recent judicial developments affecting investments into and

TRANSCRIPT

69

Recent Judicial Developments Affecting Investments Into and Out of the United Kingdom Michael McGowan and Andrew Thomson*

This article reports on two sets of judicial developments in the United Kingdom of interest to U.S. companies and investors con-sidering investing in them. First, the authors discuss the U.K. Upper Tribunal’s reversal of a lower court decision dealing with the U.K. classifi cation for tax purposes of a Delaware limited lia-bility company (LLC), which creates the potential for double taxa-tion and thus might dissuade a taxpayer considering investment in such an LLC. Second, the authors look at a U.K. Supreme Court decision on the concept of residence for U.K. tax purposes. As the global economy expands, and more and more individuals work abroad, the U.K. residency question is of importance to “expat” employees and their employers, in the U.S. and elsewhere.

Continuing Uncertainty Regarding Entity Classifi cation for U.K. Tax Purposes: Is a Delaware LLC “Tax-Transparent”? The question as to whether a non-U.K. entity such as a Delaware limited liability company (LLC) should be treated as transparent or opaque for U.K. tax purposes can make a signifi cant difference to the amount and timing of tax incurred by a taxpayer investing in it. The U.K. Upper Tribunal has now reversed the 2010 fi rst instance decision (reported as Swift v. HMRC , 1 and discussed in a previous issue of this journal 2 ) and has concluded that a Dela-ware LLC should be treated as opaque for U.K. foreign tax credit purposes. The decision creates economic double taxation. The LLC in this case does not seem to have had any particularly unusual features. Given the large num-ber of companies structured as Delaware LLCs and the increasingly global

* Michael McGowan is a partner and Andrew Thomson is a senior associate in the London offi ce of Sullivan & Cromwell LLP. They may be contacted by email at [email protected] and [email protected], respectively.

1 [2010] UKFTT 88 (TC).

2 Michael McGowan & Andrew Howard, “Ongoing Uncertainty Regarding Entity Classi fi cation for U.K. Tax Purposes: Swift v. HMRC ,” 27(4) J. Tax’n Invs. 77 (Summer 2010).

© 2012 Civic Research Institute

Authorized Reprint

©

JOURNAL OF TAXATION OF INVESTMENTS70

nature of business fi nance, how jurisdictions outside the U.S. view these vehicles can be very signifi cant.

The decision itself may be further appealed by the taxpayer but it clari-fi es the income tax treatment of a U.K. investor in an LLC. There are also other long-standing questions on the U.K. treatment of non-U.K. entities, such as whether inserting an LLC in a corporate chain can disrupt a U.K. tax “group,” and the decision may be relevant to these.

This part of the article sets out some of the issues that a U.K. taxpayer considering an investment in an LLC will need to consider by reference to the decision in this case. U.K. taxpayers face similar issues when considering investment in other non-U.K. entities that are not clearly equivalent to com-panies formed under English law.

HMRC v. Anson . HMRC v. Anson 3 has underlined the risk of economic double taxation that will be faced by a U.K. investor in a Delaware LLC, espe-cially if that investor is an individual relying on U.K. foreign tax credit relief to avoid double taxation. The U.K. does not have clear rules about whether to treat an investment in an LLC as equivalent to an investment in a partnership (tax transparent) or in a company (tax opaque) for tax purposes. The pub-lished guidance of the U.K. tax authority, HMRC (formerly the Inland Rev-enue), while recognizing that the individual facts must be considered in each case, indicates that the default position is that an LLC should be treated as opaque. 4 The outcome of the case (which may be further appealed) was that the LLC in question was opaque. This is consistent with HMRC’s view but contrary to the view of the First Tier Tribunal (when it ruled in the same case, there anonymized as Swift v. IRC ) in early 2010.

The difference in treatment can signifi cantly affect the amount of tax payable, as the facts of the case illustrate. Mr. Anson is a venture capital-ist who, together with his colleagues, set up HarbourVest Partners LLC (HVLLC), which acted as an investment manager to various venture capital funds, receiving fee income. All profi ts were distributed to the members. The key question in the case was whether Mr. Anson was able to credit U.S. tax paid on the LLC’s activities against his U.K. tax liability on the distributions made to him by the LLC. If he was entitled to a credit, out of a profi t share of 100, he would have suffered roughly 45 of U.S. tax on dis-tributed or undistributed profi ts, but would have no U.K. tax to pay (given U.K. tax rates at that time). If, as HMRC contended and the Upper Tribunal ruled, he was not entitled to a credit, he would be liable for further U.K. tax of 22, on top of the U.S. tax of 45, as and when profi ts were distributed to him.

3 [2011] UKUT 318 (TCC).

4 HMRC International Manual (INTM) at 180030.

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 71

A U.K. foreign tax credit was available if the U.K. tax and the U.S. tax were computed by reference to the same profi ts. 5 The Upper Tribunal found that Mr. Anson paid tax in the U.S. on his share of the profi ts of the LLC (dis-tributed or undistributed) on the basis that HVLLC was treated as a partner-ship for U.S. federal and state tax purposes. If the LLC was opaque for U.K. tax purposes, the U.K. tax would have been on the equivalent of a dividend, a separate income source which would not constitute the same profi ts as those subject to U.S. tax. Therefore no foreign tax credit would be available for a U.K.-resident non-corporate taxpayer.

