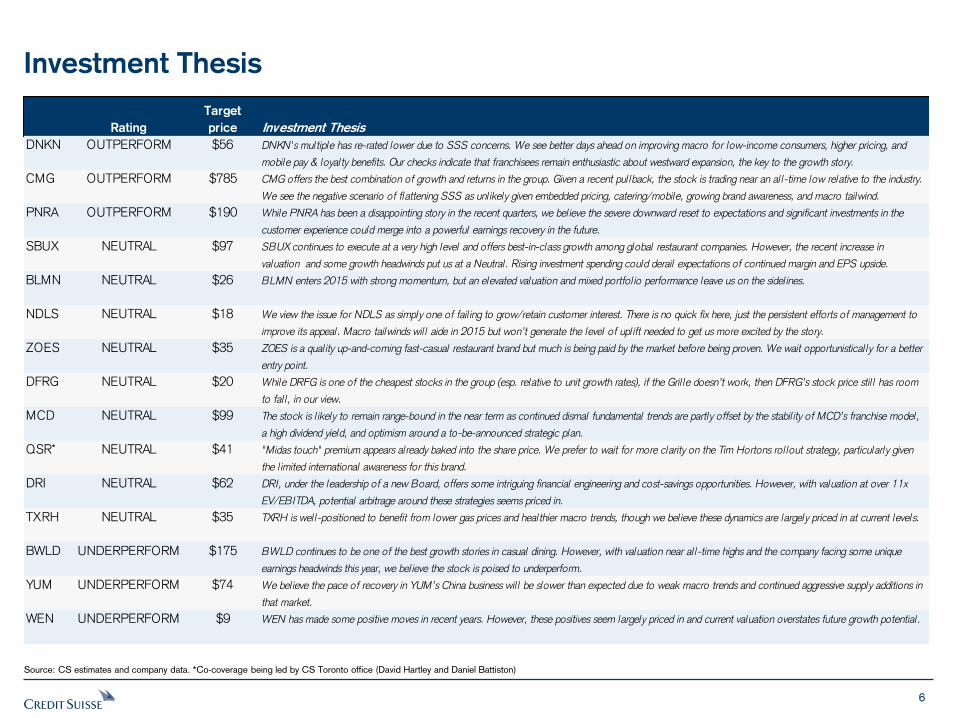

Investment Thesis

Source: CS estimates and company data. *Co-coverage being led by CS Toronto office (David Hartley and Daniel Battiston)

