real-time fx sentiment feed - bloomberg customer service

TRANSCRIPT

A Bloomberg Professional Services OfferingE

vent-D

riven

Feeds

Co

nten

t & D

ata Solu

tion

sReal-time FX Sentiment Feed Part 2 of 2

Contents

02 Event studies

04 Method

04 Results and discussion

While the research on and adoption of automated analysis of newsfeeds for trading, fund management and risk control systems are well-established in equities, automated analysis is still in the early stages for foreign exchange markets. In this paper, we conduct quantitative studies to understand news and Twitter sentiment — with a focus on their application to major currencies. We propose and test sentiment-driven portfolios of G-10 USD crosses based on the three streams of Bloomberg’s FX sentiment datasets:

1. News/single-currency model: this model extracts single-currency sentiment from news that is related to fundamental driving factors for FX, including interest rates, monetary policies, economic conditions, politics, global trades, geopolitical risks, etc.

2. News/currency-pair model: this model extracts currency-pair sentiment from news that is related to technical analysis, including price trends, bullish or bearish technical patterns, support or resistance levels, flows, positioning, etc.

3. Tweet/currency-pair model: this model extracts currency-pair sentiment from FX-related tweets. Unlike news articles, tweets are usually bite-sized, lightly edited text generated by broad base of handlers.

Introduction

Bloomberg Event-Driven Feeds (EDF)

2

Event studies

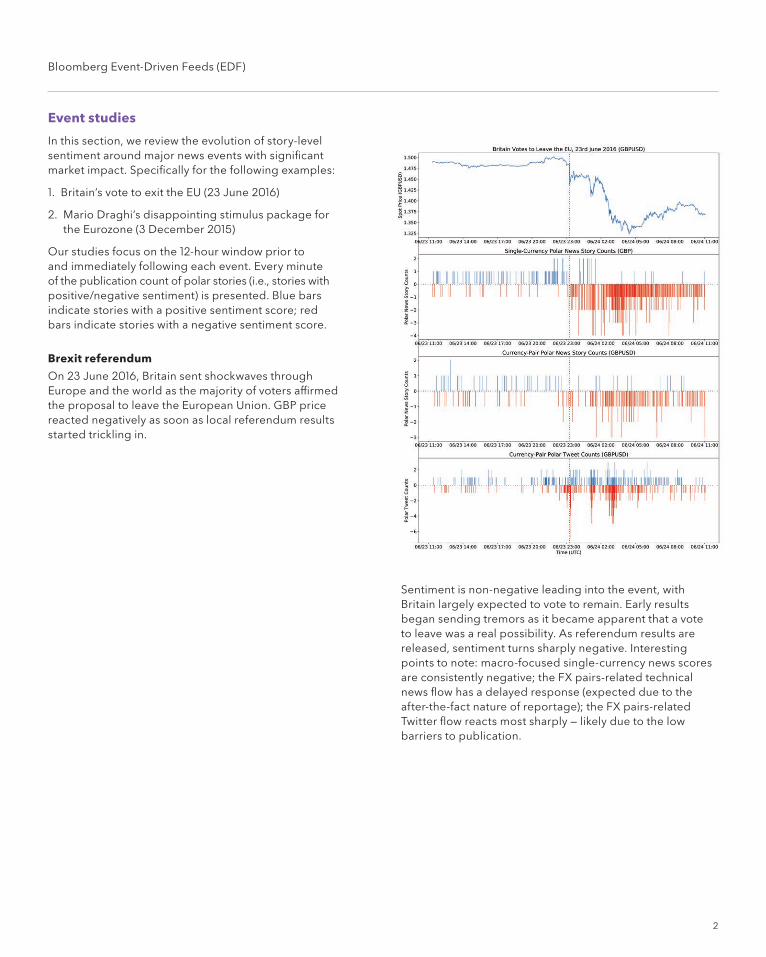

In this section, we review the evolution of story-level sentiment around major news events with significant market impact. Specifically for the following examples:

1. Britain’s vote to exit the EU (23 June 2016)

2. Mario Draghi’s disappointing stimulus package for the Eurozone (3 December 2015)

Our studies focus on the 12-hour window prior to and immediately following each event. Every minute of the publication count of polar stories (i.e., stories with positive/negative sentiment) is presented. Blue bars indicate stories with a positive sentiment score; red bars indicate stories with a negative sentiment score.