Entity Classifi cation. The essential question for U.K. tax purposes was whether to treat the U.K. taxpayer as being taxable on his share of the LLC’s underlying income (whether or not distributed) or whether to recognize the LLC as a separate corporate entity and treat the U.K. taxpayer as receiving some form of distribution from the LLC (only taxable in the U.K. if distribu-tions are actually received). In the former case, the U.K. would give credit for the U.S. tax paid by Mr. Anson; in the latter it would not. In the handful of decided cases, the U.K. courts have approached this question on an ad hoc basis, largely by asking whether non-U.K. entities are suffi ciently similar to U.K. partnerships to be treated as “transparent” for the purposes of U.K. tax. U.K. partnerships include types where some partners have limited liability 6 and types with legal personality. 7 Hence, despite uncertainties in the past, the fact that an entity has legal personality does not mean that it cannot be viewed as a partnership for U.K. entity classifi cation purposes. However, legal persona lity does complicate matters when deciding whether an entity can be treated as “transparent” for U.K. tax purposes.

Confusingly, a U.K. limited liability partnership (as opposed to a lim-ited partnership) is a form of U.K. body corporate, not a partnership as such, under the separate statute creating U.K. limited liability partnerships. How-ever, such an entity is expressly treated as a partnership for U.K. tax purposes in most cases (although not for stamp duty purposes). It will not be one of the partnerships to which the courts will have regard in making the comparison mentioned in the previous paragraph.

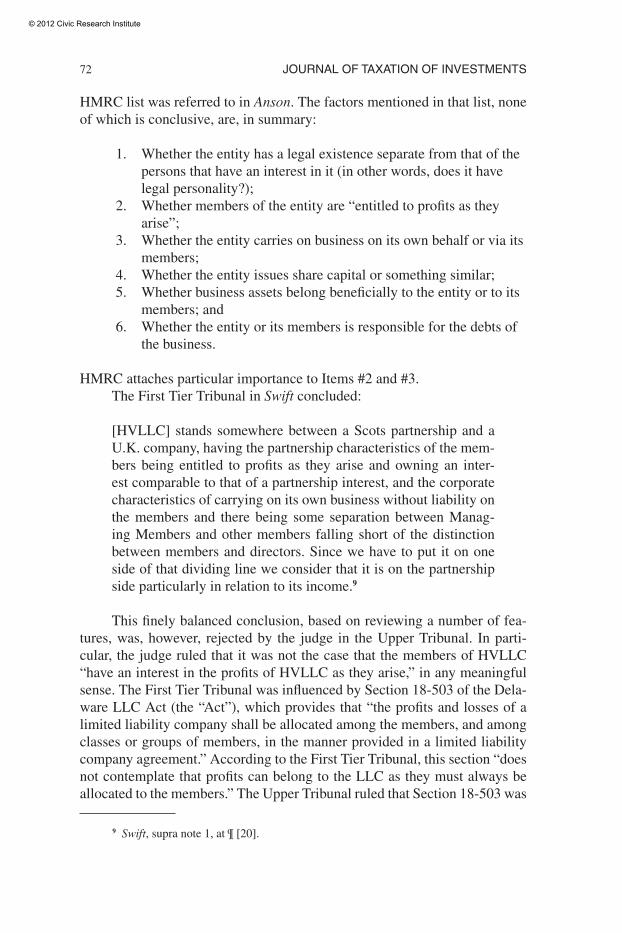

HMRC has published a list of relevant factors for the purposes of clas-sifying non-U.K. entities. 8 These factors have no statutory force but repre-sent HMRC’s distillation of the limited guidance provided by the courts. The

5 Article 24(4) of the U.K./U.S. Double Tax Convention of 24 July 2001 (SI 2002/2848) (the “Treaty”).

6 That is, partnerships under the U.K.’s Limited Partnership Act of 1907.

7 That is, Scottish partnerships, although these are rarer than English partnerships, which lack legal personality.

8 INTM, supra note 4, at ¶ 180010.

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS72

9 Swift, supra note 1, at ¶ [20].

HMRC list was referred to in Anson . The factors mentioned in that list, none of which is conclusive, are, in summary:

1. Whether the entity has a legal existence separate from that of the persons that have an interest in it (in other words, does it have legal personality?);

2. Whether members of the entity are “entitled to profi ts as they arise”;

3. Whether the entity carries on business on its own behalf or via its members;

4. Whether the entity issues share capital or something similar; 5. Whether business assets belong benefi cially to the entity or to its

members; and 6. Whether the entity or its members is responsible for the debts of

the business.

HMRC attaches particular importance to Items #2 and #3. The First Tier Tribunal in Swift concluded:

[HVLLC] stands somewhere between a Scots partnership and a U.K. company, having the partnership characteristics of the mem-bers being entitled to profi ts as they arise and owning an inter-est comparable to that of a partnership interest, and the corporate characteristics of carrying on its own business without liability on the members and there being some separation between Manag-ing Members and other members falling short of the distinction between members and directors. Since we have to put it on one side of that dividing line we consider that it is on the partnership side particularly in relation to its income. 9

This fi nely balanced conclusion, based on reviewing a number of fea-tures, was, however, rejected by the judge in the Upper Tribunal. In parti-cular, the judge ruled that it was not the case that the members of HVLLC “have an interest in the profi ts of HVLLC as they arise,” in any meaningful sense. The First Tier Tribunal was infl uenced by Section 18-503 of the Dela-ware LLC Act (the “Act”), which provides that “the profi ts and losses of a limited liability company shall be allocated among the members, and among classes or groups of members, in the manner provided in a limited liability company agreement.” According to the First Tier Tribunal, this section “does not contemplate that profi ts can belong to the LLC as they must always be allocated to the members.” The Upper Tribunal ruled that Section 18-503 was

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 73

10 Memec plc v. IRC, [1998] STC 754.

11 Defi ned in Section 1119 of the U.K.’s Corporation Tax Act of 2010 to include all share capital other than fi xed-rate preference shares.