DNKN OUTPERFORM $56

CMG OUTPERFORM $785

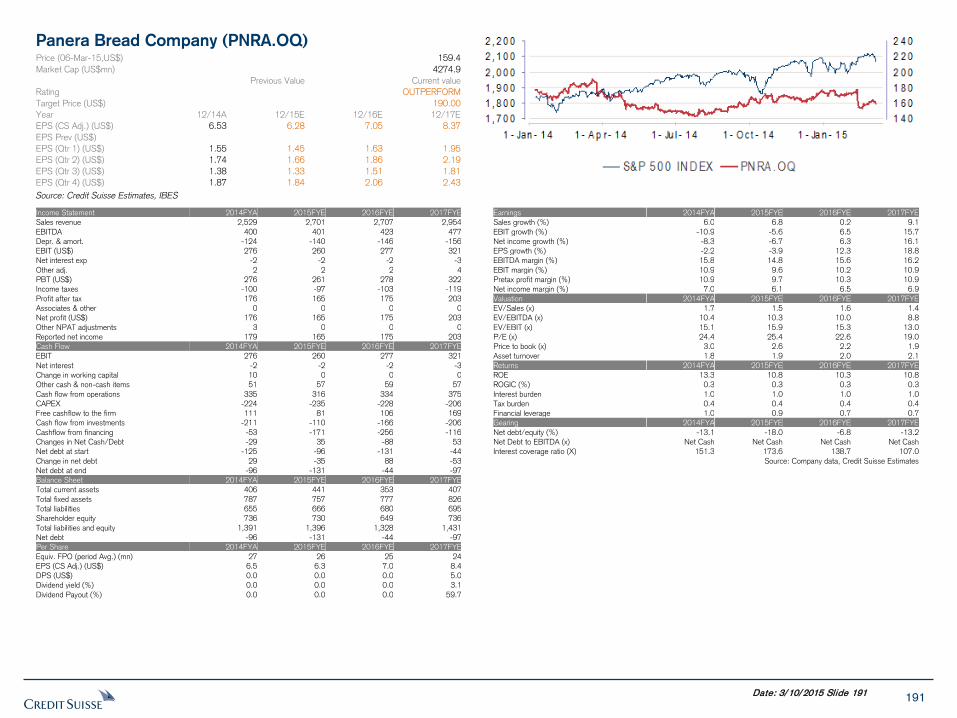

PNRA OUTPERFORM $190

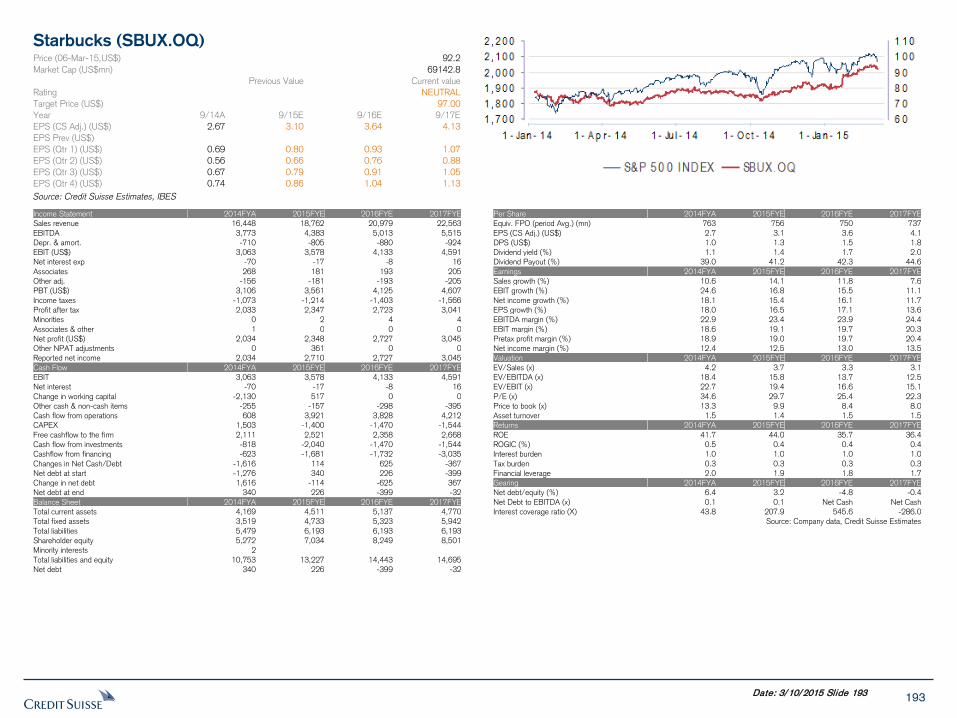

SBUX NEUTRAL $97

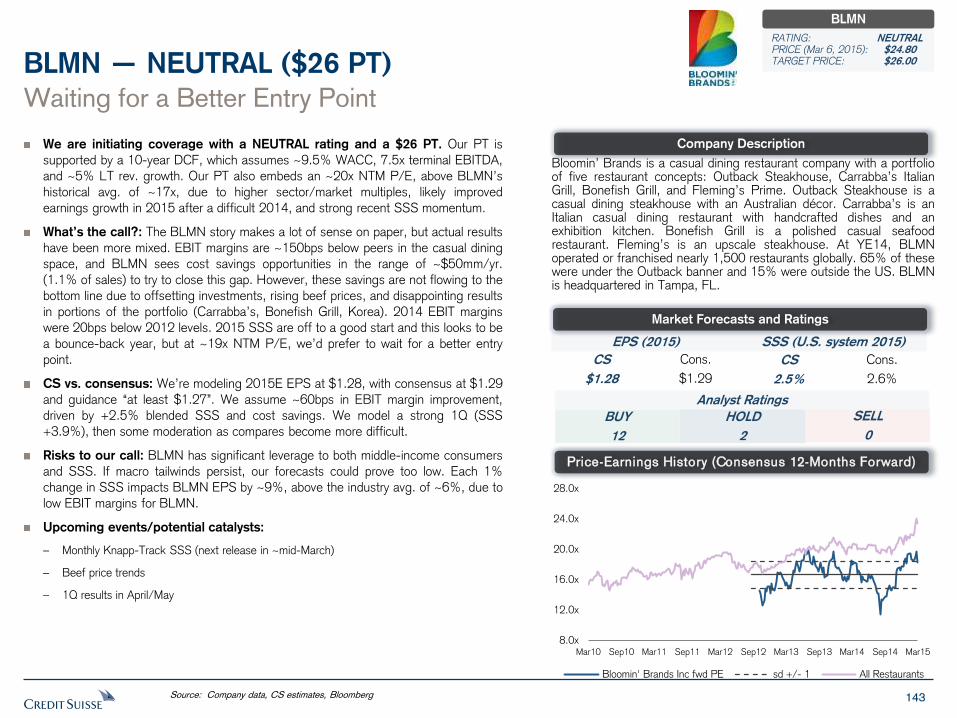

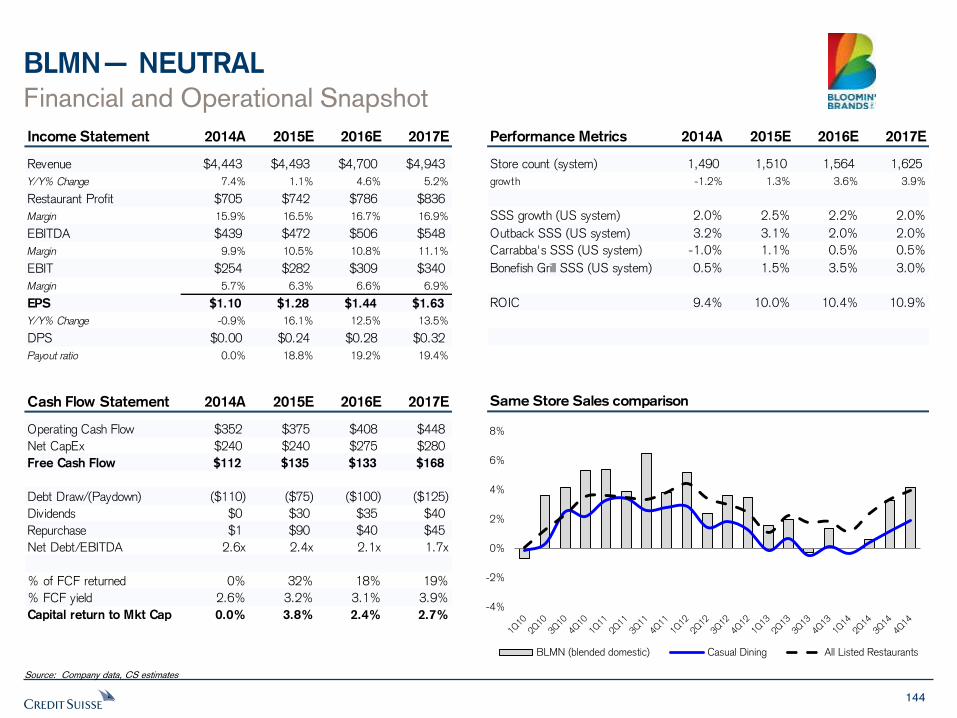

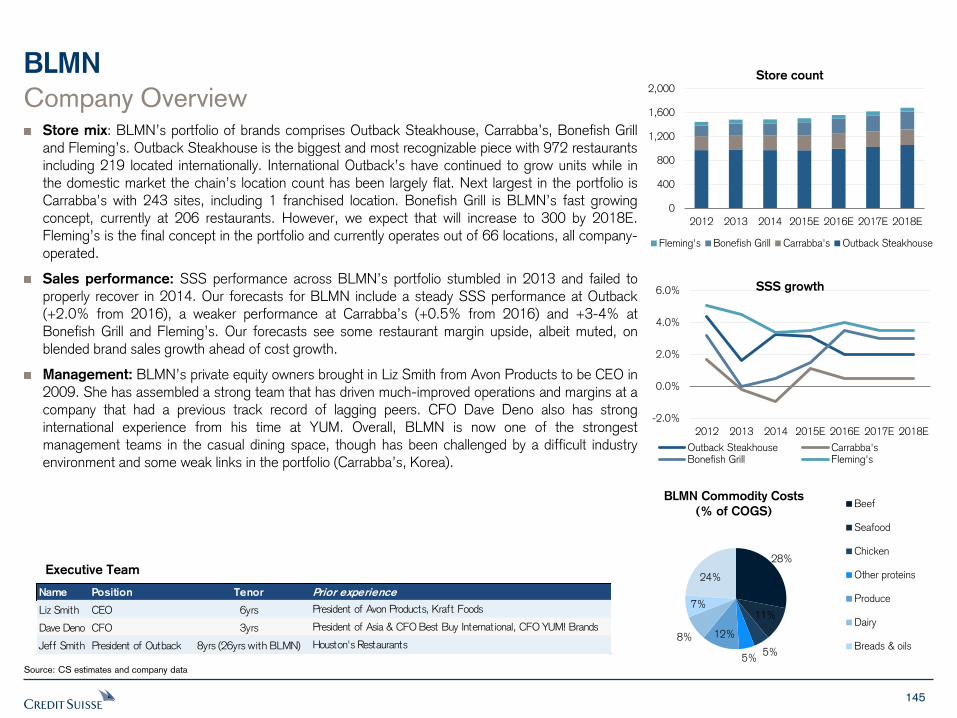

BLMN NEUTRAL $26

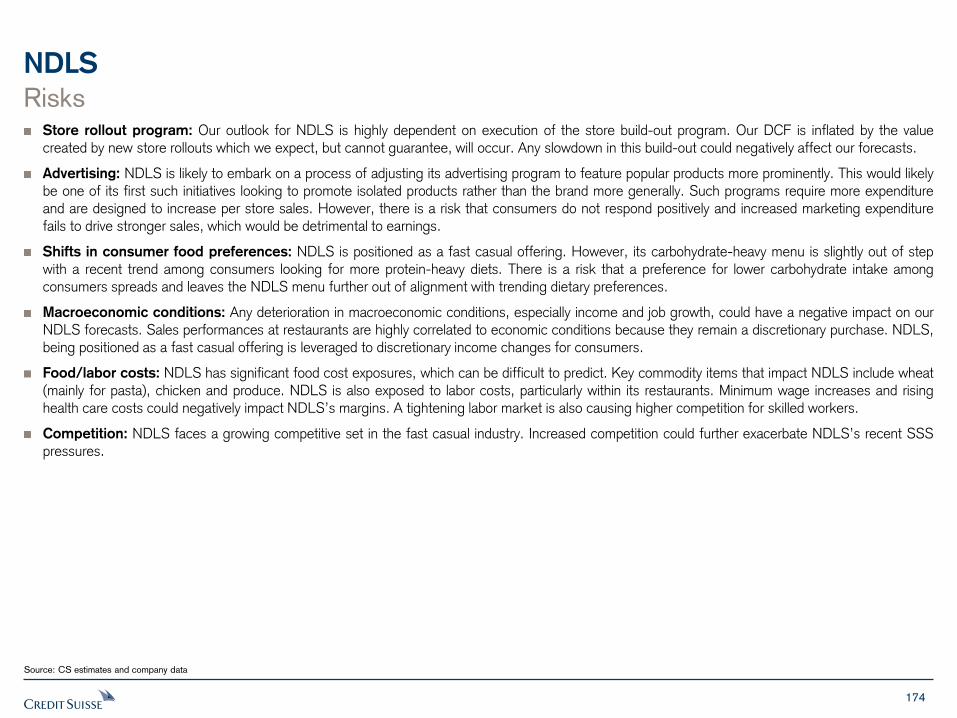

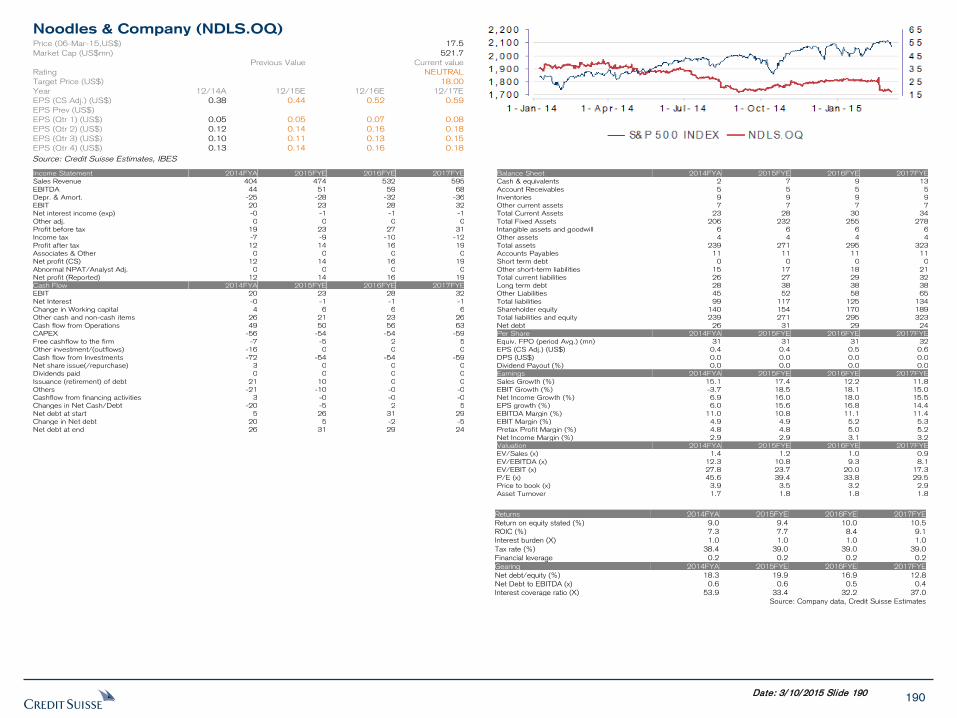

NDLS NEUTRAL $18

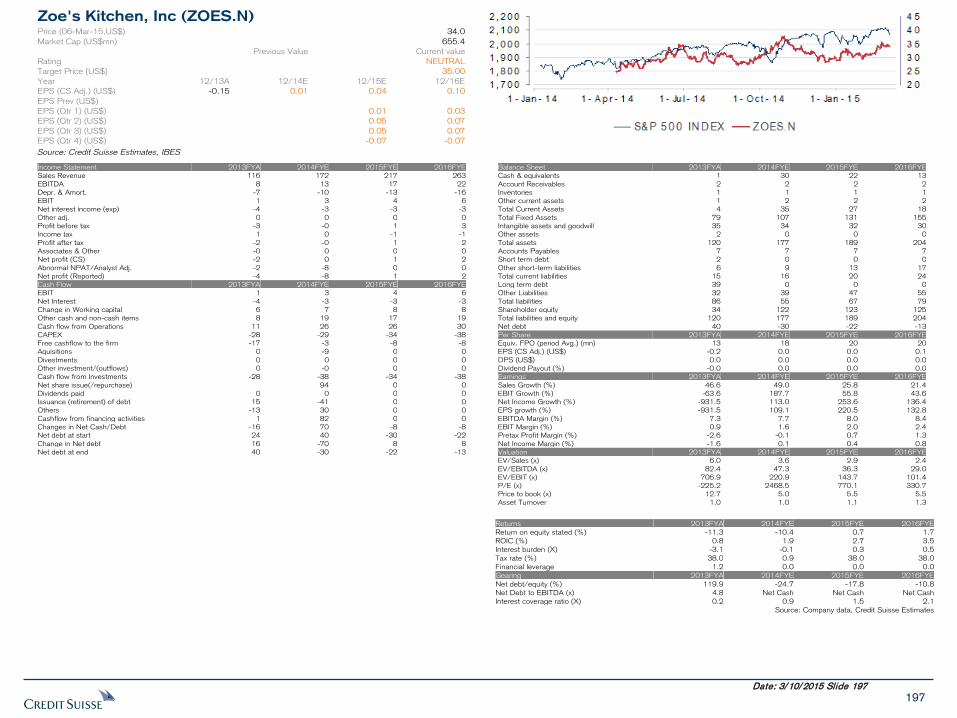

ZOES NEUTRAL $35

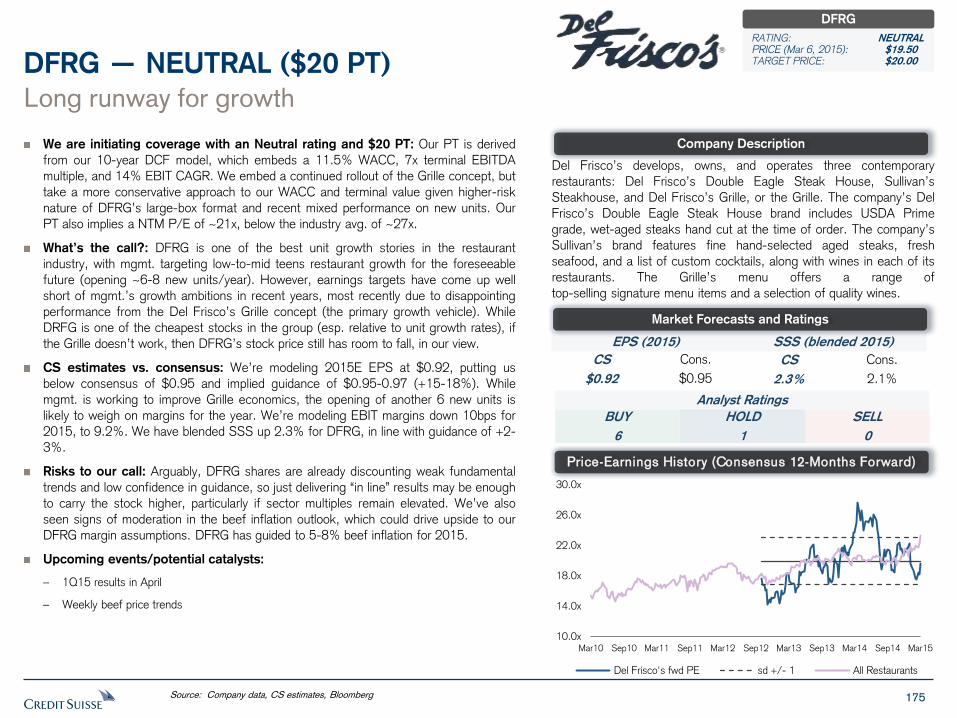

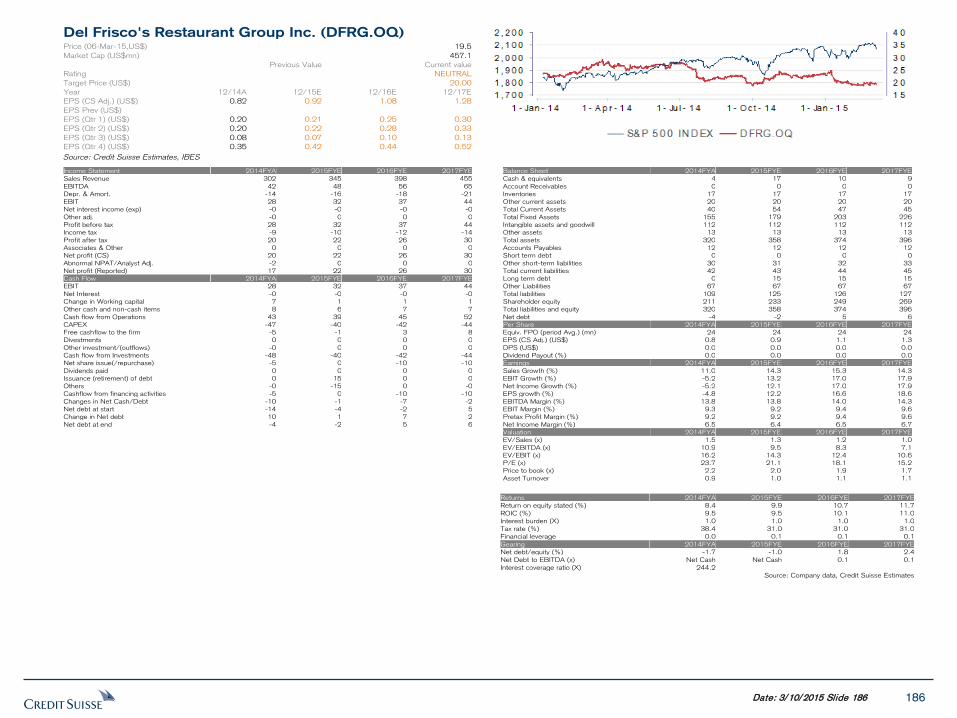

DFRG NEUTRAL $20

MCD NEUTRAL $99

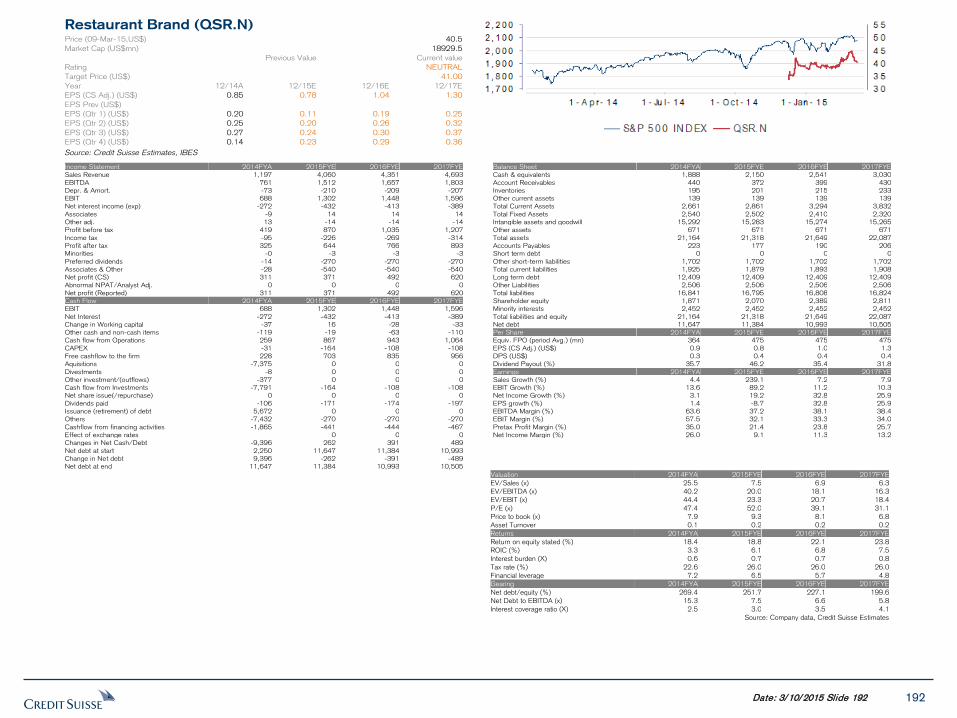

QSR* NEUTRAL $41

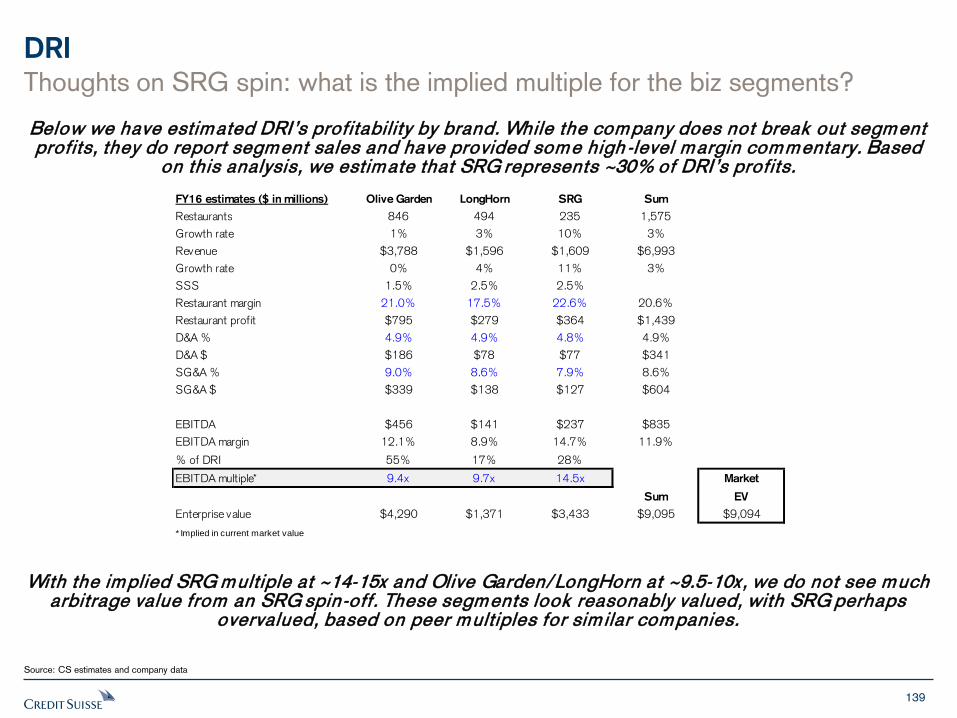

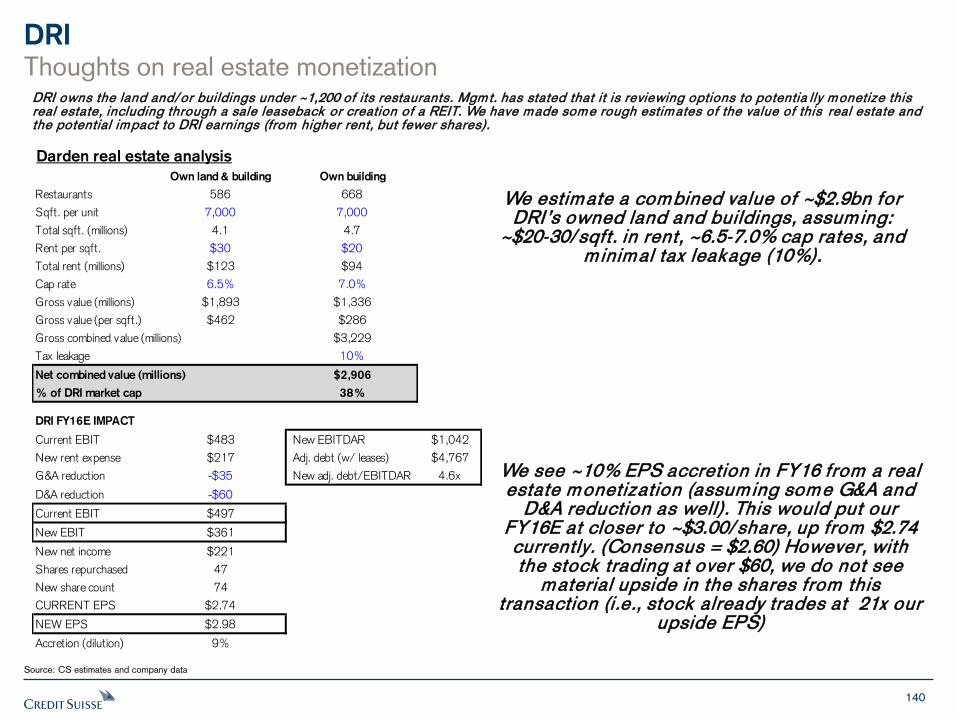

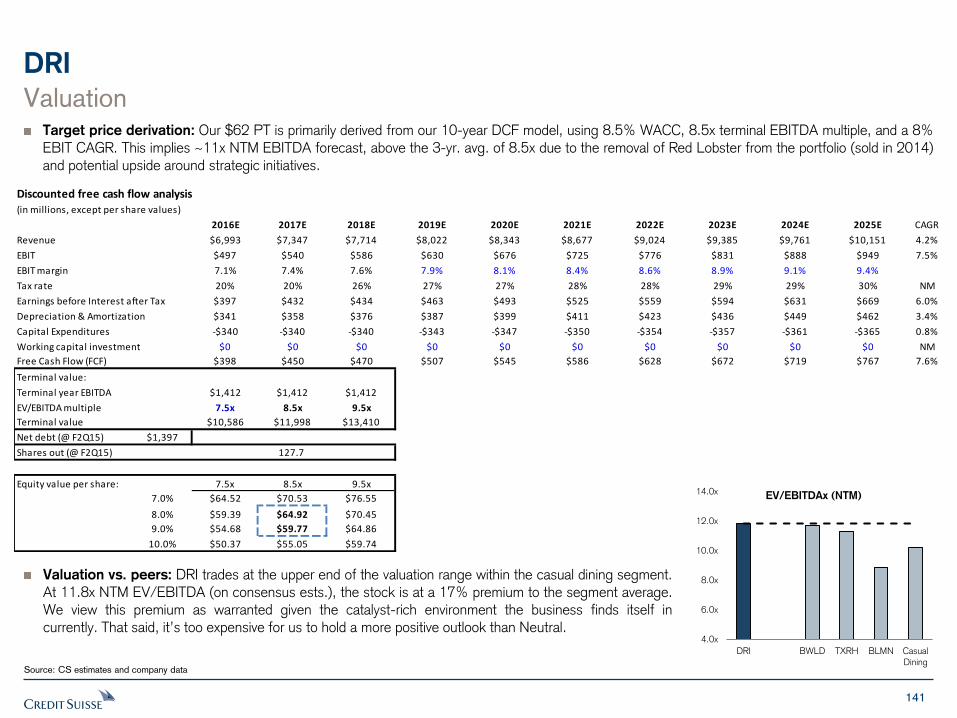

DRI NEUTRAL $62

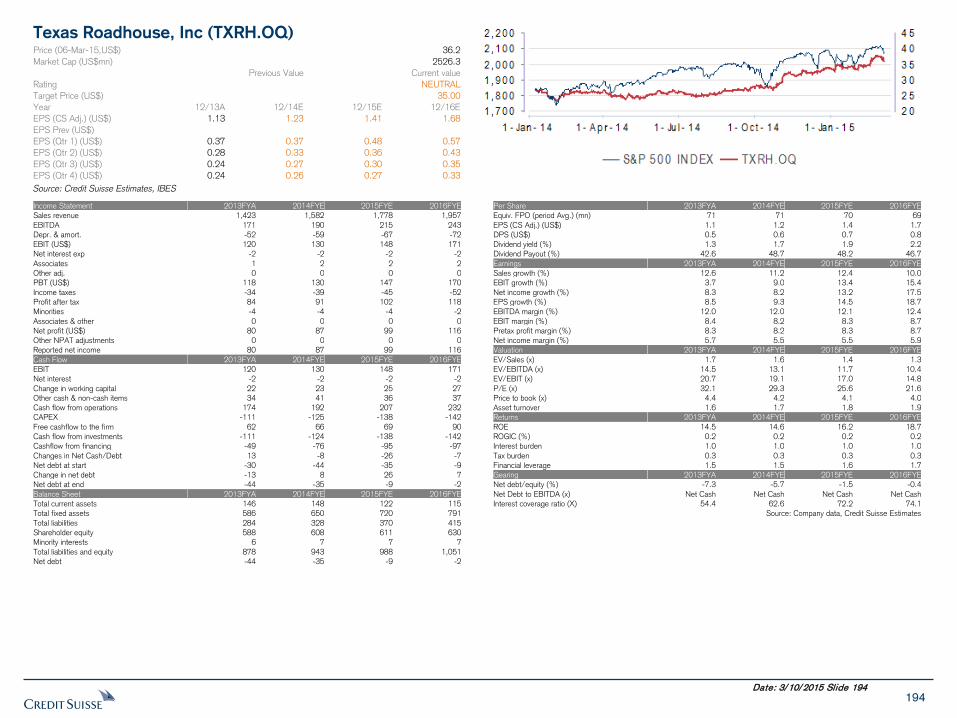

TXRH NEUTRAL $35

BWLD UNDERPERFORM $175

YUM UNDERPERFORM $74

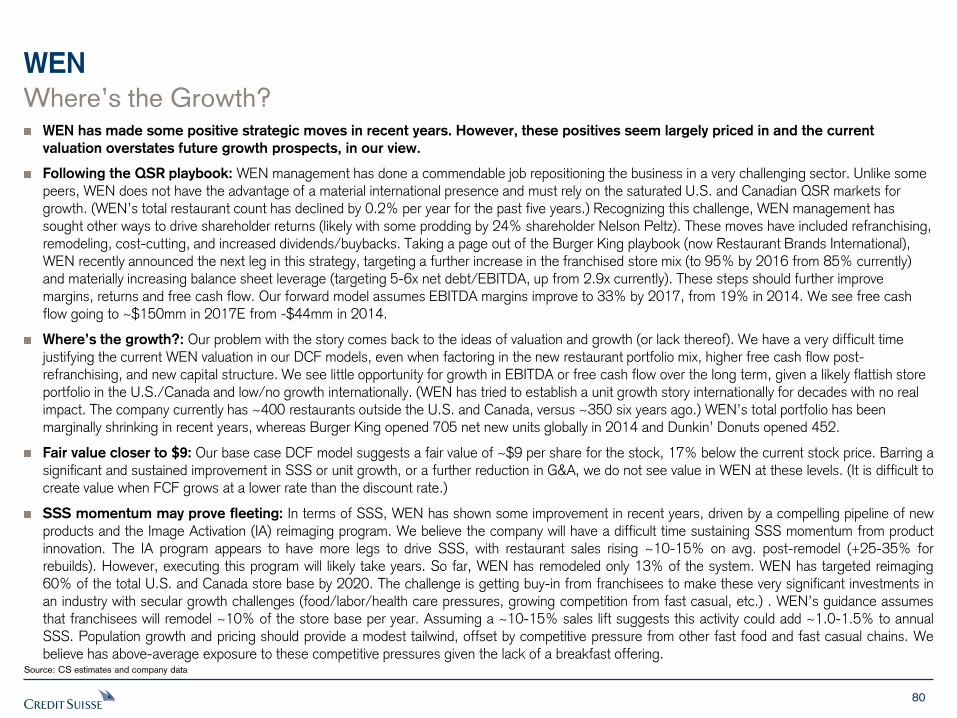

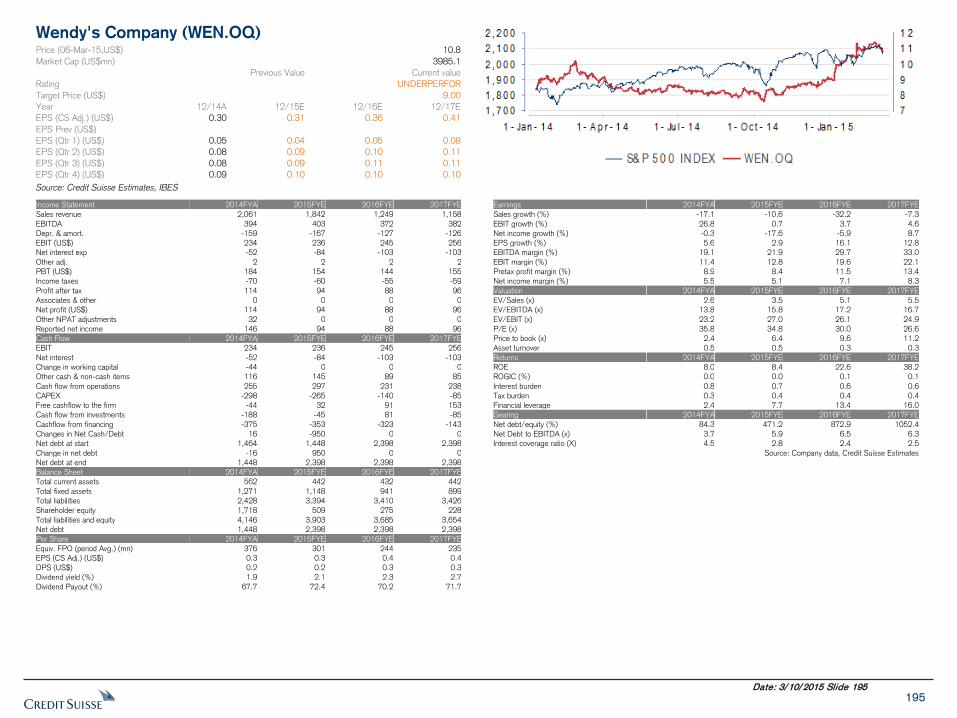

WEN UNDERPERFORM $9 WEN has made some positive moves in recent years. However, these positives seem largely priced in and current valuation overstates future growth potential .

TXRH is wel l-positioned to benefit from lower gas prices and healthier macro trends, though we bel ieve these dynamics are largely priced in at current levels.

We view the issue for NDLS as simply one of fail ing to grow/retain customer interest. There is no quick fix here, just the persistent efforts of management to

improve its appeal. Macro tailwinds wil l aide in 2015 but won’t generate the level of upl ift needed to get us more excited by the story.

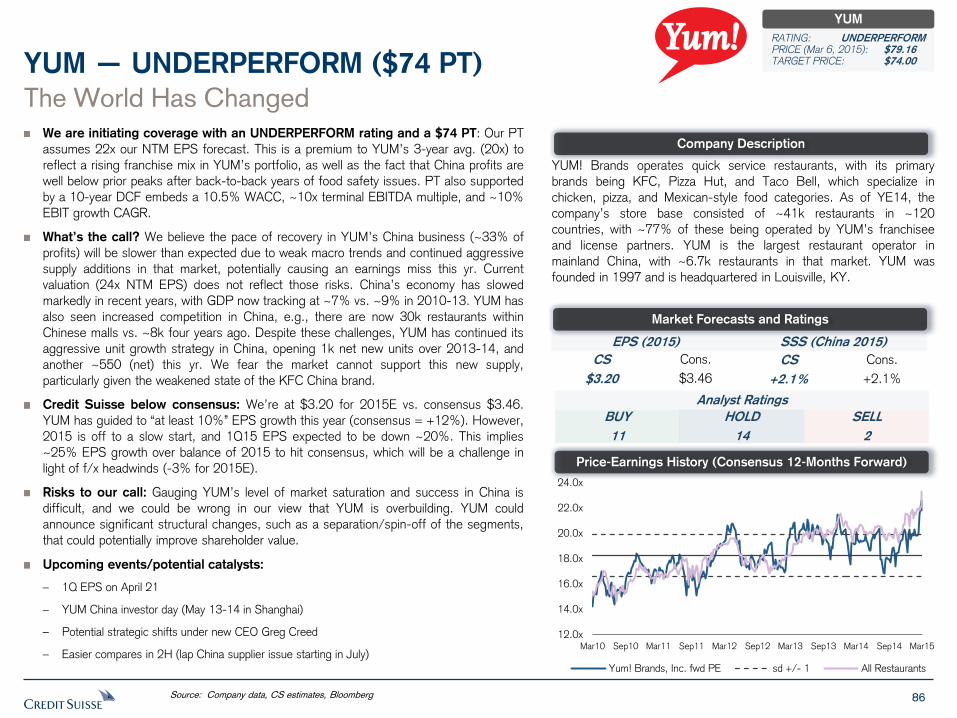

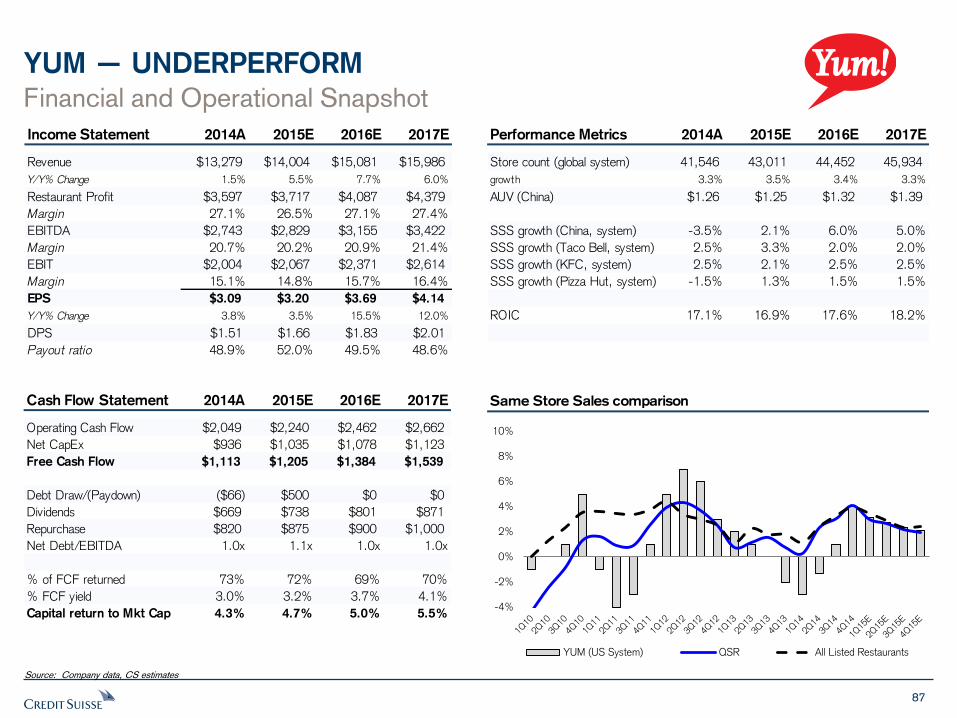

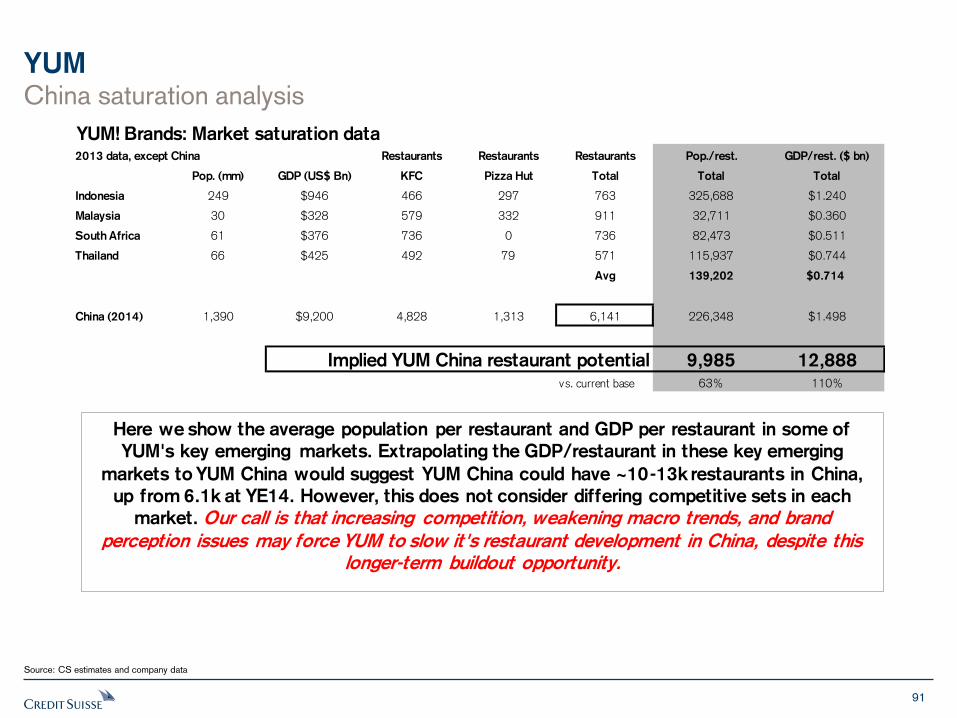

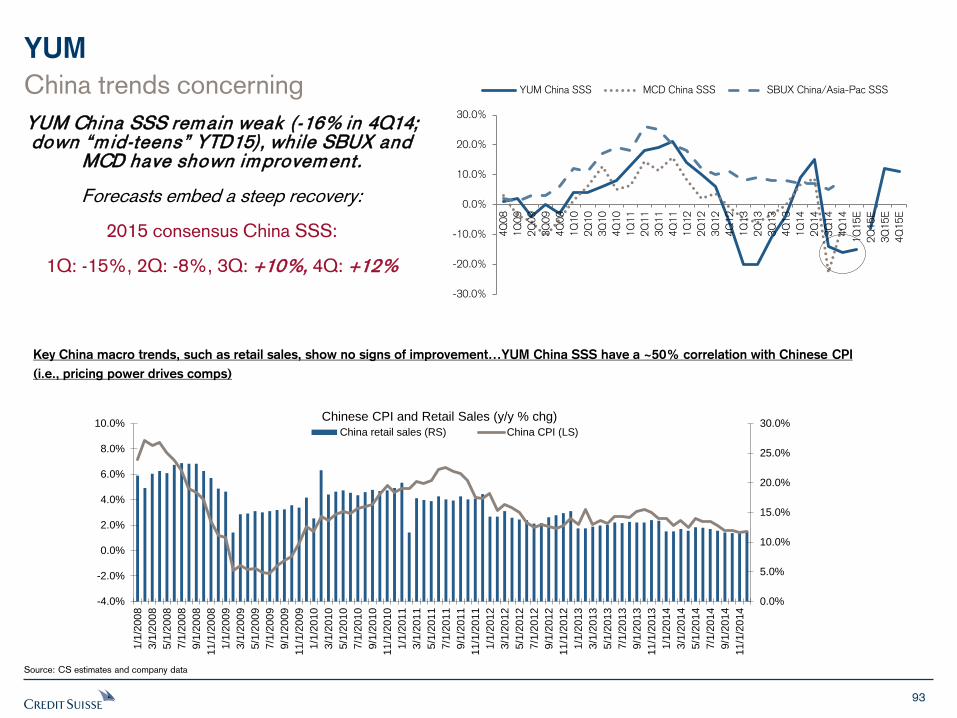

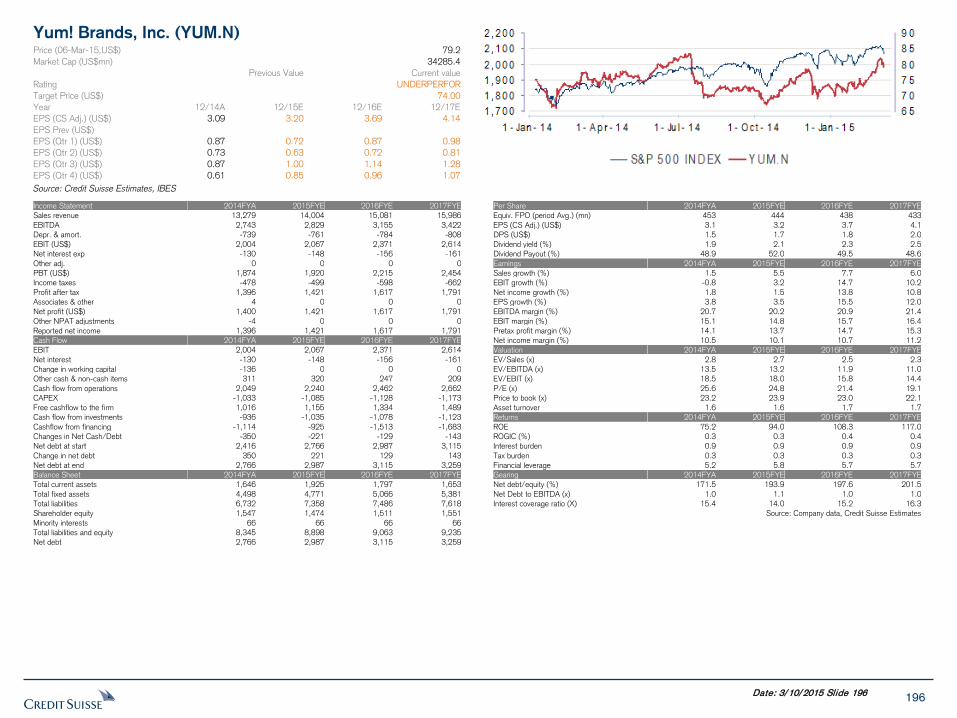

We bel ieve the pace of recovery in YUM’s China business wil l be slower than expected due to weak macro trends and continued aggressive supply additions in

that market.

The stock is l ikely to remain range-bound in the near term as continued dismal fundamental trends are partly offset by the stabil ity of MCD’s franchise model,

a high dividend yield, and optimism around a to-be-announced strategic plan.

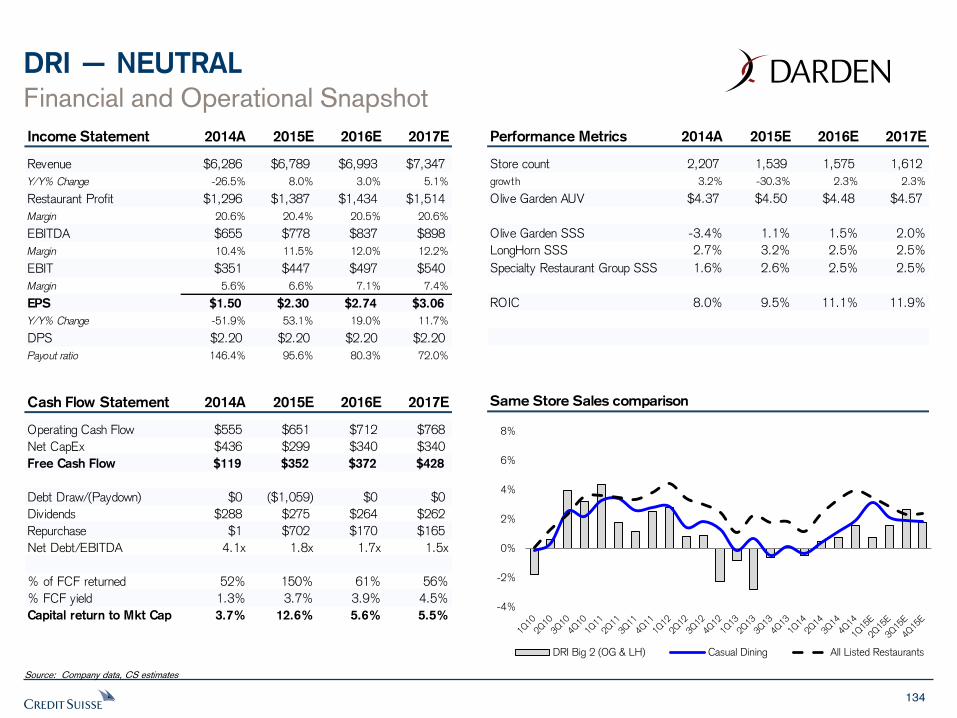

DRI, under the leadership of a new Board, offers some intriguing financial engineering and cost-savings opportunities. However, with valuation at over 11x

EV/EBITDA, potential arbitrage around these strategies seems priced in.

While DRFG is one of the cheapest stocks in the group (esp. relative to unit growth rates), if the Gril le doesn’t work, then DFRG’s stock price stil l has room

to fal l , in our view.

BWLD continues to be one of the best growth stories in casual dining. However, with valuation near al l-time highs and the company facing some unique

earnings headwinds this year, we bel ieve the stock is poised to underperform.

"Midas touch" premium appears already baked into the share price. We prefer to wait for more clarity on the Tim Hortons rol lout strategy, particularly given

the l imited international awareness for this brand.