Brexit referendum

On 23 June 2016, Britain sent shockwaves through Europe and the world as the majority of voters affirmed the proposal to leave the European Union. GBP price reacted negatively as soon as local referendum results started trickling in.

Sentiment is non-negative leading into the event, with Britain largely expected to vote to remain. Early results began sending tremors as it became apparent that a vote to leave was a real possibility. As referendum results are released, sentiment turns sharply negative. Interesting points to note: macro-focused single-currency news scores are consistently negative; the FX pairs-related technical news flow has a delayed response (expected due to the after-the-fact nature of reportage); the FX pairs-related Twitter flow reacts most sharply — likely due to the low barriers to publication.

Bloomberg Event-Driven Feeds (EDF)

3

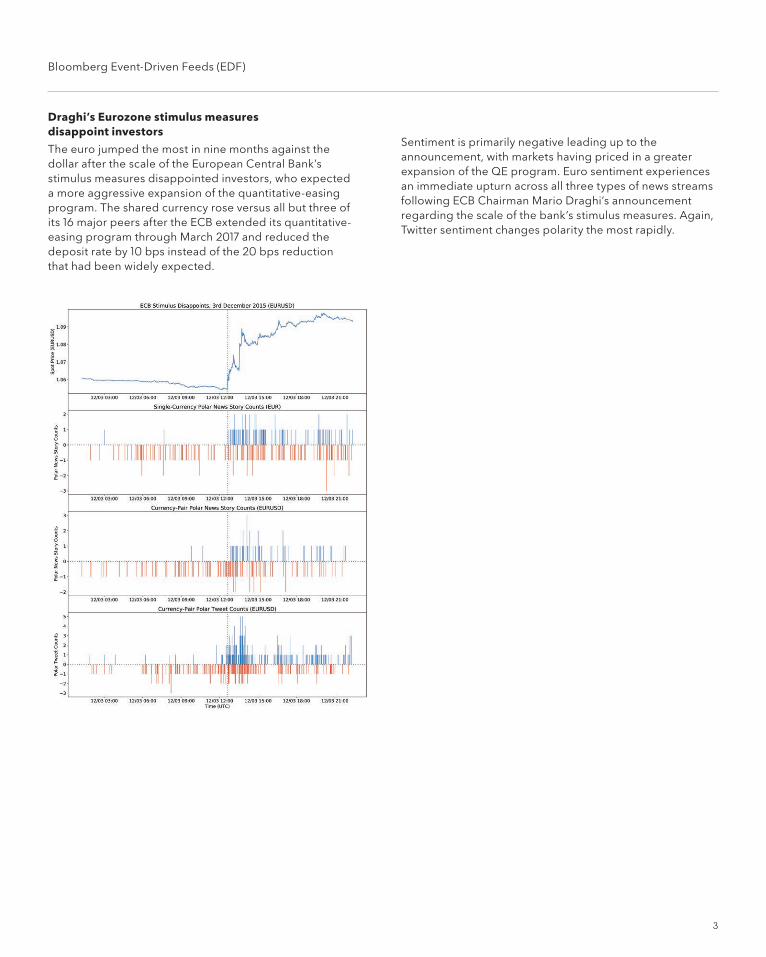

Draghi’s Eurozone stimulus measures disappoint investors

The euro jumped the most in nine months against the dollar after the scale of the European Central Bank’s stimulus measures disappointed investors, who expected a more aggressive expansion of the quantitative-easing program. The shared currency rose versus all but three of its 16 major peers after the ECB extended its quantitative-easing program through March 2017 and reduced the deposit rate by 10 bps instead of the 20 bps reduction that had been widely expected.

Sentiment is primarily negative leading up to the announcement, with markets having priced in a greater expansion of the QE program. Euro sentiment experiences an immediate upturn across all three types of news streams following ECB Chairman Mario Draghi’s announcement regarding the scale of the bank’s stimulus measures. Again, Twitter sentiment changes polarity the most rapidly.