12 HMRC Business Brief 87/09; this is another non-statutory distillation of the few relevant judicial decisions.

irrelevant, dealing merely with profi t allocation and not with the distinct—but for U.K. foreign tax credit purposes essential—question of whether an LLC member had an underlying proprietary interest (if only indirect) in the assets of the LLC. On the evidence, the Upper Tribunal ruled that there was no such proprietary interest. Instead, the Upper Tribunal described an LLC member’s interest as a mere contractual claim against the LLC entity. It equated it with the “silent partner’s” interest in the Memec case, 10 which also did not entitle the holder to a credit for non-U.K. tax in respect of underlying profi ts. Less convincingly, the Upper Tribunal held that a partner’s interest in a Scottish partnership (which also has separate legal personality) was different from an LLC member’s interest because, in a “real sense,” the profi ts and assets of a Scottish partnership belong to its partners and the partnership is their “alter ego,” despite its separate legal persona.

One other factor that pointed the First Tier Tribunal toward transparent treatment was that a member “owns an interest comparable to that of a part-nership interest,” not least because of the requirement for consent from other members before that interest could be transferred. The Upper Tribunal did not attach any signifi cance to this feature.

Tax Grouping. Another area of U.K. tax law in which the classifi cation of non-U.K. entities is important is that of grouping. In order to be part of a group for most U.K. tax purposes (including capital gains, group relief, and stamp duty), an entity must be a “body corporate” having “ordinary share capital.” 11 Not only will an entity without ordinary share capital (e.g., a com-pany limited by guarantee) not form part of the group, but HMRC may also take the view that it is not possible to trace a wider group through it, with the possible exception of instances where all the members of the entity are also part of the group. The inclusion of an entity without ordinary share capital can therefore cause the unexpected loss of the various group reliefs which would otherwise be available. Indeed, avoiding the creation of groups or splitting them by inserting companies limited by guarantee is a standard tax-planning technique.

The U.K. approaches this question by asking whether a member’s inter-est is analogous to a holding of ordinary share capital in an English company. Again this is not a bright-line test but a question of fact and degree to be determined by reference to the relevant non-U.K. corporate law and a number of factors set out in HMRC guidance. 12

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS74

Since 2007, HMRC has taken the view that it is not necessary for a member to have availed itself of the possibility provided under Section 18-702c of the Act (which allows for a member’s interest to be evidenced by a certifi cate issued by the LLC) in order for the LLC to be regarded as having ordinary share capital. The Upper Tribunal did not discuss this issue, presum-ably because corporate grouping was not directly in point.

Nonetheless, an LLC which issues certifi cates and has transfer provi-sions similar to those of an English company, where transfers are registered (whether or not subject to approval by the other members), is in our view likely to be considered as having ordinary share capital. This is separate from the question of whether an LLC should be treated as opaque for the purposes of taxing its members in the U.K.

Practical Implications of Anson . Although it is closer to most practitio-ners’ views than the First Tier Tribunal decision, the Upper Tribunal decision in Anson illustrates the unsatisfactory nature of U.K. tax law in its approach to entity classifi cation: unless all factors point in the same direction, there is always going to be some scope for argument and therefore some uncertainty for the taxpayer. That uncertainty is compounded by the need for detailed review of non-U.K. legal documents (often not in English) and the need to obtain expert evidence on non-U.K. legal questions. Evidence of the relevant non-U.K. law is crucial and, so far as a U.K. court is concerned, is a matter of fact. However, the ultimate question of entity classifi cation is a U.K. legal question.

By the time this case came to court, HVLLC (presumably because Mr. Anson had become aware of his tax exposure) had restructured to become a limited partnership. HMRC has historically tended to accept that a Delaware limited partnership is “transparent” even though it has legal personality. In many cases, a U.K. investor’s best hope for certainty may be to use a different vehicle for which the law, or at least HMRC’s practice, is clearer. Of course, in many cases, this option will not be available. There may also be problems fi nding an appropriate vehicle whose treatment is clear. It is not automatically the case that a non-U.K. entity described as a partnership will be treated as a partnership for U.K. tax purposes. The strong focus of the Upper Tribunal on whether an LLC member has a direct or indirect proprietary interest in the entity’s assets makes it harder (though not impossible) to treat a non-U.K. “partnership” entity with legal personality as a partnership or otherwise transparent for U.K. tax purposes.

Taxpayers and their advisers have diffi cult choices to make because uncertainty may be the price of potentially benefi cial tax treatment. In this case, the taxpayer was not entitled to credit for underlying tax under the Treaty because the Treaty only gives credit for underlying tax to a corporate taxpayer, not to an individual. However, in other cases or under other treaties,

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 75

13 Memec , supra note 10.

14 Part 9A of the Corporation Tax Act of 2009.

15 A recent U.K. Supreme Court decision on the tax residence of individuals is discussed in the second part of this article.