DNKN's multiple has re-rated lower due to SSS concerns. We see better days ahead on improving macro for low-income consumers, higher pricing, and

mobile pay & loyalty benefits. Our checks indicate that franchisees remain enthusiastic about westward expansion, the key to the growth story.

BLMN enters 2015 with strong momentum, but an elevated valuation and mixed portfol io performance leave us on the sidel ines.

ZOES is a qual ity up-and-coming fast-casual restaurant brand but much is being paid by the market before being proven. We wait opportunistical ly for a better

entry point.

Investment ThesisRating

Target

price

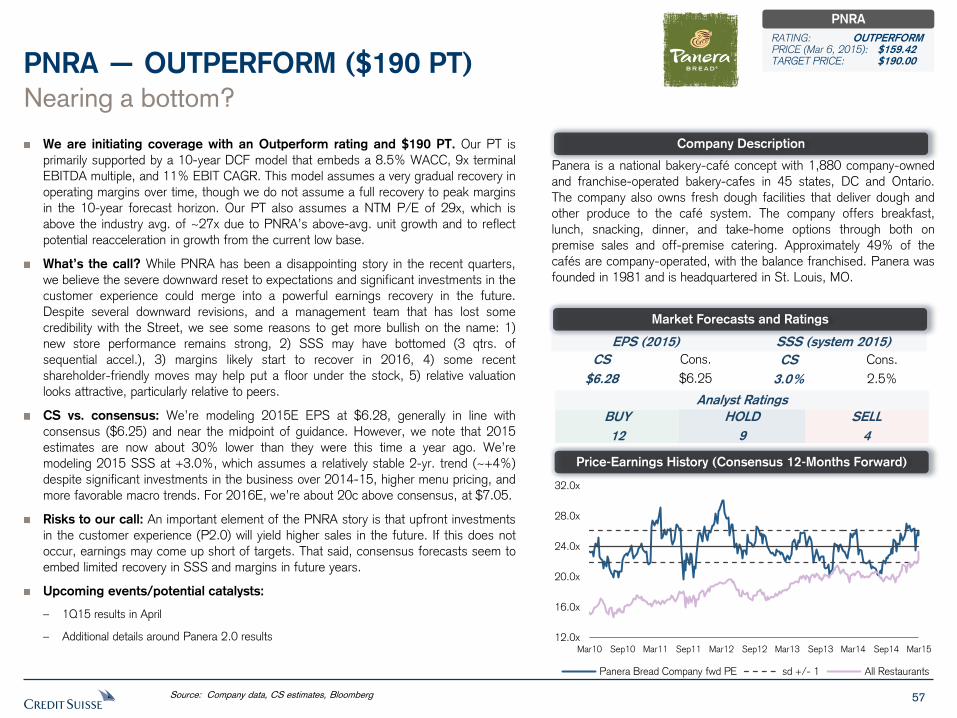

While PNRA has been a disappointing story in the recent quarters, we bel ieve the severe downward reset to expectations and significant investments in the

customer experience could merge into a powerful earnings recovery in the future.

CMG offers the best combination of growth and returns in the group. Given a recent pul lback, the stock is trading near an al l-time low relative to the industry.

We see the negative scenario of flattening SSS as unl ikely given embedded pricing, catering/mobile, growing brand awareness, and macro tailwind.

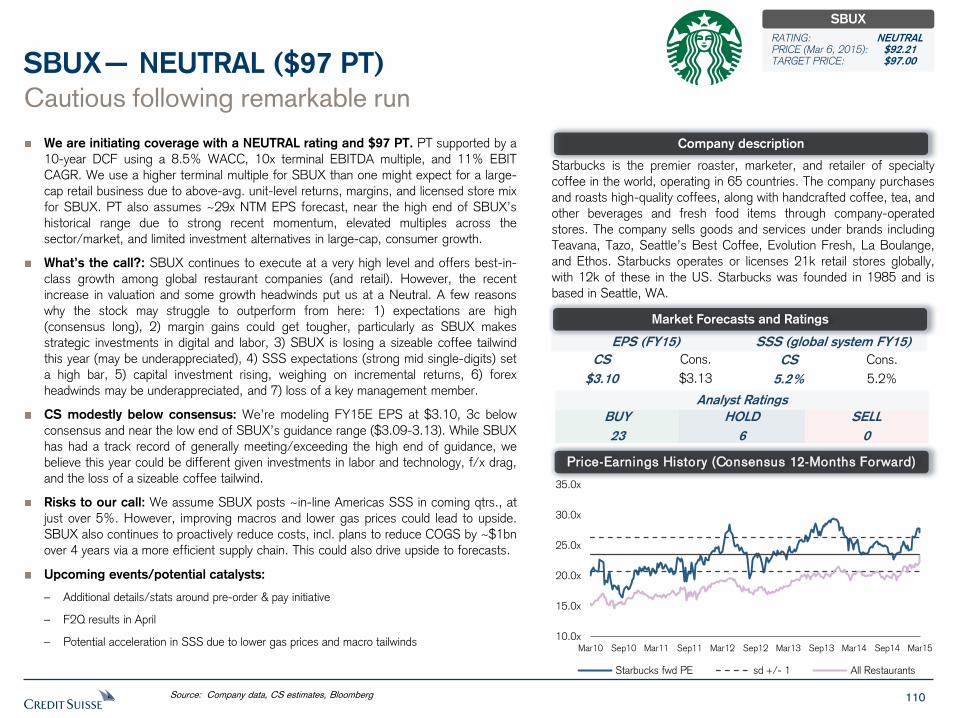

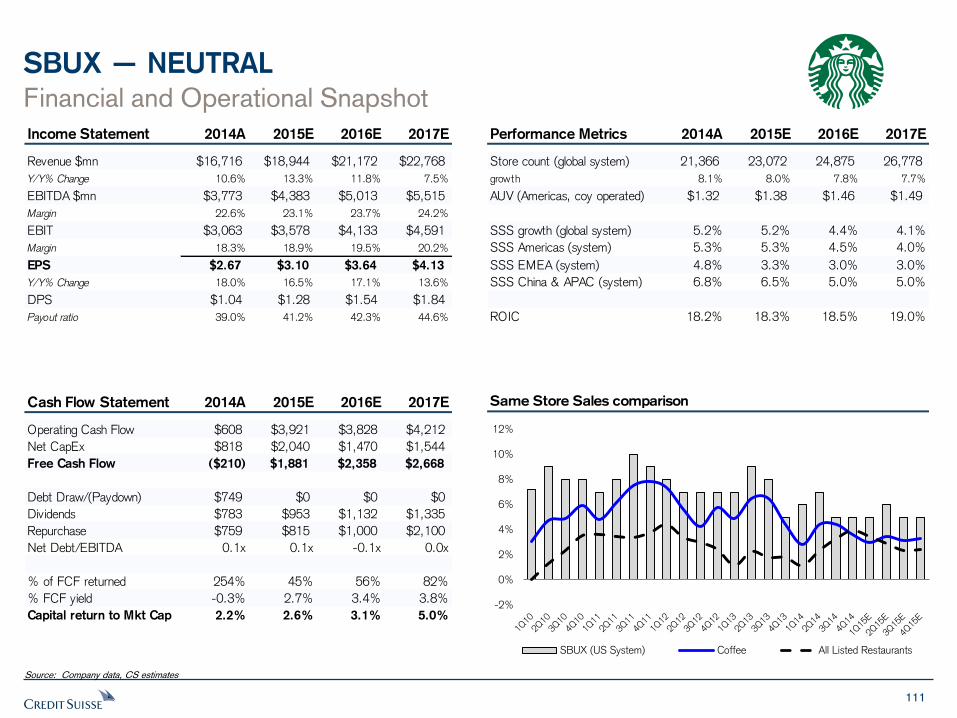

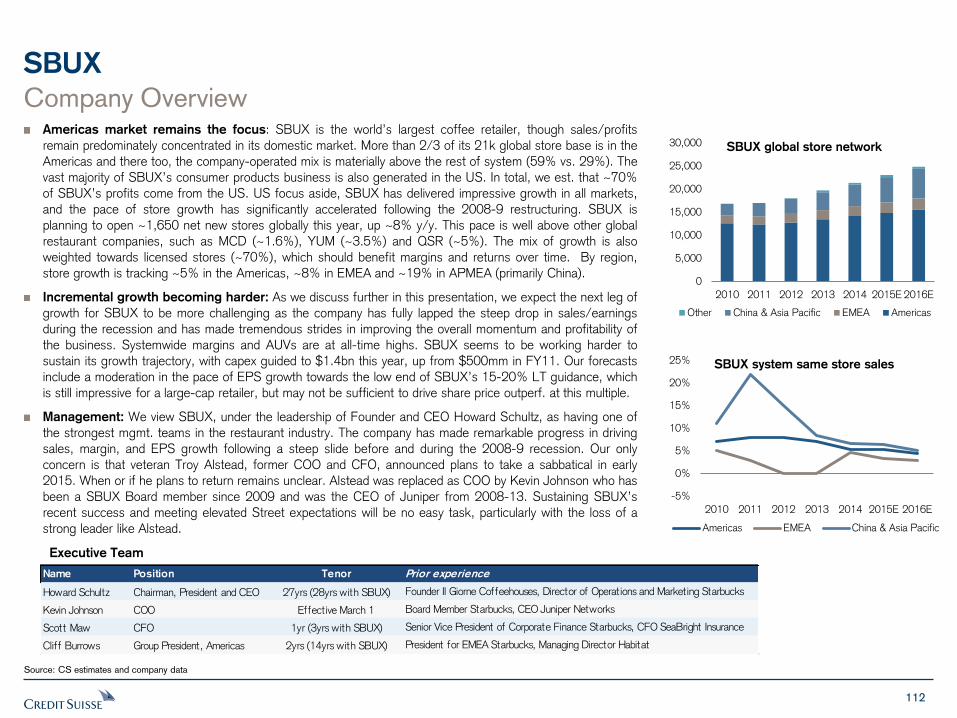

SBUX continues to execute at a very high level and offers best-in-class growth among global restaurant companies. However, the recent increase in

valuation and some growth headwinds put us at a Neutral. Rising investment spending could derail expectations of continued margin and EPS upside.

7

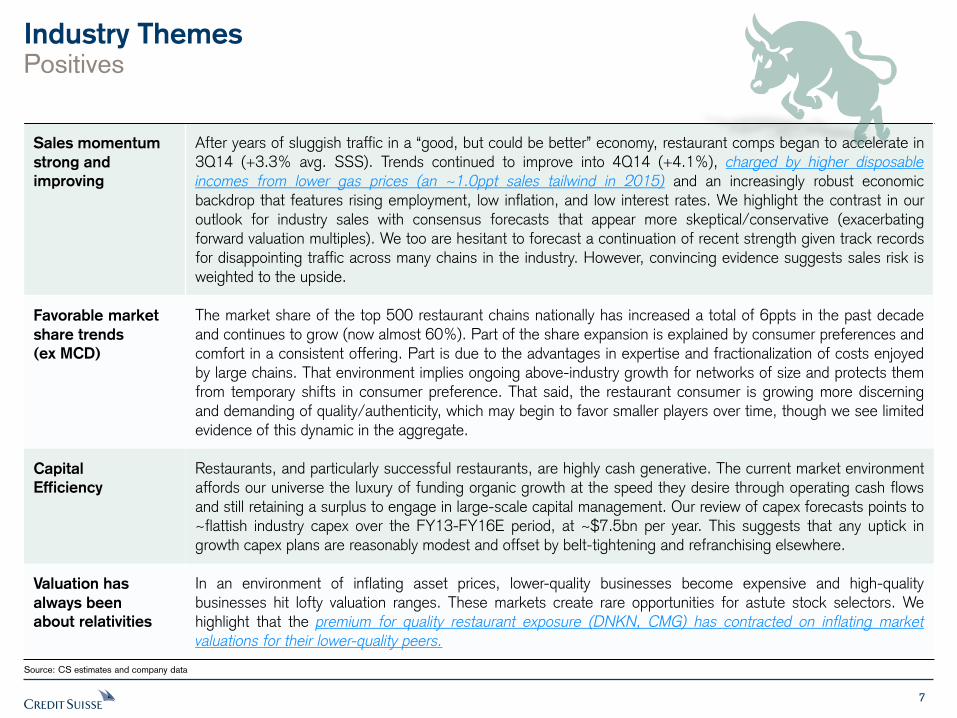

Industry Themes Positives

Source: CS estimates and company data

Sales momentum

strong and

improving

After years of sluggish traffic in a “good, but could be better” economy, restaurant comps began to accelerate in 3Q14 (+3.3% avg. SSS). Trends continued to improve into 4Q14 (+4.1%), charged by higher disposable

incomes from lower gas prices (an ~1.0ppt sales tailwind in 2015) and an increasingly robust economic backdrop that features rising employment, low inflation, and low interest rates. We highlight the contrast in our outlook for industry sales with consensus forecasts that appear more skeptical/conservative (exacerbating forward valuation multiples). We too are hesitant to forecast a continuation of recent strength given track records for disappointing traffic across many chains in the industry. However, convincing evidence suggests sales risk is

weighted to the upside.

Favorable market

share trends

(ex MCD)

The market share of the top 500 restaurant chains nationally has increased a total of 6ppts in the past decade and continues to grow (now almost 60%). Part of the share expansion is explained by consumer preferences and

comfort in a consistent offering. Part is due to the advantages in expertise and fractionalization of costs enjoyed by large chains. That environment implies ongoing above-industry growth for networks of size and protects them from temporary shifts in consumer preference. That said, the restaurant consumer is growing more discerning

and demanding of quality/authenticity, which may begin to favor smaller players over time, though we see limited

evidence of this dynamic in the aggregate.

Capital

Efficiency

Restaurants, and particularly successful restaurants, are highly cash generative. The current market environment

affords our universe the luxury of funding organic growth at the speed they desire through operating cash flows and still retaining a surplus to engage in large-scale capital management. Our review of capex forecasts points to

~flattish industry capex over the FY13-FY16E period, at ~$7.5bn per year. This suggests that any uptick in growth capex plans are reasonably modest and offset by belt-tightening and refranchising elsewhere.

Valuation has

always been

about relativities

In an environment of inflating asset prices, lower-quality businesses become expensive and high-quality businesses hit lofty valuation ranges. These markets create rare opportunities for astute stock selectors. We highlight that the premium for quality restaurant exposure (DNKN, CMG) has contracted on inflating market valuations for their lower-quality peers.

8

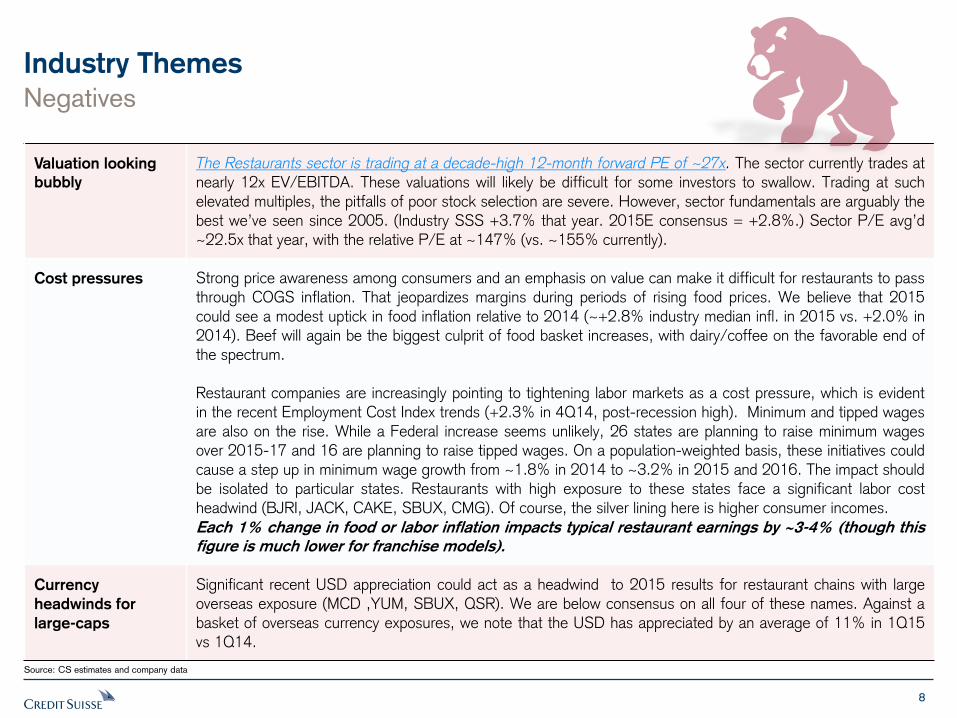

Industry Themes

Negatives

Source: CS estimates and company data

Valuation looking

bubbly

The Restaurants sector is trading at a decade-high 12-month forward PE of ~27x. The sector currently trades at nearly 12x EV/EBITDA. These valuations will likely be difficult for some investors to swallow. Trading at such elevated multiples, the pitfalls of poor stock selection are severe. However, sector fundamentals are arguably the best we’ve seen since 2005. (Industry SSS +3.7% that year. 2015E consensus = +2.8%.) Sector P/E avg’d ~22.5x that year, with the relative P/E at ~147% (vs. ~155% currently).

Cost pressures Strong price awareness among consumers and an emphasis on value can make it difficult for restaurants to pass through COGS inflation. That jeopardizes margins during periods of rising food prices. We believe that 2015

could see a modest uptick in food inflation relative to 2014 (~+2.8% industry median infl. in 2015 vs. +2.0% in 2014). Beef will again be the biggest culprit of food basket increases, with dairy/coffee on the favorable end of

the spectrum. Restaurant companies are increasingly pointing to tightening labor markets as a cost pressure, which is evident in the recent Employment Cost Index trends (+2.3% in 4Q14, post-recession high). Minimum and tipped wages are also on the rise. While a Federal increase seems unlikely, 26 states are planning to raise minimum wages

over 2015-17 and 16 are planning to raise tipped wages. On a population-weighted basis, these initiatives could

cause a step up in minimum wage growth from ~1.8% in 2014 to ~3.2% in 2015 and 2016. The impact should

be isolated to particular states. Restaurants with high exposure to these states face a significant labor cost headwind (BJRI, JACK, CAKE, SBUX, CMG). Of course, the silver lining here is higher consumer incomes.

Each 1% change in food or labor inflation impacts typical restaurant earnings by ~3-4% (though this

figure is much lower for franchise models).

Currency

headwinds for

large-caps

Significant recent USD appreciation could act as a headwind to 2015 results for restaurant chains with large overseas exposure (MCD ,YUM, SBUX, QSR). We are below consensus on all four of these names. Against a

basket of overseas currency exposures, we note that the USD has appreciated by an average of 11% in 1Q15 vs 1Q14.

9

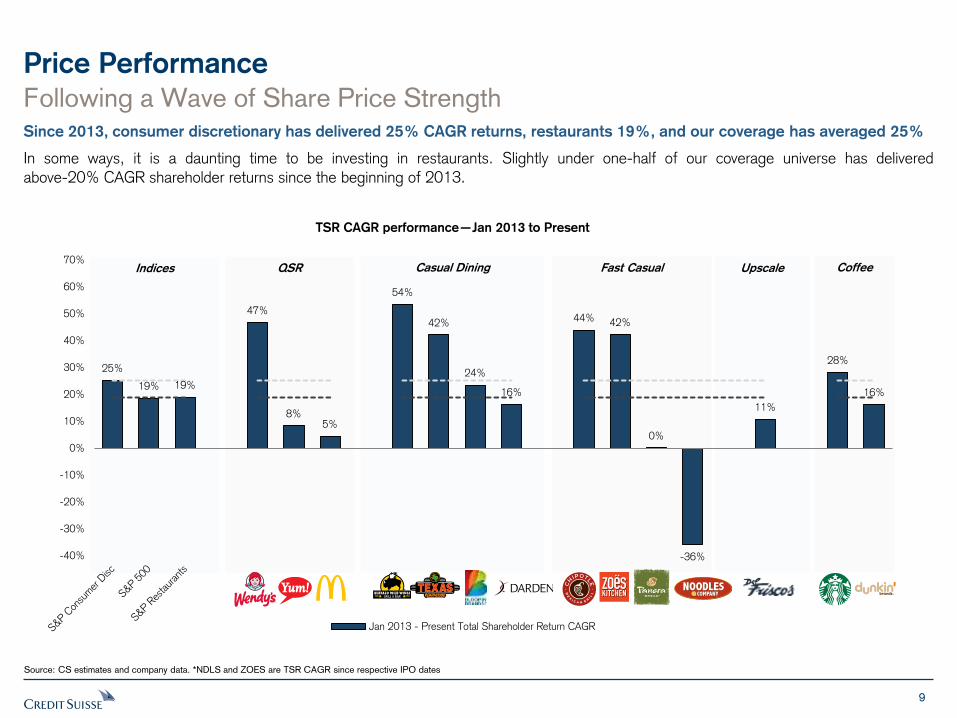

Price Performance

Following a Wave of Share Price Strength Since 2013, consumer discretionary has delivered 25% CAGR returns, restaurants 19%, and our coverage has averaged 25%

In some ways, it is a daunting time to be investing in restaurants. Slightly under one-half of our coverage universe has delivered

above-20% CAGR shareholder returns since the beginning of 2013.

Source: CS estimates and company data. *NDLS and ZOES are TSR CAGR since respective IPO dates

TSR CAGR performance—Jan 2013 to Present

25%

19% 19%

47%

8% 5%

54%

42%

24%

16%

44% 42%

0%

-36%

11%

28%

16%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Jan 2013 - Present Total Shareholder Return CAGR

Indices QSR Casual Dining Fast Casual Upscale Coffee

10

4

6

8

10

12

14

2005 2007 2009 2011 2013 2015

Restaurants NTM EV/EBITDA 10 yr Avg sd +/-1

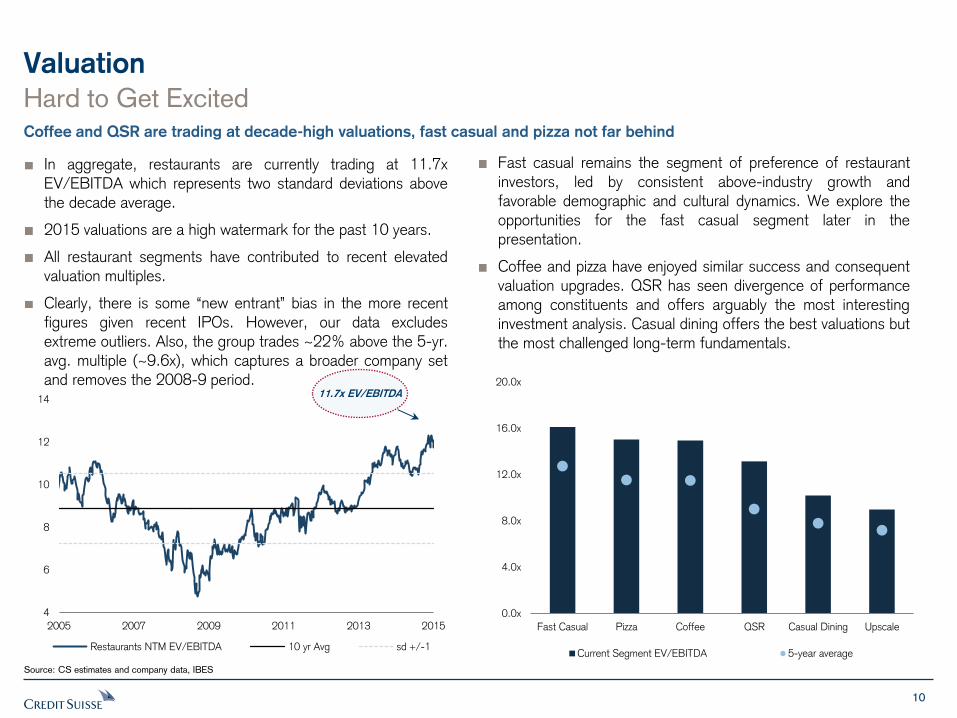

Valuation

Hard to Get Excited Coffee and QSR are trading at decade-high valuations, fast casual and pizza not far behind

Fast casual remains the segment of preference of restaurant investors, led by consistent above-industry growth and

favorable demographic and cultural dynamics. We explore the opportunities for the fast casual segment later in the presentation.

Coffee and pizza have enjoyed similar success and consequent valuation upgrades. QSR has seen divergence of performance

among constituents and offers arguably the most interesting investment analysis. Casual dining offers the best valuations but the most challenged long-term fundamentals.

In aggregate, restaurants are currently trading at 11.7x EV/EBITDA which represents two standard deviations above the decade average.

2015 valuations are a high watermark for the past 10 years.

All restaurant segments have contributed to recent elevated valuation multiples.

Clearly, there is some “new entrant” bias in the more recent figures given recent IPOs. However, our data excludes

extreme outliers. Also, the group trades ~22% above the 5-yr. avg. multiple (~9.6x), which captures a broader company set and removes the 2008-9 period.

Source: CS estimates and company data, IBES

11.7x EV/EBITDA

0.0x

4.0x

8.0x

12.0x

16.0x

20.0x

Fast Casual Pizza Coffee QSR Casual Dining Upscale

Current Segment EV/EBITDA 5-year average

11

6.0x

10.0x

14.0x

18.0x

22.0x

26.0x

30.0x

1999 2001 2003 2005 2007 2009 2011 2013 2015

Restaurants NTM PE 10 yr Avg sd +/-1

Valuation

Hard to Get Excited On P/E the sector trades two standard deviations from its historic norm

A strong start to 2015 leaves the restaurants sector at 27.0x EPS, a high watermark multiple for the past 15 years.

Looking at the past 5 yrs., which captures a more robust data

set of companies and excludes the 2008-9 swoon, the group is trading at an ~30% premium (~27x vs. ~20.5x).

Relative P/Es are less inflated vs. recent history, with the group at 155% of market multiple vs. ~152% 5-yr. avg. (15-yr. avg.

= ~125%).

Below we show restaurant sector multiples relative to non-restaurant consumer peers.

Here again, restaurants appear expensive, although not by

quite as much. The sector currently trades at a 35% premium to consumer peers, slightly more than one standard deviation above its historical average 12% premium.

Restaurants carry some advantages over other consumer

segments, including higher unit growth opportunities

(particularly in fast casual), lower inventory/seasonality

risk, lower Internet exposure, lower mall exposure, and

better international reach.