Bloomberg Event-Driven Feeds (EDF)

4

Method

Ticker universe

The asset universe consists of the nine G-10 USD crosses:

• EUR/USD

• GBP/USD

• AUD/USD

• NZD/USD

• USD/JPY

• USD/CHF

• USD/CAD

• USD/NOK

• USD/SEK

Sentiment aggregation

In the real-time feed, story-level sentiments are published as soon as a relevant news story or tweet is processed by the sentiment classification engine. Each story-level message contains a pair of values: sentiment label (Si ε {-1,0,1}, i.e., negative/neutral/positive) and confidence score (Ci ε [0,100]). In our analysis, stories from the same ticker are aggregated on a rolling basis, using the confidence-weighted mean sentiment scores over a fixed lookback window τ with no time decay.

Portfolio construction

With aggregated sentiment, different currencies can be compared cross-sectionally to form periodically rebalanced portfolios with trend-following or contrarian strategies. Such a portfolio aims to capture systematic patterns — either underreaction or overreaction — of currency prices to news developments.

An equal long and short leg is used. For each currency pair, the position weight is proportional to the deviation of its sentiment score from the cross-sectional mean.

Here are the key parameters:

• Rolling window for aggregation: the rolling lookback window where story-level sentiment scores are aggregated into currency-level sentiment.

• Rebalance frequency: the interval at which a portfolio is rebalanced based on the cross-sectional ranking of the aggregated sentiment. If no new stories/tweets are published within a given window, the last known sentiment score is carried over.

Trading rules

Different trading rules are used based on the model:

For News/single-currency model:

• short USD/X (X = {JPY,CHF,CAD,NOK,SEK}) pairs with scores above the cross-sectional mean; long USD/X pairs with scores below the cross-sectional mean.

• long X/USD (X = {EUR, GBP, AUD, NZD}) pairs with scores above the cross-sectional mean; short X/USD pairs with scores below the cross-sectional mean.

• No net USD exposure; effectively trading the 9 non-USD G-10 currencies against each other

• Positions are flipped for a contrarian strategy.

For News/currency-pair and Tweet/currency-pair model:

• long all pairs with scores above the cross-sectional mean; short all pairs with scores below the cross-sectional mean

• Net USD position may exist.

• Positions are flipped for a contrarian strategy.

Pricing data

Spot price data consists of intraday Bloomberg Generic (BGN) Last Prices sampled at a 30-minute frequency — this is a lower bound on the scoring frequency. BGN prices are a single-security composite derived from electronic dealer contribution; both executable and indicative levels are considered.

Results and discussion

We tested both contrarian and momentum-following strategies to identify the profitable style. No transaction costs have been considered.

Following high-volatility events are overlaid to the long-term performance curve:

• 2008-10-08: AUD, NZD crash against the greenback on concerns frozen credit markets will stall the global economy.

• 2009-03-12: The Swiss National Bank cuts its main lending rate to close to zero and announces it will buy corporate bonds as well as currencies in its first solo intervention in exchange markets since 1992.

• 2010-05-06: Popular safe haven play, the yen, spikes against the dollar.

• 2011-09-06: The Swiss National Bank announces intervention to keep the Swiss franc pegged to the euro.

• 2012-06-03: AUD, NZD fall sharply after a report indicates China’s manufacturing industry is slowing more than anticipated.

Bloomberg Event-Driven Feeds (EDF)

5

• 2013-06-19: The U.S. dollar rallies sharply versus its peers as Federal Reserve Chairman Ben Bernanke says the central bank could reduce its bond buying this year and end it the next year if economic improvement continues.

• 2014-07-03: Sveriges Riksbank cuts Sweden’s repo by 50 bps, double the 0.25% ease expected.

• 2015-01-15: The Swiss National Bank unexpectedly announces the end of its minimum exchange rate.

• 2016-06-24: Britain votes to leave the European Union.

• 2017-06-08: The GBP crashes due to looming political uncertainty after Conservatives fail to win a majority.