16 Although there are now situations where partnership-type arrangements for collective investment are required by Section 103A of the Taxation of Chargeable Gains Act of 1992 to be treated as opaque, but only for the purposes of U.K. tax on capital gains, not income.

17 See, for example, the 2008 agreement with France.

the conditions for underlying tax relief may be fulfi lled. Underlying tax relief is typically limited to underlying tax paid by a “company.” An earlier case illustrates that an entity that fails to meet the conditions for transparency will not necessarily be treated as a company for these purposes. 13 Hence the dis-tinction between a partnership and a company is not always the same as the distinction between a transparent and an opaque entity. A similar issue needs to be considered by corporate taxpayers in determining whether the U.K.’s distribution exemption 14 will apply to distributions received from a non-U.K. entity that is treated as opaque.

For U.K.-resident individuals, 15 the availability of a credit under the Treaty means that in most circumstances they are likely to prefer transparent entities. However, there are a number of other factors to consider if a choice of entity is available. If an entity is transparent for income purposes, it is also likely to be transparent for the purposes of U.K. tax on capital gains on the basis that it is a “partnership” within Section 59 of the U.K.’s Taxation of Chargeable Gains Act of 1992. 16 This means that a member will be treated as disposing of his fractional share of any capital asset disposed of by the entity (a credit for any non-U.K. tax should be available). The amount and timing of the income inclusion will also be different if an entity is transparent. This will be particularly signifi cant if the entity rolls up its income rather than distributing it.

The rules are similar for U.K. corporation taxpayers but they are likely to have a different perspective, particularly as distributions from opaque vehicles will be tax-exempt in most cases. Hence, they are less likely to be concerned about the availability of credit under a double taxation agreement. They will also want to have regard to the tax grouping issues mentioned above.

Wider Implications. While the Anson case related to a Delaware LLC, the same principles are applicable to other non-U.K. entities. Other entities which give rise to particular uncertainty include Dutch CVs, LLCs estab-lished under the laws of other U.S. states, and German silent partnerships.

There are detailed provisions dealing with the treatment of fi scally transparent entities in the Treaty and in other more recent U.K. double tax agreements. 17 Hence, entity classifi cation issues are to some extent reduced

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS76

18 See the Report of the OECD Committee on Fiscal Affairs on the Application of the OECD Model Tax Convention to Partnerships, 1999.

19 R (on the application of Davies and James) and R (on the application of Gaines-Cooper) v. HMRC, [2011] UKSC 47.

in the U.K./U.S. context. However, tax authorities have traditionally had some trouble with the treatment of such entities, particularly under double tax agreements where the jurisdictions in question treat an entity differently for tax purposes. 18 The U.K. now has legislation overriding attempts by U.K. residents to exploit the U.K.’s tax treaties so that fi scal transparency leads to income being taxable in neither jurisdiction. On the other hand, as Anson shows, it is not necessarily the case that the U.K. tax rules will be effective to prevent economic double taxation where such hybrid treatment of non-U.K. entities arises.

The overall result remains highly unsatisfactory. Not only are the law and HMRC guidance unclear but there is also a lack of guiding principle as to when entities should be treated as “transparent” for U.K. tax purposes and what this means. Key classifi cation questions can turn on very fi ne distinc-tions requiring detailed examination of non-U.K. law and the constitutional documents of non-U.K. entities. It was the cost, complexity, and uncertainty of such an approach which led the U.S. to adopt the “check-the-box” rules in 1997. Unfortunately, the U.K. still seems a long way from adopting an equally practical solution, notwithstanding the general focus of HM Treasury on making the U.K. corporate tax system more user-friendly for international investors.

U.K. Tax Residence The U.K. Supreme Court has handed down its judgment in Davies and Gaines-Cooper , 19 two judicial review cases on the tax residence of indi-viduals. The taxpayers argued that HM Revenue and Customs had said in guidance, and consistently taken the view in practice, that it would treat indi-viduals in their circumstances as not resident in the United Kingdom; since HMRC was refusing to apply that treatment, the court should intervene and hold HMRC to its word. HMRC, however, succeeded in convincing the court that the taxpayers had misunderstood the guidance and that there was no settled practice of the sort the taxpayers claimed.

The guidance itself has now been extensively revised. However, the Supreme Court’s judgment and the litigation leading up to it do raise wider issues:

• The decision underscores the risks in relying on HMRC guidance and—even more so—any supposed general HMRC practice. It will

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 77

20 Levene v. The Commissioners of Inland Revenue, (1928) 13 TC 486, 502 (Viscount Sumner).

21 Most recently Grace v. Revenue and Customs Commissioners, [2011] UKFTT 36 (TC).

be an uphill struggle for taxpayers to convince the courts that HMRC has bound itself to take any particular approach.

• The judgment also offers a reminder of the current law on what a taxpayer must do to shed U.K.-resident status: among other things, the taxpayer must show a distinct break from his or her life in the U.K. (going abroad to work full-time will often qualify).

• The case points up the pressing need to move to a clearer statutory defi nition of residence, as the government proposes to do.

• Finally, the litigation has raised points on (1) whether a taxpayer should apply for judicial review of the way HMRC has exercised its discretion before it begins a dispute on the law through an appeal to the Tribunal (in the circumstances, yes); and (2) whether the public is entitled under the Civil Procedure Rules to see the skeleton argu-ments HMRC provides to judges (in general, yes).