Source: CS estimates and company data, IBES

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

Feb-05 Feb-07 Feb-09 Feb-11 Feb-13 Feb-15

Restaurant PE relative to other Consumer Average sd +/-1

27.0x NTM EPS

35% premium to Consumer

12

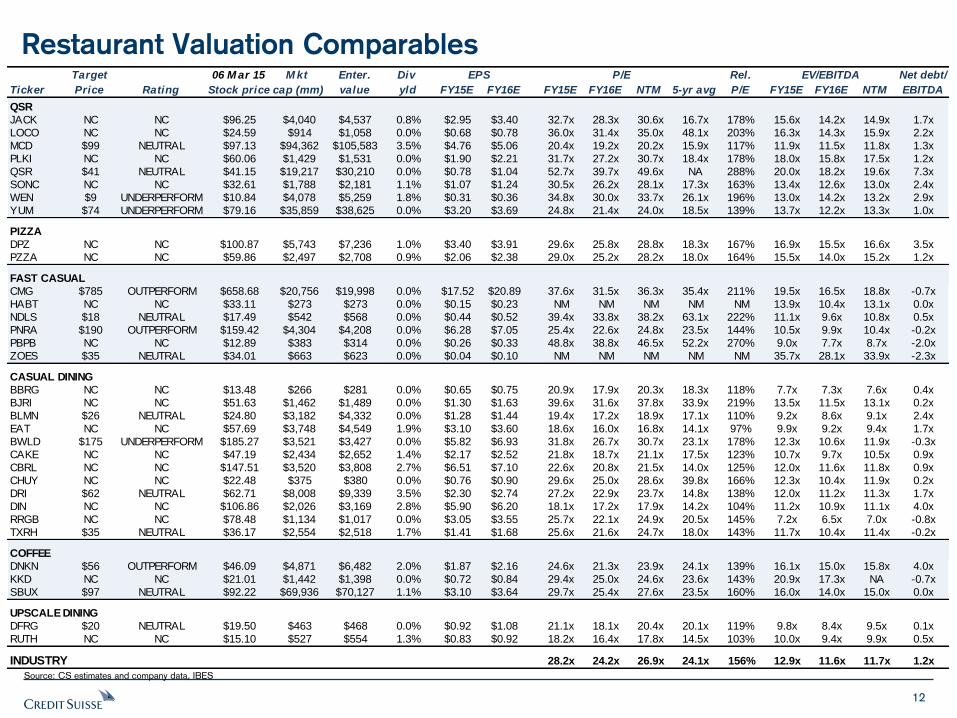

Restaurant Valuation Comparables

Source: CS estimates and company data, IBES

Target 06 M ar 15 M kt Enter. Div Rel. Net debt/

Ticker Price Rating Stock price cap (mm) value yld FY15E FY16E FY15E FY16E NTM 5-yr avg P/E FY15E FY16E NTM EBITDA

QSR

JACK NC NC $96.25 $4,040 $4,537 0.8% $2.95 $3.40 32.7x 28.3x 30.6x 16.7x 178% 15.6x 14.2x 14.9x 1.7x

LOCO NC NC $24.59 $914 $1,058 0.0% $0.68 $0.78 36.0x 31.4x 35.0x 48.1x 203% 16.3x 14.3x 15.9x 2.2x

MCD $99 NEUTRAL $97.13 $94,362 $105,583 3.5% $4.76 $5.06 20.4x 19.2x 20.2x 15.9x 117% 11.9x 11.5x 11.8x 1.3x

PLKI NC NC $60.06 $1,429 $1,531 0.0% $1.90 $2.21 31.7x 27.2x 30.7x 18.4x 178% 18.0x 15.8x 17.5x 1.2x

QSR $41 NEUTRAL $41.15 $19,217 $30,210 0.0% $0.78 $1.04 52.7x 39.7x 49.6x NA 288% 20.0x 18.2x 19.6x 7.3x

SONC NC NC $32.61 $1,788 $2,181 1.1% $1.07 $1.24 30.5x 26.2x 28.1x 17.3x 163% 13.4x 12.6x 13.0x 2.4x

WEN $9 UNDERPERFORM $10.84 $4,078 $5,259 1.8% $0.31 $0.36 34.8x 30.0x 33.7x 26.1x 196% 13.0x 14.2x 13.2x 2.9x

YUM $74 UNDERPERFORM $79.16 $35,859 $38,625 0.0% $3.20 $3.69 24.8x 21.4x 24.0x 18.5x 139% 13.7x 12.2x 13.3x 1.0x

PIZZA

DPZ NC NC $100.87 $5,743 $7,236 1.0% $3.40 $3.91 29.6x 25.8x 28.8x 18.3x 167% 16.9x 15.5x 16.6x 3.5x

PZZA NC NC $59.86 $2,497 $2,708 0.9% $2.06 $2.38 29.0x 25.2x 28.2x 18.0x 164% 15.5x 14.0x 15.2x 1.2x

FAST CASUAL

CMG $785 OUTPERFORM $658.68 $20,756 $19,998 0.0% $17.52 $20.89 37.6x 31.5x 36.3x 35.4x 211% 19.5x 16.5x 18.8x -0.7x

HABT NC NC $33.11 $273 $273 0.0% $0.15 $0.23 NM NM NM NM NM 13.9x 10.4x 13.1x 0.0x

NDLS $18 NEUTRAL $17.49 $542 $568 0.0% $0.44 $0.52 39.4x 33.8x 38.2x 63.1x 222% 11.1x 9.6x 10.8x 0.5x

PNRA $190 OUTPERFORM $159.42 $4,304 $4,208 0.0% $6.28 $7.05 25.4x 22.6x 24.8x 23.5x 144% 10.5x 9.9x 10.4x -0.2x

PBPB NC NC $12.89 $383 $314 0.0% $0.26 $0.33 48.8x 38.8x 46.5x 52.2x 270% 9.0x 7.7x 8.7x -2.0x

ZOES $35 NEUTRAL $34.01 $663 $623 0.0% $0.04 $0.10 NM NM NM NM NM 35.7x 28.1x 33.9x -2.3x

CASUAL DINING

BBRG NC NC $13.48 $266 $281 0.0% $0.65 $0.75 20.9x 17.9x 20.3x 18.3x 118% 7.7x 7.3x 7.6x 0.4x

BJRI NC NC $51.63 $1,462 $1,489 0.0% $1.30 $1.63 39.6x 31.6x 37.8x 33.9x 219% 13.5x 11.5x 13.1x 0.2x

BLMN $26 NEUTRAL $24.80 $3,182 $4,332 0.0% $1.28 $1.44 19.4x 17.2x 18.9x 17.1x 110% 9.2x 8.6x 9.1x 2.4x

EAT NC NC $57.69 $3,748 $4,549 1.9% $3.10 $3.60 18.6x 16.0x 16.8x 14.1x 97% 9.9x 9.2x 9.4x 1.7x

BWLD $175 UNDERPERFORM $185.27 $3,521 $3,427 0.0% $5.82 $6.93 31.8x 26.7x 30.7x 23.1x 178% 12.3x 10.6x 11.9x -0.3x

CAKE NC NC $47.19 $2,434 $2,652 1.4% $2.17 $2.52 21.8x 18.7x 21.1x 17.5x 123% 10.7x 9.7x 10.5x 0.9x

CBRL NC NC $147.51 $3,520 $3,808 2.7% $6.51 $7.10 22.6x 20.8x 21.5x 14.0x 125% 12.0x 11.6x 11.8x 0.9x

CHUY NC NC $22.48 $375 $380 0.0% $0.76 $0.90 29.6x 25.0x 28.6x 39.8x 166% 12.3x 10.4x 11.9x 0.2x

DRI $62 NEUTRAL $62.71 $8,008 $9,339 3.5% $2.30 $2.74 27.2x 22.9x 23.7x 14.8x 138% 12.0x 11.2x 11.3x 1.7x

DIN NC NC $106.86 $2,026 $3,169 2.8% $5.90 $6.20 18.1x 17.2x 17.9x 14.2x 104% 11.2x 10.9x 11.1x 4.0x

RRGB NC NC $78.48 $1,134 $1,017 0.0% $3.05 $3.55 25.7x 22.1x 24.9x 20.5x 145% 7.2x 6.5x 7.0x -0.8x

TXRH $35 NEUTRAL $36.17 $2,554 $2,518 1.7% $1.41 $1.68 25.6x 21.6x 24.7x 18.0x 143% 11.7x 10.4x 11.4x -0.2x

COFFEE

DNKN $56 OUTPERFORM $46.09 $4,871 $6,482 2.0% $1.87 $2.16 24.6x 21.3x 23.9x 24.1x 139% 16.1x 15.0x 15.8x 4.0x

KKD NC NC $21.01 $1,442 $1,398 0.0% $0.72 $0.84 29.4x 25.0x 24.6x 23.6x 143% 20.9x 17.3x NA -0.7x

SBUX $97 NEUTRAL $92.22 $69,936 $70,127 1.1% $3.10 $3.64 29.7x 25.4x 27.6x 23.5x 160% 16.0x 14.0x 15.0x 0.0x

UPSCALE DINING

DFRG $20 NEUTRAL $19.50 $463 $468 0.0% $0.92 $1.08 21.1x 18.1x 20.4x 20.1x 119% 9.8x 8.4x 9.5x 0.1x

RUTH NC NC $15.10 $527 $554 1.3% $0.83 $0.92 18.2x 16.4x 17.8x 14.5x 103% 10.0x 9.4x 9.9x 0.5x

INDUSTRY 28.2x 24.2x 26.9x 24.1x 156% 12.9x 11.6x 11.7x 1.2x

P/E EV/EBITDAEPS

13

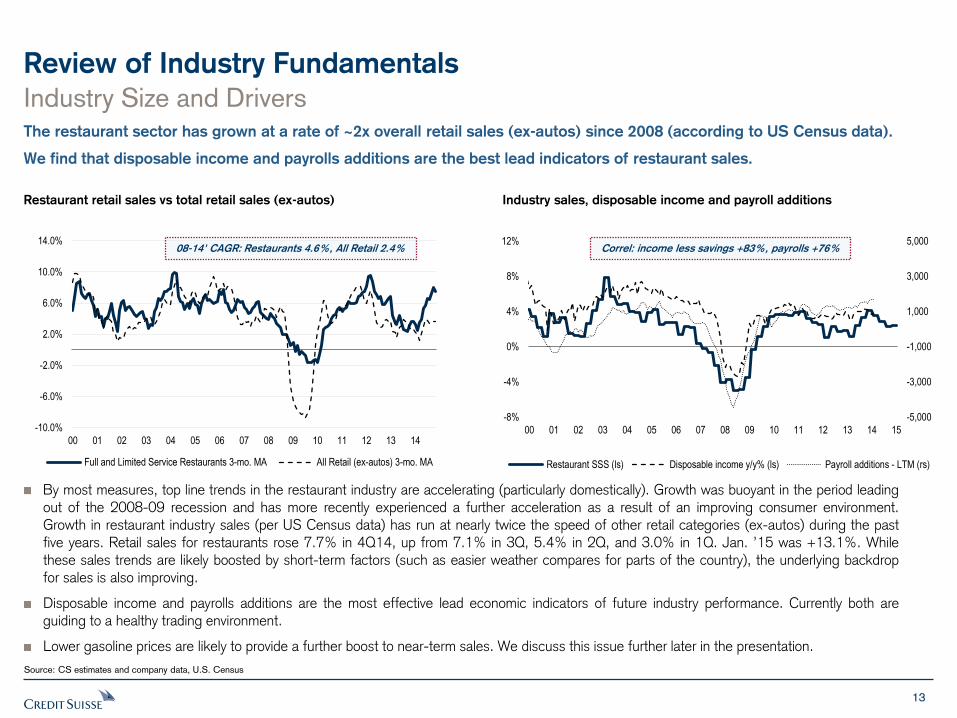

Review of Industry Fundamentals

By most measures, top line trends in the restaurant industry are accelerating (particularly domestically). Growth was buoyant in the period leading out of the 2008-09 recession and has more recently experienced a further acceleration as a result of an improving consumer environment. Growth in restaurant industry sales (per US Census data) has run at nearly twice the speed of other retail categories (ex-autos) during the past five years. Retail sales for restaurants rose 7.7% in 4Q14, up from 7.1% in 3Q, 5.4% in 2Q, and 3.0% in 1Q. Jan. ’15 was +13.1%. While these sales trends are likely boosted by short-term factors (such as easier weather compares for parts of the country), the underlying backdrop for sales is also improving.

Disposable income and payrolls additions are the most effective lead economic indicators of future industry performance. Currently both are guiding to a healthy trading environment.

Lower gasoline prices are likely to provide a further boost to near-term sales. We discuss this issue further later in the presentation.

Industry Size and Drivers The restaurant sector has grown at a rate of ~2x overall retail sales (ex-autos) since 2008 (according to US Census data).

We find that disposable income and payrolls additions are the best lead indicators of restaurant sales.

Restaurant retail sales vs total retail sales (ex-autos) Industry sales, disposable income and payroll additions

Source: CS estimates and company data, U.S. Census

Correl: income less savings +83%, payrolls +76%

-5,000

-3,000

-1,000

1,000

3,000

5,000

-8%

-4%

0%

4%

8%

12%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Restaurant SSS (ls) Disposable income y/y% (ls) Payroll additions - LTM (rs)

-10.0%

-6.0%

-2.0%

2.0%

6.0%

10.0%

14.0%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Full and Limited Service Restaurants 3-mo. MA All Retail (ex-autos) 3-mo. MA

08-14' CAGR: Restaurants 4.6%, All Retail 2.4%

14

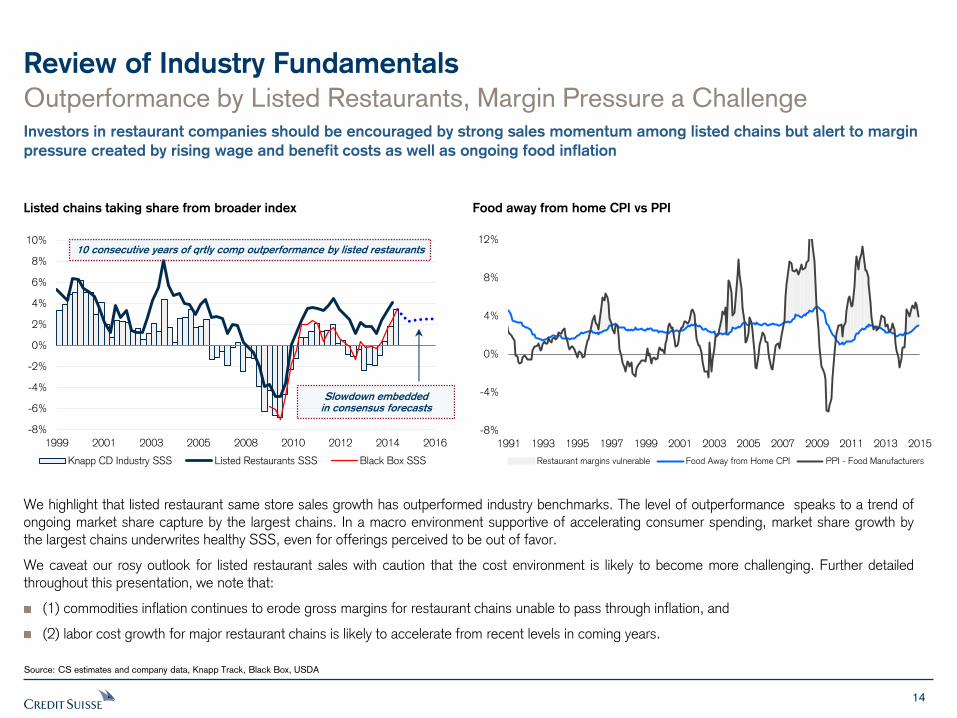

Review of Industry Fundamentals

We highlight that listed restaurant same store sales growth has outperformed industry benchmarks. The level of outperformance speaks to a trend of ongoing market share capture by the largest chains. In a macro environment supportive of accelerating consumer spending, market share growth by the largest chains underwrites healthy SSS, even for offerings perceived to be out of favor.

We caveat our rosy outlook for listed restaurant sales with caution that the cost environment is likely to become more challenging. Further detailed throughout this presentation, we note that:

(1) commodities inflation continues to erode gross margins for restaurant chains unable to pass through inflation, and

(2) labor cost growth for major restaurant chains is likely to accelerate from recent levels in coming years.

Outperformance by Listed Restaurants, Margin Pressure a Challenge Investors in restaurant companies should be encouraged by strong sales momentum among listed chains but alert to margin

pressure created by rising wage and benefit costs as well as ongoing food inflation

Listed chains taking share from broader index Food away from home CPI vs PPI

Source: CS estimates and company data, Knapp Track, Black Box, USDA

-8%

-4%

0%

4%

8%

12%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Restaurant margins vulnerable Food Away from Home CPI PPI - Food Manufacturers

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1999 2001 2003 2005 2008 2010 2012 2014 2016

Knapp CD Industry SSS Listed Restaurants SSS Black Box SSS

Slowdown embedded in consensus forecasts

10 consecutive years of qrtly comp outperformance by listed restaurants

15

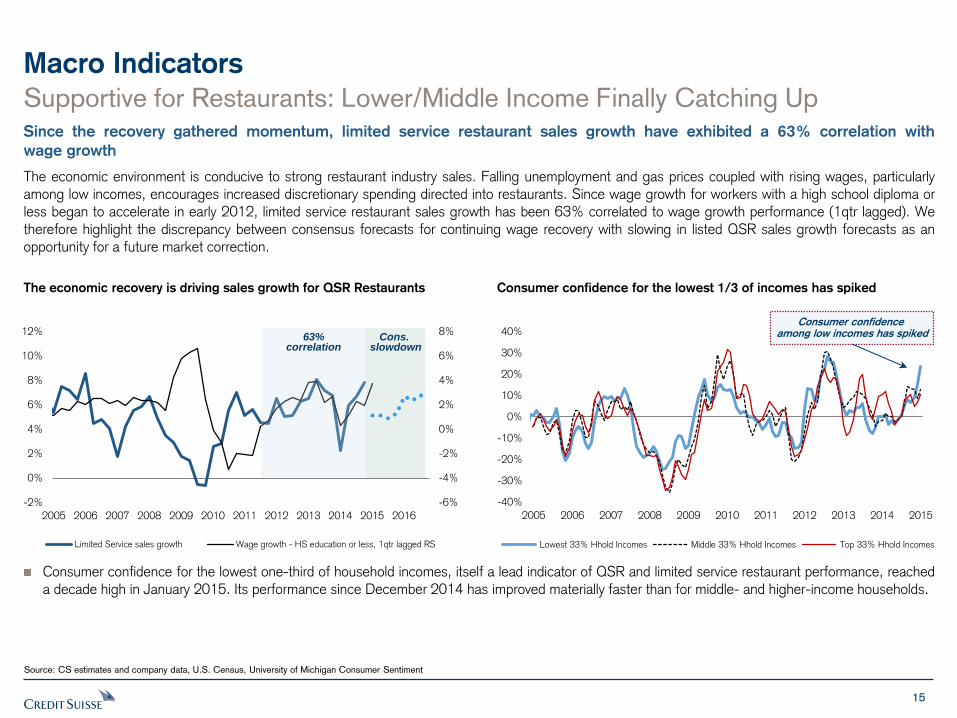

Macro Indicators

Supportive for Restaurants: Lower/Middle Income Finally Catching Up Since the recovery gathered momentum, limited service restaurant sales growth have exhibited a 63% correlation with

wage growth

The economic environment is conducive to strong restaurant industry sales. Falling unemployment and gas prices coupled with rising wages, particularly among low incomes, encourages increased discretionary spending directed into restaurants. Since wage growth for workers with a high school diploma or less began to accelerate in early 2012, limited service restaurant sales growth has been 63% correlated to wage growth performance (1qtr lagged). We therefore highlight the discrepancy between consensus forecasts for continuing wage recovery with slowing in listed QSR sales growth forecasts as an opportunity for a future market correction.

The economic recovery is driving sales growth for QSR Restaurants Consumer confidence for the lowest 1/3 of incomes has spiked

Consumer confidence for the lowest one-third of household incomes, itself a lead indicator of QSR and limited service restaurant performance, reached a decade high in January 2015. Its performance since December 2014 has improved materially faster than for middle- and higher-income households.

Source: CS estimates and company data, U.S. Census, University of Michigan Consumer Sentiment

-6%

-4%

-2%

0%

2%

4%

6%

8%

-2%

0%

2%

4%

6%

8%

10%

12%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Limited Service sales growth Wage growth - HS education or less, 1qtr lagged RS

63% correlation

Cons. slowdown

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Lowest 33% Hhold Incomes Middle 33% Hhold Incomes Top 33% Hhold Incomes

Consumer confidence among low incomes has spiked

16

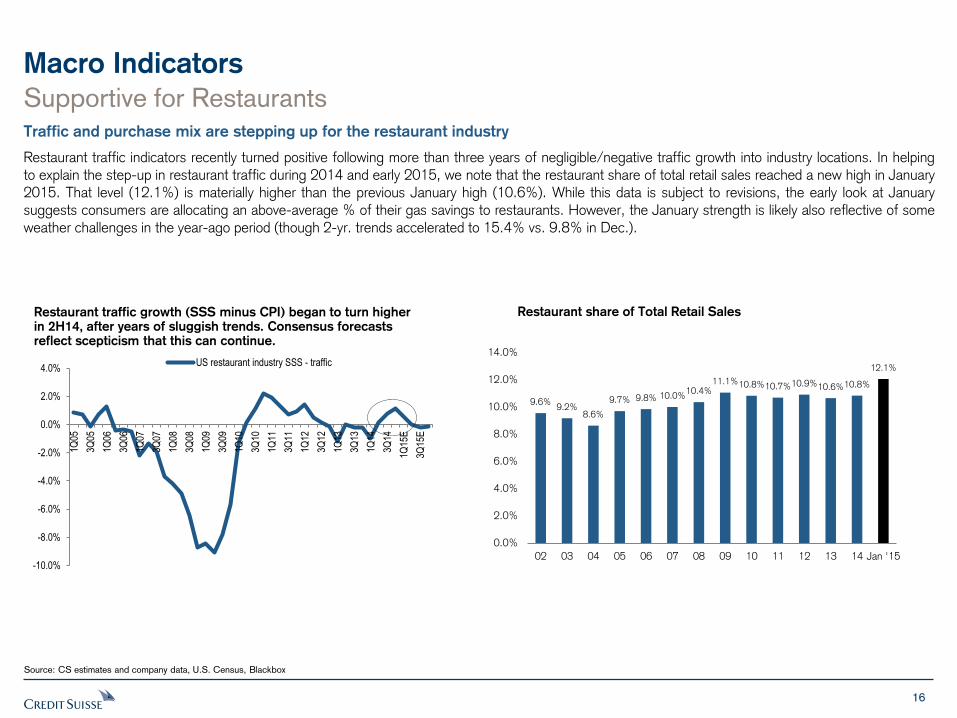

Macro Indicators

Supportive for Restaurants Traffic and purchase mix are stepping up for the restaurant industry

Restaurant traffic indicators recently turned positive following more than three years of negligible/negative traffic growth into industry locations. In helping to explain the step-up in restaurant traffic during 2014 and early 2015, we note that the restaurant share of total retail sales reached a new high in January 2015. That level (12.1%) is materially higher than the previous January high (10.6%). While this data is subject to revisions, the early look at January suggests consumers are allocating an above-average % of their gas savings to restaurants. However, the January strength is likely also reflective of some weather challenges in the year-ago period (though 2-yr. trends accelerated to 15.4% vs. 9.8% in Dec.).

Source: CS estimates and company data, U.S. Census, Blackbox

9.6% 9.2%

8.6%

9.7% 9.8% 10.0% 10.4%

11.1% 10.8% 10.7% 10.9% 10.6% 10.8%

12.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

02 03 04 05 06 07 08 09 10 11 12 13 14 Jan '15

Restaurant traffic growth (SSS minus CPI) began to turn higher in 2H14, after years of sluggish trends. Consensus forecasts reflect scepticism that this can continue.

Restaurant share of Total Retail Sales

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

E

3Q15

E

US restaurant industry SSS - traffic

17

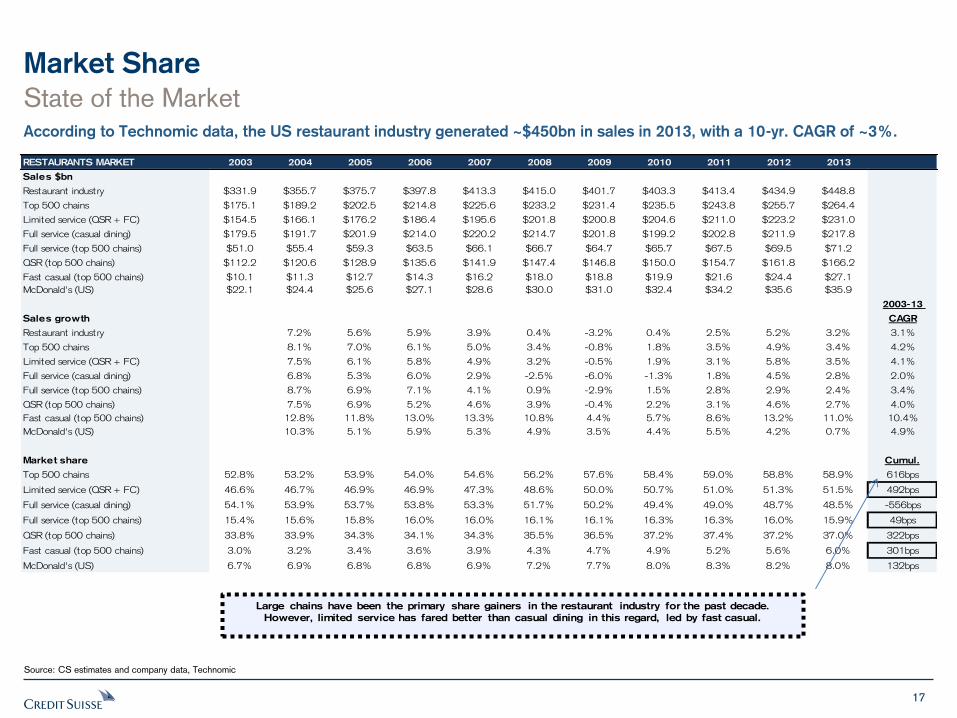

Market Share

State of the Market According to Technomic data, the US restaurant industry generated ~$450bn in sales in 2013, with a 10-yr. CAGR of ~3%.

Source: CS estimates and company data, Technomic

RESTAURANTS MARKET 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sales $bn

Restaurant industry $331.9 $355.7 $375.7 $397.8 $413.3 $415.0 $401.7 $403.3 $413.4 $434.9 $448.8

Top 500 chains $175.1 $189.2 $202.5 $214.8 $225.6 $233.2 $231.4 $235.5 $243.8 $255.7 $264.4

Limited service (QSR + FC) $154.5 $166.1 $176.2 $186.4 $195.6 $201.8 $200.8 $204.6 $211.0 $223.2 $231.0

Full service (casual dining) $179.5 $191.7 $201.9 $214.0 $220.2 $214.7 $201.8 $199.2 $202.8 $211.9 $217.8

Full service (top 500 chains) $51.0 $55.4 $59.3 $63.5 $66.1 $66.7 $64.7 $65.7 $67.5 $69.5 $71.2

QSR (top 500 chains) $112.2 $120.6 $128.9 $135.6 $141.9 $147.4 $146.8 $150.0 $154.7 $161.8 $166.2

Fast casual (top 500 chains) $10.1 $11.3 $12.7 $14.3 $16.2 $18.0 $18.8 $19.9 $21.6 $24.4 $27.1

McDonald's (US) $22.1 $24.4 $25.6 $27.1 $28.6 $30.0 $31.0 $32.4 $34.2 $35.6 $35.9

2003-13

Sales growth CAGR

Restaurant industry 7.2% 5.6% 5.9% 3.9% 0.4% -3.2% 0.4% 2.5% 5.2% 3.2% 3.1%

Top 500 chains 8.1% 7.0% 6.1% 5.0% 3.4% -0.8% 1.8% 3.5% 4.9% 3.4% 4.2%

Limited service (QSR + FC) 7.5% 6.1% 5.8% 4.9% 3.2% -0.5% 1.9% 3.1% 5.8% 3.5% 4.1%

Full service (casual dining) 6.8% 5.3% 6.0% 2.9% -2.5% -6.0% -1.3% 1.8% 4.5% 2.8% 2.0%

Full service (top 500 chains) 8.7% 6.9% 7.1% 4.1% 0.9% -2.9% 1.5% 2.8% 2.9% 2.4% 3.4%

QSR (top 500 chains) 7.5% 6.9% 5.2% 4.6% 3.9% -0.4% 2.2% 3.1% 4.6% 2.7% 4.0%

Fast casual (top 500 chains) 12.8% 11.8% 13.0% 13.3% 10.8% 4.4% 5.7% 8.6% 13.2% 11.0% 10.4%

McDonald's (US) 10.3% 5.1% 5.9% 5.3% 4.9% 3.5% 4.4% 5.5% 4.2% 0.7% 4.9%

Market share Cumul.