• 2018-01-24: The Kiwi dollar falls sharply after weaker-than-expected CPI numbers.

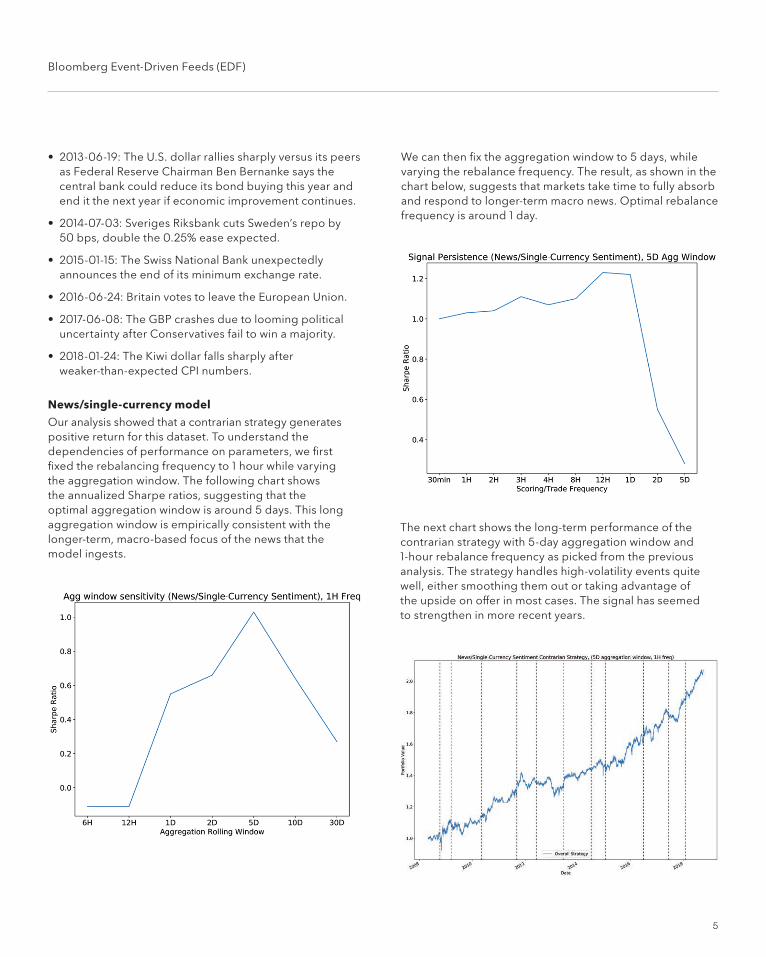

News/single-currency model

Our analysis showed that a contrarian strategy generates positive return for this dataset. To understand the dependencies of performance on parameters, we first fixed the rebalancing frequency to 1 hour while varying the aggregation window. The following chart shows the annualized Sharpe ratios, suggesting that the optimal aggregation window is around 5 days. This long aggregation window is empirically consistent with the longer-term, macro-based focus of the news that the model ingests.

We can then fix the aggregation window to 5 days, while varying the rebalance frequency. The result, as shown in the chart below, suggests that markets take time to fully absorb and respond to longer-term macro news. Optimal rebalance frequency is around 1 day.

The next chart shows the long-term performance of the contrarian strategy with 5-day aggregation window and 1-hour rebalance frequency as picked from the previous analysis. The strategy handles high-volatility events quite well, either smoothing them out or taking advantage of the upside on offer in most cases. The signal has seemed to strengthen in more recent years.