As the global economy expands, and more and more individuals work abroad, the U.K. residency question gains importance for both “expat” employees and their employers, in the U.S. and elsewhere. Untoward tax treatment could, for example, lead to tax problems for a U.S. employee work-ing in her fi rm’s London branch, or for a U.K. employee deployed to a New York offi ce.

Statutory Law on Residence. “Residence” and “ordinary residence” are key connecting factors for U.K. income tax, capital gains tax, and some-times inheritance tax. Nonetheless, the U.K. Parliament has never fully defi ned what it means for an individual to be “resident or ordinarily resident in the United Kingdom” for tax purposes. Even the judges have complained: “[t]he facility of communications, the fl uid and restless character of social habits, and the pressure of taxation have made these intricate and doubtful questions of residence important and urgent in a manner undreamt of by Mr. Pitt, Mr. Addington or even Sir Robert Peel. The legislature has, however, left the language of the acts substantially as it was in their days.” 20 In 1936 the income tax codifi cation committee proposed a statutory defi nition. But this was never enacted.

Prior Case Law on Residence. The task of defi ning what it is for an indi-vidual to be “resident” in the U.K. has fallen, by default, to the courts. Many of the cases are old, although there has been a fresh spate since 2000. 21 Judges have identifi ed several factors as relevant:

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS78

22 Or, in a couple of cases, “her.”

23 Gaines-Cooper v. Commissioners for HMRC, (2006) SpC 568.

24 “Guidance on Residence, Domicile and the Remittance Basis,” available at www.hmrc.gov.uk/cnr/hmrc6.pdf . A version of IR20 including Business Brief 1/2007 as an appen-dix and noting that it is no longer current is available at www.hmrc.gov.uk/pdfs/ir20.pdf .

• Whether an individual has accommodation available to him 22 in the U.K.;

• Whether he is employed abroad; • The length, purpose, and frequency of his visits to the U.K.; and • The extent of his ties to the U.K.

The result is a test which is highly fact-sensitive and diffi cult to apply in practice. It causes most problems for the many peripatetic individuals who visit the U.K. for extended periods and/or work here but also live and work elsewhere. The test does not simply depend on counting days spent in the U.K. In particular, the strict legal position is that taxpayers leaving the U.K. and claiming to be non-U.K. resident/ordinarily resident must make a “dis-tinct break” with the pattern of their lives in the U.K., unless they are leaving to work abroad full-time.

Guidance. In practice, however, HMRC has played a signifi cant role, both by adopting extra-statutory concessions and by publishing guidance. It is the guidance known as IR20 which was at issue in Davies and Gaines-Cooper. The Inland Revenue published the fi rst edition of IR20 in 1973 and the one at issue in 1999. In January 2007, following the Special Commissioners’ decision in Gaines-Cooper, 23 HMRC issued Business Brief 1/2007, giving HMRC’s interpretation of IR20 (which HMRC claimed had always been the same). HMRC then replaced IR20 with HMRC6 in 2009. 24

Consultation. Since 1928 “the facility of communications, the fl uid and restless character of social habits, and the pressure of taxation” have increased by leaps and bounds. This, coupled with the inadequacy of HMRC’s guid-ance and the lack of clear law, has given rise to a general concern that the existing rules are unacceptably vague, especially for the many internationally mobile individuals whose role is so important to the U.S. and U.K. econo-mies. On June 17, 2011, HM Treasury and HMRC published a consultation document entitled “Statutory defi nition of tax residence: a consultation.” The government proposed that a new statutory defi nition of residence for individ-uals would be included in the Finance Bill of 2012 and apply from April 6, 2012. The proposals were not intended to change the position of most taxpay-ers. The consultation closed on September 9, 2011, and received a broadly positive response. Timing has since slipped, however: on December 6

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 79

25 The appellate body now superseded for most purposes by the First-tier Tribunal (Tax).

26 [2007] EWHC 2617 (Ch).

27 The appeal is a statutory process; judicial review is an administrative law process deriving from the inherent jurisdiction of the court to review the exercise by public bodies (like HMRC) of their statutory powers. Different procedures apply to the two remedies. What the appellant/applicant must prove also differs: at its very simplest, a taxpayer should win an appeal if HMRC’s decision on the law is technically wrong; he should win on judicial review if HMRC is being (suffi ciently) unreasonable.

the government announced that the consultation had raised “a number of detailed issues,” so the new defi nition would not be brought in until 2013.

The Gaines-Cooper Case. Mr. Gaines-Cooper was born in the U.K. and remains a British citizen. A serial entrepreneur, Mr. Gaines-Cooper left the U.K. in the mid-1970s to live overseas, principally in the Seychelles, where he was granted a residence permit in 1976. Since the 1970s he has had business interests in several countries outside the U.K. Mr. Gaines-Cooper retained properties in the U.K. and returned to the U.K. to visit family; further, his wife and son maintained a home in the U.K. from 1998 until 2005 while his son attended school.

HMRC Determination. HMRC issued assessments and amendments against Mr. Gaines-Cooper’s self-assessments for the tax years 1992-1993 to 2003-2004, claiming that throughout that period his domicile, residence, and ordinary residence were in the United Kingdom.