Top 500 chains 52.8% 53.2% 53.9% 54.0% 54.6% 56.2% 57.6% 58.4% 59.0% 58.8% 58.9% 616bps

Limited service (QSR + FC) 46.6% 46.7% 46.9% 46.9% 47.3% 48.6% 50.0% 50.7% 51.0% 51.3% 51.5% 492bps

Full service (casual dining) 54.1% 53.9% 53.7% 53.8% 53.3% 51.7% 50.2% 49.4% 49.0% 48.7% 48.5% -556bps

Full service (top 500 chains) 15.4% 15.6% 15.8% 16.0% 16.0% 16.1% 16.1% 16.3% 16.3% 16.0% 15.9% 49bps

QSR (top 500 chains) 33.8% 33.9% 34.3% 34.1% 34.3% 35.5% 36.5% 37.2% 37.4% 37.2% 37.0% 322bps

Fast casual (top 500 chains) 3.0% 3.2% 3.4% 3.6% 3.9% 4.3% 4.7% 4.9% 5.2% 5.6% 6.0% 301bps

McDonald's (US) 6.7% 6.9% 6.8% 6.8% 6.9% 7.2% 7.7% 8.0% 8.3% 8.2% 8.0% 132bps

Large chains have been the primary share gainers in the restaurant industry for the past decade.

However, limited service has fared better than casual dining in this regard, led by fast casual.

18

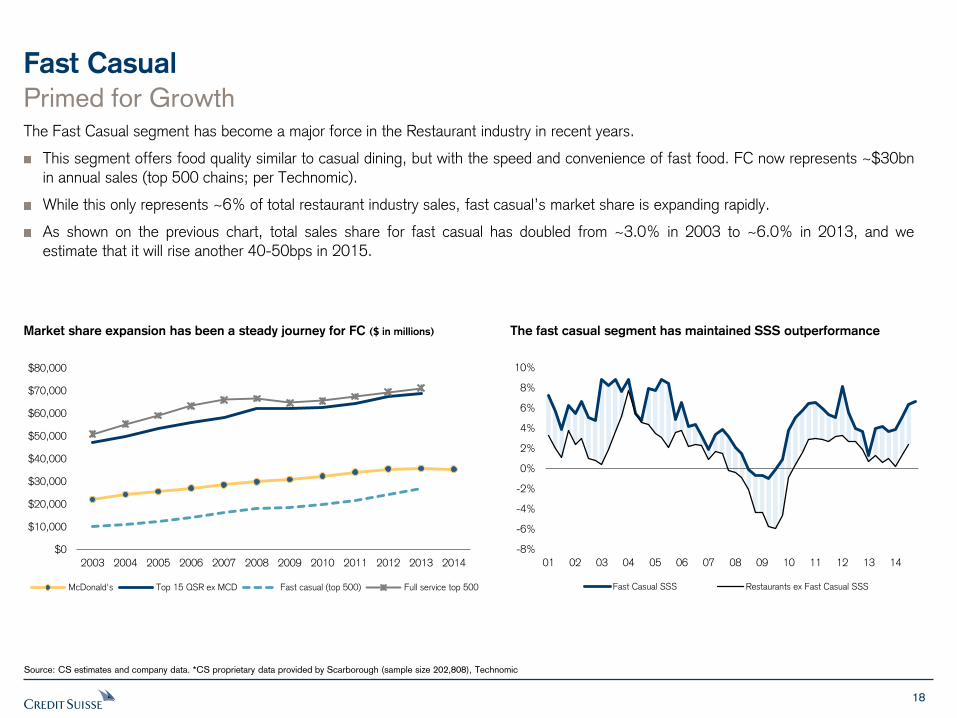

Fast Casual

Primed for Growth The Fast Casual segment has become a major force in the Restaurant industry in recent years.

This segment offers food quality similar to casual dining, but with the speed and convenience of fast food. FC now represents ~$30bn

in annual sales (top 500 chains; per Technomic).

While this only represents ~6% of total restaurant industry sales, fast casual’s market share is expanding rapidly.

As shown on the previous chart, total sales share for fast casual has doubled from ~3.0% in 2003 to ~6.0% in 2013, and we estimate that it will rise another 40-50bps in 2015.

Source: CS estimates and company data. *CS proprietary data provided by Scarborough (sample size 202,808), Technomic

Market share expansion has been a steady journey for FC ($ in millions)

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

McDonald's Top 15 QSR ex MCD Fast casual (top 500) Full service top 500

The fast casual segment has maintained SSS outperformance

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

01 02 03 04 05 06 07 08 09 10 11 12 13 14

Fast Casual SSS Restaurants ex Fast Casual SSS

19

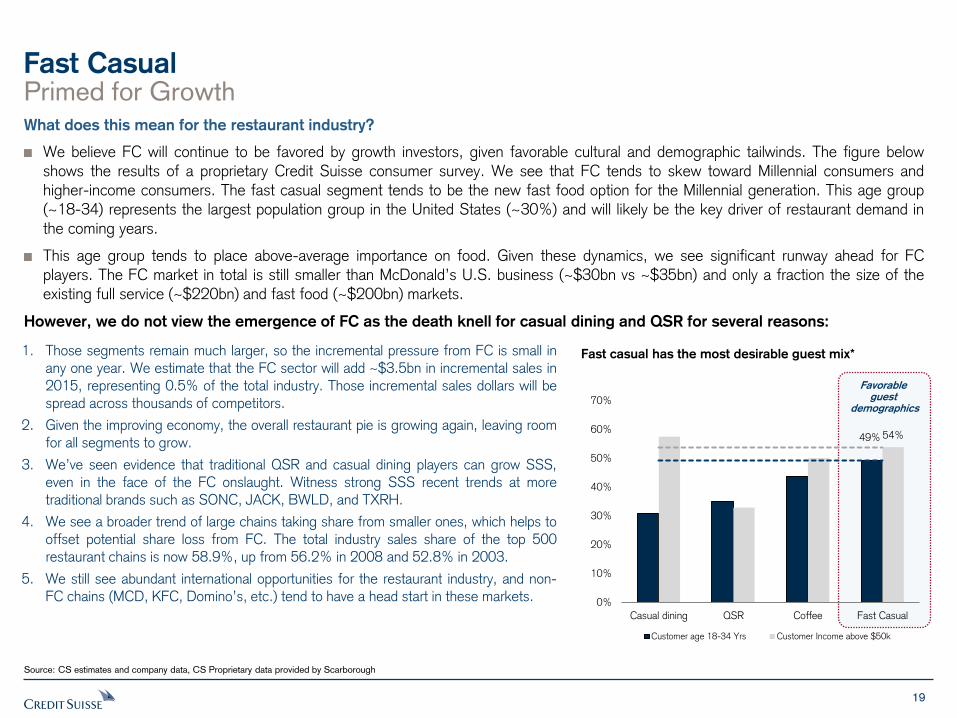

Fast Casual Primed for Growth What does this mean for the restaurant industry?

We believe FC will continue to be favored by growth investors, given favorable cultural and demographic tailwinds. The figure below shows the results of a proprietary Credit Suisse consumer survey. We see that FC tends to skew toward Millennial consumers and higher-income consumers. The fast casual segment tends to be the new fast food option for the Millennial generation. This age group

(~18-34) represents the largest population group in the United States (~30%) and will likely be the key driver of restaurant demand in

the coming years.

This age group tends to place above-average importance on food. Given these dynamics, we see significant runway ahead for FC players. The FC market in total is still smaller than McDonald’s U.S. business (~$30bn vs ~$35bn) and only a fraction the size of the existing full service (~$220bn) and fast food (~$200bn) markets.

However, we do not view the emergence of FC as the death knell for casual dining and QSR for several reasons:

Source: CS estimates and company data, CS Proprietary data provided by Scarborough

Fast casual has the most desirable guest mix*

Favorable guest

demographics

1. Those segments remain much larger, so the incremental pressure from FC is small in any one year. We estimate that the FC sector will add ~$3.5bn in incremental sales in 2015, representing 0.5% of the total industry. Those incremental sales dollars will be spread across thousands of competitors.

2. Given the improving economy, the overall restaurant pie is growing again, leaving room for all segments to grow.

3. We’ve seen evidence that traditional QSR and casual dining players can grow SSS, even in the face of the FC onslaught. Witness strong SSS recent trends at more traditional brands such as SONC, JACK, BWLD, and TXRH.

4. We see a broader trend of large chains taking share from smaller ones, which helps to offset potential share loss from FC. The total industry sales share of the top 500 restaurant chains is now 58.9%, up from 56.2% in 2008 and 52.8% in 2003.

5. We still see abundant international opportunities for the restaurant industry, and non-FC chains (MCD, KFC, Domino’s, etc.) tend to have a head start in these markets.

49% 54%

0%

10%

20%

30%

40%

50%

60%

70%

Casual dining QSR Coffee Fast Casual

Customer age 18-34 Yrs Customer Income above $50k

20

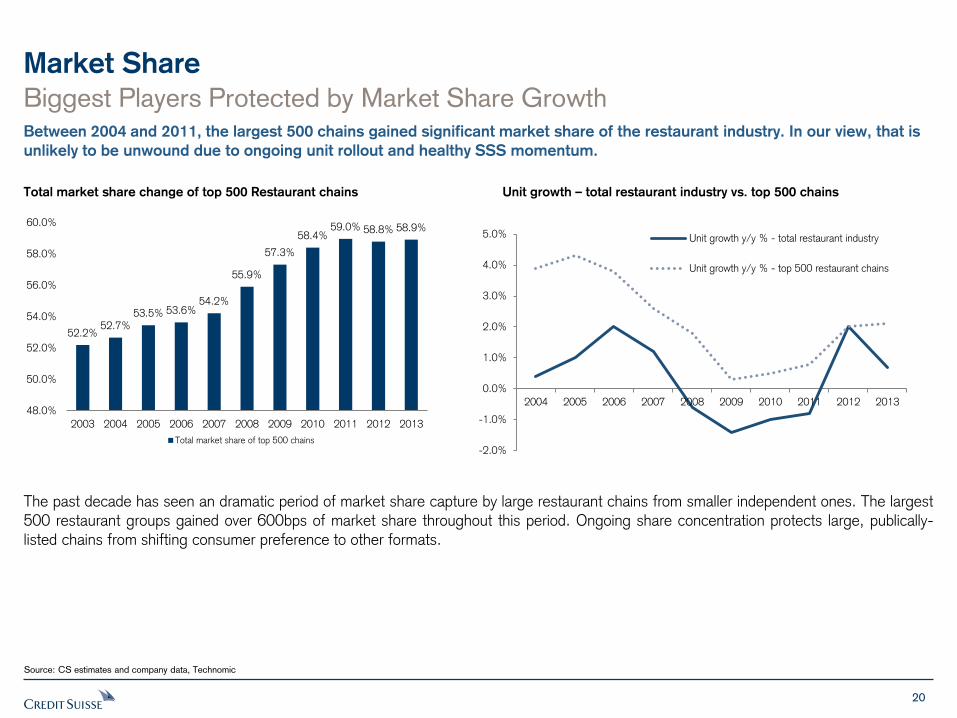

Market Share

The past decade has seen an dramatic period of market share capture by large restaurant chains from smaller independent ones. The largest

500 restaurant groups gained over 600bps of market share throughout this period. Ongoing share concentration protects large, publically-listed chains from shifting consumer preference to other formats.

Biggest Players Protected by Market Share Growth Between 2004 and 2011, the largest 500 chains gained significant market share of the restaurant industry. In our view, that is

unlikely to be unwound due to ongoing unit rollout and healthy SSS momentum.

Total market share change of top 500 Restaurant chains Unit growth – total restaurant industry vs. top 500 chains

Source: CS estimates and company data, Technomic

52.2% 52.7%

53.5% 53.6% 54.2%

55.9%

57.3%

58.4% 59.0% 58.8% 58.9%

48.0%

50.0%

52.0%

54.0%

56.0%

58.0%

60.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Total market share of top 500 chains-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Unit growth y/y % - total restaurant industry

Unit growth y/y % - top 500 restaurant chains

21

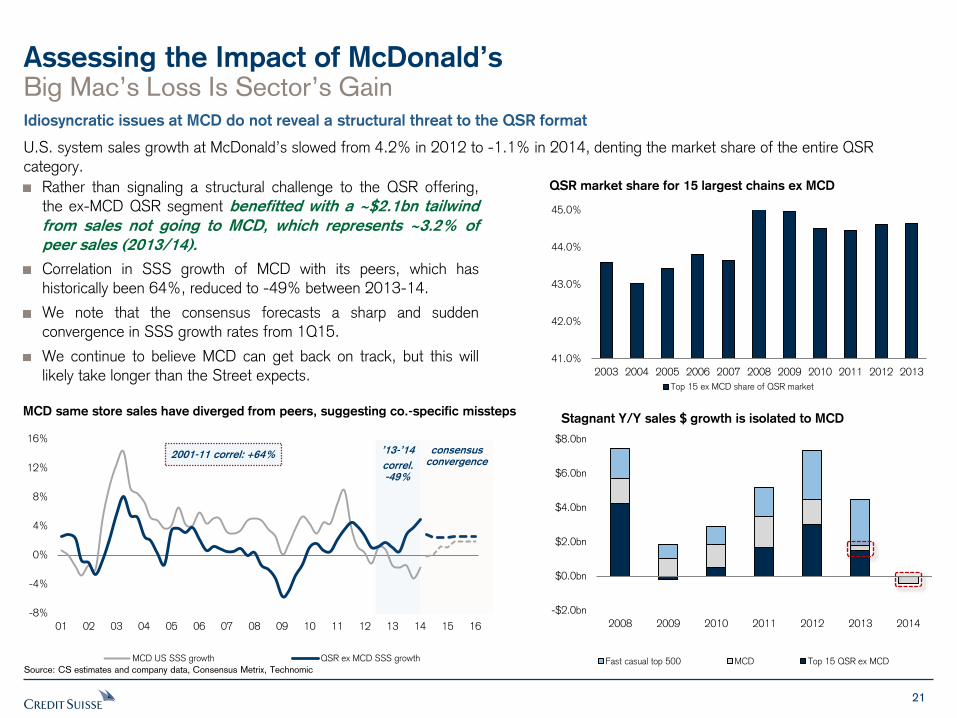

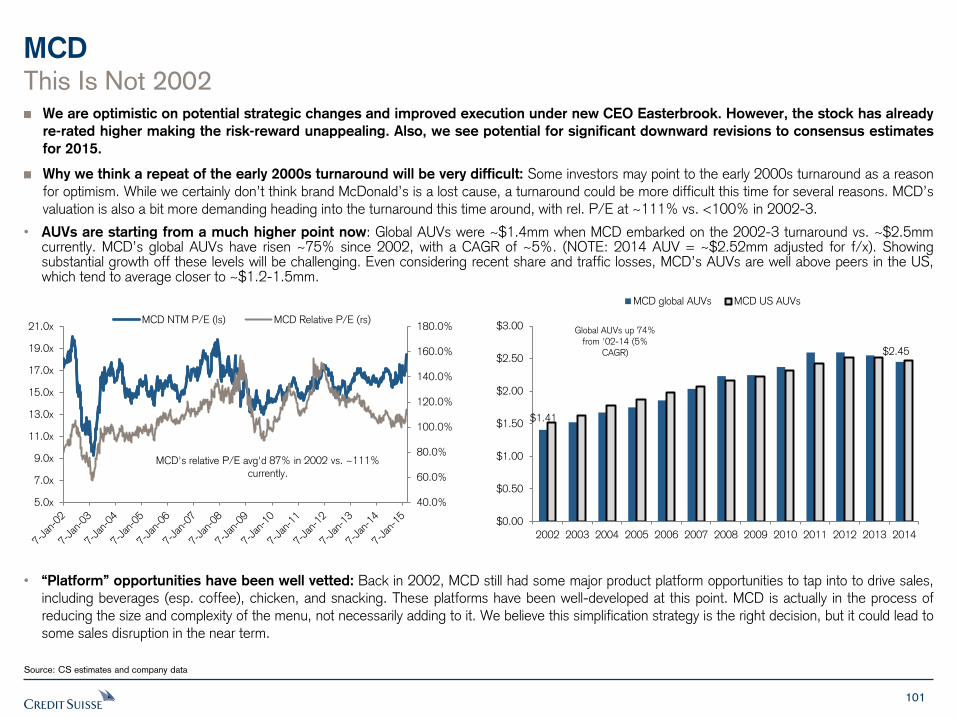

Assessing the Impact of McDonald’s

Rather than signaling a structural challenge to the QSR offering, the ex-MCD QSR segment benefitted with a ~$2.1bn tailwind

from sales not going to MCD, which represents ~3.2% of

peer sales (2013/14).

Correlation in SSS growth of MCD with its peers, which has historically been 64%, reduced to -49% between 2013-14.

We note that the consensus forecasts a sharp and sudden convergence in SSS growth rates from 1Q15.

We continue to believe MCD can get back on track, but this will likely take longer than the Street expects.

QSR market share for 15 largest chains ex MCD

Big Mac’s Loss Is Sector’s Gain Idiosyncratic issues at MCD do not reveal a structural threat to the QSR format

U.S. system sales growth at McDonald’s slowed from 4.2% in 2012 to -1.1% in 2014, denting the market share of the entire QSR

category.

Source: CS estimates and company data, Consensus Metrix, Technomic

Stagnant Y/Y sales $ growth is isolated to MCD

-8%

-4%

0%

4%

8%

12%

16%

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

MCD US SSS growth QSR ex MCD SSS growth

2001-11 correl: +64% ’13-’14

correl. -49%

consensus convergence

MCD same store sales have diverged from peers, suggesting co.-specific missteps

41.0%

42.0%

43.0%

44.0%

45.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Top 15 ex MCD share of QSR market

-$2.0bn

$0.0bn

$2.0bn

$4.0bn

$6.0bn

$8.0bn

2008 2009 2010 2011 2012 2013 2014

Fast casual top 500 MCD Top 15 QSR ex MCD

22

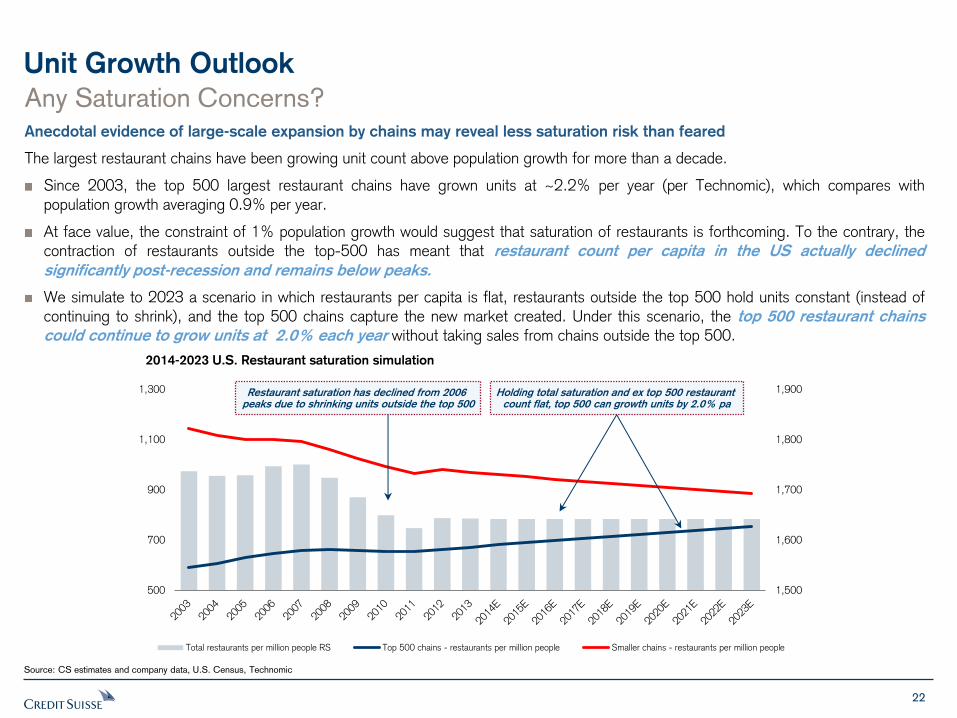

Unit Growth Outlook

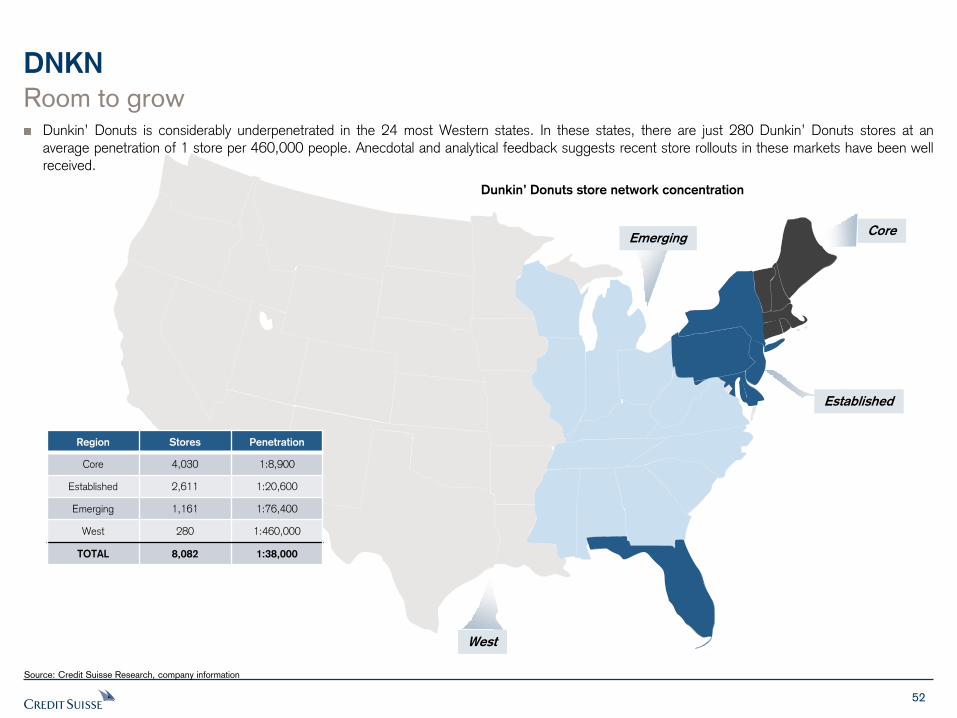

Any Saturation Concerns? Anecdotal evidence of large-scale expansion by chains may reveal less saturation risk than feared

The largest restaurant chains have been growing unit count above population growth for more than a decade.

Since 2003, the top 500 largest restaurant chains have grown units at ~2.2% per year (per Technomic), which compares with population growth averaging 0.9% per year.

At face value, the constraint of 1% population growth would suggest that saturation of restaurants is forthcoming. To the contrary, the contraction of restaurants outside the top-500 has meant that restaurant count per capita in the US actually declined

significantly post-recession and remains below peaks.

We simulate to 2023 a scenario in which restaurants per capita is flat, restaurants outside the top 500 hold units constant (instead of continuing to shrink), and the top 500 chains capture the new market created. Under this scenario, the top 500 restaurant chains

could continue to grow units at 2.0% each year without taking sales from chains outside the top 500.

Source: CS estimates and company data, U.S. Census, Technomic

2014-2023 U.S. Restaurant saturation simulation

1,500

1,600

1,700

1,800

1,900

500

700

900

1,100

1,300

Total restaurants per million people RS Top 500 chains - restaurants per million people Smaller chains - restaurants per million people

Restaurant saturation has declined from 2006 peaks due to shrinking units outside the top 500

Holding total saturation and ex top 500 restaurant count flat, top 500 can growth units by 2.0% pa

FOCUS ISSUE: Minimum Wage Analysis

24

Wages Are on the Rise

Should Restaurant Investors Be Concerned? On a population-weighted basis, we estimate the U.S. minimum wage was ~$7.76/hr. in 2014, up 1.8% from 2013. Based on

announced min. wage changes, we expect the U.S. avg. minimum wage to rise to $8.00 in 2015 (+3.2%) and to $8.26 by

2016 (+3.2%).*

We estimate that a 3% (25c/hr) increase in the national minimum wage could add 30-40 bps of margin pressure to a typical

restaurant chain

We have analyzed current and proposed minimum and tipped wages across each of the 50 states, through 2017. We went state by state and tracked past, current, and future min. wage levels.

While the vast majority of restaurant employees are paid above the minimum wage, even at QSRs, a rising wage at the lowest rung will likely lead to wage pressure throughout the hourly employee base.

The U.S. Federal minimum wage is $7.25/hr. The Fed tipped wage = $2.13/hr

Pres. Obama has pushed for an increase in the national minimum wage to ~$10.10/hr., while grass roots efforts across the country have

pushed for a $15 min. wage. We believe a Federal min. wage increase is unlikely with Congress controlled by the Republican party. However, many states are taking the matter into their own hands, with 26 states planning to raise minimum wages over 2015-16 and 16 planning to raise tipped wages. There are 29 states that have min. wages that are already above the Fed level.

These growth rates are triple the pace of minimum wage growth in recent years (+1.1% CAGR from 2012-14). This means minimum wage pressures are building for the restaurant industry.

How does this compare with the last Federal minimum wage hike? This pace of minimum wage growth is below the rate seen when

the Federal minimum wage was raised from $5.15-7.25 over 2007-09. Minimum wage grew ~7% annually over 2008-9 on a population-weighted basis.

Source: CS estimates and company data. *This data does not capture some minimum wage increases at the local level, such as in Seattle, San Francisco and Chicago

All else being equal, we estimate that an ~3% (~25c/hr) increase in national minimum wage could add

~30-40bps of margin pressure to the typical restaurant chain. This adjusts for the fact that most employees

already make above the minimum wage.

25

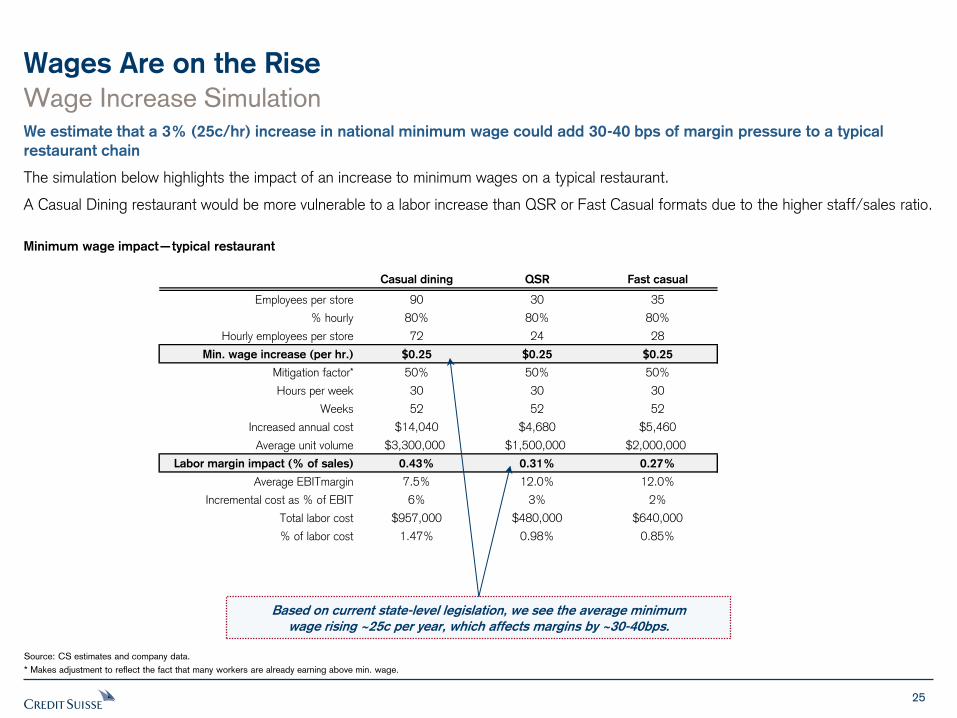

Wages Are on the Rise

Wage Increase Simulation We estimate that a 3% (25c/hr) increase in national minimum wage could add 30-40 bps of margin pressure to a typical

restaurant chain

The simulation below highlights the impact of an increase to minimum wages on a typical restaurant.