Bloomberg Event-Driven Feeds (EDF)

6

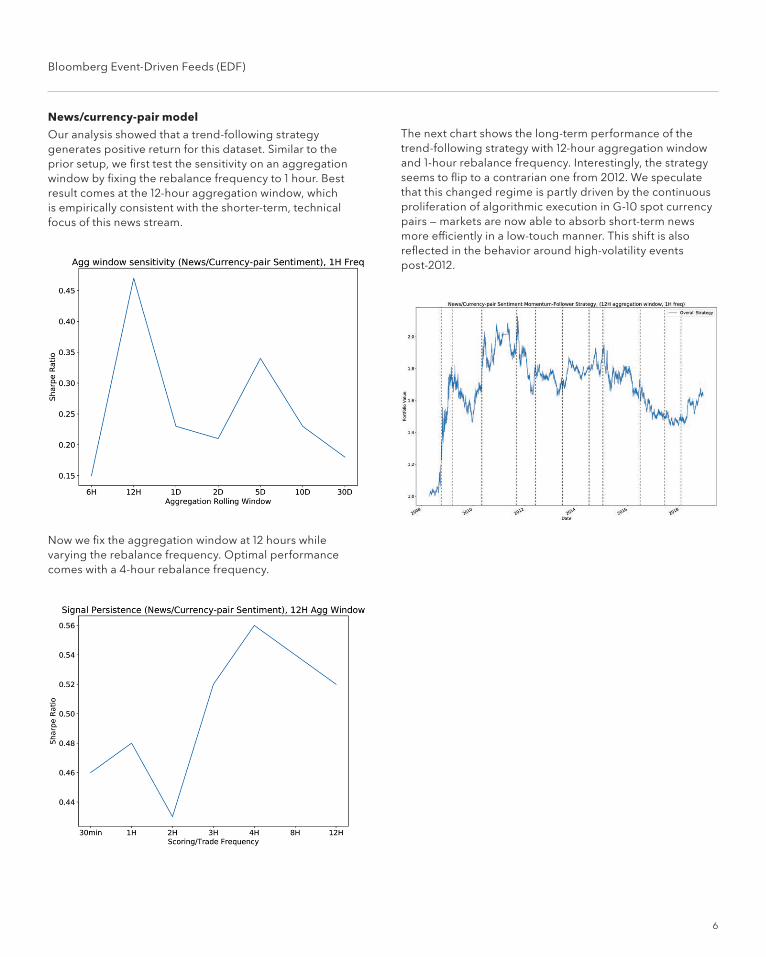

News/currency-pair model

Our analysis showed that a trend-following strategy generates positive return for this dataset. Similar to the prior setup, we first test the sensitivity on an aggregation window by fixing the rebalance frequency to 1 hour. Best result comes at the 12-hour aggregation window, which is empirically consistent with the shorter-term, technical focus of this news stream.

Now we fix the aggregation window at 12 hours while varying the rebalance frequency. Optimal performance comes with a 4-hour rebalance frequency.

The next chart shows the long-term performance of the trend-following strategy with 12-hour aggregation window and 1-hour rebalance frequency. Interestingly, the strategy seems to flip to a contrarian one from 2012. We speculate that this changed regime is partly driven by the continuous proliferation of algorithmic execution in G-10 spot currency pairs — markets are now able to absorb short-term news more efficiently in a low-touch manner. This shift is also reflected in the behavior around high-volatility events post-2012.

Bloomberg Event-Driven Feeds (EDF)