Appeals. Mr. Gaines-Cooper’s case before the Special Commissioners 25 was that he was not domiciled, resident, or ordinarily resident in the U.K. for the period in question. (There was one exception: he accepted that he was resident in the U.K. in the tax year 1992-1993. For that year only, the fact that he had a house in the U.K. made him resident automatically. That rule was then abolished.) The Special Commissioners found that, as a question of fact, Mr. Gaines-Cooper had not demonstrated a suffi cient break with the U.K. to shed his U.K. domicile, or to establish that he was neither resident nor ordi-narily resident in the U.K. for those periods. Mr. Gaines-Cooper appealed to the High Court on the question of U.K. domicile. The High Court 26 upheld the Special Commissioners’ fi nding that Mr. Gaines-Cooper remained U.K.-domiciled. Mr. Gaines-Cooper did not appeal this decision.

Application for judicial review. Between those two appeals Mr. Gaines-Cooper also applied to the High Court for judicial review of HMRC’s conduct in determining his residence and ordinary residence. 27 HMRC had failed, he said, to apply to him the policy set out in IR20 or (alternatively) HMRC’s settled practice. It was this that fell to be considered by the Court of Appeal, and subsequently by the Supreme Court.

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS80

28 The fi rst day of the U.K. tax year for individuals.

29 An appeal would now usually be heard fi rst by the First-Tier Tribunal (Tax).

30 [2008] EWHC 2608 (Admin) and [2008] EWHC 1218 (Admin) respectively.

31 [2010] EWCA Civ 83. A judicial review procedure is actually in two stages: the appli-cant must fi rst apply for permission to apply for judicial review, then apply for judicial review itself. Before the High Court the taxpayers failed at the fi rst hurdle. The Court of Appeal fi rst granted the taxpayers permission to apply and then heard the application for judicial review itself. This is why it was the Court of Appeal which heard evidence from HMRC and the taxpayers’ witnesses.

The Davies and James Case. Mr. Davies and Mr. James are both Brit-ish citizens and property developers who moved from the U.K. to Brussels in 2001 in order to set up a new property development business. They left the U.K. (and claimed that their full-time employment abroad began) before April 6, 2001. 28 They rented apartments in Brussels and worked full-time for the Brussels business for a number of years. Mr. Davies and Mr. James retained their homes in the U.K., and returned to the U.K. to attend local functions and to visit their families, who remained in the U.K.

HMRC Determination. HMRC issued determinations against Mr. Davies and Mr. James, claiming that they were resident and ordinarily resident in the U.K. in the tax year 2001-2002, when they had made signifi cant asset disposals for capital gains tax purposes. HMRC considered that their work did not start until after April 5, 2001: as they were not employed full-time for the whole tax year 2001-2002, they could not establish non-residence in the U.K. for the 2001-2002 tax year either as a legal matter or on the basis of the IR20 practice on full-time work abroad.

Application for Judicial Review and Appeal. Mr. Davies and Mr. James followed a different path than did Mr. Gaines-Cooper, applying to the High Court for judicial review before any appeal was heard. Like Mr. Gaines-Cooper, they claimed that HMRC had improperly failed to apply its guidance in IR20 or its settled practice.

They also fi led an appeal with the Special Commissioners to dispute HMRC’s conclusions as a matter of law. They succeeded in convincing the Court of Appeal that the judicial review should be heard fi rst, on the basis that a decision of the Special Commissioners against them would pre-empt the result of the judicial review. The appeal was therefore stayed until the application for judicial review could run its course. 29

Combined Judicial Review at the Court of Appeal. Mr. Gaines-Cooper and, separately, Mr. Davies and Mr. James, applied to the High Court for judicial review of HMRC’s failure (as they saw it) to apply IR20 or its settled practice. 30 In both cases the High Court refused permission to apply for judicial review. The taxpayers appealed. The Court of Appeal decided to hear both appeals together. 31

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 81

32 In R v. Inland Revenue Commissioners, ex parte MFK Underwriting Agencies Ltd and related applications, [1989] STC 873.

33 For example, R v. Inland Revenue Commissioners, ex parte Wilkinson, 77 TC 78; Al Fayed v. Advocate General for Scotland, 77 TC 273.

Legitimate Expectation. As far back as 1990 the Court of Appeal had established the principle that HMRC could be bound to honor statements made to the public as to how it would treat a taxpayer, if those statements gave rise to a legitimate expectation that it would fulfi l them. 32 Subsequent cases have clarifi ed the limits to that principle. 33 HMRC had placed some emphasis on these limitations and on disclaimers at the beginning of IR20 in the early stages of the litigation. By the time the case reached the Court of Appeal, however, HMRC was explicitly accepting that “the taxpayer has a legitimate expectation that it will apply the guidance in IR20 to the facts of his particular case and if satisfi ed that the facts fall within one of the circum-stances in Section 2 indicating a certain residence treatment, will treat him accordingly.”

Working Abroad. Mr. Davies and Mr. James argued that they were non-resident on two alternative grounds under IR20. The fi rst was that they should be treated as non-resident for the tax year 2001-2002 because they had worked abroad full-time for at least one tax year. Their primary argument on this was that they left the U.K. before the beginning of that tax year and their employment abroad covered a complete tax year in 2001-2002. HMRC said that they were not employed abroad until after the 2001-2002 tax year had started. This question of fact was not at issue in the application for judi-cial review. However, Mr. Davies and Mr. James had a fallback argument using IR20. This was that, even if their full-time employment abroad began after the start of the 2001-2002 tax year, they should still be treated as non-resident for that tax year because their full-time employment continued for a complete tax year in 2002-2003. This, they said, was the effect of paragraph 2.2 of IR20 and HMRC should be held to it. The Court of Appeal disagreed: IR20 did not mean that working abroad full-time for the whole of the tax year 2002-2003 was enough to establish non-residence for the previous year if the taxpayers had not worked abroad full-time for the whole of 2001-2002.