A Casual Dining restaurant would be more vulnerable to a labor increase than QSR or Fast Casual formats due to the higher staff/sales ratio.

Minimum wage impact—typical restaurant

Source: CS estimates and company data.

* Makes adjustment to reflect the fact that many workers are already earning above min. wage.

Casual dining QSR Fast casual

Employees per store 90 30 35

% hourly 80% 80% 80%

Hourly employees per store 72 24 28

Min. wage increase (per hr.) $0.25 $0.25 $0.25

Mitigation factor* 50% 50% 50%

Hours per week 30 30 30

Weeks 52 52 52

Increased annual cost $14,040 $4,680 $5,460

Average unit volume $3,300,000 $1,500,000 $2,000,000

Labor margin impact (% of sales) 0.43% 0.31% 0.27%

Average EBITmargin 7.5% 12.0% 12.0%

Incremental cost as % of EBIT 6% 3% 2%

Total labor cost $957,000 $480,000 $640,000

% of labor cost 1.47% 0.98% 0.85%

Based on current state-level legislation, we see the average minimum

wage rising ~25c per year, which affects margins by ~30-40bps.

26

Wages Are on the Rise

What about the Tipped Minimum Wage? The tipped minimum wage has not been increased since 1991

We are seeing more states move to raise the tipped minimum wage alongside the non-tipped minimum wage. The tipped minimum wage

is currently $2.13/hr at the Federal level, but closer to ~$4.23/hr on a population-weighted basis nationally.

There are 31 states that have tipped wages that are already above the Federal level of $2.13/hr.

Tipped wage increases have lagged the minimum wage in recent decades. The tipped wage was last increased in 1991 (to $2.13 from $2.09). At that time, the tipped wage was 50% of the minimum wage vs 29% currently.

Pres. Obama has called for an increase in the tipped wage to 70% of the minimum wage, which would bring the tipped wage to $5.08/hr

(+138%), assuming no increase in the min. wage. In our view, movement here also seems unlikely with Republican control of Congress; however, the pressure is clearly building.

Increases in tipped wage could obviously have a material impact on labor costs for chains that employ tipped servers (i.e. casual and upscale dining).

We believe that a more significant increase at the Fed level could have a much more material impact.

For example, if the Federal tip wage were to move to $5.08, as previously mentioned, this could affect EBIT margins by ~250bps (assuming no other moves at the state level).

Source: CS estimates and company data.

Based on our analysis of state-level legislation, the population-wtd. tipped wage is scheduled to rise to

$4.35 in 2015 (+2.7%) and $4.52 in 2016 (+3.9%). We estimate that an increase of this magnitude could affect

the typical casual dining restaurant margin by ~30bps.

27

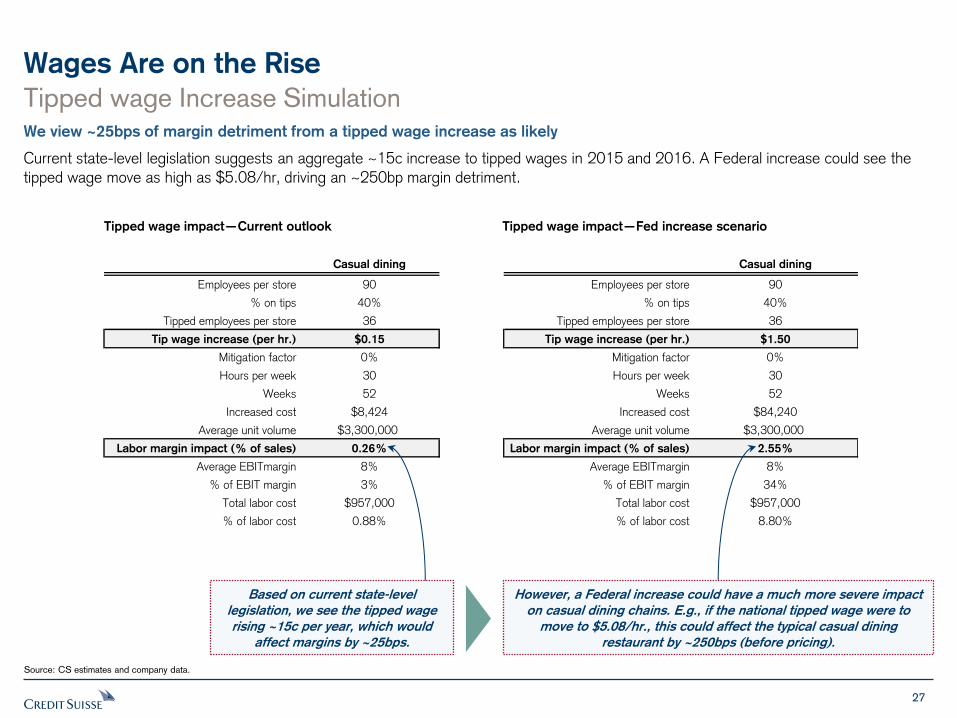

Wages Are on the Rise

Source: CS estimates and company data.

Tipped wage Increase Simulation We view ~25bps of margin detriment from a tipped wage increase as likely

Current state-level legislation suggests an aggregate ~15c increase to tipped wages in 2015 and 2016. A Federal increase could see the

tipped wage move as high as $5.08/hr, driving an ~250bp margin detriment.

Tipped wage impact—Current outlook Tipped wage impact—Fed increase scenario

Casual dining

Employees per store 90

% on tips 40%

Tipped employees per store 36

Tip wage increase (per hr.) $0.15

Mitigation factor 0%

Hours per week 30

Weeks 52

Increased cost $8,424

Average unit volume $3,300,000

Labor margin impact (% of sales) 0.26%

Average EBITmargin 8%

% of EBIT margin 3%

Total labor cost $957,000

% of labor cost 0.88%

Casual dining

Employees per store 90

% on tips 40%

Tipped employees per store 36

Tip wage increase (per hr.) $1.50

Mitigation factor 0%

Hours per week 30

Weeks 52

Increased cost $84,240

Average unit volume $3,300,000

Labor margin impact (% of sales) 2.55%

Average EBITmargin 8%

% of EBIT margin 34%

Total labor cost $957,000

% of labor cost 8.80%

Based on current state-level

legislation, we see the tipped wage

rising ~15c per year, which would

affect margins by ~25bps.

However, a Federal increase could have a much more severe impact

on casual dining chains. E.g., if the national tipped wage were to

move to $5.08/hr., this could affect the typical casual dining

restaurant by ~250bps (before pricing).

28

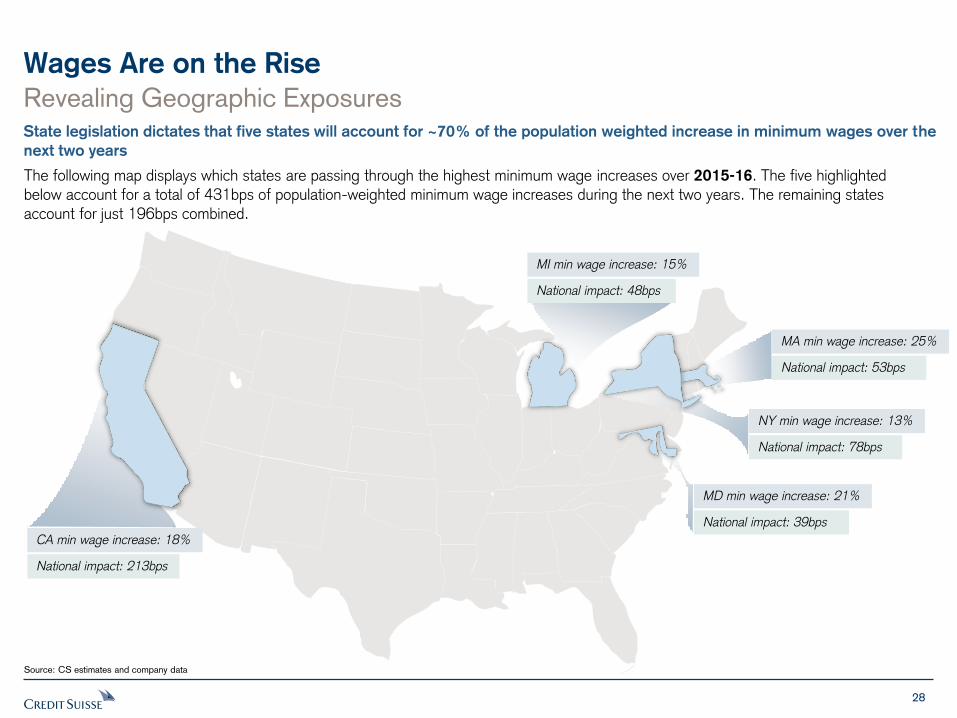

Wages Are on the Rise

The following map displays which states are passing through the highest minimum wage increases over 2015-16. The five highlighted below account for a total of 431bps of population-weighted minimum wage increases during the next two years. The remaining states account for just 196bps combined.

Revealing Geographic Exposures State legislation dictates that five states will account for ~70% of the population weighted increase in minimum wages over the

next two years

Source: CS estimates and company data

MI min wage increase: 15%

National impact: 48bps

NY min wage increase: 13%

National impact: 78bps

MD min wage increase: 21%

National impact: 39bps

CA min wage increase: 18%

National impact: 213bps

MA min wage increase: 25%

National impact: 53bps

29

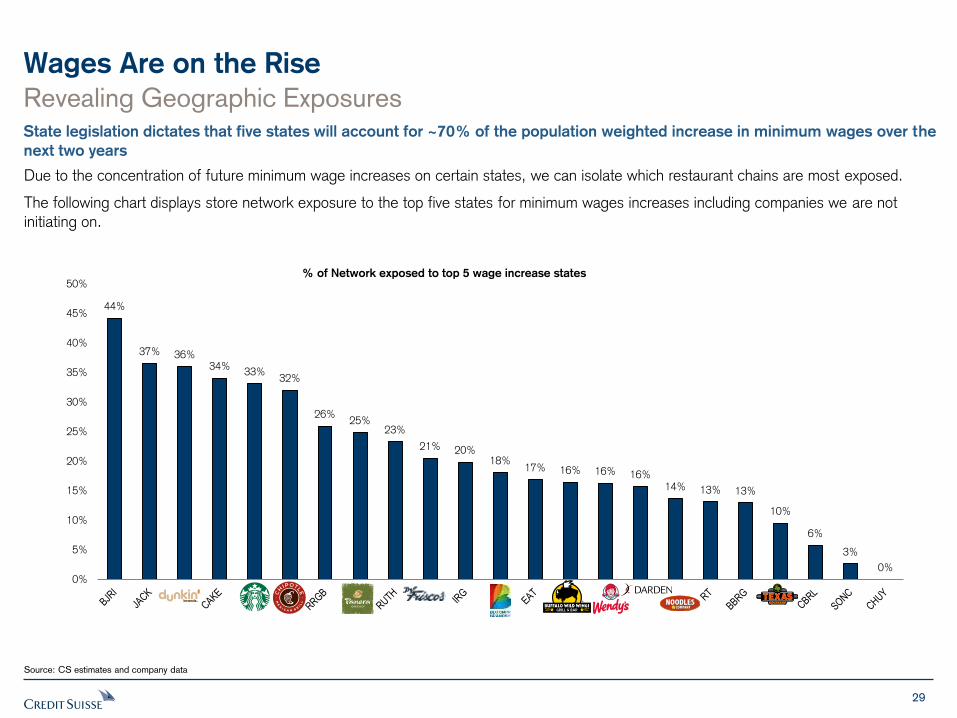

Wages Are on the Rise

Due to the concentration of future minimum wage increases on certain states, we can isolate which restaurant chains are most exposed.

The following chart displays store network exposure to the top five states for minimum wages increases including companies we are not initiating on.

Revealing Geographic Exposures State legislation dictates that five states will account for ~70% of the population weighted increase in minimum wages over the

next two years

Source: CS estimates and company data

44%

37% 36% 34%

33% 32%

26% 25%

23%

21% 20% 18%

17% 16% 16% 16% 14% 13% 13%

10%

6%

3%

0% 0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%% of Network exposed to top 5 wage increase states

30

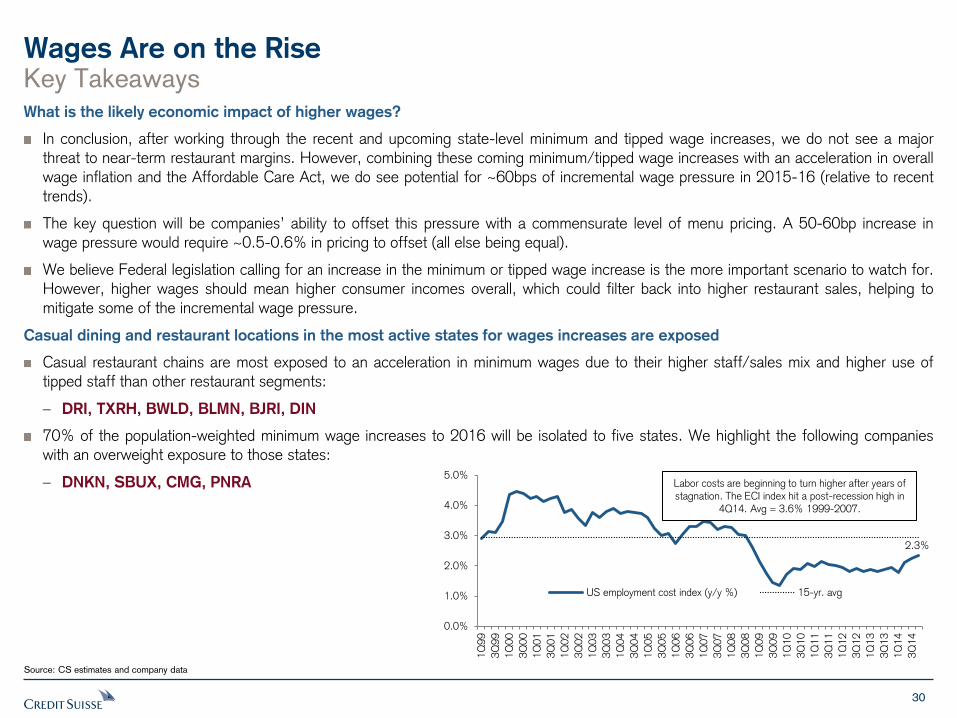

Wages Are on the Rise Key Takeaways What is the likely economic impact of higher wages?

In conclusion, after working through the recent and upcoming state-level minimum and tipped wage increases, we do not see a major threat to near-term restaurant margins. However, combining these coming minimum/tipped wage increases with an acceleration in overall wage inflation and the Affordable Care Act, we do see potential for ~60bps of incremental wage pressure in 2015-16 (relative to recent

trends).

The key question will be companies’ ability to offset this pressure with a commensurate level of menu pricing. A 50-60bp increase in wage pressure would require ~0.5-0.6% in pricing to offset (all else being equal).

We believe Federal legislation calling for an increase in the minimum or tipped wage increase is the more important scenario to watch for.

However, higher wages should mean higher consumer incomes overall, which could filter back into higher restaurant sales, helping to mitigate some of the incremental wage pressure.

Casual dining and restaurant locations in the most active states for wages increases are exposed

Casual restaurant chains are most exposed to an acceleration in minimum wages due to their higher staff/sales mix and higher use of

tipped staff than other restaurant segments:

– DRI, TXRH, BWLD, BLMN, BJRI, DIN

70% of the population-weighted minimum wage increases to 2016 will be isolated to five states. We highlight the following companies

with an overweight exposure to those states:

– DNKN, SBUX, CMG, PNRA

Source: CS estimates and company data

2.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

US employment cost index (y/y %) 15-yr. avg

Labor costs are beginning to turn higher after years of stagnation. The ECI index hit a post-recession high in

4Q14. Avg = 3.6% 1999-2007.

31

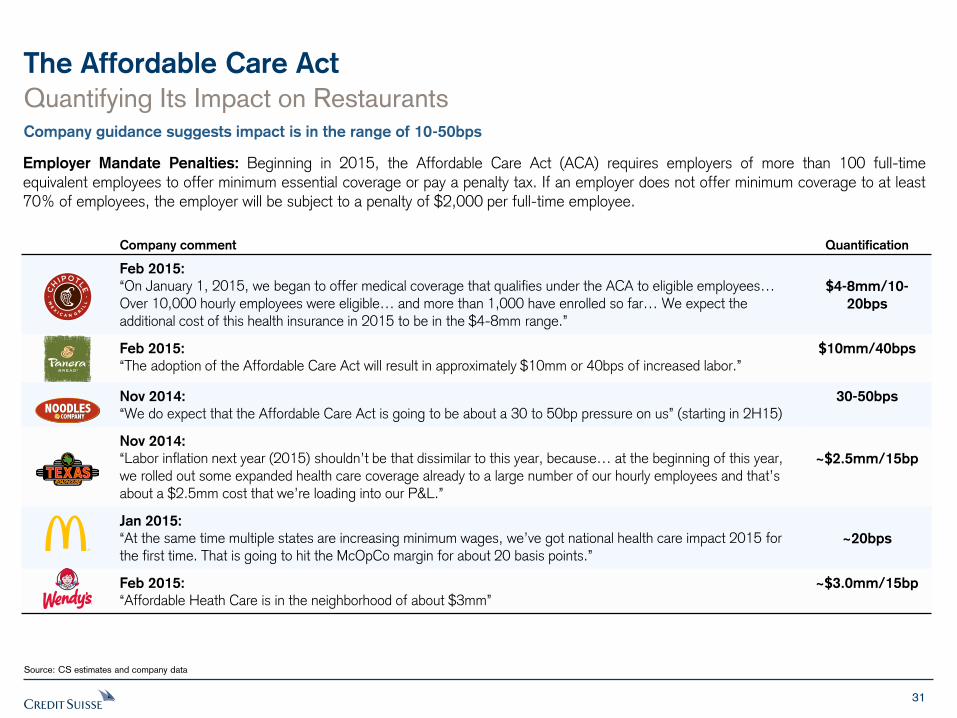

The Affordable Care Act

Quantifying Its Impact on Restaurants Company guidance suggests impact is in the range of 10-50bps

Employer Mandate Penalties: Beginning in 2015, the Affordable Care Act (ACA) requires employers of more than 100 full-time equivalent employees to offer minimum essential coverage or pay a penalty tax. If an employer does not offer minimum coverage to at least

70% of employees, the employer will be subject to a penalty of $2,000 per full-time employee.

Source: CS estimates and company data

Company comment Quantification

Feb 2015:

“On January 1, 2015, we began to offer medical coverage that qualifies under the ACA to eligible employees… Over 10,000 hourly employees were eligible… and more than 1,000 have enrolled so far… We expect the additional cost of this health insurance in 2015 to be in the $4-8mm range.”

$4-8mm/10-

20bps

Feb 2015:

“The adoption of the Affordable Care Act will result in approximately $10mm or 40bps of increased labor.” $10mm/40bps

Nov 2014:

“We do expect that the Affordable Care Act is going to be about a 30 to 50bp pressure on us” (starting in 2H15) 30-50bps

Nov 2014:

“Labor inflation next year (2015) shouldn’t be that dissimilar to this year, because… at the beginning of this year, we rolled out some expanded health care coverage already to a large number of our hourly employees and that’s about a $2.5mm cost that we’re loading into our P&L.”

~$2.5mm/15bp

Jan 2015:

“At the same time multiple states are increasing minimum wages, we’ve got national health care impact 2015 for the first time. That is going to hit the McOpCo margin for about 20 basis points.”

~20bps

Feb 2015:

“Affordable Heath Care is in the neighborhood of about $3mm” ~$3.0mm/15bp

FOCUS ISSUE: Gasoline Price Impact

33

Closer Look at Gas Prices & Restaurant Demand

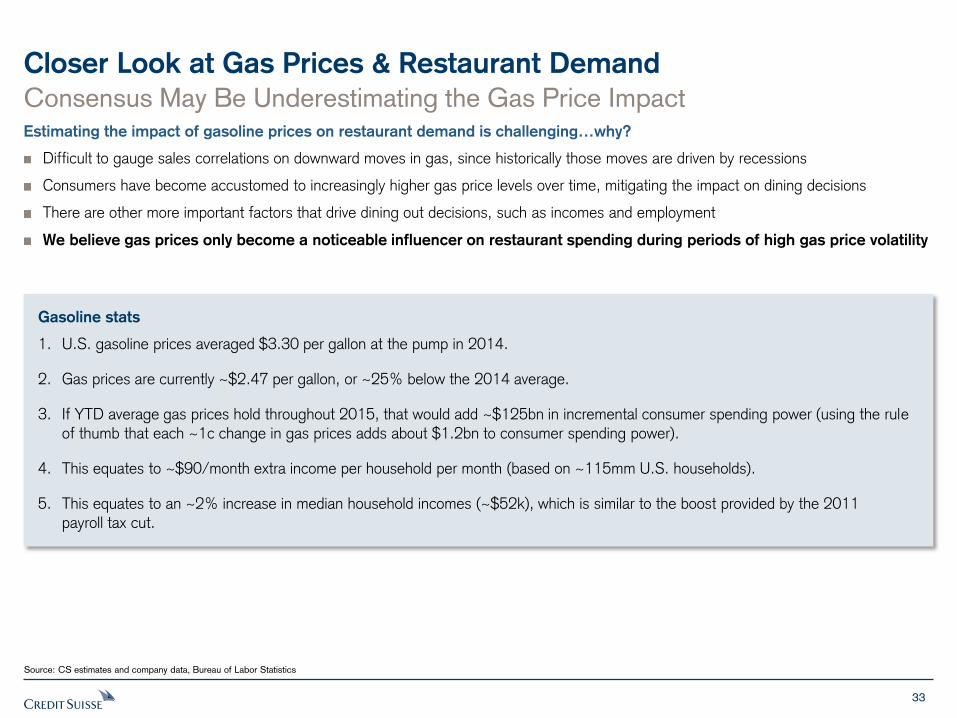

Consensus May Be Underestimating the Gas Price Impact Estimating the impact of gasoline prices on restaurant demand is challenging…why?

Difficult to gauge sales correlations on downward moves in gas, since historically those moves are driven by recessions

Consumers have become accustomed to increasingly higher gas price levels over time, mitigating the impact on dining decisions

There are other more important factors that drive dining out decisions, such as incomes and employment

We believe gas prices only become a noticeable influencer on restaurant spending during periods of high gas price volatility

Source: CS estimates and company data, Bureau of Labor Statistics

Gasoline stats

1. U.S. gasoline prices averaged $3.30 per gallon at the pump in 2014.

2. Gas prices are currently ~$2.47 per gallon, or ~25% below the 2014 average.

3. If YTD average gas prices hold throughout 2015, that would add ~$125bn in incremental consumer spending power (using the rule

of thumb that each ~1c change in gas prices adds about $1.2bn to consumer spending power).

4. This equates to ~$90/month extra income per household per month (based on ~115mm U.S. households).

5. This equates to an ~2% increase in median household incomes (~$52k), which is similar to the boost provided by the 2011 payroll tax cut.

34

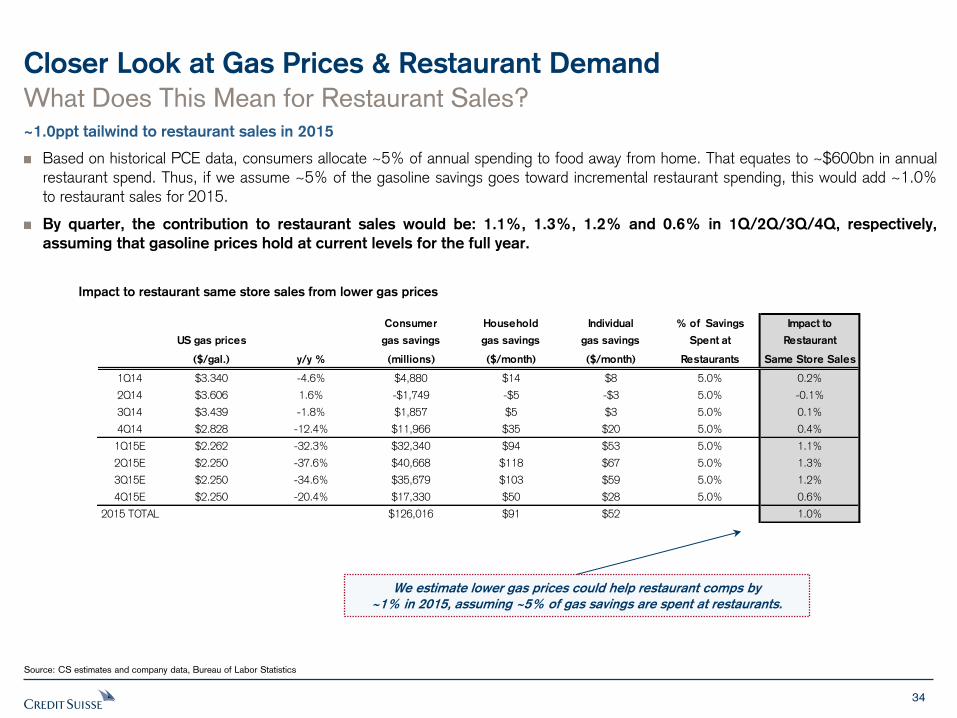

Closer Look at Gas Prices & Restaurant Demand

What Does This Mean for Restaurant Sales? ~1.0ppt tailwind to restaurant sales in 2015

Based on historical PCE data, consumers allocate ~5% of annual spending to food away from home. That equates to ~$600bn in annual

restaurant spend. Thus, if we assume ~5% of the gasoline savings goes toward incremental restaurant spending, this would add ~1.0% to restaurant sales for 2015.

By quarter, the contribution to restaurant sales would be: 1.1%, 1.3%, 1.2% and 0.6% in 1Q/2Q/3Q/4Q, respectively,

assuming that gasoline prices hold at current levels for the full year.

Impact to restaurant same store sales from lower gas prices

Source: CS estimates and company data, Bureau of Labor Statistics

We estimate lower gas prices could help restaurant comps by

~1% in 2015, assuming ~5% of gas savings are spent at restaurants.

Consumer Household Individual % of Savings Impact to

US gas prices gas savings gas savings gas savings Spent at Restaurant

($/gal.) y/y % (millions) ($/month) ($/month) Restaurants Same Store Sales

1Q14 $3.340 -4.6% $4,880 $14 $8 5.0% 0.2%

2Q14 $3.606 1.6% -$1,749 -$5 -$3 5.0% -0.1%

3Q14 $3.439 -1.8% $1,857 $5 $3 5.0% 0.1%

4Q14 $2.828 -12.4% $11,966 $35 $20 5.0% 0.4%

1Q15E $2.262 -32.3% $32,340 $94 $53 5.0% 1.1%

2Q15E $2.250 -37.6% $40,668 $118 $67 5.0% 1.3%

3Q15E $2.250 -34.6% $35,679 $103 $59 5.0% 1.2%

4Q15E $2.250 -20.4% $17,330 $50 $28 5.0% 0.6%

2015 TOTAL $126,016 $91 $52 1.0%

35

Closer Look at Gas Prices & Restaurant Demand

What’s the Correlation Between Restaurant Demand and Gas Prices? Correlations vary with the economic cycle

Over the long run, restaurant SSS have shown a LOW correlation with gas prices. We believe it is more useful to focus on the

aforementioned spending ratios rather than correlations to sales

We also looked at specific periods during which gas prices moved sharply up or down to better gauge potential correlations. The data were mixed here as well, with some periods showing POSITIVE correlations with gas prices. Overall, it was difficult to find a period similar

to the current environment of plummeting gas prices and a healthy economy.