7

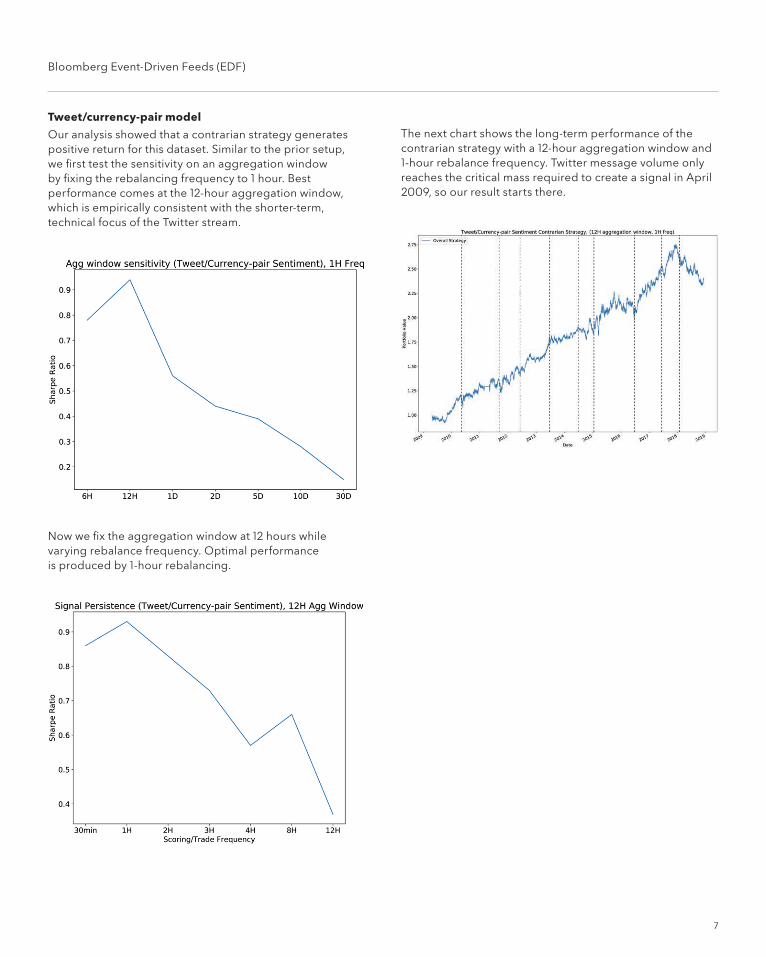

Tweet/currency-pair model

Our analysis showed that a contrarian strategy generates positive return for this dataset. Similar to the prior setup, we first test the sensitivity on an aggregation window by fixing the rebalancing frequency to 1 hour. Best performance comes at the 12-hour aggregation window, which is empirically consistent with the shorter-term, technical focus of the Twitter stream.

Now we fix the aggregation window at 12 hours while varying rebalance frequency. Optimal performance is produced by 1-hour rebalancing.

The next chart shows the long-term performance of the contrarian strategy with a 12-hour aggregation window and 1-hour rebalance frequency. Twitter message volume only reaches the critical mass required to create a signal in April 2009, so our result starts there.

About Bloomberg.We are the central nervous system of global finance. Born in 1981, Bloomberg is a forward-looking company focused on building products and solutions that are needed for the 21st century. As a global information and technology company, we connect decision makers to a dynamic network of data, people and ideas — accurately delivering business and financial information, news and insights to customers around the world.

Take the next step.

For additional information, press the <HELP> key twice on the Bloomberg Terminal®.

Beijing +86 10 6649 7500

Dubai +971 4 364 1000

Frankfurt +49 69 9204 1210

Hong Kong +852 2977 6000

London +44 20 7330 7500

Mumbai +91 22 6120 3600

New York +1 212 318 2000

San Francisco +1 415 912 2960

São Paulo +55 11 2395 9000

Singapore +65 6212 1000

Sydney +61 2 9777 8600

Tokyo +81 3 3201 8900

bloomberg.com/professional

The data included in these materials are for illustrative purposes only. The BLOOMBERG TERMINAL service and Bloomberg data products (the “Services”) are owned and distributed by Bloomberg Finance L.P. (“BFLP”) except (i) in Argentina, Australia and certain jurisdictions in the Pacific islands, Bermuda, China, India, Japan, Korea and New Zealand, where Bloomberg L.P. and its subsidiaries (“BLP”) distribute these products, and (ii) in Singapore and the jurisdictions serviced by Bloomberg’s Singapore office, where a subsidiary of BFLP distributes these products. BLP provides BFLP and its subsidiaries with global marketing and operational support and service. Certain features, functions, products and services are available only to sophisticated investors and only where permitted. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or other information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP, BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to “buy”, “sell” or “hold” an investment. Information available via the Services should not be considered as information sufficient upon which to base an investment decision. The following are trademarks and service marks of BFLP, a Delaware limited partnership, or its subsidiaries: BLOOMBERG, BLOOMBERG ANYWHERE, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG PROFESSIONAL, BLOOMBERG TERMINAL and BLOOMBERG.COM. Absence of any trademark or service mark from this list does not waive Bloomberg’s intellectual property rights in that name, mark or logo. All rights reserved. ©2019 Bloomberg 394840 DIG 0319