Leaving the U.K. Permanently, Indefi nitely, or for a Settled Purpose. The second ground advanced by Mr. Davies and Mr. James, and the sole argument of Mr. Gaines-Cooper, was that HMRC should treat them as non-resident under paragraph 2.9 of IR20. This, they said, simply required them:

• To go abroad (1) for at least one whole tax year for a “settled pur-pose”; or (2) permanently; or (3) for at least three years (once those three years had elapsed); and

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS82

34 A couple of points are worth noting on the day-count test. First, the “91-day test” is not found either in statute or case law. Second, IR20 expressly excluded days of arrival and departure from day-counting calculations (at least outside cases where the practice was being abused). However, the Special Commissioners in the case of Mr. Gaines-Cooper declined to be bound by the position in IR20, and held that days of arrival and departure should be included for the purposes of day-counting. This caused a stir among taxpayers and advisers. (From April 6, 2008, a day is counted if the individual is in the U.K. at midnight. Days of transit spent in the U.K. are, however, excluded provided that the individual does not engage in substantial activities unconnected to his or her transit during the time spent in the U.K.)

35 Lord Wilson gave the leading judgment for the majority; Lord Mance dissented at length.

36 This test was fi rst set out in R v. Inland Revenue Commissioners, ex parte MFK, supra note 32.

• To visit the U.K.: (1) for fewer than 183 days in any tax year; and (2) for fewer than 91 days per tax year on average. 34

The taxpayers argued that paragraph 2.9, unlike the strict legal position estab-lished by case law, did not include or suggest any requirement that they make a “distinct break” with the pattern of their life in the U.K.

HMRC disagreed, saying that paragraph 2.9 should be read with para-graphs 2.7 and 2.8 and bearing in mind the heading of that section of IR20: “Leaving the U.K. permanently or indefi nitely.”

The Court of Appeal agreed with HMRC, holding that the correct con-struction of IR20 required a value judgment as to whether a taxpayer has demonstrated a distinct break with the U.K. and severed social and family ties. Lord Justice Moses, giving the leading judgment, said, “[A]ny settled purpose . . . must be consistent with a distinct break, suffi cient to cut pre-existing ties. Absence for 3 years must equally be consistent with such a break.”

The taxpayers failed to convince the court that HMRC had a settled practice (irrespective of the wording of IR20) of ignoring any requirement for a “distinct break” before a taxpayer could become non-resident. Lord Justice Moses was clear that a switch by HMRC from a “laissez-faire” attitude to applying greater scrutiny was not a change in settled practice to which the taxpayer had a right to object. Lord Justice Ward agreed that the evidence given by a cross-section of tax professionals claiming a change in HMRC policy was in fact “the effect of a closer and more rigorous scrutiny . . . of claims.”

Supreme Court Judgment. The Supreme Court handed down its judg-ment on October 19, 2011, siding with HMRC by a 4–1 majority. 35

The taxpayers needed to show that the statements they relied on in IR20 were “clear, unambiguous and devoid of relevant qualifi cation.” 36 According to the majority, the statements should be read in the context of the booklet

© 2012 Civic Research Institute

INVESTMENTS INTO AND OUT OF THE U.K. 83

37 This was a reference to the preface of IR20. The preface actually states that it is intended to refl ect the law and practice .

as a whole and through the eyes of an “ordinarily sophisticated taxpayer” who might or might not be getting professional advice. The dissent gave this a stronger emphasis: “The primary issue in each appeal is . . . how, on a fair reading, IR20 would have been reasonably understood by those to whom it was directed.” Lord Justice Moses had drawn support for his reading of IR20 from the fact that it was designed to refl ect the law. 37 In the Supreme Court, however, it was agreed by the parties—and accepted by the judges—that the task of the court was “not to compare [IR20] with the law but to construe it by reference to its own terms.”

Whether the majority succeeded in viewing the guidance through the eyes of the taxpayer without reference to the law is open to question. Lord Wilson considered that there was enough in the guidance, badly drafted though it was, to alert the hypothetical taxpayer that he had to make a “dis-tinct break” in the pattern of his life in the U.K., and that various factors (implicitly including factors not mentioned in the guidance) would be rel-evant. There was therefore no representation that meeting the day-count cri-teria was enough. If he were wrong on that, Lord Wilson said, he would still conclude that IR20 was not clear enough for the taxpayer to rely on it. This conclusion rather undercuts the practical purpose of publishing IR20.

The secondary argument for Mr. Davies and Mr. James was that they should be treated as non-resident for the tax year 2001-2002 because they had left before the beginning of that tax year and their employment abroad covered a complete tax year in 2002-2003. Lord Wilson thought that this was an irrational reading of paragraph 2.2 of IR20.