In terms of companies, we found no clear trends when looking at individual company correlations.

Correlations: Restaurant same store sales vs gasoline prices

Source: CS estimates and company data, Bureau of Labor Statistics

Period Total Casual Fast Upscale

Gas price change Industry QSR Dining Casual Dining

Long-term: 1Q98-1Q15E -34% -14% -58% -31% -17%

$1.09 TO $2.10 (+93%)

1Q05-2Q06 -78% 5% -74% -60% -40%

$1.92 TO $2.79 (+45%)

3Q10-3Q11 59% 47% 65% -33% 66%

$2.68 TO $3.60 (+34%)

1Q99-3Q00 20% -80% 48% NA 86%

$0.97 TO $1.56 (+61%)

3Q08-4Q09 68% 44% 47% 50% 77%

$3.82 TO $2.56 (-33%)

Correlations between gas price and Restaurant industry

1. Since 1998, the correlation b/t industry SSS and gas prices is -34% (R-sq. 12%).

2. Casual dining has the highest correlation with gas prices (-58%), followed by fast casual (-31%) and QSR (-14%).

3. The correlation can turn positive during periods of severe economic recession (+68% in 2008-9).

4. Since 1990, there has only been one other period in which gas prices moved ~50% in a three-month window (3Q-4Q08).

5. Sharp upward gas price moves have resulted in inconsistent correlations with industry SSS (-78% in

2005-6 vs. positive in 1999-00 and 2010-11). The Restaurant industry has shown mixed correlations with gas

prices over time, even during periods of sudden price moves.

36

Closer Look at Gas Prices & Restaurant Demand

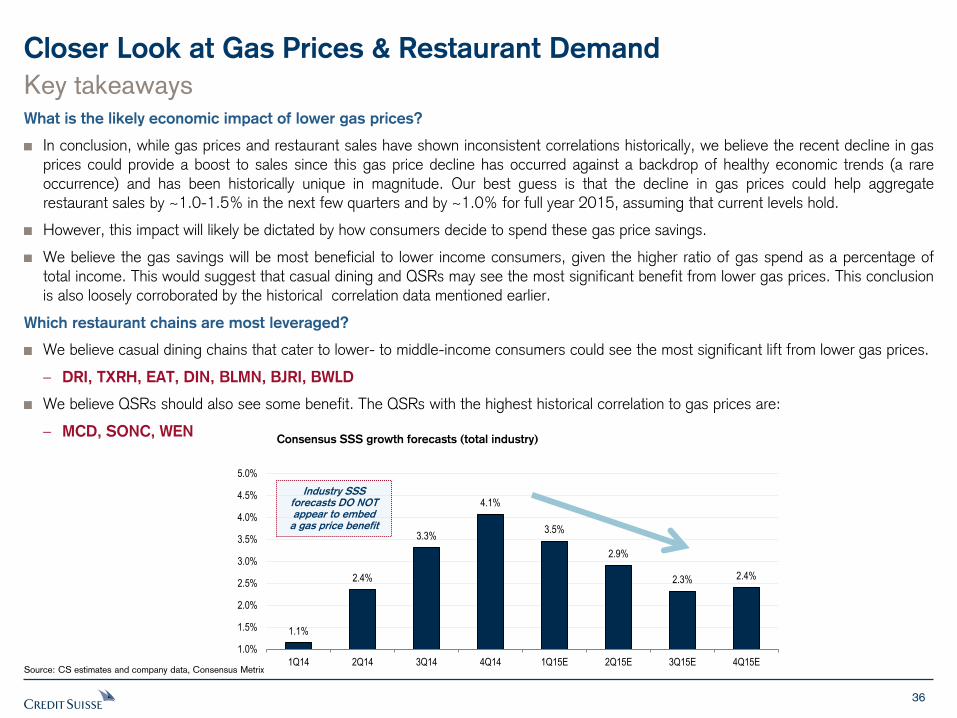

Key takeaways What is the likely economic impact of lower gas prices?

In conclusion, while gas prices and restaurant sales have shown inconsistent correlations historically, we believe the recent decline in gas prices could provide a boost to sales since this gas price decline has occurred against a backdrop of healthy economic trends (a rare occurrence) and has been historically unique in magnitude. Our best guess is that the decline in gas prices could help aggregate

restaurant sales by ~1.0-1.5% in the next few quarters and by ~1.0% for full year 2015, assuming that current levels hold.

However, this impact will likely be dictated by how consumers decide to spend these gas price savings.

We believe the gas savings will be most beneficial to lower income consumers, given the higher ratio of gas spend as a percentage of

total income. This would suggest that casual dining and QSRs may see the most significant benefit from lower gas prices. This conclusion is also loosely corroborated by the historical correlation data mentioned earlier.

Which restaurant chains are most leveraged?

We believe casual dining chains that cater to lower- to middle-income consumers could see the most significant lift from lower gas prices.

– DRI, TXRH, EAT, DIN, BLMN, BJRI, BWLD

We believe QSRs should also see some benefit. The QSRs with the highest historical correlation to gas prices are:

– MCD, SONC, WEN

Source: CS estimates and company data, Consensus Metrix

Consensus SSS growth forecasts (total industry)

1.1%

2.4%

3.3%

4.1%

3.5%

2.9%

2.3% 2.4%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1Q14 2Q14 3Q14 4Q14 1Q15E 2Q15E 3Q15E 4Q15E

Industry SSS forecasts DO NOT appear to embed

a gas price benefit

37

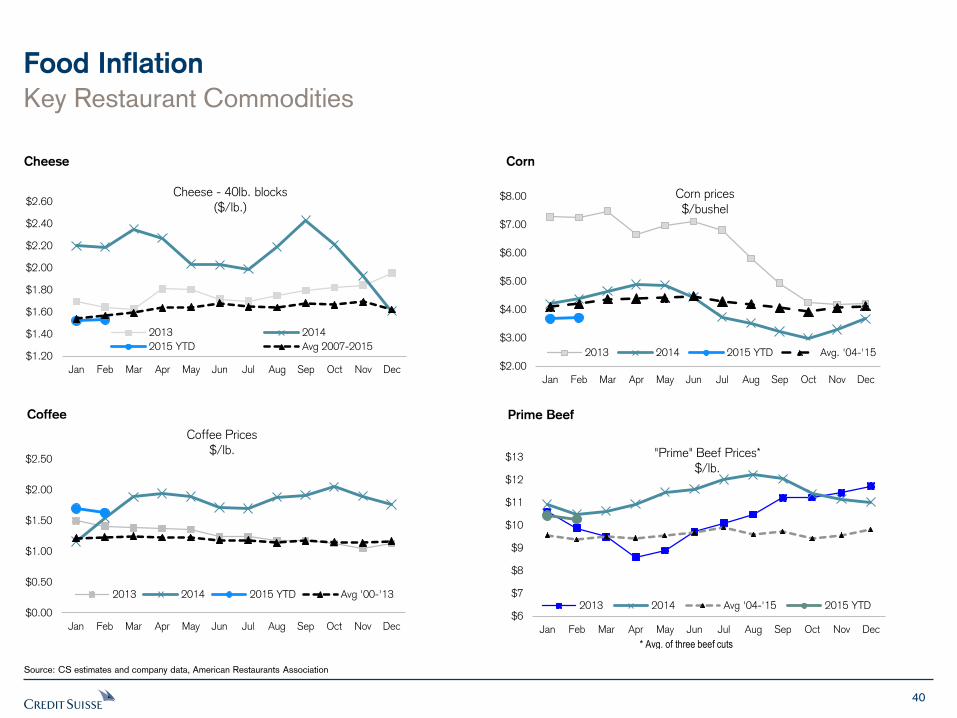

Food Inflation

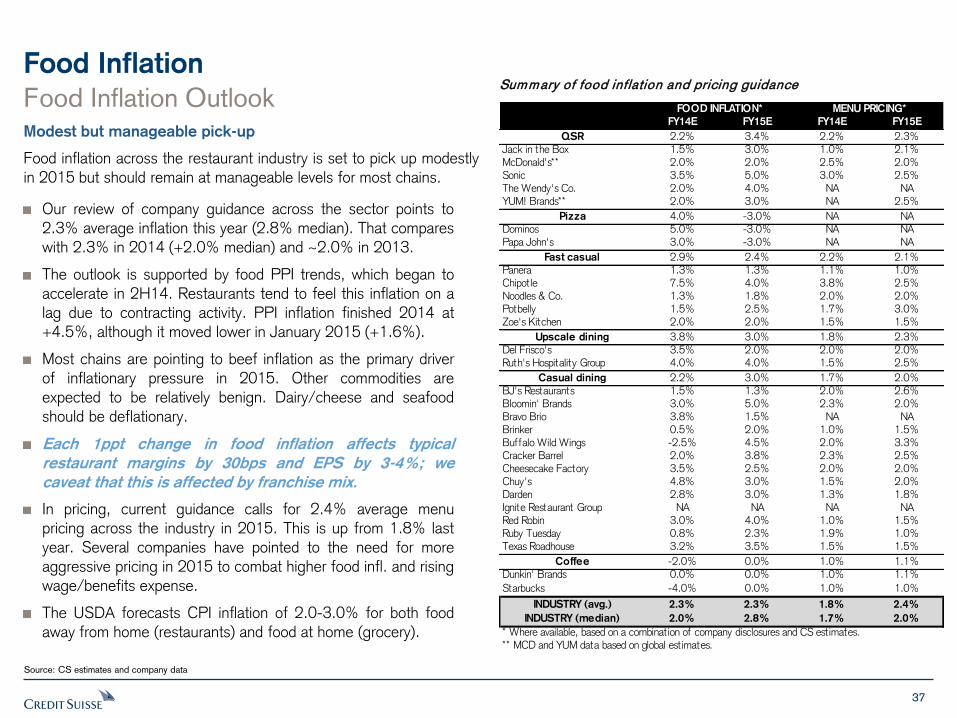

Our review of company guidance across the sector points to 2.3% average inflation this year (2.8% median). That compares with 2.3% in 2014 (+2.0% median) and ~2.0% in 2013.

The outlook is supported by food PPI trends, which began to accelerate in 2H14. Restaurants tend to feel this inflation on a

lag due to contracting activity. PPI inflation finished 2014 at +4.5%, although it moved lower in January 2015 (+1.6%).

Most chains are pointing to beef inflation as the primary driver of inflationary pressure in 2015. Other commodities are

expected to be relatively benign. Dairy/cheese and seafood should be deflationary.

Each 1ppt change in food inflation affects typical

restaurant margins by 30bps and EPS by 3-4%; we

caveat that this is affected by franchise mix.

In pricing, current guidance calls for 2.4% average menu pricing across the industry in 2015. This is up from 1.8% last

year. Several companies have pointed to the need for more aggressive pricing in 2015 to combat higher food infl. and rising

wage/benefits expense.

The USDA forecasts CPI inflation of 2.0-3.0% for both food

away from home (restaurants) and food at home (grocery).

Summary of food inflation and pricing guidance

Food Inflation Outlook Modest but manageable pick-up

Food inflation across the restaurant industry is set to pick up modestly

in 2015 but should remain at manageable levels for most chains.

Source: CS estimates and company data

FOOD INFLATION* MENU PRICING*

FY14E FY15E FY14E FY15E

QSR 2.2% 3.4% 2.2% 2.3%Jack in the Box 1.5% 3.0% 1.0% 2.1%McDonald's** 2.0% 2.0% 2.5% 2.0%Sonic 3.5% 5.0% 3.0% 2.5%The Wendy's Co. 2.0% 4.0% NA NAYUM! Brands** 2.0% 3.0% NA 2.5%

Pizza 4.0% -3.0% NA NADominos 5.0% -3.0% NA NAPapa John's 3.0% -3.0% NA NA

Fast casual 2.9% 2.4% 2.2% 2.1%Panera 1.3% 1.3% 1.1% 1.0%Chipotle 7.5% 4.0% 3.8% 2.5%Noodles & Co. 1.3% 1.8% 2.0% 2.0%Potbelly 1.5% 2.5% 1.7% 3.0%Zoe's Kitchen 2.0% 2.0% 1.5% 1.5%

Upscale dining 3.8% 3.0% 1.8% 2.3%Del Frisco's 3.5% 2.0% 2.0% 2.0%Ruth's Hospitality Group 4.0% 4.0% 1.5% 2.5%

Casual dining 2.2% 3.0% 1.7% 2.0%BJ's Restaurants 1.5% 1.3% 2.0% 2.6%Bloomin' Brands 3.0% 5.0% 2.3% 2.0%Bravo Brio 3.8% 1.5% NA NABrinker 0.5% 2.0% 1.0% 1.5%Buffalo Wild Wings -2.5% 4.5% 2.0% 3.3%Cracker Barrel 2.0% 3.8% 2.3% 2.5%Cheesecake Factory 3.5% 2.5% 2.0% 2.0%Chuy's 4.8% 3.0% 1.5% 2.0%Darden 2.8% 3.0% 1.3% 1.8%Ignite Restaurant Group NA NA NA NARed Robin 3.0% 4.0% 1.0% 1.5%Ruby Tuesday 0.8% 2.3% 1.9% 1.0%Texas Roadhouse 3.2% 3.5% 1.5% 1.5%

Coffee -2.0% 0.0% 1.0% 1.1%Dunkin' Brands 0.0% 0.0% 1.0% 1.1%

Starbucks -4.0% 0.0% 1.0% 1.0%

INDUSTRY (avg.) 2.3% 2.3% 1.8% 2.4%

INDUSTRY (median) 2.0% 2.8% 1.7% 2.0%

* Where available, based on a combinat ion of company disclosures and CS est imates. ** MCD and YUM data based on global est imates.

38

Food Inflation

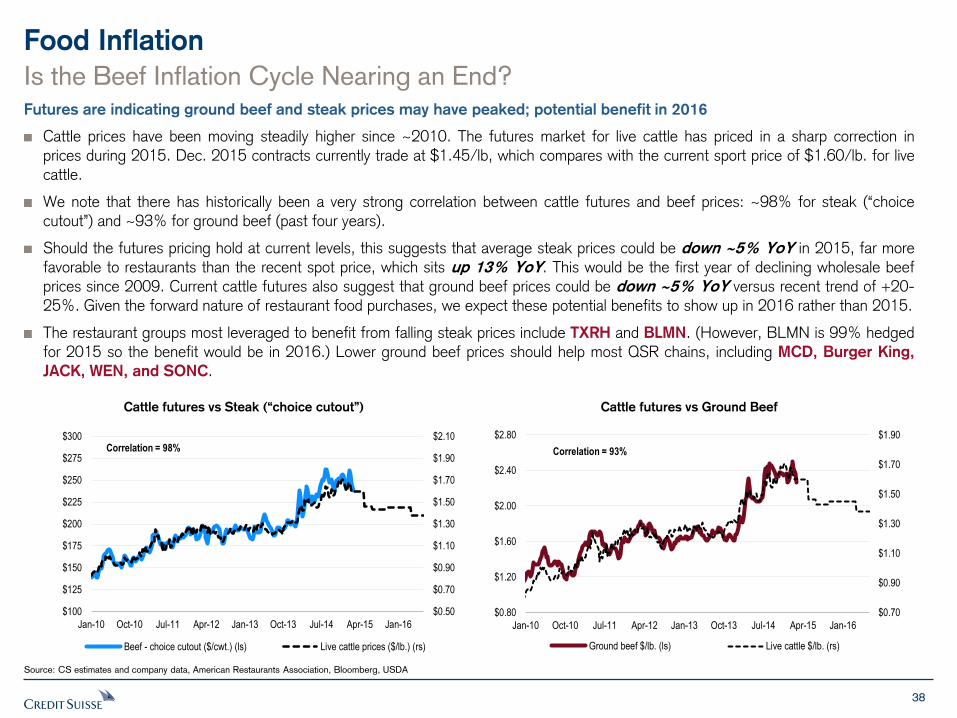

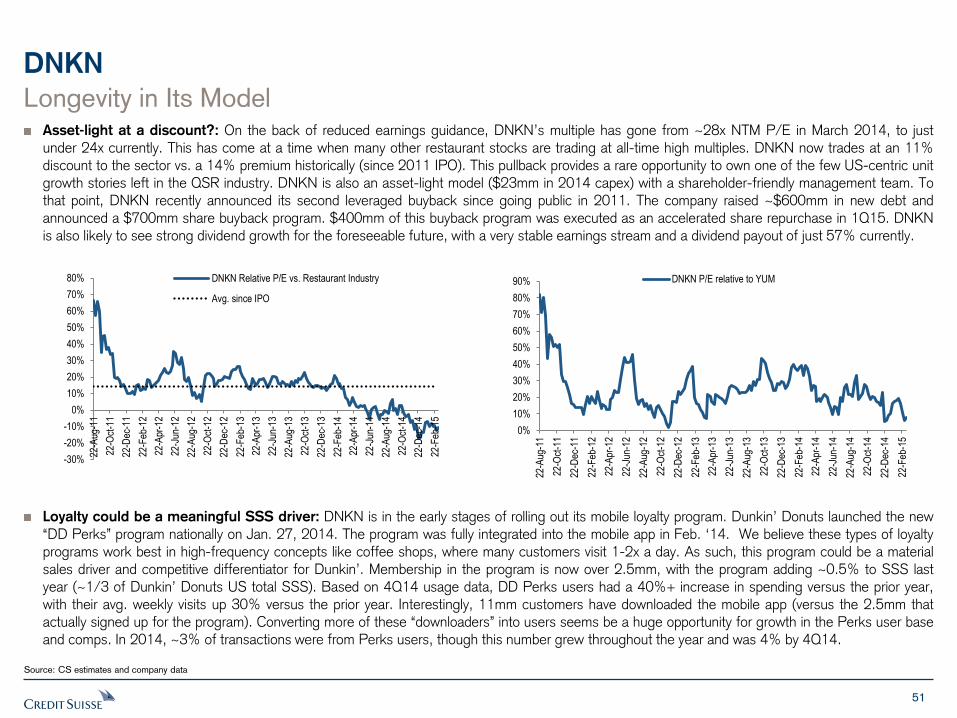

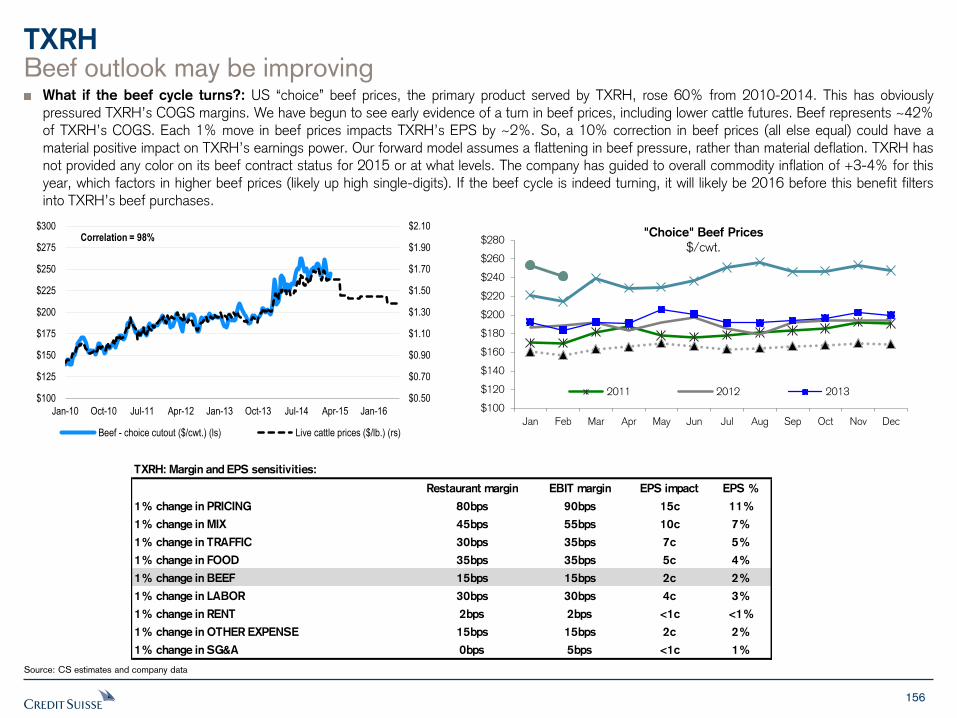

Is the Beef Inflation Cycle Nearing an End? Futures are indicating ground beef and steak prices may have peaked; potential benefit in 2016

Cattle prices have been moving steadily higher since ~2010. The futures market for live cattle has priced in a sharp correction in

prices during 2015. Dec. 2015 contracts currently trade at $1.45/lb, which compares with the current sport price of $1.60/lb. for live cattle.

We note that there has historically been a very strong correlation between cattle futures and beef prices: ~98% for steak (“choice

cutout”) and ~93% for ground beef (past four years).

Should the futures pricing hold at current levels, this suggests that average steak prices could be down ~5% YoY in 2015, far more favorable to restaurants than the recent spot price, which sits up 13% YoY. This would be the first year of declining wholesale beef prices since 2009. Current cattle futures also suggest that ground beef prices could be down ~5% YoY versus recent trend of +20-

25%. Given the forward nature of restaurant food purchases, we expect these potential benefits to show up in 2016 rather than 2015.

The restaurant groups most leveraged to benefit from falling steak prices include TXRH and BLMN. (However, BLMN is 99% hedged for 2015 so the benefit would be in 2016.) Lower ground beef prices should help most QSR chains, including MCD, Burger King,

JACK, WEN, and SONC.

Source: CS estimates and company data, American Restaurants Association, Bloomberg, USDA

$0.50

$0.70

$0.90

$1.10

$1.30

$1.50

$1.70

$1.90

$2.10

$100

$125

$150

$175

$200

$225

$250

$275

$300

Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-14 Apr-15 Jan-16

Beef - choice cutout ($/cwt.) (ls) Live cattle prices ($/lb.) (rs)

Correlation = 98%

Cattle futures vs Steak (“choice cutout”)

$0.70

$0.90

$1.10

$1.30

$1.50

$1.70

$1.90

$0.80

$1.20

$1.60

$2.00

$2.40

$2.80

Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-14 Apr-15 Jan-16

Ground beef $/lb. (ls) Live cattle $/lb. (rs)

Correlation = 93%

Cattle futures vs Ground Beef

39

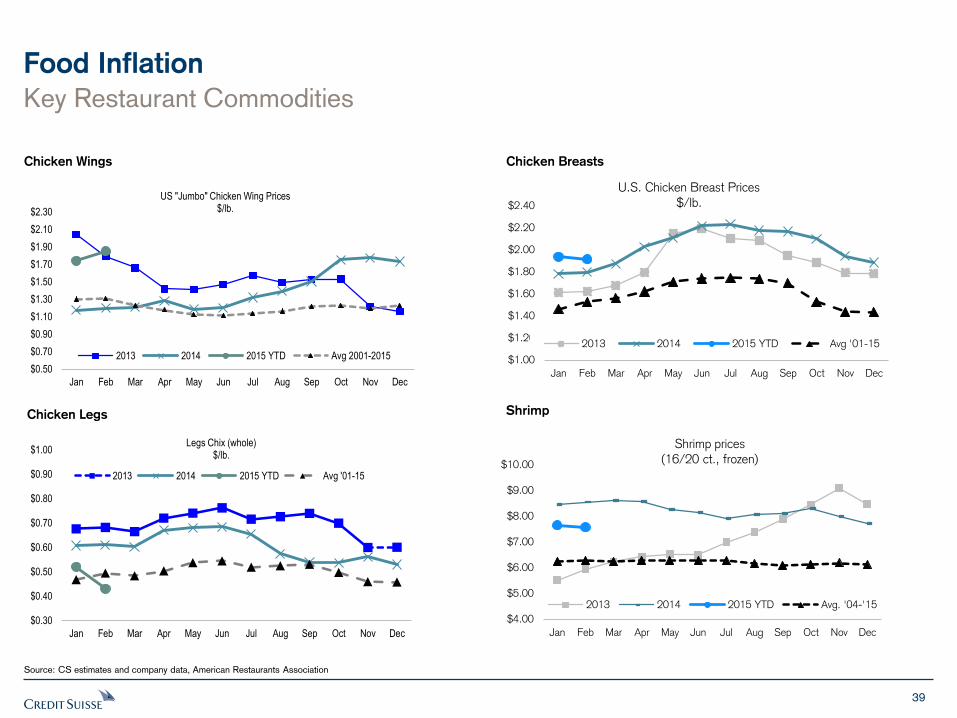

Chicken Legs

Chicken Breasts Chicken Wings

Food Inflation

Shrimp

Key Restaurant Commodities

Source: CS estimates and company data, American Restaurants Association

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

U.S. Chicken Breast Prices $/lb.

2013 2014 2015 YTD Avg '01-15

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Shrimp prices

(16/20 ct., frozen)

2013 2014 2015 YTD Avg. '04-'15

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Legs Chix (whole) $/lb.

2013 2014 2015 YTD Avg '01-15

$0.50

$0.70

$0.90

$1.10

$1.30

$1.50

$1.70

$1.90

$2.10

$2.30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

US "Jumbo" Chicken Wing Prices $/lb.

2013 2014 2015 YTD Avg 2001-2015

40

Coffee

Corn Cheese

Food Inflation

Key Restaurant Commodities

Source: CS estimates and company data, American Restaurants Association

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

$2.60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Cheese - 40lb. blocks ($/lb.)

2013 2014

2015 YTD Avg 2007-2015

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Corn prices $/bushel

2013 2014 2015 YTD Avg. '04-'15

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Coffee Prices

$/lb.

2013 2014 2015 YTD Avg '00-'13

Prime Beef

$6

$7

$8

$9

$10

$11

$12

$13

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

"Prime" Beef Prices*

$/lb.

2013 2014 Avg '04-'15 2015 YTD

* Avg. of three beef cuts

41

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

EA

TM

CD

CA

KE

RU

TH

DIN

DR

IS

BU

XC

BR

LR

TS

ON

CB

LMN

PZ

ZA

YU

MJA

CK

DN

KN

CM

GT

XR

HK

KD

IRG

DP

ZLO

CO

BW

LDQ

SR

PN

RA

PLK

IB

JRI

WE

NC

HU

YP

BP

BR

RG

BZ

OE

SD

FR

GN

DLS

HA

BT

Free cash flow yield (FCF/EV)

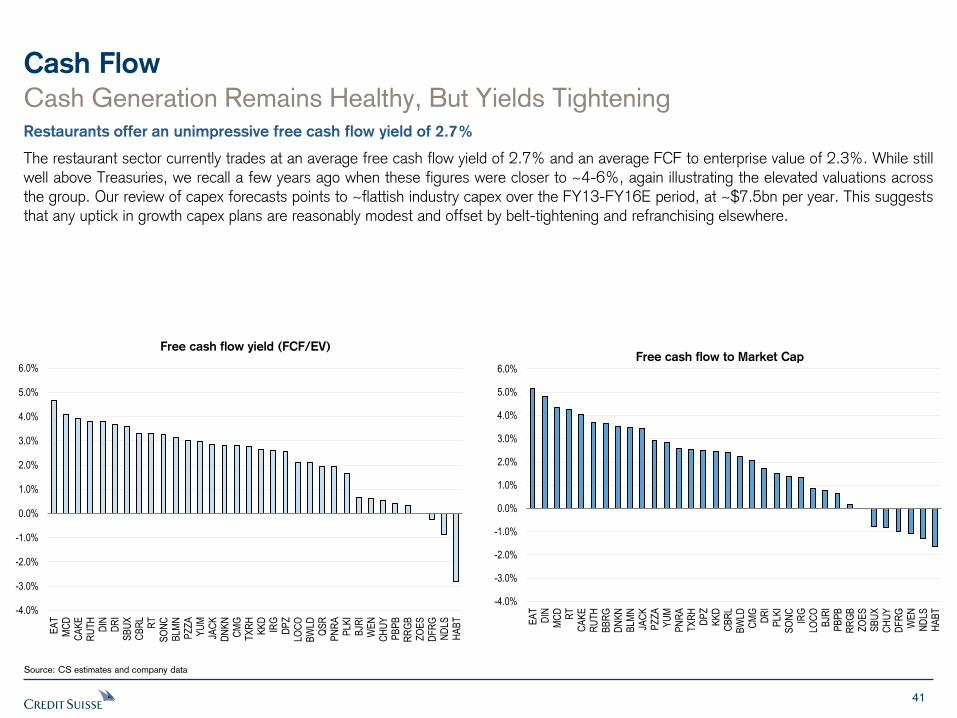

Cash Flow

Cash Generation Remains Healthy, But Yields Tightening Restaurants offer an unimpressive free cash flow yield of 2.7%

The restaurant sector currently trades at an average free cash flow yield of 2.7% and an average FCF to enterprise value of 2.3%. While still

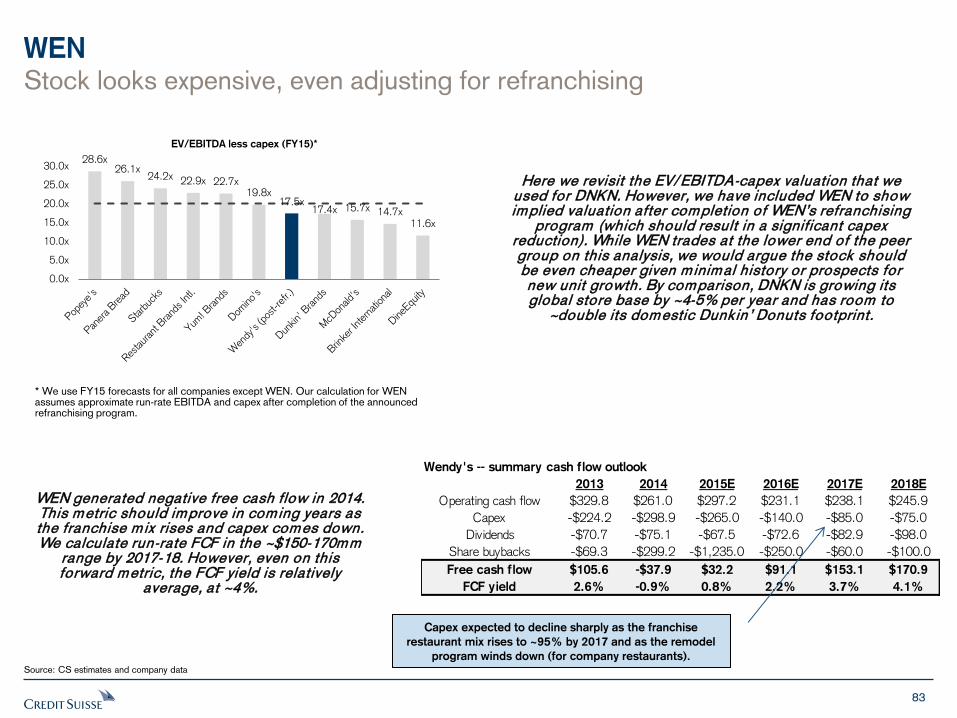

well above Treasuries, we recall a few years ago when these figures were closer to ~4-6%, again illustrating the elevated valuations across the group. Our review of capex forecasts points to ~flattish industry capex over the FY13-FY16E period, at ~$7.5bn per year. This suggests that any uptick in growth capex plans are reasonably modest and offset by belt-tightening and refranchising elsewhere.

Source: CS estimates and company data

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

EA

TD

INM

CD

RT

CA

KE

RU

TH

BB

RG

DN

KN

BLM

NJA

CK

PZ

ZA

YU

MP

NR

AT

XR

HD

PZ

KK

DC

BR

LB

WLD

CM

GD

RI

PLK

IS

ON

CIR

GLO

CO

BJR

IP

BP

BR

RG

BZ

OE

SS

BU

XC

HU

YD

FR

GW

EN

ND

LSH

AB

T

Free cash flow to Market Cap

42

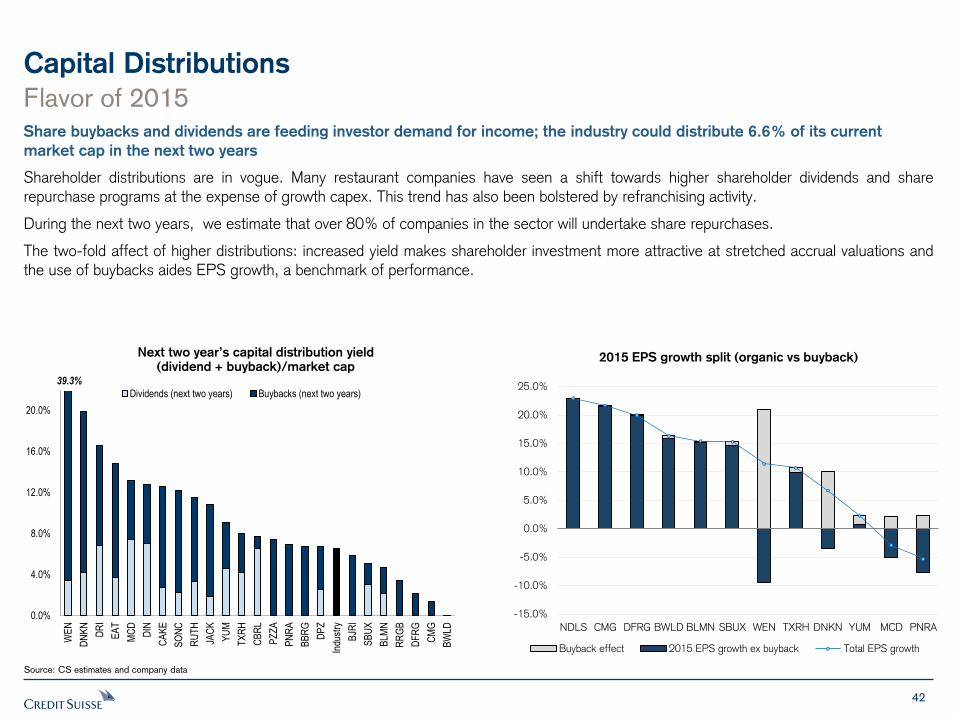

Capital Distributions

Flavor of 2015 Share buybacks and dividends are feeding investor demand for income; the industry could distribute 6.6% of its current

market cap in the next two years

Shareholder distributions are in vogue. Many restaurant companies have seen a shift towards higher shareholder dividends and share repurchase programs at the expense of growth capex. This trend has also been bolstered by refranchising activity.

During the next two years, we estimate that over 80% of companies in the sector will undertake share repurchases.

The two-fold affect of higher distributions: increased yield makes shareholder investment more attractive at stretched accrual valuations and the use of buybacks aides EPS growth, a benchmark of performance.

Source: CS estimates and company data

Next two year’s capital distribution yield (dividend + buyback)/market cap

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

NDLS CMG DFRG BWLD BLMN SBUX WEN TXRH DNKN YUM MCD PNRA

Buyback effect 2015 EPS growth ex buyback Total EPS growth

2015 EPS growth split (organic vs buyback)

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

WE

N

DN

KN

DR

I

EA

T

MC

D

DIN

CA

KE

SO

NC

RU

TH

JAC

K

YU

M

TX

RH

CB

RL

PZ

ZA

PN

RA

BB

RG

DP

Z

Indu

stry

BJR

I

SB

UX

BLM

N

RR

GB

DF

RG

CM

G

BW

LD

Dividends (next two years) Buybacks (next two years)

39.3%

43

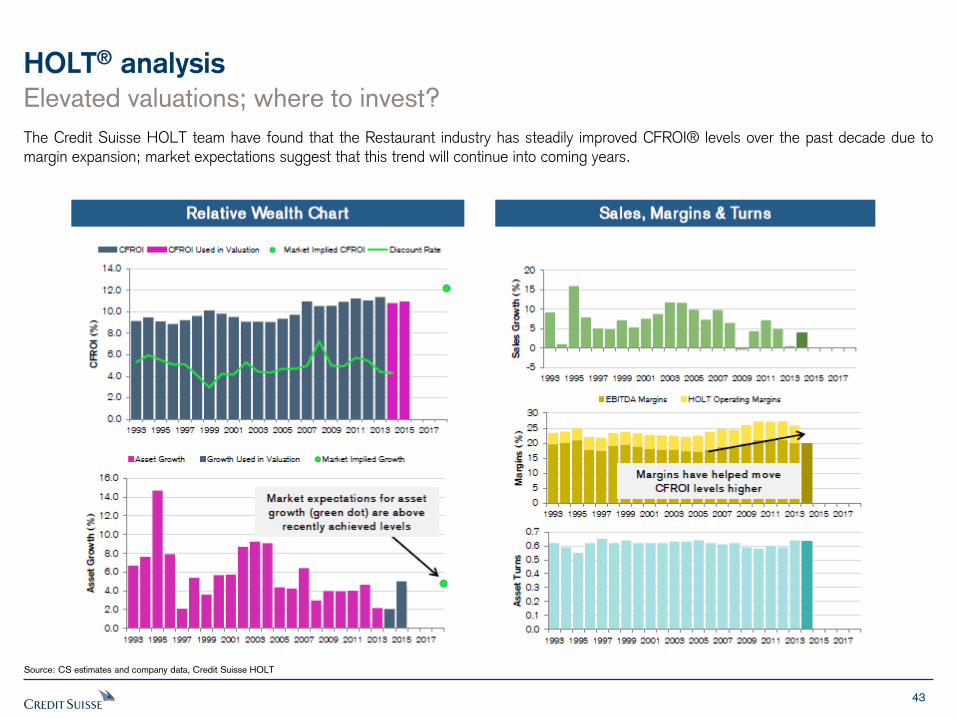

HOLT® analysis

Elevated valuations; where to invest?

Source: CS estimates and company data, Credit Suisse HOLT

The Credit Suisse HOLT team have found that the Restaurant industry has steadily improved CFROI® levels over the past decade due to margin expansion; market expectations suggest that this trend will continue into coming years.

44

HOLT analysis

Elevated valuations; where to invest?

Source: CS estimates and company data, Credit Suisse HOLT

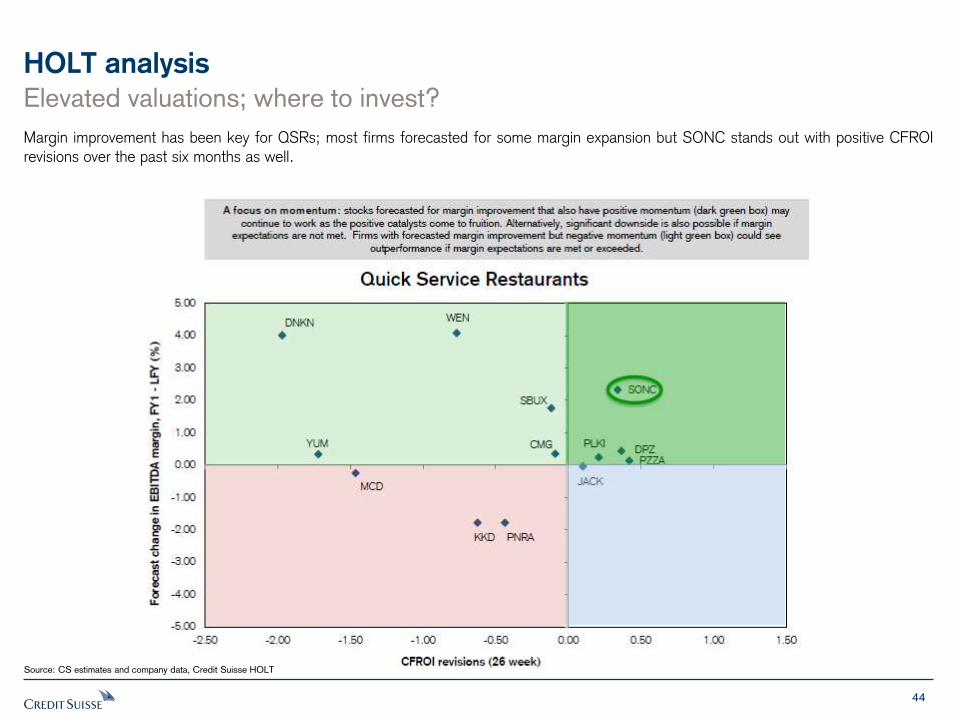

Margin improvement has been key for QSRs; most firms forecasted for some margin expansion but SONC stands out with positive CFROI revisions over the past six months as well.

45

HOLT analysis

Elevated valuations; where to invest?

Source: CS estimates and company data, Credit Suisse HOLT

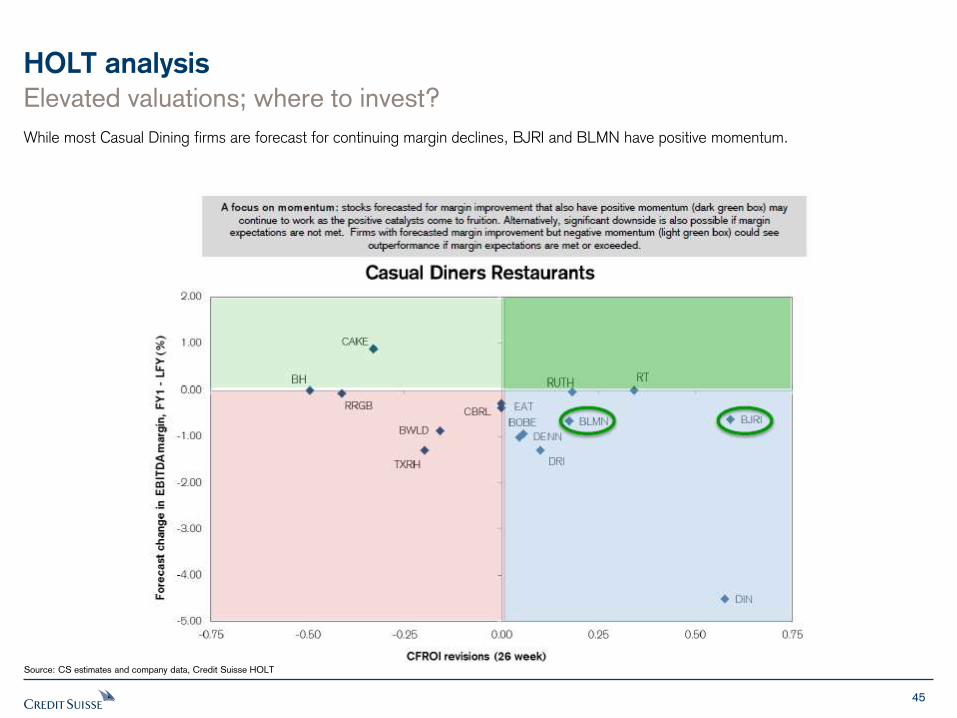

While most Casual Dining firms are forecast for continuing margin declines, BJRI and BLMN have positive momentum.

Stock Picks / Company Tear Sheets

47

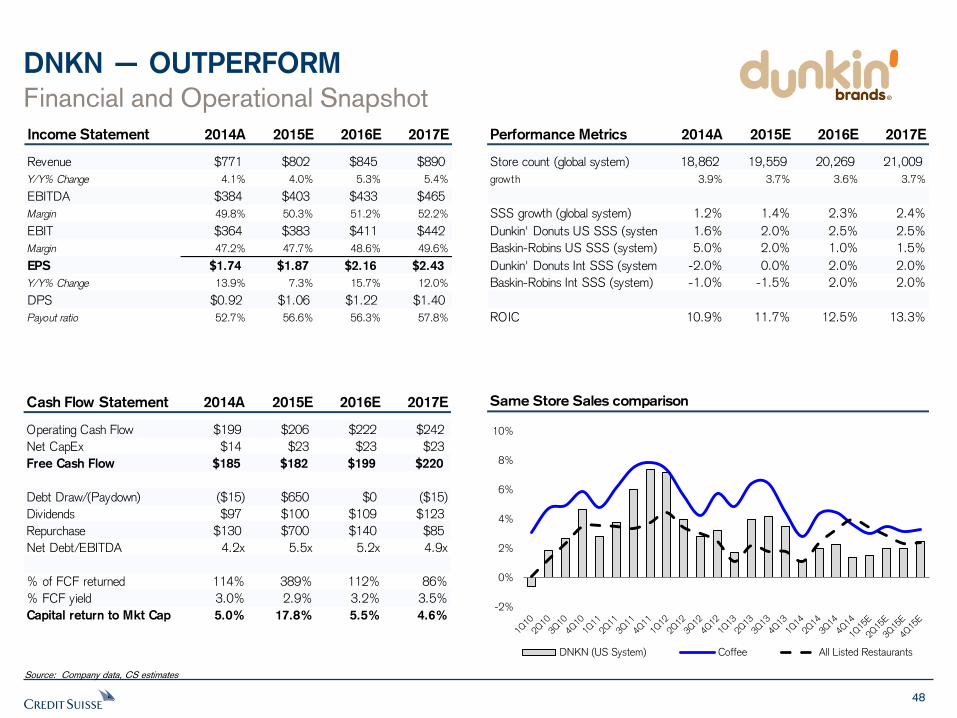

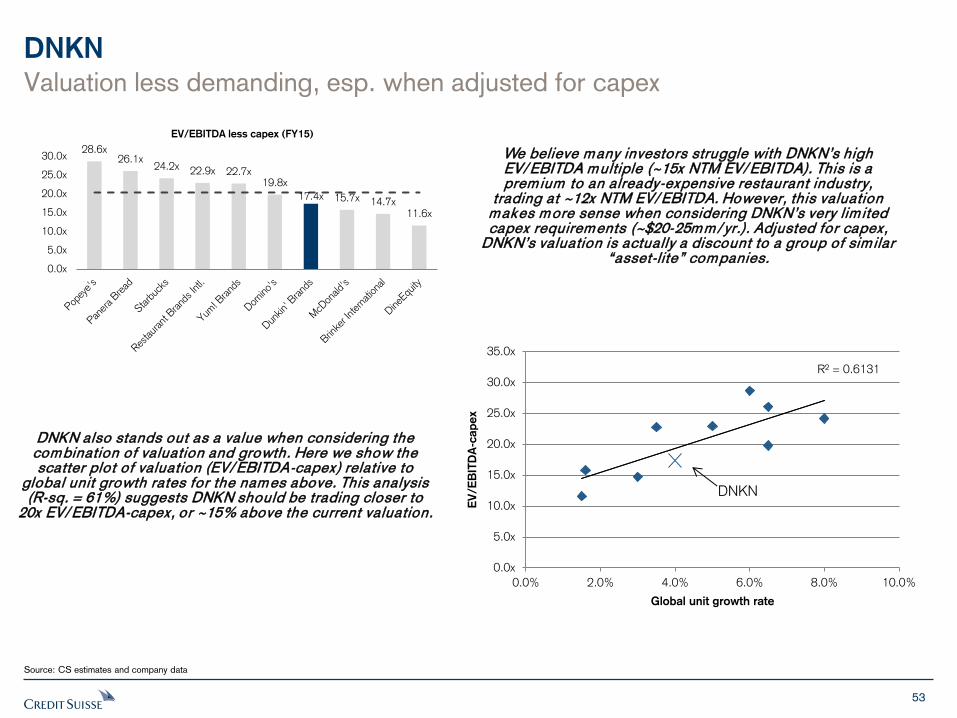

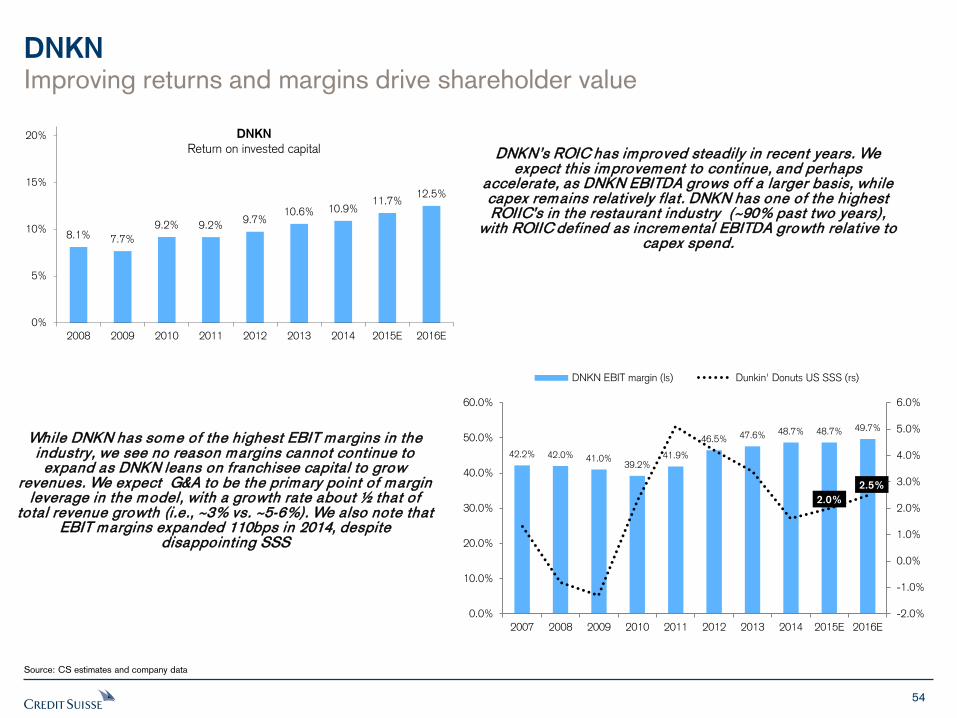

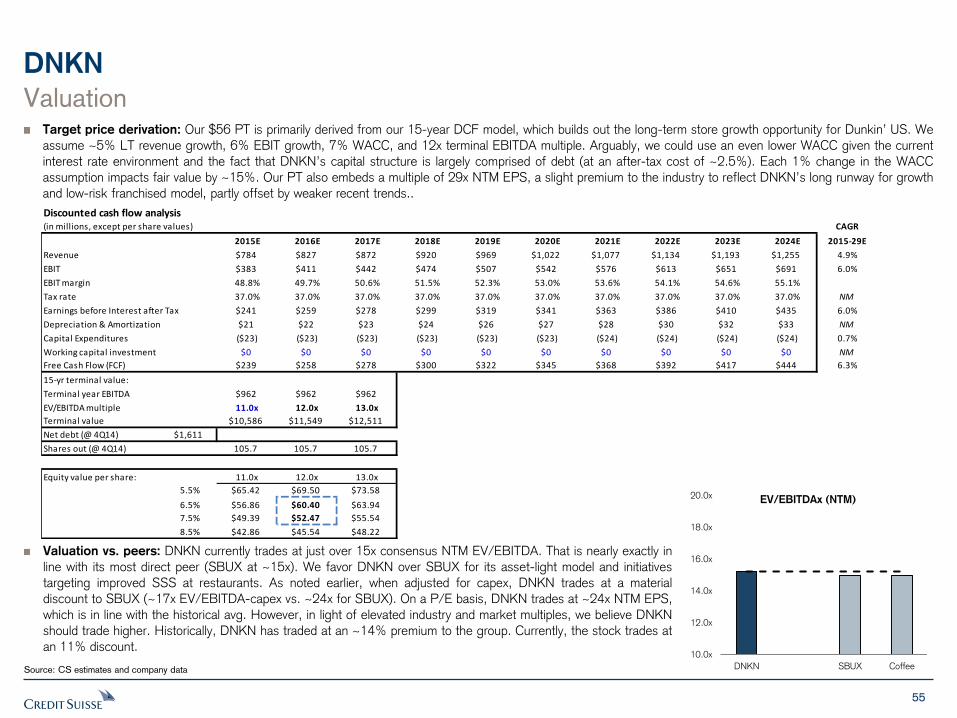

We are initiating coverage with an OUTPERFORM rating and a $56 PT. Our PT is

primarily derived from our 15-year DCF model, which builds out the long-term store growth

opportunity for Dunkin’ US. We assume ~5% LT revenue growth, 6% EBIT growth, 7%

WACC, and 12x terminal EBITDA multiple. Arguably, we could use an even lower WACC

given the current interest rate environment and the fact that DNKN’s capital structure is

largely comprised of debt (at an after-tax cost of ~2.5%). Each 1% change in the WACC

assumption impacts fair value by ~15%. Our PT also embeds a multiple of 29x NTM EPS,

a slight premium to the industry to reflect DNKN’s long runway for growth and low-risk

franchised model, partly offset by weaker recent trends.

What’s the call?: 1) Despite the disappointing 2014 comps, we believe DNKN’s domestic

unit expansion story remains on track. Franchisee profit $ and margins hit all-time highs in

2014. Our franchisee checks point to very strong demand for westward expansion, which is

the key to the DNKN story. 2) DNKN’s multiple has gone from ~28x NTM P/E to ~24x in

the past yr. This has come at a time when many other restaurant stocks are trading at or

above all-time high multiples. This discount seems unwarranted. 3) Investors are concerned

about recent SSS weakness. However, we see better days ahead, driven by improving

macro conditions for low-income consumers (incl. lower gas prices), menu pricing, and

continued adoption of mobile pay and loyalty. Dunkin’ US is in the early stages of loyalty

(Perks) expansion. Perks only represented 3% of transactions in 2014 though drove a

50bps lift to 2014 SSS. 4) DNKN has one of the most shareholder-friendly mgmt. teams

in the industry. We’re modeling $700mm in buybacks this yr. (14% of mkt. cap.).

CS vs. consensus?: We’re modeling 2015E EPS at $1.87, 1c above consensus and at

the high end of the guidance range ($1.83-1.87). Our model embeds the leveraged

buyback announced in 1Q15 but does not reflect any benefit from the broader distribution

of K-Cups (announced 2/26/15), which we estimate could add ~1-2c to ’15 estimates.

Risks to our call: The recent deceleration in Dunkin’ Donuts U.S. SSS is a concern

(+1.6% SSS in 2014). Our outlook assumes trends improve through 2015, though

weather will likely be a negative factor in 1Q15 (CS modeling +1.5% vs. cons. +1.9%).

Upcoming events/potential catalysts:

– 1Q results in April

– Investor day in Sept. ’15 (tentative)

Longevity in Its Model

DNKN — OUTPERFORM ($56 PT)

Dunkin’ Brands is a franchisor of quick service restaurants serving hot

and cold coffee and baked goods, as well as hard-serve ice cream.

The company franchises restaurants under its Dunkin' Donuts and

Baskin-Robbins brands, with nearly 100% of system restaurants

franchised. The company has nearly 19k points of distribution in nearly

60 countries. The company operates in four segments: Dunkin' Donuts

U.S., Dunkin' Donuts International, Baskin-Robbins International, and

Baskin-Robbins United States. DNKN is headquartered in Canton, MA.

Source: Company data, CS estimates, Bloomberg

Company Description

Price-Earnings History (Consensus 12-Months Forward)

EPS (2015) SSS (Dunkin’ US 2015)

CS

$1.87

Cons.

$1.86

CS

2.0%

Cons.

2.1%

Analyst Ratings

BUY

13

SELL

1

HOLD

13

Market Forecasts and Ratings

DNKN