Lords Hope and Clarke agreed with Lord Wilson. Lord Walker seems to have agreed with Lord Wilson’s fall-back position that the guidance was unclear. In a short speech he noted that the taxpayers (or their advisers) had not approached HMRC for its view on the position, in spite of the invitation in the guidance to do so where the tax treatment was unclear.

Lord Mance gave a powerful dissenting speech, disagreeing with the reasoning of both the Court of Appeal and the majority in the Supreme Court. The paragraphs in dispute did not suggest that a “distinct break” from family and social ties in the U.K. was necessary; in fact, some statements actually ran counter to such a requirement. Lord Mance did agree with Lord Wilson on the meaning of paragraph 2.2, however.

As a fall-back, the taxpayers had argued that they had a legitimate expec-tation of being treated as non-resident because of HMRC’s settled practice on the point. The bar the taxpayers had to clear here was higher than the bar for their IR20 argument. They had to prove that HMRC operated a practice of treating individuals who passed the day-count tests as non-resident and

© 2012 Civic Research Institute

JOURNAL OF TAXATION OF INVESTMENTS84

38 OAO Neftyanaya Kompaniya Yukos v. Russia, [2011] ECHR 1342.

then had to show that the “practice was so unambiguous, so widespread, so well-established and so well-recognised as to carry within it a commitment” to treat them as non-resident. Lord Wilson upheld the Court of Appeal’s view. Although there was some evidence to support the taxpayers’ contentions, there was also evidence the other way. The taxpayers had failed to prove the existence of the requisite settled practice. The dissent expressed no view on this point.

Where to From Here? The Supreme Court is—as its name suggests—the fi nal court in the U.K. judicial system. No appeal can be made from its decision. Mr. Gaines-Cooper, however, has said that he is considering whether to take the case to the European Court of Human Rights. To succeed there Mr. Gaines-Cooper would at a minimum have to persuade the European Court that the Supreme Court’s interpretation of IR20 was incorrect. In its recent judgment in Yukos , the European Court stressed that it was not its task “to take the place of the domestic courts, which are in the best position to assess the evidence before them, establish the facts and to interpret the domestic law.” 38 So a victory there would be quite an achievement.

Conclusions Relevance of the Supreme Court Judgment. We now know how the IR20 guidance in issue from 1999 to 2009 should be interpreted. A taxpayer who claims to have ceased to be resident in the U.K. cannot use it to shield him-self from the case law requirement that there be a “distinct break” in the pat-tern of his life. (In fact, even before the decision, this was clearly the effect of HMRC’s guidance from the publication of Business Brief 1/2007.) Although this affects a number of individuals, it relates only to past tax years.

Residence and HMRC6. HMRC completely recast its guidance on resi-dence and how to shed it in HMRC6. It is now closer to a summary of the case law. HMRC6 should, if all goes according to plan, be superseded by the statutory test from the tax year 2013-2014.

Relying on HMRC’s Published Guidance. By the time the case reached the Supreme Court, it was common ground that taxpayers were entitled to rely on HMRC guidance in appropriate circumstances. The statements in the pref-ace to IR20—that it was not binding in law, that whether it was appropriate to apply it would depend on the facts of the case, that taxpayers should con-sult HMRC in diffi cult cases—did not mean that the guidance could never be

© 2012 Civic Research Institute

Authorized Copy

Copyright © 2012 Civic Research Institute, Inc. This article was originally published in Journal of Taxation of Investments, Vol. 29, No. 3, Spring 2012 and is reproduced with permission. All other reproduction or distribution, in print or electronically, is prohibited. All rights reserved. Journal of Taxation of Investments is a quarterly journal devoted to analyzing important tax law developments related to the full range of investments. For more information, write Civic Research Institute, 4478 U.S. Route 27, P.O. Box 585, Kingston, NJ 08528 or call 609-683-4450. Web: http://www.civicresearchinstitute.com/jti.html.

©

INVESTMENTS INTO AND OUT OF THE U.K. 85

39 R v. Commissioners of Inland Revenue ex parte Mattessons Wall’s Ltd, 68 TC 205.

binding where it was clear and unqualifi ed. On the other hand, if the guidance were qualifi ed or simply unclear, it would not bind HMRC. This in itself is not really new. The signifi cance of the Supreme Court decision is threefold:

1. The courts may construe HMRC’s guidance very differently from a large body of tax professionals;

2. While IR20 was designed as practical guidance to alleviate the problems of applying the concept of residence, the courts in fact interpreted it almost as if it were legislation; and

3. As a result, actually enforcing HMRC guidance is in practice very diffi cult.

Relying on HMRC Practice. The decision underlines the diffi culty in making out a case that HMRC has departed from a general settled practice. Lord Justice Moses in the Court of Appeal contrasted the position of the tax-payers here with that of the Unilever group in a previous case. 39 There, Uni-lever was arguing that HMRC had a settled practice for dealing with it. Here the question was how HMRC had dealt with other taxpayers. This caused evidential diffi culties.

Lord Justice Moses also said, “There is no public law obligation of fairness which prevents the Revenue from increasing, without warning, the intensity of inquiry or scrutiny of claims to be non-resident.” Lord Wilson accepted that HMRC had intensifi ed its scrutiny of claims to be non-U.K.-resident, probably because of changes in 1998 to U.K. income tax law. Nei-ther he nor the other Supreme Court judges explicitly addressed the legal point made by Lord Justice Moses, but this must be because it is obviously right.

© 2012 Civic Research Institute

© 2012 Civic Research Institute